- UBS Turns Bearish On Stocks For First Time Since Financial Crisis

With more than $2.48 trillion AUM, UBS Global Wealth Management is one of the world’s largest asset managers. And now, for the first time since the financial crisis, the Swiss bank has dropped its rating on equities to ‘underweight’ as it braces for a recession spurred by a worsening trade war and slowing economic growth in Europe, Bloomberg reports.

The Swiss asset manager cut its equity positioning relative to investment-grade bonds, said Global Chief Investment Officer Mark Haefele, to reduce its exposure to all of the factors mentioned above.

More specifically, the change incorporates a new underweight position in emerging-market stocks.

“Risks to the global economy and markets have increased, following a renewed escalation in U.S.-China trade tensions,” Haefele said.

UBS had resisted turning outright bearish on stocks, even as the the trade war between the world’s two largest economies intensified, leading up to President Trump on Friday declaring his plans to raise tariffs on $250 billion of Chinese goods to 30% from 25%.

“With talks between the US and China dominating market moves over the near term, investors should brace for higher volatility,” Haefele said.

“We believe it is prudent to take action to neutralize part of this event risk.”

Additionally, UBS has been recommending clients go long gold for months now, and lately, it raised its price target on the precious metal to $1,600/oz, per BBG.

Haefele reiterated that emerging-market stocks are the most vulnerable because they are “the most exposed to heightened market volatility.”

- In 2019, Bombings And Explosions Up 45% In Sweden

Authored by Jon Hall via FMShooter.com,

Compared to the same period from January to July in 2018, the occurrence of explosive incidents and bombings in Sweden sky-rocketed 45 percent this year.

Statistics revealed by authorities show that Sweden saw 120 explosive events, whereas that same number from 2018 was only 83. Different sources report different numbers for the entire length of 2018, however. According to paper Dagens Nyheter, 157 explosions took place across the country in 2018 while the Crime Prevention Council BRÅ reported 108 instances of destruction via explosion last year.

The numbers differ but all of the organizations agree that 2019 has seen a rise in bombings.

Criminologist Sven Granath detailed on the explosions, explaining:

Yes, unfortunately, it has increased. Why we do not know, this may be due to the increase in gun violence at the national level. In individual locations, there may be one or more conflicts between criminal networks, but it is very difficult to know.

“You can really only speculate. It may be stolen from a building site and sold, or maybe smuggled in,” Granath continued, noting that investigators never know for certain what materials were used in the explosions or what their origins were.

According to police, the nature of explosions have shifted in recent years. At one point, hand grenades were more common in Swedish bombings but now dynamite, stolen from construction sites, has become the new norm.

Experts claim that the explosions are likely linked to organized crime and could be increasing due to stricter regulations on firearms in Sweden.

Sweden’s southern city of Malmö has been faced with a high number of explosion cases in the last several years with 58 cases in 2017, 45 last year, and 23 so far this year. Notably, the city saw three explosions in the span of just 24 hours earlier this year.

It seems that authorities willingly bury their head in the sand regarding the similar correlation of an increase in migrants and refugees as bombings and explosions also rise. Experts and officials can call it “organized crime” if it makes them feel better, but it is wholly ignoring the true problem at hand.

The reality of the situation is that the importation of third-world invaders into a once prosperous and stable first-world country has turned it into an unsafe and tumultuous battle zone where the threat of explosions place high in the minds of citizens.

After all, you reap what you sow – and Sweden is doing that, tenfold.

- Why Are Russian Special Forces Training With American Assault Rifles?

One of the most unusual stories to start the week is coming from VladTime, a Russian news agency, who reported Russian Special Forces have been exercising with American M4 carbines this month, with additional reports of how some of these soldiers are currently buying western weapons.

Military officers of the 45th Spetsnaz Airborne Brigade, a special reconnaissance and special operations military unit of the Russian Airborne Troops, said soldiers practiced shooting targets, reloading, and assembly and disassembly of the M4 last week.

Officers said NATO Response Forces have been familiarizing and training with Russian weapons for some time. The latest move to train forces with western carbines is a direct result of NATO testing Russian assault rifles.

According to one officer, special forces units were surprised by the accuracy of the M4 and even said, it’s more comfortable to shoot than the AK-74M, the main service rifle in use in the Russian Army. These elite soldiers said the ergonomics and compactness of the American assault rifle were appealing.

“It should be noted here that it was precisely such courses on familiarizing with foreign weapons that preceded the mass appearance of American and German rifles with FSB special forces. The special forces officers who appreciated the advantages of modern Western weapons, with the permission of the leadership, began to purchase them with their own money,” VladTime said (translated via Google).

Another officer of the special forces told the publication that upper command has been speaking with local gunsmiths to make the Kalashnikov rifles more like western carbines. The report goes on to say special forces are already acquiring modern Western rifles and carbines, ahead of the possibility that upper command approves the use of these weapons.

The main reason Russian Special Forces like the M4 firing a 5.56 X 45 NATO round, versus the Kalashnikov AK-47 firing a 7.62X39, is that the weapon is more lightweight, ergonomic, and more accurate.

- Obamas' "American Factory" Film Backfires, Exposes "Damning Snapshot Of American Labor Entitlement"

Authored by Peter Earle via The American Institute for Economic Research,

The Inconvenient Truth of American Factory

Higher Ground, the production company founded by Michelle and Barack Obama, has released the first of a planned seven-film series on Friday.

American Factory chronicles the opening of a Chinese factory near Dayton, Ohio, where a GM plant closed in 2008. It’s reasonable to suppose that the point was to alarm us about the wiles of global capitalism. Oddly, the film might have the opposite effect on many viewers. It certainly did for me.

The documentary opens with a prayer on the day the plant closes as tearful workers see the last vehicle come off of the production line. A few years later, Fuyao Glass announced its intent to open a glass-production facility in the shuttered facility. One of our first glimpses is of a question and answer as American employees of the Chinese firm speak about the goals of the firm to prospective employees: they plan to employ several thousand people in all capacities, but mostly blue-collar work of the type that disappeared when the local GM plant shut down. One prospect asks if this will be a union shop. No, he is told. The plan is to be non-union.

Perhaps because of their proximity to widespread unemployment, everyone who heard that answer nods in agreement. This new factory is the only game in town, and the best news most of these out-of-work machinists and factory hands have heard in years.

Initially, most of the senior managers are Americans, but alongside the American workers are a group of Chinese workers. Also initially, most of the U.S. workers are deeply appreciative of the new opportunity. We follow one who, since the closing of the GM plan, has been reduced to living in her sister’s basement. Others have been out of work for some time, barely getting by on part-time work and odd jobs.

We don’t know how much of the documentary’s production choices were under the specific direction of the former president. Mr. Obama is sometimes astonishingly tone-deaf, as when, despite his regular trafficking with the global warming/climate change crowd — and more specifically in light of their incessant warnings about massive impending changes in sea levels and coastlines — he nevertheless purchased a $15 million estate on Martha’s Vineyard. If this is a story largely seeking to highlight differences in workplace culture, that objective is vastly overshadowed by the incredible arc that the formerly unemployed workers’ attitudes travel over a fairly short amount of time.

Initially, the woman who has been living in her sister’s basement has moved into an apartment. She extols her reacquired independence. Other employees bemoan their non-union pay and conditions but seem contented; they or friends and family have lost houses, have seen communities torn apart, and know firsthand the double impact of the so-called Great Recession and increasing competition from China. But even that wears off over time.

The work is sometimes dangerous, and the pay is lower than many of the workers have previously received, and before long thankfulness is replaced by myopia. Despite the company’s warnings, there are rumblings about unionization, and a United Automobile Workers agitator is caught walking through the private workspace with a “Union Yes” sign held aloft. The ineffectiveness of American managers to quash the unionization efforts leads to their sudden termination, and the Chinese CEO threatens to close the plant if it continues.

The same workers who, a short time before, were deeply appreciative of their unlikely bounty then begin to badmouth the company. Some are meeting secretly with union officials. Ultimately employees hold a vote, and the result is somewhat surprising.

There are two particularly telling moments in the film.

In one, a Chinese manager teaches a class on how to deal with Americans, whom the Chinese line employees are training. Americans, he explains, need constant encouragement. It’s a hilarious and somewhat cringeworthy section.

In another, an employee at a local union hall complains to a cheering crowd that while he earned $27,000 last year, his nail-polishing daughter earned $40,000. Apparently, this man is unaware that there is absolutely no prohibition against his learning to paint nails for higher compensation — and with a daughter who does so, he has ready access to a highly cost-effective apprenticeship.

Despite intense lobbying and enthusiasm, the union effort is defeated. A number of the labor organizers are fired; most just sheepishly return to their duties. In one of the last scenes, we overhear plans to automate many of the jobs at the factory, which would eliminate more positions. There’s no way of knowing whether this was the plan all along or whether the shift in workers from contentment to intrigue was a key part of the decision-making calculus of the Chinese owners, but it wouldn’t be surprising if the collective bargaining bid accelerated automation plans. None of this is surprising, especially given Fuyao’s clearly stated position against collective bargaining from the very beginning.

It’s difficult for people to unlearn things they’ve grown up seeing, they’ve been told for decades, and for which they have apparent confirmation: the idea that union work naturally paid well and provided a generous raft of benefits was feasible in decades when international competition was virtually nonexistent. Throughout the ’50s, ’60s, and early ’70s, owing to the need for most of the rest of the world to rebuild after World War II, the establishment of the Iron Curtain, and the spread of collectivism throughout Asia, billions of potential competitors were simply out of the global mix. The dollar was king, and all of the major financial centers were in the Western Hemisphere.

But this period was an anomaly, even if wishful thinking sought to enshrine it as an indication of intrinsic American superiority: by the ’70s and ’80s, what was true all along finally became practicable. Markets opened, information began flowing, capital aggregated, and most of all people in other parts of the world proved that they were willing and able to do the work that Americans firmly believed only we could do. And our upstart labor competitors were willing, indeed appreciative of, the opportunities that sprung up.

There’s a common refrain from labor unionists and union members: the American worker is the best in the world — better than any of his international counterparts. It’s a feel-good, self-congratulatory sentiment, but it crumbles upon even superficial consideration. Here, it’s empirically untrue: the Chinese workers alongside Fuyao’s American employees work harder, for longer hours — they’re often at the factory working on evenings, weekends, and holidays, and do so for less pay and fewer benefits. This may not make them better people, but it absolutely makes them better employees and thus better economic prospects for firms. Even they, though, have limits, and machines are more efficient and productive.

The Obamas may have intended to make a film about workplace culture clashes. However, as it turns out, American Factory is at its core a damning snapshot of American labor entitlement. In an era where painful truths about the declining relevance of blue-collar work and the potential of automation are becoming evident in many fields, it will undoubtedly remain instructive over time. The events depicted are not a fleeting glimpse of a changing past, but an indication and warning of a rapidly oncoming future.

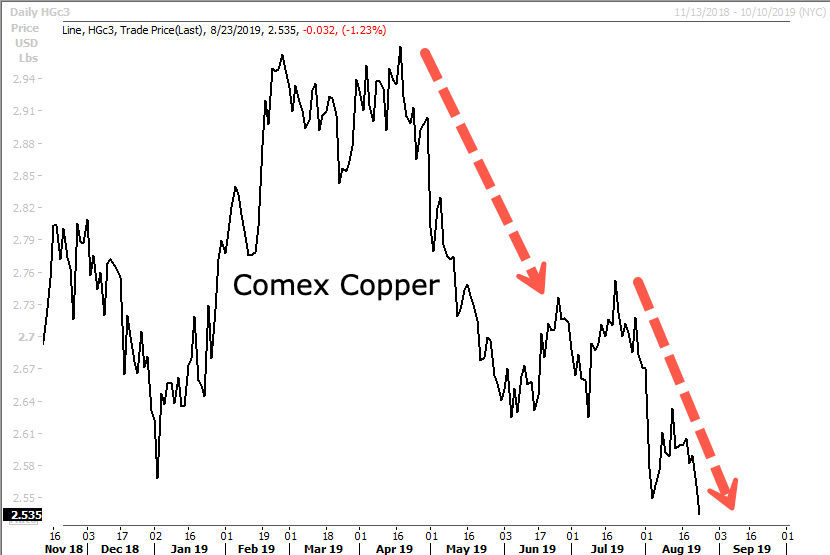

- (Dr.) Copper Collapses To 2-Year-Low As Global Macro Deteriorates

Industrial metals such as copper continue to stagnate this year as major funds take an increasingly bearish view on global macro.

The spot price of Comex copper on Friday fell 1.23% to 2.535, the lowest level in at least 115 weeks, dating back to the summer of 2017.

Copper dropped 3.34% this past week amid new fears the US economy is quickly slowing. IHS Markit’s flash reading for the manufacturing purchasing managers index, recorded 49.9 for August on Thursday, the first contraction since 2009. This is an indication a manufacturing recession could be imminent, seems plausible since a freight recession across is already underway; explains how the Trump bump in the economy has been exhausted and reveals further why President Trump is demanding 100bps rate cuts, quantative easing, and emergency payroll taxes: it’s because the cycle is rolling over. We even mentioned last week how President Trump might hold an emergency meeting next week with advisors and top donors about how a mild recession could materialize before the 2020 election.

In the last 89 days, copper is down nearly 15% from its high in April.

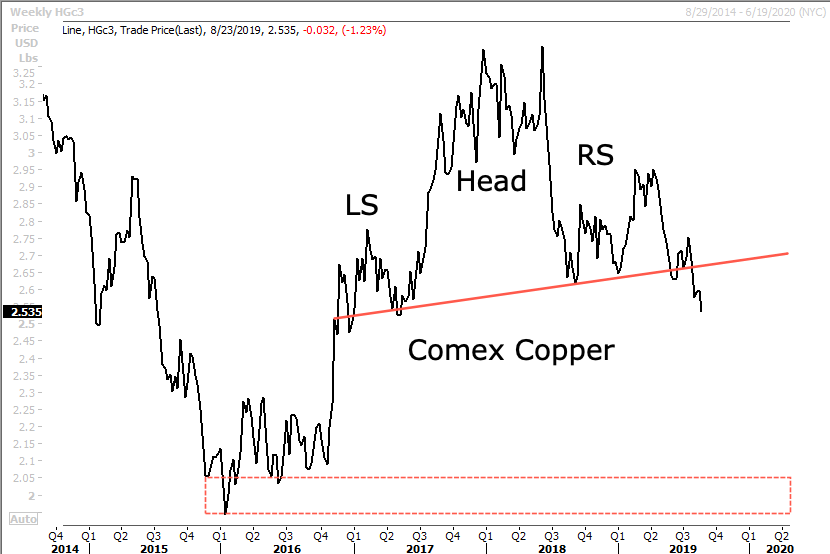

On a longer perspective, copper crashed -58% from early 2011 to January 2016. Copper prices eventually troughed at 1.94 around mid-January 2016, as global central banks pumped the world with liquidity in 2016, and then the Trump administration in 2017 and 2018 injected fiscal stimulus into the domestic economy, which helped copper prices soar 62% until June 2018. Prices then plunged into late summer and fall of 2018, by 21% as the world realized a global slowdown was developing.

The rollercoaster in prices, up and downs, created a massive head and shoulder pattern that could be completed in 2H19, or at least some time in 1H20. This would be due to another growth scare that could shock world markets. If copper was to break the head and shoulders neckline, a possible retest of 2016 levels, around 2-2.15, could be likely.

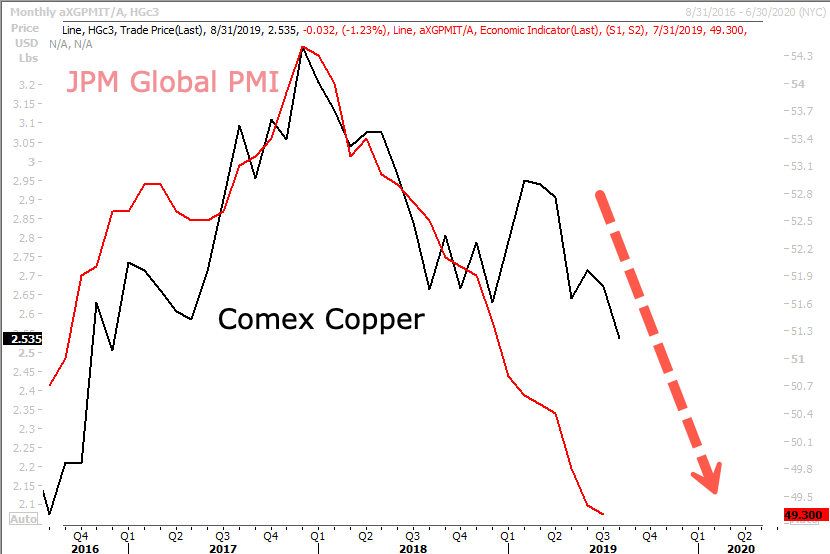

In textbook commodity market fashion, the price slump has been associated with a J.P.Morgan Global Manufacturing PMI plunging to sub 50, a harbinger that a global manufacturing recession could be imminent, or is already underway.

The Wall Street Journal said, “Net bearish bets on copper in futures markets hit their highest level in around three years earlier this month, a sign that investors have grown increasingly pessimistic on the outlook for the metal in the midst of slowing global growth and a weakening Chinese economy.”

China is the world’s largest copper user, accounting for almost 50% of global demand.

So when copper prices slump, it’s also a proxy of the health of the Chinese economy.

Earlier last week, Fathom Consulting, a global independent macro research consultancy, said its proprietary China Momentum Indicator 2.0 has slowed to 4.6% in June, the lowest reading since Aug. 2016.

There is also a growing gap between the China Momentum Indicator 2.0 at 4.6% and official GDP data at 6.2%. Might suggest China’s economy hasn’t yet bottomed, could continue to decline through 2H19 into 1H20.

And on Friday, to make matters worse for the global macro outlook, China’s Ministry of Finance said in a statement that it would levy retaliatory tariffs on another $75BN in US goods with rates anywhere between 5 and 10%, with the tariffs set to be implemented in two batches, one at midnight on Sept 1 and another at midnight on Dec 15.

Additionally, China said it would resume 25% tariffs on US autos, stating that “China’s adoption of tariff-adding measures is a forced move to deal with US unilateralism and trade protectionism.”

Then in a retaliatory move, President Trump announced starting Oct 1, the existing 25% tariffs on $250BN in Chinese goods would rise to 30%, and the 10% tariffs on $300 billion in Chinese goods set to begin on Sept 1 will be 15%.

With that being said, the global macro outlook looks set to deteriorate further into 1H20, sending copper prices tumbling much further.

- Is Silicon Valley Building A Chinese-Style Social Credit System?

Authored by Mac Slavo via SHTFplan.com,

Companies in the United States, and more specifically, Silicon Valley, are building a social credit system for individuals. Much like the social credit system communist China uses to control its population, this authoritarian control is different in one way: it is being done by corporations as opposed to the government.

Make no mistake though, the corporations building a social credit system in the U.S. are already another arm of the government. They are lobbying and using the money made to get certain politicians elected. This is the very definition of crony corporatism. If anyone thinks we live in a democracy or constitutional republic, they are either wholly uninformed, brainwashed or willfully ignorant.

China’s tyrannical social credit system is a technology-enabled, surveillance-based nationwide program designed to nudge citizens toward better behavior (or government-approved behavior). The ultimate goal is to “allow the trustworthy to roam everywhere under heaven while making it hard for the discredited to take a single step,” according to the Chinese government

According to Fast Company, China’s social credit system has been characterized in one pithy tweet as “authoritarianism, gamified.” And it’s already here in the United States.

While many Westerners are disturbed by what they read about China’s social credit system, they need to realize that they live under a system that is similar. Such systems are not unique to China. In fact, a parallel system is developing in the United States, in part as the result of Silicon Valley and technology-industry user policies, and by surveillance of social media activity by private companies. Big Tech is helping advance totalitarian control over the population by censoring information they deem goes against the government’s agenda.

For example:

The New York State Department of Financial Services announced earlier this yearthat life insurance companies can base premiums on what they find in your social media posts. That Instagram pic showing you teasing a grizzly bear at Yellowstone with a martini in one hand, a bucket of cheese fries in the other, and a cigarette in your mouth, could cost you. On the other hand, a Facebook post showing you doing yoga might save you money.

Airbnb can disable your account for life for any reason it chooses, and it reserves the right to not tell you the reason. The company’s canned message includes the assertion that “This decision is irreversible and will affect any duplicated or future accounts. Please understand that we are not obligated to provide an explanation for the action taken against your account.” The ban can be based on something the host privately tells Airbnb about something they believe you did while staying at their property. Airbnb’s competitors have similar policies.

It’s now easy to get banned by Uber, too. Whenever you get out of the car after an Uber ride, the app invites you to rate the driver. What many passengers don’t know is that the driver now also gets an invitation to rate you. Under a new policy announced in May: If your average rating is “significantly below average,” Uber will ban you from the service.

You can be banned on WhatsApp if too many other users block you. You can also get banned for sending spam, threatening messages, trying to hack or reverse-engineer the WhatsApp app, or using the service with an unauthorized app.

An increasing number of societal “privileges” related to transportation, accommodations, communications, and the rates we pay for services (like insurance) are either controlled by technology companies or affected by how we use technology services all while Silicon Valley’s rules for being allowed to use their services are getting stricter. All of the companies participating in these types of behavioral controls want one thing, and it’s the same thing the government wants: power over people.

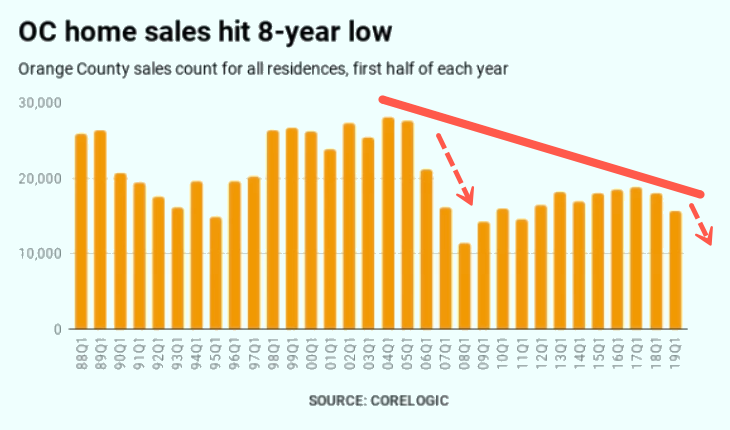

- Orange County Homebuying Plunges To 8-Year Low As Home Prices Stall

Orange County homebuying in the first six months of this year was awful, signals the top could be in as a correction in the overall California housing market could be nearing.

CoreLogic homebuying data shows 1H19 sales in and around Huntington Beach, Fountain Valley, Garden Grove, and Westminster fell 12% to the slowest pace since 1H11, just after the Great Recession ended, reported Orange County Register.

The report noted how the countywide median selling home price plateaued in 1H19, indicating a resistance level with what homebuyers are willing to pay for properties has been met.

Another concern is that lower interest rates over the last two quarters didn’t spark a revival in homebuying. It’s becoming more evident that a cyclical downshift in the regional housing market is gaining momentum.

Countywide, 15,792 homes were sold, down 12% in 1H19 YoY. It marked the slowest first half for selling since 2011. Sales were up in only 17 of the county’s 83 zip codes. The median home price of $735,000 was flat in 1H19.

Single-family home sales sank 9% in 1H19 YoY, with 9,912 sold, the slowest since 1H11. The median price fell 2% in the period to $780,000.

Condo sales in the county were down 11% in the first two quarters, with 1,572 sold — the slowest since 1H09.

Newly built home sales were down 34% in 1H19 YoY, with 1,572 sold, the slowest first half since 2013. However, the median price was up 6% in the period.

CoreLogic data pointed out several interesting neighborhood trends:

-

Seven-figure neighborhoods: 12 zip codes out of 83 with median selling prices at $1 million or more vs. 14 ZIPs a year ago. Sales in these high-end ZIPs totaled 1,900 — down 27% in a year.

-

Sub-half-million communities: Just six zip codes medians were below $500,000 compared with four ZIPs a year ago. Sales in these more-affordable ZIPs totaled 651 — up 5% in a year.

Here are more homebuying trends for Huntington Beach, Fountain Valley, Garden Grove, and Westminster:

-

Fountain Valley 92708: $805,000 median, up 2.9% in a year. Price rank? 24th of 83. Sales of 234 vs. 266 a year earlier, a decline of 12% over 12 months.

-

Garden Grove 92840: $552,500 median, down 4.5% in a year. Price rank? No. 72 of 83. Sales of 197 vs. 196 a year earlier, a gain of 0.5% over 12 months.

-

Garden Grove 92841: $615,000 median, down 0.8% in a year. Price rank? No. 62 of 83. Sales of 94 vs. 92 a year earlier, a gain of 2.2% over 12 months.

-

Garden Grove 92843: $560,000 median, up 4.7% in a year. Price rank? No. 67 of 83. Sales of 96 vs. 118 a year earlier, a decline of 18.6% over 12 months.

-

Garden Grove 92844: $485,000 median, down 14.5% in a year. Price rank? No. 79 of 83. Sales of 64 vs. 83 a year earlier, a decline of 22.9% over 12 months.

-

Garden Grove 92845: $659,000 median, down 0.9% in a year. Price rank? No. 53 of 83. Sales of 100 vs. 100 a year earlier, flat in the period.

-

Huntington Beach 92646: $742,750 median, up 0.4% in a year. Price rank? No. 38 of 83. Sales of 314 vs. 369 a year earlier, a decline of 14.9% over 12 months.

-

Huntington Beach 92647: $740,500 median, down 1.9% in a year. Price rank? No. 39 of 83. Sales of 168 vs. 197 a year earlier, a decline of 14.7% over 12 months.

-

Huntington Beach 92648: $988,000 median, up 4.9% in a year. Price rank? No. 13 of 83. Sales of 231 vs. 303 a year earlier, a decline of 23.8% over 12 months.

-

Huntington Beach 92649: $790,000 median, up 1.3% in a year. Price rank? No. 29 of 83. Sales of 182 vs. 196 a year earlier, a decline of 7.1% over 12 months.

-

Midway City 92655: $665,000 median, up 5.6% in a year. Price rank? No. 51 of 83. Sales of 24 vs. 13 a year earlier, a gain of 84.6% over 12 months.

-

Stanton 90680: $425,500 median, down 1.0% in a year. Price rank? No. 81 of 83. Sales of 91 vs. 95 a year earlier, a decline of 4.2% over 12 months.

-

Westminster 92683: $659,000 median, down 3.2% in a year. Price rank? No. 53 of 83. Sales of 228 vs. 277 a year earlier, a decline of 17.7% over 12 months.

Housing markets across California and much of the West Coast have been deteriorating in the last 8 to 12 months. On the East Coast, it’s much of the same, with Manhattan condos and Hamptons mansions stagnating in the past year.

The downturn in real estate isn’t just centralized to Orange County or West Coast markets, but it’s very board, from coast to coast to be exact, and hitting more luxurious markets the hardest.

The real estate market downturn could be one of the reasons why President Trump is begging the Federal Reserve for 100bps rate cuts, quantitative easing, and even trial ballooning headlines of emergency payroll tax cuts.

To sum up, the housing downturn is here.

-

- Will Central Banks Survive?

Authored by Tuomas Malinen via GnSEconomics.com,

Almost all economists and the vast majority of the general population erroneously believe that central banks are, basically, indestructible. And most fail to appreciate that central banks are different from normal commercial banks in just two respects: their ability to earn seigniorage revenue, and to distort accounting rules.

With the current level of liabilities central banks hold those may not be enough. We might be closing in the end of the central banking era.

The income structure of a central bank

Central banks earn seigniorage from the difference between the “printing” costs of the legal tender (monetary base) and its nominal value. In a simplified balance sheet of a central bank, money is visible in the liabilities-side, which also holds the government’s bank account (domestic liabilities) and the reserves of commercial banks and net worth. Net worth includes the capital of the central bank and valuation adjustments for changes in the foreign-exchange rate and investments. A central bank’s assets include securities, foreign-exchange reserves (net foreign assets) and loans (to commercial banks).

Thus, when a central bank buys assets, such as government bonds, it simply either creates money directly or debits the reserves of commercial banks to maintain balance. In the programs of quantitative easing (“QE”, see Q-Review 1/2018), the latter option has been used. The central bank earns income in the form of interest from these holdings. If the liabilities contain required reserves and currency, the central bank has “zero-cost” financing. If the liabilities contain excess reserves and or domestic liabilities, the central bank will need to pay interest.

Losses of a central bank

The central bank can, naturally, also incur a loss. The value of foreign and domestic assets have a significant role in a central bank’s income stream. Usually, losses result from interest obligations, subsidy payments, multiple exchange-rate practices, “guarantee” schemes and unfavorable changes in net asset valuations. With the advent of QE programs, central banks have made themselves vulnerable mostly to the latter (see the Figure).

Figure. The balance sheets of the Bank of Japan, European Central Bank, Federal Reserve and the People’s Bank of China in billions US dollars. Source: GnS Economics, BoJ, ECB, Fed, PBoC

When central bank accrues a loss beyond its stream of net interest rate income (gross interest income minus expenses) and seigniorage, it starts to eat through its capital. A central bank thus follows normal accounting practice. But, because the central bank has a control over the monetary base, it can create demand for its liabilities (currency) by buying government securities and earn seigniorage.

This is the crucial difference between a central bank and a commercial bank. The central bank can claim to be solvent, based on its future income stream from seigniorage, even with negative net worth.

But, covering a large loss from seigniorage will lead to a large growth in its monetary base and thus to very high inflation (see Q-Review 2/2019 for historical examples). So, a central bank can, technically, cover all losses, but it can only be accomplished through very high inflation and, eventually, by destroying the monetary system.

Central bank and the negative net worth

If, alternatively, a central bank continues to operate with negative net worth and/or without acknowledging its losses, it will interfere with its own monetary management (the setting of interest rates) and eventually jeopardize its independence and credibility. What this means as well is that financial market participants cannot be sure whether a central bank is conducting monetary policy according to its mandate or in an effort to cover its losses.

When trust in a central bank is broken, it loses any control it has over the markets and, eventually, the economy. A central bank operating with negative capital is also a sign that the economy is not doing well. Volatility increases and, eventually, panic is likely to take hold especially if the asset markets are over-valued.

For these reasons, all major modern central banks have rules in place concerning re-capitalization. However, recapitalization is a political decision, which has its own risks and limitations. For example, if losses are very large, the government is unlikely to be willing to cover them, because of the likely political backlash. It can let the central bank fail and start to issue currency by itself or set up a new bank.

Recapitalization of a central bank cannot therefore be considered to be “automatic”, although cases where recapitalization is not undertaken probably require exceptional considerations, such as very large losses, public anger towards central banks, and the political consequences such resentment is likely to produce.

Central bank failures

History knows of few examples of the technical bankruptcies of central banks. The Reserve Bank of Zimbabwe reached insolvency in early 2010, due to hyperinflation and accumulated foreign liabilities. The National Bank of Tajikistan fell into insolvency in late 2007 because of its external debt.

In both cases, the liabilities of the central banks exceeded their assets, and a recapitalization was needed. These examples and the process of central bank failure is described in detail an excellent article by W. Buiter. Now, with hugely-bloated balance sheets, central bank losses are almost guaranteed.

Central banks may ’disappear’

People tend to forget that central banks, compared to the economy, are a fairly new invention. They assumed their current role as setters of interest rates only in the 1920s, and became the guardians of inflation in the 1980s. In the 2010s, they became the unwitting destroyers of the pricing mechanism in the capital markets. Their evolutionary path seems clear, and it is very detrimental to the overall economy.

In the case of a recession, their only remaining (effective) stimulus option is some form debt monetization, á la “Modern Monetary Theory”. If enacted, this will signal the end of the monetary system as we know it, but also ensure the end of central bank hegemony because of the inflationary crisis which will ensue.

That’s why we should not be surprised if central banks are not around after the coming crisis has passed. Their pernicious asset buying-programs and negative rates have left them vulnerable politically to any larger shock, such as a crash in the asset markets or a global recession. Venturing into debt monetization would seal their fate.

In either case, a political reckoning for years of reckless central bank policy is fast approaching, and they may not survive what is about to hit.

- "It's A Shame For Argentina" – Workers Escape To Jobs Abroad As Economic Crisis Worsens

Shocked by President Mauricio Macri’s drubbing in elections this month many Argentines have begun calling and emailing in droves in search of work in Brazil, Chile and Colombia, head hunters told Reuters.

The issue spans the the entire employment spectrum, from graduate students looking for their first job in a new field, to executives. Some head hunters can name the executives, and some search specialists say the resumes that have deluged their offices in those countries peaked after Macri lost ground to a center-left Peronist challenger in the Aug. 11 primary elections, causing the peso to plummet in value.

Unfortunately for Macri, leftist Alberto Fernandez is now the front-runner in the upcoming Oct. 27 general election and has said he will seek to renegotiate a $57 billion loan International Monetary Fund deal agreed by Macri amid growing fears of a default.

Next door, in Chile, recruitment firm Randstad said the pressure for jobs among Argentine applicants has been building for months as the Argentine economy has sputtered out. Their rate of applications for jobs in Chile increased by 246% between May and August this year compared to last.

“I think people feel a bit of despair,” said Nicholas Schmidt, department head of executive search firm Spencer Stuart’s financial services division in Chile, who received a flood of emails and phone calls after the primaries.

“I get a sense that going forward we are going to be seeing a lot of very bright Argentine candidates. It’s a shame for Argentina,” he said.

Inside Argentina, companies helping to export workers are experiencing a boom.

Bernardo Carignano, creator of the visa assistance website “Yo me animo y vos”, said he saw traffic to his site increase the week after the primary election to the highest levels since it went online in 2008.

“On Instagram, too, in these last weeks, we have noticed our followers are increasing much more daily than in previous weeks,” he said.

A spokesman for Argentina’s Ministry of Labor, Employment and Social Security said it did not have access to migration data.

When he was first elected back in 2015, Macri was greeted as a breath of fresh air for the economy. Recruiters said they were confident that Macri would work out: However, that feeling of pervasive optimism has faded.

Several Argentine candidates told potential recruiters that Macri, elected in 2015 on a pledge to “normalize” Latin America’s third largest economy, had been their hope for an economic turnaround after a decades-long cycle of peso weakness and inflation.

“There was a sense of hope with him, a lot of people went back (to Argentina) and worked in government,” Schmidt said. “People wanted to stay and felt things were going to improve significantly going forward.”

Instead, Macri has been accused of failing to attract sufficient foreign direct investment while underestimating the inflationary effect caused by cuts to utility subsidies that Argentines had long taken for granted.

Today, unemployment stands at 10 percent, inflation at 55 percent and the poverty rate between 27 and 35 percent.

But many of Macri’s promises never panned out. His decision to devalue the country’s currency destroyed the wealth accumulated by millions of retirees. And his decision to beg the IMF for the biggest bailout in the organization’s history.

Kevin Gibson, chief of the Latin American division of Robert Walters, a large British head-hunting firm, said he had seen a steady upwards trajectory since 2017 in applicants for roles in Brazil, Mexico and Chile from Argentine candidates.

In the week after the primary vote alone, the number of applicants doubled. Colombia has also attracted interest from Argentines.

In Brazil, Gibson said the potential further losses of Argentina’s human capital would be other economies’ gain.

“Argentines are extremely flexible salary wise and have a very good reputation in the region,” he said. “It’s been gradual as different people have different pain points and family commitments but this most recent news will definitely bring a huge spike.”

Digest powered by RSS Digest

Saving...

Saving...