- What Is the REAL Risk from Terrorism?

Preface: Bad government policy has increased the level of terrorism. And corruption in our security agencies has allowed attacks to succeed which should have been stopped.

Even so, the levels of terrorism are still much lower than many assume. Government officials and counter-terror experts may hype the terror threat to promote their agendas. But – as shown below – your risk of being killed in a terror attack is actually much lower than being killed by virtually any other cause.

Daniel Benjamin – the Coordinator for Counterterrorism at the United States Department of State from 2009 to 2012 – noted in January (at 10:22):

The total number of deaths from terrorism in recent years has been extremely small in the West. And the threat itself has been considerably reduced. Given all the headlines people don’t have that perception; but if you look at the statistics that is the case.

Time Magazine noted in 2013 that the chance of dying in a terrorist attack in the United States from 2007 to 2011, according to Richard Barrett – coordinator of the United Nations al Qaeda/Taliban Monitoring Team – was 1 in 20 million.

Let's look at specific numbers …

The U.S. Department of State reports that only 17 U.S. citizens were killed worldwide as a result of terrorism in 2011.* That figure includes deaths in Afghanistan, Iraq and all other theaters of war.

In contrast, the American agency which tracks health-related issues – the U.S. Centers for Disease Control – rounds up the most prevalent causes of death in the United States:

Comparing the CDC numbers to terrorism deaths means:

– You are 35,079 times more likely to die from heart disease than from a terrorist attack

– You are 33,842 times more likely to die from cancer than from a terrorist attack

– You are 4,311 times more likely to die from diabetes than from a terrorist attack

– You are 3,157 times more likely to die from flu or pneumonia than from a terrorist attack

– You are 2,091 times more likely to die from blood poisoning than from a terrorist attack

– You are 1,064 times more likely to die as your lungs swell up after your food or beverage goes down the wrong pipe

(Keep in mind when reading this entire piece that we are consistently and substantially understating the risk of other causes of death as compared to terrorism, because we are comparing deaths from various causes within the United States against deaths from terrorism worldwide.)

Wikipedia notes that obesity is a a contributing factor in 100,000–400,000 deaths in the United States per year. That makes obesity 5,882 to 23,528 times more likely to kill you than a terrorist.

The annual number of deaths in the U.S. due to avoidable medical errors is as high as 100,000. Indeed, one of the world’s leading medical journals – Lancet – reported in 2011:

A November, 2010, document from the Office of the Inspector General of the Department of Health and Human Services reported that, when in hospital, one in seven beneficiaries of Medicare (the government-sponsored health-care programme for those aged 65 years and older) have complications from medical errors, which contribute to about 180 000 deaths of patients per year.

That’s just Medicare beneficiaries, not the entire American public. Scientific American noted in 2009:

Preventable medical mistakes and infections are responsible for about 200,000 deaths in the U.S. each year, according to an investigation by the Hearst media corporation.

And a new study in the Journal of Patient Safety says the numbers may be up to 440,000 each year. But let’s use the lower – 100,000 – figure. That still means that you are 5,882 times more likely to die from medical error than terrorism.

The CDC says that some 80,000 deaths each year are attributable to excessive alcohol use. So you’re 4,706 times more likely to drink yourself to death than die from terrorism.

Approximately 38,329 Americans die each year from drug overdoses. That's 2,255 times more than from terrorists.

Wikipedia notes that there were 32,367 automobile accidents in 2011, which means that you are 1,904 times more likely to die from a car accident than from a terrorist attack. As CNN reporter Fareed Zakaria wrote last year:

“Since 9/11, foreign-inspired terrorism has claimed about two dozen lives in the United States. (Meanwhile, more than 100,000 have been killed in gun homicides and more than 400,000 in motor-vehicle accidents.) “

President Obama agreed.

According to a 2011 CDC report, poisoning from prescription drugs is even more likely to kill you than a car crash. Indeed, the CDC stated in 2011 that – in the majority of states – your prescription meds are more likely to kill you than any other source of injury. So your meds are thousands of times more likely to kill you than Al Qaeda.

The financial crisis has also caused quite a few early deaths. The Guardian reported in 2008:

High-income countries such as the UK and US could see a 6.4% surge in deaths from heart disease, while low-income countries could experience a 26% rise in mortality rates.

Since there were 596,339 deaths from heart disease in the U.S. in 2011 (see CDC table above), that means that there are approximately 38, 165 additional deaths a year from the financial crisis … and Americans are 2,245 times more likely to die from a financial crisis that a terrorist attack.

Financial crises cause deaths in other ways, as well. For example, the poverty rate has skyrocketed in the U.S. since the 2008 crash. For example, the poverty rate in 2010 was the highest in 17 years, and more Americans numerically were in poverty as of 2011 than for more than 50 years. Poverty causes increased deaths from hunger, inability to pay for heat and shelter, and other causes. (And – as mentioned below – suicides have skyrocketed recently; many connect the increase in suicides to the downturn in the economy.)

The number of deaths by suicide has also surpassed car crashes. Around 35,000 Americans kill themselves each year (and more American soldiers die by suicide than combat; the number of veterans committing suicide is astronomical and under-reported). So you’re 2,059 times more likely to kill yourself than die at the hand of a terrorist.

The CDC notes that there were 7,638 deaths from HIV and 45 from syphilis, so you’re 452 times more likely to die from risky sexual behavior than terrorism. (That doesn't include death by autoerotic asphyxiation … discussed below.)

The National Safety Council reports that more than 6,000 Americans die a year from falls … most of them involve people falling off their roof or ladder trying to clean their gutters, put up Christmas lights and the like. That means that you’re 353 times more likely to fall to your death doing something idiotic than die in a terrorist attack.

The same number – 6,000 – die annually from texting or talking on the cellphone while driving. So you're 353 times more likely to meet your maker while lol'ing than by terrorism.

The agency in charge of workplace safety – the U.S. Occupational Safety and Health Administration – reports that 4,609 workers were killed on the job in 2011 within the U.S. homeland. In other words, you are 271 times more likely to die from a workplace accident than terrorism.

Approximately 4,000 Americans drown each year … 235 times more than from terror attacks.

The CDC notes that 3,177 people died of “nutritional deficiencies” in 2011, which means you are 187 times more likely to starve to death in American than be killed by terrorism.

About 2,200 Americans die each year from acute alcohol poisoning (i.e. extreme binge drinking) … 129 times more than from terror attacks.

Some 2,000 Americans die each year from heat or cold. That's 118 times more than from terrorism.

Approximately 1,000 Americans die each year from autoerotic asphyxiation. So you're 59 times more likely to kill yourself doing weird, kinky things than at the hands of a terrorist.

There were an average of 928 Americans killed by police officers in the United States each year in "justifiable homicides". That means that you were more than 55 times more likely to be killed by a law enforcement officer than by a terrorist. That number does not include unjustifiable homicides.

Some 411 Americans are electrocuted each year … 24 times more than die from terrorism.

Nearly 400 Americans die each year due to drug allergies from penicillin. More than 200 deaths occur each year due to food allergies. Nearly 100 Americans die due to insect allergies. And 10 deaths each year are due to severe reactions to latex. See this. There are many other types of allergies, but that totals 710 deaths each year from just those four types of allergies alone … making it 42 times more likely that you'll die from an allergic reaction than from a terror attack.

Some 450 Americans die each year when they fall out of bed, 26 times more than are killed by terrorists.

Scientific American notes:

You might have toxoplasmosis, an infection caused by the microscopic parasite Toxoplasma gondii, which the CDC estimates has infected about 22.5 percent of Americans older than 12 years old

Toxoplasmosis is a brain-parasite. The CDC reports that more than 375 Americans die annually due to toxoplasmosis. In addition, 3 Americans died in 2011 after being exposed to a brain-eating amoeba. So you’re about 22 times more likely to die from a brain-eating zombie parasite than a terrorist.

Around 34 Americans a year are killed by dog bites … around twice as many as by terrorists.

The 2011 Report on Terrorism from the National Counter Terrorism Center notes that Americans are just as likely to be “crushed to death by their televisions or furniture each year” as they are to be killed by terrorists.

Statistics from the Centers for Disease Control show that Americans are 110 times more likely to die from contaminated food than terrorism. And see this.

The Jewish Daily Forward noted in May that – even including the people killed in the Boston bombing – you are more likely to be killed by a toddler than a terrorist. And see these statistics from CNN.

Reason notes:

[The risk of being killed by terrorism] compares annual risk of dying in a car accident of 1 in 19,000; drowning in a bathtub at 1 in 800,000; dying in a building fire at 1 in 99,000; or being struck by lightning at 1 in 5,500,000. In other words, in the last five years you were four times more likely to be struck by lightning than killed by a terrorist.

The National Consortium for the Study of Terrorism and Responses to Terrorism (START) has just published, Background Report: 9/11, Ten Years Later [PDF]. The report notes, excluding the 9/11 atrocities, that fewer than 500 people died in the U.S. from terrorist attacks between 1970 and 2010.

Scientific American reported in 2011:

John Mueller, a political scientist at Ohio State University, and Mark Stewart, a civil engineer and authority on risk assessment at University of Newcastle in Australia … contended, “a great deal of money appears to have been misspent and would have been far more productive—saved far more lives—if it had been expended in other ways.”

Mueller and Stewart noted that, in general, government regulators around the world view fatality risks—say, from nuclear power, industrial toxins or commercial aviation—above one person per million per year as “acceptable.” Between 1970 and 2007 Mueller and Stewart asserted in a separate paper published last year in Foreign Affairs that a total of 3,292 Americans (not counting those in war zones) were killed by terrorists resulting in an annual risk of one in 3.5 million. Americans were more likely to die in an accident involving a bathtub (one in 950,000), a home appliance (one in 1.5 million), a deer (one in two million) or on a commercial airliner (one in 2.9 million). [Let's throw a couple more fun facts into the mix … The risk of choking to death on food is 1 in 4,404, and the risk of dying by falling out of furniture (including couches, chairs and beds) is 1 in 4,238. So you're almost a thousand times more likely to die from one of these rare causes of death than terrorism.]

Mueller and Stewart noted that, in general, government regulators around the world view fatality risks—say, from nuclear power, industrial toxins or commercial aviation—above one person per million per year as “acceptable.” Between 1970 and 2007 Mueller and Stewart asserted in a separate paper published last year in Foreign Affairs that a total of 3,292 Americans (not counting those in war zones) were killed by terrorists resulting in an annual risk of one in 3.5 million. Americans were more likely to die in an accident involving a bathtub (one in 950,000), a home appliance (one in 1.5 million), a deer (one in two million) or on a commercial airliner (one in 2.9 million). [Let's throw a couple more fun facts into the mix … The risk of choking to death on food is 1 in 4,404, and the risk of dying by falling out of furniture (including couches, chairs and beds) is 1 in 4,238. So you're almost a thousand times more likely to die from one of these rare causes of death than terrorism.]The global mortality rate of death by terrorism is even lower. Worldwide, terrorism killed 13,971 people between 1975 and 2003, an annual rate of one in 12.5 million. Since 9/11 acts of terrorism carried out by Muslim militants outside of war zones have killed about 300 people per year worldwide. This tally includes attacks not only by al Qaeda but also by “imitators, enthusiasts, look-alikes and wannabes,” according to Mueller and Stewart.

Defenders of U.S. counterterrorism efforts might argue that they have kept casualties low by thwarting attacks. But investigations by the FBI and other law enforcement agencies suggest that 9/11 may have been an outlier—an aberration—rather than a harbinger of future attacks. Muslim terrorists are for the most part “short on know-how, prone to make mistakes, poor at planning” and small in number, Mueller and Stewart stated. Although still potentially dangerous, terrorists hardly represent an “existential” threat on a par with those posed by Nazi Germany or the Soviet Union.

In fact, Mueller and Stewart suggested in Homeland Security Affairs, U.S. counterterrorism procedures may indirectly imperil more lives than they preserve: “Increased delays and added costs at U.S. airports due to new security procedures provide incentive for many short-haul passengers to drive to their destination rather than flying, and, since driving is far riskier than air travel, the extra automobile traffic generated has been estimated to result in 500 or more extra road fatalities per year.”

The funds that the U.S. spends on counterterrorism should perhaps be diverted to other more significant perils, such as industrial accidents (one in 53,000), violent crime (one in 22,000), automobile accidents (one in 8,000) and cancer (one in 540). “Overall,” Mueller and Stewart wrote, “vastly more lives could have been saved if counterterrorism funds had instead been spent on combating hazards that present unacceptable risks.” In an e-mail to me, Mueller elaborated:

“The key question, never asked of course, is what would the likelihood be if the added security measures had not been put in place? And, if the chances without the security measures might have been, say, one in 2.5 million per year, were the trillions of dollars in investment (including overseas policing which may have played a major role) worth that gain in security—to move from being unbelievably safe to being unbelievably unbelievably safe? Given that al Qaeda and al Qaeda types have managed to kill some 200 to 400 people throughout the entire world each year outside of war zones since 9/11—including in areas that are far less secure than the U.S.—there is no reason to anticipate that the measures have deterred, foiled or protected against massive casualties in the United States. If the domestic (we leave out overseas) enhanced security measures put into place after 9/11 have saved 100 lives per year in the United States, they would have done so at a cost of $1 billion per saved life. That same money, if invested in a measure that saves lives at a cost of $1 million each—like passive restraints for buses and trucks—would have saved 1,000 times more lives.”

Mueller and Stewart’s analysis is conservative, because it excludes the most lethal and expensive U.S. responses to 9/11. Al Qaeda’s attacks also provoked the U.S. into invading and occupying two countries, at an estimated cost of several trillion dollars. The wars in Afghanistan and Iraq have resulted in the deaths of more than 6,000 Americans so far—more than twice as many as were killed on September 11, 2001—as well as tens of thousands of Iraqis and Afghans.

***

In 2007 New York City Mayor Michael Bloomberg said that people are more likely to be killed by lightning than terrorism. “You can’t sit there and worry about everything,” Bloomberg exclaimed. "Get a life."

Indeed, the Senior Research Scientist for the Space Science Institute (Alan W. Harris) estimates that the odds of being killed by a terrorist attack is about the same as being hit by an asteroid (and see this).

Terrorism pushes our emotional buttons. And politicians and the media tend to blow the risk of terrorism out of proportion. But as the figures above show, terrorism is a very unlikely cause of death.

Indeed, our spending on anti-terrorism measures is way out of whack … especially because most of the money has been wasted. And see this article, and this 3-minute video by professor Mueller:

Indeed, mission creep in the name of countering terrorism actually makes us more vulnerable to actual terrorist attacks. And corrupt government policy is arguably more dangerous than terrorism.

Indeed, the terrorism deaths Americans have suffered were unnecessary … and were largely due to corruption in our security agencies. And see this.

* Note: Subsequent official reports – published in 2012 and 2013 – show that even fewer Americans were killed by terrorists than in the previous year.

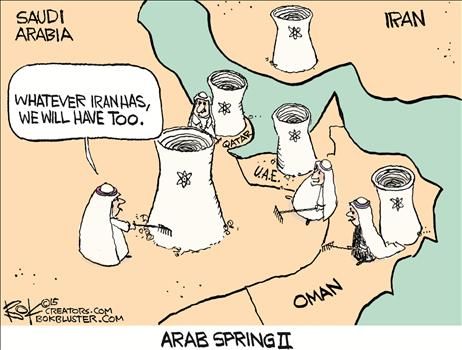

- Saudi Ambassador Warns West On Iran Deal: "All Options On Table…" Including Nukes

We previously warned of the risks of escalation in The Middle East to something much more dangerous, but, as the Saudi ambassador to UK confirmed today, the risk of Wahhabis going nuclear is even higher than many expected, “…if [Iran will not offer assurances it will not pursue nuclear weapons], then all options will be on the table for Saudi Arabia… Iran’s nuclear program poses a direct threat to the entire region and constitutes a major source and incentive for nuclear proliferation across the Middle East, including Israel.”

Saudi Arabia is ready to acquire nuclear weapons if diplomatic talks aimed at halting Iran’s nuclear ambitions break down, the Saudi ambassador to the UK has said. As RT reports,

Prince Mohammed bin Nawwaf bin Abdulaziz al-Saud said the oil-rich Gulf kingdom hoped negotiations being led by US President Barack Obama would result in a “watertight” deal with Iran.

However if does not happen, then “all options are on the table,” he said.

…

Prince Mohammad told The Telegraph: “We have always expressed our support for resolving the Iranian nuclear file in a diplomatic way and through negotiation.”

“We commend the American president’s effort in this regard, provided that any deal reached is watertight and is not the kind of deal that offers Iran a license to continue its destabilizing foreign policies in the region. The proof is in the pudding.”

The Saudi ambassador said the kingdom hopes Iran will offer assurances it will not pursue nuclear weapons.

“But if this does not happen, then all options will be on the table for Saudi Arabia.”

“Iran’s nuclear program poses a direct threat to the entire region and constitutes a major source and incentive for nuclear proliferation across the Middle East, including Israel,” he added.

Saudi Arabia is believed to have funded up to 60 percent of Pakistan’s nuclear program, on the condition it could buy warheads at short notice.

If the Gulf state were to activate the deal, it would see Saudi Arabia become the first nuclear power in the Arab world.

Finally, if this ‘threat’ were to become true… what would be the Saudi catalyst of the hair-trigger big red button of doom? This perhaps?

In Major Escalation, Yemen Rebels Fire Scud Missile Into Saudi Arabia

This won’t end well…

Source: Townhall via Sunday Funnies

- The New World Order – A Faustian Bargain

Submitted by Jeff Thomas via Doug Casey's International Man blog,

Faustian bargain: An agreement in which a person abandons his or her spiritual values or moral principles in order to obtain wealth or other benefits. A deal with the devil.

The argument over the existence of an Elite, who plan to control the entire world under a New World Order like some great yo-yo, has been around for a long time. Not surprisingly, events created by world leaders of all stripes in recent years give rise to an increasing belief in the likelihood of the existence of such an effort.

There are two great dangers in attempting to describe this perceived secret endeavour, and they are at opposite ends of the spectrum: a) being so naive as to assume that no collusion exists amongst various groups of leaders to further their respective ends, and b) over-simplifying such alliances to suggest that there is an Elite Master Plan that all members implicitly agree upon and follow in every respect.

Assumption A

In any country, the citizenry are accustomed to such acts of collusion as all the petrol suppliers raising the price by the same amount, overnight. Few individuals would doubt that the two companies get together well in advance to agree on the price hike.

The same sort of collusion can be expected between banks and governments, etc. However, most people in any given country seem to believe that the political parties that rule them do not collude in their own collective interest and against the best interests of their respective constituents.

Similarly, they are unlikely to accept that fascism exists in their country—that members of their favoured party collude with industries. Further, most people seem to disbelieve that the leaders of their own country collude with the leaders of their country’s enemies in such a way that might create loss or danger to their own people. This is naive. Such collusions are the norm rather than the exception.

Assumption B

Those who tend to be more informed, readily acknowledge that collusion exists between all of the above, to one degree or another. If this group errs, it is often in the opposite assumption—that the collusion is all-encompassing.

There can be no doubt that a New World Order is being sought by some—this has been made clear for at least a hundred years by many who regard themselves as an Elite. It is therefore an open secret. As stated by David Rockefeller in his memoirs:

Some even believe we are a part of a secret cabal working against the best interests of the United States, characterizing my family and me as ‘internationalists’ and of conspiring with others around the world to build a more integrated global political and economic structure—one world, if you will. If that’s the charge, I stand guilty and I am proud of it.

But the error that is most common amongst those who oppose a New World Order is the extent to which they believe the collusion exists. Many believe the collusion is total. That is, a Master Plan exists amongst the world’s leaders (the heads of the central banks, the Bilderberg Group, the leaders of the most powerful nations—or the whole gang of them—take your pick) that all members agree upon in detail and in full.

Still, when any New World Order opponent rails against the latest perceived move by the Elite, if asked the question, “Do you really think that these people are so unified that several hundred of them get together every week around a conference table to decide who to victimise this week?,” most will say that, no, they may act in concert, but not in so total a fashion.

Option C

So, is there a third perception as regards those in high positions who collude on a large scale? In my opinion there is.

In my experience in dealing with political leaders (and political hopefuls) from several jurisdictions, I’ve found there to be a consistent sociopathology (by definition, the desire for dominance over others, undeserved self-confidence, lack of empathy, a sense of entitlement, lack of conscience, etc.). Whether they are British members of Parliament or US members of Congress, they tend to display the same sociopathic traits.

Sociopaths are drawn to political leadership for obvious reasons. First, they’re prone to collusion, as they recognise that it may further their interests (agreements with a small group of individuals that would allow for dominance over another, larger group of individuals). And this, of course, fits well into Assumption B.

Trouble is, the same sociopathology would drive the same individuals to seek to dominate each other. Yes, they would enter into agreements with one another, but even as they are making them, they would be planning to deviate from them.

Any agreement regarding increased power for all members, defining what seat each would have at the table, may be agreed, but immediately after, each would begin jockeying for a better seat. Further, whatever agenda is agreed upon, each would already have a secondary agenda for his own betterment even as the agreement is being forged.

Any attempt at a New World Order, if it were to succeed in creating unified dominance, would never reach full fruition, as so many disparate individuals would be plotting for a bigger piece of the pie from the outset.

As regards the desire to follow a Grand Plan, we are not describing the meek Kool-Aid drinkers of Jonestown, Guyana, whose willingness to follow a Master Plan was unquestioningly due to their extremely low self-esteem. We are describing those with the opposite mental makeup—those who are compulsive in their desire for dominance of others (first their minions, then their partners).

Further, each would promote his own sphere of power. A banker would seek to have the group’s means of control be economically based; a general would seek to have the means of control be militarily based; etc.

Dissent Among the Ranks

The push-and-pull of sociopathic leaders is unending. Their very makeup dictates that each one individually will always be vying for more. In order to achieve that, they will form subversive subgroups that will agree on a separate direction from what has been agreed by the primary group, and along the way, each one, in his lack of conscience and loyalty, might betray both the primary group and the subgroup.

In the end, there’s no question that there are those who consider themselves to be part of a New World Order, as so many have publicly stated so themselves, for generations. Also, there can be little doubt that each member expects to come out of the deal as a ruler, not as one of the ruled. Further, the effort is ongoing and growing, and will result in great damage for the average person who, in most cases, simply wishes to be left alone to run his own life.

It has been postulated by many that those who see themselves as an Elite are nearing the completion of what they perceive as world dominance. However, should they succeed, they will betray their partners the very next day, as it’s their nature to do so. Their behaviour would likely be that of a group of cats with their tails tied together.

So, what might we take away from this discussion? First, that there most assuredly are extremely domineering forces (regardless of how closely associated they might be), which, in the near future, will do immense damage to the cause of freedom in the world, particularly in those countries where they are most dominant, or will become most dominant. Second, the situation does appear to be reaching a head.

The two greatest uncertainties will be how much damage will be done before the dust has settled, and how protracted the period of destruction and struggle for dominance might be.

Ultimately, for the reasons stated above, I don’t believe the New World Order concept can fully prevail, but it can and will do damage of unprecedented proportions in the attempt to implement it. Those involved will not be swayed from their individual or collective objectives (consider Adolf Hitler or Josef Stalin).

The best that can be done is to work at placing ourselves as far outside of their sphere of influence as possible.

- When It Rains It Pours: Shares Of Chinese Umbrella Manufacturer Rise 2,700%

As mentioned previously, China’s world-beating equity rally is the gift that keeps on giving, and not just for those who are riding the inexorable, margin-fueled rally. The mania also provides quite a bit of comic relief for those of us who are, on a daily basis, inundated with hundreds of depressingly absurd Greek soundbites and hoplessly clueless central banker ruminations.

Valuations have skyrocketed in China, with the median PE on the Shenzhen sitting at a cool 108X, which looks impressive until you consider that the ChiNext trades at 133X. The siren song is in fact so alluring that some US-listed Chinese tech firms are repatriating because they feel they aren’t getting the valuations they ‘deserve.’

“American investors don’t understand the business model,” one Chinese tech executive recently told Reuters.

One business model that’s easy to understand is that of Hong Kong-listed Jicheng Umbrella Holdings Limited. As you might have guessed from the name, the company designs, researches, manufactures and sells plastic umbrellas. That’s really all you need to know to appreciate the following chart which shows that shares have risen some 2,700% since February 13 (also note the annualized figure)…

* * *

What bubble?

- Major Medical Journal Retracts Numerous Scientific Papers After Fake Peer-Review Scandal

A major publisher of scholarly medical and science articles has retracted 43 papers because of “fabricated” peer reviews amid signs of a broader fake peer review racket affecting many more publications. As The Washington Post reports, BioMed Central – a well-known publication of peer-reviewed journals – shows a partial list of the retracted articles suggests most of them were written by scholars at universities in China. The Committee on Publication Ethics stated, it "has become aware of systematic, inappropriate attempts to manipulate the peer review processes of several journals… that need to be retracted."

Peer review is the vetting process designed to guarantee the integrity of scholarly articles by having experts read them and approve or disapprove them for publication. With researchers increasingly desperate for recognition, citations and professional advancement, the whole peer-review system has come under scrutiny in recent years for a host of flaws and irregularities, ranging from lackadaisical reviewing to cronyism to outright fraud.

And as The Washington Post reports, BioMed Central, based in the United Kingdom, which puts out 277 peer-reviewed journals of scholarly medical and science articles has retracted 43 papers because of “fabricated” peer reviews amid signs of a broader fake peer review racket affecting many more publications…A partial list of the retracted articles suggests most of them were written by scholars at universities in China. But Jigisha Patel, associate editorial director for research integrity at BioMed Central, said it’s not “a China problem. We get a lot of robust research of China. We see this as a broader problem of how scientists are judged.”

Meanwhile, the Committee on Publication Ethics, a multidisciplinary group that includes more than 9,000 journal editors, issued a statement suggesting a much broader potential problem.

The committee, it said, “has become aware of systematic, inappropriate attempts to manipulate the peer review processes of several journals across different publishers.” Those journals are now reviewing manuscripts to determine how many may need to be retracted, it said.

Ivan Oransky and Adam Marcus, the co-editors of Retraction Watch, a blog that tracks research integrity and first reported the BioMed Central retractions, have counted a total of 170 retractions in the past few years across several journals because of fake peer reviews.

“The problem of fake peer reviewers is affecting the whole of academic journal publishing and we are among the ranks of publishers hit by this type of fraud,” Patel of BioMed’s ethics group wrote in November.

“The spectrum of ‘fakery’ has ranged from authors suggesting their friends who agree in advance to provide a positive review, to elaborate peer review circles where a group of authors agree to peer review each others’ manuscripts, to impersonating real people, and to generating completely fictitious characters. From what we have discovered amongst our journals, it appears to have reached a higher level of sophistication. The pattern we have found, where there is no apparent connection between the authors but similarities between the suggested reviewers, suggests that a third party could be behind this sophisticated fraud.”

In a blog post yesterday, Elizabeth Moylan, BioMed Central’s senior editor for research integrity, said an investigation begun last year revealed a scheme to “deceive” journal editors by suggesting “fabricated” reviewers for submitted articles. She wrote that some of the “manipulations” appeared to have been conducted by agencies that offer language-editing and submission assistance to non-English speaking authors.

Perhaps most astonishing was the fact that…

Ultimately, when they tracked down some of the scientists in whose names reviews were written, they found that they hadn’t written them at all. Someone else had, using the scientists’ names.

But that Chinese Micro-cap Biotech stock is definitely still worth buying… even after rising 3000% YTD.

- China's Deficient Deflator Math Is One More Reason To Distrust Data

It’s no secret that Beijing’s ‘official’ GDP prints likely overstate the pace at which China’s economy is growing. In fact, the numbers may be grossly exaggerated, as some analysts say the real rate of expansion is somewhere on the order of 4% (as opposed to 7%).

We’ve noted on any number of occasions that multiple key indicators — such as rail freight volume, industrial production, electricity consumption, etc. — suggest the dreaded “hard landing” is in fact here, and if Beijing fails to figure out how to balance a sharp decrease in shadow financing with the need to boost credit creation (i.e., if China can’t navigate the impossible task of deleveraging and re-leveraging simultaneously), things could get materially worse before they get better for an economy that’s attempting to mark a very difficult transition from investment-led growth to a consumption-driven model. For more on transparency and why the real rate of growth in China’s economy is “anybody’s guess”, see “Guessing Game: China’s ‘Real’ GDP Growth Could Be As Low As 3.8%.”

Beyond intentional misrepresentations however, China’s GDP data may suffer from a calculation error that at least one firm claims is endemic across emerging markets thanks to data collection limitations.

FT has more:

The issue centres on the so-called “GDP deflator”, the inflation measure used to convert estimates of nominal GDP into real, inflation-adjusted terms.

The deflator is a broader measure than indicators such as consumer or producer price inflation and is therefore often considered a more useful gauge of overall price pressures in an economy. It is the preferred inflation measure of the US Federal Reserve.

Since GDP is a measure of domestic output, arguably this deflator should only reflect the prices of domestically produced goods and services.

In practice, this means netting out the price of imports in the calculation of the GDP deflator, a routine practice in countries with “robust statistical systems”, as Chang Liu, China economist at Capital Economics, puts it.

For much of the time, a failure to do this might not matter too much. However, at times when import price inflation varies markedly from domestic inflation, such as when global commodity prices are rising or falling rapidly, it matters more..

Because China does not net off shifts in import prices when calculating the deflator for most sectors of its economy, its deflator tracks producer price inflation much more closely.

As a result, Mr Liu says: “China’s GDP deflator is not an accurate measure of changes in domestic output prices. It exaggerates inflation when import prices are rising, and understates it when import prices fall”.

In the first quarter of the year, China’s deflator turned negative for the second time since 2000, coming in at -1.1 per cent. In comparison, consumer price inflation was +1.2 per cent. This means its inflation gap has jumped to 2.3 percentage points, even as it has fallen sharply in the likes of the US, as the chart shows.

If the deflator is, as a result, understated, then real GDP growth is overstated by the same amount.

“A reasonable guess might be that true inflation was 1-2 percentage points higher than the deflator shows. In that case, real GDP growth in Q1 would have been 5-6 per cent [rather than 7 per cent],” said Mr Liu, who added that the lower rate was closer to Capital Economics’ own estimate, based on activity data, of 4.9 per cent.

In other words, when commodity prices are falling, China (and other EMs) may be routinely overstating GDP growth. As a reminder, here are some estimates for ‘actual’ (i.e. not emanating from Beijing) Chinese economic output:

While Capital Economics is careful to suggest that this statistical ‘error’ is baked into estimates like the ones shown above, one is certainly left to wonder whether the understated deflator should be simply one more factor to consider on the way to estimating what the real growth rate in China actually looks like.

In other words, considering the above, it could well be that GDP growth in China is closer to flatlining than anyone cares to admit.

- Land Of The Debt Serf: How "Auto Title Loan" Companies Ruthlessly Prey On America's Growing Underclass

Submitted by Mike Krieger via Liberty Blitzkrieg blog,

Short-term lenders, seeking a detour around newly toughened restrictions on payday and other small loans, are pushing Americans to borrow more money than they often need by using their debt-free autos as collateral.

Their hefty principal and high interest rates are creating another avenue that traps unwary consumers in a cycle of debt. For about 1 out of 9 borrowers, the loan ends with their vehicles being repossessed…

But Jordan said it wouldn’t make a loan that small. Instead, it would lend her $2,600 at what she later would learn was the equivalent of 153% annual interest — as long as she put up her 2005 Buick Rendezvous sport utility vehicle as collateral.

State law limits payday loans to $300, minus a maximum fee of $45. California also caps interest rates on consumer loans of less than $2,500 on a sliding scale that averages about 30%. Consumer loans above $2,500 have no interest rate limit.

For that reason, essentially all auto title loans in the state are above that level, according to the state’s business oversight department.

– From the excellent LA Times article: More Auto Title Lenders are Snagging Unwary Borrowers in Cycle of Debt

Last week, I published an article highlighting how the use of “alternative financial services” has continued to increase despite the so-called economic “recovery.” These services include payday loans, refund-anticipation loans, pawnshops, rent-to-own services, and the little known, but recently surging, category called auto title loans. Here’s an excerpt from that post, titled Use of Alternative Financial Services, Such as Payday Loans, Continues to Increase Despite the “Recovery”:

Families’ savings not where they should be: That’s one part of the problem. But Mills sees something else in the recovery that’s more disturbing. The number of households tapping alternative financial services are on the rise, meaning that Americans are turning to non-bank lenders for credit: payday loans, refund-anticipation loans, pawnshops, and rent-to-own services.

According to the Urban Institute report, the number of households that used alternative credit products increased 7 percent between 2011 and 2013. And the kind of household seeking alternative financing is changing, too.

It’s not the case that every one of these middle- and upper-class households turned to pawnshops and payday lenders because they got whomped by an unexpected bill from a mechanic or a dentist. “People who are in these [non-bank] situations are not using these forms of credit to simply overcome an emergency, but are using them for basic living experiences,” Mills says.

In that article, the category of auto title loans was just a minor blip on the radar, but it seems poised to take a growing share of the legalized American loanshark market.

Yesterday, the LA Times published an excellent article on the topic of auto title loans describing what they are, and how they are being used to prey on America’s growing underclass of debt serfs. We learn that:

Cash-strapped consumers are being shown a new place to find money: their driveways.

Short-term lenders, seeking a detour around newly toughened restrictions on payday and other small loans, are pushing Americans to borrow more money than they often need by using their debt-free autos as collateral.

So-called auto title loans — the motor vehicle version of a home equity loan — are growing rapidly in California and 24 other states where lax regulations have allowed them to flourish in recent years.

Think about how troubling this is for a second. In the run-up to the last crisis, Americans borrowed on their home equity and used the proceeds to remodel kitchens, etc. Now these same Americans are so completely broke, the only asset they can borrow against is their cars, and they are desperately using the money to purchase groceries, pay cable bills, etc. Thank you Ben.

Even worse, more than 10% of these debt serfs end up losing their cars. What will they end up borrowing against after the next crisis, their organs?

Their hefty principal and high interest rates are creating another avenue that traps unwary consumers in a cycle of debt. For about 1 out of 9 borrowers, the loan ends with their vehicles being repossessed.

“I look at title lending as legalized car thievery,” said Rosemary Shahan, president of Consumers for Auto Reliability and Safety, a Sacramento advocacy group. “What they want to do is get you into a loan where you just keep paying, paying, paying, and at the end of the day, they take your car.”

Jordan, 58, said she needed about $400 to help her pay bills for cable TV and other expenses that had been piling up after her mother died.

She turned to one of a proliferating number of storefront title lenders, Allied Cash Advance, which promises to help “get the cash you need now.”

But Jordan said it wouldn’t make a loan that small. Instead, it would lend her $2,600 at what she later would learn was the equivalent of 153% annual interest — as long as she put up her 2005 Buick Rendezvous sport utility vehicle as collateral.

Nice to see how the 0% interest rate Ben Bernanke and his fellow criminals at the Federal Reserve instituted is trickling down so generously to average Americans.

Why would the company want to lend her much more money than she needed? The key reason is that California has no limit on interest rates for consumer loans of more than $2,500, and it otherwise doesn’t regulate auto title loans.

Six months later, unable to keep up with the loan payments, Jordan said, she was awakened at 5 a.m.

“My neighbor came pounding on my door and said, ‘They’re taking your car!'” she recalled.

In California, the number of auto title loans jumped to 91,505 in 2013, the latest data available, from 64,585 in the previous year and 38,148 in the first year, 2011, that was tracked by the state Department of Business Oversight.

The study, one of the first comprehensive looks at the issue, found that the average loan was for $1,000 and a typical borrower paid $1,200 in fees a year on top of the principal.

Loan sizes and fees vary by state, but the most common annual percentage rate on a one-month loan was 300%, according to Pew, which surveyed borrowers and analyzed regulatory data and company filings.

“Your auto is in many cases one of your only assets. Be careful signing away the ownership of that car for some short-term cash,” said Jan Lynn Owen, the state’s commissioner of business oversight.

The terms of auto title loans vary widely by state. But they all center on using the vehicle’s title, also known as the pink slip, as collateral. The borrower usually must have full ownership of the vehicle, and its value must be well above the amount of the loan.

Because the loan is secured by the vehicle, lenders often don’t consider a consumer’s income or ability to repay. If the borrower falls behind, the car will be repossessed and sold to pay off the loan.

State law limits payday loans to $300, minus a maximum fee of $45. California also caps interest rates on consumer loans of less than $2,500 on a sliding scale that averages about 30%. Consumer loans above $2,500 have no interest rate limit.

For that reason, essentially all auto title loans in the state are above that level, according to the state’s business oversight department. Most range from $2,500 to $5,000. Of those, about 45% carried annual percentage rates of at least 100%, according to state data for 2013.

How can this practice be seen as anything other than predatory?

Meanwhile, the Fed continues to holds interest rates for financial oligarchs at 0%, patting itself on the back as America’s underclass grows and the oligarchy consolidates all wealth and power. Bernanke and his colleagues at the Federal Reserve have committed ongoing crimes against humanity, and nobody with any ability to stop it seems to care.

* * *

For related articles, see:

Just Another Tale from the Oligarch Recovery – $100 Million Homes Being Built on Spec

Pennsylvania Looks to Legalize Payday Loans by Calling Them “Mirco-Loans”

TBTF Banks Enter Payday Loan Business with 500% Interest Rates

Portrait of the American Oligarchy – The Very Troubling Income and Wealth Trends Since 1989

- "One Belt, One Road" May Be China's 'One Chance' To Save Collapsing Economy

In April, Chinese President Xi Jinping marked a historic visit to neighboring Pakistan. China, via Beijing’s “One Belt, One Road” initiative, will invest some $50 billion in Pakistani infrastructure, including power plants, roads, railways, and, perhaps most importantly, the Iran-Pakistan natural gas pipeline. The vast sum represents 53% more than the US has given Islamabad over the past 13 years combined. China is also set to invest an equally large sum in Brazil and is even considering the construction a railroad over the Andes, which would connect Brazil to China via the Pacific and ports in Peru.

On Sunday, Hungary became the first European country to sign a Silk Road MOU. Reuters has more:

Hungary has become the first European country to sign a cooperation agreement for China’s new “Silk Road” initiative to develop trade and transport infrastructure across Asia and beyond, China’s foreign ministry said late on Saturday.

China welcomes more European countries to look East, and strengthen cooperation with China and other Asian countries, and participate in the “One Belt, One Road” in various ways, said Wang Yi, China’s foreign minister, according to a separate statement on the website.

Hungary hopes to closely cooperate with China and push on with the Hungarian-Serbia railway and other major construction projects, Hungary’s President Janos Ader was quoted as saying by the Chinese foreign ministry.

China is helping fund and build a railway connecting Hungary and Serbia.

Projects under the plan include a network of railways, highways, oil and gas pipelines, power grids, Internet networks, maritime and other infrastructure links across Central, West and South Asia to as far as Greece, Russia and Oman, increasing China’s connections to Europe and Africa.

Although highly publicized, “One Belt, One Road” isn’t well understood (which partly reflects the sheer size and scope of the initiative). The program has been cast, by some, as a Chinese Marshall Plan, an interesting characterization, given that we’ve cast the AIIB as an implicit attempt by Beijing to institute a kind of Sino-Monroe Doctrine.As an aside, this also demonstrates an overwhelming tendency (and we may be guilty here as well), to view the world through glasses tinted by the unipolarity that has dominated global politics for more than six decades. Or perhaps it’s a reflection of the fact that China is indeed a rising hegemon, and as such its policies and programs resemble those of the US at critical historical moments when Washington seized opportunities to expand American influence.

Here, to cast some light on “The Yi Dai Yi Lu”, is Barclays:

* * *

Not just a Marshall Plan – bigger, more comprehensive and more inclusive

The Yi Dai Yi Lu (YDYL) initiative has been labelled a “Chinese Marshall plan” in some global commentary. There are some similarities between China’s new initiative and the post World War II US-driven European Recovery Program (popularly known as the Marshall Plan after US Secretary of State George Marshall).

- The emphasis on infrastructure and heavy industry as a mode to kick-start growth or recovery.

- The Marshall Plan amount of US$13bn (c.US$120bn in current dollar value) is in the same order of magnitude as the initial US$40bn envisaged for the New Silk Road Fund.

- The establishment of the Asian Infrastructure Investment Bank (AIIB) could be perceived to be analogous to the formation of the IMF and the World Bank to aid the structural transformation of economies.

- The perception (in some quarters) of potential for Chinese hegemony in the YDYL countries.

However, there are some obvious differences as well.

- The world is not recovering from the aftermath of a world war. In fact, most of the countries that are potential YDYL project recipients could do just fine without the project impetus (though growth rates arguably would be lower).

- The YDYL initiative is open to all countries, regardless of their political or economic regime.

We note that the Chinese government has expressed its displeasure at the Marshall Plan moniker. A government spokesman said in early March 2015 “It is inappropriate to simply describe the Belt and Road initiatives as another Marshall Plan. These initiatives seek common development of countries with different ethnicities, religions and cultures, focusing on wide consultation, joint contribution and shared benefits.”

More than just a political slogan – this concept has potential, in our viewWe expect companies in China from SOEs to private enterprises to embrace the YDYL initiative, indentifying the value it could bring to their businesses, rather than simply paying lip service to the leadership’s latest pronouncements. We believe YDYL has captured the imagination of the market. During the FY14 results season, around 70% of the companies in our Chinese metals & mining coverage universe – including both SOEs (eg, Shenhua, Chalco, Jiangxi Copper) and private companies (eg, Hongqiao) – had YDYL formulated in their strategy and plans in some form or other.Not just about big projects – infrastructure building is just the startWe believe it would not be overstating the case to say that China’s economic power to date has not been reflected in its influence on the world. China’s economic power has not translated into “soft power” being projected into the outside world.We see three phases of the YDYL initiative beginning to mould China’s influence overseas over the course of a few decades:- (Predominantly) China-funded infrastructure using plenty of Chinese-made materials and machinery, ‘adopted’ technology and Chinese construction companies (with a high contribution of Chinese workforce as well – at least in the initial stages).

- Increasing awareness and demand for Chinese brands, consumer products and cultural products as a result of increased interaction between the countries that receive YDYL investment increases and China (in short, China becoming “cool”). Chinese consumer goods companies could capitalize on the international growth phase – very similar to Coca Cola and Disney as they became US exports in prior decades.

- Full integration of China with the global economy as global influences (not just from the economically successful countries) seep back into China. Creation of international companies out of China that are truly transnational in character (eg, the likes of Unilever), rather than those that are just “China-plus”.

Our China Economist, Jian Chang, also believes that development along the New Silk Road could contribute to sustainability of China’s growth at 5-7% in the coming years and have a positive impact on China’s industrial upgrading and economic transformation.

* * *

As you can see, One Belt, One Road has far-reaching implications for China. For Chinese state-owned companies, return on investment is falling (diminishing returns in the face of overcapacity) and now sits just above 4%. Investments in US Treasurys yield even less.

On the other hand, Barclays estimates ROIC on YDYL projects to be between 10-15%, an obvious improvement over both domestic investment and money parked in US safe haven assets.

On the other hand, Barclays estimates ROIC on YDYL projects to be between 10-15%, an obvious improvement over both domestic investment and money parked in US safe haven assets.Meanwhile, embarking on large infrastructure projects with YDYL recipients can also help alleviate one of China’s pressing problems. The transition away from investment-led growth to a consumer-driven economy and a dearth of global demand have combined to leave China’s industrial sector in a state of perpetual overcapacity.

YDYL countries offer a potential outlet (a pressure valve, if you will) as there is a pressing need for FAI in the form of roads, railways, and power generation. While infrastructure development in these countries has the potential to provide a short-term economic boost for China, an expanded Chinese presence could also yield medium- and long-term benefits. Here’s how Barclays sums things up:

China could benefit in the short, medium and long term from achieving various levels of the targets outlined in YDYL. Many sectors could benefit from increased revenue, while non- monetary benefits such as goodwill and political clout could arise if China successfully helps developing countries improve their economies.- Short term: Ease industrial overcapacity, create demand for Chinese capital and consumer goods. Help reduce the economic disparity between inland and coastal China as YDYL land-based projects are focused on central and western China.

- In the medium term: Raise demand for Chinese capital goods and Chinese products in general, effectively helping China transition to a consumption-driven economy. Maintain export growth.

- Medium to long term: Internationalization of China’s currency as some loans to YDYL countries will include RMB in the basket of currencies used to denominate and settle loans, versus using US dollars.

- Long term: Promote travel, cultural exchange and long-term cooperation in geopolitical, military and trade areas. Improve general image of China on the world stage. Increase returns for the portion of China’s reserves contributed to the development funds and diversify risks. Potentially ease tension between countries over territorial disputes.

In sum, China benefits economically from YDYL in three important ways. First, investing in countries where FAI is needed to improve infrastructure not only helps China’s SOE’s achieve a higher ROIC than they could get domestically, but also helps to alleviate China’s industrial overcapacity. Second, establishing a Chinese presence in emerging, rapidly-growing economies will boost demand for Chinese products, which will aid the country in its transition to a consumption-driven economic model. Third (and we’ve mentioned this on a number of occasions in the past), using the yuan to settle AIIB loans will help establish the renminbi and decrease dependence on the US dollar on the way to ushering in a new era characterized by yuan hegemony.

* * *

Bonus: More from Barclays on the extent to which YDYL will relieve China’s industrial overcapacity problem and a bit on the differences between the Silk Road Fund and the AIIB.

YDYL demand should help China export overcapacity

We estimate that YDYL projects would absorb some of the overcapacity in Chinese industries such as cement, steel and aluminium, even under conservative assumptions. If we envisage a scenario assuming that roads, railway, power generation and power distribution assets grow by 5% from their existing asset base among YDYL countries, this could create 137mt of steel demand based on the existing asset base. This represents around 14% of China’s total steel production capacity as of 2014. Such a boost to demand could effectively give back steel producers in China pricing power, as the industry would go from 22% oversupplied to 8%, based on our estimates.

Asian Infrastructure Investment Bank (AIIB)

The AIIB was proposed by President Xi in his speech at the Indonesian Parliament on 3 October 2013. It was proposed to finance infrastructure construction and promote regional interconnectivity and economic integration. Application to be a founding member of AIIB ended on 31 March 2015 and 57 countries have been approved to be founding members. China has stated that it will not seek to be the single majority shareholder and is aiming to dilute its 50% of capital as other countries join and contribute their own capital. The bank is expected to be set up at the end of 2015.

Silk Road Infrastructure Fund

The US$40bn Silk Road Infrastructure Fund is to provide funding to carry out infrastructure, resources, industrial cooperation, financial cooperation and other projects related to YDYL. The company that manages the fund, The Silk Road Fund Co. Ltd, is backed by China’s foreign exchange reserves, China Investment Corp, Export-Import Bank of China, and China Development Bank. The fund started operation in February 2015 with US$10bn in capital, which was 65% contributed by China’s SAFE, which manages China’s Foreign Reserve. The fund is chaired by Jin Qi, the assistant governor of PBOC.

Jin Qi, the chief executive of the Silk Road Fund, said in March 2015 that the fund will invest in projects with reasonable mid- and long-term returns, and it is not an aid agency that does not consider returns. She added that the Silk Road Fund will not be the sole financer of projects; rather it will seek to cooperate with other financial institutions when investing in projects in the future.

- Ex-US Intelligence Officials Confirm: Secret Pentagon Report Proves US Complicity In Creation Of ISIS

Two weeks ago, courtesy of the investigative work of Nafeez Ahmed whose deep dig through a recently declassified and formertly Pentagon documents released earlier by Judicial Watch FOIA, we learned that Western governments deliberately allied with al-Qaeda and other Islamist extremist groups to topple Syrian dictator Bashir al-Assad. In his words: “According to the newly declassified US document, the Pentagon foresaw the likely rise of the ‘Islamic State’ as a direct consequence of the strategy, but described this outcome as a strategic opportunity to “isolate the Syrian regime.”

Now, in a follow up piece to his stunning original investigative report titled “Secret Pentagon report reveals West saw ISIS as strategic asset Anti-ISIS coalition knowingly sponsored violent extremists to ‘isolate’ Assad, rollback ‘Shia expansion“, Nafeez Ahmed reveals that according to leading American and British intelligence experts, the previously declassified Pentagon report confirms that the West accelerated support to extremist rebels in Syria, despite knowing full well the strategy would pave the way for the emergence of the ‘Islamic State’ (ISIS).

The experts who have spoken out include renowned government whistleblowers such as the Pentagon’s Daniel Ellsberg, the NSA’s Thomas Drake, and the FBI’s Coleen Rowley, among others.

Their remarks demonstrate the fraudulent nature of claims by two other former officials, the CIA’s Michael Morell and the NSA’s John Schindler, both of whom attempt to absolve the Obama administration of responsibility for the policy failures exposed by the DIA documents.

This is Nafeez Ahmed’s follow up story, originally posted in Medium

Ex-intel officials: Pentagon report proves US complicity in ISIS

Renowned government whistleblowers weigh in on debate over controversial declassified documen

Foreseeing ISIS

As I reported on May 22nd, the US Defense Intelligence Agency (DIA) document obtained by Judicial Watch under Freedom of Information confirms that the US intelligence community foresaw the rise of ISIS three years ago, as a direct consequence of the support to extremist rebels in Syria.

The August 2012 ‘Information Intelligence Report’ (IIR) reveals that the overwhelming core of the Syrian insurgency at that time was dominated by a range of Islamist militant groups, including al-Qaeda in Iraq (AQI). It warned that the “supporting powers” to the insurgency?—?identified in the document as the West, Gulf states, and Turkey —?wanted to see the emergence of a “Salafist Principality” in eastern Syria to “isolate” the Assad regime.

The document also provided an extraordinarily prescient prediction that such an Islamist quasi-statelet, backed by the region’s Sunni states, would amplify the risk of the declaration of an “Islamic State” across Iraq and Syria. The DIA report even anticipated the fall of Mosul and Ramadi.

Divide and rule

Last week, legendary whistleblower Daniel Ellsberg, the former career Pentagon officer and US military analyst who leaked Pentagon papers exposing White House lies about the Vietnam War, described my Insurge report on the DIA document as “a very important story.”

In an extensive podcast interview, he said that the DIA document provided compelling evidence that the West’s Syria strategy created ISIS. The DIA, he said, “in 2012, was asserting that Western powers were supporting extremist Islamic groups in Syria that were opposing Assad…

“They were not only as they claimed supporting moderate groups, who were losing members to the more extremist groups, but that they were directly supporting the extremist groups. And they were predicting that this support would result in an Islamic State organization, an ISIS or ISIL… They were encouraging it, regarding it as a positive development, because it was anti-Assad, Assad being supported by Russia, but also interestingly China… and Iran… So we have China, Russia and Iran backing Assad, and the US, starting out saying Assad must go… What he [Nafeez Ahmed] is talking about, the DIA report, is extremely significant. It fits into a general framework that I’m aware of, and sounds plausible to me.”

Ellsberg also noted that “it’s pretty well known” in the intelligence community that Saudi Arabia sponsors Islamist terrorists to this day:

“It’s kind of a deal that the Saudis will support various Islamic extremists, all around the world, and the deal is that they [extremists] will not try to overthrow the corrupt, alcohol-drinking clique in Saudi Arabia.”

Ellsberg, who was a former senior analyst at RAND Corp, also agreed with the relevance of a 2008 US Army-commissioned RAND report, quoted in my Insurge story, and also examined in-depth for Middle East Eye.

The US Army-funded RAND report advocated a range of policy scenarios for the Middle East, including a “divide and rule” strategy to play off Sunni and Shi’a factions against each other, which Ellsberg describes as “standard imperial policy” for the US.

The RAND report even confirmed (p. 113) that its “divide and rule” strategy was already being executed in Iraq at the time:

“Today in Iraq such a strategy is being used a tactical level, as the United States now forms temporary alliances with nationalist insurgent groups that it had been fighting for four years… providing carrots in the form of weapons and cash. In the past, these nationalists have cooperated with al-Qaeda against US forces.”

The confirmed activation of this divide-and-rule strategy perhaps explains why the self-defeating US approach in Syria is fanning the flames of both sides: simultaneously allying with states like Turkey who have continued to covertly sponsor ISIS, while working with Assad through the Russians to fight ISIS. Ellsberg added:

“As Assad is the main opponent of ISIS, we are covertly coordinating our airstrikes against ISIS with Assad. So are we against Assad, or not? It’s ambivalent… I think that Obama and everybody around him is clear that they do not any longer as they’ve been saying want Assad to leave power. I don’t believe that that is their intention anymore, as they believe anyone who succeeds Assad would be far worse.”

If true, Ellsberg’s analysis exposes the deep-rooted hypocrisy of the previous campaign against Assad, the current campaign against ISIS, and why both appear destined for failure.

Frankenstein script

Coleen Rowley, retired FBI Special Agent described my report on the DIA document as “excellent.”

Rowley, who was selected as TIME ‘Person of the Year’ in 2002 after revealing how pre-9/11 intelligence was ignored by superiors at the FBI, said of the document:

“It’s like the mad power-hungry doctor who created Frankenstein, only to have his monster turn against him. It’s hard to feel sorry when the insane doctor gets his due. But in our case, that script is constantly repeating. The quest for ‘full spectrum dominance’ and blindness of exceptionalism seems to mean we are doomed to keep repeating the ‘Charlie Wilson’s Frankenstein War’ script… The various neocon warmongers and military industrial complex, most of them inept Peter Principles, just don’t care.”

Also commenting on the declassified Pentagon report, former NSA senior executive Thomas Drake?—?the whistleblower who inspired Edward Snowden?—?condemned “the West’s role in ISIS and threat of ‘violent extremists’, justifying surveillance and libercide at home.”

Wedge strategy

Alastair Crooke, a former senior MI6 officer who spent three decades at the agency, said yesterday that the DIA document provides clear corroboration that the US was covertly pursuing a strategy to drive an extremist Salafi “wedge” between Iran and its Arab allies.

The strategy was, Crooke confirms, standard thinking in the Western intelligence establishment for about a decade.

“The idea of breaking up the large Arab states into ethnic or sectarian enclaves is an old Ben Gurion ‘canard,’ and splitting Iraq along sectarian lines has been Vice President Biden’s recipe since the Iraq war,” wrote Crooke, who had coordinated British assistance to the Afghan mujahideen in the 1980s. After his long MI6 stint, he became Middle East advisor to the European Union’s foreign policy chief (1997–2003).

“But the idea of driving a Sunni ‘wedge’ into the landline linking Iran to Syria and to Hezbollah in Lebanon became established Western group think in the wake of the 2006 war, in which Israel failed to de-fang Hezbollah,” continued Crooke. “The response to 2006, it seemed to Western powers, was to cut off Hezbollah from its sources of weapons supply from Iran…

“… In short, the DIA assessment indicates that the ‘wedge’ concept was being given new life by the desire to pressure Assad in the wake of the 2011 insurgency launched against the Syrian state. ‘Supporting powers’ effectively wanted to inject hydraulic fracturing fluid into eastern Syria (radical Salafists) in order to fracture the bridge between Iran and its Arab allies, even at the cost of this ‘fracking’ opening fissures right down inside Iraq to Ramadi. (Intelligence assessments purpose is to provide ‘a view’?—?not to describe or prescribe policy. But it is clear that the DIA reports’ ‘warnings’ were widely circulated and would have been meshed into the policy consideration.)

“But this ‘view’ has exactly come about. It is fact. One might conclude then that in the policy debate, the notion of isolating Hezbollah from Iran, and of weakening and pressurizing President Assad, simply trumped the common sense judgment that when you pump highly toxic and dangerous fracturing substances into geological formations, you can never entirely know or control the consequences… So, when the GCC demanded a ‘price’ for any Iran deal (i.e. massing ‘fracking’ forces close to Aleppo), the pass had been already partially been sold by the US by 2012, when it did not object to what the ‘supporting powers’ wanted.”

Intel shills

Crooke’s analysis of the DIA report shows that it is irrelevant whether or not “the West” should be included in the “supporting powers” described by the report as specifically wanting a “Salafist Principality” in eastern Syria. Either way, the report groups “the West, Gulf countries and Turkey” as supporting the Syrian insurgency together?—?highlighting that the Gulf states and Turkey operated in alliance with the US, Britain, and other Western powers.

The observations of intelligence experts Ellsberg, Rowley, and Drake add further weight to Crooke’s analysis. They come in addition to comments I had previously received on the DIA document from former MI5 counter-terrorism officer, Annie Machon, and former counter-terrorism intelligence officer, Charles Shoebridge.

The comments undermine the recent claims of disgraced US national security commentator, John Schindler, a retired NSA intelligence officer, to the effect that the August 2012 DIA report is “almost incomprehensible,” “so heavily redacted that its difficult to say much meaningful about it,” “Nothing special here, not one bit,” “routine,” “a single data point,” and so on.

Schindler cites the DIA’s use of ‘Curveball’?—?the Iraqi informant who fabricated claims about Saddam Hussein’s weapons of mass destruction (WMD)?—?as evidence of the agency’s “less than stellar reputation.” But this misrepresents the fact noted by the CIA’s Valerie Plame Wilson that “it was widely known [in the intelligence community] that CURVEBALL was not a credible source and that there were serious problems with his reporting.”

As I’ve documented elsewhere, the WMD threat mythology was not the outcome of an ‘intelligence failure’, as Schindler and his ilk like to claim, but a consequence of the corruption and politicization of intelligence under the influence of dubious vested interests.

Also contrary to Schindler’s misinformation, an IIR provides raw intelligence data from human sources (HUMINT), not simply rumour, gossip or opinion. Before wider distribution, the IIR is vetted to determine whether it is worthy of dissemination to the intelligence community. IIRs then provide a source basis for evaluation, interpretation, analysis and integration with other information.

Far from justifying the dismissal of the relevance of the declassified DIA documents, this shows that urgent questions must be asked:

What happened to this raw intelligence data, described by six US UK intelligence experts as providing damning confirmation of how Western strategy led to the rise of ISIS?

And why did it not lead to a change in policy, despite DIA analysts’ clear warning of the outgrowth of an ISIS-entity from Western allies’ desire to see a ‘Salafist Principality’ in the region?—?a warning which was, in hindsight, quite accurate?

Are intel critics traitors?

Schindler previously characterized NSA whistleblower Edward Snowden as a traitor and “pawn… of America’s adversaries.”

He now declares that those who cite the DIA report as proof the intelligence community “knew more about the rise of the Islamic State than they let on” are at best “fools; at worst, they’re deceivers who have lied to the American people.”

On the contrary, six decorated former senior US and British intelligence officials, many with direct experience of IIRs and their function, agree that the DIA report provides significant insight into the kind of intelligence available to the US intelligence community at the time.

Yet for Schindler, it seems, Ellsberg, Drake, Rowley, Crooke, Machon and Shoebridge are all, effectively, traitors simply for lending their expertise to public understanding of the newly declassified documents.

As Marcy Wheeler points out in Salon, the large corpus of secret DIA documents obtained by Judicial Watch demonstrates, at the least, that:

“The Intelligence Community (IC) knew that AQI had ties to the rebels in Syria; they knew our Gulf and Turkish allies were happy to strengthen Islamic extremists in a bid to oust Assad; and CIA officers in Benghazi (at a minimum) watched as our allies armed rebels using weapons from Libya. And the IC knew that a surging AQI might lead to the collapse of Iraq. That’s not the same thing as creating ISIS. But it does amount to doing little or nothing while our allies had a hand in creating ISIS. All of which ought to raise real questions about why we’re still allied with countries willfully empowering terrorist groups then, and how seriously they plan to fight those terrorist groups now. Because while the CIA may not have deliberately created ISIS, it sure seems to have watched impassively as our allies helped to do so.”

However, Wheeler overlooks that the reliance on foreign allies is a standard proxy war strategy?—?as Ellsberg explained in his interview?—?used by the covert operations arm of the US government to guarantee ‘plausible deniability.’

As I noted in my Middle East Eye analysis of the DIA document, there is extensive evidence against which to contextualize the DIA report’s assertions. This evidence shows that the CIA did not merely watch “impassively” as the Gulf states and Turkey supported violent extremists in Syria, but actively supervised, facilitated and accelerated this policy.

The August 2012 DIA document further corroborates this by repeatedly pointing out that the support to the Syrian insurgency from its allies was itself backed by “the West”?—?despite awareness of their intent to establish an extremist Salafi political entity.

While the DIA document was, indeed, just one data-point, analyzing it in context with the other DIA reports along with incontrovertible facts in the public record, establishes that the Pentagon was complicit in its allies’ support of Islamist terrorists, despite recognizing this could create an “Islamic State” in Iraq and Syria.

These revelations show that the real traitors are not the courageous whistleblowers who sacrifice everything to speak out on behalf of the public interest, but shameless shills like Schindler and Morell who willfully sanitize a dysfunctional and dangerous ‘national security’ system from legitimate public scrutiny.

Dr Nafeez Ahmed is an investigative journalist, bestselling author and international security scholar. A former Guardian writer, he writes the ‘System Shift’ column for VICE’s Motherboard, and is also a columnist for Middle East Eye. He is the winner of a 2015 Project Censored Award, known as the ‘Alternative Pulitzer Prize’, for Outstanding Investigative Journalism for his Guardian work, and was selected in the Evening Standard’s ‘Power 1,000’ most globally influential Londoners.

Nafeez has also written for The Independent, Sydney Morning Herald, The Age, The Scotsman, Foreign Policy, The Atlantic, Quartz, Prospect, New Statesman, Le Monde diplomatique, New Internationalist, Counterpunch, Truthout, among others. He is the author of A User’s Guide to the Crisis of Civilization: And How to Save It (2010), and the scifi thriller novel ZERO POINT, among other books. His work on the root causes and covert operations linked to international terrorism officially contributed to the 9/11 Commission and the 7/7 Coroner’s Inquest.

- How Obama Spells 'Respect'

- Markets, Not Janet Yellen, Should Set Interest Rates

Submitted by Dr. Richartd Ebeling via EpicTimes.com,

Financial markets in the United States and around the world are all waiting with “bated breath” for when the Federal Reserve modifies its “easy money” policy and starts to raise interest rates. No one, however, asks a simple question: Why is the American central bank in the interest rate setting business?

In May 20th, the minutes were released of the April 2015 meeting of the Open Market Committee (OMC) of the Federal Reserve. The Open Market Committee decides when and by how much America’s central bank should intervene into the financial markets to influence the amount of money and credit in the banking system and, therefore, over time, in the U.S. economy as a whole.

The members, it seems, were still divided as to whether or not the OMC should start nudging interest rates up through monetary policy, or keep them at the low levels they have been at for years, with a majority leaning to not doing so until maybe September.

In its usual ambiguous language, the published summary of the OMC meeting stated that, “Many participants . . . thought it unlikely that the data available in June would provide sufficient confirmation that the conditions for raising the target range for the federal funds rate had been satisfied, although they generally did not rule out this possibility.”