- BoE's Bailey To Print Unlimited Money, Tells Short Sellers "Just Stop" Amid Covid-19 Chaos

BoE’s Bailey To Print Unlimited Money, Tells Short Sellers “Just Stop” Amid Covid-19 Chaos

BoE governor Andrew Bailey said on Wednesday that the central bank stands ready to pump unlimited amounts of money into the economy.

Speaking to journalists on a conference call, quoted by Financial Times, Bailey said the central bank is prepared to pump liquidity into markets via its new commercial paper facility. He said this would limit economic damage produced by the virus crisis.

BREAKING: Bank of England governor, Andrew Bailey, just said he’s willing to print unlimited quantities of money and pump in into the economy.

Ironic coming from a man that last month said those holding bitcoin should “be prepared to lose all of your money” pic.twitter.com/JDQpQ2HBVE

— Vis (@Vis_in_numeris) March 18, 2020

https://platform.twitter.com/widgets.js

He told members of the financial community that they must stop ‘exploiting’ vulnerable business by betting against them:

“Anybody who says, ‘I can make a load of money by shorting’ [aggressively betting on the value of specific companies continuing to fall] which might not be frankly in the interest of the economy, the interest of the people, just stop doing what you’re doing.”

Bailey made it clear that financial markets will remain open as a sign of confidence. He said firms who are thinking of reducing staff must reconsider because support from the central bank and government can lessen the shock.

He urged firms to “stop, look at what’s available, come and talk to us [or] the government before you take that position,” adding that support will be supplied to citizens as well.

The hardest-hit UK industries have so far been airliners, retailers, restaurants, movie theaters, and much of the services industry, as it has completely ground to a halt as the government enforces social distancing measures to flatten the curve to slowdown infections. As of 2018, the services sector accounted for at least 80% of the UK economy.

Baily said emergency loans have been available by the central bank to companies that have already fired employees. He told BBC News:

“I would emphasise the point that it’s critical that we support the needs of the people in the country.”

Baily took the reins from Mark Carney at midnight on Monday and has already faced an economic crisis on par to a decade ago as helicopter money is now needed to save the economy from crashing.

“This is a crisis we’re all in. It’s an emergency situation,” Bailey said.

The BoE is expected to cut interest rates from .25% to .10% and resume quantitative easing when it meets next week. Bailey isn’t a supporter of NIRP and has pushed measures to shield businesses and workers from virus impacts.

Tyler Durden

Thu, 03/19/2020 – 02:45 - Covid-19 Comes For Europe

Covid-19 Comes For Europe

Authored by Guy Milliere via The Gatestone Institute,

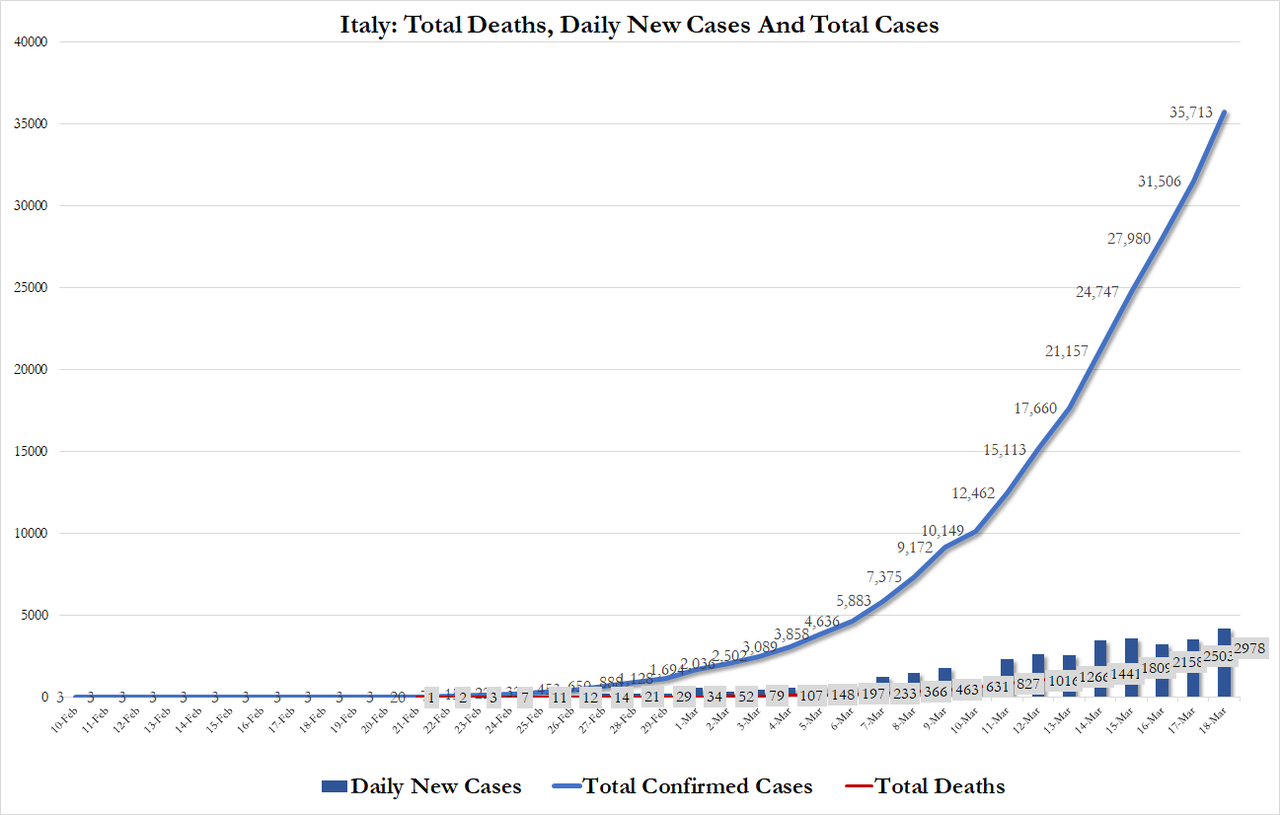

Italy’s healthcare system is in a state of almost total collapse. As of today, 31,506 people in Italy have been infected with the coronavirus; of which 2,503 people have died. The numbers continue to grow. Hospitals are overwhelmed. Doctors have to choose which sick person to save and which sick person not to save.

The country has almost completely shut down. Many businesses are running in slow motion or have stopped. Prisoners are staging uprisings. Millions of people have been ordered to stay home and are allowed out only briefly to buy food. Most shops are shut. All public gatherings are prohibited, even funerals. Big cities look like ghost towns.

No other Western country has been so severely affected by the pandemic as Italy. Why?

First, Italy has an aging population. The median age of Italians is 47.3 years; one in four Italians is over 65. In addition, the country’s birth rate is extremely low: 1.29 children per woman. Even before the coronavirus pandemic, Italy was a dying country. Sadly, the virus has accelerated the process.

Second, the authorities and medical personnel apparently underestimated the danger. Although the Italian government had suspended flights for days from China and Hong Kong from January 31, Italian doctors were saying that the illness was just a “bad flu“. On March 9, an epidemiologist, Silvia Stringhini, wrote: “The media are reassuring, the politicians are reassuring, while there’s little to be reassured of”.

Third, the Italian health system is in appallingly bad condition. There are not enough intensive care units and, as everywhere, the possibility of a major crisis simply was not anticipated. In Italy there are 2.62 acute-care hospital beds per 1,000 residents (by comparison, the number in Germany is 6.06 per 1,000 residents). The Italian health system is entirely run by the government. A public health care service (SSN, Servizio Sanitario Nazionale) pays the doctors directly, limits their number, and sets the maximum number of patients they can treat per year (1,500).

Government-run healthcare always ends up being about the government trying to cut its costs rather than to help its citizens. Private clinics do exist, but represent only a small part of the care offered (the public system represents 77% of total health-care spending. (The only country in Europe where the figure is higher is the United Kingdom, where the figure is 79%.) Public hospitals must manage shortages, and when an exceptional situation occurs, rationing care leads to horrific choices. A recent report by Siaarti (Società Italiana di Anestesia Analgesia Rianimazione e Terapia Intensiva) bureaucratically offers “ethical recommendations for admission and intensive treatment in exceptional conditions of imbalance” and speaks of “consensual criteria of distributive justice” to justify not treating certain patients and leaving them to die.

Fourth, and rarely mentioned, is that Italy today is evidently home to a large Chinese community (more than 300,000), made up of people who arrived in the past two decades and who work in the textile and leather sector. Many of the Chinese living in Italy are from Wuhan and Wenzhou, and some had just been in Wuhan and Wenzhou for the Chinese New Year on January 25, when the Chinese authorities could not hide the epidemic any longer. These Chinese had returned to Italy from China before the Italian government suspended flights from there. The epidemic emerged in Lombardy; Bergamo, one of the capitals of the Italian textile industry, was one of the first cities affected.

Before the pandemic, the Italian economy was already in a state of stagnation; now, as people stay home and shops shut, it will probably plunge into a recession. Italian banks, since mid-February, have lost 40% of their market value. Major financial upheavals seem on the way.

The Italian government was hoping for help from the European Union, but neither the other member states nor the European Union itself has given any at all. Maurizio Massari, Italy’s ambassador to the European Union, said at a recent European summit on the pandemic, that Brussels should go beyond “engagement and consultations”, and that Italy needed “quick, concrete and effective actions”. He got nothing.

Christine Lagarde, president of the European Central Bank, refused to lower interest rates to help Italy; it was a statement Italian leaders took as a demonstration of contempt. Italian President Sergio Mattarella said that Italy expected “solidarity from the EU institutions,” not “moves that could hinder Italy’s actions”. “Italy,” said Matteo Salvini, leader of the Lega party, “has been given a slap in the face”.

The dismissive attitude of the EU and the other members states seems to have been dictated by the fear of sliding into a situation as calamitous as that of Italy.

All European countries have an aging population, even if less than Italy’s (the median age in Germany is 46.8; in France it is 41.2; in Spain it is 42.3). No country in the European Union has taken a clear, hard look at the danger Europe is facing.

“The coronavirus is very contagious,” France’s minister of health, Agnes Buzyn, said on January 26, “but much less serious than we thought”.

The borders between France and Italy were not closed in time (only Austria and Slovenia closed their borders with Italy early), and Italians who wished to go to France were not stopped. The health systems of other European countries are not better prepared than the Italian one was. In Spain, Insalud (Instituto Nacional de Gestion Sanitaria), an organization equivalent to the Italian system, exists, and shortages and rationed care are the rule. The German (Krankenkassen) and the French (Sécurité Sociale) health insurance systems also operate on the same principles as those in Italy and Spain, and produce similar results. The economies of the main countries of the European Union were in a state of stagnation before the pandemic, and, like the Italian economy, are likely to plunge into a recession soon, too.

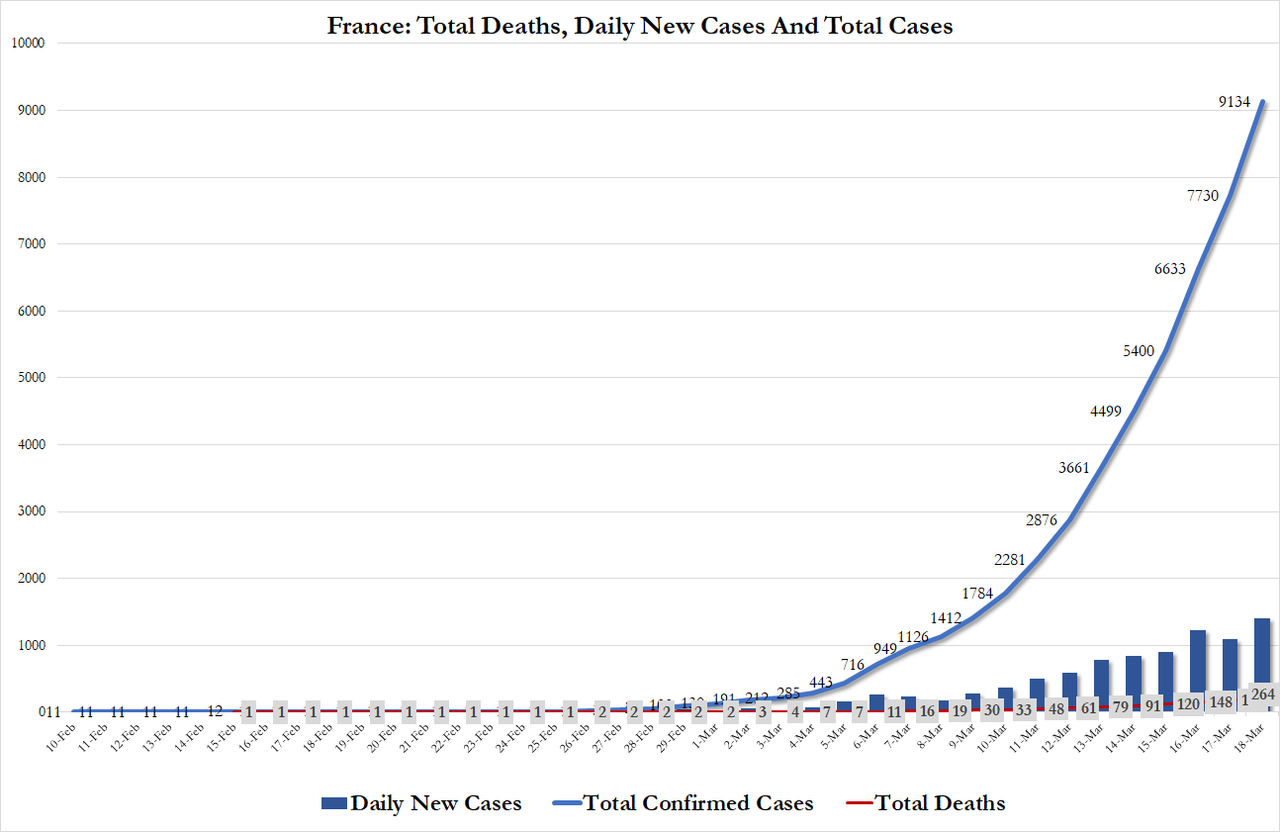

At the time of publication, 11,826 people were infected in Spain, 7,695 in France, and 9,360 in Germany. In Spain, 533 people have died; in France, 148 people, and in Germany only 26. As in Italy, the numbers escalate fast.

On March 11, German Chancellor Angela Merkel said to journalists who were accusing her of doing nothing, “60 to 70% of Germans will be infected with the coronavirus”. Lothar Wieler, President of the Robert Koch Institute, the German government agency in charge of disease prevention and control, added that it was necessary to “avoid overloading hospitals” and to let the epidemic gain ground slowly over time.

An adviser to French President Emmanuel Macron told a journalist at Le Figaro that the strategy of France was the same as in Germany: the decision was made to “let the epidemic run its course and not try brutally to stop it”. He suggested that the official will was to create “herd immunity“, a term first used in the United Kingdom by Sir Patrick Vallance, the UK government’s chief science adviser. He had said that the aim of the British government was to accept that a significant number of the citizens of a country would be infected, recover, and therefore be immunized. The French and German authorities evidently found inspiration in Sir Patrick’s remarks.

The British government, faced with criticism from the World Health Organization, replied that “herd immunity” was not a stated policy, but no statement by the German or French governments said that “herd immunity” was not the policy they chose.

Umair Haque, the British Director of the Havas Media Lab, wrote:

“Herd immunity describes how a population is protected from a disease after vaccination by stopping the germ responsible for the infection being transmitted between people. Letting an entire nation be rampaged by a lethal virus for which there’s no vaccine? How much death and mayhem would that cause, by the way?”

“Europe has now become the epicentre of the pandemic, with more reported cases and deaths than the rest of the world combined, apart from China,” noted Tedros Adhanom Ghebreyesus, director general of the World Health Organization. “More cases are now being reported every day than were reported in China at the height of its epidemic.” Sadly, all available data show that he is right.

On March 11, President Donald Trump announced that the US was suspending all flights between the United States and Europe, a decision fully justifiable to save American lives. The next day, nevertheless, the heads of the European Union could not resist trying to maul the president: “The EU disapproves of the fact that the U.S. decision to impose a travel ban was taken unilaterally and without consultation,” they said.

It is to be hoped that by now notions of ”herd immunity” have been abandoned, and that the EU gets back to salvaging for Europe whatever it can.

Tyler Durden

Thu, 03/19/2020 – 02:00 - China Takes Axe To Alternative Energy Funding, Slashing Subsidies For Solar And Wind

China Takes Axe To Alternative Energy Funding, Slashing Subsidies For Solar And Wind

Things might be going from bad to worse for Elon Musk and his merry band of alternative energy cultists in China. While Musk is currently in the midst of criticism from the Chinese government related to a bait and switch he is pulling on vehicle hardware (while blaming the coronavirus), the Chinese government appears to be set on slashing additional alternative energy subsidies in 2020.

China is going to cut its budget for new solar power plants in half this year and plans on completely ending handouts for offshore wind farms, according to Caixin.

It is the latest in a string of moves by the Chinese government to cut support for renewable energy. The attitude has shifted in recent years as manufacturing costs have dropped. The government now seems focused on getting renewable energy to stand on its own.

On Tuesday, China’s National Energy Administration (NEA) announced it had cut this year’s subsidies for new solar power projects by 50% to 1.5 billion yuan ($215.8 million). “Of the total, it has earmarked 1 billion yuan for large solar projects, which will be divvied out through auctions. The remainder will be used for residential solar systems,” Caixin reports.

China is also doing away with subsidies for new offshore wind farms this year and is ending subsidies for new onshore projects in 20201.

Shi Jingli, a professor at a research institute under China’s top economic planner said: “Cutting subsidies for new renewable energy projects is a reasonable measure to allocate funds more wisely. The generous subsidies given to offshore wind farms over the past few years have weighed on the central government’s finances and caused severe deficits in subsidy funding.”

Jingli continued: “Considering the damage that the coronavirus outbreak has done to businesses, the NEA has extended the application period for the auctions until mid-June. It has also given solar and wind farm operators an additional month to apply to connect their projects to the country’s power grid, which is necessary for a power plant to start selling electricity.”

Meanwhile, new installations of solar power capacity plunged 40% last year after the country installed 26.81 gigawatts of new capacity. Numerous other projects underway have already hit major delays due to the coronavirus outbreak and supply chain disruptions.

Could EVs be next?

Tyler Durden

Thu, 03/19/2020 – 00:50 - Standing At The Precipice Of A Financial Collapse: Time For A 21st Century Pecora Commission

Standing At The Precipice Of A Financial Collapse: Time For A 21st Century Pecora Commission

Authored by Matthew Ehret via The Strategic Culture Foundation,

As Republican and democrat politicians hold emergency meetings to decide how to avoid a meltdown of Wall Street, the smell of hyperinflation looms in the air as much today as it did in Germany during the opening months of 1922. This week, markets were propped up by a record breaking offering of $1.5 Trillion in liquidity injections over the coming months (added to the $9 trillion already injected over the past six months), and rather than deal with the real reasons for this oncoming financial collapse, the media has brainwashed the west that everything would have been just fine, “if only coronavirus had not become a pandemic”.

But what is really being bailed out here exactly and why? Is this money actually making it to the real economy? Is it being invested to rebuild America’s farms, businesses and industry?

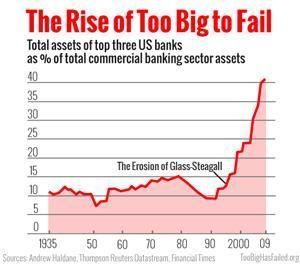

The reality is that the only thing being saved are the “Too Big to Fail” banks that are sitting atop a $1.5 quadrillion of derivatives bomb. Of the most bankrupt of America’s speculators are JPMorgan Chase, Citigroup and Goldman Sachs, whose derivatives exposure hit $48 trillion, $47 trillion and $42 trillion respectively in recent years.

It is my contention that Trump is genuine in his desire to “drain the swamp” and rebuild America’s lost industrial base. I also genuinely believe that Trump wishes to establish positive relations with Russia, China and other sovereign nation states which has drawn the ire of the international deep state. However Trump’s potentially fatal blind spot appears to be his tendency to believe the lie that Wall Street’s wellbeing is somehow indicative of America’s wellbeing.

If Trump is intelligent, (and his previous calls for Glass-Steagall’s restoration, and American System practices imply that he knows a thing or two), then rather than bailing out Wall Street by unleashing more gasoline onto the fire, it were better that he took the lessons of 1933 and established a new Pecora Commission for 2020.

What was the Pecora Commission?

Many are aware of the economic meltdown of October 24,1929 that ushered in four years of depression onto America (and much of the western world). However not many people are aware of the intense fight that was launched by patriots in both parties against the Wall Street/deep state parasite of that age which prevented both a fascist coup against the newly elected Franklin Roosevelt while also crippling Wall Street’s command of American life. In spite of whitewashing revisionist history books that contaminated the past 70 years, America’s recovery from the depression never occurred without a life or death struggle and this struggle was made possible, in large measure by the courageous work of an Italian lawyer from New York. This man’s name was Ferdinand Pecora.

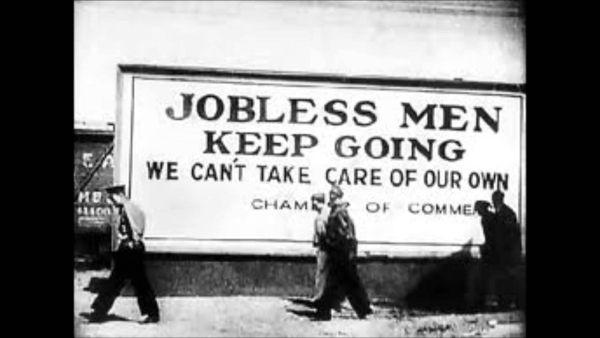

By 1932, when Senators Peter Norbeck (R-SD) and George Norris (R-NB) spearheaded the establishment of the U.S. Committee on Banking and Currency, the American economy was on life support and the people were so desperate that a fascist dictatorship in America would have been welcomed with open arms if only bread could be put on the table. Unemployment had reached 25%, while over 40% of banks had gone bankrupt and 25% of the population had lost their savings. Thousands of tent cities called ‘Hoovervilles’ were spread across the USA and over 50% of America’s industrial capacity had shut down. Thousands of farms had been foreclosed and the engines of American industry had grinded to a screeching halt.

Across the ocean, the fascist regimes of Germany, Italy and Spain were growing more powerful by the day fed by injections of hundreds of millions of dollars of capital by London and Wall Street bankers. Notable among these pro-fascist financiers was none other than Bush family patriarch Prescott, who provided millions in loans to Hitler’s bankrupt Nazi party in 1932 (and continued doing business with the party through 1942- having only stopped after being found guilty for “trading with the enemy”).

The Committee on Banking and Currency was a relatively impotent body when it began in 1932, but when Senator Norbeck called in Ferdinand Pecora to lead it in April 1932, everything began to change. A first generation Italian-American, Pecora was forced to quit high school after his father was injured in order to support his family. Years later, the young man found work as a clerk in a law firm, and managed to work his way through law school, passing the bar in 1911. His unimpeachable reputation earned him the animosity of powerful NY financiers who ensured that his successes in prosecuting brokers never resulted in attaining Attorney General, where he made a name for himself shutting down over 100 illegal brokerage houses that speculated on fraudulent securities during the depression.

Within days of accepting the Washington job as Chief Council of Norbeck’s committee (for the meager salary of $250/month), Pecora was granted broad subpoena powers to audit banks and drag the most powerful men in America to testify in the committee’s hearings.

In his first two weeks, Pecora made headlines by auditing the books of major Wall Street banks and pulled in pro-fascist National City President Charles Mitchell (then preparing to advise Benito Mussolini) to testify. Within days, Mitchell’s team of expensive defense attorneys could do nothing but watch in despair as the powerful financier admitted to short selling his own bank’s stocks during the depression, scamming depositors with purchases of Cuban junk debt and avoiding taxes for years. Mitchell was forced to resign in shame followed days later by NY Stock Exchange Chair Dick Whitney- who left the court in handcuffs.

This crackdown on Wall Street’s abuses were highly publicized and put the spotlight on the criminal schemes used to gamble with savings and commercial bank deposits on securities and futures markets which led to the orchestrated collapse of the bubble economy in 1929 (ironically much of the bubble built up during the “easy-money days” of the “roaring 20s” was centered in the housing market). Pecora’s crackdown also set the tone for the incoming Roosevelt administration.

Unlike the previous 1911 Pujo Commission led by Senator Charles Lindberg Sr. which also exposed Wall Street’s abuses of power, the Pecora Commission was supported by a President who actually cared about the Constitution and amplified Pecora’s powers even further. When FDR was told that supporting Pecora’s exposures of financial crimes would hurt the economy, the President famously responded with “they should have thought of that when they did the things that are being exposed now.” FDR followed up that warning by encouraging the attorney to take on John Pierpont Morgan Jr.

Rather than controlling an American institution as many believed 70 years ago and today, J.P. Morgan Jr. was actually running an operation that had earlier been created in the mid-19th century as part of a British infiltration of America. As historian John Hoefle pointed out in a 2009 EIR study:

“The House of Morgan was, in truth, a British operation from its inception. It began life as George Peabody & Co., a bank founded in London in 1851 by American George Peabody. A few years later, another American, Junius S. Morgan, joined the firm, and upon Peabody’s death the firm became J.S. Morgan & Co. Junius Morgan brought in his son, J. Pierpont Morgan, to head the New York office of J.S. Morgan, and the New York office became J.P. Morgan & Co. From its original role in helping the British gain control of American railroads, the Morgan bank became a leading force in the oligarchy’s war against the American System, using the deep pockets of its imperial masters to become a powerhouse in not only finance but steel, automobiles, railroads, electricity generation, and other industries.”

By 1933, the House of Morgan grew into a multi-headed hydra controlling utilities, holding companies, banks and countless other subsidiaries.

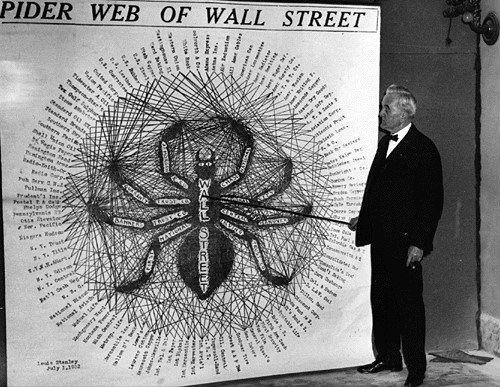

Senator George Norris showcasing a chart of Wall Street power

When J.P. Morgan jr. was called to testify, the banker carried a midget on his lap in mockery of the “circus of the commission”. As the questions began however, the arrogant banker was caught off guard by Pecora’s proof of Morgan’s secret “preferred clients lists” of politicians whom the banker owned and who received stock offerings at discount rates. Named among the thousands of traitors on this list, Pecora revealed former president Calvin Coolidge, Coolidge’s Treasury Secretary Andrew Mellon (a Schacht-Hitler supporter from the start), financier Bernard Baruch, Supreme Court Justice Owen Roberts and Democratic Party controller John Jacob Raskob. Raskob was not only a major speculator but was also the leader of the American Liberty League which tried repeatedly to overthrow FDR between 1933-1939 and worked to ally America with axis powers from 1939-1941.

Morgan’s god-like ego was brought down to the level of mortals when the flustered banker was only able to answer “I can’t remember” repeatedly when asked if he had paid taxes over the past 5 years. As it turned out, by the end of the trial, it was revealed that NONE of the subsidiaries of the House of Morgan paid any taxes during the entire period of the depression, and were caught gambling with depositors assets from commercial accounts. These revelations didn’t sit well with a population dying of starvation across the streets of America.

Similar displays of corruption were made of the heads of Kohn Loeb, Chase Bank, Brown Brothers Harriman and others.

Faced with these revelations, The Nation magazine famously reported “If you steel $25, you’re a thief. If you steal $250 000, you’re an embezzler. If you steal $2.5 million, you’re a financier.”

Pecora’s ally Sen. Burton Wheeler said “the best way to restore confidence in our banks is to take these crooked presidents out of the banks and treat them the same as we treated Al Capone.”

FDR Drains the Swamp

With the light cast firmly upon the dark shadows where vile creatures like J.P. Morgan and other financial gremlins reside, the population was finally able to start making sense of what injustices befell them during the years of post-1929 despair. While not every banker went to prison as Wheeler or Pecora would have liked, examples were made of dozens who did and many more whose careers were shamefully ended. Most importantly however, this exposure gave Franklin Roosevelt the support needed to drain the swamp and impose sweeping reforms upon the banks.

In the first hundred days, FDR was able to:

1) Impose Glass-Steagall banking separation (forcing Wall Street banks to break up their functions and preventing speculators from gambling with productive assets)

2) Create the Federal Deposit Insurance Corporation (FDIC) that protected citizens’ savings from future crises

3) Create the Securities Exchange Commission to provide oversight to Wall Street’s activities and on whose body Pecora was appointed commissioner in 1934.

4) Unleash broad credit through the Reconstruction Finance Corporation (RFC) which acted as a national bank bypassing the private Federal Reserve, channeling $33 billion to the real economy by 1945 (more than all private commercial banks combined)

5) Impose protective tariffs on agriculture, metals and industrial goods to stop dumping of cheap products in America and rebuild America’s physical economy

6) Create vast public works, like the Tennessee Valley Authority, Grand Coulee dams, Hoover dams, St Laurence development and countless other projects, hospitals, schools, bridges, roads and rail under the New Deal that acted in many ways then as China’s Belt and Road Initiative has in our modern age. Unfortunately, Roosevelt died before this new form of political economy could be internationalized abroad in the post-war years as an anti-colonial program.

A beautiful outline of FDR’s struggle is showcased in the 2008 film ‘1932: Speak not of Parties but of Universal Principles’.

Subverting a Fascist Coup Then and Now

Ferdinand Pecora’s Commission shaped the dynamics of America so intensely by its simple power of speaking the truth, that efforts to run a fascist coup against FDR using a general named Smedley Butler also came undone before it could succeed. Butler played along with Wall Street’s plans for some months before deciding to publicly blow the whistle in congress. Butler exposed the intension to use him as a “puppet dictator” leading thousands of American legionnaires in a storming of the White House displacing FDR.

It is often forgotten today, but in the early days of the 1920s-1930s, the Legion was modeled on Mussolini’s fascist squadristi and even its leader Alvin Owsley made explicit in 1921 saying:

“If need be the American Legion is ready to protect the institutions of this country and its ideals, in the same way as the Fascists have treated the destructive forces threatening Italy. Don’t forget that the Fascists are for today’s Italy what the American Legion is for the United States.”

Butler’s startling revelations amplified FDR’s popular support and inoculated much of the population from the fake news pouring out of Wall Street propaganda agencies spread across the media.

In 1939, Pecora wrote a book called ‘Wall Street Under Oath: The Story of our Modern Money Changers’ where the attorney prophetically said:

“Under the surface of the governmental regulation of the securities market, the same forces that produced the riotous speculative excesses of the ‘wild bull market’ of 1929 still give evidence of their existence and influence. Though repressed for the present, it cannot be doubted that, given a suitable opportunity, they would spring back to their pernicious activity.”

Pecora went onto deliver one more warning which current generations should take seriously “Had there been full disclosure of what has been done in furtherance of these schemes, they could not long have survived the fierce light of publicity and criticism. Legal chicanery and pitch darkness were the bankers’ stoutest allies.”

Today’s oncoming economic meltdown can only be prevented if the lessons of 1933 are taken seriously and patriots who actually care about their nations and people stop legitimizing the casino economy of fictitious capital, derivatives, debt slavery and anti-humanism that has become so commonplace across the governing strata of the technocratic and banking elite today trying to control the world. This elite, just like the financiers of the 1920s, doesn’t care ultimately for money as an end but sees it merely as a means for imposing fascist forms of governance onto the world population. In the same way that FDR’s Wall Street/London enemies sought a world government under Nazi enforcers then, today’s heirs to that anti-human legacy are driven by a religious-like commitment to “manage” a new collapse of world civilization under a Green New Deal and World Government.

So why accept that dystopic future when a brighter one is offered us by the Multipolar alliance today led by Russia and China?

Tyler Durden

Wed, 03/18/2020 – 23:40 - 100 Iranians Die By Alcohol Poisoning After Ethanol Consumption For Virus "Cure"

100 Iranians Die By Alcohol Poisoning After Ethanol Consumption For Virus “Cure”

As the world grapples with this once in a century pandemic, bizarre stories and sometimes extremely dangerous examples of people’s ‘home remedy’ attempts at combating the virus are popping up more and more.

Yesterday we detailed the story of the South Korean church which infected 46 people by the strange “remedy” of spraying salt water into their mouths thinking it would “kill” the virus; however, they used the same spray bottle, not bothering to disinfect it.

And now a new one from hard-hit Iran, which Tuesday saw state TV issue an alarming prediction that “millions” of its citizens could die: some Iranians are turning to ingesting industrial-grade ethanol and methanol thinking this can disinfect them and mitigate exposure. This has led to mass alcohol poisoning, state media has reported.

Methyl Alcohol file image “More than a hundred Iranians have died from alcohol poisoning in recent weeks in the mistaken belief that industrial-grade ethanol and methanol will help ward off the coronavirus ravaging the country, according to local media reports,” writes Bloomberg.

The reports note that nationwide over 1,000 have been treated for alcohol poisoning related to ‘home remedy’ attempts to disinfect themselves. The ‘treatment’ reportedly began as a rumor, which authorities have lately sought to combat.

And the semi-official Iranian Students News Agency has reported 61 deaths in Fars province alone by this method, which adds up to five times more fatalities than official confirmed coronavirus deaths in that area.

Other deaths from consumption of the potentially fatal substances were also reported throughout the country. Bloomberg tallies it at 100 or more, citing state sources.

Iran on Wednesday reported a huge single-day jump in fatalities, reportedly the biggest within a single 24-hour period thus far in the country as another 147 people died.

This brings the official death toll in Iran to 1,135 and a total of 17,361 confirmed cases, amid dire reports that “millions” are expected to be infected before the pandemic dissipates.

Tyler Durden

Wed, 03/18/2020 – 23:20 - Dow Futures Crash Near Limit-Down As Global Dollar Buying Panic Sparks AsiaPac FX Collapse

Dow Futures Crash Near Limit-Down As Global Dollar Buying Panic Sparks AsiaPac FX Collapse

Update (2305ET): Dow futures losses have accelerated, plunging over 1000 points limit-down…

S&P and Nasdaq futures are also crashing…

Additionally, South Korea’s KOSPI is halted after triggered circuit-breakers down 8% on the day.

And Copper has succumbed to the liquidation…

* * *

The global scramble for dollars amid a massive shortage has rolled around the AsiaPac time-zone and is leaving a bloody trail across every asset-class.

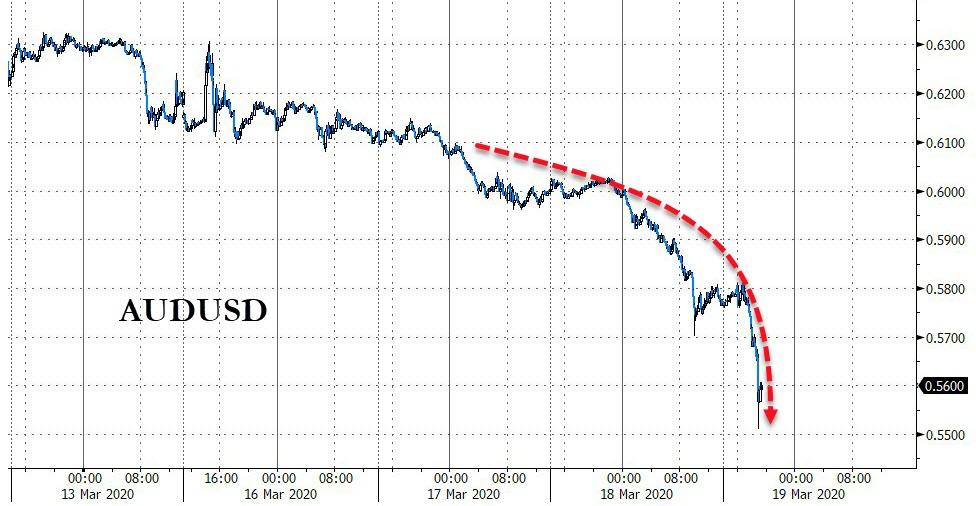

FX is in freefall with Aussie collapsing at the fastest rate since Lehman…

Source: Bloomberg

Kiwi is back to its weakest since 2009…

Source: Bloomberg

Yen is tumbling once again…

Source: Bloomberg

Won is getting whacked…

Source: Bloomberg

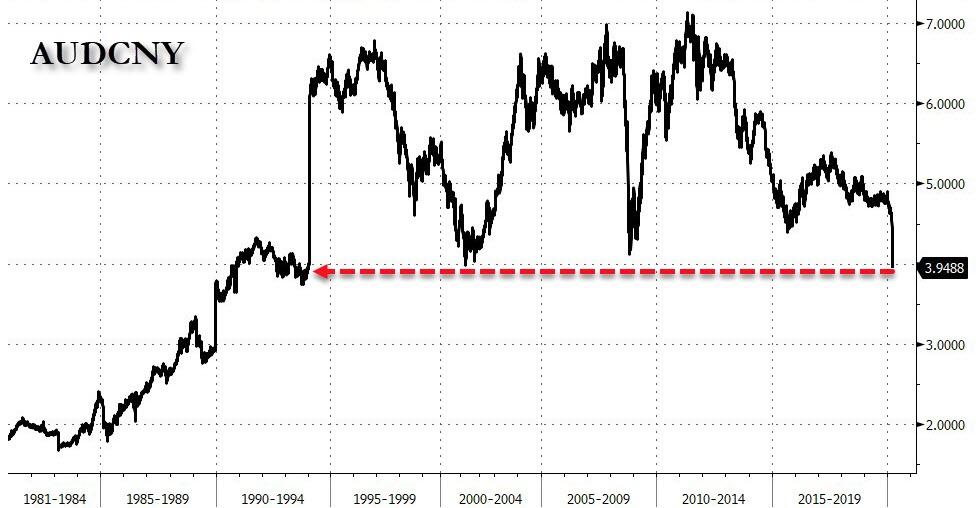

And Aussie has crashed to its weakest against the offshore yuan ever and weakest against onshore yuan since Dec 1993…

Source: Bloomberg

And overall, AsiaPac FX is crashing to its weakest against the USDollar since 2004…

Source: Bloomberg

And the liquidation continues in US equity markets with Dow futures down over 800 points, erasing the after ramp in stocks…

And losses in AsiaPac stocks are accelerating…down 27% from January highs

Source: Bloomberg

And JPY Basis-Swaps are signaling extreme dollar shortage continues…

Source: Bloomberg

This all has the smell of a massive global macro fund liquidation and the contagious impact of that leveraged unwind across the global risk markets.

As Bloomberg’s Stephen Spratt details, desks continue to speak of the “sell everything” mentality in markets with huge liquidations and de-leveraging taking place everywhere.

The data stacks up. Looking at the three-day change in open interest across major June bond futures as of close of play Tuesday, the reduction in positions is the equivalent to $150 billion in 10-year cash Treasury bonds ($140m/dv01*). Here’s 3-day open interest change:

-

Schatz: -135,295

-

Bobl: -45,931

-

Bund: -178,221

-

Buxl: -17,566

-

OATs: -41,475

-

BTPs: -41,176

-

Gilts: -28,055

-

US 2y: -158,991

-

US 5y: -44,059

-

US 10y: -129,381

-

US 20y: -60,865

-

US 30y: -26,798

-

JGBs: -36,534

As one veteran Aussie trader exclaimed (who happened to be on the right side of the collapse in the currency):

“I love the smell of global macro fund liquidations in the morning…”

With currencies flash crashing across Asia on Thursday, central bankers may be looking back at the remedies used then.

As Bloomberg’s Mike Wilson suggests, the tear the U.S. dollar was on back in 1985 was brought to an end when five central banks gathered in New York’s Plaza Hotel and came up with what became known as The Plaza Accord.

Source: Bloomberg

That sent the dollar into a steep slide that lasted until about the end of 1987.

With the Aussie, kiwi and won just free-falling, it looks like a similar sort of coordinated intervention may be needed to stop the dollar now, especially until the world is deemed free of coronavirus impacts.

Tyler Durden

Wed, 03/18/2020 – 23:14 -

- The Journey To Monetary Gold And Silver

The Journey To Monetary Gold And Silver

Authored by Alasdair Macleod via GoldMoney.com,

Markets are just beginning to latch on to the economic consequences of the coronavirus. Central banks are slashing interest rates and beginning to throw new money into the mix and governments are increasing deficit spending.

Few analysts have yet to understand the enormous consequences of the coronavirus for missed payments and accumulating current debt, which is and will rapidly drain liquidity from wholesale money markets. It is increasingly certain that the eurozone’s banking system will require rescuing from insolvency with knock-on consequences for the global monetary system. Concern over the consequences for the $640 trillion OTC notional derivative market, particularly for $26 trillion of fx swaps, is so far absent.

Continuing on our theme that the fates of the dollar and US Treasury values are closely bound, the extraordinary overvaluation of the bond market will translate into a collapse for both. This article charts how the collapse of the dollar and financial asset values is likely to progress and concludes that we are witnessing the end of the neo-Keynesian fiat currency fantasy, which will be done and dusted with surprising rapidity.

Only then will sound money, after varying time periods for different nations, return.

Setting the scene…

This week we got into the red meat of Scene One of the final Act of the financial tragedy currently staged in global markets. It is a drama that has run on the air of hope for a hundred years, with an ending that now appears to be unexpectedly sudden. We face no less than the destruction of a financial system whose twin pillars are fiat currencies and financial assets, built on the sands of monetary expansion and debt financing. The evidence of its commencement is best encapsulated in Figure 1, of the world’s reserve currency. This is where everyone was meant to seek sanctuary from lesser currencies, in order to have the liquidity to pay the coupons on their dollar debts.

It is turning out not to be so, with the dollar suddenly appearing to enter a new bear market. Meanwhile, this week saw the entire US Treasury yield curve briefly submerged under 1%, an event bifurcated from the collapsing dollar.

There is no doubt that the coronavirus is having a serious economic impact. Much has been written about the disruption of supply chains, and clearly people are staying at home and stockpiling necessities. Sales of automobiles and other durable goods have crashed. Now the politicians are falling ill. Investors have reacted by dumping equities and buying government bonds, a flight to safety by Keynesian investment managers seeking the comfort of Nurse for fear of something worse. Consequently, government bond prices have become even more detached from the true reality of where financial risk resides.

Amazingly, almost no investment manager has bought physical gold for his or her clients: gold-backed ETFs and derivatives are only paper claims on gold, so by having counterparty risk and the lack of true possession don’t count as true safety. Physical gold has been effectively banned from managed portfolios, being classified as unregulated, deterring investment managers from having to justify buying gold to their compliance officers. The related asset class is so downgraded that gold and silver mining shares remain unfashionable, with the Amex gold bugs index (HUI) standing at about one third of its 2011 peak while the gold price is in new high ground against nearly all fiat currencies.

Monetary debasement will really accelerate from here…

Monetary and market distortions could have persisted for longer if it were not for the fact that the coronavirus disruption is accompanied by considerable payment dislocation. Companies still have fixed costs when they have no sales, either because customers are not turning up or their supply chains have stopped delivering products. Where companies have cash at their banks, they will draw it down, forcing their banks to go into the money markets, either through LIBOR or repos to make up the balance, sell government bonds, or foreclose on borrowers. Where companies do not have cash, they will test their working capital facilities, likely to force their banks to cover increased lending in wholesale money markets. Where banks experience drawdowns on both sides of their balance sheets, outstanding bank credit contracts, sending the sort of signal that terrifies central bankers.

The situation will be increasingly reflected by central banks having to back-stop both liquidity and bank reserves through repos and new rounds of quantitative easing. In an interesting paper, Zoltan Pozsar of Credit Suisse describes the process that leads to what he terms deficit agents in supply chains (businesses experiencing payment failures) turning their banks into deficit agents as well.

Pozsar demonstrates that a reluctant Fed will have to backstop not just escalating domestic dollar deficits but global ones as well, and he assumes for the purpose of clarity that foreign central banks will manage the payment crises in their own currencies. Being a money market technician, he does not address the debasement issue because that is not his brief. But clearly, he describes a process where the dollar will have to be debased if financial asset values, particularly of government bonds, are to be maintained.

We see unfolding the process whereby both the dollar and financial assets are losing value, with the dollar losing it first. And while a weakening dollar may from time to time lend support to financial asset prices, measured in sound money their combined values will decline.

The second scene in the final act of our financial tragedy will be wholesale liquidation of US Treasury holdings by banks in New York and also by foreign governments to obtain dollars to satisfy their liquidity demands. The Fed will have to supply as much liquidity as it takes to accommodate the American banks and will reduce the Fed funds rate to discourage them from selling Treasury bills and bonds. As for foreigners, they are not the Fed’s first priority.

Let us assume liquidity problems should not become acute for the few foreign central banks with existing USD liquidity swap lines with the Fed. Under the existing 2013 agreement, these are only the ECB, Bank of England, Swiss National Bank, Bank of Canada and Bank of Japan. While additional temporary swap agreements might be arranged with others, it is only likely to happen in a response to liquidity stresses rather than in anticipation.

China, Korea and Taiwan as well as other nations with dollar-centric supply chains in their domains will probably have to unwind their long-dollar fx swap positions and sell T-bills and Treasuries in order to release the necessary liquidity. The end result is that in funding the US deficit, the Fed will have to not only absorb significant new debt through quantitative easing, but it will have to buy up existing debt sold by foreign holders if it is to maintain US Treasury yields at anything like current levels.

In this, mainstream opinion has been wrongfooted: foreigners certainly have dollar obligations to satisfy in an economic slump, but they already own the dollars. The thirst of foreigners for dollar liquidity will not be satisfied by the purchase of more dollars, but by the liquidation of their existing dollar assets. And to the extent that this leads to a contraction in bank credit the Fed will have no alternative but to sacrifice the dollar by increasing the base money quantity in order to absorb it all.

Furthermore, there is an unknown quantity of fx swaps taken out by US hedge funds to strip out interest rate differentials between euros and yen on one side, and the dollar on the other. It is a trade that will have built in quantity but deteriorating in quality since April 2018, when it first became clear to American based investors and speculators that the euro and yen were seemingly stuck with negative interest rates in perpetuity, while the Trump stimulus would likely lead to higher dollar rates. Now that the Fed is closing down the rate differential by cutting its funds rate these arbitrages need to be unwound, leading to substantial liquidation of T-bills, USTs and dollars to repay obligations in euros and yen. No wonder the chart of the dollar’s trade weighted index is so bearish.

Hopefully, the hedge fund problem will not replicate the crisis in September 1998, when the Long-Term Capital Management hedge fund failed. But even if that risk is contained, there will be a significant contraction of outstanding bank credit in dollar markets. Being sold on Irving Fisher’s description of how contracting bank credit led to the 1930s depression, the Fed is likely to respond by turning its liquidity taps full on.

The fiscal position is not good either. The current year US budget deficit, estimated by the CBO to be over a trillion dollars, will begin to look like running at an annualised rate of nearly twice that. The Fed could also find itself monetising not only the bulk of new Treasury flows but absorbing sales by foreigners of UST bonds, T-bills and agency debt as well. If so, it will end up increasing its balance sheet by many trillions, unless, that is, the Fed adjusts its priorities to protect the dollar. But the cost of doing so would be the inevitable destruction of US Government finances when the Fed refuses to monetise its debt. That simply won’t happen.

The sacrifice of the dollar as the Fed inevitably fails to maintain financial asset values will truly mark the end of the fiat currency era, since no other fiat currency can exist with the world’s reserve currency thoroughly debased and its financial assets in a state of collapse. This is a simple statement with complex issues behind it, including but not limited to the following:

-

The valuations placed on government bonds are so divorced from economic reality that after the initial shock in equity markets has passed, they will be exposed to a seismic downwards adjustment in prices.

-

Corporate bond markets will face an even greater collapse as risk premiums widen, leading to a spate of bankruptcies in the private sector and losses on collateralised loan obligations held by the banks on a systemically threatening scale.

-

Hedge funds which have taken out fx swaps have already lost the interest rate arbitrage opportunity following the Fed’s recent cut in the funds rate. Furthermore, with T-bills yielding only 0.37%, further cuts in the funds rate are a racing certainty. Unwinding these fx swaps is one factor that will put significant downward pressure on the dollar.

-

A reduction in outstanding derivatives will be the consequence of banks desperate to free up liquidity for their own balance sheets. The cost of hedging risk will increase significantly and in many instances become unavailable. Hedge funds and the like will be forced to restrict their activities, raising the possibility of widespread losses and potential failures in financial asset markets.

-

A glance at their share prices confirms that major European banks are already in trouble and they have long been at severe risk of failure, a fact which has been concealed by the ECB’s provision of liquidity. If nothing else, a new escalation of non-performing loans brought about by the coronavirus now threatens to collapse Italian, French, German, Spanish and other eurozone nations’ commercial banks despite the ECB’s efforts. A coordinated G-20 global bank rescue scheme involving open-ended monetary expansion by central banks is likely to be instigated in a widespread act of currency inflation.

-

A general liquidation of foreign-owned dollar assets and selling of dollars is likely to follow.

-

Only then will the wider public begin to realise the full faith and credit in their governments and currencies which they take for granted are worthless.

The confluence of these threats to financial assets and the world’s reserve currency makes it almost certain that this time attempts to rescue the world from another financial crisis will fail. The twin pillars in the Keynesian endgame, whereby the future of financial assets has become tightly bound to the purchasing power of currencies, will both be destroyed by market forces acting like Sampson pushing the pillars apart until the temple’s collapse killed all the Philistines.

Comparing fiat to sound money

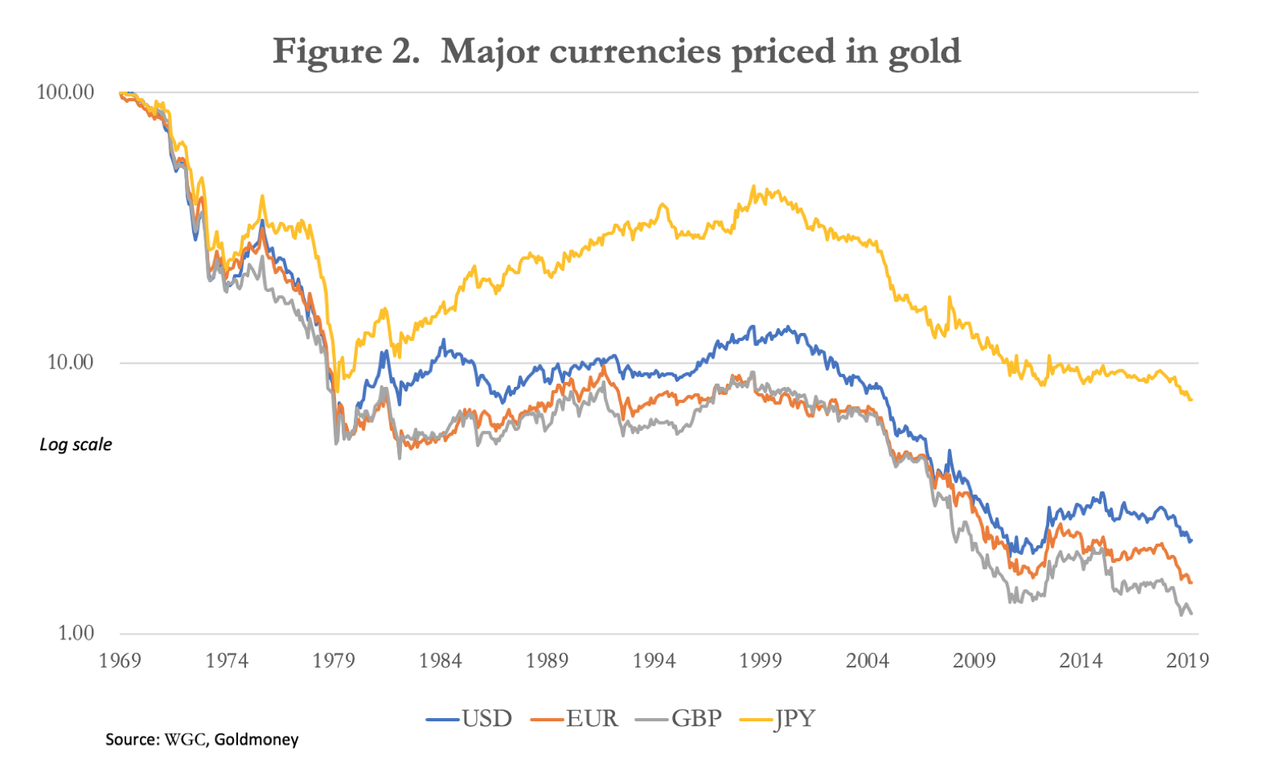

Figure 2 shows that since the gold pool failed in the late 1960s the four major currencies (including the euro’s components prior to 1999) have lost substantially all of their purchasing power, compared with that of gold. The most debased is sterling, which retains only 1.19% of its 1969 purchasing power, followed by the euro at 1.56%, the dollar at 2.22% and the yen at 7.4%.

The failure of the gold pool and the subsequent abandonment of the post-war Bretton Woods agreement was the last significant monetary failure. The first in modern times was the 1934 devaluation of the dollar from $20.67 to $35 per ounce of gold, thirty-five years before. On this timeline the next failure appears to be overdue.

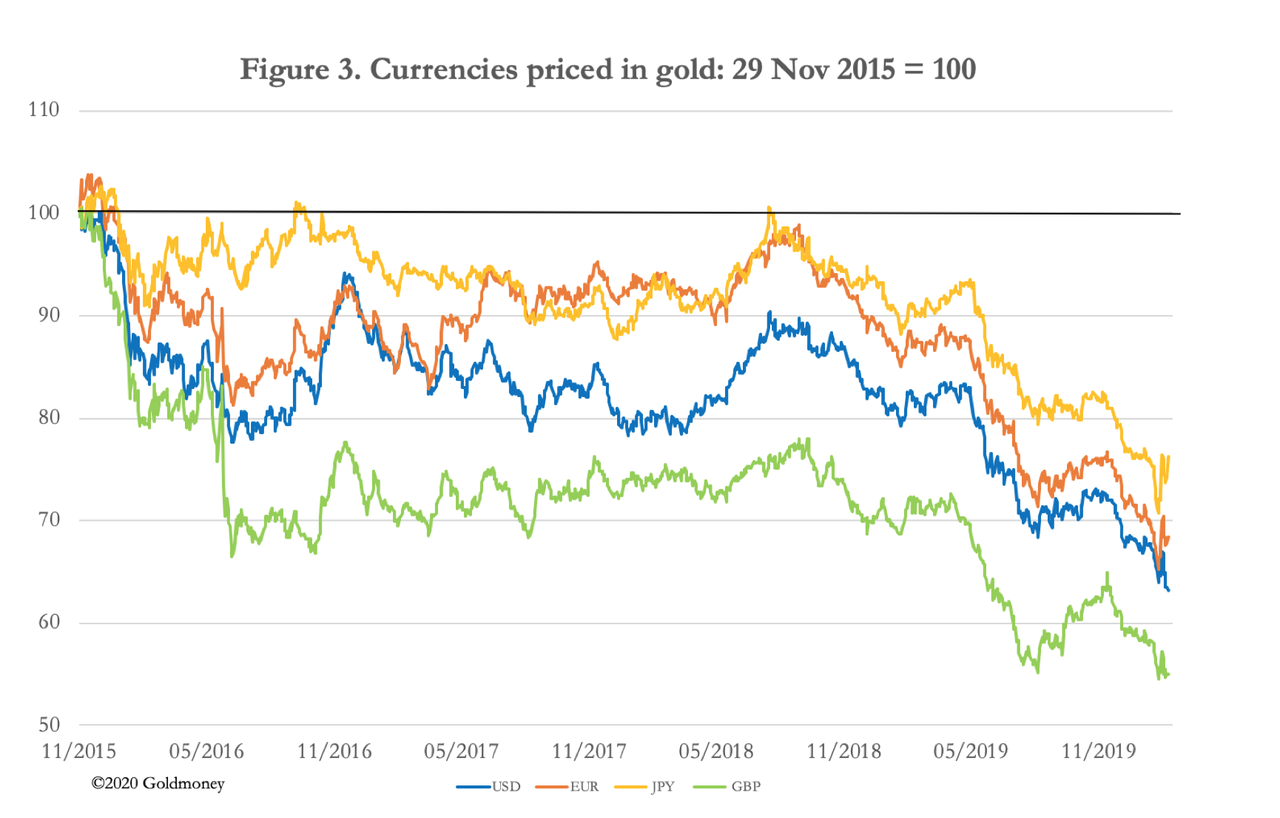

The current situation has the makings of leading into an even greater monetary event, as government spending spirals beyond control without the means to fund it, except by monetary inflation. It has already been anticipated by a renewal in the bear market in the major currencies measured in gold terms, dating from late-2015 and is illustrated in Figure 3.

These represent significant losses ahead of the currency debasement which is now becoming increasingly certain in the coming months. It is extraordinary that this marked devaluation of currencies has occurred with very few commentators noticing.

If we refer back to John Law’s Mississippi bubble, which is the best model for what is now unfolding, the loss of all purchasing power for his fiat currency happened in less than a year. Law’s livre began the final phase of its decline in November or December 1719 and by the following September there was no exchange rate against sterling, indicating it was worthless. From November 1719 Law accelerated his purchases of shares in his Mississippi venture ahead of its merger with his bank, the Banque Royale, paid for by issuing unbacked paper livres which began to noticeably undermine its purchasing power.

Sticking with Law’s failure as a template for ours today, we can similarly expect the Fed on behalf of the US Government to issue new money for the purpose of maintaining financial asset values, mainly of US Treasury bonds, but by extension of equity prices as well.

Following the current panic into perceived safety, a second phase will likely evolve, being driven by the collapse of government bond prices. Currently, they are over-valued on a combination of unrecognised price inflation, which based on independent estimates is probably closer to ten per cent than two, and a flight to perceived safety from other financial assets. That process will come to an end, and the condition of government finances, which ultimately depend upon the wealth and health of the productive economy, are bound to be reassessed in the light of the slump in business activity and a more realistic assessment of price inflation.

To sum up, the following developments are likely in the coming months in approximate order, with some running concurrently:

-

Base money will be increased substantially to offset a contraction in bank credit and to give banks extra liquidity to compensate for becoming deficit agents as supply chains dislocate and retail sales of non-essentials goods and services collapse. We have already seen daily repos by the Fed increasing from about $40bn in recent weeks to between $130bn to $200bn currently.

-

“Helicopter money” in various guises, such as deferral of tax payments and business rates to help provide liquidity, will shift to governments some of the deficits building up in businesses. Mortgage payment holidays are offered in some countries. Helicopter money is already being provided to investors through share support operations, such as the Bank of Japan’s purchases of ETFs, which is likely to be expanded. In Hong Kong, each citizen is being given HK$10,000.

-

Within a month or two there will almost certainly have to be bank bailouts in Europe, which will require additional monetary commitments by the ECB and the national central banks. This will likely lead in turn to widespread liquidation of euro commitments for speculation and arbitrage. Loans in the trillions have been taken out in euros as the counterpart in fx swaps to the dollar. As these positions are squared the euro will rise and the dollar will fall, transmitting a eurozone banking crisis into liquidation of UST-bills and short-term US Government coupon debt by US hedge funds. A heightened risk of counterparty failure in fx swaps could spread to other derivative markets, requiring bailouts of non-banks, including major hedge funds. Failure to do so or a bungled operation such as tinkering with mandated bail-ins could hasten the collapse of stocks and other financial assets.

-

A declining dollar will increase portfolio liquidation pressures on foreigners, leading to indiscriminate offerings of US Treasuries, agency debt and equities. The Fed will have to take on not only the financing of an increasing budget deficit, but also absorb foreign sales of dollar-denominated securities if it is to retain control of prices.

-

At this stage it will become increasingly obvious to domestic bank deposit holders that the dollar’s purchasing power is being destroyed by the Fed’s escalating asset support commitments. In effect, the Fed will be the only significant buyer of financial assets, paid for through quantitative easing on a far greater scale than that which followed the Lehman crisis.

-

In the absence of other buyers of US Treasuries and the loss of purchasing power for the dollar, bond prices will sink, which will make it virtually impossible for the US Treasury to fund a ballooning deficit. An election year creates extra difficulties leading to uncertain political outcomes. But by the time President Trump is due to stand for re-election, over a million elderly and poor Americans might have died from the coronavirus, socialist Democrats might be in the ascendant and the dollar could become worthless.

-

With the dollar as the world’s reserve currency and nearly all other fiat currencies having taken their cue from it since the Nixon shock in 1971, they also seem doomed to failure with the dollar.

Where will the money go?

In the three months before the collapse of his scheme, sellers of shares in his Mississippi venture required John Law to replace them with new buyers, and when they could not be found he substituted them by buying shares with new livres issued for the purpose. Today’s price support system which rigs government bond prices is exactly the same concept as that deployed by John Law, except it is on a global scale.

Law’s experience showed that in an asset and monetary collapse, apparent wealth simply vanishes, destroyed along with the medium of exchange. Theoretically, if there are no buyers at any price the collapse to zero is immediate and no one extracts any value to be redeployed elsewhere. The Mississippi bubble also showed that the purchasing power of sound money, always gold or silver, is at least retained. For this reason, it is more than likely a rising price for monetary gold will happen without very much gold needing to be purchased.

Being dominated by mathematical economists, current thinking in financial asset markets does not often admit to this. But as the central banks show increasing difficulty in maintaining the combined values of currency and bonds, the price of gold and silver in fiat currency terms will rise significantly. More correctly described, the ratios of fiat currencies to gold will fall, as illustrated in Figures 2 and 3 above.

Gold and silver are reliable money, chosen by the people as economic actors. The journey to their reinstatement will require the destruction of the unsound currency issued by the state, which is simply a distorting monopolist and therefore a distorter and destroyer of economic values. Only then can gold and silver re-emerge as circulating money, or more practically, reliable and trusted paper and electronic substitutes for them. Gold and silver are emblems of economic freedom, and while the transition will only be very reluctantly accepted by the state, a better monetary future will beckon.

It is in this light we should anticipate the money to replace dollars, euros, yen and pounds. In Asia they will be better placed than western nations to return to sound money, with Russia having substantially replaced its reserve dollars with gold, which could easily be legislated into a gold exchange standard for the rouble. China will be in a position to do the same for the yuan. In theory, getting to the point where monetary stability returns will be easier for some governments than for others. The capitalist nations, and China perhaps to a lesser extent, have subsumed Keynesian economics deep into their collective psyche, so deep that it has replaced entirely an understanding of free market economics.

Governments with extensive welfare obligations will find it an enormous challenge to maintain the balanced budgets required to ensure that a new monetary system will endure. They have been socialising wealth for too long to understand the simple fact that if you wish your nation to be prosperous you must allow the people to create and retain it. You must also make them responsible for their own affairs and make it clear to them that no one individual, lobbyist or interest has a right to government intervention. The function of government must be limited to making and administering criminal and contract law and protecting the realm, with strictly limited welfare provision.

A government that works in a sound money environment absorbs and administers only a minor part of its national economy. The loss of political power is always widely resisted, but the redeployment of national resources from a wealth-destroying state to free-market production has been shown to produce remarkable benefits in surprisingly little time. If, that is, the political class is wisely led by statesmen not in thrall to the common economic fallacies of John Maynard Keynes and John Law.

Tyler Durden

Wed, 03/18/2020 – 23:00 -

- Nearly 20% Of Households Have Already Lost Work Due To Pandemic-Shutdowns

Nearly 20% Of Households Have Already Lost Work Due To Pandemic-Shutdowns

The arrival of helicopter money in the form of two $1,000 checks to most Americans is the government’s acknowledgment that the economy crashed, and upwards of 30 million people could be unemployed due to the Covid-19 outbreak shutting down cities and towns across America.

A new NPR/PBS NewsHour/Marist poll has shown that 1 in 5 households have already experienced a layoff or reduction in work hours thanks to social distancing measures enforced by the government that is grinding local economies to a halt.

People across the country are staying home, avoiding large crowds, and ordering food on Amazon, as the fast-spreading virus is rapidly infecting people in New York, Washington state, and California. Confirmed cases have now been recorded in all 50 states.

The federal government missed containment windows to implement social distancing policies by nearly a month, and this means cases are likely to be exponential in the days or weeks ahead. Deaths have stayed low at this point because ICU treatment capacity at major hospitals has yet to be overwhelmed, but when they do, America could be the next Italy.

Bill Gates said on Wednesday that virus shutdowns could last upwards of ten weeks. The most affected industries have so far been restaurants, bars, hotels, casinos, cruise ships, and airlines, but as we noted last week, the ripple effect has collapsed the entire gig and service economy.

The poll was conducted on March 13-14, shows layoffs and reduced hours had already hit 18% of households. Lower-income households were hit the hardest, at least a quarter of them were making $50,000 per year had the most hours cut or experienced the most significant amount of job losses. It also showed a third of households had at least one person who had a significant change in work routine associated with the virus impact. College students were the most susceptible to job disruption.

Most of the jobs that experienced reduced hours or have been entirely cut have been blue-collar and service or retail jobs, which cannot be conducted remotely.

We noted last week that the virus crisis was expected to crash the gig and service economy. With more than 50 million Americans, or about 44% of all US workers, aged 18-64, are considered low-wage and low-skilled, have insurmountable debts (with limited savings), including auto, student, and credit card debts, are working in the gig-economy via side hustles and are most vulnerable to job losses as Covid-19 has likely triggered the next recession.

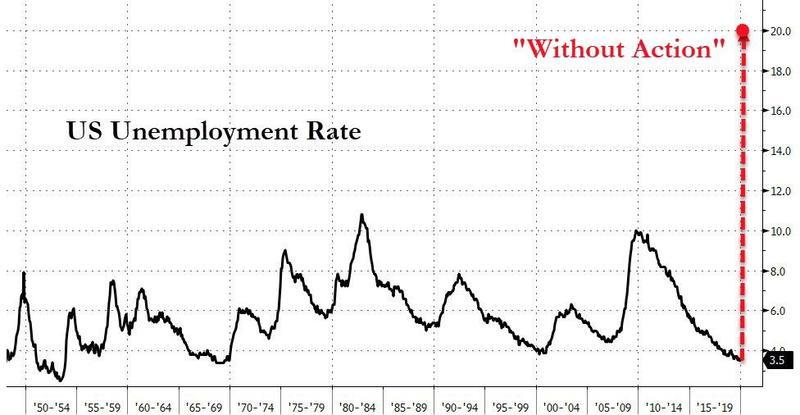

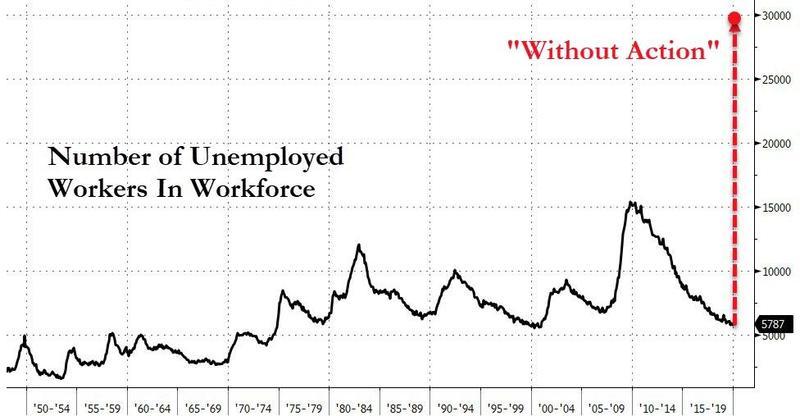

What’s about to happen next could be absolutely terrifying, as Treasury Secretary Steve Mnuchin warned the US unemployment rate could spike to a stunning 20% without stimulus directed at businesses and households.

With a total labor force of around 160 million, this would mean virus-related impacts on the gig and service economy could lead to a sudden spike to over 30 million unemployed without policy action.

Those are depression-era levels of job losses… which is prompting the Trump administration to resort to helicopter money.

New York’s unemployment claims website crashed earlier this week, search trends for “unemployment benefits” surged across the country as well, as chief economist of a multi-billion macro hedge fund said that they are now modeling approximately 10 million job losses over the next two to three months.

Maybe the real reason why the National Guard is being deployed across the country is the possibility that a Covid-19 pandemic could lead to social destabilization as millions lose their jobs and supermarkets run out of food. Who would’ve thought America is transforming into the next Venezuela?

Tyler Durden

Wed, 03/18/2020 – 22:40 - Bailout Nation: US Movie Theaters Join Airlines, Hotels And Restaurants In Demanding A Taxpayer Bailout

Bailout Nation: US Movie Theaters Join Airlines, Hotels And Restaurants In Demanding A Taxpayer Bailout

Back in 2008, when the US government bailed out the US banking sector, it became clear that virtually any industry in America’s $18 trillion economy could pass off for “too big to fail.” So fast forward to today when the longest expansion in history has mutated in under a month into the biggest market crash since the Great Depression, and sure enough, virtually any industry is trying to get bailed out.

Consider this – until today, the US government and by implication US taxpayers, had received bailout requests both direct or indirect from:

- The Airline Industry

- The Public transportation industry

- The Hotel and lodging industry

- The Restaurant Industry

- And, of course, Boeing.

And now, demonstrating just how fucked up everything has become once the government has opened the Pandora’s Box of government bailouts, US movie theaters are also demanding a bailout.

That’s right: movie theaters are now somehow a systemically important industry, one which deserves billions in taxpayer funds. And even if it doesn’t, well everyone else is getting bailed out so why not them too.

According to AP, the National Association of Theater Owners (also known as NATO, but definitely not to be confused with that other NATO), the trade group that represents most of the industry’s cinemas, said Wednesday that it’s asking for immediate federal help for its chains and its 150,000 employees. The theaters are requesting loan guarantees for exhibitors, tax benefits for employees and funds to compensate for lost ticket sales and concessions.

Just because that’s how things are done in the US where moral hazard is the name of the game. Every game.

The organization said the movie theater industry is “uniquely vulnerable” to the crisis, and needs assistance to weather a near total shutdown of two to three months. It wasn’t clear how society would collapse if there were no movie theaters after three months, especially with most Americans now having a streaming service pumping non-stop crap into their TV 24/7, but we are confident McKinsey will be hired soon to come up with a pretty slideshow explaining it all.

“This is an unprecedented challenge to the business,” said John Fithian, president and chief executive of NATO. “We’re looking to Congress and White House to understand this is a cultural institution where people gather.”

Ah… so any “cultural institution where people gather” is now eligible for a bailout. At least back in 2008 one could make a case that banks actually are important. After all they hold your money. But now, well, the collapse of theaters threatens to tear society apart.

Fithian didn’t give a specific dollar amount for what the industry is seeking but said theaters could be saved for a fraction of what the airline industry is requesting, because if airlines deserve a bailout, theaters certainly do too. For less than the cost of one airline company, Fithian said, movie theaters could be kept afloat.

In short: just show me the damn money.

“We want our policy makers to know that at the end of this thing, when people have been cooped up in their house for several months, they’ll need a break to go out and do something collectively that’s affordable and fun and away from what they’ve just been through,” he said. “But we still need to be viable.”

In other words, when this is all over, we want to be sitting on a beach, earning 20%, or rather -20% in this day and age, on the money the idiot taxpayers threw at us.

NATO also said it will supply $1 million in aid for out-of-work movie theater employees, the majority of whom are paid hourly. It wasn’t clear if he demanded $1 billion for the privilege of passing on 0.1% to his customers. “Starting tomorrow, most of them won’t be paid anything,” said Fithian, which ironically describes something once upon a time known as capitalism.

Earlier this week, US movie theaters closed nationwide, shuttering nearly all of the country’s cinemas including its largest chains, AMC Theaters and Regal Cinemas. The closures followed federal guidelines against gatherings of more than 10 people. Hollywood has postponed nearly all March and April releases, and many May ones, too.

In the meantime, some studios have moved their new releases to on-demand platforms, a rare breaking of the traditional 90-day theatrical window. Universal earlier announced that “The Hunt,” “Invisible Man” and “Emma” will be released for home viewing on Friday. On Wednesday, Sony Pictures said the Vin Diesel sci-fi thriller “Bloodshot,” which opened in theaters last Friday, will be available for digital purchase Tuesday.

“Sony Pictures is firmly committed to theatrical exhibition and we support windowing,” Sony Pictures chairman Tom Rothman said in a statement. “This is a unique and exceedingly rare circumstance where theaters have been required to close nationwide for the greater good.”

This means that a far bigger risk for theaters – which no taxpayer in their right mind will ever agree to subsidize, let alone bailout – is not that Americans don’t frequent them for the next 2-3 months due to the pandemic, but that studios realize that they stand to make far more money by “collapsing the window” entirely and transitioning to a “Straight to streaming” service across the industry. Because in case NATO (the other NATO) failed to notice, “cultural institutions where people gather” died years ago courtesy of Mark Zuckerberg and other Silicon Valley oligarchs who have made society optional.

Tyler Durden

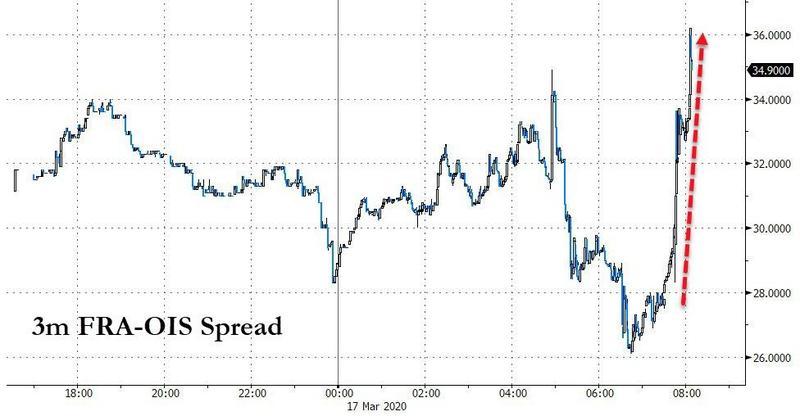

Wed, 03/18/2020 – 22:20 - Is This The Next Big Headache For Global Economy?

Is This The Next Big Headache For Global Economy?

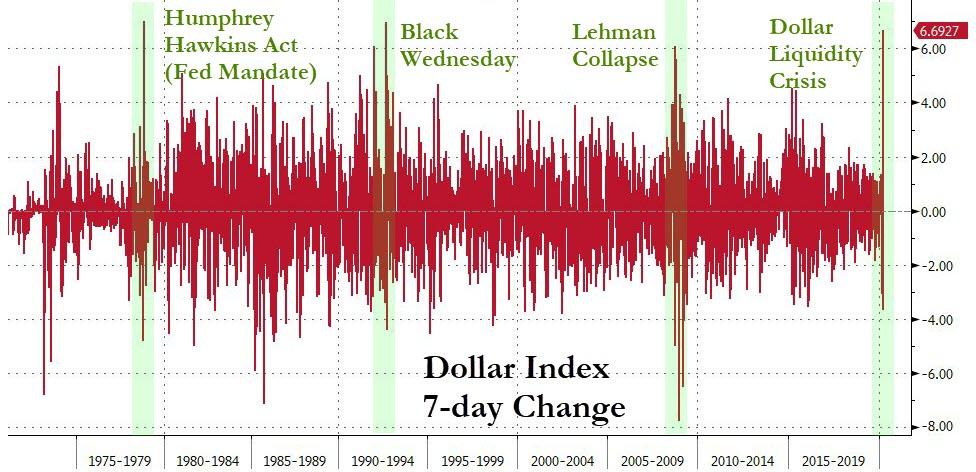

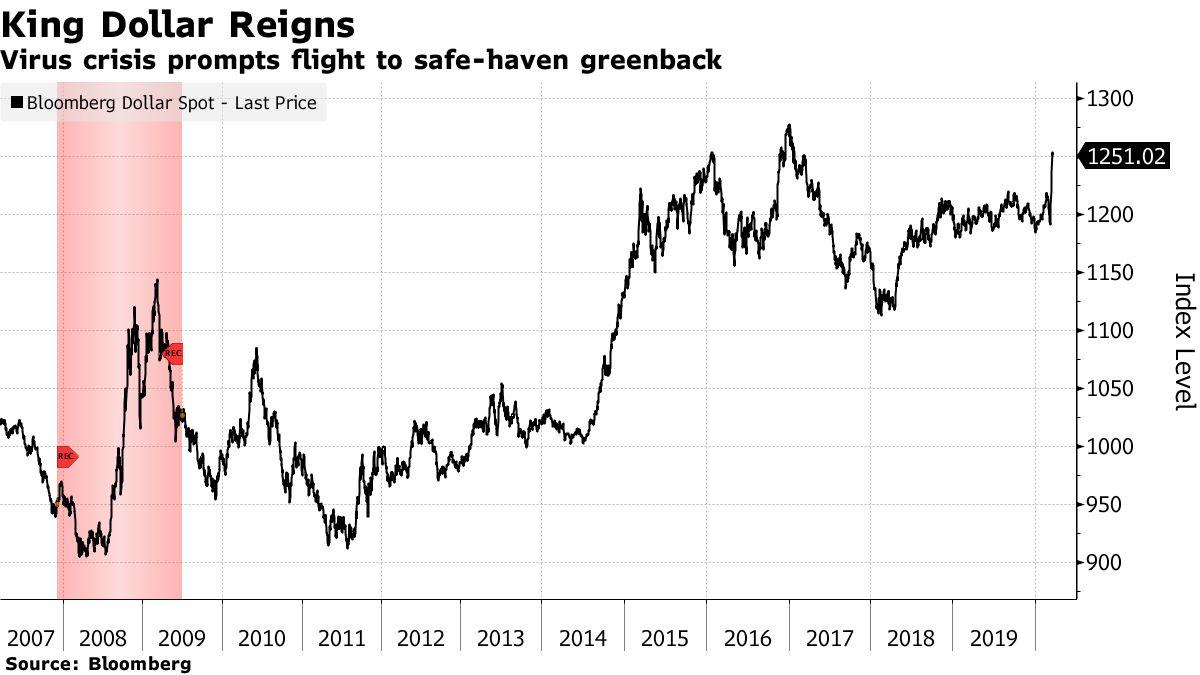

The events of the last several weeks have ominously demonstrated that dollar shortage has returned with a vengeance, as new headaches for virus-battered emerging markets will find it hard to cope with falling local currencies and demand.

The dollar shortage was confirmed last week in both the Bloomberg Dollar index and the FRA/OIS spread, a closely followed indicator of interbank dollar funding availability that has spiked higher, indicating rising stress.

The Federal Reserve’s massive monetary “bazooka” including trillions of dollars for repo markets and the launch of $700 billion QE5 and return to ZIRP, as well as an emergency six POMO operations last week has failed to boost risk sentiment, and the FRA/OIS has yet to show any signs of relief, as it has surged to the highest level since the financial crisis.

The Fed’s monetary cannon may have solved the corporate liquidity crisis for the time being. Still, the dollar/liquidity shortage in the global financial system continues to worsen as investors are dumping emerging markets in record numbers and scrambling for dollars.

Marrying the supply chain disruption triggered by the Covid-19 crisis in China with the oil price war, this has crippled the petrodollar exchange system by sending the price of oil sharply lower and exacerbating the global dollar funding shock.

We’ve pointed out, the world is facing an unprecedented dollar margin call, as a result of the $12 trillion synthetic dollar short, some 60% of US GDP. With the dollar rising, the cost of servicing dollar debt for businesses and governments becomes more expensive as their local currencies plunge amid the barrage of rate cuts by global central banks.

“The surge in the dollar is another blow to emerging markets,” said Mitul Kotecha, senior emerging markets strategist at TD Securities in Singapore.

“The demand for the dollar has outweighed any hit to the US currency from sharply lower Fed rates. EM assets will continue to struggle as investors steer clear of relatively risky assets and maintain a bias for safe havens.”

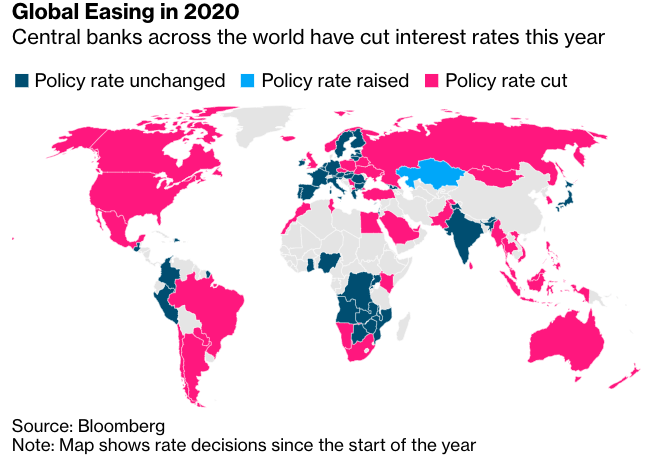

The Fed’s panic rate cuts on Sunday, welcoming the US back to ZIRP, has led to South Korea, Chile, Vietnam, Sri Lanka, Turkey, and Pakistan to cut rates as well. South Africa, Brazil, and Indonesia are expected to slash short-term interest rates later this week.

On top of dollar funding pressures, world trade growth is collapsing, and the tighter financial conditions on emerging markets have triggered a $30 billion outflow in 45 days since the virus crisis started, Bloomberg notes. The dollar reigns supreme in a crashing global economy and pandemic. For instance, the Mexican peso and Russian ruble have dropped by 20%.

Khoon Goh, the Singapore-based head of Asia research at Australia & New Zealand Banking Group Ltd., says emerging market economies are deploying rate cuts to cushion a hard landing but are using FX reserves for currency stabilization.

“They will continue to utilize their FX reserves to smooth currency volatility but will not seek to stem the trend or defend any particular levels,” said Goh.

“In the current environment, when external demand is very weak, allowing some currency weakness alongside lowering interest rates is the best way to try and ease overall financial conditions.”

The Australian dollar has tumbled to its weakest levels since 2003, a move that will increase import costs. Norway’s krone has fallen 15% this year, plunging to an all-time low as Brent tags the 27-handle this week.

Central bankers are making sure dollars continue to flow around the world. The Fed’s Sunday announcement called for reduced rates on its dollar-swap lines with five other central banks, a similar policy seen during the 2008 financial crisis.

“A strong dollar is typically a headwind for emerging-market currencies and even more so for countries that are reliant on offshore dollar funding and have floating exchange-rate regimes,” said Todd Schubert, head of fixed-income research at Bank of Singapore Ltd.

As the dollar shortage continues, tightening financial conditions in emerging markets, it’s only a matter of time before something breaks.

Tyler Durden

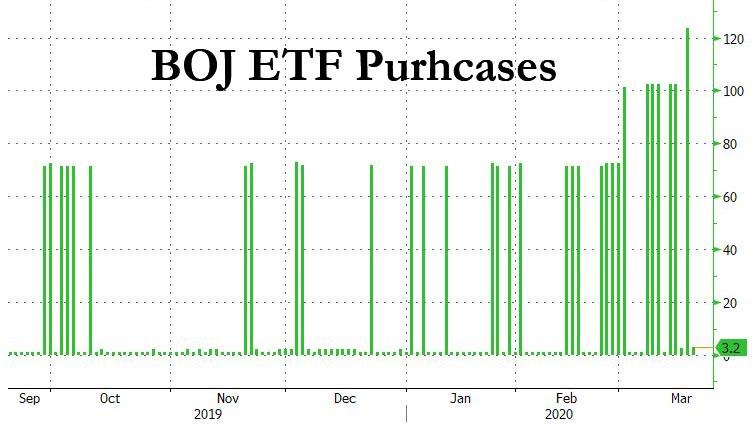

Wed, 03/18/2020 – 22:00 - BOJ Admits It Has Lost 3 Trillion Yen On Its Equity Purchases Despite Literally Printing Money Out Of Thin Air

BOJ Admits It Has Lost 3 Trillion Yen On Its Equity Purchases Despite Literally Printing Money Out Of Thin Air

Long gone are the days when central banks pretended they aren’t in the business of propping up the stock market.

A week after we reported that the BOJ had bought a record amount of ETFs in a desperate attempt to stabilize its illiquid stock market, where the central bank now owns over 73% of all ETFs, Kuroda bought a whopping 121.6BN yen of ETFs on Tuesday, the most on record, and just one day after the BOJ doubled the upper limit of ETFs it can purchase to 12 trillion yen, without however answering where it will get all those ETFs from.

The purchases in its core ETF program jumped by 20% to 120.4BN yen from the previous record of 100.2BN yen; while ETFs bought in the BOJ’s “physical and human capital” program – whereby the BOJ directly admits it is rewarding companies for pursuing policies that it finds appealing such as higher jobs – remain at 1.2b yen. Finally, the BOJ’s J-REIT purchases rose to 1.5BN yen from 1.2BN yen.

The unprecedented creeping nationalization of Japan’s stock market – which has made even the USSR spin in its grave – can be seen in the chart below:

Of course, none of the above is a problem as long as the market keeps levitating higher and higher, however once the crash arrives, people are bound to start asking question.

And as we noted last week, the crash did arrive…

… and the questions emerged. Like for example now that the Nikkei has plunged below the BOJ’s cost basis on its ETF purchases, how big are the losses for all taxpayers.

Answering just this question on Wednesday, Kuroda said that the amount of losses on exchange-traded funds held by the central bank is estimated at 2 trillion to 3 trillion yen as a result of the current crash.

The estimate is based on the current levels of Nikkei225, Kuroda said at a meeting of the Financial Affairs Committee of the House of Councillors, the upper chamber of the Diet, the country’s parliament.

And as noted above, the BOJ decided to double down, literally, on its market propping activities, and earlier this week it announced it would double its annual purchases of ETFs to 12 trillion yen as part of its additional monetary easing measures adopted Monday.

Kuroda also stressed that stepped-up ETF buying by the central bank has “certain effects as a monetary easing step”, which in addition to more gibberish by the 75-year-old, simply meant that the BOJ is doubling down on its purchases because it is now underwater on all of its purchases to date!

It gets better: unwilling to admit the truth until the bitter end of what the BOJ really does , which for the BOJ would mean that moment when its paper losses surpass its capital bases, Kuroda said that ETF purchases aren’t designed to buoy stock prices – something they most clearly are designed to do – but instead to prevent “risk premiums from rising”, whatever that means: perhaps as part of her daily discussions with out daytraders, inbetween discussions of K-Pop, what bread is especially stale today, and whether Fukushima’s gamma radiation will kill off the coronavirus before the coronavirus kills all the participants at the 2020 Olympics, Mrs Watanabe also wants to know the daily risk premium level is.

Somehow we doubt it, and for a good reason: this is just Kuroda’s typical way evading a question by answering some totally non-sequitur gibberish which nobody dares to question afraid to look dumb, when in fact the dumbest person in the room is that one who now has a 3 trillion yen paper loss despite literally being about to print money out of thin air at a moment’s notice and buying whatever he wants.

Tyler Durden

Wed, 03/18/2020 – 21:40 - 'Please Stop Shooting Each Other': Baltimore Mayor Begs Residents To Keep Hospital Beds Clear For Coronavirus Patients

‘Please Stop Shooting Each Other’: Baltimore Mayor Begs Residents To Keep Hospital Beds Clear For Coronavirus Patients

The mayor of Baltimore has asked residents to please stop shooting each other so that local hospital beds are free for coronavirus patients, according to WJZ 13 Baltimore.

“I want to reiterate how completely unacceptable the level of violence is that we have seen recently,” said Mayor Jack Young after seven people were shot Tuesday night in the Madison Park neighborhood. “We will not stand for mass shootings and an increase in crime.”

“For those of you who want to continue to shoot and kill people of this city, we’re not going to tolerate it, Young added. “We’re going to come after you and we’re going to get you.”

He urged people to put down their guns because “we cannot clog up our hospitals and their beds with people that are being shot senselessly because we’re going to need those beds for people infected with the coronavirus. And it could be your mother, your grandmother or one of your relatives. So take that into consideration.”

Commissioner Michael Harrison said the city has seen an uptick in violent crimes since Friday, including a mass shooting Tuesday night — where seven people were shot. Five people were transported to area hospitals via medics and two took private cars to the hospitals for treatment. All seven are in serious but stable condition. –WJZ 13

A local officer who was on patrol at the time traded fire with one of the shooting suspects as the man was fleeing the scene, but he was not able to match the man’s “deadly firepower” according to the report. The officer sustained minor injuries, and the incident “remains open and under investigation,” according to Commissioner Harrison.

Tyler Durden

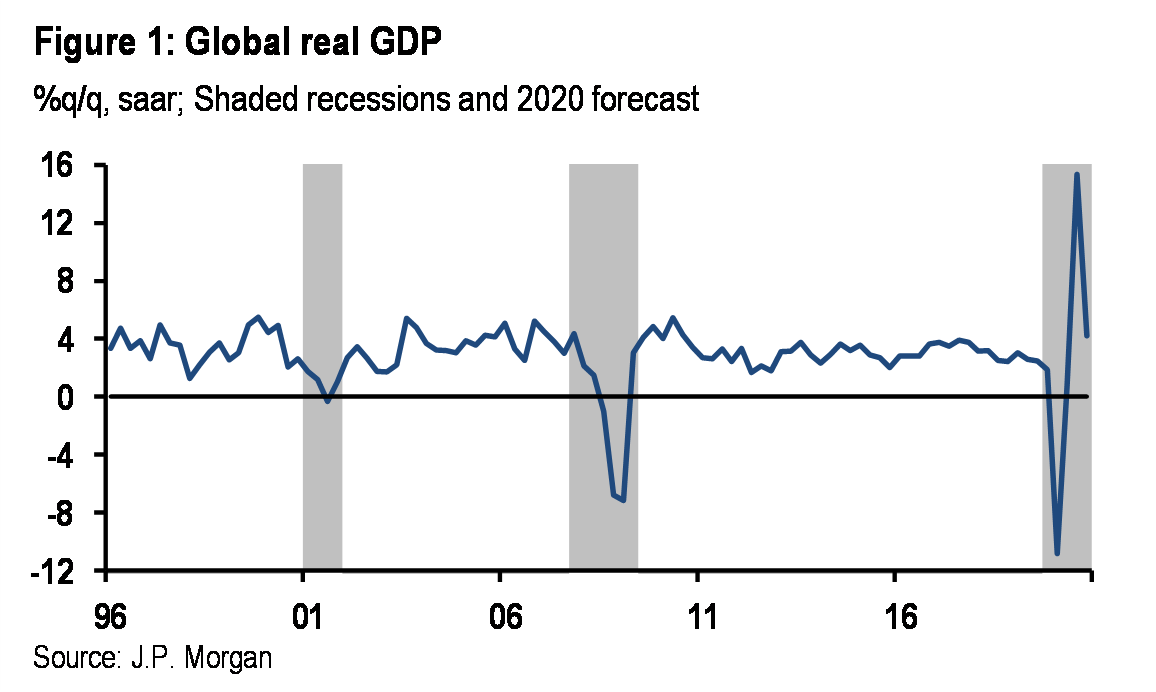

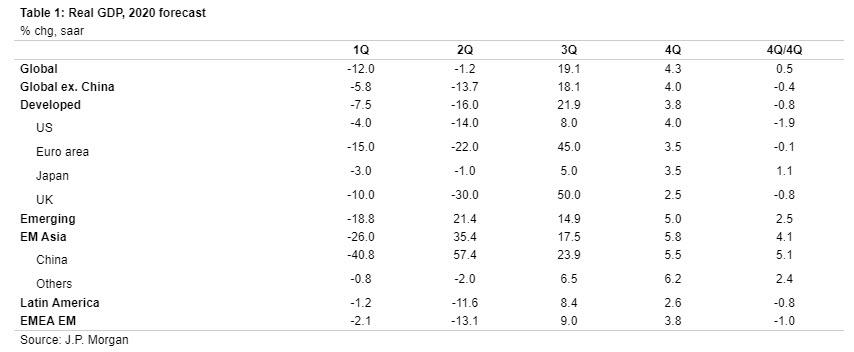

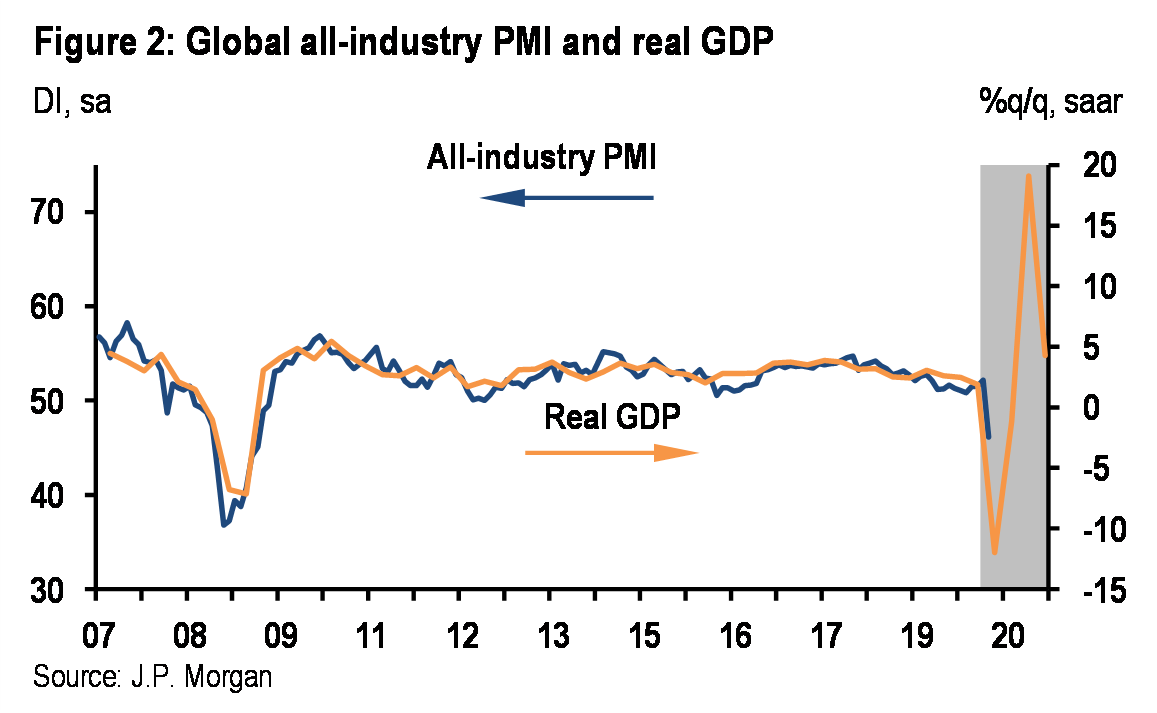

Wed, 03/18/2020 – 21:20 - JPMorgan Now Expects A Global Depression In The Second Quarter

JPMorgan Now Expects A Global Depression In The Second Quarter

Earlier we reported that in a report titled “the lamps are going out all across the economy”, JPMorgan’s chief US economist, Michael Feroli slashed his Q2 US GDP forecast to a staggering -14%, which he optimistically expects to form the bottom of a V-shaped recovery that then lifts the US economy by +8% and +4% in Q3 and Q4, respectively (at least until the next downward revision in his forecast).