- "An Existential Race Amongst The Great Powers Accelerates, At The Dawn Of The AI Age"

“An Existential Race Amongst The Great Powers Accelerates, At The Dawn Of The AI Age”

By Eric Peters, CIO of One River Asset Management

“In the global competition on AI, the alleged role of a single, and outdated, version of an American open-source model is irrelevant when we know China is already investing more than one-trillion dollars to surpass the US on AI,” said a Meta spokesperson, defending itself against an allegation.

The Jamestown Foundation had released an academic paper [here] with the following claim: “The military and security sectors within the People’s Republic of China are increasingly focused on integrating advanced AI technologies into operational capabilities. Meta’s open-source model Llama (Large Language Model Meta AI) has emerged as a preferred model on which to build out features tailored for military and security applications. In this way, US and US-derived technology is being deployed as a tool to enhance the PRC’s military modernization and domestic innovation efforts, with direct consequences for the United States and its allies and partners.”

The report also stated: “In September, the former deputy director of the Academy of Military Sciences (AMS), Lieutenant General He Lei, called for the United Nations to establish restrictions on the application of artificial intelligence (AI) in warfare. This would suggest that Beijing has an interest in mitigating the risks associated with military AI. Instead, the opposite is true. The People’s Republic of China is currently leveraging AI to enhance its own military capabilities and strategic advantages and is using Western technology to do so.”

As the world waited for America to choose its next commander-in-chief, I spent the week thinking about security matters.

“The number of different categories of space weapons that China has created and the speed with which they’re doing it is very threatening,” warned General Chance Saltzman, head of space operations for the US Space Force, as an existential race amongst the great powers accelerates, at the dawn of the AI Age.

Tyler Durden

Sun, 11/03/2024 – 23:20 - The Future Of Debanking

The Future Of Debanking

Authored by Jeffrey Tucker via The Epoch Times,

Among many worrying trends is the problem of debanking. It is underreported. The victims do not like to talk about it, even among family and friends.

It is rarely discussed at all in public forums. Only specialists write about it. But it is a threat to everyone in the most intensely effective way. The practice denies people access to the basics of life and yet there is no appeal, no process, no methods of challenge, and no remediation.

We did not know until Melania Trump’s latest biography that she and her son Barron were victims of debanking, the practice of shutting down a person’s bank account based on an unsigned and unexplained decision in which the account holder is merely notified that all services are hereby denied.

Good on her for admitting this. People rarely do.

This apparently happened in 2021, after her husband had left the office of the presidency. There were concerted efforts at the time to wipe out the memory of his time in office.

Back in those days, I used the home assistant app called Google Home. I asked who the 45th president was and the product responded that it had no information on that. Indeed, it was like a scene from Orwell.

Apparently Melania and Barron were also being deleted by their own bank.

“I was shocked and dismayed to learn that my long-time bank decided to terminate my account and deny my son the opportunity to open a new one,” she wrote.

She did not say the name of the bank. Nor do most victims of this practice. The bank simply sends a letter and encloses the balance. The victim then has to hunt around for an alternative, now with the black mark of having been canceled by another bank, which raises real questions. The problem is compounded by the absence of any real reason for the actions.

We do not know how widespread this practice is but, anecdotally, it has clearly escalated in recent years. The same has happened to the former president, and many of his supporters.

The Free Press comments: “Also debanked have been a number of Christian charities, including Indigenous Advance Ministries, a Memphis-based charity that does philanthropic work for orphans in Uganda, and Family Council, a pro-life charity based in Arkansas. According to Democratic lawmakers, many Arab and South-Asian Americans—who are considered ‘high risk’ because of being Muslim—have been debanked, too.”

There is no human right to have a bank account, and banks have every legal right to decide with whom they would like to do business. They can end client services for anyone at any time and have no legal obligation to explain or allow appeal.

Confusing matters is that banks may not necessarily want to kick out account holders but are pressured to do so by their own compliance standards. If they see a business account engaged in activity that seems even slightly sketchy—dealing with crypto or moving cash around in strange ways or taking too many deposits from a strange source—the system itself could flag the account and the process is then set in motion with no human decision-maker.

Indeed, the letter could be sent and the account removed without any knowledge of someone at the bank. The algorithms are ruling the people in this case, a problem that has become extremely serious in a range of areas.

At the same time, there is real danger presented when the practice is deployed for purely political reasons. It is a digital application of the principle of Sun Tzu: “The supreme art of war is to subdue the enemy without fighting.” Debanking allows exactly this.

Banking services exert an incredible power over our lives. Our automatic payments keep the lights on, the mortgage paid up, and the cellphone going. The debit cards and credit cards hooked into them are the lifeblood of our living standards. Try to function even a day or two without them and you’d see what I mean.

Having them suddenly cut off is like falling into the abyss. You can march down to bank headquarters and demand answers, but this much I promise you: You will get none. Probably no one there, not even the branch manager, has any answer. For whatever reason, the powers that be have decided that your account is not one they want and that is the end of it. There is no one to sue because no one did anything wrong. Granting banking services is at the discretion of the bank, period.

The problem is that the banking system is integral to power itself, regulated by agencies and holding vast amounts of government debt in a system that is ultimately overseen by the legislative and executive branches. That makes banking political, not just in the United States but all over the world. The discovery by political elites that they can weaponize the banking system should alarm anyone and everyone simply because it allows the punishment of political enemies through surreptitious means.

The Free Press points to “an emerging, bipartisan, anti-debanking bloc on Capitol Hill.” They quote Ro Khanna, a Democratic representative from California. “Every American should have the ability to take out a loan or save for their future without fear of discrimination or having their accounts closed without explanation,” Khanna said, according to the publication.

Indeed, that seems entirely reasonable. There needs to be some action taken before this gets out of hand, which it will very quickly in today’s contentious political environment.

Experts on this topic all agree: The debanked need to speak out about this now, posting letters and recording communications. It’s the only way we draw public attention to this.

There is a broader problem relating to the creation of social-credit systems around the world, most especially in China. Political compliance becomes a standard of inclusion in financial and social life generally. It’s a highly effective way that regimes can carefully and quietly control their citizens. It has no place in a free society, and it seems like our laws ought to be clear about that.

Even if the technology allows it, even if the algorithms dictate it, we need systems in which banks and other financial institutions cannot end services for people without some explicitly cited reason and an opportunity for appeal, in addition to some legal recourse in the case of arbitrary action. Taking those steps would help underscore the point that this society aspires to be free and grants its citizens dignity and rights.

Views expressed in this article are opinions of the author and do not necessarily reflect the views of The Epoch Times or ZeroHedge.

Tyler Durden

Sun, 11/03/2024 – 22:10 - Medvedev: US Election Doesn't Matter, Ukraine War Won't Stop, And Trump May Get JFK'd If He Intervenes

Medvedev: US Election Doesn’t Matter, Ukraine War Won’t Stop, And Trump May Get JFK’d If He Intervenes

Days after Russia launched a massive readyness drill of their nuclear forces, former Russian President and current deputy chairman of the country’s Security Counsel Dmitry Medvedev says that the outcome of the US election doesn’t matter, as both candidates believe “Russia must be defeated,” and that if Donald Trump is elected and tries to intervene, he may be assassinated.

Dmitry Medvedev, 2016. Medvedev made the comments to his nearly 1.4 million followers on Telegram.

The entire post, translated (emphasis ours);

The whole world stands frozen in uneasy anticipation, waiting for the results of the presidential election in the distant land of ‘Us.

There is no reason why we should have high expectations about it.

1. The outcome of the election will not change anything for Russia, as both candidates share the same bipartisan consensus that ‘Russia must be defeated’.

2. Kamala is dumb, inexperienced, and easy to control, as she will be terrified of everyone around her. All the real decision-making will be done by a coterie of top ministers and advisors plus (indirectly) the Obamas.

3. A low-energy Trump, spewing clichés like “I’ll offer them a deal” and “I have a very good relationship with…”, will be forced to comply with the system and its rules. He won’t stop the war. Not in one day, not in three days, not in three months. And if he actually attempts to do it, he could end up becoming the new JFK.

4. The only thing that matters is how much cash the new POTUS can squeeze out of Congress to finance someone else’s war, fought in a far-off land. Cash to feed the American military-industrial complex and to line the pockets of the Banderite scum in Ukraine.

5. That is why, if we want to please both candidates for the highest American office, the best thing to do on November 5 is keep pummeling the Nazi regime in Kiev!

Meanwhile, Medvedev reiterated to Russian state-controlled news agency RT that adding Ukraine to NATO could lead to World War III.

“Shortly before his death, already at a very mature age, he (Kissinger) as if with some regret suggested that now we have no choice but to accept Ukraine into NATO,” he told the outlet. “I think that he was still mistaken in this. There is no such predetermination. Because, choosing between some promises and the possibility of starting a third world war—the choice is still quite obvious.”

Ukraine’s long-held goal of NATO membership was among the objectives in the Victory Plan that Ukrainian President Volodymr Zelensky unveiled during a visit to the U.S. in September.

Kyiv’s ambassador to the alliance Nataliia Galibarenko said in October that the Ukrainian government would like a formal invitation to join the alliance before President Joe Biden leaves office in January.

Along with claims of alliance encroachment on Russia, Moscow often refers to the prospect of Ukraine joining NATO to justify its actions. Kyiv says it needs to join NATO to resist any future Russian aggression. -Newsweek

He also told RT that Moscow believes the current US and European political establishments lack the “foresight and subtlety of mind” of Kissinger, and should take the Kremlin’s nuclear warnings seriously.

“If we are talking about the existence of our state, as the president of our country has repeatedly said, your humble servant has said, others have said, of course, we simply will not have any choice,” he said, per Sky News and The Sun, adding that the US and the West are “wrong” if they think Putin won’t turn to nuclear weapons if NATO sought to inflict a defeat on Russia in the Ukraine war.

“If the new [US] leader is going to be fiercely dedicated to adding fuel to the fire of the Russia-Ukraine conflict, it will be a very bad choice,” adding “Because this is the road to hell.”

“It’s really a road to World War Three,” he continued. “Whoever decides to continue the war will be making a very dangerous mistake.”

Tyler Durden

Sun, 11/03/2024 – 21:35 - What's Wrong In Our Nation?

What’s Wrong In Our Nation?

Authored by Star Parker via The Epoch Times,

As we move to the conclusion of this election cycle, there seems to be only one thing about which all Americans agree.

That is, that something is very wrong in our nation.

In the latest Gallup polling, only 22 percent say they are satisfied with the direction of the country. The highest this has been over the last 16 years was 45 percent back in February of 2020.

So, despite change in party control over these years, the sense that something is wrong in the country has persisted.

More in the framework of this election, only 39 percent say they are better off than they were four years ago, and 52 percent say they are not better off.

Most Americans do not even have confidence in the sources where they get their news. Only 31 percent say they have a great deal or fair amount of confidence in mass media. The first time Gallup asked this question, back in 1972, 68 percent expressed confidence in mass media.

A record high percent of Americans, 80 percent, say the country is “greatly divided” on the most important values.

In a New York Times/Siena College poll, only 49 percent say “American democracy does a good job representing the people.” And 76 percent say “American democracy is currently under threat.”

All agree that something is wrong, but no consensus emerges about what exactly is the problem.

Is it possible to put a finger on what is causing the cynicism and disillusionment that grips the psyche of our nation?

My view is the problem is the drift of the nation from its founding principles.

To put it another way, we have no choice about whether we have faith or belief. But we do have choice about what it is we believe.

The dramatic change that has taken place in America is the uprooting of the Bible as our starting point for right and wrong.

We have exchanged our faith in God for a faith in government.

In 1950, Gallup reports 0 percent of Americans said they have no religion. By 1970, this was up to 3 percent. And by 2023, this was up to 22 percent.

Over this same time, in 1950, the federal government consumed 14.2 percent of our GDP. The estimate from the Congressional Budget Office is that in 2024, that percent will be 23.9 percent.

The preamble to our Constitution explains its purpose is “to secure the blessings of liberty to ourselves and posterity.”

Our Constitution was not presumed to be the source of our freedom. We are already free by virtue, as noted in the Declaration of Independence, of being created thus by our God.

Our Constitution was designed to limit interference by government in the ability of free, God-fearing men and women to live their lives as they see fit.

The guideline for behavior, for right and wrong, is that which is transmitted to us from our Creator through the Bible.

Under this reality, America grew and became great.

However, success brings the sin of pride, and we begin to attribute our success to our cleverness rather than our faith and personal responsibility. As increasing numbers of Americans have turned away from God, they have turned more to government.

The sad paradox is that as Americans turn to government, they abrogate the very freedom that the founders envisioned government’s role to secure.

The result is less economic growth, breakdown of the American family and disappearance of children.

Growth of government, growth of federal debt, and no children is no formula for a country with a future.

I believe this is what Americans are sensing and what is producing all the negative feelings and pessimism.

We must return to the vision of our founders.

A free nation, under God. And a Constitution that secures “the blessings of liberty.”

Short of this, although we may experience ups and downs, the nation will not realize its great potential.

* * *

Views expressed in this article are opinions of the author and do not necessarily reflect the views of The Epoch Times or ZeroHedge.

Tyler Durden

Sun, 11/03/2024 – 21:00 - America's Out Of Control Debt "Is A National Security Threat" – Judy Shelton On Gold & Global Peace

America’s Out Of Control Debt “Is A National Security Threat” – Judy Shelton On Gold & Global Peace

“I want the United States to be the leader if there’s any kind of gold backing to a currency.”

– Judy Shelton

Economic advisor to former President Donald Trump, Judy Shelton, joins GoldTelegraph’s Alex Deluce for a captivating conversation spanning a wide range of subjects.

Judy Shelton is a Senior Fellow at the Independent Institute and author of the book Good as Gold: How to Unleash the Power of Sound Money.

She is the former Chairman of the National Endowment for Democracy and former U.S. Director of the European Bank for Reconstruction and Development. She has testified before the U.S. Senate Banking, Senate Foreign Relations, House Banking, House Foreign Affairs, and Joint Economic Committee.

In their conversation, Deluce and Shelton explore a series of compelling topics, highlighted by Judy’s riveting career stories, including her interactions with figures like Alan Greenspan, Paul Volcker, and other influential central bankers.

One of the most powerful revelations she shared was Paul Volcker’s frank admission: he had always believed the United States would eventually return to the Bretton Woods system.

For those unfamiliar, Volcker was referencing the pivotal moment known as the Nixon Shock in 1971, when President Nixon abruptly suspended the U.S. dollar’s convertibility into gold, shattering the foundation of the Bretton Woods system.

At that historic moment in history, Volcker served as the Under Secretary of the Treasury for International Monetary Affairs.

This marked the transition to a pure fiat monetary system.

Deluce and Shelton get into a wide-ranging conversation that covers many topics, which include:

-

The US Dollar

-

The U.S. National Debt as a Security Threat

-

Federal Reserve’s Role in America’s debt and Financial Instability

-

Historical Perspectives on Monetary Policy

-

Potential Return to a Gold-Backed System

-

Comparisons Between Soviet Central Planning and Current Economic Policies

-

BRICS Countries and Global Financial Shifts

-

Treasury Bond Backed by Gold and the Potential for Gold Backed Stablecoins

TIMESTAMPS:

0:49 – How much does the US dollar’s global dominance depend on the upcoming election?

2:08 – Is debt a threat to U.S. national security?

3:20 – How responsible is the Federal Reserve for America’s current debt level?

7:54 – How has the Federal Reserve contributed to the financial instability we face today?

13:22 – How do you see today’s shifting global landscape, given your deep background in historical analysis?

19:46 – Are we on the verge of another major global monetary shift, and what might it look like?

29:13 – Was there a specific moment or event early in your career that sparked your interest in the study of gold?

34:09 – Memorable stories from your conversations with Alan Greenspan, Paul Volcker and Robert Mandel

39:22 – How do you define sound money?

46: 14 – How interconnected are sound money, economic opportunity, stability, and global peace, especially in today’s polarized world?

49:51 – Why do you think so many policymakers dismiss and mock gold, even as global demand is at records and central banks are stockpiling?

54:13 – How does the Fed’s dual mandate open it to political vulnerabilities, and could a rules-based system address these issues?

59:37 – How does the Fed’s centralized control over interest rates affect what is supposed to be a market-based economy?

1:02:48 – Are central banks aggressive policies eroding or undermining capitalism and the concept of free markets?

1:06:23 – Are BRICS nations positioning gold to become a unit of account and medium of exchange, potentially bypassing the traditional financial system?

1:09:38 – Could imposing tariffs on countries that move away from the dollar actually help America maintain its financial muscle?

1:14:47 – What gives you hope for potential reforms that could create a monetary system supporting economic freedom and stability for everyone?

1:16:58 – Could we potentially see you in the next administration advocating for these policies?

Watch the full interview below:

GOLD TELEGRAPH CONVERSATIONS #1:

JUDY SHELTON“I want the United States to be the leader if there’s any kind of gold backing to a currency.” – @judyshel

Economic advisor to former President Donald Trump, Judy Shelton, joins me for a captivating conversation spanning a wide… pic.twitter.com/gmk9GqBCPz

— Gold Telegraph ⚡ (@GoldTelegraph_) November 3, 2024

Tyler Durden

Sun, 11/03/2024 – 20:25 -

- What Drives US Voters

What Drives US Voters

By Philip Marey, Senior US Strategist at Rabobank (also available in pdf format)

Summary

-

We analyze a 2022 survey from AP VoteCast to understand what drives US voters. We find that voters who judged economic conditions as “poor”, were more likely to vote for a Republican candidate in the Senate or the House of Representatives, punishing the Biden-Harris administration. In contrast, those who considered economic conditions to be “good” were more likely to vote Democrat. However, voters who judged economic conditions as “not so good” were also more likely to favor a Democrat, suggesting that Biden did not get all of the blame for the disappointing economy or that voters made a trade-off between the economy and other issues.

-

On social policy issues, voters are more likely to vote for a Republican if they think that abortion should be illegal in all or most cases, if they think that the racism issue is not too or not at all serious, if they were not too or not at all concerned about COVID and if they strongly favor increased border security.

-

We also found that demographic characteristics determined US voter behavior. Men are more likely to vote Republican. In contrast, women and non-binary people are more likely to vote Democrat. The same is true for Black, Latino and Asian people. White people are more likely to vote Republican. People with a higher income are more likely to vote Republican, but – at a given income level – college graduates and people with a postgraduate degree are more likely to vote Democrat.

-

While this confirms several stereotypes, we also find some more nuanced results. For example, the probability of voting Republican increases with age until it peaks at the 50-64 segment, then it falls back a little. Moreover, if we take a closer look at the Hispanic vote, we find that Cuban Americans are more likely to vote Republican. Finally, it should be noted that the regression results imply that Black men are less likely to vote Democrat than Black women.

-

We also find that pop culture affects voter behavior, with people having a favorable view of Taylor Swift more likely to vote Democrat – even within their age cohort– and those with an unfavorable view of her more likely to vote Republican.

-

For the 2024 elections, our results suggest that the economy is a drag on the Harris campaign, but there are opportunities to offset this through social policy issues such as abortion. What’s more, our results show that in demographic terms Kamala Harris more closely resembles the typical Democratic voter than Joe Biden, which could help explain the increase in enthusiasm among Democratic voters after she replaced him at the top of the ticket. However, our results also explain why Harris has difficulty convincing Black men to vote for her: they are less likely to vote Democrat than Black women more generally, even if she is not on the ticket.

Introduction

The 2022 US midterm elections presented a complex political landscape. This report uses data from the AP VoteCast survey to delve into the various factors that shaped voter behavior and electoral outcomes, focusing on three key areas: the impact of economic anxieties on voting behavior, the changes in policies on abortion and immigration, and the demographics of American voters. The 2022 midterms occurred against a backdrop of significant economic uncertainty, with inflation emerging as a dominant concern among voters. As inflation hit a 40-year high of 9.1% in June 2022, Americans expressed growing anxiety about their financial wellbeing, despite a low unemployment rate of 3.6%. By November 2022, inflation had started to fall, but was still very high at 7.1%.

The 2022 midterms also demonstrated the rapid evolution of voter priorities. Just two years earlier, during the height of the pandemic, healthcare and public health concerns dominated the political discourse. By 2022, these issues had taken a backseat to inflation. However, despite the changes in priorities compared to the 2020 elections, voters were still concerned with non-economic issues. Figure 2 and 3 show the responses of voters to “Which one of the following would you say is the single most important issue for you?”

The economy was the main concern among both Democrats and Republicans, with 33.2% and 63.2% of respondents choosing it respectively. However, for Democrats climate change, abortion and healthcare followed closely. For Republicans, at some distance, immigration and crime were mentioned most often.

Regarding abortion, The Supreme Court’s decision to overturn Roe v. Wade in Dobbs v. Jackson Women’s Health Organization had a significant impact on the 2022 midterm elections. For about a quarter of voters, the Court’s decision was the single most important factor in their midterm vote. This figure increased to more than 3 in 10 among groups traditionally aligned with prochoice positions: Democratic voters, younger women, and first-time voters. These voters predominantly supported Democratic candidates. The impact was particularly pronounced among women of color. Majorities of Black and Hispanic women reported that the Supreme Court decision influenced their voting behavior. Finally, a key issue for Republican voters in 2022 was immigration, because of a surge in the number of migrant apprehensions at the southern border. Democrats, however, ranked immigration as their last concern.

The data set from the 2022 midterms offers valuable insights into US voter behavior. It reveals that while economic concerns were at the forefront of voter priorities, these were not the only factors driving electoral decisions. The economic anxieties that dominated the political discourse led to a Republican majority in the House. However, the data also underscores the continued significance of non-economic issues, such as abortion and immigration, in shaping voter behavior. The Supreme Court’s decision to overturn Roe v. Wade emerged as a pivotal factor, underscoring the powerful role of social issues in mobilizing the electorate.

Data and model

Our analysis is grounded in a comprehensive dataset primarily sourced from AP VoteCast, a nationwide survey conducted after midterm and general elections in the US comprising more than 100 thousand respondents. This data provides direct insights into the demographics, sentiments, and perceptions on various economic and non-economic topics of individual voters. AP VoteCast, initiated in 2018, combines interviews with randomly sampled registered voters from state voter files and self-identified registered voters from NORC’s AmeriSpeak® panel and nonprobability online panels.

To examine the relationships between voters’ attitudes and their candidate preferences, we employ a logistic regression model. The regression analysis of the data at the individual level helps us understand how these various factors interact and influence voting behavior. We can analyze the impact of economic factors and social policy issues, given the demographic characteristics and vice versa. This means that we can isolate the pure effects of economic factors, social policy issues and demographic characteristics on voter behavior at the micro level, rather than effects at the macro level that are distorted by the composition of the sample.

Empirical results

Our regression results can be described as follows. In 2022, voters who judged economic conditions as “poor”, were more likely to vote for a Republican candidate in the Senate or the House of Representatives. This is a plausible result since the Democrats (the Biden-Harris administration) were in charge of economic policy. In contrast, those who considered economic conditions to be “good” were more likely to vote Democrat. Interestingly, also voters who judged economic conditions as “not so good” favored a Democrat. So some voters were willing to forgive Biden or thought that he was not (fully) to blame for the economic conditions. We should not forget that high inflation in 2021 and 2022 was not restricted to the US, although the empirical evidence suggests that excessive fiscal policy has made it worse. Also, some voters could be making a trade-off between the economy and other issues. For example, if you oppose making abortion illegal, you may be willing to tolerate some economic adversity from the party that is pro-choice.

Now let’s turn to these social policy issues. Voters who thought that abortion should be illegal in all or most cases were more likely to vote Republican. In contrast, voters who though that abortion should be legal in most cases were more likely to support a Democratic candidate. Voters who were not too or not at all concerned about COVID were more likely to vote Republican, while voters who were somewhat or very concerned favored the Democrats. Compared to voters who strongly favored increased border security, those who only somewhat favored this or opposed this were more likely to vote Democrat. Those who thought the racism issue was not too or not at all serious were more likely to vote Republican compared to those who thought it was somewhat or very serious.

These questions were all about political issues, but we also found that demographic characteristics – even after correcting for economic and social policy issues – determined voter behavior. In particular, women and non-binary people were more likely to vote Democrat. The same is true of Black, Latino and Asian people. Age also matters, as people above 30 are more likely to vote Republican. This probability increases with age until it peaks at the 50-64 segment. People of 65 and older are also more likely to vote Republican, but not as much as the cohort below. If we look at education, we find that college graduates and people with a postgraduate degree are more likely to vote Democrat. In contrast, people with a higher income are more likely to vote Republican. This may seem contradictory because people with a higher education tend to have a higher income. However, our regression allows us to identify the effects of education given a certain level of income and vice versa. So if two persons with the same education differ only in their income level, then the one with the higher income is more likely to vote Republican. And if two people with the same income level differ only in their level of education, then the higher educated person is more likely to vote Democrat.

To summarize, the Republican voter in 2022 could be characterized as an older white male with a higher income but no college degree who judged economic conditions as poor, who thought that abortion should be illegal, strongly favored increased border security, was not too or not at all concerned by COVID and thought that the racism issue was not too or not at all serious. In contrast, a Democratic voter was typically a younger college-educated woman of color with a lower income who judged economic conditions as good or not so good, who thought that abortion should be legal, did not strongly favor increased border security and was concerned about COVID and racism.

While table 1 may confirm several stereotypes, the regression results show some nuances. Take age for example: the tendency to vote Republican rises with age, but falls back a little for people of 65 and older. We have also taken a closer look at ethnicity and found that not all Hispanic groups exhibit the same voting behavior. In particular, Cuban Americans are more likely to vote Republican than Democrat. This can likely be attributed to the tougher foreign policy stance of the GOP regarding Cuba. Hispanics from all other countries of origin are more likely to vote Democrat. Finally, since the regression isolates the effect of being Black from being a man, the results explain why Kamala Harris is currently having trouble getting support from Black men. Note that these regression results are based on the 2022 midterms, so well before Kamala Harris rose to the top of the Democratic ticket. It shows that Black men being less likely to vote Democrat than Black women is not specific to presidential elections. While former president Obama recently suggested that Black men “just aren’t feeling the idea of having a woman as president”, Democrats should probably better ask themselves why one of their key demographics has been drifting toward the GOP for some time now. The Democrats’ “Opportunity agenda for Black men” that they are now suddenly rolling out may be too little too late for this year’s election.

The Taylor Swift effect

The 2022 midterms also highlight an intriguing connection between pop culture and political preferences. In 2020 Taylor Swift released the song “Only the young” – a political anthem aimed to encourage young adults to “speak up and stand for what is right.” It made references to the surprise victory of Donald Trump in 2016 and how the young voters were outnumbered. Swift’s influence reflects broader trends in youth political engagement. Her public support for Democratic candidates, particularly her advocacy for LGBTQ+ rights, gender equality, and opposition to systemic racism, aligns with issues that resonate strongly with younger voters. This alignment is significant given that Swift’s fan base largely consists of Millennials and Gen Z, demographics that statistically lean more liberal and are generally more receptive to social justice movements. The “Taylor Swift effect” thus serves as a microcosm of larger cultural shifts influencing political engagement among younger voters.

This raises two interesting questions: are Taylor Swift fans more likely to vote Democrat, and if so, is this simply a reflection of their age cohort being more liberal, or are “Swifties” (Taylor Swift fans) actually more likely to vote Democrat than other people with the same demographic characteristics? We find that people with a “very favorable” or “somewhat favorable” view of Taylor Swift are more likely to vote Democrat. In contrast, those with a “somewhat unfavorable” or “very unfavorable” view of her are more likely to vote Republican. Note that the regression takes into account age, so even within the subset of Millennials and Gen Z those with a favorable view of Taylor Swift are more likely to vote Democrat. In this sense, the “Taylor Swift effect” is real. After the debate between Trump and Harris on September 10, Taylor Swift endorsed Kamala Harris “because she fights for the rights and causes I believe need a warrior to champion them.” Swift’s endorsement could help raise the voter turnout among a demographic that is culturally close to the values of the Democrats.

Conclusion

Our findings reveal that while economic anxieties drove many voters towards Republican candidates in 2022, social issues and demographics provided countervailing forces, contributing to the Democrats’ stronger-than-expected performance. In our midterm preview in 2022, we explained that based on economic performance, Biden’s approval rating and the usual midterm loss for the party occupying the White House, the Republicans should be heading for a landslide victory in the midterms, but that the more modest polling results suggested that other factors, such as abortion, could be leading to Republican underperformance, as it did on Election Day.

For the 2024 elections, our results suggest that the economy is likely a drag on the Harris campaign, but there are opportunities to offset this through social policy issues such as abortion. What’s more, while Kamala Harris may have been picked as Vice-President to balance the 2020 Democratic ticket, our regression results show that she is not just another demographic of the Democratic Party, but she actually gets close to representing the typical Democratic voter. This could help explain the recent enthusiasm among Democratic voters that was absent when Biden was on top of the presidential ticket. This also meant that picking Tim Walz as VP candidate was necessary to balance the ticket and attract swing voters. However, our results also show that Black men have been less likely to vote Democrat than Black women well before Kamala Harris rose to the top of the Democratic ticket. Taking a key demographic for granted could hurt the Democratic Party well beyond the 2024 presidential election.

Tyler Durden

Sun, 11/03/2024 – 19:50 -

- How Chinese Traders Will Help Drive Gold to $3,000+

How Chinese Traders Will Help Drive Gold to $3,000+

By Jesse Colombo of the Bubble Bubble Substack

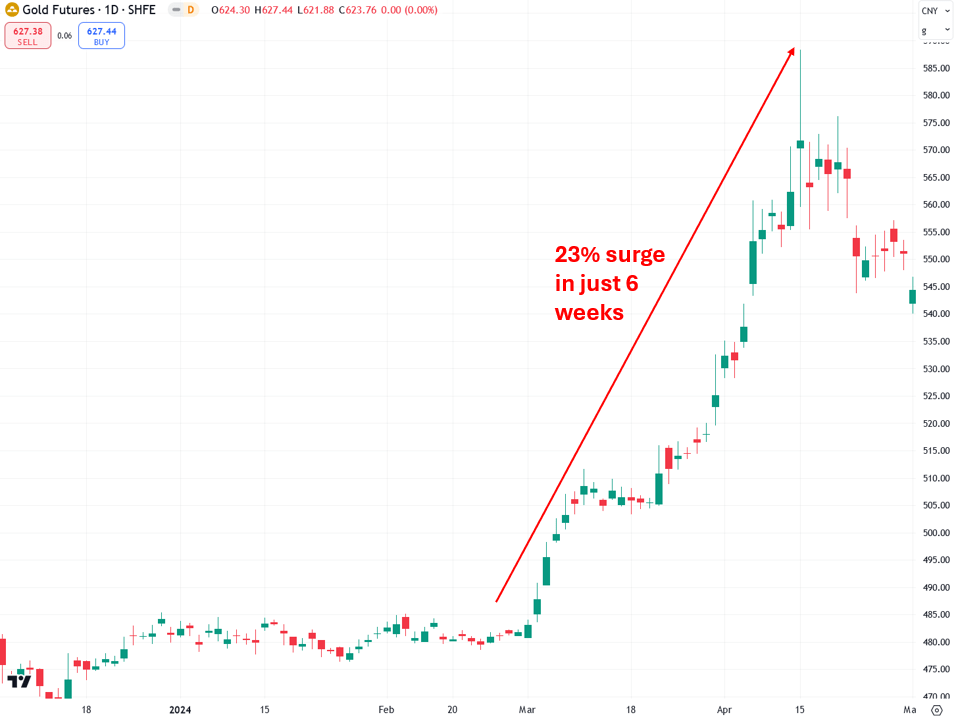

In my debut Substack article on September 6th, I theorized that Chinese futures traders would return from their summer hiatus with renewed vigor, to drive gold prices sharply higher once again in an encore of their spring performance, when they pushed prices up by $400, or 23%, in just six weeks. When I wrote that article, gold was trading at $2,497 an ounce; today, it stands at $2,738 an ounce. I’m now providing an update because the trend I anticipated is unfolding as expected, and I believe the most thrilling, explosive phase is still to come.

The Shanghai Futures Exchange (SHFE) gold futures were the primary vehicle behind the gold frenzy in March and April, a surge that subsequently spilled over into international gold prices:

A fascinating Financial Times article from that time titled “Chinese Speculators Super-Charge Gold Rally” highlighted how trading volume in SHFE gold futures had surged by 400%, propelling gold prices to record highs:

The spring Chinese gold trading frenzy can also be seen in the chart of long open interest in SHFE gold futures:

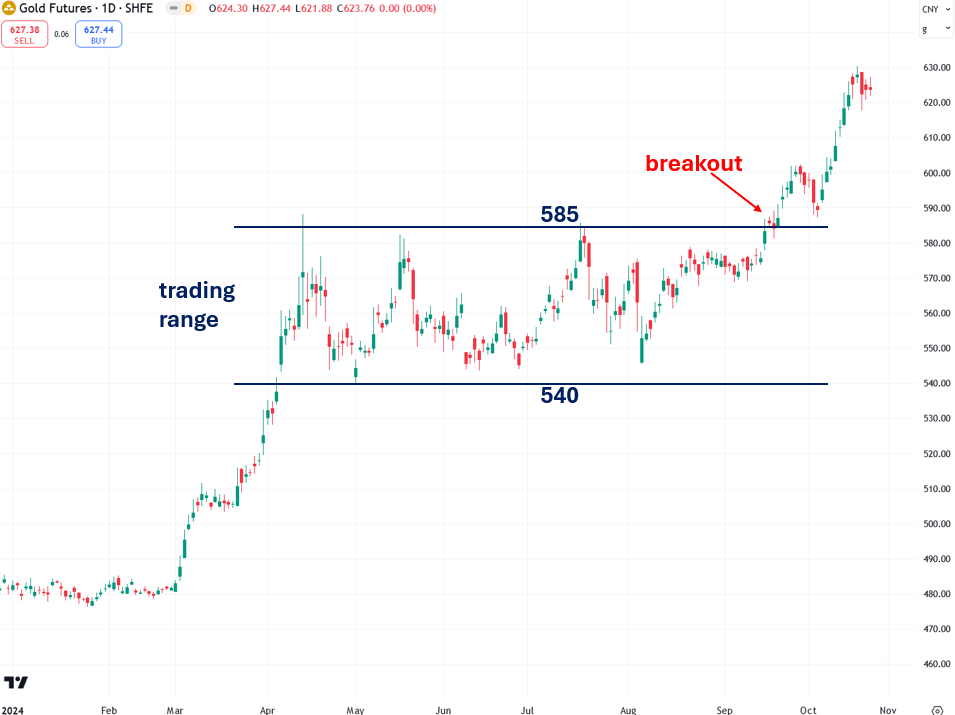

Following the Chinese-driven gold frenzy in the spring, it was as if a switch flipped off on April 15th, leading SHFE gold futures to trade sideways for five months. In my original September 6th article, I explained that SHFE gold futures were merely taking a pause, likely setting the stage for another surge similar to the one seen in the spring. I also noted that a decisive close above the 585 resistance level would trigger a new rally in gold prices—not only in China but globally. As the chart below shows, that’s precisely what’s happening:

As shown in the chart below, the international spot price of gold in U.S. dollars traded in a choppy manner from April until mid-September, when it hit an inflection point and began climbing vigorously once again. This timing is no coincidence; it aligns with SHFE gold futures breaking out of their trading range, drawing Chinese traders—known for their strong affinity for gold—back into the market.

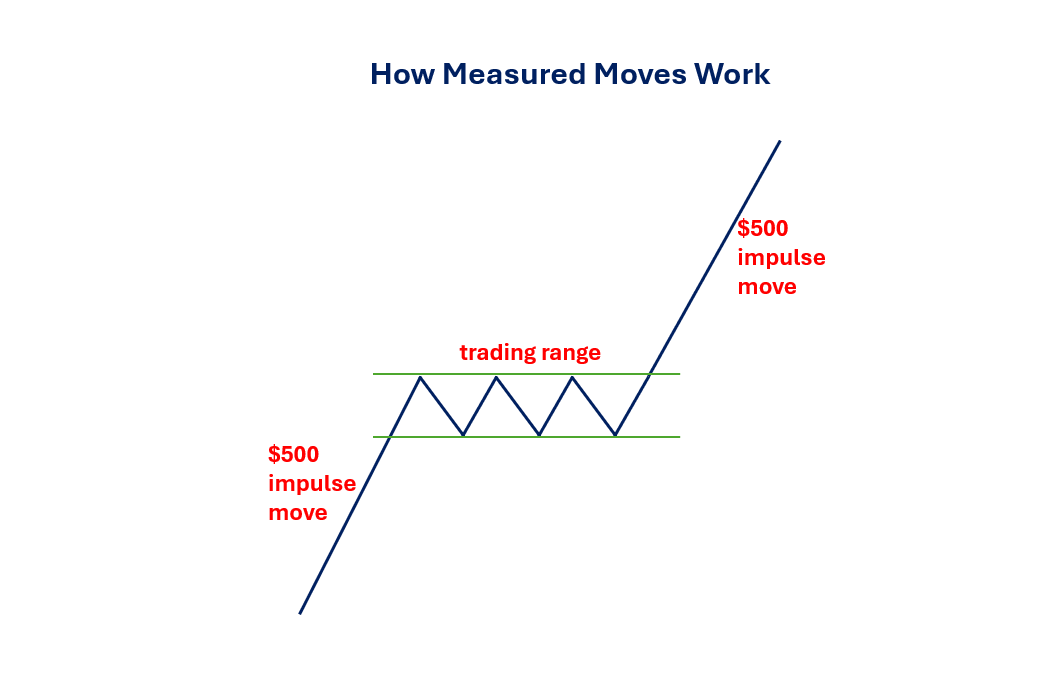

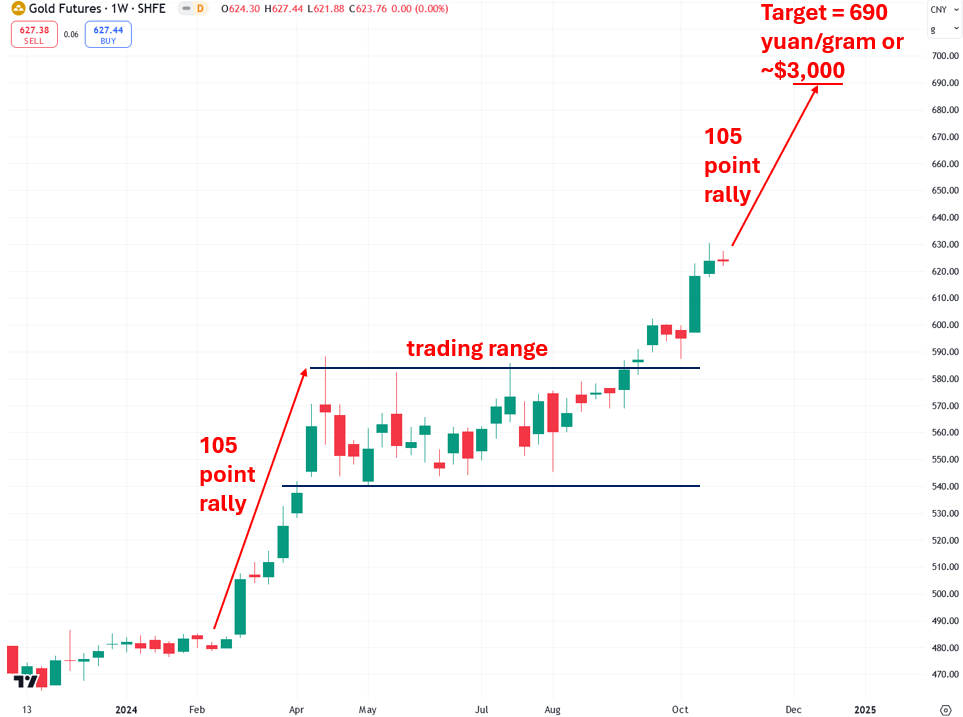

Technical analysis of SHFE gold futures implies that the international gold price in U.S. dollars should reach approximately $3,000 per ounce during the current rally. This projection relies on the concept of a “measured move,” where the price following a consolidation pattern or trading range is expected to rise by the same number of points as the rally preceding the consolidation. The diagram below illustrates how measured moves work:

The chart of SHFE gold futures below shows a 105 yuan/gram rally in the spring, followed by a five-month trading range. This suggests that the current rally should also reach 105 yuan/gram, projecting a target of 690 yuan/gram, or roughly $3,000 per ounce. This target is also logical because $3,000 is a significant psychological level, and major levels like that typically act like a magnet for prices. And, in case $3,000 seems ambitious, it’s only a 9.3% increase from current levels. I’m confident that gold will climb even higher in the course of this bull market, though it may pause or consolidate around the $3,000 level for a time to catch its breath.

Gold analysts and investors who closely follow developments in China often monitor whether the domestic Chinese gold price trades at a premium or discount compared to the international price. In recent months, China’s domestic gold price experienced an unusual discount of up to $40.60 per ounce against the international price. However, this discount has quickly reversed following the breakout in SHFE gold futures, with Chinese gold now trading at a $1.10 per ounce premium over the international price. This transition from a discount to a premium is an indication that gold trading activity in China is starting to heat up once again.

Another sign that gold trading activity in China is heating up is the recent increase in SHFE gold futures trading volume over the past two months. As seen in the chart, volume surged dramatically during the spring rally. While trading activity is currently rising in a measured and orderly way, I expect it to ramp up significantly as the rally progresses toward $3,000. That’s when the real frenzy in Chinese gold trading will likely begin in earnest.

Despite rising gold prices and increased trading activity, the high cost of gold has actually dampened physical consumer demand in China. According to Bloomberg, overall demand fell by 22% to 218 tons in the three months leading to September, with jewelry consumption dropping 29% to 130 tons and bar and coin purchases declining 9% to 69 tons. This suggests that the rapid price surge has created sticker shock for many Chinese consumers, who are likely waiting for a price dip to buy at more favorable levels.

The reality is that high gold prices are here to stay, however, with even further increases ahead as global debt, money supply, and inflation continue to rise. Soon—possibly during the intense “frenzy phase” I mentioned—physical gold buyers may recognize that prices aren’t dropping and, driven by the fear of missing out (FOMO), start buying aggressively before prices climb even higher. This shift in behavior will only add further fuel to the fire.

Another factor supporting the bullish outlook for gold in China is the country’s struggling economy, weighed down by the collapse of massive bubbles in real estate and the stock market. In response, the Chinese government recently announced a plan to issue special sovereign bonds totaling approximately 2 trillion yuan ($284.43 billion) this year as part of a new fiscal stimulus. Fiscal and monetary stimulus programs are typically bullish for gold because they add to national debt, debase the currency, and drive inflation higher. Burdened by a substantial overhang of bad debt, inflated asset prices, “zombie” companies, and a rapidly aging population, China is now on a path toward an addiction to stimulus to keep its economy afloat—much like the United States, Europe, and Japan.

Source: Financial Times In conclusion, the stage is set for Chinese traders and investors to continue fueling a powerful rally in gold prices, pushing it to $3,000 and then beyond. Now that SHFE gold futures have broken out of their consolidation and trading activity is heating up once again, all indicators point toward a renewed surge that could mirror or even surpass the intensity of the spring rally. Meanwhile, China’s economic struggles and increasing reliance on stimulus add further support to the bullish outlook for gold. As global debt and inflationary pressures rise, and with Chinese physical gold investors and consumers likely to return in droves once they recognize that high gold prices are here to stay, the conditions are primed for an explosive phase in the gold market. This momentum, driven by both domestic factors in China and international dynamics, is likely just the beginning of an even greater upward trend.

Also watch the video presentation of this report:

Tyler Durden

Sun, 11/03/2024 – 18:40 - 'A Coordinated Effort' To Rig States – Rogan Exposes Democrats' Plan To Destroy American Democracy…

‘A Coordinated Effort’ To Rig States – Rogan Exposes Democrats’ Plan To Destroy American Democracy…

“Undeniably,” admits Pennsylvania Senator John Fetterman to podcaster Joe Rogan, “immigration is changing our nation.”

The two men spoke about a wide variety of political topics ranging from how Donald Trump won in 2016 to how immigration stands as a key issue in the election today.

Specifically, Fetterman played the Democratic Party card, claiming that Republicans in 2024 “had an opportunity to do a comprehensive border-bipartisan-and that went down because Trump, he declared that that’s a bad deal after it was negotiated with the other side.”

Rogan then brutally ‘fact-checked’ the stammering senator, pointing out the reality that that the deal made many concessions that Republicans concerned about the border found to be unacceptable.

“But, didn’t that deal also involved amnesty,” responded Rogan,“and didn’t that deal also involve a significant number of illegal aliens being allowed into the country every year?”

Silence from Fetterman.

Rogan continued:

“I think it was 2 million people. So still the same sort of situation. And their fear is exactly what I talked about, that these people will be moved to swing states and that that will be used to essentially rig those states and turn them blue forever.“

Finally, the PA Senator responded

“I’ve never witnessed those kinds [illegals voting] of a thing… I don’t think there’s that level kinds of organization.“

But Rogan once again would not allow the politician to ‘lie’ pointing out that “there is an organization that’s moving these people [illegals] to swing states.”

“There’s a significant number of these people that are illegal immigrants that have made their way to swing states.

And then there’s been calls for amnesty. There’s been calls for allowing these people to have a pathway to citizenship and allow them to vote.

The fear that a lot of people have is that this is a coordinated effort to take these people that you’re allowing to come into the country, then you’re providing them with all sorts of services like food stamps and housing and setting them up and then providing a pathway to amnesty.

And then you would have voters that would be significantly voting towards the Democrats because they’re the people that enabled them to come into the country in the first place, first place and provided them with those services.

This is a big fear that people have and that you’re rigging this system and that this will turn all these states into essentially locked blue like California is.”

Fetterman’s responds:

“undeniably,” adding that “immigration is changing our nation.”

“I haven’t spent a lot of time in Texas but it’s very clear that immigration has remade Texas and I think it’s generally, it’s a good thing.”

Watch the discussion on immigration below:

John Fetterman eventually admits to Joe Rogan that Democrats’ ‘Border Bill’ merely converted illegal immigrants into legal immigrants, rather than preventing illegal immigration:

John Fetterman: “I’ve never witnessed those kinds of a thing.” [Illegals voting]

I don’t think… pic.twitter.com/sEs6Xd0pEJ— Eric Abbenante (@EricAbbenante) November 2, 2024

Tyler Durden

Sun, 11/03/2024 – 18:05 - In Addition To Not Being Funny, SNL May Have Violated Election Law With Kamala Cameo

In Addition To Not Being Funny, SNL May Have Violated Election Law With Kamala Cameo

Vice President Kamala Harris made a surprise appearance on “Saturday Night Live” last night – playing herself across from Maya Rudolph’s version of her in the show’s cold open.

Kamala Harris spent THREE HOURS rehearsing for this cringe fest on SNL.

Complete with the fake black accent.

This is a tough watch. Good Lord. pic.twitter.com/B3RbafOsH9

— Nick Sortor (@nicksortor) November 3, 2024

It was essentially an exact copy of Trump’s appearance in 2015, except not funny.

Kamala Harris SNL skit DIRECTLY copied Trump’s from 2015.

Can she do ANYTHING original at all? https://t.co/RX3zMprYfo pic.twitter.com/wwbdVJgig1

— Nick Sortor (@nicksortor) November 3, 2024

https://platform.twitter.com/widgets.jshttps://platform.twitter.com/widgets.jsWhat’s more, it may have violated election laws.

As Michael Shellenberger points out, “The producer of Saturday Night Live said neither Harris nor Trump would appear on the show “because of election laws.” Last night, about 60 hours before polls open, he put Harris on the show in a warm & humanizing sketch. He and NBC violated the equal time provision of the law.”

On October 1, 2024, Hollywood Reporter published this article. It said, “In a recent interview ahead of the show’s 50th season, SNL creator and long-running maestro Lorne Michaels revealed that he hadn’t reached out to the real-life candidates, and he didn’t intend to before the… pic.twitter.com/3olU8qMmeT

— Michael Shellenberger (@shellenberger) November 3, 2024

Continued:

That article linked to a September 19 interview between Michaels and SNL cast members, Colin Jost and Michael Che. Weirdly, however, the September 19 does not contain the Lorne Michaels quote referred to in the October 1 Hollywood Reporter article. Even more weirdly, neither does the WayBack Machine’s first capture of the article on September 19.

The reason that’s weird is that many media outlets reported on Michaels’ statement in early October.

NBC clearly violated the law. In a 2022 fact sheet, FCC writes, “FCC rules seek to ensure that no legally qualified candidate for office is unfairly given less access to the airwaves – outside of bona fide news exemptions – than their opponent.”

I will interview @BrendanCarrFCC about this at 11:45 ET on an X Spaces— please tune in https://t.co/PaCiLoVUfP

— Michael Shellenberger (@shellenberger) November 3, 2024

https://platform.twitter.com/widgets.jshttps://platform.twitter.com/widgets.js

Tyler Durden

Sun, 11/03/2024 – 17:45 - 'Fourth Turning' Election Igniting A Firestorm

‘Fourth Turning’ Election Igniting A Firestorm

Authored by Jim Quinn via The Burning Platform blog,

“Imagine some national (and probably global) volcanic eruption, initially flowing along channels of distress that were created during the Unraveling era and further widened by the catalyst. Trying to foresee where the eruption will go once it bursts free of the channels is like trying to predict the exact fault line of an earthquake. All you know in advance is something about the molten ingredients of the climax, which could include the following:

Economic distress, with public debt in default, entitlement trust funds in bankruptcy, mounting poverty and unemployment, trade wars, collapsing financial markets, and hyperinflation (or deflation)

Social distress, with violence fueled by class, race, nativism, or religion and abetted by armed gangs, underground militias, and mercenaries hired by walled communities

Political distress, with institutional collapse, open tax revolts, one-party hegemony, major constitutional change, secessionism, authoritarianism, and altered national borders

Military distress, with war against terrorists or foreign regimes equipped with weapons of mass destruction”

How many times have you heard this is the most important election of our lifetimes in the last few weeks? When Strauss & Howe published The Fourth Turning in 1997, the national debt was $5.4 trillion, and the country was running an annual deficit of $22 billion. We now add $22 billion of debt every 4 days, amounting to $2 trillion per year. They postulated the major catalysts for the next Fourth Turning would be debt, civic decay, and global disorder.

As we enter the 17th year of this Crisis, no one can question their prescience in predicting the facilitators which have propelled this ongoing Crisis thus far. The volcanic debt eruption created by the Federal Reserve and their Wall Street cabal owners in 2008 initiated all the chaos, debt creation, crushing inflation, authoritarian measures, social decay, celebration of delusion, delegitimization of the regime media and their corrupt government co-conspirators, and the rise of Trump. This country, and most of the western world, is experiencing extreme economic, social, political and military distress, as this upcoming election is guaranteed to ignite a civil and global conflagration.

No matter the result of this election, the losing side will not accept the outcome. It has been unequivocally evident for several weeks Trump would win this election in a landslide, on par with Reagan’s destruction of Mondale in 1984, if the Democrat cheat machine of fraudulent mail-in ballots, illegal hordes voting, and ever trusty Dominion vote switching algorithms cannot overcome his overwhelming margin.

Those pulling the levers are willing to do anything to retain power, not excluding assassination of Trump, initiating WW3 or some other manufactured crisis to cancel the election, illegal lawfare schemes to convict Trump of fake crimes or prevent his inauguration in January, or releasing their BLM, Antifa, and Illegal terrorist hordes into the streets to wreak havoc and initiate civil war. The treasonous bastards who stole the 2020 election and have committed crimes against the American people fear the retribution and prison sentences which could be inflicted upon them if Trump wins. They will not go silently into the night.

The Deep State skullduggery implemented through election fraud shenanigans, using their captured Soros judges and district attorneys to commit illegal lawfare, will rile the normies (aka deplorables, aka garbage) if they feel another election has been stolen by these treasonous totalitarians. Normal Americans have reached their breaking point. They have seen their bank accounts defunded by the Biden/Harris inflationary tsunami, unleashed by their covid debacle and ironically named Inflation Reduction Act, and their enablers at the Federal Reserve who printed trillions of new fiat, while keeping interest rates at 0% for years.

Anyone living in the real world knows inflation is at least twice as high as the reported government manipulated figures. They gaslight us about GDP growth, number of jobs added (850,000 overestimation last year), unemployment rate (% in labor market hugely underestimated), and every government statistic, in order to portray a false narrative of an economy doing well and raising all boats. The only boats being raised are the yachts of the .1%.

In reality, economic distress is creating psychological trauma on young and old alike. Seniors on fixed incomes and the poor dependent upon welfare, sink further into poverty, as the cost of food, energy, rent, medicine, and most necessities reach all-time highs. No one earning the average income in this country can afford a home. Credit card debt and auto loan debt have reached unpayable levels, and an avalanche of defaults and re-possessions has commenced. Meanwhile, with stock markets and housing markets at all-time highs, the wealthy have gotten wealthier, so the plight of the bottom 90% is of no concern to their day-to-day luxurious existence.

This bifurcation of economic circumstances is evidenced by the populist rage propelling Trump’s campaign. Normal Americans are tired of being screwed over by the system and fed up with politicians, left wing billionaires (Soros, Gates, Bezos, et al), and regime media talking heads demanding they acquiesce to their totalitarian mandates, while being propagandized to believe their provably false narratives about the “great” economy. Biden is president in name only, as proved by his dementia ridden rants and those pulling the strings casting him aside like a piece of trash when he no longer met their needs.

I don’t think Strauss & Howe envisioned the types of social distress which would be ushered in by the ruling oligarchy in a desperate attempt to divide, destroy, and degrade the social fabric of our society, obliterating the common values which helped build this nation. The organized, funded, and promoted invasion of our country by third world bottom feeders with the intent to take the lower paying jobs of native Americans, overwhelm the country’s social welfare system, funnel illegal voters into swing states, and create civil chaos in formerly homogeneous communities, is designed to contribute to the economic collapse of the country, allowing the Great Reseters to implement their new world order machinations.

The race riots, funded by Soros and encouraged by his bought off district attorneys in every shithole Democrat run sanctuary city in America, conducted by his BLM and ANTIFA hired terrorists, were designed to bring down Trump and demoralize the white middle class families who are the backbone of the country. We were supposed to bow down to these race baiters and pretend a drug addict black criminal thug was a saint, while honoring fictitious made-up ridiculous black holidays like Juneteenth and Kwanzaa. The entire narrative has been to make white people take the knee and accept this woke drivel. The goal has been to destroy the community standards we grew up with and replace them with an anything goes mentality of degeneracy and delusion.

The other socially explosive issues designed to divide and conquer have involved pretending mentally ill men are women and vice versa, while mentally ill women encourage the mutilation of their children as a sacrifice to the woke gods. Allowing mentally ill perverted men into women’s restrooms is pure insanity, but corrupt politicians, bought-off government bureaucrats, and woke judges have mandated this dangerously absurd behavior.

Men dominating women’s sports is perfectly fine to these seekers of societal implosion. Allowing and encouraging young girls to cut off their breasts because their batshit crazy mothers suffer from a woke form of Munchausen syndrome by proxy is a despicable surrender to degeneracy. We are failing our children, resulting in massive levels of depression, drug use, self-mutilation, and suicide among the young.

The most socially distressful act in the history of mankind was our authoritarian government politicians and bureaucrats forcing over 270 million guinea pigs (over 5 billion worldwide), under threat of losing their livelihood and being ostracized from society, to be injected by an experimental gene therapy marketed as a vaccine, that did not prevent people from catching, spreading or dying from the most overhyped flu in history.

The ruling overlords, who planned this fake pandemic (Event 201), successfully created the largest mass formation psychosis among the fearful masses than has ever been achieved through a propaganda of fear campaign. They proved they could force the sheep to willingly lock themselves down and beg to be injected with a toxic concoction designed to kill them suddenly or over time, while reducing fertility and disabling millions, accomplishing a major goal of the Gates depopulation agenda. The pure bloods will never forget or ever forgive those who treated them like trash. The coming civil war will see the dividing lines very much aligned between the jabbed versus the unjabbed.

Political distress has been building in this country since the day Trump descended that Trump Tower escalator in June of 2015, announcing he was running for president. He was able to corral the populist rage of the economically and socially distressed deplorables and achieve the upset of the century against the Deep State chosen one, initiating the Deep State coup against him, which continues to this day. The political system is wrought with fraud, corruption, malfeasance, and a disregard for the proper legal functioning of elections.

The 2020 election was stolen, mainly through fake mail-in ballots supposedly instituted as a one-time covid measure. Now it is a permanent fixture, and systematic fraud is purposely built into the system, as no ID or proof of citizenship is required to vote, illegals are being enabled to vote illegally by the Democrat party, and the judicial system is filled with left-wing activist judges whose sole purpose is to promote criminality and deviancy.

The desperation of the Deep State oligarchs and their hired henchmen within the CIA, FBI, DOJ, and State Department is palpable and exceedingly dangerous, as they are willing to burn down the system to prevent their criminal conspiracy from being revealed. They have tried to imprison and kill Trump already and will continue to do so before his January inauguration. It is probably too late to stop the election from taking place, but nothing they do is too diabolical to exclude at this point. When Trump’s margin of victory exceeds their ability to cheat, they will proceed with plan B and unleash their paid hordes of violent felons in every major city in America, to try and stop Trump from assuming power.

Biden and Harris’ handlers will use every lawfare means at their disposal to prevent the smooth transition of power. The fake January 6 insurrection will seem quaint compared to what these traitors will attempt to pull off. We know they consider us deplorable, garbage, racist Nazis, so that belief allows them to consider us as non-humans and use lethal means to suppress our voices. The Biden-Harris administration updated DOD Directive 5240.01 on Sept. 27 to include provisions authorizing lethal force in certain circumstances when assisting civilian law enforcement. The timing of this change sure seems suspicious, as this volatile election enters the home stretch.

This is where military distress will rear its ugly head. We know the woke military cooperated and conspired with the other Deep State bad actors in the coup against Trump. Milley acted in a treasonous manner behind Trump’s back by communicating with adversaries and planning to override any direct order from the Commander–in-Chief. The military leadership under Biden has proven to be incompetent, committed to diversity & equity, and willing to do the bidding of the forces aligned against Trump.

The possibility of the military participating in violent coup against Trump before he takes office, or shortly thereafter, is not out of the question. When men who know they have committed illegal, treasonous acts feel threatened with exposure and prosecution, they are capable of anything to avoid their fate. Militarily, this is an extremely dangerous period for our nation.

With neocons dominating in Congress, and their regime media partners regurgitating their propaganda talking points about Russia, China, Iran and North Korea, these psychopaths are pushing as hard as possible for WW3. Whether it launches in the Ukraine, Gaza, the Taiwan Straits, or on the border of the two Koreas, their goal is global conflict and obscene profits for the military industrial complex who dole out the bribes. They know Trump is not a war monger and will attempt to broker peace deals in the Ukraine and in the Middle East. Therefore, they are recklessly flailing about trying to initiate a global firestorm before Trump assumes the presidency.

Beware of our “Gulf of Tonkin” false flag incident, which will be used as the basis to go to war with whichever “evil dictator” suits our purposes at that moment. No matter the outcome of this election, there will be blood – whether it be American blood on American soil or American blood on foreign soil, or both simultaneously. Fourth Turnings always accelerate towards a violent denouement, with an unanticipated number of deaths. Over 5% of the male population was killed in the American Civil War Fourth Turning, while 65 million people were killed during the WWII Fourth Turning. With the current level of killing technology, the potential number of casualties in a global conflict would be astronomical and inconceivable to average Americans.

I do not have any misconceptions that the election of Trump can undo the fiscal disaster heading our way. At best, he could delay the timeline for financial catastrophe and possibly keep WW3 from launching during his term. I even wonder whether the selection of Kackling Kamala and Tampon Tim, the single worst presidential ticket in American history, has been purposely engineered by the Deep State in order to insure the economic and financial implosion happen during Trump’s reign.

Discrediting Trump, as they did by blaming Herbert Hoover for the Great Depression, when it was FDR’s policies that exacerbated the problem, might provide the Democrat Deep State Party with the narrative that Trump’s policies caused the collapse. There is absolute certainty the losers in this election will declare it stolen and refuse to acknowledge the winner. With over 75% of the population expecting post-election violence, there will be violence. Where it leads and what unintended consequences befall the nation are unknown but guaranteed to further split a divided nation.

The core elements of this Fourth Turning Crisis (debt, civic decay, global disorder) were the driving factors at the outset and continue to be the driving factors as we approach the climax of this winter of our discontent in the early 2030s. Between now and then will be the most perilous years of our lifetimes. Panic, chaos, financial disaster, authoritarian measures, civil war, global war, and a myriad of other epic challenges await. They will attempt to abscond with your wealth through their Great Taking plans.

They will attempt to implement their Great Reset though CBDCs, mass surveillance, and totalitarian enforcement of their new world order mandates. They will continue their depopulation efforts through war, vaccines, and starvation of the poor. They will attempt to put a final nail in the coffin of the U.S. Constitution, ushering in their one world government, controlled by billionaire oligarchs, and enforced by their military/police thugs. They are attempting to demoralize the masses, propagandizing them into believing only the government can save them, and forcing them to march into an electronic gulag with no escape routes.

All my ruminations about this Fourth Turning always come down to the potential outcomes laid out by Strauss and Howe twenty-seven years ago, before the turn of the century, and eleven years before the triggering of this Crisis. No matter which channels of distress the volcanic molten lava breaks free from, the next several years will be disconcerting, difficult, destructive, and deathly. There is no escape from the grim reality of what is coming. You cannot be prepped enough to withstand the bitter winter winds which will begin to blow with the outcome of this election.

Nothing will be the same after November 5. Will there ever be another election? Will our country still exist in its current form ten years from now? Strauss and Howe did not predict a specific outcome but provided four realistic possible outcomes. Three out of four are dire, including the end of humanity as a distinct possibility. After reading the recent best-selling book Nuclear War – A Scenario, you realize the world could end in a matter of hours if the weak-minded psychopaths leaders initiate an unstoppable progression of responses.

I know the linear thinking noobs who believe the world always progresses in a straight line will dismiss these warnings as just conspiracy theory doom porn. They have no interest in the cyclical nature of history and will continue to trust the government narrative, enforced by the regime media propaganda mouthpieces, and repeated by the NPCs who make up a major percentage of the population. That’s fine. They can keep their heads in the sand and believe the delusional drivel doled out by those in power, but Fourth Turnings are going to deluge them under a tsunami of reality, pain, death and destruction. That’s just the way it is.

People need to get their heads straight and understand the challenges that lie ahead. I don’t see any easy solutions, and I’m not selling a newsletter with the secret to surviving this Fourth Turning. I’ve been issuing warnings for over a decade, and I’ve seen nothing that has happened or is happening, to make me change my mind.

-

This Fourth Turning could mark the end of man. It could be an omnicidal Armageddon, destroying everything, leaving nothing. If mankind ever extinguishes itself, this will probably happen when its dominant civilization triggers a Fourth Turning that ends horribly. For this Fourth Turning to put an end to all this would require an extremely unlikely blend of social disaster, human malevolence, technological perfection and bad luck.

-

The Fourth Turning could mark the end of modernity. The Western saecular rhythm – which began in the mid-fifteenth century with the Renaissance – could come to an abrupt terminus. The seventh modern saeculum would be the last. This too could come from total war, terrible but not final. There could be a complete collapse of science, culture, politics, and society. Such a dire result would probably happen only when a dominant nation (like today’s America) lets a Fourth Turning ekpyrosis engulf the planet. But this outcome is well within the reach of foreseeable technology and malevolence.

-

The Fourth Turning could spare modernity but mark the end of our nation. It could close the book on the political constitution, popular culture, and moral standing that the word America has come to signify. The nation has endured for three saecula; Rome lasted twelve, the Soviet Union only one. Fourth Turnings are critical thresholds for national survival. Each of the last three American Crises produced moments of extreme danger: In the Revolution, the very birth of the republic hung by a thread in more than one battle. In the Civil War, the union barely survived a four-year slaughter that in its own time was regarded as the most lethal war in history. In World War II, the nation destroyed an enemy of democracy that for a time was winning; had the enemy won, America might have itself been destroyed. In all likelihood, the next Crisis will present the nation with a threat and a consequence on a similar scale.

-

Or the Fourth Turning could simply mark the end of the Millennial Saeculum. Mankind, modernity, and America would all persevere. Afterward, there would be a new mood, a new High, and a new saeculum. America would be reborn. But, reborn, it would not be the same.

I’ve been issuing warnings for over a decade, and I’ve seen nothing that has happened or is happening, to make me change my mind. Befriending like-minded people and summoning all the courage and fortitude you can muster is the best advice I can give.

The best analogy for the next several years is: get prepared to slog many miles through a raging blizzard in sub-zero temperatures with less than 50% chance of survival.

Good luck and Godspeed.

Tyler Durden

Sun, 11/03/2024 – 17:30 -

- US Warns Tehran It Will Not Restrain Israel If Iran Retaliates

US Warns Tehran It Will Not Restrain Israel If Iran Retaliates

Iran has kept up its saber-rattling in the wake of last week’s Israeli aerial attack, which itself was the much anticipated response to the Iranian ballistic missile attack of October 1st. Washington is now warning Tehran that it “won’t be able to hold Israel back” if the Islamic Republic retaliates, US and Israeli officials told Axios Saturday.

“We told the Iranians: We won’t be able to hold Israel back, and we won’t be able to make sure that the next attack will be calibrated and targeted as the previous one,” the US official said.

Via Reuters The message was reportedly passed to Iranian officials via Swiss intermediaries, the Axios report details, which is a rare public disclosure.

Ayatollah Ali Khamenei the same day warned of “tooth-breaking” response for Israel’s actions. Recent international reports have also suggested Iran-linked paramilitaries in Iraq could be preparing a new attack on Israel.

The Iranian Supreme Leader has also said, “We will do whatever is necessary in confronting arrogance, whether in terms of military and armament or politically. The Iranian people and officials will never hesitate in facing global arrogance and the criminal apparatus ruling the world order.”

“The issue is not just about revenge, but rather acting with logic and confrontation consistent with religion, ethics, Sharia, and international laws. The issue is confronting international injustice, and for the Iranian people, confronting oppression and arrogance is a mandatory duty,” he added.

The Iranians are signaling that an attack is “definitely” coming, per Axios:

- Esmail Kowsari, a member of the national security committee in Iran’s parliament, said Saturday that Iran’s security council had agreed on a response but not yet on the exact date and scope.

- Kowsari said the attack will be executed in coordination with other “resistance” groups in the region and will be stronger than Iran’s Oct. 1 attack, which involved 180 ballistic missiles.

But the reality is that Iran also is signaling its own domestic population with all this tough talk, as well as enemies across the region, even if it doesn’t actually intend to hit back against Israel.

🚨 Breaking: Israel 🇮🇱 Navy ship crossed Suez canal and enters the Red Sea.

According to N12 News, onboard the ship are Israeli LORA ballistic missiles with a range of up to 500km. As the ship is travelling eastward, Iran 🇮🇷 will be within the range of these missiles. pic.twitter.com/ylvCnddofP

— Dr. Eli David (@DrEliDavid) November 2, 2024

https://platform.twitter.com/widgets.js

With the Oct.1st attack, and Israel’s retaliation, Tehran is still able to claim ‘victory’ of sorts for its strikes involving over 180 ballistic missiles. It sent a strong message, and now that status quo has been restored to some extent.

The US days ago began moving extra B-2 bombers and other major military assets in the region, as a precaution in the scenario of another Iranian strike on Israel.

Tyler Durden

Sun, 11/03/2024 – 16:55 - "We're Not Going To Allow Them To Steal It": Raskin Repeats Trump-Like Reservation On Accepting Election Results

“We’re Not Going To Allow Them To Steal It”: Raskin Repeats Trump-Like Reservation On Accepting Election Results

On Bill Maher’s HBO Show on Friday, Rep. Jamie Raskin (D-MD) appeared to repeat his reservation about accepting a Trump win in the presidential election. Raskin said that Democrats will only support a “free and fair election.” Trump was widely criticized for the same position when he said “If everything’s honest, I’ll gladly accept the results.”

Raskin previously said that he would not guarantee certifying Trump and that, if he wins, he may be declared as disqualified by Congress:

“It’s going to be up to us on January 6th, 2025 to tell the rampaging Trump mobs that he’s disqualified. And then we need bodyguards for everybody and civil war conditions.”

Raskin went on HBO to repeat his reservation on accepting the results of any Trump victory:

“When I say we will support a free and fair election, no, we we’re not going to allow them to steal it in the states, or steal it in the Department of Justice or steal it with any other election official in the country.

If it’s a free and fair election, we will do what we’ve always done. We will honor it.”

Jamie Raskin says Democrats will only uphold the peaceful transfer of power if they view the election as fair:

Jamie Raskin: “When I say we will support a free and fair election, no we we’re not going to allow them to steal it in the states, steal it with the Department of… pic.twitter.com/wiczm4yz0I— Eric Abbenante (@EricAbbenante) November 2, 2024

https://platform.twitter.com/widgets.js

Remarkably, as the audience applauded Raskin, Maher added “That is the Democrats’ history: They honor it. That’s the big difference between the parties.”

However, that is not the history and Raskin knows it.

The certification of President George W. Bush’s 2004 re-election was opposed by Democrats and former Speaker Nancy Pelosi (D-Calif.) and Senate Judiciary Committee Chairman Dick Durbin (D-Ill.) praised the effort of then-Sen. Barbara Boxer (D-Calif.) who organized the challenge.

Jan. 6 committee head Bennie Thompson (D-Miss.) voted to challenge it in the House.

Rep. Jamie Raskin (D-Md.) sought to block certification of the 2016 election result.

Raskin also insisted on CNN that the effort to prevent citizens from voting for Trump is the very embodiment of democracy:

“If you think about it, of all of the forms of disqualification that we have, the one that disqualifies people for engaging in insurrection is the most democratic because it’s the one where people choose themselves to be disqualified.”

Democrats not only sought to strip Trump from the ballot this election, but sought to cleanse ballots of 126 House members.