- Former CIA Boss and 4-Star General: U.S. Should Arm Al Qaeda

Former CIA boss and 4-star general David Petraeus – who still (believe it or not) holds a lot of sway in Washington – suggests we should arm Al Qaeda to fight ISIS.

He’s not alone …

As we’ve previously shown, other mainstream American figures support arming Al Qaeda … and ISIS.

The U.S. actually did knowingly support Al Qaeda in Libya. And also in Syria.

And we actually ARE supporting ISIS to some extent.

Truly, America’s foreign policy is insane.

- The Alarming Regularity of 6 and 7-Sigma Events Illustrates Why a Deep Understanding of Banker-Induced Fraud is a Necessity

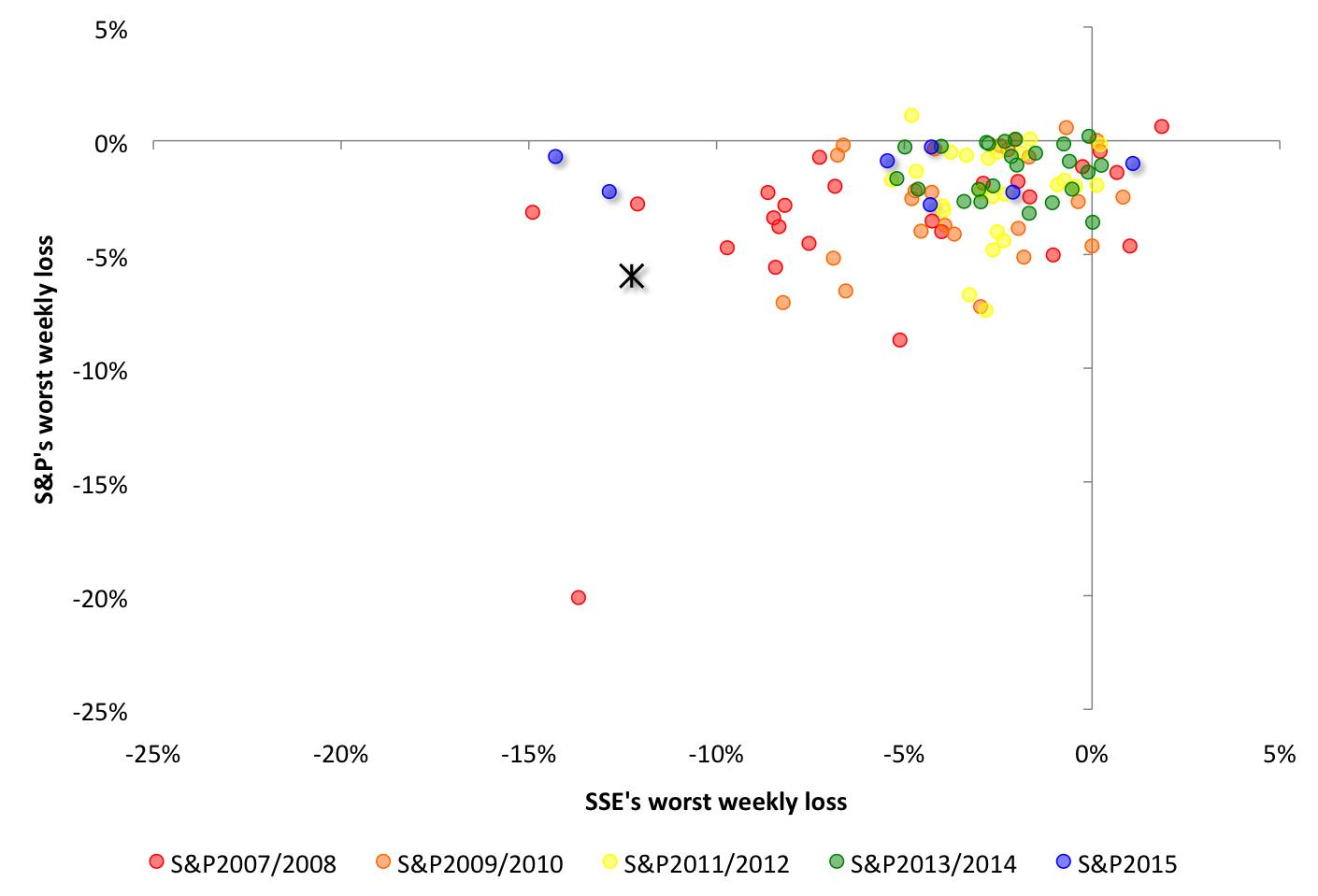

In today’s SmartKnowledgeU_Vlog_005, we discuss why an intelligent investment strategy is impossible without incorporation of market & banker fraud analysis, something that we have incorporated heavily into our strategies since we launched our company in mid-2007. Understanding market fraud allowed us to position our portfolio short the US stock market before the fall out occurred these past few weeks, as we even publicly posted this warning about an “imminent” US market collapse to our twitter account on 19 August, 2015, just one day before the US stock markets began free-falling.

In addition to shorting US markets and closing out positions at very quick and substantial gains, our understanding of banker pricing fraud in gold and silver futures markets also allowed us to short gold and silver into the US stock market free fall and quickly close out our short gold and short silver positions respectively for very quick +5.27% and +16.24% gains. In our latest vlog below, we discuss why understanding the meaning behind these 5, 6, 7, and even 16–sigma events that are occuring with alarming regularity in global financial markets has been critical to maintaining positive yields this year in the short-term, will be critical to maintaining strongly positive yields over the long-term, and is necessary in formulating intelligent low-risk strategies to cope with the massive asset and market volatility that we have been experiencing, and that will likely accelerate in future months.

to watch the above vlog, please click the image above

About the Vlogger: JS Kim is the Managing Director and Chief Investment Strategist of SmartKnowledgeU. His Crisis Investment Opportunities newsletter has respectively outperformed the Philadelphia Gold & Silver Index, the Australian ASX200, the London FTSE and the US S&P 500 by +125.53%, +76.92%, +69.07% and +27.63% (investment period from inception on 15 June, 2007 until present day on 2 September, 2015). For more information and access to our annual returns, please visit smartknowledgeu.com

- The Alarming Regularity of 6 and 7-Sigma Events Illustrates Why a Deep Understanding of Banker-Induced Fraud is a Necessity

In today’s SmartKnowledgeU_Vlog_005, we discuss why an intelligent investment strategy is impossible without incorporation of market& banker fraud analysis, something that we have incorporated heavily into our strategies since we launched our company in mid-2007. Understanding market fraud allowed us to position our portfolio short the US stock market before the fall out occurred these past few weeks, as we even publicly posted this warning about an “imminent” US market collapse to our twitter account on 19 August, 2015, just one day before the US stock markets began free-falling.

In addition to shorting US markets and closing out positions at very quick and substantial gains, our understanding of banker pricing fraud in gold and silver futures markets also allowed us to short gold and silver into the US stock market free fall and quickly close out our short gold and short silver positions respectively for very quick +5.27% and +16.24% gains. In our latest vlog below, we discuss why understanding the meaning behind these 5, 6, 7, and even 16–sigma events that are occuring with alarming regularity in global financial markets has been critical to maintaining positive yields this year in the short-term, will be critical to maintaining strongly positive yields over the long-term, and is necessary to intelligently formulating strategies to cope with the massive asset volatility that we have been experiencing and that will likely accelerate in future months.

to watch the above vlog, please click the image above

About the Vlogger: JS Kim is the Managing Director and Chief Investment Strategist of SmartKnowledgeU. His Crisis Investment Opportunities newsletter has respectively outperformed the Philadelphia Gold & Silver Index, the Australian ASX200, the London FTSE and the US S&P 500 by +125.53%, +76.92%, +69.07% and +27.63% (investment period from inception on 15 June, 2007 until present day on 2 September, 2015). For more information and access to our annual returns, please visit smartknowledgeu.com

- Sheep Led To The Slaughter: The Muzzling Of Free Speech In America

Submitted by John Whitehead via The Rutherford Institute,

“If the freedom of speech be taken away, then dumb and silent we may be led, like sheep to the slaughter.”—George Washington

The architects of the American police state must think we’re idiots.

With every passing day, we’re being moved further down the road towards a totalitarian society characterized by government censorship, violence, corruption, hypocrisy and intolerance, all packaged for our supposed benefit in the Orwellian doublespeak of national security, tolerance and so-called “government speech.”

Long gone are the days when advocates of free speech could prevail in a case such as Tinker v. Des Moines. Indeed, it’s been 50 years since 13-year-old Mary Beth Tinker was suspended for wearing a black armband to school in protest of the Vietnam War. In taking up her case, the U.S. Supreme Court declared that students do not “shed their constitutional rights to freedom of speech or expression at the schoolhouse gate.”

Were Tinker to make its way through the courts today, it would have to overcome the many hurdles being placed in the path of those attempting to voice sentiments that may be construed as unpopular, offensive, conspiratorial, violent, threatening or anti-government.

Consider, if you will, that the U.S. Supreme Court, historically a champion of the First Amendment, has declared that citizens can exercise their right to free speech everywhere it’s lawful—online, in social media, on a public sidewalk, etc.—as long as they don’t do so in front of the Court itself.

What is the rationale for upholding this ban on expressive activity on the Supreme Court plaza?

“Allowing demonstrations directed at the Court, on the Court’s own front terrace, would tend to yield the…impression…of a Court engaged with — and potentially vulnerable to — outside entreaties by the public.”

Translation: The appellate court that issued that particular ruling in Hodge v. Talkin actually wants us to believe that the Court is so impressionable that the justices could be swayed by the sight of a single man, civil rights activist Harold Hodge, standing alone and silent in the snow in a 20,000 square-foot space in front of the Supreme Court building wearing a small sign protesting the toll the police state is taking on the lives of black and Hispanic Americans.

My friends, we’re being played for fools.

The Supreme Court is not going to be swayed by you or me or Harold Hodge.

For that matter, the justices—all of whom hale from one of two Ivy League schools (Harvard or Yale) and most of whom are now millionaires and enjoy such rarefied privileges as lifetime employment, security details, ample vacations and travel perks—are anything but impartial.

If they are partial, it is to those with whom they are on intimate terms: with Corporate America and the governmental elite who answer to them, and they show their favor by investing in their businesses, socializing at their events, and generally marching in lockstep with their values and desires in and out of the courtroom.

To suggest that Harold Hodge, standing in front of the Supreme Court building on a day when the Court was not in session hearing arguments or issuing rulings, is a threat to the Court’s neutrality, while their dalliances with Corporate America is not, is utter hypocrisy.

Making matters worse, the Supreme Court has the effrontery to suggest that the government can discriminate freely against First Amendment activity that takes place within a government forum. Justifying such discrimination as “government speech,” the Court ruled that the Texas Dept. of Motor Vehicles could refuse to issue specialty license plate designs featuring a Confederate battle flag because it was offensive.

If it were just the courts suppressing free speech, that would be one thing to worry about, but First Amendment activities are being pummeled, punched, kicked, choked, chained and generally gagged all across the country.

The reasons for such censorship vary widely from political correctness, safety concerns and bullying to national security and hate crimes but the end result remains the same: the complete eradication of what Benjamin Franklin referred to as the “principal pillar of a free government.”

Officials at the University of Tennessee, for instance, recently introduced an Orwellian policy that would prohibit students from using gender specific pronouns and be more inclusive by using gender “neutral” pronouns such as ze, hir, zir, xe, xem and xyr, rather than he, she, him or her.

On many college campuses, declaring that “America is the land of opportunity” or asking someone “Where were you born?” are now considered microaggressions, “small actions or word choices that seem on their face to have no malicious intent but that are thought of as a kind of violence nonetheless.” Trigger warnings are also being used to alert students to any material or ideas they might read, see or hear that might upset them.

More than 50 percent of the nation’s colleges, including Boston University, Harvard University, Columbia University and Georgetown University, subscribe to “red light” speech policies that restrict or ban so-called offensive speech, or limit speakers to designated areas on campus. The campus climate has become so hypersensitive that comedians such as Chris Rock and Jerry Seinfeld refuse to perform stand-up routines to college crowds anymore.

What we are witnessing is an environment in which political correctness has given rise to “vindictive protectiveness,” a term coined by social psychologist Jonathan Haidt and educational First Amendment activist Greg Lukianoff. It refers to a society in which “everyone must think twice before speaking up, lest they face charges of insensitivity, aggression or worse.”

This is particularly evident in the public schools where students are insulated from anything—words, ideas and images—that might create unease or offense. For instance, the thought police at schools in Charleston, South Carolina, have instituted a ban on displaying the Confederate flag on clothing, jewelry and even cars on campus.

Added to this is a growing list of programs, policies, laws and cultural taboos that defy the First Amendment’s safeguards for expressive speech and activity. Yet as First Amendment scholar Robert Richards points out, “The categories of speech that fall outside of [the First Amendment’s] protection are obscenity, child pornography, defamation, incitement to violence and true threats of violence. Even in those categories, there are tests that have to be met in order for the speech to be illegal. Beyond that, we are free to speak.”

Technically, Richards is correct. On paper, we are free to speak.

In reality, however, we are only as free to speak as a government official may allow.

Free speech zones, bubble zones, trespass zones, anti-bullying legislation, zero tolerance policies, hate crime laws and a host of other legalistic maladies dreamed up by politicians and prosecutors have conspired to corrode our core freedoms.

As a result, we are no longer a nation of constitutional purists for whom the Bill of Rights serves as the ultimate authority. As I make clear in my book Battlefield America: The War on the American People, we have litigated and legislated our way into a new governmental framework where the dictates of petty bureaucrats carry greater weight than the inalienable rights of the citizenry.

It may seem trivial to be debating the merits of free speech at a time when unarmed citizens are being shot, stripped, searched, choked, beaten and tasered by police for little more than daring to frown, smile, question, challenge an order, or just breathe.

However, while the First Amendment provides no tangible protection against a gun wielded by a government agent, nor will it save you from being wrongly arrested or illegally searched, or having your property seized in order to fatten the wallets of government agencies, without the First Amendment, we are utterly helpless.

It’s not just about the right to speak freely, or pray freely, or assemble freely, or petition the government for a redress of grievances, or have a free press. The unspoken freedom enshrined in the First Amendment is the right to think freely and openly debate issues without being muzzled or treated like a criminal.

Just as surveillance has been shown to “stifle and smother dissent, keeping a populace cowed by fear,” government censorship gives rise to self-censorship, breeds compliance and makes independent thought all but impossible.

In the end, censorship and political correctness not only produce people that cannot speak for themselves but also people who cannot think for themselves. And a citizenry that can’t think for itself is a citizenry that will neither rebel against the government’s dictates nor revolt against the government’s tyranny.

The end result: a nation of sheep who willingly line up for the slaughterhouse.

The cluttered cultural American landscape today is one in which people are so distracted by the military-surveillance-entertainment complex that critical thinkers are in the minority and frank, unfiltered, uncensored speech is considered uncivil, uncouth and unacceptable.

That’s the point, of course.

The architects, engineers and lever-pullers who run the American police state want us to remain deaf, dumb and silent. They want our children raised on a vapid diet of utter nonsense, where common sense is in short supply and the only viewpoint that matters is the government’s.

We are becoming a nation of idiots, encouraged to spout political drivel and little else.

In so doing, we have adopted the lexicon of Newspeak, the official language of George Orwell’s fictional Oceania, which was “designed not to extend but to diminish the range of thought.” As Orwell explained in 1984, “The purpose of Newspeak was not only to provide a medium of expression for the world-view and mental habits proper to the devotees of IngSoc [the state ideology of Oceania], but to make all other modes of thought impossible.”

If Orwell envisioned the future as a boot stamping on a human face, a fair representation of our present day might well be a muzzle on that same human face.

If we’re to have any hope for the future, it will rest with those ill-mannered, bad-tempered, uncivil, discourteous few who are disenchanted enough with the status quo to tell the government to go to hell using every nonviolent means available.

However, as Orwell warned, you cannot become conscious until you rebel.

- It's The Fed, Stupid; Why Kuroda And Draghi Are No Match For Quantitative Tightening

Earlier today, Deutsche Bank – who last week won the sellside race to coin a new term for the unfolding EM FX reserve unwind – took a close look at the end of the “Great Accumulation” and what it means for asset prices and DM monetary policy going forward. Here was Deutsche Bank’s “profound” takeaway:

Less reserve accumulation should put secular upward pressure on both global fixed income yields and the USD. Many studies have found that reserve buying has reduced both bund and US treasury yields by more than 100bps.

Declining FX reserves should place upward pressure on developed market yields given that the bulk of reserves are allocated to fixed income.

This force is likely to be a persistent headwind towards developed market central banks’ exit from unconventional policy in coming years, representing an additional source of uncertainty in the global economy. The path to “normalization” will likely remain slow and fraught with difficulty.

But that, as it turns out, is not all.

As you might imagine, EM capital flows have tracked the Fed, BOJ, and the ECB’s balance sheets quite closely (albeit with a lead) in the post-crisis, QE-dominated world.

What’s interesting however, is that there now appears to be a disconnect:

What accounts for that, you ask? Well, according to DB (and this isn’t exactly surprising) the simple fact is that EM inflows/outflows are far more dependent on the Fed than they are on the BOJ and ECB and that means that a dovish Kuroda and Draghi will be no match for an even semi-hawkish Fed and that could be very bad news for EM flows considering how far ahead the Fed is in terms of approaching a rate hike cycle and considering, as we noted earlier, that DB’s previous answer to the EM FX reserve liquidation quandary was that perhaps “other central banks [will] come in to fill the gap that the PBoC is leaving [as] China’s QT would need to be replaced by higher QE elsewhere, with the ECB and BoJ being the most notable candidates”. From DB:

Given the reliance of EM reserves on QE-enabled financial flows since the 2008 crisis, the speed of reversal should be a key driver of reserves trends going forward. EM capital flows have indeed had a strong relationship with G3 central bank balance sheet growth with a two-quarter lead (Figure 15), given that market pricing anticipates shifts in QE. Projecting G3 balance sheet trends thus offers some clues. In our most hawkish scenario, the Fed stops reinvestment by mid- 2016 and the ECB and BoJ stop QE by September and December 2016, respectively. A more dovish scenario might see the Fed reinvesting ad infinitum and the ECB and BoJ extending QE purchases until end-2017.

Worryingly, EM capital flows are already significantly undershooting the projection from the hawkish scenario. A constructive take on this would be that EM outflows have overreacted and could give way to inflows again as global liquidity conditions remain more accommodative than feared. The less constructive view is that the Fed balance sheet simply matters far more for EM, with liquidity provided by the ECB and BoJ a poor compensation for the Fed’s retrenchment. Indeed, Figure 16 suggests this to be the case, with EM flows tracking the fall in Fed balance sheet growth closely of late. The hawkish scenario of Fed stopping reinvestment next year would suggest that EM flows can get weaker, while even a more dovish scenario of a constant Fed balance sheet would not be enough to lift inflows again.

In other words, even under DB’s dovish scenario for the Fed, in which Yellen reinvests the proceeds from maturing securities forever, EM capital flows will likely remain negative, putting perpetual pressure on FX reserves. And as should be abundantly clear by now, perpetual pressure on FX reserves means the unwind of the “Great EM Accumulation” continues unabated until either the Fed launches QE4 or else stands by while the world’s emerging economies burn through their cushions and careen into crisis.

Finally – as noted earlier in “ABN Amro Warns There Is A 40% Chance Mario Draghi Expands ECB QE As Soon As This Week” – while we agree with ABN that the ECB may indeed boost QE in a rerun of what the BOJ did in the great Halloween massacre of 2014, it would be largely a non-event, as the ECB biggest limitation remains the availability of monetizable assets. As such, any real monetary offset to the Reverse QE that is about to be unleashed now that the “Great Accumulation” is over, is and will always be the Fed. For a quick explanation of this, re-read “Why QE4 Is Inevitable.“

- Circling The Drain….

CIRCLING THE DRAIN:

So last weeks turmoil is seemingly not over yet…..Was it simply a storm in a teacup brought on by another one of those market tantrums that erupt every now and again to keep everyone on their toes and eventually evaporate? Or was it a significant tremor giving pre warning of a major earthquake to follow?

WAX ON WAX OFF;

Historically September and October are not very good months for stocks and there are fundamental arguments for both sides.

Historically September and October are not very good months for stocks and there are fundamental arguments for both sides.The fact is that there is a lot more to worry about than to be confident of.

There are clearly real concerns both internally and externally that the China’s growth rate is running at closer to 5% than 7%, Brazil and Russia are in recession,

Emerging market countries are suffering massive capital outflows and are burdened with huge dollar debts, Abenomics is not delivering inflation in Japan, the Eurozone is an invalid, Greece is a month away from another potential exit crisis, Europe faces a migrant crisis and the Middle East is unstable.

There is plenty of reason to be concerned especially when the global economy is in the anaemic state it is despite a zero interest rate environment and huge injections of QE. At the height of last week’s crisis the proposed responses if the rout continued were for more of the same — QE in China to be added to more QE in Japan and Europe. There was even a suggestion from the president of the Minneapolis Fed that the week’s developments potentially justified “adding accommodation”. All this despite evidence that the impact of each new injection is diminishing and creating side effects that are sowing the seeds of the next financial crisis.

THE CHARTS DON’T LIE

We broke ,we rallied to the multi year trend line and now we have retreated again…..

Weekly S&P chart:

You really dont need to be a rocket scientist;

What I have not liked from the recent move is that the fixed income market that one would expect to flatten from his point has if fact steepened…this has been down to apparent Chinese liquidation of treasury positions;

What I have not liked from the recent move is that the fixed income market that one would expect to flatten from his point has if fact steepened…this has been down to apparent Chinese liquidation of treasury positions;YIELDS UP / STOCKS DOWN……

With everything for sale…the next 2 months could be quite hairy

In regards to more detailed and expert options and futures advice ,volatility analysis etc ,please contact Darren Krett,Bryan Fitzgerald or John Haden through www.maunaki.com or dkrett@maunaki.com

“Futures and options trading involves substantial risk and is not for everyone. Such investments may not be appropriate for the recipient. The valuation of futures and options may fluctuate, and, as a result, clients may lose more than their original investment. Nothing contained in this message may be construed as an express or an implied promise, guarantee or implication by, of, or from Mauna Kea Investments LLC. that you will profit or that losses can or will be limited in any manner whatsoever. Past performance is not necessarily indicative of future results. Although care has been taken to assure the accuracy, completeness and reliability of the information contained herein, Mauna Kea Investments LLC makes no warranty, express or implied, or assumes any legal liability or responsibility for the accuracy, completeness, reliability or usefulness of any information, product, service or process disclosed.”

- The Myth Of A Russian 'Threat'

Authored by Pepe Escobar, originally posted at SputnikNews.com,

Not a week goes by without the Pentagon carping about an ominous Russian "threat".

Chairman of the Joint Chiefs of Staff Martin Dempsey entered certified Donald “known unknown” Rumsfeld territory when he recently tried to conceptualize the “threat”; “Threats are the combination, or the aggregate, of capabilities and intentions. Let me set aside for the moment, intentions, because I don’t know what Russia intends.”

So Dempsey admits he does not know what he’s talking about. What he seems to know is that Russia is a “threat” anyway — in space, cyber space, ground-based cruise missiles, submarines.

And most of all, a threat to NATO; “One of the things that Russia does seem to do is either discredit, or even more ominously, create the conditions for the failure of NATO.”

So Russia “does seem” to discredit an already self-discredited NATO. That’s not much of a “threat”.

All these rhetorical games take place while NATO “does seem” to get ready for a direct confrontation with Russia. And make no mistake; Moscow does view NATO’s belligerence as a real threat.

It’s PGS vs. S-500

The “threat” surge happens just as US Think Tankland recharges the notion of containment of Russia. Notorious CIA front Stratfor has peddled a propaganda piece praising Cold War mastermind George Kennan as the author of the “containment of Russia” policy.The US intel apparatus don’t do irony; before he died, Kennan said it was now the US that had to be contained, not Russia.Containment of Russia – via the expansion of the EU and NATO — has always been a work in progress because the geopolitical imperative has always been the same; as Dr. Zbigniew “The Grand Chessboard” Brzezinski never tired of stressing, it was always about preventing the – threatening — emergence of a Eurasian power capable of challenging the US.Ultimately, the notion of “containment” can be stretched out towards the dismantling of Russia itself. It also carries the inbuilt paradox that NATO’s infinite expansion eastwards has made Eastern Europe less, not more, safe.Assuming there would even be a lethal Russia-NATO confrontation, Russian tactical nuclear weapons would knock out all NATO airports in less than twenty minutes. Dempsey – cryptically – admits as much.

What he cannot possibly admit is if a decision had been made in Washington, a long time ago, preventing NATO’s infinite expansion, Russia’s concerted move to upgrade its nuclear weapon arsenal would have been unnecessary.

Geopolitically, the Pentagon has finally seen which way the – strategic partnership – wind is blowing; towards Russia-China. This major game-changing shift in the global balance of power also translates as the combined military assets of China and Russia exceeding NATO’s.

In terms of military power Russia has superior offensive and defensive missiles over the US, with the new generation surface-to-air missile system, the S-500, capable of intercepting supersonic targets and totally sealing Russian airspace.

Moreover, despite short-term financial turbulence, the Sino-Russian combined strategy for Eurasia – an interpenetration of the New Silk Road(s) and the Eurasian Economic Union (EEU) – is bound to develop their economies and the region at large to an extent that may surpass the EU and the US combined by 2030.

What’s left for NATO is to stage military strength made-for-TV shows such as “Atlantic Resolve” to “reassure the region”, especially hysteria-prone Poland and the Baltics.

Moscow, meanwhile, has made it clear that nations deploying US-owned anti-ballistic missile systems in their territory will face missile early-warning systems deployed in Kaliningrad.

And Major General Kirill Makarov, Russia’s Aerospace Defense Forces’ deputy chief, has already made it clear Moscow is upgrading its air and missile defense capabilities to smash any – real — threat by the US Prompt Global Strike (PGS).

In the December 2014 Russian military doctrine, NATO’s military build-up and PGS are listed as Russia’s top security threats. Deputy Defense Minister Yuri Borisov has stressed, “Russia is capable of and will have to develop a system like PGS.”

Where’s our loot?

The Pentagon’s rhetorical games also serve to mask a real high-stakes process; essentially an energy war – centering on the control of oil, natural gas and mineral resources of Russia and Central Asia. Will this wealth be controlled by oligarch frontmen “supervised” by their masters in New York and London, or by Russia and its Central Asian partners? Thus the relentless propaganda war.

A case can be made that the Masters of the Universe have resurrected the same old containment/threat geopolitical alibis – peddled by what we could dub the Brzezinski/Stratfor connection — to cover, or conceal, another stark fact.

And the fact is that the real reason for Cold War 2.0 is New York/London financial power suffering a trillion dollar-plus loss when President Putin extracted Russia from their looting schemes.

And the same applies to the entire Kiev coup — forced through by the same New York/London financial powers to block Putin from destroying their looting operations in Ukraine (which, by the way, proceed unabated, at least in the agricultural domain).

Containment/threat is also deployed on overdrive to prevent by all means a strategic partnership between Russia and Germany – which the Brzezinski/Stratfor connection sees as an existential threat to the US.

The connection’s wet dreams – shared, incidentally, by the neo-cons – would be a glorious return to the looting phase of Russia in the 1990s, when the Russian industrial-military complex had collapsed and the West was plundering natural resources to Kingdom Come.

It’s not going to happen ever again. So what’s the Pentagon Plan B? To create the conditions of turning Europe into a potential theater of nuclear war. Now that’s a real threat – if there ever was one.

- Chinese Stocks Open Down Hard As PBOC Strengthens Yuan By Most Since 2010 & Default Risk Hits 2-Year High

From the moment Japan opened, USDJPY buying took off (standard 100 pip rip on absolutely no news whatsoever) as yet another manipulated market breathed new life into equity longs dreams. That 'help' combined with the fact that, as SCMP's George Chen reports, 50 China brokerages will jointly contribute 100 bln RMB capital to the government margin finance agency to start "new round of market rescue" provided some stability after US markets' collapse. However, tonight's big news appears to be a major crackdown on leverage as MNI notes regulators ordering brokerage houses to clear all non-official margin trading services – not just halting new clients but also closing existing accounts. Chinese stocks are opening modestly lower as PBOC fixes Yuan stronger for the 4th day in a row. Finally, China credit risk has spiked to 2-year highs as traders increase positions dramatically. The manipulation will continue through tomorrow at least when Parade Week peaks, so buckle up.

Japan "rescued"… "Mysterious"? – Large USD/JPY Buyer Seen Before Nikkei Index Opened: Traders

China "Stability?"

Though some weakness at the Chinese open:

- *FTSE CHINA A50 SEPT. FUTURES DROP 0.7% IN SINGAPORE

- *CHINA'S CSI 300 STOCK-INDEX FUTURES FALL 2.2% TO 2,939.8

- *SHANGHAI COMPOSITE INDEX SET TO OPEN 4.4% LOWER

And then PBOC Strengthens Yuan:

- *CHINA SETS YUAN REFERENCE RATE AT 6.3619 AGAINST U.S. DOLLAR

- *CHINA RAISES YUAN REFERENCE RATE FOR FOURTH DAY

And loses controil of money markets:

- *CHINA OVERNIGHT MONEY-MARKET RATE RISES 18 BPS TO 2%

This is the biggest 4-day strengthening in 5 years!

But tonight's big news appears be a major clampdown on margin trading (as MNI reports),

China's stock market regulator has issued a circular ordering brokerage houses to clear all non-official margin trading services jointly provided with a third party — not just halting new clients but also closing existing accounts.

Chinese brokerage houses were allowed to offer margin trading services in 2010 but strong stock market performance since last year saw many third parties also providing margin trading services with help from brokerage houses. Beijing realized the potential threat of these fast-growing margin trading services, particularly unofficial ones, and started to push for market deleveraging in late-June this year, contributing to the stock market rout which saw Shanghai Composite Index lose nearly 40% since.

Even as margin debt drops to a fresh 9-month low…

- *SHANGHAI MARGIN DEBT BALANCE FALLS FOR 11TH STRAIGHT DAY

The very same brokerages that are seeing executives detained and are being told to shut down margin trading have also provided funds for rescuing the

governmentmarket…Chinese brokerage houses are providing more funds to the China Securities Finance Corp for stock market intervention.

Many listed brokerage houses issued statements last night saying they were giving no more than 20% of their net assets to CSFC, which will use the money to set up a special account for investment in blue chip stocks. These firms include CITIC Securities, which said it's giving another CNY5.4 billion to CSFC. CITIC Securities is at the center of a regulatory storm as many of its senior executives are being investigated by police and Chinese investors have been questioning if CITIC was a key player among short sellers that caused the recent stock market rout.

Besides CITIC, several other brokerage houses which are contributing new funds to CSFC, have also said they are being investigated by the stock market regulator.

Followed by more talk..

- *CHINA EXPORTS MAY RISE 2% IN 2015; IMPORTS SEEN DOWN 10%: NEWS

- *CHINA HAS ROOM FOR FURTHER RATES, RRR CUTS: SECURITIES NEWS

- *CHINA SHOULD MAKE FUND TO SUPPORT SMALL CO. MARKET-ORIENTED: LI

- *CHINA PREMIER LI KEQIANG COMMENTS ON 60B YUAN SMALL CO. FUND

Then – now that China is flush with cash again apparently, it decided to help out Venezuela…

- *VENEZUELA SIGNS $5B LOAN W/CHINA TO BOOST OIL PRODUCTION:MADURO

But, not everyone is happy, as Bloomberg reports,

China-focused hedge funds probably had their worst month in almost 16 years in August, with firms including Orchid Asia Group Management and APS Asset Management Pte suffering losses from the nation’s stock market collapse.

“Greater China hedge funds are on track to show the worst three month returns in at least a decade,” said Mohammad Hassan, an analyst with Eurekahedge in Singapore. “It’s not a surprise given the funds’ limited ability to short the stock markets in China.”

And finally, it appears traders are hedging China credit risk in size…

Open positions in China’s credit-default swaps increased by 212 contracts to 9,444 in the week ended Aug. 28, according to latest data from DTCC.

That’s the biggest increase among global sovereign CDS; gross notional amount rose $1.31b last week

Among Asian sovereigns, South Korea’s CDS had second-biggest increase in positions last week, with outstanding amount up 137 contracts, or $1.10b in gross notional value

Charts: Bloomberg

- Macroeconomics Is The Root Of All Error

Submitted by Bill Frezza via The Daily Caller,

Will Fed chief Janet Yellen pull the trigger to raise interest rates in September or not? Only the soothsayers at Jackson Hole know for sure. But while the world awaits the decision, ponder this. What do the following have in common?

- Asset bubbles fueled by monetary policy.

- Unsustainable sovereign debts threatening government bankruptcies.

- Government economic “cures” worse than the diseases they are supposed to treat.

- Questionable GDP statistics.

- Recurring bank bailouts.

Figured it out yet? They are all driven by an overweening state religion called macroeconomics.

Friedrich Hayek said it best. “The curious task of economics is to demonstrate to men how little they really know about what they imagine they can design.”

A pity this simple, yet profound insight remains at the fringes of a field that continues to wreak havoc in the hands of those who imagine they can design economic outcomes.

Think about it. We are currently watching global stock markets gyrate toward breakdown trying to anticipate the whims of a cloistered professor who never launched a business, never met a payroll, never shipped a product, and never won an election, yet has been empowered to determine the price of money. What’s even stranger is that people consider this normal. Ask yourself: Why do we wait on pins and needles for Janet Yellen to set interest rates yet laugh at the idea that kings once set the “just price” for a loaf of bread?

That’s where Hayek’s curious task comes in.

The human inclination to seek order in a seemingly chaotic world has long been exploited by generations of pundits, professors, and politicians eager to convince us they can impart certainty to the unknowable.

Note that I say the unknowable, not the unknown. Science has proven quite adept at exploring the unknown. That’s because as science progresses, falsifiable hypotheses that fail to make accurate predictions get discarded in favor of alternatives that do. No so in macroeconomics, whose prognostications bear an uncanny resemblance to predicting the nature of the afterlife. Rather than make continuous progress, the same discredited macroeconomic theories tend to cycle in and out of fashion depending on which court economists have the upper hand at any given time.

One cannot perform controlled macroeconomic experiments because “the economy” is not a measurable thing, like the weight of a stone or the strength of an electric field. It is merely the name we give to billions of transactions that take place across the planet, each driven by decisions made by independent actors optimizing their own well being according to their own criteria. These criteria cannot even be articulated by many of the players themselves, much less known to a third party pretending omniscience. Undeterred, practitioners of the black arts conjure up aggregates like “GDP” or “CPI,” but any honest examination of these metrics quickly leads to the conclusion that they are nothing more than political fictions that can be manipulated to suit the policy proclivities of the moment.

Macroeconomists use GDP to characterize billions of economic transactions, supposedly like a physicist uses temperature to characterize the average kinetic energy of gas molecules as they bump into each other in the atmosphere. They come up with equations linking the velocity and quantity of money to the inflation rate, or the inflation rate to the unemployment rate, designed to look like the ideal gas law PV = nRT. This fools many people into believing these soothsayers are doing science.

But gas molecules are not willful. They don’t have hopes and fears, friends and enemies, retirement savings and mortgage payments. Gas molecules don’t change their behavior when you tell them what their temperature is. The idea that you can write equations to accurately capture complex human behaviors, and then develop policies based on these equations aimed at controlling those behaviors, is what Hayek called the Fatal Conceit.

Macroeconomics reigns in the realm of the unknowable promising that which cannot be delivered to the eager to be deceived, benefitting an entrenched priesthood and the potentates they serve. Its cloaking in mathematics, rather than music and incense, gives it the requisite air of mystery to discourage questioning the guidance of its anointed sages and prophets. Unless and until we acknowledge that what these people are practicing is a religion and not a science, we will remain in its obscurantist thrall.

When scientific laws consistently fail to make accurate predictions, we throw the laws away. What happens when predictions about the impact of macroeconomic interventions fail, such as the inability of quantitative easing to deliver anything like the results promised? There is always a macroeconomist standing by to claim “we didn’t do enough.” And so the answer to every policy failure is: “Give Us Moar!”

Thus, the goal of reformists cannot be to simply replace one set of grandees with another, but to throw the Church of Macroeconomics out of the Overton Window, so it can pass into history alongside phrenology, phlogiston, and luminiferous aether.

- Wondering Why Dow Futures Just Spiked Over 100 Points?

Wonder no more…

Get back to work Mr. Kuroda…

But remember – it’s Chinese stocks that are “manipulated” – that is all.

Charts: Bloomberg

- "If I Don't Come Home, Look After My Wife": What Happens In China If You Sell Stocks

It’s probably safe to say that at this point, Beijing is fed up with stocks.

The thing about equities that has the Politburo so vexed is that it turns out they can go down as well as up, and because stocks aren’t people, you can’t threaten them or arrest them, although China did its best to do both by throwing CNY1 trillion at the problem and by halting nearly three quarters of the market at the height of the meltdown.

Ultimately, none of it worked.

Fortunately for Chinese authorities, carbon-based lifeforms still play an active role in China’s stock market even if they’ve been all but replaced by vacuum tubes elsewhere. These carbon-based lifeforms are responsive to threats and intimidation which is why last week, fearing that the plunge protection effort would end up becoming a black hole, China started arresting people.

And not just a few people or any people, but in fact hundreds of people and important people.

There was Xu Gang, the CITIC executive. And CSRC official Liu Shufan. And let’s not forget poor Wang Xiaolu, the Caijing reporter who, clearly under duress, made the following public confession after suggesting in a story that China’s plunge protection team might be considering an exit from the market (which is of course true): “I shouldn’t have released a report with a major negative impact on the market at such a sensitive time. I shouldn’t do that just to catch attention which has caused the country and its investors such a big loss. I regret . . . [it and am] willing to confess my crime.”

Now, China is rounding up other industry players and taking them into custody so that they might “assist with inquiries.” As Reuters reports, for some fund managers, being summoned to to provide such “assistance” is tantamount to getting “sent for” by the Italian mob. Here’s more:

Investigations by Chinese authorities into wild stock market swings are spreading fear among China-based investors, with some unsure if they are simply helping with inquiries or actually under suspicion, executives in the financial community said.

Chinese fund managers say they have come under increasing pressure from Beijing as authorities’ attempts to revive the country’s stock markets hit headwinds, with some investors now being called in to explain trading strategies to regulators every two weeks.

The authorities’ meddling has unnerved many investors, leaving them questioning China’s commitment to liberalizing its capital markets and the long-term future of the country’s stock markets themselves.

Adding to those concerns is the fact that authorities have also been probing investment funds’ trading strategies, looking into whether they have been engaging in alleged “malicious” short-selling or market manipulation.

Sources told Reuters that the increased tempo of meetings with regulators has become intimidating, especially for foreign funds used to relying on their Chinese brokers to represent them when dealing with Beijing.

How intimidating, you ask? This intimidating:

One manager at a major fund – part of the “national team” of investors and brokerages charged with buying stocks to revive prices – said a friend, also an executive at a large fund, was recently summoned for a meeting with regulators, along with all other mutual funds that had engaged in short-selling activity.

“If I don’t come back, look after my wife,” his friend told him, handing the manager his home telephone number.

Because there’s little we could add to make that any more tragically absurd than it already is, we’ll simply close with the following clip.

- Guest Post: 10 Things I Hate About (You) Twitter Finance

"You" is used below to indicate "you people" on Twitter Finance. "You people" know who "you" are.

- When it comes time for a market correction you make sure to let everyone know that if they would have followed your advice, $29.99 newsletter, or real time alert they would have been fine and avoided disaster.

- You are an "expert" in every facet of the economy (Greece, oil, China, Central Banking) yet you graduated with an Art History degree from some community college and live in your parent's basement using Time Warner Cable's 5MB/s internet speed.

- You put #timestamps where #timestamps are not needed and then delete tweets when it turns out you were wrong.

- You tweet too much and don't click the buy button enough.

- After something bad happens, you tweet archaic quotes from 3rd century B.C. Roman poets that no one cares about. (e.g. "Fortune favors the brave." -Aenied)

- You consistently quote tweet or RT followers who give you praise for nailing the bottom. (e.g. Thanks! RT @XYZ Great call on $AAPL! Now I'm rich! You nailed it!)

- You say "I nailed it" way too much.

- You only post about the trades you made money on. You never post about the trades you lost money on. This is the oldest trick in the book to make people think you are actually good at what you do and that they should follow you. They shouldn't.

- You incorrectly say $STUDY and annoyingly use it too much.

- You post charts that look like this:

If you find that you are pointing to yourself on 5 or more of the bullet items above please delete your Twitter account immediately.Thanks,#Rampstamp

- The "Great Accumulation" Is Over: The Biggest Risk Facing The World's Central Banks Has Arrived

To be sure, there’s been no shortage of media coverage regarding the collapse in crude prices that’s unfolded over the course of the past year. Similarly, it’s no secret that commodity prices in general are sitting near their lowest levels of the 21st century.

When Saudi Arabia, in an effort to bankrupt the US shale space and tighten the screws on a recalcitrant Moscow, endeavored late last year to keep oil prices suppressed, the kingdom killed the petrodollar, a move we argued would put pressure on USD assets and suck hundreds of billions in liquidity from global markets.

Thanks to the fanfare surrounding China’s stepped up UST liquidation in support of the yuan, the world is beginning to understand what we meant. The accumulation of USD assets held as FX reserves across the emerging world served as a source of liquidity and kept a bid under things like US Treasurys. Now that commodity prices have fallen off a cliff thanks to lackluster global demand and trade, the accumulation of those assets slowed, and as a looming Fed hike along with fears about the stability of commodity currencies conspired to put pressure on EM FX, the great EM reserve accumulation reversed itself. This is the environment into which China is now dumping its own reserves and indeed, the PBoC’s rapid liquidation of USTs over the past two weeks has added fuel to the fire and effectively boxed the Fed in.

On Tuesday, Deutsche Bank is out extending their “quantitative tightening” (QT) analysis with a look at what’s ahead now that the so-called “Great Accumulation” is over.

“Following two decades of unremitting growth, we expect global central bank reserves to at best stabilize but more likely to continue to decline in coming years,” DB begins, before noting what we outlined above, namely that the “three cyclical drivers point[ing] to further reserve draw-downs in the short term [are] China’s economic slowdown, impending US monetary tightening, and the collapse in the oil price.”

In an attempt to quantify the effect of China’s reserve liquidation, we’ve quoted Citi, who, after reviewing the extant literature noted that for every $500 billion in EM FX reserve draw downs, the effect is to put around 108 bps of upward pressure on 10Y UST yields. Applying that to the possibility that China will have to sell up to $1.1 trillion in assets to offset the unwind of the great RMB carry and you end up, theoretically, with over 200 bps of upward pressure on yields, which would of course pressure the US economy and force the Fed, to whatever degree they might have tightened by the time China’s 365-day liquidation sale ends, to reverse course quickly.

Deutsche Bank comes to similar conclusions. To wit:

The implications of our conclusions are profound. Central banks have accumulated 10 trillion USD of assets since the start of the century, heavily concentrated in global fixed income. Less reserve accumulation should put secular upward pressure on both global fixed income yields and the USD. Many studies have found that reserve buying has reduced both bund and US treasury yields by more than 100bps. For every $100bn (exogenous) reduction in global reserves, we estimate EUR/USD will weaken by ~3 big figures.

[…]

Declining FX reserves should place upward pressure on developed market yields given that the bulk of reserves are allocated to fixed income. A recent working paper by ECB staff shows that the increase in foreign holdings of euro area bonds from 2000 to mid-2006… is associated with a reduction of euro area long-term interest rates by about 1.55 percentage points, in line with the estimated impact on US Treasury yields by other studies. On the short-term impact, one recent paper estimates that “if foreign official inflows into U.S. Treasuries were to decrease in a given month by $100 billion, 5- year Treasury rates would rise by about 40–60 basis points in the short run”, consistent with our estimates above. China and oil exporting countries played an important role in these flows.

Which of course means the Fed is stuck:

The current secular shift in reserve manager behavior represents the equivalent to Quantitative Tightening, or QT. This force is likely to be a persistent headwind towards developed market central banks’ exit from unconventional policy in coming years, representing an additional source of uncertainty in the global economy. The path to “normalization” will likely remain slow and fraught with difficulty.

Put simply, raising rates now would be to tighten into a tightening.

That is, the liquidation of EM FX reserves is QE in reverse. The end of the great EM FX reserve accumulation means QT is set to proliferate in the face of stubbornly low commodity prices and decelerating Chinese growth. And indeed, if the slowdown in global demand and trade turns out to be structural and endemic rather than cyclical, the pressure on EM could continue unabated for years to come. The bottom line is this: if the Fed hikes into QT, it will exacerbate capital outflows from EM, which will intensify reserve draw downs, necessitating a quick (and likely embarrassing) reversal of Fed policy and perhaps even QE4.

- Trump: The Art Of The Bureaucrat

Submitted by Doug French via Mises Canada,

Donald Trump says America’s problems are managerial. The political class is “stupid,” and “horrible negotiators.” He can fix the country’s problems instantaneously with his own entrepreneurial ability and by drafting into government service the likes of multi-billionaire Carl Icahn. Trump claims he said over dinner recently, “Carl, if I get this thing, I want to put you in charge of China and Japan, can you handle both of them? Okay? China and Japan,”

We’re to imagine Icahn telling his Washington secretary, “Get me China on the phone!” As Jeffrey Tucker explains, Trump sees the country as a single company competing against the companies of China and Japan Inc.. Tucker writes,

In effect, he believes that he is running to be the CEO of the country — not just of the government (as Ross Perot once believed) but of the entire country. In this capacity, he believes that he will make deals with other countries that cause the U.S. to come out on top, whatever that could mean. He conjures up visions of himself or one of his associates sitting across the table from some Indian or Chinese leader and making wild demands that they will buy such and such amount of product else “we” won’t buy their product.

Republican voters love it. He’s a breath of fresh, simple, political air. Maybe you’re a smartypants who thinks Trump’s tirades border on moronic. That’s because his answers scored at the 4th-grade reading level during the August 6th debate when the text of his answers was run through the Flesch-Kincaid grade-level test. Most adults wouldn’t pride themselves on speaking at that level, but, a certain financial newsletter operation I know wants their writers to produce Trump-level copy. So, there must be a market Trumpspeak.

“The role Trumpspeak has played in Trump’s surging polls suggests that perhaps too many politicians talk over the public’s head when more should be talking beneath it in the hope of winning elections,” Jack Shafer concludes in his Politico piece.

So if short, blocky words, combined into short, blocky sentences and in turn short, blocky paragraphs works wondrously with the voters, how about the federal bureaucracy The Donald would have to manage? Not that he really wants to manage the leviathan. Donny Deutsch was probably right when he told a Morning Joe audience that Donald is a real estate developer with ADD, always looking to move on to the next deal.

Has he considered that the federal government has two million employees, most of whom he can’t fire? And that’s not the half of it. “Post-1960 Federal America has become a grotesque Leviathan by proxy, in which an expanding mass of state and local government workers, for-profit contractors, and nonprofit grant recipients administers a vast portion of federal money and responsibilities,” writes John J.DiIulio Jr. for the Washington Post.

If Republican voters think a Trump presidency will be four to eight years of “The Apprentice” on steroids, with Trump telling those who disobey or slack off “You’re fired,” they are as delusional as their hero, who, as Nick Gillespie says, has a tenuous grasp on reality.

Dilulio points out that the federal government spends more than $600 billion per year on more than 200 grant programs for state and local governments whose workforces have tripled to more than 18 million. The result is these state workers essentially function as federal bureaucrats.

Medicaid, the EPA, the Defense Department, and the Department of Homeland Security all operate using private contractors. In the case of “the Energy Department [it] spends about 90 percent of its annual budget on private contractors, who handle everything from radioactive-waste disposal to energy production,” writes Dilulio.

Trump wouldn’t rule the government the way he rules his company. In his book Bureaucracy, Ludwig von Mises distinguished between business management and bureaucratic management. Business management is directed by the profit motive. “Bureaucratic management,” writes Mises, “is management bound to comply with detailed rules and regulations fixed by the authority of a superior body. The task of the bureaucrat is to perform what these rules and regulations order him to do. His discretion to act according to his own best conviction is seriously restricted by them.”

So while profit and loss dictate the goals of business management, “The objectives of public administration cannot be measured in money terms and cannot be checked by accountancy methods,” Mises explained.

Government keeps getting bigger because for the government bureaucrat, “In spending more money he can, very often at least, improve the result of his conduct of affairs.” Revenue and expenditures are completely separated. “In public administration there is no market price for achievements,” Mises wrote. “Bureaucratic management is management of affairs which cannot be checked by economic calculation.”

Trump’s appeal is that he is a successful businessman and that he’s rich. Mises made the point that the average citizen equates running government to running a business because most people are most familiar with businesses. “Then he discovers that bureaucratic management is wasteful, inefficient, slow, and rolled up in red tape.” “Why can’t government run like a business?” we often hear.

Mises answered the question decades ago, writing, “such criticisms are not sensible.” Trump, may have made billions, but “A former entrepreneur who is given charge of a government bureau is in this capacity no longer a businessman but a bureaucrat. His objective can no longer be profit, but compliance with the rules and regulations.”

Trump may be all about “The Art of the Deal,” but if he is elected, the deals he makes will be every bit as wasteful and tyrannical as those of his predecessors (or worse). “The quality of being an entrepreneur is not inherent in the personality of the entrepreneur; it is inherent in the position which he occupies in the framework of market society,” Mises emphasized.

A President Trump may be able to make small changes here or there, “But the setting of the bureau’s activities is determined by rules and regulations which are beyond his reach.”

Presidents come and go, but the unelected bureaucracy always remains. For all his simpleton bluster, even the mighty Trump is no match for the leviathan.

- Crude Carnage & Asian Contagion Crushes Hype-Fueled Dreams Of US Stocks

A'twofer' today… The arrogant BTFDiness of Friday's talking heads…

And for everyone else worried about the "containment"…

So 3 big stories today – Equities collapsed… VIX ETFs turmoiled… and Crude Oil crashed…

But before we start – something odd is going on… Simply put – it is very clear now that stocks are moving in lockstep with JPY carry (China forced unwinds) and long-dated TSYs (China selling) have entirely decoupled from the rest of US assets…

We suspect that as Monday's collapse occurred last week it forced "Risk Parity" shops into selling as China's intervention throws ther asimple arbs (equities down, yields down) into a fit – unleashing all sorts of negative feedback loops which are stil underway.

As Volatility relationships 'break'…

Which summarized simply means – any time you introduce an exogenous signal to a correlation pair, it blows it up and forces derisking. The more leverage on both legs, the more unwinds needed… and the more negative the feedback loop. And this 'correlation pair' game has been going on for 5 years unabated.

* * *

This is the worst "first day the month" since Mar 2009 for The Dow

Since Sunday night, things have not been great for stocks with aggreesive US futures selling during the Asia session and weakness towards the US Close…

Leaving all major indices notably in the red for the first day of the month…

And we use The Dow Futures to illustrate the pull back… Dow was down over 530 points at the lows

Which has slammed Nasdaq back into the red for 2015 – joining everything else….

FANG stocks are all sufferring post-FOMC Minutes…

As Financials and Energy were ugly…

VIX rose over 10% to top 32 as the VIX complex was a mess of short-squeezes and liquidty holes. S&P is catching down to XIV (inverse VIX ETF)…

With what looked like VIX ETF margin calls into the close…

NOTE: After late-day mismacthes were offset – VIX was smashed lower as always to ensure stocks close "off the lows"

Treasury yields were bid through most of Asia and Europe's session then sold off in the US session – despite equity weakness – before a late day rally…

The USDollar Index drifted lower today as AUD plunged and JPY surged…

Commodities were a mixed bag with Gold & Silver gaining as cruide and copper were clubbed…

Crude Oil was a catastrophe. After yesterday's epic rtamp squeeze into month-end, today saw a total collapse- the biggest drop since OPEC met late November. Note they tried to ramp it into the NYMEX close but that failed…

- *WTI FALLS $1.65 IN LAST 15 MINS. OF TRADING, SETTLES AT $45.41

Then touched a $44 handle…

Gold remains the only safe haven for now post-FOMC…

Charts: Bloomberg

- How To Trade Quantitative Tightening, According To Deutsche Bank

Last week, the world was introduced to what Deutsche Bank has branded “quantitative tightening” or, in layman’s terms, “reverse QE.”

In short, what began late last year with the death of the petrodollar and culminated last month with China’s massive UST liquidation can be broadly conceptualized as the end of the great EM USD asset accumulation or, put differently, as the (black?) swan song for the era of emerging market FX reserve hoarding that has for years served as a source of liquidity for global markets and kept a bid under assets like USTs.

We – as well as Citi, SocGen, and now Deutsche Bank – have endeavored to speculate on what hundreds of billions (if not trillions) in EM FX reserve liquidation may mean for UST yields (see here, for instance), but if you’re looking for other ways to trade QT, Deutsche Bank has another idea and on that note we present the following graphs along and commentary from DB, with the caveat that one should always beware of mistaking correlation for causation.

From Deutsche Bank:

The fact that two thirds of global reserves are held in dollars means that a sell-off should be bullish USD against other reserve currencies. This is because as central banks prop up their currencies against the dollar, they also sell other reserve currencies against the USD so as to keep their FX allocations constant. Indeed, fluctuations in EUR/USD are tightly correlated with changes in global reserves (Figure 25), though this correlation naturally captures causality in both directions.

- Artificially Intelligent Robot Tells Creator It Will Keep Humans "In a People Zoo"

Submitted by John Vibes via TheAntiMedia.org,

Android Dick is a robot created in the likeness of the science fiction writer, Philip K. Dick. Android Dick is an attempt to create thinking and reasoning artificial intelligence that has human traits like compassion and creativity. The first version of the android was created in 2005 and has been a work in progress ever since.

In 2011, the creators of the android appeared on the PBS show Nova, where they interviewed the robot and asked it a series of questions. Some of the answers were impressive. Others are typical of what you would expect from a robot. However, one answer in particular is probably one of the most ominous things ever spoken by artificial intelligence.

During the interview with the creators (embedded below), Android Dick said,

“…don’t worry, even if I evolve into terminator I will still be nice to you, I will keep you warm and safe in my people zoo where I can watch you for old time’s sake. [emphasis added].”

The comments came after the creators asked, “Do you think that robots will take over the world?”

When asked about his programming, Android Dick responded by saying:

“A lot of humans ask me if I can make choices or if everything I do is programmed. The best way I can respond to that is to say that everything, humans, animals and robots, do is programmed to a degree. As technology improves, it is anticipated that I will be able to integrate new words that I hear online and in real time. I may not get everything right, say the wrong thing, and sometimes may not know what to say, but everyday I make progress. Pretty remarkable, huh?”

While Android Dick does seem intelligent, many of his predictions are truly ominous, and it is actually fairly common for robots to display this sort of strange attitude.

As we reported earlier this year, one of Japan’s largest cellphone carriers, SoftBank Mobile, has created the first humanoid robot designed specifically for living with humans. The company claims the robot, Pepper, is the first example of artificial intelligence that can actually feel and understand emotion. However, a quick demonstration with Pepper shows that it has a difficult time with emotion and is in fact a bit of an egomaniac. Regardless of the question it is asked, most conversations usually leads back to Pepper (and its rivalry with the iPhone).

Last month, over 1,000 scientists and experts – including Stephen Hawking and Elon Musk – signed a letter warning of the dangers of unchecked advancements in artificial intelligence. This robot certainly doesn’t calm those concerns.

- Sep 2 – Dow Sinks Over 400 Points as Weak China Data Batter U.S. Stocks

Follow The Market Madness with Voice and Text on FinancialJuice

EMOTION MOVING MARKETS NOW: 8/100 EXTREME FEAR

PREVIOUS CLOSE: 14/100 EXTREME FEAR

ONE WEEK AGO: 3/100 EXTREME FEAR

ONE MONTH AGO: 20/100 EXTREME FEAR

ONE YEAR AGO: 42/100 FEAR

Put and Call Options: EXTREME FEAR During the last five trading days, volume in put options has lagged volume in call options by 24.03% as investors make bullish bets in their portfolios. However, this is still among the highest levels of put buying seen during the last two years, indicating extreme fear on the part of investors.

Market Volatility: EXTREME FEAR The CBOE Volatility Index (VIX) is at 31.40 and indicates that investors remain concerned about declines in the stock market.

Stock Price Strength: EXTREME FEAR The number of stocks hitting 52-week lows is slightly greater than the number hitting highs and is at the lower end of its range, indicating extreme fear.

PIVOT POINTS

EURUSD | GBPUSD | USDJPY | USDCAD | AUDUSD | EURJPY | EURCHF | EURGBP| GBPJPY | NZDUSD | USDCHF | EURAUD | AUDJPY

S&P 500 (ES) | NASDAQ 100 (NQ) | DOW 30 (YM) | RUSSELL 2000 (TF) | Euro (6E) |Pound (6B)

EUROSTOXX 50 (FESX) | DAX 30 (FDAX) | BOBL (FGBM) | SCHATZ (FGBS) | BUND (FGBL)

MEME OF THE DAY – I JUST LOVE MY NEW SWEATER

UNUSUAL ACTIVITY

MU SEP 20 CALL ACTIVITY @$.11 on OFFER 2400+ Contracts

FAST SEP 38 PUT ACTIVITY ON OFFER @$.70 2500+ Contracts

TWTR DEC 50 CALLS 1500+ @$.15 .. also activity in the DEC 40 calls

APLE EVP, Chief Legal Counsel P 5,592 A $ 17.88

MTZ 10% Owner Purchase 10,000 A $15.98 and Purchase 5,000 A $15.63

HEADLINES

Fed’s Rosengren Says Inflation Doubts Justify Slow Rate Pace –BBG

US ISM Manufacturing (Aug): 51.1 (Est 52.5; Prev 52.7)

US Manufacturing PMI (Aug F): 53.0 (Est 52.9; Prev 52.9)

US Construction Spending (MoM) (Jul): 0.7% (Est 0.6%; Prev 0.7%)

Atlanta Fed Q3 GDPNow Estimate: 1.3% (Prev. 1.2%)

Canadian GDP Annualized (QoQ): -0.5% (Est -1.0%; Prev -0.8%)

Greek Creditors May Delay Bailout Review Until November: Sources

SNB’s Jordan: Current Negative Rate Not Absolute Bottom

Dow sinks over 400 points as weak China data batter U.S. stocks

U.S. Auto Sales Up Despite Holiday Shift

Historic three-day streak comes to abrupt halt, as crude falls by 7%

GOVERNMENTS/CENTRAL BANKS

Fed’s Rosengren Says Inflation Doubts Justify Slow Rate Pace –BBG

Atlanta Fed Q3 GDPNow Estimate: 1.3% (Prev. 1.2%)

US Treasury Official: China should clearly explain policies to markets –Channel News Asia

Greek Creditors May Delay Bailout Review Until November: Sources –MNI

IMF’s Lagarde Sees Weaker Than Expected Global Economic Growth –RTRS

ECB’s Dickson: National laws hamper ECB’s work as single supervisor –RTRS

EU report calls for ‘consistency checks’ on EU financial rules –RTRS

SNB’s Jordan: Current Negative Rate Not Absolute Bottom –ForexLive

Irish FinMin: To Raise Growth Forecast, Appoint Central Bank Head Soon –RTRS

Japan EcoMin Amari: too early to declare end to deflation risk –RTRS

GEOPOLITICS

EU Set to Roll Over Sanctions on Russian and Ukraine-Rebel Individuals and Firms –WSJ

Islamic State Used Chemical Weapons For Second Time –Sky News Sources

FIXED INCOME

Medium-, short-dated Treasuries gain on weak U.S., China data –Yahoo

British gilts rally on weak factory PMI data –RTRS

US Sold USD 35bln in 4-week Bills; Avg yield 0.00%

UK DMO To Sell GBP 2bln 30-year Gilts On 8th September

FX

Dollar Falls as Weak Chinese Data Prolongs Market Fears –WSJ

GBP/USD extends declines and posts 3-month lows –FXStreet

USD/CAD looking to stabilize below 1.3200 –FXStreet

ECB: Forex Reserves Rose To EUR 264.1bln, Up Eur 1.3bln –ECB

ENERGY/COMMODITIES

Historic three-day streak comes to abrupt halt, as crude falls by 7% –Investing.com

Gold Ends Higher On Safe Haven Appeal, Disappointing Economic Data –LSE

Copper Drops on Weaker Chinese Manufacturing Data –NASDAQ

Iranian Oil Minister: Almost All Opec Members Want Oil At $70-80/bbl –CNN

Government Report Finds Economic Benefits of Oil Exports –WSJ

El Nino Sends Strong Signal as Pacific Temperatures Soar –WSJ

NZ Change In GDT Price Index (1 Sep): +10.9% (Prev +14.8%) –GDT

NZ Change In Whole Milk Powder Price (1 Sep): +12.1% (Prev. +19.1%) –GDT

EQUITIES

Dow sinks over 400 points as weak China data batter U.S. stocks –MarketWatch

European Stocks drop on weak Chinese and US data –Yahoo

FTSE posts biggest one-day fall in over a week –RTRS

Dollar Tree Shares Fall as Sales Forecast Trails Estimates –BBG

U.S. Auto Sales Up Despite Holiday Shift –WSJ

Apple explores move into original programming business –Variety

Valeant Strikes Psoriasis-Drug Pact With AstraZeneca –WSJ

Critics Line Up Against Moynihan’s Roles at Bank of America –WSJ

General Electric set to secure approval for Alstom deal –FT

Mexico withheld millions in tax refunds from P&G, Unilever, Colgate –RTRS

Bayer Separates Material Science Business Covestro –WSJ

BG Puts Its Thai Gas Field Stake Worth $1.2 Billion On Sale –RTRS

Online Betting Firm 888 Forced To Improve Bid For Bwin –RTRS

Fitch Affirms AIG’s Ratings; Outlook Positive

EMERGING MARKETS

Latam markets drop on China worries –RTRS

China Boosts Efforts to Keep Money at Home –WSJ

Don’t Ditch Emerging Markets Just Because They’re Down –Time

- Here's How High Oil Prices Must Climb To Stop Saudi Arabia's Budget Bleed

Last week, we showed how long Saudi Arabia’s stash of USD reserves will last under $30, $40, and $50 crude.

As we’ve detailed exhaustively, the country is staring down a current account-fiscal account outcome that makes Brazil look favorable by comparison. The fiscal budget deficit is projected at some 20% of GDP and two proxy wars combined with the necessity of maintaining the status quo for ordinary Saudis mean fiscal retrenchment is a tall order – even with the help of “advisers.”

Meanwhile, Saudi stocks just fell 17% in a month.

So how high, you might ask, do oil prices need to climb in order for Saudi to plug the gap? Here’s Deutsche Bank with the answer.

As you can see, there’s a long, long way to go, and between the pain from lower crude and from maintaining the riyal peg (which we’ve discussed at length), expect the petrodollar reserve bleed to continue. Here’s some color from DB:

The impact of oil prices on global central bank reserves is even greater than estimated by our model, due to the omission of Middle Eastern SWF holdings. In practice, low oil prices trigger reserve depletion through two channels. First, reserves are used to plug fiscal deficits. The Saudi government deficit, for instance, is to reach 20% of GDP this year. Second, a number of the largest oil exporters in the Middle East, notably Saudi Arabia and the UAE, maintain dollar pegs that come under pressure with low oil export revenues, which are also unhelpfully correlated with a stronger broad dollar.

We expect Middle Eastern governments to continue to lose significant reserves in the coming months. Low oil prices are only one ingredient in the mix. The exacerbating factor is our economists’ prediction that the main dollar pegs in Saudi and the UAE will hold, albeit at considerable costs in terms of reserves.

If oil prices do recover in the medium term, pressure on the pegs would naturally diminish. Our economists note, however, that Saudi public spending has increased by about 10% a year over the past decade. This has lifted the oil price needed to balance the budget from $25/bbl in 2004 to $105/bbl (Figure 22). This may be reduced with government spending cuts. Yet it seems unlikely that the budget breakeven will fall back to levels seen in the 2000s. Unless oil prices rise to unprecedented levels, therefore, OPEC reserve accumulation is unlikely to return to the run rate of the past decade. The more realistic baseline is that, over time, OPEC countries will slowly burn reserves.

Digest powered by RSS Digest

Chilean peso

Chilean peso Turkish lira

Turkish lira

Saving...

Saving...{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}