- The Possible Limits Of China-Russia Cooperation

The Possible Limits Of China-Russia Cooperation

Tyler Durden

Sat, 09/19/2020 – 23:30Authored by Lawrence Franklin via The Gatestone Institute,

China and Russia’s coordinated policies in foreign affairs and economic endeavors belie deep-seated fissures that might well prevent their current period of cooperation from evolving into a sustained alliance.

Despite China’s planned participation in Russia’s annual Caucus 2020 exercises on September 21-26, Sino-Russian history is so replete with war, unequal treaties and racism, there seems little probability that their present military cooperation will succeed in developing into a military alliance.

The current Russo-Chinese cooperation seems loosely rooted in the notion that “the enemy of my enemy is my friend.” Both countries apparently believe that checking U.S. power is in their national interests. China wants the U.S. to withdraw from its military and diplomatic commitments in the Western Pacific, thereby allowing Beijing to assert primacy in Asia, at least for a start. Russia seems to want the U.S. to decouple itself from the decades-old NATO alliance, thereby enabling Moscow to re-assert its dominance in the Baltic region and Eastern Europe.

Russia’s drive eastward in the late 17th century already brought Russians into conflict with China’s Qing Dynasty. After a series of clashes in the 1680s, the two empires temporarily settled on a boundary along the banks of the Amur River, separating Manchurian China from the Russian Far East. The Chinese, however, apparently resented Russia’s intrusion into a region Beijing considered its backyard. The Chinese also seem to have felt humiliated by defeats in subsequent wars with Russia and by having been coerced into signing what Beijing still refers to as “unequal treaties.” The ill will generated between China and Russia over several military conflicts in the 18th and 19th centuries, and a fierce ideological rivalry in the late 20th century, might also be an obstacle to an enduring bilateral alliance. Some Chinese commentators allege that Russia still occupies hundreds of thousands of square miles of Chinese territory seized in Tsarist times. China even recently claimed that Vladivostok, the most prominent city in Russia’s Far East, is historically Chinese territory.

China and Russia’s profoundly different cultures might also help to limit a bilateral honeymoon. A portion of Russia’s self-image is that of protector of the Slavic World, guardian of the Orthodox Christian faith, and the lead society in the Eurasian landmass from the Urals to the Pacific. Moscow’s historical view of China further seems conflated with a contempt for the Mongols, who cruelly subjugated Russian Slavdom for centuries. Ethnic tensions took a dark turn in July 1900, when Russian soldiers in the Amur River territory of Blagoveshchensk executed a racist rampage with forced deportation, and killing roughly 5,000 Chinese in the operation.

China sees itself as synonymous with civilization and calls itself “Jungwo” or center country. The Great Wall was continuously maintained by Chinese dynasties to keep out what China viewed as the “northern barbarians”: the Russians and earlier marauders. Chinese racism seems to extend to everyone outside its civilization’s values, such as China’s current concentration camps holding more than a million Uighurs, who are Turkic, as well as against Africans doing business in China.

Today, most Russians who live in Siberia reside less than 150 miles from the Chinese border, and the Russian population in these border provinces is in decline. Siberia, larger than the continental United States and India combined, is home fewer than 35 million people, with hundreds of millions of Chinese just over the border. At some point, China may start eyeing this energy- and mineral-rich region of Russia. Chinese investors have already leased large swathes of land in Russia’s Far Eastern realms.

The only major link that connects European and Asian Russia is the Trans-Siberian Railroad. China is now building more roads and more rail connectivity.

President Vladimir Putin’s Russia is clearly the junior partner in the Sino-Russian anti-American “alliance of convenience”: China’s growth is nearly five times that of Russia. Bilateral trade is increasing with the hoped-for goal of reaching $200 billion by 2024. Most of their joint projects are being carried out in agriculture, light industry, and energy. Last month, the two countries agreed to initiate two new joint projects: a gas processing plant and a bilateral insurance company. China’s investments in Russia are largely in energy, agriculture, forestry, construction materials, textiles, and household electric goods.

China seems to see Russia less as an economic partner than as a source for extraction of energy and raw materials. In 2019, Russian exports to China consisted almost entirely of oil, mineral ores, and wood. China appears to favor procurement of technically advanced products from the West rather than from its Eurasian ally. China, for instance, awarded contracts for hydroelectric products for its massive Three Gorges Dam to two European consortia, one headed by Germany’s Siemens Corporation, the other by the British/French GEC-Alstom, evidently preferring western designs to bids by Russia’s “Energomashexport.” Additionally, the trading branch of a major Chinese oil refining enterprise has been turning down Russian crude oil exports since Moscow’s state petroleum institution, Rosneft, was sanctioned by the United States.

There seem to be problems even in the most vibrant dimension of Sino-Russian cooperation: arms sales. While China in the past purchased billions of dollars of fighter and bomber aircraft from Russia, Beijing has quickly been developing its own arms industry, sometimes reverse engineering Russian weapons systems. Russia, perhaps annoyed at China’s aggressive pattern of copying its weapons systems — such as the SU-27 fighter and the S-300 surface to air missile system — has delayed a planned shipment of its premier S-400 air defense system. Moscow, it seems, decided to deliver the system to China’s regional arch-rival India instead. China’s development of its most modern stealth fighter aircraft, the Chengdu J-20, resembles a cancelled variant of a Russian fighter aircraft.

China is already successfully challenging Russia for influence among the post-Soviet states in Central Asia, particularly in Tajikistan. China’s establishment of a military base inside Tajikistan near its border with Afghanistan appears to have bested Russia’s effort to provide the Tajik government with security against Afghanistan-based jihadists just across the border.

Another area of disagreement is China’s opposition to Russia’s seizure of Crimea and its subsequent invasion of Ukraine.

A major plank of disingenuously articulated Chinese foreign policy is the principle of non-interference in the internal affairs of other countries. While disapproving of Russia’s assaults on sovereign states, China seems to have no problem asserting its own will in and around other states, for instance, in the South and East China Seas, India and the Galapagos Islands.

Russia, in turn, has not supported China’s aggressive moves in the South China Sea, in an attempt not to alienate Vietnam, the Philippines or Malaysia.

Mainly, this bilateral condominium might be doomed to collapse because there is no trust in the relationship. Russian security officers recently arrested a Russian scientist accused of spying for China. Russia and China act far more like competitors than allies. Their common antipathy for the United States most likely presents a distorted image of a coordinated policy agreement. These two authoritarian rivals could eventually assume their normal historical role as adversaries, even enemies. Consequently, Western intelligence agencies and policymakers might want to be wary of not overestimating the solidity and longevity of the Chinese-Russian friendship.

- Popular Children's App Allegedly Requests Minor To Take Naked Pictures

Popular Children’s App Allegedly Requests Minor To Take Naked Pictures

Tyler Durden

Sat, 09/19/2020 – 23:00A shocking claim, made by one parent in Anne Arundel County, Maryland, alleges a popular smartphone app designed for children asked a 5-year-old user to take naked pictures of themselves and siblings while in the bathroom and threatened to strangle the child if they didn’t comply, reported WBAL Baltimore.

Anne Arundel County police learned about the incident on Wednesday (Sept. 16), said the child had several apps “Talking Angela,” “Talking Angela 2″, Talking Tom 2”, and “Talking Ben 2” on their smartphone device. The complaint, filed by one of the parents, though the report did not specify which one (mother or father), called police after the incident. Police are now warning parents in the county, just outside Washington, D.C., to monitor their children’s online activity of apps and social media.

“The parent reported that the app requested the child remove clothing and take photos while in the bathroom,” Anne Arundel County police Sgt. Kam Cooke said. “We are not really sure as to, did the app actually say that? Or was that some sort of other entity within that app that was able to request that?”

WBAL downloaded the popular apps but did not find “any verbal commands, only written messages or symbols pointing out what to do next.”

The local television station interviewed one parent in the county, Victoria Rodriguez, who said she would not let her young kids use smartphone apps.

“I feel it’s weird, like someone is watching my child through the game or through the camera. It gives me the heebie-jeebies,” Rodriguez said.

A Patch report said the tech company behind the app, Outfit7, has denied the claims:

“The claims have no factual basis and are completely untrue,” company spokesperson Daša Rankel told Patch in an email.

However, one of the apps, Talking Tom, was in hot water in 2015 in the U.K., after the Advertising Standards Authority received complaints from two parents that their 7-year-old and 3-year-old children saw porno ads on the app. One ad read,” “Wanna f**k?”

Besides police warning about apps possibly requesting children to take pictures of themselves and or others, there’s been a massive problem of hackers disrupting virtual classes for children with porn, guns, and threats, all across the country.

- Taibbi: The Post-Objectivity Era

Taibbi: The Post-Objectivity Era

Tyler Durden

Sat, 09/19/2020 – 22:30Authored by Matt Taibbi via taibbi.substack.com

From a speech given this week to the McCourtney Institute of Democracy, Penn State University:

We live in a time of incredible political division. Many of us have had the experience of talking to someone whose idea of reality seems to be completely different from our own. It’s become difficult to have an argument in the traditional sense. People with differing opinions are often no longer even working from the same commonly-accepted set of facts. It’s a problem that has a lot to do with changes in how we receive and digest information, especially through the news media.

I’ve worked in the press for thirty years. In my lifetime the core commercial strategy of the news business has changed radically. At the national level, companies have moved from trying to attract one big audience to trying to capture and retain multiple small audiences.

Fundamentally, this means the press has gone from selling a vision of reality they perceive to be acceptable to a broad mean, to selling division. For technological, commercial, and political reasons this instinct has become more exaggerated with time, snowballing toward the dysfunctional state we’re in today.

A story that illustrates how the old system worked involves the first major national news broadcast, the CBS radio program anchored by the legendary Lowell Thomas.

History buffs will know Thomas. His was the iconic voice on those old WWII newsreels:

Read the rest here.

- ByteDance Shocked By Trump Claims TikTok Deal Partners Will Seed $5BN Federal Education Fund

ByteDance Shocked By Trump Claims TikTok Deal Partners Will Seed $5BN Federal Education Fund

Tyler Durden

Sat, 09/19/2020 – 22:19Update (2240ET): It appears that the “pledge” unveiled earlier by Trump of a $5 billion educational fund set up by TikTok, Oracle and WalMart was nothing more than a mirage. According to wire sourcesand the Chinese local press, today’s White House/media announcement of this $5 billion education was the first time Bytedance had heard of such an arrangement where it was going to pay the US government:

In response to some media reports that #TikTok will set up a $5bn education fund in the #US, TikTok’s parent company #ByteDance said Sunday that it heard about this for the first time from the news. pic.twitter.com/dyIVd2GtVG

— The Business Source (@GlobalTimesBiz) September 20, 2020

https://platform.twitter.com/widgets.js

* * *

In an announcement made during a Saturday White House briefing with reporters, President Trump announced a plan that would effectively satisfy his demands, made during a seemingly improvised comment during a press briefing last month, that the deal include something for the American taxpayer.

Enter: A $5 billlion pledge made collectively by TikTok, Oracle, Wal-Mart and the deal’s other backers that will seed a fund dedicated toward financing American education. The fund would go toward teaching American children “the history of the real America.”

As Bloomberg reminds us, Trump delivered a speech at the National Archives in Washington on Thursday where he attacked the NYT’s pulitzer prize-winning 1619 project. In response, Trump said he wanted to establish “a national commission to promote patriotic education” that he calls the “1776 Commission”.

The companies have agreed to terms with Trump for new TikTok Global to give $5 billion to an education foundation that will be established, sources tell me. Trump told press: “They’re going to be setting up a very large fund…That’s their contribution that I’ve been asking for.”

— Jennifer Jacobs (@JenniferJJacobs) September 19, 2020

https://platform.twitter.com/widgets.js

TRUMP wants the $5 billion from the Tiktok Global deal to pay for “patriotic education” via his envisioned “1776 Commission.”

— Jennifer Jacobs (@JenniferJJacobs) September 19, 2020

https://platform.twitter.com/widgets.js

NEWS: Trump wants $5 billion from companies creating a new U.S.-based TikTok venture directed toward teaching American children “real history, not the fake history.”

Story by me, @MarioDParker @josh_wingrove https://t.co/EqzpnqtSjj

— Jennifer Jacobs (@JenniferJJacobs) September 20, 2020

https://platform.twitter.com/widgets.js

Reporters immediately responded that this kind of federal intervention was totally inappropriate, and possibly illegal, yet, here we are. How will all this work? It’s not exactly clear. Details were scant.

Trump apparently used “the fund” as fodder for an appearance in North Carolina on Saturday evening that followed the briefing with reporters.

Later, during a campaign rally in Fayetteville, North Carolina, Trump said “we’re going to be setting up a very large fund for the education of American youth.” He told his rally audience that in conversation with leaders of the companies, he said “do me a favor, could you put up $5 billion into a fund for education, so we can educate people as to real history of our country – the real history, not the fake history.”

Of course, President Trump might as well pile it on thick with the election season promises. After all, as a trial balloon published by the SCMP last week suggested, any ‘deal’ that would satisfy Trump, CFIUS and a growing group of GOP senators probably wouldn’t pass muster with Beijing.

As it stands, the Oracle-TikTok deal would involve spinning off TikTok into an independent US-based company with a plan to take it public some time next year. Oracle, Wal-Mart and a handful of American VC funds would be shareholders. ByteDance would also own a minority stake. The exact numbers aren’t clear, and GOP senators are insisting that Chinese ownership in the minority. Beijing also recently introduced new export controls on technology like the TikTok content-recommendation algorithm. Whether the new company would acquire the algorithm, build a new one, or lease back the algorithm from ByteDance, remains unclear.

With all that’s transpired this year, the notion that President Xi would feel inclined to hand Trump another election season victory seems laughable. And Beijing has opposed the “smash & grab deal” from the beginning. So have many Americans – it’s the rare Trump play that has angered many on the left, and the right.

Trump’s TikTok ban is a gross abuse of powerhttps://t.co/DnbKVxaPpx pic.twitter.com/jy2HW9mz3e

— The Verge (@verge) September 19, 2020

https://platform.twitter.com/widgets.js

President Trump’s proposed TikTok ban isn’t just bad for Gen Z. It’s bad for free speech, free markets, and US democracy.https://t.co/86F3geQfTo

— WIRED (@WIRED) August 1, 2020

https://platform.twitter.com/widgets.js

Critics are already slamming the fund as far-fetched, and some have speculated about whether Trump expects the deal to get spiked.

That’s still not a given and given Trump approval you have to wonder if the details are such he expects Beijing to spike it

— CCP Collaborator Balding 大老板 (@BaldingsWorld) September 20, 2020

https://platform.twitter.com/widgets.js

Beijing has made its position pretty clear.

Beijing has positioned itself against the deal quite clearly so far and some of my colleagues wrote that Beijing would rather see TikTok fold in the US than it be sold off. Would be quite a feat to get it past SAMR/MOFCOM etc

— Vincent Lee (@Rover829) September 20, 2020

https://platform.twitter.com/widgets.js

But the CCP isn’t the only threat to the deal. GOP senators working together with AG Barr could still sink the deal between now and tomorrow night. A US court in Washington, where ByteDance has filed its latest complaint about the impending ban, could also step in. In fact, one could argue that by tying the deal to his ‘education’ plan, Trump just sealed its fate in the eyes of the courts.

* * *

During a briefing with reporters at the White House on Saturday, President Trump confirmed that he had signed off on a proposed deal that would involve spinning off TikTok’s global business into a standalone, US-based company owned by Oracle, ByteDance, Wal-Mart, a group of Silicon Valley VC firms and other investors from China.

“I have given the deal my blessing, if they get it done that’s great, if they don’t that’s fine too,” President Trump told reporters at the White House on Saturday.

Of course, CFIUS still needs to technically sign off on the deal. But that’s not the only obstacle remaining in the way of a spinoff that company insiders say could lead to a US public offering roughly one year from now if everything works out.

Trump’s comments come after the Commerce Department on Friday issued regulations prohibiting American companies from providing downloads or updates for TikTok after 11:59 pm on Sunday. The order also applies to WeChat, another popular Chinese-owned messaging and payments app, that will be subjected to the ban – at least in the US market (the administration has promised that any restrictions won’t apply to American companies doing business in foreign markets like China).

In a statement, TikTok said its “proposal” to Washington included “unprecedented levels of transparency.”

During an earlier briefing on Friday, Trump called TikTok “a pretty incredible asset” and said that the companies appeared close to a deal that would ameliorate security concerns from a group of GOP senators.

If the deal is ultimately structured like a spinoff, regulators in Beijing will likely need to sign off as well, which could create problems. However, there’s been some talk about ByteDance selling TikTok without the content recommendation algorithm at its heart. Beijing has already confirmed, via a leak to the SCMP, that it won’t allow an American company to walk away with TikTok’s algorithm.

ByteDance has already sought help from American courts, arguing that President Trump’s ban was illegal under American law. Unfortunately for the company, invoking “national security” gives Trump broad latitude to act; the courts don’t have much latitude to restrain him, according to Bloomberg.

Following the Commerce Department’s latest order, the company filed another lawsuit late Friday seeking to stop the Commerce Department’s order forcing Apple and Alphabet to drop TikTok from their app stores. TikTok owner ByteDance said it dropped its lawsuit against the Trump Administration, which it filed in California, and filed a new lawsuit in Washington. The company argued that Trump’s ban is “political” in nature, and that Trump is only using national security as a ruse.

TikTok also claimed that the ban violates first amendment protections on free speech.

- "Nobody Is Here!" – Movie Theaters Reopen, Audiences Stay Away

“Nobody Is Here!” – Movie Theaters Reopen, Audiences Stay Away

Tyler Durden

Sat, 09/19/2020 – 22:00“If you build it, they will come.” That moto was popularized by Kevin Costner’s character in the 1989 movie Field of Dreams, but such advice today in a post-pandemic world is bullshit.

Take, for, example, Christopher Nolan’s movie Tenet, released on Sept. 3, was supposed to mark the revival of the movie theater industry, according to NYT.

Movie Tenet. h/t NYT, Jim Lo Scalzo/EPA, via Shutterstock Ahead of the opening, Robinhood traders in August piled into movie theater stocks, including Cineworld and AMC, in anticipation Americans would rush back to theaters.

But theater stocks dumped into corrections days after the movie was released, due to the fact the film collected $9.4 million in its first weekend in North America and just $29.5 million over its first two weeks. The disappointing turnout has made one thing clear:

“We have no way of forecasting how long it will take for consumer comfort with indoor movie theaters to return,” Rich Greenfield, a founder of the Lightshed Partners media research firm, wrote in a note on Monday.

Even with theater capacity limited to 50% in most of the country, and 68% of theater chains reopened by Labor Day, the promotion of Tenet still did not entice Americans to return to indoor movie theaters as coronavirus cases continue to rage in late summer, heading into fall.

We noted in May how a massive shift from indoor to outdoor movie theaters would be a hot trend for 2020.

-

Walmart Is Turning Its Parking Lots Into Drive-In Movie Theaters For Its Customers

-

Struggling Mall Owner Transforms Parking Lots Into Drive-In Movie Theaters

For some comparison, Jeff Goldstein, Warner Bros. president of distribution, said Nolan’s past films – Inception, Interstellar, and Dunkirk – opened in the $50 million range in North America and collected between $527 million and $837 million worldwide. The latest movie sales for Tenet suggest the public is not convinced they should be returning to movie theaters anytime soon.

Movie theaters have yet to persuade customers that indoor theaters are safe. Even before theaters started to reopen in late summer, there should’ve been an information campaign to educate the public about the millions of dollars theater operators spent to upgrade facilities to mitigate the virus spread.

Mark Zoradi, Cinemark’s chief executive, doesn’t expect a “sense of normality” for theaters until 2022, calling 2021 a “transition year.”

“We’ve spent millions and millions of dollars getting this stuff right,” Zoradi said. “If we can convince the consumer that we have done all of these things, they are much more likely to want to come back.

And if readers haven’t figured out, movie theaters will be dead for the next couple of years. Alastair Williamson, who was at a Regal movie theater in the Baltimore metro area on Saturday (Sept. 12), tweeted: “Nobody is here!”

Nobody is here! pic.twitter.com/Qu7EwWw84h

— Alastair Williamson (@StockBoardAsset) September 13, 2020

https://platform.twitter.com/widgets.js

In another tweet, Williamson shows the ticket counter, which by the way, appears to be automated, say goodbye to a few low-wage, low-paying jobs permanently displaced by automation, shows absolutely no one is at the cinema on a primetime Saturday evening.

No one at the movie theater. pic.twitter.com/uJrDo7KZZp

— Alastair Williamson (@StockBoardAsset) September 12, 2020

https://platform.twitter.com/widgets.js

The moral of the movie theater story is if theaters reopen with top-notch movies by big-time producers, well, the American public is still not interested because they believe facilities are not safe from the virus. To bring consumers back, a lot of convincing by theater operators will be needed.

-

- Too Much Centralization Is Turning Everything Into A Political Crisis

Too Much Centralization Is Turning Everything Into A Political Crisis

Tyler Durden

Sat, 09/19/2020 – 21:30Authored by Porter Burkett via The Mises Institute,

Is American politics reaching a breaking point?

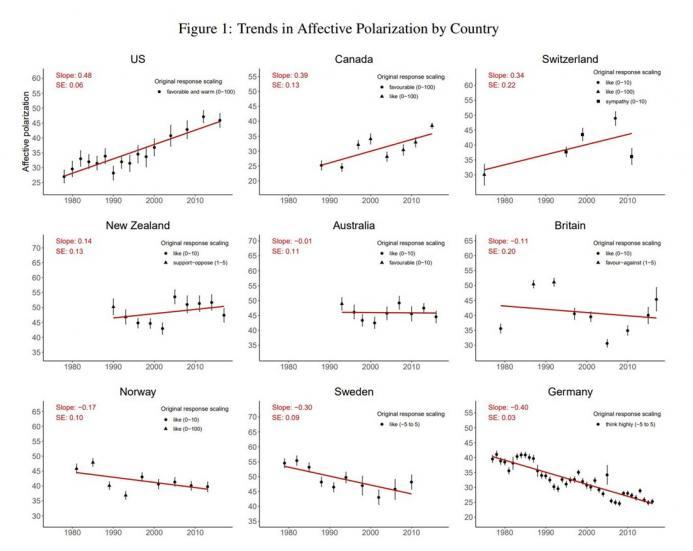

A recent study by researchers from Brown and Stanford Universities certainly paints a grim picture of the state of the national discourse. The study attempts to measure “affective polarization,” defined as the extent to which citizens feel more negatively toward other political parties than their own, in nine developed countries, including the United States.

The study authors concluded that affective polarization has risen much faster and more drastically in the United States than in any of the other countries they studied (figure 1). They then speculated on possible explanations of increasing polarization, suggesting that changing party composition, increasing racial division, and 24-hour partisan cable news are convincing possible causes. Notably, the research was completed before the coronavirus pandemic or the police killing of George Floyd, two events that have only deepened political division.

While the study is interesting and well written, the authors completely fail to consider a more fundamental potential explanation of increasing polarization, one that is likely to be understood well by libertarians and federalists, who have long railed against the trend toward ever more usurpation of local and state sovereignty in American politics.

I propose that the real culprit behind worsening polarization is the gargantuan federal government that has turned the entire country into an unceasing political battleground. When virtually all political issues are settled at the national level, the whole nation becomes a source of potential political opponents. Centralization changes the scale and with it the locus of political debate and conflict. For the average political participant, it is probably true that people with differing ideas live near you, in your city or state, but the mathematical reality is that the vast majority of your political opponents live relatively far away (spread throughout the rest of the country) and thus have no material connection to your life or your community.

Political opposition becomes just numbers on a cable news screen: 49 percent for this, 51 percent for that. Sixty-two million votes for one candidate, 65 million for another. These numbers, without names or faces, become simple objects; some are pawns to be moved around, while others are obstacles to be pushed aside. This is not just speculation: previous research has indicated that partisanship is correlated with the use of tactics to dehumanize political opponents. Centralized political decision-making amounts to a systematic dehumanization of anyone who might participate in the political process.

The effects of such a disastrous form of organization are already evident. Political polarization is not confined to academic papers, but has now manifested in the streets of Kenosha and Portland. As the 2020 election approaches, politically charged killings between members of rival factions will only become more likely. What was formerly a central promise of democratic politics—the peaceful transfer of power—has been abandoned in favor of direct action and blood.

If centralization is the cause of our problems, then decentralization is the cure. Pushing decision-making power down to state and local levels as much as possible, closer to the people actually affected by the decisions, is the only way forward. Of course, it will not solve all the problems of political culture today. Policy debates and disagreements could still be just as intense at the local level as at the federal. But it is harder to dehumanize someone who might be a part of your community. Those numbers on the screen are on your local news now, not the national news. Those percentages and vote tallies might include your neighbor down the street, your Uber driver, the person ahead of you in line at the grocery store, or the old man you saw out walking his dog this morning. Technically, this has always been true, and we would do well to remember the humanity of the people we disagree with even while political focus is at the national level. This fact is simply harder to ignore when the primary nexus for political decisions is more immediate and local.

Admittedly, I do not know exactly how decentralization can happen. There is no magic blueprint. Maybe the worst pessimists are right, and we are doomed to fight some sort of second civil war before we remember that those with whom we disagree are people too. I think the future is brighter than that. Perhaps, as Mises Institute president Jeff Deist has pointed out, de facto decentralization has already begun. Fortunately, nobody has to know exactly what the new political structure will look like, and – arguably the best part of decentralization – it does not have to look the same everywhere. Both major parties, and people of all ideological persuasions, will probably have to give up some preferred victory or vanquishing of the “other side.” Many Democrats would love to prevent all abortion laws in the state of Georgia for the rest of time. Some Republicans would love to lock down California’s southern border with an airtight seal.

A new era of decentralization means that neither of these things can be accomplished by federal imposition, and their proponents are not going to be happy about that. The task ahead is to demonstrate that whatever the sacrifices required to achieve more localized decision-making might be, centralization is too dangerous to continue.

- "Peak" SPAC: Playboy Enterprises Considering Going Public Through Blank Check Company

“Peak” SPAC: Playboy Enterprises Considering Going Public Through Blank Check Company

Tyler Durden

Sat, 09/19/2020 – 21:00Just because Playboy magazine no longer exists shouldn’t mean that the company shouldn’t have access to tap the capital markets in what is becoming the trendiest way on Wall Street: a SPAC.

Playboy Enterprises could be the next company to go public through a blank check company as the company looks to shift its model away from its magazine and onto sexual wellness products, spirits and cannabis, according to the Post.

The deal would come nine years after Hugh Hefner and Rizvi Traverse Management took the company private for $207 million. Hefner died in 2017 and his mansion in LA was divided into parcels of land. His son, Cooper, exited the business last year.

The leading SPAC candidate appears to be Mountain Crest, which has raised about $50 million and is led by Dr. Suying Liu, who is head corporate strategist at Hudson Capital, which is based in Beijing.

The company’s CEO, Ben Kohn, said Playboy would stop producing its iconic magazine in March of this year. Playboy remains a “media company” and has a website that carries much of the same content as the magazine did. The company now also focuses on Playboy branded products, including sex gels and CBD sprays.

As the Post notes, “the brand has been losing momentum in the U.S. for awhile now” – which makes it an obvious candidate to go public again.

After all, if the public markets aren’t for access to capital and socializing the losses of your cash burning company, what are they for?

- Newton, Physics, & The Market Bubble

Newton, Physics, & The Market Bubble

Tyler Durden

Sat, 09/19/2020 – 20:30Authored by Lance Roberts via RealInvestmentAdvice.com,

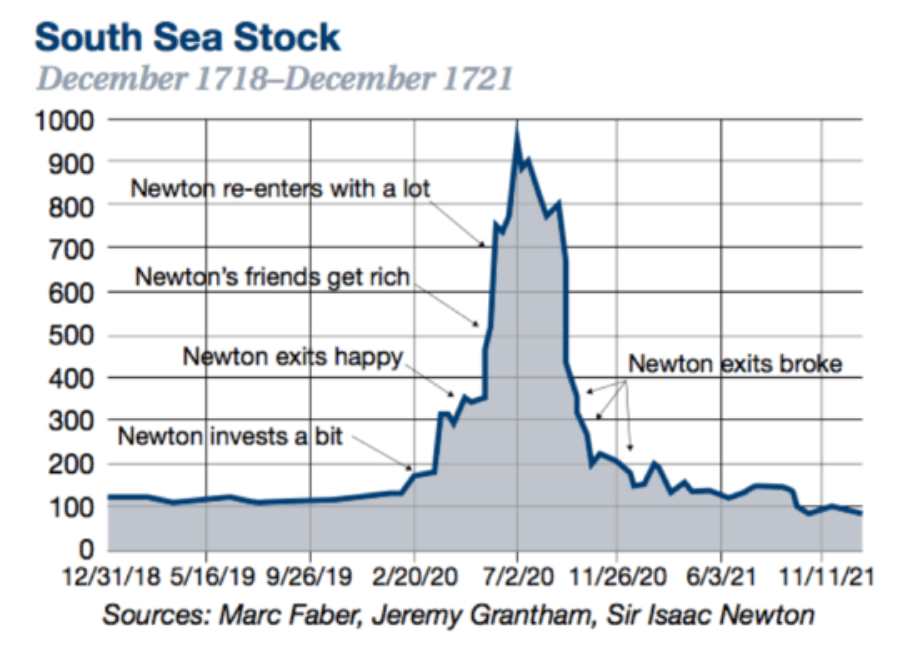

I have previously discussed the importance of understanding how “physics” plays a crucial role in the stock market. As Sir Issac Newton once discovered, “what goes up, must come down.”

Andy Kessler, via the Wall Street Journal, recently discussed a similar point with respect to the momentum in stock prices. To wit:

“Does this sound familiar: Smart guy owns stock in March at $200, sells it in June at around $600, but then buys it back in July and August for between $900 and $1,000. By September it’s back at $200. Ouch. Tesla this year? Yahoo in 2000? Nope. That was Sir Isaac Newton getting pulled into the great momentum trade of the South Sea Co., which cratered 300 years ago this month. He lost the equivalent of more than $3 million today. Newton, whose second law of motion is about the momentum of a body equaling the force acting on it, didn’t know that works for stocks too.”

To understand what happened to the South Sea Corporation, you need a bit of history.

The South Sea History

In 1720, in return for a loan of £7 million to finance the war against France, the House of Lords passed the South Sea Bill, which allowed the South Sea Company a monopoly in trade with South America.

England was already a financial disaster and was struggling to finance its war with France. As debts mounted, England needed a solution to stay afloat. The scheme was that in exchange for exclusive trading rights, the South Sea Company would underwrite the English National Debt. At that time, the debt stood at £30 million and carried a 5% interest coupon from the Government. The South Sea company converted the Government debt into its own shares. They would collect the interest from the Government and then pass it on to their shareholders.

Interesting Absurdities

At the time, England was in the midst of rampant market speculation. As soon as the South Sea Company concluded its deal with Parliament, the shares surged to more than 10 times their value. As South Sea Company shares bubbled up to incredible new heights, numerous other joint-stock companies IPO’d to take advantage of the booming investor demand for speculative investments.

Many of these new companies made outrageous, and often fraudulent, claims about their business ventures for the purpose of raising capital and boosting share prices. Here are some examples of these companies’ business proposals (History House, 1997):

-

Supplying the town of Deal with fresh water.

-

Trading in hair.

-

Assuring of seamen’s wages.

-

Importing pitch and tar, and other naval stores, from North Britain and America.

-

Insuring of horses.

-

Improving the art of making soap.

-

Improving gardens.

-

The insuring and increasing children’s fortunes.

-

A wheel for perpetual motion.

-

Importing walnut-trees from Virginia.

-

The making of rape-oil.

-

Paying pensions to widows and others, at a small discount.

-

Making iron with pit coal.

-

Transmutation of quicksilver into a malleable fine metal.

-

For carrying on an undertaking of great advantage; but nobody to know what it is.

A Speculative Mania

However, in the midst of the “mania,” things like valuation, revenue, or even viable business models didn’t matter. It was the “Fear Of Missing Out,” which sucked investors into the fray without regard for the underlying risk.

Though South Sea Company shares were skyrocketing, the company’s profitability was mediocre at best, despite abundant promises of future growth by company directors.

The eventual selloff in Company shares was exacerbated by a previous plan of lending investors money to buy its shares. This “margin loan,” meant that many shareholders had to sell their shares to cover the plan’s first installment of payments.

As South Sea Company and other “bubble” company share prices imploded, speculators who had purchased shares on credit went bankrupt. The popping of the South Sea Bubble then resulted in a contagion that spread across Europe.

Newton’s Folly

Sir Issac Newton, the brilliant mathematician, was an early investor in South Sea Corporation. Newton quickly made a lot of money and recognized the early stages of a speculative mania. Knowing that it would eventually end badly, he liquidated his stake at a large profit.

However, after he exited, South Sea stock experienced one of the most legendary rises in history. As the bubble kept inflating, Newton allowed his emotions to overtake his previous logic and he jumped back into the shares. Unfortunately, it was near the peak.

It is noteworthy that once Newton decided to go back into South Sea stock, he moved essentially all his financial assets into it. In general, Newton was intimately familiar with commodities and finance. As Master of the Mint, his post required him to make many decisions that depended on market prices and conditions.

The story of Newton’s losses in the South Sea Bubble has become one of the most famous in popular finance literature. While surveying his losses, Newton allegedly said that he could “calculate the motions of the heavenly bodies, but not the madness of people.”

For More On The History Of Speculative Bubbles: “Devil Take The Hindmost.”

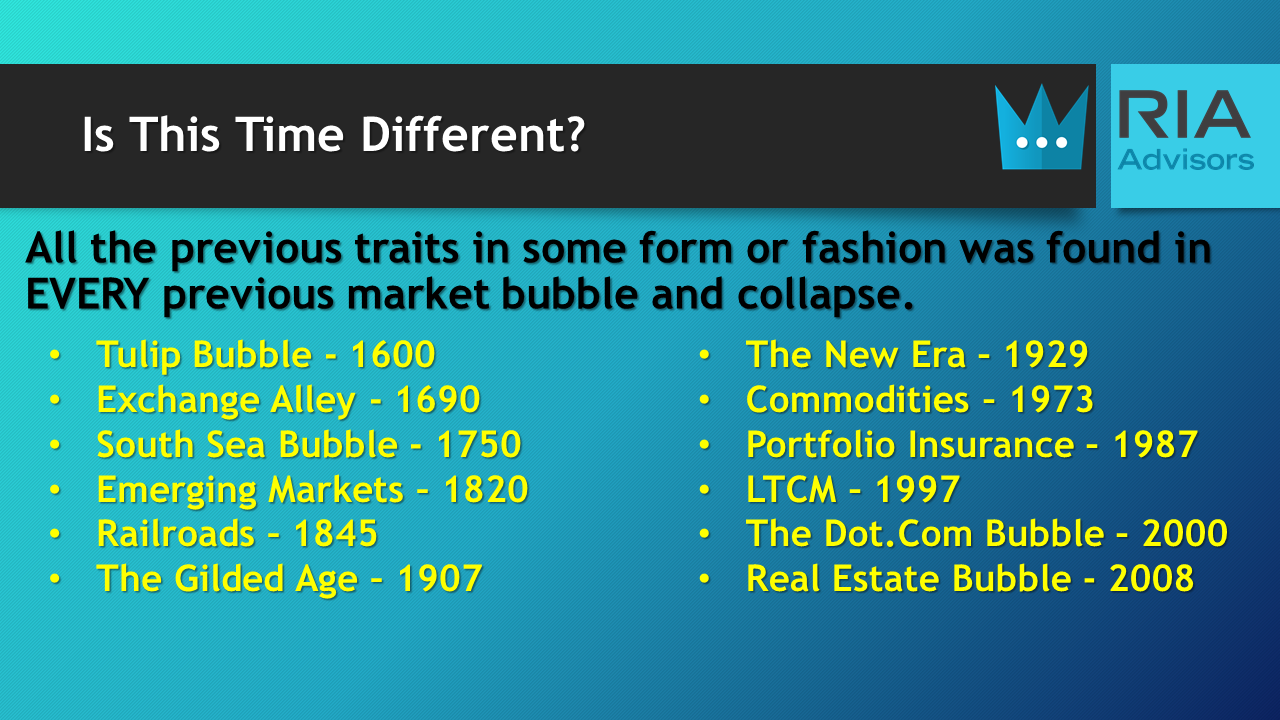

History Never Repeats, But It Rhymes

Throughout financial history, markets have evolved from one speculative “bubble,” to bust, to the next with each one being believed “it was different this time.”

The slides below are from a presentation I made to a large mutual fund company.

What we some common denominators between all previous bubbles and now.

The table below shows a listing of assets classes that have experienced bubbles throughout history, with the ones related to the current environment highlighted in yellow.

It is not hard to see the similarities between today and the previous market bubbles in history. Investors are currently chasing “new technology” stocks from Zoom to Tesla, piling into speculative call options, and piling into leverage. What could possibly go wrong?

Oh, by the way, the slides above are from a 2008 presentation just one month before the Lehman crisis.

The point here is that speculative cycles are always the same.

The Speculative Cycle

Charles Kindleberger suggested that speculative manias typically commence with a “displacement” which excites speculative interest. The displacement may come from either an entirely new object of investment (IPO) or from increased profitability of established investments.

The speculation is then reinforced by a “positive feedback” loop from rising prices. which ultimately induces “inexperienced investors” to enter the market. As the positive feedback loop continues, and the “euphoria” increases, retail investors then begin to “leverage” their risk in the market as “rationality” weakens.

The full cycle is shown below.

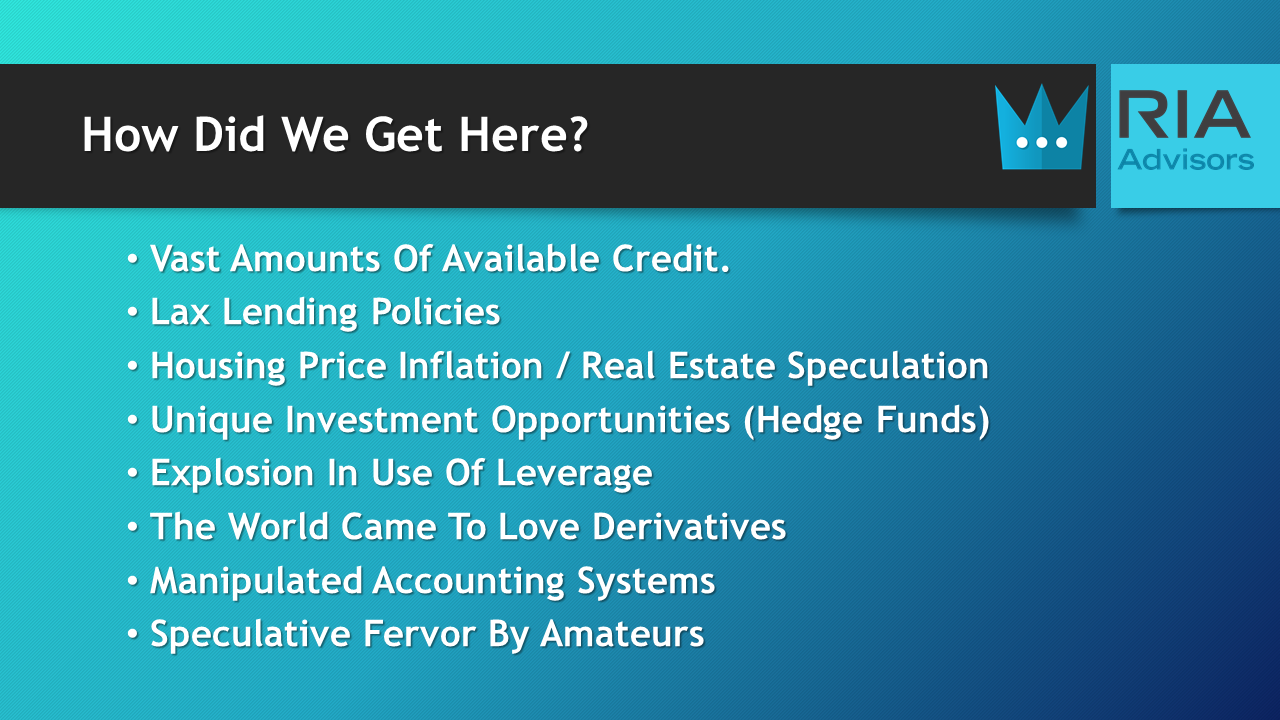

During the course of the mania, speculation becomes more diffused and spreads to different asset classes. New companies are floated to take advantage of the euphoria, and investors leverage their gains using derivatives, stock loans, and leveraged instruments.

As the mania leads to complacency, fraud and manipulation enter the market place. Eventually, the market crashes and speculators are wiped out. The Government and Regulators react by passing new laws and legislations to ensure the previous events never happen again.

The Latest Mania

Let’s go back to Andy for a moment:

“When bull markets get going, investors come out of the woodwork to pile in. These momentum investors—I call them momos—figure if a stock is going up, it will keep going up. But usually, there is some source of hot air inflating stocks: either a structural anomaly that fools investors into thinking ever-rising stock prices are real or a source of capital that buys, buys, buys—proverbial ‘dumb money.’ Think of it as a giant fireplace bellows, an accordion-like contraption that pumps in fresh oxygen to keep flames growing.” – Andy Kessler

We have seen these manias repeated throughout history.

-

In 1929 you could buy stocks with as little as a 5% down payment

-

The 1960s and ’70s had the Nifty Fifty bubble.

-

In 1987 it was a rising dollar, portfolio insurance, and major investments by the Japanese into U.S. real estate.

-

In 2000, it was the new paradigm of the internet and the influx of new online trading firms like E*Trade creating liquidity issues in Nasdaq stocks. Additionally, record numbers of companies were being brought public by Wall Street to fill investor demand.

-

In 2008, subprime mortgages, low interest rates, and lax lending policies, combined with a litany of derivative products inflated massive bubbles in debt instruments.

In 2020?

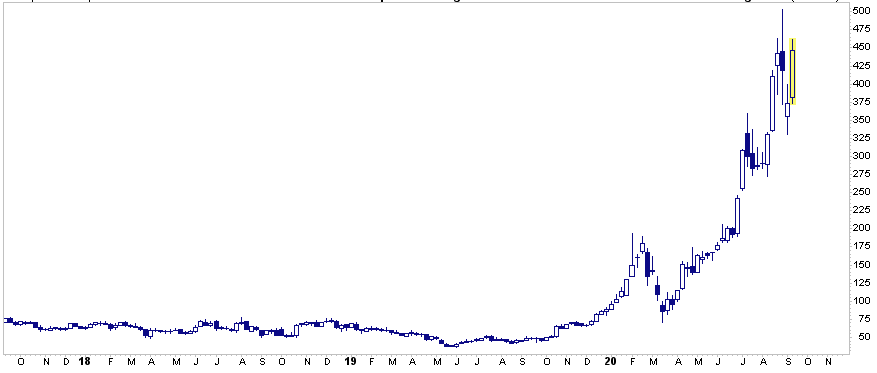

What about today? Look back at the chart of the South Sea Company above. Now, the one below.

See any similarities.

Yes, that’s Tesla

However, you can’t solely blame the Federal Reserve as noted by Andy:

“Most simply blame the Federal Reserve—especially today, with its zero-interest-rate policy—for pumping the hot air that gets the momos going. Fair enough, but that’s only part of the story. Long market runs have always allured investors who figure they’re smart to jump in, even if it’s late.

Everyone forgets the adage, ‘Don’t mistake brains for a bull market.’”

This Time Is Different

As stated, while no two financial manias are ever alike, the end results are always the same.

Are there any similarities in today’s market? You decide.

“From SPACs, or special purpose acquisition companies, which are modern-day blind pools that often don’t end well. Today’s momos also chase stock splits, which mean nothing for a company’s actual value. Same for a new listing in indexes like the S&P 500. Isaac Newton could explain the math.” – Andy Kessler

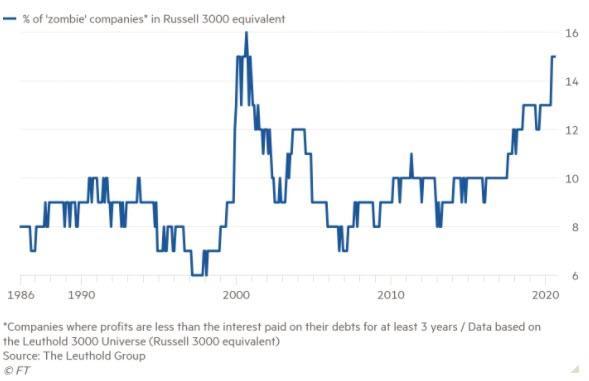

You get the idea. But one of the tell-tale indications is the speculative chase of “zombie” companies which are only still alive primarily due to the Federal Reserve’s interventions.

Fixing The Cause Of The Crash

Historically, all market crashes have been the result of things unrelated to valuation levels. Issues such as liquidity, government actions, monetary policy mistakes, recessions, or inflationary spikes are the culprits that trigger the “reversion in sentiment.”

Importantly, the “bubbles” and “busts” are never the same.

I previously quoted Bob Bronson on this point:

“It can be most reasonably assumed that markets are efficient enough that every bubble is significantly different than the previous one. A new bubble will always be different from the previous one(s). Such is since investors will only bid prices to extreme overvaluation levels if they are sure it is not repeating what led to the previous bubbles. Comparing the current extreme overvaluation to the dotcom is intellectually silly.

I would argue that when comparisons to previous bubbles become most popular, it’s a reliable timing marker of the top in a current bubble. As an analogy, no matter how thoroughly a fatal car crash is studied, there will still be other fatal car crashes. Such is true even if we avoid all previous accident-causing mistakes.”

Comparing the current market to any previous period in the market is rather pointless. The current market is not like 1995, 1999, or 2007? Valuations, economics, drivers, etc. are all different from cycle to the next.

Most importantly, however, the financial markets always adapt to the cause of the previous “fatal crash.”

Unfortunately, that adaptation won’t prevent the next one.

Yes, this time is different.

“Like all bubbles, it ends when the money runs out.” – Andy Kessler

-

- US Sends More Armored Infantry Units Into Syria Amid Increased Russian Presence

US Sends More Armored Infantry Units Into Syria Amid Increased Russian Presence

Tyler Durden

Sat, 09/19/2020 – 20:00Amid increasing tense encounters between American and Russian military convoys in northeast Syria, which in at least one recent encounter ended in a ramming incident, additional US mechanized infantry units have been ordered into Syria on Friday, including Bradley Fighting Vehicles.

“CJTF-OIR plans to position mechanized infantry assets, including Bradley Fighting Vehicles, to Syria to ensure the protection of Coalition forces and preserve their freedom of movement so they may continue Defeat Daesh operations safely,” the Pentagon said in a press release.

U.S. Army image: “Soldiers and Airmen unload Bradley fighting vehicles from a C-17 aircraft near northeastern Syria Sept.19,2020.” Ostensibly the counter-ISIS mission was offered as the prime rationale, but it’s clear it has more to do with the ratcheting cat-and-mouse encounters between US and Russian forces, which could at any moment result in an exchange of fire incident.

Ironically Trump at the same time told White House reporters that “we are out of Syria” but troops only remain solely with a mission of “guarding the oil.”

Following recent collisions b/n #US & #Russia/n troops in east of #Euphrates,US military now opts to accompany RU mil convoys from the air.The latest encounter feats 2 AH-64 Apaches flying over RU mil police in #Syria‘s Hasakah. RU military said it deems the moves as provocations pic.twitter.com/NrFwFMhhwj

— Maxim A. Suchkov (@m_suchkov) September 16, 2020

https://platform.twitter.com/widgets.js

Meanwhile Russia is appearing to get more involved in determining the future political fate of Syria, as reported by The New Arab this week:

Russian Foreign Minister Sergey Lavrov’s visit to Syria last week has been interpreted as another turning point in Moscow-Damascus relations that could have fundamental implications for Bashar Al-Assad’s rule, analysts have said.

Post-meeting comments made by the Russian delegation –

headed by Deputy Prime Minister Yury Borisov – appeared in conjunction with the Syrian regime’s own uncompromising stance towards the opposition.Amid a rapidly deteriorating economic situation given far-reaching US-led sanctions, Moscow apparently wants to arrive at a final political solution fast, ensuring stability but in a way that might end Damascus’ international isolation in order to revive the economy.

Syrian Sanctions are beginning to bite

Gasoline in Syria in short supply. This line of cars has formed in Tartus on the coast. Imports have been targeted by sanctions and Syrian oil has been impounded by US order. https://t.co/aQp4ZjrXjn

— Joshua Landis (@joshua_landis) September 19, 2020

https://platform.twitter.com/widgets.js

“Russia has now thrown its weight behind the UN supported Syrian Constitutional Committee, which involves members of the regime, opposition, and civil society and viewed as perhaps the best solution on offer to ending the war,” The New Arab report concludes.

- David Stockman: How The Stock Market Got To Be So Out Of Touch With Reality

David Stockman: How The Stock Market Got To Be So Out Of Touch With Reality

Tyler Durden

Sat, 09/19/2020 – 19:30International Man: Thanks to the shutdowns, economic activity on main street is at a standstill. Government, corporate, and personal debt is skyrocketing. Yet, the stock market is in a mania. Has the stock market become out of touch with reality, and if so, what are the consequences of that?

David Stockman: Both ends of the Acela Corridor have lost their marbles. This year, Uncle Sam borrowed $4 trillion in six months, the Fed printed $3 trillion in three months, and Wall Street drove the S&P 500 to 52X reported LTM earnings in the context of a deeper economic plunge than occurred in the worst quarter of the 1930s.

Therefore, Washington has become disconnected from any semblance of fidelity to sound money and fiscal rectitude, while Wall Street has turned into an outright casino, valuing stocks based on endless Fed liquidity injections and the delusion that momentum chasing is an investment strategy.

With respect to the rampant folly in the Imperial City, Treasury Secretary Stevie Mnuchin has always reminded us of Alfred E. Neuman of “Me Worry?” fame at Mad Magazine. Recently, he more than earned that moniker when, in the context of the current monetary and fiscal lunacy, he proclaimed that, “Now is not the time to worry about shrinking the deficit or shrinking the Fed balance sheet.”

That was the so-called Conservative Party speaking, and it is a shrill reminder that the Trumpified GOP has gone utterly AWOL when it comes to its true job in American democracy, namely, resisting the Government Party (Dems) and its affinity for feeding the Leviathan on the Potomac.

That is to say, according to even the Keynesian deficit apologists at the CBO, Uncle Sam will spend $6.6 trillion during the current fiscal year (FY 2020) while collecting only $3.3 trillion in revenue. That’s Banana Republic stuff—borrowing 50% of every dollar spent.

Yet the advisory ranks of the potentially incoming Kamala Harris regency are even worse. They are loaded with “deficits don’t matter” ideologues and MMT crackpots who noisily argue that massive monetization of the public debt is not just a virtue, but utterly imperative.

Needless to say, this bipartisan commitment to all-in stimulus is financial catnip to the Wall Street gamblers because they are actually capitalizing into today’s nosebleed stock prices, not the present drastically impaired economy on Main Street but a pro forma simulacrum of future prosperity based on the delusional presumption that massive debt and money-pumping actually create economic growth and wealth.

The fact is, industrial production in August posted at a level first achieved in March 2006, and manufacturing output weighed in at levels originally attained in December 2004. So the misbegotten lockdowns and COVID-hysteria have cost the US economy 14–16 years of industrial production growth, yet this massive setback was not caused by some mysterious Keynesian-style faltering of “demand” that can allegedly be compensated for by new Fed credits plucked from thin air.

To the contrary, the current depression is the result of the visible shutdown and quarantine orders of the state, which are likely to linger for months to come or even intensify as the fall-winter flu season arrives. Undoubtedly, the Virus Patrol will spur further outbreaks of public fear based on “bad numbers” from the CDC, which are actually an agglomeration of cases and deaths from normal influenza, pneumonia, and a myriad of life-threatening comorbidities, not pure cases of the COVID alone.

But beguiled by “stimulus” and hopium, Wall Street completely ignores the contradiction between over-the-top demand stimulus and what amounts to supply-side contraction owing to economic martial law.

So, at 3400 on the S&P 500, the current LTM price-to-earnings ratio ranges between 52.1 times the earnings CEOs and CFOs certify on penalty of jail time ($65 per share) or 27 times the Wall Street brush-stroked and curated version ($125 per share), from which all asset write-offs, restructuring charges, and other one-timers/mistakes have been finessed out.

Of course, these deleted GAAP charges reflect the consumption of real corporate resources, such as purchase price goodwill that gets written off when a merger or acquisition goes sour, or the write-down of investments in factories, warehouses, and stores that get closed. As such, they absolutely do diminish company resources and shareholder net worth over time.

But for decades now, Wall Street has so relentlessly and assiduously ripped anything that smells like a “one-timer” out of company earnings filings with the Securities and Exchange Commission (SEC) that it no longer even knows what GAAP earnings actually are.

And it pretends that these discarded debits (and credits) to income are simply lumpy things that even out in the wash over time. They do not.

If ex-items reporting was merely a neutral smoothing mechanism, reported GAAP earnings and “operating earnings” would be equal when aggregated over several years, or even a full business cycle.

Yet during the last 100 quarters, there have been essentially zero instances in which reported GAAP earnings exceeded “operating income.”

So, in aggregate terms, several trillions of corporate write-downs and losses have been swept under the rug.

During the second quarter of 2020, for example, GAAP earnings reported to the SEC totaled $145.8 billion for the S&P 500 companies, while the ex-items earnings curated by the street posted at $222.3 billion. That amounts to the deletion of nearly $77 billion of write-downs and mistakes, and it inflated the aggregate earnings number by more than 52%.

The game is all about goosing the earnings number in order to minimize the apparent price-to-earnings multiple, thereby supporting the fiction that stocks are reasonably valued and that nary a bubble is to be found, at least in the broad market represented by the S&P 500.

Still, valuing the market at 52 times trailing-12-month earnings during the present parlous moment in time—or even 27 times if you want to give the financial engineering jockeys in the C-suites a hall-pass for $77 billion of mistakes and losses this quarter alone—is nothing short of nuts.

Yet, the gamblers in the casino hardly know it.

Wall Street has already decided that current-year results don’t matter a whit: the nosebleed-level trailing P/E multiples currently being racked up are simply being shoved into the memory hole on the presumption that the sell side’s evergreen hockey sticks will come true about four quarters into the future, and if they don’t, a heavy dose of ex-items bark-stripping will gussy up actual earnings when they come in.

Still, if you think that a forward P/E multiple of, say, 17.5 times is just fine and that flushing the one-timers is OK, then you still need $193 per share of operating earnings by the second quarter of 2021 to justify today’s index level.

Then again, a 54% gain in operating earnings over the next four quarters ($193 per share in the second quarter of 2021 versus $125 per share in the second quarter of 2020) is not simply a tall order; it’s downright delusional.

International Man: What could derail the Fed’s ability to pump up the stock market casino with all this easy money? They simultaneously want zero interest rates and more inflation. It seems something has to give.

David Stockman: Yes, what’s going to “give” sooner or later is the entire house of monetary cards erected by the Fed and its fellow-traveling global central banks over the last several decades. What they are doing is based on the triple error that inflation is too low, that deeply repressed and falsified interest rates fuel real growth, and that private savers are a hindrance to optimal economic function and need to be euthanized via confiscation of the real (after-inflation) value of their capital.

In the first place, as Paul Volcker pointedly reminded, there is nothing in the pre-1990 textbooks that says 2.00% inflation is desirable and is to be pursued with fanatical intensity—even if actual inflation comes in only a few basis points below the magic target.

Indeed, if the 2% target is zealously pursued via prolonged pegging of interest rates to the zero bound and the massive purchase of bonds and other securities, the result is actually inimical to economic growth and sustainable gains in real wealth.

That’s because falsified interest rates and inflated financial asset values lead to massive malinvestment via rampant financial engineering in the corporate sector and reckless borrowing to fund transfer payments and economic waste in the public sector.

Nor is that a mere theoretical possibility. The rolling 10-year real GDP growth rate has now fallen to just 1.5% per annum, or barely one-third of the 3–4% per year rolling averages which prevailed during the heyday of reasonably sound money and fiscal rectitude prior to 1971.

Beyond that, there really hasn’t been any inflation shortfall from the 2% target, unless measured by the Fed’s flakey yardstick called the PCE deflator. For instance, since December 1996, when Greenspan uttered his irrational exuberance warning, the CPI is up by 2.09% per annum and the more stable 16% trimmed-mean CPI is up by 2.12% per annum.

That hardly constitutes a “shortfall” from target, but the Eccles Building money-printers make the claim anyway because the PCE deflator gained slightly less over that 23 year period, averaging an increase of 1.71 per annum.

The truth is, no one except groupthink besotted central bankers would think that a mere 30 basis point shortfall over more than two decades justifies the massive financial fraud of pumping trillions of fiat credit into the financial system.

That’s especially the case because the PCE deflator drastically underweights shelter costs and doesn’t even measure the purchasing power of money against a fixed basket of goods and services over time, anyway. Instead, it is actually a tool of GDP accounting that reflects the changing mix of goods and services supplied to the household sector.

That is to say, if someone chooses to live in a tepee and spend nearly all of their paycheck on computers, TVs, and other high-tech gadgets that have been rapidly falling in price, that doesn’t improve the exchange value of the dollar wages they earn; it just means that their tepee may be getting crowded with tech gadgets.

The same is true of the aggregate level. Just because the mix of goods and services changes over time, that doesn’t miraculously rescue the purchasing power of the dollar from the ravages of inflation.

Nor does it alleviate the savaging of lower- and middle-class living standards that are the direct product of the Fed’s misguided commitment to inflation targeting. In fact, during that same 23-year period, the annual rate of increase for professional services, shelter, food away from home, medical services, and education expense has been 2.6%, 2.7%, 2.8%, 3.5%, and 4.5%, respectively.

So once you set aside the foolishness of 2% inflation targeting and the Fed’s sawed-off inflation measuring stick (the PCE deflator), what you really have is growth stunting monetary madness. There is no other way to explain a Fed balance sheet that went from $4.2 trillion on March 4 this year to $7.2 trillion by June 10.

After all, the first $3 trillion of Fed balance sheet took nearly 100 years to generate, from its opening in 1914 to breaching the $3 trillion marker for the first time in March 2013. That the Fed has now become a monetary doomsday machine, therefore, is no longer in doubt.

* * *

The truth is, we’re on the cusp of a economic crisis that could eclipse anything we’ve seen before. And most people won’t be prepared for what’s coming. That’s exactly why bestselling author Doug Casey and his team just released a free report with all the details on how to survive an economic collapse. Click here to download the PDF now.

- Glenn Greenwald Shocks With Explanation On Why Mainstream Media Is Ignoring Assange Trial

Glenn Greenwald Shocks With Explanation On Why Mainstream Media Is Ignoring Assange Trial

Tyler Durden

Sat, 09/19/2020 – 19:00Well-known journalist Glenn Greenwald has once again sparked intense debate on the Left by refusing to conform to any level of group-think.

On Friday he mused about the ongoing Julian Assange extradition trial in London, offering an explanation as to why mainstream US media has seemingly dropped Assange from its radar, despite during the early years of the most bombshell WikiLeaks revelations working closely with Assange in terms of corroborating coverage.

It’s true that one reason that the Assange prosecution – despite its extreme dangers and consequences – is receiving so little media attention is that it doesn’t have a partisan angle.

But another is that many liberals believe their political adversaries deserve to be in prison. https://t.co/bViOmUAKDi

— Glenn Greenwald (@ggreenwald) September 18, 2020

https://platform.twitter.com/widgets.js

Greenwald started with a tweet acknowledging that Assange’s plight, which includes the possibility of being extradited to the United States where he faces certain life in prison, has received “little media attention” ultimately because it doesn’t have an easy partisan angle.

“But another is that many liberals believe their political adversaries deserve to be in prison,” Greenwald stated, going on the offensive.

And that’s where the most famous founding journalist at The Intercept began going off on liberals’ exaggeration of what Trump represents and how he came to power:

“If you start from the premise that Trump is a fascist dictator who has brought Nazi tyranny to the US, then it isn’t that irrational to believe that anyone who helped empower Trump (which is how they see Assange) deserves to be imprisoned, hence the lack of concern about it,” Greenwald said.

If you start from the premise that Trump is a fascist dictator who has brought Nazi tyranny to the US, then it isn’t that irrational to believe that anyone who helped empower Trump (which is how they see Assange) deserves to be imprisoned, hence the lack of concern about it.

— Glenn Greenwald (@ggreenwald) September 18, 2020

https://platform.twitter.com/widgets.js

Essentially Greenwald is saying, ‘no, Trump is not a Nazi’ — and this flawed belief will only compound errors when it comes to other pressing issues such as Assange’s fate.

Greenwald previously addressed the “authoritarian arguments” which claimed the WikiLeaks founder does not deserve journalistic protections.

One of the most dangerous and authoritarian arguments you’ll hear from those who support Trump DOJ’s attempt to imprison Assange is that it doesn’t endanger press freedoms because “Assange is not a journalist.” Leave side the huge stories he’s broken & journalism prizes he won… pic.twitter.com/J94n5E5tMO

— Glenn Greenwald (@ggreenwald) September 9, 2020

https://platform.twitter.com/widgets.js

Earlier this month President Trump shocked many national security state insiders by suggesting be might be open to pardoning Edward Snowden.

While the Assange case would no doubt be a much higher hurdle for Trump in terms of the ‘deep state’ fierce pushback that would be sure to follow any similar consideration, it remains a possibility, especially were to Trump take the White House again after November.

- Nuclear Scenario For Markets Emerges In 'Jaw-Dropping' SCOTUS/Election Plot-Twist

Nuclear Scenario For Markets Emerges In ‘Jaw-Dropping’ SCOTUS/Election Plot-Twist

Tyler Durden

Sat, 09/19/2020 – 18:00“If the script were being written, this would be the plot-twist that would drop jaws in the theater…”

That is the dramatic (and rightfully so) introduction to a tweet thread by Jake Sherman describing the potential playbook for the next few months as election campaigning and the SCOTUS-nomination-process mutate into what could potentially be a “nuclear option” for markets into year end… and the start of 2021.

Here are the highlights from Sherman’s view on the potentially cataclysmic events over the next few weeks:

45 DAYS before Election Day, the Notorious RBG — the left’s most-beloved and celebrated jurist — dies, and @senatemajldr, the left’s most-hated lawmaker who is also up for re-election, vows a floor vote on President DONALD TRUMP’S nominee to the Sup Court.

THE U.S. CAPITOL will be center stage over the next 15 weeks until the end of 2020, as the Congress considers this open Supreme Court seat.

THIS IS, QUITE LITERALLY, a mesh of MCCONNELL’S most animating interests: power and judicial nominees. The left frequently says that MCCONNELL is obsessed with power — and nothing but power. There is some truth to that — MCCONNELL is acutely aware of what is afforded to him by being the majority leader, and he says it quite frequently: He controls what comes up for a vote, and what doesn’t and when.

HE USES THAT POWER and that leverage with maximum impact. you should expect that here, w a chance to reshape the court for decades to come & a better than even chance of slipping into the minority, @senatemajldr will leverage every ounce of power afforded to him to fill this seat

MCCONNELL has made his promise plain:“President Trump’s nominee will receive a vote on the floor of the United States Senate.”

PAY ATTENTION TO WHAT MCCONNELL DOESN’T SAY: He doesn’t say when. Rushing the nomination could hurt some vulnerable senators. But it could also guarantee Republicans a Supreme Court seat. As WaPo’s put it:“[T]his is a rare moment where a congressional caucus leader’s short-term & long-term interests seriously diverge, his/her immediate interests vs legacy. Fascinating political power play ahead.”

HOW HE’S FRAMING IT TO HIS COLLEAGUES: MCCONNELL wrote GOP senators:“This is not the time to prematurely lock yourselves into a position you may later regret. … I urge you all to be cautious and keep your powder dry until we return to Washington.”

SO, EXPECT a nomination and hearings before the election, but not necessarily a vote.

-

IS IT POSSIBLE that he tries to squeeze a vote in before Election Day? Yes. Absolutely — especially if TRUMP demands it

-

IS IT POSSIBLE that he pushes the vote until after the election, both as a practical matter to help his vulnerable colleagues, and a motivating factor for his base? Yep. Absolutely.

-

IS IT POSSIBLE JOE BIDEN wins the presidency, Republicans lose the Senate and MCCONNELL jams through the nominee in the lame duck? Yes, you bet. Can Democrats do anything besides bellyache? No. They can’t.

Despite what you will hear from the left in the coming days, CHUCK SCHUMER’S power is exceedingly limited. Senate Dems have scheduled a 1 p.m. caucus call (h/t MARIANNE LEVINE) to discuss their options.

REMINDER: If MARK KELLY beats MARTHA MCSALLY in Arizona, he could be sworn in at the end of November, altering the tight majority that MCCONNELL has to work with. It would then be 52-48. This seems like a very live option.

YES, Lindsey Graham has said a number of times that Senate should not consider a nominee in the last year of a president’s term. He said it in 2016 during a Judiciary hearing. He said it to @JeffreyGoldberg in 2018 — if a nominee comes in TRUMP’S last term, he wanted to wait

DOES THAT MEAN, that GRAHAM – in a neck-in-neck race for re-election – will stay true to that? No. Absolutely not. In July, he appeared to walk back his 2018 comments in an interview with CNN’s Manu Raju:

Asked about his past opposition to moving a nominee in a presidential election year after the primary season, Graham said:

“After Kavanaugh, I have a different view of judges,” referencing the brutal 2018 confirmation process of Supreme Court Justice Brett Kavanaugh.

“I’d like to fill a vacancy. But we’d have to see. I don’t know how practical that would be,” Graham told CNN Monday. “Let’s see what the market would bear.”

YOU WILL HEAR A LOT OF REPUBLICANS say it’s dangerous to have a 4-4 court going into an election, but there was a 4-4 court going into the last election… There are a number of Republican senators to watch very closely in the coming days. They will get peppered with several questions: Should the SENATE wait until next year to confirm a nominee? And, would you vote no if MCCONNELL put it on the floor? Is a lame-duck vote appropriate?

While the script above is key, the punchline for markets is the all too real possibility of a deadlocked 4-4 SCOTUS vote deciding what may be the most contested election in US history should Republicans fail to gather the votes to fill the vacant supreme court seat before the election.

And sure enough, Republican Alaska Sen. Lisa Murkowski has already fired the proverbial first shot, confirming she would not vote to replace a Supreme Court justice until after the inauguration.

“When Republicans held off Merrick Garland because nine months prior to the election was too close, we needed to let the people decide,” Murkowski said in August, according to The Hill.

“And I agreed to do that. If we say now that months prior to the election is OK when nine months is not, that is a double standard and I don’t believe we should do it.”

Now where have we seen this before?

Murkowski’s statements echo that of Maine Sen. Susan Collins, a fellow moderate and the only other pro-choice Republican in the Senate.

“I think that’s too close, I really do,” Collins said when asked whether she would vote to confirm a Supreme Court justice in October. Collins also said that she would oppose seating a justice in the lame duck session of Congress if President Donald Trump loses the election in November.

Collins made her position official in a Saturday tweet saying the Senate should wait until after the election for the vote (although as some have noted, she doesn’t make any promises on how she would vote if/when a vote is called).

My statement on the Supreme Court vacancy: pic.twitter.com/jvYyDN5gG4

— Sen. Susan Collins (@SenatorCollins) September 19, 2020

https://platform.twitter.com/widgets.js

Add to this the outcome risk from the Mark Kelly vs Martha McSally special election in Arizona (where Kelly has a steady lead), and a 4-4 SCOTUS deciding the next president suddenly looks very real.

Simply put, the political quagmire unleashed by the passing of Ruth Bader Ginsburg leaves the market in an even more precarious position since if a contested election was a source of great uncertainty before, a 4-4 SCOTUS extends that uncertainty even further as we already know there will be no concessions for weeks, and the extensions of mail-in ballots will merely add fuel to the fire of what is shaping up as the most contested election in US history.

In short, this is the “worst case scenario” – that JPMorgan just warned about last week when envisioning a contested election’s impact on markets – on steroids, since The Fed has nothing new to offer and fiscal stimulus will definitely be off the table now until an election decision is made, a decision that may not comes for months without a SCOTUS tiebreaker vote.

Back in July, Goldman’s David Kostin wrote that one of the key concerns expressed by its clients is that a contested election could drag on, resulting in little clarity for weeks if not months, in a rerun of the contested 2000 election between Al Gore and George W. Bush, when it took a Supreme Court challenge and 34 days for the winner to be decided. This is what Goldman said then:

Health concerns and social distancing protocols suggest that more voters than ever will decide not to cast ballots at traditional polling stations on Election Day and instead vote by mail. In the case of a close election, it will take time to count – and invariably re-count – all the absentee and mail-in ballots. The deadline for each state to certify its result and finalize electors is December 8th (35 days after the election) or six days before the Electoral College convenes on December 14th (first Monday after the second Wednesday in December).

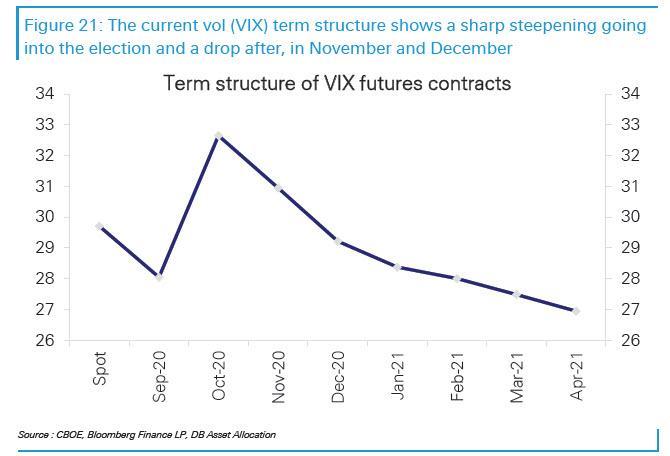

Echoing this, Deutsche Bank’s Parag Thatte wrote that the pricing of VIX futures with November and December expiries are likely too sanguine that there will be a quick and clear outcome of the elections.

Then last week, JPM’s chief equity strategist Misla Matejka joined this chorus of warnings about a contested election result, which he sees as the “worst-case scenario” for the market (Matejka also sees a contested election as the top risk for market performance into the year-end), adding that potential legislative paralysis could be “even more damaging” than Bush vs Gore for economy, as key stimulus measures to support economy could be delayed until well after the election:

The 2000 US presidential election between Bush and Gore provides a precedent for this. Equity markets struggled in the period following elections, with S&P500 dropping close to 12%.

Fast forward 20 years, when “in the current scenario,” JPM believes that “the potential legislative paralysis could be even more damaging for the economy, as key stimulus measures to support the economy might be delayed, and the partisanship is very elevated.”

Finally, the same point was underscored by Artemis Capital CIO who earlier today also wrote that “vol markets value the US election as a massive binary risk event that occurs at one point-in-time (like earnings in a stock)” However, “the real risk is a contested election and US constitutional crisis that occurs throughout time. If the latter comes to pass, forward vol is very mispriced.“

Vol markets value the US election as a massive binary risk event that occurs at one point-in-time (like earnings in a stock)

The real risk is a contested election and US constitutional crisis that occurs throughout time

If the latter comes to pass, forward vol is very mispriced

— Christopher Cole (@vol_christopher) September 14, 2020

https://platform.twitter.com/widgets.js

Putting all this into one chart, this is what the confusion and uncertainty heading into the election looked like before the death of RBG:

And now to all this add the potential “nuclear option” for markets of a contested election AND a deadlocked 4-4 SCOTUS (as Roberts again makes a “surprise” flip) failing to declare a winner, unlike the Bush v Gore 2000 election. What happens then? For the presidency, for the economy, for geopolitics, and for the stock market?

* * *

The script – as bizarre at it appears – has now been written and stocks just have to start “weighing” the risks more efficiently; Sunday night futures open will be fun to watch.

-

- ActBlue Raises Record $50 Million Following Ginsburg Death

ActBlue Raises Record $50 Million Following Ginsburg Death

Tyler Durden

Sat, 09/19/2020 – 17:30Left-wing fundraising organization ActBlue raised a staggering $50 million by 4 p.m. ET on Saturday following the death of Supreme Court Justice Ruth Bader Ginsburg, according to the Associated Press.

Hey reporters wondering if this SCOTUS news is motivating Democrats. Here is a chart of donations to our fund to help elect Democrats to the Senate. Donate (or watch the number go up) here: https://t.co/KGWmpELi2L pic.twitter.com/XCEk21Wnyh

— Tommy Vietor (@TVietor08) September 19, 2020

According to their online web tracker, donations flew in at over $100,000 per minute just hours after Ginsburg’s death – accelerated after Sen. Majority Leader Mitch McConnell (R-KY) announced that the Senate would hold a vote on Ginsburg’s seat, according to Breitbart.

“President Trump’s nominee will receive a vote on the floor of the United States Senate,” said McConnell on Friday evening.

Joe Biden’s presidential campaign also appeared to use Ginsburg’s death to raise money ahead of the election in November via an email that vice presidential candidate Sen. Kamala Harris (D-CA) sent. The email also reiterated that “voters should pick a President, and that President should select a successor” for Ginsburg. –Breitbart

“We cannot let them win this fight. Millions of Americans are counting on us to stand up, right now, and fight like hell to protect the Supreme Court — not just for today, but for generations to come,” stated the email from Harris. “The work of holding Senate Republicans accountable to the standard they set in 2016 starts now. To Joe and me, it is clear: The voters should pick a President, and that President should select a successor to Justice Ginsburg.”

“But we know, like you do, that the most important thing we can do to protect that legacy is not just winning the White House, but electing a Senate majority that will confirm fair-minded Supreme Court appointees who believe in equal justice under the law … That’s why I’m asking you today to fight alongside me and to make sure that when the time comes, President Joe Biden can appoint a justice to Justice Ginsburg’s seat who will uphold the rule of law and fight for all of us “

ActBlue has come under fire in recent weeks after nearly half of the group’s 2019 donations were revealed to be from anonymous donors who listed themselves as unemployed.

“After downloading hundreds of millions of [dollars in] donations to the Take Back Action Fund servers, we were shocked to see that almost half of the donations to ActBlue in 2019 claimed to be unemployed individuals,” said John Pudner, president of conservative political group, Action Fund. “The name of employers must be disclosed when making political donations, but more than 4.7 million donations came from people who claimed they did not have an employer. Those 4.7 million donations totaled $346 million ActBlue raised and sent to liberal causes.“

“It is hard to believe that at a time when the U.S. unemployment rate was less than 4 percent, that unemployed people had $346 million dollars to send to ActBlue for liberal causes,” Pudner continued, adding that “4.7 million donations from people without a job … raised serious concerns.”

Notably, by mid-June, ActBlue had contributed $119,253,857 to Biden – a figure which remained unchanged until at least July. As of this writing, they have contributed $194 million – an increase of $75 million.

They’ve also been scrutinized for taking a boatload of anonymous gift card donations valued at $100 or less.