- US Joins Secret Talks Between Israel & UAE Targeting Iran

Authored by Jason Ditz via AntiWar.com,

Secret talks have been ongoing between Israel and the United Arab Emirates, focused on sharing intelligence against Iran and possibly military cooperation. The talks have progressed to the point that the US is now joining the talks too.

Israel and the UAE have some security ties, but don’t have public relations. That they’re discussing Iran reflects Israel’s long-standing hostility toward Iran, and the UAE’s close proximity to Iran.

Iranian Revolutionary Guards drive speedboats at the port of Bandar Abbas. Image source: AFP While some are presenting the US joining of the talks as proof they are making progress, a lot isn’t understood about what’s going on, and particularly unclear is what the UAE is trying to work out.

The UAE seems to be trying to balance multiple interests, as they’ve tried to talk to Iran about maritime security in recent days, and seem not to be looking to pick fights with them. That’s in stark contrast to Israel, for whom picking fights with Iran is the centerpiece of decades of foreign policy.

It’s clear that the UAE has an interest in keeping the US happy, and that probably requires keeping Israel at lease sort of placated in this regard. So while they aren’t trying to start anything against Iran they’re trying to walk the tightrope of balancing both sides to keep everyone satisfied.

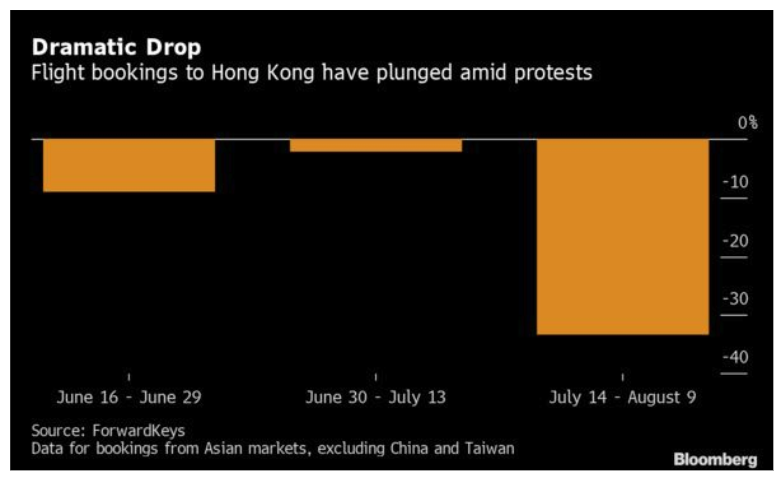

- "The Impact On Tourism Is Huge:" Hong Kong Hotel Crisis Erupts Amid Escalating Protests

Hong Kong might not be able to avoid a financial crisis this year or next despite possible stimulus packages to shore up its faltering economy amid violent protests across the city. This has led to a rapid decline in tourism, forcing major hotel chains in the city to substantially slash room prices.

Yiu Si-wing, a Hong Kong lawmaker representing the tourism industry, told Bloomberg that hotel revenue is expected to crash 50% this month thanks to escalating protests. She said visits from mainland China account for 80% of arrivals are significantly lower due to social unrest.

Yiu said hotel occupancy rates averaged 90% in 1H19, could drop by as much as 33% or more in 2H19. Arrivals from the mainland to Hong Kong, a significant source of consumption for the city, could grind to a halt.

“The impact on tourism is huge,” Yiu told Bloomberg. She said at least half of the mainland visitors due in August had canceled their plans. Yiu said top-trending topics on Chinese social media platform Weibo this week included several incidents of where violent protestors attacked government forces.

Some mainland Chinese are shunning Hong Kong because of the risks associated with its airport being closed down for an extended period of time.

Grace Huang, a 20-year-old Wuhan University student, told Bloomberg her layover at Hong Kong International Airport was horrifying earlier this week. “I fear I’m going to be beaten,” she told Bloomberg, as thousands of protestors successfully locked down the airport for several days.

Please pay attention to what’s happening in Hong Kong #HongKong #HongKongAirport

— wingless angel (@saintgreeedy) August 13, 2019

https://platform.twitter.com/widgets.js

Can you hear the people sing? ICYMI protestors at #HongKong airport singing Les Mis. #China banned track from streaming services in #PRC! #HongKongProtests pic.twitter.com/j6V5anjqMz

— Jon Williams (@WilliamsJon) August 12, 2019

https://platform.twitter.com/widgets.js

Beijing resident Jasmine Ji, 23, delayed her trip to Hong Kong because she feels protestors would target her for being a Chinese citizen.

“I feel like my personal safety could be severely threatened if they find out I speak Mandarin or am a Chinese citizen,” she said. “I won’t fly to Hong Kong airport until the situation and protests are settled there.”

Chinese officials and state-run media outlets launched an information war against the protestors, describing them as violent extremists.

Hong Kong officials have suggested a recession could be imminent due to social unrest.

Hong Kong Financial Secretary Paul Chan Mo-po on Thursday announced a $2.43 billion stimulus package to shore up the economy during the social and economic turmoil.

Paul warned that a possible recession could be imminent: “The situation we are in now is like the typhoon No 3 signal has been hoisted and the typhoon is heading towards us,” he said. “We need to get prepared before it gets worse.”

Paul downgraded Hong Kong’s GDP growth forecast for the year to 0 to 1%, from 2 to 3% previously.

He said the city could slide into a technical recession in the current quarter.

InterContinental Hotels Group Plc, a British multinational hospitality company that owns Crowne Plaza and Holiday Inn chains, said the protests in the last several months have contributed to a slowdown in business travel in the region.

Other hospitality companies with exposure to Hong Kong are also feeling the pinch: Sun Hung Kai Properties, owner of Four Seasons Hotel Hong Kong, and New World Development Co., which operates the Grand Hyatt Hong Kong, have seen their stocks enter bear markets in the last month.

Yiu said the downturn in Hong Kong hospitality industry had forced many hotels to slash their room rates by substantial amounts.

A typical room at Conrad Hotel, owned by Hilton Worldwide, is $159 per night this weekend, that’s a 40% discount versus two months ago.

Marriott International Inc. and Shangri-La Asia Ltd. have also cut room rates for their Hong Kong hotels.

Hong Kong could be the first domino to fall that kicks off the next global recession.

- The Anglo-American Origins Of Color Revolutions

Authored by Matthew Ehret via The Strategic Culture Foundation,

A few years ago, very few people understood the concept behind color revolutions.

Had Russia and China’s leadership not decided to unite in solidarity in 2012 when they began vetoing the overthrow of Bashar al Assad in Syria- followed by their alliance around the Belt and Road Initiative, then it is doubtful that the color revolution concept would be as well-known as it has become today.

At that time, Russia and China realized that they had no choice but to go on the counter offensive, since the regime change operations and colour revolutions orchestrated by such organizations as the CIA-affiliated National Endowment for Democracy (NED) and Soros Open Society Foundations were ultimately designed to target them as those rose, orange, green or yellow revolution efforts in Georgia, Ukraine, Iran or Hong Kong were always recognized as weak points on the periphery of the threatened formation of a great power alliance of sovereign Eurasian nations that would have the collective power to challenge the power of the Anglo-American elite based in London and Wall Street.

Russia’s 2015 expulsion of 12 major conduits of color revolution included Soros’ Open Society Foundation as well as the NED was a powerful calling out of the enemy with the Foreign Ministry calling them “a threat to the foundations of Russia’s Constitutional order and national security”. This resulted in such fanatical calls by George Soros for a $50 billion fund to counteract Russia’s interference in defense of Ukraine’s democracy. Apparently the $5 billion spent by the NED in Ukraine was not nearly enough.

In spite of the light falling upon these cockroaches, NED and Open Society operations continued in full force focusing on the weakest links the Grand Chessboard unleashing what has become known as a “strategy of tension”. Venezuela, Kashmir, Hong Kong, Tibet and Xinjian (dubbed East Turkistan by NED) have all been targeted in recent years with millions of NED dollars pouring into separatist groups, labour unions, student movements and fake news “opinion shapers” under the guise of “democracy building”. $1.7 million in grants was spent by NED in Hong Kong since 2017 which was a significant increase from their $400 000 spent to coordinate the failed “Occupy HK” protest in 2014.

The Case of China

In response to over two months of controlled chaos, the Chinese government has kept a remarkably restrained posture, allowing the Hong Kong authorities to manage the situation with their police deprived of use of lethal weapons and even giving into the protestors’ demand that the changes to the extradition treaty that nominally sparked this mess be annulled. In spite of this patient tone, the rioters who have run havoc on airports and public buildings have created lists of demands that are all but impossible for mainland China to meet including 1) an “independent committee to investigate the abuses of Chinese authorities”, 2) for china to stop referring to rioters as “rioters”, 3) for all charges against rioters to be dropped, and 4) universal suffrage- including candidates promoting independence or rejoining the British Empire.

As violence continues to grow, and as it has become an increasing reality that some form of intervention from the mainland may occur to restore order, the British Foreign Office has taken an aggressive tone threatening China with “severe consequences” unless “a fully independent investigation” into police Brutality were permitted. The former Colonial Governor of China Christopher Patten attacked China by saying “Since president Xi has been in office, there’s been a crackdown on dissent and dissidents everywhere, the party has been in control of everything”.

The Chinese Foreign Ministry responded saying “the UK has no sovereign jurisdiction or right of supervision over Hong Kong… it is simply wrong for the British Government to exert pressure. The Chinese side seriously urges the UK to stop its interference in China’s internal affairs and stop making random and inflammatory accusations on Hong Kong.”

The British have not been able to conduct their manipulation of Hong Kong without the vital role of America’s NGO dirty ops, and in true imperial fashion, the political class from both sides of the aisle have attacked China with Senate Majority leader Mitch McConnell and Nancy Pelosi making the loudest noise driving the American House Foreign Affairs Committee to threaten “universal condemnation and swift consequences” if Beijing intervenes. This has only made the photographs of Julie Eadeh, the head of Political Office at the American Consulate in Hong Kong meeting with leaders of the Hong Kong demonstrations that much more disgusting to any onlooker.

While both Britain and America have been caught red handed organizing this colour revolution, it is important to keep in mind who is controlling who.

The Foreign Origins of the NED

Contrary to popular opinion, the British Empire did not go away after WWII, nor did it hand over the “keys to the kingdom” to America. It didn’t even become America’s Junior Partner in a new Anglo-American special relationship. Contrary to popular belief, it stayed in the drivers’ seat.

The post WWII order was largely shaped by a British coup which didn’t take over America without a fight. Nests of Oxford-trained Rhodes Scholars, Fabians and other ideologues embedded within the American establishment had a lot of work ahead of them as they struggled to purge all nationalist impulses from the American intelligence community. While the most aggressive purging of patriotic Americans from the intelligence community occurred during the dissolution of the OSS and creation of MI6 in 1947 and the Communist witch hunt that followed, there were other purges that were less well known.

As an organization which was beginning to take form which was to become known as the Trilateral Commissionorganized by Britain’s “hand in America” called the Council on Foreign Relations and international Bilderberg Group, another purge occurred in 1970 under the direction of James Schlesinger during his six month stint as CIA director. At that time 1000 top CIA officials deemed “unfit” were fired. This was followed nine years later as another 800 were fired under a list drafted by CIA “spymaster” Ted Shackley. Both Schlesinger and Shackley were high level Trilateral Commission members who took part in the group’s 1973 formation and fully took power of America during Jimmy Carter’s 1977-1981 presidency which unleashed a dystopian reorganization of American foreign and internal policy outlined in my previous report.

Project Democracy Takes Over

By the 1970s, the CIA’s dirty hand funding anarchist operations both within America and abroad had become too well known as media coverage of their dirty operations at home and abroad spoiled the patriotic image which the intelligence community then desired. While the internal resistance to fascist behaviour from within the intelligence Community itself was dealt with through purges, the reality was that a new agency had to be created to take over those functions of covert destabilization of foreign governments.

What became Project Democracy herein originated with a Trilateral Commission meeting in May 31, 1975 in Kyoto Japan as a protégé of Trilateral Commission director Zbigniew Brzezinski named Samuel (Clash of Civilizations) Huntington delivered the results of his Task Force on the Governability of Democracies. This project was supervised by Schlesinger and Brzezinski and presented the notion that democracies could not function adequately in the crisis conditions which the Trilateral Commission was preparing to impose onto America and the world through a process dubbed “the Controlled Disintegration of Society”.

The Huntington report featured at the Trilateral meeting stated: “One might consider… means of securing support and resources from foundations, business corporations, labor unions, political parties, civic associations, and, where possible and appropriate, governmental agencies for the creation of an institute for the strengthening of democratic institutions.”

It took 4 years for this blueprint to become reality. In 1979 three Trilateral Commission members named William Brock (RNC Chairman), Charles Manatt (DNC Chairman) and George Agree (head of Freedom House) established an organization called the American Political Foundation (APF) which attempted to fulfil the objective laid out by Huntington in 1975.

The APF was used to set up a program using federal funds called the Democracy Program which issued an interim report “The Commitment to Democracy” which said: “No theme requires more sustained attention in our time than the necessity for strengthening the future chances of democratic societies in a world that remains predominantly unfree or partially fettered by repressive governments. … There has never been a comprehensive structure for a non-governmental effort through which the resources of America’s pluralistic constituencies . .. could be mobilized effectively.”

In May 1981, Henry Kissinger who had replaced Brzezinski as head of the Trilateral Commission and had many operatives planted around President Reagan, gave a speech at Britain’s Chatham House (the controlling handbehind the Council on Foreign Relations) where he described his work as Secretary of State saying that the British “became a participant in internal American deliberations, to a degree probably never practiced between sovereign nations… In my White House incarnation then, I kept the British Foreign Office better informed and more closely engaged than I did the American State Department… It was symptomatic”. In his speech, Kissinger outlined the battle between Churchill vs FDR during WWII and made the point that he favored the Churchill worldview for the post war world (And ironically also that of Prince Metternich who ran the Congress of Vienna that snuffed out democratic movements across Europe in 1815).

In June 1982, Reagan’s Westminster Palace speech officially inaugurated the NED and by November 1983, the National Endowment for Democracy Act was passed bringing this new covert organization into reality with $31 million of funding under four subsidiary organizations (AFL-CIO Free Trade Union Institute, The US Chamber of Commerce’s Center for International Private Enterprise, the International Republican Institute and the International Democratic Institute) (2).

Throughout the 1980s, this organization went to work managing Iran-Contra, destabilizing Soviet states and unleashing the first “official” modern color revolution in the form of the Yellow revolution that ousted Philippine president Ferdinand Marcos. Speaking more candidly than usual, NED President David Ignatius said in 1991 “a lot of what we do today was done covertly 25 years ago by the CIA”.

With the collapse of the Soviet Union, the NED was instrumental in bringing former Warsaw Pact nations into NATO/WTO system and the New World Order was announced by Bush Sr. and Kissinger- both of whom were rewarded with knighthoods for their service to the Crown in 1992 and 1995 respectively.

Of course, the vast web of NGOs permeating the geopolitical terrain can only be effective as long as no one says the truth and “names the game”. The very act of calling out their nefarious motives renders them impotent and this simple fact has made the recently announced China-Russia arrangement to formulate a proper strategic response to color revolutions so important in the current fight.

- Trump Reviews Controversial US-Taliban Peace Deal Which Critics Call A "Betrayal"

Critics are calling a Trump administration plan for a rapid US force draw down in Afghanistan which involves striking a peace deal with the Taliban a “betrayal”.

But administration officials have countered that this is the cost of bringing the some 14,000 US troops in Afghanistan home. Trump “has been pretty clear that he wants to bring the troops home” according to senior officials privy to ongoing negotiations.

The chief controversy behind the US-Taliban peace talks is that any deal will likely rely on the Taliban holding to counterterrorism guarantees, or that it won’t attack US coalition forces; however, there’s reportedly little in the impending deal which holds the Taliban to guarantees it won’t attack Afghan civilians or the national army.

Via Reuters According to CNN:

One source explained that the agreement is seen as paving the way for the US to leave the country without a high number of US casualties in the coming months.

President Trump said he had a “very good meeting in Afghanistan” in a tweet Friday, just after meeting with top national security advisers over the impending peace plan which seeks to end America’s longest running war, now approaching two decades.

“Discussions centered around our ongoing negotiations and eventual peace and reconciliation agreement with the Taliban and the government of Afghanistan,” a White House press spokesman said of the meeting. “The meeting went very well, and negotiations are proceeding.”

“In continued close cooperation with the government of Afghanistan, we remain committed to achieving a comprehensive peace agreement, including a reduction in violence and a cease-fire, ensuring that Afghan soil is never again used to threaten the United States or her allies, and bringing Afghans together to work towards peace,” the statement said.

CNN summarizes of the deal that it’s “expected to formalize a significant withdrawal of US forces from Afghanistan — from about 15,000 troops to 8,000 or 9,000 troops — and enshrine official commitments by the Taliban to counterterrorism efforts in Afghanistan, according to the multiple sources familiar with the plan.”

But there’s fear that the Taliban is simply looking to remove the US military from the equation, and that once the US departs, the Taliban will have free reign to attack a greatly weakened Afghan national army.

Spearheading the dialogue has been White House special envoy Zalmay Khalilzad, who has been meeting with Taliban negotiators in Qatar for months, with a desire to strike a final deal by September 1.

- Lost Within The Rate Cut: The Fed's Drive To Establish A New Payment System

Part way through delivering a press conference following the Federal Reserve’s first rate cut since December 2008, chairman Jerome Powell let it be known that the central bank was ‘looking carefully‘ at developing a new faster payments system. Unsurprisingly, his words on the subject proved the equivalent of screaming into the face of a force ten gale. Besides a handful of financial outlets, nobody heard him. All that analysts and observers were really interested in was the Fed’s stance on interest rates.

This was unfortunate because whilst they may appear banal and complex on the surface, payments systems are of far greater significance than whether a central bank opts to cut or raise interest rates. Anyone keeping pace with the myriad of speeches and publications emanating from central banks will know that globalists are working incrementally to introduce a cashless monetary system under their control. The Federal Reserve are one strand of this strategy as we will discover.

Less than a week after the rate cut, the Fed announced that they were planning to devise a new ‘round-the-clock real-time payment and settlement service.’ Called ‘FedNow‘, the system would be an RTGS run service designed to initiate faster payments.

RTGS stands for ‘Real Time Gross Settlement‘, and is the same model through which the Bank of England and the European Central Bank operate their payment systems. The BOE announced back in May 2017 a blueprint for the introduction of a ‘renewed‘ RTGS service, whilst the ECB in late 2018 launched a new system dubbed TIPS (TARGET Instant Payment Settlement). It was around the time that TIPS launched that the Fed issued a ‘request for comment‘ on reforming their own system. Taken as a whole, this is a further example of central banks working in coordination.

In a press release announcing ‘FedNow‘, the Fed justified the venture on the premise that the ‘rapid evolution of technology‘ had presented them with a ‘pivotal opportunity‘ to modernise the U.S. payment system. Exactly how long the Fed have been looking into adopting a new payment system is unclear. But if the Wall Street Journal is to be believed, they have been exploring a faster system since at least 2013.

The press release also pointed out that over 10,000 financial institutions are incorporated into the current Fed payment system known as ‘Fedwire‘, and argued that new real time infrastructure developed through the central bank would be best placed to offer full nationwide coverage.

The next stage of ‘FedNow‘ sees the Fed ‘requesting comment on how the new service might be designed‘. As for when it becomes available, the expectation is either 2023 or 2024. The Bank of England’s renewed RTGS system is due to be operational by 2025.

On the day ‘FedNow‘ was announced, Lael Brainard, a member of the Fed’s board of governors, offered up more information on the system in a speech at the Federal Reserve Bank of Kansas City. As you might expect, Brainard was there to extol the benefits. The big selling point was 365 days a year access, 24 hours a day, 7 days a week. Funds would be available immediately after payment is sent. It would be a system built on convenience and one that was fit for the speed of the 21st century.

Of greater interest than these superficial benefits, however, is the motivation behind what the Fed are seeking to achieve with ‘FedNow‘. Brainard was equally as explanatory in this regard.

We learned from her speech four key bits of information.

Firstly, fintech companies are openly supportive of the Fed’s new system. These are companies that are part of an industry that has pioneered the creation of distributed ledger technology.

Secondly, the planned implementation for either 2023 or 2024 is not a fixed objective. More important to the Fed is the goal of achieving ‘nationwide access for all‘, meaning that their overarching aim is for ‘FedNow‘ and private sector payment services to work in conjunction (or, as Brainard put it, to ‘interoperate by exchanging payments among services directly).

Thirdly, Brainard told us that no one private sector provider of a U.S. payment system has ever been able to establish nationwide reach by itself. Nationwide coverage would have to encompass the many thousands of small and medium sized banks. Hence why the Fed are now making a determined move to utilise private sector technology and incorporate it into their own system. I would contend that the Fed’s goal is to achieve full spectrum control of America’s payment infrastructure, with all digital transactions falling under their jurisdiction. ‘FedNow‘ would be the mechanism in making this happen.

Fourthly, as Brainard laid out, the path that the Fed are embracing is not one of ‘incremental‘ change. Rather, it is of ‘transformative‘ change. I would take this to mean that the infrastructure underpinning current payment systems must be overhauled to allow for the implementation of fintech devised technology.

An accompanying list of FAQ’s lent credence to the understanding that fintech is central to the construction of ‘FedNow‘. Here, the Fed expounded that the market for faster payments in the U.S. remains in the ‘early stages‘. Banks and fintech firms can provide a range of services, but the functionality of them is limited which restricts their level of coverage and reliability. They lamented the ‘lack of a universal infrastructure to conduct faster payments‘, which means that at present users who are signed up to one service such as Paypal invariably cannot send or receive payment from a user signed up to another service. As a result, the market remains ‘fragmented‘.

With the Federal Reserve system encompassing twelve regional banks, and the relationships the Fed has with 10,000 plus banking institutions, their belief is that they are ‘well positioned to overcome the challenge of extending nationwide access.’

Throughout their communications there is a preoccupation with the objective of achieving nationwide access. So much so that the Fed board are apparently intending to ‘explore interoperability and other paths to achieving the ultimate goal of nationwide reach.’

‘FedNow’ would provide the necessary universal infrastructure that the Fed are seeking, and allow banks of all description to offer real-time payments.

Undoubtedly this presents an opportunity for the Fed, and indeed central banks throughout the world, to move in and claim hegemony over the next generation of global digital payment systems. But they, along with the Bank for International Settlements and the International Monetary Fund that preside over them, cannot do this by themselves. This is where the private sector comes in, for it is here where the expertise and technological innovation is found.

Within the FAQ’s it is also stated that the ‘FedNow‘ service would ‘operate alongside private sector RTGS services for faster payments‘. Prior to the announcement of the new system, the Federal Reserve board had come to the conclusion that private sector RTGS services ‘cannot be expected to provide an infrastructure with reasonable effectiveness, scope and equity alone.’ A roundabout way of saying that whilst the Fed do not possess the technology, they do have the reach in order to disseminate private sector innovation to every corner of the U.S. The beauty for the Fed is that they would have full regulatory authority over ‘FedNow‘. In conjunction with fintech, their level of control over the payments infrastructure would be unassailable.

If central banks manage to utilise fintech successfully, it will give them a clear path to begin the gradual implementation of central bank issued digital currencies. Back in April I published an article (BIS General Manager Outlines Vision for Central Bank Digital Currencies) that looked into the subject of CBDC’s more deeply.

In regards to ‘FedNow‘, equally as interesting as what was discussed by the Fed is what was left unsaid. There was no mention throughout any of the supporting documentation of plans to incorporate distributed ledger technology. Instead, there will be ‘engagement between the Fed and the industry to inform the final service design.’ This is a process that is now getting underway.

I would expect that once the final design of ‘FedNow‘ is confirmed, it will have the capability of interacting with systems that use distributed ledgers. This would follow on from the Bank of England who in 2018 announced that their new RTGS service would enable such systems to achieve settlement in central bank money.

Once this has been achieved, the next logical step for central banks is to complete the process of digitising all financial assets through the issuance of central bank digital currency. And as BIS general manager Agustin Carstens warned back in March 2019, this would mean that people would no longer have the option of paying with cash. ‘All purchases would be electronic‘.

In a follow up article I will be exploring the process underway at the Bank of England and the European Central Bank to reform their payment systems, and how China is proving to be the test bed for fintech innovation.

- Trump's Farm Bailout Flows To "City Slickers," a D.C. Lobbyist and ‘Farms’ on Golf Courses

About 9,000 “city slickers” living in luxurious neighborhoods of the nation’s largest cities received a farm bailout from the Trump administration to minimize the impact of the trade war with China, an updated Environmental Working Group (EWG) analysis of Department of Agriculture data shows.

The EWG analysis of USDA data revealed that “many recipients live not in farm country but in the nation’s 50 largest cities or in other decidedly nonrural locations.”

Urban recipients of the bailout include members of farm families, landowners, and investors. These people provide land, capital, or equipment for farms and make high-level decessions for operations.

EWG said bailout recipients include 70 people in San Francisco, 65 residents in New York City, 63 residents in Los Angeles, 61 residents in Washington, D.C., and 19 Miami.

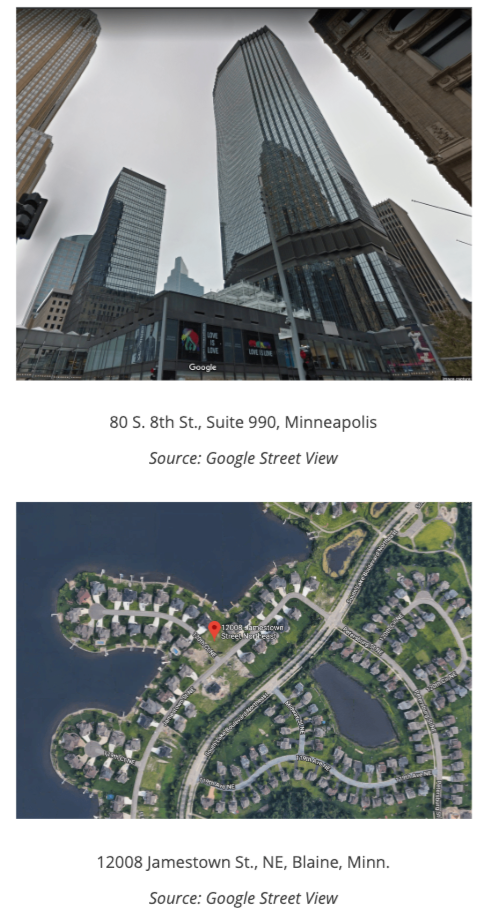

In Washington D.C., lobbyist Van R. Boyette for the sugar company Florida Crystals, and its owners, the Fanjul brothers of West Palm Beach, Fla. all collected bailouts this year. Here’s a photo of the lobbyist’s USDA address:

Another non-farm address of a bailout recipient is at a Minneapolis skyscraper, is the location of R.D. Brummond and Sons LLC., which the Trump administration handled over nearly $100,000 this spring. The second is a mansion in a wealthy lakeside community in Blaine, Minn., a Minneapolis suburb, the address of Karnik Leifker LLC., which received about $100,000.

EWG has previously reported that nearly 20,000 city slickers in the nation’s 50 largest cities received farm subsidies in 2017, including hundreds who have received payments for three decades.

One farm bailout went to the address of a mansion located on a golf course of Craig Athen, of Omaha, Neb., who received $115,000 in government money this year.

Richard M. Morgan, of Columbus, Ohio, another bailout recipient this year, had $50,000 in farm bailout money go to an address of a mansion located on a golf course.

The environmental advocacy group said 3,500 bailout recipients had collected more than $125,000 in farm bailouts through April.

In a previous report, EWG found that farm bailouts are flowing the wealthiest farmers.

They suggested that the next bailout rounds would only increase the problem of how bailouts are not protecting mom-and-pop farmers, but rather showering wealthy farmers with money.

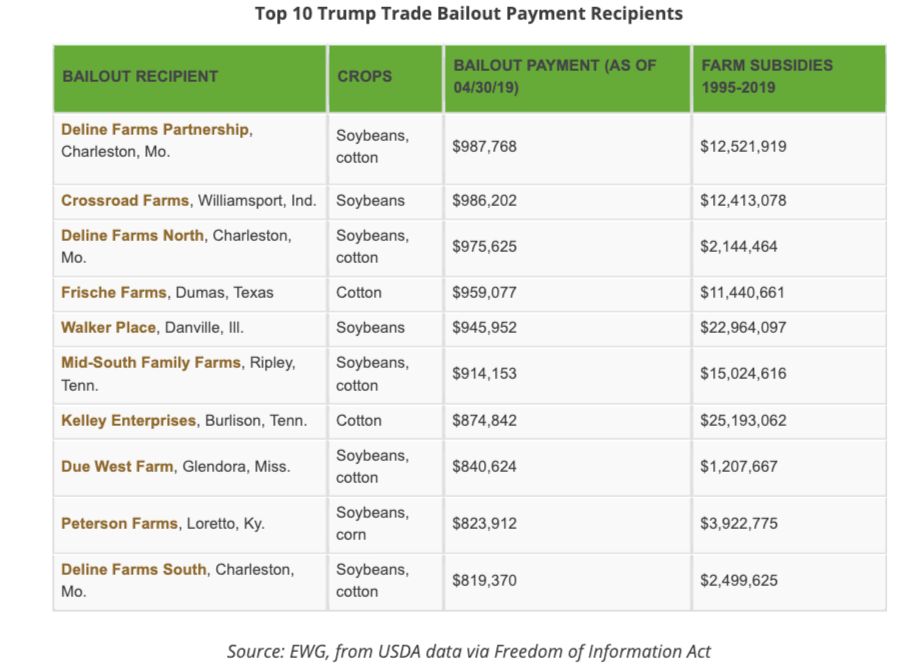

Deline Farms Partnership, a soybean farm in Charleston, Mo., was the largest bailout recipient this year receiving nearly $1,000,000.

EWG said the report is based on $8.4 billion of farm bailouts through April. The USDA data was obtained via the Freedom of Information Act.

And earlier this month, President Trump hinted at a third farm bailout.

As they have learned in the last two years, our great American Farmers know that China will not be able to hurt them in that their President has stood with them and done what no other president would do – And I’ll do it again next year if necessary!

— Donald J. Trump (@realDonaldTrump) August 6, 2019

https://platform.twitter.com/widgets.js

EWG said farm bailouts were intended to provide a level of assistance proportionate to a farm’s size and success, which have effectively crippled mom-and-pop to medium-sized farmers, by allowing more significant operations to receive the most bailout money.

This is more evidence that government interventionism in markets and socialist bailouts via the Trump administration aren’t working as farm incomes collapse, could trigger a farm bust in 2020.

- Zombie Deer Disease Rears Its Ugly Head: Canada Issues Stark Warning About "Always Fatal" Infection

Authored by Dagny Taggart via The Organic Prepper blog,

Earlier this year, an infectious disease expert warned that a deadly disease found in deer could infect humans in the near future.

Often referred to as “zombie deer” disease because of the symptoms, Chronic Wasting Disease (CWD) has been reported in at least 26 states in the continental United States and in four provinces in Canada. In addition, CWD has been reported in reindeer and/or moose in Norway, Finland, and Sweden, and a small number of imported cases have been reported in South Korea. The disease has also been found in farmed deer and elk.

To view a map that shows the distribution of CWD in North America, click here: Expanding Distribution of Chronic Wasting Disease

CWD was recently detected in a herd of deer in Canada.

On July 26, the Canadian Food Inspection Agency (CFIA) confirmed a case of CWD in a herd of white-tailed deer, reports Global News:

An Alberta deer farm recorded Canada’s third case of a so-called “zombie deer disease” last month.

While the chronic wasting disease (CWD) outbreak was contained — and no infected meat entered the Canadian food supply — experts say more needs to be done to stop the infectious disease from spreading.

The herd was “humanely destroyed on site and did not enter the food chain,” the agency told Global News in a statement. “[The farm] remains under quarantine and disease response activities have been initiated.”

This is the third case of CWD in Canada for 2019. The two other infections were also identified in Alberta — on Feb. 28 in elk and on June 21 in white-tailed deer. (source)

Before we discuss why this news is important, let’s back up a bit and talk about what CWD is and how it may eventually impact the food supply.

What is CWD?

CWD is a transmissible spongiform encephalopathy disease found in deer, elk, moose, reindeer, and caribou. It is a progressive disease that is always fatal.

The disease is believed to be caused by abnormal proteins called prions, which are thought to cause damage to other normal prion proteins that can be found in tissues throughout the body. They are most often found in the brain and spinal cord, leading to brain damage and development of prion diseases. Infected brain cells eventually burst, leaving behind microscopic empty spaces in the brain matter that give it a “spongy” look.

Prions are misfolded proteins that are somehow infectious (we’re still not really sure how or why) and for which we have no treatments or cures. If you were to catch one, you’d basically deteriorate over the course of several months, possibly losing the ability to speak or move, and eventually you would die. Doctors wouldn’t be able to do anything to save you. (source)

The disease is believed to spread through saliva, urine, or feces from live deer or through contact with high-risk parts such as the backbone, eyes, or spleen of harvested deer. The disease can spread through the natural movement of deer but it spreads farther and quicker when humans move the deer.

Symptoms develop slowly – sometimes taking years to appear – and include stumbling, lack of coordination, drooling, lack of fear of people, and aggression.

Can CWD be transmitted to humans?

While there is no direct scientific evidence to suggest that CWD can be transmitted to humans, the CFIA says the consumption of meat from contaminated animals should be avoided.

However, some experts say CWD is a concern because the disease is adapting and may become a serious threat:

Darrel Rowledge, the director of Alliance for Public Wildlife, said CWD shouldn’t be discounted as an animal-only problem.

Rowledge said that while it’s difficult for a disease to jump from one species to another, signs the disease is evolving are alarming.

“Just because it hasn’t happened yet, doesn’t mean that it hasn’t happened,” he said. “A majority of our diseases have evolved to a place where they can infect people.

“We think about 70 percent of our diseases have come to us from other animals.” (source)

Rowledge’s warning echoes that of another expert. Earlier this year, Michael Osterholm, director of the Center for Infectious Disease Research and Policy at the University of Minnesota, told lawmakers that CWD should be treated as a public health issue. Osterholm (who sat on a panel of experts tracking the emergence of mad cow disease, or BSE, decades ago) issued this warning during a hearing:

“It is my best professional judgment based on my public health experience and the risk of BSE transmission to humans in the 1980s and 1990s and my extensive review and evaluation of laboratory research studies … that it is probable that human cases of CWD associated with the consumption of contaminated meat will be documented in the years ahead. It is possible that number of human cases will be substantial and will not be isolated events.” (source)

While he is aware that skeptics will accuse him of fear-mongering, Osterholm said, “If Stephen King could write an infectious disease novel, he would write about prions like this.”

There is a very similar disease that has already killed people.

As we reported earlier this year, Osterholm noted that for years, many public health and beef industry experts did not believe a similar disease – bovine spongiform encephalopathy (BSE, also known as “mad cow disease” – could infect people:

In 1996, researchers found strong evidence that BSE can infect humans as a variant known as Creutzfeldt-Jakob disease (vCJD).

Since 1996, more than 230 vCJD cases have been identified in 12 countries, 178 of them in the United Kingdom, 27 in France, and four in the United States. Just last fall, a case of mad cow disease was confirmed in Scotland, reports Food Safety News.

Also important to note: Hunters in Kentucky contracted a version of spongiform encephalopathy from squirrels in the 1990s. (source)

CJD has killed several people. Some of the victims consumed venison – and their cases progressed rapidly. To read about those cases, please see Can “Zombie Deer” Disease Kill Humans? Research Suggests It ALREADY HAS.

Rowledge is one of 30 experts from across North America who sent a letter to the Canadian federal government in June, urging the prime minister to “mandate, fund and undertake” a number of “emergency directives” to contain the disease, prevent human exposure and expand its surveillance program of prion diseases, Global News reports:

The letter — signed by scientists, hunting groups and Indigenous advocates — labeled the spread of CWD an epidemic.

“While no human cases of CWD have been confirmed, scientists note that while low, the risk is not zero — and it is evolving,” the letter reads.

“Thousands of CWD-infected animals are being consumed by hunters and their families across North America every year. Even a single transfer to a person — proving that humans are susceptible — would bring catastrophic consequences with limited options.”

Rowledge and the other experts used mad cow as an example of what can happen when diseases evolve.

“The notion that there is insufficient proof that CWD will transfer to humans is deceptive and irresponsible, just like BSE… With the BSE inquiry, one of its key lessons was that they said that they should not have been waiting for a person to die.” (source)

There haven’t been any documented cases of CWD in Manitoba, but the government there is planning to build a health lab in Dauphin to detect the disease because experts believe it will eventually arrive in the province, CBC News reports:

Manitoba Sustainable Development posted a request for proposals online late last month to build the Dauphin Big Game Health Laboratory.

The province already has a lab in Dauphin as part of its disease surveillance programs, and chronic wasting disease is the main concern, a Sustainable Development spokesperson said.

Chronic wasting disease is a fatal neurological disease related to mad cow disease and there’s no known cure.

The province has extended the surveillance zone for the disease, in which hunters are required to submit heads of their kills for analysis. The province anticipates a rise in samples, the provincial spokesperson said. (source)

Brian Kotak, managing director of the Manitoba Wildlife Federation, told CBC News that a growing body of research suggests the diseased proteins found in deer infected with chronic wasting disease may impact human health when consumed. That’s one reason he’s pleased the province is working to build a lab. “That’s fantastic news and really proactive on their part,” he said.

There are a few things you need to know about CWD.

A 2017 study titled Chronic wasting disease: Emerging prions and their potential risk states that “CWD is one of the most contagious prion diseases”.

Plants can act as a carrier of CWD because they can uptake prions from contaminated soil and transport them to different parts of the plant.

An infected animal can shed the disease a lot over a year (via urine and feces), and its decomposing body can further infect the soil and therefore the plants.

Killing CWD is impossible. Antibiotics do not kill CWD. Neither does cooking.

To give you an idea of just how persistent prions are: In 1985, the Colorado Division of Wildlife tried to eliminate CWD from a research facility by treating the soil with chlorine, removing the treated soil, and applying an additional chlorine treatment before letting the facility remain vacant for more than a year. Those efforts failed – they were unsuccessful in eliminating CWD from the facility.

CWD prions are accumulating, and prions have a long incubation period — sometimes as long as 30 to 40 years in humans. A person can be infected and not know it for decades.

Here’s how you can avoid infection with CWD.

While CWD is scary and is spreading through cervids in North America, this doesn’t mean that you must completely avoid game. However, you have to be careful.

The CDC offers some guidelines for hunters:

Hunters harvesting wild deer and elk from areas with reported CWD should check state wildlife and public health guidance to see whether testing of animals is recommended or required in a given state or region. In areas where CWD is known to be present, CDC recommends that hunters strongly consider having those animals tested before eating the meat. (source)

In addition, the agency advises hunters to avoid eating meat from deer and elk that look sick or test positive for CWD. They should wear gloves when field-dressing carcasses and minimize the handling of brain and spinal cord tissues. As a precaution, they should avoid eating deer and elk tissues known to harbor the CWD agent (e.g., brain, spinal cord, eyes, spleen, tonsils, lymph nodes) from areas where CWD has been identified.

In addition, hunters should wash their hands and instruments thoroughly after field dressing is completed. When taking the game to be processed, they should request that their animal is processed individually, without meat from other animals being added to the meat from their animal.

If hunters notice animals that are unusually thin and exhibit behavior such as having trouble walking, as well as those acting tame around humans and allowing someone to approach them, they should notify their state wildlife agency.

The CDC also states that “a negative test result does not guarantee that an individual animal is not infected with CWD, but it does make it considerably less likely and may reduce your risk of exposure to CWD.”

Is this how the real zombie apocalypse starts?

- 12 Reasons Why Negative Rates Will Devastate The World

It has been a thesis over 20 years in the making, but with every passing day, SocGen’s Albert Edwards – who first coined the term “Ice Age” to describe the state of the world in which every debt issue ends up with a negative yield as capital markets and economies collapse into a deflationary singularity – is that much closer to having the victory lap of a lifetime. Although, we doubt he is happy about it.

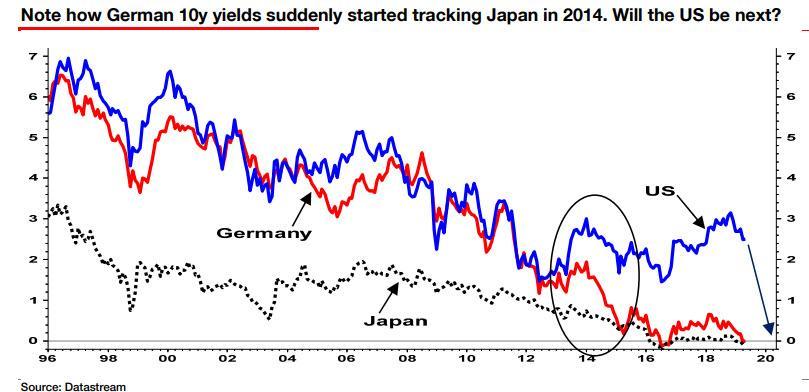

Commenting on the interest rate collapse he has been (correctly) predicting ever since he first observed Japan’s great bubble bust of the 1980s and which resulted in both NIRP and QE, and which he (correctly) expected would spread across the rest of the world, leading to a “Japanification” of every major bond market…

… Edwards said that what bond markets are telling us is “that the cycle is ending with the central banks having failed to drive core CPI inflation higher. So Japanese-style outright deflation lies ahead at a time when western economies have piled debt sky high.”

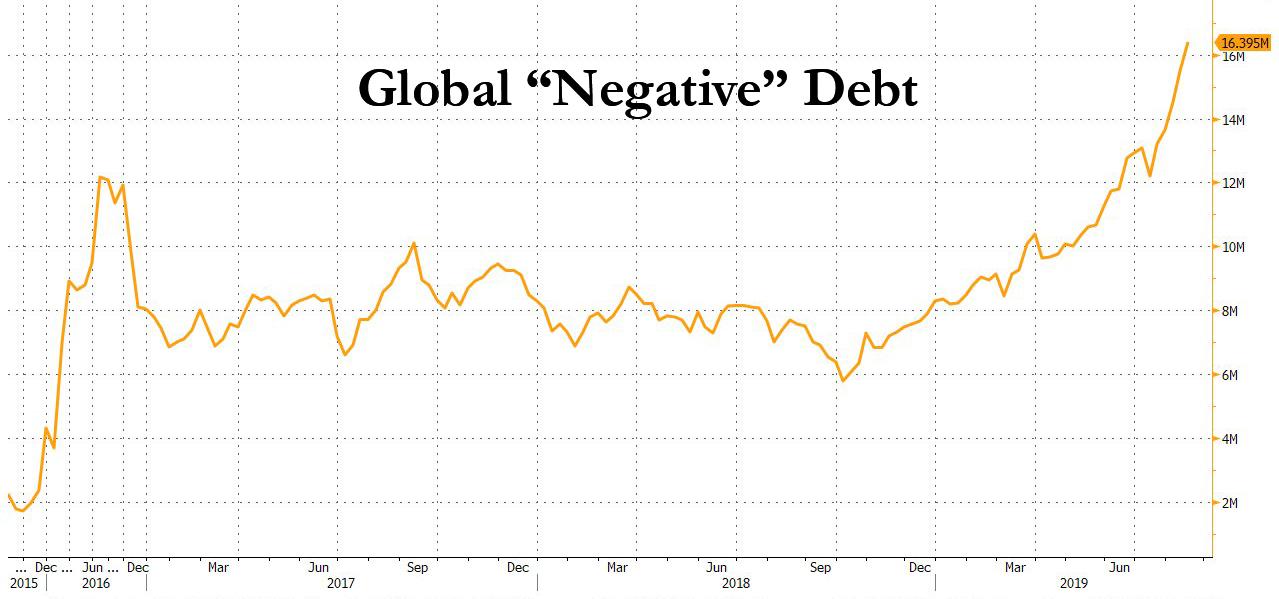

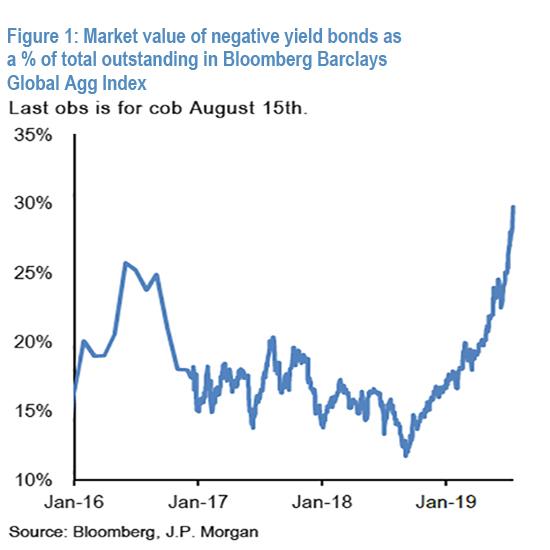

Needless to say that’s not good, not least of all because we now live in a world in which the bond universe with negative yields continued to grow at an exponential pace, rising rapidly over the past two weeks and reaching a record $16.4 trillion…

… rising significantly above the previous mid-2016 record high of around $12.2tr. The expansion of the universe of negatively yielding bonds as a percentage of total is shown below: as of the last week, this proportion increased further to around 30.0%, above the mid-2016 record high of 25.8%.

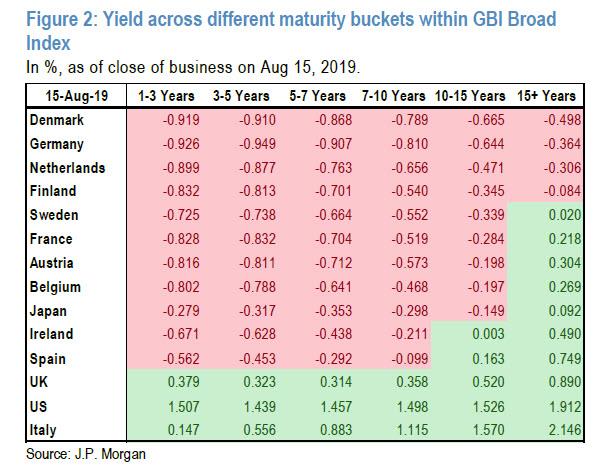

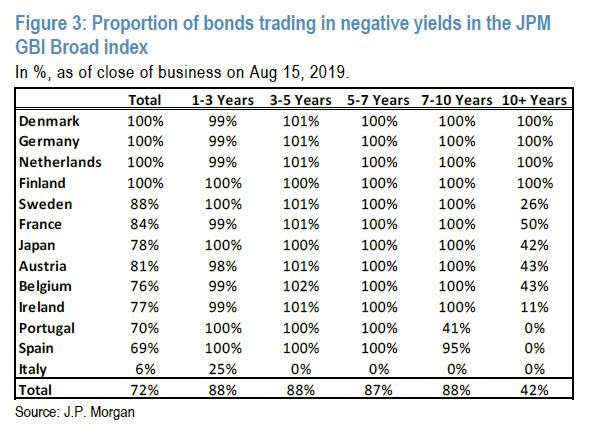

Meanwhile, as the world is blanketed by Edwards’ Ice Age, one can see the spread of negative rates both in space and in time. As JPMorgan shows, the spectrum of negative yielding universe expanded this year not only from shorter duration to longer duration government bonds but also down the risk spectrum from core Euro area government bonds to bonds issued by Peripheral countries as shown below.

The next chart shows the proportion of bonds in negative territory as a % of total bonds in each maturity bucket across various countries within the JPM GBI Broad index. In Europe, we now have four counties, Denmark, Germany, Netherlands and Finland with their full maturity spectrum trading with negative yields. Most periphery countries have at least a portion of their maturity spectrum trading with negative yields.

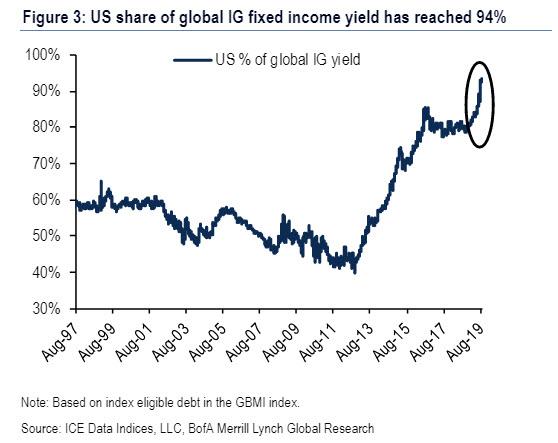

Here, a perverse “negative gamma” type of feedback loop emerges, as this growing universe of negatively yielding bonds becomes self-reinforcing as certain investors such as insurance companies and pension funds rush to avoid locking in negative yields to maturity. This has been a contributing factor to the significant flattening of the Euro area and Japanese curves, with most curves now firmly in negative territory, and leaves USTs as the last high yielder left among core bond markets. Indeed, as BofA shockingly found yesterday, the US share of global investment grade yields has climbed to 94% in the entire world, and is set to become 100% in the coming days..

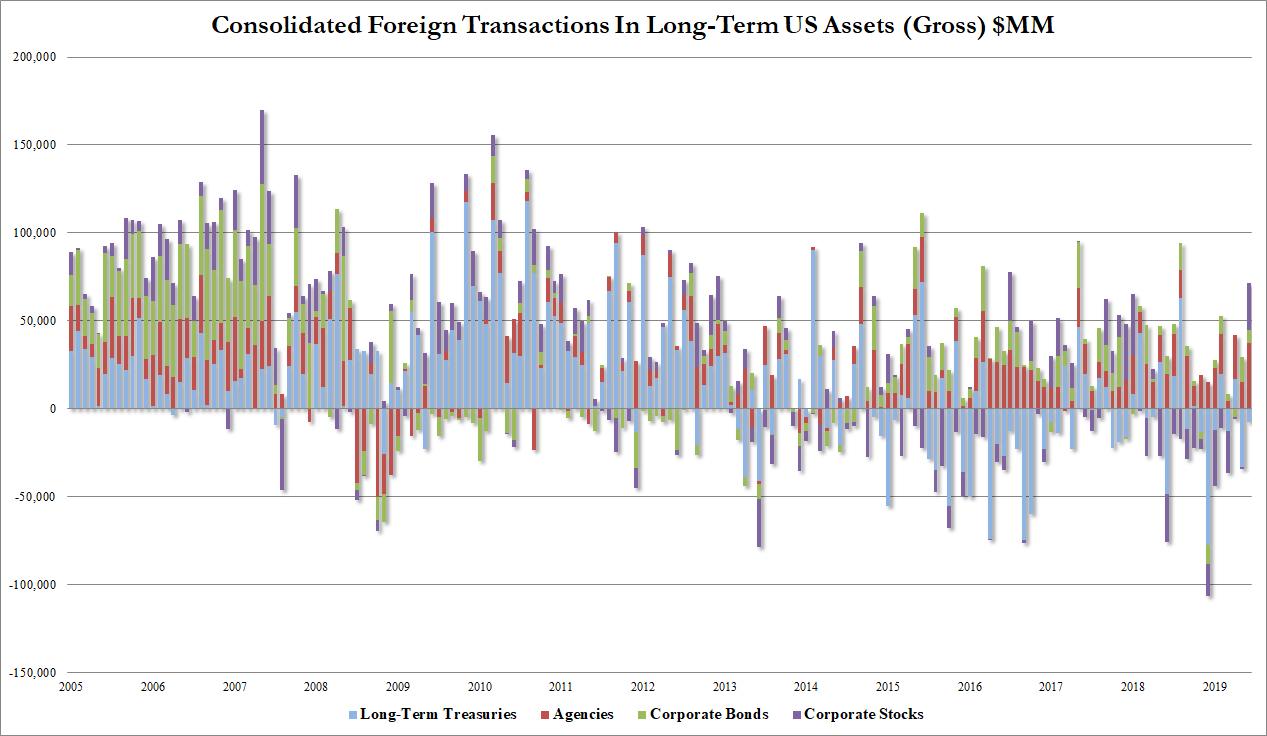

Making matters worse, when factoring in currency hedging costs, only the very long-end of the UST curve still offers a positive yield for European and Japanese investors, meaning they may be forced to consider spread product such as MBS or HG corporate bonds instead. Indeed, the latest TIC data showed that while USTs have seen cumulative outflows of nearly $30bn YTD, Agency and corporate bonds have seen inflows of $160bn.

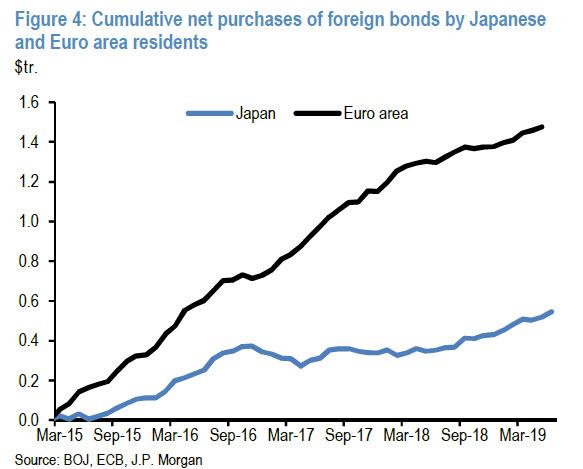

And looking at the flows from Japanese and European investors into foreign bonds, both have seen an acceleration in outflows since the turn of the year as the bond market rally has intensified, with the cumulative outflows from Japanese investors YTD in particular running at their fastest pace since January 2016 when the BoJ cut deposit rates into negative territory.

So what are the global, economic and financial implications of this gradual Japanification and relentless decline into ever more negative interest rates?

As JPMorgan Nikolaos Panigirtzoglou writes in this week’s Flows and Liquidity, a broader issue concerns the impact of negative rates on asset allocation, noting that “there is little doubt that negative yields are causing a distortion in the pricing of duration and credit risk as pension funds and insurance companies are forced to move further up the maturity and credit curve to avoid negative yields.” In other words, both duration, ie term premia and credit risk premia, are likely distorted and are likely to be distorted further if the universe of negatively yielding bonds expands further. The immediate implication is that, according to the JPM analyst, “government yield curves and credit spread curves are losing their information content.” Indeed, as Panigirtzoglou adds, “the fact that the 3m10y or 2y10y UST spreads have inverted is less of a reflection of US recession risks and more of a reflection of the desperation for yield by foreign investors flocking into USD denominated bonds as bond yields turned more negative in Europe and Japan.”

Meanwhile, US recession risks are elevated by the inversion at the front end of US money market curves which are less distorted by foreign flows, rather than the inversion of 3m10y or 2y10y UST spreads. Similarly, the fact that credit spreads have tightened, especially in Europe, is less of a reflection of an improving economy and more a reflection of European pension funds and insurance companies being forced to shift into corporate bonds to avoid very negative yields in the government space. In addition, it is likely exacerbated by expectations of the ECB restarting QE, including corporate bond purchases.

What about the impact of negative bond yields on equities?

Specifically, will negative rates force pension funds and insurance companies or other investors that dislike negative rates to move to equities? Or will pension funds and insurance companies hoover everything with positive yields in the fixed income space, including alternatives such as private debt, and avoid equity asset classes?

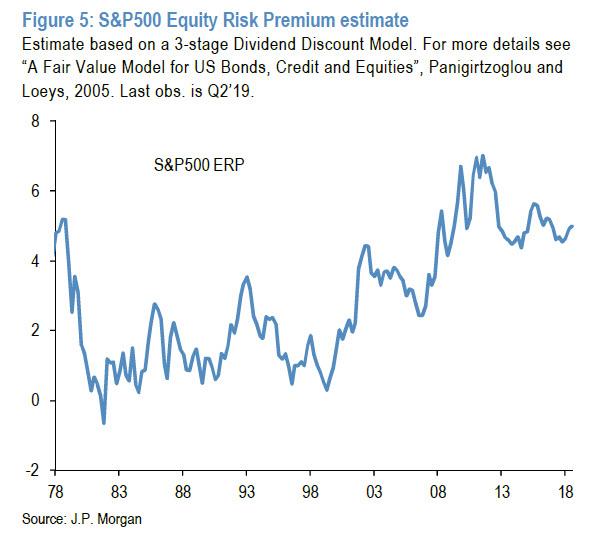

If the latter is the case and pension funds and insurance companies, a $53 trillion AUM universe in the G4 economies, avoid equities either because of regulatory constraints or demographics or simply because negative bond yields create a sense of an abnormal and uncertain environment, then the yield compression in the fixed income space could fail to spill over to equity asset classes, according to JPM. This means that the mirror image of lower bond yields would be higher rather than lower Equity Risk Premia. Indeed, the bank’s Equity Risk Premium proxy for the S&P500 index shows that since negative yields started emerging in core bond markets post the first ECB move to negative policy rate territory in June 2014, Equity Risk Premia have risen rather than fallen. This, for central banks hoping that negative rates will force stock prices to record highs, is a truly stunning development.

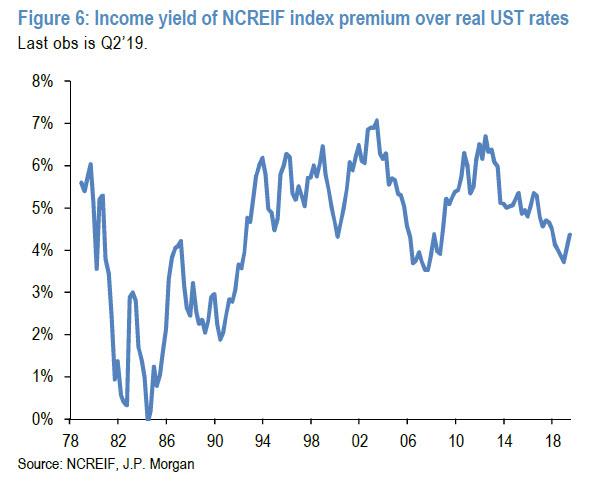

There is a similar picture with real estate. By JPMorgan estimates, property yields for the most liquid real estate markets in the world, i.e. US commercial real estate, show that yields have declined only modestly over the past year despite a compression in government bond yields. The compression in government bond yields has failed to spill over in any strong way into real estate implying that real estate risk premia vs government bonds have risen rather than fallen over the past year

In other words, as the JPMorgan strategist warns, “the hope that central banks experimenting with negative rates have that negative rates will cause a compression in risk premia in riskier asset classes beyond fixed income markets, such as equities and real estate, might not materialize.“

Needless to say this would be a historic catastrophe for capital markets, where central banks – in control over interest rates for the past century – will have officially lost control as lower rates no longer lead to easier financial conditions and higher asset prices.

A second and perhaps more important issue is about the unintended consequences of negative rates.

As readers will recall, it was back in February 2016 that we presented a JPMorgan analysis from Panigirtzoglou, in which he argued that there are several unintended consequences from very negative policy rates, with little evidence of a positive impact in Switzerland and Denmark, two of the earliest countries experimenting with very negative policy rates.

So now that there is a new record amount of negative-yielding debt, it is time revisit these unintended consequences below:

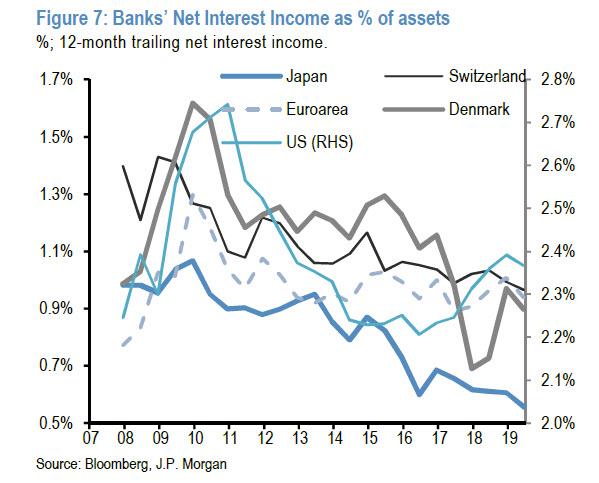

1. Lower bank profitability

It is true that a tiered deposit rate scheme, pioneered by Danish and Swiss central banks, introduced later by the BoJ and now considered by the ECB, reduces the burden on banks from taxing reserves. This is because only a portion of bank reserves are subjected to very negative interest rates. Indeed, the experience from Switzerland, Denmark and Japan is that subjecting even a small portion of reserves to the lower deposit rate could be enough to generate the marginal flow needed to push interbank rates or bond yields lower. In other words, a tiered deposit scheme can result in lower interest rates without penalizing banks too much.

However, even if the portion of reserves subjected to deeply negative rates is limited, banks are not immune to a reduction in net interest income, especially if interest rates move deeper into negative territory. This is because banks seem unable or unwilling to pass negative deposit rates to their retail customers, leaving them with few options to offset costs. These costs not only include the negative interest on their reserves with the central bank (which can be limited by a tiered scheme) but also include reduced income from security holdings as government bond yields turn negative and a potential loss in income from reduced credit creation and money market activity.

Indeed deeply negative policy rates have taken their toll on Danish, Swiss and Japanese banks’ net interest income

As JPM points out (and as it will find out soon enough personally), net interest income as % of assets has been on a declining trend since early 2015 for both Danish and Swiss banks following the introduction of very negative policy rates in these countries. In Japan, net interest margins had already deteriorated markedly by early 2016 when the BoJ adopted negative rates, but a shallower decline has continued. By contrast, net interest margins for Euro area banks appear to have held up somewhat better at least at the regional level. That said, there has been little decline in new lending rates after the ECB pushed lending rates into more negative territory in end-2015 and early 2016 even as the ECB’s second TLTRO program has helped reduce funding costs by providing funding at -40bp for banks that met relatively generous lending targets, likely supporting net interest margins.

And the contrast between banks in countries where central banks have experimented with negative deposit rates, where net interest margins have at best remained stable as in the case of the Euro area, and the US, is striking. In the latter, banks saw an improvement in net interest margins from a trough in 2016 against a background of rising central bank policy rates and despite credit creation if anything slowing modestly since early 2016, as well as a flattening in the US yield curve.

2. Reduced rather than increased credit creation to the real economy

First the good news: according to Panigirtzoglou, the introduction of modestly negative policy rates appears to have had a positive impact on credit creation. Overall credit creation improved in Denmark during 2013 and 2014 following the introduction of modestly negative policy rates in the summer of 2012. The ECB introduced negative rates in the middle of 2014 and credit creation saw a marked improvement in the Euro area with a shift from contraction to modest expansion. Sweden introduced modestly negative policy rates in 2015 and during last year credit creation to the real economy including households and non-financial corporates improved (to SEK52bn in the first three quarters of last year vs. SEK46bn for the whole of 2014).

Now the bad: there was little evidence that very negative policy rates helped credit creation further. Denmark and Switzerland introduced very negative policy rates in 2015. Credit creation to the real economy deteriorated in Denmark during 2015 vs the previous year. Indeed, it deteriorated from around DKK80bn in 2014 to DKK74bn in 2015, before subsequently increasing above DKK80bn from 2016 onward. In Switzerland the total stock of loans rose by just CHF11bn in 2015 compared to CHF31bn in 2014. Subsequently, growth in the stock of loans has risen to CHF25-40bn per year in 2016-2018, but has not surpassed the CHF46bn seen in 2013. So the evidence from Denmark and Switzerland is that the introduction of deeply negative interest rates was initially accompanied by a deterioration rather than improvement in credit creation. The subsequent recovery in lending is likely at least in part tied to an improving global growth backdrop after 2015, though at least it suggests that credit growth was not permanently weakened.

The initial evidence on credit creation from the Euro area was mixed at best: net credit creation in the Euro area declined sharply during the Euro area crisis and remained weak even as the ECB pushed deposit rates to -20bp in 2014. It subsequently recovered, though to fairly muted growth rates by historical standards. And pushing deposit rates further into negative territory at the Dec15 and Mar16 meetings did not appear to boost lending growth rates further.

So the initial experience of policy rates being pushed into very negative territory was that it was associated at best with little clear impact on credit creation and in some cases in outright contraction in loan creation, and the subsequent recovery seems subdued by historical standards.

3. Higher rather than lower bank lending rates

The message is similar to that from credit creation: the introduction of modestly negative policy rates appears to have resulted in a decline in bank lending rates to the real economy, i.e. to households and non-financial corporations. Overall bank lending rates for new loans improved in Denmark during 2013 and 2104 following the introduction of modestly negative rates in the summer of 2012. The ECB introduced negative rates around the middle of 2014, pushing the deposit rate to – 20bp, and bank lending rates also declined since then. Sweden introduced modestly negative policy rates in 2015 and bank lending rates to the real economy, including households and non-financial corporates declined during 2015.

But there was less support for the idea that deeper negative policy rates helped to further reduce bank lending rates. Denmark and Switzerland introduced very negative policy rates in 2015. In Denmark bank lending rates for new loans to non-financial corporations declined by around 40bp during 2014, but rose from late 2014 to mid-2015 by around 20bp. Bank lending rates for new loans to households declined by around 100bp during 2014 but were essentially flat during 2015 after initially rising by 60bp in 1H15. In Switzerland, bank lending rates for new investment loans to non-financial corporations went marginally higher by around 5bp during both 2015 and 2014. Bank lending rates for 10y fixed-rate mortgage loans declined until January 2015, and increased until mid-2015 before drifting towards Jan-2015 levels over the following year. Bank lending rates for variable-rate mortgage loans linked to a base rate fell until Jan15, before rising modestly by mid-2015. In the Euro area, where lending rates on new business for both households and non-financial companies declined by around 50bp during 2014, declines from late 2015 to mid-2016 when deposit rates were pushed deeper into negative territory, were more modest at around 20bp for NFCs. And while households saw larger declines in mortgage rates, rates for new loans for consumption were essentially flat.

Subsequently, the experience with deeply negative policy rates has been mixed. In Denmark, new loan rates to both NFCs and households declined by around 60bp from late 2016 to mid-2019. In Switzerland, bank lending rates for new investment loans to NFCs stabilized and were little changed in 2016-17, and declined by 5bp during 1H18 before stabilizing again. Lending rates for new 10y fixed-rate mortgages drifted 20bp higher from late 2016 to October 2018, before the bond market rally since then have seen fixed rate mortgages decline. And, despite a 50bp cut in the policy rate to -75bp in early 2015, rates on new variable interest rate mortgages linked to the policy rate declined around 10bp in total from early 2015 to late 2016 before stabilizing. In the Euro area, by contrast, loan rates on new business to NFCs and households have been relatively little changed since mid-2016. And in Sweden, new loan rates to households and NFCs have been largely stable since mid-2015.

So the evidence from Switzerland, the Euro area and Sweden appears to be that deeply negative policy rates have overall seen little further decline of lending rates as banks, whose deposit rates are largely floored at zero, struggle to avoid depressing their net interest margins further. Only in Denmark have lending rates continued to decline in subsequent years

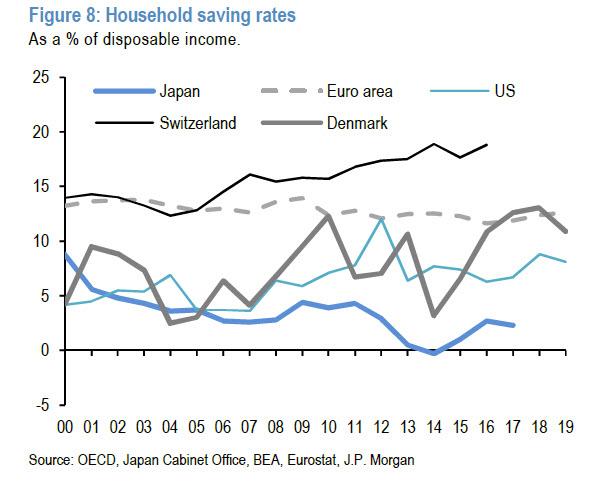

4. Higher rather than lower savings rates by households and non-financial corporates.

This was a big shock when we first pointed it out back in 2015, and quickly became one of Jeff Gundlach’s favorite talking points. For example when we look at household sector savings rates in the US, Euro area and Japan there is little evidence of lower savings rates in the Euro area and Japan, which had introduced negative policy rates in recent years, relative to the US.

Similarly there is little evidence that the non-financial corporate sectors of Euro area and Japan have reduced their financial surplus by more than the US since the introduction of negative policy rates in 2014. Higher uncertainty and the pressure to save more for retirement are likely behind persistently high savings rates by both households and companies.

5. Impaired functioning of money markets

As previously discussed, negative rates coupled with QE had caused significant slowdown in money market activity: they quite literally are an ice age . Indeed, daily data show that both unsecured (EONIA volume) and secured (GC Pooling EUR overnight index volume) money market volumes have downshifted significantly since the ECB introduced negative rates in mid-2014 and accelerated once the ECB started its bond purchase program in early 2015, and pushed rates into more negative territory in late 2015/early 2016.

And there has been at best modest signs of improvement after the ECB ended its QE program more recently. Indeed, unsecured volumes have declined further from a daily average of €4bn in 2018 to €2.4bn in 2019 to-date, though secured volumes have firmed modestly from a daily average of around €3.2bn in 2018 to €3.8bn in 2019 to-date. The collapse in money market volumes over the past years is concerning and shows that negative depo rates can make the functioning of money markets problematic even after QE is halted. Moving deeper into negative territory could exacerbate this problem.

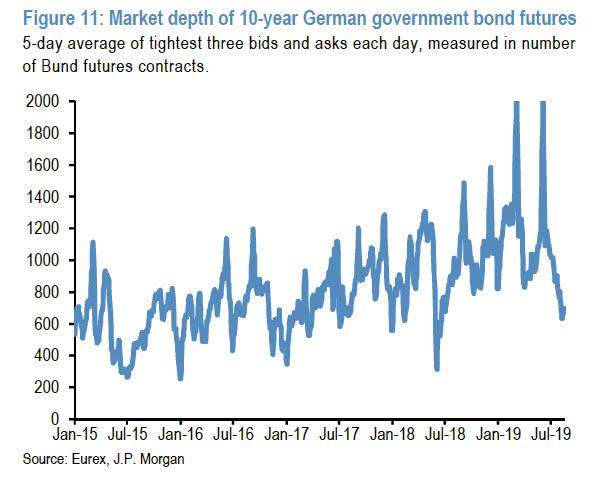

6. Reduced liquidity in bond markets

There is also a risk that, not only the functioning of money markets that becomes impaired, but that according to JPM, liquidity in bond markets could also be affected by negative bond yields as real money investors are in principle less

willing to trade bonds with negative yields. The next chart shows that the market depth of 10-year German government bond futures declined sharply this year as yields turned negative, reversing much of the improvement that occurred since mid-2016, when 10y Bund yields also turned negative. Previous sharp declines in market depth have also been associated with sharp sell-offs such as the 2015 VaR shock and in the aftermath of the US presidential election in 4Q16, but the magnitude of decline in market depth since the start of 2019 stands out nonetheless.7. Increased rather than reduced fragmentation

According to JPM’s Panigirtzoglou, there has been no improvement in the “fragmentation” of interbank markets since the first ECB depo rate cut in June 2014. ECB data show that the share of cross-border unsecured overnight interbank activity stopped improving in 2014 after rapid improvement during the second half of 2012 and during 2013. Moreover, the Euro Money Market Survey for September 2015 showed that a greater portion of the unsecured market was with national counterparties at 46% in 2015 relative to 41% in 2014. The equivalent shares for the secured market were 27% for 2015 vs. 24% in 2014; i.e. there was also deterioration in cross peripheral government paper in Euro repo markets has in fact declined between mid-2014 and mid 2015 according to the semiannual ICMA repo market survey.

Since then, the latest ECB annual financial integration indicators, from July 2019, suggest the proportion of secured and unsecured money market transactions completed with domestic counterparties has increased from 25% in 2015 to 40% in 2019. The use of cross-border collateral in ECB monetary policy operations, which had recovered from a low of around 20% in late 2013 to close to 30% by early 2015 even as policy rates moved into modestly negative territory before stabilizing, has been declining steadily since mid-2016. And the interquartile range of euro area countries’ average unsecured interbank lending rates drifted higher from mid-2014 to mid-2016 as policy rates were pushed into steadily more negative territory. From mid-2016, when the ECB’s TLTRO 2 operations were conducted, the interquartile range narrowed until early 2018, after which it has widened again sharply.

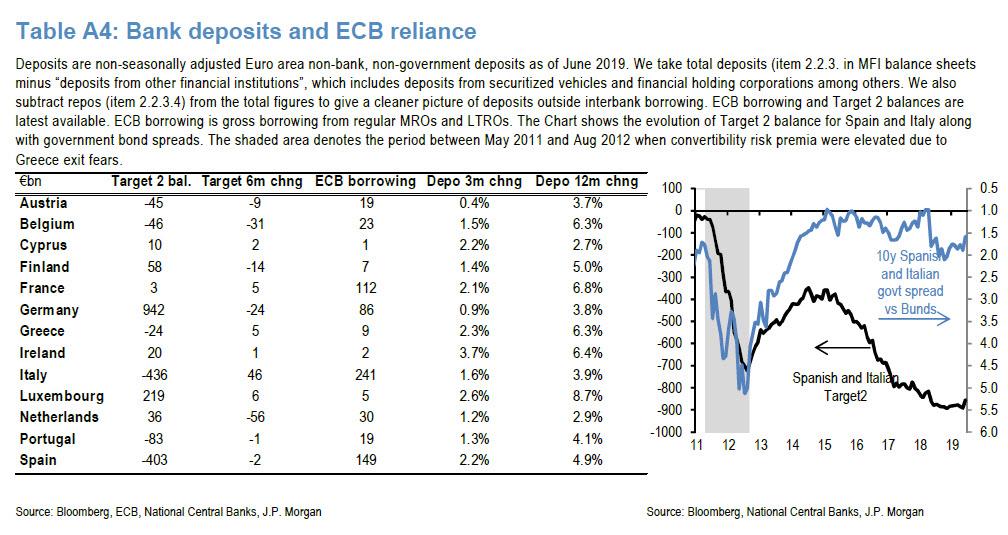

In addition, there has been deterioration in Target 2 balances since mid-2014, the broadest among quantitative measures of fragmentation. The sum of Spanish and Italian Target 2 balances has deteriorated by moving deeply into negative territory since the ECB first cut its depo rate to negative. After hitting a high of -€347bn in July 2014, the sum of Spanish and Italian Target 2 balances have been steadily declining and reached a low of €893bn in November 2018 before increasing slightly.

The reasons for the Target 2 widening have been somewhat different after the ECB started QE compared to the Euro area sovereign crisis. As we have argued previously, the more recent decline has likely been exacerbated by investors from outside the Euro area, who often hold cash accounts in core countries, selling e.g. Italian bonds to the Bank of Italy, this registers as an increase in the Target 2 liability. Nonetheless, this decline in the Target 2 balances still represents a measure of fragmentation.

In all, the evidence from money markets and Target 2 balances is at best mixed in terms of fragmentation, with some deterioration in some metrics, since the ECB introduced negative depo rates in June 2014. This is not to say that negative depo rates didn’t bolster the search for yield in the government space and the velocity of reserves, i.e. passing on the “hot potato” within the Euro area banking system. It did, as evidenced by the collapse in interest rates, the rapid expansion of the universe of negatively-yielding government bonds in the euro area core, and the concentration of reserves in core banks’ balance sheets. But while there have been capital inflows into some periphery countries, notably Spain, Italy has seen outflows particularly from bonds.

What is the channel via which negative policy rates could increase fragmentation? One potential channel is the risk appetite of banks. To the extent that negative policy rates hurt bank profitability, banks might become less willing to take risk and thus less willing to lend in interbank markets or to take credit risk in their bond portfolios. On the latter, there appears to be support from much of the academic literature that negative rates have depressed lending volumes for banks with high deposit shares. At the same time, work by the ECB (by Demiralp et al, May 2019) using Euro area bank level lending data suggests when controlled for both high retail deposit ratios and high negatively yielding excess liquidity ratios, as banks particularly exposed to negative rates, there has been a positive relationship with lending. As the ECB contemplates pushing deposit rates into even more negative territory, this is clearly a key issue – could more negative rates backfire by putting more pressure on bank profitability and curb risk-taking?

8. Lower bond yields increase pension fund and insurance company deficits putting pressure on pension funds to match assets and liabilities.

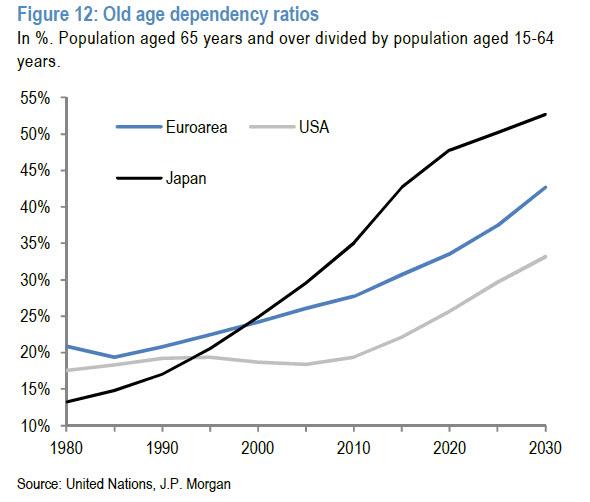

This pressure to move further away from equities and other high risk assets into fixed income is even stronger in countries like Japan where demographic pressures are more intense. For example, old age dependency ratios, i.e. the proportion of the population aged 65 years and over as a percentage of the population aged 15-64 years, have been rising steadily, with Japan aging more rapidly than the US or Europe.

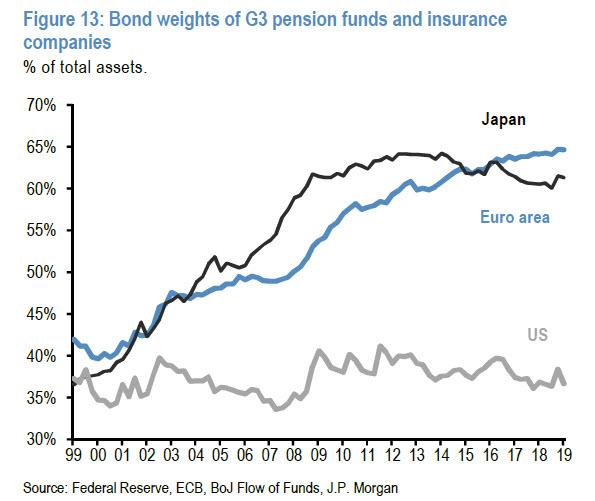

Generally, an aging population means that allocations are likely to shift towards relatively safer instruments as the ability to withstand larger drawdowns on capital diminishes as individuals age. And the effect of these demographic rends is likely a factor in the high share of total assets held in bonds by Japanese pension funds, especially relative to their US counterparts.

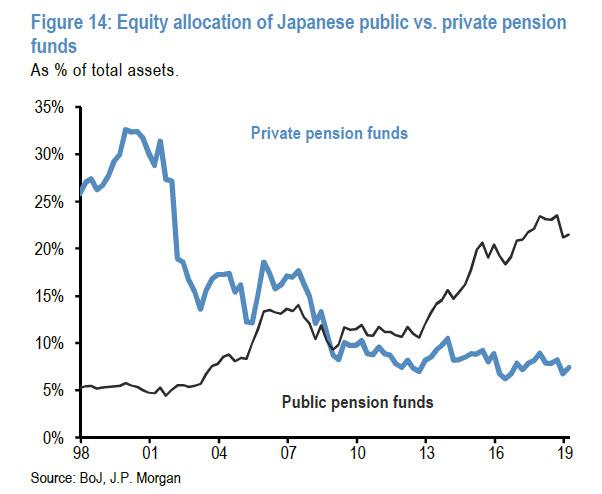

What is striking in Japan is that, in contrast to GPIF, which shifted towards equities post Abenomics most likely under political pressure, private Japanese pension funds have if anything reduced their equity allocations modestly

In general pension funds and insurance companies including those outside Japan are facing an increase in their liabilities and as a result a deterioration in their funded status. And the options pension funds and insurance companies are limited. On the asset side they can increase duration risk by shifting into even longer maturity bonds, increase credit risk by shifting into even riskier spread products, and increase fx risk by shifting into higher yielding foreign bonds. On the liability side they reduce benefits to new and sometimes existing plan beneficiaries, or they ask plan sponsors to increase their contributions.

Pension funds and insurance companies which are facing a big increase in their liabilities have limited options such as taking a lot more fx and credit risk by shifting to foreign government or corporate bond markets, reducing benefits to new and sometimes to existing plan beneficiaries, or ask plan sponsors to increase their contributions. The overall impact is that lower yields can induce households, or companies that act as plan sponsors, to save even more for the future, an argument we have made since 2014, and one which not a single economist appears able to grasp.

9. More income and wealth inequality as households and small businesses fail to benefit or are even hurt from negative rates.

The main beneficiaries of negative rates have been large corporates which have seen a collapse to their interest expense as well as private equity companies that are able to lever by even more than in previous cycles to amplify their profits. Indeed, the median debt to EBITDA ratio for both HG and HY companies has risen in recent years to well above the peaks seen in previous cycles.

10. Central banks are trapped.

Negative rates coupled with QE raise questions about central banks’ exit potentially becoming more difficult in the future and raise the risk of a policy error as well as perceptions about debt monetization. It potentially creates bond bubbles by lowering bond yields below their equilibrium or fair value, creating fears that an eventual return to normality could be accompanied by sharp price declines. Perceptions about bond bubbles can increase long term uncertainty. In turn, higher uncertainty might prevent economic agents such as businesses from spending.

11. The death of creative destruction and the zombification of corporations

Low credit spreads and corporate bond yields are an intended consequence of negative rates as pension funds

and insurance companies are forced to shift up both the maturity and credit curve, but not without distortions. By

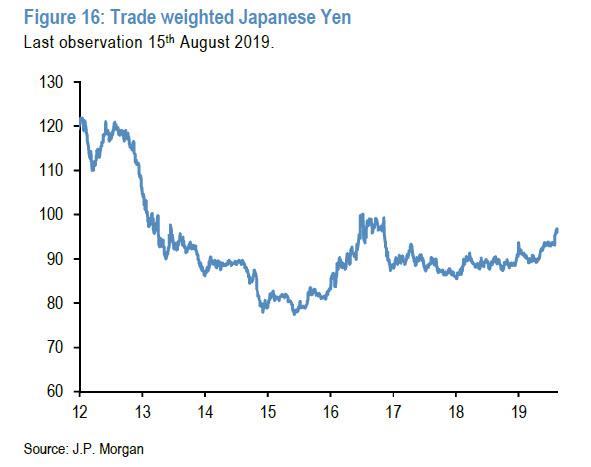

potentially allowing unproductive and inefficient companies to survive, helped by low debt servicing costs, negative rates could potentially hinder the creative destruction taking place during a normal economic cycle. In principle, similar to QE, negative rates could thus make economies less efficient or productive over time. The debate about so called “zombie” companies has been particularly intense in Japan given the low business turnover rate. According to OECD, Japan’s business startup and closure rate is about 5%, roughly a third of that in other advanced economies with several commentators blaming the BoJ’s ultra-accommodative policies for this problem.12. QE could exacerbate so called “currency wars”.

The value of the Japanese yen collapsed after Abenomics started in November 2012 and has stayed at historical lows since then helped by BoJ’s ultra-accommodative monetary policy. This is shown in the next chart by the real trade weighted index of the Japanese yen.

Japan’s main competitors across EM and DM have been feeling the pressure from this depreciation, though it is not clear that the depreciation necessarily means the yen is undervalued. Similarly, more recently, the ECB’s prospective shift towards more negative rates is currently putting downward pressure on the euro vs the dollar risking a response by the US administration

* * *

Putting all of the above together, JPMorgan warns that moving to very negative policy rates – as the world is clearly doing now – by central banks is not without risks or side effects. Modestly negative policy rates had perhaps an overall positive impact initially, but keeping rates in very negative territory for prolonged periods or navigating to even deeper negative territory could unleash more unintended consequences than benefits. Just like QE, which from an emergency medicine to prevent the world from dying became a laxative to be used daily to prop up stock markets for the better part of the past decade.

Still, in JPM’s opinion, this does not mean that central banks are without ammunition. Shifting to purchases of assets other than government bonds such as corporate bonds or bank loans has been used only sparingly so far. Even modest amounts of bank loan purchases could be more powerful than large purchases of government bonds, even if this implies central banks assuming more risk. This is especially true in the euro area where several countries face a persistent drag from non-performing loans, and where the ECB is very likely to get actively involved in reducing NPLs further by outright buying the loans.

Ironically, even the JPMorgan strategist warns that he is “rather reluctant to advocate purchases of equities given the lack of a positive impact from BoJ’s equity ETF purchases so far, either in terms of the relative performance or the liquidity of the Japanese equity market.”

Finally, in a claim that may spark a vendetta between Panigirtzoglou and Albert Edwards, the JPM strategist concludes that “negative rates are neither unavoidable nor necessary.” As he explains, “Japanization didn’t imply negative yields before the BoJ experimented with negative policy rates, following the experiment of the ECB. And negative rates do not appear to have delivered more effective stimulus and helped Japan to exit its longstanding economic malaise.”

Panigirtzoglou goes one further, and in debunking a rather vocal financial troll who somehow has a prime time presence on financial TV and media, says that according to conversations with clients “the experiments of central banks with negative rates are viewed more as a policy mistake rather than stimulus and create a sense of an abnormal and uncertain environment that damages not only banks but also consumer and business confidence.“

It is this sense of abnormality and uncertainty that makes businesses and consumers less rather than more keen to spend and banks more rather than less averse to taking risk and extending credit to the real economy.

Which is also why if and when negative rates are adopted by every central bank in the world, the consequences for society, for the economy, and for capital markets will be nothing short of catastrophic.

- Austin Slammed By Crippling Ransomware Attack

A coordinated ransomware attack has affected at least 20 local government entities in Texas, the Texas Department of Information Resources said. It would not release information about which local governments have been affected.

The Texas Division of Emergency Management is coordinating support from other state agencies through the Texas State Operations Center at DPS headquarters in Austin, according to KUT News.

City employees scrambling in the aftermath of the attack.

Press secretary for the department, Elliot Sprehe, said DIR was working to confirm which government entities are affected and which ones are still standing.

“It looks like we found out earlier today, but we’re not currently releasing who’s impacted due to security concerns,” he said.

KUT tried to contact the city of Austin for more details about the attack but the city refused to release any more information.

The Department of Information Resources advises jurisdictions that have been impacted to contact their local Texas Department of Emergency Management Disaster District Coordinator. DIR says it’s committed to providing the resources necessary to bring affected entities “back online.”