- Anything Mao Can Do I Can Do Better: Xi Jinping

Anything Mao Can Do I Can Do Better: Xi Jinping

Authored by Stu Cvrk via The Epoch Times,

For months, China watchers have been focused like laser beams on the Taiwan Strait, with much speculation on whether and when communist China will attempt a cross-Strait invasion to “absorb” Taiwan by force into the “People’s Republic.”

That speculation became a fever pitch due to two events: Nancy Pelosi’s 19-hour visit to Taipei back in July and Chinese leader Xi Jinping’s triumphant report to the Chinese Communist Party’s 20th National Congress in October.

The first event led to a surge in People’s Liberation Army (PLA) intimidation of Taiwan, while the second reemphasized “unification” as “a natural requirement for realizing the rejuvenation of the Chinese nation” to be achieved by the hundred-year anniversary of the founding of the Chinese communist dictatorship.

Will Xi pull the trigger, or won’t he? And when might that happen? Within the next year or perhaps by 2027? The opinions are all over the map.

Xi elevated himself to Mao Zedong-level status by receiving an unprecedented third five-year term as general secretary of the CCP and chairman of the Central Military Commission. The 20th Congress was a complete triumph for Xi: the constitution was modified to essentially allow him to be “emperor for life,” his allies filled all important positions in the new Standing Politburo, and former leader Hu Jintao was humiliated and frog-marched out of the plenary session by Xi’s thugs.

Furthermore, the Congress did not designate a successor to Xi. And the cult of Xi is advanced daily by state-run Chinese media in the same way they propagandized that Mao could do no wrong during his cruel reign.

Xi’s rhetoric about “peaceful unification with Taiwan” is meaningless, as reunification will be accomplished at the end of the PLA’s bayonets unless Taiwan and its allies surrender. With the continued modernization and growth of the PLA and PLA Navy, Taiwan watchers are rightfully concerned that Xi has completely consolidated political power and has the means and will to use the Chinese military to achieve his stated goals, including “reunification.”

And Xi is not afraid to use authoritarian methods to achieve his goals, as the last 10 years have shown: reeducation camps in Xinjiang, increased persecution of minority populations and religious groups, arbitrary and brutal zero-COVID lockdowns, and outright genocide against Uyghurs and others, including Tibetans.

Speaking of Tibet, could territorial gains in South China be a more immediate goal for Xi than the absorption of Taiwan?

After all, PLA ground forces have a record of success in capturing and occupying territory. In contrast, the PLA Navy is untested and faces logistics hurdles in supporting and sustaining a cross-Strait invasion.

China’s aircraft carrier Liaoning takes part in a military drill of the Chinese People’s Liberation Army (PLA) Navy in the western Pacific Ocean on April 18, 2018. (Reuters)

Mao left some unfinished business after the PLA invaded Tibet in 1949. After defeating the small Tibetan army and occupying the country, the communists imposed the sham “17-Point Agreement for the Peaceful Liberation of Tibet” on the Tibetan government in 1951. The communists annexed Tibet and began the genocide and pacification efforts that continue today, including torture, suppression of Tibetan culture, forced imprisonment and “reeducation,” and other brutality. Over a million Tibetans perished, and more than 6,000 monasteries were looted and razed as the CCP systematically destroyed Tibet’s ancient Buddhist civilization. The Dalai Lama and thousands of his followers subsequently fled to India in 1959 and established a government in exile.

Five Fingers Policy

The Chinese communists’ actions in Tibet were part of a long-expressed foreign policy developed by Mao during the 1940s—the so-called “Five Fingers Policy.” The essence of the policy is this: “While Tibet was the right hand of China, Sikkim, Arunachal Pradesh, Bhutan, Nepal, and Ladakh were its ‘five fingers’ of its periphery and that it was China’s duty to ‘liberate’ these areas,” according to India-based education tech company Byju’s. Never mind the wishes and dreams of the peaceful inhabitants of these areas!

The policy, of course, was nothing but a bald-faced characterization of communist China’s expansionist goals in the region, which could only be achieved at the expense of India—the Seven Sister States of northeast India (Arunachal Pradesh, Assam, Meghalaya, Manipur, Mizoram, Nagaland, and Tripura), Sikkim, the Siliguri Corridor, Utter Pradesh, and the western states of Jammu and Kashmir, Himachal Pradesh, and Uttar Pradesh. Previously quasi-independent, Sikkim joined the rest of India as a state in 1975—probably as much in fear of the Chinese communists as anything. These are all on the Indian side of the Line of Actual Control (LAC), a disputed demarcation that separates Indian-controlled territory from Chinese-controlled territory.

Chinese soldiers are pictured at the Nathu La Pass area at the India-China border in the north-eastern Indian state of Sikkim in August 2003. The two sides had a minor face-off at another pass called the Naku La on Jan. 20, 2021, according to the Indian army. (STR/AFP via Getty Images)

The PLA and the Indian Army have crossed swords in various military skirmishes and a border war in 1962 over LAC disputes. Here are some of those confrontations:

-

The 1962 Sino-Indian Border War, which killed 8,000 Indians and 2,000 Chinese, resulted in the establishment of a 12-mile-wide demilitarized zone along the LAC.

-

Nathu La and Cho La skirmishes near Sikkim in 1967 over India’s construction of an iron fence to prevent Chinese incursions.

-

The Tulung La Incident in 1975 along the LAC in Arunachal Pradesh.

-

The Sumdorong Chu Valley standoff in 1987 after India granted statehood to Arunachal Pradesh (claimed by China as “South Tibet”).

-

The Daulat Beg Oldi and Chumar standoffs in 2013 over the construction of various structures and encampments.

-

The Demchok standoff in 2014 over reciprocal claims of “illegal construction” in disputed areas.

-

The Burtse incident in 2015 in which India destroyed a watchtower that was “too close” to the mutually agreed-upon patrolling lane.

-

The Doklam standoff in 2017 after China began building a road through southern Bhutan that threatened the Siliguri Corridor.

-

The Sino-Indian skirmishes in 2020 near Pangong Tso Lake and the Galwan Valley in Ladakh. Beijing subsequently asserted sovereignty over the entire Galwan Valley, representing a significant change to the status quo in the western part of the LAC. During this incident, “dozens of Indian and Chinese soldiers died beating each other with sticks, clubs, and other rudimentary weapons,” Breitbart reported.

-

The 2022 standoff in Arunachal Pradesh state over a Chinese village.

And now there have been multiple reports of Indian and Chinese troops clashing on the border at the Tawang sector in the Indian state of Arunachal Pradesh on Dec. 9. “PLA troops crossed the LAC in the Tawang sector, which was contested by [India’s] own troops in a firm and resolute manner. This face-off led to minor injuries to a few personnel from both sides,” according to an Indian army spokesman.

An Indian army convoy moves on the Srinagar-Ladakh highway at Gagangeer, northeast of Srinagar, Indian-controlled Kashmir, on Sept. 9, 2020. (Dar Yasin/AP Photo)

While Mao’s “Five Fingers Policy” seemed to have died with him—as there have been no public utterances of it by subsequent Chinese leaders and diplomats since Mao’s passing—it is entirely possible that Xi has resurrected the policy, given that the preponderance of China-India skirmishes along the LAC has occurred during his tenure (and seem to be accelerating in frequency).

Concluding Thoughts

Xi has elevated himself to the stature of Mao, at least on the political level. To transcend Mao in the eyes of the CCP cadre and the Chinese people, in general, may be his ultimate personal goal. Mao left two major policies unfulfilled: the annexation of the Five Fingers and unification with Taiwan. To achieve either or both would cement Xi’s claim to be at least the equal of Mao by finishing what the Great Helmsman himself could not do.

Xi claims to have read various Western authors, including Alexander Pushkin, Leo Tolstoy, Johann Wolfgang von Goethe (Faust), Walt Whitman, Mark Twain, Jack London, Ernest Hemingway, and Victor Hugo, according to CCP mouthpiece People’s Daily. Such claims undoubtedly help cement the cult of Xi in the minds of many.

Has the apparently well-read Xi partaken of any books from ancient Greece? If so, perhaps he understands the concept of the alpha and the omega—the beginning and the end. God-willing, Mao was the alpha of the Chinese communist regime, and Xi is the omega.

Keep your eyes on Tibet and India’s Seven Sisters in the meantime.

Tyler Durden

Fri, 12/23/2022 – 23:55 -

- Putin References Ukraine "War" For 1st Time, In Response To Zelensky's D.C. Visit

Putin References Ukraine “War” For 1st Time, In Response To Zelensky’s D.C. Visit

This perhaps marks the biggest signal thus far over more than 10 months of fighting that the Ukraine conflict could grind on for years…

Russian President Vladimir Putin called his “special military operation” in Ukraine a “war” for the first time since he launched a full-scale invasion into Russia’s neighbor nearly 10 months ago.

Putin said at a Thursday televised news conference: “Our goal is not to spin this flywheel of a military conflict, but, on the contrary, to end this war,” adding that “This is what we are striving for.” The words came as the Kremlin is still reacting to Zelensky’s Wednesday speech wherein he pressed US lawmakers to authorize tanks, warplanes, and longer-range missiles while talking up future “victory”.

Getty Images The Russian president as well as all his top officials, including state media pundits, have until now been very careful in using the officially sanctioned language of “special military operation” in describing the Ukraine invasion which began on Feb.24.

All the way back in April, chairman of the Joint Chiefs of Staff Gen. Mark Milley told Congress that he expects the conflict to take “years”:

“It’s a bit early, still. Even though we’re a month-plus into the war, there is much of the ground war left in Ukraine,” he added. “But I do think this is a very protracted conflict, and I think it’s at least measured in years. I don’t know about a decade, but at least years for sure.”

“This is a very extended conflict that Russia has initiated,” Milley went on, “and I think that NATO, the United States, Ukraine and all of the allies and partners that are supporting Ukraine are going to be involved in this for quite some time.”

This week US national security spokesman John Kirby asserted that Putin is “obviously not interested in diplomacy right now.”

“Quite the contrary,” Kirby said. “He’s interested in killing more civilian Ukrainians and knocking out the lights and knocking out the heat as the winter approaches,” he alleged.

Putin is known for choosing his words very, very carefully. But for the first time publicly, the Russian president referred to the conflict in Ukraine as a “war” rather than a “special military operation.”

A slip of the tongue, or an intentional shift in rhetoric? 🇷🇺🇺🇦 pic.twitter.com/gPlVXrkBla

— Nada Bashir (@NadaaBashir) December 23, 2022

https://platform.twitter.com/widgets.js

It should also be noted that Putin’s unprecedented word choice of “war” came the day after Ukrainian President Zelensky visited Washington and met with President Biden, and gave an address before Congress, wherein he pledged “absolute victory”.

Tyler Durden

Fri, 12/23/2022 – 23:30 - Scientists Develop Gelatinous Robots To Crawl Through Human Body To Deliver Medical Payloads, Diagnose Illnesses

Scientists Develop Gelatinous Robots To Crawl Through Human Body To Deliver Medical Payloads, Diagnose Illnesses

Authored by Bryan Jung via The Epoch Times,

Scientists have developed miniature gelatinous robots that can crawl through the human body to deliver medicine or diagnose illnesses.

The “gelbot” is powered by little more than temperature changes, and its innovative design, which resembles an inchworm, is one of the most promising concepts in the field of soft robotics, according to Jill Rosen of John Hopkins University.

“It seems very simplistic, but this is an object moving without batteries, without wiring, without an external power supply of any kind—just on the swelling and shrinking of gel,” said David Gracias, a professor in the Department of Chemical and Biomolecular Engineering at Johns Hopkins University and a senior project leader.

“Our study shows how the manipulation of shape, dimensions, and patterning of gels can tune morphology to embody a kind of intelligence for locomotion.”

The 3D-printed robot, which is made out of gelatin, is intended to replace pills or intravenous injections, which could cause problematic side effects.

The prototype was announced in the journal Science Robotics, on Dec. 14.

Gelbot May Revolutionize Medicine in the 21st Century

Compared to most robots that are made out of hard materials like metals or plastics, the revolutionary “gelbot”consists an innovative water-based gel which feels like a gummy bear, making it more suitable for its task.

The team at John Hopkins said that the gels can “swell or shrink” in response to temperature, in order to be used to “create smart structures,” and they were able to demonstrate how they could move the jelly-like robots forward and backward on flat surfaces and maneuver them in certain directions, with an undulating, wave-like motion.

Gracias envisions the medical devices crawling through a patient’s body to deliver medication to a tumor, blood clot, or an infection directly, while not disturbing healthy tissue.

Unlike swallowed tablets or injected liquids, which have a time delayed effect, the tiny robot could hold back a dose of medicine and then immediately inject it when it reaches its target.

The researchers foresee the “gelbot” revolutionizing how doctors examine their patients by working as minimally invasive devices to assist with diagnoses and treatments.

Gracias is also planning to program the robots to crawl in response to variations in human biomarkers and biochemicals and test other worm and marine organism-inspired designs, along with the addition of cameras and sensors to their bodies.

He further plans to use the “gelbot” for other purposes such as marine exploration, or to patrol and monitor the ocean’s surface to fight maritime pollution.

Other Research Teams Are Working on Similar Robotic Designs

The team at John Hopkins are not the only ones looking to come up with a miniature medical robot device.

Two and a half years ago, researchers at Cornell University announced a project to develop tiny microscopic machines with legs that could move inside a patient to deliver drugs or assist with diagnoses like the “gelbot.”

This design, utilizing a mini-computer, was able to move via laser impulses and was small enough to live next to microorganisms that already lived inside a human body.

“The new robots are about 5 microns thick (a micron is one-millionth of a meter), 40 microns wide, and range from 40 to 70 microns in length,” said the Cornell report.

“Each bot consists of a simple circuit made from silicon photovoltaics—which essentially functions as the torso and brain—and four electrochemical actuators that function as legs.”

Meanwhile, another team at Stanford University earlier this year revealed a “Transformers-style robot” inspired by Japanese origami, the New York Post reported.

The “millibot,”much like the “gelbot,” is designed to carry medical payloads directly to a tumor, blood clot, or infection to dispense drugs or investigate a patient’s inner workings, said Dr. Ruike Zhao, one of the project’s co-leaders.

Zhao claims that the “spinning-enabled wireless amphibious origami millirobot” is “the most robust and multifunctional robot we have ever developed,” and that it “has broad potential application in the biomedical field.”

Tyler Durden

Fri, 12/23/2022 – 23:05 - Christmas Comes Early For 1 In 5 American Families

Christmas Comes Early For 1 In 5 American Families

Christmas traditions vary greatly across the world.

As Statista’s Felix Richter notes, while some countries hold the main celebration on Christmas Eve, others wait until Christmas Day to get festive and, most importantly at least to kids, to open presents.

In the United States, most families unwrap their gifts on Christmas Day, with the majority not waiting until breakfast to get cracking or unpacking.

You will find more infographics at Statista

According to data from Statista’s Global Consumer Survey, Santa comes early to 1 in 5 families, however, as 18 percent of respondents said they open presents on Christmas Eve in their household.

None of which makes sense since everyone knows Santa does not actually drop off his haul at your house until after you’re asleep on Christmas Eve!

Tyler Durden

Fri, 12/23/2022 – 22:40 - The Dangers Of Paper Bitcoin

The Dangers Of Paper Bitcoin

Authored by ‘Captain Sidd’ via BitcoinMagazine.com,

Are you keeping bitcoin on an exchange?

Let me tell you a story about what happens when you, and others, leave your bitcoin on exchanges. You might be surprised to hear what that means for your holdings. It might sound a lot like your own.

Let’s call our character Bill. Bill has been cautiously watching bitcoin for years, hearing about it in passing and reading a few articles. After inadvertently saving a lot of cash due to lockdowns, he decided to dive into bitcoin at last. A friend told him to check out Coinbase, Binance or another popular and “trusted” exchange in order to buy his first chunk of bitcoin.

So, Bill created an account and uploaded his face, ID, social security number, address and every other relevant detail about his life until he finally reached the “Buy Bitcoin” screen. He picked up a fraction of a bitcoin, but after all that trouble, he thought to himself:

“I don’t need to learn all these complicated technical details about hardware wallets and self custody — I just want my bitcoin safe.”

Bill reviewed the exchange’s website and decided that the security experts at the exchange, with their wiz-bang cold storage and state-of-the-art encryption, would be better at securing his bitcoin than he himself would be.

Bill was very pleased with himself after making that decision — not only did this exchange make investing in bitcoin simple, it gave him peace of mind knowing that someone else was responsible for keeping his assets safe from any kind of theft or malicious activity. After all, why should he have to worry about such things when there were professionals available who could handle them instead?

Bill has since become quite comfortable with the idea of trusting exchanges with his bitcoin — his coins are now safe from his own mistakes!

WHEN TRUST DISAPPEARS: THE FALL OF FTX

When Bill turned on the news one morning and found out that the massive crypto exchange FTX had just paused withdrawals and seemed to “accidentally” lose $10 billion, roughly a third of its market cap, he was shocked.

How could a firm with its logo on the side of a major sports stadium and a CEO who appeared on CNBC, Bloomberg and in front of the U.S. Congress(!) to talk about digital assets and regulation have lost — or likely stolen — so much from right under everyone’s nose?

Now Bill was stuck between a rock and a hard place. He was suspicious of his own exchange, but setting up his own hardware wallet seemed so difficult and scary. It would require him to invest in a physical device, acquire the necessary knowledge to secure it properly and keep track of his seed phrase backup. Even if he figured out the basics, there was still the risk of misplacing his device or improperly storing his backup and losing access to his bitcoin.

FTX was shocking, but surely Bill’s exchange would never conduct itself the same way. People would see it before it was coming, and he’d have time to get out, right?

REASONS TO TAKE YOUR BITCOIN OFF EXCHANGES

It’s clear that trusting your bitcoin to an exchange brings with it the risk that you’ll log in one morning to find that your bitcoin just isn’t there. If you hold your bitcoin yourself using a hardware wallet, this can’t happen.

However, there’s another big reason it’s important to take your bitcoin off exchanges: the bitcoin price.

How could self custody affect bitcoin’s price? Everything in economics says that buying and selling affect the market price for a good, not who holds it. However, self custody is very important to price — and it has to do with something I’ll call “paper BTC.”

INTRODUCING THE NEXT BIG THING: PAPER BTC

Let’s look at how an exchange works by considering a hypothetical exchange called ExchangeCorp, owned and operated by a jolly entrepreneur named Bernie. ExchangeCorp built an uncomplicated way to buy bitcoin, and hired a team of security experts to make sure hackers are kept at bay. Over time and through great marketing campaigns, ExchangeCorp built trust with traders and investors, drawing many in to store their bitcoin on the exchange.

When users keep their bitcoin with ExchangeCorp, the CEO Bernie and his team maintain control over those coins. Customers simply have a claim on their coins: they can log in and see their balance as well as request to withdraw their coins. However, if Bernie wants to transfer those coins owed to his customers to other Bitcoin addresses, he’s technically able to do so without any customer’s permission.

When Bernie kicks up his feet and looks at the balances in ExchangeCorp’s vault, he’s pleased to see tens of thousands of bitcoin that his customers have deposited sitting pretty. Since ExchangeCorp is doing well, more bitcoin are always coming in than going out.

So Bernie gets a wise idea. He could lend out some of those customer coins, earn some interest, and get the coins back without anyone noticing. He would get richer, and the risk of enough ExchangeCorp customers asking for withdrawals at one time to draw its vault’s massive balance down to zero is miniscule. So Bernie loans out thousands of coins here and there to hedge funds and businesses.

Source. Traditional banks are even worse than ExchangeCorp. And from March 2020, they can now lend out 100% of your money!

Now there’s another set of claims to consider. Customers have a claim on their bitcoin at ExchangeCorp, but ExchangeCorp no longer has the actual bitcoin — they only have a claim on the coin they lent out. What customers now have is a claim on Paper BTC held by ExchangeCorp, with the real bitcoin in the hands of borrowers.

This is where things get weird. All of ExchangeCorp’s customers still think they have a direct claim on real bitcoin held safely by ExchangeCorp. However, that real bitcoin is in fact in the hands of those who borrowed from ExchangeCorp, and those entities are selling it out in the market.

What happens when ExchangeCorp lends out a large quantity of the bitcoin its customers deposited? A lot of extra bitcoin starts to float around in the market, because investors who think they’re holding actual bitcoin are only holding paper BTC. All of that extra supply of bitcoin in the market absorbs buy pressure, which suppresses the price of bitcoin.

Let’s look at simple supply and demand here:

When paper BTC comes into the market, because market participants are unaware that this new supply is not real bitcoin, it has the same effect as increasing the supply of real bitcoin — until the fraud is uncovered.

Does this hypothetical story sound anything like the recent news around FTX?

THE PAPER BTC AT THE CENTER OF THE FTX FRAUD

The story of ExchangeCorp and Bernie is exactly the story of FTX and its founder Sam Bankman-Fried, with some save-the-world complexes, study drugs and polyamorous orgies redacted.

By lending out customer funds, FTX essentially inflated the supply of bitcoin by taking advantage of the trust users placed in FTX to safeguard their funds. FTX created tons of paper BTC.

Just how much paper BTC might FTX have created? We cannot be sure of the exact amounts given its absolutely horrid bookkeeping, but the estimate below suggests FTX had 80,000 paper BTC on its books — bitcoin owed to customers that is not backed by real bitcoin.

Quick math:

-330k BTC mined / year this halving era

-FTX has -$1.4B in BTC on books, meaning 80k BTC

-Assuming incurred this year, means FTX “increased” BTC supply issuance 25% this year

-Others likely did sameNo wonder we’re under prior cycle highs.

Halving math interference.— Croesus 🔴 (@Croesus_BTC) November 17, 2022

https://platform.twitter.com/widgets.js

That would represent a staggering 24% of the roughly 330,000 new bitcoin that were created over the past year through the predictable mining issuance process. That is a ton of extra bitcoin entering the market that nobody — aside from a small group of insiders at FTX — knew about!

It’s impossible to tell where the price would have gone without that extra bitcoin supply entering the market, but we can be almost certain that the price would have climbed higher than it did in 2021.

While the FTX collapse is recent and still unfolding, history has a few cautionary tales to tell about the dangers of paper assets and price manipulation. The story of gold’s failure to resist centralized capture, for instance, can tell us where Bitcoin is headed if we continue to trust exchanges and third parties to hold our bitcoin for us.

THE FALL OF GOLD

Gold was once used in daily transactions — it takes no more than a visit to a museum of ancient history to see the collections of old gold coins once circulating in local markets. The traditional view of the demise of gold as a transactional currency was that it became too cumbersome or too valuable to continue to function well as a means to buy groceries and beer.

However, this story omits a few key components that only reveal themselves when we trace the evolution that societies took from gold coins to paper bills and digital bank accounts.

Centuries ago, banks started taking customer’s gold in exchange for bank notes — giving customers a measure of security for their gold and a more convenient means of transacting. However, entrusting a bank with your precious metal meant the bank was able to lend it out or make bad investments without the depositor’s consent. When a bank was caught between bad loans and a high rate of depositor withdrawals, they had to declare bankruptcy and shut down — leaving many depositors penniless, holding paper claims on gold now worth nothing at all.

Then central banks came along to “fix” the problem of bankrupt banks leaving depositors penniless. Central banks held gold for people and commercial banks, giving them banknotes from the central bank as receipts for their gold. By 1960, central bank official holdings accounted for about 50% of all aboveground gold stocks, with their banknotes circulating freely. Commercial banks and individuals didn’t mind, since each note was convertible to a set weight of gold by the central bank that issued it.

Notice the note in the upper left? This $5 Federal Reserve note — also known as a $5 bill — is redeemable in gold. Source

This would have worked well, except that central banks — especially the Federal Reserve in the U.S. — started creating more bills than they had gold to back. Creating more bills than the Fed had gold to back was essentially creating paper gold, since each bill was a claim on gold. Doing this in secret meant the Fed was manipulating the price of gold, given the extra circulating supply which the market was not aware of. When many depositors of gold at the Federal Reserve — like the French government — started questioning the Fed’s gold holdings and creating the threat of a run on gold in the U.S., the U.S. government had to intervene.

In 1971, this came to a head with the Nixon shock. One night, President Nixon announced the U.S. would temporarily stop allowing depositors to trade in their Federal Reserve notes for the gold they promised.

This temporary halt in withdrawals was never lifted. Since all currencies were connected to gold through the U.S. dollar under the Bretton Woods agreement, the Nixon Shock meant that the entire world went off the gold standard at once. All currencies were now just pieces of paper, instead of notes giving the holder a claim on a quantity of gold.

This was only achievable because gold, over time, was deposited into commercial banks and then to central banks. Once central banks held most of the gold, they could manipulate the price of gold and remove it entirely from daily commerce. Everyday people chose the convenience of paper notes over the security of holding gold, and paid the price.

Instead of a neutral money backed by a precious metal that is difficult to dig up and impossible to synthesize, currencies became easy to print and thus highly politicized. Keeping the dollar at the top of the food chain no longer required restraint and good stewardship to ensure its backing in gold. Instead, it required military expeditions and strong policing to ensure global governments and citizens continued to use the dollar to transact.

A return to gold at this point would be impractical — the world’s commercial networks span too great a distance with transactions happening at too high a speed. With paper currency and eventually digital banking systems, what we gained in speed and convenience we lost in soundness and neutrality. We lost our savings, our social cohesion and our political institutions as a result.

PREVENTING BITCOIN’S FALL

Taking your bitcoin off of your exchange is not just good practice for your own security, it’s protecting the price of your bitcoin as well. Our freedoms depend on individuals having control over their own wealth. When we entrust our wealth to companies or states, we go down the path we witnessed with gold.

Thanks to bitcoin’s divisibility and digital nature, it overcomes the hurdles that held gold back from supporting our modern, interconnected economy. Bitcoin can support a global marketplace, but it will only get there if we each hold our own bitcoin.

Don’t let the banksters and bureaucrats manipulate the price of your bitcoin: take it off the exchange and get it on your own hardware wallet.

Tyler Durden

Fri, 12/23/2022 – 22:15 - Driver That Caused 8 Car Pile-Up In Bay Area Last Month Claims Tesla's Full Self Driving "Braked Unexpectedly"

Driver That Caused 8 Car Pile-Up In Bay Area Last Month Claims Tesla’s Full Self Driving “Braked Unexpectedly”

A driver involved in an eight car crash last month told authorities that Tesla’s “Full Self Driving” software “braked unexpectedly” and caused the pile-up.

A California Highway Patrol traffic crash report, viewed by CNN, said that the accident, which occurred in the San Francisco Bay Area and led to nine people being treated for minor injuries, happened when the Tesla slowed to a stop.

The crash report showed “the Tesla vehicle changing lanes and slowing to a stop”, CNN wrote. They obtained the report via a public records request this week.

Back in December, the California Highway Patrol was unable to confirm whether or not “Full Self Driving” was active at the time of the accident. A highway patrol spokesperson told CNN they still could not confirm, and that Tesla would have the pertinent information.

The accident took place during lunchtime on Thanksgiving Day on I-80 east of the Bay Bridge. As the report notes, the pile up happened just hours after Tesla CEO Elon Musk announced that “Full Self Driving” was available to anyone in North America who requested it.

According to CNN, the report said that “the Tesla Model S was traveling at about 55 mph and shifted into the far left-hand lane, but then braked abruptly, slowing the car to about 20 mph. That led to a chain reaction that ultimately involved eight vehicles to crash, all of which had been traveling at typical highway speeds.”

As we have noted this year, the NHTSA is in the midst of a litany of investigations into Tesla’s Autopilot, including several accidents that wound up killing motorcyclists.

The first accident was at 4:47am, July 7 on State Route 91, on a freeway in Riverside, California, the report says. A Model Y collided with a green Yamaha V-Star motorcycle that was ahead of it and the driver of the bike was ejected from his motorcycle.

Another crash happened at 1:09am on July 24, on Interstate 15 near Draper, Utah. A Model 3 was behind a Harley Davidson, the Utah Department of Public Safety said.

“The driver of the Tesla did not see the motorcyclist and collided with the back of the motorcycle, which threw the rider from the bike,” the statement says. The rider of the Harley was pronounced dead at the scene. The driver told authorities he had Autopilot on, the report says.

Tyler Durden

Fri, 12/23/2022 – 21:50 - Inflation, Recession, & Declining US Hegemony

Inflation, Recession, & Declining US Hegemony

Authored by Alasdair Macleod via GoldMoney.com,

In the distant future, we might look back on 2022 and 2023 as pivotal years. So far, we have seen the conflict between America and the two Asian hegemons emerge into the open, leading to a self-inflicted energy crisis on the western alliance. The forty-year trend of declining interest rates has ended, replaced by a new rising trend the full consequences and duration of which are as yet unknown.

The western alliance enters the New Year with increasing fears of recession. Monetary policy makers face an acute dilemma: do they prioritise inflation of prices by raising interest rates, or do they lean towards yet more monetary stimulation to ensure that financial markets stabilise, their economies do not suffer recession, and government finances are not driven into crisis?

This is the conundrum that will play out in 2023 for the US, UK, EU, Japan, and others in the alliance camp. But economic conditions are starkly different in continental Asia. China is showing the early stages of making an economic comeback. Russia’s economy has not been badly damaged by sanctions, as the western media would have us believe. All members of Asian trade organisations are enjoying the benefits of cheap oil and gas while the western alliance turns its back on fossil fuels.

The message sent to Saudi Arabia, the Gulf Cooperation Council, and even to OPEC+ is that their future markets are with the Asian hegemons. Predictably, they are all gravitating into this camp. They are abandoning the American-led sphere of influence.

2023 will see the consequences of Saudi Arabia ending the petrodollar. Energy exporters are feeling their way towards new commercial arrangements in a bid to replace yesterday’s dollar. There’s talk of a new Asian trade settlement currency. But we can expect oil exports to be offset by inward investment, particularly between Saudi Arabia, the GCC, and China. The most obvious surplus emerging in 2023 is of internationally held dollars, whose use-value is set to drop away leaving it as an empty shell. It amounts to a perfect storm for the dollar, and all those who sail with it.

Those of us who live long enough to look back on these years are likely to find them to have been pivotal for both currencies and global alliances. They will likely mark the end of western supremacy and the emergence of a new, Asian economic domination.

The interest rate threat to the west’s currencies

It is a mark of how bad the condition of Western economies has become, when interest rate rises of only a few cent are enough to threaten to precipitate an economic crisis. The blame can be laid entirely at the door of post-classical macroeconomics. And like a dog with a bone, their high priests refuse to let go. Despite all the evidence to the contrary, they would now have you believe that inflation is transient after all, though they have conceded the possibility of inflation targets being raised slightly. But the wider concern is that even though interest rates have yet to properly reflect the extent of currency debasement, they have risen enough to tip the world into recession.

In their way of thinking, it is either inflation or recession, not both. A recession is falling demand and falling demand leads to falling prices, according to macroeconomic opinions. When both inflation and a recession are present, they cannot explain it and it does not accord with their computer models. Therefore, government economists insist that consumer price rises will return to the 2% target or thereabouts, because rising interest rates will trigger a recession and demand will fall. It will just take a little longer than they originally thought.

They now saying that the danger is no longer just inflation. Instead, a balance must be struck. Interest rate policy must take the growing evidence of recession into account, which means that bond yields should stop rising and after their earlier falls equity markets should stabilise. For them, this is the path to salvation. In pursuing this line, the authorities and a group thinking establishment have had success in tamping down inflation expectations, aided by weakening energy prices.

Since March, West Texas intermediate crude has retraced 50% of its rise from March 2020 to March 2022. Natural gas has fallen forty per cent from its August high. If the western media is to be believed, Russia is continually on the brink of failure, the suggestion being that price normality will return soon. And the inflationary pressures from rising energy and food prices will disappear.

What is really happening is that bank credit is now beginning to contract. Bank credit represents over 90% of currency and credit in circulation and its contraction is a serious matter. It is a change in bankers’ mass psychology, where greed for profits from lending satisfied by balance sheet expansion is replaced by caution and fear of losses, leading to balance sheet contraction. This was the point behind Jamie Dimon’s speech at a banking conference in New York last June, when he modified his description of the economic outlook from stormy to hurricane force. Coming from the most influential commercial banker in the world, it was the clearest indication we can possibly have of where we were in the cycle of bank credit: the world is on the edge of a major credit downturn.

Even though their analysis is flawed, macroeconomists are right to be very worried. Over nine-tenths of US currency and bank deposits now face a meaningful contraction. This is a particular problem earlier exacerbated by covid lockdowns and for businesses affected by supply chain issues. It gives commercial banks a huge problem: if they begin to whip the credit rug out from under non-financial businesses, they will simply create an economic collapse which would threaten their entire loan book.

It is far easier for a banker to call in loans financing positions in financial assets. And it is also a simple matter to call in and liquidate financial asset collateral when any loan begins to sour. This is why the financial sector and relevant assets have been in the firing line so far.

Central banks see these evolving conditions as their worst nightmare. They are what led to the collapse of thousands of American banks following the Wall Street crash of 1929-1932. In blaming the private sector for the 1930s slump which followed and was directly identified with the collapse in bank credit, central bankers and Keynesian economists have vowed that it must never happen again.

But because this tin-can has been kicked down the road for far too long, we are not just staring at the end of a ten-year cycle of bank credit, but potentially at a multi-decade super-cyclical event, rivalling the 1930s. And given the greater elemental forces today, potentially even worse than that.

We can easily appreciate that unless the Fed and other central banks lighten up on their restrictive monetary policies, a stock market crash is bound to ensue. And this is what we saw when the interest rate trend began a new rising trajectory last January. For the Fed, preventing a stock market crash is almost certainly a more immediate priority than protecting the currency. It is not that the Fed doesn’t care, it’s because they cannot do both. Their mandate incorporates unemployment, and their ingrained neo-Keynesian philosophies are also at stake.

Consequently, while we can see the dangers from contracting bank credit, we can also see that the Fed and other major central banks have prioritised financial market stability over increasing interest rates to properly reflect their currencies’ loss of purchasing power. The pause in energy price rises together with media claims that Russia will be defeated have helped to give markets a welcome but temporary period of stability.

The policy of threatening continually higher interest rates must be temporary as well. In effect, monetary policy makers have no practical alternative to prioritising the prevention of bank credit deflation over supporting their currencies. Realistically, they have no option but to fight recession with yet more inflation of central bank currency funding increased government budget deficits, and through further expansion of commercial bank reserves on its own balance sheet, the counterpart of quantitative easing.

Besides central bank initiatives to keep bond yields as low as practicably possible, runaway government budget deficits due to falling tax income and extra spending to counteract the decline in economic activity will need to be funded. And given that the world is on a dollar standard, in the early stages of a recession the Fed will probably assume that the consequences for foreign exchange rates of a new round of currency debasement can be ignored. While currency debasement can then be expected to accelerate for the dollar, all the other major central banks can be expected to cooperate. The point about global economic cooperation is that no central bank is permitted to follow an independent line.

The private sector establishment errs in thinking that the choice is between inflation or recession. It is no longer a choice, but a question of systemic survival. A contraction in commercial bank credit and an offsetting expansion of central bank credit will almost certainly take place. The former leads to a slump in economic activity and the latter is a commitment too large for an inflating currency to bear. It is not stagflation, a condition which according to neo-Keynesian beliefs should not occur, but a doppelgänger rerun of what did for John Law and France’s economy in 1720. The inconvenient truth is that policies of monetary stimulation invariably end with the impoverishment of everyone.

The role of credit and the final solution

To clarify how events are likely to unfold in 2023, we must revisit the basics of monetary theory, and the difference between money and credit. It is the persistent debasement of the latter which has been the problem and is likely to condition the plans for any nation seeking to escape from the monetary consequences of a shift in hegemonic power from the western alliance to the Russian Chinese partnership.

It is probably too late for any practical solution to the policy dilemma faced by monetary policy committees in western central banks today. When commercial bankers collectively awaken to the lending risks created in large part by their earlier optimism, survival instincts kick in and they will reduce their exposure to risk wherever possible. A credit cycle of boom and bust is the consequence. Inevitably in the bust phase, not only are malinvestments weeded out, but over-leveraged banks fail as well. While the intention is to smooth out the cyclical effects on the economy, the response of the state and its central bank invariably makes things worse, with monetary policy undermining the currency.

It is important to appreciate that with a sound currency system, which is a currency that only changes in its quantity at the behest of its users, excessive credit expansion must be discouraged. The opposite is encouraged by central banks. Extreme leverage of asset to equity ratios for systemically important banks of well over twenty times in Japan and the Eurozone are entirely due to central bank policies of suppressing interest rates. It is only by extreme leverage that commercial banks, which are no more than dealers in credit, can make profits from the slimmest of credit margins when zero and negative deposit rates are forced upon them.

Since bank credit is reflected in customer deposits, a cycle of excessive bank credit expansion and contraction becomes economically destructive. The solution advocated by many economists of the Austrian school is to ban bank credit entirely, replacing mutuum deposits, whereby the money or currency becomes the bank’s property and the depositor a creditor, with commodatum deposits where ownership remains with the depositor. Separately, under these arrangements banks act as arrangers of finance for savers wishing to make their savings available to borrowers for a return.

The problem with this remedy is that of the chicken and the egg. Production requires an advance of capital to provide products at a profit in due course. The real world of free markets therefore requires credit to function. And savings for capital reinvestment are also initially funded out of credit. So, whether the neo-Austrians like it or not we are stuck with mutuum deposits and banks which function as dealers in credit.

That is as far as we can go with commercial banks and bank credit. The other form of credit in public circulation is the liability of the issuer of banknotes. To stabilise their value, the issuer must be prepared to exchange them for gold coin, which is and always has been legal money. And once the issuer has established sufficient gold reserves, the issue of any additional banknotes must be covered by additional gold coin backing.

But much more must be done. Government budget deficits must not be permitted except strictly on a temporary basis, and total government spending (including state, regional, and local governments) reduced to the smallest possible segment of the economy. It means pursuing a deliberate policy of rescinding legal obligations for government agencies to provide services and welfare for the people, retaining only a bare minimum for government to function in providing laws, national defence and for the protection of the interests of everyone without favour. All else can only be the responsibility of individuals arranging and paying for services themselves. It means that most bureaucrats employed unproductively in government must be released and made available to be redeployed in the private sector productively. A work ethic perforce will return to replace an expectation that personal idleness will always be subsidised.

Given political realities, this cannot happen except as a considered response following a major credit, currency, and economic meltdown. It is a case of crisis first, solution second. Therefore, there is no practical alternative to the continual debasement of currencies until their users reject them entirely as worthless.

Money is only gold, and all the rest is credit

For a lack of any alternative outcome, the eventual collapse of unbacked currencies is all but guaranteed. To appreciate the dynamics behind such an outcome, we must distinguish between money and credit. Currency in circulation is not legal money, being only a form of credit issued as banknotes by a central bank. It has the same standing as credit in the form of deposits held in favour of the commercial banks. The distinction between money and credit, with money wrongly being assumed to be banknotes is denied by the macroeconomic establishment today. Officially and legally, money is only gold coin. It is also silver coin, though silver’s official monetary role fell into disuse in nineteenth century Europe and America.

Gold and silver coin as money were codified under the Roman Emperor Justinian in the sixth century and is still the case legally in Europe today. In English law, the unification of the Court of Chancery and common law in 1875 formally recognised the Roman position, and gold sovereigns, which were the monetary standard from 1820, became unquestionably recognised as money in common law from then on.

Attempts by governments to restrict or ban ownership of gold as money must not be confused with the legal position. FDR’s executive order in 1933 banning American citizens from owning gold did not change the status of money. Nor did similar government moves elsewhere. And the neo-Keynesian denigration of a gold standard doesn’t alter its status either. Nor do the claims from cryptocurrency enthusiasts that their schemes are a modern replacement for gold’s monetary role. As John Pierpont Morgan stated in his testimony before Congress in 1912, “Gold is money. Everything else is credit”. He was not expressing an opinion but stating a legal fact.

That gold does not commonly circulate as a medium of exchange is explained by Gresham’s law, which states that bad money drives out the good. Originally describing the difference between clipped coins and their wholly intact counterparts, Gresham’s law also applies to gold’s relationship with currency. Worldwide, unrelated societies hoard gold coin, spending currency banknotes and bank deposits first, which are universally recognised as lower forms of media of exchange. Even central banks hoard gold. And as they have progressively distanced themselves from their roles as servants of the public, they refuse to allow the public access to their gold reserves in exchange for their banknotes.

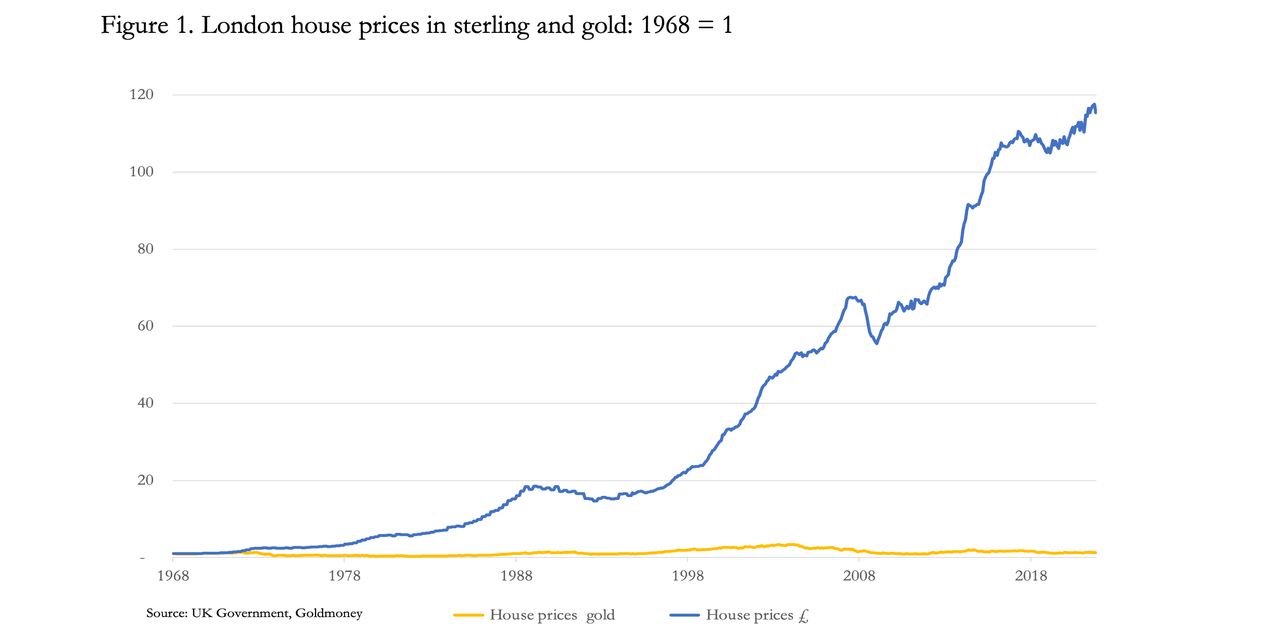

The importance of gold as a store of value, that is as sound money, appears to be difficult to understand for people not accustomed to regarding it as such. Instead, they regard it is a speculative investment, which can be held in securitised or derivative form while it is profitable to do so. When it comes to hedging a declining currency’s purchasing power, the preference today is for assets that outperform the cost of borrowing. As an example of this, Figure 1 shows London’s residential housing priced in fiat sterling and gold. Housing is the most common form of public investment in the UK, further benefiting from tax exemptions for owner-occupiers.

According to government data, since 1968 when house price statistics began median house prices in London have risen on average by 115 times. But priced in gold, they have risen only 29% in 54 years. With prices having generally risen by less outside London and its commuter belt, some areas might have seen falls in prices measured in gold.

It is virtually impossible to get people to understand the implications. They correctly point out the utility of having somewhere to live, which is not reflected in prices. They might also point out that property held by landlords produces a rental income. Furthermore, most buyers leverage their investment returns by having a mortgage.

In investing terms, these arguments are entirely valid. But they only prove that the purpose of owning an asset is to obtain a return or utility from it, with which we can all agree. The purpose of money or currency is different: it is a medium for purchasing an asset which will give you a benefit. What is not understood is that far from giving property owners a capital return which exceeds the debasement of the currency, they have just about kept pace with it. And if you had bought property elsewhere in the UK, your capital values might even have fallen, measured in real legal money, which is gold.

Since the end of the Bretton Woods agreement, the consequences of currency debasement for asset prices such as residential property have hardly mattered. The debasement of currencies has never been violent enough to undermine assumptions that residential property will always retain its value in the long run. Other assets, such as a portfolio of financial equities are seen to offer similar benefits of apparent protection against currency debasement. But we now appear to be on the cusp of a major currency upheaval. The global banking system is more highly leveraged on balance sheet to equity measures than ever before, and bank credit is beginning to contract. All the major central banks have undeclared loses which wipe out their nominal equity, affecting their own credibility as backstops to their commercial banking systems. Systemic risks are escalating, even though market participants have yet to realise it. And as economic activity turns down, government budget deficits are going to rapidly escalate. A practical remedy for the situation cannot be entertained, so the debasement of currencies is bound to accelerate. Mortgage borrowing costs are already rising, undermining affordability of residential property in fiat money terms.

The relationship between currency and real money, which is gold coin, will almost certainly break down. Measured in gold, a banking and currency crisis will have the effect of driving residential property prices significantly lower, while they could be maintained or even move somewhat higher measured in more rapidly depreciating fiat currencies.

The transition from financialised fiat currencies to… what?

There is an overriding issue which we must consider now that the long-term decline of interest rates appears to have come to an end, and that is how the dollar will fare in future. While the dollar has lost 98% of its purchasing power since the ending of Bretton Woods, it has generally been gradual enough not to undermine its role as the world’s international medium of exchange and for the determination of commodity prices. It has retained sufficient value to act as the world’s reserve currency and is the principal weapon by which America has exercised her hegemony.

It is in its role as the weapon for waging financial wars which may finally lead to the dollar’s undoing, as well as undermining the purchasing powers of the currencies aligned with it. By cutting Russia off from the SWIFT settlement system, thereby rendering her fiat currency reserves valueless, the western alliance hoped that together with sanctions Russia would be brought to her knees. The policy has failed, as sanctions usually do, while the message sent to all non-aligned nations was that America and its western alliance could render national currency reserves valueless without notice. Consequently, there has been a worldwide rethink over the dangers of relying on dollars, and for that matter the other major currencies issued by member nations of the western alliance.

At this time of transition away from a weaponised dollar, there is a general uncertainty in nations aligned with the Russian Chinese axis over how to respond, other than to sell fiat currencies to buy more gold bullion. But the sheer quantities of fiat currency relative to the available bullion suggests that at current values the bullion is not available in sufficient quantities to credibly turn fiat currencies into gold substitutes. Nevertheless, it would be logical for the gold-rich Russian Chinese axis and nations in their sphere of influence to protect their own currencies from a rapidly developing fiat currency catastrophe. So far, none of them appear to be prepared to do so by introducing gold standards for the benefit of their citizens.

Only Russia, under pressure from currency and trade sanctions has loosely tied its rouble to energy and commodity exports. In the vaguest of terms, it might be regarded as a synthetic equivalent of linking the rouble to gold. Why this is so is illustrated in Figure 2.

Measured in fiat currencies, the oil price is exceedingly volatile, while in true money, gold, it is relatively stable. Measured in gold, the oil price today is about 20% lower than it was in 1950. Since then, the maximum oil price in gold has been a doubling and the minimum a fall of 85%. That compares with a rise in US dollars of 5,350% and no fall at all. Undoubtedly, if gold had traded free from statist intervention and speculation in currency and commodity markets and from the effects of fiat-induced economic booms and busts, the price of oil in gold would most likely have been even steadier.

By insisting that those dubbed by Putin as the unfriendly nations must buy roubles to pay for Russian oil, demand for roubles on the foreign exchanges became linked to demand for Russian oil, which in turn is linked more closely to gold than the unfriendlies’ currencies. But it seems that in official minds, making this link between the rouble, oil, and gold is a step too far. When it comes to replacing the dollar with a new trade currency for the Asian powers, their initial discussions have suggested a more broadly based solution.

The Eurasian Economic Union (EAEU), consisting mainly of a central Asian subset of the Shanghai Cooperation Organisation (SCO) earlier this year announced that plans for a trade settlement currency were being considered, backed by a mixture of commodities and the currencies of member states.

So far, members of the SCO have restricted their discussion to ways of replacing the dollar for the purpose of transactions between them, a long-term project driven not so much by change in Asia but by US trade aggression and American hegemonic dollar policies over time. Following Russian sanctions imposed by the West, it is likely that the dangers of an immediate dollar crisis are now being more urgently addressed by governments and central banks throughout Asia.

With the West plunging into a combined systemic and currency crisis, no national government outside the dollar-based system appears to know what to do. Only Russia has been forced into action. But even the Russians are feeling their way, with vague reports that they are looking at a gold standard solution, and others that they are considering Sergey Glazyev’s EAEU trade currency project. As well as heading a committee set up to advise on a new trade settlement currency, Glazyev is a senior economic advisor to Vladimir Putin.

From the little information made available, it appears that Glazyev’s EAEU monetary committee is ruling out a gold standard for the new trade currency. Instead, it has been considering alternative structures without achieving any agreement so far. But for the project to go ahead, proposals reported to include national currencies in its valuation basket must be abandoned. Not only is this an area where Glazyev is unlikely to obtain a consensus easily from member states, but to include a range of fiat currencies is unsound and will not satisfy the ultimate objective, which is to find a credible replacement for the US dollar for cross-border trade settlements. For confidence in the new currency to be maintained, the structure must be both simple and transparent.

Since the currency committee’s press release earlier this year, there have been further developments likely to influence it construction. Led by Saudi Arabia, the Gulf Cooperation Council is turning its back on the dollar as payment for oil and gas. Again, this development is attributable to climate change policies of the US-led western alliance. Not only has the alliance demonstrated that foreign reserves held in its fiat currencies can be rendered valueless overnight, but climate change policies send a clear message that for the GCC the future of their trade is not with the western alliance. For long-term stable trade relationships, they must turn to the Russian Chinese axis.

It is happening before our eyes. China has signed a 27-year supply agreement with Qatar for its gas. President Biden attempted to secure a agreement with Saudi Arabia for additional oil output. He left with nothing. President Xi visited earlier this month and secured a long-term energy and investment agreement, whereby Saudi’s currency exposure to the yuan is minimised through Chinese capital investment programmes in the kingdom

Already, an increase in China’s money supply is an early indication that propelled by cheap energy and infrastructure investment programmes, her economy is in the early stages of a new growth phase, while the western alliance faces a potentially deep recession. The currency effect is likely to be supportive of the yuan/dollar cross rate, which the Saudis are likely to have factored into their calculations. But they will almost certainly need more than that. They will want to influence settlement currencies for the balance of their trade. Their options are to minimise balances on the back of inward investment flows, as mentioned above. They can seek to influence the construction of the proposed EAEU trade settlement currency. Or they can build their gold reserves, to the extent they might wish to hedge currencies accumulating in their reserves.

For the western alliance, the death knell for the petrodollar means that 2023 will see a substantial reduction of dollar holdings in the official reserves of all nations in the Russian Chinese axis and those friendly to it. The accumulation of dollars in foreign reserves since the end of the Bretton Woods regime is considerable, and its reversal is bound to create additional difficulties for the US authorities. Foreign owned US Treasuries are starting to be sold, and the $32 trillion mountain of financial assets and bank deposits are set to be substantially reduced. The potential for a run on the dollar, driving up commodity input prices in dollars, is likely to become a considerable problem for both the US and the entire western alliance in 2023.

Conclusion

We have noted the deteriorating systemic and monetary prospects for fiat currencies, predominantly those of the dollar-based Western currency system. Both sound economic and Marxist theory indicates that a final crisis leading to the end of these fiat currencies was going to happen anyway, and the financial war against Russia has become an additional factor accelerating their collapse.

After suppressing interest rates to zero and below, rising interest rates are finally being forced upon the monetary authorities by markets. With good reason, it has become fashionable to describe developments as an evolution from a currency environment driven by and dependent on financial assets into one driven by commodities — in the words of Credit Suisse’s Zoltan Pozsar, Bretton Woods II is ending, and Bretton Woods III is upon us.

For this reason, there is growing interest in how a new world of currencies based somehow on commodities or commodity-based economies will evolve. This year, Russia successfully protected its rouble by linking it to energy and commodity exports and in the process undermined Western currencies.

While it is always a mistake to predict timing, the fact that no one in the financial establishment is debating how to use gold reserves to protect their currencies clearly indicates that we are still early in the evolution of the developing fiat currency crisis. Officially at least, the forward thinkers planning a new pan-Asian trade settlement currency alternative to the dollar are looking at backing it with commodities and not a gold standard. Since Sergei Glazyev announced an enquiry into the matter, the Middle Eastern pivot away from the petrodollar to Asian currencies not only injects a new urgency into his committee’s deliberations but is bound to have a significant bearing on its outcome.

The implications for the western alliance play no part in current monetary policies. Their central banks act as if there’s no danger to their own currencies from these developments. But any doubt that fiat currencies will be replaced by currencies linked to tangible commodities, whether represented by gold or not, is fading in the light of developments.

With neither the economic establishment nor the public having a basic understanding of what is money and why it is not currency, it is hardly surprising that current financial and economic developments are so poorly understood, and the correct remedies for our current monetary and economic conditions are so readily dismissed.

These errors and omissions are set to be addressed in 2023.

Tyler Durden

Fri, 12/23/2022 – 21:25 - China's Post-Zero-COVID Surge Is Infecting 37 Million People Per Day

China’s Post-Zero-COVID Surge Is Infecting 37 Million People Per Day

In a stunning admission, according to estimates from the government’s top health authority, nearly 37 million people in China may have been infected with Covid-19 on a single day this week.

This is a shockingly stark divergence from the extremely low ‘official’ case count (which reported just 62,592 symptomatic) and utterly dwarfs the previous global daily record of about 4 million, set in January 2022, as Omicron spread…

The new data was provided in a closed-door meeting by Sun Yang, a deputy director of the Chinese Center for Disease Control and Prevention, on Wednesday.

According to two people familiar with the matter, The FT reports that Chinese officials estimate about 250mn people or 18 per cent of the population were infected with Covid-19 in the first 20 days of December as Beijing abruptly abandons its Zero-COVID strategy that for almost three years has crushed economic growth (and citizens’ freedoms).

As @MrSeanHaines noted on Twitter, it’s amazing the 180 Chinese state media have done on their Covid messaging of late.

“Omicron is not flu.”

… until it was. pic.twitter.com/L9z07Aprs5

— Whipling (@MrSeanHaines) December 19, 2022

https://platform.twitter.com/widgets.js

Bloomberg notes that it is unclear how the Chinese health regulator came up with its estimate, as the country shut down its once ubiquitous network of PCR testing booths earlier this month. Precise infection rates have been difficult to establish in other countries during the pandemic, as hard-to-get laboratory tests were supplanted by home testing with results that weren’t centrally collected.

Sun said the rate of Covid’s spread in the country was still rising and estimated that more than half of the population in Beijing and Sichuan were already infected, the people briefed on the meeting said.

And, of course, 99.9% of those people will be just fine.

This is extremely notable obviously as while China is experiencing its first real wave of infection, it is massive and will likely mean almost the entire nation will have natural immunity in two to three months… which will allow the economy to restart fully.

Chen Qin, chief economist at data consultancy MetroDataTech, forecasts China’s current wave will peak between mid-December and late January in most cities, based on an analysis of online keyword searches.

The lack of information made public by China on its Covid wave has led Washington and the World Health Organization to push Beijing to be more transparent on case counts, disease severity, hospital admission figures and other health statistics that have been made widely available by other countries.

“It is very important for all countries, including China, to focus on people getting vaccinated, making testing and treatment available and, importantly, sharing information with the world about what they’re experiencing,” U.S. Secretary of State Anthony Blinken said at a Dec. 22 press briefing.

“It has implications not just for China, but for the entire world. So we would like to see that happen,” he added.

Finally, we note that The Epoch Times reports ten famous Chinese medical experts passed away soon after Beijing lifted its zero-COVID policy. Most of them were members of the Chinese Communist Party (CCP), and two were allegedly involved in the live organ harvesting of prisoners of conscience.

While the Chinese media reported the deaths resulting from “illness,” they didn’t provide additional information, causing Chinese netizens to speculate.

A Chinese netizen commented, “It is indeed a bit strange that they died in December one after another—especially on the 16th, 17th, 18th, and 19th.” Another said: “They all died of ‘illness’ without specific reasons. It’s hard not to contemplate why.”

Tyler Durden

Fri, 12/23/2022 – 21:00 - Unleashing Clean Fusion Power Is America's Best Defense Against Tyranny

Unleashing Clean Fusion Power Is America’s Best Defense Against Tyranny

Authored by Lawrence Kadish via The Gatestone Institute,

It may prove to be as historic as the harnessing of fire, invention of the wheel, or the channeling of electricity. It will certainly rank on a par with the first release of nuclear energy in an experimental Chicago reactor or its first test as an atomic weapon near Los Alamos, New Mexico.

It is the first successful experiment to extract power from controlled fusion.

It may take a decade or more to convert their successful experiment into commercially available power, but what it offers is an inexhaustible, readily available source of clean energy that eliminates pollution, greenhouse gases, or radioactive waste from the current generation of nuclear reactors.

In short, it has the means to be as powerful and transformative than any advance in energy technology mankind as ever deployed to run its society.

Fusion occurs within our Sun and the stars that fill our night sky. The process combines hydrogen atoms, turning it into helium and producing the sunlight that allows civilization to exist orbiting some 93 million miles from the Sun. In an effort to replicate that law of physics, American scientists have used reactors and lasers to determine how they can harness its enormous power. (It has been estimated that a modest container of the “fusion fuel” is equivalent to one million gallons of oil, generating some 9 million kilowatt hours of electricity.)

As we discovered with the invention of the atomic bomb, physics can’t be kept as a national security secret.

The Soviets were working on trying to figure out how to harness fusion for something other than a hydrogen bomb more than half a century ago. Before the fall of the Soviet Union, there was even a mutual assistance program announced by Ronald Reagan and Mikhail Gorbachev.

But leadership in energy technology is crucial to a nation that is founded on freedom and committed to remaining a global superpower for good. America has already invested hundreds of millions of dollars into fusion research and it is beginning to pay off in this most recent announcement of a breakthrough. New and expanded research efforts are being announced by America’s scientific community in concert with universities such as MIT and with Western nations. They are suggesting the first commercial power station might come online as early as the 2030s.

Smart oil company executives who also recognize the power of physics will immediately understand that fossil fuels could very well become a museum curiosity if the key to unlocking the power of fusion has just been found. If that is the case, they too should begin to invest in these advances, accelerating our leadership in fusion while ensuring they have a seat at the table when the Oil Age comes to an end.

It is rare for us to recognize a turning point in humankind’s history. Too often it comes with the declaration of war. In this case, it is the sharp light of lasers illuminating a power as old as creation, one that is about to change the course of civilization for the better.

Tyler Durden

Fri, 12/23/2022 – 20:35 - Sen. Lindsey Graham: Someone Must "Take Out" Putin For War To End

Sen. Lindsey Graham: Someone Must “Take Out” Putin For War To End

Senator Lindsey Graham this week repeated his call for Russian President Vladimir Putin to be assassinated, telling Fox News in a live interview that the Ukraine war will only end if someone “takes Putin out”.

“How does this war end? When Russia breaks, and they take Putin out. Anything short of that, the war’s gonna continue,” Graham said on Wednesday’s America Reports on Fox.

Getty Images Graham said Moscow’s invasion won’t succeed because the United States is “in it to win it, and the only way you’re gonna win it is to break the Russian military and have somebody in Russia take Putin out to give the Russian people a new lease on life.”

He also called on Washington and NATO to keep up arms and support for Ukraine “completely, all in without equivocation,” and further that ramping up long-range missile transfers to Kiev would help “dislodge” Russian forces from the Donbas, and even Crimea.

He additionally said that larger drones would “kill tons of Russians without losing any Ukrainians in the endeavor” – and essentially called for giving Zelensky everything he’s asking for.

During Zelensky’s Wednesday address to Congress, which actually saw less than half of House Republicans show up, which was in part due to holiday travel and weather given also the visit was unannounced until the day prior, the Ukrainian leader suggested the US should even send tanks and aircraft. “I can assure you that Ukrainian soldiers can perfectly operate American tanks and planes themselves,” he had said during the 30-minute speech.

Lindsey Graham on Fox News: “How does this war end? When Russia breaks and they take Putin out.” pic.twitter.com/yaWt0vpRNV

— Aaron Rupar (@atrupar) December 21, 2022

https://platform.twitter.com/widgets.js

It wasn’t the first time Graham called for Putin’s assassination on a national news program. In March he made similar statements.

At the time this prompted an official reaction from the White House distancing President Biden from the assassination comments. The White House Press Secretary had said “that is not the position of the United States government and certainly not a statement you’d hear come from the mouth of anybody working in this administration.”

Tyler Durden

Fri, 12/23/2022 – 20:10 - FDA Approves Monoclonal Antibody To Treat COVID-19 For First Time

FDA Approves Monoclonal Antibody To Treat COVID-19 For First Time

Authored by Mimi Nguyen Ly via The Epoch Times (emphasis ours),

The U.S. Food and Drug Administration (FDA) has, for the first time, approved a monoclonal antibody to treat COVID-19 in hospitalized patients.

The logo of Swiss pharmaceutical giant Roche in Basel on Feb. 2, 2011. (Fabrice Coffrini/AFP/Getty Images) Healthcare company Roche’s Actemra (tocilizumab) intravenous (IV) was approved by the FDA to treat severe COVID-19 in adults, the company announced on Wednesday.

Specifically, the drug is approved in cases where the patient is hospitalized and is receiving systemic corticosteroids, as well as requiring supplemental oxygen, non-invasive or invasive mechanical ventilation, or extracorporeal membrane oxygenation.

It is the first FDA-approved monoclonal antibody to treat COVID-19, the company stated.

Monoclonal antibodies are laboratory-created proteins that mimic natural antibodies the body produces to fight off harmful pathogens, such as the SARS-CoV-2 virus that causes COVID-19.

Actemra does not directly target SARS-CoV-2 but addresses the inflammation that occurs from COVID-19 infection. The monoclonal antibody reduces inflammation by blocking the interleukin-6 receptor.

The drug is recommended to be administered as a single 60-minute IV infusion.

According to Roche, more than one million hospitalized COVID-19 patients have been treated with Actemra worldwide since the start of the pandemic.

The drug was previously FDA-authorized for emergency use in hospitalized adults and pediatric COVID-19 patients (above 2 years of age) back in June 2021.

Right now, the FDA has not approved Actemra to treat hospitalized patients aged 2 to under 18, but the Emergency Use Authorization (EUA) still applies.

Actemra is not authorized or approved for the treatment of outpatients with COVID-19.

According to Roche, Actemra is approved for use in more than 30 countries for patients hospitalized with severe COVID-19. This includes the European Union, Japan, the United Kingdom, New Zealand, Russia, and Brazil. It is also provisionally approved in Australia, and authorized for emergency use in Ghana, Mexico, and Korea for certain patients hospitalized with severe or critical COVID-19.

The drug has also been recommended and prequalified by the World Health Organization (WHO).

In the United States, Actemra is the seventh FDA-approved indication since it was launched in 2010. It has been approved for use against other inflammatory diseases, including rheumatoid arthritis.

Tyler Durden

Fri, 12/23/2022 – 19:45 - Great News NFL Fans: Avocado Prices Have Crashed

Great News NFL Fans: Avocado Prices Have Crashed

After surging to record highs in the first half of 2022, wholesale avocado prices crashed in late summer into fall time, just as the NFL season kicked off. Guacamole is the star player at any football party, and this season, there’s a sign of relief that avocado prices are back to affordable levels.

For a 20-pound box of avocados from the state of Michoacan, Mexico (the central hub of Mexican avocado production), prices jumped as high as $51 in May. Some main drivers in igniting prices to record highs were production woes and import issues at the border. Even during the Super Bowl in February, we pointed out Americans were paying some of the highest costs ever for the fruit.

Now Mexican wholesale avocado prices have collapsed from $51 to $16, or a 70% drop, because of oversupplied conditions in US markets.

After border trade was resolved and shipments restarted earlier this year, Mexican farmers produced bumper crops.