- Why The COVID-19 Model That Inspired UK's Lockdown May Be "The Most Devastating Software Mistake Of All Time"

Why The COVID-19 Model That Inspired UK’s Lockdown May Be “The Most Devastating Software Mistake Of All Time”

Tyler Durden

Mon, 05/18/2020 – 02:45While Democrats in the US and progressives in the UK continue to push back against efforts to gradually reopen their respective economies, more evidence is emerging that calls into question the models (what the public often refers to as the “science”) which inspired governments across the world to impose crippling lockdowns on their populations.

Case in point: Since Neil Ferguson and the authors of the Imperial published its modeling for non-pharmaceutical intervention for COVID-19, a number of data scientists have taken a close look and found gaping oversights that seriously undermine the model’s credibility. Of course, this isn’t the first time we have written about Ferguson and his exploits.

Neil Ferguson

In this weekend’s Telegraph, two of these critics, David Richards, the founder and CEO of global big data leader WANdisco which is jointly headquartered in Silicon Valley and Sheffield, and Dr. Konstantin Boudnik, a pioneering big-data engineer, WANdisco’s VP of architecture and author of 17 US patents, published an editorial in which they carefully examined the model’s shortcomings. Keep in mind, the Imperial model is what ultimately inspired PM Boris Johnson to make a U-turn and adopt what has been an economically devastating lockdown – was nothing short of a catastrophe. Millions have been plunged into hardship and poverty unnecessarily, they explained. Johnson himself was infected by the virus and the public is furious with the government over its rollout of a plan to reopen.

Given the influence the model had during the early days of the outbreak, the two men argued that the software issues underpinning the model could be ‘the most devastating software mistake of all time’.

Apparently, the model’s problems are rooted in its most fundamental components. The model was written using a coding language called Fortran which has been in use for decades.

Due to its age and inflexibility, Fortran has many inherent problems. But on top of the language itself, the code in the model was sprawling, sloppily written and extremely inefficient, the two men said, claiming it would never pass muster in the private sector.

Using straightforward, jargon-free language, the two authors explain how the model ran into a problem called “CACE”, or, ‘changing anything changes everything’ – a problem that software engineers and data scientists trying to model, well, anything, really, often encounter.

The approach ignores widely accepted computer science principles known as “separation of concerns”, which date back to the early 70s and are essential to the design and architecture of successful software systems. The principles guard against what developers call CACE: Changing Anything Changes Everything.

Without this separation, it is impossible to carry out rigorous testing of individual parts to ensure full working order of the whole. Testing allows for guarantees. It is what you do on a conveyer belt in a car factory. Each and every component is tested for integrity in order to pass strict quality controls.

It’s just the latest reminder that President Barack Obama’s advice to this year’s graduates rings true: You can’t just blindly accept what the experts and the people in charge tell you.

Read the full editorial below:

* * *

In the history of expensive software mistakes, Mariner 1 was probably the most notorious. The unmanned spacecraft was destroyed seconds after launch from Cape Canaveral in 1962 when it veered dangerously off-course due to a line of dodgy code.

But nobody died and the only hits were to Nasa’s budget and pride. Imperial College’s modelling of non-pharmaceutical interventions for Covid-19 which helped persuade the UK and other countries to bring in draconian lockdowns will supersede the failed Venus space probe and could go down in history as the most devastating software mistake of all time, in terms of economic costs and lives lost.

Since publication of Imperial’s microsimulation model, those of us with a professional and personal interest in software development have studied the code on which policymakers based their fateful decision to mothball our multi-trillion pound economy and plunge millions of people into poverty and hardship. And we were profoundly disturbed at what we discovered. The model appears to be totally unreliable and you wouldn’t stake your life on it.

First though, a few words on our credentials. I am David Richards, founder and chief executive of WANdisco, a global leader in Big Data software that is jointly headquartered in Silicon Valley and Sheffield. My co-author is Dr Konstantin ‘Cos’ Boudnik, vice-president of architecture at WANdisco, author of 17 US patents in distributed computing and a veteran developer of the Apache Hadoop framework that allows computers to solve problems using vast amounts of data.

Imperial’s model appears to be based on a programming language called Fortran, which was old news 20 years ago and, guess what, was the code used for Mariner 1. This outdated language contains inherent problems with its grammar and the way it assigns values, which can give way to multiple design flaws and numerical inaccuracies. One file alone in the Imperial model contained 15,000 lines of code.

Try unravelling that tangled, buggy mess, which looks more like a bowl of angel hair pasta than a finely tuned piece of programming. Industry best practice would have 500 separate files instead. In our commercial reality, we would fire anyone for developing code like this and any business that relied on it to produce software for sale would likely go bust.

The approach ignores widely accepted computer science principles known as “separation of concerns”, which date back to the early 70s and are essential to the design and architecture of successful software systems. The principles guard against what developers call CACE: Changing Anything Changes Everything.

Without this separation, it is impossible to carry out rigorous testing of individual parts to ensure full working order of the whole. Testing allows for guarantees. It is what you do on a conveyer belt in a car factory. Each and every component is tested for integrity in order to pass strict quality controls.

Only then is the car deemed safe to go on the road. As a result, Imperial’s model is vulnerable to producing wildly different and conflicting outputs based on the same initial set of parameters. Run it on different computers and you would likely get different results. In other words, it is non-deterministic.

As such, it is fundamentally unreliable. It screams the question as to why our Government did not get a second opinion before swallowing Imperial’s prescription.

Ultimately, this is a computer science problem and where are the computer scientists in the room? Our leaders did not have the grounding in computer science to challenge the ideas and so were susceptible to the academics. I suspect the Government saw what was happening in Italy with its overwhelmed hospitals and panicked.

It chose a blunt instrument instead of a scalpel and now there is going to be a huge strain on society. Defenders of the Imperial model argue that because the problem – a global pandemic – is dynamic, then the solution should share the same stochastic, non-deterministic quality.

We disagree. Models must be capable of passing the basic scientific test of producing the same results given the same initial set of parameters. Otherwise, there is simply no way of knowing whether they will be reliable.

Indeed, many global industries successfully use deterministic models that factor in randomness. No surgeon would put a pacemaker into a cardiac patient knowing it was based on an arguably unpredictable approach for fear of jeopardising the Hippocratic oath. Why on earth would the Government place its trust in the same when the entire wellbeing of our nation is at stake?

* * *

Source: The Telegraph

- The 2006 Origins Of The 'Lockdown' Idea

The 2006 Origins Of The ‘Lockdown’ Idea

Tyler Durden

Mon, 05/18/2020 – 02:00Authored by Jeffrey Tucker via The American Institute for Economic Research,

Now begins the grand effort, on display in thousands of articles and news broadcasts daily, somehow to normalize the lockdown and all its destruction of the last two months. We didn’t lock down almost the entire country in 1968/69, 1957, or 1949-1952, or even during 1918. But in a terrifying few days in March 2020, it happened to all of us, causing an avalanche of social, cultural, and economic destruction that will ring through the ages.

There was nothing normal about it all. We’ll be trying to figure out what happened to us for decades hence.

How did a temporary plan to preserve hospital capacity turn into two-to-three months of near-universal house arrest that ended up causing worker furloughs at 256 hospitals, a stoppage of international travel, a 40% job loss among people earning less than $40K per year, devastation of every economic sector, mass confusion and demoralization, a complete ignoring of all fundamental rights and liberties, not to mention the mass confiscation of private property with forced closures of millions of businesses?

Whatever the answer, it’s got to be a bizarre tale. What’s truly surprising is just how recent the theory behind lockdown and forced distancing actually is. So far as anyone can tell, the intellectual machinery that made this mess was invented 14 years ago, and not by epidemiologists but by computer-simulation modelers. It was adopted not by experienced doctors – they warned ferociously against it – but by politicians.

Let’s start with the phrase social distancing, which has mutated into forced human separation. The first I had heard it was in the 2009 movie Contagion. The first time it appeared in the New York Times was February 12, 2006:

If the avian flu goes pandemic while Tamiflu and vaccines are still in short supply, experts say, the only protection most Americans will have is “social distancing,” which is the new politically correct way of saying “quarantine.”

But distancing also encompasses less drastic measures, like wearing face masks, staying out of elevators — and the [elbow] bump. Such stratagems, those experts say, will rewrite the ways we interact, at least during the weeks when the waves of influenza are washing over us.

Maybe you don’t remember that the avian flu of 2006 didn’t amount to much. It’s true, despite all the extreme warnings about its lethality, H5N1 didn’t turn into much at all. What it did do, however, was send the existing president, George W. Bush, to the library to read about the 1918 flu and its catastrophic results. He asked for some experts to submit some plans to him about what to do when the real thing comes along.

The New York Times (April 22, 2020) tells the story from there:

Fourteen years ago, two federal government doctors, Richard Hatchett and Carter Mecher, met with a colleague at a burger joint in suburban Washington for a final review of a proposal they knew would be treated like a piñata: telling Americans to stay home from work and school the next time the country was hit by a deadly pandemic.

When they presented their plan not long after, it was met with skepticism and a degree of ridicule by senior officials, who like others in the United States had grown accustomed to relying on the pharmaceutical industry, with its ever-growing array of new treatments, to confront evolving health challenges.

Drs. Hatchett and Mecher were proposing instead that Americans in some places might have to turn back to an approach, self-isolation, first widely employed in the Middle Ages.

How that idea — born out of a request by President George W. Bush to ensure the nation was better prepared for the next contagious disease outbreak — became the heart of the national playbook for responding to a pandemic is one of the untold stories of the coronavirus crisis.

It required the key proponents — Dr. Mecher, a Department of Veterans Affairs physician, and Dr. Hatchett, an oncologist turned White House adviser — to overcome intense initial opposition.

It brought their work together with that of a Defense Department team assigned to a similar task.

And it had some unexpected detours, including a deep dive into the history of the 1918 Spanish flu and an important discovery kicked off by a high school research project pursued by the daughter of a scientist at the Sandia National Laboratories.

The concept of social distancing is now intimately familiar to almost everyone. But as it first made its way through the federal bureaucracy in 2006 and 2007, it was viewed as impractical, unnecessary and politically infeasible.

Notice that in the course of this planning, neither legal nor economic experts were brought in to consult and advise. Instead it fell to Mecher (formerly of Chicago and an intensive care doctor with no previous expertise in pandemics) and the oncologist Hatchett.

But what is this mention of the high-school daughter of 14? Her name is Laura M. Glass, and she recently declined to be interviewed when the Albuquerque Journal did a deep dive of this history.

Laura, with some guidance from her dad, devised a computer simulation that showed how people – family members, co-workers, students in schools, people in social situations – interact. What she discovered was that school kids come in contact with about 140 people a day, more than any other group. Based on that finding, her program showed that in a hypothetical town of 10,000 people, 5,000 would be infected during a pandemic if no measures were taken, but only 500 would be infected if the schools were closed.

Laura’s name appears on the foundational paper arguing for lockdowns and forced human separation. That paper is Targeted Social Distancing Designs for Pandemic Influenza (2006). It set out a model for forced separation and applied it with good results backwards in time to 1957. They conclude with a chilling call for what amounts to a totalitarian lockdown, all stated very matter-of-factly.

Implementation of social distancing strategies is challenging. They likely must be imposed for the duration of the local epidemic and possibly until a strain-specific vaccine is developed and distributed. If compliance with the strategy is high over this period, an epidemic within a community can be averted. However, if neighboring communities do not also use these interventions, infected neighbors will continue to introduce influenza and prolong the local epidemic, albeit at a depressed level more easily accommodated by healthcare systems.

In other words, it was a high-school science experiment that eventually became law of the land, and through a circuitous route propelled not by science but politics.

The primary author of this paper was Robert J. Glass, a complex-systems analyst with Sandia National Laboratories. He had no medical training, much less an expertise in immunology or epidemiology.

That explains why Dr. D.A. Henderson, “who had been the leader of the international effort to eradicate smallpox,” completely rejected the whole scheme.

Says the NYT:

Dr. Henderson was convinced that it made no sense to force schools to close or public gatherings to stop. Teenagers would escape their homes to hang out at the mall. School lunch programs would close, and impoverished children would not have enough to eat. Hospital staffs would have a hard time going to work if their children were at home.

The measures embraced by Drs. Mecher and Hatchett would “result in significant disruption of the social functioning of communities and result in possibly serious economic problems,” Dr. Henderson wrote in his own academic paper responding to their ideas.

The answer, he insisted, was to tough it out: Let the pandemic spread, treat people who get sick and work quickly to develop a vaccine to prevent it from coming back.

AIER’s Phil Magness got to work to find the literature responding to this 2006 and discovered: Disease Mitigation Measures in the Control of Pandemic Influenza. The authors included D.A. Henderson, along with three professors from Johns Hopkins: infectious disease specialist Thomas V.Inglesby, epidemiologist Jennifer B. Nuzzo, and physician Tara O’Toole.

Their paper is a remarkably readable refutation of the entire lock-down model.

There are no historical observations or scientific studies that support the confinement by quarantine of groups of possibly infected people for extended periods in order to slow the spread of influenza. … It is difficult to identify circumstances in the past half-century when large-scale quarantine has been effectively used in the control of any disease. The negative consequences of large-scale quarantine are so extreme (forced confinement of sick people with the well; complete restriction of movement of large populations; difficulty in getting critical supplies, medicines, and food to people inside the quarantine zone) that this mitigation measure should be eliminated from serious consideration…

Home quarantine also raises ethical questions. Implementation of home quarantine could result in healthy, uninfected people being placed at risk of infection from sick household members. Practices to reduce the chance of transmission (hand-washing, maintaining a distance of 3 feet from infected people, etc.) could be recommended, but a policy imposing home quarantine would preclude, for example, sending healthy children to stay with relatives when a family member becomes ill. Such a policy would also be particularly hard on and dangerous to people living in close quarters, where the risk of infection would be heightened….

Travel restrictions, such as closing airports and screening travelers at borders, have historically been ineffective. The World Health Organization Writing Group concluded that “screening and quarantining entering travelers at international borders did not substantially delay virus introduction in past pandemics . . . and will likely be even less effective in the modern era.”… It is reasonable to assume that the economic costs of shutting down air or train travel would be very high, and the societal costs involved in interrupting all air or train travel would be extreme. …

During seasonal influenza epidemics, public events with an expected large attendance have sometimes been cancelled or postponed, the rationale being to decrease the number of contacts with those who might be contagious. There are, however, no certain indications that these actions have had any definitive effect on the severity or duration of an epidemic. Were consideration to be given to doing this on a more extensive scale and for an extended period, questions immediately arise as to how many such events would be affected. There are many social gatherings that involve close contacts among people, and this prohibition might include church services, athletic events, perhaps all meetings of more than 100 people. It might mean closing theaters, restaurants, malls, large stores, and bars. Implementing such measures would have seriously disruptive consequences…

Schools are often closed for 1–2 weeks early in the development of seasonal community outbreaks of influenza primarily because of high absentee rates, especially in elementary schools, and because of illness among teachers. This would seem reasonable on practical grounds. However, to close schools for longer periods is not only impracticable but carries the possibility of a serious adverse outcome….

Thus, cancelling or postponing large meetings would not be likely to have any significant effect on the development of the epidemic. While local concerns may result in the closure of particular events for logical reasons, a policy directing communitywide closure of public events seems inadvisable. Quarantine. As experience shows, there is no basis for recommending quarantine either of groups or individuals. The problems in implementing such measures are formidable, and secondary effects of absenteeism and community disruption as well as possible adverse consequences, such as loss of public trust in government and stigmatization of quarantined people and groups, are likely to be considerable….

Finally, the remarkable conclusion:

Experience has shown that communities faced with epidemics or other adverse events respond best and with the least anxiety when the normal social functioning of the community is least disrupted. Strong political and public health leadership to provide reassurance and to ensure that needed medical care services are provided are critical elements. If either is seen to be less than optimal, a manageable epidemic could move toward catastrophe.

Confronting a manageable epidemic and turning it into a catastrophe: that seems like a good description of everything that has happened in the COVID-19 crisis of 2020.

Thus did some of the most highly trained and experienced experts on epidemics warn with biting rhetoric against everything that the advocates of lockdown proposed. It was not even a real-world idea in the first place and showed no actual knowledge of viruses and disease mitigation. Again, the idea was born of a high-school science experiment using agent-based modelling techniques having nothing at all to do with real life, real science, or real medicine.

So the question becomes: how did the extreme view prevail?

The New York Times has the answer:

The [Bush] administration ultimately sided with the proponents of social distancing and shutdowns — though their victory was little noticed outside of public health circles. Their policy would become the basis for government planning and would be used extensively in simulations used to prepare for pandemics, and in a limited way in 2009 during an outbreak of the influenza called H1N1. Then the coronavirus came, and the plan was put to work across the country for the first time.

The Times called one of the pro-lockdown researchers, Dr. Howard Markel, and asked what he thought of the lockdowns. His answer: he is glad that his work was used to “save lives” but added, “It is also horrifying.” “We always knew this would be applied in worst-case scenarios,” he said. “Even when you are working on dystopian concepts, you always hope it will never be used.”

Ideas have consequences, as they say. Dream up an idea for a virus-controlling totalitarian society, one without an endgame and eschewing any experienced-based evidence that it would achieve the goal, and you might see it implemented someday. Lockdown might be the new orthodoxy but that doesn’t make it medically sound or morally correct. At least now we know that many great doctors and scholars in 2006 did their best to stop this nightmare from unfolding. Their mighty paper should serve as a blueprint for dealing with the next pandemic.

- Chinese NEV Sales Plunge 43%, Falling For The Tenth Straight Month

Chinese NEV Sales Plunge 43%, Falling For The Tenth Straight Month

Tyler Durden

Mon, 05/18/2020 – 01:00The auto industry has been under pressure from all angles as a result of the global coronavirus lockdowns. And it looks as though while Elon Musk has been busy melting down, faux-libertarian style, about the re-opening of his California factory, things may have taken a turn for the worse for the EV market overseas.

In addition to the pandemic crippling demand, there seem to be far too many players in China’s NEV market, and that has caused sales to come under pressure, according to Automotive News. China’s market now has about 50 established EV startups competing with larger companies like Geely and Tesla.

In fact, new energy vehicle sales fell for a tenth straight month in April, plunging 43%.

Brian Gu, president of Alibaba-backed Xpeng Motors said: “The difficulties that EV start-ups have encountered, such as the auto sales decline, harsh fundraising environment and subsidies reduction, all started last year. The outbreak will aggravate these issues that already had existed.”

He continued: “Only the top-tier EV makers will be able to attract attention from investors in this environment.”

Experts believe the hit to the EV market could get even worse with the plunging price of oil, even despite subsidies and tax breaks.

One anonymous investor said: “Those who had not launched mass production of their car models by 2019 would probably die. The outbreak is going to accelerate their death.”

The headwinds could make it difficult for China to reach its goal of having EVs account for 25% of all auto sales by 2025, according to the report. Currently, the number stands at about 5%.

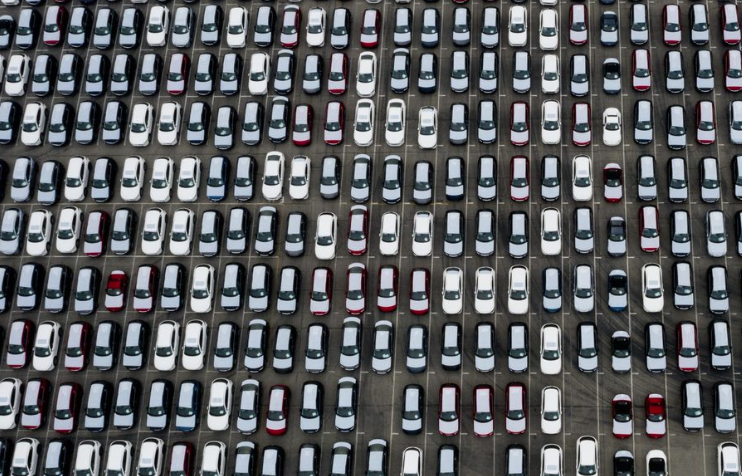

We’ve previously noted that auto dealers in the U.S. are losing billions of dollars in fleet sales, which we documented just last week.

The lack of fleet sales, combined with a massive demand drop off, has led to a massive inventory glut for auto dealers, who are being forced to consider major incentives across the board to try and sell vehicles when the consumer makes their way back to the showroom.

The inventory glut has gotten so bad that we reported on ships of SUVs coming from Japan being turned away at California ports several weeks ago.

- Goldman Spots A Huge Problem For The Fed

Goldman Spots A Huge Problem For The Fed

Tyler Durden

Sun, 05/17/2020 – 23:57Update: In implicit confirmation of everything said below, in his 60 Minutes appearance, Jerome Powell said that “There’s a lot more we can do. We’ve done what we can as we go. But I will say that we’re not out of ammunition by a long shot,” he said. Powell noted the Fed can increase its emergency lending programs and make monetary policy more supportive through forward guidance and by adjusting the Fed’s asset-purchase strategy. Which, as explained extensively below, is precisely what the Fed will have to do: by as much as $3 trillion in additional QE just to offset the flood of new debt coming to the market in the next 6 months.

And just to remove confusion, there was this exchange which the “pajama traders” appear to have focused on:

Scott Pelley: Fair to say you simply flooded the system with money?

Jerome Powell: Yes. We did. That’s another way to think about it. We did.

Scott Pelley: Where does it come from? Do you just print it?

Jerome Powell: We print it digitally. So we– you know, we– as a central bank, we have the ability to create money digitally and we do that by buying Treasury Bills or bonds or other government guaranteed securities. And that actually increases the money supply. We also print actual currency and we distribute that through the Federal Reserve banks.

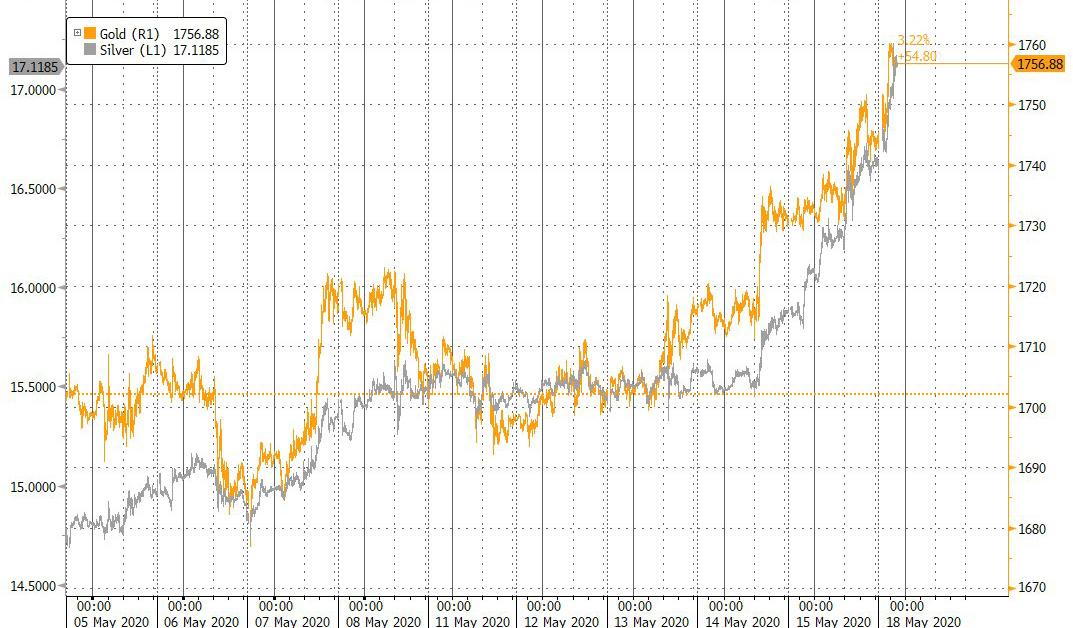

To give Powell the credit, at least he was being somewhat honest: unlike Bernanke who claimed the Fed does not “print” digital bills, Powell no longer felt compelled to make the obvious lie. And judging by the ongoing surge in gold and silver overnight, the market seems to appreciate Powell’s honesty.

* * *

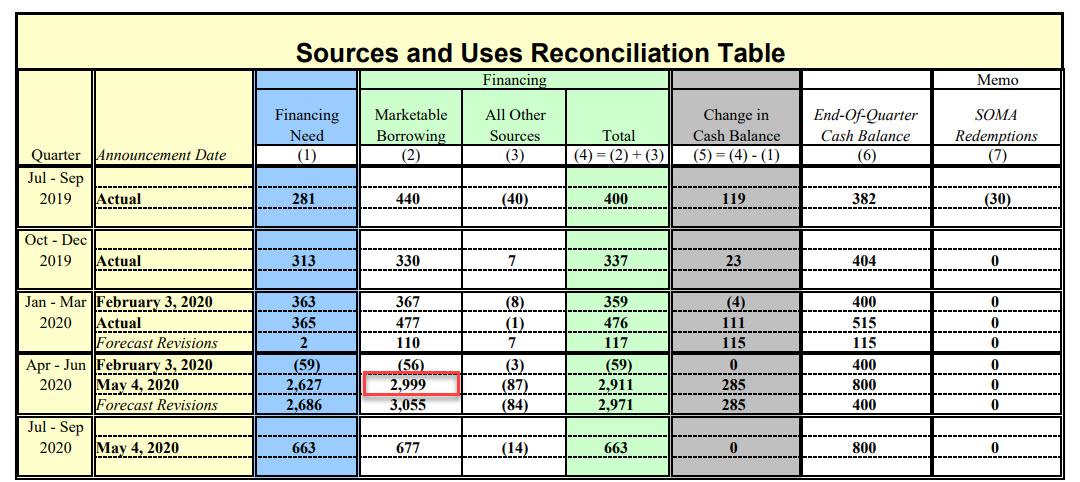

Last week, the Treasury shocked the world when it announced that in the current quarter (the 3rd of the fiscal year), the US will need to sell a mindblowing, record $3 trillion (pardon, $2.999 trillion) in Treasurys to finance the US money helicopter.

This, after selling $807 billion in the first half of the fiscal year, and another $677 billion in the quarter ending Sept 30.

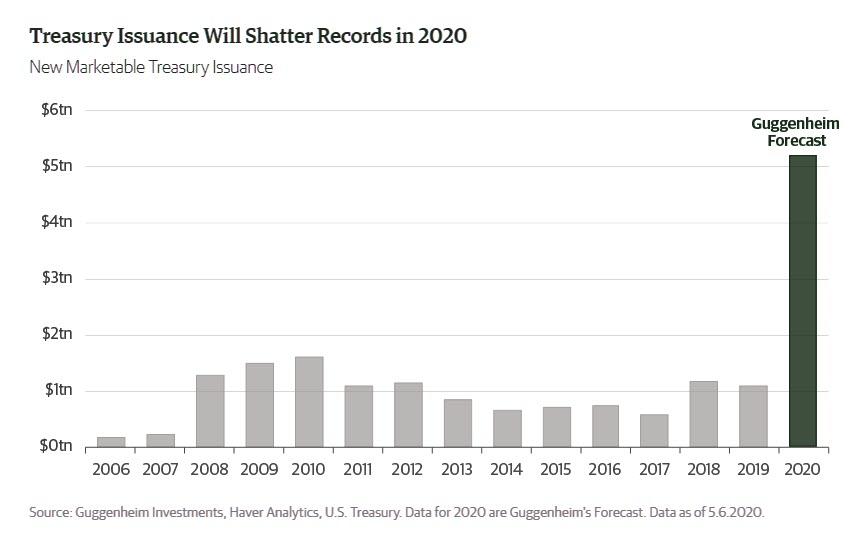

And since it is just a matter of time before Congress has to pass yet another fiscal package which will be at least another trillion dollars, and up to $3 trillion if the Democrats get their wish, one can say that Guggenheim’s projection of over $5 trillion in debt issuance this calendar year will be wildly conservative.

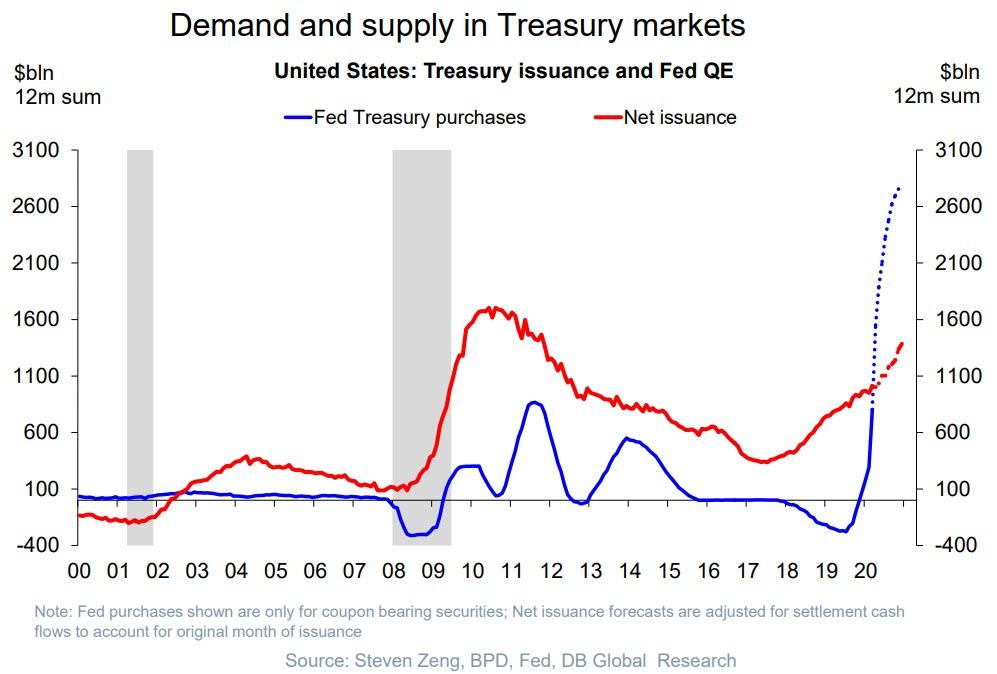

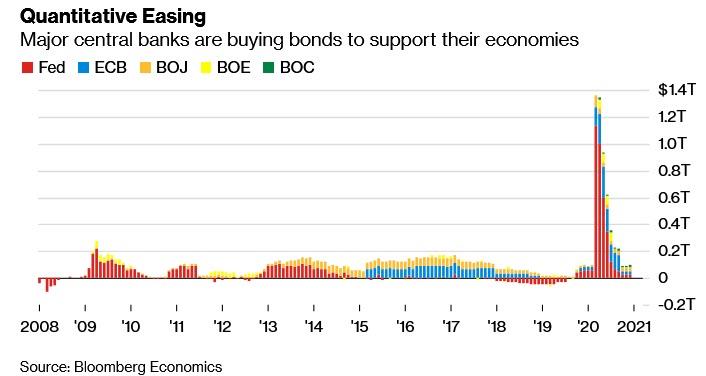

Now here’s the thing: as Deutsche Bank recently showed, so far this new debt avalanche was entire monetized exclusively by the Fed, whose debt purchasing operations have been far greater than the net Treasury issuance.

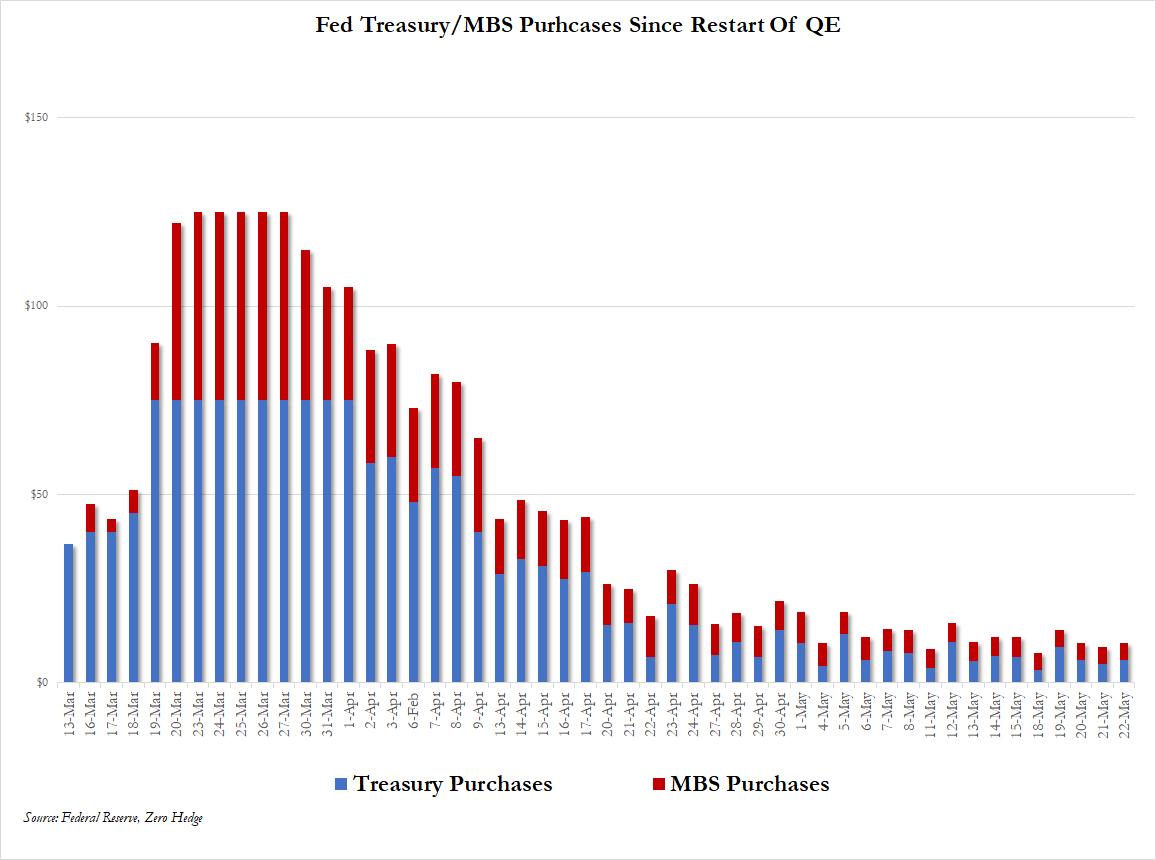

But this was only the case when the Fed was buying a massive $75 billion in TSYs per day in the late March crash, when Powell dumped a monetary nuclear bomb on the market to stabilize the biggest panic selling an entire generation of traders had ever seen, and nearly doubling the Fed’s balance – which is now just shy of $7 trillion, in a few months:

Since then, however, the Fed’s daily and weekly POMO has shrunk substantially, and as discussed earlier, it is down to just $30BN in Treasury purchases per week as of next week, which amounts to around $1.5 trillion per year.

There’s just one problem: $30BN per week in TSY monetization is nowhere near enough to consume the trillions in Treasury issuance that is about to hit. In fact, all else equal, the Fed will very soon have to find a pretext to aggressively ramp up its treasury purchases.

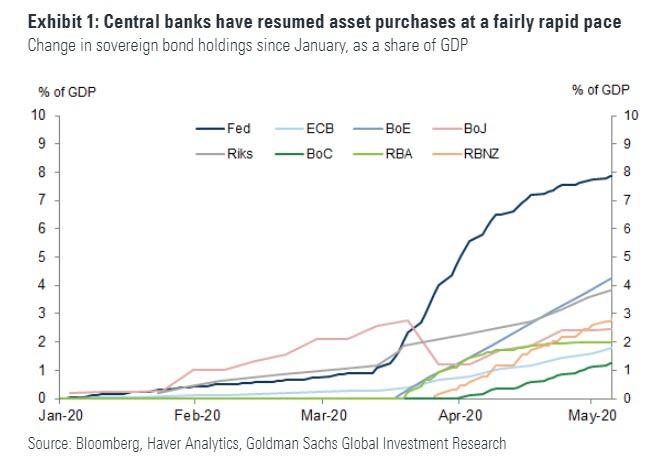

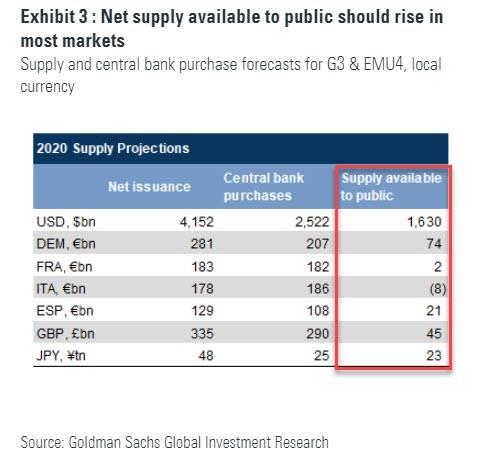

As Goldman writes overnight, putting the problem in its proper context, “Central banks have been purchasing sovereign bonds at a rapid pace (Exhibit 1), faster than past QE programs in most cases. These purchases are occurring against a backdrop of a surge in fiscal deficits, which will require enormous amounts of additional sovereign supply to finance them.”

Which makes sense, of course: after all helicopter money, which is what we have now that MMT (Magic Money Theory) has been shoved down everyone’s throat without any debate, only works when there is coordination between the Treasury and the central bank. And while until now Fed purchases have generally offset Treasury issuance, that coordination is about to end. As Goldman puts it, “Central bank buying should absorb a substantial amount of upcoming issuance, though we expect increases in “free float” across most markets, most notably in the US, which adds to the medium-term case for higher yields and steeper curves there.”

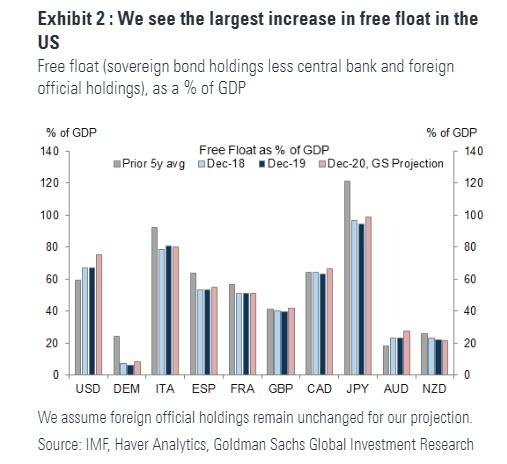

Next, Goldman estimates this so-called free float, defined as the amount of sovereign debt outstanding less central bank and foreign official holdings, across major DM markets, and shows it in the chart below. Through the end of last year, free float was on a downward trend in Germany and Japan, as ECB and BoJ purchases absorbed the bulk of new supply. In contrast, free float had been trending higher for much of the year in the US and UK.

So with record fiscal deficits and resumption of asset purchases in several markets, where is free float headed this year? In Exhibit 3, Goldman lays out its expectations for total purchase amounts on a net basis along with net supply. It finds the largest increase in free float in the US, as Fed purchases continue to slow; in fact according to Goldman calculations the US public (now that foreign investors have hit the breaks on US TSY purchases), will be on the hook to fund the $1.6 trillion needed to bridge the full amount of US funding needs.

A similar picture emerges in the Euro area, where supply is also expected outpace ECB purchases, particularly in Italy, Spain and France (absent further increases in ECB purchases). Bizarrely, a similar picture emerges in Japan where even the always ravenous BoJ is expected to absorb a large portion (about ¥25tn) of incoming supply in the upcoming year as Japan is boosting its debt sales by 18.2 trillion yen ($170 billion) to fund a spending package equivalent to a fifth of its annual economic output; but according to Goldman, the scale of supply is likely to exceed even the BOJ’s QE purchases.

It continues: foreign-ownership of New Zealand sovereign debt has fallen to 50% from 70% just five years ago as central bankers in Wellington snap up bonds as part of a quantitative-easing program.

In short, even with central banks unleashing $7.9 trillion in QE so far in 2020 (according to Bank of America calculations) of which the Fed accounts for over $2.8 trillion in debt purchases alone, this won’t be enough to monetize the tsunami of debt that is coming to fund the biggest global rescue operation in history, and if investors find that suddenly the bond market has to clear without the only true backstop – the central bank – willing and able to mop up all the supply, a critical precondition for the continuation of “helicopter money”, the outcome could be disastrous.

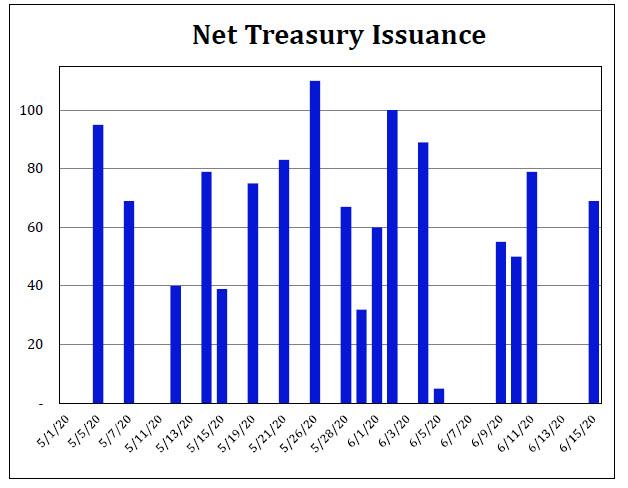

Incidentally, we first warned about the urgent need for the Fed to aggressively step up and boost its QE (instead of continuing to taper it by $1 billion week after week as it did again today) on Wednesday when we quoted Curvature Securities’ rates strategist and repo expert Scott Skyrm, who calculated that “there are $689 billion net new Treasurys settling during the month of May and $992 billion net new Treasurys settling between now and June 15. Yes, almost one trillion new Treasury securities hitting the market within the next month!”

His conclusion: “That means the market needs to come up with about one trillion dollars to pay for those securities over the next month.” Which, of course, is a euphemism because we all know who in the market needs to come up with one trillion dollar – the only one who literally prints money: the Federal Reserve.

Conveniently, Goldman’s argument allows us to recycle our conclusion from two days ago, in which we said that here is the layman’s version of what was just said: “the Fed has flooded the system with liquidity… and it is not enough, because the way helicopter money works, is that liquidity supply (the Fed), and liquidity demand (Treasury via debt issuance) go hand in hand, and periods of too much supply, as was the cash with the Fed’s massive QE in late March and early April, are promptly followed by periods of dramatic liquidity demand, such as the next month when $1 trillion in liquidity will be drained to fund the US government “money helicopter.”

Goldman’s own calculations suggest that the shortfall net of the Fed’s ongoing QE tapering could be as much as $1.6 trillion.

As a result, Powell faces a two-fold problem: since the Fed chair has taken negative rates off the table, Powell has no choice but too boost QE again, and unleash another firehose of debt monetizing liquidity in the financial system. However, any such reversal to the Fed’s current posture of shrinking QE will be met with howls of rage, especially among what’s left of the conservative political establishment. Which means that, just like in March when the Fed used the first pandemic-induced market crash to unleash unlimited QE, the Fed will soon have to go for round 2 and spark a new market crash, one which it then uses as an alibi for the next massive liquidity injection. Failing to do that, watch as the dollar takes off as markets sniff out that another major dollar squeeze is imminent. And since this will accelerate the liquidity crunch, one way or another, the coming $1.6 trillion in Treasury issuance – which has already been generously greenlighted by Congress – will serve as a trigger for the next market shock, one which the Fed will quickly reverse by expanding the already unlimited QE by trillions on very short notice.

The only question we have is whether this will be the market crash that the Fed uses to unveil it will also buy equity ETfs next, or if Powell will save this final bullet in its ammo for whatever comes next.

Finally, it’s not just us reaching this conclusion: yesterday – one day after our dire assessment – Bloomberg reached the same conclusion, and in “An $8 Trillion Spree Sets Clock Ticking for Bonds’ Judgment Day” in which it wrote that “investors are mopping up the sales as long as central banks engage in so-called quantitative easing, buying an unlimited amount of debt to counter the ravages of the pandemic. But at the first whiff of a recovery, or a pullback from policy makers, all bets may be off. Throw in the threat of inflation amid a global fiscal splurge exceeding $8 trillion, and bond investors look set for a toxic cocktail of risks in the not-too-distant future.”

Well, today we got another pullback when the Fed tapered its weekly QE to just $30BN from $35BN last week, and a record $75 billion per day two months ago.

“Given the massive central bank easing, which includes a lot of bond-buying QE in many places, there will be a lot of demand right now to buy government bonds,” said Eric Stein, co-director of global income at Eaton Vance Management, effectively describing what can simply be called “frontrunning” the Fed, a strategy that even BlackRock said is the only one left in this idiotic market.

“However, if it was a year or two from now and the economy was picking up and inflation had started to pick up, the story could be different.”

Actually, the economy doesn’t even have to be picking up: an unexpected – and unexplained – slowdown in the pace of the Fed’s “unlimited QE” purchases would be sufficient to throw the bond market into unprecedented turmoil as all those socialists who pretend that MMT makes sense, realize that the only thing permitting their idiotic “theory” to persist is the Fed’s money printer.

Yet while the Fed’s QE expansion is just a matter of time, whether catalyzed by another market crash or not, the bigger question is what happens after that?

“Can governments continue to borrow at such record levels? No,” said George Boubouras, head of research at hedge fund K2 Asset Management. “Central-bank support is key in the massive bond buying we’ve seen for now. But if they blink then at some point, in the medium term, it will all likely unravel – with unforgiving consequences for some countries.”

Ironically, this also means that an end to the coronavirus crisis is the worst possible thing that could happen to a world that is now habituated to helicopter money and virtually unlimited handouts, which however need a state of perpetual crisis.

“Once there is an end to the crisis in sight, they will be less and less willing to provide support and it will fall more on the street to absorb paper,” said Mediolanum money manager Charles Diebel, who’s adding bond steepeners in anticipation of a coming inflationary supernova.

That, incidentally, would be the endgame for the current monetary regime, which is why anyone hoping that officials, policymakers and the establishment in general, will allow the coronavirus crisis to simply fade away, is in for the shock of a lifetime.

- China's Disappeared Heroes & The Silence Of The West

China’s Disappeared Heroes & The Silence Of The West

Tyler Durden

Sun, 05/17/2020 – 23:55Authored by Giulio Meotti via The Gatestone Institute,

Three Chinese internet activists have disappeared and are believed to have been detained by police. They have reportedly been charged with preserving articles that were removed by China’s online censors. Chen Mei, Cai Wei and Cai’s girlfriend went missing on April 19.

A few days earlier, Beijing police formally arrested retired professor Chen Zhaozhi for “picking quarrels and provoking trouble” in a speech about the pandemic. The former Beijing University of Science and Technology professor had posted comments online, including that “Wuhan pneumonia is not a Chinese virus but Chinese Communist Party virus”. In addition, Wang Quanzhang, a Chinese human rights lawyer, who ended his prison sentence after more than four years for “subversion against the state”, immediately after leaving the penitentiary, was placed in “quarantine“, meaning under arrest.

These are just the latest Chinese dissidents who were concerned about the virus that began in Wuhan, the ground zero of the Covid-19 pandemic, who have vanished. They were evidently “disappeared” because they were searching for, and telling the truth about, what happened, as well as the Chinese regime’s attempt to bury it.

Frances Eve, deputy director of research at the Hong Kong-based watchdog group, Chinese Human Rights Defenders, said:

“Everyone who has disappeared is at very high risk of torture – most likely to try to force them to confess that their activities were criminal or harmful to society. Then, as we’ve seen in previous cases, people who have been disappeared will be brought out and forced to confess on Chinese state television”.

A Chinese citizen journalist, Li Zehua, recently reappeared after having vanished two months previous, while investigating the Wuhan coronavirus cover-up. The Chinese regime made him tame and silenced him. In contrast to the tone of his reporting from Wuhan, Zehua’s new video shows him heaping praise on the regime that detained him:

“Throughout the whole process, police officers acted civil and legally, making sure that I was resting and eating well, they really cared for me, I had three meals a day, felt safe with guards, and got to watch the news every day.”

His video shows the tragic consequence of China’s repression.

In his pre-arrest reports from Wuhan, Zehua had a far more aggressive tone against the authorities:

“I don’t want to remain silent, or shut my eyes and ears. It’s not that I can’t have a nice life, with a wife and kids. I can. I’m doing this because I hope more young people can, like me, stand up.”

These Chinese journalists know that the price will be terrible. Beijing just sentenced a journalist, Chen Jieren, to a 15-year prison term for “vilifying the Chinese Communist Party” after state media released his “confession”. China, the world’s largest prison for journalists, has been accused of now having entered a “total censorship era“.

The “patient zero” of this Chinese repression was Dr. Li Wenliang, an ophthalmologist, who was the whistleblower for Covid-19, and who died, purportedly of the virus, at the age of 34. First, was detained by police in Wuhan for “spreading false rumors” and, for telling the truth, forced to sign a document that he had “told untruthful information online.” Hours after state media reported Dr. Li’s death,” noted Physicians for Human Rights, “official censors scrubbed the Chinese Internet of any mention of his passing without explanation.”

Another doctor from Wuhan, Ai Fen, head of the emergency room at Wuhan Central Hospital, was apparently also one of the whistleblowers, who had “sounded the alarm” about the virus on December 30, 2019. Ai Fen was “disappeared” after criticizing the censorship concerning the epidemic. “If I had known what was to happen, I would not have cared about the reprimand. I would have fucking talked about it to whoever, where ever I could”, she said. She has not been seen or heard from since early April.

Chen Qiushi, a citizen journalist who reported from Wuhan, has also been missing since February. “I’m scared, I have the virus in front of me and behind me China’s law enforcement”, Chen said in a video dated January 30. “But I will keep my spirits up, as long as I’m alive and in this city I will continue my reports. I’m not afraid of dying. Why should I be afraid of you, Communist Party?”

A Wuhan clothing salesman, Fang Bin, apparently committed the crime of counting “too many” body bags. “This is too many, so many dead”, Bin said in a 40-minute video about the virus outbreak. He then disappeared as well. Bin filmed bodies piling up at a crematorium. Two months later, the world discovered that China had lied about the number of victims in Wuhan. Bin was right and Beijing had to raise its coronavirus official death toll in Wuhan by 50 percent.

A university student in Shandong, Zhang Wenbin, called on President Xi to step down. “When I look at the courage with which Hong Kong and Taiwan stand up to the Communist Party, I want my own voice to be heard”, he said. “I call on you all to look upon the true colors of the Communist Party, and stand together to bring down this wall”. Then Zhang Wenbin disappeared.

A property tycoon in Beijing, Ren Zhiqiang, also disappeared after writing an essay in which he described Chinese President Xi Jinping as a “clown,” and suggested that the Communist Party’s attack on freedom of speech had exacerbated the epidemic.

Wang Fang, a native of Wuhan, who won China’s prestigious Lu Xun Literary Prize, faces harassment and death threats after publishing a diary in the West about what happened in her native city. “I have fought the good fight, I have finished the race, I have kept the faith”, Fang wrote, quoting the Bible. She explained that today’s China reminds her of the Cultural Revolution, when Mao Zedong imposed fanaticism and obedience in the country and when dissidents were humiliated in public, killed by mobs or forced to commit suicide on streets.

A Chinese law professor at Tsinghua University, Professor Xu Zhangrun, was also placed under investigation after publishing an essay that railed against repression under President Xi. “I don’t know what they’ll do next,” Professor Xu said. “I’ve been mentally preparing for this for a long time. At the worst, I could end up in prison”. He also published a long essay in which he denounced Xi Jinping and the Communist Party. “The coronavirus epidemic has revealed the rotten core of Chinese governance”, Professor Xu wrote. He added that the Chinese system now “values the mediocre, the dilatory and the timid” and that the mess caused by officials in Wuhan who covered up early signs of the virus “has infected every province and the rot goes right up to Beijing”.

Friends say that since those remarks were published, Professor Xu’s social account was suspended, his name scrubbed from Weibo, a Chinese blogging platform, and that now only articles from official websites show up on the country’s largest search engine, Baidu.

A prominent Chinese legal activist, Xu Zhiyong, who urged Xi Jinping to resign — “You’re just not smart enough,” he said — was also arrested.

A pro-democracy activist, Ren Ziyuan, was sent to administrative detention for criticizing the government’s management of the epidemic, Freedom House reported. Additionally, Tan Zuoren, an online activist and former political prisoner, has received multiple visits by police and had his account on the WeChat social media platform frozen. Former professor Guo Quan , after publishing articles about the outbreak, was also arrested for “inciting subversion of state power”.

These intrepid dissidents showed how fragile, vacuous and dangerous is the edifice of the Chinese regime. The Chinese Communist Party “is the biggest and most serious virus of all”, said the blind activist and dissident Chen Guangcheng, now a refugee in the US. “It is time”, he said, “to recognize the threat the Chinese Communist Party poses to all humanity. The CCP represses and manipulates information to strengthen its hold on power, regardless of the toll on human lives”. Also apparently regardless of the number of victims in the world.

An open letter from parliamentarians, academics, advocates and policy leaders states:

“As an international group of public figures, security policy analysts and China watchers, we stand in solidarity with courageous and conscientious Chinese citizens including Xu Zhangrun, Ai Fen, Li Wenliang, Ren Zhiqiang, Chen Qiushi, Fang Bin, Li Zehua, Xu Zhiyong, and Zhang Wenbin, just to name a few of the real heroes and martyrs who risk their life and liberty for a free and open China”.

The letter was signed by, among others, Judith Abitan, Executive Director of the Raoul Wallenberg Centre for Human Rights; Lord Alton of the British House of Lords; the French historian Jean-Pierre Cabestan of the Hong Kong Baptist University; Irwin Cotler, Emeritus Professor of Law at McGill University and former Minister of Justice and Attorney General of Canada; and Giulio Terzi di Sant’Agata, Italy’s former minister of Foreign Affairs.

While many in the West thought that the Soviet Union was a heaven, it only took a handful of heroes beyond the Iron Curtain to let us know about the gulags, the secret police, the hunger, the repression — in short, they showed us that the heaven was a hell. These heroes included, the Czech writer Václav Havel, the nuclear scientist Andrei Sakharov and the author Alexander Solzhenitsyn in the Soviet Union; and the physicist Robert Havemann in East Germany, to name just a few. They paid with arrest, exile, prison and even their lives, such as Czech philosopher Jan Patočka, who died after being interrogated.

Today, similarly, if we know something about China, we owe it to China’s vanished heroes. We have, horribly, chosen to abandon them. Very few in the very free West call out the Chinese authorities and ask these great men and women to be released. For its acquiescence, the West will pay dearly.

The University of Queensland, Australia, which has close links to China, is actually trying to take disciplinary action, including the possible expulsion, against a student, Drew Pavlou, for his criticism of Beijing. Are we already playing Beijing’s game of repressing dissent?

Bloomberg News is said to censor articles that might anger China and expose Xi’s personal wealth. And the European Union recently softened criticism of China in a report on disinformation about the pandemic. The EU’s High Representative for Foreign Affairs, Josep Borrell, admitted that China had “pressured” Brussels.

“We’re almost extinct,” said Liu Hu, a journalist detained for nearly a year after investigating corrupt politicians. “No one is left to reveal the truth”.

It looks as though free thought is more valued among China’s daring dissidents than in many corners of the West.

To paraphrase Leon Trotsky: You may not be interested in China, but China is interested in you.

- Portland To Vote On $2.5 Billion Homeless Aid Tax Amid COVID Economy

Portland To Vote On $2.5 Billion Homeless Aid Tax Amid COVID Economy

Tyler Durden

Sun, 05/17/2020 – 23:30As the COVID-19 pandemic continues to bring the economy to a screeching halt, progressive cities dealing with a large and growing homeless populations face increased pressure to provide assistance amid budget shortfalls and dwindling or delayed tax revenues.

“Businesses and households are racking up huge amounts of debt. You have people who aren’t paying their rent and who are delaying their mortgages,” according to Eric Fruits, a research director at the Cascade Policy Institute.

Given this backdrop, voters in Portland, Oregon will decide on Tuesday to approve taxes on personal income and business profits which would raise $2.5 billion over a decade for the city’s homelessness initiatives, according to KATU.

The ballot measure was planned before the pandemic reduced the U.S. economy to tatters. Proponents, including many business leaders and major institutions, argue the taxes are needed now more than ever in a region that has long been overwhelmed by its homeless problem.

How voters in the liberal city react amid the pandemic will be instructive for other West Coast cities struggling to address burgeoning homeless populations as other sources of revenue dry up. The measure is believed to be one of the first nationwide to ask voters to open their wallets in a post-COVID-19 world. –KATU

Instead of housing, the money would be spent on so-called “wrap around services” to help with rent assistance, job training, mental health and substance abuse treatment, and case management and outreach.

“I think it’s really going to give you a sense about how concerned are people, still, about homelessness as an issue — and what are they willing to pay in to solve that issue,” said Marisa Zapata, head of the Homelessness Research & Action Collaborative (HRAC) at Portland State University.

“We know government budgets are going to be eviscerated, so what does this mean for additional revenue-raising opportunities?” she added. “Who could we turn to to bear some of that responsibility and how will voters react?”

According to HRAC, there are approximately 40,000 people in the greater Portland area who have experienced at least one period of homelessness, and 105,000 households which face housing insecurity.

Those who oppose the $2.5 billion bill are shocked that organizers continue to push the effort while the economy is stalled and much of Oregon’s population remains under lockdown.

“People are frustrated. They’re out of work, they’re angry and the last thing they’re thinking about right now is raising taxes,” according to Amanda Dalton, legislative director of the Northwest Grocery Association.

Voters in the three counties that make up the greater Portland metro region will be asked to consider a 1% marginal income tax on the wealthiest residents and a 1% tax on gross profits for the region’s biggest businesses.

The measure would apply to individual filers with a taxable income of more than $125,000 or joint filers with taxable income of more than $200,000. Joint filers making $215,000 a year, for example, would be taxed 1% on $15,000, or $150 a year. –KATU

Approximately 90% of Portland residents and 94% of businesses will be exempt from the tax, says Angela Martin, campaign director for HereTogether – the organization which created the measure.

Supporting the bill is the Portland Business Alliance, whose members have repeatedly cited homelessness as a ‘critical factor affecting its ability to expand and recruit,’ according to the report. Also backing the measure are the Portland Trail Blazers and other major sports franchises, as well as several local government leaders.

Last week Gov. Kate Brown asked all state agencies to find a way to cut nearly 20% of their budgets, while the city of Portland is expecting a $75 million drop in revenue.

- "Overshoot" – Understanding Our Pandemic-Economy Predicament

“Overshoot” – Understanding Our Pandemic-Economy Predicament

Tyler Durden

Sun, 05/17/2020 – 23:05Authored by Gail Tverberg via Our Finite World blog,

The world’s number one problem today is that the world’s population is too large for its resource base. Some people have called this situation overshoot. The world economy is ripe for a major change, such as the current pandemic, to bring the situation into balance. The change doesn’t necessarily come from the coronavirus itself. Instead, it is likely to come from a whole chain reaction that has been started by the coronavirus and the response of governments around the world to the coronavirus.

Let me explain more about what is happening.

[1] The world economy is reaching Limits to Growth, as described in the book with a similar title.

One way of seeing the predicament we are in is the modeling of resource consumption and population growth described in the 1972 book, The Limits to Growth, by Donella Meadows et al. Its base scenario seems to suggest that the world will reach limits about now. Chart 1 shows the base forecast from that book, together with a line I added giving my impression of where the economy really was in 2019, relative to resource availability.

Figure 1. Base scenario from 1972 Limits to Growth, printed using today’s graphics by Charles Hall and John Day in “Revisiting Limits to Growth After Peak Oil,” with dotted line added corresponding to where the world economy seems to be have been in 2019.

In 2019, the world economy seemed to be very close to starting a downhill trajectory. Now, it appears to me that we have reached the turning point and are on our way down. The pandemic is the catalyst for this change to a downward trend. It certainly is not the whole cause of the change. If the underlying dynamics had not been in place, the impact of the virus would likely have been much less.

The 1972 model leaves out two important parts of the economy that probably make the downhill trajectory steeper than shown in Figure 1. First, the model leaves out debt and, in fact, the whole financial system. After the 2008 crisis, many people strongly suspected that the financial system would play an important role as we reach the limits of a finite world because debt defaults are likely to disturb the worldwide financial system.

The model also leaves out humans’ continual battle with pathogens. The problem with pathogens becomes greater as world population becomes denser, facilitating transmission. The problem also becomes greater as a larger share of the population becomes more susceptible, either because they are elderly or because they have underlying health conditions that have been hidden by an increasingly complex and expensive medical system.

As a result, we cannot really believe the part of Figure 1 that is after 2020. The future downslopes of population, industrial production per capita, and food per capita all seem likely to be steeper than shown on the chart because both the debt and pathogen problems are likely to increase the speed at which the economy declines.

[2] It is far more than the population that has overshot limits.

The issue isn’t simply that there are too many people relative to resources. The world seems to have

-

Too many shopping malls and stores

-

Too many businesses of all kinds, with many not very profitable for their owners

-

Governments with too extensive programs, which taxpayers cannot really afford

-

Too much debt

-

An unaffordable amount of pension promises

-

Too low interest rates

-

Too many people with low wages or no wages at all

-

Too expensive a healthcare system

-

Too expensive an educational system

The world economy needs to shrink back in many ways at once, simultaneously, to manage within its resource limits. It is not clear how much of an economy (or multiple smaller economies) will be left after this shrinkage occurs.

[3] The economy is in many ways like the human body. In physics terms, both are dissipative structures. They are both self-organizing systems powered by energy (food for humans; a mixture of energy products inducing oil, coal, natural gas, burned biomass and electricity for the economy).

The human body will try to fix minor problems. For example, if someone’s hand is cut, blood will tend to clot to prevent too much blood loss, and skin will tend to grow to substitute for the missing skin. Similarly, if businesses in an area disappear because of a tornado, the prior owners will either tend to rebuild them or new businesses will tend to come in to replace them, as long as adequate resources are available.

In both systems, there is a point beyond which problems cannot be fixed, however. We know that many people die in car accidents if injuries are too serious, for example. Similarly, the world economy may “collapse” if conditions deviate too far from what is necessary for economic growth to continue. In fact, at this point, the world economy may be so close to the edge with respect to resources, particularly energy resources, that even a minor pandemic could push the world economy into a permanent cycle of contraction.

[4] World governments are in a poor position to fix the current resource and pandemic crisis.

In our networked economy, too low a resource base relative to population manifests itself in a strange way: It appears as an affordability crisis that leads to very low prices for oil. It also appears as terribly low prices for many other commodities, including copper, lithium, coal and even wholesale electricity. These low prices occur because too large a share of the population cannot afford finished goods, such as cars and homes, made with these commodities. Recent shutdowns have suddenly increased the number of people with low income or no income, pushing commodity prices even lower.

If resources were more plentiful and very inexpensive to produce, as they were 50 or 70 years ago, wages of workers could be much higher, relative to the cost of resources. Factory workers would be able to afford to buy vehicles, for example, and thus help keep the demand for automobiles up. If we look more deeply into this, we find that energy resources of many kinds (fossil fuel energy, nuclear energy, burned biomass and other renewable energy) must be extraordinarily cheap and abundant to keep the system growing. Without “surplus energy” from many sources, which grows with population, the whole system tends to collapse.

World governments cannot print resources. What they can print is debt. Debt can be viewed a promise of future goods and services, whether or not it is reasonable to believe that these future goods and services will actually materialize, given resource constraints.

We are finding that using shutdowns to solve COVID-19 problems causes a huge amount of economic damage. The cost of mitigating this damage seems to be unreasonably high. For example, in the United States, antibody studies suggest that roughly 5% of the population has been infected with COVID-19. The total number of deaths associated with this 5% infection level is perhaps 100,000, assuming that reported deaths to date (about 80,000) need to be increased somewhat, to match the approximately 5% of the population that has, knowingly or unknowingly, already experienced the infection.

If we estimate that the mean number of years of life lost is 13 years per person, then the total years of life lost would be about 1,300,000. If we estimate that the US treasury needed to borrow $3 trillion dollars to mitigate this damage, the cost per year of life lost is $3 trillion divided by 1.3 million, or $2.3 million dollars per year of life lost. This amount is utterly absurd.

This approach is clearly not something the United States can scale up, as the share of the population affected by COVID-19 relentlessly rises from 5% to something like 70% or 80%, in the absence of a vaccine. We have no choice but to use a different approach.

[5] COVID-19 would have the least impact on the world economy if people could pay little attention to the pandemic and just “let it run.” Of course, even without mitigation attempts, COVID-19 might bring the world economy down, given the distressed level of today’s economy and the shutdowns experienced to date.

Shutting down an economy has a huge adverse impact on that economy because quite a few workers who are in good health are no longer able to make goods and services. As a result, they have no wages, so their “demand” goes way down. If the economy was already having an affordability crisis for goods made with commodities, shutting down the economy tends to greatly add to the affordability crisis. Prices of commodities tend to fall even lower than they were before the crisis.

Back in 1957-1958, the Asian pandemic, which also started in China, hit the world. The number of deaths was up in the range of the current pandemic, relative to population. The estimated worldwide death rate was 0.67%. This is not too dissimilar from a death rate of 0.61% for COVID-19, which can be calculated using my estimate above (100,000 deaths relative to 5% of the US population of 33o million).

Virtually nothing was shut down in the US for the 1957-58 pandemic. When doctors or nurses became sick themselves, wards were simply closed. Would-be patients were told to stay at home and take aspirin, unless a severe case developed. With this approach, the US still faced a short recession, but the economy was soon growing again. Populations seemed to soon reach herd immunity quite quickly.

If the world could somehow have adopted a similar approach this time, there still would have been some adverse impact on the economy. A small percentage of the population would have died. Some businesses might have needed to be closed for a short time when too many workers were out sick. But the huge burden of job loss by a substantial share of the economy could have been avoided. The economy would have had at least a small chance of rebounding quickly.

[6] The virus that causes COVID-19 looks a great deal like a laboratory cross between SARS and HIV, making the likelihood of a quick vaccine low.

In fact, Professor Luc Montagnier, co-discoverer of the AIDS virus and winner of a Nobel Prize in Medicine, claims that the new coronavirus is the result of an attempt to manufacture a vaccine against the AIDS virus. He believes that the accidental release of this virus is what is causing today’s pandemic.

If COVID-19 were simply another influenza virus, similar to many we have seen, then getting a vaccine that would work passably well would be a relatively easy exercise. At least one of the vaccine trials that has been started could be reasonably expected to work, and a solution would not be far away.

Unfortunately, SARS and HIV are fairly different from influenza viruses. We have never found a vaccine for either one. If a person has had SARS once, and is later exposed to a slightly mutated version of SARS, the symptoms of the second infection seem to be worse than the first. This characteristic interferes with finding a suitable vaccine. We don’t know whether the virus causing COVID-19 will have a similar characteristic.

We know that scientists from a number of countries have been working on so-called “gain of function” experiments with viruses. These very risky experiments are aimed at making viruses either more virulent, or more transmissible, or both. In fact, experiments were going on in Wuhan, in two different laboratories, with viruses that seem to be not too different from the virus causing COVID-19.

We don’t know for certain whether there was an accident that caused the release of one of these gain of function viruses in Wuhan. We do know, however, that China has been doing a lot of cover-up activity to deter others from finding out what actually happened in Wuhan.

We also know that Dr. Fauci, a well-known COVID-19 advisor, had his hand in this Chinese research activity. Fauci’s organization, the National Institute for Allergy and Infectious Diseases, provided partial funding for the gain of function experiments on bat coronaviruses in Wuhan. While the intent of the experiments seems to have been for the good of mankind, it would seem that Dr. Fauci’s judgment erred in the direction of allowing too much risk for the world’s population.

[7] We are probably kidding ourselves about ever being able to contain the virus that causes COVID-19.

We are gradually learning that the virus causing COVID-19 is easily spread, even by people who do not show any symptoms of the disease. The virus can spread long distances through the air. Tests to see if people are ill tend to produce a lot of false negatives; because of this, it is close to impossible to know whether a particular person has the illness or not.

China is finding that it cannot really contain the virus that causes COVID-19. A recent South China Morning Post article indicates that roughly 14 million people are to be tested in the Wuhan area in the next ten days to try to control a new outbreak of the virus.

It is becoming clear, as well, that even within China, the lockdowns have had a very negative impact on the economy. The Wall Street Journal reports, China Economic Data Indicate V-Shaped Recovery Is Unlikely. Supply chains were broken; wholesale commodity prices (excluding food) have tended to fall. Joblessness is increasingly a problem.

[8] If we look at deaths per million by country, it is difficult to see that lockdowns are very helpful in reducing the spread of disease. Masks seem to be more beneficial.

If we compare death rates for mask-wearing East Asian countries to death rates elsewhere, we see that death rates in mask-wearing East Asian countries are dramatically lower.

Figure 2. Death rates per million population of selected countries with long-term exposure to the virus causing COVID-19, based on Johns Hopkins death data as of May 11, 2020.

Looking at the chart, a person almost wonders whether lockdowns are a response to requests from citizens to “do something” in response to an already evident surge in cases. The countries known for their severe lockdowns are at the top of the chart, not the bottom.

In fact, a preprint academic paper by Thomas Meunier is titled, “Full lockdown policies in Western Europe countries have no evident impacts on the COVID-19 epidemic.” The abstract says, “Comparing the trajectory of the epidemic before and after the lockdown, we find no evidence of any discontinuity in the growth rate, doubling time, and reproduction number trends. . . We also show that neighboring countries applying less restrictive social distancing measures (as opposed to police-enforced home containment) experience a very similar time evolution of the epidemic.”

It appears to me that lockdowns have been popular with governments around the world for a whole host of reasons that have little to do with the spread of COVID-19:

-

Lockdowns give an excuse for closing borders to visitors and goods from outside. This was a direction in which many countries were already headed, in an attempt to raise the wages of local workers.

-

Lockdowns can be used to hide the fact that factories need to be closed because of breaks in supply lines elsewhere in the world.

-

Many countries have been faced with governmental protests because of low wages compared to the prices of basic services. Lockdowns tend to keep protesters inside.

-

Lockdowns give the appearance of protecting the elderly. Since there are many elderly voters, politicians need to court these voters.

[9] A person wonders whether Dr. Fauci and members of the World Health Organization are influenced by the wishes of vaccine and big pharmaceutical companies.

The recommendation to try to “flatten the curve” is, in part, an attempt to give vaccine and pharmaceutical makers more time to work on their products. Is this really the best recommendation? Perhaps I am being overly suspicious, but we recently have been dealing with an opioid epidemic which was encouraged by manufacturers of Oxycontin and other opioids. We don’t need another similar experience, this time sponsored by vaccine and other pharmaceutical makers.

The temptation of researchers is to choose solutions that would be best from the point of their own business interests. If a researcher gets much of his funding from vaccine and big pharmaceutical interests, the temptation will be to “push” solutions that are beneficial to these interests. In some cases, researchers are able to patent approaches, even when the research is paid for by governmental grants. In this case they can directly benefit from a new vaccine or drug.

When potential solutions are discussed by Dr. Fauci and the World Health Organization, no one brings up improving people’s immunity so that they can better fight off the novel coronavirus. Few bring up masks. Instead, we keep being warned about “opening up too soon.” In a way, this sounds like, “Please leave us lots of customers who might be willing to pay a high price for our vaccine.”

[10] One way the combination of (a) the activity of the virus and (b) our responses to the virus may play out is as a slow-motion, controlled demolition of the world economy.

I think of what we are experiencing as being somewhat similar to a toggle bolt going around and around, moving down a screw. As the toggle bolt moves around, I picture it as being similar to the virus and our responses to the viruses hitting different parts of the world economy.

Figure 3. Image of how the author sees COVID-19 as being able to hit the economy multiple times, in multiple ways, as its impact keeps impacting different parts of the world.

If we look back, the virus and reactions to the virus first hit China. China’s recovery is moving slowly, in part because of reduced demand from outside of China now that the virus is hitting other parts of the world. In fact, additional layoffs occurred after Chinese shutdowns ended, because it then became clear that some employers needed to permanently scale back operations to meet the new lower demand for their product.

Commodity prices, including oil prices, are now depressed because of low demand around the world. These low prices can be expected to gradually lead to closures of wells and mines extracting these commodities. Processing centers will also close, making these commodities less available even if demand temporarily rises.

As one country is hit by illnesses and/or shutdowns, we can expect supply lines for manufacturing around the world to be disrupted. This will lead to yet more business closures, some of them permanent. Debt defaults tend to happen as businesses close and layoffs occur.

With all of the layoffs, governments will find that their tax collections are lower. The resulting governmental funding issues can be expected to lead to new rounds of layoffs.

Natural disasters such as hurricanes, tornadoes, floods, earthquakes and forest fires can be expected to continue to happen. Social distancing requirements, inadequate tax revenue and broken supply lines will make mitigation of all of these disasters more difficult. Electrical lines that fall down may stay down permanently; bridges that are damaged may never be repaired.

Initially, rich countries can be expected to try to help as many laid-off workers as possible with loans and temporary stipends. But, after a few months, even with this approach, many individual citizens and businesses will likely not be able to pay their rent. Default rates on home mortgages and auto loans can be expected to rise for a similar reason.

We can expect to see round after round of business failures and layoffs of employees. Financial systems will become more and more stressed. Pensions are likely to default. Death rates will rise, in part from epidemics of various kinds and in part from growing problems with starvation. In fact, in some poor countries, lower-income citizens are already having difficulty being able to afford adequate food. Eventually we can expect collapsing governments (similar to the collapse of central government of the Soviet Union) and overthrown governments.

Longer-term, after this demolition ends, there may be some surviving pieces of economies. These new economies will be much smaller and less dependent upon each other, however. Currencies are likely to be less interchangeable. The remaining people will need to learn to make do with many fewer goods than are available today. It will be a very different world.

-

- Can't Make This Up: Beijing Begins Construction Of A P-3 Biolab

Can’t Make This Up: Beijing Begins Construction Of A P-3 Biolab

Tyler Durden

Sun, 05/17/2020 – 22:56As the new trade/tech/diplomatic/cultural (in fact, everything but kinetic) war between the US and China is heating up by the hour, one would think that China would do everything in its power to defuse one of the core accusations by the Trump administration, namely that the Wuhan Institute of Virology (WIV) in China was the source of the global coronavirus pandemic (going so far as to spark unofficial demands for hundreds of billions in reparations from Beijing for its “criminal” actions), an allegation which Peter Navarro on Sunday expanded when he accused China of deliberately “seeding” the world with the “China virus”:

“The Chinese behind the shield of the World Health Organization – for two months – hid the virus from the world and then sent hundreds of thousands of Chinese on aircraft to Milan, New York and around the world to seed that,” Navarro said on ABC. “They could have kept it in Wuhan. Instead it became a pandemic.”

Well, one would be wrong, because in a “completely unexpected” twist – assuming China was indeed telling the truth and that the WIV had nothing to do with the original viral release – on Friday, a senior Chinese official confirmed Secretary of State Mike Pompeo’s allegation that Beijing had told labs in the country to destroy coronavirus samples in early January.

Recall that in a May 6 press briefing, Pompeo accused China of covering up the Covid-19 outbreak as it emerged in the central city of Wuhan, saying China’s National Health Commission had ordered destruction of samples of the virus on Jan. 3.

Asked about those comments at a press briefing in Beijing on Friday, NHC official Liu Dengfeng confirmed that the commission had issued these guidelines at that time “for pandemic prevention and control, which also played an important role in preventing biosafety risks.”

“If the laboratory conditions cannot meet the requirements for the safe preservation of samples, the samples should be destroyed on the spot or transferred to a professional institution for safekeeping,” said Liu, supervisor of the commission’s Department of Health Science, Technology and Education.

Chinese law has clear rules for the handling of highly pathogenic samples, he said, and we are sure that it does… but wait a gosh darned minute? According to Dengfeng, China is basically admitting that the coronavirus samples – which were held in China’s P-4 rated, top “biosafety” lab in Wuhan which incidentally is also where the virus was leaked from according to a mountain of circumstantial evidence – were not safe in the Wuhan lab and thus had to be destroyed?

Considering that one of the core arguments made by the Trump administration (and this website) is that the virus (whether genetically engineered or otherwise) was released (hopefully without premeditation although there is no way of knowing for certain) by the Wuhan lab, China’s actions essentially confirm that the Wuhan Institute of Virology was unsafe, and thus every last sample of the virus had to be destroyed.

Of course, the real reason why China destroyed the samples was different, and it had to do with not only destroying all the evidence but crushing any hope of finding what the real source of the pandemic was. As the WSJ reported, “Public health experts say it is likely too late to investigate the role of the market in Covid-19’s spread and that proving its origin might now be impossible.” And with China destroying the last remaining coronavirus samples, well – there goes any hope of proving or disproving that the virus emerged from the Wuhan Institute of Virology.

Just as China wanted.

So with all that in mind, and with China’s track record in biotechnology, “gain of function” experiments and reputation of deadly viral “containment” destroyed, what does China do? Why it plans to build an entirely new biolab, only this time not in the industrial backwater of Wuhan, but in the capital itself.

According to the Global Times, China’s capital Beijing will build its own, P-3 rated laboratory “to improve and explore infectious disease detection capacity” Lei Haichao, director of Beijing Municipal Health Commission, said at a press conference on Sunday, Chinanews reported.