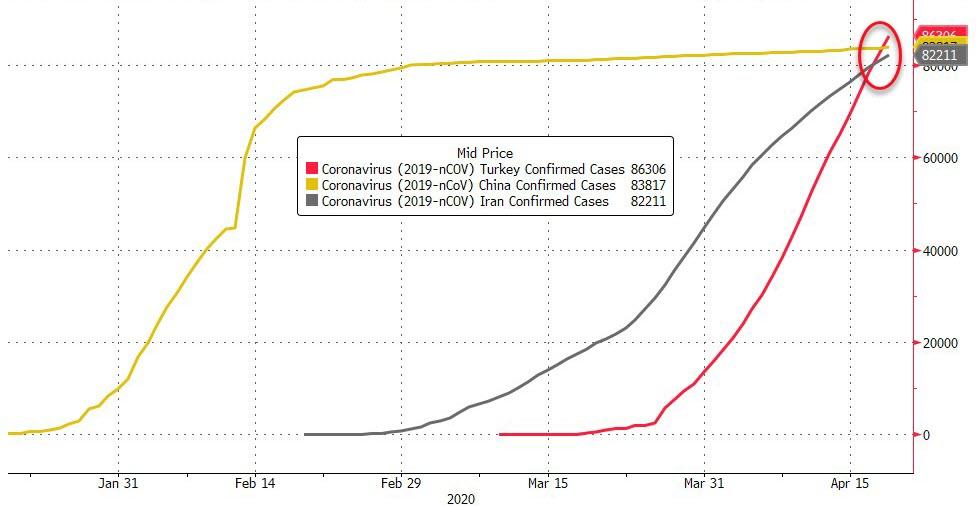

- Turkey Overtakes China & Iran In Total COVID-19 Cases But Still Resists Lockdown

Turkey Overtakes China & Iran In Total COVID-19 Cases But Still Resists Lockdown

For the first time going back to February 25 when Iranian leaders first publicly admitted they had a serious outbreak on their hands, and with the country establishing itself with the grim distinction of remaining the Middle East epicenter, another regional country now leads in total infection numbers outside the US and Europe. As of Monday morning, Turkey has 86,306 cases, surpassing China’s 83,817 and Iran’s 83,505 reported cases.

Turkey on Saturday confirmed that its numbers had risen to over 82,000 – a jump of nearly 4,000 cases from Friday, surpassing Iran for the first time ever, making it the new regional epicenter.

Line outside of Istanbul market, AFP via Getty. Like Iran before, Turkey is another country which has come under scrutiny and criticism for not only its slow response since cases began growing last month, but lack of testing and under-reporting numbers as well.

Over the weekend the Interior Ministry announced it was extending travel ban orders between 31 major cities for at least 15 more days.

Ankara has still held out against ordering a nationwide lockdown like other countries with its high numbers of cases, only opting to close schools and bars and imposing a weekend curfew only. It’s also imposed various age-restricted curfews.

“At [Turkey’s] level, most countries are implementing a full lockdown,” one virology expert was quoted in CNN as saying. “A partial lockdown can be good, it can balance keeping some of the economy functioning while still trying to contain the outbreak.”

The government has maintained its hospitals and heath care system is still functioning optimally and is nowhere near capacity, as Foreign Policy describes:

As the number of coronavirus cases has increased, Turkish Health Minister Fahrettin Koca has sought to allay fears of an overwhelmed health system. Speaking on Friday, Koca said that unlike Western nations, Turkey’s hospitals still hold excess capacity and that intensive care units were not exceeding 60 percent occupancy. A licensed physician, Koca’s daily briefings have made him a star on social media over the course of the pandemic; he has gained over 4 million followers on Twitter since the beginning of the year.

“Turkey’s problems with containing the virus came into focus on April 10, when a late announcement of a weekend curfew led to panic buying across the country,” FP adds.

The already battered Turkish economy looks to be pummeled further by the crisis, as the Turkish lira’s recent plummet to a near-historic low of 6.95 lira to the dollar demonstrates.

Recall too this report from ten days ago: “Turkey has held talks with the United States about possibly securing a swap line from the U.S. Federal Reserve and has discussed other funding options to mitigate fallout from the coronavirus outbreak, Turkish officials said on Friday.”

As recently as Sunday Presidents Trump and Erdogan spoke on the phone and agreed to continue pursuing “close cooperation” to contain the pandemic.

Tyler Durden

Tue, 04/21/2020 – 02:45 - Merkel May Survive The Coronapocalypse, But The EU Won't

Merkel May Survive The Coronapocalypse, But The EU Won’t

Authored by Tom Luongo via The Strategic Culture Foundation,

No matter how hard I try to dig German Chancellor Angela Merkel’s political grave she proves more adept at staying alive than a cockroach in a woodpile. And the recent fight amongst European Union members over “Coronabonds” has proven yet another escape path for her to avoid political termination.

Thanks to Merkel holding the line on debt mutualization and EU fiscal integration, which is very unpopular in Germany, her Christian Democratic Union (CDU) is now polling at levels it hasn’t enjoyed since before the last general election in 2017.

According to Europe Elects, the latest polling out of Germany has the CDU commanding around 35-37% of German voters. This is a party that was in shambles not two months ago after Merkel heir apparent Annagret Kramp-Karrenbauer stepped down as CDU leader, prompting a new leadership vote, which, conveniently for Merkel, has now been postponed indefinitely thanks to the COVID-19 crisis.

Germany, INSA poll:

CDU/CSU-EPP: 37.5% (-0.5)

GRÜNE-G/EFA: 16% (-2)

SPD-S&D: 16%

AfD-ID: 10.5% (+0.5)

LINKE-LEFT: 7.5% (+0.5)

FDP-RE: 7% (+1.5)+/- vs. 3-6 Apr.

Fieldwork: 9-14 Apr. ’20

Sample size: 2,108

➤ https://t.co/obOCVirbpF pic.twitter.com/VBIblbijEh— Europe Elects (@EuropeElects) April 14, 2020

https://platform.twitter.com/widgets.js

Some of that is the normal “rally around the current leader” that occurs during any crisis. President Trump’s numbers in the U.S. have been strong despite the twin crises here. Even marginal leaders like Prime Minister Giuseppe Conte in Italy have seen their numbers rise.

But a 15-point bump for Merkel is tremendous and it only happens in conjunction with her refusing to cave on Germany being seen bailing out southern Europe. It may win her support domestically, but it sets up a disastrous future for the European Union.

As COVID-19 rages across Europe the two major factions within the EU have been fighting a desperate battle for its future with the issue of debt mutualization being the fulcrum. Now, I believe wholly that the use of lock downs and draconian measures to fight the disease have been more political than practical. Using a public health care crisis to advance a political agenda is the height of cynicism and megalomania.

On the one side we have the Euro-integrationists, led by French President Emmanuel Macron. On the other are the fiscal conservatives led by Merkel, who has given way to Dutch Prime Minister Mark Rutte to be the point man for Macron’s derision.

Trapped in the middle is the real human tragedy in northern Italy where thousands of people have died from the toxic mix of a lack of medical infrastructure, high concentration of high-risk people and lack of knowledge of how to fight the disease.

Worse than that, the government in Italy was put together to spearhead this fight for Eurobonds since Conte was kept in power to ensure Lega’s Matteo Salvini didn’t and fight Macron and Merkel by threatening to leave the euro-zone.

Whether you believe the EU’s response, or, more accurately, lack thereof, to Italy’s plight was motivated by malice or incompetence the result is the same. Thousands of Italians died and weakened already weak bonds between Italy and the rest of the EU technocracy.

As I said in an article back on March 14th:

So in the midst of this mess comes COVID-19 and the uncoordinated and inept response to it from the political center of Europe to date. Only now are they coming to the conclusion they need to restrict travel, after sitting on their hands for a few weeks while Italians died by the hundreds.

And do you think that’s engendering waves of love and affection among Italians towards Germans?

If you do then you don’t know Italians… at all.

And this is your signal that this is the beginning of the real crisis. Because while COVID-19 may have been the catalyst for the breakdown of capital markets, capital markets were simply waiting for that spark to occur.

Honestly I wasn’t harsh enough in my assessment of what was happening back then, but it was clear that this crisis was being used to push forward EU integrationist plans of Macron and ECB President Christine Lagarde trying to strongarm the Germans and the Dutch into their position.

By the meeting on March 26th that plan failed. Rutte, Merkel, Austrian Chancellor Sebastain Kurz and Norway all held their ground and the meeting would have ended in a fistfight had it not been held using social distancing rules via teleconference.

That meeting set up last week’s which saw Italy cave to German and Dutch intransigence. Macron and Lagarde lost, securing just $500 billion in new loans but no ECB bond issuance. And the issue now is whether Conte will partake of the program or not.

His failure to act as Macron’s Agent of Shame to secure the EU’s future now puts the whole European project in jeopardy because Conte’s government is in serious trouble in Italy. Moreover, this failure was likely unexpected because now even the hardest-core EU integrationists in Italy’s government are wondering why they are part of the EU.

Meanwhile the polls in Italy haven’t really budged with Salvini’s Lega holding onto around 30% of the electorate with the Brothers of Italy holding onto recent gains in the mid-teens.

Italy, Termometro Politico poll:

LEGA-ID: 31%

PD-S&D: 22%

M5S-NI: 14%

FdI-ECR: 13%

FI-EPP: 6%

IV-RE: 4% (+1)

Azione-S&D: 3%

LS-LEFT: 2%

EV-G/EFA: 2%

+E-RE: 1% (-1)

PC-NI: 1%+/- vs. 1-2 Apr. ’20

Fieldwork: 8-9 April 2020

Sample size: 2,200 pic.twitter.com/QTCcUpCffP— Europe Elects (@EuropeElects) April 11, 2020

https://platform.twitter.com/widgets.js

Moreover, now the question of EU membership in Italy is a coin flip. Two different polls (here and here) have it well within the margin of error.

Lastly, and most importantly, Conte’s coalition government is split on whether to avail itself of the newly-approved loans. Reuters reported that the divisions within the Italian coalition are rising and portend a split. In a show of political spine not seen in over a year senior partner Five Star Movement (M5S) is opposed while the Eurocentric Democrats are all for it since, as of right now, there are no strings attached to the money.

Conte will have to settle the dispute before a video conference among European leaders on April 23 when Italy will be expected to make its position clear.

He tried to defuse the quarrel on Wednesday, warning in a Facebook post that the ESM “risks dividing the whole of Italy,” and adding that more information was needed on the terms of any credit lines before a final decision could be taken.

Until these details are clear, discussing whether an ESM loan is in Italy’s interests is “a merely abstract and schematic debate,” Conte said.

But we all know there will be strings in the end. If you doubt that assertion, I suggest you ask Greece how about this. So, Conte has his work cut out for himself. There is real urgency now in the EU to get even token Eurobonds approved before Germany takes over the Presidency of the European Commission in July, where it will set the agenda on the EU’s next seven-year budget.

After years of kicking the can down the road to avoid a messy political upheaval, which is Merkel’s trademark move, nothing has changed in the EU when it comes to fixing its untenable structure. And for this reason, as long as Angela Merkel is on the stage, there will be no European dream.

All Merkel ever does is manipulate events back to the previous status quo. She has no capacity or stomach to face the German voters nor will she allow anyone else to fully express themselves. Her handling of Brexit negotiations was a fiasco for the EU, thankfully, and her handling of Italy today is just as inept.

With Salvini waiting in the wings, the people ready to revolt over Germany’s handling of the crisis and a weak coalition government put in place by Merkel to hold things together, the probability of Italeave occurring rises daily.

So, while Merkel may have won this latest battle in the end she may lose the war for the EU. And, in the ultimate irony, the people of Europe may have her to thank for their deliverance from its dysfunction.

Tyler Durden

Tue, 04/21/2020 – 02:00 - Watch: Russian Fighter Buzzes US Spy Plane Near Syria For 2nd Time In Four Days

Watch: Russian Fighter Buzzes US Spy Plane Near Syria For 2nd Time In Four Days

For the second time in four days a Russian jet has intercepted a US plane over the Mediterranean, bringing tensions between the two countries to boiling point at a moment Moscow is appearing to flex in defense of its ally Syria.

The Pentagon confirmed the latest “unsafe and unprofessional” intercept incident in international airspace Sunday, after an incident the prior Wednesday involving a US P-8A Poseidon reconnaissance aircraft, which was similarly “buzzed” by an aggressive Russian SU-35, which reportedly performed a high-speed, inverted maneuver.

A Russian SU-35 aircraft is seen over the Mediterranean Sea in new footage released by the US military. “The unnecessary actions of the Russian SU-35 pilot were inconsistent with good airmanship and international flight rules, seriously jeopardizing the safety of flight of both aircraft,” the US Navy said Monday. “While the Russian aircraft was operating in international airspace, this interaction was irresponsible. We expect them to behave within international standards set to ensure safety and to prevent incidents.”

However, a Russian Defense Ministry (MoD) statement framed the latest incident as one in which the Russian fighter, scrambled from Hmeymim air base in Syria, “shadowed” the US spy plane which apparently came too close to the Syrian coast for comfort.

The Navy’s 6th Fleet released video of Sunday’s incident in which a Russian SU-35 Flanker came dangerously close to a Navy P-8A surveillance aircraft:

The Russian MoD said Monday: “On April 19, the Russian equipment controlling the airspace over the neutral waters of the Mediterranean Sea detected an air target performing a flight towards Russia’s military facilities in the Syrian Arab Republic,” according to TASS. “A fighter jet from the air defense alert quick reaction force of the Hmeymim air base was scrambled to identify the target.”

“The aircraft of Russia’s Aerospace Force performed and perform all flights in strict compliance with the international rules of using the airspace over neutral waters,” the statement added.

Gen. Tod Wolters, Commander of US European Command and NATO’s Supreme Allied Commander, has subsequently said he’s protested Russia’s “unprofessional” and potentially dangerous maneuvers involving US planes over the Mediterranean directly with counterparts in Moscow.

Tyler Durden

Tue, 04/21/2020 – 01:00 - Revolutionary Times & Regime Collapse – "The System Cannot Handle It"

Revolutionary Times & Regime Collapse – “The System Cannot Handle It”

Authored by Alastair Crooke via The Strategic Culture Foundation,

Some have queried how it could be that President Putin would co-operate with President Trump to have OPEC+ push oil prices higher – when those higher prices precisely would only help sustain U.S. oil production. In effect, President Putin was being asked to underwrite a subsidy to the U.S. economy – at the expense of Russia’s own oil and gas sales – since U.S. shale production simply is not economic at these prices. In other words, Russia seemed to be shooting itself in the foot.

Well, the calculus for Moscow on whether to cut production (to help Trump) was never simple. There were geo-political and domestic economic considerations – as well as the industry ones – to weigh. But, perhaps one issue trumped all others?

Since 2007, President Putin has been pointing to one overarching threat to global trade: And that problem was simply, the U.S. dollar.

And now, that dollar is in crisis. We are referring, here, not so much to America’s domestic financial crisis (although the monetisation of U.S. debt is connected to threat to the global system), but rather, how the international trading system is poised to blow apart, with grave consequences for everyone.

In other words, Covid-19 may be the trigger, but it is the U.S. dollar – as President Putin has long warned – that is the root problem:

“We’re looking at a commodity-price collapse and a collapse in global trade unlike anything we’ve seen since the 1930s”, said Ken Rogoff, the former chief economist of the IMF, now at Harvard University. An avalanche of government-debt crises is sure to follow, he said, and “the system just can’t handle this many defaults and restructurings at the same time”.

“It’s a little bit like going to the hospitals and they can handle a certain number of Covid-19 patients but they can’t handle them – all at once”, he added.

“More than 90 countries have inquired about bailouts from the IMF—nearly half the world’s nations—while at least 60 have sought to avail themselves of World Bank programs. The two institutions together [only] have resources of up to $1.2 trillion”.

Just to be clear, this amount is not nearly sufficient.

Rogoff is saying that $1.2 trillion is a drop in the ocean – for what lies ahead. The health of the global economy thus has attenuated down to a race between dollars flooding out of this ‘complex self-organising’ system amidst the coronavirus pandemic, versus the very limited resources of the IMF and World Bank to pump dollars in.

Simple? Just ramp up the dollar flow into system. But whoa there! This would mean the U.S. providing a flow of dollars sufficient to meet ‘rest of world’ needs – ‘during the biggest collapse since the 1930s’? There is $11.9 trillion of U.S. denominated debt out there alone, plus the dollar float required to finance day-to-day international trade (usually held as national, foreign exchange reserves).

That however, is only a fraction of the dollar-denominated debt ‘problem’, since a part of that debt takes the characteristics of a distinct ‘currency’ used in international trade, called Eurodollars. Mostly (but not exclusively), they present themselves as if ordinary dollars, but what distinguishes them is that they are overseas dollar deposits that exist outside of U.S. regulation, in one sense.

But which – in the other sense – they become the tools extending U.S. jurisdiction (think Treasury sanctions), across the globe, through the use of U.S. dollars, as its medium of trade. That is to say, this huge Eurodollar market serves Washington’s geo-political interests by enabling it to sanction the world. Hence, the Eurodollar market is a main tool to the U.S.’ covert ‘war’ against China and Russia.

Eurodollars just ‘emerged’, (initially) in Europe after WW2 (no-one is sure quite how), and they grew organically to huge size, by the European banking system simply electronically creating more of them. The Achilles’ Heel is that it lacks any Central Bank to supply it with liquid dollars, as and when, payments into the U.S. sphere are sucked out of it.

This happens especially in times of crisis, when there is flight to the onshore dollar. Oh, no. Oh yes: It’s another self-organising dynamic system that can only ‘grow’ under the right conditions, but will be prone to dynamic de-construction if too many dollars are withdrawn from it. And now, with the Covid-19 pandemic, the Eurodollar market is in a near panic for dollars: liquid dollars.

The U.S. Fed does ‘help out’, at its own discretion, but mainly through offering to swap other currencies for dollars, and by extending short term dollar loans. But this ‘swap bandage’ cannot of course staunch full-blown global trade blowout – in the same way that the Fed is ‘supporting’ U.S. domestic financial system – by throwing trillions of dollars at it.

President Putin saw this eventuality long ago, and predicted the dollar’s ultimate collapse, as a result of the world’s trade becoming too large and too diverse to be sustained on the slender back of the U.S. Fed. And because the world is no longer ready for the U.S. to be able to sanction it, willy-nilly, and at will.

And here ‘is’ that moment – very possibly. So, the collapse in the oil price is a piece to this much bigger story. Putin – not so surprisingly – thus cooperated with Trump’s OPEC initiative, no doubt guessing that the attempt to ramp prices higher would never ‘fly’. Putin may not want to see the dollar hegemony renewed, but nor would he want Russia to be viewed as a main contributor to a global blow-out. The blame being heaped on China over coronavirus serves as a potent alert in this context.

This – emphatically – is not an essay about barely-understood Eurodollars. It is about real global risk. Take the Middle East, as one example. Oil is trading currently at $17 (Friday’s WTI). No producer state’s Middle East business-model is viable at this price level. National budget ‘break-evens’ require a price of oil to be at least three times higher – maybe more. And this, comes on top of the collapse of the Gulf air-travel hub business and tourism. The northern tier of states additionally, is being pressed hard by U.S. sanctions, with the latter tightening the sanctions tourniquet, as Covid-19 strikes, rather than relaxing it. Lebanon, Jordan, Syria – and Iraq. All have national business-models that are bust. They all require bail-outs.

And into this bleak picture, coronavirus has gripped precisely that class of expatriates and migrant workers that sustain the Gulf ‘way of life’ and its business model. NGOs presently are scouring the UAE for empty buildings, and Bahrain is re-purposing closed schools in order to re-house migrant-labourers from cramped accommodation where one room with bunk-beds would sleep a dozen workers.

The virus has also spread to densely populated commercial districts of cities, where many expatriates share housing to save on rent. Many have lost jobs and are struggling. The authorities are trying to deport the migrants home; but Pakistan and India both are refusing them immediate entry. These victims have lost their livelihood, and any chance to escape their misery.

Just to be clear: Gulf élites are not exempt from Covid-19. The al-Saud have been particularly hit by what they sometimes call the “Shi’i virus”. The situation is turning explosive. Gulf economies are held aloft by expatriates, migrant workers and domestic help, and coronavirus has upended the pillars of their economies.

The state looms large over the financial sector in the Gulf, and this makes financial institutions especially vulnerable, because the proportion of loans that local banks extend to the government or to government-related entities, has been rising since 2009. As the authorities draw further on these institutions, so the Gulf economies will prove more vulnerable to Eurodollar stress – absent huge Fed bail-outs.

The global impact of Covid-19 is only beginning, but one thing is abundantly clear: Middle Eastern states will be needing a great deal of spending money, just to fend off social disorder. An economic breakdown is more than just economic. It leads quickly to a social breakdown that involves looting, random violence, fraud and popular anger directed at authorities. Global trade is going to be hit hard, and U.S. imports are going to tumble, which threatens one of the main USD liquidity channels into the Eurodollar system.

This fear of a systemic dynamic destruction of the trading system has led the BIS (Bank for International Settlements: the Central Bankers’ own Central Bank) to insist that:

“… today’s crisis differs from the 2008 GFC, and requires policies that reach beyond the banking sector to final users. These businesses, particularly those enmeshed in global supply chains, are in constant need of working capital, much of it in dollars. Preserving the flow of payments along these chains is essential if we are to avoid further economic meltdown”.

This is a truly revolutionary warning. The BIS is saying that unless the Fed makes bail-outs and working capital available on a massive scale – all the way down, and through, the supply-pyramid to nitty-gritty individual enterprises – trade collapse cannot be avoided. What is hinted at here is the concern that when multiple dynamic complex systems begin to degrade, they can, and often do, enter into a spiralling feedback-loop.

There may be agreement in the G7 on the principle of a limited debt moratorium to be offered to struggling economies, but an approach à outrance – on the BIS lines – apparently is being blocked by U.S. Treasury Secretary Mnuchin (the U.S. enjoys a veto at the IMF by virtue of its quota): No more U.S. cash is being offered to the IMF by Mnuchin, who prefers to keep the U.S. Fed front and centre of the USD liquidity roll-out process.

In other words, Trump wishes to keep intact the scaffolding of the ‘hidden’ dollar-based, sanctions and tariff ‘war’ against China and Russia. He wants the Fed to be able to determine who does, and who does not, get help in any ‘liquidity roll-out’. He wants to continue to be able to sanction those he wants. And he wants to maintain as large an external footprint of the dollar as possible.

Here then, is the crux to Putin’s complaint:

“At root, the Eurodollar system is based on using the national currency of just one country, the U.S., as the global reserve currency. This means the world is beholden to a currency that it cannot create as needed”.

When a crisis hits, as at present, everyone in the Eurodollar system suddenly realizes they have no ability to create fiat dollars, and can rely only on that which exists in national foreign exchange reserves, or in ‘swap lines’. This obviously grants the U.S. enormous power and privilege.

But more than subjecting the world to the geo-political hegemony of Washington, the crucial point is made by Professor Rogoff:

“We’re looking at a commodity-price collapse – and a collapse in global trade unlike anything we’ve seen since the 1930s. An avalanche of government-debt crises is sure to follow, he said, and “the system just can’t handle this many defaults and restructurings – at the same time”.

This simply is beyond the U.S. Fed, or the U.S. Treasury’s capacities, by a long shot. The Fed is already set to monetize double the total U.S. Treasury debt issuance. The global task would overwhelm it – in an avalanche of money-printing.

Does Mnuchin then, believe his and Trump’s narrative, that the virus will soon pass, and the economy will rapidly bounce-back? If so, and it turns out that the virus does not rapidly disappear, then Mnuchin’s stance portends a coming, tragic débacle. And with further massive money issuance, a collapse in confidence in the dollar. (President Putin would have been proved right, but he will not welcome, assuredly, being proved right in such a destructive manner).

In a parallel sphere, the global trade plight is being mirrored in the microcosm by that of EU states, such as Italy, whose economies similarly have been racked by Covid-19. They too, are beholden to a currency – the Euro – that Italy and others cannot create as needed.

With this crisis hitting Europe, everyone in the Euro system is experiencing what it means to have no ability to create fiat currency, and be entirely subject to a non-statutory body, the Eurogroup, which – like Mnuchin – simply says ‘no’ to any BIS-like approach.

Again, it is about scale: this is not business as usual, as in some neo-‘Greek’ eruption, to be countered with EU ‘discipline’. This crisis is much, much greater than that. The absence of monetary instruments – in crisis – can become existential.

Some muse might recall to Mnuchin and the Eurogroup, Alexander del Mar’s 1899 Monetary History, in which he observes how the manoeuvres of the British Crown, in constricting the export of gold and silver (i.e. money) to its American colonies, led to the Crown’s ‘war’ on the paper monetary instruments – Bills of Credit – issued by the Revolutionary Assemblies of Massachusetts and Philadelphia, to compensate for this British monetary starvation.

Finally, it left the desperate colonists with but one resort: “to stand by their monetary system. Thus the Bills of Credit of this era … were really the standards of The [American] Revolution. They were more than this: They were the Revolution itself!”

Tyler Durden

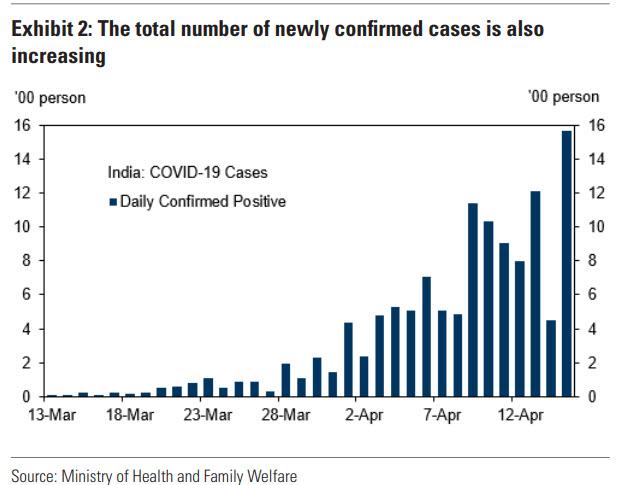

Mon, 04/20/2020 – 23:55 - India Reports Record Spike In Coronavirus Cases Just As It Starts Reopening Economy

India Reports Record Spike In Coronavirus Cases Just As It Starts Reopening Economy

With increasingly politicized debates raging across developed countries whether or not to reopen economies as new coronavirus cases and deaths appear to be plateauing, India has made the decision to ease one of the world’s strictest lockdowns to allow some manufacturing and agricultural activity to resume after the economy suffered a sharp slowdown in recent weeks.

Homeless people wait for free food during a nationwide lockdown to curb the spread of new coronavirus in Gauhati, India, Sunday, April 19, 2020. India’s shelter-in-place orders were imposed on March 24 and halted all but essential services, sparking an exodus of migrant workers and people who survive on daily wages out of India’s cities and toward villages in rural areas. Authorities picked up travelers in a fleet of buses and quarantined many of them in empty schools and other public buildings for 14 days. An even bigger problem, however, was the freefall in the Indian economy.

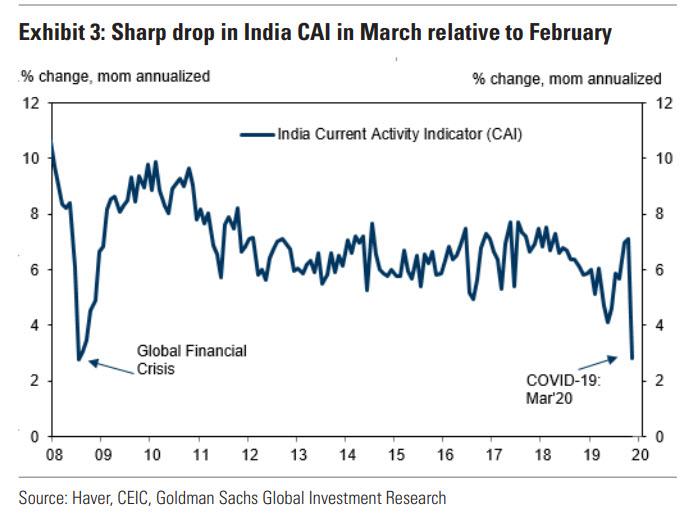

Here is why India is in a rush: according to Goldman’s current activity indicator (CAI), growth in India was reported at 2.8% in March, a 4.2% plunge relative to February, and the slowest uptick since the financial crisis. The sharp fall in March, is driven by both industrial and services, with the decline in exports, imports, auto sales, and PMI services being the biggest drivers.

Goldman also gathered a variety of high-frequency economic indicators, similar to how the banks looked at China’s economy in February to gauge the slowdown. Here are some of the findings across various sectors:

Industrial:

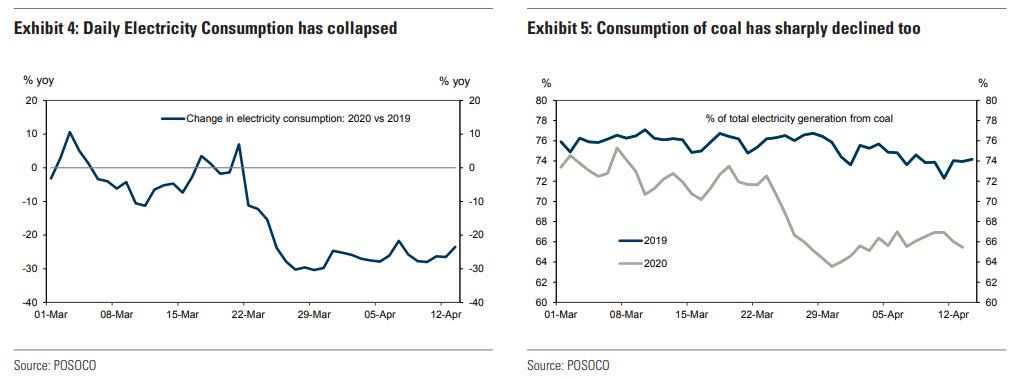

- Daily electricity consumption collapsed in March (-30% yoy on March 27), and remains at low levels since then. (Exhibit 4).

- The relative usage of coal also fell sharply in March. The fraction of total electricity generation through coal declined by almost 10 percentage points between 1st and 31st March 2020. Our rough estimate showed coal consumption was almost 11% weaker in the last week of March and first 12 days of April, relative to last year (Exhibit 5).

- Air pollution, which is an indicator of industrial activity, has fallen in several cities. The Air Quality Index (AQI) (which is positively related to air pollution; higher values for the AQI indicate greater air pollution) decreased in April for major Indian cities such as Bengaluru, Chennai, Kolkata and New Delhi, as per the data from the Central Pollution Control Board.

Services:

- Railway transportation: Railway passenger volume contracted by 7.4% in the first 10 days of March 2020, according to the Indian Railways data, and is expected to decrease for the rest of March and April.

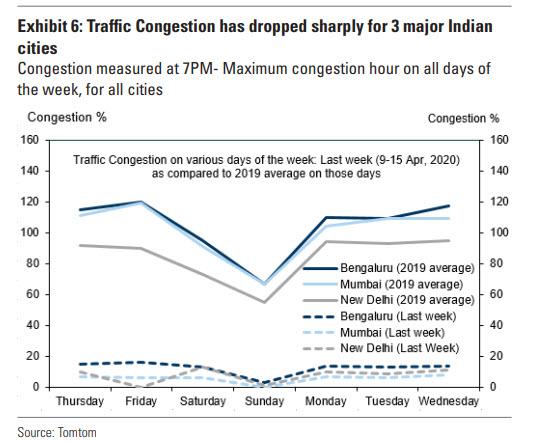

- Traffic congestion data shows that congestion has reduced to very low levels in three major Indian cities, indicating reduction in movement (Exhibit 6).

- Mobility tracker from Apple. Mobility trend reports from Apple are based on changes in routing requests of ~12 mn Iphone users in India. Based on the latest reported data, walking and driving mobility have contracted by 73% and 81% between January 13 and April 14, 2020 (Exhibit 7).

- Daily unemployment and labor force participation rates from the Center for Monitoring Indian Economy. Daily unemployment shows a sharp spike since March 29th, driven by both rural and urban areas. Not only has unemployment (defined as the number of people, 15 years of age or more, who are part of the labor force but unemployed) spiked, but labor force participation rates (number of people, 15 years of age or more, employed or actively seeking employment as % of total working age population) has also collapsed (see Exhibit 8).

In other words, just like in China in February and early March, much of India has shut down, and just like China, India is now scrambling to reboot its economy, as the alternative for the country with a population of 1.4 billion is a social upheaval that would likely be far worse than letting the coronavirus run rampant.

However, unlike China which largely reopened only after the number of reported new cases had collapsed, India is starting to ease its lockdown just as the number of single-day new cases spiked the most yet, as an additional 1,553 cases were reported over 24 hours compared with 1,334 reported on Sunday morning, raising the national total to 17,265, potentially resulting in an even faster breakout in new cases in the world’s most densely-populated nation.

As AP further adds, at least 543 people died from the Wu-Flu and epidemiologists forecast the peak may not be reached before June.

And while New York City has emerged as the global case study for rampant disease spread so far, skeptics warn that a full blown pandemic in India would be orders of magnitude more catastrophic.

However, starting Monday, limited industry and farming were allowed to resume where employers could meet social distancing and hygiene norms, and migrant workers were allowed to travel within states to factories, farms and other work sites.

This is taking place even as government surveys in the central Indian state of Maharashtra, the worst-hit by the virus, have suggested few companies eligible to restart operations can do so because they are required to transport and shelter workers as a virus-prevention measure.

“In the event a group of migrants wish to return to their places of work within the state where they are presently located, they would be screened and those who are asymptomatic would be transported to their respective places of work,” India’s home ministry said in a letter to state governments.

While a partial lifting of a curfew permitted the restart of coal plants and oil refineries, animal feed and agro-industry, and other labor-intensive manufacturing such as brick kilns, much of the country remained under lockdown.

A group of Indians distribute free food and water to homeless people during a nationwide lockdown to curb the spread of new coronavirus in Gauhati, India, Sunday, April 19, 2020. Additionally, India’s airspace was closed to commercial traffic, its passenger rail system, buses and metros were halted, e-commerce was restricted to food and other essentials, and schools, stadiums and houses of worship remained closed until May 3.

In hopes of preventing an even faster breakout, India is also continuing to ramp up testing, build up stocks of ventilators and personal protective equipment and prepare makeshift isolation wards and dedicated COVID-19 hospitals.

Yet one difference between India and the rest of the world that may help India contain the pandemic is that in Mumbai, the capital of Maharashtra and home to Asia’s largest slum, city authorities were planning to administer hydroxycloroquine to thousands of slum-dwellers over 14 days to gauge whether the drug helped to slow the spread of the disease in a place where social distancing norms aren’t possible to achieve. It was unclear how many people would participate in the experiment, or when it would begin.

Tyler Durden

Mon, 04/20/2020 – 23:35 - How To Get Rid Of A POTUS

How To Get Rid Of A POTUS

Authored by ‘John Quincy Adams’ via The Strategic Culture Foundation,

In the Soviet Union there was an expression “The Organs of State Security” or “Organs” for short. Their supposed power in the USSR was one of the things that separated them from what we used to call “the free world”. Not so much any more – the American Organs came very close to getting rid of the so-called Most Powerful Man in The World. They made only one mistake; they probably won’t next time.

The impeachment of US President Donald Trump is over, or at least this iteration is. This was not a normal impeachment, it was an attempt by the Deep State, the Organs of State Security, the Blob, the Borg – later we will learn what its members call it – to remove a president of the United States. After some false starts, it succeeded at every step except the very last one. But, as they say, practice makes perfect and the Organs have learned from their mistake.

Note that such a removal only becomes necessary when the Organs have failed to block a challenger, a Bernie Sanders or Tulsi Gabbard for example, who might question the status quo. But, in 2016 they failed and, to the amazement of the wise ones, Trump won the election. His remarks about getting along with Russia showed that he might wander off the path The Organs had laid out. The Organs got to work. They first stirred up opinion that he was so unfit for office that getting rid of him would be laudable, no matter how it was done. Not so difficult given the small number of “news” media owners in the USA well trained to take their lead from “anonymous sources in the intelligence community” and not so difficult because the losers were so bitter. He was -phobic – islamo-, trans-, homo-. He was -ist – rac-, sex-, class-. Limited mental abilities, psychological instability, personal deficiencies,incapable, dangerous. An entire theory of incapacity was built on a typo. Each attempt faded and was forgotten – faithless Electors, 25th Amendment, Logan Act – nobody remembers the details, but the stink remains.

But these produced no effective actions. There are only two ways to get rid of an American president if you are unwilling to wait until the next election – murder or impeachment. Media hysteria creates an atmosphere but it doesn’t get anything done.

It’s an experiment – this fails, that fails, try something else.

So the Organs moved to another idea – treason as grounds for impeachment. The seeds had been planted – “All 17 intelligence agencies” agreed that he was the nominee of a hostile foreign power. Three years on an inquiry intended to provoke him, but he resisted the provocations and, eventually the inquiry had to admit it found nothing. But the accusation is always there – enemies of the Organs, Tulsi Gabbard, Bernie Sanders, Jill Stein are accused of being puppets of the foreign power.

Trump talks a lot and, sooner or later, will say something the Organs can seize on and twist. And he did. A phone call to a subservient foreign leader provided the opportunity and The Organs of State Security took it. One operative became a “whistleblower” – he didn’t overhear the phonecall, didn’t know what it said but did know that a fellow operative was “visibly shaken“. Another operative actually said it out loud:

In the Spring of 2019, I became aware of outside influencers promoting a false narrative of Ukraine inconsistent with the consensus views of the interagency. This narrative was harmful to U.S. government policy. While my interagency colleagues and I were becoming increasingly optimistic on Ukraine’s prospects, this alternative narrative undermined U.S. government efforts to expand cooperation with Ukraine.

Read that again because it’s an important stage in the History of the Decline and Fall of America.

“Inconsistent with the consensus views of the interagency”.

That’s what they think should make foreign policy, not transient presidents (never mind Art 2 Sec 2). This is the moment when even the dullest should have understood that yes there is a Deep State, the Organs do exist and its operatives call it The Interagency.

The president is already unpopular, many think he must be removed and now The Interagency says he is a traitor. The opposing party stages a show in which “witnesses” from The Interagency testify that he is a traitor because he says or will say, does or will do something that violates “the consensus views of The Interagency”. Like trade Alaska to Russia for support. The House brings bills of impeachment charging that he has weakened national security (The Interagency told us so) and obstruction of justice (many members are ex-prosecutors and built their careers on plea bargains and obstruction of justice charges; that charge is an automatic reflex.)

But the plot failed in the Senate. The Interagency must be wondering what would have happened had it produced, at the right time, compromising information on 20 or 30 senators.

We recapitulate. Should someone who threatens The Interagency manage the improbable feat of climbing over the obstacles and becoming president, The Interagency will

-

Start a campaign at which obedient media scribes, quoting “people familiar with the matter“, throw all the accusations they can find or imagine. Details will be forgotten but surely, with such clouds of smoke, there must be some fire somewhere. Easier still if members of The Interagency become TV pundits themselves.

-

Gather all the compromising information The Interagency has – the NSA keeps everything – on Congressmen and be prepared to deploy it. Easier still if members of The Interagency become members themselves.

-

Wait for some event in which the POTUS goes against The Interagency Consensus.

-

Use the compromising information in the House to start an inquiry which listens to testimony from Interagency operatives that the POTUS has violated The Interagency consensus and threatened national security

-

The House charges him with 1) endangering national security and 2) obstruction of justice.

-

Use the compromising information to get enough Senators to vote to remove.

-

Repeat as necessary until every candidate understands who really runs things.

And that’s how how do it.

And The Interagency nearly pulled it off – 20 or 30 Senators, confronted with evidence of sexual or financial peccadilloes (or, these days, -isms or -phobias), could have been “persuaded” to do the right thing.

And so, as Adams foresaw two centuries ago, step by step, America, having bound “an imperial diadem” to her forehead, has ceased to be “the ruler of her own spirit”. The Interagency – built up for the pursuit of monsters – very nearly ate the government. It failed only at the very last step.

Tyler Durden

Mon, 04/20/2020 – 23:15 -

- Big Brother Bezos Is Now Tracking Amazon Factory Workers With Thermal Imaging Camera

Big Brother Bezos Is Now Tracking Amazon Factory Workers With Thermal Imaging Camera

Amazon is installing thermal cameras at its warehouses across the country to detect feverish employees in a bid to speed up screening of potential COVID-19 carriers, reported Reuters.

The new cameras measure how much heat a person releases relative to their surroundings, Amazon workers told Reuters, adding that the new process of screening is a much quicker approach than forehead thermometers.

“We implemented daily temperature checks in the locations of our operations as an additional preventative measure to support the health and safety of our employees who continue to provide a critical service in our communities,” Amazon spokesperson Kristen Kish told The Verge via an email statement.

“We are now implementing the use of thermal cameras for temperature screening to create a more streamlined experience at some of our sites,” Kish said.

Screening tents have also been erected at some warehouse entrances. Thermal cameras are expected to be installed at Amazon’s Wholefood stores.

Several employees said if the cameras flag someone, they will be given a second round of checks via a thermometer to determine if they exhibit signs of coronavirus.

The move by Amazon to increase health monitoring of its workforce comes as 50 warehouse employees in the US have contracted the virus.

We’ve reported in recent weeks that employees have conducted several strikes at a New York Amazon warehouse, many of whom demanded the company close the facility for disinfecting after several employees fell ill.

One warehouse employee in Los Angeles said a screening line wrapped around the facility one day. After the thermal cameras were installed, there was no more line as the process was streamlined.

Shown below, here is the alleged thermal cameras Amazon has deployed at some locations. It appears Infrared Cameras Inc in Texas powers the device.

Amazon has also been distributing masks and gloves to employees while disinfecting workstations. Other reports note the company is developing a testing lab to screen its employees for COVID-19.

We’ve noted before the virus has been a cover for corporate America to increase surveillance in the workplace. Now Big Brother Bezos is deploying advanced optical sensors to monitor employees’ health.

Tyler Durden

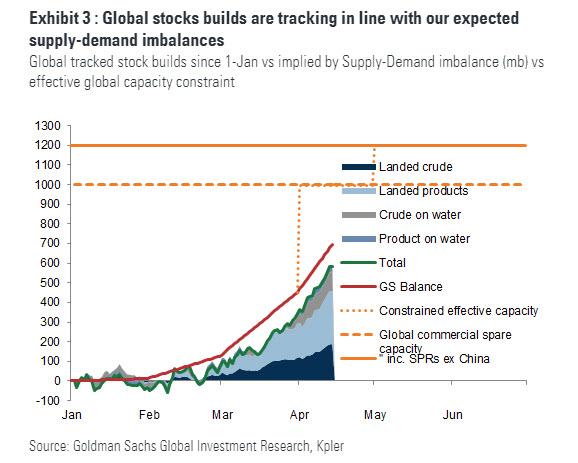

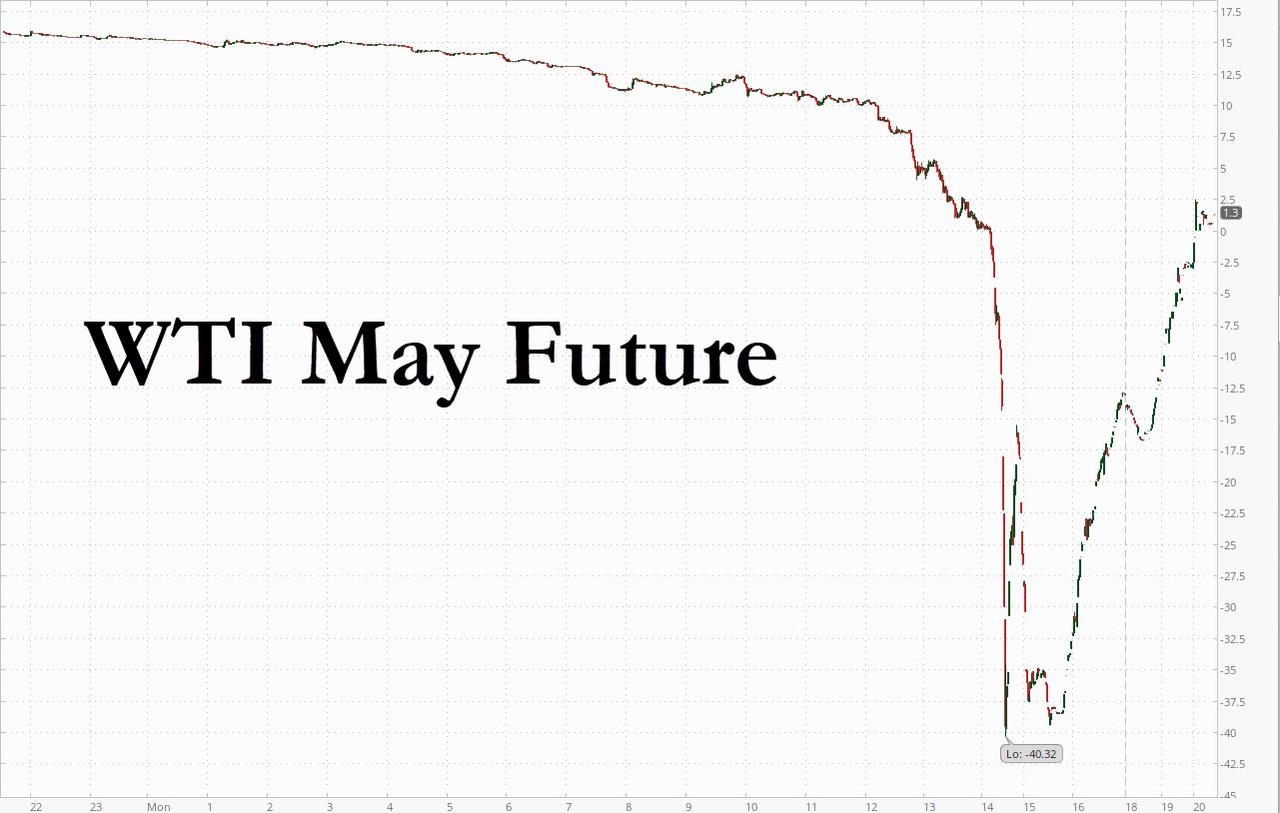

Mon, 04/20/2020 – 22:55 - Here Is The Full Explanation Behind Today's Unprecedented Negative Oil Price

Here Is The Full Explanation Behind Today’s Unprecedented Negative Oil Price

Courtesy of IHSMarkit’s energy vice president Roger Diwan

How did you end up with negative oil prices today? This happens when a physical futures contract find no buyers close to or at expiry.

Let me explain what that means:

A physical contract such as the NYMEX WTI has a delivery point at Cushing, OK, & date, in this occurrence May. So people who hold the contract at the end of the trading window have to take physical delivery of the oil they bought on the futures market. This is very rare.

It means that in the last few days of the futures trading cycle, (which is tomorrow for this one) speculative or paper futures positions start rolling over to the next contract. This is normally a pretty undramatic affair.

What is happening today is trades or speculators who had bought the contract are finding themselves unable to resell it, and have no storage booked to get delivered the crude in Cushing, OK, where the delivery is specified in the contract.

This means that all the storage in Cushing is booked, and there is no price they can pay to store it, or they are totally inexperienced in this game and are caught holding a contract they did not understand the full physical aspect of as the time clock expires.

The contract roll and liquidity crunch that made the extreme sell-off today possible but it DOESN’T necessarily represent futures market conditions: NYMEX June settled today at $21.13.

The June contract is not out of the woods either: today’s action indicate that physical oil markets at Cushing are not in good shape and that storage is getting very full.

A decline of over 15% in the June contract price points to real worries that the physical stress will continue to reverberate, and will force a lot more production shutdowns during May than the ones announced so far.

So today negative prices are the reflection of dire market conditions for producers, with the hope that demand restart before the middle of May and that the June contract does not face the same fate.

Tyler Durden

Mon, 04/20/2020 – 22:40 - Mike Krieger: "The Whole System Is Breaking Down Under Its Own Weight"

Mike Krieger: “The Whole System Is Breaking Down Under Its Own Weight”

Authored by Mike Krieger via Liberty Blitzkrieg blog,

We find ourselves at a moment where the financial and political systems that have dominated for decades are failing in a spectacular and irredeemable fashion. Those who pull the levers are (as usual) attempting to take advantage of the situation by rapaciously snatching and consolidating more wealth and power, while leaving the general public to rot. When faced with such a historic moment, one should assume a certain degree of responsibility to make sure the next paradigm ends up better than the one we’re leaving. If we fail to think deeply about an improved vision and framework for the future, someone else will do it for us.

From my perspective, humanity remains stuck within antiquated paradigms that generally function via predatory and authoritarian structures. We’ve been taught — and have largely accepted — that the really important decisions must be handled in a centralized manner by small groups of technocrats and oligarchs. As a result, we basically live within feudal constructs cleverly surrounded by entrenched myths of democracy and self-government. We’d prefer to be lazy rather than take any responsibility for the state of the world.

Empires are not democratic.

The U.S. is an empire.

The idea the U.S. is a democracy is a myth. https://t.co/LlCvzbgzbL— Michael Krieger (@LibertyBlitz) April 20, 2020

https://platform.twitter.com/widgets.js

We’re now at a point where simply recognizing current structures as predatory and authoritarian isn’t good enough. We require a distinct and superior political philosophy that can appeal to others likewise extremely dissatisfied with the status quo. My belief is humanity’s next paradigm should swing heavily in the direction of decentralization and localism.

Decentralization and localism aren’t exactly the same, but can play well together and offer a new path forward. The simplest way to describe decentralization to Americans is to look at the political framework laid out in the U.S. Constitution.

As discussed in the 2018 piece, The Road to 2025 (Part 4) – A Very Bright Future If We Demand It:

At the federal level, a separation of powers between the three branches of government: the legislative, the executive and the judicial was a key component of the Constitution. The specific purpose here was to prevent an accumulation of excessive centralized power within a specific area of government…

Beyond a separation of powers at the federal level, the founding founders made sure that the various states had tremendous independent governance authority in their own right in order to further their objective of decentralized political power.

Localism takes these Constitutional ideas of political decentralization and pushes them further, by viewing the municipality or county as the most ethical and logical seat of self-governance. The basic idea, which I tend to agree with, is that genuine self-government does not scale well. A one-size fits all approach to governance not only ends up making everyone unhappy, it also entrenches a self-serving political and oligarchical class at the top of a superstate which makes big decisions for tens, if not hundreds of millions, with little accountability or oversight. This is pretty much how the world functions today.

While localism implies relative political decentralization, decentralization is not always localism. One of the best examples of this can be found in bitcoin. Unlike traditional monetary policy, which is handled in a topdown manner by a tiny group of unelected technocrats working on behalf of Wall Street, there’s no bitcoin politburo. There’s no CEO, there’s no individual or organization to call or pressure to dramatically change things out of desire or political expediency. The protocol is specifically designed to prevent that. It’s designed to operate in a way that makes all sorts of people uncomfortable because they’re used to someone “being in control.” We’ve been taught that centralization works well, but the reality is political and economic centralization concentrates power, makes the public lazy and ultimately winds up in a state of authoritarian feudalism.

Bitcoin also demonstrates how decentralization and localism, though not quite the same, can complement each another well in an interconnected planet. Imagine a world where governance is largely occurring at a local level, but global trade remains desirable. You’d want a politically neutral, decentralized and permissionless money to conduct such transactions. Similarly, a free and decentralized internet allows the same sort of thing in the realm of communications. Regions that can’t grow coffee will still want coffee, and people in New York will still want to chat with people in Barcelona. Decentralized systems allow for the best of both worlds — localism combined with continued global interconnectedness.

The big question all of us should be asking ourselves right now is: When should small groups of people be making extremely important decisions for the masses? My answer would be almost never, yet that’s the world most of us live in irrespective of which nation-state we call home.

The pendulum has swung so far in the direction of centralization, oligarchy and authoritarianism that the whole thing is breaking down down under its own weight.

Those in charge are doing everything possible to keep it going in that same direction, but we can’t let that happen. What we need is a new era defined by decentralization and localism.

* * *

For more, see my 5-part series on localism.

Liberty Blitzkrieg is an ad-free website. If you enjoyed this post and my work in general, visit the Support Page where you can donate and contribute to my efforts.

Tyler Durden

Mon, 04/20/2020 – 22:35 - Trump Temporarily Suspends All Immigration Into The United States

Trump Temporarily Suspends All Immigration Into The United States

In a stunning turn of events, late on Monday, president Trump tweeted that “In light of the attack from the Invisible Enemy, as well as the need to protect the jobs of our GREAT American Citizens, I will be signing an Executive Order to temporarily suspend immigration into the United States!”

In light of the attack from the Invisible Enemy, as well as the need to protect the jobs of our GREAT American Citizens, I will be signing an Executive Order to temporarily suspend immigration into the United States!

— Donald J. Trump (@realDonaldTrump) April 21, 2020

https://platform.twitter.com/widgets.js

Trump did not offer specifics, such as the time frame or the scope of who would be affected.

As some noted, Trump’s decision to escalate the US response to the coronacrisis is at odds with his desire to rush in reopening the country:

Trump, who says the country is ready to begin reopening, says the crisis is so bad that he is signing an order to “temporarily suspend immigration into the United States!”

— Peter Baker (@peterbakernyt) April 21, 2020

https://platform.twitter.com/widgets.js

And while we wait for more details, we wonder if this executive order will be followed by Trump canceling the November elections.

Tyler Durden

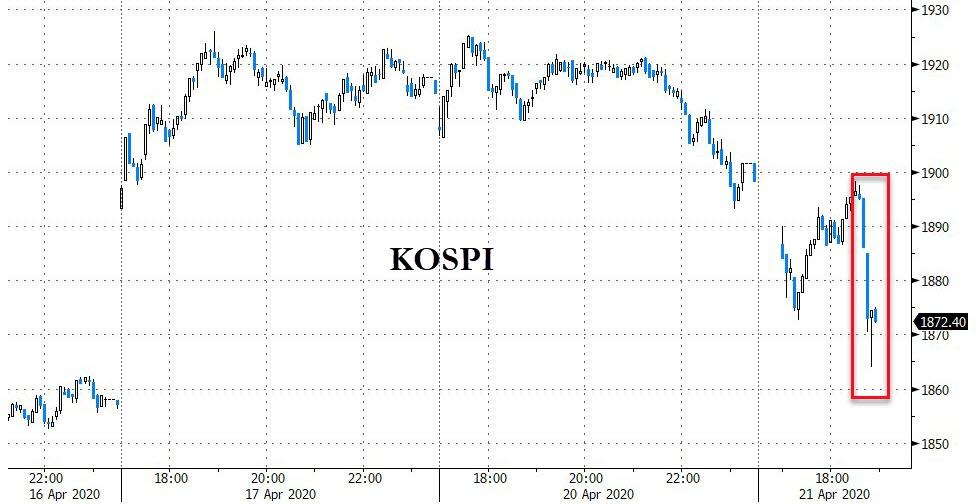

Mon, 04/20/2020 – 22:16 - Futures Whipsaw After Conflicting Reports That NKorea's Kim Is In Critical Condition

Futures Whipsaw After Conflicting Reports That NKorea’s Kim Is In Critical Condition

Update (2252ET): Futures rebounded sharply after South Korea’s Yonhap refuted reports that Kim Jong Un is seriously ill.

Yonhap cites an official as saying there’s no particular sign pointing to Kim Jong Un being in grave danger. The Korean rumor about a coma is exactly the same as one from 2014. While it’s indeed odd Kim didn’t show up on April 15, we should calm down. https://t.co/yZ2tJDC71N pic.twitter.com/Ep5cAlZDs8

— Sam Kim (@samkimasia) April 21, 2020

https://platform.twitter.com/widgets.js

Update (2240ET): Bloomberg is now reporting that Kim is in a ‘critical state,’ according to a US official speaking on condition of anonymity.

US officials are now studying the North Korean line of succession.

Trump administration officials are looking into who would be in the line of succession if Kim Jong Un dies or is already dead, I’m told.

— Jennifer Jacobs (@JenniferJJacobs) April 21, 2020

https://platform.twitter.com/widgets.js

S&P futures are sliding on the reports.

Update (2215ET): NBC’s Katy Tur was quick to respond to being scooped by CNN and tweeted the following:

“@KatyTurNBC

🚨 North Korean leader Kim Jong Un is brain dead, according to two US officials. He recently had cardiac surgery and slipped into a coma, according to one US current and one former US official.

@NBCNews confirms and adds to CNN scoop from me, @ckubeNBC @carolelee”

Only to delete it shortly after:

I’ve deleted that last tweet out of an abundance of caution. Waiting on more info. Apologies.

— Katy Tur (@KatyTurNBC) April 21, 2020

https://platform.twitter.com/widgets.js

* * *

South Korea’s KOSPI stock market index and the Won are tumbling as uncertainty grows over the health of their northern neighbor’s leader.

Earlier headlines from Daily NK – a website run mostly by North Korean defectors – reported that North Korean leader Kim Jong Un recently had cardiovascular surgical procedure and is now mostly recovered, citing unidentified sources inside the isolated state saying Kim is recovering at a villa in the Mount Kumgang resort county of Hyangsan on the east coast after getting the procedure on April 12 at a hospital there.

However, CNN has upped the ante and reported that the US is monitoring intelligence that North Korea’s leader, Kim Jong Un, is in grave danger after a surgery, according to a US official with direct knowledge.

Kim last appeared in North Korean state media on April 11. April 15 – North Korea’s most important holiday, the anniversary of the birth of the country’s founding father, Kim Il Sung – came and went without any official mention of Kim Jong Un’s movements or explanation of his absence.

CNN notes that Kim Jong Il’s absence from a parade celebrating North Korea’s 60th anniversary in 2008 was followed by rumblings that he was in poor health.

So who to believe – “mostly recovered” from NK defectors or “in grave danger” from CNN’s intel sources.

As Seoul Bureau Chief for VOA, William Gallo tweeted:

Bottom line: there is a hell of a difference between “US officials think Kim Jong Un is in grave danger” and “US officials have read unconfirmed media reports about Kim Jong Un being in grave danger.” We need to know which this is.

The market for now appears to be erring on the side of CNN’s warnings as stocks tumble…

And Korea’s Won hits a two-week low…

We wonder, of course, if President Trump will send Kim a “Get Well Soon” card (and we note that Kim Jong Un is only ~36. His father lived to be 82).

Tyler Durden

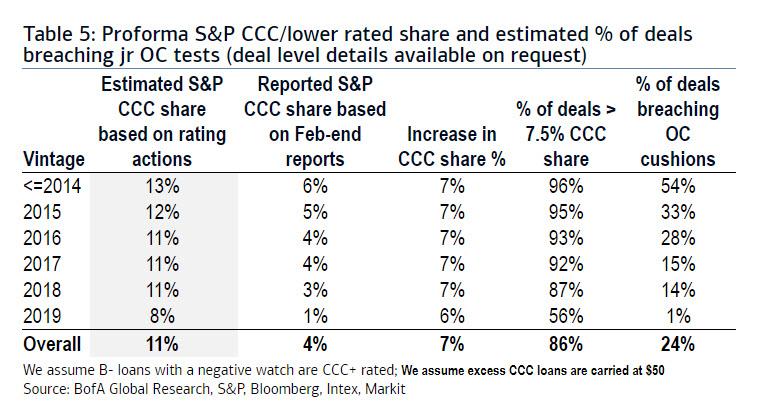

Mon, 04/20/2020 – 22:11 - Something Impossible Just Happened: A CLO Failed Its AAA Overcollateralization Test

Something Impossible Just Happened: A CLO Failed Its AAA Overcollateralization Test

Over the weekend, we reported that in its quest to bailout the richest Americans and the country’s financial system, the Fed unleashed an unprecedented array of actions meant to backstop capital markets, going so far as buying investment grade, high yield bonds and even AAA-rated CLO bonds.

However, as we warned, it won’t be enough, for two reasons: first, recall that the expanded Term Asset-Backed Securities Loan Facility (TALF) announced by the Fed last Thursday only buys AAA-rated bonds of CLOs, which after the coming tsunami of CLO downgrades is complete, will not only collapse in nominal size but will mean that any further attempts to stabilize the CLO space will require yet another Fed backstop of even riskier – i.e., rated AA and lower – structured products.

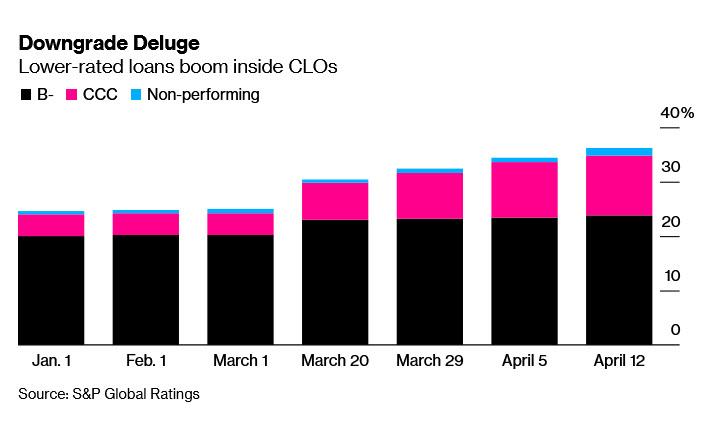

The second reason – one which Bloomberg called a “bigger and more ominous force at work that has investors bracing for the kind of pain they’ve never experienced in the decades that the [CLO] market has existed” – is that late on Friday, in the most draconian and widespread ratings action since the financial crisis, Moody’s warned it may cut the ratings on $22 billion of U.S. collateralized loan obligations – a fifth of all such bonds it grades – as a result of the collapse in cash flows due to the Covid-19 pandemic.

The ratings agency took action on 859 bonds from 358 CLOs that package leveraged loans into securities of varying degrees of risk and return. The step – which according to Bloomberg affects about 19% of Moody’s-rated CLOs that purchase broadly syndicated loans – comes as the underlying debt gets downgraded at a record pace.

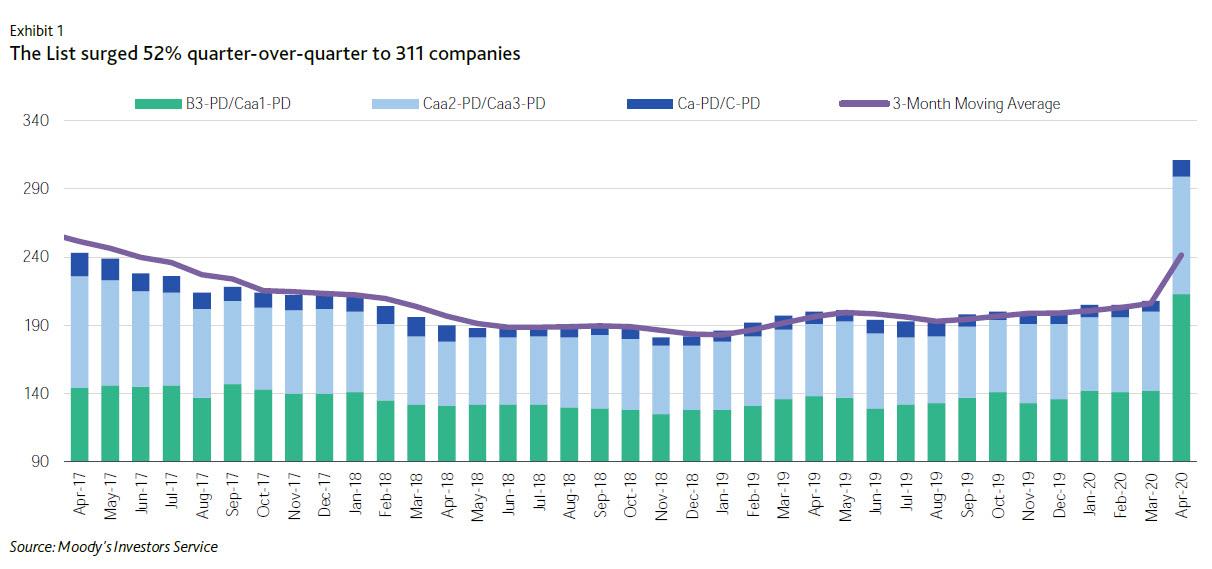

The action followed a report by Moodys earlier in the week in which it reported that its “B3 Negative and lower list” soared to its highest tally ever — 311 companies. That tops a former peak of 291 companies, reached during the credit crisis of 2009 and the commodity-related downturn in April 2016. At 20.7% of the total rated spec-grade population, the list also shot up above its long-term average of 14.8%, and closing in on its all-time high of 26.1%. This spike is the result of the confluence of a coronavirus outbreak, plunging oil prices, and mounting recessionary conditions, which created severe and extensive credit shocks across many sectors, regions and markets, the effects of which are unprecedented.

And with the underlying bonds set to suffer an unprecedented collapse in solvency, it is only a matter of time before the products where they are packaged are also hammered. Products such as CLOs.

Today, picking up on this growing risk of widespread impairments across the CLO deal stack, Bloomberg echoes what we said, namely that credit ratings on risky corporate loans that were stuffed into the CLOs “are being downgraded at a pace so frenetic that it threatens to overwhelm safeguards that were put in place to ensure the securities’ financial strength.”

And “if that happens” Bloomberg continues, “the firms that manage the CLOs will be forced to dump under-performing debt at fire-sale prices or suspend the cash payments they hand over to their investors.”

It just happened.

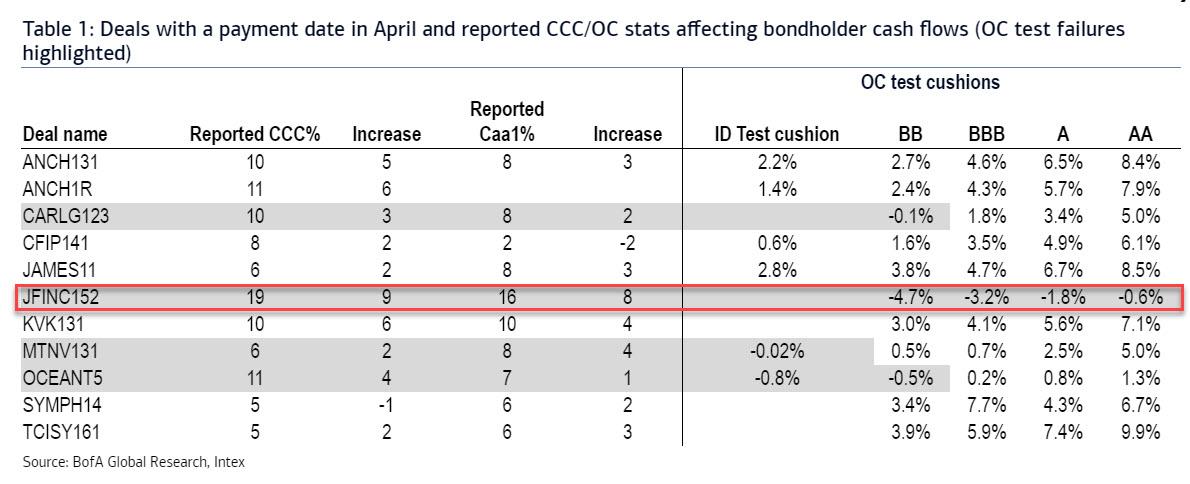

In yet another case of something that was previously deemed impossible becoming reality thanks to the Coronavirus depression – like oil trading at a negative $14 per barrel – Bank of America’s Chris Flanagan writes that with some deals already reporting late March/early April data, we find that some deals are failing, not just the junior overcollateralization (OC) test but in one case, even the AAA/AA OC test!

According to Flanagan, this will be the likely be the first “CLO 2.0” deal failing the senior most OC test; as a reminder, not even during the financial crisis were the supersafe AAA tranches impaired. This time it took just a few weeks for the cash flow collapse to impair the very top of the stack!

The CLO deal in question is JFINC152, where downgrades have sent the reported CCC percentage to 19%, up 9%, and the result is that every single test cushion is now showing impaired results, from BB (-4.7%) all the way to AA (-0.6%).

Those seeking the reason for this unprecedented development will find it in the dramatic deterioration of CLO credit ratings: for the deals that failed any one of the tests, the increase in CCC is almost 2x over the past month, BofA notes adding that the lack of reinvestment flexibility for some of the transactions as the deals were post the RP period implied managers could not take advantage of the volatile loan market condition in March.

Looking at the past month, since March, S&P and Fitch have placed around 100 tranches on negative watch. The vast majority of these deals were initially rated BB/B and there are 8 IG-rated tranches (mostly BBB). BBB bonds continue to face a high risk of downgrade in the near term considering the increasing CCC share and the recent uptick in defaults. According to an analysis by S&P, should CCC’s increase to 18%, defaults to 5% and OC declines of 2pts, around 46% of BBB bonds could be downgraded to Non-IG.

This has important ramifications for both bondholders and investors as many deal documents initiate a restricted trading condition if any IG-rated bond is downgraded. This will further limit manager’s ability to trade in/out of loans.

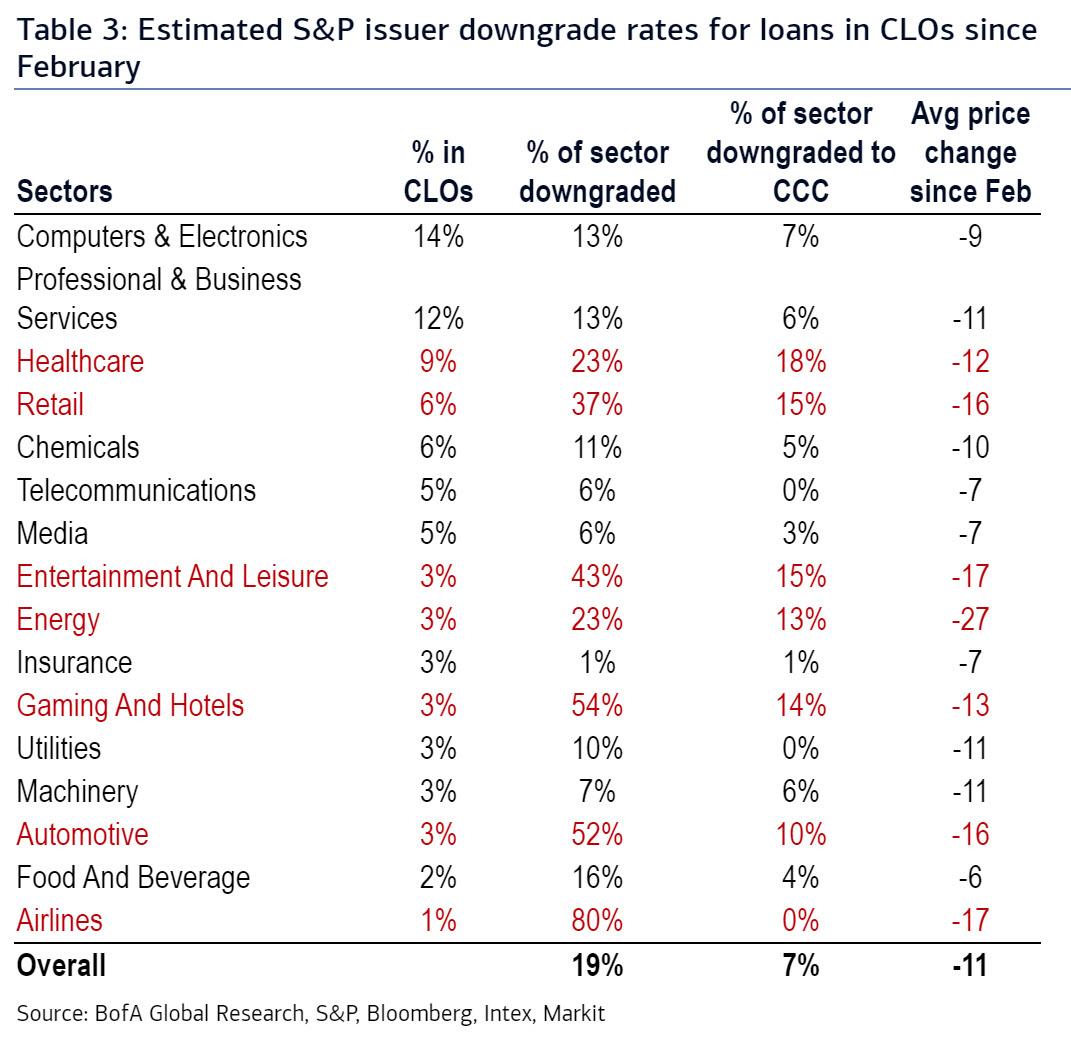

Additionally, the surging share of CCC downgrades has caused many deals to have lower OC ratios as a result of CCC excess and/or par burn as managers traded out of lower priced/lower rated loans. BofA currently estimates that around 17-19% (and counting) of loans in CLOs have been downgraded by both Moody’s and S&P since February, and many more downgrades are coming. Currently, the share of CCC+/lower rated issuers is estimated to be 10.5% and the share of Caa1/lower rated loans is estimated to be around 8.5% across CLO portfolios (assuming loans with a negative watch have been downgraded by a notch lower).

BofA also highlights the average price across each rating cohort currently (after adjusting for downgrades). There has been an increased dispersion between high/low quality names with B+/BB issuers trading around $90 and CCC issuers, around $60. As a result, to swap from a CCC name into a B or higher rated asset still implies taking a $25 hit to par.

Next, looking at updated CCC concentrations, BofA estimates that as many as 20-30% of deals are now potentially breaching their OC tests (assuming a $40-50 price for excess CCC assets and based off March portfolios). In some cases, the BB bonds may PIK as well. With April determination dates beginning and around the corner, managers have very less room/time to trade out of loans and cure these breaches.

Looking ahead, BofA thinks further OC breaches are likely to occur as more deals that make their payment in April report. With the estimated CCC share reaching 10.5%, roughly 20-30% of deals could breach their junior OC tests, and increasingly more deals will likely impair the AAA tranche as well – that’s where Japanese pensioners’ money is currently allocated – an outcome that until just a few weeks ago was inconceivable.

* * *

With the safest tranches facing impairments, the riskiest – or equity – tranches are set for a historic wipeout. According to Bloomberg, analysts expect as many as one in three CLOs may soon have to limit payouts to holders of the equity portion.

The loan downgrades have come so fast that Stephen Ketchum of Sound Point Capital Management compared it to a spill “at the Daytona 500, where the cars are crashing into each other.” It’s a lot different, he said, than the 2008 financial crisis, which “was a slow-moving train wreck.”

Another major difference between the financial crisis and now is that back in 2008, the CLO market emerged largely unscathed – especially the AAA tranches – an outcome which we now know will not happen. Corporate loans were far enough removed from the epicenter of the 2008 crisis – a housing bubble – to avoid much of the collateral damage and, besides, the CLO market back then was a fraction of its size today.

Ironically, the strong track record, the lack of major CLO impairments, along with the fact that the securities provided juicy returns in an era of near-zero global rates; fueled a boom in demand over the past decade. The same boom will now lead to hundreds of billions in losses.

Worse, it means that a key pillar of the credit market will be crushed for years: CLOs have been the biggest buyers in the $1.2 trillion leveraged loan market, helping fuel a surge in debt-fueled buyouts and other transactions.

In sympathy with the broader market, prices on CLOs have recovered some in recent days with AAA securities recouping most of their declines since the selloff began largely thanks to the Fed’s promise to backstop the supersafe tranche. However, as cash flows plunge and as a flood of downgrades hit the underlying loans which then leads to even more AAA tests being missed, the entire CLO space is in for a very violent repricing and unless the Fed is prepared to backstop the entire $1.2 trillion market, the consequences – for both the loan and broader bond market – will be catastrophic, while the Fed ends up holding paper that in a few months will be insolvent, at which point the Congressional hearings why Powell bought worthless securities with freshly printed dollars will be the hottest thing on TV.

Tyler Durden

Mon, 04/20/2020 – 21:58 - Who Was Panic Selling Oil Today? Goldman Answers

Who Was Panic Selling Oil Today? Goldman Answers

In the annals of market history, April 20, 2020 will be forever remembered the day when, for the first time ever, the deliverable WTI future contract plunged 50%, 60% – the drop accelerating – then 70%, 80%, 90%, 99%, … and then the unthinkable happened: after the May WTI contract dropped to $0.00, meaning it was free to get delivery of oil, it proceeded to slide into negative territory – a never before seen event in market history – as oil producers were paying their customers to take delivery of physical oil in a world in which oil storage has essentially run out.

And so the price of oil tumbled, dropping further into negative territory, before finally stopping at -$40.32, the lowest price ever recorded for a barrel of WTI.

In many ways, the move was a mirror image of what happened during the legendary Volkswagen short squeeze, when countless shorts found out there were not enough freely floating shares to cover all existing short positions, unleashing a scramble to buy shares at any price and avoid being the last man standing, as the alternative was – in theory – a stock price hitting infinity (it almost did: very briefly, Volkswagen became the world’s most valuable company destroying dozens of iconic shorts in the process and leading to the suicide of one of Germany’s richest people). Today’s move was similar, as many inexperienced traders suddenly realized that instead of an asset, oil had become a liability, having only hours to find a place where to receive delivery of physical barrels of oil, and failing to do that, finding a greater fool to dump the deliverable obligation to. Only it wasn’t so easy.

As a result, a game of explosive hot potato (or rather highly flamable black gold) ensued around noon, when the deliverable WTI contract hit $10, its drop accelerating in an increasingly bidless market, before triggering hundreds of $0.01 stops, at which point oil plunged vertically, crashing $40 dollars in minutes.

As Roger Diwan explained in further detail, “speculators found themselves unable to resell the WTI contract, and have no storage booked to get delivered the crude in Cushing, OK, where the delivery is specified in the contract. This means that all the storage in Cushing is booked, and there is no price they can pay to store it, or they are totally inexperienced in this game and are caught holding a contract they did not understand the full physical aspect of as the time clock expires.”

So what happens now?

Well, some stability appears to have been restored, because since its settlement close around -$37, May WTI has recovered all its losses for the day and was last trading just above $0.

But don’t count on the relative stability lasting into tomorrow’s contract expiration – or the next month – because as Goldman’s commodity strategist, Damien Courvalin, who first predicted one month ago that negative oil prices are coming for landlocked producers, warns of “potential further distress ahead of the settlement window” tomorrow for the May WTI contract.

It gets worse from there because as we discussed earlier, the pain will then shift to the June contract, which expires on May 19:

The June contract will then become the prompt contract until its expiration on May 19. While it has outperformed significantly today, down only $4.60 to $+20.43/bbl, it will nonetheless likely see downward pressure in coming weeks

In other words, there will be more fireworks tomorrow for the May future, for the simple reason that there are likely still tens of thousands of maturing May contracts that need to find a literal home, which – with Cushing effectively full – is a problem, to wit:

The May CME WTI contract expires tomorrow, April 21. Any holder of a long position going into settlement would then be obligated to take delivery of crude in Cushing during the month of May (either by transfer into a designated pipeline or storage facility or by in-tank transfer). This means that an investor long a WTI May contract would be forced to sell out of this position (at any price) before tomorrow’s settlement to avoid being stuck having to find room for barrels in the Cushing storage hub which will likely be completely full by then (it is 77% full as of last Friday with the last 2-week builds pointing to stock-out by the first week of May).

Goldman then lists the following three reasons why the June future will be crushed next:

- the potential exit of spooked long retail investors given the violence of today’s move (and the negative carry incurred at each contract roll),

- the negative impact of investors rolling their long positions from the June to the July contract in early May (the USO rolls on May 5-8), and ultimately

- the still unresolved market surplus that will hit binding storage capacity in coming weeks.

Finally, here is Goldman’s answer to the question on everyone’s lips: who was left long heading into today’s record price drop, and who was selling at any price?

Given the difficulty and costs of storing oil (even in normal times), investors typically never keep positions into expiration. The size of the long positions in May WTI had therefore already shrunk significantly as all the major commodity indices and ETFs rolled earlier this month into the June contract. Illustrating that point, the unprecedented collapse in May WTI prices occurred with only 100k contracts trading today, a tenth of the June contract volumes.

In terms of holders, the surge in retail interest in recent weeks — as illustrated by the USO ETF which now represents 30% of the June WTI contract open interest — suggests that retail positions (in outright WTI contracts rather than systematically rolling products) were likely still long May WTI contracts into this week and now forced sellers (consistent with the sell-off accelerating in the 30 minutes ahead of the close and the sharp rebound that followed).

And so it was once again the mom and pop daytraders and r/wallstreebets amateurs, who however have felt quite professional if not invincible, thanks to the Fed’s constant market manipulation and bailout out of every crash… but not in the commodity sector. It was they that suffered unprecedented losses having held on to a contract they did not understand, and without realizing that they faced not only a total wipe out, but a wipe out more than 100% of their invested capital, a privilege traditionally only reserves for short sellers.

And while we agree with Goldman that retail was the biggest victim of today’s crash, we doubt it’s the only one, because if there is one thing this market has created – if not real value (sorry but rising nominal stock prices due to printing money is the opposite of value creation) – it is an army of professional money-managing idiots who think they are geniuses whenever they are not on CNBC declaring how brilliant they are. And in the next few days we will find out not only just how many of them were wiped out, but also the names of all those “pros” who at the end of the day were as clueless as 23-year-old reddit discussion board “traders.”

Tyler Durden

Mon, 04/20/2020 – 21:42 - Uber Sticks Former Star Engineer With $180 Million Legal Bill After Google Ruling

Uber Sticks Former Star Engineer With $180 Million Legal Bill After Google Ruling

Uber says it will not be indemnifying former star engineer Anthony Levandowski for a $180 million legal award won against him by Google. The company instead claims that Levandowski’s guilty plea confirms he’s a liar and that he should not be entitled to have the company help with his legal fees.

Levandowski was brought on in 2016 from Alphabet’s self-driving car program but Uber wound up firing him after the two companies went to war over trade secrets, according to Bloomberg.

This year, Google won a contract-breach arbitration case against him and Levandowski agreed to plead guilty to trade-secret theft. He was driven into bankruptcy as a result. Levandowski had been counting on Uber’s promise for indemnification, but Uber now says they have no obligation to support him.

Instead, in a legal filing, the company said: “Levandowski secretly committed a crime by stealing trade secrets with the intent to use them at Uber. If Uber had known that, it never would’ve entered into any agreements with Levandowski.”

Sure. Because that’s not why you hire people directly from Google’s competing self-driving program, right?

Levandowski’s lawyer claims that Uber is not allowed to renege on the indemnification because it vetting Levandowski before hiring him and know there was a reasonable chance he had taken information from Google. He claims Uber is trying to protect itself from an unfavorable legal outcome, and nothing more.

“Uber’s assertion that Anthony did not disclose material information to Uber is false,” Levandowski’s lawyer said.

Uber says Levandowski forfeited his indemnification when he asserted his 5th Amendment right and refused to testify. Levandowski will likely argue in the future that Uber was so eager to hire him, they offered to buy his $680 million in stock and looked the way when red flags arose during his vetting report.

Their vetting report on Levandowski showed he had “highly confidential Google proprietary information,” including source code, design files, engineering documents and software related to self-driving cars.

Which is probably why they hired him in the first place…

Tyler Durden

Mon, 04/20/2020 – 21:35 - "The Hit Is Huge": Colleges Brace For 'Fatal' Blow Of Next Fall As Face-To-Face Instruction Uncertain

“The Hit Is Huge”: Colleges Brace For ‘Fatal’ Blow Of Next Fall As Face-To-Face Instruction Uncertain

A viral post written by a veteran professor on Medium recently grabbed prospective students’ attention in saying provocatively: “This is a message to all high school seniors (and their parents). If you were planning to enroll in college next fall — don’t.”

“No one knows whether colleges and universities will offer face-to-face instruction in the fall, or whether they will stay open if they do,” University of La Verne law professor Diane Klein wrote. “No one knows whether dorms and cafeterias will reopen, or whether team sports will practice and play.”

“It’s that simple. No one knows. Schools that decide to reopen may not be able to stay that way. A few may decide, soon, not even to try. Others may put off the decision for as long as possible — but you can make your decision now,” the veteran teacher said, making the case that it’s the worst time ever for families to make the massive financial commitment. After all, who wants to drop an initial $50K or more to potentially sit at home for Fall 2020 and take online classes?