- "Bracing For Impact" – China Shock To Strike Germany's Largest Port In Days, As Trade Volumes Collapse 40%

“Bracing For Impact” – China Shock To Strike Germany’s Largest Port In Days, As Trade Volumes Collapse 40%

The worst-case coronavirus scenario is now being realized for German ports, as collapsing trade volumes from China could push Europe’s largest economy into recession.

For the last three weeks, global markets have been obsessed with economic paralysis that is quickly spreading across Asia, Europe, and the Americas. An economic shock combined with a virus outbreak is what triggered a macro matters moment for investors, who sold first and are asking questions later, as it appears a global trade recession could be on the horizon.

The port of Hamburg, Germany’s largest trading hub, reported a 40% plunge in trade volumes for February. The weakness was a combination of the Chinese New Year festivities and the onset of economic shocks triggered by the virus shutting down two-thirds of China’s economy.

Axel Mattern, CEO of the Port of Hamburg Marketing, told Reuters that German ports are bracing for a continuation of declining trade volumes in the days and weeks ahead. The cause of this weakness is purely coronavirus disruptions that caused China’s economy to collapse.

“We’re currently bracing for the impact. It will hit us with full force from mid-March,” Mattern said, adding that “the entire supply chains have been thrown completely off balance…we expect container volumes to drop sharply due to the coronavirus.”

What’s troubling is that at least a quarter of Hamburg’s trade volumes in 2019 originated from China. This could suggest that Germany’s economy is highly exposed to foreign shocks, with limited buffers to cushion the blow.

“And this period of weakness has now been extended due to the coronavirus – and there is no end in sight. Nobody can say how long this weak phase will last,” Mattern said.

The trade and supply chain shock is expected to tilt Germany into recession for the first half of the year. Chancellor Angela Merkel is running out of options on how to stimulate the economy.

Merkel has signaled that she is ‘open’ to suspending Germany’s ‘zero-deficit rule’ – better known as the ‘debt break’ – to bolster the fight against the coronavirus.

The shock was not a black swan, but rather a black bat in Wuhan, which is turning out to be one of the biggest economic shocks in decades to strike the global economy. Now the shock has infected global supply chains and traveling towards Western countries.

We noted last week that the Port of Los Angeles, the busiest seaport not only in the US but in the entire Western hemisphere, is also bracing for a “substantial hit” in trade volumes from China.

Mattern pointed out bright spots are developing in China as some businesses have increased output but far away from full capacity.

“What we hear from on site in Shanghai is that there are first signs of normalisation. In Shanghai, more than 50% of employees now go to work. But then again, this also shows that we’re still a long way from normal and a ‘business as usual’.”

German Economy Minister Peter Altmaier said the shock is expected to hit Germany’s industrial sector over the next few weeks.

Shipping giant Maersk warned last month that containerized flows across the world would likely stay muted in the first half.

“As factories in China are closed for longer than usual in connection with the Chinese New Year as a result of the COVID-19, we expect a weak start of the year,” Maersk warned.

Reuters noted that the decline in trade volume between China and Germany has led to a shipping container shortage in the country.

“I have just spoken to an important customer from the greater Hamburg area. They just can’t get hold of containers anymore,” Mattern said. “If you currently want to ship a container, you have to expect higher prices.”

Duisburg, Europe’s biggest inland port, has warned rail volumes from China have been reduced, and will likely remain in a slump for the first half.

To sum up, the bat shock from Wuhan has taken a little more than a month to reach Europe and could start hitting Germany’s industrial base this week, if not next. This all suggests that twin shocks are about to strike Europe’s largest economy, one being an industrial shock from China, and the other being a demand shock in services, as tens of millions of people in Europe avoid public areas as virus cases and deaths erupt on the continent. Europe is the new China; its economy is set to crash.

Tyler Durden

Thu, 03/12/2020 – 02:45 - 30,000 US Soldiers Arrive In Europe Without Masks

30,000 US Soldiers Arrive In Europe Without Masks

Authored by Manlio Dinucci via VoltaireNet.org,

The United States are demonstrating their power by organising the largest transfer of their troops in Europe on the occasion of the Defender Europe 20 exercises. This country, which only a few years ago sacrificed its soldiers without warning in its nuclear tests, is taking no precautions for its soldiers faced with the coronavirus epidemic.

The United States have raised the alert for the corona virus in Italy to level 3 – (« avoid non-essential travel »), and taken it to level 4 for Lombardy and Veneto (« do not travel »), the same level as for China. The airline companies American Airlines and Delta Air Lines have cancelled all their flights between New York and Milan. US citizens who are travelling to Germany, Poland and other European countries are at alert level 2, and must take « increased precautions ».

But there is a category of US citizens which is exempt from these standards : the 20,000 soldiers who have begun to arrive from the United States to the ports and airports of Europe for the Defender Europe 20 exercises, the greatest deployment of US troops in Europe in the last 25 years. With those who are already present, approximately 30,000 US soldiers will be participating in the execises in April and May, alongside 7,000 others from the 17 member countries and partners of NATO, including Italy.

The first armoured unit arrived from the port of Savannah, USA at Bremerhaven in Germany. A total of 20,000 pieces of military equipment are arriving from the USA at six European ports (in Belgium, Holland, Germany, Latvia and Estonia). 13,000 others are provided by the stocks that were pre-positioned by the US Army Europe, mainly in Germany, Holland and Belgium.

These operations, explains the US Army Europe, « require the participation of tens of thousands of soldiers, military personnel and civilians from numerous nations ». At the same time, the majority of the contingent of 20,000 soldiers arrive from the USA, landing at seven European airports. Among this number are 6,000 from the National Guard of 15 States : including Arizona, Florida, Montana, New York and Virginia. At the start of the exercise in April – explains the US Army Europe – the 30,000 US soldiers « will deploy throughout the European region » in order to « protect Europe from any potential threat », with a clear reference to the « Russian menace ». General Tod Wolters – who commands US forces as well as the NATO forces in Europe, as Supreme Allied Commander – assures that the European Union, NATO and the United States European Command, have worked together to improve the infrastructures ». This will allow military convoys to move quickly along the 4,000 kilometres of transit routes.

Tens of thousands of soldiers will cross the frontiers to perform exercises in ten countries. In Poland, US soldiers will arrive in twelve training areas, equipped with approximately 2,500 vehicles. US paratroopers from the 173rd Brigade based in Venetia, and Italians from the Brigade Folgore based in Tuscany, will go to Latvia for a joint launching exercise.

Defender Europe 20 is being carried out in order to « increase the capacity of deploying a major combat force in Europe from the United States ». It is taking place according to times and procedures which make it practically impossible to submit tens of thousands of soldiers to the sanitary standards set up to deal with the coronavirus, and prevent their contact with local inhabitants during their rest periods. Furthermore, the US Army Europe Rock Band will be giving a series of free concerts in Germany, Poland and Latvia, which are sure to attract a large public.

The 30,000 US soldiers, who will « deploy throughout the European region », are thus exempt from the preventative standards set up to deal with the coronavirus crisis which, on the other hand, do apply to civilians. The assurance given by the US Army Europe suffices : « we have the coronavirus under surveillance » and « our forces are in good health ».

At the same time, no-one is considering the environmental impact of a military exercise of this scale. US Abrams tanks will be taking part – each of them weighs 70 tonnes, with armour-plating made of depleted uranium, and consumes 400 litres of fuel for 100 kilometres, producing heavy pollution in order to achieve maximum power.

In this situation, what is the reaction of the European Union and national authorities, and what is the WHO doing about it? They are covering their faces with masks, not only to cover their mouths and noses, but also their eyes.

Tyler Durden

Thu, 03/12/2020 – 02:00 - The Moral Panic About Capitalism Threatens American Potential

The Moral Panic About Capitalism Threatens American Potential

Authored by Joseph Sorrentino via HumanEvents.com,

We need to trust in the free enterprise system – now more than ever…

According to Alexandra Ocasio Cortez, “No one ever makes a billion dollars. You take a billion dollars.” At least, that’s what the Representative from New York recently argued at a Martin Luther King, Jr. Day event in Harlem.

Speaking hypothetically about billionaires making widgets, she added: “You didn’t make those widgets. You sat on a couch while thousands of people were paid modern-day slave wages, and in some cases real modern-day slavery.” According to AOC, the mechanisms of capitalism not only allow, they mandate theft. In her view, business success is synonymous with the mass exploitation of labor.

AOC is far from alone. Many leading Democrats have condemned the wealthy and blamed them for nearly all modern-day plights–a tactic that has proved useful at arousing populist anger on the campaign trail. It appears to be working, and not just in places or with demographics we would expect. A recent CBS News poll revealed that Texas Democratic primary voters view capitalism (in comparison to Socialism) even less favorably than California Democratic primary voters.

If this poll is to be believed, Texas Democratic primary voters view capitalism less favorably than California Democratic primary voters (?!) https://t.co/iSyzgt4CUE

— Michael Tracey (@mtracey) March 1, 2020

https://platform.twitter.com/widgets.js

The rhetoric and debates coming out of the left—and, at times, even the right—have fixated on how much to tax wealth, instead of how to help create wealth. With Andrew Yang’s exit from the Democratic primary, we lost one of the few candidates who talked openly about declining entrepreneurship and the importance of business creation as an antidote to economic decline.

And it’s not just the politicians that have scapegoated capitalism. Plastered across our newspapers, there are headlines like, “Capitalism is in crisis,” “Capitalism is failing,” or “Capitalism, as we know it, is dead.” (The latter was most recently expressed in a New York Times editorial by billionaire Salesforce CEO, Marc Benioff, who amassed his considerable wealth thanks to … capitalism).

This consistent bombardment is not only reshaping political discourse but impacting how young Americans view the future. At a time when global competition is heating up, and America’s innovation boom from decades past has slowed, the need to inspire faith in free markets has never been more urgent.

THE STARTUP DEFICIT

A recent YouGov poll revealed that nearly half of all millennials and gen-Xers hold an unfavorable view of capitalism. The same poll also found that more than 70 percent of millennials would, if given the opportunity, vote for a socialist candidate. According to a recent poll from Gallup, less than half of young Americans—45 percent—view capitalism positively. “This represents a 12-point decline in young adults’ positive views of capitalism in just the past two years and a marked shift since 2010, when 68 percent viewed it positively,” notes Gallup.

This ideological shift comes at a perilous time. The world is in retreat from the failures of globalization, and, as resurgent nationalism takes hold in its place, cooperation between economies is morphing into fierce competition. For evidence of this, one need look no further than the recent fiery exchanges between the UK and the EU over Brexit terms. It is becoming clear that a nation’s economic strength, more so than military power, will determine standing in the world order. And America is no exception.

Unfortunately, entrepreneurship and innovation have been steadily declining in the U.S. for years. We have fewer high-growth firms, especially in high-tech sectors, and those firms that do achieve high growth have been creating fewer jobs. According to economist Tyler Cowen, “These days Americans are less likely to switch jobs, less likely to move around the country, and, on a given day, less likely to go outside the house at all […] the economy is more ossified, more controlled, and growing at lower rates.”

Regardless of how you assess it, all indicators point to a downward trend. Measured as the ratio of new firms to total firms, entrepreneurship in the U.S. declined by around 50% between 1978 and 2011. Meanwhile, people working for big firms (those employing more than 250 people) rose from 51% to 57% of the overall workforce, and the average firm size increased from 20 to 24 people over the same period. These are indicators that people have grown more risk-averse and are increasingly reluctant to trade off stability to start something new—something called the startup deficit.

Several measures also indicate that entrepreneurs are less innovative. The ratio of patents to GDP in the US is declining, and the cost of patenting is increasing. The age of inventors, and when they registered their first patent, are on the rise— signaling an increasing barrier to entry for the young and cash-strapped. Plus, as economist Nicholas Bloom and his co-authors have found, “research productivity for the aggregate US economy has declined by a factor of 41 since the 1930s, an average decrease of more than 5% per year.”

It’s easy not to focus on these metrics when we’ve recently been showered with positive news about the economy. But the startup deficit means lower productivity, and less wealth creation over the long term. This is a trajectory that is certain to see us displaced from atop the world’s leader-board.

TRADING IN AMERICA’S ECONOMIC FUTURE … FOR VOTES

As far as policies are concerned, the solutions are reasonably straightforward: break up monopolies, improve competition, allow markets to work better, and (perhaps most importantly), incentivize the young and ambitious to take risks, lots of them. As financier and author Nicholas Nassim Taleb notes: “the reason free markets work is because they allow people to be lucky, thanks to aggressive trial and error.”

That trial and error is the backbone to a healthy and growing economy. Entrepreneurs discover unmet needs in society and fill them with new goods or services. They take risks without certainty of reward. They improve on existing technologies and invent whole new ones—the iPhone AOC uses to vilify billionaires on Twitter among them. And in difficult economic times, entrepreneurs help create new jobs and find unique ways to provide society with the goods and services they desire.

Policy can only take us so far. This is why we also need a shift at the level of political rhetoric.

At a time when we should be relentlessly focused on stimulating business creation, our would-be future innovators are learning that to be a successful entrepreneur is akin to being a modern-day slave driver. They learn that to take the risk to start a business, or to pursue material wealth, is to start down a road that inevitably leads to a life of immorality.

We’re in desperate need of a different dialogue. As Warren A. Stephens notes:

“By virtue of living in the United States, we are all capitalists … I hope for a day when young people no longer reject that concept but revel in it. As a country, we need to reclaim our pride in capitalism and remember that the markets have the greatest power when they are free, and that free markets empower one and all, not just the few and the select.”

Leaders and politicians have a choice: continue to denigrate examples of financial and entrepreneurial success for short term political gain—or leverage them as powerful tools for inspiration. America’s economic potential hangs in the balance.

Tyler Durden

Wed, 03/11/2020 – 23:45 - US Issues Global Level 3 Health Advisory: Reconsider Travel Abroad

US Issues Global Level 3 Health Advisory: Reconsider Travel Abroad

Following President Trump’s decision to ban all travel from Europe to the US for 30 days, The State Department has issued a Level 3 Global Health Advisory, urging Americans to reconsider travel abroad:

Global Level 3 Health Advisory – Reconsider Travel

The Department of State advises U.S. citizens to reconsider travel abroad due to the global impact of COVID-19.

Many areas throughout the world are now experiencing COVID-19 outbreaks and taking action that may limit traveler mobility, including quarantines and border restrictions.

Even countries, jurisdictions, or areas where cases have not been reported may restrict travel without notice.

For the latest information regarding COVID-19, please visit the Centers for Disease Control and Prevention’s (CDC) website.

* * *

This is one step away from an official travel ban.

This is escalating very quickly.

Tyler Durden

Wed, 03/11/2020 – 23:26 - 22 Year Old FX Trader Pleads Guilty To Fraud He Started While In His Teens

22 Year Old FX Trader Pleads Guilty To Fraud He Started While In His Teens

22 year old FX trader Kevin Perry has pleaded guilty to defrauding his investors in an FX scam that started when he was just a teenager.

A release from the U.S. Attorney’s Office in the Northern District of Georgia on Friday said that “Perry led investors to believe that his investment company, Lucrative Pips, was successfully earning substantial profits by investing in the foreign currency (or “forex”) market.”

He told investors’ that their initial investments were secure from loss, but his company was never even registered as a commodity pool operator with the Commodity Futures Trading Commission, the Department of Justice said in their complaint.

He falsified historical returns that he represented to investors while turning around and using investor cash to enrich himself or pay off his other investors. He also falsely promised an undercover agent that an investment of $10,000 would return a profit of $19,000 to $25,000 per month.

U.S. Attorney Byung J. Pak said: “Clients that invested with Perry’s company were assured they were secure from loss. Actually, Perry was enriching himself and paying off other investors. We encourage citizens to be cautious with investments, and to remember that if it sounds too good to be true, it probably is.”

Chris Hacker, Special Agent in Charge of FBI Atlanta said: “This guilty plea will be little solace to the victims who lost their savings because of Perry’s personal greed. The FBI is determined to root out and prosecute anyone who undermines investor confidence at the expense of innocent victims.”

Tyler Durden

Wed, 03/11/2020 – 23:25 - Banking Crisis Imminent? Companies Scramble To Draw Down Revolvers

Banking Crisis Imminent? Companies Scramble To Draw Down Revolvers

Earlier today, we reported that Boeing shocked the investing community when it announced that due to “market turmoil”, it would immediately draw down on its full $13.825 revolving credit facility, an unprecedented move for a company Boeing’s size and valuation, and one which was some took as an indication of how frail Boeing’s liquidity state was, ostensibly confirmed by Boeing’s surging default odds measured by its 5Y CDS.

We disagreed: after all, why would Boeing rush to draw attention to its own funding challenges by fully drawing on its revolver when it knew full well that it had access to the money, safe and sound, located at its syndicate banks… unless of course Boeing was in fact worried about the viability of said banks. AS a result, we said that the real reason Boeing did what it did was simple, especially to those who recall what happened in 2008 all too well: Boeing is worried that banks will pull their committed funding, which in turn means that Boeing appears to be worried that a 2008-style financial crisis is imminent, and is shoring up all the liquidity it can, so as not to remain at the mercy of its banks which may refuse to extend it credit at any one moment if their own liquidity is threatened.

Which is why we also concluded that now that Boeing, “one of America’s most valuable companies, has shown which way the wind blows, expect thousands of less creditworthy companies to follow suit as they scramble to cash in on every dollar in available revolver funding before the banks pull it.“

We had to wait just a few hours for this prediction to come true, because later on Wednesday, Bloomberg reported that two of the world’s biggest PE firms, Blackstone and Carlyle, have told their portfolio companies to immediately do what Boeing did earlier in the day: “Do whatever it takes to stave off a credit crunch”, which as in the case of Boeing, is a polite way of saying: your banks may pull their liquidity (i.e., fail), so get whatever cash you can now when you can, and not when you have to.

According to the report, the dozens if not hundreds of businesses – all smaller than Boeing of course – controlled by the PE titans are joining a growing wave of corporations drawing down bank credit lines to help prevent any liquidity shortfalls amid signs of mounting stress in markets. At Blackstone, which has weathered a variety of crises in its 35 years, the focus is on sectors hurt by the coronavirus, such as the hospitality industry, as well as energy firms facing a slump in oil prices.

At Carlyle the measures aren’t quite as widespread yet, although the firm has been having broad discussions with management teams at portfolio companies and recommended drawing credit lines in certain instances, with the “decisions are based on industries, regions and other factors.”

Beside Boeing, Blackstone and Carlyle, other companies which announced plans to drawdown on their full revolver were Hilton Worldwide and Wynn Resorts, all reflecting the uncertainty coursing through corporate America as the US economy hurtles into recession.

Think of it, as companies lining up at their favorite ATM machine to pull all the money that is in the account. It works until suddenly it doesn’t.

And here is Bloomberg confirming, through clenched teeth, what we said earlier: “A sudden and sustained increase in companies tapping credit lines could eventually strain banks if conditions become so dire that borrowers won’t be able to meet their obligations.“

See, it’s not market conditions, but a loss of faith in the banking sector, and the reason why it was so difficult for Bloomberg to admit it is that while toilet paper runs do not lead to a collapse of the financial system, fiat paper runs to, and all that would take for those to begin is a loss of faith in the US banking system…. just like that exhibited by Boeing and some of the smartest financial professionals in the world.

The big irony of course, is that by pulling down on revolvers en masse, US companies can trigger just the liquidity crunch they are seeking to protect themselves again, because as we noted earlier, liquidity in the US financial sector is already dismal and getting worse with every passing day, hence today’s latest expansion to the Fed’s repo cailities among a surging FRA/OIS spread.

As Bloomberg explains, “lenders offer revolving credit lines to strengthen relationships with companies and don’t typically intend for them to be drawn upon en masse.”

In normal times, revolvers serve as the corporate equivalent of credit cards, giving companies room to borrow as needed and repay when shortfalls ease. Under normal circumstances, the lines are seldom maxed out. Extensive use can be seen as a harbinger of distress.”

The fact that everyone is drawing down on their revolver, however, shows three things:

- these are not normal circumstances

- the US financial situation is on the verge of distress, and

- they remember what happened in 2008, when one bank after another collapsed the availability on their revolver to troubled companies and sectors, and this time it will be the banks left with holding the short stick.

That said, oil and natural gas companies are under particular focus as they tend to suffer a spike in funding stress when prices fall, because their credit lines are periodically updated based on market prices, motivating companies to tap them early.

But why Boeing? The company’s cash flow is one of the most stable in the world… except of course when a global viral pandemic and its ongoing 737 MAX fiasco has sent its cash flow plunging to the most negative levels in decades.

Meanwhile, Blackstone’s private equity operation is the firm’s largest business by assets, at $183 billion, of which energy accounts for almost 10% of the total portfolio.

Blackstone won’t be the last as rival private equity firms – many of which have purchased shale companies in recent years funded with staggering levels of junk debt – also are weighing similar actions.

“From an economic perspective, the virus has created dislocation in the market and fear among the people,” Blackstone co-founder Stephen Schwarzman said in an interview in Mumbai last week. “Once that starts, one has to find the impact of negative consequences. But the turbulence can also have an upside for firms with a war chest, he said.

“It creates a substantial opportunity to buy assets and give credit.” Or, in the case of Blackstone’s portfolio companies, to take it.

Tyler Durden

Wed, 03/11/2020 – 22:57 - 9 Years Later – How Fukushima Changed Japan's Energy Mix

9 Years Later – How Fukushima Changed Japan’s Energy Mix

The March 11, 2011, Fukushima nuclear incident in Japan made international headlines for months, but it also changed Japanese attitudes towards nuclear energy. As Statista’s Katharina Buchholz notes, after a devastating tsunami hit Japan on March 11, 2011, emergency generators cooling the Fukushima nuclear power plant gave out and caused a total of three nuclear meltdowns, explosions and the release of radioactive material into the surrounding areas.

Before the incident, the Japanese had been known as steadfast supporters of nuclear energy, taking previous nuclear catastrophes at Three Mile Island (USA) or Chernobyl (Ukraine) in stride. But a meltdown on their own soil changed the minds of many citizens and kicked the anti-nuclear power movement into gear.

After mass protests, the Japanese government under then Prime Minister Yoshihiko announced plans to make Japan nuclear free by 2030 and not to rebuild any of the damaged reactors. New Prime Minister Shinzo Abe has since tried to change the nation’s mind about nuclear energy by highlighting that the technology is indeed carbon neutral and well suited to reach emission goals.

You will find more infographics at Statista

Despite one reactor restart at Sendai power plant in Southern Japan in 2015, nuclear energy has almost vanished from Japanese electricity generation. In 2018 (latest available), only 6 percent of energy generated in Japan came from nuclear power plants. Coal and natural gas picked up most of the slack, but renewable sources, mainly solar energy, also grew after 2011.

Tyler Durden

Wed, 03/11/2020 – 22:45 - US Prosecutors Seeking Legal "Options" Against Epstein "Co-Conspirator" Prince Andrew

US Prosecutors Seeking Legal “Options” Against Epstein “Co-Conspirator” Prince Andrew

Authored by John Vibes via TheMindUnleashed.com,

The FBI has spent months trying to get an interview with Prince Andrew about his relationship with Jeffrey Epstein, but investigators have had no luck getting him to speak on the record about the case.

New York prosecutors told the press this week that the prince has “completely shut the door” on cooperating with authorities. They are now considering what further legal action can be taken.

Andrew continues to deny any wrongdoing or knowledge of Epstein’s many crimes, despite a growing body of evidence indicating that he was involved.

Manhattan Attorney Geoffrey Berman described the prince as a “co-conspirator.”

“Contrary to Prince Andrew’s very public offer to cooperate with our investigation into Epstein’s co-conspirators, an offer that was conveyed via press release, Prince Andrew has now completely shut the door on voluntary cooperation and our office is considering its options,” Berman said, according to the Guardian.

Andrew has previously promised to help investigators with the case, but has since removed himself from public life. He has also refused requests for interviews that investigators have sent him.

When asked about the recent statement from New York prosecutors, a spokesperson for the palace told the Guardian, “The issue is being dealt with by the Duke of York’s legal team.”

Virginia Giuffre, one of the many girls trafficked by Jeffrey Epstein, has become one of his most outspoken victims. She has also accused the prince of raping her while she was underage. Giuffre has appeared on dozens of interviews with broadcasters around the world to share her story.

Andrew has made no public comments on the matter since promising to speak with investigators after his BBC interview where he made numerous claims that were later exposed as lies.

Most notably, the prince claimed that he never met Giuffre or even heard the name before. A leak of private emails where he mentioned Virginia Giuffre surfaced just days after the interview, proving his claims false.

During his BBC interview, Prince Andrew claimed that he was at a Pizza Express in Woking on the night Giuffre says he raped her after the pair visited a nightclub together. However, eyewitnesses have now come forward to support Giuffre’s claims about being at the club with him on the evening in question.

Andrew was also found in the flight logs of Epstein’s notorious private airplane, booked on flights that went to his property in the Virgin Islands, where the Attorney General for the territory has claimed that Epstein “held underage girls captive” as recently as 2018.

Tyler Durden

Wed, 03/11/2020 – 22:25 - Trump Bans All Travel From Europe For 30 Days; Tom Hanks Infected; NBA Suspends Season: Live Updates

Trump Bans All Travel From Europe For 30 Days; Tom Hanks Infected; NBA Suspends Season: Live Updates

Summary:

- WHO declares Covid-19 is a pandemic

- President Trump declares a travel ban from all European countries (not UK)

- Tom Hanks, wife announce they have the Coronavirus

- NBA suspends all games until further notice

- Utah Jazz player Rudy Gobert has tested positive for coronavirus.

- LA confirms first death

- Seattle schools close for two weeks

- Italy closes stores

- MGM says guest at Vegas’s ‘The Mirage’ tested positive

- Denmark closes schools, will send ‘non-critical’ public employees home to work

- New Jersey case total climbs to 23

- Juve player Daniele Rugani

- DC Mayor declares public health emergency

- Congressional doctor says up to

- Cuomo confirms 39 new cases in NY, raising total to 212

- First death in Indonesia

- Confirmed cases in France top 2,000

- Washington State to ban events over 200

- Details of cruiseline industry’s ‘health and safety proposal’ leak

- ‘Waffle House’ employee in Atlanta confirmed

- UK reports 7th death

- Chicago cancels St. Paddy’s Day parade

- NY sends in National Guard

- IADB cancels meeting in Colombia as virus spreads across Latin America

- Mnuchin says first part of virus stimulus plan will be ready in 2 days

- Utah reportedly planning to shut public college and university campuses

- Dr. Fauci warns virus 10x more deadly than flu and could infect millions if not handled early

- Australia passes A$18 billion stimulus package

- Seoul says 99 cases tied to call center

- FEMA evacuates Atlanta office over coronavirus scare

- 3 Boeing workers test positie

- Washington DC advises cancellation or postponement of all gatherings with more than 1,000 people

- Harvard to prorate room and board for students

- US cases surpass 1,000

- UK Health Minister catches virus

- Ireland, Bulgaria, Sweden report first deaths

- Connecticut declares state of emergency

- UK total hits 456 following largest daily jump on record (83 new cases)

- Global cases pass 120,000

- South Korea reports new outbreak in call center

- Japan reportedly planning to declare state of emergency

* * *

Update (2130ET): Tom Hanks and his wife, Rita Wilson, have tested positive for the coronavirus during a trip to Australia, he said in a Wednesday Instagram post.

Hello, folks. Rita and I are down here in Australia. We felt a bit tired, like we had colds, and some body aches. Rita had some chills that came and went. Slight fevers too. To play things right, as is needed in the world right now, we were tested for the Coronavirus, and were found to be positive.

Well, now. What to do next? The Medical Officials have protocols that must be followed. We Hanks’ will be tested, observed, and isolated for as long as public health and safety requires. Not much more to it than a one-day-at-a-time approach, no?

We’ll keep the world posted and updated.

Take care of yourselves!

Hanx!In separate news, Utah Jazz All-Star Rudy Gobert tested positive for coronavirus; “sources say Gobert is feeling good, strong and stable — and was feeling strong enough to play tonight.” The NBA’s reaction was instant: the game Gobert was playing in was canceled, and both the Jazz and the Oklahoma City Thunder teams and lockerrooms are currently quarantined. Nobody has left Chesapeake Arena.

Both teams and lockerrooms are currently quarantined. Nobody has left Chesapeake Arena

— Tony Jones (@Tjonesonthenba) March 12, 2020

https://platform.twitter.com/widgets.js

Moments later the NBA announced it would suspend the season until further notice.

* * *

Update (2110ET): President Trump has ordered a complete travel ban from European nations for the next 30 days (beginning at midnight on Friday). The ban does not include the United Kingdom. Speaking from the Oval Office, Trump called the coronavirus a “horrible infection” and said he was addressing the nation to talk about the “unprecedented response to the coronavirus outbreak.”

#BREAKING: President @realDonaldTrump announces a new travel ban on all of Europe for 30 days. pic.twitter.com/ALBWcNx5ke

— Washington Examiner (@dcexaminer) March 12, 2020

https://platform.twitter.com/widgets.jshttps://platform.twitter.com/widgets.js

While Trump initially announced that the ban would also include “trade and cargo”, a subsequent clarification from the White House, perhaps upon seeing the market’s reaction, made it clear that Trump misspoke, and the ban does not apply to goods and trade.

Hoping to get the payroll tax cut approved by both Republicans and Democrats, and please remember, very important for all countries & businesses to know that trade will in no way be affected by the 30-day restriction on travel from Europe. The restriction stops people not goods.

— Donald J. Trump (@realDonaldTrump) March 12, 2020

https://platform.twitter.com/widgets.js

Additionally, Trump laid out his plans for taking emergency action to provide relief for those suffering financial hardship due to the virus.

The President also said health insurance companies had agreed to waive all co-payments for coronavirus treatments and extend insurance coverage to cover coronavirus treatments.

* * *

Update (1950ET): As states around the country mull whether to follow Washington and shutter their schools, we’ve received a reader tip claiming that Utah Gov Gary Herbert will announce on Thursday at 9 am MT that the state is shutting down all its public campuses of higher education. A press release will follow. The official date and duration is not know at this time.

Again, that’s according to an as-yet-unconfirmed tip, so treat it accordingly.

Of course, if this is accurate, that’s just another ~20,000 college kids about to go on an extended, cut-rate spring break.

* * *

Update (1937ET): Seoul has just confirmed that 99 cases have now been tied to an outbreak at a call center in Seoul’s Guro district, one of the busiest and most crowded parts of town. Low paid workers commuting from far away helped pass the infection along their route, creating another outbreak just as South Korea was getting the outbreak in the city of Daegu under contol.

Seoul Mayor Park Won-soon made the announcement early Thursday in Seoul. It’s unclear whether these constitute new, or already counted cases.

Australia just announced a A$17.7 billion stimulus package to bolster its economy against the fallout from the virus, joining what’s becoming a growing list of developed countries that have acted more quickly than the White House to address that aspect of the crisis.

To be sure, the Trump administration deserves credit for swiftly working out a compromise with Democrats to pass an $8.3 billion spending package that increases funding for the CDC, FDA and the other agencies within DHHS, dole out money to the states, buy vaccines when they’re available and $1.25 billion for “international activities.”

* * *

Update (1820ET): Juventus, a football club based in Turin, a city in Piedmont situated just outside Italy’s initial exclusion zone, just confirmed that center-back Daniele Rugani has tested positive for the coronavirus, though it’s not yet clear who.

BREAKING: Juventus centre-back Daniele Rugani has tested positive for coronavirus, the Serie A club have confirmed.https://t.co/PWNnhoOE5z

— Sky Sports News (@SkySportsNews) March 11, 2020

https://platform.twitter.com/widgets.js

This is the first time a Serie A football club has confirmed that one of its top players has been infected.

Juventus’ leaked line-up next game: https://t.co/6rQ1HZkzKk pic.twitter.com/PNlbg9TMfA

— J (@ln1982) March 11, 2020

https://platform.twitter.com/widgets.js

And suddenly, it seems clear that Italian soccer’s plan to ban fans at league contests is truly inadequate.

Juventus played Lyon recently.

Lyon played PSG recently.

PSG played Dortmund tonight.

Etc etc etc.

— Stan Collymore (@StanCollymore) March 11, 2020

https://platform.twitter.com/widgets.js

Immediately, most fans thoughts probably turned to Cristiano Ronaldo, the club’s star player.

Earlier in the US, Texas reported that a toddler was among its latest batch of confirmed cases for Covid-19. Another characteristic that differentiates Covid-19 from the flu is that young children are also at risk.

* * *

Update (1650ET): Italy has confirmed that it will order all stores in the country that sell items other than medicine and food to close. Factories can continue working, but all restaurants and bars must close as well. The prime minister stressed that there is “no need for a run on supermarkets.”

Watch Conte’s address live:

* * *

Update (1635ET): NJ Governor and former Goldmanite Phil Murphy just announced 8 more cases in the state, bringing its total to 23. The state has also confirmed its first case of “community spread”.

UPDATE: We now have 8 more presumptive positive cases of #COVID19 in New Jersey.

• 3 female cases, 5 male cases

• 4 cases from Bergen County, 2 cases from Middlesex County, and 2 cases from Monmouth County

• Range in age from 17- to 66-years-old— Governor Phil Murphy (@GovMurphy) March 11, 2020

https://platform.twitter.com/widgets.js

Current #COVID19 statewide stats:

• Presumptive Positive Tests: 23

• Negative Tests: 57

• Tests in Process: 20

• Persons Under Investigation: 37

• Deaths: 1For regular updates: https://t.co/UyohzX5yGk

— Governor Phil Murphy (@GovMurphy) March 11, 2020

https://platform.twitter.com/widgets.js

We’ve received $14 million in federal grants from @CDCgov to assist in our ongoing efforts to contain the spread of #COVID19. We’re working around the clock with our local, state, and federal partners to protect the health of New Jerseyans.

— Governor Phil Murphy (@GovMurphy) March 11, 2020

https://platform.twitter.com/widgets.js

Watch the rest of the press conference below courtesy of 10 Philly:

In other news, the NCAA’s annual “March Madness” basketball tournament games in Ohio will be played in front of empty crowds, with only essential staff present and “limited family attendance,” NCAA President Mark Emmert said in a statement:

NCAA President Mark Emmert statement on limiting attendance at NCAA events: https://t.co/TIHHJjdse5 pic.twitter.com/8I1HdceDfN

— NCAA (@NCAA) March 11, 2020

https://platform.twitter.com/widgets.js

Effectively cancelling dozens of live basketball games is just one ore huge blow to consumption at a very testy time. Though we suspect millions will still tune in from home.

Full panic. Making a recession inevitable https://t.co/NUcRtNvtyi

— GreekFire23 (@GreekFire23) March 11, 2020

https://platform.twitter.com/widgets.js

Sports games are being cancelled around the globe: Italian soccer made a similar determination earlier.

* * *

Update (1625ET): Washington DC Mayor Muriel Bowser has declared a public health emergency in order to access emergency funds to help her city combat the crisis.

Watch the rest of today’s live update below:

LIVE: Providing an update on coronavirus (COVID-19) cases in the District. For a stream with captions visit https://t.co/44CwI7bWqr. To learn more visit https://t.co/MEWs6uPfsI. https://t.co/Z3TuyCZEHf

— Mayor Muriel Bowser (@MayorBowser) March 11, 2020

https://platform.twitter.com/widgets.js

* * *

Update (1535ET): MGM Resorts said a female guest at the Mirage, one of its Las Vegas casinos, has tested positive for the coronavirus. The woman, who visited the city for an event featuring many bold-faced names recently, is from New York. The news comes after the company announced plans to shut down its buffets at seven of its resorts in Las Vegas.

The company said it’s tracing contacts that the patient might have had, and is in the process of doing a “deep clean” of the room.

* * *

Update (1522ET): LA County health officials announced on Wednesday that one of their patients had succumbed to the virus, marking the second death in California from the virus and the first in LA County, a local TV station reports. They also announced another 6 confirmed cases, bringing the county total to 27.

County health officials announced the unfortunate news during a press update:

#BREAKING: Los Angeles County reported its first death related to the #coronavirus outbreak on Wednesday, as county health officials announced six additional cases, bringing the county’s total to 27. https://t.co/3mZiAyy5iw

— FOX 11 Los Angeles (@FOXLA) March 11, 2020

https://platform.twitter.com/widgets.js

The victim was a woman over the age of 60 who died after contracting the virus, according to County Health Director Dr. Barbara Ferrer. The woman, who has not been publicly identified, was visiting Los Angeles County and had underlying health conditions.

As one observer noted about Ferrer during the press conference…

#BREAKING: Los Angeles County reported its first death related to the #coronavirus outbreak on Wednesday, as county health officials announced six additional cases, bringing the county’s total to 27. https://t.co/3mZiAyy5iw

— FOX 11 Los Angeles (@FOXLA) March 11, 2020

https://platform.twitter.com/widgets.js

The doctor reporting the LA county death was sniffling for her life lord god help us

— mariah smith (@mRiah) March 11, 2020

https://platform.twitter.com/widgets.js

Meanwhile, the CDC’s Dr. Nancy Messonnier is delivering her daily update:

CDC Briefing Room: Dr. Nancy Messonnier gives an update on #COVID19. For more info visit https://t.co/rObN2b0O9V pic.twitter.com/1kkqI7HJy9

— Dr. Robert R. Redfield (@CDCDirector) March 11, 2020

https://platform.twitter.com/widgets.js

In a first for major cities, the Seattle Times just reported that all Seattle schools will close on Friday for “a minimum of two weeks” to thwart the virus’s spread. The reporters cited a copy of an email sent to school administrators.

The decision was reportedly made after “conferring” with county and school officials. Inslee earlier urged all schools in the state to prepare for having students finish their studies for the year online.

On Wednesday, two schools in Seattle were already closed due to virus exposure fears.

The email instructs principals to treat the closure as if they were going on spring break, and lists some guidance for going forward.

“We know you do not have time to do everything and we trust that you will do your best given the circumstances,” the email said.

The announcement comes after the district’s early move to stay open in an effort to make sure children don’t suddenly see a loss in services.

NY Gov. Cuomo said earlier that the state would do everything it could to avoid shutting NYC schools (NYC schools rarely close, due to the fact that many students who are on subsidized lunch wouldn’t eat without school).

Further north in Denmark, officials announced that all schools and universities in the country would be closed until further notice.

And additionally, one twitter user just tallied up a breakdown of all the cases confirmed in Italy:

Coronavirus cases, Italy:

Lombardy: 7,280

Emilia-Romagna: 1,739

Veneto: 1,023

Piedmont: 501

Marche: 479

Tuscany: 320

Liguria: 194

Campania: 154

Lazio: 150

Friuli-VG: 126

Sicily: 83

Puglia: 77

Trento: 77

Bolzano: 75

Umbria: 46

Abruzzo: 38

Sardinia: 37

Aosta Valley: 20— Norbert Elekes (@NorbertElekes) March 11, 2020

https://platform.twitter.com/widgets.js

* * *

Update (1445ET): The UK has just reported its 7th death, another elderly patient, according to media reports.

In other news, the House Oversight Committee meeting where Dr. Fauci and Dr. Redfield were answering questions won’t resume until tomorrow.

Chairwoman Maloney says Fauci and Redfield have been “unavoidably detained” at the White House and we don’t know what is going on but they cannot come back.”

The House Oversight Committee hearing on #COVID2019 response will resume Thursday at 11 a.m.

— Brianna Ehley (@Briannaehley) March 11, 2020

https://platform.twitter.com/widgets.js

* * *

Update (1430ET): France has just announced roughly 500 new coronavirus infections, and more than a dozen more deaths, bringing the total above 2,000.

- FRANCE CONFIRMS 2281 CORONAVIRUS CASES, 48 DEATHS AS OF WED.

* * *

Update (1410ET): During his Wednesday press conference, Cuomo confirmed that the state had succeeded in contracting with 28 private labs to speed up coronavirus tests. He also confirmed 39 new cases in NY, bringing the state total to 212, adding that “numbers will continue to go up dramatically.”

Giving New Yorkers an update on #Coronavirus. Watch live: https://t.co/JuLCeU2Po9

— Andrew Cuomo (@NYGovCuomo) March 11, 2020

https://platform.twitter.com/widgets.js

NYS will start contracting with private labs in New York to increase our #Coronavirus testing capacity. I have spoken with 28 labs today.

We are quickly mobilizing to get these private labs online as soon as possible.

— Andrew Cuomo (@NYGovCuomo) March 11, 2020

https://platform.twitter.com/widgets.js

Meanwhile, CNBC’s Eamon Javers reported that President Trump is considering an emergency declaration for all of the US under the “Stafford Act”, which would open up more federal money via FEMA

A White House official tells me President Trump is considering issuing a disaster declaration for the entire United States under the Stafford Act. No decision yet but this would free up a lot of funding and put FEMA fully in the fight against the virus.

— Eamon Javers (@EamonJavers) March 11, 2020

https://platform.twitter.com/widgets.js

This would put FEMA “fully in the fight” against the virus.

In other news, just a few days after confirming that it had reopened nearly all of its stores on mainland China, Apple said Wednesday that all stores in Italy would be closed “until further notice.”

Boeing employees saw more bad news on Wednesday as the troubled aerospace maker said Wednesday that it would halt hiring until further notice.

Meanwhile, in Senegal, officials reported their 5th case of the virus as it continues its creep across Latin America and Africa.

* * *

Update (1350ET): As we previewed earlier, Washington State Gov. Jay Inslee has announced plans to ban gatherings with 250 people or more in the counties worst affected by the virus in his state, CNBC reports. The counties include: King, Snohomish and Pierce.

In addition, he’s asking all school districts to prepare for online instruction, and closures that might last “longer than initially thought”.

Just minutes after Inslee’s announcement, San Francisco health officials announced they would ban public and private events with 1,000 people or more to slow the spread of the new coronavirus there.

“We know that this order is disruptive, but it is an important step to support public health,” San Francisco Mayor London Breed said in a statement. “We know cancelling these events is a challenge for everyone and we’ve been talking with venues and event organizers about the need to protect public health.” She said she spoke with the Warriors NBA team and “they are in support of our efforts.”

Washington State is the hardest-hit in the country, with more than 267 confirmed cases across the state with 258 of those concentrated between the three counties, according to the state health commission.

Even more alarming: Seattle-area officials announced late Tuesday that residents or employees of 10 long-term care facilities have been infected.

Last month, Inslee declared a state of emergency to free up funding for communities combating the outbreak.

* * *

Update (1330ET): Politico reports that President Trump is looking into making an Oval Office address, presumably to share the details from his stimulus “plan”.

*TRUMP LOOKING AT OVAL OFFICE ADDRESS: POLITICO

— Jim Bianco (@biancoresearch) March 11, 2020

https://platform.twitter.com/widgets.js

Meanwhile, USAToday has published the details from a proposal delivered to the White House about how they can update health and safety measures to stop employees from getting infected. Stocks dropped on news of the details from the plan, which hadn’t been previously disclosed since the industry delivered the proposal to the White House after a meeting yesterday.

- CRUISE LINE INDUSTRY PROPOSES PLAN TO WHITE HOUSE THAT WOULD BAR PEOPLE AGE 70 AND OLDER FROM BOARDING SHIPS WITHOUT A DOCTOR’S NOTE

The proposal reportedly includes barring entry to anyone over the age of 70, or with an underlying condition, unless a doctor’s note is supplied.

* * *

Update (1315ET): One day after recording its largest increase in deaths on record, Italy has reported yet another 30%+ increase in deaths, bringing its death toll to 827 from 631. They also reported a record-breaking 2,000+ new cases on Wednesday.

- ITALY DEATH TOLL FROM CORONAVIRUS OUTBREAK RISES TO 827 FROM 631 ON TUESDAY – OFFICIAL

- ITALY CORONAVIRUS DEATHS JUMP 31% TO 827

- TOTAL NUMBER OF CONFIRMED CASES OF CORONAVIRUS IN ITALY RISES TO 12,462 FROM 10,149 ON TUESDAY – OFFICIAL

Though the jump in deaths reported yesterday (168) was larger in terms of percentage (36% vs. 31%), today’s increase is larger by the numbers.

Coronavirus update, Italy:

– 2,313 new cases today

– 12,462 cases in total

– 5,838 hospitalized

– 1,045 recovered

– 827 deaths

– 1,028 in intensive care— Norbert Elekes (@NorbertElekes) March 11, 2020

https://platform.twitter.com/widgets.js

In other news, Norway bans indoor events with more than 500 people. Russia earlier said it would ban most flights between Russia and Italy, Germany, Spain and France. Meanwhile, Washington State has confirmed plans to ban large events.

* * *

Update (1350ET): Follow the WHO’s major admission just a few minutes ago, which took the air out of a modest market rally as stocks moved off their session lows, we suspect that Wednesday will be remembered as a critical day in the development of the outbreak outside Asia.

We’ve heard no shortage of alarming predictions today – remember earlier when Merkel said up to 70% of Germans might catch the virus, or Dr. Fauci’s warning that “millions” of Americans could contract it if the US doesn’t act quickly – and Axios has just brought us one more: It reports, citing two sources briefing on the meeting, that Congress’ in-house doctor told Capitol Hill staffers at a close-door meeting this week that he expects 75-150 million people in the US, roughly one-third of the country, to contract the coronavirus.

And here’s Axios telling us “why it matters”:

Why it matters: That estimate, which is in line with other projections from health experts, underscores the potential seriousness of this outbreak even as the White House has been downplaying its severity in an attempt to keep public panic at bay.

Dr. Brian Monahan, the attending physician of the U.S. Congress, told Senate chiefs of staff, staff directors, administrative managers and chief clerks from both parties on Tuesday that they should prepare for the worst, and offered advice on how to remain healthy.

He added that 80% of people who contract the virus will ultimately be fine.

As Axios also reminds us, statistical modeling from Harvard epidemiologist Marc Lipsitch, have said that somewhere between 20% and 60% of adults worldwide might catch the virus.

During an interview with CNBC following the declaration from the WHO,

“The epidemic is always further ahead than what you perceive at the moment,” Dr. Scott Gottlieb said.

It’s possible that we have thousands of cases here possibly tens of thousands,” Dr. Gottlieb said.

In other news, Reuters reports that the White House is weighing travel bans against Italians and other Europeans.

* * *

Update (1230ET): With WHO’s major funding partner China perhaps having turned the corner, WHO Chief Tedros has finally decided to declare Covid-19 a Pandemic…

🚨 BREAKING 🚨

“We have therefore made the assessment that #COVID19 can be characterized as a pandemic”-@DrTedros #coronavirus pic.twitter.com/JqdsM2051A

— World Health Organization (WHO) (@WHO) March 11, 2020

https://platform.twitter.com/widgets.js

Full Tedros Transcript:

In the past two weeks, the number of cases of #COVID19 outside 🇨🇳 has increased 13-fold & the number of affected countries has tripled.

There are now more than 118,000 cases in 114 countries, & 4,291 people have lost their lives.

Thousands more are fighting for their lives in hospitals.

In the days and weeks ahead, we expect to see the number of #COVID19 cases, the number of deaths, and the number of affected countries climb even higher

WHO has been assessing this outbreak around the clock and we are deeply concerned both by the alarming levels of spread and severity, and by the alarming levels of inaction

We have therefore made the assessment that #COVID19 can be characterized as a pandemic

Pandemic is not a word to use lightly or carelessly. It is a word that, if misused, can cause unreasonable fear, or unjustified acceptance that the fight is over, leading to unnecessary suffering and death

Describing the situation as a pandemic does not change WHO’s assessment of the threat posed by this coronavirus. It doesn’t change what WHO is doing, and it doesn’t change what countries should do”

We have never before seen a pandemic sparked by a coronavirus. And we have never before seen a pandemic that can be controlled at the same time.

WHO has been in full response mode since we were notified of the first cases.

We have called every day for countries to take urgent and aggressive action.

We have rung the alarm bell loud and clear

As I said on Monday, just looking at the number of COVID19 cases and the number of countries affected does not tell the full story

Of the 118,000 COVID19 cases reported globally in 114 countries, more than 90 percent of cases are in just four countries, and two of those have significantly declining epidemics

81 countries have not reported any COVID19 cases, and 57 countries have reported 10 cases or less.

We cannot say this loudly enough, or clearly enough, or often enough: all countries can still change the course of this pandemic”

If countries detect, test, treat, isolate, trace, and mobilize their people in the response, those with a handful of COVID19 cases can prevent those cases becoming clusters, and those clusters becoming community transmission

Even those countries with community transmission or large clusters can turn the tide on this coronavirus.

Several countries have demonstrated that this virus can be suppressed and controlled.

The challenge for many countries who are now dealing with large COVID19 clusters or community transmission is not whether they can do the same – it’s whether they will.

Some countries are struggling with a lack of capacity. Some countries are struggling with a lack of resources. Some countries are struggling with a lack of resolve.

We are grateful for the measures being taken in Iran, Italy and South Korea to slow the virus and control their COVID19 epidemics.

We know that these measures are taking a heavy toll on societies and economies, just as they did in China.

All countries must strike a fine balance between protecting health, minimizing economic & social disruption & respecting human rights

WHO’s mandate is public health. But we’re working with many partners across all sectors to mitigate the social and economic consequences of this COVID19 pandemic

This is not just a public health crisis, it is a crisis that will touch every sector – so every sector and every individual must be involved in the fight

I have said from the beginning that countries must take a whole-of-government, whole-of-society approach, built around a comprehensive strategy to prevent infections, save lives and minimize impact

Let me summarize it in 4 key areas.

-

Prepare and be ready.

-

Detect, protect and treat.

-

Reduce transmission.

-

Innovate and learn”

I remind all countries that we are calling on you to (1):

-

activate & scale up your emergency response mechanisms

-

communicate with your people about the risks & how they can protect themselves

-

find, isolate, test & treat every #COVID19 case & trace every contact”

I remind all countries that we are calling on you to (2):

-

ready your hospitals

-

protect and train your #healthworkers

-

let’s all look out for each other”

There’s been so much attention on one word.

Let me give you some other words that matter much more, & that are much more actionable:

Prevention. Preparedness. Public health. Political leadership.

And most of all, People”

“We’re in this together, to do the right things with calm and protect the citizens of the world. It’s doable”

And just like that – $425 million dollars worth of pandemic bonds all got trggered.

* * *

Update (1220ET): Three Boeing workers have tested positive for the virus, the company said. Though Boeing offered few details, we suspect the employees are probably based in Washington State, where Boeing builds its planes.

In Washington DC, authorities are recommending the cancellation or postponement of all “non-essential” gatherings over 1,000.

As students leave campuses around the country either heading back home or hunkering down finish their classes on line, Harvard just announced that it would “pro-rate” students’ room and board.

* * *

Update (1220ET): With the committee in charge of the Tokyo Olympic Games reportedly planning to suggest that the games be delayed, more images of the coronavirus fears’ impact on international travel are circulating online. Check out this.

Airline passengers shared images on social media showing flights with rows of empty seats amid coronavirus concerns. https://t.co/48iJCgnlxM pic.twitter.com/0FS1zq6OgX

— ABC News (@ABC) March 11, 2020

https://platform.twitter.com/widgets.js

* * *

Update (1200ET): The CDC has released its latest batch of “confirmed” US figures: 29 deaths, 987 cases and cases confirmed in 39 states as of 10 pm last night.

- U.S. CDC – 39 STATES HAVE REPORTED CASES AS OF MARCH 10 AT 4 PM ET VS PREVIOUS REPORT OF 36 STATES

- U.S. CDC – 29 TOTAL DEATHS DUE TO NEW CORONAVIRUS AS OF MARCH 10 AT 4 PM ET VS 25 DEATHS AS OF PREVIOUS REPORT

- U.S. CDC REPORTS ITS COUNT OF 987 CASES OF NEW CORONAVIRUS AS OF MARCH 10 AT 4 PM ET, VS PREVIOUS REPORT OF 696 CASES

Around the world, the virus has produced many “isn’t it ironic?” moments, and we just got another in the US when FEMA announced that it would close its Atlanta office after an employee was exposed to the virus.

- FEMA ATLANTA OFFICE CLOSED AFTER EMPLOYEE EXPOSED TO VIRUS

Over in the UK, a total of 456 people have tested positive for coronavirus in the UK as of 9am on Wednesday, up from 373 at the same point on Tuesday, the Department of Health said. The jump of 83 new cases is the largest daily jump yet, following the previous ‘largest daily increase’ by only a few days.

Six have died in the UK and tested positive for the virus. Over in Ireland, authorities reported their first death on Wednesday. A 66-year-old Bulgarian woman also succumbed to the virus in the Balkan state, marking the first death there as well.

After the UK Health Minister Nadine Dorries tested positive for the virus, and started showing symptoms on Thursday, the same day she attended an event with the prime minister. Though the UK has elected to keep parliament open, Dorries and a Labour lawmaker who may have been exposed via a meeting with Dorries have decided to self-quarantine.

UK Chief Medical Officer Catherine Calderwood stressed that “we are still in the containment phase” despite an increased number of Covid-19 cases.

She said: “We have identified the first case of community transmission in Scotland which is unrelated to contact or travel. This was identified through our enhanced surveillance scheme.

Sweden has reported its first death from the coronavirus today, with a hospital in Stockholm saying an elderly patient had died in intensive care. Belgium has reported its first three deaths, with 314 cases of coronavirus. Ivory Coast has confirmed its first case of coronavirus, a 45-year-old Ivorian man who had recently travelled to Italy, the health ministry said in a statement. Denmark confirmed a batch of new cases, raising its total to 442.

While Washington State is apparently planning to ban all events with over 250 people, Washington DC has advised citizens to avoid such gatherings.

Last night, Connecticut Gov. Ned Lamont declares a state of emergency, joining a growing list of other states to do the same.

* * *

Update (1150ET): Rencap’s Charlie Robertson points out that it took 5 days since the first indication of human-to-human transmission happening at a wide scale in the US, and if our numbers track Germany’s, we should have 3,000 cases confirmed by Friday, and 6,000 by Monday.

Though that rate could double if many new clusters are discovered.

It took 5 days for the number of US #coronavirus cases to get to 1k, within the predicted range. US tracking Germany with 6 day lag implies 2K cases tomorrow, 3k by Friday, nearly 6k by Monday. Could be double this if clusters are found like Korea did in late February https://t.co/LpX2uoBhrr

— Charlie Robertson (@RencapMan) March 11, 2020

https://platform.twitter.com/widgets.js

* * *

Update (1100ET): With another day of non-stop breaking news headlines about the outbreak as it spreads across the US, Europe and Latin America, we’ve been having troubled keeping up.

Switzerland reported 148 new cases of coronavirus on Wednesday, with 645 cases in total, 58 cases in Zürich and 78 cases in Geneva.

Indonesia, an Asian nation that didn’t report its first case until more than a month after the global outbreak began reported its first death linked to the virus on Wednesday as well.

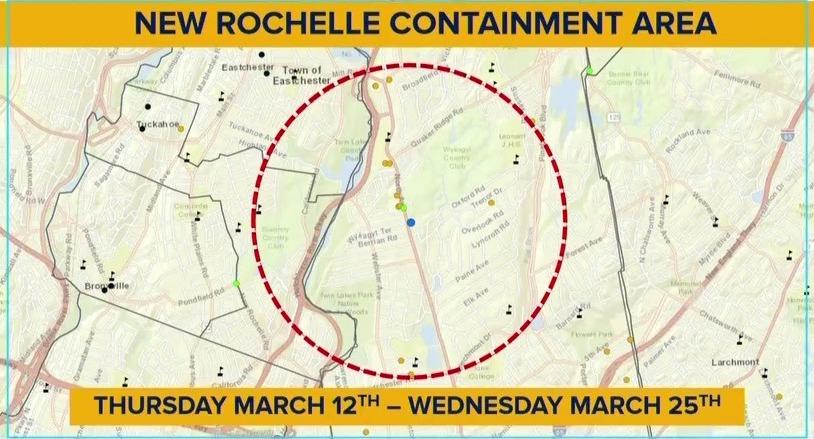

National Guard troops have been deployed to a Health Department command post in New Rochelle. Chicago has followed San Francisco and cancelled its St. Patrick’s Day Parade. In NYC, schools will not close, but parent-teacher conferences will be held via phone.

An employee at a ‘Waffle House’ in Metro Atlanta (Cherokee County) has tested positive for the virus, raising fears about a mass outbreak in Georgia. The store has been closed and 12 employees are quarantining and will continue for a few more days.

Oh well, I guess it’s back to the Chinese restaurants! https://t.co/kzovj0lC2a

— Mark B. Spiegel (@markbspiegel) March 11, 2020

https://platform.twitter.com/widgets.js

The Inter-American Development Bank postponed its annual meeting in Colombia, which had been scheduled for next week, over coronavirus fears as the virus spreads across Latin America. The Washington-based bank, the top development institution dedicated to Latin America and the Caribbean, announced the decision with Colombian President Ivan Duque on Tuesday evening.

La decisión conjunta con @el_BID, de aplazar Asamblea de Barranquilla por situación mundial del coronavirus la tomamos con responsabilidad. Queremos tener alta representación internacional y garantizar que asistentes puedan regresar a sus hogares sin problema #VisitaOficialMéxico pic.twitter.com/sJsV00zDiv

— Iván Duque (@IvanDuque) March 10, 2020

https://platform.twitter.com/widgets.js

With transports and financials leading equities lower on Wednesday, Treasury Secretary Mnuchin, who testified to Congress on Wednesday tried to offer some reassuring details about the White House plan, which remains very much in the ‘brainstorm’ phase. Still, Mnuchin insisted that Trump is standing by the payroll tax holiday to put more money in the hands of workers. The Treasury is also hoping to delay tax payments and leave $200 billion of “temporary liquidity” in the hands of Americans.

Mnuchin said the White House hopes to strike a deal on the first part of the virus stimulus plan within the next 48 hours. His testimony follows rumors about the administration offering a potential ‘bailout’ to the American shale energy industry. Other stimulus actions will take “a week or two” he added.

Importantly, the Treasury Secretary also insisted that no market interventions are being planned (so no PPT?).

In remarks on Tuesday, CDC Director Robert Redfield said that America had lost valuable time tracking the virus; some regions now can merely try to cope with its spread rather than stop it. And during testimony on Wednesday, Dr. Fauci said that when it comes to the outbreak in the US, “the worst is yet to come” because the virus is “10x more lethal than the seasonal flu”.

If the US doesn’t handle the virus outbreak correctly, “many, many millions of people” will get the virus, he said.

Rep. Carolyn Maloney on coronavirus spreading: “Is the worst yet to come, Dr. Fauci?”

“Yes, it is,” Dr. Fauci says, adding that whenever you have an outbreak where there’s “community spread,” you won’t be able to “effectively and efficiently contain it.” https://t.co/wVchsY7g1y pic.twitter.com/dhSS6joXrW

— ABC News Politics (@ABCPolitics) March 11, 2020

https://platform.twitter.com/widgets.js

Remember to wash your hands, folks.

* * *

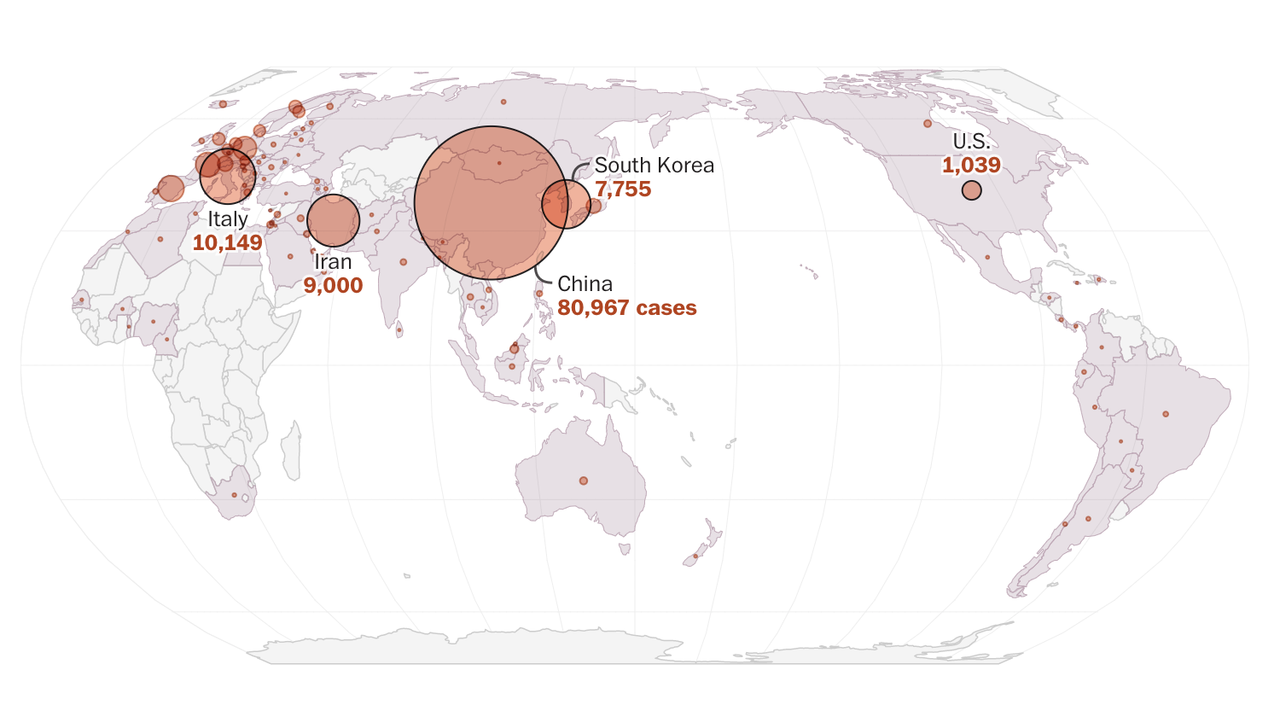

The global coronavirus outbreak has hit a new milestone: It surpassed 120,000 cases overnight. For anybody who’s still bothering to keep track, that’s 15x the number of cases from the SARS outbreak, which continued for nearly a year before it finally petered out.

In the US, the coronavirus outbreak has reached a grim new milestone. Thanks to the administration’s scramble to bring dozens of private and public labs on-line for testing across the country, the CDC has managed to confirm more than 1,000 cases of the virus. In the Westchester County town of New Rochelle, the epicenter of the outbreak in New York State, and the largest on the east coast, woke up to a 1-mile exclusion zone and national guard soldiers in the streets.

The town now looks like a “ghost town” according to several reports.

As the number of cases topped 1,000, the number of deaths has also climbed: Officially, there are 31 deaths and 1,039 confirmed cases, according to the Washington Post, which is significantly more than the number confirmed by Dr. Anthony Fauci during last night’s press conference.

Across the US, Washington State’s King County remains the epicenter of America’s worst outbreak, with 273 cases . New York is No. 2 with 176 (13 additional cases have just been announced). After hinting about ‘mandatory measures’ last night that set tongues wagging about the possibility of Italy-style travel restrictions, Washington Gov. Jay Inslee is reportedly planning to announce a plan to…ban all events with more than 250 people, according to MyNorthwest.

At a press conference scheduled for Wednesday at 10:15 a.m., it is expected that Gov. Jay Inslee along with regional leaders and city mayors could announce a ban on large gatherings and events of 250 people or more in at least three counties. Any ban would affect upcoming sporting events in the area, including a home game for the XFL’s Seattle Dragons on Sunday.

Inslee has been hinting at this for the past week as a possible preemptive move to curb the spread of coronavirus. Over the weekend, he stated that his office was considering enacting “mandatory measures” in the days ahead.

Monday night on MSBNC, the Washington governor spoke to Rachel Maddow, admitting that soon, the state was “going to have to make some hard decisions.”

He further elaborated on that point during a Tuesday press conference, when he cited the need to “look forward ahead of the curve in Washington state.”

“We need to look at what is coming, not just what is here today,” he detailed, estimating that given limits on testing capacity, experts have told him there could be at least 1,000 untested coronavirus cases across the state.

So much for ‘hard decisions’….

This immense build up, only to announce restrictions that are only ‘slightly’ more comprehensive than the milquetoast event bans embraced by Germany, France, Switzerland and others, brings to mind a tweet we noticed earlier highlighting the sometimes unintended consequences that half-measures can create.

When 90% of Americans get the coronavirus, we’ll look back & say, “Man, that was pretty dumb making all college classes ‘remote’ while airfare and hotels are super cheap. Who would’ve thought 20 yr olds don’t give a fuck and just ended up traveling everywhere spreading disease.”

— Fat Tail Capital (@FatTailCapital) March 11, 2020

https://platform.twitter.com/widgets.js

On the east coast, the State of New York is asking businesses to voluntarily consider having employees work two shifts as well as allowing telework, Gov. Andrew Cuomo said in an interview with CNN, the network that employs his brother, where he has been making near-daily appearances in addition to his daily press conferences.

Gov. Inslee

“This is about reducing the density,” Cuomo said. “The spread is not going to stop on its own.”

He also announced 20 new cases of virus, bringing total in state to about 193, with most of the new cases diagnosed in New Rochelle, where the virus has clearly been circulating for weeks.

There have been reports that Democrats are pushing for a national emergency declaration which would trigger tens of billions of dollars in funding from FEMA to help with the containment effort, and possibly to help grappled with the economic fallout from the outbreak.

Despite a few notable screwups lately (including a collapsed ad hoc quarantine that left roughly one dozen dead and many trapped in the rubble for days, Beijing continues to insist that it is winning the war against the virus, and while the true scope of China’s outbreak might never be known for sure (some have estimated 1 million cases throughout China), officials did report a slight rise in cases on Wednesday which they blamed on ‘imports from abroad.’

Officials reported 24 additional cases of coronavirus and 22 additional deaths on March 10, compared with 19 additional cases and 17 additional deaths on March 9, bringing the total number of cases in mainland China to 80,778 and death toll at 3,158. China’s Hubei province said it will mandate a return to work according to different levels of risk in an orderly manner, adding that key areas of the Wuhan economy will be allowed to return.

After 11 days of falling case numbers, South Korea reported 242 additional coronavirus cases early Wednesday, bringing its total to 7,555, and 6 additional deaths, increasing the death toll to 60, reversing a streak of declines that had convinced many that Korea’s outbreak had ended.

The South has made remarkable progress in fighting the outbreak, however, a new mass infection incident has popped up that is jeopardizing the government’s widely praised response. Earlier, South Korean authorities told Reuters that they had tested hundreds of staff at a Seoul call center where the disease broke out this week. 13 of the infected workers at the Seoul call center used public transportation to commute, leading to at least 90 other people who had close contact with them being infected. Of the 90 cases mentioned earlier, 62 were in Seoul, and all were located near a public transportation hub connecting Seoul with Incheon and other major cities, via which the virus spread.

The spread has even made it into the armed forces, raising new fears about an outbreak in tightly packed barracks.

Yonhap: A conscript South Korean Army soldier has been confirmed as a coronavirus patient in Seoul. His mother works at a call center in the city where a mass infection event has been confirmed. https://t.co/DvSP8RvoBS

— Vincent Lee (@Rover829) March 11, 2020

https://platform.twitter.com/widgets.js

Elsewhere, Japan is reportedly planning to declare a state of emergency due to the coronavirus outbreak after the number of domestic cases rose by the largest daily number yet, with 59 new cases bringing the total to 1,278, while the total death toll has climbed to 19 and there were 427 discharged from hospital on Tuesday.

Italy’s total coronavirus cases rose to 10,149, from 9172, and the death toll increased to 631 yesterday from 463 in its largest daily jump yet.

Tyler Durden

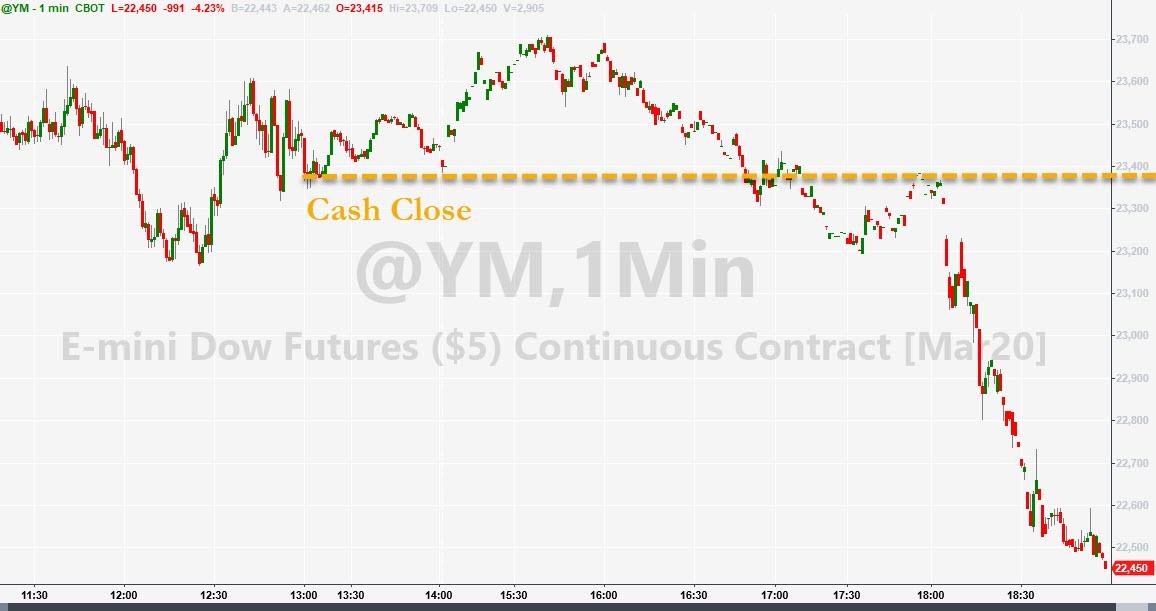

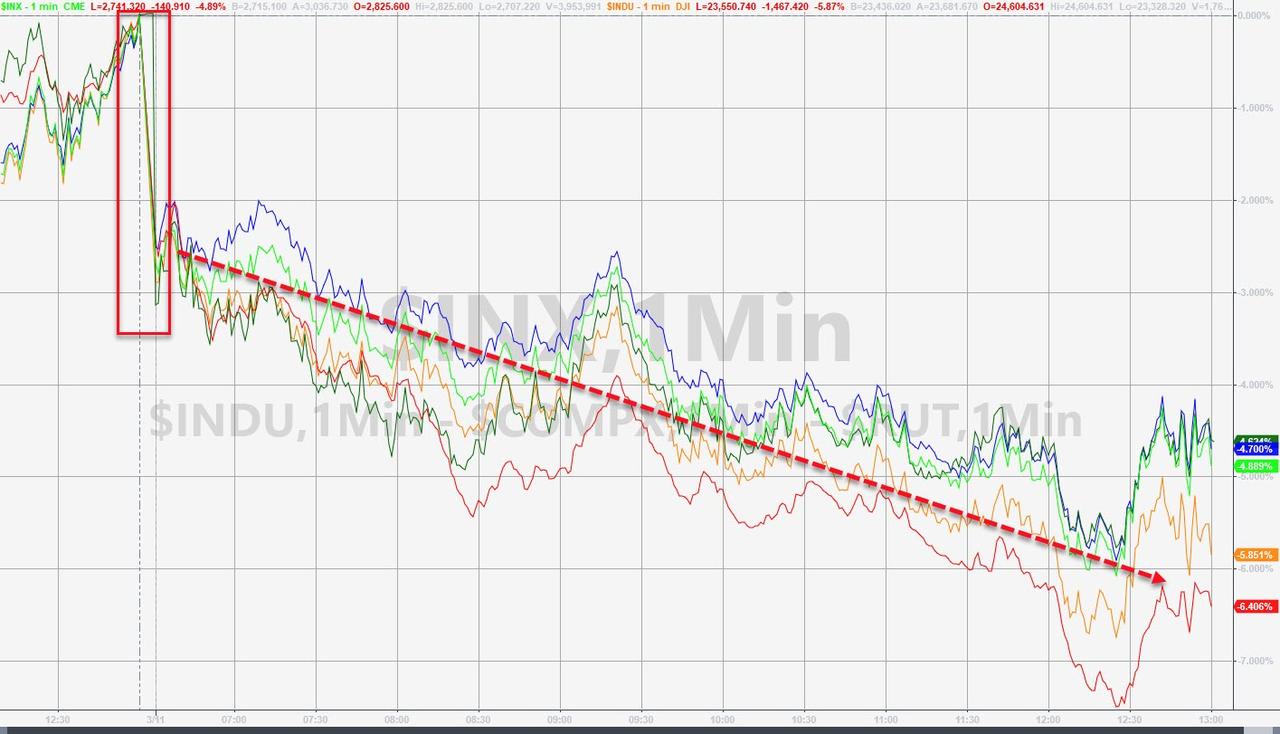

Wed, 03/11/2020 – 22:10 - Nasdaq Futures Limit-Down, Crude Crashes After Trump Announces EU Travel Ban

Nasdaq Futures Limit-Down, Crude Crashes After Trump Announces EU Travel Ban

Shortly after President Trump began his address to the nation, enacting a full travel ban from European nations for the next 30 days, the markets started to get upset.

-

S&P 500, Nasdaq and Dow futures fall 4-4.5%

-

Both Brent and WTI futures down more than 6%

-

Nikkei 225 drops 4.5%, Australia’s benchmark slumped 5% to confirm bear market status

-

Main China stock indexes all fall at least 1%

-

Kospi, Hang Seng, Taiex slide 3% or more

-

Treasury 10-year yields decline 14 bps to 0.73%

-

AUD/USD falls 0.3%, EUR/USD jumps 0.4%

-

Malaysia, Korea, Philippine currencies all retreat 0.5%; Mexican peso tumbles more than 1%

Dow futures are down over 1000 points…

Japan’s Nikkei 225 is down over 350 points…

Nasdaq futures are limit down…

S&P is close to its 2,601 limit down…

And for the cash open tomorrow:

-

7% limit down (RTH only) : 2546.50

-

13% limit down (RTH only) : 2382.00

-

20% limit down (RTH only) : 2190.00

10Y Treasury yields are down 15bps…

The Euro is strengthening against the dollar…

WTI Crude is collapsing, hitting a $30 handle

European Stoxx 50 futures are down 7.3%

It appears Trump did not offer enough detail and immediacy to appease the market’s need for funds to stop the collapse. Additionally, the uncertainty over the impact on European supply chains is also weighing on markets.

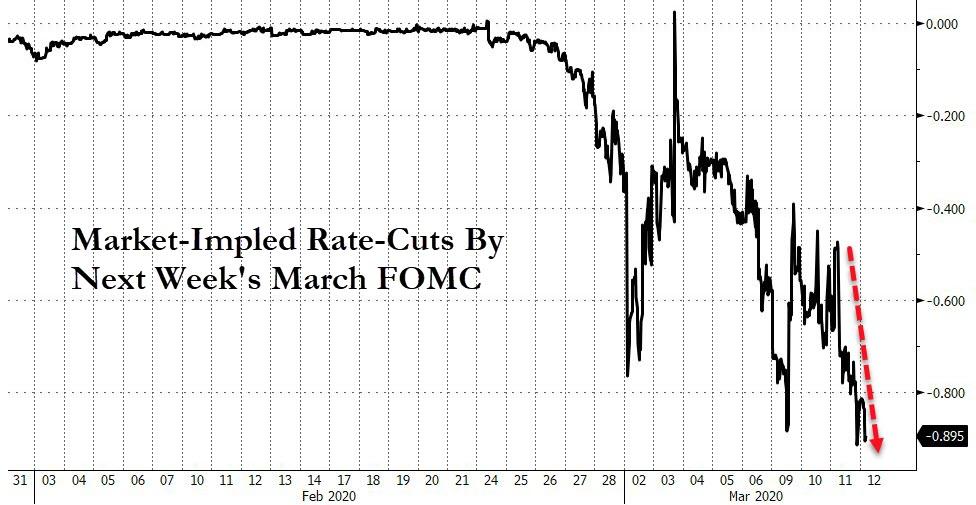

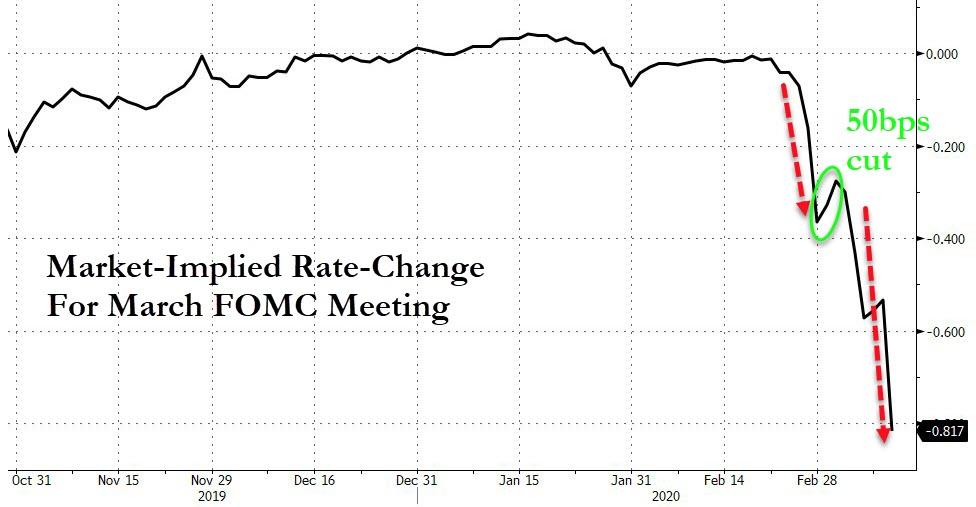

The market is now demanding 90bps of rate-cuts for next week’s FOMC…

Chris Martenson and John Rubino explain why the virus is the catalyst not the cause of the crash…