- Welcome To The Inversion

Welcome To The Inversion

Authored by Robert Gore via Straight Line Logic blog,

Getting along by going along with the patently absurd…

A seamless web, they all believe because they all believe.

– The Gordian Knot, Robert Gore, 2000

If it seems like the world has turned upside down it’s because it has. Right is wrong and wrong is right. Truth is lies and lies are truth. Knowledge is ignorance and ignorance is knowledge. Success is failure and failure is success. Reality is illusion and illusion is reality.

It would be comforting to say that this inversion is a plot by nefarious others. Comforting, but not true, in the pre-inversion meaning of the word true. Rather it stems from answers to questions that confront everyone. To think for yourself or believe with the group? To stand alone or cower with the crowd? It’s the conflict between the individual and the collective, and between what’s true and what’s believed.

We live in an age of fear. It’s not fear of germs, war, poverty or any other tangible threat that most besets humanity. It’s the fear of being disliked and ostracized by the group.

If every age has its emblematic technology, ours is social media, with its cloying likes and thumbs up and its vicious cancellations, doxing, and deplatforming. No longer must you wander through life plagued by that nagging insecurity—am I liked? Now you can keep virtual score: you not only know if you’re liked or disliked, you know how much and by whom. Unfortunately, that knowledge doesn’t seem to help; the scoreboards only amplify the insecurity. What was once an occasionally troubling question, privately asked of one’s self, has become a widely held, public obsession.

The official Covid-19 response is the apotheosis of inversion and probably the one that runs it off the rails. There’s a model that has repeatedly erred predicting infection and death rates by orders of magnitude. Use it! Politicians and bureaucrats, the two most power-hungry groups on the planet, are clamoring for unlimited powers to destroy jobs, businesses, economies, lives, and liberty. Give it to ’em, no questions asked! Sunshine, Vitamin D, fresh air, and exercise prevent diseases and lessen their symptoms’ severity. Lock ’em up! Lockdowns aren’t working. Lock ’em up harder! Masks don’t prevent or hinder viral transmission, their packaging says so. Double, triple, or better yet, quadruple mask! At high cycle thresholds, the PCR test throws off many false positives, inflating case counts. Crank up the cycle thresholds until Biden gets in office! Cheap medicines hydroxychloroquine, and ivermectin both prevent and cure the disease, provided it’s not too far advanced. Discourage their use! They work better than expensive vaccines. Make vaccinations mandatory! Scores of reputable and eminent doctors and scientists are questioning and criticizing the protocols. Censor them and follow our shapeshifting science! Death counts are inflated because hospitals have a financial incentive to attribute deaths to Covid-19 and anybody who has tested positive and subsequently dies of whatever cause is labeled a Covid-19 death. If they scare people into saving just one life…. The cure is far worse than the disease. Shut up or we’ll shut you up! There’s always germs out there and they constantly mutate, this horseshit could last forever. New Normal, Great Reset. It will last forever, and it will get worse, won’t it? We’ll circle back on that.

Peer pressure is the fundamental force of the social universe. Anyone who’s part of a collective will be pressured to accept its consensus on matters trivial and important. Congruence between what a collective believes and truth is happenstance. The larger the group, the higher the chance of incongruence.

Groups don’t think, they perpetuate and enforce belief. Collectives collectivize what passes for thought, none more so than governments. There’s always the danger that someone might ask why those who rule get to club everyone else into submission. Rulers either suppress that question or try to provide a nominal justification. If they have the clubs, what are they worried about?

The ruling caste is always small compared to the ruled. No matter how many clubs it has and how overmatched the subjects may be, the ruling caste knows its position is more secure if their subjects believe their propaganda and consent to their rule. The underpinnings of frightened compliance with, “Do as you’re told or else!” are rickety compared to a chorus chanting in unison “We’re all in this together!” or some such rot.

None are so enslaved as those chained to group belief. Truth is irrelevant, group acceptance paramount. Belief is unquestioned and unchallenged, truth the shunned and hated enemy. Governments have promoted this inversion for centuries, always telling the same lies. Faith in government may be the strongest and longest-lived secular religion, and it’s certainly the one most resistant to questions, investigation, or contrary evidence.

The script never varies. We’re good, they’re bad, exterminate them. Conquest, domination, and empire are our nation’s greatness. Need not greed: those who earn it are selfish for trying to keep it; we’re virtuous for taking it away. Our pieces of paper are good as gold. Your squalor has nothing to do with our opulent lifestyles; be grateful for your bread and circuses. Dissidence must be suppressed; opposition is traitorous. Ruination and death are everyone’s fault but ours. You just weren’t good enough to live up to our ideals.

Inversions can only last so long. People consciously or unconsciously reject them, and reality doesn’t invert. A small coterie in Washington may believe they run a global empire, but Russia and China refuse to kowtow, even nominal allies are backing away, and the costs of maintaining its crumbling empire are helping drive the US into bankruptcy. What US cheerleaders call the best military in the world hasn’t won a significant war since World War II and its fighting forces are being ideologically culled or indoctrinated in wokesterism, systematically rendering it even less fit to fight.

The censors no longer hide their censorship. There are stories that cannot be reported, questions that cannot not be asked, investigations that cannot be launched, platforms that cannot be allowed, and issues that cannot be discussed within the captured media. It cried foul when Donald Trump made “fake news” a catch phrase, but it caught on because it confirmed what millions know: much of today’s “news” is fraudulent propaganda.

After a month-and-a-half of one-party rule it’s clear that suppression is only going to get worse. Among those who intellectually stand outside the collective, suppression neither decreases belief in what is suppressed nor increases belief in the party line. They know the truth lies in what’s being kept from them.

Subconsciously, even adherents to the party line never completely believe it. Fully “woke,” you may “know” that Western civilization is a discredited product of the white male patriarchy. However, do you throw yourself from the top of a tall building because the properties of gravity were first described by white English patriarch Isaac Newton?

Psychological dissonance plagues true believers. What are they going to believe: dogma or their own senses and thought processes, such as they are? It’s the root cause of their psychic brittleness: the inability to answer questions or engage in debate, the insistence on ostensible agreement, and the need to suppress anyone who doesn’t go along.

The fragility that tries to adjust reality to belief runs head-on into the desire among those whose behaviors are to be adjusted to live their own lives as they see fit, not to mention reality itself. America’s divide is between those who want to be left alone and those who want to tell them what to do. It’s so much easier for the latter if they can impose at least the appearance of consent on the former through suppression, fraud, or force.

Reality doesn’t invert, no matter how many people believe otherwise. Governments and central banks will debase their fiat debt instruments until the illusion that they’re worth something is discarded. They have every incentive to do so and it’s happening now as governments go broke. Empires crumble because they require more energy and resources to maintain than they generate. The American empire will be no exception. The more production is taxed. regulated, and otherwise penalized, the less production you get. The more indolence is rewarded, the more indolence you get. As government’s power expands, people’s freedom shrinks. You can make people engineers or brain surgeons based on their race, ethnicity, gender, sexual preference or any other irrelevant factor, but it increases the likelihood that the bridge collapses and the patient dies on the operating table.

A society that corrupts science, the basis for discovering, describing, and employing reality, is doomed. Honest science requires free inquiry and debate. It is a never-ending process of proposing, testing, evaluating, revising and discarding hypotheses for new ones with more explanatory and predictive power. There is no such thing as settled science. The claims that there is with regards to climate, coronaviruses, or any other scientific issue are nothing more than admissions that the purported science is propaganda. Unchallenged science is a contradiction in terms; challenge is the lifeblood of science.

So add science that isn’t science to the long list of inversions that collectively could spell humanity’s doom. Consequences don’t recognize wishful thinking or political diktat. Climate and coronavirus dogma masquerading as science is the Trojan horse ushering in the great reset of a new world order. Global governance, state-approved science, political and cultural canons enforced with jihadist zeal, top down economic command and control, the eradication of any vestiges of liberty, and billions of unthinking adherents will destroy rather than build, compounding today’s inversions and creating new ones.

The danger to all this is individuals who think and act for themselves, those who are woke to the woke, so to speak. The key to standing on the outside, critically examining what’s within, is to abandon any desire to be on the inside. The docile dreck and their puppet-masters within are usually sufficient inducement to stay outside. Once that decision is made, independence of thought is almost assured. (Those who see the inside for what it is and still want in are corrupt beyond redemption.)

Challenge dogma and propaganda and you’re a dissident. Not always a comfortable position, but the dissidents will have the best shot at surviving the coming collapse. The insiders will suffer shattering disillusionment as reality obliterates cherished belief…and the insiders.

The historically unprecedented scale of present inversions guarantees upheaval and change beyond reckoning when reality’s full force can no longer be denied or subverted. Even those who see things as they are and regard themselves as fully prepared will be shocked by what’s to come. At least they will retain the existential essentials of observational power and logic as they sort through the smoldering intellectual landscape, discard the inversions, and get on with the rebuilding.

Tyler Durden

Mon, 03/08/2021 – 00:00 - China's 7,500-Mile Undersea 'Peace Pipe' To Connect Belt And Road Countries

China’s 7,500-Mile Undersea ‘Peace Pipe’ To Connect Belt And Road Countries

The Trump administration spent the last several years bashing China’s Belt and Road Initiative (BRI) and called it a ‘debt trap’, and urged countries worldwide to resist allowing China to build infrastructure projects in their respected countries. With the Biden administration now in power, there has yet to be a visible protest from the White House of Beijing’s new plan to construct a 7,500-mile submarine communications cable from Pakistan to Africa to Europe.

The high-speed, 7,500-mile Pakistan and East Africa Connecting Europe (PEACE) subsea communication cable system will offer high-capacity, low-latency routes connecting China, Europe, and Africa. In addition to France, the cable will land in Malta, Cyprus, Egypt, Djibouti, Kenya, Pakistan, and other countries with ultimate connectivity to China.

Some of the countries listed above are part of the BRI. China’s motive behind the new undersea project is to provide high-speed internet connectivity to Chinese companies doing business in Europe and Africa.

“This is a plan to project power beyond China toward Europe and Africa,” Jean-Luc Vuillemin, the head of international networks at Orange SA, the French telecommunications that will operate the PEACE cable landing station in Marseille, France, told Bloomberg.

More interesting, Huawei Technologies Co. is the third-largest investor in Hengtong Optic-Electric Co., the company building the PEACE pipe. Huawei is expected to provide critical telecommunications equipment for the project – some of Huawei telecommunications equipment has been cited as a national security risk by the US.

Despite the Trump administration’s hard stance against the BRI and Huawei and other Chinese companies – the Biden administration has yet to visibly criticize China’s new ambitions to construct a global undersea cable network. Much of the internet around the world is transmitted in 400 undersea cables stretching worldwide, controlled mostly by US companies. Chinese encroachment on the US’ dominance would likely usher in a response from the White House.

Bloomberg sources said the French government is prepared to take flak from US officials over the PEACE cable.

“It could look to mollify the US by keeping certain types of traffic off the cable,” another source said.

French President Emmanuel Macron told the Atlantic Council in February that France doesn’t want to isolate itself from China. German Chancellor Angela Merkel also had similar remarks last month.

Some European leaders objected to requests by the past administration to “decouple” from China despite security risks. According to security experts, risks are brewing that China could create backdoors into the PEACE pipe to siphon data.

“Any time that you have your data traveling over their switches, their cables—these are the source of redirecting traffic and eavesdropping,” said Robert Spalding, a senior fellow at the Hudson Institute policy group in Washington. “It’s just common sense.”

China’s attempt to control the world’s internet could be realized in the next couple of decades. The Institute of Peace and Conflict Studies and the Netherlands-based Leiden Asia Center estimates China could be the owner of at least 20% of undersea communication cables worldwide by the end of the decade.

The great power competition between the world’s two largest economies is now spilling into the internet’s physical layers.

Tyler Durden

Sun, 03/07/2021 – 23:30 - So Much For A 'National Healing'

So Much For A ‘National Healing’

Authored by Peter R. Quinones via The Libertarian Institute,

We were told the nation was in desperate need of “healing” because a large portion of the population wanted Donald Trump to “lead” the country. And if you believe that the “national healing would begin” because the “adults” are in the White House…well, you’re a dupe. The response by the corporate press and their supporters to the first freeze to happen in Texas in decades should put to rest any thoughts that the elites, especially the journalists, desire unity. Mass power outages were experienced throughout Texas and the establishment didn’t even attempt to hide their joy.

The situation many Texans faced over that week couldn’t be because freezes like this are so rare in Texas that the grid is not designed to handle the overload in demand or the freezing of its physical infrastructure. No, that can’t be it. The only reason millions of “bumbling hicks” were forced to endure power outages is because so many of them believe CNN and MSNBC are “fake news” and this belief caused them to vote for Trump. It’s amazing to me that a segment of the population that is so anti-religion adopts such a “wrath of God” or “Karma’s a bitch” stance so often when it comes to their adversaries.

I know many people who live in Texas and have been in constant contact with them. Thankfully they’re fine. But, was I shocked by this incident? As someone who lived through “Snowmageddon” in Atlanta in 2014, the answer to that is…hardly. In that year Atlanta was shut down by two inches of snow. Seriously, look it up. The snow started in the middle of the work day – roughly 11:30 AM EST – at which time school buses were loaded to take kids home and everyone left work. If you are at all familiar with Atlanta traffic, on a normal day we do not need multiple accidents to experience the second worst commute in the United States. It’s just every day congestion.

Now, imagine everyone within the city limits and surrounding areas leaving work at the same time. Add in two inches of snow which many people are not used to driving in and it was like a scene from The Walking Dead. People slept in their cars on the freeways and side streets, with many not able to get home for 24 hours. And guess what? The coastal elites went to social media and their news outlets to talk about what a bunch of hicks we were.

Why did Snowmageddon happen? It was a perfect storm of events that all occurred at once. If the storm had occurred at 3 AM, the majority of people would’ve been peacefully sleeping and the number of people trapped in cars would’ve been minimal. Atlanta wasn’t prepared because what happened during Snowmageddon had never before occurred. Apply that “not the norm” occurrence to the freeze in Texas and you have your answer to the state’s recent problems. Atlanta now has snow plows, but more importantly, schools close and businesses are asked to not open if there’s a threat of a midday snow storm.

I expect the freeze in Texas will cause the local and state governments there to have similar plans in place so that the power outages, with all the associated impacts, will not occur in the future. Or they’ll devise some scheme that will mitigate how widespread the outages will be.

Even if they don’t construct a plan for the future, the fact that the “enemy class” is using the freeze as an opportunity for ad hominem attacks against Texans should tell you everything you need to know about their so-called plans to “heal the divides.” If anything, I expect the attacks to escalate and hope they do. Popcorn futures are booming!

Tyler Durden

Sun, 03/07/2021 – 23:00 - Robo-Waiters Prove To Be A Necessity For Contactless Portland-Area Bistro

Robo-Waiters Prove To Be A Necessity For Contactless Portland-Area Bistro

About one-year into the virus pandemic, the return to normalcy for the restaurant industry is unlikely. More than 100,000 restaurants have already failed, revenues remain collapsed, and millions of workers are laid off. There was a glimmer of hope on Friday when some 75% of all US job gains in February were waiters and bartenders; besides that, COVID-19 has cleared the way for restaurant automation.

Automated kiosks, robotic bartenders, flippy the hamburger robot, automated pizza kitchens, and the list go on and on how restaurant operators who survived lockdowns are finding digital solutions for ordering, food preparations, delivery, and even serving.

While health experts are suggesting people stay at least 6 feet from others, one restaurant in Portland, Oregon, has found an innovative way to serve food without face-to-face interactions with patrons.

At Bistro Royale in Beaverton, the restaurant uses autonomous robots to minimize customer interaction between staff and customers while serving food.

Kalvin Myint, a co-owner of Bistro Royal, told the local newspaper Mail Tribune that he began using the robot last August.

“I love to actually play with all these new technologies,” said Myint. “So, when we were looking for a solution, in terms of providing a safer dining experience, my tendency is actually to lean towards technology and see what’s available out there.”

Myint and his wife, Poe, opened Bistro Royale during the pandemic last year. The couple owns another restaurant and divided staff between both to minimize layoffs during lockdowns.

“It was challenging, no doubt about it, but at the same time, it was also exciting in a way,” he said of opening a restaurant during a pandemic. “We love problem-solving, and it gives you a sort of motivation or push to try harder.”

Myint said: “We have to keep evolving and changing and coming up with new things to sort of forge ahead of everybody.”

That’s when he decided to employ three robots (Milo, Navi, and the Beast). The serving robots use mapping software to navigate between customers and obstacles in the restaurant.

Myint clarifies that he does not believe robots can — or should — fully replace human servers.

“In the robotic industry, there’s a lot of worry about robots taking jobs away,” he explained. “They’re like a cellphone, right? You have your cellphone as a tool. So, we’re using them as a tool to sort of amplify what they do best.”

The robots are “celebrities,” he said. “We have families just come here for Milo. I guess he’s getting more popular than the restaurant.”

Robotic servers, Kiosks and apps, and all other sorts of automation introduced to restaurants to maintain social distancing are job killers. While last month’s surge in restaurant jobs was inevitable, don’t get too excited that a “V-shape” recovery in bartenders and servers will be seen anytime soon – due to the deep scarring caused by the pandemic.

The ushering in of automation and artificial intelligence into the industry will eventually result in entire restaurants controlled without humans – that could happen as early as the end part of this decade.

What does this all mean? Well, technological unemployment will continue to rise for years to come.

Tyler Durden

Sun, 03/07/2021 – 22:30 - Money And Statistical Delusions

Money And Statistical Delusions

Authored by Alasdair Macleod via GoldMoney.com,

“I can prove anything with statistics, except the truth”

— Lord Canning, c. 1819

Does Canning’s aphorism still hold true, given that data collection and statistical analysis have progressed beyond all recognition in the last two hundred years? This article tests that proposition.

It is still true, because of the interests for which statistics are deployed. We know, or should know, that CPI indexation of prices fails to reflect the true rate of decline in the purchasing power of fiat currencies. That is at least a simple case of governments saving money on indexation. But being economical with the statistical truth is a far wider practice encompassing input suppression, misleading deployment, and their use to support beliefs and preferred outcomes instead of backing up properly reasoned economic and monetary a priori theory.

This article finds that the application of all these methods corrupt monetary statistics, including the three principal components of the equation of exchange. This analysis is sparked by recent changes to the definition of M1 money supply in the US.

Introduction

Monetarists have long held that there is a relationship between changes in the quantity of circulating currency and the general level of prices. It is not the only factor governing the relation, but it has been generally established to be true. So persuasive is the theoretical case, that no one — not even modern monetary theorists — deny it. We generally assume that the monetary statistics, the sheet anchor to the equation of exchange that emerged over a century ago, are reliable. But even monetary statistics whose components drop out of accounting identities end up being sliced and diced at the behest of the authorities, raising the question as to what we should regard as money at a time of unprecedented peacetime global monetary expansion. And the monetary policy planners moving the goal posts question by their actions the macroeconomic habit of relying solely on statistical evidence for predicting outcomes.

In February, the Fed changed the definition of M1 to include “Savings deposits” and “Other checkable deposits”. They are now combined and reported as “Other liquid deposits”. The effect is to increase M1 but to leave M2 unchanged, as illustrated in Figure 1.

The change accepts the reality, long recognised in the Austrian school’s definition of money supply (AMS), that depositors and banks assume savings accounts are just another form of money available for spending on day-to-day transactions. Monetary policy planners generally circumvent such considerations, looking at monetary definitions from their policy viewpoint instead of the perspective of money’s users.

For statistics junkies, there is a disadvantage in that the new M1 is only readily available as a retrospective monthly average instead of a more current weekly average. This has the effect of under recording the increase of M1 in this statistic at times of rapidly rising monetary inflation. And importantly, M1 is so much modified by these changes as to be rendered useless as a statistical record of monetary inflation.

This raises other questions, such as should we regard broad money or narrow money as the primary indicator of changes in the money supply? And, more deeply, should we ignore the statistical detail and try to understand money from an a priori analysis of the theory of exchange? This is the key difference in the approach of establishment monetarists compared with the Austrian school. Monetarists today, in common with other macroeconomic schools, test propositions by statistical correlation, thereby avoiding the necessity of sound theoretical analysis. Consequently, the definition of money rarely progresses beyond simplistic propositions. And its true use value, which is defined by less predictable human action, is ignored.

The Austrian school generally disregarded the statistical approach to money, until Murray Rothbard attempted to define circulating currency solely in the context of US monetary statistics, work that was consolidated by Joseph Salerno.[i] But slotting different monetary statistics into any combination has never been standardised, so what applies in America, which cannot be precisely defined anyway, doesn’t apply elsewhere. Nor does it when the makeup of a monetary component is altered, excluded or included, such as the current modifications to M1.

Therefore, whatever statistical evidence there is can only be used to corroborate a theoretical analysis, and not be accepted as prima facie evidence. As Lord Canning put it two centuries ago, you can prove anything with statistics but the truth.

Defining money

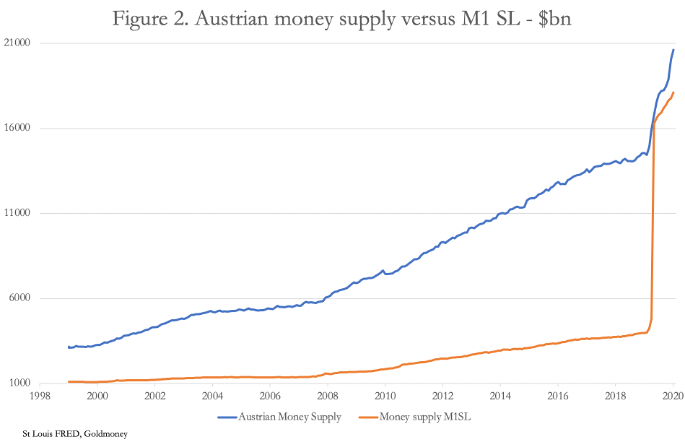

A theoretical approach to understanding money must start by defining it. This definition is taken from the glossary to von Mises’s Human Action:“The most commonly used medium of exchange in society. A community’s most marketable economic good, which people seek primarily for the purpose of later exchanging units of it for the goods or services they prefer. The circulating media most readily accepted for the payment for goods, services and outstanding debts. Money is an indispensable factor in the development of the division of labour and the resulting indirect exchanges upon which modern civilisation is based.”In other words, money is the medium that links production with consumption through the division of labour. It must be immediately available for that purpose. That certainly includes cash in circulation and money in the bank. Correctly, it is now argued by the Fed that because in practice savings are instantly available to bank depositors, that they are cash equivalents. But there are other important aspects of money, such as unspent government balances. Because that can be drawn down at any time, it is money as well, just as if it were money due to an ordinary depositor. But that is not included in the Fed’s definition of M1 (renamed M1 SL), which is an important omission given recent balances on the government’s general account of as much as $1.7 trillion. If, as well as savings deposits, unspent government balances had been included, M1 SL money supply would have looked more like Rothbard’s Austrian money supply (AMS) in Figure 2.

There are good theoretical grounds behind the Austrian money supply calculation, but the absence of the government’s general account in the official M1 calculation disqualifies it from being a true reflection of cash and cash alternatives available for spending. Consequently, official M1 has not yet caught up with AMS, having risen from $3,977bn in January 2020 to $18,105 exactly a year later, an increase of 355%. Over the same timescale AMS rose from $14,082 to $20,614, an increase of 46% — less dramatic perhaps, but genuine.

When it comes to managing expectations, a genuine increase in narrow money of 46% is of greater concern than a far larger increase due to changes in the statistic. This appears to be the reason for the Fed’s part-conversion to Austrian money supply. But they chose a halfway house, which signals perhaps less of a comprehension about what money represents to the wider public and more of a desire to conceal the true state of monetary affairs. And by suppressing interest rates, monetary policy attempts to increase the circulation of money which, the planners appear to believe, would otherwise sit in bank deposits unutilised. The fact that bank deposits are the backing for bank credit whose expansion is also desired escapes this line of reasoning, but that does not stop planners trying to increase the circulation of money.

The velocity myth

Even with M1 money supply at a lower figure that AMS, velocity of circulation is close to unity. Velocity is a widely accepted concept, used as a statistic to promote macroeconomic discourse. The St Louis Fed defines it as follows:

The velocity of money is the frequency at which one unit of currency is used to purchase domestically produced goods and services within a given time period. In other words, it is the number of times one dollar is spent to buy goods and services per unit of time. If the velocity of money is increasing, then more transactions are occurring between individuals in an economy.

This is patently untrue. For it to be correct there would be no relation between production and consumption, and consumers would somehow end up with money to spend without earning it. Money-printing might appear to satisfy this condition, because some money is produced out of thin air instead of being genuinely earned by economic actors. It does not excuse this calumny. What makes this statistical approach acceptable to neo-Keynesians is the denial of Say’s law, which describes the rationale behind the division of labour and points out that money is the most marketable intermediate good whose primary function permits production to be turned into consumption.

If there is one concept that illustrates the difference between a top-down macro-economic approach and the reality of everyday life it is concepts such as the velocity of circulation of money.

Compare the following statements:

“Whenever the interest rate on financial assets is low, the desire to hold money falls as people try to exchange it for other goods or financial assets. As a result, the velocity of circulation rises. Hence, when the money demand is low, the velocity will be high. Conversely, when the opportunity cost/alternate cost is low, money demand is high, and the velocity of circulation is low”.

– Corporate Finance Institute – What is velocity of circulation?

This is in line with monetary planners’ policy of interest rate suppression. They suppress the interest rate to encourage monetary circulation. But if this is valid, then the opposite cannot be true. Yet today, falling velocity to approximately unity with GDP has been accompanied by falling interest rates, even to the zero bound, disproving macroeconomic assumptions.

The next statement is from an economist in the classical, Austrian tradition:

“The mathematical economists refuse to start from the various individuals’ demand for and supply of money. They introduce instead the spurious notion of velocity of circulation according to the pattern of mechanics.”

– Ludwig von Mises, Human Action.

In effect, von Mises is saying it is free markets that decide how money is used, not state management of interest rates.

The mathematical economist might attempt to argue that interest rates affect the relationship between consumption and savings, with higher rates reducing immediate consumption. But that is a red herring, because GDP includes business investment and government spending financed by savings and therefore money not spent on direct consumption. To further understand the errors in the velocity concept we must delve into its origins.

The notion of velocity of circulation arose from the quantity theory of money, which links changes in the quantity of money to changes in the general level of prices. This is set out in the equation of exchange. The basic elements are money, velocity and total spending, represented by GDP. The following is the simplest of a number of ways it has been expressed:

Money x Velocity = Total Spending (or GDP)

Assuming we can measure both the quantity of money and total spending, we end up with velocity. But this does not tell us why velocity might vary: all we know is that it must vary in order to balance the equation. You could equally state that two completely unrelated metrics can be put into a mathematical equation, so long as a variable is included whose only function is to always make the equation balance. In other words, velocity is not a valid expression of the relationship between money and prices; it is merely there to balance an equation that otherwise does not exist.

Von Mises’s criticism is based on the philosopher’s logic that economics is a social and not a physical science. Therefore, mathematical relationships must be strictly confined to accounting and not be confused with resolving economic issues. Unfortunately, economists and commentators have the concept of velocity so ingrained in their thinking that this vital point escapes them.

The only apparent certainty in the equation of exchange is the quantity of money, assuming it is all recorded. No one seems to allow for unrecorded money or assets that can be assumed to be held as readily accessible cash alternatives. Furthermore, if the money is sound, as it was when the quantity theory of money was devised, one could deduce that after a time lag to allow it to fully circulate, an increase in its quantity would more directly tend to raise prices, because changes in the general level of personal liquidity in a population whose money is sound tend to be more stable than that under a fiat money regime.

Today we no longer have sound money, whose purchasing power was regulated by human preferences across national boundaries without impediment. Instead, we have fiat currencies whose purchasing power is formalised in foreign exchanges and corrupted by state intervention. An illustrative example of the consequences is given to us from the Icelandic krona, which on 8th October 2008 suddenly halved in value, which had nothing to do with changes in the quantity of money, its velocity of circulation or Iceland’s GDP.

In economic history, Iceland’s currency collapse was not an isolated event. The purchasing power of a fiat currency varies continually, even to the point of losing it altogether irrespective of changes in its quantity. The truth of the matter is that the utility of a fiat currency in the short-term is entirely dependent on the subjective opinions of individuals expressed through markets and has little to do with a mechanical quantity relationship. In this respect, merely the potential for unlimited currency issuance or a change in perceptions of the issuer’s financial stability, as Iceland discovered, can be enough to destabilise it.

According to the equation of exchange, this is not how things should work. The order of events is first you have an increase in the quantity of money and then prices rise, because monetarist logic states that prices rise as a result of the extra money being spent, not as a result of money yet to be spent. With a mechanical theory there can be no room for subjectivity.

It is therefore nonsense to conclude that velocity is a vital signal of some sort. Linking the relationship between changes in the quantity of money to the effect on prices is certainly more justified in the case of sound money, backed by and freely exchangeable into gold coin. But no material changes to the original concept have allowed for the different characteristics between sound and fiat moneys.

Monetarist theory in its current form is at the very least still a red herring until monetarists finally discover velocity is no more than a factor to make their equation balance. It is indicative of the false mechanisation of human behaviour by modern macro-economists. However, it should also be noted that it is impossible to square the concept of velocity of circulation with one simple fact of everyday life: we earn our salaries and make our profits once and we dispose of them. That’s a constant velocity of exactly one, assuming no change in cash levels over the period under consideration.

This is the irrefutable conclusion of Say’s law. But it was dismissed by Keynes in his General Theory to make way for his macroeconomic fallacies.

The implications of monetary expansion

Following Rothbard’s logic, that money and its immediately encashable equivalents in the mind’s eye of the individual are together the true money supply, we can see from Figure 2 above that in an economy whose annualised GDP is estimated at $21.5 trillion and with Austrian money supply standing at $20.6 trillion, it is 95% of all transactions, suggesting that the average economic actor holds almost a year’s worth of cash liquidity. Clearly, as a result of continual monetary expansion, the US economy is awash with money that hardly, on average, circulates.

In addition to AMS, there is credit money, which is rightly excluded, because being on the other side of a bank’s balance sheet from deposits it is not necessarily available for immediate payments — the bank can always restrict issues of undrawn credit. In this category we can also include shadow banking balances. And payments by credit card are not instantaneous, the payment for goods being deferred by up to a month, so these and similar credit facilities must be excluded as well.

Obviously, there is a link between bank credit expansion and the growth of deposits, raising the question of whether deposits so created should be included in AMS. The answer is no distinction should be made between deposits and those that result from credit expansion, because for the user all bank deposits are regarded as money, whatever their origin.

Left to free markets and sound money, money would undoubtedly be scarce, but plentiful enough to act as the medium of exchange between production and consumption. Therefore, fiat dollar money existing in the quantity that it does is the consequence of easy money policies. Rather than assuming that negative rates will stimulate the population to use it, which is undoubtedly behind official thinking, efforts should be put into considering how to reduce the danger of excess money being unexpectedly mobilised for goods.

The inconvenience of the current position is explained by von Mises’s description of money’s role as “a community’s most marketable economic good, which people seek primarily for the purpose of later exchanging units of it for the goods or services they prefer”. The risk is that substantial quantities of money will be mobilised for that function if people decide to reduce their relationship between owning money in reserve and owning goods which they do not immediately need.

But with covid lockdowns knocking out swathes of industrial production, the goods and services are not available to satisfy this potential demand. Consequently, prices can only rise significantly until the money relationship rebalances. In other words, nominal GDP, being no more than a money total, which we discuss below, will appear to rise dramatically. And with official estimates of price inflation blatantly suppressed, officially recorded “real” GDP will be declared as evidence of the success of monetary policy in rescuing the economy. But remember Canning’s aphorism: I can prove anything with statistics, except the truth…

GDP fallacies

So far, we have shown the errors in official monetary statistics and explained why velocity of circulation is meaningless. Ignorance over velocity of circulation can perhaps be understood because the reasoning behind the equation of exchange predates macroeconomics and is a belief only partially backed by reasoning. We now turn our attention to the third and final component of the equation of exchange. Ignorance cannot so easily be justified about GDP, which was invented in the 1930s, and whose only practical use is to indicate to the state the potential for tax revenues. Its role in the equation of exchange as a substitute for prices is misleading.

GDP is no more than a money total of recorded transactions during a period, usually over a year or annualised. It does not reveal the quality of transactions and economic progress as commonly supposed. It is consistent with what von Mises described as an evenly rotating economy. Again, we can refer to the glossary in his Human Action:

“An imaginary economy in which all transactions and physical conditions are repeated without change in each similar cycle of time. Everything is imagined to continue exactly as before, including all human ideas and goals. Under such fictitious constant repetitive conditions, there can be no net change in any supply or demand and therefore there cannot be any change in prices.”

By deflating it for officially recorded price inflation, GDP appears to meet all the conditions of an evenly rotating economy. Plainly, it does not accord with reality. Furthermore, if the quantity of money was constant and the balance of trade meant it was contained within a community, then that community’s GDP would also remain constant. The logic of this statement is unchallengeable.

Therefore, numerical increases in an evenly rotating economy must come from the money side. In other words, if the quantity of money and credit in an economy is increased, so will GDP. And none of its increase can be attributed to an improvement in economic conditions, because it is modelled on a constantly rotating economy. This is clearly illustrated by removing monetary expansion from the GDP statistic, as illustrated in Figure 3.

Deflating nominal GDP by broad money tells us that US GDP is indeed evenly rotating and has been doing so with not much variation for over four decades. The only notable exceptions were following the Lehman crisis when the US economy entered a brief downturn greater than the expansion of broad money, and in 2020. The latter reflects a large increase in unemployed and underemployed individuals who are still receiving direct payments from the government while locked down due to the coronavirus.

The severity of economic contraction last year was thereby concealed by the expansion of broad money. And its further expansion since the last data point (Q3 2020) will continue to mask the true depth of the economic slump. And for further confirmation, Figure 4 shows the same relationship between GDP and money supply for the UK, where similar factors are at play.

Establishment economists make no differentiation between the real economy and GDP. One never hears or reads any distinction between the two, and Mises’s evenly rotating economy is almost exclusively confined to a few unread pre-Keynesian texts. But its expansion being linked entirely to increases in the money supply reveals that its increase is completely meaningless. But then, monetary and economic policies need to deliver something to justify their existence, not to mention the livings of all the government economists and statisticians and of their opposite numbers in financial and banking institutions.

But with all the inflation money being funnelled into economies today, there can be little doubt that GDP will increase accordingly. But as the charts in Figures 3 and 4 show, with productive capacity cut, the US and UK economies are in a depression.

Canning calls out to us. Forget the statistics, just look around you.

Tyler Durden

Sun, 03/07/2021 – 22:00 - Ted Cruz Rage-Tweets 'Fact-Check' Of "Lefty Press" & Sen. Durbin's "Lies" About Stimmies For Illegal Immigrants

Ted Cruz Rage-Tweets ‘Fact-Check’ Of “Lefty Press” & Sen. Durbin’s “Lies” About Stimmies For Illegal Immigrants

The passing, by The Senate, of the Biden admin’s $1.9 trillion package of pork and payoffs has apparently triggered Senator Ted Cruz. Having attempted to insert an amendment that would disallow the $1400 handouts to illegal immigrants (paid for by legal US taxpaying residents), he was attacked as a “liar” by Senator Dick Durbin

Cruz had asked, “The question for the American people to answer is, should your money, should taxpayer money, be sent, $1,400, to every illegal alien in America?”

Durbin said, “Undocumented immigrants do not have social security numbers. And they do not qualify for stimulus relief checks, period. And just in case you didn’t notice, they didn’t qualify in December… To stand up there and say the opposite is just to rile people up.”

As is clear by the Twitter thread below – Cruz was none too happy about Durbin’s lies (which were dutifully repeated by the mainstream media)…

Cruz begins by asking (rhetorically): “Want to understand why we’re so divided? Why each side seems to live in alternate universes?”

Take a moment & examine the misinformation here (both deliberate & inadvertent)…

FACT 1: Dem spending bill sends $1400 to each adult in US.

FACT 2: Dems voted against my amendment to prohibit sending those $$ to criminals (murderers, rapists, child molesters) currently IN PRISON. EVERY Dem voted to send criminals the $$.

FACT 3: I then called up my amendment to prohibit illegal aliens from getting the $1400 checks.

FACT 4: Durbin then screamed “liar!” and insisted no illegal immigrants would get $$ because the bill requires social security numbers.

FACT 5: Lefty “press” outlets, like Daily Beast, dutifully repeated Durbin’s charge. They did ZERO fact checking of their own, just said that my claim that illegal immigrants would get the $$ was “false.”

FACT 6: Lefty pundits & celebrities like Morgan Fairchild happily repeat the charge that I “lied.” They know none of the facts, but in this politically charged world, the other side must always be wrong.

Sen. Durbin Blasts Sen. Ted Cruz Over False Claims About Immigrants and Stimulus Checks https://t.co/WSZajbWzyU via @thedailybeast

— Morgan Fairchild (@morgfair) March 7, 2021

https://platform.twitter.com/widgets.js

FACT 7: As it so happens, it was Durbin who was lying, and he knew it. Why?

FACT 8: There are 12mm or more illegal immigrants. 60% of them are from visa overstays. Many (if not most) of them have social security numbers.

FACT 9: When Durbin said “illegal immigrants don’t have social security numbers,” he was deliberately saying something false, knowing it would be repeated.

FACT 10: Under the bill’s language, MILLIONS OF ILLEGAL IMMIGRANTS will get the $1400 checks.

FACT 11: My amendment required that recipients would be “lawfully present,” i.e., legal.

FACT 12: When Durbin falsely said ZERO illegal immigrants would get $$, I asked if he would yield for a question. Schumer, sitting next to him, bellowed “no!!”

FACT 13: If Durbin had taken my Q, I would have asked, “if you’re right that no illegal aliens will get $$ under this bill…WHY ARE YOU AND EVERY DEM OPPOSING MY AMENDMENT TO DO JUST THAT?”

The answer is that Durbin was lying, and he knew that Lefty partisans would reflexively believe his gals charge that I was the one lying.

FACT 14: When the checks go out, millions of illegal immigrants WILL GET $1400 checks.

PREDICTION: the Lefty press & pundits won’t cover it, and won’t care.

Cruz ended by rather ominously – but accurately – pointing out that:

“Sadly, that’s why we’re so divided. Facts don’t matter.

Journalists don’t care about truth.

Everyone is a partisan warrior.

And we only believe news from our own side.”

Unity?

For America to come together, this must change.

Tyler Durden

Sun, 03/07/2021 – 21:30 - PIMCO Rings The Alarm Over China's Sliding Credit Impulse

PIMCO Rings The Alarm Over China’s Sliding Credit Impulse

Three months after Zero Hedge subscribers were first made aware of the biggest risk for the global economy, Pimco has finally caught up and is ringing the alarm as noted in the latest observations from Bloomberg macro commentator Ye Xie titled “Pimco Warns of Risks From Beijing’s Credit Curtail.”

1. Beijing sounds less sanguine about 2021.

The government set the growth target this year at “above 6%,” well below economists’ forecasts of 8%. A 6% year-on-year GDP expansion implies zero growth from Q4 2020. Meanwhile, the budget deficit is pegged at 3.2% of GDP, lower than the record 3.6% last year, but higher than the 3% consensus. Taken together, the government seems less upbeat than most economists.

Granted, 6% is the floor, not the ceiling for growth. Beijing may have intentionally set a low bar this year so that it could target a similar growth rate in 2022 to project the image of stability. The economy may turn out to be stronger.

In any case, even if the government ensures it won’t yank stimulus abruptly, gradual tapering in credit growth is already well under way. As first discussed in December in “In Historic Reversal, China’s Credit Impulse Just Peaked: What This Means For Global Markets“, China’s credit impulse, or the change of new credit as a percentage of GDP, peaked in October and is following the similar downward path of the previous two credit cycles in 2013 and 2016. At this rate, the gauge could turn negative in the second half of the year.

In a note on Friday, Pimco estimated that the credit impulse will fall to -3.5% of GDP by year-end, from a peak above 9% in 2020. All else equal, it may slow China’s economy to below-trend levels by late 2022, the firm’s Gene Frieda and Carol Liao wrote.

What does this mean? Tighter liquidity is likely to lead to stress in China’s corporate debt market, they wrote (echoing what Zero Hedge wrote in December). While a soft-landing is achievable and the yuan remains attractive, the drag from China’s economy next year suggests that “developed economies may require stimulus for longer than currently appreciated.”

2. The path of least resistance is for bond yields to move higher.

Jerome Powell reiterated that the Fed is in no rush to reduce stimulus, but declined to say that rising bond yields are inconsistent with the central bank’s objective. That essentially gives the market a free rein to push yields higher, keeping Treasuries as the potential source of volatility for other markets.

Chinese bonds remain insulated from the global bond rout, given they have largely priced in economic normalization.

3. The trade-weighted yuan rose amid a stronger dollar.

While rising yields lifted the dollar, the yuan managed to outperform other currencies, sending the trade-weighted yuan close to the highest since 2018. The foreign bond inflows continue to be supportive. “Real money” investors, such as pension funds, have boosted their overweight on the yuan to the highest level since JPMorgan included Chinese bond in its benchmarks in February 2020, according to Bank of America.

Tyler Durden

Sun, 03/07/2021 – 21:00 - "We'll Level Tel Aviv": Iran Responds To Israel 'Preparing' Strike Plans Against Nuclear Sites

“We’ll Level Tel Aviv”: Iran Responds To Israel ‘Preparing’ Strike Plans Against Nuclear Sites

Iran has responded to a Fox News interview from late last week wherein Israeli Defense Minister Benny Gantz said that Israel is currently updating its plans to strike Iran’s nuclear program and is prepared to act independently if the United States is not willing. The interview was unusually blunt even for Israel in terms of the defense chief openly stating war plans.

Iranian Defense Minister Amir Hatami promptly fired back with a counterthreat on Sunday. He said Iran’s military will level Tel Aviv and Haifa should Israel do anything “out of desperation”.

Iranian Defense Minister Amir Hatami, via Wiki Commons “Sometimes, the Zionist regime [Israel] out of desperation makes big claims against the Islamic Republic of Iran to allegedly threaten it,” Hatami said as cited in The Times of Israel via Iranian state media.

“It must know that if it does a damn thing, we will raze Tel Aviv and Haifa to the ground,” he followed up with according to an English translation. Hatami was addressing a military ceremony.

He further assured that Iran possesses all the power it needs to “maintain the stability of the country” and said the Islamic Republic can strike close to Israel also via “resistance groups” – which is no doubt a reference to Lebanese Hezbollah and militia groups that have been fighting in Syria.

During Gantz’s Fox News statements two days ago, the defense chief had spelled out to the American correspondent that “If the world stops them [Iran] before, it’s much the better. But if not, we must stand independently and we must defend ourselves by ourselves.”

“The Iranian nuclear aspiration must be stopped… We must defend ourselves by ourselves,” Gantz had asserted.

NEW: Israel is improving plans to strike Iranian nuclear targets, Defense Minister Benny Gantz tells mehttps://t.co/19GiARhYoy

— Trey Yingst (@TreyYingst) March 4, 2021

https://platform.twitter.com/widgets.js

Prime Minister Netanyahu has also issued similar warnings recently, however, Gantz’s words were the most specific and forceful thus far. He had even handed the Fox reporter what was purported to be a classified target list against Iranian assets that Israel prepared.

Gantz had also touted that Israel stands ready to attack Hezbollah positions throughout Lebanon and Syria – the latter country has been on the receiving end of Israeli airstrikes on a near weekly basis for much of the past year. The defense minister claimed that Hezbollah has “hundreds of thousands” of missiles aimed at Israel and is bent on the Jewish state’s destruction.

Tyler Durden

Sun, 03/07/2021 – 20:30 - Hedge Fund CIO: The 1929 Crash Sparked A Chain Reaction That Led To WWII In 1939

Hedge Fund CIO: The 1929 Crash Sparked A Chain Reaction That Led To WWII In 1939

By Eric Peters, CIO of One River Asset Management

Lost Arks

“Illiquidity is creeping into credit markets,” said Indiana, the industry’s leading archaeologist, explorer. “Credit risks of the type Minsky identified have migrated from the banking system into capital markets.”

Corporate borrowings through bond issuance, in turn captured in exchange traded funds, are an important part of that risk migration. “Even with the stability of credit spreads, this rate rise battered credit funds.” LQD is -6% YTD. “Fund outflows are $6.8bln YTD – the pandemic outflow from mid-Feb to mid-Mar 2020 was just $4.5bln.”

“This week saw the return of credit ETFs trading at a discount to net asset values,” continued Indiana. “Small for now, averaging less than 20 basis points in the past three days.” As liquidity in underlying assets lessens, so too does the ability of participants to provide that liquidity through ETFs. “The discounts are capturing a marginal fray in liquidity conditions, an early warning,” said Indy.

“And the crown jewels of global financial markets – Treasuries – saw a surge in the cost of borrowing securities this week. Illiquidity in Treasuries rose sharply.”

Rapid Unplanned Disassembly (RUD)

The 1929 market crash sparked a chain reaction that lasted a decade, a rapid unplanned disassembly, leading humanity to WWII in 1939. US unemployment averaged 18.2% in the 1930s, CPI averaged -2.0%. The S&P 500 lost 42% in the decade (real return was -29%). The 1970s RUD produced two brutal recessions, US unemployment averaged 6.4% and CPI averaged +7.25%. The S&P 500 gave the illusion of health with a 17% gain. The real return was worse than the 1930s, with a 42% decline.

- In 1930, the US CPI was -2.7%, the S&P 500 inflation-adjusted return was -23% (the inflation adjusted 10yr Treasury note return was +7.4%). In 1931, CPI was -8.9%, S&P 500 real return -38%, 10yr note real return 7.0%. In 1932 (CPI -10.3%, S&P 2%, 10yr 21.3%). 1933 (CPI -5.2%, S&P 58%, 10yr 7.4%). 1934 (CPI 3.5%, S&P -5%, 10yr 4.3%). 1935 (CPI 2.6%, S&P 43%, 10yr 1.9%). 1936 (CPI 1.0%, S&P 31%, 10yr 3.9%). 1937 (CPI 3.7%, S&P -38%, 10yr -2.3). 1938 (CPI -2.0%, S&P 32%, 10yr 6.4%). 1939 (CPI -1.3%, S&P flat, 10yr 5.8%).

- In 1970, the US CPI was +5.8%, the S&P 500 inflation-adjusted return was -2% (the inflation adjusted 10yr Treasury note return was +10.3%). In 1971, CPI was 4.3%, S&P 500 real return 10%, 10yr note real return 5.3%. In 1972 (CPI 3.3%, S&P 15%, 10yr -0.4%). 1973 (CPI 6.8%, S&P -19%, 10y -2.4%). 1974 (CPI 11.1%, S&P -33%, 10yr -8.2%). 1975 (CPI 9.1%, S&P 25%, 10yr -5.0%). 1976 (CPI 5.7%, S&P 17%, 10yr 9.7%). 1977 (CPI 6.5%, S&P -13%, 10yr -4.9). 1978 (CPI 7.6%, S&P -1%, 10yr -7.8%). 1979 (CPI 11.3%, S&P +6.5, 10yr -9.5%).

In both the 1940s and 1980s, investors who had emerged from the preceding decade with their capital intact made vast fortunes, equity markets boomed.

Anecdote

“The 19th century was defined by the formation of nation states. The US had just emerged from its UK ties, the treaty of Vienna created countries such as the Netherlands, France just had its revolution and rid itself of Napoleon, Germany unified and Italy became a nation state,” said the Dutchman, a private investor, his fortune built in the markets, trade, finance.

“The 20th century was the era of the establishment of institutions, alliances, internal, global, the US Federal Reserve, the United Nations, many others in between.” International Monetary Fund, World Bank, World Health Organization, NATO, the list goes on. Programs too: Social security, Medicare, Medicaid, state pensions. Countless agencies: CIA, FBI, NSA, NASA, EPA, FDA and so on.

“A number of those institutions have come under siege in recent times and the level of trust embedded in them has eroded,” said the Dutchman, images of America’s horned Shaman seared in the global consciousness.

History moves slowly, then fast, all at once. We read books, watch movies, and they compress years, even decades, into tight chapters, creating the illusion that periods of great change are apparent as they unfold, obvious to those living through them. And this then allows us to ignore today’s seismic shifts even as the ground beneath our feet trembles.

“This erosion of trust can also be said about the Fed at a time when the need for credibility is perhaps greater than it has ever been, which makes the trajectory for financial markets going forward particularly difficult and potentially very volatile,” he said.

“And it appears that forces are now in motion that will redistribute wealth, shifting it from capitalists to the workers,” said the Dutchman, taking a moment to consider it all.

“There tend to be couple decades each century when it is a victory to have preserved your real wealth. This looks to be one of them.”

Tyler Durden

Sun, 03/07/2021 – 20:00 - Outrage Mob Goes After Cartoon Skunk Pepe Le Pew For "Normalizing Rape Culture"

Outrage Mob Goes After Cartoon Skunk Pepe Le Pew For “Normalizing Rape Culture”

The woke cancel culture mob continues trucking along with their crusade against free speech, targeting popular Dr. Seuss books last week as they said some of these beloved children’s books contain racist imagery. As the mob continues to look for stuff to burn figuratively, cartoon characters like Pepé Le Pew, a character from the Warner Bros. Looney Tunes and Merrie Melodies series of cartoons from the 1940s, is the next target.

New York Times liberal columnist Charles Blow recently argued in an op-ed and in a series of tweets how Pepé Le Pew “normalized rape culture.” He tweeted Saturday a scene from the cartoon: “Let’s see, he grabs/kisses a girl/stranger repeatedly, without consent and against her will. She struggles mightily to get away from him, but he won’t release her. He locks a door to prevent her from escaping.”

RW blogs are mad bc I said Pepe Le Pew added to rape culture. Let’s see.

1. He grabs/kisses a girl/stranger, repeatedly, w/o consent and against her will.

2. She struggles mightily to get away from him, but he won’t release her

3. He locks a door to prevent her from escaping. pic.twitter.com/CbLCldLwvR— Charles M. Blow (@CharlesMBlow) March 6, 2021

https://platform.twitter.com/widgets.js

In a separate tweet, Blow continued: “This helped teach boys that “no” didn’t really mean no, that it was a part of “the game,” the starting line of a power struggle. It taught overcoming a woman’s strenuous, even physical objections was normal, adorable, funny. They didn’t even give the woman the ability to SPEAK.”

This helped teach boys that “no” didn’t really mean no, that it was a part of “the game”, the starting line of a power struggle. It taught overcoming a woman’s strenuous, even physical objections, was normal, adorable, funny. They didn’t even give the woman the ability to SPEAK.

— Charles M. Blow (@CharlesMBlow) March 6, 2021

https://platform.twitter.com/widgets.js

The Media Research Center, a top media watchdog, responded to Blow’s op-ed following the recent cancel mob’s assault on Dr. Seuss, who said:

“Congrats to anyone who had “liberals try to cancel Looney Tunes” on their 2021 bingo card.”

In his op-ed, Blow said, “racism must be exorcised from culture, including, or maybe especially, from children’s culture. Teaching a child to hate or be ashamed of themselves is a sin against their innocence and weight against their possibilities.” He wrote that he “cheered” when he heard the news six of Dr. Seuss’ books were discontinued by its publisher because of “racist and insensitive imagery.”

Some social media users were not thrilled with Bow’s op-ed and tweets:

One Twitter user said: 1. “It’s…a…f**king…cartoon. 2. It was made in the 1950s, when this society’s values and mores were a wee bit different. 3. Pepe always gets clowned by the cat in the end…every time. 4. It’s a fucking cartoon. 5. For those of you unclear on the point, see #1 and #4 above.”

“I’ve never gotten relationship advice from a cartoon. Not now, and for damned sure, not when I was six. Jesus H. Christ,” someone said.

“Wait until people realize that Frosty The Snowman is naked and smokes a pipe in front of children. This never ends. Cancel culture is internet cancer,” another user said.

… and there’s this.

5. He doesn’t even know WTF he’s talking about. They’ve been multiple times in which Penolope the cat Loves Him. But He smelled Like what he was. A skunk. pic.twitter.com/hXI0KShYsQ

— ScarletEmber (@Nightdragonx1) March 6, 2021

This Twitter user makes an interesting point:

“Yeah, this was on TV. it was normal to show it to children in an ‘evolving society’ it’s easy (for most of us) to see how messed up and wrong a cartoon from 80 years ago feels today, but few of us will imagine how what we are doing TODAY may look like 80 years from now.”

Perhaps, what the future will show is today’s mob-canceling crowd as “the digital equivalent of the medieval mob roaming the streets looking for someone to burn,” said Rowan Atkinson, famous for portraying the characters Mr. Bean and Blackadder.

The former secretary of Housing and Urban Development, Ben Carson, calls the left’s attempt to cancel culture a “poison.”

So every week, the left will cancel a book, cartoon, or anything that displeases them?

How about for a change, the left does something constructive – such as – cancel violent video games. Today’s youth are playing games such as “Grand Theft Auto” and or “Call of Duty” – teaching them murder and destruction is okay. While on the streets of America, millennial anarchists, for almost a year, have been destroying tens of millions of dollars in property through destructive riots.

Focus on today not what happened decades ago…

Tyler Durden

Sun, 03/07/2021 – 19:30 - Sen. Blackburn Wants NBA To "Come Clean" On Its Deal With Chinese State Television

Sen. Blackburn Wants NBA To “Come Clean” On Its Deal With Chinese State Television

Authored by Cathy He via The Epoch Times,

Sen. Marsha Blackburn (R-Tenn.) is questioning the National Basketball Association’s (NBA) reported new deal with Chinese state television, the latest official to raise concerns over the league’s relationship with the Chinese regime.

The NBA famously drew the wrath of the Chinese communist regime in late 2019 after then-Houston Rockets General Manager Daryl Morey tweeted in support of the pro-democracy protesters in Hong Kong. Chinese businesses cut ties with the league, and state broadcaster CCTV stopped airing games.

But Chinese media recently reported that CCTV will resume regular broadcast of the NBA starting with the All-Star Game on March 7.

“Commissioner Silver cut a deal to air NBA games on the same station that regularly broadcasts Communist propaganda and forced prisoner confessions,” Blackburn told The Epoch Times in an email, referring to NBA Commissioner Adam Silver.

“Commissioner Silver needs to come clean – did he agree to censor players’ free speech to return to Chinese state-run airwaves?”

Silver said last year that the league faced hundreds of millions in losses from the Chinese backlash.

Blackburn wrote to Silver on March 4, signaling concern over the league’s alleged television deal with CCTV at a time when the Chinese regime faces increasing scrutiny over its coverup of the COVID-19 pandemic and rampant human rights abuses.

“While investigations into the origin of COVID-19 continue in Wuhan, the NBA seems solely focused on mending its relationship with CCTV even though it’s clear Communist China will distort, censor or terminate any CCTV broadcast that is seen as a threat to the Chinese Communist Party (CCP),” the senator wrote in her letter (pdf).

Last October, CCTV temporarily resumed its broadcast for the last two games of the NBA finals, a result of the “goodwill” expressed by the NBA for some time, a spokesperson for CCTV said at the time. “The NBA has made active efforts to support the Chinese people in their fight against COVID-19,” the spokesperson said.

“It is safe to assume that ‘goodwill’ included the $1 million in medical supplies the NBA sent to the CCP,” Blackburn said in the letter.

“China dominates PPE production worldwide, so it is deeply troubling that the NBA would send this aid, especially after witnessing the lack of transparency shown by the CCP throughout the entire pandemic and their continued grave human rights violations.”

Blackburn asked Silver to provide details about the CCTV deal by March 30, including whether the agreement bars the NBA from speaking on topics deemed unacceptable to the Chinese regime such as Tibet, Hong Kong, Taiwan, and Xinjiang, and the financial impact of the CCTV’s broadcast ban.

Last May, the NBA announced a new head of its China operations, Michael Ma, whose father, Ma Guoli, is a co-founder of CCTV Sports. Blackburn also asked the NBA to detail what roles Ma and his father played in the negotiations.

The NBA did not immediately respond to a request for comment.

The league also sparked controversy in July 2020, when an ESPN investigation revealed that Chinese coaches at the NBA youth training academy in the region of Xinjiang physically abused players. The NBA later confirmed that it had terminated its relationship with the academy.

Tyler Durden

Sun, 03/07/2021 – 19:05 - Another Market Paradox: Wall Street Struggles To Explain Record Equity Inflows Amid Stock Turmoil

Another Market Paradox: Wall Street Struggles To Explain Record Equity Inflows Amid Stock Turmoil

Something bizarre is happening in the stock market: for the past three weeks stocks – and especially tech – has gotten hammered, with the Nasdaq briefly sliding into a 10% correction while the S&P has also been hard hit (although one can’t say the same for reflation stocks such as energy which have soared in recent weeks). Some other notable casualties: Apple has tumbled 15% since late January. Tesla has lost more than a quarter-trillion dollars in market value in three weeks, and more than $1.5 trillion has been wiped off the Nasdaq in less than a month.

And yet, despite this hit to risk assets on the back of the recent in surge in interest rates, accompanied by a parallel spike in both the VIX, and its bond market equivalent, the MOVE index…

… on Friday we reported that according to the latest EPFR fund flow data, $22.2Bn in new money flowed into equities last week, following the previous week’s massive $46.2Bn inflow which was the 3rd biggest on record, bringing the total 16 week inflow to $436BN, a stunning burst of inflows as shown in the chart below.

So bizarre has been this divergence – historically, investors have always pulled money during times of stress and heightened volatility, instead they are plowing record amounts of cash into stocks now – that Goldman’s David Kostin dedicated his Weekly Kickstart report to the topic. In a note titled “Rising rate anxiety roils share prices but also supports outlook for strong equity inflows”, the Goldman chief equity strategist writes that as “rates rose, and equities fell, long-duration growth stocks plummeted, but equity funds continued to see large net inflows.”

Equity mutual fund and ETF inflows have totaled $163 billion since the start of February, the largest five-week inflow on record in absolute dollar terms and third largest in a decade relative to assets. Even though the recent backup in rates has weighed on equity prices broadly, the pace of inflows into equity funds during the last few weeks has accelerated compared with the start of the year.

In contrast, weekly flows into bond funds averaged roughly $10 billion in February, 50% less than weekly inflows in January. In addition, money market funds have seen net outflows of $34 billion during the past month.

It is worth noting that retail investors are not indiscriminately plowing cash into all stocks, and instead the rotation into equity funds has most favored strategies that benefit from accelerating economic growth, in other words there has been a rotation of new money from growth and to value. Indeed, when looking in absolute dollar terms, while US equity funds have seen large inflows during the past month (+$62 billion), relative to assets, EM, Value, small-cap, and Materials equity funds have seen the largest inflows, consistent with the outperformance of economic growth-sensitive equities.

And here Kostin makes a curious observation in trying to explain this flood of new capital just as stocks – well, mostly tech and growth stocks – get hammered – according to the Goldman strategist, “history shows that equity funds generally experience inflows when real rates are rising. During the past 10 years, the most favorable backdrop for equity fund inflows has been when both real rates and breakeven inflation were rising (Exhibit 2).”

This, Kostin adds, is intuitive given that the dynamic typically occurs when growth expectations are improving. However, equity funds usually experienced inflows when real rates rose and breakeven inflation fell. In short, equity fund flows have been more clearly delineated by the trajectory of real yields than by inflation during the past decade.

This certainly appears to be confirmed by the data: in his latest “Investor Positioning and Flows” report (available to pro subs), Deutsche Bank’s Parag Thatte also picks up on this divergence and writes that “bond fund flows slowed sharply this week as rates rose, but equity inflows continue to roll in” and like Kostin, concludes that “the rising rates environment continues to propel large inflows into equity funds (+$22.2bn this week)” although as one would expects, “equity inflows this week went heavily towards cyclical sectors and styles, while Growth funds saw outflows”

Whether or not the chart above ends in tears will ultimately depend on just how much capital investors have to throw at reflation assets, oblivious of how painful the high duration crash in growth/tech stocks could be (and since FAAMGs still account for about 25% of the S&P500, it could be very painful indeed).

Alternatively, it may well be that yields, inflation or growth concerns have nothing to do with the massive retail inflows we are observing, and it is all due to tidal wave of Robinhood/Reddit investors who have now habituated to buying every single dip. Indeed, as Bloomberg points out over the weekend, no amount of market turmoil has been enough to rattle retail investors who are now so habituated to Fed bailouts, they have yet to find a dip they won’t buy.

According to Bloomberg, even though the market peaked almost a month ago, retail traders have plowed cash into U.S. stocks at a rate 40% higher than they did in 2020, which was a record year. Yet one way retail capital allocation differs from the charts above, is that “they’re opting for parts of the market that have suffered the most, doubling down in arguably risky ways with triple-leveraged tech funds and options galore.”

Could it be that nothing but sheer stupidity and/or certainty in yet another Fed bailout is behind the record inflows? And is Powell to blame?

Retail traders, many of them newbie investors, have consistently held strong, buying virtually every dip during what’s been the best start to a bull market in nine decades. But now the world is wondering how much it’ll take for them to call it quits, especially after a year in which retail traders were right way more often than wrong.

“Historically it’s been a bad signal that retail investors are piling into the market and a signal of a top,” said Art Hogan, chief market strategist at National Securities Corp. And yet, as he admits in the very next sentence, “every time we tried to call a top in 2020 because of retail participation, it was wrong.”

Just how aggressive has retail buying been? According to data from VandaTrack, which monitors retail flows in the U.S. market, retail investors snapped up an average of $6.6 billion in U.S. equities each week, up from an average $4.7 billion in net weekly purchases in 2020 even as stocks swooned over the last three weeks.

They’ve doubled down on areas of the market that have been hit the hardest. Apple, which has plunged 15% since late January, was the most-popular retail buy this past week. NIO Inc., the electric-vehicle maker down almost 40% since Feb. 9, was the second-most popular. Next up were exchange-traded funds tied to the Nasdaq 100, the Invesco QQQ Trust Series 1 (ticker QQQ) and a triple leveraged version (ticker TQQQ).

Because in a centrally-planned “market” where the Fed guarantees no losses ever, why not buy any and every dip? Sure enough, that’s what they did and boy did they buy the dip:

On Thursday, when the Nasdaq 100 fell as much as 2.9%, almost 32 million bullish call options traded across U.S. exchanges, the fifth-most on record. The other four have all occurred within the last four months.

There is one fundamental reason why retail investors are buying: the just passed $1.9TN Biden stimulus ensures lots and lots and lots of stimmy checks are about be deposited to daytraders’ checking accounts:

“There’s a lot of excess liquidity and we just had this $600 check going to many families in January,” said Jimmy Chang, chief investment officer of Rockefeller Global Family Office. “We’re going to get an additional liquidity injection in the $1,400 check and part of that money is going into risk assets.”

Incidentally, the question of how much of Biden’s $1.9TN stimulus will end up in the market is one we discussed last week in the context of a recent Deutsche Bank survey:

“Given stimulus checks are currently penciled in at c.$405bn in Biden’s plan, that gives us a maximum of around $150bn that could go into US equities based on our survey.

Obviously only a proportion of recipients have trading accounts, though. If we estimate this at around 20% (based on some historical assumptions), that would still provide around c.$30bn of firepower – and that’s before we talk about any possible boosts to 401k plans outside of trading accounts.”

Clearly, frontrunning that number is enough to get retail daytraders to flood the market with yet another round of dip buying for the likes of Karim Alammuri, a 31-year-old marketing strategy manager, who is one of many retail investors who’s been snapping up stocks. In recent days, he bought shares of fuboTV Inc. and SPAC Churchill Capital Corp IV. Fubo TV has plunged more than 50% since a December peak. Churchill Capital has lost almost 60% of its value in 11 trading sessions. He is not giving up however:

“I plan on sticking around because I don’t want to take a loss,” he said by phone from New York. “A lot of very attractive stocks are on crazy discount right now, so I’m just looking to see how I can re-shuffle things to be able to buy them.”

Naturally, with an army of retail investors standing ready to buy any dip, those declines have grown shallower and shallower. As shown in the chart below, the S&P 500 has gone without a 5% pullback since early November, or 83 straight days, the longest streak in a year. The end result of this persistent dip buying, as Bloomberg notes, “is a market with little downside. At its lowest closing level of 2021, the S&P 500 was only down 1.5% year-to-date. That’s the smallest drawdown at this time of a year since 2017.”

So is this time different?