- First Massachusetts Poll Shows Trump With 'Yuuge' Lead

With nine days until the Massachusetts Primary on March 1st (Super Tuesday), the first polls show Donald Trump with an enormous lead over his rivals for the GOP nomination (with Ted Cruz suffering the biggest setback). So much for all those Jeb supporters 'swinging' away from Trump.

According to The Emerson College Polling Society…

New #Massachusetts Poll#GOP@realDonaldTrump– 50%@marcorubio– 16%@JohnKasich– 13%@tedcruz– 10%@RealBenCarson– 2%

— ECPS (@EmersonPolling) February 22, 2016

His largest lead yet heading into a vote.

On the other side, Bernie and Hillary are all tied up – time for a card-cutting or coin-toss…

New #Massachusetts Poll#Democrats@BernieSanders– 46%@HillaryClinton– 46%

— ECPS (@EmersonPolling) February 22, 2016

- Were We Lied Into War?

Submitted by Justin Raimondo via AntiWar.com,

Donald Trump threw down the gauntlet at the last GOP presidential debate with his declaration that the Bush administration lied us into war, and the reverberations are still roiling the political waters on both the right and the left. If his candidacy does nothing else, it will have performed a great service to the nation by re-litigating this vitally important issue and drawing attention to the outrageous lack of accountability by the elites who cheered as we turned the Middle East into a cauldron of death and destruction. Trump has ripped the bandage off the gaping and still suppurating wound of that ill-begotten war, and the howls of rage and pain are being heard on both sides of the political spectrum.

On the neoconservative right, Bill Kristol’s sputtering outrage is a bit too studied to be taken at face value: is he really shocked that no one is coming to the defense of himself and his fellow neocons, who elaborated (with footnotes) the very lies that led us down the primrose path to what the late Gen. William E. Odom called “the worst strategic disaster in our history”?

Kristol’s Weekly Standard magazine promoted every conceivable narrative pointing to Saddam Hussein as the perpetrator of the 9/11 attacks, no matter how fantastic and bereft of evidence. Here he is accusing the Iraqis of being behind the dissemination of anthrax through the mails. Here is his subsidized magazine denying that the forged Niger uranium documents – the basis of George W. Bush’s claim in his 2003 State of the Union that Iraq was building a nuke – were an attempt to lie us into war. Here is neocon propagandist Stephen Hayes retailing a leaked “secret” memo to give credence to the debunked story of a meeting between 9/11 hijacker Mohammed Atta and Iraqi intelligence.

Every single one of these tall tales has been so thoroughly disproved that it’s enough to recall them in order to embarrass the perpetrators beyond redemption. Kristol & Co. served as a clearing house for these outright fabrications, which were then utilized by the Bush administration to make the case for war. And yet we have Peter Suderman, a senior editor over at Reason magazine, deriding Trump’s calling out of George W. Bush and his neocon intelligence-fabricators as a “conspiracy theory” on a par with birtherism and the weirdo 9/11 “truth” cult:

“[H]e is flirting with a kind of 9/11 trutherism when he accuses the Bush administration of having knowingly lied in order to push the country into war in Iraq, as he did in Saturday’s GOP debate.

“Now, as Byron York wrote on Twitter yesterday, you can reasonably interpret that charge as a general nod toward the idea that the Bush administration hyped the war effort beyond what the actual evidence could support, that the case for the war was, well, trumped up and ultimately misleading, built on insufficient proof, overconfidence, and mistaken assumptions. But Trump’s attack also leaves room for more radical, less grounded conspiracies about Bush and the war as all, and I suspect this is not an accident.

I would respectfully suggest that it is Suderman who needs “grounding” in the facts of this case. I would refer him to a project undertaken by our very own Scott Horton, whose radio program is essential listening for anyone who wants to be so educated: Scott has prepared a reading list on the occasion of the anniversary of the Iraq war, one that Suderman might want to make use of.

Of special interest is Seymour Hersh’s account of the Office of Special Plans, run by Abram Shulsky. This denizen of the murkier depths of the US intelligence community is a devotee of the philosopher Leo Strauss, who believed – as one scholar cited by Hersh put it – “that philosophers need to tell noble lies not only to the people at large but also to powerful politicians.” The OSP, set up in order to do an end run around the official intelligence community, specialized in retailing the tallest tales of Iraqi “defectors,” later proven to be self-serving fiction.

In another account of the administration’s tactics, Hersh describes how raw (and cherry-picked) “intelligence” marked “secret” was “funneled to newspapers, but subsequent C.I.A. and INR [State Department] analyses of the reports – invariably scathing but also classified – would remain secret.” Hersh points out that when the crude forgeries known as the Niger uranium papers – the basis for George W. Bush’s contention that Iraq was seeking uranium in “an African country – were exposed by the IAEA, Vice President Dick Cheney went on television and denounced the UN agency as being biased in favor of Iraq. Is this someone who was concerned with the truth?

Karen Kwiatkowski, who worked in close quarters with this parallel intelligence operation, says "It wasn’t intelligence‚ – it was propaganda. They’d take a little bit of intelligence, cherry-pick it, make it sound much more exciting, usually by taking it out of context, often by juxtaposition of two pieces of information that don’t belong together." Those who didn’t toe the neocon party line were purged, and replaced with compliant apparatchiks.

So was this simply ideological blindness, or outright lying? Robert Dreyfuss and Jason Vest, writing in Mother Jones, cite neoconservative foreign policy expert Edward Luttwak, who “says flatly that the Bush administration lied about the intelligence it had because it was afraid to go to the American people and say that the war was simply about getting rid of Saddam Hussein. Instead, says Luttwak, the White House was groping for a rationale to satisfy the United Nations’ criteria for war. ‘Cheney was forced into this fake posture of worrying about weapons of mass destruction,’ he says. ‘The ties to Al Qaeda? That’s complete nonsense.’”

Yet the American people didn’t know that at the time. The pronouncements of the Bush administration, and the War Party’s well-placed media network, led 70 percent of them to believe that the Iraqi despot was behind the worst terrorist attacks in American history – to the point that, even after this canard had been debunked (and denied by the White House) a large number of Americans still believed it. Not only that, but they believed the Iraqis had those storied “weapons of mass destruction,” and that the Bush administration was entirely justified in launching an invasion.

This is what Max Fisher’s account of the Trump-generated imbroglio fails to take into account. Fisher, who analyzes foreign policy issues for the left-of-center Vox.com, writes:

“Trump’s 10-second history of the war articulated it as many Americans, who largely consider that war a mistake, now understand it. And, indeed, Bush did justify the war as a quest for Iraqi weapons of mass destruction, which turned out not to exist.

“The other Republican candidates, who have had this fight with Trump before, did not defend the war as their party has in the past, but rather offered the party’s standard line of the moment, which is that Bush had been innocently misled by ‘faulty intelligence.’

“But neither version of history is really correct. The US primarily invaded Iraq not because of lies or because of bad intelligence, though both featured. In fact, it invaded because of an ideology.”

“…This is perhaps not as satisfying as the ‘Bush lied, people died’ bumper sticker history that has since taken hold on much of the left and elements of the Tea Party right. Nor is it as convenient as the Republican establishment’s polite fiction that Bush was misled by "faulty intelligence."

Fisher’s long account of how the neoconservatives agitated for war in the name of an “idealistic” ideology that sought to transform the Middle East into a “democratic” model is accurate as far as it goes. Yet the idea that the neocons were – or are – above fabricating evidence to make their case is naïve, at best. “If the problem were merely that Bush lied,” says Fisher, “then the solution would be straightforward: Check the administration’s facts. But how do you fact-check an ideology …?”

What if the ideology justifies lying for a “noble” end? And of course the Bush administration’s facts were checked, both during and after the war (see above): what we can conclude from this fact-checking is that the policymakers 1) Started out with an agenda, 2) Suppressed all evidence that contradicted it, and 3) Made up “factoids” out of whole cloth, the most egregious being those contained in the Niger uranium forgeries and the outright lies disseminated by Ahmed Chalabi and his Iraqi National Congress.

We can see how the neoconservatives within the administration constructed a parallel intelligence-gathering apparatus, independent of – and usually in opposition to – the CIA and the rest of the intelligence community. We can further see how their intelligence product was “stovepiped” up to the highest echelons, and landed on the President’s desk unvetted and unconfirmed. All the safeguards against compromising the US intelligence stream were dismantled – to what purpose? Fisher doesn’t think to ask this vital question. Instead, he attributes it to “ideology”;

“It does not appear that the administration encouraged them to lie, but rather that deep-rooted biases led top officials to dismiss the mountains of intelligence that undercut their theories and to favor deeply problematic intelligence that supported it.

“… By all appearances, administration officials believed their allegations of Iraqi WMDs were true and that this was indeed sufficient justification. Why else would the US launch a desperate, high-profile search for WMDs after invading – which only ended up drawing more attention to how false those allegations had been?

“Rather, they had deceived themselves into seeing half-baked intelligence as affirming their desire for war, and then had sold this to the American people as their casus belli, when in fact it was secondary to their more high-minded and ideological mission that would have been too difficult to explain. That, more than overstating intelligence on WMDs, was the really egregious lie.”

But of course they had to launch a hunt for the WMD they knew weren’t there – after all, they had justified the war on this basis. And so what if they were never found? They got away with it, didn’t they? There was never any real investigation into the intelligence-gathering activities of the Office of Special Plans, or of efforts to suppress dissent within the mainstream intelligence agencies. This was scotched by the politicians, who never followed through with their “phase two” investigation of the murky circumstances surrounding the administration’s activities.

By the time it was revealed that the war critics were right and that there weren’t any WMD in Iraq, the neocons’ goal had already been accomplished – the destruction of Iraq and the establishment of a permanent pretext for a US military presence in the region. Whatever consequences would follow the revelation of the deception – and deception it was – would be borne by the hapless George W. Bush, who was never the sharpest blade in the drawer to begin – and whom the neocons soon threw overboard as someone not willing or able to carry out their full agenda.

The US intelligence stream had been contaminated for a purpose: some entity with an agenda that included getting us inextricably involved in the Middle East over the long term. But who?

Karen Kwiatkowski, who worked in the office that was to become the Office of Special Plans, is an eyewitness:

“In early winter, an incident occurred that was seared into my memory. A coworker and I were suddenly directed to go down to the Mall entrance to pick up some Israeli generals. Post-9/11 rules required one escort for every three visitors, and there were six or seven of them waiting. The Navy lieutenant commander and I hustled down. Before we could apologize for the delay, the leader of the pack surged ahead, his colleagues in close formation, leaving us to double-time behind the group as they sped to Undersecretary Feith’s office on the fourth floor. Two thoughts crossed our minds: are we following close enough to get credit for escorting them, and do they really know where they are going? We did get credit, and they did know. Once in Feith’s waiting room, the leader continued at speed to Feith’s closed door. An alert secretary saw this coming and had leapt from her desk to block the door. ‘Mr. Feith has a visitor. It will only be a few more minutes.’ The leader craned his neck to look around the secretary’s head as he demanded, ‘Who is in there with him?’

“This minor crisis of curiosity past, I noticed the security sign-in roster. Our habit, up until a few weeks before this incident, was not to sign in senior visitors like ambassadors. But about once a year, the security inspectors send out a warning letter that they were coming to inspect records. As a result, sign-in rosters were laid out, visible and used. I knew this because in the previous two weeks I watched this explanation being awkwardly presented to several North African ambassadors as they signed in for the first time and wondered why and why now. Given all this and seeing the sign-in roster, I asked the secretary, ‘Do you want these guys to sign in?’ She raised her hands, both palms toward me, and waved frantically as she shook her head. ‘No, no, no, it is not necessary, not at all.’ Her body language told me I had committed a faux pas for even asking the question. My fellow escort and I chatted on the way back to our office about how the generals knew where they were going (most foreign visitors to the five-sided asylum don’t) and how the generals didn’t have to sign in.”

Israeli generals walking in and out of Feith’s office was the least of it. Feith himself, along with Richard Perle, David Wurmser and his wife Meyrav (all with links to Feith’s Office of Special Plans), had once prepared a strategy paper for Prime Minister Benjamin Netanyahu during his first term in office. Entitled “A Clean Break: A New Strategy for Securing the Realm,” the paper recommended a general offensive against Israel’s neighbors:

“Israel can shape its strategic environment, in cooperation with Turkey and Jordan, by weakening, containing, and even rolling back Syria. This effort can focus on removing Saddam Hussein from power in Iraq – an important Israeli strategic objective in its own right – as a means of foiling Syria’s regional ambitions.”

Stephen Walt and John Mearsheimer showed in their book, The Israel Lobby and US Foreign Policy, that the Jewish state’s American amen corner played an instrumental role in agitating for the Iraq war. As they pointed out, “A Clean Break”

“[C]alled for Israel to take steps to reorder the entire Middle East. Netanyahu did not follow their advice, but Feith, Perle and Wurmser were soon urging the Bush administration to pursue those same goals. The Ha’aretz columnist Akiva Eldar warned that Feith and Perle ‘are walking a fine line between their loyalty to American governments … and Israeli interests.’”

Whose interests were they pursuing while they manufactured talking points based on “faulty” intelligence in order to bamboozle Congress and the American people into fighting Israel’s war on Saddam Hussein?

But that was just the beginning of the long tortured road they led us down. As Ariel Sharon told a visiting delegation of American congressmen at the time, Iran, Libya, and Syria were next on Israel’s agenda:

“’These are irresponsible states, which must be disarmed of weapons mass destruction, and a successful American move in Iraq as a model will make that easier to achieve,’ said the Prime Minister to his guests, rather like a commander issuing orders to his foot-soldiers. While noting that Israel was not itself at war with Iraq, he went on to say that ‘the American action is of vital importance.’”

Two down, one to go.

Much of the “faulty” intelligence that found its way to the desks of Bush and Cheney originated with foreign intelligence agencies, and there is plenty of evidence that much of it came straight from Tel Aviv. Certainly the Israelis had an interest in using the United States military as a cat’s-paw against their traditional Arab enemies, notably Iraq. And the defense of Israel was often cited by the administration as a justification for targeting Saddam Hussein. This wasn’t the first time a foreign entity launched a covert operation to lure the United States into an overseas conflict, and it certainly won’t be the last – that is, unless and until we learn the real lesson of the Iraq war.

Yes, it was ideology that led us to commit ourselves to become the policemen of the Middle East – but the adherents of that ideology utilized methods that included fabricating “evidence” of Iraqi WMD. One aspect of neoconservative ideology conveniently left out of Fisher’s otherwise comprehensive analysis of the neocon mindset is their dedication to Israel as a model “democracy” and our ideal ally which must always be defended. An odd omission, to say the least.

If we look at the Iraq war as a wildly successful covert operation to lure us into a position from which it is almost impossible to extricate ourselves – all to the advantage of a certain Middle Eastern “democracy” beloved by the neocons – then the whole disastrous episode begins to make sense. If such is the case, then why should the perpetrators care if no WMD were found after the invasion? It would be no skin off the Israelis’ noses: Bush would get the blame, not Bibi. And of course the operatives inside the administration responsible for skewing the intelligence could always claim to have been mistaken: after all, everybody thought the WMD were there, and in any case they would never be held to account. Since when is anybody in our government held accountable for anything?

Yes, I know, this is a “conspiracy theory,” and therefore we aren’t allowed to consider it, let alone examine the facts that back it up. Nations never engage in conspiracies, and government officials never lie.

And if you believe that, there’s a bridge in Brooklyn you might be interested in purchasing….

- Germans Cheer As Refugee Center Burns, Crowds Stop Firefighters From Extinguishing Blaze

Over the past two months, Europeans have become completely fed up with the wave of refugees streaming into the bloc from the Mid-East.

After demonstrating a remarkable degree of restraint and tolerance in the wake of the attacks that left 130 people dead in Paris in November, the string of sexual assaults that swept Cologne, Germany on New Year’s Eve was the last straw for a German populace that had, until this year anyway, largely remained supportive of Angela Merkel’s “yes we can” approach to settling the 1.1 million asylum seekers that the country took in last year.

That’s not to say that there aren’t still large swaths of the German population that support the migrant cause. It’s simply to note that the general consensus is no longer teddy bears, water bottles, and hugs. Discontent with the Iron Chancellor’s approach is growing and the tension is palpable. Renewed support for PEGIDA is emblematic of the direction in which the country is headed and this weekend we got the latest evidence that Germany’s patience with migrants is wearing increasingly thin.

Residents of Bautzen (in Saxony) cheered on Saturday night as a planned migrant center burned in what very well may have been an arson. “Some people reacted to the blaze with derogatory comments and undisguised joy,” Deutsche Welle notes, before adding that “the incident in Bautzen comes shortly after a mob shouting anti-migrant slogans blocked a bus full of refugees in Clausnitz, also in Saxony.” Here’s the video of the Clausnitz incident:

Reports indicate that a number of witnesses in Bautzen attempted to prevent firefighters from extinguishing the blaze.

Saxony’s chief minister, Stanislaw Tillich, called both incidents “disgusting and hateful.“

Yes, “disgusting and hateful,” which is precisely what the German people are saying about the string of sexual assaults and the threat of Islamic terrorism.

Needless to say, when German citizens are actively attempting to keep firefighters from curtailing a blaze, it says something profound about public opinion. Then again, we suppose this isn’t anything new. As Deutsche Welle goes on to report, “there were more than 1,000 arson attacks on planned and completed refugee shelters across Germany in 2015.”

Perhaps support for Merkel’s open-door approach was never that strong in the first place.

- South Dakota Is The 'Sleepiest' State In America

Americans are not getting enough sleep, according to a new report from The CDC. More than one-third of adults in the US get less than the 'required' 7 hours sleep per night, leading to greater chance for obesity, high blood pressure and other diseases related to the digestion of food into energy. Interestingly it is the laid-back Hawaiians that get the least sleep, but South Dakota has the highest percentage of those getting seven hours of sleep each night, at 71.6%.

“People just aren’t putting sleep on the top of their priority list,” Dr. Anne Wheaton, an epidemiologist at the CDC, told CNN.

“They know they should eat right, get exercise, quit smoking, but sleep just isn’t at the top of their board. And maybe they aren’t aware of the impact sleep can have on your health. It doesn’t just make you sleepy, but it can also affect your health and safety.”

The breakdown of who gets most (and least) sleep is as follows…

On a geographic level, those in South Dakota have the highest percentage of those getting seven hours of sleep each night, at 71.6%, while those laid back Hawaiians living on the islands are getting the least amount, with just 56.1% getting seven hours of slumber. Virginia, Washington D.C. and those in the New England region are getting decent amounts of nighttime regeneration, while people in Indiana, Ohio, Michigan, Kentucky, and West Virginia are not getting much slumber.

White Americans are getting the highest level of sleep, at 66.8%, followed by Hispanics with 65.5%, Asians 62.5%, American Indians and Alaska Natives 59.6% and non-Hispanic blacks at 54.2% and Native Hawaiians and Pacific Islanders at only 53.7%.

Those with college degrees are resting at night seven hours at higher than average numbers, at 71.5%, as do those who are married, at 67.4%, while only 55.7% of those divorced, widowed or separated sleep seven hours.

To promote optimal health and well-being, adults aged 18–60 years are recommended to sleep at least 7 hours each night. Sleeping <7 hours per night is associated with increased risk for obesity, diabetes, high blood pressure, coronary heart disease, stroke, frequent mental distress, and all-cause mortality.

Insufficient sleep impairs cognitive performance, which can increase the likelihood of motor vehicle and other transportation accidents, industrial accidents, medical errors, and loss of work productivity that could affect the wider community.

Perhaps that is why US productivity is so poor?

The solution is entirely untenable… Put The Gadgets down!!

recommended lifestyle changes including going to bed at the same time each night, rising at the same time each morning as well as removing televisions, computers, mobile devices from the bedroom.

Where does your state rank?

- Trump: Finally, The Acceptance Comes… And The Gloating

On Saturday night, all doubts about whether Donald Trump was a serious contender for the White House were erased.

That’s not to say he’s locked up the nomination.

But with last night’s decisive victory in South Carolina, Trump served notice that this is no longer a matter of whether he can make a serious run at the presidency, it’s now a matter of whether Ted Cruz or Marco Rubio can mount a serious challenge.

As was the case in New Hampshire, Trump came into last night’s primary as the runaway favorite. Still, the political punditry (not to mention the GOP establishment) was incredulous and seemed to think that the electorate would “come to its senses” at the last minute and cast their votes for Jeb Bush or Marco Rubio or at the very least for Ted Cruz who isn’t exactly popular with the GOP elite, but at least he’s not telling stories about executing Muslims with bullets dipped in pig’s blood.

(pig’s blood comments begin at 33:00)

No dice. Trump “schlonged” the rest of the field and it’s looking more and more like the unthinkable will soon become reality.

Donald Trump – with his Mexican border wall, Muslim ban, and red, “Make America Great Again” baseball cap in tow – is about to secure the Republican nomination, in what amounts to the surest sign yet that public sentiment no longer bears any resemblance to establishment politics.

Against that backdrop, have a look at the following graphic which shows that while nearly three quarters of GOP voters couldn’t see themselves supporting Trump for the nominaiton last March, the tables have completely turned with nearly the same number now saying they could indeed envision supporting the controversial billionaire.

And make no mistake, Trump didn’t waste an opportunity to rub salt in the wounds of Megyn Kelly, Fox News, and the GOP establishment with this classic tweet:

“@mikeliberation: This is the best reaction shot I’ve ever seen lol #Trump2016” pic.twitter.com/jqxI7QoxEY

— Donald J. Trump (@realDonaldTrump) February 21, 2016

Finally, Trump retweeted the following from Matt Drudge:

OMG! Looks like the latest DRUDGE REPORT poll results! How can that be? ???? pic.twitter.com/PZ0CxiAh6O

— MATT DRUDGE (@DRUDGE) February 21, 2016

Get ready America. Your country is going to be “great again” in T-minus 9 months.

- NYSE Short Interest Nears Record, Pre-Lehman Level

In the last two months, NYSE Short Interest has risen 4.5%, back over 18 billion shares near the historical record highs of July 2008 (and up 7 of the last 9 months).

There are two very different perspectives on could take when looking at this data…

- Either a central bank intervenes, or a massive forced buy-in event occurs, and unleashes the mother of all short squeezes, sending the S&P500 to new all time highs, or

- Just as the record short interest in July 2008 correctly predicted the biggest financial crisis in history and all those shorts covered at a huge profit, so another historic market collapse is just around the corner.

The correct answer will be revealed in the coming weeks or months… but we know what happened last time…

Charts: Bloomberg

- French President Threatens To "Suspend" Nations That Elect "Far-Right" Polticians

Last month, we documented the burgeoning spat between Brussels and Poland over the latter’s move to approve new laws that allow the conservative (and eurosceptic) Law and Justice (PiS) government to name the chiefs of public TV and radio, and select judges for Poland’s constitutional court.

In response to a bloc-wide backlash, Polish minister Zbigniew Ziobro sent a letter to EU commissioner Gunther Oettinger in which Ziobro dismissed criticism of the new laws as “silly.”

Oettinger earlier suggested that Poland be put under supervision for possible violations of democratic principles and after the Polish Wprost weekly ran a cover depicting Angela Merkel, Jean Claude-Juncker, and other eurocrats as Nazis who “want to supervise Poland again,” Brussels hit back by launching a review of the country’s new media laws. Under the “rule of law” mechanism, the EU Commission can compel member states to change measures that pose “a systematic threat” to democracy.

But that’s not all. According to comments from French President Francois Hollande on Friday, Europe could move to “suspend” countries in which far-right governments rise to power.

“French President Francois Hollande warned Friday that an EU member state could be sanctioned if the extreme-right came to power there — and could even be suspended from the bloc,” AFP reports.

“A country can be suspended from the European Union,” the President told France Inter radio.

“Human rights watchdog the Council of Europe last week expressed concern at legislative changes proposed by Poland’s new right-wing government that have been described both at home and abroad as unconstitutional and undemocratic,” AFP goes on to say, adding that “similar concerns have been expressed about Hungary’s right-wing Prime Minister Viktor Orban.”

“When the freedom of the media is in danger, when constitutions and human rights are under attack, Europe must not just be a safety net. It must put in place procedures to suspend (countries) — it can go that far,” Hollande said.

“Checks,” he said, are necessary on Poland.

There are a couple of things to note here. First, it’s not at all clear why it should be up to France how another country’s citizens vote. Indeed, there’s something terribly ironic about the idea of punishing a country for their voting preferences in the name of democracy. There’s certainly nothing democratic about telling entire countries who they’re allowed to elect.

Second, Hollande’s comments seem to reflect fears that the worsening refugee crisis has led to a revival of nationalism in Europe. Between the growing support for PEGIDA, which staged bloc-wide rallies earlier this month)…

…and the popularity of groups like the “Soldiers of Odin” in Finland…

…it’s clear that the far-right is indeed staging a comeback. One wonders how many nations Hollande and Brussels are prepared to “suspend.”

Or perhaps it’s the other way around. Given the shifting sentiment, perhaps the far-right will “suspend” the bloc’s Francois Hollandes for failing to keep Western Europe secure in the face of myriad threats to the bloc’s territorial inegrity and cultural heritage.

- Germany's Looming Demographic Cliff

Having shown that the world is turning Japanese with tales of economic malaise, extreme monetary policy, and negative rates, Visual Capitalist's Jeff Desjardins shows that Germany, with its 5-yr government bond currently trading at a -0.33% yield, is no exception to this story. However, negative yields are not the only concern that the country has in common with Japan.

It’s the overall demographic picture that is worrying, and it could have a big effect on Germany’s economic future as well as the tough choices that must be made today.

Courtesy of: Visual Capitalist

Courtesy of: Visual CapitalistGERMANY’S IMPORTANCE

Germany is the most populous and productive economy in Europe, with 80 million people and a GDP of almost $4 trillion. It’s also the world’s third largest exporter, and that’s why it had the largest trade surplus globally in 2014 with $285 billion.

For all of its economic power, Germany has a key weakness that could potentially be its Achilles heel: it’s projected that Germany’s population will decline significantly over the coming decades, and the ratio of workers to dependents will become one of the worst in the world.

THE MATH

Every year, there are 8.4 births and 11.3 deaths per 1,000 people in Germany. The way this plays out over time is that the percentage of Germans under 15 will fall to 13% of the population by 2050, while the amount of people over 60 years old is to rise to 39%.

In the future, it is likely that there will not be enough youth or workers in the country. As Baby Boomers retire, there will be a larger burden placed on those paying into the government’s social safety net and other programs. Further, this widening gap will also mean a significant loss of experience, skill, and know-how in the workforce that will create coinciding economic challenges for the population.

In many Western nations, immigration plays a key role in keeping a population with low birth rates to be sustainable. However, in Germany’s case, both the high and low immigration scenarios look dire for future numbers. Germany’s state statistical authority currently projects a “high immigration” trend resulting in a drop to 73.1 million people by 2060, while a low-end estimate sees the population falling all the way to 67.6 million.

CHOICES

The U.N. projects that one in every six Germans will be over 80 years old by 2050. Are Germans comfortable with their nation remaining on this path?

If yes, then they must also be comfortable with a significant decrease in Germany’s economic role in the future. The country will almost certainly be on a more level stage with the U.K. and France, and it will have a diminished place on the world stage as Asia and Africa continue their rise. Tax rates will surge as a decreasing amount of workers pay into the system, and economic growth could stall in such a way that Germany has its own “Lost Decade”.

If no, then Germans must accept that there is only one realistic way to combat this trend: to open the immigration floodgates even more. While this is not what many Germans want to hear, especially as the current migrant and refugee crisis progresses, it is an option that must be weighed with careful consideration.

Either way, there are difficult choices to be made. How Germany proceeds with this question has implications both today and tomorrow on cultural, economic, and political levels.

- Iraqis Celebrate As Threat Of 3rd Bush Presidency Is Over

The New Yorker’s Andy Borowitz unleashes his satirical tongue after Jeb’s departure from the Presidential race…

Baghdad – Thousands of Iraqis poured out into the streets to celebrate in the early hours of Sunday morning, as the threat of a third Bush Presidency was declared over at last.

Iraqis, on edge about the prospect of another Bush in the White House since former Governor Jeb Bush entered the race last year, had been watching returns from the South Carolina primary with a mixture of anxiety and cautious optimism.

Moments after the first evidence of Bush’s dismal finish began trickling in, however, Iraqis roared with glee as spontaneous festivities erupted across the country.

Observers were stunned to see Sunnis, Shiites, and Kurds dancing together in the streets, putting aside their enmity to celebrate an outcome that they never dreamed possible.

“You must understand, we Iraqis have been living with the fear of a third Bush Presidency for months now,” Sabah al-Alousi, a Baghdad shoemaker, said. “Now we can begin to think about a future, for ourselves and our families.”

Asked about the possibility of a Trump Presidency, he waved off the question. “This is the greatest day for my country,” he said. “I will let nothing spoil this day.”

Fact or Fiction?

- Fannie, Freddie May Need Another Bailout As Washington Drags Feet On Housing Finance Reform

Back in March of last year, the FHFA warned that Fannie and Freddie may well go bankrupt at which point taxpayers would once again be on the hook for subsidizing their own bad mortgage debt.

As you might recall, the Treasury changed the rules when it came to the GSEs a while back.

Whereas previously, the companies paid a dividend to the government on the preferred stock Washington owned, the Feds decided instead to implement a quarterly profit sweep. As Bloomberg notes, “the payments count as a return on the U.S. investment and not as repayment of the aid, leaving no existing mechanism for them to exit government control.” That’s irked equity investors who swear they’re being illegally swindled by the government.

On Thursday, we learned that Fannie was set to pay the Treasury some $3 billion after reporting $2.5 billion in profit for Q4. The company – which has received more than $116 billion from US taxpayers since 2008, has paid the government $147.6 billion to date.

“Fannie Mae’s 2015 net income was $11 billion, down from $14.2 billion in 2014,” Bloomberg wrote on Thursday. “One reason for the decline was higher income in 2014 following settlement agreements on lawsuits related to private-label mortgage-related securities.”

Because of the arrangement which prevents Fannie from holding onto its profits, the company’s capital buffer could be completely wiped out by 2018, CEO Tim Mayopoulos warns. “At that point it would be unable to weather quarterly losses and would need to draw on Treasury funds to avoid being placed into receivership.”

So ironically, the government’s attempt to extract payments from the GSEs in perpetuity has left them without a capital cushion which in turn will force them to … wait for it… ask for another government bailout.

This is reminiscent of the rather absurd scenario the companies were in before Washington transitioned to the profit sweep model. Previously, when Fannie and Freddie owed the Treasury a dividend on the government’s preferred shares but didn’t make enough money to cover it, the Treasury would loan the GSEs the money they needed to make the payment. Obviously, that’s completely absurd but as you can see from the above, the alternative (forcing taxpayers to bail the companies out again because the government commandeers the entirety of the companies’ profits) is equally ridiculous.

“The most serious risk and the one that has the most potential for escalating in the future is the enterprises’ lack of capital,” Fannie’s top regulator, and FHFA director Mel Watt said.

As FT recounts, Fannie CEO Tim Mayopoulos said “a range of options for solving the capital problem were available, such as allowing Fannie Mae to retain earnings, changing the terms on what gets Treasury support via preferred stock purchases, and taking it out of conservatorship so it could be recapitalised in another way.”

Of course all of that is politically sensitive. Taxpayers aren’t exactly excited about seeing these bastions of cronyism and outright waste and corruption privatized again and allowing them to hang onto a porition of their profits is the first step in that direction.

Whatever the case, Americans should probably go ahead and come to terms with the fact that both Fannie and Freddie will be drawing from the Treasury over the next few years. Housing finance reform isn’t exactly moving at a breakneck pace and it’s not at all clear that income guarantee fees can offset losses from the decline in the GSEs’ retained portfolios.

As for what further bailouts would mean for the health of the US housing market, we close with the following passages from Watt:

“Future draws would reduce the overall backing available to the Enterprises, and a significant reduction could cause investors to view this backing as insufficient. It’s unclear where investors would draw that line, but certainly before these funds were drawn down in full.”

“Investor confidence is critical if we are to have, as we do today, a well-functioning and highly liquid housing finance market that makes it possible for families to lock in interest rates, obtain 30-year, fixed-rate mortgages, and prepay a mortgage if they want to refinance or need to move. If investor confidence in Enterprise securities went down and liquidity declined as a result, this could have real ramifications on the availability and cost of credit for borrowers.”

* * *

Full comments from Watt to the bipartisan policy center

Thank you, Secretary Cisneros, for your opening remarks and introduction. I also want to thank the Bipartisan Policy Center for extending the invitation for me to speak today on our work at the Federal Housing Finance Agency (FHFA). I think all of you will agree that the things I am going to talk about deserve bipartisan attention and collaboration like we have seldom seen in recent years.

This speech has two parts, an easy part and a difficult part. Both parts reflect a philosophy that I hope all of you agree we have tried to encourage since I became the Director of FHFA – a philosophy of open, honest, and transparent discussion and decision making that helps demystify what FHFA, Fannie Mae, and Freddie Mac do and how those things relate to housing finance stakeholders.

The first part of my speech is easy because it looks retrospectively at some of the things we have accomplished and how we have managed Fannie Mae and Freddie Mac (the Enterprises) in conservatorship to accomplish them. By saying that this part of the speech is easy, however, I want to be careful not to suggest that all the decisions I will highlight were easy or noncontroversial when they were being considered. It has been my experience that when decisions produce positive results down the road, we tend to forget how controversial or complicated these decisions might have been at the time they were made.

The second part of the speech is difficult, both because it looks forward – something I have shown much less inclination to do up to this point in my time as Director of FHFA – and because looking forward is inherently more difficult and almost always tends to generate more controversy. After two full years as Director of FHFA, however, I think it’s timely for me to talk not only about our accomplishments, but also about some of the challenges and risks we face, some of which will surely become more difficult for us to control the longer the conservatorships continue. While my primary responsibility as conservator may be to manage the Enterprises in the present as I have said on a number of occasions, I believe that I have an obligation, both in my role as conservator and in my role as regulator, to be frank and transparent about our challenges and risks. By doing so, I hope these remarks will ignite some dialogue that could well be difficult, but I believe is also critically needed.

The Unprecedented Conservatorships of Fannie Mae and Freddie Mac

Some background is necessary to frame both parts of the speech. Congress established FHFA in 2008 during the height of the financial crisis, and one of the Agency’s first acts was to place the Enterprises into conservatorship. Under the Senior Preferred Stock Purchase Agreements (PSPAs), the U.S. Department of the Treasury (Treasury Department) has provided essential financial commitments of taxpayer funding to support the Enterprises’ compromised financial status. During the first four years of conservatorship, the Enterprises drew a total of $187.5 billion from Treasury, but neither Enterprise has made a further draw since 2012. Fannie Mae has approximately $118 billion of its PSPA commitment remaining, and Freddie Mac has approximately $141 billion remaining. Since the beginning of conservatorship through the end of 2015, the Enterprises paid approximately $241 billion in dividends to the Treasury Department. Under the provisions of the PSPAs the Enterprises’ dividend payments do not offset the amounts drawn from the Treasury Department.Virtually everyone would agree that today we have a much safer and more stable housing finance system than when FHFA placed the Enterprises in conservatorship. I also think that most people would attribute a significant part of these improvements to decisions made in conservatorship. Guarantee fees have increased by two and a half times since 2009, and our review last year concluded that overall guarantee fee levels are now appropriate. Stronger credit standards have removed unsound risk layering and, in a manner consistent with safety and soundness, we have increasingly focused on how to support sustainable access to credit for homeowners, one of the Enterprises’ statutory obligations.

Delinquencies and foreclosures have gone down on the Enterprises’ legacy books of business, and the number of REO properties held by the Enterprises has decreased significantly. The number of HARP refinances has surpassed 3.3 million and the Enterprises have taken more than 3.6 million other actions to prevent foreclosures. The Enterprises’ retained portfolios have decreased by over half since March 2009, and their portfolios are now more focused on supporting their core business operations. The Enterprises’ multifamily programs had strong performance through the crisis, and they continue to share risk with private investors. Their multifamily purchases provide needed liquidity for the general multifamily market, with an increasing focus on affordable rental housing.

We have completed efforts to revamp and improve the Representation and Warranty Framework, and we have strengthened counterparty standards for mortgage insurers and non-bank Seller/Servicers. We have started and significantly ramped up credit risk transfer programs at both Freddie Mac and Fannie Mae, with both Enterprises now regularly transferring substantial credit risk to private investors on over 90 percent of their typical 30-year, fixed-rate acquisitions. We have a target for Freddie Mac to start using the Common Securitization Platform (CSP) in 2016, and a target for the Single Security to go into effect with both Enterprises using the CSP to support their major securitization activities in 2018.

In all of these things, we have also placed greater attention on diversity and inclusion in the Enterprises’ business operations, consistent with legal standards and with projections that the future composition of homeowners, renters, and the country as a whole will be more diverse.

FHFA’s Role as Regulator and Conservator. As this list highlights, FHFA’s role as conservator of Fannie Mae and Freddie Mac has been unprecedented in its scope, complexity, and duration – especially when you consider Fannie Mae and Freddie Mac’s role in supporting over $5 trillion in mortgage loans and guarantees. This is an extraordinary role for a regulatory agency also because we are obligated to fulfill both the role of supervisor and the role of conservator at the same time, and because we are now approaching eight full years of having these obligations. So let me also describe briefly how FHFA has managed these dual responsibilities.

Like other federal financial regulators, FHFA conducts safety and soundness supervision with a deliberate distance between FHFA and the Enterprises. Members of our supervision staff, many of whom are located onsite at Fannie Mae and Freddie Mac, conduct examinations that focus on areas of highest risk to the Enterprises. They produce reports of examination and make findings as to whether the Enterprises need to make corrective actions in particular areas.

In contrast, our role as conservator involves a different kind of relationship with the Enterprises. Under the Housing and Economic Recovery Act of 2008, FHFA has the full authority of the Enterprises’ boards of directors, management, and shareholders while the Enterprises are in conservatorship. This means that FHFA has ultimate authority and control to make business, policy, and risk decisions for the Enterprises, and the Enterprises’ boards know that their job is to meet our expectations.

However, managing these Enterprises in conservatorship requires much more of a joint effort than would occur under a normal regulatory relationship. For example, while an examiner would review board or management minutes after the meetings have taken place, members of FHFA’s Division of Conservatorship team attend management and board meetings as part of our conservatorship functions, and I personally attend and preside at executive sessions of Enterprise board meetings.

FHFA’s Management of Fannie Mae and Freddie Mac in Conservatorship. There are four key approaches that we use to manage the unique nature of these conservatorships. Using these approaches, we have been able to fulfill our statutory obligations to ensure safety and soundness, to preserve and conserve Enterprise assets, to ensure liquidity in the housing finance market, and to satisfy the Enterprises’ public purpose missions.

First, we set the overall strategic direction for the Enterprises in FHFA’s Conservatorship Strategic Plan and in annual scorecards that outline our policy expectations. We set quarterly and year-end milestones for our scorecard objectives, and we conduct regular evaluations of whether the Enterprises are on track or behind in meeting our targets. Our final scorecard assessments at the end of each year factor into the compensation calculations for Fannie Mae and Freddie Mac executives.

Second, we delegate the day-to-day operations of the companies to their boards and senior management. With over 12,000 employees at the two Enterprises and considering the nationwide scope and technical nature of their businesses, we can’t pull every lever and make every day-to-day operating decision. If we tried, I’m quick to acknowledge that their operations would grind to a halt. Under conservatorship, the Enterprises continue to operate as business corporations with boards of directors subject to corporate governance standards. The Enterprise boards are responsible – like boards of directors at other companies – for overseeing their business activities. They review budgets and set risk limits. They examine business plans and oversee senior management.

When FHFA first placed the Enterprises into conservatorship, FHFA selected new chief executive officers, reestablished their boards of directors, and approved new board members. FHFA has continued to approve all new CEOs and board members throughout conservatorship, and they are responsible for meeting our expectations and effectively running the companies. I meet several times a month with the CEOs of Freddie Mac and Fannie Mae. In addition to my attendance at board meetings, I have regular conversations and engagement with each Enterprise’s board chair to help elevate issues that need to be resolved.

Third, we have carved out actions that are not delegated to the Enterprises that require advance approval by FHFA. Deciding which items we should delegate to the Enterprises and which should require FHFA approval is a judgment call and finding the right balance is an ongoing process. There are decisions that are obvious choices for FHFA to make, such as setting the core components of the guarantee fees charged by Fannie Mae and Freddie Mac. Others are closer calls. While we retain the authority to step in and make the call on any issue, even ones that we previously delegated, we have found that providing as much clarity as possible about roles and responsibilities serves everyone better.

The fourth prong of our conservatorship model is oversight and monitoring of Enterprise activities, and this is something that happens on an on-going basis – it’s probably not an overstatement to say this takes place constantly. In addition to attending meetings of the management committees, FHFA staff members engage in regular dialogue with the management and operational teams at the Enterprises, regularly review information submitted by the Enterprises, and take action where appropriate.

Managing the Enterprises in conservatorship through this four-step approach – with regular adjustments to account for changing circumstances – has worked well. FHFA’s conservatorship decisions have helped navigate the Enterprises through a financial crisis and, despite the substantial negative impact of the crisis, helped prevent it from being far worse.

?The Challenges and Risks of a Protracted Conservatorship

However, an eight-year conservatorship is unprecedented, and managing the ongoing, protracted conservatorships of Fannie Mae and Freddie Mac poses a number of unique challenges and risks. This leads me to the more difficult part of these remarks.I have consistently stated that our responsibility and role at FHFA as conservator is to manage in the present. However, as we work to appropriately manage challenges and risks in the present, we also have a responsibility to assess when these challenges and risks may escalate to the point that they negatively impact the Enterprises and the broader housing finance market in the future. By giving this speech today, I am signaling my belief that some of the challenges and risks we are managing are escalating and will continue to do so the longer the Enterprises remain in conservatorship. Consequently, I believe that I have a responsibility, both as regulator and as conservator, to identify and discuss this concern more openly.

Enterprises’ declining capital buffers. The most serious risk and the one that has the most potential for escalating in the future is the Enterprises’ lack of capital. FHFA suspended statutory capital classifications when the Enterprises were placed in conservatorship, and Fannie Mae and Freddie Mac are currently unable to build capital under the provisions of the PSPAs. The agreements require each Enterprise to pay out comprehensive income generated from business operations as dividends to the Treasury Department, and the amount of funds each Enterprise is allowed to retain is often referred to as the Enterprises’ “capital buffer.” This capital buffer is available to absorb potential losses, which reduces the need for the Enterprises to draw additional funding from the Treasury Department. However, based on the terms of the PSPAs, this capital buffer is reducing each year. And, we are now over halfway down a five-year path toward eliminating the buffer completely.

Starting January 1, 2018, the Enterprises will have no capital buffer and no ability to weather quarterly losses – such as the non-credit related loss incurred by Freddie Mac in the third quarter of last year – without making a draw against the remaining Treasury commitments under the PSPAs. There are a number of non-credit related factors that could lead to a loss and result in a draw on those commitments: interest rate volatility; accounting treatment of derivatives, which are used to hedge risk but can also produce significant earnings volatility; reduced income from the Enterprises’ declining retained portfolios; and, the increasing volume of credit risk transfer transactions, which transfer both the risk of future credit losses as well as current revenues away from the Enterprises to the private sector. A disruption in the housing market or a period of economic distress could also lead to credit-related losses and trigger a draw.

It is, of course, impossible to predict the exact ramifications of future draws of funds from the PSPA commitments. But let me offer a few observations.

First, and most importantly, future draws that chip away at the backing available by the Treasury Department under the PSPAs could undermine confidence in the housing finance market. The remaining funds available under the PSPAs provide the market with assurance that the Enterprises can meet their guarantee obligations to investors in mortgage-backed securities even while they are in conservatorship and don’t have the ability to build capital. In effect, the Treasury Department’s financial commitment to each Enterprise under the PSPAs is a source of capital that supports mortgage market liquidity. However, under the terms of the PSPAs, these funds can only go down and cannot be replenished. Future draws would reduce the overall backing available to the Enterprises, and a significant reduction could cause investors to view this backing as insufficient. It’s unclear where investors would draw that line, but certainly before these funds were drawn down in full.

Investor confidence is critical if we are to have, as we do today, a well-functioning and highly liquid housing finance market that makes it possible for families to lock in interest rates, obtain 30-year, fixed-rate mortgages, and prepay a mortgage if they want to refinance or need to move. If investor confidence in Enterprise securities went down and liquidity declined as a result, this could have real ramifications on the availability and cost of credit for borrowers.

Second, future draws could lead to a legislative response adopted in haste or without the kind of forethought it should be given. I have been clear that conservatorship is not a desirable end state and that Congress needs to tackle the important work of housing finance reform. However, because of the intricacies of our housing finance system and the extremely high stakes for the housing finance market and for the economy as a whole if reform is not done right, I continue to hope that Congress can engage in the work of thoughtful housing finance reform before we reach a crisis of investor confidence or a crisis of any other kind. While it’s not my place to meddle in political discussions, I’m also not hearing much discussion of housing finance reform in any of the presidential campaigns.

The role of market discipline in conservatorship. A less discussed, but related, challenge posed by a continuing conservatorship is Fannie Mae and Freddie Mac’s insulation from normal market forces that would otherwise inform their operations and business practices. There are differing views about the Enterprises’ business models leading up to the financial crisis, but in conservatorship the responsibility to create a regime of market discipline and appropriate competition falls squarely on FHFA’s shoulders. The longer the Enterprises remain in conservatorship, the greater and more complicated this responsibility becomes.

This challenge presents itself in multiple decisions, including pricing. Although the Enterprises are not building capital while they are in conservatorship, FHFA expects Freddie Mac and Fannie Mae to determine their pricing as though they were holding capital and seeking an appropriate economic return on this capital. This is something that was very important to FHFA as we started to review and make adjustments to guarantee fees. We worked with the Enterprises to review the cost of capital as part of our assessment of the correct level of overall guarantee fees charged by the Enterprises. Without such an approach, it would be challenging to decide what guarantee fee levels to approve. Through our 2016 Scorecard priority to finalize a risk management framework, we are working to further our ability to evaluate these kinds of Enterprise business decisions.

Another challenge related to market discipline is the question of how the Enterprises should or should not compete against one another. As I discussed earlier, we have consciously structured the conservatorships of Freddie Mac and Fannie Mae so they continue to run as going concerns. We want them to continue to innovate and to compete on the kind of customer service they provide to lenders and on the quality of their business practices. We believe that competition in these areas is healthy for the Enterprises, good for the housing finance market, and good for borrowers.

However, we have also made a number of decisions that require the Enterprises to adopt aligned standards in certain areas, such as aligned counterparty requirements, to avoid excessive risk being placed on taxpayers. In conservatorship, we carefully determine when to allow competition and when to require alignment, requiring, of course, that all operations be executed in a safe and sound manner.

Planning amidst an uncertain future. A final challenge that being in protracted conservatorships forces us to face is how to manage and plan for the future when there is tremendous uncertainty about what the future holds. Experience demonstrates that it is difficult to manage the Enterprises in the present without establishing some kind of plans for the future. Here, I’m not talking about plans for housing finance reform, but plans for everyday operations, including strategic planning that every well-run business does and project planning that’s necessary to continue key initiatives. Without looking somewhat down the road, FHFA and the Enterprises would both lose their momentum and jeopardize day-to-day success. The key dilemma when you have an uncertain future, however, is how far down the road to look and how to retain the necessary talent to implement either short- or longer-term plans.

This challenge drove my decision to authorize the increases in compensation for both Enterprise CEOs that proved to be so controversial. First, I recognized that our delegated model relies heavily on strong management teams to uphold their side of conservatorship. Second, I decided that to be responsible we needed to have the Enterprises engage in operations-focused strategic planning over a three-to-five year horizon. To do both of those things, we needed to ensure continuity by retaining senior-level staff and having reliable succession plans that minimized disruptions.

Of course, we have implemented the legislation that Congress passed to reinstate the prior CEO compensation limits, and it is not my intention here to debate the wisdom of the decision that Congress made. Having served in Congress, I understand that it was an easy political decision. However, the issue of reliable succession planning is another example of the many challenges presented by a long-term conservatorship. The fact is that the Enterprises run businesses that rely on a highly specialized and technically skilled workforce. Retaining that workforce is essential to the Enterprises’ success and to FHFA’s success as conservator. With continuing uncertainty about conservatorships of indefinite duration and what role the Enterprises will play in the future of housing finance, retaining skilled employees will be an increasing challenge.

Conclusion

We have made these ongoing conservatorships work thus far through the dedication of staff at FHFA and the staffs of both Enterprises and we, of course, remain committed to continuing this task. We know that the stakes are high for the housing finance market and for the broader economy. However, as I have indicated in my remarks today, there are substantial challenges and risks associated with the unprecedented size, complexity, and duration of the conservatorships of Fannie Mae and Freddie Mac. After more than two years at FHFA, I can assure you that these challenges are certainly not going away, and some of them are almost certain to escalate the longer the Enterprises remain in conservatorship.

- Greek Attempt To Force Use Of Electronic Money Instead Of Physical Cash Fails

While the “developed world” is only now starting its aggressive push to slowly at first, then very fast ban the use of physical cash as the key gating factor to the global adoption of NIRP (by first eliminating high-denomination bills because they “aid terrorism and spread criminality”) one country has long been doing everything in its power to ween its population away from tax-evasive cash as a medium of payment, and into digital transactions: Greece.

The problem, however, is that it has failed.

According to Kathimerini, “Greek businesses are not ready for the expansion of plastic money through the compulsory use of credit and debit cards for everyday transactions.”

Unlike in the rest of the world where “the stick” approach will likely to be used, in Greece the government has been more gentle by adopting a “carrot” strategy (for now) when it comes to migrating from cash to digital. The government has told taxpayers that they will have to spend up to a certain amount of their incomes via bank and card transactions in order to qualify for an annual tax-free exemption.

This appears to not be a sufficient incentive however, as a large proportion of stores still don’t have the card terminals, or PoS (Points of Sale), required for card payments, while plastic is accepted by very few doctors, plumbers, electricians, lawyers and others who tend to account for the lion’s share of tax evasion recorded in the country.

Almost as if the local population realizes that what the government is trying to do is to limit at first, then ultimately ban all cash transactions in the twice recently defaulted nation as well. It also realizes that an annual tax-free exemption means still paying taxes; taxes which could be avoided if one only transacted with cash.

For the government this is bad news, as the lack of tracking of every transaction means that the local population will pay far less taxes: a recent study by the Foundation for Economic and Industrial Research (IOBE) showed that increasing the use of cards for everyday transactions could increase state revenues by anything between 700 million and 1.6 billion euros per year, and that the market’s poor preparation means that the tax burden has been passed on to lawful taxpayers. As a reminder, in Greece, the term “lawful taxpayers” is not quite the same as in most other countries.

What is more surprising is that according to data seen by Kathimerini, PoS terminals in Greece amount to just 220,000, and that despite the fact these were effectively forced on enterprises with the imposition of the capital controls, an estimated half of all businesses do not have card terminals.

Almost as if the Greeks would rather maintain capital controls than be forced into a digital currency by their Brussles overlords.

According to Finance Ministry calculations , the number of terminals the market requires for a satisfactory geographical coverage in the basic categories of small enterprises and of the self-employed to 450,000-500,000, which appears impossible for 2016.

As for consumers, the increase in the number of debit cards after the government imposed the capital controls has brought their total to 1.7 million across Greece.

And yet, despite the aggressive push to force everyone out of physical cash and into digital money, the experiment has so far failed. How long until the IMF, Troika, or Quadriga or whatever it is called these days, uses Greece as the Guniea Pig for the next monetary experiment, and “advises” the Syriza government that if it wants the bailout money to flow, it will have to do away with all physical cash within its borders. A successful implementation, first in Greece, would then mean that the global decashification process can continue in other western nations.

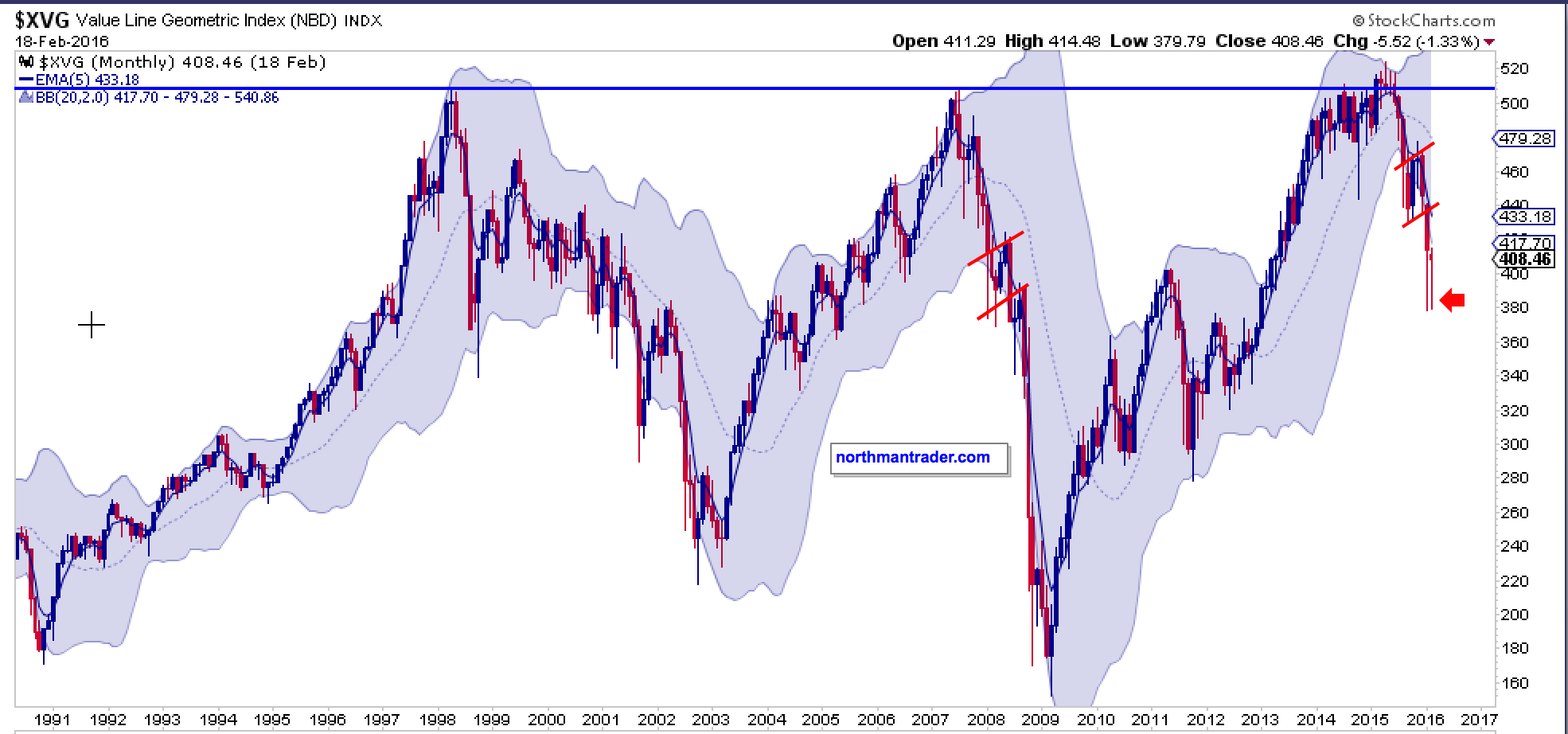

- You Know It's Over When…

Even The Economist is forced to admit to all the misplaced faith in the economic-healers…

Via @TheEconomist

- Disruption Right Where They Don’t Want It

Prosthetic eyeballs go for anywhere from $2,000 to $9,000 at an ocularist. You’ll be thanking me for this information, as the US election ramps into high gear and the deluge of political propaganda, I mean advertising, puts sane people everywhere at severe risk of stabbing their own eyes out with knitting needles.

Controlling the thoughts of over 300 million people takes some doing. For the last few decades the choice of medium has been the idiot box, specifically mass media.

But mass media costs mass money.

If you’re wondering how much, recent estimates by Kantar Media, an ad tracking firm, suggest that the price tag for political TV ads will clock in at $4.4 billion for the 2016 circus. This is up from $3 billion in 2012. Hey, what’s another 1.4 billion amongst friends?

When it comes to politics, controlling the media is all-important since the media is the all important leverage into the populace’s minds. Amassing power and personal fortunes begins with grabbing attention.

Our bent here is not to follow the political campaign, or to bother trying to figure out which podium doughnut gets the clown crown at the end of the charade. As far as I can tell, leading political candidates are selected for having no manners, no humour, no humility, and the sort of IQ commonly found in farmyard animals.

Those are the good ones. The bad ones are pure psychopaths and if I had my way they’d be thrown into cells sans plumbing or heating and forced to eat only what they can cultivate in their body hair. Predicting the outcome of this circus impresses me as a waste of time. It’s a good thing they’re performing for a populace, the majority of which have no intellect at all.

The political process formula, like most things that work well, is simple. Mass media distracts mass populace and mass populace in turn votes for all manner of absurdity.

The Controlling Elite

Contrary to popular belief, there’s no conspiracy of a group of grumpy old men in smoky rooms, sipping Chivas, wearing stripy cardigans and pushing the buttons; but rather there’s a distributed elite group of people who went to the right schools, joined the right organisations, who understand how things work and employ lobby groups to further their interests.

Nothing formal but rather the elite who’ve managed to figure out the system for their benefit and who use their influence to create ever more influence. Power clusters under the system and those who acquire power manipulate more of the system accruing ever more power in a continuous repetitive cycle.

The GFC provided some insights into how the system works.

Investment bankers managed to defraud first pension funds and institutions and, when caught out, managed to coerce the tax payer to pay them bonuses.

As I mentioned in last week’s post when discussing the criminal activities by Wall Street in the GFC.

“The bankers involved should all have landed up in jumpsuits, allowed out of their cells only for a moments man-love in the showers. They, of course, didn’t and instead paid themselves billions in bonuses.”

So the system never changes from the inside no matter what any of the political groups may promise.

Nope, change comes always from the outside; from left-field, from the unexpected to those who are caught in the trees without understanding they’re in a forest.

What the Arab Spring taught us was the tidal wave like power of a what disruptive technology can do. Social media not only undermined mass media but completely usurped it.

Just as the Berlin Wall fell with the disruption brought about by the fax machine, the great enabler that is technology is changing the political landscape in the US under our very eyes.

How so?

Attention has been found in mass media, specifically television, and newspapers.

What the elites haven’t yet figured out is that these are antiquated forms of communication. Youtube, Twitter, Facebook, Snapchat and the likes are competing. These channels allow for EVERYONE to have a voice, no permission needed, no filters, and instantaneously.

Resisting technology is as futile as the East German police resisting the populace once they had access to a different set of information. Change becomes inevitable. The elites have built centralized systems because centralized systems concentrate power. And when centralized systems come up against decentralized systems they are overwhelmed due to simple laws of distribution and economics.

The Arab Spring taught us this. The Washington Post explained it succinctly:

“During the week before Egyptian president Hosni Mubaraks resignation, for example, the total rate of tweets from Egypt — and around the world — about political change in that country ballooned from 2,300 a day to 230,000 a day. Videos featuring protest and political commentary went viral – the top 23 videos received nearly 5.5 million views. The amount of content produced online by opposition groups, in Facebook and political blogs, increased dramatically.”

Trump understands this new game and doesn’t even bother trying to play the old game, spending millions on political advertising.

Bernie spends a few million on political ads. Trump just tweets.

Bernie waits for the political debate to end, then spends money on delivering his message via mass media as a follow up. Trump live tweets on the fly.

Poor Bernie can’t keep up.

Mass media costs a ton of money but the distribution laws have changed. The barrier of money to participate is being eroded.

Trump also understands the value of “shock and awe” better than George Bush ever could.

What shock and awe?

Megyn Kelly, a reporter from Fox News, isn’t going to be inviting the Don over for dinner anytime soon.

Shock value?

You bet.

Tell me, would you re-tweet Trump calling someone any of the above or would you re-tweet Bernie discussing immigration reform or tax policy? Be honest now.

The truth is, the more vile, the more shocking, and the more crazy and offensive Trump becomes the more his message goes viral. Couple that with his political insensitivity and he makes for a character so clearly different from all of his opposition. Many who disagree with him still see him as bit of breathe of fresh air as he plays by his own rules and ostensibly at least appears not to be bought and paid for:

“Trump raked in nearly 13.5 million Twitter mentions since Dec. 30, according to SocialFlow, a social media publishing platform. This put the real estate developer well ahead of virtually every major celebrity in the United States including Justin Bieber who brought in roughly 8 million, Kanye West with 6.2 million and Rihanna with 5.7 million.”

The elites are mad and sneer and jibe. Trump doesn’t care. He’s not playing by their rules.

The age of disruption is here and mass media will not be spared.

Begging for disruption is the financial mass media.

We have some thoughts around that which I’ll be discussing on an up-and-coming podcast for subscribers.

– Chris

============

Liked this article? Read more from us and get access to

free subscriber only content here.

============

- After Blowing Up Its Clients With Its "Top 6 Trades For 2016", Goldman Has A New Trade Recommendation

After refusing to even consider the possibility of a recession in the US for over a year, the first cracks in Goldman’s armor are starting to appear. Over the weekend chief equity strategist David Kostin said that while the probability of a recession according to GS economists remains low, saying that “their model suggests the US has an 18% probability of recession during the next year and 24% likelihood during the next two years”, Goldman’s clients and investors “continue to inquire about the impact a contraction would have on the US equity market.”

Displeased with this inquiry into the worst case scenario, one which nobody at Goldman predicted as recently as a few months ago, Kostin is forced to present Goldman’s sensitivity “of our existing earnings and valuation forecasts to a US recession scenario.” Here is Goldman’s take of what may be the worst case scenario for stocks in a recession:

We estimate the S&P 500 index will generate $117 in EPS in 2016, a rise of 11% from last year, although EPS growth excluding the Energy sector will equal just 5%. Our baseline earnings forecast assumes the US economy expands by an average of 2.0% in 2016 while world ex-US growth averages 3.6%. We forecast sales, margins, and earnings for each sector of the S&P 500 based on assumptions for US GDP growth, global GDP growth, inflation, interest rates, crude oil, and the US Dollar.

From a sensitivity perspective, we estimate a 100 bp shift in US GDP growth will affect our S&P 500 EPS forecast by roughly $5 per share. For example, holding other macro variables constant, if US GDP growth averages +1.0% then EPS would equal approximately $111.

And here the humor begins:

However, if the US falls into recession and GDP actually declines by 1.0% (300 bp below our baseline forecast) then EPS would equal just $100 per share, a decline of 6% from last year and a 13% drop from the recent EPS peak of $115 in 2014. Coincidentally, the median peak-to-trough fall in EPS around the 13 recessions over the past 80 years equals 12%. Most investors find the sensitivity of our EPS forecast to shifts in GDP growth much smaller than they expect.

Perhaps it has something to do Goldman’s absolutely abysmal forecasting track record – as we reported before, 5 of Goldman’s top 6 trades for 2016 – all of which were bullish – were closed out at a loss just 6 weeks into 2016. Maybe “investors” are finally warming up to Goldman’s “predictive” powers.

That however doesn’t faze Kostin who says that “simply put, many sectors have low economic sensitivity. The profits for Telecom, Utilities, Health Care, and Consumer Staples firms are relatively immune to swings in GDP.”

Right, and just exclude energy, materials, and everything else that is nearing the biggest default wave since 2008, then just apply Tesla’s Non-GAAP adjustment, and all shall be well.

It gets better: apparently not only are investors overly worried about GDP growth, they are also panicking about EPS:

As is the case for changes in GDP growth, the EPS sensitivity to interest rates is much smaller than most investors expect. While the sensitivity of profits of Financials stocks to interest rates is high, with each 100 bp change in bond yield affecting the sector’s EPS by roughly 4%, the impact on EPS of other sectors offsets about 60% of the Financials’ change (see Exhibit 3). The sensitivity of our 2016 S&P 500 EPS forecast to changes in crude oil price has a similar offsetting impact between profits of the Energy sector and earnings of the other nine sectors. We estimate that every $10 shift in the average price per barrel of crude oil has a 29% change in Energy EPS but just a 0.8% or $1.00 per share impact on overall S&P 500 EPS. Our baseline assumption is that Brent averages $44 per barrel (18% below last year). If oil averages $34 per barrel, our EPS estimate would be $116.

We are #timestamping that and we promise to revisit in one year what EPS will be if (and when) oil averages $34 (or less).

And while we are amused by Goldman’s relentless optimism according to which even a recession will barely impact the US economy, we were truly amazed by the following:

If the US falls into recession and GDP actually declines by 1.0% (300 bp below our baseline forecast) then EPS would equal just $100 per share, a decline of 6% from last year and a 13% drop from the recent EPS peak of $115 in 2014. Coincidentally, the median peak-to-trough fall in EPS around the 13 recessions over the past 80 years equals 12%.