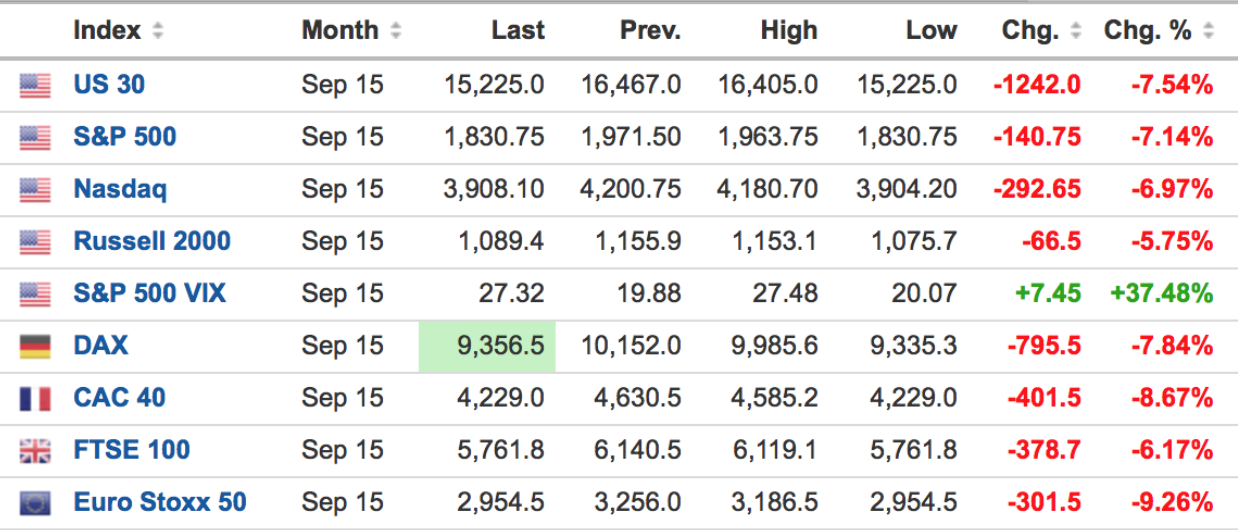

- China Halts Stock Trading For Day After Entire Market Crashes

Following the initial halt in CSI-300 Futures at the 5% limit down level, the afternoon session opened to more carnage and amid the worst 'first day of the year' in at least 15 years, Chinese stocks collapsed further to a 7% crash. At 1334 local time, stock trading was halted for the rest of the day across all exchanges (at least two hours early).

As Bloomberg reports,

Chinese stock trading was halted for the rest of the day after the CSI 300 Index plunged more than 7 percent.

Trading of shares and index futures was halted from about 1:34 p.m. local time, according to data compiled by Bloomberg.

Stocks fell as manufacturing contracted for a fifth straight month and investors anticipated the end of a ban on share sales by major stakeholders.

Under the mechanism which only became effective Monday, a move of 5 percent in the CSI 300 triggers a 15-minute halt for stocks, options and index futures, while a move of 7 percent close the market for the rest of the day. The CSI 300 of companies listed in Shanghai and Shenzhen fell as much as 7.02 percent before trading was suspended.

Not a happy new year…

Dow futures are now down over 150 points from NYE close, Gold and Treasuries are bid, and offshore Yuan has plunged most since the August devaluation.

- Murphy’s Law of Gold Analysis, Report 3 Jan

by Keith Weiner

Perhaps it may be lesser known than his other Laws, but Murphy wrote one for the basis analysis. It goes like this. If we observe that the fundamental price of a metal is far removed from the market price, the two won’t likely converge the next week. On the other hand, suppose we say this (as we did last week):

“The Monetary Metals fundamental price is measuring just that, the fundamentals. As with stocks or any other asset, our centrally banked, government-distorted markets can experience price volatility and even prices that deviate from the fundamentals for a long period of time. Just because we have been calculating a fundamental price for gold that is well over a hundred bucks above the market price, does not mean that the market price has to spike up $100 tomorrow morning. It might—and we certainly would not short gold when the market is in such a state. But as the market has proven since August, it might remain depressed for quite a while.”

Then something is bound to happen the next week.

No, the price of gold did not shoot up to approach our published fundamental. The gold-silver ratio promptly moved up +2.3%. As readers will recall, we have been calling for a ratio value over 80 for a while.

Read on for the only true look at the fundamentals of gold and silver…

But first, here’s the graph of the metals’ prices.

The Prices of Gold and Silver

We are interested in the changing equilibrium created when some market participants are accumulating hoards and others are dishoarding. Of course, what makes it

exciting is that speculators can (temporarily) exaggerate or fight against the trend. The speculators are often acting on rumors, technical analysis, or partial data about flows into or out of one corner of the market. That kind of information can’t tell them whether the globe, on net, is hoarding or dishoarding.One could point out that gold does not, on net, go into or out of anything. Yes, that is true. But it can come out of hoards and into carry trades. That is what we study. The gold basis tells us about this dynamic.

Conventional techniques for analyzing supply and demand are inapplicable to gold and silver, because the monetary metals have such high inventories. In normal commodities, inventories divided by annual production (stocks to flows) can be measured in months. The world just does not keep much inventory in wheat or oil.

With gold and silver, stocks to flows is measured in decades. Every ounce of those massive stockpiles is potential supply. Everyone on the planet is potential

demand. At the right price, and under the right conditions. Looking at incremental changes in mine output or electronic manufacturing is not helpful to predict the future prices of the metals. For an introduction and guide to our concepts and theory, click here.Next, this is a graph of the gold price measured in silver, otherwise known as the gold to silver ratio. The ratio jumped up this week.

The Ratio of the Gold Price to the Silver Price

For each metal, we will look at a graph of the basis and cobasis overlaid with the price of the dollar in terms of the respective metal. It will make it easier to provide brief commentary. The dollar will be represented in green, the basis in blue and cobasis in red.

Here is the gold graph.

The Gold Basis and Cobasis and the Dollar Price

The cobasis (i.e. scarcity of gold) rose more than the dollar (which is the inverse of the price of gold). In other words, the gold price fell a few bucks but the metal became more scarce. By the way, the above graph had to be rescaled to make the higher cobasis fit. The move in the cobasis would appear larger on the scale used last week.

Not only is the Feb contract backwardated, but so is Apr. As long speculators are selling Feb to buy Apr, the latter backwardation is more notable.

The fundamental price jumped up this week, with most of the action on Wednesday.

Now let’s look at silver.

The Silver Basis and Cobasis and the Dollar Price

The price of the dollar in silver terms moved up considerably more than the price in gold terms. Conventional analysis would say that silver fell 52 cents, but we reject that view. The dollar is not the economic constant.

While the scarcity of silver rose a bit in response, it didn’t rise that much. The May silver contract is nowhere near backwardated.

Unfortunately for silver bugs, the fundamental price for silver fell 25 cents this week. This puts it above the market price, but not by a large margin.

It also means the fundamental price of the gold-silver ratio went up. We are almost embarrassed to say what it is now. Suffice to say, quite a lot higher than the market ratio of 76.7, as of Thursday…

© 2016 Monetary Metals

- Dow Futures Dump 300 Points From New Year's Eve Highs As China Crashes

With China closing the morning session limit down, US equity futures are extending their losses (even though crude futures are holding some of their gains). The initial knee-jerk jump as crude rose on Saudi tensions has been entirely erased and Dow Futures are now down 300 points from New Year’s Eve highs… Happy New Year.

China closed the morning session “not off the lows” with a bloodbath in ChiNext and Shenzhen…

With Offshore Yuan crashing over 440 pips – the most since the August deval…

And US futures are tumbling…

But bonds and bullion are bid…

- Puerto Rico Is Greece, & These 5 States Are Next To Go

As Wilbur Ross so eloquently noted, for Puerto Rico "it's the end of the beginning… and the beginning of the end," as he explained "Puerto Rico is the US version of Greece." However, as JPMorgan explains, for some states the pain is really just beginning as Municipal bond risk will only become more important over time, as assets of some severely underfunded plans are gradually depleted.

Wilbur Ross discusses Puerto Rico's debt struggles and where it goes from here…

But, as JPMorgan details, Muni risk is on the rise for US states, but broad generalizations do not apply (in other words, these five states are 'screwed')…

The direct indebtedness of US states (excluding revenue bonds) is $500 billion. However, bonds are just one part of the picture: states have another trillion in future obligations related to pension and retiree healthcare. In the summer of 2014, we conducted a deep-dive analysis of US states, incorporating bonds, pension obligations and retiree healthcare obligations. After reviewing over 300 Comprehensive Annual Financial Reports from different states, we pulled together an assessment of each state’s total debt service relative to its tax collections, incorporating the need to pay down underfunded pension and retiree healthcare obligations.

While there are five states with significant challenges (Illinois, Connecticut, Hawaii, New Jersey, and Kentucky) , the majority of states have debt service-to-revenue ratios that are more manageable.

As a brief summary, we computed the ratio of debt, pension and retiree healthcare payments to state revenues. The blue bars show what states are currently paying. The orange bars show this ratio assuming that states pay what they owe on a full-accrual basis, assuming a 30-year term for amortizing unfunded pension and retiree healthcare obligations, and assuming a 6% return on pension plan assets. States below the green bar are spending less than 15% of total revenues on debt, which seems manageable from an economic and political perspective. When this ratio rises above 15%, harder discussions in the state legislature about difficult choices begin.

It would take a long time for underfunded pension plans (e.g., 60% funded) to run out of cash, given the long duration of plan liabilities. But as investors learned in Puerto Rico and Greece, bond markets can drift along unconcerned with mounting fundamental problems, only to experience a rapid repricing at times that cannot be predicted. As a reminder, this analysis applies to states and not to city, county and other in-state issuers.

- Oregon Standoff: A Terrible Plan That We Might Be Stuck With

Submitted by Brandon Smith via Alt-Market.com,

Well, there is whole host of things wrong with this situation, which is why I never supported or endorsed "Operation Hammond Freedom" to begin with. There is a lot of misinformation out there at this time on the debacle in Oregon, and certain alternative media outlets seem to be conveniently overlooking particular facts. I suspect that some people in the movement simply want to "kick it off" (a second American revolution), and they don't care if the circumstances of that kick-off are favorable or terrible (I realize "favorable" is relative, but starting this fight from a much stronger position is more than possible). This attitude was prevalent among some at Bundy Ranch, as certain groups refused to dig in positions for a real fight in the hopes that they would be "martyred" for the cause. This, in case you were wondering, is idiotic.

Oath Keepers including founder Stewart Rhodes was the only organization to predict how Ammon Bundy's vague calls for action on the part of the Hammond Family would actually play out. They received a lot of ignorant attacks in response, and yet, they were absolutely right.

Ammon, apparently trying to recreate what cannot be recreated, is looking for another Bundy Ranch stand-off. First, I would point out that such events can't be artificially fabricated. They have to happen in an organic way. Whenever a group of people attempt to engineer a revolutionary moment, even if their underlying motivations are righteous, it usually ends up kicking them in the ass (Fort Sumter is a good example). Ammon's wingmen appear to be Blaine Cooper aka Stanley Blaine Hicks (a convicted felon), and Ryan Payne (who claimed falsely during the Bundy Ranch standoff that he was an Army Ranger and who worked diligently to cause divisions between involved parties on the ground). This was the first sign that nothing good was going to come from the Hammond protest.

I have watched extensive video from the event in Oregon and am privy to accounts from participants. From the information at my disposal, it would appear that Ammon and team did NOT make clear their intentions to occupy the federal wildlife refuge building except to a select few, inviting protesters to "take a hard stand" without revealing what this would entail until they were already in the middle of it all. OPSEC? No, I think not. Obviously the goal was to lure as many protesters to Oregon as possible to the event in the hopes that they would jump on board with the stand-off plan once they were more personally involved. Numerous protesters were rightly enraged once they discovered the ultimate motives behind the event.

The plan is basically this – use the Hammond family as a vehicle (yes, this is what is being done) even though they did not want any kind of standoff to result and specifically refused aid. Occupy federally owned buildings which have little to do with anything of importance and have no symbolic power as did Bundy Ranch. Elicit federal response. Wash, rinse, repeat.

Bundy Ranch had many positive elements going for it, which is why it ended the way it did. This standoff has none of the same elements. I suppose one could ask, though, why do I care?

It's true, these people have every right to make positively naive strategic errors and I don't have to participate directly if I don't like it. The problem, however, is that Ammon and friends have decided they want to be the "tip of the spear" (his words, not mine). I do not think they understand what this means, or they don't care. What it means is, even though I think the entire Oregon plan is ill conceived; literally the WORST possible way to launch a fight against federal corruption, if the federal government moves in a heavy handed manner to kill these people, I and many others will have to fight as well by default when a FAR better tactical and social position could have been achieved. My conscience simply will not allow the rationalization of the deaths of liberty minded people even if their stupidity brought about the circumstances. And frankly, that pisses me off.

As a student of asymmetrics, I understand that choosing the time, place and circumstances is 95% of the battle ahead against an advanced opponent. More organization is needed. More preparedness. More training. More public awareness. The Oregon standoff could steal away what little time we had left.

The Oregon standoff potentially forces the hand of the Liberty Movement, not the hand of corrupt government – the exact reverse of what should be happening.

Mike Vanderboegh has outlined similar thoughts expertly in this article. Everything he has written is exactly what was going through my own mind when I heard of the happenings in Oregon. Ammon Bundy and companions are not the tip of the spear. Not even close. What I do fear is that they are cannon fodder beckoning a nationwide government crackdown to which I and others will then be forced to personally respond to with equal f*cking measure. And all of this on the worst possible terms and at a very inconvenient time (executive actions on gun control mere weeks from now).

And here's the best part; those of us who remain critical of the clinically retarded maneuver being executed here are going to be called cowards and "keyboard warriors"; it's a given. We are all ready to fight for the future of this country, we have been training diligently for it and helping many others along the way. But, because we do not support two dimensional planning there are those that will say – "Now we find out who the real patriots are!"

Against stupid plan = coward against freedom and action. Just watch.

If the Feds use brutality to handle the Oregon conflict, it will indeed "kick-off". There wont be any way to stop it. Just don't get too excited, folks. This is no Lexington or Concord. I really don't know what to call it…

- 2016 Off To A Miserable Start: Asian Stocks Drop; Futures Slide After China PMI Tumbles On Dire Commentary

Earlier in the session, after the surge in oil prices on fears of a spike in belligerence between Saudi Arabia and Iran, bulls were hopeful that after a poor close to 2015, at least the first trading day of 2016 would set a positive mood: after all, if there is one thing war is good for, it is to lift stock markets. And it did… for about 3 hours.

Then moments ago, Caixin Media and Markit Economics released China’s December manufacturing purchasing managers’ index. It was a doozy, falling to 48.2 from 48.6 in November, well below the 48.9 consensus estimate and even lower than the 49.6 printed a year ago, its tenth consecutive month in contraction territory and the lowest reading since September 2015.

The trend is clearly not one's friend, especially if one is part of Beijing's political oligarchy.

As the report noted, there was a renewed contraction of output, with total new work continuing to fall, while new export work declines for first time in three months; finally, companies continued to shed staff as the greatest threat facing China, a massive labor revolt, continues to slowly simmer.

The details were quite frankly, stunning, in their negativity: as if Markit wanted to paint China's economy in the worst way possible:

Adjusted for seasonal factors, the Purchasing Managers’ Index™ (PMI™) – a composite indicator designed to provide a single-figure snapshot of operating conditions in the manufacturing economy – registered below the neutral 50.0 value at 48.2 in December, down from 48.6 in the previous month. Business conditions have now worsened in each of the past 10 months. That said, the latest deterioration was modest overall.

A renewed contraction of manufacturing output weighed on the headline index reading in December. Although the rate of reduction was modest overall, it was the seventh time in the past eight months that production has fallen, and contrasted with a stabilisation in November. Anecdotal evidence suggested that relatively weak market conditions and reduced client demand had prompted firms to cut output in the latest survey period.

Indeed, total new business declined again in December, and at a similarly modest rate to those seen in the prior two months. Data suggested that softer domestic and international demand led to lower overall new work, with new export business also falling in December. Furthermore, this was the first time that new work from overseas had fallen since September.

Lower output requirements underpinned a further fall in purchasing activity in December. Moreover, the rate of contraction quickened slightly since November and was marked overall. As a result, stocks of inputs also declined over the month, while fewer sales led to a slight accumulation of stocks of finished goods.

Manufacturing companies continued to cut their payroll numbers at the end of 2015 and at a moderate rate. According to panellists, lower staff numbers were the result of company down-sizing policies and cost-saving initiatives. Fewer employees contributed to an accumulation of outstanding work in December, with the rate of growth quickening to an eight-month high.

December data signalled a further fall in average cost burdens faced by Chinese manufacturers. Moreover, the rate of reduction eased only slightly since November and remained sharp overall. Panellists that reported decreased input costs widely attributed this to lower raw material prices. Manufacturers generally passed on their cost savings to clients in the form of lower selling prices, while some companies mentioned that greater market competition had led them to cut their tariffs.

The summary from He Fan, Caixin's Chief Economist was downright dire:

“The Caixin China General Manufacturing PMI for December is 48.2, down 0.4 points from the reading for November. This shows that the forces driving an economic recovery have encountered obstacles and the economy is facing a greater risk of weakening. More fluctuations in global markets are expected now that the U.S. Federal Reserve has started raising interest rates. The government needs to pay more attention to external risk factors in the short term and fine-tune macroeconomic policies accordingly so the economy does not fall off a cliff. It needs to simultaneously push forward the supply-side reform to release its potential and reap the benefits.”

Here, again, is the key part: "The government needs to fine-tune macroeconomic policies accordingly so the economy does not fall off a cliff."

But… 7% GDP.

Incidentally, all this is happening as China's set the Yuan's fixing at 6.5032, another multi-year low for the currency as China's devaluation is accelerating with every passing day.

Furthermore, offshore Yuan is collapsing… breaking above 6.6100…

As a result, algos quickly got the hint that nothing has changed from the deteriorating trends of late 2015, and promptly applied that pattern to the E-mini, which after optimistically rising as high as 2043, has since dropped 11 points and was trading at the lows of the session, well in the red…

… and following its favorite carry trade partner, the USDJPY, which has likewise dumped, below the key 120.00 support, and is currently trading at a 2-month low.

Which reminds us of what Goldman said just on December 20: "we continue to expect $/JPY higher. We recommend being long $/JPY as part of our 2016 top trade recommendation (along with short EUR/$) and forecast $/JPY at 130 in 12 months."

It really never fails.

And speaking of things that are falling, it wasn't just US equity futures and the USDJPY. It was everything, with Asia largely down by 1% or more as of this writing:

- MSCI AP Index -1.2% to 130.46; telecoms services, IT fall most

- MXAPJ Index -1.4%; S&P 500 Futures +0.2%

- Nikkei 225 -1.1%; Topix -0.8%; yen +0.3% to 120.3/USD

- Hang Seng Index -1.5%, HSCI -1.4%, HSCEI -1.6%; H.K.’s HSI falls most in 3 weeks.

- ASX 200 -0.1%

- Kospi -1.2%

- Straits Times Index -1%

- KLCI -0.7%

- TWSE -2%

- Philippines Composite -0.4%

Finally, remember when "bad news was good news"? Well, as of this moment the Shanghai Composite is down -4% and sliding fast… and the broader CSI-300 is limit down 5%…

- Trump Vs Hillary: The ISIS Perspective

- Nassim "Black Swan" Taleb On The Real Financial Risks Of 2016

Authored by Nassim Nicholas Taleb, publish op-ed via The Wall Street Journal,

Worry less about the banking system, but commodities, epidemics and climate volatility could be trouble

How should we think about financial risks in 2016?

First, worry less about the banking system. Financial institutions today are less fragile than they were a few years ago. This isn’t because they got better at understanding risk (they didn’t) but because, since 2009, banks have been shedding their exposures to extreme events. Hedge funds, which are much more adept at risk-taking, now function as reinsurers of sorts. Because hedge-fund owners have skin in the game, they are less prone to hiding risks than are bankers.

This isn’t to say that the financial system has healed: Monetary policy made itself ineffective with low interest rates, which were seen as a cure rather than a transitory painkiller. Zero interest rates turn monetary policy into a massive weapon that has no ammunition. There’s no evidence that “zero” interest rates are better than, say, 2% or 3%, as the Federal Reserve may be realizing.

I worry about asset values that have swelled in response to easy money. Low interest rates invite speculation in assets such as junk bonds, real estate and emerging market securities. The effect of tightening in 1994 was disproportionately felt with Italian, Mexican and Thai securities. The rule is: Investments with micro-Ponzi attributes (i.e., a need to borrow to repay) will be hit.

Though “another Lehman Brothers” isn’t likely to happen with banks, it is very likely to happen with commodity firms and countries that depend directly or indirectly on commodity prices. Dubai is more threatened by oil prices than Islamic State. Commodity people have been shouting, “We’ve hit bottom,” which leads me to believe that they still have inventory to liquidate. Long-term agricultural commodity prices might be threatened by improvement in the storage of solar energy, which could prompt some governments to cancel ethanol programs as a mandatory use of land for “clean” energy.

We also need to focus on risks in the physical world. Terrorism is a problem we’re managing, but epidemics such as Ebola are patently not. The most worrisome fact of 2015 was the reaction to the threat of Ebola, with the media confusing a multiplicative disease with an ordinary one and shaming people for overreacting. Cancer rates cannot quadruple from one month to the next; epidemics can. We are clearly unprepared to deal with such threats.

Finally, climate volatility will produce some nonlinear effects, and these will be compounded in our interconnected world, in which disruptions are more acute. The East Coast blackout of August 2003 was nothing compared with what may come.

- The Movies Are Becoming Just Like The Markets: A Handful Of Blockbusters And Tons Of Losers

Back in July we first revealed something troubling: leadership breadth was collapsing not just across the Nasdaq…

… but the broader market as well:

As the WSJ had calculated, out of a total of 500 stocks, just Amazon, Google, Apple, Facebook, Gilead and Walt Disney accounted for more than all of the $199 billion in market-capitalization gains in the S&P 500. In fact, as of July, just these six firms were responsible for more than half of the $664 billion in value added to the Nasdaq Composite Index as of July.

Since then, the situation became more acute as the leadership thinned even further and as Goldman updated in November, only five firms – AMZN, GOOGL, MSFT, FB, and GE – totaling 9% of the equity cap of the index have accounted for more than 100% of the S&P 500 YTD return. Without these stocks the index would have posted a 220 bp lower total return or -2.2% YTD.

Of course, in the end, not even the thinning leadership was enough to offset the market being dragged down to a negative print, its first since 2008.

While all of the above should be well-known to regular readers, what may come as a surprise is that as go the markets, so go the movies.

According to the WSJ, Hollywood just had its biggest-ever year at the box office in 2015, collecting $11.1 billion in ticket sales, up 7% from the previous year and surpassing the record of $10.92 billion set in 2013. All of the growth, however, occurred at the top of the heap, or in other words, 2015 was a record year “thanks to a handful of blockbusters that left a whole lot of duds in the dust.”

‘Jurassic World,’ left, was one of 2015’s blockbusters, Disney’s

‘Tomorrowland’ was among the year’s costly disappointmentsBut the runaway success of “Star Wars: The Force Awakens” and “Jurassic World” raises questions about the overall health of the movie business. The problem: More films that don’t have the muscle to be megahits are struggling to attract any audience at all.

What may be also little known is that for every megahit like Star Wars there were countless just as expensive flops:

A startling number of big-budget movies bombed in 2015, proving that no amount of marketing can pull audiences into theaters at a time when Netflix queues are long and social media spreads word about a stinker in a heartbeat. The year’s costly disappointments included “Pan” and “Jupiter Ascending” from Time Warner Inc. ’s Warner Bros., “Fantastic Four” from 21st Century Fox ’s Twentieth Century Fox studio, Walt Disney Co. ’s “Tomorrowland,” and “Pixels” from Sony.

It wasn’t just a question of marketing: in 2015 eight movies failed to gross even $10 million despite full-fledged advertising campaigns, a record in recent years. In the past, spending $20 million or more to promote a film almost always guaranteed a respectable performance, said Chris Aronson, president of domestic distribution for Fox. But “there is no bottom anymore,” he said.

Another curious parallel: just like the middle class is disappearing in US society, so that staple of solidly profitable, if not blockbuster, 2nd tier movies is also on the extinction list: “worrisome to some in Hollywood is the disappearance of second-tier movies—those that aren’t blockbusters but are solidly profitable. Last year, 22 movies grossed between $100 million and $350 million domestically, down from 31 in 2014 and the fewest since 2006.”

“Gigantic hits are actually becoming more common and the midsize hits are becoming rarer,” said Adam Goodman, a producer and former film group president of Viacom Inc.’s Paramount Pictures.

In total, the WSJ calculates that the five most successful movies of 2015 grossed $2.47 billion, accounting for 22% of the year’s total box office. The previous high for the top five was $2.05 billion, or 19% of the overall take, in 2012.

And here comes the punchline: for the other 129 films released nationally last year, the results were anything but impressive. They brought in a collective $8.65 billion, the lowest total for non-top-five movies since 2008, when ticket prices were 14% lower.

In other words, just like in the stock market, a record high portion of Hollywood “gains”, or rather box office ticket sales, came from just five movies.

How to explain this curious schism?

Audiences have become “very binary” in their moviegoing choices, said Tom Rothman, chairman of Sony Pictures Entertainment’s motion picture business. “Either a film is relevant to them and penetrates the pop-cultural zeitgeist, in which case the upside is enormous, or it doesn’t rise to that level and they’re out altogether.”

“Many younger people no longer feel compelled to go to the movies as an activity in general,” said Sony’s Mr. Rothman. “Instead, they go to see a particular movie.”

One silver lining: overseas ticket sales, which rose an estimated 5% last year to $27.5 billion according to Rentrak, can help make up for losses at home. “Terminator: Genisys,” for instance, grossed $351 million internationally, compared with $90 million in the U.S. and Canada. But foreign box office more often exacerbates domestic trends. The top five domestic movies were all among the eight highest grossing internationally.

Consider this the movies’ equivalent of the “least dirty shirt” phenomenon in markets where foreign capital flows enter the US “just because.”

But what is most troubling for Hollywood is the evaporation of creativity and originality when it comes to box office success.

As they have for a number of years, sequels and reboots continued to rule the box office last year. The only exceptions that made the top 10 were animated features, such as Pixar Animation Studios’ “Inside Out,” and Fox’s surprise hit adaptation of best-selling book “The Martian.”

The trend toward sequels, reboots, computer-animated films and adaptations of comic books, toys or videogames is likely to accelerate in coming years as the major studios, increasingly focused on big-budget “event” movies they hope will become blockbuster hits, rely on formulas that have worked for them before.

This trend toward mindless recreation of a successful formula which has worked while undergoing minor tweaks will continue:

there were about 27 such films last year, and nearly 40 are scheduled for release this year and in 2017. Some of them are new installments of successful movie series like “X-Men” and “Fast and Furious” while others, such as “Wonder Woman” and “Ghostbusters” are attempts to create or refresh big-screen franchises.

The appropriate market analogy? Since nothing else is working, take the one thing that still does work, namely parasitic frontrunning of order flow by HFTs and make it better, faster, more profitable: in short – change HFTs technology from microwaves to lasers.

The only good news is that at least unlike the “market”, humans are at least still directly involved in the creation of movies. When algos start typing up movie scripts and participating in the obligatory sex scenes, that’s when Hollywood execs should quietly exit stage left.

- Spot The Difference: Salafist Edition

Earlier today, we highlighted comments from the Ayatollah who spoke out yesterday against the execution of prominent Shiite cleric Nimr al-Nimr.

The Sheikh was killed by the Saudis for his role in anti-government protests during the Arab Spring. His execution sent shockwaves across the Shiite world as protesters took to the streets from Bahrain to Pakistan in a dramatic outpouring of grief and anger.

On Saturday evening, protests in Tehran turned violent as Iranians firebombed and ransacked the Saudi embassy while police struggled to contain crowds near the consulate in Mashhad where the outcry continued on Sunday. Here’s an excerpt from a statement posted to the Ayatollah’s webpage:

“Strongly criticizing the silence of the self-proclaimed advocates of freedom, democracy and human rights, and their support for the Saudi regime, who spills the blood of the innocent only for criticism and protest, Ayatollah Khamenei said: “The Muslim world and the entire world must feel responsible towards this issue. Those who honestly care for the future of humanity and the fate of human rights and justice must pursue these issues and should not remain indifferent vis-à-vis this situation.”

This has become a familiar refrain of late. In short, it’s becoming difficult for the Western world to obscure the fact that the poisonous ideology espoused by the Saudis is virtually identical to that promoted and promulgated by ISIS, al-Qaeda, and many other Sunni extremist groups that the world at large generally identifies with terrorism.

As Kamel Daoud, a columnist for Quotidien d’Oran, and the author of “The Meursault Investigation” put it in an op-ed for The New York Times, Saudi Arabia is simply “an ISIS that made it.” On that note, we present a passage from Daoud’s article followed by an image posted by the Ayatollah on Saturday.

Black Daesh, white Daesh. The former slits throats, kills, stones, cuts off hands, destroys humanity’s common heritage and despises archaeology, women and non-Muslims. The latter is better dressed and neater but does the same things. The Islamic State; Saudi Arabia. In its struggle against terrorism, the West wages war on one, but shakes hands with the other. This is a mechanism of denial, and denial has a price: preserving the famous strategic alliance with Saudi Arabia at the risk of forgetting that the kingdom also relies on an alliance with a religious clergy that produces, legitimizes, spreads, preaches and defends Wahhabism, the ultra-puritanical form of Islam that Daesh feeds on.

And for good measure:

- Unmanageable Money: Hedge Funds Keep Losing (And Closing) – Why It Matters

Submitted by John Rubino via DollarCollapse.com,

How do you make money in a world where history is meaningless? The answer, for a growing number of big fund managers, is that you don’t.

Hedge funds, generally the most aggressive species of money manager, do a lot of “black box” trading in which bets are placed on previously-identified patterns and relationships on the assumption that those patterns will repeat in the future.

But with governments randomly buying stocks and bonds and bailing out/subsidizing everything is sight, old relationships are distorted and strategies that worked in the past begin to fail, as do the money managers who rely on them. A few recent examples:

Whitebox Closes Its Mutual Funds Ahead Of January Liquidation

(Value Walk) – Ending its foray into mutual funds, Whitebox Advisors LLC, said it has shuttered all three of its three mutual funds after poor results. According to Amara Kaiyalethe, a spokeswoman, the three mutual funds, which collectively held over $300 million, were closed on December 17th, and will be liquidated January 19th. She said the decision to close the mutual funds was related to performance and the concentration risk investors that remained in the funds faced as redemptions accelerated.

The Whitebox Tactical Opportunities Fund is the biggest among the three mutual funds, which less than two years ago managed over $1 billion, but tumbled by over 21% this year. The fund has suffered a rush of investors heading towards the exits. The fund managed about $240 million at the time it was closed.

Hedge Fund Lutetium Plans to Liquidate, Return Investor Cash

(Bloomberg) – Lutetium Capital LLC, a hedge-fund firm that invests in distressed securities, is liquidating its two credit funds and returning all of the money it was managing to investors by next month, according to co-founder Michael Carley.

The Stamford, Connecticut-based business told investors it would liquidate the funds in a letter last week following redemption requests from some of its clients and losses, Carley said. Investors in Lutetium’s liquid alternatives product had wanted their money back and the firm decided to liquidate its hedge fund holdings as well, he said.

“We returned capital to every one of our investors to treat all investors equally,” said Carley, the former co-head of distressed debt at UBS Group AG. The firm invested money from its liquid-alternatives fund and its hedge fund in the same debt securities, meaning that selling the holdings from one of the funds would likely push down the value of the assets in the other, Carley said.

The firm’s funds lost 4 percent this year, Carley said. Hedge funds that invest in distressed debt globally have lost an average of nearly 6.8 percent this year, according to data compiled by Bloomberg.

Bommer Is Returning Money From Hedge Fund SAB After 17 Years

(Bloomberg) – Scott Bommer, founder of SAB Capital Management LP, is returning all client money from his hedge fund after 17 years so that he can focus on managing his own wealth.

SAB Capital will return most money before mid January, Bommer said in an investor letter Tuesday, a copy of which was obtained by Bloomberg. The firm posted a 10.6 percent loss in the first eight months of the year in its SAB Overseas Fund, according to an investor document. Bommer started New York-based SAB Capital in 1998, and oversaw $1.1 billion as of the end of last year, according to a government filing.

Hirsch to Close Hedge Fund Seneca After Almost 20 Years

(Bloomberg) – Doug Hirsch, one of the founders of the Sohn Investment Conference, is returning money to clients from his hedge fund after almost 20 years.

Seneca Capital Investments, which managed about $500 million, is returning most capital by today, according to a client letter obtained by Bloomberg. Seneca, which made wagers on corporate events such as mergers, spinoffs and restructurings, a strategy called event-driven, said it lost 6 percent this year in its domestic fund.

The Year the Hedge-Fund Model Stalled on Main Street

(Wall Street Journal) – More “liquid alternative” mutual funds closed in 2015 than in any year on record, according to research firm Morningstar Inc., as inflows dwindled and performance weakened.

The results show that enthusiasm is fading for what had emerged in recent years as one of the hottest products in asset management—funds that combine hedge-fund strategies like shorting stock with the daily liquidity of mutual funds.

In all, 31 liquid-alternative funds have been closed this year, up from 22 a year earlier, according to Morningstar.

The host of funds liquidated this year included strategies run by J.P. Morgan Asset Management and Guggenheim Partners LLC. The closed funds were a range of unconstrained bond funds; managed future funds, which bet on futures contracts in a number of markets; and equity funds that bet on stocks rising and falling.

“You had so many funds that were launched in the last couple of years and hadn’t really been tested by market volatility and you’re starting to see the cracks in them,” said Jason Kephart, an analyst at Morningstar.

Fund companies aggressively pitched liquid-alternative products, saying they could help protect investors from volatility and offer better returns.

Assets in liquid-alternative funds grew to $310.33 billion at the end of 2014 from $124.44 billion at the end of 2010. But the inflows have slowed as performance faltered this year.

The average liquid-alternative fund was down 1.64% this year through the end of November, compared with losses of 0.38% for the average actively managed stock fund and 0.5% for the average actively managed bond fund. Just $85.1 million has flowed into liquid-alternative funds this year, down from $37.7 billion in 2014, according to Morningstar.

The MainStay Marketfield Fund, managed by Michael Aronstein, exemplifies the sector’s struggles. Started in 2007, MainStay Marketfield rose quickly to become the largest liquid-alternative mutual fund, with $21.5 billion of assets at its peak in February 2014, according to Morningstar. But the fund has been hit by poor performance and heavy withdrawals since then. It had $2.9 billion in assets at the end of November.

Why should regular people care about the travails of the leveraged speculating community? Because these guys are generally considered to be the finance world’s best and brightest, and if they can’t figure out what’s going on, no one can. And if no one can, then risky assets are no longer worth the attendant stress.

In response, a system that had previously embraced leverage and “alternative” asset classes will go risk-off in a heartbeat, and all those richly-priced growth stocks and trophy buildings and corporate bonds will find air pockets under their prices. And since pretty much everything else now depends on high asset prices, things will get ugly in the real world.

A case can be made that such a contagion is already underway but is being hidden from Americans by the recent strength of the dollar. According to Deutsche Bank, when measured in dollars the rest off the world is now deeply in recession and falling fast.

In other words, Main Street is vulnerable to leveraged trading algorithms and Brazilian bonds because it’s not just exotica that is overleveraged. Virtually all governments have to refinance trillions of short-term debt each year. Corporations have borrowed record amounts of money in this expansion (and wasted much of it on share buy-backs). Pension funds (the last remaining leg of the middle-class stool for millions of Americans) are grossly underfunded and will have to slash benefits if their portfolios decline from here.

Risk-off, in short, is no longer just a temporary swing of the pendulum, guaranteed to reverse in a year or two. As amazing as this sounds, we’ve borrowed so much money that as hedge funds go, so goes the world.

- "Now Is The Time To Stand Up": Armed Activists, Militiamen Seize Federal Wildlife Refuge Office In Oregon

On Saturday, militants seized a remote government outpost following a protest by hundreds of angry citizens.

That could very easily be the opening line for a story about a Mid-East country beset by civil war. Instead, it’s a description of what happened in Oregon yesterday.

It all started back in 2001 when Dwight Hammond and his son Steven set fire to leased government land in what they said was an effort to beat back invasive plant species and – ironically – prevent wildfires. They set more fires in 2006 and were later convicted of arson.

(the elder Hammond)

Both men served time in prison but a judge eventually determined that their sentences were too light and ordered them back to jail.

Some folks were displeased with the ruling and staged a protest that saw some 300 people march through Burns, a city of around 3,000. The procession made a stop by the Hammond residence and proceeded to make an appearance at the local sheriff’s office as well.

“As marchers reached the courthouse, they tossed hundreds of pennies at the locked door. Their message: civilians were buying back their government,” AP recounts. “A few blocks away, Hammond and his wife, Susan, greeted marchers, who planted flower bouquets in the snow [after which they] sang some songs, Hammond said a few words, and the protesters marched back to their cars.”

Enter Ammon Bundy.

Ammon is the son of Nevada rancher Cliven Bundy who famously clashed with the government last year after his cattle were kidnapped by the Feds. Around 400 of Cliven’s cows were busy grazing on land Bundy said he owned when the Bureau of Land Managment began to round them up and ship them off to a bovine internment camp at Bunkerville.

The government says the cattle were grazing on public rangeland, which is legal as long as the owner pays a fee. Bundy allegedly racked up some $1 million in such fees and so, the government decided to seize the cows, which the Nevada Bureau of Land Management accused of “trespassing.”

Evenutally, the cavalry arrived (literally) as cowboys rode in and broke the cows out of jail. No, really.

Fast forward to November and Bundy’s son Ammon was busy trying to come up with a way to keep Dwight Hammond and his son from going back to jail. “Ammon Bundy met with Dwight Hammond and his wife in November, seeking a way to keep the elderly rancher from having to surrender for prison,” The Oregonian writes, adding that “the Hammonds professed through their attorneys that they had no interest in ignoring the order to report for prison.”

But while the Hammonds have apparently come to terms with their fate, Bundy hasn’t and in a brazen move, he and an unspecified number of “outside militants” seized control of the Malheur Wildlife Refuge headquarters, which is a short drive from Burns (where the protest took place).

The federal outpost fell to the militants without a fight presumably because it was deserted for the holidays. Here’s more from the Oregonian:

“The facility has been the tool to do all the tyranny that has been placed upon the Hammonds,” Ammon Bundy said.

“We’re planning on staying here for years, absolutely,” he added. “This is not a decision we’ve made at the last minute.”

“The best possible outcome is that the ranchers that have been kicked out of the area, then they will come back and reclaim their land, and the wildlife refuge will be shut down forever and the federal government will relinquish such control,” he said. “What we’re doing is not rebellious. What we’re doing is in accordance with the Constitution, which is the supreme law of the land.”

“After the peaceful rally was completed today, a group of outside militants drove to the Malheur Wildlife Refuge, where they seized and occupied the refuge headquarters. A collective effort from multiple agencies is currently working on a solution. For the time being please stay away from that area. More information will be provided as it becomes available. Please maintain a peaceful and united front and allow us to work through this situation,” Harney County Sheriff Dave Ward said, in a statement. The elder Bundy weighed in as well, noting that the occuption isn’t “exactly what [he] thought should happen.” “But I didn’t know what to do,” he added. “You know, if the Hammonds wouldn’t stand, if the sheriff didn’t stand, then, you know, the people had to do something. And I guess this is what they did decide to do. I wasn’t in on that.”

Ammon Bundy explained the rationale for the occupation as follows:

Got that? This wildlife refuge office will become “a base place where patriots from all over the country will live and be housed.” Although from the looks of it, space is limited so reserve your spots now:

The Guardian apparently stopped by the refuge for a visit:

The occupation appears to have begun at about 2pm. Two hours later, the Guardian approached the refuge, which lies about 60 miles south of the town of Burns and is only accessible via a lakeside road slick with ice and banked with snow.

There were no law enforcement agents visible in the area around the refuge. A man with a goatee beard and wraparound sunglasses stood guard, armed with an AR-15-style rifle, and refused entry to the federally owned facility.

He declined to give his name or affiliation, citing “operational security”. He did confirm, however, that the men – several of whom were openly carrying assault weapons – would be camping on the site. “This public land belongs to ‘we the people’,” he said. “We’ll be here enjoying the snow and the scenery.”

This is as close as I was allowed to get to the armed militia occupying the Malheur Wildlife Refuge HQ. #burnsoregon pic.twitter.com/DPztu0VsVU

— Jason Wilson (@jason_a_w) January 3, 2016

The Guardian was allowed to take a few photographs, and then it was strongly advised to leave the scene. Within hours, police had descended on the remote corner of Harney county, blocking roads and urging members of the public to stay away.

Ammon Bundy, whose father became a folk hero among rightwing constitutionalists after his previous confrontation with federal authorities in Nevada, appeared to be a key figure.

He called for other likeminded US citizens to travel to the refuge in solidarity and to support what he said would be a symbolic showdown between impoverished farmers and overzealous federal authorities.

“We’re out here because the people have been abused long enough,” he said in a video interview posted on his Facebook page on Saturday night.

It isn’t entirely clear how these “patriots” plan to last “years” in the small building without supplies but that’s probably irrelevant because it’s difficult to imagine the oppressors in Washington will let this go on for very long. On that note, we’ll close with two quotes, one from The Oregonian and one from US Army veteran Ryan Payne who is among the occupiers.

From The Oregonian: “In phone interviews from inside the occupied building Saturday night, Ammon Bundy and his brother, Ryan Bundy, said they are not looking to hurt anyone. But they would not rule out violence if police tried to remove them, they said.”

From Payne: “When local and federal authorities arrive whatever else is going to happen will happen”.

- Why Silicon Valley May Be At "DEFCON 1" Status

For anyone not familiar with the term “DEFCON 1” it’s a military term used to identify the most sever military condition in the U.S. The degrees of severity range from “5” being the least severe or, at general peaceful conditions, and “1” representing the threat of imminent nuclear war. As I look out and extrapolate many of the warning signs that have been showing their hands over 2015 when it comes to everything “Silicon Valley.” I can’t help but use this military descriptor as an overlay of what’s taking place there currently. For I truly believe as I’ve written and spoken over these last 5 years – things are really about to hit the fan.

Over the last 5 years in “The Valley” (meaning everything representing tech and disrupting) there has been no other land of opportunity that lived, created, self defined, along with redefined its business metrics than the tech world. Unicorns, Non-GAAP, IPO’s, and more were the terms bandied or used to encapsulate what it was to be a “disrupter.”

Start a company (or idea) and make the rounds to get funded first – net profits are a trivial after thought. And for some they were an outright theory altogether. Then if you’re successful (i.e., you haven’t burned through all your start-up cash) turn your sagging or profitless business into a “We’re killing it!” fairy tale using Non-GAAP accounting. Once steps one and two are complete – IPO, cash out, and buy an island, yacht, McMansion, and more with the proceeds. Boom – done – next!!!

Yes the example is over-simplistic – but it’s not far off the mark. This has pretty much been the meme and/or state of business prevalent within the Valley for quite some time. However, as I’ve stated during all of that time; without the intervention of the Fed’s QE (quantitative easing) free money enabling risk taking to supersede business fundamentals to fund and fuel speculative investments in ways that mirror the dot-com days: there would be no “Valley” as it currently stands.

The amount of wasteful over investment on companies and ideas that should have never seen the light of a ledger book, let alone day, has been astounding. Billions upon Billions upon Billions (I could go on a billion more times) of $Dollars thrown at companies like it were water has been literally breathtaking. Need I remind you of WhatsApp™?

The only thing that challenged this sensation was the jaw-dropping rationales by nearly everyone involved in how, or why, it all made sense. And I mean everyone from the founders, investors, right down to the financial media et al. To say they’ve all been drinking the Kool-Aid® is being kind. Let me put a few things down for some context.

Uber™ for all intents and purposes; is an app that let’s you hail a cab. Current valuation? $50+ BILLION dollars looking to finance another round bringing it up to over $60 BILLION. The reaction, analysis and commentary? “Absolutely! Sounds logical and reasonable. After all They’re killing it!” Fair enough. I’ll just ask you this:

This business model and plan is worth more than 80% of all the companies listed in the S&P?

I mean maybe its’ me for here I am, myself, a once lowly card-carrying taxi driver. Does this now mean I surpassed all those other kids in school who dreamed of rocket science, and engineering to gain the ability as to then work at a predominant innovator? e.g., Lockheed Martin™ or Dow™ or Merck™. Little did anyone know in 2015 driving a car, not a rocket or science was the way to hang out with the stars. For when it comes to “innovative companies” do the numbers now lie? Or tell half truths? See what I mean.

This is just one of the myriad of examples currently contained within the “Unicorn” club for there’s still many more such as AirBnB™, Snapchat™, Dropbox™, Pintrest™ and over 100 others. Yet, there is another interesting data point that coincides with this currently heralded club.

Of the current 130+ that fall into this category (a valuation of $1 Billion or more) 60 of those were created in 2015 alone. To my eyes – that’s a glaring problem. Why? Well, think of it this way:

Nearly half of all the current unicorns that were/are praying, dreaming, and hoping for their day in the rainbow garden of IPO heaven with some big pay-out that was previously near-a-given when they gained their coveted title of recognition in 2015, are slowly waking up with a hangover from that Kool-Aid induced drunken stupor to a reality not based on the unicorn meme and metrics they were so drunk with. No: 2015 ended with a cold dose of reality with IPO letdowns, valuation markdowns, and a whole lot more putting many of these unicorn ambitions or dreams out to pasture. Some are now mulling around within an area that contains a building that ominously resembles a glue factory yet seem oblivious to the implications.

Another metric (as in inescapable reality) that is going to work against everything which previously “The Valley” hasn’t needed to contend with is the overarching result or knock-on effect that had yet occurred when the “free money” (QE) spigot was turned off but, as a direct consequence, and in combination with the raising of interest rates, may in fact push a global rush headlong into the $Dollar sending it skyward, causing balance sheets of companies around the globe into a complete an utter tizzy.

Some might think, “Oh, well that will only pertain if you’re a commodity company and such.” No, I’m sorry, it will influence far more sectors than just that. And the Valley is going to face this in ways just like many of the commodity producers have. A fact that for many have remained absolutely oblivious to. Or better yet; behave just like many are viewing that building at the edge of the unicorn meadow. Content to mull around under the watchful gaze of another animal friendly face (e.g., that of a bull) that adorns the building’s facade never contemplating for a moment the implications of the business contained within is called Elmer’s™.

If the $Dollar does indeed grow stronger from here it will add to the ever challenging issue of earnings reporting where revenue will take place front-and-center in a more pronounced way than ever before in the life of not only today’s Unicorn club – but the Valley as a whole.

User growth, eyeballs for dollars, and all the other metrics that were spun in a vortex of idiotic reasoning’s and rationales will not only not help – they’ll hurt if not outright maim any investor confidence if it’s coupled with the all but inevitable “foreign exchange conversion.” i.e., Had it not been for the $Dollar we would have made money rather than losing it.

Couple the $Dollar paradigm with another (now even more prevalent) “user growth was X coming in less than our projected Y” and you have a prescription for an investor revolt with a ticking time bomb laced with nuclear styled repercussions on your hands in my estimation. And that countdown clock has already started and is easily view-able as the first earnings season of 2016 is already making its presence known with an ever growing/worsening reporting of retailing metrics.

However, the $Dollar issues don’t stop there. They will fall even harder on companies that make things and sell them around the world. And, more importantly – buy the ads to sell them with.

Many advertisers will be hit with $Dollar issues to their own revenue sides of the ledger, and with that, all expenses will become more acute in their reasoning and rationale. And just like a company that needs to cut personnel to help bolster values. (i.e., send the Wall St. signal to buy, buy, buy) So to will ad expenditures fall into this same category. And with the holiday season now in the rear view mirror, just throwing money onto any and all platforms in a “hail Mary” fashion will no longer be expedient or allowed. And this will hit right at the heart of many of not only today’s Unicorns, but rather right at the bell-weathers such as Facebook™ and others.

If this happens the fallout will not be contained within the Valley itself in my estimation. It will be a global, all out nuclear winter in the ad space. How severe, and long is the only question.

So what does all this have to do with a comparison to something like a DEFCON 1 you maybe asking. Or, you might be thinking “That’s all a little hyperbolic” when talking about issues concerning Silicon Valley. Well, may be it is, yet, maybe it isn’t so far-fetched if you think about it using the following:

Back in September of 2014 I penned the following article titled “The Shot Heard Round The Valley World.” At that time my viewpoint on the issues I saw facing Unicorns and IPO’s was anathema to anything emanating not only from the Valley itself, but across all of the financial media. In that article I made the following statements:

“Problem is for a great many, they have never seen the real Jeckyll and Hyde personality of “investor funding.”

“IPO is not going to have the same term of endearment it now has. I believe it will turn into the last and most dreaded three-letter acronym no one ever imagined in Silicon Valley.”

There was more but, it was all predicated or inspired by tweet-storm unleashed at that time when Marc Andreessen ended his viewpoint about conditions within the space with the word “WORRY” too which I agreed was spot on. The resulting backlash to his argument took on rebuttals more in line with condescension rather than informed push-back in my opinion. And that viewpoint resumed with an attitude of retrenchment for much of 2015 rather, than viewing the unfolding reality objectively.

Yet, if I were to classify that period using the headline induced classification we were then at DEFCON 5. Over the subsequent 12 months we have moved progressively up the scale passing 4, and 3 jumping directly to 2 when the IPO’s of Square™ and Match™ showed the undeniable scary truth of the markets ending bewilderment of horns-over-hooves stampede to “get in-front of the IPO bandwagon.” But if that was “2” what causes a call of “1” you’re asking? Fair enough, for that happened just days ago.

It’s been reported or at least rumored to be that Peter Thiel and/or others are trying to cash out of Palantir™ (a current member in the Unicorn club) without an IPO. They cite many reasons and rationales why this may be good, bad or indifferent and that’s fine. However, I’m just going to throw this in for your own contemplation:

Do you think this argument, rational, or anything else resembling it would be taking place if we were still in a QE driven market circa mid 2014?

Welcome to DEFCON 1 is how I’m viewing it. For just this change in mindset with all the implications it can unleash within the Valley itself is enough to compound the impending fear of an all out debacle off the horizon – and straight into one’s own back yard.

And speaking of “back yard.” If anyone remembers, I also said not all that long ago you’ll know everything has changed when “I’m going to live in this shipping container till we IPO and then I’m going to get myself a McMansion!” looks more and more plausible that one might be looking at life as – living in a shipping container! This was in direct response to the current supposed craze of people opting to live out of metal storage containers in San Francisco as they pursued their IPO dreams.

Now with iconic Silicon Valley impresarios such as Theil or others being reported that they may be looking for ways as to NOT IPO rather that too? Those shipping containers may morph far faster than anyone previously thought straight into indefinite fallout shelters rather, than the start-up kits many view them as. For a nuclear winter pertaining to the world of Unicorns may be as “1” is said to represent: imminent.

- Meanwhile In Texas: Celebrating The New Open-Carry Gun Law

As reported previously, in addition to celebrating the new year, starting January 1, Texans also celebrated a new open-carry gun law which took effect in the new year. Handgun license holders in Texas will now be allowed to carry their guns in visible holsters on their hip or shoulder.

Previously, Texans wanting to carry a handgun had to obtain a concealed handgun license and conceal their weapon. With the new law, the more than 826,000 state license holders will be allowed to openly display their handguns in most public places.

Proponents of the new open carry law say making guns more visible will deter mass shootings. The bill became law after a spirited debate.

However, not everyone was in favor of the idea to discourage violence through demonstrating weapons: a majority of the state’s police chiefs opposed it.

“The question is: Does it make sense and is it good judgment to have a bunch of people running around with guns visible? And I think the answer is: Absolutely not,” said Chief Art Acevedo of Austin.

Others are for it: Perkins owns Dallas-based The Slow Bone, a barbecue spot, and Maple & Motor, which specializes in burgers. He says his weapon of choice is a Glock 43, and he frequently carries it in his front pocket. He doesn’t object to customers bringing concealed weapons into his restaurants.

“Carrying a concealed weapon is all about eventualities — things that might happen, and protection in that case,” he says. “There’s a lot of cash in my business. I have employees too. Restaurants get robbed, businesses get robbed, and I have employees that I would like to protect.”

“Carrying a gun outside, on your person where it’s visible, is at least an implied threat,” he says. “If deadly force is your final threat, you’re making it right away, visibly. … I just really don’t want that kind of threat feeling in either of the restaurants.”

Even with the new state legislation, the number of people with handgun permits makes up only about 4 percent of Texas’ population of more than 27 million. Out of these, Perkins thinks the number of people who want to openly carry weapons is pretty small.

Furthermore, private businesses are allowed to ban guns if they choose. In response, chains including Starbucks, Jack In The Box, Chili’s, Sonic and Chipotle have asked customers to leave weapons at home.

If private businesses want to prevent people from bringing weapons inside, they are required by the law to display a sign with 1-inch block lettering. Separate signs are required for banning open carry and concealed carry. Perkins says he plans to put one up, but he doesn’t foresee it causing any issues. “I don’t think it’s going to be a problem for us,” Perkins says. “I don’t think we’re going to have confrontations.”

Hopefully he is right and openly displayed weapons will indeed deter violence.

In the meantime Texans should get accustomed to sights such as this one which over the coming weeks and months will become increasingly recurring.

- Comcast, We Have a Problem

By EconMatters

The bigger news in the cable industry is that the U.S. Justice Department’s threat to block the purchase/merger of Comcast (NASDAQ: CMCSA) and Time Warner Cable (NYSE: TWC) did result in Comcast withdrawing its stock-swap proposal to acquire TWC in April, 2015. However, TWC soon afterwards entered into an agreement to be acquired by Charter Communications in May.

The Charter’s deals totaling $67.1 billion for TWC and Bright House Networks is still under review by Federal Regulators. If approved, that merger would create the country’s second-largest cable operator, with about 24 million customers in 41 states, after Comcast.

I personally think it is insane that anyone would even entertain the idea that a merger of any cable companies would be a good thing to consumers. On the surface, the cable industry is not entirely “consolidated”. Nonetheless, the fact is that almost all cable companies operate as de facto monopolies in the United States since frequently only one cable company offers cable service in a given community. Things have gotten worse as cable also has become one of the very few choices for residential Internet services.

For example, in Houston, the fourth most populous city in the nation, Comcast has a virtual monopoly over residential cable services. Leveraging its cable TV monopoly, Comcast is also the more popular choice for Internet service within the city (cable modem is supposed to have better speed than phone lines). With this kind of dominance, would any business strive to “innovate” or “improve the quality of customer service?

Comcast already had several widely reported customer service related scandals in 2014 and 2015 (there’s a whole section on Wikipedia). Since EconMatters is based in Houston, I will share some of my personal experience.

Before Comcast, Houston market was served by TWC. Then TWC and Comcast did a swap in 2006 so Comcast is now serving Houston cable TV. Although both have horrible customer service, Comcast is even worse due to the increasing complexity of service tiers and “billable” items requiring much higher skilled employees.

To sum it up, it seems a common cable industry practice to have a very cumbersome and “labor intensive” billing system coupled with poorly trained employees. EconMatters are made up of market analysts, so believe it when we say cable bills are hard to understand and reconcile. I almost think this is intentional so to kills two birds with one stone:

- Customers are less likely to call and dispute if they cannot make sense of a bill.

- Poorly trained employees not only serve as good “gatekeepers” to frustrate customers but also less likely to grant ‘disadvantageous” (to Comcast) adjustments regardless of the merit.

Due to various factors (moving, homeowner association change, etc.) at one time or another within the past 12 months, I had to go through a few rounds with Comcast either to correct billing errors or to properly reflect prices agreed upon over the phone. “Onerous” does not even begin to describe the process.

First, Comcast makes you jump through hoops to get to a live person, and Comcast outsources part of the Customer Call Center to places like Jamaica (there’s a serious frustrating communication issue here). This live customer service person serves as a gatekeeper that can only handle routine issues from a script. So discussing non-routine issues over the phone is very time-consuming, repetitive and frustrating exercise.

And get this, Comcast does not give email confirmation of what was agreed upon over the phone. I encountered a situation where I was triple assured everything was fully documented in my account (Comcast rep even gave me a “confirmation number”) and nothing to worry about since everything was noted. However, I later found out the so-called “documentation” or note consists of one sentence “Customer called to discussed pay service package”, so with nothing to go back on, I ended up repeating the same process again.

It takes about two months for any billing adjustments to appear on your account, so by the time you realize the expected adjustment fails to appear (like I said, most of Comcast employees I’ve encountered are poorly trained), two months would have gone by. Because Comcast does not give email confirmation or document properly what’s agreed on over the phone, you need to repeat the same process of explaining and diligently monitoring your account. At this stage, most of the customers would have given up.

EconMatters does not like to give up anything without a fight. In my experience, it took up to six months and very long (up to 1.5 hours) five phone calls escalated to the manager level to resolve one of the more complicated billing issues. And because of several issues taking place one after the other, it has become almost a full-time job to call, reconcile and monitor monthly bills to ensure everything goes as expected.

In addition to billing, Comcast has serious technical issues as well. I have made at least 5 trips to Comcast service centers swapping out cable boxes due to mal-function. Then, I got charged almost $250 for the technician visit that did not solve any problem. That ended up taking me 2 long phone calls and 3 months to get the credit back from Comcast.

This is where Comcast is penny wise, pound foolish. Yes, I can see how some brainy act at Comcast think they have a virtual monopoly and outsourcing customer service to Jamaica, saving employees training costs could be beneficial to the bottom line. What Comcast fails to see is that providing bad service in a service business means the days of the current business model are numbered. Brick and mortar companies such as Fidelity, Discover Card (NYSE: DFS), CitiCorp (NYSE: C), and TriEagle Energy are able to move with the latest consumer trend without sacrificing customer service. These companies understand customers should be the most important part of their business and a wide spread negative consumer response will be like a tsunami crushing the entire industry.

One thing for certain is that the core cable part of Comcast business is facing increasing downward pressure. It is no accident that 2015 is The year Wall Street Discovered Cord-Cutting. There’s a growing number of Americans either migrate to cheaper packages with fewer channel, watch shows via online services like Netflix (Nasdaq: NFLX), or drop cable altogether. This new cord-cutting consumer trend is killing the business model of an entire industry from cable providers to program producers. Disney (NYSE: DIS) sparked a panic sale of media stocks in August after revealing its ESPN sports network had lost subscribers and cutting its cable-TV outlook.

For 2015, Comcast stock seems to have held up better than some other media stocks. However, this is mostly due to Comcast’s entertainment properties like Universal Pictures that had a banner year with three films — Minions, Furious 7, and Jurassic World — exceeding $1 billion in global box office. In addition, the company experienced record attendance at its theme parks. That being said, movie and theme park business is quite cyclical, and it’s unrealistic to expect Universal and theme parks to come through for Comcast year after year as they did in 2015.

Comcast only acquired Universal NBC in 2006, and most likely retain the legacy operation model and talents. It is likely, or even already happening, that Comcast brings its failing cable operation model into the entertainment part of the business. Bad management believing in bad business model will take down any company regardless how lucrative it is going.

I think the only part of Comcast business that may have some customer-retention power is in the Internet Service. But companies like Google already saw that void and started its Google Fiber business. With consumers moving towards cord-cutting, and the line expansion like Google Fiber and other players, it is only a matter of time the entire cable industry could become obsolete real quick.

- Crude Oil Opens Above $38, Takes Out 1-Week Highs

With hedge fund short positions near record highs and speculators at their least bullish in almost five years, oil prices have spurted higher in the early trading as the diplomatic gloves come off in The Middle East. Despite record levels of crude inventory around the world, WTI Crude is trading above $38, up over 3% from its $37.07 close on New Year's Eve. Algos ran the stops above last week's highs ($38.32) but for now prices are not as excited as many would have expected. Brent, for now, is outperforming and trade 45c rich to WTI.

WTI tags last week's highs but is holding for now…

Some context – back to the early December inventory build levels…

As expected, Brent is outperforming – now trading 45c above WTI…

Hedge fund shorts near record highs may get hurt…

But don't forget that while a "war premium" makes sense in the marginal production barrel sense, with inventories at their limits amid a record glut, unless this escalates even more, the physical demand/supply divergence remains vast…

And of course, if oil prices are higher then US equity prices are higher because "lower oil prices are unequivocally good for America"… oh wait.

Source: Bloomberg

- Gail Tverberg: Something Has Got To Break

Submitted by Adam Taggart via PeakProsperity.com,

Actuary Gail Tverberg explains the tight correlation between the rates of GDP growth and growth in energy supply. For decades, energy has been becoming more costly to obtain, and instead of accepting lower GDP growth, we have been using debt to fund further energy exploration and extraction.

That strategy has diminishing returns, Tverberg warns. And we are close to the moment of reckoning:

The more we look at it the more we see that the rate of growth and energy supply is very closely correlated with the rate of GDP growth. And I know on some of my recent posts I’ve included a chart that goes back to 1820 that shows the same correlation. You have to have an increasing supply of energy in order to get GDP growth. The GDP growth tends to be a little higher than the energy growth. That’s especially the same when we made the change in the mid 70’s, when we had the big first oil crisis and we realized that Japan had already started making small cars, and so we could make smaller cars, too, and save quite a bit of oil very quickly. And we realized then that we didn’t have to burn oil to create electricity; there were a lot of other alternative approaches, including nuclear. So we pulled those off line, and where home heating had been done by oil it was easy to transfer that to other types of energy. So we had a number of different things we could do very quickly back then — and I think people got the idea that because we could pick the low-hanging fruit, then somehow or other we could do the same thing again. But we’re not getting that same kind of effect any more.

I think the thing that people don’t realize is how closely the growth in debt is tied to the growth in the economy. Even back many years ago we needed to add more debt as the economy attempted to grow, and what you would see very often back then was some country would add debt to fund a war. And if they were successful, maybe they would get some increment into the economy so that the debt made sense. And if they lost the war then somebody got their bonds written off. But what’s happened is that, as the cost of energy has gone up, especially since about the mid 70’s, the amount of debt required to find GDP growth has gone way, way up. And I think this is because it takes a given quantity of energy in terms of BTU’s or in terms of how far it can make a truck go — if it now costs a whole lot more to do that, we’re going to have to borrow a whole lot more money in order to make the whole system operate. We have a seen a spiraling of debt since the mid 70’s, and I think that’s very much related to the higher cost of energy since then.

That only works for a while. You can dial up your debt growth for a while but then you discover that debt growth has a lot of adverse effects. And one of the big ones is that it tends to funnel money to the wealthier class and take money away from the poor members of society.

I’m afraid what it means is that at some point there’s got to be a discontinuity. Something has got to break.

Click the play button below to listen to Chris' interview with Gail Tverberg (61m:03s):

- Saudi Arabia "Doesn't Care" If White House Angered As US Urges 'Ally' To Ease Tensions

Hours ago, in the latest sign that tensions between Riyadh and Tehran are set to spiral into a full blown diplomatic crisis of historic proportions, Saudi Foreign Minister Adel Al-Ahmad Al-Jubeir announced that the kingdom has cut diplomatic ties with the Iranians. The Iran mission was ordered to leave Saudi Arabia within 48 hours.

Al-Jubeir went on to accuse Iran of stoking sectarian violence in the region (a contention that represents the worst kind of hypocrisy) and suggested Riyadh may need to do more to counter the expansion of Iranian influence.

As we put it, this an exceptionally serious situation that could well mushroom into a direct conflict between the two countries which are already on opposite sides of multiple regional proxy wars.

Washington is caught in the middle. Saudi Arabia and the US have a “special” relationship that neither side is keen on damaging while the Obama administration has been walking on egg shells vis-a-vis the Iranians in order to ensure that the “historic” nuclear accord doesn’t end up falling apart in Obama’s last year in The White House.

On Sunday, Washington responded to Saudi Arabia’s decision to cut diplomatic ties with Iran by encouraging diplomatic engagement and calling for leaders throughout the region to take “affirmative steps” to reduce tensions, Reuters reports.