- The David Einhorn Podcast: The Fed Is Monetizing Debt Again

The David Einhorn Podcast: The Fed Is Monetizing Debt Again

It was back in 2012 that famed contrarian and value investing hedge fund icon, David Einhorn, first took aim at the pinnacle of market manipulation when he slammed the Fed for creating the ultimate toxic cocktail: something he called the Jelly Donut Policy. As the Greenlight founder wrote in May 2012, the Fed is “presently force-feeding us what seems like the 36th Jelly Donut of easy money and wondering why it isn’t giving us energy or making us feel better. Instead of a robust recovery, the economy continues to be sluggish.”

Seven years later, the recovery is just as sluggish and yet nothing has changed; in fact, just two months ago, the Fed launched what Fed Chair Powell sternly refuses to admit is QE4 but… is QE4. And while Einhorn has been right that the Fed is ultimately destroying the very fabric of not only the US economy, but taking down society with it as the growing wealth and income disparity chasm will eventually culminate in civil war, by fighting the Fed, Einhorn has seen his AUM plummet in recent years, his hedge fund a shadow of what of what it once was, largely due to the relentless ascent of the so-called “bubble basket” of stocks, those names which benefit entirely due to the Fed’s monetary generosity, and which have seen their stocks prices explode in the past decade.

Which brings us to another Jelly Donut – that’s the name of a new podcast service, which in recent weeks has interviewed, Julian Brigden, Ben Hunt, Miles Kimball, and others. Most notably, among those interviewed is that man responsible for the concept in the first place: David Einhorn.

While David Einhorn has recently been in the press for yet another feud he is currently waging, this time with Elon Musk, in which he first accused the Tesla CEO of “Significant fraud”, followed up with even more specific accusations of accounting irregularity profiled here, in the podcast with Ryan – which marked the Greenlight CEO’s first appearance in two years – Einhorn goes back to his roots and takes on his primary nemesis, the Federal Reserve, which is why among the topics covered are QE, ZIRP, MMT, fiscal and central bank stimulus. Oh, and gold, because seven years after the “Jelly Donut policy” was first coined, Einhorn remains just as bullish on the precious metal as the following excerpt confirms:

We’re running a very high deficit to GDP. And this is many years into an economic recovery with something that’s very close to full employment… In the event that the economy weakens, there’s going to be an enormous, both natural fiscal stimulus that comes from higher benefits, and less tax revenue, as well as an urge for Congress to do things to help people out in tougher economic times. So, what you have is a deficit right now that is very high and then you combine that with an accumulation of debt. You have a situation where the debt to GDP is much higher going into whatever the next down cycle is, and where we’ve had before similarly you have of monetary policy, which has been very aggressive. The balance sheet is much larger than it used to be and the rates going into down cycle are much lower than they used to be. There will be enormous pressure on the central bank to be very aggressive. And, so when you combine aggressive fiscal policy with aggressive monetary policy, historically that can lead to a problem with the currency and then when you realize that the same dynamic is essentially in place and in some cases worse in all of the other major developed currencies, it seems to me it’s a situation where sooner or later it might be good to have a fraction of your assets in gold, which is not subject to appropriation by the whim of the central banks.

Or rather, it is not yet subject to appropriate by central banks. Because all it takes is another Executive Order 6102 for all that to change.

All this and much more in the podcast below (phonetic transcript attached below):

Transcribed:

Ryan: David welcome to the podcast.

David: Hi Ryan. Thanks for having me.

Ryan: Well, it’s great to have you here. Really appreciate you coming on. First off, I wanted to explain a little bit to the audience of why we have you here, and when I decided to launch this podcast, I was trying to think of a great name that captured the subject of the show everything related to macro and monetary policy and I immediately thought about your article. So, going back to 2012 you wrote an article called The Fed’s Jelly Donut Policy in The Huffington Post and used a story about The Simpsons to explain a long periods of QE and zero interest rates may actually be harmful to the real economy. And it turns out a lot of what you said, they’re panned out inefficient allocation of Capital stock Buybacks with no urgency for corporations to invest to reach for yield from all investors, especially to Retirees so a lot has happened since then take us back to the feedback you got from the article and if your views have changed since.

David: Well honestly, I think the best feedback I got from the article is somebody’s naming their podcast after it. How can how can you beat that? And I’m honored to be here for the first one of these and I expect after I speak today, you’ll probably get all kinds of feedback and I will hopefully learn from listening to the feedback you get because I’m not a trained Economist. I’m not a macro-economist, I’ve never worked in the plumbing of the fed or any of these things. I’m basically an equity Market investor, and I think I have a few observations on some of these things from time to time, but I don’t profess to be a technical expert in all the mechanics of everything.

Ryan: Right and what was considered unconventional monetary policy over decade ago is really now seen as normal not just for the FED but central banks around the world and these policies seem to only be going on for longer and longer and uh others talked about using these tools and definitely what’s your view on these policies as far as do you ever imagine that balance sheet still being over $4.5T, you know taking up towards there right now and before the crisis was $800B. Did you see this still going on this long? And what’s your thoughts on the Fed using these tools and definitely?

David: Yeah. I don’t know how to predict what the FED is going to do with the size of the of the balance sheet, you know, basically, I think there’s two main parts of fed uh policy one is the interest rate policy and then the uh other is the balance sheet size the main thrust of the jelly donut thesis is that the interest rate policy by setting rates too low at some point you have a diminishing return from lower rates and eventually ultimately a marginally negative return from low rates, which is kind of separate from what you just raised which has to do with the size of the FED balance sheet and the monetary base and how they choose to implement that.

Ryan: Yes, so separating those out a little bit, obviously with the all the easing, you know, short-term rates, they’re able to target and bring down low and now we’re having some issues in the repo Market obviously some change some things change with paying interest on excess reserves and there’s been some other issues that brought up as far as the tax bill and things like this. What’s your thoughts right now on the current issues with the repo market and can the Fed really keep a hold of rates at this point?

David: Well, I think the FED ultimately can control whatever chooses to control within certainly within rates or whatever markets it’s willing to intervene in because it has unlimited fire power in order to enforce whatever policies that it wants . Sometimes eventually if the fed or a central bank over overdoes it, then people can take it out on the currency, which would be the normal reaction, but within the domestic economy in terms of control…. The Fed can set any rate that wants actually almost anywhere on the curve by, you know directly intervening in the market with unlimited firepower.

Ryan: Right, and going back to a Bloomberg interview did in 2014, you told a story about how you ask Ben Bernanke and a private dinner about QE and he talked about how these policies would lead to higher inflation talking about usually it only happens after a war and he talked about Japan has done a lot more QE than the US and they don’t have inflation. Recently Fed officials have said it’s kind of a mystery why. CPI claims inflation hasn’t gone up more but we have seen inflation in certain pockets: Healthcare, Housing, College tuition and you mentioned the currency piece. So what’s your thoughts as far as, where inflation goes and how long it can actually stay where it is right now?

David: When the Fed creates money and whether it’s from what you would call money printing or what they want to call quantitative easing, and most recently they’re doing the same thing and they want to tell us that it’s not quantitative easing. I don’t really know what the difference between all of these things is except for semantics and messaging in an attempt to, kind of control things. When the Fed increases the money the money has to go somewhere. It doesn’t have the same impact that it did when there were fewer excess reserves in the system, but we can come back to that later. I’ll just skip over that for the moment, but when they create money, the money does have to go somewhere. Now, the thing is, they don’t have any control over where that is. So it could be that the price of corn goes up or it could be the price of healthcare goes up or it could be the price of stocks go up or the price of bonds or art or Real estate or oil or what not but it doesn’t have to be any of those particular things. So as price levels in general go up it may or may not be prices that are measured within the CPI basket, which is only, you know, its a subset of possible places where new money can go.

Ryan: That makes sense. And you mentioned kind of the mechanics of how QE works. So one camp says that this is just an asset Swap and that this is a swap for bank reserves for Treasuries, and this is kind of normal operations. Where the other camp says this is something more like money printing and really something like debt monetization since all the interests gets remitted back to the Treasury and the so far a lot of these assets haven’t actually rolled off. How do you actually view that piece?

David: Yeah. I think it’s a little bit of a semantic game. By only looking at one side of a transaction, in other words, like what happens after a treasury is issued, you can decide, you know, that this isn’t money printing. But when you think about it in the totality how do treasuries get issued, a treasury is issued because the government needs to borrow money. And when the government needs to borrow money, there’s two places they can borrow it. They can borrow it in the private sector or effectively they can borrow it from the central bank. Now, there’s a rule that says they can’t sell the debt directly to the central bank, so they instead issue a T-bill to a leading commercial bank and then the central bank can buy the T-bill and you’re kind of in the same place. What’s happened is that the Federal government has borrowed money and ultimately that loan is held by the central bank which increases the central bank’s balance sheet size and thereby in there for the monetary base. So it’s the equivalent of a debt monetization. When you question whether its quantitative easing whether the current Fed chairman says it’s something different from that , whether it’s money printing, it’s really all the same things because all it is, it’s the Fed increasing the size of its balance sheet by buying Treasuries in one form or another. The difference is some people want to look at it as a two-step thing where the treasuries are issued by the Treasury Department to the private sector and then the Fed buys it as opposed to the Treasury issuing it directly to the Fed which is illegal, but the fact that there’s two steps in the transaction—I don’t think it makes any economic relevance. So think you have to look through it and when you look through it, when the Fed buys Treasuries, they’re increasing the balance sheet. They’re increasing the monetary base and effectively its debt monetization.

Ryan: Right, that makes a lot of sense. Now going back to interest rates and kind of what your article focused on, it’s arguable that interest rates are really the price of money and the price of money has been manipulated. Now, as far as rates rising on the longer end, you mentioned the Fed can kind of control not just the short-end, but also the longer-end. We saw recently when the repo market spiked up to a 10 from 2, that people said, okay, the price of money is not really what the Fed says is it is the price should be this. So, the question is, could the Fed lose control as far as people losing faith in their ability to just start tinkering and really micromanage. And will that show up maybe on the long end of the curve or how could that crisis of confidence happen?

David: I don’t know that you’ll have a crisis of confidence. But when you think about what just happened in the repo Market essentially, there wasn’t a huge amount of active intervention in the exact moment that it spiked. It spiked and the Feds saw what was happening relatively quickly after and announced new programs with extraordinary firepower in order to make sure that the problem doesn’t persist and that’s what I mean by their having the ability to control the rate. So, it spiked for a moment, but beyond that, you know, they managed to put it back together. As for Relating to the long end the curve, it has to do with how much intervention this the Fed is willing to do. Presently, I don’t know that they’re doing a lot of intervention on the long-end, but if you look at other central banks around the world, Japan and Europe and so forth, there’s huge amounts of intervention at the long-end of the curve and those banks have effectively cornered and controlled those rates as well.

Ryan: Yeah, that’s interesting when you look at Japan buying up huge amount of the JGBs is outstanding and obviously buying ETFs and things like Apple stock and seemingly distorting markets and doing so. Now, going back to the article again, the thesis laid out talking about with the Simpsons, it was actually really enjoyable to read for people who are trying to understand how this is all working. And, I think when you look at retirees, when you look at savers and obviously pension plans and insurance companies, a lot of these types of things have really caused a big problem as far as rates being low, and obviously for all investors going out on the curve to bid up risk assets. Do you see a path to normalization as far as rates or concerned? And what should the Fed be doing right now, and can they normalize rates or should they right now?

David: Well, I think it depends on what one thinks about as normalized rates. We’re certainly in a situation that there’s a lot more leverage in the financial system than 20 or 30 years ago, which means that the debt that’s in the system can’t support nominal rates that are higher than a certain amount, you know, if you think about what the deficit looked like when Volcker raised the short rates up into the teens, the debt to GDP was nowhere near what it is today. So you didn’t create a question about the government’s ability to repay the even in as rates went even a short rates went up at a at a good clip and ultimately even cost for long bonds. They wanted to sell at the time became quite expensive right once you have debt to GDP or incorporate case debt to EBITDA at higher ratios. It becomes much more sensitive to increase rates in terms of, from a solvency perspective. And so the situation is much different today than it used to be.

Ryan: Yeah, I’m looking at equity markets, especially here in the U.S., when you look at share buybacks and other things that have been going on. How are you looking at this the market based on these share buybacks uh and a lot of people have been talking about it. We’ve seen this many times before and it’s only a matter of time until the cycle has turned and you’ve talked a little bit about this over the past couple of years, but it really seems we’re almost kind of out of breaking point. How do you feel about the market right now?

David: I have no opinion as to whether the market is anywhere near a breaking point. Not the type of forecasting or thinking about things that I think about, you know, and in terms of things like share repurchases from my perspective, they are a tax efficient way to return capital and businesses to their owners and to the extent that there aren’t investment opportunities at better returns than returning capital to their owners, I think it’s a perfectly appropriate thing for businesses to do.

Ryan: Okay, that makes sense and you mentioned as far as going back to 2008 and even previous with the derivatives and all the debt built up in the system. How are you looking at the current environment compared to 2008. Obviously, it was built up more so in the mortgage market. How are you looking at the market now compared to back then. We now have some of these banking regulations after Dodd-Frank and others. Are we actually worse off or more levered up?

David: Well, there’s leverage, but the leverage is in a different place than it was last time last time. I believe (in 2008) that the leading part of the leverage was in the real estate market both commercial and residential and I think today it’s more in the public market meaning sovereign debt, municipal debt, and also corporate debt.

Ryan: Right and we’ve seen corporates levered up to some of the highest they’ve been…The last thing to touch on is, you’ve held a position in physical gold for a while now. Other investors have talked about hedging against inflation or even a “Black Swan” type event with real assets. How are you seeing a position in real assets as far as hedging against inflation?

David: Yeah. I don’t know that it’s a hedge against inflation or a particular Black Swan event. But, our theory relating to gold is that monetary and fiscal policies combined are very aggressive. Just take the United States as an example right now. We’re running a very high deficit to GDP. And this is many years into an economic recovery with something that’s very close to full employment… In the event that the economy weakens, there’s going to be an enormous, both natural fiscal stimulus that comes from higher benefits, and less tax revenue, as well as an urge for Congress to do things to help people out in tougher economic times. So, what you have is a deficit right now that is very high and then you combine that with an accumulation of debt. You have a situation where the debt to GDP is much higher going into whatever the next down cycle is, and where we’ve had before similarly you have of monetary policy, which has been very aggressive. The balance sheet is much larger than it used to be and the rates going into down cycle are much lower than they used to be. There will be enormous pressure on the central bank to be very aggressive. And, so when you combine aggressive fiscal policy with aggressive monetary policy, historically that can lead to a problem with the currency and then when you realize that the same dynamic is essentially in place and in some cases worse in all of the other major developed currencies, it seems to me it’s a situation where sooner or later it might be good to have a fraction of your assets in gold, which is not subject to appropriation by the whim of the central banks.

Ryan: Right, that makes a lot of sense. Well David, thank you so much for coming on, I really appreciate it.

David: You’re welcome and good luck with the whole podcast series.

The full podcast can be found here.

Tyler Durden

Sat, 12/07/2019 – 23:38 - Luongo: "Pelosi's Mask Just Slipped"

Luongo: “Pelosi’s Mask Just Slipped”

Authored by Tom Luongo via Gold, Goats, ‘n Guns blog,

Nancy Pelosi is a bitch. And in saying that I’m actually being sexist against female dogs, since every one of them I’ve ever met is a higher quality individual than Pelosi.

So, my apologies to dogs everywhere.

Just when you thought this power-mad harpy couldn’t sink any lower she responds to a simple question from a reporter with the kind of lame, stuttering virtue-signaling that has become her signature move, to attack when confronted with the truth.

This screed is a masterclass in diversion and doublespeak. Her self-righteous anger is a dead giveaway that she was lying about her motivations for proceeding with this impeachment while scolding the CSPAN reporter who asked the question like he was an impudent child.

If there is one thing Nancy Pelosi hates it is being called a liar.

She’s the ultimate keeper of the status quo, of the political order as she sees it and she has determined it shall be.

But she damns herself by wrapping herself in the false flag of her Catholicism. The false flag of her love for humanity. She is so desperate to deflect away from the truth that she does, in fact, hate the president and all that his election represents, she uses that to debunk the idea that she can hate anyone.

You know, except for all those unborn children that she advocates murdering or the people overseas she spends zero time stopping from being bombed by the administration.

This coming from the woman whose own daughter described her as capable of cutting off your head and not know you’re bleeding.

So, we all have to suffer because of this outrageous woman’s all-consuming love for humanity? That’s what she’s trying to sell now?

In a word, yes. The mask slipped when she had to run back to the podium to look into the camera and unconvincingly proclaim her love of children. And that she’ll fight anyone who gets in her way, clutching her rosary the entire time.

Yup, that’s love all right.

The tough broad act plays well with the bi-coastal shitlib set but the rest of us just look at her and shake our heads wondering who in the holy hell does she think she’s fooling with this stuff?

Please, I’ve seen more believable acting in your average 1990’s porn flick.

That thin veneer of compassion masks a cold and cruel calculation and psychopathology which is abhorrent to anyone with any shred of a soul left.

The sad truth is that Pelosi in her near-dementia might actually now believe some of this stuff she’s spouting. Here she does a CNN Town Hall in which she parrots the current climate hysteria saying that civilization itself depends on removing Donald Trump from the White House.

Even if this is true, and this is how she sees herself, acting out of a love for humanity rather than her own narrow interests, then she’s simply a classic villain archetype who is willing to break a few eggs to make her omelette.

And Pelosi, like the people she ultimately represents, are telling us that they will ‘love us all to death‘ to achieve their goals. It’s the most sick and twisted form of manipulation possible.

She’s morphed from the tough broad from San Francisco to the epitome of Toxic Femininity, the over-bearing mother archetype. And any threat to her power will be met with the cruelest counter-attack.

She’s Nurse Ratched with Botox.

And Donald Trump is her R. P. McMurphy.

And in every way Pelosi knows that she’s locked in an existential battle for control over the future of America. She knows that she’s been tasked with delivering results on destroying Trump and if she doesn’t she’ll be cast aside.

No rational person can actually think the world is going to end in twelve years when they take even a cursory look at the climate data. But Pelosi is an order-taker not an order-maker in the hierarchy of political dominance.

And the call has come from above her pay-grade to sell this climate hysteria as the way to keep the program on track to finish the globalist’s dream of universal serfdom for us and perpetual power for them.

That’s your tell that Pelosi simply does what she’s told. It’s her job to sell whatever it is she’s been told to sell.

Every religion has it’s apocalypse story and the latest one from the Climate Crazies is this insane notion that time has run out and we need to act now or face extinction.

You know someone is lying to you when they only present you ultimatums, which are always a false binary choice. Follow our prescriptions or we’re all going to die!

And Pelosi truly is the enforcer of this edict.

In her heart she knows this impeachment process is a sham. She knows the premise is faulty and the results for the Democratic Party will be catastrophic. She can see the poll numbers.

But in her single-mindedness to save the world from itself, Pelosi will do everything she can to force us wayward and mentally-ill citizens back into her institution because her cause is righteous.

That’s why it’s now a life or death struggle to get rid of Trump. That’s why she’s willing to sell Climate hysteria and that’s why she lost her mind when asked the simplest of questions which she could have brushed off with a wave and a “No.”

Her vehement denial is her admission of guilt. For a moment, Speaker Ratched lost control and the results were a glimpse into the depths of her evil.

* * *

Join my Patreon to help me identify the true villains of humanity. Install the Brave Browser if you want to divert capital away from those protecting them.

Tyler Durden

Sat, 12/07/2019 – 23:00 - “Where In The World Is Inigo?”: The Mysterious Disappearance Of The Billionaires’ Art Dealer

“Where In The World Is Inigo?”: The Mysterious Disappearance Of The Billionaires’ Art Dealer

Where in the world is 32 year old art dealer Inigo Philbrick?

The mysterious young dealer burst onto the art scene years ago, bidding for million-dolllar works before age 30, his name written down in the rolodex of every art-collecting billionaire.

But now, he has vanished. And as Bloomberg reports, his name was one of the biggest topics of discussion in Miami Beach this week, where Art Basel – one of the biggest events in the art industry – is taking place.

His disappearance comes after a wave of lawsuits filed against him for fraud in London, New York and Miami. The aftershock has left the Art Basel crowd fearing that it could stoke broader fears about the often-opaque industry globally.

The story, not unlike the industry itself, stretches around the globe. It has links and ties to major auction houses, including an art-finance firm backed by George Soros. Los Angeles-based art dealer Timothy Blum said: “It checks every box in a bad way. So gross.”

The scandal centers around allegations that Philbrick sold the same art works to different investors, often at inflated prices. Just like with rehypothecated collateral, companies in Asia, Europe and the U.S. have all staked claims to the same art pieces.

The allegations emerged in October which is when Philbrick disappeared. His gallery in Miami has been closed and he hasn’t been spotted for weeks at the trendy Japanese restaurant where he was once a regular. There was a “For Rent” sign hanging outside of his London gallery.

Meanwhile, he failed to appear for court last month in both Miami and London and his lawyers in Miami have stopped representing him; his whereabouts have raised questions across the industry.

Wendy Goldsmith, a London-based art adviser, asked: “What was he thinking?”

Adam Lindemann, a dealer and collector, said: “Philbrick seemed to come out of nowhere, and [I] was never quite sure where he got his funding. He had this charming, rogue manner about him. The art world always has people like this.”

Lowell Pettit, an art adviser in New York, said: “Philbrick seemed to have a lot of money behind him at a very early point in his career. In short order, his name started to light up.”

But the lawsuits paint a picture that Philbrick was not who he appeared. One company suing him says he holds $70 million in assets and put the combined value of the art managed by his business at $150 million. His collection includes a single painting, by Jean-Michel Basquiat, that Philbrick agreed to “buy” with a partner at an inflated price of $18.4 million. The price was inflated by about $6 million, the partner later found out.

Another contested work by Yayoi Kusama is worth about $3.4 million and is drawing crowds in Miami next to Philbrick’s gallery, at Miami’s Institute of Contemporary Art. A German company that bought the work through Philbrick now wants it back. There is just one problem: piece was sold months ago “to the Royal Commission for AlUla in a private transaction through Phillips auction house.”

The allegations have also shocked those that know Philbrick. He grew up in an artistic family, but had been estranged from his father for almost a decade. One classmate of his described him as “quiet and artsy”. The mother of his child said they hadn’t been together “in years” and declined to comment.

In 2010, Philbrick joined the prestigious White Cube gallery in London as an intern and quickly became a favorite of its owner, Jay Jopling. Jopling said: “He struck me as a smart, ambitious young man with a good eye for art and an impressive commercial sense. He progressed quickly and in 2012 launched Jopling’s secondary-market business.”

Jopling said he “agreed to support him financially” when Philbrick wanted to go out on his own.

Now, Jopling finds himself just another person on the long line of those suing Philbrick.

Tyler Durden

Sat, 12/07/2019 – 22:30 - "See You After Jail Guys": Art World Stunned After Man Eats $120,000 Banana Duct Taped To Wall

“See You After Jail Guys”: Art World Stunned After Man Eats $120,000 Banana Duct Taped To Wall

Let them eat duct-taped bananas

– The US Federal Reserve, probably

On Friday, we reported on the latest bizarre milestone in the “art” world, when a banana duct-taped to a wall sold for $120,000 at that excess-liquidity conclave of ultra rich and other wannabe poseurs known Art Basel Miami Beach. Worse, a second banana duct-taped to a wall also sold for $120,000. Yet even worse than that, a third banana duct-taped to a wall is expected to sell for $150,000 and so on.

Then on Saturday, at around 1:45pm, the art world was shocked when a random man, allegedly a performance artist, ate said duct-taped banana that sold earlier this week for $120,000.

New York-based performance artist David Datuna ate the banana early on Saturday afternoon in front of a stunned convention full of “art” lovers most of whom had no idea whether they were witnessing even more “art”, of just some clueless rando eating the world’s most discussed “art” exhibit, the gallery told the Miami Herald.

This happened and here’s the video: someone ripped the Maurizio Cattelan banana off the wall at @ArtBasel and ATE IT 🍌 pic.twitter.com/JOL41jLoeY

— JiaJia Fei 费嘉菁 (@VAJIAJIA) December 7, 2019

https://platform.twitter.com/widgets.js

Perrotin Gallery spokesman Lucien Terras told the Herald that Datuna did not “destroy” the artwork because “the banana is the idea”, or as Magritte would say “Ceci n’est pas une banane.”

The controversial piece, called “The Comedian,” was created by Maurizio Cattelan, an Italian artist who had also entertained art lovers from around the globe in 2017 with his “America” 18-carat-gold toilet. The $6-million throne was stolen from England’s Blenheim Palace over the summer according to CBS.

Emmanuel Perrotin, the gallery founder, told CBS News that Maurizio’s work is not just about objects, but about how objects move through the world.

“Whether affixed to the wall of an art fair booth or displayed on the cover of the New York Post, his work forces us to question how value is placed on material goods,” he said, although he could have also added “or eaten.”

He added that “the spectacle is as much a part of the work as the banana.”

Perrotin was about to head to the airport when he heard about the banana being eaten and rushed back, according to the Herald. An attendee tried to cheer him up by handing him a banana. A borrowed replacement banana was eventually re-adhered to the wall, because “art.”

Whereas the “art” world was briefly outraged after the 120,000 rotting banana was calmly eaten, unaware that they themselves were the joke, normals argued this piece is a perfect representation of what the art world has become with its gaping wealth inequalities and where idiotic “art” such as a banana duct taped to a wall sells for $120,000. Others, however, chose not to go as deep and appreciate the simplicity of the art piece. Yet others blamed the Fed for flooding the world with so much money that a banana duct taped to a wall was actually bought by someone for $120,000.

The artist first came up with the idea a year ago. He “was thinking of a sculpture that was shaped like a banana,” according to a press statement from Perrotin.

“Every time he traveled, he brought a banana with him and hung it in his hotel room to find inspiration. He made several models: first in resin, then in bronze and in painted bronze (before) finally coming back to the initial idea of a real banana.”

The artist reported no clear instructions for buyers on whether the bananas start to decompose.

As for Datuna, who calmly ate the banana in front of a room full of shocked “art” fans before he was confronted by an art gallery worker, his parting words were “see you after jail, guys.”

“Are you kidding me?”

“It’s performance.”

“It’s absolutely not performance.”

…

“See you after jail, guys!” pic.twitter.com/BHsCtNLki2— JiaJia Fei 费嘉菁 (@VAJIAJIA) December 7, 2019

Tyler Durden

Sat, 12/07/2019 – 21:42 - "We Are All George Zimmerman Now…"

“We Are All George Zimmerman Now…”

Authored by George Zimmerman via AmericanThinker.com,

Most people know my name, George Zimmerman, largely due to negative stereotypes propagated by the media as a result of the 2012 incident in Sanford, Florida, in which Trayvon Martin died.

Unfortunately, most people don’t recall the fact that I was exonerated of any wrongdoing after a thorough investigation by the Sanford Police Department in March 2012. They had interviewed dozens of witnesses, analyzed 911 calls, and examined the physical evidence of my broken nose, the lacerations on the back of my head, as well as the bruised knuckles of my assailant.

George Zimmerman in 2012, following the incident (Photo via the State of Florida)

This was all backed up by eyewitness Johnathan Good who told police that he saw me screaming for help while blows were coming down on me “MMA style.”

At the conclusion of the police investigation, Sanford Chief of Police Bill Lee announced that my actions were taken in self-defense and there were no grounds for my arrest. It was not even a “stand your ground” case. What followed immediately was a campaign of race-based defamation and incitement against me, led by Martin family attorney Benjamin Crump.

I am the last person who ever expected to be accused of being a bigot. I am Hispanic. My mother is from Peru. I speak fluent Spanish. I was an Obama supporter and a social activist. Just a year earlier, I had led a community-wide effort to get justice for Sherman Ware, a homeless black man who had been attacked by the son of a white police officer. I was also active in a mentoring program where I spent my spare time (and money) with black teens whose parents were in prison.

The Martin family attorney, Benjamin Crump, quickly recruited for his incitement efforts Al Sharpton, a man who was infamous for the 1989 Tawana Brawley race hoax and other incidents of mayhem based on racial incitement over the years. Then, Obama’s Department of Justice sent representatives to Sanford to “investigate,” but they instead helped organize protests demanding my arrest. As the protests heated up and Crump’s false narrative was repeated by the media ad nauseam, even fair-minded people began to demand my arrest without cause. Then, out of the blue, Crump produced a recorded interview of a “phone witness,” whom, he said, was Trayvon Martin’s 16-year-old girlfriend, “Diamond Eugene.”

In the recorded interview with Diamond Eugene, Crump openly led the witness. She mostly just echoed everything Crump said. Two weeks later, prosecutors went to Miami to interview 16-year-old Diamond Eugene under oath. That’s when, as I recently learned, 18-year-old Rachel Jeantel appeared, claiming she was Diamond Eugene. Despite the discrepancy in name and age, prosecutors interviewed Rachel Jeantel anyway and used her obviously false statements to issue an affidavit of probable cause for my arrest. The rest is history.

Hollywood filmmaker Joel Gilbert just released a film and book of the same name, The Trayvon Hoax: Unmasking the Witness Fraud that Divided America. He investigated the public records and made a discovery – Rachel Jeantel was an imposter. She was not “Diamond Eugene.” She was not Trayvon’s girlfriend. She was not on the phone with him before our altercation. She lied in court about everything she claimed to have heard over the phone in order to send me to prison for life.

In The Trayvon Hoax, Gilbert not only proves that Rachel was a fraud, he actually finds Trayvon’s real girlfriend, Diamond Eugene, studying Criminal Justice at Florida State University, of all things! Gilbert also identifies those who knew about the witness fraud, such as Trayvon Martin’s mother Sybrina Fulton, now a 2020 Miami Dade Commissioner candidate. Gilbert also identifies the attorneys who likely knew and/or should have known about the witness switch.

The damage the trial did to me and my family has been devastating. I suffered from PTSD and, as a result, acted out for a few years before finally returning to the person I was. I was kicked out of college due to threats against the staff by the New Black Panthers. I lost my career path to become an attorney, and to this day I cannot work or even circulate in public. In 2015, someone tried to kill me. The bullet missed my head by inches, and the shooter got 20 years in prison. Today I remain in hiding, as does my family due to constant threats, which appear almost daily in rap songs and social media rants.

Ironically, Trayvon Martin and I ended up having much in common. We were both used to divide America for a political agenda. Since the trial, I have watched in horror as those who incited against me have divided America along racial lines. Black Lives Matter started as a result of my acquittal. BLM took its vigilante act to Ferguson, and the resulting “Ferguson Effect” led to a sharp rise in homicides in black neighborhoods. Even today, Benjamin Crump continues his false race narrative (and defames me) in his new book entitled, Open Season: Legalized Genocide of Colored People.

I have now taken up the cause of bringing America back together again, and I intend to do it by revealing how the country was deceived. I feel that if I can expose and hold accountable those at the origin of this evil witness fraud, the healing can begin.

I have hired attorney Larry Klayman in his private capacity, founder of Judicial Watch and now Freedom Watch. I am suing Rachel Jeantel, Brittany “Diamond” Eugene, Sybrina Fulton, Tracy Martin, Benjamin Crump, prosecutors Angela Corey, Bernie de la Rionda, John Guy, the state of Florida, the FDLE, and HarperCollins Publishing for in excess $100 million. I don’t care about the money as much as I care about the truth coming out in discovery and at trial.

Racheal Jeantel lied under oath to deprive me of my constitutional rights and send me to prison for life. The others either suborned perjury or lied under oath to hide their knowledge of the switch of the legitimate phone witness, Diamond Eugene, for Rachel Jeantel, whom they knew was an imposter. My lawsuit is online and can be viewed or downloaded here: Zimmerman v Sybrina Fulton, Crump et al.

I am bringing this action not only to get justice for myself, but for all those Americans who are falsely accused of racial animus as well as those victimized by fake witnesses and unscrupulous prosecutors.

This lawsuit is also for the Bell family, whose sons were falsely accused of involvement in a tragic gym accident that caused the death of Kendrick Johnson. This lawsuit is for Officer Darren Wilson of Ferguson, whom even Eric Holder had to admit was falsely accused of shooting a man who allegedly put his hands up. This lawsuit is for the police officers in Baltimore, both black and white, who were falsely accused of harming Freddy Gray in order to justify mob violence. This lawsuit is for Brett Kavanaugh and any future Supreme Court nominees falsely accused of crimes they did not commit to prevent their nominations.

More than anything else, this lawsuit is for the America I grew up in and still believe in, an America of equal justice for all, where race hoaxes and fake witnesses have no place, an America where the content of one’s character, not race, is the basis for one’s judgement of another.

With my lawsuit, I hope to make a strong statement that false witnesses will not be tolerated, not in Seminole County Court or any court, and not in the United States Senate chambers. False witnesses must face consequences, or they will continue to ruin lives of innocent people. There is nothing more un-American and irreligious under the Ten Commandments than to bear false witness.

I look forward to succeeding in my court actions and hope to have enough funds to found a center for falsely accused persons of all races, those railroaded by charlatans, prosecutors, and an all too willing establishment media.

Tyler Durden

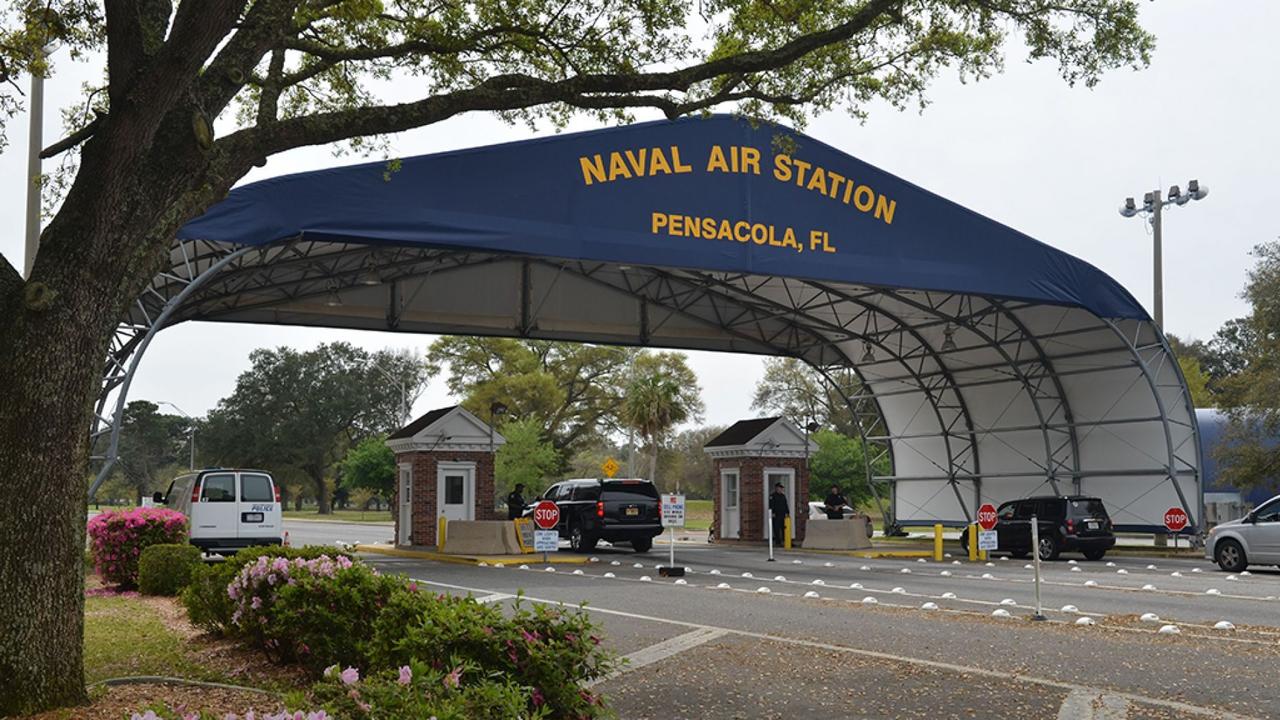

Sat, 12/07/2019 – 21:00 - Saudi Terrorist Hosted Dinner Party To Watch Mass Shooting Videos Night Before Naval Base Attack

Saudi Terrorist Hosted Dinner Party To Watch Mass Shooting Videos Night Before Naval Base Attack

Update: The Saudi student who shot and killed three people at a US naval base in Florida hosted a dinner party the night before the attack where he and others watched videos of mass shootings, according to the Associated Press, citing a US official.

One of the three students at the dinner recorded the shooting outside the building at Naval Air Station Pensacola on Friday. According to the report, two other Saudi students watched from a car.

***

Six Saudi nationals were taken into custody for questioning near the Florida naval base where an Air Force trainee – also from Saudi Arabia – opened fire Friday morning, killing three before a sheriff’s deputy shot and killed him.

According to the New York Times, three of the Saudis were filming the attack. It is unknown whether they were students at the base, or whether they are connected to the gunman.

Mohammed Saeed Alshamrani (via the Daily Mail) The shooting spanned two floors in a classroom, according to Sheriff David Morgan of Escambia Country. Two deputies were shot in the ensuing gun battle and are expected to recover.

The gunman, identified as Saudi Air Force second lieutenant Mohammed Saeed Alshamrani, used a locally bought Glock 45 9mm handgun with an extended magazine, and was carrying between four and six more magazines.

In his last message on Twitter confirmed by AFP, Alshamrani wrote that America is a nation of evil.

Pensacola terrorist’s last tweet. pic.twitter.com/B9qLnYuTwH

— Rising serpent (@rising_serpent) December 7, 2019

https://platform.twitter.com/widgets.js

The FBI is leading the investigation into the incident at Naval Air Station (NAS) Pensacola in Florida, and initially withheld Alshamrani’s name.

He was allegedly a student enrolled in a Navy training program designed for ” immersing international students in our U.S. Navy training and culture ” to help “build partnership capacity for both the present and for the years ahead,” accoring to Fox News, citing 2017 comments by Cmdr. Bill Gibson, who is the center’s officer in charge.

“These relationships are truly a win-win for everyone involved,” he added at the time.

Governor Rick Scott (R-FL) called for a “full review” of the Navy training programs in the wake of the shooting, while investigators have said they are exploring whether the attack was an act of organized terrorism.

“I’m very concerned that the shooter in Pensacola was a foreign national training on a U.S. base. Today, I’m calling for a full review of the U.S. military programs to train foreign nationals on American soil. We shouldn’t be providing military training to people who wish us harm,” said Scott.

Defense Secretary Mark Esper told reporters Friday that although his first priority is supporting the ongoing investigation and determining the shooter’s motives, he also said: “I want to make sure we’re doing our due diligence to understand what are our procedures” concerning the training programs.

“Is it sufficient [et cetera, et cetera] and it may not be — it may be the vetting — are we also screening persons coming to make sure that they have, you know, their life in order, you know, their mental health is adequate,” Esper said. “So we need to look at all that.”

Esper referred to the shooter as a Saudi national who was a second lieutenant in flight training.

Sources told Fox News that the scene of the shooting — a classroom, where students usually spend three months at the beginning of the program — indicated that the shooter was a student who was “early” in his training. –Fox News

Approximately 1,500 pilots are enrolled in the Naval training program – with Saudis having attended courses at the Pensacola site since the 1970s. According to the report, as many as 20 students from the Islamic Republic are in any given class – with many of them belonging to the Royal Family.

Following the shooting, the Saudi Arabian Ministry of Foreign Affairs conveyed “its deep distress,” offering “its sincere condolences to the victims’ families, and wishes the injured a speedy recovery.”

“The perpetrator of this horrific attack does not represent the Saudi people whatsoever. The American people are held in the highest regard by the Saudi people,” reads a statement from the Ministry. “Building upon the strong ties between the Kingdom of Saudi Arabia and the United States of America, and in continuation of the ongoing cooperation between the two countries’ security agencies, the Saudi security agencies will provide full support to the US authorities to investigate the circumstances of this crime.”

President Trump, meanwhile, relayed King Salman of Saudi Arabia’s “sincere condolences,” and gave his “sympathies to the families and friends of the warriors who were killed and wounded in the attack…”

“The King said that the Saudi people are greatly angered by the barbaric actions of the shooter, and that this person in no way shape or form represents the feelings of the Saudi people who love the American people,” said Trump.

Tyler Durden

Sat, 12/07/2019 – 20:55 - Papa John's Wife Files For Divorce Same Day He Sues Ad Agency For Leaking Racial Slur

Papa John’s Wife Files For Divorce Same Day He Sues Ad Agency For Leaking Racial Slur

After 32 years of marriage, the wife of Papa John’s founder John Schnatter has filed for divorce, claiming their marriage is “irretrievably broken” and that Schnatter is “not employed.”

“The marriage between petitioner and respondent is irretrievably broken,” wrote Cox’s attorney, Melanie Straw-Boone.

The couple was married in 1987, just three years after Schnatter founded Papa John’s Pizza out of a modified broom closet in the back of his father’s Jeffersonville, Indiana tavern. Schnatter sold his 1971 Camaro Z28 to buy used pizza equipment – which he tracked down in 2009 and bought back for $250,000.

While the pizza chain’s margins have always been razor thin, Schnatter’s real troubles began in February 2018, when he blamed the NFL kneeling demonstrations for sagging pizza sales. The NFL subsequently canceled their sponsorship agreement, awarding it instead to Pizza Hut.

Then, in July of that year news outlets reported that Schnatter used the n-word during a conference call with marketing agency ‘Laundry Services,’ saying “Colonel Sanders called blacks niggers and Sanders never faced public backlash.” Shortly after the call, the agency severed ties, while Schnatter stepped down as Chairman the day the story broke – and maintains that he was trying to illustrate that he’s not racist.

To that end, Schnatter filed a separate lawsuit Thursday against Laundry Services, claiming they broke a nondisclosure agreement when they leaked excerpts of the conference call, according to NBC News.

A sweat-drenched Schnatter raised eyebrows two weeks ago when he claimed in an interview that the pizza chain is now making substandard pizza, and that they’ve failed at their own slogan of “Better Ingredients, Better Pizza.”

“I’ve had over 40 pizzas in the last 30 days, and it’s not the same pizza,” he told Louisville, Kentucky Fox affiliate WDRB. “It’s not the same product. It just doesn’t taste as good.”

The Papa John interview is lovely pic.twitter.com/bpDMDm9t9G

— Timothy Burke (@bubbaprog) November 26, 2019

Tyler Durden

Sat, 12/07/2019 – 20:30 - Is Russia Overtaking The US In The Realm of Strategic Bombers?

Is Russia Overtaking The US In The Realm of Strategic Bombers?

Authored by South Front

The Russian Armed Forces put into action an ambitious program to modernize and expand the strategic bomber fleet.

In March 2018, Russia announced that it would completely overhaul its entire Tu-160 long-range strategic bomber fleet by 2030. According to Deputy Defense Minister Yuri Borisov, the entire fleet of Tu-160 bombers will be replaced with the newer Tu-160M2 version, in addition to heavy upgrades of all operational aircraft. All on-board radio-electronic equipment and engines will be replaced.

Serial production of the Tu-160M2 will begin in 2023 and the plan is for it to remain a state of the art warplane for the next 40 years. The Russian Aerospace Forces intend to purchase no less than 50 such aircraft.

The first such warplane is to be delivered in 2021, with 3 more in 2023. Afterwards serial production will continue with 3 Tu-160M2s being produced per year.

The Tupolev Tu-160 (NATO codename: Blackjack) is a long range, supersonic, variable geometry wing, strategic bomber -designed to penetrate sophisticated air defense systems at low altitude and supersonic speed. It is the Soviet counterpart to the US Air Force B-1B Lancer strategic bomber.

Armament (typically nuclear short range and long-range cruise missiles) is carried inside two weapons bays located at the middle of the fuselage.

The Tu-160M2 is a further development of the Tu-160 strategic bomber with state-of-the-art sensors and weapons.

In all, the Tu-160M2 is a highly upgraded version featuring detection reduction coatings, new more powerful and efficient engines giving it greater operational range, new avionics, electronics, glass cockpit, communications & control systems, a number of weapons, as well as improved thrust and unrefueled range. It will also be equipped with a new defensive system protecting it from missiles.

It will boast four new Kuznetsov NK-32 engines. The Kuznetsov NK-32 is an afterburning, three-spool, low bypass, turbofan jet engine, the largest and most powerful engine ever fitted on a combat aircraft. In maximum afterburner it produces 245 kN of thrust (55,000 lbf).

It is expected that the Tu-160M2 will be armed with long-range standoff cruise missiles, including the Kh-101/Kh-102 (nuclear variant) air-launched cruise missile and the Kh-55 subsonic air-launched cruise missile.

The maiden flight of the first Tu-160M2 took place in January 2018.

The initial contract, signed on January 25, 2018, is for the production of 10 Tu-160M2s and the modernization of all other Tu-160s in the Russian Aerospace Forces by 2030.

The contract with United Aircraft Corporation’s Tupolev, for the first 10 warplanes, stands at 160 billion rubles (nearly $2.8 bn) and stipulates that the first Tu-160M2 should be delivered by 2023. Delivery of the final bomber in the first buy, according to the contract, is slated for 2027. Relaunching production itself required an investment of 37 billion rubles ($577 mil.).

The plan is for another 40 units of the Tu-160M2 to be delivered under future contracts yet to be signed.

In the meantime, the Russian Aerospace Forces operate 10 Soviet-era Tu-160s, and 7 modernized Tu-160M1s, commissioned in 2018. The Tu-160 was first introduced into service in 1987 and was the last supersonic strategic bomber to enter service with the Soviet military.

The Tu-95 is the oldest strategic bomber in service with the Russian Aerospace Forces. There are 48 of the Tu-95MSs and 12 of the modernized Tu-95MSMs.

The Russian Aerospace Forces also operate Tu-22M strategic bombers which are much smaller than the Tu-160 and Tu-95. All 63 Tu-22s in service underwent modernization. Sixty-one were modernized to the Tu-22M3 variant, 1 to the Tu-22M3M and the last one was turned into a Tu-22MR, which is currently being overhauled.

The current fleet of strategic bombers in the Russian Aerospace Forces numbers 140 warplanes. The Soviet strategic bomber fleet was much larger. As of 1982, the USSR had 110 Tu-95s, 140 Tu-22s, 70 Tu-22Ms, 75 M4s, and 425 Tu-16s.

Currently, the US operates three types of strategic bombers – the B-1B, the B-2, and the B-52. The US Air Force has 62 B-1Bs, out of which, according to data from August 2019, only 6 were fully operational, with the others being grounded or undergoing maintenance. They have been in service since 1985.

The longest serving bomber in the US Air Force is the B-52A which was commissioned back in 1955. The existing fleet was upgraded to the B-52H Stratofortress, commissioned in 1961. It is planned for this warplane to be operated until 2050. As of June 2019, there were 58 B-52 bombers in operation, with 18 more in reserve.

The B-2 is the only stealth bomber in operation anywhere in the world. It was commissioned in 1993. Thef US Air Force operates 20 such warplanes. There is also the B-21 Raider stealth bomber in development by Northrop Grumman. The first test aircraft is being built in Northrop Grumman’s Palmdale, California, facility and has yet to make its maiden flight. The optimistic forecast is that the first bomber should enter service by 2025.

As of the end of 2019, the US and Russia operate comparable fleets of strategic bombers, with the US being technically ahead of Russia if we focus only on dry figures and do not question the forecast of expected progress for the B-21 Raider program.

At the same time, a challenge for the US Air Force is that its assets are dispersed all around the world in preparation for possible conflicts with a wide range of possible adversaries, including Russia, China and Iran. In turn, strategic bombers of the Russian Aerospace Forces’ are mainly needed to deter the United States. This factor negates the numerical advantage of the US strategic bomber fleet.

As of early 2013, Russia had only 16 Tu-160 strategic bombers. Now, it has 17. Seven of them underwent deep modernization. If the Tu-160M2 program succeeds, and if Russia procures 50 Tu-160M2 bombers by 2030, that will not only put Russia on par with the US, it might put it ahead. All this depends on progression of the US’s B-21 development and modernization of its strategic bombers.

Tyler Durden

Sat, 12/07/2019 – 20:00 - Epstein Was A Mossad Agent Used To Blackmail American Politicians, Former Israeli Spy Claims

Epstein Was A Mossad Agent Used To Blackmail American Politicians, Former Israeli Spy Claims

Authored by Paul Joseph Watson via Summit News,

Jeffrey Epstein was a Mossad asset who was used by Israeli intelligence to blackmail American politicians, according to a former Israeli spy.

Ari Ben-Menashe, a former Israeli spy and alleged “handler” of Robert Maxwell, told the authors of a new book, Epstein: Dead Men Tell No Tales, that Epstein ran a “complex intelligence operation” at the behest of Mossad.

Believing that Epstein planned to marry his daughter, Maxwell introduced him and Ghislaine Maxwell to Ben-Menashe’s Mossad circle.

“Maxwell sort of started liking him, and my theory is that Maxwell felt that this guy is going for his daughter,” Ben-Menashe said.

“He felt that he could bless him with some work and help him out in like a paternal [way].”

Israeli intelligence bosses gave the green light and Epstein then became a Mossad asset.

“They were agents of the Israeli Intelligence Services,” said Ben-Menashe.

When it became clear that Epstein wasn’t very competent at doing much else, his primary role became “blackmailing American and other political figures.”

“Mr. Epstein was the simple idiot who was going around providing girls to all kinds of politicians in the United States,” said Ben-Menashe.

“See, fucking around is not a crime. It could be embarrassing, but it’s not a crime. But fucking a fourteen-year-old girl is a crime. And he was taking photos of politicians fucking fourteen-year-old girls — if you want to get it straight. They would just blackmail people, they would just blackmail people like that.”

There’s also a Mossad connection to a different kind of sex offender; Harvey Weinstein.

Weinstein reportedly hired ex-Mossad agents to suppress allegations against him. Working for an Israeli firm called Black Cube, these agents pressured witnesses and tried to intimidate journalist Ronan Farrow in order to “bury the truth” about Weinstein’s activity.

Tyler Durden

Sat, 12/07/2019 – 19:55 - How The Dems & The Fed Ensured Trump's Re-Election

How The Dems & The Fed Ensured Trump’s Re-Election

Authored by Chris Hamilton via Econimica blog,

The story I’m not hearing…

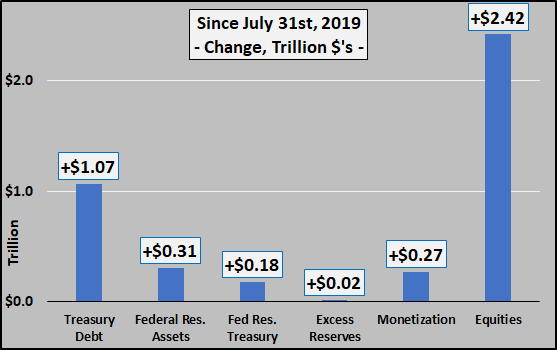

July 31…Debt Ceiling Deal – July 31st of this year, Senate Democrats carried President Trump’s budget deal eliminating the debt ceiling through July 31st of 2021. This after a majority of Trump’s House Republicans voted against the budget deal but House Democrats overwhelmingly passed it. And thus the debt ceiling was no more. Since July 31st, the Treasury has issued over $1 trillion in net new debt but that is just the start.

July 31…Federal Reserve begins series of interest rate cuts – On July 31st, the Federal Reserve begins cutting rates and has cut rates from 2.4% to 1.55% or a 35% reduction on the cost of overnight intra-bank lending, the foundation of credit.

August 21.. Federal Reserve restarts QE – Since August, the Fed ceased quantitative tightening (QT) and restarted quantitative easing (QE). The Federal Reserve balance sheet has expanded by over $300 billion in short order, with an $180 billion increase in Treasuries held.

Excess Reserves Not Restarted – With all the new QE, hardly any of it has been added to bank excess reserves…just a paltry $16 billion out of the $306 billion in new currency digitally conjured.

Direct Monetization – That is $290 billion in new dollars directly in banks hands…and banks do what banks do, which is leverage those dollars by 5x’s to 10x’s (or more), resulting in…

Asset Explosion – Using the Wilshire 5000 as a proxy (as it represents all publicly traded US equities), US equities have risen $2.42 trillion over the 4 month period as all the new digitally conjured cash has been passed to large banks for the “assets” they held…or about a 8.5x the quantity of new “not QE” and “not excess reserves”.

What does that look like?

In dollar terms over the past four months, US debt up over $1 trillion, Federal Reserve held assets up over $300 billion, Fed held Treasuries up $180 billion, Excess Reserves up only $16 billion, direct monetization of $270 billion…resulting in an increase of $2.4 trillion in the Wilshire 5000 market weighted capitalization (chart below).

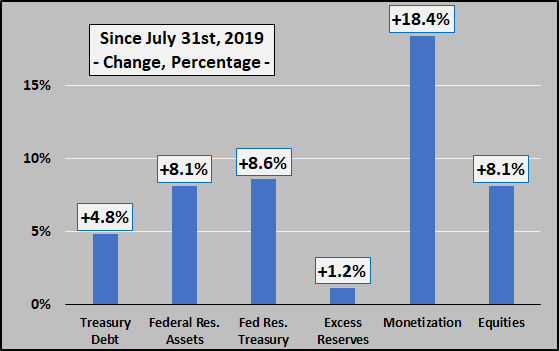

In percentage terms in just four months, total US debt is up 4.8%, Federal Reserve held assets up over 8%, Fed held Treasuries up 8.6%, excess reserves up just 1.2%, direct monetization up over 18%, and equities up over 8% (chart below).

Not shown is in addition to all this, the Federal Funds rate was also reduced by 35%.

Summary

Trump and the Democrats agreed to spend without limits, Trump and the Federal Reserve agreed to QE4 and mainlining the digitally created cash into the economy (errr…financial assets) via direct monetization. The result has been to massively enrich the few who own the vast majority of all assets which are surging upwards and pass all the debt along to the working stiffs.

Trump is truly an evil genius…Dem’s are truly self serving dolts…and the Fed is truly the best central bank money can buy. Or the Fed is the evil genius, Dem’s still self serving dolts, and Trump is the best president money can buy. Either way, Trump, the Democrats, Republicans, and the ultra-wealthy are laughing all the way to the bank. And the vast majority of Americans have been sold into debt slavery.

Post Script – Context

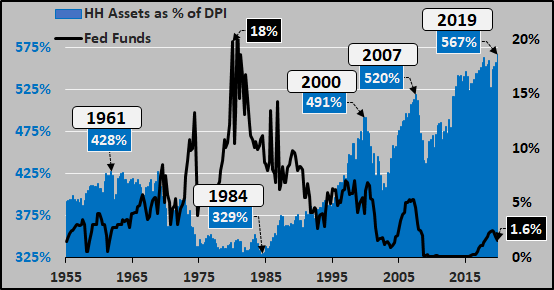

And for those who stuck around, I’ll try and put the above in a wider context. The chart below details why this is the greatest asset bubble in modern history. The chart shows the market value of all household assets (stocks, bonds, real estate, etc.) as a percentage of disposable personal income (simply put, the value of all assets held by US citizens versus their total national income that may be invested or saved after all taxes are paid). As the chart below details, as rates go up, asset valuations go down…and vice versa. And never have asset valuations been so far beyond underlying incomes to support those valuations as now.

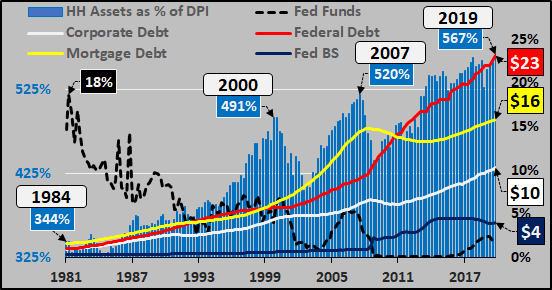

Since 1981, household assets as a percentage of disposable personal income versus federal funds rate with primary sources of debt detailed below. The breakdown of mortgage debt and surge of federal debt since 2008 are not so hard to see. Plus the Federal Reserve balance sheet is included as those assets will only be increasing from here on out.

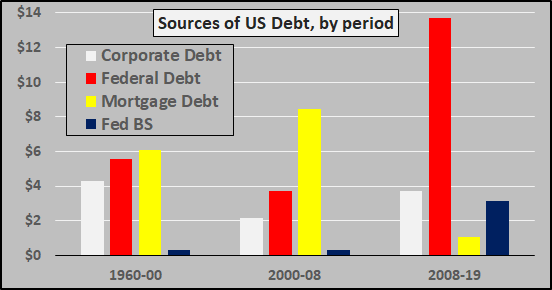

Debt creation by periods, 1960 through 2000, 2000 through 2008, and 2008 through 2019. Relatively stable corporate debt creation, collapsing mortgage debt, and surging federal debt. And collapsing mortgage debt and surging federal debt is only just getting started, because…

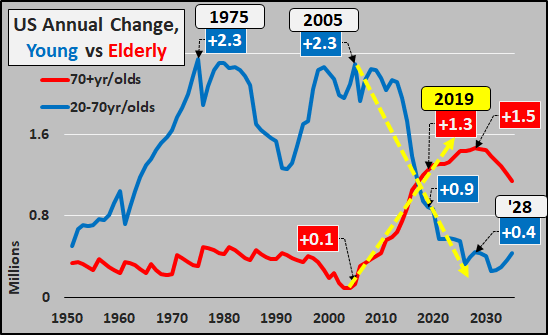

And finally, why mortgage debt won’t be rising anytime soon and all debt creation will be up to the federal government. The chart below shows the annual change in young (working age) versus elderly…a surging population of elderly versus huge deceleration of growth among the working age population.

Just a reminder, elderly earn and spend half as much as working age persons and “destroy money” via deleveraging while working age persons “create money” via undertaking new loans (debt). The current and future situation is one of collapsing credit and collapsing money creation as the growth of deflationary elderly overwhelms inflationary working age growth…and into that entirely predictable situation, steps the Federal government, Federal Reserve, and ludicrous politicians to serve the interests of the few at the expense of the many.

Tyler Durden

Sat, 12/07/2019 – 19:30 - How To Re-Elect Trump In One Easy Lesson

How To Re-Elect Trump In One Easy Lesson

Authored by Mike Shedlock via MishTalk,

Radical progressives are up in arms. Ironically, if Trump wins again, they will be the reason…

Not Getting It

Wall Street Journal writer Jason Riley laments “Bloomberg’s past accomplishments in business and politics are liabilities among today’s Democrats.”

With that lead-in, Riley tries to explain Why Bloomberg’s Candidacy Is Terminal.

It isn’t that Mr. Bloomberg doesn’t have a solid record of accomplishments as a private citizen and elected official. He built one of the world’s most successful financial-media companies and is now worth an estimated $54 billion. According to the Chronicle of Philanthropy, last year he donated $767 million to various charities, second only to Amazon’s Jeff Bezos. And as mayor of New York from 2002 to 2013, he oversaw an expansion of school choice for low-income minorities and sharp reductions in violent crime and incarceration.

Mr. Bloomberg’s problem is that these past accomplishments in business and politics are liabilities among today’s Democrats. To win the support of teachers unions, Sens. Bernie Sanders and Elizabeth Warren have attacked the charter-school movement that Mayor Bloomberg championed. And the social-justice activists now ascendant in the party are far more interested in racial parity among people arrested than in reducing crime rates and keeping the streets safe. Progressives view the Mike Bloombergs of the world primarily as rhetorical punching bags who should have their wealth confiscated by politicians and then sprinkled among others in society who are considered more deserving.

Mr. Bloomberg is very much aligned with today’s Democrats on any number of other issues. He can check off all the right boxes on climate change, tax hikes and gun control, for example. But none of those views distinguish him in the current field or justify his decision to join the race.

Pandering to the Radicals

Riley is correct that a majority of Democrats don’t like Bloomberg.

So what?

Forget the Base

Why appeal to the radicals? Where are they going? I ask the same questions of Republicans and Democrats alike.

If given a choice between Biden or Bloomberg vs Trump, Progressives will vote for Biden or Bloomberg.

Q: Why?

A: Under no circumstances will they vote for Trump.

So how is Bloomberg a liability?

What About Independents?

Independents might easily vote for Biden or Bloomberg. In contrast, they might not easily vote for Kamala Harris or Elizabeth Warren.

In fact, Harris and Warren, darlings of the Progressives, might be the only people that Trump could beat.

These kinds of honest assessments get me in hot water.

Flashback 2008

In February of 2008, before Obama even won the nomination, I made this post: Obama: The Next President Of The United States

I discussed “Yes We Can“, an excellent campaign slogan, and concluded “Destiny: Barack Obama will be the next president of the United States of America.“

It was a political opinion, and a correct one. I didn’t even vote for Obama (I did not vote Republican either), but I was accused of being an Obama lover for years.

Hot water

I am again in hot water today. I responded to a Tweet about Kamala Harris. I called her unqualified.

Why? Because, and I explained, I do not believe she can be elected. This of course brought out all sorts of Tweets about me being a racist male, especially from a self-proclaimed black feminist.

Both Extremes

This post, no doubt will bring attacks from Republicans who believe Trump to be invincible and radical progressives on the other end.

Simple Question

Q: Why did Trump Win?

A: Democrats nominated, Hillary Clinton, the most radical lightning rod at the time. Then Clinton ran what is likely the worst campaign in history.

Let’s get to the heart of the matter.

Republicans Cannot Re-Elect Trump, Democrats Can!

Trump has upset so many people, even in his own party, that I believe the only way he can win is if Democrats nominated another lightning rod.

At the top of the list are Elizabeth Warren and Kamala Harris.

The US simply is not ready for an extreme radical leftist person like Warren.

Independents would not vote for her. Independents did vote for Obama, en masse.

Merely making such statements gets me in hot water.

But It’s not my desire to elect another white male boomer fogey. I could care less. I do care about ideas.

Candidate Appeal

I am a staunch anti-war, fiscal conservative, Libertarian, who does not give a damn about race, religion, sex, or age. I believe in equal rights. I also believe in the right to choose. If two women or two men want to get married, I believe it’s none of my business.

If either party nominated such a person, young or old, black or white or purple, I would vote for that person.

I believe many independents feel the same way.

None of these candidates appeal to me. Among other things, Trump fails the fiscal conservative test.

Electoral Crapshoot

Q: Once again, where are the radicals going?

A: Nowhere, in both parties. The core will vote core.

To win the election then, a candidate must appeal to the middle. Otherwise, it’s an electoral crapshoot as Democrats found out with Hillary.

So, if Democrats want to help re-elect Trump, they should nominate the most radical person they can find. One of them just backed out. Elizabeth Warren is still in the batter’s box.

This does not mean I back Biden. I don’t. Nor do I back Bloomberg. Nor do I back men.

I back ideas, not people. Age, race, or sex, does not matter.

Tyler Durden

Sat, 12/07/2019 – 19:00 - Biden And Pelosi Snap On The Same Day, Anti-Impeachment Witness Threatened; What's Going On With Democrats?

Biden And Pelosi Snap On The Same Day, Anti-Impeachment Witness Threatened; What’s Going On With Democrats?

As public support for impeachment continues to fade, Democrats appear to be coming unglued – with rabid outbursts in public, and privately threatening anyone who might derail their ill-advised gambit.

To wit, George Washington University Law School professor Jonathan Turley says he’s been “inundated with threatening messages” following his Wednesday testimony in front of the House Judiciary Committee, where he argued that Democrats have launched a “slipshod impeachment” based on flimsy evidence against President Trump.

“Before I finished my testimony, my home and office were inundated with threatening messages and demands that I be fired from George Washington University for arguing that, while a case for impeachment can be made, it has not been made on this record,” Turley wrote in a Thursday Op-Ed.

Turley was the lone expert at Wednesday’s hearing to warn Democrats that pushing forward with impeachment would be ill-advised because they can’t prove that Trump inappropriately pressured Ukrainian President Volodomyr Zelensky to investigate 2020 Democratic candidate Joe Biden and his son Hunter. Moreover, Zelensky has stated multiple times that there was no pressure, no quid pro quo, and that he didn’t know that nearly $400 million in US military aid had been paused until after his discussions with Trump.

On edge

On the same day that Joe Biden snapped at an Iowa voter who pressed him on his son’s sweetheart board seat in Ukraine – calling the man a “damn liar” and challenging him to a push-up contest and an IQ test (his go-to, apparently) – House Speaker Nancy Pelosi bit a reporter’s head off for asking why she hates Trump.

Q: “Do you hate the president?”@SpeakerPelosi: “I don’t hate anybody…As a Catholic, I resent your using the word hate in a sentence that addresses me. I don’t hate anyone…So, don’t mess with me when it comes to words like that.”

Full video: https://t.co/l9peY9RTzl pic.twitter.com/zpqUaCcVrS

— CSPAN (@cspan) December 5, 2019

I’m an Energy / Vibe guy.

How do Democrats FEEL?

Pelosi isn’t melting down because she feels like she’s winning.

If you’ve ever won, you know how winners act.

Some are composed and good sportsmen.

Others are “sore winners,” they are smug.

Pelosi is shook.

— Mike Cernovich (@Cernovich) December 5, 2019

https://platform.twitter.com/widgets.js

Meanwhile, a growing number of Democrats have backed away from impeachment.

🚨BREAKING🚨

Democrat Jeff Van Drew says he plans to vote against all the articles of impeachment “unless there’s something that I haven’t seen, haven’t heard before.” pic.twitter.com/swsGl9k7Bz

— Benny (@bennyjohnson) December 5, 2019

Perhaps Democrats are losing it because they’re effectively trapped in their own catch-22, thanks to Rep. Adam Schiff – who hired a former colleague of alleged whistleblower Eric Ciaramella the day after the Trump-Ukraine call.

If House Democrats move forward with impeachment, it will mean a trial in the GOP-controlled Senate, exposing their leading 2020 candidate and his crackhead son to potentially disastrous testimony next year. We’re guessing the Bidens, like several Trump administration officials, will refuse to comply with Congressional subpoenas and instead ask the courts to decide. Not a good look for two guys who supposedly did nothing wrong.

https://platform.twitter.com/widgets.jshttps://platform.twitter.com/widgets.js

If Democrats back down from impeachment and instead censure Trump – avoiding a Senate trial which would ‘exonerate’ Trump, they will look weak for backing down, and exonerate Trump just the same.

Nancy Pelosi warned her party that this is exactly what would happen if they pushed forward with impeachment. Now, much like Hunter Biden, they’ve gone in unprotected and can’t pull out.

Today’s strong jobs numbers are going to make it even harder for the 31 House Dems in Trump-leaning districts to vote for his impeachment. If Pelosi was wigging out yesterday, imagine her angst today.

— Paul Sperry (@paulsperry_) December 6, 2019

Tyler Durden

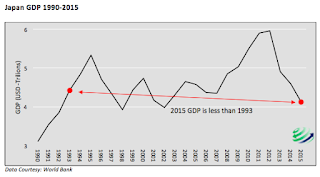

Sat, 12/07/2019 – 18:30 - Japan Is Again Forced To Stimulate Its Troubled Economy

Japan Is Again Forced To Stimulate Its Troubled Economy

Submitted by Bruce Wilds of Advancing Time

Japan faces a wall of debt that can only be addressed by printing more money and debasing its currency. This means they will be paying off their debt with worthless yen where possible and in many cases defaulting on the promises they have made. Japan currently has a debt/GDP ratio of about 250% which is the highest in the industrialized world. With the government financing almost 40% of its annual budget through debt it becomes easy to draw comparisons between Greece and Japan. While adding to the markets move higher across the globe the latest move by Prime Minister Shinzo Abe should do little to boost confidence in the small island nation.

Entering the third quarter of 2019 Reuters reported their monthly Tankan survey showed that Japanese manufacturers had again turned pessimistic about business prospects. Confidence in the service sector also plunged. Amid the escalating Sino-U.S. trade war, and problems in China the prospects for a global downturn remain large.

Survey results showed the weakest sentiment reading since April 2013. Concerns about weakening global demand intensified after a closely watched bond market indicator pointed to the growing risk of a U.S. recession, and data revealed Germany’s economy was in contraction.

Japan. the world’s third-largest economy is highly dependent on exports. The U.S.- China trade war in conjunction with Japan’s export curbs to South Korea and the rising yen has put a lid on sales. This has stoked the fears of recession and raised questions over how much longer domestic demand can remain resilient enough to offset rising external pressures. Private consumption constitutes about 60% of the Japanese economy. Adding to the stress is the fact Japan’s economy is now under pressure from a hike in the consumption tax to 10 percent from 8 percent. This increase took place on Oct 1st. The Bank of Japan has estimated this will generate a net burden of 2.2 trillion yen on households in fiscal 2020.

As a result of its economic growth slowing down and slumping to its weakest point in a year, Japan has put together a large-scale stimulus package totaling 26 trillion yen to prop up the domestic economy. Please note, this is equal to $239 billion. For a country the size of Japan, this is massive. This is the first stimulus package in three years and centers on measures to ignite consumer spending by promoting “cashless sales” and public works spending to bolster infrastructure. “We have crafted a powerful policy package aimed at…helping overcome economic downside risks,” Prime Minister Shinzo Abe said.

As part of its economic package to spur consumer spending, the government has created a program to give rebates for cashless payments at small shops from October through June next year. For this, the government will set aside about 280 billion yen. To stimulate personal spending the government is also thinking about giving 5,000 yen to consumers they can spend at stores across Japan if they load 20,000 yen in their account for purchases to be made through their smartphone. This would start in September next year say people familiar with the matter. The stimulus package also contains public sector spending of 13.2 trillion yen which would include low-interest loans to companies involved in building infrastructure projects. Nearly half of the outlay will be used for reconstruction from recent natural disasters and strengthening infrastructure to reduce future damage.

Abe’s package broadly aims to improve labor conditions, support small companies and promote advanced technology development. This means the government will increase job training services to help people in their 30s and 40s as well as provide subsidies to small and medium-sized companies to spur their capital spending. It will also supply more computers to public schools and support companies in developing wireless technologies that will follow 5G networks. The package also contains steps to help expand exports of farm products to take advantage of a bilateral trade agreement between Tokyo and Washington that is set to take effect next year.