- Russian Electricity Imports Halted To Another EU Nation

Russian Electricity Imports Halted To Another EU Nation

Lithuania has become the second European country within a month to have electricity supplies from Russia halted.

Inter RAO, the only importer of electricity from Russia to Lithuania, confirmed the suspension of deliveries would begin on Sunday, according to Russian state-media Tass News Agency. Earlier this month, Inter RAO’s Nordic branch stopped sending power to Finland after formally applying to join NATO.

“According to the decision of the electricity exchange operator Nord Pool, trading in electricity generated in Russia, which was carried out by Inter RAO (through its subsidiary Inter RAO Lietuva), is terminated” starting from May 22, Lithuania’s Energy Ministry said in a statement.

It wasn’t immediately clear why power trading between both countries was halted, though it comes as the Baltic nation (and NATO member) was the first European Union member to slash natural gas imports from Russia last month.

Lithuanian Energy Minister Dainius Kreivys said Friday that cutting imports of Russian energy supplies, including oil, electricity, and natural gas, has allowed it to become “energy independent.”

While Lithuania says halting Russian energy imports is a move toward energy freedom, Inter RAO explained that the country could not pay for electricity.

“Inter RAO has received notices from [exchange operator] Nord Pool about the suspension of trading by subsidiaries due to the risk of being unable to pay for Russian electricity,” the company told TASS.

Russian President Vladimir Putin recently declared that “unfriendly countries” countries must pay for energy products in rubles. He said if any country refuses to settle in Russian currency, “existing contracts will be suspended.”

Form Sunday, Lithuania will ramp up domestic electricity generation and increase imports from other EU countries. The latest figures show Lithuania, in 2021, imported 17% of all its domestic electricity demand from Russia.

What’s apparent is that Russian energy supplies are being reduced towards NATO countries or countries attempting to join NATO, along with ones who refuse to pay rubles.

Tyler Durden

Mon, 05/23/2022 – 02:45 - Meet The Globalists: Here Is The Full Roster Of Davos 2022 Attendees

Meet The Globalists: Here Is The Full Roster Of Davos 2022 Attendees

The infamous World Economic Forum (WEF) will host its annual meeting in Davos this week, and Jordan Schachtel,via ‘The Dossier’ Substack, is going to make sure you know who is attending the invite-only gathering.

For those of you who are new to this nefarious organization:

The World Economic Forum (WEF), through its annual Davos conference, acts as the go-to policy and ideas shop for the ruling class. The NGO is led by a comic book villain-like character in Klaus Schwab, its megalomaniac president who articulates a truly insane, extremist political agenda for our future.

Heard one of your politicians declaring support for the “Build Back Better” agenda?

How about the “Great Reset?”

All of those bumper sticker political narratives were popularized by the World Economic Forum.

Have you read about the ESG (Environmental, Social, and Governance) movement?

That’s also a WEF favorite.

Davos 2022 includes the usual components of WEF’s “you’ll own nothing and you’ll be happy” totalitarian eco statist agenda. Topics discussed and panels at the 2022 meeting will include:

-

Experience the future of cooperation: The Global Collaboration Village

-

Staying on Course for Nature Action

-

Future-proofing Health Systems

-

Accelerating the Reskilling Revolution (for the “green transition”)

-

The ‘Net’ in Net Zero

-

The Future of Globalization

-

Unlocking Carbon Markets

-

And of course, a Special Address by Volodymyr Zelenskyy, President of Ukraine

The American contingent will include 25 politicians and Biden Administration officials. US Secretary of Commerce Gina Raimondo will join Climate Czar John Kerry as the White House representatives there. They will be joined by 12 democrat and 10 republican politicians, including 7 senators and two state governors

Without further delay, I’ve provided the entire list of attendees who are showing up to Davos next week. I’ll list the Americans below and the rest are linked below that in an attached document.

-

Gina Raimondo Secretary of Commerce of USA USA

-

John F. Kerry Special Presidential Envoy for Climate of the United States of America

-

Bill Keating Congressman from Massachusetts (D)

-

Daniel Meuser Congressman from Pennsylvania (R)

-

Madeleine Dean Congresswoman from Pennsylvania (D

-

Ted Lieu Congressman from California (D)

-

Ann Wagner Congresswoman from Missouri (R)

-

Christopher A. Coons Senator from Delaware (D)

-

Darrell Issa Congressman from California (R)

-

Dean Phillips Congressman from Minnesota (D)

-

Debra Fischer Senator from Nebraska (R)

-

Eric Holcomb Governor of Indiana (R)

-

Gregory W. Meeks Congressman from New York (D)

-

John W. Hickenlooper Senator from Colorado (D)

-

Larry Hogan Governor of Maryland (R)

-

Michael McCaul Congressman from Texas (R)

-

Pat Toomey Senator from Pennsylvania (R)

-

Patrick J. Leahy Senator from Vermont (D)

-

Robert Menendez Senator from New Jersey (D)

-

Roger F. Wicker Senator from Mississippi (R)

-

Seth Moulton Congressman from Massachusetts (D)

-

Sheldon Whitehouse Senator from Rhode Island (D)

-

Ted Deutch Congressman from Florida (D)

-

Francis Suarez Mayor of Miami (R)

-

Al Gore Vice-President of the United States (1993-2001) (D)

Full list of confirmed attendees of 2022 World Economic Forum Annual Meeting

Here’s the PDF File in case the link goes down.

There is one member of the ‘elites’ that is not going to be there (and never has).

As Mohamed El-Erian writes in an op-ed at Bloomberg, Davos meetings are full of potential but rarely full of solutions.

I have never taken up the opportunity to attend the Davos meeting and I will pass again this year.

That, however, does not mean that I do not follow its evolution and outcomes. I am certainly interested in what could emerge from a meeting that brings together so many leaders of governments, civil society and business.

In an ideal world, this year’s meeting would prove catalytic in two important ways.

-

First, it would trigger greater awareness of ongoing watershed developments in the global economy and draw attention to how differently these are viewed around the world.

-

And second, it would point to ways in which an increasingly “zero-sum” view of international coordination can be reshaped to contribute to collective resilience and inclusive prosperity.

The list of ongoing watershed developments in the global economy is long, extending well beyond the horrific war in Ukraine and the associated human tragedies. Here is an example of what is on such a list:

-

Due to the convergence of food, energy, debt and growth crises, a growing number of poorer countries face a rising threat of famine — and this is but one part of the “little fires everywhere” phenomenon undermining lives and livelihoods around the world.

-

Inflation at 40-year highs in wealthier countries is undermining standards of living and growth engines, hitting the poor particularly hard, fueling political anger, eroding institutional credibility, and undermining the effectiveness of economic and financial policy.

-

The inability to deal with critical secular challenges, including climate change, is seeing short-term distractions compound what already are meaningful long-term challenges.

-

Private- and public-sector efforts to strike a better balance between highly interconnected supply chains and national/corporate resilience are complicated by a global economy that lacks sufficient momentum for this to be done in an orderly fashion.

-

The western weaponization of international finance, while effective in bringing the eleventh largest economy in the world to its knees, has been pursued without a global framework of standards, guidelines and safeguards.

I suspect that, while the vast majority of Davos participants will agree on this list (and, indeed, add a few more items), there will be quite a bit of disagreement on the causes and longer-term consequences. Such disagreement is problematic in two ways.

-

First, it undermines the shared responsibility needed to address challenges with important international dimensions;

-

and second, it erodes even more trust in the existing international order. Unless the disagreements can be resolved, the damaging effects will deepen and spread.

On paper, the upcoming Davos meeting would be perfectly suited for resolving these conflicts. History, however, does not provide much encouragement or optimism.

Time and time again, Davos has fallen victim to a lack of focus and actionable unifying vision. Individual and collective interests have remained unreconciled. Distractions abound. As a result, the output has been, at best, backward-leaning.

Given the multiple crossroads facing the global economy, this would be a particularly good time for Davos to fulfill its considerable potential — to look ahead, not back. To identify solutions instead of just problems. Otherwise, the forum will evolve even more into a network and social club that is, and is widely perceived to be, even more decoupled from the realities of many and the challenges of most.

Tyler Durden

Mon, 05/23/2022 – 02:00 -

- Gave: The End Of The Unipolar Era

Gave: The End Of The Unipolar Era

Authored by Louis-Vincent Gave via Gavekal Research,

Investors today must deal with the effects of not one, but two wars, as my Gavekal-IS colleague Didier Darcet pointed out in April (see Tick,Tock Tick,Tock).

-

The first is the one we can see playing out each day on our television screens, with all the tanks, deaths and human suffering.

-

The second is a financial war, with the unprecedented weaponization of the Western banking system and Western currencies aimed at bringing Russia to its financial knees (see CYA As A Guiding Principle (2022)).

To the surprise of most people in the West, resistance against both of these war efforts has proved far stronger than expected. Almost 11 weeks into the war on the ground in Ukraine, Russian troops still seem to be taking heavy losses for relatively small territorial gains. And a little over six weeks after US president Joe Biden boasted that the ruble had been “reduced to rubble” by Western sanctions, the Russian currency is close to a two-year high against the US dollar and near a post-Covid high against the euro. At this point, both the euro and the yen appear to be bigger casualties of the Ukraine war than the ruble.

The US boast that the ruble had been “reduced to rubble” is looking premature

In this paper, I shall review the implications of this stronger-than-expected resistance – both on the battlefield and in the financial markets – and attempt to draw some salient conclusions for investors.

The evolution of warfare

In October 1893, some 6,000 highly-disciplined warriors of King Lobengula’s Ndebele army launched a night-time attack on a camp occupied by 700 British South Africa Company police near the Shangani river in what is now Zimbabwe. It was a massacre. The BSAC “police” killed more than 1,500 Ndebele for the loss of just four of their own men. A week later, they did it again, killing some 3,000 Ndebele warriors for just one policeman dead. These one-sided victories were not won by courage or superior discipline, but because the British were armed with five machine guns and the Ndebele had none. As Hillaire Belloc wrote in The Modern Traveller: “Whatever happens, we have got / The Maxim gun, and they have not”.

The technological superiority of the machine gun allowed Britain, and France, Germany and Belgium, to subjugate almost all of Africa, even though outnumbered by the Zulu, Dervish, Herero, Masai and even Boer forces they opposed. All were rendered helpless by the machine gun’s firepower.

I revisit this ancient history to illustrate how military technology is a lynchpin of the geopolitical balance.

Dominance of military technology is also a key factor underpinning the strength and resilience of a reserve currency. Today, one of the main reasons why Taiwan, South Korea, Japan, Saudi Arabia, the United Arab Emirates and others keep so much of their reserves in US dollars is that the US is widely regarded as being a generation (if not more) ahead of the competition in the design and production of smart bombs, anti-missile systems, fighter jets and naval frigates. In short, the superiority of US weaponry has been one of the principal factors underpinning the US dollar’s status as the world’s reserve currency. However, recent events raise important questions about whether the US can retain this superiority.

-

In September 2019, drones allegedly deployed by Yemeni Houthi forces took out the Saudi Aramco oil processing facilities at Abqaiq.

-

Between late September and early November 2020, Armenia and Azerbaijan fought a war over the Nagorno-Karabakh region. The conflict ended in near-total victory for the Azeris. This result stunned the military world. Observers had assumed that Armenia, with a bigger army, larger air force, more up-to-date anti-aircraft and anti-missile systems, and a history of Russian support, would easily triumph. But all Armenia’s expensively-acquired military “advantages” were quickly taken out in the early days of the fighting by Azerbaijan using Turkish-made drones costing no more than US$1mn each.

-

On successive occasions between March 2021 and March 2022, Houthi drones attacked Saudi Arabian oil facilities, notably the giant terminal at Ras Tanura on the Persian Gulf.

-

In December 2021, Turkish-made drones allowed the Ethiopian government to tip the balance in a civil war that until then had been going badly for government forces.

-

In January 2022, Houthi drones hit oil facilities in the UAE.

Now, imagine being Saudi Arabia or the UAE. Over the years you have spent tens, if not hundreds, of billions of US dollars purchasing anti-missile and anti-aircraft systems from the US. Now, you see relatively cheap drones penetrating these defense systems like a hot knife through butter. This has to be frustrating. What is the point of spending up to US$340mn on an F-35c (and US$2mn on pilot training), or US$200mn on an anti-aircraft system, if these can be taken out by drones at a fraction of the cost?

This evolution in warfare may help to explain the impressive resilience of the Ukrainian army in the face of Russia’s onslaught. When the Russian troops marched into Ukraine, consensus opinion was that the Ukrainian forces would crumble before the Russian military juggernaut. It is always hard to know what is happening on the ground amid the fog of war. But judging by the number of tanks destroyed, warships sunk and the apparent failure of the Russian air force to establish control over Ukraine’s skies, it seems the invasion of Ukraine is proving far more costly in terms of blood and treasure than Russian president Vladimir Putin had imagined.

Could this be because Putin failed to factor the impact of drones into his military outlook? It may be premature to jump to that conclusion. But judging from afar, it appears inexpensive Turkish drones have helped level the battlefield in the Ukrainian-Russian David versus Goliath confrontation— the biggest and bloodiest on European soil since World War II.

This helps to explain why the US military assistance package for Ukraine Biden announced this month included 700 Switchblade drones. These are surprisingly cheap—the Switchblade 300 reportedly carries a price tag as low as US$6,000—yet highly effective. In essence, they are single-use kamikaze drones. Apparently, they fly faster than the Turkish Bayraktar TB2 drones that the Ukrainians, like the Azeris before them, have used to such devastating effect. This suggests the Switchblades should be able to evade the air defenses that Russia has attempted to maintain over its troops.

The US military deployed Switchblades sparingly in Afghanistan, so it is hard to know whether these will perform as billed in combat conditions. But before this shipment to Ukraine, only the UK was permitted to purchase Switchblades. This implies that the Pentagon considers the Switchblade a valuable and potent weapon.

David Petraeus, the former Central Intelligence Agency director who, as a four star general, commanded the US campaigns in both Iraq and Afghanistan, singled out the weapon in a recent interview with historian Niall Ferguson:

“I’ll mention one item in particular: the Switchblade drone. It’s a loitering munition that takes a one-way trip. The light version can loiter for 15 to 20 minutes. Heavy version, 30 to 40 minutes with a range of at least 40 km. The operator selects a target, it locks on and it follows. Then it strikes when the operator gives that order. This is extraordinarily effective because you can’t hear it on the ground. The first time the enemy knows it’s there is when it blows up. If we can get enough of those into Ukraine, they could be a true game-changer.”

However, I digress.

Returning to the discussion about why drones might matter for financial markets:

1) If ever-cheaper and more readily available drones are going to revolutionize war, much as the Maxim gun did 140 years ago, then it is questionable whether it still makes sense to invest in tanks, airplanes, anti-aircraft and anti-missile systems. If it does not, what does this mean for the value of the large, listed death-merchants?

Cheap drones are bad news for the stocks of defense giants

Historically, buying the merchants of death after a big rally in oil made sense, if only because so much of the world’s high-end weapon consumption occurs in the Middle East. But in the world of tomorrow, will Middle Eastern oil kingdoms still line up to buy multibillion US dollar systems from Raytheon, Boeing, Lockheed and the like, if those systems are vulnerable to attacks from relatively cheap drones?

2) Talking of Middle Eastern regimes, the deal prevailing in the Middle East for the past five decades has been that oil would be priced in US dollars, and that the oil-exporting regimes in Saudi Arabia, the UAE or Kuwait would use these US dollars to buy US-made weapons (and US treasuries). With this bargain, the US implicitly guaranteed the survival of the Gulf Arab regimes. Fast forward to 2022, and following the invasion of Ukraine, countries such as Saudi Arabia and the UAE have failed to condemn Russia. What’s more, Saudi Arabia let it be known that it might start to accept payment for its oil in renminbi. Perhaps this makes sense if Saudi Arabia feels it no longer needs US$340mn F-35s, but instead more US$1mn Turkish-made drones?

3) If, as the Azeri-Armenian and the Ukrainian-Russian wars suggest, drones have radically leveled the battlefield in war, this profound development has a multitude of implications. Does it undermine the long-held superiority of vastly expensive armament systems, tilting the balance in favor of much cheaper and much more widely-available weapons? If so, does this mean another pillar supporting the US dollar’s reserve currency status is crumbling in front of our eyes?

In a world where military might is no longer the monopoly of a single superpower, or the duopoly of two, does the world become, de facto, multipolar? In such a world, would there still be a compelling reason for trade between Indonesia and Malaysia to be settled in US dollars, rather than in their own currencies? Wouldn’t trade between China and South Korea now be settled in renminbi and won?

Drone tactics are a radically different form of warfare, and they are evolving fast. So, it would be premature to offer any definitive conclusions about the extent to which drones will dominate warfare in the future. However, their recent use in Ukraine (and Yemen, Azerbaijan and Ethiopia) means that investors have to be open to the idea that drones will change the battlefield of the future. Because if they are going to change the battlefield of the future, then they will also change the economic and financial realities of today.

In this sense, drones might well be the modern-day equivalent of aircraft carriers. In World War II, aircraft carriers made big-gun battleships and other traditional naval warships obsolete, or at least highly vulnerable. Two early Pacific battles proved the point. The Battle of the Coral Sea in May 1942, generally considered by historians to have been a draw, was the first naval engagement ever fought in which the opposing fleets never made visual contact with each other. Carrier-based aircraft drove the action. A month later, the far more consequential Battle of Midway established the new reality beyond all doubt. The Imperial Japanese Navy was ambushed northwest of Hawaii and lost the bulk of its carrier force in a single action. It would be on the defensive for the rest of the war.

With hindsight, Midway marked the start of US dominance over the world’s oceans. In short order, this translated into US dominance over global trade. But with the nature of warfare again changing, is this dominance of the oceans and of other battlefields guaranteed to last?

Investors need to consider the uncomfortable possibility that it might not.

The dramatic shift in the global financial landscape

We are all the offspring of our own experiences. One important formative event in my own modest career was the Asian financial crisis of 1997-98. Witnessing how quickly things could unravel left a deep mark. I highlight this because I am not alone in having lived through the shock of 1997-98. Pretty much every emerging market policymaker aged 50-75 (which is most of them) went through a similar trauma. Seeing your country’s entire middle class wiped out in the space of a few weeks—which is what happened in Thailand, Indonesia, Russia, Argentina and others in the period from 1997 to 2000—is bound to leave a few scars.

Among emerging market policymakers these scars took the form of a deepseated conviction of “never again” (see Our Brave New World). To ensure their countries’ middle classes were never again wiped out, they adopted a straightforward set of policy prescriptions that in the early 2000s Gavekal dubbed the The Circle Of Manipulation. It went something like this:

1) To avoid a future crisis, your central bank needs to maintain a healthy safety cushion of hard currency bonds, mostly US treasuries and bunds.

2) The more you become integrated with the global economy, the larger this cushion should be.

3) To build up this safety cushion, you need to run consistent and large current account surpluses.

4) To run consistent large current account surpluses, you need to maintain an undervalued currency.

Among the results of these policy prescriptions were charts looking like this:

By all previous standards, this was an odd state of affairs: an economic arrangement under which poorer countries with high savings rates and vast infrastructure investment needs ended up subsidizing consumption in rich countries with low savings rates and ever-accelerating twin deficits.

To cut a long story short, for the last 25 years, we have lived in a world in which undervalued currencies in emerging markets allowed Western consumers to buy attractively priced goods and services imported from developing countries. Meanwhile, the individuals, companies and governments in the emerging markets which earned capital from these sales largely recycled their earned capital into Western assets—because Western assets were perceived to be “safe.”

But this perception of safety may now be changing in front of our eyes.

Consider the following changes:

1) Developed economy government bonds have proved anything but safe. As stresses of increasing severity have affected the world economy over the last 12 months, investors in local currency Indonesian and Brazilian government bonds and in gold have generated positive returns of between 3% and 4% in US dollar terms. Chinese government bonds are up by just over 1.5%. Meanwhile, Indian and South African government bonds have lost -4%. These performances contrast with US treasuries, which have lost -9%, and the train wrecks suffered by investors in eurozone bonds and Japanese government bonds, which are down anywhere between -17% and -23%. Of these, which can be considered the safest?

2) The confiscation of Russia’s reserves. I will not repeat here arguments I have made at length elsewhere (see What Freezing Russia’s Reserves Means). But in a nutshell, the decision to freeze Russia’s central bank reserves has been the most important financial development since US president Richard Nixon closed the gold window in 1971. From now on, any country that is not an outright US ally—China, Malaysia, South Africa and others—and even some historical friends—Saudi Arabia? The UAE? India?—will think twice before reflexively accumulating US treasuries from fear they may get canceled.

Over the course of a weekend, with no discussion in the US Congress, and no discussion with the Federal Reserve, the US administration unilaterally turned the US treasury market on its head. From that moment on, the whole nature of a US treasury security would depend entirely on who owned it.

3) Running roughshod over property rights. It is hard to pin down what the West’s single most important comparative advantage might be. Having the world’s strongest military? Being the seat of almost all the world’s greatest universities? Issuance of the world’s reserve currencies? The list goes on. But surely somewhere near the top of the list should be the sanctity of property rights, guaranteed by rock-solid “rule of law.” The main reason Chinese tycoons for years purchased Vancouver real estate, the Emirati central bank bought US treasuries and Saudi princes parked their wealth in Zurich was the knowledge that, whatever happened, and wherever you came from, you were guaranteed property rights, and a fair trial to ascertain those rights, in any courtroom in New York, London, Zurich or Paris.

Better still, since the implementation over the last 850 years in the West of habeas corpus and various bills of rights, you have been able to have confidence that you would be judged as an individual. One of the fundamental tenets of Western democracies’ legal systems is that there is no such thing as a collective crime—or collective punishment. You can only be held responsible and punished for what you have done as an individual.

Unless – all of a sudden – you are a Russian oligarch. This is a dramatic development, if only because every Chinese tycoon, Saudi prince, or emerging market billionaire will now wonder whether he will be next to get canceled. If the wealth of Russian oligarchs can be confiscated so abruptly, then why not the assets of Saudi princes?

Stretching this a little further, maybe it shouldn’t just be Saudi princes or Chinese billionaires who should be worried. If wealth can be seized without any trial, but simply because of guilt by association, maybe in the not-too distant future Western governments could confiscate the wealth of anyone who mined coal or pumped oil out of the ground. Don’t they have blood on their hands for causing tomorrow’s climate crisis? And while we are about it, perhaps we should also confiscate the wealth of social media barons for failing to prevent a mental health crisis among our youth?

4) Russia’s counter-attacks. Older readers may remember how in the days that preceded the Lehman bust, US Treasury secretary Hank Paulson walked around proclaiming that he had “a big bazooka,” and that if the market pushed too hard, he would fire this bazooka and blow shortsellers out of the water. Unfortunately, with Lehman it became obvious to all and sundry that Paulson’s bazooka was firing blanks.

Today’s situation is similar. In the wake of the Russian invasion of Ukraine, the US decided to go for full weaponization of the US dollar, proclaiming the ruble had been turned to rubble. Last week, the ruble hit two-year highs against both the US dollar and euro. Biden’s financial bazooka seems to have been no more potent than Paulson’s. Why? Because Russia decided to fight back, requiring buyers from “unfriendly” countries to pay for their purchases of Russian commodities in rubles. And in effect, the only way unfriendly customers can acquire rubles is by offering gold to the Russian central bank (see The Clash Of Empires Intensifies).

This has created a sudden and profound shift in the global trading and financial architecture. For decades, global trade was simple. If Russia produced commodities that China needed, then China first had to earn US dollars by selling goods and services to the US consumer. Only in this way could it acquire the US dollars it needed to purchase commodities from Russia. But what happens now that China or India can purchase their commodities from Russia or Iran for renminbi or Indian rupees? Obviously, their need to earn and save US dollars is no longer so acute.

Conclusion

Warfare is changing and the financial system has been weaponized like never before. However, the weaponization of the financial system has so far failed to deliver the intended results. At this point, investors can adopt one of two stances. The first might be described as “nothing to see here; move along.” The second is to accept that the world is changing rapidly, and that these changes will have deep and lasting impacts on financial markets. Different war, different world, different consequences

For now, there are some clear takeaways.

1) The Ukraine war may be telling us that modern history’s unipolar age is now well and truly over. As big as the Russian army is, and as powerful as the US Treasury might be, the current crisis has demonstrated that neither is powerful enough to impose its will on its perceived enemies. This includes even relatively weak enemies; Ukraine’s army was hardly thought of as formidable, while Russia was supposed to be a financial pygmy.

2) This is a very important message. In an age of drones and parallel financial arrangements, there is no longer such a thing as absolute power—nor even the perception of absolute power. The pot has been called, each player has had to show his cards, and all are sitting with busted flushes! The fact that military and financial dominance may be harder to assert in the future opens the door to a much more multipolar world.

3) For 25 years, emerging market workers have subsidized consumption in developed markets, as emerging market policymakers kept their currencies undervalued and recycled their current account surpluses into “hard” currencies. If this arrangement now comes to an end, then the developed market consumer will struggle while the emerging market consumer will thrive.

4) Much consumption in emerging markets tends to occur at the “low end” of the product chain. This plays into a theme I have been harping on about for the last year: that investors should focus on companies that deliver products that consumers “need to have” rather than products that are “nice to have.”

5) Over the last two years, US treasuries and German bunds have failed in their job of providing the antifragile element in portfolios. There are few reasons to think that this failure is about to reverse any time soon. Today, investors need to look elsewhere for antifragile attributes. Precious metals, emerging market government bonds, high-yield energy assets and foodstuffs are all leading candidates.

6) High-end residential real estate in Western economies will lose the emerging market money-recycling bid and will struggle.

7) New safe destinations for emerging markets’ excess capital will emerge. Obvious candidates include Dubai, Singapore, Mauritius, and perhaps even Hong Kong (should China eventually decide to follow the rest of the world and to live with Covid). It is hard to be too bullish on these destinations. They are so small that even a marginal, influx of financial and human capital will have a disproportionate impact.

The world’s unipolar era is over. Few portfolios reflect this reality – and definitely not the indexed portfolios that are today massively overweight an overvalued US and a desperately ill-omened Europe.

Tyler Durden

Sun, 05/22/2022 – 23:50 -

- Record Rate Cut Shows Beijing Pursues Shock-and-Awe

Record Rate Cut Shows Beijing Pursues Shock-and-Awe

By Ye Xie, Bloomberg markets live commentator and analyst

The record reduction in China’s key interest rate on Friday was a rare positive policy surprise from Beijing since the Omicron variant of Covid began to wreak havoc on the economy in the past two months.

It’s a clear policy U-turn that aims to offset some of the self-imposed constraints, such as housing restrictions, to boost business and household confidence. If so, more policy easing for the housing market and more fiscal spending are likely to come.

China’s banks lowered the five-year loan prime rate (LPR), which is tied to the mortgage rate, by a record 15 bps on Friday, triple the amount that economists had forecast. It was the second policy move in a week that was aimed at propping up the ailing property market, after the People’s Bank of China cut the floor of the mortgage rate a week earlier.

Until now, Beijing’s plan to save the economy had been conservative, focusing on liquidity injections and tax reductions. That had fallen short of what’s required to offset the destruction caused by Covid restrictions and the property slump. Take the housing sector: New home sales for the top 100 developers tumbled 59% in April from a year earlier. Goldman Sachs on Friday raised the default forecast for high-yield property developers’ bonds to 32% from 19%.

The efforts to lower mortgage rates show a clear sense of urgency to turn around the housing market. As Zhaopeng Xing, senior China strategist at ANZ Bank, said: “The cut signals that the leadership has ended discussion over the property sector and decided to rescue it as soon as possible.”

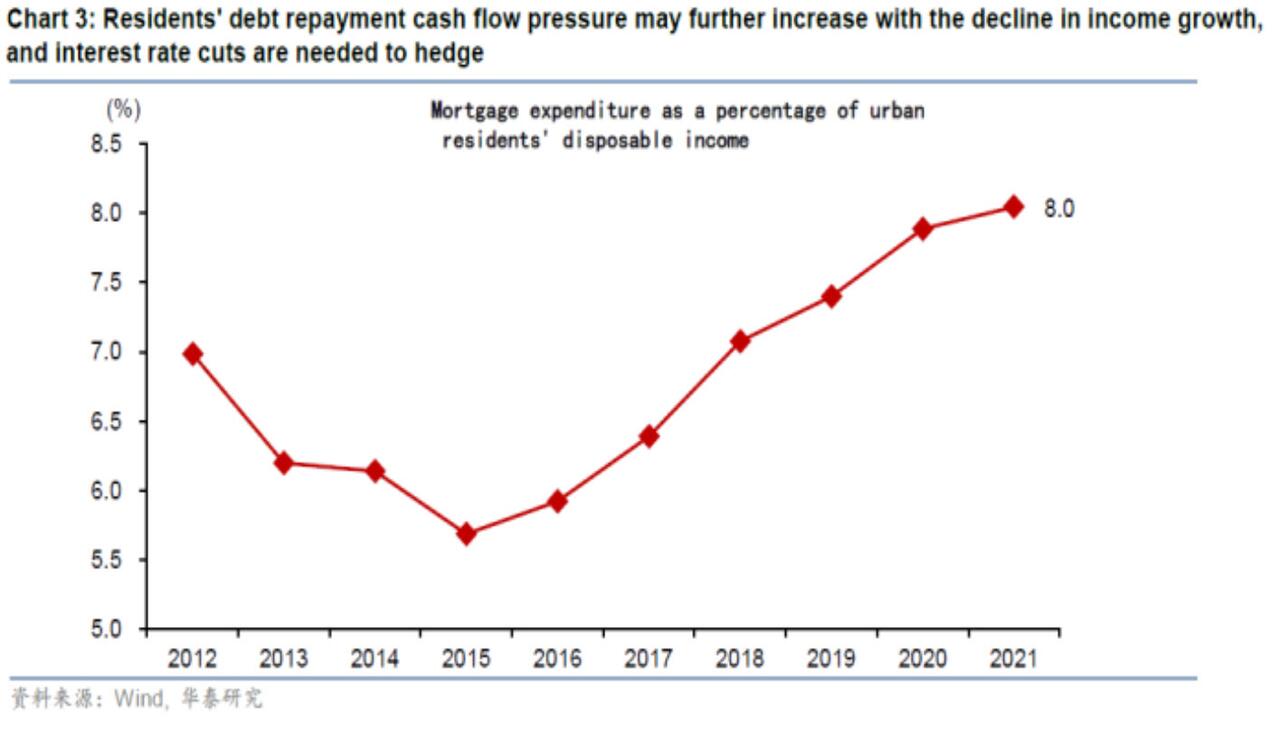

Source: Huatai Securities There are a few reasons to believe that the impact of the LPR cut alone will be limited. As Nomura’s Lu Ting pointed out, mortgage rates had already started to decline, even before recent policy moves. That did little to arrest the sales decline, in part because Covid restrictions limited mobility, jobs, income and confidence of residents. In addition, when consumer leverage is already high, the willingness and ability to borrow remains in question. In fact, property stocks fell Friday, even as the benchmark CSI 300 rallied.

What’s clear, then, is more policy follow-ups are likely needed to boost income, save jobs and lift confidence. Here’s is a laundry list from Citigroup on what Beijing could do to revive the housing and the broader economy:

- Ease restrictions on presale deposits, maybe even tinker with the “three red lines” on funding curbs to improve cash flow for developers

- Advance part of the 2023 special local-government bond quota to support investment

- Consumer subsidies or vouchers funded by the central government

- Special Treasuries to cover Covid expenses, as was done in 2020 (1 trillion yuan)

- General budget revision to expand stimulus as in 2016 (for tax reform), 2008 (Sichuan earthquake) and 1998 (Asian financial crisis)

Bloomberg Economics now forecasts China’s growth will trail the U.S. for the first time since 1976, when Chairman Mao died. President Xi reportedly aims to avoid such a scenario in a year when he is expected to retain power for a third term.

The rate cut on Friday may be the beginning of a shock-and-awe attack to get ahead of sagging expectations.

Tyler Durden

Sun, 05/22/2022 – 23:25 - Gen. Milley Warns West Point Graduates On Likelihood Of War With Russia And China

Gen. Milley Warns West Point Graduates On Likelihood Of War With Russia And China

Authored by Frank Fang via The Epoch Times (emphasis ours),

The top U.S. general told the U.S. Military Academy West Point’s class of 2022 that the nature of war is changing and the current rules-based international order is being threatened by Russia and China.

“Right now, at this very moment, a fundamental change is happening in the very character of war,” Chairman of the Joint Chiefs of Staff Gen. Mark Milley said on May 21.

“We are facing, right now, two global powers: China and Russia, each with significant military capabilities, and both fully intend to change the current rules-based order.”

Mark A. Milley, chairman of the Joint Chiefs of Staff, arrives for the 2022 West Point Commencement Ceremony at West Point Military Academy in West Point, N.Y., on May 21, 2022. (Michael M. Santiago/Getty Images) He made the remarks during a speech to the graduating cadets at a commencement ceremony in West Point, New York.

“The world you’re being commissioned into has the potential for significant international conflict between great powers,” Milley said.

“And that potential is increasing, not decreasing.”

He reminded the cadets that Russia’s invasion of Ukraine was a lesson that “aggression left unanswered only emboldens the aggressor.”

As for China, Milley pointed out that the communist regime has a “revisionist foreign policy,” and now boasts an “increasing capable military.”

Details of China’s growing military capabilities were disclosed by the Office of the Director of National Intelligence in its annual threat assessment report (pdf) released in March. One area of concern is China’s ongoing construction of hundreds of new intercontinental ballistic missile silos.

Another concern centers around China’s push to develop space capabilities in order to “erode the U.S. military’s information advantage.” The report states that the communist regime is “fielding new destructive and nondestructive ground- and space-based antisatellite weapons.”

Adm. John Aquilino, commander of U.S. Indo–Pacific Command, in his prepared statement (pdf) for a congressional hearing on May 17, warned about the threat posed by China’s expansion and modernization of its air force, navy, and rocket force.

For instance, China is expected to increase its battle force ships to 420 by 2025, even though the communist regime currently already boasts the largest navy in the world, according to Aquilino. China’s new generation of mobile missiles, some of which rely on hypersonic glide vehicles, is designed to evade U.S missile defenses, he added.

Mark A. Milley, chairman of the Joint Chiefs of Staff, shakes the hands of West Point graduates as they receive their diplomas during the 2022 West Point Commencement Ceremony at West Point Military Academy in West Point, N.Y., on May 21, 2022. (Michael M. Santiago/Getty Images) Technology

Milley said the character of war has also changed in the kinds of weapons being used.

“The maturity of various technologies that either exist today or are in the advanced stages of development, when combined, are likely to change the character of war just by themselves,” Milley said.

“You’ll be fighting with robotic tanks, ships, and airplanes,” he added. “We’ve witnessed a revolution in lethality and precision munitions. What was once the exclusive province of the U.S. military is now available to most nation states with the money and will to acquire them.”

According to Milley, the mother of all technologies is artificial intelligence (AI), which is resulting in “the most profound change ever in human history.”

In recent years, the Chinese Communist Party (CCP) has repeatedly identified AI as one of the top priorities for its national development. It was one of the key industries outlined in China’s industrial road map known as “Made in China 2025.” Two years later, Beijing rolled out the “New Generation Artificial Intelligence Development,” that sets out strategic goals by 2020, 2025, and 2030.

According to a Congressional Research Service report (pdf) published in April, Beijing is developing AI tools for cyber operations and advancing AI in various types of air, land, sea, and undersea autonomous military vehicles.

“China is actively pursuing swarm technologies, which could be used to overwhelm adversary missile defense interceptors,” the report added. Swarm intelligence is having machines communicate and work together to achieve a certain objective.

A People’s Liberation Army air force WZ-7 high-altitude reconnaissance drone is seen a day before the 13th China International Aviation and Aerospace Exhibition in Zhuhai in southern China’s Guangdong province on Sept. 27, 2021. (Noel Celis/AFP via Getty Images) Future

Milley reminded the cadets that the United States is losing ground militarily.

“Whatever overmatch we, the United States, enjoyed militarily for the last 70 years is closing quickly,” he said. “And the United States will be, in fact, we already are challenged in every domain of warfare in space and cyber, maritime, air, and, of course, land.”

The cadets should be prepared for a future that is different from the past, Milley emphasized.

“So in short, the next 20 or 25 years, is not going to be like the last 20 or 25,” he said.

“Globally, there’s an increase in nationalism and authoritarian governments, regional arms races and unresolved territorial claims, ethnic and sectarian disputes, and an attempt by some countries to return to an 18th-century concept of balance of power politics with spheres of influence,” Milley added, without naming any country.

The CCP is expanding its sphere of influence, particularly over developing countries, through its infrastructure and investment scheme known as the Belt and Road Initiative. At the same time, the communist regime is aiming to take over Taiwan—a de facto independent entity that Beijing considers a part of its territory—in order to expand its sphere of influence in East Asia and the western Pacific.

Tyler Durden

Sun, 05/22/2022 – 23:00 - Everything You Want To Know About Monkeypox, But Were Afraid To Ask

Everything You Want To Know About Monkeypox, But Were Afraid To Ask

With the COVID-19 pandemic still fresh in the minds of the people around the world, it comes as no surprise that recent outbreaks of another virus are grabbing headlines.

Monkeypox outbreaks have now been reported in multiple countries, and it has scientists paying close attention. For everyone else, numerous questions come to the surface:

-

How serious is this virus?

-

How contagious is it?

-

Could Monkeypox develop into a new pandemic?

Below, Visual Capitalist’s Nick Routely and Mark Belan answer these questions and more.

What is Monkeypox?

Monkeypox is a virus in the Orthopoxvirus genus which also includes variola virus (which causes smallpox) and cowpox virus. The primary symptoms include fever, swollen lymph nodes, and a distinctive bumpy rash.

There are two major strains of the virus that pose very different risks:

-

Congo Basin strain: 1 in 10 people infected with this strain have died

-

West African strain: Approximately 1 in 100 people infected with this strain died

At the moment, health authorities in the UK have indicated they’re seeing the milder strain in patients there.

Where did Monkeypox Originate From?

The virus was originally discovered in the Democratic Republic of Congo in monkeys kept for research purposes (hence the name). Eventually, the virus made the jump to humans more than a decade after its discovery in 1958.

It is widely assumed that vaccination against another similar virus, smallpox, helped keep monkeypox outbreaks from occurring in human populations. Ironically, the successful eradication of smallpox, and eventual winding down of that vaccine program, has opened the door to a new viral threat. There is now a growing population of people who no longer have immunity against the virus.

Now that travel restrictions are lifting in many parts of the world, viruses are now able to hop between nations again. As of the publishing of this article, a handful of cases have now been reported in the U.S., Canada, the UK, and a number of European countries.

On the upside, contact tracing has helped authorities piece together the transmission of the virus. While cases are rare in Europe and North America, it is considered endemic in parts of West Africa. For example, the World Health Organization reports that Nigeria has experienced over 550 reported monkeypox cases from 2017 to today. The current UK outbreak originated from an individual who returned from a trip to Nigeria.

Could Monkeypox become a new pandemic?

Monkeypox, which primary spreads through animal-to-human interaction, is not known to spread easily between humans. Most individuals infected with monkeypox pass the virus to between zero and one person, so outbreaks typically fizzle out. For this reason, the fact that outbreaks are occurring in several countries simultaneously is concerning for health authorities and organizations that monitor viral transmission. Experts are entertaining the possibility that the virus’ rate of transmission has increased.

Images of people covered in monkeypox legions are shocking, and people are understandably concerned by this virus, but the good news is that members of the general public have little to fear at this stage.

I think the risk to the general public at this point, from the information we have, is very, very low.

–TOM INGLESBY, DIRECTOR, JOHNS HOPKINS CENTER FOR HEALTH SECURITY

Finally, as Infectious Disease expert Muge Cevik notes in a detailed Twitter thread, as the monkeypox virus (MPX) outbreak continues, a lot of data emerging in real-time & being rapidly disseminated (as well as misinformation).

Confirmed and suspected cases of #MonkeyPox now reached 200 among 14 countries with 20 confirmed cases in the UK.

The main concern is that there are non-travel associated cases in Europe, meaning there is likely unnoticed community transmission.

This is the biggest outbreak outside of Africa, and there will be more cases to come. The concern is not necessarily a global pandemic like what we’ve seen w/ coronaviruses or influenza. But a growing & large MPX epidemic is a concern especially if PH measures are delayed.

So, the most important thing is to inform our communities & healthcare workers about the clinical presentation, incubation period, so that people can be diagnosed at an earlier possibility, isolated and contacts are protected. This is the range of skin lesions.

In conclusion, monkeypox is not really a rare disease & is a public health concern.

According to prelim evidence there is no indication that current outbreak is due to a new MPX variant & epidemiological data suggest that it’s been introduced to male-to-male sexual networks, likely sometime in late-April.

We have observed MXP outbreaks in many countries mainly in Africa, this is the first time that we are observing wide transmission in Europe. MPX remains an under-recognized and underreported emerging disease. Good clinical management can limit disease severity or death.

We are in an unknown territory as individuals who have prior smallpox vaccination do have some degree of protection against monkeypox, but we don’t really know the degree of protection it provides to individuals who had vaccination 50, 60 years prior.

Tyler Durden

Sun, 05/22/2022 – 22:35 -

- Gun-Parts Dealer Sues ATF Over 'Secret And Unannounced Policy Changes'

Gun-Parts Dealer Sues ATF Over ‘Secret And Unannounced Policy Changes’

Authored by Ken Silva via The Epoch Times (emphasis ours),

Pennsylvania firearms product dealer JSD Supply filed for a temporary restraining order against the Bureau of Alcohol, Tobacco, Firearms, and Explosives (ATF) on May 19, asking a federal judge to block “secret and unannounced policy changes” that restrict the sale of gun parts.

A “ghost gun” is displayed before the start of an event about gun-related violence in the Rose Garden of the White House in Washington on April 11, 2022. (Drew Angerer/Getty Images)

The dispute stems from the ATF ordering JSD Supply to stop dealing “80 percent receivers”—a colloquial term used within the firearms industry for incomplete and unfinished firearm frames or receivers.

“Those engaged in the business of selling these complete kits, as your company does, are in fact engaged in the business of dealing firearms,” the ATF’s May 9 order said, referencing the company’s “JSD 80% Lower Receivers, Jigs, and Gun Parts Kits.”

While the ATF has a history of approving the sale of 80 percent receivers—as documented in JSD Supply’s motion for a restraining order—the two parties apparently disagree about what exactly the company is selling. In response to an email inquiry for this article, ATF Special Agent Robert Cucinotta declined to comment but referenced The Epoch Times to the Biden administration’s April 11 order to crack down on “ghost guns.”

“This final rule bans the business of manufacturing the most accessible ghost guns, such as unserialized ‘buy build shoot’ kits that individuals can buy online or at a store without a background check and can readily assemble into a working firearm in as little as 30 minutes with equipment they have at home,” the order said. “This rule clarifies that these kits qualify as ‘firearms’ under the Gun Control Act.”

However, JSD Supply contends that the ATF’s May 9 cease-and-desist order has nothing to do with the White House ghost gun rule, which doesn’t go into effect until August. To the company’s point, ATF said in its cease-and-desist order that JSD Supply’s 80 percent receivers “have always been firearms pursuant to the [Gun Control Act] … notwithstanding the recently announced regulations.”

Instead, JSD Supply contends that the ATF’s cease-and-desist order resulted from “secret and unannounced policy changes” from years ago.

According to JSD Supply, in 2018, the ATF began to “implement a series of secret and unannounced policy changes regarding the sale of ‘80% frames and receivers,’ the tools used to manufacture them, and the firearm parts used in the assembly process.” Internal ATF records obtained by JSD Supply via the Freedom of Information Act (FOIA) show the bureau refusing to categorize a gun kit as “not a firearm” in 2018—evidence that the policy shift occurred behind closed doors around that time, JSD Supply’s attorney, Stephen Stamboulieh, told The Epoch Times.

According to Stamboulieh and his client, gun product dealers weren’t made aware of the secret change until the ATF raided a manufacturer in late 2020.

“Suddenly, without warning, in December of 2020, ATF paid a visit to the nation’s largest manufacturer of 80% frames and receivers, Polymer80, Inc.,” JSD Supply’s motion said.

“Each time since then, ATF has moved the goalposts by changing its policy. The industry—including plaintiff—has attempted in good faith to adapt to and comply with ATF’s demands, despite the lack of any legal authority for ATF’s position.”

To support its theory about moving the goalposts, JSD Supply noted that the ATF did not seize from Polymer80 some of the same 80 percent receivers that are subject to the bureau’s cease-and-desist order. JSD Supply also argued that it was being singled out by the ATF when numerous other retailers offer the same products.

“Indeed, there are dozens, if not hundreds (or possibly thousands) of other companies across the country and internet which offer for sale ‘all the component parts’ necessary for a customer to manufacture a complete firearm,” JSD Supply said quoting from the ATF’s order.

“This raises the obvious question as to why ATF made the decision to target Plaintiff with a cease-and-desist order, effectively shutting down its business, for doing nothing more than following standard industry practice.”

JSD Supply said the ATF has not clarified how the company can comply with its policy on 80 percent receivers, which is why a restraining order is necessary.

“If ATF had wanted to change (again) its secret, unsupported policy on 80% frames and receivers, the agency had the option of issuing an open letter to all manufacturers and retailers of 80% receivers and firearm parts, giving notice to all of the change,” the company said.

“Defendants’ vague C&D order, without any statutory authority, has forced plaintiff to immediately suspend all retail sales of its entire product line, causing immediate and substantial financial losses, violating the Fifth Amendment, and infringing on the Second Amendment rights of Plaintiff and its customers. Accordingly, Plaintiff is seeking emergency relief, in the form of a temporary restraining order.”

A hearing date has yet to be set for the matter.

Tyler Durden

Sun, 05/22/2022 – 22:10 - Bullwhip Effect Ends With A Bang: Why Prices Are About To Fall Off A Cliff

Bullwhip Effect Ends With A Bang: Why Prices Are About To Fall Off A Cliff

It was exactly a year ago, when Deutsche Bank strategist Luke Templeman said that amid the panicked scramble by US wholesalers to stock up on scarce inventory as a result of snarled supply chains, it was only a matter of time before the US economy was roiled by a “bullwhip” (or whiplash) effect.

Some details for those unfamiliar with this concept: the bullwhip effect occurs when a drop in customer demand causes retailers to under stock. In turn, wholesalers respond to a lack of retail orders by understocking themselves. That then causes manufacturers to slow production. Eventually the reverse occurs. As customer demand comes back, retailers quickly order more goods, often too much, and wholesalers and factories are caught short. Shortages occur, prices increase. Eventually production ramps up at levels that are far beyond equilibrium levels and this cascades down the chain. These violent swings in availability of goods then continue back and forth until an equilibrium is eventually established.

Last May, the beginning of the bullwhip effect was seen in the way retailers and wholesalers managed their inventory levels since the outbreak of covid. Specifically, retailers kept a supply of inventory at a relatively constant level, above that of wholesalers. As covid hit, supply chains from Asia were cut which caused a fright amongst retailers in the West who immediately began to put in orders for more inventory. A whole lot more of it. Subsequent lockdowns saw demand plummet and inventories along with it. In both cases, the actions of wholesalers followed those of retailers by a month or so.

In the context of a starting bullwhip effect, Templeman’s conclusion was accurate: “As inventory levels have fallen to multi-decade lows at retailers, there are likely many businesses that will not have enough inventory to satisfy customers as economies recover and pent-up demand is unleashed. This is particularly the case as retailers are far more reliant on just-in-time supply chains than they were in decades past.”

Among other things, this is also why last May is when a historic bout of inflation was unleashed (one which not a single career economist or Fed official predicted correctly) as collapsing inventories and lack of restocking by jammed up supply chains meant that prices for goods would keep rising and rising and rising. And they did.

Of course, for much of the past year, the big story was the congestion at west coast ports due to both external (China covid breakouts, port closures, changing legislation) and internal factors (lack of port workers, downstream supply jams including trucking and trains, etc) but that has now changed and as the latest Supply Chain Congestion Monitor report from JPMorgan (available to pro subscribers in the usual place) shows, the number of ships at anchor and on approach to L.A. and Long Beach has collapsed since the January high mark, and is back to levels first seen at the start of the covid pandemic.

Why does this matter? Well, for a simple but critical reason: if one year ago we saw the hyperinflationary start of the bullwhip effect, we have entered the terminal phase of the “bullwhip effect”, where plunging inventory-to-sales ratios reverse violently higher, where supply chains unclog suddenly and rapidly amid a sudden chill in the economy, and where prices for so-called “core” goods collapse almost overnight, even as non-core prices (food and energy) explode even higher.

This is how Freight Waves discussed this effect on Friday when commenting on the recent dire earnings (and outlook) from the largest US retailers such as Walmart and Target, which saw their prices crater as management warned that inflation is now crippling demand and snuffing profit margins:

“furniture, home furnishings and appliances, building materials and garden equipment, and a category known as “other general merchandise,” which includes Walmart and Target, among others, reported higher inventory-to-sales ratios, according to government data analyzed by Michigan State.”

How much higher? A quick look at the latest data reveals the following stunning chart of the Inventory to Sales ratio at the Walmarts of the world at the highest level since just before the deflationary flashbang that was the Global Financial Crisis:

Think: widespread inventory liquidations.

As Freight Waves continues, “the change has happened fast, according to Jason Miller, logistics professor at MSU’s Eli Broad College of Business. As of November, inventory-to-sales ratios were at pre-COVID levels, Miller said. They have since exploded upward. Miller said he expects a “cooldown” in retailer order volumes, even if inflation-adjusted sales stay constant, as retailers look to reduce their existing stock.”

And here is the punchline: Miller “also expects retailers to launch major discounting programs to expedite the inventory burn.”

In short: we are about to see the mother of all liquidations as retailers scramble to unload inventory in a time off rampant demand destruction. The immediate result is the freight recession that was first (correctly) forecast by FreightWaves CEO Craig Fuller at the end of March and which is now coming true as the crashing stock price of countless trucker and other freight stocks has demonstrated. Some more on this:

high inventory levels are an expected occurrence and should be welcomed. In a Tuesday note, Amit Mehrotra, transport analyst at Deutsche Bank, said rising buffer stock is part of retailers’ desire to have goods available when consumers scan the shelves. Mehrotra added, however, that the data points translate into a likely slowdown in freight flows in the coming months and quarters.

He said that a recession is already priced into most transportation equities, noting that the shares of most trucking companies are higher over the past 30 days while the broader market is about 7% lower.

The latest data also confirms what FreightWaves’ Fuller said in a subsequent post when he wondered if “Deflation Was Next” as “the Bullwhip was about do the Fed’s job on inflation.”

To be sure, not every product will see its price cut: commodities, whose bullwhip effect take much longer to manifest itself, usually lasting several years in either direction, are only just starting to see their price cycle higher. However, other products – like those carried by the Walmarts and Targets of the world – are about to see a deflationary plunge the likes of which we have not seen since the global financial crisis as retailers commence a voluntary destocking wave the likes of which have not been seen in over a decade.

Tyler Durden

Sun, 05/22/2022 – 21:45 - Turkey's Chief Statistician Quits For "Health Reasons" After Inflation Hits 70%

Turkey’s Chief Statistician Quits For “Health Reasons” After Inflation Hits 70%

Three months after Turkey’s president Erdogan fired his statistics chief as inflation hit a mere 36%, now that inflation has almost doubled since then, the latest official in charge of compiling Turkish inflation statistics has decided to do the smart thing and step down on his own, becoming the latest prominent departure at an institution that’s facing harsh criticism over the reliability of its economic data.

On Friday, the Turkish Statistical Institute said Cem Bas resigned as head of the department of price statistics for “health reasons.” Furkan Metin, who previously oversaw the digital transformation and projects department at the agency known as TurkStat, has replaced Bas, who’ll remain on staff in a lower-profile role.

The personnel change, first reported by Bloomberg, adds to a period of ongoing turmoil at TurkStat, whose president was replaced in January less than a year after his appointment.

Turkish inflation data has been in the spotlight at a time when consumer prices are exploding at the fastest pace since the turn of the century, a key concern for President Recep Tayyip Erdogan’s government just over a year before elections.

Furthermore, according to Bloomberg, concerns have swirled among researchers over what they call a divergence between the agency’s price statistics and the surge in the cost of living felt by wage earners. While TurkStat reported an annual inflation of 70% in April, ENAGroup, an independent group of scholars who’ve put together an alternative consumer price index, put the figure at as high as 157%.

While both numbers are ridiculous, what is even more ridiculous is that until recently the central bank was cutting rates to avoid angering the president whose “Erdoganomics” theory of upside down economics recommends cutting rates when inflation rises, effectively setting the country on a path to suicide, something the Turkish lira has clearly grasped, as it has resumed plunging after cratering in 2021 and only a massive intervention by the central bank preventing an all-out economic collapse.

The government is meanwhile seeking to pass legislation that would bar independent researchers from publishing their own data without seeking approval from TurkStat and potentially face a jail term if they violate the law. That should answer any questions whether the government or the shadow stat inflation data is the correct one.

Tyler Durden

Sun, 05/22/2022 – 20:55 - Bloated Inventories Hit Walmart, Target And Other Retailers' Profits, Trucking Demand

Bloated Inventories Hit Walmart, Target And Other Retailers’ Profits, Trucking Demand

By Mark Solomon of FreightWaves

There’s little in retailing that Walmart and Target aren’t prepared to handle. So it was jarring that over a 24-hour period the two scions of the trade posted weak first-quarter profits that appeared to blindside management at both.

Part of the bottom-line blowup was due to fuel, which soared to record highs following Russia’s Feb. 24 invasion of Ukraine. Part of it was due to margin pressures caused by an unfavorable sales mix as consumers shifted their buying from higher-margin goods like electronics to less profitable items like groceries. An extension of that was an overshoot of inventory-stocking activity, which came back to bite the retailers after waning concerns over the COVID-19 pandemic pushed more consumer buying toward services and “experiences” and away from goods.

There’s little that retailers can do about fuel prices. It can be argued they should have expected the pandemic-driven buying spree from March 2020 until the end of 2021 to peter out and that they should have planned their inventory strategies accordingly. Yet demand forecasting has always been a tough nut to crack, and the market is where it is. Inventory build may also have been the result of supply chain delays at the start of the year that resulted in some late deliveries of impaired freight.

Inventory levels as of March, when compared to activity in March 2019 after inventories stabilized following a major pull-forward in 2018 ahead of the Trump administration’s China tariffs, produce a mixed bag of results. Unsurprisingly given the current dearth of motor vehicles, the ratio of vehicle and parts inventories to sales has fallen considerably, according to federal government data analyzed by Michigan State University. Apparel inventories to sales also declined over those periods, as did e-commerce.

However, furniture, home furnishings and appliances, building materials and garden equipment, and a category known as “other general merchandise,” which includes Walmart and Target, among others, reported higher inventory-to-sales ratios, according to government data analyzed by Michigan State.

For the latter sectors, the change has happened fast, according to Jason Miller, logistics professor at MSU’s Eli Broad College of Business. As of November, inventory-to-sales ratios were at pre-COVID levels, Miller said. They have since exploded upward.

Miller said he expects a “cooldown” in retailer order volumes, even if inflation-adjusted sales stay constant, as retailers look to reduce their existing stock. He also expects retailers to launch major discounting programs to expedite the inventory burn. Fewer orders within certain categories bodes ill for carriers whose networks are strongly tied to inbound lanes to retailers’ distribution centers, Miller said.

In a Friday note, Bascome Majors, analyst for Susquehanna Investment Group, said that the spread between year-over-year sales and inventories — a rough barometer of the impact of higher sales on restocking activity — turned positive in spring 2020 and accelerated in favorable territory for four consecutive quarters. Gradually, however, the spread has turned negative, according to Majors. In this year’s first quarter, inventory growth exceeded sales growth by 200 basis points. The recent surge in inflation, Majors wrote, has severely distorted inventory and sales trends.

Freight recession priced in?

For some, high inventory levels are an expected occurrence and should be welcomed. In a Tuesday note, Amit Mehrotra, transport analyst at Deutsche Bank, said rising buffer stock is part of retailers’ desire to have goods available when consumers scan the shelves. Mehrotra added, however, that the data points translate into a likely slowdown in freight flows in the coming months and quarters.

He said that a recession is already priced into most transportation equities, noting that the shares of most trucking companies are higher over the past 30 days while the broader market is about 7% lower.

In an unusual world, Walmart, Target and other retailers are likely to turn to the one area where they’ve traditionally found leverage: their shipping bill. During the quarter, Target faced freight and transportation costs that were hundreds of millions of dollars above already-elevated expectations, COO John Mulligan said on the company’s Wednesday analyst call. It was essentially the same story at Walmart.

Retailers’ efforts to rein in transportation costs will translate into an unprecedented third and even fourth round of truckload contract negotiations, with users getting more aggressive in their bids to extract greater cost savings, according to industry experts.

The discussions could get contentious. In a LinkedIn post on Friday, Jason Ickert, president of trucking firm Sonwil Logistics, said a large shipper that Ickert wouldn’t identify suggested on a conference call this week with truckload carriers that they were “artificially propping up their rates” above accepted market levels. The shipper “stated clearly” that the carriers were expected to adjust their rates during what would be an “unprecedented and unplanned” third round of request for proposals, Ickert wrote.

A potential shift to intermodal

Pressures to drive down transport expenses will also trigger increased interest in intermodal, whose all-in costs are cheaper relative to contract truckload than at any time since 2018. Intermodal rates have risen at a slower pace than truckload contract rates, a turnabout from the 2019 freight recession when higher intermodal rates allowed over-the-road transport to gain market share.

The shift to intermodal, if it happens, would benefit the railroads and intermodal marketers like J.B. Hunt Transport Services, Hub Group and Schneider. However, experts caution that intermodal capacity remains constrained, as does warehouse space needed to store the stuff.

“Walmart, Target and other retailers will soak up every drop of intermodal capacity that Hunt, Hub, Schneider and the rails deliver in 2022 and probably in 2023,” said Majors of Susquehanna Investment Group. The elevated level of activity, he said, should occur even if retailers are working through a multiquarter process of de-stocking.

Tyler Durden

Sun, 05/22/2022 – 20:30 - 2022 Has Been The Worst Year Ever For Hedge Funds, Who Are Now Massively Shorting To Chase Stocks Lower

2022 Has Been The Worst Year Ever For Hedge Funds, Who Are Now Massively Shorting To Chase Stocks Lower

Some were stunned to see stocks surge in the last hour of trading on Friday in the illiquid vacuum that saw the S&P earlier tumble into a bear market, sliding more than 21% from its January all time high (a level that equates with 3,855 in the e-mini) briefly before bouncing back above 3900, and rejecting the third attempt to enter a bear market in the past week.

We were not, and the reason why is that as has been the case every time a short base builds up, there was a sharp short squeeze. And how did we know that enough of a short pile up had been built up to be toppled by even the smallest spike higher? Why the latest Goldman Prime Brokerage data (full report available to zh pro subscribers). Here are the highlights:

- US equities on the GS Prime book were net sold for the first time in 4 days driven by short sales and to a lesser extent long sales (2.5 to 1).

- Wednesday’s net selling on the Prime book, driven by short sales, was relatively modest (1-Year Z score -1.4) compared to the sharp market losses (SPX -4%, largest drop in nearly 2 years), suggesting that hedge funds collectively were not the main driver of the price declines; and also suggesting that they had been already substantially short heading into the -4% abyss.

- At the same time, quantitative measures tracked by Goldman Research indicates retail investors have become sellers in the past few months, reversing ~26% of the cumulative positions net bought in SPX stocks since Jan ’19 (link ).

Looking at the composition of trades, Goldman Prime finds that both single stocks and macro products (Index and ETF combined) were net sold and made up 67% and 33% of the $ net selling, driven by short sales.

Furthermore, single stocks saw the largest $ net selling in the past month (1-Year Z score -1.4). 9 of 11 sectors were net sold led in $ terms by Info Tech, Comm Svcs, Industrials, Health Care, and Materials.

Which is not to say that hedge funds refuse to take profits: indeed, Consumer Discretionary and Consumer Staples – the worst performing sectors on Wednesday – were both modestly net bought on the Prime book, driven by long buys and short covers, respectively.

On the other hand, long-suffering Info Tech stocks were net sold for a second straight day – following 5 straight days of net buying from 5/10 to 5/16 – and saw the largest $ net selling in the past month (1-Yearr Z score -1.2), driven by short sales and to a lesser extent long sales (3.2 to 1)

But the easiest way to visualize the growing bearish sentiment is by looking at the red line in the top left chart (US equities trading flows) , which is now at the lowest level (most shorts) in 2022:

Ok, so we now that hedge funds have been piling up shorts (not to mention puts), which also explains the lack of a violent VIX surge or a capitulation lower in stocks. What may be just as notable is that despite the rise in short positions, both gross and net hedge funds exposures have collapsed. Indeed, the latest Goldman PB data reflects some of the largest reduction of leverage on record (more in the full latest Goldman prime broker weekly note available to pro subscribers).

According to Goldman’s Tony Pasquariello, the huge underperformance of implied volatility traces back to this point (which, he calls an “immense oddity” – over the past 15 years, there have been 36 daily selloffs of 4% or more, and the VIX was never as low as it was on Wednesday).

Finally, here are the five top highlights from the latest quarterly Hegde Fund Tracker report from Goldman (also available to professional zero hedge subs in the usual place):

PERFORMANCE: Both alpha and beta have posed large headwinds to hedge fund returns so far in 2022. The worst start to a year for the S&P 500 since 1932 has created a challenging beta environment. In terms of alpha, Goldman’s Hedge Fund VIP basket of the most popular long positions (GSTHHVIP) has lagged the S&P 500 by 28 pp since early 2021, its worst stretch on record.

Funds have fared better with shorts; the most concentrated short positions are down 31% YTD, lagging both the S&P 500 and VIPs. Nonetheless, the median S&P 500 stock still carries short interest equivalent to just 1.5% of market cap, a 25-year low.

LEVERAGE AND FLOWS: As noted above, the decline in hedge fund net leverage that began in 2021 has accelerated in recent months. Exposure data calculated by Goldman Sachs Prime Services show net leverage in the 30th percentile vs. the past 5 years compared with record highs in spring 2021.

Despite recent selling pressures, equity allocations across a number of investor groups – most notably households – still appear elevated, suggesting the potential for more selling pressure if the macro outlook does not become more friendly for equities.

HEDGE FUND VIPS: Despite the sell-off in technology stocks, FAAMG remains atop Goldman’s list of the most popular hedge fund long positions. MSFT maintains its position as #1. The VIP list contains the 50 stocks that appear most often among the top 10 holdings of fundamental hedge funds. Four new Energy stocks entered the basket (CHK, VAL, OXY, and LNG) and the sector now has a 10% weight.

The basket has outperformed the S&P 500 in 58% of quarters since 2001 with an average quarterly excess return of 40 bp. 16 new constituents: ANTM, APO, ATVI, CHK, CHNG, CRWD, EQT, FIVN, GPN, HUM, MRVL, OXY, PLAN, T, VAL, Z.

GROWTH STOCKS: Hedge funds continued to reduce exposures to Growth sector and stocks. Rising real interest rates and declining leverage have weighed in particular on the valuations of long-duration stocks with extremely high multiples.

SECTORS: Hedge funds added to Industrials and Materials while cutting exposures to former favorite Growth sectors. Fund tilts to Information Technology and Consumer Discretionary are now at the lowest levels in at least a decade. “Big Tech” drove much of the reduction in positions across Tech and Discretionary, with funds incrementally rotating away from AAPL, AMZN, and TSLA.

Putting it all together, Goldman’s Ben Snider summarizes that “a plummeting equity market and the even worse performance of the most popular long positions have led to the worst start of a year on record for hedge fund returns. HFR data show the average equity hedge has returned -9% YTD and GS Prime Services estimates an asset-weighted decline of -17%. As a result of these struggles, in recent months hedge funds have accelerated the reduction in leverage and rotation away from Growth stocks they began several quarters ago” while at the same time piling up shorts.

However, as Goldman notes, this adjustment has not been quick enough and despite four Energy stocks entering Goldman’s Hedge Fund VIP list of the most popular long positions (CHK, VAL, OXY, and LNG), Tech still represents over a third of the basket’s 50 constituents. The five FAAMG companies remain at the top of the list. The basket has declined by -27% YTD vs. -18% for the S&P 500 after underperforming the S&P 500 by 17 pp in 2021. During this period, hedge fund VIPs have effectively given back all the excess return they had generated since 2014.

Concluding, Goldman writes that the sharp recent reduction in hedge fund length and rotation in long portfolios reflects a broader asset reallocation taking place across the market. In recent years, low interest rates have supported the investment philosophy that There Is No Alternative to equities (“TINA”). Long-duration Growth stocks have benefited most as both institutional and household investors lifted their equity exposures.

Today, in contrast, positive real interest rates, growing recession fears, and declining equity prices have signaled to investors that There Are Reasonable Alternatives to stocks (“TARA”). Investors have been reallocating accordingly. This ongoing adjustment is reflected in household and institutional flows away from equities broadly and from Growth stocks in particular.

For hedge funds, this has exacerbated the vicious cycle of falling share prices, declining leverage, and poor liquidity that has created such a challenging market environment this year.

All reports mentioned above are available to zero hedge professional subs.

Tyler Durden

Sun, 05/22/2022 – 20:05 - How Did Mueller's $40 Million Trump-Russia Investigation 'Miss' Hillary's Hoax?

How Did Mueller’s $40 Million Trump-Russia Investigation ‘Miss’ Hillary’s Hoax?

Authored by Sundance via The Last Refuge (emphasis ours),

One of the public revelations created by the trial of Clinton lawyer Michael Sussmann is that Hillary Clinton’s campaign, Hillary Clinton’s lawyers, and Hillary Clinton’s contracted opposition research firm, Fusion GPS, manufactured the Trump-Russia collusion hoax. How did Robert Muller not find this?