- Think Media Won't Help Lead US Into War With Iran Based On False Intelligence? Looks Like They Already Are

Authored by Jake Johnson and Jon Queally via Common Dreams

If there were any lingering hopes that the corporate media learned from its role in perpetuating the lies that led to the 2003 invasion of Iraq and would never again help start a Middle East war on the basis of false or flimsy evidence, the headlines that blared across the front pages of major U.S. news websites Thursday night indicated that such hopes were badly misplaced.

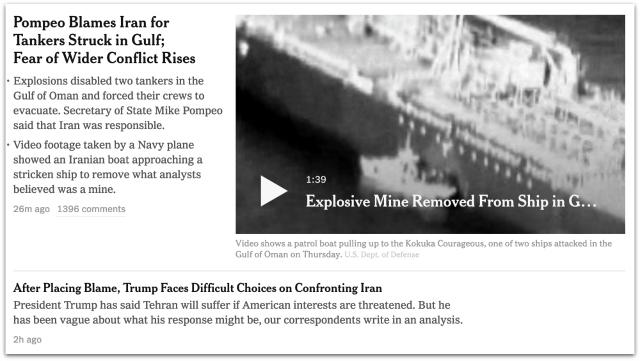

The U.S. military late Thursday released blurry, black-and-white video footage that it claimed — without any underlying analysis or further details — to show an Iranian patrol boat removing an unexploded limpet mine from the Japanese-owned Kokuka Courageous, one of the oil tankers damaged in attacks in the Gulf of Oman.

Here’s how CNN presented the U.S. military’s video:

Iran has denied any involvement in the attacks, and Yutaka Katada — the owner of the Kokuka Courageous — contradicted the Trump administration’s account during a press conference on Friday.

“Our crew said that the ship was attacked by a flying object,” Katada said. “I do not think there was a time bomb or an object attached to the side of the ship.”

Independent critics were quick to call for extreme skepticism in the face of U.S. government claims, given the quality of the “evidence” and the warmongering track records of those presenting it.

But the media displayed no such caution.

Just taking a random sample of screenshots after the news broke Thursday night, major outlets largely did the Pentagon’s dirty work by posting uncritical headlines that took the claims at face value.

The Washington Post used the word “purported” in its headline, but erroneously reported that the video was taken “before” the explosion on the vessel, not after. The headline was later changed, but was made no more critical of the military’s claim:

The U.K.-based Guardian also offered a simple “U.S. says” headline construction:

In the New York Times rendition — which appeared prominently on their homepage — the claim of what the U.S. military intelligence “believed” the video to show was framed with the more objective-sounding and vague phrase “what analysts believed”:

Like the Guardian, Politico made no attempt to go beyond the “U.S. says” framework:

Fox News, of course, went further than most by characterizing the Pentagon video as a “major clue” to who was behind the alleged attack:

CNN, meanwhile — specifically in the subhead of the headline story that appeared at the top of their page late Thursday night — took the military’s claim of what the video showed as actual fact:

The Hill‘s version, similar to the error made by the Post, reported that the video was taken before the explosion — a detail likely to leave readers much more suspicious of Iran’s involvement than if one of its vessels had approached the ship in the wake of the incident:

Though no single headline could be construed as explicit pro-Pentagon propaganda on its own, the uncritical nature of the coverage and ensuing echo chamber effect — or what is sometimes referred to as “propaganda reinforcement” — is one of the ways that the U.S. government and its intelligence agencies are empowered to turn a flimsy claim into a pervasive and widely-accepted fact.

Classic BBC propaganda reinforcement:

‘The footage released by the US on Thursday is rather more convincing…’

And ascribe doubts *solely* to the accused ‘Bad Guys’:

‘There will likely be doubts in Tehran as to whether this video is genuine.’ https://t.co/aXZVSS3XJL

— Media Lens (@medialens) June 14, 2019

https://platform.twitter.com/widgets.js

In a blog post on Friday, historian and Middle East expert Juan Cole wrote that the Trump administration’s narrative that Iranians were removing an unexploded mine from the damaged oil tanker “doesn’t make any sense at all” and said the video footage released by the U.S. “needs to be carefully analyzed” before any conclusions are drawn.

“[Secretary of State Mike] Pompeo alleged that only the Iranians had the expertise to deploy these mines,” Cole wrote. “We heard this crock for 8.5 years in Iraq—all shaped charges had to be Iran-backed, even those of al-Qaeda, because Iraqis didn’t have the expertise…. Sure. Had to be Iran, helping those hyper-Sunni al-Qaeda. Very likely story.”

On Twitter, Sina Toossi, research associate at the National Iranian American Council, echoed Cole’s call for skepticism and an investigation.

“What we need is an impartial investigation,” Toossi wrote, “and to be highly skeptical of claims and intel assessments from Bolton/Pompeo.”

Head of the tanker says two drones caused the damaged, contradicting this “dozen men on a boat” narrative.

What we need is an impartial investigation & to be highly skeptical of claims & intel assessments from Bolton/Pompeo. https://t.co/i0s3Nnsiwm

— Sina Toossi (@SinaToossi) June 14, 2019

https://platform.twitter.com/widgets.js

In a column published last month as the U.S. aggressively escalated military tensions with Iran and pushed the two nations to the brink of all-out war, The Intercept‘s Mehdi Hasan asked a straightforward question that remains relevant in the present: “Do U.S. reporters, anchors, and editors really want more Middle Eastern blood on their hands?”

“If not,” Hasan wrote, “they need to fix their rather credulous and increasingly hawkish coverage of Iran and the Trump administration — and fix it fast.”

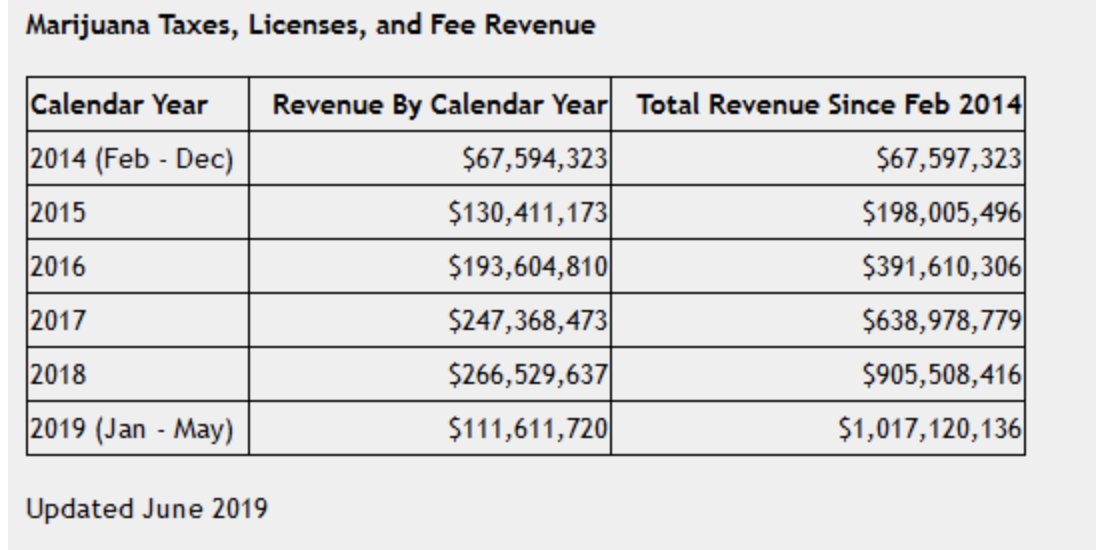

- Colorado Hits $1 Billion In Marijuana State Revenue

Colorado has passed another major marijuana milestone, surpassing $1 billion in state revenue since it legalized the drug in 2014.

Source: Colorado.gov

Up to May of this year, Statista’s Niall McCarthy notes that the state has seen more than $6 billion in total marijuana sales since the industry was given the green light.

You will find more infographics at Statista

According to CNBC, Colorado now has 2,917 licensed marijuana businesses and 41,076 people licensed to work in the industry.

As SafeHaven.com’s Alex Kimani notes, marijuana companies face a pretty hostile tax environment.

First off, they are not allowed any tax deductions or credits for business expenses which can mean effective federal tax rates of as high as 90 percent. Hemp producers are luckier since recent changes to the law now allows them to deduct ordinary business expenses for tax purposes on condition that their products contain no more than 0.3 percent THC.

Second, most banks and financial institutions will not touch them with a 10-foot pole, meaning they have to pay their taxes in cash and not through checks or electronic means.

Yet, they continue to tough it out, making an important mark where they are officially recognized. According to the Tax Policy Center, states with marijuana taxes are obligated to put a portion of their funds toward important social programs ranging from education programs in Colorado and Nevada to administrative costs in California and crime reduction in Alaska.

Luckily, the IRS is trying to get a handle on the situation and hopefully, cannabis companies will soon be able to enjoy the same benefits that other industries take for granted.

- Why The S-400 Is A More Formidable Threat To US Arms Industry Than You Think

Authored by Federico Pieraccini via The Strategic Culture Foundation,

Generally, when discussing air-defense systems here, we are referring to Russian devices that have become famous in recent years, in particular the S-300 (and its variants) and the S-400. Their deployment in Syria has slowed down the ability of such advanced air forces as those of the United States and Israel to target the country, increasing as it does the embarrassing possibility of having their fourth- or fifth-generation fighters shot down.

Air-defense systems capable of bringing down fifth-generation aircraft would have a devastating effect on the marketability and sales of US military hardware, while simultaneously boosting the desirability and sales of Russian military hardware. As I have often pointed out in other analyses, Hollywood’s role in marketing to enemies and allies alike the belief that US military hardware is unbeatable (with allies being obliged to buy said hardware) is central to Washington’s strategies for war and power projection.

As clashes between countries in such global hot spots as the Middle East increase and intensify, Hollywood’s propaganda will increasingly struggle to convince the rest of the world of the continued efficacy and superiority of US weapons systems in the face of their unfolding shortcomings.

The US finds itself faced with a situation it has not found itself in over the last 50 years, namely, an environment where it does not expect to automatically enjoy air superiority. Whatever semblance of an air defense that may have hitherto been able to pose any conceivable threat to Uncle Sam’s war machine was rudely dismissed by a wave of cruise missiles. To give two prime examples that occurred in Syria in 2018, latest-generation missiles were intercepted and shot down by decades-old Russian and Syrian systems. While the S-400 system has never been employed in Syria, it is noteworthy that the Serbian S-125 systems succeeded in identifying and shooting down an American F-117 stealth aircraft during the war in the Balkans.

There is a more secret aspect of the S-400 that is little disclosed, either within Russia itself or without. It concerns the S-400’s ability to collect data through its radar systems. It is worth noting Department of Defense spokesman Eric Pahon’s alarm over Turkey’s planned purchase of the S-400:

“We have been clear that purchasing the S-400 would create an unacceptable risk because its radar system could provide the Russian military sensitive information on the F-35. Those concerns cannot be mitigated. The S-400 is a system built in Russia to try to shoot down aircraft like the F-35, and it is inconceivable to imagine.

Certainly, in the event of an armed conflict, the S-400’s ability to shoot down fifth-generation aircraft is a huge concern for the United States and her allies who have invested so heavily in such aircraft. Similarly, a NATO country preferring Russian to American systems is cause for alarm. This is leaving aside the fact that the S-400 is spreading around the world, from China to Belarus, with dozens of countries waiting in line for the ability to seal their skies from the benevolent bombs of freedom. It is an excellent stick with which to keep a prowling Washington at bay.

But these concerns are nothing when compared to the most serious threat that the S-400 poses to the US arms industry, namely, their ability to collect data on US stealth systems.

Theoretically, the last advantage that the US maintains over her opponents is in stealth technology. The effectiveness of stealth has been debated for a long time, given that their costs may actually outweigh their purported benefits. But, reading between the lines, what emerges from US concerns over the S-400 suggests that Moscow is already capable of detecting US stealth systems by combining the radars of the S-400 with those of air-based assets, as has been the case in Syria (despite Washington’s denials).

The ability of the S-400 to collect data on both the F-35 and F-22 – the crown jewels of the US military-industrial complex – is a cause for sleepless nights for US military planners. What in particular causes them nightmares is that, for the S-400 to function in Turkey, it will have to be integrated into Turkey’s current “identification friend or foe” (IFF) systems, which in turn are part of NATO’s military tactical data-link network, known as Link 16.

This system will need to be installed on the S-400 in order to integrate it into Turkey’s defensive network, which could potentially pass information strictly reserved for the Russians that would increase the S-400’s ability to function properly in a system not designed to host such a weapon system.

The final risk is that if Turkey were to fly its F-35s near the S-400, the Link 16 system would reveal a lot of real-time information about the US stealth system. Over time, Moscow would be able to recreate the stealth profile of the F-35 and F-22, thereby making pointless Washington’s plans to spend 1.16 trillion dollars to produce 3,000 F-35s.

What must be remembered in our technological age is that once the F-35’s radar waveform has been identified, it will be possible to practice the military deception of recreating fictitious signals of the F-35 so as to mask one’s own aircraft with this shape and prevent the enemy’s IFF systems from being able to distinguish between friend or foe.

Of particular note is the active cooperation between China and Russia in air-defense systems. The S-400 in particular has already been operational in China for several years now, and it should be assumed that there would be active information sharing going on between Moscow and Beijing regarding stealth technology.

It turns out that the S-400 is a weapon system with multiple purposes that is even more lethal than previously imagined. It would therefore not be surprising that, were S-400s to be found in Cuba and Venezuela, Washington’s bellicose rhetoric against these two countries would come to an abrupt halt.

But what US military planners fear more than the S-400 embarrassing their much-vaunted F35 and F22 is the doubts they could raise about the efficacy of these stealth aircraft in the minds of allies and potential buyers. This lack of confidence would deal a mortal blow to the US arms industry, a threat far more real and devastating for them than a risk of conflict with Moscow or Beijing.

- Trade War Nightmare Causes Collapse In Demand For US Industrial Space, Says Cushman & Wakefield

The latest Cushman & Wakefield commercial real estate report shows demand for US industrial space collapsed 60% on year in 1Q19, reflecting the global synchronized decline and the deepening trade war.

Cushman & Wakefield’s economists warned President Trump’s trade war is unraveling complex supply chains around the world that have led to a slump in demand for industrial space. They also said the restocking trend by importers forced by the tariffs is likely over. There is also another possibility that the slowdown could be linked to some seasonal factors, the economist said.

“It is possible that the trade dispute is causing disruptions to supply chains which are causing demand for industrial space to slow. Another possibility is companies may have overstocked before the implementation of tariffs in 2018. Seasonality, a general slowing in the global economy and lagging supply may also have been the main culprits,” economists Kevin Thorpe and Rebecca Rockey said in the report.

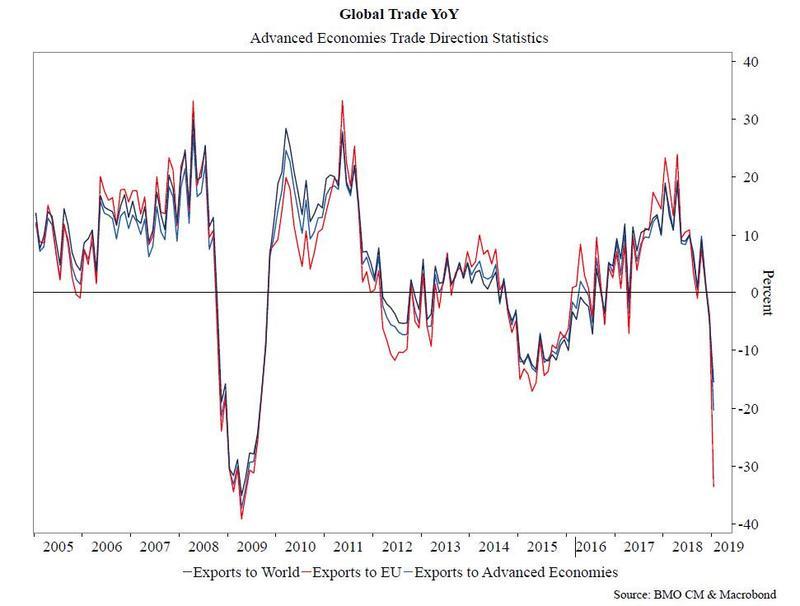

The report said world export volumes are expected to have no growth this year, dropping from a 5% annual expansion rate in the last two years.

To best visualize the global slowdown is YoY changes in global trade as measured by the IMF’s Direction of Trade Statistics, courtesy of BMO’s Ian Lyngern. It shows the collapse in global exports as broken down into three categories:

-

Exports to the world (weakest since 2009),

-

Exports to advances economies (also lowest since 2009), and

-

Exports to the European Union (challenging 2009 lows).

President Trump slapped 25% tariffs on $200 billion of Chinese goods last month. Trump then threatened to slap tariffs on another $300 billion of Chinese exports if China’s leader Xi Jinping doesn’t meet him at the 2019 G20 Osaka summit in Japan. If the meeting doesn’t occur, this could mean a full-blown trade war would be in effect, would spark a global trade recession and lead to a further collapse in demand for US industrial space.

The economist noted that the trade war has driven up construction costs and has damaged global business confidence for the year.

“There are also anecdotal reports in the US that construction costs for steel, aluminum, cabinetry, flooring, etc, are being driven up as China is ‘taken out’ as a supplier… Although it is challenging to parse out the impact, it is not difficult to conclude that the longer the trade war drags out the more disruptive it will be,” the report said.

<!–[if IE 9]><![endif]–>

Separately, the trade war has left corporate America uncertain about the future by pulling back investments, Eugene Seroka, executive director of the Port of Los Angeles, said.Tariffs are having the most significant impact on Los Angeles and Long Beach ports, the nation’s busiest container ports, which both handle about 47.5% of US containerized trade with China. But it’s not just the ports that are feeling the pressure from the trade war, trucking, railroads, warehousing, construction, manufacturing, and farming, have also been impacted. About one million jobs related to international trade around the port are also in question as the trade war continues to deepen.

As the US economy cycles down through summer with the threat of a full-blown trade war, industrial space demand is likely to drop further, which could suggest that the commercial real estate bubble is about to burst.

-

- Goldman: Here's Why The Fed Is About To Shock The Market

As discussed earlier, and as both Bank of America and JPM explained, the biggest risk for the market next week is if the Fed not only doesn’t cut – the market assigns a very low probability to such a “pre-emptive” move – but fails to signal an aggressive dovish reversal in the form of a rate cut in July. And yet, despite its upbeat outlook – it still expects the S&P to close the year at 3,000, Goldman’s strategists are certainly taking the over on how hawkish the Fed will sound next week.

As Goldman’s chief economist Jan Hatzius writes, the bank expects “unchanged” policy at the June 18-19 FOMC meeting and sees the subjective odds of a June cut at only 10%. More importantly, while Goldman looks for a dovish tilt to the proceedings it won’t be nearly enough to appease markets that have aggressively priced rate cuts in the fall.

Barring an unlikely surprise on the funds rate, we expect the market to focus on four key developments:

- the statement’s policy stance/balance of risks paragraph,

- the number of participants projecting cuts in the Summary of Economic Projections (SEP),

- the extent of dovish changes to the statement and economic forecasts, and

- the tone of Powell’s press conference.

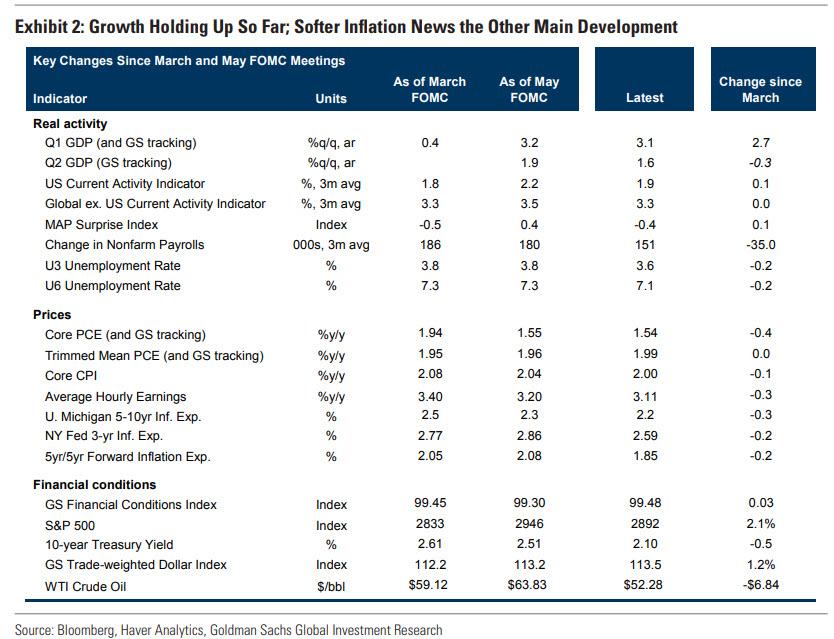

In Goldman’s view, the main reason why the Fed is poised to disappoint markets is simply that not enough has changed to warrant a clear signal of an upcoming cut. Indeed, “since the March SEP meeting, stock prices are higher, the unemployment rate fell to a 50-year low, consensus growth forecasts are unchanged, and the very tariffs on Mexico that prompted the latest calls for rate cuts have been taken off the table.” Not only that, but the economy continues to chug along largely as expected: outside of May payrolls, the growth data still look decent: Goldman’s Q2 GDP tracking estimate has rebounded to +1.6%, Atlanta Fed GDPNow is +2.1%, and the bank’s own tracker of private final demand is at an even healthier pace (+2.8%).

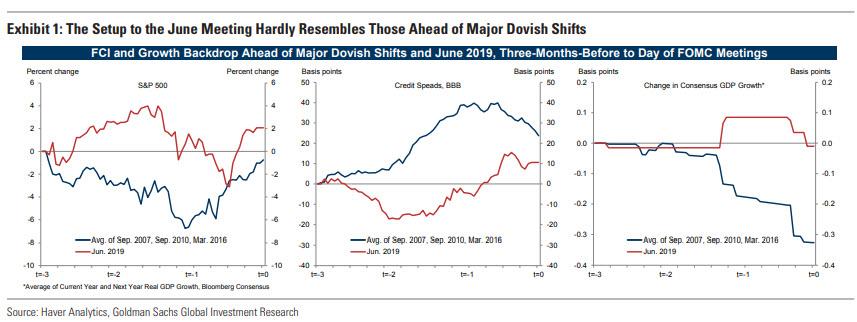

Rather than Goldman’s standard “Then and Now” table, the chart below “plots the setup for next week’s meeting across three dimensions, as well as their averages ahead of three major dovish shifts: September 2007 (at which the Fed abandoned the hiking bias and cut 50bps in response to subprime turmoil), September 2010 (formally signaled QE2), and March 2016 (scuttled the hiking cycle until global risks abated). Here, Hatzius also shows the three-month evolution of these four variables: stock prices, IG credit spreads, and consensus GDP growth.

What is remarkable, is that the June 2019 values show little resemblance ro prior dovish reversals: “risk assets performed much better, and annual GDP forecasts are little changed, vs. -0.3pp on average across the three alternate episodes.“

So how do one reconcile this with the outspoken consensus forecasting major dovish changes next week? According to Hatzius, one possibility is that most salient changes over the last 6 weeks “relate to investor sentiment and global news headlines” instead of the actual economy and market conditions. If so, there may not be sufficient reasons to expect or implement changes in the path of monetary policy, Goldman concludes in what may be a major disappointment for the market bulls.

So what about all those predictions of an upcoming recession? Here, too, Goldman is skeptical and writes that it remains to be seen whether US growth will fall below potential in the back half of the year because of the trade war and related uncertainty. But, as shown in the first chart above, outside of May payrolls, the growth data still look decent —particularly the solid rise and significant upward revisions in Friday’s retail sales report.

Taken together, Goldman’s chief economist thinks Fed officials “will view recent data as evidence that growth has indeed slowed from its brisk mid-2018 clip (of 3.5-4.0%) but remains at a healthy pace (of around 1.75%-2.0%).“

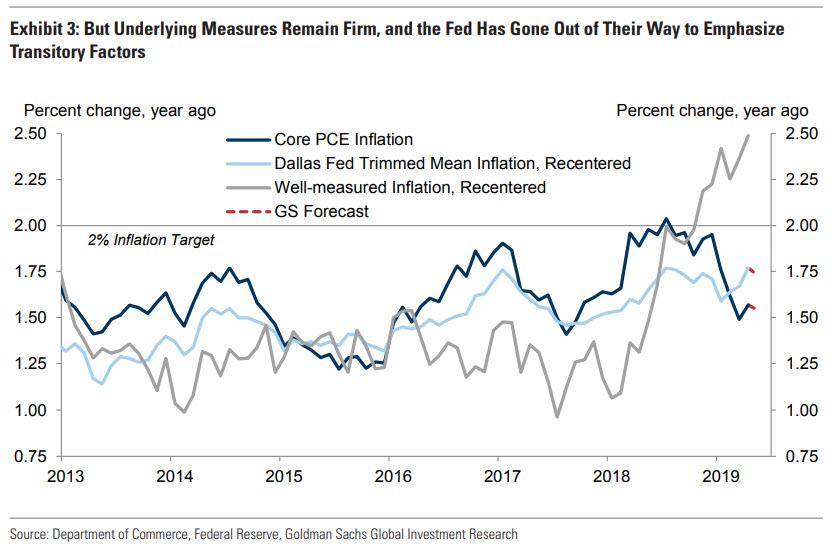

Will this be sufficient to sway those expecting a major dovish concession by the Fed? Probably not, and they will point to the recent slowdown in inflation. And while inflation it has undoubtedly been soft (four consecutive core CPI misses, core PCE inflation hovering just above 1.5%), the Committee has gone out of their way recently to attribute the weakness to transitory factors, Hatzius writes. In fact, the FOMC has emphasized the Dallas Fed trimmed-mean measure—which based on CPI and PPI source data is similar to its levels at the March and May meetings (in fact, slightly higher at 1.99%).

Furthermore, as shown in Exhibit 4, the Dallas Fed measure is consistent with core inflation of 1.75%, and it has also more clearly trended up in recent years. Such well-measured inflation (also adjusted for its average gap vs. core PCE) is consistent with above-target inflation for the first time since 2010 (of around 2.5%).

Looking ahead, the inflationary outlook is even more conflicted, and Goldman believes core PCE inflation is on its way back to 2% by late 2019, especially given the 0.3-0.4% boost from tariffs that is expected to hit shortly after Trump hikes tariffs on the remaining $300BN in Chinese imports. On the other hand, don’t expect a hike either:

But even if inflation has resurfaced as a predominant concern on the Committee in recent weeks, now would be a curious time to launch a reflation campaign, given vocal pressure from the White House to cut rates and the fact that the framework review itself won’t be completed for another 6+ months.

But while all this is known, why is the market pricing in roughly 4 rate cuts by the end of 2020, and why does Goldman refuse to drink the Dove-Aid? Playing Devils’ advocate, Hatzius explains that “one common pushback to our view is that if the Fed fails to deliver the rate cuts now priced, financial conditions will tighten and force the Fed’s hand anyway” To this, Goldman counters that it expects Fed officials to be “very careful not to deliver an unconditional hawkish message, but to continue emphasizing that they will respond to shocks as needed to attain their mandate.” And so, with hikes very unlikely (for now, although the market has started to price in rising rates in 2020 and early 2021), this would keep the market priced for a reasonable amount of easing.

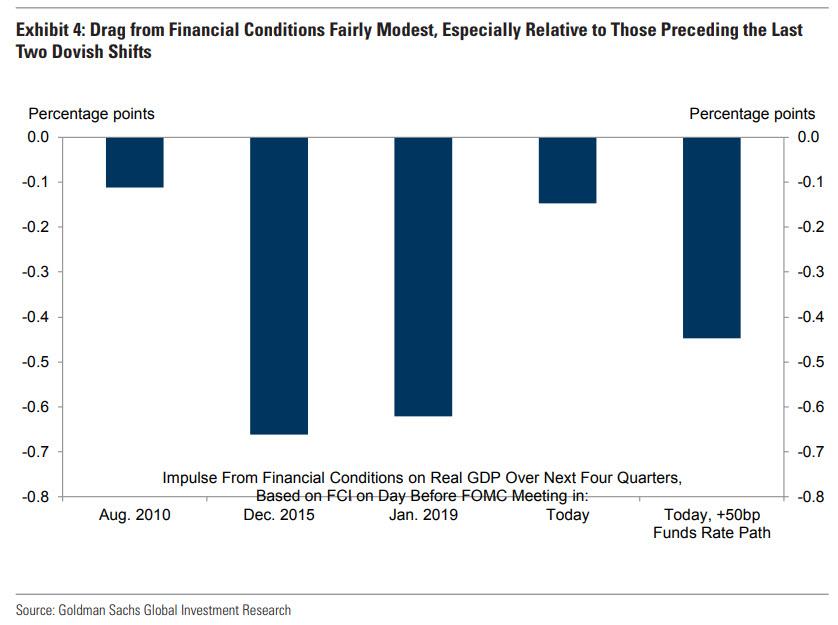

Meanwhile, even if the Fed does shock the market in the opposite direction, and the Committee disappoints markets this summer and Treasury yields rebound sharply, Goldman’s statistical estimates, identified via changes in bond yields around FOMC meetings, suggest that a 50bp exogenous rise in short-term rate expectations tightens our FCI by 30-40bp on average. This is not insignificant, but neither is it dramatic when measured against the last two major FCI tightening episodes, according to Goldman.

Some examples: the index moved up by 150bp in 2018 Q4, and even that change affected only the expected pace of monetary tightening as opposed to producing outright increases in accommodation.

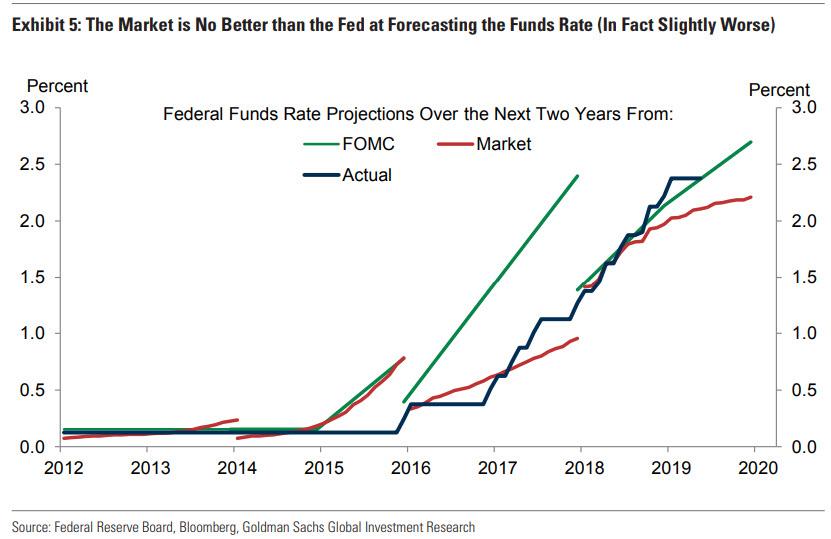

Here Goldman brings up another key consideration: the market has recently been even more inaccurate in its predictions than the notoriously terrible at forecasting Federal Reserve.

Case in point: market pricing implies four rate cuts by the end of next year, a sharp divergence to the FOMC’s median projection at that horizon (one hike as of March). Goldman next compares the policy rate paths implied by the median SEP dot with those of Fed funds futures. And over the seven years that the Committee has tracked and published their projections (an admittedly small sample), the bank finds that the Fed’s two-year-ahead forecasting performance has actually been somewhat better than the market’s: more accurate forecasts in both 2012 and in 2018, a comparable forecast in 2014, and a less accurate one in 2016.

Which brings us to perhaps the biggest concern of all: will the Fed’s own rate cuts telegraph that a recession is about to commence? Goldman’s answer is that history suggests that the hurdle for mid-cycle easing is rather high (perhaps as opposed to late-cycle, as a recession looms anyway). The 1990s saw two such episodes, in 1995 and 1998, the former of which represented a normalization in policy from clearly restrictive levels (from 6.0% to 5.25% from July 1995 to February 1996). At the same time, pre-emptive ”insurance” cuts of 1998 seem more relevant today, as interest rates are low, global risks appear to be rising, and US data has shown only pockets of weakness. Chairman Greenspan said at the time, “There are only limited hard data that suggest any loss of momentum in the current expansion… The crucial development… is that we are observing an important shift in attitudes toward risk… a change in psychology clearly is what we are observing. The opening up of risk spreads is a very significant indication of increased risk aversion.”

But, Hatzius observes, just as today’s FCI evolution and growth outlook look very different from those that preceded the Fed’s dovish pivots in 2007, 2010, and 2016, the tightening in credit spreads in summer 1998 was nearly 10 times as large as that of recent experience (+102bp in the three months leading up to the Sep ‘98 meeting vs. +11bps currently, US IG). And even in that instance (1998), fixed income markets too aggressively priced the Fed’s intentions: markets priced more than a 125bp cumulative decline in Fed Funds, whereas the Fed only cut by 75bps and resumed the hiking cycle less than a year later.

The bottom line, according to Goldman, is that:

“…while markets are aggressively priced for rate cuts, we believe the dovish shift indicated by Fed commentary has been more marginal in nature. For example, we take much less signal than other commentators and market participants from Chair Powell’s promise that “as always, we will act as appropriate to sustain the expansion.” In our view, this was not a strong hint of an upcoming cut but was simply meant to provide reassurance that the FOMC is well aware of the risks.

Additionally, Hatzius sees the “as always” caveat declaring an ever-present ability to ease policy if the situation warrants—as opposed to an imminent rate cut this summer, and furthermore doubts it is a coincidence that New York Fed President John Williams used the same language two days later: “My baseline is a very good one but at the same time we obviously, as always, need to be prepared to adjust our views.”

In sum, and broadening the analysis to all participants that have offered a view on monetary policy since the May meeting, Goldman – unlike the majority of the market – has trouble finding more than a couple outright endorsements of easier policy.

The importance of this caveat is also visible in the history of the FOMC statement itself, Hatzius writes, and shows in the next chart that “act as appropriate” / “act as needed” is a strong signal of imminent policy change (in contrast to, “monitor/closely monitoring,” which has been used over 30 times since 2010 alone). For the Fed-watching pedants, since 1999, Goldman has found only four examples of “as needed” or synonymous verbiage that did not signal a policy action at the upcoming meeting, out of 34 meetings in which this language was used to explain the policy outlook. In each of these four exceptions, the statement included strongly worded caveats that leaned in the other direction (slowing “aggregate demand” in June 2006 and the “uncertain” inflation outlook in April, June, and August 2008). This may underscore just how important Powell’s and Williams’s “as always” caveats truly are.

One final semantic note: when the “as needed” language includes a qualification (that leans against the policy bias), Goldman has found that since 1999, there is only one instance where the Committee followed through at the next meeting, and those were truly exceptional circumstances (Lehman Brothers bankruptcy in September/October 2008).

So unless a major bank defaults in the next few days, Goldman is confident that the odds of a major dovish signal by the Fed are virtually nil, and in that case, should Trump fail to strike a trade war deal with Xi Jinping at the G-20, then the worst case scenario as laid out by Bank of America…

… is in play, which to those who may have missed it, is the following:

… the worst possible outcome would be if there is a 1) a hawkish Fed surprise and 2) no Deal at the G-20, which would send the S&P below 2,650, or potentially resulting in a 12% drop in the market, while slamming 10Y yields to 1.50% and helping gold rise above its 5 year breakout zone as the VIX surges.

In short: if Goldman is right (and that’s a big if), brace for market correction.

- Credit Card Debt Spikes In Hawaii As Economy Falters

Total credit card debt among American consumers jumped 29% since 2015, reaching a whopping $807 billion in 1Q19, according to the latest Experian data. In the past year, as the economy cycles down, overall credit card debt rose 6%.

More than 60% of Americans used credit cards for basic purchases in 1Q19. That’s an 11% increase when compared to 1Q16, and a 3% increase from 1Q18.

The average American carries four credit cards with a balance of $6,028.

Experian said all 50 states plus Washington, DC, saw an increase in its average credit card debt on a YoY basis.

Hawaii had an average credit card debt increase of 3.4% over the past year, experienced the most significant growth in credit card usage among any state.

Experian said the average credit card debt in Hawaii is approximately $6,500, which is $500 more than the national average.

Separately, a report from WalletHub suggests why Hawaiians are increasingly using their credits cards. The report collected data from 28 key indicators of economic performance and growth from the island state, determined its economy is the worst in the country because of slow GDP growth, low exports per capita, and relatively few tech jobs.

US Bankruptcy Court District of Hawaii reported last week that the number of Hawaiians filing for bankruptcy in May jumped by double digits over the same month the previous year. May cases showed a 14.3% increase from 2018, with 144 cases filed last month as compared to 126 cases in May last year. May’s readings are the highest since 2014, a sign that the consumer is experiencing financial stress.

Some of the stress is due to massive student loan debt, the housing affordability crisis, and out of control living costs.

Growth in student loan debt is expected to outpace mortgage debt in the state in the near term. Student debt also exceeds credit card debt.

Hawaii ranked 26th in the country for its household income, even though the cost of living is the highest in the country.

The sobering reports come as travel experts warn Hawaii could see an imminent downturn, as tourism dollars are expected slow and the labor market softens.

Americans, and more importantly, Hawaiians, continue to drown even deeper in debt as the economy cycles down.

- Williams: How To Create Conflict

Authored by Walter Williams, op-ed via Townhall.com,

We are living in a time of increasing domestic tension. Some of it stems from the presidency of Donald Trump. Another part of it is various advocacy groups on both sides of the political spectrum demanding one cause or another. But nearly totally ignored is how growing government control over our lives, along with the betrayal of constitutional principles, contributes the most to domestic tension.

Let’s look at a few examples…

Think about primary and secondary schooling. I think that every parent has the right to decide whether his child will recite a morning prayer in school. Similarly, every parent has the right to decide that his child will not recite a morning prayer. The same can be said about the Pledge of Allegiance to our flag, sex education and other hot-button issues in education. These become contentious issues because schools are owned by the government.

In the case of prayers, there will either be prayers or no prayers in school. It’s a political decision whether prayers will be permitted or not, and parent groups with strong preferences will organize to fight one another. A win for one parent means a loss for another parent. The losing parent will be forced to either concede or muster up private school tuition while continuing to pay taxes for a school for which he has no use. Such a conflict would not arise if education were not government-produced but only government-financed, say through education vouchers. Parents with different preferences could have their wishes fulfilled by enrolling their child in a private school of their choice. Instead of being enemies, parents with different preferences could be friends.

People also have strong preferences for goods and services. Some of us have strong preferences for white wine and distaste for reds while others have the opposite preference — strong preferences for red wine. Some of us love classical music while others love rock and roll music. Some of us love Mercedes-Benz while others love Lincoln Continentals. When’s the last time you heard red wine drinkers in conflict with white wine drinkers? Have you ever seen classical music lovers organizing against rock and roll lovers or Mercedes-Benz lovers in conflict with Lincoln Continental lovers?

People have strong preferences for these goods just as much as they may have strong preference for schooling. It’s a rare occasion, if ever, that one sees the kind of conflict between wine, music and automobile lovers that we see about schooling issues. Why? While government allocation of resources is a zero-sum game — one person’s win is another’s loss — market allocation is not. Market allocation is a positive-sum game where everybody wins. Lovers of red wine, classical music and Mercedes-Benz get what they want while lovers of white wine, rock and roll music and Lincoln Continentals get what they want. Instead of fighting one another, they can live in peace and maybe be friends.

It would be easy to create conflict among these people. Instead of market allocation, have government, through a democratic majority-rule process, decide what wines, music and cars would be produced. If that were done, I guarantee that red wine lovers would organize against white wine lovers, classical music lovers against rock and roll lovers and Mercedes-Benz lovers against Lincoln Continental lovers.

Conflict would emerge solely because the decision was made in the political arena. Again, the prime feature of political decision-making is that it’s a zero-sum game. One person’s win is of necessity another person’s loss. If red wine lovers win, white wine lovers would lose. As such, political allocation of resources enhances conflict while market allocation reduces conflict. The greater the number of decisions made in the political arena, the greater the potential for conflict. That’s the main benefit of limited government.

Unfortunately, too many Americans want government to grow and have more power over our lives. That means conflict among us is going to rise.

- 2.2 Million Homes In America Still Have Negative Equity, Despite Record High Prices

As the boom in mortgage applications and refinancing activity last week would suggest, the return of interest rates toward multi-year lows this year is helping to pump more froth into the already bubblicious American housing market.

But while somebody will inevitably be left holding the bag when the bubble bursts, for now, at least, the inexorable rise in American home prices has bequeathed an outsize benefit on at least one group of people: American homeowners who were stuck with underwater mortgages following the last housing bust.

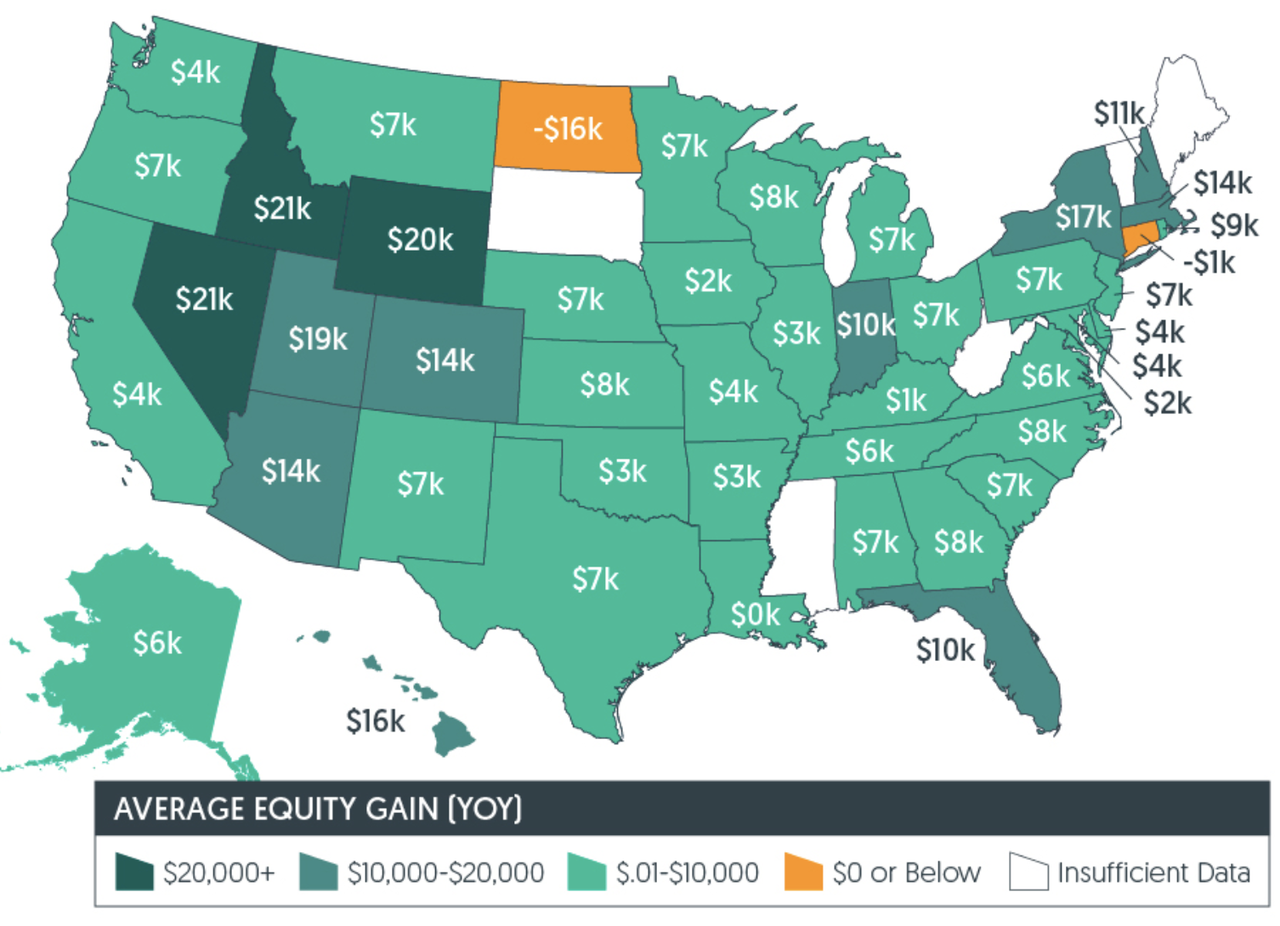

However, even with average national home values back above their pre-crisis highs, CoreLogic’s most recently quarterly survey of national homeowner equity found that there are still 2.2 million homes underwater in the US – a sign of just how bad the last bubble was, and a warning for where we might be headed.

The percentage of homes with underwater mortgages in the US has shrunk between Q4 2018 and Q1 2019 by a full percentage point to just 4% of all mortgaged properties (or just 2.2 million homes). On a YoY basis, negative equity fell 11% from 2.5 million homes, or 4.7% of all mortgaged properties.

However, in terms of national aggregate value, negative equity climbed slightly to approximately $304.4 billion at the end of the first quarter of 2019, an increase of $2.5 billion, from $301.9 billion in the fourth quarter of 2018.

To be sure, this represents a massive shift from the final quarter of 2009, when negative equity peaked at 26% of all mortgaged residential properties.

The national aggregate value of negative equity was approximately $304.4 billion at the end of the first quarter of 2019. This is up QoQ by approximately $2.5 billion, from $301.9 billion in the fourth quarter of 2018. Over the full year, the average homeowner gained approximately $6,400 in equity. Nevada homeowners saw the highest increase, with an average of $21,000 (likely thanks to that flood of California refugees fleeing to Sun Belt states for more affordable lifestyles.

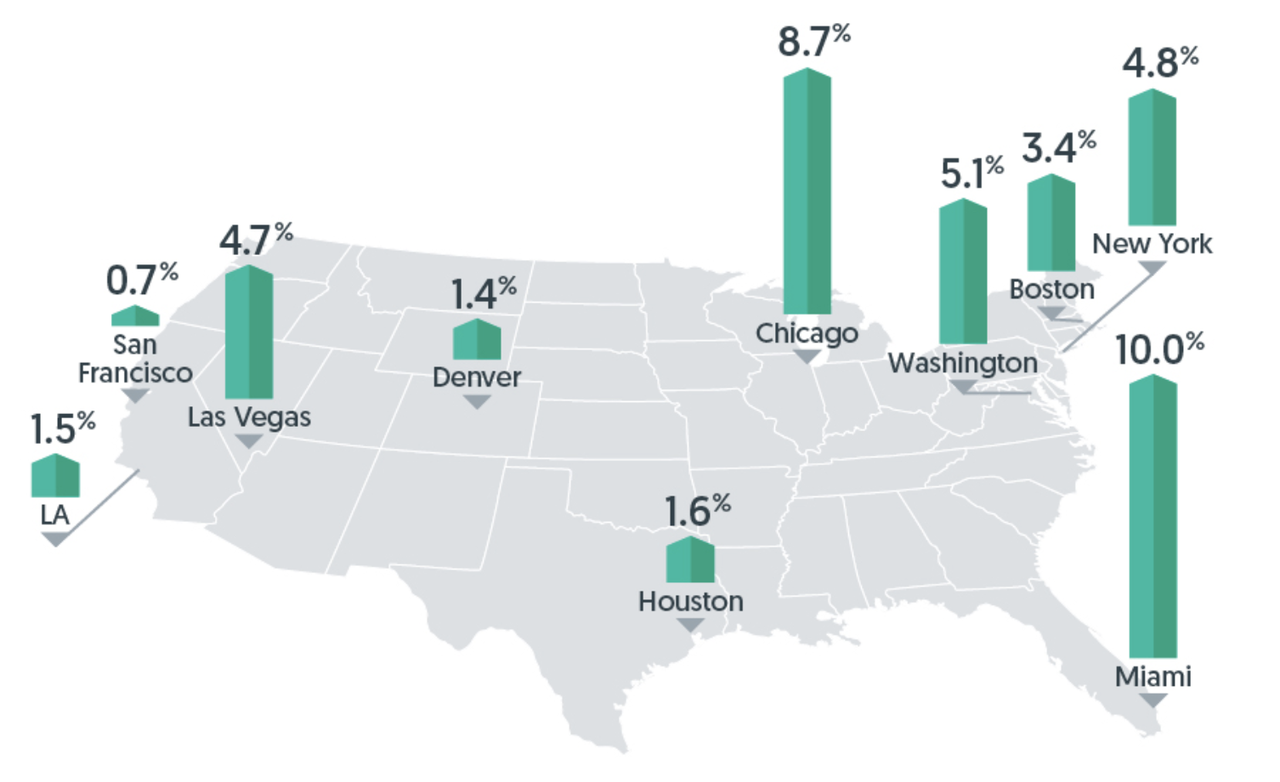

Some of the frothiest housing markets (think San Francisco and the rest of the Bay Area) are now the least burdened by negative equity. But it’s almost more surprising that even in San Francisco, still nearly a full 1% (0.7%) of mortgaged properties are underwater, though that is the lowest rate in the nation. The scars of the housing crisis are even more visible in some of the hardest hit markets, despite the torrid recovery: Las Vegas (4.7%), Chicago (8.7%) and Miami (10%) still have among the highest rates of underwater mortgages in the country.

Either way, with home prices at such unaffordable level, homeowners who suffered through the crisis might be thinking one of two things: Those who were underwater but have seen their equity miraculously right-sized might be so amazed by the turnaround in their fortunes, that they might soon start seeking buyers, hoping to get out ahead (and possibly downsize) before the whole thing comes crashing down again.

And those whose homes are still under might finally be ready to cut their losses, before another down turn drags them all the way back to square one.

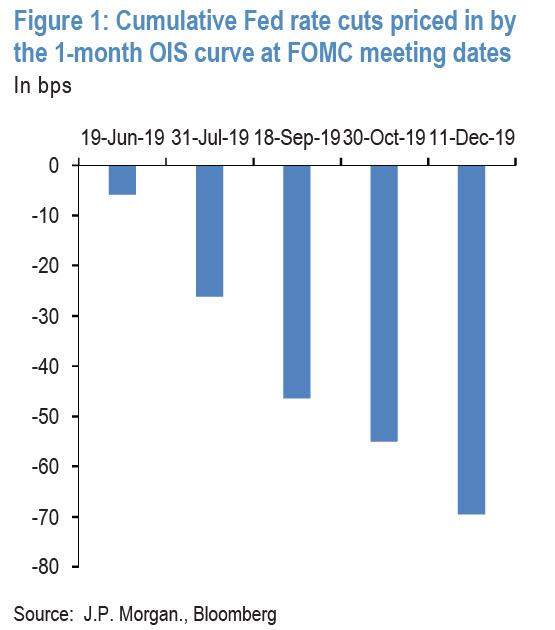

- JPMorgan: "Significant Risk" Is Coming Next Week… And Nobody Is Prepared

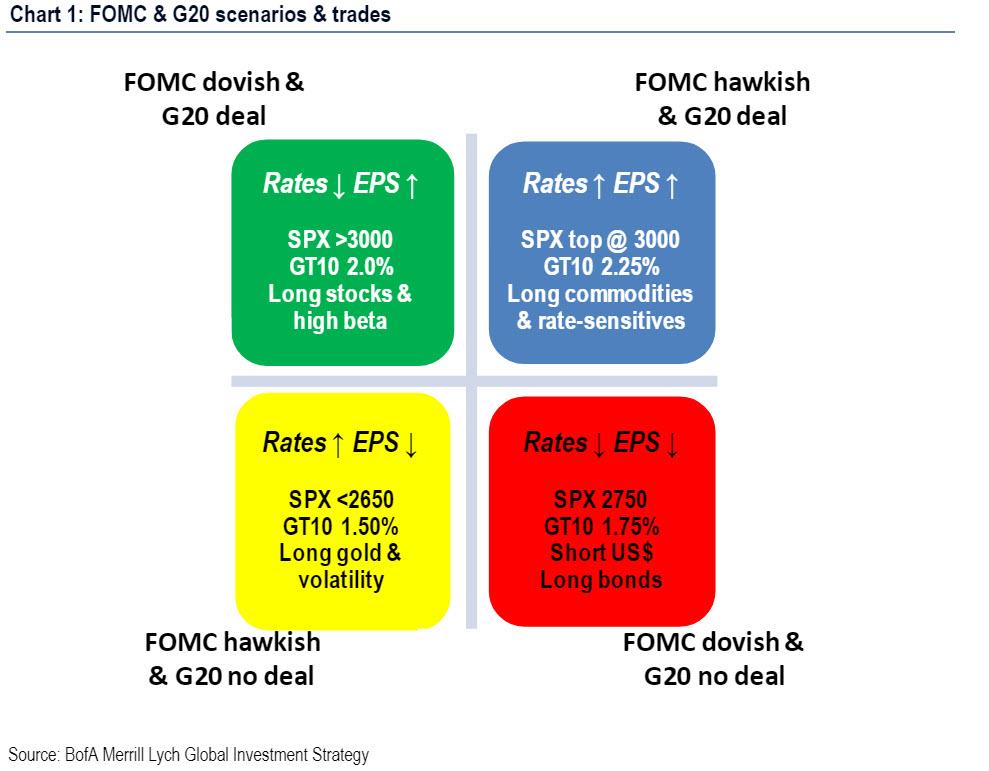

With arguably the most important two weeks of the year looming, on Friday Bank of America’s Chief Investment Officer, Michael Harnett, laid out a 2-by-2 matrix summarizing the four possible scenarios that could result from the Fed’s announcement next week, and the G-20 meeting on June 28-29, where there is a chance (if minuscule) that Trump and Xi will announce the trade war ceasefire, although far more likely, will simple lead to further trade war escalation.

Of these 4 scenarios, two are most remarkable: the best/best and the worst/worst cases. The first one sees a Dovish Fed statement, coupled with a G-20 deal, which according to BofA will send the S&P > 3000, and the 10Y yield to 2.00%, while the worst possible outcome would be if there is a 1) a hawkish Fed surprise and 2) no Deal at the G-20, which would send the S&P below 2,650, or potentially resulting in a 12% drop in the market, while slamming 10Y yields to 1.50% and helping gold rise above its 5 year breakout zone as the VIX surges.

And yet while the market’s reaction to a favorable outcome from the G-20 meeting will undoubtedly be bullish, and vice versa, we disagree that a dovish Fed would necessarily push stocks higher (recall that the Fed cut rates on average 3 months before the last three recessions, effectively telegraphing a start to the economic contraction), because as JPMorgan noted last week, the trajectory for the equity market during Fed rate cut cycles has differed historically depending on whether the Fed was seen as preemptive and cutting rates to provide insurance or seen as simply reacting to weak growth.

So, in picking up where Hartnett left off, JPMorgan’s Nikolas Panigirtzoglou writes in his latest Flows and Liquidity report, that next week’s FOMC meeting provides an opportunity where the Fed can act pre-emptively in the current cycle. Considering how little probability of a cut is priced in next week (as opposed to July), a cut by the Fed would surprise markets while signaling an openness to a July cut, closer to JPM’s house view which expects rate cuts in 2019, and could essentially ‘validate’ market pricing. So a rate cut next week which is not priced in, JPM argues, “would show that the Fed is moving ahead rather than staying behind the curve.”

But what if Powell doesn’t cut?

By remaining on hold and failing to convey an overall dovish message, JPM echoes what Hartnett said, warning that “there is a risk of a shift in equity market thinking away from a preemptive towards a reactive Fed.”

The resilience of the equity market is in our opinion showing that equity investors have been leaning towards the thesis of a preemptive Fed, i.e. a Fed that is keen to provide insurance against downside growth risks in the current cycle similar to the 1995 and 1998 rate cut cycles.

As a result, a more “cautious and patient” Fed next week could cast doubt on the above thesis, creating what JPM simply calls “the risk of an equity market correction”… and which BofA quantified as a potential drop of as much as 12% from current levels.

Further complicating the picture is the feedback loop between deteriorating trade and monetary policy (with Trump chiming in periodically on his twitter account). Which is why a negative outcome in US-China trade talks into the G20 meeting on June 28th-29th could further raise the hurdle for the Fed in the future by intensifying rate cut expectations for the July meeting and beyond, according to JPM. In turn, if the Fed does nothing next week, it would add to the perception of a policy error, as a collapse in G-20 talks “could make it even more difficult to surprise markets and move ahead of the curve in future FOMC meetings.”

But wait there’s more, because if the next US payroll report at the beginning of July is as weak as the one released in early June could intensify fears in markets of a US downturn or recession, which in turn could require an even larger cut for the Fed not to be seen by equity investors as reacting belatedly to weak economic data.

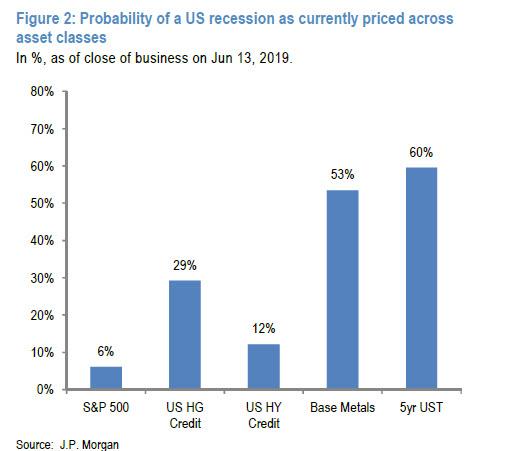

Yet the biggest paradox remains that fear of a US recession seems to be far from priced in equity markets. Indeed, as JPM calculates, its framework of assessing the probability of a US recession embedded across asset classes “is still showing a large disconnect between equity and rate markets with equity markets still pricing in very little probability of a US recession.”

This complacency is also consistent with consensus earnings expectations. The S&P500 earnings per share expectations at $167 for this year are pricing a modest 3% increase from last year, i.e. far from a severe contraction likely to be seen in a recession.

The above discussion, according to the JPM strategist, exposes what he calls “the significant event risk” markets are facing over the coming weeks, which will likely result in a spike in volatility, especially if rate vol finally spills over into equities.

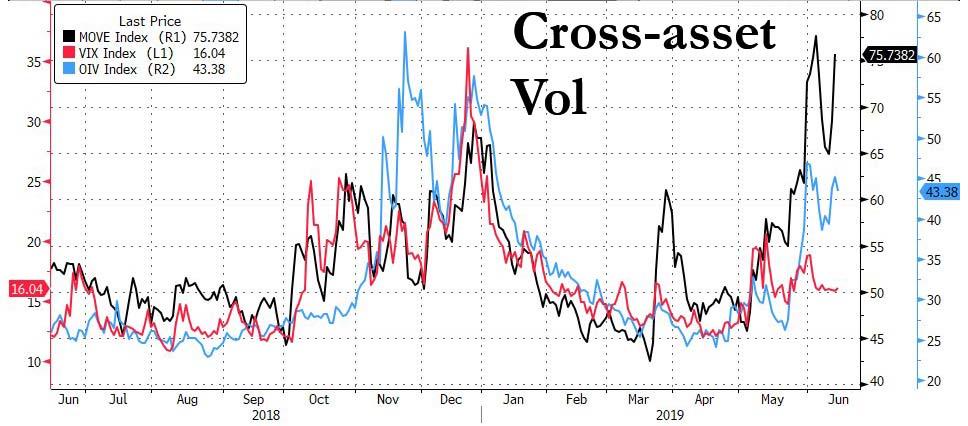

This leaves us with one last question: are markets (especially option and vol) anticipating this potential rise in volatility, something we touched on yesterday when we showed that equity vol remains stubbornly low even as equity and oil vol has been rising sharply.

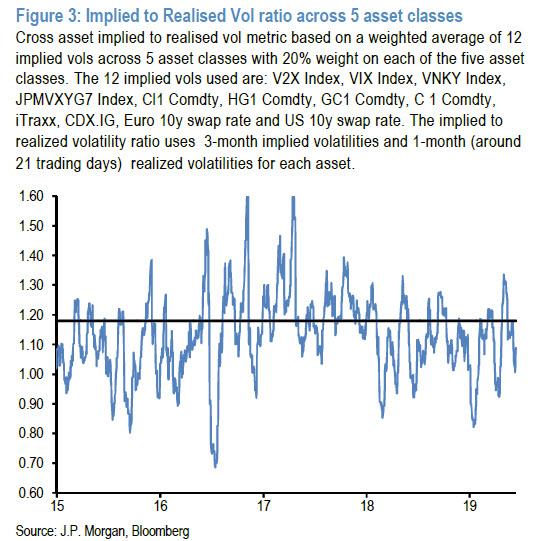

To JPMorgan, one way of answering this question is by assessing the volatility premium embedded in option markets via calculating the implied to realized volatility ratio across asset classes. This is shown in the next chart which depicts a cross asset implied to realized vol metric based on a weighted average of 12 implied vols across 5 asset classes with 20% weight on each of the five asset classes. The 12 implied vols used are: V2X Index, VIX Index, VNKY Index, JPMVXYG7 Index, Cl1 Comdty, HG1 Comdty, GC1 Comdty, C 1 Comdty, iTraxx, CDX.IG, Euro 10y swap rate and US 10y swap rate. The implied to realised volatility ratio uses 3-month implied volatilities and 1-month (around 21 trading days) realized volatilities for each asset. Figure 3 shows that the cross-asset implied to realized ratio stands significantly below its historical average of 1.2x pointing to little volatility risk premium embedded in option markets.

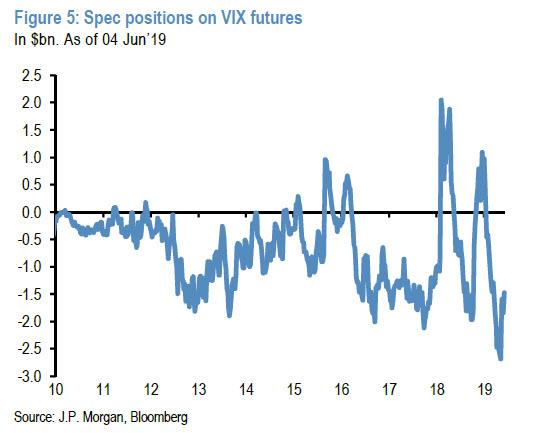

Of course, that’s not all, and other vol-related indicators are also pointing to complacency; for example a simple inspection of the spec positions on VIX futures suggest that there still a large short base not different from the levels seen in September 2018 or January 2018 which at the time were followed by a sharp rise in vol (Figure 5).

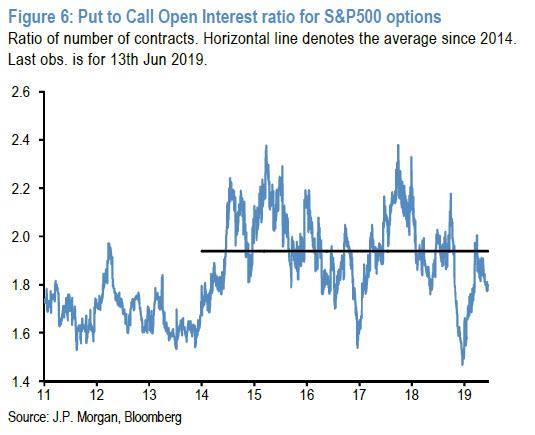

Finally, the Put to Call Open Interest ratio for S&P500 options points to low rather than high hedge ratios (Figure 6).

Putting it all together, JPM finds that “option markets do not appear to embed enough cushion against the significant event risk markets are facing over the coming weeks.” In other words, if Powell for some reason unveils a hawkish surprise next week, it’s going to get very, very messy.

Digest powered by RSS Digest

Saving...

Saving...