- "The Race In This Cold Is Not About FX Devaluation; It's Technological – Like The Ones Before"

“The Race In This Cold Is Not About FX Devaluation; It’s Technological – Like The Ones Before”

By Marcel Kasumovich of One River Asset Management

“Membership in the WTO, of course, will not create a free society in China overnight or guarantee that China will play by global rules,” President Bill Clinton said in pitch-mode. “But over time, I believe it will move China faster and further in the right direction.” Leadership requires risk. Being in a position of command demands that you adjust to the new realities decisively, tossing ego aside. WTO may have been the inevitable start of the next cold war. Or it may have been, as Clinton intimated, the alternative was worse. No matter – a strong China is a reality.

China seized its moment with rapid export growth, a well-narrated story. The world economy has advanced at a 5% annualized pace since 2000, growing to $100 trillion last year. China’s goods exports, at $2.7 trillion, may not seem particularly exciting as a share of world GDP. But the growth since 2000 has averaged 12% per annum. And China exports share of world GDP leapt 4x since then. It is not nuts and bolts, either – it is higher value-add. China export complexity is now 25th place, on par with rich European countries and up from 54th in 2000.

“I believe that my bilateral meetings served as a step forward in our effort to put the US-China relationship on surer footing,” Yellen said after two days and ten hours of meetings. “We believe that the world is big enough for both of our countries to thrive,” the Secretary of the Treasury emphasized in a clear effort to deescalate tensions. Yellen is left to navigate growing frictions, inheriting a shaky position. She also left plenty of those behind. That’s the job – decide to take the pain today for better outcomes tomorrow or punt it forward.

China has a voice again. And Beijing is using it – mostly through actions. Yellen’s visit follows the China Commerce Ministry imposing export restrictions on two key inputs for semiconductor production – gallium and germanium. Those start August 1. It’s not a ban – Chinese exporters will now need licenses to explain how the metals are being used by importers. But it is a clear warning shot. The political playing field is more level than in 2000 or even 2018. Yellen getting on a plane to visit Premier Li already made that point, emphatically.

Royalty? China’s launch up the value curve is evident in subtle ways – like royalties and licensing. China came first in nuclear fusion patents on a careful survey by Japanese researchers. Patent trade has exploded – China royalties’ exports are up nearly 100x since the start of WTO. It has never been about FX devaluation as the path to prosperity. And now it is explicit – China policy is setting CNY to higher valuations against the USD than where it trades in the market. The race in this cold war is technological – like the ones before.

Tyler Durden

Sun, 07/23/2023 – 23:00 - 'Serious Doubt' About COVID-19 Vaccine Safety After Forced Release Of 15,000 Pages Of Clinical Trial Data

‘Serious Doubt’ About COVID-19 Vaccine Safety After Forced Release Of 15,000 Pages Of Clinical Trial Data

Authored by Tom Ozimek via The Epoch Times (emphasis ours),

The COVID-19 Moderna Vaccination prepared at Lestonnac Free Clinic in Orange, Calif., on March 9, 2021. (John Fredricks/The Epoch Times) Conservative public interest advocacy group Defending the Republic (DTR) has obtained almost 15,000 pages of Moderna’s COVID-19 vaccine clinical trial data, claiming the data show an “utter lack of thoroughness” of the trials and calls the vaccine’s safety into “serious doubt.”

As a result of successful Freedom of Information Act (FOIA) litigation against the U.S. Food and Drug Administration (FDA), the group recently announced it had obtained—and is releasing—nearly 15,000 pages of documents relating to testing and adverse events associated with “Spikevax,” Moderna’s COVID-19 vaccine.

Since 2022, the group has been involved in litigation against the FDA relating to the production of data submitted by Moderna in support of its application to federal regulators for approval of its vaccine.

As a result, the FDA agreed to produce around 24,000 pages of the Moderna records by the end of this year, with the 15,000 pages being the first installment.

The records, some of which relate to adverse events related to the vaccine, include important information related to the safety profile of Spikevax, which was first authorized for emergency use in the United States in December 2020 and in January 2022 received full approval for adults.

“The public can be assured that Spikevax meets the FDA’s high standards for safety, effectiveness and manufacturing quality required of any vaccine approved for use in the United States,” Acting FDA Commissioner Dr. Janet Woodcock said in a statement earlier this year.

But the new data call this view into question. The advocacy group says that the tens of thousands of pages of clinical trial data released by the FDA supports the conclusion that there is “serious doubt” about both the safety of Spikevax and the FDA’s standards for approval.

Neither Moderna nor the FDA immediately responded to a request for comment.

More Details

DTR filed its FOIA lawsuit after the FDA rejected requests to produce the Moderna COVID-19 records, justifying its decision by claiming there was no pressing need for the public to review the information.

The documents obtained as part of the group’s litigation against the FDA are the first significant release of data from Moderna’s COVID-19 clinical trials.

The studies reveal the causes of deaths, serious adverse events, and instances of neurological disorders potentially associated with Spikevax.

One of the key takeaways from the documents is that many of those who died after receiving the Moderna vaccine were not given an autopsy.

“According to one study, 16 individuals died after being administered the Moderna vaccine. The study’s authors indicated that out of those 16 deaths, only two autopsies were performed, five of the dead were not autopsied, and the autopsy status of nine of the dead was ‘unknown,’” DTR said in a statement.

“Yet this did not stop those running these ‘studies’ from concluding, despite the absence of evidence, that the Moderna vaccine was not related to these deaths,” the group added.

As an example, the group gave the case of a 56-year-old woman who experienced ‘sudden death’ 182 days after receiving the second dose of the Moderna vaccine.

“The cause of death was unknown, and no autopsy was conducted. It seems they purposely decided not to investigate suspicious deaths in case the Moderna vaccine might be the cause,” the group stated.

There were also numerous examples in the clinical trial data of participants diagnosed with post-vaccination Bell’s Palsy and Shingles, with numerous vaccinated trial participants seeing the onset of Shingles less than 10 days after getting the shot.

The studies also showed that there were a number of serious adverse events noted in the vaccinated groups, with a number of participants experiencing heart attacks, pulmonary embolisms, and spontaneous miscarriages.

Read more here…

Tyler Durden

Sun, 07/23/2023 – 22:15 - 'The Perfect Crime': Tech Companies Are Manipulating Our Elections And Indoctrinating Our Children — How We Can Stop Them

‘The Perfect Crime’: Tech Companies Are Manipulating Our Elections And Indoctrinating Our Children — How We Can Stop Them

Authored by Robert Epstein via the Gatestone Institute,

Big Tech companies are deliberately manipulating the outcomes of our elections and the thinking and beliefs of our children. And they are having an enormous impact.

If you doubt that, consider this latest snippet of data from my lab, the American Institute for Behavioral Research and Technology (AIBRT).

Consider this: The GOP currently has a slim 10-seat majority in the House of Representatives. Without Google’s interference in 2022, it would likely now have a majority of between 27 and 59 seats.

The 2022 midterm elections that gave the Democrats a two-vote majority in the U.S. Senate had quite a bit of help from Google, and, to a lesser extent, from a couple of other major tech companies.

If Google had not interfered in the 2022 midterm elections, the GOP would likely have ended up with a Senate majority of up to eight seats.

The Big Tech companies that exploded into existence over the past 20 years — as some of their prominent insiders have stated – have undermined our democracy, indoctrinated our children, and increasingly turned our freedom into an illusion.

Tristan Harris, a former “design ethicist” at Google, says that he was a member of a team at the company, whose job it was to influence “a billion people’s attention and thoughts every day.” Jaron Lanier, a computer scientist and one of the early investors in Google and Facebook, claims that Big Tech content has “morphed into continuous behavior modification on a mass basis.” Another early investor in these companies, the prominent author and venture capitalist Roger McNamee, has said that he now regrets having financed them, and asserts that they constitute “a menace to public health and to democracy.”

Rigorous Research

Such concerns are valid and the Senate numbers correct: we have been using rigorous, scientific methods to study Google and other tech companies for more than 10 years. During this time, we have discovered and quantified about a dozen powerful new forms of influence that the internet has made possible. We have also developed and deployed monitoring systems that track, record, and analyze the personalized content that Google and other tech companies send to voters and children 24 hours a day – in other words, we are monitoring their systems and doing to them what they do to us.

Our basic scientific, peer-reviewed studies clearly show the power that Google and other companies have to alter thinking and behavior. Our monitoring systems confirm that these companies are actually using these techniques, as confirmed by company whistleblowers, as well as by leaks of documents, emails, videos, and other materials from Google, Facebook, and Twitter.

The techniques we have discovered – the Search Engine Manipulation Effect, the Answer Bot Effect, the Targeted Messaging Effect, and others – can easily shift the opinions and voting preferences of undecided voters by between 20% and 80% after just one manipulation. Google can also repeat these manipulations many times over a period of months prior to an election.

Assuming the effects of these techniques are additive, Google can likely produce even larger shifts in opinions and voting preferences than the ones from a single manipulation used just once.

Google also knows exactly who is vulnerable to these manipulations – who is still undecided before Election Day, for example – so they can target and bombard just the right people on a massive scale 24 hours a day.

Our research has shown repeatedly that the manipulations used can make them invisible to people, and can often produce shifts of 40% or more in the voting preferences of undecided voters without anyone having the slightest idea they have been manipulated. They feel free, even while they are being strongly controlled. As one journalist wrote, “It really is the perfect crime.”

Finally, our research measures the influence of “ephemeral experiences” –– their term — meaning content that is seen briefly, affects the user, and then disappears forever, leaving no paper trail for authorities to trace, Most online content – search results, newsfeeds, video sequence, and so on – are ephemeral.

Can Google deliberately use ephemeral content to manipulate people? You bet. If you doubt that, read this 2018 article from the Wall Street Journal about some leaked emails from the company. In that email exchange, Googlers are discussing how they might use “ephemeral experiences” to change people’s views about Trump’s temporary 2017 travel ban on visitors from seven majority-Muslim countries.

Rapidly Growing Monitoring Capabilities

In the days leading up to the 2022 midterms, the American Institute for Behavioral Research and Technology monitored Big Tech content through the computers of 2,742 registered voters in 10 swing states, and preserved more than 2.5 million ephemeral experiences – data that is normally lost forever – on Google and other platforms.

We preserved overwhelming evidence of Google’s manipulations on their search engine, on their video recommendations on YouTube (owned by Google), and even on their homepage on Election Day. On that day in Florida, for example, 100% of liberals received go-vote reminders on their version of Google’s homepage (Figure 1), but only 59% of conservatives did (Figure 2).

The Tried and Tested Solution: a Permanent, Self-Sustaining Monitoring System

Google can, overall, easily shift the votes of between 20-80% of undecided voters; right now, that is about 40% of the electorate. This could be enormously consequential. By mid-2024, 20% of voters will likely still not have made up their minds on who to support. At that point, Google will still be able to shift up to 80% of the votes of those individuals — or up to 16% percent of the electorate.

If, in 2024, 158 million people cast ballots, as they did in 2020, it means Google could likely shift the votes of between 6.4 and 25.5 million people, thereby easily controlling the outcome of any election in which the projected win margin is less than 4%. No laws or regulations are in place to stop them, but our monitoring can. We are monitoring their systems and doing to them what they do to us. When the Big Tech companies know that their manipulations are being watched, they back off. It has already worked to completely shut down manipulations in one important election.

On November 5, 2020, three U.S. Senators sent a strong warning letter to the CEO of Google expressing concern about the extreme political bias our monitoring system had detected in the days leading up to the presidential election – bias sufficient to have shifted at least 6 million votes to Joe Biden.

As a result, Google immediately shut down its election manipulations in the two upcoming Senate runoff elections in Georgia.

We were monitoring Google content through the computers of a politically-balanced group of more than 1,000 registered voters in that state. Go-vote reminders ceased, and so did bias in Google search results.

In other words, monitoring, combined with political pressure from our leaders and our public, can and will force Google and other tech companies to stay clear of our elections and our children. It will also give legislators, regulators, and litigants the ammunition they need to challenge both the company and its executives in court.

Since 2016, we set up six election monitoring systems, for only the weeks leading up to each election. After the 2022 midterms – with the results being so blatant and disturbing – we decided that the time had finally come to set up a permanent monitoring system in all 50 states – a $50 million project that we were able to launch with $3 million indentations from some patriotic Americans.

Without a permanent system like this in place, we will never know the extent to which Google-and-the-Gang are messing with our elections, our kids, or even with our own heads.

Yes, they do mess with us. As explained in “How Google Stopped the Red Wave,” whenever you see online content screaming about Democrats who have perpetrated widespread ballot harvesting or ballot box stuffing, you are being manipulated by Google-and-the-Gang. It is their algorithms – controlled very precisely by their employees – that decide what content goes viral and what content is suppressed. If stories about other election irregularities are spreading like wildfire online and then being echoed on the news, it is because Google-and-the-Gang want them to. Why?

So you will not look at them – at the tech companies themselves.

As of this writing, we are preserving and analyzing Big Tech content through the computers of a politically-balanced group of 9,838 registered voters in all 50 states, and we have met our minimum “representative sample” thresholds in 5 states. We are also now monitoring and preserving content – some of which is quite alarming – through the phones and mobile devices of children and teens.

Best of all, we have now preserved more than 25 million ephemeral experiences on Google and other platforms – content that is normally lost forever. Our goal is to make our findings available to the public in real time, 24 hours a day, through dashboards such as America’s Digital Shield.

The problem is: unless we can find additional major funding soon, we will have to start scaling down our effort in August and may have to shut it down completely soon after.

If this type of election interference continues unmonitored and unchallenged, could the GOP itself – and ultimately all of American democracy – become ephemeral experiences?

Note from the author: If you are concerned about the dangers the Big Tech companies pose to our democracy, our children, and our autonomy, please contribute at https://MyGoogleResearch.com. All donations are fully tax-deductible.

Robert Epstein earned his Ph.D. at Harvard University in 1981. He is currently Senior Research Psychologist at the American Institute for Behavioral Research and Technology. He has published 15 books and more than 300 articles in both mainstream media outlets and scientific journals, among them, Science, Nature, and the Proceedings of the National Academy of Sciences USA. He is the former editor-in-chief of Psychology Today magazine and was a longtime contributing editor at Scientific American. His 2019 Congressional testimony about Google can be viewed at https://EpsteinTestimony.com. To support or learn about his work, visit https://MyGoogleResearch.com or https://TechWatchProject.org.

Tyler Durden

Sun, 07/23/2023 – 20:45 - Texas' Operation Lone Star Seizes 422 Million Doses Of Fentanyl, Nearly 400K Migrants Arrested

Texas’ Operation Lone Star Seizes 422 Million Doses Of Fentanyl, Nearly 400K Migrants Arrested

Republican Texas Gov. Gregg Abbott’s operation to halt the influx of illegal immigrants, weapons and drugs into the United States has resulted in the seizure of more than 422 million lethal doses of fentanyl, and the apprehension of 394,200 illegal immigrants.

Dubbed Operation Lone Star, the mission launched in March 2021 between the Texas National Guard and the Texas Department of Public Safety.

“Since the launch of Operation Lone Star, the multi-agency effort has led to over 394,200 illegal immigrant apprehensions and more than 31,300 criminal arrests, with more than 29,100 felony charges reported. In the fight against fentanyl, Texas law enforcement has seized over 422 million lethal doses of fentanyl during this border mission,” Abbott’s office said in a Friday statement.

Operation Lone Star continues to fill the dangerous gaps created by the Biden Administration’s refusal to secure the border. Every individual who is apprehended or arrested and every ounce of drugs seized would have otherwise made their way into communities across Texas and the nation due to President Joe Biden’s open border policies.

Meanwhile, the Abbott administration has bused more than 27,260 migrants to Democrat-run sanctuary cities across the nation – with most ending up in Washington DC and New York City.

As Just the News notes, “The announcement about the operation’s achievements comes as the Justice Department plans to sue Texas over the state’s use of a floating barrier to stop illegal migration across the Rio Grande River, which separates Texas from Mexico. Abbott has fired back against the federal government, stating that his state has the authority to defend its border.”

Tyler Durden

Sun, 07/23/2023 – 20:00 - It’s Time To Acknowledge America’s Education Crisis

It’s Time To Acknowledge America’s Education Crisis

Authored by Tina Blum Cohen via American Greatness,

The recent Supreme Court ruling regarding college admissions has once again thrust America’s educational system into the spotlight. A major question that has come from this ruling is whether America’s children are being intellectually and academically prepared to even enter or succeed in these colleges and universities. The tragic answer is that America’s public education system is failing to equip our youth with the tools necessary to succeed in higher education and in their future professional lives. We are failing America’s most valuable asset—our children.

According to the Department of Education’s own report on the state of education in America, we are experiencing what is essentially an educational crisis. Scores in every subject and grade level have been declining over the years. While illogical and unscientific Covid policies certainly worsened the crisis to a point that lawmakers can no longer ignore the problem, the situation has actually been declining for years. Especially concerning are scores in reading and mathematics, with close to one third of students in elementary school behind in grade-level reading and only about a third of fourth graders able to perform grade-level math.

Earlier this year, the nation was shocked to hear that 55 Chicago schools reported zero proficiency in math or reading despite billions of dollars of federal funding for the schools. But this crisis is not unique to Chicago. In my own Houston community, the Texas Education Agency has had to intervene in the leadership of the state’s largest public school district after years of failing to adequately educate our community’s children.

Unfortunately for America’s youth and the future of our nation, public schools have put core educational instruction on the back burner, instead prioritizing culturally sensational philosophies. We now see schools artificially inflating grades in order to ‘pass’ students who do not have the educational tools necessary to succeed in higher grades. While this is done under the guise of “equity,” it is unfortunately setting kids up for future failure when they find themselves unprepared for the next steps in their education, and ultimately, for adulthood and success in society.

Likewise, we see schools ditching the concepts of expectations and consequences, both educational and behavioral, including things like homework deadlines. Besides the negative effect this has on mastering educational principles that will be used to learn more difficult concepts later, this lack of personal accountability and consequences has our youth growing accustomed to an unrealistically lenient reality which does not exist in our society. We do our children a disservice when we do not intellectually and emotionally prepare them to deal with reality, including things like personal consequences or meeting deadlines. Imagine their shock when their first employer sets a hard deadline for a project, and they have no experience with being required to meet a deadline. They will have been set up for anxiety and potential failure rather than confidence and success.

Beyond these misguided but culturally relevant philosophies that are failing to prepare our students for success, core educational instruction also has been eclipsed by ideological indoctrination. Instead of focusing time and attention on improving reading and mathematics, or even introducing practical principles of finance and economics, teachers and administrations prioritize the woke Marxist principles of social-emotional learning. Even as their students are unable to adequately read and write, teachers give classroom time and attention to discussing gender and sexuality, often behind the backs of parents who they know would not appreciate public school teachers having such discussions with their children.

Even after-school clubs for practical skills or intellectual enrichment are being replaced by secret gender identity clubs, while activist educators go out of their way to entice vulnerable students to join and even encourage them to lie to their parents about their participation. These radical gender ideologies endanger both the minds and bodies of impressionable and developing youth, and yet parents who object are either vilified or kept in the dark entirely. In an effort to undermine parental rights and advance woke social agendas, schools go so far as to implement policies to keep secrets from parents, who are primarily responsible for the health and development of their children.

The rising generation is America’s most valuable asset. They will carry on the legacy of the freest and greatest nation in the world, both enjoying and safeguarding our rights and liberties as they make valuable contributions to society. But this can only happen if parents, neighbors, and lawmakers come together to acknowledge and address the potentially catastrophic educational crisis which is already having a negative impact on America’s youth and their future. We must take the steps necessary to restore practical education to our public schools. We must protect the rights and facilitate the involvement of parents in every aspect of their children’s development and education rather than allowing public schools to go behind their backs. Now is the time to stand together in defense of our children and our nation.

Tina Blum Cohen is a Republican running for Congress in Texas District 7. She is a graduate of Boston University. Education is a top priority for Cohen, a married mother of three.

Tyler Durden

Sun, 07/23/2023 – 19:30 - California Demographers Forecast Population To Stagnate By 2060

California Demographers Forecast Population To Stagnate By 2060

Elon Musk was right when he told a Wall Street Journal forum in 2021: “One of the biggest risks to civilization is the low birth rate and rapidly declining birthrate.”

The billionaire has since encouraged the public to make more babies as concerns of a population collapse or “Demographic Winter” mount.

In a tweet in late March, Musk said that the US would face consequences due to a declining birth rate and that “Japan is a leading indicator.”

Big reckoning coming due to low birth rate. Japan is a leading indicator.

— Elon Musk (@elonmusk) March 31, 2023

https://platform.twitter.com/widgets.js

“Population collapse is a major risk to the future of civilization,” the billionaire entrepreneur tweeted.

Musk’s comments should not surprise readers — as we’ve explained over the years, the Western world was already stumbling into a Demographic Winter.

In a more in-depth view of America’s Demographic Winter, we focus on a new report from California demographers who warn that the state’s population might plateau in the coming decades.

The California Department of Finance released a startling report about its forecasted total population of the state will be around 39.5 million people in 2060 — or about the same level as it’s currently. State demographers were projecting 45 million just three years ago — and a decade ago, these folks were expecting a surge in population to 53 million.

A combination of a higher-than-normal death rate, a declining birthrate, a fall in international migration, and a flow of Californians moving to other states sent the total population down to 38.94 million in 2022, or minus 138,400 people, the first annual decline in more than a century.

“You don’t have those people, and those people don’t have kids,” Andres Gallardo, a demographer who works for the state government, told Bloomberg. He said this report is the first time California’s long-term population forecast has flatlined.

Even though California remains the nation’s most populous state, the economic impact of stagnating total population will mean municipalities will likely need help balancing their budgets.

Tyler Durden

Sun, 07/23/2023 – 19:00 - Higher Military Spending Will Save Democracy, Says NY Times

Higher Military Spending Will Save Democracy, Says NY Times

Authored by William Astore via AntiWar.com/Bracing Views,

Days ago, I got a story in my New York Times email feed on “A Turning Point in Military Spending.” The article celebrated the greater willingness of NATO members as well as countries like Japan to spend more on military weaponry, which, according to the “liberal” NYT, will help to preserve democracy. Interestingly, even as NATO members have started to spend more, the Pentagon is still demanding yet higher budgets, abetted by Congress. I thought if NATO spent more, the USA could finally spend less?

No matter. Russia’s invasion of Ukraine, as well as the hyping of what used to be called the “Yellow Peril,” today read “China,” is ensuring record military spending in the USA as yearly Pentagon budgets approach $900 billion. That figure does not include the roughly $120 billion or more in aid already provided to Ukraine in its war with Russia. And since the Biden administration’s commitment to Ukraine remains open-ended, you can add scores of billion more to that sum if the war persists into the fall and winter.

Image source: NATO Here’s an excerpt from the New York Times piece that I found especially humorous in a grim way:

[Admittedly,] The additional money that countries spend on defense is money they cannot spend on roads, child care, cancer research, refugee resettlement, public parks or clean energy, my colleague Patricia points out. One reason Macron has insisted on raising France’s retirement age despite widespread protests, analysts believe, is a need to leave more money for the military.

But the situation [in Europe of spending more on butter than guns] over the past few decades feels unsustainable. Some of the world’s richest countries were able to spend so much on social programs partly because another country – the U.S. – was paying for their defense. Those other countries, sensing a more threatening world, are now once again promising to pull their weight. They still need to demonstrate that they’ll follow through this time.

Yes, Europe could continue to invest in better roads, cleaner energy, and the like, but now it’s time to buckle down and build more weapons. Stop freeloading, Europe! Dammit, “pull your weight”!

You’ve had better and cheaper health care than Americans, stellar educational systems, child care benefits galore, all sorts of social programs we Americans can only dream of, but that’s because we’ve been paying for it! Captain America’s shield has been protecting you on the cheap! Time to pay up, you Germans, you French, you Italians, and especially you cheap Spaniards.

Above: Look at all those cheap Spaniards. They have good stuff because of Captain America. Freeloaders! (NYT Chart, 7/12/23)

As the NYT article says: NATO allies need to “follow through this time” on strengthening their militaries. Because strong militaries produce democracy. And European “investments” in arms will ensure more equitable burden sharing in funding stronger cages and higher barriers to deter a rampaging Russian bear.

Again, you Americans out there, that doesn’t mean we can spend less on “defense.” What it means is that the US can “pivot to Asia” and spend more on weaponry to “deter” China. Because as many neocons say, the real threat is Xi, not Putin.

We have met the enemy, and he is us. That’s an old saying you won’t see in the “liberal” NYT.

Tyler Durden

Sun, 07/23/2023 – 18:30 - "Nobody Understands Where Bottom Is" For Commercial Real Estate

“Nobody Understands Where Bottom Is” For Commercial Real Estate

Starwood Capital Group’s Barry Sternlicht recently told Bloomberg’s David Rubenstein about the ongoing crisis in the commercial real estate sector, equating it to a severe “Category 5 hurricane“. He cautioned, “It’s sort of a blackout hovering over the entire industry until we get some relief or some understanding of what the Fed’s going to do over the longer term.”

Currently, the biggest problem in the CRE space is sliding office and retail demand in downtown areas. Couple that with high-interest rates, and there’s a disaster lurking for building owners. According to Morgan Stanley, the elephant in the room is a massive debt maturity wall of CRE loans that totals $500 billion in 2024 and $2.5 trillion over the next five years.

Senior markets editor for Bloomberg, Michael Regan, chatted with John Fish, who is head of the construction firm Suffolk, chair of the Real Estate Roundtable think tank and former chairman of the board of the Federal Reserve Bank of Boston, in the What Goes Up podcast to discuss the biggest problems in the CRE market.

Fish warned that “capital markets nationally have frozen” and “nobody understands value.” He said, “We can’t evaluate price discovery because very few assets have traded during this period of time. Nobody understands where the bottom is.”

For a sense of recent price discovery trends, we were the first to point out to readers of a wicked firesale of office towers in the downtown area of Baltimore City:

- Beginning Of CRE Firesale? Baltimore Office Tower Dumped At 63% Discount

- CRE Panic Hits Baltimore As Second Office Tower Dumped At 69% Discount

As for the overall CRE industry, Goldman Sachs chief credit strategist Lotfi Karoui recently told clients, “The most accurate portrayal of current market conditions with Green Street indicating a 25% year-over-year drop in office property values.”

Here’s the transcript of the interview between Regan and Fish:

Michael Regan’s question: Can you talk to us about why this rise in interest rates that we’ve experienced is so dangerous to this sector?

John Fish’s answer: When you talk about these large structures, especially in New York City, you get all these buildings out there, almost a hundred million square feet of vacant office spaces. It’s staggering. And you say to yourself, well, right now we’re in a situation where those buildings are about 45%, 55%, 65% occupied, depending where they are. And all of a sudden, the cost of capital to support those buildings has almost doubled. So you’ve got a double whammy. You’ve got occupancy down, so the value is down, there’s less income coming in, and the cost of capital has gone up exponentially. So you’ve got a situation where timing has really impacted the development industry substantially.

The biggest problem right now is because of that, the capital markets nationally have frozen. And the reason why they’ve frozen is because nobody understands value. We can’t evaluate price discovery because very few assets have traded during this period of time. Nobody understands where bottom is. Therefore, until we achieve some sense of price discovery, we’ll never work ourselves through that.

Now, what I would say to you is light at the end of the tunnel came just a little bit ago, back in June when the OCC, the FDIC and others in the federal government provided policy guidance to the industry as a whole. And that policy guidance I think is very, very important for a couple reasons. One, it shows the government with a sense of leadership on this issue because it’s this issue that people don’t want to touch because it really can be carcinogenic at the end of the day. It also provides a sense of direction and support for the lending community and the borrowers as well. And by doing such, what happens now is the clarity.

Basically what they’re saying is similar to past troubled-debt restructuring programs. They’re saying, listen, any asset out there where you’ve got a qualified borrower and you’ve got a quality asset, we will allow you to work with that borrower to ensure you can re-create the value that was once in that asset itself. And we’ll give you an 18- to 36-month extension, basically ‘pretend and extend.’ Whereas what happened in 2009, that was more of a long-term forward-guidance proposal and it really impacted the SIFIs (systemically important financial institutions). This policy direction is really geared toward the regional banking system. And why I say that is because right now the SIFIs do not have a real big book of real estate debt, probably less than 8% or 7%. Whereas the regional banks across the country right now, thousands of them have over probably 30% to 35% and some even up to 40% of the book in real estate. So that guidance gave at least the good assets and the good borrowers an opportunity to go through a workout at the end of the day.

Michael Regan’s question: This “extend and pretend” idea seems to me almost like a derogatory phrase that people use for this type of guidance from the Fed, or this type of approach to solving this problem. But is that the wrong way to think about it? Is “extend and pretend” actually the way to get us out of this mess?

John Fish’s answer: Let me say this to you: I think some well-known financial guru stated that this was not material to the overall economy. And I’m not sure that’s the case. When I think about the impact that this has on the regional banking system, basically suburbia USA, we had Silicon Valley Bank go down, we had Signature Bank go on, we saw First Republic go down. If we have a systemic problem in the regional banking system, the unintended consequences of that could be catatonic. In addition to that, what will happen is when real-estate values go down? 70% of all revenue in cities in America today comes from real estate. So all of a sudden you start lowering and putting these buildings into foreclosure, the financial spigot stops, right? All of a sudden, the tax revenues go down. Well, what happens is you talk about firemen, policemen and teachers in Main Street, USA, and at the end of the day, we’ve never gone through something as tumultuous as this. And we have to be very, very cautious that we don’t tip over the building that we think is really stable.

Tyler Durden

Sun, 07/23/2023 – 18:00 - CDC Changed Definition Of Breakthrough COVID-19 After Emails About 'Vaccine Failure'

CDC Changed Definition Of Breakthrough COVID-19 After Emails About ‘Vaccine Failure’

Authored by Zachary Stieber via The Epoch Times,

The U.S. Centers for Disease Control and Prevention (CDC) altered its definition of COVID-19 cases among the vaccinated, leading to a lower number of cases classified as a breakthrough, according to documents obtained by The Epoch Times.

The CDC in early 2021 defined the post-vaccination cases as people testing positive seven or more days after receipt of a primary vaccination series, according to one of the documents.

The definition was changed on Feb. 2, 2021, to only include cases detected at least 14 days after a primary series, another document shows.

“We have revised the case definition,” Dr. Marc Fisher, the lead of the CDC’s Vaccine Breakthrough Case Investigation Team, wrote to colleagues at the time.

The rationale for the change was redacted.

A CDC spokesperson defended the altered definition.

“CDC made the change to the definition of a breakthrough infection time period due to the most current data that showed that the 14-day period was required for an effective antibody response to the vaccines,” Scott Pauley, the spokesman, told The Epoch Times in an email.

“That, in combination with the data showing that many cases of COVID-19 were incubating for up to two weeks before becoming symptomatic, required the change to refine the time period to eliminate cases where exposure happened before the vaccination response would be effective,” Mr. Pauley added.

Dr. Harvey Risch, professor emeritus of epidemiology at the Yale School of Public Health, said there was “no cogent rationale” for excluding early cases and other events among the vaccinated, whether they occurred within seven days or 14 days.

“With either of these delays, CDC addressed what is the theoretical best that the vaccination could achieve. If the vaccines don’t work for the first 7 or 14 days or increase risk of getting Covid-19 during that period, that is part of what happens when they are deployed in a population,” Dr. Risch told The Epoch Times via email.

Dr. Jay Bhattacharya, professor health policy at Stanford University, said that the CDC should have been focused on advising people that they weren’t as protected immediately after vaccination.

“Rather than playing games with the definition of breakthrough cases,” Dr. Bhattacharya told The Epoch Times in an email, the CDC should have warned “recently vaccinated vulnerable older people that they were at higher risk for being infected during that period.”

An internal CDC email obtained by The Epoch Times. (The Epoch Times)

Undercount

The CDC excluded some post-vaccination cases because they did not meet the updated definition, the documents show, providing an inflated view of vaccine effectiveness.

One document, for instance, shows that Kansas in early 2021 reported 37 cases among the vaccinated.

Thirty-four were not counted because they occurred after receipt of one dose, not two. A primary series for both vaccines was two doses until recently, with the second dose not advised until at least 21 days after the first dose.

The other three cases happened after a second dose, but they were not counted as breakthrough cases by the CDC because they happened within 13 days of completion of a primary series, Dr. Fisher informed colleagues in an email.

On Jan. 29, 2021, the CDC learned in a call with Maryland health officials that a cluster appeared to stem from a person who was vaccinated with a single dose before experiencing symptoms. A CDC official said it was a “possible breakthrough case,” but the case would not have been counted under the earlier or later breakthrough definition.

In another likely form of suppression of the true number of cases, states weren’t able to report cases through the National Notifiable Diseases Surveillance System until February 2021, according to one of the emails.

Kansas was the first state to send info through the system, according to a Feb. 1, 2021, email reporting the 37 cases.

States could also report cases outside of the system through calls, as could health care providers, according to another email. Reports to the Vaccine Adverse Event Reporting System were also analyzed for possible inclusion.

The CDC started reporting the number of breakthrough cases on April 15, 2021. Some of the breakthrough cases led to hospitalization and death. CDC officials discussed breakthrough cases sporadically in public settings, but also made false claims about vaccine effectiveness, including claiming in March 2021 that vaccinated people did not get sick.

COVID-19 vaccines in Washington in a Dec. 14, 2020, file photograph. (Jacquelyn Martin/Pool/AFP via Getty Images)

Change Came After Emails About ‘Vaccine Failure’

The breakthrough case definition was revised after multiple CDC officials emailed about the vaccines failing to prevent infection.

Dr. Fisher said in one missive on Dec. 21, 2020, that he was directed by a superior “to start working on a protocol to evaluate COVID vaccine failures or breakthrough cases.”

Dr. Rochelle Walensky, the CDC director at the time, highlighted an editorial on Jan. 30, 2021, that described variants as a “growing threat” of escaping the protection from vaccines and said she’d spoken to the head of the U.S. National Institutes of Health about the matter.

Around the same time, CDC officials circulated a one-page document about investigating post-vaccination cases.

“What? There is a 1-pager from Tom about vaccine failures?” Dr. Nancy Messionnier, another top CDC official, said on Jan. 27, 2021, after hearing about the document, which was being distributed by CDC medical officer Dr. Thomas Clark.

The version of the document The Epoch Times received was fully redacted. After Dr. Clark was asked for an unredacted version, the CDC declined to provide any other versions of the document.

Dr. Fisher also made a presentation near the end of January 2021 on breakthrough cases and sent those slides to colleagues after emphasizing he’d developed them “for internal use” and that the slides “have not been reviewed or cleared by anyone.” Dr. Fisher did not respond when asked for the slides.

Soon after the change, the CDC was alerted to a college athlete who tested positive for COVID-19 about three weeks after completing a Pfizer primary series. One CDC official described it as a “potential breakthrough case” and said data would have to be reviewed to see whether it would be counted.

In a document distributed to states, the CDC outlined a number of ways post-vaccination cases, even one detected at least 14 days after a primary series, would not be counted. That included excluding people who received a vaccine that was not authorized in the United States, people with only a positive antibody test, and people who tested positive within 44 days of their latest test.

Time Exclusion

The CDC initially floated (pdf) counting a person as “fully vaccinated” as early as seven days after completion of a primary series but ultimately settled on 14 days after completion.

The CDC declined to provide the name of the official who decided on the definition of fully vaccinated. The agency, in response to a Freedom of Information Act, also said it did not have any records on deciding to exclude cases that occur in what amounts to at least 35 days after the first vaccine dose.

Officials pointed to U.S. Food and Drug Administration (FDA) materials that outlined the results from clinical trials from Pfizer and Moderna, which make the vaccines that the FDA authorized in 2020.

The trials found efficacy against symptomatic COVID-19 was much lower within days of vaccination. In Pfizer’s trial, for instance, suspected cases within seven days of a vaccine dose were 409 among the vaccinated versus 287 among placebo recipients. Moderna estimated a 50.8 percent efficacy within 14 days of dose one, compared to 92 percent efficacy 15 or more days after the dose.

Observational data have also indicated lower or negative shielding in the days after vaccination, and almost immediately after the vaccines were rolled out, some vaccinated people were reporting getting infected anyways.

Tyler Durden

Sun, 07/23/2023 – 17:30 - Tesla Attempts To Stoke Demand With 84-Month Loans Amid Affordability Crisis

Tesla Attempts To Stoke Demand With 84-Month Loans Amid Affordability Crisis

Most consumers rely on auto loans to finance new vehicle purchases. Tesla Inc. has offered an 84-month auto loan after Elon Musk said ‘something needs to be done’ about the auto affordability crisis, according to Bloomberg.

In general, 84-month loans are less common than 36 – 48 or 72-month auto loans, but with new vehicle borrowing rates at two-decade highs and prices at record-high levels, the solution has been to stretch out the payment for seven years to stoke demand. There’s one problem with these loans: the period is much longer, and the interest cost will be much higher.

Financing options for Tesla Model S Plaid

“When interest rates rise dramatically, we actually have to reduce the price of the car, because the interest payments increase the price of the car,” Musk said in a July 19 earnings call. “So we have to do something about that,” he said.

According to Bankrate, a new car’s average 60-month auto loan rate peaked at 7.64%, not seen since December 2001. There are many Americans with +$1,000 payments.

Tesla’s chief executive officer has been critical of the Federal Reserve’s 16-month aggressive interest rate hiking cycle. Musk tweeted late last year that hiking interest rates were “massively amplifying the probability of a severe recession.”

While there is no recession yet, used car prices have slid due to mounting affordability concerns. High borrowing costs have done exactly what the Fed’s goal has been, which is to stymie demand. We’ve covered the latest trends in used car prices in notes titled Used-Car Prices Continue Slide As Signs Of Normalcy Start To Reemerge and Used-Car Prices Tumble Most Since Start Of Pandemic, Record Drop For Month of June.

The move to offer 84-month loans is to stoke demand amid an EV price war with other carmakers.

Tyler Durden

Sun, 07/23/2023 – 17:00 - And Now, The Climate Gang Is Coming For Our Thermostats

And Now, The Climate Gang Is Coming For Our Thermostats

Authored by J. Kennerly Davis via RealClear Wire,

In 2019, candidate Joe Biden pledged to voters that, if elected president, “We’re going to end fossil fuel.” Since taking office, he has worked ceaselessly with the radical environmentalists who call the shots and set the agenda to make good on his campaign promise by waging an all-out war against the production, distribution, and use of fossil fuels.

The Biden administration immediately cancelled the Keystone pipeline and then blocked other pipeline projects. It has drastically curtailed the issuance of leases and permits needed to develop fossil resources on public lands and offshore. It has denied applications to expand refinery capacity. And it has issued unattainable carbon dioxide emission limitations designed to force the closure of hundreds of fossil-fueled electric power plants currently in operation.

The Biden administration and its political allies in state and local governments have launched a series of aggressive regulatory initiatives designed to drastically restrict the availability and increase the cost of a wide range of fossil-fueled consumer products: gas stoves and furnaces, gasoline and diesel-powered vehicles, gasoline-powered lawn care equipment, wood stoves, and more.

The openly stated utopian goal of all these regulatory actions is to “decarbonize” the entire American economy and somehow smoothly transition the whole country to a supposedly climate-friendly “sustainable” future that is powered and heated and cooled by electricity produced by renewable wind and solar generators.

The Biden administration’s decarbonization campaign poses a grave threat to the reliability of the nation’s electric system. Electricity, unlike oil and gas and other forms of energy, cannot be stored in significant amounts. It must be produced by generators and supplied to customers in amounts precisely equal to the amounts demanded by customers at any given point in time. If the supply of electricity is not kept continuously in balance with the demand for it the electric system will crash, and a widespread blackout will result.

Electric system operators can easily adjust the output of fossil-fueled generators, and nuclear generators, to meet customer demand as that demand fluctuates throughout each day. With electricity available to everyone “at the flick of a switch,” each of us is free to manage our daily affairs in the way that we find most convenient. The overall economic efficiencies and societal benefits that result from such flexibility are enormous.

With renewables, it’s an entirely different story. Electric system operators have no such control over the output of wind turbine generators and solar panels. The amount of power supplied by these technologies depends entirely on the availability of steady wind and clear sunlight.

Widespread smoke from the recent wildfires in Canada cut solar output across the U.S. Northeast by 90%. Calm weather cuts the output of a wind farm to a faction of its specified production capability. If the wind drops unexpectedly, system operators have to scramble to purchase replacement power from neighboring systems, or they must quickly cut power to customers enough to maintain system balance.

Emergency power supply cuts are enormously disruptive for commercial customers, and tremendously expensive. Power cuts associated with wildfires in California have cost customers billions of dollars.

Independent regulators responsible for maintaining the reliability of the electric system are warning with increasing urgency that the forced retirement of fossil-fueled power plants and the growing reliance on weather dependent renewables pose a serious threat to the nation’s power supply. They are predicting that emergency power cuts will become more and more common in the future.

Faced with such a threat, any responsible administration would moderate its energy and environmental policies. But that’s not what progressives do. They never change course, regardless of the objective evidence confronting them. They double down.

If system operators cannot control the output of wind turbine generators and solar panels to meet fluctuating customer demand then, to advance the decarbonization agenda, system operators must be given the authority and resources they need to control customer demand on an ongoing basis and limit that demand to levels that can be meet by the fluctuating capabilities of weather dependent generators.

Under pressure from environmentalists, more and more electric companies are installing equipment and implementing protocols that will allow them to remotely control customer demand continuously, not just during emergencies. California regulators have announced a goal to place 7,000 megawatts of customer demand under centralized control by 2030.

To sell this normalization of power cuts, the companies have launched sophisticated media programs designed to convince customers that flick-of-the-switch power is an irresponsible indulgence that must be foregone, and demand “flexibility” must be embraced, to save the planet from catastrophic climate change.

They came for our gas stoves and furnaces. They came for our cars and trucks, our wood stoves and firepits, our lawn mowers and leaf blowers. And now, they are coming for our thermostats.

J. Kennerly Davis (Ken) is a regulatory attorney with over 40 years of experience in the electric and gas power industry. He can be reached at j.kendavis@verizon.net

Tyler Durden

Sun, 07/23/2023 – 16:30 - Woke Researchers Spin Mockery Of STEM/Trans Survey Into Laughable 'Online Fascism' Paper

Woke Researchers Spin Mockery Of STEM/Trans Survey Into Laughable ‘Online Fascism’ Paper

After a national survey meant to assess the representation of “transgender and gender nonconforming” undergrads in science, technology, engineering and math fields elicited a major dose of sarcasm and insults, five woke researchers have written a paper arguing the responses are proof that “fascist ideologues” are “living ‘inside the house’ of engineering and computer science.”

Researcher Andrea Haverkamp lived in a van for five months while pursuing a doctorate in environmental engineering with a minor in queer studies (Street Roots) Of 723 responses, only 299 were considered valid, and 50, or 15%, were classified as “malicious.” True to form, the researchers — all associated with Oregon State University — also claim injury from unwelcome words:

“The malicious words and slurs directed towards our research team had a profound impact on [our] morale and mental health…particularly for one of our graduate student researchers…who was already in therapy for anxiety and depression regarding online anti-trans rhetoric” and “had to be taken off the project to heal from traumatic harm.”

Asked about their gender, many respondents identified as attack helicopters, a long-standing meme that mocks woke culture’s encouragement of people to “identify” as whatever they want. Comically, the authors took special offense that many respondents specifically chose the best-known attack helicopter:

“It is notable that the specific descriptor of an Apache Attack Helicopter is referenced by several different participants—itself a synthesis and reflection of U.S. military force and the appropriation of Indigenous language by colonizers.”

The 28-page paper is titled “Attack Helicopters and White Supremacy: Interpreting Malicious Responses to an Online Questionnaire about Transgender Undergraduate Engineering and Computer Science Student Experiences.” It was rejected by multiple engineering-education journals before finding a home at “Bulletin of Applied Transgender Studies,” which Northwestern University alumni can proudly claim as their alma mater’s contribution to society.

“Online memes associated with white nationalist and fascist movements were present throughout the data, alongside memes and content referencing gaming and ‘nerd’ culture,” wrote the authors, who call for academia to face STEM’s surging fascist menace head-on, as the survey results demonstrate “social justice STEM education must include perspectives on online hate radicalization and center anti-colonial, intersectional solidarity organizing as its opposition.”

There are plenty more word-salads strewn through the 28-page paper. Rather than ranch dressing, they’re served with a splash of Marxism:

- “The university at its most ideal can be envisioned as ‘a central site for revolutionary struggle, a site where we can work to educate for critical consciousness’ using ‘a pedagogy of liberation.’”

- “Identities such as transgender status in STEM teaching should similarly not be taught as ‘single issues’ but be conceptualized as one component of our multifaceted experiences with power and oppression—and that categories such as race, gender, and sexuality have roots in European colonial logics shared by fascist movements.”

- “Engineering graduates in the U.S. frequently work in fields such as fossil fuels, defense, construction, and technology upon graduation, and could be taught about these field’s relationships with national and global racial capitalism.”

One of the authors, Qwo-Li Driskill, is Oregon State University’s director of Women, Gender and Sexuality Studies and asks that you use “them” to refer to him (Arts Everywhere) Keeping in mind that $5 Amazon gift cards were used as an enticement to participate, here’s a sampling of the responses that sent the study’s lead data analyst fleeing into the arms of a therapist…

Gender:

- I identify as a gift card

- Apache Attack Helicopter

- Cis gender lizard king

- A human being

- F**king white male

- V22 Osprey

- DID YOU JUST F**KING ASK FOR MY GENDER

- F-16 Fighter Jet

- Pansexual attack helicopter

- Non-cookie-cutter cis-furry dragonkin. Don’t judge.

- Quasi-Demi-poney; bankai-released state queercopter with a hint of faggotdrag lesbian and homosexual upside-down Frappuccino cake

- I’m just here for the gift card

Race/Ethnic Identity

- I’m an ethnic gift card.

- My skin color is not important

- Afro/Klingon-Asicatic Galapogayation

- AH-64 Apache

- Republican

- Come on man, these questions are stupid. Everyone is a grab bag of genetics from all over the world

- I’m a Swedish Muslim

- Native American (Elizabeth Warren)

- Pansexual attack helicopter

- Cracker

- Colored Native Mix w/oppressed ancestors

- Born white but I spend a lot of time in the sun so I identify as a light skin black male

- My skin is blue, I think I might be a smurf

Disability

- I don’t have enough gift cards

- My country is run by communists

- Being 2.86% white

- Pedophilia

- Gender disphoria

- Thinking I’m not a man

- Being trans

- That I’m a tranny

- I’m mentally retarded

- I have hands where my feet are and feet where my hands are

- Like all transgenders, my disability is the inability to come to terms with biological reality. Madness, essentially.

Open-Ended Responses

- I am trans obviously I will have a job regardless of my skills thanks to diversity quotas inspired by surveys such as these

- I don’t actually have any skills I’m just a diversity “affirmative action” student

- You’re ruining genuine scientific disciplines here. There are two genders, male and female. If an engineer creates a bolt and a nut but then whimsically labels them, then they’re not that great of an engineer.

- I wish people in universities (especially the faculty) would not focus so much on gender and identity. That doesn’t matter. Just let people do their thing and teach them how to do Gauss eliminations and whatnot

Just think: If your wisecracks in our comments are potent enough, you too may find yourself quoted in an alarmist paper at the esteemed Bulletin of Applied Transgender Studies.

Tyler Durden

Sun, 07/23/2023 – 16:00 - Asahi Gold Vault 30 Miles Outside Manhattan Added To COMEX Approved Vault List

Asahi Gold Vault 30 Miles Outside Manhattan Added To COMEX Approved Vault List

Submitted by Ronan Manly, BullionStar.us

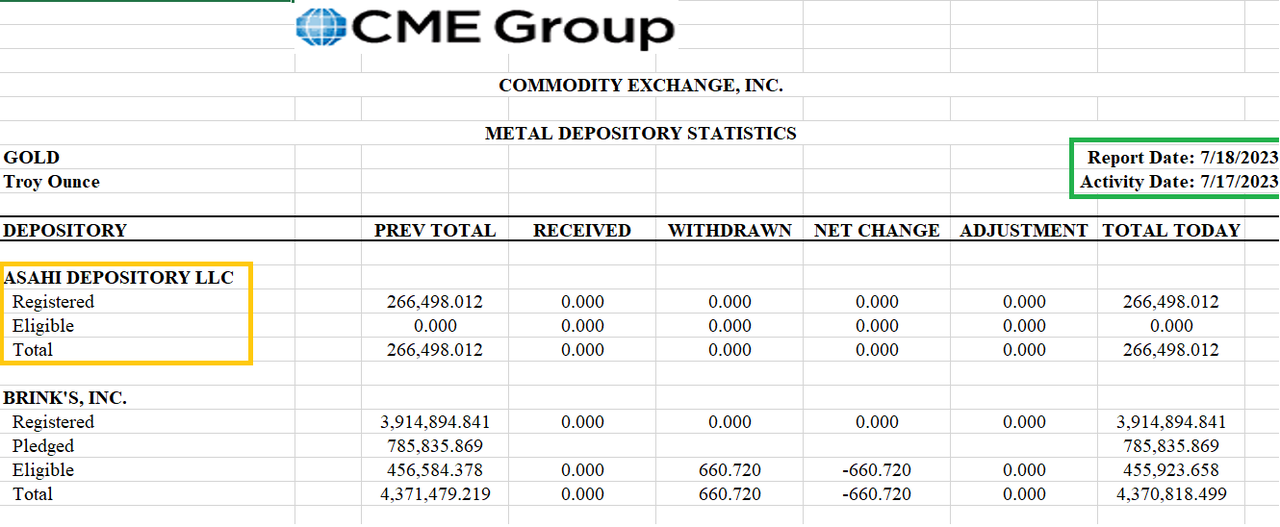

Those who keep an eye on the well-known COMEX daily gold and silver inventory reports, (officially titled CME’s “Warehouse and Depository Stocks”) will by now have noticed that a new depository / vault called “ASAHI DEPOSITORY LLC” has recently made an appearance on the reports, specifically since May of this year.

COMEX inventory reports are always of keen interest in the precious metals space because they show, at least in theory, how much physical gold and silver in held within a group of ‘approved’ depositories / vaults in and around New York City to backstop or meet delivery obligations connected to the trading of gold futures and silver futures contracts on the Commodity Exchange (COMEX).

Note that in addition to gold and silver, ‘Asahi Depository’ is also now an approved CME depository for storing platinum and palladium metals connected to the trading of CME platinum futures and palladium futures contracts on the NYMEX (New York Mercantile Exchange).

Given that a new depository / precious metals vault joining the list of COMEX/NYMEX approved vaulters is quite a rare occurrence, it’s worth examining Asahi Depository and its approval by the CME Group (owner of COMEX and NYMEX), as well as looking at where the Asahi Depository vault is located in the US.

COMEX SILVER VAULT TOTALS RISE OVER 2.2 MILLION OUNCES

– Registered rose almost 1.2M oz. as the newly added Asahi Depository begins adding silver for the first time.

– Open Interest is now equal to 254% of all vaulted silver and 2,252% of Registered silver. pic.twitter.com/JZgU1oPyY9— Michael #silversqueeze (@mikesay98) May 18, 2023

https://platform.twitter.com/widgets.js

As per the CME website, we find that Asahi Depository made an application to CME to become an approved depository for precious metals storage all the way back on March 15, 2022:

“Application for Gold, Silver, Platinum and Palladium Regularity

Notice is hereby given that Asahi Depository LLC. has applied to become an Approved Depository for gold, gold (enhanced delivery), silver, platinum, and palladium at the following location:

Asahi Depository LLC Location Blauvelt, NY”

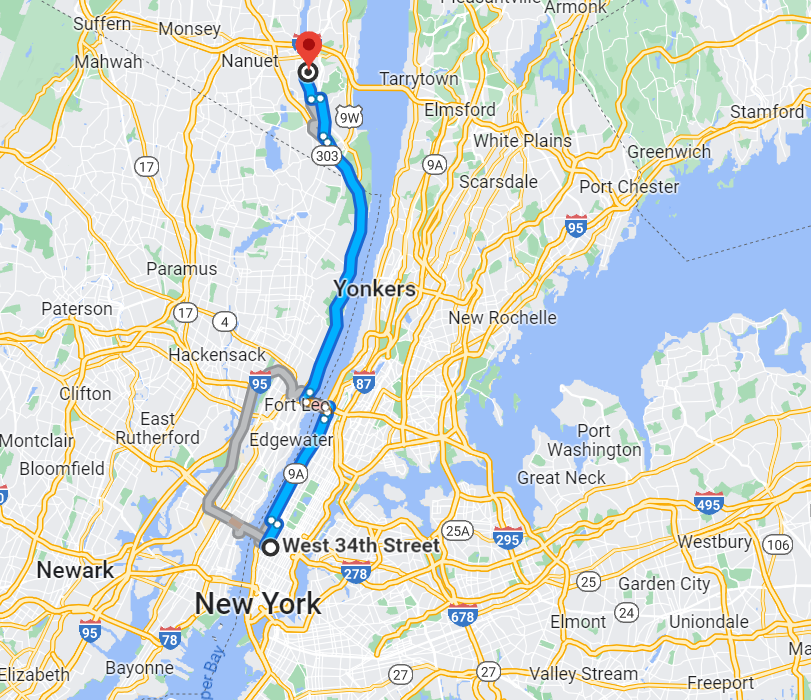

Blauvelt is a municipality in Rockland County, New York, in the town of Orangetown, 30 miles from midtown Manhattan, and about 40 minutes drive from midtown via the NY-9A North/Henry Hudson Pkwy and then Palisades Interstate Pkwy North taking the Orangeburg exit.

Following the application to CME in March 2022, NYMEX and COMEX then approved the Asahi Depository application on May 01, 2023:

“Regularity Approval for Gold, Silver, Platinum, and Palladium

New York Mercantile Exchange, Inc. (“NYMEX”) and Commodity Exchange, Inc. (“COMEX”) (collectively, the “Exchanges”) has approved the application of Asahi Depository LLC. to become an Approved Depository for gold, silver, platinum, and palladium at their facility in Blauvelt, NY.

This approval is effective immediately.”

While this might seem like a long delay between applying for approval (March 2022) and securing approval (May 2023), the delay – as you’ll see below – was probably due to the fact that the Asahi storage facility in Blauvelt, New York, was not fully up and running until early Q2 2023.

COMEX Gold Inventory report with Asahi entry – July 17, 2023 Asahi Refining

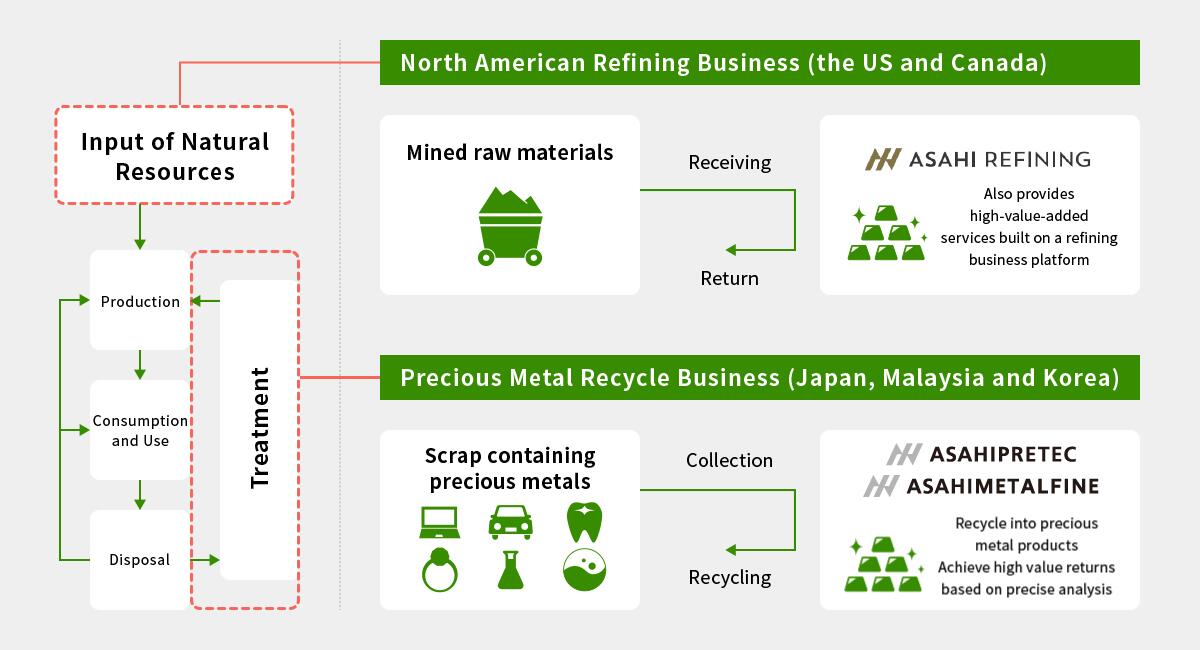

So who or what is Asahi Depository LLC?

Asahi Depository LLC is a subsidiary of Asahi Refining, which itself is a wholly owned subsidiary of Japan’s Asahi Holdings, Inc. So technically speaking, a Japanese owned depository has now entered the COMEX precious metals storage market.

For those who thought that Asahi is a Japanese beer, you’re not wrong. But … it’s not the same Asahi, and not even the same holding company. Japan’s famous Asahi beer is manufactured by similarly named Asahi Group Holdings. Asahi Depository is part of Asahi Holdings.

Coincidentally, Asahi Holdings, Inc very recently rebranded as ‘ARE Holdings’, actually on July 01, 2023, so any confusion over Asahi Group Holdings vs Asahi Holdings will from now on be purely historical.

Asahi Refining itself came into existence in March 2015 when Asahi Holdings Inc completed the acquisition of the Johnson Matthey Gold & Silver refining businesses in North America, following Johnson Matthey’s decision in 2014 to divest of its nearly 200 year old precious metals refining business.

The Asahi acquisition included Johnson Matthey’s US precious metals refinery located in Salt Lake City, Utah, and the Johnson Matthey precious metals refinery located in Brampton, Ontario, Canada.

As per the Asahi Refining press release about the acquisition on March 06, 2015:

“Asahi Holdings is a Tokyo, Japan based precious metals recycling company (collection, recovery, refinement) founded in 1952. “

“Asahi Holdings is proud to announce on March 5, 2015 that it has finalized the acquisition of the former Johnson Matthey Gold & Silver refining businesses.”

“The Salt Lake City, USA and Brampton, Canada refineries will collectively operate as “Asahi Refining.”

The Johnson Matthey Salt Lake City refinery is now known as the ‘Asahi Refining USA, Inc’ while the Johnson Matthey Brampton, Ontario refinery is now known as ‘Asahi Refining Canada Limited’.

Japanese gold refiner Asahi wins auction for the assets of bankrupt Republic Metals Corp (RMC) of Miami, with a bid of $25.5 million, after Asahi outbid the Swiss Valcambi refinery on Thursday – Reuters https://t.co/0MPkBLMGQx

— BullionStar (@BullionStar) February 1, 2019

https://platform.twitter.com/widgets.js

Both refiners are on the London Bullion Market Association (LBMA) Good Delivery Lists for both gold and silver. Asahi Refining Canada is a full member of the London Bullion Market Association (LBMA). Asahi Refining also operates a precious metals mint located in Miami, Florida and fabricates a range of gold and silver cast bars and minted bars as well as silver rounds.

Further details about the precious metals recycling business of Asahi Holdings (collection, recovery, refinement) can be read here.

Asahi Holdings’ precious metals refining and recycling business. Source Asahi Depository

Let’s look at Asahi Depository LLC. The company Asahi Depository LLC was registered on December 17, 2021 New York State Department of State (NYSDOS).

Looking at the Asahi Refining website, a press release published on June 02, 2023 refers to “Asahi Refining’s expansion into vaulting and storage services” where it “looks to establish itself as a leader in the precious metals storage industry”. This expansion is being done via Asahi Depository LLC.

Specifically:

“Asahi Depository LLC (ADL) is proud to announce its approval by the CME Group (CME) as a storage facility for Gold, Silver, Platinum, and Palladium.

This is a significant achievement as the approval, which is dually applicable for both the Commodities Exchange (COMEX) and the New York Mercantile Exchange (NYMEX), ensures that ADL meets strict standards for security, transparency, and accuracy in the storage and handling of precious metals.”

As regards the location of the vaulting facility, the press release goes on to say that:

“Located in Blauvelt, NY, ADL is located within 30 miles of the CME in New York. ADL’s near proximity to the New York metropolitan area provides easy access to a range of financial institutions, and other industry professionals.

Likewise, the location, just outside of Manhattan, offers a distinct advantage of accessibility without the hassle of navigating the city’s logistical challenges.”

PDF version of press release here.

Map of route from Manhattan midtown to Asahi’s Blauvelt depository 875 Western Highway – Hudson Crossing

Its very easy, using publicly available information on the web, to pinpoint exactly where this Asahi Depository vault is located. A quick Google search of “Asahi Depository” and “Blauvelt” reveals that the Asahi Depository is located at 875 Western Hwy, Blauvelt, NY 10913.

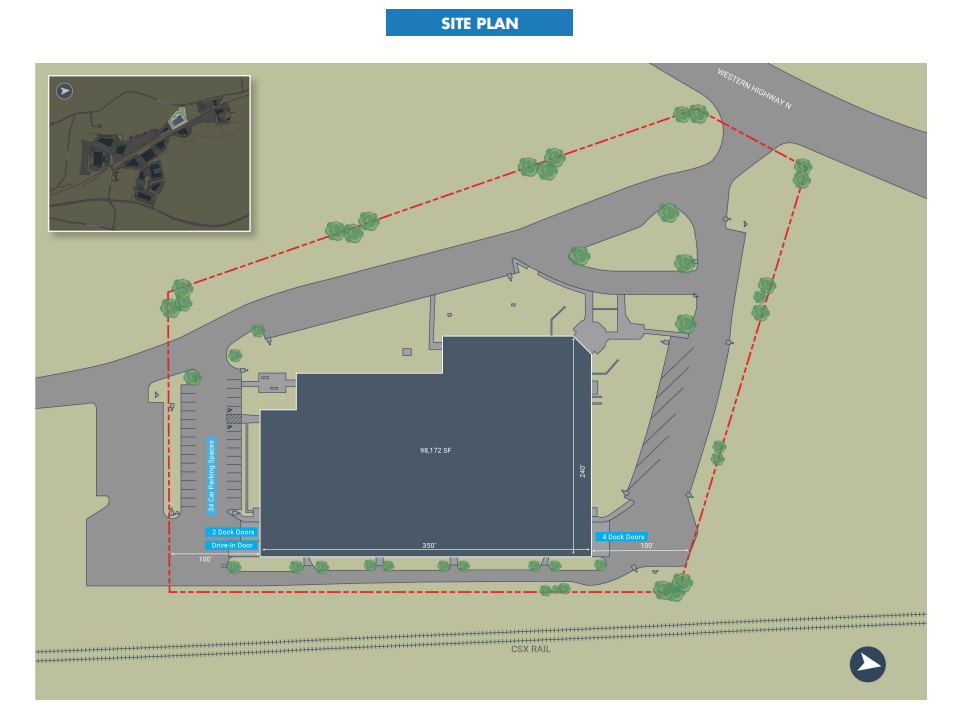

The location 875 Western Highway is in the Hudson Crossing industrial park. The building is Building 11, and is 98,172 sq feet in area with a ceiling height of 23 feet.

Asahi Depository LLC bought its building in Hudson Crossing in February 2022 from Partners Group & Onyx Equities LLC for US$ 24.565 million. The building is described as “100% leased, wet sprinklers, 6 docks, 1 drive-in door, CSX rail line spots”. See Lee & Associates Q1 2022 Industrial market snapshot here.

You can also see plans of the building on the Hudson Crossing website, where it also says that the building, built in 1981, also has a 18,839 square foot mezzanine floor, and 40’ x 40’ column spacing. The site plan is also here on the CBRE website.

Hudson Crossing – 875 Western Highway – Asahi Depository LLC Also in February 2022, Asahi then entered into a set of lease agreements with the County of Rockland Industrial Development Agency (IDA) so as to obtain tax relief, in which Asahi leased the property to IDA, and IDA leased it back to Asahi, and IDA promised to grant Asahi an exemption from sales tax up to US$ 711,000 for qualified expenditures up to US$ 8.5 million.

Asahi Depository, Hudson Crossing – Source On the Orangetown Tax Map, the Asahi Depository property (located at 875 Western Highway, Blauvelt, New York) is identified as Section 65.13, Block 1, Lot 2; in the LO zoning district.

After buying the building in February 2022, Asahi also submitted some planning requests to the town of Orangetown on June 3, 2022 for modifications to the property:

“Applicant is proposing to utilize the existing building for a NY based corporate office and for the storage of gold and silver”.

“Applicant is proposing a new 8’-0” high fence which requires a 5’-4” setback from the property along the side yards and rear yard.”

A more detailed letter on June 23, 2022 from Asahi’s architect to the Zoning Board of Appeals expanded on this request:

“The building at 875 Western Highway, Blauvelt, NY was purchased by the Owner Asahi Depository LLC to be used as an office & storage facility where rare metals will be stored on site. The need for heightened security on the site is crucial for the operation of the facility. A new 8.0’ high fence is thus proposed along the side and rear yards of the property to ensure the controlled access into the facility.”

Asahi also requested expansion of loading docks and expansion of turning radius area for armored delivery trucks.

This request was heard by the zoning board on September 07, 2022 and the minutes of the hearing can be seen here, which include such facts as that Asahi’s armored delivery trucks are 75 feet long, that Asahi Depository wanted 4 loading docks (2 of which will be in use all the time), that they have trucks coming from Utah and Canada twice a week that are loading and unloading metal bars that are stored in the Blauvelt facility.

Here the references to Utah and Canada refer to Asahi’s Salt Lake City refinery in Utah and Asahi’s Brampton, Ontario refinery in Canada.

Asahi Depository has also recently been hiring staff for the Asahi Depository in Blauvelt, for example “full-time Security Guard positions available at our new facility in Blauvelt”, and also “full-time Material Handler positions available at our new facility in Blauvelt, New York“, and also a “a full-time Inventory & Logistics Administrator position available at our new facility in Blauvelt”.

Conclusion

You can see from these timelines that Asahi bought the Hudson Crossing warehouse property in February 2022, then applied for COMEX / NYMEX approval in March 2022, but then also needed to wait to receive local planning approvals and tax relief, and then presumably made security and other modifications to the property, and then CME granted the application for COMEX/NYMEX vault approval by May 2023.

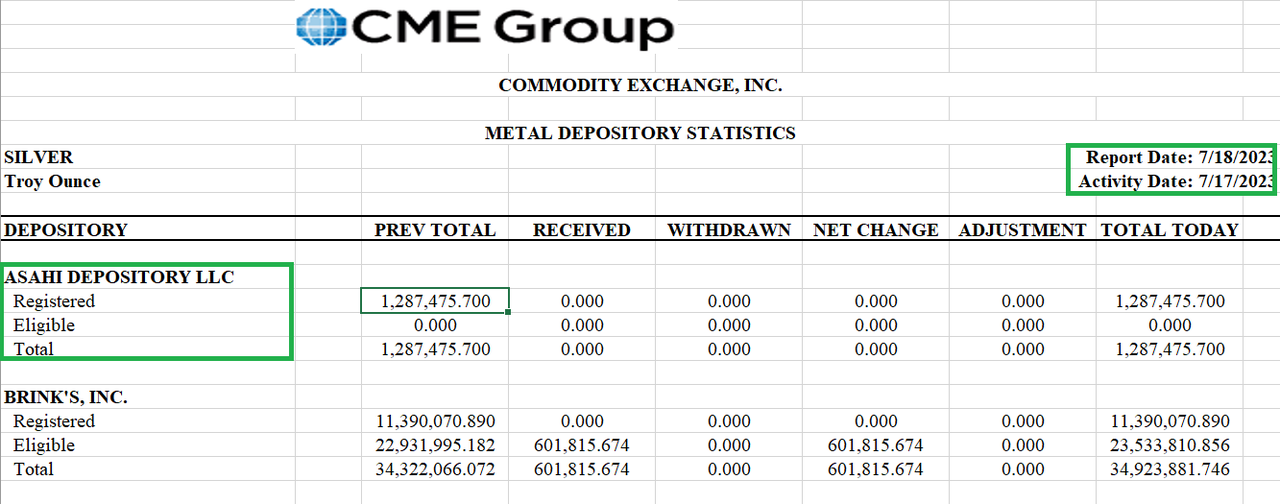

COMEX Silver Inventory report with Asahi entry – July 17, 2023 According to the COMEX inventory reports, as of July 20, 2023, the Asahi Depository in Blauvelt is storing 266,498 troy ounces of gold (8.29 tonnes) and 1,880,973 troy ounces of silver (58.5 tonnes), all of which is in the ‘registered category’ meaning that all of this metal has COMEX warrants attached.

Interestingly, on July 18, a deposit of 593,497 troy ozs of silver (18.46 tonnes) was added to Asahi’s ‘registered’ silver category, which boosted the previous total of 1,287,476 ozs (40 tones) to 58.5 tonnes.

COMEX SILVER VAULT TOTALS RISE 1.14M OUNCES

– Registered rises 593K oz., courtesy of a deposit (not a transfer from Eligible) into the new-ish Asahi depository.

– Open Interest is now equal to 264% of all vaulted silver and 2,076% of Registered silver. pic.twitter.com/JKulQqIgb8— Michael 🏳️🌈 #silversqueeze (@mikesay98) July 19, 2023

https://platform.twitter.com/widgets.js

https://platform.twitter.com/widgets.js

The CME inventory reports show that the Asahi Depository has no gold or silver in the ‘eligible’ category. Apart rom the 18.46 tonnes inflow of silver, the quantities of gold and silver in the Asahi vault look static and don’t seem to be changing regularly at this point in time. But presumably that will change as the Asahi Despository at Hudson Crossing gets more business.

CME warehouse inventory reports for platinum and palladium also show that the Asahi Depository, although listed on the reports, is holding no platinum or palladium in either the ‘registered’ or eligible categories.

While most of the COMEX approved vaults are in New York City, not all of them are. This is because the CME (COMEX) Rulebook allows approved vaults to be within 150 miles og New York City.

As per CME Rulebook – Chapter 7, 703 (11):

” The depository for gold deliverable against the Gold futures (GC) contract must qualify and be designated a weighmaster and must be located within a 150-mile radius of the City of New York”

For appoved gold depositories, the vaults of JP Morgan, HSBC, MTB, Loomis, Brinks and Malca-Amit are in New York City. But the vaults of Delaware Depository and IDS Delaware, are, as the names suggest, in Delaware. Now you can add Asahi to that list.

For appoved silver depositories, the COMEX list is identical to gold, except that the CNT Depository in Bridgewater, Massachusetts is also an approved depository for silver. While Bridgewater is about 220 miles from midtown Manhattan, the 150 mile rule does not apply to silver.

This article was originally published on the BullionStar.us website under the same title “Asahi vault 30 miles outside NYC added to COMEX approved vault list“

Tyler Durden

Sun, 07/23/2023 – 15:30 - Visualizing America's $20 Trillion Economy By State

Visualizing America’s $20 Trillion Economy By State

A sum of its parts, every U.S. state plays an integral role in the country’s overall economy.

Texas, for example, generates an economic output that is comparable to South Korea’s, and even a small geographical area like Washington, D.C. outputs over $129 billion per year.

The visualization below by Visual Capitalist’s Avery Koop and Joyce Ma uses 2022 annual data out of the U.S. Bureau of Economic Analysis (BEA) to showcase each state or district’s real gross domestic product (GDP) in chained 2012 dollars, while also highlighting personal income per capita.

A Closer Look at the States

California is by far the biggest state economy in the U.S. at $2.9 trillion in real GDP—and when comparing its nominal value ($3.6 trillion) with national GDPs worldwide, the Golden State’s GDP would rank 5th overall, just below Germany and Japan.

Here’s an up-close look at the data:

Rank State Real GDP (chained 2012 dollars) 1 California $2.9 trillion 2 Texas $1.9 trillion 3 New York $1.6 trillion 4 Florida $1.1 trillion 5 Illinois $798 billion 6 Pennsylvania $726 billion 7 Ohio $639 billion 8 Georgia $591 billion 9 Washington $582 billion T9 New Jersey $582 billion 11 North Carolina $560 billion 12 Massachusetts $544 billion 13 Virginia $513 billion 14 Michigan $490 billion 15 Colorado $386 billion 16 Maryland $369 billion 17 Tennessee $368 billion 18 Arizona $356 billion 19 Indiana $353 billion 20 Minnesota $350 billion 21 Wisconsin $312 billion 22 Missouri $301 billion 23 Connecticut $253 billion 24 Oregon $235 billion 25 South Carolina $226 billion 26 Louisiana $217 billion 27 Alabama $213 billion 28 Kentucky $201 billion 29 Utah $192 billion 30 Oklahoma $191 billion 31 Iowa $177 billion 32 Nevada $165 billion T32 Kansas $165 billion 34 District of Columbia $129 billion 35 Arkansas $127 billion 36 Nebraska $124 billion 37 Mississippi $105 billion 38 New Mexico $95 billion 39 Idaho $84 billion 40 New Hampshire $83 billion 41 Hawaii $75 billion 42 West Virginia $72 billion 43 Delaware $66 billion 44 Maine $65 billion 45 Rhode Island $55 billion 46 North Dakota $53 billion 47 South Dakota $50 billion T47 Montana $50 billion T47 Alaska $50 billion 50 Wyoming $36 billion 51 Vermont $31 billion United States $20 trillion Altogether, California, New York, and Texas account for almost one-third of the country’s economy, combining for $6.3 trillion in real GDP in 2022. The only other state that reached the trillion dollar mark is Florida with $1.1 trillion.

Texas’ economy is driven largely by industries like advanced manufacturing, biotech, life sciences, aerospace, and defense. The state is also home to a number of large companies, like Tesla and Texas Instruments, which make it a hub for jobs, innovation, and opportunity.