- US Urgently Mediating Between Turkey & Syrian Kurds To Prevent Ground Offensive

US Urgently Mediating Between Turkey & Syrian Kurds To Prevent Ground Offensive

Turkey has reportedly laid out its conditions for refraining from a ground offensive against the US-backed Syrian Democratic Forces (SDF) in Syria, Kurdish media reported.

According to local sources, the Turkish bombardment – although ongoing – has decreased significantly as of the last few days. The sources added that this is due to the current US mediation between Turkey and the Kurdish militant group. “Turkish Defense Minister Hulusi Akar received the US ambassador, Jeffry L. Flake, at the ministry’s headquarters in Ankara,” the Turkish Defense Ministry said in a statement on 24 November, without further clarification.

Turkish Defense Ministry/Twitter During the meeting, the US ambassador reportedly offered a 30-kilometer pullback of Kurdish forces to prevent Turkey from launching its promised ground offensive. According to a Kurdish media report, however, Ankara has not only demanded a 30-kilometer withdrawal of the SDF from Turkey’s borders, but also that all members of the Kurdistan Workers Party (PKK) in Syria be handed over to Turkish custody.

The report also states that Turkey has demanded “the allocation of partial oil revenues in SDF-controlled areas for the benefit of factions loyal to Ankara [and the areas under their control],” referring to the Syrian National Army (SNA) and the Free Syrian Army (FSA).

Ankara has also requested the establishment of “observation points,” either independent ones or joined by the US coalition, to allow Turkey to “monitor weapons transfers [following the SDF withdrawal].”

The Kurdish report also states that Ankara is willing to “substitute” all of its conditions with a handover “of the entire area” to the Syrian Arab Army (SAA). The report also accused Turkey of having a secret agreement with Russia that would allow it to occupy more Syrian territory. This could be due to Russian pressure on the Kurdish militants to withdraw.

While the US mediates between Turkey and the Kurds, President Recep Tayyip Erdogan announced Friday that a Turkish ground offensive in Syria is still imminent and will begin “when the time comes.”

Moreover, Erdogan identified the northern Syrian towns of Ras al-Ain, Manbij, and Ain al-Arab (Kobane), as the site of the upcoming ground offensive. According to Turkish Interior Minister Suleiman Soylu, the order for the Istanbul bombing was taken in Manbij.

1/3 At the meeting held in #Qamishli, Russia asked the YPG to withdraw all its military presence from the Turkish border to the M4 road (and leave the entire region to the government). https://t.co/2qN8C95pYa pic.twitter.com/oh3nEG4EPr

— Balanche (@FabriceBalanche) November 26, 2022

https://platform.twitter.com/widgets.js

Erdogan also announced that Turkey would initiate its plans to establish a 30-kilometer “security zone” on its southern border, which has been the longstanding goal of the Turkish military occupation in northern Syria.

Turkey has accused the US of supporting Kurdish ‘terrorism,’ while the SDF has accused the US of turning a blind eye to Turkish aggressions. Washington’s mediation is likely to be a form of appeasement for the two opposing sides, which are considered US allies.

Tyler Durden

Sun, 11/27/2022 – 23:30 - 1.8M Chickens Slaughtered In Nebraska As Bird Flu Pecks Away At Food Supply

1.8M Chickens Slaughtered In Nebraska As Bird Flu Pecks Away At Food Supply

Another 1.8 million chickens were ordered to be culled in Nebraska after agriculture officials analyzed yet another bird flu outbreak on a farm.

The latest culling comes after 50 million birds have been slaughtered nationwide to try and contain the ongoing outbreak according to AP, so who knows if it’s actually true.

Fortunately the Nebraska Department of Agriculture (NDA) issued a report, which adds that this is the 13th farm in the state to suffer an outbreak this year. According to the report, 6.8 million birds have been killed in Nebraska – the second-most behind Iowa, which has killed 15.5 million.

After the affected flock is culled, the NDA will establish a 6.2-mile control zone around the affected premises.

Highly pathogenic avian influenza (HPAI) is a highly contagious virus which spreads easily among birds via nasal and eye secretions, along with manure, the NDA said in a statement. Symptoms include a lack of energy and appetite, decreased egg production or malformed eggs, and sudden death in birds even if they aren’t showing symptoms.

The disease can survive ‘for weeks’ in contaminated environments.

According to Yahoo, Turkey and chicken farms aren’t the only facilities affected by bird flu this year – as a petting zoo in Utah had an outbreak in recent days.

Tyler Durden

Sun, 11/27/2022 – 23:00 - Plane Crashes Into High Voltage Power Lines Leaving 120,000 Without Power In Maryland

Plane Crashes Into High Voltage Power Lines Leaving 120,000 Without Power In Maryland

Approximately 120,000 customers in Montgomery County, Maryland were without power Sunday night after a small plane crashed into high-voltage power lines just north of Montgomery Village.

The pilot and passenger, identified as Patrick Merkle, 65, of Washington, and Jan Williams, 66, of Louisiana, are reportedly alive and unharmed in the aircraft, and authorities are in cell phone contact with them according to Montgomery County Fire Chief Scott Goldstein.

Update – Gaithersburg, Maryland, @MontgomeryCoMD small plane into powerlines & tower plow, suspended about 100 feet in the air, two persons on board uninjured at this time, @mcfrs on scene, Widespread power outages, some roads closed in area, https://t.co/VRLGfpyFaA pic.twitter.com/3iCMW0v94j

— Pete Piringer (@mcfrsPIO) November 27, 2022

https://platform.twitter.com/widgets.js

Rescue personnel have had to wait until crews can ground the lines before attempting to extract the plane, with Goldstein saying that crews would need to go up the lines themselves in order to put clamps or cables onto the wires to ensure there is no static electricity or residual power that could pose danger to any involved, according to DC News Now.

Authorities say they are in communication with the two people stuck in a plane that hit a power transmission tower in Gaithersburg. Tap here for more: https://t.co/jjq2Wdqlnn . pic.twitter.com/cE7CGcccDR

— NBC4 Washington (@nbcwashington) November 28, 2022

https://platform.twitter.com/widgets.js

Bascially: Crews have to go up to the wires and ground them. then secure plane to the tower. Large crane about to arrive. They’re awaiting additional resources arriving around 9:30. the occupants in airplane are okay.

— I’m Glad I Don’t Look Like What I’ve Been Through (@CosmicKitty143) November 28, 2022

https://platform.twitter.com/widgets.js

The power outage is limiting the number of patients that two nearby hospitals can take, according to the report.

Tyler Durden

Sun, 11/27/2022 – 22:38 - Fauci's 7-Hour Deposition: What We Know So Far

Fauci’s 7-Hour Deposition: What We Know So Far

The transcript is not yet available and no reporters were allowed. But from the Attorneys General who brought the suit, the plaintiffs in the case and their attorney, and other parties to the lawsuit against the Biden administration, we have some information about the deposition provided by Anthony “I am the Science” Fauci. He has been the face of the pandemic response and stands accused of colluding with Big Tech to suppress dissent in violation of the First Amendment.

The question of whether the deposition was to be public was itself the subject of legal attention. The Department of Justice filed to block all recording and personally identifiable information for fear of public harassment, and this condition was granted. As a result, we have no transcript (yet) and one senses a great skittishness even from those who were there to explain the fullness of what transpired. Major national media have shown no interest in getting the story.

Nonetheless, we do have information thanks to some candid tweets and an article by one of the plaintiffs. The main takeaway is that Fauci has come down with a serious case of amnesia. Over seven hours, reported Louisiana Attorney General Jeff Landry, he mostly stonewalled detailed questioning by answering that he has no clear memory of details that would shed light on his involvement in speech suppression.

“Wow! It was amazing to spend 7 hours with Dr. Fauci. The man who single-handedly wrecked the U.S. economy based upon ‘the science.’ Only to discover that he can’t recall practically anything dealing with his Covid response!”

This is despite the hundreds of pages and many public statements that seem to confirm that the White House and many government agencies worked very closely with Google, Facebook, Twitter, and others, to control the narrative for the better part of two years. And these efforts are probably ongoing.

Eric Schmitt, the Attorney General of Missouri and now Senator-Elect, bought the suit along with the Attorney General of Louisiana. Schmitt tweeted “some takeaways from the deposition of Fauci: Fauci knew the Lab Leak theory had merit but it’d come back to him & sought to immediately discredit it; He defended lockdowns; The rest of us ‘don’t have the ability’ to determine what’s best for ourselves.”

In addition, he wrote: “In the Fauci depo this week the court reporter sneezed. Fauci wanted her to wear a mask. This is the mentality in Nov 2022 of the guy who locked down our country & ruined countless lives & livelihoods.The Experts followed suit. Dissent was censored. In America. Never Again.”

Plaintiff Aaron Kheritary, Brownstone Senior Scholar and Fellow, explains as follows:

UPDATE: from our deposition of Fauci yesterday in the MO v. Biden case. Fauci confirmed that in Feb 2020, Fauci sent Clifford Lane, his deputy at the NAIAD, as the U.S. representative for the WHO delegation to China. Lane convinced Fauci we should emulate China’s lockdowns.

The CCP had announced China had contained the virus through draconian lockdowns–a claim now known to be false. Given the (sic) China’s pattern of falsified information, Lane and Fauci should have approached this claim with skepticism. Lockdowns were wholly untested & unprecedented.

As our lawyer, @Leftylockdowns1 put it, Fauci “was apparently willing to base his lockdown advocacy on the observations of a single guy relying on reports from a dictator.” Not exactly a double-blind randomized trial level of evidence, or indeed, any level of evidence.

Days after Lane returned, WHO published its report praising China’s strategy: “China’s uncompromising and rigorous use of non-pharmaceutical measures [lockdowns] to contain transmission of the COVID-19 virus in multiple settings provides vital lessons for the global response.

“This rather unique and unprecedented public health response in China reversed the escalating cases,” the report claimed. My colleague @jeffreyatucker at the @brownstoneinst gave a tongue-in-cheek gloss of WHO’s misty eyed report: “I’ve seen the future—and it is Wuhan.”

Lockdowns quickly spread from China to the West, as a troubling number of Western apologists besides the WHO also looked to the Chinese Communist Party’s covid response for guidance.

The U.S. & U.K. followed Italy’s lockdown, which had followed China, and all but a handful of countries around the globe immediately followed our lead. Within weeks the whole world was locked down.

From the very beginning, the evidential basis for this global policy catastrophe was always paper-thin. We are now living in the aftermath.

Jim Hoft of Gateway Pundit added direct quotes from Fauci fully confirming Brownstone’s report on the NIH junket to China in February 2020:

John Sauer, “And Mr. Lane, after returning from the trip, said the Chinese were managing this in a very structured, organized way; correct?… Did you discuss Mr. Lane’s experience on the trip with him when he got back from the WHO trip?”

Dr. Fauci, ” The answer is I did… Dr. Lane was very impressed about how from a clinical public health standpoint, the Chinese were handling the isolation, the contact tracing, the building of facilities to take care of people, and that’s what I believed he meant when he said [they] were managing this in a very structured organized way.”

Sauer: “So he drew the conclusion that there might have to be extreme, in his word, measures to mandate social distancing to bring the outbreak under control; correct?”

Fauci: “That’s what this is implying, yes… He did discuss with me that the Chinese 19 had a very organized way of trying to contain the spread in Wuhan and elsewhere. He didn’t get a chance to go to Wuhan, but he was in Beijing, and I believe other cities — at least Beijing — and he mentioned that they had a very organized, well regimented way of handling the outbreak.

Sauer: “And so he had a kind of positive reaction to that. There might be lessons to be learned for the United States in its response to the outbreak?”

Fauci: “I believe Dr. Lane came to the conclusion that when you have a widespread respiratory disease that a very common and effective way to curtail the rapid spread of the disease is by implementing social distancing measures… Dr. Lane is a very astute clinician, and I have every reason to believe that his evaluation of the situation was accurate and correct.”

Just to be clear, Fauci has here described a policy response that included welding shut the doors to people’s apartments and full totalitarian controls on movement as a “very organized” and “well regimented” implementation of “social distancing measures.”

Just let that sink in.

Hoft provided in addition the most detailed observations yet. Quoting here from his report in full:

-

Fauci is a skillful liar. As we have seen now for months in his public comments, he lies when he feels he can get away with it or when he feels there will be no meaningful consequences.

-

Fauci frequently lied unless and until he was confronted with alternate facts. For example, he claimed he really wasn’t familiar with Ralph Baric (creator of the COVID virus) or Peter Daszak (who brokered Fauci’s NIAID grant money to the Chinese biolab in Wuhan), until he was confronted with evidence that his own chief of staff emailed him describing Daszak and Baric as being part of Fauci’s team!

-

Fauci claimed that he had no knowledge that his communications team did not coordinate with social media companies to stop “misinformation and disinformation” until he was forced to admit that he actually did know of certain instances of coordination.

-

Fauci continued to push the now-debunked assertion that COVID-19 was a naturally occurring virus.

-

Fauci said disinformation and misinformation (information he disagrees with) puts lives at risk.

-

Fauci refused to define “gain of function” research saying it was too broad of a term to define.

-

FUN FACT: until VERY recently, Fauci’s daughter worked for Twitter.

-

FUN FACT: Fauci is a hypochondriac. In a bizarre and stunning segment during the deposition, Fauci blew off some of his frustration on the poor court reporter. The court reporter transcribing the deposition sneezed, and Fauci stopped the deposition and scolded the court reporter: “WHAT’S WRONG WITH YOU??? Do you have some sort of respiratory illness, because in the era of COVID, I’m concerned about being near you.” Court Reporter: “I’m not sick, I just have allergies. I can wear a mask though.” Fauci: “Ok. Thank you, because the last thing I want is to get COVID. [notably, (1) Fauci himself did not wear a mask at any point during the deposition, and (2) he appeared to be several feet away from the court reporter].

-

FUN FACT: in another Fauci hypochondria spasm, Fauci conspicuously mean-mugged Louisiana Attorney General Jeff Landry after Landry sneezed into his suit coat jacket.

-

Gamesmanship. Whenever introduced to a difficult topic, he dishonestly refused to define key terms so he could avoid being pinned down and held accountable. For example, when discussing the topic of “gain of function” research, he refused to acknowledge what the term meant, objecting that it was a term so broad it could not be defined.

-

Fauci repeatedly claimed that he “couldn’t recall” or “couldn’t remember,” and attempted to bolster these incredible statements by appealing to the volume of emails he would receive or issues or studies that would come across his desk. This is simply not credible for nearly all of such statements, because the incidents in question were either recent or within the past three years, and they were all highly politically charged.

-

Fauci’s other method of lying was simply to pretend that he didn’t understand something, and then hope the lawyer asking the question wouldn’t be able to catch him in the lie. For example, he very obviously lied at one point when he claimed he didn’t know what Meta (parent company of Facebook) was, until he was forced to admit that he did, in fact, know what Meta was.

-

Another Fauci tactic: when forced to admit he had made a communication or reviewed a key record at a key time, or knew or worked with a key individual, he would try and downplay each negative fact by (1) downplaying the significance of the communication, (2) suggest that while he reviewed the key record, he didn’t really read it carefully, or (3) with false humility suggest that he was not an expert in X field and so did not fully understand the scientific study at issue, or (4) claim that, while he did “know” said individual, he doesn’t really know them that well because he meets so many doctors and scientists as part of his job.

-

Other Fauci deceit tactics: throwing subordinates under the bus. Fauci is a famous survivor among bureaucrats. One way he has survived this long is by only taking credit for wins and pawning off losses on hapless subordinates. This trend continued in his deposition, in which he brazenly argued that, while he is the head of the NIAID and its $6 billion budget, he repeatedly didn’t have any knowledge about what his immediate direct reports were doing right under his nose. Fauci supports accountability, so long as he has a subordinate to sacrifice.

-

Fauci argued that Hydroxychloroquine was “dangerous” and had “toxic” side effects…. Fauci claimed HCQ was ineffective in treating COVID, but couldn’t cite a single study to support his claim. Fauci also rejected the list of 371 studies on HCQ and its effectiveness in treating the disease when he was presented with the list.

-

Fauci admitted lying to the public. In one of the more amazing segments during his deposition, Fauci admitted that he knowingly made false public health statements at the beginning of the pandemic, advising people against using masks in order to discourage the public from depleting the supply of masks.

-

Fauci admitted he got his ideas of a lockdown from the Communist Chinese who implemented their extreme lockdowns in January 2020.

Jenin Younes, attorney for the plaintiffs who works with the New Civil Liberties Alliance, wrote on Twitter: “One of my favorite quotes from Fauci’s deposition today: “I have a very busy day job running a six billion dollar institute. I don’t have time to worry about things like the Great Barrington Declaration.”

Keep in mind that we have full records of emails in which Fauci took credit for coming “out very strongly publicly against the Great Barrington Declaration.”

In conclusion, we have here a revealing account of astonishing testimony from Fauci, which, to those of us who have followed this case closely from the very beginning, is only shocking because it confirms the fullness of the treachery we have long suspected was at the very heart of the US lockdown experience. We also have confirmed that the phrase “social distancing” really is nothing but a euphemism for a China-style full assault on everything we once called freedom in the West.

Tyler Durden

Sun, 11/27/2022 – 22:30 -

- Futures, Crude, Crypto, Yuan Tumble Amid Violent China Covid Protests As Goldman Warns Of "Disorderly" Early Exit From Covid Zero

Futures, Crude, Crypto, Yuan Tumble Amid Violent China Covid Protests As Goldman Warns Of “Disorderly” Early Exit From Covid Zero

It finally happened.

After markets had ignored for months the rising tension between China’s artificial Covid Zero lockdowns – which are there not to protect the economy from covid as even the wokest mask-breathers realize by now that the latest diluted iteration of Wuhan’s most infamous export is no different than the flu…

Packaging update 🙄 pic.twitter.com/ErkMMdnQit

— Bernie’s Tweets (@BernieSpofforth) November 26, 2022

https://platform.twitter.com/widgets.js

Lockdown protests reported in Beijing as well https://t.co/QoqFu4dxfN

— Austin Ramzy (@austinramzy) November 26, 2022

https://platform.twitter.com/widgets.js

… but to provide the Xi regime with a scapegoat for China’s slow-motion implosion, over the weekend said tension finally erupted as millions of Chinese took to the streets in protest of Beijing’s ongoing lockdown lunacy which late last week led to multiple fire deaths in a building whose doors were literally bolted down as China’s ingenious “covid quarantine”, in many cases accompanied by violence.

As reported earlier, protests spread over the weekend as citizens in major cities including Beijing and Shanghai took to the streets to express their anger on the nation’s Covid controls in a rare show of defiance which some believe raises the threat of a government crackdown, prompting investors to re-think investment plans after jumping back in on reopening hopes.

This culminated in a violent selloff across Chinese stocks, the yuan, US equity futures, crude oil, and cryptos, which all tumbled as China’s protests cast a shadow over the nation’s reopening path and putting investors on edge.

The Hang Seng China Enterprises Index was hardest hit, tumbling more than 4% out of the gate, and paring this month’s sharp advance to less than 16%.

The onshore yuan plunged 1%, the most since May, to 7.2592 per dollar as risk appetite faded.

“We might see some derisking around Chinese markets,” said Chris Weston, head of research at Pepperstone Group Ltd. “We are seeing some outflows of the offshore yuan, which I think is a pretty good indication of how Chinese markets may fare.”

In a note from Goldman China economist Hui Shan (available to pro subs in the usual place), he warned that there is some chance of a “disorderly” exit from Covid Zero in China, as the “central government may soon need to choose between more lockdowns and more Covid outbreaks.” The bank added that “the current situation imposes further downside risk to our Ielow-consensus Q4 GDP forecast.”

Ironically, the Chinese rioting takes place right after the PBOC cut RRR by 25bps last Friday unleashing (a paltry) RMB 500bn in long-term liquidity. While the economic impact may be more limited if the PBOC offsets it with a partial rollover of maturing MLF loans next month, the significance of the RRR cut lies in its signal value: policymakers are attentive to incoming data and the central bank will likely keep monetary policy accommodative in the face of a challenging growth outlook in the next quarter or two.

Needless to say, widespread rioting across China will not ensure peaceful and prosperous golden years for China’s dictator-for-life, Xi Jinping. On the contrary, the latest developments underscore China’s rocky path to reopening as the nation grapples with a record number of Covid cases. Just as ironically, Chinese assets rallied in November as directives for a less-restrictive pandemic approach, coupled with strong support for the property sector, gave investors confidence that the worst is well behind.

But not any more: Hong Kong’s Hang Seng Index fell as much as 4.2% and a separate gauge of Chinese tech stocks down more than 5%. On the mainland, the CSI 300 Index declined as much as 2.8%, while yields on the benchmark note gained one basis point to 2.83%.

The shockwave from China’s riots quickly spread across the Pacific as US equity futures tumbled as much as 0.7% to hit a session low of just above the “nice, round number”, at 4,001.5.

Oil was slammed too, with WTI tumbling as much as $3 from Friday’s close to a session low of $73.75, or right above the level when the Biden admin lied it would restart purchasing oil to refill the SPR which it has drained by more than 200 million barrels in the past year.

Finally, and not like anyone will be surprised by this, crypto which now tumbles to any news, both good and bad, tumbled right on cue, with bitoin sliding from the $16,500 level right back down to $16,000, as even the faintest attempt to reverse the relentless selling of 2022 is promptly crushed.

Tyler Durden

Sun, 11/27/2022 – 21:53 - What The #$%& Is A Shallow Recession

What The #$%& Is A Shallow Recession

This week, DataTrek founder Nick Colas is visiting his in-laws in Memphis for the Thanksgiving holiday, and as he notes, contact with what New York finance types call “the real world” is always an educational experience, given his usual cloistering in midtown Manhattan. To celebrate his brief freedom from the Big Apple, if only for a few days, are two brief thoughts based on a few interactions during his time here.

Below we excerpt from the latest Morning Briefing by Nick Colas of DataTrek

#1: What the #@$% is a shallow recession? My hotel’s breakfast area had business TV on this morning, and one of the hosts said, “markets are expecting a shallow recession next year”. She was not wrong. US equities trade for 18x current earnings, which strongly implies either no diminishment of corporate earnings or, at worse, a dip sometime in 2023 but then a swift recovery.

An older gentleman sitting opposite me at group table shook his head and grumbled the question noted above. His observation, implying that any recession can be “shallow” is at best euphemistic and at worst delusional, is also not wrong.

Since World War II, the shallowest recessions in terms of their effect on US GDP growth were in 1990 and 2001. The chart below shows quarterly real GDP growth from 1947 to 2019, with the 11 official NBER recessions over that period noted by the gray bars. We have put a dotted line across the 1 percent contraction level. All but the 1990/2001 recession exceeded that number.

Many readers will recall the 1990 and 2001 recessions, and I am fairly sure none would think of them as “shallow”. The first was due to an oil shock caused by Iraq’s invasion of Kuwait. US unemployment went from 5 to 8 percent over 2 years. The second was caused by the bursting of the dot com stock bubble and the 9-11 terror attacks. Unemployment rose from 4 to 6 percent.

The lesson here is that even “shallow” recessions have real world outcomes and, in the case of 1990 and 2001, came with other problems. Yes, perhaps the Fed can thread the needle of reducing inflation without causing a steep recession. We certainly hope it can. But I think it will pay to have some of the skepticism offered by my dining companion until that result becomes somewhat clearer.

* * *

#2: Help wanted. There are still many small businesses in the Memphis area looking for workers, especially those with seasonal labor needs heading into the holidays. The shortage of workers is evident here, as it is across the country. It has been thus for over 2 years, with wage inflation a necessary byproduct of that phenomenon.

The chart below shows US labor force participation (people in the workforce divided by the total population) for 25 – 54-year-olds (in red, left axis) and all adults (black line, right axis) from 2015 to the present.

Two points on this data:

- Prior to the pandemic, aggregate and 25 – 54 LFP was rising. The former hit 63.4 percent in February 2020, its highest level since June 2013. The latter got up to 83.1 percent, the best level since May 2013. A strong, late cycle US economy was pulling Americans into the workforce.

- Today, both LFP levels remain below their pre-pandemic highs. Working-age (25 – 54-year-olds) LFP is 0.4 points lower, which translates into 520,000 “missing” prime-aged workers. Total LFP is down 1.2 percentage points, or 3.2 million people.

The upshot here is that, despite population growth, there are scarcely more workers in the US now than at the start of the Pandemic Crisis. According to BLS data, the civilian non-institutional American population has grown by 1.9 percent since February 2020. The total number of Americans in the workforce has only grown by 0.5 percent.

Linking this discussion to the prior point about recessions, it is worth noting that every economic downturn since the 1980s has seen labor force participation either stay flat or decline. In the 1970s/early 1980s, LFP was stable through recessionary periods primarily because women were still entering the American workforce. In the 1990, 2001, and 2007 – 2009 recession, LFP fell by 2 points or more during/after each downturn.

The lesson here is that a recession does not draw people into the workforce, so the current labor shortage is unlikely to ease very much in a “shallow” recession. An economic downturn should, however, reduce wage inflation to some degree if employees feel they no longer have bargaining power with respect to their pay. Still, this may not be enough to bring wage growth in line with productivity growth if the supply of labor contracts over the next 1-2 years.

Tyler Durden

Sun, 11/27/2022 – 21:30 - After 15 Break-Ins, A Portland Business Finally Calls It Quits

After 15 Break-Ins, A Portland Business Finally Calls It Quits

Progressives are hell bent on fixing the world, climate, capitalism and every form of social injustice…. just don’t look at the destruction in the cities under their control.

Take Portland resident, Marcy Landolfo, who finally hit her breaking point. As KATU reports, this week marked the 15th break-in at her PDX store within a year and a half in the city that spawned the radical-leftist Antifa movement.

Landolfo said most of those repairs at the Northeast Portland location were paid for out of pocket. Other times, she just left the windows boarded up. “It’s just too much with the losses that are not covered by insurance, the damages, everything. It’s just not sustainable,” Landolfo said.

The owner at Rains tells me after five break-ins in about three weeks, she made the sudden decision to permanently close. Staff here are putting pressure on the city to look after small businesses dealing with ongoing challenges with crime. pic.twitter.com/XyP2p6PR6W

— Megan Allison (@mallisonKATU) November 26, 2022

KATU asked why Landolfo decided to close now, instead of keeping doors open through the holiday shopping season.

“The products that are being targeted are the very expensive winter products and I just felt like the minute I get those in the store they’re going to get stolen,” she said.

Landolfo said she’s worried about her employees, and no longer sees this location as a feasible business model.

“The problem is, as small businesses, we cannot sustain those types of losses and stay in business. I won’t even go into the numbers of how much has been out of pocket,” she said. If only the progressives who effectively run her city were aware of the hellhole they have made it into, maybe this could have been avoided, but alas – anyone who speaks out against the idiotically socialist practices of these “progressive” ghettos is immediately blasted as a racist, white supremacist, etc, and promptly canceled.

When Rains was broken into in late October, KATU reached out to Mayor Ted Wheeler’s office; his team responded that they’re working to increase funding for business repair grants through Prosper Portland. Because somehow for socialists it makes more sense to pay fore reparations instead of preventing the crime from occurting in the first place. Then again, all such Democrat strongholds are all about reparations.

Needless to say, for Landolfo that was not enough.

“Paying for glass that’s great, but that is so surface and does nothing for the root cause of the problem, so it’s never going to change,” she said, gradually realizing why socialism never works.

The mayor’s office also said they participated in a retail safety summit in October, and cited recent efforts to streamline the permitting process for things like storefront lighting. News channel KATU asked how that work is going, and it was still waiting to hear back.

Tyler Durden

Sun, 11/27/2022 – 21:00 - FTX Post Mortem Part 2 Of 3: How Did We Get Here?

FTX Post Mortem Part 2 Of 3: How Did We Get Here?

Authored by Scott Hill via BombThrower.com,

Last week we covered the collapse of FTX as it happened but there’s a lot more to the story.

How did FTX grow from a tiny Hong Kong bucket shop into a top three Crypto exchange over the course of just a few years?

What was Alameda research and were they ever legitimate?

Most importantly, how exactly does an exchange lose track of up to $10 billion worth of customer deposits?

Most of this material is still an educated guess, but the guessers are out there putting together clues from private discussions which have been leaked, the bankruptcy proceedings and first hand dealings shared on Crypto Twitter.

It’s worth noting that there is a whole deep state angle to this story.

I won’t go into it in this article because so little is known (see endnote)

What we do know is mostly confined to the fact that FTX CEO Sam Bankman-Fried (SBF) was the second largest donor to Democrat political campaigns since 2019. His Co-CEO for part of the FTX Empire, Ryan Salame, was a top 10 donor to the Republican party in the same period.

Sam Bankman-Fried met with SEC Chairman Gary Gensler seeking a “no action” letter on an enforcement matter in April, shortly before SBF began pushing the DCCPA, a bill which the Crypto industry mainly saw as a subtle crackdown on DeFi wrapped in a reasonable sounding regulatory framework.

The biggest question mark is the identity of FTX CTO and co-founder Garry Wang. The man is a ghost with very little online presence and only a handful of photos. Famed short seller Marc Cohodes is under the impression that Wang is a state actor for the CCP.

These questions are important and interesting, but they don’t make for a useful article because of the complete absence of detail.

Alameda Research

Alameda Research, the market maker or crypto hedge fund founded by SBF in Hong Kong during the bull run of 2017 is the start of the rot. The official story is that the firm was formed from a team of young hotshots who learned to trade at Jane Street, a notoriously secretive global market maker which trades more than $10 trillion in securities volume each year.

In January 2018 as Bitcoin was collapsing, Alameda research were performing the Japan arbitrage trade. They purchased Bitcoin in the US, moved it onto Japanese exchanges and cashed in on the gap between markets. The spread was often as wide as 10%. SBF claimed the firm made $10M on the arbitrage over the course of several weeks.

This was a complicated trade. Japanese capital controls are strict with only Japanese nationals allowed to hold bank accounts, making it extremely difficult to get the money out of Japan and requiring a reasonable level of sophistication and corporate legitimacy to pull off.

Following the Japan arbitrage, Alameda went after the “Kimchi Premium”. This was the same type of arbitrage trade, with Bitcoin on South Korean exchanges worth up to 20% more than Bitcoin on US exchanges. The capital controls were tighter, the ability to set up corporate infrastructure in the nation was more restricted and Bitcoin was in the middle of collapsing making trading the asset much more risky.

Some people are suggesting that Alameda lost $10 million on the Kimchi Premium trade, but no one really knows whether any of this story is even true.

I’m deeply skeptical of this entire backstory given what we have now seen about how careful SBF is with his public image.

It’s entirely possible that this whole story was a fabrication to paint the picture of a boy genius trader with a Jane Street pedigree striking out on his own in Crypto land.

Completely Absurd Fundraising

In early 2018, Alameda Research established headquarters in Hong Kong. While SBF was a complete unknown to Crypto insiders at the time, Alameda Research was making a name for itself, frequently up the top of the Bitmex trading leaderboard.

Crypto markets in 2018 were very different to the last few years. While 2017 had seen a burst of activity during Bitcoin’s bull run, volumes were still tiny and there were very few professional firms taking the asset class seriously.

It’s completely plausible that in the absence of professional market makers, Alameda Research could have done very well. It also seems likely that the edge that such a small team had would have disappeared quickly as the market became more professional. Alameda Research only had a handful of employees. Nowhere near enough to build and execute a sophistical algorithmic market making strategy, such as those employed at Jane Street.

In December 2019 an investment pitch deck for Alameda Research circulated among Crypto insiders. The firm was seeking to raise $200 million in debt funding and was offering 15% payments on the debt. The pitch itself made ridiculous claims about the firm’s edge and was riddled with red flags.

“High Returns with no risk – These loans have no downside”

Insiders that viewed the pitch deck were confused. The whispers within the industry were that this firm was highly profitable yet they seemed desperate to raise $200 million. Most stayed away and it’s unclear whether or not the fundraising was successful.

Launch of FTX

FTX was founded in May 2019 but had very little volume until the following year when they established the regulatory status to allow US customers to trade. FTX later acquired Blockfolio to obtain additional US licensing and the bones of a trading app. Even with this boost in volume, FTX was considered an unfavorable exchange to make markets for among established industry participants.

The presumption was that Alameda Research was an embedded market maker that was given an unfair advantage on the platform and rival firms stayed clear.

At the time SBF was still the CEO of both companies. There were claims of a separation of the firms, but it was known that they both operated out of the same offices in Hong Kong. It was rumored that Alameda had full access to customer position data and would hunt for liquidations.

FTX was seen as a shady offshore bucket shop.

By early 2021 little had changed in the industry perception of FTX, but volume was growing. In January SBF was busy arguing on Twitter, leading to the infamous “I’ll buy as much Solana as you have, right now, at $3” tweet. He was not taken seriously until later that year when this huge Solana bet seemed to pay off.

FTX gains Legitimacy

By the middle of 2021, with Crypto in a raging bull market and FTX capturing significant market share, the exchange became too large to ignore. A big part of the story was China putting in place another round of Crypto bans in September which forced many major Crypto traders and market makers to find new venues to trade.

Zhu Su, founder of disgraced Crypto Hedge fund Three Arrows Capital said recently that he had moved his fund’s trading from Huobi and Okex to FTX and Binance in the wake of the China ban.

FTX gave them extremely favorable terms.

A big reason that firms began to feel comfortable with FTX was the splashy fundraising FTX was able to pull off. Market participants assumed that among the billions of dollars of venture capital money that had been invested in FTX, someone had done basic due diligence on the firm. We now know that during these heady days of free money SBF was demanding investment commitments quickly from VCs or he would move on to the next phone call.

There was a giant line of VCs desperate to get into an FTX round.

The July fundraising list was a who’s who of Silicon Valley VC. Led by Sequoia, the round included Softbank, Temasek and VanEck. Apparently none of these firms insisted on even the most basic corporate controls, like installing a board of directors. A later round included a strategic investment from Blackrock. FTX was a blue ribbon investment.

They all needed Crypto exposure now and FTX was the hottest Crypto startup in town.

The other piece of the puzzle was that trading firms were now making money on FTX, when before they were simply getting their positions hunted by Alameda. Leverage was handed out in ample servings. Compliance was lax. Payouts were quick. It seemed to most that FTX had moved on from its shady beginnings to become a legitimate venue for market makers to use.

Tokens

A giant part of understanding exactly what went down at FTX is understanding the Tokens they had launched or partnered with. In 2019 FTX launched FTT, an Ethereum ecosystem token which represented a cut of exchange fees and offered discounts to traders for holding it. It was the same model that Binance launched their token with in 2017. Tokens would be bought out of the market with a portion of exchange profits on a regular basis, delivering a return to investors.

A huge portion of FTT tokens were held on the FTX balance sheet as an asset.

Even more egregious were the Solana ecosystem tokens which FTX helped launch. The leaked balance sheet showed that FTX had large holdings of Serum, Maps and Oxy.

It showed Serum tokens marked as a $2.2 billion asset. Available market cap at the time was less than $500 million.

We don’t know for sure, but it seems likely that loans were taken out backed by FTT and other minor tokens.

Essentially, it seems that SBF invented his own currency from this air and then took out US dollar loans against it from anyone that would offer.

We haven’t heard from any major Crypto lender about whether or not they took FTT as collateral. We may never hear an admission on that point. What we do know is that Solana DeFi, where SBF had significant influence, largely took these minor tokens as collateral for loans on much more generous terms than seems reasonable now.

And why wouldn’t Crypto lenders offer loans to FTX on whatever collateral was offered? FTX was the fastest growing exchange in industry history. It had prestigious investors. Its CEO was throwing around cash on advertising and political donations. Surely FTX was profitable enough to service their loans.

So what happened to the money?

When FTX blew up there was a balance sheet hole of somewhere between $6-10 billion. It was reported as “missing customer funds” but judging from recent public comments made by SBF it seems more likely that there was a complex web of loans and cross company funding arrangements than just straight up theft of customer assets.

An underreported part of this story which fills in a key gap is that the offshore FTX entity apparently didn’t have its own bank account. Wires to the offshore exchange would go directly into a bank account held by Alameda Research. It seems that FTX didn’t secretly transfer customer funds to its associated hedge fund, it probably didn’t even make loans between companies.

The most likely explanation is that Alameda Research just had direct access to customer funds which were wired to them.

While shocking, it wouldn’t be as egregious if the FTX terms didn’t explicitly say that assets were held on trust for customers. FTX wasn’t supposed to touch customer funds once they were deposited. Maybe that’s the whole point, that SBF was relying on some bizarre technicality or legal fiction to convince himself that he had the right to deal with customer assets. Did I mention that both of his parents are compliance lawyers, with one a leading expert on tax havens.

If there’s anyone that could access the advice to set up a complex piece of legal fiction entitling him to pilfer customer funds in a defensible way, it’s SBF.

Liquidations

That only explains how Alameda Research got access to customer funds, but how did they lose the funds? Alameda Research is a market maker primarily and was the key integrated market maker on FTX. Among other things that gave Alameda the ability to purchase liquidated positions of customers, likely at a huge discount.

In a bull market this is a hugely advantaged position to be in. Say Bitcoin drops 5% in an hour and longs get liquidated, Alameda was able to purchase those long Bitcoin positions and then resell them later, after the liquidation cascade was over and price had recovered.

Alameda was exempt from liquidation on FTX, so they could hold underwater positions for as long as they wanted without being forced to close them.

In a bear market, Alameda would likely accumulate underwater positions that they couldn’t get out of without incurring a large loss. Other market makers will generally sell a liquidated position off as soon as possible, to avoid being liquidated themselves. This doesn’t appear to be a check and balance that was in place for Alameda’s operations on FTX.

Another key feature of the leverage trading offered at FTX was cross asset collateral. Essentially this means that leverage was offered on the entire portfolio of a customer. There wasn’t a segregation of collateral, users could simply offer up a mixed list of tokens and take margin loans against the whole pie. This included FTT and Serum at much more generous collateral ratios than other exchanges offered.

Whatever low quality collateral you had, FTX would take it, and it seems that it would end up on Alameda’s books when a customer was liquidated.

Luna Eclipse

In a collapsing market, this lack of controls over Alameda is potentially disastrous. Luna had the most high profile collapse in the history of Crypto tokens in May this year, losing 99.7% of its value in a week before getting as close to absolute zero as possible. FTX and Binance were the major venues for trading the Luna collapse. Traders bought the dip on leverage all the way down.

It seems likely that Alameda took all of those liquidated positions onto their own balance sheet.

Luna started its collapse at around $90. The following week it was at essentially zero. There is no way that Alameda could have sold off all of those liquidated customer positions as the token collapsed. This type of liquidation transaction is known as “toxic flow” and is a surefire way to bankrupt a market maker.

If FTX’s famously specialized liquidation engine simply meant that customer positions were shunted onto the Alameda balance sheet to be cleared at a later date, then the amount of toxic flow from junk tokens in the last year would build up quickly.

This seems to be the only way the size of the hole makes any sense.

Other Problems

If we assume that Luna blew a giant hole in the balance sheets within the FTX empire then what happened next makes a whole lot more sense. SBF went on a buying spree as Crypto lenders collapsed, backstopping insolvent firms and being proclaimed as Crypto’s JP Morgan.

In the cold light of day a more likely explanation than wanting to save the industry is wanting to save himself.

If insolvent Crypto lenders like Voyager and Celsius had given loans to FTX, taking FTT and other minor tokens as collateral then those tokens would be seized and sold into the market during a bankruptcy, cratering the price and liquidating FTX loans with other lenders. Don’t forget, for tokens like Serum, FTX held and likely pledged as collateral more than the entire free float on the market.

All of this isn’t to say that funds didn’t go missing in other ways though.

According to the Bankruptcy filings, FTX had loaned more than $1 billion to SBF individually and $2.3 billion to his investment company, Paper Bird Inc. There were also 9 figure loans to other executives and Bahamas real estate purchased by SBF’s parents and associates worth $300 million. There are even suggestions that the $420 million meme fundraise in October 2021 basically just ended up in the pocket of SBF, rather than productively invested in the company.

It seems like the FTX balance sheet was used as a slush fund for SBF.

None of this in any way can add up to $6-10 billion in stolen customer funds and it’s unlikely that the mechanism was brazen theft. The scenario outlined above, poor trading controls at Alameda creating bad debt within the corporate structure and a CEO that was scrambling to keep the empire afloat, is far more likely. This also casts a new light on the “generous terms” offered to other major market participants in 2021.

Taking VC money

What if Alameda’s goal wasn’t to make money, but to lose money to other traders in a perverse growth hack used to attract the next round of “smart money” investors?

After all, at best Alameda had been making a few hundred million from trading over the course of its existence and likely much less than that. As spreads closed with more market makers flooding into the asset class it’s much easier to take money from Sequoia and Softbank than it is to make money trading.

Running an unprofitable casino is a terrible business, but selling an unprofitable casino that looks extremely busy to a private investor is a fantastic business.

This part of the story seems like the inevitable end state of the 2010s dominance of Venture Capital and private investing. After a decade of easy money, low interest loans and an insatiable appetite for tech investments we were bound to see someone game the system. In 2021 VCs were not doing diligence, they were shoving newly raised funds into startups as fast as possible. Venture capital firms invested $643 billion in 2021. Almost double the pace of 2020 and five times as much as was committed in 2012.

For context, noted scam company Theranos raised $1.4 billion over 13 years. FTX raised $1.8 billion in only 3 years.

The entire story of the growth of FTX is a story of the driving forces of tech stock investing being applied to Crypto and fintech. The problem is that when a social media company blows up, users just lose their photos and social graph. When a fintech or Crypto company blows up, customers lose their funds and lives are ruined.

A big part of the problem with FTX was that tech growth hacking and the infinite pot of VC money was applied to financial services with little regard for the safety of users. No one did the diligence. The regulators were asleep at the wheel.

“Grow fast and break things” isn’t an appropriate model for the financial sector.

We Have Questions…

This article mostly dealt with how FTX managed to grow so fast and then blow up so spectacularly but it didn’t touch on the why. As stated in the introduction, there are some major question marks about state entanglement, potential involvement of intelligence operatives and the corruption of captured regulators are all major open questions that I just don’t have answers to.

Was FTX a plant to bring down the Crypto industry and justify tighter regulation?

Was FTX a front for money flowing from Crypto traders and Tech VCs into Democrat coffers?

Why is the mainstream media reporting on this event as if SBF is just a failed entrepreneur who dreamed too big, rather than a fraud who appropriated customer funds?

Who was behind the success of FTX? Who is Gary Wang?

We likely won’t ever get satisfactory answers to these questions. The family political links between major characters in this story are deeply suspicious. As one Crypto Twitter account that has been covering the news relentlessly said:

“This FTX fiasco is *really* doing its best to confirm every single conspiracy theory anyone has ever had about anything.”

Next week in the conclusion of this three part article I’ll cover some of the fallout surrounding the FTX collapse that is important to understand and the lessons being learned by the industry in its attempt to rebuild.

[A good place to start down the deep state rabbit hole in all this is Mathew Crawford’s ‘A Grand Unified Theory of FTX’ – which I printed off to read and it clocks in around 65 pages – markjr]

* * *

Today’s post is from contributing analyst Scott Hill. To receive further updates of this series and our overall investment thesis for digital assets (even in this climate), subscribe to the Bombthrower mailing list.

Tyler Durden

Sun, 11/27/2022 – 20:30 - IRS Warns Americans To Report Annual PayPal, Venmo Transactions Exceeding $600 Per Year

IRS Warns Americans To Report Annual PayPal, Venmo Transactions Exceeding $600 Per Year

The Internal Revenue Service is warning Americans that they need to prepare to report transactions of at least $600 per year through ‘third-party’ payment processors such as Venmo and PayPal.

Transactions made with popular online payment apps may be subject to taxation. (Tada Images/Shutterstock) In a notice posted Tuesday to irs.gov, businesses and the self-employed are warned that cumulative income of at least $600 per year through apps – which also include Zelle and Cash App – will need to be reported on a tax form known as 1099-K, according to Marketwatch.

According to the agency, the notice is primarily aimed at part-time workers, those with side-gigs and people selling goods. It does not apply to non-commercial transactions such as reimbursing people, or one-off transactions such as selling old furniture, Marketwatch reports.

That said – considering that the 3rd party providers are going to start reporting transactions exceeding $600, how will the IRS know you’re selling ‘old furniture’ versus, say, sweaters made out of cat hair on Ebay?

Before this year, the threshold for filing a Form 1099-K report was at least 200 transactions totaling an aggregate of at least $20,000.

When Congress passed the American Rescue Plan Act of 2021, it included a provision that reduced the reporting threshold to a single transaction over $600.

The Biden administration hopes that by reducing the threshold, the measure will crack down on Americans evading taxes by not reporting the full extent of their gross income. -MarketWatch

In short, this will undoubtedly raise taxes on people making under $400,000 per year.

Tyler Durden

Sun, 11/27/2022 – 20:00 - Bans On "Assault" Weapons Do Not Reduce Crime

Bans On “Assault” Weapons Do Not Reduce Crime

Authored by Benjamin Williams via The Mises Institute,

Prominent Democrats, including President Joe Biden, have repeatedly expressed interest in reinstating a federal assault weapons ban.

Biden himself included an assault weapon ban in his 1994 crime bill, which lasted ten years until its expiration in 2004.

Biden has claimed that the ban did its job and reduced mass shootings:

“When we passed the assault weapons ban, mass shootings went down. When the law expired, mass shootings tripled.”

But a detailed review of the data demonstrates that the ban had no real benefits whatsoever, and neither did it lessen the frequency of major shootings.

What Is an Assault Weapon?

Contrary to popular belief, an assault weapons ban does not ban AR- or AK-style rifles. Assault weapons bans focus primarily on the specific functions of these rifles. The 1994 ban described assault weapons as semiautomatic rifles that

had the ability to accept a detachable magazine and possessed two of the following five features: (1) a folding or telescopic stock; (2) a pistol grip that protrudes conspicuously beneath the action of the weapon; (3) a bayonet mount; (4) a flash suppressor or threaded barrel designed to accommodate a flash suppressor; or (5) a grenade launcher.

This definition permits some adjustments to be made to rifles, such as an AR-15, that would make them completely legal (or “compliant”). Rifles that comply must have a fixed stock. Stocks cannot be telescopic or folding. A pistol grip is incompatible with a compliant rifle. Compliant rifles typically have a stock that has additional material added to it, so the pistol grip is attached to the stock or is extended far enough to prevent the shooter from wrapping around it with their thumb. The maximum number of rounds the rifle’s magazine can hold is 10. Any more than that is regarded as a high-capacity magazine. The rifle may not have a flash suppressor.

Many creative minds have discovered countless ways to transform basic AR-style rifles into completely compliant weapons. Today, several states have their own assault weapons bans with similar or identical provisions as the 1994 federal ban. In these states, the ownership of AR-15s and such is not at all uncommon. The same went for gun owners during the federal ban from 1994–2004.

The reality of compliant assault weapons is a strong indicator that the assault weapons ban did not work, outside of some inconveniences for gun owners. Any owner could easily convert a compliant rifle into a fully functional (and illegal) one using minimal tools and labor. And many, including mass shooters, take advantage of this. The 1994 ban led to a sharp increase in the demand for assault weapons, which initially increased prices. But after an increase in production, prices began to fall to their previous state. A 2002 study showed:

In the short-term, the federal AW ban reduced the availability of AWs to criminal users by increasing the cost of these weapons in primary and, presumably, secondary markets. However, the ban also stimulated production increases for AWs and legal substitute models, resulting in a post-ban decline in prices.

Proponents of a renewed ban completely overlook the rise in the ownership of assault weapons both before and after the 1994 ban. Any positive benefits cited by Biden and other politicians and talking heads are seriously called into question in light of this fact.

Did the Ban Decrease Mass Shootings?

When we closely examine the facts, Biden’s assertion that the ban will reduce the number of mass shootings is shown to be, to put it mildly, an excessive exaggeration. It is safe to assume that Biden derived this claim from a 2019 study that references the Mother Jones mass shootings database, or possibly he obtained it directly from Mother Jones. Either way, there are numerous flaws in citing this data as evidence. The methodology Mother Jones utilized to create their dataset on mass shootings and the conclusions that were made using this data have garnered criticism from criminologists such as Grant Duwe, who points to underreporting problems and says that “the Mother Jones list relied exclusively on news reports as a source of data, and news coverage tends to be less accessible for the older cases.”

He anchored the hunt for more in-depth news reporting on mass homicides in his own study of homicide using the FBI’s Supplementary Homicide Reports (SHR) data. The SHR data has several shortcomings, but it is the most complete homicide dataset currently accessible that sheds light on, among other things, when and where the majority of mass shootings have occurred in the United States. Duwe’s research revealed that mass shootings are “roughly as common now as they were in the 1980s and ’90s.”

But what about the frequency of assault weapons used in mass shootings? Did that change? Economist John R. Lott says: “There was no drop in the number of attacks with assault weapons during the 1994 to 2004 ban. There was an increase after the ban sunset, but the change is not statistically significant.”

Did the Ban Decrease Gun Homicides?

Assault rifles (and rifles in general) are very rarely used in gun crimes, so we would not expect to see any significant decrease in gun homicides or gun crimes due to the 1994 ban. Multiple studies have been done examining the effects of the ban on gun homicides and the results are generally inconclusive. A 2016 review published in JAMA found that four different studies, “do not provide evidence that the ban was associated with a significant decrease in firearm homicides.”

Between 1991, when violent crime reached an all-time high, and 2017, the country’s overall violent crime rate decreased by 47 percent, with a murder rate decline of 34 percent. Meanwhile, it appears foolish to attempt to count the almost two hundred million new firearms purchased by Americans, including the more than twenty million AR-15s and the hundreds of millions of “large” pistol and rifle magazines.

Conclusion

The assumption that the 1994 assault weapons prohibition was successful in lowering gun homicides, mass shootings, or even the possession of assault weapons is not backed by strong evidence. Most likely, those who advocate for the ban’s reintroduction are unaware of the compelling evidence against the prohibition, whether on purpose or accidentally. When the police and ATF start enforcing a new ban, there may even be an uptick in violence.

Tyler Durden

Sun, 11/27/2022 – 19:30 - Binance's 'CZ' Says Half Billion WhatsApp User Records For Sale On Dark Web

Binance’s ‘CZ’ Says Half Billion WhatsApp User Records For Sale On Dark Web

Nearly half a billion WhatsApp users’ mobile phone numbers are allegedly for sale on a dark web community forum, according to multiple sources, including Binance’s billionaire Changpeng “CZ” Zhao.

“A new set of 487 million WhatsApp phone numbers for sales in the Dark Web,” CZ tweeted Sunday. He said a sample of hacked data “indicates the phone numbers are legit.”

CZ warned users on the Meta-owned platform that “threat actors downstream will use this data to conduct smishing (phishing messages) campaigns.”

A new set of 487 million WhatsApp phone numbers for sales in the Dark Web. A sample indicates the phone numbers are legit. Please stay vigilant as threat actors downstream will use this data to conduct smishing (phishing messages) campaigns. Stay SAFU. 🙏 pic.twitter.com/ZuDVXlzz4F

— CZ 🔶 Binance (@cz_binance) November 27, 2022

https://platform.twitter.com/widgets.js

Cybernews initially confirmed the hack. They said:

On November 16, an actor posted an ad on a well-known hacking community forum, claiming they were selling a 2022 database of 487 million WhatsApp user mobile numbers.

The dataset allegedly contains WhatsApp user data from 84 countries. Threat actor claims there are over 32 million US user records included.

Another huge chunk of phone numbers belongs to the citizens of Egypt (45 million), Italy (35 million), Saudi Arabia (29 million), France (20 million), and Turkey (20 million).

The dataset for sale also allegedly has nearly 10 million Russian and over 11 million UK citizens’ phone numbers.

The threat actor told Cybernews they were selling the US dataset for $7,000, the UK – $2,500, and Germany – $2,000.

Cybernews also posted a screenshot of the seller’s post on the forum featuring the total number of phone numbers per country.

Cybernews investigated a sample of the stolen database and concluded this is legit.

The report adds massive data sets “could be obtained by harvesting information at scale, also known as scraping, which violates WhatsApp’s Terms of Service.” The seller claims all numbers belong to active users.

“In this age, we all leave a sizeable digital footprint – and tech giants like Meta should take all precautions and means to safeguard that data.

“We should ask whether an added clause of ‘scraping or platform abuse is not permitted in the Terms and Conditions’ is enough. Threat actors don’t care about those terms, so companies should take rigorous steps to mitigate threats and prevent platform abuse from a technical standpoint,” head of Cybernews research team Mantas Sasnauskas said.

This is not the first time Meta and its platforms have had users’ personal data published on the dark web. Last year, someone on a low-level hacking forum published the phone numbers and personal data of 533 million Facebook users from 106 countries for free.

Meta has vowed to crack down on data-scraping after Cambridge Analytica scraped the data of over 80 million users to target them with political ads in the 2016 election.

Tyler Durden

Sun, 11/27/2022 – 19:00 - EU Accuses Washington Of Making A Fortune From Ukraine War

EU Accuses Washington Of Making A Fortune From Ukraine War

“Nine months after invading Ukraine, Vladimir Putin is beginning to fracture the West,” Politico observes in a surprising admission which marks a stark reversal from prior mainstream media optimism and cheerleading of the White House’s blank check approach to supporting Ukraine. “Top European officials are furious with Joe Biden’s administration and now accuse the Americans of making a fortune from the war, while EU countries suffer.”

There’s clearly growing frustration among European officials over Washington’s refusal to push the Zelensky government to the negotiating table while an unprecedented billions worth of weaponry and defense aid pours in, risking unpredictable escalation between NATO and Russia. Meanwhile European populations will continue being the first to pay the price amid frigid winter temperatures and a simultaneous severe energy supply crisis even as some leaders still spout abstract ideals of “sacrifice”.

Macron and Biden on sidelines of a G20 meeting earlier this month in Indonesia, via AFP. And all the while Biden has continued rolling out his controversial green subsidies and taxes which are widely perceived as unfairly punishing European industries at this most sensitive juncture.

A senior European official speaking to Politico additionally blasted the White House policy of in effect using the Ukraine war to line the pockets of American defense contractors while at the same turning a deaf ear on European pleas for some relief to the no-win situation.

“The fact is, if you look at it soberly, the country that is most profiting from this war is the U.S. because they are selling more gas and at higher prices, and because they are selling more weapons,” the senior official said.

The person acknowledged a large-scale shift in sentiment happening, largely driven by the intractable ‘win in Ukraine at all costs’ stance of the US administration:

The explosive comments — backed in public and private by officials, diplomats and ministers elsewhere — follow mounting anger in Europe over American subsidies that threaten to wreck European industry. The Kremlin is likely to welcome the poisoning of the atmosphere among Western allies.

“We are really at a historic juncture,” the senior EU official said, arguing that the double hit of trade disruption from U.S. subsidies and high energy prices risks turning public opinion against both the war effort and the transatlantic alliance. “America needs to realize that public opinion is shifting in many EU countries.”

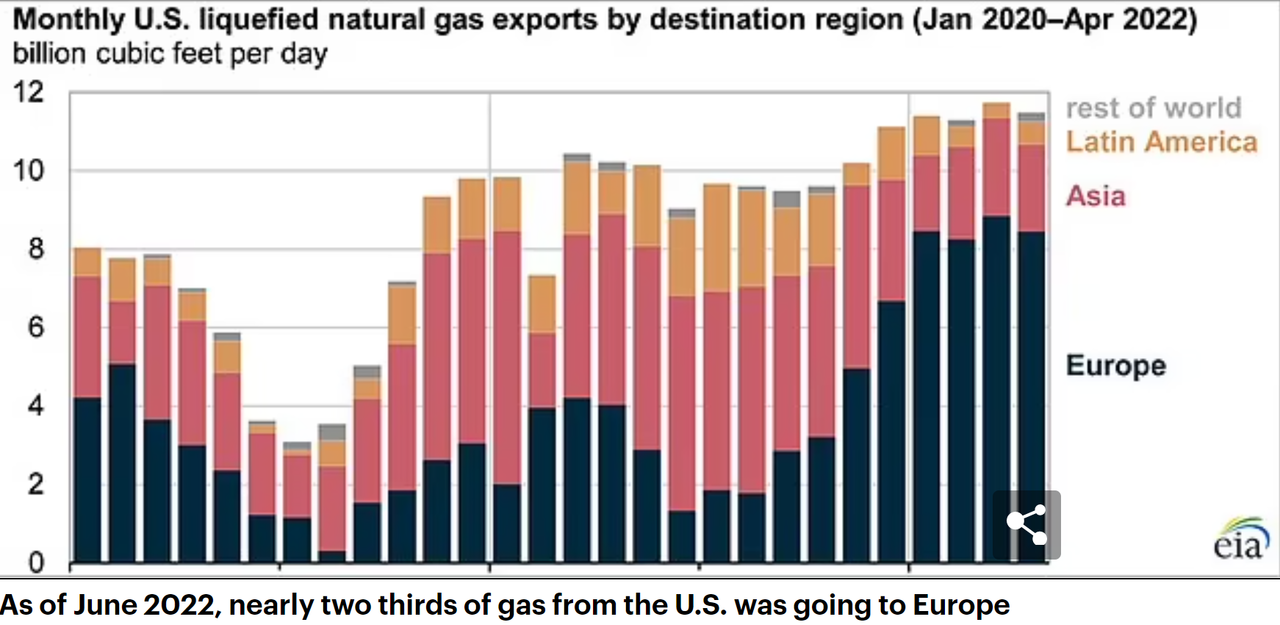

But the US National Security Council has lately reiterated its position that the crisis is solely on Putin’s shoulders full-stop, while Washington is simply presenting ramped-up US liquefied natural gas delivery to Europe as fulfilling the need to “diversify away from Russia,” according to a NSC statement.

Via EIA/Daily Mail Even the typically compliant EU foreign policy chief Josep Borrell is now questioning and showing hints of losing faith in ‘united’ efforts to support Ukraine, acknowledging to Politico, “Americans — our friends — take decisions which have an economic impact on us.”

And for a more pointed breakdown of the problem as Brussels sees it…

“The United States sells us its gas with a multiplier effect of four when it crosses the Atlantic,” European Commissioner for the Internal Market Thierry Breton said on French TV on Wednesday. “Of course the Americans are our allies… but when something goes wrong it is necessary also between allies to say it.”

Another EU diplomat cited in the Politico report described that Biden’s $369 billion industrial subsidy scheme to support green industries as part of the Inflation Reduction Act unleashed panic across European capitals.

“The Inflation Reduction Act has changed everything,” the EU diplomat said. “Is Washington still our ally or not?” This rising fury could spill into the streets as more European households are likely to experience shortages in electricity and heat this winter, further intensifying the pressure on EU politicians.

Tyler Durden

Sun, 11/27/2022 – 18:35 - True Colors: J6 Staff Lash Out At Liz Cheney For Allegedly Burying Parts Of The Investigation

True Colors: J6 Staff Lash Out At Liz Cheney For Allegedly Burying Parts Of The Investigation

There is a deepening division on the J6 Committee as staffers turn on Liz Cheney over the final report on the January 6th riot. Angry rhetoric is flying with staffers accusing the Committee of becoming a “Cheney 2024 campaign” while both the Cheney spokesperson and Committee spokesperson lashed out at the staff members as “disgruntled” and producing shoddy or biased work. The underlying issue, however, is important and revealing. The Committee’s color coated teams include a “Blue Team” on the failure to prepare adequately for the riot. That part of the investigation is reportedly being dumped or reduced. Members of the “Green” and “Purple” teams are also reportedly irate.

Cheney was soundly defeated in her primary in Wyoming and will soon leave Congress. She is being pushed by some Democrats as a possible surprise candidate for House Speaker if they could get a few Republican votes. That seems highly unlikely. The Republicans are likely to end up with the identical margin held by the Democrats for the past two years. Alternatively, some Democrats want Cheney to run for president either to dog Donald Trump in the primary debates or to run as an independent to siphon off votes in the general election.

That seems to be the suspicion for some staffers in the Washington Post story.

Fifteen former and current staffers, who spoke on the condition of anonymity to discuss internal deliberations, expressed concerns that important findings unrelated to Trump will not become available to the American public…

Several committee staff members were floored earlier this month when they were told that a draft report would focus almost entirely on Trump and the work of the committee’s “Gold Team,” excluding reams of other investigative work.

Potentially left on the cutting room floor, or relegated to an appendix, were many revelations from the “Blue Team” — the group that dug into the law enforcement and intelligence community’s failure to assess the looming threat and prepare for the well-forecast attack on the Capitol. The proposed report would also cut back on much of the work of the Green Team, which looked at financing for the Jan. 6 attack, and the Purple Team, which examined militia groups and extremism.

“We all came from prestigious jobs, dropping what we were doing because we were told this would be an important fact-finding investigation that would inform the public,” said one former committee staffer. “But when [the committee] became a Cheney 2024 campaign, many of us became discouraged.”

If true, the report will largely track the virtual exclusive focus of the hearings with open references to the 2024 election as an overriding concern.

Some of us have lamented that the J6 Committee could have been so much more than a one-sided, highly partisan investigation. House Democrats barred two Republican members originally selected by GOP leaders, who then boycotted the panel in response.

Even with the GOP boycott, the Committee could have followed the type of balanced inquiry that pursued allegations tied to the Pearl Harbor attack or Watergate. It could have insisted on balanced hearings with witnesses and dissenting views.

Nevertheless, the committee revealed important, often disturbing details. It was important for Americans to hear from figures like former attorney general Bill Barr and White House lawyers who struggled to counter unfounded advice given to Trump by outside lawyers on challenging the 2020 election. There were painful scenes of Capitol police overwhelmed at barricades and members of Congress hunkered down in offices.

Yet, the focus on a single approved narrative gave the hearings the feel of an infomercial selling a product that most of us bought two years earlier.

Now, staffers are turning on Cheney who appears to have objected to parts of the final report and wants the report to focus on Trump. Cheney’s spokesman Jeremy Adler said that the staffers in the other teams produced “subpar material” full of “liberal biases.”

Tim Mulvey, the spokesperson for the committee, criticized the staffers speaking to the media as “disgruntled” and added that “they’ve forgotten their duties as public servants and their cowardice is helping Donald Trump and others responsible for the violence of January 6th.”

It is obviously hard to address the alleged shoddy work on these other teams or claims of liberal bias. However, the “Blue Team” was a particular interest for some of us. The J6 Committee virtually ignored the issue despite ample questions over decisions by Congress leading to the riot.

The Democrats in the final hearing hammered away at documents showing that the agency knew about violent threats in the days leading up to Jan. 6th. However, the Democrats have refused to pursue the lack of preparations on Capitol Hill as a focus of the hearing. On the day of the riot, many of us noted (before the breach of security) that there was a relatively light police presence around the Capitol despite the obvious risk of a riot. Once the crowd surged, they quickly were able to gain access to the building. Conservative media have featured a video showing an officer standing by as crowds poured into the building.

That obviously does not mean that there was not violence or that Capitol police did not bravely fight to protect the building. Most of us have denounced the riot as a desecration of our constitutional process.

Moreover, at some point, officers may have shifted to deescalating as crowds surged into the building. The question is why there were not more substantial barriers, like those used at the White House. Instead, some barriers were composed of a few officers using their bikes.

The available evidence indicates that the House was warned and that the need for National Guard deployments were discussed.

There is a concern that, after criticizing such deployment and fencing around the White House in the earlier riots, the Democrats did not want to be seen following the same course.

An Inspector General report indicated that police were restricted by Congress in what they could use on that day. Previously, it was disclosed that offers of National Guard support were not accepted prior to the protests. The D.C. government under Mayor Muriel Bowser used only a small number of guardsmen in traffic positions.

That focus was rejected by the Committee members and there were no dissenting views voiced on the Committee as well as a virtual bar on opposing explanations or interpretations of evidence.

The GOP is now expected to fully investigate what the Congress knew and what it did in the days leading to the breach of the Capitol. Clearly, Cheney and others did not believe that the Blue Team full findings were ready to be released. However, those findings could be reviewed by the new GOP majority as it seeks full disclosure on why the Capitol was so quickly overrun on January 6th.

Tyler Durden

Sun, 11/27/2022 – 18:30 - When Crypto Bros Hit Miami: "It Was Like Revenge Of The Nerds" Booking Tables For $50,000

When Crypto Bros Hit Miami: “It Was Like Revenge Of The Nerds” Booking Tables For $50,000

In the grand scheme of the post-FTX collapse, millions of depositors in the exchange will suffer terminal losses and countless other investors will see much if not all of their crypto gains wiped out. But we doubt anyone will shed a tear for the Miami nightclubs which made an absolute killing for much of 2022 only to see their crypto spoils evaporate as the bitcoin bubble burst.

As the FT recalls, it was the spring of 2021, and Miami’s hottest night clubs were inundated with phone calls from cryptocurrency entrepreneurs that no one had heard of. They wanted to reserve lots of tables, or rent the entire venue for a whole evening at a cost of half a million dollars or more.

As bitcoin hit a then-record high of $60,000 and as crypto became mainstream, the biggest beneficiaries descended on the Florida city to flaunt their wealth at lavish parties.

“Out of the blue, all these kids from crypto started coming down and spending a lot of money — like, an insane amount of money,” said Andrea Vimercati, director of food and beverage at Moxy Hotel group.

“They were booking tables for $50,000, and it was like, who the hell are these people,” added Vimercati, former director of Groot Hospitality, which operates some of the hottest night clubs in Miami including Liv, Story and Swan.

The new partygoers were “95 per cent men, young . . . with a kind of nerdy style,” he said. “You couldn’t tell they had a lot of money if they were just walking around.”

A little more than a year later, the phones have stopped ringing with the value of the crypto universe tumbling over 70% from its all time highs, culminating with the collapse of Sam Bankman-Fried’s fraudulent FTX exchange which has cast a pall over the industry. As a result, the FT reports that according to Vimercati, the crypto revellers frequenting Miami’s clubs have “completely disappeared”,

Those on the dance floor had behaved as though there was no tomorrow. In the event, it turns out they might have been right. “They wanted to show that they didn’t have any limits,” recalled Vimercati. “They were ordering 12 or 24 bottles of the most expensive champagne and just showering themselves without even drinking.”