- How Will Boris Johnson 'Deliver Brexit'? These Are His Best Options

There are 99 days left between now and Oct. 31 – the day the UK is set to leave the European Union. And newly elected Tory leader Boris Johnson (soon to be prime minister, barring some unforeseeable circumstance) will need every one of them to try and negotiate his way out of the mess that Theresa May is leaving behind.

Unlike May, Johnson is a leading voice in the “Brexiteer” faction of the Conservative Party. He has insisted that the UK will leave the EU on Oct. 31 with or without a deal. Of course, he would prefer to succeed where his predecessor failed and strong-arm the EU into a deal that excludes the troublesome Irish Backstop – the contingency in the prior agreement which would have allowed for the border between Ireland and Northern Ireland to remain open. But EU officials have insisted in recent days that they have no plans to change the withdrawal agreement negotiated with May; they are only open to making changes to the political declaration that accompanied it.

Moving forward, only one thing is clear right now: May’s deal is dead. Johnson, who will officially take over as prime minister this afternoon, and who is currently scrambling to fill the top jobs in his government, is giving off the impression that he would have no problem with taking the UK over the no-deal cliff, and President Trump is dangling a US-UK trade deal in front of Johnson that would make such an outcome slightly more palatable, politically.

Among the personnel rumors circulating early on Wednesday were that Sajid Javid might be tapped to serve as Chancellor, while Dominic Raab might be tapped to serve as foreign secretary.

So, what are the options available to Johnson? These are four of the most likely scenarios, according to Bloomberg:

Renegotiate Withdrawal Deal

Johnson wants to scrap the deal Theresa May struck and restructure the whole negotiation that was agreed at the start of the process.

The most controversial element of May’s deal is the so-called Irish backstop, a fallback measure to ensure the border with Ireland remains open whatever future trading terms the two sides eventually agree on. He wants to postpone any talks about the border until after the U.K. has left the bloc, arguing they should be part of future trade negotiations. He also suggests using the 39-billion-pound ($49 billion) divorce settlement as leverage in the talks, making payment contingent on the terms negotiated.

Obstacles: The EU has repeatedly said it’s not prepared to renegotiate the Withdrawal Agreement, and it’s the only deal on the table. It’s also said a backstop must be part of any withdrawal accord, because it wants to lock in a guarantee that no hard border will emerge. The exit bill is also part of the divorce deal, and is due to be paid whatever trade terms are eventually negotiated. EU law dictates that Brexit should happen in two parts: First the exit negotiation, and once the U.K. has left, formal trade talks can begin.

Leave on Oct. 31

Johnson has said that after May twice delayed Brexit, the U.K. must now leave the bloc on Oct. 31, “do or die,” whether a new deal has been negotiated or not. He’s refused to rule out suspending Parliament – known as proroguing – to achieve that.

Obstacles: The timetable is tight to negotiate an entirely new deal. And the U.K. Parliament is opposed to a no-deal Brexit. That was made clear again last week when Conservative rebels joined the opposition to pass an amendment aimed at preventing Johnson suspending Parliament. The EU side has indicated it would prefer another extension to a no-deal split.

Standstill Period After Brexit

Johnson is seeking to negotiate a “standstill” period with the European Union after Oct. 31, during which there would be zero tariffs and zero quotas to “smooth things over for business” – much the same as the transition period negotiated by May. He said it would end “well before the next election,” which is due in 2022.

Obstacle: The EU has said any form of transition period is contingent on there being a withdrawal agreement, which must contain an Irish backstop.

Use WTO rules if EU won’t cooperate

Johnson has said that if the EU won’t offer a new deal, the U.K. will be able to use Article 24 of the World Trade Organization’s General Agreement on Tariffs and Trade to ensure the terms of commerce remain the same after Brexit.

Obstacles: The clause Johnson cites applies to countries negotiating a trade deal rather than a country leaving a trading bloc. It would also require the agreement of the EU, and a clear timetable for the negotiation of a trade agreement — neither of which would be guaranteed in the event of an acrimonious no-deal Brexit. The WTO and EU have said this won’t work, and Johnson revealed a hazy understanding during the campaign as to why it would.

Oddly, Bloomberg’s options don’t include ‘general election’, which is widely seen as possible as the Conservatives’ majority is set to shrink to just one vote (and that’s with Northern Irish DUP’s votes included). Many expect that Johnson will be stuck in a similar impasse to May’s and that he will need to call a general election – much like May once did – to strengthen his mandate. A group of strategists at UBS believe a general election toward the end of the year has the highest probability of all these outcomes, and many suspect that the odds of a vote and, once it’s declared, the polls, will have a similar impact on UK markets that the original pre-referendum Brexit polls had.

If an election is called, the strategists believe the Bank of England is more likely to cut rates to boost sentiment, stocks with international exposure would outperform domestically focused shares and the FTSE 100 would move modestly lower.

Before Johnson takes over, May will preside over her last PMQs. Watch live coverage here.

- Russian-Chinese Air Patrol Near S.Korea Was 'Show Of Force' To US Hawks

The recent violation of the South Korean airspace during a joint patrol of Russian and Chinese strategic bombers, resulting in scrambled South Korean jets reportedly firing hundreds of warning shots, may have been a message to US hawks. On Tuesday, a group of Russian and Chinese warplanes, including strategic bombers, conducted a joint patrol mission near South Korea’s territory under the annual cooperation plan, the Chinese Defense Ministry’s official spokesman Col. Wu Qian said on Wednesday:

“As far as the air incident is concerned, I would like to reiterate that China and Russia are engaged in all-encompassing strategic coordination. This patrol mission was among the areas of cooperation and was carried out within the framework of the annual plan of cooperation between the defense agencies of the two states. It was not directed against any other ‘third state,’” the Chinese military official said during the presentation of the white paper headlined ‘China’s National Defense in the New Era.’

The Defense Ministry said further:

“As far as the practice of joint strategic patrols is concerned, both sides will make a decision on the matter on the basis of bilateral consultations. Under the strategic command of the heads of states, the armed forces of the two nations will continue developing their relations. The sides will support each other, respect mutual interests and develop corresponding mechanisms of cooperation,” he added.

Two Russian strategic bombers Tu-95MS and two Chinese strategic bombers Xian H-6 carried a scheduled flight over the neutral waters of the Sea of Japan and the East China Sea.

South Korean said that a Russian plane breached the republic’s airspace near the Dokdo (Takeshima) islands, which are disputed by Seoul and Tokyo. In response, South Korea’s F-15 and F-16 fighter planes were scrambled.

On Wednesday, Yoon Do-han, a spokesman for the South Korean president, told reporters that a Russian military attaché in Seoul had conveyed Moscow’s “deep regret” about the incident and had said that the Russian plane mistakenly deviated from its flight plan.

The news agency Interfax quoted the press officer of the Russian Embassy in South Korea, Dmitry Bannikov, as saying that Russian officials had seen reports on Mr. Yoon’s comments, and that “there are many things in them that aren’t true.”

“The Russian side did not issue an official apology,” Mr. Bannikov noted, according to the agency.

That appeared to leave open the possibility that the Russians were apologetic in private. Such appologies are beyond general attitude of states in similar cases. Taking into account this and the Chinese statement, it appears that Russia and China do not see South Korea as a potential enemy. Rather they see it as an equal partner on the international scene.

China and Russia demonstrated that they are ready to employ jointly their strategic bombardment capability in the event of confrontation.

Crucially, the July 23rd incident happened a day ahead of meeting between US national security adviser John Bolton with South Korean officials.

Bolton was set to meet with South Korea’s chief of National Security Office Chung Eui-yong, Defense Minister Jeong Kyung-doo, and Foreign Minister Kang Kyung-wha in Seoul to discuss issues including denuclearisation of the Korean Peninsula and ways to strengthen the South Korea-US cooperation.

Above: Newly published Russian media footage showing clips of Russian bombers encountering South Korean fighter jets during the air patrol

Of course, Bolton is among the most hawkish voices of the Washington establishment that calls for a further confrontation with China and Russia.

- Clark: Don't Mourn May, She Was One Of Britain's Worst-Ever PMs

It’s a crowded field but, by any objective standard, outgoing British Prime Minister Theresa May must rate as one of the worst – if not the worst – occupants of the office of all time.

Spare us the Uriah Heep-style hypocrisy and gushing ‘tributes.’ The truth is an Op-Ed on the achievements of Theresa May would be the shortest one ever written.

Winston Churchill helped defeat the Nazis in World War Two. Clement Attlee gave Britain the NHS. Harold Wilson established the Open University. Ted Heath saved Rolls Royce. Gordon Brown gave over-60s and disabled people free nationwide bus travel. What did Theresa May give us except a Brexit impasse and the worst movements to Abba’s Dancing Queen ever seen?

May boasted about delivering “strong and stable” leadership but in reality she was as weak and wobbly as a plate of jelly.

Given the task of implementing the EU referendum vote of 2016, she gave the horse named ‘Brexit’ such a terrible ride that if she’d been a jockey she’d have been hauled before the stewards.

Of course every one was to blame for this debacle except Theresa herself. But as Prime Minister, the buck stopped with her. She prevaricated and this prevarication emboldened the ‘Stop Brexit’ campaign.

In 2017, she needlessly called a general election, and fought the most unimpressive election campaign any sitting prime minister has ever fought. Mr Bean himself couldn’t have ballsed it up more.

May would in normal circumstances have gone the morning after she lost her party’s Parliamentary majority, but the Establishment’s fear of Jeremy Corbyn kept her hanging on for two more excruciating years.

On the foreign policy front May did her bit to stoke up Cold War 2.0 tensions with Russia and in April 2018 rushed to join in with Trump’s punishment bombing of Syria before chemical weapons experts could carry out a proper investigation into reports of an attack in Douma.

New revelations of a leaked but hitherto unpublished report cast doubt on but do not conclusively prove that it wasn’t Syrian government forces that carried out an attack, but May preferred to bomb first and wait for evidence later.

At home, she continued policies of austerity, which have caused great misery across the land. Drug trade-fuelled knife crime has spiralled horrifically following cuts to frontline police services – which began in 2010 when one Theresa May was Home Secretary. Hundreds of local libraries, the hallmark of a civilized society, have closed during May‘s period in power. In December 2018 it was reported that almost 130 of Britain’s public libraries had closed during the previous year.

Even under Thatcher it was never this bad.

Promises to the electorate were broken even before they were made.

In 2017, the Tory Manifesto pledged to ‘maintain’ pensioner benefits “including free bus passes, eye tests, prescriptions and TV licences, for the duration of this Parliament”.

Yet a month before it was published, May’s government had already handed over the power to the BBC to take TV licences away from over-75s in 2020 – a full two years before the new Parliament’s expiry date. Last month, the BBC said they would be withdrawing free TV licenses for up to 3.7 million over-75s. May could have said ‘the government will step in to keep good our promise made to pensioners’ but she didn’t. Instead we just got a government minister saying the BBC ‘should do more to support older people.’ Meaningless waffle when instead action was needed.

May posed as a ‘moderate‘ – to contrast herself both from her own ‘right-wing’ and Jeremy Corbyn’s ‘left-wing extremism’ but there was, in truth, nothing moderate about her or her policies. Under her watch the gradual privatization of the NHS has continued. In March it was reported that the number waiting more than 18 weeks for operations had tripled in five years. Early this year, NHS chiefs asked May to reverse pro-privatization reforms.

In October 2018 May declared ‘austerity is over,’ but the situation on the ground was very different.

Just take a tour of Britain’s town and city centers and count the number of boarded-up retail outlets, to see the impact austerity has had.

Theresa Mayhem inspired no-one but demoralized millions.

Britain is best rid of her.

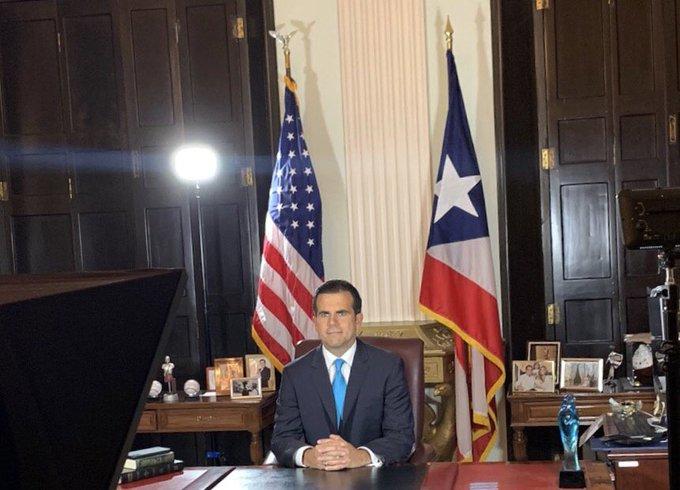

- Puerto Rico Governor Ricardo Rosselló Resigns After Weeks Of Protest

Following weeks of unrest amid a corruption scandal and damning text messages, Puerto Rico Governor Ricardo Rossello announced his resignation on Wednesday in a videotaped address which aired just before Midnight.

After discussing his “laundry list of accomplishments,” Rossello said he ‘did his best,’ and ‘worked during vacations, weekend and long days to make Puerto Rico more just.’ His resignation will take effect August 2nd.

Now he’s talking about hurricanes Irma and Maria and praising his response to it.

— claudia irizarry aponte (@clauirizarry) July 25, 2019

https://platform.twitter.com/widgets.js

He just announced his resignarion effective August 2, 2019.

— claudia irizarry aponte (@clauirizarry) July 25, 2019

Rossello’s resignation comes days after thousands of demonstrators took to the streets of Old San Juan, calling for his ouster.

Following the announcement, crowds broke out into celebration, exclaiming “Ricky, te botamos!” (“Ricky, we threw you out!”).

Demonstrators chant slogans as they wave Puerto Rican flags during ongoing protests calling for the resignation of Governor Ricardo Rossello in San Juan, Puerto Rico July 24, 2019.Marco Bello / Reuters “After the birth of my son, this is the happiest day of my life,” said Puerto Rican reggaton star René Pérez Joglar, also known as Residente. Joglar released a song last week calling for protesters to take to the streets, rapping “This is coming out early so you can eat it for breakfast … Sharpening the knives. Fury is the only political party that unites us.“

As we noted last week, protesters broke past a barricade at the governor’s mansion on Wednesday, resulting in the deployment of tear gas. “By early hours Thursday, the old city of San Juan resembled a war zone, with police chasing protesters through the streets while firing rubber bullets, gas canisters and what appeared to be flash bombs,” according to NPR.

- We Will Have To Reboot Our Standard Of Living To Survive As A Nation

Authored by Tom Chatham via Project Chesapeake,

In 1940 you could buy a nice cape cod style home for around $2,500. Someone entering the job market likely started out at $25 a week. A 1940 Buick with a straight 8 would run you $895 and up.

Why this stroll down memory lane? Because it is meant to show how much inflation has changed the price of things. When we still used money that was based on gold and silver, inflation was kept in check to some degree. Fractional reserve banking and excessive credit creation have distorted the value of things we depend on for life and we are coming to the end of that failed experiment. All of our recent prosperity has been paid for with our ability to print dollars out of thin air.

If you want to know where we are being led you only have to stroll down any city street where the homeless live, or you can look through the many pictures of the great depression. The American people are being systematically impoverished and it is being done knowingly by those in charge and is allowed by a dumbed down, apathetic public too busy staring at their iphone to notice.

If this nation is to survive and retain a reasonable standard of living and quality of life, we will have to downsize to a level that we can actually afford. We will need to forego the 2,000 sq. ft. $300,000 homes we all like so much and settle for a more affordable 900 sq. ft. $30,000 home we can actually pay for. We will have to give up the $40,000 autos coming out of Detroit now and settle for a smaller inexpensive model that can actually get 60 mpg.

We will also need to return to a financial system that is based on real value. This being gold and silver money. If we try to use anything else we are simply trying to fool ourselves. You cannot use a currency that does not act as a store of wealth over the long term.

We can do this by choice and salvage what is left of our country or we can continue on the current path and end up an impoverished country with a dictator in charge like most other failed nations in the world.

If we want to continue having a country worth living in we need to go back to what we know works and try to build up from there. We no longer have sufficient manufacturing capacity to employ all of the people in this country and any kind of welfare will not work without debasing the currency.

This will necessitate 20% of the population going back to living on small farms to insure they have a job and sufficient resources to care for their families. Nothing else in our current situation will work. We have too many unemployed people living off of the state and this will end soon. We will either have a mass exodus from the country or a mass extinction within it. As unpleasant as it sounds that is our future if we do not make substantial changes while we still have time. That time is nearly up.

Downsizing our lives and our wants will be a necessary change if we want to salvage something of our future. We have lived too long in fantasy land and now we must come back to reality. The west line has moved and we will never get back all of the production jobs we once had. We must accept that and accept that our country will be less productive and less prosperous in the future and learn to live within our means.

- US Sends Warship Through Taiwan Strait Hours After China Warns It Is Ready For War

The US military said on Wednesday that a guided-missile cruiser had sailed through the Taiwan Strait just hours after the Chinese military criticized Washington for “adding complexity to regional security” and warned it to stay clear of the island or else risk war.

Trump’s support for Taiwan, which recently was cleared by Congress to purchase over $2 billion in US weapons, is among a growing number of flashpoints in the U.S.-China relationship, which include a trade war, U.S. sanctions and a growing geopolitical conflict in the South China Sea, where China has been expanding its military presence while the United States conducts freedom-of-navigation patrols.

The warship sent to the 112-mile-wide Taiwan Strait was identified as the Antietam. “The (ship’s) transit through the Taiwan Strait demonstrates the U.S. commitment to a free and open Indo-Pacific,” Commander Clay Doss, a spokesman for the U.S. Navy’s Seventh Fleet, said in a statement. “The U.S. Navy will continue to fly, sail and operate anywhere international law allows,” he added, quoted by Reuters.

USS Antietam The defiant move comes shortly after China warned that it is ready for war if necessary, to prevent any attempts to split the island from the mainland, or any push toward Taiwan’s independence, and accusing the United States of undermining global stability and denouncing its arms sales to the self-ruled island.

While the voyage will further escalate tensions with China, it will also be viewed by self-ruled Taiwan as a sign of support from U.S. President Donald Trump’s administration amid growing friction between Taipei and Beijing.

While the United States has no formal ties with Taiwan but is bound by law to help provide the island with the means to defend itself and is its main source of arms. Meanwhile, China has been ramping up pressure to assert its sovereignty over the island, which it considers a wayward province of “one China” and sacred Chinese territory.

On Wednesday, Chinese Defense ministry spokesman Wu Qian told a news briefing on a defense white paper, the first like it in several years to outline the military’s strategic concerns, that China would make its greatest effort for peaceful reunification with Taiwan.

“If there are people who dare to try to split Taiwan from the country, China’s military will be ready to go to war to firmly safeguard national sovereignty, unity and territorial integrity,” he said, in a clear warning to the US.

Commenting on the white paper’s implications, China’s notorious twitter troll, Hu Xijin, editor in chief of the nationalist Global Times, said “there are few possibilities and necessities for China to possess military power to provoke the US. But if attacked by the US, China must be able to cause unbearable losses to the US.“

There are few possibilities and necessities for China to possess military power to provoke the US. But if attacked by the US, China must be able to cause unbearable losses to the US. https://t.co/mx3Naqvpui

— Hu Xijin 胡锡进 (@HuXijin_GT) July 24, 2019

https://platform.twitter.com/widgets.js

There are few possibilities and necessities for China to possess military power to provoke the US. But if attacked by the US, China must be able to cause unbearable losses to the US.

In recent years, China has repeatedly sent military aircraft and ships to circle Taiwan on exercises – usually around the time US had sent its own ships in the vicinity – and worked to isolate it internationally, whittling down its few remaining diplomatic allies.

- Epstein Found "Nearly Unconscious" In Prison Cell After Possible Suicide Attempt

Jeffrey Epstein has been found “nearly unconscious in a fetal position inside his New York City jail cell, according to the New York Post, citing sources close to the investigation.

The 66-year-old convicted pedophile is being held in the Metropolitan Correctional Center (MCC) in lower Manhattan pending trial. He was found semi-conscious with ‘marks on his neck,’ according to the report – which adds that investigators are still trying to figure out what happened.

As NBC New York also reports, “Two sources tell News 4 that Epstein may have tried to hang himself, while a third source cautioned that the injuries were not serious and questioned if Epstein might be using it as a way to get a transfer.”

A fourth source told the outlet that assault has not been ruled out – as investigators have questioned former Orange County police officer Nicholas Tartaglione in connection with the incident. Tartaglione was arrested in December 2016 on suspicion of killing four men in an alleged cocaine distribution conspiracy, before burying their bodies in his Otisville yard, according to court records.

Sources told News 4 investigators questioned Tartaglione, and the former cop claimed not to have seen anything and didn’t touch Epstein, sources said.

The attorney for Tartaglione denied all the claims that his client attacked the financier, saying he and Epstein get along and saw each other recently. –NBC New York

MCC isolated cell via the Daily Mail Epstein was arrested on July 6 for allegedly sex-trafficking minors, and was denied bail on July 18 by US District Judge Richard Berman after prosecutors said he poses an “extraordinary risk of flight” due to his “exorbitant wealth.” He has notified the court that he will appeal the decision.

Berman said prosecutors established a “preponderance” of evidence of Epstein being a flight risk, calling the fake Saudi passport “concerning,” and said the government also established community danger by “clear and convincing evidence” — which led to his decision to keep the financier behind bars.

Epstein’s lawyers had wanted him released on house arrest with electronic monitoring at his $77 million Manhattan mansion. They said he wouldn’t run and was willing to pledge a fortune of at least $559 million as collateral.

That said, Epstein would likely be in solitary confinement for 23 hours per day, lawyer Andrew Laufer, who has represented MCC inmates, told Reuters earlier this month.

“When you have someone that’s allegedly a sexual predator like Jeffrey Epstein, he’ll need to be in protective custody,” said Laufer.

“The sex offenders have a hard time,” said former BOP employee Jack Donson. “He’s definitely going to get ostracized.”

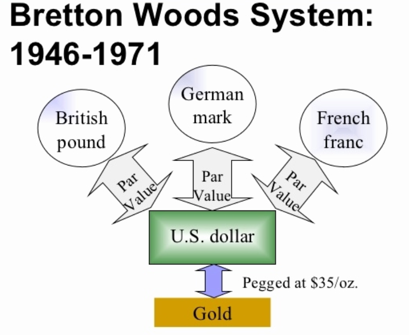

- Bretton Woods At 75: Has The System Reached Its Limits?

75 years ago, the Bretton Woods conference laid the foundations for much of today’s global economic order. But the system is facing a serious threat from growing nationalism and protectionism worldwide.

In July 1944, as it appeared that World War II would be coming to an end with victory for the Allies, senior finance officials from 44 countries huddled in a luxury hotel in Bretton Woods, in the US state of New Hampshire, to put in place the post-war economic order.

The decades prior to Bretton Woods were characterized by commercial conflict, trade wars and military conflict. Restrictions on global commerce and “beggar-thy-neighbor” economic policies had deepened the reach of the Great Depression in the 1930s, imposing huge economic and social costs, which contributed to the rise of nationalist movements, resulting in the outbreak of World War II.

The delegates, including the principle architects of Bretton Woods — John Maynard Keynes of the UK Treasury and Harry Dexter White of the US Treasury — were acutely aware of the adverse effects of the depression, two world wars, economic chaos and poverty.

They set forth to bring about change by promoting international monetary cooperation, supporting the expansion of trade and economic growth, and discouraging policies like trade protectionism and competitive currency devaluations.

The mission of Bretton Woods, in the words of then US Treasury Secretary Henry Morgenthau, was that it should “do away with the economic evils — the competitive devaluation and destructive impediments to trade — which preceded the present war.”

The delegates agreed to create a new international monetary system, underpinned by open markets and fixed exchange rates. The agreement pegged the value of other nations’ currencies to the US dollar, which, in turn, was pegged to the price of gold, fixed at $35 (€31.2) an ounce.

The International Monetary Fund (IMF) was established to monitor and enforce a rules-based system of exchange rates and financial stability, while the International Bank for Reconstruction and Development, now part of the World Bank Group, was set up to provide assistance to countries that had been physically and financially devastated by the war.

The conference at Bretton Woods thus laid the foundations for much of today’s global economic order.

Shaping economic agenda

By the early 1970s, the regime of fixed, but adjustable, exchange rates came under heavy pressure. It ultimately collapsed in 1971 when US President Richard Nixon, following large US trade deficits, broke the dollar’s link to gold. It marked the effective end of the Bretton Woods monetary arrangement.

But the Bretton Woods institutions – the IMF and the World Bank – have continued to shape the international economic agenda. And the objective and spirit of Bretton Woods have continued to guide global policymakers.

In terms of overall economic development, the decades since have been a success, say many economists, although the world has had to deal with inevitable economic and social challenges.

For the 75th anniversary, the Washington-based Bretton Woods Committee organized a compendium of 50 essays – Revitalizing the Spirit of Bretton Woods – examining the 1944 conference’s legacy and challenges ahead.

In their chapter, Nicholas Stern of the London School of Economics and Amar Bhattacharya of the Brookings Institution pointed out that “overall, world income per capita has grown by a factor of 4 since 1950 as population has roughly trebled, so that total output has gone up by a factor of around 12.”

They also noted, “inequality between countries has fallen as a result of the more rapid growth of the large populous emerging markets.” Adding, “however, there has been an increase in inequality within many countries, particularly in terms of the shares of income and wealth going to the top 1%.”

Governance issues

Overall, the Bretton Woods ideal of multilateral cooperation and open markets worked well. Paul Volcker, former chairman of the US Federal Reserve, once said: “Bretton Woods is not a particular institution — it is an ideal, a symbol, of the never-ending need for sovereign nations to work together to support open markets in goods, in services, and in finance, all in the interest of a stable, growing and peaceful economy.”

But for decades, the Bretton Woods institutions have drawn hefty criticism for imposing “neoliberal” economic policies, involving financial deregulation, mass privatizations and austerity. The IMF has faced flak for forcing debtor countries around the world to open their markets and weaken labor protection.

Prior to the 2008 financial crisis, some even questioned the continued need for the IMF. But the crisis changed all that, and the institution played a key firefighting role in cooperation with central banks and finance ministries. Today countries from Pakistan to Argentina continue to knock on the doors of the IMF for help when they find themselves in dire financial straits.

And countries from Asia to South America continue to seek funds from the World Bank to carry out all sorts of developmental projects, despite increased competition from the likes of other institutions, such as the China-led Asian Infrastructure Investment Bank (AIIB).

The Bretton Woods institutions have been grappling with governance issues for years, with many emerging economies maintaining that they’re being denied adequate representation in the organizations’ governing bodies.

Another irritant is the informal arrangement between the US and Europe to name the heads of the institutions, where Europe chooses the IMF’s managing director and the US selects the head of the World Bank.

Many emerging economies are calling for an increase in their IMF shares, while also protecting the shares of African countries. Experts say that would mean reducing the shares of European countries.

‘Reached its limits’

China’s economic rise and the global shift away from US dominance have also strained the system.

“The Bretton Woods order as we know it has reached its limits,” French Finance Minister Bruno Le Maire recently said. “Unless we are able to reinvent Bretton Woods, the New Silk Roads might become the new world order,” Le Maire stated, referring to China’s Belt and Road Initiative, which envisions rebuilding the old Silk Road to connect China with Asia, Europe and beyond with massive infrastructure spending largely financed by China.

“And Chinese standards — on state aid, on access to public procurements, on intellectual property — could become the new global standards,” Le Maire said.

Meanwhile, US President Donald Trump’s “America First” policies and trade protectionist measuresare viewed as a rejection of the spirit of multilateralism and international cooperation that defined Bretton Woods. Many fear that could ultimately lead to instability and conflict.

As Richard A. Debs, the international council chair of the Bretton Woods Committee, wrote in his chapter in the compendium: “History has proven that a nationalistic, isolationist, protectionist approach to dealing with other countries of the world can lead, and has often led, to instability, conflict and wars.”

- $1.6 Trillion Fund Spots A New, Ticking Time Bomb In The Market

First it was the shocking junk bond fiasco at Third Avenue which led to a premature end for the asset manager, then the three largest UK property funds suddenly froze over $12 billion in assets in the aftermath of the Brexit vote; two years later the Swiss multi-billion fund manager GAM blocked redemptions, followed by iconic UK investor Neil Woodford also suddenly gating investors despite representations of solid returns and liquid assets, and most recently the ill-named, Nataxis-owned H20 Asset Management decided to freeze redemptions.

By this point, a pattern had emerged, one which Bank of England Governor Mark Carney described best when he said last month that investment funds that promise to allow customers to withdraw their money on a daily basis are “built on a lie.”

And now, the chief investment officer of Europe’s biggest independent asset manager agrees with him, because while for much of 2019 the biggest risk bogeymen were corporate credit, leveraged loans, and trillions in negative yielding debt, gradually consensus is emerging that investment funds themselves may be the basis for the next liquidity crisis.

“There is no point denying we are faced with a looming liquidity mismatch problem,” said Pascal Blanque, who oversees more than 1.4 trillion euros ($1.6 trillion) as the CIO of Amundi SA, according to Bloomberg’s Mark Gilbert who in a Bloomberg View piece writes that Blanque told him that the prospect of melting liquidity is one of “various things keeping me awake at night.”

Continuing the discussion of illiquid institutions, Blanque said that market making, where firms generate prices at which they are willing to either buy or sell financial products, is effectively “a public good” (or “public bad”, if it is being done by HFTs who disappear at the first sign of volatility, and them having to take on real positional risk). Of course, as that activity declines, the drop in turnover reduces the banking industry’s exposure to a collapse in prices or a surge in volatility. But the dangers are simply transferred, rather than diminished.

“Market making is falling off a cliff at the level of individual banks, but creating a systemic problem,” Blanque told Gilbert. “The banks are less risky – but the risks have been shifted to the buy side.”

As we have discussed extensively in the past, and as Gilbert reminds us, following the global financial crisis, as part of their macroprudential duties, regulators forced investment banks to bolster their balance sheets, which in turn reduced the amount of capital those institutions are able to commit to the securities markets, resulting in a creeping shortage of liquidity when it comes to market making, not only at buyside institutions but also market making banks.

“Market making is falling off a cliff at the level of individual banks, but creating a systemic problem,” Blanque says. “The banks are less risky – but the risks have been shifted to the buy side.”

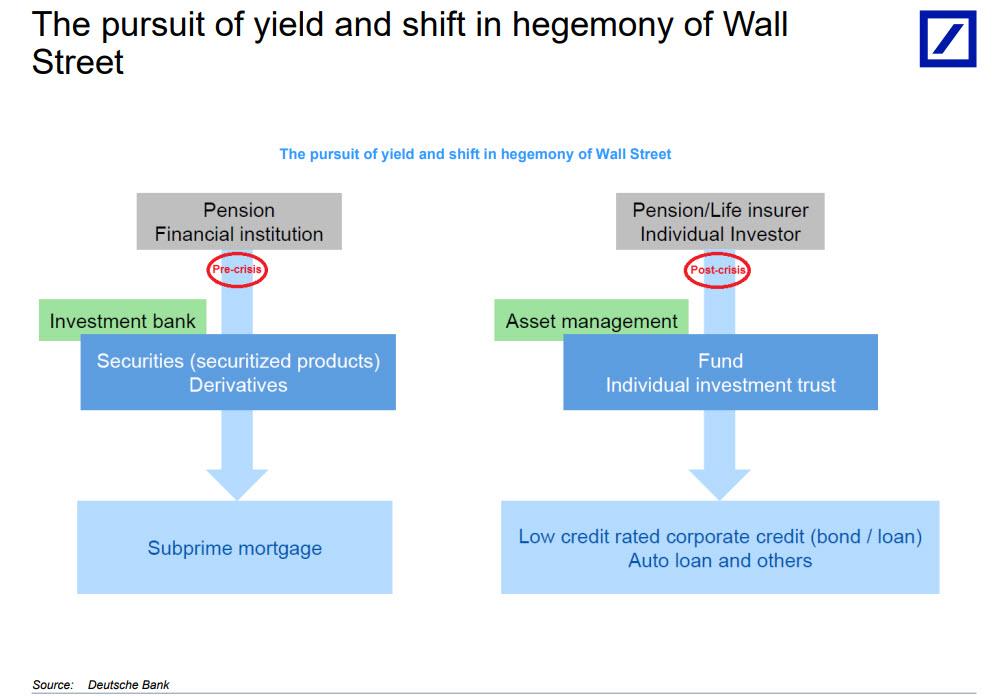

Blanque is probably referring to a recent report from Deutsche Bank (which should know systemic risks better than anyone), which last month published a report titled “Investment Funds – The next liquidity crisis”, in which it wrote that recent events, i.e. the abovementioned collapse of GAM, Woodford and H20, have been “a timely reminder of the potential risks of illiquid securities within open-ended mutual funds offering daily liquidity.” Citing the FSB (Financial Stability Board), Deutsche Bank noted that over half of global intermediation now happens outside the banking system, and that the assets of NBFIs (Non-bank financial Institutions) have grown by over 50% since 2008.

The bank showed this transformation in the pursuit of yield and “shift in the hegemony of Wall Street” in the following chart showing the transition from pension and financial institutions (mediated by investment banks), to pension insurers and individual investors (mediated by at times extremely illiquid asset managers) in the following chart.

Deutsche goes on to show how liquidity risks have shifted, highlighting – like Blanque noted – that while post-crisis banking regulations have materially reduced liquidity (and other) risks within the banking system, some of these risks have been merely transferred to the unregulated NBFI ecosystem, notably mutual funds.

And this is where sudden, unexpected blow ups like Woodford, GAM and H20 are especially jarring as they are an indication of what to expect once the broader market locks up.

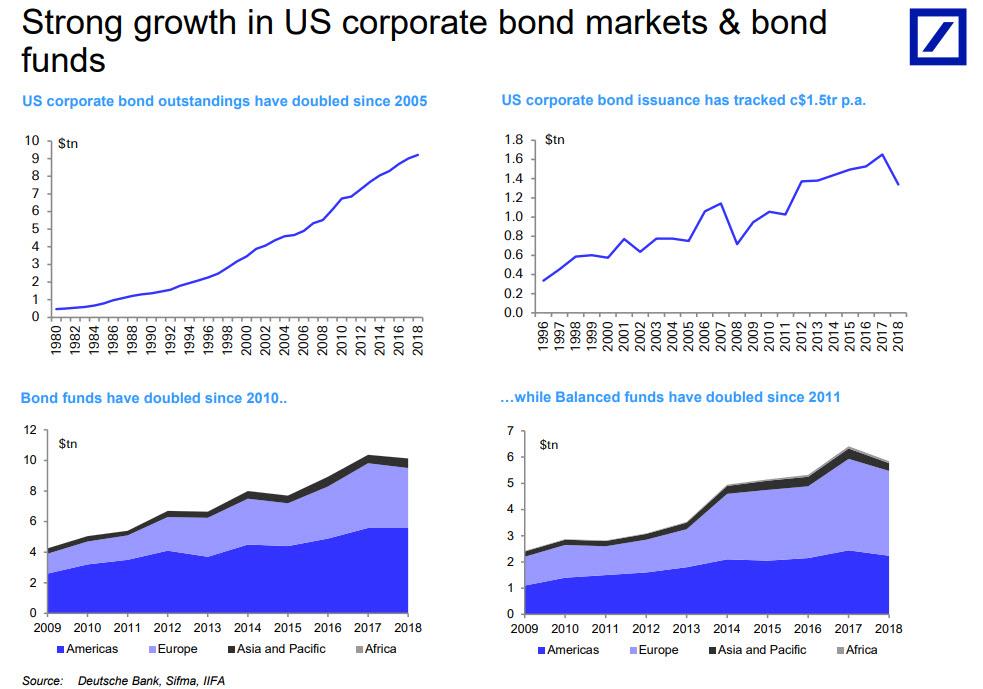

And speaking of the above funds, there is a reason why they are went from liquid to illiquid overnight: they have all geared into corporate bonds. As DB notes, US corporate bond outstandings have doubled since 2005 with recent issuance running at $1.5trn each year.

Over the same period, mutual funds’ ownership of corporate bonds has increased from 12% to almost 30%, or $2.6 trillion…

… with the balance is largely held by insurance and pension funds 45%.

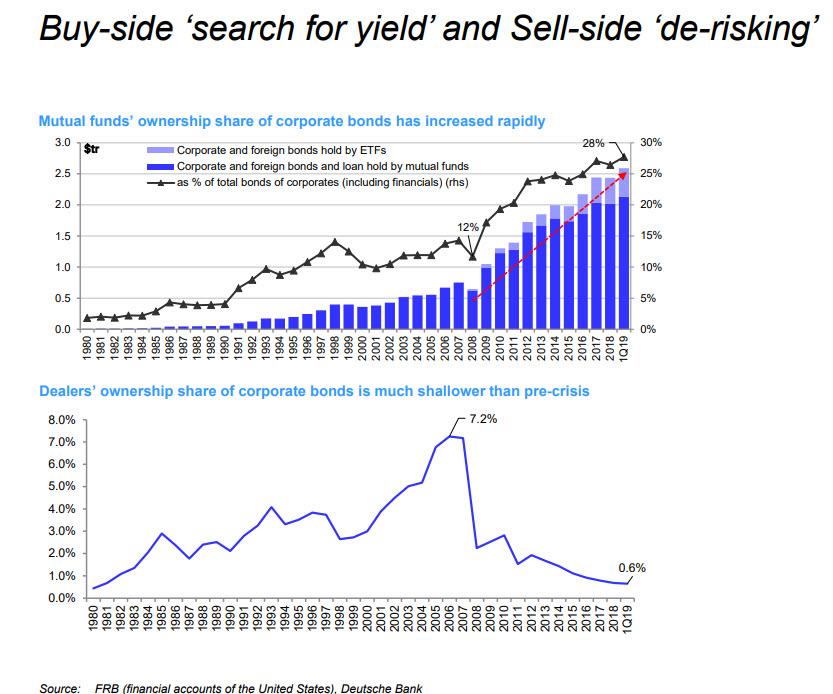

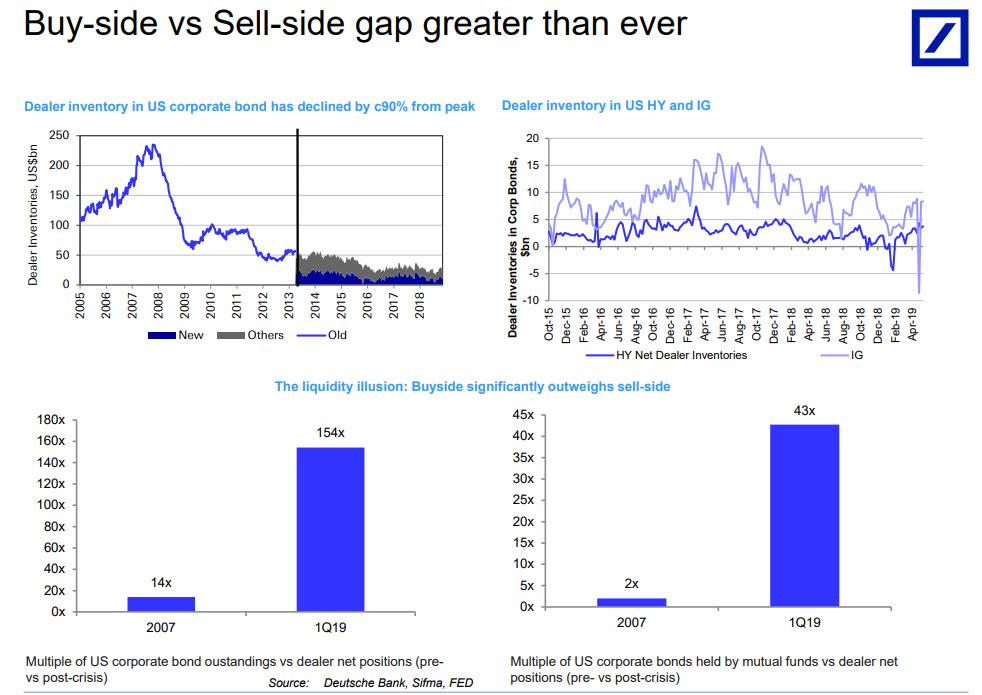

But the biggest reason why liquidity has become an illusion (or rather mass delusion), is that while the dealer inventory of corporate bonds has declined by 90%…

… the ratio of corporate bonds held by mutual funds vs dealer inventory has increased from 2x in 2007 to 43x currently.

In short, as DB highlights, the buy-side significantly outweighs the sell-side and the gap has never been bigger. Worse, this comes at a time when BBB represents 60% of the Investment Grade and 250-300% of the High Yield market.

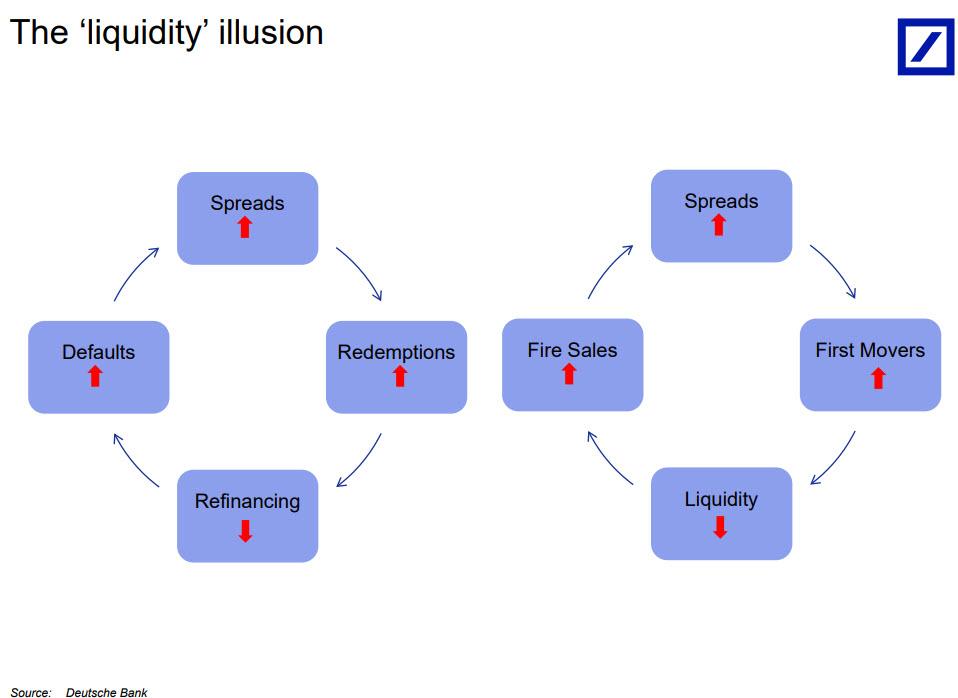

Incidentally, for those wondering if liquidity remains an illusion – a test that can only be confirmed when there is a crash and the market is indefinitely halted, an outcome that is now virtually inevitable – Deutsche has a simple test: it all has to do with the sequence of events unleashed by widening spreads, where redemptions and first movers rush to sell, collapsing the market’s liquidity, freezing refinancings, and resulting in a surge in defaults and firesales, which in turn leads to even wider spreads and so on, until central banks have to step in to short circuit this toxic loop.

This also explains why GAM, Woodford, H20 and many more funds (in the near future), will be similarly gated once their investors discover there is no liquidity to sell into and the only “real time” liquidity is offered to those who have a “first

sellermover advantage”, to wit:- If investors anticipate severe losses on the fund’s investments, they could be incentivised to “run for the exit” to be the first to redeem their shares.

- The first-mover advantage in open-ended funds arises because losses on asset sales to meet redemptions are incurred by investors which remain in the fund.

- As in a ‘bank run’, the asset manager is, in principle, forced to sell assets in a fire sale in order to meet its short-dated liabilities

As an aside, while the above is 100% correct,we find it ironic that it comes from none other than Deutsche Bank, a financial institution which due to a similar considerations among its clients, has itself become the target of a mini “bank run” one targeting the bank’s prime brokerage assets, and which as we explained last week, is reportedly draining roughly $1 billion per day from the German lender.

In any case, this dramatic imbalance of asset holdings at market making banks and buyside “bagholders” of illiquid securities, is now posing a major problem for regulators, something the Bank of England acknowledged in a working paper published earlier this month, and highlighted by Mark Gilber, to wit: “as the funds industry has supplanted banks as a source of credit in the past decade, households and companies have benefited from a useful alternative source of financing. But, the report warned, we don’t know how this market-based system will respond under stress.”

Modelling such a scenario “can generate an adverse feedback loop in which lower asset prices cause solvency/liquidity constraints to bind, pushing asset prices lower still,” the BOE found. In other words, the new market structure may be worse than the old.

The feedback loop discussed by the BOE is the one we showed above. Here it is again:

And, as recent notable fund “gates” and/or collapses have shown, the difficulty for asset managers in such an eventuality is finding sufficient cash to repay exiting investors while preserving the structure of the portfolio without distorting market prices, according to Amundi’s Blanque.

According to Bloomberg, part of Amundi’s response to this seemingly intractable issue is to include liquidity buffers in its portfolios, which may mean holding securities such as German bunds and U.S. Treasuries, which should always trade freely. But the industry needs to come up with a common definition so that liquidity is included along with risk and return when assessing a portfolio’s robustness, Blanque says. Additionally, this band aid only works for modest redemptions. A wholesale liquidation would crush even the most “buffered” up fund.

For now, asset managers have to cope with what Blanque called “the sacred cow” – although a better phrase would be “constant risk” of allowing clients to withdraw funds on a daily basis.

“It is a bomb, given the risks of liquidity mismatch,” he warns. “We don’t know if what is sellable today will be sellable in six months’ time.”

That’s not the only we don’t know. As Blanque concluded, “we don’t know the channels of transmission, we don’t know how the actors will act. It is uncharted territory.”

And that, precisely, is why central banks can never again allow risk asset prices to drop: the alternative means gating not one, or two, or a hundred funds, but halting the entire market, because once everyone start selling and price discovery finally returns to a market that has been dominated by central banks for the past decade, several generations of traders and investors who have grown up without price discovery will be shocked to discover just where “fair” market prices reside.

Digest powered by RSS Digest

Saving...

Saving...![<!–[if IE 9]><![endif]–>](https://www.zerohedge.com/s3/files/inline-images/threw%20out.jpg?itok=PJdoBBnY){kind=link}

![<!–[if IE 9]><![endif]–>](https://www.zerohedge.com/s3/files/inline-images/antietam.jpg?itok=wMwhgYWr){kind=link}

![<!–[if IE 9]><![endif]–>](https://www.zerohedge.com/s3/files/inline-images/mcc%20cell%20%282%29.jpg?itok=6-HaBRwy){kind=link}