- Escobar: The 'Doomsday Clock' Is Speeding Up

Escobar: The ‘Doomsday Clock’ Is Speeding Up

Authored by Pepe Escobar via PressTV,

The Doomsday Clock, set by the US-based magazine Bulletin of the Atomic Scientists, has been moved to 90 seconds to midnight…

That’s the closest ever to total nuclear doom, the global catastrophe.

The Clock had been set at 100 seconds since 2020. The Bulletin’s Science and Security Board and a group of sponsors – which includes 10 Nobel laureates – have focused on “Russia’s war on Ukraine” (their terminology) as the main reason.

Yet they did not bother to explain non-stop American rhetoric (the US is the only nation that adopts “first strike” in a nuclear confrontation) and the fact that this is a US proxy war against Russia with Ukraine used as cannon fodder.

The Bulletin also attributes malignant designs to China, Iran and North Korea, while mentioning, only in passing, that “the last remaining nuclear weapons treaty between Russia and the United States, New START, stands in jeopardy”.

“Unless the two parties resume negotiations and find a basis for further reductions, the treaty will expire in February 2026.”

As it stands, the prospects of a US-Russia negotiation on New START are less than zero.

Now cue to Russian Foreign Minister Sergei Lavrov making it very clear that war against Russia is not hybrid anymore, it’s “almost” real.

“Almost” in fact means “90 seconds.”

So why is this all happening?

The Mother of All Intel Failures

Former British diplomat Alastair Crooke has concisely explained how Russian resilience – much in the spirit of Iranian resilience past four decades – completely smashed the assumptions of Anglo-American intelligence.

Talk about the Mother of All Intel Failures – in fact even more astonishing than the non-existent Iraqi WMDs (in the run-up to Shock and Awe in 2003, anyone with a brain knew Baghdad had discontinued its weapons program already in the 1990s.)

Now the collective West “committed the entire weight of its financial resources to crushing Russia (…) in every conceivable way – via financial, cultural and psychological war, and with real military war as the follow-through.”

And yet Russia held its ground. And now reality-based developments prevail over fiction. The Global South “is peeling away into a separate economic model, no longer dependent on the dollar for its trading needs.”

And the accelerated collapse of the US dollar increasingly plunges the Empire into a real existential crisis.

All that hangs over a South Vietnam scenario evolving in Ukraine after a rash government-led political and military purge. The coke comedian – whose only role is to beg non-stop for bags of cash and loads of weapons – is being progressively sidelined by the Americans (beware of traveling CIA directors).

The game in Kiev, according to Russian sources, seems to be that the Americans are taking over the Brits as handlers of the whole operation.

The coke comedian remains – for now – as a sock puppet while military control over what is left of Ukraine is entirely NATO’s.

Well, it already was – but now, formally, Ukraine is the world’s first de facto NATO member without being an actual member, enjoying less than zero national sovereignty, and complete with NATO-Nazi Storm troopers weaponized with American and German tanks in the name of “democracy”.

The meeting last week of the Ukraine Defense Contact Group – totally controlled by the US – at the US Air Force base in Ramstein solidified a sort of tawdry remix of Operation Barbarossa.

Here we go again, with German Panzers sent to Ukraine to fight Russia.

Yet the tank coalition seems to have tanked even before it starts. Germany will send 14, Portugal 2, Belgium 0 (sorry, don’t have them). Then there’s Lithuania, whose Defense Minister observed, “Yes, we don’t have tanks, but we have an opinion about tanks.”

No one ever accused German Foreign Minister Annalena Baerbock of being brighter than a light bulb. She finally gave the game away, at the Council of Europe in Strasbourg:

“The crucial part is that we do it together and that we do not do the blame game in Europe because we are fighting a war against Russia.”

So Baerbock agrees with Lavrov. Just don’t ask her what Doomsday Clock means. Or what happened after Operation Barbarossa failed.

The NATO-EU “garden”

The EU-NATO combo takes matters to a whole new level. The EU essentially has been reduced to the status of P.R. arm of NATO.

It’s all spelled out in their January 10 joint declaration.

The NATO-EU joint mission consists in using all economic, political and military means to make sure the “jungle” always behaves according to the “rules-based international order” and accepts to be plundered ad infinitum by the “blooming garden”.

Looking at The Big Picture, absolutely nothing changed in the US military/intel apparatus since 9/11: it’s a bipartisan thing, and it means Full Spectrum Dominance of both the US and NATO. No dissent whatsoever is allowed. And no thinking outside the box.

Plan A is subdivided into two sections.

1. Military intervention in a hollowed-out proxy state shell (see Afghanistan and Ukraine).

2. Inevitable, humiliating military defeat (see Afghanistan and soon Ukraine). Variations include building a wasteland and calling it “peace” (Libya) and extended proxy war leading to future humiliating expulsion (Syria).

There’s no Plan B.

Or is there? 90 seconds to midnight?

Obsessed by Mackinder, the Empire fought for control of the Eurasian landmass in World War I and World War II because that represented control of the world.

Later, Zbigniew “Grand Chessboard” Brzezinski had warned: “Potentially the most dangerous scenario would be a grand coalition between Russia, China and Iran.”

Jump cut to the Raging Twenties when the US forced the end of Russian natural gas exports to Germany (and the EU) via Nord Stream 1 and 2.

Once again, Mackinderian opposition to a grand alliance on the Eurasian landmass consisting of Germany, Russia and China.

The Straussian neo-con and neoliberal-con psychos in charge of US foreign policy could even absorb a strategic alliance between Russia and China – as painful as it may be. But never Russia, China and Germany.

With the collapse of the JCPOA, Iran is now being re-targeted with maximum hostility. Yet were Tehran to play hardball, the US Navy or military could never keep the Strait of Hormuz open – by the admission of the US Joint Chiefs of Staff.

Oil price in this case would rise to possibly thousands of dollars a barrel according to Goldman Sachs oil derivative experts – and that would crash the entire world economy.

This is arguably the foremost NATO Achilles Heel. Almost without firing a shot a Russia-Iran alliance could smash NATO to bits and bring down assorted EU governments as socio-economic chaos runs rampant across the collective West.

Meanwhile, to quote Dylan, darkness keeps dawning at the break of noon. Straussian neo-con and neoliberal-con psychos will keep pushing the Doomsday Clock closer and closer to midnight.

Tyler Durden

Sun, 01/29/2023 – 23:30 - Mixed Oil Momentum Signals To Persist Until Impact Of War Fades

Mixed Oil Momentum Signals To Persist Until Impact Of War Fades

By Ryan Fitzmaurice of Marex

As many traders would agree, sometimes it’s not the data that is important but rather the price reaction to the data. We believe this is the case with oil prices recently. Looking at US inventory statistics, crude oil stocks have built by an incredible +27mb over the past two reports, yet oil prices have rallied more than 10% over the same timeframe in a classic case of sell the rumor, buy the fact. As for the sharp rise in US crude inventories, it’s not as if oil fundamentals have shifted on a dime, but rather it’s the result of the extreme cold weather that ravaged the US energy corridor in late December. The cold forced several major US refineries to shut down due to operational issues related to the freezing temperatures. Additionally, end of year tax on inventory in Texas and Louisiana caused oil imports to come onshore in early January.

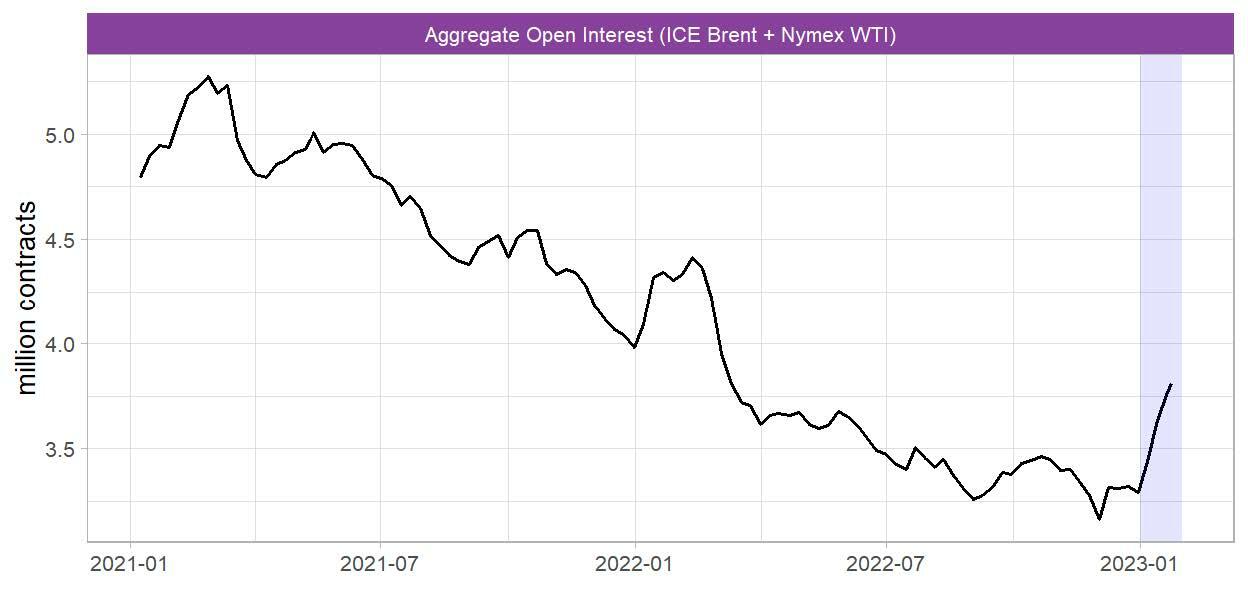

So, despite what seems to be very bearish data points, the oil market appears focused on China’s abrupt reopening plans and the improving macro backdrop as opposed to backward looking inventory that was impacted by weather. In fact, the spot Brent contract is now trading in the mid to high $80s and above many moving averages. The oil rally has also coincided with a notable increase in futures open interest and managed money buying. The combined aggregate futures open interest for ICE Brent and Nymex WTI has climbed by +440mb since the start of the year while the net managed money position has increased by +68mb since last Tuesday, the latest reporting period for the CFTC positioning data. Also, about half of the net buying has come from “short”covering due to the big shift in momentum the past two weeks.

Oil prices have now turned higher on the year despite oil stocks climbing by +27mb for the first two reports of January, as the focus shifts to China’s reopening… Mixed Signals

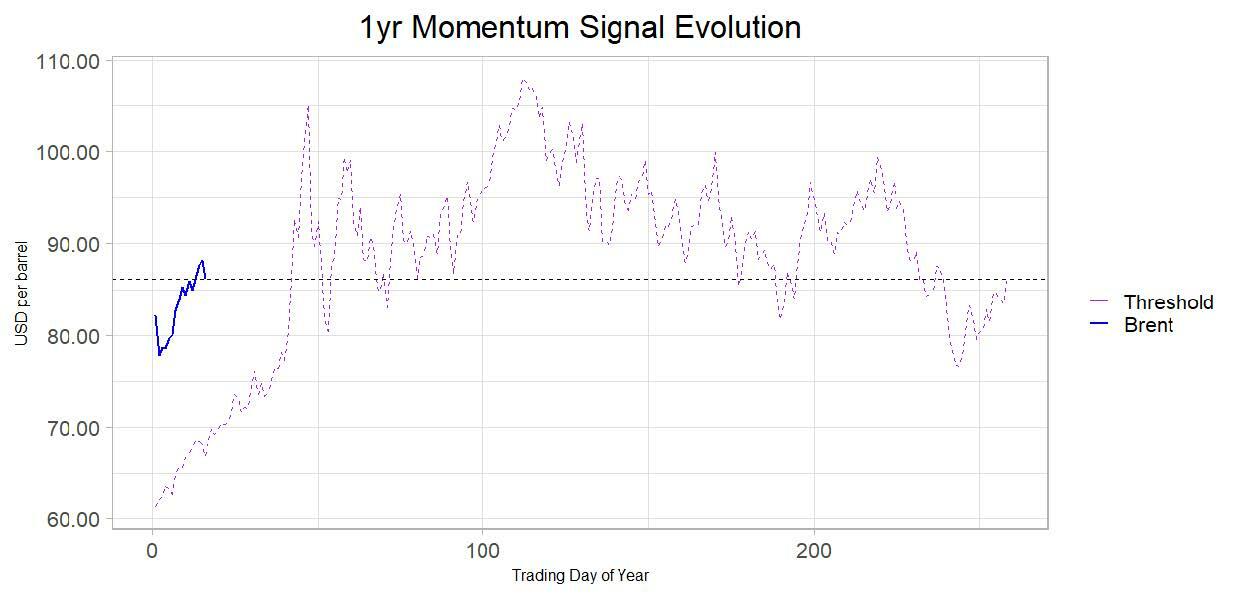

Last week we discussed momentum traders, and how their herd-like behavior can impact oil prices at times. Today we want to expand on that topic while discussing the impact the war in Ukraine has had on the momentum factor. To reiterate our point from last week, momentum is a very simple and straight forward trading strategy, buying commodities or assets with positive returns and selling those with negative returns over a pre-defined timeframe. For example, the one-year momentum signal tends to be a popular long-term indicator that measures the roll-adjusted return of the past year. Given we are dealing with historical prices, it is possible to look at the price development of the prior year to formulate a roadmap of how this key hurdle will change with time. It is worth noting that roll-adjustments will alter the momentum indicator somewhat, with contango increasing the signal threshold over time while backwardation decreases it.

With that in mind, we are all aware of how erratic oil prices were last year, and particularly in the early stages of the Russian invasion of Ukraine in late February. In fact, spot Brent prices spiked from below $80 at the start of 2022 to more than $135 by early March. This is important to remember because the huge spike in oil prices is going to make for an increasingly higher bar with respect to the one-year momentum signal as we approach the anniversary of the start of the war. Importantly, the forward curves shifted into a strong state of backwardation for several months after the price spike, which has worked to lower this key hurdle, but the current contango could work to offset that in the coming months should it hold. On the flip side, the weak price action more recently could make for a low bar with respect to shorter-term signals. As a result, mixed oil momentum signals are likely to persist until the impact from the war fades.

The threshold for the 1-year momentum signal will become increasingly higher over the first half of the 2023, before declining in the second half of the year… Thinking Ahead

Oil prices are now higher on the year after a very sharp decline the first week of January and despite some sizable US inventory builds. Notably, open interest has also increased alongside prices as new money enters the fray. So far, there has been little in the way of commodity index inflows this year, however, one would assume “long-only” investor dollars are likely to be chasing oil prices given the past two years of stellar returns. This group of institutional investors should gain more influence as the war-inspired volatility begins to filter out of risk models, allowing for increased position sizes. This dynamic should become more apparent in 2H23 though.

Fundamentally, all eyes remain on the Chinese reopening and its potential demand implications for this year. As we have been highlighting recently, Chinese crude imports already climbed to more than 11mb/d in November and December, even before the abrupt pandemic policy reversal took place. This supports the notion that China will likely need record oil imports this year to meet its refining demand. In addition, we believe the US will also need to increase crude imports this year to fill the void left by the cessation of SPR releases and as the US refining system bounces back from the cold related outages.

Aggregate futures open interest for the two benchmark crude oil contracts has increased sharply to start the new year, albeit from a low base… Tyler Durden

Sun, 01/29/2023 – 23:00 - A Tale Of Two Presidents: Biden Vs Trump

A Tale Of Two Presidents: Biden Vs Trump

Highly appreciated Automatic Earth commenter TAE Summary presents another one of his series “A Tale of Two..”, and if only just for the obvious effort he put into it, let’s dig in.

How do you feel about what each president has achieved? No wrong answers.

TAE Summary:

Biden is a Great President and Trump was an Awful President

Biden

-

Appointed a diverse cabinet

-

Signed executive orders addressing systemic racism and discrimination

-

Passed the infrastructure bill to repair roads and bridges and improve internet access

-

Reduced the deficit

-

Led NATO in its support of Ukraine and opposition to Vladimir Putin

-

Lowered the child poverty rate by increasing the tax credit for children

-

Launched a program to protect earth from killer asteroids

-

Officially recognized Turkish genocide of Armenians in 1915

-

Sidelined the court-packing movement of the left

-

Stepped up US support for Taiwan

-

Announced a historic trilateral security agreement with Australia and Britain to counter Chinese hegemony

-

Accelerate Covid vaccine delivery at home an abroad

-

Improved the American economy by championing competition and reining in the power of big business which helped create millions of jobs

-

Gave Medicare the power to negotiate drug prices and made the price of things like insulin and hearing aids cheaper

-

Attacked hunger and fostered better nutrition in the US

-

Funded opioid recovery programs

-

Eliminated the statute of limitations for child sex abuse

-

Tried to reform student loans

-

Issued important cybersecurity regulations

-

Chose humanity over politics when getting Brittney Griner released

Trump

-

Colluded with the Russians to get elected in 2016

-

Appointed unqualified family members to important positions in his administration

-

Tried to ban TikTok

-

Withdrew the US from the Paris Climate Accords

-

Increased the deficit every year of his presidency

-

Approved the Keystone Pipeline through native lands

-

Disallowed transgender students from using the bathroom of their choice

-

Attacked John McCain as a loser

-

Ended curbs on auto emissions

-

Cracked down on legal immigrants

-

Impeded regulation against toxic chemicals

-

Shrank the food safety net so that over 700K Americans lost their access to food stamps

-

Suggested vaccines cause autism

-

Accused Barack Obama of spying on his campaign

-

Cut corporate taxes to the lowest level since 1939

-

Oversaw the longest government shutdown in US history

-

Acted as a racist and xenophobe when he implemented a travel ban from Muslim countries, blamed the Chinese for Covid, separated families at the US border, tried to build a wall between the US and Mexico and gave racist speeches

-

Tried to repeal the Affordable Care Act which would have left millions without healthcare

-

Inadequately responded to Covid, downplaying the dangers

-

Use his influence as president to try to get Ukraine to provide damaging narratives about his political opponent

-

Challenged the outcome of the 2020 election undermining democratic institutions and the public’s trust in elections which led to the events of January 6th and the deaths of 5 people

Trump was a Great President and Biden is an Awful President

Trump

-

Negotiated three Arab-Israeli peace accords

-

Fostered a strong economy and stock market by signing into to law the Tax Cuts and Jobs Act and other policies

-

Started the Space Force

-

Attempted the first Defense Department wide audit

-

Cracked down on unwanted robo-calls

-

Attempted to build a wall on the border with Mexico to stop illegal immigration

-

Helped American farmers with billions of dollars in aid

-

Tried to fix health technology by removing rules blocking the sharing of medical information

-

Rescinded rules for federal contractors that protected them from sexual harassment claims

-

Made it easier to prosecute financial crimes like money laundering

-

Renegotiated trade deals with Mexico, Canada and China which benefitted American workers and businesses

-

Appointed three Supreme Court justices and many other conservative judges to federal courts leading to pro-Constitutional decisions like the overturning of Roe

-

Passed the VA MISSION Act which improved healthcare access and services for veterans

-

Oversaw the defeat of the Islamic State’s territorial caliphate in Syria and Iraq

-

Kept us out of war

-

Signed executive orders and laws combating human trafficking

Biden

-

Opened the borders to illegal immigrants

-

Discharged thousands of troops for refusing the Covid vaccine

-

Opposed efforts to stop biological males from competing in women’s sports

-

Lied about border patrol agents whipping migrants

-

Claimed that January 6th rioters were a bigger threat to democracy than Confederates in the Civil War

-

Described terrorism from white supremacy as the most lethal threat to the US

-

Oversaw the disastrous withdrawal of American troops for Afghanistan

-

Mis-handled the response to Covid mandating vaccines and dividing the nation on the basis of vaccination status

-

Supported lockdowns and other pandemic polices which damaged the supply chain and the world economy

-

Supported violent protesters instead of the police during the BLM riots

-

Lied about Hunter’s laptop saying it was Russain disinformation

-

Stated that election reform is the new Jim Crow

-

Suppressed first amendment rights by influencing policies of social media outlets

-

Supported the war in Ukraine and vilified Russia as our enemy

-

Blocked American energy production

-

Illegally attempted to forgive student loans

-

Printed massive amounts of money causing massive inflation

I have one comment: I don’t think that “Joe Biden” (in Jim Kunstler language) only “supported the war in Ukraine and vilified Russia as our enemy”, “Joe Biden” did a lot more to poke the bear and instigate and fire up the war. But that’s just me. You can be the judge of that too.

Also just me: when Trump left and Biden came, we were at peace. Look at us now.

* * *

Tyler Durden

Sun, 01/29/2023 – 22:30 -

- Air Force General Tells His Officers 'War With China' Only 2 Years Away

Air Force General Tells His Officers ‘War With China’ Only 2 Years Away

In recent years there have been at least a handful of high-ranking US military commanders which in some form or fashion have sounded the alarm over a “coming war with China”… with the latest warning being the most unusual, issued in the form of a memo by an active four-star general and circulated with an official order.

This case is particularly significant given he took the rare step of passing it down through military command and to the chief officers he oversees, giving a greater urgency to the warning:

A four-star Air Force general sent a memo on Friday to the officers he commands that predicts the U.S. will be at war with China in two years and tells them to get ready to prep by firing “a clip” at a target, and “aim for the head.”

In the memo sent Friday and obtained by NBC News, Gen. Mike Minihan, head of Air Mobility Command, said, “I hope I am wrong. My gut tells me will fight in 2025.”

General Mike Minihan, a four-star officer, sent the memo Friday. Getty Images Various reports have counted some 50,000 service members and nearly 500 planes total under Gen. Minihan’s command.

The message is particularly alarming given it instructed commanders under him to “consider their personal affairs and whether a visit should be scheduled with their servicing base legal office to ensure they are legally ready and prepared.”

He explained that he sees Beijing as desirous of moving against the self-ruled island of Taiwan within that time period, and that it would trigger a large US military response.

The Air Force general further urged “a fortified, ready, integrated, and agile Joint Force Maneuver Team ready to fight and win inside the first island chain.” And in the memo Gen. Minihan issued an order, requiring that all major efforts in preparation for a coming China fight to be reported to him directly by Feb. 28.

As for why he thinks China will invade Taiwan within the next two years, NBC described the following:

Minihan said in the memo that because both Taiwan and the U.S. will have presidential elections in 2024, the U.S. will be “distracted,” and Chinese President Xi Jinping will have an opportunity to move on Taiwan.

🚨Here is the memo which Four Star General Mike Minihan predicts the US will be at war with China in 2025. pic.twitter.com/tXO7JhjtpB

— The Calvin Coolidge Project (@TheCalvinCooli1) January 28, 2023

https://platform.twitter.com/widgets.js

As for Beijing, it has long claimed it is only interested in pursuing peaceful reunification with Taiwan based on political means. China has further laid blame on Washington for militarizing the island and thus creating current tensions, and by stoking independence forces through high-level visits, such as Nancy Pelosi’s ultra-provocative August trip to Taipei.

It should be noted that Gen. Minihan has a reputation for being among the Pentagon’s most outspoken and hawkish top generals. In this latest memo, he directed all Air Mobility Command personnel to “fire a clip into a 7-meter target with the full understanding that unrepentant lethality matters most. Aim for the head.”

Tyler Durden

Sun, 01/29/2023 – 22:00 - The New York Times Is Orwell's Ministry Of Truth

The New York Times Is Orwell’s Ministry Of Truth

Authored by Edward Curtin via Off-Guardian.org,

“Ingsoc. The sacred principles of ingsoc. Newspeak, double-speak, the mutability of the past.”

– George Orwell, 1984

As today dawned, I was looking out the window into the cold grayness with small patches of snow littering the frozen ground. As light snow began to fall, I felt a deep mourning in my soul as a memory came to me of another snowy day in 1972 when I awoke to news of Richard Nixon’s savage Christmas bombing of North Vietnam with more than a hundred B-52 bombers, in wave after wave, dropping death and destruction on Hanoi and other parts of North Vietnam.

I thought of the war the United States is now waging against Russia via Ukraine and how, as during the U.S. war against Vietnam, few Americans seem to care until it becomes too late. It depressed me.

Soon after I was greeted by an editorial from The New York Times’ Editorial Board, “A Brutal New Phase of the War in Ukraine.” It is a piece of propaganda so obvious that only those desperate to believe blatant lies would not fall down laughing. Yet it is no laughing matter, for The N.Y. Times is advocating for a wider war, more lethal weapons for Ukraine, and escalation of the fighting that risks nuclear war. So their title is apt because they are promoting the brutality. This angered me.

The Times’ Editorial Board tells us that President Putin, like Hitler, is mad. “Like the last European war, this one is mostly one man’s madness.” Russia and Putin are “cruel”; are conducting a “regular horror” with missile strikes against civilian targets; are “desperate”; are pursuing Putin’s “delusions”; are waging a “terrible and useless war”; are “committing atrocities”; are responsible for “murder, rape and pillaging,” etc.

On the other hand, “a heroic Ukraine” “has won repeated and decisive victories against Russian forces” who have lost “well over 100,000 Russian soldiers killed and wounded,” according to the “reliable” source, chairman of the U.S. Joint Chief of Staff, Gen. Mark A. Milley. To add to this rosy report, the Ukrainians seem to have suffered no causalities since none are mentioned by the cozy Times’ Editorial Board members from their keyboards on Eighth Avenue.

When you support a U.S. war, as has always been The Times’ modus operandi as a stenographer for the government, mentioning the dead pawns used to accomplish the imperialists’ dreams is bad manners. So are the atrocities committed by those forces, so they too have been omitted. Neo-Nazis, the Azov Battalion? They too must never have existed since they are not mentioned.

But then, according to the esteemed editorial writers, this is not a U.S. proxy war waged via Ukraine by U.S./NATO “to strip Russia of its destiny and greatness.” No, it is simply Russian aggression, supported by “the Kremlin’s propaganda machinery” that has churned “out false narratives about a heroic Russian struggle against forces of fascism and debauchery.” U.S./NATO were “horrified by the crude violation of the postwar order,” so we are laughingly told, and so came to Ukraine’s defense as “Mr. Putin’s response has been to throw ever more lives, resources and cruelty at Ukraine.”

Nowhere in this diatribe by the Times’ Board of propagandists – and here the whole game is given away for anyone with a bit of an historical sense – is there any mention of the U.S. engineered coup d’état in Ukraine in 2014. It just didn’t happen. Never happened. Magic by omission.

The U.S., together with the Ukrainian government “led” by the puppet-actor “President Volodymyr Zelensky,” are completely innocence parties, according to the Times. (Note also, that nowhere in this four page diatribe is President Putin addressed by his title, as if to say that “Mr. Putin” is illegitimate and Zelensky is the real thing.)

All the problems stem from when “Mr. Putin seized Crimea and stirred up a secessionist conflict in eastern Ukraine n 2014.”

Nowhere is it mentioned that for years on end U.S./NATO has been moving troops and weapons right up to Russia’s borders, that George W. Bush pulled the U.S. out of the Anti-Ballistic Missile Treaty and that Trump did the same with the Intermediate-Range Nuclear Forces Treaty, that the U.S. has set up so-called anti-ballistic missile sites in Poland and Rumania and asserted its right to a nuclear first-strike, that more and more countries have been added to NATO’s eastern expansion despite promises to Russia to the contrary, that 15,000 plus mostly Russian-speaking people in eastern Ukraine have been killed by Ukrainian forces for years before February 2022, that the Minsk agreements were part of a scheme to give time for the arming of Ukraine, that the U.S. has rejected all calls from Russia to respect its borders and its integrity, that the U.S./NATO has surrounded Russia with military bases, that there was a vote in Crimea after the coup, that the U.S. has been for years waging economic war on Russia via sanctions, etc.

In short, all of the reasons that Russia felt that it was under attack for decades and that the U.S. was stone deaf to its appeals to negotiate these threats to its existence. It doesn’t take a genius to realize that if all were reversed and Russia had put troops and weapons in Mexico and Canada that the United States would respond forcefully.

This editorial is propaganda by omission and strident stupidity by commission.

The editorial has all its facts “wrong,” and not by accident. The paper may say that its opinion journalists’ claims are separate from those of its newsroom, yet their claims echo the daily barrage of falsehoods from its front pages, such as:

-

Ukraine is winning on the battlefield.

-

“Russia faces decades of economic stagnation and regression even if the war ends soon.”

-

That on Jan.14, as part of its cruel attacks on civilian targets, a Russian missile struck an apartment building in Dnipro, killing many.

-

Only one man can stop this war – Vladimir Putin – because he started it.

-

Until now, the U.S. and its allies were reluctant to deploy heavy weapons to Ukraine “for fear of escalating this conflict into an all-in East-West war.”

-

Russia is desperate as Putin pursues “his delusions.”

-

Putin is “isolated from anyone who would dare to speak truth to his power.”

-

Putin began trying to change Ukraine’s borders by force in 2014.

-

During the last 11 months Ukraine has won repeated and decisive victories against Russian forces …. The war is at a stalemate.”

-

The Russian people are being subjected to the Kremlin’s propaganda machinery “churning out false narratives.”

This is expert opinion for dummies. A vast tapestry of lies, as Harold Pinter said in his Nobel Prize address. The war escalation the editorial writers are promoting is in their words, “this time pitting Western arms against a desperate Russia,” as if the U.S./NATO does not have CIA and special forces in Ukraine, just weapons, and as if “this time” means it wasn’t so for the past nine years at least as the U.S. was building Ukraine’s military and arms for this very fight.

It is a fight they will lose in the days to come. Russia was, is, and will triumph.

Everything in the editorial is disingenuous. Simple propaganda: the good guys against the bad guys. Putin another Hitler. The good guys are winning, just as they did in Vietnam, until reality dawned and it had to be admitted they weren’t (and didn’t). History is repeating itself.

Little has changed and so my morning sense of mourning when I remembered Nixon and Kissinger’s savagery at Christmas 1972 was appropriate. As then, so today, we are being subjected to a vast tapestry of lies told by the corporate media for their bosses, as the U.S. continues its doomed efforts to control the world. It is not Russia that is desperate now, but propagandists such as the writers of this strident and stupid editorial. It is not the Russian people who need to wake up, as they claim, but the American people and those who still cling to the myth that The New York Times Corporation is an organ of truth. It is the Ministry of Truth with its newspeak, double-speak, and its efforts to change the past.

Let Harold Pinter have the last words:

The crimes of the United States have been systematic, constant, vicious, remorseless, but very few people have actually talked about them. You have to hand it to America. It has exercised a quite clinical manipulation of power worldwide while masquerading as a force for universal good. It’s a brilliant, even witty, highly successful act of hypnosis.

Tyler Durden

Sun, 01/29/2023 – 21:30 -

- Ahead Of The Fed – Ugh!

Ahead Of The Fed – Ugh!

By Peter Tchir of Academy Securities

I really didn’t want to write about the Fed this weekend and have the 10,000th report that barely gets glanced at. I would much rather have followed up on Academy’s latest Around the World report from Thursday (which addresses Russia/Ukraine, Japan’s Military, Iran/Russia, Turkey/Greece, and Brazil & Peru) with World War v3.1. World War v3.1 will explore the shift from a “Commodity War” (which is being fought) to the potential for a “Semiconductor War”. Fortunately, that report can wait a couple of days and I cannot hide from how powerful the equity rally was last week. The S&P 500 was up 2.5% and the Nasdaq was up 4.3%. ARKK was up 10%, though that segment had been washed out, so outperformance there was more in line with views. I did say that “if there was a gun to my head” the move could be higher for stocks, but no one put the gun to my head. Ugh!

The stock market returns were accompanied by Treasuries doing very little (2s through 30s moved less than 3 bps in most cases on the week). That was interesting.

Energy futures were down 1% to 4% across the board last week (heating oil was down 6%, but I can guarantee that this won’t get passed on to me by my provider). Even copper was down on the week despite the near frantic hype about China’s re-opening (it is up 11% on the month though, giving some credence to the importance of the China re-opening).

We also have a market where literally everyone (yes, even my mom) is talking about the 200-day moving average! It is one of those rare occasions when even “fundamentalists” (those who look down on “mere technicians”) are spouting technical levels especially if they are bullish, which is the direction fundamentalists seem to be leaning the vast majority of the time.

When we broke below the 200 DMA the morning after MSFT’s earnings call (triggered by the warning of future cloud earnings, which fits my 5 steps forward, 2 steps back theme), I thought that we would catch a lot of weak longs and the breakdown would continue. I was wrong and Tesla (among others) propelled us right back above the 200 DMA and set a true “feeding frenzy” into motion.

The “Weirdest” Venn Diagram Ever

Technically, I don’t think that it is a Venn diagram, and I eventually gave up trying to make the chart, but there is an interesting subset of people out there.

-

Initially, they were in the “inflation is transitory” camp.

-

Then, they morphed into the “inflation is here for a long time” camp because wages will drive it and it will be incredibly difficult to contain.

-

Now, they’ve joined the “soft-landing” camp. However, if you once thought that inflation was going to be difficult to tame, then this might be the next logical step now that inflation has been reduced, but it still feels like an awkward shift to me.

-

What makes this subset interesting is the credibility it maintains. I’m not sure how this subset got it wrong twice, so how can they be so certain that they are correct this time around? Anyways, just me moaning out loud, but it really does strike me as interesting that this subset exists (and how large it is).

At least Larry Summers, who was panicking about inflation, seems to have jumped all the way into “the Fed needs to slow” camp.

Coulda, Shoulda, Woulda

At this point, the Fed’s options boil down to a couple simple scenarios. It has a “woulda, coulda, shoulda” feel to it.

-

What the Fed “should” do (which they should have done two or three meetings ago) is hike 25 bps and focus on data dependence for future hikes. The market will use that as code for no more hikes given the direction that most of the data is moving.

-

The Fed funds terminal rate is at 4.91%. That doesn’t get hit until June now! At the start of this year, it was expected to be 4.97% in May. So, despite the Fed promising/threatening to hike to 5.25% or more, the markets haven’t believed them and believe them less so now compared to a mere month ago (amazing what data will do). I completely agree that the terminal rate will not get above 5%, though I think that the rate is already too high.

-

The market is now pricing in 4.4% by January 2024, which means that the market is pricing in rate cuts later this year. In fact, there was supposedly a very large SOFR options trade that went through this week betting on the policy rate being as low as 2.5% by the December meeting. As much as I believe that rates are already too high, I’m not sure how willing the Fed will be to reverse course after so much “higher for longer” rhetoric.

-

-

What the Fed “will” do. At this point, it seems like most people have fallen into the same camp about what the Fed “should” do. But, as I’ve learned the hard way, figuring out what the Fed “should” do doesn’t pay the bills. To generate alpha and good returns, we must divine what the Fed “will” do.

-

I revert back to last weekend’s The Fed’s Demons report. While it is one thing for pundits and the mainstream media to shift camps almost willy-nilly, it is far more difficult for the Fed to do that. This group is dealing with mistakes made by the Fed a long time ago and even their own mistakes during the “transitory” phase. For a little change of pace, we discussed this and some other subjects on Fox Business.

-

There was just enough inflation in Friday’s PCE data (4.4% YOY for Core) that the Fed could be tempted to remain more hawkish than they should. However, they really should be looking at the direction of change as opposed to the annual rate.

-

Financial conditions are not the Fed’s friend. The Fed has consistently referenced financial conditions. However, I’m not sure why they let the stock market (which is a large component of financial conditions) influence them so much.

-

-

- According to the Bloomberg Financial Conditions index, we are “looser” now vs. when we did the first hike, or even when Powell slammed everyone at Jackson Hole. That is consistent with other measures of financial conditions. In the Bloomberg index, we are in outright “easy” territory. Not just relatively easy, but actually easy! This, to me, would be the most compelling reason why the Fed would have to be more hawkish. The Fed also focused our attention on the dot plots (rather than downplaying them) and it would seem weird to shift the dot plots too dramatically right after the Fed made them the star of the show. If the demons are getting to the Fed, the financial conditions give them a real world metric to support them being more hawkish than markets have priced in.

At this point I believe that markets have priced in what the Fed “should” do and not what the Fed “will” do.

All-In Corporate Bond Yields and New Issue

Let’s start with the new issue calendar. We are almost 1 month into the year and we are at $138 billion, which is down 8% from last year. That is an especially slow start when you consider Q4 finished with an anemic $205 billion.

Many investors were expecting a much higher new issue volume to start the year (and they presumably set aside dry powder for those expected new issues).

The entire Treasury curve is around levels last seen in September.

The Bloomberg Corporate OAS, at 119, is lower than at any time since April.

I’m looking at all-in corporate yields and telling investors to be very cautious here. Issuers should be taking advantage of not only reasonable all-in yields, but the dry powder that asset managers were hoping to put to work and presumably need to (or want to) put to work now!

For all-in yields to do better, we need lower Treasury yields with spreads close to today’s levels. That could happen with a small move in rates, but I suspect that for 10s to get back to sub-3% it will take serious recession fears and that will not be good for corporate credit.

As Treasury yields move lower, spreads will widen at something close to a ½ bp for every bp. However, spreads could easily blow out faster on any real concerns. One nice thing is that some of the companies experiencing the biggest re-valuations in their equity prices are incredibly stable from the credit side.

If Treasury yields go higher (for any number of reasons) it is extremely difficult for spreads to compress. This would be under a “normal” scenario of yields rising because the economy and growth both look good. Spreads can tighten, but there isn’t a ton of room. If Treasury yields were to go higher on some dearth of dollar denominated debt buying, then spreads could widen while Treasury yields go higher. Not my base case, but it is possible. I am hearing that the strong auctions this week were not only due to the Fed’s potentially less hawkish message, but also because people want to buy debt before the debt ceiling debate potentially affects issuance.

I just don’t find all-in corporate bond yields compelling here, and I’d be taking advantage of the dry powder out there if I was an issuer.

Inventories and the Consumer

Retail sales have been weak (even adjusted for inflation). Credit card usage has been increasing. These are all signs of a consumption spree that is very long in the tooth. This spending would have already died without strong discounting from retailers during the holiday season.

We can quibble about sales and the strength of the consumer, but I don’t see the strength and I’ve discounted the “bank deposit” argument because it hasn’t captured the concept of “deferred payments” that I think affects many individuals.

There is no debating inventories.

Business inventories are far larger than any “Covid catchup” would warrant. This is occurring as the cost of financing those inventories increases. China’s “re-opening” and shipping more “cheap” goods here is a “good” thing? Hmmmmm.

According to NAPM, inventories are increasing every month. Greater than 50 means increased inventories. There have been some big increases and while they have slowed a bit, that is from high overall inventory levels (see previous chart).

What has never fully made sense to me is why inventories are considered a “good” thing in data. NAPM and ISM treat inventory builds as positive. GDP treats inventories the same way. I can see it from this perspective, but at a time when we have big existing stockpiles and evidence that consumption is slowing (especially ex-inflation), then we are setting ourselves up for a bigger fall!

My single biggest concern is “inventory build versus consumption” and I think that this (in hindsight) will be what turns the “soft landing” chatter into real recession fears!

Bottom Line

I am far from convinced that the Fed “will” do what the markets think it “should” do.

Good luck with the FOMC on Wednesday and I hope that you find World War v3.1 interesting when it comes out later this week.

Tyler Durden

Sun, 01/29/2023 – 20:30 -

- The Furious Squeeze That Sent Nasdaq To Its Best Start In Over 20 Years, And Why Bears Are Really Sweating Now

The Furious Squeeze That Sent Nasdaq To Its Best Start In Over 20 Years, And Why Bears Are Really Sweating Now

Back on January 9, despite a wave of raging pushback (putting it mildly) as the consensus bearish call was dead certain that the bottom was about to fall out of the market – after all, who in their right mind would fight the Fed when the Fed has clearly telegraphed that it wants risk lower – we warned that “We Are Setting Up For A Tech-led Squeeze Higher As Shorting Gets Extreme.”

What happened next was a historic tech-led squeeze as shorts got steamrolled over and over, and every attempt to push stocks lower was met with furious dip-buying (mostly by retail) which pushed S&P futs above all key resistance levels (50DMA, CTA trigger, 200DMA, descending channel) which sent it to a two month high of 4,100.

The bear-capitulating result, as Goldman’s Michael Nocerino puts it in his latest market note (available to pro subs), is that with just two trading days left in the month, “the January effect has come to fruition as the SPX is +6.02% and NDX is +11.2%, making this Nasdaq’s best start in over 20 years.”

As shorts were squeezed – with Goldman’s most shorted basket rising 23% since our Jan 9 post…

… and as markets melted up, here is what the bank’s clients were focused on this week: i) the pull forward of a soft landing; ii) better than feared earnings so far; iii) reduction in wages; iv) declining dollar; v) light positioning; vi) CTA demand resurgence and vi), retail returning.

Most importantly, this all comes as corporate are starting to exit their buyback blackout window (more on this shortly).

To be sure, the recent trend can still reverse – especially since much of the “real $” is still waiting for the big earnings week ahead (and risking to miss the train entirely if the rally accelerates), and next Wednesday is the Fed, followed by GOOGL, AMZN, and AAPL reporting on Thursday (+12%, 22%, 12% on the year), which to Nocerino “feels like a set up for a fade, but with the caveat that investors are not “full” and retail and technicals continuing to fuel price action.”

And speaking of technicals, the most important one by far this year, remains ever present. Here is how Goldman derivatives guru Brian Garrett describe market action 20 (long) sessions in 2023:

What we are talking about on the desk and seeing in markets 20 trading sessions down, and 232 trading sessions to go?

Bottom line… implied vols have retraced to 2 year lows and we yet not seen an increase in demand (in fact the desk has seen the opposite) …

… correlation is breaking down as stocks behave like individual corporations and factor vol decreases (nothing shows this better than the earnings surprise miss/beat chart we showed previously – even if trading “wrong way”) …

… the rest of the world is decoupling from the US in terms of both absolute return and positioning (PM survey suggests this could keep going).

Garrett’s bottom line: “US stock exposures are not set up for a continued rally and one could argue that if this squeeze continues, there is no shortage of single stock positions that would need to be covered (ie: potential for early innings).”

One final last chart from Garrett before we shift back to Nocerino, just because the numbers are – as the Goldman trader puts it, “staggering” – the 50 day average $ notional traded in SPX options is remains above $1 trillion.

Meanwhile, for those who think that the shorts have had enough getting spanked and are finally covering, guess what: wrong. As Nocerino writes referencing the latest Goldman Prime data, “Gross and Net leverage for the overall Prime book increased on the week. Fundamental L/S Gross leverage increased while Net leverage finished slightly down.” Some more color:

Overall Prime book was modestly net sold, driven by risk-off flows with long sales outpacing short covers. Macro Products were net sold led by long sales, while Single Stocks were net bought for a 3rd straight week driven entirely by short covers. Hedge funds net bought Energy stocks amid continued optimism over China demand. Aggregate US Energy long/short ratio increased +3% week/week.

Ironically, so ingrained is the bearish mindset that pro investors would rather short any rip than buy any dip (that’s what retail has been doing for the past two weeks after 17 weeks of selling). As Brian Garrett states in his latest note, Positioning Remains Light, and notes that “the GS prime brokerage data shows that the professional investor community is not ready to chase this rally … chart below of the GS PB l/s ratio vs rolling SPX returns.”

And while this tactic served well in 2022, others at Goldman admit that everything has changed in just a few short weeks (see Goldman’s Biggest Bear Capitulates: “The Market Is In No Mood To Go Down Right Now“, Goldman Trader: Market Dynamics Have Shifted Dramatically Again, Here’s Why) and so institutions and hedge funds – who remain largely short – may soon be forced to chase the rally higher.

But it’s not just the relentless short squeeze that threatens the mental stability of bears (see Hartnett’s latest note: “Another 3-5% Will Feel Like Bathing In Lava If You’re A Bear“), there are many other bullish technicals on deck starting with…

CTAs: here is some more in depth color from Goldman’s Futures Strats Desk: the recap is that Equity positioning is still to BUY, but demand slowing as positioning is getting full.

CTAs are at a 100% rank for positioning on a 1-yr scale within our work. That is to say that positioning is at the highest it’s been on a rolling 1-yr basis. To round out the week, we estimate CTAs bought $34bn of equities this week bringing the total positioning to long $91bn. Of the simulated buying, purchasing was heaviest in TOPIX ($13.6bn), followed by SPX ($12.5bn), with continued N. America buying in other products like RTY and TSE. SPX has rebalanced decidedly long in our work where we now estimate CTAs are long $9.1bn. N. America, however, has not yet caught up to EMEA, which holds its title for heaviest long in our model.

Flows scenarios over the next week:

- Baseline (flat prices and vols): $20bn of which 4.6bn is SPX, $11.2bn in TOPIX, $2.5bn in Nasdaq

- Prices up 2s and vol down: $17.78bn of which $5.4bn in SPX, $11.7bn in TOPIX, $2.5bn in Nasdaq

- Prices down 2.5s and vol up: -$14.4bn of which -$8.0bn SPX, +$5.0bn in TOPIX, -$3.4bn in FTSE

Threshold Levels (short/medium/long): SPX: 3937/3970.5/4073 … RTY: 1830/1841/1954

EARNINGS…As we first discussed last Thursday in “When Stocks Don’t Go Down On Bad News, That’s A Bullish Signal“, when the market/stocks dont go down on bad news (MSFT guide) typically a bullish signal. As Goldman wrote then, “we learned a lot from this price action today: this market is more resilient than most of us are giving it credit for (be very thoughtful/selective with your short positions as squeezes will be common this Q).” To this, Nocerino adds that we have been seeing weaker report being bought (ie: MSFT). And as we pointed out on Friday, “companies who miss earnings on EPS have outperformed at the largest pace on record.” Hardly a bearish signal.

BUYBACKS…Needless to say, this is the most important driver as we exit buyback blackout. We will have more to say on this shortly, but as Goldman calculates, the current blackout window ended Friday and the bank estimates that ~23% of the S&P 500 will be in open window. When the window is open Goldman estimates ~$4B/day in demand.

WHERE IS THE MONEY FLOWING… Net flows into global equity funds accelerated in the week ending January 25 (+$14bn vs +$8bn in the previous week)…a lot of this comes in Emerging Mkts, but importantly the outflows out of US turned positive and money market fund assets declined by $2bn.

Meanwhile, Money Market Funds just hit a new all-time high cash level. As Goldman points out, “5% cash yields make the bar higher for a re-allocation to risk assets; but if the Fed’s done, the incentive to reallocate is done.”

RETAIL…Last but not least, retail is back in full force and after selling for 17 straight weeks, retail investors have been buying aggressively for the past two. Here’s a good example: TSLA now accounts for roughly 7% of all options trading on an average day, with nearly 3mm contracts changing hands on an avg — up from 1.5 million a year ago and more than any other stock (WSJ). TSLA gained +33% last week, its best week in >10 years, largely thanks to an epic retail-driven gamma squeeze.

And as Vanda Research adds, “retail investor appetite returns as stocks recover from last week’s slump. Indeed, retail flows remained resilient and continued ticking higher, helping broad indices recover from a two-day dip last Wednesday and Thursday. Moreover, with the earnings calendar getting busier and some of retail’s favorite names beating expectations, flows into single names have kept climbing. The two charts below depict these dynamics, with the average daily inflow across all securities rebounding toward US$ 1.2bn/day…

… and with full-week flows into single stocks estimated to approach ~US$ 5.3bn.

Moreover, intraday action shows that retail traders gave a needed hand to US stocks after the initial dip post MSFT earnings. Beyond the usual flurry of buying at the open, retail crowds leaned against downward pressure on stocks – all of it coming from institutions – for the entire first two hours of trading while adding extra support on the way up in the early afternoon as well

Bottom line: if retail is once again a more powerful price setter than institutions and hedge funds (thank you zero market liquidity), and we are facing another Jan 2021-type meltup, then watch out above even if none of the abovementioned technicals go into play.

More in the full note available to pro subs.

Tyler Durden

Sun, 01/29/2023 – 20:00 - How Two Conflicting COVID Stories Shattered Society

How Two Conflicting COVID Stories Shattered Society

Authored by Gabrielle Bauer via The Brownstone Institute,

The story went like this:

There is a virus going around and it’s a bad one. It’s killing people indiscriminately and will kill many more. We must fight it with everything we’ve got. Closing businesses, closing schools, canceling all public events, staying home…whatever it takes, for as long as it takes. It’s a scientific problem with a scientific solution. We can do this!

There was another story simmering under the first one.

It went like this:

There is a virus going around. It’s nasty and unpredictable, but not a show stopper. We need to take action, but nothing so drastic as shutting down society or hiding out for years on end. Also: the virus is not going away. Let’s do our very best to protect those at higher risk. Sound good?

[Editor: this is an excerpt from Blindsight Is 2020, by Gabrielle Bauer, now available from Brownstone.]

The first story traveled far and wide in a very short time. People blasted it on the nightly news and shouted it to each other on Twitter. They pronounced it the right story, the righteous story, the true story. The second story traveled mainly underground. Those who aired it in public were told to shut up and follow the science. If they brought up the harms of closing down society, they were reminded that the soldiers in the World War 1 trenches had it much worse. If they objected to placing a disproportionate burden on children and youth, they were accused of not caring about old people. If they breathed a word about civil liberties, they were told that freedumbs had no place in a pandemic.

The first story was a war story: an invisible enemy had invaded our land and we had to pour all our resources into defeating it. Everything else—social life, economic life, spiritual life, happiness, human rights, all that jazz—could come later. The second story was an ecological story: a virus had entered and recalibrated our ecosystem. It looked like we couldn’t make it go away, so we had to find a way to live with it while preserving the social fabric.

The two stories continued to unfold in tandem, the gulf between them widening with each passing month. Beneath all the arguments about the science lay a fundamental difference in worldview, a divergent vision of the type of world needed to steer humanity through a pandemic: A world of alarm or equanimity? A world with more central authority or more personal choice? A world that keeps fighting to the bitter end or flexes with a force of nature?

This book is about the people who told the second story, the people driven to explore the question: Might there be a less drastic and destructive way to deal with all this?

As a health and medical writer for the past 28 years, I have a basic familiarity with infectious disease science and an abiding interest in learning more. But my primary interest, as a journalist and a human taking my turn on the planet, lies in the social and psychological side of the pandemic—the forces that led the first story to take over and drove the second story underground.

Many smart people have told the second story: epidemiologists, public health experts, doctors, psychologists, cognitive scientists, historians, novelists, mathematicians, lawyers, comedians, and musicians. While they didn’t always agree on the fine points, they all took issue with the world’s single-minded focus on stamping out a virus and the hastily conceived means to this end.

I have selected 46 of these people to help bring the lockdown-skeptical perspective to life. Some of them are world famous. Others have a lower profile, but their fresh and powerful insights give them pride of place on my list. They lit up my own way as I stumbled through the lockdowns and the byzantine set of rules that followed, bewildered at what the world had become.

I see them as the true experts on the pandemic. They looked beyond the science and into the beating human heart. They looked at the lockdown policies holistically, considering not only the shape of the curve but the state of the world’s mental and spiritual health. Recognizing that a pandemic gives us only bad choices, they asked the tough questions about balancing priorities and harms.

Questions like these: Should the precautionary principle guide pandemic management? If so, for how long? Does the aim of stopping a virus supersede all other considerations? What is the common good, and who gets to define it? Where do human rights begin and end in a pandemic? When does government action become overreach? An article in the Financial Times puts it this way: “Is it wise or fair to impose radical limits on the freedom of all with no apparent limits in sight?”

Now that three years have gone by, we understand that this virus doesn’t bend to our will. Serious studies (detailed in subsequent chapters) have called the benefits of the Covid policies into question while confirming their harms. We’ve entered the fifty shades of moral grey. We have the opportunity—and the obligation—to reflect on the world’s choice to run with the first story, despite the havoc it wreaked on society.

I think of the parallel Covid stories as the two sides on a long-playing vinyl album (which tells you something about my age). Side A is the first story, the one with all the flashy tunes. Side B, the second story, has the quirky, rule-bending tracks that nobody wants to play at parties. Side B contains some angry songs, even rude ones. No surprise there: when everyone keeps telling you to shut up, you can’t be blamed for losing patience.

Had team A acknowledged the downsides of locking up the world and the difficulty of finding the right balance, team B might have felt a tad less resentful. Instead, the decision makers and their supporters ignored the skeptics’ early warnings and mocked their concerns, thereby fueling the very backlash they had hoped to avoid.

Side A has been dominating the airwaves for three years now, its bellicose tunes etched into our brains. We lost the war anyway and there’s a big mess to clean up. Side B surveys the damage.

Many books about Covid proceed in chronological order, from the lockdowns and vaccine rollout through the Delta and Omicron waves, offering analysis and insight at each stage. This book takes a different approach, with a structure informed by people and themes, rather than events.

Each chapter showcases one or more thought leaders converging on a specific theme, such as fear, freedom, social contagion, medical ethics, and institutional overreach. There’s oncologist and public health expert Vinay Prasad, who explains why science—even very good science—cannot be “followed.” Psychology professor Mattias Desmet describes the societal forces that led to Covid groupthink.

Jennifer Sey, whose principles cost her a CEO position and a million dollars, calls out the mistreatment of children in the name of Covid. Lionel Shriver, the salty novelist of We Need To Talk About Kevin fame, reminds us why freedom matters, even in a pandemic. Zuby, my personal candidate for world’s most eloquent rapper, calls out the hubris and harms of zero-risk culture in his pithy tweets. These and the other luminaries featured in the book help us understand the forces that shaped the dominant narrative and the places where it lost the plot.

Along with the featured 46, I’ve drawn from the writings of numerous other Covid commentators whose sharp observations cut through the noise. Even so, my list is far from exhaustive. In the interest of balancing perspectives from various disciplines, I’ve left out dozens of people I admire and no doubt hundreds more I don’t know about. My choices simply reflect the aims of the book and the serendipitous events that placed some important dissenting thinkers in my path.

To maintain the book’s focus I’ve stepped away from a few subplots, notably the origin of the virus, early treatments, and vaccine side effects. These topics merit separate analyses by subject matter experts, so I respectfully cede the territory to them. And what they find under the hood, while obviously important, doesn’t alter the core arguments in this book. I also steer clear of speculations that the lockdown policies were part of a premeditated social experiment, being disinclined to attribute to malice what human folly can readily explain (which is not to say that malfeasance didn’t occur along the way).

In case it needs to be said, the book does not discount the human toll of the virus or the grief of people who lost loved ones to the disease. It simply argues that the path chosen, the Side A path, violated the social contract underpinning liberal democracies and came at an unacceptably high cost. If there’s a central theme running through the book, it’s exactly this. Even if lockdowns delayed the spread, at what cost? Even if closing schools made a dent in transmission, at what cost? Even if mandates increased compliance, at what cost? In this sense, the book is more about philosophy and human psychology than about science—about the trade-offs that must be considered during a crisis, but were swept aside with Covid.

The book also calls out the presumption that lockdown skeptics “don’t take the virus seriously” or “don’t care.” This notion infused the narrative from the get-go, leading to some curious logical leaps. In the spring of 2020, when I shared my concerns about lockdowns with an old friend, the next words out of her mouth were: “So you think Covid is a hoax?” Some two years later, a colleague gave me a thumbs-up for hosting a woman from war-torn Ukraine, but not without adding that “I didn’t expect it from a lockdown skeptic.” (I give her points for honesty, if nothing else.)

You can take the virus seriously and oppose lockdowns. You can respect public health and decry the suspension of fundamental civil liberties during a pandemic. You can believe in saving lives and in safeguarding the things that make life worth living. You can care about today’s older people and feel strongly about putting children first. It’s not this or that, but this and that.

The pandemic is both a collective story and a collection of individual stories. You have your story and I have mine. My own story began in the Brazilian city of Florianópolis, known to locals as Floripa. I lived there for five months in 2018 and returned two years later to reconnect with the gaggle of friends I had made there. (It’s ridiculously easy to make friends in Brazil, even if you’re over 60 and have varicose veins.)

March was the perfect month to visit the island city, signaling the end of the summer rains and the retreat of the tourist invasion. I had a tight schedule: Basílico restaurant with Vinício on Monday, Daniela beach with Fabiana on Tuesday, group hike along the Naufragados trail on Wednesday, just about every day of the month packed with beaches and trails and people, people, people.

Within three days of my arrival, Brazil declared a state of emergency and Floripa began folding in on itself. One after the other, my favorite hangouts closed up: Café Cultura, with its expansive sofas and full-length windows, Gato Mamado, my go-to place for feijão, Etiquetta Off, where I indulged my sartorial cravings… Beaches, parks, schools, all fell like dominoes, the world’s most social people now cut off from each other.

My friend Tereza, who had introduced me to ayahuasca two years earlier, offered to put me up in her house for the next month, amid her rabbits and dogs and assorted Buddhist and vegan lodgers. I would be lying if I said I wasn’t tempted. But Prime Minister Trudeau and my husband were urging me to come home, and as much as I loved Brazil I couldn’t risk getting stranded there. I hopped on a plane to São Paulo, where I spent 48 hours awaiting the next available flight to Toronto.

When I finally got home and flung open the front door, Drew greeted me with his right arm stretched out in front of him, his hand facing me like a stop sign. “Sorry we can’t hug,” he said, fear traveling across his face. He pointed to the stairs to the basement. “See you in two weeks.”

There wasn’t much natural light in the basement, but I did have my computer, which kept me abreast of the memes of the moment. Stay home, save lives. We’re all in this together. Don’t be a Covidiot. Keep your social distance. The old normal is gone. It felt alien and graceless and “off” to me, though I couldn’t yet put my finger on why. Ignoring my misgivings, I slapped a “stay home, save lives” banner on my Facebook page, right under my cover photo. A few hours later I took it down, unable to pretend my heart was in this.

Every once in a while I would go upstairs to get something to eat and find Drew washing fruits and vegetables, one by one. Lysol on the kitchen counter, Lysol in the hallway, paper towels everywhere. “Six feet,” he would mumble as he scrubbed.

The fourteen days of quarantine came and went, and I rejoined Drew at the dining table. On the face of it, the restrictions didn’t change my life much. I continued to work from home, as I had done for the past 25 years, writing health articles, patient information materials, medical newsletters, and white papers. All my clients wanted materials on Covid—Covid and diabetes, Covid and arthritis, Covid and mental health—so business was brisk.

Even so, the new culture forming around the virus troubled me mightily: the pedestrians leaping away if another human passed by, the taped-up park benches, the shaming, the snitching, the panic… My heart ached for the young people, including my own son and daughter in their dreary studio apartments, suddenly barred from the extracurricular activities and gigs that made university life tolerable for them. People said it was all part of the social contract, what we had to do to protect each other. But if we understand the social contract to include engaging with society, the new rules were also breaking the contract in profound ways.

Stay safe, stay safe, people muttered to each other, like the “praise be” in The Handmaid’s Tale. Two weeks of this strange new world, even two months, I could countenance. But two months were turning into the end of the year. Or maybe the year after that. As long as it takes. Really? No cost-benefit analysis? No discussion of alternative strategies? No regard for outcomes beyond the containment of a virus?

People told me to adapt, but I already knew how to do that. Job loss, financial downturn, illness in the family—like most people, I put one foot in front of the other and powered through. The missing ingredient here was acquiescence, not adaptability.

I connected with an old-school psychiatrist who believed in conversation more than prescriptions, and scheduled a string of online sessions with him. I called him Dr. Zoom, though he was more of a philosopher than a medical man. Our shared quest to understand my despair took us through Plato and Foucault, deontology and utilitarianism, the trolley problem and the overcrowded lifeboat dilemma. (Thanks, Canadian taxpayers. I mean that sincerely.)

And then, slowly, I found my tribe: scientists and public health experts and philosophy professors and lay people with a shared conviction that the world had lost its mind. Thousands and thousands of them, all over the planet. Some of them lived right in my city. I arranged a meetup, which grew into a 100-strong group we called “Questioning Lockdowns in Toronto,” or Q-LIT. We met in parks, on restaurant patios, at the beach, and between meetings stayed connected through a WhatsApp chat that never slept. Zoom therapy has its place, but there’s nothing more healing than learning you’re not alone.

To those who have traveled a similar path, I hope this book provides that same sense of affirmation. But I’ve also written it for the Side A people, for those who sincerely upheld the narrative and despaired at the skeptics. Wherever you fall along the spectrum of viewpoints, I invite you to read the book with a curious mind. If nothing else, you’ll meet some interesting and original thinkers. And if their voices help you understand Side B, even a little, we all win.

Tyler Durden

Sun, 01/29/2023 – 19:30 - If WW3 Breaks Out, Tanks Or Fighter Jets Won't Matter: Kremlin

If WW3 Breaks Out, Tanks Or Fighter Jets Won’t Matter: Kremlin

Fresh off getting the West to sign off on the main battle tanks he’s long sought from the US and Germany, Ukraine’s President Volodymyr Zelensky is already pressing for more, and specific, advanced systems from his external backers.

In his Saturday night address, he pleaded for deliveries of the US Army Tactical Missile System, known as ATACMS, to protect cities which are far from front line fighting. “There can be no taboo in the supply of weapons to protect against Russian terror,” he said.

On the same day, Russian Security Council Deputy Chairman Dmitry Medvedev issued a scathing condemnation in reaction to the Biden administration and other Western officials claiming that ramped-up arms deliveries are actually helping to prevent a world war.

“Firstly, defending Ukraine, which nobody needs in Europe, will not save the senile Old World from retribution if anything occurs. Secondly, once the Third World War breaks out, unfortunately it will not be on tanks or even on fighter jets. Then everything will definitely be turned to dust,” Medvedev wrote on Telegram Saturday.

Kremlin officials have of late made the point that the US M1 Abrams as well as German Leopard tanks will make little difference on the battlefield, other than to ensure rapid escalation between NATO and Russia.

Medvedev was also specifically responding to remarks out of Italy’s defense chief, as Russian state media writes:

In this post, Medvedev commented, in particular, on Italian Defense Minister Guido Crosetto’s remarks that the Third World War would erupt if Russian tanks reached Kiev and “the borders of Europe”, and that the weapons sent to Ukraine were meant to stop the escalation. Medvedev equated his remarks to the calls from the United Kingdom to provide Kiev with all the weapons NATO has.

Medvedev’s reference to everything being “turned to dust” was without doubt reference to potential nuclear exchange as a result of runaway escalation. The former president and close Putin confidant has repeatedly warned of things going nuclear in Ukraine if the West keeps pumping heavier arms to the Ukrainians, and if Moscow loses the war.

Interestingly, a fresh lengthy report by RAND Corporation seems to agree that continued escalation on the part of Washington could prove disastrous. RAND, though notoriously hawkish as essentially the Pentagon’s think tank arm, now argues that in Ukraine “US interests would be best served by avoiding a protracted conflict,” and that “costs and risks of a long war…outweigh the possible benefits.”

Tyler Durden

Sun, 01/29/2023 – 19:00 - Raise The Social Security Age To (At Least) 75

Raise The Social Security Age To (At Least) 75

Authored by Ryan McMaken via The Mises Institute,

On January 10, the French government announced plans to raise the retirement age from 62 to 64.

The change would mean that after 2027, workers in France would have to work 43 years to qualify for a government pension, instead of 42 years. French workers promptly took to the street in protest decrying even this very small reduction government welfare.

Like many countries in Western Europe and North America, France faces a major demographic problem in that its population is aging and demanding ever larger amounts of public pension funds.

Meanwhile, the younger working-age population is shrinking as birth rates continue to fall. So, the French state is looking for ways to stay relatively solvent.

For Americans who follow our own old-age social benefits systems, this problem will seem quite familiar. Although the US regime is not in as dire fiscal straits as the French one, the US’s federal government nonetheless faces huge and growing obligations to current and future pensioners. This will only grow more urgent as the population continues to age and as the numbers of prime-age workers stagnates.

Indeed, the Social Security scheme is an excellent example of how government programs, once established, gradually become far more costly—in real per capita terms, not just aggregate terms—as time goes by. Many recipients now spend decades collecting benefits on a program that had been sold as a program only for people who were too old, exhausted, and injured to work at all. Meanwhile, fewer and fewer workers are called upon to foot the inflated bill.

At the center of this mission creep for Social Security is the fact that Social Security benefits originally began at age 65. Yet, at that same time, the life expectancy at birth was below 65. (It’s much higher now.) Many people lived well past 60 back then, of course, but not nearly as many as do today. In other words, a far smaller fraction of the work force collected Social Security, and for a shorter period. Today, however, more workers live long enough to collect Social Security, and they now receive payments for longer. That’s a sure way to inflate the cost to taxpayers of old-age benefits. (It’s also a sure way to encourage able-bodied workers to leave the workforce, thus tilting the economy more toward consumption rather than production.)

Even if we ignore the moral problems presented by transferring huge amounts of income from current workers to pensioners, the realities of demographics in the twenty-first century mean the minimum “retirement age” should really be at least 75. Too long has a shrinking pool of workers been forced to fund pensioners who start collecting government benefits in their 60s and can now expect to be on the dole for 20 years or more. Moreover, this phenomenon is growing. Social Security increasingly forces today’s workers to shoulder an ever-greater burden on their ability to earn a living and support their families. The days of subsidized extended vacations for able-bodied 65-year olds must come to an end, but until that day comes, the damage can at least be limited by raising the age of eligibility.

The Original Justification for Social Security

When it was being sold to the public in 1935, those promoting Social Security took advantage of sentiments that people over age 65 were essentially too old to work, and thus would soon fall into poverty. This certainly would have seemed plausible at the time. Most jobs in 1935 involved significant amounts of physical labor whether we’re talking about cleaning laundry, waiting tables, farming, mining coal, or building houses. Work was also more dangerous—as historical work injury data makes clear—and workers were more likely to sustain injuries that would render one unable to work. For example, a 65-year-old simply could not safely perform much of the work required at a steel mill. (As shown in this 1944 video on the steel industry.)

Especially important to efforts at presenting Social Security as fiscally prudent was the fact that with a minimum age of 65, the number of Social Security beneficiaries would also be limited by the realities of life expectancy. In 1940, for example—the first year that pensioners could receive benefits—life expectancy at birth was only 61 for men and 65 for women. Indeed, even if we eliminate the toll of childhood diseases on life expectancy, the numbers do not change dramatically. In 1940, total life expectancy for persons over 15 years of age was 68. Moreover, in 1940 the percentage of the population surviving from age 21 to 65 was only 54 percent for males and 61 percent for females. But what about those who actually made it to age 65? In 1940, a male at age 65 would, on average live another 13 years. A female would live another 15 years. So, when looking at the work force in 1940, we can eliminate nearly half of the men and about 40 percent of the women as likely future Social Security recipients. About half of those who actually made it to 65 would then collect benefits for no more than 15 years.

Now let’s contrast that with life expectancy realities in our own time.

Life expectancy at birth today is 78 years, and for those who reach age 15, it is 80. for both men and women, more than 75 percent of the population reaching 21 will survive to age 65. That’s an increase of 50 percent for men, and around 30 percent for women. For those reaching age 65 in 2022, males will live another 18 years on average, while females will live another 20 years.

These growing commitments from Social Security are further aggravated by the fact that while the retiree population is growing, growth in the work force is stagnating. Since 1960, the total number of Social Security recipients has increased by 364 percent. Meanwhile, the prime age population (age 25-54) has grown by only 90 percent. Put another way, in 1960, there were 4.6 prime age workers per Social Security recipient. In 2020, that number was 1.9.

Now let’s look at this in dollar terms. Per prime-age worker, inflation-adjusted dollars spent on SS amounted to $9,590 in 2022. That’s up from $4,814 in 1980, or an increase of 99 percent over the period. During the same period, inflation-adjusted weekly earnings for workers increased 16 percent. Part of this discrepancy is due to the fact SS payments are consistently—as mandated by law—bumped up by cost-of-living adjustments to account for price inflation. Wage workers enjoy no such guarantees.

Social Security benefits are rapidly outpacing both population growth and earnings growth. In the aggregate, the program is more generous (toward pensioners) than ever.