- Could Voting Out Anti-Gun Politicians Next Week Secure The Second Amendment?

Could Voting Out Anti-Gun Politicians Next Week Secure The Second Amendment?

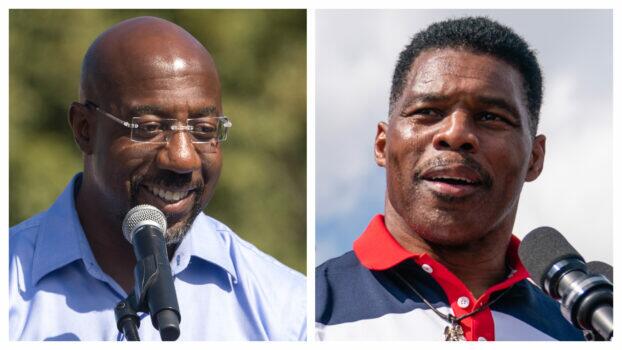

Submitted by Erich Pratt, the Senior Vice President of Gun Owners for America.,

This past year, America saw all sorts of headlines with a Second Amendment connection. From the Bruen decision at the Supreme Court and states passing more gun control in its wake, to the mass murders in Uvalde and Buffalo that prompted poorly crafted and openly unconstitutional legislation from Congress, there was a lot to digest.

Now as we approach election day next week, the debate over guns will play out in the ballot box, and we are confident which way America will go.

Despite the Bruen precedent, which is already having ripple effects on unconstitutional gun laws across the country, anti-gun legislators in both parties and at every level of government are doubling-down or even compromising away your rights because a vocal minority demands they “do something.” This phrase, while emotionally compelling, has unfortunately also led to bad policy, like the Cornyn-Murphy gun control package passed in late June.

Think about it. Just 48 hours after the Bruen decision, President Biden signed a major gun control package into law that, among other provisions, now relegates adults aged 18-21 to being second class citizens. Nothing could be more frustrating, especially with the edict that had just come from the Supreme Court – but hey, the Senate negotiators couldn’t let that get in their way.

Then we have Governor Hochul in New York, who teamed up with her legislature to quickly pass a highly restrictive concealed carry law – only after their previous (and less restrictive) law was overturned by our nation’s highest court!

In neighboring New Jersey, legislators are poised to go even further, by requiring individuals to obtain liability insurance to carry firearms! These policies will not stand judicial muster, just look at the comments from Judge Suddaby in our suit against the New York’s new concealed carry restrictions. Or look to Winchester, Virginia, where GOA won in court against a local ordinance that prohibited carry in many public locations, or Philadelphia where we secured a permanent injunction against the anti-gun Mayor’s latest gun grab in less than a week.

Frustratingly, at a time when crime is spiking across our country and sits atop voters’ minds, anti-gunners appear more focused on ensuring their constituents have no means to effectively protect themselves. In Congress, Senators from some of the most pro-gun states in the country sold your rights down the river. Voters are demanding one thing and their representatives are doing the opposite.

While the courts are a viable option, voting out anti-gun politicians is a much swifter alternative. Thankfully, We the People will soon have our say again, and it appears all but guaranteed that the Second Amendment will be more favored come January in both Washington and across the states.

Like we warned the anti-gun crowd after the Bruen decision, come into compliance and ensure our constitutional rights are protected, or we (or the voters) will force you to.

* * *

Gun Owners for America, the only no-compromise gun lobby in Washington.

Tyler Durden

Fri, 11/04/2022 – 23:40 - Meanwhile In London…

Meanwhile In London…

Here’s something you don’t see every day…

In a bizarre moment caught on video, two giant Christmas baubles bounced down London’s Tottenham Court Road this week after being swept by high winds, as passing cars attempt to avoid them…

They are reportedly part of an art installation by artist Tom Shannon which was due to remain on display in St Giles’ Square.

Tyler Durden

Fri, 11/04/2022 – 23:20 - Whitney: The One Chart That Explains Everything

Whitney: The One Chart That Explains Everything

Authored by Mike Whitney,

Look at the chart below. The chart explains everything.

It explains why Washington is so worried about China’s explosive growth. It explains why the US continues to hector China on the issues of Taiwan and the South China Sea. It explains why Washington sends congressional delegations to Taiwan in defiance of Beijing’s explicit requests. It explains why the Pentagon continues to send US warships through the Taiwan Strait and ship massive amounts of lethal weaponry to Taipei. It explains why Washington is creating anti-China coalitions in Asia that are aimed at encircling and provoking Beijing. It explains why the Biden administration is stepping up its trade war on China, imposing onerous economic sanctions on its businesses, and banning critical high-tech semi-conductors that are “are essential not just… for virtually every aspect of modern society, from electronic products and transport to the design and production of all manner of goods.” It explains why China has been singled-out in the US National Security Strategy (NSS) as “the only competitor with both the intent and, increasingly, the capability to reshape the international order.” It explains why Washington now regards China as its biggest and most formidable strategic adversary that must be isolated, demonized and defeated.

The chart above explains everything, not just the hostile diplomatic jabs that are designed to discredit and humiliate China, but also the openly belligerent policies that are aimed at Russia as well. People need to understand this. They need to see what is really going on so they can put events in their proper geopolitical context.

And what “context” is that?

The context of a Third World War; a war that was thoroughly-planned, instigated and (now) prosecuted by Washington and Washington’s proxies. That’s what’s really going on. The increasingly violent conflagrations we see cropping-up in Ukraine and Asia are not the result of “Russian aggression” or “evil Putin”. No. They are the actualization of a sinister geopolitical strategy to quash China’s meteoric rise and preserve America’s dominant role in the world order. Can there be any doubt about that?

No. None.

This is why we are experiencing the redivision of the world into warring blocs. This is why we are seeing the roll back of 30 years of Globalization and massive suppyline disruption. And this is why Europe has been thrust headlong into frigid darkness and forced deindustrialisation. All of these suicidal policies were concocted for one purpose and one purpose alone, to maintain America’s exalted spot in the global system. That is why all of humanity is presently embroiled in a Third World War; a war that is designed to prevent China from becoming the world’s biggest economy; a war that is designed to preserve US global primacy. Check out this excerpt from an article at the World Socialist Web Site:

An October 19 Financial Times article by Edward Luce, entitled “Containing China is Biden’s explicit goal,” sounded the following alarm: “Imagine that a superpower declared war on a great power and nobody noticed. Joe Biden this month launched a full-blown economic war on China—all but committing the US to stopping its rise—and for the most part, Americans did not react.

“To be sure, there is Russia’s war on Ukraine and inflation at home to preoccupy attention. But history is likely to record Biden’s move as the moment when US-China rivalry came out of the closet.”

Moreover, last week, a top Biden administration official indicated that the US was preparing new bans on China in key hi-tech areas. Speaking at the Center for a New American Security, Alan Estevez, the under-secretary of Commerce for Industry and Security, was asked if the US would ban China from accessing quantum information science, biotechnology, artificial intelligence software or advanced algorithms. Estevez admitted that this was already being actively discussed. “Will we end up doing something in those areas? If I was a betting person, I would put down money on that,” he said….

Luce concluded his Financial Times article cited above by declaring: “Will Biden’s gamble work? I’m not relishing the prospect of finding out. For better or worse, the world has just changed with a whimper not a bang. Let us hope it stays that way.”…(“Biden’s technology war against China”, World Socialist Web Site)

Once again, look at the chart. What does it tell you?

The first thing it tells you is that the hostilities we see in Ukraine (and eventually Taiwan), can be traced back to a fundamental shift in the global economy. China is growing stronger. It’s on a path to overtake the United States economy within the decade. And with growth, come certain benefits. As the world’s biggest economy, China will naturally become Asia’s regional hegemon. And, as Asia’s regional hegemon it will be able “to settle regional disputes in its own favor and to de-legitimize U.S. regional and global leadership.”

Can you see the problem here?

For nearly two decades, the US has oriented its foreign policy around a “rebalancing of forces” strategy called the “pivot to Asia”. In short, the US intends to be the dominant player in the world’s most populous and prosperous region, Asia. Can you see how China’s rise derails Washington’s plan for the future?

The United States is not going to let this happen without a fight. Washington is not going to let China muscle-it-out of the markets that it plans to dominate. That’s not going to happen. And if you think that’s going to happen, you’d better think again. The United States will go to war to avoid a scenario in which the US plays “second fiddle” to China. In fact, the foreign policy establishment has already decided that the US will engage China militarily for that very objective.

So, our thesis is simple; we think WW3 has already begun. That’s all we’re saying. The ructions we see in Ukraine are merely the first salvo in a Third World War that has already triggered an unprecedented energy crisis, massive worldwide food insecurity, a catastrophic break-down in global supply lines, widespread and out-of-control inflation, the steady reemergence of extreme nationalism, and the redivision of the world into warring blocs. What more proof do you need?

And it’s all economic. The origins of this conflict can all be traced back to the seismic changes in the global economy, the rise of China and the unavoidable decline of the United States. It is a case of one empire replacing the other. Naturally, a transition of this magnitude is going to generate tectonic changes in global distribution of power. And along with those changes will come more flashpoints, more devastation, and the looming prospect of nuclear war. And this is precisely how things are playing out.

So, how does the chart explain what is happening in Ukraine?

Washington’s proxy war in Ukraine is actually aimed at China not Russia. Russia is not a peer competitor and Russia does not have the economic wherewithal to displace the United States in the global order. NordStream, however, did pose a significant risk to the US by greatly strengthening Moscow’s economic relations with the EU and particularly with Europe’s industrial powerhouse, Germany. The Moscow-Berlin alliance—which was mutually beneficial and key to German prosperity—had to be sabotaged to prevent further economic integration that would have drawn the continents closer together into the world’s biggest free trade zone. Washington had to stop that in order to preserve its economic stranglehold on Europe and defend the dollar as the world’s reserve currency. Even so, no one expected the US to blow up the pipeline itself in—what appears to be—the greatest act of industrial terrorism in history. That was truly shocking.

In essence, Washington sees Russia as an obstacle to its “pivot” plan to encircle, isolate and weaken China. But Russia is not the greatest threat to US global primacy; not even close. That designation belongs to China.

The Third World War is being waged to contain China not Russia. What the war in Ukraine suggests is that—among foreign policy elites—there is general agreement that, The road to Beijing goes through Moscow. That appears to be the consensus view. In other words, US powerbrokers want to weaken Russia in order to spread US military bases across Asia. Ultimately, the military will be called upon to enforce Washington’s economic rule over its new Asian subjects. If that day ever comes.

We think it is extremely unlikely that Washington’s ambitious plan will succeed, but we have no doubt that it will be implemented all the same. Tens of millions of people are likely to die in a desperate attempt to turn-back the clock to the fleeting ‘unipolar moment’ and the equally short-lived American Century. It is a tragedy beyond comprehension.

Tyler Durden

Fri, 11/04/2022 – 23:00 - Getting Away With Murder In The US?

Getting Away With Murder In The US?

The share of murders going unsolved is on the rise in the United States, according to the FBI’s Criminal Justice Information Services (CJIS).

As Statista’s Anna Fleck details in the chart below, 2020 saw a record low of only 54.4 percent of the country’s homicide cases cleared – or an estimated 9,836 out of 21,570 crimes. Due to data reporting delays, this is the latest available data.

You will find more infographics at Statista

A case is “cleared” when either it is solved and the suspected killer has been arrested and formally charged or when the case has been deemed an “exception”, which means the assailant cannot be arrested, whether that’s because they are already dead, imprisoned elsewhere, or for another reason.

The sudden drop in 2020 can partly be attributed to the fact that homicides saw a nearly 30 percent increase that year, according to the FBI’s 2020 Uniform Crime Report, which meant police and sheriff’s departments were overwhelmed with cases.

The longer downward trend, however, is likely the result of a number of reasons.

For instance, analysts argue that data collection in the 1960s and 1970s is not fully reliable and so their clearance levels are likely exaggerated.

Meanwhile, more recently, a decline in police trust and willingness to work with law enforcement are also possible factors.

Jeff Asher, a crime analyst, explains in an interview with The Atlantic, that the rise in gun violence is a main contributor to the trend. Since guns can be shot from further away, gunshot homicides tend to be more difficult to solve.

“The nature of murder in America is changing in ways that we don’t really talk about enough”, he explains.

“You’ve got a bunch of cities where firearms make up 80 to 90 percent of murders today. That is the main driver. Guns make murders much harder to solve, and it leads to lower clearance rates everywhere.”

Judge the source on that last one…

Tyler Durden

Fri, 11/04/2022 – 22:40 - Macleod: The Great Global Unwind Begins, Part 2

Macleod: The Great Global Unwind Begins, Part 2

Authored by Alasdair Macleod via GoldMoney.com,

With price inflation rising out of control and interest rates rising strongly, the trading environment for commercial banks has fundamentally changed. With bad debts looming and bond prices in entrenched downtrends, procrastination is now the enemy of bankers.

We are at the beginning of The Great Unwind, and this article elaborates on my first article for Goldmoney on the subject published here.

The imperative for bankers to respond to these conditions overrides all other matters if their businesses are to survive these changed conditions. We are entering a cyclical downdraft of the bank credit cycle which promises to be cataclysmic. And the monetary policy planners at the central banks can do nothing to stop it.

After outlining the scale of the problems faced by each global systemically important bank, this article looks at the future for the $600 trillion derivatives mountain.

It was born out of the long-term decline in interest rates from the mid-eighties, which ended last year. It is almost entirely distributed through banks and shadow banks.

The question to address is, what is the future for the derivative mountain, now that the long-term trend for falling interest rates is over? And what are the economic consequences?

If it’s you in the hot seat…

Imagine, for a moment, that you are the CEO of a commercial bank involved in lending to businesses and with profit centres acting in a range of financial activities. As CEO, you are answerable to the board of directors for the bank’s performance, and ultimately the bank’s shareholders for maintaining and advancing the value of their shares.

Furthermore, let us set this imaginary exercise in the present. These are the issues that should keep you awake at night:

-

In common with your competitors, the ratio of your balance sheet assets to total equity is almost the highest in the history of the bank, in many cases for other banks over twenty times leaveraged.

-

Official inflation, measured by the CPI is about ten per cent, and producer prices are rising somewhat faster. Your central bank expects a return to the 2% target in two- or three-years’ time. But your contacts at the central bank have privately admitted to you that they cannot imagine the circumstances where this would be true without a deep recession.

-

Bond yields are rising, and losses are beginning to impact on the bank’s investments. The bank has relatively little direct exposure to corporate bonds and equities, but they are commonly held as collateral against customer loans.

-

How are higher interest rates impacting the quality of the bank’s loan book? The bank supported its business customers through the covid pandemic, which increased the indebtedness of them all. This exposes the bank to excessive default risk if rates rise further.

-

The mortgage loan book has been a profitable business for decades. But the bank is beginning to see a material rise in delinquencies. If loan guarantees are not forthcoming from government agencies, the bank may have to shut this activity down.

-

What impact will higher interest rates have on the bank’s derivative exposure? What are the counterparty risks in derivative chains? Derivatives that involve inadequately capitalised counterparties should perhaps be sold on, or where the bank has the option to do so, closed down.

The underlying problem is that the conditions that led to the bank becoming increasingly involved in diversified activities, such as investment banking, trading, and investment management have now changed. Since financial deregulation in the 1980s, the bank has expanded into these profitable areas. The whole industry moved from dealing in credit into generating fee income. The growth in fee income can be directly related to the long-term trend of falling interest rates, which apart from interruptions such as the dot-com excesses and the Lehman crisis, stimulated growth in corporate finance, underwriting, investment management, and trading in financial securities. The expansion of these activities in turn led to a massive expansion of derivative markets, with new instruments being devised, such as credit default and interest rate swaps.

If, and this is really what should worry you, the long-term trend of falling global interest rates has ended and is now set to be reversed, not just temporarily but for the rest of the decade and perhaps beyond, then the reasons justifying the bank’s expansion away from its core lending business have come to an end. As CEO, how do you unwind the deep-rooted departmental interests, and keep the shareholders onside?

It is time for the whole executive to be urgently involved in a wide-ranging debate about how serious these threats might be and where you should take actions to protect the bank’s shareholders’ interests. Given the high level of balance sheet leverage, the bank’s survival is at stake if you act indecisively or too slowly. You are facing head-on the unpleasant prospect of The Great Unwind.

Balance sheet ratios

There are two ratios that concern bankers. The first is the relationship between liquid and illiquid assets with respect to sources of balance sheet funding. These are set by regulators through Basel regulations, now in their third iteration. Banks are required to submit details of their balance sheets periodically to bank regulators in accordance with the net stable funding requirement formula as set out in Basel III.

The second ratio is of less importance to regulators, which is the relationship between Tier 1 capital and the total balance sheet, which Basel regulations simply states that the maximum leverage ratio is for Tier 1 capital to not be less than 3% of the bank’s balance sheet assets. Put another way, subject to certain conditions, a bank can theoretically leverage its assets to equity as much as thirty-three times. But it should be noted that within that leverage ratio, a bank is permitted to net off certain classifications of credit, reducing its apparent balance sheet size. The following are examples of hidden forms of balance sheet assets and liabilities:

-

Security financing transactions, which include repos and other derivatives, can be netted off where they are between the same counterparty and maturity. For a true accounting picture, a bank balance sheet should reflect credit and debt obligations on both sides of its balance sheet until they are extinguished.

-

Long and short credit derivatives can be netted so long as there is no maturity mismatch. Again, the full obligations should be reflected on both sides of the balance sheet. And valuation methods give banks enormous wriggle room, an issue which regulators are unable to properly address.

-

Off-balance sheet items are only partially recognised through standardised credit conversion factors. Where a bank has off-balance sheet activities, they should be properly reflected in its accounts.

Therefore, true bank balance sheet leverage can be considerably greater than a bank complying with Basel regulations will declare in its audited accounts. But while conforming with Basel regulations, the board of a bank has a primary duty, often forgotten even by some directors, to their shareholders.

It is changes in the ratio between a bank’s assets and its shareholders’ equity which drive the cycle of bank credit expansion and contraction, which in turn drives the business cycle.

While they have a specific expertise in assessing lending risk, bankers are human. When they perceive lending risk to decline, they increase the quantity of credit offered, recorded as assets on their bank balance sheets, without increasing shareholders’ equity. Their confidence is synchronised through individual banks’ market intelligence and commonly available information concerning lending conditions. What few bankers realise is that it is expansion of their cohort lending which creates the very confidence in the lending conditions being observed.

The benefit to the bank is enhanced by expanding the ratio of total balance sheet assets to shareholders’ equity. A gross lending margin of two per cent becomes 20% for the shareholders on a balance sheet ten-times leveraged. However, this depends on margins being maintained, which, when banks compete with each other for lending business, is unlikely. Furthermore, the trend for declining rates over the decades due to the policies of the monetary authorities has led to a general increase in shareholder leverage as banking cohorts try to maintain profitability on slimming margins.

We all know that this recently reached an extreme position, with unnaturally negative interest rates imposed by central banks principally in Japan, the Eurozone, and Switzerland. In response to heavily compressed rate margins, the large commercial banks in the Eurozone were leveraging up through repos to gear up the slimmest of lending margins. The European repo market has been rolling over in excess of €9 trillion in all currencies with euros the largest component by far.

For these reasons, the most highly leveraged G-SIBs (global systemically important banks) are in the Eurozone and Japan. Table 1 below shows their balance sheet leverage from highest to lowest (the third column), and the price to book rating upon which the market values this leverage risk. Share prices were as of last weekend.

With the Eurozone’s and Japan’s G-SIBs heading the list of most highly leveraged banks, the question before us is now that interest rates are rising, how will these banks adjust their balance sheet ratios to more normal levels, which are probably in the region of eight to ten times or even less? True balance sheet gearing in all cases is likely to be far, far higher principally because of the accounting treatment of derivative obligations. These are the banks leading involvement in repos, have significant derivative positions, have netted out foreign exchange, commodity, and credit derivatives, and have only partially reflected off-balance sheet obligations through standardised credit conversion factors.

In general terms, in the new interest rate environment banks are almost certain to restrict counterparty risk by reducing their exposure to other banks for two reasons. Firstly, contracting balance sheets throughout the banking industry enhance systemic risk significantly, and a significant number of the banks in Table 1 are highly likely to fail. And secondly, as a cohort bankers are motivated to act the same way for the same reasons at the same time, even for banks without derivative exposure. The contraction and consequences of interbank obligations should not be ignored.

The problems of rising inflation, interest rates, and bond yields

After decades of minimal price inflation, central banks were caught unawares when consumer prices started to rise and continued to do so. Initially, they said it was transient. When they were laughed at, they then merely pushed back their forecasts of consumer price inflation returning to the 2% target back a year. The chart below, of the current UK’s Office for Budget Responsibility forecast is typical. It is due to be updated on 17 November, but it is a racing certainty that the OBS will still expect it to return to 2%, a little further delayed. To admit otherwise is to acknowledge a complete failure of monetary policy.

The US Congressional Budget Office is similarly unrealistically optimistic about the outlook for consumer price inflation. The illustration below is lifted from the CBO’s website.

But with consumer prices already rising in the US, UK, and Europe at a 10% clip and likely to go higher in the coming months, the interest rate disconnection is substantial and can only be bridged with interest rates doubling or even tripling from current levels. Even if they only double, business plans for all manufacturers and service providers will go out of the window. And with that catastrophe, bad debts for the banks will simply soar.

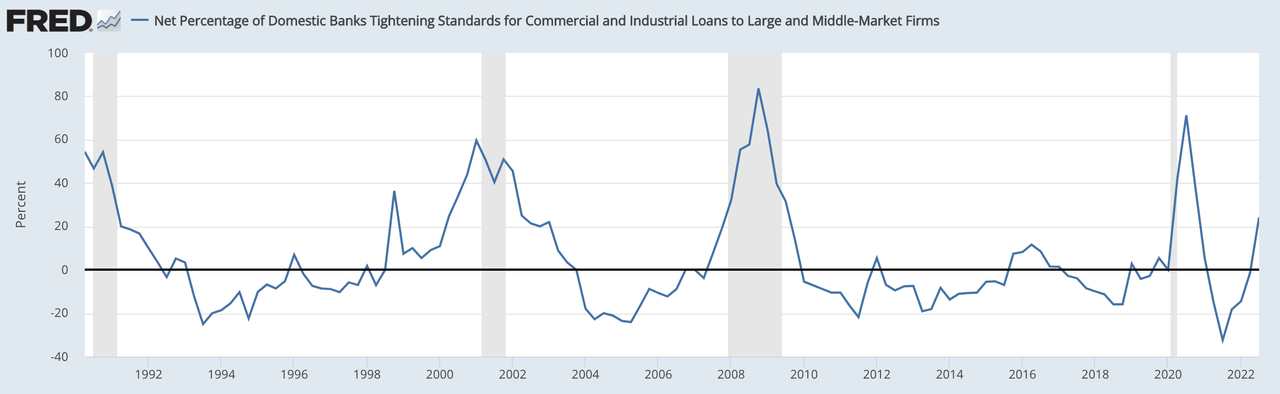

The effect on financial securities will be no less devastating. While banks generally limit their bond exposure to shorter maturities — typically bills and bonds maturing in less than a year — it is likely that banks in the Eurozone and Japan will have some exposure to longer maturities. They might have some exposure to corporate bonds and collateralised debt obligations as well, which will be at risk from rising interest rates. This is not to be ignored, and the evidence of a downturn in credit availability for corporates is already evident in loan officer surveys. Our next chart, of US banking sentiment towards corporate borrowers confirms that credit contraction for non-financial borrowers is already underway.

Clearly, bank credit is set to contract mightily, and together with higher interest rates it is likely to lead to escalating non-performing loans, insolvencies, and rising unemployment. These conditions are likely to develop before interest rates can properly reflect the debasement of the major currencies, reflected in the rise in consumer prices.

Economists commonly assume that the developing recession will restrict consumer demand, leading to an amelioration of the consumer price inflation problem. Furthermore, some supply chains are beginning to flow again, particularly with respect to computer chips. But before we can consider how a fall in demand affects prices, we should remember that the initial market effect of contracting bank credit is always to drive interest rates higher, due to accelerating credit demand arising from lost sales and accumulating inventories while banks are trying to reduce their credit obligations.

Since almost all recorded transactions that make up GDP are settled with bank credit, its contraction will reduce GDP as well. The extent to which this is the case cannot be mechanically predicted. However, since bank balance sheets are very highly leveraged and rising interest rates will force a severe credit contraction, the effect will not be trivial. If a banker is to retain control over non-performing write-offs, he must not delay in reducing his exposure.

It is for this reason that the cycle of bank credit is like a saw-tooth series of gradual increases followed by sharp declines. And the more exaggerated the increase, the more catastrophic the decline.

Mortgage loan books

It turns out that the sub-prime mortgage crisis of 2007-2009 was little more than a blip in the growth of bank lending for residential property ownership. But America with Fanny Mae and Freddy Mac is different from other jurisdictions, where banks have become highly active originators in the mortgage business.

With old memories of ruinous interest rates, borrowers have consistently gone for fixed rate mortgages in preference to floating rates. Some 80% of residential mortgages in the UK are fixed rate for between two and five years before they are reset. Until recently, to opt for fixed rates was the wrong decision. Banks have profited mightily, not by simply lending long and borrowing short, but by covering fixed rate offers with interest rate swaps allowing a healthy turn for the bank, with early termination expenses covered by penalties for the borrower.

For a bank, the beauty of this business lies in the transaction size and minimal administration. And with house prices continually rising, the collateral has been secure. But this has now changed dramatically, with mortgage rates soaring and house prices turning lower. The previous lucky minority who opted for floating rates find they face an enhanced risk of repossession of their homes. And interest rates have probably only started to increase.

From a banker’s point of view, this is turning into a very bad business. Payment defaults are certain to increase rapidly; not just for those on floating rates, but with the majority of borrowers on two- and three- fixed rate deals which are maturing at a rapid rate. A two-year fixed rate of less than two per cent faces renewal at over three times that. And no banker wants the bad publicity of foreclosing on homeowners and their families in droves, “who through no fault of their own” face eviction.

In any event, when homeowners in large numbers face eviction, the lenders have the problem more than the homeowners. It is both politically and practicably impossible for lenders to evict families in large numbers and put their homes up for sale. Apart from anything else, residential property values would collapse under the combined weight of higher borrowing costs (if mortgages are still available) and an increasing supply of liquidated housing stocks. Look no further than what happened to property prices in cities like Atlanta in 2007-2010, as the liar-loans were unwound. All that happens from the bank’s point of view is that even solvent borrowers would be pushed deeply into negative equity.

The difficulties in managing these politically toxic issues will not be the only problem facing bankers. Existing fixed-rate mortgages have been covered through credit default swaps, which are only as good as a bank’s counterparties. If, say, a British bank has a highly leveraged Eurozone bank as its counterparty, it will soon be thinking about counterparty risk in a more focused way. Where it can, it should seek to novate these obligations with more secure counterparties. But that comes with costs.

In a rising interest rate environment, this easy-come business will not be easy-go.

Wider derivative considerations

According to the Bank for International Settlements, OTC derivative market interests in the global banking system amounted to $600 trillion equivalent of notional amounts outstanding last December.[i] Being based on only seventy dealers in twelve countries reporting to their respective central banks, the statistics are not the whole picture, capturing an estimated 94% on average of their wider triannual survey covering an additional thirty nations.

To this can be added a further $40 trillion in regulated futures and options markets, in which banks play a major counterparty role. To give an idea of the sheer scale of these activities, global GDP is estimated at roughly $100 trillion.

The credit nature of OTC derivatives is poorly understood, and therefore widely ignored by commentators. Nevertheless, these are credit obligations which are only extinguished after the terms of the individual derivative contracts have been satisfied. But being purely financial, they differ from a contract which has on one side the delivery of goods or a service, and on the other a settlement invariably in bank credit. A financial transaction, be it a forward settlement, a swap, or an option exercise, involves both debt and credit obligations. And since debt is synonymous with credit because one always balances the other in both parties’ books, until a financial obligation is settled there is twice the notional credit involved.

The simplest example to take is deferred settlements, such as foreign exchange forwards. In these cases, there are two parts to the contract: there is the initial agreement, under whose terms there may or may not be a partial margin payment due immediately, and the second part is satisfaction of the entire contract by its completion.

At a notional $104 trillion — the BIS’s figure for mid-2021— foreign exchange contracts are the second largest segment of the $600 trillion OTC total. Ten per cent of that $104 trillion are options. According to the BIS’s triannual survey, only 84% of foreign exchange contracts are captured in the semi-annual statistics, so a truer figure is $124 trillion.

By maturity, they split 80% up to a year, 15% one to five years, and the rest over five years. Therefore, these are not a simple case of next day settlement, but credit obligations of material duration.

The status of options is different from forward settlements, being initial settlements for a transaction that might not eventually take place. The buyer of the option has no further credit obligation other than the initial payment of a premium to the seller of the option. But the latter party does have a continuing credit obligation which is not in his power to extinguish before it finally matures. Because all foreign exchange contracts on the BIS’s statistics represent only one side of foreign exchange contracts, the whole amount of $124 trillion are definitely credit, the majority of which, only excluding options, is duplicated by matching credit obligations for the other counterparties. Therefore, total foreign exchange derivative credit in trillions is double notional amounts outstanding less one side of notional options. This amounts to $236 trillion.

According to the BIS, the gross market value of this credit is $2.548 trillion. The BIS defines gross market value as “the sum of the absolute values of all outstanding derivatives contracts with either positive or negative replacement values evaluated at market prices prevailing on the settlement date”. In other words, to the extent to which the banking system is counterparty to these OTC derivatives, in total their balance sheets will reflect this figure, and not actual credit obligations, which are almost a hundred times greater.

It is in this context that counterparty risk must be considered. Counterparty risk is a wager that delivery of a credit obligation might not occur, and the relevant figure with respect to foreign exchange commitments alone for assessing it is $236 trillion. As an indication of the scale of these credit obligations, the BIS reports that the total of global bank credit to the non-financial sector amounted to $226.3 trillion at the date of its latest derivative statistics, similar to the scale of foreign exchange derivative credit on its own.[ii]

In round figure terms, all other OTC derivatives in the BIS statistics total about five times the recorded foreign exchange total. They include in the BIS’s notional amounts:

-

Interest rate contracts — $475.2 trillion

-

Equity-linked contracts —$7.28 trillion

-

Commodity contract — $2.22 trillion

-

Credit derivatives — $9.06 trillion

-

Credit default swaps — $8.80 trillion

-

Not otherwise classified — $337 billion.

Interest rate derivatives in rising rates

Interest rate derivatives make up the vast bulk of all OTC derivatives, with the notional contract amount of interest rate swaps totalling $397.11 trillion, and forward rate agreements adding a further $39.44 trillion. A swap is a financial derivative in which two parties agree to exchange payment streams based on a specified notional amount for a specified period. And a forward rate agreement is a contract in which the rate to be paid or received on a specific obligation is for a set period of time, beginning at some time in the future.

What concerns us here are the consequences of a rising trend of interest rates for the values of these contracts. FRAs might continue thrive if interest rate relationships along yield curves permit. But an environment of rising counterparty risk might be a hurdle too high for participating banks to overcome. A far more important consideration is the future for interest rate swaps.

Unlike the foreign exchange contracts described above, interest rate swap notional amounts are not bank credit obligations. The credit commitments of both parties are only for the income streams on a notional amount. An originator, usually a bank, funds a fixed interest stream from a floating rate, rather than the other way round.

A clue to the relationship between the gross market value of these contracts and interest rates is illustrated below, which is of interest rate swaps only originated in US dollars.

The chart confirms what we would expect: that major falls in the Fed funds rate stimulate the gross market value of interest rate swaps; and increases in the funds rate correspondingly leads to falls in their gross value. From this, we confirm that declining interest rates lead to profits for banks taking floating rates and offering fixed rates. This is the protection that customers from the gamut of pension funds to homeowners seek from higher rates. While over the long-term interest rates were declining, interest rate swaps were a profitable form of insurance product for the banks to offer. And we can now see that with sharply rising interest rates, not only will these profits vanish, but the banks are bound to exit this market entirely.

This is the heart of The Great Unwind. It will be a surprise to observers to see the BIS’s OTC derivative statistics collapse as interest rates rise further. Existing contracts with time to run can be closed down by buying out counterparties, entering offsetting swaps, selling the swap to another party, or entering an option on offsetting swaps. But these solutions to a bank withdrawing from interest rate swap obligations will be very costly, if available at all, as the entire banking cohort attempts to depart from this market.

Undoubtedly, large losses will result, threatening the entire global banking network through enhanced systemic risk.

Derivatives and the Bretton Woods III meme

That we are entering an entirely new banking and financial environment was originally put forward by a Credit Suisse analyst, Zoltan Pozsar, earlier this year. Pozsar argued that since the ending of Bretton Woods, a new financial era had dominated financial markets, which he described as Bretton Woods II. He contended that the trend for lower interest rates has now ended, that global supply chains will be repatriated, and that the era of the petrodollar is over. Instead, Bretton Woods III will be the era of commodity-based currencies.

Driving his argument was the imposition of currency sanctions against Russia. In his 3 March article, he posed the question: is the OTC commodity derivatives market the gorilla in the room?[iii] His concern was over margin calls faced by producers and others in the physical commodity business hedging physical product by carrying short positions in the futures markets. As if on cue, Trafigura, the big commodities trader, had to be refinanced within weeks of Pozsar’s note having received massive margin calls on its OTC positions.[iv]

Since Pozsar’s note, Saudi Arabia has signalled the death of the petrodollar by aligning itself with the Russia-China axis, and is scheduled to join the BRICS organisation next year. Members of the Eurasian Economic Union are planning a new trade settlement currency, said to be linked at least partly to commodities. And Moscow is setting up a new gold exchange to handle Russian and other nations’ refined gold, which will almost certainly adopt China’s 99.99% gold kilo standard.

Undoubtedly, the movement towards commodity-linked currencies, the decline of the dollar’s hegemony, and of western financial markets will have a major impact on commercial banking. One wonders how many of the banks weaned on financial activities can make the transition back to traditional lending. And if global supply chains are a thing of the past, will they be prepared to provide the credit for investment in replacement component production in the advanced economies?

As a subset of commodity derivatives, the London Bullion Markets’ forward contracts were estimated to be $781bn on 31 December 2021, of which gold forwards and swaps represented $528bn. At that date, this was the equivalent of 8,975 tonnes compared with 1,595 tonnes in the main gold contract on Comex — a ratio of 5.6 to one

The other side of the LBMA banks’ derivative positions is unallocated customer accounts, originally devised and expanded as a means of diverting demand for gold that would have otherwise driven up the price of bullion. The trend towards increasing quantities of paper bullion relative to the physical is likely to be reversed, because suppression of the gold price is now leading to accelerating demand for physical bullion.

While Keynesian hedge fund managers claim that higher interest rates are bad for the gold price, rising interest rates are bound to render derivative trading unprofitable for banks which find themselves both short of derivatives, and technically short to their unallocated bullion account holders. As quickly as the London bullion market developed in the 1980s, it is likely to diminish as interest rates increase.

Economic consequences of contracting bank credit

Today, the priority for commercial banks is to reduce their balance sheets to more normal conservative levels in their shareholders’ interests. Without considering secondary factors, the likely consequences of a severe credit contraction for the nominal GDP statistic could be to reduce it by a third or more in major jurisdictions. Realistically, central banks will have no option but to finance the losses of tax revenue and the increased welfare burdens falling on their government’s shoulders. The expansion of central bank currency and credit will replace the contraction of commercial bank credit.

Empirical evidence suggests that a population is more alert to the inflationary implications of central bank credit expanding than that of commercial bank credit. Essentially, if the public deems the currency to be stable, it will respond to higher prices when it is the result of bank credit expansion by moderating their spending. But if the public sees the currency as being unstable, they will vary their spending, and therefore their liquidity reserves accordingly.

Clearly, the political imperative will be to replace lost commercial bank credit with central bank credit. Nor can we rule out “helicopter drops” in an attempt to stimulate recovery. But having tried these measures during the covid pandemic, the public reaction to central bank debasement in a deep recession is almost certain to be less tolerant.

Central banks, which are already ceding control of interest rates to market forces will find they continue to rise as currencies’ purchasing powers continue to quicken their collapse.

Conclusion

As dealers in credit, banks face the most difficult times in living memory. Austrian economists have long understood that the business cycle is driven by a cycle of bank credit. The root of the credit cycle has been ignored by statist economists and policymakers who respond by suppressing the evidence. This has been going on with increasing intensity since the 1980s, when the Fed under Paul Volcker broke with interest rate suppression to slay the 1970s inflation dragon.

Since then, the era of pre-Bretton Woods price stability has been replaced by the fiat dollar as the reserve currency, with demand for it engineered by Triffin’s dilemma: balancing the export of dollars through budget and trade deficits with global demand for it. The expansion of derivative markets served to conceal the inflationary effects by shifting the supply of dollar credit into financial markets, away from non-financial activities. This lessened the consequences of currency expansion on the prices of goods and services, allowing the monetary authorities to suppress interest rates without apparent ill effects.

That period has now ended, and The Great Unwind of all the distortions accumulated over the last four decades has begun. No one in government and central banking circles saw it coming, and they are still in denial.

Commercial bankers are becoming acutely aware of the dangers to their business models. At the moment, they have only a growing fear of the consequences of interest rates seemingly out of control. Having been protected from free markets by central banks and their regulators, this loss of statist control is immensely worrying for them.

It is now dawning on commercial bankers that they have been left high and dry, with over-leveraged balance sheets, loan business rapidly souring, loan collateral falling in value, and a derivative merry-go-round about to implode. They must stop pandering to regulators and public opinion, and now protect their shareholders from The Great Unwind by dumping credit obligations as rapidly as possible ahead of the wider banking crowd.

From banking deregulation in the mid-eighties, it took nearly four decades to get to this point. The Great Unwind might take only as many months.

Tyler Durden

Fri, 11/04/2022 – 22:20 -

- Dear Liberals, How Many Of These MSM Hoaxes Did You Fall For?

Dear Liberals, How Many Of These MSM Hoaxes Did You Fall For?

How many recent mainstream media hoaxes did you fall for? … and/or still believe?

-

Russian collusion

-

Trump called neo-nazis “fine people”

-

Jussie Smollett

-

Bubba Wallace garage pull

-

Covington kids

-

Governor Whitmer kidnapping plot

-

Kavanaugh rape

-

Trump pee tape

-

COVID lab leak was a conspiracy theory

-

Border agents whipped migrants

-

Trump saved nuclear secrets at Mar-a-Lago

-

Steele Dossier

-

Russian bounties on US soldiers in Afghanistan

-

Trump said drinking bleach would fight COVID

-

Muslim travel ban

-

Hunter Biden’s laptop was Russian disinformation

-

Andrew Cuomo best COVID leadership

-

Trump built cages for migrant kids

-

“Austere religious scholar”

-

Trump overfed Koi fish in Japan

-

Build Back Better will pay for itself

-

Trump tax cuts benefited only the rich

-

Cloth masks prevent COVID

-

If you get vaccinated you won’t catch COVID

-

SUV killed parade marchers

-

Trump used teargas to clear a crowd for a bible photo

-

“Don’t Say Gay” was in a bill

-

Putin price hike

-

Ivermectin is a horse dewormer and not for humans

-

“Mostly peaceful” protests

-

Trump overpowered secret service for wheel of “The Beast”

-

Officer Sicknick was murdered by protesters

-

January 6th was an insurrection

-

BYU students hurled racist insults at Duke volleyball player

-

And don’t forget “democracy is under threat…”

h/t Mitch P.

Tyler Durden

Fri, 11/04/2022 – 22:00 -

- School Choice Is About To Revolutionize K-12 Education

School Choice Is About To Revolutionize K-12 Education

Authored by Brian McGlinchey via starkrealities.substack.com

Since the beginning of the Covid-19 pandemic, America’s parents have shifted nearly 2 million students from public schools to alternatives that include private schools and home schooling. For public schools, that represents a loss of about 4% of their enrollment.

Expect the exodus to grow larger, as the United States is undergoing a major change in philosophy regarding publicly-funded K-12 education, away from funding government-run school systems and toward funding individual students—with parents getting to choose where their children learn.

In June, Arizona put itself at the leading edge of that shift: Every Arizona family can now direct about $7,000 a year per student toward the education solution of their choice. Funds can be used for private schools, home schooling, tutoring and online learning.

Arizona Governor Doug Ducey at a celebration of his signing of the law allowing all students to use pubic funds to attend the school of their choice (Photo: Governor’s office) Arizona also provides free choice among public schools — rather than being forced into a particular school by neighborhood, parents who prefer public schools can pick whichever one they want, first-come first-served.

Defenders of the status quo typically characterize school-choice laws as “taking money away” from public schools, recoiling at the very idea that government money would be spent anywhere other than a government institution.

However, that’s already how the great majority of publicly-funded education and other entitlements work, without uproar.

“We have Pell Grants for low-income students for higher eduction, we have the Head Start program for pre-K where you can pick public, private, religious or non-religious,” said Corey DeAngelis, a senior fellow at the American Federation for Children, on Michael Malice’s “Your Welcome” podcast.

“We have food stamps where the money goes to the person and you can pick Walmart or Trader Joe’s…it doesn’t go to a residentially-assigned, government-run grocery store. That would be absolutely ridiculous.”

Meanwhile, those who say school choice programs will drain public schools of huge sums of money are implicitly asserting that, were it not for a system that protects public schools from competition — by granting them a monopoly on the use of public K-12 funds — a great many more parents would send their children elsewhere.

For decades, public school monopolies have been protected by a particular, self-reinforcing power dynamic:

-

Powerful teacher unions overwhelmingly favor Democratic politicians. Exhibit A: Democrats have received 99.94% of congressional contributions from the American Federation of Teachers in 2022.

-

Democratic politicians protect public school monopolies by opposing voucher and other school choice programs, while relentlessly pushing for increased public school funding

-

Increased funding enables the hiring of more public school staff

-

Larger staffs mean more union dues, enriching teacher unions and increasing their political power…and the cycle repeats

Today, however, there are large cracks in the foundation of this monopoly-protecting fortress, and the government response to the Covid-19 pandemic has been a big factor.

With public schools closed to in-person instruction, parents were suddenly much more engaged in their children’s education, and many didn’t like what they were seeing as they observed remote teaching.

As the pandemic ground on, relentless union opposition to school re-openings, and the insistence on masking children despite the many collateral harms of doing so, made it all too clear to enlightened parents that public teacher unions — and public school boards — can’t be trusted to always put children’s interests first.

Mask-free GA gubernatorial candidate Stacy Abrams surrounded by children forced to wear masks Though the government’s destructive responses to the pandemic are now largely behind us, the impact on parent attitudes about public schools is still growing, as a steady stream of reports illuminates the massive learning setbacks experienced by K-12 victims of school shutdowns.

At the same time, new data shows that students in private schools — which were much more eager to provide in-person instruction — fared significantly better.

The ongoing culture wars are another reason more people are embracing the idea of funding students rather than systems.

Parents understandably have strongly differing ideas about what’s appropriate for the classroom. Rather than forcing opposing parents into the same school and having them fight at board meetings about which curriculum will be forced onto everyone, each family should be free to seek out a school arrangement that best matches their own philosophy — and use public money to do so.

Austin elementary school kids forced to mask and join a Pride Month march (via Libs of TikTok) Many politicians who oppose school choice are themselves private school products or send their own children to private schools. One of the most notorious such hypocrites is Democratic Senator Elizabeth Warren.

Pandering to teacher unions as a presidential candidate, Warren said she not only wanted to stop school choice programs, but also end federal funding for charter schools and make it harder to open new ones.

Yet Warren sent her son to private schools — including one on Philadelphia’s wealthy Main Line where total fees today are $42,600. Worse, she actually denied it when confronted about her hypocrisy by a group of black Atlanta activists, who know the worst-performing public schools tend to be in poor, minority communities — and that wealthier people like Warren have the disposable income to afford private schools without using government money.

Nebraska state senator Justin Wayne, a black Democrat who supports school choice, knows all that too. Wayne told his colleagues he’d vote against school choice if they moved their children to a school in his neighborhood “so we can go through the transformation — that you keep telling my community to wait for — together.”

BREAKING: Nebraska Senator Justin Wayne (D) again calls out his colleagues for sending their kids to private school while opposing school choice for others. pic.twitter.com/WiXAmcBRN8

— Corey A. DeAngelis (@DeAngelisCorey) January 11, 2022

https://platform.twitter.com/widgets.js

Arizona’s 2022 expansion is distinguished from other school-choice experiments by its universality — all children are eligible to use a stipulated amount of state school dollars for education at a public school, private school or home school, regardless of where they live or the incomes of their parents.

Having witnessed what Arizona has done, activist parents in other states are now pressuring their own legislatures. As they do, they’re backed by polls showing 72% of Americans now support school choice programs, including 82% of Republicans and 68% of Democrats.

Look for the school choice movement to take a major step forward in 2023 — most impactfully in Texas. The Lone Star State’s public school population is a close second in size to California’s, and nearly double the third largest, which is Florida’s.

In the wake of Arizona’s school choice expansion, Governor Greg Abbott said he too wants to let parents “send their children to any public school, charter school or private school with state funding following the student,” and the next biennial legislature section starts on Jan. 10.

While private school enrollments will surge, the rise of school choice will also stimulate a novel education approach that existed before the pandemic but was greatly popularized by it — learning pods.

When parents were let down by public school closures — with working parents suddenly scrambling to manage day-long supervision of their children — many of them formed collaborative learning pods, where small groups of children would gather at a single home to do schoolwork together and have social interaction.

Before the pandemic, other parents had already used a pod approach to home-schooling. As school choice programs allow the use of state money to cover the cost of home schooling, look for pods to proliferate.

Those pods won’t all be led by parents. The concept could turn into an ideal career alternative for public school teachers yearning to break free from public school system bureaucracy.

Consider the math in Arizona for a former public school teacher who sets out on her own and assembles a pod of 15 children to teach. With parents able to tap up to about $7,000 per student per year for education, that teacher could charge $105,000 for her services with no out-of-pocket expense for the parents. In 2021, public school teacher salaries in Arizona ranged between $40,554 and $68,910.

Particularly for middle and high schools, where deeper subject-matter knowledge is required, groups of specialist teachers could collaborate to form their own “micro-schools.”

Of course, when comparing income, teachers will have to factor in expenses and the loss of public school system employee benefits — as well as intangible changes in quality-of-life they realize by leaving a public school system behind.

Parents will have their own pros and cons to consider, which is one reason why school choice shouldn’t be equated with the wholesale destruction of public schools. Indeed, it’s likely to bring about long-needed improvements — especially when programs like Arizona’s let parents who stay in the public system choose which public school their child attends.

“Twenty-five of 27 studies suggest that…school-choice competition leads to better outcomes in the public schools,” said DeAngelis. “Why? Because school choice is a rising tide that lifts all boats. Competition works.”

* * *

Stark Realities undermines official narratives, demolishes conventional wisdom and exposes fundamental myths across the political spectrum. Read more and subscribe at starkrealities.substack.com

Stark Realities: Invigoratingly unorthodox perspectives for intellectually honest readers

Tyler Durden

Fri, 11/04/2022 – 21:40 -

- Take A Rare Glimpse Inside China's Zero-Covid Madhouse

Take A Rare Glimpse Inside China’s Zero-Covid Madhouse

The western world has been given a rare, intimate look inside the confines of a Chinese Covid-19 concentration camp, after Financial Times Shanghai correspondent Thomas Hale was ensnared by the President Xi Jinping’s zero-Covid regime.

It’s not that Hale had tested positive. Merely being designated as a “close contact” was enough to sentence him to 10 days of confinement on a secret island camp identified only as “P7.”

Hale provides a primer on framework of China’s system works:

“PCR testing in China is an almost daily ritual and testing booths are common on many street corners. They look vaguely like food stalls, except they’re larger and cube-shaped and a worker inside sits behind Plexiglas cut with two arm holes.

They are merely the surface machinery of a vast monitoring system. China’s digital Covid pass resembles track-and-trace programmes elsewhere, except it’s mandatory and it works. Using Alipay or WeChat, the country’s two major apps, a QR code is linked to each person’s most recent test results. The code must be scanned to get in anywhere, thereby tracking your location. Green means you can enter; red means you have a problem.”

Hale’s journey into Covid madness started with an innocent outing at a Shanghai bar. Apparently, someone who’d also been at the bar tested positive. Via the tracking system, the authorities knew Hale had been there too.

Hale had “won” some kind of terrible lottery: On the day he was in the bar, there were only 18 cases in all of Shanghai that day — a city of 26 million people.

A few days after his bar outing, authorities called to confirm he’d been at the bar. The next day, a caller from the Shanghai Municipal Center for Disease Control and Prevention alerted him that authorities were on their way. Hale was about to be “taken away” — an expression Chinese use when describing the phenomenon.

Next, a hotel staffer called to say he couldn’t leave, and that the hotel was in lockdown due to his mere presence in it. Then came the men in hazmat suits, who escorted him down a deserted hallway to a staff elevator and out through the cordoned-off hotel entrance. He was directed to board a small bus driven by another man in a hazmat suit.

Hale joined the other condemned passengers — none of whom had actually tested positive. His hopes that he’d be taken to a quarantine hotel were dashed. A drive of more than an hour ended on a small road in the middle of a field, with several large buses queued up ahead of his.

The driver got out, locked the bus behind him and wandered off. A fellow passenger was surprised to hear that Hale was from the UK: “They brought you here? With a foreign passport?” Hours of waiting on the increasingly chilly bus went by, until it finally moved again at 2 am.

As he was trudging along to his assigned quarters, a fellow detainee pointed to three rows of wire above the perimeter fences, beyond which were only tall trees.

Hale counted 10 alleyways, each with some 26 cabins (Thomas Hale/Financial Times) Hale’s new home was a box similar to a shipping container, elevated by short stilts. His and every door was monitored by a camera. There was no hot water.

“Inside my 196-sq-ft cabin there were two single beds, a kettle, an air-conditioning unit, a desk, a chair, a bowl, two small cloths, one bar of soap, an unopened duvet, a small pillow, a toothbrush, one tube of toothpaste and a roll-up mattress roughly the thickness of an oven glove

The floor was covered in dust and grime. The whole place shook when you walked around, which I soon stopped noticing. The window was barred, though you could still lean out. There was no shower.

…The bed was made of an iron frame and six planks of wood, and the mattress was so thin you had to lie completely flat. The bed frame, meanwhile, was impossible to lean against.”

Hale was sentenced to live here for 10 days, only because he allegedly was in loosely-defined “contact” with some unknown person who tested positive (Thomas Hale/Financial Times) He was pleasantly surprised, however, to find the internet connection was 24 times speedier than what he had at his hotel. Like Hale, the camp staff were prohibited from leaving or receiving deliveries there. A worker said he earned the equivalent of about $32 a day.

A camp staffer in hazmat gear walks by Hale’s cabin (Thomas Hale/Financial Times) Hale tried to see if his status as a foreign journalist might spring him from detention. The worker he approached with that question was baffled by the mere premise…but we can’t blame Hale for trying.

Hale describes key aspects of daily life in Covid detention:

- Every morning, he was awakened by a “lawnmower-like noise,” as an industrial-grade machine sprayed the cabin windows and front steps with disinfectant

- Around 9 am, two workers came to administer PCR tests. A positive result would have meant being taken to a different type of detention

- Meals were delivered at 8 am, noon and 5 pm

- Hale pursued a strict routine of language study, writing, exercise, music, online chess, and then reading or watching Amazon Prime entertainment

The routine served him well. Over time, he noticed his neighbors stopped eating breakfast, while some could be heard pacing their shaky boxes at night.

He did endure some psychological discomfort, in the form of not knowing when he’d get out. He was originally told seven days but it ended up being 10.

Upon his release and return to civilization, Hale savored the hot water of the hotel’s shower and the softness of its bed. When he went out for a celebratory meal, however, he faltered — pacing the street as he contemplated the fact that entering China’s contact-tracing matrix brought the peril of a return to confinement.

He settled on takeout from a steak restaurant, where an employee said there’d be no need for his code to be swiped — if he ordered takeout.

* * *

Check out Hale’s full tale at the Financial Times (subscription required)

Tyler Durden

Fri, 11/04/2022 – 21:20 - Opponents Setting Out Unintended Consequences Of Oregon’s Gun Control Measure

Opponents Setting Out Unintended Consequences Of Oregon’s Gun Control Measure

Authored by Scottie Barnes via The Epoch Times (emphasis ours),

If voters approve a pending ballot measure, Oregon would have the strictest gun laws in the nation—which opponents claim would virtually end the legal sale of firearms in the state.

Sales clerk Courtney Manuring, shows an AR-15 semi-automatic gun to buyer at Action Target in Springville, Utah, on June 17. (George Frey/Getty Images) The “Reduction of Gun Violence Act” (Measure 114) would require a permit to obtain any type of firearm.

Magazines capable of holding more than 10 rounds would be outlawed. Commonly used pump shotguns would be banned. And state police would be required to maintain an electronically searchable, publicly available database of all permit applications.

Backers of the measure, including a coalition of faith-based leaders and Ceasefire Oregon, say the new restrictions would help prevent guns from getting into the wrong hands, as well as reduce gun homicides, suicides, and trafficking.

The ballot measure is currently polling at 51 percent.

But opponents say the measure was poorly written and the explanatory language in the voters’ pamphlet was misleading.

They argue that the measure would create a bureaucratic nightmare that would only impact law-abiding gun owners, be impossible to comply with, violate the Second Amendment, and put an onerous burden on law enforcement.

And, though the pamphlet says the “financial impact is ‘indeterminate,” opponents claim it would cost taxpayers hundreds of millions of dollars.

“The main problem with the ‘Reduction of Gun Violence Act’ is it doesn’t address violent crime,” Aiobheann Cline, National Rifle Association of Oregon state director wrote. “That’s because it ignores criminals who break the law and instead penalizes law-abiding citizens.”

“The law fails to mandate sentences for gun-related criminals or put an end to the soft-on-crime policies that have made many Oregon cities into nightmares,” she added.

The Oregon State Sheriff’s Association (OSSA) cites the burden it would place on financially-strapped law enforcement agencies.

The measure would enact a law that requires a permit issued by a local law enforcement agency in order to purchase any type of firearm. Applicants would have to pay a fee, be fingerprinted, complete safety training, and pass a criminal background check.

“This measure will require law enforcement agencies to create and operate a massive permit-to-purchase and training program out of local budgets,” explained OSSA president and Deschutes County Sheriff Shane Nelson in a video message shared on social media.

“It will move very scarce resources away from protecting our communities to doing background checks and issuing permits at a time when crime is skyrocketing and law enforcement numbers are at their lowest in decades.”

Leonard Williamson, an Oregon trial attorney who specializes in firearms law and who served on the explanatory statement committee shares OSSA’s concerns.

“In order to obtain the permit, an applicant would have to show up with a firearm to demonstrate the ability to load, fire, unload, and store the firearm,” he told The Epoch Times.

“But you can’t get a firearm without the permit. And under Oregon’s highly restrictive gun storage laws, no one can legally loan a firearm to another. That creates an impassable barrier.”

The permit and training programs also create an unfunded mandate with no enforcement measures, opponents claim.

“The measure calls upon the Oregon State Police to come up with these [permitting and training] programs, but there’s no consequence if they don’t and there’s no timeframe for coming up with them,” explained H.K. Kahng, an engineer and NRA firearms instructor.

Nelson said that implementing the measure would cost local law enforcement agencies just over $49 million annually, with expected permit fees covering only $19.5 million. That means local law enforcement would need to shift about $30 million of their budgets to fund the programs.

Amy Patrick, the policy director for the Oregon Hunters Association, told The Epoch Times that it will take at least two years to set up the permitting system.

“In the meantime, federal, firearm license, gun sales would cease until purchase permits could be issued, potentially putting gun shops out of business,” she claims.

In Oregon, the sporting arms and ammunition industry is responsible for 3,668 jobs with an average wage of $59,541 and total economic contribution to the state of $1.78 billion annually, Michael Findlay, the National Shooting Sports Foundation’s director of government affairs told The Epoch Times.

Loss of that revenue could have a devastating impact on fish and wildlife conservation funding through the Pittman-Robertson Act.

Enacted in 1937, that act collects an 11 percent federal excise tax on all firearms, ammunition, and archery equipment. Those funds are then remitted to states.

Oregon is among the top 10 recipients of those funds.

“Pittman-Robertson funding brought $44 million to Oregon Department of Fish and Wildlife in the last biennium,” Patrick explained. “Those funds are specifically used for fish and wildlife conservation.”

A record setting high of more than $1 billion was collected in the past year and has yet to be distributed to the states, Findlay added.

Those economic contributions to the state budget would cease unless a court grants a legal injunction.

“I don’t think you’ll find any precedent in U.S. history in which a citizen has to go through so many hoops to exercise Constitutional rights,” Williamson said. “This is the first of its kind and, if it passes, it will wind up in court.”

Taxpayers will pay for the litigation.

Tyler Durden

Fri, 11/04/2022 – 21:00 - Scholz's China-Appeasing Visit With Xi Triggers Backlash In Europe

Scholz’s China-Appeasing Visit With Xi Triggers Backlash In Europe

German Chancellor Olaf Scholz met with Chinese President Xi Jinping on Friday in Beijing, where the German leader was on the ground for just 11 hours, and he focused his talking points on the war in Ukraine and containing Russian aggression. But looming large was the symbolism and controversial messaging back home of such a high-level visit, Scholz’s first as German chancellor. After all, he arrived with a team of top CEOs by his side. As CNN put it, the message is clear: “business with the world’s second-largest economy must continue”…

Accompanying Scholz on the whirlwind visit was a “delegation of 12 German industry titans, including the CEOs of Volkswagen (VLKAF), Deutsche Bank (DB), Siemens (SIEGY) and chemicals giant BASF (BASFY), according to a person familiar with the matter. They were expected to meet with Chinese companies behind closed doors,” CNN continued in describing the optics. They also were given a rare exemption to China’s typically strict quarantine and Covid measures for anyone entering the country.

Scholz’s trip, despite being only a day-long, marked the first time a European head of state has visited China since Russia launched its invasion. It was further Scholz’s first major foreign trip as Germany’s chancellor, and comes just after Xi secured a third term as Communist party secretary and president of China.

Scholz and Xi, Pool via AP “We are seeing discussions in China tending more towards autonomy and less economic ties. And these views are ones that need discussing,” Scholz told a press briefing in Beijing. The trip was seen as an attempt to maintain cozy relations with China after key pillars of a successful German economic machine evaporated this year – namely cheap energy from Russia and a prior relaxed approach to security spending.

But as Politico points out, “To his critics, he’s making exactly the same mistakes of overreliance on China as Berlin previously made with Russia.”

Foremost among them is German Foreign Minister and Greens party member Annalena Baerbock, who didn’t hide her disapproval and discomfort with Scholz’s meeting in stating just ahead of the trip, “The federal chancellor has decided the time of his trip. Now it is crucial to make clear in China the messages that we laid down together in the coalition agreement,” as cited in Der Spiegel newspaper. She and others are piling on pressure for a new, more assertive stance toward China.

“As is well known, we clearly stated in the coalition agreement that China is our partner on global issues, that we cannot decouple in a globalized world, but that China is also a competitor and increasingly a systemic rival,” said Baerbock. She added: “And that we will base our China policy on this strategic understanding and also align our cooperation with other regions in the world.”

Seeking to defend himself against such growing criticisms, also as the EU is seeking to put pressure on Beijing to turn more definitively against Russia’s war aims in Ukraine, Scholz wrote in an op-ed this week, “When I travel to Beijing as German chancellor, then I do so also as a European” – suggesting the trip in no way compromised the EU’s united front.

However, he acknowledged, “It is here that new centers of power are emerging in a multipolar world, and we aim to establish and expand partnerships with all of them.” And he noted, “Thus, in recent months, we have carried out in-depth coordination at the international level — with close partners such as Japan and Korea, India and Indonesia, and countries in Africa and Latin America too. At the end of next week, I will travel to Southeast Asia and the G20 summit, and while I’m visiting China, Germany’s federal president will be in Japan and Korea.”

The op-ed just written by Olaf Scholz 🔽 is worth a read.

Biggest bombshell: “New centers of power are emerging in a multipolar world, and we aim to establish and expand partnerships with all of them”

👉 New – multipolar – world order is now reality.https://t.co/jSqpagD6MC

— Arnaud Bertrand (@RnaudBertrand) November 4, 2022

https://platform.twitter.com/widgets.js

Following the Friday meeting with President Xi, Scholz said he urged the Chinese side to remove barriers for closer economic ties:

Scholz said he had told Xi that China was becoming “more difficult” for German companies, in terms of market access, the protection of intellectual property and the “interruption of economic relationships” as the country moved towards “autarky”. He said he had told his hosts “how important it is in our view to rectify these imbalances”.

Scholz later told reporters that he and Xi had discussed what could be done to ensure a “level playing field” for German investors in China. In his press statement, premier Li Keqiang acknowledged Germany and China had “differences” and said these had been discussed. “But we still respect each other,” he said.

And on the foreign policy front, Scholz urged President Xi Jinping the Beijing must use its “influence” on Moscow to halt the ongoing invasion of Ukraine. “I told President (Xi) that it is important for China to use its influence on Russia,” Scholz said in a statement after the meeting. “Russia must immediately stop the attacks under which the civilian population is suffering daily and withdraw from Ukraine.”

Scholz reminded the Chinese leader that all major global powers, including the West, had vowed to respect the UN charter and “principles such as sovereignty and territorial integrity,” which is being violated by Russia in Ukraine, according to the statement.

The two leaders also talked about the deeply alarming possibility of nuclear escalation, as well as the newly restored but tenuous Ukraine grain export deal. Sholz at a news conference lashed out at the Kremlin, saying “Hunger must not be used as a weapon.”

when Xi meets Scholz

he does not even address him as name or title for the ’greeting‘

he just said “哎你好 Ah hello”— 巴丢草 Bad ї ucao (@badiucao) November 4, 2022

https://platform.twitter.com/widgets.js

Chinese state media affirmed that Xi Jinping called on all world powers to “reject the threat of nuclear weapons and advocate against a nuclear war to prevent a crisis on the Eurasian continent” – while leaving his words somewhat vague regarding Russia or Putin and the West’s accusations of nuclear saber-rattling. Both agreed that nuclear threats and potential use related to the Ukraine crisis must be out of the question:

…Scholz told reporters he was “glad” that he and Xi had “reached an understanding . . . that there can be no escalation through the use of tactical nuclear weapons”.