- Mass Shootings, Mass Psychology, And Self-Defense

Authored by Brandon Smith via Alt-Market.com,

There is an unfortunate correlation between crises and catastrophes and mass psychology.

For those with a decent long-term memory, you may have noticed that the frequency of attacks and tragedies taking place today around the world is far above and beyond what occurred 10 years ago. So much so that many in the public have moved beyond the point of outrage and have now embraced complacency.

The mass shooting issue, for example, once inspired fevered debate over gun rights. Not so much anymore. While I am happy that the relentless attempts by leftists to exploit every shooting as a tool for their gun grabbing agenda have taken a backseat, I see a trend in another direction which is equally dangerous. That trend is a move towards acceptance that "these things happen," instead of a healthy discussion on real solutions (and no, more gun control is not one of them).

A decade ago the Vegas shooting would have inspired media and social discussion for at least a year. Now, the story disappears in two weeks and is replaced with 10 others. I will be surprised if the latest church shooting in Texas in which 26 people were killed stays on the news feeds for more than a few days.

Where does this complacency come from?

It is a complex problem, but one that I think relates to the state of decline within any particular society. In Carl Jung's The Undiscovered Self, Jung mentions a consistent element of latent sociopathy and psychopathy within most cultures. Perhaps 10% of people within a society are latent sociopaths and psychopaths, and around 1% or less represent full blown sociopaths/psychopaths. Most of the latent people will never become truly dangerous if they are living within a culture that is healthy and morally balanced. In fact, those with inherent sociopathic traits can become very high functioning human beings who are adept at careers that many other people avoid (surgeons and career soldiers are two examples).

However, in the event that there is cultural rot and a degradation of principles, environmental influences come into play and latent sociopaths/psychopaths have the potential to mutate into something far more dangerous. Jung examines this dynamic as an explanation for the sudden and accelerated decline of Germany in the 1920s and 1930s into totalitarianism and moral relativism. When the mentally disturbed 1% turns into 10% or more, entire nations can be dragged along into the abyss.

As a litmus test I find it valuable to look at popular culture when trying to determine if a society is on the brink of collapse into a singularity of moral relativism, because popular culture often reflects these elements more honestly than the supposed "experts" will. When examining Germany before its fall, I recommend studying the films of Fritz Lang; particularly his movie 'M' released in 1931, which depicts a serial killer with a penchant for children being put on trial by a group of underworld criminals, not because they abhor what he does on moral grounds, but because his activities are drawing too much unwanted attention from authorities on their own criminal enterprises. If the dark world of 'M' doesn't perfectly showcase the decline of Germany, I don't know what does.

Today, we are constantly surrounded by popular culture which leans towards the morally relative; stories in which the heroes must become monsters in order to defeat other supposedly worse monsters.

At another level, our popular culture tells us that it is only the fantastical, the super powered and the government contracted heroes that have the ability to affect change and disrupt disaster. Underlying all of this seems to be a narrative of defeat; the notion that there is nothing the average person can do. And, of course, we are also bombarded with stories in which gluttony and decadence are applauded while anyone that takes a more responsible path is portrayed as unhappy or joyless in the long run.

Translate this to the developing trend of mass shootings around the world and the public reaction to them. On one end of the spectrum, in the past it was the sociopathic left that saw mass death as an opportunity to enforce political control over gun rights advocates, with the goal of eventually achieving total disarmament. These people do not care about the dead, let alone logic, they only care about furthering their agenda. They see government power as the answer to every problem.

If you were to hold up examples like the Paris or Mumbai attacks to gun grabbers and point out that disarmament only makes mass shootings EASIER for criminals and terrorists, they would not listen. Obviously, if any of the citizens including the off-duty police officers had been armed in Paris, the attack might have been stopped much sooner.

In the case of the church shooting near San Antonio, that attack WAS interrupted by an armed neighbor of the church who used his rifle to fend off Devin Kelley, forcing him to escape in his vehicle. Had that neighbor not been armed, the massacre might have gone on much longer. Had one of the people within the church been armed, the attack might have ended in seconds, as we saw in Denver in 2007.

Now, as I said earlier, there are sociopathic members of the political left that seek to take advantage of these scenarios, but these people have fallen by the wayside recently.

On the political right, sadly, I have seen another brand of sociopathy rising, with some arguing that all the people within the San Antonio church that were unarmed "deserved to die." This is just as dangerous a mentality as the exploitations of the left. If the liberty movement itself sets aside empathy and resorts to sensationalist or morally relative methods to drive forward a political agenda, then we are only hastening the fall of our culture, not protecting it. And, we become no better that the leftist disarmament thugs we abhor.

In between these two extremes sits a coagulated mass of people who simply don't care much as long as a particular disaster doesn't involve them. These are the folks who are uninterested in solutions and don't really want to hear anything about it. It is these people who tend to become wreckage floating on the tides of history; their lack of concern eventually comes back to haunt them in the future.

So, if these are the wrong ways to approach the mass shooting problem, then what are the right ways?

I think it is vital that Americans in particular maintain our care and concern for the victims of these events. The solution to mass shootings is clearly a responsibly armed populace. According to all the stats on active shooters, defense by citizens is the only factor that seems to make much difference. But to convince more and more people of this requires a level of conscience and empathy that inspires confidence, and perhaps brotherhood. When people know that you give a damn and aren;t simply pursuing an agenda like the political left does, it is more likely that they will listen to what you have to say.

As I noted in my article How To Stop All Future Mass Shootings, the Vegas attack was organized by someone who was smart enough to avoid a point-blank engagement in a city and state in which concealed-carry firearms are more common. Point-blank attacks are by far the most common because they are generally attempted by people who have minimal training or because the attackers are relatively certain that their victims will be disarmed in the area they have chosen (gun free zones).

The Vegas attacker (or attackers) chose to use sniper-like tactics to prolong the massacre. However, what this shows is that an armed citizenry is a factor or barrier in how an attack is planned. With properly trained and armed security overwatching major events along with an armed population, there may never be another mass shooting again.

This is what Americans should be talking about, yet, there is no practical discussion on solving the problem. Is this a symptom of impending collapse within our society? Possibly. If there was ever an honorable task for the liberty movement today, it is to inspire solutions and to maintain moral balance. These shootings and other crisis events should not be forgotten within a week. They should at the very least be a learning process, a means by which we evolve our way of life and become more self reliant and by extension more safe.

If you are not a conceal- or open-carry proponent, then you should be. If you understand that the majority of shooting events that are stopped are stopped by average citizens that are armed, then it should only follow that you should become one of those armed citizens. In the meantime, it is not for us who are consistently armed to admonish disarmed victims as if they "deserve what they got." Their failure is our failure as well. For if we are not working diligently to convince others of the importance of citizen self defense, then we have contributed to the conditions that led to these massacres taking place.

There are methods of stemming the tide of social collapse. There are in fact solutions. They begin with each individual acting in small ways and big ways everyday. Complacency and zealotry are the enemy, as well as those that would encourage such mentalities.

- 35 Chinese Cities Have Economies As Big As Countries

Gaining perspective on China’s monstrous economy isn’t always the easiest thing to do.

As Visual Capitalist's Jeff Desjardins notes, with 1.4 billion people and the third-largest geographical area, the country is a vast place to begin with. Add in explosive economic growth, a market-oriented but Communist government, a longstanding and complex cultural history, and self-inflicted demographic challenges – and understanding China can be even more of a puzzle.

Courtesy of: Visual Capitalist

Courtesy of: Visual CapitalistCITY BY CITY

To truly grasp the emergence of China, one approach is to look at the impressive economic footprint made by the country’s cities.

Of course, cities like Shanghai, Beijing, and Hong Kong are the metro economic powerhouses that most people are familiar with. But have you heard of cities like Shijiazhuang, Wuxi, Changsha, Suzhou, Ningbo, Foshan, or Yantai?

There are literally dozens of Chinese cities that most people in Western countries have never heard of – yet they each hold millions of people and have an economic output comparable to nations.

The infographic above illustrates 35 of them, but here’s a list of 10 of them, the size of their local economy, and a comparably sized national economy:

MEGAREGIONS

It’s also important to remember that these cities don’t exist in isolation, and are instead cogs in the wheels of larger megaregions. Such areas would be comparable to the Northeast U.S., in which New York City, Philadelphia, Boston, Baltimore, and Washington, D.C. are all hours apart and remain largely integrated as a regional economy.

In China, there are three main megaregions worth noting:

Yangtze River Delta

With a combined GDP of $2.17 trillion, which is comparable to Italy, the Yangtze River Delta contains cities like Shanghai, Suzhou, Hangzhou, Wuxi, Ningbo, and Changzhou.Pearl River Delta

With a combined GDP of $1.89 trillion, which is comparable to South Korea, the Pearl River Delta has cities like Hong Kong, Guangzhou, Shenzhen, Foshan, Dongguan, and Macao.Beijing-Tianjin

With a combined GDP of $1.14 trillion, which is comparable to Australia, this megaregion holds the two largest cities in northern China, Beijing and Tianjin. The two cities are a 30-minute bullet train ride apart. - Paul Craig Roberts Laments "I Don't Recognize My Country Today"

Authored by Paul Craig Roberts,

Having grown up during the second half of the 20th century, I don’t recognize my country today. I experienced life in a competent country, and now I experience life in an incompetent country.

Everything is incompetent.

The police are incompetent. They shoot children, grandmothers, cripples, and claim that they feared for their life.

Washington’s foreign policy is incompetent. Washington has alienated the world with its insane illegal attacks on other countries. Today the United States and Israel are the two most distrusted countries on earth and the two countries regarded as the greatest threat to peace.

The military/security complex is incompetent. The national security state is so incompetent that it was unable to block the most humiliating attack in history against a superpower that proved to be entirely helpless as a few people armed with box cutters and an inability to fly an airplane destroyed the World Trade Center and part of the Pentagon itself. The military industries have produced at gigantic cost the F-35 that is no match for the Russian fighters or even for the F-15s and F-16s it is supposed to replace.

The media is incompetent. I can’t think of an accurate story that has been reported in the 21st century. There must be one, but it doesn’t come to mind.

The universities are incompetent. Instead of hiring professors to teach the students, the universities hire administrators to regulate them. Instead of professors, there are presidents, vice presidents, chancellors, vice chancellors, provosts, vice provosts, assistant provosts, deans, associate deans, assistant deans. Instead of subject matter there is speech regulation and sensitivity training. Universities spend up to 75% of their budgets on administrators, many of whom have outsized incomes.

The public schools have been made incompetent by standardized national testing. The purpose of education today is to pass some test. School accreditation and teachers’ pay depend not on developing the creativity or independent thinking of those students capable of it, but on herding them through memory work for a standardized test.

One could go on endlessly.

Instead, I will relate a story of everyday incompetencies that have prevented me from writing this week and for a few more days yet.

Recently, while away from my home, a heavy equipment operator working on a nearby construction site managed to drive under power lines with the fork lift raised. Instead of breaking the wire, it snapped the pole in half that conveyed electric power to my house. The power company came out, or, as I suspect, an outsourced contractor, who reestablished power to my home but did not check that the neutral wire was still attached. Consequently for a week or so my house experienced round the clock surges of high voltage that blew out the surge protection, breaker box, and every appliance in the house. Expecting my return, the house was inspected, and the discovery was that there was no power. Back came the power company and discovered that high voltage was feeding into the house and had destroyed everything plugged in.

So. Here we have a moron operating heavy equipment who does not understand that he cannot drive under power lines with the lift raised. We have a power company or its outsourced contractor who does not understand that power cannot be reconnected without making certain that the neutral wire is still connected.

So every appliance is fried. Glass everywhere from blown out light bulbs. We are talking thousands of dollars.

This is America today.

And the incompetents ruling incompetents want war with Iran, Korea, Russia, China. Considering the extraordinary level of incompetence throughout the United States, I guarantee you that we will not win these wars.

- More New Normal – Buy Bloomberg's "Bubblicious" Index Of Bubbles – Make Out Like A Bandit

If only every year was this “easy”.

Unfortunately, the old adage of the trend being your friend becomes harder to adhere to as a guidepost as one asset market after another goes into bubble territory. As we discussed here, Alberto Gallo of Algebris Investments has ranked (see here) the top 14 bubbles worldwide, according to characteristics such as duration, appreciation, valuation and the degree of irrational behaviour.

When we started in this industry, we were taught by those with the gray hair of experience that betting against the herd was the key to success. Turning up on January 1, imagine the look on their faces if you’d told them you’d bought a portfolio of everything that had gone parabolic (or almost) the previous year. Luckily for them, markets were relatively free and absent $15 trillion of price insenstive asset purchases by central banks. Fundamentals counted for somethiing – and will again (we hope) – there’s just the small matter of getting to the other side of the current bubble, sorry bubble(ssssssssssssssssssssssssssss).

In 2017, the strategy of buying bubbles has obviously worked almost perfectly or, as Bloomberg notes,“Investors can either buy bubbles or be left far behind”. Indeed, it’s gone to the trouble (see here) of creating ts own “Bubblicious” index, which includes an equal weighting of a host of the “usual suspects”. These include:

- Sunac China Holdings Ltd.: perhaps the poster child of the real-estate frenzy in the world’s second-largest economy, this company’s aggressive acquisition strategy has been met with raised eyebrows among regulators at a time when China is trying to rein in the country’s financial risk.

- Tencent Holdings Ltd.: A 2,600 percent rise in the past decade? Tencent is the leader of the pack when it comes to Asian tech stocks that have made the sector the biggest component of the MSCI Asia Pacific Index for the first time since the internet bubble.

- Tesla Inc. and Netflix Inc.: two U.S. tech companies that have both been branded with the b-word by hedge fund manager Einhorn.

- VelocityShares Daily Inverse VIX Short-Term ETN, ticker XIV: this exchange-traded note is a proxy for the presumed “short volatility” bubble that’s seen investors bet billions of dollars on the prospect of not much happening in markets.

- Bitcoin Investment Trust, ticker GBTC: the cryptocurrency fund that typically trades at a substantial premium to its net asset value. Bitcoin itself has been called a bubble by bank CEOs including JP Morgan Chase & Co.’s Jamie Dimon, ethereum co-founder Joseph Lubin and many more.

- ETF Industry Exposure & Financial Services ETF, ticker TETF: this meta exchange-traded product holds a basket of firms poised to benefit the most from the explosion in ETFs — a proxy for the “passive bubble.”

- Lots of long bonds: The iShares 20+ Year Treasury Bond ETF has enjoyed $1.8 billion worth of inflows in a year that saw former Federal Reserve Chair Alan Greenspan warn of a massive bubble in the space. Meanwhile yields on German sovereign debt maturing in 2048 and Japanese bonds maturing in 2050 have dipped ever lower, sealing the latter’s reputation as a ‘widow maker’ for frustrated shorts. The portfolio also includes the infamous Argentinian century bond.

Bloomberg observes that its broad range of choices mean that its Bubblicious portfolio is “fairly well diversified” across the many bubbles. Actually, it could have been more diversified. While we don’t disagree with the inclusion of any of Bloomberg’s picks, it’s worth noting that compared with Gallo’s list, the Bubblicious portfolio does not include European high yield, EM high yield or any of the obvious property bubbles outside China. London, for example, and Australian cities, such as Sydney and Melbourne. Unlike Gallo, we might have chosen New Zealand property instead of London property (where prices have started falling) and, while Bloomberg has chosen Sunac as its “poster child” for Chinese real estate, China Evergrande and others would be equally valid.

Anyway, as Bloomberg explains, the “Bubblicious” index has risen by well more than 120% so far this year.

The best way to crush the crowd in 2017? Buy the things everyone insisted would never keep going up. A portfolio stuffed with allegedly over-inflated assets would have returned more than 120 percent so far in 2017, trouncing the S&P 500 Index and underscoring the challenge for investors facing a plethora of pricey securities.

As the chart shows, if you’d gone “Bubblicious” on 1 January 2017, you’d have smashed the S&P 500 "out of sight" by more than 100%.

As Bloomberg laments.

The hypothetical ‘Bubblicious’ portfolio includes Chinese real estate and internet names, a pair of U.S. tech behemoths, a cryptocurrency fund, the ETF industry, bonds that mature decades from now, and a dash of short volatility bets just to make things more interesting.

The out-performance is a testament to the momentum mania prevalent in today’s markets, a dynamic which has prompted the likes of Greenlight Capital’s David Einhorn, Goldman Sachs Group Inc., and Sanford C Bernstein & Co. LLC to mull whether value investing is in the midst of an existential crisis given ultra-low interest rates and abundant liquidity.

Of course it is, but the nature of markets is that they move in cycles. This cycle happens to be the most unpleasant cycle for value investors, active managers and contrarian thinkers, but it’s still a cycle.

- 13 Baltimore High Schools Have Zero Students That Are Proficient In Math

For the past several weeks, one Fox affiliate in Baltimore has been publishing some staggering stories about the Baltimore public school system under an investigative series called “Project Baltimore.” Just a few weeks ago we noted one of those stories in which an undercover teacher admitted that public schools routinely pass kids that never even bother to show up for class a single day during the school year.

Now, a stunning new installment of the Project Baltimore series from Fox 45 reveals that 13 public high schools sprinkled around Baltimore, of the city’s 39 total, had exactly 0 kids that tested proficient in math.

An alarming discovery coming out of City Schools. Project Baltimore analyzed 2017 state testing data and found one-third of High Schools in Baltimore, last year, had zero students proficient in math.

Project Baltimore analyzed 2017 state test scores released this fall. We paged through 16,000 lines of data and uncovered this: Of Baltimore City’s 39 High Schools, 13 had zero students proficient in math.

- Achievement Academy

- Carver Vocational-Technical High

- Coppin Academy

- Excel Acadamy @ Francis M. Wood High

- Forest Park High

- Frederick Douglass High

- Independence School Local 1

- Knowledge and Success Academy

- New Era Academy

- New Hope Academy

- Northwestern High

- Patterson High

- The Reach! Partnership School

Meanwhile, digging a bit deeper, Fox 45 also found that of the 3,804 students in Baltimore’s worst 19 high schools, only 14 of them, or less than 1%, were proficient in math.

Digging further, we found another six high schools where one percent tested proficient. Add it up – in half the high schools in Baltimore City, 3804 students took the state test, 14 were proficient in math.

- Ben Franklin H.S. at Masonville Cove

- ConneXions: Community Based Arts SchoolDigital Harbor High School

- Edmondson-Westside High

- Renaissance Academy

- Vivien T. Thomas Medical Arts Academy

Not sursprisingly, only one Baltimore school replied to Fox 45 with a generic comment suggesting that improvement is difficult and “will take time.” That said, why do we suspect that ‘improvement’ will also take just a little more taxpayer money despite the fact that Baltimore already spends $16,000 per year per student…which, mind you, is more than many private schools that deliver far better results.

With these eye-opening results, Project Baltimore reached to North Avenue. But no one inside the building would sit down to answer our questions. Instead, we got a statement. Concerning our investigation, it read, “These results underscore the urgency of the work we are now pursuing. We must do more to meet the needs of all our students.”

That work, according to the statement, involves a new math curriculum started this year, enhanced teacher development and expanded partnerships to provide opportunities for students.

The statement concludes, “There is no simple answer that will close the achievement gap for Baltimore’s students. Though we all want to see results quickly, the work is hard and will take time.”

Of course, we’re almost certain that these poor results have absolutely nothing to do with Baltimore’s stellar, unionized teachers and administrators who will undoubtedly get to maintain their jobs and exorbitant public pensions despite the complete failure of their students.

- Facebook Founder Warns "God Only Knows What It's Doing To Kids' Brains"

38-year-old founding president of Facebook, Sean Parker, was uncharacteristically frank about his creation in an interview with Axios. So much so in fact that he concluded, Mark Zuckerberg will probably block his account after reading this.

Confirming every 'big brother' conspiracy there is about the social media giant, Parker explained how social networks purposely hook users and potentially hurt our brains…

"When Facebook was getting going, I had these people who would come up to me and they would say, 'I'm not on social media.' And I would say, 'OK. You know, you will be.' And then they would say, 'No, no, no. I value my real-life interactions. I value the moment. I value presence. I value intimacy.' And I would say, … 'We'll get you eventually.'"

"I don't know if I really understood the consequences of what I was saying, because [of] the unintended consequences of a network when it grows to a billion or 2 billion people and … it literally changes your relationship with society, with each other … It probably interferes with productivity in weird ways. God only knows what it's doing to our children's brains."

"The thought process that went into building these applications, Facebook being the first of them, … was all about: 'How do we consume as much of your time and conscious attention as possible?'"

"And that means that we need to sort of give you a little dopamine hit every once in a while, because someone liked or commented on a photo or a post or whatever. And that's going to get you to contribute more content, and that's going to get you … more likes and comments."

"It's a social-validation feedback loop … exactly the kind of thing that a hacker like myself would come up with, because you're exploiting a vulnerability in human psychology."

"The inventors, creators — it's me, it's Mark [Zuckerberg], it's Kevin Systrom on Instagram, it's all of these people — understood this consciously. And we did it anyway."

In this 'confessional', it appears Parker has become "something of a conscientious objector" on social media.

Howeever , as Axios notes, Parker ends with just enough crazy to make you wonder…

"Because I'm a billionaire, I'm going to have access to better health care so … I'm going to be like 160 and I'm going to be part of this, like, class of immortal overlords. [Laughter]

Because, you know the [Warren Buffett] expression about compound interest. … [G]ive us billionaires an extra hundred years and you'll know what … wealth disparity looks like."

- "Lull Before The Storm" – Will China Bring An Energy-Debt Crisis?

Authored by Gail Tverberg via Our Finite World blog,

It is easy for those of us in the West to overlook how important China has become to the world economy, and also the limits it is reaching. The two big areas in which China seems to be reaching limits are energy production and debt. Reaching either of these limits could eventually cause a collapse.

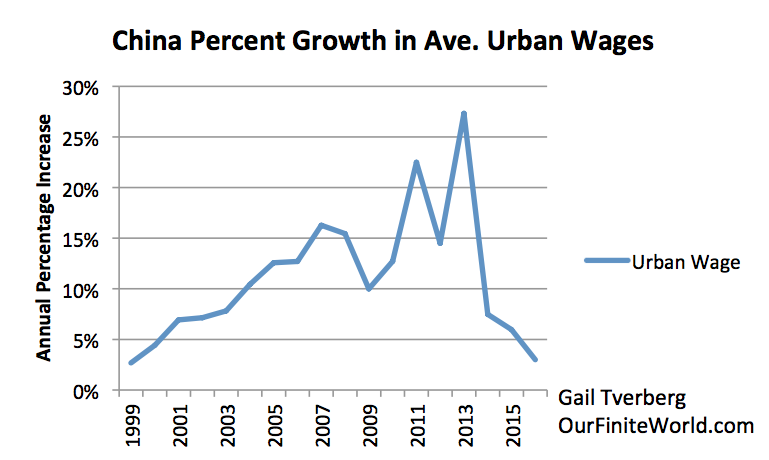

China is reaching energy production limits in a way few would have imagined. As long as coal and oil prices were rising, it made sense to keep drilling. Once fuel prices started dropping in 2014, it made sense to close unprofitable coal mines and oil wells. The thing that is striking is that the drop in prices corresponds to a slowdown in the wage growth of Chinese urban workers. Perhaps rapidly rising Chinese wages have been playing a significant role in maintaining high world “demand” (and thus prices) for energy products. Low Chinese wage growth thus seems to depress energy prices.

(Shown as Figure 5, below). China’s percentage growth in average urban wages. Values for 1999 based on China Statistical Yearbook data regarding the number of urban workers and their total wages. The percentage increase for 2016 was based on a Bloomberg Survey.

The debt situation has arisen because feedback loops in China are quite different from in the US. The economic system is set up in a way that tends to push the economy toward ever more growth in apartment buildings, energy installations, and factories. Feedbacks do indeed come from the centrally planned government, but they are not as immediate as feedbacks in the Western economic system. Thus, there is a tendency for a bubble of over-investment to grow. This bubble could collapse if interest rates rise, or if China reins in growing debt.

China’s Oversized Influence in the World

China plays an oversized role in the world’s economy. It is the world’s largest energy consumer, and the world’s largest energy producer. Recently, it has become the world’s largest importer of both oil and of coal.

In some sense, China is the world’s largest economy. Usually we see China referred to as the world’s second largest economy, based on GDP converted to US dollars. Economists use an approach called GDP (PPP) (where PPP is Purchasing Power Parity) when computing world GDP growth. When this approach is used, China is the world’s largest economy. The United States is second largest, and India is third.

Figure 1. World’s largest economies, based on energy consumption and GDP based on Purchasing Power Parity. Energy Consumption is from BP Statistical Review of World Energy, 2017; GDP on PPP Basis is from the World Bank.

Besides being (in some sense) the world’s largest economy, China is also a country with a very significant amount of debt. The government of China has traditionally somewhat guaranteed the debt of Chinese debtors. There is even a practice of businesses guaranteeing each other’s debt. Thus, it is hard to compare China’s debt to the debt level elsewhere. Some analyses suggest that its debt level is extraordinarily high.

How China’s Growth Spurt Started

Figure 2. China’s energy consumption, based on data from BP Statistical Review of World Energy, 2017.

From Figure 2, it is clear that something very dramatic happened to China’s coal consumption about 2002. China joined the World Trade Organization in December 2001, and immediately afterward, its coal consumption soared.

Countries in the OECD, whether they had signed the 1997 Kyoto Protocol or not, suddenly became interested in reducing their own greenhouse gas emissions. If they could outsource manufacturing to China, they would be able to reduce their reported CO2 emissions.

Besides reducing reported CO2 emissions, outsourcing manufacturing to China had two other benefits:

- The goods being manufactured in China would be cheaper, allowing Americans, Europeans, and Japanese to buy more goods. If more “stuff” makes people happy, citizens should be happier.

- Businesses would suddenly have a new market in China. Perhaps the people of China would start buying goods made elsewhere.

Of course, a major downside of moving jobs to China and other Asian nations was the likelihood of fewer jobs elsewhere.

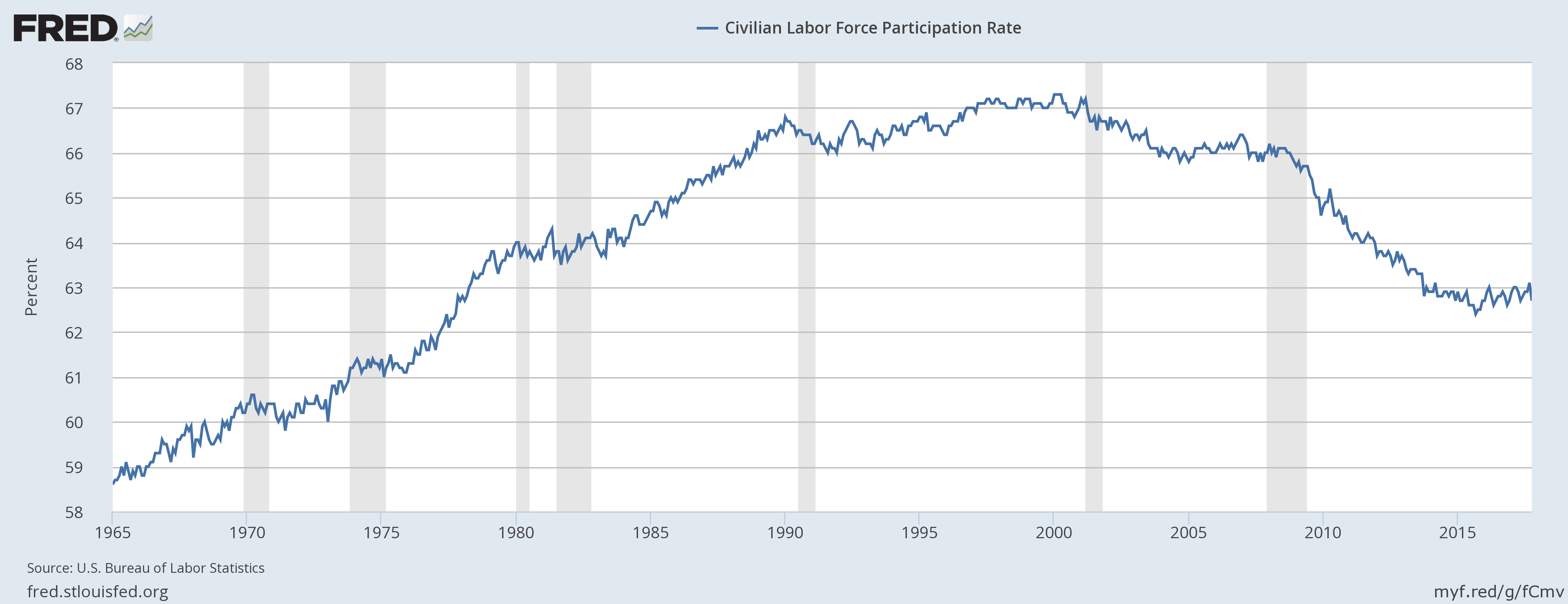

Figure 3. US Labor Force Participation Rate, as prepared by Federal Reserve Bank of St. Louis.

In the early 2000s, when China started competing actively for jobs, the share of people in the US workforce started shrinking. The drop-off in labor force participation did not level out until mid-2014. This is about when world oil prices began to fall, and, as we will see in the next section, when China’s growth in average wages began to fall.

Another downside to moving jobs to China was more CO2 emissions on a worldwide basis, even if emissions remained somewhat lower locally. CO2 emissions on imported goods were not “counted against” a country in its CO2 calculations.

Figure 4. World carbon dioxide emissions, split between China and Rest of the World, based on BP Statistical Review of World Energy, 2017.

At some point, we should not be surprised if countries elsewhere start pushing back against the globalization that allowed China’s rapid growth. In some sense, China has lived in an artificial growth bubble for many years. When this artificial growth bubble ends, it will be much harder for China’s debtors to repay debt with interest.

China’s Rapid Wage Growth Stopped in 2014

Rising wages are important for making China’s growth possible. With rising wages, workers can increasingly afford the apartments that are being built for them. They can also increasingly afford consumer goods of many kinds, and they can easily repay debts taken out earlier. The catch, however, is that wage growth cannot get ahead of productivity growth, or the price of goods will become too expensive on the world market. If this happens, China will have difficulty selling its goods to others.

China’s wage growth seems to have slowed remarkably, starting in 2014.

Figure 5. China’s percent growth in average urban wages. Values for 1999 based on China Statistical Yearbook data regarding the number of urban workers and their total wages. The percentage increase for 2016 was estimated based on a Bloomberg Survey.

This is when China discovered that its high wage increases were making it uncompetitive with the outside world. Wage growth needed to be reined in. Its growth in productivity was no longer sufficient to support such large wage increases.

China’s Growth in Energy Consumption Also Slowed About 2014

If we look at the annual growth in total energy consumption and electricity consumption, we see that by 2014 to 2016, their growth had slowed remarkably (Figure 6). Their growth pattern was starting to resemble the slow growth pattern of much of the rest of the world. Energy growth allows an economy to increasingly leverage the labor of its workforce with more energy-powered “tools.” With low energy growth, it should not be surprising if productivity growth lags. With low productivity growth, we can expect low wage growth.

Figure 6. China’s growth in consumption of total energy and of electricity based on data from BP Statistical Review of World Energy, 2017.

It is possible that the increased rate of electricity consumption in 2016 is related to China’s program of housing migrant workers in unsalable apartments that took place at that time. The fact that these apartments were otherwise unsalable was no doubt influenced by the slowing growth in wages.

This decrease in energy consumption most likely occurred because the price of China’s energy mix was becoming increasingly expensive. For one thing, the mix included a growing share of oil, and oil was expensive. The proportion of coal in the mix was falling, and the replacements were more expensive than coal. There was also the issue of the general increase in fossil fuel prices.

Lower Wage Growth in China Likely Affected Fossil Fuel Prices

Affordability is the big issue with respect to how high fossil fuel prices can rise. The issue is not just buying the oil or coal or natural gas itself; it is also being able to afford the goods made with these fuels, such as food, clothing, appliances, and apartments. If wages were depressed in the developed countries because of moving production to China, then rising wages in China (and other similar countries, such as India and the Philippines) must somehow offset this problem, if fossil fuel prices are to remain high enough for extraction to continue.

Figures 7 and 8 (below) show that oil, natural gas, and coal prices all started to slide, right about the time China’s urban wages growth began shrinking (shown in Figure 5).

Figure 7. Oil and natural gas prices, based on BP Statistical Review of World Energy data.

Figure 8. Coal prices between 2000 and 2016 from BP Statistical Review of World Energy. Chinese coal is China Qinhuangdao spot price and Japanese coal is Japan Steam import cif price, both per ton.

The lower recent increases made China’s urban wage growth look more like that of the US and Europe. Thus, in 2014 and later, Chinese urban wages present much less of a “push” on the growth of the world economy than they had previously. Without this push of rising wages, it becomes much harder for the world economy to grow very rapidly, and for it to have a very high inflation rate. There is simply not enough buying power to push prices very high.

It might be noted that the average Chinese urban wage increases shown previously in Figure 5 are not inflation adjusted. Thus, in some sense, they include whatever margin is available for inflation in prices as well as the margin that is available for a greater quantity of purchased goods. Because of this, these low wage increases may help explain the recent lack of inflation in much of the world.

Quite likely, there are other issues besides China’s urban wage growth affecting world (and local) energy prices, but this factor is probably more important than most people would expect.

Can low prices bring about “Peak Coal” and “Peak Oil”?

What does a producer do in response to suddenly lower market prices–prices that are too low to encourage more production?

This seems to vary, depending on the situation. In the case of coal production in China, a decision was made to close many of the coal plants that had suddenly become unprofitable, thanks to lower coal prices. No doubt pollution being caused by these plants entered into this decision, as well. So did the availability of other coal elsewhere (but probably at higher prices), if it is ever needed. The result of this voluntary closure of coal plants in response to low prices caused the drop in coal production shown in Figure 8, below.

Figure 8. China’s energy production, based on data from BP Statistical Review of World Energy, 2017.

It is my belief that this is precisely the way we should expect peak coal (or peak oil or peak natural gas) to take place. The issue is not that we “run out” of any of these fuels. It is that the coal mines and oil and gas wells become unprofitable because wages do not rise sufficiently to cover the fossil fuels’ higher cost of extraction.

We should note that China has also cut back on its oil production, in response to low prices. EIA data shows that China’s 2016 oil production dropped about 6.9% compared to 2015. The first seven months of 2017 seems to have dropped by another 4.2%. So China’s oil is also showing what we would consider to be a “peak oil” response. The price is too low to make production profitable, so it has decided that it is more cost-effective to import oil from elsewhere.

In the real world, this is the way energy limits are reached, as far as we can see. Economists have not figured out how the system works. They somehow believe that energy prices can rise ever higher, even if wages do not. The mismatch between prices and wages can be covered for a while by more government spending and by more debt, but eventually, energy prices must fall below the cost of production, at least for some producers. These producers voluntarily give up production; this is what causes “Peak Oil” or “Peak Coal” or “Peak Natural Gas.”

Why China’s Debt System Reaches Limits Differently Than Those in the West

Let me give you my understanding regarding how the Chinese system works. Basically, the system is gradually moving from (1) a system in which the government owns all land and most businesses to (2) a system with considerable individual ownership.

Back in the days when the government owned most businesses and all land, farmers farmed the land to which they were assigned. Businesses often provided housing as part of an individual’s “pay package.” These homes typically had a shared outhouse for a bathroom facility. They may or may not have had electricity. There was relatively little debt to the system, because there was little individual ownership.

In recent years, especially after joining the World Trade Organization in 2001, there has been a shift to more businesses of the types operated in the West, and to more individual home ownership, with mortgages.

The economy acts rather differently than in the West. While the economy is centrally planned in Beijing, quite a bit of the details are left to individual local governments. Local heads of state make decisions that seem to be best based on the issues they are facing. These may or may not match up with what Beijing central planning intended.

Historically, Five-Year Plans have provided GDP growth targets to the various lower-level heads of state. The pay and promotions of these local leaders have depended on their ability to meet (or exceed) their GDP goals. These goals did not have any debt limits attached, so local leaders could choose to use as much debt as they wanted.

A major consideration of these local leaders was that they also had responsibility for jobs for people in their area. This responsibility further pushed them to aim high in the amount of development they sought.

Another related issue is that sales of formerly agricultural land for apartments and other development are a major source of revenue for local governments. Local leaders did not generally have enough tax revenue for programs, without supplementing their tax revenue with funds obtained from selling land for development. This further pushed local leaders to add development, whether it was really needed or not.

The very great power of local heads of state and their administrators made these leaders tempting targets for bribery. Entrepreneur had a chance of getting projects approved for development, with a bribe to the right person. There has been a recent drive to eliminate this practice.

We have often heard the comment, “A rising tide raises all boats.” When the West decided to discourage local industrialization because of CO2 concerns, it gave a huge push to China’s economy. Almost any project could be successful. In such an environment, local rating agencies could be very generous in their ratings of proposed new bond offerings, because practically any project would be likely to succeed.

Furthermore, without many private businesses, there was little history of past defaults. What little experience was available suggested the possibility of few future defaults. Wages had been rising very rapidly, making individual loans easy to repay. What could go wrong?

With the central government perceived to be in control, it seemed to make sense for one governmental organization to guarantee the loans of other governmental organizations. Businesses often guaranteed the loans of other businesses as well.

Why the Chinese System Errs in the Direction of Overdevelopment

In the model of development we are used to in the West, there are feedback loops if too much of anything is built–apartment buildings (sold as condominiums), coal mines, electricity generating capacity, solar panels, steel mills, or whatever else.

In China, these feedback loops don’t work nearly as well. Instead of the financial system automatically “damping out” the overcapacity, the state (or perhaps a corrupt public official) figures out some way around what seems to be a temporary problem. To understand how the situation is different, let’s look at three examples:

Apartments. China has had a well-publicized problem of building way too many apartments. In about 2016, this problem seems to have been mostly fixed by local governments providing subsidies to migrant workers so that they can afford to buy homes. Of course, where the local governments get this money, and for how long they can afford to pay these stipends, are open questions. It is also not clear that this arrangement is leading to a much-reduced supply of new homes, because cities need both the revenue from land sales and the jobs resulting from building more units.

Figure 9 shows one view of the annual increase in Chinese house prices, despite the oversupply problem. If this graph is correct, prices have increased remarkably in 2017, suggesting some type of stimulus has been involved this year to keep the property bubble growing. The size of an apartment a typical worker can now afford is very small, so this endless price run-up must end somewhere.

Figure 9. Chinese house price graph from GlobalPropertyGuide.com.

Coal-Fired Power Plants. With all of the problems that China has with pollution, a person might expect that China would stop building coal-fired power plants. Instead, the solution of local governments has been to build additional power plants that are more efficient and less polluting. The result is significant overcapacity, in total.

A May 2017 article says that because of this overcapacity problem, Beijing is forcing every coal-fired power plant to run at the same utilization rate, which is approximately 47.7 % of total capacity. A Bloomberg New Energy Finance article estimates that at year-end 2016, the “national power oversupply” was 35%, considering all types of generation together. (This is likely an overestimate; the authors did not consider the flexibility of generation.)

Beijing is aware of the overcapacity problem, and is cancelling or delaying a considerable share of coal-fired capacity that is in the pipeline. The plan is to limit total coal-fired capacity to 1,100 gigawatts in 2020. China’s current coal-fired generating capacity seems to be 943 gigawatts, suggesting that as much as a 16% increase could still be added by 2020, even with planned cutbacks.

It is not clear what happens to the loans associated with all of the capacity that has been cancelled or delayed. Do these loans default? If “normal” feedbacks of lower prices had been allowed to play out, it is doubtful that such a large amount of overcapacity would have been added.

If China’s overall growth rate slows to a level more similar to that of other economies, it will have a huge amount of generation that it doesn’t need. This adds a very large debt risk, it would seem.

Wind and Solar. If we believe Darien Ma, author of “The Answer, Comrade, Is Not Blowing in the Wind,” there is less to Beijing’s seeming enthusiasm for renewables than meets the eye.

According to Ma, China’s solar industry was built with the idea of having a product that could be exported. It was only in 2013 when Western countries launched trade suits and levied tariffs that China decided to use a substantial number of these devices itself, saving the country from the embarrassment of having many of these producers go bankrupt. How this came about is not entirely certain, but the administrator in charge of wind and solar additions was later fired for accepting bribes, and responsibility for such decisions moved higher up the chain of authority.

Figure 10. China current view of solar investment risk in China. Chart by Bloomberg New Energy Finance.

Ma also reports, “Officials say that they want ‘healthy, orderly development,’ which is basically code for reining in the excesses in a renewable sector that has become yet another emblem of irrational exuberance.”

According to Ma, the Chinese National Energy Administration has figured out that wind and solar are still about 1.5 and 2.5 times more expensive, respectively, than coal-fired power. This fact dampens their enthusiasm for the use of these types of generation. China plans to phase out subsidies for them by 2020, in light of this issue. Ma expects that there will still be some wind and solar in China’s energy mix, but that natural gas will be the real winner in the search for cleaner electricity production.

Viewed one way, we are looking at yet another way Chinese officials have avoided closing Chinese businesses because the marketplace did not seek their products. Thus, the usual cycle of bankruptcies, with loan defaults, has not taken place. This issue makes China’s total electricity generating capacity even more excessive, and reduces the profitability of the overall system.

Conclusion

We have shown how low wages and low energy prices seem to be connected. When prices are too low, some producers, including China, make a rational decision to cut back on production. This seems to be the true nature of the “Peak Coal” and “Peak Oil” problem. Because China is reacting in a rational way to lower prices, its production is falling. China is already the largest importer of oil and coal. If there is a shortfall elsewhere, China will be affected.

We have also given several examples of how the current system has been able to avoid defaults on loans. The issue is that these problems don’t really go away; they get hidden, and get bigger and bigger. At some point, all of the manipulations by government officials cannot hide the problem of way too many apartments, or of way too much electricity generating capacity, or of way too many factories of all kinds. The postponed debt collapse is likely to be much bigger than if market forces had been allowed to bring about earlier bankruptcies and facility closures.

Chinese officials are now talking about reining in the growth of debt. There is also discussion by heads of Central Banks about raising interest rates and selling QE securities (something which would also tend to raise interest rates). China will be very vulnerable to rising interest rates, because of stresses that have been allowed to build up in the system. For example, many mortgage holders will not be able to afford the new higher monthly payments if rates rise. If interest rates rise, factories will find it even harder to be profitable. Some may reduce staff levels, to try to reach profitability. If this is done, it will tend to push the system toward recession.

We likely now are in the lull before the storm. There are many things that could push China toward an energy or debt crisis. China is so big that the rest of the world is likely to also be affected.

- "This Is Crazy" – Antarctic Supervolcano Is Melting The Ice-Caps From Within

As we’ve pointed out, the supervolcano phenomenon is hardly unique to Yellowstone National Park, where a long dormant volcano with the potential to cause a devastating eruption has been rumbling since mid-summer, making some scientists uneasy.

Surprisingly active supervolcanos have been documented in Italy, North Korea and, now, Antarctica after scientists at NASA’s Jet Propulsion Laboratory (JPL) have found new evidence to support a theory that the breakup of Antarctic ice may be caused in part by a massive geothermal heat source, with output close to the scale of Yellowstone National Park.

Of course, if accurate, this theory would help rebut the notion that man-made climate change is in part responsible for the melting ice, Russia Today reports.

A geothermal heat source called a mantle plume, a hot stream of subterranean molten rock that rises through the Earth's crust, may explain the breathing effect visible on Antarctica's Marie Byrd Land and elsewhere along the massive ice sheet.

While the mantle plume is not a new discovery, the recent research indicates it may explain why the ice sheet collapsed in a previous era of rapid climate change 11,000 years ago, and why the sheet is breaking up so quickly now.

"I thought it was crazy. I didn't see how we could have that amount of heat and still have ice on top of it," said Hélène Seroussi of NASA's Jet Propulsion Laboratory in Pasadena, California.

Seroussi and Erik Ivins of JPL used the Ice Sheet System Model (ISSM), a mathematical depiction of the physics of ice sheets developed by scientists at JPL and the University of California, Irvine. Seroussi then tweaked the ISSM to hunt for natural heat sources as well as meltwater deposits.

This warm water lubricates the ice sheet from below, allowing glaciers to slide off into the sea. Studying meltwater in western Antarctica may allow scientists to estimate how much ice will be lost in future.

During their initial work, Seroussi and Ivins created simulations using higher heat flows than 150 milliwatts per square meter, which did not align with their space-based readings, except for one area: The Ross Sea.

Scientists to study 120,000yo ecosystem uncovered after 1tn-ton iceberg break (PHOTOS) https://t.co/8byRh7kD1J pic.twitter.com/Ey8l1Tviap

— RT (@RT_com) October 11, 2017

https://platform.twitter.com/widgets.js

Their calculations showed that, in certain sections of the sea, a heat flow of at least 150-180 milliwatts was required to create sufficient meltwater flows that matched with observations. They now believe the mantle plume is responsible for these higher-than-average readings.

The Marie Byrd Land mantle plume formed 50 to 110 million years ago, predating the Western Antarctic ice sheet. The mantle plume theory was initially proposed 30 years ago, but it’s not the only theory. Another posits that the sheer weight of the ice sheets causes melting deep below the surface.

- Deutsche Bank CEO Says AI Will Help Him Cut Tens Of Thousands Of Jobs

While many in the financial services industry are dreading the day that AI technology becomes advanced enough to render broad swaths of the human workforce obsolete, Deutsche Bank’s John Cryan ironically sees the technology as something that might help him save his job.

The leader of the biggest German lender has been tasked with putting the bank back on sound footing, regaining market share and – of course – reining in costs, including the bank’s bloated headcount. DB has 97,000 employees worldwide, about double the number of employees at many of its European peers.

And as the bank has made about half of the 9,000 cuts promised by Cryan in a five-year restructuring plan, the CEO told the Financial Times that machine learning and automation technology could help him cut tens of thousands of additional jobs, particularly in the bank’s back office.

Deutsche has made about 4,000 of the 9,000 job cuts promised under a five-year restructuring plan announced in late 2015. Mr Cryan said many of the additional cuts would come through using technology to boost efficiency in the bank’s processes.

“There we’ve got the most to gain,” he said. “We’re too manual, which can make you error-prone and it makes you inefficient. There’s a lot of machine learning and mechanisation that we can do."

Mr Cryan said the ratio of front office, revenue-generating staff, to back office people who keep the bank’s systems running, was “out of kilter” at Deutsche.

When asked about the specific number of employees at risk of being replaced, he told Laura Noonan at the Financial Times it would be a "big number."

Cryan’s remarks come after the bank reported a tangible return on equity of just 4% for the third quarter, far short of its medium-term target of 10%. Of course, hitting that goal will be virtually impossible as long as the European Central Bank is embracing NIRP. As we noted yesterday, DB’s investment bank is looking to the risky leveraged loan market, where it can collect juicy fees from US corporates.

While the bank’s headcount has been reduced elsewhere, the Frankfurt-based lender added 24 managing directors and directors to its US corporate finance business this year.

As the FT points out, DB’s staff has taken umbrage in some of Cryan’s more critical remarks about the staff bloat at the bank. Back in September, Cryan said the bank’s accountants “sped a lot of time basically being abacuses” and are ripe for being automated.

As the bank works to integrate its retail network with Postbank, its German retail banking subsidiary, Cryan said he closing retail branches and pushing more of its customers to do their banking online could help the bank cut costs.

Furthermore, Cryan believes entire industries will be able to replace workers with robots, not just Deutsche Bank. "We have to find new ways of employing people and maybe people need to find new ways of spending their time," he said, according to CNBC. "The truthful answer is we won't need as many people."

Cryan’s views on AI are diametrically opposed to Elon Musk’s warnings that AI is the “single biggest threat to humanity” and that governments should immediately move to regulate the technology.

However, some experts say that any meaningful advancements in AI that would render a significant portion of the US labor force obsolete are still far in the future, and that the technology has been incredibly overhyped. According to Gartner Inc.’s hype cycle for new technologies, the hype surrounding machine learning is at the “peak of inflated expectations” and heading to the “trough of disillusionment"…

Digest powered by RSS Digest

Saving...

Saving...