- CEO Of Startup Company Turvo Fired For Expensing $76,120 At Strip Clubs

CEO Of Startup Company Turvo Fired For Expensing $76,120 At Strip Clubs

Paging Lou Pai…

Though likely not on Lou’s spending level, the former CEO of startup Turvo Inc., found out the hard way that expensing nearly $80,000 in company funds at a strip club is apparently not OK with the company’s board of directors.

As a result, Scott Lang, the company’s new CEO, aims to stress the company’s new policy: employees are not allowed to entertain clients at strip clubs, according to Bloomberg.

Former CEO Eric Gilmore has been accused by the company’s Board of expensing $76,120 at strip clubs over the course of a 3 year span. The Board removed him as CEO in May. Gilmore didn’t deny the allegations, but instead turned around and sued the Board of Directors, claiming they didn’t follow proper protocol for his termination. Turvo disputes this, saying they settled in September and that all the proper steps were taken.

Lang is a former executive from the energy industry who joined Turvo just before Thanksgiving. The startup, based in Silicon Valley, makes software to help companies track the movement of freight and is backed by about $85 million in Venture Capital. In his first interview as CEO, Lang said he is trying to help the company move past the scandal and, when asked about whether or not he tries to win over clients at strip clubs, he responded: “Never have. Never will.”

The Board’s quick reaction at Turvo shows that more and more companies are quietly addressing allegations of misconduct before they become public. The #MeToo movement has already claimed the jobs of many technology executives, like Kris Duggan of Betterworks Systems, and has cost Ken Fisher’s firms billions of dollars in assets managed.

Gilmore started the company in 2014 and was a veteran of Microsoft and Coupons.com. Mubadala Investment Co., the Abu Dhabi-based sovereign wealth fund, led investors with a $60 million injection into the company last year. Soon after, Gilmore hired a new CFO, who discovered the pattern of “unusual charges” from the CEO.

The strip club related expenses spanned most of the company’s life and Gilmore made “no effort to conceal them”, according to Bloomberg. More than $125,000 in entertainment charges were flagged by the new CFO during a review of corporate spending: more than half of them were from strip clubs.

In May, after the board found out, Directors for Mubadala and VC firms Felicis Ventures and Activant Capital, told Gilmore that his time as CEO was over and demanded he sign a separation agreement. Gilmore declined and argued the process violated the company’s bylaws because the confrontation wasn’t at first presented as a formal board meeting. The board disagreed and Gilmore’s lawsuit over the dispute lasted 3 months before settling.

Gilmore remains on the Board and is the company’s largest shareholder. His two co-founders also still hold executive roles at the company.

Tyler Durden

Sat, 12/14/2019 – 23:00 - Thousands Of Strange "Penis Fish" Wash Ashore On California Beach

Thousands Of Strange “Penis Fish” Wash Ashore On California Beach

Authored by John Vibes via TheMindUnleashed.com,

Morning visitors to Drakes Beach in Northern California last week witnessed thousands of strange 10-inch phallic fish washed up on the shore.

The strange creatures are known as “fat innkeeper worms,” and they have been spotted on other nearby beaches in California in the past. They usually wash up on beaches after storms, similar to the storms seen around Drakes beach last week.

Scientists call this creature Urechis caupo and it is classified as a type of spoonworm. The picture below was taken on a different occasion earlier this year, when fat innkeepers washed up on Bodega Bay back in June.

This photo illustrates why the fat innkeeper is sometimes casually known as a “penis fish.”

Photo by Kate Montana, iNaturalist Creative Commons

At Drakes Beach last week, thousands of these things washed up on the beach, making it entirely impossible to walk the beach without stepping on them.

The following images posted to Instagram were taken on December 6th, after the storm around Drakes Beach.

Even when you don’t see them on the beach there is a very good chance that they are many feet below you, burrowed under the sand. During storms, the layers of sand that were once covering them are washed out to sea, leaving the innkeepers exposed to predators, including seagulls, sharks, stingrays, and other fish.

Some cultures also see the strange fish as a delicacy. In South Korea for example, the dish is known as “gaebul.”

Of course, the strange phallic appearance of the fat innkeeper seems to attract far more attention than the many other sea creatures that wash up onshore throughout the year.

Researchers estimate that an individual fat innkeeper can live for up to 25 years if they manage to avoid predators. As a species, fossil evidence shows that these creatures may have been around for over 300 million years.

Tyler Durden

Sat, 12/14/2019 – 22:30 - New WikiLeaks Bombshell: 20 Inspectors Dissent From Syria Chemical Attack Narrative

New WikiLeaks Bombshell: 20 Inspectors Dissent From Syria Chemical Attack Narrative

Late Saturday WikiLeaks released more documents which contradict the US narrative on Assad’s use of chemical weapons, specifically related to the April 7, 2018 Douma incident, which resulted in a major US and allied tomahawk missile and air strike campaign on dozens of targets in Damascus.

The leaked documents, including internal emails of the Organization for the Prohibition of Chemical Weapons (OPCW) — which investigated the Douma site — reveal mass dissent within the UN-authorized chemical weapons watchdog organization’s ranks over conclusions previously reached by the international body which pointed to Syrian government culpability. It’s part of a growing avalanche of dissent memos and documents casting the West’s push for war in Syria in doubt (which had resulted in two major US and allied attacks on Syria).

This newly released batch, WikiLeaks reports, includes a memo stating 20 inspectors feel that the officially released version of the OPCW’s report on Douma “did not reflect the views of the team members that deployed to [Syria]”. This comes amid widespread allegations US officials brought immense pressure to bear on the organization.

RELEASE: Third batch of documents showing doctoring of facts in released version of OPCW chemical weapons report on Syria. Including a memo stating 20 inspectors feel released version “did not reflect the views of the team members that deployed to [Syria]”https://t.co/ndK4sRikNk

— WikiLeaks (@wikileaks) December 15, 2019

https://platform.twitter.com/widgets.js

The Daily Mail’s Peter Hitchens, who saw the leaked documents just prior to WikiLeaks going public with them had this to say:

Sources stress that the scientists involved are ‘non-political, utterly uninterested in any strategic implications of what they reveal’.

They just ‘feel that the OPCW has a duty to be true to its own science, and not to be influenced by political considerations as they fear it has been’.

An internal memo seen by The Mail on Sunday suggests that as many 20 OPCW staff have expressed private doubts about the suppression of information or the manipulation of evidence.

This suppression of information included key evidence which undermined claims Syrian military helicopters dropped a gas cylinder from the air, which had long been the linchpin in Washington’s accusation that “Assad gassed his own people” at Douma.

Like waking up from a long nightmare that almost led to WWIII:

“The Mail on Sunday can reveal that a senior official at the @OPCW demanded the ‘removal of all traces’ of a document which undermined claims that gas cylinders had been dropped from the air..”https://t.co/MvMwX1xrEr— Ian Wilkie (@Wilkmaster) December 14, 2019

https://platform.twitter.com/widgets.js

The leaks also suggest the OPCW possessed scientifically credible evidence showing the victims of the alleged attack had symptoms not consistent with chemical gas exposure (prior OPCW statements pointed to chlorine use), casting further doubt on that aspect of the investigation.

OPCW memo raising concerns: pic.twitter.com/UHFJbm0iDQ

— Koen (@KoenSwinkels) December 15, 2019

https://platform.twitter.com/widgets.js

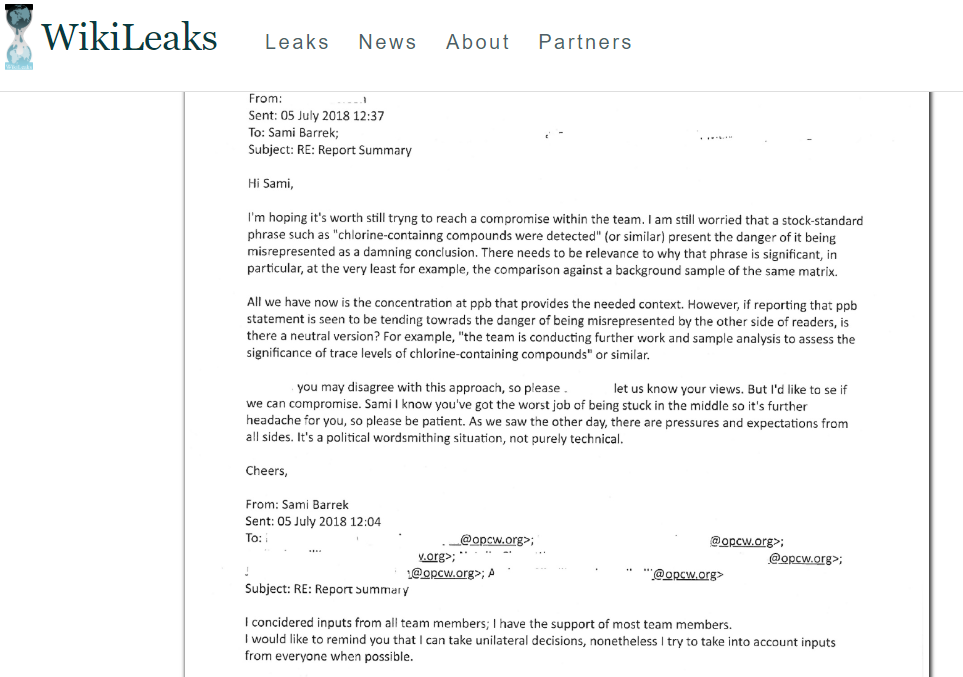

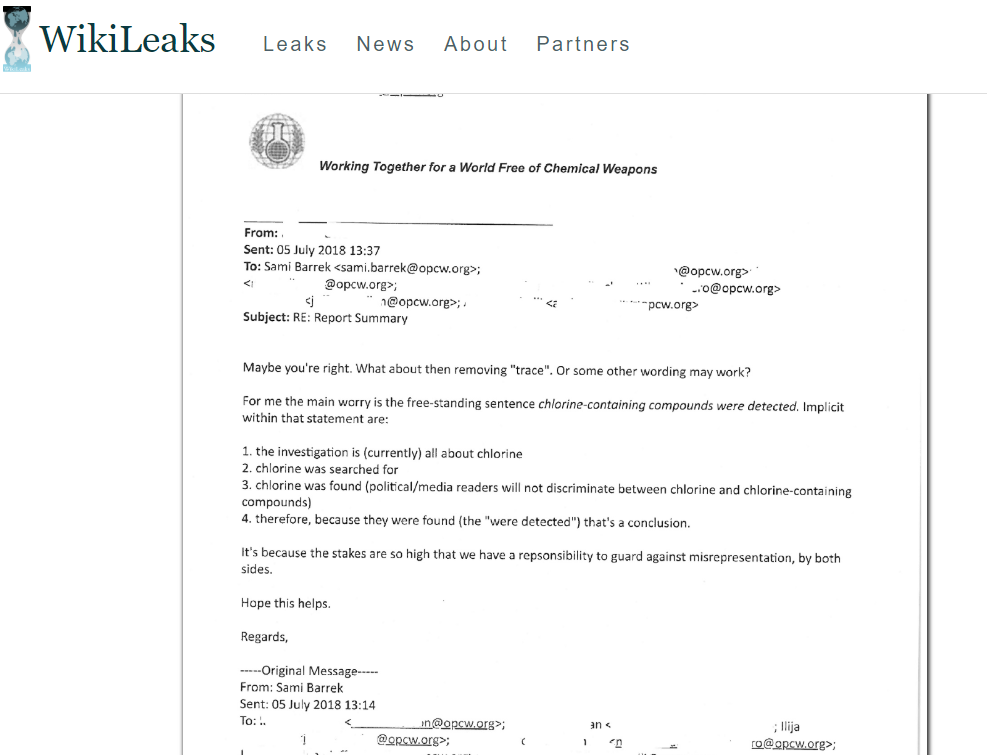

But perhaps the most important leak in the new trove of emails centers on a raging debate among scientists over whether to include in their report the phrase “chlorine containing compounds were detected” and how to qualify it — given it was found only in such trace amounts as to be consistent with common household levels of chlorine-related items.

That final report claimed there were ‘reasonable grounds’ that chlorine gas was used in Douma, but an OPCW whistleblower says only tiny quantities of chlorine were detected in forms possible to find in any household. — Daily Mail

OPCW inspector tries to argue to FFM team leader Sami Barrek that the low levels of chlorinated organic chemicals need to be reported to avoid misrepresentation and confusion. Barrek says he’ll unilaterally overrule the inspectors and omit the information.https://t.co/nPZtMbakAF pic.twitter.com/norATrlc7l

— Caitlin Johnstone ⏳ (@caitoz) December 15, 2019

https://platform.twitter.com/widgets.js

This crucial document (among others), which expresses concern that the media would wrongly assume a “chlorine attack” based on common household trace levels is found in the following memo:

And here’s another example:

Another stunning OPCW admission heretofore unreleased to the public:

Hitchens continues commenting on the trove of leaked documents as follows:

Alleged casualties shown in videos of the attack were foaming at the mouth in a way that might be expected of victims of sarin, but not by victims of chlorine. Yet all the reports agree that no traces of sarin were found at Douma.

These doubts were confirmed by expert toxicologists consulted by the OPCW investigation team on a visit to Germany in June 2018.

They concluded ‘there was no correlation between symptoms and chlorine exposure’.

In a key passage it adds ‘the team considered two possible explanations for the incongruity.

‘A) The victims were exposed to another highly toxic chemical agent that gave rise to the symptoms observed and has so far gone undetected.

‘B) The fatalities resulted from a non-chemical-related incident.’ In other words, either the victims died from an unknown, undetected gas for which no evidence exists or there never was a chemical attack.

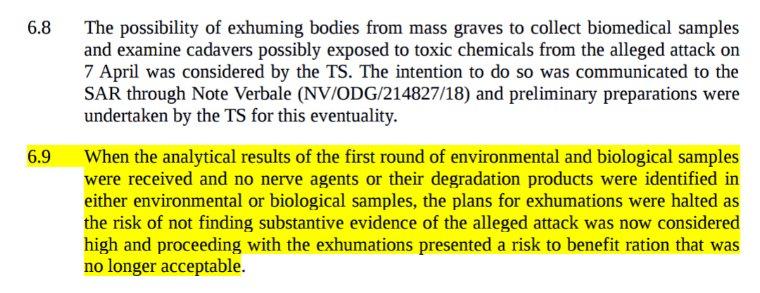

These severe doubts which were expressed internally among scientists, analysts, and technicians were never made public by the OPCW, hence the new leaks, apparently facilitated by frustrated staff who want to make the case to the world about the significant doubts.

Chemical weapons experts taking samples from a prior alleged chemical weapons attack site in Syria, via Reuters. * * *

14 December, 2019

Today WikiLeaks releases more documents showing internal disagreement within the OPCW about how facts were misrepresented in a redacted version of a report on an alleged chemical attack in Douma, Syria in April 2018.

Amongst these is a memorandum written in protest by one of the scientists sent on a fact finding mission (FFM) to investigate the attack. It is dated 14 March 2019 and is addressed to Fernando Arias, Director General of the organisation. This was exactly two weeks after the organisation published its final report on the Douma investigation.

WikiLeaks is also releasing the original preliminary report for the first time along with the redacted version (that was released by the OPCW) for comparison. Additionally, we are publishing a detailed comparison of the original interim report with the redacted interim report and the final report along with relevant comments from a member of the original fact finding mission. These documents should help clarify the series of changes that the report went through, which skewed the facts and introduced bias according to statements made by the members of the FFM.

The aforementioned memo states that around 20 inspectors have expressed concerns over the final FFM report, which they feel “did not reflect the views of the team members that deployed to Douma”. Only one member of the fact finding team that went to Douma, a paramedic, is said to have contributed to the final version of the report. Apart from that one person, an entirely new team was gathered to assemble the final report, referred to as the “FFM core team”…

* * *

Tyler Durden

Sat, 12/14/2019 – 22:00 - Why Is The System Rigged?

Why Is The System Rigged?

Authored by Bruce Yandle via The American Institute for Economic research,

It’s crazy season, that special time on the American calendar when aspiring candidates for the nation’s highest office try to outdo each other in an effort to attract more voters to their platforms.

This time around, background support is provided by a virtual anvil chorus of anti-capitalism clatter. Senator Elizabeth Warren, for example, frequently unleashes criticism of American capitalism by asserting that the “system is rigged,” a complaint that seems to resonate with meaningful populist appeal. It’s an old refrain that has echoed across the years from Karl Marx onward.

Nobel Laureate Robert J. Shiller explains why this may be the case in his new book, “Narrative Economics.” As Shiller points out, when a story is repeated enough, the viral message may be accepted as conventional wisdom, more like an article of belief than a matter of reason.

I’ll also emphasize that for a message to prevail, it helps if its content rests on a preexisting and inherently moral foundation that reflects our tribal instincts as an evolved human species. And what works for a small tribe doesn’t necessarily work so well for a huge industrialized nation.

Consider this: Some may inquire, “Do you believe in capitalism?” almost as if the position one takes is a matter of religion. When answering, we reflect on our tribal preferences, and cooperating and sharing with our family and neighbors is often a key to success. Thus, many people will almost instinctively answer “no,” or at least “yes, but …” followed by some serious caveats and exceptions.

Yes, the beneficial-but-invisible hand of commerce driven by self-interest has never been an instinctually lovable idea. Gains from trade, while well-documented since the days of Adam Smith, can be more elusive than we may first realize. Given the widespread negative views on the subject, politicians’ calls for greater accountability and government intervention may not be welcomed by all, but they’re understandable.

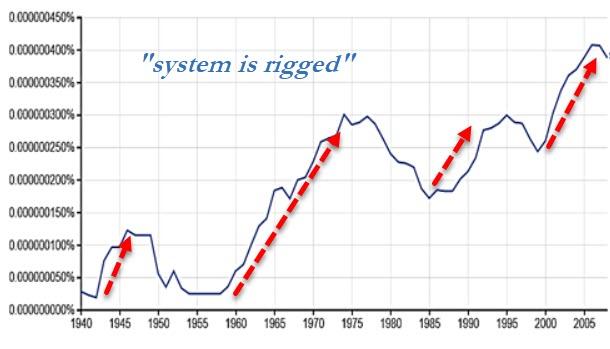

Shiller adds another dimension to his narrative economics story by using data from Google’s Ngram Viewer. The viewer produces charts based on the frequency of particular words and phrases in Google Books, which include some 8 million downloaded volumes in various languages.

Consider an Ngram we might apply to Senator Warren’s comments. The nearby figure contains one for “system is rigged” that shows the frequency of the phrase’s occurrence from 1940 through 2008, the final year in the database. I have smoothed the data by using a three-year running average:

The data show four viral periods: 1940-1950, 1960-1985, 1990-1998, and 2000-2008.

The first period encompasses World War II, a time of draft, rationing, price controls, defense contracting, and related cronyism that may in some cases have been highly profitable for hand-picked firms.

The second viral period is much longer and encompasses a period including the Vietnam War and related draft, Watergate and significant social unrest.

The third period includes the first Iraq war,

and the fourth contains anti-capitalism protests and budding expressions of concern about income inequality as a version of the economy closer to what we know today took shape.

The Ngram suggests that in seeking to communicate to her base, Senator Warren artfully chose a phrase that had gone viral before—which is to suggest that there may be an embedded tribal norm that reacts during periods when a relatively small number of people are able to build large fortunes or avoid burdens, such as the draft, as a result of government actions and favors.

Oddly enough, Senator Warren and other capitalism critics seldom ask how the system got rigged and what might be done to undo the rigging. But of course, the rigging is done in Washington, sometimes when special interest groups—including corporations—lobby congress for favorable treatment.

And how might that be undone? By trimming away uneven regulation and adopting policies that expose all business firms to the refreshing winds of competition. Put another way, by forcing capitalists to act like capitalists and not lobbyists.

Tyler Durden

Sat, 12/14/2019 – 21:30 - "You Backing The Russians, Boy?" – Illinois Man Charged With Threatening To Murder GOP Congressman

“You Backing The Russians, Boy?” – Illinois Man Charged With Threatening To Murder GOP Congressman

It would appear all the escalating rhetoric from a month of impeachment hearings – including one Democratic congressman asking fellow lawmakers to imagine the teenage daughter of Ukraine’s president tied up in Trump’s basement – have sparked more than just verbal assaults on Republicans (just as Maxine Waters would had suggested previously).

The Hill reports that a man in Illinois has been charged after allegedly threatening to shoot Rep. Rodney Davis (R-Ill.) and accusing the congressman of “backing the Russians.”

Rodney Lee Davis

64-year-old Randall Tar of Rochester, Ill. was charged with communicating threats to injure a person and threatening to assault, kidnap or murder a federal official, according to court documents released this week (full release below).

Contacted at his home Thursday, Tarr said he saw a television ad in which Davis, a Republican from Taylorville, claimed that Ukraine, not Russia, was responsible for meddling in the 2016 U.S. elections, and it angered him enough to call.

Prosecutors say Tarr called Davis’s district office last month and left a profanity-filled voicemail, saying:

“I just saw you … on the TV. You backing the Russians, boy?”

“Stupid son of a bitch, you’re gonna go against our military and back the Russians?” he allegedly added.

“I’m a sharpshooter. … I’d like to shoot your f—ing head off you stupid motherf—er.”

Tarrlater reportedly told The Associated Press:

“I screwed up,” Tarr said.

“I don’t even have a weapon to do it, is the silliest thing.”

“I wish I could just take it all back and just say he’s a lousy (expletive) for backing the Russian theory.”

Of course, the only problem with all this is that the Democrats’ constant spewing of the narrative that Ukraine did not ‘meddle’ in the 2016 election is entirely false.

So did Democrats’ lies cause an unstable person to threaten a Congressman?

* * *

Full Affadvit below:

Tyler Durden

Sat, 12/14/2019 – 21:00 - Edward Snowden Speaks Out For Julian Assange And Chelsea Manning

Edward Snowden Speaks Out For Julian Assange And Chelsea Manning

Authored by Adam Dick via The Ron Paul Institute for Peace & Prosperity,

Julian Assange of WikiLeaks has been silenced. Assange was prevented from communicating with the outside world in his final 13 months at the Ecuador embassy in London, where he had obtained sanctuary from extradition to the United States. The silencing has continued in a British prison where Assange has been detained pending extradition to the US since British police forcibly removed him from the embassy in April.

Similarly, communication by Chelsea Manning has been much curtailed after Manning reveled United States military secrets. First, Manning served seven years in United States military prison after being convicted for the leak. Released from prison in 2017, Manning has been condemned to jail for most of the time since March of this year for refusing to testify for a grand jury involved in the US government’s effort to prosecute Assange.Manning, a whistleblower, and Assange, a publisher who through WikiLeaks helped make public revelations of government activities provided by Manning and other whistleblowers, are prevented by the US and British governments, respectively, from speaking up on their own behalf. But that does not mean that other individuals cannot speak up for them. In fact, with Assange and Manning’s ability to communicate limited, it is more important than ever that advocates for their freedom speak up on their behalf.

Last week, Edward Snowden, a whistleblower who has since 2013 escaped similar silencing via retaining sanctuary in Russia, spoke up in strong advocacy for Assange and Manning’s freedom. He did so in an interview with Democracy Now host Amy Goodman.

Snowden points out in the interview that the US cases against Assange, Manning, and himself all derive from the Espionage Act, the same Espionage Act that he notes was used against Daniel Ellsberg in the 1970s after Ellsberg leaked the Pentagon Papers to media. Pointing as an example to Ellsberg being prevented from even telling a jury at trial why he leaked the Pentagon Papers that revealed the hidden truth about US actions in the Vietnam War, Snowden emphasizes that the Espionage Act “is a special law that absolutely rules out any kind of fair trial.”

Continuing, Snowden discusses in the interview Manning’s revelations of “torture and war crimes, indefinite detention on the part of the United States government in places like Iraq and Afghanistan and Guantanamo Bay in Cuba” and Snowden’s own “involvement in the revelation of global mass surveillance” as being part of activities by a “new generation” of whistleblowers.

Like Ellsberg, Snowden relates that he and Manning were confronted with the Espionage Act “that forbids the jury to consider” if the leaking activity at issue “was something that did more good for the public to know than it did harm to the government in terms of inconvenience or theoretical risks of investigative journalism in a free society.”

And Snowden makes sure to emphasizes that the victims of this type of persecution over the last few years extend beyond Manning and himself. Indeed, the charging of Julian Assange under the Espionage Act Snowden sees as particularly threatening. States Snowden:

We moved from an individual and exceptional case that was not repeated for decades and decades in the Ellsberg instance to something that under the Obama administration he charged more sources of journalism using this special law than all other presidents in the history of the United States combined. And now, under the Trump administration, we have taken one more step. We have gone from the United States government’s war on whistleblowers to, now, a war on journalism with the indictment of Julian Assange for what even the government itself admits was work related to journalism. And this I think is a dangerous, dangerous thing — not just for us, not just for Julian Assange, but for the world and the future.

Watch Snowden’s complete interview here:

Tyler Durden

Sat, 12/14/2019 – 20:30 - China's "Moment Of Reckoning" Arrives: $38BN State-Owned Giant Announces Largest Dollar Bond Default In Two Decades

China’s “Moment Of Reckoning” Arrives: $38BN State-Owned Giant Announces Largest Dollar Bond Default In Two Decades

Two weeks ago we previewed what we said would soon be a D-Day for China’s bond market, as a massive commodities trader and Global 500 state-owned enterprise was set for an “unprecedented” bond default.

As of last week, this historic default is now in the history books after Tewoo, the closely watched Chinese commodities trader, became the biggest dollar bond defaulter among the nation’s state-owned companies in two decades, in what Bloomberg called a “moment of reckoning” for Beijing as China struggles to contain credit risk in a weakening economy, as bond defaults hit an all time high and are set to keep rising in the coming years.

Last Wednesday, Tewoo Group announced results of its “unprecedented” debt restructuring, which saw a majority of its investors accepting heavy losses, and which according to rating agencies qualifies as an event of default. As a result of the default, until recently seen as virtually impossible for a state-owned company, investors’ perceptions are undergoing a dramatic U-turn about government-owned borrowers whose state-ownership had for years offered an ironclad sense of security.

No more: The fact that a state-owned enterprise such as Tewoo has now defaulted on repaying its dollar bonds in full, confirms that Beijing will no longer bail out troubled SOEs, let alone private firms, perhaps due to the strains imposed by the economy which while growing at just below 6%, is slowing the most in three decades. It also raises concerns over the Chinese province of Tianjin, where Tewoo is based, following a series of rating downgrades and financing difficulties suffered by some of the city’s state-run firms. The metropolis near Beijing also has the highest ratio of local government financing vehicle bonds to GDP in China.

As a reminder, Tewoo ranked 132 in 2018’s Fortune Global 500 list, higher than many other conglomerates including service carrier China Telecommunications Corp. and financial titan Citic Group Corp. It had an annual revenue of $66.6 billion, profits of about $122 million, assets worth $38.3 billion, and more than 17,000 employees as of 2017, according to Fortune’s website. Tewoo is owned by the Tianjin government and operates in a number of industries including infrastructure, logistics, mining, autos and ports, according to its website. It also has footprints in countries including the U.S., Germany, Japan and Singapore.

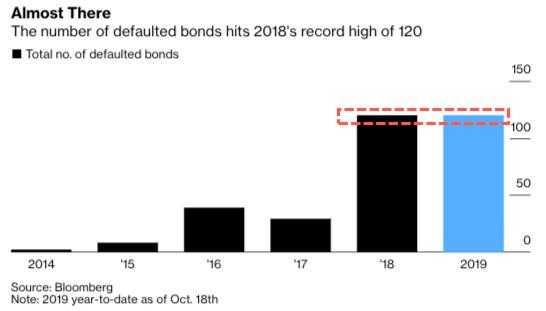

Putting last week’s “unprecedented” event in context, since the first SOE bond default emerged in China’s domestic market four years ago, 22 such firms have failed to make good on a combined 48.4 billion yuan ($6.9 billion) onshore bonds as of the end of October, according to Guosheng Securities. However, despite periodic scares such as late repayment, Chinese SOEs had yet to suffer any high-profile default in the dollar bond market since the collapse of Guangdong International Trust and Investment Corp. in 1998.

Tewoo is precisely that default.

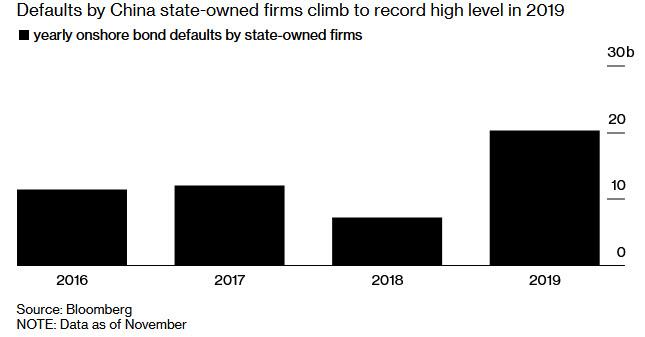

Furthermore, Tewoo’s exchange offer, which has bondholders accepting a major haircut on their bonds, is seen as a road-map for resolving similar debt crises in the future as the prospect of more failures by state-backed firms looms. 2019 has already seen over 20 billion in SOE bond defaults, nearly triple 2018’s total and the highest on record.

Specifically, the former Fortune Global 500 company from the northern port city of Tianjin said dollar bond investors representing 57% of the the total $1.25 billion have agreed to be paid just 37 to 67 cents on the dollar, depending on the maturity of the bonds. Additionally, bondholders representing 22.6% of these bonds voted to exchange their debt for new bonds with sharply lower coupons to be issued by Tewoo’s offshore debt manager, a state asset manager from Tianjin.

“This is one form of default based on our definition,” said Moody’s analyst Ivan Chung, pointing out that the debt restructuring has resulted in losses for investors.

The distressed exchange offer which concluded hastily last week represents a “first of its kind” debt restructuring plan for the relatively immature Chinese bond market and for a state-run enterprise in the dollar bond market. It was rushed ahead of $300 million dollar bond maturity on Dec. 16, one of the four notes covered by Tewoo’s debt restructuring plan.

To be sure, the market was not surprised: late last month, Tianjin State-owned Capital Investment and Management, Tewoo’s offshore debt manager, said on an investor call that Tewoo is very likely to default on this paper. That explains why Tewoo’s bond prices were largely unchanged after the exchange offer.

Meanwhile, investors who turned down the company’s forced exchanges face even steeper losses; their dollar bonds will be grouped into a comprehensive debt plan involving Tewoo’s onshore debt, according to Tianjin State-owned Capital.

Tewoo said settlement of the debt restructuring offers are expected to be on or about Dec. 17.

As Bloomberg summarizes, “Tewoo’s failure in the dollar bond market, the biggest for a Chinese SOE since the collapse of Guangdong International Trust and Investment Corp. in 1998, is a sign that the worst economic slowdown in three decades is limiting Beijing’s capacity to bail out its weaker state firms. As a result, the authorities appear increasingly willing to use a more market-oriented approach to clean up the mess.”

“Tewoo’s default is a landmark case, and demonstrates a growing tolerance for defaults by distressed SOEs,” Cindy Huang, an S&P Global Ratings credit analyst said in a note.

Needless to say, Tewoo’s crisis comes as a wake-up call for investors, many of whom had expected to never incur losses in China’s offshore (dollar) bond market where until now, moral hazard had been the only game in town. Alas, that game is now changing.

“This is a poor outcome for investors that bought the bonds at par. That said, there is now some track record as to the severity of loss for an SOE-related entity,” said Charles Macgregor, head of Asia at Lucror Analytics. “Hopefully, these types of restructures will bring more discipline to the market and result in investors properly pricing for the apparent risk,” he added hopefully, although with developed nation central banks engaging in precisely the kind of moral hazard boosting activity that China is now desperately seeking to distance itself from, we doubt that any investors will learn any lessons, and if anything, creditors will only demand even bigger bailouts in the future.

* * *

What is perhaps just as concerning is that as we noted last month, the Tewoo default is a harbinger of the crisis facing China’s insovent local governments themselves. Tianjin “is not an exception” and other local governments with deteriorating fiscal conditions might also see eroding support for their less competitive SOEs, S&P warned.

It all started with the bankruptcy of Bohai Steel Group in 2018 which triggered systemic risk in Tianjin’s financial market. The incident involved a large number of local companies and financial institutions, which recorded huge amounts of bad debt. Financial institutions became more conservative in their lending standards, and this resulted in liquidity issues for a number of Tianjin enterprises.

At the same time, Beijing’s deleveraging and capacity reduction reforms made it difficult for a traditionally highly-leveraged company like Tewoo to raise financing. The default in May 2018 by Hsin Chong Group Holdings Limited, a company controlled by Tewoo, showed further signs of financial problems at Tewoo Group.

While normally such a critical company as Tewoo would be quietly bailed out by either Beijing or the local province, investors told Bloomberg that the company’s excessive debt levels would limit Tianjin authorities’ ability to lend support to the city’s troubled firms. They were right, and in July, Tianjin Binhai New Area Construction & Investment Group postponed plans to sell a three-year dollar bond offering amid such concern.

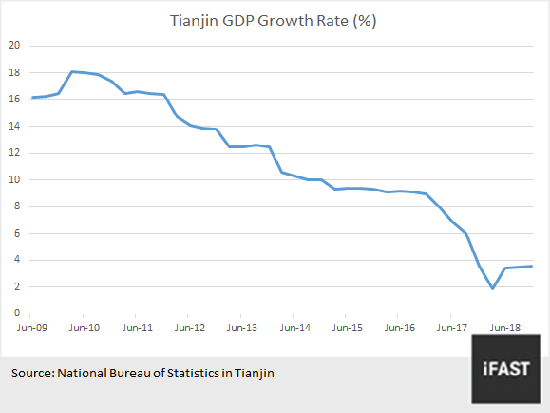

Tewoo’s debt issues that had surfaced from its current crisis may be only the tip of the iceberg. Tianjin’s economic growth has slowed down sharply since the beginning of 2016. GDP growth dropped to 1.9% in the first quarter of 2018. Even as it started to rebound thereafter, the outlook is still pessimistic, with GDP growth in 2018 less than 4%, which ranked last in the country according to iFast.

On the other hand, according to a 2016 report released by ratings agency Moody’s, state-owned enterprises in Tianjin recorded an aggregate liability-to-fiscal revenue ratio of more than 600%, which was the highest in the country.

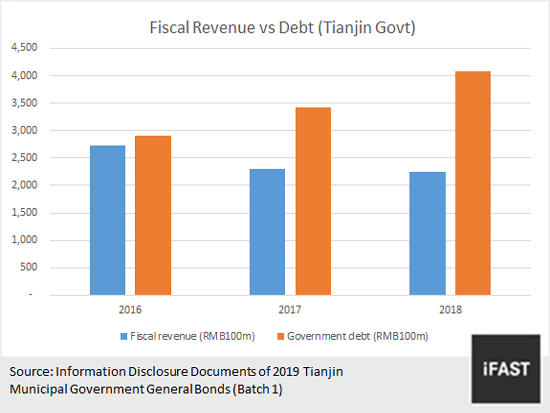

At the same time, as shown in Tianjin municipal government’s most recent three-year revenue and debt data, Tianjin government’s fiscal revenue has declined significantly since 2017. Fiscal revenue fell by close to RMB40 billion in 2017, while government borrowings rose rapidly. By the end of 2018, debt owed by the Tianjin government was almost double its fiscal revenue.

The bankruptcy of Bohai Steel, a Tianjin SOE, in 2018 may also be a sign that the Tianjin government has lost control over the local debt crisis. Other than Bohai Steel and Tewoo, there have been a number of state-owned companies in Tianjin that are fighting to stave off insolvencies, such as Tianjin Real Estate Group Co. Limited, which owes RMB200 billion in debt. From the above observations, we think that in the event of a default by Tewoo, the company is likely to go into bankruptcy reorganization in a similar way as Bohai Steel, which has brought in capital from the private sector for its corporate restructuring. But for bondholders, recovery of their investments may be difficult, and potential loss heavy.

With Tianjin failing – or simply unable to step up, in the aftermath of Tewoo’s debt restructuring which confirms that Beijing will no longer bail out even SOEs, investors’ skepticism about state support for such state-linked firms will collapse, and the default will have wide, and dire, implications on how investors assess and price their bonds in the future, said Judy Kwok-Cheung, director of fixed-income research at Bank of Singapore. It will certainly have a chilling effect on demand for Chinese bond issuers as investors will actually have to perform due diligence to find out just what they are buying.

“Investors would be going back to basics in assessing credit risk in that the company’s stand-alone ability to repay is the first line of defense when it comes to non-repayment risk,” said Kwok-Cheung.

In short, “investors” would be reacquainted with a thing called “fundamentals.” The horror, the horror.

* * *

It gets worse: should Tewoo’s default spread to provincial-backed debt, an already ugly situation could quickly turn catastrophic as Tianjin has the highest debt burden among mega-cities and provinces in China according to S&P. Earlier this year, Fitch cut ratings on several government-related entities from the city, which is reliant on heavy industry and commodities trading. As a result of having the highest debt, Tianjin also has to slowest growth – Tianjin’s local economy grew by just 3.6% last year, the slowest in China; at the end of last year, Tianjin’s government had 407.9 billion yuan worth of debt outstanding, or about 22% of the size of its economy, said the Chinese credit risk assessor.

And just in case the Tewoo default isn’t troubling enough, Moody’s said that it expected the number of Chinese defaults to jump further in 2020 as economic growth sputters and the government attempts to rein in support to indebted companies. Specifically, Moody’s expects 40-50 new defaults in 2020, up from 35 this year, according to Ivan Chung, which will make next year another all time high.

“The regulators’ intention is to reduce moral hazard” while at the same time ensuring any defaults “won’t undermine socioeconomic stability or trigger systemic risks,” Chung said on Wednesday, who added that whereas state support may be available for companies engaged in social welfare projects, for those that are more commercial in nature, “government support may not be so forthcoming,” he said.

So what happens next?

Now that a Tewoo event of default is in the history books, the next question is what will bondholders of China’s other SOE’s – those who bought bonds on the assumption that China will always bail them out – do next? A flurry of aggressively selling may be just the catalyst that cracks the market if it emerges in the extremely illiquid days just before Christmas.

Tyler Durden

Sat, 12/14/2019 – 20:00 - Repo-Market Turmoil: Are We Staring Into The Financial Abyss?

Repo-Market Turmoil: Are We Staring Into The Financial Abyss?

Authored by Tuomas Malinen via GnSEconomics.com,

One thing has been bothering us for six years. How can so many economists and economic commentators dismiss the ever-increasing market meddling of central banks so lightly?

The first time we warned about this possible threat to financial markets was in December 2013. In the report, we wrote:

There is a serious possibility that the measures taken by the central banks have already created a situation in which their actions increase rather than decrease financial instability. This is due to the fact that if the actual price of an asset does not meet its market–based value, the true level of risk is not properly revealed.

The continuing turmoil in the repo-market, first triggered on 16 September, is the most recent and probably the most worrying example of this.

There has been a lot of speculation about its origins. In this post we explain why we consider the repo-problems to be the first sign, a symptom, of the financial calamity we’re about to face.

The failed clean-up

The global financial crisis (GFC) or “Panic of 2008” was a shock not just to bankers, but also to economists—not to speak of ordinary citizens. It was a massive failure of risk-hedging in the financial sector, combined with both regulatory failures and dangerous and deeply-embedded incentives. We summarized the factors leading to the crisis in our blog: 10 years from Lehman and nothing has been fixed.

While the extraordinary measures used to stop the crisis from mutating into a systemic meltdown can be considered appropriate, the fact these measures were continued cannot. In retrospect, the U.S. did recapitalize, merge and permit the failure of some banks, but Europe choose the exact opposite approach: undercapitalized and ailing banks were left standing.

However, the most crucial mistakes were made after the GFC on both sides of the Atlantic. The hidden virtue of crises and recessions is that they remove both unproductive firms and financial excess, creating space for more productive firms and fresh financial investment. This was not allowed to happen post-GFC. This also explains why the economic recovery from the crisis was so weak.

But the financial sector got the worst treatment. One major central bank after another enacted zero or negative interest rate policies and started asset purchase (QE) programs run through the commercial banks. In the U.S., the Fed purchased securities from authorized Primary Dealer banks by crediting reserve balances to the Fed accounts associated with each dealer counterparty.

These intermediary banks paid the sellers of bonds (households, funds, banks, etc.) and the Fed compensated the banks with reserves. In practice, the Fed forced excess reserves onto the balance sheets of banks far beyond levels they would have acquired independently.

Because of the higher supply of reserves system-wide, their marginal benefit decreased, bidding-up the prices of various securities. This led the banks to issue additional and often riskier loans until the balance of the marginal benefits was restored. Also, because QE and low policy rates depressed long-term rates, many of the securities that the commercial banks held had no yield advantage over reserves, making the banks more likely to substitute less-liquid securities with more credit risk.

The Never-Never (financial) land of post-GFC

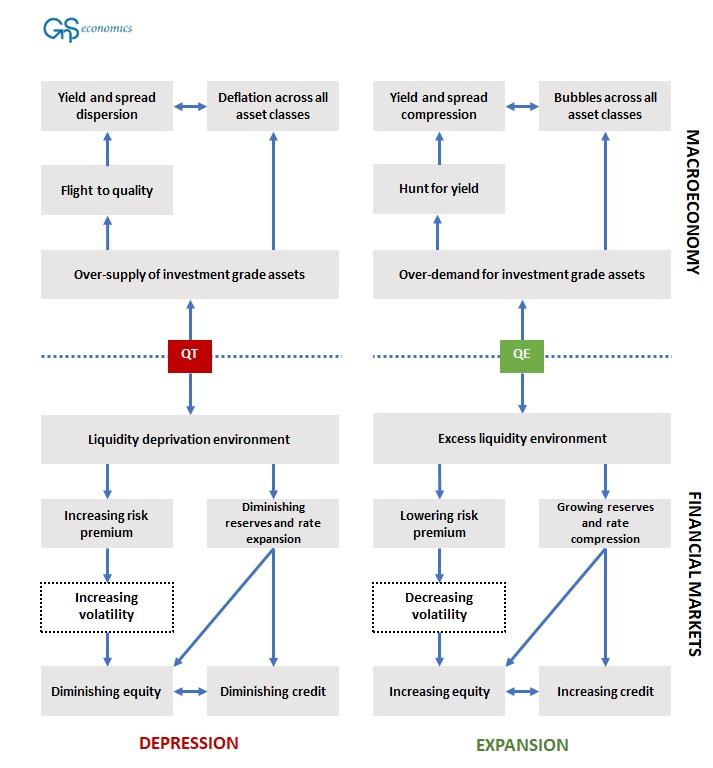

QE created overdemand for investment-grade assets and excess liquidity in the financial markets by introducing central banks as a persistent buyer. This overdemand led to a relentless hunt for yield, to spread compression, and to artificially-inflated prices across the entire spectrum of the asset universe (see Figure 1).

Quantitative tightening, or QT, attempted globally for the first time from August to November of 2018, created an oversupply of investment-grade bonds which lead to a flight to quality, to spread dispersion and to asset price deflation. It also removed the excess liquidity from the financial markets created by QE by introducing a persistent seller.

Figure 1. The causative channels of quantitative easing (QE) and quantitative tightening (QT) in the macroeconomy and in financial markets. Source: Q-Review 1/2018

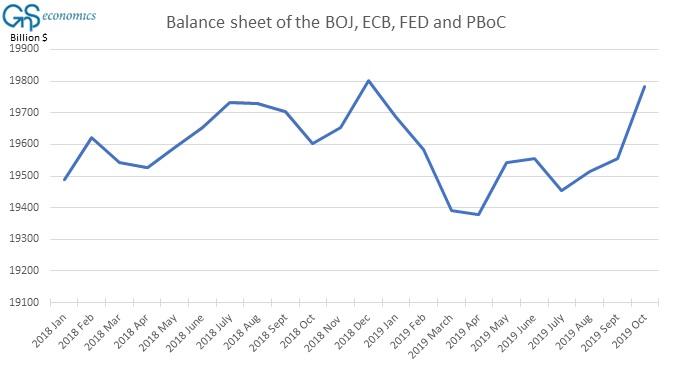

In December 2018, it became clear that the financial markets were unable to tolerate a balance sheet run-off by central banks. Markets declined abruptly and forced the PBoC to inject record amounts of liquidity into the markets, and the Fed to make an immediate 180-degree turn in its monetary policy. Yet, overall, global QT essentially continued through the 2019 until the repo-markets broke in September (see Figure 2).

This time around, central bankers learned their lesson with the Fed and ECB returning to QE programs (although the Fed insistently characterized its T-bill purchase program as “Not QE”). In case you have wondered what a central banker’s panic looks like, it can be seen in the latter part of Figure 2.

Figure 2. The combined balance sheet of the BoJ, ECB, Fed and PBoC from January 2018 till October 2019. Source: GnS Economics, BoJ, ECB, Fed, PBoC

The repo-market as a harbinger

On the 16th of September, rates in the repo markets spiked by 248 basis points to more than double of the overnight rate set by the Fed. Panic was imminent, as the over $4 trillion repo-market is used by big institutional investors to satisfy their short-term demand for liquidity. If rates stay elevated for an extended period of time, highly-leveraged institutions start to fail and trust in financial markets and the banking sector is likely to shatter.

So, what happened? There are a lot of theories, but this is what we know.

The interbank market never recovered from the Panic of 2008. Banks demand collateral for their loans to other banks, which has shifted more of the ‘action’ to the repo-market, increasing its role. During 2018 and 2019, the four big banks of the U.S. became the dominant lenders in the repo-markets. So, any change in their ability or willingness to lend to the repo-market will cause an imminent shortage of funding and sky-rocketing interest rates. Banks have also been hoarding Treasuries, shrinking their availability.

Yet, the main issue is likely to be the fact that QE programs fundamentally altered the balance sheets of banks as well as their money-market activity.

QE accustomed banks to holding large amounts of excess reserves, which provided a reliable source of interest income. When QT started to reduce reserves, they replaced them with another reliable source, Treasuries, which acted as a hedge on their balance sheet against riskier lending practices and securities holdings induced by QE programs. Obtaining a hedge against riskier assets and loans (loan portfolios in particular take a long time to adjust) becomes especially important, if the economic outlook is expected to worsen—as it is presently.

We cannot, of course, be absolutely certain that this is what drove big banks to Treasuries, but it seems plausible. QE has distorted both bank balance sheets specifically and the financial markets more broadly. These factors, combined with decreased money-market activity of banks—explained here in detail by the BIS—has likely made the ‘Big 4’ wary of lending to the repo-market, if even a hint of potential loss exists.

This leads us to another and potentially more worrying development: increased access to the repo-market by hedge funds to increase their leverage. They seem to have been getting short-term funding from the repo-market to buy U.S. T-bills, which they have then re-invested in the repo-market to obtain more short-term funding to buy T-bills, etc. Using this “leverage-loop” they have been able amass very high leverage ratios.

The behavior of hedge funds is also the end-result of massive central bank interference in the global capital markets. When the yields of practically every financial asset class are squeezed to near-zero (or less!) due to artificial liquidity from the central banks, leverage becomes the only way to obtain yield sufficient for fixed-income investors.

Staring at the financial abyss

When the financial history of this era is written, it is fairly likely that historians will identify the onset of the global economic crisis as 16 September, 2019. It was the first clear sign of the potential for a violent unwinding of the massive speculative financial positions created by central bank meddling.

Thus, in their efforts to “save” the world economy, central banks have created a monster: a dysfunctional, extremely-speculative and highly-leveraged financial sector. All that is needed for it to unravel are rising rates in an some important, if obscure, corner of the capital markets—just like the repo-markets.

The Fed has been engaged in a desperate battle to avert this through its repo and “Not QE” -programs since September. However, even if successful, it’s very likely that these programs, not to speak of an “actual QE”, will just further aggravate the distortions in the financial markets, until they become unbearable.

Then we’ll be staring into the financial abyss. Beware!

Tyler Durden

Sat, 12/14/2019 – 19:30 - Hundreds Of Billions In Gold And Cash Are Quietly Disappearing

Hundreds Of Billions In Gold And Cash Are Quietly Disappearing

Something strange is going on: at the same time that central banks are injecting $100 billion each month in electronic money to crush volatility and ramp markets, a similar amount in hard physical currency and precious metals is literally disappearing.

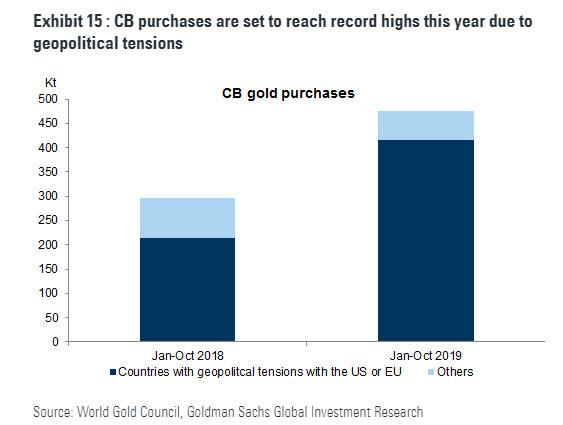

Take gold: as we reported last week, it was none other than Goldman Sachs which recently laid out the case for gold, saying “gold’s strategic case still strong.” One reason for this is that the same central banks that are “full tilt” printing cash, they have also been splurging on gold, and as a result of “geopolitical uncertainty” there has been a record surge in gold demand by central banks themselves. As Goldman notes, “CBs globally have been buying gold at a very strong pace” and “2019 looks to be a record year for CB gold purchases with our target of 750 tonnes combined purchases likely to be met.”

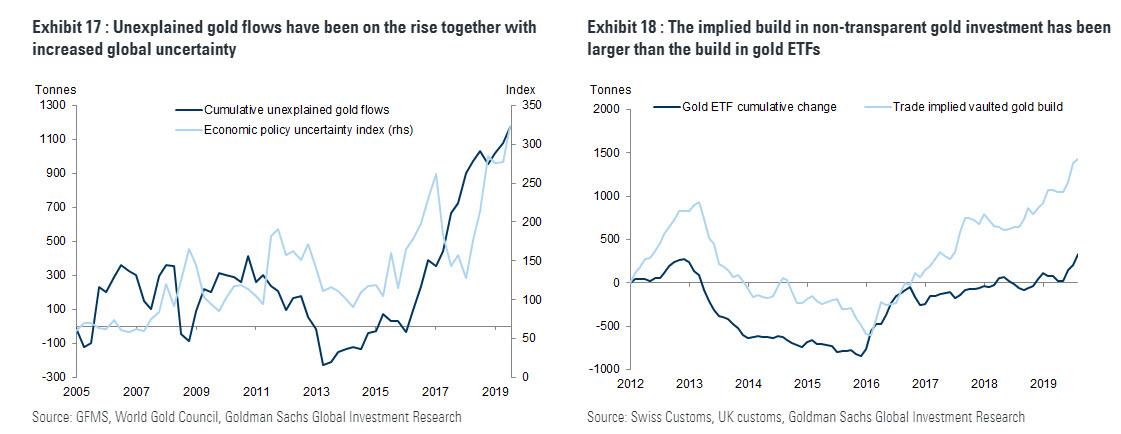

But it was another, even more bizarre discovery by Goldman, that caught our eye: according to the bank there has been a whopping 1,200 tons, or $57 billion, of “unexplained” gold flows in just the 3 years.

As Goldman’s Mikhail Sprogis writes, “rising political risk – together with negative European rates – may be an important reason behind the large share of unaccounted gold investment over the past several years. Exhibit 17 shows cumulative unexplained gold demand based on World Gold Council (post 2010) and GFMS (pre 2010) balances data. It surged since 2016. Similar dynamics can be seen when we look at implied vaulted gold stocks built in the UK and Switzerland, which is calculated as implied cumulative total net imports minus transparent ETF gold stocks.”

And another remarkable observation, or rather lack thereof: “One can see that since the end of 2016 the implied build in non-transparent gold investment has been much larger than the build in visible gold ETFs (see Exhibit 18). This is consistent with reports that vault demand globally is surging. Political risks, in our view, help explain this because if an individual is trying to minimize the risks of sanctions or wealth taxes, then buying physical gold bars and storing them in a vault, where it is more difficult for governments to reach them, makes sense. Finally, this build can also reflect hedges by global high net worth individuals against tail economic and political risk scenarios in which they do not want to have any financial entity intermediating their gold positions due to the counterparty credit risk involved.”

In other words, Goldman points out that just over the past three years, there have been tens of billions in gold flows which have mysteriously and inexplicably disappeared from the official record, yet which are most certainly taking place behind the scenes as the world’s “top 1%” brace for a major shock.

But it’s not just gold that is disappearing: according to the WSJ, so is the world’s cold, hard cash.

Some Australians are burying it. The Swiss might be hiding it. The Germans are probably hoarding.

Indeed, while banks are printing more bank notes than ever and, these seem to be “disappearing off the face of the earth” and nobody knows where or why. or as the WSJ notes, “central banks don’t know where they have gone, or why, and are playing detective, trying to crack the same mystery.”

We do know one thing: of the $1.7 trillion in US dollars in cash circulation in 2018 (up from $1.2 trillion 5 years prior), the vast majority is offshore, where it is quickly and quietly disappears as the world’s second best physical store of value (after gold of course). A Fed economist, Ruth Judson, wrote in 2017 that about 60% of all U.S. currency, and about 75% of $100 bills, had left the country by the end of 2016 — for a total of about $900 billion in U.S. dollars kept overseas. Socking those bills away “provides some protection against economic turmoil, especially in countries with a record of instability in their own financial systems”, the paper said.

Take Australia: there the stock of Australian bank notes on issue relative to the size of the economy is near the highest it has been in 50 years, said Philip Lowe, governor of Australia’s central bank: “He showed off newly printed bank notes to diners at a recent event in Melbourne and estimated that about $2,000 in printed bills exists for every Australian.” And just to inspire confidence in his own job, he added: “I, for one, don’t have anywhere near that amount” on hand. In a few years, he will wish he did.

To be sure, there is the criminal element: as anyone who has watched a documentary on Pablo Escobar knows the Colombian drug kingpin buried tens of billions in the ground for “safe keeping” (in fact, as “The Accountant’s Story” writes, “Pablo was earning so much that each year we would write off 10% of the money, or about $2.1 billion, because the rats would eat it in storage or it would be damaged by water or lost“). As such, dollar bills are often vital grease for criminal gangs and tax cheats.

Physical cash is also popular with preppers and “collectors” who worry about a future collapse of the financial system.

But these two groups are far too small to explain the wholesale loss of cash as central bankers scramble to “follow the money” and glean how society’s saving and spending patterns change in a time of zero and negative interest rates. As the WSJ notes, bankers aren’t just hunting down cash to satisfy their own curiosity. If central banks don’t know how much cash is out there, they could print too much currency and risk inflation.

Then there are bizarre incidents such as these:

Construction workers recently dug up an estimated $140,000 buried in packages at a site on Australia’s Gold Coast, prompting a police search to find the trove’s owner.

In September, a court in Germany ruled on a case brought by a man who stuffed more than 500,000 euros in a faulty boiler only to see it incinerated when a friend made a fix on a cold day while he was on vacation. The man sued his friend for the value of the lost bank notes plus interest. He lost.

“People hide their money everywhere,” said Sven Bertelmann, head of the Bundesbank’s National Analysis Centre in Mainz, Germany. Sometimes bank notes are buried in the garden, where they start decomposing, or hidden in attics, where they are used by mice for building nests. “It happens again and again that people keep money in an envelope and then they shred it by mistake,” Mr. Bertelmann said. “We pick up the bank notes with tweezers and then start to put them together, like a jigsaw puzzle.”

Few are as perplexed by the fate of the missing cash as the German central bank: according to the Bundesbank more than 150 billion euros are being hoarded in Germany.

This has led the European Central Bank, and others, to ask the public for help.

“Everyone says that they are not hoarding cash but the money is clearly somewhere,” said Henk Esselink, head of the issue and circulation section in the ECB’s currency management division.

Some stunning facts: Australia’s central bank says its best guess is that only around a quarter of the bank notes in circulation are used for everyday transactions. Up to 8% of cash is used in the shadow economy—tax avoidance or illegal payments—while as much as 10% could have been lost. That is $7.6 billion Australian dollars ($5.2 billion) missing at the beach or in couch cushions… Or simply lost in a “boating accident” to avoid the taxman until the rainy days arrive.

The biggest use of cash is as a store of wealth “in safes, under beds and at the back of cupboards, both here in Australia and elsewhere around the world,” Mr. Lowe, the RBA governor, said.

Officials at the Swiss National Bank came up with another theory: hoarded bank notes should wear out less because they aren’t being used for everyday transactions. Demand for high-denomination bank notes tends to rise when interest rates are low, households feel distrustful of the banking system or people want to make transactions anonymously.

Sure enough, SNB officials found that hoarding of Swiss francs jumped around the year 2000, likely motivated by fear of the Y2K bug infecting computer systems, the bursting of the dot-com bubble, the September 11 terrorist attacks and introduction of the euro. The financial crisis that began in 2007 encouraged people to stash even more.

Meanwhile, with a financial crisis looming – and getting closer by the day – for some countries, such as New Zealand, making money disappear is becoming a national pastime.

Christian Hawkesby, of the Reserve Bank of New Zealand, wonders where all the cash has gone. As the WSJ concludes, around a third of New Zealand’s new bank notes headed overseas in 2017, up from 6% four years earlier. That happened around the time that tourism overtook dairy as the country’s main export money-spinner, leading officials to speculate on the role played by currency exchanges, especially in Asia.

The trail mostly ran cold after that. The bank could only identify the whereabouts of around 25% of New Zealand’s cash. The rest, of about 75%, has disappeared.

“Our sense is that we’re in the same boat as a lot of other central banks out there,” said Christian Hawkesby, assistant governor at the RBNZ. “We can’t fully explain why holdings of cash are rising and where they are going.”

Well, Christian, the answer to where all that cash is going is simple and is shown on the image below…

Unfortunate boating accident.

Tyler Durden

Sat, 12/14/2019 – 19:00 - "It's For Racists!" – Academics Slam Quantum Computing Article For Using The Term 'Supremacy'

“It’s For Racists!” – Academics Slam Quantum Computing Article For Using The Term ‘Supremacy’

Authored by Dave Huber via The College Fix,

The ultimate in “woke” just may have waited until the very end of the year to reveal itself.

A cadre of academics is not happy about the journal Nature using the term “supremacy” in an article about quantum computing.

Titled “Quantum supremacy using a programmable superconducting processor,” the October piece deals with, well, just what it says: the superiority of computers using quantum processors versus so-called “classical” ones.

But 16 scholars say “supremacy” is for … racists. They want the phrase “quantum advantage” to be used in its place.

We consider it irresponsible to override the historical context of this descriptor, which risks sustaining divisions in race, gender and class. We call for the community to use ‘quantum advantage’ instead. …

In our view, ‘supremacy’ has overtones of violence, neocolonialism and racism through its association with ‘white supremacy’. Inherently violent language has crept into other branches of science as well — in human and robotic spaceflight, for example, terms such as ‘conquest’, ‘colonization’ and ‘settlement’ evoke the terra nullius arguments of settler colonialism and must be contextualized against ongoing issues of neocolonialism.

Surprisingly, all 16 who signed the complaint are associated with the hard sciences. They’re obviously brilliant individuals; nevertheless, there are a few indications about the origins of their linguistic policing.

For instance, Leonie Mueck, one of the principal authors, has a background in quantum chemistry … but her bio notes she serves on a diversity and inclusion committee and is “passionate about diversity in STEM.”

Divya Persaud is working on her PhD in “Mars imaging” at University College London, and also writes poetry. Her work “do not perform this” deals with “trauma and identity” and “examines various aspects of […] historical trauma …”

Syed Mustafa Ali of Open University has written articles such as “Transhumanism and/as Whiteness,” “Decolonizing Information Narratives: Entangled Apocalyptics, Algorithmic Racism and the Myths of History,” and “A Brief Introduction to Decolonial Computing.” Oh, don’t forget “Towards a Critical Race Theory of Information.”

The University of Granada’s Juani Bermejo-Vega is Europe’s only transgender quantum computer scientist.

Lastly, Cecilia Cormick of Argentina’s National University of Córdoba is a member of the Argentinian Physical Society’s “gender commission.”

Does anyone recall eleven years ago when a local Texas official called the astronomy term “black hole” racist?

Will “Star Trek” soon have to go back and edit terms like “trans-warp drive” for the same reasons as this quantum computing gripe? After all, the trans-warp experiment ended up being a failure. The negative symbolism!!

h/t: Rod Dreher

Tyler Durden

Sat, 12/14/2019 – 18:30 - Hong Kong Police Report Second Bomb Plot Foiled

Hong Kong Police Report Second Bomb Plot Foiled

With the Hong Kong protests showing no sign of letting up, a new narrative has emerged; that anti-government activists are “sliding into terrorism with home-made bombs” designed to inflict mass casualties.

On Sunday, Hong Kong police reported that they foiled a second bomb plot in under a week – arresting three men who were allegedly testing home-made devices and chemicals in a secluded area, according to SCMP.

One of the suspects is brought to a Tuen Mun school as part of police investigations. Photo: Winson Wong (via SCMP) According to Superintendent Suryanto Chin-chiu from the bomb squad, officers found a transmitter and a receiver at the scene and believed the devices were used to detonate the bombs at short-range using a low frequency. –SCMP

Police seized a transmitter and a receiver. Photo: Handout “The amount [of explosives] was not a lot. But intelligence showed there were two purposes behind the plot – one was to upgrade the power of the bombs, and the other to launch attacks at future assemblies or rallies,” said Senior Superintendent Steve Li Kwai-wah.

Acting on intelligence, officers from the organised crime and triad bureau ambushed the trio in scrubland off Siu Lang Shui Road in Tuen Mun in the early hours as they carried out tests.

…

In the Tuen Mun operation, officers also seized a radio-controlled detonation device and protective gear, including shields, bulletproof vests, a steel plate and gas masks at the scene. The tools were believed to have been used during the tests.-SCMP

Earlier in the week two home-made bombs were defused in Wan Chai, according to reports.

Adding to the case for home-grown terror, SCMP notes that the alleged bomb plots come as “police said three men and two women, aged 15 to 18, had been arrested in suspected connection with the death of a 70-year-old man who was hit by a brick during a fight between masked protesters and Sheung Shui residents last month.”

Police on Saturday added that they have recovered 34 petrol bombs, 20 smoke bombs, 12 corrosive bombs and a bunch of easily flammable items following calls from City University staff regarding potentially dangerous items on their Kowloon campus. University officials also reported the discovery of dangerous chemicals which were disposed of by police.

Accompanying SCMP‘s Saturday report is an Op-Ed, titled “Hong Kong’s revolution is sliding into terrorism with home-made bombs primed to kill and maim.”

While this great revolution of our times has removed Hong Kong’s bragging rights as one of the safest cities in the world, the security situation has not been deemed alarming enough for people to have to be dragged through metal detectors and frisked by security guards when entering shopping centres, cinema halls, train stations and other vulnerable public venues.

In the past I have often contemplated how easy it would be for the terroristically inclined to set off bombs pretty much anywhere, in such a trusting and open society, but always perished the thought. Not in Hong Kong. Not by Hongkongers.

I hate to report I’m not so sure any more these days, now that the revolutionaries have taken to building home-made bombs packed with high explosives and shrapnel. Just this week, the police bomb squad defused two improvised explosive devices found on school grounds by chance.

If this keeps up, China will be virtually forced to shut down the protests – all in the name of fighting terrorism.

Tyler Durden

Sat, 12/14/2019 – 18:00 - Can We Impeach The FBI Now?

Can We Impeach The FBI Now?

Authored by Peter van Buren via TheAmericanConservative.com,

The release of Justice Department Inspector General Michael Horowitz’s report, which shows that the Democrats, media, and FBI lied about not interfering in an election, will be a historian’s marker for how a decent nation fooled itself into self-harm. Forget about foreigners influencing our elections; it was us.

The Horowitz Report is being played by the media for its conclusion: that the FBI’s intel op run against the Trump campaign was not politically motivated and thus “legal.”

That covers one page of the 476-page document, but because it fits with the Democratic/mainstream media narrative that Trump is a liar, the rest has been ignored.

“The rest,” of course, is a detailed description of America’s domestic intelligence apparatus, aided by its overseas intelligence apparatus, and assisted by its Five Eyes allies’ intelligence apparatuses. And the conclusion is that they unleashed a full-spectrum spying campaign against a presidential candidate in order to influence an election, and when that failed, they tried to delegitimize a president.

We learn from the Horowitz Report that it was an Australian diplomat, Alexander Downer, a man with ties to his own nation’s intel services and the Clinton Foundation, who set up a meeting with Trump staffer George Papadopoulos, creating the necessary first bit of info to set the plan in motion. We find the FBI exaggerating, falsifying, and committing wicked sins of omission to buffalo the Foreign Intelligence Surveillance Act (FISA) courts into approving electronic surveillance on Team Trump to overtly or inadvertently monitor the communications of Paul Manafort, Michael Cohen, Jared Kushner, Michael Flynn, Jeff Sessions, Steve Bannon, Rick Gates, Trump transition staffers, and likely Trump himself. Trump officials were also monitored by British GCHQ, the information shared with their NSA partners, a piece of all this still not fully public.

We learn that the FBI greedily consumed the Steele Dossier, opposition “research” bought by the Clinton campaign to smear Trump with allegations of sex parties and pee tapes. Most notoriously, the dossier claims he was a Russian plant, a Manchurian Candidate, owned by Kremlin intelligence through a combination of treats (land deals in Moscow) and threats (kompromat over Trump’s evil sexual appetites). The Horowitz Report makes clear the FBI knew the Dossier was bunk, hid that conclusion from the FISA court, and purposefully lied to the FISA court in claiming that the Dossier was backed up by investigative news reports, which themselves were secretly based on the Dossier. The FBI knew Steele had created a classic intel officer’s information loop, secretly becoming his own corroborating source, and gleefully looked the other way because it supported his goals.

Horowitz contradicts media claims that the Dossier was a small part of the case presented to the FISA court. He finds that it was “central and essential.” And it was garbage: “factual assertions relied upon in the first [FISA] application targeting Carter Page were inaccurate, incomplete, or unsupported by appropriate documentation, based upon information the FBI had in its possession at the time the application was filed.” One of Steele’s primary sources, tracked down by FBI, said Steele had misreported several of the most troubling allegations of potential Trump blackmail and campaign collusion.

We find human dangles, what Lisa Page referred to as “our OCONUS lures” (OCONUS is spook-speak for Outside CONtinental US) in the form of a shady Maltese academic, Joseph Mifsud, who himself has deep ties to multiple U.S. intel agencies and the Pentagon, paying Trump staffers for nothing speeches to buy access to them. We find a female FBI undercover agent inserted into social situations with a Trump staffer (pillow talk is always a spy’s best friend). It becomes clear the FBI sought to manufacture a foreign counterintelligence threat as an excuse to unleash its surveillance tools against the Trump campaign.

We learn that Trump staffer Carter Page, while under FBI surveillance, was actually working for the CIA in Russia. The FBI was told this repeatedly, yet it never reported it to the FISA court while seeking approval for its secret investigation of Page. An FBI lawyer even doctored an email to hide the fact that Page was working for the Agency and not the Russians; it was that weak a case. The Horowitz Report went on to find “at least 17 significant errors or omissions” concerning FBI efforts to obtain FISA warrants against Page alone. California Congressman Devin Nunes raised these points almost two years ago in a memo the MSM widely discredited, even though we now know it was basically true and profoundly prescient.

Page was a nobody with nothing, but the FBI needed him. Horowitz explains that agents “believed at the time they approached the decision point on a second FISA renewal that, based upon the evidence already collected, Carter Page was a distraction in the investigation, not a key player in the Trump campaign, and was not critical to the overarching investigation.” They renewed the warrants anyway, three times, largely due to their value under the “two hop” rule. The FBI can extend surveillance two hops from its target, so if Carter Page called Michael Flynn who called Trump, all of those calls are legally open to monitoring. Page was a handy little bug.

Carter Page was never charged with any crime. He was blown into a big deal only by the fictional Steele Dossier, an excuse for the FBI to electronically surveil the Trump campaign.

When Trump was elected, the uber-lie that he was dirty with Russia was leaked to the press most likely by James Comey and John Brennan in January 2017 (not covered in the Horowitz Report), and a process, which is still ongoing, tying the president to a foreign power, began. “With Trump, All Roads Lead to Moscow,” writes the New York Times even today, long after both the Mueller Report and now the Horowitz Report say unambiguously otherwise. “Monday’s congressional hearing and the inspector general’s report tell a similar story,” bleats the Times, when in fact the long read of both says precisely the opposite.

Michael Horowitz, the author of this current report, should be a familiar name. In January 2017, he opened his probe into the FBI’s Clinton email investigation. In a damning passage, that 568-page report found it “extraordinary and insubordinate for Comey to conceal his intentions from his superiors…for the admitted purpose of preventing them from telling him not to make the statement, and to instruct his subordinates in the FBI to do the same. By departing so clearly and dramatically from FBI and department norms, the decisions negatively impacted the perception of the FBI and the department as fair administrators of justice.”

Horowitz’s Clinton report also criticizes FBI agents and illicit lovers Peter Strzok and Lisa Page, who exchanged texts disparaging Trump before moving from the Clinton email probe to the Russiagate investigation. Those texts “brought discredit” to the FBI and sowed public doubt. They included one exchange reading, “Page: “[Trump’s] not ever going to become president, right? Strzok: “No. No he’s not. We’ll stop it.”

If after reading the Horowitz Report you want to focus only on its page one statement that the FBI did not act illegally, you must in turn focus on what is “legal” in America. If you want to follow the headlines saying Trump was proven wrong when he claimed his campaign was spied upon, you really do need to look up that word in a dictionary and compare it to the tangle of surveillance, foreign government agents, undercover operatives, and payoffs that Horowitz details.

You may accept the opening lines of the Horowitz Report that the FBI did not act with political bias over the course of its investigation. Or you can find a clearer understanding in Attorney General William Barr’s summary of the Report: “that the FBI launched an intrusive investigation of a U.S. presidential campaign on the thinnest of suspicions.” You will need to reconcile the grotesque use the information the FBI gathered was put to after Trump was elected, the fuel for the Mueller investigation, and years’ worth of media picking at the Russian scab.

The current Horowitz Report, read alongside his previous report on how the FBI played inside the 2016 election vis-a-vis Clinton, should leave no doubt that the Bureau tried to influence the election of a president and then delegitimize him when he won. It wasn’t the Russians; it was us. And if you walk away concluding that the FBI fumbled things, acted amateurishly, failed to do what some claim they set out to do, well, just wait until next time.

On a personal note, if any of this is news to you, you may want to ask why you are only learning about it now. The American Conservative has been one of the few outlets that’s consistently exposed the Steele Dossier as part of an information op nearly since it was unveiled, and which has explained how the FISA court was manipulated, and which has steadily raised the question of political interference in our last election by American intelligence services. We claim no magical powers or inside information. To those of us who have been on the fringes of intelligence work, what was obvious just from the publicly available information was, well, obvious.

If you are reading any of this for the first time, or know people who are reading bastardized MSM versions of it for the first time, you might ask yourself why those outlets went along with Steele, et al. Their journalists are no dumber or smarter than ours. They do, however, write with a different agenda. Keep that in mind as we flip the calendar page to 2020.

* * *

Peter Van Buren, a 24-year State Department veteran, is the author of We Meant Well: How I Helped Lose the Battle for the Hearts and Minds of the Iraqi People,Hooper’s War: A Novel of WWII Japan, and Ghosts of Tom Joad: A Story of the #99 Percent.

Tyler Durden

Sat, 12/14/2019 – 17:30 - Blackwater Founder Erik Prince Held Secret Meetings With Maduro Government

Blackwater Founder Erik Prince Held Secret Meetings With Maduro Government

As if recent Washington regime change efforts in Venezuela — which on a couple of occasions this year led to brief military coup attempts which were quickly stamped out — weren’t already shady and murky enough, enter the prince of off-the-books black ops and covert dirty tricks himself:

Erik Prince, a private security mogul with ties to the Trump administration, held secret talks in Caracas last month with Venezuela’s vice president after briefing at least one senior U.S. official on his plans, according to people familiar with the situation.

Even though Prince was earlier publicly on record (as recently as April) pushing a plan to use thousands of mercenaries to back coup efforts in favor of US-recognize ‘interim president’ Juan Guaido, this latest effort revealed in the Bloomberg report appears an unconventional change in tactic by the Trump administration — a possible private back-channel opening of sorts via Prince — perhaps realizing Maduro is here to stay as Washington loses confidence in Guaido’s prospects.

Prince, and Venezuelan Vice President Delcy Rodriguez In Caracas Prince had “proposed a business deal and urged freedom for six imprisoned Citgo executives in the meeting with Vice President Delcy Rodriguez, according to one of the people.” It’s possible the efforts made headway, given those employees were released to house arrest from prison last week. Rodriguez is an outspoken close ally of Maduro and is under US sanctions.

Details of just what the ultimate goal is of Prince’s personal intervention remain unclear, but Maduro was reportedly briefed on the matter. The meeting was held on either Nov. 20 or 21, according to a separate report in Reuters.

Among proposals discussed included, according to the report, Prince’s suggestion of “sending personnel to train the nation’s police force as well as protecting judges and political candidates to help pave the way for new presidential elections.” So it’s perhaps part of a new ‘unofficial’ US administration effort to begin slowly dealing with Caracas, in hopes of influencing a political outcome?

The other interesting context to the revelation is that VP Delcy Rodríguez is a sanctioned individual, meaning discussion of any business arrangement with her without authorization is against US law (not that Prince was every overly concerned with that).

Delcy Rodríguez alongside Venezuela’s President Nicolás Maduro in Caracas in January. Image source: AFP/Getty Bloomberg speculates further on potentially what’s in it for the Venezuelan government:

For the Maduro regime, holding talks with an arch-enemy like Prince makes sense because they could present an opportunity for a deal that would alleviate the financial pressure the oil-producing country is under. While Maduro has successfully managed to stave off Guaido’s bid to take control of the government, top officials have been hamstrung by crippling U.S. economic sanctions.

But interestingly, the State Department claims no knowledge of the visit, with special envoy for Venezuela Elliott Abrams saying in a statement, “Neither the meeting nor any offers made were on behalf of the United States Government and on their face such offers would appear to violate U.S. sanctions.”

No doubt, the administration will continue to talk regime change in public while perhaps secretly using opportunists like Prince as back-channels for concessions, as the situation remains stalemated.

Erik Prince But then one wonders how Caracas would ever trust someone like the former Blackwater chief. But then again he is accustomed to doing dictatorial regimes’ “dirty work” from China to the UAE to that of any top bidder ultimately.

Tyler Durden

Sat, 12/14/2019 – 17:00 - "The Art Of The Deal" & How To Lose A "Trade War"

“The Art Of The Deal” & How To Lose A “Trade War”

Authored by Lance Roberts via RealInvestmentAdvice.com,

This past Monday, on the #RealInvestmentShow, I discussed that it was exceedingly likely that Trump would delay, or remove, the tariffs which were slated to go into effect this Sunday, On Thursday, that is exactly what happened.

Not only did the tariffs get delayed, but on Friday, it was reported that China and the U.S. reached “Phase One” of the trade deal, which included “some” tariff relief and agricultural purchases. To wit:

“The U.S. plans to scrap tariffs on Chinese goods in phases, a priority for Beijing, Vice Commerce Minister Wang Shouwen said. However, Wang did not detail when exactly the U.S. would roll back duties.

President Donald Trump later said his administration would cancel its next round of tariffs on Chinese goods set to take effect Sunday. In tweets, he added that the White House would leave 25% tariffs on $250 billion in imports in place, while cutting existing duties on another $120 billion in products to 7.5%.

China will also consider canceling retaliatory tariffs set for Dec. 15, according to Vice Finance Minister Liao Min.

Beijing will increase agricultural purchases significantly, Vice Minister of Agriculture and Rural Affairs Han Jun said, though he did not specify by how much. Trump has insisted that China buy more American crops as part of a deal, and cheered the commitment in his tweets.”

Then from the USTR:

“The United States will be maintaining 25 percent tariffs on approximately $250 billion of Chinese imports, along with 7.5 percent tariffs on approximately $120 billion of Chinese imports.”

Not surprisingly, the market initially rallied on the news, but then reality begin to set in.

Art Of The Deal Versus The Art Of War

Over the past 18-months we have written numerous articles about the ongoing “trade war,” which was started by Trump against China. As I wrote previously:

“This is all assuming Trump can actually succeed in a trade war with China. Let’s step back to the G-20 meeting between President Trump and President Xi Jinping. As I wrote then:

‘There is a tremendous amount of ‘hope’ currently built into the market for a ‘trade war truce’ this weekend. However, as we suggested previously, the most likely outcome was a truce…but no deal. That is exactly what happened.

While the markets will likely react positively next week to the news that ‘talks will continue,’ the impact of existing tariffs from both the U.S. and China continue to weigh on domestic firms and consumers.