- The Geopolitics Of Biological Weapons, Part 3: Population Control & The Doomsday Vault

The Geopolitics Of Biological Weapons, Part 3: Population Control & The Doomsday Vault

Authored by Larry Romanoff via GlobalResearch.ca,

GM seeds and GM food carry great risks for all nations, so much so that for many reasons it is probably imperative these foods be banned outright. This subject is too large to be discussed here, but one aspect requires brief notice. If we were to ask about the origin of GM seeds, how the idea was conceived and developed, who did the research and who provided the funding, how would we reply? We might reasonably suggest that perhaps the concept originated in the Biology or Agricultural Department of some university, or that a government lab doing research on food supplies might have conceived and pursued the idea. Or, we might suggest a private company in the agricultural field was looking for more productive varieties of grains and stumbled on this process.

We might suggest all those answers, but in each case we would be wrong. GM seed was conceived, promoted, researched and funded by the US Department of Defense – the American War Department. GM seed was never meant as a way to feed the hungry, but was instead conceived and developed as a weapon or, more precisely, as a weapons-delivery system. Genetically-Modified seed was never intended to support human life, but to eliminate it.

GM seed is neither more productive nor healthier than traditional heritage crops, and is far more expensive and destructive, but it presents almost irresistible military advantages against any nation that becomes dependent on this source of food grains. One is that the US can use it as a political weapon, refusing to supply seed to a disfavored nation, perhaps causing widespread famine and dislocation. The other is more sinister, in that many groups have experimented with gene-splicing technology, inserting unrelated DNA into various seeds.

In one case in Canada, a government department discovered an “anti-freeze” gene contained in the blood of fish living in Arctic waters, permitting them to survive in waters of sub-zero temperature. The scientists spliced this gene into Canadian wheat crops, permitting the wheat to withstand freezing temperatures without damage. Monsanto also forced these genes into tomatoes, resulting in the first GMO tomato. An American research lab spliced the genes from fireflies into tobacco plants, producing a tobacco field that glowed in the dark.

These examples may be harmless, but others are much less so. The US Defense Department has invested huge sums in research directed to splicing lethal genes into these GM crop seeds, including smallpox, bird and swine flu viruses, coronaviruses, the plague, AIDS, and more. As a military weapon, such science is priceless. Why begin a shooting war when Monsanto or Cargill can sell rice, corn and soybeans that contain smallpox, H5N1, or a coronavirus? When the seed is harvested and passes into the nation’s food supply it could, within weeks, exterminate 50% or more of the population without firing a single shot.

And this was precisely the reason GM seed was conceived and developed by the Americans. It is a weapon of war, designed and meant to deliver to a nation’s entire population a lethal virus or other disease, to literally exterminate an enemy with no risk to the aggressor. Many scientists and US military documents have demonstrated that seeds are far cheaper and much more effective than bombs in the search for military domination. One such military document I’ve discussed elsewhere stated the cost per death of an enemy population by nuclear, conventional and biological weapons, the latter being orders of magnitude less than the former.

In 2001 scientists at the Epicyte bio-lab in San Diego created a GM contraceptive corn, having discovered a rare class of human antibodies that attack sperm. Their researchers isolated the genes that regulate the manufacture of these antibodies and inserted them into corn plants, creating horticultural factories that make contraceptives. Shortly after the 2001 Epicyte press release, all discussion of the breakthrough vanished. The company was taken over by Biolex and nothing more was heard in any media about the development of spermicidal corn. Epicyte, DuPont and Syngenta (sponsors of the Svalbard Seed Vault) had a joint venture to share and use this technology. Silvia Ribeiro, of the NGO ETC Group, warned in a column in the Mexican daily La Jornada, that “The potential of spermicidal corn as a biological weapon is very high”, and reminisced about the use of forced sterilizations against indigenous peoples.

The Doomsday Seed Vault at Svalbard

A new and serious cause for concern is the recently-announced seed vault built on a piece of barren rock named Svalbard, which is owned by Norway, is very remote near the North Pole, and virtually inaccessible. According to press releases, this seed vault has dual blast-proof doors with motion sensors, two airlocks, and walls of steel-reinforced concrete one meter thick. There are no full-time staff, but the vault’s relative inaccessibility will facilitate monitoring any human activity. The stated purpose is to store the entire world’s heritage seeds so that crop diversity can be saved for the future, but that crop diversity is already “saved”, stored in vaults all around the world. What do these people foresee, that such a remote and secure facility should be developed?

The promoters and financiers of this venture are the same people who control the world’s GM seeds and who have been among the most outspoken proponents of drastically reducing the world’s population: the Rockefeller and Gates Foundations, Syngenta, DuPont, Monsanto and CGIAR. These are the same people who are actively destroying crop diversity all over the planet. Why would they suddenly get religion and decide to save in Norway the same seeds they are destroying everywhere else?

Some time ago, William Engdahl wrote an excellently researched article on this subject of the seed vault and arrived at the same conclusion, that the vault was created as a storehouse for lethal biological pathogens, the DNA of which can be combined with GM seed and unleashed anywhere with the help of these same seed companies. No other use would explain the list of participants or the need for the remote location and virtually nuclear-proof security. Engdahl asked, “Is it a coincidence that these same organizations, from Norway to the Rockefeller Foundation to the World Bank are also involved in the Svalbard seed bank project?”

Tyler Durden

Mon, 02/17/2020 – 00:00 - "This Is Just Chauvinism": Oklahoma Woman Upset After Being Thrown Out Of All-Male Barbershop

“This Is Just Chauvinism”: Oklahoma Woman Upset After Being Thrown Out Of All-Male Barbershop

Today in “private business owners are allowed to do whatever they want at their own business and tough sh*t if you don’t like it” news…

An Oklahoma woman took her story to the media when she was asked to leave an all-male barbershop in Ponca City, Oklahoma last week. The barbershop, called Kings Kuts, says it has a “strict no girlfriends or wives policy”, according to ABC.

Maliki Skowronski and her husband came into the shop to get him a haircut and beard trim when the owner informed her that she had to leave.

“The man kind of ignores my husband, directly approaches me and says, ‘I’m sorry, but we have a strict no women policy. You can’t be here,'” she said. She was kicked out before her husband had a chance to sit in the chair, she said.

Barbershop owner Daxton Nichols admitted that some people have trouble understanding his rules, but compares it to many women-only salons.

Nichols said:

“In New York City, there’s over 17 women’s only clubs where women can go and do the salon thing. They can go get their nails done, hair done, talk business amongst each other, and do that whole women’s power hear me roar stuff.”

Nichols says he considers his barbershop a “private club”. When a reporter asked him if men paid a membership fee to get their haircut there, Nichols responded: “Yeah, when they pay a $20 fee.”

Nichols says people get offended at his rule just “because they can”. The barber who asked Skowronski to leave, Scott Seagraves, said he threw her out to “preserve the shop’s ‘man cave’ environment”.

He continued:

“We want guys to be able to come in here and be guys and not have to worry what they say or what they talk about because there’s a lady present.”

Skowronski called it chauvinism: “It’s not cute, no matter how you describe it. It’s not cute, you can’t treat people that way.”

Tyler Durden

Sun, 02/16/2020 – 23:30 - Mapping Out The Banking Elite's Goal For A Cashless Monetary System, Part 1

Mapping Out The Banking Elite’s Goal For A Cashless Monetary System, Part 1

Back in 2014 the Bank of England became the first central bank to publish research on digital currencies through their quarterly bulletin (Innovations in payment technologies and the emergence of digital currencies). A leading focus was on the use of distributed ledger technology, with the research declaring that ‘the key innovation of digital currencies is the ‘distributed ledger’ which allows a payment system to operate in an entirely decentralised

way, without intermediaries such as banks‘.One of the main draws of this technology is the belief that cryptocurrency and stablecoins offer a genuine route out of the traditional centralised model of banking that epitomises fiat currency. But is bypassing central banks and being able to make and receive payments independent of these institutions really what the rise in digital currencies is all about?

Six years on from the BOE’s research, the digital currency agenda has advanced significantly in the face of increased geopolitical instability. An area of interest that has garnered scant attention is the ‘utility settlement coin‘ (USC) project that several global banks have been heavily invested in. It is a project that has now evolved through the inception of Fnality International, a consortium of shareholders that includes UBS, Barclays and Lloyds Banking Group.

Here is a breakdown of some of the key events which have taken place in regards to USC since the BOE’s research was published:

2015

In September of 2015 a partnership consisting of Swiss bank UBS and UK based blockchain firm Clearmatics was announced that officially launched the concept of a Utility Settlement Coin. As detailed by Bitcoin Magazine, USC would be utilised for ‘post-trade settlements between financial institutions on private financial platforms built on blockchain technology.’

With blockchain underpinning the foundations of USC, payments would be settled in a matter of seconds rather than days. It would operate using a ‘permissioned‘ blockchain network, meaning access to the network must be granted by participants. This is in contrast to the likes of Bitcoin which uses a permissionless network that anyone can access. As discussed in previous articles, central banks openly advocate permissioned blockchain for the future development of digital currencies.

2016

A year on from the original announcement on USC, Santander, BNY Mellon and Deutsche Bank all issued press releases to confirm that they had gone into partnership with UBS and Clearmatics to develop the Utility Settlement Coin.

Reacting to the news, Julio Faura, head of Blockchain R&D at Santander, said:

Recent discussion of digital currencies by central banks and regulators has confirmed their potential significance. The USC is an essential step towards a future financial market on distributed ledger technologies.

Expanding on the definition of USC, Deutsche Bank’s press release stated:

USC is an asset-backed digital cash instrument implemented on distributed ledger technology for use within global institutional financial markets. USC is a series of cash assets, with a version for each of the major currencies (USD, EUR, GBP, CHF, etc.) and USC is convertible at parity with a bank deposit in the corresponding currency. USC is fully backed by cash assets held at a central bank.

The Financial Times quoted David Treat, head of Accenture’s capital markets blockchain practice, as saying the technology behind USC would be ‘three to five years before we get things adopted at scale and several more years before it goes mainstream.’

2017

Exactly twelve months after Santander, BNY Mellon and Deutsche Bank announced their involvement in USC, more banks came on board in the shape of Barclays, Credit Suisse, HSBC, the Canadian Imperial Bank of Commerce (CIBC), Mitsubishi UFJ Financial Group (MUFG) and State Street.

It was here where links were made between USC and the future development of central bank digital currencies. Speaking to CoinDesk, Hyder Jaffrey, the director of strategic investment and fintech innovation at UBS, said:

It may well inform the way central banks choose to move things forward. We see it as a stepping stone to a future where central banks issue their own [cryptocurrency] at some point.

Head of fintech partnerships and strategy at HSBC, Kaushalya Somasundaram, added to Jaffrey’s comments:

It is a very good step forward in terms of going for more ambitious projects such as central bank digital currencies in the future.

In September of 2017 the Bank for International Settlements released their quarterly review that contained a section titled, ‘Central bank cryptocurrencies‘. It was here where the BIS presented an illustration called ‘The Money Flower: a taxonomy of money‘, which consisted of a mix of universally accessible money, electronic money, central bank issued money and peer to peer transactions. Located in the middle of the flower was the Utility Settlement Coin, this despite how relatively under advanced the venture was at the time. The review did not present any details for why USC was included, other than to reaffirm the definition of the term by linking to a press release issued by UBS in August 2016.

Nonetheless, for the BIS to take notice of USC shows that the technology was being actively considered at the highest levels of central banking.

2019

With the USC project progressing, in February 2019 JP Morgan announced that they had become the first U.S. bank to create and test a digital coin (known as JPM Coin). Characterised as a stablecoin, the JPM Coin is underpinned by blockchain technology and runs on a permissioned blockchain network. For the time being it is restricted to ‘institutional clients‘ only. As with other stablecoins, the value of one JPM Coin is equivalent to one U.S. Dollar, but the plan is to extend the use of the coin beyond the dollar and encompass other leading currencies around the world.

Far from being averse to the technology, JP Morgan are fully behind cryprocurrencies, provided they are ‘properly controlled and regulated.’

A few months later and the first soundings began to emerge of the Utility Settlement Coin entering a new phase of development. In May Reuters reported that some of the largest banks in the world were in the process of investing up to $50 million to ‘create a digital system using blockchain technology to settle financial transactions.’ A spokeswoman from Barclays confirmed at the time that the research and development phase of USC was ‘coming to an end.’

The $50 million in funds would make up a new entity called ‘Fnality‘, which would be tasked with running the project.

In June came confirmation of the evolvement of USC into ‘Fnality International‘. In a subsequent press release the founding shareholders of Fnality were listed as:

-

Banco Santander

-

BNY Mellon

-

Barclays

-

Canadian Imperial Bank of Commerce (CIBC)

-

Commerzbank

-

Credit Suisse

-

ING

-

KBC Group

-

Lloyds Banking Group

-

MUFG Bank

-

Nasdaq

-

Sumitomo Mitsui Banking Corporation

-

State Street Corporation

-

UBS

UK Blockchain firm Clearmatics were confirmed as maintaining their role as the technology partner to the project.

Here is an extract from the press release:

The focus for Fnality is now to create and deploy a solution incorporating legal, regulatory, operational. and technical aspects to create a regulated network of distributed Financial Market Infrastructures (dFMIs) to support global exchange of value transactions. Initially, five currencies are in scope: USD, EUR, GBP, JPY, and CAD. Further currencies will likely be added in due course.

USC envisages being 100% backed by fiat currency held at the respective central bank with convertibility into fiat currency at par guaranteed at all times.

The CEO of Fnality, Rhomaios Ram, stated that the launch of Fnality was ‘the commercial realisation of the USC Project‘, and that ‘USC will be an enabler for tokenised markets.’ Speaking a few months later, Ram said that one of the main areas of interest was in ‘establishing a digital currency capability in each currency‘. This is why Fnality is preparing to open accounts with all the major central banks, with the aim of having one account operational in early 2020 and for a digital currency to go live by the summer.

The potential significance of Fnality was illustrated in September when senior officials from public authorities gathered at the Bank for International Settlements in Basel, Switzerland. Up for discussion during the ‘Conference on global stablecoins‘ was ‘the regulatory issues posed by the emergence of ‘stablecoin’ initiatives backed by financial institutions and large technology companies.’

Recall how two years previously the BIS quarterly report included ‘The Money Flower‘ with USC as part of the network. Now as Fnality International, they were invited to give a presentation hosted by the BIS. JP Morgan and the Libra Association also gave their own presentations.

This was an event convened by the Group of Seven Working Group on stablecoins, which at the time was chaired by Benoit Coeure. Having been chair of the Committee on Payments and Market Infrastructures, Coeure is now head of the BIS Innovation Hub.

The BIS have since run two other conferences on digital money, the first being in September 2019 – ‘Fintech and Digital Currencies‘ – in conjunction with the Asian Bureau of Finance and Economic Research (ABFER) and the Centre for Economic Policy Research based in Britain. The second was in October – ‘Digital currencies, central banks and the blockchain: policy implications‘ – and was co sponsored by the Oesterreichische Nationalbank (central bank of Austria) and the Central Bank Research Association (CEBRA).

As I have written about before, the BIS are central to the agenda of digitising money at the expense of tangible assets. Exactly how instrumental Fnality could be to that agenda is something we will look at in part two of this series.

Tyler Durden

Sun, 02/16/2020 – 23:00 -

- Buzzkill: Many Public Marijuana Companies Have Just Several Months Worth Of Cash Left

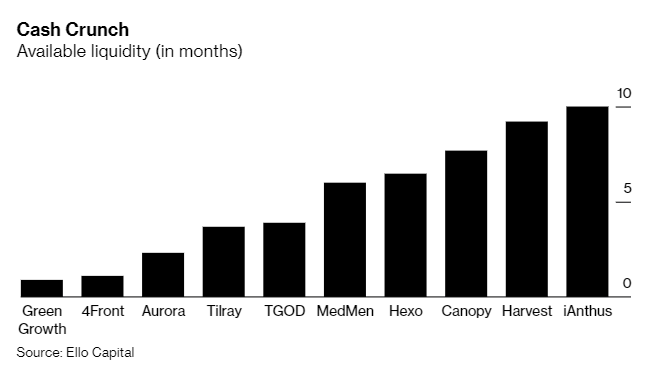

Buzzkill: Many Public Marijuana Companies Have Just Several Months Worth Of Cash Left

While the idea of marijuana companies has certainly been a hot topic in the public market space – especially since Tilray’s epic short squeeze in late 2018 – companies in the sector have been silently burning through their war chests of cash, leaving many just months away from being completely out of cash altogether.

Large Canadian pot producers have a median of just 6.5 months of cash left, according to Bloomberg. This compares to 14.4 months for most U.S. multi-state operators. For operators in both countries, the clock is ticking for them to raise capital and likely cut costs.

Names like Aurora Cannabis are going to have to address the problem sooner, rather than later. The company has the worst cash position of Canadian producers with just 2.3 months of liquidity remaining. Tilray isn’t far behind, with just 3.7 months of liquidity.

Aurora announced this week that it was going to be cutting 500 jobs as part of a major cost cutting effort. It also announced that its CEO would be stepping down. Regardless of the changes internally, the reality of the situation is that the company is still going to be in dire need of cash soon.

Another option for cannabis companies that don’t want to go to the market and raise cash is to merge or find a partner in the future. Investors may be more likely to deploy capital to marijuana names under better circumstances than traditional equity raises or bond issues. And there has undoubtedly been an appetite for mergers and acquisitions in the space, with names like Altria taking a $1.8 billion stake in Cronos Group in 2019.

Hershel Gerson, chief executive officer of Ello Capital, said: “I think people are looking for quality management teams that can effectuate a turnaround and have experience operating in a tighter environment than some of these early C-level teams.”

“There’s a switch going on related to the management teams that is potentially going to benefit the industry going forward,” he concluded.

The clock is officially ticking and we’ll check back in several months to see just how beneficial these changes really are…

Tyler Durden

Sun, 02/16/2020 – 22:30 - Are Web Traffic Trends The Best Way To See What's Happening In The World?

Are Web Traffic Trends The Best Way To See What’s Happening In The World?

Submitted by Market Crumbs

For most people, it’s hard to imagine a day going by without using the internet. Without it, you wouldn’t be reading this. It’s estimated that nearly 4.8 billion people, or about 61% of the world’s population, currently have internet access.

With such a large portion of the world depending on the internet for so many aspects of their lives, studying trends in web traffic can provide a lot of valuable insights. Web analytics company SimilarWeb has done just that in its recently released 2020 Digital Trends report. Many of the top digital trends aren’t too surprising, but are interesting to analyze further nonetheless.

Global web traffic continues its steady increase, with the total traffic to the top 100 websites averaging 223 billion monthly visits last year. This represents growth of 8.0% and 11.8% from 2018 and 2017, respectively. Mobile traffic continues to outgrow desktop traffic, with mobile traffic now representing 52% of total traffic. Mobile traffic has grown 30% since 2017, while desktop traffic has declined 3% over the same period.

Just like the gains in the S&P 500 are increasingly driven by a few stocks, the same can be said about web traffic for the top 100 websites. The top ten websites saw a 10.7% increase in traffic last year compared to a 2.3% increase for the remaining 90. Google, YouTube, Facebook, Baidu and Wikipedia are the top five most popular websites, with Amazon, Twitter and Instagram following. Thankfully for Facebook it acquired Instagram, because Facebook’s traffic fell 7% from 2018 and nearly 20% from 2017.

As United States total household debt surpassed $14 trillion last year for the first time, web traffic to shopping websites shows that’s not all too surprising. All nine online shopping categories showed growth last year, with Amazon receiving 69% of total shopping traffic since 2017. After jumping nearly 12% from 2017 to 2018, daily web traffic during the week of Black Friday actually declined 0.1% over the last year. Interestingly, daily web traffic during the week of Amazon’s Prime Day, which is in July, jumped more than 8% over the last year after declining by 4% from 2017 to 2018.

One of the not-so-surprising findings in the report is that news publishers are having a very difficult time. Traffic to the top 100 media websites dropped 5.3% over the last year and 7% since 2017. Finance and Business and Women’s Interest are the only two categories that have seen increases in web traffic. Interestingly, websites that are left- or right-leaning have seen traffic grow while those that are politically centered have seen traffic fall.

Web traffic to the top 100 finance websites was essentially flat last year. Traffic to cryptocurrency websites jumped in 2017 as they hit all-time highs, only to subsequently fall the last two years. While “too big to fail” banks have shown essentially flat web traffic, which is expected, there’s been a notable increase in traffic to fintech companies such as mobile only banks, personal financial management apps and payment apps.

With so much time spent on the internet these days, analyzing web traffic trends is an invaluable resource to see what is going on in the world. It will be interesting to see how these trends change in the years to come and the implications they’ll have on society and the economy.

Tyler Durden

Sun, 02/16/2020 – 22:00 - "It's Winter-Time For Capital Flow" – Outbreak Sparks Collapse In Chinese Tech Venture Funding

“It’s Winter-Time For Capital Flow” – Outbreak Sparks Collapse In Chinese Tech Venture Funding

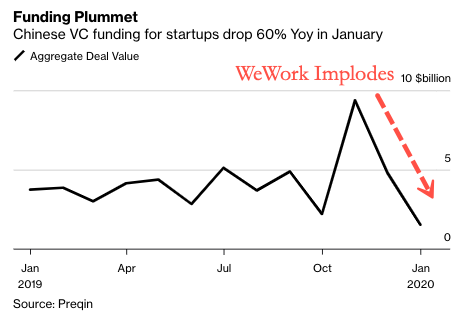

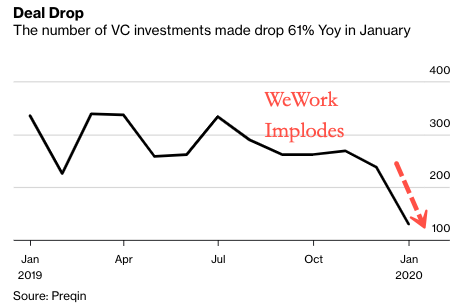

Hundreds of startups in China failed in 2019 as macroeconomic headwinds flourished. But now, the Covid-19 outbreak in the country crippled the already deteriorating venture capital industry, as funding freezes last month, according to Bloomberg, citing a new report from London-based consultancy Preqin.

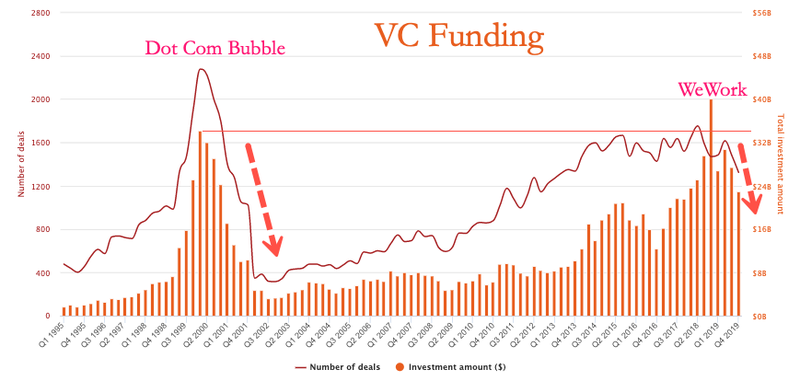

Tech companies in China faced a “capital winter” last year, where funding shortages increased as the global economy continued to decelerate. The implosion of WeWork in Sept 2019, as it attempted to IPO and subsequently ran out of cash, sent jitters through the global startup industry.

Startups in China, just like the ones in the U.S., had trouble last year supporting their lofty valuations, driven sky-high after global central banks printed an obscene amount of money, which allowed speculators to bet in greater size in these companies. With macroeconomic headwinds mounting, and the global IPO market faltering last year, it was a sign that investors were turning to the exits, out of trash unicorns, and into cash or defensive plays, such as value companies, or ones that had stable cash flows.

By the time 2020 turned the corner, the Covid-19 outbreak in China delivered a deadly blow to startups.

Preqin estimates that venture capital firms slashed investments in money-losing startups by 60% in January from a year ago. This means all the startups with negative cash flows and high burn rates, who are currently not operating at the moment because two-thirds of China’s economy is halted for virus containment purposes, could undergo a severe cash crunch in the near term.

Without proper funding, there could be a surge of companies that could start failing, driving up non-preforming loans for banks, and lead to the next big financial crisis.

Neil Shen, the founding partner of Sequoia Capital China, told Bloomberg that “we will fully stand by to provide help and support to the companies we backed in any way possible,” which he outlined some firms could undergo a cash crunch because the economy is shutdown.

Ee Fai Kam, head of Preqin Asian operations, said the setback in the venture capital industry is “coming on the back of a bruising 2019 when trade and tech tensions with the U.S. caused investors to exercise an abundance of caution.”

The bust of the global venture capital industry was likely accelerated by the blowup of WeWork last Sept.

Last fall, a month or so after WeWork’s IPO attempt ended in disaster, which resulted in a valuation collapse and was bailed out by its largest investor, SoftBank; top U.S. venture capitalists called an emergency meeting of startups in Oct to discuss the evolving and downshifting industry.

C.B. Insights and PWC noted last month that venture capital-backed companies in the U.S. raised $23 billion in 4Q19, down 42.5% over the prior year.

Wang Jun, chief financial officer for Chinese fresh produce delivery firm Missfresh, warned that early 2020 would be a challenging time for startups to obtain liquidity. Jun said, “It’s winter time for capital flow,” he added that “companies need to produce blood on their own to become cash-positive.”

To sum up, the venture capital industry across the world is headed for a possible bust cycle. An exogenous shock, like the trade war or a virus outbreak, is crippling startups from China to the U.S. The funding taps for these companies are shutting off; this is evident on both sides of the world as investors plow into defensive assets.

Tyler Durden

Sun, 02/16/2020 – 21:30 - Fedophilia: The Intellectual Disease And Cure

Fedophilia: The Intellectual Disease And Cure

Authored by George Selgin via Alt-M.org,

Although the movement to “End the Fed” has a considerable popular following, only a very tiny number of economists—our illustrious contributors amongst them—take the possibility seriously. For the rest, the Federal Reserve System is, not an ideal currency system to be sure (for who would dare to call it that?), but, implicitly at least, the best of all possible systems. And while there’s no shortage of proposals for reforming it almost all of them call only for mere tinkering. Tough though their love may be, the fact remains that most economists are stuck on the Fed.

This veneration of the Fed has long struck me as perverse. Its record can hardly be said, after all, to supply grounds for complacency, much less for the belief that no other system could possibly do better. (Indeed that record, as Bill Lastrapes, Larry White and I have shown, even makes it difficult to claim that the Fed has improved upon the evidently flawed National Currency system it replaced.) Further, as the Fed is both a monopoly and a central planning agency, one would expect economists’ general opposition to monopolies and to central planning, as informed by their welfare theorems and by the general collapse of socialism, to prejudice them against it. Yet instead of ganging up to look into market-based alternatives to the Fed, the profession, for the most part, has relegated such inquiries to its fringe.

Why? The question warrants an answer from those of us who insist that exploring alternatives to the Fed is worthwhile, if only to counter people’s natural but nevertheless mistaken inclination to assume that the rest of the profession isn’t interested in such alternatives because it has already carefully considered—and rejected—them.

It’s tempting to blame Fedophilia, and the more general phenomenon of what Larry White calls “status quo” bias in monetary research, on the Fed’s direct influence upon the economics profession. According to White, in 2005 the Fed employed about 27 percent more full-time macro- and monetary (including banking) economists than the top 50 US academic economics departments combined, while disseminating much of their research gratis through various in-house publications or as working papers. Perhaps not surprisingly, despite a thorough review of such publications, White could not find “a single Fed-published article that calls for eliminating, privatizing, or even restructuring the Fed.” That professional monetary economics journals are not much better may, in turn, reflect the fact, also documented by White, that Fed-affiliated economists also dominate those journals’ editorial boards.

But I doubt that a reluctance to bite the hand that feeds them is the only, or even the most important, reason why most economists seldom question the Fed’s desirability.

Another reason, I suppose, is their desire to distance themselves from… kooks. Let’s face it: more than a few persons who’d like to “End the Fed” want to do so because they think the Rothschilds run it, that it had JFK killed because he planned to revive the silver dollar, and that the basic plan for it was hatched not by the Congressional Committee in charge of monetary reform but by a cabal of Wall Street bankers at a top-secret meeting on Jekyll Island.

Oh, wait: the last claim is actually true. But claims like the others give reasonable and well-informed Fed critics a bad name, while giving others reason for wishing to put as much space as possible between themselves and the anti-Fed fringe.

I’m convinced that imagination, or the lack of it, also plays a part. To some extent, the problem is too much rather than too little imagination. With fiat money, and a discretionary central bank, it’s always theoretically possible to have the money stock (or some other nominal variable) behave just like it ought to, according to whichever macroeconomic theory or model one prefers. In other words, a modern central bank is always technically capable of doing the right thing, just as a chimpanzee jumping on a keyboard is technically capable of typing-out War and Peace.

Just as obviously, any conceivable alternative to a discretionary central bank, whether based on competition and a commodity standard or frozen fiat base or on some other “automatic” mechanisms, is bound to be imperfect, judged relative to some—indeed any—theoretical ideal. Consequently, an economist need only imagine that a central bank might somehow be managed according to his or her own particular monetary policy ideals to reckon it worthwhile to try and nudge it in that direction, but not to consider other conceivable arrangements.

That there’s a fallacy of composition of sorts at play here should be obvious, for a dozen economists might hold as many completely different monetary policy ideals; yet every one might be a Fedophile simply because the Fed could cater to his or her beliefs. In actual fact, of course, the Fed’s conduct can at most satisfy only one of them, and is indeed likely to satisfy none at all, and so might actually prove distinctly inferior to what some non-central bank alternative would achieve. So in letting their imaginations get the best of them, all twelve economists end up endorsing what’s really the inferior option.

If you don’t think economists are really capable of such naivete, I refer you to the literature on currency boards, in which one routinely encounters arguments to the effect that central banks are always better than currency boards because they might be better. Or how about those critics of the gold standard who, having first observed how, under such a standard, gold discoveries will cause inflation, go on to conclude, triumphantly, that a fiat-money issuing central-bank is better because it might keep prices stable?

But if economists let their imaginations run wild in having their ideal central banks stand in for the real McCoys, those same imaginations tend to run dry when it comes to contemplating radical alternatives to the monetary status quo. Regarding conventional beliefs concerning the need for government-run coin factories, which he (rightly) dismissed as so much poppycock, Herbert Spencer observed, “So much more does a realized fact influence us than an imagined one, that had the baking of bread been hitherto carried on by government agents, probably the supply of bread by private enterprise would scarcely be conceived possible, much less advantageous.” Economists who haven’t put any effort into imagining how non-central bank based monetary systems might work find it all too easy to simply suppose that they can’t work, or at least that they can’t work at all well. The workings of decentralized markets are often subtle; while such markets’ ability to solve many difficult coordination problems is, not only mysterious to untrained observers, but often difficult if not impossible even for experts to fathom except by means of painstaking investigations. In comparison monetary central planning is duck soup—on paper, anyway.

Nor does the way monetary economics is taught help. In other subjects, the welfare theorems are taken seriously. In classes on international trade, for example, time is always spent, early on, on the implications of free trade: never mind that the world has never witnessed perfectly free trade, and probably never will; it’s understood that the consequences of tariffs and other sorts of state interference can only be properly assessed by comparing them to the free trade alternative, and no one who hasn’t studied that alternative can expect to have his or her pronouncements about the virtues of protectionism taken seriously.

In classes in monetary economics, on the other hand, the presence of a central bank—a monetary central planner, that is—is assumed from the get-go, and no serious attention is given to the implications of “free trade in money and banking.” Consequently, when most monetary economists talk about the virtues of this or that central bank, they’re mostly talking through their hats, because they haven’t a clue concerning what other institutions might be present, and what they might be up to if the central bank wasn’t there.

Since monetary systems not managed by central banks, including some very successful ones, have in fact existed, economists’ inability to envision such systems is also evidence of their ignorance of economic history. That ignorance in turn, among younger economists at least, is a predictable consequence of the now-orthodox view that history can be safely boiled down to a bunch of correlation coefficients, so that they need only gather enough numbers and run enough regressions to discover everything worth knowing about the past.

Those who’ve been spared such “training,” on the other hand, often have a purblind view of the history of money and banks—one that brings to mind Saul Steinberg’s famous New Yorker cover depicting a 9th-Avenuer’s view of the world, with its almost uninhabited desert between the Hudson and the Pacific, and China, Japan, and Russia barely visible on the horizon. If he or she knows any monetary history at all, the typical (which is to say American) economist knows something about that history in the U.S., and perhaps considerably less about events in Great Britain. Theirs is, in short, just the right amount of knowledge to be very dangerous indeed.

And dangerous it has been. In particular, because the U.S. before 1914, and England before the Bank of England began acting as a lender of last resort, happened to suffer frequent financial crises, economists’ historical nearsightedness has given rise to the conventional wisdom that any fractional-reserve banking system lacking a lender of last resort must be crisis-prone, and two clever (if utterly fantastic) formal models serving to illustrate the same view (or, according to economists’ twisted rhetoric, to “prove” it “rigorously”). It has, correspondingly, led economists to ignore or at least to underestimate the extent to which legal restrictions, including unit banking laws in the U.S. and the six-partner rule in England, contributed to the deficiencies of those countries’ banking systems. Finally, and most regrettably, it has caused economists to overlook altogether the possibility that the monopolization of paper currency has itself been more a cause of than a cure for financial instability.

The good news is that Fedophilia is curable. Milton Friedman, for one, was a recovering Fedophile: later in his career, he repudiated the mostly-conventional arguments he’d once put forward in defense of a currency monopoly. Friedman, of course, was a special case: a famous proponent of free markets, he had more reason than most economists do to view claims of market failure with skepticism, even if he’d once subscribed to them himself. Even so, his was only a half-hearted change of heart, in part (I believe) because he still hadn’t drawn the lessons he might have from the banking experiences of countries other than the U.S. and England.

Friedman’s case suggests that it will take some pretty intense therapy to deprogram other Fed inamoratos, including a regimen of required readings.

Charles Conant’s History of Modern Banks of Issue will help them to overcome their historical parochialism.

Vera Smith’s The Rationale of Central Banking will do more of the same, while also exposing them to the lively debates that took place between advocates and opponents of currency monopolies before the former (supported by their governments’ ravenous Treasuries) swept the field.

The Experience of Free Banking, edited by Kevin Dowd (with contributions by several Alt-M contributors including yours truly) gathers studies of a number of past, decentralized currency systems, showing how they tended to be more stable than their more centralized counterparts, while another collection, Rondo Cameron’s Banking in the Early Stages of Industrialization, shows that less centralized systems were also better at fostering economic development. Finally, instead of being allowed to merely pay lip service to Walter Bagehot’s Lombard Street, Fedophile’s should be forced, first to read it from cover to cover, and then to re-read out-loud those passages (there are several) in which Bagehot explains that there’d be no need for lenders of last resort had unwise legislation not created centralized (“one reserve”) currency systems in the first place. The last step works especially well in group therapy.

Of course, even the most vigorous deprogramming regimen is unlikely to alter the habits of hard-core Fed enthusiasts. But it might at the very least make them more inclined to engage in serious debate with the Fed’s critics, instead of allowing the Fed’s apologists to go on believing that they answer those critics convincingly simply by rolling their eyes.

Tyler Durden

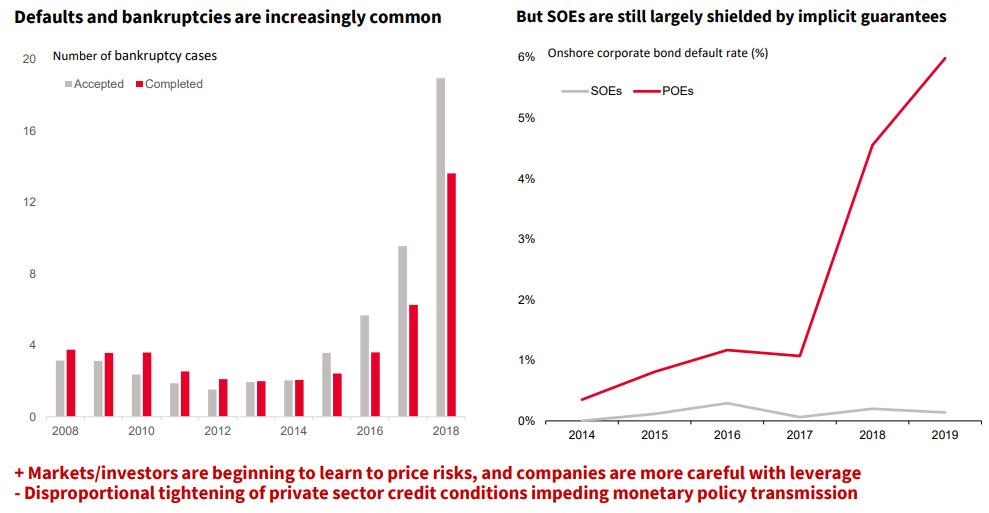

Sun, 02/16/2020 – 21:00 - China Central Bank Orders Lenders To "Tolerate" Higher Bad Debt Levels To Avoid Financial Cataclysm

China Central Bank Orders Lenders To “Tolerate” Higher Bad Debt Levels To Avoid Financial Cataclysm

Last week we reminded readers that unless Beijing manages to contain the coronavirus epidemic, China faces a fate far worse than just reported its first ever 0% (or negative) GDP print in history. For those who missed it, here it is again: back in November, we reported that as part of a stress test conducted by China’s central bank in the first half of 2019, 30 medium- and large-sized banks were tested; In the base-case scenario, assuming GDP growth dropped to 5.3% – nine out of 30 major banks failed and saw their capital adequacy ratio drop to 13.47% from 14.43%. In the worst-case scenario, assuming GDP growth dropped to 4.15%, some 2% below the latest official GDP print, more than half of China’s banks, or 17 out of the 30 major banks failed the test. Needless to say, the implications for a Chinese financial system – whose size is roughly $41 trillion – having over $20 trillion in “problematic” bank assets, would be dire.

Well, with GDP set to print negative if Goldman is right (with risk clearly to the downside as China’s economy remains completely paralyzed)…

… every single Chinese bank is set to fail a “hypothetical” stress test, and the immediate result is an exponential surge in bad debt. The result, as we discussed in detail last week, is that the bad loan ratio at the nation’s 30 biggest banks would soar at least five-fold, and potentially far, far more, flooding the country with trillions in non-performing loans, and unleashing a tsunami of bank defaults.

Of course, regular readers are well aware that China’s banks are already suffering record loan defaults as the economy last year expanded at the slowest pace in three decades while bankruptcies soared. As extensively covered here previously, the slump tore through the nation’s $41 trillion banking system, forcing not only the first bank seizure in two decades as Baoshang Bank was nationalized , but also bailouts at Bank of Jinzhou, China’s Heng Feng Bank, as well as two very troubling bank runs at China’s Henan Yichuan Rural Commercial Bank at the start of the month, and then more recently at Yingkou Coastal Bank.

All that may be a walk in the park compared to what is coming next.

“The banking industry is taking a big hit,” You Chun, a Shanghai-based analyst at National Institution for Finance & Development told Bloomberg. “The outbreak has already damaged China’s most vibrant small businesses and if it prolongs, many firms will go under and be unable to repay their loans.”

According to a recent Bloomberg report, S&P estimates that a worst-case scenario (one which however saw GDP remain well in positive territory) would cause bad debt to balloon by 5.6 trillion yuan ($800 billion), for an NPL ratio of about 6.3%, adding to the already daunting 2.4 trillion yuan of non-performing loans China’s banks are sitting on (a number which, like the details of the viral epidemic, is largely massaged lower and the real number is far higher according to even conservative skeptics).

S&P also expects that banks with operations concentrated in Hubei province and its capital city of Wuhan, the epicenter and the region worst hit by the virus, will likely see the greatest increase in problem loans. The region had 4.6 trillion yuan of outstanding loans held by 160 local and foreign banks at the end of 2018, with more than half in Wuhan. The five big state banks had 2.6 trillion yuan of exposure in the region, followed by 78 local rural lenders, according to official data.

Meanwhile, exposing the plight of small bushiness, most of which are indebted to China’s banks, a recent nationwide survey showed that about 30% said they expect to see revenue plunge more than 50% this year because of the virus and 85% said they are unable to maintain operations for more than three months with cash currently available. Perhaps they were exaggerating in hopes of garnering enough sympathy from Beijing for a blanket bailout; or perhaps they were just telling the truth.

Finally, the market is increasingly worried that all this bad debt will have a dire impact on bank assets: consider that the “big four” state-owned lenders, which together control more than $14 trillion of assets, currently trade at an average 0.6 times their forecast book value, near a record low. This also means that in the eyes of the market, as much as $6 trillion in bank assets are currently worthless.

All of this led us to conclude last week that “nothing short of a coronavirus cataclysm faces both China’s banks and small businesses if the coronavirus isn’t contained in the coming weeks.”

In retrospect, there is one thing we forgot to footnote, and that is that China could buy some extra time if the central bank suspend financial rules and moves the goalposts once again.

And so, just three days after our first article on China’s looming bad debt catastrophe, that’s precisely what the PBOC has opted to do, because as Reuters writes, on Saturday the PBOC said that the country’s lenders will tolerate higher levels of bad loans, part of efforts to support firms hit by the coronavirus epidemic.

“We will support qualified firms so that they can resume work and production as soon as possible, helping maintain stable operations of the economy and minimizing the epidemic’s impact,” Fan Yifei, a vice governor at the People’s Bank of China, told a news conference.

He added that the problem will be manageable as China has a relatively low bad loan ratio.

What the PBOC really means is that China’s zombie companies are about to take zombification to a preciously unseen level, as neither the central bank nor its SOE-commercial bank proxies will demand cash payments amounting to billions if not trillions of dollars from debtors, who will plead “force majeure” as part of their debt default explanation. In other words, we may be about to see the biggest “under the table” debt jubilee in history, as thousands of companies are absolved from the consequences of having too much debt.

Separately, during the same briefing, Liang Tao, vice chairman of the China Banking and Insurance Regulatory Commission, said that lending for key investment projects will be sped up, while Xuan Changneng, vice head of the country’s foreign exchange regulator, said China was expected to maintain a small current account surplus and keep a basic balance in international payments. We wouldn’t hold our breath for a surplus if China is indeed producing nothing as real-time indicators suggest.

And just so the message that debt will flow no matter what is heard loud and clear, on Friday, said Liang Tao, vice-chairman of the China Banking and Insurance Regulatory Commission said that financial institutions in the banking sector had provided more than 537 billion yuan ($77 billion) in credit to fight against the novel coronavirus outbreak as of noon on Friday.

“The regulator will soon launch more measures to give stronger credit support to various industries,” said Liang at a news conference held by the State Council Information Office on Saturday. “It will continue to lead banks’ efforts on increasing loans to small and micro enterprises, making loans accessible to a larger number of small businesses, and further lowering their lending costs.”

Hilariously, Liang highlighted the importance for banks to take accurate measures to renew loans for small businesses to reduce their financial pressure. It wasn’t clear just how burdening the small businesses with even more debt they will never be able to repay reduces financial pressure, but we can only assume that this is what is known as financial strategy with Chinese characteristics.

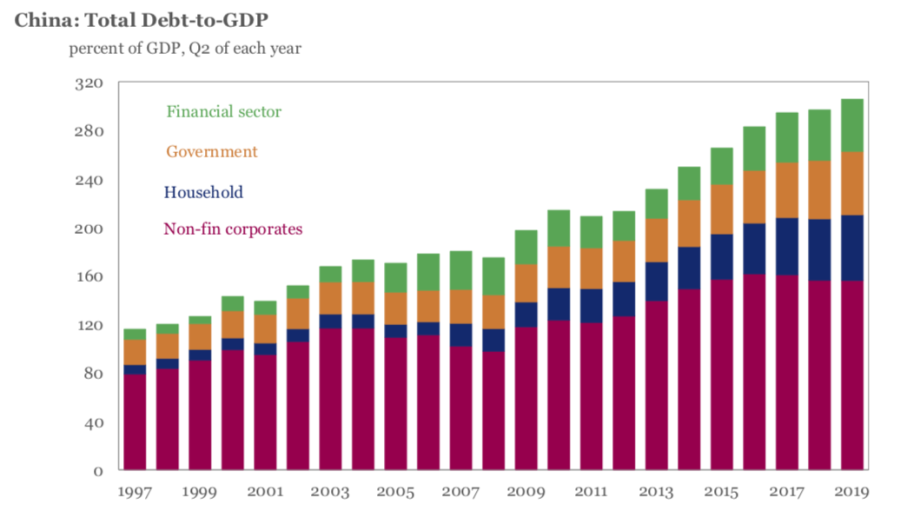

The bottom line is simple: no matter how or when the coronavirus epidemic ends, the outcome for China – which already toils under an gargantuan 300% debt/GDP burden…

… will be devastating as more companies are encumbered by even more debt which they will never be able to repay, and once rates jump or the Chinese economy hits another pothole – viral or otherwise – the avalanche in defaults will be a sight to behold.

Tyler Durden

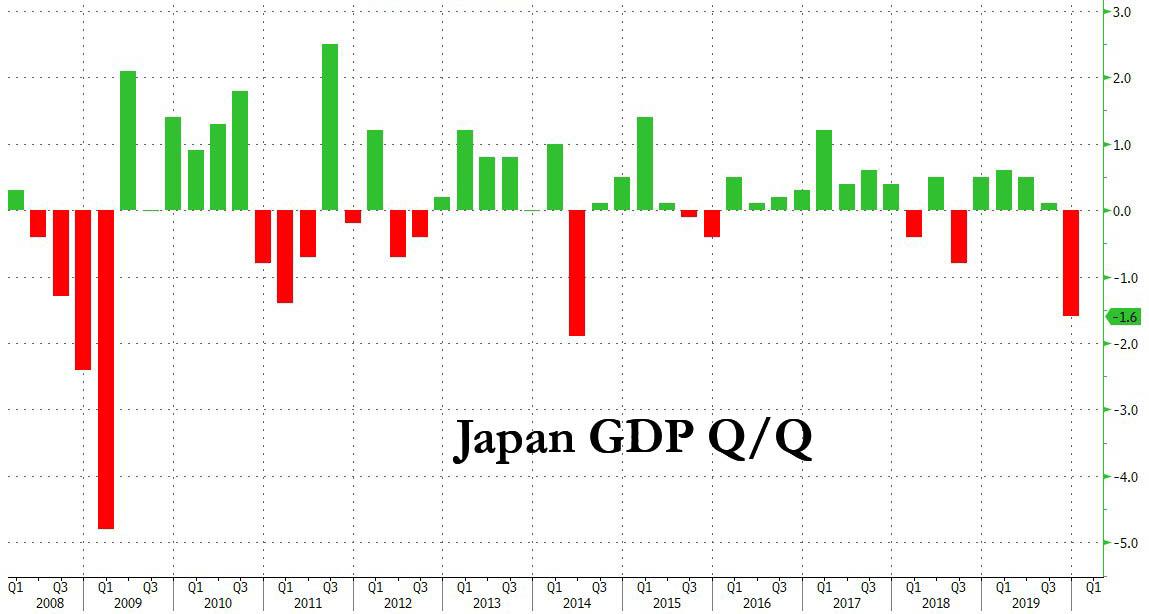

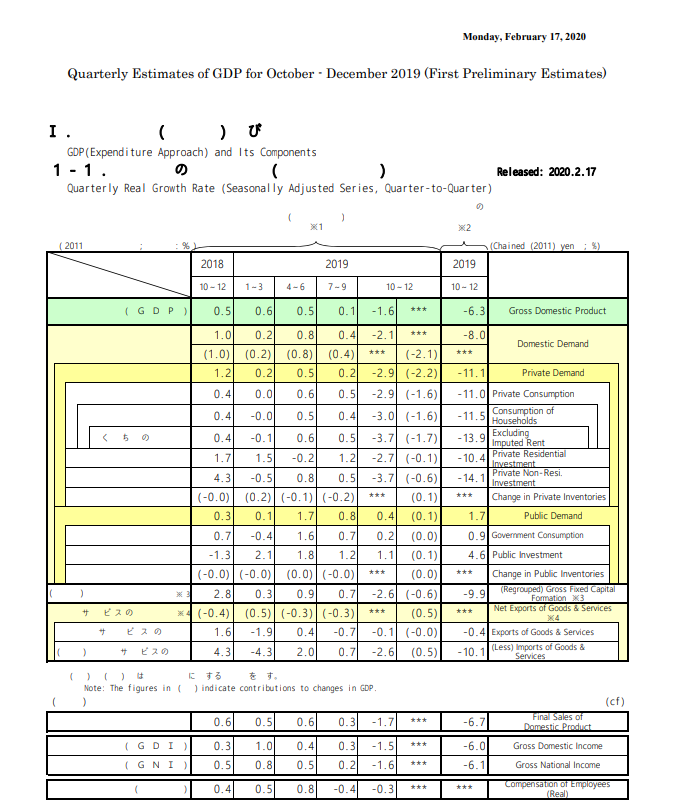

Sun, 02/16/2020 – 20:30 - Japan Unexpectedly Reports Terrible GDP As It Slides Into Recession

Japan Unexpectedly Reports Terrible GDP As It Slides Into Recession

One look at the latest GDP print out of Japan, and one would think the country’s economy was already being ravaged by the coronavirus: at -1.6% Q/Q and a whopping -6.3% annualized – nearly double the 3.8% estimated drop – this was the second worst GDP print since the financial crisis and the second-worst quarter of the Shinzo Abe era, surpassing even the drop in the aftermath of the Fukushima disaster.

Of course, the latest plunge in Japan’s GDP has nothing to do with the coronavirus as it took place in Q4, and the drop was largely a byproduct of the sale tax hike, which led to a similar collapse in Q2 2014 GDP, following the first such tax hike.

One look at the GDP components confirms that the plunge was largely the result of collapsing consumption, with Houshehold Consumption plunging at an 11.5% annualized pace, the second biggest drop that Private Demand plummeted at an -11.1% annualized basis…

… the second worst on record, and also just behind the -18.1% drop recorded after the first sales tax hike in 2014.

It wasn’t just households who retrenched, however, and as the following breakdown from Japan’s cabinet office reveals, in Q4, Japan’s capex fell fore the first time in 3 quarters, dragged down by construction and production machinery. Finally, the economic misery was complete as a result of a second consecutive drop in exports led by cars, as the global automotive sector remains mired in the deepest recession since the financial crisis.

And since Q1 GDP will likely be even worse due to the paralysis in Chinese supply chains which have knocked out a good part of Japanese domestic manufacturing indefinitely, today’s bleak GDP report means that a Japanese recession – definied as two quarters of negative GDP – is now just a matter of time.

The unexpected plunge in Japan’s GDP triggered a kneejerk reaction of selling on the Topix, which slid more than 1% in early trading, though bond yields and the yen showed little reaction to the worst nominal GDP performance since Prime Minister Shinzo Abe took office (U.S. futures were of course higher, because the closer the world gets to depression, the more likely central bankers are to start buying, well, everything).

Tyler Durden

Sun, 02/16/2020 – 20:22 - Why Wasn't Andrew McCabe Charged?

Why Wasn’t Andrew McCabe Charged?

Authored by Andrew McCarthy via National Review.com,

The proof that he willfully deceived investigators appears strong, but the Justice Department likely felt there were too many obstacles to convicting him.

The Justice Department announced Friday that it is closing its investigation of Andrew McCabe, the FBI’s former deputy director, over his false statements to investigators probing an unauthorized leak that McCabe had orchestrated. McCabe was fired in March 2018, shortly after a blistering Justice Department inspector general (IG) report concluded that he repeatedly and blatantly lied — or, as the Bureau lexicon puts it, “lacked candor” — when questioned, including under oath.

Why not indict McCabe on felony false-statements charges? That is the question being pressed by incensed Trump supporters. After all, the constitutional guarantee of equal justice under the law is supposed to mean that McCabe gets the same quality of justice afforded to the sad sacks pursued with unseemly zeal by McCabe’s FBI and Robert Mueller’s prosecutors.

George Papadopoulos was convicted of making a trivial false statement about the date of a meeting.

Roger Stone was convicted of obstruction long after the special counsel knew there was no Trump–Russia conspiracy, even though his meanderings did not impede the investigation in any meaningful way.

And in the case of Michael Flynn’s false-statements conviction, as McCabe himself acknowledged to the House Intelligence Committee, even the agents who interviewed him did not believe he intentionally misled them.

I emphasize Flynn’s intent because purported lack of intent is McCabe’s principal defense, too. Even McCabe himself, to say nothing of his lawyers and his apologists in the anti-Trump network of bureaucrats-turned-pundits, cannot deny that he made false statements to FBI agents and the IG. Rather, they argue that the 21-year senior law-enforcement official did not mean to lie, that he was too distracted by his high-level responsibilities to focus on anything as mundane as a leak — even though he seemed pretty damned focused on the leak while he was orchestrating it.

The “he did not believe he intentionally misled them” defense is not just implausible; it proved unavailing on McCabe’s watch, at least in General Flynn’s case. Hence, McCabe has a back-up plan: To argue that it would be extraordinary — and thus unconstitutionally selective and retaliatory — for the Justice Department to prosecute a former official for false statements in a “mere” administrative inquiry (which the leak probe was), as opposed to a criminal investigation. Again, tell that to Flynn, with whom the FBI conducted a brace-style interview — at the White House, without his counsel present, and in blithe disregard of procedures for FBI interviews of the president’s staff — despite the absence of a sound investigative basis for doing so, and whom Mueller’s maulers squeezed into a guilty plea anyway.

It will be a while before we learn the whole story of why the Justice Department walked away from the McCabe case, if we ever do. I have some supposition to offer on that score. First, however, it is worth revisiting the case against McCabe as outlined by the meticulous and highly regarded IG, Michael Horowitz.

If you want to know why people are so angry, and why they are increasingly convinced that, for all President Trump’s “drain the swamp” rhetoric, a two-tiered justice system that rewards the well-connected is alive and well, consider the following.

In October 2016, McCabe directed his counsel, Lisa Page, to leak investigative information about the FBI’s Clinton Foundation probe to reporter Devlin Barrett, then of the Wall Street Journal. The leak had the effect of confirming the existence of the investigation, something the FBI is supposed to resist. While his high rank gave him the power to authorize such a disclosure if it were in the public interest, the IG found that McCabe’s leak “was clearly not within the public interest.”

In fact, the Bureau’s then-director, James Comey, had tried to keep the Clinton Foundation probe under wraps, refusing to confirm or deny its existence even to the House Judiciary Committee. Comey had been right to stay mum: Public revelation would have harmed the probe and thrust the FBI deeper into the politics of the then-imminent 2016 presidential election, in which Hillary Clinton was the Democratic candidate and her investigation by the Bureau was an explosive campaign issue.

Notwithstanding these concerns, according to Horowitz’s report, McCabe orchestrated the leak “to advance his personal interests” — to paint himself in a favorable light in comparison to Justice Department officials amid an internal dispute about the Clinton Foundation probe (specifically, about the Obama Justice Department’s pressure on the Bureau to drop it). As the IG put it: “McCabe’s disclosure was an attempt to make himself look good by making senior department leadership . . . look bad.”

McCabe’s account has been contradicted by Comey, a witness who is otherwise sympathetic to him and hostile to the Trump Justice Department, and whose actions — like his — are being examined in prosecutor John Durham’s probe of the Trump-Russia investigation. Comey’s testimony is directly at odds with McCabe’s version of events, and the IG painstakingly explained why the former director’s version was credible while his deputy’s was not. (Comey was, nevertheless, exceedingly complimentary of McCabe after the IG report was published.)

Page is regarded by McCabe backers as key to his defense. She reportedly told the grand jury that, because McCabe had authority to approve media disclosures, he had no motive to lie about the leak. That’s laughable. McCabe did serially mislead investigators, so plainly he had some reason for doing so. But even putting that aside, the IG’s conclusion was not that McCabe lacked authority to leak; it was that he lacked a public-interest justification for exercising that authority. He leaked for self-promotion purposes, and then he lied about it because it was humiliating to be caught putting his personal interests ahead of the Bureau’s investigative integrity. That said, Page’s account does illuminate a problem for prosecutors: It’s tough to win a case when your witnesses are spinning for the defendant. (Oh, and have you seen Page’s tweet toasting McCabe in the aftermath of the news that the DOJ had closed the investigation?)

McCabe’s Multiple False Statements

Barrett’s Journal article appeared on October 30, 2016. The very next day, McCabe deceived Comey about it, indicating that he had not authorized the leak and had no idea who its source was. In Comey’s telling, credited by the IG, McCabe “definitely” did not acknowledge that he had approved the leak.

Thereafter, the FBI’s Inspection Division (INSD) opened an investigation of the leak. On May 9, 2017, McCabe denied to two INSD investigators that he knew the source of the leak. This was not a fleeting conversation. McCabe was placed under oath, and the INSD agents provided him with a copy of Barrett’s article. He read it and initialed it to acknowledge that he had done so. He was questioned about it by the agents, who took contemporaneous notes. McCabe told the agents that he had “no idea where [the leaked information] came from” or “who the source was.”

On July 28, 2017, McCabe was interviewed by the IG’s office — under oath and recorded on tape. In that session, he preposterously claimed to be unaware that Page, his FBI counsel, was directed to speak to reporters around the time of the October 30 Journal report. McCabe added that he was out of town then, and thus unaware of what Page had been up to. In point of fact, McCabe had consulted closely with Page about the leak. A paper trail of their texts and phone contacts evinced his keen interest in Page’s communications with Barrett. Consequently, the IG concluded that McCabe’s denials were “demonstrably false.”

Clearly concerned about the hole he had dug for himself, McCabe called the IG’s office four days later, on August 1, 2017, to say that, shucks, come to think of it, he just might have kinda, sorta told Page to speak with Barrett after all. He might even have told her to coordinate with Mike Kortan, then the Bureau’s top media liaison, and follow-up with the Journal about some of its prior reporting.

As the IG observed, this “attempt to correct his prior false testimony” was the “appropriate” thing for McCabe to do. Alas, when he was given an opportunity to come in and explain himself, he compounded his misconduct by making more false statements while under oath: In an interview with investigators on November 29, 2017, McCabe purported to recall informing Comey that he, McCabe, had authorized the leak, and that Comey had responded that the leak was a good idea.

These were quite stunning recollections, given that the deputy director had previously disclaimed any knowledge about the source of the leak. But McCabe took care of that little hiccup by simply denying his prior denial. That is, he insisted that he had not feigned ignorance about the leak when INSD interviewed him on May 9. Indeed, McCabe even denied that the May 9 interview had been a real interview. To the contrary, he claimed that agents had casually pulled him aside at the conclusion of a meeting on an unrelated topic, and peppered him out of the blue with a question or two about the Journal leak. As General Flynn could tell you, that sort of thing can be tough on a busy top U.S. government official . . . although Flynn did not get much sympathy for it when McCabe was running the FBI.

Again, the IG concluded that McCabe’s version of events was “demonstrably false.”

McCabe Covers His Tracks

As an old trial lawyer, I’d be remiss if I failed to rehearse my favorite part of the IG’s report — the part that would tell a jury everything they needed to know about good ol’ Andy McCabe.

Again, the Journal story generated by McCabe’s leak was published on October 30, a Sunday. Late that afternoon, McCabe called the head of the FBI’s Manhattan office. Why? Well . . . to ream him out over media leaks, that’s why. McCabe railed that New York agents must be the culprits. He also made a similar call to the Bureau’s Washington field office, warning its chief to “get his house in order” and stop these terribly damaging leaks.

It is worth remembering McCabe’s October 30 scolding of subordinates when you think about how he later claimed that, on the very next day, he’d freely admitted to his superior, Comey, that he himself was the source of the leak. Quite the piece of work, this guy: To throw the scent off himself after carefully arranging the leak, McCabe dressed down the FBI’s two premier field offices, knowing they were completely innocent, and then pretended for months that he knew nothing about the leak.

This is the second-highest-ranking officer of the nation’s top law-enforcement agency we’re talking about, here.

The Non-Prosecution Decision

We may never get a satisfying explanation for the Justice Department’s decision to drop the McCabe probe. That’s the way it is when such complicated reasons and motives are at play.

The aforementioned challenge of hostile witnesses is not to be underestimated. In addition, there are growing indications that the Justice Department had lost confidence in the U.S. attorney who was overseeing the probe, Jesse Liu. As I noted this week, while Liu was once seen as a rising Trump administration star, she was quietly edged out of her post last month, and the White House just pulled her nomination to fill an important Treasury Department post.

There have been rumblings that the McCabe investigation was botched. Kamil Shields, a prosecutor who reportedly grew frustrated by her supervisors’ inordinate delays in making decisions about the McCabe probe, ultimately left the Justice Department to take a private-practice job. Another prosecutor, David Kent, quit last summer as DOJ dithered over the decision on whether to prosecute. Things became so drawn out that the investigating grand jury’s term lapsed. Meanwhile, the Justice Department endorsed Liu’s aggressive decision to bring a thin, politically fraught false-statements case against former Obama White House counsel Greg Craig, in connection with lobbying for a foreign country — the sort of crime that is rarely prosecuted. Craig was swiftly acquitted. Reportedly, Liu advocated charging McCabe, but the DOJ may have harbored doubts about her judgment.

No matter the outcome, the Justice Department stood to take some hits if McCabe had been charged. Focus on McCabe’s leak would have drawn attention to pressure DOJ officials had put on the Bureau over the Clinton Foundation investigation (which, reportedly, is likely to be closed without charges). It would also renew interest in the question of whether the FBI improperly allowed McCabe to play a role in Clinton-related investigations when his wife, as a political candidate, got major funding from Clinton-tied sources.

Moreover, new Freedom of Information Act disclosures — made to meet a deadline set by District Judge Reggie Walton, which may explain the timing of the non-prosecution announcement — indicate that the Justice Department and FBI did not comply with regulations in what appears to be the rushed termination of McCabe, adding heft to the former deputy director’s claim that he was being singled out for abusive treatment, potentially including prosecution, because of vengeful politics.

On that score, Judge Walton took pains to decry the fusillade of tweets directed at McCabe by President Trump. I must note here that if a district U.S. attorney publicly labeled as a liar a suspect the Justice Department had indicted for false statements, that U.S. attorney would be sanctioned by the court. The U.S. attorneys, like the rest of the Justice Department, work for Trump. The president is correct when he insists, as he did this week, that he has the constitutional power to intervene in Justice Department matters. But that means he is subject to the same legal obligations that inhibit his Justice Department subordinates. Those obligations include protecting McCabe’s right to a fair trial — a duty the president may chafe at, but which is part of the deal when you take an oath to preserve the Constitution and execute the laws faithfully.

If you envision Judge Walton as part of the Obama-appointed robed resistance, check your premises. He is a no-nonsense jurist originally named to the D.C. Superior Court by President Reagan, and then to the federal district court by President George W. Bush. As Politico reports, he had this to say about President Trump’s commentary on the McCabe investigation:

The public is listening to what’s going on, and I don’t think people like the fact that you got somebody at the top basically trying to dictate whether somebody should be prosecuted. . . . I just think it’s a banana republic when we go down that road. . . . I think there are a lot of people on the outside who perceive that there is undo inappropriate pressure being brought to bear. . . . It’s just, it’s very disturbing that we’re in the mess that we’re in in that regard. . . . I just think the integrity of the process is being unduly undermined by inappropriate comments and actions on the part of people at the top of our government. . . . I think it’s very unfortunate. And I think as a government and as a society we’re going to pay a price at some point for this.

If you want to know why Attorney General Barr was warning this week that the president’s tweets are undermining the Justice Department’s pursuit of its law-enforcement mission, Judge Walton’s words are worth heeding. I have been making this point since the start of the Trump presidency. If you want people held accountable for their crimes, you have to ensure their fundamental right to due process. When the government poisons the well, the bad guys reap the benefits.

Finally, we must note that when the District of Columbia is the venue for any prosecution with political overtones, Justice Department charging decisions must factor in the jury pool, which is solidly anti-Trump.

The proof that McCabe willfully deceived investigators appears strong — it is noteworthy that IG Horowitz, who has strained to give the FBI the benefit of the doubt in many dubious contexts, was unequivocal in slamming McCabe. Nevertheless, a D.C. jury would be weighing that evidence, as discounted by whatever pro-McCabe slant reluctant prosecution witnesses put on it. And the jury would be weighing against that evidence (a) whatever problems caused prosecutors at the U.S. attorney’s office to beg off, and more significantly, (b) defense arguments that McCabe would not have been fired or prosecuted if not for the fact that he had gotten crosswise with a president of the United States whom at least some of the jurors are apt to dislike.

Looking at all that baggage, the Justice Department must not have liked its chances.

McCabe is not out of the woods yet, of course: The Durham investigation is a separate matter, and it is continuing. But it is unclear whether he will face any criminal charges arising from that inquiry, whereas the now-dead-and-buried false-statements case against him looked cut-and-dried.

The FBI’s former deputy director, though he undeniably misled investigators, remains a commentator at CNN. In the meantime, Papadopoulos is a felon convicted and briefly imprisoned for misleading investigators, while Flynn and Stone are awaiting sentencing on their false-statements charges. That covers both tiers of our justice system.

Tyler Durden

Sun, 02/16/2020 – 20:00 - Venezuela Stages Massive Live-Fire War Drill Amid Invasion Threats

Venezuela Stages Massive Live-Fire War Drill Amid Invasion Threats

A week after President Trump met with Venezuelan opposition leader Juan Guaidó at the White House and reiterated his support to remove President Nicolás Maduro from power, Venezuela’s armed forces and civilian militias staged a massive war drill over the weekend, reported Telesur.

The meeting between Trump and Guaidó on Feb 5 was nothing short of historic, suggests that the US could support a future military intervention to remove the Maduro regime.

The Trump administration has been tightening political, diplomatic, and economic screws on Maduro, but despite a crashed economy and hyperinflation, the regime continues to survive.

Back in 2017, Trump said he is “not going to rule out a military option” to confront the Venezuelan president.

Tensions in 2019 ran high after Guaido’s failed attempt to overthrow the regime.

Last month, Guaido was denied entry into the country’s National Assembly for his re-election as head of Congress, only to be reelected for a second term as speaker of parliament hours later.

The country continues to descend into chaos, and it appears that Maduro understands military intervention by Washington, or at least maybe a proxy force of some sort, could be imminent.

Maduro’s response to this lingering threat was to launch one of the most massive war drills the country has seen in years this weekend, called Bolivarian Shield 2020.

The objected of the exercise is to strengthen national defenses against armed aggressions:

“We started the Bolivarian Shield 2020 Exercise, with the deployment of our glorious FANB (Bolivarian National Armed Forces) in a Civic Military Union, with more than 2 million 300 thousand combatants mobilized to defend territorial integrity, independence and national sovereignty. We will preserve the Peace!” Maduro said.

Venezuelan Minister of Defense Vladimir Padrino tweeted that Bolivarian Shield 2020 Exercise will be conducted through the weekend and across the country. It will help Maduro prepare and face future threats of “aggression” from Washington.

¿Cómo negarle al pueblo su derecho a defender a la Patria? Vaya que acto de justicia la plena incorporación de la Milicia a la Fuerza Armada Nacional Bolivariana, hacen ustedes indestructible el #EscudoBolivariano2020 para proteger a nuestra amada Venezuela. pic.twitter.com/Qp1c6jHrWy

— Vladimir Padrino L. (@vladimirpadrino) February 15, 2020

https://platform.twitter.com/widgets.js

Padrino tweeted another video of the drills that shows an assortment of weapons being used, from small arms to surface to air missiles.

¡Febrero Rebelde! Hoy en desarrollo el segundo día del Ejercicio Militar #EscudoBolivariano2020. Tremendo balance hasta ahora, hemos conseguido, junto a la Milicia, aumentar el nivel de cohesión de la FANB. Felicitaciones a toda FANB. #EnDefensaDeLaPatria. ¡Venceremos! pic.twitter.com/i68hoWVa8h

— Vladimir Padrino L. (@vladimirpadrino) February 16, 2020

https://platform.twitter.com/widgets.js

AFP’s Yuri Cortez tweets pictures of an infantry battalion securing streets in Caracas.

Member of 311 mechanized infantry battalion Liberator Simon Bolivar points their Ak 103 rifles next to a 120mm mortar during military exercises for the “Bolivarian Shield 2020 Operation’ in #Caracas #photography #photojournalism #EscudoBolivariano2020 #Venezuela #FANB #15Feb pic.twitter.com/5JvCXy3i91

— Yuri Cortez (@YuriYurisky) February 15, 2020

https://platform.twitter.com/widgets.js

Ahead of this weekend’s mass military exercises across the country, CNW tweeted pictures of heavy military equipment being deployed.

AMX 13 F3 self propelled artillery being transported on autopista 1 in Maracaibo pic.twitter.com/QyD7KWPSPi

— CNW (@ConflictsW) February 11, 2020

https://platform.twitter.com/widgets.js

A quick video related to the BUK at La Carlota airbase. Video showing the radar was active today pic.twitter.com/onnQPOtXGd

— CNW (@ConflictsW) February 11, 2020

https://platform.twitter.com/widgets.js

Somewhere in Táchira ( I will geolocate at a later date) an S-125 air defence convoy including 2 loaders with 2 missiles each and the command and control vehicles, launchers possibly at the back of the convoy pic.twitter.com/um0D8J6kba

— CNW (@ConflictsW) February 12, 2020

https://platform.twitter.com/widgets.js

From the above post, the Full S-125 convoy in Táchira near San Cristobal including 2 launchers. Interesting to note is the motorbikes escorting the convoy with milicia holding Iglas pic.twitter.com/luolx5G889

— CNW (@ConflictsW) February 12, 2020

https://platform.twitter.com/widgets.js

More photos of the BUK at La Carlota, as well as a ZU-23. A full BUK squad is deployed including radars, command and control and 2 launchers. pic.twitter.com/UmueJZLvJ5

— CNW (@ConflictsW) February 12, 2020

https://platform.twitter.com/widgets.js

Venezuelan BUK with 2 launchers still located on the side of the Caracas- La Guaira Highway next to Caracas Maiquetia airport pic.twitter.com/yjBVbqPPLe

— CNW (@ConflictsW) February 14, 2020

https://platform.twitter.com/widgets.js

Mi-35 from the 712 attack helicopter batallón in Barinas pic.twitter.com/tC8b3TZWDh

— CNW (@ConflictsW) February 14, 2020

https://platform.twitter.com/widgets.js

S-125 and low blow radar deployed next to the Puente general rafael Urdaneta in Maracaibo pic.twitter.com/cEXfOag5f9

— CNW (@ConflictsW) February 14, 2020

https://platform.twitter.com/widgets.js

VN-18s live firing in Bahia de Turiamo, Aragua pic.twitter.com/0Ce9IqTeCY

— CNW (@ConflictsW) February 15, 2020

https://platform.twitter.com/widgets.js

S-125 convoy arriving at the Alcasa aluminium factory in Guayana city. Same location as the above photos pic.twitter.com/raqoZn8bUR

— CNW (@ConflictsW) February 16, 2020

https://platform.twitter.com/widgets.js

So, could a military intervention in Venezuela to rid Maduro of power be the next big distraction from a recession-prone US economy?

Tyler Durden

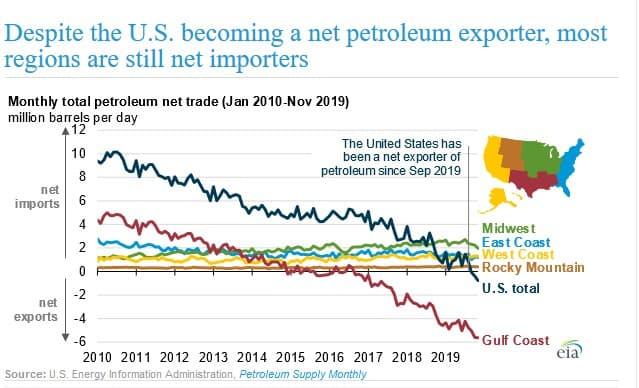

Sun, 02/16/2020 – 19:30 - Real Energy Independence Is An Illusion

Real Energy Independence Is An Illusion

Authored by Anes Alic via OilPrice.com,

Ultimately, energy independence is an illusion in the era of globalization because the hyper connectedness of the market makes it impossible. Still, it’s a never-ending battle cry that ends up being an argument of semantics, the outcome of which depends on how you define “independence”.

America’s ongoing oil and shale boom has reignited the debate about something that the nation had long come to consider a far-off dream: energy independence.

The notion that the country could become self-sufficient by producing enough energy to sustain the entirety of its population and industries was first floated by Nixon when he declared war on foreign oil during the oil crisis of the 1970s.

It was later popularized by Bush in a state of the union address in February 2006 when he decried United States’ addiction to oil, which is often imported from unstable parts of the world before announcing plans to break this addiction by developing several alternatives, including a multibillion-dollar subsidized ramp-up of biofuels.

Bush went on to boldly declare that by 2025, America would “…make our dependence on Middle Eastern oil a thing of the past” by cutting imports from Gulf states by three-quarters.

Well, it turns out the former president was prescient on some key predictions, which in hindsight appears quite remarkable when you consider that back then, the shale industry was barely on its feet. The shale era now is in full swing, with Trump, uncharacteristically, preferring to describe it using the somewhat less boisterous moniker of a “new era of American energy dominance”.

But the devil is in the details in any discussion as to whether America is any closer to true energy independence than during Nixon’s time or whether it is a populist charade masquerading as an energy strategy. There’s a third option, too: It’s simply misunderstood.

Net Oil Exporter

For many years, the United States has been the leader in the $6 trillion global energy market, and is currently the world’s largest oil producer accounting for about 18 percent of global oil supply. But it has also been a leading importer of energy with foreign markets supplying about 20 percent of its needs.