- Whitehead: "We, The People" Are The New, Permanent Underclass In America

Whitehead: “We, The People” Are The New, Permanent Underclass In America

Authored by John W. Whitehead & Nisha Whitehead via The Rurtherford Institute,

“We are now speeding down the road of wasteful spending and debt, and unless we can escape we will be smashed in inflation.”

– Herbert Hoover

This is financial tyranny.

The U.S. government—and that includes the current administration—is spending money it doesn’t have on programs it can’t afford, and “we the taxpayers” are the ones who must foot the bill for the government’s fiscal insanity.

We’ve been sold a bill of goods by politicians promising to pay down the national debt, jumpstart the economy, rebuild our infrastructure, secure our borders, ensure our security, and make us all healthy, wealthy and happy.

None of that has come to pass, and yet we’re still being loaded down with debt not of our own making.

Let’s talk numbers, shall we?

The national debt (the amount the federal government has borrowed over the years and must pay back) is $30 trillion and growing. That translates to roughly $242,000 per taxpayer.

Now the Biden administration is proposing a $5.8 trillion spending budget that notably includes $813 billion for national defense, $30 billion to “fund the police,” and a plan to reduce the national deficit by roughly $1 trillion over 10 years through additional tax hikes.

It’s estimated that the amount this country owes is now 130% greater than its gross domestic product (all the products and services produced in one year by labor and property supplied by the citizens).

The U.S. ranks as the 12th most indebted nation in the world, with much of that debt owed to the Federal Reserve, large investment funds and foreign governments, namely, Japan and China.

Essentially, the U.S. government is funding its very existence with a credit card.

In 2021, we paid more than $562 billion in interest on that public debt, which according to journalist Rob Garver, “is more than the annual budget of every individual federal agency except for the Treasury, the Department of Health and Human Services (which manages the Medicare and Medicaid government health insurance programs), and the Department of Defense.”

According to the Committee for a Reasonable Federal Budget, the interest we’ve paid on this borrowed money is “nearly twice what the federal government will spend on transportation infrastructure, over four times as much as it will spend on K-12 education, almost four times what it will spend on housing, and over eight times what it will spend on science, space, and technology.”

Clearly, the national debt isn’t going away anytime soon, especially not with government spending on the rise and interest payments making up such a large chunk of the budget.

Still, the government remains unrepentant, unfazed and undeterred in its wanton spending.

Indeed, the national deficit (the difference between what the government spends and the revenue it takes in) remains at more than $1.5 trillion.

If Americans managed their personal finances the way the government mismanages the nation’s finances, we’d all be in debtors’ prison by now.

Despite the government propaganda being peddled by the politicians and news media, however, the government isn’t spending our tax dollars to make our lives better.

We’re being robbed blind so the governmental elite can get richer.

We’re not living the American dream. We’re living a financial nightmare.

In the eyes of the government, “we the people, the voters, the consumers, and the taxpayers” are little more than pocketbooks waiting to be picked.

“We the people” have become the new, permanent underclass in America.

Consider: The government can seize your home and your car (which you’ve bought and paid for) over nonpayment of taxes. Government agents can freeze and seize your bank accounts and other valuables if they merely “suspect” wrongdoing. And the IRS insists on getting the first cut of your salary to pay for government programs over which you have no say.

We have no real say in how the government runs, or how our taxpayer funds are used, but we’re being forced to pay through the nose, anyhow.

We have no real say, but that doesn’t prevent the government from fleecing us at every turn and forcing us to pay for endless wars that do more to fund the military industrial complex than protect us, pork barrel projects that produce little to nothing, and a police state that serves only to imprison us within its walls.

If you have no choice, no voice, and no real options when it comes to the government’s claims on your property and your money, you’re not free.

It wasn’t always this way, of course.

Early Americans went to war over the inalienable rights described by philosopher John Locke as the natural rights of life, liberty and property.

It didn’t take long, however—a hundred years, in fact—before the American government was laying claim to the citizenry’s property by levying taxes to pay for the Civil War. As the New York Times reports, “Widespread resistance led to its repeal in 1872.”

Determined to claim some of the citizenry’s wealth for its own uses, the government reinstituted the income tax in 1894. Charles Pollock challenged the tax as unconstitutional, and the U.S. Supreme Court ruled in his favor. Pollock’s victory was relatively short-lived. Members of Congress—united in their determination to tax the American people’s income—worked together to adopt a constitutional amendment to overrule the Pollock decision.

On the eve of World War I, in 1913, Congress instituted a permanent income tax by way of the 16th Amendment to the Constitution and the Revenue Act of 1913. Under the Revenue Act, individuals with income exceeding $3,000 could be taxed starting at 1% up to 7% for incomes exceeding $500,000.

It’s all gone downhill from there.

Unsurprisingly, the government has used its tax powers to advance its own imperialistic agendas and the courts have repeatedly upheld the government’s power to penalize or jail those who refused to pay their taxes.

While we’re struggling to get by, and making tough decisions about how to spend what little money actually makes it into our pockets after the federal, state and local governments take their share (this doesn’t include the stealth taxes imposed through tolls, fines and other fiscal penalties), the government continues to do whatever it likes—levy taxes, rack up debt, spend outrageously and irresponsibly—with little thought for the plight of its citizens.

To top it all off, all of those wars the U.S. is so eager to fight abroad are being waged with borrowed funds. As The Atlantic reports, “U.S. leaders are essentially bankrolling the wars with debt, in the form of purchases of U.S. Treasury bonds by U.S.-based entities like pension funds and state and local governments, and by countries like China and Japan.”

Of course, we’re the ones who will have to repay that borrowed debt.

For instance, American taxpayers have been forced to shell out more than $5.6 trillion since 9/11 for the military industrial complex’s costly, endless so-called “war on terrorism.” That translates to roughly $23,000 per taxpayer to wage wars abroad, occupy foreign countries, provide financial aid to foreign allies, and fill the pockets of defense contractors and grease the hands of corrupt foreign dignitaries.

Mind you, that staggering $6 trillion is only a portion of what the Pentagon spends on America’s military empire.

The United States also spends more on foreign aid than any other nation, with nearly $300 billion disbursed over a five-year period. More than 150 countries around the world receive U.S. taxpayer-funded assistance, with most of the funds going to the Middle East, Africa and Asia. That price tag keeps growing, too.

As Forbes reports, “U.S. foreign aid dwarfs the federal funds spent by 48 out of 50 state governments annually. Only the state governments of California and New York spent more federal funds than what the U.S. sent abroad each year to foreign countries.”

Most recently, in response to Russia’s military aggression against Ukraine, the Biden Administration approved $13.6 billion in military and humanitarian aid for Ukraine, with an additional $200 million for immediate military assistance.

As Dwight D. Eisenhower warned in a 1953 speech, this is how the military industrial complex will continue to get richer, while the American taxpayer will be forced to pay for programs that do little to enhance our lives, ensure our happiness and well-being, or secure our freedoms.

This is no way of life.

Yet it’s not just the government’s endless wars that are bleeding us dry.

We’re also being forced to shell out money for surveillance systems to track our movements, money to further militarize our already militarized police, money to allow the government to raid our homes and bank accounts, money to fund schools where our kids learn nothing about freedom and everything about how to comply, and on and on.

It’s tempting to say that there’s little we can do about it, except that’s not quite accurate.

There are a few things we can do (demand transparency, reject cronyism and graft, insist on fair pricing and honest accounting methods, call a halt to incentive-driven government programs that prioritize profits over people), but it will require that “we the people” stop playing politics and stand united against the politicians and corporate interests who have turned our government and economy into a pay-to-play exercise in fascism.

Unfortunately, we’ve become so invested in identity politics that pit us against one another and keep us powerless and divided that we’ve lost sight of the one label that unites us: we’re all Americans.

Trust me, we’re all in the same boat, folks, and there’s only one real life preserver: that’s the Constitution and the Bill of Rights.

The Constitution starts with those three powerful words: “We the people.”

There is power in our numbers.

As I make clear in my book Battlefield America: The War on the American People and in its fictional counterpart The Erik Blair Diaries, that remains our greatest strength in the face of a governmental elite that continues to ride roughshod over the populace. It remains our greatest defense against a government that has claimed for itself unlimited power over the purse (taxpayer funds) and the sword (military might).

Where we lose out is when we fall for the big-talking politicians who spend big at our expense.

Tyler Durden

Thu, 04/14/2022 – 23:40 - How Many People Live In A Political Democracy Today?

How Many People Live In A Political Democracy Today?

Governments come in all shapes and sizes, but can ultimately be divided into two broad categories: democracies and autocracies.

Using the Regimes of the World classification system developed by political scientists Anna Lührmann, Marcus Tannenberg, and Staffan Lindberg and data from V-Dem, it’s estimated that 2.3 billion people – about 29% of the global population – lived in a democracy in 2021.

By contrast, as Visual Capitalist’s Dorothy Neufeld details below, that means 71% of people lived under what can be considered an autocratic regime.

In fact, the number of people considered to be living under a type of autocracy is at its highest total in the last three decades.

To see how this split has changed over time, the chart from Our World in Data, which uses data from the aforementioned sources, highlights how many people have lived under political democracies versus autocracies since the 18th century.

Forms of Political Democracies and Autocracies

First, let’s look at the four types of political regimes shown in the chart, based on criteria from the classifications of Lührmann et al. (2018):

-

Liberal democracies: Judicial and legislative branches have oversight of the chief executive, rule of law, and individual liberties.

-

Electoral democracies: Hold multiparty de-facto elections that are free and fair, have an elected executive, and institutional democratic freedoms such as voting rights, clean elections, and freedom of expression.

-

Electoral autocracies: Hold de-facto elections; democratic standards are lacking and irregular.

-

Closed autocracies: No elections are held for the chief executive or no meaningful competition is present.

It’s important to note that this is a fairly stringent and specific classification system. Many countries consider themselves an electoral democracy or strive to appear as one, but are still considered autocratic based on this criteria.

Using this categorization scheme, 34 countries can be considered liberal democracies, 55 are electoral democracies, 60 are electoral autocracies, and 30 are closed autocracies as of early 2022.

Over 200 Years of People Living in a Political Democracy

Many political systems around the world have made clear transitions in the last two centuries, but even in the last decade they’ve shifted substantially.

In 2010, the global population was split about 50/50 between democratic and autocratic regimes. Since then, there has been a clear trend towards autocratization.

Note: Missing regime data not included

Though modern democracies have roots in the 1700s and 1800s in Europe and the United States, governments have only more recently been able to check the boxes of the stringent democratic criteria highlighted above.

According to the data, liberal democracies and electoral democracies only emerged in Switzerland and Australia in the 1850s and in France in the 1870s after the Franco-Prussian war.

Following both World Wars, the number of democracies in the world increased, spreading across Europe, Latin America, and parts of Asia. After the Cold War, countries across Eastern Europe also adopted democracies, with the total populations shown in the table below.

On the flipside, it’s estimated that 5.5 billion people live in autocratic countries.

Electoral autocracies make up the majority of this total, with 3.5 billion people or about 45% of the global population today. Russia, Turkey, and Venezuela are considered electoral autocracies, as well as India since 2019.

Closed autocracies are the second-most common, and in the last decade, the number of closed autocracies rose from 25 to 30 countries.

One report estimates that as much as 20% of European countries are autocratizing as of 2021, including Hungary, Greece, Poland, and Croatia.

Changes in Political Systems

What countries became more autocratic in 2021, and why?

Coups, involving the overthrow of a government in power, played a large role behind the most recent autocratic shifts. Of the five coups that occurred in 2021, four—Chad, Mali, Guinea, and Myanmar—became classified as closed autocracies. Meanwhile, Nigeria, Tunisia, and El Salvador became classified as electoral autocracies.

Meanwhile, Austria, Portugal, Ghana, and Trinidad & Tobago shifted from liberal democracies to electoral democracies, as the transparency of laws and enforcement waned.

Moving in the opposite direction, both Armenia and Bolivia started being classified as democracies in 2021.

Current Obstacles

Reinforcing the current shift to autocracies is increasing polarization around the world. Research shows that political polarization is linked with democratic decline. Since 1950, 26 of the 52 instances of countries facing deep polarization saw their democratic systems downgraded.

At the same time, misinformation reinforces polarization. With democratic institutions facing headwinds, it remains unclear if current autocratic trends will continue.

Tyler Durden

Thu, 04/14/2022 – 23:15 -

- Israeli Spyware Maker NSO Group Asks SCOTUS For Sovereign Immunity

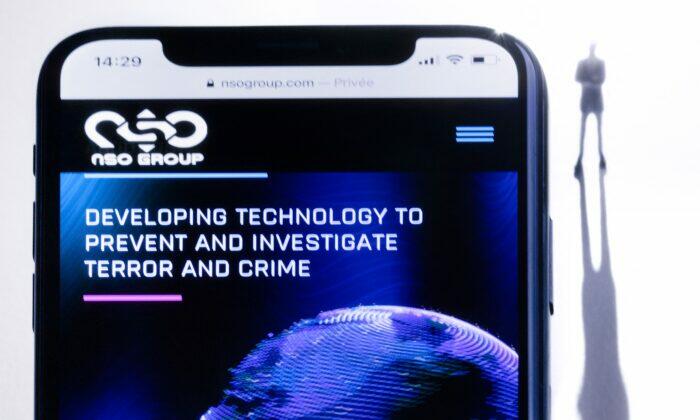

Israeli Spyware Maker NSO Group Asks SCOTUS For Sovereign Immunity

Authored by Matthew Vadum via The Epoch Times (emphasis ours),

Israeli spyware developer NSO Group is urging the Supreme Court to recognize it as a foreign government agent, a move it says would give it immunity under U.S. laws restricting lawsuits against foreign countries.

A smartphone with the website of Israel’s NSO Group, which features ‘Pegasus’ spyware, is displayed in Paris on July 21, 2021. (Joel Saget/AFP via Getty Images) NSO’s leading software product, Pegasus, allows operators to clandestinely surveil a suspect’s mobile phone—access contacts and messages, as well as the built-in camera, microphone, and location history. NSO says it deals only with government law enforcement agencies and that all sales are approved by the Israeli Defense Ministry. It refuses to identify its clients.

WhatsApp parent Facebook, which renamed itself Meta Platforms Inc., filed suit against NSO in 2019, claiming the company targeted about 1,400 users of its encrypted messaging service using sophisticated spyware. Meta wants to prevent NSO from accessing Facebook platforms and servers and is seeking unspecified damages.

WhatsApp accused NSO of wrongdoing in a statement.

“NSO’s spyware invades the rights of citizens, journalists, and human rights activists around the globe, and their attacks must be stopped,” WhatsApp said. Two U.S. courts have already rejected “NSO’s contrived bid for immunity, and we believe there is no reason for the Supreme Court to hear their last-ditch attempt to avoid accountability.”

Apple sued NSO in 2021, claiming it needed to do so to prevent NSO from hacking its products, calling the company’s employees “amoral 21st century mercenaries.”

Critics claim some NSO clients, including Poland, Saudi Arabia, and Jordan have used the company’s products to spy on adversaries and repress dissent. The U.S. Department of Commerce blacklisted NSO, saying its products have played a role in “transnational repression.”

But NSO, which is close to the Israeli government, says it cannot control what users do with its products and that it has done nothing wrong.

“NSO products are used exclusively by government intelligence and law enforcement agencies to fight crime and terror,” the company’s website states. Its products have been used to prevent car and suicide bombings, break up pedophilia rings, and help locate survivors trapped under collapsed buildings, the website continues.

Bestowing sovereign immunity on NSO would make it harder for WhatsApp to move forward and could shield NSO from a discovery process that could identify its customers and trade secrets.

The petition (pdf) in NSO Group Technologies Ltd. v. WhatsApp Inc., court file 21-1338, was docketed April 8 by the Supreme Court. The company is appealing an adverse ruling by the U.S. Court of Appeals for the 9th Circuit.

On Nov. 8, 2021, the 9th Circuit voted 3-0 (pdf) to deny NSO’s motion to throw out the lawsuit.

Circuit Judge Danielle Forrest, who was appointed by then-President Donald Trump, wrote: “[t]he question presented is whether foreign sovereign immunity protects private companies. The law governing this question has roots extending back to our earliest history as a nation, and it leads to a simple answer—no. Indeed, the title of the legal doctrine itself—foreign sovereign immunity—suggests the outcome.”

But in its petition, NSO states that many national governments, including the United States, rely on private contractors to carry out or support core governmental activities.

“If such contractors can never seek immunity, as the Ninth Circuit held, then the United States and other countries may soon find their military and intelligence operations disrupted by lawsuits against their agents,” the petition continues.

The respondents, WhatsApp and Meta, have until May 9, to file a response with the Supreme Court.

Tyler Durden

Thu, 04/14/2022 – 22:50 - "Not A Peak" – Manhattan Apartment Rents Hit Another Record High

“Not A Peak” – Manhattan Apartment Rents Hit Another Record High

The red-hot Manhattan apartment rental market continues to get even more challenging for tenants as average rents soar to another record high, according to Bloomberg, citing a new report from appraiser Miller Samuel Inc. and brokerage Douglas Elliman Real Estate.

Tenants paid an average rent price of $3,644 on new leases signed in March. Rents have soared 23% from a year earlier and are up $14 from the previous record high recorded in February.

A year ago, Manhattan apartment rents slumped as an exodus of urbanites from the borough fled to the countryside, cheaper communities, or even tax-haven Florida. However, since last spring, rental demand has surged. In March, about 20% of rents were signed at a 9.7% premium to their asking prices, suggesting a bidding war continues.

Even with most white-collar NYC workers still out of the office and remotely working or on some hybrid work schedule, people continue to flood the borough.

Landlords have had the upper hand in negotiating as the vacancy rate remained below 2% for a fourth consecutive month. In 2019, vacancies were around 2% but jumped to 10% after the pandemic.

“There’s a fair amount of growth in front of us, this is not a peak yet,” Jonathan Miller, president of Miller Samuel said.

“Right now, it’s ramping up into the spring and summer, and I would suspect we’re going to continue atypical rent growth until then,” Miller continued.

A separate report by real estate firm Corcoran Group noted that inventory is rising. However, they said listings are significantly down compared with last year.

Corcoran said last month that a shortfall of new apartment buildings in the borough could add to tighter inventory and further boost prices.

Tyler Durden

Thu, 04/14/2022 – 22:25 - Twitter's Chickens Come Home To Roost

Twitter’s Chickens Come Home To Roost

By Matt Taibbi of the TK News Substack

Elon Musk has reportedly attempted to purchase Twitter, and I have no idea whether his influence on the company would be positive or not.

I do know, however, what other media figures think Musk’s influence on Twitter will be. They think it will be bad — very bad, bad! How none of them see what a self-own this is is beyond me. After spending the last six years practically turgid with joy as other unaccountable billionaires tweaked the speech landscape in their favor, they’re suddenly howling over the mere rumor that a less censorious fat cat might get to sit in one of the big chairs. O the inhumanity!

A few of the more prominent Musk critics are claiming merely to be upset at the prospect of wealthy individuals controlling speech. As more than one person has pointed out, this is a bizarre thing to be worrying about all of the sudden, since it’s been the absolute reality in America for a while.

as someone who isn’t a fan of Elon Musk, I still find it darkly funny that billionaire-owned media is suddenly having a moral panic about a billionaire possibly buying Twitter

— David Sirota (@davidsirota) April 14, 2022

https://platform.twitter.com/widgets.js

Probably the funniest effort along those lines was this passage:

We need regulation… to prevent rich people from controlling our channels of communication.

That was Ellen Pao, former CEO of Reddit, railing against Musk in the pages of… the Washington Post! A newspaper owned by Jeff Bezos complaining about rich people controlling “channels of communication” just might be the never-released punchline of Monty Python’s classic “Funniest Joke in the World” skit.

Many detractors went the Pao route, suddenly getting religion about concentrated wealth having control over the public discourse. In a world that had not yet gone completely nuts, that is probably where the outrage campaign would have ended, since the oligarchical control issue could at least be a legitimate one, if printed in a newspaper not owned by Jeff Bezos.

However, they didn’t stop there. Media figures everywhere are openly complaining that they dislike the Musk move because they’re terrified he will censor people less. Bullet-headed neoconservative fussbudget Max Boot was among the most emphatic in expressing his fear of a less-censored world:

I am frightened by the impact on society and politics if Elon Musk acquires Twitter. He seems to believe that on social media anything goes. For democracy to survive, we need more content moderation, not less.

— Max Boot 🇺🇦 (@MaxBoot) April 14, 2022

https://platform.twitter.com/widgets.js

In every newsroom I’ve ever been around, there’s always one sad hack who’s hated by other reporters but hangs on to a job because he whispers things to management and is good at writing pro-war editorials or fawning profiles of Ari Fleischer or Idi Amin or other such distasteful media tasks. Even that person would never have been willing to publicly say something as gross as, “For democracy to survive, it needs more censorship”! A professional journalist who opposed free speech was not long ago considered a logical impossibility, because the whole idea of a free press depended upon the absolute right to be an unpopular pain in the ass.

Things are different now, of course, because the bulk of journalists no longer see themselves as outsiders who challenge official pieties, but rather as people who live inside the rope-lines and defend those pieties. I’m guessing this latest news is arousing special horror because the current version of Twitter is the professional journalist’s idea of Utopia: a place where Donald Trump doesn’t exist, everyone with unorthodox thoughts is warning-labeled (“age-restricted” content seems to be a popular recent scam), and the Current Thing is constantly hyped to the moronic max. The site used to be fun, funny, and a great tool for exchanging information. Now it feels like what the world would be if the eight most vile people in Brooklyn were put in charge of all human life, a giant, hyper-pretentious Thought-Starbucks.

My blue-checked friends in media worked very hard to create this thriving intellectual paradise, so of course they’re devastated to imagine that a single rich person could even try to walk in and upend the project. Couldn’t Musk just leave Twitter in the hands of responsible, speech-protecting shareholders like Saudi Prince Alwaleed bin Talal?

Saudi Prince Alwaleed bin Talal and his company Kingdom Holding, which have held big stakes in Twitter, dismissed Elon Musk’s offer to buy the social-media platform https://t.co/0snqiLPtlu

— The Wall Street Journal (@WSJ) April 14, 2022

https://platform.twitter.com/widgets.js

Interesting. Just two questions, if I may.

How much of Twitter does the Kingdom own, directly & indirectly?

What are the Kingdom’s views on journalistic freedom of speech?

— Elon Musk (@elonmusk) April 14, 2022

https://platform.twitter.com/widgets.js

Even though it hasn’t happened yet, why wait to start comparing Musk’s Twitter takeover to the Fourth Reich? Journalism professor Jeff Jarvis of CUNY certainly thinks it isn’t too soon:

Today on Twitter feels like the last evening in a Berlin nightclub at the twilight of Weimar Germany.

— Jeff Jarvis (@jeffjarvis) April 14, 2022

https://platform.twitter.com/widgets.js

The most incredible reaction in my mind came not from a journalist per se, but former labor secretary Robert Reich. His Guardian piece, “Elon Musk’s vision for the internet is dangerous nonsense,” is a marvel of pretzel-logic, an example of what can happen to a smart person who thinks he’s in Plato’s cave when he’s actually up his own backside. The opening reads:

The Russian people know little about Putin’s war on Ukraine because Putin has blocked their access to the truth, substituting propaganda and lies.

Years ago, pundits assumed the internet would open a new era of democracy, giving everyone access to the truth. But dictators like Putin and demagogues like Trump have demonstrated how naive that assumption was.

Reich goes on to argue… well, he doesn’t actually argue, he just makes a series of statements that don’t logically follow one another, before dismounting into a remarkable conclusion:

Musk says he wants to “free” the internet. But what he really aims to do is make it even less accountable than it is now… dominated by the richest and most powerful people in the world, who wouldn’t be accountable to anyone for facts, truth, science or the common good.

That’s Musk’s dream. And Trump’s. And Putin’s. And the dream of every dictator, strongman, demagogue and modern-day robber baron on Earth. For the rest of us, it would be a brave new nightmare.

Reich starts by talking about how Vladimir Putin is cracking down using overt censorship, progresses to talking about how making the Internet less “accountable” is bad, then ends by saying Musk is like Putin, and Trump, and every evildoer on earth, again before Musk has even done anything at all. He may be trying to say that Musk could use algorithms to silently push reality in the direction he favors, but this is the exact opposite of Vladimir Putin passing laws outlawing certain kinds of speech. Any attempt to argue that dictators are also speech libertarians is automatically ridiculous.

More to the point, where has all this outrage about private control over speech been previously? I don’t remember people like Reich and Jarvis, or Parker Molloy, or Scott Dworkin, or Timothy O’Brien at Bloomberg (“Elon Musk’s Twitter Investment Could Be Bad News for Free Speech”), bemoaning the vast power over speech held by people like Sergei Brin, Larry Page, or even Jack Dorsey once upon a time. That’s because the Bluenoses in media and a handful of hand-wringers on the Hill successfully paper-trained all those other Silicon Valley heavyweights, convincing them to join on with their great speech-squelching project.

It’s become increasingly clear over the last six years that these people want it both ways. They don’t want to break up the surveillance capitalism model, or come up with a transparent, consistent, legalistic, fair framework for dealing with troublesome online speech. No, they actually want tech companies to remain giant black-box monopolies with opaque moderation systems, so they can direct the speech-policing power of those companies to desired political ends.

When someone like Reich says, “Billionaires like Musk have shown time and again they consider themselves above the law. And to a large extent, they are,” he’s talking about an authoritarian framework that already exists in the speech world, just with different billionaires at the helm. What’s got him cheesed off isn’t the concept of privatized civil liberties — we’re already there — but the idea that one particular billionaire might not be on board with the kinds of arbitrary corporate decisions Reich likes, like removing Trump (“necessary to protect American democracy,” he says).

When I first started to cover the content-moderation phenomenon back in 2018, I was repeatedly told by colleagues that I was worrying over trivialities, that there couldn’t possibly be any negative fallout to coordinated backroom deals to de-platform the likes of Alex Jones, or to the Senate demanding Facebook, Twitter, and Google start zapping more “Russian disinformation” accounts. Even when I pointed out that it wasn’t just right-wingers and Russians vanishing, but also Palestinian activists and police brutality sites and a growing number of small independent news outlets, most of my colleagues didn’t care. Because they were so sure they’d never be targeted, the credentialed media were mostly all for the most aggressive possible conception of “content moderation.”

It was beyond obvious that self-described progressives would eventually regret hounding people like Mark Zuckerberg to start getting into the editorial business, and that pushing Silicon Valley to take a bigger interest in controlling speech was flirting with disaster. Of course they would someday wake up to find these companies owned by people less sympathetic to their niche political snobbery, and be horrified, and wish they’d never urged virtually unregulated tech oligopolies to start meddling in the speech soup.

Now, here we are. To all those people who are flipping out and shuddering over the possibilities (CNBC: “If he owns the whole place…? The Orange man is probably going to be back!”), remember that you didn’t mind when other unaccountable tycoons started down this road. You cheered it on, in fact, and backlash from someone with different political opinions and real money was 100% predictable. This is the system you asked for. Buy the ticket, take the ride, you goofs!

Tyler Durden

Thu, 04/14/2022 – 22:20 - "The West Needs WWIII" – Martin Armstrong Warns "There's No Return To Normal Here"

“The West Needs WWIII” – Martin Armstrong Warns “There’s No Return To Normal Here”

Via Greg Hunter’s USAWatchdog.com,

Legendary financial and geopolitical cycle analyst Martin Armstrong thinks the New World Order’s so-called “Great Reset” plan for humanity now needs war to try and make it work.

It could happen in the next few weeks.

Armstrong explains, “What they are trying to do is deliberately poke the bear…”

“They are increasing the pressure on just about everything under the sun. The West needs World War III. They just need it. The real problem here is they went to negative interest rates in 2014 in Europe. They have been unable to stimulate the economy, and Keynesian economics have completely failed…

I would say this is mismanagement of government on a global scale. The problem is that central banks have no control over the economy.

Add to this, this type of inflation is substantially different than a speculative boom. This inflation is based upon shortages. These morons with covid… with lockdowns, ended up destroying the supply chains…

Things that are there, I buy extra of because next time it might be gone. So, everybody is increasing their hoarding…

So, what we have with Europe, with its negative interest rates, they have wiped out all the pension funds. They need 8% to break even, not negative rates. There is not a pension fund in Europe that is solvent at this stage of the game. . . . The European government is collapsing. If they end up defaulting, you are going to have millions of people down there with pitch forks storming the parliament. So, to avoid that, they need war…

The Biden Administration has deliberately destroyed the world economy.”

If there is war in Europe, the “U.S. dollar will get stronger initially and not weaker” according to Armstrong. Armstrong also says,

“This is all deliberate. There is no return to normal here. Unfortunately, this is where we are headed.”

Armstrong contends, war in Europe could break out in a couple of weeks, and the EU and NATO are pushing this. Armstrong says,

“They want Russia to do something. . . . This thing with Russia is the same thing all over again. Unfortunately, we are headed for war.”

Armstrong also talks in detail about the following subjects: Digital currency and why the Deep State is pushing so hard for it; gold, silver, food and just about everything going way up in price because of shortages.

Armstrong recommends that people “stockpile two years of food.” Armstrong has other tips for what the common man needs to stock up on; Armstrong also says President Trump is the only President he knew that cared about U.S. soldiers dying in combat. This is why Trump wanted to bring the troops home, and the Deep State warmongers hated him for it.

Armstrong also gives his predictions on who wins the midterm election this coming November. Will it matter which party comes out on top?

In closing, Armstrong says,

“We are not getting back to normal. The system is crumbling from within, and it’s just like the fall of Rome, basically.”

(There is much more in the nearly 1 hour interview.)

Join Greg Hunter of USAWatchdog.com as he goes One-on-One with Martin Armstrong cycle expert and author of the popular book “Manipulating the World Economy,” for 4.12.22.

* * *

To Donate to USAWatchdog.com Click Here

There is some free information, analysis and articles on ArmstrongEconomics.com.

Tyler Durden

Thu, 04/14/2022 – 22:00 - Does 'Dark Tetrad' Of Personality Traits Drive Some To Buy Crypto?

Does ‘Dark Tetrad’ Of Personality Traits Drive Some To Buy Crypto?

Having blown their efforts to leverage the ESG ‘movement’ to attack cryptocurrencies (‘mining is killing the climate’) and failed to find any actual evidence that cryptocurrencies are a major source of illicit finance (especially relative to dollar dollar bills and the banking system) it appears the skeptics have found a new FUD angle to attack the ‘freedom’ of decentralized currency.

The last few years have seen cryptos soar to record highs with a multi-trillion-dollar ‘market cap’ and an accelerating rate of adoption, despite the extreme volatility of the ‘young’ asset-class.

So, five ‘scientists’ set about to find out what kind of person is attracted to this kind of volatility, fear, uncertainty, and doubt.

What they found is perfect for headline-writers – there is a link between “dark tetrad” personality traits and attitudes towards cryptocurrency.

The “dark tetrad” – a term used in psychology – refers to a group of four personality traits – Machiavellianism, narcissism, and psychopathy (together known as the “dark triad”), plus sadism.

All four dark tetrad traits correlated with an affinity for investing, each for their own reasons.

According to the researchers, dark tetrads are partly drawn to crypto because they are prepared to take risks.

Based on a pre-registered survey of the main research question rather than hypotheses (N = 566), it was found that:

-

Narcissism was positively associated with crypto attitude which was mediated by positivity.

-

Machiavellianism was associated with buying intention which was mediated by conspiracy beliefs. Machiavellians were more distrustful of government which was associated with a greater desire to buy crypto.

-

Psychopathy affected crypto judgments through FoMO and a negative effect on positivity.

-

Sadism is associated with FoMO and a lack of positivity which affects crypto judgments.

So there you have it folks – if you’re a conspiracy theorist, distrust government, are overly positive or over-confident, and/or have a fear of missing out (in other words, if you’re a psychopath, narcissist, or a sadist); you’re highly likely to be a fan of crypto…

Crucially, as TheConversation notes – deep in their report – the ‘scientists’ admit this is not a two-way causal relationship – i.e. while many ‘reporters’ would like to claim this study shows that crypto-enthusiasts are all psychos, the study in fact only suggests the causality runs from being a pyscho narcissist to liking crypto (and not necessarily the other way around)…

“We are not suggesting that everyone interested in crypto displays dark tetrad traits.“

So if you find yourself inexplicably drawn to the ‘escape hatch from tyranny’ that is the crypto-world, have no fear – it doesn’t make you a crazy person, as Dr. Wang said: “If you happen to be a Bitcoin or other crypto holder, you may or may not exhibit [these traits].”

Tyler Durden

Thu, 04/14/2022 – 21:35 -

- Ukraine War Revives Supply Chain Crisis

Ukraine War Revives Supply Chain Crisis

By Maartjie Wijffelaars and Erik-Jan van Harn of Rabobank

Summary

The Ukraine war has sparked another supply chain crisis, just as pandemic-related disruptions had started to ease.

- Europe depends on Russia, Ukraine and Belarus for its energy imports, but also for some chemicals, oilseeds, iron and steel, fertilizers, wood, palladium and nickel, amongst others.

- Especially the energy dependency is a vulnerability, now that Russia is demanding ruble payments for its exports. It is unlikely that Europe would be able to fully replace Russian gas in the short term, whilst most of the Russian oil and solid fossil fuels could be replaced.

- Besides energy goods, disrupted supply of pig iron and several other iron and steel products, nickel and palladium will likely have the largest impact on EU industry.

- EU supply chains could also be distorted via war-related production disruptions in third countries. The EU could face challenges in importing e.g. electronic circuits from third countries, as these require inputs such as nickel and neon gas sourced from the warzone.

- Germany and Italy are relatively vulnerable to the crisis because of their relatively large industrial sectors, strong reliance on Russian energy, and in case of Italy strong reliance on Russia and Ukraine for certain iron and steel imports and gas in its total energy mix

Will we ever catch our breath?

Just as supply chain issues caused by the pandemic were starting to ease (Figure 1), the next crisis has presented itself. The war in Ukraine is making clear that large parts of the world depend on Russia, Ukraine and Belarus for basic necessities such as food, energy and other commodities.

Trade with Russia, Belarus and Ukraine (referred to as the warzone in the remainder of this piece) has come close to a halt due to a wide range of sanctions, self-sanctioning (mainly by western companies), and strongly disrupted production and transport in Ukraine. Although the overall share in world trade is limited for those countries, trade disruptions can have large implications for both specific firms and industries as well as entire economies. Disruptions (both actual and feared) to imports from the warzone will hurt the EU more than less exports to the warzone. Not only because the warzone accounts for a larger share in the EU’s imports than exports (Figure 2), but especially because less imports of commodities and intermediate products can have knock-on effects on multiple production processes in the EU.

In Part I of this research note we will zoom in on the EU’s direct and indirect dependence on non-food commodities and goods imported from the warzone. We will assess which EU industry subsectors are most vulnerable for the disruptions caused by the war. In Part II we compare the vulnerability of the largest Eurozone countries.

The revival of supply chain disruptions

On top of oil and gas, Russia, Belarus and Ukraine are producers of a number of key commodities that are used in everyday items or in the production thereof– such as pig iron, palladium and neon. Next to commodities, certain industries also depend on these countries for intermediate products. A striking example is the dependence of several German car factories on certain car parts produced in Ukraine. This has already led to the closure of several German car factories.

We can split up the effects on supply chains into first order and second order effects. First order effects are caused by a reduction in direct trade between the warzone and the European Union. There are two types of second order effects. The first is less trade between the warzone and third countries that results in fewer supply of products to the EU from those third countries. The second

is less EU production of intermediate goods due to higher energy prices -or even shortages- as a result of the war and, consequently, less production of downstream goods for which these intermediates serve as inputs (Figure 3).

Part I: EU dependence on goods from the warzone

We start our analysis by looking for products for which the EU27 depends heavily on Russia, Ukraine and Belarus. We then omit those products that can easily be imported from other parts of the world and those which do not play a vital economic role. For example, Germany is quite dependent on Russia for raw fur skins, but it is safe to say that Germans and the German economy will survive without fur coats.

Table 1 lists the most exposed vital economic goods based on these principles, with a minimum net import volume of EUR1bn. In the table we have aggregated certain product lines that came out on top in this analysis, to prevent getting lost in too much detail. Note that the row ‘chemicals’, for example, does not encompass all chemicals, yet only those that fulfil the above criteria. A list of the specifics for each product group can be found in the appendix. Apart from food products, the EU extensively depends on the warzone for several energy goods, chemicals, fertilizers, and metals – such as iron, nickel and palladium. And apart from, perhaps, chemicals, it seems rather difficult for the EU to find alternative suppliers for these goods and will likely at least cause price rises.

Below we will elaborate on usages and the consequences of reduced availability of the non-agri products listed in table 1 and where necessary, on specific products within those product groups. We also give some indication on the relative ease or difficulty to substitute these products.

All in all, we find that many sectors are likely to face disruptions to the supply of inputs and/or higher prices thereof. Most vulnerable seem to be production of basic metals and fabricated metal products. Other sectors that will certainly be impacted as well are construction, machinery and equipment, and transport equipment.

EU dependence on Russian energy

The most obvious link with Russia is on the part of energy commodities. The EU relies on Russia for 21% of its oil imports, 37% of its gas imports and roughly 45% of its solid fossil fuels imports. Energy imports are not yet subject to outright sanctions in the EU and are still flowing, but the possibility of sanctions is talk of the town. In any case, fear of reputational damage and of accidently breaching sanctions has already led to some reduction of Russian oil imports in the EU. Meanwhile, Russia is demanding ruble payments for its exports, which the EU is currently refusing to pay. For the time being, Gazprombank will help European companies to convert their euro payments to rubles, but it is still possible that gas deliverance will be weaponized. Finally, the EU has presented a plan to cut back on Russian energy dependence over the coming year(s). In other words, it is useful to dive into the EU’s dependence on Russian energy, to grasp if we could do without. Not surprisingly it appears that it won’t be easy to get rid of Russian energy altogether and it would certainly lead to a shock effect in the short run if energy trade with Russia came to a sudden standstill. It would lead to energy shortages, possibly requiring rationing of energy consumption for the industry, leading to a substantial drop in industrial production. Special thanks to our energy strategist, Ryan Fitzmaurice, for providing us with the much needed background on energy markets.

Gas

It is unlikely that Europe could replace Russian gas with alternative gas in the short run.

The most obvious way to cope with a halt of Russian gas imports, would be to replace Russian gas with non-Russian gas imports. Yet as we have already explained in a recent research note, there probably isn’t enough available gas to, suddenly, replace Russian supply. Moreover, switching to different gas suppliers also faces technical constraints. Much of Europe’s gas is supplied through pipelines in Central- and Eastern-Europe from the east to the west, which are not suitable for sending gas the other way around -at least not on a short notice.

It is also unlikely that LNG imports will fill the gap in the short run. Apart from a lack of availability -certainly in the short run-, some EU countries lack the infrastructure needed to import LNG. LNG needs to be converted to a gas state in LNG terminals before it can be transported through a network of pipelines. Germany, for example, does not have any LNG terminals and neither do landlocked countries such as Czech Republic.

Were it to come to gas shortages, switching to alternative fuels, like coal, is potentially necessary to avoid an energy shortage in the winter. But it goes without saying that increasing coal consumption is not in line with Europe’s green ambitions.

A full report on Europe’s gas dependency can be found here.

Oil

Replacing oil could be somewhat easier than replacing gas, although it would come at a higher cost. Even though some oil is transported via pipelines, it can also be transported via ship or railway, without the need to liquify it first (as is the case with gas). This means that, if Europe can get its hands on oil of a similar grade, Russian oil that is transported through pipelines in central and eastern Europe, could be replaced, albeit at a higher price. Europe would have to compete with countries that currently rely on those types of oil, potentially pushing those countries, such as India or China, to importing the (cheaper) oil from Russia.

That is a big if however. Oil can differ strongly depending on its origin. Usually different oils are characterized by their sulphur content and density. Ural oil is a medium sour crude oil (figure 6). The closest replacement crudes are from Saudi Arabia, Iran and Oman. In addition, the medium sweet barrels from the North Sea, West Africa and the United states would also be suitable alternatives, with less need to desulfurize the crude (a process that is very natural gas intensive). Refineries are usually tailored to a specific kind of oil, but could switch their operations to accommodate other types of oil in a relatively short period of time, but testing and blending of the new crudes are required to ensure smooth operations.

Solid fossil fuels

Friday 8 April, the EU announced a ban on Russian solid fossil fuel imports from August. While this has induced the price for coal to increase and can hurt specific factories, in our view, the omittance of Russian coal won’t be a major problem on a macro scale.

The EU also gets about one-third of its imported solid fossil fuels -mainly coal- from Russia. At first sight, this seems to imply the EU is rather dependent on Russia for this part of its energy consumption too. But the figure overstates the importance of Russian coal imports for the EU. First, coal is not as important to most European countries as gas or oil. On average, solid fossil fuels -mostly coal- are good for 11% of total EU energy consumption (Figure 4). Second, while a couple of countries, especially in the eastern part of Europe, still rely on coal for a significant part of their energy consumption (Figure 9), most of these countries are either pretty self-reliant or mainly import their coal from countries other than Russia. Major consumer Poland for example, produces around 98% of its coal consumption domestically. Moreover, although clearly in contradiction with the green ambitions of the European Union, the EU could decide to produce more coal if push comes to shove.

Halted EU production due risen energy prices

As mentioned, gas and oil imports are not yet subject to outright sanctions in the EU. Yet energy prices have jumped (Figure 7) upon uncertainty over the future of Russian energy imports in the EU, a ban on Russian oil in the US, and a voluntary drop in purchases of especially Russian oil by European buyers, amongst other things -data on the coal price is from before the announcement of the ban on Russian coal imports. Despite a drop since their war-peak, energy prices are still higher than at the start of the year and just prior to the start of the war. These higher energy prices, in turn, have led to production cuts of energy intensive products in the EU such as aluminium, zinc, steel, ceramics, concrete, bricks, glass, asphalt, paper and fertilizers – especially large gas consumers had also already taken a hit from surging prices last year. This will not only hamper the production of these specific products, but also frustrate downstream production for which these goods serve as inputs.

The disruptions will certainly hit the construction sector, a sector that was already dealing with lengthy delivery times for several inputs. Furthermore, higher input prices will likely hit margins of construction companies and project developers, raise consumer prices of construction projects, and lead to delays and cancelations of projects.

Other sectors that will see the costs of their non-energy inputs rise are for example machinery and equipment, consumer appliances, and transportation due to less steel and aluminium production. Meanwhile, less production of paper -or higher prices- will be felt across many sectors that need packaging material. And finally, lower fertilizer production in the EU adds to less supply from the warzone countries (see below), impacting especially the agricultural sector.

EU dependence on chemicals, fertilizers and wood imports

Apart from energy commodities, the EU quite extensively depends on the warzone for certain chemicals, fertilizers, certain types of wood, rubber and several types of metal.

Chemicals include carbon (black) which is used, to strengthen rubber in tires for example, and ammonia which is mostly used to produce fertilizers. Combining the former with the EU’s dependence on Russia for the ‘end product’ rubber (12% import market share), there could be an impact on the car sector. That said, based on world market shares it should not be too difficult to shift to other suppliers if importers are ready to pay a somewhat higher price. Limited availability of fertilizers due to lower imports from the warzone and less production in the EU poses a challenge for agriculture and hence ultimately the food sector. Meanwhile, Russia is the world’s largest exporter of lumber and is an important supplier of different types of wood for the EU’s construction sector and fuel wood. Although we do not expect any shortages here, due to the wide availability of wood from other parts of Europe, we do expect higher prices.

EU dependence on metal imports

Table 1 also shows a large dependence on the warzone for different metals with in some cases limited diversification possibilities. Should the prices of products mentioned below rise, delivery times are likely to lengthen as it usually takes time to find alternative suppliers. In some cases actual shortages could arise -although it is difficult to get a grip on the timing thereof due to missing details on the size of stocks.

Most vulnerable in this respect are sectors making use of iron and steel, nickel, palladium and aluminium: basic metals and fabricated metal products, machinery and equipment, transportation, computer and electronic products, and construction.

Iron and steel

To illustrate, more than 50% of EU imports of pig iron -used to make steel-, ferrous ore products, semi-finished iron and non-alloy steel products, and waste from iron and steel production comes from the warzone. Especially for pig iron and waste there are few alternatives as the warzone has a world export market share of respectively 63% and 52%. But also for the ferrous and semi-finished products diversification will be difficult, given the world market share of 30% and 40%. Fewer steel imports from the warzone adds to pressure in the market from less production in the EU itself due to the risen energy prices. Iron and steel have a broad range of destinations. They not only end up in the basic and fabricated metal industry, but also construction, production of machinery, equipment (that obviously includes ‘military’) and automotive.

Nickel and aluminium

Another important metal with availability at risk is nickel. Nickel is essential for rechargeable batteries, medical devices, automotive, and electrical and electronic equipment. It is also used in construction and to make stainless steel. The EU gets 90% of its nickel mattes’ imports from the warzone and 20% of its unwrought nickel. Russia is in the top three of global exporters of nickel -playing musical chairs with the US and Canada- and has a global export market share of 15%. Moreover, it’s a very tight market, especially due to nickel being required in rechargeable batteries, with ever growing demand due to the world’s push for electrification. Hence it is likely to be challenging -at best- to replace nickel imports from Russia and will for sure induce higher costs. With regards to aluminium, Russia is the steady number 2 exporter in the world, with a market share of 10%. Some 12% of EU imports of unwrought aluminium is sourced from Russia. Fewer aluminium imports from Russia adds to pressure in the market from less production in the EU itself due to the risen energy prices. Aluminium has a broad range of applications and is used for, for example, wires and cables in electrical equipment, in construction, transportation, machinery and equipment and electronic products, e.g. consumer appliances.

Palladium and platinum

The final metal we will highlight is the rare metal palladium. EU import dependence on Russia is 27%, with Russia having a world export market share of 23%. Palladium is a by-product of nickel and platinum mining, amongst others, and hence it is tough to ramp up production. In other words, the EU is both very dependent on Russia and it won’t be easy to get a grip on alternative supplies -at least not at favourable costs. Importantly, palladium is used as a catalytic converter in cars: in both gas engine cars to reduce the emission of polluting gasses and as a catalyst in hydrogen fuel cell vehicles. It is also used in multilayer ceramic capacitors and hard disks, which in turn can be found in laptops and phones for example. Other uses of palladium are in sensors, chips, surgical instruments and dentistry. For most applications there are alternatives such as platinum, although opinions on the quality of substitutes differ. Currently, the EU gets 9% of its platinum imports from Russia, and the latter’s world export market share is 7%. Yet, if palladium is being replaced by e.g. platinum, clearly the price of the latter would likely explode as well -unless the world’s largest platinum producer South Africa more or less doubles its platinum production.

To sum it all up

So, in short, the EU -and also the world- depends heavily on Russia, Ukraine and Belarus for several key inputs to its industrial sector. Among those commodities are gas, oil, iron and steel products, nickel, palladium, several chemicals and aluminium. Combined, the products in table 1 only account for some 1% of EU GDP. Yet their value alone does not give the full picture of their importance to lengthy industrial value chains -and food security as far as the agri-related commodities are concerned.

Gas and oil are still flowing, but a sudden stop in Russian gas imports would clearly have significant ramifications for the entire industrial sector. Risen energy prices have already curtailed EU production of energy intensive products. Meanwhile, halted or limited inflows of the non-energy commodities certainly has an impact on the price of these products and lengthens delivery times, which will be felt by multiple industrial subsectors.

Topping the list of most exposed sectors are basic metals and fabricated metal products. Thereafter we find construction, chemicals, coke and refined petroleum products, wood and paper, machinery and equipment, and transport equipment with more or less the same impact score. Whereas risen energy prices have a higher impact on some, commodity shortages and higher prices of non-energy goods are more problematic for others.

Second order effects via non-EU countries

Apart from vulnerabilities due to direct trade links between the EU and the warzone, the EU will likely also be impacted via trade with third countries. In this respect, vulnerable product groups are motorcycles, electronic circuits, batteries and electronics and electrical machines.

To get a feeling for second order effects that run via non-EU countries, we adopt a two-step approach. First, we look at the product categories for which the European Union is not self-sufficient. Unfortunately, it is hard to find any consumption data on this level of detail, so we look at the average ratio of imports to exports over the last couple of years. Second, we filter the data to exclude product groups with a trading volume smaller than EUR 1bn. Third, we have excluded the goods that already popped up in the analysis of direct trade links between the EU27 and Russia, Belarus and Ukraine.

The second step is to look at whether these products -are likely to- consist of inputs coming from the warzone and/or include inputs which have experienced large price rises due to the war. Due to the globally intertwined supply chains and data gaps in this respect we have to resort to proxies in some cases. We start by listing products for which the warzone countries have a significant world market share. The larger their combined market share, the larger the chance that producers depend on the warzone countries. And even if producers don’t rely on the warzone themselves, they are likely to be confronted with price increases if manufacturers in other countries start looking for alternatives for their inputs from the warzone. For products where the warzone countries have a combined world market share above 10%, we check whether these products are commonly used in the production process of the goods in table 2.

We also have to take into account whether the dependency relies on goods and commodities from Russia or Ukraine. China, for example, has not yet joined the west in imposing sanctions on Russia, and thus for now Russian goods will continue to flow to China. For Ukraine it is different, however, given that production has (partially) come to a standstill.

Some of the product groups listed in table 2 are vulnerable due to the current sanctions or the production fallout in the warzone. This mainly holds for motorcycles, electronic circuits, batteries and electronics and electrical machines.

Motorcycles

Motorcycles production is dependent on long, optimized supply chains and is therefore vulnerable to any disruption whatsoever. Moreover, most new motorcycles are packed with chips (see below) and other electronics (which were already in short supply before the war started!) and are built using steel, aluminium, plastics and rubber. Russia is a global player when it comes to steel and aluminium production, but China as well. Japan depends on imports when it comes to aluminium and articles thereof, yet has a major steel industry itself.

Electronic circuits and diodes

(Electronic) circuits and diodes are mostly made of purified silicon. Silicon is the second most abundant element on earth after oxygen, so silicon is not the constraint for circuits. The production process also requires an inert gas, for which neon, krypton and xenon gases are often used- in fact, these gases are said to be essential for the semiconductor manufacturing industry. With some 70% of world supply, Ukraine is the world’s largest producer of the required purified form of neon gas. It also supplies respectively 40% and 30% of global demand for krypton gas and xenon gas. Two major Ukrainian producers of purified neon gas in Odessa and Mariupol have already halted production. Meanwhile, Russia is a major player when it comes to the production of the crude version of neon gas, given that the latter is a by-product of the steel industry. China, with its large steel industry, is another major player in both the crude and refined production, although it would need to increase its activities to be able to fulfil domestic demand and it is uncertain at what pace it could expand production -China currently also imports neon gas from Ukraine. At the start of the invasion, stocks at major semiconductor manufacturers worldwide were estimated to be enough for some 6 months of chip production.

Batteries

Batteries are currently in high demand since they pay a vital role in the energy transition. Batteries are mostly made from steel and nickel. We have already touched upon the former above. Especially the latter could prove to be an issue. Nickel is currently in a really tight spot, given that Russia supplies roughly 18% of the worldwide nickel exports and high demand due to the world’s push for electric vehicles. Whilst buying nickel from Russia could be an issue for Japan, for now it is unlikely to be an issue for China, however. Other materials used in batteries, such as zinc, manganese, and graphite are mainly produced in China, whilst again others such as cobalt are produced in Congo, but are directly controlled by China.

Electronics and electrical machines

Electronics and electrical machines will likely be impacted indirectly through a crunch of the already tight market for electronic circuits. Additionally, some of the appliances make use of rechargeable batteries, which in turn are affected by shortages and/or higher prices in nickel markets. Other inputs for these type of products with tighter world supply are aluminium, palladium and steel. But, again, for the time being China -which is the EU’s major supplier of electronics and electrical machines-, need not to be harshly impacted as it is still refraining from sanctioning Russia and is one of the largest global aluminium and steel producers itself.

To conclude, the EU might be confronted with lengthened delivery times or higher prices of some final goods imports from third countries, such as motorcycles and electrical machines. Yet also intermediate imports from third countries such as chips and batteries could become more difficult to get by. This, in turn, could hamper EU production of transport equipment, machinery, and electronic products and electrical equipment.

Conclusion part I

Even though the imports from Russia, Ukraine and Belarus only make up a small share of the total imports and exports of the European Union, it is clear that the war in Ukraine is wreaking havoc in supply chains. The most obvious impact is from higher energy prices, and maybe, if sanctions escalate, an outright energy shortage. Sanctions on gas imports are the most likely catalyst for such a crisis, whilst oil and coal imports are easier to replace.

As we will show in the second part of this publication, Germany and Italy are worst suited to deal with such a crisis because of their relatively large industrial sector and heavy reliance on Russian energy, gas in particular. France and Spain on the other hand, are better equipped to deal with such a crisis, although it needs to be said that no country will be left unscathed.

But it’s not just energy that is posing a serious threat to supply chains. As we have shown in the report, there are plenty of other materials and products, such as nickel, palladium, iron, wood and neon (and agri-commodities of course!), that threaten supply chain disruptions in some industries, especially in the short run as it takes time to find supply elsewhere. Some supply chains will be directly impacted through their dependence on Russia, Ukraine and Belarus, whilst others may be impacted indirectly, through second order effects.

Part II: Which member state is the most vulnerable?

In the second part of this publication, we compare the exposure of the five largest EU economies to distortions caused by the war. We find that the German economy is most exposed, followed by the Italian economy.

Direct trade linkages between member states and the warzone

Just looking at the macro picture for the EU27 might understate some of the problems in specific member states. Since, even if there is a surplus in timber in Poland for example, that doesn’t necessarily mean that that surplus can be exported to Spain easily if the infrastructure isn’t there. Additionally, it would be naïve to assume it can be done at a similar price and ease. As such it is useful to zoom in on member states to see for what goods they rely on the warzone the most.

To compare member states we adopt a similar methodology as we did to create table 1 for the EU 27, but use z-scores to compare the relative vulnerability for the five biggest economies in the EU. Table 3 presents the relative vulnerabilities related to non-energy products for which at least one of the five large member states strongly depends on the warzone, via direct trade linkages. Given the importance of energy security we will dedicate a separate section to the reliance on Russian energy. The products in table 3 are ranked based on the combined z-scores of the member states for that product group.

Semi-finished products of iron or non-alloy steel top the list, due to Italy’s strong links with the warzone in this respect. Maize, sunflower-seed and oil, and pig iron are other products that stand out.

Out of the five largest member states, Italy seems most exposed to the war through direct trade linkages with the warzone. It relies heavily on the warzone for pig iron and semi-finished products of iron or non-alloy steel. Some 84% of its imports of the former come from the warzone and 77% of the latter. Italy also gets 82% of its ferrous products imports from the warzone, yet the (net) trade value of this category is substantially smaller. Finally, its dependence on warzone sunflower seeds and oil stands out.

Spain is relatively dependent on the warzone for agri-commodities, like maize and sunflower seeds. Respectively, some 32% and 66% of Spain’s imports of these products comes from the warzone at relatively large net-volumes. It also substantially relies on the warzone for pig iron and ferrous products.

The Netherlands is especially dependent on the warzone for ‘maize or corn’. Roughly half of Dutch maize/corn imports are from the warzone. This could severely impact the price and availability of animal fodder, as is evident from the fact that Dutch farmers have already begun to hoard animal fodder.

For Germany, the biggest vulnerabilities (next to energy) are unwrought nickel and copper, metals that are vital to German industry. Roughly 45% of Germany’s nickel imports and 24% of its copper imports come from the warzone.

France seems least vulnerable to the war-induced supply crunch. Yet it is exposed to a halt in oilcake imports; oilcake can be used as fodder and fertilizer.

Energy dependence of member states on Russia

In order to gauge the vulnerability of European countries to a potential collapse in Russian energy exports, we have gathered data on the consumption, trade and domestic production of oil, gas and solid fossil fuels. Based on this data, we can compute the share of energy consumption for which alternative sources would need to be found if imports of Russian energy come to a halt.

Looking at figure 8 it is evident that especially countries in Eastern and Central Europe are set to lose in case of an energy boycott. These countries have been able to acquire Russian fossil fuels for attractive prices in the past decades, partially because of the large network of pipelines that run through Eastern and Central Europe. This has given them no incentive to diversify their energy mix or decrease the reliance on Russia. Yet also, Finland, Germany, Italy and Greece get more than 20% of their energy consumption out of Russia, while in the Netherlands it is only slightly less.

Meanwhile, Scandinavian countries rely on Norway for gas and oil imports, whilst they simultaneously have relatively large shares of renewable energy; the Iberian Peninsula relies on Algeria for gas and France but also Belgium are relatively large producers and users of nuclear heat (Figure 9).

As we have argued before in the section on Europe’s energy dependence, replacing all of these fossil fuels will not be easy. Replacing Russian oil and solid fossil fuels may be possible, albeit at a higher price, but replacing Russian gas will not be as easy. Simply supplying more LNG, if this is even possible, will not do the trick in the short run. Whilst some countries, such as Spain, the Netherlands and Italy, have the terminals to convert LNG to regular gas, landlocked countries such as Czechia, but also Germany do not. Currently, the infrastructure is lacking to transport freshly converted gas to those countries and hence those countries are even more vulnerable to a stop in Russian gas imports than others -which explains Germany’s most outspoken resistance to banning such imports. For the full report on Europe’s gas dependency, we refer to this publication.

Importantly, this analysis is primarily focussed on the availability of energy, but even if we don’t get to the point where energy availability is an acute issue, high energy prices impact all countries, whether they are dependent on Russia or not. Especially member states with a large share of gas in their energy consumption such as Italy and the Netherlands have seen their energy bills rise substantially -already last year. Relatively large coal consumers also seem to have a cost disadvantage compared to those consuming more oil. If current prices would be sustained until the end of the year, gas, coal and oil bills would on average be about, 9, 4 and 1.7 times larger this year than in 2019, respectively. Compared to last year, bills would increase less, but still be 1.6 times larger in case of gas and oil and 2.5 times in case of coal.

How about the sectoral composition?

Next to the vulnerability related to certain key commodities and (intermediate) products, the economic impact of the war in Ukraine is also determined by the economic composition of a country. Basically every sector in an economy is impacted by the higher energy prices, but some are more than others3. Additionally, some sectors rely heavily on commodities that are currently in tight supply and are unable to transfer some of the higher commodity prices to consumer prices.

Most service sectors are left relatively unscathed, whilst the industrial sector is feeling the pinch. Based on the energy intensity, exposure to commodities for which prices have risen, and exposure to commodities that are in short supply, we have ranked industrial subsectors from most to least likely to be impacted (Table 4).

It needs to be said that while it is clear that basic metals and fabricated metal products rank at the top and textiles at the bottom, there is a broader ‘middle’ group with more or less the same impact score. In table 4 this group ranges from construction to electrical equipment. Whereas risen energy prices have a higher impact on some, commodity shortages and higher prices of non-energy goods are more problematic for others. If we combine the ranking with the relative size of the industrial subsector per country, we can compare the relative vulnerability for the industries of the five biggest Eurozone member states.

Based on their composition, industries in Germany and the Netherlands seem most vulnerable, but the differences are small. The fact that Germany has a relatively large transport and machinery sector for example, is compensated for by the fact that the German food industry is relatively small.

Conclusion part II

The economic fallout of the Ukraine war is felt by the entire EU, with higher volatility in commodity markets, lengthened delivery times and higher prices for a range of commodities. Highly intertwined supply chains make it difficult to isolate the exact economic impact of the war on different member states, but we explored a method to grasp the relative vulnerabilities of the five largest EU member states.

According to our analysis the German economy is most at risk to face headwinds caused by the war due to the composition and size of its industrial sector, and its dependence on Russian energy. Next in line is Italy. Italy’s industrial composition seems slightly more favorable, but it is relatively large as well. Furthermore, Italian industry extensively depends on Ukraine and Russia for certain industrial steel inputs and energy. Finally, Italy is a large gas consumer, and hence relatively more impacted by the increase in energy prices so far.

Tyler Durden

Thu, 04/14/2022 – 21:10 - "These Are Record Numbers" – Wall Street Interns Now Earning $16,000 A Month As Talent War Heats Up

“These Are Record Numbers” – Wall Street Interns Now Earning $16,000 A Month As Talent War Heats Up

Goldman junior associates who are complaining about the ‘5-0’ in-office work schedule should keep this in mind: an army of well-heeled interns are ready and willing to take your spots.

As the rapid pandemic-era wage growth (well, real wages, that is) for blue-collar and public-facing workers (in service and other industries) sputters as average hourly wages fail to keep pace with inflation, white-collar workers who are being aggressively courted with lavish bonuses and wage hikes are seeing those benefits trickle down to even the lowest workers on the totem poll.

Bloomberg reported Thursday that even the lowly Wall Street investment banking interns are earning up to $16K per month as Wall Street’s epic battle for talent reaches a new level of intensity. To put that in perspective, for the upcoming summer intern season, the top investment banks have boosted compensation by nearly 40% over the prior year.

We suspect that all of this discontent over being required to report to the office has something to do with it. One Wall Street compensation expert told BBG that this is the biggest jump in comp year-to-year that he has ever seen.

Wall Street Oasis founder Patrick Curtis said the growth in compensation for prospective junior bankers over the past year is the highest he’s seen since launching the company in 2006. And it’s not just the banks: interns at high-frequency trading firm Jane Street are making an average salary of $16,356 a month – the equivalent of nearly $200,000 a year. Jane Street didn’t respond to a request for comment.

[…]

“These are record numbers for intern pay, especially what we are seeing in 2022,” Curtis said.

A breakdown of average intern comp from BBG shows that the highest compensation is going to interns at infamous HFT market makers Jane Street and Citadel, followed by Bridgewater.

Source: Bloomberg

Top compensation is going to software engineers, quantitative researchers and interns. For now, at least, it appears Wall Street is winning in the eternal battle with the tech industry for top talent. But so far at least, Glassdoor says Roblox is the No. 1 source of compensation for interns.

Source: Bloomberg