- The World Is Not Enough

Earth Overshoot Day came on July 29 this year.

As Statista’s Katharina Buchholz notes, this is only the second time the day, which marks the time at which humanity has used up its allotment of natural planetary resources for the year, occurred in the month of July. It had occurred in August between 2010 and 2017.

The day, whose existence is highlighted by the NGO Global Footprint Network, means that all humans on Earth for this year have already used up more natural resources than mother nature can reproduce annually. Emissions, but also of resources like wood or fish and the use of land for crops, are among the things counted in when calculating Earth Overshoot Day.

Industrialized nations have the biggest share in pushing its date forward, as seen in the organization’s country profiles. The U.S. is the biggest offender.

You will find more infographics at Statista

If all nations lived like U.S. residents, the resources of five Earths would be needed each year in order for the natural environment to regenerate. The U.S. overshoot day is therefore on March 15.

Australia, which had been ahead of the U.S. for some years, now had its overshoot day on March 31, with 4.1 “Earths” used annually.

India was among the countries whose style of living would use up less than a whole Earth each year if practiced globally, which also has to do with poverty still being widespread in the country.

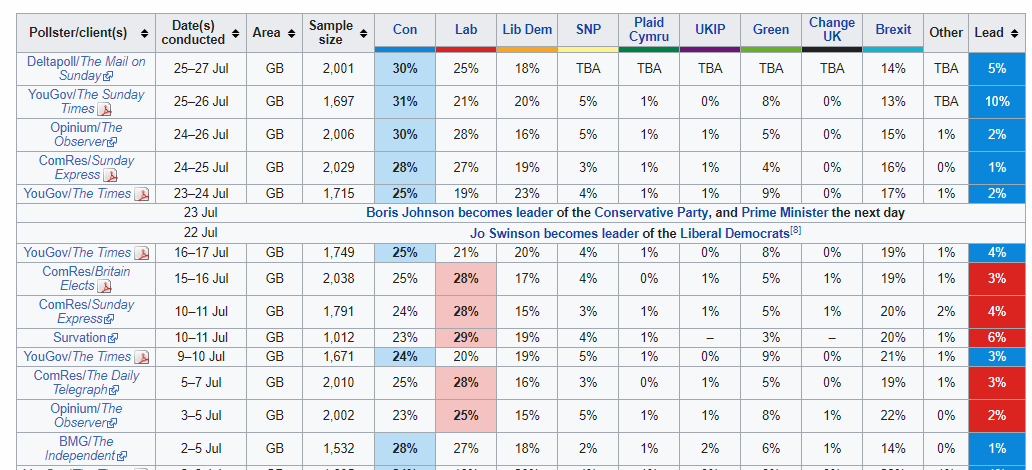

- Nigel Farage Offers Boris Johnson A Chance To Work Together To "Smash Labour"

Authored by Mike Shedlock via MishTalk,

Nigel Farage wants to help Boris Johnson deliver Brexit. Boris should accept the offer gratefully.

In a Telegraph Op-Ed Nigel Farage says Boris, the country is crying out for leadership – but with my party’s help, we can resolve Brexit.

The European elections were a sobering experience for the Tories. Their support fell to only 10 per cent of the vote and I already know of several large-scale Tory donors who switched to the Brexit Party overnight. Arguably, the Conservatives’ future is already in doubt. Suddenly, it is ‘do-or-die’ not just for Brexit, but for the Conservative Party as well.

Mr Johnson should realize that he is going to have to risk his longed-for position as PM to ensure Brexit is enacted properly. There is no prospect of a meaningful Brexit thanks to the views of most sitting MPs. And any attempt to prorogue Parliament will lead to the PM being brought down by his own side. The inescapable truth, therefore, is that he must hold an Autumn general election. That is his only way out. Doing so will take enormous courage. Inevitably, it will trigger a split in the Conservative Party. But the country is crying out for leadership and a resolution to the Brexit crisis.

Even on Brexit, he was very late to the cause. He will have a lot of convincing to do to persuade us that an early election will lead to a clean-break Brexit on 31 October.

If he is able to convince us, then together we would electorally smash the Labour Party, he would assume a big working majority, and he would go down as one of the great leaders in British history. All this is possible, but is Boris Johnson brave enough?

Johnson Should Accept

Johnson should accept this offer, just not quite yet. I propose mid-September.

Johnson should delay long enough there is no mathematical chance an election can stop Brexit.

By Common’s math, assuming an election is on a Thursday, an election is already too late to stop Brexit. But there is no requirement for a Thursday election.

My calculation says BJ can seek an election any time after September 10 secure that it cannot be held in time to prevent Brexit on October 31.

Johnson Bounce

The Tories have had a bounce following Johnson’s election. And his message is “Deliver Brexit – Do or Die.

What’s Jeremy Corbyn going to offer? Another referendum!

That’s supposed to carry the day?

It won’t.

Meet Jo Swinson

She is the new head of the Liberal Democrats.

The Guardian reports Jo Swinson rules out Lib Dem pact with Labour under Jeremy Corbyn

If that holds, a coalition between Farage and the Tories would indeed smash Labour and the Liberal Democrats to boot.

Of course, we only know what she says she would do not what she would really do.

But the Liberal Democrat platform is to return to the EU. Corbyn wants a “People’s Choice”.

67 Labour Party Members Attack Corbyn’s Anti-Jewish Leadership in Newspaper Ad

Also recall 67 Labour Party Members Attack Corbyn’s Anti-Jewish Leadership in Newspaper Ad.

Finally, at least 25% of Labour membership voted for Brexit. It was on those grounds that Corby said he would honor the referendum.

A significant number of Tories wanted to remain, but Labour has the far bigger problem.

Early Elections Coming

I commented on July 20: Early Elections Coming, But How Early?

The pieces are now falling together nicely. The EU is About to Face 2 Realities: Johnson Will Deliver Brexit, Eurozone in Recession

Johnson just needs a little more time to meet with German Chancellor Angela Merkel and French President Emmanuel Macron.

He can easily kill a week or two, come back and say they won’t listen, and opt for an election right after he delivers Brexit.

People’s Choice?

Will a majority of UK really vote for Corbyn or any other Labour leader if the platform is another People’s Choice referendum?

I think not.

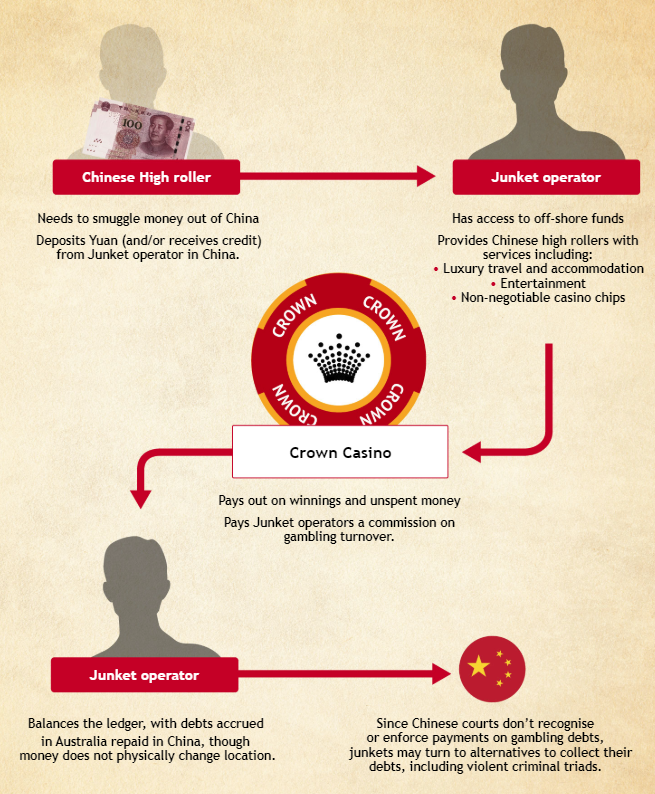

- Australia's Largest Casino Exposed: Chinese Whales Washed Money With Triads & Drug Traffickers

A year-long investigation that examined tens of thousands of leaked emails has revealed the secret inner workings of Australia’s biggest casino, Crown. The investigation, a collaborative effort led by 60 Minutes Australia, highlighted links to Chinese crime bosses and communist party figures in addition to drugs syndicates, money laundering and alleged sex trafficking rings.

After setting up offices across mainland China in 2010, Crown offered big incentives to its staff to break Chinese law to lure high rollers. When authorities closed in, the company reportedly abandoned its employees.

Crown employee Jenny Jiang, along with of her 18 colleagues, were arrested on October 13 and 14, 2016 and held in custody, convicted of breaching mainland Chinese laws that ban gambling and its promotion. She lives in Shanghai and now has a criminal record in China. As a Crown employee, her pay was based on incentives that were paid out when their high roller customers reached “appraisal targets” by gambling billions of dollars.

Jiang claimed that Crown’s promise to bring revenue to the Australian government led to hundreds of visas being stamped for Chinese nationals because they promised to gamble tens or hundreds of millions of dollars on trips to casinos.

EXCLUSIVE: #60Mins and @Ageinvestigates can reveal Former Border Force Commissioner Roman Quaedvlieg says he was encouraged by several members of parliament to fast track Crown’s Chinese high-rollers through Australian borders. pic.twitter.com/HuVgDjKVxS

— 60 Minutes Australia (@60Mins) July 28, 2019

https://platform.twitter.com/widgets.js

Jiang became a whistleblower that refused a $60,000 payment from Crown for her silence.

The investigation highlighted that Crown was prepared to cooperate with Asian organized crime syndicates, including the Triads and the most powerful drug trafficking syndicate in the world, in order to encourage business at their casinos. Current and former government officials also said that Crown helped bring criminals through the nation’s border in a way that raised serious national security concerns for Australia.

Chinese high rollers and criminals would look for ways to either “clean” money or smuggle it out of the country. They would work with “junket operators”, who had access to offshore funds and would provide luxury services to high rollers including non-negotiable casino chips. Many of these “junket operators” were familiar with the territory in Macau, the only place in China where you can legally bet in a casino.

From there, Crown casino would pay out winnings and unspent money. The junket operator got a commission and the high rollers and criminals would leave the casino with “clean” money.

Junket operators would then “balance the ledger” by having Australian debts repaid in China. Since Chinese courts don’t recognize gambling debts, this would occasionally lead to junkets seeking “alternatives” to collecting on debts, including violence.

In 2013, when authorities looked into one Melbourne financial adviser who was licensed by Crown to work as a representative for an Asian junket operator, Roy Moo, they found CCTV video of him passing bundles of $50 notes from a plastic shopping bag to a Crown staff member.

He claimed that “Crown offered its junkets a financial service with all the hallmarks of an underground banking operation.”

The money wound up totaling $969,000 and wound up being the proceeds of a drug syndicate’s trafficking operation in Melbourne and Sydney.

Crown said: “Crown does not comment on its business operations with particular individuals or businesses. However, it has a ‘comprehensive’ anti-money laundering and counter-terrorism financing program in place which is subject to regulatory supervision by AUSTRAC.”

You can watch the entire investigation here:

In Australia, there was some outrage over how the segment was promoted by 60 Minutes, who, in teasers called it a story that would “rock the foundation of Australia”. Viewers noted that a similar investigation had also taken place in 2017 by ABC and some said that the story was “overhyped”.

- Meet Peter Listerman: Epstein's "World Famous Seller Of Young Models To Oligarchs"

Authored by Jerry Lambe via LawandCrime.com,

Back in 2016, the New York Post ran a story alleging that convicted pedophile Jeffrey Epstein had moved beyond having his assistants “troll local high schools” for girls, and instead had begun “importing his playmates from Russia.”

One of the men who allegedly “procured” such girls for Epstein and other affluent men is Peter Listerman, was reportedly “running scared” when reporters approached him earlier this month at a film festival asking questions about his ties to Epstein, according to a report from the Daily Beast Monday.

According to the report, Listerman’s reputation for “matchmaking,” in which he would connect rich men to young models, has been notorious for decades, citing multiple interviews wherein Listerman brags about the number of women he’s hooked up with rich men.

The 10th annual Odesa International Film Festival in Ukraine, has been described as a haven for young Russian and Ukrainian models who partake in events organized for the festival’s Fashion Weekend. It was here reporters from the Daily Beast were able to find Listerman and question him about allegations that had connected Epstein with young foreign girls. According to the report, Listerman, whom the reporter was able to find based on his social media posts from the party, first responded to questions by attempting to turn the situation into a joke.

“I invented myths and fairy tales to entertain people,” Listerman said.

But when reporters refused to relent about his supposed role in exploiting teen models, Listerman refused to respond, eventually blocking the Daily Beast reporter from his Instagram and Facebook pages. But the online news outlet did catch up with model Krista Goncharova, who provided further details regarding Listerman’s reputation and behavior, referring to him as “the world famous seller of young models to oligarchs.”

Listerman began sending Goncharova private messages in 2016, allegedly trying lure her to become one of his girls.

“I had enough of a brain to turn him down when I was a minor but many girls look for a chance to meet with him, say yes to his offers, as he is paying them much more than [$334], the average of what we make per day working as professional models in Europe,” she said.

It’s doubtful that any of the Russians or Ukrainians that Page Six noticed around Epstein were there to be life partners; and, as for Goncharova herself, the Daily Beast concludes by noting that after a lifetime of modeling, at 24 she is disillusioned and says she is planning to quit the business.

- Chinese Duck Farmers Become Overnight Millionaires As Half Of China's Pigs Die

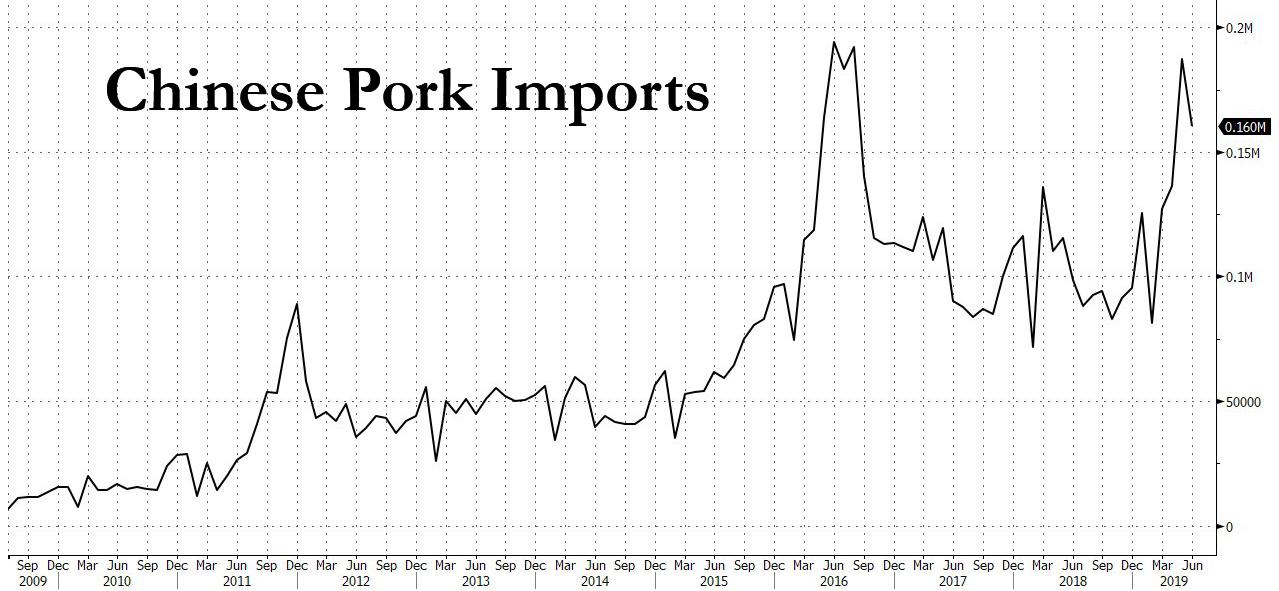

The price of China’s favorite food is about to hit all time highs.

As a result of the decimation of Chinese pig herds, which have been crippled by the ongoing spread of so-called “pig ebola”, i.e. African swine fever which has crippled domestic pork production, RaboBank expects China’s pork prices to hit a record high by the fourth quarter of 2019 even as imports continue to surge.

Last Tuesday China’s customs data showed that pork imports in June surged from the previous year, as the world’s top consumer of the meat stocked up on supplies after African swine fever swept across the country’s pig herds. China brought in 160,467 tonnes of pork in June, up 62.8% from the same month last year, according to data from the General Administration of Customs. This was down 14% from 187,459 tonnes imported in May.

China’s pork imports for the first six months of the year came in at 818,703 tonnes, up 26.3% from a year earlier according to Reuters. Meanwhile, pork prices rose by nearly 30% in June compared with a year earlier, according to the Ministry of Agriculture and Rural Affairs, with the spread of African swine fever showing no sign of abating, causing domestic production to plunge.

Retail pork prices have also increased in recent weeks but at a slower pace than whole sale prices, with prices up 34.6% from a year earlier at 27.29 yuan per kg as of July 10. And while China’s agriculture ministry is investigating local veterinary authorities in 10 provinces as it tries to slow the ongoing spread of the deadly African swine fever virus, few analysts expect it to succeed, and instead see prices rising even higher:

“China’s pork and hog prices are likely to break the previous record high in 2016 by the fourth quarter,” said Pan Chenjun, senior analyst for animal protein at Rabobank. He also expects pork production to fall by 30% or about 16 million tonnes, leaving a gaping hole in the country’s protein supply. Analysts warn the disease could hit some farms more than once, and ratings agency Fitch forecasts pork output will stay below 2018 levels through 2021.

Rabobank pointed out that Chinese data showed that sow, or mother pig, inventory had dropped 26.7% and the number of hogs had fallen 25.8% at the end of June compared with a year ago. But it believes that the herd losses in specific regions are much worse, down by 40 to 60 per cent since last August. For 2019, the bank expects the total herd loss to exceed 50 per cent.

Since the first African swine fever outbreak in Liaoning province in August 2018, the disease has affected animals across the country, forcing China to cull more than 1.1 million pigs. China began to import more pork in March when domestic wholesale prices started to rise. Imports of US pork – which fell 75% to 1,609 tonnes between July and December 2018 after China retaliated with tariffs in response to US duties on Chinese goods – have soared. Since January, imports from the US have more than tripled from 5,788 tonnes to 17,603 tonnes in May. While US pork imports to China face a 62% tariff, Bloomberg has cited unnamed sources saying that Beijing has approved duty waivers for some Chinese companies.

African swine fever will also put downward pressure on middle-class consumer spending, which Beijing is counting on to help boost growth in an economy that is expanding at its slowest pace in nearly three decades. China’s middle class accounts for around 400 million people, or 28.6% of the 1.4 billion population.

According to SCMP, economists at Capital Economics warned that Chinese consumption growth will be weighed down in the near term by consumer price inflation which is set to reach an eight-year high, due in large part to rising pork prices resulting from African swine fever.

“This will drag down real income growth and likely lead to a further deterioration in consumer sentiment,” they said in a report this month.

This also means that China is facing its first stagflationary episode since 2011: last month, China’s consumer price index

rose 2.7% Y/Y, driven by higher food prices in pork and fruits, according to the National Bureau of Statistics. And with spending curtailed, China’s economy will likely continue to contract even as prices of food stables rise.* * *

Meanwhile, and as a result, prices for other meats including chicken and duck, are also expected to rise substantially, putting further pressure on the discretionary spending of Chinese consumers.

One direct – and soon to be very rich – beneficiary of China’s pig ebola are duck farmers. As the SCMP reports, on a 30-hectare (74-acre) plot of land in China’s Shandong province poultry hub, more than half a million white-feathered ducks are busy eating, chattering and laying eggs to produce cheap meat for thousands of factory canteens.

With birds already packed into around 60 open-sided buildings, farm owner Shenghe Group is expanding further, aiming to raise output by 30 per cent this year to capture record profits as a plunge in pig numbers shrinks production of pork, China’s favourite meat.

“The market prospects are very good now because of African swine fever,” said Shenghe Chairman Wang Shuhong, whose firm sells about 300,000 ducklings a day for fattening and slaughter.

Expect demand for ducks to soar, for the simple reason that the deadly pig disease has already reduced China’s hog herd by more than a quarter, according to official data, however as many as half of the country’s breeding sows are thought to have died or been slaughtered to cope with disease outbreaks.

A farmer surrounded by ducklings at a duck farm on the outskirts of Jiaxing in Zhejiang province on April 5, 2011. Photo: Reuters Meanwhile, soaring pork prices have already fueled a surge in poultry meat demand. Chicken breast is about 20% more expensive than a year ago, while duck breast has nearly tripled in price to 14,600 yuan (US$2,125) a tonne, according to Shenghe. While this is still only about half the cost of pork, but such prices are unheard of in China, where breast is typically the cheapest part of the bird.

As the SCMP also reports, about 80% of the world’s ducks are raised in China, but are traditionally eaten in the south, where fried duck tongues, braised feet and spicy duck neck are popular snacks, and duck intestines make up a hotpot.

In recent years, as pork prices spiked, more ducks have been processed for use by cost-conscious catering firms, supplying large canteens feeding schools, factories, businesses and the military. These buyers are now switching as much pricey pork as they can to duck.

A procurement manager with a catering firm that supplies about 100 large clients around China said he has replaced about 20 per cent to 30 per cent of the pork on menus with either chicken or duck meat. He declined to be identified because of the sensitivity of the issue.

“We may switch even more. But our concern is that the poultry price is now going up as well,” he said.

The price of day-old ducklings, sold by farms like Shenghe, has hovered around 6 yuan, three times the usual level, since July last year. While the torrid price surge eased last month as farmers held off restocking during hot summer weather, they are rising again and set to go higher, said Dong Xiaobo, China general manager for French genetics company Orvia, the No. 2 supplier of breeding ducks.

Orvia is sold out six months ahead and has even had calls from pig farmers considering raising ducks after losing their hogs to African swine fever.

“I’ve never seen this in our 10 years in this market,” said Dong.

As swine fever continues to spread, China’s vice-premier Hu Chunhua has urged poultry farmers to help fill the protein gap to maintain social and economic stability.

Meanwhile, with output of about 5 million tonnes last year, less than half China’s chicken production, duck meat has plenty of room for growth, especially since the barrier to entry is lower for ducks than broiler chickens and breeding stock is more available, said Rabobank analysts.

Ironically, any rapid expansion carries its own disease risks, as in densely stocked farms, diseases like bird flu, several strains of which are circulating in China, will spread easily.And it remains to be seen whether duck farmers can hold on to a bigger share of the meat market when pork output recovers. As a reminder, in 2012 and 2016, duck farmers were forced out of the industry in droves when overproduction killed profits, and most people still want more pork dishes than any other meat, said the catering company manager.

But Shenghe’s Wang, who is planning to expand downstream with a slaughterhouse later this year, is not worried. “Pork output won’t go up in the next three years and will take at least five years to recover,” he said.

The bottom line: as China’s pork farmers face a dismal future, their duck farming friends are making more money than ever.

- Weaponizing Space Is The New Bad Idea Coming From Washington D.C.

Authored by Federico Pieraccini via The STrategic Culture Foundation,

When considering the possibility of great-power conflict in the near future, it is difficult to bypass space as one of the main areas of strategic focus for the major powers. The United States, Russia and China all have cutting-edge programs for the militarization of space, though with a big difference.

Donald Trump’s announcement of a “Space Force” is by no means a new idea. During the Reagan presidency, a similar idea was proposed in the form of the famous “Star Wars“ program, formally known as the Strategic Defense Initiative. It aimed to do away with the concept of mutually assured destruction (MAD) by positioning anti-ballistic-missile (ABM) interceptors in low-Earth orbit in order for them to be able to easily intercept ballistic missiles during their entry into orbit and before their re-entry phase. The costs and technology at the time proved prohibitive for the program, but military planners retained the dream of negating the concept of MAD in Washington’s favor, especially with the dawning of the unipolar era following the collapse of the Soviet Union.

The decisions taken in the years since, such as the US withdrawal from the ABM Treaty in 2002 during Bush’s presidency and from the INF Treaty during Trump’s, follows Reagan in trying to invalidate MAD, a balance of terror that has served to maintain a strategic stability.

This hope of doing away with MAD so that the unthinkable may become thinkable has guided the missile developments of Russia and China, which through the development of hypersonic missiles aim to nullify the US’s ABM systems and thereby make the thought of an unreciprocated nuclear first strike MAD again. With Russia’s recent successes in testing hypersoning technologies, and the fast-tracking of other new strategic weaponsannounced by Putin less than 12 months ago, strategic stability seems to have been restored through Russia’s strengthened deterrence posture.

The weaponization of space is a less known and talked about aspect of Washington’s mad attempts to make mutually assured destruction no longer mutual and therefore thinkable. During the peak of the unipolar moment, the idea of the Pentagon and the lobbyists of the military-industrial complex was to develop the so-called Prompt Global Strike system, which envisioned being able to deliver an air strike with conventional weapons anywhere in the world in the space of an hour. The dream (or delusion) of the US was to have the unique ability to determine the course of events around the globe within an hour. Such experimental craft as the Orbital Test Vehicle seem to confirm that serious efforts have been underway to realize this objective.

Neither China nor Russia has been sitting idly by waiting to be struck undefended. Russia’s development of its S-500 system has been quite timely. The S-500 system is often considered an upgrade to the better-known S-400 system, but these are in reality different systems with different aims and objectives. The main task of the S-500 is to engage long-distance targets in low-Earth orbit. We are therefore talking about the ability to take out military or any future ABM satellites as those originally conceived with Reagan’s “Star Wars” program.

Unlike Washington, Moscow and Beijing do not appear to be developing space-based weaponry; they are certainly not going to increase their military budgets to create a space force. On the contrary, both countries have been working for more than a decade on a proposed Prevention of an Arms Race in Outer Space (PAROS) treaty that seeks to ban the weaponization of space. The aims are summarized as follows:

“Under the draft treaty submitted to the [Conference on Disarmament] by Russia in 2008, State Parties would have to refrain from carrying out such weapons and threatening to use objects in outer space. State Parties would also agree to practice agreed confidence-building measures.

A PAROS treaty would complement and reaffirm the importance of the 1967 Outer Space Treaty, which aims to preserve space for peaceful uses by prohibiting the use of space weapons, and technology related to ‘missile defense’. The treaty would prevent any nation from gaining a military advantage in outer space.”

The intentions of the draft treaty clearly go against Washington’s plans. It is therefore not surprising that Washington has no intention of acceding to PAROS, and it is probably only a matter of time before Washington withdraws from the 1967 Outer Space Treaty.

Trump is looking at things from a practical point of view. He wants to give a major boost to the military-industrial complex, which is salivating at the prospect of being showered with tens or even hundreds of billions of US taxpayer dollars in a quest to weaponize space. But the policy makers in Washington and in think-tanks look at the weaponization of space from a different perspective. They look at it from the point of view of Washington as a superpower that must seek to prolong its unipolar moment through the use of force, even from space. While it is delusional nonsense, it has nevertheless been the prevailing outlook in Washington for at least the last 25 years.

The reason why China and Russia have proposed and continue to discuss the PAROS lies in their political and military philosophies that contrast with that of the US. As an imperial power bent on global domination, the US is always looking for ways to subjugate and dominate what it considers to be its underlings, while Russia and China act to hold back and counterbalance US aggression, in the process serving to enhance global stability.

The proposal for the non-militarization of space is the latest example of what unites and guides the Eurasian strategy of China and Russia without having any illusions about Washington’s intentions. The development of the SR-72 system seems to confirm that Washington wants to also bridge the gap with its Eurasian competitors in the field of hypersonic technology in addition to wishing to weaponize space.

Realistically, however, global powers in a multipolar context will seek to defend their territorial and economic sovereignty with every means at their disposal. Likewise, those seeking global hegemony will try to exploit any existing domain to gain an advantage over their rivals.

China and Russia seek to weaponize distance and speed to make any possible US attack on them impracticable, both in terms of the logistics required and the revivified cost-benefit calculus of MAD. The US, on the other hand, is trying to weaponize all conceivable domains of conflict by all means possible, hoping to be able to find a chink in its opponents’ armor.

Beijing and Moscow seem to have studied extensively how to respond. All the various defensive systems produced in recent years, from hypersonic anti-ship missiles to multi-layered defense systems like the S-400, S-500 and A-135/A-235, seem to meet the challenge.

Beijing fears US naval strength, and while seeking to achieve parity and surpass the US in the future, it aims above all to prevent the use of aircraft carriers as launching platforms through the employment of defensive area-denial weapons. In this sense, speed (Mach 10) and extending the range of Chinese anti-ship missiles (DF-21) are fundamental to the success of this strategy. Similarly, Moscow intends to seal Eurasia’s skies, and the S-500 seems to be the final flourish, able to protect up to 800 kilometers above sea level.

The weaponization of space is the latest issue that the US is exploiting for various political purposes. Be that as it may, this creates an adversarial environment that compels the US’s peer competitors to develop weapons capable of countering US belligerency. Instead of sitting down and defining the parameters of major-power interaction so as to reduce the likelihood of war, we are witnessing an intentional US policy of pursuing an arms race in every possible domain of warfare.

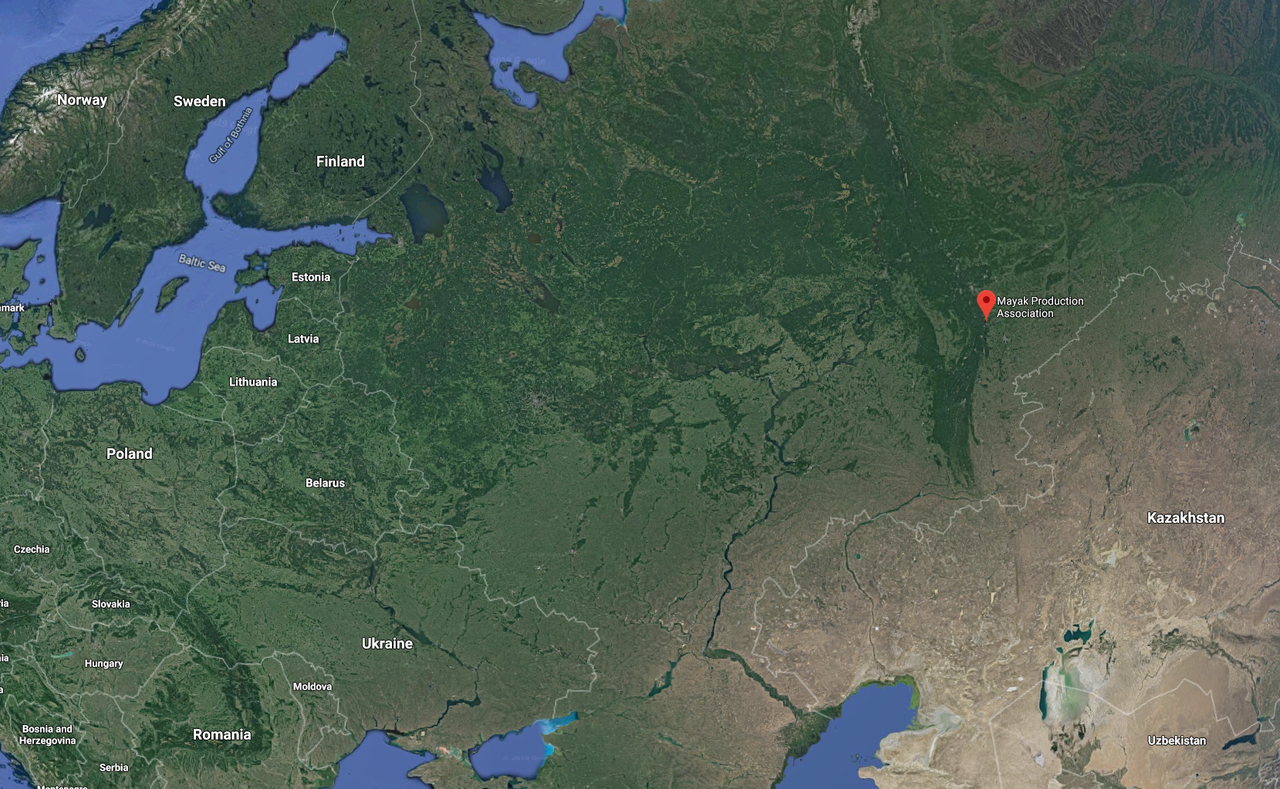

- Massive Radiation Leak Dwarfing Fukushima Traced To Russian Research Facility

A massive, unexplained cloud of radiation that swept across Europe in 2017 has been traced to one of Russia’s largest nuclear facilities, according to NewScientist.

Located between the Volga river and the Ural mountains, the leak coming from the Mayak nuclear development facility released up to 100 times the amount of radiation into the atmosphere as the Fukushima disaster.

Italian scientists were the first to raise the alarm on 2 October, when they noticed a burst of the radioactive ruthenium-106 in the atmosphere. This was quickly corroborated by other monitoring laboratories across Europe.

Georg Steinhauser at Leibniz University Hannover in Germany says he was “stunned” when he first noticed the event. Routine surveillance detects several radiation leaks each year, mostly of extremely low levels of radionuclides used in medicine. But this event was different.

“The ruthenium-106 was one of a kind. We had never measured anything like this before,” says Steinhauser. –NewScientist

After the radioactivity was detected, the Institute for Radioprotection and Nuclear Security in Paris soon concluded that the most likely source of the leak was the Mayak facility – something Russian officials denied at the time, instead suggesting that the source may have been emissions from a radionuclide satellite battery burning up during re-entry.

The team which tracked down the source of the emission ruled out a satellite because no space organizations reported missing any at the time, and the pattern of radiation in the atmosphere didn’t match that of a satellite’s reentry.

The report claims that despite being so much higher than the Fukushima release, the radiation level in the Mayak incident wasn’t high enough to impact human health.

A nuclear fuel processing facility in Russia looks to have been been the source of the leak

ITAR-TASS News Agency / Alamy Stock PhotoAfter further investigation of 1300 measurements from hundreds of monitoring stations across Europe, Steinhauser and colleagues found that radiation levels were “between 30 and 100 times higher than those measured after Fukushima.”

The leak was unusual because the release was limited to radioactive ruthenium. “If there is a reactor accident, one would expect the release of radioactive isotopes of many different elements,” says Steinhauser. Exactly why such a specific element was released remained a mystery until Steinhauser learned that an Italian nuclear research facility had ordered a consignment of cerium-144 from Mayak before the incident. “There are several indications that the release of ruthenium-106 was linked to this order,” he says. –NewScientist

“This was indeed quite alarming,” said Steinhauser.

- Gun Violence In California

Authored by Jacob Hornberger via The Future of Freedom Foundation,

Upon hearing that a man dressed in a military-style outfit was shooting people with an assault rifle at the Gilroy Garlic Festival in California on Sunday, I imagine that there were at least some Californians saying to themselves, “That’s impossible. It’s illegal in California to take an assault rifle into a public festival.” Indeed, according to Wikipedia, “The gun laws of California are some of the most restrictive in the United States.”

So, what are gun-control advocates in California going to do now? Make their gun laws even more restrictive?

For 20 years, I have been writing that people who are going to kill other people with guns don’t give a hoot about gun laws. After all, at the risk of belaboring the obvious, if a person doesn’t care about obeying a law against murder, he’s not going to care about violating a law against taking an assault rifle into a food festival.

But ordinary, law-abiding people do care about obeying gun laws. That’s because many of these laws make it a felony offense to violate them. That means jail time, big fines, and a serious criminal record. Even when it’s just a misdemeanor offense, oftentimes a conviction can also mean jail time.

For most people, violating the law in order to have a means of self-defense is just not worth the risk. The chances of being caught in a place where some mass murderer is indiscriminately shooting people is relatively low and, therefore, not enough to justify the risk of a felony conviction if caught with, say, a concealed handgun for self-defense.

Thus, as we learn, once again, gun-control laws destroy people’s natural, God-given right of self-defense by disarming them, while, at the same time, do nothing to dissuade a mass murderer from wreaking his deadly mayhem on innocent, disarmed victims.

[ZH: And judging by the avalanche of virtue-signaling demands that “enough is enough” and “gun reform” is needed immediately by any and all politicians able to fog a mirror, that is exactly what we see…]

U.S. Sen Kamala Harris

“Simply horrific. I’m grateful to the first responders who are on the scene in Gilroy, and my thoughts are with that community tonight. Our country has a gun violence epidemic that we cannot tolerate.”

House Speaker Nancy Pelosi

“This brutal killing targeting children and families enjoying a day of community breaks the heart of America. We thank the heroic first responders who provided aid and support to those in need, and we send our prayers to all who are mourning the lives that were cruelly cut short by this shocking attack.

“Enough is enough. Congress has a responsibility to every family torn apart by gun violence to act, and help advance a future that is finally free from this senseless violence. Every day the Senate refuses to act is a stain on the conscience of our nation.

“May it bring some measure of comfort to the friends and loved ones of those whose lives were cut short that all of America mourns with and prays for them during this sad time.”

U.S. Rep. Eric Swalwell, D-Dublin

“My heart breaks for all of our Bay Area neighbors who attended the Gilroy Garlic Festival. We need gun reform and we need it now. Enough is enough.”

Assemblyman Marc Berman, D-Palo Alto

“Instead of sending racist tweets and stoking hate in America, how about Donald Trump put in a real day of work for once and bring legislative leaders together to find real solutions to the gun violence epidemic that’s plaguing our communities? Or is it more thoughts & prayers?”

Assemblywoman Buffy Wicks, D-Oakland

“As news unfolds of another tragic mass shooting — at the Gilroy Garlic Fest— our communities weep, we grapple with both anger and heartbreak, and we hold our children closer. We send love to those whose lives are forever changed — we must match it with political courage to end this epidemic.”

Assemblyman Rob Bonta, D-Alameda

“Unacceptable. Thoughts and prayers are not enough. Bold action on gun safety is required.You’ve (President Donald Trump) failed to adequately address gun violence even as mass shootings have repeatedly occurred on your watch. Unless you will act to make the US safe from gun violence, don’t talk. Action.”

Los Angeles Mayor Eric Garcetti

“Our hearts go out to the victims of the shooting in Gilroy. It is devastating that families cannot enjoy a community festival without fear of gun violence. We have a moral imperative to end this epidemic.”

Assemblyman Phil Ting, D-San Francisco

“No more thoughts and prayers. Time to take more action so we can go to work, school and festivals in peace without fear of getting shot.”

State Sen. Scott Wiener, D-San Francisco

My heart goes out to the people of Gilroy, to the victims of this act of domestic terrorism, and to the families and community that will be impacted forever. Our country must take action — must stop ignoring — the flood of guns plaguing our country. These murders are avoidable.

“We’ve dramatically tightened access in California to guns whose purpose is to kill as many people as possible as quickly as possible. But, we can’t do it alone. Congress must act and take this tidal wave of gun violence seriously. Too many people, too many of our kids, are dying.”

Of course, the deeper question is why this sort of thing continues to happen in the United States.

Here is my personal thesis as to the series of mass killings in America, one that I have set out in previous articles.

Keep in mind that I am not a psychiatrist and, therefore, that this is just a personal theory. But I remain convinced that it is a valid one.

I believe that America’s forever wars, sanctions, embargoes, and assassinations overseas are triggering some sort of mechanism within the minds of people who are bit off kilter mentally, which is causing them to wreak the same sort of violent and deadly mayhem here at home that the U.S. government, specifically the Pentagon and the CIA, is wreaking in the Middle East, Afghanistan, and elsewhere.

For some 30 years, U.S. officials have led the American people into believing that all the death and destructive wreaked on people overseas would have no effect on American society. After all, since the killings happen thousands of miles away from American shores, how could that affect the American people?

For three decades, there have been two separate worlds.

One world is thousands of miles away and entails constantly killing people with sanctions, embargoes, bombs, shootings, invasions, occupations, wars of aggression, occupations, undeclared wars, coups, and alliances with violent dictators. Hundreds of thousands of people killed, maimed, or exiled or have their homes and businesses destroyed by U.S. forces.

The other world is here at home. Americans go to work. They go on vacation. They go to sports events and concerts. They engage in their hobbies. And whenever they see a person in military uniform, they go out of their way to thank him for his service, which purportedly consists of protecting the freedoms here at home by killing people abroad.

But the truth is that the freedom of the American people has never been threatened by any of the hundreds of thousands of people they have killed overseas. At worst, Americans have been threatened by terrorist strikes in retaliation for the death and destruction the U.S. government wreaks overseas.

Through it all, there has been a remarkable lack of concern for the sanctity of human life over there. Who cares, for example, about the hundreds of thousands of Iraqi who have been killed at the hands of U.S. forces, beginning with the Persian Gulf War, continuing through the 11 years of deadly sanctions, followed by the invasion and occupation of Iraq based on those supposed WMDs? The deaths of all those people just don’t matter.

During the many years of the Iraq occupation (labeled “Operation Iraqi Freedom”), church ministers all across the country exhorted their congregations to pray for U.S. troops in Iraq but never for their victims, even though it is undisputed that neither the Iraqi people nor their government ever attacked the United States. Even while constantly reminding people of the sanctity of life when it comes to the unborn, church ministers have forgotten that in the eyes of God, the lives of the born, including the foreign born, is just as sacred as the lives of the unborn.

U.S. sanctions and embargoes target innocent foreign citizens with death, with the aim of achieving a political end, i.e., regime change. And there is never an upward limit on the number of people who can be killed in the process of trying to achieve that political end. Any number of deaths is considered “worth it,” the words used by U.S. Ambassador to UN Madeleine Albright to justify the deaths of half-a –million Iraqi children from U.S. sanctions.

What does all this have to do with the California shooting and, for that matter, other instances of mass violence in America?

I believe that when a nation’s government has been killing people continuously for three decades, all that death and destruction is inevitably going to seep into the subconscious of individual citizens, even though it’s happening thousands of miles away and even though the government tries to keep us immune from it. Most of us can handle it but my thesis is that there are some people who are a bit off-kilter mentally who cannot handle it. I believe that the massive death and destruction ultimately triggers something within them that causes them to mirror here in the United States what the U.S. government is doing overseas. In their off-kilter minds, they are unable to do what U.S. officials do — place a high value on the sanctity of American life and no value on foreign life. For the off-kilter people, all life is equally valueless. The fact that some of these mass killers are military veterans and may even have participated in the oversea death, destruction, and mayhem makes the psychological situation even more problematic.

There is an easy way to test my thesis: bring the forever wars to an immediate end and bring all U.S. soldiers home immediately. Even if my thesis isn’t correct, it’s the morally right thing to do anyway.

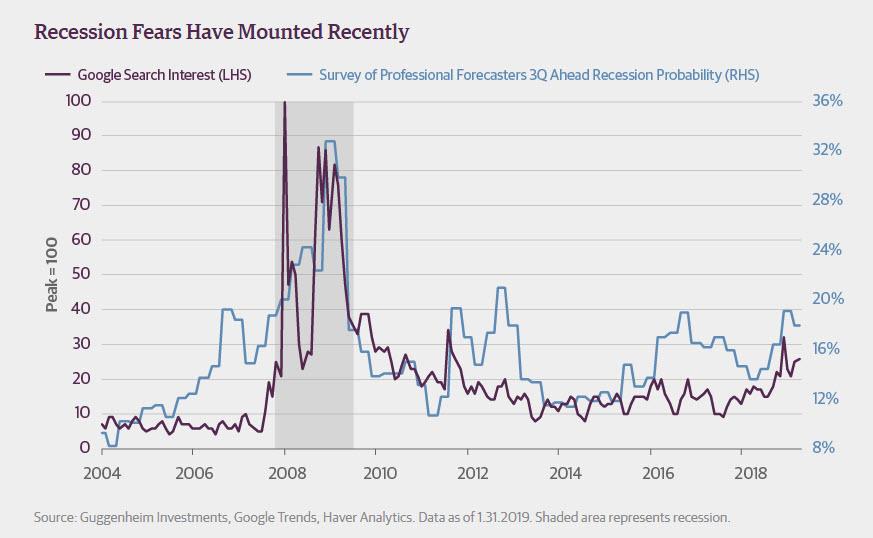

- Guggenheim Expects Stocks to Crash 50% In The Next Recession

One could get whiplash listening to Guggenheim’s Scott Minerd’s rapidly changing opinions these days.

Back on May 29, the weightlifting CIO of the $265 billion asset manager, made a gloomy forecast on CNBC, predicting that the stock market sell-off is likely far from over, and said stocks would go “somewhere below the lows in December.” Near term, he saw an “immediate move” down to around 2,730 on the before it drops further. Oh, and he also said the next move by the Fed will be a rate hike.

Oops.

Not even two months later, everything miraculously changed, and on July 15, again on CNBC, Minerd changed his tune by 180 degrees, and no longer seeing any crash, said that he now thinks the S&P 500 could rise 15% and approach 3,500 before the end of year, comparing the current market environment to a 1998 rally amid interest rate cuts.

“This rally — whether you’re looking at bonds, you’re looking at stocks, high yield, pick whatever you want — is all being driven by liquidity. And the central banks around the world have basically signaled that they are going to step on the accelerator,” Minerd said adding that the Fed has “kind of hit the panic button” and that “you’re going to see the money flow out of the central banks into bonds, which will free up capital and that will naturally find another place to migrate to and ultimately it will end up in the hands of stocks.”

And so, Minerd now had all bases covered, with a soundbite to say he was right if stocks crashed, and another if they melted up by another 500 points. Actually, there was one base that needed covering: the same one that Trump has been pounding every single day, namely that if it all goes pear-shaped, it will be the Fed’s fault (he is actually right about that), and today, Minerd – undaunted by his recent dismal track record in making public predictions – slammed the Fed saying that the Fed should hike interest rates, not cut them.

The consequences of the Fed’s actions in the next week – the U.S. central bank is expected to cut interest rates by a quarter of a percentage point – could be with us for much longer than we think, culminating in the next recession and increasing the risk to financial stability.

In the meantime, the Fed could be delivering yet another sugar high to the economy that doesn’t address underlying structural problems created by powerful demographic forces that are constraining output and depressing prices.

Like we said, this time Minerd was correct, though we wonder: why does it take all these sophisticated financial professionals a decade to realize (or admit) what we have been saying since 2009. Must have something to do with vested year-end bonus options…

In any case, just in case everyone wasn’t completely confused yet, today’s Minerd released yet another research report in which he tried to predict not only when the next recession would hit (“we maintain our view that the recession could begin as early as the first half of 2020, but will be watching for signs that the dovish pivot by the Federal Reserve (Fed) could extend the cycle”), but also how severe it will be.

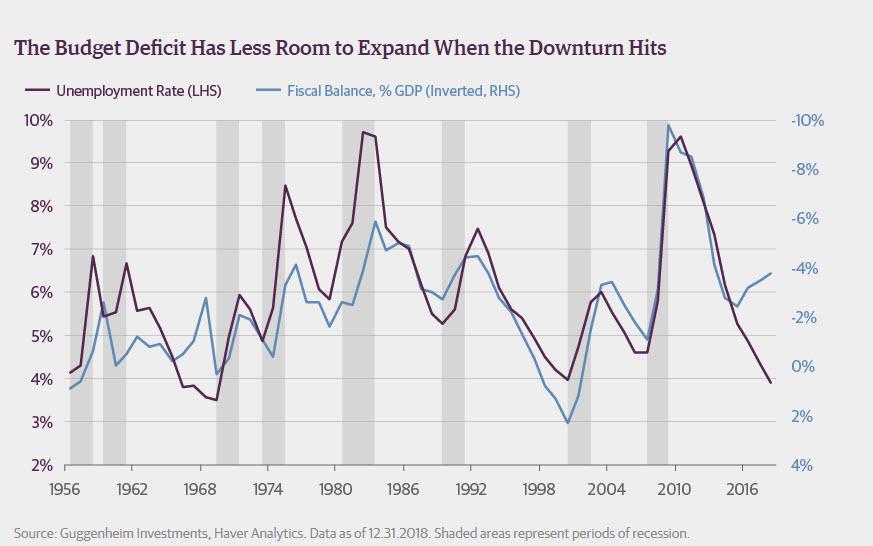

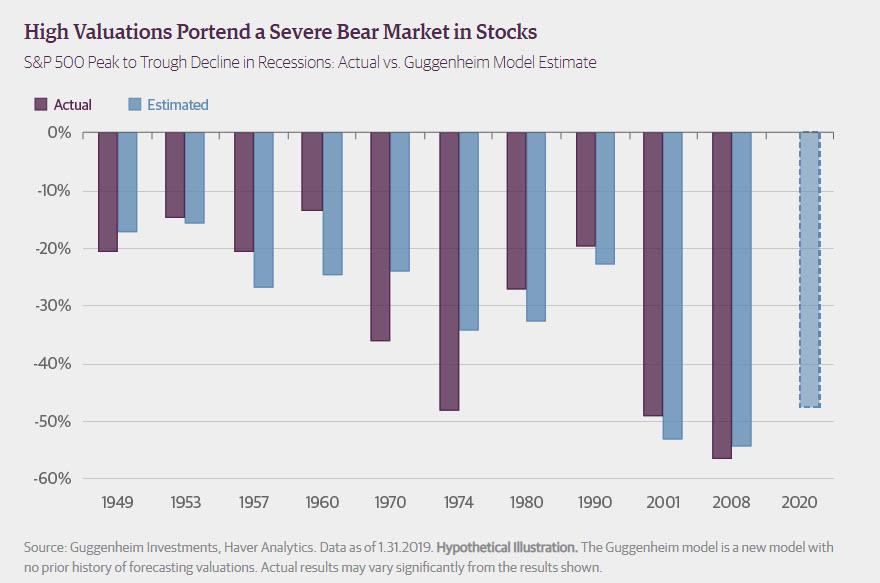

It is here that things get ugly, because as Guggenheim notes, credit markets “are likely to be hit harder than usual in the recession. This stems from the record high ratio of corporate debt to GDP and the likelihood of a massive fallen angel wave.” With that in mind, the bank notes that “when recessions hit, the magnitude of the associated bear market in stocks is driven by how high valuations were in the preceding bull market.” And given that valuations reached quite elevated levels in this cycle, Guggenheim expects “a severe bear market of 40–50 percent in the next recession.”

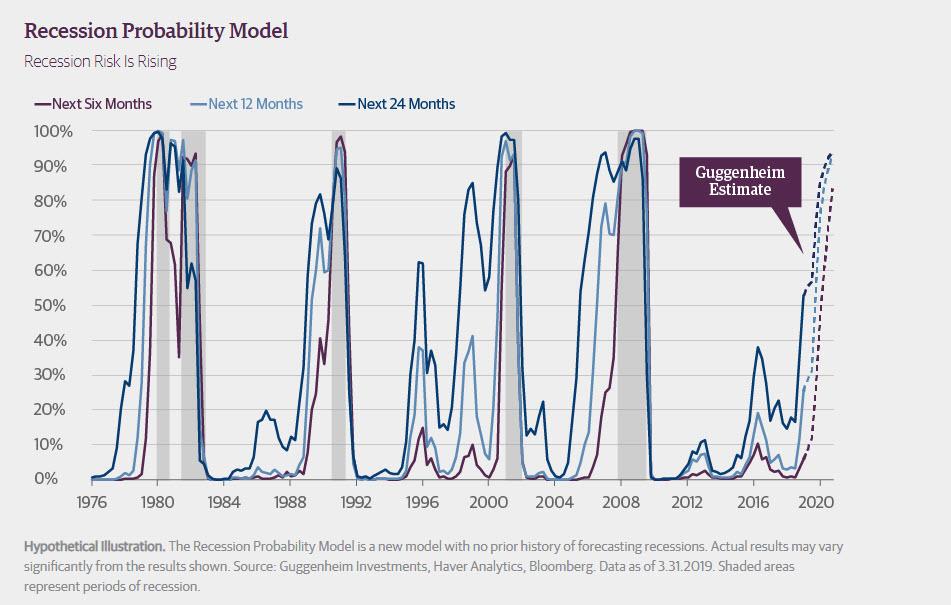

Here are some additional details, starting with Guggenheim’s framework for when the next recession will hit: here, the bank notes that its Recession Probability Model rose across all horizons in the first quarter of 2019, and while near-term the recession probability remains subdued, over the next 24 months recession probability more than doubled compared to the third quarter reading. The deterioration in leading indicators, further flattening of the yield curve, and tightening of monetary policy all contributed to rising recession risks through the first quarter. And since Guggenheim expects these trends to continue and growth to weaken in 2019, it expects recession risk to rise throughout the year.

The bank’s Recession Dashboard also continues to point to a recession starting by mid-2020. Recession probability estimates rose across all horizons in the fourth quarter of 2018, most notably in the 24 month time frame.

The pace of decline in the unemployment rate is beginning to slow, with the unemployment rate holding steady, on net, over the last nine months. Past Fed rate increases and balance sheet runoff mean that monetary policy may already be tight enough to induce a recession. Additionally, yield curve flattening is now back in line with the average of prior cycles, with the three-month to 10-year Treasury yield curve having inverted recently (see our previous report, The Yield Curve Doesn’t Lie, for our analysis showing that the yield curve may not be unduly flat due to quantitative easing, but rather unduly steep due to outsized Treasury issuance). The strength of the Leading Economic Index has faded, putting it in line with the range of prior cycles. Hours worked and real retail sales have also cooled, and “these trends will continue this year as fading fiscal stimulus, tighter financial conditions, and rising policy uncertainty increasingly weigh on economic activity.”

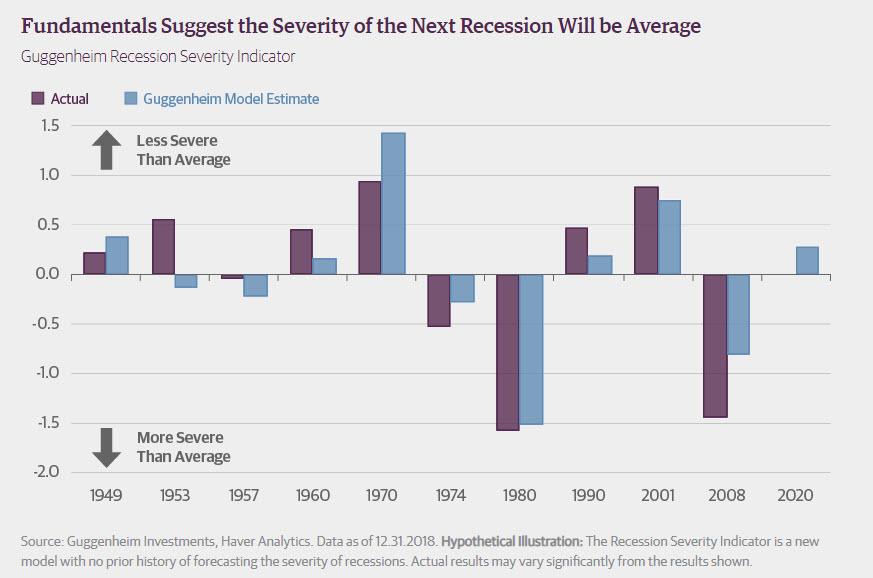

So with a recession coming as soon as under a year from now, there is some good news. First, Guggenheim notes that its work shows that the next recession will not be as severe as the last one, “but it could be more prolonged than usual because policymakers at home and abroad have limited tools to fight the downturn.”

Recession severity can be defined a number of ways: either by focusing on the i) magnitude of the contraction (the peak to trough decline in real gross domestic product (GDP)), ii) the size of the output gap (the difference between real GDP and potential output), iii) the peak unemployment rate relative to the natural rate, or iv) the length of time the recession lasts. Combining these four indicators to create a recession severity indicator that shows unsurprising results: the 2007–2009 recession was one of the worst of the post-war period, exceeded only by the “double dip” recession of 1980–1981. In contrast, the 2001 recession was mild by comparison.

Several factors play a role in determining the severity of a recession. From a sectoral basis, an overheated housing market has a strong relationship with severe recessions, reflecting the fact that housing is the largest asset for most households and is closely tied to the banking system. A related factor is stress on the banking system, which also makes recessions worse. Beyond housing, overinvestment (as measured by the private capital stock relative to GDP) contributes to more severe downturns. Other factors that can make recessions worse are monetary policy tightness (and degree of subsequent easing) and weaker global growth. Perhaps surprisingly, Guggenheim found that neither the length nor the magnitude of an expansion seem to have a relationship with the severity of the subsequent contraction. Also contrary to conventional wisdom, there is not a straightforward relationship between debt levels and recession severity, whether debt is measured by sector or from a total economy perspective. This is likely due to debt cycles lasting longer than business cycles, as the negative effects of debt accumulation can sometimes be put off in a downturn as borrowers simply take on even more debt.

Guggenheim’s analysis of these factors indicates that “the next recession should be about average. On the positive side, the housing market is not currently overheated, the banking system is sound, and the capital stock is only somewhat elevated.” In addition, Fed policymakers will likely act more quickly in response to signs of a slowdown than in the prior cycles, as evidenced by the recent Fed reaction to weaker economic data.

That’s the good news.

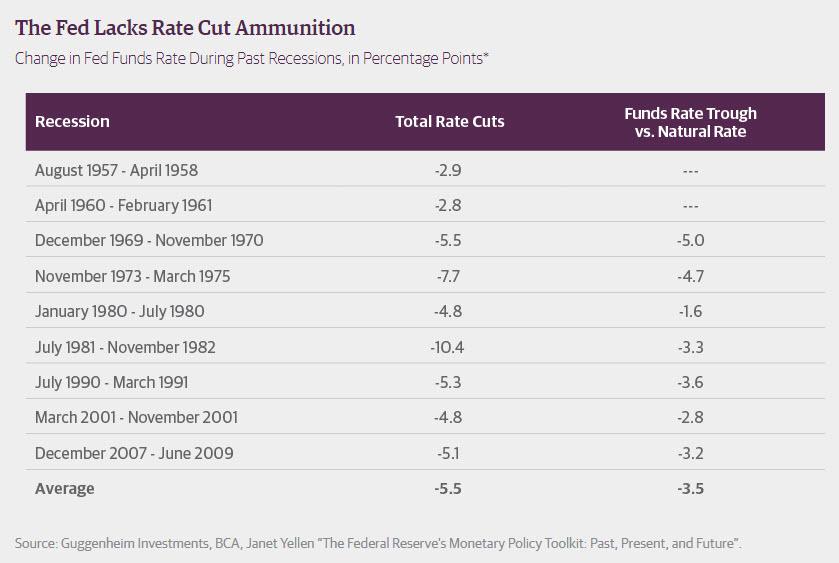

On the negative side, Guggenheim is worried about the limited scope for policy response once the recession hits. From a monetary policy perspective, Fed policymakers will be unable to ease to the same degree that they have in previous recessions, as cumulative rate cuts have averaged 5.5 percentage points in past downturns. Even with another hike or two in this cycle, per the Fed’s March 2019 Summary of Economic Projections, the Fed would have less than 3 percentage points of rate cuts available to combat the next recession.

With limited room to cut rates, it is therefore likely the Fed will again turn to unconventional policy tools, namely forward rate guidance and quantitative easing (QE). While another round of QE will undoubtedly provide some incremental stimulus, the efficacy of QE remains in question, according to Guggenheim. Furthermore, QE could also again come under fire from politicians looking to blame the Fed for economic woes, which could limit the size or duration of future QE programs. Moreover, the bank expects problems to center on corporate credit markets in the next downturn, but unlike some other central banks, the Fed lacks statutory authority to buy corporate debt or loans, at least for now. Policymakers are not likely to seek—nor would we expect Congress to pass—changes to the Federal Reserve Act that would permit the Fed to buy corporates. With these limitations in mind, the Fed is embarking on a review of its policy framework in 2019. This review will explore, among other things, the possibility of adding additional tools to the toolkit. These could include a version of Japan’s yield curve control policy and/or negative short-term rates, though both face hurdles to being deployed in the United States.

At the same time, since the monetary policy’s ability to stimulate the economy is limited, Guggenheim is also worried that fiscal policy will be constrained. Typically, the fiscal balance is countercyclical, meaning that when economic times are good we have small deficits or even surpluses that allow us to run large deficits when recessions occur, in part due to automatic stabilizers, and in part due to discretionary stimulus. However, over the past few years this relationship has reversed, with deficits widening even as the economy has strengthened due to discretionary spending increases and tax cuts.

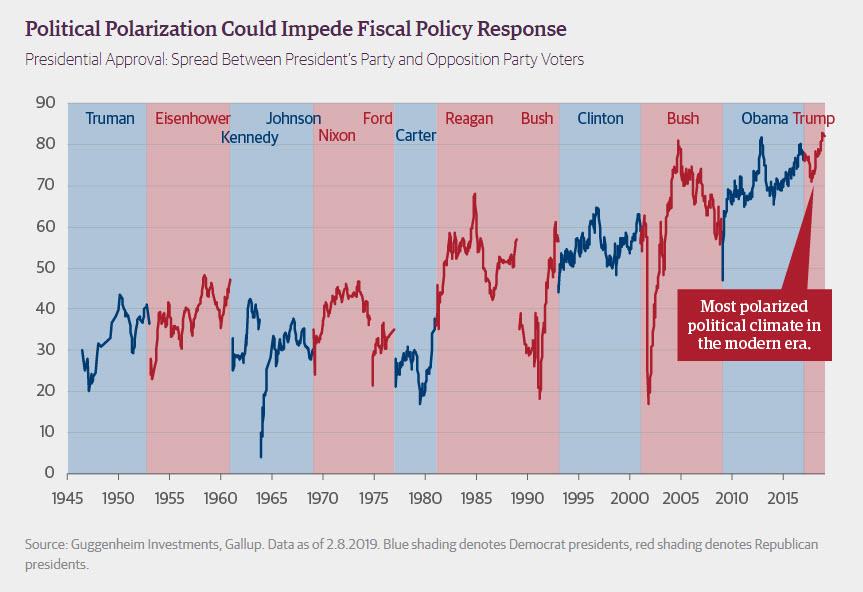

It gets worse: when the next recession finally hits, the starting point for the federal deficit will likely be much worse than it typically is at the end of an expansion, raising the prospect that fiscal hawks will resurface to raise concerns about deficits and debt. Furthermore, the expected recession interval comes at a particularly challenging time in the political calendar given the presidential election in November 2020. If growth continues to slow, will the Democrat-controlled House really want to pass a spending bill that would stimulate the economy right before the election? Guggenheim see significant obstacles to the bipartisan enactment of proactive fiscal policy measures, which is informed by our analysis of polling data that reveals a historically high degree of political polarization.

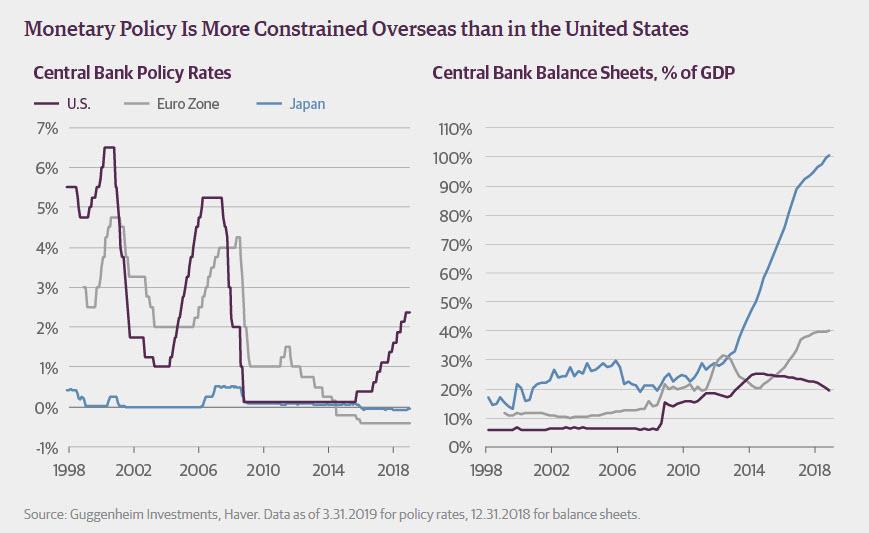

But if the US is bad, the rest of the world is far worse as policy space is even more limited overseas. As constrained as Fed policy is likely to be, the problem is much worse for the European Central Bank (ECB) and Bank of Japan (BOJ), where the starting point for inflation is lower, policy rates are still negative, and central bank balance sheets hold a much larger share of eligible assets. Given the Japanese yen’s status as a global safe-haven asset, the BOJ faces an especially difficult challenge in fending off what will likely be a deflationary exchange rate appreciation, with fiscal policy unlikely to offer much support.

Nor is fiscal policy the answer in northern Europe, where austerian ideas still hold sway. In southern Europe, fiscal tools are limited as political pressure from the north and sovereign spread widening will likely force pro-cyclical belt-tightening measures. Meanwhile, the ECB will have limited ability to cushion the downturn. If politicians in Spain, Portugal, Greece and especially Italy are not able to deliver the fiscal tightening that markets will demand, then concerns about the viability of the eurozone are likely to resurface. Advanced economies are therefore likely to be mired in a protracted downturn, spilling back into the U.S. economy by way of weak export demand, tighter financial conditions and potential concerns about exposures to weaker foreign banks.

But most importantly, during the last recession a major source of global stimulus was China’s massive credit easing and infrastructure spending, without which the global recession would have been even more severe. China has, until recently, actively been working to deleverage its economy, where debt growth over the past 10 years has been on par with some of the biggest debt bubbles in history. When the global economy slows, Chinese policymakers are unlikely to deliver nearly as much stimulus as last time around, even if China manages to avoid a debt crisis or “hard landing” scenario. Other emerging markets (EM) are also unlikely to deliver the needed global stimulus, as balance of payments pressures in many EM countries will limit domestic policy space and force them to intervene in foreign exchange markets to avoid disorderly currency depreciations. This would reduce their net demand for U.S. Treasury and Agency securities, which could further complicate the Fed’s ability to deliver an appropriate degree of monetary stimulus.

Taking these factors together, Guggenheim anticipates a scenario where the magnitude of the decline in the U.S. economy is not especially severe when the recession hits, given the lack of major imbalances and relative soundness of the banking system. However, this downturn is likely to be more prolonged than usual, given the limited ability of policy to respond and the potential spillback from economic weakness abroad. The result could be a cycle that is more “U-shaped” than “V-shaped”.

Yes but…

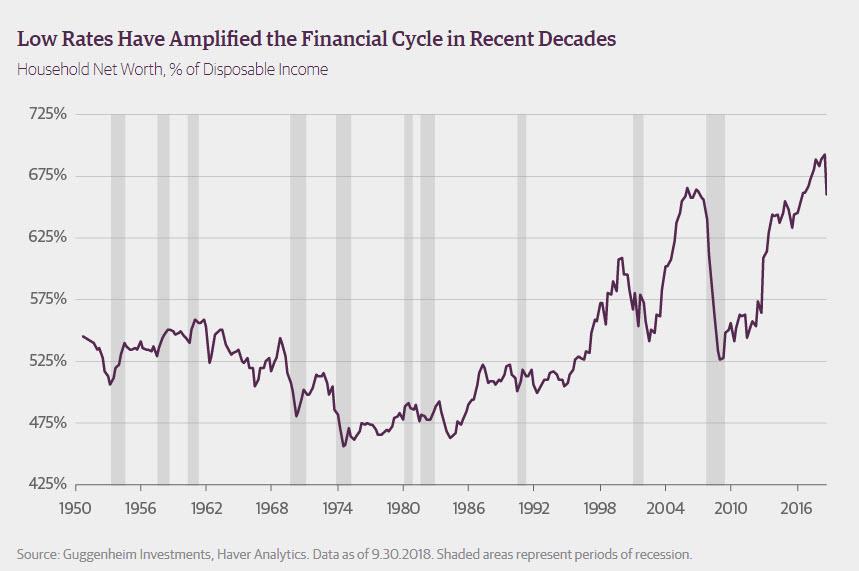

Prepare for a Steep Decline in Risk Assets: On the surface, this scenario may not seem particularly dire for investors, but Minerd would caution that market behavior is only loosely correlated with economic conditions, and a moderate recession does not mean moderate market movements. On the contrary, as he cautions “years of low interest rates have served to amplify the financial cycle over the past few decades, and this amplification has been further heightened in the current cycle by asset purchases by global central banks.”

Worse, as Minerd’s work shows, when recessions hit, the severity of the downturn has a relatively minor impact on the magnitude of the associated bear market in stocks. A far more important factor is how high valuations were in the preceding bull market. A good example is the 2001 recession, which was relatively modest economically, but saw one of the worst bear markets on record given the sky-high valuations of the tech bubble.

So given that valuations reached elevated levels in this cycle, Guggenheim’s CIO now expects a severe equity bear market of 40–50 percent in the next recession, consistent with the bank’s previous analysis that pointed to low expected returns over the next 10 years.

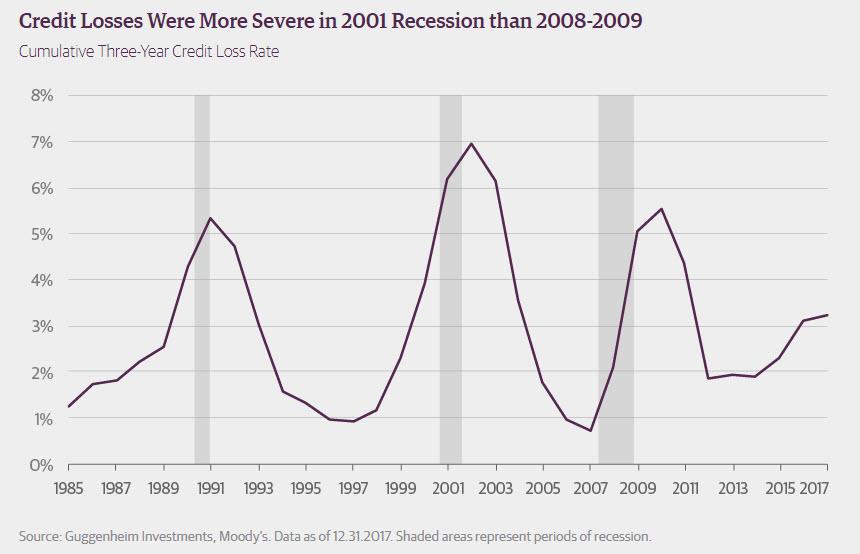

Credit markets are also likely to be hit harder than usual in the recession due to the record high ratio of corporate debt to GDP and the upcoming massive fallen angel wave that could cause forced selling in an environment where liquidity will already be poor. The 2001 recession offers a relevant case study, as cumulative corporate defaults and realized credit losses were greater than in 2008, which saw a much more severe recession and a higher peak in the annual default rate.

Finally, from a purely asset allocation standpoint, given this historical lesson and the fact that the exits tend to shrink when investors need them most, Guggenheim has been steadily upgrading portfolio credit quality and reducing spread duration in the lead up to the next recession. As Guggenheim concludes last quarter, the Fed’s dovish pivot has supported risk assets, which afforded investors a window of opportunity to further recession-proof client portfolios.

And the punchline: as Minder concludes, he will be looking to add rate duration this year given his firm’s view that policy rates will return to the zero lower bound during the upcoming recession. In other words, ZIRP is coming back, and NIRP may follow shortly after.

Digest powered by RSS Digest

Saving...

Saving...![<!–[if IE 9]><![endif]–>](https://www.zerohedge.com/s3/files/inline-images/china%20pigs%203.jpg?itok=G-5wzKEf){kind=link}

![<!–[if IE 9]><![endif]–>](https://www.zerohedge.com/s3/files/inline-images/duck%20farmers.jpg?itok=EhtlH7Tb){kind=link}

![<!–[if IE 9]><![endif]–>](https://www.zerohedge.com/s3/files/inline-images/fuel%20proc.jpg?itok=dPQTejny){kind=link}