- Many Volkswagen EVs Are Already Sold Out For The Second Half Of 2020

Many Volkswagen EVs Are Already Sold Out For The Second Half Of 2020

Tyler Durden

Tue, 05/19/2020 – 02:45While the auto market has been falling apart, Volkswagen has been crushing it in the EV market.

The automaker’s CEO said on a podcast on Monday morning that many of its EVs are already “sold out far into the second half of the year,” according to Bloomberg.

The company’s market share for EVs more than doubled to almost 4% and could rise as high as 5% or 6% by the end of 2020 with help from incentives and tax breaks, CEO Herbert Diess said. The company has a longer-term target of EVs accounting for about 40% of deliveries by 2030.

And the target for VW is clear: the company is “very confident” that it “won’t lose sight of Tesla,” Deiss said.

He continued, saying that the company’s “ability to boost technology skills and software operations quickly is more important to compete than leveraging industrial scale.”

Diess expects “very strong” competition from Chinese firms in the future and reiterated his call for economic stimulus in Germany to help the country steer clear of a prolonged recession.

This targeted move, taking aim at Tesla, shouldn’t be a surprise to Zero Hedge readers, as we recently predicted that Volkswagen would become a major player in the EV market, posing a threat to Tesla.

Recall, just days ago, we wrote about the Volkswagen ID3, which, with a price point of $33,000 possibly represents the biggest challenge to Tesla’s dominant EV status yet. The vehicle goes on sale in Europe and the UK this summer, despite the coronavirus and offers the same amount of range and storage space as a Tesla Model 3.

The ID3 is going to offer three different battery choices and two power outputs. It has a claimed range of 260 miles.

Volkswagen has been taking pre-orders for the car and more than 35,000 people have placed deposits so far, according to Autocar. Those who placed deposits will be able to buy their cars starting June 17 in Europe. The UK will follow in mid-July due to the time it takes to get approval for right hand drive models.

Volkswagen sales boss Jürgen Stackmann said at the time deliveries are on track and that the ID3 is the company’s sole focus right now: “The focus of the company now is on ID 3. We’re almost ready, and we just need a few more weeks to get the software to where we need it to be. The entire team are working on this topic, and we want to deliver a great quality product on time – and that time is this summer.”

Volkswagen is aiming to build 100,000 ID3s this year and prices in the will start from around £27,500 before the government grant for the entry-level 45kWh version.

The storage capabilities of the ID3 make it a formidable competitor to the Model Y. The ID3 also features two digital dashboard displays and, as Business Insider says “…seems to offer a bit more familiarity” than the Tesla Model 3.

It also offers adaptive cruise control and lane assist, similar to Tesla’s autopilot. And again, the price point could be the car’s best selling point. Its $33,000 (USD) tag compares to about $48,000 for the Model 3 and $52,990 for the Model Y.

A video comparison of the ID3 and the Model 3 can be seen here:

- United Nations Claims It's Politically-Incorrect To Say "Husband" Or "Wife"

United Nations Claims It’s Politically-Incorrect To Say “Husband” Or “Wife”

Tyler Durden

Tue, 05/19/2020 – 02:00Authored by Paul Joseph Watson via Summit News,

The United Nations has put out a tweet asserting that people shouldn’t use politically incorrect terms like “boyfriend,” “girlfriend,” “husband” and “wife” in order to “help create a more equal world.”

<!–[if IE 9]><![endif]–>

“What you say matters. Help create a more equal world by using gender-neutral language if you’re unsure about someone’s gender or are referring to a group,” states the tweet.

“What you say matters. Help create a more equal world by using gender-neutral language if you’re unsure about someone’s gender or are referring to a group,” states the tweet.It then lists a number of terms alongside their politically correct alternative.

These include mankind, chairman, congressman, policeman, landlord, boyfriend/girlfriend, manpower, maiden name, fireman and husband/wife.

What you say matters.

Help create a more equal world by using gender-neutral language if you’re unsure about someone’s gender or are referring to a group. https://t.co/QQRFPY4VRn #GenerationEquality via@UN_Women pic.twitter.com/koxoAZZuxq

— United Nations (@UN) May 18, 2020

https://platform.twitter.com/widgets.js

A faceless globalist bureaucracy telling people what sounds are allowed to come out of their mouths surprisingly didn’t go down too well.

“Stop trying to control people’s language. It’s creepy and unnecessary,” said Lucy Harris.

Stop trying to control people’s language. It’s creepy and unnecessary.

— Lucy Harris (@Lugey6) May 18, 2020

https://platform.twitter.com/widgets.js

“Are we allowed to say son or daughter or will my spouse and I get a visit from a police officer?” asked another.

Are we allowed to say son or daughter or will my spouse and I get a visit from a police officer?

— Wes Butler 🐝 (@WButler77) May 18, 2020

https://platform.twitter.com/widgets.js

“Are we still allowed to say manhole cover?” joked another.

* * *

My voice is being silenced by free speech-hating Silicon Valley behemoths who want me disappeared forever. It is CRUCIAL that you support me. Please sign up for the free newsletter here. Donate to me on SubscribeStar here. Support my sponsor – Turbo Force – a supercharged boost of clean energy without the comedown.

- The Coming Nuclear Menace: Hypersonic Missiles

The Coming Nuclear Menace: Hypersonic Missiles

Tyler Durden

Tue, 05/19/2020 – 00:05Authored by Karl Grossman via Counterpunch.org,

The United States is seeking to acquire “volumes of hundreds or even thousands” of nuclear-capable hypersonic missiles that are “stealthy” and can fly undetected at 3,600 miles per hour, five times faster than the speed of sound.

Why so many?

A Pentagon official is quoted in the current issue of Aviation Week & Space Technology as saying “we have to be careful we’re not building boutique weapons. If we build boutique weapons, we won’t—we’ll be very reluctant to—use them.”

The article in the aerospace industry trade journal is headlined: “Hypersonic Mass Production.” A subhead reads: “Pentagon Forms Hypersonic Industry ‘War Room.’”

On March 19, 2020, the U.S. conducted its first hypersonic missile test from its Pacific Missile Range Facility on Kauai, Hawaii.

“Fast and Furiously Accurate” is the title of an article about hypersonic missiles written by a U.S. Navy officer which appeared last year on a U.S. Naval Institute website.

The piece declares that by “specifically integrating hypersonic weapons with U.S. Navy submarines, the United States may gain an edge in developing the fastest, most precise weapons the world has ever seen.”

“Hypersonic weapons,” explains the article by U.S. Navy Lieutenant Andrea Howard, “travel faster than Mach 5—at least five times the speed of sound, around 3,600 mph, or one mile per second….They are similar to but faster than existing missiles, such as the subsonic U.S. Tomahawk missile, which maxes out around 550 mph.”

“While hypersonic weapons can carry conventional or nuclear warheads, they differ from existing technologies in three critical ways,” writes Howard. “First…a one-kilogram object delivered precisely and traveling multiples of the speed of sound can be more destructive than one kilogram of TNT. Second, the low-altitude path helps mask HCMs [Hypersonic Cruise Missiles] when coupled with the curvature of the Earth” and so “they are mostly invisible to early warning radars. And third…they can maneuver during flight; in contrast with the predictable ballistic-missile descend, they are more difficult to intercept, if even detected.”

“By offering the precision of near-zero-miss weapons, the speed of ballistic missiles, and the maneuverability of cruise missiles, hypersonic weapons are a disruptive technology capable of striking anywhere on the globe in less than an hour,” declares the Navy officer.

The article also notes that Russian “President Vladimir Putin unveiled six new” what he called “invincible” hypersonic missiles as part of a March 2018 “state of the nation” speech. “Russia has successfully tested the air-to-ground hypersonic missile” named Kinzhal for dagger, “multiple times using the MIG-31 fighter.” It’s “mounting the Kinzhal on its Tu-22M3 strategic bomber.” The article also says “China, too, is working on hypersonic technologies.”

The piece concludes:

“As the tradition of arms control weakens with the breakdown of the Intermediate-Range Nuclear Forces (INF) agreement, it would be naïve to anticipate anything other than full-fledged weapon development by Russia and China in the coming decades….The bottom line is that hypersonic weapons will determine who precisely is ‘prompt’ enough in 21st century conflict.”

The U.S. under President Trump withdrew last year from the INF treaty, a landmark agreement which had banned all land-based ballistic and cruise missiles with ranges of from 310 to 3,420 miles. It had been signed in 1987 by President Reagan and Soviet General Secretary Mikhail Gorbachev. The treaty “marked the first time the superpowers had agreed to reduce their nuclear arsenals, eliminate an entire category of nuclear weapons, and employ extensive on-site inspections for verification,” notes the Arms Control Association.

“Hypersonic missiles may be unstoppable. Is society ready?” was the headline of an article in March in The Christian Science Monitor. This piece notes: “Hypersonic missiles are not just very fast, they are maneuverable and stealthy. This combination of speed and furtiveness means they can surprise an adversary in ways that conventional missiles cannot, while also evading radar detection. And they have injected an additional level of risk and ambiguity into what was already an accelerating arms race between nuclear-armed rivals.”

The article raises the issue of the speed of hypersonic missiles miring military decisions. “For an incoming conventional missile, military commanders may have 30 minutes to detect and respond; a hypersonic missile could arrive at that same destination in 10 minutes.” Thus “artificial intelligence” or “AI” would be utilized.

The Christian Science Monitor article quotes Patrick Lin, a professor of philosophy at California Polytechnic State University in San Luis Obispo, as noting:

“Technology will always fail. That is the nature of technology.”

And, says the article: “Dr. Lin argues that the benefits of hypersonic weapons compared to the risk they create are ‘widely unclear,’ as well as the benefits of the AI systems that inform them.”

It quotes Dr. Lin as saying, wisely:

“I think it’s important to remember that diplomacy works and policy solutions work…I think another tool in our toolbox isn’t just to invest in more weapons, but it’s also to invest in diplomacy to develop community.”

The Aviation Week & Space Technology article begins: “As the U.S. hypersonic weapons strategy tilts toward valuing a quantity approach, the new focus for top defense planners—even as a four-year battery of flight testing begins—is to create an industrial base that can produce missiles affordably enough that the high-speed weapons can be purchased in volumes of hundreds or even thousands.”

It continues: “To pave the way for an affordable production strategy, the Pentagon’s Research and Engineering division has teamed up with the Acquisition and Sustainment branch to create a ‘war room’ for the hypersonic industrial base, says Mark Lewis, director of research and engineering the modernization.”

The piece then quotes Lewis as saying:

“At the end of the day, we have to be careful we’re not building boutique weapons. If we build boutique weapons, we won’t—we’ll be very reluctant to—use them. And that again factors into our plans for delivering hypersonics at scale.”

The article says that “Air Force and defense officials have been promoting concepts for operating air-launched hypersonic missiles in swarm attacks. The B-1B [bomber], for example, will be modified to carry” six hypersonic missiles.

“I think it’s a poorly posed question to ask about affordability per unit,” the piece quoted Lewis as saying.

“We have to think of it in terms of the affordability of the capability that we’re providing. By that I mean: If I’ve got a hypersonic system that costs twice as much as its subsonic counterpart but is five times more effective, well, clearly, that’s an advantageous cost scenario.”

The hypersonic missiles will indeed likely be “invincible.” And they would be at the ready because of the withdrawal by the Trump administration of the INF treaty and other international arms control agreements, one after another.

With the vast numbers of hypersonic nuclear-capable missiles being sought, the world will have fully returned to the madness in the depths the Cold War—as presented in the 1964 film Dr. Strangelove or: How I Learned to Stop Worrying and Love the Bomb.

Apocalypse will be highly likely. Artificial intelligence is not going to save us. These weapons need to be outlawed, not produced and purchased en masse. And we must, indeed, “invest in diplomacy to develop community”—a global community at peace, not a world of horrific and unstoppable war.

- Watch: 'City Of 400 Foreign Ships' Illegally Fishing Off Argentina Comes To Life Each Night

Watch: ‘City Of 400 Foreign Ships’ Illegally Fishing Off Argentina Comes To Life Each Night

Tyler Durden

Mon, 05/18/2020 – 23:45The Argentine newspaper Clarín has published footage highlighting a growing problem for the government and the country’s unique surrounding ecology — illegal fishing.

Each night multiple hundreds of international fishing vessels descend on an area of ocean not far off Argentina’s coast, often crossing into the country’s Exclusive Economic Zone (EEZ) and thus illegally, in order to take advantage of waters seemingly endlessly full of squid and other fish.

Stillframe from newspaper Clarín newspaper footage. New footage shows what the publication dubs “a city of foreign ships” after reporters boarded a recent Argentine military flight to do surveillance on the illegal fishing below.

The video shows ships with bright lights piercing the pitch dark ocean surface for as far as the eye can see, as if one is looking down on mysterious planet from space.

They fish often using bottom trawlers, and most are after the abundance of squid in these far southern waters, popular especially in East Asia.

Clarín describes that:

In the 200 miles there is a real city of foreign ships, estimated at between 350 and 400. They come to stay in these remote sectors of the sea for up to two years. They are generally of oriental origin. There are Chinese and Korean ships. But also Russians, Spanish, English and South Africans. They are tangoneros (those that fish only squid) and trawlers (fishing with a net).

‘City of foreign ships’ within 200 miles off Argentina’s coast lit up at night:

“These are factory ships. They freeze and process on board. Then they transfer the product to another that takes them to the ports of their countries or disembarks them in Uruguay,” the report reads.

And separate coverage, showing the ‘city of ships’ from the water’s surface:

“They are true floating freezers. And they are preying on the whole area that is a true sanctuary. Because trawlers don’t make any selections,” an environmental activist was quoted in the Spanish language report as saying.

“In this biological corridor there are orcas, whales, elephants and sea lions and dolphins. They all fall into the nets,” the spokesman added.

Satellite image of a “city” of boats fishing illegally in the Argentine Sea, via Clarín. The vessels are commonly estimated capable of catching up to a whopping 50 tons a night, especially some of the more massive boats measuring at up to 70 meters.

“The streets are emptied by the coronavirus, but the sea fills with ships, some without a flag to prey on our resources,” a Greenpeace spokesman said ironically.

Prior satellite photo showing the clusters of foreign vessels look like cities from space:

The problem has been ongoing for years, with one publication previously featuring satellite imagery of the fishing boat clusters.

“These ships emit more light into space than almost all Argentine cities, including urban centers such as Córdoba or Rosario,” the publication said.

- Big Tech Is Turning Hospitals Into Real-Time Surveillance Centers

Big Tech Is Turning Hospitals Into Real-Time Surveillance Centers

Tyler Durden

Mon, 05/18/2020 – 23:25via Mass Private I blog,

Recent events have come to light about hospital surveillance that should concern everyone.

Big Tech is using the pandemic as an excuse to turn hospitals into mirror images of law enforcement’s real-time crime centers.

When Google announced that they were donating 10,000 Nest cameras to hospitals, my jaw dropped.

“With these Nest Cams, nurses and doctors will be able to check in on patients, supplementing in-person checks. This means there will be a reduction of physical contact, and therefore less of a need for personal protection equipment (PPE), which has fast become a scare resource.”

What makes Google’s donation so jaw dropping is how Big Tech companies are using the pandemic to make them appear magnanimous.

“With both contact tracing and the Nest Cam solution, however, Google needs to rebuild a reputation as a privacy concerned company due to the sensitive nature of both projects. It’s not going to be an easy task, but one that should remain at the forefront of all such efforts.”

Because nothing says reputation builder, like putting real-time surveillance cameras in patients rooms. Not only will hospitals record patients but they will record, nurses, doctors, hospital staff and anyone else who enters a patients’ room. That also includes minors, so no one will be safe from Big Brother’s prying eyes.

As The Guardian discovered, it also sends that information to Google servers.

“However, Nest admits that when connected to Google’s “Works with Nest integration” system, which allows other devices such as ceiling fans, washing machines and car sensors to integrate with Nest’s products, it does share personal information with Google.”

Why would Google donate 10,000 Nest cameras to 6,146 hospitals? Because they are hoping that the staff and patients will grow accustomed to being surveilled 24/7, and they hope hospitals will eventually purchase a Nest Aware subscription.

Nest cameras also record audio, making them the perfect hospital surveillance tool for law enforcement. Although a Google search of ‘total hospital police departments in the U.S.’ turned up nothing, we know that there are more than 6,000 hospitals and there are more than 17,000 law enforcement agencies in the U.S.

So if we were to make a conservative guess and say that at least half of America’s hospitals have police departments, that puts the number at roughly 3,075. Does anyone really think that 3,075 hospital police departments will return Google’s Nest cameras after the pandemic?

A recent Wall Street Journal article warned that hospitals are also using thermal imaging to scan everyone entering hospitals.

It is reprehensible to see how the mass media portrays Big tech in such a positive light as they slowly turn our hospitals into real-time surveillance centers.

A recent news release by Care.ai revealed that the largest hospital association in the country, the Texas Hospital Association (THA) is using Artificial Intelligence (AI) to monitor patients in real-time.

“Through this new partnership with care.ai, Texas hospitals will have the opportunity to experience the use of AI in a hands-on local lab environment. They will get to see in real time the value that autonomous monitoring can bring to their facilities. We’re proud to connect our members to cutting-edge technologies that have a transformative impact on healthcare delivery in Texas,” Fernando Martinez, Ph.D., president and CEO of the Texas Hospital Association Foundation said.

As THA’s “history” page notes, they are easily the largest health care association in the country.

“Today, THA is one of the largest, most respected health care associations in the country, and the only association that represents the entire Texas hospital industry. The Texas Hospital Association serves as the political and educational advocate for more than 430 hospitals and health systems statewide.”

If the “most respected health care association in the country” thinks it is OK to use AI to monitor patients in real-time then America’s hospitals have truly become real-time surveillance centers.

Care ai’s business model is not built on helping patients recover from the coronavirus: it is built on monitoring patients in real-time.

“Continuous monitoring that can locate and identify individuals and their behaviors in real time, minimizing risks before they happen.”

According to Care ai they are continuously monitoring everyone in every Texas hospital room. Care ai calls it a “the self aware room”, I call it the real-time surveillance room.

Care ai has taken smart devices and perverted them into three real-time surveillance devices.

The AMS-M1, AMS-M2 and AMS-M2R smart devices are packed with cameras and deep learning sensors.

Question, if Google is donating 10,000 Nest Cameras and Care ai is using multiple smart devices equipped with cameras at what point do we ask, how many surveillance devices are too many?

There is no word if Google plans to “donate” Nest Hub Max’s to hospitals but if they do, they would turn America’s hospitals into real-time facial recognition centers.

Do we really want to live in a future where hospitals mirror police department real-time crime centers? Once hospitals acquire surveillance technology, mission creep dictates that it will grow and grow until there is no turning back.

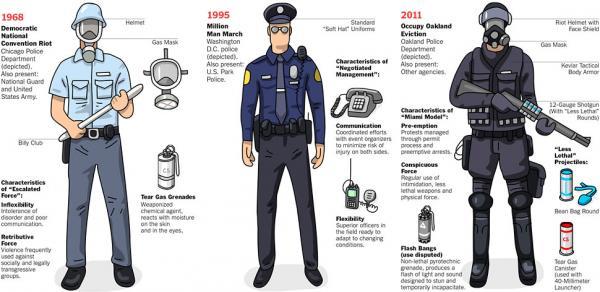

- Veterans Affairs Police Buy Riot Gear, Citing COVID-19 Pandemic

Veterans Affairs Police Buy Riot Gear, Citing COVID-19 Pandemic

Tyler Durden

Mon, 05/18/2020 – 23:05The federal government is ramping up new purchases of riot gear, citing the virus pandemic, comes at a time when the economy has plunged into recession, and high unemployment has led to increased anxieties across the country.

The Intercept says a recent order made by the Department of Veterans Affairs (VA) shows “disposable cuffs, gas masks, ballistic helmets, and riot gloves, along with law enforcement protective equipment” were bought for federal police assigned to guard VA facilities. The order was quickly fulfilled under a special authorization “in response to the Covid-19 outbreak.”

The VA department operates 1,243 health care facilities, including 170 VA Medical Centers and 1,063 outpatient sites of care in the US, which serves millions of veterans.

Redcon Solutions Group is the supplier of the latest contract. The Intercept says the firm received $1.6 in contracts to supply equipment for “Covid-19 screening security guard services.” Other security firms have been awarded similar contracts, providing defensive equipment for federal police who guard VA buildings in San Francisco, Des Moines, and Fayetteville.

The purchase order can be explained by the latest Inspector General (IG) report that said a shortage of VA workers and VA police created additional strain on the agency during lockdowns. The IG report said some VA facilities became the site of “COVID-19-related screenings,” which meant the VA needed to beef up security.

The Intercept notes federal police at VA facilities were not armed until after 2011, which was around the time the Pentagon started militarizing police forces across the country.

“Between 2005 and 2014, VA police departments acquired millions of dollars’ worth of body armor, chemical agents, night vision equipment, and other weapons and tactical gear,” The Intercept said.

Within the $2.2 trillion CARES Act, there was $850 million for the Coronavirus Emergency Supplemental Funding program, which is a federal grant program that injects new capital into the nation’s police forces. It has been used to cover overtime, increase personal protective equipment, and cover additional expenses related to the virus.

The militarization of America’s police forces shown below:

President Trump signed an executive order in 2017 allowing police forces to receive military weapons. More recently, President Trump signed an executive order that allows activating up to one million troops.

As to why the VA police would need riot gear is beyond anyone’s guess. However, the rapid militarization of police forces over the last decade shows the federal government could be preparing for social unrest.

- Can Debt Be Inflated Away?

Can Debt Be Inflated Away?

Tyler Durden

Mon, 05/18/2020 – 22:45By Paul Donovan, Chief Economist at UBS Global Wealth Management

-

Government debt to GDP ratios rarely fall in periods of high inflation. Since the 1970s, debt reduction has almost always taken place with low inflation.

-

Government spending is strongly linked to inflation. This can be formal (as with the US social security budget) or just because the government is a consumer in the market place and must pay the higher price.

-

If bond investors are hit with unexpected, high inflation they are unlikely to be happy. When this has happened in the past, investors have demanded an insurance against future inflation shocks. This risk premium raises the real cost of borrowing for a government, making it difficult to lower debt ratios over time.

-

Financial repression—a form of taxation where savers are forced to hold bonds—can be combined with inflation to reduce debt ratios. However, this hurts companies and threatens growth. Financial repression without inflation is a more effective solution. Governments are likely to use this method in the future.

Inflation is a complex topic. Entire books can be written about it. One of the myths that exist about inflation is that governments can easily inflate away their debt levels. In the modern world, government debt-to-GDP ratios rarely fall significantly in periods of high inflation. Since the 1970s, successful debt reduction has almost always taken place with low inflation.

What inflation should we use?

When talking about debt, it is income inflation not price inflation that matters. Income inflation makes it easier to pay down debt. If a person has a fixed rate mortgage that is three times their income, and their wages rise three times, then it is a lot easier to pay off the mortgage. Their debt to income ratio goes from 300% to 100%. Their income has “inflated” away their debt ratio.

For governments, the inflation rate that matters is also income inflation. How much a government’s tax revenue is growing tells you how easily they can pay down debt. This is why government debt is normally measured by the debt-to-GDP ratio. Because governments can tax the income of the domestic economy, the growth of the domestic economy is a quick way of measuring how easily debt can be managed.

The big difference between people and governments is that people are expected to repay their debt at the end of the mortgage. Governments are not. Governments need to borrow again and again. It is that fact that makes it so difficult for governments to inflate away their debt. It creates two problems.

Problem one – deficits grow with inflation

Government spending is increasingly tied to inflation. In the 1970s the US began to formally link social security payments to consumer price inflation. Japan’s pension payments have formally been tied to inflation since the 1970s as well. Even if there is not a formal tie, the government is a consumer in the market just like individuals. If prices go up, the consumer pays more. If building costs go up, then governments will pay more to build infrastructure, for example.

So while a government’s tax revenues will tend to increase with inflation, a significant part of government spending will also increase with inflation. This means that deficits will increase with inflation. Inflation is unlikely to help reduce the amount of money spent each year. This makes it harder to reduce the overall debt level. But the fact that deficits rise with inflation does not stop debt reduction. It just makes it harder. The real damage is done by the second problem—the reaction of bond markets.

Problem two – bond markets’ punishment offsets inflation’s help

Inflation itself is not a problem for bond investors. If investors were sure inflation will be 10% a year for ten years, they would happily buy bonds that covered the inflation cost. Bond yields would be 11.5%, guaranteeing a 1.5% real rate of return. But investors cannot be sure inflation will be 10% a year for ten years. Inflation uncertainty is a problem. If you think inflation is going to be 1% and it turns out to be 10% that is very bad news for the investor.

In reality, inflation cannot be kept absolutely stable. But if there is an expectation that it will not move much, and tend to get back to trend over time, investors are happy. If inflation starts to rise rapidly, that happiness disappears. Investors start demanding some kind of insurance against the unpredictable nature of inflation. Thus, if inflation jumps from 3% to 6% investors will want payment. They will want a real yield (in normal times, perhaps 1.5%). They will want payment for the inflation (6%). They will also want an insurance premium in case inflation does not turn out to be 6%, but comes in at 8% or 10%. That insurance is known as inflation uncertainty risk. It is worth somewhere between 1% and 1.5%.

In other words, if governments try to inflate their way out of debt, bond markets will demand a price. And because when a bond matures a new bond takes its place, that inflation uncertainty risk will eventually be charged for all the outstanding debt. It is not just new debt that costs government more. Eventually the existing debt will cost more money too.

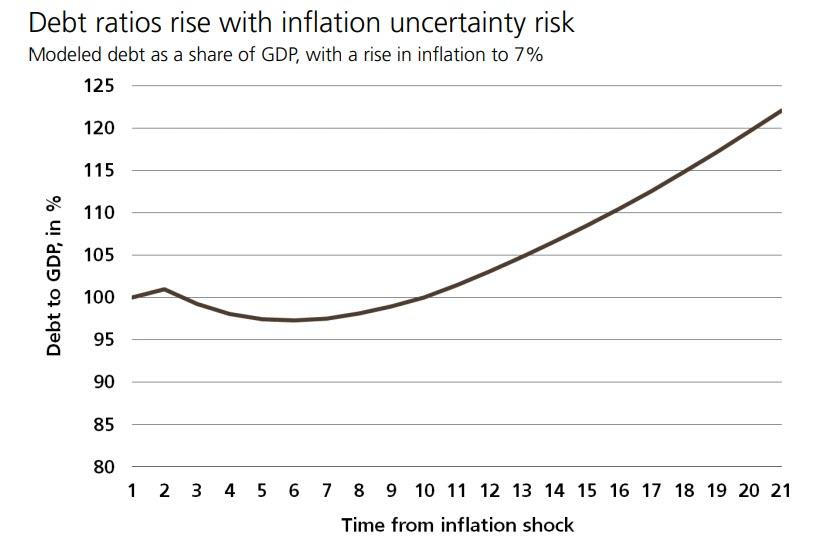

This chart is a simulation of what inflation uncertainty risk will do. This shows that inflation reduces debt ratios a little in the short term. As more and more bonds need to be refinanced, the inflation uncertainty risk raises the cost of borrowing for a larger and larger proportion of the debt. The debt-to-GDP ratio starts to rise, in spite of the inflation.

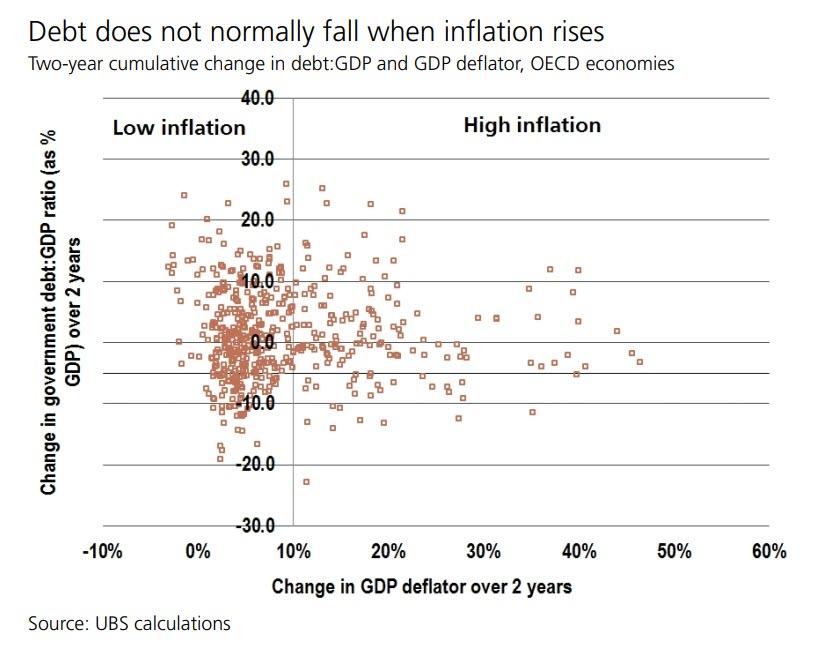

This chart shows the two-year change in government debt plotted against the two-year change in inflation, for each OECD country. The data covers 1970 to 2019, where available. Nearly all the debt reductions take place when inflation is low (below 5% per year). High inflation and debt reduction almost never take place at the same time.

Repression and inflation

Governments are likely to try to reduce debt levels after the virus by taxation. There is one particular form of tax that is likely to be popular— financial repression. Financial repression is when investors are forced to hold government bonds, at a lower yield than they would freely accept. Investors have been forced to give up some of the yield that they want to the government. Giving up money to the government is a tax, however much it may be disguised.

Financial repression has been effective in cutting debt in the past. Financial repression also means that bond markets cannot punish governments for inflation (at least, not as easily). Bond yields are forced lower under financial repression. So why not mix repression and inflation together?

While this mix would cut debt ratios, it would come at quite a high price. Financial repression normally only applies to government bonds. The inflation uncertainty risk would apply to corporate bonds. Without financial repression to help, the real cost of borrowing for companies would rise, hurting economic growth.

For a government it makes more sense to tax savers through financial repression, while keeping inflation moderate. Adding inflation does not reduce debt in the long term.

-

- America's First-Ever Jury Trial By Zoom Streamed Live Today

America’s First-Ever Jury Trial By Zoom Streamed Live Today

Tyler Durden

Mon, 05/18/2020 – 22:25Seemingly everyone knows about videoconferencing software company Zoom. Friends, family, co-workers, grandparents, and neighbors have stayed connected with video chat during the pandemic. Now a Texas court is preparing to conduct a jury trial by Zoom this week.

In a first, lawyers in an insurance dispute in Collin County District Court will present their case on Monday via Zoom to court officials, which will be available to watch on YouTube (click here for live stream — video will be streamed at some point on Monday). Jurours will be able to hear a “condensed version of a case and deliver a non-binding verdict,” reported Reuters.

“So we are going to have the jurors report through zoom,” 470th District Court Judge Emily Miskel told NBC DFW last week. “Doing a short trial through zoom. Having them deliberate through zoom and give a verdict.”

Texas Supreme Court Chief Justice Nathan Hecht recently said, “it’s just too dangerous” to have people in a “courthouse and make them sit together for days at a time.”

Judge Miskel said the Zoom trial could serve as a pilot program to see if the future of trials could one day be virtual.

“We’re open to creatively thinking about any way to be able to get the jury trials that they need, to allow citizens to participate in their jury service, and to do it through creative remote ways,” she said.

US courts have limited operations since mid-March when the pandemic lead to soaring virus cases and deaths. Many states locked down economies and enforced stay-at-home orders for citizens to flatten the pandemic curve. Some courts have already experimented with videoconferencing platforms, but the trial on Monday is a first.

Monday’s case is a dispute involving commercial property damages during a severe weather event in 2017. The summary jury trial is non-binding, which means lawyers could settle the matter. If there’s no agreement, a full jury trial will be slated an unknown date.

As concerns emerge about a second wave of the virus, courts might have to quickly adopt videoconferencing for trials.

If all goes well on Monday, virtual trials could soon become the norm.

- Ron Paul Rages: Listening To Virus "Experts" Has Led To Death & Despair

Ron Paul Rages: Listening To Virus “Experts” Has Led To Death & Despair

Tyler Durden

Mon, 05/18/2020 – 22:05Authored by Ron Paul via The Ron Paul Institute for Peace & Prosperity,

On April 21st the Washington Post savaged Georgia governor Brian Kemp’s decision to begin opening his state after locking down for weeks. “Georgia leads the race to become America’s No. 1 Death Destination,” sneered the headline.

The author, liberal pundit Dana Milbank, actually found the possibility of Georgians dying to be hilarious, suggesting that, “as a promotion, Georgia could offer ventilators to the first 100 hotel guests to register.”

Milbank, who is obviously still getting paid while millions are out of work, sees his job as pushing the mainstream narrative that we must remain in fear and never question what “experts” like Dr. Fauci tell us.

Well it’s been three weeks since Milbank’s attack on Georgia and its governor, predicting widespread death which he found humorous. His predictions are about as worthless as his character. Not only has Georgia not seen “coronavirus…burn through Georgia like nothing has since William Tecumseh Sherman,” as Milbank laughed, but Covid cases, hospitalizations, and deaths have seen a steep decline since the governor began opening the state.

Maybe getting out in the fresh air and sunshine should not have been prohibited in the first place!

In fact, as we now have much more data, it is becoming increasingly clear that the US states and the countries that locked down the tightest also suffered the highest death rates. Ultra locked-down Italy suffered 495 Covid deaths per million while relatively non-locked down South Korea suffered only five deaths per million. The same is true in the US, where non lockdown states like South Dakota were relatively untouched by the virus while authoritarian-led Michigan, New York, and California have been hardest hit.

In those hardest hit states, we are now seeing that most of the deaths occurred in senior care facilities – after the governors ordered patients sick with Covid to leave the hospitals and return to their facilities. There, they infected their fellow residents who were most likely to have the multiple co-morbidities and advanced age that turned the virus into a death sentence. Will these governors be made to answer for this callous disregard for life?

Yesterday, Health and Human Services Secretary Alex Azar admitted the obvious:

“We are seeing that in places that are opening, we’re not seeing this spike in cases.”

So why not open everything? Because these petty tyrants cannot stand the idea of losing the ability to push people around.

Shutting down the entire United States over a virus that looks to be less deadly than an average flu virus – particularly among those under 80 who are not already sick – has resulted in mass unemployment and economic destruction. More Americans may die from the wrong-headed efforts to fight the virus than from the virus itself.

Americans should pause and reflect on the lies they are being sold. Masks are just a form of psychological manipulation. Many reputable physicians and scientists have said they are worthless and potentially harmful. Lockdowns are meant to condition people to obey without question.

A nation of people who just do what they are told by the “experts” without question is a nation ripe for a descent into total tyranny.

This is no empty warning – it’s backed up by history. Time to stand up to all the petty tyrants from our hometowns to Washington DC. It is time to reclaim our freedom.

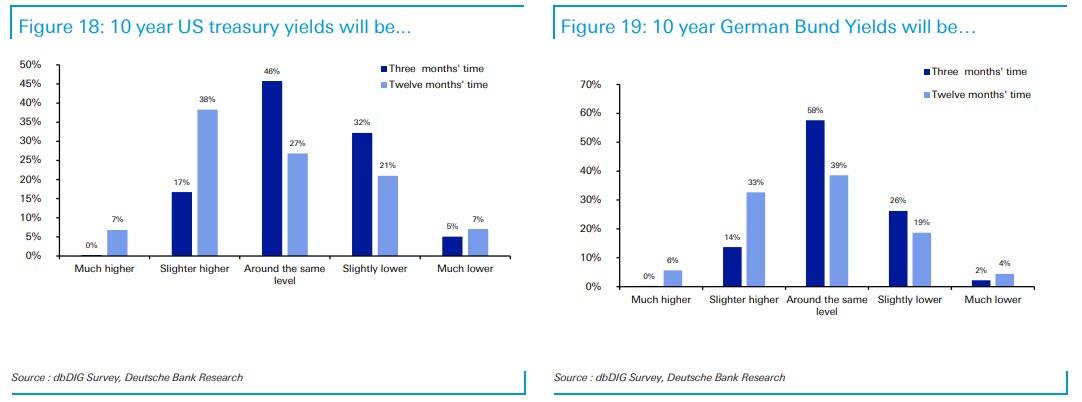

- Majority On Wall Street Expects Stocks Lower In 3 Months, Braces For Second Virus Wave

Majority On Wall Street Expects Stocks Lower In 3 Months, Braces For Second Virus Wave

Tyler Durden

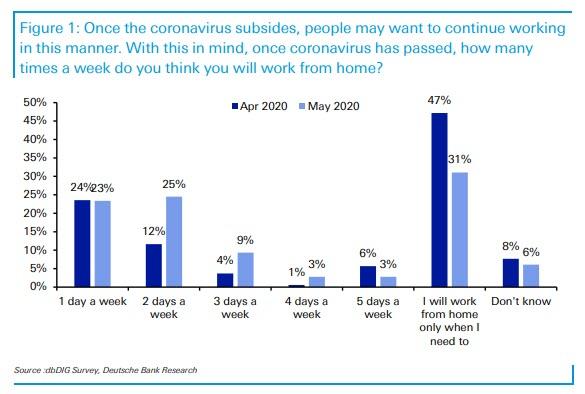

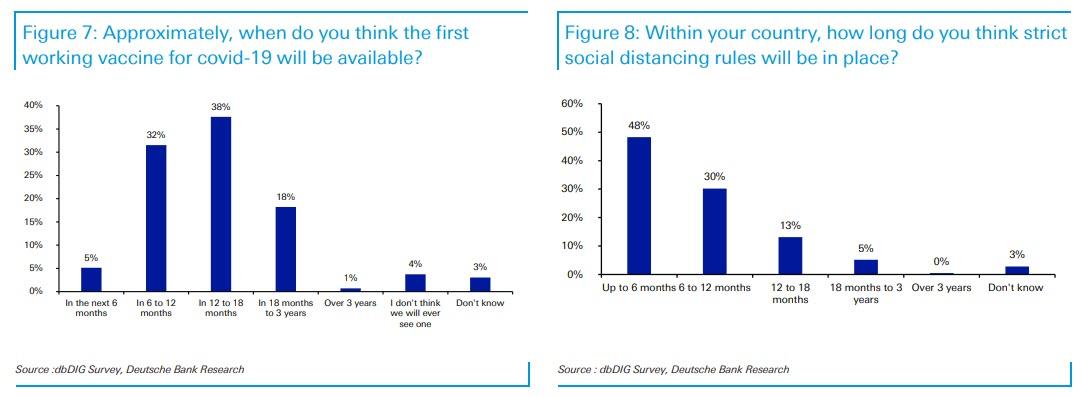

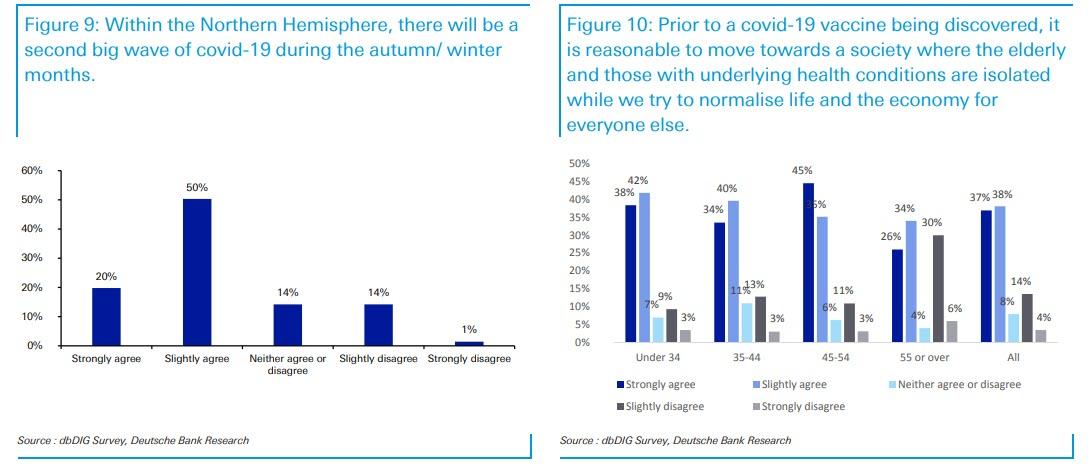

Mon, 05/18/2020 – 21:45Between May 13 -15th, Deutsche Bank conducted its seventh monthly market sentiment survey covering 450 market professionals across the world, in which questions emphasized the covid-19 pandemic around the working from home (WFH) experience as well as also people’s thoughts on the duration of this pandemic, and how that will impact various parts of their lives as well as how market expectations have evolved.

In terms of WFH it seems that more people are getting comfortable with this being a more regular feature post covid relative to last month. 57% (39% last month) think they’ll do 1-3 days per week WFH in a post-covid world. Those thinking they’ll only do it when they need to has dropped to 31% from 47% last month.

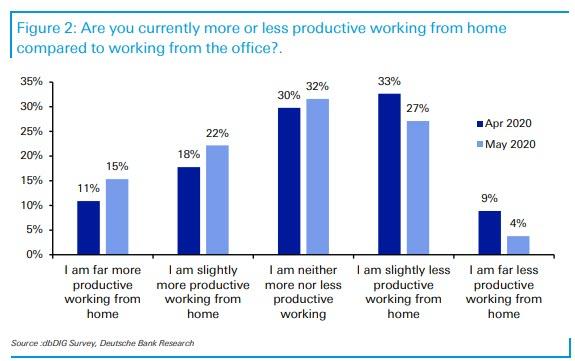

According to DB’s Jim Reid, “this reflects an improvement in productivity in month two of shutdowns. We’ve seen the net balance of more productive vs less productive WFH increase from -13% to +7%. The amount who claim to be as productive or more productive WFH has gone up from 58% to 69%.” This may reflect IT departments getting more able to handle the vast increase in traffic and end users ensuring their set-up has improved. However, 31% say they are less productive WFH (42% last month), so it’s not for everyone.

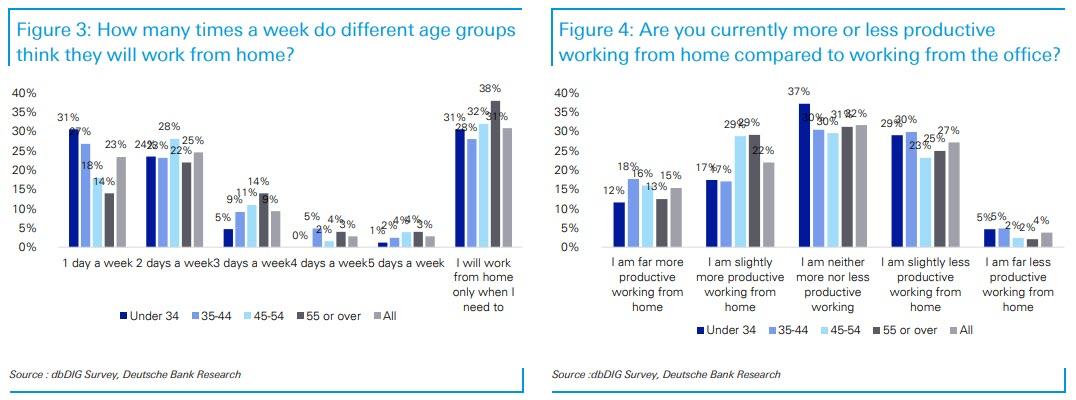

The survey reveals an age bias: under 34 year olds were net -5% more productive at home. For 35-44yrs this was flat (0%). For 45-55 yr olds (+19%) and over 55 yr old (+15%) the pendulum swings to them being more productive. This is perhaps a reflection of younger people more likely to live in smaller city flats with less space for an optimum set up. They may also require more mentoring and guidance to thrive. The answer may also be skewed to whether people have young kids at home at the moment? Interestingly across all ages the answer “I am far less productive at home” only received 2-5%. I am “far more productive” saw answers of 12-18% across the ages.

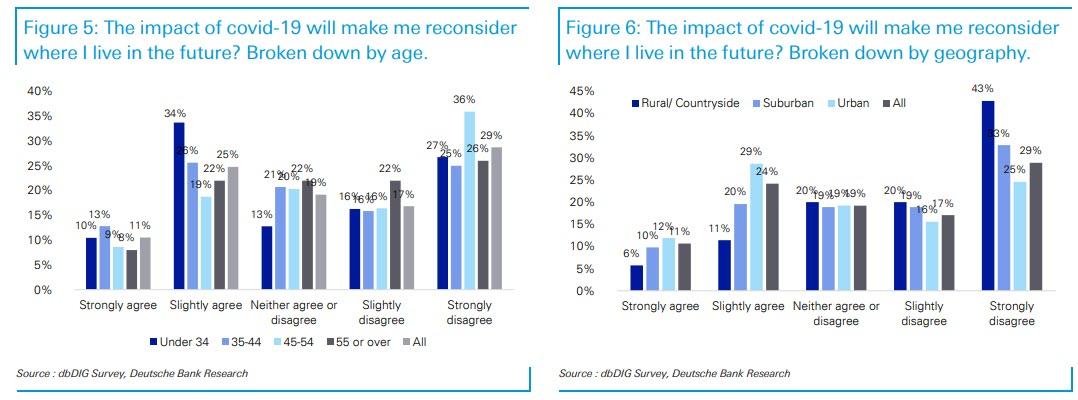

The under 34-year-olds are also the one group most likely to review where they live as a result of covid-19 but on balance they are just about net (+1%) happy with where they live. The older we get, though, the less likely we are to reconsider where we live due to the virus with this peaking forv45-55 year olds (-25%). Urban dwellers of all ages are neutral on balance (0%) as to whether covid-19 will make them assess where they live. Suburban (-22%) and Rural (-46%) dwellers are far less inclined to review where they live post covid-19 though.

In terms of the virus, people are generally optimistic (74%) on a vaccine being available within 18 months even if only 5% think within six months. Only 4% think that we’ll never see one. 48% think social distancing will only last for the next 6 months with a further 30% thinking an extra 6 months on top.

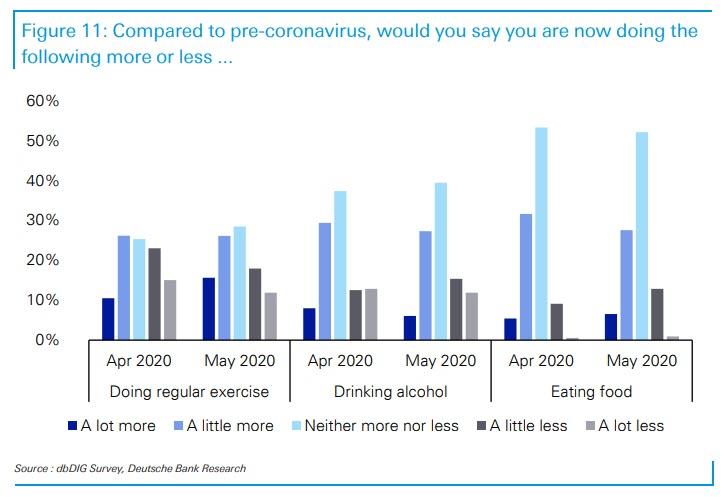

A net 55% agree with Lloyd Blankfein that there will be a second wave of the virus and a net 58% agree with shielding the elderly and those with underlying conditions and trying to restart the economy prior to a vaccine being available. Unsurprisingly a net 67% of under 34 year olds agreed with this compared to a net 24% for over 55 year olds.

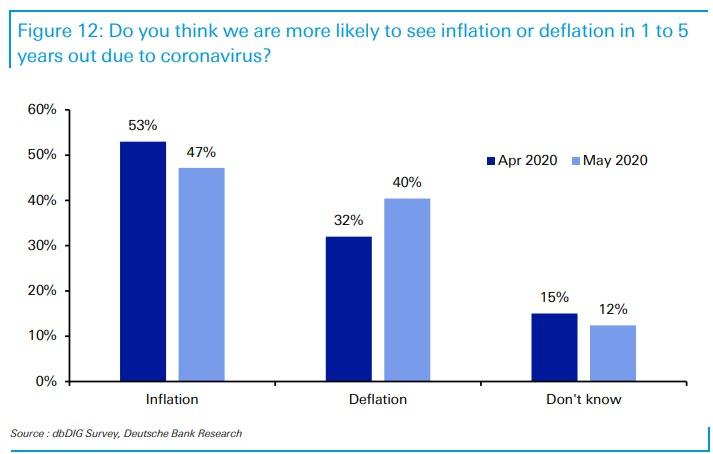

Some good news: in month two of lockdown it seems people are getting healthier relative to month one. Exercise is up on pre-covid levels now with +12% doing more than they were pre-lockdown (-1% balance last month) and whilst alcohol consumption is up (+6%), it’s less than it was last month (+12%). People are still eating more food (+20% balance) but it’s less than last month (+27%).

Moving to our more markets-based questions, people still think the covid crisis will be inflationary (47% to 40%) but this has narrowed relative to last month (53% to 32%).

Now that there are seven months’ worth of data on S&P 500 expectations, Jim Reid was able to see how net expectations measure matches up with market performance through the survey history period. 3-month expectations were closely aligned with price action into the market decline during March but seem to not have caught the rebound through April and so far in May. 12-month expectations had been roughly the inverse, but we have seen long-term expectations roll over this month along with the short-term views.

Given the recent rally in equities and lack of improving economic data in Europe and the US, sentiment has gotten more bearish in the last month, especially in the short term. A majority (42%) see equity prices slightly lower over the next 3 months for the S&P 500 and Stoxx 600, before improving over the next 12 months. However, it is the lowest net higher expectation for the S&P 500 since February as ‘only’ 13% on balance believe the index will be higher a year from now, down from 47% two months ago as the crisis was causing the first big dip in markets. Respondents were torn on 12 month expectations for the Stoxx 600, with an equal number thinking the index would be higher or lower.

With Treasury yields near all-time lows and further conversations over negative US rates (even as they are opposed by the Fed), expectations lean toward US core rates falling further over the next 3 months (37% vs 17% to rise) but then rising again over 12 months (45% rise against 28% lower). Similarly bund yields are expected to fall by 28% of respondents over 3 months (14% rise), but over 12 months, 38% expect a rise against only 23% expecting further falls.

There continue to be fairly strong expectations that Italian yields to bunds will widen over the next 3 and 12 months. Net 34% expect wider spreads in 3 months, the most one-sided that short term expectations have been in 5 months of asking. Meanwhile, a net 26% expect wider in 12 months. In terms of Italy being in the Eurozone in 5 years, 14% think it won’t be, which is up from 7% when first asked back in November last year. The budgetary pandemic shock is certainly knocking confidence on this measure.

Finally, with the US election just under 6 months away, a net of 23% believe President Trump will receive a second term, though respondents continue to become steadily more bearish on his re-election chances. Our survey has always heavily favored Trump’s electoral chances but more and more doubts are emerging. The economic fallout of covid-19 and the country’s lingering and sizeable case numbers seem to have dulled any polling bounce Mr. Trump received at the beginning of the outbreak. This is the lowest that respondents have thought his re-election was “extremely likely”. This is now at 14%, having peaked at 63% in February.

- "This Is Not A Costless Exercise" – The Unintended Consequences Of Monetary Inflation

“This Is Not A Costless Exercise” – The Unintended Consequences Of Monetary Inflation

Tyler Durden

Mon, 05/18/2020 – 21:25Authored by Alasdair Macleod via GoldMoney.com,

“In short, the Fed is committed to rescue businesses from the greatest economic catastrophe since the great depression and probably even greater than that, to fund the US Government’s rocketing budget deficits, fund the maintenance of domestic consumption directly or indirectly through the US Treasury, while pumping up financial markets to achieve these objectives and preserve the illusion of national wealth.

Clearly, we stand on the threshold of an unprecedented monetary expansion.”

Introduction

President Reagan memorably said that the nine words you don’t want to hear are “I’m from the government and I’m here to help.” Governments in all the major jurisdictions are now making good on that unwanted promise and are taking responsibility for everything from our shoulders.

Those receiving subsidies and loan guarantees are no doubt grateful, though they probably see it as the government’s duty and their right. But someone has to pay for it. In the past, by the redistribution of wealth through taxes it meant that the haves were taxed to give financial support to the have-nots, at least that was the story. Today, through monetary debasement nearly everyone benefits from monetary redistribution.

This is not a costless exercise. Governments are no longer robbing Peter to pay Paul, they are robbing Peter to pay Peter as well. You would think this is widely understood, but the Peters are so distracted by the apparent benefits they might or might not get that they don’t see the cost. They fail to appreciate that printing money is not just the marginal source of finance for excess government spending, but it has now become mainstream.

There is almost a total absence in the established media of any commentary on the consequences of monetary inflation, and in a cry for more we even have financial experts warning us of a deflationary collapse and the need for the Fed to introduce negative interest rates to stave off deflation. Yes, there are deflationary forces, because banks wish to reduce their loan exposure at a time of increasing risk. But we can be sure central banks and their political masters will do everything they can to counter the trend of contracting bank credit by increasing base money. There can only be one outcome: the debasement and eventual destruction of fiat currencies.

It was the nineteenth century French economist, Frederic Bastiat, who pointed out there were unseen consequences from violating property. He took the biblical approach of a parable, famous as the broken window fallacy. It is not what is seen, but what is unseen. He told of a boy breaking a window, its destruction giving business to the glazier which he would not otherwise have had. That is seen; unseen is the constructive spending that otherwise would have occurred if the cost of the broken window had not been incurred.

We see the helicoptered money, the furlough support, and the businesses helped not to go bust. But we do not see the cost. We don’t see how the resources taken up might otherwise be constructively deployed. We are told that the government is paying for it all, but taxes are not being raised.

Was Reagan’s aphorism wrong after all? If so, the government employee on our doorstep with his offer of help is to be welcomed. He comes bearing gifts. And without an increase in taxes what is not to like?

Bastiat gave us the answer. Unfortunately, the unseen consequences of apparently costless inflationary financing are myriad, as we will painfully discover.

The Cantillon effect

Over a century before Bastiat, an Irish banker in France, Richard Cantillon, observed that new money drove up prices as it was spent. He had experienced John Law’s Mississippi bubble, which was fueled by printed money and the issuance of bank credit, so Cantillon had observed the effect. It made well-connected speculators their fortunes, whose profligate spending drove up prices for everyone else. The effect at that time was that in real terms insiders became rich and the poor got poorer. To this day the process by which this happens is known as the Cantillon effect.

Now that it is official policy, the lesson for today is that a rapid increase in monetary inflation will, as the effects trickle through the economy, further impoverish the poor. It will do this by driving up prices of their essentials and reducing the purchasing power of their salaries, if they are lucky enough to still be employed. But as Cantillon pointed out in his Essai, reflecting the increased quantity of circulating money prices rise unevenly. Never has it been truer than today, when we face the combination of an unprecedented slump in economic activity combined with a sharp escalation in monetary inflation: the rich whose stocks are rising can buy their expensive toys at knockdown prices, while the poor, increasing numbers of which are newly unemployed, struggle to make ends meet with rising prices for life’s essentials.

It gets worse. Just as in Cantillon’s day, modern monetary policy is aimed at maintaining and increasing financial asset values. John Law’s puffery attempted to inflate the combination of his Banque Royale and his Mississippi ventures. Today it is all government bond markets, corporate debt, and stocks and shares. The intention is to maintain and further a wealth effect to replace the true wealth that has been lost, originally accumulated by entrepreneurs and businessman serving the consumer successfully. All we have now is John Law-style puffery.

The enrichment of the few at the expense of the many is a finite process. The outcome will inevitably be the same: Law’s scheme began to run into headwinds in December 1719, and by the following September his unbacked currency had failed. It was dead, worthless, an ex-currency. The empirical evidence is clear. Central banks emulating Law’s scheme today will destroy their currencies and everything that floats on their seas of paper credit and debt. The rapidity of the collapse of the Mississippi scheme strongly suggests that once control over bond prices is lost the contemporary financial and monetary collapse will be similarly swift.

For this reason, understanding the consequences of monetary inflation spiralling out of control has never been more important. We should know what they are from a study of sound economic theory and empirical evidence. The poor will starve and many of those who became rich through financial asset inflation will eventually join them. For the latter class, there will come a point where they abandon a failing dollar-based inflation scheme to save what they can from the financial wreckage.

Distortions and misallocations of capital

There is an aspect of the destruction brought about by monetary policy, which is almost never considered by policy makers, and that is how it distorts the allocation of capital and leads to its misallocation. In free markets, capital is scarce and must be used to greatest effect if the consumer is to be properly served and the entrepreneur is to maximise his profits.

Capital comes in several forms and encompasses every aspect of production; principally an establishment, machinery, labour, semi-manufactured goods and commodities to be processed, and money. An establishment, such as a factory or offices, and the availability of labour are relatively fixed in their capacity. Depending on their deployment and capacity they produce a limited amount of goods. It is just the one form of capital, that is money and credit, which central banks and the banking system now provide, and which in its unbacked form is infinitely flexible. Consequently, attempts to stimulate production by monetary means run into the capacity constraints of the other forms of capital.

Monetary policy has been increasingly used to manipulate capital allocation since the early days of the great depression in the 1930s. The effect has varied but it has generally come up against the constraints of the other forms of capital. Where there is excess labour, it takes time to retrain it with the specialist skills required, a process hampered by trade unions ostensibly protecting their members, but in reality, resisting reallocation of labour resources. Government control over planning and increasingly stifling regulations, again putting a brake on change, meant that changes and additions to the use of establishments lengthen the time before entrepreneurial investment was rewarded with profits. Government intervention has also discouraged the withdrawal of monetary capital from unprofitable deployment, or malinvestments, lengthening recessions needlessly.

When the advanced nations had strong industrial cores, the periodic expansions of credit and their subsequent sudden contractions led to observable booms and busts in the classical sense, since production of labour-intensive consumer goods dominated production overall.

There were then two further developments. The first was the abandonment of the Bretton Woods agreement in 1971, which led to a substantial rise in prices for commodities. According to the broad-based UN index of commodities rose from 33 to 157 during the decade, a rise of 376%. This input category of production capital compared unfavourably with US consumer price increases over the decade of 112%, the mismatch between these and other categories of capital allocation making economic calculation a fruitless exercise. The second development was the liberation of financial controls in the mid-eighties, London’s big-bang and the repeal of America’s Glass Steagall Act of 1933, allowing commercial banks to fully embrace and exploit investment banking activities.

The banking cartel increasingly directed its ability to create credit towards purely financial activities mainly for their own books, thereby financing financial speculation, while de-emphasising bank credit expansion for production purposes for all but the larger corporations. Partly in response, the nineties saw businesses move production to low-cost centres in South-East Asia where all forms of production capital, with the exception of monetary capital, were significantly cheaper and more flexible.

There then commenced a quarter-century of expansion of international trade replacing much of the domestic production of goods in the US, the UK, and Europe. It was these events that denuded America of its manufacturing, not unfair competition as President Trump has alleged and Germany’s retention of manufactures proves. But the effect has been to radically alter how we should interpret the effects of monetary expansion on the US economy and others, compared with Hayekian triangles and the like.

Business cycle research had assumed a capitalistic structure of savers saving and thereby making monetary capital available to entrepreneurs. Changes in the propensity to save sent contrary signals to businesses about the propensity to consume, which caused them to alter their production plans. Based on the ratio between consumer spending and savings, this analytic model has been corrupted by the state and its licensed banks by replacing savers with former savers now no longer saving, and even borrowing to consume.

Today, the inflationary origins of investment funds for business development are hidden through financial intermediation by venture capital funds, quasi-government funds and others. Being mandatory, pension funds continue to invest savings, but their beneficiaries have abandoned voluntary saving and run up debts, so even pension funds are not entirely free of monetary inflation. Insurance funds alone appear to be comprised of genuine savings within an inflationary system.

Other than pension funds and insurance companies, Keynes’s wish for the euthanasia of the saver has been achieved. He went on to suggest there would be a time “when we might aim in practice… at an increase in the volume of capital until it ceases to be scarce, so that the functionless investor will no longer receive a bonus…”

Now that everywhere bank deposits pay no interest, his wish has been granted, but Keynes did not foresee the unintended consequences of his inflationist policies which are now being visited upon us. Among other errors, he failed to adequately account for the limitation of non-monetary forms of capital, which leads to bottlenecks and rising prices as monetary expansion proceeds.

The unintended consequences of neo-Keynesian policy failures are shortly to be exposed. The checks and balances on the formation and deployment of monetary capital in the free market system based on the division of labour have been completely destroyed and replaced by inflation. So, where do you take us from here, Mr Powell, Mr Bailey, Ms Lagarde, Mr Kuroda?

Taking stock

We can now say that America, the nation responsible for the world’s reserve currency, has encouraged policies which have turned its economy from being a producer of goods with supporting services as the source of its citizens’ wealth into little more than a financial casino. The virtues of saving and thrift have been replaced by profligate spending funded by debt. Unprofitable businesses are being supported until the hoped-for return of easier times, which are now gone.

Cash and bank deposits (checking accounts and savings deposits) are created almost entirely by inflation, and currently total $15.2 trillion in the US, while total commercial bank capital is a little under $2 trillion. This tells us crudely that $13 trillion sitting in customer accounts can be attributed to bank credit inflation. Increasing proportions of those customers are financial corporations and foreign entities, and not consumers maintaining cash and savings balances.

On the other side of bank balance sheets is consumer debt, mostly off-balance sheet, but ultimately funded on-balance sheet. Excluding mortgages, the total comprised of credit cards, autos and student debt was $3.86 trillion in mid-2019, amounting to an average debt of $27,571 per household, confirming the extent to which consumer debt has replaced savings.

At $20.5 trillion, bank balance sheets are far larger than just the sum of cash and bank deposits, giving them a leverage of over ten times their equity. Bankers will be very nervous of the current economic situation, aware that loan and other losses of only ten per cent wipes out their capital. Meanwhile, their corporate customers are either shut down, which means most of their expenses continue while they have no income, or they are suffering payment disruptions in their supply chains. In short, bank loan books are staring at disaster. Effectively, the whole banking system is underwater at the same time as the Fed is extolling them to join with it in rescuing the economy by expanding their balance sheets even more.

The sums involved in supply chains are considerably larger than the US’s GDP. Onshore, it is a substantial part of the nation’s gross output, which captures supply chain payments at roughly $38 trillion. Overseas, there is a further mammoth figure feeding into the dollar supply chain, taking the total for America to perhaps $50 trillion. The Fed is backstopping the foreign element through currency swaps and the domestic element mainly through the commercial banking system. And it is indirectly funding government attempts to support consumers who are in the hole for that $27,571 on average per household.

In short, the Fed is committed to rescue all business from the greatest economic collapse since the great depression, and probably greater than that, to fund the US Government’s rocketing budget deficits, fund the maintenance of domestic consumption directly or indirectly through the US Treasury, while pumping financial markets to achieve these objectives and preserve the illusion of national wealth.

Clearly, we stand on the threshold of an unprecedented monetary expansion. Part of it will be, John Law style, to ensure inflated prices for US Treasuries are maintained. At current interest rates debt servicing was already costing the US Government 40% of what was expected to be this year’s government deficit. That bill will now rise beyond control even without bond yields rising. Assistance is also being provided to the corporate debt market. Blackrock has been deputed to channel the Fed’s money-printed investment through ETFs specialising in this market. So not only is the Fed underwriting the rapidly expanding US Treasury market, but it is underwriting commercial dollar debt as well.

In late-1929, a rally in the stock market was prolonged by a similar stimulus, with banks committed to buying stocks and the Fed injecting $100m liquidity into markets by buying government securities. Interest rates were cut. And when these attempts at maintaining asset prices failed, the Dow declined, losing 89% of its value from September 1929.

Today, similar attempts to rescue economies and financial markets by monetary expansion are common to all major central banks, with the possible exception of the ECB, which faces the unexpected obstacle of a challenge by the German Constitutional Court claiming primacy in these matters. There is therefore an added risk that the global inflation scheme will unravel in Europe, which if it does will rapidly lead to funding and banking crises for the spendthrift member states. Doubtless, any financial contagion will require yet more money-printing by the other major central banks to ensure there are no bank failures in their domains.

Whither the exit?

So far, few commentators have grasped the implications of what amounts to the total nationalisation of the American economy by monetary means. They have only witnessed the start of it, with the Fed’s balance sheet reflecting the earliest stages of the new inflation which has seen its balance sheet increase by 61% so far this year. Not only will the Fed battle to fund everything, but it will also have to compensate for contracting bank credit, which we know stands at about $18 trillion.

The Fed must be assuming the banks will cooperate and pass on the required liquidity to save the economy. Besides the monetary and operational hurdles such a policy faces, it cannot expect the banks will want responsibility for the management of businesses that without this funding would not exist. The Fed, or some other government agency has to then decide one of three broad options: further support, withdrawing support, or taking responsibility for business activities. This last option involves full nationalisation.

We must not be seduced into thinking this is an outcome that can work. The nationalisation of failing banks and their eventual privatisation is not a good precedent for wider nationalisation, because a bank does not require the entrepreneurial flair to estimate future consumer demand and to undertake the economic calculations to provide for it. The state taking over business activities fails for this reason, demonstrated by the collapse of totalitarian states such as the USSR and the China of Mao Zedong.

That leaves a stark choice between indefinite monetary support or pulling the rug from under failing businesses. There are no prizes for guessing that pulling rugs will be strongly resisted. Therefore, government support for failing businesses is set to continue indefinitely.

At some stage, the dawning realisation that central banks and their governments are steering into this economic cul-de-sac will undermine government bond yields, despite attempts by central banks to stop it, even if the deteriorating outlook for fiat currencies’ purchasing power does not destroy government finances first.

Earlier in the descent into the socialisation of money, nations had opportunities to change course. Unfortunately, they had neither the knowledge nor the guts to divine and implement a return to free markets and sound money. Those opportunities no longer exist and there can be only one outcome: the total destruction of fiat currencies accompanied by all the hardships that go with it.

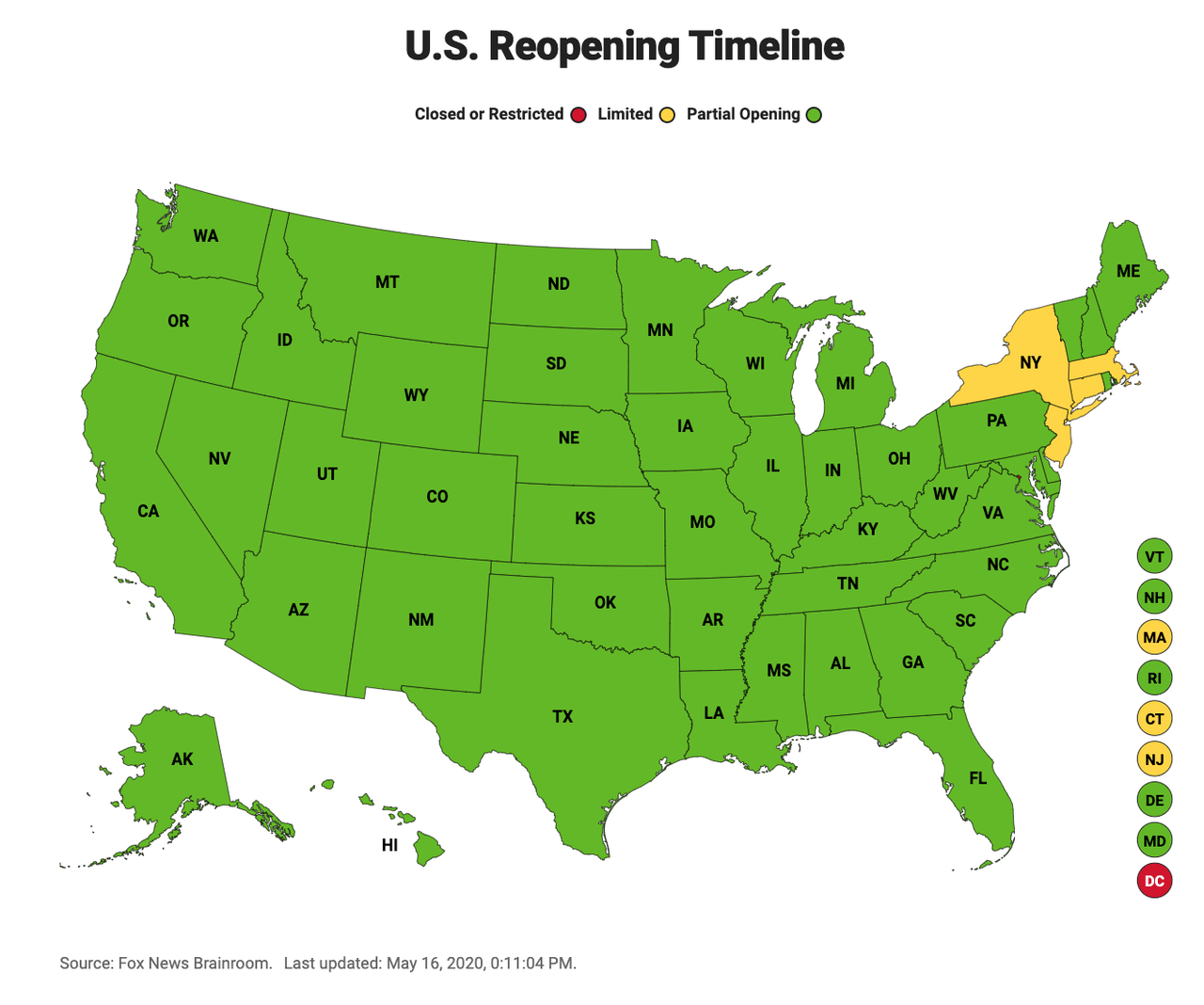

- "Bumper Tables" For Socially-Distant Dining Appear In Maryland

“Bumper Tables” For Socially-Distant Dining Appear In Maryland

Tyler Durden

Mon, 05/18/2020 – 21:05Vistors are headed back to Ocean City, Maryland’s beach and boardwalk after Gov. Larry Hogan relaxes the stay-at-home order. At one restaurant over the weekend, a post-corona world was recognized with what is being called a socially distant dining experience, reported The Baltimore Sun.

Shaped like a giant donut with an outer perimeter lined with an inner tube, the socially distant tables were custom made for Fish Tales waterfront restaurant. The restaurant posted a Facebook Live video of employees unloading the new tables from a large box truck.

“It’s like a bumper boat, but it’s a table,” Fish Tales owner Shawn Harmon told Delmarva Daily Times, referring to the design of the table, which was created by a Baltimore-based design firm.

A customer stands in the center of the table surrounded by a rubber barrier that keeps patrons about six-feet apart. The tables have wheels and allow patrons to move around the restaurant.

Several months of lockdowns have led to restaurants and bars shuttering operations across Maryland — except for carryout and delivery service. The state inched into phase one of its Roadmap to Recovery, dining in could become a reality later this year, that is if a second virus wave doesn’t materialize.

Fish Tales is providing curbside and carryout service at the moment, with preparations to reopen its restaurant and bar when restrictions are lifted.

This restaurant in Maryland intends to use bumper tables to keep customers six feet apart once it begins to take seated diners. pic.twitter.com/ReCLbzcowF

— CBS News (@CBSNews) May 18, 2020

Erin Cermak, the owner of Revolution, the firm responsible for designing and producing the tables, said: “we’re an event company, and events have taken a hard hit, so we’ve been trying to figure out a way that events and things can still happen.”

She said they’ve gotten an “incredible reaction” so far and are in discussions with other restaurants.

Hogan made the announcement last week to relax stay-at-home orders and reopen the state. Though reopening the state will not return Maryland nor any other part of the country back to 2019 growth levels. Businesses and households have been finally damaged because of lockdowns.

Current US reopening timeline

At least a quarter of restaurants in the US are expected to fail. Many that remain open will have to develop creative technologies with social distancing in mind to attract patrons.

We noted last week, McDonald’s opened a prototype restaurant outfitted with a new social distancing layout. The move is to test new safety measures for guests and employees that will limit the spread of the virus once lockdowns are relaxed.

The restaurant industry will be severely impacted and might not return to 2019 activity levels for years.

- Nasdaq Imposes Restrictions On Chinese IPOs, Halting Futures Rally

Nasdaq Imposes Restrictions On Chinese IPOs, Halting Futures Rally

Tyler Durden

Mon, 05/18/2020 – 21:00In a move that anyone who has ever invested in a Chinese fraud stock (which one can argue are most of them) will argue is long overdue, late on Monday Reuters reported that the Nasdaq is set to unveil new restrictions on initial public offerings, in a move that will make it more difficult for some Chinese companies to debut on its stock exchange.

While Nasdaq will not cite Chinese companies specifically in the changes, according to Reuters, the move is being driven by concerns about some of the Chinese IPO hopefuls’ lack of accounting transparency and close ties to powerful insiders.

And since the Nasdaq move, which may well be prompted by legitimate widespread concerns about shady Chinese accounting, comes just days after the Trump administration barred a government retirement fund from investing in Chinese equities, it will be seen by Beijing as another political intervention in soft capital controls imposed by the US vis-a-vis Chinese equities, inviting further retaliation from China against this “latest flashpoint in the financial relationship between the world’s two largest economies.”

Nasdaq also unveiled some restrictions on listings last year, seeking to curb IPOs by small Chinese companies. Their shares often trade thinly because most stay in the hands of a few insiders. Their low liquidity makes them unattractive to many large institutional investors, to whom Nasdaq is seeking to cater.

Whatever the reason behind the move, it has been a long time coming, considering the ease with which countless Chinese frauds are allowed to list in the US and soak up capital of gullible US investors. Last month, Luckin Coffee which had a U.S. IPO in early 2019, announced that an internal investigation had shown its chief operating officer and other employees fabricated sales deals.

The new rules will require companies from some countries, including China, to raise $25 million in their IPO or, alternatively, at least a quarter of their post-listing market capitalization, the Reuters sources said. This would represent the first time Nasdaq has put a minimum value on the size of IPOs. The change would have prevented several Chinese companies currently listed on the Nasdaq from going public. Out of 155 Chinese companies that listed on Nasdaq since 2000, 40 grossed IPO proceeds below $25 million, according to Refinitiv data.

And while it was not immediately clear how many of these IPOs were Chinese, Reuters notes that Chinese firms have historically pursued such small IPOs because they allow their founders and backers to cash out, rewarding them with U.S. dollars they cannot easily access because of China’s capital controls. And they have US bagholders, and lax exchange listing standards to thank. At the same time, these newly IPOed frauds would also use their Nasdaq-listed status to convince lenders in China to fund them and often get subsidies from Chinese local authorities for becoming publicly traded.

Finally, the proposed rules will also require auditing firms to ensure that their international franchises comply with global standards, and Nasdaq will also inspect the auditing of small U.S. firms that audit the accounts of Chinese IPO hopefuls, the sources added.

The news of the restriction hit S&P futures – which were on their way to regaining the 2950 handle that had failed twice – slid to session lows below the key resistance level on a day when there was no talk of trade war, and instead the market was obsessing over what in retrospect will end up being one giant “Made in the US” bait-and-switch by Moderna, which sold $1.25BN in stock after soaring earlier in the day on news of a “successful” Phase 1 coronavirus vaccine trial which involved eight “young and healthy” people.

Meanwhile, ahead of the Nasdaq news and perhaps sensing what was coming, China has been urging domestic companies to look at listing in London, Reuters also reported earlier in the day, as the country aims to revive deals under a Stock Connect scheme and strengthen overseas ties in the wake of the coronavirus crisis.

The Shanghai-London Stock Connect scheme, which began operating last year, aims to build links between Britain and China, help Chinese companies expand their investor base and give mainland investors access to UK-listed companies.

The original plan was for several companies to take part in the scheme in the first couple of years, but so far only one company — Huatai Securities — made the trip from Shanghai to London last June.

But now Chinese authorities have given the go-ahead for China Pacific Insurance and SDIC Power to move ahead with their London-listing plans, the sources said, after both deals were halted last year.

They also gave the nod to China Yangtze Power (600900.SS) to begin preparations for a secondary listing on the London Stock Exchange, the sources said, speaking on condition of anonymity as the matter is confidential.

The sources, including officials from banks, government and exchanges, said that the aim was to push for a resumption of listings under the Stock Connect scheme as China seeks to improve ties with the outside world and help to fund its post-lockdown recovery. “In the second half of this year, we could see one or maybe two Chinese companies list in London,” said one of the sources, who is closely involved in the process.

“China is among the first countries to come out of lockdown, and is keen to get back on track with plans to improve trade relations with the UK,” he added, by which he of course meant finding more gullible, naive investors to part with their money after investing in the next Chinese Luckin-like fraud, especially if the US window is closing.

- The Revenge Of "Bobo The Clown"? How The Media Is Inadvertently Reelecting Donald Trump

The Revenge Of “Bobo The Clown”? How The Media Is Inadvertently Reelecting Donald Trump

Tyler Durden

Mon, 05/18/2020 – 20:45Various media outlets are struggling with recent polls that not only show President Trump at the same popularity as this time last year but actually rising in states like Ohio. When one poll found him leading by 7 points in battleground states, John King cautioned viewers to “be careful not to invest too much in any one poll” especially amid the coronavirus.

It was a CNN poll and, while Biden leads in other polls, it is not unique.

The media seems honestly confused. It was not supposed to work this way. With unrelentingly negative coverage of an impeachment, a pandemic, and an economic collapse, voters were supposed to be angry. There is even a psychological model for such social cognitive learning or conditioning called “Bobo the Clown” and, while this experiment by psychologist Albert Bandura, these polls suggest that conditioning does not work nearly as well in politics as it does on playgrounds.

In 1961, Bandura used a goofy inflatable clown named Bobo and had children watch adults as they acted aggressively toward it. Soon the children followed the adults’ example and beat the clown. Conversely, when children watched the clown being treated without aggression, they were less aggressive toward it.

For many voters, Donald Trump and Joe Biden are not so funny clowns, and voters are being conditioned by some in the media to treat one aggressively and the other not aggressively. It is not the first attempt at media conditioning: In 2016, when every poll indicated that voters wanted outsider candidates, Democratic leaders pushed through one of the two most unpopular presidential candidates in history, Hillary Clinton.

She was beaten by the other most unpopular figure on the Republican side, Trump. Yet, after largely positive treatment of Clinton and correspondingly negative coverage of Trump, the election results stunned experts who predicted an easy win for Clinton — and why not? Voters had been exposed to unyielding, continual media conditioning against Trump.

The conclusion of the media today appears to be that the scathing treatment in 2016 was not aggressive enough. Trump is routinely called an actual clown by some in the media. More importantly, there are now consistent attacks on Trump supporters. Washington Post “conservative columnist” Jennifer Rubin has declared that Trump supporters as a whole are racists. That common stereotyping of Trump supporters is uncontested, even as the media objects to Trump’s generalizations about other groups.

Columnist Leonard Pitts wrote a recent column entitled, “No, it’s not the economy, stupid. Trump supporters fear a black and brown America.” The narrative has moved beyond Clinton’s description of Trump supporters as a “basket of deplorables” to now portraying all Trump supporters as open racists. “Make America Great Again” hats are denounced by academics as the symbol of “modern day hitlerjugend” and hate speech.

It is all part of media-cognitive learning, and it is working in a curious way. Recent polls show Trump at the exact same spot as he was last year, with roughly 43 percent support. In Ohio he actually is ahead by 3 percentage points in a survey from Emerson College and Nexstar Media; he and Biden are in a statistical dead heat in Wisconsin. In other words, as in 2016, the media campaign is forcing Trump supporters into the closet, but not away from Trump.

Meanwhile, the media has been working hard at non-aggressive treatment of Biden. His frequent gaffes are quickly dismissed; when he was accused of sexual assault, the media reluctantly noted the story. Even when Biden recently espoused a conspiracy theory that Trump was going to halt the November election, the media called it a “prediction” and ignored that it was based on a fundamental misunderstanding of the Constitution.