- China's Global Power Tops The US? New Measures Say No!

China’s Global Power Tops The US? New Measures Say No!

Tyler Durden

Sun, 12/13/2020 – 23:30Authored by Hal Brands, op-ed via Bloomberg.com,

GDP and military spending matter, but so do networks of allies and “resilience”…

Ever since the U.S. reached the pinnacle of global power after World War II, Americans have worried it wouldn’t remain there. Waves of “declinism” rolled across the country after Sputnik in the late 1950s, the Vietnam War, the oil shocks of the 1970s, the rise of Japan in the 1980s, and the Iraq War and the global financial crisis of the 2000s.

Now, amid a global pandemic and at the onset of a long struggle with China, the question of American decline has taken on renewed urgency.

The trouble with these debates is that power is as elusive as it is essential: It can be devilishly hard to measure outside of major war. (In war, it’s easy: Who won?) Recently, though, several innovative studies have sharpened our understanding of what power is and how to measure it — studies that are mostly, but not entirely, reassuring for a status-obsessed superpower.

Traditionally, measures of power focused on attributes such as population, energy consumption and production of steel or other indicators of industrial strength. In the information age, these indices tell us relatively little about whether a country can get its way in world affairs.

It is still common, though, to assess power through blunt measures like gross domestic product or military spending. Analysts who argue that Beijing is overtaking the U.S. habitually note that China’s GDP may soon surpass America’s. But GDP is a snapshot of activity rather than a measure of overall wealth. Some countries that spend massively on military power, such as Saudi Arabia, are quite useless in projecting it.

So how can we determine the balance of advantage in a long rivalry? The groundbreaking academic work is giving us better answers.

The first category focuses on refining our grasp of economic and military might. Michael Beckley of the American Enterprise Institute (where I am also a fellow) has developed a model that measures net power rather than gross power by accounting for things such as security costs (“the price a government pays to police and protect its citizens”) and production costs (how much it costs, in material and environmental degradation, to build that coal power plant).

He finds, not surprisingly, that the U.S. fares far better than China, an authoritarian state with vast internal security costs and a prodigiously wasteful approach to stimulating growth. Similarly, it is critical that American per capita GDP dwarfs China’s, because that means the U.S. has more wealth left over, after it feeds its population, to pursue global influence. Other work has better accounted for the way wealth accrues over time, and found that the U.S. will still have far more overall economic power than China even after China’s GDP eclipses America’s.

The second category better captures the reality of “network power.” In a landmark paper published in 2019, Abraham Newman of Georgetown University and Henry Farrell, my colleague at the Johns Hopkins School of Advanced International Studies, argue that the centrality of the dollar to international financial networks — which persists, despite decades of handwringing about its decline — gives the U.S. outsized coercive leverage. Scholars have also affirmed something that policymakers have long understood: America punches far above its own weight in global affairs, because of the network of military, economic and diplomatic partners it leads. China has nothing equivalent.

The third category accounts for less tangible forms of power. For decades, analysts have grasped that soft power — the degree of admiration and emulation a country inspires — matters enormously.

An intriguing study by Ted Hopf of the National University of Singapore, Bentley Allan of Johns Hopkins and Srdjan Vucetic of the University of Ottawa demonstrates that, even though America’s global favorability ratings have plummeted under President Donald Trump, there remains strong global support for democracy and free-market economic policies.

That’s a body blow for an authoritarian, mercantilist China, which, the authors predict, “is unlikely to become the hegemon in the near term.” It also helps explain why European states are systematically turning away from Beijing even amid enormous turbulence in their relations with the U.S.

So does all this imply smooth sailing for the reigning superpower? Not necessarily. The U.S. could deplete its network power by abusing it: Overusing financial sanctions and trade barriers, particularly against allies, could encourage countries to seek ways of opting out of networks America dominates. (The European Union made tentative moves in this direction after the U.S. withdrew from the Iran nuclear deal and threatened sanctions against European companies that did business with Tehran.)

If Washington steps back from leading an open world economy, as it did under Trump, it will lose some of the influence that comes with that role. And if the U.S. damages its democracy at home, as the president is trying desperately to do on his way out of office, that would have vast implications for U.S. soft power abroad.

Finally, there is at least one category of power in which the U.S. is struggling. This would be the concept of “resilience.” A globalized world creates vulnerability to international shocks, whether caused by financial instability, climate change or disease. Resilience is a measure of how well a country can rebound.

The U.S. has demonstrated one extremely powerful form of resilience during the coronavirus pandemic: Its fantastically innovative private sector, in coordination with the federal government, is helping to lead the world out of this nightmare with vaccines developed at, well, “warp speed.”

But the fact that U.S. society is so crippled right now (millions of kids are “attending” school from their living rooms or dining rooms), that per capita deaths are relatively high compared with the toll in many advanced democracies, and that political polarization has prevented Americans from even coming to a common understanding of the threat Covid-19 poses, is more alarming.

According to Bloomberg’s pandemic resilience rankings, the U.S. is only 18th — well behind China — in its response to the pandemic. That’s a flashing red light in an age in which so many transnational threats will test America’s capacity to adapt.

The more we learn about power, the more we realize the U.S. still has great advantages in the contest for global leadership. The longer the pandemic goes on, the more we learn about America’s vulnerabilities, as well.

Override Early AccessOn - Michael Jordan's New Golf Course Uses Drone To Deliver Beer To Golfers

Michael Jordan’s New Golf Course Uses Drone To Deliver Beer To Golfers

Tyler Durden

Sun, 12/13/2020 – 23:00Michael Jordan’s new golf course in Florida is the latest example of robots, drones, and the uncertain future of work for humans.

The course, called The Grove XXIII, has opted to deliver snacks and beer to golfers via a drone.

Traditionally, food and beverages on courses are delivered to golfers on refreshment golf carts, operated with one or two servers.

As shown in the video below, the last-mile delivery, from the clubhouse to the golfer, is conducted by drone.

Here’s video Caroline Wozniacki posted yesterday of the food and drink delivery by drone out at Michael Jordan’s newish golf course, Grove XXIII. (Also the scooters in the background) pic.twitter.com/QEAyUCI0yO

— Brendan Porath (@BrendanPorath) December 7, 2020

https://platform.twitter.com/widgets.js

Drone deliveries on the course will likely be huge cost-savings for the club, increasing margins because golf carts and servers are no longer required – just a drone operator.

As for all those teenagers working courses during the summer break – well, be careful in this decade, technology will not just result in a displacement of their jobs – it will also lead to the displacement of millions of other jobs, in other industries, in the coming years.

Override Early AccessOn - Why Michael Morell Cannot Be CIA Director

Why Michael Morell Cannot Be CIA Director

Tyler Durden

Sun, 12/13/2020 – 22:30Authored by Ray McGovern via ConsortiumNews.com,

As President-elect Joe Biden names his cabinet and other chief advisers, what has escaped wide attention is the fact that none of his hawkish national security advisers — except for his nominee for defense secretary, Gen. Lloyd Austin — has served in the military.

Former CIA Deputy Director Michael Morell, who is reportedly on Biden’s short list for CIA director, shares that non-veteran status, one of the reasons along with other skeletons from Morell’s past that make him singularly unfit to lead the CIA.

During my 27 years at the CIA, I worked under nine CIA directors — three of them (Stan Turner, Bill Colby, and George H.W. Bush) at close remove — and served in all four of the agency’s main directorates.

Having closely followed the past-two-decade corruption of my profession — in particular, what the chair of the Senate Intelligence Committee called the “uncorroborated, contradicted, or even non-existent” intelligence manufactured to “justify” the attack on Iraq, I have on occasion offered suggestions for remediation, particularly during transition periods like this one. (Links to five such efforts in the past appear below.)

Whiz Kids

Decades of unfortunate experience show that over-dependence on bright, but inexperienced “best and brightest” can spell disaster. War gaming and theorizing at Princeton and Johns Hopkins have yielded knights with benightedly naive, politics-drenched decisions that get U.S. troops killed for no good reason.

Michael Morell, acting director of the CIA, Feb. 14, 2013. (DoD Photo By Glenn Fawcett)

Even if Gen. Lloyd Austin is confirmed as secretary of defense, the whippersnappers already appointed by Joe Biden will probably be able to outmaneuver the general and promote half-baked policies and operations bereft of needed military input — not to mention common sense from the likes of Gen. Austin who knows something of war.

The current generation of “whiz kids” — the well-heeled, politically astute chickenhawks Biden has appointed — will always “know better” and — if past is precedent — are likely to pooh pooh what Gen. Austin may advise, assuming he is able to get a word in edgewise.

Moreover, ambitious former generals like David Petraeus — many of them now on the outside of the proverbial revolving door making big bucks in the MICIMATT (Military-Industrial-Congressional-Intelligence-Media-Academia-Think-Tank) complex — will not hesitate to weigh in with their own self-interested support to the chickenhawks, fostering the notion that military threats from notional enemies warrant still more funding for the defense contractors on whose boards so many alumni generals sit.

Who does not remember the braggadocio accompanying the criminal attack on Iraq, the full-throated support of journalists like David Sanger of The New York Times, and the chest-thumping of Bush/Cheney neocons saying “Real men go to Tehran?” (Sanger is still at it, sitting on the “Judith Miller Chair for Journalism”.)

Clearly, one does not have to go as far back as Vietnam for noxious examples of the harm that can be done by these “best and brightest,” albeit inexperienced advisers — whether out of the myth of American exceptionalism, ignorance of post-WWII military history, or pure arrogance.

It may be helpful to recall that Vice President Dick Cheney, the archdeacon of the chickenhawks, acquired five draft deferments during Vietnam. (So did his successor as vice president, the president-elect.)

Cheney, Tenet and Bush (White House photo)

Cheney, of course, was the driving force behind the attack on Iraq. He had appointed himself Bush’s principal intelligence officer (usurping the role of CIA Director George Tenet who made not a murmur of protest) and went first and biggest with the Big Lie on (ephemeral) weapons of mass destruction in Iraq. Here’s Cheney in his kick-off speech to the Veterans of Foreign Wars on Aug. 26, 2002: “Simply stated, there is no doubt that Saddam Hussein now has weapons of mass destruction.”

Simply stated, Tenet dutifully followed White House orders to “fix” the intelligence to support Cheney’s accusations against Iraq. Tenet did so formally in the deceitful National Intelligence Estimate of Oct. 1, 2002 — which earned the sobriquet “The Whore of Babylon.”

It was successfully used to get Congress to enable Bush/Cheney to make war on Iraq, and eventually create havoc in the whole region. In his memoir Tenet gave the laurels to Morell for “coordinating the CIA review” of Secretary of State Colin Powell’s UN speech that let slip the dogs of war. (Details on that below)

Cakewalks and Cubbyholes

Cheney, the quintessential chickenhawk, surrounded himself with advisers of the same bent. One pitiable example was armchair warrior Kenneth Adelman, who had been director of the U.S. Arms Control and Disarmament Agency under President Reagan. In a Washington Post op-ed of Feb. 13, 2002, Adelman wrote: “I believe demolishing Hussein’s military power and liberating Iraq would be a cakewalk.”

Two years later, Adelman wrote an equally pathetic op-ed, insisting that he and his neoconservative friends had been right on everything except Iraq possessing WMD, Iraqi factions cooperating after Saddam Hussein was deposed, and “probably” on close ties between Saddam and al-Qaeda.

As for Cheney himself, he did memorize some weapons nomenclature vocabulary, but could not avoid an occasional faux pas betraying his lack of familiarity with things on the ground. Nine months after the attack on Iraq, when WMD were still nowhere to be found, NPR asked Cheney whether he had given up on finding them.

“No, we haven’t,” he said. “It’s going to take some additional, considerable period of time in order to look in all the cubbyholes and ammo dumps and all the places in Iraq where you’d expect to find something like that.” (The continued, quixotic search cost not only a billion dollars but the lives of U.S. troops.).

The amateur but opinionated Cheney was the largest fly in the intelligence ointment. Four months into the war it got so blatantly bad that we Veteran Intelligence Professionals for Sanity (VIPS) sent a Memorandum to President Bush entitled “Intelligence Unglued”, recommending that he “ask for Cheney’s immediate resignation.”

Naiveté on War

In a recent, disturbingly graphic article entitled “Biden’s young Hawk: The Case Against Jake Sullivan,” retired Army Maj. Danny Sjursen broadly hinted that President Biden’s national security adviser should at least look at the photos. (An editor’s note in the piece explained that such photos are almost totally absent from Establishment media: “Graphic images of war and suffering are included with this text. We believe it is important for the world to witness what their taxes, votes and apathy may be supporting.” )

Jake Sullivan, seated farthest back, as national security advisor to vice president, in a meeting with President Barack Obama and advisers, Aug. 29, 2013. (White House, Pete Souza)

In his article Sjursen finds himself wondering “whether Sullivan’s ever seen a dead child, gazed upon the detritus of American empire, waded through the sights and smells of our indecency. And, worse still, I wondered whether it’d matter much if he had. …”

The national security adviser is gatekeeper to the president, with the gate strong or weak depending — at least in concept — on what the president wants. In the normal course of business, the CIA director and the director of national intelligence would go through the security adviser to get to the president. Cabinet secretaries in the national security arena and, when appropriate, FBI directors often use the same channel.

What seems important here, though widely overlooked, is that no Biden national security appointee/nominee except Gen. Austin has apparently served a day in the military. Not Sullivan, not DNI nominee Avril Haines, not secretary of state nominee Antony Blinken, and not FBI Director Christopher Wray.

This is just one factor that should disqualify Morell for director of Central Intelligence (DCI). There are already far too many fledgling warhawks-without war experience. In Morell’s case, though, there are many other factors — some even more important — that disqualify him. His playing fast and loose regarding the legality and effectiveness of torture has been in the headlines recently, thanks to Senate Intelligence Committee member Ron Wyden (D-OR), who called Morell a “torture apologist.”

It has been a challenge to record Morell’s many artful dodges, but Consortium News did publish “On Iraq/Torture, Still in Denial”, as Morell began to peddle his memoir in May 2015.

Two of Morell’s tours de force with Charlie Rose in 2016, in which Morell advocates killing Russians and Iranians in Syria, were covered by CN.

More revealing still — and damning of his chances for another try at CIA — is an article, “Rise of Another CIA Yes Man.” That piece was written when Morell was picked to be Gen. David Petraeus’s deputy at CIA; it ends with personal comments by intelligence professionals who knew Morell well.

The article also includes citations from Tenet’s own memoir, including encomia he threw in Morell’s direction, one of which should actually be enough to bar Morell from any future role in intelligence.

Tenet to the left of Powell at the United Nations on Feb. 5. 2003. (Wikimedia Commons)

In Tenet’s book, At the Center of the Storm, he writes that Morell “coordinated the CIA review” of the intelligence used by Secretary of State Colin Powell in his infamous Feb. 5, 2003 speech to the UN Security Council on the threat from (non-existent) WMD in Iraq.

Tenet, who sat directly behind Powell on that day, pointed out that Morell had served as regular briefer to President George W. Bush. It has been reported that, of the CIA’s finished intelligence product on Iraq, it was The President’s Daily Brief delivered by Morell that most exaggerated the danger from Iraq.

Morell fluttered quickly up CIA ranks as the yes-sir protege of two CIA directors who were, arguably, the worst of them all — “Slam-Dunk” Tenet and the-Russians-hacked-so-Trump-won John Brennan. During the presidential campaign of 2016, as Brennan and his accomplices in the National Security State worked behind the scenes to sabotage candidate Donald Trump, Morell dropped any pretense of nonpartisanship — which used to be the hallmark of an intelligence professional.

From retirement (but with eyes on the big prize he coveted in a new Democratic administration), Morell openly backed the Democratic candidate in a highly unusual op-ed in The New York Times on August 5, 2016: “I Ran the C.I.A. Now I’m Endorsing Hillary Clinton.”

Iraq: the Crucible

In my view, the key gauge in weighing qualifications for a national security position like CIA director is whether a candidate showed good judgment before the misbegotten, calamitous attack on Iraq.

Morell flunks that test outright. Accordingly, he can hardly be expected to be one of the calmer voices in a room of still less experienced fledgling hawks who, to quote Maj. Sjursen, have never “waded through the sights and smells of our indecency” in killing and maiming abroad. With Morell in the room, there would be greater risk of the U.S. getting sucked into still more misadventures overseas.

What did Morell tell Bush about Iraq? In Tenet’s memoir, he describes Morell as “the perfect guy” to brief President Bush, noting that Morell and Bush hit it off “almost immediately”. Morell added later: “I was President Bush’s first intelligence briefer, so I briefed him kind of the entire year of 2001.”

‘The Entire Year 2001’

So, was Iraqi President Saddam Hussein trying to acquire “weapons of mass destruction” during 2001? The first (and honest) answer was ”No” — if Powell and National Security Adviser Condoleezza Rice are to be believed. Here’s what they said at the time — Powell publicly during a speech in Cairo and Rice to CNN five months later.

Powell on Feb. 24, 2001:

“He [Saddam Hussein] has not developed any significant capability with respect to weapons of mass destruction. He is unable to project conventional power against his neighbors.”

Rice told CNN’s John King on July 29, 2001:

“We are able to keep arms from him [Saddam Hussein]. His military forces have not been rebuilt.”

Is this what Morell told Bush just six weeks before 9/11? Did Morell ever explain how Iraq could have developed, purchased, or stolen copious WMD in one year’s time?

Rice. (Wikipedia)

And when Morell briefed Bush right after 9/11, was the president fixated on Saddam Hussein, as counterterrorism chief Richard Clarke describes him in his book Against All Enemies? According to Clarke, on 9/12 Bush told him “to go back over everything, everything. See if Saddam did this. See if he’s linked in any way.”

Clarke says he was incredulous, replying, “But, Mr. President, al-Qaeda did this.” In later interviews Clarke added that he felt he was being intimidated to find a link between the attacks and Iraq.

Did Morell play it straight and tell Bush (as Clarke did) that Iraq had nothing to do with al-Qaeda or the attacks of 9/11? Did Clarke share that vignette at the time with Tenet and Morell?

And what about those notional Weapons of Mass Destruction in Iraq? After 9/11, did Morell take his cue from Cheney, Defense Secretary Donald Rumsfeld, and Tenet and give President Bush the impression that Iraq already had all manner of WMD and was on the threshold of acquiring a nuclear weapon?

Sham Dunk

Later, in December 2002 when Morell’s boss Tenet assured Bush and Cheney that CIA could prove, slam-dunkedly, the existence of WMD in Iraq, did Morell ever ask himself how both Powell and Rice could have been so far off base the year before?

Far more likely, Morell knew what the game was, as he watched Rice do a fancy pirouette, telling CNN’s Wolf Blitzer on Sept. 8, 2002 that “Saddam Hussein is actively pursuing a nuclear weapon. We do know that there have been shipments into Iraq of aluminum tubes that really are only suited to nuclear weapons programs.”

The most accomplished engineers and technical intelligence analysts in the intelligence community knew that the aluminum tubes story was BS. In the finest tradition of intelligence analysis, they remained impervious to the political winds. They insisted that associating those aluminum tubes with nuclear weapons development was wrong and they could not be persuaded to go along. And yet that bogus information got into Powell’s February 2003 speech at the UN.

In Morell’s memoir he wrote that he wanted to apologize to Powell. Morell says, “We said he [Saddam Hussein] has chemical weapons, he has a biological weapons production capability, and he’s restarting his nuclear weapons program. We were wrong on all three of those.”

But not my fault, wrote Morell, who tried to shift the blame by claiming he was not a senior official at the time.

How does that square with Tenet writing that Morell “coordinated the CIA review” of Powell’s speech? Whom to believe? However begrudging must be any trust given “slam-dunk” and “we-do-not-torture”Tenet, he presumably would have less reason to dissimulate than Morell in this particular case.

Assuming Morell did “coordinate the CIA review” of Powell’s speech, did Morell know about the strong dissent on the infamous aluminum tubes?

More important, did he know that CIA operators had recruited and “turned” Naji Sabri, the Iraqi foreign minister (who Saddam Hussein continued to believe was still working for him) and, with the help of British intelligence, had “turned” the chief of Iraqi intelligence, Habbush, as well.

After the reporting from these two sources on other issues and after their access to secret information was evaluated and judged to be genuine, President Bush was told that Sabri and Habbush both said there were no weapons of mass destruction in Iraq. Sabri’s information was given to the president by Tenet on Sept. 18, 2002; Habbush’s in late Jan. 2003.

Did Tenet not share that with Morell before he coordinated CIA input into Powell’s speech?

Clearly, this first-hand intelligence from proven sources with excellent access did not suit the Cheney/Bush narrative for war on Iraq. The president’s staff told CIA operatives not to forward additional reporting on this issue from these sources, explaining that Bush did not want more information about weapons of mass destruction; rather, it was now about “regime change.”

McGovern questions Clapper at Carnegie Endowment in Washington. (Alli McCracken)

Did Morell know about this when he was “coordinating” input into Powell’s disastrous speech? It is a safe bet that Morell was fully aware of the con job he was “coordinating” — as did other senior intelligence officials.

In his own memoir, former Director of National Intelligence (and, during Iraq, director of imagery analysis), James Clapper takes a share of the blame for the Iraq WMD fiasco. Clapper puts the blame for “the failure” to find the (non-existent) WMD “squarely on the shoulders of the administration members who were pushing a narrative of a rogue WMD program in Iraq and on the intelligence officers, including me, who were so eager to help that we found what wasn’t really there.” (emphasis added) .

Regarding Morell’s “I-confess-they-did-it” apology to Powell, the still-youngish Morell has not stopped lusting for an eventual seat at the table, so he apparently thought it a smart move politically. Typically, Powell did not react — as far as is known. Nor has the conflict-averse Powell summoned the cohones to say clearly what he thinks of how Tenet, Morell, et al. sold him a bill of goods on Iraq.

In the “where-are-they-now?” department, Tenet quit in July 2004 and fled to Wall Street to be joined the following year by Jami Miscik, who was deputy director for intelligence during the Iraq fiasco. She “lucked into” a nice job at Lehman Brothers before it went bust.

Note to readers: If you know someone advising the Biden team on selecting a director for CIA, please pass this along.

Finally, those interested in suggestions from the experience of previous transition teams, please click on one or two of the links below. The key issues tend to remain the same. Above all, integrity counts.

* * *

Additional Readings

1 — A Compromised Central Intelligence Agency: What Can Be Done?

By Ray McGovern, 2004

Chapter 4 in “Patriotism, Democracy, and Common Sense: Restoring America’s Promise at Home and Abroad”, Rowman & Littlefield, 2004

Ray’s chapter follows chapters by Alan Curtis (editor), Gary Hart, and Jessica Mathews.

Link to Chapter 4 text:

2 — Sham Dunk: Cooking Intelligence for the President?

By Ray McGovern, 2005

Chapter 19 in “Neo-CONNED! Again: Hypocrisy, Lawlessness, and the Rape of Iraq”, Light in the Darkness Publications, 2005?https://drive.google.com/file/d/1vBsKG1CRHTpqKrtOm4_bftQSOWtjF_PE/view?usp=sharing

3 — Try These on Your CIA Briefer, Mr. President-Elect

By Ray McGovern, November 8, 2008

https://www.commondreams.org/views/2008/11/08/try-these-your-cia-briefer-mr-president-elect

4 — What Needs to Be Done in Intelligence (a memo for the Bush-to-Obama transition team)

By Ray McGovern. December 4, 2008

https://drive.google.com/file/d/1mfT70D90UrNxAWhpy_SKtF4NkSmmHxmn/view?usp=sharing

5 — US Intelligence Vets Oppose Brennan’s CIA Plan

By Veteran Intelligence Professionals for Sanity (VIPS), March 9, 2015

https://consortiumnews.com/2015/03/09/us-intel-vets-oppose-brennans-cia-plan/

* * *

Please Contribute to Consortium News During its 2020 Winter Fund Drive

Override Early AccessOn - Aussie Media Claims Massive Leak Of CCP Members "Lifts The Lid" On Global Surveillance State

Aussie Media Claims Massive Leak Of CCP Members “Lifts The Lid” On Global Surveillance State

Tyler Durden

Sun, 12/13/2020 – 22:00Just days after leaked video from China exposed details of China having “people at the top of America’s core inner circle of power and influence,” which was followed by Eric Swalwell’s ‘fang-banger-gate’ debacle, Sky News Australia reports that a major leak containing a register with the details of nearly two million CCP members has occurred – exposing members who are now working all over the world, while also lifting the lid on how the party operates under Xi Jinping..

This report reinforces details exposed in 2018, when a series of leaked internal documents revealed that China’s military reforms are aimed at allowing Beijing to “manage a crisis, contain a conflict, win a war” and overtake the United States in military strength:

“As we open up and expand our national interests beyond borders, we desperately need a comprehensive protection of our own security around the globe,” read the leaked documents, which adds that a strong military is the best way to “escape the obsession that war is unavoidable between an emerging power and a ruling hegemony”.

Which led to recent concerns about China’s increasingly ‘hyrbid’ war efforts around the world.

As ABC reported in September, a Chinese company with links to Beijing’s military and intelligence networks has been amassing a vast database of detailed personal information on thousands of Australians, including prominent and influential figures.

A database of 2.4 million people, including more than 35,000 Australians, has been leaked from the Shenzhen company Zhenhua Data which is believed to be used by China’s intelligence service, the Ministry of State Security.

Zhenhua boasts of having the People’s Liberation Army and the Chinese Communist Party among its main clients.

Information collected includes dates of birth, addresses, marital status, along with photographs, political associations, relatives and social media IDs.

Zhenhua’s chief executive Wang Xuefeng, a former IBM employee, has used Chinese social media app WeChat to endorse waging “hybrid warfare” through manipulation of public opinion and “psychological warfare”.

All of which leads to today’s breaking news from Australia’s Sky News who claim that the leak is a significant security breach likely to embarrass Xi Jinping, noting that the data was extracted from a Shanghai server by Chinese dissidents, whistleblowers, in April 2016, who have been using it for counter-intelligence purposes.

“It was then leaked in mid-September to the newly-formed international bi-partisan group, the Inter-Parliamentary Alliance on China – and that group is made up of 150 legislators around the world.

#IPAC comment on the leaked database of the Chinese Communist Party Shanghai branch member register. pic.twitter.com/ReKT9Ge8Hd

— Inter-Parliamentary Alliance on China (@ipacglobal) December 13, 2020

https://platform.twitter.com/widgets.js

“It was then provided to an international consortium of four media organisations, The Australian, The Sunday Mail in the UK, De Standaard in Belgium and a Swedish editor, to analyse over the past two months, and that’s what we’ve done”.

TimesNowNews.com reports that the data analysis also revealed that:

…more than 600 party members were working at 19 branches of British banks like HSBC and Standard Chartered in 2016.

Similarly, pharmaceutical giants Pfizer and AstraZeneca, currently involved in the development of coronavirus vaccines, had employed 123 CCP loyalists.

Defence firms like Airbus, Boeing and Rolls-Royce also employed hundreds of party members.

Sky News added that it, “is worth noting that there’s no suggestion that these members have committed espionage – but the concern is over whether Australia or these companies knew of the CCP members and if so have any steps been taken to protect their data and people”.

But, as ABC reported in September, a Five Eyes intelligence officer, who uses the pseudonym Aeneas, has pored over the data, and described the technique as “mosaic intelligence gathering” – sourcing vast tracts of information from a wide variety of sources.

“The individual pieces of intelligence are like tiles in a mosaic, which make sense when they are arranged the right way,” Aeneas said.

He argued it was a different way to collect information than how many western agencies went about their work.

The narrative does confirm recent comments by US Secretary of State Mike Pompeo, who slammed China for stealing research and intellectual property, calling China’s Communist Party the “central threat of our time.”

Still, the blaring headlines from Australian media do, however, smack a little of McCarthyism amid increasing tensions with the Chinese (wine tariffs, for example) as the nation’s largest trading partner rattles it hybrid sabre over disagreeable comments from Aussie politicians/media about the pandemic’s spread. Among the 2.4 million ‘CCP members’ in the leaked database, we simply have no idea how many are ‘bad actors’ and how many are merely little-red-book-carrying Chinese citizens, living and working abroad.

Override Early AccessOn - "A Final Middle Finger From Trump" – Dems Furious About White House COVID Vaccine Access: Live Updates

“A Final Middle Finger From Trump” – Dems Furious About White House COVID Vaccine Access: Live Updates

Tyler Durden

Sun, 12/13/2020 – 21:33Summary:

- White House gets priority vaccine access

- NY cases top 10K for 5th day

- US cases decline slightly from record; 7-day still at record highs

- NJ Gov: winter “going to be hell”

- Germany enters 3-week hard lockdown

- Portugal sees another record

- Half of Brazilians wouldn’t take vaccine

- Malaysia announced 1.3K new case

* * *

Update (0900ET): News broke a few hours ago that White House staff, starting with senior staffers who are the closest to the president, will be included in the first wave of essential workers who receive priority access to vaccines.

Though it’s not clear how many doses are being allocated to the White House, the NYT says that given the number of staffers who have already tested positive, it’s likely the number could be minimal, and it’s likely Trump won’t be receiving the vaccine since he’s already repeatedly claimed to be “immune” (claims that, we should point out, have been backed up by “the science”, but are still treated with skepticism by the NYT).

Senior staffers will in theory have priority, though, as we said, many have already been infected and likely have enough naturally occurring antibodies (for at least a little while longer, from what we know from various studies).

Unsurprisingly, top Dems lept on Trump right away, with Tim Hogan, a Democratic consultant and a former top aide on Senator Amy Klobuchar’s presidential bid, said Washington “will not come close to covering every health care worker with its first allotment of the vaccine, but a White House that downplayed the virus and held a half-year nationwide super spreader tour gets to cut the line, ” calling the WH vaccinations “a final middle finger to the nurses and doctors on the front lines from the Trump administration.”

So, will Joe Biden, who has already committed to taking the vaccine on video in the coming days/weeks, now commit to barring his staff from priority access?

* * *

Following Friday’s latest record daily tally in the US, the number of new cases pulled back a bit on Saturday (though the 7-day average remained at a record high), while the number of total hospitalizations continued its ascent to new records. According to the COVID Tracking Project, nationwide hospitalizations climbed to a new record: 108,487, with some projecting that number to more than double before the spring arrives, and with it, more of the temperate weather that can help slow the spread of viruses like SARS-CoV-2 and the flu (readers may remember a few months back, Goldman Sachs analysts ran a detailed analysis of temperatures vs. COVID-19 infection data) .

Deaths were just below 2.5K, remaining above the 2K threshold for the 5th straight day (every day since Dec. 8).

California reported another daily record, as we noted last night. New York has now joined the states with more than 10K new cases for the 4th straight day.

In other news, New Jersey Gov. Phil Murphy offered up his optimistic outlook on the COVID-19 vaccine on Sunday, while still cautioning that the next few weeks are “going to be hell” during an appearance on ABC’s “This Week”.

New Jersey Gov. Phil Murphy says despite “good news” on a COVID-19 vaccine, “the next number of weeks are going to be hell, I fear, so we’re begging with people to please, please, please don’t let your guard down even when you’re in private settings.” https://t.co/8pO0laHwTB pic.twitter.com/mLMnT29Vg0

— This Week (@ThisWeekABC) December 13, 2020

https://platform.twitter.com/widgets.js

Murphy also noted that Moderna is up for its EUA this week, and that “God willing, they get it,” as if the outcome wasn’t already virtually preordained. Or that seems to be the perception, anyway.

With the first trucks loaded with vaccines trundling on to their destinations Sunday, Moncef Slaoui (the head of “Operation Warp Speed” is at it again with the increasingly sunny projections, claiming as many as 8 in 10 Americans could be vaccinated by June during an appearance on “Fox News Sunday” (public opinion polls suggest only 50% of the population plans to get a vaccine immediately once they become available). In Europe, the first COVID vaccines will probably be approved in the coming weeks, official said.

Here’s some more COVID news from overnight and Sunday morning:

- Portugal on Sunday reported 98 deaths, more than the previous daily record of 95 announced on Friday, and taking the total number of fatalities to 5,559 (Source: Bloomberg).

- Half of Brazilians wouldn’t take the Covid-19 vaccine being developed by China’s Sinovac Biotech Ltd. with Instituto Butantan in Sao Paulo, a Datafolha poll shows (Source: Bloomberg).

- Malaysia announced 1,229 new coronavirus cases on Sunday, bringing the total number of infections in the Southeast Asian country to 83,475, according to a health ministry statement. Four deaths were recorded, pushing up the death toll to 415 (Source: Bloomberg).

- Israel will likely begin to make Covid-19 vaccines available to the population ahead of schedule (Source: Bloomberg).

* * *

Finally, the biggest news out of Europe so far on Sunday is Chancellor Angela Merkel’s decision to plunge the country back into a full-fledged lockdown, despite growing opposition to another economy wrecking shutdown. Even schools will close, something that European nations have largely tried to avoid.

Germany cancels Christmas: Angela Merkel plunges country into new national lockdown over the festive season in desperate bid to drive down Covid infection rate

— The Gammon Dave to friends (@TheGammon3) December 13, 2020

https://platform.twitter.com/widgets.js

For now, at least, the lockdown will be short-lived, Under new measures which will last from Dec. 16 until Jan. 10, schools and non-essential shops across the country will be closed, including during the Christmas holiday. Hairdressers, beauty salons and tattoo parlours will also close while drinking alcohol in public will be banned until Jan. 10.

Override Early AccessOn - "Reformed" Criminal Hired To Curb Violence In DC Charged With Murder

“Reformed” Criminal Hired To Curb Violence In DC Charged With Murder

Tyler Durden

Sun, 12/13/2020 – 21:30Via Judicial Watch (emphasis ours)

In a curious twist, a “reformed” criminal hired by the District of Columbia’s chief legal officer to help curb violence has been arrested and charged with murder. The case involves a taxpayer-funded public safety program known as Cure the Streets launched by D.C. Attorney General Karl Racine to reduce gun violence by treating it as a disease that can be interrupted and stopped from spreading. Cure the Streets typically hires men and women with criminal histories as violence interrupters because they know first-hand about the challenges that residents of crime-infested communities live with. Racine, who was reelected to a second term in 2018, says the transformed criminals hired by his program perform community-driven public safety work that can avoid using police.

Here is how they carry out the task, according to Racine’s office: By interrupting potentially violent conflicts because they have relationships and influence within targeted neighborhoods. Violence interrupters “engage with the community to learn about brewing conflicts and resolve them peaceably before they erupt in violence,” the program’s website states. Violence interrupters also identify and treat individuals at high risk for involvement with violence by meeting with them and implementing individualized risk reduction plans. “They also help connect participants with needed services, such as housing, counseling and employment assistance, and develop action plans for a positive future.” Finally, the D.C. Attorney General claims violence interrupters mobilize communities to change norms by engaging residents, local businesses, community leaders and faith leaders to work with high-risk individuals to reduce violence. “CTS works with these partners to organize forums and public events where residents can gather and interact safely without fear of conflict and violence,” the D.C. government website claims. It is not clear what impact Cure the Streets is having on violent crime in the District, but the Metropolitan Police Department reports that homicides are up 20% from last year.

The program operates in notoriously high-crime sections throughout D.C., which are broken down by wards. They include Eckington/Truxton and Trinidad in Ward 5, Marshall Heights/Benning Heights in Ward 7 and Bellevue, Washington Highlands, and Congress Heights in Ward 8. The Cure the Streets employee recently charged with murder was a supervisor who led a team of six violence interrupters and outreach workers. His name is Cotey Wynn, an ex-con with an extensive rap sheet who served a decade in prison before D.C.’s chief legal officer hired him. Wynn’s record includes felony murder, first degree murder, possession with intent to distribute crack cocaine, and distribution of a controlled substance, according to the Metropolitan Police Department. On December 4, the agency’s Capital Area Fugitive Task Force arrested the 39-year-old Wynn and charged him with second degree murder while armed. At the time of his arrest Wynn was under the supervision of the Pretrial Services Agency for the District of Columbia, a federal agency that believes preventative detention should only be a last resort for defendants, who should live in the least restrictive conditions while awaiting court.

Police say Wynn fatally shot a 53-year-old man named Eric Linnair Wright in 2017 near the Trinidad neighborhood in Northeast Washington. The violence interrupter was identified by multiple witnesses after viewing security camera footage from nearby homes, according to police. Authorities also tracked Wynn’s cell phone to the location of the crime. In a statement issued to local media, Racine’s spokesperson said this: “The Office of the Attorney General is aware of Mr. Wynn’s arrest for a homicide he is alleged to have committed in 2017, prior to his employment with Cure the Streets. This case will now proceed through our criminal justice system where Mr. Wynn is presumed innocent. We are confident that justice will be served once this process is complete. Our hearts go out to the family of Mr. Wright, the victim in this case, and to the affected members of the community. The important work of the Cure the Streets team will continue.”

It was not that long ago that the same office, charged with enforcing D.C. laws and protecting the interest of its citizens, bragged about what a great guy Wynn is. In a profile posted on the Attorney General’s website over the summer, Wynn was portrayed as somewhat of a saint. “When observing Cotey at work, you see a respected professional, a loving father, a devoted friend, and a pillar of the community,” according to the piece which includes a photo of the accused murderer delivering resources to D.C. residents during COIVD-19. The story also reveals that Wynn could not find a job after a decade in prison since “the damage to his reputation made it hard for him to find employment” so D.C. government hired him as a violence interrupter for Cure the Streets.

Override Early AccessOn - China Tells Cabin Crews To Wear Diapers And Avoid Using Bathrooms On Risky Covid Flights

China Tells Cabin Crews To Wear Diapers And Avoid Using Bathrooms On Risky Covid Flights

Tyler Durden

Sun, 12/13/2020 – 21:00In one of the most absurd post-covid developments, last week China’s aviation regulator recommended that cabin crew on charter flights to high-risk Covid-19 destinations – such as the US – reduce the risk of infection by using the bathroom. Their solution: use disposable diapers. The advice, first reported by Bloomberg, was published in a 38-page list of guidelines for airlines to prevent the spread of coronavirus.

The Civil Aviation Administration of China said the recommendation applies for charter flights to and from countries and regions where infections exceed 500 in every one million people. According to the latest data, that would include most countries, and certainly the US where the official number is some 4,400 cases per 1 million people on a rolling 7 day basis.

In addition to wearing diapers, the regulator suggests cabin crew use such personal protective equipment including:

- Medical protective masks

- Double-layer disposable medical rubber gloves

- Goggles

- Disposable caps

- Disposable protective clothing

- Disposable shoe covers

So far there is no mandatory requirement for cabin crew to wear full hazmat suits, although we assume as the global panic rages unabated, this is coming too. The regulator also said that flight crew should wear masks and goggles, but they don’t need diapers.

Other advice for the flights includes dividing the cabin into “clean area, buffer zone, passenger sitting area and quarantine area,” separated by disposable curtains. The last three rows should be designated as an emergency quarantine area, said CAAC. CAAC declined to disclose any more details on the guidelines.

While China’s aviation market was hit hard at the onset of the outbreak in Wuhan, it has since recovered to close to pre-pandemic levels as China’s cases remain laughably low, even as the diseases reportedly rages unabated in other regions such as Europe and the U.S. struggle to bring Covid-19 under control.

Override Early AccessOn - The Renminbi Will Gain Wider Use Globally, Gavekal's CEO Says

The Renminbi Will Gain Wider Use Globally, Gavekal’s CEO Says

Tyler Durden

Sun, 12/13/2020 – 20:35Authored by Resham Kapadia via Barrons.com,

Louis-Vincent Gave, CEO of Gavekal, is a go-to source for institutional investors trying to interpret global macro risks such as the financial implications of China’s rise. Gave, 46, was born in Paris, educated at Duke University, and based in Hong Kong before the pandemic. Gavekal provides independent research and manages $1.7 billion in Asian fixed-income and equities strategies, primarily for European institutions.

Barron’s: What investment trends will be most prominent after the pandemic?

Louis-Vincent Gave: If I ask what the most important development was in 2001, most people would say it was 9/11. With the benefit of hindsight, it was China joining the World Trade Organization, which changed the world for the following 20 years. If I ask about 2007, you’d say it was the start of the subprime crisis. With the benefit of hindsight, it was the launch of the smartphone.

With hindsight, what will people say about 2020?

So far, the Covid response in the U.S. has been a $12,800 increase in debt per capita; in the United Kingdom, it’s $7,000, and in Germany and France, $5,300. In China, it’s $1,200. The Western world responded with massive increases in budget deficits, which could constrain future policy options, while Asia, especially China, hasn’t.

Western policy makers have no choice but to embrace yield-curve controls; they can’t let interest rates go back up. You had Japan and Europe in the yield-curve control gang. The big change now is that the U.S. has joined them. Once the European Central Bank went down this [path], the euro tanked. Once we are on the other side of Covid-19 and it becomes clear the U.S. has no other choice, the dollar will collapse.

What will be the best investment opportunity post-Covid?

Investing in Asian fixed-income markets, in local currencies. Governments there have broadly been more efficient at dealing with Covid-19. Central-bank balance sheets and government spending haven’t grown out of control. Just as water flows downhill, capital is attracted to positive real [inflation adjusted] rates. Today, these are mostly found in Asia.

What is the most pressing public policy issue the U.S. will face?

How to fund runaway debt. For now, everyone’s answer is through modern monetary theory [which posits that governments that control their own currency can spend freely]. Once the debt is monetized by the central bank, there are no historical examples, outside of Japan, where that doesn’t lead to massive and very fast inflation, massive currency debasement, or both.

What does that mean for the dollar’s reserve-currency status?

I look at currencies like computer operating systems. Most Gavekal clients use Microsoft because everyone else uses it. The dollar is Microsoft. Go back to 2005-06, when Apple was trading at nine times earnings and viewed as making a niche product. In 2007, Apple said it would create a parallel system and went straight to the consumer, who took [Apple] not because it was cheaper but because it was easier.

So the renminbi is Apple.

We are seeing the rollout of Chinese fintech solutions across Southeast Asia, the Middle East, and Africa through WePay and Alipay. Then, tack on the digital renminbi and look forward to a future where an Indonesian businessman goes to Singapore and pays for his taxi with Alipay and the transaction isn’t settled through Swift or the dollar but through digital renminbi. The pushback I get is that no one is going to trust the digital RMB—or, who wants the Chinese government to know how and where you spend your money? That’s a big roadblock, but if you told me 10 years ago people would put Alexa in their homes voluntarily….

Aren’t you worried about China’s debt or social instability?

For the past 10 years, I’ve been told that Chinese debt was about to implode and there would be riots in the street. In the past 10 years, we have seen riots in France and the U.S—and in Hong Kong—but China has been remarkably stable. We have been told that the Chinese government would have no choice but to nationalize big parts of the economy and the renminbi would collapse. That scenario has unfolded in Europe and the U.S. [The U.S.] has increased debt by $4.2 trillion, three-quarters of which was funded by the Fed. Meanwhile, the renminbi has been the strongest currency year to date and over 10 years.

What is a key concern for Asia-based investors?

The decoupling of the U.S. and China is a massive change, and Taiwan is an important fault line. Taiwan wasn’t too much of an issue when the U.S. and China got along and all China produced were cheap plastic toys and bicycles. But this year, the market cap of the global semiconductor industry is above that of the energy sector. Taiwan Semiconductor Manufacturing [ticker: TSM] said it is already manufacturing a generation of chips that Intel [INTC] has said it won’t be able to fabricate until as late as 2023. If you think semiconductors matter more than energy, Taiwan Semi is one of the most important companies in the world.

What are the longer-term ramifications of President Xi’s crackdown in Hong Kong?

The core thesis is that Xi is a transformational president—the first imperialist president since the Ming Dynasty. If you are Xi and you hear your companies won’t have access [to U.S. markets], Hong Kong sounds like a great way to internationalize the renminbi and do a digital renminbi. Most Westerners saw the intervention as the death of Hong Kong, but China guaranteed Hong Kong would be China’s capital markets for the foreseeable future. [Xi] has no choice but to make it a success, which is why the Hong Kong dollar is stuck at the high end of its [trading] band.

Chinese internet stocks have been hit by increased regulatory scrutiny, including the scuttling of the oversubscribed planned public offering of Ant Group. Does this mark a turning point for these companies?

Since the [suspension] of the Ant IPO and new antitrust [guidelines], we also had a state-owned coal company default on one billion renminbi, or $150 million. One big issue for China has been a trade surplus of $60 billion and enormous inflows into China tech and bonds driving the renminbi higher.

In the Western world, we would raise rates [to deal with potential bubbles]. In China, they have regulatory weapons. They managed to cool the tech stocks in China and inflows into Chinese bonds. They got their message through.

You have been living in Vancouver during the pandemic. What is the one place on Earth that you’d most like to visit when the pandemic ends?

I have to get back to my Hong Kong and Beijing offices. I miss my colleagues and my friends there.

Thank you.

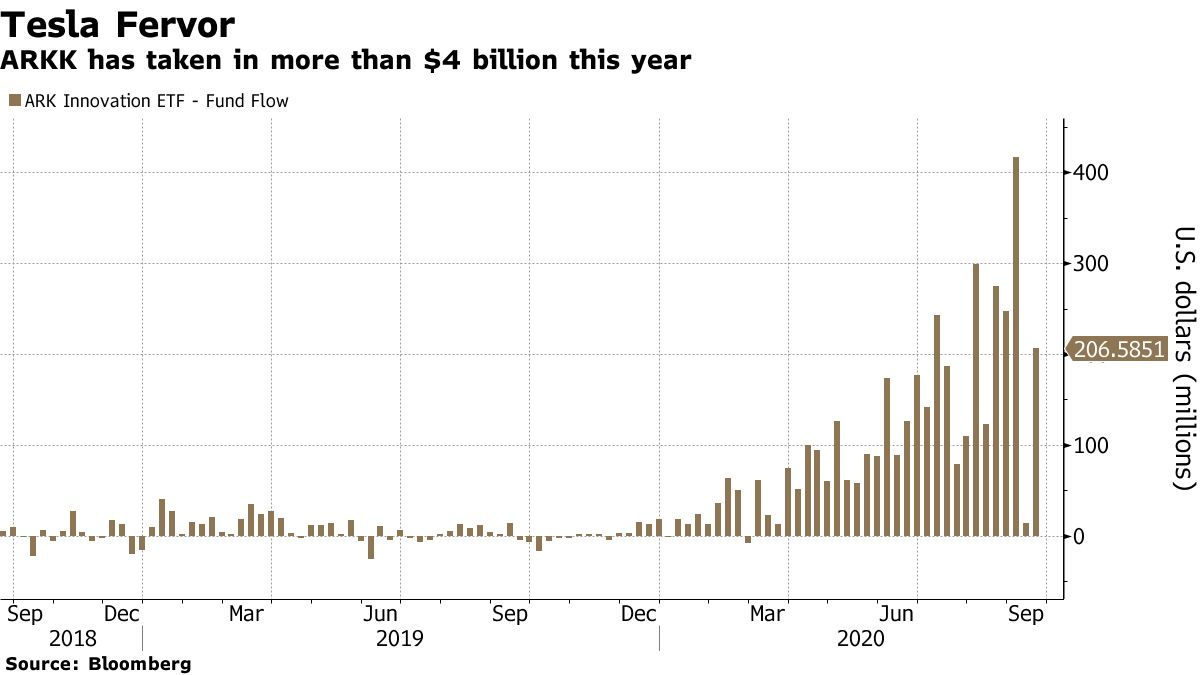

Override Early AccessOn - Cathie Wood's ARKK ETF Passes JP Morgan For Largest Active ETF

Cathie Wood’s ARKK ETF Passes JP Morgan For Largest Active ETF

Tyler Durden

Sun, 12/13/2020 – 20:10No sooner did we just write about ARK Invest’s Cathie Wood involuntarily losing majority control of her own firm than it has been revealed that her firm – known for its massively outsized investments in Tesla (and numerous other tech companies that are vastly overpriced and incapable of generating consistent cash) has now surpassed JP Morgan “for the largest actively managed exchange-traded fund.”

According to Bloomberg, the ARK Innovation ETF (ARKK) saw a record inflow of $275 million on Thursday that helped boost it to just under $16 billion in total assets. This surpasses the $15.2 billion JPMorgan Ultra-Short Income ETF (JPST).

The firm is just one of the financial assets that the everyday working-man doesn’t even know exists, yet was the major beneficiary of a “rising tide” created by the Fed injecting trillions of dollars of liquidity (colloquially known as QE Infinity) that caused a massive boom in tech stocks off their lows in March.

The ARKK ETF, which has a

insanestrategic 10% weighting in Tesla, is up 150% year-to-date. Tesla is up 650% this year, totally not as a result of Softbank and Goldman Sachs options buying schemes and definitely as a result of their super-duper financials, we’re sure.This outperformance comes from the same visionary who, back in November, was delivered notice from Resolute Management Investors that they would be taking control of her firm due to an option in a deal Wood had negotiated back in 2016.

The question for ARK is how long can it defy gravity AND history, which is littered with supernovas like $ARKK a la The CMG Focus Fund, which shot up 900%, got $8b aum, only to drop 50% in ’08, now only $300m (despite bounce back & lifetime perf > SPX). Once bitten twice shy.. pic.twitter.com/7z1SsM5A4K

— Eric Balchunas (@EricBalchunas) December 9, 2020

https://platform.twitter.com/widgets.js

The power shift, which Pensions & Investments notes isn’t especially amicable, came due to a 2016 agreement between Resolute and ARK, where RIM acquired a minority stake in the investment manager – with a call option “to purchase a controlling voting and equity interest in (ARK) that is exercisable in 2021.”

While the financial terms of the deal had not been made available, ARK’s founder, CEO and CIO, Wood, who currently owns 50% to 75% of the firm, didn’t seem happy with RIM’s decision.

Wood said in a statement: “On behalf of the employee-owners of ARK, we are disappointed that Resolute Investment Managers and its private equity owner, Kelso & Co., have chosen to issue this unwelcome notice that they intend to seize control of our business.”

“As reported by Morningstar, ARK has delivered top one-percentile returns for multiple products over one-, three- and five-year periods. Thanks to our research and investing success, paired with our innovative digital marketing strategies, ARK now ranks among the largest ETF issuers in the U.S.,” Wood continued.

She concluded: “The remarkable success of our team is rooted firmly in a culture of transparency, collaboration, and employee ownership. We do not believe that equity ownership by a party tangential to our business is in the best interest of ARK’s stakeholders.”

As we said last month: “Regardless, the deal may actually be a blessing in disguise for Wood, who is likely going to receive a large payday and gets a chance to potentially exit on top – with the added bonus of a scapegoat to blame any future implosion by the firm on.”

And hey, we were going to congratulate Cathie on passing J.P. Morgan, but we guess what we meant to say was, “Congratulations, Resolute Investment Managers!”

Override Early AccessOn - After Trump, The Flood…

After Trump, The Flood…

Tyler Durden

Sun, 12/13/2020 – 19:45Authored by Ghassan and Intibah Kadi for the Saker Blog,

Whether there was indeed voter fraud and rigging, and I personally believe there was and at a huge scale, it seems that, by hook or by crook, Joe Biden will become the next President of the United States of America; and we should prepare ourselves for this, regardless of our political points of view and inclinations.

The presence of Biden in the Whitehouse will definitely change course on a number of issues, both domestically within the USA and overseas, but the objective of this article is to shed a bit of light on what is likely to happen to the current pro-Biden camp and the diverse array of supporters who have helped elevate him to this position.

In more ways than one, I have always seen in Syria a microcosm of world politics and conflicts. Long before the enemies of Syria decided to launch their attack in March 2011, the masterminds of the conspiracy put the most unlikely allies together, only united by their hatred of Syria. Back then I called them the ‘Anti-Syrian Cocktail’. Those allies each had their own agenda regarding Syria and had nothing in common other than their desire to remove President Bashar Al-Assad from office. Among the issues they disagreed on was his replacement, how to share the spoils, not to mention the alternative political system to install, Syria’s future position in the region, international alliances, and so forth.

With a whole array of enemies, Trump inadvertently caused a rounding up of a very loosely-united anti-Trump-cocktail; only united by their hatred of him. So, let’s face it and acknowledge it; they will never let him win the November 2020 elections. Though only united by their hatred of Trump, there are too many of them, they are powerful; extremely powerful, and they are very determined to get rid of him by any means possible, legal, illegal, using tactics like bribery, intimidation, threats, thuggery, and they have no one to fear because, collectively they have given each other impunity, covering each other’s backs and producing a culture where criticizing them is taboo. Crucially, the ‘law’ and the media are on their side.

With the exception of the Clintons and Bidens perhaps, the other Democrats have their traditional political opposition to Trump, even when they see and know he is making good decisions. This is the golden rule of political duopoly. But the Clintons and the Bidens have personal dirt on them and even blood on their hands that they want to keep the lid on in order to avoid prosecution and possibly even jail. They are likely to remain united after a Trump loss, but the same cannot be said about other odd couples.

Most of the other November 2020 Biden supporters are destined to be on a collision course, and they will soon enough realize that their differences are much stronger than what united them and that they were taken for fools. None will be disappointed more than the so-called ‘Progressives’.

The definition of the term progressive has morphed quite significantly over the last decade or so. Currently, it seems to include any one who stands up against Trump; and this is the primordial cause of the confusion and reason for future conflict between them. In reality, what defines the term ‘progressive’ in any existing progressive movement can be totally different from that of another movement; and the difference is not necessarily marginal. Being ‘progressive’ in the 21st Century implies the presence of a very specific agenda or slogan that may or may not be compatible with other ‘progressive’ agendas.

Take the Assange supporters for example. The moment they wake up from their deep slumber, they will realize that the man they supported to become President is actually the leader of the political party that has put Assange in jail for exposing his party’s dirt. I hope that Trump pulls the rug from underneath their feet and pardons Assange before the 20th of January 2021. But will this show the Assange supporters who is who? Not necessarily because if they wanted to open up their eyes and see, they would have seen from day one that Assange’s biggest enemy is none but Hillary Clinton and that she is the one responsible for his demise; not Trump.

But the Assange supporters did not play a major role in the elections; at least not directly, and at least not as much as their closest ‘progressives’; the peace activists.

The Democrats and their cohorts have portrayed Trump as a warmonger. When peace activists eventually see that Biden will have to serve his warlord masters and start new wars across the globe, they will have to think again. He is already touting hiring well known hawks in key positions in his forthcoming cabinet and team of advisors, with his Defense Secretary reportedly selected.

When it comes to street power however, none has been more powerful and effective as the combination of BLM and the environmentalists.

BLM activists have just fallen a tad short of blaming Trump for an American five-century long history of racism. But how much do BLM activists really care about Climate Change and specifically about Greta-type environmental vision of how the world should run? Moreover, most environmentalists, if not all of them, are anti-vaxxers. When they see that Biden is the trump card for the vaccine empire, they may wish they didn’t take to the streets to unseat the Trump card they had in the Whitehouse. If there is/was one person standing up against the malevolent “Gates vaccine”, it has to be Trump, and the single-issue anti-vaxxers are against Trump. Try to make sense of this.

This is not to forget and ignore that the Climate Change activists will soon find out, the hard way, that Biden will not come clean on the zero-emission promise; not only because he doesn’t want to, not only because he goes to bed with the petro-dollar lobby, but also because he does not have the alternative technology to replace fossil fuel with.

In and out and in between the BLM and Climate Change activists, what do the Climate Change activists have in common ideologically with BLM and at what stage will they break ranks and decide to go against one another? What will happen after either one of them accuses the other, rightfully I must say, that they have been used as pawns by the ‘Deep State’?

And who said that the BLM has more in common with the LBGTI community and activists than it does with the gun lobby? Sections of the BLM likely also love guns.

And speaking of Greta, for how much longer will she able to keep up the fallacy that her agenda and those of her friends Soros and the World Economic Forum (WEF), and its members that include Monsanto, are actually compatible?

And for the right or wrong reasons, who is to guarantee that the tens of millions of Trump supporters are going to sit and accept that the election win of Biden is legitimate and that they have to swallow it? Will this cause social strife, violence on the streets, even worse perhaps civil war and much more? We don’t know. What we do know is that a controversy about election results should have been dealt with in total transparency in order to put all concerns to rest. But this is not happening, and it is not going to happen because a decision has been made against Trump dictating that he must lose.

But the after-Trump-effect is not necessarily going to affect only America. Right-wing politics, including the extreme version of it, have been on the rise in the world, and especially in Western Europe. And if the Neo-Nazis look threatening because their ideology is based on a very dark chapter in human history, what do we really know is on the agenda of the forces that have combined the very diverse elements of the anti-Trump cocktail in order to serve its objective(s)? What is it really that they want?

Hitler was at least clear about his mission statement. He wanted an Aryan Third Reich to rule the world for a thousand years. The rest of the world did not have to wonder and ponder about his intentions. He sent a very clear message to rest of the world, a message clear enough to unite the West with the Bolsheviks against him.

But today, we have an invisible driving force that has managed to put together an array of the most unlikely partners in order to fight a common cause. Do we not at least ask the question ‘why?’

In the case of Syria, the answer to the ‘why’ question was to topple Assad, albeit without having a plan that went further, at least as a united coalition. It would have been impossible for the plotters and planners to each disclose what they had in mind. In reality, they did not have any plan at all other than replacing him with a void. Fast-forward; the get-rid-of-Trump plan is very similar; get rid of him without having a plan so as to ensure all participants are pleased and appeased, because the plan seems to also be based on replacing Trump with chaos and anarchy.

The irony here is that the anti-Trump-cocktail is not only comprised of his political opponents, mainstream media, social media, but also includes government agencies such as the DOJ, the CIA, the FBI and even some American Republicans.

Briefly put, Trump has been chosen to lose, but after him, the flood is imminent. The current allies who lobbied against him will very shortly come to the realization that they are no longer united, and some will even turn into enemies fighting over the spoils of the win.

In more ways than one, they will harvest the fruit of the seeds they planted, and they will rightfully deserve all consequences. A Biden win is the most befitting ‘punishment’ of the anti-Trump cocktail.

Apart from the hapless American populace, the biggest loser of this all is the international stature of America as the leader of the so-called Democratic Free World. In a fitting blowback for these pernicious actors, Trump would have proven without a shadow of doubt, that the Deep State is so deep and powerful, powerful enough to mobilize its own enemies to serve it.

At that point, to quote the rhetoric of the “Great Reset” agenda, but again, as blowback, things will never be the same again for these dangerous characters.

Override Early AccessOn - Bravery Is…

Bravery Is…

Tyler Durden

Sun, 12/13/2020 – 19:20Having trouble interpreting what’s really going on in the world? JP Sears and his fellow ‘thinkers’ explain what the media would like you to think…

Of course you can always trust the media to lead the way to the promised land of truth.

Override Early AccessOn - Cornell Offers "Person Of Color"-Exemption For Flu Vaccine Requirement

Cornell Offers “Person Of Color”-Exemption For Flu Vaccine Requirement

Tyler Durden

Sun, 12/13/2020 – 18:55Authored by Benjamin Zeisloft via Campus Reform,

Students at Cornell University can use their status as a “person of color” to be exempt from the university’s flu vaccine requirement.

“Students who identify as Black, Indigenous, or as a Person of Color (BIPOC) may have personal concerns about fulfilling the Compact requirements based on historical injustices and current events,” explains Cornell Health’s vaccine requirement FAQ.

Students can send a private message to Cornell Health in order to request a non-medical or non-religious exemption for the immunization.

For more information, the FAQ links to a page “especially for students of color,” which is meant to help minority students concerned about the flu vaccine requirement.

“We recognize that, due to longstanding systemic racism and health inequities in this country, individuals from some marginalized communities may have concerns about needing to agree to such requirements,” explains the page. “For example, historically, the bodies of Black, Indigenous, and other People of Color (BIPOC) have been mistreated, and used by people in power, sometimes for profit or medical gain.”

The university, therefore, considers it “understandable that the current Compact requirements may feel suspect or even exploitative to some BIPOC members of the Cornell community.”

Nevertheless, Cornell strongly encourages minority students to receive immunizations.

“Away from campus community, BIPOC individuals are not as likely to have access to preventive services or quality health care,” continues the page.

“The systems, services, and policies being implemented at Cornell seek to address these inequalities as well as the differential impacts.”

One Cornell undergraduate, who spoke to Campus Reform on the condition of anonymity, said that “all students deserve equal treatment regarding what healthcare choices they are allowed to make at Cornell.”

Because students of all identities may have personal concerns about taking a mandatory vaccine, “having a policy statement that singles out BIPOC students for requesting an exemption” is unfair for other students.

Campus Reform contacted Cornell University for more information and will update this article accordingly.

Override Early AccessOn - Here Is The Little-Known Provision In The CARES Act That Could Trigger A Year-End "Selling Deluge"

Here Is The Little-Known Provision In The CARES Act That Could Trigger A Year-End “Selling Deluge”

Tyler Durden

Sun, 12/13/2020 – 18:30One week before the end of November, JPMorgan issued a startling warning: according to calculations by the bank’s quant, Nick Panigirtzoglou, some $160 billion in negative equity rebalancing (read selling) was on deck by various pension and balanced mutual funds, and – should the rally continued into December – an additional $150 billion in forced selling could emerge from funds who have to keep their 60/40 stock/bond asset allocation. While many on Wall Street braced for a late November drawdown following this note, expecting a deluge of selling into an extremely illiquid market, with Emini top-of-book depth near the lowest levels on record…

… aside from a modest dip on Nov 30, stocks continued their upward ascent with the S&P hitting an all time high last week, just above 3,700.

That said, it may be too early to give the “all clear”, for two reason: first, it is possible that the rebalancing fund “forced selling” has merely been pushed back to December, and year-end, and if JPM’s calculation that we could be facing over a $100 billion in forced selling in the coming, even more illiquid days is correct, it is unlikely there will be enough buying interest to offset the coming pension rebalancing. The second reason why we may experience market turbulence in the last days of the year, is over a little noticed piece of legislation which according to Larry McDonald’s Bear Traps Report, could open the floodgates to 401K selling, leading to a “selling deluge.”

As McDonald writes, buried deep in the CARES Act (the Corona Aid, Relief and Economic Security Act) which was enacted on March 27, 2020, and provided $2.2 Trillion of fiscal stimulus to offset the impact of the coronavirus on the U.S. economy, “is a clause that gives temporary flexibility on early withdrawals from retirement accounts. These temporary changes to the rules give more leeway to make emergency withdrawals from tax-deferred retirement accounts without incurring a penalty.”

Specifically, Section 2022 of the CARES Act eliminates the 10 percent early withdrawal penalty if you are under the age of 59 ½ and withdraw up to $100,000. It also allows for the spread out of your income tax liability over three years rather than the same year you withdraw the money. And since the window to make these penalty-free early withdrawals closes by the end of 2020, millions of cash-strapped households may have no choice but to sell tens, if not hundreds of billions in passively-managed funds to take advantage of this one-time offer to avoid a 10% early withdrawal charge.

McDonald then goes on to highlight the importance of passive investing which over the past decade has emerged as the dominant price setter in a world where actively managed funds have been fading. As the Bear Traps author writes, “the explosive impact of passive investing is significant. In recent years, passive equity funds have enjoyed inflows of more than $2T, even as traditional, active ones have suffered outflows of over $1.5T, according to data provider EPFR.” Indeed, the main story on Bloomberg this morning picks up on this, writing that “roughly $427 billion has poured into U.S. exchange-traded funds this year, divided almost evenly between equity and fixed-income funds, according to Bloomberg Intelligence data. Meanwhile, mutual funds have bled roughly $469 billion of assets in 2020, on track for the worst year on record in Investment Company Institute data going back to 1990.“

While we have for years covered the staggering divergence between active outflows and passive inflows – which threaten to make conventional stock pickers obsolete and make market prices meaningless – and thus the topic is familiar to regular readers, Bloomberg writes that “this stark divergence in fortunes is part of a tectonic shift that’s seen investors favor ETFs over mutual funds for nine consecutive years, lured by the industry’s ultra-low fees and tax advantages. That trend was accelerated further in 2020, thanks to a well-timed rule from the Securities and Exchange Commission and the Federal Reserve’s first foray into the $5.3 trillion U.S. ETF market. Combined with another rocky performance from active managers, it’s clear why ETFs are winning out, according to State Street Global Advisors.”

In any case, as McDonald summarizes, “there is now over $12T in index funds globally —either passive mutual funds or the increasingly popular ETFs.”

And while the 401(k) provision is intended for those hardest hits by the pandemic, such as people who lost their jobs, the rules are applied rather loosely. For example, a qualified person includes those that “experience adverse financial consequences from being quarantined, being furloughed or laid off or having their work hours reduced.” Also qualified are those who “experienced adverse financial consequences as a result of being unable to work due to lack of childcare [or] closing or reducing hours from a business that you own or operate due to SARS Cov-2 or Covid-19”. Since virtually anyone can argue that they are qualified under these criteria, the language is open to interpretation and the IRS is unlikely to enforce the limits of this provision to the letter of the law according to McDonald, especially since banks and retirement management companies – who have themselves benefited greatly from the CARES act – are giving considerable leeway to allow their customers to use the CARES Act early withdrawal exemption.

McDonald then makes one final point – the same one we noted three weeks ago – namely the lack of market depth or liquidity, to wit:

This potential selling deluge comes as positioning in U.S. equities is becoming stretched and implied volatility for the Georgia runoffs is above average. Year-end rebalancing by pension funds is still expected to create supply in equities as funds rebalance their (now) overweight in equities. Overall, for 2021 we should expect volatility to grind lower as the removal of trade war risk, the declining corona risk with the advent of the vaccines, the removal of the uncertainty of the elections, and rebounding GDP growth with 0% Fed funds rates provide a supportive backdrop for risk assets. Notwithstanding that, we first need to pass the year-end hurdle of retirement withdrawals, pension rebalancing, and Georgia runoffs.

Ultimately, The Bear Trap report’s conclusion is identical to that of Morgan Stanley’s Michael Wilson, who has recently cautioned that a near-term “drawdown” is coming, but that would be followed by a brisk episode of BTFD and new highs in 2021, or as McDonald puts it, while the coming selling deluge “could take an overstretched market by surprise…. we would then use a meaningful pullback to prudently add to the risk.”

Override Early AccessOn - The 'Hannibal Trap' Will Crush Global Wealth

The ‘Hannibal Trap’ Will Crush Global Wealth

Tyler Durden

Sun, 12/13/2020 – 18:05Authored by Egon von Greyerz via GoldSwitzerland.com,

Is the global investment world about to be caught in the Hannibal trap?

Hannibal was considered as one of the greatest military tacticians and generals in history. He was a master of strategy and regularly led his enemies into excruciating defeats.