- Taiwan Election: How a DPP Win Would Tick Off China

By EconMatters

Taiwan will elect a new president and parliament on January 16. The current President Ma Ying-jeou, from the Nationalist party (Kuomintang, KMT, led by Chiang kai-shek before his demise in 1975), will complete his second term in May. During the eight years President Ma has been in power, he has focused on improving relations with China, and achieved the most cordial terms since the end of the Chinese civil war in 1949. But since Ma cannot run again after serving the maximum of two terms, there are three fresh presidential candidates ducking it out in Taiwan.

Candidate #1: Tsai Ing-wen, the Chairperson of the Democratic Progressive Party (DPP)

Tsai has a master’s degree from Cornell Law, and a PhD in Law from the London School of Economics. So far, she was top of the last opinion poll at 45.2% last Tuesday before a polling blackout begins ahead of the Jan. 16 elections. Tsai previously served as DPP chair from 2008 to 2012 and is no stranger to a presidential campaign. She was the DPP’s presidential candidate in 2012 before losing to Ma Ying-jeou.

Read – Taiwan: The Democratic China

Candidate #2: Eric Chu from the Nationalist party (KMT)

Chu is the chairman of KMT and the current mayor of New Taipei with a master’s degree in Fiance and a PhD in Accounting from New York University. Chu declared his candidacy very late (in October, about 3 month before the election) to replace Hung Hsiu-chu at the last minute.

This unusual debacle came as the KMT party miscalculated thinking it would be better off with a female candidate to run against the more popular female candidate Tsai Ing-wen from the Democratic Progressive Party (DPP). Unfortunately, Hung Hsiu-chu does not have the support base like Tsai and had been unpopular with voters, trailing badly in opinion polls. This last minute switch of candidate looks bad for the KMT party but also increases the odds of a complete loss in the presidential and general election.

Candidate #3: James Soong from the People’s First Party (PFP)

Soong has a Phd in political science from Georgetown University and is the founder and chairman of the PFP, part of the the KMT-led Pan-Blue Coalition. Soong was a KMT senior official before he left the party to run as an independent in the 2000 presidential election. Many has blamed Soong’s departure splitting the votes supporting KMT which resulted in KMT’s defeat in the 2000 election. He ran again in 2004 as Vice President to Lien Chan. The pair lost narrowly to the Chen Shui-bian from DPP seeking a second term. Now 73, Soong is at it again dividing the KMT’s support and sympathetic base. Not that it makes much of a difference as both KMT candidates fell miserably in the poll behind the DPP’s Tsai.

DPP’s Scandalous Legacy

The liberal DPP had its shot at running Taiwan. Chen Shui-bian, the party’s former Chairman, won both the 2000 and 2004 presidential elections. During his two terms, the popularity of Chen and DPP sharply dropped due to alleged corruption within his administration. Chen was later convicted, along with his wife, on two bribery charges and was sentenced to 19 years in Taipei Prison. Tsai Ing-wen, the DPP current presidential candidate, is one of the very few highly educated DPP members and has been credited with picking up the pieces restoring DPP’s credibility and image after Chen’s scandal.

DPP & Taiwan’s Legislative Violence

DPP has a tendency of resorting to violence and many times exhibited traits of a mob group. Taiwan has mostly DPP to thank for the headlines and Youtube gone viral on “legislative violence” over the past decade. Below is the infamous picture back in 2006 when the then ruling party DPP deputy Wang Shu-hui chewed up a proposal to halt voting on opening direct transport links with Mainland China. Here is how Reuters describes the aftermath:

Wang later spat out the document and tore it up after opposition lawmakers failed to get her to cough it up by pulling her hair. During the melee, another DPP woman legislator, Chuang Ho-tzu, spat at an opposition colleague.

Taiwan rulling party DPP deputy chews up a porposal to halt voting in Parliarment in 2006

“Violence Is Normal in a Democratic Society”

Tsai Ing-wen was dubbed by Time magazine cover as the one that could “lead the Only Chinese democracy”. However, during a lecture at Harvard University in 2011, when asked about why DPP seems to use violence as a tool to gain political power, Tsai’s reply won a round of applause and laughter when she said “Your definition of violence in a democratic society, that seems to be normal when you speak louder.” (Youtube here, English starts at 0:49).

I don’t think I need to waste more writing on how DPP has gone above and beyond simply “speaking louder”, and Tsai of all people knows it, which I think is why she dodged and made light of the question. That actually makes me queasy as she seems to endorse handling conflicts in a country bumpking style.

DPP’s liberal view has gained a grassroot massive support base in the youth, farming and working class, which is evidenced by Tsai’s overwhelming lead in the poll. Nevertheless, political views aside, judging from DPP’s conflict resolution skill, I personally has much reservation about how DPP could bring more progress and achieve true democracy as many seem to believe.

Read: 90 Years of Communist China

Status Quo with China?

DPP has long held the position of pro-independence regarding Taiwan’s status and wanted to sever all ties (historic, cultural, economic, etc.) with Mainland China. But this time around, DPP and Tsai is signaling a more pragmatic approach. “We want to maintain the status quo. We want to maintain the current democratic way of life,” says Joseph Wu, Tsai’s No. 2 and the DPP secretary.

Based on DPP’s history, I have serious doubt DPP would be contend with “status quo” regarding the cross-Taiwan-Strait relationship with China achieved by the KMT and Ma Ying-jeou.

Will DPP Cross China’s Bottom Line?

Even though Taiwan has its own military, foreign diplomacy and government services, Mainland China sees it as nothing more than a renegade province, and has threatened many times to overtake the island by force. China’s stance has softened quite a bit in recent years partly due to President Ma’s effort; however, an independent Taiwan remains the final “bottom line” not to be trifled with.

Taiwan president Ma Ying-jeou (left) and China’s president Xi Jinping (right) shaking hands on Nov. 7, 2015 in Singapore

Between the KMT and DPP, China would rather deal with the KMT. Leaders in China actually have as much to lose as the KMT with an unprecedented win by the liberal DPP. To show support to the KMT and also send a message to DPP, president Xi Jinping of China met with president Ma Ying-jeou of Taiwan in Singapore in November, 2015 (aka 2015 Xi-Ma Meeting, although Taiwan calls it Ma-Xi Meeting). This is the first time the leaders of China and Taiwan met in more than six decades, and Singapore was chosen as a neutral ground.

Bad Economy Keeps Idle Hands Busy

China has its own economic problems and authorities recently had to make a move to stablize currency, buy share, suspend circuit-breaker. Meanwhile, Taiwan’s export-oriented economy is currently in recession sharing the pain from China marred by near-zero growth, stagnant wages and rising prices. There’s also the looming threat of an energy shortage, low domestic investment and overdependence on China, according to a new report by the the US-China Economic and Security Review Commission.

Tsai is now regarded as a virtual shoe-in to win in the 2016 presidential election while DPP is expected to sweep the majority in the parliarment as well. This suggests Taiwan could revert back to a one-party political system with its own social and economic implications.

Needless to say, things will also get ever more complicated and tricky between China and Taiwan. The sucess of both administrations depends on how their economic policies could turn things around for the Chinese people in Mainland China and Taiwan. So perhaps neither would have much time and energy to make good on their previous political rhetoric.

- Chinese Immigrant Turned Citizen Defies Obama Gun Grab: "I Will Never Be A Slave Again"

Submitted by Mac Slavo via SHTFPlan.com,

President Obama knows that the American people have not embraced his radical, leftist gun control agenda.

That’s why he took to the stage at a town hall spectacle hosted by CNN’s Anderson Cooper in attempt to defend his unconstitutional executive actions for stealth gun control, and try to convince Americans once and for all that he is not enacting some kind of gun grabbing conspiracy.

But his “common sense” policies – made law under the force of executive order – and his crocodile tears for exploited victims of gun violence are not going to shift pubic opinion.

There is clearly a line in the sand, and a bold Chinese immigrant, who became an American citizen by choice, is the latest to remind the government what it shall not infringe.

Lily Tang Williams happens to be the state chair of the Colorado Libertarian Party and has made a splash with her January 5th Facebook post, which has now received thousands of comments and shares. Williams vows to defy all government attempts at disarmament, citing the authoritarian abuses of China, her native country.

She declares, “I will always stand with my AR, no matter what my President signs with his pen.”

Lily Tang Williams posted this on her Facebook account with the above picture of her holding a rifle against the backdrop of an American flag:

If you believe more gun control by your government is going to save lives, you are being naïve. The champion of all the mass killings in this world is always a tyrannical government.

Where I came from, China had killed thousands of the students by its own government during the massacre of Tian An Men square in 1989. I surely wish my fellow Chinese citizens back then had guns like this one I am holding in the picture.

I am a Chinese immigrant and an American citizen by choice. I once was a slave before and I will never be one again.

I will always stand with my AR, no matter what my President signs with his pen.

Posted by Lily4Liberty on Tuesday, January 5, 2016

Chinese immigrant on recent Obama's gun control move: "I once was a slave before and I will never be one again" pic.twitter.com/c6GYokIjQI

— Wisconsin 4 Guns (@Wisconsin4Guns) January 7, 2016

Live free, or die standing on your feet.

Lily Tang Williams has actually lived as a slave under an oppressive government, and like other immigrants who came to the U.S. fleeing such conditions, she is appalled at seeing the same pattern come home to America.

But it isn’t over yet.

By the look of determination in this freedom fighters’ eyes, the resistance won’t soon die, and government will still face an intense fight if it intends to completely eradicate freedom.

Despite decades of indoctrination and mass media propaganda, millions and millions of Americans are still aware of what this country was founded upon, and what principles it stands for.

And. They. Will. Never. Give. Up. Their. Guns. Period.

- The Death Of The Canadian Oil Dream, A Firsthand Account

We’ve spent quite a bit of time over the past 12 months documenting the trainwreck that is Alberta’s economy.

Most recently, we brought you “This Is Canada’s Depression: Surging Crime, Soaring Suicides, Overwhelmed Food Banks” and “For Canadian Repo Men, Business Has Never Been Better“, but you can review the story in its entirety by revisiting the following posts:

- Canada Crude Contagion: Calgary home Prices Drop Most In 2 Years

- “Canada’s Biggest Oil Casualty To Date: Calgary’s Nexen Shutters Oil Trading Desk”

- “The Canadian Housing Bubble Has Begun To Burst”

- “Canada’s Oil Patch Confidence Crashes”

- “Canada Mauled by Oil Bust, Job Losses Pile Up – Housing Bubble, Banks at Risk”

- “The Stage Is Set For A Massive Housing Market Correction in Canada’s Oilpatch”

In short, Alberta is at the center of Canada’s oil patch and has suffered mightily in the wake of crude’s seemingly inexorable decline.

Going into last year, Alberta expected its economy to grow at a nearly 3% clip. That forecast was reduced to 0.6% in March and further to -0.6% in the latest fiscal update. Oil and gas investment has fallen by a third while rig activity has been cut in half.

The fallout is dramatic. Food bank usage in Alberta is up sharply and so, unfortunately, is property crime in places like Calgary where vacancy rates in the downtown area are at their highest levels since 2010. Suicide rates are on the rise as well while the outlook for unemployment continues to darken with each passing month of “lower for longer” oil prices.

Below, find excerpts from an excellent account of the malaise penned by Jason Markusoff who writes about Alberta, lives in Calgary, and has spent 12 years reporting for the city’s largest newspapers.

* * *

From “The Death Of The Alberta Dream,” by Jason Markusoff as originally published at Macleans

Late last year, Brandon MacKay listed his Kawasaki dirt bike for sale on Kijiji, the online classifieds site. It was the only treat the 25-year-old had given himself in three years living in Fort McMurray. The rest he’d spent on supporting and visiting his wife and kids in Pictou County, N.S. But in crafting the ad for the bike—$4,400 or best offer—MacKay did what any sales agent would advise against: he revealed his desperation to sell. “I lost my job and am in need of money for my wife and kids for Christmas.”

Energy companies are preparing for a grim 2016. Analysts predict budgets will get slashed further, and that more energy firms may have to cut staff, having already laid off thousands. Ongoing oil sands construction projects will continue to wind down with little to replace them, hitting both the residential and commercial real estate sectors hard. For instance, in nearly one-sixth of all the office space in downtown Calgary, the fluorescent lights now shine on empty cubicles, and it’s forecast to get worse. Reports of the symptoms pop up almost daily: more insolvencies, more business for moving trucks and repo crews, even a noticeable uptick in suicides. The Calgary Stampede itself has been forced to lay off staff, as its offseason event bookings dried up. In November, the Alberta unemployment rate came within one-tenth of a percentage point of the national average, the closest it’s been since 1989. Those trend lines are expected to cross over next year, making it more clear to Canadian job-seekers that the Alberta dream is in decline.

The rest of the country isn’t immune from those ominous grinding sounds coming from Canada’s longtime economic engine. Canadian GDP dipped into recession territory in the first half of 2015 on the oil shock, and though the country managed a rebound in the third quarter, Alberta’s troubles—as well as slumps in other oil-rich provinces like Saskatchewan and Newfoundland—have left a gaping wound. The energy sector had long driven Canada’s trade surplus, papering over weakness elsewhere while soaking up large numbers of unemployed and underemployed people from regions like the Maritimes and hard-hit southwestern Ontario.

But even average growth seems a ways off, as troubles keep filtering through the province. In Alberta’s southeast, Medicine Hat drew international acclaim in the spring of 2015 after it became the first city in Canada to eliminate homelessness, having pursued an ambitious five-year agenda to put people into subsidized housing within 10 days of them landing in emergency shelters. After so much progress, Medicine Hat’s Salvation Army shelter is back to averaging 17 clients a night, up about one-third since 2014—too many to promptly find them all affordable housing. Local demand for donated clothing and household items also rose by more than a quarter over the last year, says manager Murray Jaster. But donations slumped too, and he had to reduce staff.

To Jaster’s point, there is much his province used to have that now seems gone. Most noticeable is Alberta’s eroding status as the Promised Land for so many Canadians from other parts of the country. Over the last decade, net interprovincial migration by 18- to 44-year-olds, the key working demographic, swelled Alberta’s population by 200,000, according to a report by a rather envious Business Council of British Columbia. (That province netted fewer than 40,000 over that stretch, while all other provinces were net losers.) The momentum has shifted. While 1,200 more Canadians still moved to the province than left it during the third quarter of 2015, that was the smallest gain since 2010—when the province was recovering from the 2009 oil price collapse—and less than half the average of the last 50 years.

“Seeing that there’s no real light at the end of the tunnel right now, more [companies] are turning to job cuts,” says Wendy Giuffre, the president of Wendy Ellen, a human resources consultancy. “It seems that there’s another wave right now. I think people were kind of hopeful things were going to pick up sooner, but it’s not looking too promising.”

Statistics Canada’s payroll survey shows Alberta shed 63,500 jobs over the year leading up to October. That doesn’t account for lost potential—the Canadian Association of Petroleum Producers estimates 40,000 jobs that were expected to be created never materialized.

It’s no secret that Alberta’s economy is closely linked to the peaks and craters of oil prices—nominal GDP (not adjusted for inflation) swings in tandem with crude prices. It’s why Fort McMurray is like a wounded beast these days. MacKay’s neighbour got laid off this fall. “I watched the bank come and take his truck,” he recalls—it was that or not feed the kids. Home prices in November were 20 per cent below last year’s average, with even townhouses and duplexes losing $100,000 in value. According to reports, a number of people who used to regularly donate to the city’s food bank have become clients.

What happens in the oil fields directly affects one of Canada’s largest business cores. Elevator trips to Beaver’s small ninth-floor Calgary office have gotten lonelier. Nearly one-third of the office space in the 32-storey highrise is listed for lease or sublease. The asking rate to rent downtown Calgary’s “Class A” office space is down nearly 42 per cent from last year, the result of “a complete lack of demand,” according to a report by real estate advisers Jones Lang Lasalle.

The hollowing out of Calgary offices has decimated the corporate lunch crowd. Regulars who would come to Jalapeno’s Mexican Grill three times a week now visit once, or not at all, owner Doug Hernandez says. “We’re not making any money; we’re just floating right now,” he says. “The problem would be when I’m not wearing my lifejacket anymore. Then I’d drown.”

Much more in the full article here

- Raoul Pal Explains What Indicators He Looks At To Decide If The Next Crisis Has Arrived

Two months ago, RealVision’s Raoul Pal brought our readers an interview excerpt with “The Fourth Turning” author Neil Howe in which the author and current head of Saeculum Research explained “what keeps him up at night.”

Today, we bring our readers another RealVision excerpt of a reflexive “interview” in which Pal himself is in the hot seat, and is challenged by Ken Monahan to lay out the market shifts he expects in 2016. In the full interview Raoul goes into detail on the indicators he will be watching throughout 2016 that will suggest that a liquidity crisis is imminent. He emphasizes that if this scenario occurs, most people are in investments that “they should absolutely not be in.”

One such metric closely followed by Pal is the ISM. This is what he says:

The ISM to me is the global guide to the business cycle. I think that [with the ISM below 50] we have a 65% chance or probability of a recession. We’ve seen that the cycle peaked back in 2011. It troughs at some point. The cycle always does this. We look back at the probabilities. We have a reasonable chance of a recession. Again, I don’t deal in certainties. It’s not like it’s definitely going to happen.

… the probability is now that we crossed 50, that over due course, the business cycle will continue lower, and therefore we should see the ISM coming through 47 which is the recession level – maybe much lower than that depending on the severity of the recession. So that would mean that the year on year rate of change of the S&P would be negative.

… if I’m right and the ISM, for example, gets down to 47, 45 then you’d start to see the year on year rate of change on the S&P at -10%

A way of visualizing Pal’s point comes courtesy of BofA, which shows that once the ISM drops below 45, it virtually always results in a recession, with just two false positives: in 1951 and 1968.

And then there is another indicator which Pal watches, one which we have been warning about since early 2014 when it first started to slide because it is the most important leading indicator into any global recession, namely trade – for the simple reason that while central banks can print asset prices, “they can’t print trade.”

The ISM is my basic framework, you then need to further increase the probability of success of what you’re trying to do. So what you look at, for example, is all the other economic indicators around what’s happening in the global economy. For example, if I look at exports – global exports. Global exports around the world are the second lowest levels since 1958. There’s something going on that the world is slowing down. Some of it is dollar translation effect. And the other is volume loss. So there’s something going on that wasn’t going on in 2012.

Yes, something is indeed going on, and after years of ignoring it because it was masked by the “wealth effect” of central bank manipulation, the markets are starting to realize it. Pal then touches on all the other deteriorating economic data points we have covered over the past year.

Then we look at other things like freight shipments. We look at retail sales. We look at industrial production. Once you start putting all the data series together many of them are at levels – durable goods – that are only seen in recessions.

Correct, and yet the question is: why does Janet Yellen ignore it and continue to push on with the “recovery” narrative, because ultimately is all about the “narrative” to boost confidence:

Its the Fed’s job to say things are good because it’s about expectations management. Whether we like it or not it’s a behavioral economics world and I’m realizing that more and more that you need to look at how behavior and incentive schemes are done. Soshe has to say that. She’s not going to say, “Oh, my God, the economy is looking terrible” until she has to because then you flip around the expectations.

Of course, with every passing day, the moment when Yellen will say the “economic is looking terrible” draws closer, and with it brings not only a return to ZIRP, and then NIRP, but also presents the question: will the Fed do another round of QE, or will it finally proceed to what Bernane said back in 2002 was the endgame all along: helicopter money. Or non-helicopter money is on the latter.

There is more in the Raoul Pal interview excerpt can be watched below, and much more in the full hour-long interview. Furthermore, Raoul Pal has again given Zero Hedge readers an exclusive weekly trial so both the full Howe, and all the other fascinating interviews in RealVision’s database can be watched in their entirety. To do so, please click here and use the “zerohedge” trial code.

- "Death To Saudi Arabia": Thousands Of Iranians Pour Into The Streets In Anti-Saudi Protests

It’s now been nearly a week since Saudi Arabia set the Muslim world on fire (both figuratively and literally) by executing prominent Shiite cleric Nimr al-Nimr.

The Sheikh was a leading figure in the 2011 anti-government protests staged in the kingdom’s Eastern Province and when the House of Saud moved to silence a dissident voice once in for all last Saturday, demonstrators poured into the streets from Bahrain to Pakistan to decry the execution.

For the Saudis, Nimr is a “terrorist,” but for the Shiite community he has now become a symbol of the oppression embodied by the Sunni Gulf monarchies. For those interested in a bit of background, here are some excerpts from The Atlantic:

The State Department cable added Nimr was gaining popularity among young people. His stature grew in spring 2009, after Shia pilgrims clashed with security forces in Medina over access to holy sites; Nimr denounced the security forces, but then was forced to go into hiding to avoid arrest. By January 2010, the State Department reported in another cable that Nimr had returned home and was living under something like house arrest. The diplomat, who wrote that cable, judged that Nimr had overestimated his sway, gone too big, and as a result had lost his influence. A neighbor said that the government “chose not to pursue him further out of concern they would elevate his status.”

The government changed its ignore-them-and-they’ll-go-away stance on Shia rabble-rousers once the Arab Spring began. In Bahrain, Shia protests threatened the stability of the regime, and the Sunni regimes of Saudi Arabia and the United Arab Emirates sent troops to help quell uprisings. But protests also spread from Bahrain into the kingdom. Nimr preached forcefully against the regime, and was rare in speaking up both in favor of the domestic protests and those in Bahrain.

In another 2011 speech, Nimr said, “From the day I was born and to this day, I’ve never felt safe or secure in this country. We are not loyal to other countries or authorities, nor are we loyal to this country. What is this country? The regime that oppresses me? The regime that steals my money, sheds my blood, and violates my honor?”

That was all too much for the regime, and in 2012 it moved to arrest him. But during his apprehension, police claimed they came under fire. Nimr was shot in the leg. He was charged with sedition and various terrorism-related crimes.

In the six days since his death, Saudi Arabia and its allies have been busy cutting all ties (both diplomatic and commercial) with Iran. “Enough is enough”, was the message from Riyadh after protesters firebombed the Saudi embassy in Tehran last Saturday.

Now, with tensions running higher than ever, the feud threatens to derail a fragile peace “process” in Syria on the way to plunging the region into an all-out sectarian shooting war.

Each side accuses the other of being a state sponsor of terror and each side blames the other for fomenting sectarian discord. Needless to say, it’s difficult to look past the fact that Saudi Arabia’s promotion of Wahhabism is almost unquestionably to blame for the rise of extremist elements throughout the Islamic World. At the very least, Riyadh’s contention that Iran promotes sectarian strife is an egregious case of the pot calling the kettle black.

In any event, Iranians are in no mood to forgive and forget. “Iranians held mass protests on Friday across the Islamic Republic, angered by Saudi Arabia’s execution of a Shiite cleric that has enflamed regional tensions between the Mideast rivals,” AP reports, adding that “after Friday prayers in Tehran, thousands of worshippers joined the rally, carrying pictures of al-Nimr and chanting “Death to Al Saud,” referencing the kingdom’s royal family.” They also chanted “down with the US” and “death to Israel.”

Below, find the visuals which underscore the fact that the sense of outrage is palpable – to say the least.

- Why Is North Korea Our Problem?

Submitted by Patrick Buchanan via Buchanan.org,

For Xi Jinping, it has been a rough week.

Panicked flight from China’s currency twice caused a plunge of 7 percent in her stock market, forcing a suspension of trading.

Kim Jong Un, the megalomaniac who runs North Korea, ignored Xi’s warning and set off a fourth nuclear bomb. While probably not a hydrogen bomb as claimed, it was the largest blast ever in Korea.

And if Pyongyang continues building and testing nuclear bombs, Beijing is going to wake up one day and find that its neighbors, South Korea and Japan, have also acquired nuclear weapons as deterrents to North Korea.

And should Japan and South Korea do so, Taiwan, Vietnam and Manila, all bullied by Beijing, may also be in the market for nukes.

Hence, if Beijing refuses to cooperate to de-nuclearize North Korea, she could find herself, a decade hence, surrounded by nuclear weapons states, from Russia to India and from Pakistan to Japan.

Still, this testing of a bomb by North Korea, coupled with the bellicosity of Kim Jong Un, should cause us to take a hard look at our own war guarantees to Asia that date back to John Foster Dulles.

At the end of the Korean War in July 1953, South Korea was devastated, unable to defend herself without the U.S. Navy and Air Force and scores of thousands of U.S. troops.

So, America negotiated a mutual security treaty.

But today, South Korea has 50 million people, twice that of the North, the world’s 13th largest economy, 40 times the size of North Korea’s, and access to the most modern U.S. weapons.

In 2015, Seoul ran a trade surplus of almost $30 billion with the United States, a sum almost equal to North Korea’s entire GDP.

Why, then, are 25,000 U.S. troops still in South Korea?

Why are they in the DMZ, ensuring that Americans are among the first to die in any Second Korean War?

Given the proximity of the huge North Korean Army, with its thousands of missiles and artillery pieces, only 35 miles from Seoul, any invasion would have to be met almost immediately with U.S.-fired atomic weapons.

But with North Korea possessing a nuclear arsenal estimated at 8 to 12 weapons and growing, a question arises: Why should the U.S. engage in a nuclear exchange with North Korea, over South Korea?

Why should a treaty that dates back 60 years commit us, in perpetuity, to back South Korea in a war from the first shot with Pyongyang, when that war could swiftly escalate to nuclear?

How does this comport with U.S. national interests?

In 1877, Lord Salisbury, commenting on Great Britain’s stance on the Eastern Question, noted that “the commonest error in politics is sticking to the carcass of dead policies.”

Is this not true today of America’s Asian alliances?

North Korea’s tests of atomic weapons and development of land-based and submarine-launched missiles should cause us to reconsider strategic commitments that date back to the 1950s.

President Nixon, ahead of his time, understood this.

As he began the drawdown of U.S. forces in Vietnam in 1969, he declared in Guam that while America would meet her treaty obligations, henceforth, Asian nations should provide the ground troops to defend themselves. Gen. MacArthur had told President Kennedy, before Vietnam, not to put U.S. foot soldiers onto the Asian mainland.

Now that we have entered a post-post Cold War era, where many Asian nations possess the actual or potential military power to defend themselves, something like a new Nixon Doctrine is worth considering.

Take all of the major territorial quarrels between China and its neighbors — the dispute with India over Aksai Chin and Arunachal Pradesh, the dispute with Japan over the Senkaku Islands, with Vietnam over the Paracels, with the Philippines over the Spratlys.

In none of these quarrels and conflicts does there seem to be any vital U.S. national interest so imperiled that we should risk a clash with a nuclear power like Beijing.

Once, there was a time when Hitler, Stalin, Mussolini and Tojo ruled almost all of Eurasia. And another time when a monolithic Sino-Soviet Communist bloc ruled from the Elbe to the Pacific.

As those times are long gone, is it not time for an exhaustive review of the alliances we have entered into and the war guarantees we have issued, to fight for nations and interests other than our own?

Under NATO, we are committed to go to war against a nuclear-armed Russia on behalf of 27 nations, including tiny Estonia.

One understood the necessity to defend West Germany and keep the Red Army on the other side of the Elbe, but when did Estonia’s independence become so critical to U.S. security that we would fight a nuclear-armed Russia rather than lose it?

Indeed, how many of the dozens of U.S. war guarantees we have outstanding would we honor by going to war if they were called?

- China's Largest Bank Is Mystery Buyer Of Massive 1,500 Ton Gold Vault In London

Back in June 2013, when Deutsche Bank opened a gold vault in Singapore which could hold up to 200 metric tons, the German bank was euphoric about the prospects for storing physical gold: “Gold has traditionally been stored in London, Zurich and New York, but there is a serious shift in dynamics going on as the global financial crisis continues to evolve,” Mark Smallwood, Deutsche Asset & Wealth Management’s head of wealth planning in the Asia-Pacific region, told The Wall Street Journal.

This is what the outside, and inside, of the state of the art Singapore vault looked like:

Mark was correct and thanks to the ongoing decline in gold prices, Chinese and Indian demand for the metal, the physical metal that is, not its various paper manifestations, has risen to record levels. Alas, one thing Mark did not know is that in early 2014, a German regulator would reveal that “precious metals manipulation was worse than the Libor scandal” and as a result the largest German bank (and largest bank in the world by notional derivative exposure) – which has been probed and found guilty for rigging virtually every market, including gold – would quietly liquidate its entire physical precious metals trading group.

Which meant that Deutsche Bank’s Singapore gold vaul, was about to be sold.

But while the sale of DB’s Singapore gold vault was to be expected with China’s ravenous apetite for warehousing physical gold around the Pacific Rim, what may have escape popular attention is that Deutsche Bank’s even more massive, and even newer, gold vault in London was also “on the block” as of December 2014 when we reported that Deutsche Bank is “open to offers for its London-based gold vault following the closure of its physical precious metals business.” As Reuters noted: “If the right offer came along, then the bank would sell the London vault,” one source close to the situation said.

Most curiously, the bank’s London gold vault only became operational in June of 2014, more than two years after launching the project. It can store some 1,500 tonnes of gold and was built and managed by British security services company G4S.

As Reuters further noted, with other banks withdrawing from the commodities business to cut costs and reduce their regulatory burden, it might be difficult for Deutsche Bank to find buyers amongst its nearest peers. However, one possible buyer is general LBMA-member, Chinese bank ICBC, which we said at the end of 2014, was trying to build a presence in London.

In any case, the list of potential buyers for DB’s brand new vault lease remained a mystery, and perhaps our revelation of the exact location of this vault, something potential buyers tend not to appreciate especially when said vault will house up to 1,500 tons of gold, or over $50 billion worth of “inventory”, may have dissuaded some. As a reminder, the “secret” location of the Deutsche Bank vault, which as revealed in the G4S building application, is located in the Park Royal complex, and specifically at the 291 Abbey Road, London NW10 7SA location.

As it turns out, one persistent buyer failed to be dissuaded.

According to Reuters, as was rumored one year ago, China’s largest bank – and in fact the world’s largest bank – by assets, ICBC Standard Bank, is buying the lease on Deutsche Bank’s London gold and silver vault, enlarging its footprint in the city’s bullion market, four industry sources close to the companies told Reuters.

China’s ICBC, which took a controlling stake in Standard Bank’s London-based Global Markets business last year, has also applied to become a clearing member of the London gold and silver over-the-counter business.

From Reuters:

The Chinese and South African lender is aiming to fill the gap left by Western banks, which are retreating from commodities to cut costs and reduce regulatory burden. “They (ICBC Standard Bank) have taken on the lease for the vault,” the first source said.

Currently, five banks – JP Morgan, HSBC, Bank of Nova Scotia, Barclays and UBS – settle daily bullion transactions between dealers, amounting to more than $5 trillion worth of metal each year in the London over-the-counter market.

These banks are shareholders of the London Precious Metals Clearing (LPMCL) company. They will decide whether to accept or reject ICBC Standard Bank’s application within the next few months. The LPMCL declined to comment.

“They are applying for clearing membership at the moment, but that’s still subject to a vote, which has not taken place yet,” the source said.

Should the vote go in its favor, ICBC will be ready with what may be one of the largest gold vaults in London, if not the world, to park local gold which will then be promptly shipped over to the mainland to be dealt with as seen fit. Unless, of course, the vault is there for the reverse migration: to house quietly escaping Chinese gold as part of the local oligarchy’s attempts to circumvent China’s capital controls, a task so far accomplished relatively painless with bitcoin.

Only time will tell.

What is perhaps most surprising is how cheaply ICBC acquired the massive gold vault: “The figure that was initially talked about may have been around $4 million, but it’s way lower now,” a second source said, without disclosing the figure paid for the vault.

So what does “way less” than $4 million buy you nowadays? Here is the answer, courtesy of Google Maps:

Finally, for those curious, here is precisely where the brand new gold vault of the world’s biggest bank will be located.

- Americans Can't Wait To Get Out Of These Five States

A low cost of living, no sales tax, and beautiful scenery (oh, naked bike rides, more strip clubs per capita than any other US city, and legalized weed) means Oregon is the "top moving destination" for Americans for the third year running, according to United Van Lines, with 69% of moves inbound. But, which states are Americans leaving in droves?

Americans continue to pack up and head West and South, according to new data from United Van Lines.

Oregon is the most popular moving destination of 2015 with 69 percent of moves to and from the state being inbound. The state has continued to climb the ranks, increasing inbound migration by 10 percent over the past six years. New to the 2015 top inbound list is another Pacific West state, Washington, which came in at No. 10 with 56 percent inbound moves.

Moving In – The top inbound states of 2015 were:

- Oregon

- South Carolina

- Vermont

- Idaho

- North Carolina

- Florida

- Nevada

- District of Columbia

- Texas

- Washington

The Northeast continues to experience a moving deficit with New Jersey (67 percent outbound) and New York (65 percent) making the list of top outbound states for the fourth consecutive year. Two other states in the region — Connecticut (63 percent) and Massachusetts (57 percent) — also joined the top outbound list this year. The exception to this trend is Vermont (62 percent inbound), which moved up two spots on the list of top inbound states to No. 3.

Moving Out – The top outbound states for 2015 were:

- New Jersey

- New York

- Illinois

- Connecticut

- Ohio

- Kansas

- Massachusetts

- West Virginia

- Mississippi

- Maryland

Simply put, Americans are moving from heavily-regulated, bureaucratic, high cost-of-living states to more affordable states.

This year's data from United Van Lines…

And the interactive version from the last 39 years…

Finally, as The Daily Signal concludes,

Moving patterns show how important cost of living is to American families.

With perfect weather and a booming, high-tech economy, California ought to be the #1 destination. Instead, more moving trucks are leaving the state than entering.

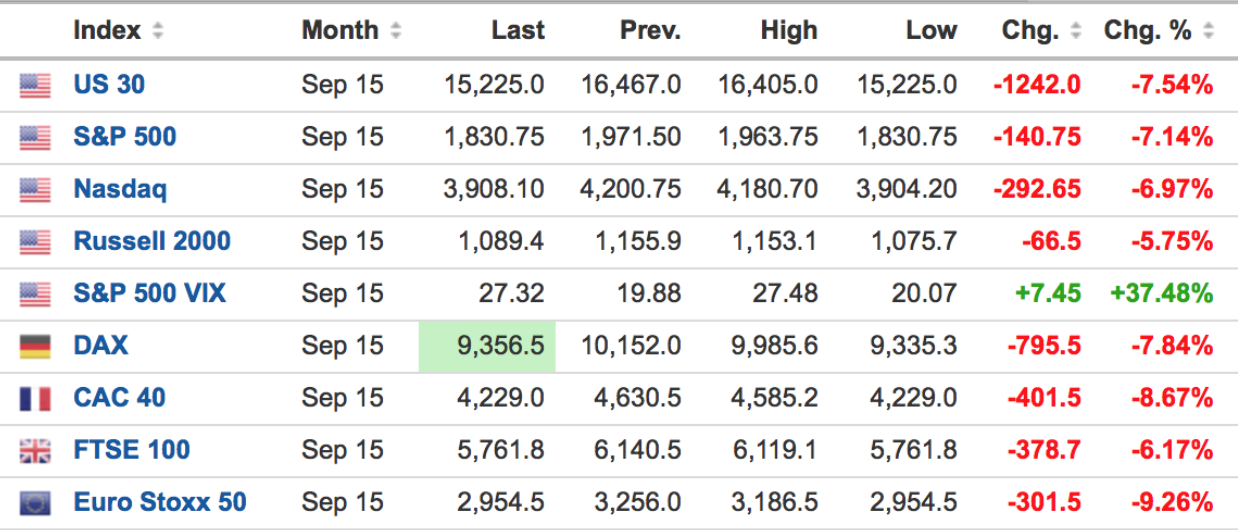

- Market Massacre: Worst Ever First Week Of Trading

What better analogy than this…

This was the worst first week of the year for US equities… ever!

Dow… (even worse than 2008)

S&P…

Europe was a disaster…

And epic for China…

And while only Trannies are in a bear market (down 20%) in the US, these 7 developed world markets are already there…(h/t SocGen's Andrew Laphthorne)

* * *

So let's look at the week in stocks…

It was all looking so awesome last night…

Futures show the swings better (with China weakness as an early week driver and US as late-week driver)…

Small Caps and Trannies are down around 7% this week, S&P best but still down over 5% (and down 6 of the last 7 days)

- S&P down 5.3% – worst week since Black Monday

- Dow Industrials down 5.6% – worst week since Black Monday

- Small Caps down 6.9% – worst week since Nov 2011 – Russell 2000 lowest close since since Oct 2014

- Dow Transports down 7.1% – worst week since Sept 2011 – lowest close since Nov 2013

The Dow is down 1400 points in a week (from 17,660 to 16,250)

Utes managed to end the week unchanged but Homebuilders collapsed… Financials and Materials were next worst…

- Financials down 6.6% – worst week since May 2012

- Materials down 7.4% – worst week since Sept 2011

- Homebuilders down 8.6% – worst since Aug 2011

VIX broke back above 25… (VIX up 60% in 2 weeks – biggest jump since Black Monday)

What did Janet do? Post Fed rate-hike – S&P down 6.5%, Gold up 3%, 30Y Bonds up 1.6%

Stocks are about half-way there…

Since the end of QE3, Trannies are down 20% and only Nasdaq is holding any gains…

The FANTAsy stocks are all red since the end of 2015 (with TSLA and AMZN worst)…

Energy Stocks finally woke up to reality in the credit underlying commodity…

US financials have started to plunge back to credit/yield curve reality…

With MS and GS back below Tangible Book Value for first time in 2 years…

Away from stocks…

Treasury Yields tumbled, closing at their low yields of the year with the belly of the curve outperforming… 10Y yields dropped 14bps this week – the biggest drop in 3 months.

FX markets were volatile but by the end The Dollar Index closed unchanged (against the majors)…

But the USDollar surged 1.5% against Asian FX – its best week in 5 months… (Asian FX is its weakest since April 2009 against the USD)

But AUDJPY – probably the world's most-levered carry trades – collapsed 6.7% this week!! It's worst week since May 2010…

Commodities were very mixed this week…

Gold rallied 4% this week – its best 'first week of the year' since 2008… (best week in 5 months) – breaking 2 key technical levels…

Crude down 5 days in a row touching a $32 handle at the lows… biggest weekly drop since Nov 2014

In Summary – Sell The Dips!

See you all Sunday night!

Charts: Bloomberg

Bonus Chart: Investors seeking safety are greatly rotating from Triple AAA stocks to Gold stocks (h/t SocGen's Andrew Laphthorne)

- Islamic Radicalism: A Consequence Of Petro-Imperialism

Submitted by Nauman Sadiq

Islamic radicalism, a consequence of Petro-imperialism:

In its July 2013 report [1] the European Parliament identified the Wahhabi-Salafi roots of global terrorism, but the report conveniently absolved the Western powers of their culpability and chose to overlook the role played by the Western powers in nurturing Islamic extremism and jihadism during the Cold War against the erstwhile Soviet Union. The pivotal role played by the Wahhabi-Salafi ideology in radicalizing Muslims all over the world is an established fact as mentioned in the EU report; this Wahhabi-Salafi ideology is generously sponsored by Saudi Arabia and the Gulf-based Arab petro-monarchies since the 1973 oil embargo when the price of oil quadrupled and the contribution of the Arab sheikhs towards the “spiritual well-being” of the Muslims all over the world magnified proportionally; however, the Arab despots are in turn propped up by the Western powers since the Cold War; thus syllogistically speaking, the root cause of Islamic radicalism is the neocolonial powers’ manipulation of the socio-political life of the Arabs specifically and the Muslims generally in order to appropriate their energy resources in the context of an energy-starved industrialized world. This is the principal thesis of this write-up which I will discuss in detail in the following paragraphs.

Prologue:

Peaceful or not, Islam is only a religion just like any other cosmopolitan religion whether it’s Christianity, Buddhism or Hinduism. Instead of taking an ‘essentialist’ approach, which lays emphasis on ‘essences,’ we need to look at the evolution of social phenomena in its proper historical context. For instance: to assert that human beings are evil by ‘nature’ is an essentialist approach; it overlooks the role played by ‘nurture’ in grooming human beings. Human beings are only ‘intelligent’ by nature, but they are neither good nor evil by nature; whatever they are, whether good or evil, is the outcome of their nurture or upbringing. Similarly, to pronounce that Islam is a retrogressive or violent religion is an ‘essentialist’ approach; it overlooks how Islam and the Quranic verses are interpreted by its followers depending on the subject’s socio-cultural context. For example: the Western expat Muslims who are brought up in the West and who have imbibed the Western values would interpret a Quranic verse in a liberal fashion; an urban middle class Muslim of the Muslim-majority countries would interpret the same verse rather conservatively; and a rural-tribal Muslim who has been indoctrinated by the radical clerics would find meanings in it which could be extreme. It is all about culture rather than religion or scriptures per se.

Moreover, I said that Islam is only a religion just like any other religion. But certain reductive neo-liberals blame the religion, as an institution and ideology for all that is wrong with the world. I have not read much history since I am only a humble student of international politics; that’s why I don’t know what the Crusades and the Spanish Inquisition were all about? Although, I have a gut feeling that those were also political conflicts which are presented to us in a religious garb. However, I am certain that all the conflicts of the 20th and 21st centuries were either nationalist (tribal) conflicts; or they had economics and power as their goals. Examples: First and Second World Wars; Korea and Vietnam wars; Afghanistan and Iraq wars; and Libya and Syria wars.

When the neo-liberals commit the fallacy of blaming religion as a root factor in the contemporary national and international politics, I am not sure which ancient global order they conjure up in their minds, the Holy Roman Empire perhaps? Religion may have been a paramount factor in the ancient times, if at all, but the contemporary politics is all about economics and power: the Western corporations rule the world and politics and diplomacy is all about protecting the trade and energy interests of the Corporate Empire. Thus, the root of all evil in the contemporary politics is capitalism, not religion, which has been reduced to a secondary role and at times to complete irrelevance especially in the liberal and secular Western societies.

More to the point, when the neo-liberals blame religion for all that is wrong with the world, they are actually engaging in a peculiar kind of juvenile thinking: a child mistakenly assumes that the world can only be seen from his eyes; and that all the people think exactly like he does. He does not understands that the outlooks and worldviews and the preferences and priorities of the people could be very different depending on their upbringing, circumstances and stations in life. You are not supposed to put yourself in another person’s shoes because sizes vary; you are supposed to put that other person in his own shoes, keeping in view his upbringing and mindset and then prescribe a viable future course of action for his individual and social well-being.

As we know that politics is a collective exercise for creating an ideal social matrix in which individuals and their families can live peacefully and happily, and in which they can maximally actualize their innate potentials. The first priority of the liberals, especially the privileged liberal elite of the developing countries, seems to be to create a liberal society in the developing countries in which they and their families can feel at home. I don’t have anything against a liberal society, especially if looked at from a feminist, inclusive and egalitarian angle, but the ground reality of the developing world is very different from the reality of the developed world. The first and foremost preference of the developing world isn’t social liberalization; it is reducing poverty, ensuring equitable distribution of wealth and economic growth. Liberal ethos and values, important as they are, can wait; our first preference ought to be to create a fair and egalitarian social and economic order on a national and international level, only then can our interests and priorities converge on a single and common goal.

If the liberals are willing to compromise on the foremost goal of equitable distribution of wealth, then the heavens won’t fall if they could show a little flexibility and maturity on the subject of the enforcement of liberal values too, which affects them on a personal level, more than anything. The socialist liberals of ‘60s and ‘70s at least made sense when they promoted liberalism along with the promise of radical redistribution of wealth. But the neo-liberals of 21st century are a breed apart who shrug off abject poverty and gross inequality of wealth in the developing nations as a secondary preference and espouse liberal values as their first and foremost priority.

The mainspring of Islamic extremism:

If we look at the evolution of Islamic religion and culture throughout the 20th and 21st centuries, it hasn’t been natural. Some deleterious mutations have occurred somewhere which have negatively impacted the Islamic societies all over the world. Social selection (or social conditioning) plays the same role in the social sciences which the natural selection plays in the biological sciences: it selects the traits, norms and values which are most beneficial to the host culture. Seen from this angle, social diversity is a desirable quality for social progress; because when diverse customs and value-systems compete with each other, the culture retains the beneficial customs and values and discards the deleterious traditions and habits. A decentralized and unorganized religion, like Sufi Islam, engenders diverse strains of beliefs and thoughts which compete with one another in gaining social acceptance and currency. A heavily centralized and tightly organized religion, on the other hand, depends more on authority and dogma than value and utility. A centralized religion is also more ossified and less adaptive to change compared to a decentralized religion.

The Shia Muslims have their Imams and Marjahs (religious authorities) but it is generally assumed about the Sunni Islam that it discourages the authority of the clergy. In this sense, Sunni Islam is closer to Protestantism theoretically, because it promotes an individual and personal interpretation of scriptures and religion. It might be true about the educated Sunni Muslims but on a popular level of the masses of the Third World Islamic countries, the House of Saud plays the same role in Islam that the Pope plays in Catholicism. By virtue of their physical possession of the holy places of Islam – Mecca and Medina – they are the de facto Caliphs of Islam. The title of the Saudi King, Khadim-ul-Haramain-al-Shareefain (Servant of the House of God), makes him the vice-regent of God on Earth. And the title of the Caliph of Islam is not limited to a nation-state, he wields enormous influence throughout the Commonwealth of Islam: that is, the Muslim Ummah.

Islam is regarded as the fastest growing religion of the 20th and 21st centuries. There are two factors responsible for this atavistic phenomena of Islamic resurgence: firstly, unlike Christianity which is more idealistic, Islam is a more practical religion, it does not demands from its followers to give up worldly pleasures but only to regulate them; and secondly, Islam as a religion and ideology has the world’s richest financiers. After the 1973 collective Arab oil embargo against the West, the price of oil quadrupled; the Arabs petro-sheikhs now have so much money that they don’t know where to spend it? This is the reason why we see an exponential growth in Islamic charities and madrassahs all over the world and especially in the Islamic world. Although the Arab sheikhs of the oil-rich Saudi Arabia, Qatar, Kuwait and some emirates of UAE generally sponsor the Wahhabi-Salafi brand of Islam but the difference between the numerous sects of Sunni Islam is more nominal than substantive. The charities and madrassahs belonging to all the Sunni sects get generous funding from the Gulf states as well as the private Gulf-based donors.

After sufficiently bringing home the fact that Islam as a religion isn’t different from other cosmopolitan religions in regard to any intrinsic feature and that the only factor which differentiates Islam from other mainstream religions is the abundant energy resources in the Muslim-majority countries of the Persian Gulf and the Middle East and North Africa (MENA) region; and the effect of those resources and the global players’ manipulation of the socio-political life of the inhabitants of those regions to exploit their resources culminated in the emergence of the phenomena of Petro-Islamic extremism and violent Takfiri-Jihadism, our next task is to examine the symbiotic relationship between the illegitimate Gulf rulers and the neo-colonial powers.

The global neocolonial political and economic order:

Before we get to the crux of the matter, however, let us first cursorily discuss that why is it impossible to bring about a major fundamental change: political, social or economic, on a national level under the existing international political and economic dispensation? As we know that the Western so-called liberal-democracies could be liberal, however, they are anything but democracies; in fact, the right term for the Western system of government is plutocratic oligarchies. They are ruled by the super-rich corporations whose wealth is measured in hundreds of billions of dollars, far more than the total GDPs of many developing nations; and the status of those multinational corporations as dominant players in their national and international politics gets an official imprimatur when the Western governments endorse the Congressional lobbying practice of the so-called ‘special interest’ groups, which is a euphemism for ‘business interests.’

Moreover, since the Western governments are nothing but the mouthpieces of their business interests on the international political and economic forums, therefore, any national or international entity which hinders or opposes the agenda of the aforesaid business interests is either coerced into accepting their demands or gets sidelined. In 2013 the Manmohan Singh’s government of India had certain objections to further opening up to the Western businesses; the Business Roundtable which is an informal congregation of major US businesses and which together holds a net wealth of $6 trillion (6000 billion) held a meeting with the representatives of the Indian government and made them an offer which they couldn’t refuse. The developing economies, like India, are always hungry for the Foreign Direct Investment (FDI) to grow further, and that investment comes mostly from the Western corporations.

When the Business Roundtables or the Paris-based International Chamber of Commerce (ICC) form pressure groups and engage in ‘collective bargaining’ activities, the nascent and fragile developing economies don’t have a choice but to toe their line. State ‘sovereignty’ that the sovereign nation-states are at liberty to pursue an independent policy, especially an economic and trade policy, is a myth. Just like the ruling elites of the developing countries who have a stranglehold and a monopoly over domestic politics; similarly the neo-colonial powers and their multinational corporations control the international politics and the global economic order. Any state who dares to transgress becomes an international pariah like Castro’s Cuba, Mugabe’s Zimbabwe or North Korea; and more recently Iran, which had been cut off from the global economic system, because of its supposed nuclear aspirations. Good for Iran that it has one of the largest oil and gas resources, otherwise it would have been insolvent by now; such is the power of global financial system especially the banking sector, and the significance of petro-dollar because the global oil transactions are pegged in the US dollars all over the world, and all the major oil bourses are also located in the Western world.

There is an essential precondition in the European Union’s charter of union according to which the under-developed countries of Europe who joined the EU allowed free movement of goods (free trade) only on the reciprocal precondition that the developed countries would allow the free movement of labor. What’s obvious in this condition is the fact that the free trade only benefits the countries which have a strong manufacturing base, and the free movement of workers only favors the under-developed countries where labor is cheap. Now when the international financial institutions, like the IMF and WTO, promote free trade by exhorting the developing countries all over the world to reduce tariffs and subsidies without the reciprocal free movement of labor, whose interests do such institutions try to protect? Obviously, such global financial institutions espouse the interests of their biggest donors by shares, i.e. the developed countries.

Some market fundamentalists who irrationally believe in the laissez-faire capitalism try to justify this unfair practice by positing Schumpeter’s theory of ‘creative destruction’ that the free trade between unequal trade partners leads to the destruction of the host country’s existing economic order and a subsequent reconfiguration gives birth to a better economic order. Whenever one comes up with gross absurdities such as these, they should always make it contingent on the principle of reciprocity: that is, if free trade is beneficial for the nascent industrial base of the underdeveloped countries, then the free movement of labor is equally beneficial for the labor force of the developed countries. The policy-makers of the developing countries must not fall prey to such deceptive reasoning, instead they must devise a policy which suits their national interest. But the trouble is that the governments of the Third world are dependent on the global loan sharks, such as IMF and World Bank, that’s why they cannot adopt an independent economic and trade policy.

From the end of the Second World War to the beginning of the 21st century the neo-colonial powers have brazenly exploited the Third world’s resources and labor, but after China’s accession to the World Trade Organization in 2001 things changed a little. Behind the “Iron Curtain” of international isolation, China successfully built its manufacturing base by imparting vocational and technical education to its disciplined workforce and by building an industrial and transport infrastructure. It didn’t allow any imports until 2001, but after entering the WTO it opened up its import-export policy on a reciprocal basis; and since the labor in China is much cheaper than its Western counterparts, therefore, it now has a comparative advantage over Western bloc which China has exploited in its national interest.

Asking the neo-colonial powers to act in the interests of the developing world is incredibly naïve. It’s like asking the factory-owners to act in the interest of their factory-workers on altruistic grounds. This is not the way forward, the factory-workers must strengthen their own labor unions and claim what’s rightfully theirs. The developing countries must form regional blocs and settle things among themselves. If a country takes interest in the affairs of its regional neighbor; like if India takes interest in the affairs of Pakistan, or if Pakistan is wary of the happenings in Afghanistan and Iran, their concerns are understandable. But what “vital strategic interests” does the US has in the Middle East where 35,000 of its troops are currently stationed, ten thousand kilometers away from its geographical borders? ‘Humanitarian imperialism’ is merely a charade, it’s the trade and energy-interests of the corporate empire which are ‘vitally’ important to the neo-colonial powers.Cold War and the birth of Islamic Jihad:

The Western powers’ collusion and conflicted relationship with the Islamic jihadists (aka moderate rebels) in Syria isn’t the only instance of its kind. The Western powers always leave such pernicious relationships deliberately ambiguous in order to fill the gaps in their self-serving diplomacy and also for the sake of “plausible deniability.” Throughout the late ‘70s and ‘80s during the Cold War, they used the jihadists as proxies in their war against the Soviets. The Cold War was a war between the Global Capitalist bloc and the Global Communist bloc for global domination. The Communists used their proxies the Viet Congs to liberate Vietnam from the imperialist hegemony. The Global Capitalist bloc had no answer to the cleverly executed asymmetric warfare.

Moreover, the Communist bloc had a moral advantage over the Capitalist bloc: that is, the mass appeal of the egalitarian and revolutionary Marxist and Maoist ideologies. Using their: “Working men and women of all the countries, unite!” rhetoric, the Communists could have instigated an uprising anywhere in the world; but how could the Capitalists retaliate, through “the trickle-down economics” and “the American way of life” rhetoric? The Western policy-makers faced quite a dilemma, but then their Machiavellian strategists, capitalizing on the regional grassroots religious sentiment, came up with an equally robust antidote: that is, the Islamic Jihad.

During the Soviet-Afghan conflict from 1979 to 1988 between the Global Capitalist bloc and the Global Communist alliance, Saudi Arabia and the Gulf Arab petro-monarchies took the side of the former; because the USSR and the Central Asian states produce more energy and consume less of it; thus they are net exporters of energy; while the Global Capitalist bloc is a net importer of energy. It suits the economic interests of the Gulf Cooperation Council (GCC) countries to maintain and strengthen a supplier-consumer relationship with the Capitalist bloc. Now the BRICS are equally hungry for the Middle Eastern energy but it’s a recent development; during the Cold War an alliance with the Western countries suited the economic interests of the Gulf Arab petro-monarchies. Hence, the Communists were pronounced as Kafirs (infidels) and the Western capitalist bloc as Ahl-e-Kitaab (People of the Book) by the Salafi preachers of the Gulf Arab states.

All the celebrity terrorists, whose names we now hear in the mainstream media every day, were the products of the Soviet-Afghan war: like Osama bin Laden, Ayman al Zawahiri, the Haqqanis, the Taliban, the Hekmatyars etc. But that war wasn’t limited only to Afghanistan; the NATO-GCC alliance of the Cold War had funded, trained and armed the Islamic Jihadists all over the Middle East region; we hear the names of Jihadists operating in the regions as far afield as Uzbekistan and North Caucasus. In his 1998 interview [2], the National Security Adviser to President Carter, Zbigniew Brzezinski, had confessed that the President signed the directive for secret aid to the Afghan Mujahideen in July 1979 while the Soviet Army invaded Afghanistan in December 1979. Here is a poignant excerpt from his interview:

Question: “And neither do you regret having supported the Islamic Jihadis, having given arms and advice to future terrorists?”

Brzezinski: “What is most important to the history of the world? The Taliban or the collapse of the Soviet empire? Some stirred-up Moslems or the liberation of Central Europe and the end of the cold war?”

Despite the crass insensitivity, you got to give credit to Zbigniew Brzezinski that at least he had the guts to speak the unembellished truth. The hypocritical Western policy makers of today, on the other hand, say one thing in public and do the opposite on the ground. However, keep in mind that the aforementioned interview was recorded in 1998. After the WTC tragedy in 2001, no Western policy-maker can now dare to be as blunt and honest as Brzezinski.

The Anglo-Wahhabi alliance:

All the recent wars and conflicts aside, the unholy alliance between the Anglo-Americans and the Wahhabi-Salafis of the Gulf petro-monarchies, which I call “the Anglo-Wahhabi alliance,” is much older. The British stirred up uprising in Arabia by instigating the Sharifs of Mecca to rebel against the Ottoman rule during the First World War. After the Ottoman Empire collapsed, the British Empire backed King Abdul Aziz (Ibn-e-Saud) in his struggle against the Sharifs of Mecca; because the latter were demanding too much of a price for their loyalty: that is, the unification of the whole of Arabia under their suzerainty. King Abdul Aziz defeated the Sharifs and united his dominions into the Kingdom of Saudi Arabia in 1932 with the support of the British. However, by then the tide of British Imperialism was subsiding and the Americans inherited the former possessions and the rights and liabilities of the British Empire.

At the end of the Second World War on 14 February 1945, President Franklin D. Roosevelt held a historic meeting with King Abdul Aziz at Great Bitter Lake in the Suez canal onboard USS Quincy, and laid the foundations of an enduring Anglo-Wahhabi friendship which persists to this day; despite many ebbs and flows and some testing times especially in the wake of 9/11 tragedy when 15 out of 19 hijackers of the 9/11 plot turned out to be Saudi citizens. During the course of that momentous Great Bitter Lake meeting, among other things, it was decided to set up the United States Military Training Mission (USMTM) to Saudi Arabia to “train, advise and assist” the Saudi Arabian Armed Forces.

Aside from USMTM, the US-based Vinnell Corporation, which is a private military company based in the US and a subsidiary of the Northrop Grumman, used over a thousand Vietnam war veterans to train and equip the 125,000 strong Saudi Arabian National Guards (SANG) which is not under the authority of the Saudi Ministry of Defense and which acts as the Praetorian Guards of the House of Saud. The relationship which existed between the Arab American Oil Company (ARAMCO) and the House of Saud is no secret. Moreover, the Critical Infrastructure Protection Force, whose strength is numbered in tens of thousands, is also being trained and equipped by the US to guard the critical Saudi oil infrastructure along its eastern Persian Gulf coast where 90% Saudi oil reserves are located. Furthermore, the US has numerous air bases and missile defense systems currently operating in the Persian Gulf states and also a naval base in Bahrain where the Fifth Fleet of the US Navy is based.

The point that I am trying to make is that left to their own resources, the Persian Gulf’s petro-monarchies lack the manpower, the military technology and the moral authority to rule over the forcefully suppressed and disenfranchised Arab masses, not only the Arab masses but also the South Asian and African immigrants of the Gulf Arab states. One-third of Saudi Arabian population is comprised of immigrants; similarly, more than 75% of UAE’s population is also comprised of immigrants from Pakistan, Bangladesh, India and Sri Lanka; and all the other Gulf monarchies also have a similar proportion of the immigrants from the developing countries; moreover, unlike the immigrants in the Western countries who hold the citizenship status, the Gulf’s immigrants have lived there for decades and sometimes for generations, and they are still regarded as unentitled foreigners.

Petroimperialism and the Western energy interests:

A legitimate question arises in the mind of a curious reader , however, that why do the Western powers support the Gulf’s petro-monarchies, knowing fully well that they are the ones responsible for nurturing the Takfiri-Jihadi ideology all over the Islamic world; does that not runs counter to their professed goal of eliminating Islamic extremism and terrorism? When you ask this question, you get two very different and contradictory responses depending on who you are talking to. If you ask this question from a Western policy-maker or a diplomat that why do you support the Gulf’s despots? He replies that it’s because we have vital strategic interests in the Middle East and North Africa region; by which he means abundant oil and natural gas reserves and also the fact that the Arab Sheikhs have made substantial investments in the Western economies at a time of global recession and the outsourcing of most of manufacturing to China. Thus, the Western policy-makers’ defense is predicated on self-interest, i.e. the Western national interests.

When you ask the same question, however, from the constituents of the Western liberalism that what is the Western policy in the Middle East region? The constituents’ response is quite the opposite, they don’t think that the Western powers control the Middle East, or the global politics and economics in general, for their trade and energy interests; they believe that the motives of the Western powers are more altruistic than selfish. The constituents of the Western liberalism mistakenly believe in the counterfactual concepts of humanitarian and liberal interventionism and the responsibility to protect.

Coming back to the question, why do the Western powers prop up the Middle Eastern dictators knowing fully well that they are the ones responsible for nurturing Islamic jihadism and is it possible that in some future point in time they will withdraw their support? It is highly unlikely at least in the foreseeable future. The Western powers have become so dependent on the Arab petro-dollars that they would rather fight the Arab tyrants’ wars for them against their regional rivals. Presently, there are two regional powers vying for dominance in the Middle East: Saudi Arabia and Iran. The Syrian civil war is basically a Sunni Jihad against the Shi’a Resistance axis. The Shi’a alliance is comprised of Iran and Syria, the latter is ruled by an Alawi (Shi’a) regime, even though the majority of Syria’s population is Sunni Muslims and the Alawites constitute only 12% of the population. Lebanon-based Hezbollah (which is also Shi’a) is an integral part of the Shi’a Resistance axis. And recently the Nouri al Maliki and Haider al Abadi administrations in Iraq, which also has a Shi’a majority, have formed a tenuous alliance with Iran.

Moreover, Saudi Arabia has long-standing grievances against Iran’s meddling in the Middle Eastern affairs, especially the latter’s support to the Palestinian cause, the Houthis in Yemen, the Bahraini Shi’as and more importantly the significant and restive Shi’a minority in the Eastern Province of Saudi Arabia where 90% of Saudi oil reserves are located along the Persian Gulf’s coast. On top of that Saudi Arabia also has grievances against the US for toppling the Sunni Saddam regime in Iraq in 2003 which had formed a bulwark against the Khomeini influence in the Middle East because of Saddam’s military prowess. Furthermore, in the wake of political movements for enfranchisement during the Arab Spring of 2011, Saudi Arabia took advantage of the opportunity and militarized the peaceful and democratic protests in Syria with the help of its Sunni allies: the Gulf monarchies of Qatar, UAE, Kuwait and Jordan and Turkey (all Sunnis) against the Shi’a regime of Bashar al Assad.

However, why did the Western powers preferred to join this Sunni alliance against the Shi’a Resistance axis? It’s because the Assad regime has a history of hostility towards the West; it had also formed a close working relationship with the erstwhile Soviet Union and it still hosts a Russian naval facility at Tartus; and its proxy in Lebanon, Hezbollah, has emerged over the years as the single biggest threat to the Israel’s regional security. On the other hand, all the aforementioned Sunni states have always been the steadfast allies of the Western powers along with Israel; don’t get misled by the public posturing, all the aforementioned Sunni states along with the Western support are in the same boat in the Syrian civil war as Israel.

Hypothetically speaking, had the Western powers not joined the ignoble Syrian Jihad which has claimed 250,000 lives so far and made millions of Syrians refugees, what could have been an appropriate course of action to force the Gulf monarchies, Turkey and Jordan, not to engage in fomenting trouble in Syria? This is a question of will, if there is will there are always numerous ways to deal with the problem. However, after what has happened in Afghanistan, Iraq, Libya and Syria only a naïve neoliberal will prescribe a Western military intervention anywhere in the world. But if military intervention is off the table, is there a viable alternative to enforce justice and to force the states to follow moral principles in international politics? Yes there is.

The crippling “third party” economic sanctions on Iran in the last few years may not have accomplished much, but those sanctions have brought to the fore the enormous power which the Western financial institutions and the petro-dollar as a global reserve currency wields over the global financial system. We must bear in mind that the Iranian nuclear negotiations were as much about Iran’s nuclear program as they were about its ballistic missile program, which is a much bigger “conventional threat” to the Gulf’s petro-monarchies just across the Persian Gulf. Despite the sanctions being unfair, Iran felt the heat so much that it remained engaged in the negotiations throughout the last few years, and finally the issue was amicably settled in the form of the Iran nuclear deal in April 2015. However, such was the crippling effect of those “third party” sanctions on the Iranian economy that had it not been for Iran’s enormous oil and gas reserves, and some Russian, Chinese and Turkish help in illicitly buying Iranian oil, it could have defaulted due to those sanctions.

All I am trying to suggest is, that there are ways to arm-twist the Gulf’s petro-monarchies to implement democratic reforms and to refrain from sponsoring the Takfiri-Jihadist terror groups all over the Islamic world, provided that we have just and upright international arbiters. However, there is a caveat: Iran is only a single oil-rich state which has 160 billion barrels of proven crude oil reserves and around 4 million barrels per day (mbpd) production. On the other hand, the Persian Gulf’s petro-monarchies are actually three oil-rich states: Saudi Arabia with its 265 billion barrels of proven reserves and 10 mbpd of daily crude oil production; and UAE and Kuwait with 200 billion barrels (100 billion barrels each) of proven reserves and 6 mbpd of daily crude oil production; together their share amounts to 465 billion barrels, almost one-third of the world’s 1477 billion barrels of total proven crude oil reserves; and if we add Qatar to the equation, which isn’t oil-rich, as such, but has substantial natural gas reserves, it must take a morally very very upright arbiter to sanction all of them.

Therefore, though sanctioning the Gulf petro-monarchies sounds like a good idea on paper, but bear in mind that the relationship between the Gulf’s petro-monarchies and the industrialized world is that of a consumer-supplier relationship: the Gulf Arab states are the suppliers of energy and the industrialized world is its consumer, therefore, the Western powers cannot sanction their energy-suppliers and largest investors, if anything, the Gulf’s petro-monarchies have in the past “sanctioned” the Western powers by imposing an oil embargo in 1973 after the Arab-Israel war. The 1973 Arab oil embargo against the West had lasted only for a short span of six months but it had such a profound effect on the psyche and the subsequent strategy of the Western powers that after the embargo the price of crude oil in the international market quadrupled; the US imposed a ban on the export of indigenously produced crude oil outside the US’ borders which is still in place; and the US started keeping a strategic oil reserve amounting to two months of fuel supply for its total energy needs for the military purposes that includes jet fuel for its aircrafts and petrol and diesel for the armored personnel carriers, battle tanks and naval vessels.

Recently, some very upbeat rumors about “the Shale Revolution” [3] have been circulating the mainstream media. However, the Shale revolution is primarily a natural gas revolution: it has increased the ‘probable-recoverable’ resources of natural gas by 30%. The ‘shale oil’ on the other hand, refers to two very different kinds of energy resource: one, the solid kerogen, though substantial resources of kerogen have been found in the US’ Green River formations, but the cost of extracting liquid crude from solid kerogen is so high that it is economically unviable for at least another 100 years; two, the tight oil which is blocked by the shale, it is a viable energy resource, but the reserves are so limited, around 4 billion barrels in Texas and North Dakota, that it will run out in a few years.