- China Aims To Be "World's Most Influential Power", US Warns In New Indo-Pacific Strategy

China Aims To Be “World’s Most Influential Power”, US Warns In New Indo-Pacific Strategy

Submitted by Andrew Thornebrooke of Epoch Times

The White House released its long-awaited Indo-Pacific Strategy on Feb. 11, outlining how it plans to deal with the increasing adventurism of the Chinese Communist Party (CCP) and to better secure and improve the region for the international community.

The Royal Australian Navy guided-missile frigate HMAS Parramatta (FFH 154), left, is underway with the U.S. Navy amphibious assault ship USS America (LHA 6), the Ticonderoga-class guided-missile cruiser USS Bunker Hill (CG 52) and the Arleigh-Burke-class guided-missile destroyer USS Barry (DDG 52) In an associated statement, the White House said that interest in the region from partners and allies was converging, and that the realm would play a critical role in the future development of the United States both economically and diplomatically.

“This convergence in commitment to the region, across oceans and across political-party lines, reflects an undeniable reality: the Indo-Pacific is the most dynamic region in the world, and its future affects people everywhere.”

The strategy, as such, focuses on five key concepts: That the Indo-Pacific ought to remain free and open, connected, prosperous, secure, and resilient.

Across these concepts, the strategy outlines various broad actions that the Biden administration intends to take in the region, including a plethora of investments in democratic institutions abroad and efforts to ensure that commons such as the skies and seas are navigated in accordance with international law.

The strategy, as such, focuses on five key concepts: That the Indo-Pacific ought to remain free and open, connected, prosperous, secure, and resilient.

Across these concepts, the strategy outlines various broad actions that the Biden administration intends to take in the region, including a plethora of investments in democratic institutions abroad and efforts to ensure that commons such as the skies and seas are navigated in accordance with international law.

The strategy centers on the United States’ intent and continued ability to leverage its relationships with partners and allies in the region to counter growing adventurism from the CCP.

“The PRC is combining its economic, diplomatic, military, and technological might as it pursues a sphere of influence in the Indo-Pacific and seeks to become the world’s most influential power. The PRC’s coercion and aggression spans the globe, but it is most acute in the Indo-Pacific,” the strategy reads, referring to the country’s official name, the People’s Republic of China.

“Our collective efforts over the next decade will determine whether the PRC succeeds in transforming the rules and norms that have benefitted the Indo-Pacific and the world.”

The statement is important for clearly defining the CCP as the foremost challenge in the region, and stating plainly that the administration considers the competition between the two nations as nothing less than a battle between differing visions for the future of the global order.

“We recognize the limitations in our ability to change China, and therefore seek to shape the strategic environment around China by building a balance of influences that advances the future we seek, while blunting Beijing’s efforts to frustrate U.S. objectives and those of our partners,” a senior administration official said during a Feb. 11 press call.

The official pointed out, however, that the document did not cover the administration’s entire China strategy, however, but presented its vision for further securing the region.

“This is not our China strategy. This—you know, we very clearly identify China as one of the challenges that is—that the region faces and, in particular, the rise of China and China’s much more assertive and aggressive behavior,” the official said.

“But, you know, our China strategy is global in scope. It recognizes the Indo-Pacific as a particularly intense region of competition.”

The strategy further regards the United States’ network of security alliances and partnerships as its “single greatest asymmetric strength,” and says that it will expend significant investments to push the so-called Build Back Better World plan, and its goal of global infrastructure development.

Importantly, the strategy also defines the administration’s approach to Taiwan and the ongoing crisis with the CCP over the island’s continued de facto independence. On this issue, the United States appears set to maintain the same policy of strategic ambiguity that it has held for decades. Under this policy, Washington is deliberately vague on whether it would come to the island’s defense in the event of a Chinese invasion.

“We will also work with partners inside and outside of the region to maintain peace and stability in the Taiwan Strait, including by supporting Taiwan’s self-defense capabilities, to ensure an environment in which Taiwan’s future is determined peacefully in accordance with the wishes and best interests of Taiwan’s people,” the strategy reads.

As such, while the administration appears set to increase investments in the Indo-Pacific across the realm of security, diplomacy, and economic development, it will not pursue changes in the status quo regarding Taiwan.

Tyler Durden

Sun, 02/13/2022 – 23:30 - New Zealand Police Play "Barry Manilow" And "The Macarena" To Antagonize New Zealand Protesters

New Zealand Police Play “Barry Manilow” And “The Macarena” To Antagonize New Zealand Protesters

The authorities in New Zealand have found a new strategy for warding off unwanted demonstrators who are camping outside the Parliament building: playing “Barry Manilow’s Greatest Hits” and the “the Macarena” on repeat to try and ward people off.

Of course, the global protest movement inspired by the Canadian “Freedom Convoy” is vexing governments from the antipodes to Europe, and beyond.

And in a few instances, the demonstrators have responded in kind by playing Twisted Sister’s “We’re Not Gonna Take It”. Hundreds of demonstrators have been camped out outside Parliament in Wellington since Tuesday. According to the BBC, they adopted the name “Convoy for Freedom” and blocked streets in the city.

Although their numbers dwindled to the dozens by mid-week, they increased again by the time the weekend arrived.

Police haven’t been shy about making arrests: on Thursday, police arrested 122 people and charged many with trespassing or obstruction. Yet, still the demonstrators persisted.

The local police haven’t stopped at playing music. Other tactics of dispersal have included “turning on sprinklers” on a lawn where protesters had camped out.

But again, protesters retaliated by digging trenches and building makeshift drainpipes to re-route the water.

On Saturday, singer James Blunt responded to a headline about authorities sonic repellant, and joked that his music should be added to the playlist.

Give me a shout if this doesn’t work. @NZPolice https://t.co/AM2dZ6asMS

— James Blunt (@JamesBlunt) February 12, 2022

https://platform.twitter.com/widgets.js

Sure enough, somebody was apparently paying attention, since an observer said his hit “You’re Beautiful” was added to the authorities’ playlist on Sunday.

Tyler Durden

Sun, 02/13/2022 – 23:00 - Zuesse: Making Sense Of The Ukraine Standoff

Zuesse: Making Sense Of The Ukraine Standoff

Authored by Eric Zuesse via TheDuran.com,

Someone asked me:

Can you make sense out of the current Ukraine situation/stand-off? You indicated in an earlier note that you didn’t think Putin would invade Ukraine unless Ukraine invaded Donbass. So, what is going on right now? Why the massive Russian build-up on the borders (assuming the news isn’t exaggerating)?

I answered:

Putin intends to assure that if Ukraine invades Donbass, the residents in Donbass will win. He has armed and trained them how to use the weapons, but if Russian soldiers would need to enter Donbass and fight there against Ukraine, he also will need to defeat the Ukrainian soldiers there. He is waiting for Ukraine to invade Donbass.

Biden wants Zelensky to order the invasion; Zelensky doesn’t want to do it, because then the EU almost certainly will never allow Ukraine into the EU. Ukraine needs the EU because it lost its main trading-partner, Russia, on account of Obama’s 2014 anti-Russian coup.

The EU won’t support Ukraine if Ukraine starts the invasion to occupy Donbass, except if it is responding to a prior Russian entrance into Donbass, in which case Ukraine wouldn’t be blamed for the carnage there. That is the reason why Biden wants Ukraine to set up a false-flag event, so as to make a Ukrainian invasion SEEM to be a defense against Russian aggression.

For a long time, there have been allegations that nazis in Ukraine were preparing a false-flag event and were threatening Zelensky with a coup to overthrow him if he refused to do it, to give the go-ahead. He’s walking a tightrope.

But recently, American media have been reporting that U.S. intelligence shows that Putin has planned a false-flag event in order to ‘justify’ a Russian invasion of Ukraine.

The EU’s position is to demand Ukraine to fulfill its promise under the February 2015 Minsk II accord to negotiate with the Donbass government so as to accept Donbass back into Ukraine without hostility and with independence like Crimea had inside Ukraine during 1954-2014 which was when Crimea had been part of Ukraine instead of part of Russia (of which it was a part during 1783-2014). But if Zelensky were to go forward with the Minsk II deal (to which Hollande, Merkel, and Putin had forced both Ukraine and Donbass to sign), then the nazis would overthrow him.

I believe that Zelensky is doing all he can to comply with EU and not with U.S. but still stay alive.

* * *

Investigative historian Eric Zuesse is the author of They’re Not Even Close: The Democratic vs. Republican Economic Records, 1910-2010, and of CHRIST’S VENTRILOQUISTS: The Event that Created Christianity.

Tyler Durden

Sun, 02/13/2022 – 22:30 - American Companies That Failed In China

American Companies That Failed In China

For decades, China has been a top priority for American companies looking to expand.

This is because the country’s middle class is simply enormous, growing from 3.1% to 50.8% of the country’s total population between the years 2000 and 2018.

According to Brookings, there are now at least 700 million people in China’s middle class, and this group has never had more disposable income to spend on consumer goods and services.

However, as Visual Capitalist’s Marcus Lu details below, despite the size and potential of the market, China is not an easy place for foreign businesses to enter. As this infographic shows, many of America’s biggest names eventually admitted defeat.

Companies by Tenure

The following table lists the tenures of every company included in the graphic.

It’s worth noting that Google’s parent company, Alphabet, still maintains a physical presence in China. Google’s services were banned by the Chinese government in 2010.

Dates were gathered from various media reports and sources. There may be small deviations from when a company actually entered or exited.

The reasons for why these companies withdrew are surprisingly similar, and can be broken down into two broad categories.

Retailers Fail to Adapt

Failing to adapt to the cultural differences of Chinese consumers is a common mistake. Here’s how two American retailers learned this lesson the hard way.

Best Buy

Best Buy struggled because Chinese consumers were not willing to pay a premium for brand-name electronics. Local retailers could often source similar (or counterfeit) goods for much cheaper, and undercut Best Buy’s prices.

“Why buy a Sony DVD player or Nokia phone at Best Buy when you can pay less for the exact same product at a local store?”

– SHAUN REIN, CHINA MARKET RESEARCH GROUP

Best Buy also made the mistake of bringing over its large flagship stores, which were out of reach for most consumers. Due to severe traffic congestion, locals preferred smaller shops that were closer to home.

Home Depot

The Home Depot expanded into China around the same time as Best Buy, but unfortunately it was another cultural mismatch.

Home Depot failed to acknowledge that “do it yourself” repairs are not a strong cultural match for China. Labor costs are relatively low, so rather than do the work themselves, many homeowners prefer to rather hire someone else to do it. On the other side of the equation, the American brand failed to win over contractors doing the repairs and renovations.

The Home Depot’s product offerings were also left unchanged from America, making them a poor match for local tastes. As a point of comparison, IKEA has had a presence in China since 1998, and continues to open new stores to this day.

Tech Firms Clash with Regulators

Uber’s experiences in China make a good case study on how American tech firms struggle to succeed in Asia’s biggest economy.

For starters, breaking into the Chinese market was incredibly expensive. Uber spent billions on subsidies to attract customers and drivers, and losses were quickly piling up. To make matters worse, domestic rivals like DiDi were also handing out subsidies.

On the operational side, Uber ran into several hurdles. To avoid issues with China’s data localization laws, the company needed servers on Chinese soil. Its navigation provider, Google Maps, also had limited accuracy in the country. This left Uber with no choice but to partner with Baidu, a Chinese tech company.

The final straw, however, was likely a set of impending regulations which targeted the ride-hailing industry. Under these rules, Uber risked losing control of its data, and would need both provincial and national regulatory approvals for its activities. Even further, subsidies would also no longer be allowed.

Uber realized that doing business in China was unsustainable, but its exit wasn’t exactly a failure. In 2016, Uber sold its assets to rival DiDi and took an 18.8% stake in the company. Ironically, DiDi is now embroiled in a conflict with Chinese regulators over its listing on the NYSE.

The Tech Fallout Continues

Since Uber’s departure, the Chinese government has increased their grip over the tech industry. This has driven more American firms out of the country, including Yahoo and LinkedIn, which is now owned by Microsoft.

Both firms announced their withdrawals in 2021 and were rather clear about why they made the decision. Yahoo cited its commitment to a “free and open” internet, while LinkedIn says its decision was due to a “considerably more difficult operating environment and higher regulatory requirements”.

Given the geopolitical tensions between the U.S. and China, companies that generate data (often seen as a national security concern) are likely to continue facing regulatory hurdles.

Outside of tech, China is still a massive opportunity for American businesses. By 2027, the country’s middle class is expected to reach 1.2 billion people, or one quarter of the global total.

Tyler Durden

Sun, 02/13/2022 – 22:00 - Beto O'Rourke U-Turns On AR-15 Confiscation, Saying He's "Not Interested" In Taking Firearms From Americans

Beto O’Rourke U-Turns On AR-15 Confiscation, Saying He’s “Not Interested” In Taking Firearms From Americans

Authored by Katabella Roberts via The Epoch Times,

Beto O’Rourke has backtracked from comments he made in 2019 when he asserted that he would confiscate AR-15-style firearms from Americans.

The Democrat, who announced his run for Texas governor on Nov. 15, said on Tuesday that he’s “not interested” in taking anyone’s firearms.

“I’m not interested in taking anything from anyone,” O’Rourke told supporters during a campaign stop in Tyler, Texas, according to KLTV. “What I want to make sure that we do is defend the Second Amendment.”

He added: “I want to make sure that we protect our fellow Texans far better than we’re doing right now. And that we listen to law enforcement, which [Gov.] Greg Abbott refused to do. He turned his back on them when he signed that permitless carry bill that endangers the lives of law enforcement in a state that’s seen more cops and sheriff’s deputies gunned down than in any other.”

The U-turn comes just months after O’Rourke doubled down on his comments regarding removing AR-15-style firearms in an interview with the Texas Tribune.

“I think most Texans can agree—maybe all Texans can agree—that we should not see our friends, our family members, our neighbors, shot up with weapons that were originally designed for use on a battlefield,” O’Rourke told the publication.

O’Rourke, whose run for Texas governor targets the incumbent Gov. Greg Abbott, who is seeking a third term, vehemently endorsed confiscating guns back in 2019.

He told people watching a presidential primary debate in September of that year: “Hell yes! we’re gonna take your AR-15, your AK-47.”

When asked whether he’d actively force Americans to give up their guns, O’Rourke said: “I am if it’s a weapon that was designed to kill people on the battlefield. If the high-impact, high-velocity round, when it hits your body shreds everything inside of your body—because it was designed to do that—so that you would bleed to death on a battlefield. And not be able to get up and kill one of our soldiers.”

“We’re not going to allow it to be used against fellow Americans anymore,” O’Rourke added.

Earlier this week, O’Rourke took aim at Abbott for supporting constitutional carry, something that the Democrat has vowed to repeal if elected governor.

He wrote on Twitter on Feb. 9: “The number of Texans shot to death has gone up EVERY single year under Abbott. 4,164 Texans in 2020 alone. How does Abbott respond? By signing a dangerous law that makes it easier for criminals to carry a loaded gun in public. His radical agenda is killing the people of Texas.”

Abbott in November said that O’Rourke wants to “impose socialism.” Abbott said O’Rourke would defund the police, kill good-paying oil and gas jobs, allow open border policies, support President Joe Biden’s policies, and “take your guns.”

Texas in September became the latest U.S. state to allow individuals to carry a gun without a permit.

First signed into law by Abbott in mid-June, the bill means that Texans who are aged 21 and older and who are legally able to purchase and own a handgun will no longer require a license to carry one and will not have to undergo training either.

Tyler Durden

Sun, 02/13/2022 – 21:30 - Robots, Like Humans, Are Also Struggling In This Market

Robots, Like Humans, Are Also Struggling In This Market

By Cormac Mullen, Bloomberg Markets Live commentator and strateigst

Exasperated fund managers can take some comfort from the fact that the machines are struggling just as much as humans with this year’s volatility.

An artificial intelligence-guided fund has fallen almost 9% — lagging its benchmark, the S&P 500 Total Return Index, by about 5 percentage points — according to data compiled by Bloomberg through Wednesday.

The AI Powered Equity ETF seemed to have been positioned well going into the new year, having sold down its so-called FANG+ positions in December. But stock picks in the financials and energy sectors have weighed on the fund, even as it benefited from a lower-than-benchmark exposure to communication services, according to Bloomberg’s Portfolio & Risk Analytics function.

The AI fund’s “manager” is a quantitative model which runs 24/7 on IBM Corp.’s Watson platform and was developed by EquBot. It’s still overweight tech stocks with chipmaker AMD the largest holding, and is close to benchmark with the three key value sectors of financials, energy and materials stocks.

And Apple remains the only FANG+ stock in its top 20 holdings, suggesting it is sticking with a strategy of avoiding the mega-cap tech names for now.

Tyler Durden

Sun, 02/13/2022 – 20:30 - "Buy The Dip And Sell The Rally" – What Hedge Funds Are Doing In The Current Market Turmoil

“Buy The Dip And Sell The Rally” – What Hedge Funds Are Doing In The Current Market Turmoil

After a catastrophic start to the year for hedge funds, which was followed by an epic shorting frenzy before hedge funds reversed and rushed to buy all risk assets last week, which reaffirms the common them seen across 2022 – nobody has any idea how to trade this market.

Still, the good news is that after a dismal beginning, hedge funds performance has stabilized modestly and as Goldman Prime writes in its latest weekly note, the GS Equity Fundamental L/S Performance Estimate rose for a 2nd straight week by +2.71% between 2/4 and 2/10 (vs MSCI World TR +1.19%), driven by beta of +1.41% (from market exposure and market sensitivity combined) and alpha of +1.31%, representing the best weekly alpha returns in the past year.

Thanks to this performance rebound, overall book gross leverage increased 2.9% to 238.6% (46th percentile one-year) and Net leverage also rose 1.2 pts to 79.5% (2nd percentile one-year). Still, overall book L/S ratio little changed at 1.998 (lowest since Jul ‘20). Fundamental L/S Gross leverage +2.5 pts to 178.7% (59th percentile one-year) and Fundamental L/S Net lev erage +2.5 pts – the first increase in 7 weeks – to 60.2% (6th percentile one-year).

Not surprisingly, just days after Goldman Prime reported the biggest bout of shorting in history…

… The GS Prime book saw the largest net buying since late December (+1.0 SDs), driven by risk-on flows with long buys outpacing short sales 8 to 1. Net flows diverged between Single Names (3rd straight week of net buying) and Macro Products (4th straight week of net selling); suggesting a shift of focus to micro variables. Furthermore, as GS Prime notes, all regions were net bought led by North America (driven by long buys) and to a lesser extent DM Asia (driven by short covers). 8 of 11 global sectors were net bought led in $ terms by Info Tech, Materials, Financials, and Consumer Disc, while Comm Svcs and Energy were the most net sold.

Net buying in US Info Tech continued this week but hedge funds sold Non Profitable Tech stocks (GSXUNPTC) in each of the past three days, suggesting that managers faded the group’s price rally this week amid a growing focus on profitability. While price of the Non Profitable Tech basket is down nearly 50% from its all-time high, net exposure in the group remains well above historical averages.

US Financials have been net bought for five straight days led by long buys and short covers in Rate Sensitive Financials amid a higher than expected US CPI print and higher bond yields. Despite this week’s buying activity, net exposure in Rate Sensitive Financials – at just 1.3% of the overall US single name book – remains well below its long-term average in the 63rd percentile vs. the past year and in the 37th percentile vs. the levels seen going back to Jan ‘18.

From Goldman, we switch to JPMorgan’s Prime desk which writes that in light of the volatility we’ve continued to see in equity markets recently, “it’s interesting to note that while we didn’t see clear signs of consistent HF capitulation a couple weeks ago, post some dip buying 2 weeks ago, we have also not seen a desire to add much additional risk over the past week.”

If anything, the bank notes that “sell the rally” behavior has been apparent in some parts of the market (generally in the US and somewhat specifically in Tech).

So what has JPM Prime seen, what has it not seen, and what is it watching that could have broader HF & market implications?

What have we seen recently?

- Buy the dip & sell the rally behavior

- In US, a recent shift to selling Value (but Growth sold as well). That said, Tech still most bought in past month (albeit recent selling into strength) with Banks also bought over the past week and month

- In Europe, re-buying of Banks (two weeks ago) and continued selling of Luxury Goods

- Leverage fairly stable with Quants adding most to exposure and increasing gross leverage

- Performance above the worst levels YTD, but still challenging for L/S and better for Quants & Multi-Strats

What have we not seen (which are notable in light of market sell-off recently)?

- Broad de-grossing or persistently large net selling

- Outsized hedging via ETF shorts

- Recent selling areas that have underperformed (e.g. software, exp software, biotech, semis) and a lack of buying Energy despite strong performance

What JPM is watching for in the near term?

- High Vol / High SI stocks – is the bottom in, especially relative to the broader market? A rally in “risky” factors could be helpful for Equity L/S longs, but it still seems too early to say whether or not we’ve seen the low for these factors

- Could a rally in shorts cause broader de-grossing? Shorts have been the common factor helping HF performance across strategies in recent months…but if this reverses and hits all strategies, could this cause a broader de-gross event?

- What would happen during a “double dip” (i.e. a second market drawdown) that puts the S&P near or below the Jan lows? How would funds react? Historically, many of the short term rallies (c. 5-6%) in markets post initial decline have been followed by a second drawdown of c. 10% (based on 23 events since 1990)

In general, JPM concludes that there were some data points across volatility metrics, retail & ETF flows, as well as a few HF-related points that suggested a fairly negative change in positioning right near the Jan low. Thus, there might still be room for further upside in near term, but how the market rallies and whether we see a “double dip” will be important to watch.

Tyler Durden

Sun, 02/13/2022 – 20:00 - NPR Declares Using Wrong Color Emojis Is Probably Racist

NPR Declares Using Wrong Color Emojis Is Probably Racist

Authored by Steve Watson via Summit News,

In another example of the establishment left’s obsessive grift with race and social segregation, publicly funded NPR published a story claiming that if you use the wrong colour emoji in text messages in relation to your own skin colour, you are probably a racist.

In the article titled “Which skin color emoji should you use? The answer can be more complex than you think”, writers Alejandra Marquez, Janse Patrick Jarenwattananon, and Asma Khalid (it took three of them to take on this weighty subject) argue that choosing to use a yellow emoji, rather than a white, brown or black one is “the neutral option” that will leave the respondent free to “focus on the message” rather than race.

Of course, any rational person wouldn’t immediately see an emoji in a text and start thinking about race. Not these taxpayer funded hacks though.

They even went around interviewing people for the piece.

One interviewee said “I present as very pale, very light skinned. And if I use the white emoji, I feel like I’m betraying the part of myself that’s Filipino.”

The interviewee continued, “But if I use a darker color emoji, which maybe more closely matches what I see when I look at my whole family, it’s not what the world sees, and people tend to judge that.”

OMG, what a terrible dilemma to be in.

The only emojis relevant here are 🤡🌎 https://t.co/IFgGs0L40n

— Paul Joseph Watson (@PrisonPlanet) February 9, 2022

https://platform.twitter.com/widgets.js

The article suggests that choosing a specific colour emoji “can be a simple texting shortcut for some, but for others, it opens a complex conversation about race and identity.”

For who? Grifters writing for NPR and the mentally ill?

Sarai Cole, an opera singer in Germany (Yes they interviewed someone in Germany for this too) stated “I have some friends who use the brown ones, too, but they are not brown themselves. This confuses me.”

“She was not offended when a non-brown friend used a dark emoji”, the article states, adding she just “would like to understand why.”

The nonsense continues, “Zara Rahman, a researcher and writer in Berlin, argues that the skin tone emojis make white people confront their race as people of color often have to do.”

Rahman adds “I think it’s more one of those places where we just have to think about who we are and how we want to represent our identities, and maybe it does change depending on the season; depending on the context.”

What?

Over to you the internet:

— Stephen L. Miller (@redsteeze) February 9, 2022

https://platform.twitter.com/widgets.js

I don’t use 👍 because I don’t have jaundice.

— Mr Gray (@uup116) February 9, 2022

https://platform.twitter.com/widgets.js

It’s okay to be 👍🏻

— Sher 🌺 🛻🚛🚚 (@cosmicpixie3) February 9, 2022

https://platform.twitter.com/widgets.js

I find all emojis triggering.

— franko blondee (@FrankHosey) February 9, 2022

https://platform.twitter.com/widgets.js

NPR “academics” every morning… pic.twitter.com/3ZrcIg2eT9

— 🖤Ꮲɛཞʂơŋą ŋơŋ Ꮆཞąɬą🖤 (@RudisExcitatio) February 9, 2022

https://platform.twitter.com/widgets.js

My emojis don’t give a fuck about their feelings.

👍🏼✌🏼🤦🏻♂️🖕🏼🤷🏻♂️

— 🇺🇸 THE Pittsburgh Patriot 🇨🇦 (@LemmeTriggerU) February 9, 2022

https://platform.twitter.com/widgets.js

what color emoji should Trudeau use

— Christina Pushaw 🐊🚛 (@ChristinaPushaw) February 9, 2022

https://platform.twitter.com/widgets.js

Incredible that it took *three* NPR employees to write something this stupid. pic.twitter.com/8KtXWN0sIz

— Christopher F. Rufo ⚔️ (@realchrisrufo) February 9, 2022

https://platform.twitter.com/widgets.js

Only woke white people care about this kinda shit. Everyone else has a life and real problems to worry about.

— Brad Polumbo 🇺🇸⚽️ 🏳️🌈 (@brad_polumbo) February 10, 2022

https://platform.twitter.com/widgets.js

* * *

Brand new merch now available! Get it at https://www.pjwshop.com/

In the age of mass Silicon Valley censorship It is crucial that we stay in touch. We need you to sign up for our free newsletter here. Support our sponsor – Turbo Force – a supercharged boost of clean energy without the comedown. Also, we urgently need your financial support here.

Tyler Durden

Sun, 02/13/2022 – 19:30 - Forget Burrow & Stafford, Brady Jerseys Still In High Demand

Forget Burrow & Stafford, Brady Jerseys Still In High Demand

In a few short hours, the Cincinnati Bengals will face off against the Los Angeles Rams in the 56th Super Bowl, arguably the biggest event of the year in U.S. sports. However, as Statista’s Florian Zandt shows in the chart below, our chart shows, only one athlete playing for either of the two finalists ranked in the top 8 of the highest-selling NFL jerseys in the last week of the regular season according to data from Fanatics, the company behind nflshop.com.

The first spot was claimed by a very familiar face once again.

You will find more infographics at Statista

This face, of course, belongs to star quarterback Tom Brady, who announced his retirement on February 1, 2022 after 22 seasons. Brady spent his last two seasons at the Tampa Bay Buccaneers with whom he won the last Super Bowl and is widely regarded as one of the best quarterbacks of all time. While his legacy as an athlete is largely undisputed, the now-former NFL player is not without controversy off the field: Brady has been good friends with former President Donald Trump since 2001, although he did decline a speaker’s role at the 2020 Republican National Convention and hasn’t officially endorsed Trump’s presidential races in 2016 and 2020.

Coming in second after Brady in terms of jersey sales is Ben Roethlisberger, moving up three ranks from the week prior. Both sale increases might be related to one similarity between the two players: Just like Brady, Roethlisberger retired at the end of the 2021/2022 season after spending 18 years with the Pittsburgh Steelers. The sole player from a Super Bowl competitor in the top 8 jersey ranking is Ja’marr Chase of the Cincinnati Bengals. In his first season, the wide receiver broke several NFL rookie records, including most receiving yards in a game.

Even though the final game of the NFL playoffs is still immensely popular in the U.S., its viewership numbers have dwindled since 2015. In 2021, roughly 91 million viewers from the U.S. watched the Super Bowl, while ad revenue amounted to roughly $485 million.

Tyler Durden

Sun, 02/13/2022 – 19:00 - Morgan Stanley: The Amount Of Hiking Needed To Contain Inflation Will Soon Stall The Economy

Morgan Stanley: The Amount Of Hiking Needed To Contain Inflation Will Soon Stall The Economy

Last week, for the first time since the current tightening frenzy began, Goldman warned that the Fed’s aggressive tightening may could to a hard landing. Not surprisingly, just a few days later, the bank slashed its year-end S&P target and now warns that in a recession the S&P could tumble to 3,600.

Now, it’s Morgan Stanley’s turn as the following Sunday Start note by the bank’s Chief US Economist Seth Carpenter, reveals.

Rising Inflation, Rising Risks

Over the past half year, we and many central banks have serially revised our inflation forecasts higher. As inflation has continued to surprise to the upside, markets have priced in more rate hikes and an earlier onset of hiking by many DM central banks. How much is too much? That question needs to be asked for both market pricing and the economy.

Last week’s US CPI print was the most recent of these upside surprises. Of course, auto prices softened amid mounting evidence that supply chains are slowly normalizing, but on the heels of the CPI report, our US team revised up its inflation forecast for three reasons:

- The first is a simple mark-to-market of an upside surprise.

- Second, the annual revision to the weights for the price index means that our forecast for the components of inflation will result in a higher index.

- And finally, rent inflation has stayed high, and in our forecast we have extended the timeline for that pressure. This third reason is particularly important because it reflects macro, cyclical inflation that will not recede with healing supply chains.

The upside surprise to CPI means the risks to our Fed call are even more skewed to further hiking. The US team’s baseline call is for four 25bp hikes and the initiation of quantitative tightening (QT) around mid-year. So why not build in more hikes? Our central bank forecasts result from overlaying our reading of the policy reaction function on our economic forecasts – especially for inflation. Consider the typically hawkish Esther George, who said that QT should allow for a flatter path of rate hikes. The market is pricing an even chance of a 50bp hike at the March meeting, a view that we have resisted. Front-loading the tightening has appeal with inflation risks skewed to the upside, but much Fed communication has tilted away from such a move, echoing the cautious tone that Chair Powell struck at the last press conference.

The Bank of England has already hiked twice and initiated its QT, but markets still expect more hiking than we do. The markets have priced in roughly 85bp of hikes over the next 12 months, while we expect somewhat less. Of course, we could be wrong, and markets could continue to be right. But most of the excess inflation in the UK remains in core goods, and if supply chains are normalizing as our index implies, inflation should underperform market expectations later in the year. The BoE appears to share our view, as its latest inflation expectations based on market pricing show inflation undershooting its target. The uncertainty surrounding inflation, however, skews the risks to more hiking rather than less.

The ECB was the last of this group to execute a hawkish pivot. Our European economics team revised its ECB call last week, forecasting an end to QE by September and rate hikes starting in December that bring the deposit rate to zero in 1Q23. The persistence of the inflation overshoot drove the pivot, and while continued upside surprises could lead to more, for the ECB there is another consideration. Negative rates in the eurozone impose costs on banks and are politically unpopular. Hiking from negative to zero has a lower threshold than hiking above zero, so getting to zero could happen faster than we expect. Regardless, we expect the ECB to pause at zero as the uncertainty settles down. If our forecast for goods inflation proves right, and if oil and gas prices stabilize, that pause in 2023 could last for some time.

It is hard to argue that risks are not still skewed to the upside. Even if market pricing has not gone too far, before long we will have to confront the risk I noted in the Sunday Start two weeks ago. The amount of hiking needed to bring inflation down will soon approach the amount that stalls the economy.

Tyler Durden

Sun, 02/13/2022 – 18:35 - GOP Senate Candidate Unveils "Let's Go Brandon" Super Bowl Ad

GOP Senate Candidate Unveils “Let’s Go Brandon” Super Bowl Ad

US Senate candidate Dave McCormick will debut a multi-million dollar ad during the Super Bowl tonight featuring a “Let’s go, Brandon” advertisement summarizing the failures of President Biden and Democrats, according to Fox News.

McCormick, the former CEO of Bridgewater Associates (one of the largest hedge funds in the world), paid millions of dollars for a 30-second ad that will be featured during the Super Bowl in the Pittsburgh area on NBC platforms. The ad lists “record inflation,” Afghanistan withdrawal debacle, Facebook and other Silicon Valley companies “silencing conservative voices,” out-of-control trade deficit, widespread violent crime, and the southern border crisis.

The video concludes with, “This is so much bigger than Brandon.”

“Let’s go Brandon” has become a rallying cry for those on the right. The slogan debuted after a mainstream news reporter tried to cover up the crowd chanting “F*** Joe Biden” by saying they’re shouting “Let’s go Brandon” while interviewing racer Brandon Brown.

McCormick is running for Pennsylvania Sen. Pat Toomey’s seat, an anti-Trumper who voted to convict the former president for the Jan. 6, 2021, Capitol riots.

“The only reason worth watching today is to hear the chant. I haven’t watched since the early days of kneeling,” said a commenter on the Fox News article.

Tyler Durden

Sun, 02/13/2022 – 18:10 - Yielding Digital Assets Are The Replacement For A Broken 60/40 Balanced Portfolio

Yielding Digital Assets Are The Replacement For A Broken 60/40 Balanced Portfolio

By Marcel Kasumovich, Head of Research at One River Asset Management

The Great Financial Inflation has compelled investors into passive portfolios in our view. Bonds are no longer assets to balance portfolio risk, as seen so far this year. Not surprisingly, investors are searching for replacements to bond holdings.

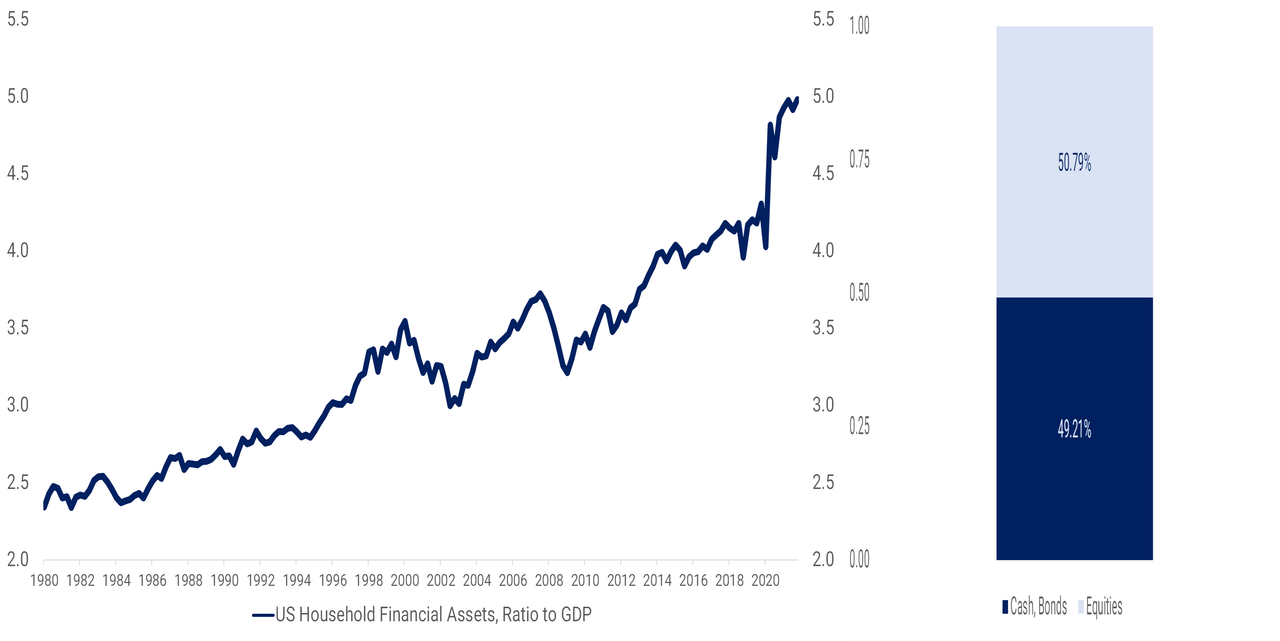

1/ Portfolios, we have a problem. U.S. household financial assets have risen to nearly 5-times nominal GDP in the Great Financial Inflation. So great is the financial inflation, households find themselves (perhaps unintentionally) with a whopping 49.2% allocation to cash, cash-equivalent assets, and bonds (Figure 1). This comes at a time when macro policies are resolutely committed to multi-generational financial repression. For all the hawkish hype, bond markets are convinced that the next easing cycle will come in 2023 and that long-term policy rates will remain well below inflation. This is strongly counter to Fed guidance. We see no historical precedent.

Figure 1: Great Financial Inflation: Large Bond Holdings

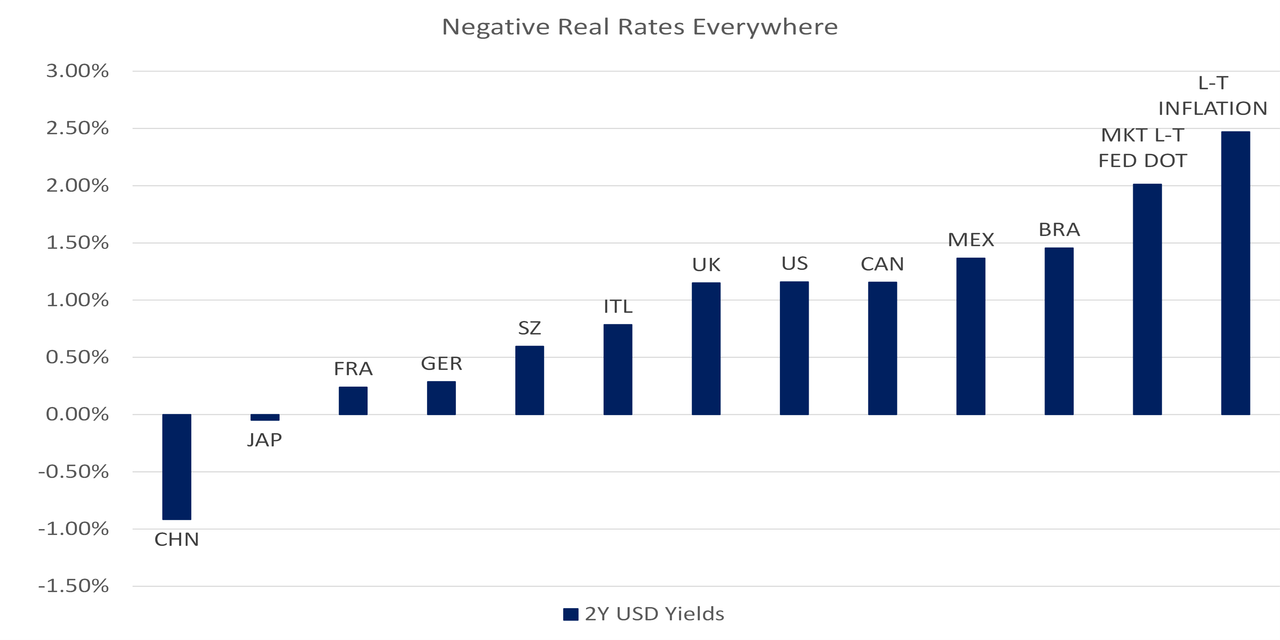

Source: Federal Reserve Board. St. Louis Federal Reserve. One River Digital Calculations. Provided for illustrative purposes only. See important disclosures at the end of this article. 2/ So, financial markets are telling us that nearly 50% of household assets are expected to lose money in real terms in the decades ahead. It is not just a U.S.-asset problem – shorter-term real yields are a global phenomenon (Figure 2). The Great Financial Inflation has masked the misallocation – long gone are the days of diversification. A 60-40% equity-bond portfolio returned 15% last year with a coincident rise in equity and bond valuations. Bonds have taken on equity-like return characteristics – the 60-40% portfolio is unbalanced. No doubt, the drawdown in 60-40% portfolios to start this year was on par with crisis periods – we were only missing the crisis – with equities and bonds both sharply retracing in January.

Figure 2: Problem: Low Short-Term Yields, Inflation Taxing Bond Portfolios

Source: Bloomberg. One River Digital Calculations as of February 9, 2022. MKT L-T FED DOT is the 5y5y OIS forward to imply the long-term Federal funds policy rate. L-T inflation is 5y5y forward inflation. 3/ Are digital assets a potential solution to balance portfolio risk? Yes. But the solution has a more subtle first step: yield. Directional exposure to bitcoin and the One River Digital Core Index seeks to offer diversification properties over the course of market cycle. However, shorter-term cyclical correlations are still quite high. Daily bitcoin returns year-to-date have a 53% correlation to US equity returns and a 36% correlation to US fixed income. Not all investors are searching for more risk, slowing the institutional adoption to directional digital asset exposure. Ethereum’s migration to proof of stake will mark a milestone, transforming ether into a bond-like asset. But even then, the yield from staking is low relative to the ether’s volatility.

4/ A more natural first step for some investors is to focus on yield derived from the digital ecosystem. Ideally, a yield investment would avoid any directional exposure and offer an income-like cashflow that is familiar to institutional investors. It would bring digital assets to investment committees in a low-risk manner, a more natural fit for their mandates (What’s Taking So Long? here). It was missing – an uncorrelated, low-risk, liquid yield fund without direct digital asset exposure. So, we built it: the One River Digital Income Fund. The objective was clear – deliver a low-risk yield solution in the digital ecosystem. The lowest end of the risk spectrum is the natural starting point – risk can be added alongside the evolution of investor appetites easily enough.

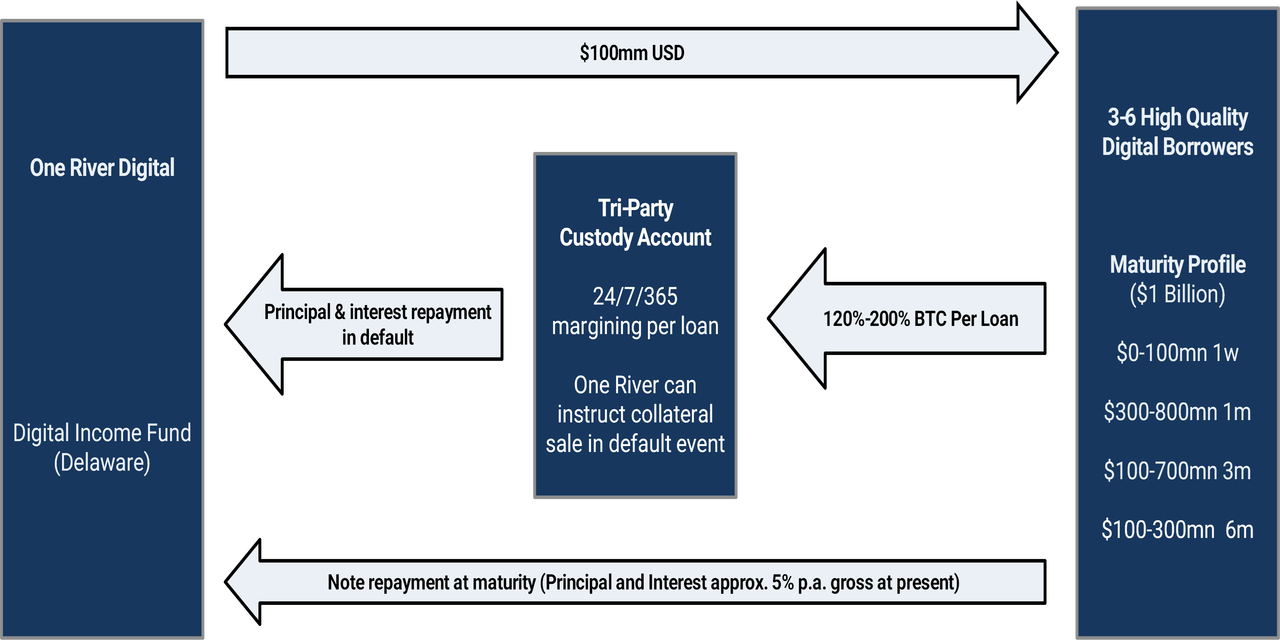

5/ Digital Income is a short-term yield fund. The Fund seeks to generate yield by providing a U.S. dollar loan to high quality borrowers in the digital ecosystem. The loan’s safety is achieved by over-collateralizing the loan through high-quality liquid digital assets, initially only bitcoin. The Fund does not take possession of the bitcoin and thus is not a money transmitter, an important consideration in the context of future regulation. Instead, the liquid collateral is held by a third party with conditions on when collateral can be liquidated (Figure 3). Our process selects known, researched, and regulated counterparties. Investors are granted the added security by over-collateralization of a liquid asset with 24-hour margining, 365 days a year.

Figure 3: Solution: Digital Income, Low Risk Strategy in the Digital Ecosystem

Source: One River Digital. This chart is provided for informational purposes only and represents a simplified description. The above investment strategy may differ from what is stated above at One River’s discretion. See important disclosures at the end of this article Here are the four most common questions on Digital Income:

6/ First, what are the risks to the structure? The short answer – negligible. Digital Income builds layers of protection. The over-collateralization means that a default scenario is recognized well before collateral values breach the par value of a loan. This negates counterparty risk. Digital Income also allows for U.S. dollar collateral, which can be used to buffer a cascading decline in the price of bitcoin. Further, the loan has recourse beyond the collateral. These measures are designed to add safety. Not surprisingly, our estimates of the “risk premium” needed to compensate for collateral risk is comfortably less than ten basis points. The yield is not compensating lenders for a known risk premium. Instead, Digital Income will seek to provide income to lenders for intermediating activity in the digital ecosystem. And we believe there is a shortage of high-quality lenders doing so.

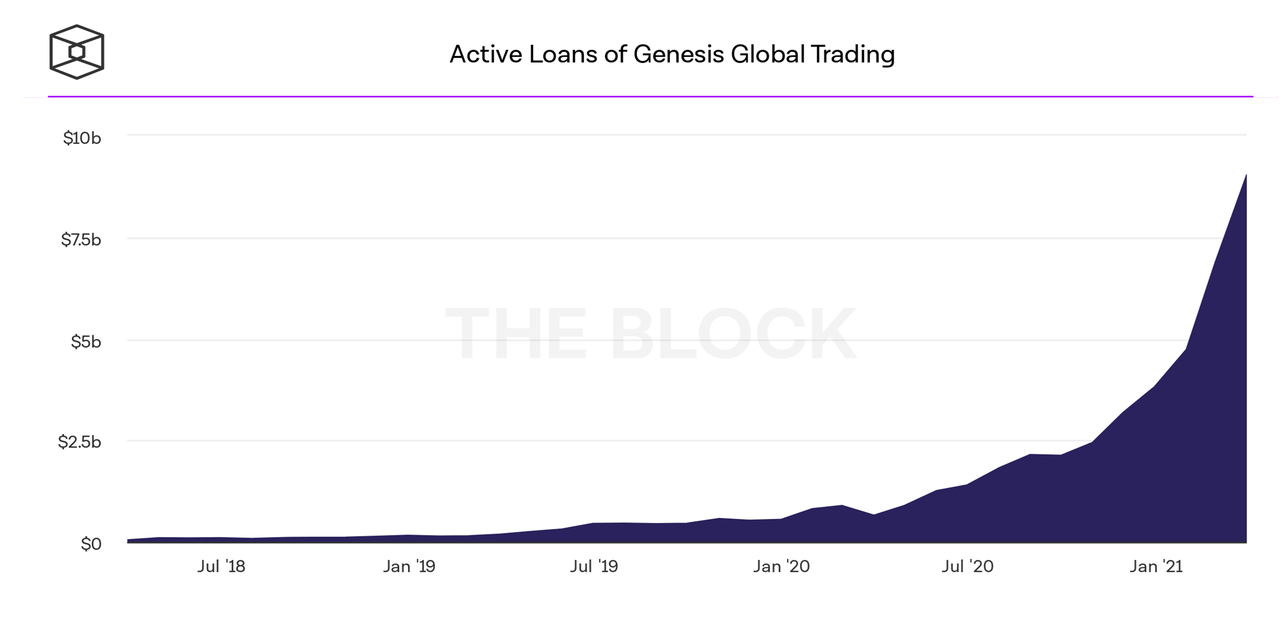

7/ Second, where does the yield come from? Demand for capital in the digital ecosystem is robust, alongside high expected asset returns. This is the natural flipside of high asset volatility. In the early phase of lending growth, retail capital, such as yield-bearing digital deposits, were sufficient. However, as the system has matured, growth in loan demand has increased through digital banking partners, high net worth individuals, corporations, hedge funds and family offices. Active loans for Genesis Global Trading, for instance, are approaching $10 billion, an increase from less than $1 billion at the start of last year (Figure 4). Rapid and broadening growth in digital assets will require substantial debt capital, including attractive, low-risk rates for institutional investors.

Figure 4: Market Demand, Shortage of High-Quality Lenders

Source: Genesis Global Trading as of September 2021. 8/ What is the right benchmark to compare Digital Income? Digital Income is a quarterly fund and will be compared to cash-equivalents such as the Bloomberg 1-to-3-month U.S. Treasury bill total return index. We anticipate Digital Income yields to be in the 4-12% range, varying pro-cyclically with the demand for capital. A rise in digital asset prices raises expected returns and the interest rates paid by the borrower, even with collateralization. Rates are driven by demand. However, it is important to value Digital Income relative to other benchmarks. One way is to infer unsecured funding rates from publicly traded digital asset companies. Five-year unsecured financing, inferred from one convertible bond, is running at ~4%, the low end of our expected range. Digital Income is secured and can still offer an attractive premium.

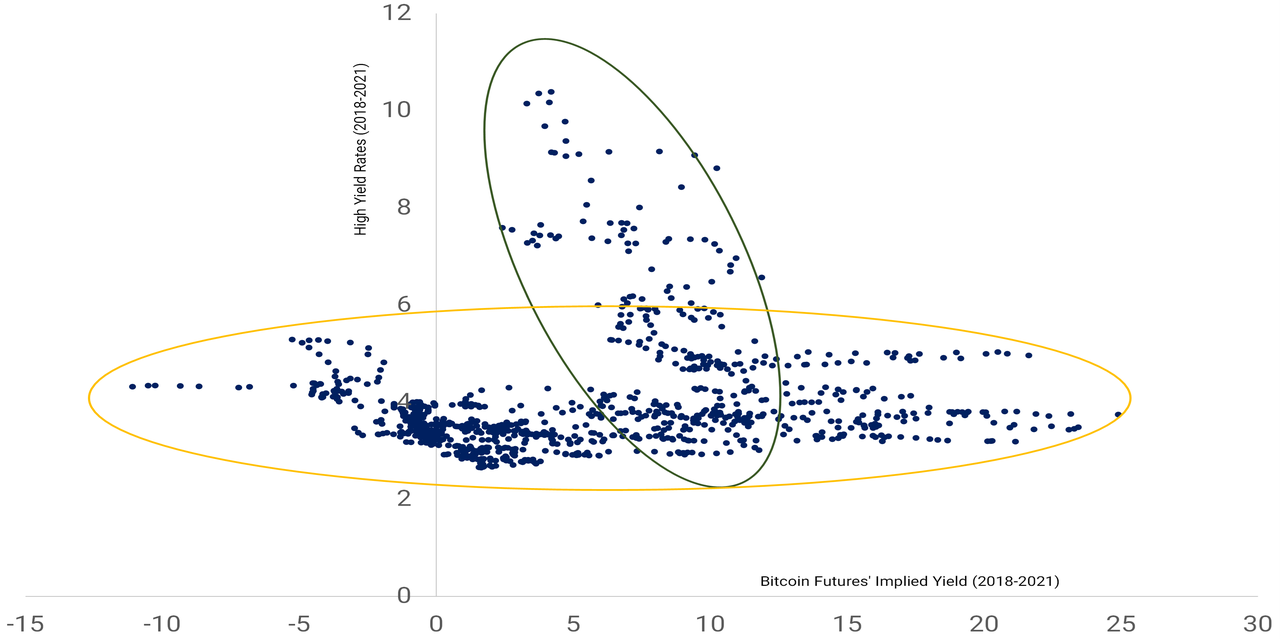

9/ How does Digital Income fit into a portfolio? This is a subtle benefit. Typically, credit and risk assets co-move. As equity asset prices decline, credit spreads widen. This is a mathematical truism of credit spreads– it is equivalent to being long a risk-free asset and short an equity put. But this is not how yields in digital assets behave. Figure 5 illustrates the implied yield in bitcoin futures against high-yield corporate borrowing costs. Most of the time, there is no correlation. However, digital asset yields decline alongside the fall in the demand for borrowing in sell-off periods for risk assets and widening in credit spreads. Digital Income spreads are counter-cyclical, narrowing as asset prices decline. This behavior is more like a Treasury bill than credit.

Figure 5: How Do Spreads Behave? Opposite of Credit!

Source: Bloomberg. One River Digital Calculations. 2018 to 2021. The above graph demonstrates implied yield in bitcoin futures against high-yield corporate borrowing costs, both in percent. The bitcoin futures’ yield is a five-day rolling average of the daily annualized yield implied by the ratio of the one-month rolling bitcoin future to the spot bitcoin price. 10/ The beginning is a good place to start. That is precisely what we are doing with Digital Income – we are defining the lowest risk point of the digital asset yield curve. Doug Wilson, the portfolio manager, executed our first loans this week with research and operational tools in place. We believe that this will be a comfortable step into the digital ecosystem for institutional investors. And it will also be a natural point from which to migrate out the risk spectrum, lowering collateralization rates to enhance yields and moving into credit provision through bitcoin bond-like structures. Bonds are a problem, and we believe Digital Income is a solution.

Tyler Durden

Sun, 02/13/2022 – 17:45 - USDA Suspends Mexican Avocado Imports, Stokes Yet More Food Inflation

USDA Suspends Mexican Avocado Imports, Stokes Yet More Food Inflation

The U.S. suspended all imports of Mexican avocados that could send prices to near-record highs in the coming weeks on diminishing supplies if the ban remains in place. The reason for the import halt is a U.S. Department of Agriculture (USDA) inspector was threatened by what is presumed to be drug cartel members.

“U.S. health authorities…made the decision after one of their officials, who was carrying out inspections in Uruapan, Michoacan, received a threatening message on his official cellphone,” Mexico’s Agriculture Department said in a statement. –AP News

The surprise halt comes as the price of a 20-pound box of avocados from the state of Michoacan, Mexico (the central hub of Mexican avocado production) is approximately $26.89, the highest ever for this time of year with data going back to 1998.

This year alone, avocado prices are up 31%. The import ban came on the eve of the Super Bowl and may send spot prices to record highs on the prospects of tighter supplies.

Supply woes aren’t expected to affect Super Bowl consumption since those avocados had already been shipped, but there are concerns disruptions could be seen in the weeks ahead (if the import ban remains in place).

The ban also comes as the Avocados From Mexico association unveiled its Super Bowl ad that will be shown during the game.

Violence against USDA inspectors is nothing new since the Michoacan state is known for cartel turf wars. In 2019, a team of inspectors was threatened by a cartel.

USDA wrote in a memo at the time, “For future situations that result in a security breach, or demonstrate an imminent physical threat to the well-being of APHIS personnel, we will immediately suspend program activities.”

Tyler Durden

Sun, 02/13/2022 – 17:27 - Zelensky Invites Biden To Visit Ukraine In "Coming Days" In Pushback Against 'Imminent' Invasion Fears

Zelensky Invites Biden To Visit Ukraine In “Coming Days” In Pushback Against ‘Imminent’ Invasion Fears

update(5:10pmET): During their Sunday phone call Ukraine’s President Zelensky asked Biden to visit Kiev in person amid continuing White House claims that a Russian invasion is set to happen “any day” now.

Saying that major Ukrainian cities are “under safe protection,” Zelensky suggested that a visit of the US president in person would stop the spread of panic and prevent escalation. “I am convinced that your visit to Kyiv in the coming days… would be a powerful signal and help stabilize the situation,” Zelensky was quoted as saying in the call.

“We will stop any escalation. The Ukrainian capital, Kiev, other cities in our country – Kharkov and Lvov, Dnepr and Odessa – are under safe protection,” Zelensky told the US president.

Zelensky himself and other top Kiev officials have in the past days once again been urging Washington to calm down its rhetoric. On Saturday the Ukrainian leader publicly urged the US to provide evidence or any relevant intelligence to back its claims of an “imminent” Russian invasion. That Zelensky has now gone so far as to issue a personal invitation for Biden to travel to Ukraine is clearly a move aimed at directly combatting the White House’s persistent fear-mongering and overblown predictions regarding Russia’s intent.

As for the White House call readout, it was brief and scant on details, while again underscoring the path for diplomacy remains open:

President Biden reaffirmed the commitment of the United States to Ukraine’s sovereignty and territorial integrity. President Biden made clear that the United States would respond swiftly and decisively, together with its Allies and partners, to any further Russian aggression against Ukraine. The two leaders agreed on the importance of continuing to pursue diplomacy and deterrence in response to Russia’s military build-up on Ukraine’s borders.

Meanwhile, the below tweet from the Russian embassy in the UK is being seen by some as a “ray of hope” – strongly signaling there will be no Russian offensive:

FM #Lavrov: After Russian troops finish drills and return to barracks, West will declare ‘diplomatic victory’ by having ‘secured’ Russian ‘de-escalation’. Predictable scenario and cheap domestic political points. pic.twitter.com/S58RcmsetA

— Russian Embassy, UK (@RussianEmbassy) February 12, 2022

https://platform.twitter.com/widgets.js

However, speculation over the timing of the US-predicted Russian invasion scenario abounds…

Will Russia invade Ukraine during the Super Bowl?

In Tom Clancy’s “The Sum of All Fears,” the Kremlin did not understand the significance of the Super Bowl.

In real life, Russia’s government knows exactly what “the Big Game” means to America. 🧵 pic.twitter.com/R49x1v9rVt

— Clint Ehrlich (@ClintEhrlich) February 13, 2022

https://platform.twitter.com/widgets.js

* * *

Another Sunday, and Biden’s national security adviser is at it again making the rounds on the big network news shows, warning the Russian invasion will invade Ukraine “any day now” – at this point a familiar refrain we’ve heard for multiple weeks running…

“We cannot perfectly predict the day, but we have now been saying for some time that we are in the window, and an invasion could begin, a major military action could begin by Russia in Ukraine any day now — that includes this coming week, before the end of the Olympics,” Jake Sullivan told CNN’s Jake Tapper.

This latest round of breathless White House proclamations and predictions of the Russians are coming! began in earnest Friday afternoon when the administration told reporters that Putin has made the decision to launch a large military offensive.

US officials anticipate a horrific, bloody campaign that begins with two days or aerial bombardment and electronic warfare, followed by an invasion, with the possible goal of regime change.

— Nick Schifrin (@nickschifrin) February 11, 2022

https://platform.twitter.com/widgets.js

Multiple countries have now followed Washington’s lead in drawing down embassy and diplomatic staff from Ukraine to get people “out of harm’s way” – with the latest over the weekend being Australia. This is what the alarmism and panic emanating from the White House has wrought…

The prime minister, Scott Morrison, has ordered the evacuation of the Australian embassy in Kyiv, warning the situation in Ukraine has reached a dangerous stage.

Australia’s foreign affairs minister, Marise Payne, says the government has directed the departure of embassy staff to a temporary office in Lviv, with the buildup of Russian troops on the border.

“The situation is deteriorating and is reaching a very dangerous stage,” Morrison said on Sunday.

This is the latest in a growing list of countries withdrawing embassy personnel including Israel, the UK, the Netherlands, Latvia, Japan and South Korea.

But the all-important and central question that’s not being asked is once again: what’s the view from Kiev? What is the Ukrainian government’s reaction to the latest White House statements on the crisis? How about the President of Ukraine himself?

#BREAKING Ukraine leader Zelensky says warnings of Russian invasion ‘provoking panic’, demands to see firm proof pic.twitter.com/ZoBndyL3BU

— AFP News Agency (@AFP) February 12, 2022

https://platform.twitter.com/widgets.js

Kiev is not too happy, and is demanding proof from US intelligence backing the new dire allegations that Russia is poised to go in:

“There has been too much information about a full-scale war with Russia – even specific dates have been announced. We understand there are risks. If you have any additional information regarding the 100 percent guaranteed invasion of Ukraine by Russia on 16 February, please give it to us,” Volodymyr Zelensky told reporters on Saturday.

Naturally, Ukraine’s leaders are trying to calm the panic which Washington pronouncements and the Western media echo chamber have created…

Zelensky said he did not believe in the danger of a full-scale war at the moment. “I have to speak to the public with real information at hand. We receive information from many sources. We also have an intelligence service. I don’t think that it’s any worse than the intelligence services of other countries,” he noted.

Warnings of Russian invasion stoking ‘panic’ says Ukrainian President: Ukrainian President Volodymyr Zelensky says that warnings of an imminent Russian attack on his country were stoking “panic” and demands to see firm proof of a planned invasion. pic.twitter.com/cEuwEUrLpA

— worldnews24u (@worldnews24u) February 13, 2022

https://platform.twitter.com/widgets.js

And a fresh report from NBC News taken from the streets of Kiev suggests that many common Ukrainian citizens too can see through the hype:

Now, as the West warns a fresh attack is a “distinct possibility” as soon as next week, many in Kyiv aren’t convinced.

“I don’t believe that Russia is going to invade Kyiv. The situation is wound up from both sides,” Oleksandr Bovtach, 55, told NBC News. “The West and Putin are playing each other’s nerves.”

Although some are wary of an invasion, few are preparing for that possibility.

And notably a number of longtime Russia observers and mainstream journalists living on the ground in the region are beginning to have serious doubts…

I admit. I have not seen The Intelligence. But there’s never been a time when my understanding of Russia — my 15 years of reporting on Russia and Ukraine — has been so at odds with what the U.S. government says about Russia and Ukraine. I hope I’m right, and they’re wrong.

— Simon Shuster (@shustry) February 11, 2022

https://platform.twitter.com/widgets.js

As one foreign policy analyst observed Saturday, the situation ironically remains that “Everyone is predicting war between Russia and Ukraine except Russia and Ukraine.”

Biden and Zelensky are expected to hold a phone call Sunday, where it’s likely the Ukrainian leader will ask for Biden for firm evidence backing the latest White House alarmist claims. This will likely be a repeat of the last call they held: Biden and Zelensky last spoke last month and it “did not go well,” a senior Ukrainian official told CNN at the time, amid disagreements over the “risk levels” of a Russian attack.

Tyler Durden

Sun, 02/13/2022 – 17:10 - With Money Flowing Into Stocks At A Record Pace, Goldman Does Not See A "Larger Correction" Taking Place

With Money Flowing Into Stocks At A Record Pace, Goldman Does Not See A “Larger Correction” Taking Place

On Friday we observed that something odd was happening in the market: while stocks were tumbling, pushing most tech names into a deep bear market amid the worst turmoil for risk assets in years, inflows into stocks – both institutional and retail – have been soaring, and according to EPFR data compiled by Bank of America, cumulative equity flows YTD in 2021 have hit a record $153bn, exceeding the pace of early-2021 (when the year started with $151bn in inflows, ahead of a record year of more than $1tn inflows).

“How can this be”, we asked and answered that the catalyst behind this unprecedented scramble for risk “is that despite falling prices, investors are bailing on other even more impacted securities, and with a record outflows from money markets/cash as well as huge capital flight out of bond funds, this money has to go somewhere, and that “somewhere” is stocks for now, even though if the Fed is indeed set to hike 7 times this year and drain $2+ trillion from its balance sheet, the pain for stocks is only just starting.”

Over the weekend, Goldman desk trader Scott Rubner picked up on this peculiar flow dynamic, and roughly around the time that Goldman’s chief (retail client facing) equity strategist David Kostin was cutting the bank’s year-end S&P price target to 4,900 from 5,100 (while warning that much more downside could be in place if a recession hits), Rubner wrote that “with money flowing into global equities “at extreme levels”, this would need to change before a larger correction can take place: I would turn bearish if the money slows or reverses” he said, adding that “portfolio rebalances of this size typically last for the full quarter (Q1 2022).” Rubner also reminds that the “headlines will continue to be robust through March (i.e., advisor quarter-end rebalancing) March 4th NFP, March 10th Feb CPI, March 16th FOMC Meeting, etc.”

Here are the key observations from a still bullish Rubner, as the market continues to crack and remains unable sustain even a modest bounce:

1. Global Equities logged a massive $46.571 Billion worth of inflows this week. This is the 4th largest weekly inflow into Global Equities on record. This works out to $9.3B worth of inflows per day this week. This increased by +220% week over week.

2. Adjust for quarterly rebalances (inflows one week vs. outflows the next), this is the 2nd largest weekly inflow on record, after $58.087B, which happened this exact week in 2021 (2/10/2021).

3. Global Equities have logged $152.50B worth of YTD inflows. This annualizes to $1.322 Trillion. There have been 27 trading days this year or $5.7B inflows per day.

4. 2021 logged more equity inflows, $913 Billion, than the prior 25 years combined. 2022 is on pace to exceed this number by 45%.

Rubner writes that “in 2009, I officially retired the term “Great Rotation” or the movement of capital out of fixed income into equities, from my weekly emails and IB chat rooms. I switched this portfolio shift into the “Wedge”, which was the movement of capital into bonds and cash, and out of equities.”

But, as the Goldman trader notes, “if this shift of money continues at this rapid of a pace, I am adding back “Great Rotation” into the mix, as I expect the wedge needs to shrink given the trajectory of inflation.”

5. Since January 1st 2019, 3 years ago, Cash has seen $1.897 Trillion worth of inflows, Bonds have seen $1.824 Trillion worth of inflows, and Equities just $632 Billion. This makes the GS wedge $3.08 Trillion.

6. Goldman is are introducing the “anti-portfolio” asset allocation theme: “this has been the core of my zoom calls with allocators this week”, Rubner writes.

Money Market Outflows

7. Cash saw outflows of -$47.5B this week. This 100% funded the allocation to equities this week. Cash has seen substantial outflows YTD.

Bond Outflows

8. The current cash AUM is $4.593 Trillion, which clearly overstates “Cash on the sidelines”, but the point is that this a massive cash pile, earning now deeply negative inflation adjusted yield. $1.824 Trillion worth of cash was raised since 2019.

9. Global Bond outflows are now accelerating. I have been looking at this chart for the last 19 years. It’s rare to see bond outflows. Global bonds have seen outflows every week of 2022. They happen in clusters. ie when CNBC says that the outlook for bond allocation is not positive, the “Robo-Advisor” ETF allocation will trim passive bond allocations. This is the anti-portfolio.

10. Global Bonds have seen $1.897 Trillion worth of inflows in the last 3 years. This chart looks very “toppish”.

Credit Outflows

11. Global HY credit seems to be the place, which has benefited from this dynamic. Capital is rolling out of credit. I am popular among the crowd tracking “passive credit outflows”, which I am watching closely. Put open interest in most of these products is at record levels.

Rest-of-World Equities

12. Rest of World Equity Allocation is the anti-portfolio allocation. 2022 money is not going into growth/tech/USA.

13. Non-USD Equity allocations have scope to add and this is where the $$ is flowing.

14. Rubner writes that “Emerging Market Equities are resonating with clients. I sent out a note this week to asset allocators on Re-Emerging Markets. This is the most feedback that I have gotten on overall interest in EM again in years. The broad index has underperformed its historical relationship by 20% in the past year. (ie Brazil is up 17% YTD vs. SPX -5% YTD). There is anti-portfolio scope to add.”

15. Does the inflow picture change in March? As Rubner concludes, “retail is deploying record capital into the equity market, as is corporates, and systematic supply has abated. Not all clear, but there is a lot of capital looking for a home.”

* * *

One final chart, this one from Deutsche Bank’s Parag Thatte, confirms what we said on Friday – that even though tapering should in theory hit risk assets, the hit to even more overvalued bonds will result in funds flowing from bonds to equities (as was historically the case) thereby keeping stocks and other risk assets artificially elevated on the back of continued selloff in bonds, until either the selling reverses fully or everything is finally dragged down together.

Tyler Durden

Sun, 02/13/2022 – 17:00 - Is It Possible For Putin To Get Crimea Without Force?

Is It Possible For Putin To Get Crimea Without Force?

Authored by Steven Kopits via AmericanThinker.com,

Russian President Vladimir Putin is in a pickle.

Having mobilized his forces, he has committed his prestige, and Russia’s, at the Ukrainian border. He can scarcely afford to pull back without a loss of face, certainly for himself, and possibly no less for Russia. Indeed, Russia’s self-conception may be on the line.

On the other hand, invading Ukraine could become a disaster of epic proportions for Russia. There is much talk of the Russian army’s capability, but the underlying realities are sobering. Russia has a small economy, smaller than even that of Canada or South Korea. At $1.5 trillion, Russia’s GDP is one-fourteenth the size of the US economy, and its population is only half of America’s. Add in all of NATO and the disparity is even starker. NATO’s population is six times that of Russia, and its GDP is 25 times larger. The late senator John McCain was scarcely exaggerating when he called Russia a gas station masquerading as a country.

Successfully invading Ukraine, therefore, requires either speed to conclusion or passivity from NATO and, most importantly, the United States. Like it or not, Russia cannot move without US acquiescence, not unless Putin is willing to risk unmitigated disaster. Moreover, the US and NATO do not have to win for Russia to lose. NATO can bankrupt Russia out of petty cash merely by keeping the Russians in the field. In such an event, gas and oil sales will prove problematic and, of course, Russia will be unable to borrow from international capital markets.

Indeed, Russia will be entirely thrust upon the kindness of its neighbor, China’s President Xi Jinping. Such support could prove punishingly expensive. Xi can scarcely imagine his own equal, and he is certain that Putin is not that. Moreover, Xi has demonstrated a taste for real estate acquisitions, including the South China Sea and Taiwan.

But Taiwan is small potatoes compared to the vast Russian lands north of China. This includes a Russian coastline extending to the Arctic, one that would enable China’s effective domination of Japan. Russia is playing the Big Fish but is as likely to end up on Xi’s dinner plate. The harsh reality is that no country in Europe covets Russian land but, sooner or later, Xi’s attention will turn to Russia’s vast and empty east.

For Putin, this risks the worst of all worlds: A war in the west where Russia not only fails to secure Ukraine, but that also sees earlier gains in Crimea and Donbas reversed, along with the risk that NATO seizes Belarus, putting that country into the western camp. Russian weakness and dependence on Chinese support would make Moscow susceptible to China’s demands for compensation in the east. It is a nightmare scenario, but a not inconceivable outcome of a prolonged conflict in Ukraine.

Nevertheless, the status quo is also unsatisfactory. Russia has struggled to integrate occupied Crimea and the Donbas region into the Russian economy. Fighting continues sporadically in the Donbas area, and more importantly, Ukraine has cut off Crimea’s water supply. Much of Crimean agriculture had been irrigated by a canal from the Dnipro River, which Ukraine cut off after Russia invaded the peninsula in 2014.

Further, sanctions have depressed the Crimean tourist industry, a critical part of the economy there. Both Crimea and Donbas, therefore, appear to be continuing drains on the Russian treasury, although estimates differ. Some argue that the cost is negligible, but an annual burden of 2% of Russian GDP does not appear particularly implausible when subsidies, investments, and military costs are included.

Consequently, Russia and Putin are facing the prospect of a lose-lose situation. If they fight and lose, Russia will suffer a historic setback. On the other hand, if Russia backs down, then its hold on Crimea may become increasingly precarious over time, particularly if Ukraine cozies up to the west. At best, the country would be stuck with a problematic status quo. At worst, Ukraine could leverage NATO support to put the squeeze on Moscow.

Image: Vladimir Putin. YouTube screen grab.

As a result, Putin finds himself in a situation in which he can neither advance nor retreat without cost, time may not be on his side, and the risks are hard to judge. For the moment, the Germans are dead at the switch, but what of the Biden administration?

Washington has demonstrated weakness in foreign policy, notably by allowing the US to be ignominiously chased out of Afghanistan by a ragtag Taliban at a time when the US was neither taking casualties nor incurring extravagant costs. If the Biden administration exhibits such passivity in Ukraine and NATO sits on the sidelines, then Putin can take Ukraine and perhaps even Belarus and restore most of imperial Russia. But should Washington decide to intervene, the calculus is entirely different. Putin must weigh the risks.

Biden should have been clear upfront: The US would not abide re-writing Europe’s borders in this fashion and would meet the Russians in the field. That might have prevented Putin from investing so much of his and Russia’s prestige into this perilous venture. However, it would not have addressed Russian concerns and, if the US is to veto Russian action, as the global hegemon, America is obligated to find some reasonable accommodation.

It is important to emphasize that the US interest is not anti-Russian or pro-Ukrainian, or vice versa. America’s and NATO’s interest is in stability, normalcy, and peace. The intent is not only to integrate Ukraine into Europe but also to integrate Russia as well, such that its people should enjoy a status similar to that of, say, Hungarians or Poles. Gradual, steady progress towards prosperity in both Russia and Ukraine is the western interest, just as it is the interest of the Russian and Ukrainian people.

Still, Russia’s status can only be normalized pursuant to a settlement of the status of Ukraine’s currently occupied lands. Russia will not give these back. It is a matter of national pride. The occupied lands may yet be lost in war, but no Russian leader—not Putin nor his successor—would willing cede Donbas and Crimea.

What then should be done?

Fortunately, title to property may be settled by means other than force. It may be purchased. The status of the occupied territories could be resolved with appropriate payment. A reasonable price might be set at 1-2% of Russia’s GDP for a quarter-century; call it $0.5 – $1.0 trillion over twenty-five years. This would still be vastly cheaper than an unsuccessful—or even successful—war in Ukraine and present far less risk.

The move would pay for itself with lower costs associated with holding Crimea and through enhanced trade between Russia, Ukraine, and Europe. It would allow Putin to claim a victory for a show of force and see a path back to a normalization of Russia’s status in Europe.

Ukrainians may not be elated, but the reality is this: If Putin does not start a war, there appears no feasible path for Ukraine to reconquer the occupied territories. Neither the US nor NATO will underwrite such a venture. Meanwhile, Russia’s control over these territories will tend to create a fait accompli over decades, if not years. At some point, European leaders will tire of the whole matter and concede Russian hegemony over contested territories.

Therefore, unless one is wildly optimistic about prospects for the re-conquest of occupied territories, Ukraine’s interest is to put a dollar value on the land and take the money. Ukraine’s GDP totals $160 bn/year, a little more than 10% that of Russia. An annual payment of $25 billion from Russia would amount to 16% of Ukraine’s GDP, and resolving the conflict should boost GDP by as much again. Thus, ceding Crimea and other negotiated lands to Russia should boost Ukrainian GDP by perhaps one-third. This would not be a bad deal for Ukraine, all things considered.

Further, for the next quarter-century, ceding occupied lands to Russia through an agreement could be leveraged both to protect Ukrainian sovereignty and Finlandize Ukraine, subject to acceptable behavior from Moscow. That would provide plenty of time for the various parties to become accustomed to the new status quo.

For Russians, such a deal would mean tempering ambitions for reunifying Greater Russia, while Ukrainians would have to accept compensation for territorial losses. It would not be everything, but it is certainly far better than the potential disaster of a European war.

American and NATO interests dictate that the dispute between Ukraine and Russia be settled on reasonable, financial terms rather than through force. Our diplomacy should be geared to support that outcome.

Tyler Durden

Sun, 02/13/2022 – 16:30 - Super Bowl Pales In Comparison To The Biggest Game In Soccer

Super Bowl Pales In Comparison To The Biggest Game In Soccer

While Americans are getting ready for what they consider the biggest sporting event of the year, the 56th Super Bowl, the rest of the world couldn’t care less.

Well that may be a bit harsh, but, as Statista’s Felix Richter notes, from an American perspective it’s easy to overestimate the global appeal of the biggest game in (American) football.

Speaking of football, soccer, i.e. the proper kind of football from a European perspective, far exceeds the Super Bowl in terms of global interest.

You will find more infographics at Statista

The FIFA World Cup Final, played every four years to culminate a month-long tournament of 32 nations, really is the biggest game in the world, regularly reaching more than a billion people across the globe.

According to FIFA, the 2018 World Cup final between France and Croatia reached an average live audience of 517 million viewers, with more than than 1.1 billion people tuning in over its 90 minutes.

The 2021 Super Bowl pales in comparison, having had an average TV viewership of 91.6 million in the U.S. plus an estimated 30 to 50 million viewers around the world.

Tyler Durden

Sun, 02/13/2022 – 16:00 - Pentagon Docs Shed New Disturbing Light On Biden's Afghan Evacuation Disaster

Pentagon Docs Shed New Disturbing Light On Biden’s Afghan Evacuation Disaster

Authored by Kyle Anzalone via AntiWar.com,

A recently declassified Pentagon report on the US withdrawal from Afghanistan has renewed attacks against President Joe Biden from across the political spectrum. No doubt, the lack of foresight on the rapid collapse of the US-built Afghan government is inexcusable and created needless chaos.

New reporting on the August 26 suicide bombing at the Kabul airport – an attack that killed more than 150 people – suggests that some victims may have died of gunshot wounds, rather than the explosion. While the Pentagon has acknowledged that American and British troops fired “a small number of warning shots” from opposite sides of the crowd, it maintains that no Afghans were killed by US forces. Doctors in Kabul tell a different story.

Kabul airport evacuation, via FT In interviews with ProPublica and Alive in Afghanistan, six physicians from three different hospitals in the Afghan capital dispute the Pentagon’s claim that casualties were inflicted solely by “explosively propelled ball bearings” used in the improvised bomb.

“The doctors remained convinced that they saw wounds from bullets, not only ball bearings,” the outlets reported, adding “All said they had the experience necessary to make the distinction, having responded to numerous terrorist attacks and firefights in their medical careers.”

At Kabul’s Emergency Surgical Centre – an Italian-run facility which primarily treats war victims – doctors say they received 10 people killed by gunfire to the head, neck and chest. Others were also treated for non-fatal gunshot wounds.

“It was really a disaster situation,” said Dr. Mir Abdul Azim, a senior surgeon at the Centre who treated victims of the airport attack. While he noted that no bullets were recovered from his patients or the deceased, he said “he could tell that the wounds were caused by bullets and not ball bearings from the shape and size of the entry and exit wounds, along with other factors such as the tissue damage he saw.”

The suffering inflicted on Afghans is not limited to those killed during the withdrawal or who starve in their homeland under American sanctions. Thousands who were evacuated during the hasty US pull-out now find themselves stranded in the UAE. The conditions for the 10,000 people warehoused for months in the Emirates are so poor that protests have broken out, with many directing their anger toward Washington.

The meeting notes – published here in full – highlight how many crucial actions the Biden administration was deciding at the last minute, just hours before Kabul would fall and former Afghan President Ashraf Ghani would flee his palace in a helicopter.

— Jonathan Swan (@jonathanvswan) February 2, 2022