- Japandemonium – Is Kuroda Losing Control Of JGB Market?

For the first time since February, 5Y JGB yields have spiked above BOJ policy rates (to -9.5bps), but despite a policy of maintaining 10Y yields and attempting to steepen the yield curve, it appears Kuroda and his cronies have lost control as the short-end of the Japanese bond market is collapsing.

Broadly speaking it seems investors are dumping JGBs in favor of 'cheap' US Treasuries once again…

As the UST-JGB spread is at 6 year highs…historically an attractive relative-value entry…

2Y JGB yields are up 5 days in a row soaring 16bps to 9-month highs

But 10Y yield are breaking notably above the policy rate of 0.00%…

And the JGB yield curve is bear flattening dramatically… not what the BOJ wanted (despite the bank stocks spike post-Trump)…

With a market bereft of liquidity, and rapidly losing its anchor to BOJ policy rates, Kuroda and his pals better start praying for some divine intervention to stall this inflationary burst crushing the Potemkin village of a market they have created.

- Who's Behind The Portland Riots? 60% Of Arrested Anti-Trump Protesters Were From Out Of State, Didn't Vote

Two months ago, Charlotte police confirmed that 70% of those arrested during the riots were from out-of-state. 18 months before that, as the riots flared in Ferguson, George Soros spurred the protest movement through years of funding and mobilizing groups across the U.S., according to financial records reviewed by The Washington Times. And now, amid more headlines of Soros' involvement, KGW reports that more than half of the anti-Trump protesters arrested in Portland were from out of state.

At least sixty-nine demonstrators either didn’t turn in a ballot or weren’t registered to vote in the state.

KGW compiled a list of the 112 people arrested by the Portland Police Bureau during recent protests. Those names and ages, provided by police, were then compared to state voter logs by Multnomah County Elections officials.

Records show 34 of the protesters arrested didn’t return a ballot for the November 8 election. Thirty-five of the demonstrators taken into custody weren’t registered to vote in Oregon.

Twenty-five protesters who were arrested did vote.

KGW is still working to verify voting records for the remaining 17 protesters who were arrested.

In other words over 60% of the arrested protesters in Portland were not local voters dismayed by the election of Donald Trump.

* * *

And so – just as in Ferguson and Charlotte – we see what appears to be professional agitators popping up at key times to encourage social unrest (which as we recently detailed were funded from George Soros' MoveOn.org), all of which perhaps explains why these 'professionals' were so adamant not be filmed or 'caught on tape' as GatewayPundit reports, reporters in Portland, Oregon were attacked by anti-Trump rioters Sunday night, according to Portland Police. The protesters also handed out leaflets warning people to not record the riots.

One reporter, Mike Bivins, who was threatened by the pro-Hillary mob decided to not report the threats but changed his mind after the announcement by police that a news crew had been attacked. Bivins is student at Portland State University and was reporting for PSU”s Pacific Sentinel.

Some protesters attacked a film crew. Bottles being thrown at police. Distractionary "bang" devices being used to effect arrests.

— Portland Police (@PortlandPolice) November 13, 2016

“Some protesters attacked a film crew. Bottles being thrown at police. Distractionary “bang” devices being used to effect arrests.”

I wasn't gonna mention it, but at the outset of the Pioneer Square march masked protesters warned me not to film them. #PortlandProtest

— Mike Bivins (@itsmikebivins) November 13, 2016

“I wasn’t gonna mention it, but at the outset of the Pioneer Square march masked protesters warned me not to film them. #PortlandProtest”

Fellow PSU student Andy Ngo who writes for PSU’s Vanguard student newspaper posted an image of the threatening leaflet.

Media colleague @itsmikebivins warned not to record violent anti-Trump protests. At least 1 media crew attacked last night #PortlandProtest pic.twitter.com/fVKgaLHKO5

— Andy C. Ngo (@MrAndyNgo) November 13, 2016

The text of the leaflet reads:

DON’T SNITCH, EVER.

PUT DOWN YOUR CELLPHONES AND PARTICIPATE

DO NOT HELP THE POLICE IN IDENTIFYING PERSONS ENGAGED IN ILLEGAL ACTIVITY

DON’T POST PROTEST VIDEOS TO SOCIAL MEDIAA FEW THINGS YOU CAN DO:

JOIN, CELEBRATE, SHOW YOUR RAGE

YELL FUCK THE POLICE

DRINK SOME WATER AND CHILL

SHARE FOOD

COLLABORATE

FIND ONE ANOTHER

KEEP PEOPLE SAFE FROM PHYSICAL HARMSTOP FILMING.

CONSIDER THIS A WARNING.Bivins said he also was threatened on Twitter via Direct Messages.

@MrAndyNgo that flier also came through my direct messages :-/. It's definitely dangerous out there.

— Mike Bivins (@itsmikebivins) November 13, 2016

“@MrAndyNgo that flier also came through my direct messages :-/. It’s definitely dangerous out there.”

Bivins also noted a film crew camera had been destroyed by rioters.

@fredamoon a local news camera was smashed, and threatening fliers have been circulating. The danger is no secret. Perhaps you're not…

— Mike Bivins (@itsmikebivins) November 13, 2016

“@fredamoon a local news camera was smashed, and threatening fliers have been circulating. The danger is no secret. Perhaps you’re not…”

Bivins posted video of Portland police dropping in to clear out a group of rioters (wait for it). Being a student reporter, Bivins ran away from the story (cussing up a storm) instead covering it, but he captured the intensity of the police action.

LIVE on #Periscope: #PortlandProtest. I'm here coincidentally https://t.co/NaoDUuCz84

— Mike Bivins (@itsmikebivins) November 14, 2016

“LIVE on #Periscope: #PortlandProtest. I’m here coincidentally”

On Thursday night a Portland news crew was attacked by rioters with a baseball bat.

Anarchists hit one of the @KGWNews cameras. w/ bat #BlackLivesMatter protesters came to their aid & chased the anarchists off #Portland #PDX

— Nattering Nabob of N (@phpress) November 11, 2016

“Anarchists hit one of the @KGWNews cameras. w/ bat #BlackLivesMatter protesters came to their aid & chased the anarchists off #Portland #PDX”

On Saturday night another news crew was attacked.

@WashCoScanner @AlertSalem @aliceem36 Anarchists just attacked the KOIN cameraman.

— Alan (@PepsiDad) November 13, 2016

“@WashCoScanner @AlertSalem @aliceem36 Anarchists just attacked the KOIN cameraman.”

Talked with our cameraman… Thankfully, he didn't get hurt. https://t.co/pnqNb39NDD

— KOIN Assignment desk (@KOINdesk) November 13, 2016

“Talked with our cameraman… Thankfully, he didn’t get hurt.”

Cue media outrage “if these were Trump supporters”…

- 5 Stunning Facts About the 2016 Election

- President Obama Leaves Behind A Deplorable Civil Liberties Legacy

Submitted by Mike Krieger via Liberty Blitzkrieg blog,

More disappointing than the Obama administration itself (which was very disappointing), were the seemingly endless hordes of fake liberals constantly justifying and making excuses for his well documented litany of civil liberties abuses. Naturally, I likewise expect countless Trump supporters to instinctively make similar excuses for Trump if he should end up naming former Goldman Sachs Partner, and overall finance miscreant, Steve Mnuchin as Treasury Secretary. This is a huge part of our problem as a nation. Rather than having well defined principles and defending them, we tend to pick personalities we like and then cheer them on as uncritically as our favorite sports teams.

Moving along, a New York Times article published yesterday highlighted some of the extremely illiberal policies perpetrated by so-called “liberal” champion, Barack Obama.

Here are a few key excerpts:

Over and over, Mr. Obama has imposed limits on his use of such powers but has not closed the door on them — a flexible approach premised on the idea that he and his successors could be trusted to use them prudently. Mr. Trump can now sweep away those limits and open the throttle on policies that Mr. Obama endorsed as lawful and legitimate for sparing use, like targeted killings in drone strikes and the use of indefinite detention and military tribunals for terrorism suspects.

And even in areas where Mr. Obama tried to terminate policies from the George W. Bush era — like torture and the detention of Americans and other people arrested on domestic soil as “enemy combatants” — his administration fought in court to prevent any ruling that the defunct practices had been illegal. The absence of a definitive repudiation could make it easier for Trump administration lawyers to revive the policies by invoking the same sweeping theories of executive power that were the basis for them in the Bush years.

Two decisions by Mr. Obama in 2009 set the tone for his leave-it-on-the-table approach. They involved whether to keep indefinite wartime detentions without trial and to continue using military commission prosecutions — if not at the Guantánamo prison, which he had resolved to close, then at a replacement wartime prison.

Told that several dozen detainees could not be tried for any crime but would be particularly risky to release, and that a handful might be prosecutable only under the looser rules governing evidence in a military commission, Mr. Obama decided that the responsible policy was to keep both the tribunals and the indefinite detentions available.

The president refused to use either power on newly captured terrorism suspects, instead prosecuting them in civilian court. But by leaving the options open, he helped normalize them and left them on a firmer legal basis.

Mr. Obama followed a similar course with several national security practices that became controversial during his first term. After his use of drones to kill terrorism suspects away from war zones led to mounting concerns over civilian casualties and other matters, he issued a “presidential policy guidance” in May 2013 that set stricter limits. They included a requirement that the target pose a threat to Americans — not just to American interests — and that there would be near certainty of no bystander deaths.

But the Obama administration also successfully fought in court to establish that judges would not review the legality of such killing operations, even if an American citizen was the target. Mr. Trump — who has said he would “bomb the hell out of ISIS,” beyond what Mr. Obama is doing, and go after civilian relatives of terrorists, prevailing over any military commanders who balked — could scrap the internal limits while invoking those precedents to shield his acts from judicial review.

Similarly, after a surge of criminal prosecutions against people who leaked secret information to the news media and bipartisan outrage at aggressive investigative tactics targeting journalists, the Obama Justice Department issued new guidelines for leak investigations intended to make it harder for investigators to subpoena reporters’ testimony or phone records. It also decided not to force a reporter for The New York Times to testify in a leak trial or face prison for contempt.

But the Obama administration also successfully fought in court to establish that the First Amendment offers no protection to journalists whom the executive branch chooses to subpoena to testify against confidential sources. Mr. Trump, who has proposed changing libel laws to make it easier to sue news organizations, could abandon the Obama-era internal restraints and invoke the Obama-era court precedent to adopt more aggressive policies in leak investigations.

Well done Obama.

- First India, Now Australia Should Abolish Big Bank-Notes According To UBS

Despite widespread chaos, bank runs, tumbling currency, and economic uncertainty in India following its surprise announcement last week, UBS analysts think Australia should follow India’s lead and scrap its biggest bank notes, extending the war on cash further across the globe.

The war on cash really began to escalate in February when The European Central Bank said it was considering withdrawing 500-euro notes because of an “increased conviction in world public opinion” such high-value notes are used for criminal purposes.

And as a reminder, here is what happened in India this week after they abolished large denomination banknotes, (via Reuters)…

Anger intensified in India on Saturday as banks struggled to dispense cash following the government's decision to withdraw large denomination notes in an attempt to uncover billions of dollars in undeclared wealth.

Tempers frayed as hundreds of thousands of people queued for hours outside banks for a third day to swap 500 and 1,000 rupee bank notes after the notes were abolished earlier in the week.

The banned bills made up more than 80 percent of the currency in circulation, leaving millions of people without cash and threatening to bring much of the cash-driven economy to a halt.

"There's chaos everywhere," said Delhi Chief Minister Arvind Kejriwal, a rival of Prime Minister Narendra Modi, accusing the premier of wreaking havoc on poor and working Indians while the wealthy found ways to skirt the new rules.

Customers argued and banged the glass doors at a Standard Chartered branch in southern Delhi after security guards blocked the entrance, saying there were too many people inside already.

And now, as Bloomberg reports, UBS analysts thin Australia should follow the same path towards abolishing banknotes…

“Removing large denomination notes in Australia would be good for the economy and good for the banks,” UBS analysts led by Jonathan Mott said in a note to clients on Monday. Benefits would include reduced crime and welfare fraud, increased tax revenue and a “spike” in bank deposits, he said.

In Australia, 92 percent of all currency by value is in A$50 ($38) and A$100 notes, the larger of which is “rarely seen,” according to the UBS report. Removing bigger denominations would boost digital payments in a country where the use of cash payments is continuing to fall, the analysts wrote.

Since 2009, ATM transactions in Australia have fallen 3.4 percent a year, while credit-card transactions have increased 7.3 percent a year, UBS said.

The program would also be positive for banks. If all the A$100 notes were deposited into accounts at the lenders, household deposits would rise by about 4 percent, the UBS analysts said. That would likely be enough to fill the big banks’ regulatory-mandated net stable funding ratios and reduce reliance on offshore funding, they said.

We have one warning for all those pushing the war on cash – and using the "coorruption" excuse – be careful what you wish for… trust only lasts so long. As Devashang Datta concludes,

Our entire monetary system depends on trust. A banknote is a piece of paper that says the RBI will give the bearer another similar piece of paper, or make an entry in an electronic ledger for that amount. The system works because everybody believes that those pieces of paper will be accepted by everybody else and therefore, money serves as an useful medium of exchange. This move has shaken that trust.

And sure enough gold prices in India have skyrocketed since the currency ban.

- Surge In Online Loan Defaults Sends Shockwaves Through The Industry

Online lenders were supposed to revolutionize the consumer loan industry. Instead, they are rapidly becoming yet another “the next subprime.”

We first started writing about the P2P sector in early 2015 with cautionary pieces like and “Presenting The $77 Billion P2P Bubble” and “What Bubble? Wall Street To Turn P2P Loans Into CDOs.” Things accelerated in February of this year when we first noted that substantial cracks were starting to show in the world of P2P lending, and more specifically, with LendingClub’s inability to assess credit risk of its borrowers that were causing the company to experience higher write-off rates than forecast.

Below is a chart that was used in a LendingClub presentation showing just how far off the company was in predicting write-off rates – the bread and butter of its business. It was evident then that their algorithms weren’t “working very well.”

At the time we said that what the slide above shows is that LendingClub is terrible at assessing credit risk. A write-off rate of 7-8% may not sound that bad (well, actually it does, but because P2P is relatively new, we don’t really have a benchmark), it’s double the low-end internal estimate. That’s bad. In other words, we said, the algorithms LendingClub uses to assess credit risk aren’t working. Plain and simple.

Three months later, in May of 2016, our skepticism was proven right when the stock of LendingClub – at the time the largest online consumer lender – imploded when the CEO resigned following an internal loan review.

Since then, despite a foreboding sense of deterioration behind the scenes, there were few material development to suggest that the cracks in the surface of the online lending industry were getting bigger.

Until today, that is, when we learned that – as expected – there has been a spike in online loan defaults by US consumers, sending a shockwave through the online lending industry: a group of online loans that were packaged into bonds is going bad faster than lenders and bond underwriters had expected even after the recent volatility in the P2P market, in what Bloomberg dubbed was “the latest sign that some startups that aimed to revolutionize the banking industry underestimated the risk they were taking.”

In a page taken right out of the CDO book of 2007, delinquencies and defaults on at least four different sets of bonds have reached the “triggers” points. Breaching those levels would force lenders or underwriters to start paying down the bonds early, redirecting cash from other uses such as lending and organic growth. According to Bloomberg, one company, Avant Inc. and its underwriters, will have to begin to repay three of its asset-backed notes, which have all breached trigger levels.

Two of Avant’s securities breached triggers this month for the first time, the person said, asking for anonymity because the data is not public. Another bond, tied to the subprime lender CircleBack Lending Inc., may also soon breach those levels, according to Morgan Stanley analysts. When the four offerings were originally sold last year, they totaled more than $500 million in size. Around $2.8 billion of bonds backed by online consumer loans were sold in 2015, according to research firm PeerIQ.

The breach of trigger points is merely the latest (d)evolutionary event attained by the online lending industry, whose fall promises to be far more turbulent than its impressive rise. Prior to the latest news, LendingClub last month raised interest rates and tightened its standards for at least the second time this year after seeing higher delinquencies among its customers, especially those with the most debt.

However, that was a linear deterioration which had no impact on mandatory cash covenants, at least not yet. With the breach of trigger points, online lenders have officially entered the world of binary outcomes, where the accumulation of enough bad loans will have implications on the underlying business and its use of cash.

Breaching triggers typically forces a company to divert cash flow from assets to paying off bonds instead of making new loans, which often means it has to find new, more expensive funding or to scale down its business. Avant, based in Chicago, cut its monthly target for lending this summer by about 50 percent, and decided to shrink its workforce in line with that, while CircleBack Lending, based in Boca Raton, Florida, stopped making new loans earlier this year.

Setting bond triggers is often up to the security’s underwriters. Some lenders have been working more closely with Wall Street firms to make sure the banks know how loans will probably perform and set triggers at reasonable levels, said Ram Ahluwalia, whose data and analytics firm PeerIQ tracks their loan data.

Indicatively, in the “old days” John Paulson would sit down with

Goldman Sachs and determine the “triggers” on CDOs, also known as

attachment and detachment points, so he could then be the counterparty on the trade, and short it while Goldman syndicated the long side to its clients, also known as muppets. It would be interesting if a similar transaction could take place with online loans as well.Other industry participants aren’t doing better: “There was a rush to grow,” said Bryan Sullivan, chief financial officer of LoanDepot, a mortgage company that last year began making unsecured loans to consumers online. In the true definition of irony, while Sullivan was speaking about the industry in general, LoanDepot’s own loan losses on a bond in September broke through the ceilings that had been set by underwriters at Jefferies Group.

We are not the only ones to have warned early about the dangers of online lending: Recently Steve Eisman, a money manager who predicted the collapse of subprime mortgage securities, said some firms have been careless and that Silicon Valley is “clueless” about the work involved in making loans to consumers. Non-bank startups arranged more than $36 billion of loans in 2015, mainly for consumers, up from $11 billion the year before, according to a report from KPMG.

And while P2P may be the “next” subrpime, there is always the “old” subprime to fall back on to get a sense of the true state of the US consumer :as Bloomberg adds, the percentage of subprime car loan borrowers that were past due reached a six-year high in August according to S&P Global Ratings’ analysis of debts bundled into bonds.

Lenders themselves are talking about the heavy competition for customers. Jay Levine, the chief executive officer of OneMain Holdings Inc., one of America’s largest subprime lenders, said last week that “the availability of unsecured credit is currently the greatest that has been in recent years,” although he said much of the most intense competition is coming from credit card lenders.

And in a surprising twist, OneMain, formerly part of Citigroup, is taking steps to curb potential losses by requiring the weakest borrowers to pledge collateral. In other words, what was until recently an unsecured online loan industry is quietly shifting to, well, secured. Alas, for most lenders it may be too late.

* * *

For those curious, the deals that have or are expected to breach triggers include:

- MPLT 2015-AV1, a bond deal backed by Avant loans that Jefferies bought and securitized.

- AVNT 2015-A, a bond deal issued by Avant and underwritten by Jefferies.

- AMPLT 2015-A, a bond deal backed by Avant loans and underwritten by Morgan Stanley.

- MPLT 2015-CB2, backed by subprime loans made by CircleBack Lending Inc. and underwritten by Jefferies.

- Did President-Elect Trump Just Inadvertently Kill The Golden Goose?

Submitted by Gordon T Long via MATASII.com,

President-Elect Trump may have just unwittingly sowed the seed of an equity market draw-down which will send even more protesters into the streets of America. Donald Trump's stated economic policies are clearly pro-growth and if he manages to implement his pro-business, anti-regulation agenda, in the longer term they have the potential to surpass the bold and successful initiatives of Ronald Reagan. However, in the near term he has already unknowingly just shot himself in the foot.

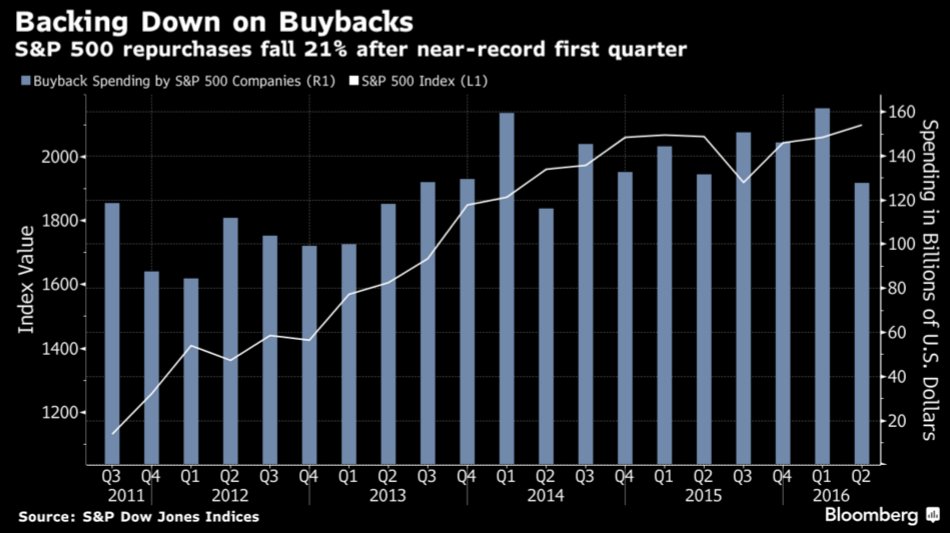

To understand this we need to look at some charts from the FRED system which we unearthed in trying to understand what the future presently entails for corporate stock buybacks and dividend payouts. Shown in the chart below we see how Corporate CEO / CFO's have increased their debt loads by historically unprecedented levels of 20-30% Y-o-Y since just after the GFC (Great Financial Crisis). You will notice that in the last year that rate of growth has gone negative.

The next chart we found astounding regarding the degree of correlation of the above corporate debt growth (primarily being used for buybacks and dividend payouts) compared to the movement of the S&P 500 on a Quarterly Y-o-Y change basis. There can be little doubt about what has been sustaining the artificial levels of US equity markets!

You will also notice that recently this correlation has begun to falter, as equities diverged staying positive from the falling rate of debt growth.

To put this into perspective our analysis indicated that corporate cashflows (EBITDA) and debt levels had now reached a level where they were potentially impacting corporate credit & lending ratings. As you would suspect, corporations as a consequence have began to slow their rate of buybacks (shown below).

SWISS NATIONAL BANK (A LIKELY PROXY) TEMPORARILY TO THE RESCUE

The question is; what allowed US equities to continuing rise? We sense this can best be answered by showing how mysteriously, at the same time as the above divergence, we witnessed the Swiss National Bank buying US stocks. The SNB acquired to almost the exact level required to keep markets temporarily levitated. Obviously nothing more than a coincidence and certainly not something that anyone might suspect they could be potentially acting as a proxy for the US Federal Reserve or US Treasury?

ENTER PRESIDENT-ELECT DONALD TRUMP

But now we have a new President and the political pressures on the Federal Reserve to keep markets from falling prior to the US Presidential & Congressional election are over. Based on President-Elect Trump's campaign rhetoric, Janet Yellen knows she is likely not to have her term renewed in 2018 and knows the Fed's historical independence may in fact be exposed.

IMMEDIATELY on Trump's victory we have witnessed A Global Bond debacle as yields have shot skyward. Suddenly corporate borrowing has become even more expensive and most importantly, perceived low-risk Treasury yields are now the same or slightly higher than stock yields! Investors have been forced to buy US equity stocks (other than the FANGs & NOSH) for the dividends in a yield hungry world controlled by policies of Financial Repression.

This dramatic post election development may be the "spanner" in the corporate stock buyback program that many have been anticipated, but were unsure what exactly would trigger it.

Trump's aggressive $1 Trillion Infrastructure Plan may have released the "inflation genie" based on his vowed spending and tax cut programs.

BOTTOM LINE

With bond prices having removed $1 Trillion globally the expectations and pressures are now for the equity market correlation to more closely align with bond values.

Courtesy of ZeroHedge.com

Expect the correction of an over-valued US Equity market to be summarily and quickly blamed by the liberal media on the new Trump Administration before it has even taken office.

- Violent Clashes Erupt Between Greek Police And Demonstrators Protesting Obama's Visit

It appears that no matter what outgoing US president Barack Obama does, he can’t get anything right. In the US, it is mostly the right that detests the president, who threw his entire weight behind Hillary Clinton’s failed campaign (a sentiment shared by many Bernie Sanders supporters who feel that the presidency was complicit in Hillary Clinton’s theft of the primary from their preferred candidate).

Meanwhile, in Greece – the first stop of Obama’s farewell global tour – it is the left that appears to be disgusted with Obama. As the following videos and photos show, leftist demonstrators took to the streets to protest against US President Barack Obama’s visit to Athens, clashing with police, who used tear gas to disperse the crowd as people tried to break through cordons.

According to Reuters, the clashes broke out just a few kilometers from the presidential mansion where Greek leaders were hosting a state banquet for visiting U.S. President Barack Obama. About 7,000 people, among them many hooded protesters and members of the Communist-affiliated group PAME, marched through the streets of central Athens holding banners reading “Unwanted!”

Protesters are rallying against US policy that is “creating tensions” with various countries around the world, starting with China and Russia, as well as against the US attempts to “overthrow the government in Ukraine,” Greek journalist Aris Chatzistefanou told RT. Apart from that, protesters are blaming the US for supporting“Islamic extremists”which led to“well-known consequences.”

???? ??????? ??? ?????? ?????????? pic.twitter.com/WpLJhSmB5N

— Aris Chatzistefanou (@xstefanou) November 15, 2016

“While the Greek government is trying to present the visit of Obama as a visit of a peacemaker, thousands of demonstrators came onto the streets to protest US policy in [such] parts of the world from Latin America to Middle East, Afghanistan and Syria,” Chatzistefanou said.

“The government was trying to present to the Greek public that Barack Obama will come and help with the austerity policy that was imposed by the Troika,” Chatzistefanou said, also adding that there is “no direct connection” between Obama’s promises and what the IMF is planning to do.

The police clashed with the protesters after they tried to break through cordon lines to reach the parliament building and the U.S. embassy. In traditional Greek fashion, some demonstrators threw two petrol bombs at police before dispersing into nearby streets close to Athens’s main Syntagma Square.

????? ????… ??? ??? ????? ????? pic.twitter.com/4CR8j0d7Dm

— Aris Chatzistefanou (@xstefanou) November 15, 2016

“We don’t need protectors!” one of the banners carried by the demonstrators read. Some could be heard exclaiming: “Yankees go home!”

All public gatherings were banned in the central part of Athens due to Obama’s two-day visit, however that did not prevent protesters from appearing. Riot police parked buses along Obama’s route and erected cordons.

No injuries or arrests have been reported so far, according to AP.

More than 5,000 police officers were deployed in central Athens to maintain order.

In a separate protest in the northern city of Thessaloniki, more than 1000 people took place in a similar protest, where one of the participants was caught burning a U.S. flag.

?? ???????? ????? ??? ??????????? ?????? ??? ????????? ?? #skouries ??????? ???? ????????????. #obama_athens #ObamaGr pic.twitter.com/qVC2uOKZCI

— Chris Avramidis (@Chris_Avramidis) November 15, 2016

Authorities had to step up security measures “as the circumstances require,” with a number of protests planned, a police source told AFP earlier today.

Obama left Washington on Monday, embarking on his last trip across Europe before President-elect Donald Trump assumes his post in January 2017.

He is to spend one more day in Greece to continue the discussion of Greece’s economic situation and Europe’s migration crisis. He will then leave for Germany on Wednesday, intending to soothe concerns over Trump’s upcoming presidency

This was the first time that Obama has visited Greece during his eight years in office. Last time Greece was visited by a US president when Bill Clinton held the office in 1999. His visit also saw extensive street fighting between anarchists and riot police.

The visit comes only two days before the anniversary of a bloody 1973 student revolt that helped topple the 1967-1974 military junta which was backed by the U.S. government.

- The Secular Trend In Rates Remains Lower: The Yield Bottom Is Still Ahead Of Us

Donald Trump’s victory sparked a tremendous sell-off in the Treasury market from an expectation of fiscal stimulus, but more broadly, from an expectation that a unified-party government can enact business-friendly policies (protectionism, deregulation, tax cuts) which will be inflationary and economically positive. It doesn’t take too much digging to show that the reality is different. The deluge of commentaries suggesting 'big-reflation' are short-sighted. Just as before last Tuesday we thought the 10yr UST yield would get below 1%, we still think this now.

[single left-click to enlarge]

Business Cycle

No matter the President, this economic expansion is seven and a half years old (since 6/2009), and is pushing against a difficult history. It is already the 4th longest expansion in the US back to the 1700’s (link is external). As Larry Summers has pointed out (link is external), after 5 years of recovery, you add roughly 20% of a recession’s probability each year thereafter. Using this, there is around a 60% chance of recession now.

History also doesn’t bode well for new Republican administrations. Certainly, the circumstances were varied, but of the five new Republican administrations replacing Democrats in the 19th and 20th centuries, four of them (Eisenhower, Nixon, Reagan, and George W. Bush) faced new recessions in their first year. The fifth, Warren Harding, started his administration within a recession.

Fiscal Stimulus

Fiscal stimulus through infrastructure projects and tax cuts is now expected, but the Federal Reserve has been begging for more fiscal help since the financial crisis and it has been politically infeasible. The desire has not created the act. A unified-party government doesn’t make it any easier when that unified party is Republican; the party of fiscal conservatism. Many newer House of Representatives members have been elected almost wholly on platforms to reduce the Federal debt. Congress has gone to the wire several times with resistance to new budgets and debt ceilings. After all, the United States still carries a AA debt rating from S&P as a memento from this. Getting a bill through congress with a direct intention to increase debt will not be easy. As we often say, the political will to do fiscal stimulus only comes about after a big enough decrease in the stock market to get policy makers scared.

Also, fiscal stimulus doesn't seem to generate inflation, probably because it is only used as a mitigation against recessions. After the U.S. 2009 Fiscal stimulus bill, the YoY CPI fell from 1.7% to 1% two years later. Japan has now injected 26 doses (link is external) of fiscal stimulus into its economy since 1990 and the country has a 0.0% YoY core CPI, and a 10yr Government bond at 0.0%.

Rate sensitive world economy

A hallmark of this economic recovery has been its reliance on debt to fuel it. The more debt outstanding, the more interest rates influence the economy’s performance. Not only does the Trump administration need low rates to try to sell fiscal stimulus to the nation, but the private sector needs it to survive. The household, business, and public sectors are all heavily reliant on the price of credit. So far, interest rates rising by 0.5% in the last two months is a drag on growth.

[single left-click to enlarge]

Global mooring

Global policies favoring low rates continue to be extended, and there isn’t any economic reason to abandon them. Just about every developed economy (US, Central Europe, Japan, UK, Scandinavia) has policies in place to encourage interest rates to be lower. To the extent that the rest of the world has lower rates than in the US, this continues to exert a downward force on Treasury yields.

[single left-click to enlarge]

Demographics

As Japan knows and we are just getting into, aging demographics is an unmovable force against consumption, solved only with time. The percent of the population 65 and over in the United States is in the midst of its steepest climb. As older people spend less, paired with slowing immigration from the new administration, consumer demand slackens and puts downward pressure on prices.

[single left-click to enlarge]

Conclusion

We haven’t seen such a rush to judgement of boundless higher rates that we can remember. Its noise-level is correlated with its desire, not its likelihood. While we cannot call the absolute top of this movement in interest rates, it is limited by these enduring factors and thus, we think it is close to an end. In a sentence, not only will the Trump-administration policies not be enacted as imagined, but even if they were, they won't have the net-positive effect that is hoped for. We think that a 3.0% 30yr UST is a rare opportunity buy.

Digest powered by RSS Digest

Saving...

Saving...