- They Will Lock You Down Again

They Will Lock You Down Again

Authored by Jeffrey Tucker via The Brownstone Institute,

The lords of lockdown barely escaped their worst possible fate, namely that the topic would become the national and international source of scandal that it should be. And let’s add the vaccine mandates here too: even if such had been morally justified, which they were not, there is absolutely no practical reason for them at all.

To have imposed both of these within the course of one year – with zero evidence that they achieved anything for public health and vast amounts of unfolding evidence that they ruined life quality for countless millions – qualifies as a scandal for the ages. It was in the US but also in nearly every country in the world but a few.

Might that have huge political implications? One would suppose so. And yet today it appears that truth and justice are further off than ever. The most passionate of the anti-lockdown governors – those who never locked down or opened earlier than the rest of the country – won on their record. Most of the rest joined the entire political establishment in pretending that all of this is a non-issue. Tragically, this tactic seems to have worked better than it should have.

Meanwhile, a few points to consider:

The US government, through the Transportation Safety Administration, has signed yet another order extending the ban on unvaccinated international visitors until January 8, 2023. This means that no person who has managed to refuse the shot is allowed to come to the US for any reason. This is 30% of the world’s population, banned even to enter the US on their own dime. Something like this would have been inconceivably illiberal three years ago, and been a source of enormous controversy and outrage. Today, the extension hardly made the news.

The Biden administration has once again extended the Covid emergency declaration another 90 days, which continues to grant government vast powers without Congressional approval. Under a state of emergency, the Constitutional structure of the US is effectively suspended and the country remains on a wartime footing. This announcement was not controversial, and, like the above, it barely made the news.

Many colleges and universities, and also other schools and public agencies, continue to enforce the vaccine mandate even without any solid science behind the approval of the bivalent shots or any real rationale behind the push, given that most people have long ago been exposed and acquired natural immunity, and, moreover, it is very well established that the shots do not protect anyone from infection nor stop transmission. They just keep doing this anyway.

Masking is not in disrepute because we never really obtained anything like an honest admission of their failure to control the spread. Even today, there is a percentage of people out there permanently traumatized. On travels, I’m seeing perhaps 10-20% but in some Northeastern cities, regular wearing of masks is also very common. Once they became a symbol of political compliance and virtue, that sealed the deal and the culture was changed. Now we face the threat of mask mandates whenever government deems it necessary because the Transportation Safety Authority has been given the go-ahead by the courts.

The end of vaccine mandates in most areas of life, and hence also the drive for a passport to distinguish between clean and unclean people, is a good sign. But the infrastructure is still in place and becoming more sophisticated. It is hardly a final victory. It might only be a temporary respite, while all the ambitions are still extant.

More than that, the Biden administration (and all that it represents, including the World Economic Forum, the World Health Organization, and everything else called the establishment) has its own pandemic plans in place. The idea is not to dial back the mandates or cool it on them. It’s the reverse: centralize all pandemic planning to make a South Dakota, Georgia, and Florida experience impossible the next time. Also, spend tens of billions in more money.

The principle seems to have emerged among the agencies, intellectuals, and politicians who did this. Whatever you do, never admit to having made any major mistakes. And never connect the economic, cultural, health, and educational disasters all around us to anything the govenrment did in 2020 or 2021! That would be nothing but a conspiracy theory.

The pandemic racket is so huge at this point that it is even embroiled in the FTX meltdown over the weekend. Sam Bankman-Fried’s brother Gabe actually founded a nonprofit solely for the purpose of providing “support” for the $30 billion that the Biden administration has allocated to pandemic planning. The institution “Guarding Against Pandemics” is very obviously a honeypot for such funding, complete with on-the-record endorsements from many Democrat Party candidates who won election.

Meanwhile, yes, there have been many successful court challenges to many features of the pandemic response. But not enough. The main machinery that took away liberty and property in the name of virus control is still in place in all its essentials. The CDC to this day brags of its awesome quarantine powers that it can deploy any time government deems it necessary. Nothing about that has changed.

In the big picture and rendered in a philosophical sense, humanity seems to have lost its ability to learn from its own errors. Put in more gritty terms, too many people among ruling-class interests gained financially and in terms of the lust for power during the pandemic to prompt any serious rethinking and reform.

In any case, that rethinking and reform is now put off for another day. Anyone seriously concerned about the future of humanity and the civilizations it built must throw themselves into the long-term battle for truth and reason. That will require that we use every bit of what remains of free speech and what remains of the longing for integrity and accountability in public life. The group we have come to call “they” want a demoralized population and a silent public square.

We cannot allow that to happen.

Tyler Durden

Sun, 11/20/2022 – 23:30 - Texas Prepares Military Tanks For Southern Border After Governor Abbot Declares Invasion

Texas Prepares Military Tanks For Southern Border After Governor Abbot Declares Invasion

Three days after Texas Governor Greg Abbott invoked the state’s “Invasion Clauses” to tackle the record-setting influx of migrants illegally crossing the southern border, a new planning document obtained by Army Times and The Texas Tribune reveals Texas Military Department officials are planning to deploy a fleet of fully tracked armored personnel carriers and National Guard troops.

Texas Military Department officials issued the order Thursday to the headquarters leading Operation Lone Star reveals. It detailed the deployment of ten M113 armored personnel carrier vehicles to the border.

By Friday, the Texas Military Department released a statement that “aircraft flights and security efforts” will also be ramped up.

“These actions are part of a larger strategy to use every available tool to fight back against the record-breaking level of illegal immigration.

“The Texas National Guard is taking unprecedented measures to safeguard our border and to repel and turn-back immigrants trying to cross the border illegally,” the department said.

Governor Abbott launched Operation Lone Star in March 2021, deploying soldiers and Texas Department of Public Safety troopers to counter the influx of illegals crossing the border while the Biden administration turned a blind eye to the migrant crisis they sparked.

Fox News reporter Bill Melugin tweeted a shocking video from Eagle Pass, Texas, via drone outfitted with a thermal imaging system. He said the drone “shows a large group of migrants crossing illegally into private property early this morning [Thursday morning].”

Melugin said, as reported by the U.S. Customs and Border Protection, “there have been over 1,400 illegal crossings in the Del Rio sector in the last 24 hours & 69,000 since 10/1.”

NEW: Thermal drone video from our team in Eagle Pass, TX shows a large group of migrants crossing illegally into private property early this morning.

Per CBP source, there have been over 1,400 illegal crossings in the Del Rio sector in the last 24 hours & 69,000 since 10/1. pic.twitter.com/N1FjKVVuDa— Bill Melugin (@BillFOXLA) November 17, 2022

https://platform.twitter.com/widgets.js

Texas Republican Senator Ted Cruz quoted Melugin’s tweet, stating that “5,000,000 illegal aliens have crossed the border since Joe Biden was elected,” adding “over 230 illegal aliens crossed last month alone.”

5,000,000 illegal aliens have crossed the border since Joe Biden was elected.

Over 230,000 illegal aliens crossed last month alone.

And STILL Joe Biden doesn’t secure the border. https://t.co/BBSJadktHB

— Ted Cruz (@tedcruz) November 17, 2022

https://platform.twitter.com/widgets.js

Melugin has shown that migrant inflows were relatively low during the Trump years but have since erupted under Biden.

BREAKING: CBP reports there were 230,678 migrant encounters at the border in October, the first month of fiscal year 2023. It is an enormous increase over recent Octobers.

OCT FY’23 : 230,678

OCT FY’22 : 164,837

OCT FY’21 : 71,929

OCT FY’20: 45,139

OCT FY’19: 60,781 @FoxNews— Bill Melugin (@BillFOXLA) November 15, 2022

https://platform.twitter.com/widgets.js

The near-term deployment of the M113s comes as no surprise. These tanks are designed to carry infantry troops and or haul equipment. Each tank can be outfitted with a variety of weapons, heavy machine guns, grenade launchers, and antitank missiles. What weapons will be on Texas Guard’s M113s at the border is unclear.

Tyler Durden

Sun, 11/20/2022 – 23:00 - No Evidence Freedom Convoy Donations Were From Criminal Origins: GoFundMe Exec

No Evidence Freedom Convoy Donations Were From Criminal Origins: GoFundMe Exec

Authored by Peter Wilson via The Epoch Times (emphasis ours),

An executive from the online crowdfunding platform GoFundMe said in testimony before a parliamentary committee that there is no evidence suggesting that any of the funds raised for the Freedom Convoy protest through the platform were illegal or acquired through criminal means.

A person crosses the street beside a big rig parked on Metcalfe Street in downtown Ottawa during the second week of the Freedom Convoy protest against federal COVID-19 restrictions, on Feb. 7, 2022. (The Canadian Press/Justin Tang) Conservative MP Larry Brock asked GoFundMe general counsel Kim Wilford if she agreed that there was “no evidence that any of the funds originating to your platform were proceeds of crime.”

“That is correct,” Wilford told the parliamentary joint committee on the declaration of emergency on Nov. 18.

Prime Minister Justin Trudeau said in the House of Commons on Feb. 9 that there was a “flow of funds through criminal activities” being sent to the convoy.

Just over a week later, the prime minister also told the House that the convoy was “being heavily supported by individuals in the United States and from elsewhere around the world.”

“We see that roughly half of the funding that is flowing to the barricaders here is coming from the United States,” he said on Feb. 17.

Wilford said Thursday that 88 percent of the funds donated to the convoy through GoFundMe originated in Canada and 86 of the donors were from Canada. The convoy’s fundraising page raised over $10 million before GoFundMe removed it on Feb. 4 on the grounds that it violated their service terms.

Wilford confirmed that of the total 133,000 donors who gave to the fundraiser, only 18,000 originated from outside of Canada, with 14,000 of that total coming from the United States.

‘Perhaps A Handful’

A CBC broadcasting host said on Jan. 28 that there was “concern that Russian actors could be continuing to fuel things as this protest grows or perhaps even instigating it from the outside.”

The national media outlet’s ombudsman later called the comment “too bold” and said it should’ve been backed by more evidence.

Wilford told the House finance committee on March 17 that the largest single donation made to the convoy through GoFundMe totalled $30,000 and that it was from Canada.

GoFundMe’s president Juan Benitez told the committee on the same day that “there was virtually no, perhaps a handful at most, of donations from Russia.”

“In our opinion, and from the evidence that we see, there was no coordinated effort there to have any kind of contribution or impact,” he said.

On Nov. 18, Liberal MP Rachel Bendayan asked Wilford to provide the joint committee on with GoFundMe’s numbers outlining where convoy donors originated.

“Can you confirm to the committee that no donations were received from China?” Bendayan asked.

“I do not believe that any donations were received from China,” Wilford said, adding that she didn’t have the exact information at hand and couldn’t “confirm with 100 percent certainty.”

“Can you similarly confirm with respect to any donations coming from Russia?” Bendayan asked.

“Correct, yes,” said Wilford.

David Wagner contributed to this report.

Tyler Durden

Sun, 11/20/2022 – 22:30 - Worst Chinese Bond Drop Since 2016 Is Coming To An End

Worst Chinese Bond Drop Since 2016 Is Coming To An End

By Ye Xie and George Lei, Bloomberg Markets Live commentators and reporters

Three things we learned last week:

1. Good policy news is bad news for Chinese bonds. Bonds tumbled the most in six years earlier in the week amid growth optimism following the government’s loosening of Covid restrictions and support for the housing market. The selloff prompted retail investors to pull money from wealth-management bond products, which fueled a spiral of price declines and accelerating withdrawals. While redemption remains a wild card, it’s unlikely that rates will keep shooting up. The interbank borrowing costs have already converged with the central bank’s benchmark after persistently staying below. That limits the scope for further tightening unless the PBOC shifts its policy stance. On Friday, the PBOC added liquidity to the banking system for a second day, suggesting that it doesn’t want to see borrowing costs rise much further.

After the selloff, five-year swap rates are about 80 bps above the PBOC’s policy rate, surpassing levels seen in the second half of 2020. The market looks as if it is pricing in a V-shaped recovery similar to the one two years ago. Those expectations may be misplaced. “We believe the valuation is getting stretched,” Bank of America’s strategists, including Janice Xue, told their clients.

2. That’s because Covid reopening takes time. A little over a week since Beijing issued 20 new guidelines for easing Covid controls, fear and confusion lingers. With daily cases near record highs, China’s largest cities saw dramatic declines in subway traffic due to movement curbs, infection and quarantine worries. That said, there have been only 61 severe cases across the country out of hundreds of thousands of infections in recent weeks. Both authorities and the public may feel more confident in resuming a normal life if severe cases stay low.

Source: Bank of America 3. Tech companies still trade with lower valuations than utilities. The three large Chinese tech firms reported mixed earnings last week. Alibaba posted a surprise loss, while Tencent saw revenue shrink for the second straight quarter. JD.com fared better, reporting higher sales. Even after the recent rally, Alibaba and Tencent are trading at valuations below utility companies in China and the US, underscoring investors’ skepticism toward big tech’s future under Beijing’s “common prosperity” drive.

Tyler Durden

Sun, 11/20/2022 – 21:30 - The No Normal

The No Normal

By Eric Peters, CIO of One River Asset Management

The No Normal:

“Restoring price stability will take some time and requires using our tools forcefully to bring demand and supply into better balance,” reminded Powell this past summer, on Aug 26. The equity market had just jumped 15% from the lows on hopes of a gentler Fed. The Fed doesn’t tighten into weaker equity markets and a contracting economy. Ever. It’s a rule. Powell changed the rule, an opportunity to win back inflation credibility. And the market listened. The swap market anticipates inflation will collapse to an average of 2.28% next year from 7.02% this year.

Hard landing. Soft landing. No landing. Investors are dusting off playbooks from the past. There is a little bit for everyone.

-

Hard landing? Housing demand has fallen off a cliff. Prospective homebuyer traffic is down 49 points since the start of the year, the largest decline ever.

-

Soft landing? Credit markets are showing almost no sign of strain, even in areas where activity is weak.

-

No landing? There are too many job openings to talk about landings. Real wages have a lot of room to rise, and this could allow the global economy to fumble along.

The Fed keeps hiking until policy rates are above inflation. It’s a bear market until credit cracks. The Fed pivots when something breaks, and nothing has broken yet. Equity valuations are bloated, and earnings-per-share are too high. EPS always declines sharply in recession. S&P 500 EPS is tracking growth of 6% in 2022 and consensus expected to rise another 4% next year. When the Fed is easing into recession, equity markets are usually in decline. Bear-market rallies are noise, not signal. This is the hard-landing playbook.

The soft-landing playbook sees 2022 markets anticipating a recession that never comes. Inflation was driven by temporary supply constraints. The US has withstood three quarters of housing contraction. Credit markets are fine because nominal GDP is running 7.3% annualized for the year, whereas real GDP is flat. The rapid rise in the US dollar is typically tied to foreign credit events. None have occurred. The fall in inflation will give a big boost to real incomes. Policy returns predictable path. All is forgiven – global risk climbs the wall of worry.

These are normal debates in a world that is far from normal. There is no tidy fundamental equilibrium. Balance sheets add complexity, the blind spot of most investors and policymakers. Balance sheets mostly don’t matter. Those who care about them are often in the shadows of institutions, fretting over left tails being underwritten when buying credit. The Fed’s balance sheet is merely a window into deeper challenges. Reserve balances with Fed district banks are $3.13trln. It is the symbol of decades of policy preventing financial failure.

Capital was drawn to duration assets of all varieties in that world. This came at the expense of real investment. Emerging market countries were charged with filling that gap – an epic geopolitical miscalculation. And now, whatever the type of landing that lies ahead, decades of financial imbalances need to be reconciled. Markets need to incentivize a shift to tangible investment. People will hold on to their iPhones longer, keep that ThinkPad an extra year or two. You see, the landing isn’t the problem – it’s that we need to rebuild the runway.

Tyler Durden

Sun, 11/20/2022 – 21:00 -

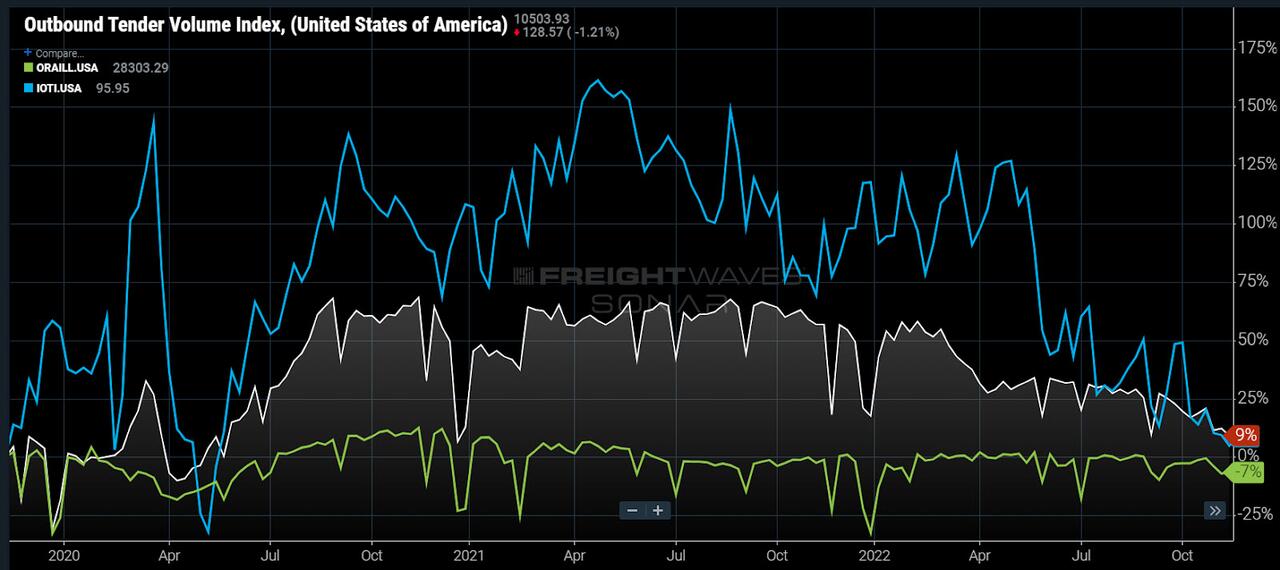

- Freight Demand Has Not Found The Floor

Freight Demand Has Not Found The Floor

By Zach Strickland of FreightWaves,

Container imports, rail intermodal shipments and truckload demand have fallen from their lofty peaks during the pandemic era and may be a better indicator of how inflation will be tamed in the coming months than the Consumer Price Index (CPI) itself.

Container import bookings measured by FreightWaves’ Inbound Ocean TEUs Index (IOTI) are now only roughly 6% higher than they were in November 2019 after averaging 80% above pre-pandemic levels through most of 2021.

Loaded intermodal container volumes on the rails (ORAILL) are down 7% versus mid-November 2019 levels.

The Outbound Tender Volume Index (OTVI), a measure of shipper requests for truckload capacity, is now only 9% higher than it was the week before Thanksgiving in 2019 after averaging nearly 50% above pre-pandemic norms from July 2020 to March 2022.

Chart of the Week: Outbound Tender Volume Index, Outbound Loaded Rail Containers, Inbound Ocean TEUs Index – USA SONAR: OTVI.USA, ORAILL.USA, IOTI.USA Demand destruction has occurred at a much more significant level than suggested by the dollar figures that drive a lot of the macroeconomic data. Dollar values are noisy and measure emotion as well as supply and demand imbalances. The scarcity effect is a prime example of this and has been one of the main drivers of inflation over the past two years.

The CPI that is representative of inflation, the Fed’s No. 1 enemy, is still moving higher from an annual basis thanks to rising supply costs and companies still passing along upstream cost increases that occurred over the past two years.

Looking at the Producer Price Index (PPI), which is focused more on upstream production costs, that direction has already changed and has been slowing since June. Transportation costs are a portion of this figure.

The point is that scarcity is diminishing. Supply chain congestion is easing. Consumer conditions have diminished from a purchasing power perspective. It takes time for this all to fully work its way into macroeconomic figures and behavior to change fully.

The transportation sector has been on the front end of both the economic boom and its recent decline. The reason for this is that transportation is the backbone of the goods economy. All goods, unfinished and finished, need to be moved at some point.

Raw materials move ahead of production and represent the furthest upstream view of aggregate demand. Finished goods moving to brick-and-mortar stores and fulfillment centers are also represented in transportation data.

While truckload and import demand may not have fully eroded back to pre-pandemic levels, the direction and time of the year suggest that it won’t be long until we are there. Seasonally speaking, retail volumes tend to spike just prior to and around the holidays, but there is little evidence of that at this point.

December and January are the slowest months of the year for domestic freight movements, meaning that it will probably get worse for transportation providers this winter without some sort of black swan event.

It is hard to tell how long this downward trend will last, as a lot of it will hinge on fiscal policy and investment sentiment. There is some surprising strength in labor numbers, which the Fed cites as a reason for continued rate increases, but this is a lagging figure that may still be reflecting past conditions.

About the Chart of the Week

The FreightWaves Chart of the Week is a chart selection from SONAR that provides an interesting data point to describe the state of the freight markets. A chart is chosen from thousands of potential charts on SONAR to help participants visualize the freight market in real time. Each week a Market Expert will post a chart, along with commentary, live on the front page. After that, the Chart of the Week will be archived on FreightWaves.com for future reference.

SONAR aggregates data from hundreds of sources, presenting the data in charts and maps and providing commentary on what freight market experts want to know about the industry in real time.

The FreightWaves data science and product teams are releasing new datasets each week and enhancing the client experience.

Tyler Durden

Sun, 11/20/2022 – 20:30 - Trump-Era Treasury Secretary Calls G7 Russian Oil Price Cap "Ridiculous"

Trump-Era Treasury Secretary Calls G7 Russian Oil Price Cap “Ridiculous”

Authored by Bryan Jung via The Epoch Times,

Former U.S. Treasury Secretary Steven Mnuchin has called the Group of Seven’s plan to place a price cap on Russian oil “ridiculous.”

The veteran cabinet member from the Trump administration was speaking with CNBC’s Hadley Gamble on a panel at the Milken Institute’s Middle East and Africa Summit.

In addition to being a former Goldman Sachs partner, Mnuchin now works in private equity investing.

Mnuchin panned the proposal to cap prices as “not only not feasible, I think it’s the most ridiculous idea I’ve ever heard.”

He explained that that imposing sanctions on Russia and its officials now would have far less of an impact than if they were implemented before the war started.

“Sanctions would have had a big impact back then. I think the problem now is that there’s limited options … there’s parts of the world that are now buying Russian oil outside of U.S. sanctions,” Mnuchin said.

“But look, a price cap, the market is going to set the price. So if you put sanctions on at higher prices, in a way, you’re just making the situation worse, in my opinion.”

The G7, which includes the United States, Canada, France, Germany, Italy, Japan, and the United Kingdom, are trying to set a fixed price cap on Russian oil from Dec. 5. Australia will also participate.

Meanwhile, American and European officials are still trying to decide upon the exact cap level, which has delayed the implementation of the plan.

The price caps, which were first proposed in July, would restrict shipping-related services that involve oil, including maritime transport, insurance, and financing to buyers of Russian oil supplies, unless it was sold at or below the limit.

The scheme is intended to hurt Russia financially, while protecting Western businesses and households from the effect of skyrocketing energy prices.

G7 Continue Stepping Up Sanctions on Kremlin

The United States and its allies have repeated that they are fully committed to rolling out more sanctions on Russia due to the Kremlin’s invasion of Ukraine.

Additional sanctions by the European Union will also take effect in early December and will terminate Russian crude oil deliveries to the bloc by sea, in time for a ban on all refined energy imports from Moscow next year.

The EU is imposing the energy sanctions in solidarity with President Volodymyr Zelensky’s government in Kyiv, despite the hardship it will cause on already suffering European residents and businesses.

The Kremlin has been pressed to look for new customers in Asia, and has since boosted its oil exports to countries like India and China, as it loses its main export base in Europe.

However, analysts have said that the price cap plan will not work without cooperation from the Asian nations, which both have strong ties with Moscow.

If the Indians and Chinese agreed to follow the price caps, American policymakers anticipate a relaxation in global oil prices, while hitting Russian oil export revenues where it hurts.

The United States said that it has no problem with India still buying oil from Russia, as long as it agrees to abide by the G7 price caps, Treasury Secretary Janet Yellen said, while visiting her counterparts in New Delhi last week.

Indian energy companies “can also purchase oil at any price they want as long as they don’t use these Western services and they find other services. And either way is fine,” Yellen told Reuters.

The Russians have threatened retaliatory measures against any country that imposes price caps on its energy exports and will terminate oil shipments to them.

Peace Negotiations Long Overdue

It currently looks uncertain that the two Asian giants would even go along with the proposed price caps, due to major political and economic factors.

Mnuchin stated that negotiations between Moscow and Kyiv were “long overdue,” and that the best case scenario to avoid an escalating crisis for now would be a truce between both combatants.

Ukraine has repeatedly expressed it will only enter negotiations following the “restoration of Ukraine’s territorial integrity,” financial reparations, and the handing over of Russian soldiers and officials for alleged war crimes.

The Russians have outright rejected those offers.

A spokesman for Russian President Vladimir Putin’s government said on Nov. 18, that “one thing is for sure: the Ukrainians do not want any negotiations,” CNBC reported.

Biden Administration Should Push For Energy Self-Sufficiency

Mnuchin also criticized President Joe Biden for having an “extreme focus on the issue of global warming.”

He said that while he was “not minimizing” climate change, he stated that the White House should not “discourage investment in the carbon economy.”

“With approvals, and again this stuff doesn’t need legislation, there are things the current administration could do, you know, there’s a need for pipeline, there’s a need for infrastructure, there’s a need for more drilling,” Mnuchin said.

He then stated that cheap and secure domestic energy supplies still remain critical to U.S. national security interests.

Mnuchin called for a return to the years of energy self-sufficiency under his former boss, President Donald Trump, and blasted Biden for hypocritically complaining about insufficient oil supplies from exporting nations.

“We can’t turn around and say to OPEC+, ‘Why are you not producing more oil?’ when we’re not doing it ourselves,” the former treasury secretary said.

“There’s plenty of shale oil and at these numbers, it’s very economic to produce,” he said, while noting that the U.S. energy sector was being “starved of capital.”

Mnuchin said that when he was still Treasury Secretary, he wanted to acquire more funding to fill up the National Petroleum Reserve, when prices were still low in the first months of the pandemic.

That oil reserve since has been severely depleted by a decision of the Biden administration to tap it in order to lower U.S. gas prices.

Tyler Durden

Sun, 11/20/2022 – 20:00 - "You Can't Put It Back Together" – Jim Rickards Warns Of 'Unstoppable Crisis Worse Than 2008'

“You Can’t Put It Back Together” – Jim Rickards Warns Of ‘Unstoppable Crisis Worse Than 2008’

Via Greg Hunter’s USAWatchdog.com,

Six-time, best-selling financial author James Rickards says the upcoming book “Sold Out” lays out the case why a huge crash is already a certainty sometime in 2023.

In a nutshell, broken supply chains have already caused big inflation, and the Fed is raising rates to tamp it back down. On top of the perfect storm of inflation and prolonged supply problems, we have the recent meltdown of the FTX crypto currency exchange. Rickards says,

“It is definitely going to cause sequential collapses in the crypto world, but will it jump the fence into the broader financial world? My expectation is it will, but it can take six months or more to play out…

We probably have an acute global financial crisis coming anyway. If FTX never existed, I would say we are staring at a worse financial crisis than 2008. Throw FTX on top of that, and it’s like throwing gasoline on a fire. It will accelerate the fire. So, we’re probably going to have problems anyway, but the FTX implosion just makes it worse.”

As far as the dwindling supply chains, Rickards says, “The old supply chain has collapsed. A new supply chain will emerge, and I talk about that in my book and what it will look like…”

” Right now, we are in a very messy middle period where things don’t work well. It’s like a vase. You knock over a vase, and it breaks into 5,000 pieces. You can’t put it back together. You’ve got to go get a new vase. We broke the vase, and we are shopping for a new one. We are not there yet. We are just cleaning up the mess. . . . Russia invades Ukraine. The Ukrainian plastic conduit factory shuts down, and all of a sudden, the BMW production lines are shut down because they cannot get a part. Again, this is another example of how this is all falling apart, and it’s not going to be put back together quickly. There will be a new supply chain, and I call it supply chain 2.0, but we are in that in between time, and it’s going to be just a mess.”

Rickards says the Fed is going to keep raising rates because that is what they keep telling the public. Rickards says, “They are telling us what they are going to do, and you should believe them.”

Rickards says we do have inflation, and it’s going to be with us for awhile, but we are also going to get deflation too. Rickards points out,

“Why does Warren Buffett and Berkshire Hathaway have $130 billion in cash? Buffett is one of the greatest investors of all time. Why isn’t he out there buying stocks? Again, why does he have $130 billion in cash? It’s because Buffett sees what I see. Yes, this thing is going to completely crash.

It’s a really good idea to have cash because you can go shopping in the wreckage and pick up some bargains. My point is, we don’t have to guess. Look at the Treasury yield curve. Look at the euro/dollar futures yield curve. Look at other metrics, and guess what it looks like? It looks like 2007. Everything I am describing, but not quite as extreme by the way, was true in 2007…

These euro/dollar futures were behaving then exactly as they are now. Except now, the inversion is even worse, which means we are in for a worse crisis than 2008. It’s coming. Everything I said has nothing to do with FTX. Throw FTX on top, and as I said, you are throwing gasoline on a fire.”

After the inflation, Rickards says count on big deflation. He will explain exactly how that happens in the 58-minute interview.

Join Greg Hunter of USAWatchdog.com as he goes One-on-One with six-time, best-selling author James Rickards. Rickards’ new book “Sold Out” will be coming out in early December.

* * *

To Donate to USAWatchdog.com Click Here

If you want to pre-order a copy of “Sold Out,” click here.

Tyler Durden

Sun, 11/20/2022 – 19:30 - What's Behind The Explosion In 0DTE Option Trading

What’s Behind The Explosion In 0DTE Option Trading

In recent weeks there has been much discussion of the unprecedented explosion in 0DTE (0-days to expiry), or options with less than 24 hours to maturity, which have become an extremely levered way to bet on even the smallest market gyrations (of course, the past month has seen some very major market gyrations, so imagine those magnified by 100x or more when it comes to P&L impact).

Just last week we quoted Goldman’s derivative strategist Rocky Fishman explaining that “the strongest area of volume growth has been ultra-short-dated” options, and that “measured in notional volume terms, S&P options with less than 24 hours to maturity now represent 44% of the index’s trading volume, and have been averaging $470BN notional per day over the past month.”

Roughly around the same time, JPMorgan quant Peng Cheng also picked up on this fascinating topic, writing that the increase in the volume of 0 day to expiry (0DTE) options on the S&P 500 (SPX) has attracted a lot of questions.

To analyze the topic, he published two reports (both available to pro subs), the first of which focused on 0DTE SPX index options and found that 1) the flow is not retail driven; 2) the order flow is biased towards seller initiated; and 3) proposed a framework is proposed for measuring the market impacts of 0D options. The second report looked at the tradability of 0D options.

Let’s start at the top with Peng’s response to several client questions:

Q1: Are retail traders driving up the volume?

Based on JPM’s retail classification algorithm, around 5.6% of all market volume on 0DTE options is attributable to retail market orders. This may be higher than the average for all SPX options (3.3%), but far from dominating the flow.

According to Peng, it is tempting to overestimate the retail activity in 0DTE options, given one observes a large number of small trades in 0DTE options. However, due to the proliferation of algo trading, trade size is no longer a good classifier for retail vs. institutional. Moreover, the average 0DTE trade size is not smaller than regular options, for the most part. To illustrate, the average trade size of 0DTE options is 3.6 contracts vs 5.7, for all SPX options. However, as Figure 2 shows, the distributions of 0DTE and regular option trade sizes are largely indistinguishable besides the very right tail (largest trades).

Q2: Are these options bought or sold, and are they held to maturity?

After estimating the directions of all +trades on 0DTE options, Peng does not observe an overwhelming bias toward either buying or selling. Despite the large volume traded, only a small percentage of the trades result in imbalances, and most of them are in fact net sold. Moreover, JPM estimates that only around 6% of the options are kept open until maturity.

Q3: Do 0DTE option trades move markets?

Since 0DTE options are traded at such a high frequency, their delta hedging behavior becomes much less predictable. Therefore, the gamma on 0DTE options is less meaningful than gamma on longer dated options. Instead, the JPM strategist looks at the market impact of delta: he partitioned market trading hours (9:30AM – 4:00PM) into 5-minute intervals. All 0DTE option trades are assigned an estimated trade direction, and their deltas at trade initiation are aggregated into the 5-minute bars. These aggregated deltas are then merged with the S&P 500 returns over the same interval. A regression between these two quantities tells us the market impacts emanating from 0DTE option delta imbalance. The relationship can be seen in Figure 5, whose positive slope suggests that there is indeed some market impact on the SPX from 0DTE delta. To wit, JPM estimates that market impact in any 5 minutes is between [-0.6%, +1.1%] over the last month.

With that background in mind, Cheng next looks at a transaction cost analysis and profitability of trading 0DTEs.

Transaction cost analysis

Q4. Is it more expensive to trade 0D options than longer-dated options, and if so, by how much?

Using tick level data during regular trading sessions from the month of October, JPM measured the cost of trading at-the-money 0D options. Specifically, it filtered for options with |delta| between [0.45, 0.55] at trade inception and eliminated those that are traded exactly at the mid. For comparison, we run the same analysis on 1 day to expiry options. The chart below shows the average effective spread, defined as the difference between traded level and mid, by trade size. For trades that are 10 contracts or fewer, the transaction costs are relatively invariant with respect to size. However, the transaction cost for 0D options is 3 times as much as 1D options on these trades.

Specifically, for 0D options, the volume-weighted effective spread is approximately 0.35 vega for trades 10 contracts or fewer (95% of all trades). For the 5% largest trades, the effective spread is 0.65 vega. In comparison, for 1D options, the average effective spread of is only about 0.11 vega for the lower 95% of all trades (11 contracts or less), and 0.66 vega for the 5% largest trades.

In terms of the intraday profile, there is significant volatility in the 0D option effective spread throughout the day. Notable volatility is observed at the market open, and again after 15:00 as time to expiry approaches 0. The profile of 1D options is much better behaved and exhibits little intraday seasonality.

Profitability

As pointed out in Q2 above, most of the 0D options are net sold by end users. This begs the question, who are the end users, and how are they using these options? In our view, these options are likely to be used by high-frequency directional traders, rather than volatility arbitrage traders. This is based on our analysis below, for which we find outright option returns to be profitable, but volatility premium strategies to be unprofitable.

First, consider the outright performance of the end users of 0D options, who are assumed to pay the bid-ask spread to enter into these trades. Let’s limit the analysis to ATM options (|delta| between 0.45 and 0.55 at the time of trade). Figure 4 shows the performance of estimated P&L shortly after trade initiation, based on the best bid or offer of the traded option 1 and 10 minutes later. These trade level P&Ls are then aggregated into a daily volume weighted average. It’s notable that not only is the performance strong, but also that 2/3 of the 10-minute P&L is earned in the first minute. Moreover, profitability disappears if these trades are held to expiry. It further supports the hypothesis that 0D options are unlikely to be held to expiry.

On the flip side, assume the market makers supply liquidity to the order flow and hedge out delta, their estimated P&L is 1 and 10 minutes after trade initiation is shown in Figure 5. They also show a strong performance, implying that volatility premium is captured by taking on the opposite positions of the order flow. The difference between delta hedged and unhedged performance suggests that end users of 0D options are unlikely to be volatility arbitrage traders.

In summary, JPM finds that trading 0DTE options cost up to three times as much as trading 1D options. However, it appears that the end users of 0D options profit from directional, high-frequency trading strategies even after incorporating the wider bid-ask spread. In other words, in a time when conventional HFT frontrunning of orderflow is far less profitable than it was a decade ago, HFTs are forced to resort to such market reflexivity schemes as 0DTE to boost their returns. At the same time, market makers are willing to supply liquidity thanks to the wider bid-ask and are able to systematically profit from delta hedged positions.

More in the full 0DTE notes available to pro subs.

Tyler Durden

Sun, 11/20/2022 – 19:00 - Entire Gender Industry Is Based On A Failed Study That Disproved Scientist’s Theory: Psychiatrist

Entire Gender Industry Is Based On A Failed Study That Disproved Scientist’s Theory: Psychiatrist

With schools teaching sex and gender ideology beginning in kindergarten, the Biden administration encouraging early medical treatments for gender dysphoria, and social media influencers discussing the topic, a record number of adolescent girls believe they are transgender and are transitioning to live as males.

Miriam Grossman, a child and adolescent psychiatrist, in New York on Sep. 23, 2022. (Blake Wu/The Epoch Times) Concerned adults are sounding the alarm on the lack of scientific studies to support transgender medical treatments that permanently alter a young person’s physiology and leave their mental health issues unresolved.

Child and adolescent psychiatrist Miriam Grossman, who has been a mental health professional for 40 years, said the gender industry is built on the lies of one troubled psychologist.

“The person who came up with the theory was Dr. John Money, and he came up with this idea that a person’s biology—their body, their chromosomes—is completely separate from their feeling of whether they are male or female,” Grossman said during a Sept. 23 interview for EpochTV’s “American Thought Leaders” program.

Grossman said the industry surrounding gender ideology—from gender clinics and hospitals to transgender pride flags and the emergence of a transgender civil rights movement—is based on a concept that was never proven to be true.

“In fact, the opposite was proven,” she said. “This whole concept of having an identity as male or female being completely separate from your biology has actually been proven incorrect by John Money’s experiment.”

Money was instrumental in establishing the first clinic to perform gender reassignment surgeries on children and adults at the Johns Hopkins Gender Identity Clinic.

In the 1960s, Money set out to prove his theory of gender identity to the world, and the perfect case study showed up in his office, Grossman said. But instead, his theory was disproven, and it was later revealed that his gender theory came from a study that was seriously corrupted.

The Canadian Twins

Grossman told the story of Janet and Ron Reimer, a Canadian couple with twin boys who consulted Money in the mid-1960s after one of the twins, Bruce, suffered a botched circumcision as an 8-month-old that permanently disfigured his genitals.

After seeing Money speak on a TV program about his research, the parents thought their grievously injured son could—like Money was promoting—change the sex he was born with and live a happy life as a girl.

Money’s hypothesis was that humans are born with a blank slate in terms of gender.

“He told the parents that they must immediately change Bruce’s name to a girl’s name, put him in girl’s clothing, tell everybody that he’s a girl, and never, ever tell him the truth about his birth and what happened to him,” Grossman explained.

Money advised the parents to have Bruce castrated and for doctors to construct an elementary female genitalia for the boy, Grossman said. Bruce was renamed Brenda and raised as a girl.

However, after many years of being treated by Money, at about the age of 10 the twins refused to see him again. It was later revealed that Money sexually abused the twins during their appointments. Bruce was reportedly never happy as a girl and had masculine inclinations that disturbed him throughout his life.

When the parents finally revealed the truth to the twins as they were entering puberty, Bruce (who was living as Brenda at that time) chose to revert to living as a male and took the name David.

“We have to acknowledge the unbelievable arrogance of a professional high-standing academic—widely respected, accomplished—the arrogance that he had to exploit this family in order to hold them up as proof of his theory,” said Grossman.

Money received a slew of awards during his treatment of the twins, including 25 years of continuous funding from the National Institutes of Health, Grossman said.

“His ideas about gender were institutionalized, were immediately adopted within an entire field of medicine—within mental health, psychiatry—and outside of medicine as well,” she said.

Indoctrination

Children have been indoctrinated with Money’s gender ideology, and now most young people do not believe there is a fundamental connection between biology and gender, which Grossman said is troubling.

She cited a poll published in September by The New York Times which found that over 60 percent of respondents aged 30 and older said they believe gender is determined by a person’s biological sex at birth, but 61 percent of respondents aged 18 to 29 said they believed that gender identity is distinct from biological sex.

The different between the younger and older group is directly due to the spread of gender ideology, Grossman said. This is because children as young as 5 years old have been indoctrinated with Money’s gender ideology in schools.

A transgender children’s book in Irvine, Calif., on Aug. 30, 2022. (John Fredricks/The Epoch Times) Kids are repeatedly being told that gender identity is separate from biology and that one can choose one’s gender identity, and it’s being presented as fact in the same way children are taught that the capital of California is Sacramento, she said.

Children are being told that a person can choose their own gender and that “gender-affirming care” is available for them if they want to become a different sex.

The “care” starts with puberty blockers and later progresses to opposite sex hormones and finally sex reassignment surgeries, at which point there is no room for the children to change their minds, Grossman said.

Researchers at Vanderbilt University in Nashville, Tennessee, published a study in JAMA Pediatrics (from the Journal of the American Medical Association) and reported that the number of gender-affirming chest surgeries performed in the United States on adolescents aged 13 to 17 years—the majority of which were elective mastectomies on girls—increased from 100 surgeries in 2016 to 489 surgeries in 2019, a difference of 389 percent.

Adolescents are constantly changing and trying to discover who they are, so allowing them to make a drastic change to their bodies during or before puberty is having a devastating impact on many young people and families, said Grossman.

A person holds a transgender pride flag in New York on June 28, 2019. (Angela Weiss/AFP/Getty Images) Dutch Protocol Run Amok

Prior to the 1990s, the majority of those seeking medical treatment for gender dysphoria were men in their 30s and 40s, Grossman said. Doctors were finding that opposite-sex hormones and surgeries were less effective after puberty, so they thought if they started these treatments before puberty, the patient might have better outcomes in the sex change.

Researchers in Holland came up with a study that’s now referred to as the Dutch protocol. Children were only chosen to participate in the study if they had discomfort with their biological sex from an early age and their discomfort became worse when they reached puberty. They also could not have any other mental health issues.

“They took those kids and they put them on puberty blockers at age 12. And those puberty blockers had never been used before for that purpose, and to this day, puberty blockers are not licensed or FDA approved in any country to be used with gender dysphoria,” said Grossman. They are only approved for disorders or medical conditions like precocious puberty, she said.

The researchers then gave opposite-sex hormones to the 55 children in the study, and later the children could have surgeries if they wanted them. There were problems with this study, including the fact that there was no control group alongside the transitioning kids, said Grossman.

Grossman said there is a lot of evidence to suggest that if the kids who were uncomfortable with their sex at adolescence had been left alone, the majority of the cases of gender dysphoria would have resolved on their own after puberty.

“This Dutch protocol was immediately adopted in other countries, including in the U.S., as ‘this is the solution for these kids,’” said Grossman.

Dr. Rachel Levine, the first transgender state secretary of health, meets with the media at the Pennsylvania Emergency Management Agency headquarters in Harrisburg, Pa., on May 29, 2020. (Joe Hermitt/The Patriot-News via AP) ‘Gender Affirming Care’

The phrase “gender-affirming care” is a euphemism for radical medical experiments that are leaving patients with long-term physical health problems, and they don’t address the more important mental health issues these young people have, Grossman said.

“You’ll have to note, again, the manipulation of language and the Orwellian use of language, when the term ‘gender affirming’ is used. They’re experimenting on the body, and people are paying a massively high price for these medical experimentations,” she said.

“Gender-affirming care means that whatever the child comes up with in terms of their identity, no matter how old they are or what other conditions they may suffer from, that is their identity and we accept it. We affirm it. And we give them the treatment that they would like to get,” said Grossman.

President Joe Biden and Health and Human Services Assistant Secretary Dr. Rachel Levine are promoting these treatments, and the majority of U.S. professional organizations are backing it, leaving parents to fight an uphill battle should they oppose their child’s wishes to change their gender, said Grossman.

Further, there are not enough long-term studies regarding the impact of “gender-affirming care” on children, but there is evidence about the dangerous outcomes, including being left sterile and developing blood clots, heart attacks, cancers, kidney failure, and early menopause, said Grossman.

Even with all the adverse effects of “gender-affirming care,” the Biden administration is trying to mandate that all medical professionals participate and support children to get these types of treatments, Grossman said.

Chloe Cole, an 18-year-old woman who regrets surgically removing her breasts, holds testosterone medication used for transgender patients in Calif. on Aug. 26, 2022. (John Fredricks/The Epoch Times) Rapid Onset Gender Dysphoria

The Tavistock gender clinic in London has seen an exponential increase in kids seeking sex changes, most with rapid onset gender dysphoria.

Read more here…

Tyler Durden

Sun, 11/20/2022 – 18:30 - Heavy Shelling At Ukraine's Largest Nuclear Plant: "You Are Playing With Fire!"

Heavy Shelling At Ukraine’s Largest Nuclear Plant: “You Are Playing With Fire!”

Concerns are mounting over the potential for radioactive fallout and disaster at the Russian-occupied Zaporizhzhia nuclear power plant in Ukraine following large explosions heard at the site over the weekend.

Like with prior incidents of shelling and fighting coming near the sensitive facility, each warring side is blaming the other for these latest attacks. “Explosions shook the Zaporizhzhia nuclear power plant in Ukraine over the weekend in what appeared to be renewed shelling of the facility and the surrounding area, according to the United Nations’ International Atomic Energy Agency (IAEA),” The Hill reports Sunday.

The BBC cites local sources who say over a dozen powerful explosions were heard Saturday night at or in the vicinity of Zaporizhzhia plant, which remains Europe’s largest nuclear facility.

Image via AP IAEA Director General Rafael Grossi called the reports “extremely disturbing” and “completely unacceptable”. He urged for fighting to halt there immediately. “Whoever is behind this, it must stop immediately. As I have said many times before, you’re playing with fire!”

The IAEA said that in prior weeks there had been a “period of relative calm” in the area, which has now ended. “I’m not giving up until this zone has become a reality. As the ongoing apparent shelling demonstrates, it is needed more than ever,” Grossi stated.

The UN atomic watchdog still has a team of experts on location at the plant, but there’s been no definitive word on which side was behind the renewed shelling which risks destabilizing the plant.

Most Western media reports have blamed Russia for the powerful explosions which reportedly continued into Sunday, despite Russian troops still being the ones to occupy and oversee the actual site. Ukrainian state energy company Energoatom charged that Russia is “once again… putting the whole world at risk.”

“This morning on Nov. 20, 2022, as a result of numerous Russian shelling, at least 12 hits were recorded on the territory of the Zaporizhzhia nuclear power plant,” Energoatom said.

“You are playing with fire!”

Director General of the international Atomic Energy Agency reacted to reports that the Zaporizhzhia nuclear power plant is being shelled and said: “whoever is behind this, it must stop immediately.”

Latest: https://t.co/X3flQUBL0r

📺 Sky 501 pic.twitter.com/L9897zapHB

— Sky News (@SkyNews) November 20, 2022

https://platform.twitter.com/widgets.js

Russia fired back, with its own nuclear agency Rosatom saying the following:

Kyiv “does not stop its provocations aiming at creating the threat of a man-made catastrophe at the Zaporizhzhia nuclear power plant,” the Russian army said in a statement on Sunday.

Despite the shelling, radiation levels “remain normal,” the army added.

It said missiles exploded around a power line that feeds the plant, the fourth and fifth power units and “special building number 2.”

Renat Karchaa, an adviser to the Russian nuclear agency Rosatom, told state-run agency TASS that the “special building” contained nuclear fuel.

As for assessed damage as a result of the weekend explosions, the IAEA said at this point the damage to the buildings is not “critical.”

However, there fears this means escalation in fighting around the plant, with the IAEA statement underscoring the shelling is “abruptly ending a period of relative calm at the facility and further underlining the urgent need for measures to help prevent a nuclear accident there.”

Tyler Durden

Sun, 11/20/2022 – 18:00 - Hedge Fund CIO: This Isn't The 1920s Or The 1970s… Today's Starting Points Are Like None We Have Ever Seen

Hedge Fund CIO: This Isn’t The 1920s Or The 1970s… Today’s Starting Points Are Like None We Have Ever Seen

By Eric Peters, CIO of One River ASset Management

“Buyer traffic is becoming increasingly scarce,” explained the Chairman of the National Homebuilder Association. “Even as home prices moderate, building costs have yet to follow.”

When prospective homebuying is this weak, the Fed is typically cutting rates. Yet markets are prepared for another 100bps of rate hikes through next Spring.

US existing home prices were down each of the past four months across all four regions. Price discounts aren’t enough – inventory ratios are higher as nobody wants to move unless they must.

Bond markets are convinced that inflation is going to fall hard – higher real rates, a weaker economy, a stronger US dollar, and a massive deflationary impulse from global trade make it a safe bet.

But there are oddities in the background. Labor is gaining strength. This doesn’t usually happen with a weaker economy and falling inflation. But it is happening.

“Overtime and minimum wage violations are common violations found in food service industry investigations,” said the Department of Labor. Krispy Kreme quickly settled damages filed by 516 workers on Nov 7th. Starbucks workers staged their largest labor action on Red Cup Day, one of their busiest of the year.

“If the company won’t bargain in good faith, why should we come to work,” the mood captured by a shift manager. US rail strikes are scheduled to start on Dec 5 – key chemicals shipments will stop days before. “Congress must quickly intervene to ensure a disruption does not occur,” the National Retail Federation warned. And it isn’t just the US – labor tensions are rising in the UK, Canada, Finland. Central bank balance sheets make unusual the new normal.

The QT theme continues; the “T” for tightening bit has paused. Fed excess reserves rose again last week, having bottomed seven weeks ago. It’s a complication that policy has never experienced. Demand for US dollars has declined as investors fish for an equity bottom, pushing excess liquidity back onto the Fed’s balance sheet.

Warren Buffet is one of those investors on the hunt for value. Berkshire’s 13F focused on cyclical infrastructure – semiconductors, energy companies, transportation over banks and technology stocks.

What to make of this mix of marbles?

There is a thirst to place current circumstances into a package that resembles the past, to give some comfort that the future isn’t as unknown as it seems. But it isn’t the 1920s or the 1970s, pre-war or post-war. There is no analog. Today’s starting points are like none we have seen.

The biggest risk is extrapolating to the future from a past that feels comfortable, confirmed by recent data. Disequilibrium is the new equilibrium.

Tyler Durden

Sun, 11/20/2022 – 17:30 - Top Contender To Replace Kuroda As BOJ Head Urges Removal Of Emergency Central Bank Support

Top Contender To Replace Kuroda As BOJ Head Urges Removal Of Emergency Central Bank Support

Central banks must remove emergency support measures once financial crises are over to avoid causing moral hazard in the market, former Bank of Japan deputy governor Hiroshi Nakaso said on Thursday. Which is ironic coming from the one central bank that not only institutionalized moral hazard and MMT, keeping rates at or below zero for the past 30 years, but also ushered in QE and now owns more than half of the entire JGB market, and even the merest hint of a pull back in BOJ support would spark financial armageddon for Japan where the country’s pensions would be wiped out in a millisecond should a central bank backstop ever be removed.

According to Reuters, Nakaso, who is considered one of the top candidates to become next BOJ governor, also said that once an economy was running below potential capacity, a central bank could more easily normalize ultra-loose monetary policy. Which is easy for him to say now that he is in the running for next BOJ head: we just somehow doubt he will demonstrate the same conviction if and when he becomes the next BOJ head.

Hiroshi Nakaso Echoing what we have said for the past 13 years, Nakaso said that investors had come to (correctly) assume that central banks would always come to the rescue when financial markets destabilized because of the massive monetary support deployed during the COVID-19 crisis, Nakaso said.

“This moral hazard must be removed once the crisis is over, though this is easier said than done because it’s a contradictory issue,” Nakaso said in a seminar hosted by the University of Tokyo and International Monetary Fund. And yet he said it, because the wave against relentless central bank intervention – which sparked record inflation across the world in the aftermath of the Covid crisis – is turning. Then again, it will promptly make another U-turn the moment tens of millions are left without a job as the financial tightening spawned by central banks in the past year finally hits the economy instead of just markets.

“Crisis management is like creating … artificial moral hazard,” he said. “It shouldn’t stay forever.” Yes it shouldn’t, which is precisely what we said in 2009, and yet no official or politician will ever have the guts to pull the plug knowing very well that the alternative is overnight collapse of the financial system.

None of this fazed Nakaso who continued citing what monetary policy should look like, not what it looks like now: to avoid moral hazard, central banks could design their lending facilities so they were less costly to tap for investors in crisis situations but became more costly when the market normalised. Oh you mean like ending QE 2, 3, Twist and so on, instead of holding on to them for years and for dear life. Yes, well, we tried suggesting that pretty much every single year since 2009 and it didn’t work. It won’t work now either, and it’s why – as Elliott correct predicted – we are facing tens of trillions more in monetary stimulus as the alternative is total collapse.

“Maybe this is something we can revisit and study” in preparing tools to combat the potential next financial crisis, Nakaso said. Maybe. Or maybe not, because once it is up to Nakaso to pull the plug on Japan’s unprecedented easing and collapse what’s left of Japan’s economy and market – as it is now far too late to try and “normalize” – he will never dare to do it.

Nakaso’s remarks come amid growing debate about how and when the next BOJ governor will reduce its massive stimulus, considered by some to be distorting market pricing.

“Inflation pressure that proved persistent … can be attributed at least … to generous monetary and fiscal support by the authorities,” Nakaso said, debunking relentless lies by central bankers in Europe and the US who have feigned ignorance and claimed none of the galloping inflation observed today is the result of their actions.

Nakaso and incumbent BOJ deputy governor Masayoshi Amamiya are considered among top candidates to succeed BOJ Governor Haruhiko Kuroda, whose current term will end in April.

Nakaso was speaking at the online symposium from Bangkok, where he was joining a meeting of national economic leaders along with Kishida. Their being there together may stoke speculation about Nakaso’s closeness to the premier.

Of course, all of this is just posturing and jawboning: as analysts quoted by Reuters note, neither would rush into tightening monetary policy, given the fragility of Japan’s economy and the need to keep low the cost of funding its huge public debt. And if they don’t tighten now, they never will.

Still, compared with Amamiya, Nakaso is seen more in favor of dialing back Kuroda’s radical stimulus. In a book published this year, he laid out in detail how the BOJ could end ultra-loose policy. What he left out is how JGBs go bidless, how trillions in Japanese pensions evaporate overnight, and how a global financial shockwave crushes the western financial system which is inextricably linked to the continued stability of the Japanese bond market.

Tyler Durden

Sun, 11/20/2022 – 17:00 - Don't Make Taylor Swift Fans Angry

Don’t Make Taylor Swift Fans Angry

By Matt Stoller, author of the BIG Substack

“It’s truly amazing that 2.4 million people got tickets, but it really pisses me off that a lot of them feel like they went through several bear attacks to get them.” – Taylor Swift

Over the past week, there has been fiasco in the sale of Taylor Swift tickets, with millions of angry fans despondent at not being able to see their favorite singer, and frustrated at the incredibly poor service, inexplicable pricing, and high fees of the Ticketmaster software system used to sell them.

Swift is the most popular artist in America, and hadn’t done live shows for four years. When she announced a tour, Ticketmaster was the ticketing agent. Due to under-investment in its platform, the corporation’s site and app crashed, unable to handle the demand for tickets. Somehow, though, scalpers managed to get plenty of tickets and put them on sale for much more than the original list price.

Why was Ticketmaster’s system so poorly structured? To answer that it helps to look at the firm’s stock price. In the face of such a high-profile embarrassment, a firm without market power would suffer in the marketplace. Investors would assume that customers would switch to a competitor’s services, much as, say, Ford’s stock drops when it has to do a recall of a line of cars. But Live Nation’s stock didn’t move at all. No investors were afraid that artists or venues would use a competitor’s software system. Because they can’t. There aren’t any meaningful rivals.

The problem, as this new generation of fans is learning, isn’t just that Ticketmaster is a bad system. The problem is Ticketmaster is the only system. It’s a monopoly.

And so Swifties, as they are known, demanded answers. These kinds of bitter cries tend to go into the void, just one more piece of evidence we have too many greedy people at the top and a government that cannot act. But this time, something different happened. Yesterday, David McCabe reported that the Department of Justice Antitrust Division has been investigating Live Nation, the parent company of Ticketmaster, for antitrust violations. And THAT revelation caused the stock to drop.

Members of the antitrust division’s staff at the Justice Department have in recent months contacted music venues and players in the ticket market, asking about Live Nation’s practices and the wider dynamics of the industry, said the people, who spoke on the condition of anonymity because the investigation is sensitive. The inquiry appears to be broad, looking at whether the company maintains a monopoly over the industry, one of the people said.

The Ticketmaster monopoly story goes back to the 1990s. It started with a merger. In 1991, Ticketmaster acquired its main rival in computerized ticketing, Ticketron, which put 90% of the ticketing business in the hands of one firm. This was a milestone. Indeed, Ticketmaster brags about this unlawful merger on its own website.

Three years later, the fees for ticketing had gotten out of hand. So Pearl Jam, then the biggest band in the world, got mad. The band was angry at the high prices and hidden fees the firm charged their fans, and they wanted a straightforward ticket price – $1.80 service fees clearly spelled out on $18 tickets, which was lower than what Ticketmaster sought. But Ticketmaster refused. So the band boycotted what was the then-new Ticketmaster monopoly. They ran a pressure campaign, testifying to Congress, embarking on a lobbying campaign, and pointing to the firm’s acquisitions of rivals and other underhanded tactics in its attempt to control the industry.

Ticketmaster struck back, bribing music venues to only accept Ticketmaster as a booking system, which meant that Pearl Jam couldn’t play at most normal locations. Pearl Jam’s 1995 tour was thus a catastrophe, because they had to play in places like sporting fields which couldn’t hold concerts, so most of their shows were canceled. The cost to Pearl Jam was in the millions, and it devastated the band. This was a remarkable potential moment for antitrust enforcement, with the biggest music act in the world brought to its knees by a ticketing monopoly.

And yet, enforcers did nothing. Under Clinton, Bush, Obama, and Trump, Ticketmaster grew, buying up rivals, becoming more and more powerful. Then, enter the other major powerhouse of the industry, Live Nation, a firm that rolled-up live events until it ultimately became the world’s largest concert promotion company. Live Nation was sick of paying Ticketmaster’s fees, and the two firms had been battling at the bargaining table. Finally Live Nation simply built its own ticketing software and threatened to compete directly with Ticketmaster. Competition would have hit profits for both firms. So instead the two worked out a deal to merge, so the combined entity could have all the fees – and more – to itself.

This new giant of the industry would open the door to an array of opportunities to grab cash. The merger combined the biggest owner of venues, the monopolist of ticketing software, and Front Line Management, a roll-up of artist management firms that came to control most of the biggest names in the business, making Live Nation the most powerful live entertainment firm America had ever seen.

Assistant Attorney General Christine Varney, Deputy Assistant Attorney General William Cavanaugh (right) and Chief Counsel for Competition Policy and Intergovernmental Relations Gene Kimmelman (left) discuss the Ticketmaster/Live Nation settlement with reporters. The deal was so outrageously arrogant that the combined firm was to be chaired by Irving Azoff, who – in a New York Times profile – confessed himself a serial liar and talked about how he put pictures of himself giving the middle finger on his own stationary. Initially, people thought Obama, who had talked tough on antitrust on the trail, would block the merger. Not doing so would look weak. If you weren’t going to go after Ticketmaster, the scourge of the 1990s, then would you go after anyone?

But the Obama administration approved the merger, with Antitrust Assistant Attorney General Christine Varney leading negotiations over what concessions Live Nation would have to offer. Immediately after the merger, Live Nation began violating its consent decree with the Antitrust Division, charging outrageous fees, and not stopping the sale of tickets to bots. It suppressed competitors who had developed ways of blocking scalpers, like Songkick. Live Nation acted in such bad faith that the Trump Antitrust Division eventually had to rework the consent decree.

Today, the choice by the Obama administration looks inexplicable. “The people who came in to oversee this transaction were very interested in doing everything imaginable to create more competition in ticketing in the marketplace,” said former Antitrust Division chief counsel Gene Kimmelman, who worked on the deal. “We were frustrated that the options were unbelievably limited.”

The concerns of Obama-era enforcers weren’t outlandish. From the 1980s onwards, it had become increasingly hard to prevail in antitrust claims. This ideological turn is one reason Clinton didn’t act despite Pearl Jam’s advocacy, and why the Bush, Obama, and Trump administrations allowed it to fester and worsen.

The post-1982 model used in antitrust cases, known as the consumer welfare standard, made it hard to show harm, because large firms could claim they were large not because they engaged in predatory behavior, but because they were efficient. And plenty of bought-off people in the industry would validate Live Nation, and very few opponents – after seeing what had happened to Eddie Vedder – would be willing to speak out publicly for fear of retribution. By the Obama administration, antitrust enforcers had come to see themselves as deal-makers, working with merging firms to help them make deals, rather than law enforcers trying to constrain corporate power.

But then something changed. Starting in the early 2010s, but then picking up steam over the decade, a new anti-monopoly movement began challenging the standard by which dominant firms such as Google and Amazon acquired their power. A range of writers, lawyers, businesspeople, workers, and ordinary citizens began learning, reading, researching, and talking. While a lot of people assumed that big tech was the only focus, the target was much broader. In 2021, my organization released a report called Courage to Learn, in which we highlighted a litany of Obama antitrust failures, including allowing the Ticketmaster/Live Nation merger. We recommended that the incoming Biden administration appoint new enforcers and engage in a far more aggressive strategy, including “unwinding” that merger.

Joe Biden listened. He appointed Jonathan Kanter to the Antitrust Division, and Lina Khan to the Federal Trade Commission. And they embarked on a series of new choices within the agencies, sparking controversy and in some cases bitterness within the white collar antitrust bar. A month ago, we published a research report on Live Nation, and were part of a coalition of fans and artists called Break Up Ticketmaster. 40,000 people have since asked for action.

And then came the Taylor Swift fiasco. It’s deeply embarrassing for the antitrust enforcers who facilitated the Live Nation merger, because the premise of their merger was that bigness begat efficiency. And yet the firm couldn’t handle an easily predicted demand spike that it induced by sending out marketing codes to Swift fans.

Politicians began speaking out, such as the state attorneys general of Tennessee and North Carolina, who pledged investigations. Members of Congress wrote letters to the Department of Justice, and Senators Amy Klobuchar and Mike Lee said they would hold hearings. And yet, the firm itself acted as a monopolist would, treating the fiasco as something of a joke. The first words out of a Live Nation executive at the Liberty Investor meeting two days ago was “Everyone has a Taylor swift ticket underneath their seat.” The harm Live Nation caused was irrelevant to its owners, who profited mightily regardless. Then, when the Chair of Live Nation, Greg Maffei, was asked on CNBC about the ticketing fiasco, he blamed… Taylor Swift.

Finally, Swift herself spoke out. On Instagram, she expressed anger at the exploitation of her fans. “It’s really difficult for me to trust an outside entity with these relationships and loyalties,” she said, “and excruciating for me to just watch mistakes happen with no recourse.” The statement was mostly heartfelt and personal, but the ‘no recourse’ phrase suggests something else. ‘Recourse’ is not the word choice of a songwriter, but of a lawyer trying to make a point about market power. Swift – or perhaps Swift’s lawyer – is saying that Ticketmaster is, as it was when Pearl Jam was the biggest act in the world, a monopoly. “We asked them,” she said, “multiple times, if they could handle this kind of demand and we were assured they could.” Even Swift, as the most powerful artist in music, could not prevent her fans from being cheated by Ticketmaster.

And now we know the Antitrust Division is on the case. It’s going to take time for this suit to move forward. They’ve been doing interviews for months, but there’s more work needed to put together a complaint. To some extent the lawyers can short-circuit the process since there’s a consent decree, but a judge will still drag it out. There are many more wrinkles to the Live Nation antitrust case. But that’s the gist of it.

It’ll be interesting to see if Live Nation decides to throttle back a bit on its fees, alleged coercive practices, and rumored retaliatory behavior. Firms in the crosshairs often do, and that’s probably why the stock went down, an expectation from investors that Live Nation might have to eat some margin loss for PR purposes. Somehow, though, I suspect they won’t. Live Nation is still guided by its original chairman’s love of putting up a middle finger to the world.

That’s what at least two generations of music fans have experienced.

Tyler Durden

Sun, 11/20/2022 – 16:30 - FTX Hacker Starts Dumping Massive Haul Of Ether Tokens

FTX Hacker Starts Dumping Massive Haul Of Ether Tokens

Last weekend, we reported on the mysterious $662 million outflow of tokens that suddenly hit FTX.

At the time, Nansen’s Alex Svanevik said, “It’s unclear exactly who’s making the transactions, but you wouldn’t expect to see these on-chain trades at this time.”

He said FTX’s main wallet was entirely drained of FTT.

Additionally, Reuters reported that SBF had a “backdoor” in FTX’s book-keeping system, which allowed him to move customer money around without triggering internal compliance or accounting red flags.

During the week, more details came out that suggested at least some of this outflow was in fact an apparently sanctioned transfer from FTX to Bahamian regulators – who rejected the exchange’s US bankruptcy filing and took possession of some of the assets.

“[There is] credible evidence that the Bahamian government is responsible for directing unauthorized access to the Debtors’ systems for the purpose of obtaining digital assets of the Debtors—that took place after the commencement of these cases,” read the filing, signed by new FTX CEO John Ray, famous for handling the liquidation of Enron.

The company went on to say that its co-founders Sam Bankman-Fried and Gary Wang were recorded saying that Bahamanian regulators instructed the pair to make “certain post-petition transfers” and that such assets were “custodied on FireBlocks under control of [the] Bahamian government.”

Securities Commission Addresses FTX Statement on Bahamian Withdrawals pic.twitter.com/OZKWwicSuN

— Securities Commission of The Bahamas (@SCBgov_bs) November 12, 2022

https://platform.twitter.com/widgets.js