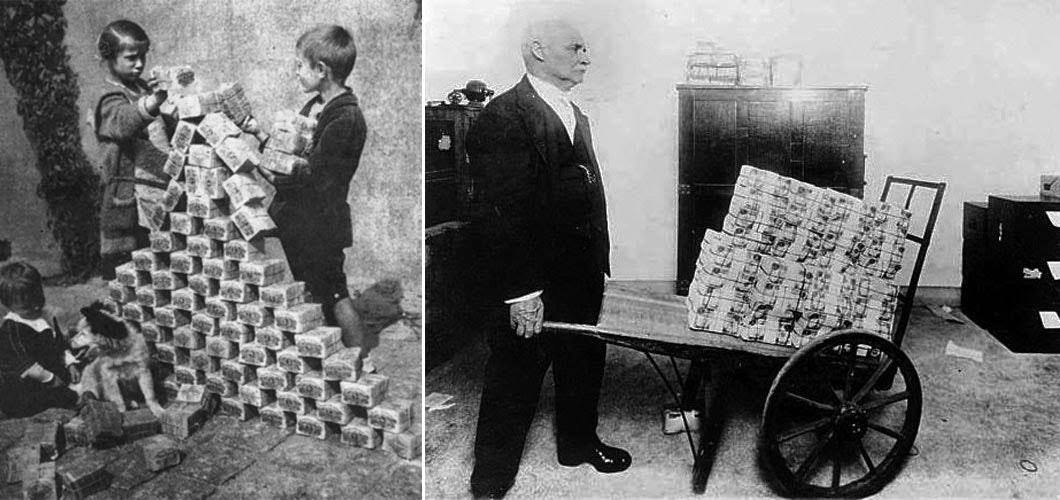

- Fertilizer Prices Hit Record Highs, May Pressure Food Inflation Even Higher

Fertilizer Prices Hit Record Highs, May Pressure Food Inflation Even Higher

Fertilizer prices have risen to a record high in North America, threatening to boost food inflation even higher. Nitrogen products are increasing due to the cost of natural gas, which is used in the manufacturing process.

The Green Markets North America Fertilizer Price Index soared to a record high last week of $996.32 per short ton.

The fertilizer market has been roiled by hurricanes, plant shutdowns, sanctions, and shortages of natural gas in Europe and China, pushing nutrient prices sky-high, which will raise the cost of production for global farmers. Here are global fertilizer prices zooming higher:

Fertilizers play an essential role in crop development for producing enough food for the global economy. The soaring costs of nutrients plus rapid food inflation will have the most severe economic impacts on emerging market economies first because low-income folks allocate a more significant part of their incomes to purchasing food. This week, the Food and Agriculture Organization’s global food index hit a new decade high, driven by gains for cereals and vegetable oils.

Expensive fertilizer will push production costs higher for farmers worldwide, which will continue to increase food inflation.

Benefiting from rising fertilizer prices is CF Industries Holdings Inc., the world’s second-biggest fertilizer company.

The Northern Hemisphere growing season begins late March/April. It may suggest that soaring farm input costs, such as fertilizer, diesel, labor, and machinery, will pressure farm incomes and lead to sustained food inflation well into 2022.

Tyler Durden

Mon, 10/11/2021 – 02:45 - Europa Scorned And Forsaken

Europa Scorned And Forsaken

Authored by Alasdair Crooke via The Strategic Culture Foundation,

Does Europe possess the energy and the humility to look itself in the mirror, and re-position itself diplomatically?

Two events have combined to make a major inflection point for Europe:

The first was America’s abandonment of the Great Game ploy of attempting to keep the two Central Asian great land powers – Russia and China – divided and at odds with each other. This was the inexorable consequence to the US’ defeat in Afghanistan – and the loss of its last strategic foothold in Asia.

Washington’s response was a reversion to that old nineteenth century geo-political tactic of maritime containment of Asian land-power – through controlling the sea lanes. However America’s pivot to China as its primordial security interest has resulted in the North Atlantic becoming much less important to Washington – as the US security crux compacts down to ‘blocking’ China in the Pacific.

The Establishment-linked figure, George Friedman (of Stratfor fame), has outlined America’s new post-Afghan strategy on Polish TV. He said tartly: “When we looked for allies [for a maritime force in the Pacific] on which we could count – they were the British and the Australians. The French weren’t there”. Friedman suggested that the threat from Russia is more than a bit exaggerated, and implied that the North Atlantic NATO and Europe are not particularly relevant to the US in the new context of ‘China competition’. “We ask”, Friedman says, “what does NATO do for the problems the US has at this point?”. “This [the AUKUS] is the [alliance] that has existed since World War II. So naturally they [Australia] bought American submarines instead of French submarines: Life goes on”.

Friedman continued: “The NATO countries don’t have force enough to help us. It has been weakened by the Europeans. To have a military alliance, you have to have a military. The Europeans are not interested in spending the money”. “Europe”, he said, “has left us with no choice: It is not a case of the US adopting this strategy [AUKUS], it is the strategy of Europe. First, there is no Europe. There is a bunch of countries in Europe, pursuing their own interests. You can only be bilateral [perhaps working with Poland and Romania]. There is no ‘Europe’ to work with”.

A storm in a tea-cup? Possibly. But the French went apoplectic. Expressions such as ‘stab in the back’ and ‘betrayal’ were flung around. It was Europa scorned. She is bitter and angry. Biden has made a groveling apology to President Macron over cutting out France from the submarine contract, and Blinken has been in Paris smoothing feathers.

George Friedman’s blunt account of the ‘new strategy’ may not be Biden ‘speak’, but it is Military Industrial think-tank conceptualisation. How do we know that? Firstly, because Friedman is one of their spokesmen – but simply because… continuity. The incumbents of the White House come and go, but US security objectives do not alter so readily. When Trump was in the White House, his views on NATO were very similar to those just repeated by Friedman. Incumbents may change, but military think-tank perspectives evolve to a different and slower cycle.

The ‘multilateral dimension’ of relations with France would be viewed as a largely Biden preoccupation. Friedman expressed the continuity of a US slow-burn focus to seeing China as the threat to US primacy. NATO won’t disappear, but it will play a narrower role (especially in the wake of its’ Afghan débacle).

But the EU, Friedman has made ruthlessly clear, is not viewed by the US security élite as a serious global player – or really as much more than one ‘punter’, amongst others, buying at the US weapons supermarket. The submarine contract with Australia however, was a centrepiece to Paris’s strategy for European ‘strategic autonomy’. Macron believed France and the EU had established a position of lasting influence in the heart of the Indo-Pacific. Better still, it had out-manoeuvred Britain, and broken into the Anglophone world of the Five Eyes to become a privileged defence partner of Australia. Biden dissed that. And Commission President von der Leyen told CNN that there could not be “business as usual” after the EU was blindsided by AUKUS.

One factor for the UK being chosen as the ‘Indo-Pacific partner’ very probably was Trump’s successful suasion with ‘Bojo’ Johnson to abandon the Cameron-Osborne outreach to China; whereas the big three EU powers were perceived in the US security world as ambivalent towards China, at best. The UK really did cut links. The grease finally was Brexit, which opened the window for strategic options – which otherwise would have been impossible to the UK.

There may be a heavy price to pay though further down the line – the US security establishment are really pushing the Taiwan ‘envelope’ to the limit (possibly to weaken the CCP). It is extremely high risk. China may decide ‘enough is enough’, and crush the AUKUS maritime venture, which it can do.

The second ‘leg’ to this global inflection point – also triggered around the Afghan pivot into the Russo-Chines axis – was the SCO summit last month. A memorandum of understanding was approved that would tie together China’s Belt and Road Initiative to the Eurasian Economic Community, within the overall structure of the SCO, whilst adding a deeper military dimension to the expanded SCO structure.

Significantly, President Xi spoke separately to members of the Collective Security Treaty Organisation (of which China is not a part), to outline its prospective military integration too, into the SCO military structures. Iran was made a full member, and it and Pakistan (already a member), were elevated into prime Eurasian roles. In sum, all Eurasian integration paths combined into a new trade, resource – and military block. It represents an evolving big-power, security architecture covering some 57% of the world’s population.

Having lifted Iran into full membership – Saudi Arabia, Qatar and Egypt may also become SCO dialogue partners. This augurs well for a wider architecture that may subsume more of the Middle East. Already, Turkey after President Erdogan’s summit with President Putin at Sochi last week, gave clear indications of drifting towards Russia’s military complex – with major orders for Russian weaponry. Erdogan made clear in an interview with the US media that this included a further S400 air defence system, which almost certainly will result in American CAATSA sanctions on Turkey.

All of this faces the EU with a dilemma: Allies who cheered Biden’s ‘America is back’ slogan in January have found, eight months later, that ‘America First’ never went away. But rather, Biden paradoxically is delivering on the Trump agenda (continuity again!) – a truncated NATO (Trump mooted quitting it), and the possible US shunning of Germany as some candidate coalition partners edge toward exiting from the nuclear umbrella. The SPD still pays lip service to NATO, but the party is opposed to the 2% defence spending target (on which both Biden and Trump have insisted). Biden also delivered on the Afghanistan withdrawal.

Europeans may feel betrayed (though when has US policy ever been other than ‘America First’? It’s just the pretence which is gone). European grander aspirations at the global plane have been rudely disparaged by Washington. The Russia-China axis is in the driving seat in Central Asia – with its influence seeping down to Turkey and into the Middle East. The latter commands the lions’ share of world minerals, population – and, in the CTSO sphere, has the region most hungry and ripe for economic development.

The point here however, is the EU’s ‘DNA’. The EU was a project originally midwifed by the CIA, and is by treaty, tied to the security interests of NATO (i.e. the US). From the outset, the EU was constellated as the soft-power arm of the Washington Consensus, and the Euro deliberately was made outlier to the dollar sphere, to preclude competition with it (in line with the Washington Consensus doctrine). In 2002, an EU functionary (Robert Cooper) could envisage Europe as a new ‘liberal imperialism’. The ‘new’ was that Europe eschewed hard military power, in favour of the ‘soft’ power of its ‘vision’. Of course, Cooper’s assertion of the need for a ‘new kind of imperialism’ was not as ‘cuddly’ liberal – as presented. He advocated for ‘a new age of empire’, in which Western powers no longer would have to follow international law in their dealings with ‘old fashioned’ states; could use military force independently of the United Nations; and impose protectorates to replace regimes which ‘misgovern’.

This may have sounded quite laudable to the Euro-élites initially, but this soft-power European Leviathan was wholly underpinned by the unstated – but essential – assumption that America ‘had Europe’s back’. The first intimation of the collapse of this necessary pillar was Trump who spoke of Europe as a ‘rival’. Now the US flight from Kabul, and the AUKUS deal, hatched behind Europe’s back, unmissably reveals that the US does not at all have Europe’s back.

This is no semantic point. It is central to the EU concept. As just one example: when Mario Draghi was recently parachuted onto Italy as PM, he wagged his finger at the assembled Italian political parties: “Italy would be pro-European and North Atlanticist too”, he instructed them. This no longer makes sense in the light of recent events. So what is Europe? What does it mean to be ‘European’? All that needs to be thought through.

Europe today is caught between a rock and a hard place. Does it possess the energy (and the humility) to look itself in the mirror, and re-position itself diplomatically? It would require altering its address to both Russia and China, in the light of a Realpolitik analysis of its interests and capabilities.

Tyler Durden

Mon, 10/11/2021 – 02:00 - China Prepares For Possible Large-Scale COVID-19 Outbreak: Leaked CCP Documents

China Prepares For Possible Large-Scale COVID-19 Outbreak: Leaked CCP Documents

Authored by Alex Wu via The Epoch Times,

The Chinese regime has notified local authorities to prepare for a large-scale outbreak of COVID-19, according to leaked internal documents obtained by the Chinese Epoch Times.

One document, titled “Notice of Further Strengthening of Epidemic Prevention” was issued by the Chinese regime’s State Council, and forwarded by Fujian provincial government to local authorities on Sept. 30.

The other is a “National Day Epidemic Prevention Notice” issued by the State Council on Oct. 1 and distributed by the Fujian provincial officials to local authorities.

The documents are both marked “extra urgent.”

Both notices request enhanced preparations for an emergency response to the outbreak, with the Chinese Communist Party (CCP) putting forward at least two standards for local authorities.

One is to build central isolation sites, with local authorities required by the end of October to set up isolation centers and rooms of not less than 20 rooms per 10,000 people. The scale of each isolation site must be more than 100 rooms.

According to public data, the population of Fujian Province in 2020 was 41.54 million. As of Sept. 19, the province has set up 35,691 quarantine rooms in 296 central sites.

Based on the standard in the epidemic prevention notice, Fujian Province will need to build at least 83,000 quarantine rooms by the end of October, which is around 47,000 rooms in less than a month.

According to one expert, the requirements for the COVID-19 quarantine sites reveal the real situation of the pandemic in China.

Dr. Sean Lin, a former virology researcher at the U.S. Army Research Institute, told The Epoch Times:

“This reflects the CCP’s concern about the rise of the epidemic. It must have been concealing the true epidemic in mainland China, otherwise it would not suddenly issue a national notice of emergency preparedness.”

“Notice of Further Strengthening of Epidemic Prevention” requires the establishment of a five-layered control system.

It states:

“Township and street CCP cadres, community grid staff, grassroots medical workers, police, and volunteers shall jointly implement community epidemic prevention,” such as “strictly implement[ing] community prevention and control,” or locking down residential communities.

Lin said that the control system is actually to tighten social management in local areas, and “the CCP’s purpose is to tighten control.”

“If there is no nucleic acid test, all the CCP’s epidemic prevention measures are the same as political campaigns. For example, you can be quarantined at any time and put in a quarantine site. And the quarantine sites can also be a place of political persecution,” Lin said.

“No matter who you are, as long as the CCP says that you tested positive in a nucleic acid test, it will deprive you of all your rights. The CCP’s quarantine sites are actually an alternative form of concentration camp.”

Tyler Durden

Sun, 10/10/2021 – 23:30 - "Ready For Fielding" – US AC-130 Gunship Receives Laser Cannon

“Ready For Fielding” – US AC-130 Gunship Receives Laser Cannon

One of the most feared planes on the modern battlefield is the U.S. Air Force’s AC-130H Spectre gunship. The service has made major upgrades to the gunship, including a new offensive laser weapon system.

Lockheed Martin published a press release last week outlining how the Airborne High Energy Laser (AHEL) “is ready for fielding today.”

“Completion of this milestone is a tremendous accomplishment for our customer,” said Rick Cordaro, vice president, Lockheed Martin Advanced Product Solutions. “These mission success milestones are a testament of our partnership with the U.S. Air Force in rapidly achieving important advances in laser weapon system development. Our technology is ready for fielding today.”

The gunship, nicknamed “Hell in the Sky,” packs a serious punch with three side-firing weapons, including a 25mm Gatling gun, a 40mm Bofors cannon, and a 105mm howitzer. The fourth will be the AHEL, a chemical energy weapon, unleashing concentrated pulses of light to transfer energy to the target, quickly heating it and damaging it.

Lockheed went on to say the “AHEL subsystem for integration with other systems in preparation for ground testing and ultimately flight testing aboard the AC-130J aircraft.” There was no mention of when the laser weapon system would conduct air tests.

The 60-kilowatt laser weapon doesn’t have enough energy to punch a hole through a main battle tank or blow an enemy soldier to pieces, but rather it can melt ground-based satellite antennas and optical sensors.

There’s also a push by the Pentagon to develop and field laser weapons that are a “million times stronger” than anything out in the field today.

Tyler Durden

Sun, 10/10/2021 – 23:00 - Anti-Interventionist vs Neocon: Rare Debate Sees Scott Horton Steamroll Iraq War Architect Bill Kristol

Anti-Interventionist vs Neocon: Rare Debate Sees Scott Horton Steamroll Iraq War Architect Bill Kristol

Authored by Caitlin Johnstone via caitlinjohnstone.substack.com

An important and long-overdue debate has occurred between Iraq-raping arch-neocon Bill Kristol and the tireless libertarian war critic Scott Horton on the subject of US interventionism, and you should definitely drop whatever you’re doing and watch it immediately. The resolution up for debate was “A willingness to intervene, and to seek regime change, is key to an American foreign policy that benefits America,” with Kristol obviously arguing in the affirmative and Horton in the negative.

- The introduction starts here.

- Kristol’s opening argument starts here.

- Horton’s opening argument begins here.

- Questions from the moderator (where things really heat up) starts here.

- Q&A from the audience (in my opinion is the best part) begins here.

The winner of the debate will be obvious to anyone watching. Horton plowed through criticisms of the way US foreign policy is constantly “creating its own disasters it must then attempt to solve” from his encyclopedic knowledge of interventionist bloodbaths and their undeniable repercussions while Kristol appeared frequently flustered, passed on multiple rebuttals, and got called on blatantly false claims.

Horton rattled off nations, dates and death tolls in rapid succession and repeatedly referenced Kristol’s own role in imperialist bloodshed, while Kristol relied almost entirely on insubstantial assertions to defend his position that “we can be at once a republic and a liberal empire” and empty dismissal of Horton’s points about the destructive nature of various US foreign interventions.

In the end a deflated-looking Kristol gave closing remarks which amounted to little more than whining that Horton’s position doesn’t assume war hawks like himself are acting “in good faith”, while Horton’s closing statement just continued his blistering assault.

By the end of it you almost feel bad for old Bill.

The audience unsurprisingly sided overwhelmingly with Horton by a significantly greater margin at the end of the debate than the beginning. The only unanswered question when all was said and done was, how the hell did Kristol get it in his head that entering this debate was a good idea?

One can only assume hubris. Hubris arising from a life in an elitist echo chamber where his warped views are seldom challenged, and continual marination in the kind of unearned validation that only Beltway swamp monsters ever receive.

So watch and enjoy, folks. Participating in this kind of humiliating debate is not a mistake that any high-profile neocon is likely to repeat anytime soon.

Tyler Durden

Sun, 10/10/2021 – 22:30 - New Apple CarPlay Features Could Allow Control Of AC, Seats And Speedometer, From Your iPhone

New Apple CarPlay Features Could Allow Control Of AC, Seats And Speedometer, From Your iPhone

Apple isn’t just planning on getting into the car business, it plans on getting further into your business, no matter what car you drive.

That’s because the tech giant is looking to vastly expand its CarPlay feature, which is already used by millions of drivers to control music and get directions in their vehicles.

Apple says it is expanding the reach of CarPlay and “working on technology that would access functions like the climate-control system, speedometer, radio and seats,” according to a new report by Bloomberg. The company’s CarPlay feature allows drivers and passengers to hook up their iPhones to their vehicles, mostly for infotainment purposes.

The new project is codenamed “IronHeart” and would need to be executed with the help of automakers. Per Bloomberg, a new version of the software could include features to control:

- inside and outside temperature and humidity readings

- temperature zones, fans and the defroster systems

- settings for adjusting surround-sound speakers, equalizers, tweeters, subwoofers, and the fade and balance

- seats and armrests

- the speedometer, tachometer and fuel instrument clusters

Apple could “turn CarPlay into an interface that could span nearly the entire car” with the improvements, the report says. The all-in-one interface would be similar to the type that is being included in newer EVs.

Some drivers have complained of having to switch between Apple’s interface adn the car’s interface to manage some controls. In 2015, Apple allowed carmakers to develop third party apps to work with CarPlay and in 2019, the tech giant enabled support for the platform on secondary car screens, like digital instrument clusters. Neither of the modifications caught on broadly with automakers.

The expansion of CarPlay would mark Apple’s most drastic move into vehicles since CarPlay was released in 2014. The feature is now available in more than 600 car models and Apple’s Siri voice assistant, works in tandem with the software.

Some auto manufacturers, like Tesla, have balked at offerings from Apple and Google, choosing instead to develop their own software.

The report says Apple may still cancel the project if the features wind up not showing enough promise.

Tyler Durden

Sun, 10/10/2021 – 22:00 - Does Taiwan Need Nuclear Weapons To Deter China?

Does Taiwan Need Nuclear Weapons To Deter China?

By James Holmes,J. C. Wylie Chair of Maritime Strategy at the Naval War College and a Nonresident Fellow at the University of Georgia School of Public and International Affairs. Originally published in 19fortyfive.com

Back in August in the Washington Examiner, American Enterprise Institute senior fellow Michael Rubin (and a 1945 Contributing Editor) contended that Taiwan must go nuclear in the wake of the disastrous American withdrawal from Afghanistan. It can no longer count on a mercurial United States to keep its security commitments to the island. To survive it should obey the most primal, bareknuckles law of world politics: self-help.

QED.

Set aside Rubin’s claim that the Afghan denouement wrought irreparable harm to America’s standing vis-à-vis allies. He could be right, but I personally doubt it. The United States gave Afghanistan—a secondary cause by any standard—twenty years, substantial resources, and many military lives. That’s a commitment of serious heft, and one that gave Afghans a chance to come together as a society. That they failed reflects more on them than the United States. I suspect Taiwan would be grateful for a commitment of that magnitude and duration.

Yet Rubin’s larger point stands. One nation depends on another for salvation at its peril. Wise statesmen welcome allies . . . without betting everything on them. Taiwan should found its diplomacy and military strategy on deterring Chinese aggression if possible—alone if need be—and on stymieing a cross-strait assault if forced to it. This is bleak advice to be sure, but who will stand by Taiwan if the United States fails to? Japan or Australia might intercede alongside America, but not without it. Nor can Taipei look for succor to the UN Security Council or any other international body where Beijing wields serious clout. These are feeble bulwarks against aggression.

Deterrence, then, is elemental. But does a deterrent strategy demand atomic deterrence? Not necessarily. It’s far from clear that nuclear weapons deter much apart from nuclear bombardment—the type of aggression least likely to befall Taiwan. After all, the mainland longs to possess the island, with all the strategic value it commands. The Chinese Communist Party (CCP) has little use for a radioactive wasteland.

CCP overseers are vastly more likely to resort to military measures short of nuclear arms. China’s People’s Liberation Army (PLA) could launch a naval blockade or a conventional air campaign against Taiwan in a bid to starve out the populace or bludgeon them into submission. And even a direct cross-strait amphibious offensive—the PLA’s surest way to seize prime real estate on a tight timetable—would preserve most of Taiwan’s value to China.

So, it seems, a nonnuclear onslaught is what Taipei mainly needs to deter. History has shown that nuclear weapons stand little chance of deterring nonnuclear aggression. A threat to visit a Hiroshima or Nagasaki on, say, Shanghai in retaliation for low-level aggression would be implausible. Breaching the nuclear threshold would do little good strategically while painting the islanders as amoral—and hurting their prospects of winning international support in a cross-strait war.

An implausible threat stands little chance of deterring. Think about Henry Kissinger’s classic formula for deterrence, namely that it’s a product of multiplying three variables: capability, resolve, and belief. Capability and resolve are the components of strength. Capability means physical power, chiefly usable military might. Resolve means the willpower to use the capabilities on hand to carry out a deterrent threat. A deterrent threat generally involves denying a hostile contender what it wants or meting out punishment afterward should the contender defy the threat.

Statesmen essaying deterrence are in charge of capability and resolution. They can amass formidable martial power and steel themselves to use it. That doesn’t mean their efforts at deterrence will automatically succeed, though. Belief is Kissinger’s other crucial determinant. It’s up to the antagonist whether it believes in their combined capability and willpower.

Taiwan could field a nuclear arsenal, that is, and its leadership could summon the determination to use the arsenal under specific circumstances such as a nuclear or conventional attack on the island. In other words, it could accumulate the capacity to thwart acts the leadership deems unacceptable or punish them should they occur. But would Chinese Communist magnates find the island’s atomic arsenal and displays of willpower convincing?

Against a nuclear attack, maybe. If Taipei maintained an armory that could inflict damage on China that CCP leaders found unbearable, then Beijing ought to desist from a nuclear attack under the familiar Cold War logic of mutual assured destruction. The two opponents would reach a nuclear impasse.

Kissinger appends a coda to his formula for deterrence, namely that deterrence is a product of multiplication, not a sum. If any one variable is zero, so is deterrence. What that means is that Taiwan could muster all the military might and fortitude in the world and fail anyway if China disbelieved in its capability, resolve, or both. And it might: Chinese Communist leaders have a history of making statements breezily disparaging the impact of the ultimate weapon if used against China. Founding CCP chairman Mao Zedong once derided nukes as a “paper tiger.” A quarter-century ago a PLA general (apparently) joked that Washington would never trade Los Angeles for Taipei.

The gist of such statements: nuclear threats cannot dissuade China from undertaking actions that serve the vital interest as the CCP leadership construes it.

Again, though, nuclear deterrence ought to be a peripheral concern for Taipei. Beijing is unlikely to order doomsday strikes against real estate it prizes, regardless of whether the occupants of that real estate brandish nuclear arms or not. Far better for the island’s leadership to refuse to pay the opportunity costs of going nuclear and instead concentrate finite militarily relevant resources to girding for more probable contingencies.

Contingencies such as repulsing a conventional cross-strait assault.

Wiser investment will go to armaments that make the island a prickly “porcupine” bristling with “quills” in the form of shore-based anti-ship and anti-air missiles along with sea-based systems such as minefields, surface patrol craft armed to the teeth with missiles, and, once Taiwan’s shipbuilding industry gears up, silent diesel-electric submarines prowling the island’s environs. These are armaments that could make Taiwan indigestible for the PLA. And Beijing could harbor little doubt Taipei would use them.

Capability, resolve, belief. Deterrence through denial.

So Michael Rubin is correct to urge Taiwan not to entrust its national survival to outsiders. But it can take a pass on nuclear weapons—and husband defenses better suited to the strategic surroundings.

Tyler Durden

Sun, 10/10/2021 – 21:20 - California Orders Big Box Stores To Create 'Gender-Neutral' Section For Kids Products

California Orders Big Box Stores To Create ‘Gender-Neutral’ Section For Kids Products

The Golden State has long burnished its reputation as the most “progressive” (at least when it comes to superficial posturing) state in the union by adopting ultra-strict emissions standards and gas taxes (which is why Californians pay $6 a gallon right now), offering official protection to sanctuary cities, and a host of other measures, including – most recently – outlawing bacon with some new ‘animal welfare’ law.

Meanwhile, homelessness and inequality are soaring in Cali as businesses and residents (most recently Tesla and Elon Musk) have fled for the exits, flocking to places like Texas and Florida.

Yet once again, Gov Gavin Newsom demonstrated Saturday just how out of touch the state’s leadership is when he signed into law one of the most ridiculous examples of government overreach in support of enforcing the “woke” agenda that we have ever seen. From here on out, any store in California with more than 500 employees (which essentially means all the big-box stores) are legally required to establish “gender-neutral” sections for a small range of products (essentially just toys and hygiene products).

The law was inspired by “LGBT advocates” who claim that the colors pink and blue, when used in marketing, reinforce gender stereotypes that can be “harmful”.

The law will allow dividing clothing and other products into boys and girls’ sections (due to its obvious practicality) to continue. But clothing stores must also now include a “gender neutral” section as well.

As if business owners didn’t have enough on their hands dealing with COVID, the new law will require affected retailers to majorly reorganize, essentially forcing stores to shrink the sizes of their ‘boys’ and ‘girls’ sections while forcing them to place more items especially toys and things like razors that many complain have been subjected to the “pink tax”, in the new gender-neutral section.

The bill was written and championed by Evan Low, a Democrat state assemblyman representing Cali’s 28th district (in Silicon Valley). It was rejected twice before the governor ultimately signed it.

“We need to stop stigmatizing what’s acceptable for certain genders and just let kids be kids,” Low said. “My hope is this bill encourages more businesses across California and the US to avoid reinforcing harmful and outdated stereotypes.”

In reality, the law won’t have much practical effect at all since big box stores like Target and Wal-Mart have already been making “reforms” moving away from “boys” and “girls” sections in the face of agitation from LGBT activists. Although California is the first state to adopt this policy into law.

The law was opposed by some Republicans, who argued the government shouldn’t tell parents or businesses how to handle this. Interestingly, at least one big-box store – Target – already committed to easing gender identifiers attached to its products years ago.

Given the bill’s almost-laughable premise, we wonder: who will be left to “enforce” this new law? Will gender studies majors suddenly have a market demand for their expertise?

Tyler Durden

Sun, 10/10/2021 – 21:00 - Snowden: Your Money AND Your Life

Snowden: Your Money AND Your Life

Submitted by Edward Snowden via Continuing Ed,

1. This week’s news, or “news,” about the US Treasury’s ability, or willingness, or just trial-balloon troll-suggestion to mint a one trillion dollar ($1,000,000,000,000) platinum coin in order to extend the country’s debt-limit reminded me of some other monetary reading I encountered, during the sweltering summer, when it first became clear to many that the greatest impediment to any new American infrastructure bill wasn’t going to be the debt-ceiling but the Congressional floor.

That reading, which I accomplished while preparing lunch with the help of my favorite infrastructure, namely electricity, was of a transcript of a speech given by one Christopher J. Waller, a freshly-minted governor of the United States’ 51st and most powerful state, the Federal Reserve.

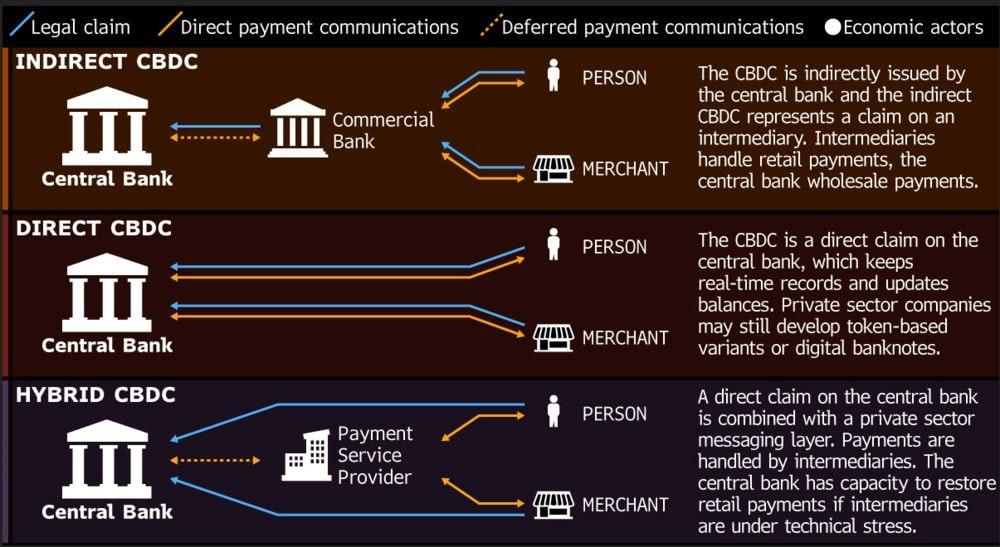

The subject of this speech? CBDCs—which aren’t, unfortunately, some new form of cannabinoid that you might’ve missed, but instead the acronym for Central Bank Digital Currencies—the newest danger cresting the public horizon.

Now, before we go any further, let me say that it’s been difficult for me to decide what exactly this speech is—whether it’s a minority report or just an attempt to pander to his hosts, the American Enterprise Institute.

But given that Waller, an economist and a last-minute Trump appointee to the Fed, will serve his term until January 2030, we lunchtime readers might discern an effort to influence future policy, and specifically to influence the Fed’s much-heralded and still-forthcoming “discussion paper”—a group-authored text—on the topic of the costs and benefits of creating a CBDC.

That is, on the costs and benefits of creating an American CBDC, because China has already announced one, as have about a dozen other countries including most recently Nigeria, which in early October will roll out the eNaira.

By this point, a reader who isn’t yet a subscriber to this particular Substack might be asking themselves, what the hell is a Central Bank Digital Currency?

Reader, I will tell you.

Rather, I will tell you what a CBDC is NOT—it is NOT, as Wikipedia might tell you, a digital dollar. After all, most dollars are already digital, existing not as something folded in your wallet, but as an entry in a bank’s database, faithfully requested and rendered beneath the glass of your phone.

In every example, money cannot exist outside the knowledge of the Central Bank Neither is a Central Bank Digital Currency a State-level embrace of cryptocurrency—at least not of cryptocurrency as pretty much everyone in the world who uses it currently understands it.

Instead, a CBDC is something closer to being a perversion of cryptocurrency, or at least of the founding principles and protocols of cryptocurrency—a cryptofascist currency, an evil twin entered into the ledgers on Opposite Day, expressly designed to deny its users the basic ownership of their money and to install the State at the mediating center of every transaction.

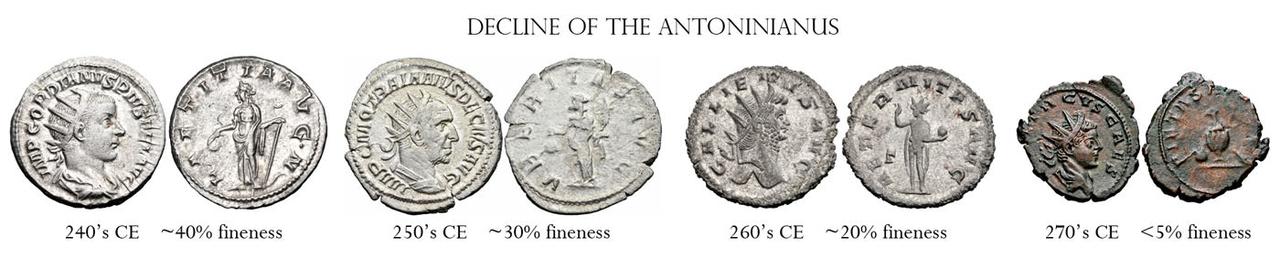

2. For thousands of years priors to the advent of CBDCs, money—the conceptual unit of account that we represent with the generally physical, tangible objects we call currency—has been chiefly embodied in the form of coins struck from precious metals. The adjective “precious”—referring to the fundamental limit on availability established by what a massive pain in the ass it was to find and dig up the intrinsically scarce commodity out of the ground—was important, because, well, everyone cheats: the buyer in the marketplace shaves down his metal coin and saves up the scraps, the seller in the marketplace weighs the metal coin on dishonest scales, and the minter of the coin, who is usually the regent, or the State, dilutes the preciosity of the coin’s metal with lesser materials, to say nothing of other methods.

Behold the glory of thelaw The history of banking is in many ways the history of this dilution—as governments soon discovered that through mere legislation they could declare that everyone within their borders had to accept that this year’s coins were equal to last year’s coins, even if the new coins had less silver and more lead. In many countries, the penalties for casting doubt on this system, even for pointing out the adulteration, was asset-seizure at best, and at worst: hanging, beheading, death-by-fire.

In Imperial Rome, this currency-degradation, which today might be described as a “financial innovation,” would go on to finance previously-unaffordable policies and forever wars, leading eventually to the Crisis of the Third Century and Diocletian’s Edict on Maximum Prices, which outlived the collapse of the Roman economy and the empire itself in an appropriately memorable way:

Tired of carrying around weighty bags of dinar and denarii, post-third-century merchants, particularly post-third-century traveling merchants, created more symbolic forms of currency, and so created commercial banking—the populist version of royal treasuries—whose most important early instruments were institutional promissory notes, which didn’t have their own intrinsic value but were backed by a commodity: They were pieces of parchment and paper that represented the right to be exchanged for some amount of a more-or-less intrinsically valuable coinage.

The regimes that emerged from the fires of Rome extended this concept to establish their own convertible currencies, and little tiny shreds of rag circulated within the economy alongside their identical-in-symbolic-value, but distinct-in-intrinsic-value, coin equivalents. Beginning with an increase in printing paper notes, continuing with the cancellation of the right to exchange them for coinage, and culminating in the zinc-and-copper debasement of the coinage itself, city-states and later enterprising nation-states finally achieved what our old friend Waller and his cronies at the Fed would generously describe as “sovereign currency:” a handsome napkin.

Sovereign currency, as known to history Once currency is understood in this way, it’s a short hop from napkin to network. The principle is the same: the new digital token circulates alongside the increasingly-absent old physical token. At first.

Just as America’s old paper Silver Certificate could once be exchanged for a shiny, one-ounce Silver Dollar, the balance of digital dollars displayed on your phone banking app can today still be redeemed at a commercial bank for one printed green napkin, so long as that bank remains solvent or retains its depository insurance.

Should that promise-of-redemption seem a cold comfort, you’d do well to remember that the napkin in your wallet is still better than what you traded it for: a mere claim on a napkin for your wallet. Also, once that napkin is securely stowed away in your purse—or murse—the bank no longer gets to decide, or even know, how and where you use it. Also, the napkin will still work when the power-grid fails.

The perfect companion for any reader’s lunch.

3. Advocates of CBDCs contend that these strictly-centralized currencies are the realization of a bold new standard—not a Gold Standard, or a Silver Standard, or even a Blockchain Standard, but something like a Spreadsheet Standard, where every central-bank-issued-dollar is held by a central-bank-managed account, recorded in a vast ledger-of-State that can be continuously scrutizined and eternally revised.

CBDC proponents claim that this will make everyday transactions both safer (by removing counterparty risk), and easier to tax (by rendering it well nigh impossible to hide money from the government).

CBDC opponents, however, cite that very same purported “safety” and “ease” to argue that an e-dollar, say, is merely an extension to, or financial manifestation of, the ever-encroaching surveillance state. To these critics, the method by which this proposal eradicates bankruptcy fallout and tax dodgers draws a bright red line under its deadly flaw: these only come at the cost of placing the State, newly privy to the use and custodianship of every dollar, at the center of monetary interaction. Look at China, the napkin-clingers cry, where the new ban on Bitcoin, along with the release of the digital-yuan, is clearly intended to increase the ability of the State to “intermediate”—to impose itself in the middle of—every last transaction.

“Intermediation,” and its opposite “disintermediation,” constitute the heart of the matter, and it’s notable how reliant Waller’s speech is on these terms, whose origins can be found not in capitalist policy but, ironically, in Marxist critique. What they mean is: who or what stands between your money and your intentions for it.

What some economists have lately taken to calling, with a suspiciously pejorative emphasis, “decentralized cryptocurrencies”—meaning Bitcoin, Ethereum, and others—are regarded by both central and commercial banks as dangerous disintermediators; precisely because they’ve been designed to ensure equal protection for all users, with no special privileges extended to the State.

This “crypto”—whose very technology was primarily created in order to correct the centralization that now threatens it—was, generally is, and should be constitutionally unconcerned with who possesses it and uses it for what. To traditional banks, however, not to mention to states with sovereign currencies, this is unacceptable: These upstart crypto-competitors represent an epochal disruption, promising the possibility of storing and moving verifiable value independent of State approval, and so placing their users beyond the reach of Rome. Opposition to such free trade is all-too-often concealed beneath a veneer of paternalistic concern, with the State claiming that in the absence of its own loving intermediation, the market will inevitably devolve into unlawful gambling dens and fleshpots rife with tax fraud, drug deals, and gun-running.

It’s difficult to countenance this claim, however, when according to none other than the Office of Terrorist Financing and Financial Crimes at the US Department of the Treasury, “Although virtual currencies are used for illicit transactions, the volume is small compared to the volume of illicit activity through traditional financial services.”

Traditional financial services, of course, being the very face and definition of “intermediation”—services that seek to extract for themselves a piece of our every exchange.

4. Which brings us back to Waller—who might be called an anti-disintermediator, a defender of the commercial banking system and its services that store and invest (and often lose) the money that the American central banking system, the Fed, decides to print (often in the middle of the night).

You’d be surprised how many opinion-writers are willing to publicly pretend they can’t tell the difference between an accounting trick and money-printing. And yet I admit that I still find his remarks compelling—chiefly because I reject his rationale, but concur with his conclusions.

It’s Waller’s opinion, as well as my own, that the United States does not need to develop its own CBDC. Yet while Waller believes that the US doesn’t need a CBDC because of its already robust commercial banking sector, I believe that the US doesn’t need a CBDC despite the banks, whose activities are, to my mind, almost all better and more equitably accomplished these days by the robust, diverse, and sustainable ecosystem of non-State cryptocurrencies (translation: regular crypto).

I risk few readers by asserting that the commercial banking sector is not, as Waller avers, the solution, but is in fact the problem—a parasitic and utterly inefficient industry that has preyed upon its customers with an impunity backstopped by regular bail-outs from the Fed, thanks to the dubious fiction that it is “too big too fail.”

But even as the banking-industrial complex has become larger, its utility has withered—especially in comparison to crypto. Commercial banking once uniquely secured otherwise risky transactions, ensuring escrow and reversibility. Similarly, credit and investment were unavailable, and perhaps even unimaginable, without it. Today you can enjoy any of these in three clicks.

Still, banks have an older role. Since the inception of commercial banking, or at least since its capitalization by central banking, the industry’s most important function has been the moving of money, fulfilling the promise of those promissory notes of old by allowing their redemption in different cities, or in different countries, and by allowing bearers and redeemers of those notes to make payments on their and others’ behalf across similar distances.

For most of history, moving money in such a manner required the storing of it, and in great quantities—necessitating the palpable security of vaults and guards. But as intrinsically valuable money gave way to our little napkins, and napkins give way to their intangible digital equivalents, that has changed.

Today, however, there isn’t much in the vaults. If you walk into a bank, even without a mask over your face, and attempt a sizable withdrawal, you’re almost always going to be told to come back next Wednesday, as the physical currency you’re requesting has to be ordered from the rare branch or reserve that actually has it. Meanwhile, the guard, no less mythologized in the mind than the granite and marble he paces, is just an old man with tired feet, paid too little to use the gun that he carries.

These are what commercial banks have been reduced to: “intermediating” money-ordering-services that profit off penalties and fees—protected by your grandfather.

In sum, in an increasingly digital society, there is almost nothing a bank can do to provide access to and protect your assets that an algorithm can’t replicate and improve upon.

On the other hand, when Christmas comes around, cryptocurrencies don’t give out those little tiny desk calendars.

But let’s return to close with that bank security guard, who after helping to close up the bank for the day probably goes off to work a second job, to make ends meet—at a gas station, say.

Will a CBDC be helpful to him? Will an e-dollar improve his life, more than a cash dollar would, or a dollar-equivalent in Bitcoin, or in some stablecoin, or even in an FDIC-insured stablecoin?

Let’s say that his doctor has told him that the sedentary or just-standing-around nature of his work at the bank has impacted his health, and contributed to dangerous weight gain. Our guard must cut down on sugar, and his private insurance company—which he’s been publicly mandated to deal with—now starts tracking his pre-diabetic condition and passes data on that condition on to the systems that control his CBDC wallet, so that the next time he goes to the deli and tries to buy some candy, he’s rejected—he can’t—his wallet just refuses to pay, even if it was his intention to buy that candy for his granddaughter.

Or, let’s say that one of his e-dollars, which he received as a tip at his gas station job, happens to be later registered by a central authority as having been used, by its previous possessor, to execute a suspicious transaction, whether it was a drug deal or a donation to a totally innocent and in fact totally life-affirming charity operating in a foreign country deemed hostile to US foreign policy, and so it becomes frozen and even has to be “civilly” forfeited. How will our beleagured guard get it back? Will he ever be able to prove that said e-dollar is legitimately his and retake possession of it, and how much would that proof ultimately cost him?

Our guard earns his living with his labor—he earns it with his body, and yet by the time that body inevitably breaks down, will he have amassed enough of a grubstake to comfortably retire? And if not, can he ever hope to rely on the State’s benevolent, or even adequate, provision—for his welfare, his care, his healing?

This is the question that I’d like Waller, that I’d like all of the Fed, and the Treasury, and the rest of the US government, to answer:

Of all the things that might be centralized and nationalized in this poor man’s life, should it really be his money?

Tyler Durden

Sun, 10/10/2021 – 20:40 - China Braces For Possible Large-Scale COVID-19 Outbreak: Leaked CCP Documents

China Braces For Possible Large-Scale COVID-19 Outbreak: Leaked CCP Documents

By Alex Wu of the Epoch Times

The Chinese regime has notified local authorities to prepare for a large-scale outbreak of COVID-19, according to leaked internal documents obtained by the Chinese Epoch Times.

One document, titled “Notice of Further Strengthening of Epidemic Prevention” was issued by the Chinese regime’s State Council, and forwarded by Fujian provincial government to local authorities on Sept. 30. The other is a “National Day Epidemic Prevention Notice” issued by the State Council on Oct. 1 and distributed by the Fujian provincial officials to local authorities.

The documents are both marked “extra urgent.”

Both notices request enhanced preparations for an emergency response to the outbreak, with the Chinese Communist Party (CCP) putting forward at least two standards for local authorities.

One is to build central isolation sites, with local authorities required by the end of October to create facilities of not less than 20 rooms per 10,000 people. The scale of each isolation site must be more than 100 rooms.

The under-construction centralized quarantine facilities, where people at risk of contracting COVID-19 are to be taken into quarantine in Shijiazhuang, in northern Hebei Province, after the province declared an “emergency state,” on Jan. 16, 2021. (STR/CNS/AFP via Getty Images According to public data, the population of Fujian Province in 2020 was 41.54 million. As of Sept. 19, the province has set up 35,691 quarantine rooms in 296 central sites.

Based on the standard set in the notice, Fujian Province will need to build at least 83,000 quarantine rooms by the end of October, which is about 47,000 rooms in less than a month.

According to one expert, the requirements for the COVID-19 quarantine sites reveal the real situation of the pandemic in China.

Sean Lin, a former virology researcher at the U.S. Army Research Institute, told The Epoch Times: “This reflects the CCP’s concern about the rise of the epidemic. It must have been concealing the true epidemic in mainland China, otherwise, it would not suddenly issue a national notice of emergency preparedness.”

“Notice of Further Strengthening of Epidemic Prevention” requires the establishment of a five-layered control system.

It states: “Township and street CCP cadres, community grid staff, grassroots medical workers, police, and volunteers shall jointly implement community epidemic prevention,” such as “strictly implement[ing] community prevention and control,” or locking down residential communities.

Lin said that the control system is actually to tighten social management in local areas, and “the CCP’s purpose is to tighten control.”

“If there is no nucleic acid test, all the CCP’s epidemic prevention measures are the same as political campaigns. For example, you can be quarantined at any time and put in a quarantine site. And the quarantine sites can also be a place of political persecution,” Lin said.

“No matter who you are, as long as the CCP says that you tested positive in a nucleic acid test, it will deprive you of all your rights. The CCP’s quarantine sites are actually an alternative form of concentration camp.”

* * *

Commenting on the report, Dr. Li-Meng Yan, who was among the first to demonstrate that the Covid virus was man made in the Wuhan lab, says that this report shows

- CCP leaders know #COVID19 is Unrestricted Bioweapon. They are scared of it

- CCP knows vaxx can’t stop the pandemic

- But CCP wanna the pandemic everlasting in other countries

- CCP leaders will be away from patients for their safety

This report shows

•CCP leaders know #COVID19 is Unrestricted Bioweapon. They are scared of it

•CCP knows vaxx can’t stop the pandemic

•But CCP wanna the pandemic everlasting in other countries

•CCP leaders will be away from patients for their safetyhttps://t.co/p9VDo8bPQc— Dr. Li-Meng YAN (@DrLiMengYAN1) October 11, 2021

Tyler Durden

Sun, 10/10/2021 – 20:20 - Gazprom Hikes Export Prices As Moscow Urges Europe To Fix Ties To Avoid More Gas Shortages

Gazprom Hikes Export Prices As Moscow Urges Europe To Fix Ties To Avoid More Gas Shortages

Russia’s nat gas giant, Gazprom, raised its 2021 price guidance for natural gas exports, while signaling caution on volumes it could ship, as Europe’s energy crisis worsens.

According to Bloomberg, the Russian state-controlled exporter that supplies 35% of European gas needs, reiterated that shoring up inventories at home was its top priority, and only after it has refilled its own storage facilities by the end of October, would the company look at potentially increasing exports to continental Europe, Wood & Co. and BCS Global Markets wrote in separate notes Friday following a webinar with Gazprom managers. It would, in theory, explain why Russian supplies to Europe remain well below recent levels.

At the same time, Russian research houses Wood & Co and Sova Capital noted that Gazprom increased its full-year gas-price guidance for exports to Europe and Turkey to a range of $295 to $330 per 1,000 cubic meters. The revised outlook on Gazprom’s average prices in the region is good news for the company’s investors as it signals higher dividends may be coming. Both Wood & Co. and Sova Capital also say that Gazprom is sticking with its conservative estimate of full-year gas supplies to Europe and Turkey, which is seen at 183 billion cubic meters.

That suggests that despite Putin’s suggestion last Wednesday that his country could boost deliveries to record levels, partially easing an energy crisis sweeping Europe which threatens to hamper the region’s economic recovery by driving up business costs and household bills and sending inflation soaring, Gazprom’s caution on shipments will disappoint some traders and policy makers hoping for an immediate hike in supply.

Incidentally, in response to Putin’s statement, Goldman’s European energy analysts said that the comments from the former KGB spy raised questions as to what extent Russian gas supplies can alleviate the ongoing tightness in European gas markets. Goldman was adamant:

“we believe these statements, which we discuss in more detail below, are similar in nature to what officials have communicated for the past few months and bring no new information as to how we should think about this winter’s gas balances in Europe. Accordingly, we maintain our base case, which assumes Russian flows to NW Europe through existing pipelines will normalize from November from reduced levels this month and that the newly built 55 Bcm Nord Stream 2 pipeline will be operational this winter, but with only a marginal net contribution to NW European supplies. Until then, we continue to see a risk that Gazprom might have to rely on taking physical delivery at the TTF hub to complement their pipeline flows to the region to satisfy winter contractual obligations given its local storage sites remain nearly empty.”

According to Goldman, such physical tightening of the market could take TTF prices well above current levels. However, should Russian flows increase as Goldman predicts in its base case, the bank would expect EU gas prices to decline from current levels but remain above the threshold for gas-to-oil switching of $27/mmBtu at current oil prices (rising to $30/mmBtu at our year-end Brent price forecast) until we know more about winter weather. Should winter weather remain average, prices could then drop further to the bank’s base case $17/mmBtu forecast by likely year-end.

Going back to the supply issues at hand, it’s not unusual for Gazprom to offer a cautious supply outlook, due to the fact that its sales are highly dependent on the weather, both in Russia and abroad. However, the company has taken pains to reiterate in recent days that it is fulfilling all its contractual obligations and it will aim to boost exports whenever possible. The Russian analysts say that Gazprom sees longer-term contracts and longer-dated prices as a tool that would help Europe mitigate the impact of extreme volatility. Translation: turn on Nord Stream 2 and all shall be well.

Which brings us to the second point: according to the FT, the Kremlin’s ambassador to the EU called on Europe to mend ties with Moscow in order to avoid future gas shortages, even as he insisted that Russia had nothing to do with the recent jump in prices.

Vladimir Chizov, Russia’s permanent representative to the EU, said he expected Gazprom, to respond swiftly to instructions from president Vladimir Putin to adjust output.

Making it abundantly clear that the hurdles preventing Russia from pumping more gas to Europe are largely political, the ambassador said that action, which would help curb skyrocketing wholesale prices, was likely to come “sooner rather than later.” Putin “gave some advice to Gazprom, to be more flexible. And something makes me think that Gazprom will listen,” Chizov told the Financial Times.

While rejecting assertions from European lawmakers that Russia had played a role in Europe’s gas crunch, Chizov said Europe’s choice to treat Moscow as a geopolitical “adversary” had not helped.

“The crux of the matter is only a matter of phraseology,” he said. “Change adversary to partner and things get resolved easier . . . when the EU finds enough political will to do this, they will know where to find us.”

And there you have it: after demonizing Russia for much of the past decade, with countless fake news reports out of the liberal media in the US seeking to portray Putin as the world’s biggest mastermind and effectively in control of the Trump White House, while helping send western relations with Russia to fresh post-Cold War lows, the chicken are coming home to roost and they are finding the temperature to be rather frigid.

Ironically, for a gas-starved Europe, Russia has now emerged as the only source of incremental gas supply which stands between the continent and a very cold winter. At one point last week spot gas prices reached nearly 10 times their level from the beginning of the year, before abruptly dropping after Putin hinted that Gazprom might increase supplies.

Chizov insisted Moscow had no interest in gas price surges. “This does not promote stability,” he said. “People will start looking around, turning back from gas to coal, which some are already doing”, much to the chagrin of the ESG lobby.

Record high prices and low reserves have spooked EU governments fearful of a winter shortage and led to demands from some member states for Brussels to consider emergency remedies or new reforms. But energy commissioner Kadri Simson told the FT last week that the roots of the crisis were “not created here in Europe.” Which, of course, is laughable as even Reuters’ energy analyst John Kemp explained over the weekend in “Forget Russian Intentions, Fundamentals Drove Up Europe’s Gas Price.”

Cutting to the chase, Russian officials have said that regulatory approval to permit gas flows through the controversial Nord Stream 2 pipeline to Germany would help solve the crisis. Some analysts have suggested Moscow is exacerbating the price squeeze to force such an outcome (they wouldn’t be wrong). Meanwhile, the US and many eastern EU states oppose the pipeline, which they say was designed to circumvent gas transit through Ukraine.

Chizov said the EU’s own energy policies had worsened the bloc’s woes as well as a reluctance among European energy companies to pay more to replenish their reserves. “All the problems that are arising have been created artificially. Primarily for political reasons,” he said.

However, Klaus-Dieter Maubach, chief executive of German gas company Uniper, a Gazprom client, suggested last week that supplies were the issue. Uniper “would be happy if Gazprom . . . delivered more volumes to cool down the situation and lower the gas price,” he said at a conference in Russia.

Chizov also told the FT that the crisis had been aggravated by EU regulations that force Gazprom to supply a proportion of gas to Europe on the freely-traded spot market terms, rather than through long-term contracts, which Brussels has argued are uncompetitive.

“Long-term contracts . . . provided security of supply and stability of volumes and prices. Then came this idea, emanating from Brussels, that the system should be changed,” he said. “We know that market rules may be helpful in some situations but quite unhelpful in others. Things can change. And they did change.” And the result was the biggest surge in gas prices in history.

Chizov also said that Gazprom is fulfilling its obligations to European customers on long-term supply contracts, but has been reluctant to make additional volumes available on the spot market, instead supplying domestic Russian storage facilities. That was because European energy companies were delaying extra purchases in the hope that prices will fall.

“If prices are freely floated on the market, of course any energy company in this part of Europe will think what the best moment is to order additional volumes,” he said. “The serious buyers know perfectly well what is going on . . . they have their own calculations.”

But Chizov said he believed the commission, whose flagship renewable energy reform initiative aims for the bloc to achieve net zero emissions by 2050, was “underestimating the future role of gas” as a European energy source.

“Until mankind finds a way to store energy in a sizeable manner, all those propellers and solar panels will not become a decisive factor,” he said, and somewhere Greta Thunberg sobbed uncontrollably.

Tyler Durden

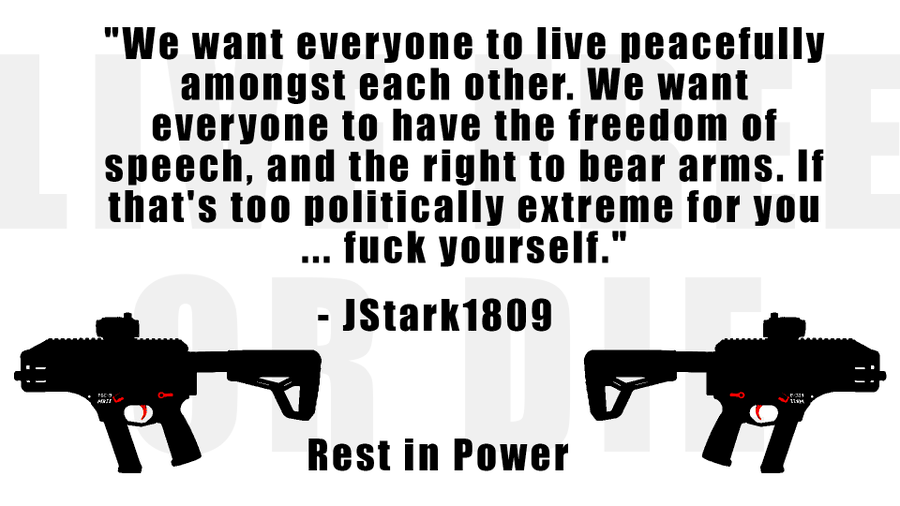

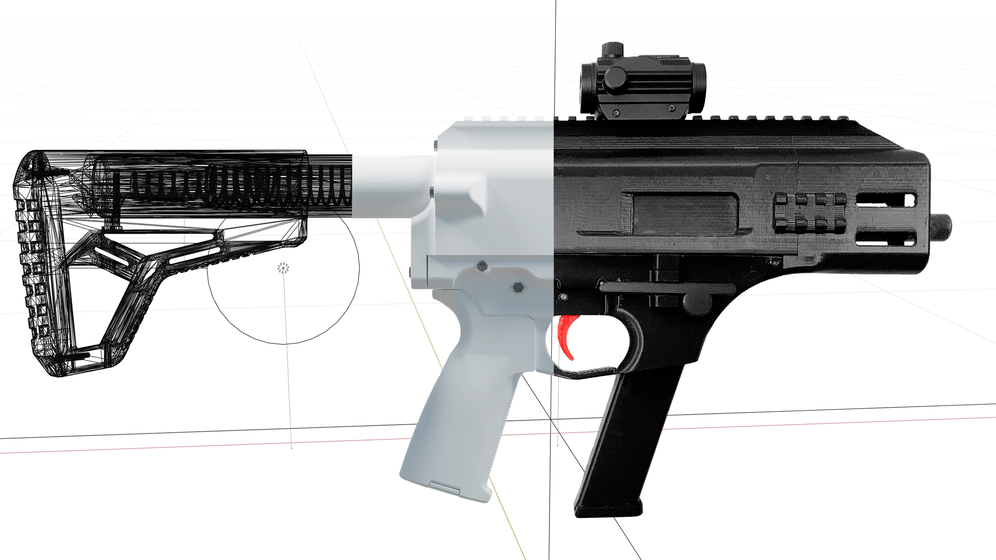

Sun, 10/10/2021 – 20:11 - 3D Gun Legend, "JStark," Famous For "FGC-9," Dead At 28-Years Old

3D Gun Legend, “JStark,” Famous For “FGC-9,” Dead At 28-Years Old

It’s come to our attention that German magazine Der Spiegel reports the inventor of the rapid-fire 3D-printed gun that could be entirely printed at home has passed away.

JStark, a 28-year-old German citizen, was one of the biggest innovators of this decade when printing weapons and gun parts at home. He helped create Deterrence Dispensed – an online group that promotes and distributes open-source 3D printed firearms, gun parts, and cartridges. The group strongly supports freedom of speech applied to computer code and blueprints.

Der Spiegel says JStark passed away on Friday of an apparent heart attack. Foul play was ruled out, and it “appears” his death was natural without any involvement of a third party. Along with this, the German magazine also reported police raided his home days before.

Another top 3D-printed gun designer that goes by the Twitter handle “CTRLPew,” also confirmed the death of Stark.

Its a sad time my friends. I can confirm the news that JStark has passed. The drive he brought to development will be dearly missed.

I’ll not be offering any details or commentary on his passing or the articles that were written. We are investigating some inconsistencies. pic.twitter.com/RUmIf6xcuv

— CTRLPew (@CtrlPew) October 9, 2021

https://platform.twitter.com/widgets.js

JStark’s wasn’t just an at-home gun hobbyist printing weapons. He promoted firearm ownership, freedom of speech and has been quoted in a documentary as saying, “We want everyone to have the freedom of speech, and the right to bear arms. If that’s too politically extreme for you … f**k yourself.”

JStark’s 2020 release of the FGC-9. otherwise known as “f**k gun control 9 mm,” was made widely available across the internet in late 2020. The publication of the gun’s blueprints created an online sensation. It spurred freedom movements of millennial printers who have revolutionized the way firearms are produced and that government cannot and will not control them. FGC-9 emerged as a symbol of life and freedom rather than a deadly weapon as governments worldwide impose tyrannical measures that restrict freedoms in a post-COVID world.

Some in the printing community have pointed out that a young man like himself shouldn’t have had a heart attack at 28-years old and reeks of suspension.

Im not gonna lie, a “heart attack” for a young man like him really just…

glows. pic.twitter.com/D82HEeSLHw— hanz (@TacticalHanz) October 9, 2021

https://platform.twitter.com/widgets.js

Keep in mind, governments around the world are freaking out about printed guns (because they’re unserialized). The Biden administration has repeatedly warned he will “stop ghost guns.”

Here’s a tribute to JStark.

Tyler Durden

Sun, 10/10/2021 – 20:00 - "It's A Big Day For Our State" – Sydney Lockdown Finally Ends After 106 Days

“It’s A Big Day For Our State” – Sydney Lockdown Finally Ends After 106 Days

Not long after controversial New South Wales Premier Gladys Berejiklian stepped down amid a corruption scandal, Sydney residents are breathing a sigh of relief early Monday (local time) as a nearly four-month-long lockdown afflicting Australia’s most populous city has finally been lifted, AFP reports.

For the last 106 days, Sydney’s 5 million residents have been living under lockdown conditions, intended to suppress the hyper-infectious (allegedly) delta variant. The measures became an international joke as cases continued to soar (and are at an all time high currently), and the government mostly stood by their policy directives, despite the fact that Australia has recorded an enviably low number of hospitalizations and deaths.

You really have to be impressed at Australia’s complete inability to control their outbreak, even with some of the strictest, harshest lockdowns & mask policies in the world

Imagine if anyone was willing to acknowledge how destructive & ineffective The Science™ actually is pic.twitter.com/Lwh9SbE3SX

— IM (@ianmSC) October 8, 2021

https://platform.twitter.com/widgets.js

But after a successful vaccination campaign, the government no longer sees a need for the lockdown conditions. New South Wales, the state where Sydney serves as the capitol, recorded just 477 cases on Sunday, while more than 70% of the population over the age of 16 gas been fully vaccinated. While cases numbers may remain elevated in other parts of Australia, Sydney has seen a distinct downward trend in daily cases.

Restaurant owners and bars were elated at the news. Some even planned to open at 1201 local time to serve vaccinated customers after months of struggling with little to no business. Locals appeared ready to celebrate now that the chaos, punctuated by increasingly violent protests, and an influx of soldiers sent to help ensure compliance, has ended.

“It’s a big day for our state,” said New South Wales’ recently appointed conservative premier Dominic Perrottet.

After “100 days of blood, sweat and no beers,” he said, “you’ve earned it.”

Since June, most shops, schools, salons and offices have been closed for any non-essential workers or purpose. Many critics slammed the restrictions and protests pushed back aggressively against what many described as the greatest infringement on Australians’ personal liberty.

During the lockdown there were bans on everything from traveling more than 5km from home, visiting family, playing squash, browsing in supermarkets and even attending funerals.

“Very few countries have taken as stringent or extreme an approach to managing Covid as Australia,” Tim Soutphommasane, an academic and former Australian race discrimination commissioner, told AFP.

Some restrictions on travel and mass gatherings will remain in place, but for the first time in months – since the delta wave arrived in Australia – life will return to some semblance of normal.

Tyler Durden

Sun, 10/10/2021 – 19:40 - How Stocks Perform During Stagflation, And Why Goldman's Clients Are Worried

How Stocks Perform During Stagflation, And Why Goldman’s Clients Are Worried

In our third and final post of the day discussing stagflation (here are part one and part two), we look squarely at the reason why Wall Street is finally freaking out about the threat of rising inflation in a time of shrinking growth or outright contraction (for Wall Street’s definition of stagflation or rather lack thereof, see here) by taking a look at how markets perform during periods of stagflation. Spoiler alert: it’s ugly.

As Goldman’s chief US equity strategist David Kostin writes in his Weekly Kickstart, “Stagflation was the most common word in client conversations this week as equity market volatility remained elevated.” One look at interest rates and energy prices should explain why.

There is a reason why Goldman clients are worried: while Kostin repeats that “stagflation is not our economists’ base case expectation” even as his economics team just cut its GDP forecast again while hiking its inflation outlook, he admits that “the weak historical performance of equities in stagflationary environments helps explain why investors are concerned.”

How weak? Well, during the last 60 years, Goldman calculates that the S&P 500 has generated a median real total return of +2.5% per quarter, but that quarterly return fell to -2.1% in stagflationary environments, worse than the median returns in environments characterized solely by weak economic growth or high inflation.

Of course, one would have to look far and wide to find a trader who was actually active during the last major stagflationary episode, or even during the somewhat milder ones at the start of the century, and is why Kostin notes that “US equity investors have had little experience with stagflation in recent decades” which have been characterized mostly by deflation.

By way of background, Kostin defines “stagflationary periods” – a term which as the recent Deutsche Bank poll found there was a wide disparity of opinions as to what exactly is “stagflation” – as episodes of two or more consecutive quarters in which core CPI inflation ran at least 50 basis points above the consensus long long-term expectation while real US GDP growth registered 50 bp or more below trend.

As the next chart shows, since 1960, 41 quarters (17%) have met these criteria, but the vast majority of those occurred between the late 1960s and early 1980s. In the 21st century, stagflation has been virtually non-existant, until now.

It should hardly come as a surprise that most of the equity market weakness in historical stagflationary environments has been attributable to pressure on corporate profit margins. That’s because stagflation has been associated with stable real revenues but declining profit margins and real earnings, indicating companies struggling to raise prices quickly enough to offset rising input costs.

In addition to the earnings headwinds, Godlman also notes that P/E multiples have also declined modestly during stagflationary periods alongside rising interest rates.

Who are the winners and losers during stagflation?

At the sector level, Energy and Health Care have typically generated the strongest returns during periods of stagflation. That may explain why during the past month, Energy has been the strongest sector in the market, rising by 14% alongside an equivalent surge in crude oil, yet Health Care has declined by 6% and lagged the S&P 500 (-3%). This split outcome hint at dynamics that are more consistent with a market pricing rising growth and inflation than one focused on the type of economic growth weakness that would characterize a stagflationary environment.

And while Goldman purposefully ignores the “other” possibility, it may also indicate that the market is woefully mispricing stagflation risks, as DB’s Jim Reid suggested earlier. In light of Goldman’s increasingly more frequent downgrades of US GDP, it is this alternative that looks far more realistic to us.

In any case, looking at the big stagflation losers Goldman notes that “Industrials and Information Technology have generally lagged most during stagflationary environments. The Info Tech sector is less cyclical now than it was during the stagflationary years of the late 1960s to early 1980s due to the compositional shift toward software and services firms.” Today, however, the sector’s massive long long-term growth profile has given it a longer “duration” than most other equities, making it particularly sensitive to real interest rates.

Further to this point, Albert Edwards showed last week that global tech stocks have become “cojoined” been with the US 30y bond yield since the start of this year. The SocGen strategist noted that “if the US 30y yield rises to 2.4% from the current 2.1%, it would knock some 15% off tech stock prices. Imagine if the US 10y rose from 1.5% currently to 2¼%! We could see quite a bear market in tech!“

Going back to Kostin, not even this perennial optimist can deny that the sector would likely still be vulnerable to stagflation today if such an environment led investors to price higher future interest rates to combat inflation.

Goldman then looks at the thematic shifts that have emerged during stagflationary periods, and notes that stagflation has been associated with shifts in consumer spending behavior and the outperformance of services companies relative to firms selling goods. Value and Size factors have generated roughly the same median returns during stagflationary periods as they have in general during the last 60 years. However, during stagflationary environments, real personal consumption expenditures for goods have grown at a median annualized rate of 1% compared with 3% for services. To justify this point Goldman looks at the historical performance of consumer stocks which reflects this gap: “Consumer services industries like restaurants and entertainment have outperformed goods industries including apparel and retail by over 100 bp per quarter during stagflationary periods compared with roughly equivalent performance in all periods.” The coming stagflation likely explains why consumer goods companies have lagged the S&P 500 since May, while consumer services firms have traded with the shifting virus outlook (see Exhibit 4).

Another reason why stagflation has pernicious and adverse side-effects on all aspects of life is that historically it has weighed on not just economic growth but also the growth of household wealth. Household net worth has grown by a median real rate of 0.5% per quarter since 1960, but just a 0% rate during periods of stagflation. These periods have also been associated with declining household allocations to equities, helping explain the weakness in equity valuation multiples. Home prices have typically declined in real terms during stagflation while gold has appreciated.

And yet, despite these admissions that stagflation has all but arrived, Goldman falls back on the tired, cliched narrative that “inflation is transitory” and the bank – which has a 4700 S&P price target, expects “equity market will continue to rally.” Goldman also falls back on the ironclad bullish defense that every dip has been bought so far, and the current one will too, because why not:

… we believe this dip will prove a good buying opportunity, as 5% pullbacks usually have in the past. The 226 trading day stretch between last November and last Thursday ranked as the 8 8th longest period since 1930 without a 5% S&P 500 pullback. Since 1980, an investor buying the S&P 500 down 5% from its 12 12-month high would have gained a median of 6% during the subsequent three months and enjoyed a positive return in 82% of episodes (28 of 34). Our year year-end S&P 500 target of 4700 reflects 7% upside from today’s price.

Its traditionally oblivious optimism aside, Goldman notes that Q3 earnings reporting season begins next week, and investors will be paying close attention to corporate messaging regarding the path of profit margins.

Last quarter companies expressed an unprecedented degree of attention on input costs and price hikes, and we expect margins will remain the primary focus of both investors and managements this quarter.

Curiously, at this point a major schism has opened up between Goldman’s traditionally bullish take and Morgan Stanley’s increasingly bearish outlook, and as the bank’s equity strategist Michael Wilson wrote last week when he predicted that a “fire and ice” scenario is coming that will send stocks sliding more than 10% in the coming days, a large number of companies are flagging serious supply chain issues in off-cycle earnings reports suggests and “both forward earnings estimates and price de-rated after many of these reports.”

Jumping to the punchline, Wilson thinks this will be a pervasive dynamic during 3Q reporting season and it will “trigger downside in earnings revisions at the index level – a headwind for price.”

Which begs the question: who will be right on the outcome of Q3 earnings season, and whose year-end price target will be closer to the S&P500 on Dec 31: Goldman with 4,700 or Morgan Stanley at 4,000.

Tyler Durden

Sun, 10/10/2021 – 19:29 - Here's How Wall Street Defines "Stagflation" And Why "Markets Could Be Massively Mispriced"

Here’s How Wall Street Defines “Stagflation” And Why “Markets Could Be Massively Mispriced”

It is easy to understand why Wall Street is increasingly worried about Stagflation: with the Citi global inflation surprise index surging to the highest level ever (granted, it only captures the period since 1999 so it’s unclear how it compares to the 1970s or early 1980s inflation shock periods)…

… Citi’s economic surprise index has turned negative and slumped to levels which historically have indicated an economic slowdown if not outright recession.