- British Doc: "Right Now, It Feels Like We're Heading Into The Abyss"

British Doc: “Right Now, It Feels Like We’re Heading Into The Abyss”

The UK government is now considering a partial lockdown in London to slow down the spread of COVID-19. Over 10,000 troops have been told they could deploy at any given time if social order deteriorates. The hospital system is being pushed to its “breaking point” with an influx of virus patients, all as the economy crashes.

On March 16, we noted that the UK missed the “critical containment window” to suppress the epidemic curve. Now cases and deaths are surging. It was also said that hospital beds and ICU-level treatment were nearing full capacity, indicating that the hospital system is nearing the point of being overwhelmed, which would result in a jump of the mortality rate.

Dr. Jessica Potter, a respiratory specialist in the UK’s National Health Service (NHS), confirmed our thoughts in a recent New York Times op-ed piece, where she said hospitals across the UK “are overwhelmed” and “on the brink of collapse.”

As people with the coronavirus flood our corridors, hospitals will be pushed to the breaking point. Britain is a rich country and may fare better than others. But the NHS is creaking at the seams after years of underfunding. A decade of cuts by successive Conservative governments has stripped the service of resources. Staff morale is low and retention is poor. We are already working at capacity.

When our hospitals are overwhelmed and we have to decide how to allocate scarce resources, how do we choose whom to ventilate and whom not to? Italy is nearly at that point, and its health service has many more intensive-care beds per person than Britain’s. Will I have to tell someone we can’t treat a loved one because we’re out of ventilators, oxygen, tubes, masks, hospitals, staff? Will we then impose an age limit, as some hospitals in Italy are considering, or will some notion of “deservingness” come into play?

Potter said there is much uncertainty surrounding where the country is in the epidemic curve:

But I worry about how we know where we are on the epidemic curve. Have we tested enough people? What if lockdown comes too late? Will we be overwhelmed too soon? Across the NHS this winter there have been patients in corridors and canceled surgeries. How many people will die because we’ve been working on the brink of collapse for too long?

She warned that the hospital system could struggle to treat the most vulnerable:

Britain has fewer intensive-care beds than most other European countries. Occupancy rates are high, and there’s a daily struggle to discharge enough people to make space for new patients. Even when a bed is available, we do not have the nurses to staff it. A decade of cuts and underfunding has left us dangerously exposed. This is the perpetual winter of the NHS.

Potter said, “right now, it feels like we’re heading into the abyss.” And that is right because the hospital system is at near full capacity, no one knows where the country stands on the epidemic curve, and until a complete lockdown of the country is seen, the virus will continue spreading.

If you thought UK’s collapsing hospital system was terrible, the economy has also crashed, resulting in the Bank of England to make a statement that said it would print unlimited amounts of money.

A secret government document was leaked earlier this week that said 80% of Britons could be infected, and the virus would not clear out of the country until Spring 2021.

Tyler Durden

Fri, 03/20/2020 – 02:45 - How The European Union Turned The Coronavirus Into A Pandemic

How The European Union Turned The Coronavirus Into A Pandemic

Authored by Con Coughlin via The Gatestone Institute,

The emergence of Europe as the new epicentre of the coronavirus pandemic has as much to do with the European Union’s inept handling of the crisis as it does with the resilience of the virus itself.

When the world first learned about the existence of coronavirus in China at the start of the year, the EU’s response, like much of the rest of the world’s, was to adopt a wait and see approach as to how it developed.

The problem for the EU, though, is that it has maintained this lackadaisical approach long after it became clear that the virus was going to develop into a global, rather than a specifically Chinese, issue. More pertinently, the EU’s failure to raise its game, after the rapid spread of the virus resulted in much of Europe coming to a standstill, means that the EU is now trying to play catch-up in terms of asserting a leadership role.

After weeks of prevarication, the EU finally imposed measures to ban travellers from outside the bloc for 30 days. The measure is expected to apply to 26 EU states as well as Iceland, Liechtenstein, Norway and Switzerland. The ban will not apply to citizens from the UK and Ireland.

“This is good,” commented European Commission President Ursula von der Leyen as she announced the new measures earlier on March 18.

“We have a unanimous and united approach [where] the external borders are concerned.”

That it has taken until now for the EU to act, when so many major European countries such as France, Italy and Spain are already in lockdown, illustrates the inadequacy of the EU’s response to the crisis. It also helps to explain why Europe has replaced Asia as the main epicentre of the pandemic.

By the time Mrs von der Leyen finally got around to announcing at the start of this week that the EU was planning to impose its travel ban, most member states had already taken matters into their own hands and made their own arrangements to restrict border access.

Moreover, by undertaking their own unilateral actions, the decision by some EU member states, such as Austria and the Czech Republic, to specifically ban citizens from other EU states, such as neighbouring Italy, represents a flagrant breach of one of the EU’s key founding principles, namely the free movement of its citizens across the borders of other member states.

Consequently, the EU’s failure to address the coronavirus issue earlier has resulted in the Schengen Agreement, which stipulates that the citizens of any EU state can travel freely throughout the union, becoming null and void.

The EU’s commitment to Schengen was one of the key factors that persuaded U.S. President Donald Trump to impose his initial travel ban on continental Europe, claiming — correctly — that the EU was being far too complacent in its response to tackling the virus.

Now, thanks to the EU’s ineptitude, the union has entered a new era in which the precedent has been established whereby it is the governments of the various constituent member states, and not Brussels, that decide who can, and who cannot, cross their borders.

The sudden imposition of new border controls in Europe is already having a serious impact on the trading arrangements between different EU member states. This week, for example, trucks trying to enter Poland from Germany have been subjected to a tailback dozens of kilometres long, as Polish border guards insisted on checking the temperatures, health and documentation of drivers seeking to enter the country.

Moreover, the EU’s inability to provide effective leadership in terms of responding to the coronavirus challenge has led to an increase in tensions between key member states, tensions that could ultimately threaten the survival of the EU in its current manifestation.

Perhaps the most shameful episode concerning inter-EU relations since the start of the coronavirus outbreak was Germany’s refusal to allow the export of much-needed face masks and ventilators to Italy after the Italian government made a direct appeal to the rest of the EU for help. Instead of demonstrating the so-called solidarity that is supposed to underpin the EU’s founding ethos, the German government issued a ban on the export of the equipment to Italy.

It was left to the Chinese government to provide the Italians with 31 tons of urgent medical supplies.

The EU’s handling of the coronavirus has not just been incompetent. It raises serious questions as to whether it is about to become yet another victim of the deadly pandemic.

Tyler Durden

Fri, 03/20/2020 – 02:00 - 50 New Infections Every Hour In Iran, One Death Per 10 Minutes: Health Ministry

50 New Infections Every Hour In Iran, One Death Per 10 Minutes: Health Ministry

Despite that between Tuesday and Wednesday of this week Iran witnessed its biggest ever single-day spike in Covid-19 cases, authorities are still struggling to get everyone to observe quarantine and self-isolation measures, especially after throngs of hardline Shia demonstrators have gathered to protest the closure of two of the country’s holiest shrines in the city of Qom.

Toward this end, Iran’s Health Ministry spokesman Kianush Jahanpur made an astounding statement to put things in perspective, saying the current soaring numbers show that—

“In Iran, every ten minutes one person dies from the coronavirus, 50 get infected.”

He added in the Twitter statement “And every 10 minutes one person dies.”

#Iran’s Health Ministry’s Spokesman: Every hour 50 Iranians contract #Covid19 and every 10 minutes 1 dies. Keep this data in your mind and think twice when you decide to visit relatives in Nowruz or travel to other cities. https://t.co/BBbYwv6czM

— Fereshteh Sadeghi فرشته صادقی (@fresh_sadegh) March 19, 2020

https://platform.twitter.com/widgets.js

He further urged citizens to think about this extreme risk every time they break national directives and go out to visit people or travel to other cities.

This as on Thursday the national number of cases climbed to 18,407 — a jump of 1,046 cases from the day prior.

The death toll in Iran from the coronavirus outbreak has risen to 1,284, state media reported on Thursday, among those 149 people dying of the virus in the last 24 hours, with 1,046 new cases emerging.

Earlier this week another top health official issued an ‘extreme scenario’ warning in order to urge citizens to stay home, saying he expects “millions” of Iranians to die of the disease.

Among other drastic measures the country has implemented, Tehran says it’s now temporarily sent some 85,000 prisoners home to ensure the pandemic doesn’t rip through the nation’s overcrowded prisons and jails.

Some countries in the West, including cities across the United States, are actually considering the temporary release of non-violent offenders from local jails for the sake of preventing the spread.

Tyler Durden

Fri, 03/20/2020 – 01:00 - Escobar: China Locked In Hybrid War With US

Escobar: China Locked In Hybrid War With US

Authored by Pepe Escobar via The Asia Times,

Fallout from Covid-19 outbreak puts Beijing and Washington on a collision course…

Among the myriad, earth-shattering geopolitical effects of coronavirus, one is already graphically evident. China has re-positioned itself. For the first time since the start of Deng Xiaoping’s reforms in 1978, Beijing openly regards the US as a threat, as stated a month ago by Foreign Minister Wang Yi at the Munich Security Conference during the peak of the fight against coronavirus.

Beijing is carefully, incrementally shaping the narrative that, from the beginning of the coronovirus attack, the leadership knew it was under a hybrid war attack. Xi’s terminology is a major clue. He said, on the record, that this was war. And, as a counter-attack, a “people’s war” had to be launched.

Moreover, he described the virus as a demon or devil. Xi is a Confucianist. Unlike some other ancient Chinese thinkers, Confucius was loath to discuss supernatural forces and judgment in the afterlife. However, in a Chinese cultural context, devil means “white devils” or “foreign devils”: guailo in Mandarin, gweilo in Cantonese. This was Xi delivering a powerful statement in code.

When Zhao Lijian, a spokesman for the Chinese Foreign Ministry, voiced in an incandescent tweet the possibility that “it might be US Army who brought the epidemic to Wuhan” – the first blast to this effect to come from a top official – Beijing was sending up a trial balloon signaliing that the gloves were finally off. Zhao Lijian made a direct connection with the Military Games in Wuhan in October 2019, which included a delegation of 300 US military.

He directly quoted US CDC director Robert Redfield who, when asked last week whether some deaths by coronavirus had been discovered posthumously in the US, replied that “some cases have actually been diagnosed this way in the US today.”

Zhao’s explosive conclusion is that Covid-19 was already in effect in the US before being identified in Wuhan – due to the by now fully documented inability of US to test and verify differences compared with the flu.

Adding all that to the fact that coronavirus genome variations in Iran and Italy were sequenced and it was revealed they do not belong to the variety that infected Wuhan, Chinese media are now openly asking questions and drawing a connection with the shutting down in August last year of the “unsafe” military bioweapon lab at Fort Detrick, the Military Games, and the Wuhan epidemic. Some of these questions had been asked – with no response – inside the US itself.

Extra questions linger about the opaque Event 201 in New York on October 18, 2019: a rehearsal for a worldwide pandemic caused by a deadly virus – which happened to be coronavirus. This magnificent coincidence happened one month before the outbreak in Wuhan.

Event 201 was sponsored by Bill & Melinda Gates Foundation, the World Economic Forum (WEF), the CIA, Bloomberg, John Hopkins Foundation and the UN. The World Military Games opened in Wuhan on the exact same day.

Irrespective of its origin, which is still not conclusively established, as much as Trump tweets about the “Chinese virus,” Covid-19 already poses immensely serious questions about biopolitics (where’s Foucault when we need him?) and bio-terror.

The working hypothesis of coronavirus as a very powerful but not Armageddon-provoking bio-weapon unveils it as a perfect vehicle for widespread social control – on a global scale.

Cuba rises as a biotech power

Just as a fully masked Xi visiting the Wuhan frontline last week was a graphic demonstration to the whole planet that China, with immense sacrifice, is winning the “people‘s war” against Covid-19, Russia, in a Sun Tzu move on Riyadh whose end result was a much cheaper barrel of oil, helped for all practical purposes to kick-start the inevitable recovery of the Chinese economy. This is how a strategic partnership works.

The chessboard is changing at breakneck speed. Once Beijing identified coronavirus as a bio-weapon attack the “people’s war” was launched with the full force of the state. Methodically. On a “whatever it takes” basis. Now we are entering a new stage, which will be used by Beijing to substantially recalibrate the interaction with the West, and under very different frameworks when it comes to the US and the EU.

Soft power is paramount. Beijing sent an Air China flight to Italy carrying 2,300 big boxes full of masks bearing the script, “We are waves from the same sea, leaves from the same tree, flowers from the same garden.” China also sent a hefty humanitarian package to Iran, significantly aboard eight flights from Mahan Air – an airline under illegal, unilateral Trump administration sanctions.

Serbian President Aleksandar Vucic could not have been more explicit: “The only country that can help us is China. By now, you all understood that European solidarity does not exist. That was a fairy tale on paper.”

Under harsh sanctions and demonized since forever, Cuba is still able to perform breakthroughs – even on biotechnology. The anti-viral Heberon – or Interferon Alpha 2b – a therapeutic, not a vaccine, has been used with great success in the treatment of coronavirus. A joint venture in China is producing an inhalable version, and at least 15 nations are already interested in importing the therapeutic.

Now compare all of the above with the Trump administration offering $1 billion to poach German scientists working at biotech firm Curevac, based in Thuringia, on an experimental vaccine against Covid-19, to have it as a vaccine “only for the United States.”

Social engineering psy-op?

Sandro Mezzadra, co-author with Brett Neilson of the seminal The Politics of Operations: Excavating Contemporary Capitalism, is already trying to conceptualize where we stand now in terms of fighting Covid-19.

We are facing a choice between a Malthusian strand – inspired by social Darwinism – “led by the Johnson-Trump-Bolsonaro axis” and, on the other side, a strand pointing to the “requalification of public health as a fundamental tool,” exemplified by China, South Korea and Italy. There are key lessons to be learned from South Korea, Taiwan and Singapore.

The stark option, Mezzadra notes, is between a “natural population selection,” with thousands of dead, and “defending society” by employing “variable degrees of authoritarianism and social control.” It’s easy to imagine who stands to benefit from this social re-engineering, a 21st century remix of Poe’s The Masque of the Red Death.

Amid so much doom and gloom, count on Italy to offer us Tiepolo-style shades of light. Italy chose the Wuhan option, with immensely serious consequences for its already fragile economy. Quarantined Italians remarkably reacted by singing on their balconies: a true act of metaphysical revolt.

Not to mention the poetic justice of the actual St. Corona (“crown” in Latin) being buried in the city of Anzu since the 9th century. St. Corona was a Christian killed under Marcus Aurelius in 165 AD, and has been for centuries one of the patron saints of pandemics.

Not even trillions of dollars raining from the sky by an act of divine Fed mercy were able to cure Covid-19. G-7 “leaders” had to resort to a videoconference to realize how clueless they are – even as China’s fight against coronavirus gave the West a head start of several weeks.

Shanghai-based Dr. Zhang Wenhong, one of China’s top infectious disease experts, whose analyses have been spot on so far, now says China has emerged from the darkest days in the “people’s war” against Covid-19. But he does not think this will be over by summer. Now extrapolate what he’s saying to the Western world.

It’s not even spring yet, and we already know it takes a virus to mercilessly shatter the Goddess of the Market. Last Friday, Goldman Sachs told no fewer than 1,500 corporations that there was no systemic risk. That was false.

New York banking sources told me the truth: systemic risk became way more severe in 2020 than in 1979, 1987 or 2008 because of the hugely heightened danger that the $1.5 quadrillion derivative market would collapse.

As the sources put it, history had never before seen anything like the Fed’s intervention via its little understood elimination of commercial bank reserve requirements, unleashing a potential unlimited expansion of credit to prevent a derivative implosion stemming from a total commodity and stock market collapse of all stocks around the world.

Those bankers thought it would work, but as we know by now all the sound and fury signified nothing. The ghost of a derivative implosion – in this case not caused by the previous possibility, the shutting down of the Strait of Hormuz – remains.

We are still barely starting to understand the consequences of Covid-19 for the future of neoliberal turbo-capitalism. What’s certain is that the whole global economy has been hit by an insidious, literally invisible circuit breaker. This may be just a “coincidence.” Or this may be, as some are boldly arguing, part of a possible, massive psy-op creating the perfect geopolitlcal and social engineering environment for full-spectrum dominance.

Additionally, along the hard slog down the road, with immense, inbuilt human and economic sacrifice, with or without a reboot of the world-system, a more pressing question remains: will imperial elites still choose to keep waging full-spectrum-dominance hybrid war against China?

Tyler Durden

Thu, 03/19/2020 – 23:45 - "He Must Resign From The Senate And Face Prosecution": Tucker Carlson Blasts Burr For Liquidating Stock While Downplaying COVID

“He Must Resign From The Senate And Face Prosecution”: Tucker Carlson Blasts Burr For Liquidating Stock While Downplaying COVID

Fox News‘s Tucker Carlson had some serious words for Sen. Richard Burr (R-NC), who sold off a significant percentage of his stocks on February 13 – raising between $628,000 and $1.72 million in 33 separate transactions.

Carlson noted Burr sold “more than a million dollars in stock in mid-February after learning how devastating the Chinese coronavirus could be.

“He had inside information about what could happen to our country – which is now happening – but he didn’t warn the public. He didn’t give a prime time address. He didn’t go on television to sound the alarm. He didn’t even disavow an op-ed he’d written just ten days before claiming America was ‘better prepared than ever for coronavirus.”

Instead what did he do? He dumped his shares in hotel so he wouldn’t lose money. And then he stayed silent.

Now maybe there’s an honest explanation for what he did. If there is, he should share it with the rest of us immediately. Otherwise, he must resign from the Senate and face prosecution for insider trading. There is no greater moral crime than betraying your country in a crisis, and that appears to be what happened.” -Tucker Carlson

Perhaps Burr was simply reading Zero Hedge’s coronavirus coverage?

Watch:

Wow. Add @TuckerCarlson to the list of folks calling on @SenatorBurr to resign. pic.twitter.com/HhTsDtP7Qv

— Andrew Feinberg (@AndrewFeinberg) March 20, 2020

https://platform.twitter.com/widgets.js

Meanwhile, a second Senator has come under fire for similarly selling stocks before the market took a dive – selling between $1,275,000 and $3,100,000 between January 24 and February 14.

Sen. Kelly Loeffler, R-Ga., has become the second lawmaker to have reportedly sold stock weeks before the coronavirus outbreak triggered a stock market downfall.

The Daily Beast reported on Thursday that Loeffler sold stock that was owned by her and her husband and January 24, which was the same day she sat in on a closed-door coronavirus briefing as a member of the Senate Health Committee with the Trump administration, which Dr. Anthonly Fauci was in attendance.

According to the report, she sold stock in Resideo Technologies “worth between $50,001 and $100,000,” whose stock price “has fallen by more than half” since January. –Fox News

27 out of 29 February transactions by Loeffler and her husband were sales. One of the buys worth $100,000 – $250,000 – Citrix, is a teleworking software company, which has risen since the pandemic has progressed.

Tyler Durden

Thu, 03/19/2020 – 23:25 - BofA Says "The Bond Market Is Broken" And Only Fed Buying Bonds Can Fix It

BofA Says “The Bond Market Is Broken” And Only Fed Buying Bonds Can Fix It

One week ago, Bank of America’s credit strategists issues a dire assessment of the current state of the bond market: the Treasury market was no longer functioning properly.

Fast forward to today, when Citi issued a similar warning about the overall state of the corporate bond market, noting that “order book has collapsed to 10% of historical average and trade impact cost has risen to more than x2 normal market function” pointing out that in terms of overall market liquidity “current levels are close to historical extremes.”

Bank of America also chimed in again, only this time instead of focusing on the Treasury market, it shifted its attention to the corporate market where its take was simple: the “market is basically broken at this point.” Why would the normally non-hyperbolic BofA credit strategist Hans Mikkelsen come out with such a shocking assessment? Simple: just like Janet Yellen and Ben Bernanke the day before, BofA is now confident that the only thing that can fix the bond market – where BofA had been busy herding its clients into corporates for the past year only to see the rug pulled from under them this week – is the Fed which should not waste any time in starting to buy corporate bonds.

Here is the section in question:

A Financial Times article [on Wednesday] – by no less than Janet Yellen and Ben Bernanke – suggested the Fed should start buying corporate bonds. That seems a small step since they just set up a facility to buy commercial paper and, if little else, would be useful to calm a market that is basically broken at this point, with large outflows that look set to continue and pent-up issuance.

Moral hazard? More like no-real hazard.

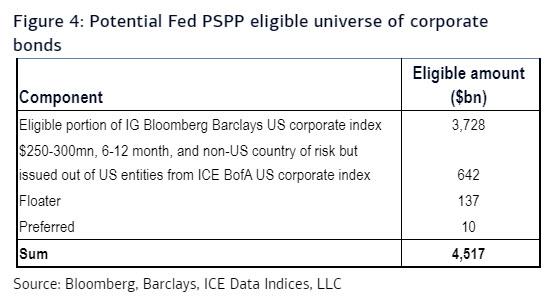

Corporate credit has become a big concern for investors and, as we have seen in Europe, central banks can sharply improve pricing given illiquidity. Obviously it will take some time for the Fed to set it up but the announcement itself would be very powerful. The ECB announced corporate bond purchases in March 2016 and began buying in June that year. Their justification was for monetary policy purposes and – unlike for the Fed – the ECB has no 13.3 requirement so there was no need to seek approval. We estimate an eligible universe in the US of $4.5tn outstanding (Figure 4) plus $49bn average monthly new issuance.

Oh wonderful, at least there is a lot of bonds the Fed can buy.

So sure is BofA that the Fed will come to its – and its clients’ rescue – that it is already preparing a list of bonds and monthly amounts that the central bank should buy:

Some of the decisions the Fed would have to make include what they buy. We assume no bank bonds for example, as that would cut a little close to home with the Fed being the regulator. In other words how do you define the eligible universe? Also, while the ECB buy anything that is eligible irrespective of what the company does, the Bank of England in their program checks that every company makes a “material contribution to the UK economy”.

The next question? How much could they purchase weekly/monthly?

Maybe $50bn/monthly. Do they buy in primary, which would give them access to a lot more bonds and hurts secondary liquidity less. Do they buy like an ETF, i.e. in a market neutrality way? If so the Fed – like the ECB – needs no credit analysts. How do you treat Auto finance units? How much of any single security can they buy as a maximum? They need to define IG – maybe one IG rating and at least two if there are more, which is similar to Bloomberg-Barclays index and the Feds methodology for the new CPFF. What happens to downgraded bonds from IG to HY? Etc.

And since we doubt that BofA is so dumb not to realize that a vast number of the corporate bonds the Fed buys will default in the next few months as a result of the coming global depression – as a reminder, buying a company’s securities does noting for its cash flow but merely drives an even bigger wedge between fundamentals and market prices – and will therefore be equitized post-reorg, BofA is now essentially working under the assumption that the Fed should be buying stocks, an assumption which we are confident all other banks will soon adopt, especially since Janet Yellen expressly said that the Fed should purchase stocks during the next crisis. i.e., right now.

Which, of course, is the final step before the nationalization endgame begins, because once monetizing corporate credit fails to lift the market and bail out both BofA’s client as well as its sellside research division whose only out now is to beg the Fed for a rescue, all that’s left is for the central bank to directly enter the stock market and end price discovery as we know it.

Come to think of it, life will be much easier when the trading day consists of just one daily press release from the Fed advising markets what the closing price is. The only possibly problem could be when just like Kuroda, the Fed chair is asked to explain how despite printing money out of thin air, the central bank is still facing trillions in paper losses.

Tyler Durden

Thu, 03/19/2020 – 23:16 - NASA Warns Two Asteroids Could Cause Atmospheric Explosion Over Earth This Week

NASA Warns Two Asteroids Could Cause Atmospheric Explosion Over Earth This Week

Authored by Aaron Kesel via TheMindUnleashed.com,

As if 2020 weren’t overwhelming enough, in addition to the potential start of World War 3, the massive fires in Australia, the locust plague in the Middle East and Africa, and the novel coronavirus, we are now dealing with multiple asteroids hurtling towards Earth. One of the asteroids may even collide with Earth’s atmosphere resulting in an atmospheric explosion tonight!

Two asteroids following Earth’s intersecting orbit known as 2020 EF and 2020 DP4 are approaching the planet, and information collected by NASA indicates the space rocks are big enough to create violent explosions in the atmosphere if they come too close to the Earth.

The asteroids are being closely monitored by NASA’s Center for Near-Earth Object Studies (CNEOS).

According to a report by IB Times, CNEOS estimates the 2020 EF asteroid has a diameter of 98 feet, making it a little longer than the distance between baseball diamond bases, with a velocity of 10,000 mph.

CNEOS sates that 2020 EF is what is known as an Aten asteroid, which means the object follows a normal orbit that crosses Earth’s path. NASA’s orbit diagram for 2020 EF shows the asteroid mimics a very wide orbit around the sun and almost follows the exact same path as Earth. The good news is NASA states in their diagram that the asteroid will have multiple near-approaches between 2020 EF and our planet—but it won’t hit us.

According to NASA, as a result of their size, 2020 EF will most likely not cause an impact event. Instead, it will break up into pieces if it enters Earth’s atmosphere. However, it will still cause an explosion in the sky that could be dangerous.

The last asteroid atmospheric explosion took place over the city of Chelyabinsk, Russia, which produced a flash 30 times brighter than the Sun and caused 180 cases of eye pain and 70 cases of temporary flash blindness.

So make sure you don’t stare at it with the naked eye, similar to how you shouldn’t stare directly at the sun, no matter how curious you may be.

2020 DP4 is coming our way and will cause a similar space spectacle this week on March 22nd at 2:36 p.m EST. Compared to 2020 EF, 2020 DP4 is much larger in diameter at 180 feet wide and traveling at a faster velocity rate at 18,000 mph according to CNEOS.

While 2020 EF is classified as an Aten asteroid, 2020 DP4 on the other hand belongs to the Apollo family of space rocks. Although the two asteroids are labeled differently, they are known to intersect Earth’s orbit as the planet makes its way around the Sun.

CNEOS states 2020 EF is expected to fly past the Earth from a distance of 0.04241 astronomical units or approximately 4 million miles. Meanwhile, 2020 DP4 will approach Earth from a much closer distance which according to CNEOS, is only 0.00901 astronomical units or around 840,000 miles.

While NASA has expressed that both asteroids won’t collide directly with the Earth, last year NASA and the U.S. government’s Federal Emergency Management Agency (FEMA) participated in an exercise with other international partners to deal with asteroids that could be a future impact danger. Last year, NASA also awarded SpaceX a $69 million contract to redirect an asteroid off its intended path under the Double Asteroid Redirection Test (DART) program, which uses a technique known as a kinetic impactor. The mission involves sending one or more SpaceX Falcon 9 rockets into the path of an approaching near-earth object, in this case, Didymos’ small moon in October 2022.

The European Space Agency (ESA) is also involved in that joint mission to slam a probe into the asteroid Didymos’ small moon.

Next month a third asteroid is expected to come close to hitting Earth called 52768 (1998 OR2). First spotted in 1998, the space rock much bigger than 2020 FE and 2020 DP4, at 1.1 – 2.5 miles wide, is expected to pass within around 4million miles—or about 17 times the distance from Earth to the Moon, moving at a velocity of 19,461 miles per hour. CNEOS states that the third asteroid will fly by the Earth on April 29, at 4:56 a.m. EST.

According to CNN, NASA also reassures that 52768 (1998 OR2) will not hit the Earth despite worries with its classification as “potentially hazardous.” However, the asteroid is “large enough to cause global effects,” according to NASA.

The next potential asteroid that could cause significant damage if it hit Earth is expected to fly through our solar system and pass near Earth on April 13, 2029. The giant icy space rock—known as 99942 Apophis, for the Egyptian God of Chaos—is 1,100 feet wide (340 meters) and will speed by at over 67,000 miles per hour. According to NASA, Apophis has a 2.7% chance to hit Earth—a very low probability.

Thankfully we shouldn’t expect an Independence Day scenario any time soon.

Tyler Durden

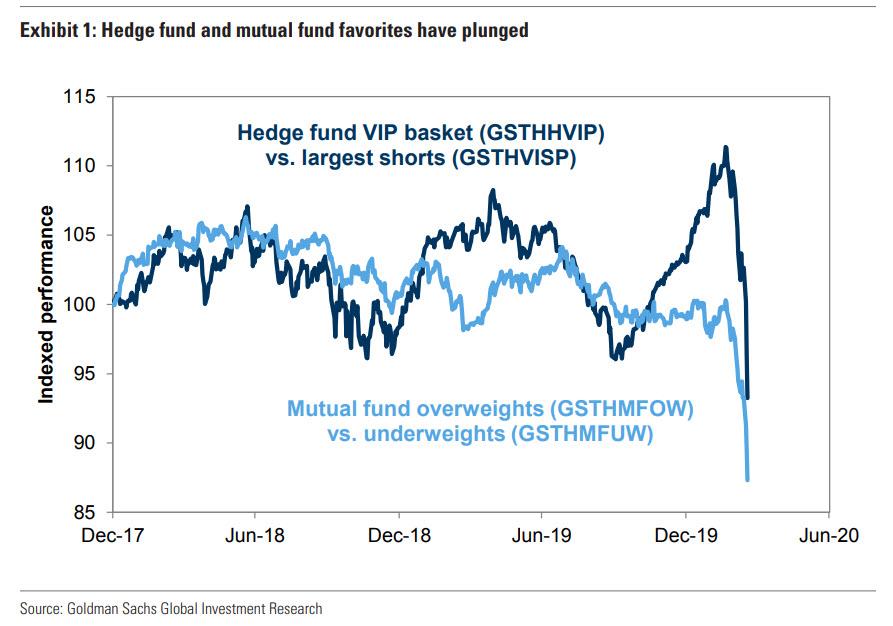

Thu, 03/19/2020 – 23:05 - "Very Intense Plunge": Top Hedge Fund Longs Suffer Historic Crash As Top Shorts Outperform… And Much More Pain Is Coming

“Very Intense Plunge”: Top Hedge Fund Longs Suffer Historic Crash As Top Shorts Outperform… And Much More Pain Is Coming

Total announced stimulus in the US, EU and UK this week was $4.2 trillion, and counting. But for those looking to buy this dip, the bears remain in control of a market paralyzed by its inability to decipher the true economic impact of the virus and the unprecedented dollar shortage just below the surface.

Meanwhile, following the fastest crash from an all time high on record and the biggest VaR shock in history, hedge fund deleveraging is now accelerating (as are mutual fund redemptions) and while realized P&L volatility remains high, and hedging with options expensive, it is unlikely to stop here, at least according to Morgan Stanley. And while the stimulus creates a better backdrop for sharp/short-lived rallies now (helped by clients’ $45bn net short in SX5E futs) the bank’s view remains that we have not yet seen the bottom in index levels.

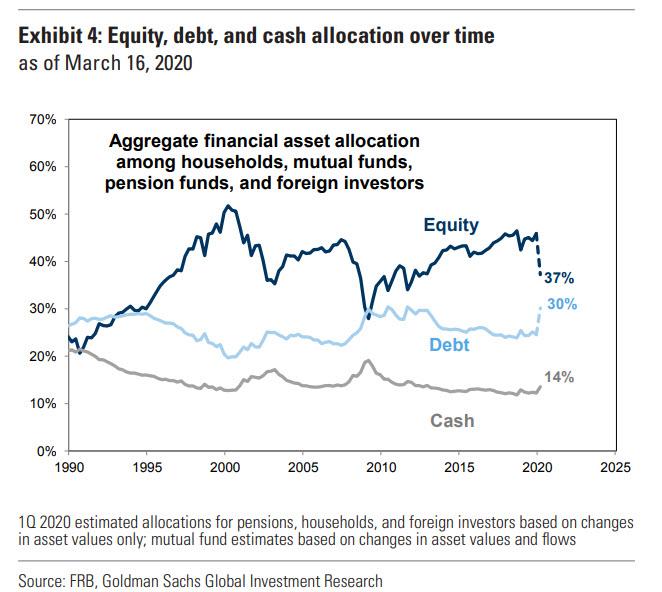

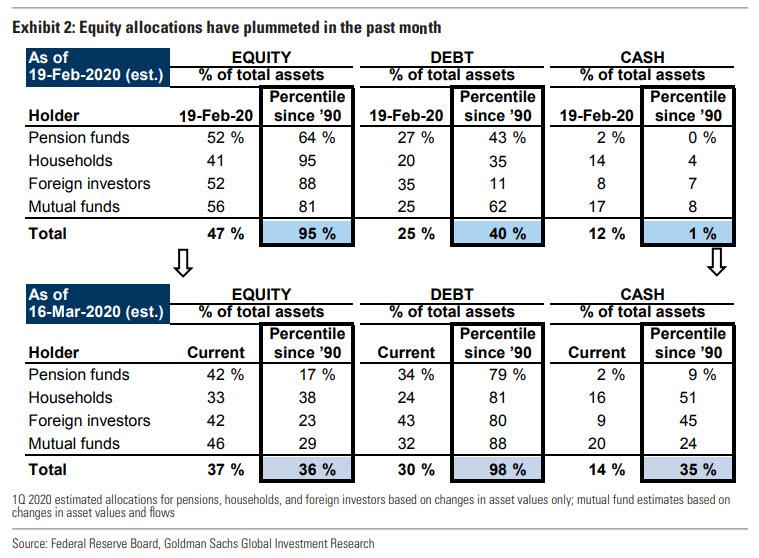

Goldman agrees, pointing out that equity allocations were near all-time highs in February but have plummeted since the start of the bear market. As we pointed out previously, in February, households, mutual funds, pension funds, and foreign investors — who collectively hold 84% of the total equity market — were more or less “all in”, and had notably overweight equity exposure in their portfolios relative to history.

In aggregate, these entities had equity allocations ranking in the 95th percentile vs. the past 30 years. In contrast, these investors had cash allocations at the very bottom of their historical allocations. However, since the all-time high on February 19, the S&P 500 has fallen by 30%, while the allocation to equities has fallen by around 10 percentage points to 37% of financial assets (36th percentile) from 47% (95th percentile). At the same time, allocation to bonds and cash have risen to 30% of assets (98th percentile) and 14% of assets (35th percentile), respectively.

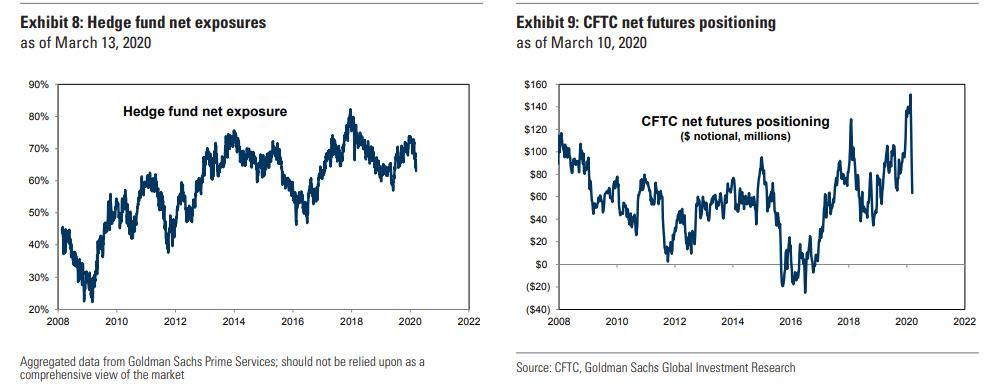

Institutional investor positioning indicators also show a significant decrease in equity exposures, but current levels remain elevated relative to the lows in past corrections. Based on data from GS Prime Brokerage, hedge fund net exposure registered 63% this week, well below the level recorded at the February 19 equity market peak (72%). Similarly, CFTC data also show a sharp decline in net futures length. However, both of these are well above the average observed during the past decade.

This 37% aggregate equity allocation among major investors currently ranks in the 36th percentile since 1990 compared with the 95th percentile in February. However, there is more selling to come, because despite the steep decline, equity allocations are still above the troughs in 2001 and 2008, and cash allocations are at just the 35th percentile vs. history.

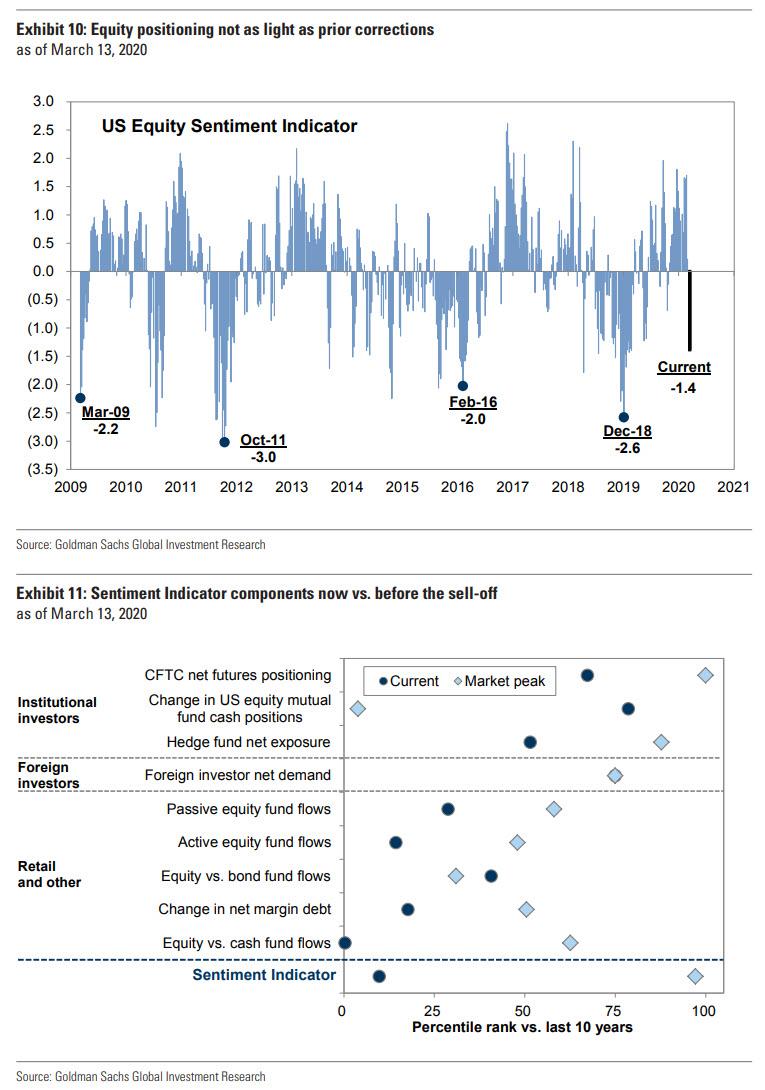

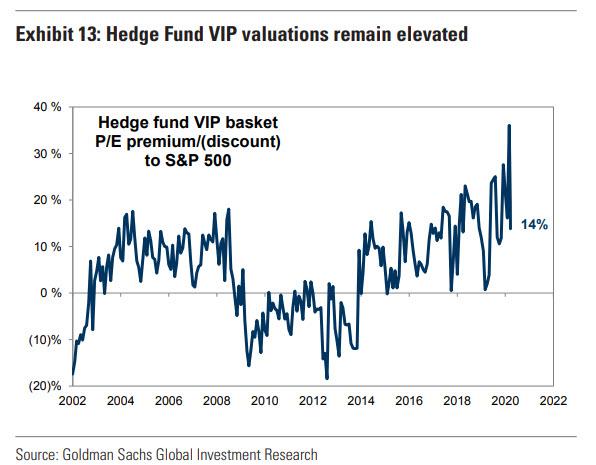

Similarly, Goldman’s high-frequency Sentiment Indicator and the valuations of favorite hedge fund stocks remain more elevated than the bank would expect at the trough of a major correction. As such, Goldman notes that it “expects that investors will continue to rotate away from equities in the near term, leading equity prices even lower.”

Of note is the sharp underperformance this week of the most popular stocks among hedge funds and mutual funds, which suggests that institutional investor selling has accelerated. That’s putting it mildly: whereas Goldman typically takes pride in its Hedge Fund VIP basket which it frequently praises for outperforming the broader market more than 95% of the time, it is now safe to rename it to the Hedge Fund Very Intense Plunge (VIP) basket.

Here’s why: after mostly outperforming the US stock market since the coronavirus started rattling investors in mid-February, the HF VIP basket is now down almost 29 per cent for the year, more than the S&P itself. At the same time, Goldman’s index of popular short positions has – as we have repeatedly told our readers– been far more resilient than the US stock market over the same period, declining only 13% this year. The five-day outperformance of the hedge fund shorts index versus the VIP index is the most extreme seen since Goldman Sachs started collecting the data in 2001. And it’s not just hedge funds: during the same period, the most popular Mutual Fund Overweights have lagged the largest Underweights by 700 bp (-20% vs. -13%), confirming once again that the only way to generate alpha is to do the opposite of what most people on Wall Street do.

And yet, hedge fund leverage curiously remains higher than typical in periods of severe market stress, and the valuations of their favorite stocks remain elevated relative to history.

In short, Goldman expects that the rotation away from equities will persist in the near-term as “uncertainty around the global spread and economic impact of COVID-19 remains high, volatility is at extreme levels across asset classes, and liquidity is thin.”

In this environment, investors are likely to continue cutting portfolio risk, particularly because current aggregate equity allocation of 37% is still above the troughs in 2001 (35%) and 2008 (28%) and cash allocations are still only at the 35th percentile vs. history, despite what the BofA self-serving, and completely meaningless Fund Managers Survey says.

To summarize, “a further decline in investor equity positioning, in concert with thin liquidity and a reduction in corporate buybacks, should cause the S&P 500 to fall” to Goldman’s estimated trough of 2000.

Tyler Durden

Thu, 03/19/2020 – 22:45 - US Airlines To Burn Through $40 Billion By Year End If No Recovery

US Airlines To Burn Through $40 Billion By Year End If No Recovery

Most Wall Street analysts are predicting a V-shaped recovery for the US economy in the second half (even if it boggles the mind how the US economy can simply spring right back from a -14% GDP depression in Q2 without missing a beat). But if they are wrong, there will be hell to pay. Or at least 40 billion dollars to pay for the US airline industry.

According to a new from Vertical Research, US airlines will burn through $40 billion in cash by year-end if passenger revenue plunges to nothing for the rest of 2020, and there is now second half rebound.

“This is a dramatization, but isn’t far from the new reality as each capacity reduction far exceeds the one that preceded it,” Vertical analyst Darryl Genovesi said in a report which was seen by Bloomberg. His “no-longer-so-extreme” scenario also assumes that bookings dry up and carriers are forced to refund all advance ticket purchases.

Genovesi expects that carriers focused on the domestic market, which have cut about 20% of available seats so far, will in the next few weeks slash capacity more along the lines of 70% as Delta has done already.

“Passenger revenue could hit zero by the end of this quarter and stay there for the rest of the year”, he wrote, with cargo revenue disappearing in the third quarter. Annual operating income would then fall about $65 billion short of what had been expected a few months ago.

Major US carriers such Delta, American Airlines and United have already halted nearly all of their international operations as the virus’s spread spurred governments to restrict travel. Carriers now are making deeper cuts in domestic operations, parking planes, offering unpaid leaves to workers and securing billions in loans. Congress is considering $58 billion in loans and other financial help for the industry.

Genovesi’s outlook, which excludes new ticket sales, government aid, new sources of capital secured and about $45 billion in existing fixed financial obligations this year, would leave Delta and United with negative cash balances in the second quarter. American would follow in the third.

In short, all those companies will need to find an additional source of funding or they will have to file for Chapter 11.

“Government hasn’t completely shut down U.S. air traffic, but it may still,” Genovesi said. “And even if it doesn’t, demand is approaching zero as U.S. citizens are staying home.”

Tyler Durden

Thu, 03/19/2020 – 22:25 - A Disgusted Nikki Haley Quits Boeing's Board In Protest Over Bailout Demand

A Disgusted Nikki Haley Quits Boeing’s Board In Protest Over Bailout Demand

While Boeing’s shareholders await to see if they will be granted a taxpayer-funded bailout, or if all those billions they greedily pocketed from the company’s stock buybacks instead of forcing the company to allocate toward a rainy day fund may have doomed if not the airplane manufacturer, which will promptly re-emerge from Chapter 11 with a clean balance sheet, then themselves, today the first casualty of the Boeing crisis emerged when Nikki Haley, the former U.S. ambassador to the United Nations, announced she was leaving Boeing’s board after less than a year, saying she opposes the planemaker’s decision to seek a U.S. bailout amid the coronavirus crisis.

“I cannot support a move to lean on the federal government for a stimulus or bailout that prioritizes our company over others and relies on taxpayers to guarantee our financial position,” Haley said in a March 16 letter that Boeing disclosed late on Thursday, one day after it was revealed that the company is seeking a $60BN bailout.

“I have long held strong convictions that this is not the role of government” she added.

Whatever one thinks of Haley, she is absolutely correct on on this issue: that Boeing wasted tens of billions to push its stock artificially higher by repurchasing its stock in hopes of lifting management equity-linked comp and making its shareholders richer instead of even pretending to plan for a less than perfect future is inexcusable, and no bailout of Boeing should ever be allowed. If Boeing needs the funds, it can sell stock and raise cash – the opposite of what it did for decades. If that is insufficient, Boeing should file a prepackaged Chapter 11 where the creditors take over all the equity and the company emerges from bankruptcy debt-free in one day. Without a dollar of debt, Boeing should be able to weather any disruption no matter how long, and once the economy normalizes it can rehire all the workers that had been laid off.

In short, Boeing will survive but its existing shareholders will be liquidated, as they should in any system even vaguely resembling capitalism.

“Covid-19 is the biggest threat of all time to the airline/aerospace ecosystem and augurs sharp production cuts and liquidity issues” for Boeing, said Cai von Rumohr, an analyst at Cowen & Co. “It’s hard to tell where the stock may bottom.”

Well, if it bottoms at 0, so be it. It’s called a bankruptcy process and countless companies have emerged from it, and gone on to a prosperous, debt-free future. And with the aid of a DIP loan – whether private or public-funded – not one Boeing employee has to lose their job, especially since with a new and clean balance sheet, Boeing will no longer face an existential crisis to produce every single day.

Haley, who was elected to two terms as South Carolina governor, is a rising star in Republican politics who is widely expected to consider a run for president herself in 2024. She is one of the few people who left President Donald Trump’s administration on good terms, finding ways to occasionally distance herself from the boss but remaining a steadfast supporter after announcing her resignation as U.N. ambassador in October 2018.

Tyler Durden

Thu, 03/19/2020 – 22:05 - US Equity Futures Tumble After California State-Wide 'Stay At Home' Order

US Equity Futures Tumble After California State-Wide ‘Stay At Home’ Order

Having been ramped up to unchanged from post-close lows, news that CA Governor Newsom has issued a state-wide “stay at home” order, futures tumbled…

Dow futures are down over 300 points…

It’s Quad Witch tomorrow so we should expect plenty of high gamma swings between now and the open tomorrow.

Tyler Durden

Thu, 03/19/2020 – 21:53 - Alphabet Soup: CPFF, PDCF And MMLF Down; TAF, TSLF, MMIFF And TALF To Go

Alphabet Soup: CPFF, PDCF And MMLF Down; TAF, TSLF, MMIFF And TALF To Go

Authored by Phillip Marey of Rabobank

Summary

-

On Sunday, the Fed set the discount window and the USD liquidity swap lines with 5 key central banks further open.

-

On Tuesday, the Fed relaunched the CPFF and a few hours later the PDCF.

-

On Wednesday, the Fed established the MMLF.

-

Today, the Fed reopened the USD liquidity swap lines with a wider set of central banks.

-

In this special we give an overview of the special lending facilities that are now in place, the special lending facilities from the previous financial crisis that are likely to make a comeback, and a few novel special lending facilities that could become reality.

Introduction

On Sunday, the Fed set the discount window and the USD liquidity swap lines with 5 key central banks further open. However, commercial paper markets were freezing up. The coronavirus outbreak is hitting the cashflow of businesses, who therefore need to raise cash. At the same time, the money market mutual funds – the regular buyers of commercial paper – are also trying to raise cash in anticipation of outflows from the mutual funds by investors. In other words, the commercial paper market had increasingly become dysfunctional. On Tuesday, the Fed relaunched two special lending facilities from the financial crisis, the Commercial Paper Funding Facility (CPFF) and the Primary Dealer Credit Facility (PDCF). While CPFF helps issuers of commercial paper, and PDCF supports primary dealers who remained stuck with large inventories of commercial paper, money market mutual funds were still in need of liquidity. So on Wednesday, the Fed established the Money Market Mutual Fund Liquidity Facility (MMLF). Today, in response to the global need for USD liquidity, the Fed reopened the USD liquidity swap lines they closed in 2010 with a range of non-G7 central banks.

As we indicated in Crash to zero a week ago, we expected the Fed to deploy a range of special lending facilities from the financial crisis. Several were indeed deployed in recent days. In this special we give an overview of the special lending facilities that are now in place, and the special lending facilities from the previous crisis that are likely to make a comeback.

The standard lending facility: the discount window

The Fed is the lender of last resort in the US financial system. In normal times, the Fed operates a standard lending facility that is accessible only to depository institutions, the discount window. This excludes a range of financial institutions and all non-financial firms, but under normal circumstances it is enough for the Fed to provide a backstop for depository institutions, who then in turn provide liquidity to other financial institutions and all non-financial businesses and households. When the US financial system comes under stress, the Fed may first try to stabilize the system by setting the discount window further open. On Sunday, the Fed extended the discount window to 90 days and slashed the primary credit rate by 150 bps to 0.25%. By providing liquidity to banks through the discount window the Fed tries to make sure that banks don’t have to withdraw credit to their customers during times of market stress. In this way, the Fed could support the smooth flow of credit to households and businesses.

Special lending facilities

The discount window is the Fed’s standard lending facility. However, it is restricted to depository institutions and there is a stigma to borrowing at the discount window. On Sunday, the Fed tried to reduce this stigma by encouraging banks ‘to turn to the discount window to help meet demands for credit from households and businesses at this time.’ In order to make this more attractive the Fed slashed the primary credit rate by 150 bps to 0.25%. This means that the spread between the primary credit rate and the top of the target range for the federal funds rate was reduced from 50 bps to zero. The discount window was also extended to 90 days.

However, when the financial system comes under stress and widening the discount window is not enough to stabilize the financial system the Fed also has the possibility to deploy special lending facilities. The special lending facilities are based on section 13(3) of the Federal Reserve Act, which is a ‘unusual and exigent circumstances’ clause. Unfortunately, after the financial crisis the US Congress – through the Dodd-Frank Act of 2010 – made it more difficult for the Fed to use this clause. The Fed needs the approval from the US Treasury Secretary. Why wasn’t CPFF included in Sunday’s emergency package when the Fed cut rates to zero, launched a new large scale asset purchase program, and set the discount window and USD swap lines wide open? Markets were screaming for CPFF. On Tuesday, Mnuchin sent a letter to Powell giving him permission to start CPFF2020. It seems that Congress has tied the Fed’s hands and this has not been beneficial to market functioning as we found out in this week. Perhaps something to reconsider once this crisis is over.

In this special, we try to discuss the ‘alphabet soup’ of special lending facilities in a systematic manner, by focussing on the beneficiaries of the special lending facilities. We start with the depository institutions, which even in normal circumstances have access to the Fed’s standard lending facility: the discount window. Then we look at the primary dealers, money market mutual funds, CP issuers, ABS issuers and foreign central banks.

Term Auction Facility (TAF)

If it turns out that the stigma of going to the discount window is holding back depository institutions too much, the Fed may relaunch a special lending facility known as the Term Auction Facility (TAF). Through TAF the Fed provided term loans to depository institutions, collateralized by standard discount window collateral. However, the funds were allocated through an auction, so that banks would not face the stigma of going to the discount window to ask for a loan. So TAF is basically the discount window without the stigma. During the financial crisis, TAF was the first and largest special lending facility employed by the Fed.

On Sunday, the Fed tried to make the discount window more attractive by slashing the primary credit rate to 0.25% and encouraging banks to use the discount window, but if these incentives would fail to get banks to the discount window – because of the stigma attached to it – then relaunching TAF could help alleviate bank funding strains. In fact, on Tuesday Loretta Mester (Cleveland Fed) mentioned TAF in addition to CPFF.

Primary Dealer Credit Facility (PDCF)

While primary dealers play a crucial role in the financial system, they have no access to the discount window if they are not part of a depository institution. The Primary Dealer Credit Facility (PDCF) provides funding to primary dealers, similar to the way the discount window provides a backup source of funding for depository institutions. On Tuesday March 17, the Fed relaunched PDCF. The PDCF will offer overnight and term funding with maturities up to 90 days. A broad range of collateral is allowed if primary dealers want to use this facility, including investment grade corporate debt securities, international agency securities, commercial paper, municipal securities, MBS, and ABS and equity securities. In case of ABS, only AAA-rated CMBS, CLOs and CDOs are accepted. In case of equity securities, ETFs, unit investment trusts, mutual funds, rights and warrants are excluded. Additional collateral may become eligible at a later date upon further analysis by the Fed. Note that PDCF supports primary dealers who remained stuck with large inventories of commercial paper in recent days when the commercial paper market became dysfunctional.

The loans under the PDCF will be made at a rate equal to the primary credit rate. So in practice this is a ‘discount window’ for primary dealers against a broad range of collateral. In this way, the Fed acts as a lender of last resort to primary dealers, who – if not part of a depository institution – have no access to the discount window. The PDCF is established under Section 13(3) of the Federal Reserve Act, with approval of the Treasury Secretary. The PDCF will be in place for at least 6 months and may be extended as conditions warrant. Note that during the financial crisis the PDCF only offered overnight funding. However, the 2020 version of PDCF offers term funding up to 90 days.

Term Securities Lending Facility (TSLF)

During the financial crisis, depository institutions had access to the discount window and TAF. Analogously, the Fed created the PDCF and the TSLF for primary dealers. The roles of the discount window, TAF, PDCF and TSLF can be summarized in the following table:

The PDCF is a standing facility for primary dealers, while TSLF is an auction for primary dealers. In TSLF auctions the Fed loaned Treasury securities to primary dealers for one month against collateral that consisted of less liquid securities. An important difference between TSLF and TAF is that in TSLF the Fed offers securities for securities, while in TAF the Fed offers funds from the Federal Reserve in exchange for securities and loans. In combination, the PDCF and the TSLF offered the primary dealers access to funds and Treasury securities against a broad range of collateral. Following the widening of the discount window and the relaunch of the PDCF, we are likely to see a relaunch of TSLF (and TAF) in the coming days or weeks.

Money Market Mutual Fund Liquidity Facility (MMLF)

After discussing the Fed’s lending facilities for depository institutions and primary dealers, now we turn to the money market mutual funds. On Wednesday, March 18, 2020 the Fed established the Money Market Mutual Fund Liquidity Facility (MMLF). The Boston Fed will make loans of up to 12 months available to eligible financial institutions secured by high-quality assets purchased by the financial institution from money market mutual funds. The aim of the MMLF is to help money market mutual funds in meeting demands for redemptions by households and other investors. Note that money market funds were scrambling for liquidity in anticipation of withdrawals. This also meant that they were not buying commercial paper from businesses. By introducing CPFF the Fed helped those businesses, but money market mutual funds kept struggling. Through the MMLF the Fed is stimulating financial institutions to buy assets from the money market mutual funds, so that they don’t have to sell them at a large discount if they are forced to sell when investors withdraw their money from the mutual funds. Eligible financial institutions are all US depository institutions, US bank holding companies, US branches and agencies of foreign banks.

Eligible collateral consists of two types with different rates at which the loan is made. The primary credit rate applies to US treasuries and fully guaranteed agencies and securities issued by US government sponsored entities. The primary credit rate plus 100 bps for ABCP or unsecured CP issued by a US issuer, rated not lower than A1, F1 or P1 if rated by at least two major rating agencies or in the top rating if rated by only one major rating agency.

The MMLF is in structure very similar to the Asset-Backed Commercial Paper Money Market Fund Liquidity Facility (AMLF) that operated from late 2008 to early 2010. The main difference is that MMLF will purchase a broader range of assets from financial institutions. The AMLF provided funding for depository institutions purchasing asset-backed commercial paper from money market mutual funds. This facility peaked at $140bn in 2008.

Money Market Investor Funding Facility (MMIFF)

Related to AMLF, in 2008-2009 the Fed also established the Money Market Investor Funding Facility (MMIFF). This facility was designed to provide liquidity for money market mutual funds, stimulating them to extend the term of their money market investments. Instead of scrambling for overnight assets because of liquidity fears, this would help maintain demand for term securities in the money market. Although no loans were made under the MMIFF, the facility could still be useful this time if MMLF would not be enough to support the money market mutual funds.

Commercial Paper Funding Facility (CPFF)

Markets were screaming for it, but finally on Tuesday, March 17, the Fed relaunched the Commercial Paper Funding Facility (CPFF) in order to deal with the freezing up of the US commercial paper market. At present, the coronavirus outbreak is hitting the cashflow of businesses, who therefore need to raise cash. At the same time, the money market mutual funds – the regular buyers of commercial paper – are also trying to raise cash in anticipation of outflows from the MMMFs by investors. In other words, the commercial paper market had increasingly become dysfunctional. The reintroduction of the CPFF brings in the Fed as a large buyer of commercial paper and should help stabilize the market.

Through this facility the Fed finances a special purpose vehicle (SPV) that purchases 3 month commercial paper from eligible users. In this way the Fed takes over the role of money market mutual funds and other buyers of commercial paper that stopped purchasing in recent days. This also reduces the pressure on banks providing credit to issuers unable to sell commercial paper anymore. By providing a liquidity backstop for issuers of commercial paper the Fed hopes to stabilize the commercial paper market. For more technical details we refer to our special report CPFF2020. Note that through this channel the Fed is also able to provide liquidity to businesses, not only depository institutions which already have access to the Fed’s discount window.

During the financial crisis the Commercial Paper Funding Facility (CPFF) was the second largest special funding facility. In this way the Fed took over the role of money market mutual funds and other buyers of commercial paper that were afraid to purchase unsecured debt during the financial crisis. This stabilized the commercial paper market and provided a liquidity backstop for issuers of commercial paper.

Term Asset-Backed Securities Loan Facility (TALF)

Stress in the financial system may also affect the market for asset backed securities (ABS). During the financial crisis the Fed came to the rescue of issuers of ABS by establishing a special lending facility. The Term Asset-Backed Securities Loan Facility (TALF) was launched in March 2009 after interest rates on ABS rose and issuance feel sharply in late 2008. Through TALF the Fed provided loans in exchange for certain AAA-rated ABS backed by newly and recently originated consumer and small business loans. The Treasury Department provided $20bn of credit protection to the New York Fed in connection with the TALF. Through this facility the Fed tried to support the issuance of ABS. Problems in the ABS markets could lead to a relaunch of TALF. USD and foreign currency liquidity swap lines

After discussing the Fed’s special lending facilities for US depository institutions, primary dealers, money market mutual funds, and issuers of CP and ABS we turn to the international dimension of liquidity provision. The crucial role that the USD plays in the international financial system is also reflected in the fact that the USD liquidity swap lines with 5 other central banks never went away.

Also, the foreign currency liquidity swap lines that came in reciprocity were never used by the Fed, except for some pre-arranged small-value test operations. On Sunday, the Board of Governors enhanced the standing USD liquidity swap line arrangements with the Bank of Canada, the Bank of England, the Bank of Japan, the ECB and the Swiss National Bank by offering 84-day maturity, in addition to the 1-week maturity operations currently offered, and by reducing the pricing by 25 bps to OIS+25bps.

On Thursday, in response to the global need for USD liquidity, the Fed reopened the swap lines they closed in 2010 with a range of central banks of non-G7 countries: the Reserve Bank of Australia, the Banco Central do Brasil, the Danmarks Nationalbank, the Bank of Korea, the Banco de Mexico, the Reserve Bank of New Zealand, the Norges Bank, the Monetary Authority of Singapore, and the Sveriges Riksbank. These USD liquidity arrangements will be in place for at least 6 months.

In the coming days and weeks, the USD liquidity swap lines could be extended to an even wider set of central banks, longer maturities could be offered and pricing could be reduced further. Of course, the main question is whether the Fed will open a USD liquidity swap line with the People’s Bank of China.

What’s next?

Now that CPFF and PDCF have been relaunched, MMLF has been established, and USD liquidity swap lines have been expanded to a range of non-G7 central banks it is only a matter of time before the rest of the Fed’s emergency toolkit from the previous financial crisis is reinstated. We may see the return of TAF, TSLF, MMIFF, TALF and the opening of new USD liquidity swap lines. We could also see new facilities, for example targeted at corporate debt, and focussed on lending to small businesses and households. After all, in contrast to the Great Recession, the current shock did not come from the financial system but from the real economy. Consequently, special lending facilities should be aimed more directly at businesses and households.

Tyler Durden

Thu, 03/19/2020 – 21:35 -

- Newsom: 56% Of Californians To Be Infected With COVID-19 Within Eight Weeks

Newsom: 56% Of Californians To Be Infected With COVID-19 Within Eight Weeks

Update (2215ET): During a Thursday evening announcement that California is now under a ‘stay at home order,’ Newsom clarified that the 22.5 million infected figure is a worst case scenario in which nothing is done (in a letter to Trump asking to borrow a Navy medical ship).

The next day he announces a major action to reduce the spread of COVID-19.

* * *

California Governor Gavin Newsom says that an estimated 56% of the state’s population – some 25.5 million people – will be infected with coronavirus within the next eight weeks.

Newsom made the sobering claim in a Wednesday letter to President Trump asking for the US Navy’s Mercy Hospital Ship to be stationed at the Port of Los Angeles until September in order to provide backup to the region’s healthcare system.

“The acquisition of the Mercy here off the coast of the state of California would provide additional 1,000 bed capacity, provides support for pharmacists and other diagnostic equipment,” said Newsom, adding “This resource will help decompress the health care delivery system to allow the Los Angeles region to ensure that it has the ability to address critical acute care needs, such as heart attacks and strokes or vehicle accidents, in addition to the rapid rise of COVID-19 cases.”

“We have community acquired transmission in 23 counties with an increase of 44 community acquired infections in 24 hours. We project that roughly 56 percent of our population – 25.5 million people – will be infected with the virus over an eight week period,” the letter continues.

A spokesperson for the governor said the projection shows why it’s so critical that Californians take action to slow the spread of the disease – and those mitigation efforts aren’t taken into account in those numbers. The spokesperson added that the state is deploying every resource at its disposal to meet this challenge and is continuing to ask for the federal government’s assistance in this fight. –ABC 7

Newsom is working closely with Los Angeles Mayor Eric Garcetti to try and protect the state’s enormous homeless population from the disease – particularly those with pre-existing conditions. The city is also working with the American Red Cross to open 6,000 beds at 52 recreation centers.

California will also supply local governments with $150 million.

“If we take these emergency shelter beds and add in our bridge shelter beds, this means we can bring 7,000 unhoused Angelenos off the streets and into emergency housing – the most in recent memory, maybe ever in the city’s history,” Garcetti said.

Ten years ago, then-Los Angeles Police Department Chief Bill Bratton “said what would it take to clean up skid row and he actually said a pandemic,” said Any Bales, CEO of the Union Rescue Mission in downtown Los Angeles. “It’s unfortunate that that’s what it’s taken, but man am I glad to see so many people making so places for people to go.“

Bales with skid row’s Union Rescue Mission praised all the resources that are coming together to protect the homeless population against COVID-19. Three hundred hand-washing stations and 120 mobile bathrooms have already been set up at encampments.

“I’m hoping we don’t return to putting people on the streets,” said Bales. “That this all teaches us that we all live a better life housed than unhoused together when we immediately help people get off the streets and stay off the streets.” –ABC 7

Newsom said that the state’s typical 2,000 unemployment insurance claims had skyrocketed to 80,000 over the last week.

Tyler Durden

Thu, 03/19/2020 – 21:15 - BMO: The Market Ponders If This Is "The Spanish Flu" Or "The Great Depression"

BMO: The Market Ponders If This Is “The Spanish Flu” Or “The Great Depression”

For the past week, it’s been virtually non-stop: one central bank after another has fired a bazooka, rushing to frontrun its peers in hopes of big impact, only to find no response from the market, forcing it to fire another, even bigger bazooka. Consider that just over the past 24 hours we have gotten the following (via Nomura):

-

Fed announced a new emergency program (MMLF) to aid money markets

-

ECB “no limits” bazooka (“Pandemic Purchase Program w/ $820B of QE)

-

RBA 25bps cut to ELB, introduces QE and targeted YCC

-

Japan discussing $276B packed including “cash payouts” to households

-

S Korea new $40B package

-

Brazilian 50bps rate cut

-

US Senate passes 2nd stimulus bill and negotiating the 3rd ($1.3T)

-

BOE emergency rate cut to 0.1% and GBP200BN QE expansion

And yet, as BMO’s rate strategist Ian Lyngen writes this morning, “central bank intervention continues to mount, but its effectiveness in containing the fear evident throughout financial markets appears to be diminishing.”

The ECB has unveiled a €750 bn bond-buying program (to run at least until year-end) which will target sovereign debt, including Greek bonds, and is in direct response to this week’s spike in Italian yields. The Fed has also followed-through with another emergency effort; through the Market Mutual Fund Liquidity Facility (MMLF) “the Federal Reserve Bank of Boston will make loans available to eligible financial institutions secured by high-quality assets purchased by the financial institution from money market mutual funds.” Providing another source of liquidity for the cash market is a crucial step in assuring the stability of the broader system, even if – as with all the efforts of monetary policymakers – it is not going to flatten the Covid-19 curve.

And, as Lyngen adds, to accomplish this objective, federal and local governments are increasingly the focus of investor angst. The initial phase of trading the official response was “wow – didn’t know things had gotten so bad. Better sell equities.” After a few weeks of gauging the actions of governments both domestically and abroad, a second phase has emerged; “wow – there isn’t enough being done or that can be done. Better sell equities.”

In short, the theme is clear – the market is pondering whether the situation is akin to the Spanish flu or the Great Depression, however facing this dire dilemma, BMO finds itself with a slightly different interpretation as the severity of the price action itself has given the bank pause. Here’s why:

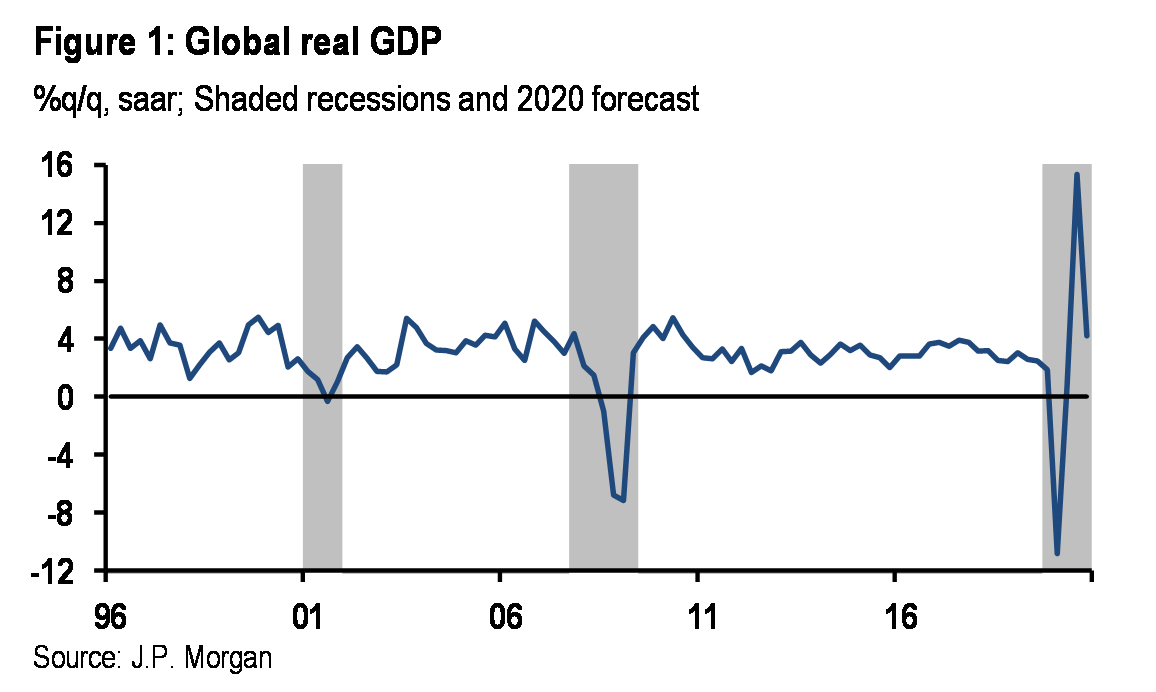

It’s now well-known that the first half of 2020 is going to experience dismal real economic growth; that much is certain. In fact, JPMorgan now predicts a depression-like plunge in US GDP of -14%.

The operating assumption is that once the coronavirus curve has finally peaked (similar to what appears to be occurring in China), cities will reopen and consumption will return anew. This is also the basis behind JPM’s very optimistic assumption of a V-shaped recovery.

However, whether this indeed triggers a v-shaped recovery or a u-shaped one will depend on three unknowns:

-

Fed/government liquidity measures,

-

ability of authorities to contain or slow the spread of Covid-19 and

-

length of the economic lockdown.

Essentially, the first ‘unknown’ is coming into focus as Powell delivers and the White House cobbles together a fiscal package that can make it through Congress.

The second, is even more difficult to judge because as more people are tested, more cases are discovered – the timeline of actual infections is unlikely to be definitively established. Said differently, even a ‘perfect quarantine’ of untested individuals will see a rise in ‘known’ cases as the testing commences.

The third element, the period of economic disruption, is the most angst inducing for investors. Every trading session that passes without either a turn in the pace of infection or a hope-inspiring development has resulted in a downward repricing of risk assets. As an alternative to the more dramatic reading of Spanish flu versus Great Depression, BMO suggests that investors are facing either Y2K (econ-ageddon that never was) or a severe v-shaped recession; akin to the 2009 financial crisis without the same degree of systemic risks.

In the near-term, the details coming out of Washington related to the fiscal response will inform the next leg for risk assets. Helicopter money has become an assumption at this point; however, the ability of businesses to stay viable during the shutdown is even more relevant.

To a large extent, this will depend on how money is funneled to small businesses and whether it is in the form of cheap financing or an outright grant. As an astute member of upper management highlighted, it isn’t in the best interest of firms to load up on debt owed to the government during a mandated closure only to use those moneys to pay workers. Why not simply furlough and rehire the workers; thereby creating a more direct path (via unemployment benefits) to the federal funds? Business owners could then simply negotiate with their landlords and creditors for bridge funding/forbearance until the economy reopens. Food for thought as the details slowly emerge on the >$1 trillion package. Punchline; grant and not cheap financing.

And speaking of the stimulus package, it is worth conetmplating what form the fiscal response from Washington will take. While the details are still unknown, some combination of a direct cash infusion, extended tax payment deadlines, money fund guarantees, and various industry bailouts are on the table. Regardless of how large the spending ultimately is, it will be funded via massive increases in Treasury issuance. This will be focused in the bill market, where the historically larger volatility in offering sizes will bear the brunt of ramp-up in borrowing. Several cash management bills of substantial heft would also follow intuitively. While on the margin, such increases in supply introduce a bearish relative value risk for the front-end, this should be at least partially offset by the flood into government money funds.

As BMO concludes, “as long as the dollar maintains its position as the global reserve currency, even with gargantuan supply sizes, a structural bid will continue to exist for Treasuries, a notion supported by 10s trading below 1.50%.”

Tyler Durden

Thu, 03/19/2020 – 20:55 -

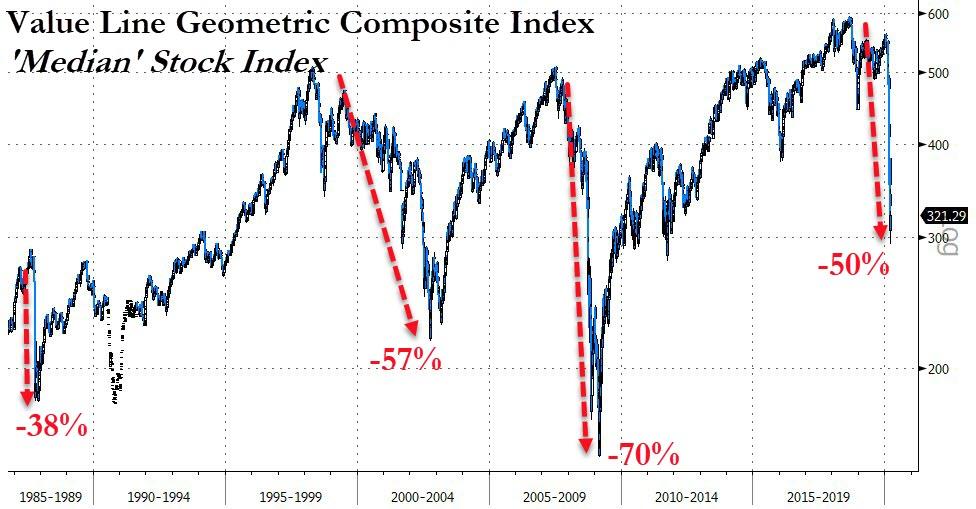

- The Median US Stock Is Now Down 50% From Its Highs As World Loses $25 Trillion In A Month

The Median US Stock Is Now Down 50% From Its Highs As World Loses $25 Trillion In A Month

Global stock and bond markets have seen $25 trillion of ‘paper’ wealth erased in the last month, wiping out all the gains from the Dec 2018 crash lows….

Source: Bloomberg

Global bonds are actually still up around $5 trillion while global stocks have lost around $5 trillion since the Dec 2018 lows, and a lot of those losses come from the US markets where the median stock is now down 50% from its highs… (because the Value Line index below is based on a geometric average the daily change is closest to the median stock price change)

Source: Bloomberg

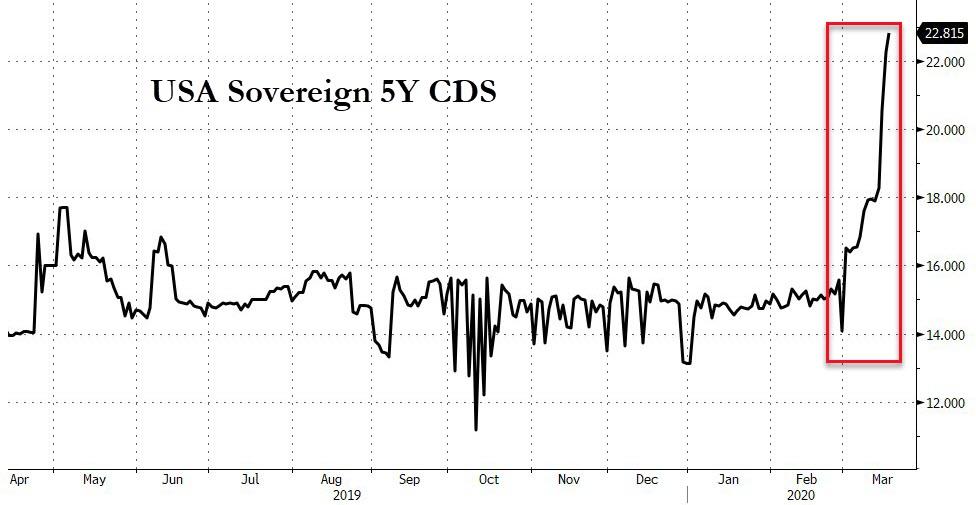

As Washington signs and promises more and more bailouts and helicopter money drops, USA sovereign risk is starting to get a little spooked…

Source: Bloomberg

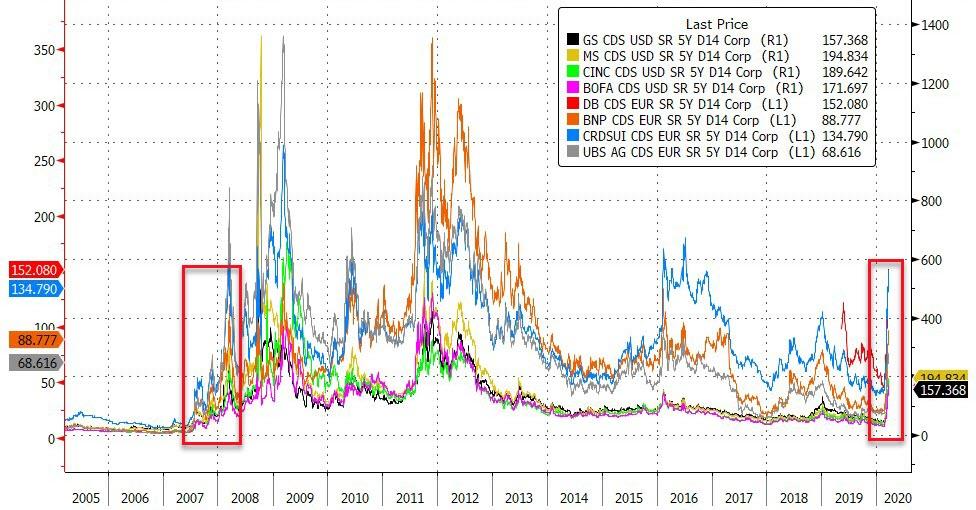

Systemic risk remains extremely elevated…

Source: Bloomberg

Which makes sense when the world’s largest banks are seeing their credit risk explode like it did ahead of the Lehman crisis…

Source: Bloomberg

And despite the endless liquidity from global central banks and polititicians, financial conditions are tightening at their fastest rate ever…

Source: Bloomberg

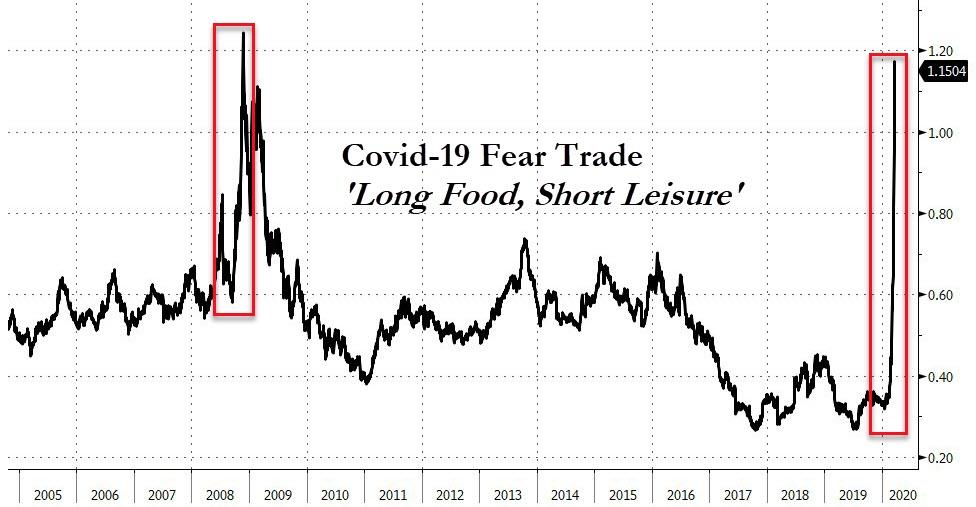

And the real ‘fear’ trade is now at its most extreme since the peak of the Lehman crisis…

Source: Bloomberg

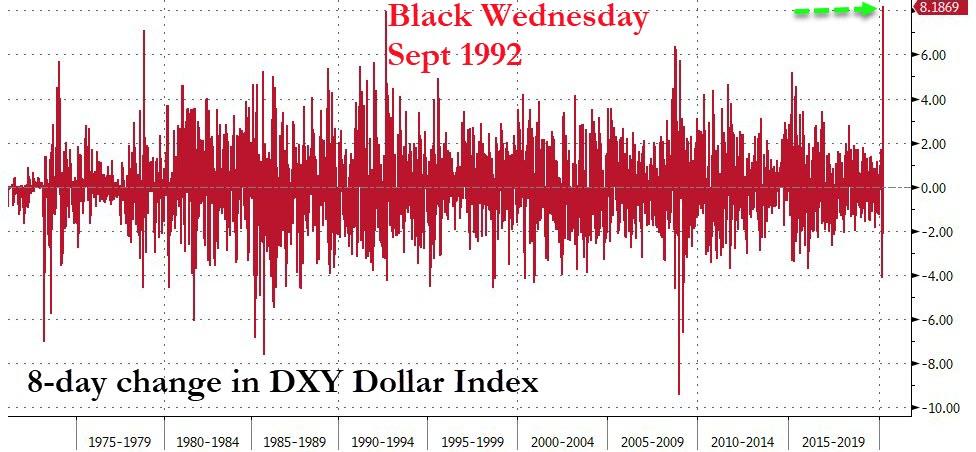

Policy Fail – The Dollar rallied for the 8th straight day, soaring to a new record high despite The Fed opening unlimited FX Swap Lines…

Source: Bloomberg

This is the largest 8-day rally in the DXY Dollar Index… ever! Greater even than when Soros broke The Bank of England in Sept 1992…

Source: Bloomberg

But The Fed will “never give in”…

Since the COVID-19 Malrarkey began, Chinese stocks remain the leaders (down only 12%), while Europe is the laggard…

Source: Bloomberg

US equity markets soared today (thanks to the biggest short-squeeze in 7 years), but failed to erase yesterday’s gains… (NOTE Nasdaq just tagged unch from Tuesday and then rolled over – algo-tom-foolery)…

On the week, it’s still a shitshow with The Dow worst, down 13%…

Today saw “Most Shorted” stocks soar 8% – the biggest short-squeeze since August 2013…

Source: Bloomberg

Directly virus-affected sectors rebounded today…

Source: Bloomberg

VIX fell notably today, testing below 70 ahead of tomorrow’s Quad-Witch option expiry…

Meanwhile, Boeing credit risk continues to soar (as questions rise about whether they should be bailed out or not)…

Source: Bloomberg

And Ford suspended its dividend and withdrew its guidance sending its credit risk soaring…

Source: Bloomberg

Credit markets were not buying what stocks were selling today…

Source: Bloomberg

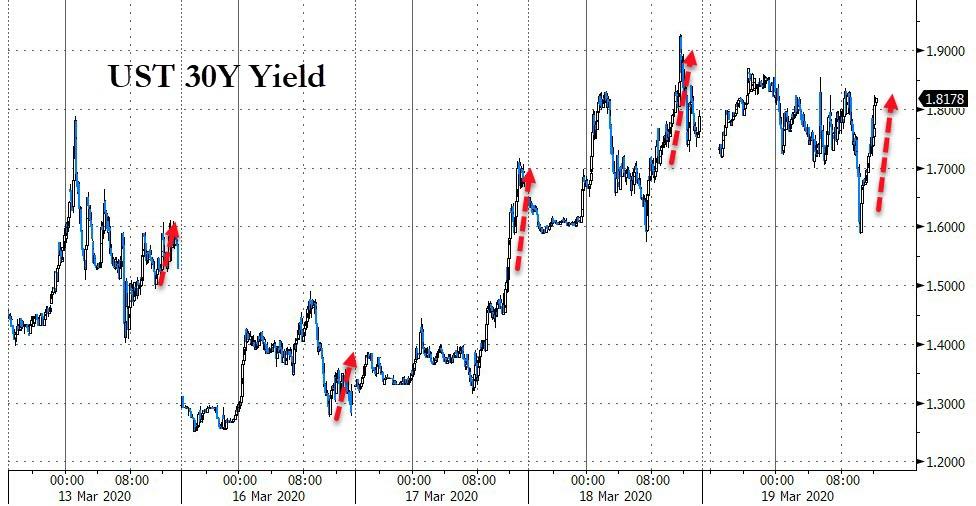

Treasury yields were mixed with the long-end higher and rest of the modestly lower (despite a huge range)… (10Y yields briefly dipped below 1.00% today)

Source: Bloomberg

Another late-day purge in yields pushed 30Y to end higher on the day…

Source: Bloomberg

Munis were massacred today – 10Y yield spiking 47bps!! (MUNI-BOND OUTFLOW ALMOST THREE TIMES PREVIOUS RECORD)

Source: Bloomberg

EUR tumbled today to 3 year lows today in biggest loss since Jan 2001 (bigger than Jun 2016 Brexit vote loss)

Source: Bloomberg

And Cable crashed to the weakest since 1985…

Source: Bloomberg

Cryptos had a big day with Bitcoin Cash outperforming…

Source: Bloomberg

Today’s commodity markets were dominate by oil’s biggest rally ever…however, given the carnage in crude, WTI is still down 20% on the week…

Source: Bloomberg

Today was oil’s biggest daily gain… ever. Bouncing off a $20 handle and helped by talk of Trump intervention, WTI was up around 25%!! However, in context, it doesn’t look like much (apart from the insane $2 spike at settlement for a 35% surge intraday)…

Oil and the dollar both rallied together late on…

Source: Bloomberg

Gold was modestly lower on the day but silver actually managed gains, bouncing off $12 again..

And on a somewhat related note, is this the other reason why gold has been sold?

Source: Bloomberg

Volatile day in PMs with Palladium best and Platinum worst…

Source: Bloomberg

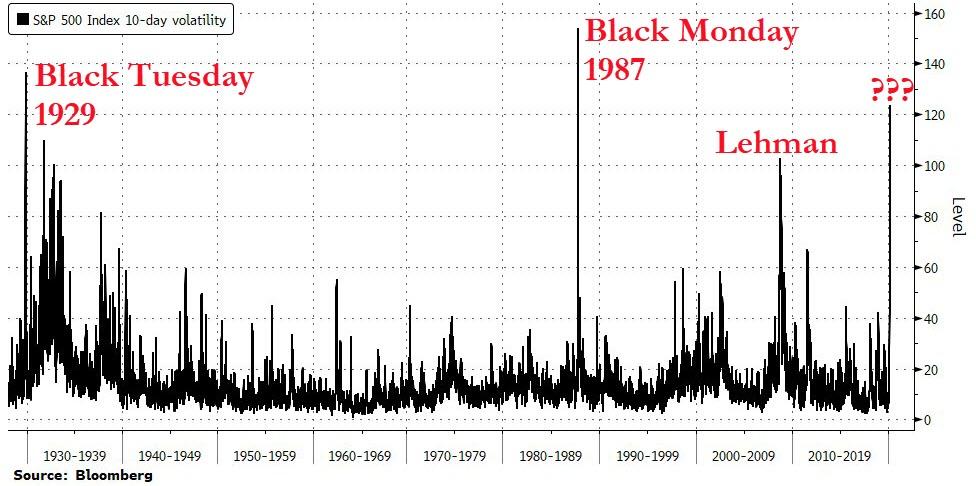

Finally, as Bloomberg notes, anyone referring to the past month’s plunge in U.S. stocks as a crash has history on their side. The S&P 500 Index’s volatility for the 10 trading days ended Wednesday was 122%, according to data compiled by Bloomberg.

Source: Bloomberg

Only two periods have produced higher readings: the aftermath of the 1929 Black Tuesday crash and the 1987 Black Monday crash. The volatility gauge climbed more than 17-fold from Feb. 19, when the S&P 500’s latest bull market ended, through Wednesday.

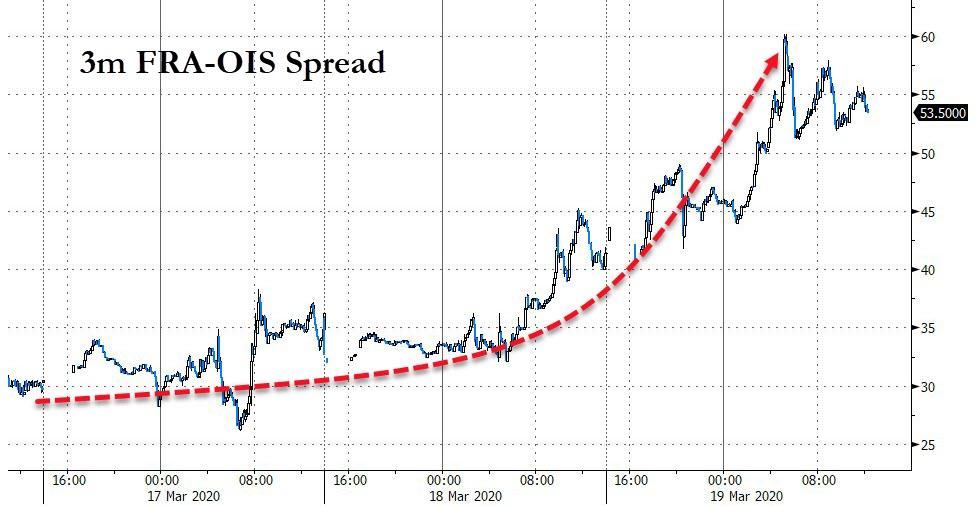

The FRA-OIS spread spiked once again today signaling major tensions in the liquidity markets remain…

Source: Bloomberg

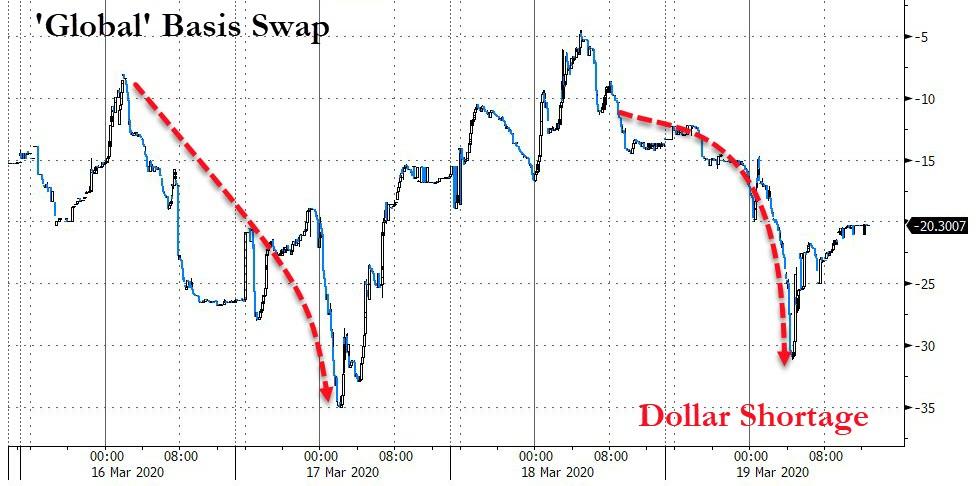

And global basis swaps spiked again (led by JPY) as the dollar shortage worsened today…

Source: Bloomberg