- BRICS Will Change The World… Slowly

BRICS Will Change The World… Slowly

BRICS, the organization that is hardly noticed in the West, more than doubled its membership at the end of August – something is happening.

Introduction

It seems to be more a rule than an exception that the most important changes in the history of financial systems either go completely unnoticed or the vast part of the public – including financial experts and investors – does not grasp the importance of such transformations.

There are several examples for this claim: On December 23, 1913 the Senate passed and President Woodrow Wilson signed the Federal Reserve Act. The FED being as “federal” as “Federal Express”, a private bank whose shareholder register is not open to the public, rules the world since 1913. The date of December 23 was wisely chosen since the public and most politicians were too engaged in Christmas preparations to realize that this event would change the order of America and then the world forever.

When Richard Nixon, on August 15, 1971, “temporarily” closed the gold window, the Sunday afternoon TV shows got interrupted – among else the TV series “Bonanza” – to inform the American people of his decision. Although, this event was called the Nixon Shock, people did not seem to grasp the importance of this deed.

Lastly, the famously brilliant Henry Kissinger managed to make a deal with King Faisal of Saudi Arabia in 1974, which gave the US unlimited financial and, therefore, geopolitical power by creating the Petrodollar, banishing the danger stemming from a U.S. dollar that was backed by nothing, by backing it with U.S. military might in exchange for nearly unlimited investments in U.S. bonds.

Now, on August 22, BRICS, an organization, which does not gather a lot of attention in the Western media, announced that, apart from the five countries, whose initials gave it its name (Brazil, Russia, India, China, South Africa), BRICS welcomed six new members (Argentina, Egypt, Ethiopia, Iran, Saudi Arabia and the United Arab Emirates) to join BRICS by January 1, 2024; therefore, BRICS becoming BRICS 11.

In this article, let us first quickly look at some facts & figures of BRICS 11. Then, we shall explore the history of the current financial system and it’s becoming in detail in order to appreciate its importance to U.S. power in the period from World War II to the present. Then we shall look at the way the U.S. abused the inherent privileges of this system, which is one reason that led to the current rise of BRICS. Finally, we shall try to answer the question whether the events of August 2023 have the potential to change the world or whether it will be one more fruitless endeavor of emerging market nations to stand-up against the Collective West.

Origin of BRICS

The term BRIC was coined by Goldman Sachs economist Jim O’Neill in a 2001 paper where he explained the future economic potential of Brazil, Russia, India and China.

In 2006, the BRIC countries met for the first time on the fringes of the UN-General Assembly in New York. A first formal meeting took place in Yekaterinburg in 2009. The aim of this initially loose community was to improve cooperation among its members. In 2010, South Africa joined, which means that this organization has since been called BRICS. This August the number of its members more than doubled and we shall call it now BRICS 11.

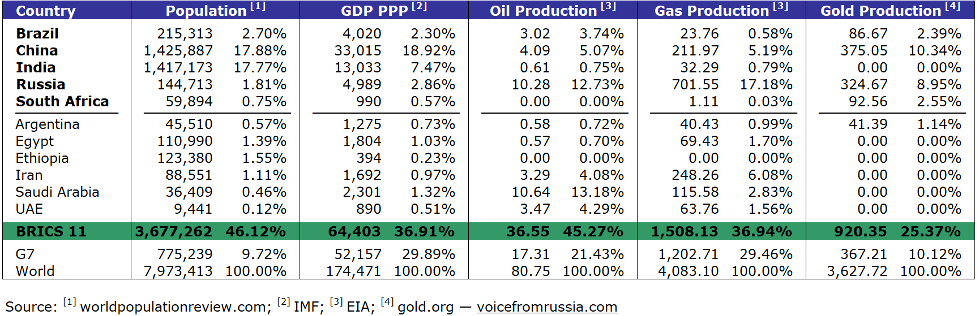

Figures

With regard to the most important economic indicators such as population, GDP (PPP), oil, natural gas and gold production, naked figures show that BRICS 11 is much stronger with regard to any of these indicators than G7 (Table 1).

These figures on their own should be a wake-up call to all the people, experts, politicians and investors who still seem to believe that it is sufficient to judge the financial world from a pure western perspective.

There are a few points I would like to draw the attention to of the readers regarding the way these naked figures could and should be read and interpreted. However, I am fully aware that I can only give you a glimpse at the reality and this exercise herein is of a very limited nature indeed.

Regarding GDP, I use purchase power adjusted figures. Why? – If you use the U.S. dollar as a tally to measure GDP, ask yourself the simple question: If I want to measure financial punch, does it matter whether, e.g., a Big Mac costs twice as much in U.S. dollar terms in one place than in the other? – In my opinion it does. The Big Mac Index should be reason enough to use PPP-adjusted figures when comparing GDP figures. The reason that Western outlets use the non-adjusted figures is pure marketing masking the debasement of the U.S. dollar and appearing stronger than one is – propaganda.

Regarding oil production figures, we should consider the following facts when assessing them: Firstly, although the U.S. is still the largest oil producer in the world with a share of about 18% of world production, the U.S. are also the largest oil consumer, using-up more than 20% of world consumption. Therefore, the U.S. are at this time not even able to cover their own consumption. Secondly, the large oil-producing members of BRICS 11 have a big influence – or better – control over OPEC. Therefore, BRICS 11 will also rule OPEC and, therefore, control the price and distribution of oil, which has not been given the nick name “Black Gold” without good reason. Thirdly, the production cost of U.S. oil are about 2.5 times higher than the production cost of Saudi oil.

Regarding natural gas one should note, that with the accession of Iran into BRICS, the two largest natural gas producers worldwide are joint members of BRICS: Russia and Iran. The largest non-BRICS gas producer is the (still) U.S. allied Qatar. BRICS is, therefore, also a powerhouse regarding natural gas indeed.

Regarding gold, it should shortly be mentioned that China and Russia are number 1 and 2 respectively regarding global gold production. Gold I mention in here since there is a rather good chance that – somewhere in the future – gold will again play a major role in future money systems, being the only manner to discipline central bankers who basically only did one thing since 1914 – printing money, debasing the U.S. dollar and cynically claiming to protect the currency. There are a lot of people in the West who actually claim that gold is a pet rock. These people do not understand the history of the past 4’000 years where gold was always king. The mere fact that Nixon abolished the gold standard in order to avoid bankruptcy is not a good argument against gold, but should be one in its favor.

Bretton Woods

In order to grasp the importance of the rather swift developments around BRICS and the rationale behind it, we shall look at the present system of the financial corset so imposed by the U.S. on the rest of the world. How did the U.S. achieve such dominance, how the hegemon behaved since, and finally the probability of a change of the system.

In 1944, the Americans reached the pinnacle of their power. They dominated the war effort together with the Russians, possessed 22,000 tons of gold, and the American industry produced 70% of the world’s manufactured goods. That is how complete dominance looks like: Military dominance, industrial dominance and gold – he who has the gold makes the rules.

On top of these facts, the Americans – as ever – being the undisputed masters of marketing, persuaded the Europeans to believe that it was actually the U.S. who liberated Europe from the evil Mr. Hitler. This was a diplomatic master stroke since cold facts and figures clearly showed that the Russians bore the largest chunk liberating Europe from the Nazis. The Russians decimated the German Wehrmacht in the East and – in this endeavor – killed around 5 times more German soldiers than all western allies together at the western front. This very ability of marketing and deception by the United States would serve them well until the present day.

Against such an overwhelming power, based on the three pillars of military might, industry and gold, the entire rest of the world – whether friend or foe – did not stand a chance to have any influence worth mentioning on influencing US intentions.

The Bretton Woods system was thus an emanation of absolute U.S. power and not – as portrayed in history books – a mechanism negotiated by the victorious powers of World War II in an atmosphere of friendly partnership.

Bretton Woods also sealed the demise of the British Empire by giving the Americans absolute power through pegging the currencies of 44 member states to the U.S. dollar, which in turn came out as the only currency of the world backed by gold.

The British Empire on which the sun finally set, proposed a system that involved the introduction of an international settlement currency called the Bancor. This idea by John Maynard Keynes foresaw the Bancor being used as an international unit of account to which participating currencies would have been pegged. The value of the Bancor itself was to be backed by gold. The gold-backed Bancor would have served as the unit of account. A fair system giving a chance to countries with merit, leading to a multipolar world. However, a multipolar world was the last thing the Americans intended to build – they wanted to become the hegemon and achieved their goal; the British had not a snowball’s chance in hell with their – in my opinion – great idea.

The Bretton Woods system gave all member states the contractual right to exchange the U.S. dollar they held for physical gold at a fix rate of U.S. dollar 35 per ounce of gold. Therefore, the Bretton Woods system should have forced the Americans to behave fiscally disciplined so that all member countries would keep confidence in the U.S. dollar believing that the U.S. dollar was indeed as good as gold.

The Americans, however, as the world power and hegemon, did not care one iota about the interests of their partners and, starting in the 1960s, printed more and more U.S. dollars to finance the Vietnam War and the Great Society project initiated by President Johnson. Both, the costs of the Vietnam War as well as the Great Society Project, the largest social program of the USA up to that time, whose main goal was to completely eliminate poverty and racial injustice, got completely out of hand.

The French were the first to realize that the U.S. dollar was losing value due to American money printing and began to exercise their contractual right to exchange their U.S. dollars for physical gold. Others followed suit. The Americans’ huge gold hoard melted away like butter in the sun. While the USA had more than 22,000 tons of gold at the end of the war, it was only over 8,000 tons in 1971.

On August 15, 1971, all major television stations in the U.S. interrupted their Sunday afternoon programming and President Nixon addressed the nation. He claimed that the speculators were waging an all-out war against the U.S. dollar and that he had thus ordered the U.S. dollar to be defended against these speculators. He informed the American people that he had instructed the treasury that the convertibility of the U.S. dollar into gold be temporarily suspended.

This all sounded very patriotic, but it was a complete lie. The speculators Nixon decried were actually member states of the Bretton Woods system who had realized that the Americans had ripped them off and were merely exercising their contractual right to exchange a debasing U.S. dollar for gold as stipulated in the Bretton Woods agreements. Nixon thus committed nothing less than breach of contract. The members of Bretton Woods were cheated and left sitting on their paper dollars being barred from getting their contractually stipulated gold.

Petrodollar – an exorbitant privilege

The deceived members of Bretton Woods decided not to hand over a declaration of war to the Americans, but kept silent like sheep and made a fist in their pockets. They probably believed that the Americans had dug their own grave by breaking the treaty.

However, they had not reckoned with the brilliant Henry Kissinger. The man was sent by Richard Nixon on Mission Impossible to save the Dollar. Kissinger convinced Saudi King Faisal to sell his oil exclusively in U.S. dollars and to invest the proceeds in American government securities. In return, smart Henry promised Faisal military protection. Other countries and commodities followed. Like Houdini, Kissinger freed the U.S. from a dire situation by making the impossible possible. Mission accomplished: The Petrodollar was born.

Now, if almost the entire world uses a single currency – the U.S. dollar – for almost all trading activities, all countries are obliged to hold this currency in reserve to pay their bills. These countries do not hold the reserves in cash, but invest them in American government securities to earn a return on their reserve holdings. In this way, the Americans managed to create the largest bond market in the world. It should be noted that the U.S. dollar is a product like any other, whose price is subject to the law of supply and demand. The U.S. dollar is not bought because it is a good investment in itself nor do most buyers purchase American products. No, U.S. dollars are required in order to buy nearly any product around the globe. This unjustifiably strengthens the price of the U.S. dollar. Why unjustifiably? – Other countries need to produce something worth buying that will hold up in the world market to keep their currencies valuable – the U.S. do not.

If now the whole world has to hold U.S. dollars and holds them in American government securities, the American government finances itself very cheaply because the price of American bonds does not depend on the strength of the American economy, but is based on compulsory buying due to the Petrodollar system – ingenious.

To put it bluntly, the U.S. could thus afford everything for over 50 years, because the bills were paid by others. Imagine a guy who goes shopping with a credit card that has not limit. He has a big mouth, buys everything he wants and never pays the credit card bill, but owes the money to those who sell him the goods, the latter never getting paid but receive an IOU only.

Only due to this – for the U.S. – brilliant system were the Americans able to increase their deficits to levels which can only be described as mind boggling: When Roland Reagan took office, US-debt was below 1 trillion, now it stands at over 33 trillion. Any other nation would have collapsed since nobody would dare to put money in such a black hole – but the whole world has to keep buying U.S. dollars due to the Petrodollar system. So, now we know how the U.S. could cultivate a lifestyle at the expense of others for over 50 years that in no way correlates with the performance of its economy. This great lifestyle is based only on the compulsion of the rest of the world to hold U.S. dollars. Giscard d’Estaing called this advantage an exorbitant privilege – rightly so.

Petrodollar, a geopolitical power tool abused by the U.S.

When it came to maintaining their privilege, the U.S. showed little squeamishness if anyone dared to break away from the Petrodollar regime. In recent history, two examples may be mentioned. We all remember the second Iraq war, when it was claimed that Saddam Hussein had weapons of mass destruction and that this put the USA in danger. Despite a unambiguous report from the UN that there were no weapons of mass destruction or even a single hint that they existed, the Americans attacked Iraq anyway in order to rid the world of the evil Saddam Hussein and bring peace and freedom to the Iraqis. A big lie. Weapons of mass destruction were not to be found in Iraq; half a million civilians were killed – their relatives were certainly thrilled about this kind of democratic gift that the U.S. forced upon them. The reason for the Iraq war was a different one: the Petrodollar. Saddam Hussein – we don’t need to dwell on his qualities as a human being here – wanted to sell his oil not only in U.S. dollars but also in Euros. That was his death sentence. Anyone who claims otherwise is either ill-informed, naive or lying. The facts are on the table.

President Gaddafi ruled Libya with a strong hand for decades. He made Libya the richest country in Africa with an excellent infrastructure. Whether Colonel Gaddafi was a do-gooder or not is also not a topic of this discussion. Gaddafi also had a plan to get away from the U.S. dollar: He wanted to create the Gold Dinar to free Africa from the shackles of the Petrodollar. This, too, did not go over well with the Americans. The result was a dead Gaddafi and a completely destroyed country.

These two examples bring us to the geopolitical might the U.S. draws from the Petrodollar. It is important to know that only the U.S. Federal Reserve can actually hold U.S. dollars. Every bank in the world that offers U.S. dollar accounts ultimately only has a booking entry for a U.S. dollar amount and a contractual claim against the US central bank. This also explains that any payment made in U.S. dollars goes through the U.S. Thus, the Americans can single-handedly cut off any party – be it a country or an individual – from the U.S. dollar or freeze or seize a party’s U.S. dollars holdings.

The U.S. has been using this tool systematically since World War II with countries deemed worthy of being punished or destroyed economically, e.g., the U.S. sanction Cuba for over 60 years or Iran for over 40 years.

This use of force was justified by the USA with flimsiest arguments like communism, terrorism, war crimes etc. Whether the accusations were or are true or not, is completely irrelevant, because the judge sits in the U.S. and the legal basis is force. Depending on the decade you live in, you gets the label of communist, terrorist, drug dealer if you have the audacity to disagree with the hegemon. And the lapdogs such as the European “rulers” agree with the empire and serve as its willing assistants.

When the Americans impose such sanctions, they regularly threaten any party that does business with the sanctioned party with sanctions as well. These so-called secondary sanctions work since most international business is transacted in U.S. dollars and the respective companies – banks, commodity buyers, industrial suppliers – have no choice, but to comply.

A lot of people in the world are of the opinion that the U.S. are not behaving fairly towards the rest of the world and completely abuse their exorbitant privilege they possess with the Petrodollar.

This concludes our journey into the world of the Petrodollar and brings us to the reasons why BRICS want to say goodbye to the U.S. dollar, as the U.S. has overstepped the mark. After the start of Russia’s invasion of Ukraine, the West, led by the U.S., not only slapped Russia with a flurry of sanctions that has no equal in history, but also froze the foreign currency reserves of the Russian Central Bank. Shortly thereafter, discussions began as to what the West intended to do with the funds. After the freeze, the robbery is now being discussed.

I strongly believe that with the freezing of the reserves of the Russian Central Bank, the U.S. triggered a reaction they did not expect. Huge nations like India and China became suddenly concerned that the freezing of Russian Central Bank assets set a precedent and could also happen to them, especially in the more than tensioned geopolitical situation of today where anybody who cares can easily observe that the strategy of weakening Russia is only a pre-course of the battle the U.S. will lead against China. This is also the reason that BRICS seems to speed-up the process. Apart from the current 11 members of BRICS around 40 further nations applied to join.

The trigger for the attack on the petrodollar

This concludes our journey into the world of the Petrodollar and brings us to the reasons why BRICS want to say goodbye to the U.S. dollar, as the U.S. has overstepped the mark. After the start of Russia’s invasion of Ukraine, the West, led by the U.S., not only slapped Russia with a flurry of sanctions that has no equal in history, but also froze the foreign currency reserves of the Russian Central Bank. Shortly thereafter, discussions began as to what the West intended to do with the funds. After the freeze, the robbery is now being discussed.

I strongly believe that with the freezing of the reserves of the Russian Central Bank, the U.S. triggered a reaction they did not expect. Huge nations like India and China became suddenly concerned that the freezing of Russian Central Bank assets set a precedent and could also happen to them, especially in the more than tensioned geopolitical situation of today where anybody who cares can easily observe that the strategy of weakening Russia is only a pre-course of the battle the U.S. will lead against China. This is also the reason that BRICS seems to speed-up the process. Apart from the current 11 members of BRICS around 40 further nations applied to join.

Consequences

We have now seen that the might of the U.S. and the fate of their economic well-being very much hinges on the Petrodollar and that the American leadership is very well aware of this fact, crushing anybody who dares not to use the U.S. dollar in international trade.

In my opinion, however, the U.S. government misjudges its own leverage to put fear into other nations at this time. The Petrodollar system only works as flawlessly as it did in the past as long as the U.S. were able to control the world with mere threats, which were – once in a while – kinetically executed as it was the case with Iraq and Libya. However, the embarrassing retreat from Afghanistan did not help the U.S. to be seen as the military force they like to portray. The loss of influence over Saudi Arabia and Iran is a painful geopolitical sign for U.S. foreign policy. The peace reached between Saudi Arabia and Iran and then between Saudi Arabia and Syria is not only an economic disaster to the U.S. regarding oil, but a geopolitical catastrophe regarding U.S. influence in the Middle East. With these peace makings, the U.S. have been deprived of their ability to play out the strategy of divide et impera since the U.S. cannot manipulate these countries anymore and it seems that the U.S. are not feared anymore. As a group the middle east nations became too powerful and do sell their commodities in other currencies other than the U.S. dollar – a scenario which was completely unthinkable just a few years ago.

BRICS 11 will have one immediate consequence: Their members will not use the U.S. dollar when trading among each other. This is a huge problem for the U.S. since these countries will reduce their U.S. dollar holdings and therefore, the refinancing of the U.S. budget becomes a problem, leading to higher interest rates, which will in turn lead to higher inflation and a further debasement of the U.S. dollar because what cannot be raised in the international markets has to be printed.

The much-discussed introduction of a new settlement currency based on gold within BRICS is not a necessary element to de-dollarization. Such introduction faces substantial hurdles also due to the heterogeneity of the BRICS members. However, the consequences for the U.S. dollar will be immediate and problematic to the U.S.

We explained the vast power of the United States since World War II. It is in my opinion a myth that the U.S. hegemony is based on its military might. Far more important is their financial hegemony which – at least until now – allowed the U.S. to more or less control the world with a relatively small army and 9 aircraft carrier groups who regularly, as a show of force, bomb the hell out of small countries which do not have air forces or air defense systems to stand a chance against U.S. force. The whole U.S. power is based on the Petrodollar – that is my belief.

Conclusion

There are authors who predict a quick demise of the Petrodollar and, therefore, of the American financial hegemony, which in turn will lead to the demise of the U.S. as the undisputed geopolitical world leader. Fact is, that a substantial part of the world will avoid using the U.S. dollar in trade. This development has already started. Therefore, the trend is set. However, it is in my opinion impossible to make any prediction as to the speed and timing of this trend. The proclaimed goal of BRICS and other organizations of the Global South, such as SCO, EEU, the Arab League and OPEC is to build a multipolar world. This seems to be a realistic goal. However, one should also take into consideration, that the larger these organizations become, the more heterogeneous they become and the difficulty of implementation of a common course of action will rise in line with the number of the respective members. Lastly, I would like to draw the attention to one historical fact a lot of people are not aware of. When the U.S. were at the peak of their might and forced Bretton Woods on the rest of the world, it still took 12 years until the U.S. dollar overtook the British pound in international trade in 1956. Some trends may be irreversible – but they take time.

* * *

This article appeared in English in the Gloom, Boom & Doom Report by Swiss financial expert Marc Faber and in abbreviated form on September 21, 2023 in the print edition of Weltwoche and on Weltwoche Online in German.

Tyler Durden

Mon, 09/25/2023 – 00:20 - Traders Brace For China's Property Slump To Drag For Years

Traders Brace For China’s Property Slump To Drag For Years

By Charlie Zhu and Helen Sun, Bloomberg Markets Live reporters and analysts

Three things we learned last week:

1. A multi-year property downturn looks increasingly likely as a raft of rescue measures have fallen flat. Disappointing home sales in China’s largest cities suggest policy supports have failed to turn around buyer sentiment. New home sales for the first two weeks of September in tier-one cities fell from August’s levels.

The fallout from the property crisis is spreading to investment-grade developers. Moody’s Investors Service put China Jinmao Holdings Group Ltd. and China Vanke Co. on review for possible downgrade, while lowering the outlook for seven other builders to negative.

Onshore investors shared the view that China’s property sector is facing a multi-year downturn and are even less optimistic on the outlook for commercial properties, Zerlina Zeng, senior analyst at Credit Sights, wrote in a note. Considering China’s aging population and slowing urbanization, a mild contraction of home construction and sales is appropriate, Zeng wrote.

Efforts to relax home-buying restrictions have continued, with 11 cities announcing such measures in September alone, according to China Index Holdings. Among the latest came from Guangzhou, which shortened the period of time non-residents need to pay tax before they’re allowed to buy homes.

2. As property woes cast a pall over the broader market, policymakers are bolstering efforts to court investors. Key Chinese stock gauges hit new 2023 lows last week, before rebounding Friday. A Bloomberg Intelligence gauge of China’s developer shares posted its biggest weekly decline since mid-August, while an index of high-yield dollar bonds, mostly developers, halted a four-week advance.

As capital flees at a pace unseen in years, the People’s Bank of China vowed to stabilize trade and improve business environment in a forum attended by top global financial institutions. China is also considering relaxing the rules that cap foreign ownership in domestic publicly traded firms, people familiar with the matter said.

Whether those efforts will bear fruit remains unclear. While onshore shares saw its biggest inflow via the trading links on Friday since the end of July, market rebounds this year have barely lasted two weeks.

3. For all the skepticism engulfing Chinese markets, investor faith in the local government financing vehicles seems intact, at least for now. Their bond issuance onshore jumped 50% in August from July to notch the third-highest monthly tally on record.

While investors are betting that LGFVs will remain relatively safe in the near term given the central government’s efforts to tackle debt problems, there’s still a risk that when the music stops, someone will need to pay the price.

In the first eight months this year, 72% of LGFVs’ bond sales were used to pay back existing debt, analysts led by Liu Yu at GF Securities Co. wrote in a report, highlighting repayment pressure.

Tyler Durden

Sun, 09/24/2023 – 23:45 - Hunter Biden Wanted To Lobby Sen. Bob Menendez On Behalf Of Foreign Client

Hunter Biden Wanted To Lobby Sen. Bob Menendez On Behalf Of Foreign Client

Hunter Biden and pals wanted to lobby indicted Democratic New Jersey Senator Bob Menendez on behalf of a Spanish rail company after regulators scrutinized the firm, according to emails found on Hunter’s infamous laptop.

According to the Daily Caller, Spanish rail company Construcciones y Auxiliar de Ferrocarriles (CAF) hired Rosemont Seneca Partners, Hunter Biden’s investment firm, to lobby the Department of Transportation (DOT) and Amtrak in order to obtain government contracts on various railway contracts, the emails reveal.

In fact, Hunter and pals spoke with Menendez’s office about CAF, and even arranged for meetings between CAF and DOT officials.

CAF hired Rosemont Seneca in June 2010 and Hunter Biden’s firm appeared to discuss potential contracts with Amtrak shortly thereafter, according to the laptop archive. Biden and his associates also appeared to work with CAF on a letter sent by the Spanish ambassador to Amtrak advocating for the firm, emails show.

Hunter Biden sat on Amtrak’s board from July 2006 to February 2009 after he was nominated by former President George W. Bush. Prior to his Amtrak position, Biden worked in former President Bill Clinton’s commerce department and at a Washington, D.C., law firm. -Daily Caller

In July 2010, the month after they hired Rosemont Seneca, Amtrak awarded CAF’s US subsidiary a $298.1 million contract to make 130 new rail cars at an Elmira, New York plant. According to the report, Hunter’s firm appeared to have negotiated a “success fee” with CAF once the contract was announced.

“We may very well be because we don’t have anything in writing, but my point has been that we be firm, have Hunter call the CEO and congratulate him, say we are looking forward to working with CAF as they implement the Amtrak contract and then follow it up with a letter to memorialize the success fee arrangement,” said Hunter business partner Eric Schwerin in a July 27, 2010 email.

“IF and only if they push back let’s not let CAF make us think we didn’t do enough work to deserve the fee, as it is a minor percentage compared to what we would normally get for working on a project like this,” he added.

Rosemont asked for a “success fee” in excess of $800,000 for their work in securing the contract.

In early August 2010, Schwerin engaged Menendez’s office – holding a call with the Senator’s Chief-of-Staff, Daniel O’Brien.

“Talked to Danny re: CAF and he is looking into it,” said Schwerin. “He was very interested in finding out more mainly because of Menendez’s chairing the U.S.-Spain Council. Also, mentioned they are doing an event in NY on Sept. 24th (when we will be up there for CGI anyway) with the Spanish President if you want to attend. I’ll hold the date.”

O’Brien communicated with Hunter Biden on multiple occasions and the pair appeared to be friends. Hunter Biden emailed O’Brien in June 2010 about attending a Washington Nationals game during a conversation about his father, then-Vice President Joe Biden, attending a forum Menendez was holding with U.S. and Spanish officials, emails show.

Hunter Biden and O’Brien spoke again in March 2011 about the younger Biden stopping by Menendez’s office, emails on the laptop archive show.

“The Senator wants to talk to you,” O’Brien wrote March 9, 2011, and Hunter Biden proceeded to send O’Brien his new cellphone number.

“You’ll hear a message from the Senator if you haven’t already. He felt badly due to his mistaking you for Beau. You were kind to stop by,” O’Brien said later that day. -Daily Caller

In other emails, Hunter appeared frustrated that the “success fee” hadn’t materialized.

“I just tell people it’s a minimum of 250k just to talk to me– you don’t show up on a call or in a room unless we are getting 20% of the deal. No overhead- no offices no salaries,” Hunter said in an email exchange regarding CAF. “I cc’d Eric b/c he gave me A big talk on how CAF really wanted him on this and didn’t really care if I was there and how we wouldn’t have to do much work and the fact he didn’t read the contract regarding success fee.”

On September 14, 2010, Rosemont and lobbyists from the Democratic lobbying firm SKDK appeared to schedule a meeting with DOT official Peter Rogoff, after the firm was hired in early September to beef up CAF’s lobbying efforts.

“Further to Hunter’s earlier email, the meeting between CAF and Rogoff is scheduled for Friday at 3:30pm at DOT. They are working on their message to Rogoff between now and then and hope to be able to persuade him to delay implementation of the ruling,” Schwerin wrote in a Sept. 14, 2010 email.

“Mentioned Florida and Tomar said they are still focused on it and in fact he has gotten some calls from other consortia this week which he took as a good sign that CAF’s image has not been affected by this Houston issue. He wants our help on this still and asked that we talk after the Rogoff meeting on Friday to figure out a plan on Florida going forward,” he added.

Menendez on Friday resigned as chairman of the Senate Foreign Relations Committee following his felony indictment for allegedly accepting bribes and providing sensitive US government information to the Government of Egypt.

Read the rest here…

Tyler Durden

Sun, 09/24/2023 – 23:10 - Scarcity Is Not Enough

Scarcity Is Not Enough

By Marcel Kasumovich, Deputy CIO of Coinbase Asset Management

“We are not dependent on the ideas of a single person, but on the combined wisdom of thousands of people who are all thinking of the same problem, each doing their little bit to add to the great structure of knowledge that is gradually being erected.” Ernest Rutherford is recognized as the father of nuclear physics, and also for his appreciation that his contributions would be invisible over time if done right – others building on them would shine.

Perhaps this is the point of Satoshi Nakamoto’s anonymity. He doesn’t matter. For bitcoin and crypto asset technologies to work requires widespread adoption from technologists to regulators and users. We are all Satoshi if bitcoin rises to reach its full potential. Could the creators be bad operators? Yes, and transparency is the solution. Bitcoin started with a bit more than 1,000 lines of code and an open architecture for all to see. And it works, with nobody in charge.

3,847. Those are the number of consecutive days the bitcoin network has operated without interruption. It covers an eventful decade – a global recession, a collapse in commodity markets, a freezing of the US repo market, a global pandemic, the fastest US monetary tightening in four decades, country bans of bitcoin mining, and the crypto Great Depression. Over $100 trillion dollars have settled on the bitcoin protocol over its lifetime. Remarkable.

It’s also the type of data that earns bitcoin the reputation as the “gold standard” of crypto asset markets. Energy is a connective tissue between gold and bitcoin. Machines and energy are needed to produce gold. Devaluation of a currency that elevates the cost of production would be captured by the local price of gold. When central banks anchored monetary policy to gold, they were anchored to those real resource constraints.

The parallels to bitcoin mining – computers and power – are self-evident. Bitcoin’s nominal anchor, like gold, are real resources dominated by energy. Now, investors are keen to see whether the parallels of bitcoin to gold extend to the financial world. After all, the introduction of the gold exchange traded product (ETF) was coincident with a decade-long bullish trend. Even if just a coincidence, what’s clear is that the “bitcoin standard” has institutional engagement.

But there is one major difference – scarcity. When the price of gold is high relative to its cost of production, there is an incentive to hunt for new gold reserves to mine. Supply rises. It’s a law of any market. Bitcoin has no supply response. When profits are high, more computers enter the network, and the bitcoin algorithm makes mining more difficult. The energy cost of bitcoin rises, and profits fall to push weakest miners out of the network.

And difficulty has surged. It’s a sign of maturity. Bitcoin mining difficulty is up nearly 60% this year and is more than double from the 2022 highs in the price of bitcoin. The secular rise in bitcoin mining difficulty means the market is becoming more efficient, more institutional than previous cycles. Part of the surge in mining difficulty is computers entering the market in anticipation of “the halving,” collecting rewards before they are reduced by 50% next year.

Bitcoin inflation is cut by half every four years or so. There will only ever be 21 million in bitcoin supply, and 92% is already in circulation. April 16, 2024 is the approximate date of the next bitcoin halving, which will reduce the bitcoin inflation rate to less than 1%. Bitcoin miners and investors are excited by the historical precedent – the price of bitcoin rose 25% on average starting from two months before past halvings and 60% three months after the event.

Not bad. But this is only the fourth cycle – it’s a small sample. Figure 1 illustrates halving cycles for bitcoin and her “silver equivalent”, litecoin. The data are a visual reminder that scarcity isn’t enough to make prices rise. Litecoin enjoyed a sharp price spike before its most recent halving on August 2, 2023, then fizzled out. Scarcity without being useful is pointless. I produce plenty of music that is scarce…and valueless. There needs to be demand.

Where’s the demand for bitcoin? The most natural is as a payment rail. The numbers are staggering. The top 100 bitcoin transactions in the past 24 hours sum to nearly $10 billion at an average cost of less than 2 basis points. Spectacular technology. What’s built on top of the bitcoin protocol will define its user experience, like the Lightning Network that allows for virtually costless micro transactions. But similar to gold, its store of value could detract it from its utility.

Gold is a remarkable conductor of electricity – it’s not afraid of oxygen, unlike copper. But gold’s price has largely destroyed its industrial use-case. Could bitcoin see the same fate? Long-term holders of bitcoin are at record highs – reluctant sellers for all of the right reasons. But how can bitcoin become ubiquitous when the top 100 of owners control 15% of its value? It can’t. But it can play the role of gold in the crypto ecosystem – the standing benchmark. And that’s the top of the heap in crypto asset markets. Halving or not.

Tyler Durden

Sun, 09/24/2023 – 22:35 - Senator Shocked By Classified Briefing On Ukraine: Warhawks Want Blank Check With No Victory In Sight

Senator Shocked By Classified Briefing On Ukraine: Warhawks Want Blank Check With No Victory In Sight

“If there is some path to victory in Ukraine, I didn’t hear it today. I also heard that there’s going to be no end to the funding requests…”

Hawley went on to indicate that Americans will be asked to spend hundreds of billions more dollars in the region with an indefinite blank check in place to protect “US standing” on the world stage. Zelensky asked Biden and Congress for another $24 billion during his latest visit, stating that if Ukraine doesn’t get the aid, they will lose the war. The information at hand suggests that Ukraine is going to lose the war anyway.

Hawley also revealed that the public is being lied to about the war footing in the region and that Ukraine is definitely ‘not winning.’ This information confirms what many Americans already suspected, with 55% of the public now in opposition to more aid according to recent polls.

The corporate media blitzkrieg bombarding the populace with tales of imminent Ukrainian victory against Russian forces has lost its momentum and reality is starting to set in. Though, this did not stop journalists from trying to insert their list of debunked talking points into the interview as they seemed to debate Hawley more than ask him questions.

These debate points have long been a part of the media’s narrative but none of them have held water so far. Assertions of an inevitable “domino effect” leading to a Russian invasion of Europe should Ukraine fall are reminiscent of the same false claims made during the Vietnam War. There is no evidence to indicate Russia has plans to attack Poland or any other NATO member, with Putin obviously aware of the danger of nuclear conflict. As Hawley points out, the warhawks can’t have it both ways – They can’t claim that arming Ukraine has led to the degradation of Russian forces “on the cheap”, and at the same time claim that Russia is strong enough to then overrun Europe should Ukraine lose.

Another disturbing takeaway from this argument is the notion that Ukrainian citizens need to be used as cost effective human shields to prevent a wider war between Russia and NATO. It is the same claim that Zelensky has been making for the past year in order to frighten the western populace into throwing billions more dollars into Ukrainian coffers – “$100 billion and hundreds of thousands of Ukrainian lives will buy you the deaths of hundreds of thousands of Russians. A proxy war is lot cheaper than engaging in a direct war with them…”

But why entertain a war with Russia at all? A false choice has been presented – Either Americans support a proxy war against Russia, or be forced to fight a direct war.

So far, there has been no quantifiable benefits for the western public. It is clear, however, that there are elements of the establishment that desire an ongoing conflict with Russia. The anti-Russian rhetoric began in 2016 well before the war in Ukraine. Propaganda surrounding Donald Trump and “Russiagate” has been thoroughly debunked. Most of the “evidence” presented to prove that the 2016 election was manipulated by Russia was in fact fabricated by groups under the watch of Democrat operatives and some Neo-cons. Of course, the aftermath of the propaganda convinced a large portion of the public (most of them on the political left) that Russia was a predator lurking at their door waiting to strike.

Hawley also notes that while public attentions have been directed at Russia, China is a much more viable threat and any effort to prevent them from invading Taiwan would at this stage be futile. The truth is, neither war is a winnable prospect for the US or NATO given the economic instability at play; a conflagration between East and West would be disastrous for both sides, but western populations have the furthest to fall. Clearly there are people within our government that see this as a good thing as they continue to press geopolitical tensions closer and closer to WWIII.

Tyler Durden

Sun, 09/24/2023 – 22:00 - CDC Refuses To Release Updated Information On Post-COVID Vaccination Heart Inflammation

CDC Refuses To Release Updated Information On Post-COVID Vaccination Heart Inflammation

Authored by Zachary Stieber via The Epoch Times,

The U.S. Centers for Disease Control and Prevention (CDC) is refusing to release updated information on reported cases of myocarditis and pericarditis following COVID-19 vaccination.

COVID-19 vaccines can cause the inflammatory conditions, the CDC has confirmed previously.

The agency has regularly conveyed the number of post-vaccination myocarditis and pericarditis cases to the Vaccine Adverse Event Reporting System (VAERS), which it helps manage, as it has consulted with its advisers on updates to the vaccines.

But during a meeting on Sept. 12, the CDC did not mention VAERS data.

Asked for the information, a CDC spokesman pointed to a CDC study that covers data only through Oct. 23, 2022.

That study identified nine reports of myocarditis or pericarditis following vaccination with one of the bivalent COVID-19 vaccines, which were introduced in September 2022. Seven of the reports were verified by medical review.

Asked for more current data, the spokesman acknowledged the agency has it but is not making it public.

“When appropriate, the updated safety data will be published,” the spokesman told The Epoch Times in an email.

He did not answer when asked why the meeting was not an appropriate time.

“The CDC has acknowledged that heart inflammation is a complication of mRNA COVID-19 shots and, yet, the only published data released by CDC officials about that complication is a seven week study that ended on Oct. 23, 2022. Where is more specific myocarditis/pericarditis data related to bivalent COVID shots for the past 10 months?” Barbara Loe Fisher, co-founder and president of the National Vaccine Information Center, told The Epoch Times via email.

The mRNA shots are made by Pfizer and Moderna. Novavax’s updated shot, which uses different technology, has not yet been authorized by the U.S. Food and Drug Administration (FDA).

“I am tired of the CDC and FDA deciding what information the public needs and doesn’t need. This is precisely the information that parents need to have especially when there are still schools and activities mandating these shots. This is evil playing out right before our eyes,” Kim Witczak, a drug safety advocate who runs the nonprofit Woodymatters, told The Epoch Times in an email.

She added, “The CDC’s response of ‘when appropriate, the updated safety data will be published’ is unacceptable and they wonder why there is vaccine hesitancy and lack of trust in public health officials.”

Presentation

During the recent meeting, CDC officials and their partners presented data on the bivalent shots to their advisory panel, the Advisory Committee on Immunization Practices. The advisers were considering which groups should be recommended to get one of the new COVID-19 vaccines, which were cleared by regulators with scant clinical trial data.

Dr. Nicola Klein, a Kaiser Permanente doctor who works closely with the CDC, gave a presentation (pdf) on COVID-19 vaccine safety. She presented data from the Vaccine Safety Datalink, a monitoring system that covers a much smaller population than VAERS.

Dr. Klein said that two cases of myocarditis after bivalent vaccination were detected in the Vaccine Safety Datalink (VSD) through March 11. It’s not clear why more current data were not presented. Dr. Klein did not respond to a request for comment. The cases did not trigger a safety signal among adults, Dr. Klein said.

The presented data were widely cited by doctors quoted in news outlets, including Dr. Andrew Pavia, who told a briefing that there did not appear to be a “detectable risk” of the bivalent shots causing myocarditis.

“What I was conveying is that in the era of the bivalent vaccine, the number of cases has fallen to where it no longer is giving a signal that is detectable,” Dr. Pavia, chief of the University of Utah’s Division of Pediatric Infectious Diseases, told The Epoch Times in an email. In response to how he could say that with the missing VAERS data, he said “the strongest data are from the controlled studies like the VSD where you have built in controls.”

Through Sept. 8, 98 cases of myocarditis, pericarditis, or myopericarditis were reported to VAERS following bivalent vaccination, according to a search of the system by The Epoch Times.

While anybody can lodge a report with VAERS, research has shown most reports are entered by health care providers. People who submit false information can face prosecution.

Five reports were for people aged 6 to 17 years while another 13 were for people aged 18 to 29.

When presenting to the panel, CDC official Megan Wallace said, “There are limited data to inform the myocarditis risk following an updated mRNA dose.” She did not mention the cases reported to VAERS but alleged the benefits of the vaccines outweigh the risks, even for young, healthy males. The Vaccine Safety Datalink, she acknowledged, did have a “relatively lower sample size” of recipients.

Panel members were taken by the data. Dr. Oliver Brooks said “Feel good about the fact that in the bivalent we saw no signal from myocarditis,” he said after the presentation. “Very important.” Dr. Brooks, chief medical officer at Watts Healthcare Corporation, did not respond to an inquiry.

Dr. Pablo Sanchez, the only member to recommend against a widespread recommendation, said the risk of myocarditis was a reason.

“I think we really need to level with our patients and say what is known and unknown, rather than make a complete recommendation,” he said, “especially for some groups that there are limited data.”

The labels for the new vaccines say they can cause myocarditis.

“Postmarketing data with authorized or approved mRNA COVID-19 vaccines demonstrate increased risks of myocarditis and pericarditis, particularly within the first week following vaccination,” the labels state. While some people have recovered, others have not. The labels also say, “Information is not yet available about potential long-term sequelae.”

Tyler Durden

Sun, 09/24/2023 – 21:25 - China's 300% Debt And Dilemmas

China’s 300% Debt And Dilemmas

By Teeuwe Mevissen, Senior Macro Strategist at Rabobank

Summary

- China’s combined debt (Government, corporate and household) is more than 300% of GDP

- China’s local government debt has been rising sharply for years and is seen as a key risk among investors in Asia.

- With declining income from land sales and increasing expenditures to service these high levels of debt, financial risks for local governments are increasing.

- Local government finance vehicles add to high levels of debt. We estimate that total local government debt is CNY 106.7 tn or USD 14.6 tn.

- Some local governments are scaling down government services and salaries of workers

- High levels of local government debt is likely to put a drain on economic growth for some time to come.

Introduction

Local governments have been a pillar of China’s economic growth model for decades. Land-sales for (commercial) real estate projects, infrastructure investments of all sorts and controlling the allocation of credit to State Owned Enterprises (SOE) have significantly contributed to economic growth. But recently, more and more investors and analysts alike worry about the sustainability of the high levels of local government debt. While the problems in the real estate sector have received much attention in the past two years, the high levels of local government debt have been somewhat overlooked, even as they are currently considered a key risk for economic growth and financial stability for 2023 and beyond. Indeed, the problems in the real estate sector are part and parcel of the problem that local governments are facing right now, but clearly there is a lot more to it. With local governments being responsible for the vast majority of total tax expenditures (estimated at almost 88% in 2023), this creates potential challenges for maintaining robust economic growth. Moreover, holders of local government bonds or bonds issued by local government finance vehicles (LGFV) might run significant credit risks.

This paper will specifically try to assess the financial situation of China’s local governments and tries to answer the question whether and to what extent the levels of local government debts are indeed alarming. We make an estimate of China’s total local government debt by comparing official data of local government debt (where available) with all outstanding local government bonds. We analyse over 11.000 securities to determine local debt to GDP for the relevant administrative levels and determine weighted average maturities and weighted average yields for the respective administrative levels. We also include all outstanding so called Chengtou bonds, i.e. urban construction development bonds. The next step is to look at corporate bonds which also include so called Municipal Corporate Bonds (MCB). We finalise our analysis by looking at balances from the financial sector (excluding the shadow banking sector) to estimate the amount of ‘hidden debt’. We conclude that for some regions there is cause for concern. At best, mitigating measures to deal with the high amount of debt is likely to weigh on China’s future growth potential.

China’s overall debt situation

China’s miraculous path of economic growth and development has received praise all over the world. Never in history was a country so successful in pulling hundreds of millions of people out of levels of absolute poverty. Clearly this could not have been realized without huge amounts of foreign and domestic investments. In other words, money was needed and lots of it. Money that also needed to be borrowed.

While borrowing money makes a lot of sense when the rate of return exceeds the costs including the costs of servicing this debt, this obviously is not always the case. In the case of China, some of the money that has been borrowed has ended up to be speculative borrowing. This includes the real estate sector, households (mainly real estate), poor investment projects by corporates and overambitious local governments that felt the need to simply make good on their economic growth targets by investing in real estate- and infrastructure projects.

Of course investing inevitably comes with risks attached and therefore some losses will have to be incurred. However, at certain levels of debt, the level itself can become a problem regardless of the quality of the loans that have been provided. Liquidity problems, for instance, can occur despite a high quality asset portfolio. Regardless, with a total level of debt of more than 300% of GDP it is clear that China’s fast rising levels of debt need to be brought under control. As can be seen from the graph below, in less than 20-years total debt-to-GDP more than doubled. Moreover, the metric shown in figure 1 is considerably lower both in the US and the Eurozone that -according to the BIS definition – have debt levels of respectively 265% and 255% of GDP

Local Government debt levels

No one knows the weight of another one’s burden

In April this year the total level of government debt was estimated at around USD 23 trillion or CNY 152tn. From this estimate, around 60% (CNY 91.7tn) is assigned as implicit government debt, i.e debt that doesn’t count as ‘official’ government debt. The absence of official data on borrowing by local governments via non-marketable assets has led to a broad range of estimates of what the total size of outstanding implicit debt issued by LGFVs could be.

According to the estimate above, CNY 60tn, or USD 9tn is to be assigned to LGFVs. An estimate by the Wall Street Journal amounts to USD 7tn, while the IMF estimated total LGFV debt at 50% of China’s GDP, which would also amount to approximately USD 9 tn. Wind estimated the total amount of outstanding LGFV debt at almost USD8tn at the end of 2021. The uncertainties that surround these estimates of the amount of implicit government debt plague both onshore and offshore bond markets for LGFV’s. These uncertainties also have received attention from China’s top leadership and recently it became known that China has started a nationwide effort to reveal the amount of hidden debt.

Doing the math: estimates, caveats and assumptions

Of course some of these differences between the estimates can be attributed to changes in the exchange rate, date of measurement or methodology. However, as we have flagged several times, China analysts often need to come up with proxies and estimates since fewer and fewer data is being published. So with this warning, we will explain our methodology, assumptions and estimates below.

In order to estimate the total amount of local government debt we will add up:

- the total amount of local government bonds outstanding,

- the amount of Chengtou bonds outstanding,

- an estimate of outstanding MCB’s, and

- our proxy for non-marketable local government loans (via financial sector)

To estimate the latter, we look at banking balances of depository corporations, foreign funded banks, rural credit cooperatives, and finance companies. We then select their claims on governments and claims to non-financial corporations.

While we are aware of the fact that not all non-financial corporations are state-owned, the total amount is relatively small compared to the claims on governments (figure 5 below). Furthermore, we also acknowledge that there are more ways in which local governments can finance themselves so that simply looking at the financial sector’s claims on governments likely underestimates total non-marketable local government debt. Furthermore, we assume that all claims on government are claims on local governments and that the central government doesn’t fund itself via non-marketable loans. In the following four sections we will simply provide the outcomes of our analyses. For those interested in our methodology we refer to the appendix at the end of this publication.

Local government bonds

Official local government debt is measured by simply adding up all outstanding amounts of bonds issued directly by local governments. This debt adds up to CNY 37.05tn on March 2023.

As we already mentioned above and as figure 4 shows, only CNY 17bn of central government debt is in the form of loans. Since this amount is negligible in comparison to the total we will not correct for this amount when analyzing loans to local governments. Figure 5 shows total outstanding corporate debt of which we assume that SOE’s account for 75% of outstanding corporate bonds. We further assume that 40% of these bonds can be assigned to LGFV.

Finally, figure 6 provides an overview of the financial sector’s claims on government excluding the shadow banking system which generally owns bonds which we exclude to avoid double counting since the bonds that they own are already included in our analyses. As with corporate bonds, we assume that 75% of financial claims on NFC can be assigned to SOE’s of which 40% can be assigned to LGFV. This adds up to CNY 55.6tn. When we add up all 4 separate categories the total amount of local government debt amounts to CNY 106.7tn or $14.6tn (based on a USD/CNH exchange rate of 7.3.

A double-edged budgetary sword

But for some local governments problems seem to go further than fast growing levels of debt. Local governments have consistently run budget deficits for years as can be seen from figure 7 and 8 below. With debt levels growing, so has the share of local government budgets that needs to be spent on interest payments on those debts. Moreover, with declining revenues from land sales as a result of the real estate crisis, local government budgets have become even more strained. While funding has generally become cheaper (see figure 9) it remains to be seen whether this trend will hold. Should market participants start to question the credit worthiness of local governments, this trend could quickly reverse.

Additionally, it is important to bear in mind that these lower levels of average yields have to be paid on a much larger amount of nominal debt. To be more specific, while in 2020 yields for standard bonds averaged around 3.50% and in 2023 approximately 3.35%, the total amount of outstanding debt went up from CNY 24tn to CNY 37tn.

This means that in 2020 total interest to be paid on outstanding standard government bonds amounted to CNY 840bn while in 2023 this would already be CNY 1,240bn. To summarize – total (interest rate) expenditures have gone up while (potential) revenues have gone down, creating a double-edged budgetary sword.

In some cases we now see that this leads to challenges for some local governments to continue to provide the usual level of government services. This could mean the delay of the salary payments for (local)government workers, lower pension benefits or downscaling of healthcare services. But local governments are also urging local companies to repay their (overdue) debts. More extreme incidents have also been reported, such as fining a restaurateur for $700 for serving a cucumber dish. For obvious reasons we assume that the more indebted regional governments run the highest risk of needing to cut expenditures or worse default.

Figure 10 shows the ratio of debt to GDP for local governments. It is important to consider that China distinguishes different levels of local government. While the constitution identifies three levels of government, in practice there are five. Here, we mainly focus at the provincial level which includes provinces, autonomous regions, municipalities and special administrative regions. Furthermore we have included a few prefecture level cities that have issued their own bonds, such as Beijing and Shanghai.

From the graph above it becomes clear that official local government debt to local GDP ratios differ wildly, from less than 10% in Shenzhen to almost 90% in Qinghai. Furthermore, if we look at the financially more vulnerable regions in 2020, we see that in 2023 not much has changed. Qinghai, Yunnan and Guizhou are still the most vulnerable regions with debt to fiscal revenue reaching 1087% in Yunnan in 2022 meaning that it would require almost 11 years of revenues to pay off Yunnan’s local government debt. Most vulnerable regions are located in the North- and South-West of China, while China’s economically vibrant East coast are generally characterized by significantly healthier debt ratio’s. As such, these regions look a lot more able to raise tax revenues. They also have more valuable assets to sell if that would ever be needed.

It is important to realize that according to the local government debt risk emergency response plan article 4.1 ‘Local governments are responsible for repaying debts they borrow, and the central government implements the principle of no bailout’. In general, the debt emergency response is dependent on the severity of the specific debt risk event but we will not elaborate much further on the legal technicalities here. The key point is that a central government bailout of a local government that risks falling into default, is anything but certain.

When we zoom in further on the amount of outstanding official local government debt, we see that, whilst there is a positive relationship between the average maturities and yields, the relative financial vulnerability of a region or province is not necessarily reflected in weighted average yields. An important reason for this is the assumption by investors that official local government debt has an implicit guarantee from the central government. But as we have concluded above, it remains to be seen whether and, if so, to what extent, the central government will bail out local governments.

Having calculated the weighted average yield we can also obtain an estimate of the amount of interest that is needed to service these outstanding official local government debts. Since we also know the total level of local government expenditures – which amounts to CNY 23.67tn – we can obtain the average percentage of debt servicing expenditures compared to total expenditures.

Our calculations show that almost exactly 4% of total official local government expenditures is spent on interest of outstanding official local government debt. Needless to say that there are significant differences between regions. Since we do not have data about individual local government budgets we calculate our estimation of debt servicing costs per region by assuming that local government budgets are divided equally based on the weight that a certain region has in total GDP. This gives us the following estimates.

While it is clear that the assumptions that we made only lead to an approximation of the true financial situation for local governments, the most fragile local governments are the usual suspects. In a previous publication that investigated the link between higher rates and government finances we assumed that if a (local) government has to spend more than 10% of the total expenditure budget to service existing levels of debt, this starts to put (local) government finances under pressure. We apply this threshold on our analyses as well. As can be observed from our estimates this includes 7 of the 36 regions. Based on an average level of debt servicing of 7.2% which is the average level of bonds rated BB by Fitch, 19 regions would face financial challenges. However it is important to realize that we included redemptions for the whole of 2024. This means that if we had used a 12 month window the outcomes would be slightly lower.

Recent developments

Looking at the most recent developments, China appears to have decided to double down on the same path that we have become so accustomed to; i.e. let local governments borrow more money to spend more on infrastructure. Indeed, as recently as 31 August it became clear that local governments are accelerating the pace of borrowing (which is not visible in figure 3 above since these are the special bonds/Chengtou bonds discussed previously). Local governments are accelerating issuance to meet their 2023 targets and are expected to raise the remainder of the 2023 target of CNY 3.8tn before the end of this month according to minister of finance Liu Kun. This would mean that local governments still have to issue approximately CNY 800bn to meet this target.

Furthermore, local governments that have not used their quota in previous years are allowed to issuance additional bonds. It is estimated that this could free up an additional amount of CNY 1tn which would then be used for debt swaps, i.e. issuing a bond to pay of bank loans or other forms of non-standard/non marketable loans. However, as we have discussed in previous publications, new infrastructure projects increasingly provide diminishing marginal returns on investments made. Additionally, while refinancing can put further pressure on average yields (figure 8), the total amount of debt is likely to increase by another 1.8tn regardless.

So what is next?

Now that we have obtained an overview of the ins and outs of China’s local government debt situation it is time to reflect on what this means for China’s economy. First, we conclude that -based on our benchmark assumption that a (local) government that spends more than 10% of the total budget on debt servicing is financially fragile – a significant share of China’s local governments have or are approaching risky levels of debt.

If the current trend of increasing debt levels continues, we believe it is a matter of time before a significant share of local governments will run into financial difficulties. At this moment it is mainly the fragile liquidity position that local governments are struggling with. While the PBOC can provide for extra liquidity in the financial system by lowering the 7-day RRR for example, it should be clear that this will not offer a structural solution.

Although higher taxes would increase local government revenues, it could also put further downward pressure on consumer demand. Currently, total consumption is already at low levels contributing only 38% to total GDP growth. If Beijing would be serious about reforming their economic model from a purely export-based economy to an economy of dual circulation – i.e. remaining open for trade and investments (external circulation) while prioritizing domestic demand (internal circulation) – raising taxes is not a policy that would help achieving that goal. Remember that China also postponed the imposition of a real estate tax in order not to aggravate the real estate crisis. Increased revenues from land sales are also not to be expected in the foreseeable future. So, with limited possibilities to raise local government revenues we are left with a number of other options. In no particular order, these options are:

- cut local government spending

- blend and extend operations of the current outstanding debt

- a bail-out of highly indebted local governments by the central government

- defaulting on debt by local governments

To date, no bond defaults have yet occurred, but local governments have already defaulted on nonstandard debt in several cases. As long as there is no risk to the broader financial system we do not expect that Beijing will come to the rescue when a local government would not be able to service its debt obligations anymore.

While some local governments have reigned in spending as we discussed above, they are also pressed to issue more debt and prop up spending. So cutting local government spending does not seem to be Beijing’s preferred strategy. Indeed, we think that blend and extend operations will turn out to be the preferred and most likely policy.

In this case, major state banks will be asked to be lenient towards local governments and the PBOC will support those state banks. This could be done by adjusting interest rate policies and/or lowering the required reserve ratio – currently at 7.6% for relevant banks (not all banks have the same RRR as this depends on the size of the balance sheet). Indeed we do see an high chance of the PBOC lowering the RRR this month.

No crisis, but weighing on growth all the same

In other words, those who are waiting for a big bazooka will likely be disappointed. However, we also do not expect an uncontrolled crisis that would put the financial system as a whole in danger. First of all because it can simply be avoided. China still has considerable amounts of foreign reserves and also has the means to increase tax revenue if necessary. Although this would go at the cost of domestic consumption. Additionally, an uncontrolled collapse would come with socioeconomic instability which is something that Beijing wants to prohibit at all costs.

In the end the current local government debt situation is an example of “choose your poison”. Losses are likely to be divided between bond holders and banks. While the amount of offshore bonds is limited, the holders of those bonds are likely to be the first ones to get hit with a haircut as we have seen in the real estate sector already. So in the end we expect a combination of different measures. The tool of preference is likely to be blend and extent operations. Still, a blend and extent approach would mean that the fragile financial position of local governments will continue to weigh on economic growth for a long time to come.

We also expect some defaults to occur and here the hybrid bonds, which invest in multiple (commercial) projects, seem to be the most risky bonds given the fact that the government is less likely to save SOE’s. Indeed the bonds that are most likely to be eligible for a bail out are bonds that are officially regarded as local government debt. Regardless, China’s economy is likely to be at the start of a long process of deleveraging that will suppress economic growth for years to come.

Appendix

Methodology

Official local government debt (issued bonds)

Starting with the official total amount of debt for local governments we see that this stood at CNY 37.05tn (USD 5.17tn) in March this year. Again, this figure excludes so-called Chengtou bonds and non-standard/non-marketable products which are generally bank loans or private placements to local governments made by (local) banks.

When looking at the development of this narrow definition of outstanding local government debt we still see that the absolute level of debt has almost doubled over the last four years. While it is understandable that government debt has risen given the huge health care costs and the government stimulus that had to be provided during the Covid Pandemic, the current pace of increasing levels of debt is unlikely to be sustainable in the future.

Chengtou Bonds

When including Chengtou bonds, which unlike ‘normal’ local government bonds are often issued for specific urban construction development purposes, we obtain a more accurate picture of local government’s total amount of outstanding debt. Chengtou bonds can be separated in two different classes: quintessential and hybrid bonds. In both cases the ownership is in the hands of local government entities, but hybrid bonds hold more diversified assets and as such are more similar to SOEs. This means that a hybrid bond can invest in both public as well as in private projects.

The idea of issuing hybrid bonds was initially stimulated by the central government to raise revenues in order to decrease reliance on local government finances. However this also led to excessive risk taking. Furthermore, from the central governments point of view, hybrids are deemed less important than the quintessential bonds that solely finance collective projects. This heightens the credit risk on hybrid bonds. Until recently, there was a tendency to attract more capital from abroad via offshore Chengtou bonds, but the Fed rate hiking cycle has made this form of funding increasingly less interesting.

Bloomberg data suggest that at the moment of writing there are 11,517 outstanding onshore securities which amount to CNY 8,818bn. When we include offshore bonds this amounts to 12,047 securities, adding up to CNY 8,887bn. Together with the amount of official outstanding government debt this totals approximately CNY 46tn of debt or about USD6.5tn. This still falls way short of the estimates by other institutions.

Municipal Corporate Bonds (MCB)

This is largely because we have not included non-standard/non-marketable government debt and MCB. We will first outline our assumptions behind our estimation of the more hidden part of local government debt. First, when we look at how the central government funds itself, we see that the vast majority of central government’s cash intake comes from issuing bonds.

In figure 4 one can observe that, indeed, only a bit more than CNY 17bn is funded through (bank) loans. We therefore assume, for simplicity, that all net claims on government are bank loans to local governments. We also include all claims on non-financial corporations since many SOEs are qualified as non-financial corporations. Indeed the bonds that are issued via LGFV’s are also known as MCB’s.

While these bonds are initially traded via the interbank market, the majority are held by wealth managers and the shadow banking system. We exclude the shadow banking sector since we have already included all bonds that have been issued by local governments (see figure 3) and we are not focusing on credit exposure in this special. Moreover, we have no means to analyse this sector because (reliable) data is absent. Finally we also exclude debt secured by stocks given that it is not considered government debt for domestic creditors according to article 3.3.3 subsection 1 which says: … “Stock secured debt is not government debt. According to the Guarantee Law of the People’s Republic of China and its judicial interpretations, except for loans from foreign governments and international economic organizations, the guarantee contracts issued by local governments and their departments are invalid, and the local government and its departments shall not bear the liability for debt repayment”…

This leaves us with estimating which share of corporate bonds should be considered as local government debt. Many estimate that as much as 40%-50% of outstanding corporate bonds are related to local government debt. The total amount of outstanding corporate bonds in China is about CNY 60tn (based on Bloomberg data). However these outstanding corporate bonds also include many Chinese banks. The Asian Development Bank reports an outstanding amount of local currency bonds for the corporate sector at CNY 44.4tn so we use this amount for our analysis. According to a IMF paper from 2019, SOE’s account for 75% of non-financial corporate debt. This would imply that 75% of CNY 44.4tn is in scope. Staying on the conservative side, and in line with other approximations, we estimate that 40% of this debt is related to LGFV’s. This amounts to CNY 13.3tn of outstanding local government debt. However we have to subtract the outstanding amount of Chengtou bonds since these are incorporated in the total amount of outstanding corporate bonds. This leaves us with CNY 4.3tn of additional outstanding debt.

Non-marketable debt (loans by financial sector)

We can now come up with our estimate/proxy of the banking sector’s exposure to local government debt. In figure 5 it can be seen that depository corporations by far hold most claims on government. The total amount is CNY 51.1tn. We keep the claims on NFC constant since data is only available until 2022. Similar to the assumption that we made earlier, we include 75% of this debt (6tn) as exposure to SOE’s. This amounts to CNY 4.5tn in additional exposure. We estimate that the financial sector’s total exposure to local governments amounts to roughly CNY 55.25tn which is close to USD 7.6tn. This is actually very comparable with other estimates that we referred to above.

If we add this up to the numbers in our previous findings this would amount to a total amount of local government debt of CNY 106.7tn or close to USD 14.6tn. This is higher than the CNY 95tn (or USD 13.2tn) estimate based on an analysis by Goldman Sachs.

Breakdown of China government debt, all 152TN yuan of it. pic.twitter.com/H5C2Jw5U71

— zerohedge (@zerohedge) June 5, 2023

https://platform.twitter.com/widgets.js

Clearly these changes can be explained by differences in methodology and a different time of measurement. As the graph below shows, the claims that depository corporations have on the government rose from CNY 47.6tn in December 2022 to 51.14tn in July 2023; an increase of almost 7.5%. This already explains almost CNY 4tn difference.

(Also available in pdf format to pro subs here)

Tyler Durden

Sun, 09/24/2023 – 20:50 - "Don't Be Intimidated" By The Censors – Tucker Carlson Urges Americans To Fight Back By 'Telling The Truth'