- Bob Farrell's (Illustrated) 10-Investment Rules

Submitted by Lance Roberts via RealInvestmentAdvice.com,

Over the weekend, it was interesting to see the number of advisors/analysts quickly rushing to defend their “buy and hold” investing philosophies following the sharp decline on Friday. As I wrote this past weekend:

“The downfall of all investors is ultimately ‘greed’ and ‘fear.’

They don’t sell when markets are near peaks, nor do they buy market bottoms. However, this does not just apply to individuals but many advisors as well.

When I read articles from advisors/managers promoting ‘buy and forget’ strategies it is for one of three reasons. They either can’t, don’t want to, or don’t know how to manage portfolio risk. Therefore, the easy message is simply:

‘You just have to ride the market out. Long-term it will go up. But hey, let me charge you a fee for holding your stuff in an account.’

The reality is that markets do not return 6%, 8% or 10% annually, and spending years making up previous losses is not a way to successfully obtain retirement goals. (Read this)

It is also worth pointing out that those promoting these ‘couch potato’ methodologies are generally out in full force near peaks of bull market cycles, and are rarely heard of near bear market bottoms. This is why, as I discussed in ‘Why You Still Suck At Investing,’ investors consistently underperform over long periods of time.”

When markets are at, or near, “record levels” those levels are records for a reason. Throughout history awe-inspiring bull markets have been followed by devastating bear markets. Like “yen and yang,” a bull cannot exist without its forever intertwined counterpart.

Despite the media, advisor and analysts rhetoric to the contrary, investors DO have the ability to manage the inherent risk in their portfolios.

Investors can capture returns and grow their “savings” versus just blindly hoping that history will not once again repeat itself. While I can’t tell you exactly when the second half of the full-market cycle will manifest itself, I can assure you it will and the negative impact to retirement goals, and the time lost, will be just as damaging.

One other question to ponder. While Wall Street tells you to “just hold on and ride the market out,” why are they managing risk, spending billions on trading platforms and algorithms, and in many instances betting against you?

With this in mind, I present Bob Farrell’s 10-Investment Rules. While these rules should be a staple for any investor who has put their hard earned “savings” at risk in the market, they are rarely heeded in the heat of bull market. Just as they are being ignored now.

Who is Bob Farrell?

Bob is a Wall Street veteran with over 50 years of experience in crafting his investing rules. Farrell obtained his master’s degree from Columbia Business School and started as a technical analyst at Merrill Lynch in 1957. Even though Farrell studied fundamental analysis under Gramm and Dodd, he turned to technical analysis after realizing there was more to stock prices than balance sheets and income statements. Farrell became a pioneer in sentiment studies and market psychology. His 10 rules on investing stem from personal experience with dull markets, bull markets, bear markets, crashes, and bubbles. In short, Farrell has seen it all and lived to tell about it.

The Illustrated 10-Rules Of Investing

1. Markets tend to return to the mean (average price) over time.

Like a rubber band that has been stretched too far – it must be relaxed in order to be stretched again. This is exactly the same for stock prices which are anchored to their moving averages. Trends that get overextended in one direction, or another, always return to their long-term average. Even during a strong uptrend or strong downtrend, prices often move back (revert) to a long-term moving average. The chart below shows the S&P 500 with a 52-week simple moving average.

The bottom chart shows the percentage deviation of the current price of the market from the 52-week moving average. During bullish trending markets, there are regular reversions to the mean which create buying opportunities. However, what is often not stated is that in order to take advantage of such buying opportunities profits should have been taken out of portfolios as deviations from the mean reached historical extremes. Conversely, in bearish trending markets, such reversions from extreme deviations should be used to sell stocks, raise cash and reduce portfolio risk rather than “panic sell” at market bottoms.

The dashed RED lines denote when the markets changed trends from positive to negative. This is the very essence of portfolio “risk” management.

2. Excesses in one direction will lead to an opposite excess in the other direction.

Markets that overshoot on the upside will also overshoot on the downside, kind of like a pendulum. The further it swings to one side, the further it rebounds to the other side. This is the extension of Rule #1 as it applies to longer term market cycles (cyclical markets).

While the chart above showed prices behave on a short term basis – on a longer term basis markets also respond to Newton’s 3rd law of motion: “For every action, there is an equal and opposite reaction.” The first chart shows that cyclical markets reach extremes when they are more than 2-standard deviations above or below the 50-week moving average. Notice that these excesses ARE NEVER worked off by just going sideways.

The second chart shows the price reversions of the S&P 500 on a long term basis and adjusted for inflation. Notice that when prices have historically reached extremes – the reversion in price is just as extreme. It is clear that the current reversion in the stock market is still underway from the 2000 peak.

3. There are no new eras – excesses are never permanent.

There will always be some “new thing” that elicits speculative interest. These “new things” throughout history, like the “Siren’s Song,” has led many investors to their demise. In fact, over the last 500 years, we have seen speculative bubbles involving everything from Tulip Bulbs to Railways, Real Estate to Technology, Emerging Markets (5 times) to Automobiles and Commodities. It always starts the same and ends with the utterings of “This time it is different”

[The chart below is from my March 2008 seminar discussing that the next recessionary bear market was about to occur.]

As legendary investor Jesse Livermore once stated:

“A lesson I learned early is that there is nothing new on Wall Street. There can’t be because speculation is as old as the hills. Whatever happens in the stock market today has happened before and will happen again.”

4. Exponential rapidly rising or falling markets usually go further than you think, but they do not correct by going sideways

The reality is that excesses, such as we are seeing in the market now, can indeed go much further than logic would dictate. However, these excesses, as stated above, are never worked off simply by trading sideways. Corrections are always just as brutal as the advances were exhilarating. As the chart below shows when the markets broke out of their directional trends – the corrections came soon thereafter.

5. The public buys the most at the top and the least at the bottom.

The average individual investor is most bullish at market tops and most bearish at market bottoms. This is due to investor’s emotional biases of “greed” when markets are rising and “fear” when markets are falling. Logic would dictate that the best time to invest is after a massive sell-off; unfortunately, this is exactly the opposite of what investors do.

6. Fear and greed are stronger than long-term resolve.

As stated in Rule $5 it is emotions that cloud your decisions and affect your long-term plan.

“Gains make us exuberant; they enhance well-being and promote optimism,” says Santa Clara University finance professor Meir Statman. His studies of investor behavior show that “Losses bring sadness, disgust, fear, regret. Fear increases the sense of risk and some react by shunning stocks.”

The index of bullish sentiment shows that “greed” is once again beginning to reach levels where markets have generally reached intermediate-term peaks.

In the words of Warren Buffett:

“Buy when people are fearful and sell when they are greedy.”

Currently, those “people” are getting extremely greedy.

7. Markets are strongest when they are broad and weakest when they narrow to a handful of blue-chip names.

Breadth is important. A rally on narrow breadth indicates limited participation and the chances of failure are above average. The market cannot continue to rally with just a few large-caps (generals) leading the way. Small and mid-caps (troops) must also be on board to give the rally credibility. A rally that “lifts all boats” indicates far-reaching strength and increases the chances of further gains.

The chart above shows the ARMS Index which is a volume-based indicator that determines market strength and breadth by analyzing the relationship between advancing and declining issues and their respective volume. It is normally used as a short term trading measure of market strength. However, for longer term periods the chart shows a weekly index smoothed with a 34-week average. Spikes in the index has generally coincided with near-term market peaks.

8. Bear markets have three stages – sharp down, reflexive rebound and a drawn-out fundamental downtrend

Bear markets often start with a sharp and swift decline. After this decline, there is an oversold bounce that retraces a portion of that decline. The longer term decline then continues, at a slower and more grinding pace, as the fundamentals deteriorate. Dow Theory suggests that bear markets consist of three down legs with reflexive rebounds in between.

The chart above shows the stages of the last two primary cyclical bear markets. The point to be made is there were plenty of opportunities to sell into counter-trend rallies during the decline and reduce risk exposure. Unfortunately, the media/Wall Street was telling investors to just “hold on” until hey finally sold out at the bottom.

9. When all the experts and forecasts agree – something else is going to happen.

This rule fits within Bob Farrell’s contrarian nature. As Sam Stovall, the investment strategist for Standard & Poor’s once stated:

“If everybody’s optimistic, who is left to buy? If everybody’s pessimistic, who’s left to sell?”

As a contrarian investor, and along with several of the points already made within Farrell’s rule set, excesses are built by everyone being on the same side of the trade. Ultimately, when the shift in sentiment occurs – the reversion is exacerbated by the stampede going in the opposite direction

Being a contrarian can be quite difficult at times as bullishness abounds. However, it is also the secret to limiting losses and achieving long-term investment success. As Howard Marks once stated:

“Resisting – and thereby achieving success as a contrarian – isn’t easy. Things combine to make it difficult; including natural herd tendencies and the pain imposed by being out of step, since momentum invariably makes pro-cyclical actions look correct for a while. (That’s why it’s essential to remember that ‘being too far ahead of your time is indistinguishable from being wrong.’)

Given the uncertain nature of the future, and thus the difficulty of being confident your position is the right one – especially as price moves against you – it’s challenging to be a lonely contrarian.”

10.Bull markets are more fun than bear markets

As stated above in Rule #5 – investors are primarily driven by emotions. As the overall markets rise; up to 90% of any individual stock’s price movement is dictated by the overall direction of the market hence the saying “a rising tide lifts all boats.”

Psychologically, as the markets rise, investors begin to believe that they are “smart” because their portfolio is going up. In reality, it is primarily more a function of “luck” rather than “intelligence” that is driving their portfolio.

Investors behave much the same way as individuals who addicted to gambling. When they are winning they believe that their success is based on their skill. However, when they began to lose, they keep gambling thinking the next “hand” will be the one that gets them back on track. Eventually – they leave the table broke.

It is true that bull markets are more fun than bear markets. Bull markets elicit euphoria and feelings of psychological superiority. Bear markets bring fear, panic, and depression.

What is interesting is that no matter how many times we continually repeat these “cycles” – as emotional human beings we always “hope” that somehow this “time will be different.” Unfortunately, it never is and this time won’t be either. The only questions are: when will the next bear market begin and will you be prepared for it?

Conclusions

Like all rules on Wall Street, Bob Farrell’s rules are not meant has hard and fast rules. There are always exceptions to every rule and while history never repeats exactly it does often “rhyme” very closely.

Nevertheless, these rules will benefit investors by helping them to look beyond the emotions and the headlines. Being aware of sentiment can prevent selling near the bottom and buying near the top, which often goes against our instincts.

Regardless of how many times I discuss these issues, quote successful investors, or warn of the dangers – the response from both individuals and investment professionals is always the same.

“I am a long term, fundamental value, investor. So these rules don’t really apply to me.”

No, you’re not. Yes, they do.

Individuals are long term investors only as long as the markets are rising. Despite endless warnings, repeated suggestions and outright recommendations; getting investors to sell, take profits and manage your portfolio risks is nearly a lost cause as long as the markets are rising. Unfortunately, by the time the fear, desperation or panic stages are reached it is far too late to act and I will only be able to say that I warned you.

- Hillary Breaks Silence; Says Whole Pneumonia, 'Stumble' Thing "Wasn't That Big A Deal", Admits Happened Before

Hillary Clinton broke her post-9/11 silence tonight with an interview with CNN’s Anderson Cooper. Claiming that she felt dizzy but did not lose consciousness (all video evidence aside), the presidential candidate proclaimed that she didn’t think the pneumonia was “going to be that big a deal,” and is now “feeling so much better.” Cooper did press Clinton on the number of times this has happened – more than once – but Clinton took the opportunity to ironically call out her opponent for his lack of transparency.

So judge for yourself. This is what happened…

And this is what she told Anderson Cooper…

As CNN reports, Hillary Clinton said Monday night she’s “met a high standard of transparency” about her health and didn’t think the pneumonia was “going to be that big a deal.”

Clinton said she felt dizzy and lost her balance Sunday, but did not lose consciousness, and is now “feeling so much better.”

“I was supposed to rest five days — that’s what they told me on Friday — and I didn’t follow that very wise advice,” Clinton told CNN’s Anderson Cooper in a phone interview.

“So I just want to get this over and done with and get back on the trail as soon as possible,” she said.

But during her interview Monday, Clinton sought to turn criticism of her secrecy over her illness into an attack on Republican rival Donald Trump.

“Compare everything you know about me with my opponent. I think it’s time he met the same level of disclosure that I have for years,” Clinton told Cooper.

She said her campaign didn’t publicly reveal her diagnosis because “I just didn’t think it was going to be that big of deal.”

Finally, Cooper asked about Bill Clinton’s remark in an interview with Charlie Rose that she has occasionally become dehydrated and gone through episodes like Sunday’s, and how many times that has happened before…

“I think really only twice that I can recall,” Clinton said.

“You know, it is something that has occurred a few times over the course of my life, and I’m aware of it, and usually can avoid it,” she said.

So a ‘stumble’ that appeared more like a full drag, leaving a shoe behind… has happened before… but “wasn’t a big deal.” Ok.

- US Think Tank Warns That Australia Is About 6 Weeks Away From Housing Collapse

Over the past couple of months, we have written frequently about the impact of Chinese money laundering operations on home prices in a couple of large cities around the globe. So far, the Vancouver market has seemingly been the hardest hit with homes prices collapsing over 20% in one month after the city passed a 15% property tax on foreign buyers on July 25, 2016 (see "As The Vancouver Housing Market Implodes, The "Smart Money" Is Rushing To Get Out Now").

Now, a U.S. based think tank, International Strategic Studies Association (ISSA), is warning that similar efforts to restrict Chinese investment in Australian real estate could send prices tumbling there as well. In speaking with news.com.au, Greg Copley, President of ISSA, predicted that Australia has about 6 weeks before real estate prices start to collapse.

"We estimate that Australia has about six weeks or so to turn this situation around, otherwise there would be a massive hit on property valuations and the building trades."

"The urgency is, I believe, based on the fact that this is about how long it will take for the banks' policies to start switching off a lot of existing and planned contracts for Australian properties."

"The banks clearly believe Australian real estate values will decline, so they are attempting to avoid that risk. They’ve learned from the US collapse that seizing real estate collateral is a no-win scenario when the volume is great and the market slow."

“In so doing, they precipitate the market collapse but are less exposed to it.”

Real estate prices in Australia's largest housing markets have soared over the past couple of years fueled, in no small part, by demand from Chinese buyers looking for offshore locations to park cash. The Sydney and Melbourne markets have been the largest beneficiaries of foreign capital with real estate prices up 53% and 51%, respectively, since 2012. That said, based on data from the Australian Bureau of Statistics it looks like home prices in Australia have already started their descent.

Back in the spring, Australian banks began cracking down on foreign purchasers of residential properties due to concerns of increasing fraud and money laundering activites. New rules enacted required borrowers to be Australian citizens and/or legal residents with a valid visa. Per ISSA, these new restrictions on lending will likely result in many foreign buyers being forced to default on new residential properties. He argues that many foreign buyers placed down payments on properties under the old banking regulations but now won't be able to secure financing to close once the properties are actually completed.

Efforts to restrict lending, came in addition to taxes imposed by many Australian cities after foreign demand was found to be pricing local buyers out of many residential markets and killing the “Great Australian Dream” of owning property. In fact, Sydney prices have risen to record levels and currently rank second only to Hong Kong in terms of major cities with the world’s least-affordable housing.

With Vancouver and Australia now cracking down on Chinese money laundering operations the only question that remains is where the next bubble will spring up to take it's place?

- Supervisor Of "Massive Fraud" At Wells Fargo Leaves Bank With $125 Million Bonus

There was a burst of righteous populist anger anger last week, when it emerged that Wells Fargo had engaged in pervasive, “massive” fraud since at least 2011, including opening credit cards secretly without a customer’s consent, creating fake email accounts to sign up customers for online banking services, and forcing customers to accumulate late fees on accounts they never even knew they had. For this criminal conduct, Wells was fined $185 million (including a $100 million penalty from the CFPB, the largest penalty the agency has ever issued). In all, Wells opened 1.5 million bank accounts and “applied” for 565,000 credit cards that were not authorized by their customers.

As “punishment” Wells Fargo told CNN that it had fired 5,300 employees related to the shady behavior over the last few years. The firings represent about 1% of its workforce and took place over several years. The fired workers went to far as to create phony PIN numbers and fake email addresses to enroll customers in online banking services, the CFPB said. What was hushed away is that not a single employee will go to prison, and that ultimately it will be Wells Fargo’s shareholders – such as Warren Buffett – who will end up footing the bill.

What Wells did not disclose publicly to anyone is that the head of the group responsible for Wells’ biggest consumer fraud scandal in years, is quietly leaving the bank with a $125 million bonus, a bonus which as Fortune’s Stephen Gandel writes today will not see even one cent clawed back as part of the dramatic revelations.

According to Gandel, Carrie Tolstedt, the Wells Fargo executive who was in charge of the unit where employees opened more than 2 million largely unauthorized customer accounts—a seemingly routine practice that employees internally referred to as “sandbagging”— is leaving the giant bank with an enormous pay day, some $124.6 million.

Carrie TolstedtTolstedt is walking away from Wells Fargo with a very full bank account, and praise: in the July announcement of her exit, which made no mention of the soon-to-be-settled case, Wells Fargo’s CEO John Stumpf said Tolstedt had been one of the bank’s most important leaders and “a standard-bearer of our culture” and “a champion for our customers.” In light of the record fine levied by the CFPB for the unit which Tolstedt headed, we wonder if Stumpf would like to retract his statement.

What is just as troubling is that despite beefed-up “clawback” provisions instituted by the bank shortly after the financial crisis, “it does not appear that Wells Fargo is requiring Tolstedt, the Wells Fargo executive who was in charge of the unit where employees opened more than 2 million largely unauthorized customer accounts—a seemingly routine practice that employees internally referred to as “sandbagging”—to give back any of her nine-figure pay.”

As a reminder, on Thursday, Richard Cordray, the head of the CFPB, said, “It is quite clear that [the actions of Tolstedt’s unit] are unfair and abusive practices under federal law. They are a violation of trust and an abuse of trust.”

However, cited by Gandel, a spokesperson for Wells Fargo said that the timing of Tolstedt’s exit was the result of a “personal decision to retire after 27 years” with the bank. The spokesperson declined to comment on whether the bank was considering clawing back Tolstedt’s back pay.

In a statement following the settlement, Wells Fargo said, “Wells Fargo reached these agreements consistent with our commitment to customers and in the interest of putting this matter behind us. Wells Fargo is committed to putting our customers’ interests first 100% of the time, and we regret and take responsibility for any instances where customers may have received a product that they did not request.”

In other words, this has become yet another instance where bank subordinates were engaged in activity that seemingly none of their supervisors was – mysteriously – aware of, a pattern observed in virtually every major crackdown against a prominent sellside bank, from Goldman’s Fab Tourre to the Libor conspiracy. While Fortune writes that it is not clear how closely Tolstedt was responsible for or even aware of the widespread abusive tactics at the bank, it is a fact that Tolstedt ran the community banking division of the bank, which included its retail banking and credit card divisions, during the entire period in which the customer abuse was alleged, which goes back to 2011. The CFPB said about three quarters of the unauthorized accounts opened by employees of Wells Fargo were bank deposit accounts. Another 565,000 were unauthorized credit card applications. Tolstedt took over the division in 2008, after Wells Fargo merged with Wachovia during the financial crisis.

Ironically, Tolstedt was a regular on Fortune‘s Most Powerful Women list. She was replaced on this year’s list by Mary Mack, who is taking over her job at the bank.

Tolstedt was regularly praised for her unit’s ability to get customers to open numerous accounts. For a number of years, Wells Fargo’s proxy statement, which details executive pay, cited high “cross-selling ratios” as a reason that Tolstedt had earned her roughly $9 million in annual pay. For instance, in Wells Fargo’s 2015 proxy statement, the company said that its compensation committee had authorized Tolstedt’s $7.3 million stock and cash bonus that year, because “under her leadership, Community Banking achieved a number of strategic objectives, including continued strong cross-sell ratios, record deposit levels, and continued success of mobile banking initiatives.”

However later in 2015, the L.A. City Attorney’s office sued the bank because of its sales tactics, saying that many of the abusive practices came from intense pressure on Wells Fargo’s employees to get customers to open up numerous accounts. A separate class action of former employees alleges they were fired for not meeting cross-selling goals, or going along with the aggressive sales tactics.

Meanwhile, the awards for Toldstedt continued piling in, and earlier in 2016, when Wells Fargo released its annual proxy statement, it once again said that in order to justify her multimillion dollar bonus, Tolstedt’s division had “achieved a number of strategic objectives.” But this time, for the first time in years, cross-selling wasn’t listed as one of them.

While one can speculate if Tolstedt decided to leave in advance of the CFPB crackdown on her division, one thing that is certain is how much money she is taking with her: according to Gendell, when Tolstedt leaves Wells Fargo later this year, on top of the $1.7 million in salary she has received over the past few years, she will be walking away with $124.6 million in stock, options, and restricted Wells Fargo shares. Some of that hasn’t vested yet. But Tolstedt gets to keep all of it because she technically retired. Had she been fired, Tolstedt would have had to forfeit at least $45 million of that exit payday, and possibly more. It is safe to assume that had she waited until after the CFPB settlement, that her parting present may have been one third smaller, and that she could have been the bank’s scapegoat, fired to placate regulators.

Alas, now we will never know what “could”have happened, which means that the only recourse Wells and its shareholders have – if they feel like bothering – is to try to recoup some of her ill-gotten bonus. As Fortune concludes, “the bank’s proxy statement says that the bank has “strong recoupment and clawback policies,” and that the bank will revoke bonus pay if it is found that the conduct of an executive resulted in representational harm to the bank, or that the executive was not able to “identify or manage” risks in his or her division. But there is no sign that Wells Fargo is going to ask Tolstedt to return even a sliver of her stock jackpot.“

As we pointed out last week, when we observed that yet again nobody is going to prison, Gandel’s parting assessment is similar: “on Wall Street, the carrots are still widely handed out. The sticks, however, remain out of sight.”

This also means that the biggest crime on Wall Street remains a more prosaic one: getting caught.

- Hillary Versus Donald: War Or Peace?

Although history does not exactly repeat itself, it does provide parallels and sometimes quite ominous ones. Such is the case with the current U.S. Presidential election and the one which occurred one hundred years earlier.

The dominating question which hung over the 1916 campaign was whether the country would remain neutral in regard to the horrific slaughter which was taking place on the European battlefields in probably the greatest act of mass insanity ever recorded, World War I.

President Wilson had maintained that the U.S. would continue a policy of strict neutrality. By all indications, the nation wanted no part of the war, with the President’s own party at his nomination delivering an emphatic “No” to any foreign intervention.

Although Wilson maintained a neutral policy through the election and briefly afterwards, his advisors and Cabinet had been lobbying for war and continued to do so even more vehemently after the President’s re-election was secured. Nearly all of them, including Wilson himself, had deep financial, family, and political ties to J.P. Morgan. Wilson received considerable Morgan financial backing for his two presidential runs.

The Morgan operatives within the Administration were pushing for war because the House of Morgan had “invested” heavily in the “Allied” cause and a defeat or a negotiated settlement with any favorable concessions to Germany would be a catastrophe for Morgan financial interests.

Germany understood the cozy Morgan relationship with the Wilson Administration and the Allied powers as Morgan representatives, especially the sinister Colonel House, had repeatedly rebuffed peace proposals from the Central Powers. The Allies and their opponents understood that Wilson’s re-election would mean U.S. entry into the conflict.

Tragically, for the U.S. and for the course of war-ridden 20th century history, Wilson capitulated and brought the U.S. into the battle despite the campaign promise of neutrality and no real German threat. The House of Morgan’s financial bacon was saved at the cost of a devastated Western world.

One hundred years later, the U.S. and the world stand at another critical juncture and face a similar choice: the election of a known war criminal who has not only shown no remorse for her murderous policies, but promises, if elected, to continue them; or the election of a candidate who has spoken of negotiating with America’s supposed principle enemy, a possible pull back in the nation’s unsustainable global empire, and the enactment of a legitimate use of federal authority – protection of the country’s borders.

It is difficult to believe that Donald Trump is not sincere in seeking accommodation and friendly relations with Russia. It would be far easier for the billionaire businessman and would most likely secure his election if he followed the bellicose policy of the Democrat and Republican Presidents of the recent past who have continued to antagonize and threaten Russia. The most hopeful sign for peace coming from the U.S. in quite a while has been Trump’s talk of de-escalation of tensions and a pledge to place American interests first in foreign policy, instead of mouthing the global domination designs of the crazed neocons.

Some of the things he has said about Vladimir Putin and Russia have been, to say the least, quite encouraging:

I think I would get along with Vladimir Putin. I just think so.

…

It is always a great honor to be so nicely complimented by a man [Putin] so highly respected within his own country and beyond.

…

I have always felt that Russia and the United States should be able to work well with each other towards defeating terrorism and restoring world peace, not to mention trade and all of the other benefits derived from mutual respect.

Although not a non-interventionist, a President Trump is unlikely to provoke Russia or China into a civilization-ending conflagration and has displayed the instincts of a true peace maker.

There is, however, little hope for a reduction of global tensions if his sociopathic opponent becomes Commander-in-Chief. Killary has repeatedly demonstrated that she is a willing tool of the neocons and the global financial forces that will profit mightily from continued U.S.- instigated conflicts. If she makes it past the finish line, either legitimately or more likely through fraud, she will surely do their bidding.

For once, politicians and pundits who routinely call every election “the most crucial of a generation” are right. This year’s Presidential election is the most significant one since at least the fall of the Soviet Union and Eastern Bloc. If the U.S. electorate wants to avoid the disaster not only to its own land and the world that followed in the wake of the 1916 election, there can be only one choice in November of 2016.

- It's Time To Bring Back Bernie

Submitted by Charles Hugh-Smith via OfTwoMinds blog,

This tells you everything you need to know about how Hillary will operate as President: there will be no honesty, transparency or truth, ever.

Hillary's bid for the presidency is no longer defensible; it's time to bring back Bernie Sanders as the Democratic nominee.

The issue isn't Hillary Clinton's health per se; what is indefensible is her response to legitimate questions of the American public regarding her health.

Hillary Clinton has disqualified herself to be President of the United States because she is incapable of telling the truth about anything. There is no such thing as truth or transparency in the Clinton persona and campaign; everything is an ongoing experiment in perception management.

First one narrative is floated; if the narrative shifts the public perception positively, it is defended to the death, and anyone questioning it is instantly accused of being a conspiracy theorist from the "vast right-wing conspiracy" that has been Hillary's favorite defense for 30 years.

If this tried-and-true attack fails, then the questioners are accused of being sexist, partisan, etc.

If the first trial balloon narrative doesn't gain public perception traction, it's quickly dropped and another explanation is unleashed on a willing-to-accept-anything-as-"fact"-from-Hillary mainstream media.

So when the "overheated" explanation in 79-degree weather doesn't get traction, then it is dropped in favor of pneumonia, which mysteriously puts most sufferers in bed but Hillary declares that she feels great.

This process of replacing explanations and narratives, interspersed with attacks on anyone who questioned the previous narrative, is repeated until the perception management result is satisfactory. Hillary is clearly incapable of honesty–the word has no meaning, because all communication is aimed at concealing or obscuring the facts of the matter and defending what is visibly indefensible as if perception management is the same as the truth. It is not the same, but Hillary is incapable of discerning the difference.

This reliance on attacking the questioner to delegitimatize what is a legitmate inquiry also disqualifies Hillary. The American public has a legitimate interest in how Hillary Clinton benefited from the Clinton Foundation's hundreds of millions of dollars in contributions from overseas donors during her stint as secretary of state.

The American public also has a legitimate interest in the health of presidential candidates. John F. Kennedy's poor health was masked by a compliant media in the early 1960s, but that sort of duplicity is no longer condoned. The American public wants an accurate accounting of the candidate's health.

As you view the clip of Hillary collapsing, study the body language of her multiple handlers. I'm not referring to the Secret Sevice agents; I'm referring to her private handlers and aides. Note their extreme defensiveness about anyone seeing what was happening to Hillary. Their way of propping her up doesn't look like it was the first time they had to prop her up; their actions were practiced, automatic.

They are accustomed to propping her up and masking her true condition from the public. Study the clip; it's all there, in plain view.

Their hyper-wary posture was not just an attempt to shield the candidate from anyone seeing a moment of weakness; their over-protective watchfulness for "eyes on the candidate" is 24/7. Their only job is to mask the truth of Hillary's condition, whatever it may be.

This tells you everything you need to know about how Hillary will operate as President: there will be no honesty, transparency or truth, ever. Life for Hillary boils down to managing perceptions and hiding facts–inconvenient or otherwise. This is not a campaign strategy–it is her default mode of existence, the only way she knows how to operate.

Hillary's health may or may not be decisive, but what is decisive is how she has banished honesty, truthfulness, candor and transparency. The issue for Hillary and her handlers is not the facts of her health; it's how to manage public perceptions of her health in a satisfactory manner.

We don't just need to know whether Hillary suffers from conditions beyond allergies and pneumonia. What counts most is whether she is capable of being honest, forthright and truthful about legitimate, important issues. She has clearly proven that she is incapable of being honest and truthful about anything, very likely because she cannot distinguish between plain, simple truth and perception management.

Let's be honest for a moment, and confess that this is a character flaw that disqualifies the candidate from holding office. The last two presidents who saw their job as hiding the truth and managing perceptions were Richard Nixon during the Watergate era, and Lyndon Johnson during the War on Vietnam.

Attacking every legitimate inquiry as a "vast right-wing conspiracy" is not governance; it's a paranoia and distrust of the American public that leads inexorably to catastrophes like Watergate and wars of choice that drag on as the bodies and lies pile up.

It's time to bring back Bernie Sanders, a candidate who can tell the difference between the truth and perception management, someone who isn't an embarrassment to the nation. I understand that Hillary's coronation as Head of the Deep State has already been scheduled by the Powers That Be, but that doesn't mean we too must lose the ability to differentiate between the truth and perception management.

* * *

My new book is #7 on Kindle short reads -> politics and social science: Why Our Status Quo Failed and Is Beyond Reform ($3.95 Kindle ebook, $8.95 print edition) For more, please visit the book's website.

- Track All Of Bankrupt Hanjin's "Ghost Ships" In Real Time

After two weeks of impenetrable legal limbo, there was some good news for owners of cargo stuck in the bowels of container ships belonging to the recently bankrupt South Korean shipping giant, Hanjin Shipping. As Bloomberg reported according to the insolvent shipper, at least some vessels are in line to unload cargo at Long Beach port in California after a U.S. court Friday granted bankruptcy protection, easing a gridlock that disrupted delivery of goods.

Three more Hanjin ships are waiting at the port to clear their freight once Hanjin Greece, which is currently offloading, clears early Sept. 12 local time, Hanjin said in response to a query. Truck drivers probably will begin moving containers from the Greece on Monday while the vessel prepares to leave late in the day for the Port of Oakland, said Teamsters spokeswoman Barbara Maynard and shipping traffic controllers, cited by Reuters. Port workers began taking Hanjin Greece’s cargo ashore at 8 a.m. local time Sunday, and the Hanjin Gdynia will follow, Noel Hacegaba, chief commercial officer of the Port of Long Beach, said in a telephone interview Sunday.

However, the Greece, and its two peer ships, carry only a fraction of the $14 billion in goods on dozens of ships owned or leased by the world’s seventh-largest container carrier. Worse, while some of Hanjin’s ships would be free to offload their cargo once they obtain the needed funding, the fate of many other ships is unknown. Charter owner Seaspan has three ships under charter with Hanjin – the Hanjin Buddha, Hanjin Namu and Hanjin Tabul – which are all due to hit the U.S. West Coast within the next few days. Chief executive Gerry Wang said he was confident the South Korean government would provide sufficient funds to pay port operators and Seaspan by the time those ships arrived to ensure they were unloaded.

“We’re keeping our fingers crossed, but South Korea is an export economy and the government needs to ensure the flow of goods to consumers,” Wang said. “I don’t think they want that supply chain to be interrupted on a permanent basis.”

Alas, it may be, if only for the time being: as Reuters notes, creditors have sought an arrest warrant against the Seaspan Efficiency, a ship hauling cargo for Hanjin that was due to arrive in Savannah.

In the meantime, two weeks after the bankruptcy was filed, most of the company’s “ghost ships” remain in limbo: it is not clear when port operators will bring others to berths in Southern California and elsewhere. One Hanjin ship off Long Beach, the Hanjin Montevideo, is under the supervision of a court-ordered custodian after two fuel companies obtained an arrest warrant for it over unpaid bills. Hanjin and the fuel providers are trying to work out an arrangement to release the vessel.

It’s no less chaotic around the globe: in Hong Kong, the Hanjin Belawan arrived from Shanghai on Monday loaded with containers and was anchored a short distance from the city’s Kwai Chung Container Terminal. Terminal operator Hongkong International Terminals, a unit of Hutchison Port Holdings Trust controlled by tycoon Li Ka-shing, has outraged local cargo owners by charging fees of between HK$10,000–HK$15,000 per Hanjin container to release them at the port.

The delays have concerned importers like Alex Rasheed, president of Pacific Textile and Sourcing Inc in Los Angeles, which has a shipment of clothing in 16 containers on Hanjin ships off Long Beach. “We’re already starting to run out of some colors and some sizes,” Rasheed said, noting Hanjin’s collapse comes as U.S. retailers prepare for the all-important holiday shopping season.

In Singapore, cargo owner AP Oil International said it had been sending replacement cargos on urgent orders.

“On the procurement side, we do also face some issues to receiving raw materials shipped on Hanjin vessels, which of course we are adjusting our supply chain and production to meet and replace the cargo due to the uncertainty of the situation now” Group Chief Executive Ho Chee Hon said.

* * *

In total, Hanjin said that as of this morning, it had 93 vessels, including 79 container ships, stranded at 51 ports in 26 countries. Readers who wish to track the fate of Hanjin’s “ghost ships” in real time – as it looks likely that many of them will remain stuck in legal and financial limbo for a long time – can do so courtesy of the following Platt’s interactive map.

- A Homerun For The Donald – Attack The Fed's War On Savers, Workers And The Unborn (Taxpayers)

Submitted by David Stockman via Contra Corner blog,

The central banks have gone so far off the deep-end with financial price manipulation that it is only a matter of time before some astute politician comes after them with all barrels blasting. As a matter of fact, that appears to be exactly what Donald Trump unloaded on bubble vision this morning:

By keeping interest rates low, the Fed has created a “false stock market,” Donald Trump argued in a wide-ranging CNBC interview, exclaiming that Fed Chair Janet Yellen and central bank policymakers are very political, and should be “ashamed” of what they’re doing to the country…

He’s completely correct. After all, they are crushing real wages with their 2% inflation targeting; destroying savers with NIRP and sub-zero rates; and burying unborn taxpayers in monumental debts that today’s politicians are pleased to issue with reckless abandon because the short-run carry cost is nil.

Interest on the Uncle Sam’s $19.4 trillion of debt, for example, is easily $500 billion lower than its true economic cost based on a normal yield after inflation and taxes and elimination of the phony $100 billion per year in so-called Fed “profits” that are booked by the treasury as negative interest expense.

Alas, when interest rates eventually normalize, the Treasury’s debt service costs will soar by hundreds of billions. At the same time, the entirety of the Fed’s “profits”, which are conjured from thin air because it buys interest-yielding government and GSE debt with printing press liabilities which cost virtually nothing, will disappear. That’s because it will be forced to take reserve charges for giant principal losses on the falling prices of its $4.5 billion portfolio of government and GSE bonds.

At that moment, the long-abused citizens of Flyover America, who have already been clobbered as savers and wage earners, will get hit with the triple whammy of soaring Federal tax bills. And this is not a matter of if or even when; it’s really just a question of how soon.

When it comes to the establishment’s monetary lunacy, of course, Mario Draghi’s is always leading the charge. So just consider what has been happening after his inartful punt during last week’s ECB meeting.

First, the casino cheerleaders have insisted that there is nothing to sweat about with respect to the incredible anomaly that now plagues the euro-bond markets. To wit, socialist Europe has apparently not issued enough qualifying debt (with a yield not below the negative 0.4% threshold) to fill the ECB’s $90 billion per month purchase target.

The solution is real simple according to Draghi’s acolytes in the casino. In addition to lowering the bond yield threshold as deep into the subzero freezer as necessary, they have proffered an even better solution. Just buy up the stock market, too!

“The obvious reason for the ECB to buy equities is they have almost run out of German bonds to buy,” said Stefan Gerlach, chief economist at BSI Bank and a former deputy governor of Ireland’s central bank. “The basic idea is that the central bank can put essentially anything on its balance sheet and there is no reason to be straight-laced about this.”

Equities offer a deep pool of assets. The market capitalization of listed eurozone companies was $6.1 trillion at the end of 2015, according to World Bank data.

And this isn’t just some whacko sell side analyst talking his book. Here’s what one of the world’s alleged leading monetary policy exports added to the mix:

When policy rates approached zero, central banks in the U.S., the U.K., Japan and the eurozone turned to bond purchases to reduce long-term interest rates. Buying equities would likely yield some of the same effects in terms of encouraging consumption and investment through higher household wealth and lower cost of capital.

“I don’t see a reason not to do this,” said Joseph Gagnon, senior fellow at the Peterson Institute for International Economics. “It isn’t obvious to me why a central bank wouldn’t always want a diversified portfolio, including equities.”

Actually, it gets even better. According to another casino player, bonds have now gotten so over-valued—-from massive central banking QE purchases, of course—-that European equities are now “under-valued” in relative terms!

Therefore, the ECB can do no less than plunge into a stock buying bacchanalia in order to set things right.

ECB stock purchases “would be justified: European equities are undervalued, while there is a bubble—that the ECB continues to inflate—in bonds,” said Patrick Artus, chief economist at French investment bank Nataxis in a research note.

Besides that, the Swiss National Bank (SNB) and the BOJ have already pioneered the way. Fully 20% of the former’s bulging portfolio consists of equities, including massive holdings of US stocks. And when we say “massive” that’s exactly what we mean.

The balance sheet of the SNB is up by nearly 7X since the eve of the financial crisis, and now totals $715 billion. That happens to be 108% of Switzerland’s GDP.

It also happens to mean that in order to fight off the exchange rate impact of Mario’s relentless campaign to trash the Euro, the Swiss monetary central planners have purchased upwards of $150 billion of global equities, making them one of the largest hedge funds in the world.

Now that the Donald has extended his talk about the “rigged” system run by our unelected financial elites to include the stock market, he surely has a point.

Nor is the SNB an outlier. The BOJ also has roughly $150 billion of equities on its balance sheet. Indeed, it already owns 55% of all Japanese ETFs; is now among the top 10 shareholders in 90% of Japan’s 225 largest companies; and is slated to become the top holder in 40 of the Nikkei 225 companies by year-end 2017 at its planned stepped-up ETF purchase rate.

But the insanity of buying up and thereby falsifying large sections of the stock and bond markets in order to pursue the will-o-wisp of 2% inflation isn’t the half of it. Having done this, the central banks have made themselves hostage to the most reckless fast money speculators in the entire casino.

That’s because the latter will sell at a moments notice anything they have been front-running via leveraged carry trades if they think the central banks’ buying binge will stop.

In the case of Japan’s 30-year bond, for example, the yield in the last few weeks has soared from 6 bps to 61 bps on fears that the BOJ may “pause” its madcap bond buying program. Since it has already purchased more than 40% of Japan’s monumental public debt, the mere hint that it might stop caused the price of the 30-year bond to plunge by upwards of 20%.

But the recent dislocations in the euro-bond market leave nothing to the imagination. Draghi’s failure last Thursday to unequivocally state that the ECB’s $90 billion per month QE program would be extended after its scheduled expirtation next March shows exactly why the central banks have turned themselves into monetary doomsday machines:

Meanwhile, yields on 10-year German Bunds turned positive for the first time since June 22. Yields were around 0.013 percent at the time of the market close, up from -0.06 percent on Thursday.

“The jolt across bond markets began when ECB president Mario Draghi said the governing council did not discuss extending its asset purchase program. Understandably, bondholders got a little nervous about holding onto a negative-yielding asset which could fall in price if there’s no central banking buying alongside them,” Jasper Lawler, market analyst at CMC Markets, said in a note on Friday.

There is all the evidence you need that the world’s financial markets are totally and completely rigged. And that’s why Donald Trump was exactly on target this morning when he uncorked another politically incorrect observation about the rigged nature of the Wall Street casino.

To wit, Yellen is still sitting on interest rates at the zero bound after 93 months for one simple reason. Even in the context of an economic recovery that is now allegedly so complete that we are actually on the cusp of full employment, according to Vice-Chairman Stanley Fischer, she is deathly fearful of a hissy fit on Wall Street, as was foreshadowed by last Friday’s sharp sell off.

Opined the Donald:

“She’s obviously political and she is doing what [President Barack] Obama wants her to do,” Trump said in an interview on CNBC. Trump predicted that the market is going to “go way down” as soon as interest rates go up.

“I believe it is a false market because money is essentially free,” Trump said.

He got that right, but needs to take it a step further. At the same time that the Fed continues placating Wall Street gamblers with an unending stint of free carry trade funding that has self-evidently not generated real breadwinners jobs or higher real incomes in Flyover America, savers and retires continue to be pounded.

In fact, our unelected monetary politburo is causing upwards of $300 billion per year to be transferred from savers to the banks and the financial system owing to its senseless pursuit of 2.00% inflation via pegging the money market interest rate on the zero-bound.

Even then, however, the true impact goes far beyond retirees and the modest share of the population that actually attempts to save. To wit, 2% inflation targeting is absolutely the stupidest thing any central bank could pursue in the context of a global economy is which goods and services are freely traded, and in which the US, Europe and Japan have the highest nominal wage rates on the planet.

What inflation targeting does is cause the domestic price level to rise, rather than fall, in DM economies. It thereby also causes the nominal wage gap with China and its EM supply chain to widen. So the Donald is right on that one, too.

Indeed, the most potent agency of off-shoring American jobs is not the USTR or bad trade deals, but the central banks. And in the middle and lower ranks of the wage market—-where the China price on goods and the India price on services bears down most heavily—-the Fed’s inflation folly is especially perverse.

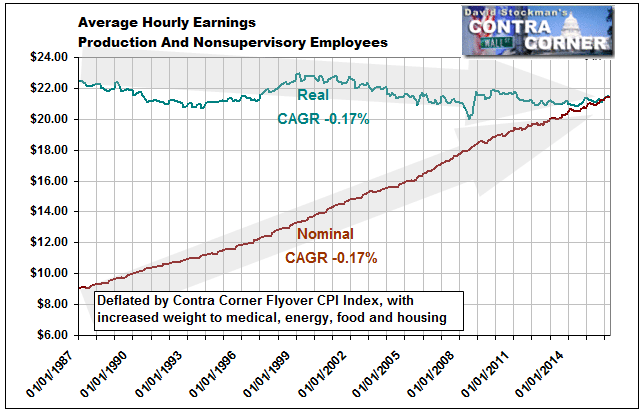

As we have demonstrated with our more accurate “Flyover CPI”, the cost of living faced by main street America—especially for the four horseman of food, energy, medical and housing prices—has risen by 3.1% annually since the late 1980s. And that is well more than hourly wage gains for production workers.

So the Fed has delivered to working class Americans the worst of both worlds. Namely, rising nominal wages which have priced them out of the world market, but even higher domestic inflation that has caused their real wages and living standards to shrink.

Here is the smoking gun. Notwithstanding a near tripling of the nominal wage rate from $9 per hour in 1987 to about $22 per hour today, real wages are lower than they were three decades ago.

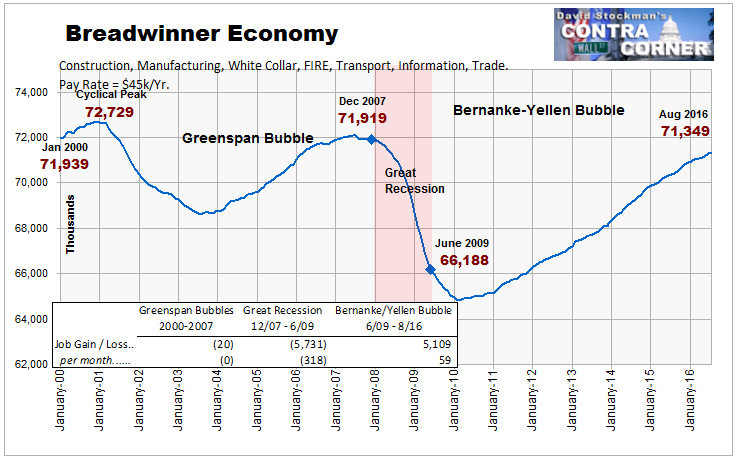

At the same time, the tripling of nominal wages has caused a relentless export of breadwinner jobs in goods and services to the China price and India price regions of the world. That’s why, in fact, there were still 1.4 million fewer full-time, full-pay breadwinner jobs at $50k per year in August than there were way back when Bill Clinton was packing his bags to shuffle out of the White House in January 2001.

In short, the “something for nothing” money printing policies inflicted on Flyover America by our unelected rulers at the central banks, and with the full support of their facilitators and supporters among the Wall Street/ Washington ruling elites, are not only bad economics; they are perverse and unjust beyond measure.

Indeed, the Fed is waging an insensible and outrageous war on savers, workers and future taxpayers – even as it pleasures the 1% with fantastic financial windfalls from the Wall Street casino.

Now that is a rigged system. And that is a beltway evil that merits the Donald’s unrelenting attack on behalf of the citizens of Flyover America who have been left behind in their tens of millions.

- What Happens If Hillary Clinton Has To Drop Out?

Submitted by Emily Zanotti via HeatSt.com,

Hillary Clinton’s doctor now says the Democratic presidential candidate, 68, was officially diagnosed with pneumonia sometime on Friday, and has been campaigning with the serious respiratory illness for a week, leading to her “medical episode” at Sunday morning’s September 11th memorial event.

When it comes to candidates (rather than office holders) the rules actually come from the political parties, not the Constitution. For Republicans, if a Presidential candidate dies or drops out, the RNC has to either convene a new convention or take an official poll of the RNC’s state representatives to select a replacement candidate. Most likely, the RNC would move the running mate up to the top of the bill, in order to preserve what fundraising has already been done for the ticket.

But for the Democrats, it’s not so clear. The Democratic National Committee reserves the right to replace a candidate who dies or drops out, and it doesn’t provide additional details in its by-laws. So presumably the Democrats would have to make up the process up as they go along. The DNC could entrust replacing Clinton to a central DNC brain trust or, more likely, replicate the RNC’s system, handing the vote over to the committee’s state delegates.

Tim Kaine

The DNC would likely want to retain the support of major donors who’ve already given to the Clinton-Kaine ticket, and would probably just bump Tim Kaine up from the Veep slot. Kaine would simply slide up the ticket, choose a new running mate, hope the ballots could be reprinted in time, and carry on just as Clinton had.

But, of course, this is 2016 and anything can happen.

The Open Slot

Donald Trump has proven to be a wild card candidate: he’s spent no money, compared to Clinton’s million-dollar ad buys, and raised virtually nothing compared to his Democratic opponents, and he’s still running neck and neck with Clinton nationwide. So the DNC would likely have to consider whether Kaine could retain Clinton’s razor-thin lead, or whether they’d need a more capable candidate.

The DNC might naturally lean towards Joe Biden who said he didn’t want to campaign, but has never said, openly, that he’d prefer not to be President. Biden is neither Clinton nor Trump, making him an easy favorite in the Presidential contest (though, it’s likely any number of cartoon characters, inanimate objects and D-list celebrities would also easily pull into the lead), and he’d have the backing of President Obama, who could unite the party with a call to action to unite behind his Vice President.

Also likely contenders: Bernie Sanders and Elizabeth Warren (both progressive candidates with a large swath of support within the Democratic party), New York governor Andrew Cuomo, Virginia’s Jim Webb, even second runner up Martin O’Malley.

Chelsea Clinton

There’s a longtstanding tradition in American politics of spouses stepping in after an unexpected death. Take Missouri’s Jean Carnahan, for instance, who stood in for her husband Mel after he died in a plane crash three weeks before the Missouri Senate election. After Mel won posthumously, she served in the Senate for two years. Future Senator Olympia Snowe first entered politics after the death of her husband, a Maine state representative, in a car wreck. Likewise, Mary Bono’s long political career began when her husband Sonny died in a skiing incident.

Bill Clinton is prohibited by the 22nd Amendment of the Constitution from running. If a Clinton were to step in for Hillary, it would likely be Chelsea, who at 36 is just old enough, in terms of the Constitution, to be president.

The Filing Deadlines

Most states’ campaign filing deadlines have already passed – and as some independent candidates, including conservative Evan McMullin are finding, states aren’t normally open to extending the period of time candidates have to file the paperwork necessary to put their names on the Presidential ballot.

For the Democratic replacement, though, as long as they have the party’s blessing, it’s likely officials could simply replace Clinton name any time up to a month before election day (ballots are usually printed and mailed about three weeks before). It’s also possible that Congress could postpone or move election day, but that would be an extreme step.

Digest powered by RSS Digest

Saving...

Saving...