- US Election "Success"… And Hey Presto "Russian Interference" Disappears

US Election “Success”… And Hey Presto “Russian Interference” Disappears

Tyler Durden

Sun, 12/06/2020 – 00:00Via The Strategic Culture Foundation,

The United States’ election victory of Democrat presidential candidate Joe Biden has yet to be officially confirmed. That requires the 500-plus Electoral College comprising the 50 federal states to cast the final vote when the constitutional body meets on December 14. Biden holds a commanding lead of over 300 delegates in the Electoral College, more than 70 above Donald Trump’s quota and decisively more than the 270 threshold required for election to the White House.

Nonetheless, already one thing is indisputably clear. Biden’s nominal victory from the popular vote tallies is glaring proof that Russia did not interfere in the American presidential ballot. Not in 2020. And not, we may discern, in 2016, nor in any other election. Yet the silence in US media over this obvious conclusion is deafening.

Four years of frenetic and unsubstantiated allegations of “Russian interference” have disappeared overnight, it seems. Poof! Gone! As if by a magic conjuring trick. Now you see it, now you don’t, so to speak.

The New York Times has declared the recent presidential contest a “great election.. a resounding success free of fraud”. The Department of Homeland Security pronounced the election to be the “most secure in American history.” Other US media outlets have jettisoned supposed political neutrality and can barely contain their elation at Biden’s electoral victory.

But hold on a moment.

In the months and weeks leading up to the November election, there was a fever pitch in US media among politicians, national security chiefs, pundits and anonymous intelligence sources that Russia was allegedly stepping up “interference efforts” to get Trump re-elected.

Those evidence-free claims were predicated on the equally absurd assertion that Trump was a Manchurian candidate for the Kremlin. That “Russiagate” fable was first spun in 2016 and for the past four years elaborated into a tangled web to “explain” how a maverick former reality TV star had been elected to the White House.

Suddenly, however, the Democrats and supportive US media are now asserting that the voting process was impeccable and unblemished by any malfeasance. Of course they would say that in order to bolster legitimacy of Biden’s win against the Republican White House incumbent Donald Trump. But the thundering takeaway which the US political class and media are bizarrely ignoring is that Russia did not interfere not in the 2020 race nor in any other election. Russia has always categorically said it is not meddling in US politics and its electoral process. Turns out that Russia is de facto vindicated in its protestations against American slander.

The “Russiagate” nonsense was hatched by Democrats, their supportive media and intelligence agencies because they could not come to terms with the reality of why Trump beat the then establishment-ordained candidate Hillary Clinton in 2016. Could it have been because Clinton and the Democrat party was repudiated by popular sentiment due to perceived corruption and overseas wars? No, another “explanation” had to be found. And the US political establishment came up with the “Russian interference” narrative.

No matter that the Mueller investigation found after 22 months of probing and hundreds of millions of taxpayer-dollars spent that there was no evidence of “Russia collusion” with the Trump campaign. Nevertheless, Mueller and the Democrats, their media and intelligence backers, persisted in the spurious notion that Russia meddled in the 2016 election and, allegedly, was continuing to meddle, purportedly with even more sophisticated, nefarious techniques.

How can US politicians, intelligence officials and media credibly claim that Russia interfered in 2016 and in mid-term congressional elections in 2018, but now in 2020 it evidently did not? The most logical explanation is simply that Russia never did.

Four years of hysterical American accusations against Russia have transpired to just that: bogus hysteria. US politicians, media and so-called intelligence gurus should be held to account for fabricating what is perhaps the biggest hoax ever played on the American public.

Though, one can be sure that they won’t be held accountable in a formal way. Venal power doesn’t work like that. And the US political system has built-in layers of self-protection for the political class never to be prosecuted. But in an informal no less real way, the system is being held to account by the wider public who are increasingly holding it in contempt and distrust. The political class and their plaything media are losing the moral authority to govern. This goes beyond mere Trump Derangement Syndrome. The systematic lying and deception over alleged Russian interference perpetrated on such a grand scale has fatally damaged the credibility of American institutions. Not just in the US, but around the world too.

Equally lamentable is the corrosive, damaging effect that the bogus hysteria has had on bilateral US-Russia relations and international tensions. Relations are at a dangerous all time low comparable to the depth of the Cold War. This has in turn sabotaged diplomatic efforts to strengthen arms controls and global security. The anti-Russia hysteria has led to the US abandonment of key nuclear weapons treaties, the Intermediate-range Nuclear Forces (INF) treaty and soon the New START.

The Russophobia that has been whipped up as a political weapon against Trump over the past four years is not something that can be easily put aside. It has engendered deep-seated hostility against Russia. During the presidential debates, Joe Biden vowed that the would take a tough stand against Russia for “interfering” in US politics. The incoming administration is being mentally held hostage by its own Russophobia which was cultivated on entirely false grounds.

It is disturbing how the US nation has been dragged into an obsession about alleged Russian malign activities, an obsession which turns out to be a mirage. Not for the first time either. Recall the Cold War Red Scares and McCarthyite witch-hunts which poisoned American society.

The implications are daunting. How can bilateral relations with Russia be restored? How can an intelligent dialogue be conducted with a nation whose leaders are so self-deluded and irrational?

Moreover, this is a nation whose leaders presume to have the prerogative to use overwhelming military force whenever they deem so. It is not unlike the driver of a juggernaut vehicle on a precipice who is hurtling along while out of his brain on misconceptions.

- Japan Set To Abolish Gas Powered Cars By Mid 2030s

Japan Set To Abolish Gas Powered Cars By Mid 2030s

Tyler Durden

Sat, 12/05/2020 – 23:30As if the speculative EV mania needed any more fuel thrown on its fire, Japan is joining numerous other countries – and California – in setting a date to make all new cars electric and “eco friendly” by the mid 2030’s.

The country’s Ministry of Economy, Trade and Industry has said they are considering abolishing conventional cars and shifting purely to hybrids and electrics within the next 10 to 20 years, according to Nikkei.

The move is part of a broader plan for the entire country to go “zero emissions” by 2050. Vehicles made up 16% of the country’s total emissions in 2018, according to the report. An official announcement is expected later this month at a conference attended by experts and car industry executives. This will be followed by more concrete plans and timelines.

“Many territories” have already said they are going to ban the sale of new ICE vehicles by 2030, the report says.

Currently, the country is focused on making car makers improve efficiency by 30% by the end of 2030. The country does not plan on banning hybrids. Key auto makers in Japan have already offered their support: Toyota has stated they will offer an electric option for all models by 2025 and Nissan aims to raise its ratio of hybrid to electric cars from 30% to 60% by as early as 2023.

The U.K. already has similar legislation planned, banning ICE cars by 2030 and hybrids by 2035. California will also ban sales of new ICE cars by 2035. France has said they will do the same by 2040.

China is considering implementing similar rules by 2035, allowing a mix of EVs and hybrids.

- This New Technology Will Dangerously Expand Government Spying On Citizens

This New Technology Will Dangerously Expand Government Spying On Citizens

Tyler Durden

Sat, 12/05/2020 – 23:00Authored by Jack Rasmus via Counterpunch.org,

If you’re worried about the capability of government to conduct surveillance of citizens engaged in political assembly and protest, or even just personal activity, then you should be aware the technological capability of government surveillance is about to expand exponentially.

The US Air Force’s Research Lab (yes, it has its own lab) has recently signed a contract to test new software of a company called SignalFrame, a Washington DC wireless tech company. The company’s new software is able to access smartphones, and from your phone jump off to access any other wireless or bluetooth device in the near vicinity. To quote from the article today in the Wall St. Journal, the smartphone is used “as a window onto usage of hundreds of millions of computers,s routers, fitness trackers, modern automobiles and other networked devices, known collectively as the ‘Internet of Things’.”

Your smartphone in effect becomes a government listening device that detects and accesses all nearby wireless or bluetooth devices, or anything that has a MAC address for that matter. How ‘near’ is nearby is not revealed by the company, or the Air Force, both of which refused to comment on the Wall St. Journal story. But with the expansion of 5G wireless, it should be assumed it’s more than just a couple steps from your smartphone.

One can imagine some scary scenarios with this capability in the hands of government snoops:

-

Not only would the government know your geographical location via the GPS signal to your cellphone. They’d know what you are doing. And with whom.

-

A political gathering would allow them to see all the owners of other cellphones in the vicinity of a protest or demonstration. How many are gathering at a particular street or location. The direction they might be heading. Or whether there’s an organization meeting in a hall or room and who (with a cellphone as well) might be attending.

-

If you’re driving on a winding coastal or mountain road, it would know, and could possibly access, your car’s various electronic systems to turn them off. It might access your car’s circuit board that governs your power steering when you’re driving in an area of winding roads. Or it might be able to just shut down your car’s electrical system and remotely lock all your doors. The police no longer have to engage in highway chases until capture.

-

The new tech would allow the government to access the data on your fitbit device while you’re jogging. Or worse, maybe even interfere with the signal on your heart pacemaker device.

-

The technology might be used to access your smartphone, and from there to turn on your home Alexa device to listen in and record conversations without you ever knowing. Or to listen in on your zoom conferencing on your laptop. Or maybe even worse, to shut down or bypass the safety features on your home furnace equipment. Or turn off your home security system.

-

And with 5G wireless broadband, the tracking might be extended well beyond the range of a bluetooth device. Add 5G broadband wireless to SignalFrame’s technology, and then wed that to the capability of machine learning and artificial intelligence, and you get instant processing of a massive amount of data on any targeted person or gathering!

This problem of government surveillance on free citizen activity is not new. It took a giant leap after 9-11 with the Patriot Act and acquisition of phone data by Homeland Security and other government agencies. It was supposed to have stopped. But it hasn’t. The snoops have continued to ignore Congressional resolutions and court decisions on privacy invasion of citizens. The latest Air Force lab testing is likely just a recent ‘tip of the iceberg’ revelation. And if the Air Force is doing it, be assured so are the Army, Navy, the NSA, CIA, FBI and all the other government snoops.

Certainly this kind of technology would be used not only by the US government. If the USA has it, you can bet other governments do too–especially China, Russia, Israel, and probably some of the Europeans as well.

Unlike in 2001, in 2020 SignalFrame’s technology takes government surveillance to a new level–given the ubiquity of smartphones, Internet of Things (IOT) devices, digital circuit board dependent autos, and all the many household devices now with MAC wireless access addresses. And now, unlike circa 2001 and the passage of the Patriot Act (and its continuation in annual NDAA legislation), we have AI, machine learning, neural nets everywhere, and massive government data processing power.

In short, Technology is becoming a growing tool and power in the hands of governments, to use to thwart democratic and constitutional rights–as well as to detect, apprehend, and ‘deal with’ those who protest and oppose those governments.

The coming decade in the USA will be not only increasingly difficult economically, increasingly unstable politically, but will prove to be a period in which technology is increasingly threatening basic civil rights as well as the very foundations of Democracy itself.

-

- Saudis Demand To Be Consulted Before Biden Reenters Iran Nucleal Deal

Saudis Demand To Be Consulted Before Biden Reenters Iran Nucleal Deal

Tyler Durden

Sat, 12/05/2020 – 22:30After President-Elect Joe Biden told The New York Times this past week that should Iran return to compliance to the 2015 nuclear deal (particularly caps placed on enrichment) he’ll return the US to participation in the Obama-era agreement, the Saudis have registered their alarm.

Saudi Arabia’s top diplomat said Saturday that Washington must consult the kingdom and Gulf state allies before moving forward with reentry to the JCPOA. The Sunni kingdom sees Shia Iran as its number one threat and enemy in the region.

Saudi Foreign Minister Prince Faisal bin Farhan told AFP, “Primarily what we expect is that we are fully consulted, that we and our other regional friends are fully consulted in what goes on vis a vis the negotiations with Iran.”

Saudi Foreign Minister Prince Saud al-Faisal with then US Vice President Joe Biden in 2011. Image: AFP via Getty “The only way towards reaching an agreement that is sustainable is through such consultation,” he emphasized while speaking to reporters at a security conference in Bahrain.

“I think we’ve seen as a result of the after-effects of the JCPOA that not involving the regional countries results in a build up of mistrust and neglect of the issues of real concern and of real effect on regional security.”

While Riyadh said it is “ready” and waiting to engage the incoming Biden administration on the issue, there’s not yet been any contacts regarding the nuclear deal.

“We are confident that both an incoming Biden administration, but also our other partners, including the Europeans, have fully signed on to the need to have all the regional parties involved in a resolution,” the Saudi FM added.

The most significant and direct military action of late involving the Iranians and Saudi remains the September 14, 2019 attack on the Aramco Abqaiq and Khurais oil processing facilities, which the US and Saudis blamed on Tehran ultimately ordering. However, who precisely was behind it remains somewhat shrouded in mystery.

The major attack involved drones and missiles, based on weapons fragments produced by the Saudis, and likely came from Yemen, possibly via Iranian proxy fighters, the Houthis.

- Minority Students Crushed By Lockdowns; 600% Increase In Math Failures, 500% English

Minority Students Crushed By Lockdowns; 600% Increase In Math Failures, 500% English

Tyler Durden

Sat, 12/05/2020 – 22:05Authored by James Bovard via the American Institute for Economic Research (emphasis ours)

In August, I reported here on how Montgomery County, Maryland, was seeking to shut down private schools as part of their Covid-19 strategy of abolishing all risk by abolishing all freedom. As more individuals have recently tested positive for Covid, the county government is responding with a new array of iron-fisted decrees. Some of the latest edicts make little or no sense, confirming the county’s nickname of LoCo Moco.

Gov. Larry Hogan blocked the county government’s effort to criminalize private teaching; Catholic, Jewish, and other schools have operated safely with no significant Covid outbreaks. But county schools remain shut down in large part due to the clout of the teachers union, a bulwark of political support for County Executive Marc Elrich.

For at least 40 years, MoCo politicians and school officials have invoked “closing the achievement gap” as a sacred goal which justifies the sacrifice of as many taxpayers as necessary. But that goal is not as sacrosanct as assuring that teachers continue to collect full pay while taking zero risks and leaving the most vulnerable students far behind.

Since the county padlocked public schools earlier this year and shifted to unreliable “distance learning,” there has been a 500%+ increase in the number of black junior high students failing mathematics and a 600%+ increase in Hispanic students failing. The percentage of black elementary school students failing English increased more than 350% and the percentage of Hispanic students failing increased more than 500%. These numbers were revealed during a County Board of Education meeting on December 3; a local activist captured screenshots of the disastrous test results. Some of the data was also reported in yesterday’s Washington Post. Shutting down public schools has done more harm to black students than anything since the end of local school segregation in 1961.

Montgomery’s results are in line with reports elsewhere that show that minority students have suffered far more harm from shutdowns justified to curtail the spread of Covid. This carnage was foreseeable. An analysis by McKinsey & Company consultants last spring estimated that if schools were entirely online until January, on average “white students would lose 6 months of learning, Hispanic students 9 months, black students 10 months and low-income students more than a year during the time school buildings have closed for the pandemic.”

MoCo leaders recite their devotion to “science and data” except when the data might curb their arbitrary power. C.D.C. chief Robert Redfield testified this week, “The data clearly shows us that you can operate these schools in face-to-face learning in a safe and responsible way.” Maryland State Schools Superintendent Karen Salmon urged local schools to bring back students five weeks ago but Salmon can deliver neither vanloads of votes nor armloads of cash to County Council members. The Washington Post, in an article on the success and safety of European school reopenings, noted, “Teachers unions, which have emerged as a powerful force of opposition to school reopenings in the United States, have generally been more acquiescent in Europe, pushing for safety measures rather than closures.”

Many kids may have unnecessarily lost practically a year of their learning lives but MoCo has compensated with a maniacal devotion to mandating masks. On April 9, Montgomery County’s chief health officer Travis Gayles decreed that any store customer who failed to wear a mask would be fined $500. Gayles discouraged local residents from acquiring and wearing the most reliable protection, such as surgical masks or N95 masks, which the county said “should be reserved for health care workers.” Mandating the wearing of unreliable masks makes about as much sense as requiring everyone to wear a dunce cap with the inscription, “Save me, Big Brother!”

On August 24, the County Council “expanded” the face mask mandate to compel everyone to cover their chins as well as their mouth or nose. (N95 masks were exempt but commoners were not supposed to be using those anyway.) Neither the Council members nor health czar Gayles revealed the secret medical data on how chins could transmit Covid. The edict was poorly publicized and mostly ignored by local residents.

On November 24, Gayles issued a new mask dictate: “Coverings must be worn outdoors and whenever coming into contact with individuals who are not members of their household, such as being within six feet.” Ordering people to wear masks when they walked alone outside, walked their dog, or went to the mailbox spurred ridicule on local forums. One cynic groused: “Gayles says he follows the science. The science he follows may be from a mad scientist but it’s science.” The following day, the county issued a “clarification” specifying that masks are not required if you are “Alone in your office or vehicle.” Also exempted were kids “Under the age of 18 and are engaged in vigorous sports – as recommended by the American Academy of Pediatrics.” But the pro-exercise health guidance apparently becomes null and void on the 18th birthday.

Maryland has a hotline number to report any violators of statewide mask mandates, and MoCo is a rich soil for raising informants. Politicians and bureaucrats have fanned mass fears which have ripened into hatred of anyone who does not comply with the latest edict. I was recently walking along the C & O Canal Towpath, talking to two friends. None of us were masked.

Coming in the opposite direction was a geezer, walking slumped forward with a long white shirt, big floppy hat, and a six-foot walking stick. He suddenly stops and points his stick at me and shouts:

“DISTANCING!”

“What?” I replied

“YOU’RE NOT DISTANCING!”“So what are you supposed to be, an Old Testament prophet?” I said. “Great – so now we got the Prophet Isaiah casting damnation on all Towpath violators.” I should have counted my blessings that he wasn’t like Coleridge’s Ancient Mariner, buttonholing people and forcing them to listen to a 45-minute poem.

Maybe I should have also felt lucky that Prophet Dude could not summon a police SWAT helicopter. Maryland has vigorously encouraged people to rat out violators and the state has no shortage of self-appointed Junior Stasi members.

County agents conducted 90 inspections of businesses on the night before Thanksgiving.

Earl Stoddard, Montgomery County’s head of emergency management, lamented to the Washington Post: “We can’t be everywhere in every store all at once.” Stoddard encouraged residents to file accusations against any business with which they had “concerns.”

Last week’s Black Friday sales were treated by government officials like a crime scene in progress. A long line of customers waited outside of a humongous Best Buy store – along with police cars from both the county and Rockville. Perhaps the police were equipped with long-distance Tasers to zap anyone not wearing a proper mask?

Businesses have no safe haven regardless of how much they have spent to protect customers and placate bureaucrats. A Harris Teeter grocery store made extensive changes after the start of the pandemic, including placing large plexiglass screens between every one of its nine self-service checkout stations. A single customer, who perhaps failed to take his Xanax that morning, complained to the Montgomery County government that he felt unsafe when he visited the store. A county inspector swooped in and threatened to shut down the grocery store unless they blocked access to half of their self-service stations. As a result, the store now sometimes has long lines of people waiting to check out – and presumably increasing their exposure to Covid while waiting. The inspector also forced the store to designate one of its two entrances as an “exit only.” One store employee feared that county inspectors could return and compel the store to dictate which direction people walk down each grocery aisle.

Trader Joe’s in Rockville, perhaps seeking favor with zealous inspectors, has imposed some of the tightest restrictions on shoppers since the pandemic began. There is usually a long line out front; shoppers are also required to form a single long line before checking out. Recently, a Hispanic lady pushed her grocery cart to bluntly cut the line. A number of black customers with their grocery carts were in line behind her, and a shouting match ensued with ethnic taunts flying thick and fast. The store manager raced to the scene to squelch the uproar. But this type of fracas never happened in that store prior to its “pandemic fixes.” This is another example of how unjustified government prohibitions are spurring pointless social conflicts.

Perhaps local residents should be grateful that Gayles or County Executive Elrich have not gone as far as the California mayor who swore that anyone not wearing a mask in public was guilty of “an act of domestic terrorism.”

Unfortunately, all the bankrupted local businesses, all the shafted young children, and the surge in cases of attempted suicide and mental illness are irrelevant to how MoCo scores its good deeds. As long as county officials can claim that things would have been worse without its destructive edicts, they can continue pretending to have saved humanity. Perhaps Elrich and Gayles are hoping that if they inflict enough misery on MoCo, the Biden administration will appoint them to prestigious positions to help impose a national Covid lockdown.

- Oliver Stone: Here's Why Trump Should Pardon Snowden, Assange

Oliver Stone: Here’s Why Trump Should Pardon Snowden, Assange

Tyler Durden

Sat, 12/05/2020 – 21:40Filmmaker Oliver Stone has joined the growing chorus of activists calling for President Trump to pardon Julian Assange and Edward Snowden – without whom we wouldn’t know about intrusive government surveillance programs, the United States’ aggressive drone strike program, or that Hillary Clinton’s 2016 campaign manager and his brother are apparently into ‘spirit cooking‘ with a satanic performance artist.

According to Stone, pardoning the pair of whistleblowers “will take the edge off his pardons for his family & loyalists by being unselfish and not self-serving. And at the least, confound his many critics — as well as future historians.”

Second, “It will drive his enemies in #DeepState and #Media absolutely nuts!“

“A pardon of @Snowden and #Assange would be a great shock to this world, and reflect well on @realDonaldTrump,” wrote Stone in a Thursday tweet. “Despite all the negatives he’s created, it will be seen as a purely merciful action. It will not be forgotten.”

2. It will drive his enemies in #DeepState and #Media absolutely nuts! A reproof to @BarackObama’s #DOJ, a shock to @JoeBiden, and a well-deserved finger to one of the worst of the bad losers, @HillaryClinton, who essentially started this 4 years of destructive disinformation.

— Oliver Stone (@TheOliverStone) December 3, 2020

https://platform.twitter.com/widgets.js

A pardon of @Snowden and #Assange would be a great shock to this world, and reflect well on @realDonaldTrump. Despite all the negatives he’s created, it will be seen as a purely merciful action. It will not be forgotten.

— Oliver Stone (@TheOliverStone) December 3, 2020

On Thursday, Edward Snowden asked President Trump to pardon Assange.

Mr. President, if you grant only one act of clemency during your time in office, please: free Julian Assange. You alone can save his life. @realDonaldTrump

— Edward Snowden (@Snowden) December 3, 2020

https://platform.twitter.com/widgets.js

Snowden — who released classified documents on surveillance programs — fled to Hong Kong, and later to Moscow, to seek asylum. He tweeted last month that he and his wife were applying for Russian citizenship.

Meanwhile, Assange faces a sentence of up to 175 years in prison if convicted of charges of conspiring to hack government computers and for violating the 1917 Espionage Act for “unlawfully obtaining and disclosing classified documents related to the national defence.” –The Hill

https://platform.twitter.com/widgets.jsMeanwhile for more on Oliver Stone, read: Oliver Stone, America Firster authored by Bill Kauffman via The American Conservative

At root, Oliver Stone is a patriot who despises the American Empire for corrupting his country, and a far cry from your run-of-the-mill Hollywood liberal.

I first became aware of Oliver Stone when in 1986 I was watching his film Salvador with an audience of left-wing Santa Barbarians. They were enjoying this madcap cinematic indictment of Uncle Sam’s imperialist crimes in Central America—until a scene in which the rebel forces, riding to town like a Marxist cavalry in the righteous cause of The People, began executing the unenlightened. Then the boos rang down.

Who is this guy, I wondered. My curiosity was whetted further when the P.C. reviewer in the Los Angeles Herald denounced Stone’s screenplays for earlier films: “Movies like Midnight Express, Scarface, and Year of the Dragon are such grand-scale xenophobic fever-dreams that they almost demand to be remade into operas, complete with belching smoke and lurid lighting and crimson-suited devils scurrying out of the wings to pitchfork lily-white Mother America.”

Ah, a left-wing America Firster!

Not quite, as his subsequent work and his entertaining new memoir, Chasing the Light, illumine, but Oliver Stone, our most political major filmmaker, evinces a rowdily heterodox vision shaped by the unusual quartet of Jim Morrison, Sam Peckinpah, Frank Capra, and Jean-Luc Godard.

What do you call a man who joins the Merchant Marine on a whim, runs up big pro football gambling debts, and takes the Old Right view of FDR’s foreknowledge of the Japanese attack on Pearl Harbor?

I’d call him an American.

Stone was a rich kid, the son of an FDR-hating Jewish Republican who had served on Eisenhower’s Supreme Headquarters Allied Expeditionary Force staff and a French Catholic party girl. He attended the Hill School, played on the tennis team, was devastated by his parents’ divorce, and then went seriously off script.

Avid for experiences, Stone dropped out of Yale, taught in a Catholic school in Taiwan, and volunteered to fight in Vietnam. He came home with a Bronze Star, shrapnel in his ass, and a taste for “powerful Vietnamese weed.”

Stone’s politics hadn’t changed all that much, though. He had supported Barry Goldwater in 1964 and would vote for Ronald Reagan in 1980. In later years he became more explicitly libertarian, expressing support for Ron Paul and making a film about Edward Snowden.

At root, Oliver Stone is a patriot who despises the American Empire for corrupting his country. JFK, his fantasia on the Deep State, echoes Dwight Eisenhower’s warning that “we must guard against the acquisition of unwarranted influence” by “the military-industrial complex.” Platoon and Salvador bespeak an old-fangled American anti-interventionism in an age when that tendency, once the default position of ordinary Americans, is a virtual thoughtcrime.

Lost innocence is as common in Stone’s films as splattered blood. In Midnight Express, the Turkish prison movie to end all Turkish prison movies, protagonist Billy Hayes is a Long Island college kid just trying to make a few bucks by smuggling two kilos of hashish to sell to his friends. Heck, it’s no different than being the guy who runs out to pick up the pizza and beer at halftime! (The real Hayes, as Stone later learned, was on his fourth smuggling run and was about as innocent as Brad Davis, the deeply troubled actor who played him.)

When his sentence is stretched from four to 30 years, Billy explodes in a Stone-penned courtroom rant that belongs in the xenophobe’s hall of fame: “For a nation of pigs it sure is funny you don’t eat ’em … I hate you, I hate your nation, and I hate your people.”

Yikes! As the husband of an Armenian I’m not overly sensitive to slights against the Turkish nation, but this was a tad intemperate. But so was the left-wing French newspaper Liberation, which reviled Stone as “a madman of the Right.”

A pithier America First line from Stone’s pen came in Year of the Dragon (1985), when a New York City cop (Mickey Rourke) responds to a Chinese gangster who is describing his culture’s ancient tolerance of gambling and extortion: “This is America you’re living in and it’s 200 years old, so you’d better get your clocks fixed.”

Stone’s co-writer on Year of the Dragon was Michael Cimino, whose Oscar-winning epic The Deer Hunter was unusual for its sympathetic treatment of small-town working-class men whose church is central to their lives. Critic Pauline Kael sneered at The Deer Hunter’s “traditional isolationist message: Asia should be left to the Asians, and we should stay where we belong, but if we have to be over there we’ll show how tough we are.” A Trumpian message, on Trump’s better days. Cimino blew up his career with the sprawling Heaven’s Gate, a commercial disaster that snuffed his long-dreamt-of goal of filming Ayn Rand’s novels The Fountainhead and Atlas Shrugged.

Liberal Hollywood, eh?

Bill Kauffman is the author of 11 books, among them Dispatches from the Muckdog Gazette and Ain’t My America.

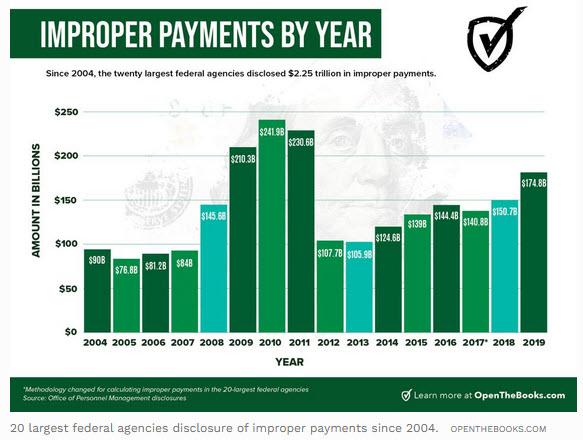

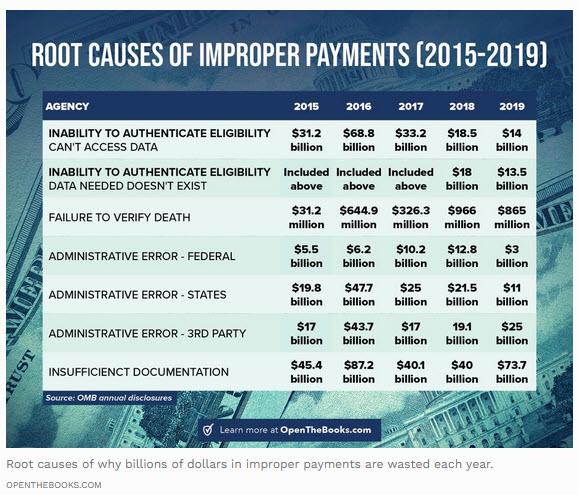

- Feds Admit $2.3 Trillion In Improper Payments

Feds Admit $2.3 Trillion In Improper Payments

Tyler Durden

Sat, 12/05/2020 – 21:15Submitted by Adam Andrzejewski,

Since 2004, twenty large federal agencies have admitted to disbursing an astonishing $2.25 trillion in improper payments. Last year, these improper payments totaled $175 billion – that’s about $15 billion per month, $500 million per day, and $1 million a minute.

But what exactly is an improper payment?

Federal law defines the term as “payments made by the government to the wrong person, in the wrong amount, or for the wrong reason.”

When people or companies receive incorrect payments, it erodes trust and hinders the government’s ability to finance everything from defense to health care.

Recently, auditors at OpenTheBooks.com published a 24-page oversight report analyzing why, how, and where federal agencies wasted our tax dollars last year.

Here are the top 10 takeaways regarding improper and mistaken payments by the 20 largest federal agencies in 2019:

1. Total Mistakes: $175 billion in estimated improper payments reported by the 20 largest federal agencies, averaging $14.6 billion per month – Total (FY2004-FY2019): $2.25 trillion.

2. Worst Programs – $121 billion (approximately 69 percent) in improper payments occurred within three program areas – Medicaid, Medicare, and Earned Income Tax Credit.

3. Claw Back – only $21.1 billion of the $175 billion improper payments during 2019 was recaptured — that’s only 14 cents on every dollar misspent. Five-year total: $103.6 billion recaptured/ $747.7 billion improperly spent

4. Biggest Offenders:

5. Dead people: $871.9 million in mistaken payments were made to dead people. Medicaid, social security payments, federal retirement annuity payouts (pensions), and even farm subsidies were sent to dead recipients. Root cause: failure to verify death. Four-year total: $2.8 billion

6. Ancient Americans: Six million Social Security numbers are active for people aged 112+; however, only 40 people in the world are known to be older than 112 years of age.

7. Worst Upward Trend: Medicaid and Medicare improper payments soared from $64 billion (2012) to $88.6 billion (2017), and, in 2019, to $103.6 billion. Five-year total: $456 billion

8. Best Turnaround: In 2018, the Education Department overpaid $6 billion to college students receiving PELL grants and student loans. In 2019, improper payments were reduced to $1.1 billion – an 85-percent reduction.

9. Improper Income Redistribution: $17.4 billion in improper payments by the Internal Revenue Service (IRS) within the Earned Income Tax Credit program. 25-percent of all payments were improper. Five-year total: $84.35 billion

10. Purchasing Power: What can $175 billion buy? Last year, the federal government wasted the equivalent of a full year of all federal salaries, perks, and pension benefits for every employee of the federal executive agencies. A stunning example of institutionalized incompetence.

Justifications for their improper payments vary by agency.

For example, Veterans Affairs (VA) says they are working on the problem and, yet, have a long way to go:

“During FY19 testing for improper payments, VA found that many root causes of improper payments still have not been remediated. While the VA is actively working corrective actions to remediate these complex problems, VA completes its statically valid testing for Improper Payments Elimination & Recovery Act) one year in arrears…”

The Internal Revenue Service (IRS) flat out admits that their improper payments ($17.4 billion FY2019) will continue:

“… the IRS does not have the resources to audit every return claiming return tax credits… Without legislative change to greatly improve effective tools to administer these credits, the improper payment rate will not drastically change.”

Over the years, improper payments is an issue that has attracted reform efforts on both sides of the aisle.

In 2009, President Barack Obama issued an executive order to stop improper payments in the core programs of the federal government. Core programs provide services such as Medicare and Medicaid.

In 2020, President Donald Trump emphasized the importance of eliminating improper payments in the President’s Budget to Congress FY2021.

But with billions of dollars misspent every year, it’s obvious that both administrations failed to successfully address the issue of improper payments and much more needs to be done.

- MicroStrategy Buys Another $50 Million In Bitcoin At $19,427; Bringing Total To Half A Billion

MicroStrategy Buys Another $50 Million In Bitcoin At $19,427; Bringing Total To Half A Billion

Tyler Durden

Sat, 12/05/2020 – 20:50Last week, just after Bitcoin’s first modest correction since the start of its March rally which prompted an amusing twitter meltdown by Nouriel Roubini, we reported that one of the world’s biggest fixed income asset managers, Guggenheim Partners, jumped on the bitcoin bandwagon when it announced that it was reserving the right for its $5.3 billion Macro Opportunities Fund to invest in the Grayscale Bitcoin Trust whose shares are solely invested in Bitcoin, and track the digital asset’s price less fees and expenses.

Guggenheim’s (partial) embrace of Bitcoin following PayPal’s announcement a few weeks later that it had enabled crypto transactions for all its clients, sparking the latest leg higher in bitcoin. It also came following glowing endorsement from legendary investors such as Paul Tudor Jones and Stan Druckenmiller, and in the aftermath of Jack Dorsey’s “other” company, Square, which said in October that it bought 4,709 bitcoins, worth approximately $50 million, about 1% of Square’s total assets.

“Square believes that cryptocurrency is an instrument of economic empowerment and provides a way for the world to participate in a global monetary system, which aligns with the company’s purpose,” the company said in a release. Square founder Jack Dorsey, whose twitter bio only includes the hashtag #bitcoin…

… has been a advocate of the digital currency, saying in 2018 the cryptocurrency will eventually become the world’s “single currency.” However the founder of Twitter said it could take a long as a decade.

Perhaps… but for others the payback from investing in bitcoin has come far sooner, most recently the publicly traded business-intel firm, MicroStrategy, which on August 11 sent a shockwave around the globe when it announced it had poured all $250 million of its planned inflation-hedging funds into the digital currency.

Not content with the 100% return its stock has generated since then, on Friday MicroStrategy announced that it has bought even more Bitcoin.

In an 8-K, the company announced that it had purchased “approximately 2,574 bitcoins for $50.0 million at an average price of approximately $19,427 per bitcoin.” As a result, as of December 4, 2020, the Company held approximately 40,824 bitcoins that were acquired at an aggregate purchase price of $475.0 million. Microstrategy CEO Michael Saylor confirmed as much in a subsequent tweet:

MicroStrategy has purchased approximately 2,574 bitcoins for $50.0 million in cash in accordance with its Treasury Reserve Policy, at an average price of approximately $19,427 per bitcoin. We now hold approximately 40,824 bitcoins.https://t.co/nwZcM9zAXZ

— Michael Saylor (@michael_saylor) December 4, 2020

https://platform.twitter.com/widgets.js

And since the current market value of the company’s bitcoin holdings is currently $770 million, or a 60% return in just a few months, one can see why the stock price of MSTR is up 165% since the day it announced its first Bitcoin purchase.

In September, Saylor told Bloomberg that the purchase were being done because he sees the cryptocurrency as less risky than cash or gold. On Monday, Bitcoin surpassed its December 2017 record high of $19,511, and even though it neared $20,000 it wasn’t able to crack that key level, and after peaking at $19,914 has bounced around mostly in a range between $18,500 to $19,500 since.

This brings us to a question we asked last weekend: “whereas in 2017 it was all the rage to pivot to “blockchain”, we wonder how long before every public company converts some (or all) of its cash and equivalents into bitcoin similar to MicrosStrategy and Square, in hopes of reaping a quick surge in its stock price” (we wonder how much of MSTR’s bitcoin purchase just a few days later was prompted by this rhetorical question).

If it’s up to Saylor, we wouldn’t have long to wait: as the CEO tweeted earlier today “If you don’t fantasize about flaunting it, floating in it, flying in it, frolicking with it, fortifying it, or fighting over it, you should probably play it safe and just buy #Bitcoin.”

If you don’t fantasize about flaunting it, floating in it, flying in it, frolicking with it, fortifying it, or fighting over it, you should probably play it safe and just buy #Bitcoin.

— Michael Saylor (@michael_saylor) December 5, 2020

- Trump Orders Withdrawal Of Nearly All US Troops From Somalia

Trump Orders Withdrawal Of Nearly All US Troops From Somalia

Tyler Durden

Sat, 12/05/2020 – 20:25President Trump has ordered the immediate withdrawal of the “majority” of American troops from Somalia, according to a Pentagon announcement made Friday. There’s an estimated 700 troops currently inside the country.

“The President of the United States has ordered the Department of Defense and the United States Africa Command to reposition the majority of personnel and assets out of Somalia by early 2021,” the Pentagon said.

US military training in Africa, Getty Images The statement indicated that “some forces may be reassigned outside of East Africa,” however remaining troops are expected to go elsewhere within Africa Command (AFRICOM) to “allow cross-border operations”. This is parallel to how the draw down from Germany is envisioned – some troops coming home to US soil with others stationed elsewhere in Europe.

The American public might be forgiven for never knowing there are American troops and bases in Somalia in the first place.

After all, the war-torn country in the Horn of Africa only sporadically hits the news when things go horribly wrong, such as with major pirate attacks on tankers in the Gulf of Aden, or last month’s death of a CIA officer reportedly during a raid on a suspected al-Shabaab bomb-maker, and then there’s the disastrous ‘Black Hawk Down’ 1993 mission wherein 18 American soldiers were killed.

CJCS Gen. Milley confirms this story, describes “brave” CIA officer and former SEAL: https://t.co/MiI1hy9oAX

— Paul D. Shinkman (@PDShinkman) December 2, 2020

https://platform.twitter.com/widgets.js

US forces are there ostensibly to help train national Somali security forces, and to conduct covert raids and drone warfare against local and regional terrorists like al-Shabab. In 2019 alone, for example, the Trump administration conducted an unprecedented 63 airstrikes in Somalia.

Trump is attempting a last-ditch effort to “bring our troops home” – something he emphasized heavily on the campaign trail. However, something like a full Syria pull-out would be seen as more significant, given that this theatre presents the greater potential for US entering a major regional war.

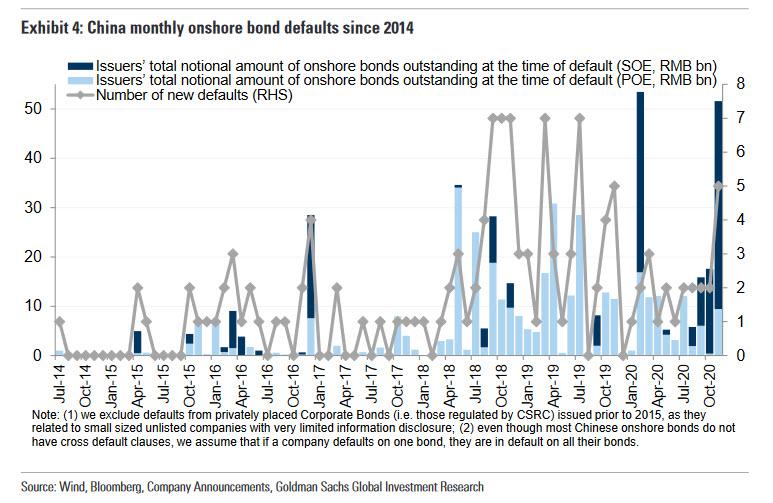

- Goldman Sees More Chinese Bond Defaults

Goldman Sees More Chinese Bond Defaults

Tyler Durden

Sat, 12/05/2020 – 20:00By Ye Xie, Bloomberg macro commentator

President Donald Trump has continued bashing China. This time, his administration restricted travel visas for members of the Chinese Communist Party and banned cotton imports from a military-linked firm it accused of “slave labor.”

So far, all of these moves, including the House bill that could lead to the delisting of Chinese companies on American exchanges, are roughly in line with market expectations. They don’t touch sensitive issues like the trade deal or sanctions on major banks. And investors have largely shrugged it off, with the yuan trading at the strongest in more than two years.

Looking at the domestic market, the fallout from the recent onshore bond defaults seems to be lessening after the government vowed to crack down on “debt evasion”. The credit spread of AA-rated bonds over government debt has stabilized after widening in recent weeks. Thus far, the default scare hasn’t caused major funding problems or market dislocation, which suggests that policy easing is unlikely.

What Beijing’s trying to do is break the implicit government guarantee and moral hazard of debt without triggering systemic and contagion risks. The net effect of this “credit cleanup” strategy will be more onshore defaults next year and more differentiation among weak and strong borrowers, according to Goldman Sachs’s Kenneth Ho and Chakki Ting.

The strategists expect the pace of new defaults to revert to the levels of 2018 and 2019, when there was an average of three to four new defaults a month. For the offshore market, strategists expect the pace of defaults to moderate because there was less forbearance this year, predicting that the high-yield default rate will drop to 4.3% next year from 4.9% this year.

It looks like 2021 is going to be another bumpy ride.

- Head Of World's Largest Sovereign Wealth Fund Forced Out Because His Wife Is Chinese

Head Of World’s Largest Sovereign Wealth Fund Forced Out Because His Wife Is Chinese

Tyler Durden

Sat, 12/05/2020 – 19:30The deputy governor of the Norwegian central bank, Jon Nicolaisen, announced on Friday he was resigning because his application for renewed security clearance had been rejected because he has a Chinese wife.

“The Norwegian Civil Security Clearance Authority informs me that the reason that I will not receive a renewed security clearance is that my wife is a Chinese citizen and resides in China, where I support her financially,” Nicolaisen said. “At the same time, they have determined that there are no circumstances regarding me personally that give rise to doubt about my suitability for obtaining a security clearance, but that this does not carry sufficient weight.”

“I have now had to take the consequences of this,” he said as he tendered his resignation.

Jon Nicolaisen, head of the Norwegian sovereign wealth fund and deputy governor of Norway’s central bank, stepped down after being denied security clearance because he has a Chinese wife. The resignation takes effect immediately, according to a statement released by the central bank. It was not immediately clear who would replace him.

In recent years, Norway has introduced stricter rules for the issuing of security clearances, making it difficult in many cases to get approval for anyone married to a person from a country with which Norway does not have security cooperation.

Jon Nicolaisen, whose wife lives in China, has been married since 2010. He had his term at the bank extended in April, having originally been appointed in 2014. In other words for over a decade it wasn’t an issue who the central banker was married, but has suddenly become grounds for effective termination.

In addition to taking part in setting monetary policy, Nicolaisen had been in charge of overseeing Norway’s $1.2 trillion sovereign wealth fund, the world’s largest.

Central Bank Governor Oeystein Olsen said Nicolaisen’s departure would be a big loss: “I will miss Jon Nicolaisen in his post as deputy governor, where he performed his duties superbly as a close colleague and competent professional,” Central Bank Governor Oeystein Olsen said in a statement.

- 'Virtuous Hypochondria': How One Man Lost A 'Friend' Of 20 Years…

‘Virtuous Hypochondria’: How One Man Lost A ‘Friend’ Of 20 Years…

Tyler Durden

Sat, 12/05/2020 – 19:00Authored by Eric Peters via EricPetersAutos.com,

I parted ways yesterday with a friend of more than 20 years’ standing over his sickness – and my refusal to indulge it or even pretend to ignore it.

This ex-friend says I should don the Holy Rag because “I might be asymptomatic” and because I ought to “show a little respect for your fellow man” and that “It’s not all about you.” He added:

“Grow your own food and you don’t need to interact with people. But if you want the benefits of society you have to participate and conform a bit.”

Italics added.

So I said good-bye.

I “have to conform a bit”? I am obliged to literally show that I (supposedly) agree with the outrageous assertion that I might be sick – i.e., “asymptomatic” – and so present an ongoing, never-ending threat to other people that requires me to wear a Face Diaper – the religious vestment of the Sickness Cult – to assuage their fears?

I attempted to reason with this friend.

It was like attempting to discuss Euclid with a rooster.

“I’m not sick,” I texted him.

“I’ve had two friends die from it,” he texted back. “And several still sick.”

Me: “Well, I’m not sick. Therefore, I cannot transmit sickness. Therefore, wearing a rag over my face serves no medical purpose.”

Him: “You might be asymptomatic.”

Me: “Okay, so you are saying that the possibility I might be sick – even though I’m not coughing or sneezing or manifesting any symptoms of sickness and so there is no evidentiary/specific reason to suppose I am in fact sick, much less contagious – obligates me to act as if I am in fact sick and contagious and to literally put on something as a ‘protective’ measure, just in case and to ease your fears?”

“In that case, why shouldn’t you be obliged to turn in your guns (my ex-friend likes guns) since many people are quite terrified of them and fear you might use them to harm them or someone they care about?”

“If my fear that you might be – or do – some thing is enough to impose an obligation on you, then how do you feel about being made to wear an armband or similar highly visible item indicating that you are gay (my ex-friend is homosexual) and thus a potential transmitter of AIDS?”

“The fact is you could possibly transmit AIDs. You might spit on me. You might rape someone. These are just as possible as ‘you might be asymptomatic’ ”…

He didn’t like that much – and that was the end of the texting and the friendship.

I do not mourn the loss.

Because I understand this person is not and may never have been my friend. A friend doesn’t threaten violence nor countenance its threat. Yet that is precisely what my ex-friend advocates – in a mewling, gas-lighting way – when he urges me to “wear a mask” to “show a little respect for (my) fellow man” and then says I am obliged to “conform a little bit.”

He means obey. And not merely obey.

I must agree.

I must show that I agree . . . by wearing a visible accoutrement of agreement.

Like the wearing of an armband, in another time.

To not wear the armband then – or the Holy Rag now – is to give visual evidence of non-agreement and that is what these creeps cannot stand.

Not that we are “asymptomatic” and might be plague carriers but that we disagree with them. That we do not share their virtuous hypochondria and by showing that we do not share it show contempt for it.

My now-ex-friend supports my being made to “conform a little bit” – and you, too. They will cheer when we are hounded by the Gesundheitpolizei for not wearing the Holy Rag and – soon – refusing to allow ourselves to be injected with god-knows-what. They will support our being excommunicated from life – not allowed to transact business, buy food.

“If you want the benefits of society you have to participate and conform a bit.”

Such people are no friends of mine.

The words attributed to Edward I – the “longshanks” – come to mind: “A man does good business when he rids himself of a turd.

* * *

If you like what you’ve found here please consider supporting EPautos. We depend on you to keep the wheels turning! Our donate button is here.

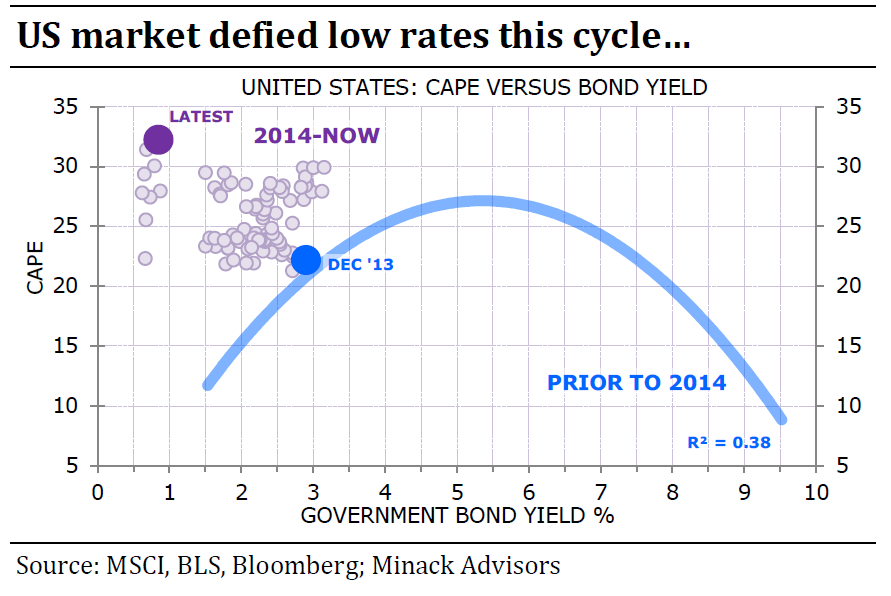

- No, Low Rates Do Not Lead To Higher Earnings Multiples: What That Means For Markets

No, Low Rates Do Not Lead To Higher Earnings Multiples: What That Means For Markets

Tyler Durden

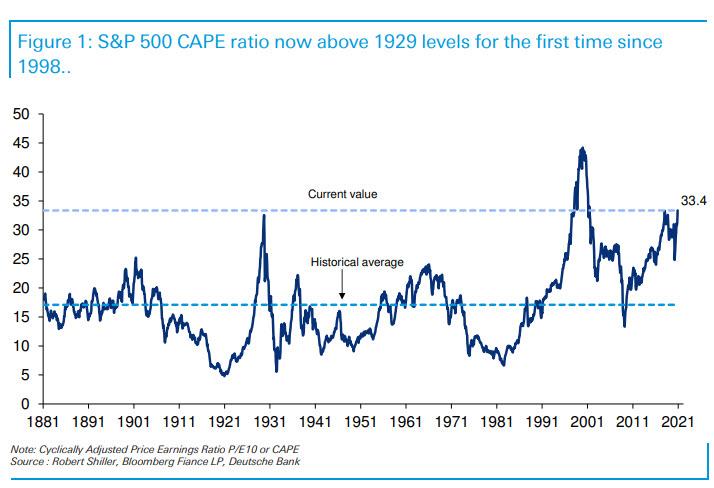

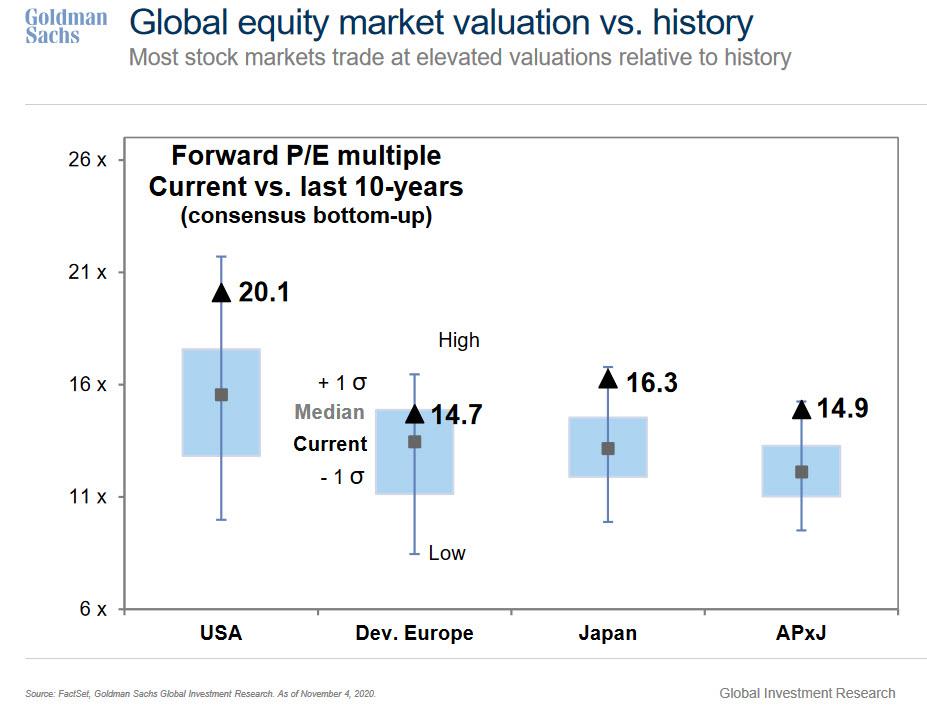

Sat, 12/05/2020 – 18:35With the S&P closing Friday at a new record high just shy of 3,700, which as we showed last week translates into a Shiller CAPE ratio now above levels where it was on the eve of the crash of 1929 for the first time since the dot com bubble…

… even Goldman has been forced to admit that stocks around the globe are at extremely elevated valuations relative to history not just on a forward P/E multiple basis…

… but across all valuation metrics…

… with one exception: the equity risk premium, which is also used in the so-called “Fed model”, both of which boil down to a simple concept: that low interest rates (and rates are now the lowest they have been in 4000 years of history) justify – and “allow” – high earnings multiples, implying that even if stocks are extremely overvalued since rates are at historic lows, investors have no choice but to keep buying stocks as there are no alternatives.

But is that true?

That’s the question which Gerard Minack, of Minack Advisors, raised this week as Bloomberg’s John Authers noted: do low interest rates on their own lead to higher earnings multiples?

Well, contrary to what Goldman, Morgan Stanley and virtually every other bank writes using the “Fed Model” as the only valuation-based justification for projecting even higher S&P500 targets in 2021 and onward (most banks predict the S&P will rise another 10-15% next year), Minack’s answer is a resounding no: it’s not rational to bid up stocks just because rates are low.

The reason is blindingly simple to anyone whose pay doesn’t depend on goalseeking a bullish narrative, namely that “all else is not equal”, or in other words, interest rates are usually low – i.e. disinflationary – because growth is bad, and as Authers redundantly clarifies, when growth is bad that tends to be bad for equities (except, paradoxically, now when collapsing global GDP has pushed world stocks to record highs).

Minack digs deeper to find that there is a curved relationship between rates and equities over time: when rates come down from very high levels, equity multiples tend to improve, but when rates then drop to very low levels, equity multiples fall because this generally means that the economy is mired in a recession.

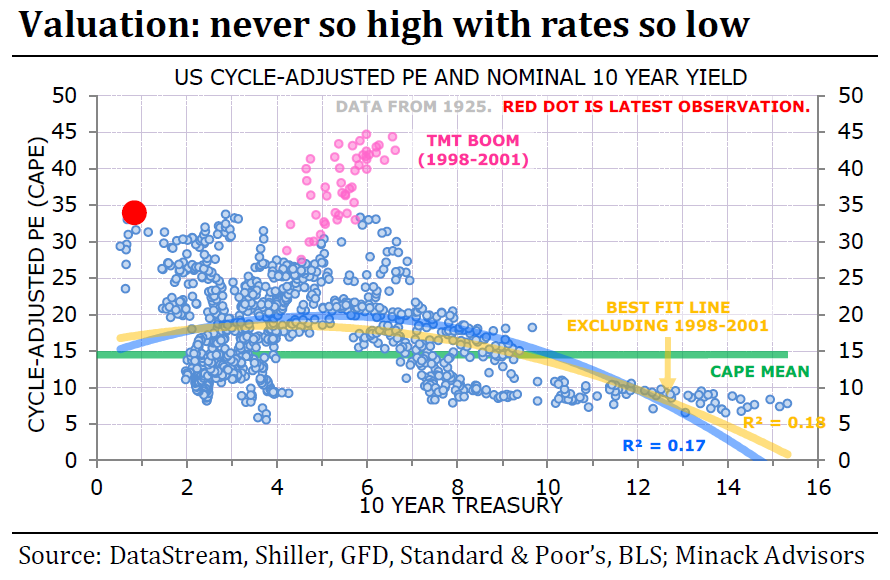

The chart below from Minack maps the CAPE on one scale against the 10-year yield on the other for every month since 1925. It shows that the relationship between the two isn’t that strong. In fact, the best fit Minack can find, excluding the bubble dot-com years, has an R-squared of only 0.12, meaning only a weak correlation:

As Authers points out the dot-com bubble readings, in pink, are almost off the chart — irrationally high multiples given the interest rates of the time (everyone knows what happened next). The current reading, shown in bright red, is clearly alarming as it’s the only time outside of the dot com bubble when the CAPE ratio was this high. This isn’t a well-explored end of the spectrum, obviously, but stocks do look expensive… and of course, Wall Street is quick to point out that this is justified due to the record low yields. Further bolstering the bullish case, one can extrapolate Shiller’s logic to show that one would expect the excess yield to rise further as rates get to extreme lows. If the relationship with rates held as anticipated in his chart, then the excess yield as calculated by Shiller would be roughly double what it is now (and stocks, on Shiller’s suggested methodology, would look like a screaming buy).

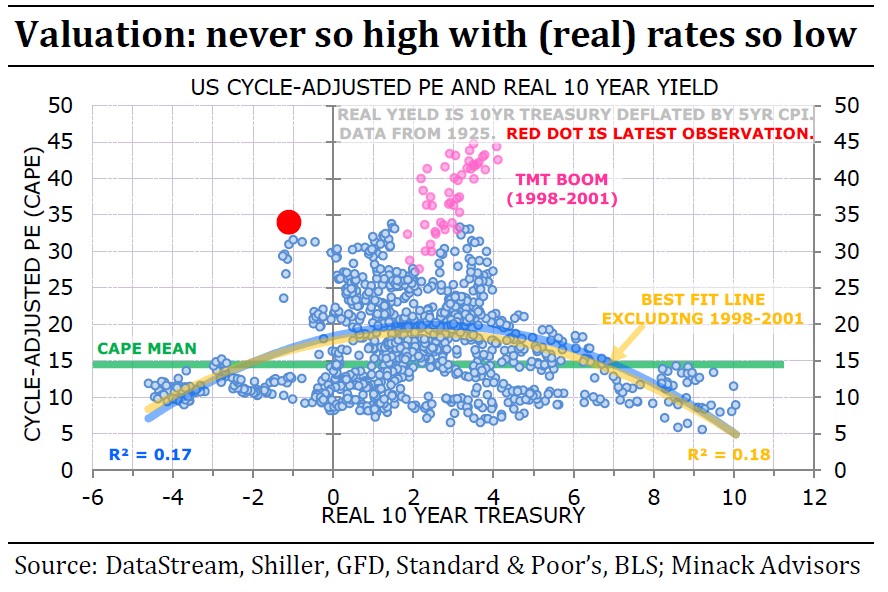

What if instead of nominal one uses real yields? Minack repeats his exercise to account for inflation, looking precisely at real yields which as one can imagine, are low present, but not historically unprecedented. As Bloomberg’s Authers writes, this exercise gives a slightly better correlation, “makes the dot-com bubble look like more of an outlier and, sadly, also makes the current point look like more of an outlier.” In short, while there have been a number of observations with 10-year nominal yields below the rate of inflation in the past, this is the most expensive that stocks have ever been during such a period:

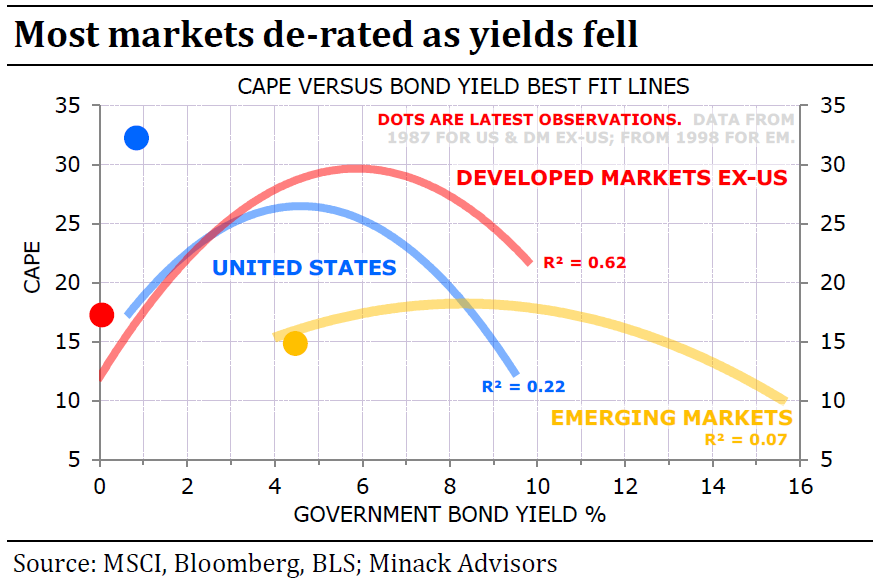

What is particularly notable is that not every market is an outlier like the US: the next chart, which uses nominal yields since 1987, compares CAPEs and 10-year yields for developed markets outside the U.S., emerging markets, and the U.S. While the US is clearly a bubble, stocks outside the U.S. appear to be reasonably valued given the level of interest rates. It is only U.S. stocks look wildly overpriced across most valuation metrics as even Goldman would agree:

And here a nuance emerges: as Authers points out, in an intriguing development, the U.S. relationship between yields and earnings multiples has started to differ from its historic pattern only in the last six years. In other words, until the end of 2013, there was a much more discernible correlation, with an R-squared of 0.38. But since the end of 2013, earnings multiples have been without exception higher than the previous relationship with interest rates would have suggested. In fact, they have never been further away. To be clear, this means that they now look unambiguously expensive, given where interest rates are, even though interest rates are so low:

According to Authers, we can learn two things from this chart:

- One is that the relationship between rates and earnings multiples changed at some point early in the last decade in the U.S., presumably when investors got used to the notion of enduring “lower for longer” rates coupled with low inflation. One possibility is that this was due to the belief that the traditional relationship between rates and the economy had broken down, in other words the advent of central planning by banks broke one of the most fundamental valuation relationships.

- The second is that whatever is driving multiples higher, it isn’t rates. As the chart shows clearly enough, rates have been on or about where they are now for nine months. Earnings have dipped and then recovered, and yet this is the most expensive that stocks have been.

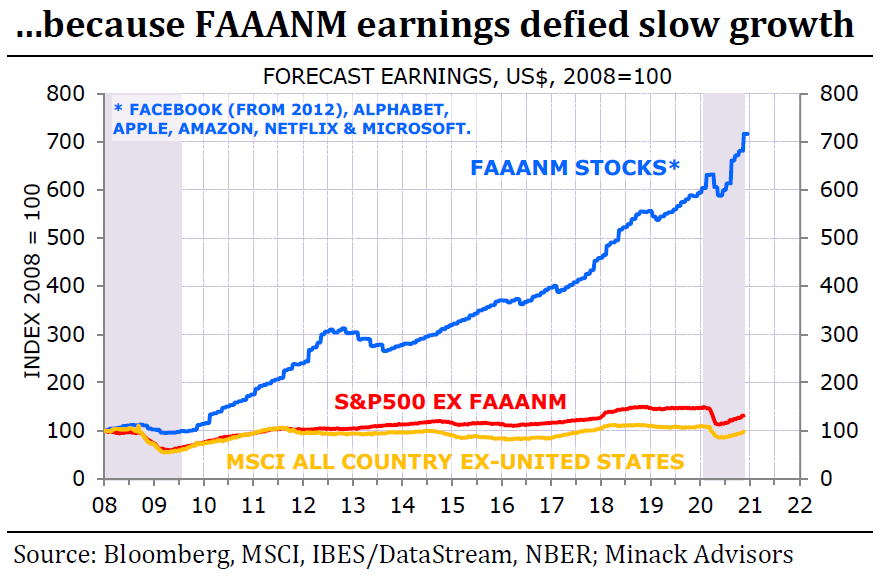

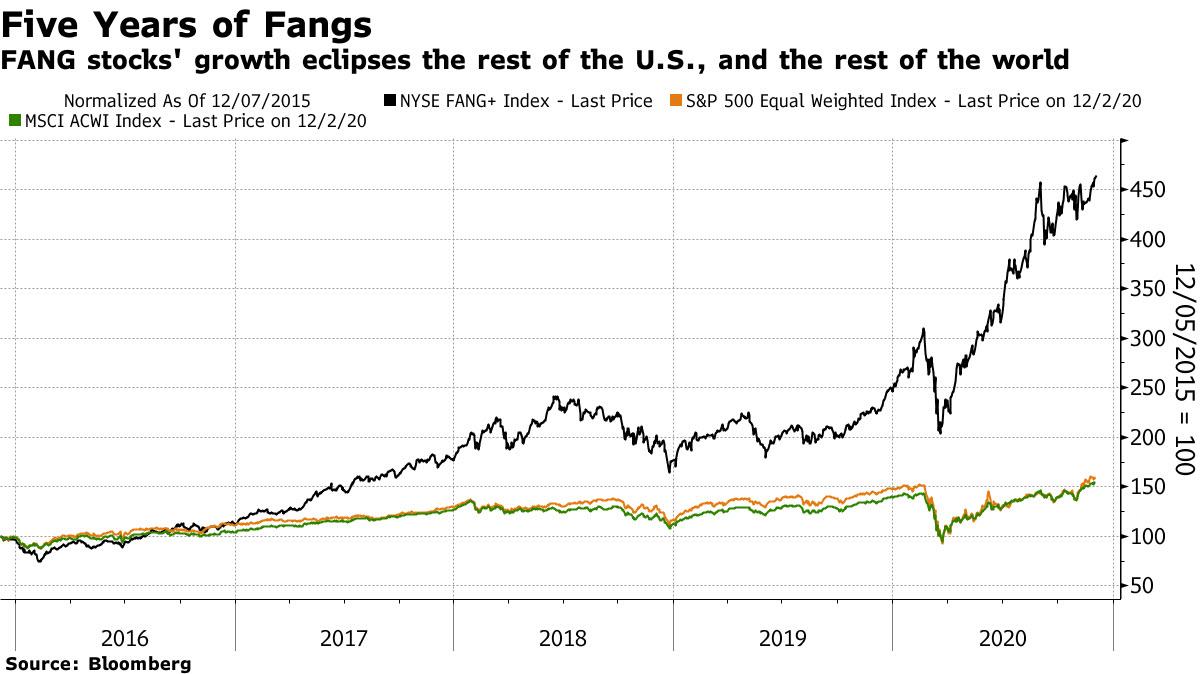

In an attempt to find out what is driving multiples, Minack next turns to the FANG stocks, which he defines as the FAAANMs (for Facebook, Amazon.com, Apple, Alphabet, Netflix and Microsoft). The key finding is that their earnings have, until now, defied slow growth that defined the developed world during the post-crisis decade, and have even defied the slump that followed the Covid shock. The rest of the S&P 500, and indeed the rest of the world, did nothing remotely similar. The following stunning chart from Minack shows the internet platform groups’ earnings, rather than their share prices.

Of course, soaring earnings also mean soaring stock prices (especially when one applies record PE multiples), and on Friday the NYSE Fang+ index hit a new all-time high. As Authers shows, over the last five years, its performance has dwarfed that of the S&P 500, and the MSCI all-world index. While smaller stocks are beginning to make a relative comeback, the FANGs’ share prices are as high as they have ever been in absolute terms.

Putting it together, while much of the world has seen corporate earnings behave just as one would expect in a world of very low interest rates (i.e., in a very sluggish economy), a tiny group of U.S. companies have managed to defy that logic completely and seen their earnings explode, dragging the US stock market higher while leaving the 494 remaining S&P companies in the dust. And now, amid growing expectations of a post-vaccine boom, earnings estimates are rising even more. That leads stocks to trade at a higher multiple of past earnings. In other words, as Authers notes, “it is earnings expectations, not rates, that have brought the market up in the last month or so, on this logic, and it would be an earnings disappointment (presumably sparked by some disappointment with distribution of the vaccine) that would bring it down again.”

As Minack summarizes:

In short, the US has been exceptional – relative to both its own history and other markets – by re-rating in the low-rate post-GFC cycle. The reason global equities are re-rating now is because of improving growth expectations, not because rates are low. If the rally were to correct – and I think it’s getting frothy – then the catalyst will be a growth scare, not a rate scare. Having said that, it’s a terrific combination for equities if growth does improve as expected next year and rates stay low. That combination would be more beneficial for de-rated non-US markets than the re-rated US market.

Indeed, anywhere one turns, one can find banks pushing the argument for favoring non-U.S. equities over the U.S. – JPMorgan did that just this week, when it downgraded US stocks and upgraded Europe.

That said, even in a world where record low rates did not justify the record high in stocks, and as we have repeatedly cautioned the last thing markets want is to find out what will happen if rates do surprise by rising, especially if they spike higher in an uncontrolled manner similar to what happened during the 2013 taper tantrum when 10Y yields soared by 150bps in months. As Authers notes, “U.S. markets have been working on the assumption that they will stay low for a while. It has been an unspoken ceteris paribus clause” and for good reason: “The sharp corrections in response to slightly higher rates in 2013 and 2018 both forced central banks into climbdowns.”

This is also the worst case conceived by Morgan Stanley’s Michael Wilson who last week said that “with our economists forecasting 7.5% nominal US GDP growth next year, a 1% 10-year Treasury bond looks awfully mispriced on a 12-month view. This has implications for equity valuations, especially longer-duration ones like the Nasdaq and S&P 500.”

Conversely, shorter-duration cyclical and value stocks get a boost from better growth and higher interest rates – hence the rotation we have been witnessing in the equity markets from the Nasdaq to the small-cap Russell 2000 over the past few months as markets contemplate a full reopening of the economy. “We think this rotation has further to go if we are right about the economy and rates” according to Wilson.

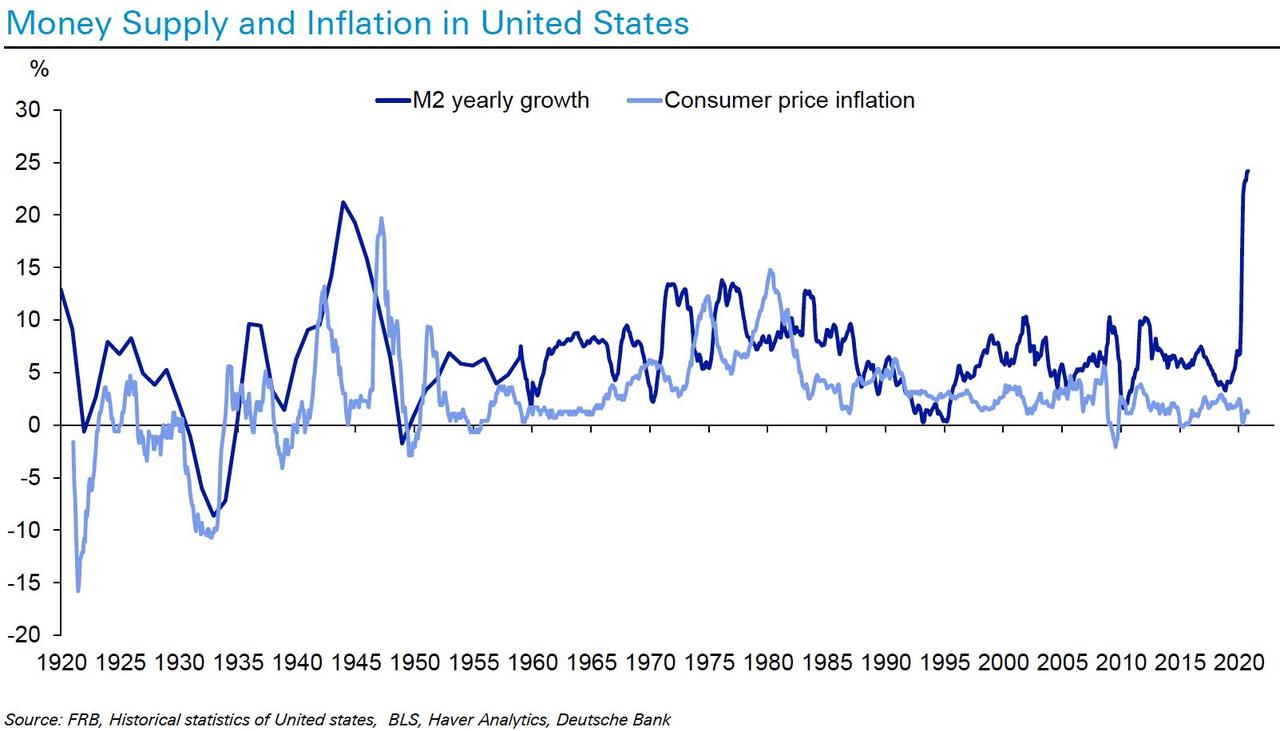

Of course, the question is just how high will rates eventually go in a world where the recent record injection of M2 would suggest it is just a matter of time before we experience a record inflationary spike:

As Authers ominously concludes, “we don’t yet know the results of an experiment in which rates rise and central banks cannot climb down because the economy is growing and inflation is back” but we may very soon have to find out.

- Why Does Bitcoin Have Value?

Why Does Bitcoin Have Value?

Tyler Durden

Sat, 12/05/2020 – 18:10Authored by Jeffrey Tucker via The American Institute for Economic Research,

Even after eleven years experience, and a per Bitcoin price of nearly $20,000, the incredulous are still with us. I understand why. Bitcoin is not like other traditional financial assets. Even describing it as an asset is misleading. It is not the same as a stock, as a payment system, or a money. It has features of all these but it is not identical to them. What Bitcoin is depends on its use as a means of storing and porting value, which in turn rests of secure titles to ownership of a scarce good. Those without experience in the sector look at all of this and get frustrated that understanding why it is valuable is not so easy to grasp.

In this article, I’m updating an analysis I wrote six years ago. It still holds up. For those who don’t want to slog through the entire article, my thesis is that Bitcoin’s value obtains from its underlying technology, which is an open-source ledger that keeps track of ownership rights and permits the transfer of these rights. Bitcoin managed to bundle its unit of account with a payment system that lives on the ledger. That’s its innovation and why it obtained a value and that value continues to rise.

Consider the criticism offered by traditional gold advocates, who have, for decades, pushed the idea that sound money must be backed by something real, hard, and independently valuable. Bitcoin doesn’t qualify, right? Maybe it does.

Bitcoin first emerged as a possible competitor to national, government-managed money in 2009. Satoshi Nakamoto’s white paper was released October 31, 2008. The structure and language of this paper sent the message: This currency is for computer technicians, not economists nor political pundits. The paper’s circulation was limited; novices who read it were mystified.

But the lack of interest didn’t stop history from moving forward. Two months later, those who were paying attention saw the emergence of the “Genesis Block,” the first group of bitcoins generated through Nakamoto’s concept of a distributed ledger that lived on any computer node in the world that wanted to host it.

Here we are all these years later and a single bitcoin trades at $18,500. The currency is held and accepted by many thousands of institutions, both online and offline. Its payment system is very popular in poor countries without vast banking infrastructures but also in developed countries. And major institutions—including the Federal Reserve, the OECD, the World Bank, and major investment houses—are paying respectful attention and weaving blockchain technology into their operations..

Enthusiasts, who are found in every country, say that its exchange value will soar even more in the future because its supply is strictly limited and it provides a system vastly superior to government money. Bitcoin is transferred between individuals without a third party. It is relatively low-cost to exchange. It has a predictable supply. It is durable, fungible, and divisible: all crucial features of money. It creates a monetary system that doesn’t depend on trust and identity, much less on central banks and government. It is a new system for the digital age.

Hard lessons for hard money

To those educated in the “hard money” tradition, the whole idea has been a serious challenge. Speaking for myself, I had been reading about bitcoin for two years before I came anywhere close to understanding it. There was just something about the whole idea that bugged me. You can’t make money out of nothing, much less out of computer code. Why does it have value then? There must be something amiss. This is not how we expected money to be reformed.

There’s the problem: our expectations. We should have been paying closer attention to Ludwig von Mises’ theory of money’s origins—not to what we think he wrote, but to what he actually did write.

In 1912, Mises released The Theory of Money and Credit. It was a huge hit in Europe when it came out in German, and it was translated into English. While covering every aspect of money, his core contribution was in tracing the value and price of money—and not just money itself—to its origins. That is, he explained how money gets its price in terms of the goods and services it obtains. He later called this process the “regression theorem,” and as it turns out, bitcoin satisfies the conditions of the theorem.

Mises’ teacher, Carl Menger, demonstrated that money itself originates from the market—not from the State and not from social contract. It emerges gradually as monetary entrepreneurs seek out an ideal form of commodity for indirect exchange. Instead of merely bartering with each other, people acquire a good not to consume, but to trade. That good becomes money, the most marketable commodity.

But Mises added that the value of money traces backward in time to its value as a bartered commodity. Mises said that this is the only way money can have value.

The theory of the value of money as such can trace back the objective exchange value of money only to that point where it ceases to be the value of money and becomes merely the value of a commodity…. If in this way we continually go farther and farther back we must eventually arrive at a point where we no longer find any component in the objective exchange value of money that arises from valuations based on the function of money as a common medium of exchange; where the value of money is nothing other than the value of an object that is useful in some other way than as money…. Before it was usual to acquire goods in the market, not for personal consumption, but simply in order to exchange them again for the goods that were really wanted, each individual commodity was only accredited with that value given by the subjective valuations based on its direct utility.

Mises’ explanation solved a major problem that had long mystified economists. It is a narrative of conjectural history, and yet it makes perfect sense. Would salt have become money had it otherwise been completely useless? Would beaver pelts have obtained monetary value had they not been useful for clothing? Would silver or gold have had money value if they had no value as commodities first? The answer in all cases of monetary history is clearly no. The initial value of money, before it becomes widely traded as money, originates in its direct utility. It’s an explanation that is demonstrated through historical reconstruction.

That’s Mises’ regression theorem.

Bitcoin’s use value

At first glance, bitcoin would seem to be an exception. You can’t use a bitcoin for anything other than money. It can’t be worn as jewelry. You can’t make a machine out of it. You can’t eat it or even decorate with it. Its value is only realized as a unit that facilitates indirect exchange. And yet, bitcoin already is money. It’s used every day. You can see the exchanges in real time. It’s not a myth. It’s the real deal.

It might seem like we have to choose. Is Mises wrong? Maybe we have to toss out his whole theory. Or maybe his point was purely historical and doesn’t apply in the future of a digital age. Or maybe his regression theorem is proof that bitcoin is just an empty mania with no staying power, because it can’t be reduced to its value as a useful commodity.

And yet, you don’t have to resort to complicated monetary theory in order to understand the sense of alarm surrounding bitcoin. Many people, as I did, just have a feeling of uneasiness about a money that has no basis in anything physical. Sure, you can print out a bitcoin on a piece of paper, but having a paper with a QR code or a public key is not enough to relieve that sense of unease.

How can we resolve this problem? In my own mind, I toyed with the issue for more than a year. It puzzled me. I wondered if Mises’ insight applied only in a pre-digital age. I followed the speculations online that the value of bitcoin would be zero but for the national currencies into which it is converted. Perhaps the demand for bitcoin overcame the demands of Mises’ scenario because of a desperate need for something other than the dollar.

As time passed—and I read the work of Konrad Graf, Peter Surda, and Daniel Krawisz—finally the resolution came. Bitcoin is both a payment system and a money. The payment system is the source of value, while the accounting unit merely expresses that value in terms of price. The unity of money and payment is its most unusual feature, and the one that most commentators have had trouble wrapping their heads around.

We are all used to thinking of currency as separate from payment systems. This thinking is a reflection of the technological limitations of history. There is the dollar and there are credit cards. There is the euro and there is PayPal. There is the yen and there are wire services. In each case, money transfer relies on third-party service providers. In order to use them, you need to establish what is called a “trust relationship” with them, which is to say that the institution arranging the deal has to believe that you are going to pay.

This wedge between money and payment has always been with us, except for the case of physical proximity.

If I give you a dollar for your pizza slice, there is no third party. But payment systems, third parties, and trust relationships become necessary once you leave geographic proximity. That’s when companies like Visa and institutions like banks become indispensable. They are the application that makes the monetary software do what you want it to do.

The hitch is that the payment systems we have today are not available to just anyone. In fact, a vast majority of humanity does not have access to such tools, which is a major reason for poverty in the world. The financially disenfranchised are confined to only local trade and cannot extend their trading relationships with the world.

A major, if not a primary, purpose of developing Bitcoin was to solve this problem. The protocol set out to weave together the currency feature with a payment system. The two are interlinked in the structure of the code itself. This connection is what makes bitcoin different from any existing national currency, and, really, any currency in history.

Let Nakamoto speak from the introductory abstract to his white paper. Observe how central the payment system is to the monetary system he created:

A purely peer-to-peer version of electronic cash would allow online payments to be sent directly from one party to another without going through a financial institution. Digital signatures provide part of the solution, but the main benefits are lost if a trusted third party is still required to prevent double-spending. We propose a solution to the double-spending problem using a peer-to-peer network. The network timestamps transactions by hashing them into an ongoing chain of hash-based proof-of-work, forming a record that cannot be changed without redoing the proof-of-work. The longest chain not only serves as proof of the sequence of events witnessed, but proof that it came from the largest pool of CPU power. As long as a majority of CPU power is controlled by nodes that are not cooperating to attack the network, they’ll generate the longest chain and outpace attackers. The network itself requires minimal structure. Messages are broadcast on a best effort basis, and nodes can leave and rejoin the network at will, accepting the longest proof-of-work chain as proof of what happened while they were gone.

What’s very striking about this paragraph is that there is not even one mention of the currency unit itself. There is only the mention of the problem of double-spending (which is to say, the problem of inflationary money creation beyond which the protocol would otherwise permit). The innovation here, even according to the words of its inventor, is the payment network, not the coin. The coin or digital unit only expresses the value of the network. It is an accounting tool that absorbs and carries the value of the network through time and space.

This network is the blockchain. It’s a ledger that lives in the digital cloud, a distributed network, and it can be observed in operation by anyone at any time. It is carefully monitored by all users. It allows the transference of secure and non-repeatable bits of information from one person to any other person anywhere in the world, and these information bits are secured by a digital form of property title. This is what Nakamoto called “digital signatures.” His invention of the cloud-based ledger allows property rights to be verified without having to depend on some third-party trust agency.

The blockchain solved what has come to be known as the Byzantine generals’ problem. This is the problem of coordinating action over a large geographic range in the presence of potentially malicious actors. Because generals separated by space have to rely on messengers and this reliance takes time and trust, no general can be absolutely sure that the other general has received and confirmed the message, much less its accuracy.

Putting a ledger, to which everyone has access, on the Internet overcomes this problem. The ledger records the amounts, the times, and the public addresses of every transaction. The information is shared across the globe and always gets updated. The ledger guarantees the integrity of the system and allows the currency unit to become a digital form of property with a title.