- Opening The CIA's Can Of Worms

Opening The CIA’s Can Of Worms

Authored by Edward Curtin via Off-Guardian.org,

“The CIA and the media are part of the same criminal conspiracy,” wrote Douglas Valentine in his important book, The CIA As Organized Crime.

This is true. The corporate mainstream media are stenographers for the national security state’s ongoing psychological operations aimed at the American people, just as they have done the same for an international audience.

We have long been subjected to this “information warfare,” whose purpose is to win the hearts and minds of the American people and pacify them into victims of their own complicity, just as it was practiced long ago by the CIA in Vietnam and by The New York Times, CBS, etc. on the American people then and over the years as the American warfare state waged endless wars, coups, false flag operations, and assassinations at home and abroad.

Another way of putting this is to say for all practical purposes when it comes to matters that bear on important foreign and domestic matters, the CIA and the corporate mainstream media cannot be distinguished.

For those who read and study history, it has long been known that the CIA has placed their operatives throughout every agency of the U.S. government, as explained by Fletcher Prouty in The Secret Team; that CIA officers Cord Myer and Frank Wisner operated secret programs to get some of the most vocal exponents of intellectual freedom among intellectuals, journalists, and writers to be their voices for unfreedom and censorship, as explained by Frances Stonor Saunders in The Cultural Cold War and Joel Whitney in Finks, among others; that Cord Myer was especially focused on and successful in “courting the Compatible Left” since right wingers were already in the Agency’s pocket.

All this is documented and not disputed. It is shocking only to those who don’t do their homework and see what is happening today outside a broad historical context.

With the rise of alternate media and a wide array of dissenting voices on the internet, the establishment felt threatened and went on the defensive. It, therefore, should come as no surprise that those same elite corporate media are now leading the charge for increased censorship and the denial of free speech to those they deem dangerous, whether that involves wars, rigged elections, foreign coups, COVID-19, vaccinations, or the lies of the corporate media themselves.

Having already banned critics from writing in their pages and or talking on their screens, these media giants want to make the quieting of dissenting voices complete.

Just the other day The New York Times had this headline:

“Robert Kennedy Jr. Barred From Instagram Over False Virus Claims.”

Notice the lack of the word alleged before “false virus claims.” This is guilt by headline. It is a perfect piece of propaganda posing as reporting, since it accuses Kennedy, a brilliant and honorable man, of falsity and stupidity, thus justifying Instagram’s ban, and it is an inducement to further censorship of Mr. Kennedy by Facebook, Instagram’s parent company.

That ban should follow soon, as the Times’ reporter Jennifer Jett hopes, since she accusingly writes that RFK, Jr. “makes many of the same baseless claims to more than 300,000 followers” at Facebook. Jett made sure her report also went to msn.com and The Boston Globe.

This is one example of the censorship underway with much, much more to follow. What was once done under the cover of omission is now done openly and brazenly, cheered on by those who, in an act of bad faith, claim to be upholders of the First Amendment and the importance of free debate in a democracy. We are quickly slipping into an unreal totalitarian social order.

Which brings me to the recent work of Glenn Greenwald and Matt Taibbi, both of whom have strongly and rightly decried this censorship. As I understand their arguments, they go like this.

First, the corporate media have today divided up the territory and speak only to their own audiences in echo chambers: liberal to liberals (read: the “allegedly” liberal Democratic Party), such as The New York Times, NBC, etc., and conservative to conservatives (read” the “allegedly” conservative Donald Trump), such as Fox News, Breitbart, etc.

They have abandoned old school journalism that, despite its shortcomings, involved objectivity and the reporting of disparate facts and perspectives, but within limits. Since the digitization of news, their new business models are geared to these separate audiences since they are highly lucrative choices. It’s business-driven since electronic media have replaced paper as advertising revenues have shifted and people’s ability to focus on complicated issues has diminished drastically.

Old school journalism is suffering as a result and thus writers such as Greenwald and Taibbi and Chris Hedges (who interviewed Taibbi and concurs: part one here) have taken their work to the internet to escape such restrictive categories and the accompanying censorship.

Secondly, the great call for censorship is not something the Silicon Valley companies want because they want more people using their media since it means more money for them, but they are being pressured to do it by the traditional old school media, such as The New York Times, who now employ “tattletales and censors,” people who are power-hungry jerks, to sniff out dissenting voices that they can recommend should be banned.

Greenwald says,

They do it in part for power: to ensure nobody but they can control the flow of information. They do it partly for ideology and out of hubris: the belief that their worldview is so indisputably right that all dissent is inherently dangerous ‘disinformation.’”

Thus, the old school print and television media are not on the same page as Facebook, Twitter, etc. but have opposing agendas.

In short, these shifts and the censorship are about money and power within the media world as the business has been transformed by the digital revolution.

I think this is a half-truth that conceals a larger issue. The censorship is not being driven by power-hungry reporters at the Times or CNN or any media outlet. All these media and their employees are but the outer layer of the onion, the means by which messages are sent and people controlled.

These companies and their employees do what they are told, whether explicitly or implicitly, for they know it is in their financial interest to do so. If they do not play their part in this twisted and intricate propaganda game, they will suffer. They will be eliminated, as are pesky individuals who dare peel the onion to its core.

For each media company is one part of a large interconnected intelligence apparatus – a system, a complex – whose purpose is power, wealth, and domination for the very few at the expense of the many. The CIA and media as parts of the same criminal conspiracy.

To argue that the Silicon valley companies do not want to censor but are being pressured by the legacy corporate media does not make sense. These companies are deeply connected to U.S. intelligence agencies, as are the NY Times, CNN, NBC, etc. They too are part of what was once called Operation Mockingbird, the CIA’s program to control, use, and infiltrate the media. Only the most naïve would think that such a program does not exist today.

In Surveillance Valley, investigative reporter Yasha Levine documents how Silicon Valley tech companies like Facebook, Amazon, and Google are tied to the military-industrial-intelligence-media complex in surveillance and censorship; how the Internet was created by the Pentagon; and even how these shadowy players are deeply involved in the so-called privacy movement that developed after Edward Snowden’s revelations.

Like Valentine, and in very detailed ways, Levine shows how the military-industrial-intelligence-digital-media complex is part of the same criminal conspiracy as is the traditional media with their CIA overlords. It is one club.

Many people, however, might find this hard to believe because it bursts so many bubbles, including the one that claims that these tech companies are pressured into censorship by the likes of The New York Times, etc. The truth is the Internet was a military and intelligence tool from the very beginning and it is not the traditional corporate media that gives it its marching orders.

That being so, it is not the owners of the corporate media or their employees who are the ultimate controllers behind the current vast crackdown on dissent, but the intelligence agencies who control the mainstream media and the Silicon Valley monopolies such as Facebook, Twitter, Google, etc. All these media companies are but the outer layer of the onion, the means by which messages are sent and people controlled.

But for whom do these intelligence agencies work?

Not for themselves.

They work for their overlords, the super wealthy people, the banks, financial institutions, and corporations that own the United States and always have. In a simple twist of fate, such super wealthy naturally own the media corporations that are essential to their control of the majority of the world’s wealth through the stories they tell.

It is a symbiotic relationship.

As FDR put it bluntly in 1933, this coterie of wealthy forces is the “financial element in the larger centers [that] has owned the Government ever since the days of Andrew Jackson.” Their wealth and power has increased exponentially since then, and their connected tentacles have further spread to create what is an international deep state that involves such entities as the IMF, the World Bank, the World Economic Forum, those who meet yearly at Davos, etc.

They are the international overlords who are pushing hard to move the world toward a global dictatorship.

As is well known, or should be, the CIA was the creation of Wall St. and serves the interests of the wealthy owners. Peter Dale Scott, in “The State, the Deep State, and the Wall Street Overworld,” says of Allen Dulles, the nefarious longest-running Director of the CIA and Wall St. lawyer for Sullivan and Cromwell:

There seems to be little difference in Allen Dulles’s influence whether he was a Wall Street lawyer or a CIA director.”

It was Dulles, long connected to Rockefeller’s Standard Oil, international corporations, and a friend of Nazi agents and scientists, who was tasked with drawing up proposals for the CIA. He was ably assisted by five Wall St. bankers or investors, including the aforementioned Frank Wisner who later, as a CIA officer, said his “Mighty Wurlitzer” was “capable of playing any propaganda tune he desired.”

This he did by recruiting intellectuals, writers, reporters, labor organizations, and the mainstream corporate media, etc. to propagate the CIA’s messages.

Greenwald, Taibbi, and Hedges are correct up to a point, but they stop short. Their critique of old school journalism à la Edward Herman’s and Noam Chomsky’s Manufacturing of Consent model, while true as far as it goes, fails to pin the tail on the real donkey. Like old school journalists who knew implicitly how far they could go, these guys know it too, as if there is an invisible electronic gate that keeps them from wandering into dangerous territory.

The censorship of Robert Kennedy, Jr. is an exemplary case. His banishment from Instagram and the ridicule the mainstream media have heaped upon him for years is not simply because he raises deeply informed questions about vaccines, Bill Gates, the pharmaceutical companies, etc. His critiques suggest something far more dangerous is afoot: the demise of democracy and the rise of a totalitarian order that involves total surveillance, control, eugenics, etc. by the wealthy led by their intelligence propagandists.

To call him a super spreader of hoaxes and a conspiracy theorist is aimed at not only silencing him on specific medical issues, but to silence his powerful and articulate voice on all issues. To give thoughtful consideration to his deeply informed scientific thinking concerning vaccines, the World Health Organization, the Bill and Melinda Gates Foundation, etc., is to open a can of worms that the powerful want shut tight.

This is because RFK, Jr. is also a severe critic of the enormous power of the CIA and its propaganda that goes back so many decades and was used to cover up the national security state’s assassination of both his father and his uncle.

It is why his wonderful recent book, American Values: Lessons I Learned from My Family, that contains not one word about vaccines, was shunned by mainstream book reviewers; for the picture he paints fiercely indicts the CIA in multiple ways while also indicting the mass media that have been its mouthpieces.

These worms must be kept in the can, just as the power of the international overlords represented by the World Health Organization and the World Economic Forum with its Great Reset must be. They must be dismissed as crackpot conspiracy theories not worthy of debate or exposure.

Robert Kennedy, Jr., by name and dedication to truth seeking, conjures up his father’s ghost, the last politician who, because of his vast support across racial and class divides, could have united the country and tamed the power of the CIA to control the narrative that has allowed for the plundering of the world and the country for the wealthy overlords.

So they killed him.

There is a reason Noam Chomsky is an exemplar for Hedges, Greenwald, and Taibbi. He controls the can opener for so many. He has set the parameters for what is considered acceptable to be considered a serious journalist or intellectual. The assassinations of the Kennedys, 9/11, or a questioning of the official Covid-19 story are not among them, and so they are eschewed.

To denounce censorship, as they have done, is admirable. But now Greenwald, Taibbi, and Hedges need go up to the forbidden gate with the sign that says – “This far and no further” – and jump over it. That’s where the true stories lie. That’s when they’ll see the worms squirm.

Tyler Durden

Sun, 02/14/2021 – 23:30 - Mapping The Wealthiest Billionaire In Each U.S. State In 2021

Mapping The Wealthiest Billionaire In Each U.S. State In 2021

It is a testament to the burgeoning wealth of the U.S. that there is a billionaire in nearly every U.S. state. As Visual Capitalist’s Avery Koop notes, the country is home to around 800 billionaires among its 330 million people.

This map from HowMuch.Net reveals the wealthiest billionaire in each U.S. state.

The Richest of the Rich

Billionaires are a constant across the United States. The only states that don’t house one of these high-net-worth individuals are: Alabama, New Mexico, North Dakota, Alaska, Vermont, New Hampshire, Rhode Island, and Delaware.

Among the richest of the rich in the U.S., most are men, but there are 10 female billionaires who are the wealthiest in their respective states.

Jeff Bezos is worth an astounding $193.8 billion. Amazon became increasingly successful during the pandemic, as lockdown orders caused many people to have to stay home and shop online rather than in stores.

The runner up, Elon Musk, is worth $191.8 billion. The recent boom in Elon Musk’s net worth was due to the sharp rise in Tesla’s share prices. Recently, Elon Musk shifted his residence to the state of Texas, a move which is indicative of a larger trend of internal migration away from America’s most pricey urban areas.

Mind the Gap

Many of these individuals have actually become more wealthy during the COVID-19 pandemic, widening the existing gap of wealth inequality within the country.

Together Jeff Bezos, Elon Musk, Mark Zuckerberg, Bill Gates, and Warren Buffet (the five richest American billionaires) experienced a collective 85% increase in their wealth since the pandemic took hold. This equates to an added $303 billion in wealth.

In contrast, the median wealth of American households is about $121,700, and due to COVID-19, there has been a rising inability to cover bills and a risk of mass home loss in the country.

Overall, while we rely on companies like Amazon for our socially-distanced shopping and Facebook to keep us connected during the pandemic, Jeff Bezos and Mark Zuckerberg will likely continue to accrue immense fortunes. The wealthiest billionaires in the U.S. are likely to continue growing their net worth, pandemic or not, and have been consistently outpacing the lower to upper-middle income groups.

Tyler Durden

Sun, 02/14/2021 – 23:00 - America's Out Of Control Teens Are On A Historic Crime Spree

America’s Out Of Control Teens Are On A Historic Crime Spree

Authored by Michael Snyder via The Economic Collapse blog,

Young people are running wild all over the country, and nobody seems to be able to come up with a solution to slow down the violence. Following the tragic death of George Floyd, teens were disproportionally involved in the rioting, looting and arson that erupted in major cities throughout the nation for the remainder of 2020. And sometimes they would just take out their frustrations on random people on the street.

But in addition to violence that was spurred by social movements, most of our urban areas also experienced dramatic spikes in their murder rates. In fact, one recently released report found that murder rates rose by an average of 30 percent in 34 of our largest cities…

THE HOMICIDE RATE across 34 American cities increased by 30% on average during 2020, according to experts, as the U.S. reeled from the coronavirus pandemic and widespread protests against police brutality.

The newly released report from the National Commission on COVID-19 and Criminal Justice found that homicides rose in 29 of the 34 cities studied and that the three largest cities in the sample – New York, Los Angeles and Chicago – accounted for 40% of the additional homicide victims in 2020.

That 30 percent average increase was the biggest one year spike ever recorded, and way too much of the time these murders are being committed by Americans under the age of 20.

For example, two Milwaukee teens were just charged with the rape and murder of a young woman named Ee Lee…

Kamare Lewis, 17, and Kevin Spencer, 15 each face one count of first-degree intentional homicide, as party to a crime and one count of first-degree sexual assault (great bodily harm), as party to a crime.

Lee was found Sept. 16, 2020 in Washington Park by “bystanders,” still breathing but unconscious, severely beaten and left for dead. She was undressed below the waist, indicating sexual assault. She suffered severe contusions to the face/head. A hospital examination confirmed the sex assault.

Lee later died from her injuries on September 19th.

But it wasn’t just Lewis and Spencer that were involved in this brutal attack. In fact, we are being told that a total of 11 youths were seen leaving the area…

Video from the Washington Park Library showed 11 people leaving the park — six in a group on bicycles; five in a separate group, some on bikes and others on foot.

Sadly, young girls are also murdering one another.

Here is an example of one young girl stabbing another young girl to death…

Lyric D. Stewart, 14, of Rock Island, was stabbed to death Dec. 30 during a fight in the 1200 block of 11th Street.

Jimena Jinez, 18, also of Rock Island, was arrested in the early morning of Dec. 31, 2020, and charged with first-degree murder in the stabbing death. She has been in custody in Rock Island County Jail since then, and is being held on $1.5 million bond.

Our nation is degenerating right in front of our eyes, and it is only going to get worse.

In Jacksonville, Florida a group of teens recently ganged up to kill three people, including a very young mother…

In the first time since a Washington Heights triple-murder, the family of one of the victims, Sara Urriola, is speaking out. The Jacksonville mother was murdered by four suspected teens at the Calloway Cove apartments.

“We have lost a loving, caring, wife, mother, daughter, niece, cousin, sister, aunt, best-friend and friend today. Sara loved her friends and family very much and the friends that knew her know she was all about the well-being of her family. She loved to dance, dress up, and enjoyed all family events,” the family said in a statement to Action News Jax.

How twisted do you have to be in order to do something like that?

Horrific murders like this happen day after day, but they barely make a blip on the news anymore because they have become so common.

Meanwhile, carjackings are on the rise all over the nation as well.

According to NPR, the number of carjackings in Minneapolis more than tripled last year…

In Minneapolis, for example, there were 405 carjackings last year — more than triple the number in 2019. The suspects arrested were often juveniles between the ages of 11 and 17.

Other cities saw huge increases too, including New Orleans; Kansas City, Mo.; Louisville, Ky.; and Washington, D.C. Last year in Chicago, there were 1,400 carjackings.

Speaking of Chicago, there are certain parts of the city that now resemble a war zone. If you are in the wrong place at the wrong time, there is a good chance that a kid could stick a gun in your face and demand the keys to your vehicle.

What would you do if this happened to you?…

On a sunny January afternoon, Amy Blumenthal drove to her Chicago home after picking up groceries. She turned off a street and into an alley, backed her car into her garage and started unloading the bags.

“All of a sudden, I heard something and looked up and there was a boy with a COVID mask on holding a gun just inches from my face,” Blumenthal says. He demanded she hand over her keys. Another young male, also wearing a mask, told her to hurry up.

Amy Blumenthal was not prepared to face this sort of a scenario.

She eventually pulled herself together enough to give her two attackers the car keys, and she was later totally shocked to find out that they were both under 16 years of age…

In shock, she fumbled as she complied — they let her keep her house keys. Then they jumped in the car and sped off. Chicago police officers noticed their erratic driving, gave chase and the two were quickly arrested after crashing the vehicle into a building.

The robbery had left her shaken, but learning more about who they were left her stunned: They were just 15 and 13 years old.

Thanks to decades of running in the wrong direction, this is what our country has become.

We have become a completely and utterly lawless nation from the very top to the very bottom, and yet we continue to refuse to see the error of our ways.

So the fabric of our society will continue to unravel, and the thin veneer of civilization that we all take for granted on a daily basis will continue to disappear.

* * *

Michael’s new book entitled “Lost Prophecies Of The Future Of America” is now available in paperback and for the Kindle on Amazon.

Tyler Durden

Sun, 02/14/2021 – 22:30 - China Shows Off "Super Soldiers" Equipped With Exoskeleton Suits On Heavily Disputed Border

China Shows Off “Super Soldiers” Equipped With Exoskeleton Suits On Heavily Disputed Border

While Beijing may already be engineering “super soldiers” through biological advancements, it’s unclear how far Chinese military researchers have gone. But what we do know is that the Chinese military has already deployed exoskeleton suits for troops along the heavily disputed Sino-Indian border.

In recent months, China has used top-secret weapons along the Ladakh Line of Actual Control (LAC), such as microwave weapons against Indian troops. Perhaps the heavily disputed border is a testing ground for the People’s Liberation Army (PLA).

According to RT News, citing a state broadcaster CCTV report, PLA soldiers were seen with exoskeleton suits that enabled them to complete challenging tasks in high altitude environments around Ngari, located in Southwest China’s Tibet Autonomous Region. These troops delivered much-needed supplies to border guards along the LAC during the Chinese New Year holiday.

It usually takes all-terrain vehicles three days to reach the high-altitude outpost, located more than 16,000 feet above sea level. With exoskeleton equipped troops, the delivery time was significantly reduced.

CCTV did not disclose much more information about the exoskeleton developer or endurance of the suit. In the past, China has displayed other types of exoskeletons that are battery-powered and allow PLA troops to carry upwards of 170 pounds.

The PLA has gone all-in to develop “super soldiers” as the US Army is not far behind with their “Ironman-like” soldier exoskeleton suit.

Bank of America’s equity strategist Haim Israel recently told clients of the increasing geopolitical tensions between the US and China and how it would likely flourish through the 2020s.

More or less, exoskeleton suits for the modern battlefield are no longer science fiction as both of the world’s superpowers are racing to deploy the suits ahead of the next conflict.

Tyler Durden

Sun, 02/14/2021 – 22:00 - Biden Initiates Process To Close Guantanamo Bay Prison Permanently

Biden Initiates Process To Close Guantanamo Bay Prison Permanently

Authored by Dave DeCamp via AntiWar.com,

The Biden administration is launching a review of the US military prison at Guantanamo Bay with the aim of closing the facility, something the Obama administration promised to do but never followed through on.

White House Press Secretary Jen Psaki announced the review on Friday. When asked if President Biden plans to shut the prison before his presidency ends, Psaki said, “That certainly is our goal and our intention,” but an exact timeline was not given.

Detainees on arrival to Camp X-Ray, the holding facility at Guantánamo Bay, Cuba. DoD image National Security Council spokeswoman Emily Horne discussed the review with Reuters. “We are undertaking an NSC process to assess the current state of play that the Biden administration has inherited from the previous administration, in line with our broader goal of closing Guantanamo,” she said.

Horne said the NSC will be working with the Pentagon, State Department, and the Justice Department to make progress towards closing Gitmo.

There are currently 40 inmates being held in Gitmo. The prison costs over $530 million to operate each year, meaning each prisoner costs about $13 million per year.

In January, a Gitmo inmate appealed to President Biden for his release in an article in the Independent. Ahmed Rabbani was kidnapped in Pakistan in 2002, sold to the CIA, and mistakenly identified as an al-Qaeda member.

The White House has started a process to figure out how to close the military prison at Guantanamo Bay, officials say. https://t.co/BggHtosO6p pic.twitter.com/wOApstWkIt

— ABC News (@ABC) February 13, 2021

https://platform.twitter.com/widgets.js

Before heading to Gitmo, Rabbani was tortured for 540 days at a CIA black site, according to the 2014 Senate Intelligence Committee Report on CIA torture.

Rabbani has been on a seven-year hunger strike to protest being detained on no charges with no trial. Each day, guards force-feed Rabani by strapping him to a chair and forcing a tube down his nose and throat.

Tyler Durden

Sun, 02/14/2021 – 21:30 - Oil Surges To Jan 2020 Highs Amid Permian Freeze, Supercycle Chatter

Oil Surges To Jan 2020 Highs Amid Permian Freeze, Supercycle Chatter

While the US cash market may be closed for holiday tomorrow, world traders aren’t wasting any time and are taking reflationary traders to the next level, starting with Brent which just rose 2% to $63.47, the highest level since January 2020.

There are many catalyst for the surge:

- As we noted last week, and as Bloomberg’s Javier Blas reminded commodity traders yesterday, “the Permian is suffering extremely low temperatures, with the worse expected the night of Sun-to-Mon with -3 Fahrenheit. Oil gathering lines may froze; NGLs / water may condense, clogging pipes. And oil trucking would be disrupted by snow and ice.” In short, a perfect storm for a sudden spike in oil.

- Last week, Dylan Grice said that the stage is set for a new bull market in oil.

- JPMorgan chimed in, and predicted that a new commodity – and especially oil – supercycle has started, and will accelerate in March once CTA cover their shorts and go long.

- Morgan Stanley said a “high-pressure economy” is about to be unleashed, resulting in a major spike in inflation in the coming months.

Among all these bullish indicators, there is just one potential downside risk: whereas OPEC has been remarkable resilient in keeping production quotas in place so far, Reuters’ John Kemp writes that “oil prices have reached a critical threshold where OPEC+ must decide whether to increase production, or risk losing market share again to U.S. shale producers.”

As he further notes, after adjusting for inflation, Brent prices are now in the 58th percentile for all months since the start of 1990, which is consistent with slow but steady increases in output by non-OPEC producers.

In the last decade, whenever Brent prices averaged more than about $57 per barrel, U.S. producers captured all the growth in global oil consumption, increasing their market share at the expense of OPEC and its allies.

Responding to the earlier rise in prices, U.S. producers have already increased the number of rigs drilling for oil to nearly 300, up from a low of just 172 in August, according to oilfield services company Baker Hughes.

More recent price increases are likely to ensure the number of active rigs increases at least until the end of June, when the count is likely to exceed 425 or even 450, if the current trend continues.

Reflecting the rising rig count, U.S. production from the Lower 48 states excluding the Gulf of Mexico is already forecast to rise from current levels by 340,000 barrels per day (bpd) by the end of 2021.

In short, if prices rise further, both drilling and production are likely to accelerate even faster in the second half of 2021 and 2022.

On the other hand, traders don’t appear especially bothered and in the oil futures market, the price for Brent delivered in April is trading more than $2.70 per barrel higher than for deliveries in November, a price structure known as backwardation.

Backwardation normally occurs when traders anticipate production will fall short of consumption and petroleum inventories are low and falling further.

As Kemp concludes, “If that expectation proves correct, Brent prices are likely to increase further, perhaps significantly. Escalating prices and intensifying backwardation are both signalling the need for more production in the rest of the year.”

And amid continued calls for sharp rises in inflation – consider the following stunning fact from Morgan Stanley…

Cumulatively, the Covid-19 recession has cost US households US$400 billion in income, but they have already received more than US$1 trillion in transfers (even before the late December and forthcoming rounds of stimulus). Households have already accumulated US$1.5 trillion in excess saving, which is set to rise to US$2 trillion (9.5% of GDP) by early March once the additional fiscal package is enacted.

… it is unlikely that the upward trajectory of oil, commodities, and the reflation trade in general will change any time soon.

Tyler Durden

Sun, 02/14/2021 – 21:00 - Lincoln Project Donors Include Romney's Bain Capital And China-Linked Companies

Lincoln Project Donors Include Romney’s Bain Capital And China-Linked Companies

Authored by Ben Wilson via SaraACarter.com,

In the wake of several scandals rocking the infamous, and now failing, Lincoln Project, reports are surfacing of the organizations that contributed major donations to the group. And those that donated are facing backlash.

The National Pulse reports that the major donors show a list of left-leaning groups, despite the group’s claims that it represents a disenfranchised Republican base.

Lincoln Project Donors Include Romney’s Bain And China-Linked Sequoia Capitalhttps://t.co/7bNrymKau8

— Jack Posobiec 🇺🇸 (@JackPosobiec) February 12, 2021

https://platform.twitter.com/widgets.js

Hollywood figures, hedge fund managers, Mitt Romney’s firm Bain Capital, and other questionable sources make up the group’s largest donors.

“The list also includes Michael Moritz, a partner at the venture capital firm Sequoia, who donated a sizable sum in three donations in May, June, and July of 2020: one worth $50,000 and two worth $25,000,” the Pulse reports.

This morning The National Pulse published the Lincoln Project donor list.

This afternoon the donors backed away from the pedo-friendly group.https://t.co/jBiP6I4qng

— Raheem Kassam (@RaheemKassam) February 12, 2021

https://platform.twitter.com/widgets.js

See the full list of donors and reporting on the China connections here.

The news comes after reports broke that the FBI is investigating allegations against Lincoln Project co-founder John Weaver.

Meghan McCain, the co-host of the The View and daughter of former U.S. Senator John McCain, said in a Tweet that “John Weaver and Steve Schmidt were so despised by my Dad he made it a point to ban them from his funeral.”

“Since 2008, no McCain would have spit on them if they were on fire,” she added.

1. I’ve been very hesitant to comment but since my deceased father keeps getting invoked I will say this:

John Weaver and Steve Schmidt were so despised by my Dad he made it a point to ban them from his funeral. Since 2008, no McCain would have spit on them if they were on fire.

— Meghan McCain (@MeghanMcCain) February 13, 2021

https://platform.twitter.com/widgets.js

Weaver was accused by at least 21 men last week for sending inappropriate messages and in some instances offering political and employment opportunities for sexual favors.

“John Weaver led a secret life that was built on a foundation of deception at every level,” the prominent never-Trump organization said in a statement last week. “He is a predator, a liar, and an abuser. We extend our deepest sympathies to those who were targeted by his deplorable and predatory behavior.”

Tyler Durden

Sun, 02/14/2021 – 20:30 - Elderly Asians Targeted In Spate Of Vicious Bay Area Attacks

Elderly Asians Targeted In Spate Of Vicious Bay Area Attacks

Civil rights groups in California’s San Francisco Bay Area are demanding action following a recent surge in attacks on Asian Americans which have left one person dead and many others badly injured.

The attacks, reminiscent of the ‘knockout game,’ typically happen during daytime – including one against a 91-year-old Asian man in Oakland’s Chinatown who was hospitalized with serious injuries after being shoved to the ground by an African American man who walked up behind him. Last week, a 64-year-old grandmother was assaulted and robbed of cash she had withdrawn ahead of the Lunar New Year. And in January, a 52-year-old Asian American woman was shot in the head with a flare gun, also in Chinatown. Weeks later, 84-year-old Vicha Ratanapakdee was tackled to the ground by an assailant running at full speed through his San Francisco neighborhood, killing him, according to NPR. A 19-year-old man was arrested and charged with murder and elder abuse.

A special response unit has been created in Oakland’s Chinatown after a string of violent attacks targeting Asian-Americans.

Some of the assaults were caught on video, including a 91-year-old man being shoved to the ground.@Weijia asked @PressSec @jrpsaki about the attacks. pic.twitter.com/CT29gsfNSo

— CBS This Morning (@CBSThisMorning) February 9, 2021

A 28-year-old man, Yaha Muslim, charged with assault in the case of the 91-year-old man and two other elderly victims. Muslim, who was in custody on other charges, has two prior felony assault convictions, according to the Alameda County Sheriff and DA’s offices.

“These attacks taking place in the Bay Area are part of a larger trend of anti-Asian American/Pacific Islander hate brought on in many ways by COVID-19, as well as some of the xenophobic policies and racist rhetoric that were pushed forward by the prior administration,” said Manju Kulkarni, executive director of the Asian Pacific Policy and Planning Council, a coalition of California community-based groups which apparently thinks black thugs have been taking direction from former President Trump (who received just 12% of the black vote).

And while the much of the NPR report suggests that Trump’s rhetoric against China is responsible for the recent attacks, Black-on-Asian violence isn’t a new thing, and has been documented in the Bay area for more than a decade.

Over two-dozen recent Bay Area assaults and robberies reportedly mirror a “national rise in hate crimes against older Asian Americans,” according to the report, which notes that there have been nearly 3,000 incidents of anti-Asian hate across 47 states and DC, according to Kulkarni’s group.

“And roughly 7 to 8% of those, unfortunately, come from elders in our community who have experienced incidents, not unlike the ones that have taken place in recent days,” Kulkarni added.

The spate of attacks have prompted many Chinatown businesses to reduce hours during an already-dire situation thanks to the pandemic, during what is normally a bustling period due to the Lunar New Year.

“The fear is not only for the patrons but also employees,” said Carl Chan, head of Oakland’s Chinatown Chamber of Commerce. “They [businesses] are so fearful they prefer to close early. We also have many juveniles driving around Chinatown and carrying guns, so they’re also hurting people before they’re being robbed.”

According to Chan, some Asians are taking matters into their own hands – with over half-a-dozen ad-hoc volunteer groups springing up in recent weeks to protect businesses and older residents when they shop.

“Some of them are young people, they want to walk Chinatown,” said Chan. “And then also helping seniors pick up the groceries and then walk them home.”

Meanwhile, over 200 people across the Oakland area have volunteered as “community strollers” in Chinatown beginning next week.

And in a tone-deaf measure aimed at ‘helping’ the situation, somehow, the Oakland Anti-Police Terror Project has been asking people to “wear yellow” clothing to show support of the Asian community.

In the wake of the attacks several Oakland city council members including Council President Nikki Fortunato Bas, whose district includes Chinatown, have joined social justice groups warning against scapegoating and calling for solidarity between Asian American and African American communities. The Oakland Anti Police-Terror Project has asked people “to wear yellow to show you’re in support of Chinatown seniors and businesses.”

The Bay Area attacks and increased harassment nationwide have rallied support from those in arts, too. Actor and director Daniel Wu, who also is an East Bay native, led an effort to help stop what he described recently as an epidemic of hate-fueled language. –NPR

Oakland Police say they’ve added foot and car patrols, as well as set up a mobile command post in Chinatown – which the community has welcomed.

Tyler Durden

Sun, 02/14/2021 – 20:00 - Taibbi: The Bombhole Era

Taibbi: The Bombhole Era

Authored by Matt Taibbi via TK News

The new paperback edition of Hate Inc. has gone to print (for details about where to find the book, click here). The excerpt below is from the new chapter in the book, looking back at the Trump years. Thanks to Leighton Woodhouse for his great work on the animated video above. From the new foreword:

A UTOPIA OF DIVISION

News in the Trump years became a narrative drama, with each day advancing a tale of worsening political emergency, driven by subplots involving familiar casts of characters, in the manner of episodic television. It worked, but news directors and editors hit a stumbling block. If you cover everything like there’s no tomorrow, what happens when there is, in fact, a tomorrow?

The innovation was to use banner headlines to saturate news cycles, often to the exclusion of nearly any other news, before moving to the next controversy so quickly that mistakes, errors, or rhetorical letdowns were memory-holed.

The American Napoleon generated controversies at such a fantastic rate that stations like CNN and MSNBC (and Fox too) were able to keep ratings high by moving from mania to mania, hyping stories on the way up but not always following them down. The moment the narrative premise of any bombshell started to fray, the next story in line was bumped to the front.

News outlets paid off old editorial promises with new headlines: Ponzi journalism.

This technique of using the next bombshell story to push the last one down a memory-hole — call it Bombholing — needed a polarized audience to work. As surveys by organizations like the Pew Center showed, the different target demographics in Trump’s America increasingly did not communicate with one another. Democrats by 2020 were 91 percent of the New York Times audience and 95 percent of MSNBC’s, while Republicans were 93 percent of Fox viewers. When outlets overreached factually, it was possible, if not likely, that the original target audience would never learn the difference.

This reduced the incentive to be careful. Audiences devoured bombshells even when aware on a subconscious level that they might not hold up to scrutiny. If a story turned out to be incorrect, that was okay. News was now more about underlying narratives audiences felt were true and important. For conservatives, Trump was saving America from a conspiracy of elites. For “liberal” audiences, Trump was trying to assume dictatorial power, and the defenders of democracy were trying to stop him.

A symbiosis developed. Where audiences once punished media companies for mistakes, now they rewarded them for serving up the pure heroin of shaky, first-draft-like blockbusters. They wanted to be in the trenches of information discovery. Audiences were choosing powerful highs over lasting ones.

Moreover, if after publication another shoe dropped in the form of mitigating information, audiences were disinterested, even angry. Those updates were betrayals of the entertainment contract, like continuity errors. Companies soon learned there was a downside to once-mandatory ethical practices. Silent edits at newspapers became common, and old standards like the italicized editor’s note at the bottom of the page letting you know this or that story had been “updated” began to disappear.

The political impact of all this was that the news watcher in the Trump years became more addicted to the experience of being outraged, while retaining less about specific reasons for outrage. Audiences remembered some big stories and big themes, but stopped digesting each story on its own, rarely bothering to look back at the meaning of various manias after they’d died down.

As George Orwell understood when he created the “memory hole” concept in 1984, an institution that can obliterate memory can control history. In the Trump era, news audiences volunteered to stop the disobedient act of remembering.

They brought a pure, virginal belief to watching news, and agreed to unquestioningly accept any new versions of the past put forward. This was Hate Inc. brought to its logical conclusion. Fox and MSNBC already knew how to monetize anger by setting audiences against one another. The innovation of the Trump era was companies learned they could operate on a sort of editorial margin, borrowing credibility for unproven stories from audiences themselves, who gave permission to play loose with facts by gobbling up anonymously-sourced exposes that tickled their outrage centers.

Mistakes became irrelevant. In a way, they were no longer understood as mistakes.

This is an excerpt from today’s subscriber-only post. To read the entire post and get full access to the archives, you can subscribe for $5 a month or $50 a year.

Tyler Durden

Sun, 02/14/2021 – 19:30 - If House Price Increases Of 10% Is Not Inflation. Then What Is it

If House Price Increases Of 10% Is Not Inflation. Then What Is it

Submitted by Joseph Carson, former chief economist Alliance Bernstein

Two Decades of Price Mismeasurement & Policy Confusion

Two decades of price mismeasurement and policy confusion have left everyone bewildered and puzzled over inflation. Inaccuracies in inflation measurement are far from being merely academic; it reopens the fundamental issue of inflation and how policymakers should use price information in its conduct of monetary policy.

Inflation – What Is It?

There has not been a general discussion about inflation and how statisticians should measure it in about 25 years. In the mid-1990s, a controversy over the consumer price index (CPI) erupted when Former Federal Chairman Alan Greenspan told Congress that the CPI overstated actual inflation by at least one percentage point. And by using it to index government entitlement programs Congress was over-spending for cost-of-living adjustments and increasing the budget deficit in the process.

Politicians always looking for an easy and quick fix jumped into the debate, calling for the Bureau of Labor Statistics (BLS) to make an immediate change in the CPI measurement. The dispute over measurement issues was not as simple or clear-cut as politicians thought it was. So the Senate created a formal Advisory Commission, under the direction of Micheal Boskin, former Chairman of the Council of Economic Advisors, to study the CPI issue.

The Commission recommended that BLS move the CPI more towards a cost-of-living index (COLI). As constructed, the CPI is a fixed-weighted index measuring price change between two periods. In contrast, a COLI would measure the prices of a comprehensive basket of goods and services that offers the same satisfaction to an average consumer as in the prior period. There is no consensus on what a true COLI is, nor is there a consensus on how such an index would be estimated.

In its final report to the Senate, the Commission made a number of recommendations (e.g., quality changes, product substitution, and new business outlets) that would purportedly lower the CPI index and ignored or overlooked changes that would result in a higher index. In time, BLS incorporated several of the Commission measurement changes and also made a change at the same time in the measurement of owners’ housing costs.

The change in owners’ housing costs had nothing to do with the CPI controversy, but it had a bigger impact on reported inflation. BLS statisticians argued that because of the ever-shrinking supply of owners’ occupied homes available for rent, data adequacy and quality did not meet their standards. BLS decided to link owners’ rent to the rental market even though the two markets were separate.

The change in the measurement of owners’ housing costs was never challenged by the Federal Reserve or politicians, but its impact proved to be far bigger than the changes made by the Boskin’s Commission. In the past two decades, house price inflation has increased twice as fast as the owners’ rent index. And all of the outperformance has occurred during the expansion years, periods when policymakers have been confused why cyclical inflation has not run faster and why inflation seemed to be at times insensitive to changes in monetary policy.

There is an old axiom in price measurement; that is, price indexes measure the rate of price change for the conditions of the index. The appropriate price index for monetary policy is an index based on market prices paid by the consumers (i.e., a buyers index). Excluding the price change for houses (or the implied rents from owners occupied homes) reduces the accuracy of reported inflation.

Policy Confusion

The Federal Reserve was one of the stakeholder groups that forced a change in the measurement of the CPI. So when it was time to select a price index initially as an informal policy tool, and later as a formal guide, policymakers were in a jam. Could policymakers select the CPI as the preferred index after saying it was flawed? No. In the end, policymakers choose the personal consumption expenditure deflator (PCE) reported by the Bureau of Economic Analysis (BEA) over BLS’s CPI.

The Fed argued that BEA’s PCE index was a superior index. It’s not. First, BEA does not measure consumer prices. That’s the responsibility of BLS. The only direct measure of prices that consumers pay for is the CPI. Second, BEA uses the CPI data for 70% of the PCE index. Third, the remaining 30% of the PCE index is for goods and services that businesses and the government provide or give to people. That creates a price measurement problem since these items are not “sold” to the consumer and should disqualify it as the appropriate price index for monetary policy since it is not based solely on market prices paid by the consumer.

Confusion over inflation and the appropriate measure of inflation has left policymakers adrift. Instead of acknowledging the errors in price measurement and the selection of the wrong price index, policymakers have doubled-down. They remain hell-bent on hitting a 2% inflation target with a flawed index and have introduced inflation-averaging as a new policy tool. Inflation-averaging doesn’t eliminate the flaws of price mismeasurement; it compounds them. In other words, a “donkey-indicator” is still a donkey after averaging!

Inflation Outlook

Several analysts have raised concerns that the recent explosion in the broad money supply is a harbinger of higher inflation. Similar comments on inflation were made nearly a decade ago when the Federal Reserve introduced quantitative easing.

During the early years of quantitative easing (almost ten years ago), I made a bet that reported inflation could never rise above 5% again based on price measurement issues with Alliance Bernstein colleague Cathy Wood, who is the founder, CEO, and CIO of ARK Investments. I have never collected on that bet. And I would make the same bet today based on the construction of the price indexes.

Reported inflation is different than experienced inflation. In 2020, core consumer prices rose 1.6%, but I would argue that experienced inflation was at least 100 to 150 basis points higher since house prices increased 500 basis points more than the owner’s rents index.

In a speech titled “Problems With Price Measurement,” Former Chairman Alan Greenspan stated, “policymakers should be cognizant of the shortcomings of our published price indexes to avoid actions on inaccurate premises that will provoke undesired consequences.”

Inflation can destabilize an economy even if faulty price indexes fail to reveal it. It already happened during the house price bubble of 2007-2009. Odds are high it will happen again because policy confusion over inflation lives on, evident by the current policy framework built upon the false premise that a single price index can identify economy-wide price imbalances. In the past two decades, reported inflation has veered off as a useful and accurate barometer of what prices matter. A flexible policy approach is needed because prices that matter nowadays have shifted from the goods and services markets to the asset markets.

Tyler Durden

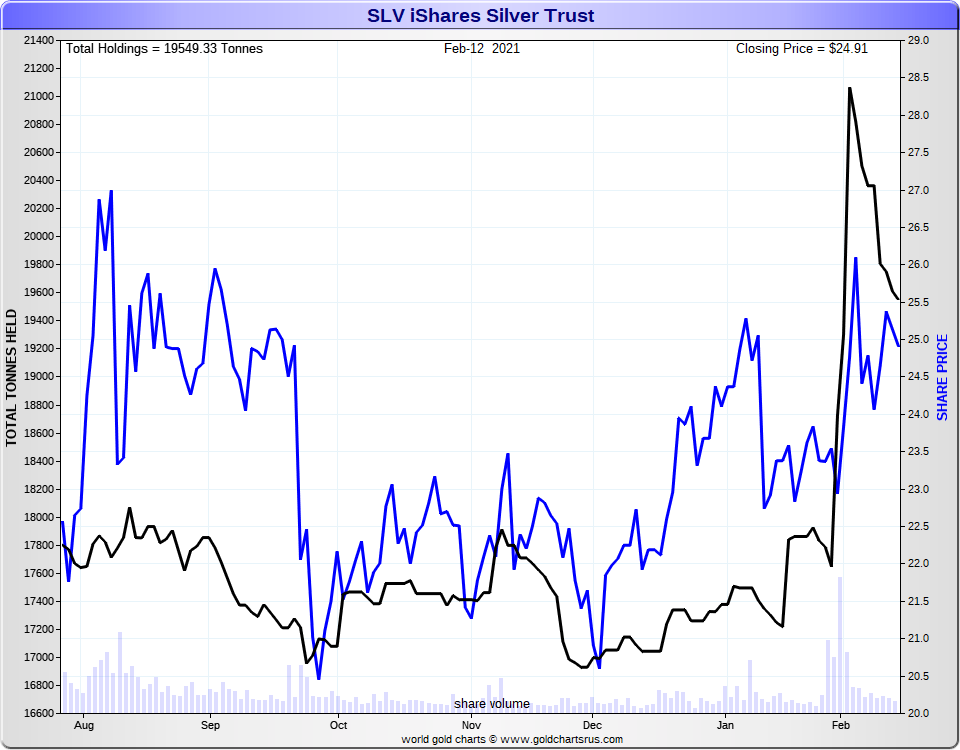

Sun, 02/14/2021 – 19:05 - #SilverSqueeze Hits London As SLV Warns Of Limited Available Silver

#SilverSqueeze Hits London As SLV Warns Of Limited Available Silver

Submitted by Ronan Manly, BullionStar.com

Less than a week ago in ‘Houston, we have a Problem”: 85% of Silver in London already held by ETFs’, we explained how with the emergence of the #SilverSqueeze, the silver-backed ETFs which claim to hold their silver in London, now account for 85% of all the silver claimed to be stored in the London LBMA vaults (over 28,000 tonnes of the LBMA total of 33,609 tonnes). This, for anyone who can out 2 and 2 together, does not leave very much available silver in London for silver ETFs or for anyone else, especially the largest silver ETF in the market the giant iShares Silver Trust (SLV), which let’s not forget has the infamous JP Morgan as custodian.

That SLV has seen massive dollar inflows in late January and early February with corresponding jumps in claimed silver holdings is now widely known, but is worth repeating here, for what’s about to come next.

3,416.11 Tonnes of Silver?

The intense market interest in the iShares Silver Trust (SLV) started on 28January when a huge volume of 152 million shares traded on NYSE Arca. Again on Friday 29January, SLV traded a massive volume of 113 million shares. This led to an increase in SLV ‘Shares Outstanding’ on Friday 29 January of 37 million shares, and a same day claim by JP Morgan, the SLV custodian, that it had increased the silver held in the SLV by 37.67 million ozs (1,171 tonnes), all claimed to be sourced in the LBMA vaults in London.

On Monday 01 February, an even larger 280 million SLV shares traded on NYSE, and by end of day SLV shares outstanding jumped by 20 million. On that day SLV claimed to add another 15.376 million ounces of silver (478.25 tonnes) within the LBMA vaults in London, about three-quarters of the value of the new SLV shares created on that day.

On Tuesday 2 February, with SLV trading still elevated on NYSE, the iShares Silver Trust created a massive 61,350,000 new SLV shares, bringing the SLV shares outstanding to 729.1 million. On the same day, JP Morgan and Blackrock claimed to have added a huge 56.783 million ozs of silver (1,766 tonnes) to the SLV (again all in London), an incredible amount by any measure, but still short of reflecting the total of 118.45 million total of new shares that had been created between Friday and Tuesday (which led them to adjust down shares outstanding by 8.6 million on Wednesday 3 February).

Over this time, you can see a nearly one for one relationship between the change in number of SLV shares outstanding and the amount of silver ounces claimed to be added to SLV.

Between Friday 29 January and Wednesday 3 February inclusive, SLV shares outstanding increased by a net 109.85 million. Over the 3-day period from Friday 29 January to Tuesday 2 February, SLV claimed to have added an incredible 109.83 million ozs of silver (3,416.11 tonnes), with holdings of silver bars rising from 567.52 million ozs of silver to 677.35 million ounces (from 17,651.77 tonnes to 21,067.88 tonnes).

According to the SLV daily bar lists, this extra 3,416.11 tonnes of silver added to SLV between 29 January and 2 February was in the form of 113,501 Good Delivery silver bars (the bars weighing approx. 1000 oz each). Again, according to the SLV bar list, these bars were added in five London vaults which SLV uses, namely Brinks vault in Premier Park London (45.5%), Loomis London vault (27.7%), Brinks Unit 7 vault Radius Park London (15.5%), Malca Amit London vault (6.0%) and JP Morgan’s own London vault (a measly 5.3%).

In fact, according to the bar lists, SLV only started tapping into silver in the Brinks Premier park vault on Monday 1 February, and only started tapping to silver held in the Loomis London vault on Tuesday 2 February. Which to some people may look like a case of desperation or maybe even panic.

SLV silver holdings over the 6 months from August 2020 to February 2021. Source: www.GoldChartsRUs.com Unable to Acquire Sufficient Silver

Adding 3,416.11 tonnes of silver to SLV between 29 January and 2 February is not something that JP Morgan can easily claim to do again.

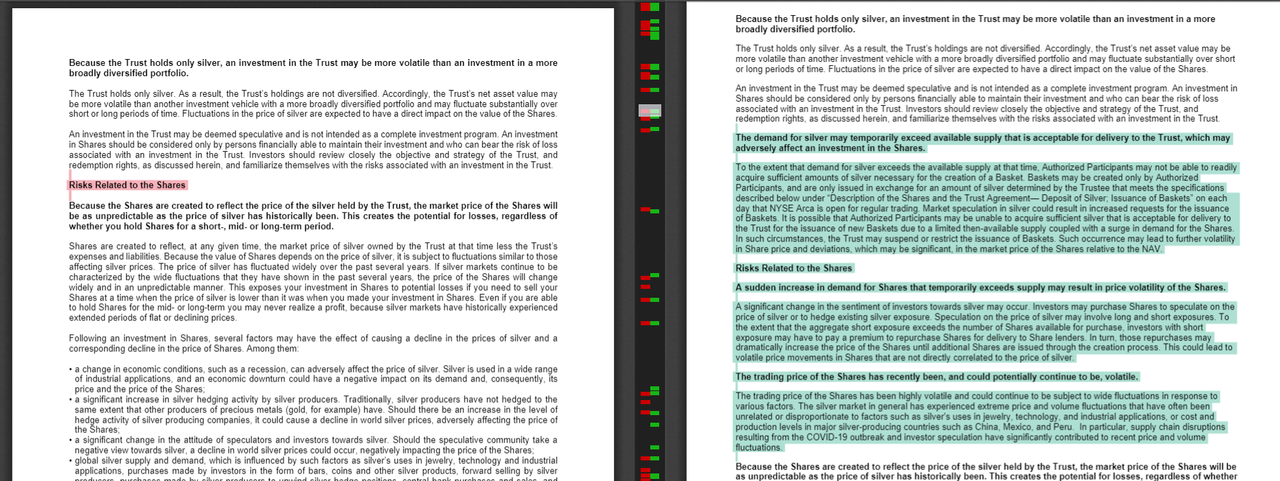

Which is why it’s particularly interesting that on Wednesday 3 February, right after claiming to add 3416 tonnes of silver to SLV by frantically tapping the LBMA vaults in London, the iShares Silver Trust prospectus was changed, and the following wording added:

“The demand for silver may temporarily exceed available supply that is acceptable for delivery to the Trust, which may adversely affect an investment in the Shares.

To the extent that demand for silver exceeds the available supply at that time, Authorized Participants may not be able to readily acquire sufficient amounts of silver necessary for the creation of a Basket.

Baskets may be created only by Authorized Participants, and are only issued in exchange for an amount of silver determined by the Trustee that meets the specifications described below under “Description of the Shares and the Trust Agreement— Deposit of Silver; Issuance of Baskets” on each day that NYSE Arca is open for regular trading. Market speculation in silver could result in increased requests for the issuance of Baskets.

It is possible that Authorized Participants may be unable to acquire sufficient silver that is acceptable for delivery to the Trust for the issuance of new Baskets due to a limited then-available supply coupled with a surge in demand for the Shares.

In such circumstances, the Trust may suspend or restrict the issuance of Baskets. Such occurrence may lead to further volatility in Share price and deviations, which may be significant, in the market price of the Shares relative to the NAV.”

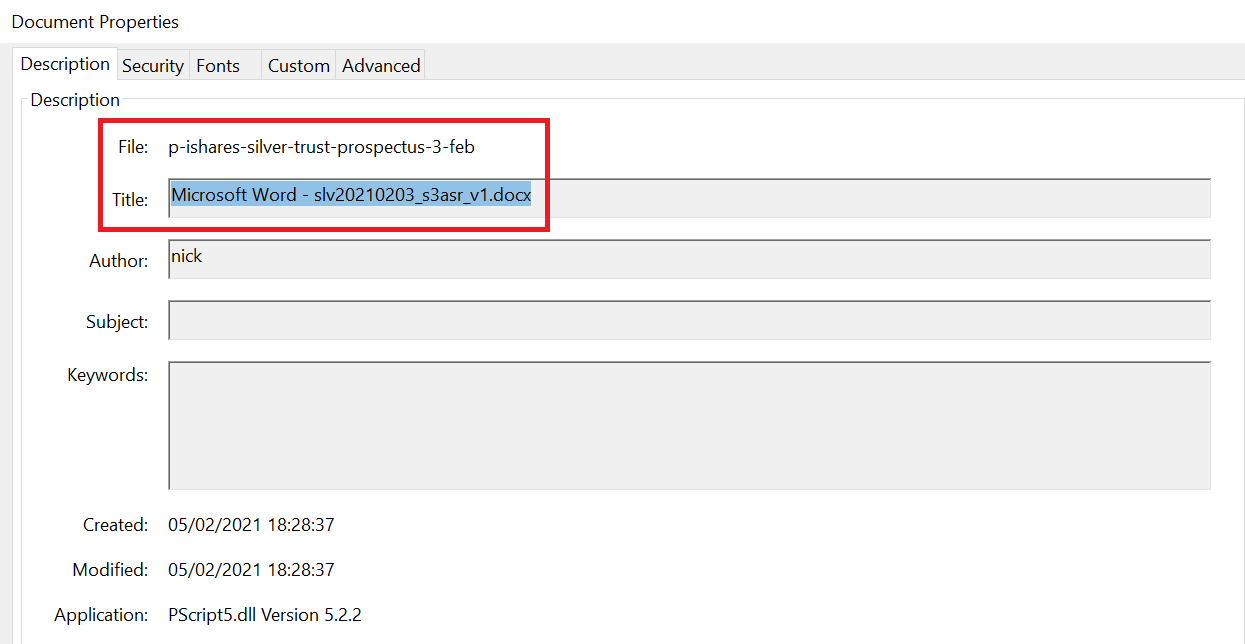

That the prospectus change was first drafted on Wednesday 3 February is clear by looking at prospectus pdf filename which is ‘p-ishares-silver-trust-prospectus-3-feb.pdf’ and the pdf title ‘Microsoft Word – slv20210203_s3asr_v1.docx’, which was authored by someone called ‘nick’. While the draft started in Word, the final version was saved as a pdf on 5 February.

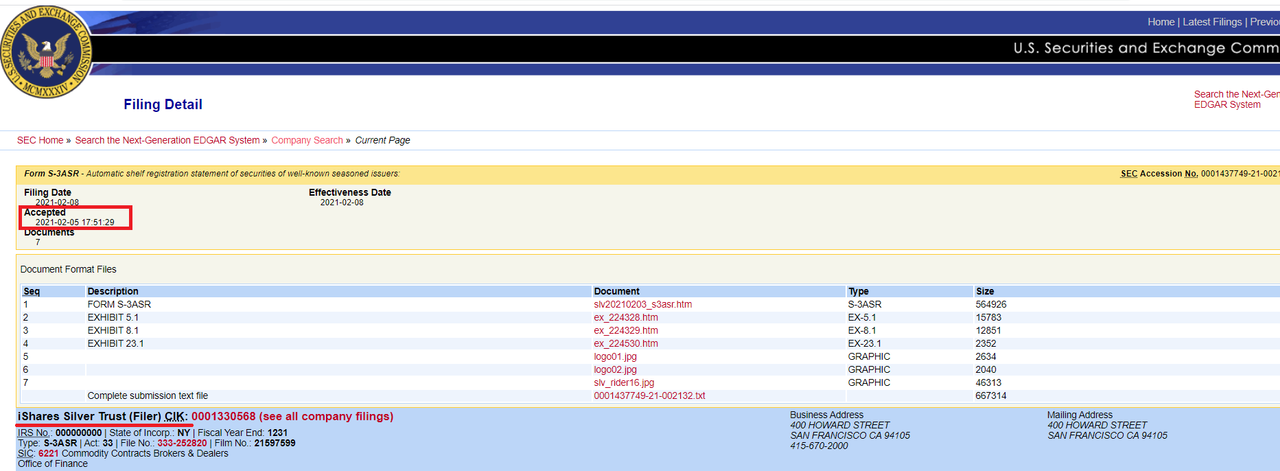

SLV Prospectus amendment draft created on Wednesday 3 February The final pdf date is the same day, 5 February, that the amended prospectus was quietly uploaded to the SEC Edgar website here with an effective date of 8 February. The previous version of the SLV prospectus was from 14 January

SLV informs SEC of its amended prospectus, 5 February Below you can see the changes in the new 8 February version of the SLV prospectus compared to the 14 January version.

SLV Prospectus” Left Hand Side – 14 January version, Right Hand Side New February version BullionStar picked up on the fact that there was a new prospectus with the suspicious 3 February date, and then a twitter user (h/t Roelzns) compared the two prospectus versions to pinpoint the amended text

iShares Silver Trust (SLV) published a new Prospectus dated 08 February 2021. From the link on its website, this is a document saved as “slv20210203_s3asr_v1.docx”, with a date of 03 February, the day after massive 3 day inflows into SLV. Suspicious timing on updated prospectus!

— BullionStar (@BullionStar) February 13, 2021

https://platform.twitter.com/widgets.js

In addition to the paragraph above about silver demand exceeding available silver supply, the SLV prospectus also added into two further paragraghs under the first, one of which ominously predicting volatile share price movements that could be uncorrelated to the silver price:

“Risks Related to the Shares

A sudden increase in demand for Shares that temporarily exceeds supply may result in price volatility of the Shares.

A significant change in the sentiment of investors towards silver may occur. Investors may purchase Shares to speculate on the price of silver or to hedge existing silver exposure. Speculation on the price of silver may involve long and short exposures. To the extent that the aggregate short exposure exceeds the number of Shares available for purchase, investors with short exposure may have to pay a premium to repurchase Shares for delivery to Share lenders.

In turn, those repurchases may dramatically increase the price of the Shares until additional Shares are issued through the creation process. This could lead to volatile price movements in Shares that are not directly correlated to the price of silver.“

Humorously, the third new paragraph inserted into the SLV prospectus explains that the silver price, which don’t forget is a paper price set by the dominance of bullion bank trading on COMEX and LBMA London, is subject to extreme fluctuations which are unrelated to physical silver demand and supply, but alas there is no mention of the years long silver price manipulations that JP Morgan and other LBMA cronies have been recently prosecuted for:

The trading price of the Shares has recently been, and could potentially continue to be, volatile.

The trading price of the Shares has been highly volatile and could continue to be subject to wide fluctuations in response to various factors. The silver market in general has experienced extreme price and volume fluctuations that have often been unrelated or disproportionate to factors such as silver’s uses in jewelry, technology, and industrial applications, or cost and production levels in major silver-producing countries such as China, Mexico, and Peru. In particular, supply chain disruptions resulting from the COVID-19 outbreak and investor speculation have significantly contributed to recent price and volume fluctuations.”

If the short squeeze on GameStop caused fireworks among a few hedge funds on Wall Street, we hate to think what a short squeeze on the global silver supply will look like as hedge funds wake up to the possibility that SLV “cannot acquire sufficient silver acceptable for delivery to the Trust”.

Tyler Durden

Sun, 02/14/2021 – 18:44 - Rickards Warns 'Green New Deal' Is Already Underway

Rickards Warns ‘Green New Deal’ Is Already Underway

Authored by James Rickards via The Daily Reckoning,

By now, you’ve heard of the Green New Deal, an ambitious agenda to decarbonize the economy. The overall Green New Deal calls for ending the use of oil and natural gas, moving to electric vehicles, solar, wind and geothermal power, imposing carbon taxes to reduce C02 emissions and providing government subsidies to non-carbon-based energy technologies.

The U.S. would also seek to embed these policies and priorities in new trade treaties and multilateral agreements. President Biden has already begun this process by rejoining the Paris Climate Accord, which actually doesn’t mean much; it’s mostly for show.

The Paris Accord is also a platform for pursuing the Green New Deal.

But it’s difficult to conceive of any other program that would do more harm to the U.S. economy and give more of a boost to the Chinese, Russians and Iranians.

Biden has temporarily halted all new oil and gas drilling leases and permits on federal lands. He’s moving quickly to make the ban permanent. This ban will kill the fracking industry and help to destroy what’s left of the coal industry. Because of reduced supply, it will raise energy prices globally. New carbon emission taxes will raise prices even further.

Why Kill the Keystone XL Pipeline?

Very significantly, Biden has also canceled the Keystone XL pipeline. This is a pipeline that brings oil from Alberta, in Canada, to the central United States. The pipeline would then go to Nebraska, where there would be a hub and a distribution center.

Killing the pipeline would cost tens of thousands of jobs. And when you count suppliers and subcontractors, it could be at least 100,000 high-paying lost jobs, mostly union jobs with benefits.

But the fact is, the oil is still coming anyway. That oil from Canada is still coming to the United States, except it comes by truck and train. That’s the reason you build a pipeline. It’s faster and cheaper to move the oil by pipeline than it is to move it by truck and train. What we have now is just a pipeline on wheels with one difference…

They release much greater CO2 emissions. All these trucks and all these trains are putting more CO2 into the atmosphere than a pipeline would. Again, that’s why you build a pipeline.

So if you’re doing this for economic reasons, it makes no sense because you destroyed maybe 100,000 high-paying jobs. If you’re doing it for environmental reasons, it makes no sense because you will have more CO2 emissions from the trains and trucks than you would from the pipeline. But they’ve done it anyway.

This is a good example of what I call the triumph of ideology over common sense. Common sense will say, build a pipeline for the reasons I just mentioned. But that doesn’t fit the ideology or their worldview. They’re immune to the facts. They just say pipelines are bad, so get rid of them.

A Propaganda Cover for the Real Objectives

Biden justifies the Green New Deal based on fear of climate change. I don’t want to dive into the climate change debate today. But there’s good science that says CO2 is more or less a harmless trace gas, not the existential threat that many environmentalists would have you believe.

Climate science provides almost no evidence that slight observable temperature changes have anything to do with C02 emissions. It is far more likely that any temperature changes are the result of solar flare cycles and volcanic eruptions. Some data strongly suggests that the earth is slowly cooling, not warming.

Scare tactics about the “costs” of hurricanes have more to do with expensive homes built on exposed barrier islands (subsidized by federal insurance programs) than the intensity of storms, which were actually greater and more frequent in the 1940s.

Climate change is a propaganda cover for the real goals of higher taxes, more regulation, slower growth and favors for tech entrepreneurs. It’s a globalist’s dream.

What About Congress?

When you add it all up, Biden’s proposals will destroy high-paying jobs with benefits in the energy sector, raise energy costs for consumers and help flat-line economic growth.

Still, given the ideological momentum behind the Green New Deal and the imperatives of getting policies enacted quickly, it seems likely that some of these misguided provisions will become law at great cost to consumers and the economy as a whole.

But the prospects of the most radical parts of the Green New Deal becoming law are problematic. The projected adverse economic and geopolitical results will possibly derail the program in Congress. But, there can be no assurance of that. This will be one of the legislative priorities that Biden puts on a fast track because a Republican takeover of the House in 2022 would stop it indefinitely.

But the climate change agenda is seeping into all aspects of policy, including monetary policy. The original role of central banks was to provide a sound currency, which, in turn, facilitated government borrowing.

By the late 19th century, a new mission was added, which was to be a lender of last resort to banks themselves in a financial crisis. It held that in a crisis, the central bank should lend freely to solvent banks against sound collateral at a high rate of interest. That’s been flipped on its head.

Today’s version is to lend freely to anyone without collateral at a zero rate of interest.

From Lender of Last Resort To Climate Savior

After 1934, the Federal Reserve and other central banks were given broad regulatory powers over the banks in their jurisdictions. Finally, in 1978 the Humphrey-Hawkins Act gave the Federal Reserve a dual mandate, which included price stability and job creation.

With the job creation mandate in its portfolio, the Fed was empowered to interfere with almost every aspect of the real economy, including jobs, inflation, interest rates, liquidity and financial regulation.

As if that weren’t enough, economist Barry Eichengreen now calls on central banks, especially the Fed, to use their regulatory powers to control climate change! Part of the agenda would address racial inequality, income inequality and credit access for underprivileged groups.

These may be laudable goals, but it’s a long way from the Fed’s role as lender of last resort.

What’s frightening about this push to expand the Fed’s mandate is not that it can’t work, but that it could. A central bank could require commercial banks to lend money to solar and wind generating companies and deny credit to oil companies.

A central bank could require more loans to disadvantaged neighborhoods and require that no credit be made available to gun manufacturers or gun dealers.

There is no aspect of the economy and business activity that could not be affected positively by mandatory credit or destroyed by the lack of credit and access to the payments system. This is already being done to some extent by cabals of commercial banks. It would be even more powerful if required by central banks.

This is exactly the outcome that has been warned about for centuries by philosophers and political scientists. It is exactly the reason Americans abolished two U.S. central banks in the 19th century.

Any party that controls money can control the world. One solution is to abolish the Fed. Another solution is to abandon the money and move to something the Fed cannot control — gold.

Tyler Durden

Sun, 02/14/2021 – 18:40 - Exposing The Robinhood Scam: Here's How Much Citadel Paid To Robinhood To Buy Your Orders

Exposing The Robinhood Scam: Here’s How Much Citadel Paid To Robinhood To Buy Your Orders

Frankly, we’ve had it with the constant stream of lies from Robinhood and neverending bullshit from the company’s CEO, Vlad Tenev.

With Tenev scheduled to testify on Thursday, alongside the CEOs of Citadel, Melvin Capital and Reddit, the apriori mea culpas have started to emerge – if a little too late – the former HFT trader spoke late on Friday on the All-In Podcast hosted by Chamath Palihapitiya, who had strongly criticized Robinhood over the trading restrictions, and Jason Calacanis, a Robinhood investor, and said that “no doubt we could have communicated this a little bit better to customers.”

What he is referring to, of course, is Robinhood’s outrageous decision to restrict the buying of 13 heavily shorted stocks on Jan 28 that had been driven to record highs, including GameStop, whose shares had surged more than 1,600%.

Tenev said the restrictions were necessary due to a large increase in collateral/deposit requirements by the DTCC, but that was not spelled out in automated emails sent to Robinhood customers early on Jan. 28.

Robinhood CEO Vlad Tenev And then he decided to pull the oldest trick and deflect attention from his own mistakes by blaming “conspiracy theories.”

“As soon as those emails went out, the conspiracy theories started coming, so my phone was blowing up with, ‘how could you do this, how could you be on the side of the hedge funds,’” he said.

What Tenev did not say, or explain, is why his company – which is merely a client-facing front of Citadel, which buys the bulk of Robinhood’s orderflow to use it perfectly legally in any way it sees fit – was so massively undercapitalized that the DTCC required several billion more in collateral to protect Robinhood’s own investors against the company’s predatory ways of seeking to capitalize on the gamification of investing making it nothing more (or less) than a trivial pursuit to millions of GenZ and millennial investors, a point which Michael Burry made so vividly.

The #mainstreetrevolution is a myth. Zero commissions and gamified apps were designed to feed flows to the two most influential WS trading houses. A few HFs got hurt, but if retail is moving toward more trading and away from fundamentals, WS owns that game. #Stonks by design. https://t.co/Y4raF0jiM3

— Cassandra (@michaeljburry) February 9, 2021

https://platform.twitter.com/widgets.js

Incidentally we know why Tenev did not mention it: it’s because Robinhood’s back office is a shambles of a shoestring operation, one which never anticipated either such a surge in trading not a multi-billion collateral requirement; had Robinhood been a true brokerage instead of pretending to be one, and run merely to open as many retail accounts as it could in the shortest amount of time, thus generating the most profit in the quickest amount of time to allow its sponsors a quick and profitable exit, it would actually have been on top of this.

It’s also why Tenev’s ridiculous pleas for immediate settlement instead of the usual T+2 arrangement, which has not been an issue for any other brokers, is nothing but a strawman argument which he hopes to present in Congress.

Which brings us to a totally separate topic, and one which Teven will one way or another have to address: the fact that Robinhood is a de facto subsidiary of Robinhood, whose entire business model is to sell retail orders to a handful of HFT market makers first and foremost… Citadel. In doing so the only ones who benefited from the surge in retail trading are Robinhood itself, by pocketing millions more from selling orderflow to Citadel, Virtu, Two Sigma, Wolverine and other HFT

frontrunning“market-making” venues, as well as Citadel which made billions by having an advance look at the biggest surge in retail stock and option orders flow in history, and being able to trade ahead of and around it.

And no, it’s not a conspiracy theory Vladimir – it is the stone cold truth, as Jeffrey Gundlach suggested last week when he said “Robin Hood (sic) should be forced to change its name to Hood Robbin’. I grow so weary of lies through nomenclature, which are ubiquitous these days” adding “To be clear, the name change would reflect Robinhood robbing the little guy, nothing else.”

To be clear, the name change would reflect Robinhood robbing the little guy, nothing else.

— Jeffrey Gundlach (@TruthGundlach) February 10, 2021

https://platform.twitter.com/widgets.js

As an aside, how dare we allege that Citadel was buying orderflow to frontrun it? After all, that very allegation…

… coupled with the reminder that Robinhood engages exclusively in a practice called payment-for-orderflow (or PFOF)…

… which is what allowed Robinhood to provide “free” trading in the first place, that nearly destroyed us when last June Citadel’s lawyer army threatened to sue us into the ground for suggesting precisely that?

Some key phrases of note from the above text:

- “‘Frontrunning’ is an industry term of art that refers to an illegal form of trading.”

- “Citadel Securites does not engage in such conduct [i.e., frontrunning] and there was no factual basis whatsoever for ZeroHedge to publish such an incendiary, false, and reckless allegation to its 742,000 Twitter followers” [it’s 771,000 now].

- “ZeroHedge’s statement obviously disparages the lawfulness and integrity of Citadel Securities’ business pratices.”

- “Quite obviously, this most recent iteration of this same harmful allegation was not made in jest.”

- “We demand that ZeroHedge immediately retract this tweet by deleting it from ZeroHedge’s Twitter page… A refusal to promptly take down these remedial steps will be seen as further evidence of actual malice and will only increase the already substantial legal risk faced by you and ZeroHedge.”

Well, we now officially know all about Citadel’s modus operandi because just a few days after we received that letter, none other than financial regulator FINRA, revealed that Citadel Securities was censured and fined for engaging in – drumroll – “trading ahead of customer orders” as Letter of Acceptance No. 2014041859401 revealed:

Now we admit that our financial jargon is a bit rusty these days, but “trading ahead of customer orders” sounds awfully similar to another far more popular “term of art“, one which we know very well: frontrunning!

Jargon aside, some of the other highlighted words we are very familiar with, such as “hundreds of thousands”… and “559 instances” in which Citadel traded ahead of customer orders.

And while we may be getting a little ahead of ourselves here, it was Citadel’s own lawyers that informed us on more than one occasion that:

“frontrunning” is an unethical and illegal trading practice.”

So, what are we to make of this? Could it be that Citadel was engaging in at least 559 instance of what its lawyer called “unethical and illegal trading practice.” Surely not: after all the lawyers would surely know very well how ridiculous and laughable their letter and threats would look if it ever emerged that Citadel was indeed frontrunning its customers.

But wait, it gets even funnier.

Back in April 2004, long before Citadel became the dominant market maker – and buyer – of retail orderflow controlling a whopping 27% of total US equity volume market share in 2020 according to Bloomberg and a staggering 46% of retail orderflow, it was Citadel’s own General Counsel, Adam Cooper, who urged the SEC to ban payment for orderflow because it “distorts order routing decisions, is anti-competitive, and creates an obvious and substantial conflict of interest between broker-dealers and their customers.“

As Cooper also revealed…

“broker-dealers accepting payment for order flow have a strong incentive to route orders based on the amount of order flow payments, which benefit these broker-dealers, rather than on the basis of execution quality, which benefits their customers. Furthermore, the parties making such payments (either voluntarily or through an exchange-mandated program) are forced to find other ways to recoup the amounts of such payments, whether through wider spreads or a reduction in other benefits that otherwise could, and should, be provided to customers.”

And the punchline:

Payment for order flow is a practice that on its face is at odds with a broker-dealer’s obligations to its customers. A broker-dealer has a fiduciary obligation to obtain the best execution reasonably available for its customers’ orders under prevailing market conditions. We do not believe that a broker-dealer that accepts payment for order flow and does not pass such payments on to its customers (either directly or through reduced execution fees or commissions) can consistently fulfill its best execution obligations.

Which leads us to the one time Citadel was actually telling the truth: