- German State Finance Minister Found Dead

German State Finance Minister Found Dead

The body of Thomas Schäfer – finance minister of the German state of Hesse, was found next to high-speed train tracks on Saturday morning in the town of Hochheim, located between Frankfurt and Mainz, according to DW, citing local police.

The remains of Schäfer, 54, were initially unable to be identified due to the extent of the injuries after witnesses reported the body. His death has been ruled a suicide by police.

According to media in the state of Hesse, the 54-year-old regularly appeared in public in recent days, for example, to inform the public about financial assistance during the coronavirus crisis. Schäfer had been finance minister of Hesse for almost 10 years

The state premier of Hesse, Volker Bouffier, said in a statement Saturday that the state’s leadership has received the news with “sadness and disbelief.” –DW

“We are all shocked and can hardly believe,” he died “so suddenly and unexpectedly” said Bouffier, adding “Our sincere condolences go to his closest relatives.”

On Thursday, “Schäfer, together with Economics Minister Tarek Al-Wazir (Greens), explained how the government wants to support the more than 200,000 small entrepreneurs and solo self-employed in the country who fear for their existence due to the corona pandemic,” according to WELT.

A bailout of 8.5 billion euros is opened and the debt brake, which Schäfer had always defended, is relaxed. The Mittelhesse from Biedenkopf near Marburg was very worried, that was obvious. The country and the whole world were facing “unforeseen challenges,” he said, and that tackling this “task of the century” would take several generations.

But he also tried to relieve fears: The country would help quickly and unbureaucratically, Schäfer promised. “The fight against the corona crisis will not fail with money.” –WELT (translated)

He leaves behind a wife, a nine-year-old son and a twelve-year-old daughter.

Schäfer isn’t the only high-profile German to meet his end on train tracks.

In 2009, 74-year-old billionaire Adolf Merckle committed suicide after pushing his business empire to the edge of ruin with a speculative bet on Volkswagen stock that went wrong. He was found dead on railroad tracks near his villa in the southern German hamlet of Blaubeuren.

Merckle lost hundreds of millions of euros after he was “caught in a brief but ferocious speculative riptide linked to a campaign by Porsche, the sports car manufacturer, to seize control of Volkswagen,” reported the New York Times at the time. As a result, he was facing a massive liquidation of his empire to cover the bad bet.

Tyler Durden

Sun, 03/29/2020 – 01:33 - The Propaganda Of Terror And Fear: A Lesson From Recent History

The Propaganda Of Terror And Fear: A Lesson From Recent History

Authored by Dr Piers Robinson, Co-Director Organisation for Propaganda Studies, via Off-Guardian.org,

The ongoing and unfolding reactions to the Coronavirus look set to have wide-ranging and long-lasting effect on politics, society and economics. The drive to close down all activities is extraordinary as are the measures being promoted to isolate people from each other.

The deep-rooted fear of contagious disease, hardwired into the collective consciousness by historical events such as the ‘Black/Bubonic Plague’ and maintained through popular culture (e.g. the Hollywood movies Outbreak and Contagion), means that people are without question highly susceptible to accepting extreme emergency measures whether or not such measures are rational or justified. The New York Times called for America to be put on a war footing in order to deal with Corona whilst former Army General Stanley McChrystal has been invoking his 9/11 experience in order to prescribe lessons for today’s leaders.

At the same time, political actors are fully aware that these conditions of fear and panic provide a critical opportunity that can be exploited in order to pursue political, economic and societal objectives. It is very likely, however, that the dangers posed by the potential exploitation of Corona for broader political, economic and societal objectives latter far outweigh the immediate threat to life and health from the virus. A lesson from recent history is instructive here.

9/11 AND THE GLOBAL ‘WAR ON TERROR’

The events of September 11 2001 represent a key moment in contemporary history. The destruction of three skyscrapers in New York after the impact of two airliners and an attack on the Pentagon, killing around 3000 civilians, shocked both American and global publics. The horror of seeing aircraft being flown into buildings, followed by the total destruction of three high rise buildings within a matter of seconds, and the spectre of a shadowy band of Islamic fundamentalists (Al Qaeda) having pulled off such devastating attacks, gripped the imagination of many in the Western world.

It was in this climate of paranoia and fear that extraordinary policies were implemented. The USA Patriot Act led to significant civil liberty restrictions whilst the mass surveillance of the digital environment became normalized.

In the United States torture was authorized in the name of preventing terrorism whilst the Guantanamo Bay facility in Cuba became a site in which accused individuals have been held without any adequate legal protection or due process.

Remarkably, the individual accused of leading the alleged 9/11 plot, Khalid Sheikh Mohammed, who ‘confessed’ to CIA interrogators after being ‘waterboarded’ 183 times, has recently received his trial date, set for January 11 2021 and 20 years after 9/11. Civil liberty restrictions, mass surveillance and torture were only a sub-strand of the major war-fighting-policy that was enabled by 9/11.

Presented at the time as America’s ‘New Pearl Harbour’, 9/11 provided the conditions for a series of major regime-change wars which persist until today.

Critically, these wars have not been primarily about combatting ‘Islamic fundamentalist terrorism’/Al Qaeda, but rather attacking ‘enemy’ states. Indeed, the evidence that the 9/11 event and the alleged threat of ‘Islamic fundamentalist’ was then exploited in order to pursue a geo-politically motivated set of regime-change wars which had little connection to the purported Al Qaeda threat is well established.

Former Supreme Allied Commander of NATO, Wesley Clark, famously went public in 2006/7 stating that immediately after 9/11 he had been informed that the US was intending to attack seven countries within five years including Iraq, Syria, Lebanon, Somalia, Sudan and Iran. Clark stated:

He [the Joint Staff officer] picked up a piece of paper, he said I just got this down from upstairs, from the Secretary of Defence’s office today, and he said this is a memo that describes how we are gonna take out seven countries in five years, starting with Iraq and then Syria, Lebanon, Libya, Somalia, Sudan, and finishing off Iran.

Clark’s claims have recently been corroborated by retired Colonel Lawrence Wilkerson (chief of staff to Colin Powell and Iraq War planner) who stated that he had actually seen the same plans Clark was referring to many months prior to 9/11:

My first briefing in the Pentagon from an Air Force three-star general in February of 2001 I almost fell of my chair because their briefing included on the one hand the Air Force’s ability to take out 80 to 90% of the targets in North Korea in the first few hours of an aerial strike on that country to hey when we do Iraq we’re gonna do Syria and Lebanon and we’re going to do Iran and maybe Egypt … but this was more than that [just contingency planning] Wes Clark is right they had these plans they were going to go right through all these countries that they felt threatened Israel all through those countries that they felt threatened 25-30% of the world’s oil passing through the Strait of Hormuz.

Documentary evidence for these claims has come by way of the UK Chilcot Inquiry into the 2003 Iraq War. For example, a report quoted a British embassy cable, dated 15 September 2001, explained that ‘[t]he “regime-change hawks” in Washington are arguing that a coalition put together for one purpose [against international terrorism] could be used to clear up other problems in the region.’ Another document released by Chilcot shows British Prime Minister Tony Blair and US President George Bush discussing phases one and two of the ‘war on terror’ and when to hit particular countries. Blair writes:

If toppling Saddam is a prime objective, it is far easier to do it with Syria and Iran in favour or acquiescing rather than hitting all three at once.

The regime-change wars that have flowed directly and indirectly from 9/11 continue to this day. War and conflict continues in Afghanistan and Iraq whilst the nine-year-long war in Syria has borne witness to extensive and illegal policies pursued by Western governments including the funding and arming of extremist groups coupled with support for groups actually aligned with Al Qaeda. Iran continues to be subjected to US hybrid warfare tactics including sanctions and covert operations whilst the threat of military action is very clear and present.

The human cost of these wars, built upon the ruthless exploitation of public fear of terrorism in order to pursue multiple ‘regime-change’ wars, has been huge. According to the Brown University ‘Costs of War Project’, the wars in Afghanistan and Iraq have killed a combined 480,000 to 507,000 civilians, coalition military members, and foreign fighters, with an untold number having been maimed and disfigured. IPPNW estimated that the first ten years of the ‘war on terror’ in Afghanistan, Iraq and Pakistan killed 1.3 million people.

Since 2011, in Syria alone, over 400,000 people have died as a result of war. The numbers of people displaced as a result of these conflicts are also extremely high; wars in Afghanistan, Iraq, Pakistan, and Syria have wrought a combined 9.39 million refugees, 10.78 million internally displaced peoples, and 830,000 asylum seekers. In addition, there are persisting and very serious concerns with respect to the possible involvement of state actors with the event of 9/11.

Recent and critical developments regarding the events of 9/11 include the publication this week of the University of Alaska study of the WTC7 Collapse which confirms that the official US government investigation was wrong if not plain fraudulent. Other important developments include publication last year of the 9/11 Consensus Panel evidence and increasing scrutiny of the official narrative from mainstream academics.

Overall, the 9/11 global ‘war on terror’ is increasingly coming to be understood particularly across the world as, first and foremost, a remarkable propaganda campaign designed to enable violent conflict in the international system and with its effects and objectives being far wider and deeper than had been suggested by official narratives regarding the need to combat Al Qaeda.

CORONA VIRUS: A NEW 9/11?

The lesson of 9/11 is that major events can become what scholar Peter Dale Scott describes as deep events which are exploited by political actors in order to precipitate and manage major political, economic and social shifts. 9/11 became, in effect, the deep event that enabled 20 years of unfettered Western warfare abroad and severe civil liberty restrictions and extensive surveillance at home.

At the time of 9/11 many people in the West were terrified of terrorism. Public opposition to the invasion of Afghanistan (the first regime war to flow within months of 9/11) was almost impossible without being accused of being reckless in the ‘fight against terrorism’ or of being an ‘Al Qaeda’ sympathizer. Muslims throughout the West were widely despised. US President George Bush declared that ‘you are either with us or against us’. The parallels with what is happening today are obvious.

Is the Coronavirus a new 9/11, a new deep event? We cannot yet be sure, as of this writing. Perhaps the current strategy of suspending basic liberties will work to effectively eliminate all threats posed by the virus. Governments will then restore the civil liberties currently being suspended and all will fairly quickly return to the way things were before. Perhaps the economy will confidently weather the fallout from the ‘lockdowns’ and everything will return to business as usual.

And perhaps a sober ‘lessons learned’ review will lead to public health officials developing reasonable and balanced plans, such as developing sufficient capacity for rapid testing and tracing, which can be deployed the next time a sufficiently dangerous virus starts to spread thus avoiding terrifying publics and implementing draconian measures that inflict significant damage to the social and economic fabric of society.

Or perhaps not. It may be that, as British journalist Peter Hitchens has been warning, the loss of liberty and basic rights will continue indefinitely as governments greedily hold on to their increased powers of control over their citizenry.

Similarly, Italian journalist Stefania Maurizi has warned about the risks in Italy of state authorities, hostile to open societies and the political left, exploiting Corona in order to increase their control.

An obvious concern here is whether there will be a permanent impact on mass gatherings and protests. James Corbett warns of a permanent state of ‘medical martial law’ and there is certainly the very real possibility of the normalization of government-imposed quarantine and other freedom of movement restrictions.

Margaret Kimberley of the US-based Black Agenda Report warns that Corona may be used as a way of covering up both economic crisis and collapse. She notes that the Federal Reserve ‘recently threw Wall Street a $1.5 trillion lifeline which only kicked the can down the road. The can has been kicked ever since the Great Recession of 2008’. The likely destruction of small businesses might allow for ever greater corporate choke-hold on the economy with more people forced into the corporate workforce.

There is certainly the danger that COVID-19 will be exploited in order to distract from severe economic problems whilst also enabling the pursuit of new economic strategies which worsen rather than mitigate the social inequalities that already tarnish Western countries.

And, of course those actors behind the regime-change wars that flowed from 9/11 may use the Coronavirus to increase pressure on the countries they have been targeting for the last 20 years and those they wish to target in the future.

Already we have seen the regime-change advocate John Bolton blaming China for the Corona Virus whilst the New York Times reported that US Secretary of State Mike Pompeo and national security adviser Robert C. O’Brien were ‘arguing that tough action while Iran’s leaders were battling the corona virus ravaging the country could finally push then into direct negotiations’.

ABC news report that, despite the Coronavirus, US and UAE troops have held a major military exercise ‘that saw forces seize a sprawling model Mideast city’. It is also worth nothing here the recent US assassination of Iranian General Solemeni and the on-going proxy battles between US forces and Iranian-backed groups in Iraq. The possibility of Corona being exploited in order to further the regime change wars we have seen over the last 20 years is extremely likely and it would be naïve in the extreme to think otherwise.

Whatever the COVID-19 event may or may not be, the fundamental lesson of the last 20 years is that governments can and do exploit, even manipulate, events in order to pursue political, social, military and economic objectives. Fearful populations are frequently irrational ones, vulnerable and malleable. Now is not the time for deference to authority and reluctance to speak out.

It is time for publics to get informed, think calmly and rationally, and to robustly scrutinize and challenge what their governments are doing. The dangers of failing to do this likely far surpass the immediate threat posed by the Coronavirus.

Tyler Durden

Sat, 03/28/2020 – 23:45 - China Suffers Economic Double-Whammy As Current Global Demand Collapse Follows Earlier Supply Crash

China Suffers Economic Double-Whammy As Current Global Demand Collapse Follows Earlier Supply Crash

As the first quarter is about to close, many Chinese factories are still operating below full capacity, have been gradually ramping up production over the last several weeks as government data suggests the country’s pandemic curve has flattened.

But as Bloomberg notes, there is a serious problem developing, one where the virus crisis is locking down the Western Hemisphere, has resulted in firms from Europe and the US to cancel their Chinese orders en masse, triggering the second shockwave that is starting to decimate China’s industrial base.

A manager from Shandong Pangu Industrial Co. told Bloomberg that 60% of their orders go to Europe. In recent weeks, manager Grace Gao warned that European clients are requesting orders to be delayed or canceled because of the virus crisis unfolding across the continent.

“It’s a complete, dramatic turnaround,” Gao said, estimating that sales in April to May could plunge by 40% over the prior year. “Last month, it was our customers who chased after us checking if we could still deliver goods as planned. Now it’s become us chasing after them asking if we should still deliver products as they ordered.”

A twin shock has emerged, one where China shuttering most of its industrial base from mid-January through early March, generated a supply shock. Now, as those Chinese firms add capacity, expecting to be met with a surge in demand from Western companies, that is not the case and is resulting in a demand shock.

“It is definitely the second shockwave for the Chinese economy,” said Xing Zhaopeng, an economist at Australia & New Zealand Banking Group. The pandemic across the world “will affect China manufacturing through two channels: disrupted supply chains and declining external demand.”

With orders canceled, supply chains disrupted, and payments delayed – the road to recovery in China is going to be a bumpy one at best. Overly optimistic analysts who have been touting a V-shape recovery in China, thus the world, in the first half of the year, will likely be wrong, and as we’ve explained several times, the best case is a U-shape or even perhaps an L-shape.

“Manufacturers are seeing many cases where overseas clients regretted their orders or where goods can’t be delivered due to customs closures in other countries,” said Dong Liu, vice president of Fujian Strait Textile Technology Co. in southeastern China. Liu’s factory was on the cusp of resuming full capacity this month until a demand shock severely dented export orders.

Nomura International HK Ltd warned earlier this week that China could be on the verge of “plummeting export growth in the coming months.”

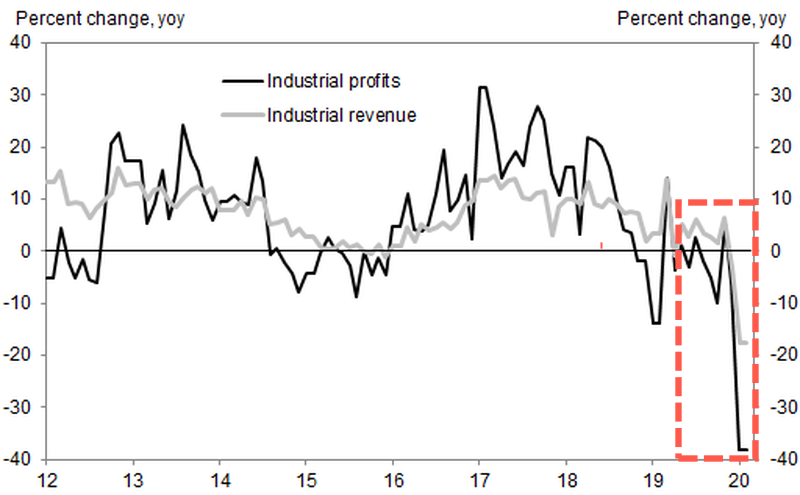

We noted on Friday morning that Chinese industrial profits crashed the most on record in January-February, due mostly because of the Lunar new year holiday, coupled with the virus outbreak and strict social distancing measures implemented by the government. This means many Chinese firms are struggling to survive, running out of cash, and on the brink of bankruptcy as demand from abroad has collapsed.

In Keqiao, Shaoxing, a district known for textile manufacturing, many firms are in rough shape after several months of shuttering operations. Have now been greeted with a collapse in demand, thwarting any hope that full capacity can arrive in the coming weeks.

The twin shocks, first being a supply shock, originating from shutdowns in China, then a demand shock, now coming from the Western world, is the evolution of the global economic crash that is unfolding right in front of us. The world is headed for a depression, if not already in one, as central banks are frantically deploying MMT and unleashing helicopter money to save the world.

Tyler Durden

Sat, 03/28/2020 – 23:20 - Is The COVID-19 Outbreak A Trojan Horse To Increase Smartphone Surveillance?

Is The COVID-19 Outbreak A Trojan Horse To Increase Smartphone Surveillance?

Authored by Aaron Kesel via ActivistPost.com,

The coronavirus outbreak is proving to be the Trojan horse that justifies increased digital surveillance via our smartphones.

All over the world, starting with China – the suspected origin of the COVID-19 outbreak – governments are increasing surveillance of citizens using their smartphones. The trend is taking off like wildfire; in China citizens now require a smartphone application’s permission to travel around the country and internationally.

The application is AliPay by Ant Financial, the finance affiliate controlled by Alibaba Group Holding Ltd. co-founder Jack Ma, and Tencent Holdings Ltd.’s WeChat. Citizens now require a green health code to travel, Yahoo News reported.

China isn’t the only country looking towards smartphones to monitor their citizens; Israel and Poland have also implemented their own spying to monitor those suspected or confirmed to be infected with the COVID-19 virus. Israel has gone the more extreme route, and has now given itself authority to surveil any citizen without a court warrant. Poland on the other hand is requiring those diagnosed with COVID-19 ordered to self-isolate to send authorities a selfie using an app. Which, if Poles don’t respond back in 20 minutes with a smiling face, they risk a visit from police, Dailymail reported.

Singapore has asked citizens to download an app which uses Bluetooth to track whether they’ve been near anyone diagnosed with the virus; and Taiwan, although not using a smartphone, has introduced “electronic fences” which alert police if suspected patients leave their homes.

Meanwhile, here in the U.S. as reported by the Washington Post, smartphones are being used by a variety of companies to “anonymously” collect user data and track if social distancing orders are being adhered to. Beyond that, the mobile phone industry is discussing how to monitor the spread of COVID-19. If that’s not enough, as this author reported for The Mind Unleashed, the government wants to work with big social tech giants like Google, Facebook, and others, to track the spread of COVID-19.

A new live index shows the increase of the police state by Top10VPN, a Digital Rights group. Top10VPN lists a total of 15 countries which have already started measures to track the phones of coronavirus patients, ranging from anonymized aggregated data to monitor the movement of people more generally, to the tracking of individual suspected patients and their contacts, known as “contact tracing.”

That’s not the only live index, a company called Unacast that collects and analyzes phone GPS location data also launched one. Except this is a “Social Distancing Scoreboard” that grades, county by county, monitoring who is following social distancing rules.

As Activist Post previously wrote while discussing the increase of a police surveillance state, these measures being put into place now will likely remain long after the pandemic has stopped and the virus has run its course. That’s the everlasting effect that COVID-19 will have on our society. The coronavirus is now classified as a pandemic by the World Health Organization, and it may very well be a legitimate health concern for all of us around the world. But it’s the government’s response that should worry us all more in the long run.

At the time of this report the COVID-19 virus has infected 640,589, killed 29,848, while 137,270 have recovered according to the Johns Hopkins map.

Tyler Durden

Sat, 03/28/2020 – 22:55 - Global Pandemic Preparedness – Which Country Is The Most (And Least) Ready For COVID-19?

Global Pandemic Preparedness – Which Country Is The Most (And Least) Ready For COVID-19?

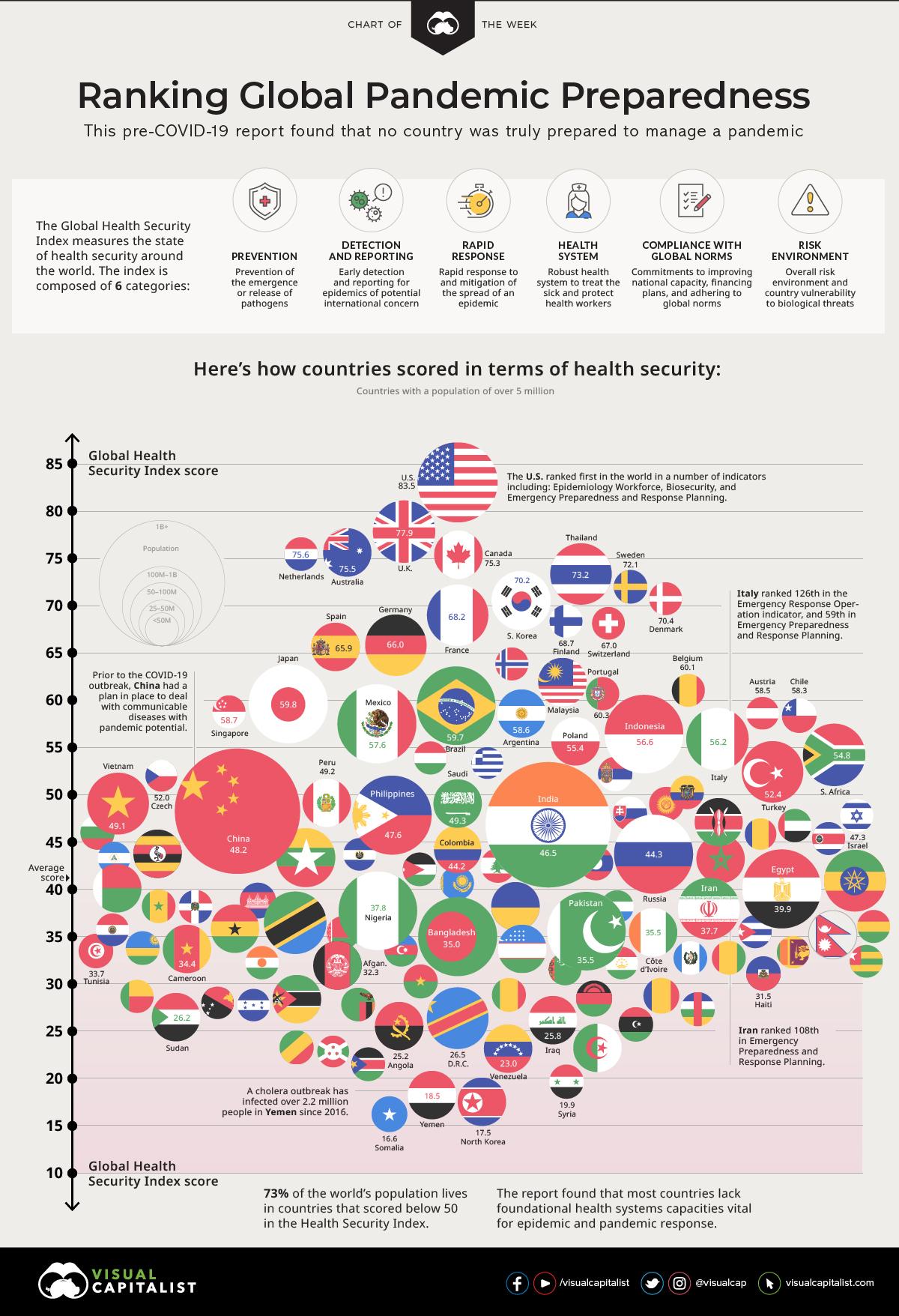

The world has experienced many pandemics throughout its history, but not every era has had the benefit of modern medicine and hindsight.

However, as Visual Capitalist’s Nichaolas LePan notes, even with the readily available medical expertise and equipment that exists today, it is still unevenly distributed throughout the globe. Combine this with a highly interconnected global economy, and large populations are still at risk from infection.

Today’s chart pulls data from the 2019 Global Health Security Index, which ranks 195 countries on health security. It reveals that while there were top performers, healthcare systems around the world on average are fundamentally weak – and not prepared for new disease outbreaks.

Pathways for Commerce and Disease

Modern transportation and trade have linked the farthest stretches of the world to fuel a global economy. Physical distance plays less a limiting role and more an enabling one to form a flat world as Thomas Friedman put it, creating opportunities for commerce anywhere in the world.

A person can sell dishware from his home in Cusco, Peru, online to a customer in Muncie, Indiana, with products manufactured in China, from materials sourced in Africa.

While these connections sound sterile, there are people interacting with one another to procure, manufacture, package, and distribute the goods. The connections are not just through products, but also people and animals across many borders.

Now, add up the interactions within the global food supply chain with plants and livestock and tourism industries and place them under the pressures of climate change, urbanization, international mass displacement, and migration—and the volume and variety of opportunities for disease transmission and mutation becomes infinite.

The same pathways of global commerce become the transmission vectors for disease. A cough in Dubai can become a fever in London with one flight and one day.

You Cannot Manage What You Do Not Measure

Despite this, we still live with national healthcare systems that look inward towards national populations, with less of a focus on integrating what is happening with the outside world.

The Global Health Security (GHS) Index is the first comprehensive effort to assess and benchmark health security and related capabilities by nation, and it tracks six key factors to come up with an overall score for each of the 195 countries in the ranking:

-

Prevention

Prevention of the emergence or release of pathogens -

Detection and Reporting

Early detection and reporting for epidemics of potential international concern -

Rapid Response

Capability of rapidly responding to and mitigating the spread of an epidemic -

Health System

Sufficient and robust and health system to treat the sick and protect health workers -

Compliance with Global Norms

Compliance with international norms by improving national capacity, financing plans to address gaps -

Risk Environment

Risk environment and country vulnerability to biological threats

Note: The GHS Index is a project of the Nuclear Threat Initiative (NTI) and the Johns Hopkins Center for Health Security (JHU), and was developed with The Economist Intelligence Unit (EIU).

Country Overall Rankings

Overall, the rankings uncover a distressing insight. Global preparedness for both epidemics and pandemics is weak, with the average score in the index sitting at 40.2 out of 100.

The countries with the highest scores have effective governance and politics systems in place, while those with the lowest scores fall down for their inadequate healthcare systems—even among high-income countries.

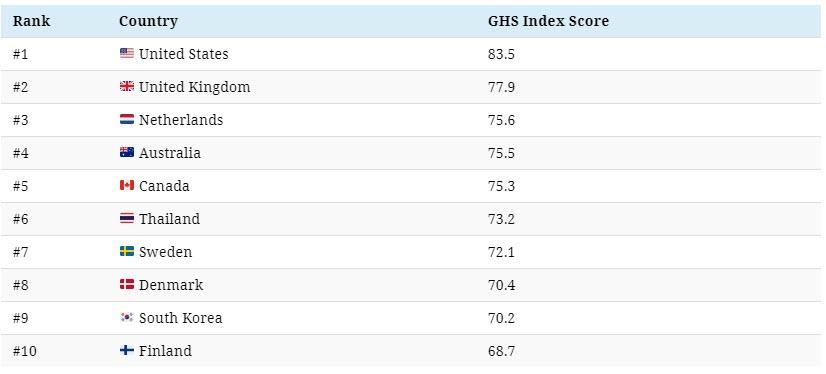

Here are the 10 highest-ranking countries in the index:

You can view the complete rankings of all 195 countries on the GHS Index website.

Interestingly, 81% of countries score in the bottom tier for indicators related to biosecurity—and worse, 85% of countries show no evidence of having completed a biological threat-focused simulation exercise in conjunction with the World Health Organization (WHO) in the past year.

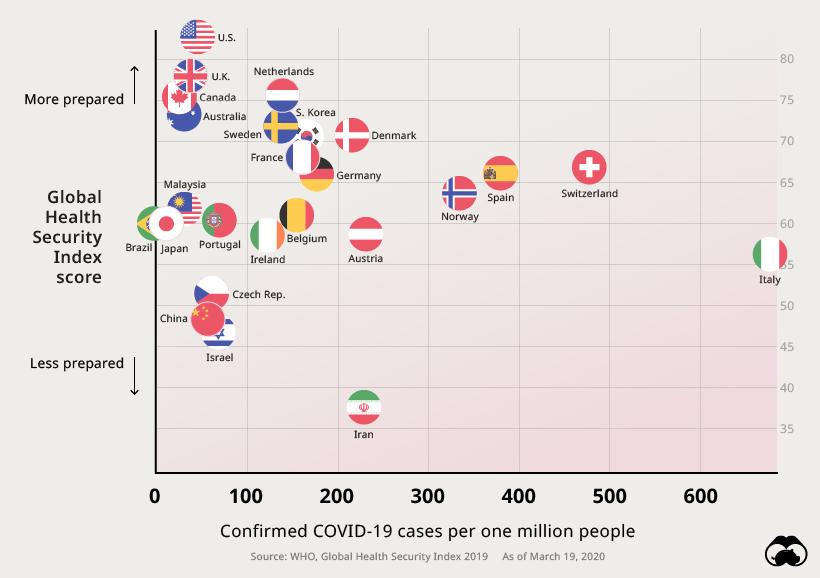

Confirmed COVID-19 Cases vs. Global Health Security Score

Many healthcare systems have had their security tested with the outbreak of COVID-19.

Although it is still extremely early, there appears to be a relationship between a nation’s health security and its ability to cope with pandemics.

Takeaways: A World Unprepared

While there may be top performers relative to other countries, the overall picture paints a grim picture that foreshadowed the current crisis we are living through.

“It is likely that the world will continue to face outbreaks that most countries are ill positioned to combat. In addition to climate change and urbanization, international mass displacement and migration—now happening in nearly every corner of the world—create ideal conditions for the emergence and spread of pathogens.”

– The Global Health Security Index, 2019

The report outlined eight critical insights about global health security in 2019 that reveal some of the problems countries are now facing.

-

National health security is fundamentally weak globally. No country is fully prepared for epidemics or pandemics, and every country has important gaps to address.

-

Countries are not prepared for a globally catastrophic biological event.

-

There is little evidence that most countries have tested important health security capacities or shown that they would be functional in a crisis.

-

Most countries have not allocated funding from national budgets to fill identified preparedness gaps.

-

More than half of countries face major political and security risks that could undermine national capability to combat biological threats.

-

Most countries lack basic health systems capacities critical for epidemic and pandemic response.

-

Coordination and training are inadequate among veterinary, wildlife, and public health professionals and policymakers.

-

Improving country compliance with international health and security norms is essential.

A Stark Reality

The intention of the Global Health Security Index is to encourage improvements in the planning and response to one of the world’s most omnipresent risks–infectious disease outbreaks. When this report was released in 2019, it revealed that even the highest ranking nations still had gaps to fill in preparing for a pandemic.

Of course, hindsight is 20/20. The COVID-19 outbreak has served as a wake-up call to health organizations and governments around the world. Once all of the curves have been flattened, the next version of this report will undoubtedly be viewed with renewed interest.

Tyler Durden

Sat, 03/28/2020 – 22:30 -

- COVID-19 Is Forcing The World To Re-Think The Idea Of "Monetary Value"

COVID-19 Is Forcing The World To Re-Think The Idea Of “Monetary Value”

Authored by Matthew Ehret via The Strategic Culture Foundation,

Western society has long been gripped by a deep seeded belief in money. Trillions of dollars of bank notes tied to ever-growing mountains of un-payable national debts has taken on a life of its own over the years. As the post-1971 years rolled by, society increasingly lost a sense that this human invention called “money” was created to serve humanity rather than rule it, and with that lost sense, money became an idol of worship.

Decades of this modern religion have resulted in an incredibly tragic situation: a disproportionate wealth distribution in the hands of the 0.1%, an over-bloated services/consumer driven economy, increased rates of poverty and despair internationally as well as a dismal loss of vital skills, and productive capacity once enjoyed by advanced industrial nations just four decades ago. Vital infrastructure built up during the 1930s-1960s has been permitted to decay through simple neglect while un-payable debts have reached record highs.

Then like a thief in the night, the illusion was ripped away.

The Confused Response to the Crisis

This ripping away took the form of an international pandemic which has resulted in western nations’ economies grinding to a halt with a new $2 Trillion government emergency spending bill unveiled on March 24. The Washington Post reports that this bill will authorize “hundreds of billions of dollars sent to Americans in the form of checks as a way to flood the country with money in an effort to blunt the dramatic pullback of spending that has resulted from the coronavirus outbreak.”

Governments across the Trans-Atlantic have also announced national interventions into banks and private industry in order to force production quotas of vital equipment like ventilators, masks and other medical necessities to meet the increased demand. Banks in Spain have been nationalized (albeit only “temporarily”) to force finance to act in accordance with the needs of society. In America, the Defense Authorization Act and broader War Powers Act passed by President Trump gives the executive broad powers to take over vital industries if needed in order to mobilize the nation to respond to the crisis.

This renewal of national sovereign powers breaks all of the monetary “laws of the neoliberal order” and with that defiance of globalization, a genuine positive potential for a paradigm shift is visible…

…but something vital is still missing.

This “missing something” is clearly demonstrated by the continued obsession with money as new bailouts of the collapsing speculative banks have now risen to a $1 trillion/day overnight repo loan to collapsing banks which is added to the $1 Trillion 14 week loans offered every week that will dramatically increase the $9 trillion already emitted since helicopter money began in earnest in September 2019. With the mass panic and economic shutdown instigated by COVID-19, markets have lost over 30% of their value and fears of a new great depression have spread far and wide. Rather than impose serious bank regulation like Glass-Steagall to break up the commercial from speculative banks as was done in 1933, the American government has merely unleashed unlimited money printing. This bipolar response is akin to trying to stop a raging fire with a combination of water and gasoline.

We thus find that the greatest crisis facing humanity is not caused by the market crisis, or even the coronavirus per se, but rather society’s profound inability to understand the source of real from fictitious value.

What is REAL Value? Lincoln and FDR Revisited

“The privilege of creating and issuing money is not only the supreme prerogative of Government, but it is the Government’s greatest creative opportunity. By the adoption of these principles, the long-felt want for a uniform medium will be satisfied. The taxpayers will be saved immense sums of interest, discounts and exchanges. The financing of all public enterprises, the maintenance of stable government and ordered progress, and the conduct of the Treasury will become matters of practical administration. The people can and will be furnished with a currency as safe as their own government. Money will cease to be the master and become the servant of humanity. Democracy will rise superior to the money power.”

These words were uttered by none other than America’s 16th president Abraham Lincoln as he fought to take federal control of credit vis a vis the “greenbacks” that not only allowed him to win the war of secession but also construct the greatest infrastructure and industrialization programs of history driven by the trans continental railway. The dramatic success of Lincoln’s “American System” not only saved the union, but spread successfully across the world from Japan’s Meiji restoration, Russia’s trans Siberian rail development, Bismarck’s Zollverein in Germany and Sadi Carnot’s France. This powerful spread of what German economist Friedrich List called “the American System of Political Economy” nearly annihilated the money-worshipping system of Adam Smith’s Free Trade doctrine from the earth and only failed in this task via a plenitude of London-directed assassinations, and a couple of imperially-orchestrated wars and revolutions along the way.

The world spun out of control between the murder of the “last Lincoln republican” William Mckinley in 1901 and the orchestrated meltdown of the U.S. economy known as the great depression of 1929.

Amidst this dark period, Franklin Roosevelt called for the Democrats to claim the legacy of Lincoln from the corrupt republican party and faced a Wall Street-backed coup d’etat, survived a freemasonic assassination attempt and subverted a City of London-orchestrated bankers’ dictatorship… all in his first year in office. During his March 4, 1933 inaugural address, the president rallied the American people saying:

“I am prepared under my constitutional duty to recommend the measures that a stricken nation in the midst of a stricken world may require. These measures, or such other measures as the Congress may build out of its experience and wisdom, I shall seek, within my constitutional authority, to bring to speedy adoption.”

As I have outlined in my recent paper How to Crush a Bankers’ Dictatorship, FDR took control of credit in a similar manner as Lincoln by forcing the Federal Reserve to obey a national mandate for the first time since the private bank was set up in 1913. He did so by imposing his ally Mariner Eccles into the position of Chairman who understood that money had to create infrastructure and industrial growth in order to acquire any claim to having actual “value”. This was a stark break from the “hands off/laissez-faire” policy of President Hoover and his JP Morgan-run cabinet. FDR also emitted Lincoln-styled productive credit through the Reconstruction Finance Corporation (RFC) to fuel the New Deal. The RFC issued over $33 billion in low-interest loans by the end of the war (more than all private banks combined).

Describing his moral philosophy of political economy, FDR stated:

“We seek not merely to make government a mechanical implement, but to give it the vibrant personal character that is the very embodiment of human charity. We are poor indeed if this nation cannot afford to lift from every recess of American life the dread fear of the unemployed that they are not needed in the world. We cannot afford to accumulate a deficit in the books of human fortitude.”

What is missing today

Today’s America is confronting an existential crisis similar to that which both Lincoln and Franklin Roosevelt battled in their time. Just as the proto-deep state of 1865 ran Lincoln’s assassination from Montreal Canada, and took over the White House minutes after FDR’s untimely death in 1945, today’s deep state has attempted in vain to overthrow President Trump while successfully undermining the political viability of other “outsiders” like Bernie Sanders and Tulsi Gabbard.

The difference is that today’s crisis combines elements of all previous crises of 1861-1865, 1929-1933 and 1938-1945: the very real new threat of chaos and civil war within, NATO-led wars with China and Russia without and economic collapse across the entire trans-Atlantic bubble economy. The other difference is located in the current presidency’s inability to FOCUS with a clear mind on principled solutions to this multi-faceted crisis while instead finding itself trapped within contradictory impulses.

While FDR and Lincoln understood that VALUE was located the physically productive forces of labor which sustained and improved the lives of people and gave the constitution’s pre-amble a real living character, today’s American leadership has displayed a far greater ignorance to this basic fact of life. The vital difference between “need” vs “want” which has been obscured by decades of free market ideology has resulted in a loss of moral judgment necessary to properly put out the fires threatening to unleashing civil war, chaos and fascist global government “solutions” across the Trans Atlantic today.

The new multipolar alliance led by Russia and China have demonstrated what modern day New Deal policies can do. The Belt and Road Initiative as well as the Strategic Eurasian Partnership, Polar Silk Road and bold space exploration projects all reflect the type of principles of win-win cooperation and long term planning that characterized both FDR and Lincoln earlier. The Health Silk Road announced earlier this week by President Xi Jinping provides a brilliant maneuver to tackle the COVID-19 pandemic under a non-Malthusian worldview. This Multipolar Alliance exists as a form of a life raft for anyone wishing to escape the fate of the Titanic and embark on a new epoch of growth and cooperation.

The question is: Do western powers have the ability to act according to a scientific (and moral) standard of value by aligning with this multipolar alliance or will they choose to remain in Orwell’s dystopic cage and succumb to a fate which Lincoln, FDR and other great leaders gave their lives to prevent?

Tyler Durden

Sat, 03/28/2020 – 22:05 - More Evidence China Is Lying; Number Of Urns More Than Double Reported Coronavirus Deaths

More Evidence China Is Lying; Number Of Urns More Than Double Reported Coronavirus Deaths

China has been caught lying once again about coronavirus figures – with the latest evidence coming from ground-zero in Wuhan, where according to official CCP data just 50,006 people were infected with COVID-19, and 2,535 dying of the virus.

Yet, Chinese investigative outlet Caixin revealed that when mortuaries opened back up this week, photos revealed a far greater number of urns than reported deaths. In one, a truck loaded with 2,500 urns can be seen arriving to the Hankou Mortuary. According to the report, the driver said he had delivered the same amount the previous day.

In another photo, seven 500-urn stacks can be seen inside the mortuary, adding up to 3,500 deaths.

This adds up to more than double the amount of reported deaths in the region – for which grieving family members waited in line for as long as five hours to collect, according to Shanghaiist.

Urns are reportedly being distributed at a rate of 500 a day at the mortuary until the Tomb Sweeping Day holiday, which falls on April 4 this year.

Wuhan has seven other mortuaries. If they are all sticking to the same schedule, this adds up to more than 40,000 urns being distributed in the city over the next 10 days.

When reporters at Bloomberg made calls to the funeral homes to check on the number of urns waiting to be collected, the mortuaries said that they either did not have that data or were not authorized to disclose it. –Shanghaiist

Given the constant, provable lies, does anyone believe that China has actually contained COVID-19?

And of course, as former White House press secretary Sean Spicer pointed out implicitly, don’t expect the mainstream media to question anything…

Reminder to all of the journalists that took China at face value when they claimed they had no more cases https://t.co/mlS0t9HvRo

— Sean Spicer (@seanspicer) March 28, 2020

https://platform.twitter.com/widgets.js

Besides they all know the truth…(but must resist)

Tyler Durden

Sat, 03/28/2020 – 21:40 - Fictional Reserve Lending Is The New Official Policy

Fictional Reserve Lending Is The New Official Policy

Authored by Mike Shedlock via MishTalk,

Official policy finally caught up with reality. Reserves are fictional.

Official Announcement

With little fanfare or media coverage, the Fed made this Announcement on Reserves.

As announced on March 15, 2020, the Board reduced reserve requirement ratios to zero percent effective March 26, 2020. This action eliminated reserve requirements for all depository institutions.

Amusingly, a few days ago yet another article appeared explaining how the Money Multiplier works. The example goes like this: Someone deposits $10,000 and a bank lends out $9,000 and then the $9,000 gets redeposited and 90% of the gets lent out and so an and so forth.

The notion was potty. That is not remotely close to how loans get made. Deposits and reserves never played into lending decisions.

What’s Changed Regarding Lending?

Essentially, nothing.

The announcement just officially admitted the denominator on reserves for lending is zero.

There are no reserve lending constraints (but practically speaking, there never were).

Fictional Reserve Lending Flashback

I wrote about this in December of 2009 in Fictional Reserve Lending and the Myth of Excess Reserves.

The flashback is amusing as I reference a number of people worried about hyperinflation.

Here are the facts of the matter as I explained in 2009.

Money Multiplier Theory Is Wrong

-

Lending comes first and what little reserves there are (if any) come later.

-

There really are no excess reserves.

-

Not only are there no excess reserves, there are essentially no reserves to speak of at all.

The rationale behind the last bullet point pertains to banks hiding losses. Regulators suspended mark-to-market accounting.

When Do Banks Make Loans?

-

They meet capital requirements

-

They believe they have a creditworthy borrower

-

Creditworthy borrowers want to borrow

All three requirements must be met.

-

Banks generally do not lend if they are capital impaired.

-

Clearly someone must want to borrow.

Point two is worthy of discussion.

Banks may not have a creditworthy borrower, they just have to believe it, or they have an alternate belief that applies. In 2007 banks knew full well they were making mortgage liar loans.

So Why Did They?

Because banks bought into the idea home prices would not go down so they did not give a rat’s ass if someone was out on the street. All they cared about was the quality of the loan. If Home prices appreciated, they were covered.

From a bank lending aspect, nothing has changed. Neither reserves nor deposits never entered into the picture.

Denominator Officially Zero

The denominator on lending is now officially zero. But nothing really changed. The Fed was always ready, willing, and able to supply unlimited reserves.

The only thing that’s new is the official announcement that reserves are fictional.

Capital Concerns in 2009

There are capital concerns, but note that in March of 2009 the Fed suspended mark-to-mark accounting.

That was the key announcement that launched the bull market.

Capital Concerns Now

There are still capital concerns, but the Fed stepped up to the plate and is willing to buy corporate bonds.

Guess who is going to unload as much questionable junk as possible and guess who will buy it.

Banks know they have losses but hey will not admit them.

All it takes to mask them is a clever swap takes the assets off the balance sheet of the banks and temporarily hides them on the balance sheet of the Fed.

What About New Lending?

Hiding junk is not new lending. It is not new production. And it is not new hiring.

To achieve real growth we need new production, not hiding of losses.

Losses and Zombies

Once again, the Fed has chosen to hide losses and shelter zombie corporations.

This will be a drag on any recovery.

All Excess Now

Hey, look on the bright side.

By definition, all reserves are now excess reserves. Banks can collect on all reserves.

The rate may not be much, but Interest on Excess Reserves = Interest on Reserves

Ain’t life grand?

But, But, But, But

But banks are saved. What more could you possibly want?

Meanwhile, Nothing is Working Now (Except for Banks)

For a 20-point discussion of where we are headed, please see What’s Next for America?

Tyler Durden

Sat, 03/28/2020 – 21:15 -

- Rosneft Abruptly Exits Venezuela, Sells Assets To Russian State, Amid US Squeeze On Maduro

Rosneft Abruptly Exits Venezuela, Sells Assets To Russian State, Amid US Squeeze On Maduro

In the past weeks the Kremlin has shown it’s willing to punch back as well as take drastic necessary defensive action in the face of Washington sanctions at a moment America is preoccupied and made more vulnerable by the coronavirus threat — first by dumping OPEC+ and MbS, effectively declaring war on US shale — and now by taking aggressive measures to insulate Russia’s state-controlled Rosneft.

On Saturday Rosneft announced it has sold off all its Venezuelan oil assets to an unnamed Russian state entity. “The government of the Russian Federation has acquired assets in Venezuela from Rosneft. A company 100% owned by the Russian Federation has become the owner,” Russia’s TASS said.

A company statement framed the move as key to protecting shareholders’ interests at a moment the Trump administration ramps up pressure on Maduro and external entities still doing business with Caracas. It’s been widely reported that Rosneft has explored exit options since early 2019 when Venezuelan assets continued rapidly losing money, leading to worsened current operating conditions.

Venezuelan President Nicolas Maduro holds a sword given as gift by Russian oil company Rosneft’s CEO, Igor Sechin. File image: AFP via Getty “As a result of the concluded agreement all assets and trading operations of Rosneft in Venezuela and/or connected with Venezuela will be disposed of, terminated or liquidated,” Rosneft said. “We took this decision in the interests of our shareholders, as a publicly traded international company,” Rosneft spokesman Mikhail Leontyev further told TASS. “And we have a right to expect, indeed, that the US regulators fulfill their public promises.”

On Thursday the White House went so far as to issue a $15 million bounty on Maduro and his inner circle over drug trafficking charges, amid sweeping indictments against what Washington dubbed a vast narco-state criminal enterprise orchestrated by the regime. It appears Rosneft took note of Trump’s willingness to press his economic war on Venezuela further even as the United States now leads the world in numbers of confirmed coronavirus cases, which threatens to decimate an economy still on “pause” and extreme uncertainty still on the horizon.

All of this follows in mid-February the US slapping new sanctions on Rosneft Trading SA, a unit of Rosneft, and the company’s executive Didier Casimiro, accusing it of being the “primary culprit” of a campaign to evade Washington’s pressure campaign on the Maduro government. But the sanctions stopped just short of naming parent company Rosneft, though the Trump administration long accused it of “actively evading sanctions — engaging in ruses, engaging in deception.”

Via AFP/Getty Bloomberg observed that “The fight over Venezuela fits into a much larger geopolitical battle between Trump and Vladimir Putin, with both turning to oil as the weapon of choice.” And the report further cited Russia’s ambassador to Venezuela, Sergey Melik-Magdasarov, as saying:

“Don’t worry! This is about Rosneft’s assets being transferred to Russia’s government directly. We keep moving forward together!,” he [Amb. Melik-Magdasarov] said, in a message that also posted on the embassy website.

The assets include Rosneft’s stakes in local upstream companies Petromonagas, Petroperija, Boqueron, Petromiranda and Petrovictoria, as well as oil-service, commercial and trading units.

The Russian Federation controls Rosneft with just over 50% of its shares, while BP Plc is the second-largest shareholder with 19.75%, and Qatar’s QH Oil Investments owns 18.93%.

Rosneft’s position has long been that US sanctions are illegal and that its own operations in Venezuela are commercial in nature, not political, after in prior months the company’s cooperation with state-run PDVSA became an “open secret”.

The ultimate strategy behind Saturday’s dramatic announcement is as yet uncertain, it should be noted:

But Russ Dallen, head of Caracas Capital Markets brokerage, cautioned that it’s too early to know for sure whether the move is intended to bolster Maduro.

“We don’t know whether the new state entity is a cemetery corporation, where companies go to die, or whether the Russians are simply doing it to take Rosneft — which is their crown jewel and provides a large portion of Russia’s income — out of the way of sanctions and Putin will use the new company to continue to help Maduro,” he said.

Rosneft has emerged as one of PDVSA’s closest joint venture partners, being crucial as a heavy lifter keeping Venezuelan oil afloat at a moment Washington tries to strangle and blockade the socialist state’s industry.

Tyler Durden

Sat, 03/28/2020 – 20:50 - Midnight On Planet Lockdown: Bob Dylan Strikes Again

Midnight On Planet Lockdown: Bob Dylan Strikes Again

Authored by Pepe Escobar via The Asia Times,

What spectacular timing. Like a shot ricocheting at Heaven’s Door as a virus pandemic rages and Planet Lockdown is the new normal, Bob Dylan has produced a stunning 17-minute masterpiece dissecting the November 22, 1963, assassination of JFK – releasing it at midnight US Eastern Standard Time on Thursday.

For baby boomers, not to mention obsessive Dylanologists, this is the ultimate sucker punch. Countless eyes will be plunged into swimming pools revisiting all the memories swirling around “the day they blew out the brains of the king / Thousands were watching, no one saw a thing.” But that’s not all: the Dylanmobile takes us on a magical mystery tour of the 60s and 70s, complete with the Beatles, the Age of Aquarius and the Who’s “Tommy.”

If there’s any cultural artifact capable of sending a powerful jolt across a discombobulated America trying to come to grips with a dystopic Desolation Row, this is it, the work of America’s undisputed, true Exceptionalist. The times, they are-a-changin’. Oh, yes, they are.

There are so many nuggets in Dylan’s lyrics they would be worthy of a treatise, tracking the vortex of music, literature, film references and interlocking Americana.

This is essentially an incantatory mantra set to piano, sparse percussion and violin. We have two narrators: a dying Kennedy (“Ridin’ in the backseat next to my wife / Headin’ straight on in to the afterlife / I’m leanin’ to the left, got my head in her lap / Oh Lord, I’ve been led into some kind of a trap”) and Dylan himself.

Or this can be read as Dylan playing Kennedy’s doppelganger, plus occasional interventions, such as Kennedy’s would-be killers

(“Then they blew off his head while he was still in the car / Shot down like a dog in broad daylight / Was a matter of timin’ and the timin’ was right / You got unpaid debts we’ve come to collect / We gonna kill you with hatred, without any respect / We’ll mock you and shock you and we’ll grin in your face / We’ve already got someone here to take your place”).

The pearl at the heart of the mantra is nothing sort of apocalyptic:

“They killed him once and they killed him twice / Killed him like a human sacrifice / The day that they killed him someone said to me, / ‘Son, The Age of the Antichrist has just only begun.’”

Extra words to define it would be idle. Wherever you are in Planet Lockdown, sit back in stay at home social distancing mode, turn on, tune in and time travel. There will be blood on the tracks.

Tyler Durden

Sat, 03/28/2020 – 20:25 - Joe Biden: "Believe All Women" (Except The One Accusing Me Of Sexual Assault)

Joe Biden: “Believe All Women” (Except The One Accusing Me Of Sexual Assault)

In September, 2018 – former Vice President Joe Biden weighed in on allegations of sexual assault against Justice Brett Kavanaugh by insisting that any woman’s public claims of sexual assault should be presumed to be true.

Except for Biden’s former Senate staffer, Tara Reade, who says Biden penetrated her with his fingers in 1993 when she was in her mid-20s, making her life “hell.”

Biden’s deputy campaign manager magically transformed “believe all women” into “all women have a right to tell their story” on Friday, saying in a statement to Fox News: “Women have a right to tell their story, and reporters have an obligation to rigorously vet those claims. We encourage them to do so, because these accusations are false.“

If you believed Kavanaugh’s accuser, why in the world would you not believe Biden’s? Believing women doesn’t end when it starts to impact your politics.

— The Gravel Institute (@GravelInstitute) March 27, 2020

https://platform.twitter.com/widgets.js

Remember when Benjamin Wittes said, “Kavanaugh himself bears the burden of proof.” Does the same apply for Biden? https://t.co/Qb53NAJI3g

— David Harsanyi (@davidharsanyi) March 27, 2020

https://platform.twitter.com/widgets.js

As we noted last week, Reade said in an interview with Rolling Stone‘s Katie Halper that Biden sexually assaulted her after she was asked to run a gym bag over to him.

Biden’s “hands were on me and underneath my clothes,” she said, after he “had me up against the wall.”

“I remember him saying first, like as he was doing it, ‘Do you want to go somewhere else,'” she said, adding “And then him saying to me when I pulled away, he got finished doing what he was doing, and I kind of just pulled back and he said, ‘Come on man, I heard you liked me.’ And that phrase stayed with me because I kept thinking what I might’ve said and I can’t remember exactly if he said ‘i thought’ or ‘I heard’ but he implied that I had done this.”

Reade then went on to say that “everything shattered in that moment” because she knew that there were no witnesses and she looked up to him. “He was like my father’s age,” she said. “He was like this champion of women’s rights in my eyes and I couldn’t believe it was happening. It seemed surreal.”

Reade then said Biden grabbed her by the shoulders and said, “You’re okay. You’re fine” and proceeded to walk away.

Reade said that Biden also told her something after the alleged assault that she initially didn’t want to share because “it’s the thing that stays in my head over and over.” But after some pressing from Halper, Reade decided to share:

“He took his finger. He just like pointed at me and said you’re nothing to me.”

Halper said she spoke with Reade’s brother and close friend, and both of them recall Reade telling them about the alleged assault at the time. –NewsOne

Reade says that after she revealed some of Biden’s inappropriate behavior, she was accused of doing the bidding of Vladimir Putin, according to The Intercept.

Listen to Reade’s interview here:

Tyler Durden

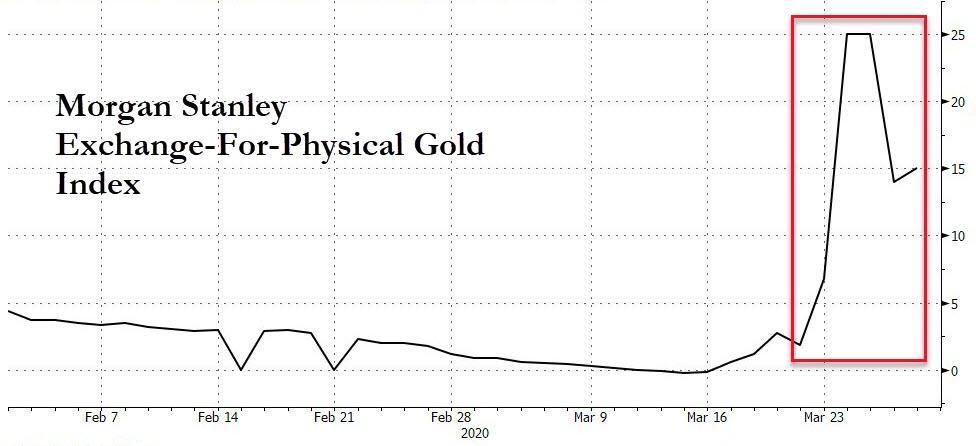

Sat, 03/28/2020 – 20:00 - "There's No Gold" – COMEX Report Exposes Conditions Behind Physical Crunch

“There’s No Gold” – COMEX Report Exposes Conditions Behind Physical Crunch

Early this week, we were among the first to report on the “break down” in precious metals markets.

While the demand for gold has been soaring as a safe haven asset amid the multiple global crises we are currently facing, forced paper gold liquidation (as leveraged funds scramble to cover margin calls) and unprecedented logistical disruptions created a frantic hunt for actual bars of gold.

Specifically, as Bloomberg details, at the center of it all are a small band of traders who for years had cashed in on what had always been a sure-fire bet: shorting gold futures in New York against being long physical gold in London. Usually, they’d ride the trade out till the end of the contract when they’d have a couple of options to get out without marking much, if any, loss.

But the virus, and the global economic collapse that it’s sparking, have created such extreme price distortions that those easy-exit options disappeared on them. Which means that they suddenly faced the threat of having to deliver actual gold bars to the buyers of the contract upon maturity.

It’s at this point that things get really bad for the short-sellers.

To make good on maturing contracts, they’d have to move actual gold from various locations. But with the virus shutting down air travel across the globe, procuring a flight to transport the metal became nearly impossible.

If they somehow managed to get a flight, there was another major problem. Futures contracts in New York are based on 100-ounce bullion bars. The gold that’s rushed in from abroad is almost always a different size.

The short-seller needs to pay a refiner to re-melt the gold and re-pour it into the required bar shape in order for it to be delivered to the contract buyer. But once again, the virus intervenes: Several refiners, including three of the world’s biggest in Switzerland, have shut down operations.

“I realized it was going to be an extremely volatile day,” Tai Wong, the head of metals derivatives trading at BMO Capital Markets in New York, said of Tuesday. “We watched this panic develop literally over the course of 12 hours. Having seen enough market dislocations, you recognize that the frenzy wasn’t likely to last, but at the same time you also don’t know how long it would extend.”

By the end of the week, the shorts had sourced the metal and chartered flights, reverting the spot-futures spread…

But Morgan Stanley’s Exchange-For-Physical Index shows a large physical premium remains…

The real price.. for real gold? Nearer $1,800. If you can get it.

“There’s no gold,” says Josh Strauss, partner at money manager Pekin Hardy Strauss in Chicago (and a bullion fan).

“There’s no gold. There’s roughly a 10% premium to purchase physical gold for delivery. Usually it’s like 2%. I can buy a one ounce American Eagle for $1,800,” said Josh Strauss. “$1,800!”

“The case for gold is simple,” says Strauss.

“You want to own gold in times of financial dislocation and or inflation. And that’s been the case since time immemorial. And gold behaves well in those cases. In those cases stocks behave poorly. It’s a great portfolio hedge. Gold does poorly when you’ve got strong economic growth and low inflation. Tell me when that’s going to happen. Gold held its value during 2008 and after all that money printing it tripled over the next three years.”

And in case you doubted this, the cost of an American Eagle one ounce coin at the US Mint is now $2,175…

But now we can see more details of what is behind this ‘shortage’ as SKWealthAcamdemy’s J.Kim details, the latest COMEX Issues and Stops reports expose conditions behind the COMEX physical gold supply problems. Though I have written about the various reasons why physical gold supply problems manifest many times in the past, this topic still remains one rarely discussed by financial journalists, and never discussed by the mass financial media.

For client accounts, when bullion banks stop more notices than issued, they, will lose physical inventory.

For house accounts, the opposite is true.

When bullion banks issue more notices than stops, then they will lose physical inventory as well. Normally, when bullion banks manufacture waterfall declines in paper gold and silver prices, as they did earlier this month, with the complicity of the CME’s largely unreported rampage in raising initial and maintenance margins on futures contracts many times within a 2-month period in the midst of a stock market crash, they load up on physical gold and silver for their house accounts while ensuring that their clients take almost zero delivery of physical gold and silver ounces. However, if they are unable to execute this clever strategy, this is when physical gold supply problems can manifest.

In fact, I have not seen a single news site in the entire world, except for my own, mention the relentless increase in initial and maintenance margins in gold and silver futures contracts (the 100-oz gold futures contract and the 5000-oz silver futures contract) for the past two months, in a desperate attempt to knock long positions out of the game and thereby prevent an increasing amount of physical delivery requests.

Just recently, the CME raised margins yet again for 100-oz gold futures contracts to $9,185/$8,350 for initial/maintenance margins, representing a massive 86% increase in margins, and for 5000-oz silver futures contracts to $9.900/$9,000 for initial/maintenance margins, representing a gigantic 73% increase in margins, in just a couple months’ time. Normally, such relentless increases in initial/maintenance margins in gold futures markets is sufficient to prevent physical gold supply problems from afflicting futures markets, but the fact that even this reliable manipulation mechanism failed recently is a sign of additional tectonic earthquakes to come in the global financial system.

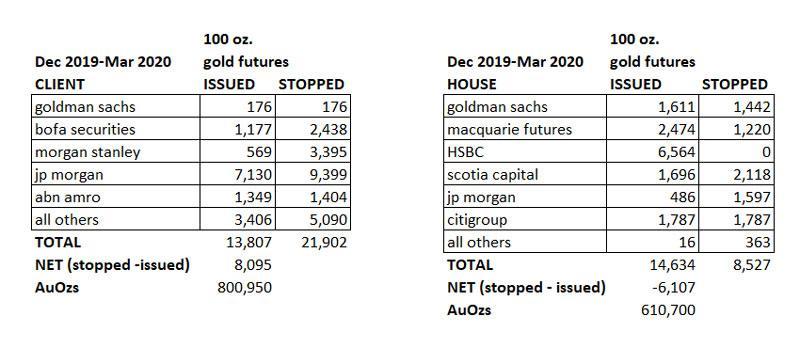

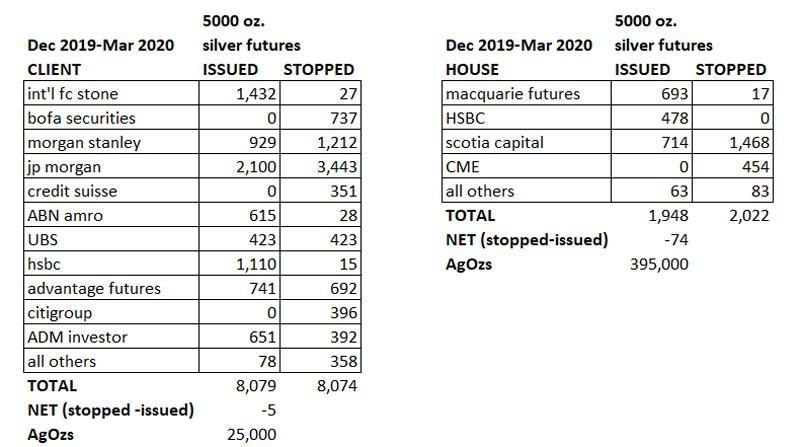

However, as you can see for the data I have compiled for the behavior of issues and stops for client and house accounts for bullion banks in gold and silver from December 2019 to March 2020, this pattern of normal behavior, in which bullion banks take advantage of their own artificially manufactured paper gold and silver price plunges to load up on physical metals at the expense of their clients, has strongly reversed during this four-month time span. I have only included data for the major gold (100-oz) and silver (5000-oz) futures contracts below and not for the mini gold (10-oz) and mini silver (1000-oz) silver futures contracts.

Furthermore, I only separated out the bullion banks by name that had several hundred to a few thousand contracts stopped or issued, and compiled all other data under the category of “all others”. For those of you that don’t understand the terminology “stopped” and “issued”, the categories refer to the number of delivery notices that were “issued” (short positions issuing notification that underlying gold/silver would be delivered) and “stopped” (long positions receiving a delivery notice).

Therefore, when delivery notices are “issued” in house accounts, the issuing bank is on the hook for delivering the physical ounces associated with the underlying contracts. On the contrary, when notices are “stopped”, then the stopping bank would receive notification of the future delivery of the physical ounces associated with the underlying contracts. The same holds true for client accounts. Thus, all bullion banks desire more stopped than issued notices for their house accounts, and desire more issued versus stopped notices for their client accounts. This way they accumulate more physical inventory during artificially engineered paper price crashes.

As you can see, the massive engineered drop in paper silver prices versus the massively higher physical silver prices for the past month backfired on the bullion banks, as it led to a frenzy of clients asking for physical delivery, whereas in the past, bankers had been able to chase client long positions out of the market without ever being on the hook for physical delivery. Thus the amount of contracts stopped versus issued for clients was nearly break even for silver futures contracts, a pattern I have not witnessed in a long time during a banker raid on paper silver prices. And in regard to house accounts, under past similar circumstances, I had always observed JP Morgan bankers taking a tremendous amount of physical silver delivery during engineered collapses in paper silver prices. However, during the last four months, this situation did not materialize, perhaps due to the stress on physical stores of silver created by so many clients asking for physical delivery. As you can see in the data I complied above, this time around, JP Morgan bankers were nearly absent in taking physical silver delivery for their house account. In fact, for the bullion bank house accounts, the amount of stopped versus issued contracts, net, was only 74 contracts, or a mere 395,000 AgOzs for their House accounts. As a basis of comparison, during similarly engineered collapses in paper silver prices in the past, JP Morgan alone was able to accumulate and take delivery of many millions of physical silver ounces.

In regard to real physical gold delivery, the situation was even worse for bullion bankers than their situation with real physical silver delivery, which likely has given rise to physical gold supply problems at the current time. In their client accounts, physical delivery requests exploded, with the net (stopped minus issued) totaling 8,095 contracts representing 800,950 AgOzs of real physical gold requested for delivery. In their house accounts, the bullion banks were unable to yield a positive net situation either, with issued contracts exceeding stopped contracts by 6,107 contracts, representing 610,700 AgOzs. Thus, when adding these two figures together, the bullion banks are on the hook for delivering more than 1.4M AgOzs.

This unexpected demand on bullion bank physical gold reserves has undoubtedly led to a disruption of physical gold delivery associated with the gold futures markets, though various COMEX spokespeople have claimed there is no shortage of physical gold whatsoever, and that the disruption of delivery is simply due to a disruption in the supply chain caused by the coronavirus pandemic, i.e., when in doubt, blame the coronavirus pandemic for all manifested stresses revealed in the global financial system. Earlier, here, on 24 February, I speculated, well before US stock markets started to crash, that the coronavirus pandemic would be scapegoated for the market crash, and I was 100% right. Is it possible that the coronavirus pandemic is now being scapegoated for shortages of physical gold as well?

Oddly, a gold analyst, Ole Hanson stated in response to the shortages of gold physical supply in the futures markets: “There is plenty of gold in the market, but it’s not in the right places. Nobody can deliver the gold because we are forced to stay home.” The explicit function of COMEX warehouses is to store the physical gold that backs gold delivery associated with gold futures contracts. Consequently, why is the physical gold “not in the right places” and in these warehouses, as if it is stored where it is supposed to be stored, and the data is accurate (1.76M registered AuOzs and an additional 6.98M eligible AuOzs in COMEX warehouses as of 26 March 2020), there should be no physical gold shortages to meet physical demand right now? Did Mr. Hanson, in his statement that gold is “not in the right places” unwittingly reveal that the reported COMEX warehouse data is fraudulent?

Secondly, some would suggest that ever since the COMEX mandate that paper gold could be used to close out physical delivery requests through EFP (Exchange For Physical) transactions by Exchange Rule 104.36 enacted on February 18, 2005, which allowed for the substitution of gold ETFs for physical gold, that no physical shortage of gold could ever result.

Since paper was allowed to replace physical, could not bullion banks just literally “paper over” any physical supply deficit? And if the answer to this question is yes, then why is the COMEX experiencing physical shortages of gold right now? Well, as I explained in an article that I published on my news site in June 2011, in which I explained how EFP transactions operate (which you can read here), “the Related Position [Physical] must have a high degree of price correlation to the underlying of the Futures transaction so that the Futures transaction would serve as an appropriate hedge for the Related Position [Physical].” Consequently, since there has been a massive price decoupling between physical and paper gold prices, perhaps this price decoupling has enabled the underlying holder of longs in gold that asked for physical delivery to reject any EFP transaction, since there is no longer a “high degree of price correlation” between paper and physical gold, and to insist on physical gold delivery with no substitution for this request. And this rejection of EFPs and EFS (exchange for swaps) as acceptable behavior is perhaps what is causing the physical gold supply problems in the futures markets right now.

Tyler Durden

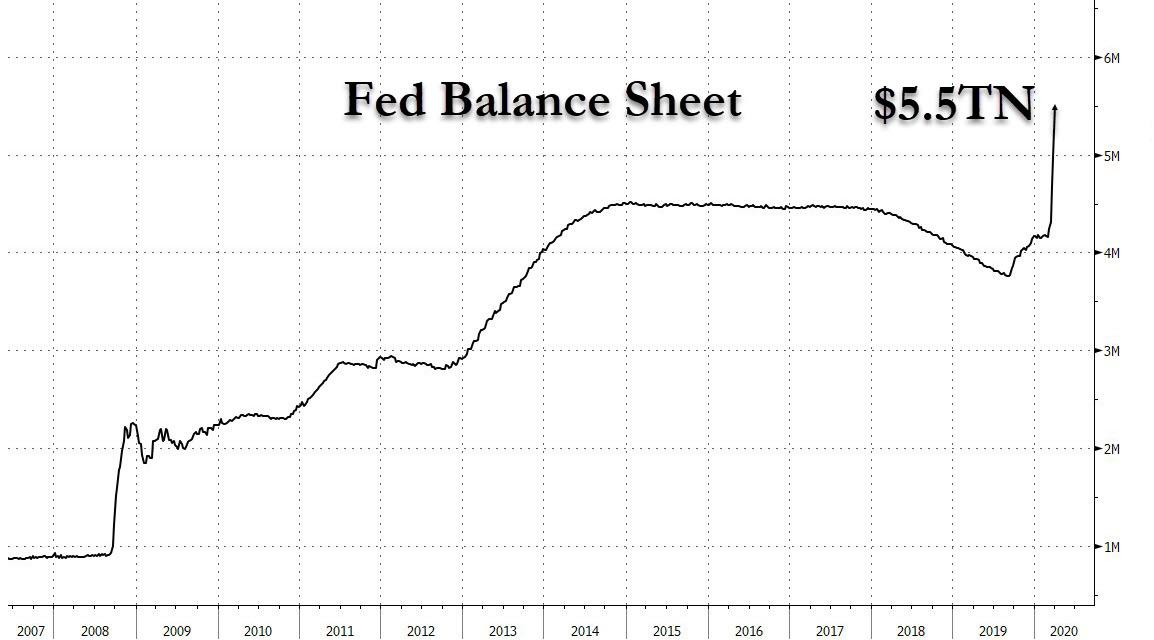

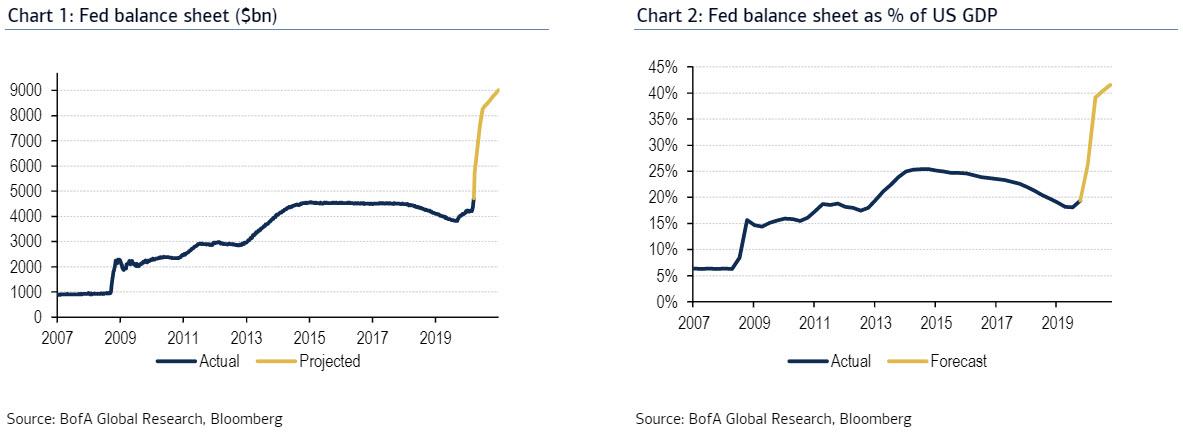

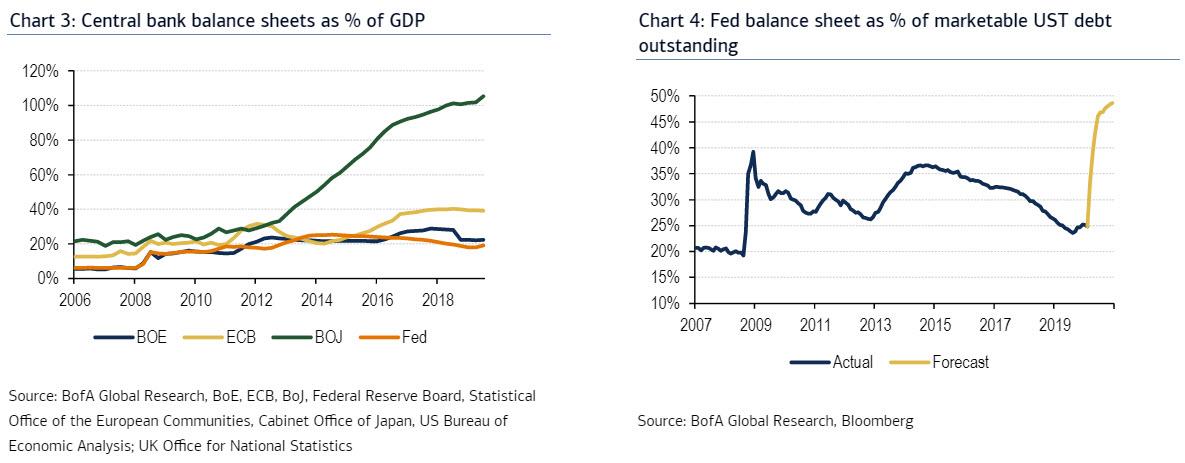

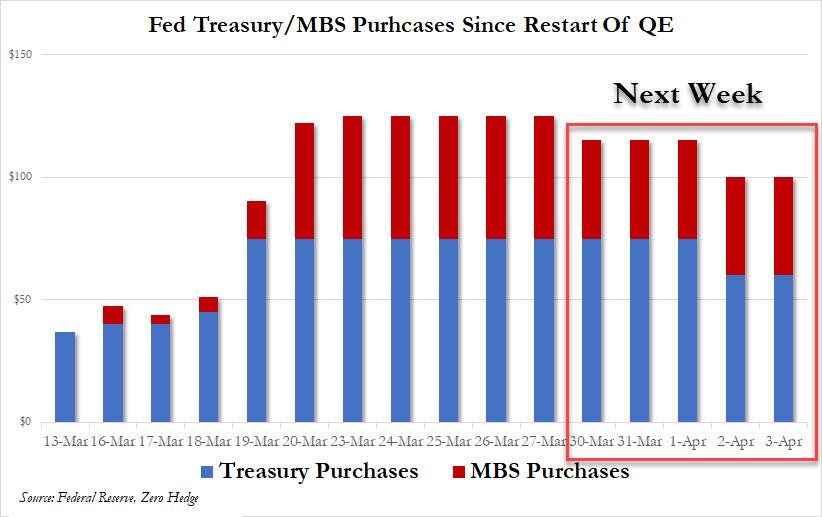

Sat, 03/28/2020 – 19:35 - $9,000,000,000,000: Former Fed Strategist Now Expects Fed's Balance Sheet To Double This Year

$9,000,000,000,000: Former Fed Strategist Now Expects Fed’s Balance Sheet To Double This Year

Late on Thursday, we calculated that as of the end of this turbulent week, the Fed will have added a record $625 billion to its balance sheet, bringing the total to $5.5 trillion, an increase of $1.3 trillion in two weeks (6% of GDP), which was the amount the Fed monetized during all of QE1 in response to the financial crisis, but which took place over a period of almost 2 years.

That’s just the start of what will soon become the most aggressive expansion in Fed balance sheet history because according to BofA’s Fed guru Mark Cabana, who was a former officer in the New York Fed’s Markets Group, the Fed’s balance sheet is now set to double to $9 trillion by the end of the year, to wit:

We acknowledge there is elevated uncertainty around the outlook for the balance sheet, but anticipate it will approximately double in size from end ’19 to end ’20.

The estimates for the Fed’s balance sheet “after unlimited QE and new programs” currently imply that between end ’19 & end ’20:

- Fed balance sheet to US GDP will rise from 20% to 40%, in the process unleashing an unprecedented liquidity tsunami that will send asset prices soaring once the pandemic is over yet the Fed refuses to shrink its balance sheet (Chart 2)

- Fed UST as percentage of marketable debt will rise from 20% to 50%, in other words the Fed will now monetize all US Treasury issuance and then some (Chart 4)

- Fed UST holdings will increase by $1.8tn and agency MBS by $700+bn

- Reserves will increase three- to four-fold

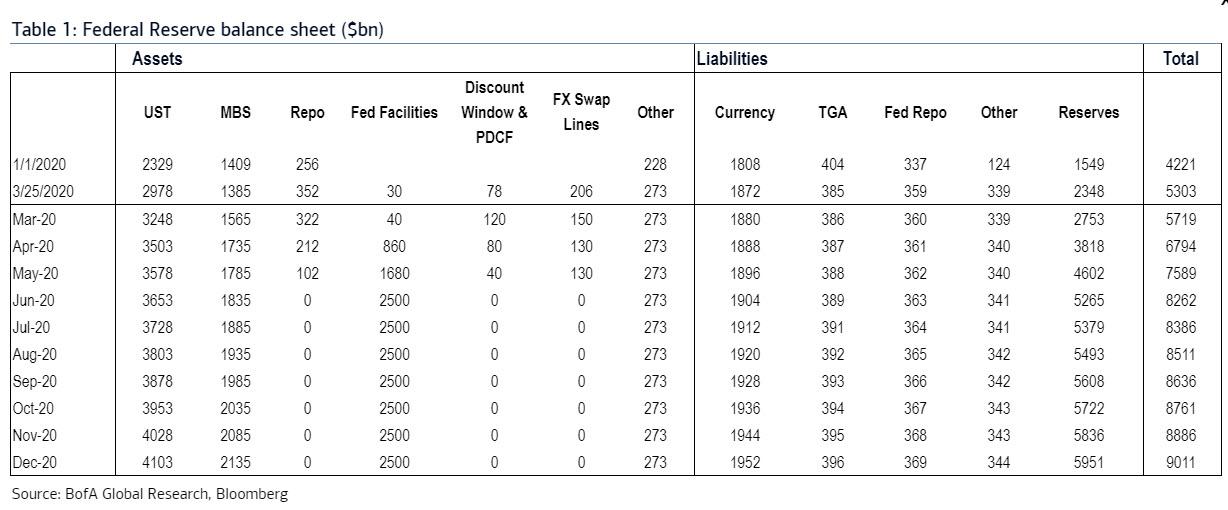

All of the above in table format:

To arrive at these estimates, Cabana make the following assumptions about Fed purchases and use of the Fed’s facilities:

UST and MBS purchases: expect two phases:

- (1) initial bazooka to support market functioning. The Fed has purchased $75bn/day of USTs and $50bn/day of MBS. Through next week Cabana anticipates an average of $60bn/day of USTs and $40bn/day of MBS, which is fascinating because Cabana published this report in the early morning hours of Friday, and just a few hours later the Fed announced that it would follow precisely this schedule, tapering TSY QE from $75BN to $60BN and MBS from $50BN to $40, which announcement sent stocks sharply lower in the last 30 minutes of trading on Friday.

- (2) standard QE from April through December with $75bn/month of USTs and $50bn/month of MBS; this would help with the glut of upcoming UST supply.

Fed facilities – The Fed has announced five facilities: CPFF, MMLF, PMCCF, SMCCF and TALF. Treasury made an initial investment of $10bn in these facilities, which can be 10x levered. Congress is set to allocate another $454bn to the Fed facilities, which can be 10x levered. This implies the max size of these facilities is roughly $5tn, and BofA anticipates 50% takeup spread across three months. In ’08, TALF saw 35% takeup, so assume about 1.5x takeup of facilities now vs ’08 levels.

Discount window and PDFC – Assume discount window and PDCF use peaks at around $120bn in the near term then gradually declines.

FX swap lines – Assume FX swap line use peaks around $200bn, and current 84 day operations roll off in June.

While the former NY Fed staffer acknowledges that there is an elevated uncertainty around these estimates, he sees the risks to his estimates “as skewed to the high side.”

In short, once you start helicopter money you never stop.

* * *

Finally, what are the market implications from the Fed going full BOJ. There are three, as the Fed’s launch of helicopter money in conjunction with the treasury should support:

- liquidity – the sharp reserve increase will allow for funding markets to operate in state of abundant liquidity

- low long-term US rates – As even Cabana admits, “the Fed’s large holdings of US Treasuries will amount to COVID-19 stimulus debt monetization and support low longer-term UST yields”, in short after 11 years of debate whether the Fed is or isn’t monetizing debt, we finally have a clear answer and guess what, the tinfoil conspiracy blog won.

- Corporate bonds (i.e. LQD) will benefit from Fed credit programs.

One final point: buy physical gold, lots of it (pay whatever premium over spot is asked), because the real purpose behind the Fed’s helicopter money which miraculously came at the “right” time – just as the economy was about to tailspin into a recession even without covid-19- courtesy of a virus which prompted a coordinated global reset and the launch of helicopter money, will allow the Fed to commence the endgame of fiat currencies. In the process, the Fed will inject $4.5 trillion into capital markets which will eventually trickle down to the economy.

The endgame is simple: an initial deflationary bust followed by hyperinflation, first in asset markets and soon after, as the Fed triples down on helicopter money until it eventually buys gold outright in the final dollar devaluation, everywhere else.

Tyler Durden

Sat, 03/28/2020 – 19:10 - Trump Says "No Quarantine Necessary" For NY, NJ And CT As US Death Toll Tops 2,000: Live Updates

Trump Says “No Quarantine Necessary” For NY, NJ And CT As US Death Toll Tops 2,000: Live Updates

Summary:

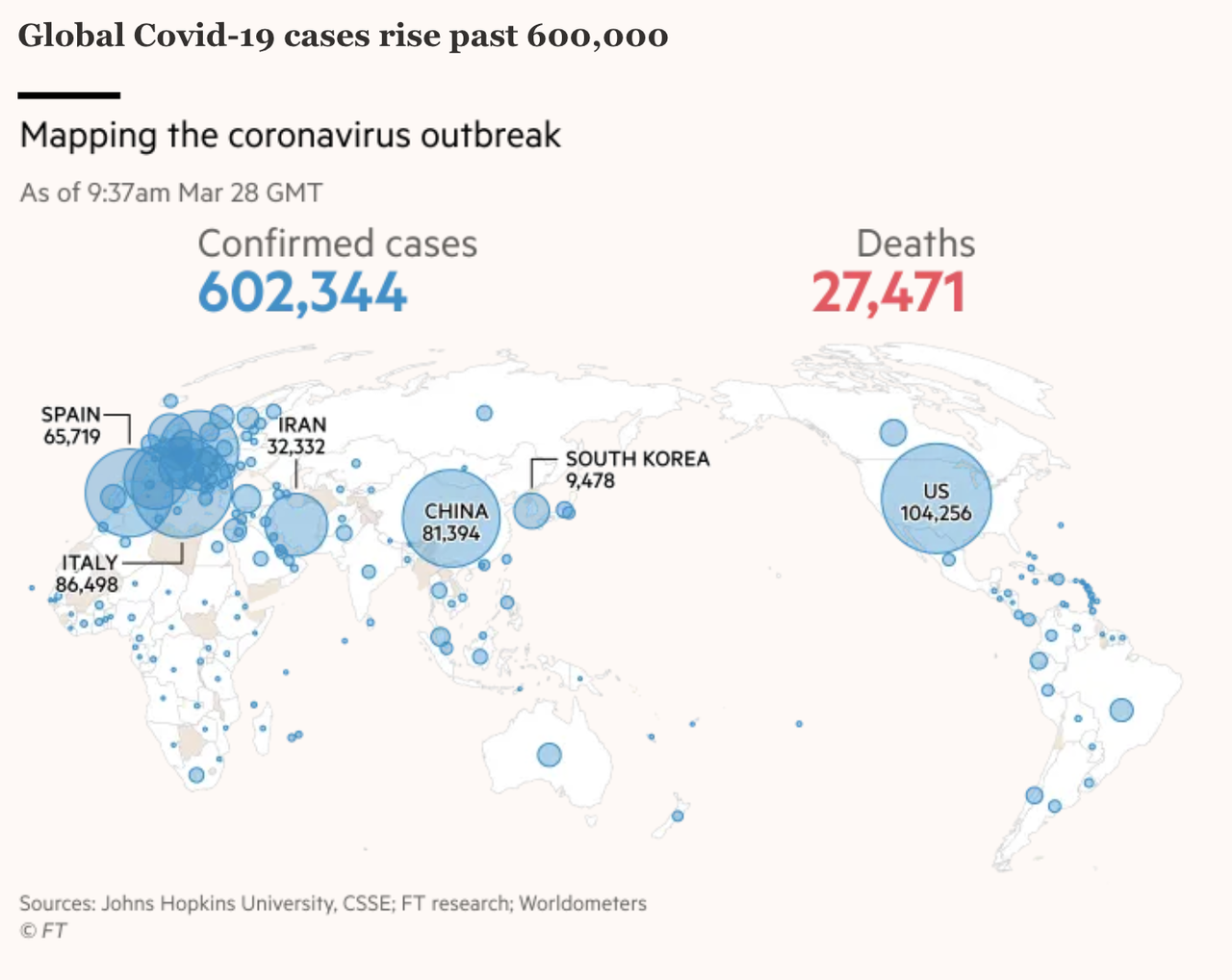

- Global case total tops 600k

- Global COVID-19 death toll tops 30k

- US death toll tops 2k

- After Trump earlier said he was weighing enforceable quarantine order for all the tri-state area, late on Sunday he said that “on the recommendation of the White House CoronaVirus Task Force, and upon consultation with the Governor’s of New York, New Jersey and Connecticut” he would not be imposing a quarantine.

- Japan fast-tracks approval of treatment drug for COVID-19

- Third UK minister self-quarantines after showing symptoms of virus

- Calif. death toll tops 100

- Trump tells NBC reporter that quarantines of New York, NJ & Conn. were “possible”

- Axios reports infant dies in Chicago after testing positive for COVID-19

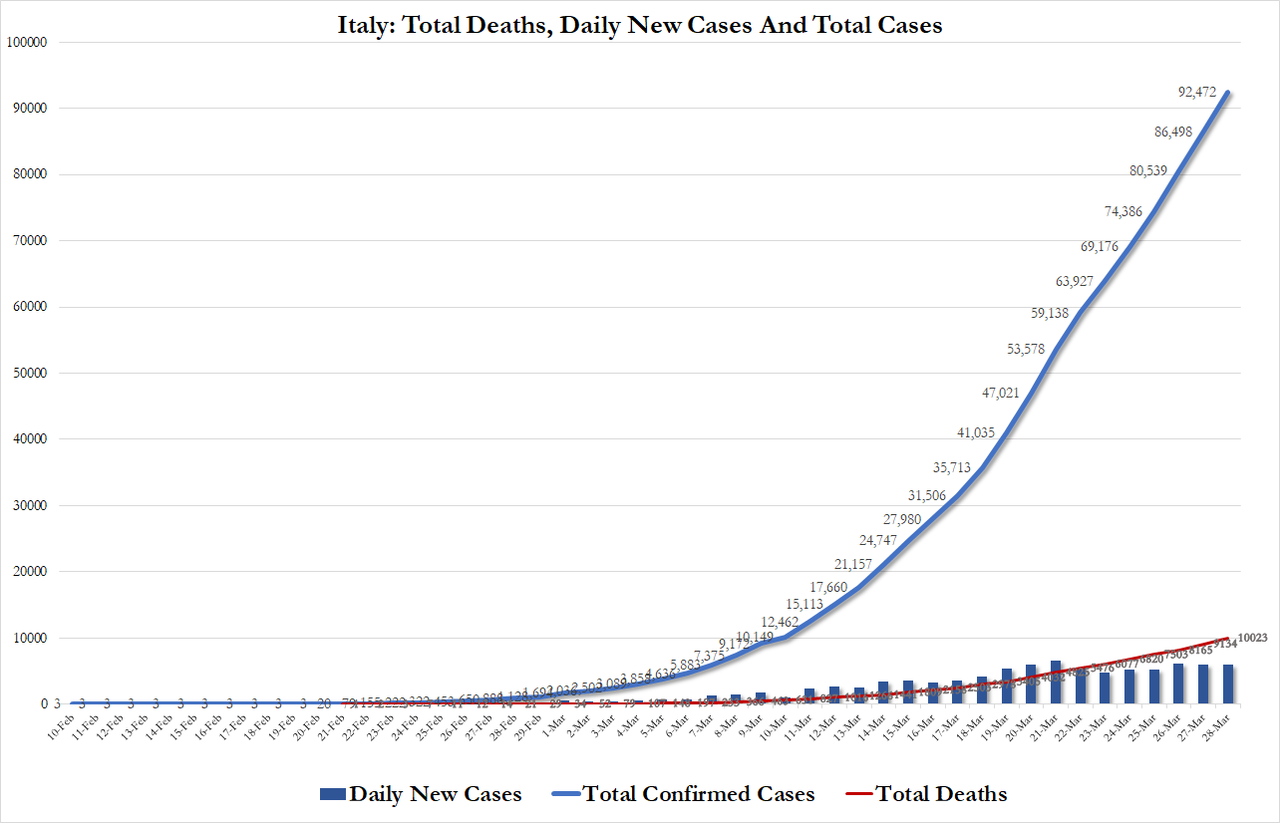

- Italy case total surpasses China

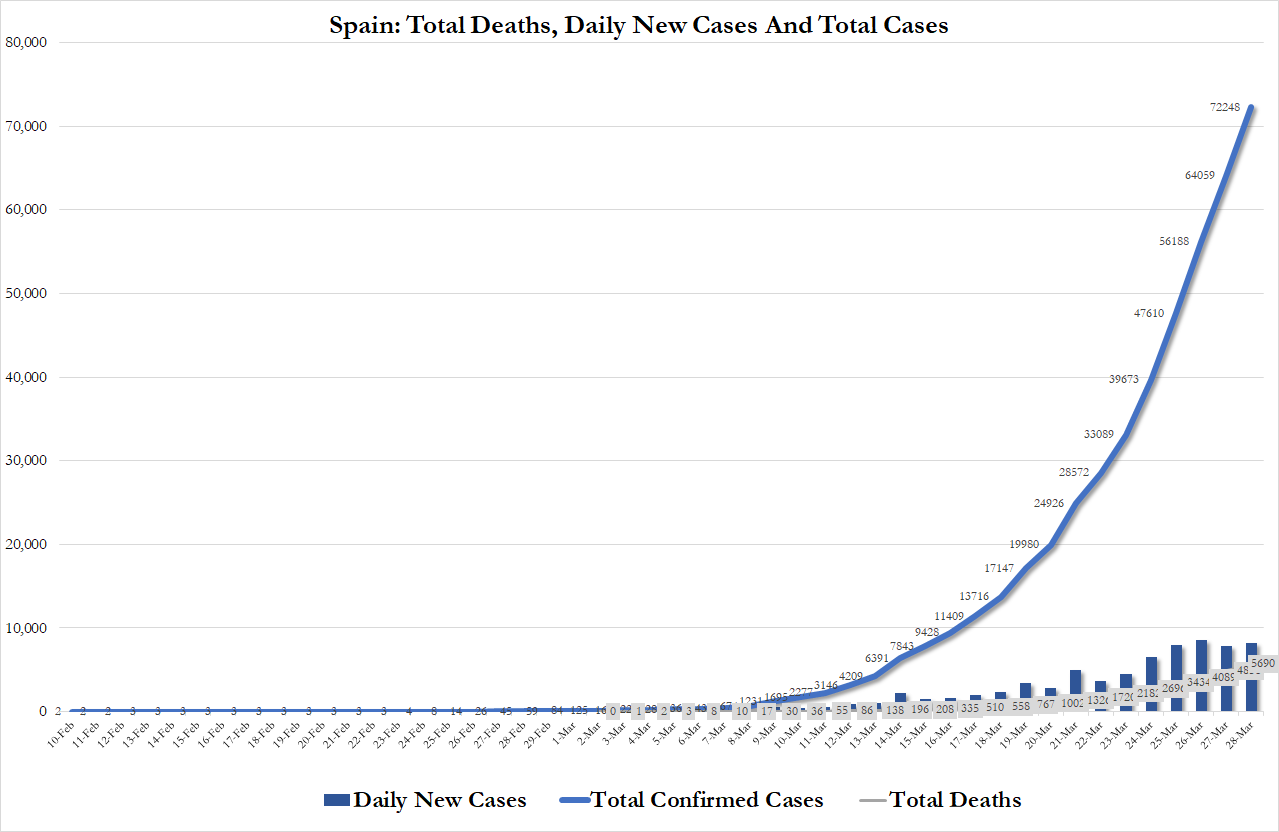

- Spain reports deadliest day yet

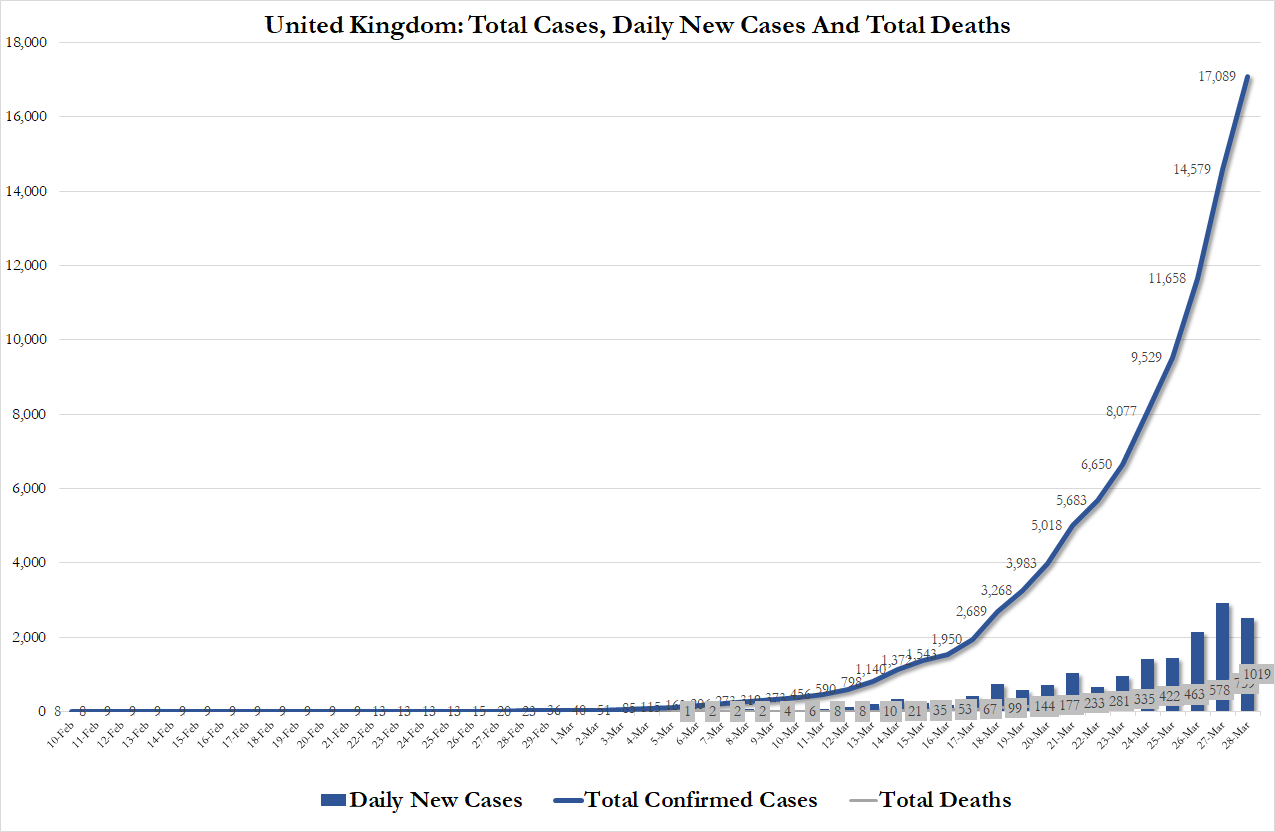

- UK case total climbs north of 17k

- France reports another 5k cases

- Navy hospital ships leave for New York, LA

- Abe says he’s “just barely avoiding” declaring a national emergency