- 19 Senior Experts Of China’s Top Academic Bodies Died In December

19 Senior Experts Of China’s Top Academic Bodies Died In December

Authored by Anne Zhang and Lynn Xu via The Epoch Times (emphasis ours),

In December, 19 experts of China’s top academies, the Chinese Academy of Sciences (CAS) and the Chinese Academy of Engineering (CAE), died of unspecified “illness,” a statistic that is six times higher than the average number of deaths in the past years.

The P4 laboratory at the Wuhan Institute of Virology in Wuhan in China’s central Hubei Province on April 17, 2020. The P4 epidemiological laboratory was built in co-operation with French bio-industrial firm Institut Merieux and the Chinese Academy of Sciences. (Hector Retamal/AFP via Getty Images) Official reports avoid mentioning the cause of these deaths, in what appears to be an attempt to cover up deaths caused by COVID-19.

But Airfinity, a UK-based Health Data Agency, updated data on Dec. 30, saying that roughly 11,000 people in China are dying every day from COVID, bringing the total number of deaths from the disease to 110,000 in December.

According to obituaries published by China’s official media, in the 12 days from Dec.15 to Dec.26, 13 members of CAE passed away due to “illness.” They are fiber optic communication expert Zhao Zisen (91), environmental engineering and environmental water quality expert Tang Hongxiao (91), rare earth metal smelting and separation expert Zhang Guocheng (91), laser technology expert Zhao Yijun (92), inorganic non-metallic materials expert Gu Zhenan (86), civil engineering and structural mechanics expert Long Yuqiu (96), ecologists and foresters Li Wenhua (90), wildlife scientist Ma Jianzhang (86), pediatric surgery specialist Zhang Jinzhe (102), thermal impeller machinery expert Wang Zhongqi (90), architect and professor at Tsinghua University Guan Zhaoye (93), welding specialist for aerospace manufacturing engineering Guan Qiao (87), and petroleum engineering expert Li Qingzhong (92).

A total of six CAS members passed away on Dec. 6, 23, and 25, including Lu Qiang (86), a Chinese expert in automatic control and dynamics of electrical systems and professor at Tsinghua University; Zhang Youshang (97), a Chinese biochemist and molecular biologist; Jiang Hualiang (57), a former director of the Shanghai Institute of Pharmaceutical Sciences; Wu Chengkang (93), a high-temperature gas dynamist; Tong Tanjun (88), a medical scientist; and Huang Kezhi (95), a physicist and a professor at Tsinghua University.

Most of the deceased were CCP members, and some were from the minority parties, such as the Democratic League and the Jiu San Society, which were recognized as existing because they explicitly supported the CCP and recognized its leadership.

Zhang Yaping, Vice Prersident of the Chinese Academy of Sciences speaks at an event announcing details of international access to lunar samples collected by China’s Chang’e-5 moon probe, in Beijing on January 18, 2021. (Greg Baker/AFP via Getty Images) Political Factors Introduced to the Selection of Academicians

In 2022, at least 53 members of the CAS and CAE passed away according to incomplete statistics.

CAS and CAE, known as the Two Academies, accumulate scientists and experts that can serve the Chinese Communist Party (CCP) and enjoy the privilege of lifetime membership. The selection system for academics inevitably reflects political factors.

Xie Yong, deputy editor-in-chief of Huanghe magazine in north China’s Shanxi Province, published an article in Modern China Study, an international journal, in 2022 discussing the differences between academician systems under CCP rule and under the Republic of China.

In 1948, before the CCP took power, the Republic of China’s way to select members of the Academia Sinica, the current national academy, was based on the sole principle of academic achievement.

Academicians were nominated by major universities, research institutions, professional societies, and respected celebrities of the academic community. Hence, the candidates were all first-class scholars at that time. Even Guo Moruo and Ma Yinchu, who were both pro-Communist in their political stance, were also elected as academicians, Xie said.

In contrast, CAS selecting methods in 1955, by then controlled by the CCP, included political considerations to the selection criteria. For academicians of Social Sciences, candidates were required to uphold socialism and the Communist Party.

At that time, all former members of the Academia Sinica who had not left the mainland in 1949, the year the CCP seized power, basically became members of CAS.

However, Hu Xianfu, a famous biologist at that time, was taken off the list because the CCP authorities thought that his academic views were anti-Soviet.

Hu then suffered physically and mentally during the Cultural Revolution, and finally passed away in 1968 at the age of 75 in a 10-square-meter (about 108 square feet) room.

During the Cultural Revolution, many academicians were branded as reactionary academic authorities and were severely criticized and even persecuted to death.

Other scholars and experts have not escaped various political campaigns and purges by the CCP. After the anti-rightist movement and the Great Leap Forward, 11 academicians were ranked as rightists and stripped of their titles as academic members.

Tyler Durden

Mon, 01/02/2023 – 23:00 - Proper Hydration "Might Slow Down Aging Process In Humans," Study Reveals

Proper Hydration “Might Slow Down Aging Process In Humans,” Study Reveals

A peer-reviewed study published by National Institutes of Health (NIH) researchers in the eBioMedicine journal on Monday reveals that adequately hydrated individuals could live longer and develop fewer age-related chronic diseases.

“The results suggest that proper hydration may slow down aging and prolong a disease-free life,” Natalia Dmitrieva, Ph.D., the study’s lead author and researcher in the Laboratory of Cardiovascular Regenerative Medicine at the National Heart, Lung, and Blood Institute (NHLBI), part of NIH, said in a statement.

Dmitrieva and her team used health data spanning three decades of 11,255 adults and analyzed their serum sodium levels which fluctuate with fluid intake. Consuming more fluid will lower serum sodium levels. They found that adults with higher sodium levels were more prone to develop chronic illnesses and show signs of advanced biological aging than those with lower sodium levels. Adults with higher sodium levels were more susceptible to death at a younger age.

Serum sodium levels above 142 mEq/L increased the risk of chronic diseases like heart failure, stroke, atrial fibrillation, peripheral artery disease, chronic lung disease, diabetes, and dementia by up to 64%. But adults with serum sodium levels between 138-140 mEq/L had a much lower risk of such fatal diseases.

“People whose serum sodium is 142 mEq/L or higher would benefit from evaluation of their fluid intake,” Dmitrieva said. She added that most people could increase their fluid intake to reduce sodium levels.

According to the National Academy of Medicine, men should ingest 125 ounces of water daily, and women consume 91 ounces.

Dmitrieva said her findings don’t prove a causal effect, and randomized, controlled clinical trials are needed to understand if proper hydration can promote healthy aging, prevent diseases, and lead to a longer life.

Tyler Durden

Mon, 01/02/2023 – 22:25 - "Should Not Live In Fear" – Chief Justice Roberts Year-End Message Focuses On Judges' Security

“Should Not Live In Fear” – Chief Justice Roberts Year-End Message Focuses On Judges’ Security

Authored by Matthew Vadum via The Epoch Times (emphasis ours),

After a difficult 2022 at the Supreme Court, Chief Justice John Roberts said in an annual report that the personal security of judges needs to be a priority.

“The law requires every judge to swear an oath to perform his or her work without fear or favor, but we must support judges by ensuring their safety,” Roberts wrote (pdf) in the “2022 Year-End Report on the Federal Judiciary,” which was made public late Dec. 31.

“A judicial system cannot and should not live in fear,” he added.

Chief Justice John Roberts at the Supreme Court Building in Washington on Nov. 30, 2018. (J. Scott Applewhite/AP Photo) In the report, Roberts paid tribute to federal Judge Ronald N. Davies, who in 1957 ruled in favor of black students in Little Rock, Arkansas, who had been barred from attending a local high school despite the Supreme Court’s landmark ruling in 1954 striking down school desegregation on constitutional grounds.

Arkansas Gov. Orval Faubus, a Democrat, ordered the state’s National Guard to block the students but “when it came time to rule in the school desegregation litigation, Davies did not flinch,” Roberts wrote.

Angry crowds resisted the desegregation effort and Republican President Dwight D. Eisenhower directed the 101st Airborne to make sure the black students could attend the school.

In his role as Chief Justice of the United States, Roberts, appointed in 2005 by President George W. Bush, both presides over the Supreme Court and oversees the federal judiciary.

The report does not reference the unprecedented leak in May 2022 of Justice Samuel Alito’s draft majority opinion in Dobbs v. Jackson Women’s Health Organization, which overturned Roe v. Wade, the 1973 precedent that legalized abortion nationwide.

The Supreme Court is said to be investigating the leak, but the identity of the leaker or leakers is still unknown. Various justices have said publicly and repeatedly in recent months that the public would be updated on the progress of the investigation but no updates have been issued.

The report also does not reference the raucous protests at the homes of the conservative justices in Maryland and Virginia, nor the attacks on justices such as Brett Kavanaugh who was the target of a foiled assassination attempt and of flash-mob harassment in public outings by left-wing activists.

Roberts defended the right of Americans to disagree with court rulings.

“Judicial opinions speak for themselves, and there is no obligation in our free country to agree with them. Indeed, we judges frequently dissent—sometimes strongly—from our colleagues’ opinions, and we explain why in public writings about the cases before us.”

Roberts said recent security legislation was a step in the right direction.

Roberts acknowledged that last month Congress passed the Daniel Anderl Judicial Security and Privacy Act to help protect judges and their families. The measure was named after the son of federal Judge Esther Salas of New Jersey, who was killed by an assailant when he answered the door to his mother’s home.

Roberts did not mention that on June 16, 2022, President Joe Biden signed the Supreme Court Police Parity Act into law. The measure gives Supreme Court officials greater authority to protect the court, members of the justices’ immediate families, and other court employees.

The report also states that caseloads for the federal judiciary, including the Supreme Court, fell over the past year.

In the 12-month period ending Sept. 30, 2022, the number of cases docketed by the Supreme Court dropped by 8 percent compared to the previous 12-month period. Similar declines were seen in federal courts of appeals, district courts, and bankruptcy courts.

The Epoch Times reached out to the U.S. Department of Justice for comment but did not receive an immediate reply.

Tyler Durden

Mon, 01/02/2023 – 21:50 - Trump Suggests He May Run On Third-Party Ticket In 2024

Trump Suggests He May Run On Third-Party Ticket In 2024

Former President Trump has last week hinted that he’ll hand-grenade the 2024 presidential election for Republicans by running as a third-party candidate.

Trump shared an American Greatness article by Dan Gelernter which suggests that establishment Republicans would do everything in their power to prevent Trump from winning again, and that voters like Gelernter would rather vote for Trump on a third-party ticket even if it means losing the election.

“They’d rather lose an election to the Democrats, their brothers in crime, than win with Trump,” Gelernter wrote of establishment GOP.

…despite the obvious differences, we’re heading for a 1912-repeat, in which the Republican Party ignores its own voters. The Republican machine has no intention of letting us choose Trump again: He is not a uniparty team player. They’d rather lose an election to the Democrats, their brothers in crime, than win with Trump.

That leads us to the inevitable question: What should we do when a majority of Republicans want Trump, but the Republican Party says we can’t have him? Do we knuckle under and vote for Ron DeSantis because he would be vastly better than any Democrat?

I say no, we don’t knuckle under. And I like DeSantis. I’d vote for him after Trump’s second term. But not before. –American Greatness

“Do I think Trump can win as a third-party candidate? No,” Gelernter added. “Would I vote for him as a third-party candidate? Yes, because I’m not interested in propping up this corrupt gravy-train any longer.”

In 2021, Trump told RNC Chairwoman Rona McDaniel that he was “done” with the party after receiving virtually no support over his claims that Democrats cheated in the 2020 election.

“You cannot do that. If you do, we will lose forever,” McDaniel reportedly told Trump regarding a 3rd party run, according to a book by ABC News reporter Jonathan Karl. “Exactly – you will lose forever without me. I don’t care. This is what Republicans deserve for not sticking up for me,” Trump allegedly shot back.

That said, DeSantis has been shooting up in the polls – and even received his own hit piece in Vanity Fair on Monday.

New Hitler just dropped. https://t.co/byESQjVJp0

— Stephen L. Miller (@redsteeze) January 2, 2023

Tyler Durden

Mon, 01/02/2023 – 21:15 - Congress Should Investigate 'Gain-Of-Function' Research

Congress Should Investigate ‘Gain-Of-Function’ Research

Authored by Bill King via RealClear Wire,

I fear that the investigations Republicans have promised in the House next year will be little more than another round of toxic partisan gamesmanship. But there is one investigation Congress should undertake, and that is into so-called “gain-of-function” research.

Before the pandemic, I suspect that most of you, like me, had never heard of gain-of-function research. What we learned during the pandemic is that scientists around the world routinely tinker with the genome of viruses to see how the induced changes will affect replication of the virus (contagiousness) and the effects it has on its host (lethality). Such research has apparently been going on for decades and is routinely funded by governments, including ours.

Within weeks of the COVID-19 virus emerging in China near the Wuhan Institute of Virology (WIV), many began to question whether the virus had been created by gain-of-function research and somehow escaped from WIV’s labs. Recently analyzed Chinese documents from early in the pandemic seem to suggest the virus might have come from WIV. To many, the proposition that the novel coronavirus just happened to naturally occur a few hundred yards from the WIV facility seemed too much of a coincidence.

But in February 2020, barely three months after the virus’s genome had been sequenced, 27 scientists signed a statement in the medical journal The Lancet, unequivocally declaring that the virus had occurred naturally and that any suggestion to the contrary was quackery and a conspiracy theory. Their statement quickly became the accepted orthodoxy for much of the world’s scientific community and virtually all the mainstream media.

However, as time wore on, circumstances regarding the origin of that statement came under scrutiny. In a 2021 Vanity Fair article, investigative journalist Katherine Eban revealed that the statement was organized by a scientist named Peter Daszak. That statement concluded with a declaration from the scientists who signed it that “we have no competing interests.” However, Eban reported in a follow-up article that Daszak was the director of EcoHealth Alliance, which in 2014 had received a $3.7 million grant from the NIH for gain-of-function research and made a sub-grant for $600,000 – to the WIV.

I wrote to the email address reserved for the statement in the Lancet post, posing a number of questions about the circumstances around the creation of the letter and the “competing interests” statement. I also reached out to two of the scientists who signed the letter asking for an interview regarding the statement. I received no responses.

Questions about gain-of-function research predate COVID. In fact, there has been a robust debate over the potential risks and benefits that dates to, at least, 2011. In 2014, a group of 300 prominent scientists, led by Harvard’s highly regarded epidemiologist Marc Lipsitch, signed a statement raising alarms about risks associated with gain-of-function research.

The academic controversy caused the Obama administration to issue a moratorium on gain-of-function research, but it included a general exception for studies “urgently necessary to protect the public health or national security.” According to Eban’s reporting, the exception quickly became a glaring loophole that essentially rendered the rule useless: the controversial research mostly continued unabated.

The Trump administration scrapped the moratorium in favor of a complex review process. But that process was mostly conducted outside of the public’s view or even significant peer review, leaving many of the critics, including Lipsitch, still wary.

The debate over the origins of COVID still rages today and unfortunately has become politicized, with Democrats and Republicans generally lining up behind the natural and lab-leak theories, respectively. In August 2021, the National Intelligence Council issued an unclassified report in response to an order from President Biden to review the origin of the virus. The report stated that the intelligence community had not been able to reach a conclusion and that the origin would likely never be known without more cooperation from the Chinese government. Of course, the more time that passes the less likely it is that the mystery will ever be solved.

While we would all like to know how the pandemic started, the mere fact that it might have originated from gain-of-function research gone awry makes it imperative to conduct a detailed investigation of the risks and potential benefits of this kind of research. Of all the things we regulate, surely tinkering with viruses to make them more contagious and more lethal should be right at the top of the list. Congress needs to pass laws closely regulating what Rutgers professor Richard Ebright described to Katherine Eban as “looking for a gas leak with a lighted match” and not leave this up to executive orders.

Congress should also investigate what appears to have been a coordinated attempt to squelch any inquiry into the legitimate questions over COVID’s origins in the early days of the pandemic. For example, the signers of the Lancet statement should be subpoenaed and questioned about what was almost certainly a false certification of “no competing interests” by at least one of the signers. (The criticism regarding potential conflicts of interest is not just coming from the right: The uber-progressive Columbia professor Jeffrey Sachs disbanded a group he had established to study the origins of COVID, citing conflicts of interest. Interestingly, Daszak was part of the group Sachs disbanded.)

I don’t know whether House Republicans can conduct such hearings without turning them into a carnival sideshow. But hopefully they will rise above partisan instincts and deliver much-needed answers for the American people.

Bill King is a businessman and lawyer, and is a former opinion columnist and editorial board member at the Houston Chronicle. He has served in a number of appointed and elected positions, including mayor of his hometown. He writes on a wide range of public policy and political issues. Bill is the author of “Unapologetically Moderate” and currently serves as the co-chair of the Forward Party of Texas.

Tyler Durden

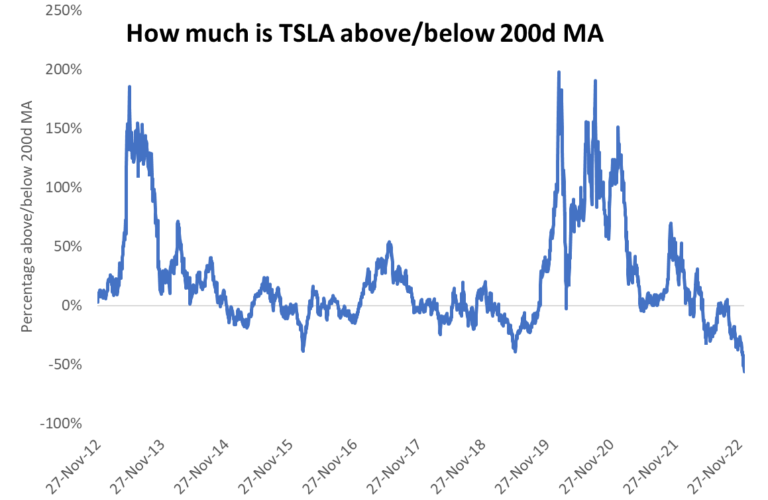

Mon, 01/02/2023 – 20:40 - Tesla Kicks Off 2023 By Continuing 10,000 Yuan Sales Incentives In China

Tesla Kicks Off 2023 By Continuing 10,000 Yuan Sales Incentives In China

It was an ugly end to 2022 for Tesla shares, to say the least. The automaker fell 37% alone in the month of December, due to fears about Elon Musk’s additional time commitments at Twitter and concerns about demand for vehicles drying up.

And it looks as though Tesla will begin 2023 by, in part, validating some concern about demand. The automaker is set to open the year in China by extending incentive offers aimed at generating sales in China, according to Bloomberg.

Bloomberg reported this weekend that Model 3 sedan and Model Y sport utility vehicle buyers will get 10,000 yuan in incentives (about $1,450) if they take delivery by February 28, 2023, per Tesla’s website.

The automaker is offering a 6,000 yuan subsidy it began early in December, in conjunction with a 4,000 yuan subsidy that is “tied to purchasing insurance through Tesla” and that was started in November 2022, Bloomberg wrote.

Tesla is also looking to stoke sales in the U.S., offering $7,500 off all of its major models. Delivery numbers for Q4 were announced this morning and missed Wall Street’s expectations.

Tesla was down 45% in December before an Adam Jonas note from Morgan Stanley encouraged buying in the waning days of the month. He lowered his price target on Tesla from $330 to $250, but maintained his overweight rating on the name and argued that the recent selloff had created an “opportunity”.

“We believe 2023 is shaping up to be a ‘reset’ year for the EV market where the last 2 years of demand exceeding supply will be substantially inverted to supply exceeding demand. Within this environment, we believe players that are self-funded (non-reliant on external capital funding) with demonstrated scale and cost leadership throughout the value chain (from manufacturing to up-stream material supply) can be relative winners,” Jonas wrote.

“We believe Tesla may bein position to extend its lead vs. the EV competition in FY23 (both legacy and start-up) even before consideration of IRA (Inflation Reduction Act) benefits where Tesla also stands out as the biggest potential winner,” he continued.

Jonas is convinced that among peers, Tesla is one of the best suited to handle the macro headwinds, writing: “On a relative basis, the reiteration of our OW rating must be seen vs. more challenged EV-related peers such as EW-rated Fisker (FSR), UW-rated Lucid (LCID),and UW-rated QuantumScape (QS). Between a worsening macro backdrop, record high unafforability,and increasing competition, there are hurdles to overcome. Yet we do believe that in the face of all these pressures, TSLA will widen its lead in the EV race, as it leverages its cost and scale advantages to further itself from the competition.”

Tyler Durden

Mon, 01/02/2023 – 20:05 - Mark McCloskey Won’t Have Guns Or Money Returned, Despite Pardon, Missouri Judge Rules

Mark McCloskey Won’t Have Guns Or Money Returned, Despite Pardon, Missouri Judge Rules

Authored by Mimi Nguyen Ly via The Epoch Times (emphasis ours),

St. Louis lawyer Mark McCloskey will not have his guns or the fines he paid returned to him even though he received a governor’s pardon in 2021, a Missouri judge has ruled.

Armed homeowners Mark and Patricia McCloskey, stand in front their house confronting protesters marching to St. Louis Mayor Lyda Krewson’s house in the Central West End of St. Louis on June 28, 2020. (Laurie Skrivan/St. Louis Post-Dispatch via AP) McCloskey and his wife, Patricia McCloskey, both personal injury lawyers, pleaded guilty in June 2021 to misdemeanor charges for assault and harassment, respectively, over an incident in 2020 where they wielded guns as self-defense measures at their property while watching Black Lives Matter protesters walk through their private, gated neighborhood.

They were required to pay maximum fines totaling $2,750. As part of the plea agreement, the two also surrendered the guns they wielded—a Colt AR-15 rifle and a Bryco pistol.

After their convictions, Missouri Gov. Mike Parson, on July 30, 2021, pardoned the couple and shortly following the move, McCloskey filed a lawsuit in St. Louis City Circuit Court seeking to have the guns returned and the fines paid back to him and his wife.

Circuit Judge Joan Moriarty rejected the request on Dec. 28, saying that the governor’s pardon doesn’t have any impact on the plea agreement the couple had agreed to.

“Plaintiff and his wife are required to follow through with their end of the bargain,” she wrote, reported the St. Louis Post-Dispatch.

“While the governor’s pardon does clear plaintiff’s record of the conviction,” she added, “his guilt remains and the terms of an agreement that predicated said guilt also remains.”

McCloskey said he plans to appeal, the outlet reported.

Law Licenses Suspended

In February 2022, the Missouri Supreme Court indefinitely suspended the McCloskeys’ law licenses. The court also stayed the suspension and put the two attorneys on probation for a year, which means they can still practice law, but the suspension would kick in if they violate their probation by not following the “Rules of Professional Conduct.”

Read more here…

Tyler Durden

Mon, 01/02/2023 – 19:30 - US Inflation: How Much Have Prices Increased In 2022?

US Inflation: How Much Have Prices Increased In 2022?

Inflation has been top of mind over the last year, looming over every aspect of the economy. But how has inflation actually impacted the prices of everyday goods like bread and butter or gas and public transportation?

In this infographic, Visual Capitalist’s Avery Koop and Bhabna Banerjee showcase select items and how inflation has impacted the price year-over-year. Additionally, we’ve charted the overall price increases across the overarching goods categories, using data from the U.S. Bureau of Labor Statistics (BLS).

Note: These numbers are assessed using the Consumer Price Index (CPI) for all Urban Consumers (CPI-U), using the U. S. city average by detailed expenditure category.

How Much has the Cost of Goods Gone Up?

Inflation has caused the cost of many goods to increase significantly compared to last year. The most dramatically affected item is elementary school lunches, a cost in the U.S. that is already unaffordable for many families.

Here’s a look at every single reported good’s change in price from last year:

Item Unadjusted Change YoY (Nov 2021 – Nov 2022) Food at elementary and secondary schools +254.1% Food at employee sites and schools +110.1% Fuel oil +65.7% Eggs +49.1% Margarine +47.4% Other motor fuels +43.3% Fuel oil and other fuels +41.7% Airline fares +36.0% Butter and margarine +34.2% Butter +27.0% Flour and prepared flour mixes +24.9% Public transportation +23.8% Other dairy and related products +22.4% Fats and oils +21.8% Canned fruits +20.9% Crackers, bread, and cracker products +19.9% Salad dressing +19.9% Lettuce +19.8% Motor oil, coolant, and fluids +19.6% Frozen and refrigerated bakery products, pies, tarts, turnovers +19.4% Cookies +19.2% Lunchmeat +18.4% Canned fruits and vegetables +18.4% Frozen vegetables +18.3% Other uncooked poultry including turkey +17.9% Cakes, cupcakes, and cookies +17.6% Ice cream and related products +17.5% Rice, pasta, cornmeal +16.8% Cereals and cereal products +16.6% Other bakery products +16.5% Cereals and bakery products +16.4% Dairy and related products +16.4% Bakery products +16.3% Other meats +16.2% Potatoes +16.2% Canned vegetables +16.2% Olives, pickles, relishes +16.1% Processed fruits and vegetables +15.8% Bread +15.7% Pet food +15.7% Fresh milk other than whole +15.6% White bread +15.5% Bread other than white +15.5% Utility (piped) gas service +15.5% Roasted coffee +15.2% Other fats and oils including peanut butter +15.2% Soups +15.0% Motor vehicle repair +15.0% Frozen fruits and vegetables +14.9% Fresh biscuits, rolls, muffins +14.8% Milk +14.7% Coffee +14.6% Other miscellaneous foods +14.6% Fresh cakes and cupcakes +14.4% Stationery, stationery supplies, gift wrap +14.3% Energy services +14.2% Transportation services +14.2% Rice +14.1% Sugar and sugar substitutes +14.1% Household paper products +14.1% Apparel services other than laundry and dry cleaning +14.1% Frozen and freeze dried prepared foods +14.0% Instant coffee +13.9% Other food at home +13.9% Delivery services +13.8% Fresh whole chicken +13.7% Beverage materials including coffee and tea +13.7% Sauces and gravies +13.7% Electricity +13.7% Vehicle accessories other than tires +13.7% Health insurance +13.5% Frankfurters +13.4% Motor vehicle insurance +13.4% Breakfast cereal +13.3% Nonalcoholic beverages and beverage materials +13.2% Nonfrozen noncarbonated juices and drinks +13.2% Poultry +13.1% Fresh whole milk +13.1% Sugar and sweets +13.1% Energy +13.1% Pets and pet products +13.0% Juices and nonalcoholic drinks +12.9% Candy and chewing gum +12.9% Other foods +12.9% Carbonated drinks +12.8% Tools, hardware and supplies +12.8% Other sweets +12.7% Cheese and related products +12.4% Oranges, including tangerines +12.4% Gasoline, unleaded premium +12.4% Housekeeping supplies +12.4% Motor vehicle body work +12.4% Energy commodities +12.2% Other beverage materials including tea +12.1% Food at home +12.0% Chicken +12.0% Miscellaneous household products +11.9% Vehicle parts and equipment other than tires +11.8% Household cleaning products +11.7% Motor vehicle maintenance and repair +11.7% Fresh and frozen chicken parts +11.6% Motor vehicle parts and equipment +11.6% Food from vending machines and mobile vendors +11.5% Snacks +11.1% Spices, seasonings, condiments, sauces +11.1% Veterinarian services +11.0% Baby food +10.9% Pet services including veterinary +10.9% Motor fuel +10.8% Miscellaneous personal goods +10.8% Gasoline, unleaded midgrade +10.7% Food +10.6% Other processed fruits and vegetables including dried +10.4% Living room, kitchen, and dining room furniture +10.3% Tires +10.3% Floor coverings +10.2% Gasoline (all types) +10.1% Tools, hardware, outdoor equipment and supplies +10% Gasoline, unleaded regular +9.8% Fruits and vegetables +9.7% Fresh vegetables +9.6% Fresh sweetrolls, coffeecakes, doughnuts +9.5% Citrus fruits +9.5% Prepared salads +9.5% Hair, dental, shaving, and miscellaneous personal care products +9.3% Motor vehicle maintenance and servicing +9.3% Tax return preparation and other accounting fees +9.1% Full service meals and snacks +9.0% Purchase of pets, pet supplies, accessories +8.9% Video discs and other media +8.9% Frozen fish and seafood +8.8% Women’s underwear, nightwear, swimwear, and accessories +8.6% Food away from home +8.5% Dishes and flatware +8.5% Outdoor equipment and supplies +8.4% Household furnishings and supplies +8.3% Fresh fruits and vegetables +8.0% Wine away from home +7.9% Rent of primary residence +7.9% Laundry and dry cleaning services +7.9% Ham +7.8% Dried beans, peas, and lentils +7.8% New cars +7.8% Breakfast sausage and related products +7.7% Processed fish and seafood +7.7% Beer, ale, and other malt beverages at home +7.7% Ham, excluding canned +7.6% Other goods +7.5% Apples +7.4% Other fresh vegetables +7.4% Personal care products +7.4% Pet services +7.4% Admission to movies, theaters, and concerts +7.4% Frozen noncarbonated juices and drinks +7.3% Medical equipment and supplies +7.3% Rental of video discs and other media +7.3% New vehicles +7.2% Rent of shelter +7.2% New trucks +7.1% Music instruments and accessories +7.1% Alcoholic beverages away from home +7.1% Shelter +7.1% Owners’ equivalent rent of residences +7.1% Owners’ equivalent rent of primary residence +7.1% Distilled spirits away from home +7.0% Salt and other seasonings and spices +6.9% Meats, poultry, fish, and eggs +6.8% Furniture and bedding +6.8% Services less energy services +6.8% Personal care services +6.8% Haircuts and other personal care services +6.8% Limited service meals and snacks +6.7% Shelf stable fish and seafood +6.6% Fresh fruits +6.6% Beer, ale, and other malt beverages away from home +6.6% Garbage and trash collection +6.6% Fish and seafood +6.5% Indoor plants and flowers +6.5% Other personal services +6.5% Cigarettes +6.4% Dental services +6.4% Video discs and other media, including rental of video +6.4% Men’s suits, sport coats, and outerwear +6.3% Tobacco and smoking products +6.3% Miscellaneous personal services +6.3% College textbooks +6.2% Legal services +6.2% All items less food and energy +6.0% Women’s suits and separates +5.9% Clocks, lamps, and decorator items +5.8% Peanut butter +5.7% Women’s apparel +5.7% Window and floor coverings and other linens +5.6% Women’s and girls’ apparel +5.6% Other fresh fruits +5.5% Other food away from home +5.5% Other household equipment and furnishings +5.5% Newspapers and magazines +5.5% Alcoholic beverages +5.5% Tobacco products other than cigarettes +5.5% Fresh fish and seafood +5.4% Nonprescription drugs +5.4% Cosmetics, perfume, bath, nail preparations and implements +5.4% Recreation services +5.4% Financial services +5.4% Sports equipment +5.3% Educational books and supplies +5.3% Day care and preschool +5.3% Other condiments +5.2% Girls’ apparel +5.2% Jewelry and watches +5.2% Watches +5.1% Jewelry +5.1% Toys, games, hobbies and playground equipment +5.1% Club membership for shopping clubs, organizations, or participant sports fees +5.1% Other linens +5.0% Other furniture +5.0% Water and sewer and trash collection services +5.0% Fees for lessons or instructions +5.0% Funeral expenses +4.9% Alcoholic beverages at home +4.5% Nursing homes and adult day services +4.5% Water and sewerage maintenance +4.4% Domestic services +4.4% Medical care services +4.4% Photographers and photo processing +4.4% Other recreation services +4.4% Residential telephone services +4.4% Meats, poultry, and fish +4.3% Video and audio services +4.2% Postage and delivery services +4.2% Cable and satellite television service +4.0% Infants’ and toddlers’ apparel +3.9% Bananas +3.8% Propane, kerosene, and firewood +3.8% Care of invalids and elderly at home +3.8% Commodities less food and energy commodities +3.7% Services by other medical professionals +3.7% Admissions +3.7% Tomatoes +3.6% Apparel +3.6% Recreation commodities +3.6% Moving, storage, freight expense +3.5% Elementary and high school tuition and fees +3.5% Photographic equipment and supplies +3.3% Other lodging away from home including hotels and motels +3.3% Recreational reading materials +3.2% Lodging away from home +3.2% Hospital and related services +3.2% Postage +3.2% Medical care commodities +3.1% Professional services +3.1% Intracity transportation +3.1% Tuition, other school fees, and childcare +3.1% Wine at home +3.0% Outpatient hospital services +3.0% Other appliances +2.9% Hospital services +2.9% Bedroom furniture +2.8% Medicinal drugs +2.8% Housing at school, excluding board +2.8% Inpatient hospital services +2.8% Sporting goods +2.7% Men’s shirts and sweaters +2.5% Window coverings +2.4% Men’s footwear +2.4% Transportation commodities less motor fuel +2.4% Checking account and other bank services +2.4% Men’s apparel +2.3% Footwear +2.3% Boys’ and girls’ footwear +2.3% State motor vehicle registration and license fees +2.3% Bacon, breakfast sausage, and related products +2.2% Women’s footwear +2.2% Education and communication services +2.2% Photographic equipment +2.0% College tuition and fees +2.0% Prescription drugs +1.9% Recorded music and music subscriptions +1.8% Eyeglasses and eye care +1.8% Motor vehicle fees +1.8% Appliances +1.7% Distilled spirits at home +1.7% Whiskey at home +1.7% Distilled spirits, excluding whiskey, at home +1.7% Pork chops +1.6% Other intercity transportation +1.6% Men’s pants and shorts +1.5% Physicians’ services +1.5% Telephone services +1.5% Audio equipment +1.4% Other recreational goods +1.4% Internet services and electronic information providers +1.4% Men’s and boys’ apparel +1.3% Pork +1.2% Meats +1.1% Women’s dresses +1.1% Sports vehicles including bicycles +1.1% Parking fees and tolls +1.1% Technical and business school tuition and fees +1.1% Wireless telephone services(1)(2) +1.0% Sewing machines, fabric and supplies +0.9% Parking and other fees +0.9% Nonelectric cookware and tableware +0.8% Men’s underwear, nightwear, swimwear, and accessories +0.8% Toys +0.6% Tenants’ and household insurance +0.6% Intracity mass transit +0.4% Laundry equipment +0.1% Recreational books 0.0% Uncooked ground beef -1.0% Major appliances -1.0% Bacon and related products -1.1% Boys’ apparel -1.7% Computer software and accessories -1.7% Women’s outerwear -2.0% Used cars and trucks -3.3% Ship fare -3.6% Computers, peripherals, and smart home assistants -4.4% Other pork including roasts, steaks, and ribs -5.1% Beef and veal -5.2% Car and truck rental -6.0% Uncooked other beef and veal -7.2% Admission to sporting events -7.2% Uncooked beef steaks -7.4% Uncooked beef roasts -8.1% Video and audio products -8.2% Other video equipment -9.5% Education and communication commodities -9.7% Information technology commodities -11.5% Televisions -17.0% Telephone hardware, calculators, and other consumer info items -17.9% Smartphones -23.4% Household operations – Gardening and lawncare services – Repair of household items – Leased cars and trucks – All items +7.1% School lunches became more expensive this year as a federal waiver program came to an end. The program had provided every school child in the country with free lunches.

After school lunches, fuel oil and eggs rank high in terms of big jumps in their prices, increasing by 66% and 49% respectively. Some other notable increases: airfares have gone up by 36%, living room, kitchen, and dining room furniture by 10.3%, and alcoholic beverages at home by 4.5%.

However, a number of goods have actually gone down in the index, including:

-

Smartphones: -23%

-

Televisions: -17%

-

Uncooked beef roasts: -8%

-

Admission to sporting events: -7%

-

Car and truck rentals: -6%

Interestingly, smartphones are not actually getting cheaper, rather the BLS adjusts for products that improve rapidly in quality year-over-year. Usually, most items are identical on a year-to-year basis, but smartphones are improving in their quality, which is why their price appears to be deflating rather than inflating.

U.S. Inflation

Overall, the items in the basket of goods under the Consumer Price Index have increased by a collective 7.1% since last year, making purchasing necessary food and energy items more difficult.

Here’s another look at how each overarching category increased, between November 2021 and November 2022:

-

Food: +10.6%

-

Energy: +13.1%

-

All other items excluding food and energy: +6.0%

Purchasing your everyday ingredients to cook with, energy to heat your home, and all other items that are standard in our everyday lives has become increasingly expensive. In an effort to counter inflation pressures, the U.S. Federal Reserve has been raising interest rates to make borrowing more difficult in order to push down demand.

Heading into 2023, many feel that a recession is on the way, and a lot of households will have to continue borrowing at higher rates to keep up with basic goods purchases. On the upside, some experts anticipate that although there will be economic downturn, it will be brief and won’t deeply impact the economy like past ones.

Tyler Durden

Mon, 01/02/2023 – 18:55 -

- Have We Seen A Peak In Pax Americana

Have We Seen A Peak In Pax Americana

By Russell Clark of The Capital Flows and Asset Markets substack

Happy New Year! Welcome to a special on the idea of a perhaps we are seeing a peak in the Pax Americana.

Pax Americana implies that America has become the dominant empire as Rome once was, or perhaps on a more comparable basis, as Britain used to be. In financial markets and elsewhere, the question is asked where we have entered an era of decline for the US.

Conventional thoughts on Pax Americana link the decline of the British Empire with the rise of the America. I think this analysis is wrong. The decline of the British Empire saw the rise of two new empires, the US and the Soviet Union. In military terms, the Soviet Union was largely responsible for the the defeat of Germany in World War II, and the Soviet Union and Chinese assistance saw US forces turned back in the Korean War of 1950 to 1955, and defeated in Vietnam War. The US centred trading system only incorporated North America, Western Europe, and some parts of East Asia. Most of the rest of the world was either socialist on non-aligned. If this is at odds with how you think of modern history, then I would recommend Eric Hobsbawm series of books: Age Of Capital 1848 -1875, Age of Empire 1875 – 1914 and Age of Extremes 1914 – 1991. Hobsbawm is probably correct in marking 1991 as the beginning of Pax Americana. Not only did it mark the collapse of the Soviet Union, it was also when the first Gulf War demonstrated to the world that US military power was far beyond the capabilities of all other powers, but also the integration of the world into a single trading system – globalization. First military domination, then financial domination. Or as in Dark Knight Rises when Bain askes Daggett, “Do you feel in charge?”, are politics and military really in charge or finance and corporates? The former is really in charge in my view. If we look at Russian invasion of Ukraine, financial sanctions matter far less than the ammunition that the US is providing.

The question of Pax Americana is whether US military can still project power? Defeat in Ukraine would almost certainly signal an end to Pax Americana. If Russia was to take control of Ukraine, the ability of the US to protect the global trade system would come under severe pressure. Could countries really rely on imports of key resources from elsewhere? Could Europe and Japan continue to have undersized armed forces? The key tenets of globalisation would fall apart, and with it the underpinnings of Pax Americana. However, a rout of Russia, and the regime change in Russia would offer the potential of an increase in Pax Americana, and a new age in European integration. In my mind, the future of Pax Americana will be decided at home, rather than on black earth of Ukraine. To confront the rising powers, US military spending will need to rise. Going back to levels seen in 1980s implies a tripling of the current military budget.

But here is the problem. Domestically will voters stand for increasing military spending as their own domestic conditions worsen? The biggest spending item for the US government is social security, but it is plain that this spending is not benefiting the majority of Americans. While most countries saw a stagnation in life expectancies during Covid, the US has seen three years of decline, wiping out at least two decades of gains.

A similar decline in visible in the relatively capitalist UK. However compared to a relatively more “socialist” Japan – the flattening out of life expectancy in the UK and the US is striking.

It is likely that the US policy makers understand these issues, which is why there has been increasing use of export controls of technology to China. How effective is this likely to be? Very hard to tell. Export controls are very unlikely to stop China from catching up to already existing technology. For example, ever since the US invented nuclear weapons, it has worked very hard to keep the technology as a monopoly and to limit other countries access to it. The Soviet Union successfully tested it first atomic bomb in 1949, China followed in 1964, France in 1968. North Korea in 2006 tested its first atomic weapon, despite severe sanctions, and very weak technological development elsewhere. But can the US stop China developing a lead in technology? Possibly, but ultimately, Pax Romana or the British Empire did not head for decline due to losing a technological lead, more that the political structure of Empire declined. That was that local politics lead to the decline of empire, and looking at the US, with high income inequality, falling life expectancy, and a Republican party that is split between free trade and Trump politics, a decline in Pax Americana seems likely.

How do we trade this? My best trade remains, long gold short treasuries, for reasons outlined many times before.

The key takeaway from all of this, is that corporates and financial markets feel like they are in charge. Financial market assumed that Russia would not invade in Ukraine and were wrong. Politics is Bane, while financial market are Daggett. Do financial markets really feel like “they are in charge?” anymore? I don’t think so. Long GLD, short TLT.

Tyler Durden

Mon, 01/02/2023 – 18:20 - Virgin Islands AG Fired Three Days After Suing JPMorgan Over Jeffrey Epstein

Virgin Islands AG Fired Three Days After Suing JPMorgan Over Jeffrey Epstein

As we noted last week, US Virgin Islands Attorney General Denise George filed a lawsuit against JPMorgan for allegedly reaping financial benefits from Jeffrey Epstein’s sex-trafficking operation – less than a month after George secured a $105 million settlement with Epstein’s estate, which agreed to liquidate Epstein’s islands and cease all business operations in the region.

Three days later, George is now unemployed, after Governor Albert A. Bryan Jr. fired her for allegedly filing the suit against JPMorgan without his permission.

According to the complaint, for “Over more than a decade, JPMorgan clearly knew it was not complying with federal regulations in regard to Epstein-related accounts as evidenced by its too-little too-late efforts after Epstein was arrested on federal sex trafficking charges and shortly after his death, when JPMorgan belatedly complied with federal law.”

JPMorgan Sued By Virgin Islands Over Jeffrey Epstein’s Alleged Sex-Trafficking Operation https://t.co/d8tH2eytdE

— zerohedge (@zerohedge) December 29, 2022

https://platform.twitter.com/widgets.js

It goes much deeper than just the JPMorgan lawsuit…

The suit against JPMorgan Chase was not the whole scope of George’s pursuit of the remnants of Epstein’s network of conspirators. Although Little St. James (“Pedo Island”) and its adjacent island owned by the Epstein estate went up for sale in March 2022, action taken by George kept the premise of any sale from going through. Acting in her former capacity as US Virgin Island Attorney General, she placed criminal activity liens on the islands from a civil racketeering lawsuit. That lawsuit was filed in 2020 following Epstein’s “death” in August of 2019. The suit alleged that Little St. James Island was used as part of a network of shell companies that Epstein manipulated to conceal the activities of his human trafficking network.

However, that suit was settled between the Epstein estate and George’s office in early December 2022. Under the agreement, Epstein’s estate would pay over $105 million to the Government of the US Virgin Islands as restitution. In addition to that sum, the liens preventing the sale of Epstein’s islands become removed under the condition that half of the proceeds from the sale will also be given to the US Virgin Islands through a trust it has opened to allocate the money to fund government programs to fight sexual abuse on the archipelago. “This settlement restores the faith of the People of the Virgin Islands that its laws will be enforced, without fear or favor, against those who break them. We are sending a clear message that the Virgin Islands will not serve as a haven for human trafficking,” Attorney General George stated upon the announcement of the settlement in one of her last acts before being fired.

Despite the resolution of the US Virgin Islands’ direct case against the assets held by the Epstein estate, questions still linger about its operations in George’s jurisdiction. One of the most mysterious and perhaps most vital to examine of those shell companies, Southern Country International, was the first internationally operating bank to be opened in the US Virgin Islands by Epstein in 2014. The bank opened when John Percy de Jongh Jr. served as the governor of the territory. During his term, de Jongh appointed present-governor Albert A. Bryan Jr. into his administration as Commissioner of the US Virgin Islands Department of Labor. Despite not having much activity on its books, Southern Country International would renew its license with the US Virgin Islands five times before Epstein’s purported demise.

By the time Epstein died, his Virgin Islands based bank had less than $700,000 in assets. However, in December of 2019, months after his purported suicide, Epstein’s estate transferred a whopping $15.5 million into Southern Country International. In under a month, the bank’s assets diminished to less than $500,000. Mark Epstein, Jeffrey’s brother and executor of his estate, stated that the bank was used to pay existing debts of the assets he had control over. Though the bank was not explicitly referenced in the press release on the December settlement, that announcement does detail the Virgin Islands action against Southern Trust Company, a holding company which points to a larger scale of Epstein owned enterprises connected to Southern Country International. It is unclear how the allegations made in George’s lawsuit against JPMorgan Chase connect to the posthumous activity conducted by Epstein’s Virgin Islands banking operation.

Following her dismissal, Assistant Attorney General Carol Thomas-Jacobs has been named to an interim position to fill George’s vacated seat. She will inherit the office as it joins an on-going list of plaintiffs who have taken action against large scale banks relating to their accounts with Epstein. Just over a month before George’s filing, multiple class action suits were filed against JPMorgan Chase and Deutsche Bank alleging each institution knowingly profited from Epstein’s criminal activity. Those suits coincided with another filed against Epstein associate Leon Black, the billionaire who previously served as CEO of Apollo Global Management before his relationship with the pedophile thrust him into the spotlight.

The civil suit against Black alleges that the disgraced financier raped the plaintiff in 2002 at a mansion owned by Epstein. A spokesman for Black told Forbes that the claims made against their client were “categorically” false. Their response to Forbes follows one of a similar like from Deutsche Bank who told the publication that the suit filed against them “lacks merit.” Despite the magnitude of these lawsuits, the gravity of George’s suit against JPMorgan Chase surely made the biggest splash in the once-stagnant waters of the cesspool of the Epstein debacle. However, the firing leaves little hope that the waves caused by her last act as Attorney General will wash any truth to shore.

Tyler Durden

Mon, 01/02/2023 – 17:45 - North Carolina Lawmakers Urge Governor To Follow Other States In Banning TikTok

North Carolina Lawmakers Urge Governor To Follow Other States In Banning TikTok

Authored by Matt McGregor via The Epoch Times (emphasis ours),

Two North Carolina representatives are pressing Gov. Roy Cooper’s office to follow other states in issuing an executive order banning TikTok from government devices.

The TikTok logo is displayed outside a TikTok office in Culver City, Calif., on Aug. 27, 2020. (Mario Tama/Getty Images) State Reps. Jason Saine and Jon Hardister, both Republicans, sent a letter to the Democrat governor (pdf) insisting that Cooper remove the Chinese video app “swiftly and decisively,” deeming it to be a “matter of national security.”

“As we know, the Chinese government is constantly working to infiltrate our communications and access intellectual data within the United States,” Saine and Hardister wrote. “If sensitive data is breached, it could pose both an economic and security threat for North Carolina. We have a responsibility to prevent this from happening, which is why we are urging an executive order as soon as possible.”

Saine and Hardister referenced past orders, such as the chief administrative officer for the U.S. House of Representatives issuing an order on Wednesday for all lawmakers to delete the app on all devices managed by the House.

The $1.7 trillion omnibus bill President Joe Biden signed into law on Thursday includes legislation banning the social media app from government devices due to concerns over national security.

State-Level Bans

State governments have also banned TikTok, which is owned by the Beijing-based ByteDance Ltd.

As of Friday, Indiana became the 20th state to block TikTok from being used on state devices.

In addition, Indiana Attorney General Todd Rokita, a Republican, filed two lawsuits against TikTok stating that the app made false claims.

“The TikTok app is a malicious and menacing threat unleashed on unsuspecting Indiana consumers by a Chinese company that knows full well the harms it inflicts on users,” Rokita said in a press release. “With this pair of lawsuits, we hope to force TikTok to stop its false, deceptive and misleading practices, which violate Indiana law.”

Rokita said the first lawsuit alleges that TikTok lured children onto the platform using misleading advertising stating that the app contains only “’infrequent/mild’ sexual content, profanity, or drug references.”

However, Rokita said the app is in fact “rife with examples of such material.”

“An essential part of TikTok’s business model is presenting the application as safe and appropriate for children ages 13 to 17,” he said.

The second lawsuit alleges that TikTok collects data from its consumers and that it “deceived those consumers to believe that this information is protected from the Chinese government and Communist party.”

“In multiple ways, TikTok represents a clear and present danger to Hoosiers that is hiding in plain sight in their own pockets,” Rokita said. “At the very least, the company owes consumers the truth about the age-appropriateness of its content and the insecurity of the data it collects on users. We hope these lawsuits force TikTok to come clean and change its ways.”

Read more here…

Tyler Durden

Mon, 01/02/2023 – 17:10 - Flu Or Stroke? Hezbollah Leader's Hospitalization Sets Off Intense Speculation

Flu Or Stroke? Hezbollah Leader’s Hospitalization Sets Off Intense Speculation

Regional media is reporting that Hezbollah Secretary-General Hassan Nasrallah is in a Beirut hospital and said to be in serious condition, setting off intense speculation over the fate and future leadership of the powerful Lebanese Shia paramilitary group with ties to Iran.

Israeli media is claiming that Nasrallah suffered a stroke after an important Friday speech was unexpectedly canceled. Nasrallah is among the most powerful and prominent leaders in Lebanon and throughout the region, seen as head of an Iran-backed terror organization by Israel, the US, and much of the West. However, he’s hailed as a “hero” by many from Syria to Iraq to Iran as part of the ‘axis of resistance’.

For years, Israeli intelligence has sought to track his whereabouts in hopes of initiating a kill or capture mission, but the Hezbollah leader is known for his secrecy and ability to evade Israeli eavesdropping measures, and also rarely does in-person speeches – instead appearing to supporters via televised feed from secret locations.

As The Jerusalem Post notes, Hezbollah officials are denying that a stroke hospitalized Nasrallah, instead saying its a bad bout of the Flu. “The reports came after Nasrallah canceled a planned Friday speech, with the Lebanese terrorist organization announcing through its affiliated media he had fallen ill with influenza and was unable to speak well,” according to the report.

“Saudi journalist Hussein al-Gawi contradicted Hezbollah’s statement, claiming that Nasrallah indeed suffered a second stroke instead of falling ill as was reported,” Jerusalem Post continues. “The Hezbollah leader was reportedly hospitalized at the Great Prophet Hospital in Beirut.”

This led to reports that he’s unconscious and in intensive care, but this was shot down by his son as “untrue”.

Hezbollah leader Hassan Nasrallah cancelled a speech scheduled for this evening due to health reasons. Hezbollah said in a statement that Nasrallah has the flu, “which hinders his Eminence from speaking in the usual and natural manner while he is receiving appropriate treatment.” pic.twitter.com/5qYlG5A33Z

— Ariel Oseran (@ariel_oseran) December 30, 2022

https://platform.twitter.com/widgets.js

Since emerging as head of Hezbollah in the early 1990’s, Nasrallah’s state of health has long been subject of intense speculation and rumors, especially when he abruptly cancels a speech or disappears from the public eye – much like the kind of close scrutiny that North Korea’s Kim Jong-Un receives.

It’s well know that Israeli and US intelligence closely monitors Hezbollah’s media arm for any indicators that would impact the military readiness and leadership of the organization. This is especially as Israel sees Hezbollah as its most immediate ‘enemy #1’ on the Jewish state’s northern border.

Tyler Durden

Mon, 01/02/2023 – 16:35 - Analysts Predict 1 Million Bpd Drop in Russian Crude Output

Analysts Predict 1 Million Bpd Drop in Russian Crude Output

By Charles Kennedy of OilPrice.com

- UBS’ Giovanni Staunovo: The European Union’s ban on Russian oil products set to come into force on February 5 could lead to a 1 million barrel per day drop in Russian crude oil output for the New Year.

- Moscow has also warned it could cut production by up to 700,000 bpd as it responds to the $60/barrel price cap on its oil implemented by the G7 in December.

- According to Energy Intelligence, Russian refineries are already struggling with a labor shortage due to conscription for Putin’s war on Ukraine.

The European Union’s ban on Russian oil products set to come into force on February 5 could lead to a 1 million barrel per day drop in Russian crude oil output for the New Year, commodity analysts for UBS told Insider on Monday.

“We expect the European ban on seaborne Russian crude and refined products (to come into force on February 5) to result in a drop of Russian production of at least 1 million barrels per day in 2023, with Russia having difficulties in finding alternative markets,” UBS’ Giovanni Staunovo, told Insider.

While Russia has been rerouting crude volumes to Asia, traders are finding it increasingly challenging to secure the necessary insured vessels to carry sanctioned Russian crude. As of the first week of December, Moscow was sending nearly 90% of its crude to Asia.

Moscow has also warned it could cut production by up to 700,000 bpd as it responds to the $60/barrel price cap on its oil implemented by the G7 in December.

Another analyst, Saxo Bank’s Ole Hansen, told Insider that global supplies will experience more tightness, leading oil prices to top $100 bpd this year, once Chinese demand improves.

“Following a soft first quarter, I see the price of Brent returning to a $90-100 dollar range. What happens later will depend on the strength of an incoming economic slowdown,” Saxo told Insider.

Russia boasts the world’s third-largest refining industry, and the EU ban that goes into effect on February 5 is expected to have a fairly significant impact.

According to Energy Intelligence, Russian refineries are already struggling with a labor shortage due to conscription for Putin’s war on Ukraine. Energy Intel analysts expect to see a further decline in Russian refining margins this year as they pay more for tankers to export further, predicting a 600,000-bpd drop in refining throughput in 2023, year-on-year.

Tyler Durden

Mon, 01/02/2023 – 16:00 - 2023 Starts Off With A Bang: Winklevoss Slams Barry Silbert's Genesis, Accuses Of Commingling Funds

2023 Starts Off With A Bang: Winklevoss Slams Barry Silbert’s Genesis, Accuses Of Commingling Funds

If anyone expected that the bursting of the crypto bubble and the resulting unprecedented tidal wave of failure and fraud would somehow be confined to 2022 we have some bad news.

As if the collapse of Sam Bankman-Fried’s crypto empire wasn’t bad enough, its fallout just got much messier after digital-asset entrepreneur and Facebook billionaire, Cameron Winklevoss, accused fellow crypto businessman Barry Silbert of “bad faith stall tactics” and the commingling of funds within his conglomerate that Winklevoss says have left $900 million in customer assets needlessly in limbo since FTX’s meltdown.

First, some background: in early November, shortly after FTX imploded, Gemini Trust which was founded by the Winklevoss twins, paused redemptions on a lending product called Earn, which offered investors the potential to generate as much as 8% in interest on their digital coins. It did so by lending them out to Genesis Global Capital, one of the companies owned by Silbert’s Digital Currency Group. The Earn halt came after Genesis suspended both redemptions and new loan originations at its lending unit because of its exposure to FTX. Genesis has told clients that it could take “weeks” to find a path forward, and that bankruptcy may be one possibility.

Which brings us to today: this morning, facing pressure of his own from angry customers locked out of their Gemini accounts and a lawsuit alleging fraud, Cameron Winklevoss published an open letter saying he had provided Silbert with multiple proposals to resolve the issue, including as recently as Dec. 25. He told Silbert “this mess is entirely of your own making,” citing some $1.675 billion owed to Genesis by DCG, which it used for other business purposes within Silbert’s conglomerate. “This is money that Genesis owes to Earn users and other creditors.”

“It’s not lost on us that you’ve been working desperately to try and firewall DCG from the problems that you created at Genesis,” Winklevoss added, strongly hinting that the relationship between DCG and Genesis is similar to that between FTX and Alameda. And in case that wasn’t clear, the next sentence strikes it home: “You should dispense with this fiction because we all know what you know — that DCG and Genesis are beyond commingled.”

Earn Update: An Open Letter to @BarrySilbert pic.twitter.com/kouAviTho4

— Cameron Winklevoss (@cameron) January 2, 2023

https://platform.twitter.com/widgets.js

An Open Letter to Barry Silbert

Barry — today marks 47 days since Genesis halted withdrawals. I am writing on behalf of more than 340,000 Earn users who are looking for answers. These users aren’t just numbers on a spreadsheet, they are real people. A single mom who lent her son’s education money to you. A father who lent his son’s bar mitzvah money to you. A husband and wife who lent their life savings to you. A school teacher who lent his children’s college funds to you. A policeman, and so many more. All together, these people entrusted more than $900 million of their assets to you. They deserve concrete answers and we are here to get them.

For the past six weeks, we have done everything we can to engage with you in a good faith and collaborative manner in order to reach a consensual resolution for you to pay back the $900 million that you owe, while helping you preserve your business. We appreciate that there are startup costs to any restructuring, and at times things don’t go as fast as we would all like. However, it is now becoming clear that you have been engaging in bad faith stall tactics.

For example, on December 2nd we expressed our belief “that getting everyone in a room together as soon as possible will be the most productive path towards reaching a resolution.” You agreed, but stated you would only do so after there was a proposal on the table. On December 17th, a proposal was delivered to you. On December 25th, Christmas Day, an updated version of this proposal was delivered to you. Despite this, you continue to refuse to get into a room with us to hash out a resolution. In addition, you continue to refuse to agree to a timeline with key milestones. Every time we ask you for tangible engagement, you hide behind lawyers, investment bankers, and process. After six weeks, your behavior is not only completely unacceptable, it is unconscionable.

The idea in your head that you can quietly hide in your ivory tower and that this will all just magically go away, or that this is someone else’s problem, is pure fantasy. To be clear, this mess is entirely of your own making. Digital Currency Group (DCG) — of which you are the founder and CEO — owes Genesis (its wholly owned subsidiary) ~$1.675 billion. This is money that Genesis owes to Earn users and other creditors. You took this money — the money of schoolteachers — to fuel greedy share buybacks, illiquid venture investments, and kamikaze Grayscale NAV trades that ballooned the fee-generating AUM of your Trust; all at the expense of creditors and all for your own personal gain. It is now time for you to take responsibility for this and do the right thing.

It’s not lost on us that you started your career as a bankruptcy restructuring associate. And it’s not lost on us that you’ve been working desperately to try and firewall DCG from the problems that you created at Genesis. You should dispense with this fiction because we all know what you know — that DCG and Genesis are beyond commingled. Everyone takes orders from you and always has. And anything you have done after the fact to pretend otherwise, won’t hold up. If instead, you had put all of this energy towards finding a resolution, we would have been done by now. Everyone would be in a better place, including you.

Earn users are tired. They’re scared. Many are now in dire straits. And yet despite all that they have had to endure, they have been remarkably patient and supportive. But there is only so much more they can take. They deserve a resolution for a recovery of the assets they lent to you and an end to this nightmare. To that end, and for the final time, we are asking you to publicly commit to working together to solve this problem by January 8th, 2023. We remain ready and willing to work with you, but time is running out.

Sincerely,

Cameron Winklevoss

Winklevoss claims the $1.675 billion borrowed by DCG from Genesis was used “to fuel greedy share buybacks, illiquid venture investments, and kamikaze Grayscale NAV trades,” referring to another of Silbert’s businesses, Grayscale Investments, whose largest vehicle is the Grayscale Bitcoin Trust. This came, he said, “all at the expense of creditors and all for your own personal gain.”

Winklevoss also asked Silbert to “publicly commit to working together to solve this problem,” which he says affects more than 340,000 Earn customers, by Jan. 8. He didn’t say what would happen if no agreement was reached by then.

Silbert prompted responded in kind, tweeting a refutation to several of Wilkevoss’s accusations, saying “DCG did not borrow $1.675 billion from Genesis” and “never missed an interest payment to Genesis and is current on all loans outstanding,” without providing more detail. Silbert also claimed DCG delivered a proposal for resolving the dispute to Genesis and Winklevoss’s advisers on Dec. 29, but had received no reply.

DCG did not borrow $1.675 billion from Genesis

DCG has never missed an interest payment to Genesis and is current on all loans outstanding; next loan maturity is May 2023

DCG delivered to Genesis and your advisors a proposal on December 29th and has not received any response

— Barry Silbert (@BarrySilbert) January 2, 2023

https://platform.twitter.com/widgets.js

That would not be the last of it, and moments later, Cameron Winklevoss doubled down, urging Silbert to “stop trying to pretend that you and DCG are innocent bystanders and had nothing to do with creating this mess. It’s completely disingenuous. So how does DCG owe Genesis $1.675 billion if it didn’t borrow the money? Oh right, that promissory note…”

And then, in an apparent attempt to avoid the nuclear option and filing a notice of default against Genesis – an event that will likely lead to even more havoc and mayhem across the crypto community – WInklevoss tweeted “Will you, or will you not, commit to solving this by January 8th in a manner that treats the $1.1 billion promissory note as $1.1 billion?”

Will you, or will you not, commit to solving this by January 8th in a manner that treats the $1.1 billion promissory note as $1.1 billion?

— Cameron Winklevoss (@cameron) January 2, 2023

https://platform.twitter.com/widgets.js

Previously Silbert’s DCG has been trying to emphasize that it’s separate from Genesis and insulated from its troubles. After Genesis suspended redemptions, DCG said in a tweet that “this temporary action has no impact on the business operations of DCG and our other wholly owned subsidiaries.”

Silbert, in a letter to shareholders last month, said that intercompany loans were made “in the ordinary course of business.” He noted that DCG has a liability of $575 million to Genesis. In the letter, he also described a $1.1 billion promissory note, due June 2032, which he said came about as the parent company stepped in to assume liabilities from Genesis related to the collapse of digital-assets hedge fund Three Arrows Capital.

As Bloomberg notes, Winklevoss’s aggressive stance comes as Gemini and its founders faces a lawsuit from investors who accuse the company of fraud, claiming the Earn product was in effect an interest-bearing account that it failed to register as a security.

As for the public spat between Winklevoss and Silbert, which is all too reminiscent of what happened between CZ and SBF in the days before the failure of FTX, as twitter user Jeremey Padawer summarizes “When these sorts of issues become public, almost every single time the worst is still to come… good luck crypto community.” Indeed.

When these sorts of issues become public, almost every single time the worst is still to come… good luck crypto community. 💔

— Jeremy Padawer (@JeremyCom) January 2, 2023

https://platform.twitter.com/widgets.js

And even Edward Snowden is bracing for what’s coming.

*sigh* gonna be a big week https://t.co/E0QQzX0rvO

— Edward Snowden (@Snowden) January 2, 2023

Tyler Durden

Mon, 01/02/2023 – 15:25 - David Stockman On The Parallels Between The COVID Hysteria And The Salem Witch Trials

David Stockman On The Parallels Between The COVID Hysteria And The Salem Witch Trials

Authored by David Stockman via InternationalMan.com,

It would not be going too far to say that the eruption of irrationality and hysteria in America during the COVID-19 period of 2020-2021 most resembled not 1954, when Senator McCarthy set the nation looking for communist moles behind every government desk, or 1919, when the notorious raids of Attorney General Mitchell were rounding up purported Reds in their tens of thousands, but the winter of 1691-1692. That’s when two little girls—Elizabeth Parris and Abigail Williams of Salem, Massachusetts—fell into the demonic activity of fortune-telling, which soon found them getting strangely ill, having fits, spouting gibberish, and contorting their bodies into odd positions.

The rest became history, of course, when a malpracticing local doctor claimed to have found no physical cause for the girls’ problems and diagnosed them as being afflicted by the “Evil Hand,” commonly known as witchcraft. Other ministers were consulted, who agreed that the only cause could be witchcraft and since the sufferers were believed to be the victims of a dastardly crime, the community set out to find the perpetrators.

Within no time, three witches who were famously accused —the Parris’ slave, Sarah Good, an impoverished homeless woman and Sarah Osborne, who had defied conventional Puritan society. Many more followed, and as the hysteria spread, hundreds were tried for witchcraft and two dozen hanged.

But there is a lesson in this classic tale that is embarrassing in its verisimilitude. Namely, one of the best academic explanations for the outbreak of seizures and convulsions which fueled the Salem hysteria was a disease called “convulsive ergotism”, which is brought on by ingesting rye grain infected with a fungus that can invade developing kernels of the grain, especially under warm and damp conditions.

During the rye harvest in Salem in 1691 these conditions existed at a time when one of the Puritans’ main diet staples was cereal and breads made of the harvested rye. Convulsive ergotism causes violent fits, a crawling sensation on the skin, vomiting, choking, and, hallucinations—meaning that it was Mother Nature in the ordinary course working her episodically unwelcome tricks, not the “Evil Hand” of a spiritual pathogen, which imperiled the community.

Similarly, in 2020 there Was no Evil Hand Sci-Fi Pathogen

The truth is, in 2020 it was also Mother Nature—likely abetted by the Fauci-sponsored gain-of-function researchers at the Wuhan Institute of Virology—who disgorged one of the nastier among ordinary respiratory viruses.

Such viruses, of course, have afflicted humankind over the ages, which, in turn, has evolved marvelous adaptive immune systems to cope with and overcome them. So again, there was no Evil Hand sci-fi pathogen at large that was something new under the sun, nor a disease that was extraordinarily lethal for 90% of the population.

In the grand scheme of things, therefore, the COVID-19 pandemic has already been recorded as an unfortunate bump on the road to longer and more pleasant lives for Americans and much of the rest of the world, too. That truth is strikingly depicted in the chart below.

While the all-cause mortality figure for 2020 did not exist when the CDC published the chart above, the green line would have depicted it as only a tiny upward blip—of which there have been several during the last 120 years shown above.

Was COVID-19 an Analogue of the Spanish Flu?

Indeed, the true analogue is the year 1918 when an estimated 675,000 Americans succumbed to the Spanish Flu from a population (100 million) just 30% of today’s level.

In that case, the green line in the chart above (all cause deaths) pushed up by nearly 400 per 100,000 population compared to the pre-war baseline (1914). By contrast, the excess rate in 2020 over 2019 was just 118 per 100,000.

And, yes, there is the sad fact of senseless dough-boy deaths on the killing fields of France embedded in these 1918 numbers, but it turns out that upwards of 45% of the conventionally reported 117,000 GI (gastrointestinal) deaths were not from German bullets, but the Spanish Flu that ripped through the massive US training camps that were hastily-assembled after Wilson foolishly declared war in April 1917 with no meaningful standing army to fight it.

So on the true measure of pandemic lethality—deaths from all causes—the COVID-19 was not even in the same ballpark as the Spanish Flu. And as the chart also shows, the former occurred way down the green line curve that is actually the ultimate rebuke to today’s on-going COVID-policy disaster.

The US age-adjusted death rate in 2020 (828 per 100,000) was actually 67% lower than it had been in 1918 (2,542 per 100,000) because since then a free capitalist society has gifted the nation with the prosperity and freedom to progress that has ushered in better sanitation, nutrition, shelter, life-styles and medical care.

It is those forces which have pushed the green line relentlessly to the lower-right corner of the chart, not the Federales atop their bureaucratic perches in Washington.

Hope for a New Great Barrington Declaration to Serve as Antidote to the Totalitarian Lockdown

At length, perhaps some future historian will need to find the “convulsive ergot” theory of 2020 to explain the COVID-Hysteria because the explanation will not be found in the “science” embedded in what will be a tiny blip in the green line of the chart above.

The Great Barrington Declaration was penned by three fearless world leading epidemiologists—Dr. Martin Kulldorff of Harvard, Dr. Sunetra Gupta of Oxford University and Dr. Jay Bhattacharya of Sanford—and was a powerful antidote to the Evil Hand theory then raging through the MSM and political class of almost every stripe.

At essence, it said the real science was that America was not being attacked by a Grim Reaper visiting death upon one and all regardless of age, health status or physical circumstances, but, instead, was a highly selective respiratory disease variant that honed-in tightly on the immunity-impaired aged and co-morbid.

Accordingly, the one-size-fits all Lockdown policy was dead wrong, and what was needed was highly targeted help, protections and treatments for the smallish minority of the vulnerable, which policy would presently lead to the attainment of “herd immunity” and the ultimate extinguishment of the pandemic in the normal way.

Colonial America found its way out of the Salem aberration in 1692, and surely 330 years and much science later it can do so again, exposing the 21st century miscreants who brought on this insensible hysteria as it does.

* * *

We’ve seen governments institute the strictest controls on people and businesses in history. It’s been a swift elimination of individual freedoms. But this is just the beginning… Most people don’t realize the terrible things that could come next, including Central Bank Digital Currencies (CBDCs), the abolition of cash, and much more. If you want to know how to survive what the central bankers and the Deep State have planned, then you need to see this newly released report from legendary investor Doug Casey and his team. Click here to download it now.

Tyler Durden

Mon, 01/02/2023 – 14:50 - Huge Death Toll After US-Supplied Himars Leveled Russian Barracks In Donetsk, Possibly Hundreds Killed

Huge Death Toll After US-Supplied Himars Leveled Russian Barracks In Donetsk, Possibly Hundreds Killed