- MeMORiaL DaY 2015: THe LaND OF THE FRee

.

Once alienated,

an “unalienable right” is apt to be forever lost, in which case we are no longer

even remotely the last best hope of earth but merely a seedy imperial state

whose citizens are kept in line by SWAT teams and whose way of death, not life,

is universally imitated.

Gore Vidal

- Bernanke Says "No Large Mispricings In US Securities"; These 5 Charts Say Otherwise

Retired central banker, blogger, bond guru and hedge fund consultant Ben Bernanke just uttered the following total rubbish…

- *BERNANKE: NO LARGE MISPRICINGS IN U.S. SECURITIES, ASSET PRICES

In an effort to save whoever it is that will pay him $250,000 next for these wise words, we offer five charts.

One of these things is not like the others…

nope, no mispricing there at all…

Almost imperceptible amount of mispricing here…

So now "relative" mispriings at all..

How about "absolute" mispricings?

Cyclically, even Yellen thinks stocks are expensive…

and the median stock has never been more expensive…

But apart from that – nope – no mispricing whatsoever.

* * *

Which is why it seems odd that Bernanke would conclude his speech with this statement:

- *BERNANKE: HOW TO MANAGE ASSET PRICE DROP SCENARIO MORE CRUCIAL

Why would asset prices drop if they are not mispriced?

- Another Decapitator-in-Chief Of America's Working Class

It is not Senators Elizabeth Warren and Bernie Sanders who don’t get it. It is our near-sighted Globalist-in-Chief who really doesn’t get it, following in the footsteps of that other Republican-lite president, William Jefferson Clinton. But what can one expect, given the advice he’s getting from a cadre of Wall-Streeters working with, or influencing, the White House? Or, from a president who has confessed to being a “great admirer” of celebrated JP Morgan Chase chief, Jamie Dimon?

A few days ago President Obama honored our Portland (Oregon) area with a visit to promote the Trans-Pacific Trade Partnership (TPP) agreement; which for all intents and purposes is but another addition to the gallery of NAFTA, CAFTA, and PNTR ugly siblings. Perhaps an even uglier sibling in this period of expanding economic inequality!

It seems comical, yet ill-omened, how Barack Obama is herding the already decimated middle class along a path sure to reach economic oblivion, while maintaining support from much of the old guard of school-government-trade unionists which has kept the Democratic Party afloat during the last five decades in a conservative sea dominated by currents of old-time religion and misguided patriotism.

Common sense and humanity, and not just blind acceptance of global economics, tell us that eventually most barriers to competition should be coming down; and that there will be a significant trend towards greater homogenization in both productivity and personal income throughout much of world. But we might still be two or three generations away from such happening, assuming changes take place in an orderly and least painful fashion… without allowing our politicians, Democrats or Republicans alike, to follow the will of the elite that place them in power… and, correspondingly, expect a payback.

And that’s where we are today in Congress, ominously on the eve of passing this terrible TPP legislation sure to reach a smiling Obama, pen in hand ready to sign, instead of rejecting it with a forceful and merited veto.

Could it be that Obama is suffering from the same illusionary political disease as Bill Clinton, after the latter’s receipt of unmerited kudos for all the low-paying jobs created during his two terms in office? Is it so difficult to understand that job numbers can have a profoundly different significance in economic, social and political terms than labor income?

Regardless of the POTUS’ misleading sermonizing on “what’s good for the United States,” the reality is acrimoniously different. The anticipated net outsource of labor income sure to come from the TPP agreement is likely to be similar in results as past global renditions initiated with NAFTA. The economic capillary effect of this agreement (TPP) will affect labor significantly, not just in the manufacturing sector (possibly losing half as many jobs as the number lost to China and the American hemisphere in the past two decades), but also in the service sector – and here, we are not referring to jobs in low remuneration call centers, but jobs with high technical skills in both medicine and engineering, which could result in the loss of half of the now existing – and anticipated increases – programmer jobs; and a reduction in overall pay of the remaining half by a third or more.

Other areas in Americans’ lives will also be affected or threatened, from food safety standards, to the environment, to increases in the already stratospheric cost of drugs, to the protection of rights and sovereignty that we’ve inherited from the sacrifice of past generations.

So who’s to gain from this TPP agreement that Barack Obama is pushing with greater fervor than that exhibited in critical domestic issues such as immigration reform and the (dirty secret) racial divide? As it’s always the case in our predatory society, Corporate America and its circle of influential friends are the culprit… and it’s beginning to look as if the villains will get their way: Wall Street, Big Pharma, and a long list of multinationals displaying their corporate flags at the top of the pole, knowing that their safety is in the good hands of the Pentagon; all international policing costs defrayed by the American taxpayer… in its incredible masochistic docility.

ISIS’ literal style of decapitation is repugnant and shocking. US’ self-imposed economic decapitation may not appear at first as shocking, but the end result will be as gruesome to America’s working class: not the proletariat of old, but most everyone holding both blue and white collar jobs.

- Hanergy Contagion Sparks Chinese Investor Rotation From Shenzhen "Ponzi" To Shanghai "Safety"

It appears the reality that we exposed in all its unbelievable ponzi-ness has filtered into the psyche of Chinese investors.. though ever so gently for now. Hanergy’s self-dealing self-referential loans collateralized by stock and Goldin financial’s farcical flop, along with 500% return year-to-date stocks by the dozen, has sparked some selling with CHINEXT down around 4%, Shenzhen down 1-2% (both heavily dominated by these high-flying idiot-maker stocks) while Shanghai Composite and CSI-300 (China A-Share proxy) is bid…

because why wouldn’t you greatly rotate to the index that is only up 47% YTD and not 92%?

Charts: Bloomberg

- From the Very Creation of the Internet, U.S. Spy Agencies Fought to Block Encryption

American spy agencies have intentionally weakened digital security for many decades. This breaks the functionality of our computers and of the Internet. It reduces functionality and reduces security by – for example – creating backdoors that malicious hackers can get through.

The spy agencies have treated patriotic Americans who want to use encryption to protect their privacy as extremists … or even terrorists.

As Gizmodo’s Matt Novak points out, this attack started at the very birth of the internet:

In the 1970s, civilian researchers at places like IBM, Stanford and MIT were developing encryption to ensure that digital data sent between businesses, academics and private citizens couldn’t be intercepted and understood by a third party. This concerned folks in the U.S. intelligence community who didn’t want to get locked out of potentially eavesdropping on anyone, regardless of their preferred communications method. Despite their most valiant efforts, agencies like the NSA ultimately lost out to commercial interests. But it wasn’t for lack of trying.

***

When the NSA got wind of the research developments at IBM, Stanford and MIT in the 1970s they scrambled to block publication of their early studies. When that didn’t work, the NSA sought to work with the civilian research community to develop the encryption. As Stowsky writes, “the agency struck a deal with IBM to develop a data encryption standard (DES) for commercial applications in return for full pre-publication review and right to regulate the length, and therefore the strength of the crypto algorithm.”

Naturally, in the Watergate era, many researchers assumed that if the U.S. government was helping to develop the locks that they would surely give themselves the keys, effectively negating the purpose of the encryption. Unlike IBM, the researchers at Stanford and MIT didn’t go along with the standard and developed their own encryption algorithms. Their findings were published (again, against the wishes of the NSA) in the late 1970s after courts found that researchers have the right to publish on the topic of cryptography even if it makes the government uncomfortable. According to Stowsky, the NSA retaliated by trying to block further research funding that Stanford and MIT were receiving through the National Science Foundation.

Novak also notes that – right from the start – people realized the potential of the internet as a tool for conducting mass surveillance on the public. And see this, this and this.

- How iTunes Destroyed The Music Business In 1 Simple Chart

The music industry was the first entertainment business to confront the digital transition, although it was not exactly a willing pioneer. Rather, it was thrust into this role as a matter of survival, as it grappled with the rapid rise of online piracy in the early 2000s.

The music industry was incredibly slow to respond to the digital transition. Napster, the original music piracy site, burst onto the scene in 1999, but it wasn’t until 2004 when Apple iTunes debuted that consumers grew more and more primed to free music.

This was a serious error and haunted the music industry for years thereafter, costing the industry multi-billions in annual sales. The rest of the entertainment industry has taken note and, as a result, all other entertainment sectors, including video, have been comparatively quick to embrace digital distribution.

The music industry, rather than focusing on a legal digital download service, initially focused all its effort on shutting down Napster by way of a copyright infringement lawsuit. Ultimately, the industry prevailed and the courts shut down Napster in mid-2001; however, this was a pyrrhic victory. By the time Napster was shut down, the pirates had moved on to the next new thing: decentralized peer-to-peer file sharing, led by Gnutella. Unlike Napster, these piracy sites were virtually impossible to shut down because there was no central server storing the files. Shutting down Gnutella would have been tantamount to shutting down the entire internet.

In addition to the failure to launch a legal alternative to the pirate sites, the music industry was, understandably, paralysed by its fear of album unbundling. Piracy had given consumers a taste for singles and there was no going back to albums.

Against this backdrop of piracy and absent a legal digital alternative, music sales plummeted. From a peak of nearly US$15 bn in 1999, US music sales declined cumulatively by 15% to US$12 bn in 2003 (previous exhibit). The decline in song units (assuming 10 songs per album) was even more dramatic, declining by 29% cumulatively to 7.7 bn over the same time. Little did the industry know that this was only the beginning of the decline. By 2004, the music industry was in dire straits. Physical sales were in free fall and its own efforts to launch a digital download service were failing.

Apple, with the dominant digital music player and superior software engineering skills, was a perfect partner (nay, savior) for the music industry, with Steve Jobs Achieving a very consumer-friendly retail price of US$0.99 per song and a wholesale price of US$0.70. This wholesale price was, in effect, a 30% price reduction from the implicit price per song on a physical album (i.e., US$10 album wholesale price, 10 songs per album).

After a small bump in sales in 2004 from the launch of iTunes, the declines resumed as the double whammy of album unbundling and a 30% wholesale price cut took its toll. From 2004 to 2014, US music unit and dollar sales declined cumulatively by another 50%, erasing US$5 bn in annual sales.

There is no rest for the weary, and the music industry is already confronting another digital transition, call it digital transition 2.0, in the form of online streaming. Song sales stabilised from 2010 to 2012, but have since resumed declining as music demand is now shifting from digital downloads (ownership) to online streaming (rentals), such as Pandora.

Source: Goldman Sachs

- Ron Paul: The Case For Truly 'Free' Trade

Submitted by Ron Paul via The Misess Institute,

With recent DC politicking on both the Export-Import Bank and the Trans-Pacific Partnership, we revisit Ron Paul's 1981 essay "The Case for Free Trade" which explains the basics of truly free trade:

Although we think of ourselves as a free-trading nation, it takes more than 700 pages just to list all the tariffs on imported goods, and another 400 to inventory all the non-tariff restraints, such as quotas and "orderly marketing agreements."

A tariff is a tax levied on a foreign good, to help a special interest at the expense of American consumers.

A trade restraint or marketing agreement—on the number of inexpensive Taiwanese sneakers that Americans can buy, for example—achieves the same goal, at the same cost, in a less forthright manner.

And all the trends are towards more subsidies for U.S. exporters, and more prohibitions and taxes on imports.

Trade is to be subsidized or restrained, not left to the voluntary actions of consumers and producers.

In 1930, Congress passed the Smoot-Hawley tariff bill, imposing heavy tariffs on imports, with the avowed motive of "protecting" U.S. companies and jobs. Within one year, our 25 major trading partners had retaliated with their own tariffs on American goods. World trade declined sharply, and the depression was made world-wide and longer-lasting.

Today the policy of protectionism is again gaining favor in Congress, and in other countries. But it must be fought with all our strength.

Not only does protectionism make everyone poorer—except certain special interests—but it also increases international tensions, and can lead to war.

"If a foreign country can supply us with a commodity cheaper than we ourselves can make it," wrote Adam Smith in 1776, "better buy it of them with some part of the pro duce of our own industry, employed in a way in which we have some advantage. The general industry of the country will not therefore be diminished… but only left to find out the way in which it can be employed to the greater advantage."

An important economic principle is called the division of labor. It states that economic efficiency, and therefore growth, is enhanced by everyone doing what he does best.

If I had to grow my own food, make my own clothes, build my own house, and teach my own children, our family's living standard would plummet to a subsistence, or below-subsistence, level.

…

Every economic intervention in trade, domestic or foreign, should be abolished, for practical and moral reasons.

Even if other countries maintain tariffs or subsidies, we would be helped, not hurt, by unilaterally ending ours.

We would improve our productivity, shift resources to those areas where we 'have an advantage, grow more pros-perous, and make a greater variety of less-expensive goods available to our people.

And we would serve the cause of peace and set a good example for the world to emulate.

"When people and goods cross borders," Ludwig von Mises used to quote, "armies do not." Free and extensive trade, unsubsidized, between the peoples of the Earth lowers tensions and makes us all better off It is, morally and economically, the only proper policy.

- McDonalds Responds To Minimum Wage Protests

But all they wanted was $15 per hour?

h/t @Stalingrad_Poor

- Lake Mead Water Level Mysteriously Plunges After Nevada Quake

A 4.8 magnitude earthquake (originally reported 5.4) shook Las Vegas and surrounding areas Friday morning causing roads and bridges to be closed. The quake went little-reported outside of local news (since there was at first glance minimum damage caused) but, since the quake’s occurrence, something considerably more worrisome has occurred.

In the 36 hours since the quake’s occurrence, water levels at Lake Mead have plunged precipitously. While we know correlation is not causation, the ‘coincidence’ of an extreme loss in water levels occurring in the aftermath of one of the largest quakes in recent Vegas history does raise a suspicious eyebrow – especially when there has been no official word on the precipitous decline.

The earthquake hit mid-morning on Friday:

A 4.8 magnitude earthquake shook Las Vegas and surrounding areas Friday morning, forcing loose a rubber casing on a bridge and leading state officials to close Spaghetti Bowl interchanges for several hours.

After the Nevada Department of Transportation inspected bridges for possible structural damage, they deemed the roads safe for travel and reopened them just before 5 p.m. Traffic had backed up for miles during the closures, which came at the start of the Memorial Day weekend.

The quake, which hit at 11:47 a.m., was centered about 23 miles south-southwest of Caliente, the U.S. Geological Survey said. The magnitude was originally reported as 5.4, but the official number was lowered twice Friday.

The ramp from southbound U.S. Highway 95 to southbound Interstate 15 was closed about 12:20 p.m. Friday, officials said.

“The joint damage was pre-existing. The tremblor simply dislodged the protective rubber encasing the bridge seam making it look much worse than it was in reality” and prompting an immediate shutdown of the ramps, NDOT engineer Mary Martini said in a news release about 3:45 p.m.

Since then, official water level data shows an incredible 8 foot plunge in water levels since the earthquake.

considering the (average drop in the last 10 years is 1 inch, this is a troubling outlier.

Source: Lake Mead Water Database, h/t Professor Doom and Quasar

There is , of course, a possibility that the drop is the result of broken sensors and we will be following up during the week to see if levels normalize.

This is crucial since, as we noted previously,

If the water level drops below 1,075 feet elevation by January 1, 2016, it will trigger a federal water emergency. And water rationing.

Las Vegas Review Journal reported that forecasters expect the level to drop to 1073 feet by June, before Lake Powell would begin to release more water. Assuming “average or better snow accumulations in the mountains that feed the Colorado River – something that’s happened only three times in the past 15 years,” the water level on January 1 is expected to be barely above the federal shortage level.

Even with these somewhat rosy assumptions of “average or better than average snow accumulations,” the water level would begin set new lows next April. But if the next winter is anything like the last few, all bets are off.

If the level drops below 1050 feet, one of the two intake pipes for the Las Vegas Valley, which gets 90% of its water that way, will run dry.

As Roman Catholic Imperialist notes, this is quite unprecedented… For a sense of just how bad things are gettiing, the following images will help…

Update: moments ago the Lake Mead National Recreation Area officially denied that the online reading was accurate blaming the water level collapse on inaccurate water levels as of this morning.

Lake Mead’s elevation has NOT dropped to 1,068 feet. Some inaccurate data was posted online. We are at 1,077 feet. http://t.co/a0YUo9iD0P

— Lake Mead (@LakeMeadNRA) May 24, 2015

@jeffreyneillong This information is not accurate. The website had incorrect data this morning. It has been updated http://t.co/0ls3f4yoC5

— Lake Mead (@LakeMeadNRA) May 24, 2015

Dare we say it: double seasonally-adjusted water levels?

- Grexit "Disaster" Looms As Greek Hospitals Run Out Of Sheets, Painkillers

The default countdown is about to go under 10 days and it is becoming increasingly apparent that both Greece and its creditors have had enough.

Months of tense negotiations have gone nowhere and yielded exactly nothing and it now looks like PM Alexis Tsipras and FinMin Yanis Varoufakis may be willing to miss a June 5 payment to the IMF if it means proving they are serious about keeping their campaign promises and forcing the troika to the bargaining table. The implications of a missed payment aren’t entirely clear but Athens is keen to predict the worst as it tries to squeeze concessions from creditors. Bloomberg has more:

A day after Prime Minister Alexis Tsipras said Greek society can’t absorb any more austerity measures, Finance Minister Yanis Varoufakis said his government has met the euro area and IMF three-quarters of the way, and that it’s up to creditors to cover the remainder.

“Greece has made enormous strides reaching a deal, it is now up to the institutions to do their bit,” Varoufakis said Sunday on BBC’s Andrew Marr Show. “It is not in their interests as our creditors that the cow that produces the milk should be beaten into submission to the extent that the milk will not be enough for them to get their money back”…

German Finance Minister Wolfgang Schaeuble, meanwhile, signaled there isn’t much wiggle room after Tsipras’s government committed to policy changes in return for aid in a euro-area accord on Feb. 20.

“That is the condition for completing the current program,” Schaeuble said in a Deutschlandfunk radio interview aired Sunday. “The problems are rooted in Greece. And now Greece does have to fulfill its commitments.”

Some members of Tsipras’s Syriza party advocate defaulting on loans rather than backing down from the anti-austerity policies that swept it to power in January even if that leads the country out of the euro.

Greece doesn’t have the money, and won’t pay what it owes the IMF in June, Interior Minister Nikos Voutsis said in a Mega TV interview on Sunday. Spiegel Online on April 1 cited Voutsis as saying Greece should delay an April 9 payment to the fund, which was made.

“We’ve done remarkably well for an economy that doesn’t have access to the money markets to meet our obligations,” Varoufakis said. “At some point we will not be able to do it.”

“Once you are in a monetary union, getting out of it is catastrophic,” Varoufakis said. “It would be a disaster for everyone involved. It would be a disaster primarily for the Greek social economy but it would also be the beginning of the end of the common currency project in Europe, whatever some analysts might be saying.”

And “whatever some analysts might be saying”, Greeks are now suffering mightily, as the €22 million per day hit to the economy has now bankrupted the country’s hospitals which have reportedly run out of painkillers and sheets. Here’s The Independent:

Greek hospitals have run out of supplies such as painkillers, scissors and sheets as budget cuts have left the health service unable to provide even basic provisions for operations and medical procedures…

Huge cuts to the healthcare budget, amid the economic turmoil which made millions unemployed, have left than 2.5m Greeks uninsured, up from 500,000 in 2008..healthcare spending has fallen by 25 per cent since 2009, creating shortages of the most basic surgical equipment and leaving too little money to pay nurses’ salaries.Reports have surfaced of patients being turned away from hospital because there was no meter to measure their high blood pressure, while others have had to do without painkillers during medical procedures. One patient was even asked to bring their own sheets to hospital.A trainee surgeon at KAT, a respected state hospital in Athens, said the situation was at “breaking point”.“There is no money to repair medical equipment, no money for ambulances to use for petrol, no money to hire nurses and no money to buy modern surgical supplies.”Meanwhile, Tsipras is steadfastly refusing to compromise on the now ubiquitous “red lines” and the most outspoken austerity advocates look to be entrenching themselves even further as the following quote from German FinMin Wolfgang Schaeuble makes clear:Greece committed itself to the fulfillment of this program on Feb. 20 and therefore we don’t need to talk about alternatives.Clearly, the end game is approaching although it’s till unclear what form it will take. The idea that a developed country cannot provide basic emergency medical care because it is in poor standing with the institutions that print a fiat currency is patently absurd and simply isn’t tenable meaning that one way or another, this ‘situation’ will resolve itself in the coming weeks, an event which will put Europe’s broken bond markets to a rather difficult test.

- The "New Era" Is An Old Story

Excerpted from John Hussman's Weekly Market Comment,

Among the recurring features of speculative episodes across history is the appearance of “new era” arguments to justify the elevated prices, coupled with arguments that historically reliable measures no longer apply. In our view, the problem is not that investors search for new, more reliable tools of market analysis – that should always be an objective. The problem is when investors adopt theories and models that embed the most optimistic assumptions possible, run contrary to historical evidence, or embed subtle peculiarities that actually drive the results (see, for example, the “novel valuation measures” section of The Diva is Already Singing). Eventually, the final refuge of speculation is to abandon historically reliable measures wholesale, resting faith instead on the advent of some new era in which the old rules simply don’t apply.

John Kenneth Galbraith noted this phenomenon decades ago in his book The Great Crash 1929: “It was still necessary to reassure those who required some tie, however tenuous, to reality. This process of reassurance eventually achieved the status of a profession. However, the time had come, as in all periods of speculation, when men sought not to be persuaded by the reality of things but to find excuses for escaping into the new world of fantasy.”

In late-1929, Business Week observed: “This is the longest period of practically uninterrupted rise in security prices in our history… The psychological illusion upon which it is based, though not essentially new, has been stronger and more widespread than has ever been the case in this country in the past. This illusion is summed up in the phrase ‘the new era.’ The phrase itself is not new. Every period of speculation rediscovers it… During every preceding period of stock speculation and subsequent collapse business conditions have been discussed in the same unrealistic fashion as in recent years. There has been the same widespread idea that in some miraculous way, endlessly elaborated but never actually defined, the fundamental conditions and requirements of progress and prosperity have changed, that old economic principles have been abrogated… that business profits are destined to grow faster and without limit, and that the expansion of credit can have no end.”

“This time” is not different. There’s no question that investors have come to believe that somehow quantitative easing has durably changed the world – that central banks have (or even can) put a floor under the markets as far as the eye can see. But if you examine the persistent and aggressive easing by the Fed during the 2000-2002 and 2007-2009 plunges, it’s clear that monetary easing has little effect once investor preferences shift toward risk aversion –which we infer from the behavior of observable market internals and credit spreads. Monetary easing only provokes yield-seeking speculation when low-interest money is viewed as an inferior asset.

It’s not monetary easing, but the attitude of investors toward risk that distinguishes an overvalued market that continues higher from an overvalued market that is vulnerable to vertical losses. That window of vulnerability has been open for several months now, and the immediacy of our downside concerns would ease (despite obscene valuations) only if market internals and credit spreads were to shift back toward evidence of investor risk-seeking.

Zero interest rate policy has two effects on the financial markets. One is legitimate – every year in which short-term interest rates are expected to be zero instead of say, a typical 4%, should reasonably warrant a 4% valuation premium in stocks and bonds, over and above run-of-the-mill historical norms (one can demonstrate this using any discounted cash flow approach). So if investors expect short-term rates to be zero for another 4 years, it would be reasonable for stocks and bonds to be about 16% higher than historical valuation norms. At present, the most historically reliable measures we identify suggest that S&P 500 valuations are more than twice their pre-bubble norms.

The other effect of zero interest rate policy is pure delusion. It is to convince investors that there is some miraculous support, "endlessly elaborated but never actually defined," that places a floor under the financial markets. By creating that delusion, investors become prone to “carry trade” speculation – buying any risky security that offers a yield better than zero. That carry trade mentality can only survive in a world where the possibility of capital loss is quietly assumed away.

Our view is simple. The U.S. stock market is in the third valuation bubble of the past 15 years, which is likely to be resolved by losses similar to the outcomes we observed in the first two. In the face of constant cheerleading in 2000 based on theories and valuation measures that were historically unfounded, I wrote in February of that year:

“If you turn off CNBC and think about the market independently for even a few minutes, it is clear that this market displays none of the conditions which have historically been followed by sustained market advances, and all of the conditions which have historically been followed by market crashes. The aphorism ‘Buy low, sell high’ has long been discarded. The replacement ‘Buy high, sell higher’ has also been abandoned. The rallying cries of investors are now just ‘Buy’ and ‘Get me in!’

“Are we the only sane people on the planet? While investors are conditioned to think that ‘extreme risk’ means 15-20% downside, let’s not be shy… we expect a 50% plunge in the S&P 500 by the time this cycle is over. Fortunately, investors who decide to buy on a 15% drop will only lose about 41%, and investors who hold out for a 20% drop before buying will only lose about 38% by the bottom. That’s how the math works… So that’s the good news. The bad news is that the more speculative sectors of the market are likely to be hit harder… The difficult part of all of this is the short term. I have no answer for that, except that in each prior instance, every scrap of short-term gain was wiped out in the eventual downturn."

As it happened, yes, we were evidently among the only sane people on the planet. The S&P 500 went on to lose half of its value by October 2002, while the Nasdaq 100 lost 83% of its value. We expressed similar concerns (and projections of potential loss for the S&P 500) in 2007, which were validated in the financial crisis that followed.

I can write this a thousand times, but we’re still regularly asked questions that implicitly assume that we’ve neither learned anything, nor addressed anything as a result our challenge in the recent half-cycle since 2009. I’ll say this again: our central challenge was not the result of our valuation methods, which didn’t miss a beat (see Why Warren Buffett is Right and Why Nobody Cares). Rather, the challenge was the inadvertent result of my 2009 insistence on stress testing our methods of classifying return/risk profiles against Depression-era data. The ensemble methods that came out of that effort, while performing even better than our pre-2009 methods in full cycles across history, also subtly reduced the impact of various components we use to infer investor risk preferences. The one thing that QE did to make things legitimately “different this time" was to reduce the overlap between overvalued, overbought, overbullish syndromes and corresponding deterioration in market internals. Because those syndromes were historically a reliable warning of subsequent deterioration in market action, we responded too strongly when they emerged. Put simply, QE made that overlap unreliable. We imposed overlays in mid-2014 that essentially rule out a hard-negative outlook until that deterioration in market internals or credit spreads becomes evident (as it has at present).

Don’t imagine that our stumble in this half-cycle makes current market valuations any less breathtaking. An advancing stock market is not evidence that stocks are not obscenely overvalued. If overvalued markets always crashed immediately, extreme overvaluation could never emerge in the first place. Instead, we have to ask a different question: what distinguishes an overvalued market that continues higher from an overvalued market that crashes? History repeatedly provides the same answer (which, like most discoveries, only seems “obvious” after you’ve figured it out). What distinguished the late-1990’s valuation bubble from the crash that followed that bubble? A shift in investor risk-preferences, as revealed by a subtle (and eventually profound) deterioration of observable market internals and risk measures. What distinguished the advance to the 2007 peak from the collapse that followed? A shift in investor risk-preferences, as revealed by a subtle (and eventually profound) deterioration of observable market internals and risk measures. The same is likely to be the case in the present instance, and on historically reliable measures, that shift has already occurred. Our concerns about market risk will become less immediate if they were to improve. At present, the market remains vulnerable to losses similar to those we observed in 2000 and 2007.

- The Best-Selling 'Monetary-Policy' Books Are All Anti-Fed

Interestingly, Amazon's list of best sellers in the "monetary policy" category is a veritable parade of anti-Fed and anti-central bank books.

Having not read all of them, I certainly can't endorse all of them, and many of them surely contain questionable economics and fanciful claims about central banks. (Jim Grant's great new book is in there, though.)

On the other hand, the fact that such books dominate the book sales in this category tells us a thing or two about how the near consensus of approval once enjoyed by the Fed (and other Western central banks) is long gone — thanks largely to Ron Paul's 2008 campaign.

Had we a list like this from 10 or 15 years ago, it probably would have been dominated by books like Bob Woodward's Maestro, which basically made the case that Alan Greenspan was an inimitable genius.

(You can pick up a hardback copy of Maestro for one cent, by the way.)

Perhaps perfectly combining the two phrases "A penny for your thoughts" and "You get what you pay for"

* * *

And Ben Bernanke's not-released-yet Memoir is already discounted by 29%…

- The Fed's Perilous "Fake It Till You Make It" Strategy May Be Coming Home To Roost

We all know the difference between reality and wishful thinking. Many of us know just how quickly the jaws of reality can crush the life out of unicorn and fairytale stories when fiction is used to cover the facts. Where the businesses and happy customers that are supposedly represented on an income statement turn out to be little more than the Non-GAAP application of a fairy’s wand and pixie dust.

However, this doesn’t stop people from buying in (literally) to the illusion. And what has far more onerous consequences is when the story tellers themselves begin to believe their own works of fiction.

Since the financial meltdown of ’08 one thing has changed in ways never before seen in its voracity, let alone the sheer breath of complacency and acceptance to it. That “change” is what used to be reported or used as benchmarks of statistical data (whether it be of the government supplied sourced or other venue) and the outright publicly displayed willingness to adulterate them.

Some will ask, “Is it really such a big deal? It’s not like reports haven’t been adjusted for decades, what’s the big deal now?”

Part of that question is correct. Yes, we’ve always tried to “smooth” out data to get a more accurate read of what is actually transpiring within an economy and more. As a matter of fact whole companies as well as individuals have built well deserved reputations for doing just that and supplying that advice to businesses and others. However, what is taking place currently (in my opinion) is the practice of “goal-seeking” as in the manipulation of that data; and moving it closer in a perilous pursuit of another methodology that may have far more disastrous consequences e.g., “Fake it till you make it.”

Personally I am all too well versed on this latter dictum. It is used extensively throughout the motivational speaking realm. The problem is not with the idea per se, it’s in the where, why, and how application that causes all the problems. Let me give you a quick example for clarity…

Want to break a habit such as smoking and more? “Fake it till you make it” works perfect here and is absolutely a useful and beneficial frame of mind to accomplish that goal. For as soon as you decide to quit you can begin living and adapting your life to that as a person who doesn’t. Want to begin and start acting like a person of success? You can do the same.

Where the dangerous version of using this example comes into play and is shouted from stages, and books too many to mention here, is when you’re advised to buy or spend (as well as kid yourself into believing this is how the rich do it) money you maybe can’t afford or, get into onerous long-term contracts and financing deals such as a high-end or exotic cars, or homes well above your current income as to “grow” into it. i.e., Fake it till you make it.

Here is where “faking it” only works for so long because someone else comes along and “takes it back” with a Sheriff’s notice for non-payment. The landscape is littered with those who bought in (again literally) to this type of advice. And yet – this is exactly what is taking place in kind at the most powerful monetary body in the world e.g., The Federal Reserve.

Just this past week the “data dependent” Fed. was supplied with the fantastic news that the Dept. of Commerce will now “double seasonally adjust” GDP data. i.e., if at first you don’t succeed – try, try again. This coincides with other reports now that have become outright jokes to anyone with a modicum of business acumen. e.g., The jobs reports, consumer spending, et al. Yet, all this data is exactly what the Fed. points to as confirmation why they should or should not alter or adjust monetary policy. I’m sorry, but this is no longer delirious or delusional economic policy and theories in action. This is out right dangerous.

For how does one now solve the dilemma when investing or anything else market related when data has been flipped from adulterated, to inverted, to an inverted adulteration? (e.g., data was at first adjusted, then it took on the caveat of “bad is now good.” to now where it’s adjusted and can literally imply both good and bad)

As much as that may seem like a play on words, I assure you it’s not. For in today’s markets all that matters is what the Fed. does and when. There is no longer anything approaching what was once known as “fundamental investing” in these markets. “Fundamental” is now nothing more – than front-running. Pure and simple.

And with that now comes another dilemma in this duopoly: Who does the Fed. now want to believe? Their own numbers? (e.g., like those of the Atlanta Fed.) Or: the double seasonally adjusted, goal-seeked versions?

One heralds: “Bad news is good, and worse is fantastic!” implying the Fed. is hamstrung to the zero bound along with keeping the narrative alive for the possibility of a resurgence of QE. And the other portends: “Bad news is now going to be adjusted to show good, and better news will be seen as “mission accomplished” releasing the Fed. to both raise rates sooner, and possibly faster, than the market anticipates. Welcome to your new version of “clarity” as portrayed by current Fed. speak.

The argument can be made (in which I’m trying to do just that) as of this week: all “clarity” as to what any relevant data point used and professed by the so-called “smart crowd” as to infer what the Fed. may, or may not do, in the coming months – has been completely and outright nullified. The Fed. by virtue of their own clarifying distinctions when they moved from “patient” to “data dependent” means one will lose their minds (as well as money) let alone patience as they now try to extrapolate what data point the Fed. now views as determinant.

Let’s use a very possible (if not plausible) example to express the above today, in real-time…

You are a fund manager with a considerable amount of money at risk within the markets whether private or customer funded. As of last Monday you were of the mindset along with the group think based upon confirmation expressed by “clarity” statements emanating from the Fed. that “data” is what will determine their policy adjustments. And so, with the narrative of “bad news is good news for stocks” you are fully exposed to equities. That has been the bread and butter trade of “insight” for nearly 6 years.

However, just days ago (going into a long holiday weekend) you just learned: the remaining “data points” that helped buttress those assumptions (i.e., deteriorating macro data points) are now going to be “double seasonally adjusted” as to show that maybe in the eyes of those discerning those numbers – they just aren’t as bad as they first portended to be. Now what?

Are you so sure the Fed. won’t raise rates in June? Maybe they won’t, maybe they won’t this year, or in our lifetime. Who knows. However, exactly who is this “data” being adjusted for to show more “clarity?” The public at large? Or – The Fed? And if it’s the latter; then all previous assumptions of what, why, when, and how are now moot. Welcome to where double speak aligns with goal-seeked expressed via Fed. speak. Good luck with any clarity in that equation. Let alone what the headline reading, algorithmic front-running arsenal of HFT vacuum tubes will now interpret it.

The Fed. embarked on the greatest experiment in the history of monetary policy based on the ultimate “fake it till you make it” strategy. They have openly stated the underlying premise (or illusion) why it was pursuing this path was for: The wealth effect. However, as with most that ever followed this type of strategy without fully comprehending the dangers – trouble is now lurking around every corner.

What was once implied as “good” can now mean just that, which in turn means bad for stocks. What was said as being “transitory” can now mean to have lasting repercussions to stock values. What was earlier programmed and algo fueled to mean “buy, buy. buy” could this Tuesday be flipped with a switch in code to mean “sell everything!” No one knows because “clarity” just took on a whole new meaning with “double seasonally adjusted.”

The only one’s that may be more surprised with the coming ramifications to a “fake it till you make it” world of monetary policy are those that still believe it’s been their investing prowess over the last 6 years that’s been the force behind their performance. For one thing will be certain.

Will JBTFD (just buy the dip) work in the markets any longer when monetary policy has more in common with trying to figure out what the definition of “is” is? And if you’re confused going forward don’t feel bad. Just take solace in how confused the HFT headline reading algo’s will be going forward. Because as the volumes as well as market data shows:

They’re the only one’s still in this market.

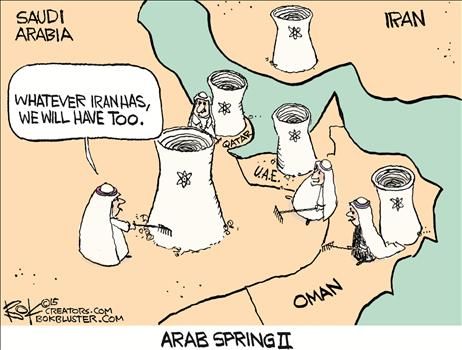

- Arab Spring 2.0: Wahhabis Go Nuclear

This won't end well…

Source: Townhall via Sunday Funnies

* * *

Pepe Escobar explains (via Global Research)…

The serious possibility of a nuclear deal between Iran and the P5+1 is only a few weeks away – on June 30.

So guess what the terminally paranoid House of Saud is up to: Lay their hands on a nuclear bomb to counteract the non-existent “Iranian bomb”, which Tehran, via Supreme Leader Ayatollah Khamenei, has consistently abhorred as un-Islamic, and wouldn’t have it anyway because of stringent inspections bound to be part of the final nuclear deal.

The proverbial “former Pentagon official” has leaked to a Rupert Murdoch paper that the House of Saud is bound to buy a ready-made nuclear bomb from Pakistan. The choice of media already offers a clue; Prince Alwaleed bin Talal is one of News Corporation’s leading shareholders.

The “why now?” concerning the leak is pretty obvious. Yet the whodunit is hazier territory.

Meanwhile, adding fuel to the jihadi fire, as the Wahhabis in Riyadh dream of going — literally — nuclear their faith brothers across “Syraq” are going figuratively nuclear, adding victory after victory on the ground; from the assault on Palmyra, the Silk Road-era jewel of the desert in Syria, to the fall of Ramadi in the former “triangle of death” in Iraq.

The “Iranian bomb” was never really an issue for successive U.S. administrations; only a convenient pretext to box in, harass, sanction and “isolate” the Islamic Republic, the former “gendarme” of the Gulf in the Shah era. The U.S. government always knew nuclear bombs can be bought on the black market; so whether Tehran could develop a nuclear weapon was irrelevant.

The House of Saud, for its part, may — and the operative concept is “may” — already have a bomb, for a long time now, to offset Israel. And they “may” have paid Islamabad for it. There is no conclusive proof.

What’s certain is that the — non-existent — “Iranian bomb” is where the House of Saud, other GCC minions and, crucially, Bibi Netanyahu’s extremist, fundamentalist Israeli government converge; they all consider it an “existential threat” to their survival.

The problem is we can’t just dismiss outbursts of the type as mere instances of geopolitical surrealism. A running myth — very popular in the Beltway — goes that Riyadh’s got some credit with Islamabad as the House of Saud invested billions of dollars in the 1970s to develop the Pakistani nuclear program, which was a counterpunch against the Indian nuclear program.

Already on December 2011, the House of Saud announced publicly that it was pursuing a nuclear bomb. But only as the possibility of an Iranian nuclear deal advanced they started to embark in a wag the dog attempt to control U.S. foreign policy.

Israel got into the game as early as November 2013, when the BBC reported on an alleged nuclear deal between Riyadh and Islamabad. A key quote was from a former head of Israeli military intel, Amos Yadlin; if Iran had a bomb, “the Saudis will not wait one month. They already paid for the bomb, they will go to Pakistan and bring what they need to bring.”

Compare this with wily Prince Turki, former Saudi intelligence chief and close pal of one Osama bin Laden, who has always waved the possibility of a nuclear House of Saud. The last time was in fact in April, at the South Korean Asan Plenum; “Whatever the Iranians have, we will have, too.”

The new Godfather of the Riyadh mob, King Salman, wanted Islamabad to provide troops for his ongoing war on Yemen. Islamabad said thanks but no, thanks. Instead, a nuclear deal might – and the operative word, once again, is “might” — have been struck. Naturally no high-ranking official in Riyadh or Islamabad will confirm any of this.

Watch the Pakistani angle

King Salman is pretty much aware that in the event of ISIS/ISIL/Daesh achieving regime change in Syria – still a pretty remote possibility – the next in line would be the House of Saud.

And then there’s the fact of Washington keeping those infamous 28 redacted pages of the 9/11 secret under wraps after all these years. So possessing a nuclear bomb might be as much an insurance policy against Washington as against the non-existent “Iranian bomb.”

Beyond propaganda, the fact remains that several Masters of the Universe VIPs are positively fed up with the House of Saud on a number of key issues, most of all the Saudi oil price war decimating the U.S. shale oil industry.

Still, the House of Saud would never be allowed to go — literally — nuclear — without a green light from Washington.

The view from Pakistan helps to clear the haze. Pakistani nuclear project chief A.Q. Khan — with some support or at least acquiescence by Islamabad — did sell nuclear weapons technology to North Korea, Iran and Libya. Yet the whole Pakistani nuclear program cost less than $450 million. Scores of Pakistani analysts stress it was that cheap because Islamabad received help from China, not the House of Saud.

Both Iran and Saudi Arabia are key Chinese energy suppliers. Both Iran and Pakistan will be key players in the emerging, Chinese-led New Silk Road(s) project. Islamabad would be extremely foolish to jeopardize its relationship with Beijing by providing a nuclear weapon which would be used to threaten a non-nuclear neighbor — Iran — that not only is a Chinese strategic ally but will play a key role into easing Pakistan’s energy problems, via the Iran-Pakistan (IP) pipeline, partly financed by — who else — Beijing.

Watch the Battle of Ramadi – remixed

Wahhabism as practiced in beheading-friendly Saudi Arabia is and will continue to be the ideological matrix of all forms of Salafi-jihadism let loose in the Middle East and beyond. That especially applies to its latest social media-friendly spectacular, ISIS/ISIL/Daesh.

ISIS/ISIL/Daesh – to the “civilized world” consternation – has seized Ancient Silk Road pearl Palymra. UNESCO is “concerned.” The White House is “worried.” Palmyra is a strategic crossroads in the center of Syria which will allows the fake Caliphate to launch attacks in all directions and harass the Syrian government’s vital axis, from Damascus to Aleppo. They have already taken over the crucial Syria-Iraq border control point of al-Walid, in Syrian territory.

Moreover, over a third of Palmyra’s 200,000 residents have already been turned into refugees. Hundreds have been made hostages. The macabre beheading show is on. Is the Empire of Chaos — which, in thesis, is at war with the fake Caliphate — doing anything to save Palmyra’s priceless Roman ruins from possible, imminent destruction by Wahhabi-drenched barbarians? Of course not.

And the same applies to Ramadi, capital of Anbar province, roughly 110 km west of Bahgdad, which the U.S. did not “lose” because it never had. While ISIS/ISIL/Daesh gloated about their victory with megaphones at all the major mosques, the Pentagon was spinning this “is a fluid and contested battlefield”, and insisted on “supporting (the Iraqis) with air power.”

Cue to gleaming Toyota convoys of Caliphate goons laughing their Kalashnikovs off while they make their mark on the “fluid and contested battlefield.” The Pentagon may “support” anything they want with “air power,” but bombing won’t disrupt the fluidity. The Pentagon has run out of targets. ISIS/ISIL/Daesh are not sitting ducks; they are an asymmetrical guerrilla very apt at redeploying in a flash.

ISIS/ISIL/Daesh invested in a lot of strategic planning to take Ramadi. The symbolism is far-reaching; a major defeat not only for Baghdad but also for the “leading from behind” Empire of Chaos, even though a clueless Barack Obama insists “we are not losing” the fight against the Caliphate.

Iraqi Prime Minister Haydar al-Abadi is finally starting to get the picture. He met with leaders of key Shi’ite militias — who will have to do the heavy lifting crossing the Euphrates and trying to retake Ramadi before the Caliphate goons decide to advance towards holy Karbala, which holds the tomb of Imam Hussein, the martyred grandson of Prophet Muhammad. It’s a race against time because ISIS/ISIL/Daesh may also try to control nearby Iraqi military bases and weapons depots.

As for Sunni tribal sheikhs around Ramadi willing to fight the Caliphate, they were — and remain — fuming because they never received promised weaponry from Baghdad. Besides, no one knows why the Iraqi Army on site did not get air support; helicopter gunships would have turned scores of Caliphate goons into minced meat.

Al-Abadi finally acted by removing his early ban for the Shi’ite militias to operate in hardcore Sunni Anbar province; they did that in the first place obeying a command by revered Ayatollah Sistani.

Meanwhile, the head of the Badr Corps and overall commander of the Shi’ite militas, Hadi al-Ameri, is sure that taking back Ramadi is easier than campaigning north of Baghdad in Salahuddin province — where the militias, alongside the Iraqi Army, recaptured Tikrit and Beiji from ISIS/ISIL/Daesh. In both cases, Empire of Chaos bombing played a minimal role.

Al-Abadi also met with Iranian defense minister, Brig. Gen. Husain Dehqan, in Baghdad; he stressed both Iran and Iraq are fighting (Sunni) terrorist extremism; and crucially, he said, “we do not support the war on Yemen,” which puts Baghdad in direct conflict with Riyadh.

It gets even better; al-Abadi has gone to Moscow, where he hopes to get plenty of support — and weapons. After all, ISIS/ISIL/Daesh is crammed with Chechens. Moscow wants the Caliphate smashed; as it thrives, there is a direct threat of a jihadi renewal in Chechnya.

So now the stage is set for the Battle of Ramadi — remixed; Shi’ite militias plus Sunni tribals, the odd American adviser, and discreet help from Iran and Russia, against Caliphate goons, many of them mercenaries, lavishly supported by assorted wealthy Wahhabis in Saudi Arabia and across the Gulf. As far as the Empire of Chaos goes, Divide and Rule remains the sweetest game in town.

- Greece Is On The Ragged Edge: Bloodied Idealogues Vs. Bloodthirsty Technocrats

Submitted by Bruno de Landevoisin via StealthFlation.org,

On the grave Greek question, it appears that the moment of truth is finally upon us. After nearly four months of frenetic, fruitless and often feckless high level deliberations and negotiations, both sides remain essentially at an impasse, right where they started. The technocrats in Brussels want to see their austerity driven reform program carried forward and implemented unconditionally. As for the idealogues in Athens, they have pledged to put forth their own enlightened approach to rescue their sinking society.

The Technocrats hold the purse strings, but the Ideologues hold the heart strings. For what it’s worth, that is typically a highly combustible combination, tick tock. With their recent cocksure bravado, are the Technocrats entirely misreading the desperate determination of the Idealogues? Get ready for yet another Euro Summer swoon………

Everyone agrees that Greece, under a corrupt political oligarchy, grossly abused its privileges as a Eurozone member. In fact, with the help of a few sleazy sophisticated Goldman Sachs financiers, they actually cheated on their application forms in order to join the exclusive club to begin with. The illegitimate Ionian books were cooked from the get go, and it only got worse and worse over time. The self serving political elites and their self-seeking sponsors at multinational banks and corporations ran up a massive tab, while their ill-fated nation did not have the wherewithal to pay the astronomical bills.

That is essentially what happened here. Oh, and the parties specifically involved all happened to personally get rather wealthy themselves along the way.

Check out the mess they left:

Along with the privilege of leadership comes responsibility. That clearly seems to have gone out the window here.

There can be little doubt that the predatory international banking institutions was clearly complicit, along with the disgracefully corrupt Greek politicians and high ranking government officials, as well as most of the Ionian elites at the highest levels of society in the near total abrogation of their financial responsibilities to their country. They completely failed the common man in this regard, who naturally assumed their leaders knew what the hell they were doing, and quite understandably counted on them for proper sustainable fiscal governance.

So, I have a simple question. Why should the brunt of the demanded reforms fall on those least responsible for the mess, and most vulnerable? Surely, the provincial woman on the streets of Athens pushing her Gyro cart up the steep hills of Kolonaki is far less responsible for the lamentable state of affairs her beloved country finds itself in, then those in the positions of leadership whom should have clearly known better. Yet, today she is the one being asked to bear the burden of the terribly onerous predicament her Nation is suffering through. Meanwhile, the bankers want more Euros, and no one is buying her Gyros.

Seems to me the wealthy Greek political class, the int’l financial establishment and the EU political leadership bear the lion share of the responsibility here. Yet, instead of facing up to the mess they presided over and largely created, by putting forth workable resolutions to the debt death spiral effectively consuming Greece, what I have mostly witnessed over the past four months is that same establishment circling the wagons, doing everything in their power to delegitimize the SYRIZA leadership and further cripple their already stressed banking system. I guess the best defense is a flat out offensive. Is this what passes for inspired leadership in this day and age?

Moreover, do we really need to hear these “free market” frauds opine from the peanut gallery on the difficult matter at hand:

A Greek exit from the euro is just a matter of time and wouldn’t lead to the breakup of monetary union, former Federal Reserve Chairman Alan Greenspan told Het Financieele Dagblad in an interview published Saturday. An exit could make the euro stronger, billionaire investor Warren Buffett said in an interview in the Euro-am-Sonntag newspaper.

I’m certainly no socialist, but if this is what today’s crony capitalism continues to spawn, I’m definitely no longer taking part. A romantic quote from Jimi Hendrix’s comes to mind…….

“When the power of love overcomes the love for power, only then will the world change.”

When are we going to wake up? It’s high time for honest enlightened free market capitalism! Enough of this crony capitalism crap already! The entire financialized abominNation is a national disgrace.

As for me, I would be more than happy to see the cradle of democracy put the imperial autocrats and financial kleptocrats in their place, teaching them a thing or two about enlightened self governance. Perhaps the ascent of Alexis Tsipras simply reflects the frustration of the everyday Greek citizen, completely fed up with their notoriously corrupt self serving political class oligarchy, the self seeking autocrats in Brussels and self interested banking elites that keep offering up the same poison pill to cure a lethal debt epidemic that they themselves were central to spreading around the globe in the first place.

- WaRReN BuFFeT EXPLaiNS NaSH EQuiLiBRiuM

- We Have Entered The Mania Phase: Market Complacency Has Never Been Higher

More than merely a subjective, psychological state, the complacency of market participants can be effectively quantified, which is precisely what Deutsche Bank’s David Bianco has done by looking at the ratio of the market’s P/E to implied vol or VIX.

As Bianco notes, “our PE/VIX market emotion indicator climbed to 1.3 on S&P trailing PE of 18 and 3m avg VIX of 14. A level between 1.2-1.5 signals complacency. There was similar complacency going into summer last year, with S&P trailing PE at 17.5 and a calm market kept VIX at 10-14. The complacency persisted to July but then faded as the risk of higher yields came on falling unemployment, but yields ultimately stayed subdued preventing any major summer sell-off. Yet a selloff began in late Sept as oil prices started cracking and the dollar climbing.”

And while the 3M trailing average may be at “only” at 1.30 suggesting prevailing complacency, the chart below shows that on a daily basis, the PE/VIX ratio just hit 1.49x – it has never been higher, and again based on DB’s estimation, market sentiment has now crossed from the complacency zone into outright Mania.

The last time this ratio was at the current level: late 2007/early 2008, just before the Fed had to launch a multi-trillion bailout to save capitalism as we know it.

So is a correction imminent? Depends on one’s definition: Deutsche sees the probability of a 5% correction as “high”, although the question is whether the S&P will slide by 10% or more in the coming months. One look a the chart below shows that it has been over three calendar years or 916 trading days since the last 10% market drop, the third longest period in history without a 10% drop, so yes: one could say we are indeed overdue.

From DB:

We believe the probability of a 5%+ dip is high this summer and our tactical call remains Down given the S&P now at an even higher PE than a year ago, heightened uncertainty in 10yr yields, weak earnings growth and continued soft economic data. We haven’t had a 5%+ dip this year. Historically 5%+ dips are common and happen at least once a year since 1960, except 1964, 1993 & 1995. It has been 916 trading days (3.6 years) since a 10% correction. Selloff triggers could be a further rise in 10yr yields especially if UE keeps falling amidst slow economic growth and Fed remains unclear on first hike timing, or a jump in the dollar upon the Fed expressing firm intentions to hike in Sept.

Of course, the time since a 10% correction would have been far, far shorter had Bullard not popped up in October when the market had plunged 9.8% in the matter of days, only for the Fed “hawk” to suggest that should the market selloff continue, the Fed can always do QE4.

Which is why even a token 10% market correction here could be catastrophic: since the BTFD and BTFATH “mentality” is now purely driven by faith that the Fed will never let the market drop again, anything suggesting a loss of control by the market could become a self-fulfilling prophecy, and all those who suggest that a 10% drop is just what the market needs, is cathartic and so on, may find that suddenly there is not a single BTFDer left once stocks do drop by 10.1% or more…

- On Memorial Day, Who Is America's True Superhero

On such a ‘patriotic’ weekend, we thought it appropriate to consider who is the ‘MVP’ superhero of our time. Captain America? No. How about Ironman? No. What about Superman? Nope… The most valuable superhero of our time is a dark, deranged masked-human dressed in black…

Batman.

Source: Goldman Sachs

- China Establishes World's Largest Physical Gold Fund

While many eagerly await the day when China will finally reveal its latest official gold holdings, a number which when made public will be orders of magnitude higher than its last 2009 disclosure of just over 1,000 tons, or less even than Russia, China continues to plough ahead with agreements and arrangements to obtain even more gold in the coming years.

Exhibit A: two weeks ago, Xinhua reported that China National Gold Group Corporation announced it has signed an agreement with Russian gold miner Polyus Gold to deepen ties in gold exploration. The companies will cooperate in mineral resource exploration, technical exchanges and materials supply, the largest gold producer of China said.

Polyus Gold is the largest gold producer in Russia and one of the world’s top 10 gold miners.

The agreement between the two gold miners is one of many deals signed between China and Russia in energy, transportation, space, finance and media exchanges during President Xi Jinping’s visit to Russia from May 8 to May 10.

“China’s Belt and Road Initiative brings unprecedented opportunities for the gold industry. There is ample room for cooperation with neighboring countries, and we have advantages in technique, facilities, cash, and talents,” said Song Xin, general manager of China National Gold Group Corporation.

In light of such developments, it is little wonder there has been increasing chatter in recent months that Russia and China are setting the stage for a gold-backed currency, in preparation for the day the Dollar reserve hegemony finally ends (a hegemony whose demise is accelerating with every incremental physical gold repatriation such as those of Germany, the Netherlands, and now Austria).

And now, Exhibit B: overnight Xinhua also reported that a gold sector fund involving countries along the ancient Silk Road has been set up in northwest China’s Xi’an City during an ongoing forum on investment and trade this weekend. (read more about the “New Silk Road” which could change global economics forever here). The fund, led by Shanghai Gold Exchange (SGE), is expected to raise an estimated 100 billion yuan (16.1 billion U.S. Dollars) in three phases. The amount of capital allocated to nothing but physical gold purchases (without plans for financial paper intermediation a la western ETFs) will be the largest in the world.

The billions of dollars in allocated funding will come from roughly 60 countries that have invested in the fund, which will in turn facilitate gold purchase for the central banks of member states to increase their holdings of the precious metal, according to the SGE.

As Xinhua notes, China is the world’s largest gold producer, and also a major importer and consumer of gold. Among the 65 countries along the routes of the Silk Road Economic Belt and the 21st-Century Maritime Silk Road, there are numerous Asian countries identified as important reserve bases and consumers of gold.

“China does not have a big say in gold pricing because it accounts for a small share of international gold trade,” said Tang Xisheng of the Industrial Fund Management Co. “Therefore, the Chinese government seeks to increase the influence of RMB in gold pricing by opening the domestic gold market to international investors.”

As a reminder, the reason why China has been aggressively building out and expanding its Shanghai Gold Exchange is precisely that: to shift the global gold trading center away from London (and certainly the US where only paper gold is relevant these days) and to its own native soil: China’s ambition is nothing short of becoming the world’s new gold trading hub.

In other to do that, it is already setting up the regional infrastructure to facilitate such a goal: according to Tang, the fund will invest in gold mining in countries along the Silk Road, which will increase exploration in countries such as Afghanistan and Kazakhstan.

The good news for China is that with the BIS and virtually all “developed” central banks in desperate need of keeping the price of gold as low as possible while they debase their own paper currencies to unprecedented levels over fears of faith in fiat evaporating, China’s gold fund will be able to procure gold for its members at a very reasonable price until such time as the lack of physical gold supply can no longer be swept away by mere paper shorting of the yellow metal.

Digest powered by RSS Digest

Saving...

Saving...{kind=link}