- Destroying The Planet To Save Ukraine?

Destroying The Planet To Save Ukraine?

Authored by Patricia Adams and Lawrence Solomon via The Epoch Times,

Saving Ukraine from Russia has become more important to Western leaders than saving the planet from climate change, more important than keeping their populations from freezing in the dark, more important than the viability of Western industries, and more important even than avoiding the risk of an all-out nuclear war between the West and Russia.

An early indication of the West’s loss of all perspective where Russia is concerned – call it Russia Derangement Syndrome – occurred in the United States after Donald Trump was elected president. Large swathes of the public, including virtually all Democrats and the legacy media, embraced a fantasy known as Russian Collusion, which asserted that Russia had colluded with the Trump campaign to install him as president.

The fantasy persisted for three years until 2019 when Russia Collusion was confirmed to be a hoax perpetrated by Trump’s rival for the 2016 presidency, Hillary Clinton.

Former Homeland Security Secretary Jeh Johnson testifies before the House Intelligence Committee in an open hearing in the U.S. Capitol Visitors Center in Washington on June 21, 2017. Johnson answered questions about Russia’s interference in the 2016 presidential elections and his department’s response to the threat. (Chip Somodevilla/Getty Images)

Earlier this year, after Russia invaded Ukraine over a territorial dispute, Russia Derangement Syndrome went into overdrive. An infuriated West sanctioned Russian goods and services helter-skelter without thinking through the consequences, chiefly those involving energy. Russia represents continental Europe’s chief energy source and is the main reason Europeans can keep the lights on.

Only after the Europeans decided to punish Russia, and only after Russia announced cuts to gas flows—temporarily, it said—on the Nord Stream 1 pipeline of 60 percent, did it dawn on Europeans that Russia could retaliate this coming winter through punitively-timed energy curtailments, putting Europe at Russia’s mercy.

In Germany, for example, Chancellor Olaf Scholz’s administration did its sums to discover that under all scenarios, Germany lacked the reserves needed to last the winter.

“That was the sobering moment,” admitted Klaus Mueller, who heads Germany’s gas network regulator.

“If we have a very, very cold winter, if we’re careless and far too generous with gas, then it won’t be pretty.”

The European Union, now in a panic, is scrambling to acquire fossil fuels from any sources in a desperate attempt to stockpile energy prior to winter. Germany is returning to coal, as are Austria, Italy, and the Netherlands. The United Kingdom is also turning to coal and reversing its ban on fracking and on North Sea oil production. The EU is endorsing Norway’s latest exploitation of the North Sea and is open to new contracts for long-term commitments of natural gas.

The United States is exporting record amounts of gas, so much so that Europe now receives more high-priced liquefied natural gas from U.S. tankers than inexpensive natural gas from Russian pipelines. Since Russia invaded Ukraine, Europeans have advanced more than 20 liquefied natural gas import projects.

In this fossil fuel free-for-all, the West has effectively abandoned its once ironclad commitment to combat climate change, which its leaders never tired of describing as an existential threat to the planet. Gone is Germany’s net-zero commitment to phase out coal plants by 2030, tenuous is the UK’s pledge to stop using coal in power stations by 2024, and shaky is the G-7’s determination to end “direct public support for the international unabated fossil fuel energy sector by the end of 2022.” Instead, the G-7, noting its determination to support Ukraine, backed increased deliveries of liquefied natural gas and urged oil-producing nations to increase their production.

Wind turbines near a coal-fired power plant are pictured near Hamm, western Germany, on June 8, 2022. (INA FASSBENDER/AFP via Getty Images)

To punish Russia, the Europeans are knowingly visiting far more severe punishments on themselves. Germany is preparing to put its population on an emergency footing by urging a rationing of energy. Its governments are responding by dimming street lights, switching off the illumination of historic buildings, and shutting off hot water in gyms, museums, and government buildings. Housing complexes are limiting the hours that hot showers can be taken and lowering the thermostats in centrally heated complexes. Industries are planning to scale back, move away from Europe, or shut down operations altogether.

“A complete halt to Russian natural gas exports would cost Germany 12.7% of economic performance in the second half of 2022,” costing some $200 billion and affecting 5.6 million jobs, the Bavaria Industry Association warned last month.

Denmark’s emergency plan involves shutting down gas heating during the summer, taking shorter showers, drying clothes outside, and suspending gas supplies to energy-intensive industries.

A greater punishment still is being voiced in the form of nuclear war. The UK, France, and the United States have all reminded Russia that they possess nuclear weapons in response to Russian reminders that it has the greatest nuclear arsenal of all.

Remarkably, before the West so uniformly came to Ukraine’s defense, Ukraine was held in low regard by Europeans, viewed as a kleptocracy run by corrupt oligarchs with only the faintest hint of the rule of law. That image was transformed overnight once Russia invaded, as Ukraine became an instant darling of the West, so worthy as to warrant the destruction of the West’s economy, environment, and possibly the West itself.

Such is the power of the Russia Derangement Syndrome.

Tyler Durden

Sun, 07/17/2022 – 23:30 - Rescue-Fund Idea Floated To Stop Mortgage Crisis

Rescue-Fund Idea Floated To Stop Mortgage Crisis

By George Lei, Bloomberg Markets Live reporter and analyst

The Chinese stock market suffered its biggest weekly loss in three months, with the benchmark CSI 300 index sinking more than 4%. Real estate and banking risks soured sentiment and surging Covid cases made matters worse.

Last week, housing ministry officials met with financial regulators and major Chinese banks to discuss lending matters. The government also censored crowd-sourced documents tallying the number of mortgage boycotts across the country. Markets, however, expect much more. Swift policy responses coordinated from Beijing are urgently needed to prevent bigger market rout.

Knee-jerk reactions from local authorities may be to tighten oversight of escrow accounts for new home sales, and for banking regulators to raise mortgage standards. After all, a key reason for the mortgage boycotts is that developers diverted homeowner payments for other purposes. Now that many developers are facing financing difficulties, construction on those unfinished homes stalled.

Such moves make perfect sense in isolation. But they might cause more troubles nationwide if implemented together. More money in escrow means less for developers, which could “lead to a sustained slowdown in housing market activity and more developer defaults,” according to a JPMorgan client note written by Tingting Ge, Haibin Zhu and Grace Ng on Friday. Relaxation of escrow management, on the other hand, would create the risk of embezzlement that could hurt more homebuyers.

Nomura also expects “stricter control over presale escrow accounts” that would “hurt sales demand further,” credit desk analyst Iris Chen said in a note on Thursday. Mortgage issuance may also face a stricter approval process that could slow down cash collection and add pressure to developers’ liquidity.

The mortgage boycott news, paradoxically, reduced concerns that accommodative macro policies might be pulled back, according to a client note from Goldman Sachs. Analysts Maggie Wei, Hui Shan and Lisheng Wang talked with clients including asset managers, private equity and hedge funds in Beijing and Shanghai. They found that domestic investors have high expectations for additional fiscal measures, such as more government bond issuance or further financial support by policy banks.

Monetary easing alone cannot provide a quick fix to property sector problems, Xu Gao, chief economist at Bank of China International told local media. He floated the idea of a 1 trillion yuan ($148 billion) relief fund to buy non-controlling equity stakes in troubled developers. Once the builders are adequately capitalized with state-backed money, banks will be more willing to lend and the public will feel more assured of their new home purchases.

There are plenty of precedents for such rescue facilities. In 2008-09, the US Treasury spent about $250 billion to stabilize banks and $46 billion to help struggling families avoid foreclosure under the Troubled Assets Relief Program. Premier Li Keqiang said in March that Beijing plans to set up a fund for ensuring financial stability without giving more details.

Now, it looks like homeowners, banks and developers all need some lifeline to see through the mortgage crisis. Policy makers in the very top will need to act swiftly and decisively. The consequences of inaction, or a piecemeal, uncoordinated approach, can be very costly.

Tyler Durden

Sun, 07/17/2022 – 22:47 - Dr. Birx Praises Herself While Revealing Ignorance, Treachery, & Deceit

Dr. Birx Praises Herself While Revealing Ignorance, Treachery, & Deceit

Authored by Jeffrey Tucker via The Brownstone Institute,

The December 2020 resignation of Dr. Deborah Birx, White House Coronavirus Response Coordinator under Trump, revealed predictable hypocrisy.

Like so many other government officials around the world, she was caught violating her own stay-at-home order.

Therefore she finally left her post following nine months of causing unfathomable amounts of damage to life, liberty, property, and the very idea of hope for the future.

Even if Anthony Fauci had been the front man for the media, it was Birx who was the main influence in the White House behind the nationwide lockdowns that did not stop or control the pathogen but have caused immense suffering and continue to roil and wreck the world. So it was significant that she would not and could not comply with her own dictates, even as her fellow citizens were being hunted down for the same infractions against “public health.”

In the days before Thanksgiving 2020, she had warned Americans to “assume you’re infected” and to restrict gatherings to “your immediate household.” Then she packed her bags and headed to Fenwick Island in Delaware where she met with four generations for a traditional Thanksgiving dinner, as if she were free to make normal choices and live a normal life while everyone else had to shelter in place.

The Associated Press was first out with the report on December 20, 2020.

Birx acknowledged in a statement that she went to her Delaware property. She declined to be interviewed.

She insisted the purpose of the roughly 50-hour visit was to deal with the winterization of the property before a potential sale — something she says she previously hadn’t had time to do because of her busy schedule.

“I did not go to Delaware for the purpose of celebrating Thanksgiving,” Birx said in her statement, adding that her family shared a meal together while in Delaware.

Birx said that everyone on her Delaware trip belongs to her “immediate household,” even as she acknowledged they live in two different homes. She initially called the Potomac home a “3 generation household (formerly 4 generations).” White House officials later said it continues to be a four-generation household, a distinction that would include Birx as part of the home.

So it was all a sleight-of-hand: she was staying home; it’s just that she has several homes! This is how the power elite comply, one supposes.

The BBC then quoted her defense, which echo the pain experienced by hundreds of millions:

“My daughter hasn’t left that house in 10 months, my parents have been isolated for 10 months. They’ve become deeply depressed as I’m sure many elderly have as they’ve not been able to see their sons, their granddaughters. My parents have not been able to see their surviving son for over a year. These are all very difficult things.”

Indeed. However, she was the major voice for the better part of 2020 for requiring exactly that. No one should blame her for wanting to get together with family; that she worked so hard for so long to prevent others from doing so is what is at issue.

The press piled on and she announced that she would be leaving her post and not seeking a position at the Biden White House. Trump tweeted that she will be missed. It was the final discrediting – or should have been – of a person that many in the White House and many around the country had come to see as an obvious fanatic and fake, a person whose influence wrecked the liberties and health of an entire country.

It was a fitting end to a catastrophic career.

So it would make sense that people might pick up her new book to find out what it was like to go through that kind of media storm, the real reasons for her visit, what it was like to know for sure that she must violate her own rules in order to bring comfort to her family, and the difficult decision she made to throw in the towel knowing that she has compromised the integrity of her entire program.

One slogs through her entire book only to find this incredible fact: she never mentions this. The incident is missing entirely from her book.

Instead at the moment in the narrative at which she would be expected to recount the affair she says almost in passing that “When former vice president Biden was declared the winner of the 2020 election, I’d set a goal for myself—to hand over responsibility for the pandemic response, with all its many elements, in the best possible place.”

At that point, the book skips immediately to the new year. Done. It’s like Orwell, the story, even though it was reported for days in the world press and became a defining moment in her career, is just wiped out from the history book of her own authorship.

Somehow it makes sense that she would neglect to mention this. Reading her book is a very painful experience (all credit to Michael Senger’s review) simply because it seems to be weaving fables on page after page, strewn with bromides, completely lacking in self awareness, punctuated by revealing comments that make the opposite point of what she is seeking. Reading it is truly a surreal experience, astonishing especially because she is able to maintain her delusionary pose for 525 pages.

Recall that it was she who was tasked – by Anthony Fauci – with doing the really crucial thing of talking Donald Trump into green-lighting the lockdowns that began on March 12, 2020, and continued to their final hard-core deployment on March 16. This was the “15 Days to Flatten the Curve” that turned into two years in many parts of the country.

Her book admits that it was a two-level lie from the beginning.

“We had to make these palatable to the administration by avoiding the obvious appearance of a full Italian lockdown,” she writes. “At the same time, we needed the measures to be effective at slowing the spread, which meant matching as closely as possible what Italy had done—a tall order. We were playing a game of chess in which the success of each move was predicated on the one before it.”

Further:

“At this point, I wasn’t about to use the words lockdown or shutdown. If I had uttered either of those in early March, after being at the White House only one week, the political, nonmedical members of the task force would have dismissed me as too alarmist, too doom-and-gloom, too reliant on feelings and not facts. They would have campaigned to lock me down and shut me up.”

In other words, she wanted to go full CCP just like Italy but didn’t want to say that. Crucially, she knew for sure that two weeks was not the real plan. “I left the rest unstated: that this was just a starting point.”

“No sooner had we convinced the Trump administration to implement our version of a two-week shutdown than I was trying to figure out how to extend it,” she admits.

“Fifteen Days to Slow the Spread was a start, but I knew it would be just that. I didn’t have the numbers in front of me yet to make the case for extending it longer, but I had two weeks to get them. However hard it had been to get the fifteen-day shutdown approved, getting another one would be more difficult by many orders of magnitude. In the meantime, I waited for the blowback, for someone from the economic team to call me to the principal’s office or confront me at a task force meeting. None of this happened.”

It was a solution in search of evidence she did not have. She told Trump that the evidence was there anyway. She actually tricked him into believing that locking down a whole population of people was somehow magically going to make a virus to which everyone would inevitably be exposed somehow vanish as a threat.

Meanwhile, the economy was wrecked domestically and then all over the world, as most governments in the world followed what the US did.

Where did she come up with the idea of lockdowns? By her own report, her only real experience with infectious disease came from her work on AIDS, a very different disease from a respiratory virus that everyone would eventually get but which would only be fatal or even severe for a small cohort, a fact that was known since late January. Still, her experience counted for more than science.

“In any health crisis, it is crucial to work at the personal behavior level,” she says with the presumption that avoidance at all costs was the only goal. “With HIV/AIDS, this meant convincing asymptomatic people to get tested, to seek treatment if they were HIV-positive, and to take preventative measures, including wearing condoms; or to employ other pre-exposure prophylaxis (PrEP) if they were negative.”

She immediately hops to the analogy with Covid. “I knew the government agencies would need to do the same thing to have a similar effect on the spread of this novel coronavirus. The most obvious parallel with the HIV/AIDS example was the message of wearing masks.”

Masks = condoms. Remarkable. This “obvious parallel” remark sums the whole depth of her thinking. Behavior is all that matters. Just stay apart. Cover your mouth. Don’t gather. Don’t travel. Close the schools. Close everything. Whatever happens, don’t get it. Nothing else matters. Keep your immune system as unexposed as possible.

I wish I could say her thought is more complex than that but it is not. This was the basis for lockdowns. For how long? In her mind, it seems like it would be forever. Nowhere in the book does she reveal an exit strategy. Not even vaccines qualify.

From the very beginning, she revealed her epidemiological views. On March 16, 2020 at her press conference with Trump, she summarized her position: “We really want people to be separated at this time.” People? All people? Everywhere? Not one reporter raised a question about this obviously ridiculous and outrageous statement that would essentially destroy life on earth.

But she was serious – seriously deluded not only about how society functions but also about infectious disease of this sort. Only one thing mattered as a metric to her: reducing infections through any means possible, as if she on her own could cobble together a new kind of society in which exposure to airborne pathogens was made illegal.

Here is an example. There was a controversy about how many people should be allowed to gather in one space, as in home, church, store, stadium, or community center. She addresses how she came up with the rules:

The real problem with this fifty-versus-ten distinction, for me, was that it revealed that the CDC simply didn’t believe to the degree that I did that SARS-CoV-2 was being spread through the air silently and undetected from symptomless individuals. The numbers really did matter. As the years since have confirmed, in times of active viral community spread, as many as fifty people gathered together indoors (unmasked at this point, of course) was way too high a number. It increased the chances of someone among that number being infected exponentially. I had settled on ten knowing that even that was too many, but I figured that ten would at least be palatable for most Americans—high enough to allow for most gatherings of immediate family but not enough for large dinner parties and, critically, large weddings, birthday parties, and other mass social events.

She puts a fine point on it: “if I pushed for zero (which was actually what I wanted and what was required), this would have been interpreted as a ‘lockdown’—the perception we were all working so hard to avoid.”

What does it mean for zero people to gather? A suicide cult?

In any case, just like that, from her own thinking and straight to enforcement, birthday parties, sports, weddings, and funerals came to be forbidden.

Here we gain insight into the sheer insanity of her vision. It is nothing short of a marvel that she somehow managed to gain the amount of influence she did.

Notice her above mention of her dogma that asymptomatic spread was the whole key to understanding pandemic. In other words, on her own and without any scientific support, she presumed that Covid was both extremely fatal and had a long latency period. To her way of thinking, this is why the usual tradeoff between severity and prevalence did not matter.

She was somehow certain that the longest estimates of latency were correct: 14 days. This is the reason for the “wait two weeks” obsession. She held onto this dogma throughout, almost like the fictional movie “Contagion” had been her only guide to understanding.

Later in the book, she writes that symptoms mean next to nothing because people can always carry around the virus in their nose without being sick. After all, this is what PCR tests have shown. Instead of seeing that as a failure of PCR, she saw this as a confirmation that everyone is a carrier no matter what and therefore everyone has to lock down because otherwise we’ll deal with a black plague.

Somehow, despite her astonishing lack of scientific curiosity and experience in this area, she gained all influence over the initial Trump administration response. Briefly, she was godlike.

But Trump was not and is not a fool. He must have had some sleepless nights wondering how and why he had approved the destruction of that which he had seen as his greatest achievement. The virus was long here (probably from October 2019), it presented a specific danger to a narrow cohort, but otherwise behaved like a textbook flu. Maybe, he must have wondered, his initial instincts from January and February 2020 were correct all along.

Still, he very reluctantly approved a 30-day extension of lockdowns, entirely on Birx’s urging and with a few other fools standing around. Having given in a second time – still, no one thought to drop an email or make a phone call for a second opinion! – this seemed to be the turning point. Birx reports that by April 1, 2020, Trump had lost confidence in her. He might have intuited that he had been tricked. He stopped speaking to her.

It would still take another month before he would fully rethink everything that he had approved at her behest.

It made no difference. The bulk of her book is a brag fest about how she kept subverting the White House’s push to open up the economy – that is, allow people to exercise their rights and freedoms. Once Trump turned against her, and eventually found other people to provide good advice like the tremendously brave Scott Atlas – five months later he arrived in an attempt to save the country from disaster – Birx turned to rallying around her inner circle (Anthony Fauci, Robert Redfield, Matthew Pottinger, and a few others) plus assembling a realm of protection outside of her that included CNN reporter Sanjay Gupta and, very likely, the virus team at the New York Times (which gives her book a glowing review).

Recall that for the remainder of the year, the White House was urging normalcy while many states kept locking down. It was an incredible confusion. The CDC was all over the map. I gained the distinct impression of two separate regimes in charge: Trump’s vs. the administrative state he could not control. Trump would say one thing on the campaign trail but the regulations and disease panic kept pouring out of his own agencies.

Birx admits that she was a major part of the reason, due to her sneaky alternation of weekly reports to the states.

After the heavily edited documents were returned to me, I’d reinsert what they had objected to, but place it in those different locations. I’d also reorder and restructure the bullet points so the most salient—the points the administration objected to most—no longer fell at the start of the bullet points. I shared these strategies with the three members of the data team also writing these reports. Our Saturday and Sunday report-writing routine soon became: write, submit, revise, hide, resubmit.

Fortunately, this strategic sleight-of-hand worked. That they never seemed to catch this subterfuge left me to conclude that, either they read the finished reports too quickly or they neglected to do the word search that would have revealed the language to which they objected. In slipping these changes past the gatekeepers and continuing to inform the governors of the need for the big-three mitigations—masks, sentinel testing, and limits on indoor social gatherings—I felt confident I was giving the states permission to escalate public health mitigation with the fall and winter coming.

As another example, once Scott Atlas came to the rescue in August to introduce some good sense into this wacky world, he worked with others to dial back the CDC’s fanatical attachment to universal and constant testing. Atlas knew that “track, trace, and isolate” was both a fantasy and a massive invasion of people’s liberties that would yield no positive public-health outcome. He put together a new recommendation that was only for those who were sick to test – just as one might expect in normal life.

After a week-long media frenzy, the regulations flipped in the other direction.

Birx reveals that it was her doing:

This wasn’t the only bit of subterfuge I had to engage in. Immediately after the Atlas-influenced revised CDC testing guidance went up in late August, I contacted Bob Redfield…. Less than a week later, Bob [Redfield] and I had finished our rewrite of the guidance and surreptitiously posted it. We had restored the emphasis on testing to detect areas where silent spread was occurring. It was a risky move, and we hoped everyone in the White House would be too busy campaigning to realize what Bob and I had done. We weren’t being transparent with the powers that be in the White House…

One might ask how the heck she got away with this. She explains:

[T]he guidance gambit was only the tip of the iceberg of my transgressions in my effort to subvert Scott Atlas’s dangerous positions. Ever since Vice President Pence told me to do what I needed to do, I’d engaged in very blunt conversations with the governors. I spoke the truth that some White House senior advisors weren’t willing to acknowledge. Censoring my reports and putting up guidance that negated the known solutions was only going to perpetuate Covid-19’s vicious circle. What I couldn’t sneak past the gatekeepers in my reports, I said in person.

Most of the book consists of her explaining how she headed a kind of shadow White House dedicated to keeping the country in some form of lockdown for as long as possible. In her telling, she was the center of everything, the only person truly correct about all things, given cover by the VP and assisted by a handful of co-conspirators..

Largely missing from the narrative is any discussion of the science gathering outside the bubble she so carefully cultivated. Whereas anyone could have noted the studies pouring out from February onward that threw cold water on her entire paradigm – not to mention 15 years, or make that 50 years, or perhaps 100 years of warnings against such a reaction – from scientists all over the world with vastly more experience and knowledge than she. She cared nothing about it, and evidently still does not.

It’s very clear that Birx had almost no contact with any serious scientist who disputed the draconian response, not even John Iaonnidis who explained as early as March 17, 2020, that this approach was madness. But she didn’t care: she was convinced that she was in the right, or, at least, was acting on behalf of people and interests who would keep her safe from persecution or prosecution.

For those interested, Chapter 8 provides a weird look into her first real scientific challenge: the seroprevalence study by Jayanta Bhattacharya published April 22, 2020. It demonstrated that the infection fatality rate – because infections and recovery was far more prevalent than Birx and Fauci were saying – was more in line with what one might expect from a severe flu but with a much more focused demographic impact. Bhattacharya’s paper revealed that the pathogen eluded all controls and would likely become endemic as every respiratory virus before. She took one look and concluded that the study had unnamed “fundamental flaws in logic and methodology” and “damaged the cause of public health at this crucial moment in the pandemic.”

And that’s it: that’s Birx grappling with science. Meanwhile, the article was published in the International Journal of Epidemiology and has over 700 citations. She saw all differences of opinion as an opportunity to go on the attack in order to intensify her cherished commitment to the lockdown paradigm.

Even now, with scientists the world over in outrage, with citizens furious at their governments, with governments falling, with regimes toppling and anger reaching a fevered pitch, while studies pour out by the day showing that lockdowns made no difference and that open societies at least protected their educational systems and economies, she is unmoved. It’s not even clear she is aware.

Birx dismisses all contrary cases such as Sweden: Americans could not take that route because we are too unhealthy. South Dakota: rural and backwater (Birx is still mad that the brave Governor Kristi Noem refused to meet with her). Florida: oddly and without evidence she dismisses that case as a killing field, even though its results were better than California while the population influx to the state sets new records.

Nor is she shaken by the reality that there is not one single country or territory anywhere on the planet earth that benefitted from her approach, not even her beloved China which still pursues a zero-Covid approach. As for New Zealand and Australia: she (probably wisely) doesn’t mention them at all, even though they followed the Birx approach exactly.

The story of the lockdowns is a tale of Biblical proportions, at once evil and desperately sad and tragic, a story of power, scientific failure, intellectual insularity and insanity, outrageous arrogance, feudalistic impulses, mass delusion, plus political treachery and conspiracy. It is real-life horror for the ages, a tale of how the land of the free became a despotic hellscape so quickly and unexpectedly. Birx was at the center of it, confirming all of your worst fears right here in a book anyone can buy. She is so proud of her role that she dares to take all credit, fully convinced that the Trump-hating media will love and protect her perfidies from exposure and condemnation.

There is no getting around Trump’s own culpability here. He never should have let her have her way. Never. It was a case of fallibility matched by ego (he has still not admitted error), but it is a case of enormous betrayal that played off presidential character flaws (like many in his income class, Trump had always been a germaphobe) that ended up wrecking hope and prosperity for billions of people for many years to come.

I’ve tried for two years to put myself in that scene at the White House that day. It’s a hothouse with only trusted souls in small rooms, and the people there in a crisis have the sense that they are running the world. Trump might have drawn on his experience running a casino in Atlantic City. The weather forecasters come to say a hurricane is on the way, so he needs to shut it down. He doesn’t want to but agrees in order to do the right thing.

Was this his thinking? Perhaps. Perhaps too someone told him that China’s President Xi Jinping managed to crush the virus with lockdowns so he can too, just as the WHO said in its February 26 report. It’s also difficult in that environment to avoid the rush of omnipotence, temporarily oblivious to the reality that your decision would affect life from Maine to Florida to California. It was a catastrophic and lawless decision based on pretense and folly.

What followed seems inevitable in retrospect. The economic crisis, inflation, the broken lives, the desperation, the lost rights and lost hopes, and now the growing hunger and demoralization and educational losses and cultural destruction, all of it came in the wake of these fateful days. Every day in this country, even two and a half years later, judges are struggling to regain control and revitalize the Constitution after this disaster.

The plotters usually admit it in the end, taking credit, like criminals who cannot resist returning to the scene of the crime. This is what Dr. Birx has done in her book. But there are clearly limits to her transparency. She never explains the real reason for her resignation – even though it is known the world over – pretending like the entire Thanksgiving fiasco never happened and thus attempting to write it out of the history book that she wrote.

There is so much more to say and I hope this is one review of many because the book is absolutely packed with shocking passages. And yet her 525-page book, now selling at a 50% discount, does not contain a single citation to a single scientific study, paper, monograph, article, or book. It has zero footnotes. It offers no go-to authorities and displays not even a hint of humility that would normally be part of any actual scientific account.

And it nowhere offers an honest reckoning for what her influence over the White House and the states foisted on this country and on the world. As the country masks up yet again for a new variant, and is gradually being groomed for another round of disease panic, she can collect whatever royalties come from sales of her book while working at her new gig, a consultant to a company that makes air purifiers (ActivePure). In this latter role, she makes a greater contribution to public health than anything she did while she held the reins of power.

Tyler Durden

Sun, 07/17/2022 – 22:30 - Where The Contraceptive Pill Is Available Over-The-Counter

Where The Contraceptive Pill Is Available Over-The-Counter

The Food and Drug Administration has for the first time received an application by a pharmaceutical firm that looks to start selling a contraceptive pill as an over-the-counter medication.

According to the BBC, the move is unrelated to the recent Supreme Court decision that overturned Roe v. Wade, the previously long-standing precedent that guaranteed the right to abortion in the U.S.

However, as Statista’s Katharina Buchholz notes, the development is nevertheless meaningful in the context of the post-Roe world where the Democrats and women’s organizations are scrambling to expand other services to those who have lost access to abortion. According to the OCs OTC Working Group, over-the-counter contraceptives can be a puzzle piece in this endeavor, especially since a codification of abortion rights on the federal level is looking evermore futile. The issue has already gained support from Democrats on Capitol Hill, but it is expected that opposition could form at least against removing the prescription requirement for minors.

Looking at a world map of sales restrictions for contraceptive pills, developed countries typically require a prescription, while the medication is – either informally or formally – available over-the-counter almost everywhere else.

You will find more infographics at Statista

According to the working group, offering the pill over-the-counter can significantly reduce unwanted gaps in contraceptive use, which can occur in areas where doctors’ appointments are hard to come by, clinics are far away or people are short on funds to pay for medical visits or extra travel. Some reasons for contraceptive gaps are more minute, according to the source, and can occur when women run out of pills at an inconvenient time or contraceptives are forgotten at home ahead of a trip.

While some medical checks can be helpful before going on the pill, the American College of Obstetricians and Gynecologists as well as the American Medical Association and the American Academy of Family Physicians have spoken out in favor of the over-the-counter pill, saving that the benefits outweighed the risks especially for modern, well-researched contraceptive pills. Research has shown that checklist can be helpful for women to self-screen for potentially adverse health conditions, like high blood pressure, and find the right pill. According to a study on U.S. women who obtained over-the-counter pills in Mexico, a large majority of them continued to attend gynecological screenings. Of course, women can also still opt to discuss the right contraceptive method with their doctors before starting a regimen, with the added benefit that refills become much easier.

Tyler Durden

Sun, 07/17/2022 – 22:00 - Bill Moves Forward That Will Legalize Psychedelic Drugs In California

Bill Moves Forward That Will Legalize Psychedelic Drugs In California

Authored by Matt Agorist via TheFreeThoughtProject.com,

Despite the overwhelming evidence showing that kidnapping and caging people for possessing illegal substances does nothing to prevent use and only leads to more crime and suffering, government is still hell bent on enforcing the war on drugs. Like a crack addict who needs to find his next fix, the state is unable to resist the temptation to kick in doors, shake down brown people, and ruin lives to enforce the drug war.

Instead of realizing the horrific nature of the enforcement of prohibition, many cities across the country double down on the drug war instead of admitting failure. As we can see from watching it unfold, this only leads to more suffering and more crime. Luckily, there are cities, and now entire states in other parts of the country that are taking steps to stop this violent war and the implications for such measures are only beneficial to all human kind.

Eight years ago, Colorado citizens—tired of the war on drugs and wise to the near-limitless benefits of cannabis—made US history by voting to legalize recreational marijuana. Then, in 2019, this state once again placed themselves on the right side of history as they voted to decriminalize magic mushrooms. But this was just the beginning and their momentum is spreading—faster and stronger, toward decriminalizing all plant-based psychedelics. Then, this year, the state of Oregon decriminalized all drugs.

Now, another state is following suit, but not just with psilocybin— a bill in California is moving forward with a legalization measure for other psychedelics like mescaline cacti, ayahuasca and ibogaine.

The California Assembly committee is holding a hearing next month on the bill to legalize the possession, personal use, and facilitated and supported use of the following substances by adults 21 and over.

-

psilocybin

-

psilocyn

-

MDMA

-

LSD

-

DMT

-

mescaline (excluding peyote)

-

ibogaine

Senate Bill 519 was proposed last year but was put on hold in August to adjust the wording in order to ensure its passage. As the Tenth Amendment Center points out:

Under the Controlled Substances Act (CSA) passed in 1970, the federal government maintains the complete prohibition of many of the drugs on SB519’s decriminalization list and heavily regulates others. Of course, the federal government lacks any constitutional authority to ban or regulate such substances within the borders of a state, despite the opinion of the politically connected lawyers on the Supreme Court. If you doubt this, ask yourself why it took a constitutional amendment to institute federal alcohol prohibition.

In effect, the passage of SB519 would end criminal enforcement of laws prohibiting the possession of these drugs in California. As we’ve seen with marijuana and hemp, when states and localities stop enforcing laws banning a substance, the federal government finds it virtually impossible to maintain prohibition. For instance, FBI statistics show that law enforcement makes approximately 99 of 100 marijuana arrests under state, not federal law. By curtailing or ending state prohibition, states sweep part of the basis for 99 percent of marijuana arrests.

Furthermore, figures indicate it would take 40 percent of the DEA’s yearly annual budget just to investigate and raid all of the dispensaries in Los Angeles – a single city in a single state. That doesn’t include the cost of prosecution either. The lesson? The feds lack the resources to enforce marijuana prohibition without state and local assistance, and the same will likely hold true with other drugs.

“With mental health issues on the rise, it is time that California take an incremental and measured step to dismantle failed war on drugs policies by ending the criminalization of people that possess and use substances with immense healing potential,” the bill’s sponsor Sen. Scott Wiener said in a statement of the bill’s purpose.

“It’s the plants that are going to bring us back to sanity. We’ve got to listen to their message and we’ve got to live reciprocally with nature and restore the natural order,” Susana Eager Valadez, director of the Huichol Center for Cultural Survival and Traditional Arts said after Oakland passed a similar decriminalization bill in 2019.

The Assembly Appropriations Committee will hear the case for SB519 on Aug. 3. It must pass the committee by a majority vote before moving to the full Assembly for further consideration. Hopefully it does and California shifts from kidnapping and caging people for these substances, to focusing on using them for therapy.

While California is certainly no bastion for freedom — especially with their draconian COVID-19 response — bills like this are a win for everyone as it requires far less money to help people than it does to incarcerate them.

Now, cops can try to focus on real crimes instead of kidnapping and caging people who are trying to heal themselves with a plant.

Supporters hope the decision will begin a nationwide discussion about decriminalizing plant-based drugs.

Tyler Durden

Sun, 07/17/2022 – 21:30 -

- In 2023, Global Emoji Count Could Grow To 3,491

In 2023, Global Emoji Count Could Grow To 3,491

Just in time for today’s World Emoji Day, new pictograms coming to phones in 2023 have been announced. As Statista’s Katharina Buchholz details below, next year will likely see the release of 31 new emojis including the pink heart, the hair pick and the Khanda, the symbol of Sikh faith. The update would grow the number of emojis to nearly 3,500 next year. The Unicode consortium has recommended the emojis for release, but a final decision is still outstanding.

You will find more infographics at Statista

While 2021 saw the release of 217 new emojis, that number was lowered to just more than 100 in 2022 and now finally to the double digits for next year. While emojis that allow users to pick different skin colors or genders drive up the size of releases as they are counted individually, the number of non-customizable emojis has also decreased with each release. 2023 will also see the addition of the moose head, the donkey, the goose, the handheld fan, the jelly fish and the maracas, among others, with the high-five hands – both left and right-facing – being the only customizable emoji in the new batch. The pink heart is reportedly the most anticipated of the release as social media users have griped for some time about the availability of the simple heart icon in white, orange and even brown, but not pink.

What emojis appear on people’s phones and on their social media platforms is not arbitrary but has been coordinated by the Unicode Consortium since 1995, when the first 76 pictograms were adapted by the U.S. nonprofit. The Consortium has been overseeing the character inventory of electronic text processing since 1991 and sets a standard for symbols, characters in different scripts and – last but not least – emojis, which are encoded uniformly across different platforms even though illustration styles may vary between providers.

Even though the first Unicode listings predate them, a 1999 set of 176 simple pictograms invented by interface designer Shigetaka Kurita for a Japanese phone operator is considered to be the precursor of modern-day emojis. The concept gained popularity in Japan and by 2010, Unicode rolled out a massive release of more than 1,000 emojis to get with the burgeoning trend – the rest is history.

Different skin colors have been available for emojis since 2015. 2014 saw the release of the anti-bullying emoji “eye in speech bubble” in cooperation with The Ad Council, which produces public service announcements in the United States. Regional flags came to the service in 2017. Same-sex couples and same-sex families have been available since the first major emoji-release in 2010. The 2021 release also included the rollout of non-binary options and interracial couples.

Tyler Durden

Sun, 07/17/2022 – 21:00 - "Weakest Links": March 2020 Was A Preview, Fragilities Are Now In Capital Markets And Liquidity Channels

“Weakest Links”: March 2020 Was A Preview, Fragilities Are Now In Capital Markets And Liquidity Channels

By Marcel Kasumovich, Head of Research at One River Asset Management

Weakest Link I: Weak links lie within sectors and economies experiencing uninterrupted growth. Expectations are extrapolated from recent realities. Underwriting standards relax as growth hides risks. New Century Financial grew mortgage originations from $357mm in 1996 to $60bln in 2006. $1.2bln of capital. $17.4bln in credit lines. “CloseMore University” was the internal nickname. Originate. Sell. 60% dividend yield to discourage short-sellers. The sudden-stop in mortgage buying was the end of the line – the largest non-bank mortgage originator filed for bankruptcy April 2, 2007.

Weakest Link II: Weak links exist without systemic financial risks. Take Freeport-McMoRan (FCX). Emerging markets, China, and commodities recovered swiftly from the 2008 crisis. Strong free cashflow encouraged FCX to diversify into shale oil and gas just as China was tightening credit, sparking a global recession. The market put high odds on FCX default – long-term debt fell to 40 cents on the dollar. The company deleveraged. Terrible for shareholders. Today’s supply constraints are born from the underinvestment in those weak-link moments.

Weakest Link III: Commodities cratered in the 2015 downturn, expectations for terminal policy rates collapsed, and bond curves flattened. Long duration assets – broadly, like intellectual property – were the preferred investment. Buyouts surged: leverage companies with high free-cash-flow yields and use ‘cost synergies’ to deleverage. Even with rates low, those deals can be challenging. The Kraft-Heinz marriage in 2015 was funded by ballooning debt. But deleveraging was too slow. Shareholder value was destroyed. Another weak-link case study.

Weakest Link IV: The clues for the next crisis are usually found in the solutions to the previous one. The post-GFC macro megatrend was to issue more debt and less equity. Less equity is less principal risk. Less principal risk lends itself to weaker underwriting. That trade was funded through capital markets after the GFC, not by banks who were in a regulatory penalty box. Dealers now have less than one-tenth the credit inventory than 2007. Fragilities are now in capital markets and liquidity channels. March 2020 was a preview. Policy either accommodates or intervenes.

Weakest Link V: The leverage lending market – high yield bonds and leveraged loans – exploded to $3trln in 2021, double a decade earlier. Underwriting standards eroded. Covenants to protect creditors vanished. Opportunistic refinancing surge. But the tide is turning. JP Morgan took a $257mm write-down in Q2, stuck with loans they couldn’t move. Flexible pricing to discount unwanted loans is the new normal. Companies need to adjust – end buybacks, retain earnings. More principal risk. Fast or slow – excesses in leverage lending will be resolved.

Weakest Link VI: Debtor countries are driving inflation. Creditor countries are not immune. Inflation flips the narrative – US dollar reserves are a captive tax against creditors, savers. China gross national savings is 45% of GDP versus 18% for the United States. Chinese households flocked to what they could – physical assets are an extreme 69.3% of their wealth. Real estate dominates. Underwriting is weak. Highly indebted builders are funded by presale deposits. Credit downgrades are now rampant. Demographics are a severe headwind. Regional economies are unbalanced, fueled by coal. Political, financial, and environment threats are acute.

Weakest Link VII: The digital ecosystem is living its version of the GFC. Losses – some expected, many unforeseen – are being crystalized. It is small enough today with few direct linkages to the ‘real’ economy that digital is a spectator sport. But the areas of resiliency are the ones that can make the broader financial system stronger. Decentralized Autonomous Organizations brought risk-management changes to protocols at an unprecedented pace. It is for the public to see and learn from – its integration into the mainstream is part of the solution.

Tyler Durden

Sun, 07/17/2022 – 20:30 - Relentless Heat Wave Pummeling Texas And Central Plains To Bring Hottest Temperatures Of Year

Relentless Heat Wave Pummeling Texas And Central Plains To Bring Hottest Temperatures Of Year

Extreme heat threatens Texas and the Southern Plains to start the new work week, with temperatures forecasted to exceed 100 degrees Fahrenheit.

This new round of heat could be the hottest yet. Large swaths of interior Texas, Oklahoma, and Kansas could see predicted highs reaching 110 degrees Fahrenheit and heat indexes much higher.

Although triple-digit temperatures are typical for the Central Plains and Texas in July and August, the frequency in the number of 100-degree days is above average.

Take, for instance, Tulsa, Oklahoma. The metro area has just recorded its 11th 100-degree day of the season — the average for the entire season is ten.

The National Weather Service (NWS) tweeted Sunday afternoon, “Excessive heat will continue this week across parts of Southern Region. Heat advisories and excessive heat warnings are in effect today across TX/OK.”

The heat will increase days after the Electric Reliability Council of Texas (ERCOT), which operates Texas’ electric power grid, asked customers to conserve energy on Monday and Wednesday. ERCOT blamed grid strains on record high electric demand and the lack of wind and solar power.

Reuters noted that a handful of manufacturers, including Toyota Motor Corp., Samsung Electronics Co Ltd., General Motors Co., and LyondellBasell’s Houston refinery, dialed back energy usage to preserve grid stability.

Tesla Motors even asked owners of its electric cars not to charge “between 3 pm and 8 pm … to help statewide efforts to manage demand.”

The same areas are under a dangerous and expanding worsening drought.

ERCOT could be forced to take emergency action and ask customers to conserve power Monday to avoid rolling blackouts as a relentless heatwave strains power supplies.

Tyler Durden

Sun, 07/17/2022 – 20:00 - Bodycam Video, Report Exposes "Systemic, Egregious" Law Enforcement Failures In Uvalde School Mass Shooting

Bodycam Video, Report Exposes “Systemic, Egregious” Law Enforcement Failures In Uvalde School Mass Shooting

The Texas state House report into the Uvalde elementary school shooting in May that killed 21 people, including 19 children, said the massacre was unable to be stopped due to “systemic failures and egregious poor decision-making.”

The report obtained by the Texas Tribune attempts to piece together what happened during the 77 minutes after the alleged gunman, 18-year-old Uvalde High School dropout Salvador Ramos, entered Robb Elementary School until the point he was killed by a Border Patrol agent.

“There is no one to whom we can attribute malice or ill motives. Instead, we found systemic failures and egregious poor decision making,” the report said, noting “shortcomings and failures of the Uvalde Consolidated Independent School District [CISD] and of various agencies and officers of law enforcement” and “an overall lackadaisical approach.”

As Jack Phillips reports for The Epoch Times, those claims appear to coincide with statements made by top Texas officials days after the shootings.

Texas Department of Public Safety Director Steve McCraw said May 27 that it was the “wrong decision” not to engage with the shooter, Salvador Ramos.

Meanwhile, surveillance footage from Robb Elementary School released on July 12 shows officers waiting around more than 45 minutes before several officers approached the classroom where Ramos had entered.

JUST IN: Exclusive body cam video from the law enforcement response to the Uvalde, TX school shooting. @ShimonPro obtained the video from the city’s Mayor.

It shows just how chaotic the situation was: pic.twitter.com/VppNuJ1d7b— Ryan Nobles (@ryanobles) July 17, 2022

https://platform.twitter.com/widgets.js

The officers didn’t enter. It took more than 75 minutes for law enforcement to kill Ramos, 18, after he entered the building.

This goes against EVERYTHING we who were in law enforcement were trained to do….

[GUN SHOTS]

Uvalde school police chief, trying to negotiate with an active shooter: “Sir, if you can hear me, please put your firearm down, sir.” pic.twitter.com/9UjbPY8cDf

— Josh Campbell (@joshscampbell) July 17, 2022

https://platform.twitter.com/widgets.js

The report said that law enforcement failed to quickly confront the suspect and instead retreated to safety.

“In this crisis, no responder seized the initiative to establish an incident command post,” it states.

“Despite an obvious atmosphere of chaos, the ranking officers of other responding agencies did not approach the Uvalde CISD chief of police or anyone else perceived to be in command to point out the lack of and need for a command post, or to offer that specific assistance.”

Some individual officers acted without instruction to try to reach the shooter and might have been able to do so if they had more backup, according to the paper.

“Given the information known about victims who survived through the time of the breach and who later died on the way to the hospital, it is plausible that some victims could have survived if they had not had to wait 73 additional minutes for rescue,” the report reads.

A force of 376 law enforcement officers responded to the mass shooting, according to the House panel, which said that there wasn’t clear leadership as they responded.

Texas lawmakers on July 17 noted that Ramos was born in Fargo, North Dakota, before he was moved to Texas when he was a child. Ramos also may have been sexually abused as a child, the report states.

Friends of the suspect, including a girlfriend, told investigators that Ramos became increasingly depressed during the COVID-19 pandemic. At one point, Ramos told the girlfriend that he wouldn’t live past age 18.

Ramos in late 2021 also allegedly posted a video of himself holding a dead cat inside a bag. Footage also showed the future school shooter dry firing BB guns at people from a car, according to the report.

In the wake of the shooting, which left 19 students and two teachers dead, congressional lawmakers used the tragedy to pass a gun control bill that included funding to bolster red flag laws and other measures, which was signed into law on June 25 by President Joe Biden.

Tyler Durden

Sun, 07/17/2022 – 19:30 - With Bearish Sentiment Off The Charts, $5.5 Billion In Daily Stock Buybacks Set To Flood Markets

With Bearish Sentiment Off The Charts, $5.5 Billion In Daily Stock Buybacks Set To Flood Markets

On the one hand, what was the most bullish case for markets starting this month fizzled with a bang, when after a solid start to July and the best start to Q3 since 1980, stocks resumed their bear market slide, only to recover some losses toward the end of the week. In any case, the barely 1% rise in the first half of July was at best meh considering the lofty expectations for what has traditionally been the best two-week period of the year…

… for markets.

So as attention turns from what was a big dud of a strong calendar period, to what is already shaping up as a disappointing Q2 earnings season (with virtually all banks missing expectations across the board), the bulls are once again in retreat, and nowhere is this more obvious than in hedge fund positioning which according to Goldman’s Scott Rubner, “is so low, it has officially fallen off my chart.” Rubner then invites readers to take a look at some of this stuff, and points to Goldman’s Prime Broker hedge fund exposure, Futures Positioning, CTA, Risk Parity, noting that “I don’t think there is more marginal position left to sell, given large hedges vs. fundamental positions already in play.”

Indeed, digging into the dispersion between single stocks and macro products we find that a record divergence where there has been little shorting at the index and ETF level, but nearly record shorting at t the single stock level!

Meanwhile, away from increasingly bearish institutions, we noted lat week that retail investors are close to capitulating, but not quite yet, and according to Goldman, households – which represent “the most important investor in the markets” have not yet capitulated and remain in HODL mode, with “that $1.325 Trillion worth of “cumulative net inflows” remaining a cement block.”

And until that massive wall of inflows refuses to budge, there is little risk of a liquidation flush. On the contrary, with sentiment crashing through the floor, it is far more likely that stocks are due for another (bear market) rally and/or short squeeze. All they need is a catalyst, especially since markets digested the risk of a 100bps rate hike and actually rose on the news.

That catalyst may be the return of buybacks: according to Goldman, stocks will see a whopping $300B worth of US Corporate buyback execution in Q3 (Q2 data is still TBD but Q1 was $312BN for all US stocks). Some math:

- Days in Q3 = 61

- Days in Q3 open window 55

- $300B / 55 = $5.5B per day, every day, starting on July 22nd. VWAP + VOL muting.

The fundamental question, does $5.5B worth of demand, help mute overall earnings guidance weakness per diem? According to Ruber “the answer is yes” but that’s to be expected, after all he is the resident Goldman permabull and the bank’s equivalent of JPM’s Marko Kolanovic.

In conclusion, Rubner sums up current sentiment as follows:

- The bearish trade is very consensus, when I talk about very consensus, I mean very very consensus. I got more pings this week, than any week of 2022.

- The bearish view is already reflected in current market positioning and extreme over hedges.

Bonus chart from Rubner who notes that “this is cash levels (money markets + mutual fund cash) – this is elevated and looking for dip alpha.”

Tyler Durden

Sun, 07/17/2022 – 19:00 - Morgan Stanley: Central Banks Are Increasingly Out Of Balance

Morgan Stanley: Central Banks Are Increasingly Out Of Balance

By Seth Carpetner, global chief economist at Morgan Stanley

Divergences in policy rates are now in focus, accentuated by the sharp depreciation of the yen and the euro. I want to turn attention to the divergent paths for central bank balance sheets.

Fed quantitative tightening (QT) started in June, and the pace will double in September. While the ECB’s balance sheet has started to shrink a bit as targeted long-term refinancing operations (TLTROs) are repaid, the contraction is small, and prepaying TLTROs is very different than QT. And the shrinking may not last as the ECB confronts peripheral spreads. The BoJ could go in the opposite direction, and yield curve control (YCC) could turn into substantial QE if markets keep testing the Bank. These balance sheet differences will only become starker.

In absolute terms, the ECB and the Fed have the largest balance sheets, with the BoJ a distant third. But relative to GDP, the BoJ has the biggest by far, with the ECB second. The Fed is an outlier on the low side, and as its QT continues and accelerates, the Fed’s footprint will contract further while the BoJ’s will likely grow.

The Fed started trimming its balance sheet last month, and the pace of the unwind will accelerate in September to $60bn per month of Treasuries and $35bn per month of MBS. The Fed plans to let QT run in the background, and it seems very likely to me that balance sheet runoff keeps going even if the economy stalls (for a differing opinion from BofA’s Marc Cabana, see here). Chair Powell keeps reminding us that the FOMC wants the funds rate to be tool of first recourse, so if we get to the point of the economy faltering, there will be room to cut. Indeed, that narrative is priced into the futures curve already.

For the ECB, the balance sheet trajectory is complicated. QT and TLTRO prepayments are not the same. Running off securities gives the market no choice—the central bank calls the shots. With TLTROs, commercial banks have the option to prepay at their discretion. Indeed, as our Europe team has noted, prepayments have been on the low side of expectations. Proper QT for the ECB is far off. Moreover, the ECB’s vow to contain peripheral spreads with a yet-to-be defined “anti-fragmentation tool” points to a potentially significant upside risk to the size of its balance sheet.

The BoJ is at the other end of the spectrum. Relative to GDP (and even more so, relative to the size of the sovereign debt market), the BoJ’s balance sheet is already an outlier to the upside. And despite the fall in the yen, inflation is still lower in Japan than other DMs, leaving Governor Kuroda committed to his very accommodative policy stance. That mindset will confront slower global growth that weighs on Japanese growth. Against this backdrop, our Japan team revised the call for the timing of a shift in YCC. Whereas we had thought that a tweak would come in October, allowing the JGB curve to drift upward, we now expect YCC to be maintained until the second quarter of next year, after Governor Kuroda is replaced by a successor. With the market increasingly likely to test the BoJ, I see the risks to the balance sheet as skewed substantially to the upside.

Markets have a lot to digest. Following the Covid shock, all major central banks were moving in the same direction but no longer, and market liquidity will be buffeted by severe crosscurrents. The irony is that the risks come from both larger and smaller balance sheets. In dollar markets, a lot more Treasuries and MBS will have to be absorbed as financing costs are rising. In JGBs, the BoJ already owns half the market, and more might be coming.

Tyler Durden

Sun, 07/17/2022 – 18:30 - Republicans Freak As Ukrainian-Born GOP Colleague Trash Talks Zelensky

Republicans Freak As Ukrainian-Born GOP Colleague Trash Talks Zelensky

House Republicans are seriously regretting giving Ukraine-born GOP Rep. Victoria Spartz a platform to speak on the war, after she started lobbing intense criticism at president Volodomyr Zelensky and his administration, drawing a rare rebuke last weekend from the Ukrainian Foreign Ministry, which said she was “trying to earn extra political capital on baseless speculation.”

Rep. Victoria Spartz, who emigrated from Ukraine, speaks during a press conference about a Senate resolution calling for accountability for Russian President Vladimir Putin, Wednesday, March 2, 2022, at the Capitol in Washington. | Mariam Zuhaib/AP Photo According to Politico, Republicans within the GOP Conference have “widespread fear” that her outspoken posture will damage US-Ukraine relations, and that the MAGA wing of their party – which has seen growing opposition to US support of the Ukraine war – will point to Spartz’s comments as justification.

Spartz, who has traveled to Ukraine about six time since the war began, released a statement earlier this months calling on Zelensky to “stop playing politics and theater” and “start governing to better support his military and local government.”

She also accused President Joe Biden of “playing politics” and said that he needs to present a “clear strategy and align security assistance with our strategy.”

Lastly, she called on lawmakers to “establish proper oversight of critical infrastructure and delivery of weapons and aid,” a concern shared among progressives over the possibility that the weapons could end up in the wrong hands.

The extraordinary statement comes after Rep. Victoria Spartz (R-Ind.) asked President Joe Biden to brief Congress on years-old allegations against Ukrainian President Volodymyr Zelenskyy’s chief of staff, Andriy Yermak. Earlier this week, the freshman lawmaker also slammed both Biden and Zelenskyy for their approaches to the ongoing war, infuriating officials in both countries. -Politico

One anonymous GOP lawmaker who serves on the House Foreign Affairs Committee told Politico “Her naiveness is hurting our own people,” adding “It is not helpful to what we’re trying to do and I’m not sure her facts are accurate … We have vetted these guys.”

Another senior House Republican who spoke on condition of anonymity simply said “What the fuck.”

Panic Spreads:

A third House Republican granted anonymity to speak candidly about Spartz said she has a reputation for elbowing her way into briefings and meetings for committees she doesn’t belong to, like the Foreign Affairs panel, where multiple members have tried to address her comments behind closed doors.

The Biden administration is even getting involved — another sign of growing worries that Spartz’s comments may damage cohesion among the Western coalition in defense of Kyiv. A Foreign Affairs Committee aide, speaking on condition of anonymity, said the U.S. intelligence community is planning to brief Spartz about her claims in a classified setting Friday morning. -Politico

“I don’t share her criticisms,” said Seen Lindsey Graham (R-SC), who has collaborated with Spartz on legislation concerning Ukraine. “I believe that the Zelenskyy government and the Ukrainian people have risen to the moment. It is in our national security interest to stand with the Ukrainian people and their elected leadership.”

Spartz defended herself to Politico in a statement:

“Growing up in Ukraine and visiting six times since the war started, I have a comprehensive understanding of the situation on the ground,” adding “The stakes are too high to be reactive without deliberation — as intended for our institution.”

Read more here…

Tyler Durden

Sun, 07/17/2022 – 18:00 - Logistics Warehouse Activity May Cool As Interest Rates Heat Up

Logistics Warehouse Activity May Cool As Interest Rates Heat Up

By Mark Solomon of FreightWaves

Nothing in the second-quarter data indicates that the 12-year bull market for U.S. logistics warehousing, and the trends of e-commerce growth and the need for businesses to maintain high inventory levels that have driven the surge, are close to ending.

The industrial construction pipeline hit an unprecedented 699 million square feet in the quarter, up 112% from pre-pandemic levels and 177% above the 10-year average, according to Cushman & Wakefield, a real estate services firm. New leasing activity for the year is tracking to exceed 800 million square feet, which would mark only the second year ever at such a lofty perch, Cushman said.

Nationwide vacancy rates plunged in the quarter to 3.1%, 120 basis points below a year ago, according to Cushman data. Every U.S. region that Cushman canvasses reported under 4% vacancy rates for the second consecutive quarter. Twenty markets reported vacancy rates of less than 2%.

In Chicago, the country’s largest industrial market with more than 1.2 billion square feet of inventory, 8.1 million square feet were developed, the greatest second-quarter completion total in the market’s history, according to Colliers International Group Inc, a real estate services firm. According to Colliers data, 20 projects totaling 8.1 million square feet commenced during the quarter in the Chicago market.

Colliers said that the Chicago market experienced in the quarter an uptick in vacancy rates for speculative development, where projects are undertaken with no formal end-user commitment, as well as a drop in leasing activity for the category. However, those changes reflect how tight the market has become and are likely more of a blip on the radar than a meaningful trend.

Two weeks into the third quarter, though, anecdotal evidence is pointing to a break in the action. Institutional investors who have pumped billions of dollars into the industrial market in search of higher yields in a low interest rate environment have hit the pause button, concerned about how to price real estate returns in an environment of higher interest rates and of the future direction of borrowing costs with the Federal Reserve in aggressive tightening mode.

Jack Rosenberg, Colliers’ Chicago-based national director of logistics and transportation who represents industrial tenants, said that “cap rates,” which determine the annual return on a property’s investment by dividing its value with its net operating income, have begun to creep up due to the higher cost of money. A higher cap rate means the investment will likely yield less than it would have if interest rates were lower.

Lack of clarity into the speed, extent and duration of rate hikes will slow, if not stop, development, Rosenberg said. That’s because no one knows what cap rates will look like in 12 to 18 months when the project is leased and is ready to be sold. One major developer and a significant investor, neither of whom Rosenberg would identify, are in “pencils down” mode, industry lingo for a corporate pause. Projects slated to begin this fall are being pushed into next spring. In the meantime, sale prices per square foot have been dropping, and buyers are requesting changes in their favor to contractual terms of projects currently under contract.

The angst over the Fed’s actions extends to developers as well. Lisa DeNight, national industrial research director at Newmark Group, a real estate services firm, said higher capital costs are leading some developers to halt or abandon projects. Some developers are even selling development sites. Unsurprisingly, “new construction starts have begun to slow, but still remain historically elevated,” she said.

A different cycle

This isn’t the first rate tightening cycle the industrial market has managed through since 2010. What’s different about this cycle is that it dovetails with construction cost inflation, labor shortages and long lead times for materials due to continued global supply chain disruptions.

As bottlenecks ease and commodity prices decline due to market expectations that higher rates will curtail end demand, more supply will hit the markets and will do so at lower prices. However, that won’t occur until 2023 at the earliest, according to Newmark.

The average permitting and construction process for new industrial projects is taking five months longer than it did in 2019, DeNight said, and the average order lead times for a critical commodity like roofing materials remain at 30 to 50 weeks. Progress on obtaining necessary building permits continues to be hamstrung by understaffed local governments.

“Every stage of the construction timeline has been hampered by two years of challenges that are unlikely to subside during the balance of 2022,” DeNight said.

Despite higher rates, most projects now underway will be seen through to completion, said John Morris, Americas president of industrial & logistics for real estate services firm CBRE Group Inc. Morris said that the 12- to 18-month lead time for end-to-end project completions means that it will take five or six quarters for the impact of rate hikes to be dramatically felt in the industrial market.

For now, occupier demand remains strong as e-commerce sales stay elevated and as tenants ensure they can occupy facilities ahead of the peak holiday season. Overall occupier demand is about 95% of what it was at this time a year ago, Morris said. Any slowdown will come from the supply side and not from demand, he said.

Rosenberg said that none of his clients have indicated they are putting their leasing needs on hold, although he acknowledged that the people he works directly with are typically the last to know if a project is being shelved.

Carolyn Salzer, Americas head of logistics and industrial research at Cushman, said the supply-demand scales continue to favor lessors. “Right now, there just isn’t enough space out there for occupiers in general,” Salzer said. “What we have heard is that if a tenant needs to be in a market, they will make it work.”

Tenants will have more leverage should supply begin to exceed demand, which, if it happens, will be a 2023 story, she added.

The variable in all this is whether higher rates will trigger a recession, which could trigger a sustainable drop in consumer demand. Should consumers pull back, occupiers’ appetites will dull quickly, leading to a decline in rents and an increase in vacancy rates. However, should the economy avoid a contraction and new development continues to slow, then competition for available space is likely to surge and rents will soar.

The many crosscurrents buffeting industrial real estate have produced a degree of murkiness that stakeholders are unaccustomed to. When asked for directional clarity, Rosenberg replied, “I’ll say, ‘Who the hell knows’ because nobody knows.”

Tyler Durden

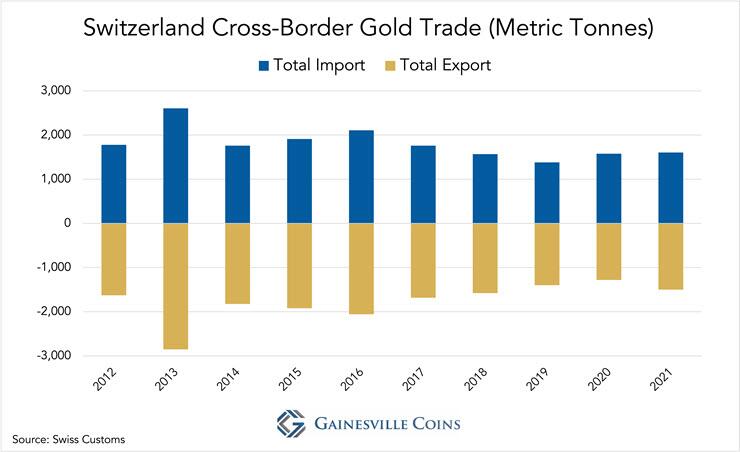

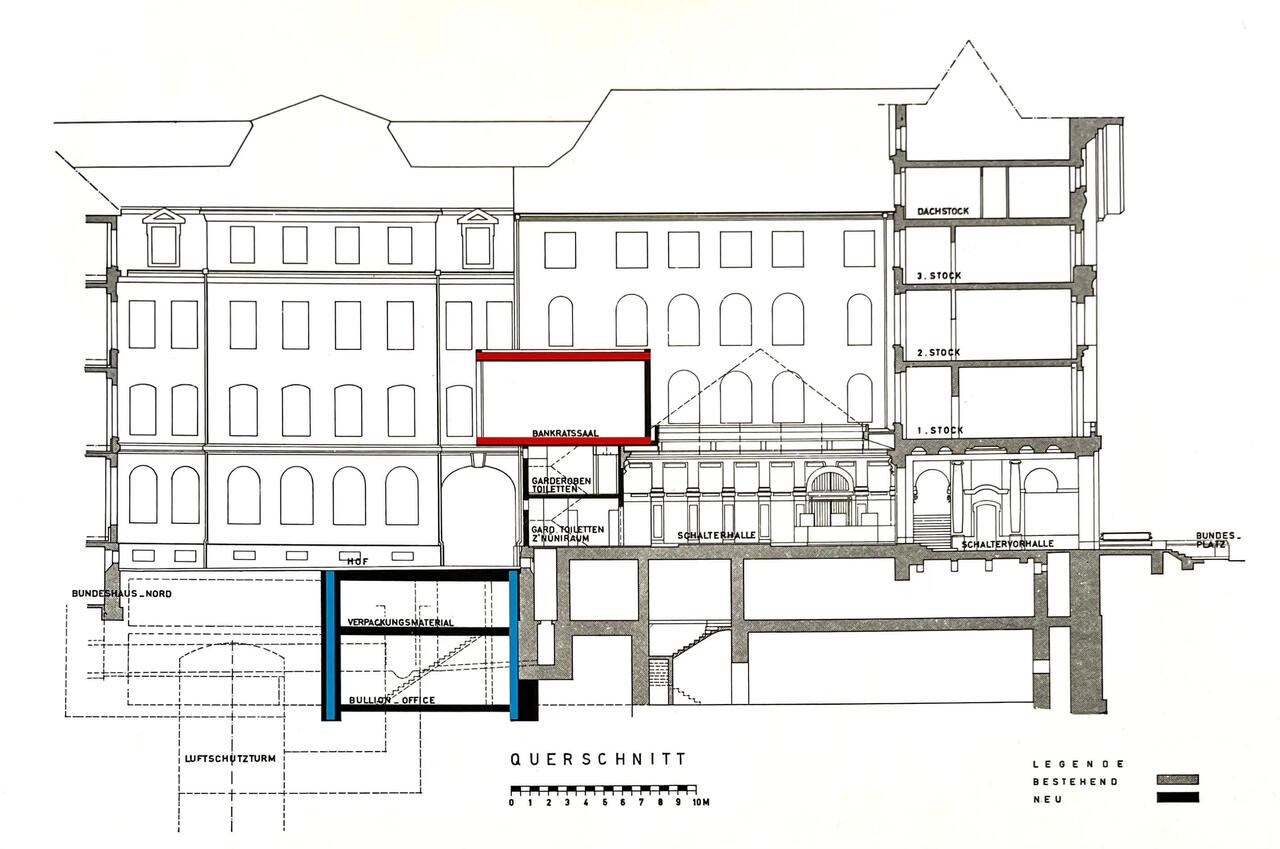

Sun, 07/17/2022 – 17:30 - Did The Swiss Central Bank Quietly Move Its Gold

Did The Swiss Central Bank Quietly Move Its Gold

By Jan Nieuwenhuijs of Gainesville Coins

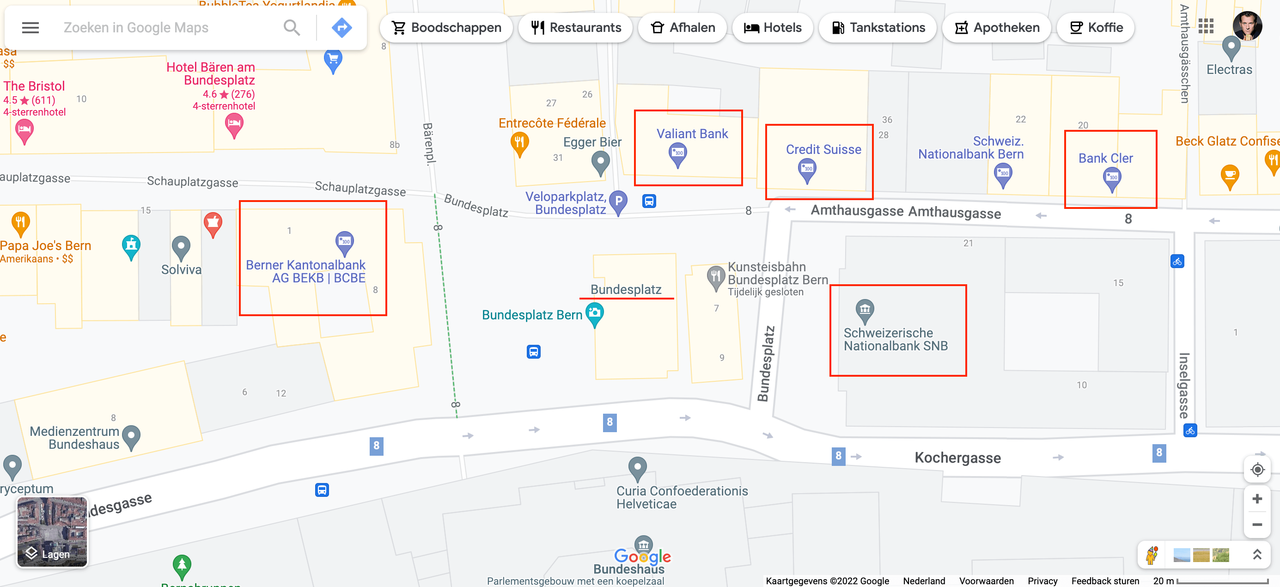

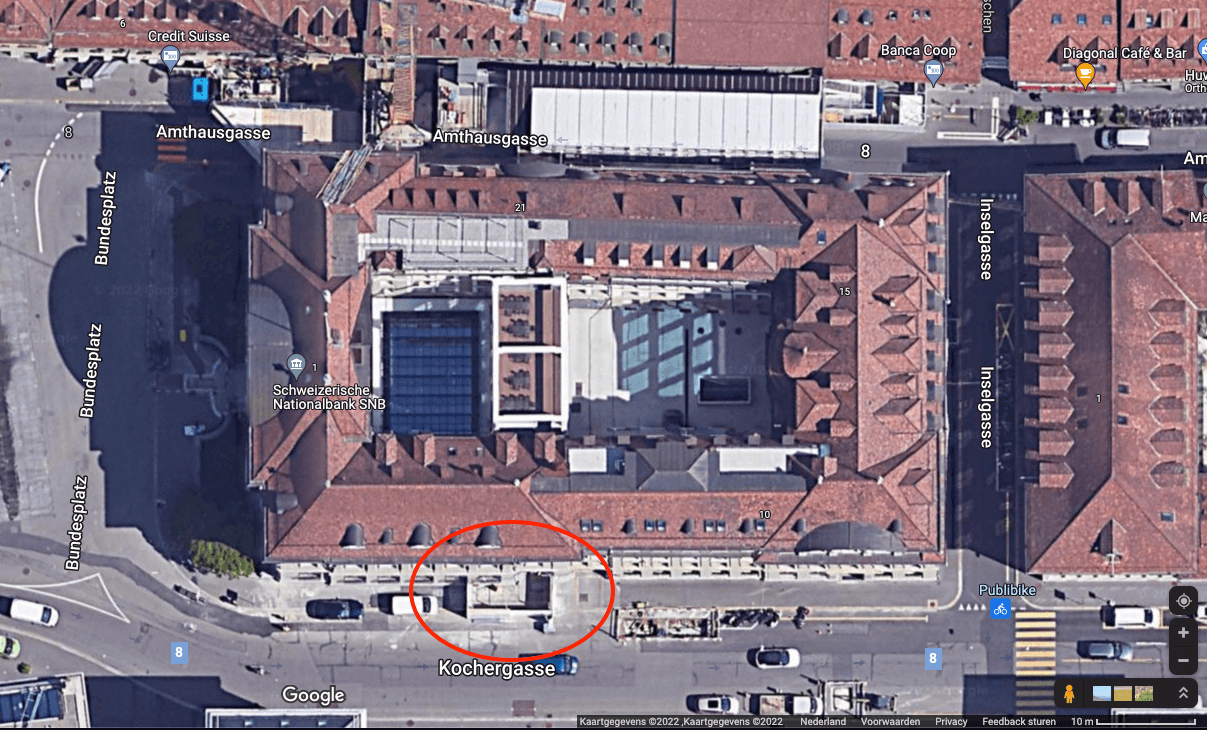

In Switzerland it’s a state secret where the central bank stores its gold domestically. From all the information I could gather I conclude the Swiss central bank primarily stores its gold—and that of foreign central banks and the Bank for International Settlements—on Bundesplatz 1 in the capital Berne.

This vault may be one of the largest globally. However, due to a renovation the vault is now empty. The metal has temporarily been transferred to a federal bunker near Kandersteg, deep in the Swiss mountains.

Source: Martin Ruetschi / Keystone. What led me to research this topic is a multi-year delay of a gold shipment by the Austrian central bank (OeNB) from London to Switzerland. From reading my previous article on this subject, some could be tempted to think OeNB’s gold is gone, or that the Bank Of England is obstructing the transfer. According to my analysis, though, London isn’t the problem. OeNB’s shipment was supposed to be in Berne by now, but due to a delay in the renovation of the vault the gold hasn’t been transferred yet.

To get to the bottom of this we will examine the vaults of the Swiss central bank in this article. In a following article I will present more proof of OeNB postponing to ship metal to the vault in Berne.

The first two chapters serve as an introduction. If you are short on time you can skip to the third.

The Swiss Have Been Digging Caves for Centuries

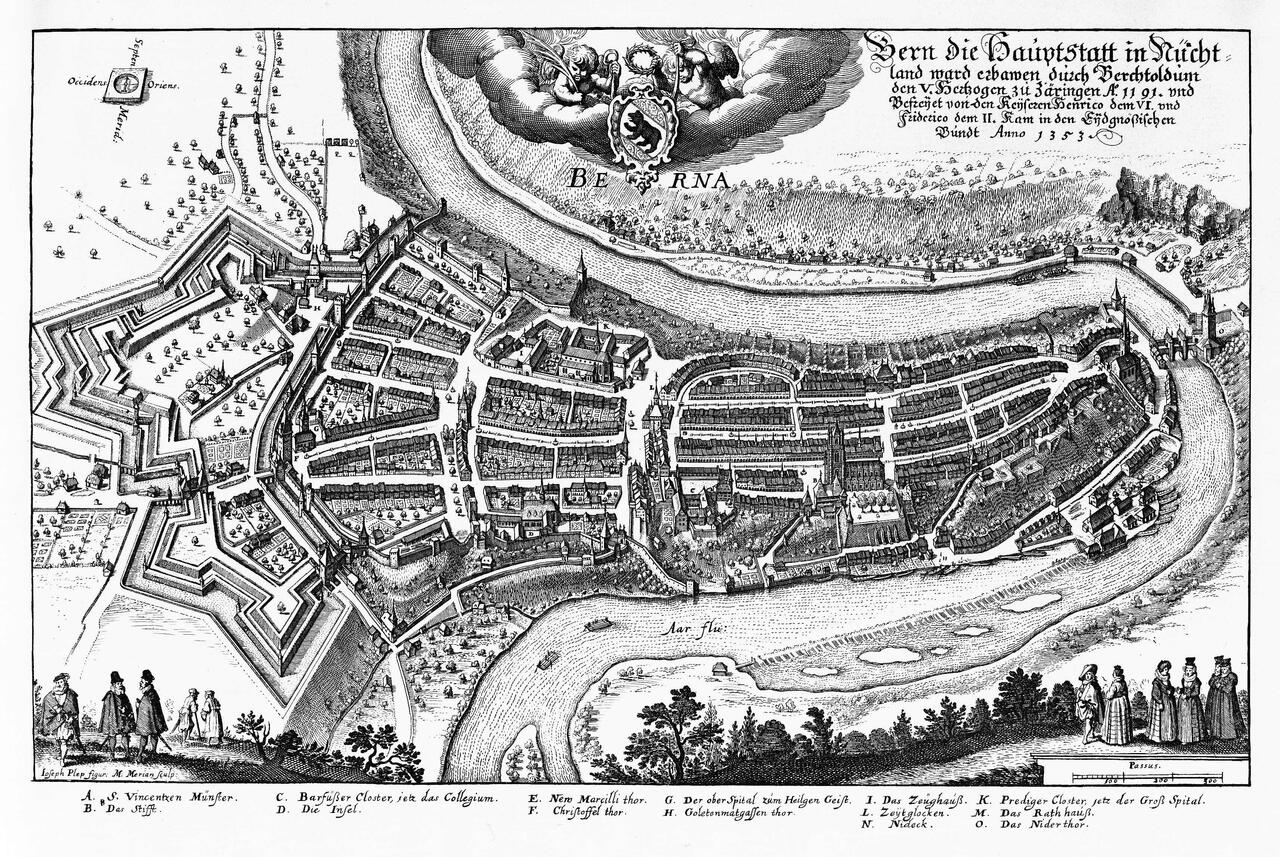

If there is one country that excels in building tunnels and caverns, it’s Switzerland. Berne was founded around 1200 on a peninsula in the river Aare. The peninsula is shaped as a hill due to the wear of the water. Enclosed by the Aare, the Old City could be easily defended by a wall at the West. The safety within this natural fortress allowed the city to flourish.

Source: Wikimedia. Map of the Old City of Berne, 1635. Many of the early inhabitants of Berne had vineyards outside of the city. Already in the 13th century cellars were being constructed below the buildings in the city, for more room and the right climate to preserve wine. The soil in Berne, consisting mostly of gravel and sand put there by glaciers during the last Ice Age, is well suited for constructing cellars. The weight of the ice caused the soil to compress¹. Today, many of the cellars are being used as bars, restaurants, shops, and more.

Source: Alamy Since 1983 the Old City of Berne is UNESCO world heritage site for its exceptionally coherent planning concept. Berne has always retained its historical character, presenting variations of the late Baroque period and Late Middle Ages. The Old City continues to be a place for living, working and commerce.

The first tunnel in Switzerland was built in 1707 to ease the passage over the Gotthard Massif Mountain in the Alps. Ever since, more road, railway, waterway, and maintenance tunnels have been built, by now totaling an astonishing 2,000 kilometers in length.

The Alps are in the South of Switzerland In the 1880s the Swiss started to build a line of fortifications in the Alps for the army to retreat and defend their country against a foreign invasion. In the Second World War a network of military tunnels and bunkers was added.