- COVID-19 Shutdown: The End Of Globalization And Planned Obsolescence – Enter Multipolarity

COVID-19 Shutdown: The End Of Globalization And Planned Obsolescence – Enter Multipolarity

Authored by Joaquin Flores via The Strategic Culture Foundation,

The coronavirus pandemic has shown that the twin processes of globalization and planned obsolescence are deficient and moribund. Globalization was predicated on a number of assumptions including the perpetuity of consumerism, and the withering away of national boundaries as transnational corporations so required.

What we see instead is not a globalization process, but instead a process of rising multipolarity and a rethinking of consumerism itself.

Normally a total market crash and unemployment crisis would usher in a period of militant labor activity, strikes, walk-outs and community-labor campaigns. We’ve seen some of this already. But the ‘medical state of emergency’ we are in, has effectively worked like a ‘lock-out’. The elites have effectively flipped-the-script. Instead of workers now demanding a restoration of wages, hours, and work-place rights, they are clamoring for any chance to work at all, under any conditions handed down. Elites can ‘afford’ to do this because they’ve been given trillions of dollars to do so. See how that works?

All our lives we’ve been misinformed over what a growing economy means, what it looks like, how we identify it. All our lives we’ve been lied to about what technical improvement literally means.

A growing economy in fact means that all goods and services become less expensive. That cuts against inflation. Rather all prices should be deflating – less money ought to buy the same (or the same money ought to buy more). Technical innovation means that goods should last longer, not be planned for obsolescence with shorter lifespans.

Unemployment is good if it parallels price deflation. If both reached a zero-point, the problems we believe we have would be solved.

In a revealing April 2nd article that featured on the BBC’s website, Will coronavirus reverse globalisation? it is proposed that the pandemic exposes the weaknesses and vulnerabilities of a global supply-chain and manufacturing system, and that this in combination with the over-arching US-China trade war would see a general tendency towards ‘re-shoring’ of activities. These are fair points.

But the article misses the point of the underlying problem facing economics in general: the declining rate of profit necessitated by automation, with the increasingly irrational policies, in all spheres, being pursued to salvage the ultimately unsalvageable.

The Karmic Wheel of Production-Consumption

The shut-downs – which seem unnecessary in the numerous widely esteemed experts in virology and epidemiology – appear to be aimed at stopping the production-consumption cycle. When we look at the wanton creation of new ‘money’, to bailout the banks, we are told that this will not cause inflation/debasement so long as the velocity of money is kept to a minimum. In other words – so long as there is not a chain reaction of transactions, and the money ‘stays still’ – this won’t cause inflation. It’s a specious claim, but one which justifies the quarantine/lock-down policy which today destroys thousands of small businesses every day. In the U.S. alone, unemployment claims will pass 30 million by mid April.

Likewise, this money appears real, it sits digitally as new liquidity on the computer screens of tran-Atlantic banks – but it cannot be spent, or it tanks the system with hyper-inflation. More to the point, the BBC piece erroneously continues to assume the necessity of the production-consumption cycle, spinning wheat into gold forever.

The elites were not wrong to shut-down the cycle per se. The problem is that they cannot offer the correct hardware in its place – for it puts an end to the very way that they make money. It is this, which in turn is a major source for the maintenance of their dopamine equilibrium and narcissist supply.

This is not an economic problem faced by ‘the 1%’ (the 0.03%) . It is an existential crisis facing the meaning of their lives, where satisfaction can only be found in ever greater levels of wealth and control, real or imagined – chasing that dragon, in search of that ever-elusive high.

So naturally, their solutions are population reduction and other such quasi-genocidal neo-Malthusian plans. Destruction of humanity – the number one productive-potential force – resets the hands of time, back to a period where profit levels were higher. The algorithmically favored coronavirus Instagram campaign of seeing city centers without people and declaring these ‘beautiful’ and ‘peaceful’ is an example of this misanthropic principle at play.

That the elites have chosen to shut-down the western economy is telling of an historic point we have reached. And while we are told that production and consumption will return somewhat ‘after quarantine’, we also hear from the newly-emerged unelected tsars – Bill Gates et al – that things will never return to normal.

What we need to end is the entire theory and practice of globalization itself, including UN Agenda 21 and the dangerous role of ‘book-talking’ philanthropists like Gates and his grossly unbalanced degree of power over policy formation in the Western sphere.

In place of waning globalization, we are seeing the reality of rising multipolarity and inter-nationalism. With this, the end of the production-consumption cycle, based upon off-shore production and international assembly, and at the root of it all: planned obsolescence towards long-term profitability.

The Problem of Globalization Theory

Without a doubt, globalization theory satisfied aspects of descriptive power. But as time marched forward, its predictive power weakened. Alternate theories began to emerge – chief among these, multipolarity theory.

The promotion of globalization theory also raises ethical problems. Like a criminologist ‘describing’ a crime-wave while being invested in new prison construction, globalization theory was as much theory as it was a policy forced upon the world by the same institutions behind its popularization in academia and in policy formation. Therefore we should not be surprised with the rise of solutions like those of Gates. These involve patentable ‘vaccines’ by for-profit firms at the expense of buttressing natural human immunities, or using drugs which other countries are using with effectiveness.

The truth? Globalization is really just a rebrand of the Washington Consensus – neo-liberal think-tanks and the presumed eternal dominance of institutions like the World Bank and the International Monetary Fund, which in turn are thinly disguised conglomerates of the largest trans-Atlantic banking institutions.

So while globalization was often given a humanist veneer that promised global development, modernization, the end of ‘nation-states’ which presumably are the source of war; in reality globalization was premised on continuing and increasing concentration of capital towards the 19th century zones – New York, London, Berlin, and Paris.

‘Internationalism’ was once rooted in the existence of nations which in turn are only possible with the existence of culture and peoples, but was hi-jacked by the trans-Atlanticist project. Before long, the new-left ‘internationalists’ became champions of the very same process of imperialism that their forbearers had vehemently opposed. Call it ‘globalization’ and show how it’s destroying ‘toxic nationalism’ and creating ‘microfinance solutions for women and girls’ – trot out Malala – and it was bought; hook, line and sinker.

This was not the new era of ‘globalization’, but rather the usual suspects going back to the 19th century; a ‘feel-good’ rebranding of the very same 19th century imperialism as described in J.A Hobson’s seminal work from 1902, Imperialism. Its touted ‘inevitability’ rested not on the impossibility of alternate models, but on the authority that flows forth from gunboat diplomacy. But sea power has given way to land power.

In many ways it aligned with the era of de-colonialization and post-colonialism. New nations could wave their own flags and make their own laws, so long as the traditionally imperialist western banking institutions controlled the money supply.

But what is emerging is not Washington Consensus ‘globalization’, but a multipolar model based in civilizational sovereignty and difference, building products to last – for their usefulness and not their repeatable retail potential. This cuts against the claims that global homogenization in all spheres (moral, cultural, economic, political, etc.) was inevitable, as a consequence of mercantile specialization.

Therefore, inter-nationalism hyphenated as such, reminds us that nations – civilizations, sovereignty, and their differences – make us stronger as a human species. Like against viruses, some have stronger natural immunity than others. If people were identical, one virus could wipe-out all of humanity.

Likewise, an overly-integrated global economy leads to global melt-down and depression when one node collapses. Rather than independent pillars that could aid each other, the interdependence is its greatest weakness.

Multipolarity is Reality

This new reality – multipolarity – involves processes which aspects of globalization theory also suggest and predict for, so there are some honest reasons why experts could misdiagnose multipolarity as globalization. Overlooked was that the concentration of capital nodes in various and globally diverse regions by continent, were not exclusively trans-Atlantic regions as in the standard globalization model of Alpha ++ or Alpha+ cities. This capital concentration along continental lines was occurring alongside regional economic development and rising living standards which tended to promote the efficiency of local transportation as opposed to ocean-travel in the production process. As regional nodes by continent had increasingly diversified their own domestic production, a general tendency for transportation costs to increase as individual per capita usage increased, worked against the viability of an over-reliance on global transit lines.

But among many problems in globalization theory was that the US would always be the primary consumer of the world’s goods, and with it, the trans-Atlantic financial sector. It was also contingent on the idea that mercantilist conceptions of specialization (by nation or by region) would always trump autarkic models and ISI (income substitution industrialization). Again, if middle-class consumer bases are rising in all the world’s inhabited continents as multipolarity explains and predicts, then a global production regimen rationalized towards a trans-Atlantic consumer base as globalization theory predicts isn’t quite as apt.

Because the present system is premised on a production-consumption and financial model, the solutions to crises are presented as population reduction and what even appears, at least in the case of Europe, as population replacement. As cliché as this may seem, this also appeared to be the policy of the Third Reich when capitalism faced its last major crises culminating in WWII.

Breaking the Wheel

The shutdown reveals the karmic wheel of production-consumption is in truth already broken. We have already passed the zenith point of what the old paradigm had to offer, and it has long since entered into a period of decay, economic and moral destruction.

Like the Christ who brings forth a new covenant or the Buddha who emerges to break the wheel of karma, the new world to be built on the ruins of modernity is a world that liberates the productive forces, realizing their full potential, and with it the liberation of man from the machine of the production-consumption cycle.

Planned obsolescence and consumerism (marketing) are the twin evils that have worked towards the simultaneous time-wasting enslavement of ‘living to work’, and have built globalization based on global assembly and global mono-culture.

What is important for people and their quality of life is the time to live life, not be stuck in the grind. We hear politicians and economists talking about ‘everyone having a job’, as if what people want is to be away from their families, friends, passions, or hobbies. What’s more – people cannot invent, innovate, or address the greater questions of life and death – if their nose is to the grindstone.

Now that we are living under an overt system of control, a ‘medical state of emergency’ with a frozen economy, we can see that another world is possible. The truth is that most things which are produced are intentionally made to break at a specific time, so that a re-purchase is predictable and profits are guaranteed. This compels global supply chains and justifies artificially induced crashes aimed at upward redistribution and mass expropriations.

Instead of allowing Bill Gates to tour the world to tout a police-state cum population reduction scheme right after a global virus pandemic struck, one which many believe he owns the patent for, we can instead address the issues of multipolarity, civilizational sovereignty, and ending planned obsolescence and the global supply chain, as well as the off-shoring it necessitates – which the BBC rightly notes, is in question anyhow.

Tyler Durden

Sun, 04/12/2020 – 23:50 - JPMorgan Scrambles To Raise Mortgage Borrowing Standards Ahead Of "Biggest Wave Of Defaults In History"

JPMorgan Scrambles To Raise Mortgage Borrowing Standards Ahead Of "Biggest Wave Of Defaults In History"

Earlier this week when we reported that JPMorgan has quietly halted all non-Paycheck Protection Program based loan issuance for the foreseeable future, we said that we didn’t buy the stated reason namely – the bank was drowning in (government-backstopped) applications and would be willing to forego millions in easy, recurring net interest income and that instead the real reason why JPMorgan would “temporarily suspend” all non-government backstopped loans such as PPP, is if the bank expects a default tsunami to hit, coupled with a full-blown depression that wipes out the value of assets pledged to collateralize the loans. We went on:

Furthermore, why issue loans that will default in months if not weeks, just as bankruptcy courts fill up with millions of cases (assuming the coronavirus clears out by then, as the alternative is simply unthinkable – a default tsunami without any functioning Chapter 11 or Chapter 7 process) when JPM can simply stick to the 100% risk-free issuance of government-guaranteed small-business loans which pay a handsome 1% interest, especially if it makes JPM look patriotic by doing its duty to bail out America.

Over the weekend our skepticism was confirmed when Reuters reported that JPMorgan, the country’s largest lender by assets and which will kick off earnings season tomorrow, will raise borrowing standards this week for most new home loans as the bank “moves to mitigate lending risk stemming from the novel coronavirus disruption.”

Starting Tuesday, customers applying for a new mortgage will need a credit score of at least 700, and will be required to make a down payment equal to 20% of the home’s value (something which we thought was the norm after the last financial crisis, but apparently lending conditions had eased quite a bit in the past decade).

“Due to the economic uncertainty, we are making temporary changes that will allow us to more closely focus on serving our existing customers,” Amy Bonitatibus, chief marketing officer for JPMorgan Chase’s home lending business, told Reuters.

According to Reuters, “the change highlights how banks are quickly shifting gears to respond to the darkening U.S. economic outlook and stress in the housing market, after measures to contain the virus put 16 million people out of work and plunged the country into recession.”

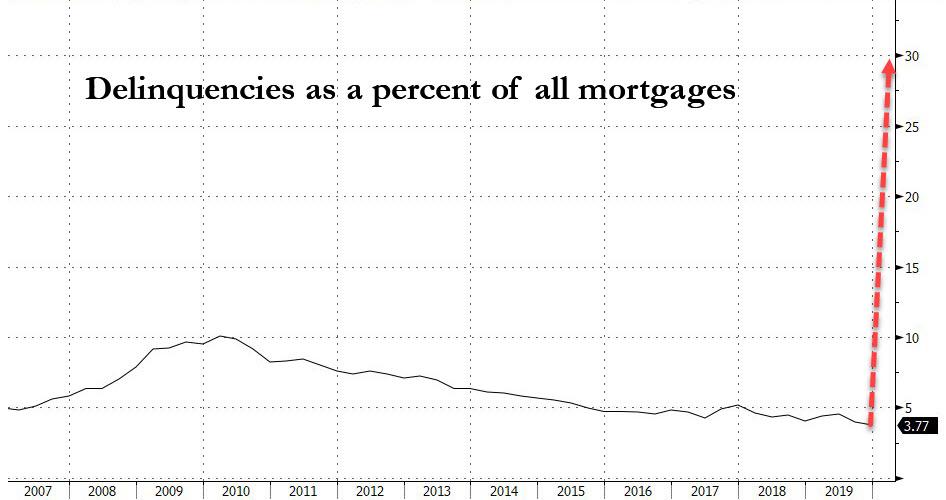

What the change really highlights is that after halting its exposure to plain vanilla, non-government guaranteed loans, JPMorgan is now quietly pulling out of that other market where it makes the bulk of its revenues – mortgages – ahead of a tsunami of mortgage defaults, which last week we dubbed “The Next Crisis” as “Up To 30% Of All Mortgages Will Default In “Biggest Wave Of Delinquencies In History.”

Sure enough, JPMorgan – the fourth largest U.S. mortgage lender in 2019 – not only agrees with this dour assessment, but is taking proactive measures to mitigate its exposure to this wave of defaults but minimizing its exposure as soon as it can. And with JPM setting the stage, it is only a matter of days before all other banks follow and lock out tens of million of even credit-worthy Americans with less than prime credit scores, out of the housing market for years.

Of course, just like in the PPP case, the bank did not dwell on the true cause for this action, but instead said the change will “free up staff to handle a surge in mortgage refinance requests, which are taking longer to process due to staff working from home and non-essential businesses being closed.” While that is certainly a factor, the biggest reason behind these changes is to help JPMorgan reduce its exposure to borrowers who unexpectedly lose their job, suffer a decline in wages, or whose homes lose value.

In short, JPMorgan wants no part of the shitstorm that is about to be unleashed on middle America.

While JPMorgan would not disclose the current minimum requirements for its various mortgage products, the average down payment across the housing market is around 10%, according to the MBA. Furthermore, the new credit standards do not apply to JPMorgan’s roughly four million existing mortgage customers, or to low and moderate income borrowers who qualify for its “DreaMaker” product, which requires a minimum 3% down payment and 620 credit score.

The U.S. housing market had been on a steady footing earlier this year, but all hell broke loose as a result of the economic paralysis and deepening depression resulting from the Coronavirus pandemic. And with would-be home buyers unable to view properties or close purchases due to social distancing measures, the health crisis now threatens to derail the sector, especially as banks are going to make it next to impossible to get a new mortgage.

To be sure, as we reported last week the residential mortgage market is already freefalling after borrower requests to delay mortgage payments exploded by 1,896% in the second half of March. And unfortunately, this is just the beginning: last week, Moody’s Analytics predicted that as much as 30% of homeowners – about 15 million households – could stop paying their mortgages if the U.S. economy remains closed through the summer or beyond. Bloomberg called this the “biggest wave of delinquencies in history.”

This would result in a housing market depression and would lead to tens of billions in losses for mortgage servicers and originators such as JPMorgan.

Tyler Durden

Sun, 04/12/2020 – 23:25 - Robert F Kennedy Jr. Exposes Bill Gates' Vaccine Agenda In Scathing Report

Robert F Kennedy Jr. Exposes Bill Gates' Vaccine Agenda In Scathing Report

Authored by Robert F. Kennedy Jr., Chairman, Children’s Health Defense,

Vaccines, for Bill Gates, are a strategic philanthropy that feed his many vaccine-related businesses (including Microsoft’s ambition to control a global vaccination ID enterprise) and give him dictatorial control of global health policy.

Gates’ obsession with vaccines seems to be fueled by a conviction to save the world with technology.

Promising his share of $450 million of $1.2 billion to eradicate Polio, Gates took control of India’s National Technical Advisory Group on Immunization (NTAGI) which mandated up to 50 doses (Table 1) of polio vaccines through overlapping immunization programs to children before the age of five. Indian doctors blame the Gates campaign for a devastating non-polio acute flaccid paralysis (NPAFP) epidemic that paralyzed 490,000 children beyond expected rates between 2000 and 2017. In 2017, the Indian government dialed back Gates’ vaccine regimen and asked Gates and his vaccine policies to leave India. NPAFP rates dropped precipitously.

In 2017, the World Health Organization (WHO) reluctantly admitted that the global explosion in polio is predominantly vaccine strain. The most frightening epidemics in Congo, Afghanistan, and the Philippines, are all linked to vaccines. In fact, by 2018, 70% of global polio cases were vaccine strain.

[ZH: The CDC has a large financial interest in pushing untested vaccines on the public and WHO is even more under the control of Big Pharma. The organization is corrupt beyond the meaning of the word. “The WHO is a sock puppet for the pharmaceutical industry.” — Robert F. Kennedy Jr.]

During Gates’ 2002 MenAfriVac campaign in Sub-Saharan Africa, Gates’ operatives forcibly vaccinated thousands of African children against meningitis. Approximately 50 of the 500 children vaccinated developed paralysis.

South African newspapers complained, “We are guinea pigs for the drug makers.” Nelson Mandela’s former Senior Economist, Professor Patrick Bond, describes Gates’ philanthropic practices as “ruthless and immoral.”

In 2010, the Gates Foundation funded a phase 3 trial of GSK’s experimental malaria vaccine, killing 151 African infants and causing serious adverse effects including paralysis, seizure, and febrile convulsions to 1,048 of the 5,949 children.

In 2010, Gates committed $10 billion to the WHO saying, “We must make this the decade of vaccines.”

A month later, Gates said in a Ted Talk that new vaccines “could reduce population”.

In 2014, Kenya’s Catholic Doctors Association accused the WHO of chemically sterilizing millions of unwilling Kenyan women with a “tetanus” vaccine campaign. Independent labs found a sterility formula in every vaccine tested. After denying the charges, WHO finally admitted it had been developing the sterility vaccines for over a decade. Similar accusations came from Tanzania, Nicaragua, Mexico, and the Philippines.

In 2014, the Gates Foundation funded tests of experimental HPV vaccines, developed by Glaxo Smith Kline (GSK) and Merck, on 23,000 young girls in remote Indian provinces. Approximately 1,200 suffered severe side effects, including autoimmune and fertility disorders. Seven died. Indian government investigations charged that Gates-funded researchers committed pervasive ethical violations: pressuring vulnerable village girls into the trial, bullying parents, forging consent forms, and refusing medical care to the injured girls. The case is now in the country’s Supreme Court.

A 2017 study (Morgenson et. al. 2017) showed that WHO’s popular DTP vaccine is killing more African children than the diseases it prevents. DTP-vaccinated girls suffered 10x the death rate of children who had not yet received the vaccine. WHO has refused to recall the lethal vaccine which it forces upon tens of millions of African children annually.

Global public health advocates around the world accuse Gates of steering WHO’s agenda away from the projects that are proven to curb infectious diseases: clean water, hygiene, nutrition, and economic development.

The Gates Foundation only spends about $650 million of its $5 billion dollar budget on these areas.

They say he has diverted agency resources to serve his personal philosophy that good health only comes in a syringe.

In addition to using his philanthropy to control WHO, UNICEF, GAVI, and PATH, Gates funds a private pharmaceutical company that manufactures vaccines, and additionally is donating $50 million to 12 pharmaceutical companies to speed up development of a coronavirus vaccine.

In his recent media appearances, Gates appears confident that the Covid-19 crisis will now give him the opportunity to force his dictatorial vaccine programs on American children.

Tyler Durden

Sun, 04/12/2020 – 23:00 - Worker Visas For Hydroxychloroquine: India Demands Quid Pro Quo To Export Tump's 'Miracle' Drug

Worker Visas For Hydroxychloroquine: India Demands Quid Pro Quo To Export Tump's 'Miracle' Drug

One of India’s leading newspapers has reported that President Trump’s much-touted ‘miracle’ coronavirus drug cocktail hydroxychloroquine, which is produced in large amounts in India, is being used by Prime Minister Narendra Modi to negotiate Indian workers’ continued ability to access employment in the United States.

It seems it’s a classic and perhaps foreseeable clash of Modi’s “India First” vs. Trump’s “America First” after New Delhi previously placed an export ban on the pill, given India is trying to contain its own COVID-19 outbreak now threatening 1.3 billion people. The popular popular Hindustan Times reported late last week of the developing quid pro quo situation:

The Indian government has asked the US to extend the validity of visas, including H-1B and other types of visas, held by Indian nationals who have been hit by the Covid-19-related economic slump, people familiar with developments said on Friday.

Foreign secretary Harsh Shringla took up the matter during his telephone conversation with US deputy secretary of state Stephen Biegun on Wednesday, when the two sides also discussed ways to enhance cooperation to counter the pandemic and ensure the availability of essential medicines [hydroxychloroquine] and equipment.

The timing is extremely sensitive, given India relies heavily on wealth earned by “Non-Resident Indians” in the US – yet at a moment tens of thousands are being forced back home amid the broader coronavirus employment crush and companies furloughing employees.

Trump in an April 4th phone call with Modi made clear America’s needs in the escalating virus lockdown emergency: “They make large amounts of hydroxychloroquine — very large amounts, frankly,” Trump told reporters of the call.

“They had a hold [on exports], because, you know, they have 1.5. billion people, and they think a lot of it. And I said I’d appreciate it if they would release the amounts that we ordered,” Trump described.

Modi was swayed, apparently, as days later he approved the export of many hydroxychloroquine pills, temporarily lifting the ban.

Via Getty Images/Vox Thus naturally New Delhi expects Washington to play ball now, as India’s Economic Times voiced late last week:

Congress chief spokesperson Randeep Surjewala said after compromising the “India First” policy in the HCQ drug climb-down, the government is again failing to secure the safety and livelihood of Indians in the US.

“Time for the prime minister to ensure that our soft power of ‘Namaste Trump’ converts into fair treatment of H-1B visa holders in the US,” Surjewala said, noting that the US has put Americans on a temporary paid leave or allowed them to work for reduced hours in the wake of the pandemic.

But “the sword of H-1B visa job terminations” looms large over an estimated 75,000 Indians, with the United States giving them only a 60-day period to find a new job in case of a lay off, he said.

It’s unclear the degree to which Modi himself made the appeal directly to the administration, but it remains that “India’s Congress is demanding that India’s Narendra Modi use his control over the hydroxychloroquine supply to protect the nation’s huge population of well-paid visa workers in the United States.”

So it appears Trump’s long-term ‘America First’ principles – seen regarding India in his prior March 2016 vow to end many American Fortune 500 companies’ reliance on the H-1B visa and the cheap labor it often provides – may have to be compromised to keep the more immediately vital hydroxychloroquine supply going.

It’ll be interesting to see if Modi pivots to playing hardball. Possibly, New Delhi’s parliament demands have already been articulated forcefully as linked directly to the vital potentially life-saving medicine behind the scenes.

Tyler Durden

Sun, 04/12/2020 – 22:35 - One Bank Explains Why No V-Shaped Recovery Is Coming, And Why The Fed Will Nationalize Everything

One Bank Explains Why No V-Shaped Recovery Is Coming, And Why The Fed Will Nationalize Everything

In the past three weeks stocks have staged a substantial rebound from their March 24 lows, in big part thanks to an unprecedented barrage of Fed-driven bailouts, backstops, and asset purchases which at last count amount to over $5 trillion in committed capital in just the past month, and also due to the growing conviction that a V-shaped recovery is imminent one the coronacrisis pandemic fades away. Setting aside concerns about a second, even more powerful infection wave, the reality is that a V-shaped recovery – the underlying narrative catalyst for the powerful bear market rally – from the current quarter’s GDP plunge which according to JPM will be as big as 40% simply will not happen, and here is Bank of America with a clear and succinct explanation why:

There is a growing narrative in the markets that the end of the crisis is in sight. By some accounts, countries are bending the COVID-19 cases curve, allowing a relatively quick reversal of social distancing policies and a V-shaped recovery in the global economy. In sum, it is time to look through the dark hours ahead and focus on the approaching dawn.

We agree with part of this narrative, but disagree with the bottom line. It does appear that a number of countries and regions are starting to bend the curve. The growth in cases has slowed significantly in most of the Euro area and the biggest hotspot in the US, New York, is showing hints of slowing. Areas that shut down early, like Austria, are now debating what a reopening should look like. Of course, the number of deaths will lag and that ugly reality will be with us longer.

Unfortunately, we are also getting more information on what a reopening looks like and the dangers of premature reengagement. China, with its authoritarian controls on population movement, has opened up significantly in the past six weeks or so and now is roughly at 80% of capacity by some metrics. However, a number of other countries have found it hard to completely reopen their economy even with a much better pandemic health system than in Europe and the US.

In addition, in our view, V-shaped optimists have forgotten a basic lesson of the business cycle. Recessions can be triggered by a variety of shocks-surging oil prices, central bank inflation fighting popping bubbles and now a health crisis-but the recession continues well after the initial shock fades. This is because the drop in activity triggers a nasty feedback loop in the economy that overwhelms the policy easing.

A two- or three-month shutdown will leave lasting scars on confidence. Economies will re-open to a greatly diminished demand environment, with high saving rates and very low discretionary spending. This argues for a U-shaped recovery and a persistent, large output gap, in our view.

If this view is correct, and if the world is indeed stuck in the mire of economic contraction not for a quarter or two, but years, it means that what the Fed has done so far will be insufficient and the next step before Powell & Co., will be to expand its nationalization of capital markets by taking full control of the yield curve – to avoid the crossover point beyond which yields on the long-end of the curve soar – a in the form of Yield Curve Control, something the BOJ has been experimenting with for the past 4 years, and a version of which was used by the Fed in the 1940s, as the NY Fed was kind enough to remind its readers last week (perhaps in a hint of what is coming next). Here is BofA on this very topic:

Global central banks have rolled out an impressive array of stimulus measures. However, as the depth of the downturn becomes clear, it will be hard for them to rest on their laurels. Easing thus far was likely predicated on a nasty recession, but not the worst recession in the post-war period. What do they do next? Negative policy rates look like the very last resort for many central banks given the hot debate over whether they do more harm than good. Therefore the obvious next potential step in our view is to take a page out of the BoJ playbook and implement yield curve control.

Will it be effective and is it worth trying? Yield curve control did not succeed in getting Japan out of its low-rates-low-inflation trap. In our view, this is not because the policy is a waste of time, but because the BoJ only implemented it after deflation psychology was deeply embedded in the economy. It did not help matters that the Japanese government has repeatedly shocked the economy with tax hikes, over the objections of many economists.

Yield curve control has many advantages, in our view. First and foremost, it makes it much easier to control the long end of the curve. Japan was able to keep bond yields low even as it slowed its bond purchases. Second, and related, it makes a replay of the 2013 taper tantrum much less likely. Third, it enhances fiscal stimulus as it prevents the normal rise in interest rates and the “crowding out” of private spending. Fourth, it ensures that as the economy crawls out of the deep hole it has fallen into, rising bond yields do not slow the rebound. Fifth, it would be particularly useful in Europe if the ECB can overcome political hurdles and direct the policy at specific bond markets.

What BofA did not mention, on purpose, is that any form of Yield Curve Control would terminally crush any forward-looking function the bond market, which is the earliest warning indicator of inflationary (or deflationary) forces across the economy, has. That means that with the yield curve frozen, inflationary imbalances will build up beneath the surface and there will be no way to either observe them or respond to them… besides asset price hyperinflation and soaring gold prices of course.

Effectively, yield curve control in a depressionary world would eliminate one of the two core market-moving drivers of risk prices – market-driven inflation/interest rates – and only leave corporate profits as an indicator of how the economy is doing. However, since the Fed has with its alphabet soup of measures disconnected risk asset prices from corporate fundamentals, i.e., profits and cash flow, by directly purchasing corporate bonds and soon stocks, it is only a matter of time before US capital markets get to a point where no economic or fundemental signals are reflected in risk assets, resulting in a “market” that is if not nationalized, then centrally-planned by the whims of a small group of Fed career economists, most of whom have never held a private sector job and have zero real world experience.

How does such ubiquItious central planning end? Look no further than the USSR for the answer.

Tyler Durden

Sun, 04/12/2020 – 22:14 - Observations Of An Anonymous UPS Driver: "Customers I've Seen Since The 'Rona'…"

Observations Of An Anonymous UPS Driver: "Customers I've Seen Since The 'Rona'…"

Authored by Daisy Luther via The Organic Prepper blog,

The other day, I shared something funny on social media. A little bit of humor is good for us, even (and especially) in times like this. If anyone knows who originally wrote this, please let me know so I can give proper credit.

If you think about it, a UPS driver with a regular route gets to know a little bit about nearly everyone who frequently places orders. I hope this brings you a giggle. (Remember, fun is not the F-Word.) I also hope it reminds you to pay strict attention to OPSEC.

Here are some observations.

From an anonymous UPS delivery driver…

5 types of customers since the “rona”:

1) Steve: He has been waiting for this moment his whole life. He has been drinking boilermakers since 10:00 am in his recliner and his AR is within arms reach. He has 6 months provisions in the basement and a bug out bag due west buried in the woods. Steve demands a handshake as I give him his package. He’s sizing me up as I deliver his ammo. Steve will survive this, and he will kill you if he needs to.

2) Brad: He is standing at his window wearing skinny jeans and a Patagonia t-shirt. He is mad because there were no organic tomatoes at Whole Foods today. He points at the ground where he has taped a 6 ft no go zone line from his porch. I leave his case of Fuji water, organic granola bites, and his new “Bernie Bro” hat at the tape. Brad will not survive. Steve will probably eat him.

3) Nancy: She has sprayed everything with Thieves oil. Bought all the Clorox wipes, hand sanitizer, toilet paper, meat, and bread from the local grocery chain. She has quarantined her kids and sprays them with a mixture of thieves, lavender, & mint essential oils daily. She has posted every link known to man about “The Rona” on her social media. She will spray you if you break the 6 ft rule. I will leave her yet another case of toilet paper. She will last longer than Brad, but not Steve.

4) Karen: She has called everybody and read them the latest news on “The Rona”. She asked for the manager at Food Lion, Walmart, Publix, McDonald’s, Chi-Fil-A, and Vons all before noon demanding more toilet paper. Karen’s kids are currently faking “The Rona” to avoid her. I’m delivering “Hello Kitchen” to her. Karen will not survive longer than Brad.

5) Mary: Is sitting in the swing watching her kids have a water balloon fight in the front yard as she is on her fourth glass of wine. She went to the store and bought 2 cases of pop tarts, 6 boxes of cereal, 8 bags of pizza rolls, And a 6 roll pack of toilet paper. There is a playlist of Bob Marley, Pink Floyd, and Post Malone playing in the background. I’m bringing her second shipment of 15 bottles of wine in 3 days. Mary will survive and marry Steve. Together they will repopulate the earth.

Got any other types to add to this?

And boy did people have other types to add to this. The responses were pretty apt and I think we all know someone who fits the bill of these characters. I also sent it to my friend, 1stMarineJarHead, who had a few characters of his own to add.

The observations of our imaginary UPS driver are continued below.

6) Aelfie: It takes me four trips to deliver all her seeds and gardening supplies. Two trips for all her sewing supplies. Her grocery order is smaller than you’d expect being mostly bulk items and alcohol.

She hands me a handmade mask after showing how to fit in the N95 filter paper. It has the UPS logo neatly embroidered on the side. She hands over 5 boxes, prepaid and with printed labels all addressed to different hospitals. They’re full of masks, she tells me cheerfully. Just doing my small bit to help.

The mail carrier walks up with a package for her from a pharmacy, seed catalogs, and a handful of assorted magazines. They’re wearing a mask with the USPS logo embroidered on it and they nod in passing. She limps back inside to get her hand truck, whistling “Good Ship Venus” as she starts to haul things to the back yard.

Aelfie will survive and Steve and Mary will barter with her for groceries. She’ll accept bribes of wine to NOT teach their offspring the lyrics to all the songs she knows.

7) Todd: He pretends to be a partner at a prestigious hedge fund firm in the city, when in reality he is a mid-level analyst. He answers the door to his East Hampton seaside 3,000sqft “cottage,” in his casual attire of slacks, Italian shoes (Corinthian leather, of course), polo shirt and a designer sweater tied around his neck. All of which costs more than I make in three months. As Todd signs for the delivery of a case of Russian caviar, his wife, Buffy, is complaining in the background of how the “help” has not shown up and how dreadful it will be to have to look at all those “townies” for the next few weeks. Faced with a possible mandatory quarantine with Todd and Buffy, the “help” all ran back to their third world Central, South American countries, and New Jersey.

The “townies” know that Todd and Buffy came from the city and storm the “cottage” with pitchforks and torches. Todd and Buffy meet a terrible fate, all the while the “townies” enjoy the well-stocked wine cellar and use the caviar as fishing bait.

8) Brenda: She follows social distancing to her own tailored interpretation. She doesn’t leave but has all walks of life come over every day for bbq’s, extended family games, birthday parties, and jigsaw puzzle nights. Brenda starts a major cluster of illness among her visitors and dies of COVID-19.

9) Shooter: He hunts people like Steve for fun, avoids everyone anyway especially people like Brad and wasn’t aware there was a social distancing issue until they started putting tape on the ground. He wasn’t specifically trained for this but he’s happy to wipe out anyone near him in his pursuit of taking care of his family or just because he’s tired of looking at them. Shooter and his family eventually relocate someplace so remote that no one ever sees them again, but rumor has it there’s a very nice, handbuilt homestead out in the boondocks somewhere that is surrounded by tripwires and homemade claymore mines.

10) Scott: He is a former Special Ops guy, currently contracted as chief of security for a CEO of a major global corporation, his wife and kids, and their grandkids in a former missile silo converted into a bunker at an undisclosed location. After only three weeks, Scott and his team are already growing tired of being referred to as the “help,” and as one teammate commented, “She orders me to make her a chocolate martini one more time and I am going to ghost her! The paycheck is not worth it!”

Within a week, the CEO and his entire family meet a most unfortunate end, and are converted into compost. Scott and his team take up with the locals, integrate, and after a few years, become a nomadic tribe, traveling throughout the wasteland of what was once the greatest nation of the 21st century.

11) Susan: Susan is Karen’s sister. She’s the one who keeps tabs on her neighbors who are out for a walk or anyone she thinks is not social distancing properly. She posts every incident on social media and can sometimes be found at Wal-Mart screaming at people who don’t have masks on. She secretly wants to call the police several times a day.

When there’s no apocalypse going on, Susan heads the locals HOA and makes some HOA kickbacks from threatening to report dead lawns.

Susan will be the first one Steve or Shooter takes out…from 100 yards

12) Kyle: Kyle is like Steve but makes his kids in camo do boot camp in the back yard, and then play Pokémon with him at night, pounds Monster in the morning and whiskey at night, cringes when his former medic wife kicks his butt for using too much TP after eating MRE’s for 2 weeks straight. Kyle likes to hide in the bushes in his ghillie suit to freak out the UPS guy. I just sigh and throw the package into the bushes.

Kyle will survive although his wife strongly considers killing him for being aggravating.

13) Dan: As I pull up the long dirt drive, Dan and his dog, Jake, step off the front porch to greet me. Dan was a high power lobbyist on K Street in Washington DC but retired early after his heart attack at the age of 42. He sold everything and moved to this remote woodland off-grid cabin, where he gardens, fishes, hunts and grows pot. When I hand over his new wheeled hand row tiller, I ask him what is he doing about the pandemic. “Pandemic? What pandemic?” I cannot help but envy him.

Dan will survive and have no idea that the death toll is as high as it is.

14) John: John lives in a small mobile home, off a county road. Half a dozen different antennas of various shapes and sizes fill his small back yard. Just beyond the back yard is the state park, all 5,000 acres of it. After I knock, the door opens a crack, and Bob looks me over and then opens the door a bit more. He looks around nervously. He is tight-lipped as he signs for the insured package of radio equipment. He mutters his thanks and closes the door. Not only was he wearing a N95 mask, as nearly everyone is nowadays, but a tinfoil hat. Once the pandemic broke out, John never appeared in public again.

John will be found years later, dead of starvation in his mobile home, with just one Twinkie left and surrounded by at least 100 empty boxes Twinkies and empty Spam cans.

13) Rachel: She is a nurse at a local hospital ER, but sells homemade candles not as a second source of income, but as something she enjoys on the side. I deliver the wicks in large spools about once an] month. She gets the wax from a local apiary. The additional income would be a bonus, but her husband insists on spending the money on firearms, ammo, and MREs. He has stockpiled enough MREs to feed him, her, and their teen daughter for a year. He has 20k rounds of ammo for each firearm. After the pandemic and the collapse of the food distribution system, I see her at the town square market place. She looks almost bewildered, even nervous as she and her daughter walk among the people who are bustling about, trading things and food. As I approach, she recognizes me, despite my beard and smiles, even giving me a half hug, as she is carrying a case of MREs. I ask her what is it she is looking to trade for, and she seems to be at a loss. I ask her what has happened to her.

She says in the name of OPSEC, her husband demanded they make their home look like it was looted, breaking some of the windows, and putting the body of a dead animal just in front to deter would-be looters/scavengers. He also ordered they dig a pit in the back of their fenced in yard and do their “business” there. After three months of nothing but MREs, OPSEC, and pooping in a hole they had to squat over, Rachel’s hubby has succumbed to an “unfortunate accident” and was disposed of in one of the poop holes.

I tell her the community has set up a daily farmers market like square where people trade for things, socialize as the pandemic has subsided for now. I help her trade MREs for two dozen fresh eggs, cabbage, carrots, apples, and two freshly slaughtered chickens. That night, they eat the best they have in three months.

Being a nurse, I help Rachel find employment as an assistant to the house call doctor that has sprung up in the community. They are paid in various things, from food to home knit wool hats. Rachel still trades her candles for other things. A few years go by, and Rachel’s daughter marries one of the doctors. Rachel later becomes a member of the community council leaders and eventually chairperson. At the age of fifty, Rachel marries a blacksmith. She allowed me the honor of giving her away. She has never been happier.

14) Me, the anonymous UPS delivery driver: Having delivered ammo, Fiji water, toilet paper, pre-made foodstuff, wine, Russian caviar, and a package of unknown origin to an undisclosed former missile silo, I had to call the ball. The food supply distribution system was collapsing. I sat in my brown truck, leaned over the steering wheel, looking at the road in front of me. Do my job or save myself and my family?

I chose the latter and took the truck back home. Had the wife and kids follow me with the dogs to family farm out in the sticks. I figured a UPS truckload of ammo, wine, water, toilet paper, and whatever else was back there would be additions at the farm. I would learn to like Russian caviar. With a good chianti, it cannot be that bad, right?

Tyler Durden

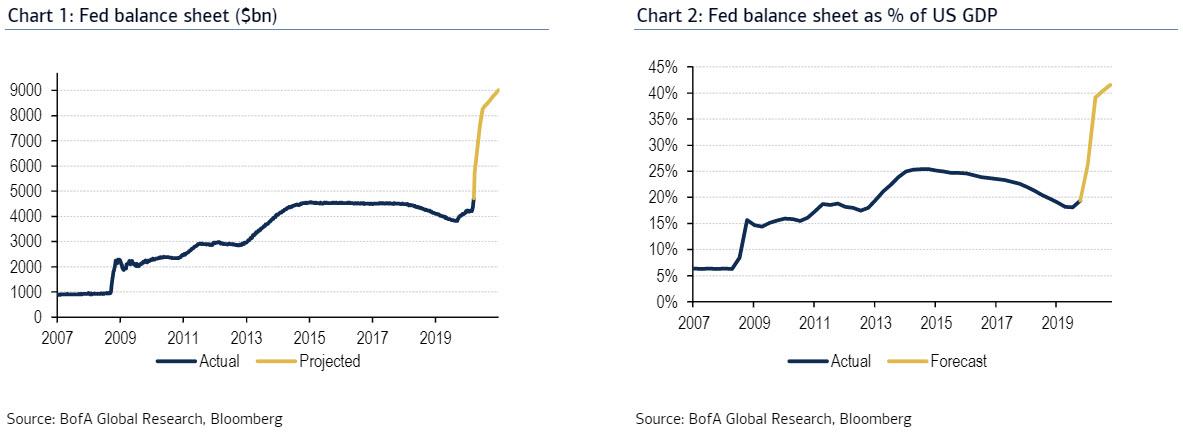

Sun, 04/12/2020 – 22:10 - Timing The "Crossover Point": The Fed Will Soon Monetize The Entire Fiscal Stimulus Package… What Happens Then

Timing The "Crossover Point": The Fed Will Soon Monetize The Entire Fiscal Stimulus Package… What Happens Then

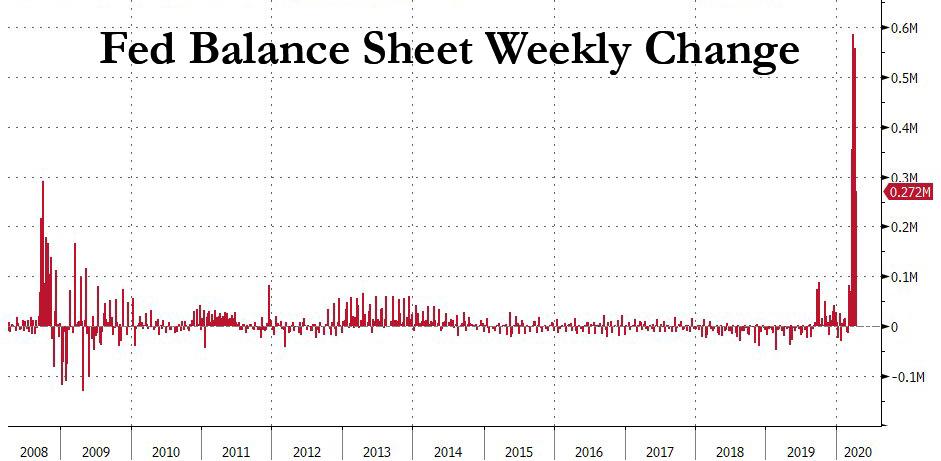

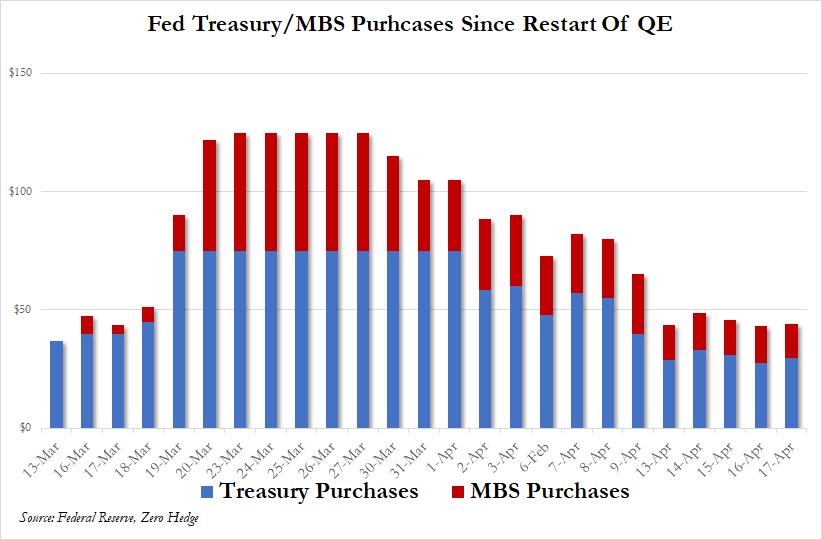

As we noted late last week, the Fed’s money printer has been going brrrr in overtime, and in the past month alone, Powell & Co. has purchased nearly $2 trillion in Treasury and MBS securities, far more than during any of the previous QE episodes (either in the first month or their entirety)…

… which together with the Fed’s POMO schedule which sees the Fed purchasing another $225BN in securities this week…

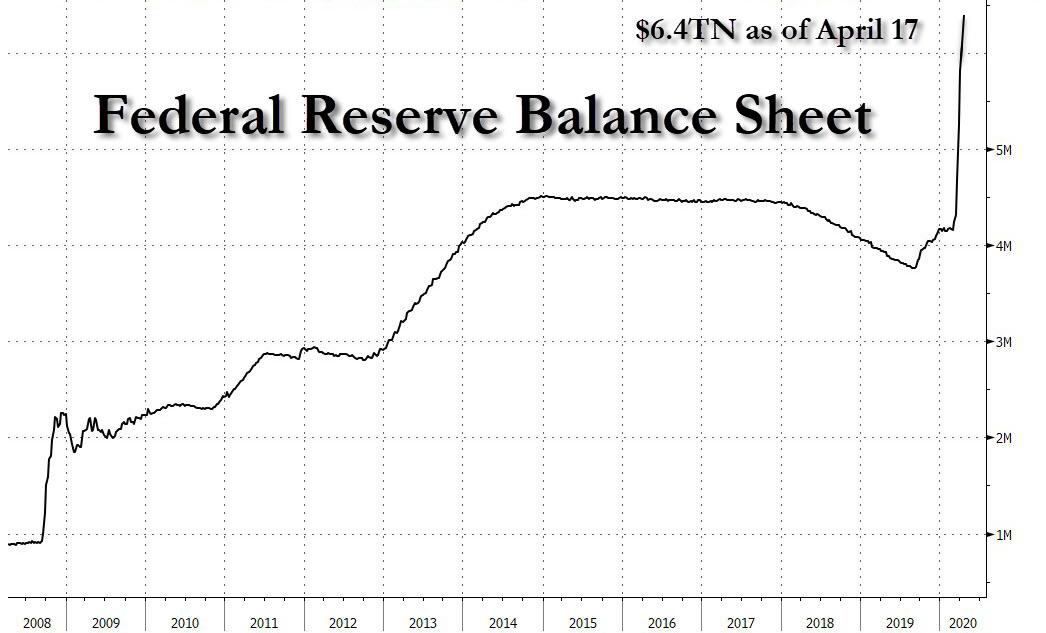

… will push the Fed’s balance sheet (currently at $6.1 trillion) to $6.4 trillion by next Friday, up more than 50% in the span of just weeks.

That’s just the beginning, because as we showed two weeks ago, BofA strategist and former Fed guru, Mark Cabana expects the Fed’s balance sheet to double to $9 trillion by the end of the year.

What does this mean for Treasury issuance? Well, for one thing it means that the Fed will monetize not only all the debt issuance for 2020 that was scheduled before the coronavirus pandemic broke out, but also the entire fiscal stimulus package (currently $2.2 trillion, soon $3+ trillion). Which is hardly a surprise: last week the Bank of England became the first bank to officially announce it would openly monetize the UK’s deficit. In other words, the central bank and the Treasury are now one and the same, which also means that helicopter money has arrived, first in the UK and soon everywhere else.

It also means that, as DB’s Stuart Sparks puts it “these are administered markets” (or perhaps “administerrrrrred” markets).

Yet while the Fed has unleashed an unprecedented buying spree across the curve, traders are starting to ask when and how will markets price in a “crossover point” when there is more supply than demand (if such a thing is possible), potentially resulting in a violent bear steepening in the yield curve and a spike in long-term yields as the Fed loses control over long-term inflation expectations.

Commenting on this, DB’s rates strategists write that the narrative for bearish curve steepening is rooted in the idea of a crossover point at which the duration impact of additional Treasury supply exceeds that of demand stemming from Fed QE purchases. This is particularly true in the long end, where the Treasury is still expected to begin 20y issuance in the May refunding. The “crossover” argument is illustrated on the chart below: coupon supply net of Fed purchases is likely to turn positive during Q3, even if the Fed monetizes the entire fiscal stimulus package as it currently stands.

That said, the crossover argument is inherently a flow argument, rather than a stock argument. To mitigate fears that the deluge of Treasurys – now that helicopter money has been unleashed – will lead to a chaotic spike in long-rates, Deutsche Bank writes that an immediate issue with the flow argument that increasing Treasury supply will push yields higher and the term premium steeper “is that it ignores the flows between the present and the time at which this crossover occurs.” That is, large purchase volumes at higher than market WAM should flatten the term premium and push yields lower until the crossover point. Yields might rise and the term premium steepen, but from lower and flatter levels.

At the same time, the Fed’s thought process around QE is inherently more stock-based (an argument that the Fed lost long ago when it was demonstrated conclusively by the like of Goldman and others that only the flow matters): QE “permanently” reduces the stock of risk free government debt, which should cause that government debt to richen. In order to enhance returns, private investors are then obliged to extend duration, flattening the term premium. When the term premium is flat, investors must move out the risk spectrum to enhance returns. This is the Fed’s portfolio balance channel.

Deutsche take a middle ground, and notes that pragmatically, one would expect the effects of large asset purchases to be cumulative, and to occur at a lag. For this reason QE is something of a hybrid between stock and flow. Intuitively, Fed purchases of, say, $100 billion/month should have a different impact on the market if they were preceded by a period in which the Fed bought $2 trillion in total than they would had the Fed bought nothing previously. Here DB is quick to note that, at its projection of QE demand, the Fed will have fully monetized the first three phases of fiscal stimulus totaling

around $2.2 trillion. Likewise the bank expects Fed purchases to increase to absorb any “phase 4” stimulus as is currently being debated in the US Congress.In short, without the Fed actively monetizing US debt, the long end would have disconnected long ago.

A second issue is that there is still a reasonable amount of uncertainty about the magnitude of flows on both the supply and demand sides. Let’s start with the supply side.

While a fourth installment of fiscal stimulus of $1 trillion or more would clearly add to potential supply, it is somewhat less clear where on the curve it might come. Specifically, there is a possibility that the Treasury might elect to delay its inaugural 20y issue due to poor liquidity and stretched dealer balance sheets. According to DB, the entire 2040 maturity sector is trading extremely cheap to the fitted curve (chart below).

The bank’s view is that the Treasury will proceed, but the “long end supply thesis” is subject to both the risk that the issue will be delayed for better market conditions, and to the risk that if the issue comes, a smaller issue size could reduce long end supply pressures.

Perhaps the key issue in the “crossover thesis” is what is the true goal of the Fed’s QE program. One argument is that the immense initial size of Fed Treasury purchases was intended as a powerful short term market stabilizer, but a “V”-shaped recovery could obviate the need for an extended program to stimulate the economy (not that one is coming as we will discuss in a subsequent post). This argument is perhaps the most consistent with Treasury cheapening as it could be consistent with a rapid taper of QE purchases in the relatively near term. That said, the probability of this scenario is low as the Fed will not do anything to send rate volatility (MOVE) soaring again.

As a result, DB’s central expectation is that while QE purchase volumes are indeed likely to be tapered further, they will remain sufficiently large to exert further downward pressure on the level of real yields and the term premium. In short: once helicopter money start, it can never again stop.

The fundamental reason the Fed will target these variables is that rising real yields and real term premium run contrary to their policy goals. First, the level of r* has likely fallen due to the acute demand shock caused by virus mitigation. As DB strategists argue, the equity/bond correlation suggests that r* could be as low as -1% (chart below).

And with short rates already at the effective lower bound (at least until we get NIRP), the Fed must ease further by growing its balance sheet (i.e., targeting longer maturities). Suppressing the term premium crowds return-seeking investors first out the curve, and ultimately out of Treasuries into riskier assets, which means the Fed is now back to blowing the biggest asset bubble ever. The chart below illustrates that the ACM term premium has been reasonably well correlated with a proxy for the equity risk premium. When the term premium is low, all else equal, equities look cheaper, and price appreciation tightens the equity risk premium.

Second, high real yields keep the dollar strong, which keeps downward pressure on commodity prices and hence headline inflation. Note that the spike in real yields as BEI declined coincided with the sharp dollar appreciation during March. Moreover, we think it is important that the broad dollar is stronger than before the Fed began to ease, and remains higher than end-2019 levels in spite of the fact that 10y real yields have fallen 50 bp. The implication is that real yields likely need to fall further to stabilize the dollar and improve the prospects for persistent increases in headline and core inflation, the Fed’s true stated mission.

Which brings us to the key question: what happens once we reach the Treasury supply/demand crossover point, and the answer is most that either the Fed doubles down voluntarily, or the Fed loses control and doubles down because it is forced to keep on monetizing all US debt issuance, which is now in its exponential phase (a lot of exponential curves in recent weeks)…

… as the alternative is that everything that the Fed has been working on for the past decade (and really, 107 years) can be thrown out, and the US – and global – economy implodes.

How long can this can-kicking last? Simple: as long as the world has faith in the dollar as a reserve currency (as discussed earlier) – while that particular fiction persists, the now co-joined Fed and Treasury will be able to pick the US economy up by its bootstarps while giving everyone the impression that printing money somehow makes people richer, when in reality it just devalues purchasing power, cripples labor and makes the “top 0.1%” holders of assets wealthier beyond their wildest dreams.

Tyler Durden

Sun, 04/12/2020 – 21:45 - Westward No! A Bitter Land-Office Business In Taming Federal Bureaucrats

Westward No! A Bitter Land-Office Business In Taming Federal Bureaucrats

Submitted by Vince Bielski, of RealClearInvestigations

The Trump administration’s big strike against the federal bureaucracy is quietly unfolding at the Bureau of Land Management, where its senior managers and scientific staff have been told to pack up their desks in Washington, D.C., and move to its new headquarters in Grand Junction, Colo. and other western offices. Most employees aren’t climbing aboard the wagon train.

Environmental protesters in Vail, Colo., 2019, greet Interior Secretary David L. Bernhardt at a Western Governors Association meeting.

Dean Krakel/The Colorado Sun via AP, FileThe shake-up, meant to make the bureaucracy more accountable to the drillers, cattle ranchers, hunters and hikers who use America’s public lands, is part of the sweeping deregulation that has fueled a boom in U.S. energy production through last year. In its earliest days, the administration declared energy independence a top priority and two years later oil production on federal and tribal lands and offshore hit record highs — a surge that will likely slow as the coronavirus pandemic cuts demand and rocks the industry.

“It’s more efficient now,” says Kathleen Sgamma, president of Western Energy Alliance, a trade group representing 300 oil and gas companies that pushed for the BLM move. “You can be productive without fighting for years to get a permit. They are processed more efficiently in less time.”

The gusher that has been feeding the coffers of states like Wyoming and New Mexico, however, is also raising concerns about the impact on some of the country’s spectacular landscapes and wildlife. Noting that only 80 of 174 employees have agreed to move west, environmental groups and some former BLM managers warn that relocating the agency’s headquarters reflects a broader shift of authority to political appointees, from career bureaucrats with years of expertise.

“The relocation will have a substantial impact on the management of our public lands,’’ says Ray Brady, a retired senior manager and minerals specialist who worked in the Washington headquarters for 23 years. “We view it as a dismantling of the organization and turning major decisions on public lands over to political people who have agendas.” The department and bureau didn’t respond to requests for comment.

The move began in November 2019 with a target completion date of July 1, and the pandemic, which may provide an unexpected rationale for getting out of a major population center, is not expected to significantly slow it down. But nonessential BLM travel is on hold for now.

William Perry Pendley: “Sagebrush Rebel” and Bureau of Land Management acting director. It represents tests both of the power of the administrative state and of striking a balance between the competing forces of development and conservation on public lands. It also promises to be a key regional issue in the 2020 election. At a campaign rally in Colorado in February, a state Donald Trump lost in 2016, the president touted the BLM relocation as part of his effort to end “the tyranny of Washington bureaucrats.” Joe Biden, the likely Democratic nominee, would have the bureau flex its regulatory muscles like never before. He would ban new oil and gas permitting on public lands and waters to reduce the threat of climate change. Carbon emissions from energy produced on federal lands amount to one quarter of the U.S. total.

Americans have a lot riding on the outcome. BLM manages 245 million acres of public lands – 10% of the U.S. land mass — primarily in 12 Western states. The iconic sagebrush deserts, grasslands and rugged mountains hold rich oil and gas deposits, robust elk and antelope herds, desert monuments and tribal cultural sites. Federal and tribal property produce about 10% of U.S. oil and gas sales. BLM also cares for 28 national monuments and other conservation areas encompassing red-rock deserts, jagged coastline and remote tundra.

The bureau was founded in 1946, and in its first three decades quietly served cattle ranchers and coal miners who needed permits to use public lands. The rise of environmentalism and increased pressure on the lands changed the game by the 1970s: The National Environmental Policy Act forced federal agencies to examine ecological and health impacts — and take public input — before making decisions. A few years later the Federal Land Policy and Management Act gave BLM new and broader marching orders to manage public lands under a multiple-use principle. It now had to balance the interests of many competing groups – conservationists, drillers, hunters, miners and ranchers – in carving up lands for grazing, historical preservation, recreation, resource extraction and wildlife protection.

Herding wild horses in Idaho: BLM manages 245 million acres – 10% of the U.S. land mass — primarily in 12 Western states.

Darin Oswald/Idaho Statesman via APThe “Sagebrush Rebellion” sprung up in the West in the 1970s to challenge the government’s tightening grip on public lands and the movement still reverberates today. William Perry Pendley, who was appointed BLM’s acting chief by Interior Secretary David L. Bernhardt, calls himself a “Sagebrush Rebel.” The firebrand property-rights attorney rose to prominence by suing BLM and other federal agencies on behalf of ranchers and drillers who depend on public lands.

BLM has wiggle room in striking that balance between development and conservation, making its job tricky. Its offices spread throughout the West in cities like Boise, Billings and Carson City solicit input from groups with opposing land-use agendas. Staffers then apply scientific expertise to assess the best use of the resources and impact on the environment, and try to reach a consensus. But the hardest part of the balancing act can be navigating Washington politics, as Democratic and Republican administrations zealously push their priorities onto BLM decision-making. The radical swing from Barack Obama to Donald Trump is the latest example

“The Obama administration was laser focused on conservation and I wasn’t a fan of that. It was too far left and not enough in the middle,” says Mary Jo Rugwell, who retired as BLM Wyoming state director in August after 46 years of federal service. “The Trump administration is all about removing barriers and restrictions to development.”Soon after Trump took office, then-Interior Secretary Ryan Zinke announced a shift in the balance. While Zinke’s strategic plan includes fishing, hunting and recreation, it stresses drilling above all else: “An American-First energy policy is one that maximizes the use of American resources in freeing us from dependence on foreign oil,” wrote Zinke, who resigned in late 2018 amid investigations into his conduct and was succeeded by Bernhardt, his like-minded deputy.

David L. Bernhardt, right, Trump Interior Secretary: Put political appointees in charge of major land-use decisions. Photo: doi.gov To speed up energy production, the department significantly streamlined BLM regulations. In January 2018 officials ended the requirement for public input during environmental review of potential leases and cut the days for protests of lease offerings by more than half to 10. The number of new acres leased shot up by 117% in fiscal 2018 compared with two years earlier. And the time it takes to get a drilling permit on leased land was slashed by almost three months in that period. In 2019, oil production on federal and tribal lands and offshore hit a record of more than 1 billion barrels, almost a 30% jump.

The BLM move shifts more than 200 filled and unfilled career positions in Washington to Grand Junction and other Western outposts — primarily the bureau’s top leaders and staffers with training in biology, geology, forestry, rangelands and archeology. As the experts leave Washington, major decisions will be made by political appointees who lack scientific training, say current and former BLM managers.

Retiree Brady said the agency’s renewable-energy program, which he helped create and oversaw, requires scientific expertise and collaboration that may be lost in the relocation. The large wind and solar energy developments on public lands can disturb the ecology and cultural sites, threaten endangered species like the desert tortoise and bald eagle and impinge on military installations and parklands. Brady said a technical staff is needed in Washington to collaborate with the National Park Service, Fish & Wildlife Service and the Defense and Energy departments to reduce possible harm from the renewable-energy projects.

Bernhardt has already put political appointees in charge of major BLM land-use decisions. In 2018, he said a team of six political appointees and one career professional must review all actions that involve an environmental impact statement. This includes pivotal resource management plans created by field and state offices that divide up public lands for conservation, drilling, recreation and other uses for 20-year periods. The appointees on the team are lawyers and former Capitol Hill and department staffers with little or no scientific training. Before the order, BLM experts in Washington had played the leading role in reviewing plans, with occasional input from political appointees on major decisions, says Steve Ellis, who retired in 2016 as BLM deputy director, the top career post.

The Bureau of Land Management is moving a long way from D.C.;blm.gov “The review has been taken over by political people who are not scientists and have never worked in the field,” says Ellis, a forester by training.

State offices that have submitted plans to headquarters for review have been told to open more land to oil and gas leasing. In Wyoming, the biggest energy exporting-state in the country, the Rock Springs field office developed a draft plan that fenced off a limited number of acres from leasing in its region while allowing drilling in other areas. The restrictions, which were requested by local officials and groups, were meant to protect the city’s aquifer and some sensitive big-game habitat. When the plan was presented to headquarters in 2018, the then-BLM director shot it down. He told Wyoming staffers to go back to the drawing board and make a plan that was less restrictive to drilling, says Rugwell, who was in the meeting.

“He said, ‘Are you trying to turn BLM into the National Park Service?’” Rugwell said. “That insulted me. I take pride in trying to be balanced. When I tried to explain that we had listened to the people of Wyoming, that didn’t make a difference.” The field office is now revising its plan.

In Montana, the Lewistown field office’s draft plan called for setting aside about 100,000 acres because of its wilderness characteristics. The land is next to the Charles M. Russell National Wildlife Refuge, some of Montana’s wildest habitat with robust herds of bugling elk and mule deer. While this land surface would be off-limits to development, the plan sought to strike a balance by permitting oil and gas drilling on more than 1 million acres in the district.

The political team in Washington asked for changes in the plan that eliminated the wilderness characteristics’ protections. The final 2020 plan allows for drilling and road building under controlled conditions in the wilderness area.

The tradeoff between energy production and wildlife conservation is evident in New Mexico, an epicenter of the U.S. surge in energy production. The state’s San Juan Basin is one of the country’s most prolific oil and gas regions. But the drilling infrastructure in the area has disrupted mule deer migration from Colorado to winter feeding grounds in New Mexico. That prompted Sen. Tom Udall, Democrat of New Mexico, to introduce a bill last year with bipartisan backing giving federal agencies authority to create national wildlife corridors to protect the state’s big game and other animals around the country hurt by the loss of habitat.

Chaco Culture National Historical Park is another flashpoint in New Mexico. Navajo Nation leaders oppose drilling close to Chaco Canyon where ancient ruins have been preserved. After Bernhardt visited the park last year, he said, he “walked away with a greater sense of appreciation of the magnificent site” and announced a one-year moratorium on leasing within a 10-mile radius of Chaco while BLM revised its resource management plan for the area.

Greater sage grouse: The thing with feathers, and lawyers.

Pacific Southwest Region U.S. Fish and Wildlife Service /WikimediaThe stakes are also high for the greater sage grouse. A 2015 plan from the Obama administration covering 10 states established restrictions on development to keep the bird from being listed as an endangered species. Last year, BLM revised the plan to permit more drilling and other development by reducing restrictions on millions of acres of sensitive habitat. But a federal judge in Idaho blocked the revisions from going into effect, citing a wildlife biologist who found that the bureau ignored analyzing how its changes would impact sage grouse habitat in a way that’s “inconsistent with standard practices and the best available science.” The bureau responded in February with supplemental environmental analysis to justify its revisions.

Amid a string of legal challenges, BLM’s Pendley points to the benefits of the U.S. becoming the world’s largest producer of crude oil.

People in states that depend heavily on energy production — such as Wyoming, New Mexico and North Dakota — are the winners. An astonishing 50% of Wyoming’s revenue comes from energy industry taxes and royalties. Job growth in oil and gas extraction has been robust until a recent slowdown, made worse by the pandemic that has caused oil prices to plunge.

“Barack Obama says you cannot drill your way out of energy dependence. And the president came in and said, ‘We are going to do it,’ and we have done it,” Pendley said in mid-February on a Colorado radio show. “It’s an unprecedented accomplishment.”

BLM employees in Washington appear to be the losers. Brady, the retired minerals expert, says far fewer employees, only about 20%, will end up making the move, based on a survey he has done will most of the leadership and staff. Many of them are disillusioned over their diminished role at BLM and are either retiring or finding positions at other agencies.

“A lot of good people are fleeing the agency,” a BLM senior manager with extensive experience in Washington wrote in an email before retiring in February. “This administration does not respect career employees.”

Colorado Sen. Cory Gardner, who spearheaded the effort to move the agency to his state, isn’t concerned about the experts the bureau is losing. The Republican lawmaker said BLM is hiring to fill those spots and that it is more important to have career employees living in the West where they’ll learn about the local issues and take a more common-sense approach to regulation.

“If people don’t want to live and work in the West, on the land that they’re regulating, that’s probably a good decision” to leave the BLM, he says. “I find it offensive and elitist that somebody would refuse to live on the land they regulate.”

Tyler Durden

Sun, 04/12/2020 – 21:20 - Global 'Jubilee' Looms As G20 Finalizes Debt Relief Program For World's Poorest Countries

Global 'Jubilee' Looms As G20 Finalizes Debt Relief Program For World's Poorest Countries

Hours after Pope Francis on Easter Sunday morning said the debt burden on the most impoverished countries should be forgiven (aka debt jubilee), the Financial Times is now reporting that the G20 group is nearing a critical “action plan” to freeze debt servicing payments for poor countries to stave off an emerging-market meltdown.

The new relief program could be finalized on April 15 on a videoconference of finance ministers and central bank governors. The plan would “freeze on sovereign debt repayments for six or nine months, or possibly through to 2021,” the official told the Times.

The official said developed countries and multilateral institutions would use this period to write up “very clear criteria, country-by-country of what exactly is going to happen. Is it debt relief totally? Is it just a deferment, a rescheduling?”

“For debt relief to happen, it would take time for it to be co-ordinated,” the official said.

“But what is immediately needed is to give these people space so they don’t need to worry about the cash flow and debt servicing going to other countries, and they can use that money for their immediate needs,” the official said, who did not want to be named due to the sensitivity of the discussions.

Last week, the British-based Jubilee Debt Campaign called for a worldwide debt jubilee to avoid some of the world’s poorest countries from collapsing into chaos amid the COVID-19 crisis.

Sarah-Jayne Clifton, director of the Jubilee Debt Campaign, said: “The suspension on debt payments called for by the IMF and World Bank saves money now, but kicks the can down the road and avoids actually dealing with the problem of spiraling debts.”

Clifton is urging for the immediate cancellation of 69 of the world’s poorest countries’ debt payments this year, which would free up at least $25 billion for the countries in 2020, and up to $50 billion if the jubilee was extended to the end of 2021.

“This is the fastest way to keep money in countries to use in responding to Covid-19, and to ensure public money is not wasted bailing out the profits of rich private speculators,” added Clifton.

Much of the debt crisis concern is situated around the poorest countries that line China’s Belt and Road Initiative.

The official said there is “very clear recognition that a global co-ordinated approach is a must” to avoid an emerging market debt crisis.

Odile Renaud Basso, chair of the Paris Club, a group of the 22 largest creditor nations, told the Times that all creditor nations and China should work closely with G20 negotiations to resolve emerging market woes.

“There must be a level playing field so that all creditors agree to the same key parameters,” she said. “But with that in place there is always a need for bilateral discussions between each creditor and debtor nation, and China could work within that framework. They are very much involved and I think they will be part of an agreement.”

The IIF has also been vocal in calls “to forbear payment default for the poorest and most vulnerable countries significantly affected by Covid-19 and related economic turbulence for a specified time period, without waiving the payment obligation”.

The official also said that governments would not make it mandatory for private creditors to offer relief programs for the poorest countries.

“You cannot force individual investors to waive their rights. That could distort the markets, and could have the negative consequences of liquidity problems. They would not lend if they see any sign that they can be forced to let go of their assets.”

And it appears the world is at the end of a decade’s long monetary experiment, where ushering in more quantitative easing to fix below-trend growth or instabilities in the financial casino will not work this time.

Daniel Lacalle, CIO at fund manager Tressis Gestión, recently said: “QE will not fix this. Swap lines will not fix this. A debt jubilee would fix this or multiple trillions of dollars in write-downs and defaults.”

Internet search term for “debt jubilee” has surged to the highest level not seen since late 2012.

Increasing calls for a debt jubilee suggests the 100-year debt-super cycle’s “kick the can down the road” plan may have finally hit a wall .

Tyler Durden

Sun, 04/12/2020 – 20:55 - "Down The Rabbit Hole" – The Eurodollar Market Is The Matrix Behind It All

"Down The Rabbit Hole" – The Eurodollar Market Is The Matrix Behind It All

Submitted by Michael Every of Rabobank

Summary

- The Eurodollar system is a critical but often misunderstood driver of global financial markets: its importance cannot be understated.

- Its origins are shrouded in mystery and intrigue; its operations are invisible to most; and yet it controls us in many ways. We will attempt to enlighten readers on what it is and what it means.

- However, it is also a system under huge structural pressures – and as such we may be about to experience a profound paradigm shift with key implications for markets, economies, and geopolitics.

- Recent Fed actions on swap lines and repo facilities only underline this fact rather than reducing its likelihood

What is The Matrix?

A new world-class golf course in an Asian country financed with a USD bank loan. A Mexican property developer buying a hotel in USD. A European pension company wanting to hold USD assets and swapping borrowed EUR to do so. An African retailer importing Chinese-made toys for sale, paying its invoice in USD.

All of these are small examples of the multi-faceted global Eurodollar market. Like The Matrix, it is all around us, and connects us. Also just like The Matrix, most are unaware of its existence even as it defines the parameters we operate within. As we shall explore in this special report, it is additionally a Matrix that encompasses an implicit power struggle that only those who grasp its true nature are cognizant of.

Moreover, at present this Matrix and its Architect face a huge, perhaps existential, challenge.