- Germany To Prioritize Coal Shipments Across Rail Network Over Passenger Trains Amid Worsening Energy Crisis

Germany To Prioritize Coal Shipments Across Rail Network Over Passenger Trains Amid Worsening Energy Crisis

The latest sign lawmakers in Europe’s industrial heartland are preparing for what could be a disastrous winter of reduced natural gas supplies from Russia and record high electricity prices is a new proposal to prioritize Germany’s rail network for coal shipments over passenger services, according to Bloomberg, citing local newspaper Welt am Sonntag.

Even though Germany has promised to eliminate coal-fired power generation in the coming years, the historic energy crisis has made it more dependent on coal than ever as Russian flows of NatGas slump ahead of winter.

Economy Minister Robert Habeck recently said increased reliance on coal is bitter but necessary.

And we must give our readers a spoiler alert: there’s no way Germany will eliminate coal as a power source by 2030. If anything, it will be more reliant on it than ever unless it extends the life of its nuclear power plants.

“Priority is normally given to passenger transport in Germany, and timetables are geared toward it. As a result, there’s a risk of chaos on the rails from making the change,” Bloomberg said, citing the draft.

There’s a strong possibility the draft will be passed as a way to accelerate coal shipments via rail to power plants ahead of winter to ensure there are adequate supplies. Coal power generation is expected to soar in Europe’s largest economy this winter as a move to boost energy security.

The draft plan comes as German year-ahead power, a European benchmark, skyrocketed last week to a record 570 euros per megawatt-hour, with French prices rising as much as 3% to 720 euros. Coal prices in Europe also hit a record of 310 euros a ton.

Russia continues to squeeze NatGas flows to Europe as a heat wave limits hydroelectric and nuclear production. Rhine River levels have dropped to dangerously low levels, disrupting commodity cargos on the continent’s most important inland waterway. However, the good news this weekend is water levels have risen.

Germany’s increasing coal use this winter will be made possible by the rail system delivering supplies to power plants.

So much for the Europeans spearheading efforts toward green energy as Putin’s energy insecurity strategy appears to be a major success where it has caused stagflation and chaos across Germany.

Tyler Durden

Mon, 08/22/2022 – 02:45 - Geopolitics: The World Is Splitting In Two

Geopolitics: The World Is Splitting In Two

Authored by Alasdair Macleod via GoldMoney.com,

While we are being distracted by Ukraine, President Putin has advanced his geopolitical goals materially. Aided and abetted by President Xi, Putin is taking the Asian continent into his control. That mission is well on its way to being achieved. He now awaits the winter months to finally force the EU to reject America’s hegemony. Only then, will the western end of the Eurasian continent be truly free of American interference.

This article explains how he is achieving his strategic goals. It examines the geopolitics of the Asian landmass and the nations tied to it, which are commercially and financially turning their backs on the US-led western alliance.

I look at geopolitics from President Putin of Russia’s viewpoint, since he is the only national leader who seems to have a clear grasp of his long-term objectives. His active strategy conforms closely with Halford Mackinder’s predictive analysis of nearly 120 years ago. Mackinder is regarded by many experts as the founder of geopolitics.

Putin is determined to remove the American threat to his Western borders by squeezing the EU to that end. But he is also building political relationships based on control of global fossil-fuel supplies — a pathway opened for him by American and European obsessions over climate change. In partnership with China, the consolidation of his power over the Eurasian landmass has progressed rapidly in recent weeks.

For the Western Alliance, financially and economically his timing is particularly awkward, coinciding with the end of a 40-year period of declining interest rates, rising consumer price inflation, and a deepening recession driven by contracting bank credit.

It is the continuation of a financial war by other means, and it looks like Putin has an unbeatable hand. He is on course to push our fragile fiat currency based financial system over the edge.

Mackinder’s legacy

In a paper presented to the Royal Geographic Society in 1904, the father of geopolitics, Halford Mackinder, effectively predicted what is happening today. In his presentation, he asked:

“Is not the pivot region of the world’s politics that vast area of Euro-Asia which is inaccessible to ships, but in antiquity lay open to the horse-riding nomads, and today is about to be covered with a network of railways?

“Outside the pivot area, in a great inner crescent, are Germany, Austria, Turkey, India, and China. And in an outer crescent, Britain, South Africa, Australia, the United States, Canada, and Japan.”

This is shown in Figure 1, taken from the original paper presented to the Society.

In 1919 after the First World War, in his Democratic Ideals and Reality he summarised his theory in slightly different language thus:

“Who rules East Europe commands the Heartland;

Who rules the Heartland commands the World-Island;

Who rules the World-Island commands the world.”

This is Putin’s destiny. In conjunction with China (rather than a united Germany, which is what worried politicians such as Balfour before the First World War), Russia appears to be successfully pursuing her goal of control of Mackinder’s World Island. Today, we can expand on the inner crescent concept to include Iran, the Middle East, as well as the new nations spun out of the old Soviet Union. Of Mackinder’s original inner crescent, only Germany and Austria are omitted today. Austria was the centre of the Hapsburg Empire at that time and so is no longer geopolitically important.

Of the outer circle, we can now include most of Africa and some of South America, which are increasingly dependent on the World-Island for demand for their commodities. Without the West’s media and public seeming to realise it, there has been and continues to be an extension of Russian power through Asian partnerships which now eclipses America’s in terms of the global population covered. And if we add in China’s diaspora in South-East Asia, America and her NATO allies look like a somewhat isolated minority.

As well as political power ebbing away from the West, economic power is as well. Hampered by increasingly expensive and anti-capitalist democratic socialism, their economies are struggling under the burden of their governments. And as the West declines, the World-Island is enjoying its own industrial revolution. The network of railways, to which Mackinder referred in 1904, has expanded from the trans-Siberian railway to China’s new overland silk roads, linking China with Western Europe and the great nations south of the original silk road.

Russia and its ex-Soviet satellites occupy half the Eurasian continent. The Eurasian continent is 21 million square miles, or more than three times the size of all North America. Central and North America together measure some 9 million square miles, more than twice the area of Europe. Even without its ex-Soviet satellites, Russia is still by far the largest nation by land area. And together with China, Russia is nearly three times the size of the United States.

Russia is the world’s largest single source of energy, commodities, and raw materials and as we now see can control the prices the West pays for them. As a consequence of recent sanctions, the west is paying top-rouble, while Russia’s Asian allies have energy and commodities offered at a discount payable in their own currencies, undermining the West’s relative economic position even more.

As to whether Putin has studied Mackinder, this must be supposition. But there is no doubt that if he is not so guided, Putin is following the same predicted course. As Russia’s undisputed leader, he has played the geopolitical game masterfully. He does not fall into the traps which bedevil Western socialism. He follows foreign guidelines in the mould of the British at the time of Lord Liverpool’s Prime Ministership two hundred years ago, when the policy was not to interfere in the domestic affairs of foreign nations, except to the extent that they affected British interests.

It is a fact of life for Putin that his allies include some very unpleasant regimes. But this does not concern him — their domestic affairs are not his business. His business is Russia’s interests, and like the British in the 1820s, he pursues them single-mindedly.

The rationale behind Ukraine

Ukraine was an unusual instance of Putin taking the initiative in acting against the American-led NATO alliance. But in the run-up to Ukraine, he had seen Britain leave the EU. Britain was America’s vicar on the EU’s earth, so Brexit represented a significant decline in the US’s ability to influence Brussels. Following Brexit, President Biden precipitously exited Afghanistan, taking the rest of NATO with him. Therefore, America was on the run from the Heartland. The way was open for Putin to push further and expel America from Russia’s western borders.

To do this, he needed to confront NATO. And there is little doubt this was on Putin’s mind when he escalated his “special military operation” against Ukraine. He must have anticipated NATO’s reaction to impose sanctions, from which Russia has profited greatly. At the same time, it is the EU which has been badly crushed, a squeeze which he can intensify at will.

The drama is still playing out. He needs to keep up some pressure on Ukraine to keep the squeeze going. He is not ready to compromise. Winter in the EU will be tougher still, with energy and food shortages likely to lead to increasing riots by the EU’s citizens. Putin will only stop when the Europeans realise that America is sacrificing them in the pursuit of its hegemony. Zelensky is little more than a puppet in this drama.

With respect to the war on the ground, Russia has already secured its access from the Black Sea by cultivating her relationship with Turkey. As a NATO member, Turkey is hedging its bets. The Black Sea is vital to her economic interests. For this reason, Turkey is maintaining her relationship with Russia, while cooling down her antipathy to Israel (President Herzog visited Ankara in March) and mending her fences with the UAE — it’s all part of the World Island coming together.

For the US, Erdogan is an unreliable NATO partner. Allegedly, the US tried to remove him by instigating a failed coup attempt in 2016, when he was tipped off by Russian intelligence and the coup failed. While he owes a favour to Putin, Turkey’s NATO membership leads him to be cautious. And as a born-again Sunni, he appears keen to extend Turkish influence into the Moslem nations in Central Asia, dreaming perhaps of the glory days of the Ottoman Empire.

To further Russia’s power over energy sources upon which the Western belligerents depend, Putin has cultivated Iran, and has also made welcoming overtures to Saudi Arabia and the UAE. Sergei Lavrov, Putin’s foreign minister, took care to fully brief members of the Arab league of Russia’s energy policy in Cairo last month. The argument is simple: the West has turned its back on fossil fuels, planning to phase them out entirely in a decade or so. As producers of oil and gas, their future is to stick together with Mackinder’s World Island and its Inner Crescent. This is so obviously the case, that even Saudi Arabia is said to be seeking an association through the BRICS group.

Whatever the merits of climate change driven policies, with respect to energy the West seems to be hell-bent on a suicide mission. But Russia’s message to its partners is that you can have oil and natural gas at a discount to what Europe has to pay. Putin is offering to release them fully from the West’s climate change ideology.

With the pressure he is applying on Western Europe, Putin almost certainly assumes European politicians will be driven from supporting US sanctions to a more neutral position. And Russia probably expects that non-aligned nations suffering from grain shortages will also pressure the West to bring sanctions to an end. But before Putin relinquishes the pressure on EU nations, he is still likely to insist that American influence from Western Europe is withdrawn, or at the least it is withdrawn from Russia’s western borders.

Phase 1 has concluded. Let Phase 2 begin

We must now turn from Putin’s supposed megalomania to the conditions faced by his Western enemies, particularly the nations in Europe and the Eurozone. Figure 2, which is of a basket of commodities and raw materials priced in euros, shows that after a significant rise, for Europe prices have eased in recent months.

For the beleaguered Europeans, the pause in a substantial rise in commodity prices since the Fed’s introduction of zero interest rates in March 2020 has given them temporary and minor relief from an escalating inflation headache. Perhaps it is premature, but investors in western markets are taking the pullback in commodity prices as evidence that the commodity squeeze is probably over, and that with it the problem of consumer price inflation will diminish as well.

Indeed, in his 1 August report for Credit Suisse, Zoltan Pozsar reported that he had visited 150 investment managers in eight European cities recently, and the consensus was just that: they think inflation is licked, recession is due, and therefore interest rates will shortly decline.

But so long as he holds the pricing reins for energy, Putin can play with the euro to his heart’s desire. By manipulating his quasi-monopoly on energy, grains, and fertilisers he can increase pressure on the EU’s leaders to reject US hegemony. And to fully appreciate the power in Putin’s hands, it is important to understand the true relationship between fiat currencies and commodities.

The evidence is that the volatility of commodity prices is in the fiat currency they are priced in, and not the commodities themselves. Figure 3 shows this relationship, by comparing the price of oil measured in legal money (gold) and the fiat euro currency.

The most the price of oil in gold has varied on the upside is double at the time of the Lehman failure, whereas in euros at that time it was sixteen times. So far this year, it has been even more volatile when the price in gold fell to 70% of the 1950 price, while in euros it hit 15 — that’s 21 times as volatile.

This finding turns all energy pricing assumptions upside-down. The chart shows that what was true before the ending of Bretton Woods was no longer true after 1971. [The euro only commencing in 2000, the currency taken before then was the German mark]. Since oil prices are wholly determined in markets whose participants all assume price volatility is in the commodity, the entire basis of price forecasting becomes undermined. That being so, if an analyst gets a forecast half right it is more by luck than judgement.

This is the whole point behind sound money. With sound money, dealers in commodities and all other goods justifiably assume that the intermediating medium is a constant. They assume that when they receive payment, its utility is invariable. But with unbacked fiat it is different. For individual transactions, while we still assume a dollar is a dollar and a euro is a euro we all know that a currency’s utility varies. Why, then, for analytical purposes do forecasters always assume it does not? Why do analysts never take this into account in their forecasts?

Figure 3 above proves that conventional approaches to pricing and economic forecasts involving them are nonsensical. The same is demonstrably true for all other commodities, not just oil. In current circumstances, the basis for an incorrect analysis is being used to support expectations that prices are beginning to reflect an increasing prospect of recession, which to a Keynesian or monetarist mind, means falling demand for commodities and energy leads to lower prices. But the fact remains that overnight, Putin can put the squeeze on the EU again. And armed with the knowledge that price volatility is in the currency, we know that the falling euro will do most of his work for him.

As we approach Europe’s winter, it will not take much to drive energy prices in euros considerably higher. Putin is unlikely to make the mistake of being seen to do this deliberately. But in all probability, he need not take any significant action at all to see Western currency prices for energy and food rise again as winter approaches.

There is a further misjudgement common to Western capital markets: this time over interest rates. In almost every piece of analysis forecasting recession, the underlying assumption is that with economies turning down demand for goods, services and credit will diminish. For these reasons, interest rate pressures are expected to decline.

This misunderstands the nature of credit. Almost all circulating media is commercial bank credit. Consequently, GDP is simply the sum of all bank credit used for qualifying transactions. Therefore, nominal GDP is set by the availability of bank credit, and not, as commonly supposed driven by a slowdown in economic activity. When the banking cohort contracts its collective balance sheet, interest rates initially rise because of a shortage of credit.

These conditions are now faced by financial markets. Commercial banks are bound to seek ways to protect themselves in uncertain times. They are already looking to reduce the ratio of their assets to equity before bad debts really escalate. Banks in the Eurozone are not alone with this change in outlook. The so-called global recession is not being driven much by other economic factors, but mainly by the tendency for bank credit to be withdrawn from both financial and non-financial economic sectors.

It is a problem poorly understood and never mentioned by analysts in their economic forecasts. But in the current economic and financial environment, the consequences lead to a conclusion about interest rates the opposite of that commonly supposed.

We can see from the foregoing that contrary to expectations expressed everywhere by western governments and their central banks along with the whole investment establishment, the inflation and interest rate problem is not going away. Because interest rates had been suppressed and could go no lower and for no longer, there has been a fundamental shift from a long-term decline in them, to what is increasingly sure to turn out to be a long-term trend for interest rates to rise. As it is elsewhere, the bank lending environment in Europe is deteriorating for obvious reasons. Furthermore, it comes at a time when bank balance sheet leverage is at record levels, leaving banks badly exposed to the change.

A severe contraction in bank credit is only in its initial stages. A second phase in the economic and financial war against Putin’s Russia will shortly emerge. Currently, we appear to be in a summer pause after the first, indicated by consolidating commodity prices. Government bond yields have declined from earlier highs. Stock markets have rallied. Bitcoin has rallied. Gold, which is the only legal money from which to escape from all this, has declined. It all indicates a false optimism, vulnerable to the rudest of shocks.

China may be Putin’s only wildccard

With its economy based on commodities whose values are aligned with gold and so long as the current geopolitical situation does not escalate into a wider military conflict, Russia appears to be in a strengthening economic position while her adversaries are in decline. If there is a threat to its position, it probably comes from her alliance with China, which is exposed to the West’s follies through trade. China has some wildcard problems.

Since the death of Mao, in its rapid development China has relied on the expansion of credit through state owned banks. Bank executives are state functionaries, instead of managers on behalf of profit-seeking shareholders. It is this difference which has insulated the domestic economy from the cycles of bank credit which have plagued the West’s economic model with repetitive credit crises.

While this lack of destructive cyclicality might be seen as a good thing, it has allowed malinvestments to build up uninterruptedly over recent decades. So, while the Chinese authorities still exercise significant control over lending, the degree of economic distortion has become a threat to further progress.

This is being manifest in a growing property crisis, with developers going to the wall in droves. It’s not that there is unlikely to be demand for commercial and residential properties in the future: the savers are there to buy, the middle classes are growing in number, and the economy has some way to go in its development. The problem is that the property market has got ahead of itself.

As a sector, property and related activities make up an estimated one-third of China’s economic activity. Developers have suspended completions of pre-sold properties, which citizens have bought on a pre-payment basis. Consequently, mortgage payments are being suspended by angry purchasers. Private banks have been affected, with bank runs against some of them. Some thirty real estate companies have missed foreign debt payments, with Evergrande being the most high-profile defaulter on $300bn of debt.

Problems in property were and are still being compounded by Beijing’s zero tolerance covid policy. More so than in other jurisdictions, strictly enforced clampdowns have hit production and undermined logistics, factors that have inevitably undermined economic performance. While exports to other nations have held up well — mostly due to foreign governments’ spending deficits escalating and not being matched by increased personal savings — China’s exporters’ profits are bound to become squeezed by the West’s deepening recession. Unless, that is, China’s foreign exchange policy is to deliberately weaken the yuan against western currencies. But that will only end up destabilising the domestic economy as consumer price increases accelerate.

And lastly, if Beijing follows up on its threats to annex Taiwan — if only to detract from domestic economic failures — a train of events is likely to be set in motion which could escalate tensions with America and its defence allies to the detriment of everyone.

But despite the headlines from China’s property crisis, it is too early to assume China is descending into much deeper trouble. It must abandon macroeconomic policies driven purely by statistics and ensure its citizens and their business have a stable currency. Whether this is understood in Beijing is not clear.

The fundamental difference from its Russian partner is its greater economic dependence on consumption of commodities as opposed to their production. The consequences of western economic policies set to undermine their own currencies’ purchasing power will be felt more by China than Russia. Nevertheless, an increasingly likely banking and currency crisis in the West can be weathered by China with the correct economic approach.

The era of the dollar is ending

While Putin appears to be gaining control of the World Island, leaving a few nations on its fringes adhering to the US and its currency’s hegemony, much of what he has achieved is through the abject failure of the West in playing this greatest of great geopolitical games. A notable feature of the West’s decline is in its embrace of anti-capitalistic and woke cultures. In this article, it would lose our focus if we drifted into the climate change debate, other than to point out that by seeking to eliminate fossil fuels in the next decade or so, the West is on a course of economic self-destruction relative to Russia’s partners, who are being offered discounted oil, gas, and coal for the foreseeable future.

When President Nixon turned the dollar into an entirely fiat currency in August 1971, he set off a train of events which is now ending. From establishing the dollar as the world’s reserve currency, and his agreement with Saudi Arabia which led to the creation of the petrodollar, global fiat currency instability commenced as shown in Figure 3 to this article. But the fiat dollar gave both the US Government and the American banking system enormous power. That was effectively wielded, forcing recalcitrant nations to kowtow to the mighty dollar.

The power was not used judiciously, leading to an alliance between Russia and China to protect themselves from US actions. The lessons they learned from American imperialism were not lost. Despite earlier promises to Russia not to do so, the US military directly threatened her western border. For China, though her economic and industrial revolution having been initially praised, she began to be seen as a threat to the American interests.

This imperialism has made America few friends and many latent enemies. With repeated failures in US foreign policy in the Middle East, North Africa, Ukraine, and most recently Afghanistan, the US can now count on nations representing only about 19% of the world’s population of 8 billion people, compared with 54% allied to the World Island. This is shown in Figure 4.

While allocating nations into these categories is somewhat subjective, it gives an approximation of the relative power of the World Island partnership compared with that of US/NATO. As the US-led partnership’s grip slackens, vested interests are sure to drive non-aligned nations towards the World Island camp, particularly when they have commodities to sell.

Before Russia’s invasion of Ukraine and the sanctions that followed, none of the 170 nations in the table could do without the dollar. Russia has been forced to find alternative settlement currencies and its close allies in the Eurasian Economic Union are planning a new trade settlement currency to cut out the dollar. But the international pricing of commodities and raw materials in dollars is impossible to overcome, even for Russia.

The World Island cannot side-line the dollar completely — it is too entrenched. While the dollar’s power is declining, the destruction of its virtual monopoly in international trade will have to come from US monetary policy itself, a process that is arguably under way.

Since the financialisation of Western economies in the mid-eighties, the dollar has retained its credibility as the world’s reserve currency. It was achieved by ensuring a ready supply for international use, as forecast by Robert Triffin by his description of the dollar’s dilemma in the late fifties. The demand side was bolstered by the development of regulated and unregulated derivative markets, which forced foreigners to purchase dollars in order to purchase derivatives. Essentially, it was synthetic dollar demand created to satisfy speculator demand for commodities, including precious metals, by creating synthetic supply.

When this concept is grasped, the importance of the ending of the long-term trend of interest rate suppression becomes better understood. The suppression of commodity prices by increasing synthetic supply became part and parcel of interest rate declines. Interest rates are no longer declining but rising. There will be unexpected consequences for commodity prices, which we will come to in a moment.

There are two immediate consequences for bank lending: their lending margins improve, and the incidents of bad and doubtful debts increases. Consequently, overleveraged bank balance sheets are being cut back by banks no longer having to work them so hard to maintain bottom-line profits. And with lending risk escalating, this is a further reason to contract bank credit overall. Credit is going to be in increasingly short supply.

There are the consequences for financial markets, including synthetic commodity supply, to be considered as well. Under the new Basel 3 regulations which were recently introduced, trading and market-making in derivatives is an inefficient use of balance sheet capacity, so these activities are bound to be reduced over time under pressure from banks’ treasury departments. In effect, the conditions that allowed banks to expand credit to finance the increase of derivative trading activities between 1985 and 2021 are being reversed.

According to the Bank for International Settlements, the notional value of global regulated futures totalled $40. 7 trillion last March, and in options totalled a further $54 trillion. To this must be added over $610 trillion in over-the-counter derivatives. For now, it is variations in this synthetic supply which drive pricing relationships between fiat currencies and commodities. But the impact of contracting bank credit will almost certainly lead to higher commodity prices, as this synthetic supply dries up and is increasingly withdrawn.

Furthermore, contracting bank credit invariably leads to banking failures. And with the Eurozone’s and Japanese global systemically important banks leveraged over 20 times on average, the scale of banking failures is likely to be significantly larger than that of Lehman when it failed fourteen years ago next month.

And finally, as insurance against a widespread fiat currency catastrophe, both Russia and China have stockpiled physical bullion. Russia is known to have about 12,000 tonnes, of which 2,300 tonnes are held as monetary reserves. It mines 330 tonnes annually, which it is now adding to its hoard. Having accumulated the bulk of its hoard before permitting the Chinese public to buy gold, China’s state probably has over 30,000 tonnes, of which only 1,776 tonnes are declared official reserves. Since its inception in 2002, China’s citizens have taken delivery of a further 20,000 tonnes from the Shanghai Gold Exchange, some of which will have returned as scrap.

Therefore, the Russian and Chinese states between them command over 40,000 tonnes, which compares with America’s reserves, officially listed as 8,133 tonnes. As nations, they are also the two largest gold miners by output.

There can be no doubt that both China and Russia have a better understanding than western central banks of the relationship between money, which legally and in actuality is gold, and credit. They can only have built their reserves and mining capacity in anticipation that their currencies will need, one day, protection from a fiat currency crisis. First it was China, which accumulated most of her stash during the 1980-2002 bear market at prices as low as $275, before letting her citizens buy gold. With Russia, the accumulation has been more recent, undoubtedly seen by Putin as an essential part of his geopolitical ambitions. Both countries have concealed their true gold position, presumably so as to not threaten the dollar’s hegemony directly and to allow them to secretly add to their hoards.

In the event of a fiat currency crisis for the dollar, both the rouble and yuan have more monetary projection backing them than in any of the currencies of their adversaries. And while the jury might be out with respect to President Xi’s geopolitical nous, there can be little doubt that Putin will do whatever it takes to protect Russia, the rouble, and his geostrategic plans from any crisis which might envelop the West.

Tyler Durden

Mon, 08/22/2022 – 02:00 - Weaponizing The Bureaucracy: Who Will Protect Us From The Government's Standing Army?

Weaponizing The Bureaucracy: Who Will Protect Us From The Government’s Standing Army?

Authored by John & Nisha Whitehead via The Rutherford Institute,

“A standing military force, with an overgrown Executive will not long be safe companions to liberty.”

– James Madison

The IRS has stockpiled 4,500 guns and five million rounds of ammunition in recent years, including 621 shotguns, 539 long-barrel rifles and 15 submachine guns.

The Veterans Administration (VA) purchased 11 million rounds of ammunition (equivalent to 2,800 rounds for each of their officers), along with camouflage uniforms, riot helmets and shields, specialized image enhancement devices and tactical lighting.

The Department of Health and Human Services (HHS) acquired 4 million rounds of ammunition, in addition to 1,300 guns, including five submachine guns and 189 automatic firearms for its Office of Inspector General.

According to an in-depth report on “The Militarization of the U.S. Executive Agencies,” the Social Security Administration secured 800,000 rounds of ammunition for their special agents, as well as armor and guns.

The Environmental Protection Agency (EPA) owns 600 guns. And the Smithsonian now employs 620-armed “special agents.”

This is how it begins.

We have what the founders feared most: a “standing” or permanent army on American soil.

This de facto standing army is made up of weaponized, militarized, civilian forces which look like, dress like, and act like the military; are armed with guns, ammunition and military-style equipment; are authorized to make arrests; and are trained in military tactics.

Mind you, this de facto standing army of bureaucratic, administrative, non-military, paper-pushing, non-traditional law enforcement agencies may look and act like the military, but they are not the military.

Rather, they are foot soldiers of the police state’s standing army, and they are growing in number at an alarming rate.

According to the Wall Street Journal, the number of federal agents armed with guns, ammunition and military-style equipment, authorized to make arrests, and trained in military tactics has nearly tripled over the past several decades.

There are now more bureaucratic (non-military) government agents armed with weapons than U.S. Marines. As Adam Andrzejewski writes for Forbes, “the federal government has become one never-ending gun show.”

While Americans have to jump through an increasing number of hoops in order to own a gun, federal agencies have been placing orders for hundreds of millions of rounds of hollow point bullets and military gear. Among the agencies being supplied with night-vision equipment, body armor, hollow-point bullets, shotguns, drones, assault rifles and LP gas cannons are the Smithsonian, U.S. Mint, Health and Human Services, IRS, FDA, Small Business Administration, Social Security Administration, National Oceanic and Atmospheric Administration, Education Department, Energy Department, Bureau of Engraving and Printing and an assortment of public universities.

Add in the Biden Administration’s plans to grow the nation’s police forces by 100,000 more cops and swell the ranks of the IRS by 87,000 new employees (some of whom will have arrest-and-firearm authority) and you’ve got a nation in the throes of martial law.

The militarization of America’s police forces in recent decades has merely sped up the timeline by which the nation is transformed into an authoritarian regime.

What began with the militarization of the police in the 1980s during the government’s war on drugs has snowballed into a full-fledged integration of military weaponry, technology and tactics into police protocol. To our detriment, local police—clad in jackboots, helmets and shields and wielding batons, pepper-spray, stun guns, and assault rifles—have increasingly come to resemble occupying forces in our communities.

As Andrew Becker and G.W. Schulz report, more than $34 billion in federal government grants made available to local police agencies in the wake of 9/11 “ha[ve] fueled a rapid, broad transformation of police operations… across the country. More than ever before, police rely on quasi-military tactics and equipment… [P]olice departments around the U.S. have transformed into small army-like forces.”

This standing army has been imposed on the American people in clear violation of the spirit—if not the letter of the law—of the Posse Comitatus Act, which restricts the government’s ability to use the U.S. military as a police force.

A standing army—something that propelled the early colonists into revolution—strips the American people of any vestige of freedom.

It was for this reason that those who established America vested control of the military in a civilian government, with a civilian commander-in-chief. They did not want a military government, ruled by force.

Rather, they opted for a republic bound by the rule of law: the U.S. Constitution.

Unfortunately, with the Constitution under constant attack, the military’s power, influence and authority have grown dramatically. Even the Posse Comitatus Act, which makes it a crime for the government to use the military to carry out arrests, searches, seizure of evidence and other activities normally handled by a civilian police force, has been greatly weakened by exemptions allowing troops to deploy domestically and arrest civilians in the wake of alleged terrorist acts.

The increasing militarization of the police, the use of sophisticated weaponry against Americans and the government’s increasing tendency to employ military personnel domestically have all but eviscerated historic prohibitions such as the Posse Comitatus Act.

Indeed, there are a growing number of exceptions to which Posse Comitatus does not apply. These exceptions serve to further acclimate the nation to the sight and sounds of military personnel on American soil and the imposition of martial law.

Now we find ourselves struggling to retain some semblance of freedom in the face of administrative, police and law enforcement agencies that look and act like the military with little to no regard for the Fourth Amendment, laws such as the NDAA that allow the military to arrest and indefinitely detain American citizens, and military drills that acclimate the American people to the sight of armored tanks in the streets, military encampments in cities, and combat aircraft patrolling overhead.

The menace of a national police force—a.k.a. a standing army—vested with the power to completely disregard the Constitution, cannot be overstated, nor can its danger be ignored.

Historically, the establishment of a national police force accelerates a nation’s transformation into a police state, serving as the fundamental and final building block for every totalitarian regime that has ever wreaked havoc on humanity.

Then again, for all intents and perhaps, the American police state is already governed by martial law: Battlefield tactics. Militarized police. Riot and camouflage gear. Armored vehicles. Mass arrests. Pepper spray. Tear gas. Batons. Strip searches. Drones. Less-than-lethal weapons unleashed with deadly force. Rubber bullets. Water cannons. Concussion grenades. Intimidation tactics. Brute force. Laws conveniently discarded when it suits the government’s purpose.

This is what martial law looks like, when a government disregards constitutional freedoms and imposes its will through military force, only this is martial law without any government body having to declare it.

The ease with which Americans are prepared to welcome boots on the ground, regional lockdowns, routine invasions of their privacy, and the dismantling of every constitutional right intended to serve as a bulwark against government abuses is beyond unnerving.

We are sliding fast down a slippery slope to a Constitution-free America.

This quasi-state of martial law has been helped along by government policies and court rulings that have made it easier for the police to shoot unarmed citizens, for law enforcement agencies to seize cash and other valuable private property under the guise of asset forfeiture, for military weapons and tactics to be deployed on American soil, for government agencies to carry out round-the-clock surveillance, for legislatures to render otherwise lawful activities as extremist if they appear to be anti-government, for profit-driven private prisons to lock up greater numbers of Americans, for homes to be raided and searched under the pretext of national security, for American citizens to be labeled terrorists and stripped of their rights merely on the say-so of a government bureaucrat, and for pre-crime tactics to be adopted nationwide that strip Americans of the right to be assumed innocent until proven guilty and creates a suspect society in which we are all guilty until proven otherwise.

All of these assaults on the constitutional framework of the nation have been sold to the public as necessary for national security.

Time and again, the public has fallen for the ploy hook, line and sinker

We’re being reeled in, folks, and you know what happens when we get to the end of that line?

As I make clear in my book Battlefield America: The War on the American People and in its fictional counterpart The Erik Blair Diaries, we’ll be cleaned, gutted and strung up.

Tyler Durden

Sun, 08/21/2022 – 23:30 - "Population Will Rebel" – Swiss Police Chief Fears Social Unrest From Winter Power Shortages

“Population Will Rebel” – Swiss Police Chief Fears Social Unrest From Winter Power Shortages

The Swiss government is preparing rapidly for the possibility of power shortages this winter with Jan Flückiger, Secretary General of the Energy Directors’ Conference, warning that “internal security then becomes a problem,” arguing that the federal government has not yet recognized the urgency in this regard.

In an interview with Swiss German-language daily newspaper Blick, Fredy Fässler, the Police Chief of one of Switzerland’s largest Cantons, warned that people may revolt and resort to looting if the Alpine nation is hit by a severe energy crunch this winter.

“Imagine, you can no longer withdraw money at the ATM, you can no longer pay with the card in the store or refuel your tank at the gas station. Heating stops working. It’s cold. Streets go dark. It is conceivable that the population would rebel or that there would be looting,” he said, adding that the country’s authorities should take measures to prepare for such extreme scenarios.

Exercises that were conducted in 2014 to prepare for a blackout scenario revealed major shortcomings, including lack of emergency generators for police, hospitals and other critical infrastructure and services, he said.

“These shortcomings have been corrected in recent years,” the police chief noted, adding rather ominously that now “the security forces are armed” and his agency is even prepared to provide the Swiss with cash if they are unable to use cards in stores, given that relevant agreements with banks have been signed.

Additionally, Fässler warned of looting:

“I don’t want to paint the devil on the wall, but it has also been seen in environmental disasters that certain people have abused the situation to plunder unprotected objects. This could also be the case if the network is switched off, for example in shops where there is something to buy.”

But he warned the federal government not to over-step its tyrannical orders pre-emptively and expected police support:

“I appeal to the federal government to only order measures that can be implemented and, above all, controlled. We certainly won’t become the sauna police.“

Earlier, Werner Luginbuhl, the head of Switzerland’s electricity regulator ElCom, complained that electricity was being used “completely thoughtlessly,” and urged citizens to stock up on candles and firewood due to possible power outages in the country this winter.

Trigger a german pic.twitter.com/QRZsNKtx29

— James Reece (@Conye91) August 12, 2022

https://platform.twitter.com/widgets.js

There has been a surge in searches in Switzerland for ‘brennholz’ (firewood)…

Fãssler’s comments come after Swiss authorities said last week that they may place restrictions on energy consumption this coming winter, signaling that “power shortages [are] among the most serious risks” for the landlocked country.

This is Swiss officials warning of revolt and urging its people to gather firewood… not central Parisian leaders or Baltimore politicians!!!

Tyler Durden

Sun, 08/21/2022 – 23:00 - Power Crunch Threatens Growth, Reinforces Weak Yuan

Power Crunch Threatens Growth, Reinforces Weak Yuan

By George Lei, Bloomberg markets live commentator and reporter

Three things we learned last week:

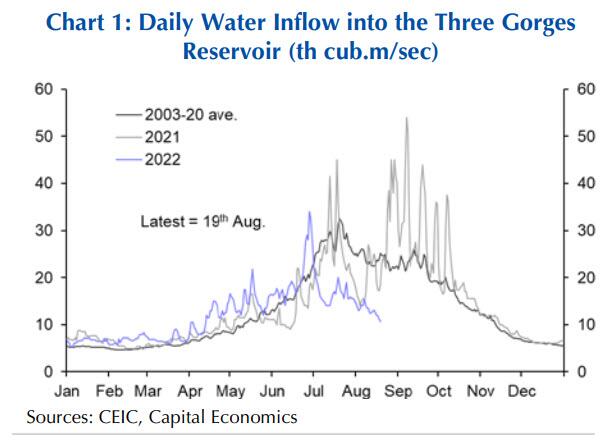

1. Electricity shortages amid a severe drought have replaced Covid lockdowns as the latest and potentially biggest threat to economic growth, at least in the month of August. Sichuan, a southwestern province with more than 83 million people, had to cut its hydropower generation by more than half as of Friday, state broadcaster CCTV reports. Dazhou, a city of more than 5 million, has implemented rolling blackouts on non-household users and is making plans for residential power cuts if the situation doesn’t improve.

Water Flow to Three Gorges Reservoir The blackout in Sichuan has led to factory closures of Toyota, Panasonic and CATL, the world’s top battery maker, while threatening supply chains to automakers including Tesla. Power generation in other parts of the country may come under pressure as well. Capital Economics noted on Friday that China’s eastern provinces — industrial hubs that normally consume power from the west — are now being asked to send electricity in the other direction, leading to a quick depletion of their thermal coal inventories.

Electricity shortages are so far at an early stage and relatively concentrated in the southwest, according to Morgan Stanley. Further deterioration, however, could start to drag on manufacturing and other economic activities, posing additional downward risks to corporate earnings and stock-market sentiment, analysts Laura Wang, Jonathan Garner and Fran Chen wrote last week.2. The Chinese yuan, trading both onshore and offshore, fell on Friday to the weakest since September 2020 and investors only see more downside ahead. The People’s Bank of China isn’t standing in the way of the currency’s devaluation path, and a raft of 2022 GDP downgrades (with the full impact of blackouts unknown) only add to negative market sentiment.

The offshore yuan has lost more than 1% so far in August, on course for the worst month since April’s 4.3% plunge. Things might be a bit different this time, however, as a “slow boil” yuan decline is the most likely scenario and runaway depreciation pressures appear less acute, JPMorgan wrote in a client note on Thursday. Investor positioning on the Chinese currency is already “extremely bearish” and foreign bond outflows have also lightened up somewhat, according to the US bank.

A gradual FX weakening could prompt the offshore yuan to first test 6.90, a level last seen in August 2020, and then onto the key 7.00 level, reached in July that year. The three-month CNH risk reversal, which measures the cost of protection against depreciation, traded around 1.3% on Friday — well above its 200-day moving average of 0.88% yet still shy of 2022 high near 1.75%, last seen on May 10.

3. Chinese banks are poised to cut their benchmark lending rates on Monday, following the PBOC’s 10 basis-point reduction to its 1-year MLF rate last week. Seven out of 20 economists polled by Bloomberg expect a 15bps cut to the five-year loan prime rate, a reference for mortgage costs, while six see an easing of 10bps.

Just don’t expect a turnaround any time soon. More policy support is on the way, yet “it will probably be too late too little to prevent output from stagnating this year,” according to Capital Economics.

Tyler Durden

Sun, 08/21/2022 – 22:30 - Ratio Of Full- And Part-Time Workers Spells Inflation Peak

Ratio Of Full- And Part-Time Workers Spells Inflation Peak

By Vincent Cignarella, Bloomberg markets live commentator and reporter

Is the US at full employment and we just don’t know it yet?

The ratio of full-time workers to part-time workers is at a near 20-year high. It may be turning, and a drop in the ratio may spell peak inflation as companies adjust to cut costs. That’d mean a better environment for stocks and bonds going forward.

If the ratio falls, it likely means companies are either looking to replace higher paid full-time workers with less expensive part-time employees or they are seeing declining sales. Either way, it is a sign of rising costs and an attempt to lower them or a slowing economy.

Both scenarios could prompt a Fed pivot. A slowing economy and peaking inflation are the signs the Fed needs to see in order to pause rate hikes.

Tyler Durden

Sun, 08/21/2022 – 22:00 - What Would A Crypto Crash Mean For Markets And The Economy

What Would A Crypto Crash Mean For Markets And The Economy

By Peter Tchir of Academy Securities

On “bitcoin infinity” day (apparently 8/21 is symbolic of ∞ infinity, the projected value of bitcoin) divided by 21,000,000 (the total number of bitcoin that can ever be mined), it seemed like a good time to explore what a crypto crash would look like and what it would mean for markets and the economy.

We all know what a mortgage bank collapse looks like (Washington Mutual). We’ve seen broker dealers collapse (Lehman), we’ve seen the stress on the system when money center banks and insurance companies come under intense pressure. Heck, we’ve even endured a sovereign default (Greece). We’ve also experienced flash crashes in equities and bond yields.

In all those cases, I would argue that having a gameplan ahead of time allowed companies and investors to profit from the events (both positive and negative). I haven’t seen much on what a crypto crash would mean, so I figured we could examine that today.

Jackson Hole

I could have written the 900th Jackson Hole primer, but I couldn’t bring myself to do that. I’ve already covered a lot that is applicable to Jackson Hole in Taxi Strategies, Orwellian Moments, Things You Won’t See, and Inversion and Inventories.

My focus right now is pretty simple:

- What is the real story on jobs?

- The weak data is a more accurate sign of the current situation.

- How bad is the inventory build?

- I think it might be the worst we’ve seen in my lifetime.

- Is the wealth effect a problem?

- I think that the concentrated nature of the wealth effect in disruptive stocks and crypto is different than anything else we’ve experienced historically, and the housing sector weakness is ominous to me.

- Inflation Fighting.

- Be careful what you wish for is all that comes to mind. Time and again, lower commodity prices have accompanied stock prices as they became much lower as well and I’m not sure why that will be different this time.

Anyways, let’s get back to being off topic and discussing a crypto crash.

6 Impossible Things Before Breakfast

I cannot come up with 6 impossible things before breakfast, but as the Queen suggested to Alice, you do need to practice.

Let’s start with the premise of a crypto crash or crypto collapse. If it is impossible, then there is no point even thinking about it. However, not only is it possible, but I put the possibility of it occurring in the next year at 10% or higher. Still unlikely, but a high enough probability that I should think about what it would mean.

Why a crypto crash or collapse seems possible:

- It has already happened. Luna/Terra is gone. Poof. XRP is down 80% from its highs, Cardano is down 85%, Bitcoin Cash (you got to love the name) is down 91%, and Dogecoin is down 90% as well. Dogecoin was allegedly started as a joke, which makes it all the more ironic (or moronic) that an SNL skit helped pump it to the moon. So, collapses and crashes have occurred in some segments of the market, which alone tells me that it is worth exploring more.

- This chart is precarious.

- Bitcoin continues to hover near levels that would ensure that no “hodler,” or someone who buys crypto and will never sell (diamond hands as opposed to lettuce hands), has made money on any purchase in almost two years. That is a long time to wait to make money (or to sit on large losses). FOMO is a big part of crypto trading, and we are on the precipice of declining to levels where many could decide to take their money and run. There is an ongoing theme in crypto that the “whales” keep buying dips, which might be possible, though it seems more likely to me that many have decided to lock in massive amounts of wealth into the much maligned (but useful) “fiat” currency. Crypto bounced here recently, but that was just the first test and I suspect that there were some heavily incentivized holders who went out of their way to support the price (there really are no rules in this space). This chart, by itself, doesn’t convince me that a crash is possible, but when I highlight the other issues, it certainly adds to that overall theme that a crash or collapse is a non-zero probability event.

- The chart isn’t much better.

- The $13.5 billion trust, GBTC, is currently at a 32% discount to NAV. This isn’t an ETF, so it has the ability to trade at a discount or premium to NAV for extended periods. A 33% discount lets you buy bitcoin at the equivalent of under $14,000 ($21,000 * 67%). There is, to some extent, over $4 billion in “free” money in this stock if the discount closes to 0. It is bizarre and scary to me that the discount continues to widen. In ETF’s, I believe that discount/premium to NAV leads the way (cheapness begets lower prices and vice versa). While that view doesn’t quite translate given the nature of GBTC, it is cautionary to me.

- A lack of interest. Recently one of the largest asset managers on the planet announced plans to collaborate with one of the largest public companies focused on crypto to work on some crypto projects. Two years ago, I can only imagine the impact that headline would have had on bitcoin. My guess is $10k in a heartbeat, but we are already back below the price when that deal was announced. Every headline like that (a year or more ago) was met with thousands (if not millions) of social media posts touting ADOPTION! While adoption is growing and more big banks have announced crypto strategies, the response seems to be more like “well, of course they are going to see if they can make money in it” rather than “OMG, XYZ just endorsed crypto, BUY!” Subtle shift in response, but an important one (albeit subjective).

- The best “use” cases are diminishing. China, to me, has always been the best use case. A large population with enough money to matter. For all the talk about banking the unbanked, etc., which sounds nice, this isn’t what will drive crypto prices higher. There are stats saying that as many as 4 billion people are unbanked across the globe. According to the World Bank, about 700 million people make less than $2.15 per day. That is depressing, scary, and almost mind-boggling, but from the crypto perspective, it is not the poor that will drive prices (there just isn’t enough money). But China, where millions of “middle class” citizens exist under a regime where they may want to keep money outside of the system, it has always been a good use case. With the property market in tatters, a slowing economy, and the government continuing to crackdown on crypto (outside of the digital Yuan), that use case may be dropping rapidly. Sanction avoidance as a use case may also be diminishing. If you were illicitly trading embargoed products (like oil), crypto may have been the “currency” of choice. But with the U.S. looking to ease restrictions on places like Iran and Venezuela (hypothetically), maybe some of the alleged trade will come back onto the books. With China and India openly buying Russian oil and Chinese currency gaining in stature (at least amongst some nations), there is less reason to use crypto when the Yuan is about 10 times less volatile than bitcoin (30-day vol of 5.4 versus 53). Criminal activity still flourishes, though the ability to track and reclaim ransomware payments seems to be increasing.

- It’s about blockchain and blockchain technology. The number of pundits, experts, and companies that seem to be doing contortions to pitch themselves as blockchain rather than crypto is high. Again, this is subtle, but it seems that re-positioning oneself as blockchain rather than crypto is occurring, which doesn’t bode well for crypto.

- It’s a Ponzi scheme, but it’s our Ponzi scheme. There were always the slogans that accompanied crypto, like “have fun staying poor” but they often included passionate explanations about the greatness of crypto. The use cases would take up pages including such themes like it is banking the unbanked (already discussed), that it is an inflation hedge (hasn’t worked on that front for some time), that it is outside the reach of the government (it is being regulated more by the day, and many in crypto, after some recent highly visible failures, now seem to embrace this), that it is lower cost (costs remain high and there is little protection against mistakes or fraud, unlike with bank accounts or credit cards), or speed (but how many people really need to instantaneously shift large amounts of money, but aren’t already served by Venmo or Zell or some similar product?) I still see those arguments being made, but with far less enthusiasm. However, there is another “use case” that seems to be getting traction (at least in my social media streams). It basically amounts to the argument that convincing more people to participate will help. Kind of like “adoption” but with a more cynical tone. Basically, it is admitting that it only really works if more people get in (so get in, and get more people in). It has the advantage of being true and seems honest, but it seems like the last vestige of a pump and dump scam.

I’m not sure about you, but that is enough for me to at least take a look at what a crypto collapse or crash would mean.

Crypto Market Cap

Let’s start with the market capitalization of crypto currencies as that is the most obvious and direct hit to investors. We will use coinmarketcap for this section (beware of using the link as it will ask to send notifications, know your location, etc., but I figured there should be a link to something to verify).

- Bitcoin at $21,262 has a market cap of $406 billion.

- Ethereum at $1,628 has a market cap of $199 billion.

- Binance Coin at $286 has a market cap of $46 billion.

- Then XRP, Cardano, and Solana come in between $13 billion and $17 billion.

- Dogecoin, Polkadot (love the name), and Shiba Inu are all about $7 billion, with Avalanche, Polygon, TRON, and Uniswap, all a bit over $5 billion.

Let’s call it about $750 billion in total market capitalization for crypto.

To make things “simple” let’s assume that after the top 3, most of the coins could disappear and people would hardly notice (I’m assuming that many of those coins are not widely held, and a few “whales” would lose a lot, but the average person wouldn’t lose much more than what they are already prepared to lose.) If you believe that this is an area where many have spent their “winnings” or took money made in bitcoin or Ethereum to really roll the dice (which I believe), that gives us further reason to argue that the hit here would be minimal on the economy (it also makes the analysis much easier as we only have to focus on a few key currencies).

Stablecoin Market Cap

We need to also consider the stablecoins. Terra/Luna was supposed to be a stablecoin. Stablecoins, in theory, are backed by assets of some sort, except those that were algorithmically backed (whatever that means).

Tether (USDT) is still the biggest at $67 billion. I love how much everything is made to sound like dollars (USD) despite the rhetoric against fiat. This stablecoin, in particular, attracts a lot of negative posts about how it is backed. The company asserts that Tether is backed by T-bills, commercial paper, etc., but to my knowledge, it has never produced a detailed list of its holdings, let alone an audited list of its holdings. This behemoth of an account ($67 billion is large even in money markets) is unknown by any money market participant I speak to (albeit that is only a handful of people outside of Academy’s strong short-term liquidity desk). Someone recently pointed out that they apparently manage that much money without a Bloomberg terminal account (there is no Bloomberg account linked to a company called “Tether,” but they could use a different name on Bloomberg to obfuscate their existence, which isn’t unheard of). Tether has seen their market cap drop from $82 billion to $67 billion, and part of that could be that some investors, given what has gone on this year, have shied away from it.

USD Coin or USDC (again, notice how much it tries to sound like the dollar) has a market cap of $52 billion. Its market cap only peaked at $55 billion, so it has gained at the expense of USDT. Circle, which is the company behind USDC, makes a big deal out of being transparent and regulated in the U.S. I’ve had brief conversations with people involved in the company and the pitch makes sense to me (though I have not yet gone through the effort of figuring out how granular that transparency is – that’s a project for another day). But they are clearly marketing themselves on the transparency issue and have surged relative to Tether over the past year or so.

Binance USD (BUSD) weighs in at $18 billion and is a distant third and seems relatively tied to the Binance ecosystem.

Vegan hotdogs. When I see all these names trying so hard to associate themselves with the dollar despite being part of an ecosystem designed to avoid the dollar, I can’t help thinking about vegan hotdogs and why vegans try to replicate an already weird food, when vegan food in its own right can be awesome! But I digress.

My view is that stablecoins and their market caps are a function of the overall utility of cryptocurrencies. If crypto crashes, we should see a decline in the market cap of stablecoins.

Two things could occur:

- Those backed by assets will have to sell the assets to meet redemptions. If it is a few billion and they are back by T-bills, then no sweat. Markets would digest that easily and no one would be impacted. But if the size is bigger (10s of billions) and the assets are less liquid (non-standard commercial paper programs for example) then we could see some friction in markets. Again, if we knew exactly what they held we could be more or less prepared. What they hold and the size of the selling would impact the knock-on effects of any unwind (Terra/Luna held nothing, so that didn’t spread to the greater financial system, but this could).

- If the stablecoins don’t truly hold sufficient assets or the assets are of low quality (there are all sorts of conspiracy theories out there on what it might be invested in that isn’t worth me repeating here, even if they intrigue me) then we could see what looks like a “bank run” occur not just in stablecoins, but ultimately in the assets they hold and asset classes that compete with what they hold. Let’s just pretend, for the moment, that they have money market lending that is off the radar screen, and presumably paid a lot, as it wasn’t standard. If they have to sell, that could cause prices to plummet, possibly to a level that more traditional players sell what they have to buy this stuff, creating that first domino effect.

There is a circularity between crypto and stablecoins. They can bring each other down.

While crypto losses themselves will be largely isolated to the holders (we still have to dig into that), the unravelling of stablecoins is likely to influence other markets, possibly quite negatively.

Direct Losses

The direct losses are relatively easy to figure out.

- Crypto losses. Let’s say $500 billion could be wiped out of crypto. While some evidence points to there being a small subset of “whales” that would bear the brunt of that loss, I think there is a broad enough swath of the population that would take a serious hit and it would affect spending in the near-term.

- Stablecoin losses. Stablecoins in theory should have an orderly unwind. If, and that remains a question, there is a disorderly unwind of one or more stablecoins, the losses would be in the 10’s of billions (which isn’t so bad). The problem is that unlike crypto losses, where investors presumably treated this as a risky portion of their portfolio, stablecoins are viewed as cash equivalents. Losing cash is always more problematic than losing risky investments. Something to watch.

- Public Company Losses. There are at least a couple of public companies that are linked to crypto. Then there are the miners, mostly listed on foreign exchanges. HIVE for example went from almost $2 billion to just over $400 million (higher than the recent lows of $237 million). Not a huge market cap loss, but only one of many miners out there. This would add up to more losses, some of which would hit mainstream funds. The bigger losses would likely be felt in the private domain as many of the companies in the space have not yet made the leap from private equity to public equity. The losses shouldn’t be material to the broader market, but would likely be concentrated enough to leave a mark disproportionate to the size of the losses. On the private equity side (even more than the public side) the losses will hit employees the hardest and that will hit spending.

- Jobs.

- If you consider day trading crypto and waiting for NFT drops to be a job, then there will be job losses.

- The companies I’ve mentioned, both the public and private ones, will be forced to let go of employees (that already will have lost significant paper wealth). These are skilled employees, so in theory, could find other jobs, but that could be more difficult to do in an environment where crypto losses cause investors (including private equity) to be more conservative across the fintech space.

- Domino or knock-on effects. Assuming the stablecoins hold liquid assets, that unwind should be handled easily (there is a risk that isn’t the case, at least for some stablecoins) but I won’t harp on it. There is not a lot of direct debt tied to crypto (though there are some bonds out there, but they are too small to have any material impact). I don’t see crypto being used as a major source of collateral. If bitcoin holdings, for example, were being used to leverage up stock investments, then I’d be very scared. I think some individuals may manage their personal wealth along those lines, but I don’t see it as a widespread issue (unlike housing in 2008, for example).

- Spending. How much spending is coming from this sector and what does that mean for us?

Spurious Correlation or Real Threat

You can take any two data series and potentially see a correlation. They may have nothing to do with each other, so we can stare at the “correlation” chart as long as we want, but it isn’t going to help us because there is no causation. Complicating matters further, we should be looking at correlations between the rate of change rather than correlations between asset classes themselves (I vaguely remember the reasons for this, but I will ignore that technicality for today).

Here is the SOX (Philadelphia Semiconductor Index) versus bitcoin. I chose to use this index because it is more likely to be spurious and highlights how much more correlated some individual semi-conductor stocks are.

Spurious correlation. The argument for “spurious correlation” is strong.

- It seems impossible that a small segment of the market, like crypto, could have a large effect on such a big diversified market.

- Many of the things that drove crypto were also driving other industries that placed huge demands on the chip industry (video conferencing, autonomous driving, big data, etc.). So crypto was just one of many things driving those industries and those industries should not be impacted by a crash in crypto.

- I could go on, but I can see heads nodding here, so I won’t spend any more time arguing what is a consensus (and probably correct) view.

What if it is correlated?

- The wealth being generated by those in crypto was large. From the miners to the “exchanges,” there was a race to capture revenue and there was plenty of revenue to capture. The spending on chips (rigs to mine, servers to provide customer service, etc.) was large. Chip companies presumably saw this demand and knew that they could charge a premium to an industry where speed and timeliness meant everything. Were chips designed specifically for the crypto industry? Was production of generics shifted to higher profit margin lines? Not only were the companies (that succeeded) spending money, but many failed business ideas (or those just not yet successful) had money to spend as well.

- What if crypto spending went to web services (seems like it would). What if it went to advertising? (It did). What if that spending caused those companies to spend more? Maybe they needed to add systems, components, and people to keep up with the demand from the crypto industry. Did that spending then create more spending and make it very difficult (if not impossible) to figure out where crypto spending ended and where “regular” spending went?

- How much money was crypto spending on energy? At one time I saw stories that in terms of energy usage, crypto, if treated as a nation, would have been the 10th largest country in terms of energy use. Commodity prices are always affected by the marginal 5% or 10% of demand. Is it possible that part of energy inflation was due to crypto? Does that mean policy makers are responding to a problem (high inflation) while ignoring one of the causes (because it isn’t on their radar screen, except in China, which has been clamping down on mining in that country?)

The case for crypto being a bigger driver than previously thought may seem weak, but I cannot help but believe that it is a risk we should be discussing more than I think we are.

What if the correlation was a driver for exciting new technologies where enormous wealth seemed possible (to such an extent) that current spending or success was irrelevant? What if crypto’s decline and potential collapse may not be causal, but is correlated to some broader move in markets and the economy? Then in that case, it might be spurious, but is still dangerous.

Impossible Things, Black Swans, and Thinking Out of the Box

I do not think a crypto collapse is impossible. It isn’t my base case, but there is a real possibility that it occurs.

Black swans are things that people didn’t think were possible (and turned out to be possible). We can get a pass on missing black swans, but not if we are looking at a grey swan and choose to ignore it.

I’m not lying awake at night thinking about a crypto collapse because:

- It “probably” won’t happen.

- If it does happen, the damage to the economy “could” or maybe even “should” be minimal.

But I am thinking more and more about it because if there is a correlation between crypto and the broader economy (and markets) or because crypto, the broader markets, and the economy are moving to the same theme, there is serious risk to the downside. Some of this risk may not be getting priced in based on some simple charts of crypto versus other asset classes. On this broader correlation theme, check out ARKK shares outstanding because something seems to have shifted in terms of the investor mentality there.

For those who celebrate, enjoy bitcoin infinity day! It really seems weird that not only is that a thing, but on 8/21/21 the CEO of a public company enjoyed tweeting it out. I’m possibly too old and jaded, but stuff like that seems silly rather than compelling.

Tyler Durden

Sun, 08/21/2022 – 21:30 - What is the real story on jobs?

- How Water Powers The World

How Water Powers The World

Discussions about the relevance and viability of renewable energy are often limited to solar and wind, two types of power sources that have risen to prominence since the turn of the century.

Hydropower and its role in certain countries’ electricity generation are often overlooked, even though even so-called developed nations like Norway, Austria and Canada generate sizeable shares of their electricity via hydropower plants.

However, as Statista’s Florian Zandt shows in the inforgraphic below, based on data from BP and Ember collated by Our World in Data, Africa and Latin America and the Caribbean, in particular, rely heavily on water power.

You will find more infographics at Statista

For example, the Central African Republic, the Democratic Republic of the Congo, Lesotho or Ethiopia generated almost 100 percent of their electricity with hydropower in 2020. The latter started construction on the Grand Ethiopian Renaissance Dam in 2011, a project expected to produce 5.15 gigawatt once finished, making it the biggest dam on the continent.

In the southern half of the Americas, Venezuela’s electricity mix consisted of 82 percent water power owed in no small part to the Guri dam with its installed capacity of 10.2 gigawatts. Ecuador, Guinea, Costa Rica and Panama also primarily rely on hydropower for electricity with shares of 78, 71 and 66 percent, respectively.

When looking at the total energy mix, hydropower takes a backseat to emission-heavy fossil fuels. In 2019, it amounted to a share of just seven percent worldwide, according to Our World in Data. Due to the high reliance on oil and gas for heating and transport, it’s unlikely this centuries-old power source will become a contender in primary energy generation. Generating power via methods like hydroelectric dams also has other drawbacks. Funneling rivers into reservoirs can impact the habitats of some aquatic species and upset the balance of river ecosystems, as well as necessitate rehoming of residents dependent on said rivers.

Tyler Durden

Sun, 08/21/2022 – 21:00 - Facebook Fact-Check Censors Factual Claim IRS Is Arming Agents To Use Deadly Force

Facebook Fact-Check Censors Factual Claim IRS Is Arming Agents To Use Deadly Force

Authored by Paul Joseph Watson via Summit News,

Facebook has deployed one of its infamous ‘fact checkers’ to suggest that the completely accurate claim that the IRS is seeking to arm more agents to use deadly force was “partly false information.”

Earlier this month, an IRS job posting was uncovered that announced the agency was looking to hire people who are ready to kill.

The job ad listed one of the “major duties” of IRS agents to be able to “carry a firearm and be willing to use deadly force, if necessary.”

The IRS subsequently deleted the job posting after it stoked controversy, but then a 2021 IRS annual report also came to light which showed heavily armed agents simulating an assault on a suburban home as part of their training.

When the Heritage Foundation and Young Americans for Liberty (YAL) posted about the issue on Facebook, the Big Tech giant, relying on a ‘fact check’ carried out by Lead Stories, slapped a warning label on posts that said they constituted “partly false information.”

Fact checks have the effect of basically blacklisting content on Facebook, burying it in the algorithm and preventing large numbers of people from viewing the content.

‘Fact Check: IRS Is NOT Trying To Arm All Its Agents’ shouted the headline of the article by Lead Stories.

However, as Christina Maas notes, “The Heritage Foundation never said the IRS was arming all of its agents.”

“In its article, Lead Stories singles out pro-liberty youth organization Young Americans for Liberty (YAL). The youth group posted a screenshot of the original job posting, and wrote: “The IRS is hiring! The government wants its IRS agents armed and its citizens disarmed. We’ll let everyone just marinate on that for a second.”

“Lead Stories tried to make it look like YAL said the IRS is arming all of its employees. “Is the IRS trying to arm all its employees?” asked Lead Stories. “No, that’s not true: A job posting from the IRS Criminal Investigation unit, which carries firearms, does refer to carrying firearms.”

As ever, fact checkers pedantically select a piece of language that was used (or not even used at all in this case) which might be slightly exaggerated to then declare that the entire story is “false information,” when it isn’t, it’s overwhelmingly true information.

As we previously highlighted, fact checkers used by Facebook previously declared the Hunter Biden laptop story to be “Russian disinformation.”

We also reported on how 11 ‘fact checkers’ are demanding that YouTube censor more videos for “misinformation,” with one of the reasons being that no one is content produced by fact checker groups.

Back in June, USA Today, which is used as a ‘fact checker’ by social media platforms, was forced to delete 23 articles from its website after an investigation found one of its reporters had fabricated sources.

* * *

Brand new merch now available! Get it at https://www.pjwshop.com/

In the age of mass Silicon Valley censorship It is crucial that we stay in touch. I need you to sign up for my free newsletter here. Support my sponsor – Turbo Force – a supercharged boost of clean energy without the comedown. Get early access, exclusive content and behinds the scenes stuff by following me on Locals.

Tyler Durden

Sun, 08/21/2022 – 20:30 - US National Institutes Of Health Ending Subaward For Wuhan Lab

US National Institutes Of Health Ending Subaward For Wuhan Lab

Authored by Zachary Stieber via The Epoch Times (emphasis ours),

The U.S. National Institutes of Health (NIH) has ended a subgrant to the laboratory in China located where the first COVID-19 cases were identified in 2019.

U.S.-based EcoHealth Alliance was granted $3.7 million, starting in 2014, to study bat-related coronaviruses. It conveyed some of the money to the Wuhan Institute of Virology (WIV), located in China.

The grant was renewed in 2019, but suspended in 2020 because of concerns the grantees were failing to comply with conditions attached to the money.

The NIH’s review of the concerns has concluded, Dr. Michael Lauer, an NIH deputy director, revealed in a letter on Aug. 19. It determined that all of the problems cannot be fixed.