- Austria's New Hate Speech Law

Austria’s New Hate Speech Law

Tyler Durden

Mon, 11/16/2020 – 02:00Authored by Judith Bergman via The Gatestone Institute,

The Austrian government has presented a draft online hate speech law, the Communication Platforms Act, which, if passed, will limit free speech in the country. The Austrian government writes in the introduction to its proposed law:

“The main reason for the development of this draft Act is the worrying development that the Internet and social media, in addition to the advantages that these new technologies and communication channels provide, have also established a new form of violence, and hate on the Internet is increasing in the form of insults, humiliation, false information and even threats of violence and death. The attacks are predominantly based on racist, xenophobic, misogynistic and homophobic motives. A comprehensive strategy and a set of measures are required that range from prevention to sanctions. This strategy is based on the two pillars of platform responsibility and victim protection, with the present draft Act relating to ensuring platform responsibility”.

The proposed law is modelled on Germany’s much criticized NetzDG law, also known as the censorship law, which came into effect in January 2018 and requires social media companies to delete or block any online unlawful content within 24 hours or 7 days at the most, or face fines of up to 50 million euros.

In May 2020, France adopted a similar law, known as the “Avia law“, also modelled on the German NetzDG law, which requires online platforms to remove reported “hateful content” — incitement to hatred, or discriminatory insult, on the grounds of race, religion, ethnicity, gender, sexual orientation or disability — within 24 hours. Failure to do so could result in fines of up to 1.25 million euros or 4% of the platform’s global revenue.

Similarly, the Austrian law requires “obviously” unlawful content to be deleted within 24 hours and other unlawful content within seven days. Failure to do so could lead to fines of up to 10 million euros ($12 million). Platforms must provide a reporting function for such content and react immediately to notifications.

Just like Germany’s NetzDG law, the Austrian censorship law privatizes state censorship by requiring social media platforms to censor their users on behalf of the state. If the proposed law is passed, the freedom of speech of Austrians online will be subject to the arbitrary decisions of corporate entities, such as Twitter, Google and Facebook.

With Austria’s draft online hate speech law, yet another European country is taking another step towards making online censorship an institutionalized feature of European hate speech laws. In Austria, according to Reuters, a surprising number of private associations would like to see even wider measures implemented: Austria’s association of digital service providers, ISPA, representing more than 200 companies including Google Austria and Facebook Germany welcomed the initiative against online hate speech but called for a joint European effort.

“Only a uniform European regulation can become a successful standard and assert itself worldwide,” ISPA said in a statement. “Uncoordinated individual courses don’t get us any further here.”

There has been, however, significant pushback against government censorship: In France, the Constitutional Council, a French court that examines legislation’s compatibility with the constitution, struck down multiple provisions of the “Avia law” in June because it infringed on freedom of expression. The Constitutional Council noted in its press release:

“[According] to Article 11 of the Declaration of the Rights of Man and of the Citizen of 1789: ‘The free communication of thoughts and opinions is one of the most precious human rights: any citizen can therefore speak, write, print freely, except to answer for the abuse of this freedom in the cases determined by the law’. It is inferred from these provisions that with the present state of the means of communication and in view of the generalized development of online communication services to the public, as well as the importance of these services for participation in democratic life and the expression of ideas and opinions, this right implies the freedom to access and express yourself in these services…”

“Freedom of expression and communication is all the more precious since its exercise is a condition of democracy and one of the guarantees of respect for other rights and freedoms. It follows that the interference with the exercise of that freedom must be necessary… and proportionate to the objective pursued”.

The court found that multiple provisions of the “Avia law” infringed on freedom of expression because they were not “necessary or proportionate”.

“We too often make bad laws with good intentions. Online platforms should not censor the freedom of expression,” said Chairman of the Senate Law Commission Philippe Bas after the Constitutional Council’s decision.

It can only be hoped that European lawmakers eager to censor free speech online will heed the ruling of the French constitutional court.

- "Rapidly Intensifying" Hurricane Iota Set To Slam Central America

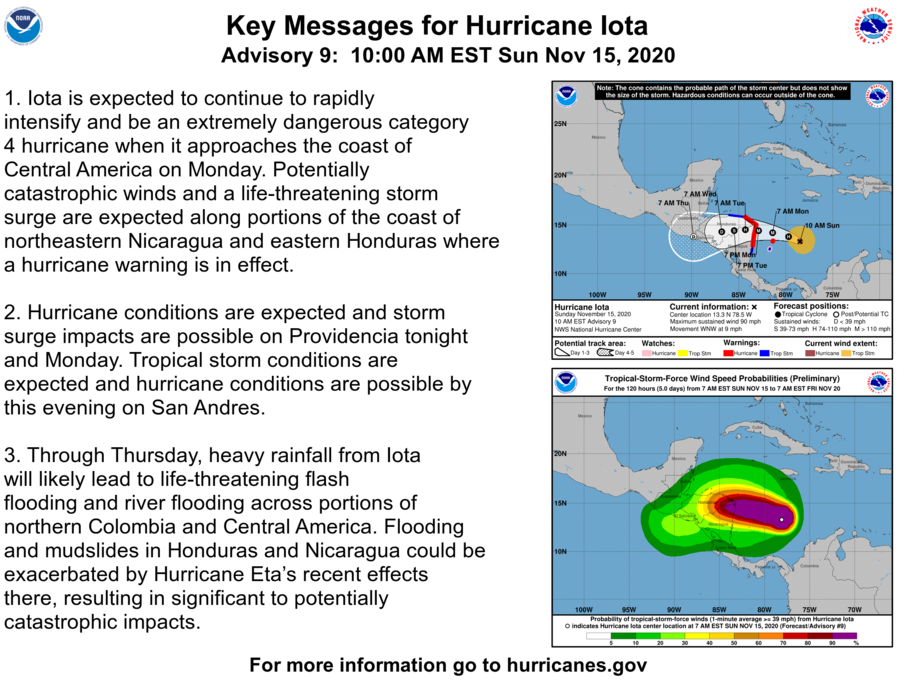

“Rapidly Intensifying” Hurricane Iota Set To Slam Central America

Tyler Durden

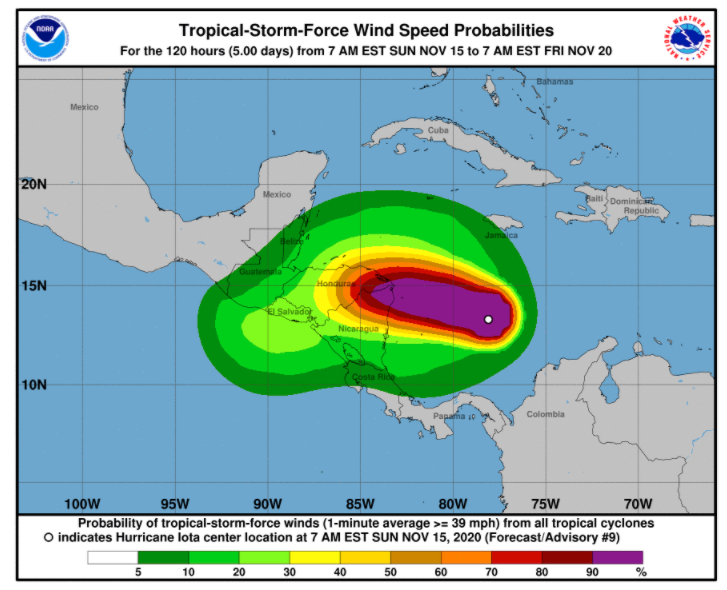

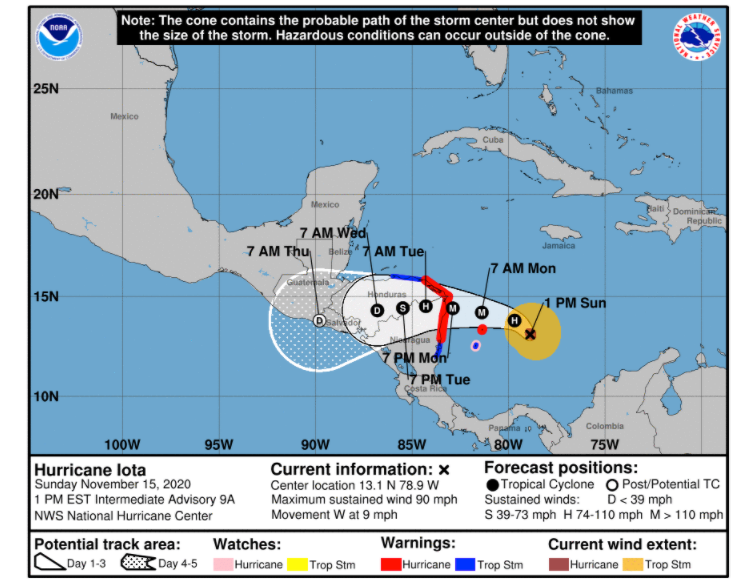

Mon, 11/16/2020 – 01:00Iota strengthened to a hurricane Sunday over the southwestern Caribbean Sea, expected to “bring potentially catastrophic winds, a life-threatening storm surge, and rainfall impacts to Central America,” reported the National Hurricane Center (NHC).

#Hurricane #Iota is expected to become an extremely dangerous category 4 hurricane tomorrow and make landfall in NE Nicaragua or E Honduras. Preparations to protect life and property should be rushed to completion in the Hurricane Warning areas. More: https://t.co/tW4KeFW0gB pic.twitter.com/mK7SpNo0IF

— National Hurricane Center (@NHC_Atlantic) November 15, 2020

https://platform.twitter.com/widgets.js

NHC’s 1000 ET Sunday update outlined how Iota is “rapidly intensifying” as it could be an extremely dangerous category 4 near the coasts of Nicaragua and Honduras.”

The current landfall forecast says tropical conditions will arrive on the coasts of Honduras and Nicaragua by Monday morning. “This is an extremely dangerous situation with Iota expected to be category 4 at landfall!” NHC warned.

Earliest Reasonable Arrive Time Of Tropical-Storm-Force Winds

Wind Speed Probabilities

Hurricane Warning For Much Of Nicaragua and Honduras Coastline

Hurricane Model

We explained on Saturday Iota would become a “major hurricane.” Weather models are forecasting the storm could dump 8 to 30 inches of rain on Honduras, northern Nicaragua, eastern Guatemala, and southern Belize by early next week.

In early November, Hurricane Eta battered the region (read: here & here), destroying upwards of 10% of the coffee crop in Central America, with Iota likely to push up the percentage to 25%.

- When Does A "Glitch" Become A Coup? It's Time to Regulate America's Fly-by-Night Voting Machine Monopoly

When Does A “Glitch” Become A Coup? It’s Time to Regulate America’s Fly-by-Night Voting Machine Monopoly

Tyler Durden

Sun, 11/15/2020 – 23:50Authored by Robert Bridge via The Strategic Culture Foundation,

It’s a frightening thing to consider, but the ultimate success of democracy in the United States largely hinges on the integrity of just three voting machine companies, which conduct their affairs with almost no government oversight and regulation. Unless that changes, the greatest democracy will start looking like a banana republic in the eyes of the world.

In January 2020, the CEOs of the three companies that produce over 80 percent of voting machines in the U.S. – Election Systems & Software (ES&S), Dominion Voting Systems and Hart InterCivic – were grilled by members of Congress over the question of security at the ballot box. Perhaps it would surprise exactly nobody that the 90-minute discussion focused almost entirely on the possibility of foreign actors, specifically China and Russia, interfering in the U.S. election system. Within such a predictably narrow frame of reference – Russia! Russia! Russia! – it becomes much easier to eliminate the possibility that domestic actors may also be tempted to tamper with the vote. At the same time, Russia provides the perfect smokescreen in the event someone gets caught with their hand in the election cookie jar. But already I digress.

Currently, Dominion Voting Systems, the supplier of voting machines in 28 states, is coming under fierce scrutiny after it was reported that thousands of votes in one Michigan country intended for Donald Trump went to his challenger, Joe Biden. Officials were quick to point out that the ‘glitch’ was due to silly “human error,” as opposed to any mechanical flaws with the voting machines.

According to Michigan state government website, “[T]he erroneous reporting of unofficial results … was a result of accidental error on the part of the Antrim County Clerk (who) accidentally did not update the software used to collect voting machine data and report unofficial results.”

While I am no computer specialist, it is hard to imagine how a software update would have done anything to prevent one candidate from receiving the votes intended for another unless it was originally programmed to behave that way. But again, I am no expert.

Another state that relies heavily on Dominion Voting Systems is Georgia, which received 30,000 new voting machines last year – “the largest rollout of elections equipment in U.S. history,” according to the Government Technology newsletter. Following the announcement of the $107 million contract, the same newsletter foretold of problems down the road, saying the “new voting system is expected to be quickly challenged in court by voters who say it remains vulnerable to hacking and tampering, despite the addition of paper ballots.”

Those fears were quickly realized on the morning of Nov. 3, Election Day, when a technological glitch wreaked havoc on voting in two Georgia counties (a side note to this story is that Georgia officials blamed the abrupt pause in vote counting on a burst pipe at Atlanta’s State Farm Arena. Thus far, however, officials have not been able to produce any evidence that such an incident took place).

While the source of the ‘glitch’ is still under investigation, one state ballot supervisor, Marcia Ridley, initially told POLITICO on Nov. 3 that Dominion, which prepares the poll books for counties before elections, “uploaded something last night, which is not normal, and it caused a glitch.” That reported incident prevented staff from programming the voter smart cards for the voting machines. Ridley continued, “That is something that they don’t ever do. I’ve never seen them update anything the day before the election.”

However, Dominion officials, while admitting there was a problem with the poll books, deny there was any last-minute update made to the poll books after Oct. 31 (a press release by Dominion countered this and other allegations, including that the Pelosi family, the Feinstein family, or the Clinton Global Initiative has any relationship with the company).

And here is where things get interesting.

Ridley went on to say that Dominion assured her that “no system can be updated remotely without the knowledge of [the company],” indicating that an update could not have been made without detection. In other words, there appears to be a backdoor channel for Dominion Voting Systems to connect to the internet, and, as everybody knows, whatever appears on the internet is fair game for hackers.

Has Pennsylvania ever sent blank ballots to constituents?

If yes, what eventually happened to those blank ballots?— Ron (@CodeMonkeyZ) November 12, 2020

https://platform.twitter.com/widgets.js

In fact, it was exactly that concern that helped dissuade the state of Texas from also purchasing the dodgy Dominion system.

In a letter from Brandon Hurley, a voting systems examiner, addressed to Keith Ingram, Director of Elections in Texas, it was determined that “some of the hardware in the Democracy 5.5-A System can be connected to the internet through Ethernet ports.”

Later in the letter, it was emphasized again that “[W]ithout question, one or more of the components of the 5.5-A System can be connected to an external communication network and this can only be avoided if the end-user takes the proper precautions to prevent such a connection.”

On Wednesday, Georgia Secretary of State Brad Raffensperger announced the state would perform a hand-recount of presidential ballots before certifying the results of its election. According to the New York Times, Biden leads the incumbent Trump by 14,000 votes.

In hindsight, how could voting software named Dominion not have a nefarious purpose?

— Keith Preston (@KeithPreston) November 12, 2020

https://platform.twitter.com/widgets.js

Whatever the outcome of the 2020 presidential election, which also had to wrangle with the influx of millions of mail-in ballots amid a pandemic, it will certainly go down in the history books as one of the most chaotic, controversial and fraud-prone contests in U.S. history. The tragedy is that this fiasco, which is making America look ridiculous on the global stage, could have been avoided. There have been numerous attempts to sound the alarm on the vulnerability of voting machines to accurately tabulate the results of an election, and not least of all the ongoing Trump-Biden showdown, which will determine the political, cultural and economic trajectory of the United States long into the future.

It is the opinion here that, judging by everything we know and don’t know about how the 2020 presidential election was organized, the only realistic option is to hold a nationwide recount. It is simply impossible to expect millions of American voters from either side of the political aisle to hold any doubts over an election of such tremendous consequence. Yes, a recount would be a massive undertaking, but the future peace and tranquility of the nation, already partisan to the breaking point, depends upon it. Once the recount is accomplished, the next task should be a congressional task force to examine ways of securing U.S. elections in the future, while holding the voting machine companies to severe government control and regulation. The days of monkey-wrenching U.S. elections must end.

- Assassination Attempt On Armenian Prime Minister Thwarted By Security Forces

Assassination Attempt On Armenian Prime Minister Thwarted By Security Forces

Tyler Durden

Sun, 11/15/2020 – 23:25Armenian security officials announced they had thwarted an active assassination attempt on Prime Minister Nikol Pashinyan plotted by a cadre of his political opponents amid widespread outrage at Armenia signing a ceasefire with Azerbaijan which Baku hailed as a “capitulation” by Yerevan, essentially admitting defeat in Nagorno-Karabakh.

The Armenian National Security Service (NSS) revealed in a statement that “one of the political opponents opposed to the government kept a large number of weapons, ammunition and explosives and reached an agreement with the leaders of the parties operating in Armenia and Karabakh to plan to seize power and kill the prime minister.”

Prime Minister Nikol Pashinyan of Armenia. Source: Armenian Prime Minister Press Service via Associated Press “The leaders of parties, antigovernmental politicians, their supporters and former senior officials were preparing to attempt to assassinate a statesman and usurp power,” the statement said.

Earlier last week enraged protesters had stormed Armenia’s parliament in Yerevan, after Pashinyan on Monday evening signed a Russia-brokered agreement with Azerbaijan and Russia for the immediate cessation of hostilities in Karabakh. This was at a moment the Azerbaijan Army had made undeniable and significant gains.

“The suspects were planning to illegally usurp power by murdering the prime minister and there were already potential candidates being discussed to replace him,” says #Armenia NSS in statement, announcing its former head, Artur Vanetsyan, and others have been arrested.

— Steve Herman (@W7VOA) November 14, 2020

https://platform.twitter.com/widgets.js

According to Reuters, “Pashinyan had come under pressure with thousands of demonstrators protesting since Tuesday and demanding he resign over a ceasefire that secured territorial advances for Azerbaijan in Nagorno-Karabakh after six weeks of fighting.”

Pashinyan has responded to widespread anger among the Armenian public by saying he had little choice but to sign the agreement to prevent further territorial losses and major loss of life.

Armenian protestors trash their parliament building. The Pashinyan gov and the Armenian media did not prepare them for this terrible defeat. | pic.twitter.com/93Qf1e55Lp

— Mike (@Doranimated) November 10, 2020

https://platform.twitter.com/widgets.js

Few details were given as to how far the assassination plot advanced or how precisely it was uncovered, but arrests were made: “The NSS said its former head Artur Vanetsyan, the former head of the Republican Party parliamentary faction Vahram Baghdasaryan and war volunteer Ashot Minasyan were under arrest,” Reuters reported.

Vanetsyan was also former head of Armenia’s national security service, suggesting the plot entered high levels of the government.

- What Is John Brennan So Worried About?

What Is John Brennan So Worried About?

Tyler Durden

Sun, 11/15/2020 – 23:00Authored by Ray McGovern via ConsortiumNews.com,

Former CIA Director John Brennan is apparently so worried that Donald Trump might release certain classified intelligence that he suggested this week that Vice President Mike Pence and the cabinet remove Trump via the 25th amendment.

Brennan appeared this week on both CNN and MSNBC to spread alarm about what Trump might do as he continues to contest the election results and appoints new people at Defense, NSA (and possibly CIA) who may do his bidding.

Brennan warned on CNN that it was “very, very worrisome” that Trump “is just very unpredictable now … like a cornered cat — tiger. And he’s going to lash out.”

Brennan told MSNBC he was worried that Trump has called for the “wholesale declassification of intelligence in order to further his own political interests.”

Whom would he lash out at and what classified documents might Brennan be referring to?

The CIA’s point man at The Washington Post, David Ignatius, has provided the answer:

“President Trump’s senior military and intelligence officials have been warning him strongly against declassifying information about Russia that his advisers say would compromise sensitive collection methods and anger key allies.

An intense battle over this issue has raged within the administration in the days before and after the Nov. 3 presidential election. Trump and his allies want the information public because they believe it would rebut claims that Russian President Vladimir Putin supported Trump in 2016. That may sound like ancient history, but for Trump it remains ground zero — the moment when his political problems began.”

Protecting “sources and methods” is a red herring. They can be redacted from a classified document. It’s the content of these files that has Brennan extremely nervous as they might reveal Brennan’s role in the Russiagate scandal. Of course, Brennan invoked the old trope of “national security” when it appears it’s his own security he’s worried about.

This new standoff over releasing Russia intel is the perfect bookend. When Trump challenged intel officials on their Russia claims in January 2017, Chuck Schumer warned that the national security state could easily retaliate against the elected president. Who will prevail? pic.twitter.com/NjMPcOIHH0

— Aaron Maté (@aaronjmate) November 11, 2020

https://platform.twitter.com/widgets.js

As we noted at a similar juncture in March 2018 (in “Former CIA Chief Brennan Running Scared”), Brennan’s foremost worry — then, as now — was that Trump was about to expose him to the disgrace that befell ex-FBI Deputy Director Andrew McCabe for malfeasance in connection with Russiagate.

The president had just fired McCabe for repeatedly lying, and Brennan had good reason to worry. That was before the true extent of the roles McCabe, his boss, former FBI Director James Comey, and Brennan played in the WMD-style fabrication of “Russiagate” had became more fully understood.

Brennan landed on his MSNBC perch as a paid commentator on Feb. 2, 2018 and was riding high with adulation from the likes of former UN Ambassador Samantha Power, who publicly warned Trump that it is “not a good idea to piss off John Brennan.”

Even back then, however, storm clouds were gathering. House Intelligence Committee Chairman Devin Nunes (R-CA), who knew much more than he revealed, was warning of legal consequences for Russiagate conspirators.

Referring to the weavers and tailors of Russiagate, Nunes told reporter Sharyl Attkisson on Feb. 18, 2018:

“If they need to be put on trial, we will put them on trial. The reason Congress exists is to oversee these agencies that we created.”

Dismissive of such warnings, Brennan accused Trump on May 17, 2018 of “moral turpitude” and predicted, with an alliterative flourish, that he would end up “as a disgraced demagogue in the dustbin of history.”

As the Russiagate saga has unfolded, however, it has become abundantly clear that there is more than enough moral turpitude to go around. As discussed below, there may be a reasonable hope that documentary evidence — chapter and verse — about Russiagate turpitude will see the light of day if Trump summons the backbone to get unimpeachable evidence into the open.

In my view, this is what seems to have Brennan on tenterhooks.

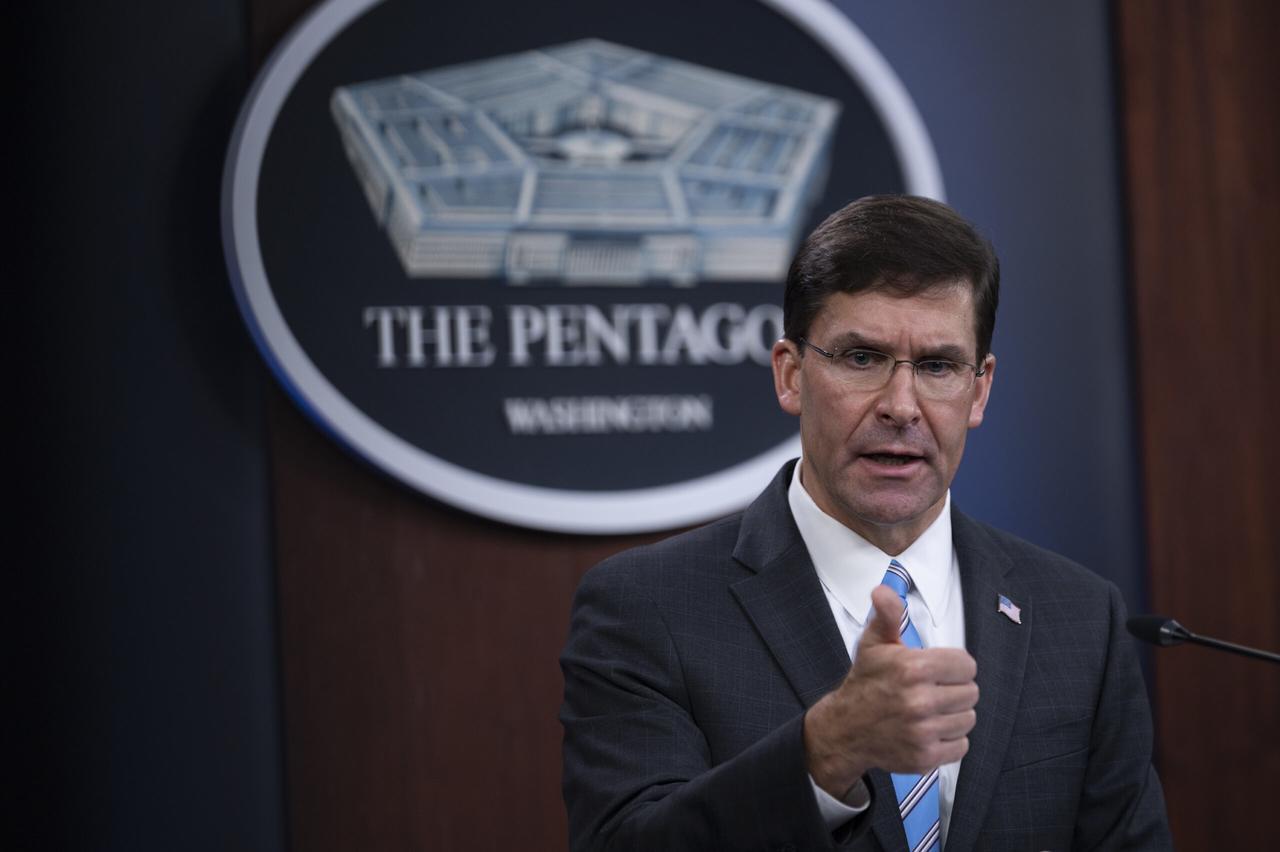

What Else Did Esper Refuse to Do?

John Brennan in Oval Office, Jan. 4, 2010. (White House photo by Pete Souza)

This is the big question. In the CNN interview, Brennan was not artful enough to disguise what seems to be his major worry. Right after complaining that complacent observers are “missing what is a very, very worrisome development,” the ex-CIA chief added:

“And I think it’s quite apparent from reporting that Mark Esper has stood up to Donald Trump repeatedly. Who knows what else has he [‘terminated’ Secretary of Defense Esper] refused to do?”

(For one thing, according to Politico, Esper clashed with Trump over pulling U.S. troops out of Afghanistan.)

Brennan added:

“Who knows what [freshly appointed Acting Secretary of Defense] Chris Miller is going to do if Donald Trump does give some kind of order that really is counter to what I think our national security interests need to be?”

There are abundant — and disquieting (to Brennan) — clues to this, in the events unfolding over the past several days.

For starters, there is the role Ignatius (as close to Brennan as a Siamese twin) played in setting an unusually transparent table to interpret Brennan’s CNN interview the morning after — curiously, without mentioning the interview itself.

(Yes, this is the same David Ignatius who reported on the leaked, late-Dec. 2016 telephone conversation between Russian Ambassador Sergey Kislyak and Gen. Michael Flynn, which was used to trap Flynn and, if possible, put him in prison. After all, Flynn was a major threat. He knew — or would have been able to find out — where most of the Russiagate bodies were buried. It was imperative that he be removed quickly from his position as Trump’s national security adviser.)

Here are Ignatius’s main points:

-

Senior military and intelligence officials have been warning Trump against declassifying information about Russia that would compromise sensitive collection methods and anger allies.

-

Trump wants the information out “because he thinks it would rebut claims that Putin supported Trump in 2016 — how his political problems began.”

-

CIA Director Gina Haspel is against release; said to be determined to “protect sources and methods.”

-

NSA Director Gen. Paul Nakasone directly opposed White House efforts to release the information.

-

Defense Secretary Mark Esper — just “terminated” on Monday — supported Nakasone’s view, warning of “harm to national security and specific harm to the military.”

-

Christopher Miller is named to replace Esper.

-

Michael Ellis, former chief counsel to Nunes, has just been installed as general counsel at NSA.

Nunes: Out From Under the Bus?

After being “thrown under the bus” by Trump more than once in his attempts to expose the crimes of Russiagate, Nunes may now harbor some hope that his patience and loyalty will be rewarded after all. In October Trump ordered Russiagate documents declassified and nothing happened. The next few weeks will tell. The omens are better than before.

Not only will Ellis be general counsel at NSA, reportedly over the objections of Gen. Nakasone, but Kashyap Patel, a longtime Russiagate skeptic and former Nunes aide on the House Intelligence Committee, is replacing Esper’s chief of staff at the Pentagon. Patel is said to already have a “very close” working relationship with Miller, the acting defense secretary. (And rumors persist that Haspel’s ouster is next.)

In addition, former National Security Council official Ezra Cohen-Watnick has been named acting undersecretary of defense for intelligence. Cohen-Watnick not only reaps close ties to Nunes; he was also a top aide to Flynn during the latter’s abbreviated tenure as national security adviser.

Have these folks been appointed to help start a new war? They seem better placed to try to finish an old one — namely, Russiagate. They would certainly be well placed to execute a Trump order to declassify and release R-gate-related documents that have been Waiting for Godot.

This sends shivers up the spines of those with much to fear from such disclosures. At the same time, the formidable ability of the bureaucracy to resist is well known to all concerned.

Esper Slow-Walked Out the Door

Former Secretary of Defense Mark Esper at the Pentagon, July 29, 2020. (DoD, Chad J.McNeeley)

It appears Esper may have been slow-walking a White House request to release information gathered and stored by the National Security Agency, which could document what Trump calls the “hoax” of Russiagate, and the criminal behavior of its perpetrators — including the role prime mover Brennan may have had.

It may be hard to believe, but the NSA intercepts and stores every electronic communication. All Trump has to do is to have newly appointed acting Pentagon chief Miller order Gen. Nakasone to release materials spelling out chapter and verse on the Russiagate operations orchestrated by Brennan, Comey, and ex-National Intelligence Director James Clapper. Nakasone reports to the secretary of defense.

Don’t be misled; virtually all of it can be released with ZERO danger to intelligence “sources and methods.” But release won’t happen if Trump continues to just whine to Fox News, or he “authorizes” release without follow-up (he’s already done that — to no effect).

What Brennan seems to fear is that it might dawn on Trump that he lost the election and has little time left to act. As a lame-duck he might want to go out with a flourish: revenge against the intelligence establishment that undermined him for four years with its Russiagate fable.

Trump might awake one day to find that someone has scrawled on his mirror, “Hey, I thought YOU were the president.” At that point, there would be an outside chance he might act like one, and Brennan and co-conspirators might find themselves going the way of McCabe.

In such circumstances, establishment media can be expected to make a Herculean effort to suppress the (highly embarrassing, including for the media) truth about Russiagate.

It certainly did an amazingly effective job suppressing “Huntergate.” Odds are they could succeed this time around too.

Like those huge banks ten years ago, Russiagate may be too-big-to-fail. But, at least, the documentary evidence would be out there for those who “can handle the truth” — and for future historians with some courage. This is not about the election, which has been decided. But about putting on the record intelligence interference in the last election and subsequent administration, so that future agencies might think twice about doing it again.

By finally ordering the release of such documents, sanitized in those few cases in which it might be necessary, Trump may enable anyone opened minded about Russiagate to be informed in a documented way, about what actually happened during that long-lingering, dark chapter of our recent history.

And, in the process, Russiagaters might be able to overcome their instinctual reluctance to accept the pernicious nature of the National Security State. And that would be for the best.

* * *

Please Contribute to Consortium News on its 25th Anniversary . Donate securely with PayPal here.

-

- 86% Of Trump Voters Say Biden 'Did Not Legitimately Win' Election

86% Of Trump Voters Say Biden ‘Did Not Legitimately Win’ Election

Tyler Durden

Sun, 11/15/2020 – 22:35The vast majority of Trump voters think that Joe Biden’s predicted election win was illegitimate, and that we’ll never know the true outcome.

According to the latest YouGov/The Economist poll, 86% of Trump voters say Biden “did not legitimately win the election,” while 73% say that we’ll “never know the real outcome of this election.”

The poll also reveals that a majority of voters (53%) thought that President Trump would win vs. Biden (47%), according to Economist data journalist, G. Elliott Morris.

Meanwhile, 88% of Trump voters say they believe that “illegal immigrants voted fraudulently in 2016 and tried again in 2020,” while 90% believed that “mail ballots are being manipulated to favor Joe Biden.“

Republicans are also exhibiting some… concerning… attitudes about the franchise, with 46% saying that “some people are not smart enough to vote” (27% among Dems) and 43% saying that people should have to pass a test before voting (15% for Dems).

— G. Elliott Morris (@gelliottmorris) November 11, 2020

Morris adds that 46% of Republicans think “some people are not smart enough to vote” (vs. 27% of Dems), and 43% of Republicans also think that people should have to pass a test before voting (vs. 15% of Dems).

89% of Republicans also think Trump should contest the outcome of the election in court, while 62% of his voters think it will change the outcome.

Less than half of those polled believe there will be a peaceful transition of power in the event Biden is sworn in.

It should be noted that this YouGov/Economist poll is in stark contrast to a recent Reuters poll, which found that 40% of Republicans say Trump won. Perhaps the difference lies in the distinction between YouGov’s sampling of “Trump voters” vs. “Republicans” – which would ostensibly include so-called ‘never-Trumpers.’

- Biden's Cancer Charity Took In Millions, Spent Big On Salaries But Nothing On Research

Biden’s Cancer Charity Took In Millions, Spent Big On Salaries But Nothing On Research

Tyler Durden

Sun, 11/15/2020 – 22:10Authored by Matt Margolis via PJMedia.com,

Fake charities are not just for the Clintons, it seems, as a report from the New York Post reveals that a cancer charity started by former Vice-President Joe Biden spent most of the millions it raised on salaries, but gave out no grants in its first two years.

The mission of the Biden Cancer Initiative, which was founded in 2017, was to “develop and drive implementation of solutions to accelerate progress in cancer prevention, detection, diagnosis, research and care and to reduce disparities in cancer outcomes.” The charity took in nearly $5 million in contributions in 2017 and 2018, according to IRS filings, but spent most of it, just over $3 million, on the salaries of former Washington D.C. aides who were hired for the charity.

The charity took in $4,809,619 in contributions in fiscal years 2017 and 2018, and spent $3,070,301 on payroll in those two years. The group’s president, Gregory Simon, raked in $429,850 in fiscal 2018 (July 1, 2018 to June 30, 2019), according to the charity’s most recent federal tax filings.

Simon, a former Pfizer executive and longtime health care lobbyist who headed up the White House’s cancer task force in the Obama administration, saw his salary nearly double from the $224,539 he made in fiscal 2017, tax filings show.

Danielle Carnival, former chief of staff for Obama’s cancer initiative, the Cancer Moonshot Task Force, who took home $258,207 in 2018.

The rest of the charity’s income was spent on expenses like travel and conferences.

Gregory Simon claims that the purpose of the charity is not to give out grants, but to “accelerate” treatment for all, whatever that means.

Joe Biden’s son Beau Biden died of brain cancer in 2015.

The charity effectively stopped running once Joe Biden started his presidential campaign. According to Simon, that’s when the “charity” floundered.

“We tried to power through but it became increasingly difficult to get the traction we needed to complete our mission,” Simon said in July 2019.

The Biden Cancer Initiative remains unrated by the Charity Navigator, an organization that analyzes charities to determine which effectively use their donations for their stated cause.

- Navy Pushes Ahead With 500-Ship Plan To 'Counter China & Russia' In Wake Of Esper Firing

Navy Pushes Ahead With 500-Ship Plan To ‘Counter China & Russia’ In Wake Of Esper Firing

Tyler Durden

Sun, 11/15/2020 – 21:45In the Washington beltway world of defense spending and expansion, there’s always room to “spend more” no matter which administration or DoD leadership is at the helm. This trend is on display following last week’s Trump firing of Secretary of Defense Mark Esper, and his replacement with Christopher C. Miller.

An ambitious plan to greatly expand the number of ships in America’s naval arsenal put in place by Esper will not be impacted by the latest dramatic turnover in top Pentagon leadership, as Military.com reports:

Plans to build a 500-ship Navy are still intact as the Trump administration ushered in a host of new leaders at the Pentagon this week – though the top admiral overseeing shipbuilding says challenges remain.

Battle Force 2045, Defense Secretary Mark Esper’s ambitious plan to nearly double the size of the Navy fleet, is still underway. Esper was fired by President Donald Trump’s this week, and several new civilian leaders were installed to replace him and other top policy staffers.

USS Roosevelt via US Navy While China for example has many more total naval ships than the United States, the US Navy is still unrivaled in the total size and technological advantage of its force, given it has nearly a dozen large nuclear-powered fleet carriers and a handful of others that can be deemed carriers, compared to China’s two.

Esper’s plan calls for an active 500-ship fleet by 2045.

Vice Adm. William Galinis, the head of Naval Sea Systems Command, recently told reporters that nothing will change in terms of Esper’s plan for naval expansion:

“I don’t see any change to that right now,” Galinis said. “We’ll have to see how things play out over the next several weeks here, but I don’t see any change.”

“The underlying analytics and the requirements [of Battle Force 2045], I think, remain sound,” Galinis said at a Thursday defense conference. “How we meet those requirements, that’s a topic for further discussion.”

Esper’s ambitious plan also calls for the construction of three Virginia-class submarines per year, including 140 and 240 unmanned ships, which in prior statements he said was necessary to counter growing Chinese and Russian maritime expansion of their fleets.

Adm. Galinis said there may be “capacity challenges” in terms of such rapid ship-building:

“In terms of the industrial base’s ability to build those ships, I think there are some capacity challenges out there,” he said. “… Especially when we start talking about maybe going to three Virginias a year, and what it takes to transition from to two to three per year.

“There’s some capacity issues not just within the shipyard, but the supply base as well.”

In September the now former Defense Secretary Esper touted that the US maintains complete naval superiority over China and that the latter will never close the gap.

He said at the time time, “I want to make clear that China cannot match the United States when it comes to naval power.”

- "This Pandemic Was The Final Blow To Our Collective Notion Of Money As Something Real"

“This Pandemic Was The Final Blow To Our Collective Notion Of Money As Something Real”

Tyler Durden

Sun, 11/15/2020 – 21:20By Eric Peters, CIO of One River Asset Management

“The shift to digital forms of currencies is inevitable,” declared PayPal CEO, Dan Schulman, introducing crypto trading to all his US customers, ahead of his payments roll-out to 26mm global merchants.

“Bringing with it, clear advantages in terms of financial inclusion and access; efficiency, speed and resilience of the payments system,” he added, talking his book. “And providing the ability for governments to disburse funds to citizens quickly,” concluded PayPal’s CEO, saving the most important bit for the end – classic Steve Jobs style.

You see, there will be many legacies of this pandemic, which miraculously “ended” with Pfizer’s announcement. Daily life will return to something more normal, perhaps even euphoric, as has been the case throughout human history when our plagues subside.

But what will never return is the way that we once looked at money. This coronavirus was the final blow to our collective notion of money as something real. After agonizing for years about multi-hundred billion-dollar deficits, America’s Treasury more or less borrowed $3 trillion from our central bank. We gave that money to ourselves.

But the world didn’t end. The dollar didn’t collapse. Interest rates remained low. Inflation did too. Stock naturally surged. The rich got richer, the poor got poorer. From this blow-off top in inequality, we begin the next stage of a transition that started with the 2016 election and surely has a decade to run.

And while no one knows precisely what will happen, we can be quite sure that governments will disburse funds to citizens quickly. Digitally. And we can be certain that a dollar in a decade’s time will be worth a fraction of what it’s worth today.

Anchors

Britain was first to devalue in Sept 1931. Others followed. The 1929 market crash had worked through the system, grinding insidiously, turning what had been a roaring boom to bust. Back then, currencies were backed by metal. Governments understandably feared that without an anchor like gold, of which there was limited supply, the nation’s citizens would easily lose faith in the value of a piece of colorful paper. And it is likely that governments also had little faith in their own prudence when it came to deficit spending, were it unconstrained by a golden anchor.

“We have gold because we cannot trust governments,” said President Herbert Hoover in early 1933 with the price of gold at $20/ounce. In April of 1933 FDR abandoned the gold standard and outlawed the hoarding of gold coins, bullion, and certificates. The dollar fell over 10% relative to European currencies that had already devalued, as it readjusted to the surprise move by the US. In 1934, FDR reset the price of gold from $20.67/ounce to $35/ounce. Each devaluation helped the US expand credit, stimulate trade, and reflate the economy.

Gold prices were then steady for 38-years. But naturally, nothing is that stable. So imbalances quietly grew. In 1971, beset by deficits, inflation and a looming gold run, Nixon ended the convertibility of the dollar to gold at the $35/ounce rate.

This freed the price to trade at whatever sellers and buyers saw fit. By 1980 the gold that traded at $35/ounce 9yrs earlier hit a high of $875/ounce. That’s what the inflationary 1970s did to the value of the US dollar. And today, after decades of policy intended to sustain slow but steady inflation, gold trades at $1,889.

- China Retail Sales Disappoint, Despite Expected Golden-Week Boost

China Retail Sales Disappoint, Despite Expected Golden-Week Boost

Tyler Durden

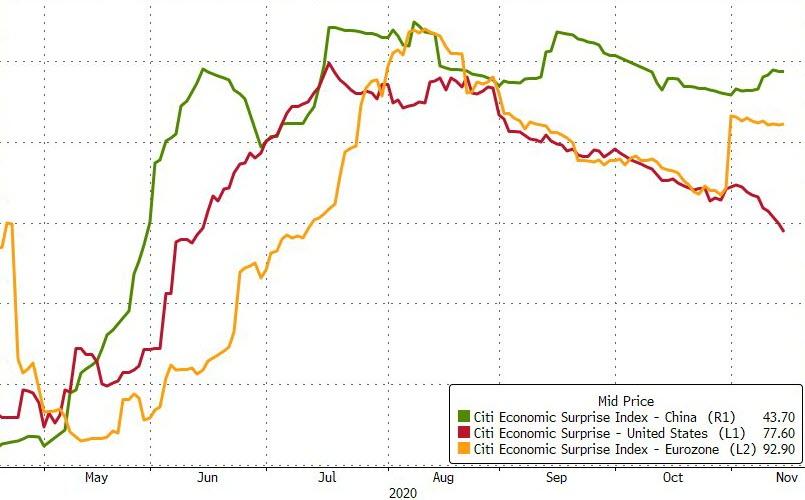

Sun, 11/15/2020 – 21:07Amid sudden domestic defaults, liquidity shortfalls, a soaring yuan, and overseas economics lockdowns, tonight’s smorgasbord of data is expected to show a continued recovery in China’s economy (after a disappointing Q3 GDP and PMI), as US data begins to falter.

Source: Bloomberg

The strongest yuan in well over two years is likely not helping the export situation…

Source: Bloomberg

But, despite the massive credit impulse, China’s engine of growth remains relatively lackluster as it appears whatever credit is being created is filling holes and being put to productive (multiplier-driving) use in the broader economy…

Source: Bloomberg

So, the question for tonight is, has the slowdown in the rest of the world started to impact China’s rebound or is a domestic revival fueling a ‘virus-free’ return to normal in the communist nation? Simply put, all eyes will be on retail sales…

Interestingly, right before the bulk of the data, China Home Prices printed a disappointing slowdown (though as can be clearly seen, prices haven’t actually fallen on MoM basis since early 2015)…

Source: Bloomberg

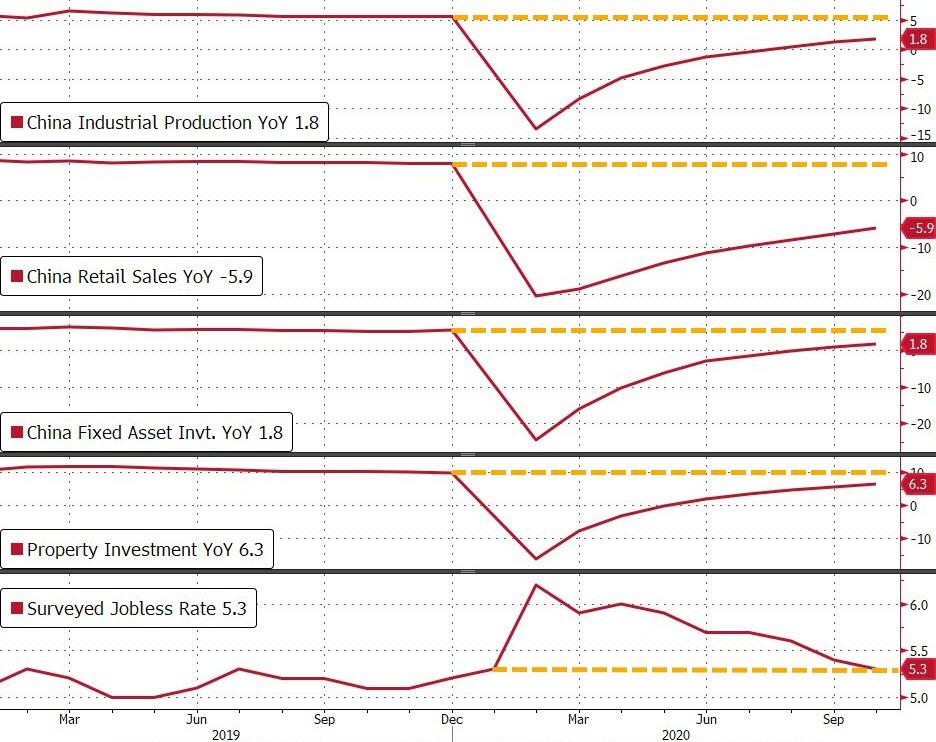

One thing to note is that the nationwide eight-day Golden Week holiday likely pushed October retail sales up by 5%, and on the other side of the coin, the longer-than-usual Golden Week holiday cut into working days (potentially impacting industrial production)

Here’s the rest of the data:

-

China Industrial Production YTD MEET +1.8% YoY vs +1.8% exp vs +1.2% prior

-

China Retail Sales YTD MEET -5.9% YoY vs -5.9% exp vs -7.2% prior

-

China Fixed Asset Investment YTD BEAT +1.8% YoY vs +1.6% exp vs +0.8% prior

-

China Property Investment YTD BEAT +6.0% YoY vs +6.0% exp vs +5.6% prior

-

China Surveyed Jobless Rate MEET 5.3% vs 5.3% exp vs 5.4% prior

Most notably the jobless rate is back at pre-COVID levels…

Source: Bloomberg

However, the biggest headline of the night is the disappointment in year-over-year retail sales, rising 4.3% YoY vs +5.0% expected (though accelerating over September’s +3.3%)…

Source: Bloomberg

Bloomberg reports the retail sales break down shows petroleum was down by 11% but the other categories were all positive. While restaurant and catering grew 0.8% there were big gains for food (8.8%), beverages (16.9%), clothing (12.2%) and cosmetics (18.3%) among others.

The supply side of the economy remains strong from the looks of things, but the consumer failed to live up to economists’ expectations.

Except, elsewhere in Asia tonight, Japan’s economy rebounded more strongly than expected from its record crash during the pandemic as businesses reopened, trade roared back and government stimulus helped fuel a jump in consumer spending. Gross domestic product grew an annualized 21.4% in the three months through September from the prior quarter, the Cabinet Office said Monday, reporting the fastest growth since 1968. Economists had forecast an 18.9% expansion.

Source: Bloomberg

Finally, we note that China’s economy is still expected to grow by 2% in 2020 and 8% in 2021 – a sharp contrast to other major economies across the region, where most are expected to contract sharply.

-

- Asia-Pacific Countries Sign World's Largest Free Trade Deal In "Coup For China"

Asia-Pacific Countries Sign World’s Largest Free Trade Deal In “Coup For China”

Tyler Durden

Sun, 11/15/2020 – 20:55Nothing less than a major milestone in global economic history and a huge victory for China over increasing US regional hegemony has been realized on Sunday with the signing of the biggest free trade deal ever among fifteen Asia Pacific Nations.

Called the Regional Comprehensive Economic Partnership, or RCEP, the agreement was signed virtually during the annual summit of the 10-nation Association of Southeast Asian Nations (ASEAN), and effectively establishes the world’s largest trading block that is expected to encompass almost one-third of all global economic activity, crucially without the United States.

Via Grain.org It’s being further seen as a massive blow to four years of both Trump’s America First policy and simultaneously the trade war and increasing attempts to convince other large regional powers like India to isolate China (though India is notably absent from the RCEP).

The trade pact involves ten ASEAN bloc member nations including Brunei, Cambodia, Indonesia, Laos, Malaysia, Myanmar, the Philippines, Singapore, Thailand and Vietnam – and additionally their trade partners Australia, China, Japan, New Zealand, and South Korea.

China’s Premier Li Keqiang was cited in state media as hailing a “victory against protectionism” and in international media reports it is being called “a coup for China” which will bolster Chinese claims that it remains a “champion of globalization and multilateral cooperation”.

“The signing of the RCEP is not only a landmark achievement of East Asian regional cooperation, but also a victory of multilateralism and free trade,” Li said, after it’s been in negotiations for eight years.

The RCEP was initiated by ASEAN, how could it be China-led? China pursues win-win and win-for-all, but Washington sees it as China wins twice and China wins all. So, China is awesome that it wins no matter what.😀 pic.twitter.com/g3ZjxanwET

— Hu Xijin 胡锡进 (@HuXijin_GT) November 15, 2020

https://platform.twitter.com/widgets.js

The AP summarized of the agreement:

The accord will take already low tariffs on trade between member countries still lower, over time, and is less comprehensive than an 11-nation trans-Pacific trade deal that President Donald Trump pulled out of shortly after taking office.

…It will take time to fully assess exact details of the agreement encompassing tariff schedules and rules for all 15 countries involved — the tariffs schedule just for Japan is 1,334 pages long.

It is not expected to go as far as the European Union in integrating member economies but does build on existing free trade arrangements.

India was the only country invited to the table but that didn’t sign the deal (and then there’s Taiwan, also not part of the deal).

Closing ceremony of ASEAN summit being held online in Hanoi on November 15, 2020. Getty Images Yet clearly this marks the final death knell for both Obama’s so-called ‘pivot to Asia’ and Trump’s anti-Chinese decoupling initiatives. In the days leading up to the expected signing on Sunday the major American networks were noticeably quiet about it.

As The Wall Street Journal now forewarns: “The deal signed Sunday increases pressure on Mr. Biden to deepen U.S. trade engagement in the Asia-Pacific region. He warned last year that if America doesn’t write the rules of the road, China will, and said he would try to renegotiate the TPP, but hasn’t taken a firm position either way.”

- Sen. Bernie Sanders Confirms He's Seeking Labor Secretary Position

Sen. Bernie Sanders Confirms He’s Seeking Labor Secretary Position

Tyler Durden

Sun, 11/15/2020 – 20:30Authored by Jack Phillips via The Epoch Times,

Sen. Bernie Sanders (I-Vt.) said he has spoken with Democratic nominee Joe Biden’s team about becoming the secretary of labor should Biden win the election.

“Have you had any conversations with anyone from the Biden transition team about a possible Cabinet post?” CNN host Jake Tapper asked the self-described socialist senator on Sunday.

Sanders responded in the affirmative and confirmed he spoke with Biden’s team, and said he “want[s] to do [his] best in whatever capacity, as a senator or in the administration, to protect the working families in this country.”

Numerous media outlets have declared the presidential winner as Biden. The Epoch Times will not call the race for either Biden or President Donald Trump until all results are certified and any legal challenges are resolved.

Sara Nelson, the head of the Association of Flight Attendants, told NBC News that Sanders reached out to her for support.

Several other progressive politicians have reportedly attempted to reach out to Biden in recent days. However, with Republicans likely to control the Senate following two runoff elections in Georgia in January, it’s entirely possible that their nominations would be blocked in the upper chamber if Biden is victorious.

Some business groups have expressed anxiety over the prospect of Sanders having a prominent role in the federal government.

“Naming such a polarizing choice would be a pretty big bait-and-switch for a president-elect who ran on bringing the country together to solve problems,” said Matt Haller, senior vice president of government relations and public affairs at the International Franchise Association, according to The Hill in a report last week.

“This election said many things, but it was not a mandate by voters to turn America into a country that rejects capitalism – just ask the House incumbents who were thrown out of office in purple districts for being unable to separate themselves from the lunatic fringe agenda,” he added.

Aric Newhouse, senior vice president of policy and government relations at the National Association of Manufacturers, added that bipartisanship is sorely needed, suggesting that he doesn’t favor a left-wing direction.

Biden’s team has not responded to a request for comment, and it also declined to comment to The Hill on the prospect of Sanders joining.

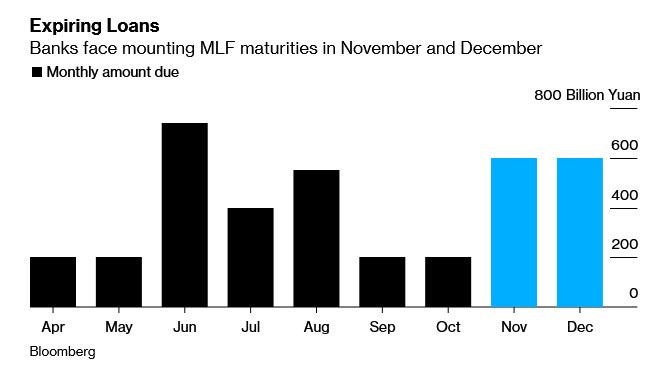

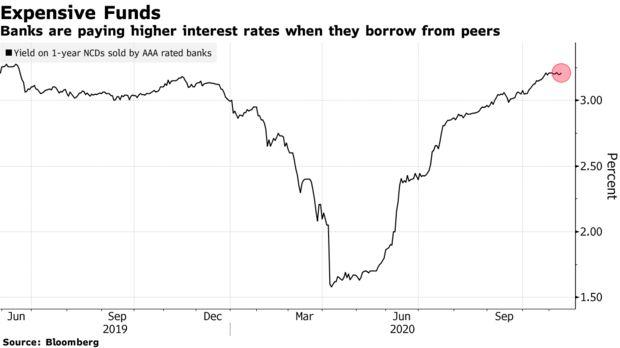

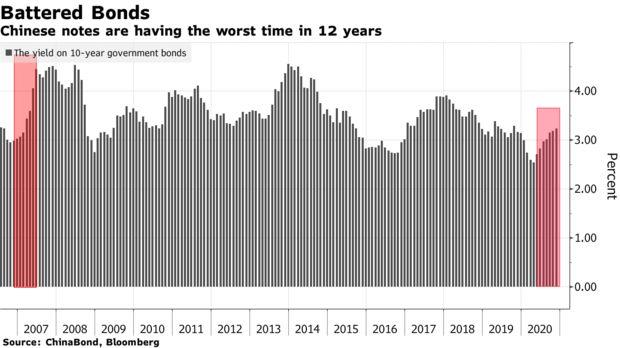

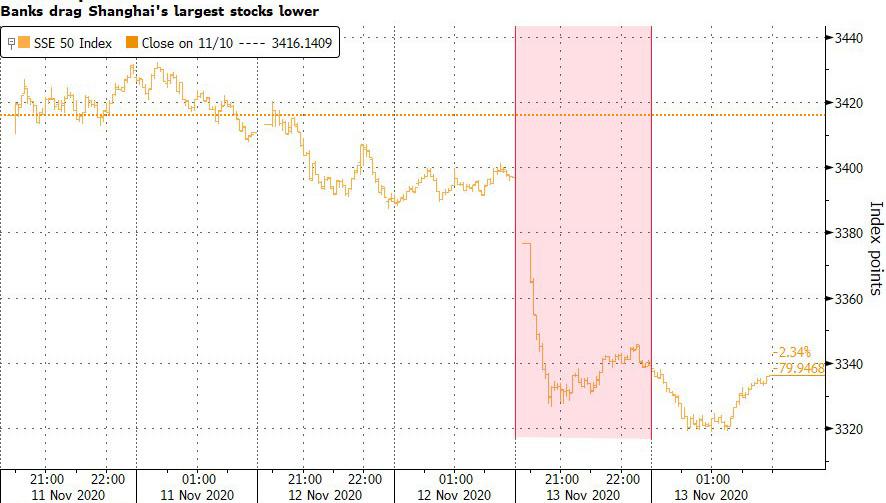

- Traders On Edge As China Faces $900 Billion Liquidity Shortage

Traders On Edge As China Faces $900 Billion Liquidity Shortage

Tyler Durden

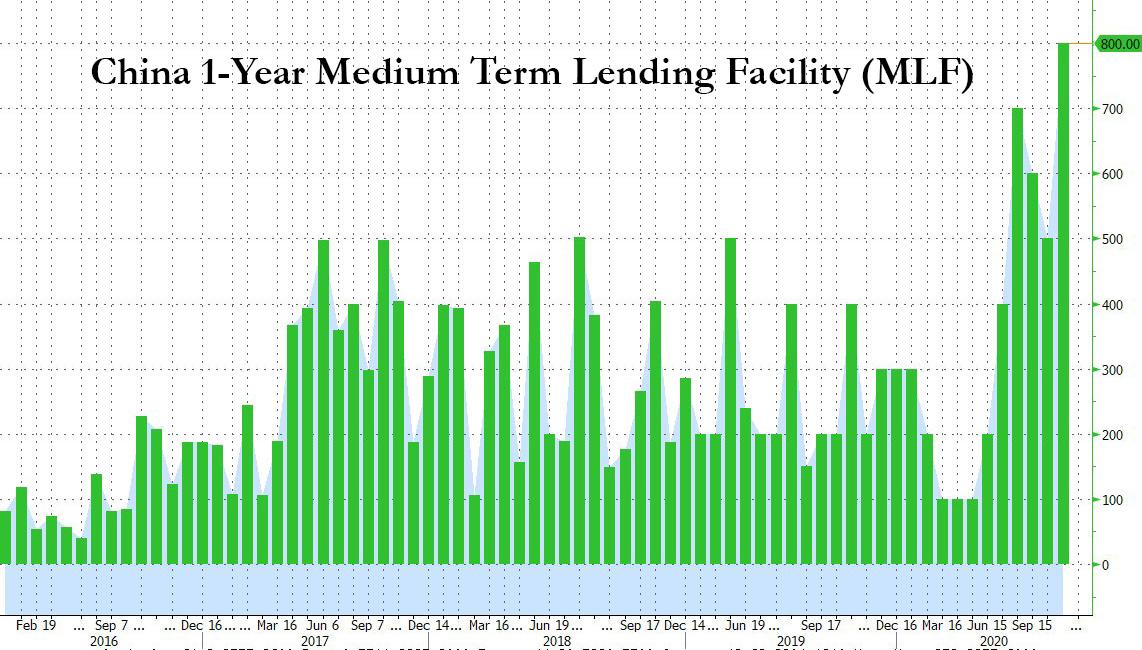

Sun, 11/15/2020 – 20:13Update: facing a potentially calamitous liquidity shortage, China buckled and despite hawkish commentary from its central bankers, moments ago the PBOC announced that it would offer a whopping 800 billion in MLF, which was not only vastly greater than the CNY 200BN whisper number, but was 200 billion more than the currently maturing MLF amount of 600 billion, indicating that what PBOC Deputy Governor Liu Guoqiang said recently when he warned that exiting easing measures was “a matter of time” and “necessary,” was just a jawboning placeholder, and with China finding itself in a funding scramble, the PBOC not only delivered but left quite a bit of liquidity on top.

* * *

In all the recent noise surrounding the presidential elections, the pandemic, the state of US fiscal stimulus, and a possible vaccine it is easy to forget that what really matters for the global economy is neither US fiscal or monetary stimulus, nor who the US president is, but rather what China does: after all, recall that it was China’s epic credit expansion in 2009 that successfully pulled the world out of the post-Lehman depression, with Chinese credit injections in the past decade putting the Fed and all other developed central banks to shame. Nowhere is this clearer than in a comparison of total assets in the US vs Chinese banking sector where some may be surprised to learn that China’s banking sector is more than twice as large as that of the US.

It’s also why we – and many others – have repeatedly said that what really matters for the world economy, and for global reflation is China’s credit impulse, which as we have shown recently has soared in recent months, and a delayed correlation with 10Y yields suggests that a major spike in real 10Y rates is coming.

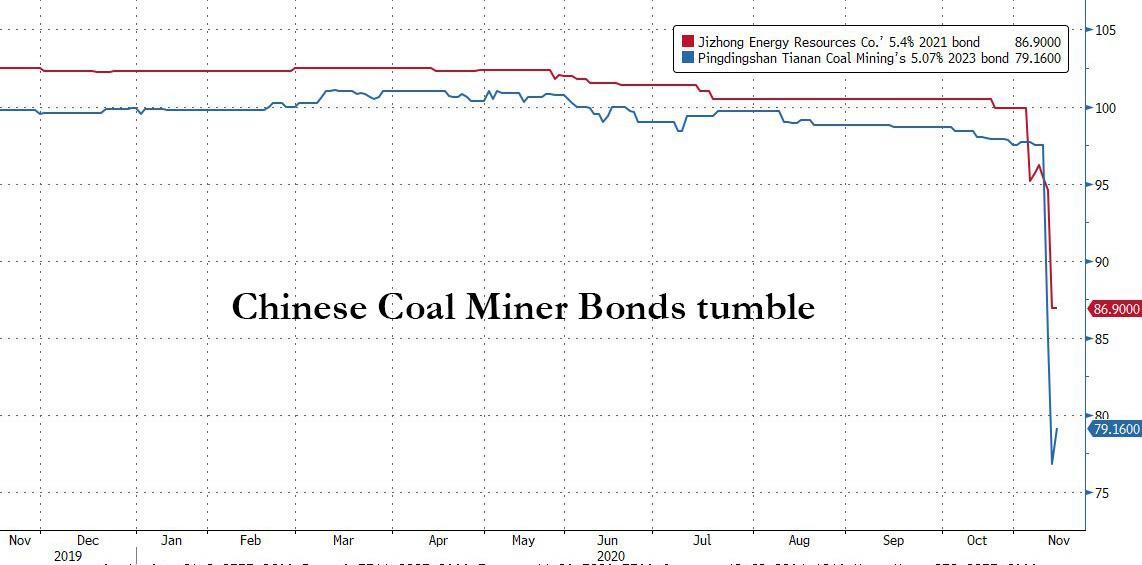

We bring all this up, because despite the recently concluded Communist Party Plenum according to which everything is great, lately China’s financial system is experiencing some major glitches starting with what we discussed earlier today, the unexpected default of the AAA-rated state-owned coal mining company, Yongcheng Coal and Electricity Holding Group, which came as a shock to most investors and sent state-backed local debt – previously seen as sacrosanct due to an implied state backstop – tumbling as markets repriced the long-running assumption that Beijing would never allow SOEs to fail.

There is another problem: as Bloomberg writes, increasingly weary trader eyes are now looking at China’s central bank for any signal of potential monetary easing, as a $900 billion funding shortage raises concerns over tighter liquidity.

The first clue should come in hours, if not minutes when early on Monday (local time) the People’s Bank of China is expected to at least offset most of the 600 billion yuan ($91 billion) of policy loans coming due this month. The funds, which were offered by the central bank a year ago via the medium-term lending facility, are just about 10% of the total amount local banks need to repay debt and buy government bonds by the end of 2020.

As China is among the first countries in the world to consider reversing emergency stimulus measures deployed to support markets in the wake of the coronavirus outbreak – now that its economy is reportedly humming – a withdrawal of liquidity by the state (which lately has been cracking down on excess leverage everywhere from Evergrande to the fintech industry) may stoke fears of tighter monetary policy as the economy recovers from the pandemic. Alternatively, a meaningful net injection would be viewed a sign that Beijing is committed to ensuring ample cash supply and is not willing to risk tipping over the boat at a time when Chinese investor nerves are already frayed in the aftermath of the shocking pulling of the 800x+ oversubscribed Ant Financial IPO (which as the WSJ reported last week, followed an order from Xi Jinping himself as China’s leader seeks to put upstart and outspoken local billionaires in their place).

However, how the PBOC treats the maturing 600bn yuan MLF (whether it rolls it in a similar size loan, or shtinks it) is just the start, because as Bloomberg explains demand for cash will surge in the coming weeks, as banks will need to repay more debt and buy newly issued government bonds, while facing yet another 600bn MLF maturity.

In total, a combined 1.2 trillion yuan in MLF funds is due in November and December, or roughly a third of this year’s total. On top of that, lenders are set to repay at least 3.7 trillion yuan of short-term interbank debt and use another 1 trillion yuan to buy sovereign bonds by end-2020.

Said otherwise, if Beijing wishes to, it could drain as much as $6 trillion, or roughly $900 billion, in liquidity from the Chinese financial system in the next 6 weeks.

While under normal conditions, traders would hardly be worried that Beijing would do anything but continue the liquidity status quo, recent comments from officials have sparked funding concerns.

Last week, PBOC Deputy Governor Liu Guoqiang said exiting easing measures was “a matter of time” and “necessary,” remarks that helped send China’s sovereign yield to a one-year high. The rhetoric came as recent data suggest the nation’s economic recovery has been on track. Furthermore, while total credit growth remained stable it took a modest seasonal dip in October.

“The PBOC’s comments struck a hawkish tone, suggesting money supply will be tightened,” said Australia & New Zealand Banking Group economist Xing Zhaopeng. This means that any net injection less than 200 billion yuan on Monday won’t be enough to soothe nerves on tight liquidity: “We see the 10-year government bond yield more likely to rise in the fourth quarter”, Xing added as traders brace for a continued tightening in China’s financial conditions.

While we will know shortly if the PBOC’s liquidity generosity persists, concerns about tighter liquidity have already driven banks to demand a higher yield when lending to each other. The interest rate on one-year negotiable certificates of deposits issued by AAA rated banks has climbed to the highest since June 2019.

The overnight repo rate also jumped to the most elevated since January on Thursday according to Bloomberg data, providing further evidence of the rising thirst for liquidity. On Friday, the PBOC responded by adding 160 billion yuan on a net basis into the financial system via seven-day repurchase agreements, the biggest injection since Sept. 22.

That’s hardly enough, however, with much more liquidity needed.

China’s massive commercial banks – the biggest buyer of Chinese government bonds – now have less idle cash to invest in the fixed-income market, and some of them even need to shed their holdings of the securities for funding, according to Bloomberg. Worries over cash supply have already led to a sell-off in sovereign bonds with short tenors, which are more sensitive to shifts in liquidity conditions.

That has helped narrow the gap between one- and 10-year yields to near the smallest since September 2019.

Naturally, the liquidity shortage has been bad news for bond bulls, and the yield on 10-year Chinese sovereign bonds has jumped about 8 basis points so far in November, in part tracking the concurrent rebound in “reflationary” sentiment in the US. That came after the notes just posted the longest stretch of monthly declines since 2007 in October, making them worst performers in Asia this year.

While US traders have not had to worry about Chinese financial conditions for a long time, having been distracted by everything from the election, to covid, to fiscal stimulus negoatiations, all those risks are well-known and priced in, the real risk is what China could do in the coming days and weeks if it decides to suddenly turn off the liquidity spigot. A worst case scenario could have dire consequences for global capital markets due to China’s position as the hub in the global liquification/reflationary apparatus.

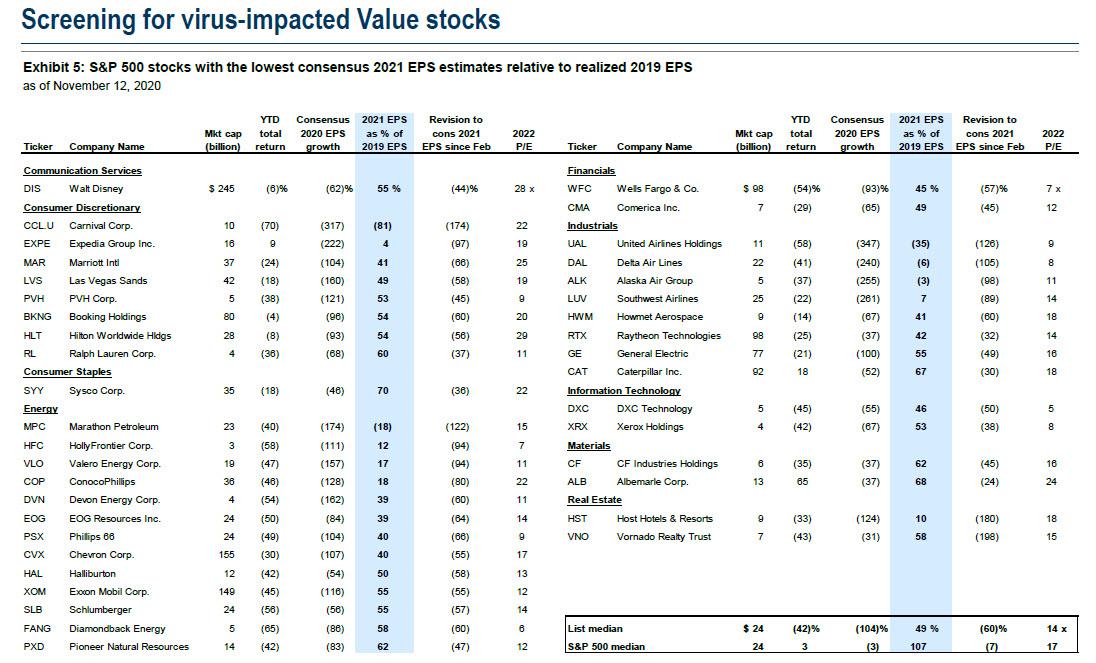

- Here Are The Companies That Will Benefit The Most From A Covid Vaccine

Here Are The Companies That Will Benefit The Most From A Covid Vaccine

Tyler Durden

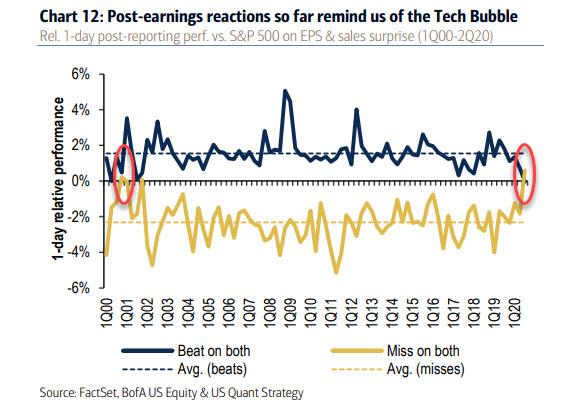

Sun, 11/15/2020 – 19:40In his latest Weekly Kickstart note published late on Friday, Goldman’s David Kostin correctly notes that with all eyes on two major macro catalysts in recent weeks –the US elections and the potential for imminent vaccine approval – investors had mostly overlooked the 3Q earnings season. According to Kostin, this “lack of focus” was reflected in the unusual price performance of stocks beating on EPS during the recently-concluded earnings season, namely that whereas in the past, stocks that surpass consensus expectations typically outperform the S&P 500 by 100bps the trading day after reporting, this quarter those firms outperformed by just 9bp, the smallest in our 15-year history outside of 2Q 2017.

Incidentally, a few weeks earlier Bank of America put its own spin on this phenomenon, writing that the lack of upside which is due to stocks being priced to perfection, “smacks of the Tech Bubble, which was the only earnings season in history when surprises saw perverse rather than intuitive reactions – beats were not rewarded and misses were not penalized.” The bank then ominously warned that “the market cracked after the 2Q earnings season when this happened.”

Whether the Q3 earnings reaction is indicative of a lack of investor focus, of euphoria having been pried-in, or is simply a rehash of the previous bubble top remains to be seen, but one notable point made by Kostin is that “margins, more than sales, were the primary source of upside surprises in 3Q” which suggests that once again companies were drastically cutting back on overhead – read laying off workers aggressively.

Some more points:

- At the start of earnings season, consensus expected S&P 500 sales to fall by 3%, and companies realized growth of -2%.

- Analysts also forecast S&P 500 net profit margins would decline by 220 bp to 8.7%, but margins actually fell by much less than expected; net margins contracted by just 83 bp to 10.1%.

- At the sector level, the divergence that occurred in 2Q continued into 3Q. Health Care and Info Tech delivered positiveEPS growth in the quarter (+7% and +5%), while Energy and Industrials saw EPS fall by 109% and 50%, respectively.

- Most notably, limited reserve builds moderated the decline in Financials EPS in 3Q (-7% y/y vs. -52% in 2Q).

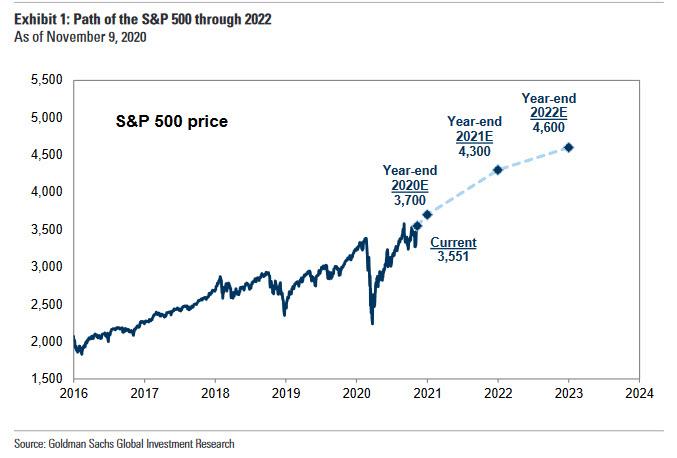

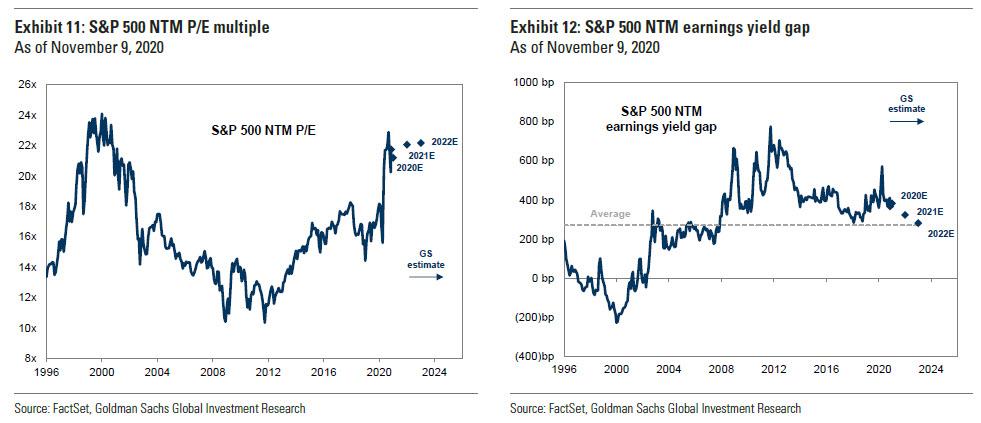

Kostin then shifts to recapping his “Roaring 20s thesis“, which as a reminder sees the S&P hitting 4,600 in 2022…

… by using a 22x P/E forward multiple…

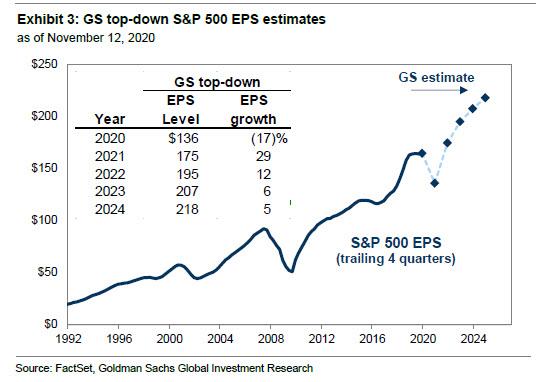

… by defending Goldman’s hyper-optimistic EPS outlook: according to the chief strategist, “strong 3Q results and our economists’ optimistic growth outlook support our above-consensus EPS estimates for 2021.” To wit, following the better-than-feared 17% decline in 2020, Kostin now forecasts S&P 500 EPS will grow by 29% in 2021 to $175, which would be 6% above the pre-pandemic level in 2019 ($165). It’s all uphill from there as the following chart forecasting even more perfection until 2024 shows:

Here’s how Kostin “gets” his ultra-cheerful numbers: “economic growth is the primary driver of earnings growth. Our US economists expect annual average real US GDP growth of 5.3% in 2020, 150 bp above consensus (+3.8%).” In addition to what even Kostin admits is an “optimistic outlook” based on above-consensus earnings estimates, the Goldman strategist also expects S&P 500 EPS to benefit from i) a weakening USD, representing a tailwind to sales, and ii) labor market slack, adding to the tailwind for profit margins.

Importantly, the forecast assumes at least one vaccine is approved by January and widely distributed across the US in 1H 2021, to wit: “We expect additional positive EPS revisions toward our forecasts in coming months as vaccines are approved and distributed and accelerate the economic and earnings rebound.”

In addition to the top-line rebound, the cost cutting evident in 3Q earnings reports suggest higher revenues should lead to a sharp margin rebound next year. Translation: don’t expect a hiring spree any time soon now that company have learned they can do more with less.

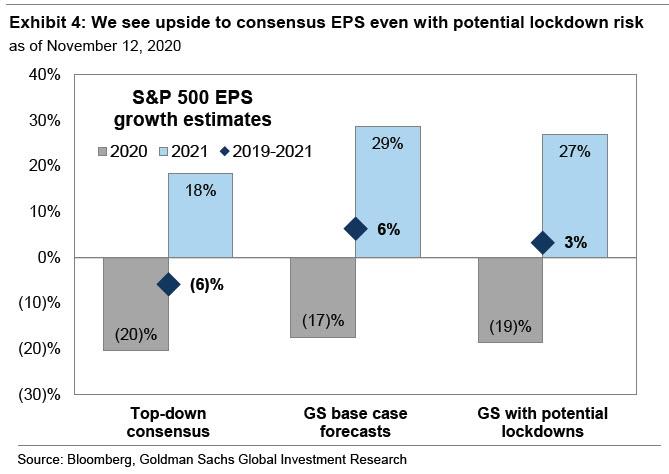

Looking even further out, Goldman forecasts S&P 500 EPS growth of 12% in 2022, 6% in 2023, and 5% in 2024, despite conceding that “in the near term, surging COVID cases and the possibility of renewed US lockdowns represent a source of downside risk to S&P 500 EPS.” All of this, however, is expected to somehow renormalize by early 2021.

One final key assumption comes in the form of Goldman’s expectation that a $1 trillion fiscal package will eventually be passed “but not until early 2021, therefore posing a potential downside risk to 4Q 2020 EPS, and potentially also longer-term risks if fiscal aid is too small or too late to avoid major economic scarring.”

Still, that risk too, is too small for Goldman to incorporate into its base case which, as shown above, see the S&P rising by over 1,000 points over the next two years.

In other words, in its base case projection, the bank sees nothing going wrong with the economy or markets until the next presidential election.

* * *

While we reserve judgment on whether Goldman is right or not (or right but for the wrong reasons, since none of this will matter once the Fed launches another major QE expansion in early 2021 as we previewed overnight) we will highlight on factual observation, namely which companies have been hit the hardest by covid, and thus stand to benefit the most from a vaccine.

Assuming a vaccine is approved – and one most likely will be approved in the coming weeks – Goldman highlights a list of stocks where the largest gap exists between the current consensus expectations for 2021 EPS and pre-pandemic EPS in 2019. Goldman expects vaccine approval and distribution to serve as a catalyst to drive positive EPS revisions in many of the hardest-hit industries and most virus-exposed companies. As context, the median company in the S&P 500 is anticipated to generate 2021 EPS that is 7% above its level of last year. In contrast, the 39 stocks shown below are anticipated to generate EPS next year that is still less than half the level of EPS realized in 2019.

Ultimately, Goldman’s recommendation is to go long some or all of these deep Value stocks as part of a barbell with long-term positions in secular growth stocks. Or in other words, the bank is long both the FAAMGs – which benefit from a continuation of the status quo – and the “deep value” names that will soar should the covid situation normalize or if sustainable reflation finally emerges.

- Watch "Historic" Event: SpaceX Rocket To Launch Astronauts To Space Station

Watch “Historic” Event: SpaceX Rocket To Launch Astronauts To Space Station

Tyler Durden

Sun, 11/15/2020 – 19:15If schedules and the weather hold up, the launch of NASA’s SpaceX Crew-1 Mission on the “Resilience” Crew Dragon spacecraft, powered by a Falcon 9 rocket, will begin at 7:27 p.m. ET on Sunday from pad 39A at NASA’s Kennedy Space Center in Florida.

🚀 We’re sending four astronauts to the @Space_Station on a U.S. rocket from U.S. soil at 7:27pm ET on Sunday, Nov. 15.

Here’s how you can watch our #LaunchAmerica coverage: https://t.co/PTHOoEbLO0 pic.twitter.com/V2MNT2aWCQ

— NASA (@NASA) November 14, 2020

https://platform.twitter.com/widgets.js

Sunday’s launch will make history as the first crewed commercial space mission to the space station. This will also be the second time in a decade that NASA has launched astronauts from the US.

In May, astronauts Doug Hurley and Bob Behnken rode the Crew Dragon spacecraft, powered by Falcon 9 rocket, to the space station, stayed for two months and returned to Earth in August.

On Friday, at a press conference, NASA Administrator Jim Bridenstine said, “this is another historic moment — it seems like every time I come to Kennedy [Space Center] we’re making history, and this is no different.”

All systems are go for tonight’s launch at 7:27 p.m. EST of Crew Dragon’s first operational mission with four astronauts on board. Teams are keeping an eye on weather conditions for liftoff, which are currently 50% favorable → https://t.co/bJFjLCzWdK pic.twitter.com/GTpvVAiLkK

— SpaceX (@SpaceX) November 15, 2020

https://platform.twitter.com/widgets.js

Bridenstine continued: “The history being made this time is we’re launching what we call an operational flight to the International Space Station.”

“The whole goal here is to commercialize our activities in low-Earth orbit,” he added. “NASA wants to be one customer of many customers in a very robust commercial marketplace for human spaceflight in low-Earth orbit.”

NASA’s website outlines today’s scheduled events:

- 3:15 p.m. – Coverage of the Launch of NASA’s SpaceX Crew-1 Mission on the “Resilience” Crew Dragon to the International Space Station (Mike Hopkins, Victor Glover, Shannon Walker, Soichi Noguchi;

- Launch scheduled at 7:27 p.m. EST; coverage will be continuous through docking and hatch opening on Sunday, Nov. 15) – Kennedy Space Center/ Hawthorne, Calif./Johnson Space Center

- 9:30 p.m. – NASA/ SpaceX Crew-1 Postlaunch News Conference (time is subject to change)- Kennedy Space Center

NASA Live: Launch Event

It remains to be seen if SpaceX CEO Elon Musk attends the launch event as he revealed Saturday evening he “likely” has a “moderate case of COIVID-19.

- A Euphoric Morgan Stanley Lists "Three Features That Will Distinguish The Global Economy In 2021"

A Euphoric Morgan Stanley Lists “Three Features That Will Distinguish The Global Economy In 2021”

Tyler Durden

Sun, 11/15/2020 – 18:50By Chetan Ahya, Morgan Stanley chief economist and global head of economics

Twice a year, the Morgan Stanley macro research team huddles in a time-honoured ritual – outlook season. We come together to debate and reassess our forecasts and narratives, challenging each other while collaborating to provide clients with a consistent and coherent view of the world.

In a few hours’ time, you will be receiving our 2021 outlooks in your inboxes. As a preview, here’s a summary of our views.

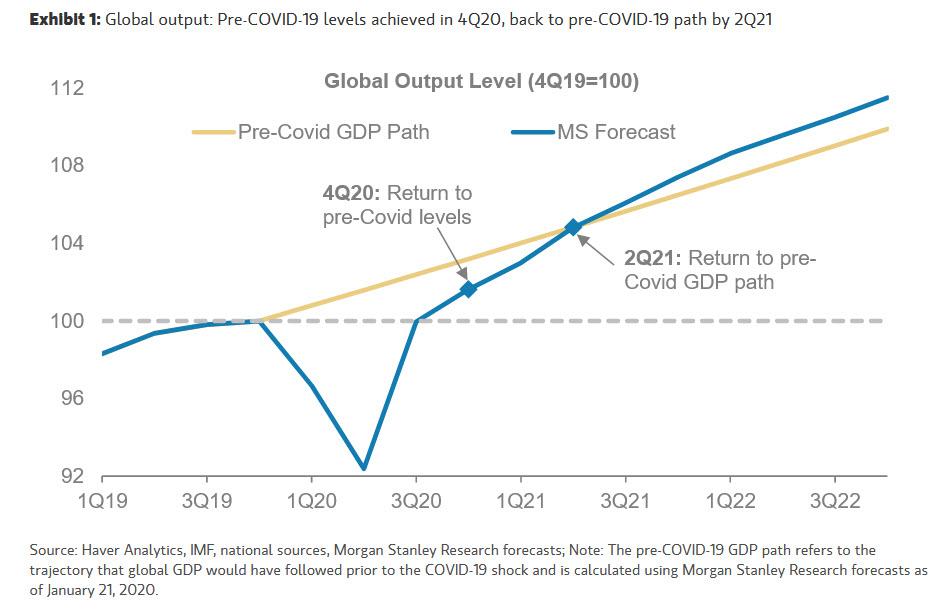

We remain constructive on the prospects for macro and markets in 2021. On the macro side, we think that the global economy will enter the next phase of the V-shaped recovery. In the first stage, the global economy has reached pre-COVID-19 output levels, a milestone we expect to pass this quarter. By 2Q21, we envision the economy getting back on its pre-COVID-19 path (i.e., where GDP would have been absent the COVID-19 shock).

Three features will distinguish the global economy in 2021:

- A synchronous global recovery: At 6.4%Y, our 2021 global growth forecast remains above consensus (5.3%Y), a stance bolstered by the news on vaccines and antibody treatments. We are more bullish than consensus because we believe that the COVID-19 shock has not dampened private sector risk appetite significantly, while policy stimulus has proved to be more than a backstop. We think that a global synchronous recovery, last seen in 2017, will unfold in 2021. While rising COVID-19 cases may lead to tighter restrictions and weigh on DM activity in the near term, EM growth will continue to accelerate. Emerging from the winter, the easing of restrictions will lift growth in DMs, which will join the rest of the world from March/April 2021. While the consumer has been driving the recovery so far, we expect the capex cycle to kick in from 2Q21.

- EMs boarding the reflation train: The past eight years have been tough for EMs, as a series of challenges have brought about a prolonged downturn. While it is tempting to blame structural issues for weak EM growth, we think that cyclical challenges and exogenous shocks (e.g., China and commodity price slowdowns, trade tensions and COVID-19) played a bigger role in keeping EM growth well below potential. However, we see a turn in 2021. The COVID-19 situation is now improving in a broad range of EMs and their recoveries are gaining momentum. In 2021, a widening US current account deficit, low US real rates, a weaker dollar, China’s reflationary impulse and EMs ex China’s own accommodative domestic macro policies will lead to a sharp rebound in growth. As this cyclical recovery takes hold, it can help create a virtuous cycle where stronger nominal GDP growth alleviates some of the pressure from structural issues like the need to consolidate public finances.

- Inflation regime change in the US: We see an altogether different inflation dynamic taking hold, especially in the US. While we argued for the return of inflation in this cycle earlier this year, 2021 will lay down the marker for this thesis. The US economy will reach both pre-COVID-19 levels and its pre-COVID-19 path over the course of 2021. Even so, both monetary and fiscal policy will remain much more accommodative relative to 4Q19. Our chief US economist Ellen Zentner expects underlying core PCE inflation to rise to 2% in 2H21 and move sustainably higher from 1H22. In contrast, the consensus doesn’t expect inflation to reach 2% until 2022.

A constructive macro view provides a supportive backdrop for risk assets: Our chief cross-asset strategist Andrew Sheets believes that while abnormality defined 2020, 2021 will be characterised by a return to more normal conditions (economic growth recovering, control of the virus improving and uncertainty declining). Markets will also follow much of the ‘normal’ post-recession playbook. Our strategy team recommends investors overweight equities and credit against government bonds and cash and sell USD. Within equities, they would overweight cyclicals and underweight defensives across regions, and expect US small-caps to outperform large-caps.

The risks to our views are twofold. In the near term, an even sharper rise in hospitalisations in the US or Europe could prompt policy-makers to adopt stricter lockdown measures than our base case, pushing near-term growth lower and also delaying the return to the pre-COVID-19 path. Looking a bit further out, US inflation could surprise to the upside from 2H21, particularly if we get a large fiscal package. This could challenge the market’s view on inflation and create a disruptive shift in expectations for Fed policy.

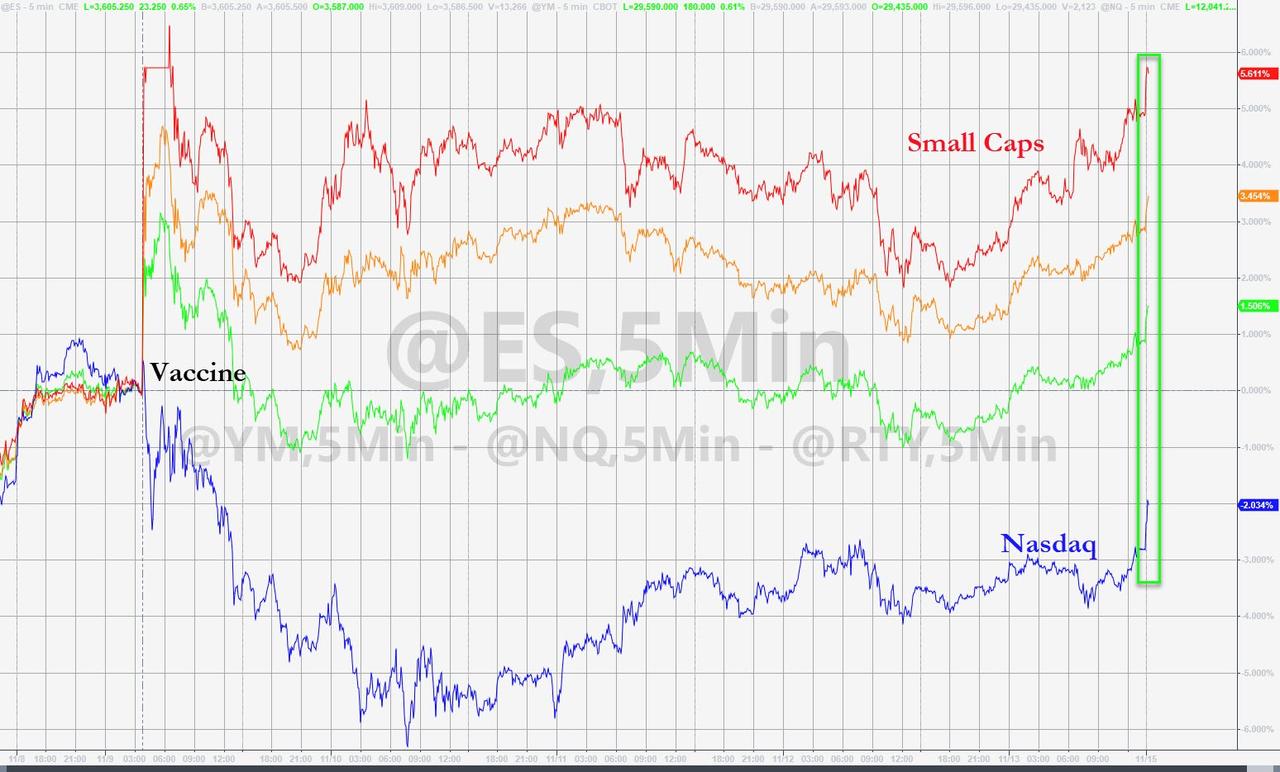

- S&P Futures Surge Above 3,600, Nasdaq Jumps 1%

S&P Futures Surge Above 3,600, Nasdaq Jumps 1%

Tyler Durden

Sun, 11/15/2020 – 18:46US equity futures surged out of the gate following the 6pm ET reopen. There was some debate as to the catalyst: according to some the Moderna covid vaccine may hit as early as tomorrow, and a favorable outcome would have a similar result to last Monday’s Pfizer surprise which sent the S&P as high as 3,668 before fading much of the losses.

As JPMorgan said over the weekend when discussing the likelihood of a continuation of the “value” stock rotation, “this makes the forthcoming vaccine announcement by Moderna particularly important as a comparable vaccine effectiveness to that of the Pfizer earlier this week “would help to sustain this week’s value rotation trade. At the same time, an announcement of vaccine effectiveness by Moderna that would be seen as significantly weaker could prompt some further reversal of the value rotation trade.”

Another explanation for the spike in early risk sentiment floated by Bloomberg is that contrary to expectations, two of Joe Biden’s coronavirus advisers said they oppose a nationwide U.S. lockdown as too blunt.

“There is certainly elevated chatter that potential shutdowns in the U.S. will weigh more in the near-term and maybe so, but investor sentiment is the most elevated since 2017,” Pepperstone head of research Chris Weston said.

Meanwhile, in an indication that the rally is not merely on the back of value stocks, the Nasdaq jumped even higher, and rose as much as 1% in early trading, which in turn would be a bet on continued deflation, and may be a result of growing trader convictions that in the absence of a sizable fiscal stimulus ($1 trillion or more), the Fed will likely step in with more QE, especially since the Treasury is facing net issuance of over $2.4 trillion in 2021 with less than $1 trillion currently monetized by the Fed under the current $80BN Treasury/month schedule.

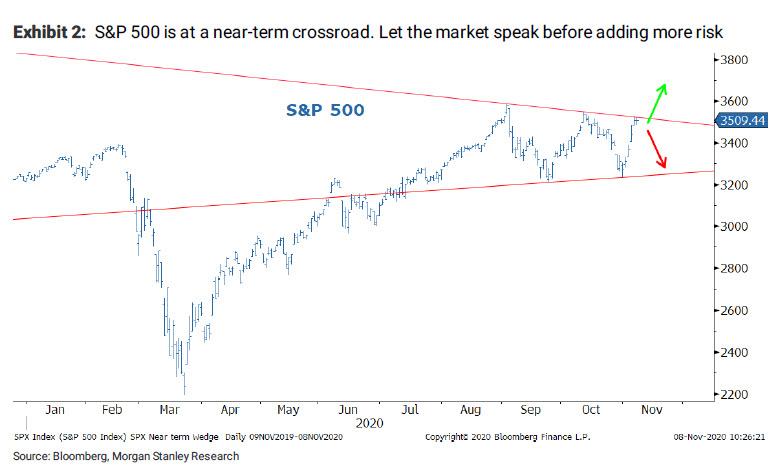

Whatever the reason, on Friday both the S&P 500 and small caps (Russell 2000), rallied to new all time highs, and if the early euphoria is any indication…

… tomorrow we should see new records across the board, especially with the S&P now having broken out to the upside of the recent wedge, a key technical according to Morgan Stanley’s Michael Wilson.

- Washington, Michigan Impose Tough New COVID-19 Restrictions; US Tops 11 Million Cases: Live Updates

Washington, Michigan Impose Tough New COVID-19 Restrictions; US Tops 11 Million Cases: Live Updates

Tyler Durden

Sun, 11/15/2020 – 18:44Summary:

- US tops 11 million cases

- Wash. Gov Jay Inslee announces restrictions to help slow the spread of COVID

- Mich. imposes tough new restrictions

- NY cases top 3,600, highest daily print since the spring

- NJ sees 2nd straight COVID record

- NYC schools to stay open

- US suffers 10th day of 100k+ new cases

- 38 states report 1k+ new cases

- Austria orders mandatory COVID tests

- Germans will live with “considerable restrictions” for months

- Tokyo reports another 350+ new cases as Japan’s outbreak worsens

* * *

Update (1830ET): It’s been an eventful afternoon for coronavirus news. As th US surpassed 11 million confirmed COVID-19 cases, Washington Gov. Jay Inslee announced strict new social distancing restrictions that will shut down bars, restaurants, gyms and other non-essential businesses for at least 3 weeks.

Meanwhile, Retail and grocery stores must limit occupancy to 25 percent, and malls are required to keep food court seating closed. Personal services, including barbershops and salons, will also be limited to 25% capacity.

“Today, Sunday, November 15, 2020, is the most dangerous public health day in the last 100 years of our state’s history,” Inslee said during a news conference. “A pandemic is raging in our state. Left unchecked, it will assuredly result in grossly overburdened hospitals and morgues; and keep people from obtaining routine by necessary medical treatment for non-COVID conditions.”

Other measures, like limiting outdoor dining to parties of 5 or under, along with requiring people to work from home if possible, were added to the proposal.

In Michigan, meanwhile, Gov. Gretchen Whitmer warned during a press briefing that her state could see as many as 1,000 fatalities a week in the coming months if something isn’t done. Starting Monday, she closed schools, colleges, sports games and other non-essential functions for three weeks.

Finally, the US topped 11 million cases on Sunday, one week after topping the 10 million mark.

* * *

Update (1415ET): New York Gov Andrew Cuomo just confirmed another 3,649 new cases, while total hospitalizations are just below 1,850.

The 3,650 or so new cases is the highest daily number since the spring.

Today’s update on the numbers:

Of the 133,202 tests reported yesterday, 3,649 were positive (2.74% of total).

Total hospitalizations are at 1,845.

Sadly, there were 30 COVID fatalities yesterday. pic.twitter.com/8ttDSwLGzW

— Andrew Cuomo (@NYGovCuomo) November 15, 2020

https://platform.twitter.com/widgets.js

The positivity rate in the state’s hardest-hit areas has notably fallen.

The test positivity rate in the focus areas under NY’s Micro-Cluster strategy is 4.05%.

The statewide positivity rate excluding these focus areas is 2.45%.

We continue to take strong action to respond to outbreaks and to stop the spread.

Mask Up.

— Andrew Cuomo (@NYGovCuomo) November 15, 2020

https://platform.twitter.com/widgets.js