- China's Exploiting The COVID-19 Pandemic To Expand In Asia

China’s Exploiting The COVID-19 Pandemic To Expand In Asia

Authored by Con Coughlin via The Gatestone Institute,

While the rest of the world is preoccupied with tackling the coronavirus pandemic, China is intensifying its efforts to extend its influence in the South China Sea by intimidating its Asian neighbours.

The arrival of China’s Liaoning aircraft carrier, together with five accompanying warships, in the South China Sea earlier this month has resulted in a significant increase in tensions in the Asia-Pacific region as Beijing seeks to take advantage of the coronavirus pandemic to flex its muscles.

So far in April, there were claims that a Chinese coast guard vessel deliberately rammed and sank a Vietnamese fishing boat operating close to the disputed Paracel Islands. All the fishermen survived and were transferred to two other Vietnamese fishing vessels operating nearby.

The incident prompted a furious response from the Vietnamese government, which accused Beijing of violating its sovereignty and threatening the lives of its fishermen. The US State Department said it was “seriously concerned” about the incident and called on Beijing “to remain focused on supporting international efforts to combat the global pandemic, and to stop exploiting the distraction or vulnerability of other states to expand its unlawful claims in the South China Sea.”

In other incidents, Chinese vessels have been accused of harassing Indonesian fishing boats, as well as tailing Malaysian oil-exploration boats.

At the same time, China has provoked a diplomatic dispute with the Philippines following Beijing’s declaration that a region over which Manila claims sovereignty in the South China Sea is Chinese territory.

The dispute concerns China’s recent announcement that it intends to administer two disputed groups of islands and reefs in the waterway. One district covers the Paracel Islands, and the other has jurisdiction over the Spratlys, where China has built a network of fortified man-made islands. The Philippines has a presence of its own on at least nine islands and islets in the area, and bitterly opposes Chinese attempts to extend its influence.

Beijing has long claimed control over the South China Sea and the surrounding area because of its strategic significance as one of the world’s busiest waterways. Around one third of the world’s shipping passes through it and carries trade worth around $3 trillion. In addition, the waters contain lucrative fisheries, and huge oil and gas reserves are believed to lie beneath its seabed.

China’s gradual encroachment on the area has been resisted by other countries in the region such as Vietnam, the Philippines, Taiwan, Malaysia and Brunei, which all have competing claims of their own.

As the region’s dominant power, China has shown little interest in seeking to resolve these conflicting claims peacefully. Instead, it has resorted to brute force, using its increasingly powerful navy to assert its dominance by harassing the shipping of rival states, even, at times, in their own territorial waters.

China’s increasingly aggressive action, known in Beijing as “Wolf Warrior diplomacy”, has prompted US Secretary of State Mike Pompeo to warn that China is taking advantage of the world’s preoccupation with the coronavirus pandemic to push its territorial ambitions in the South China Sea. At a recent briefing to foreign ministers of the 10-member Association of Southeast Asian Nations (ASEAN), Mr Pompeo stated:

“Beijing has moved to take advantage of the distraction [over Covid-19], from China’s new unilateral announcement of administrative districts over disputed islands and maritime areas in the South China Sea, its sinking of a Vietnamese fishing vessel earlier this month, and its ‘research stations’ on Fiery Cross Reef and Subi Reef.”

Despite the Trump administration’s preoccupation with tackling the coronavirus pandemic, Washington is not prepared to tolerate China’s aggressive actions. Three ships from the US Seventh Fleet, together with an Australian frigate, have responded by sailing through the disputed waters in a show of force.

China’s communist leadership may believe that they can take advantage of the coronavirus pandemic to bully their Asian neighbours. But this show of force by the US Navy should send a timely reminder to Beijing as to which country is the real military power in the region.

Tyler Durden

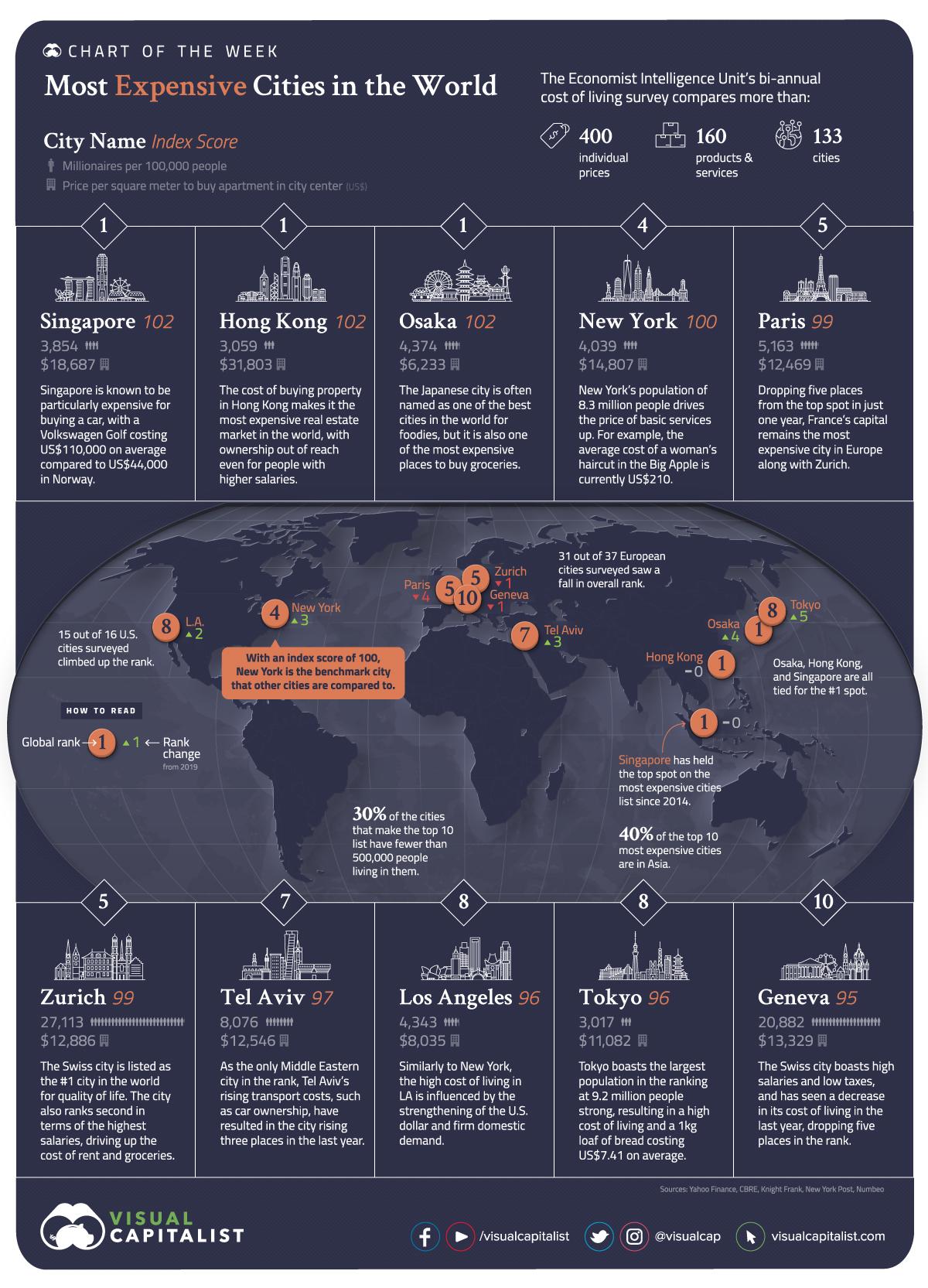

Sat, 05/02/2020 – 23:50 - These Are The 10 Most Expensive (And Cheapest) Cities In The World

These Are The 10 Most Expensive (And Cheapest) Cities In The World

Where personal wealth is concerned, there are two sides to every story.

The first of which is the amount of money a person earns, and the other is what they choose to spend their money on. As Visual Capitalist’s Katie Jones notes, the latter is influenced by the cost of living in the city where they reside – an ever-changing metric that is driven by a wide variety of factors, such as currency, population growth, or external market movements.

Today’s graphic visualizes the findings from the 2020 Worldwide Cost of Living report and uses data from 133 cities to rank the most expensive cities in the world.

Note: Report research was conducted towards the end of 2019, before the COVID-19 outbreak.

Asia Dominates the Ranking

Globally, the cost of living has fallen by an average of 4% over the last year, with much of the movement up and down the ranking being driven by currency fluctuations.

The locations with the highest cost of living are largely split between Europe and Asia. For the second time in the report’s 30-year history, three cities are tied as the top spot—Singapore, Hong Kong, and Osaka.

Source: EIU. New York City is index baseline (score = 100). Ties in index score values are denoted by (t).

Osaka is a newcomer to the top spot, climbing four places over the last year to join cost of living heavyweight champions, Singapore and Hong Kong. As Japan’s third-largest city, Osaka is a major financial hub and a breeding ground for emerging startups, with relatively low real estate costs compared to Singapore and Hong Kong.

Three European cities (Paris, Zurich, and Geneva) sit atop the most expensive city rankings, compared to seven cities only 10 years ago. Similarly, 31 of the 37 European cities have seen a decrease in cost of living overall—largely as a result of the Euro or local currencies losing value relative to the U.S. dollar.

Finally, the top 10 is rounded out with two cities from the United States (New York, Los Angeles) and one from Israel (Tel Aviv).

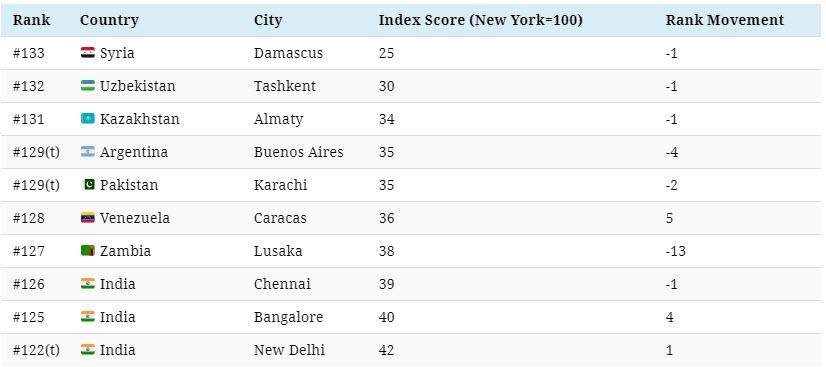

The Cheapest Cities

While East Asia is home to many of the world’s most expensive cities, South Asia hosts the largest grouping of cities with the lowest cost of living.

Source: EIU. New York City is index baseline (score = 100). Ties in index score values are denoted by (t).

Three Indian cities dominate the cheapest cities ranking due to a combination of low wages and high levels of income inequality, preventing any price increases.

Meanwhile, political and economic turmoil is a common denominator among the cheapest cities outside of South Asia. For example, the Syrian Civil War resulted in an economic collapse, leading to high inflation and a downward spiral in value for the Syrian pound.

A Spanner in the Works

The COVID-19 pandemic is estimated to cost the global economy up to $2 trillion in 2020, so while governments attempt to boost the economy, many are concerned about higher inflation rates spreading across the world.

With a recession becoming more likely, uncertainty around real estate prices will heighten for every city, regardless of their cost of living ranking.

As we navigate chaotic and uncertain times, the next cost of living survey could look very different to today—the most important question will be how permanent the damaging effects of the pandemic will be.

Tyler Durden

Sat, 05/02/2020 – 23:25 - Johnstone: Biden Is Everything The Democrats Are

Johnstone: Biden Is Everything The Democrats Are

Authored by Caitlin Johnstone via Medium.com,

Joe Biden is not an “imperfect candidate” for the Democrats.

He is the perfect candidate, because he’s everything the party is: Demented. Decrepit. Bloodthirsty. Corrupt. Cronyistic. Authoritarian. Reactionary. Rapey.

He is exactly what they deserve. He is exactly what they are.

Joe Biden is the Democrat’s Democrat. He is the perfect representative of the party. They should even take it a step further and replace that donkey with Joe Biden.

Biden is to the Democrats as Trump is to the Republicans. Everyone’s just wearing their true face now.

~

If you’re willing to sacrifice all principles, all sanity and all morality to get rid of Trump, what exactly is the point of getting rid of Trump?

~

We know Biden is a liar. He’s been pinged for lying his whole career. Everyone is trying to undermine the victim’s character in order to discredit her while ignoring Joe’s character. We know he lies. He also has a history of unwanted sexual advances. His story is not credible.

~

Nobody actually believes that Biden didn’t sexually assault Tara Reade. Nobody’s actually confident that Creepy Uncle Hair Sniffer isn’t a rapist, they’re just pretending they are. I can understand saying “It’s possible but unproven”, but saying it’s false is so gross and dishonest.

They’re accusing Reade of lying for partisan reasons, when in reality that’s exactly what they are doing: they’re pretending they believe Handsy Joe Biden is incapable of shoving his fingers into a woman without her consent, and they are lying. Out of pure partisan loyalty.

~

It’s funny how refusing to support a literal dementia patient who has been credibly accused of rape for the world’s most powerful elected office is a very, very normal thing to do, yet people are acting like it’s bizarre and freakish.

~

Which looks more likely to you? (A) That Reade seeded a bunch of vicious lies about Senator Joe Biden in the 1990s with the intention of someday sabotaging his presidential bid in the distant future for some reason, or (B) that a powerful man sexually assaulted a woman?

~

It’s so weird how Joe Biden is a spent piece of leftover 1970s beltway flotsam made of plastic donor class dinner parties and AIPAC lobbying but everyone’s all pretending they like him as a person and stuff.

~

There are no fact-based and intellectually robust arguments for working within the establishment to manifest revolutionary agendas, but there are a lot of highly effective intellectually dishonest arguments for why it’s okay for you to pretend otherwise and go back to sleep.

~

“They destroyed the economy over a virus, but the narrative about the virus is completely fake!”

Perhaps. But so is the narrative about “the economy”.

~

Terence McKenna once said “We are led by the least among us. The least intelligent, the least noble, the least visionary.” Can’t think of a better illustration of this than having Donald Trump versus Joe Biden competing for the most powerful elected office on the planet.

~

Hey remember when Trump provoked a missile retaliation that led to scores of injured US soldiers by assassinating Iran’s top military commander for no legitimate reason, lied about the whole thing, and then suffered no consequences or political repercussions of any kind? Good times.

~

Democrats are so fucking stupid and ridiculous that the Krassenstein brothers are still a thing.

~

All of humanity’s worst atrocities have been legal. Genocide. Slavery. Torture. The fact that you can squint at the imprisonment and extradition of a journalist for exposing US war crimes in such a way that makes it look “legal” does not mean it isn’t unforgivably evil.

~

It’s always about power. Power comes before everything, including profit, which is why you see escalations against nations who’d be very profitable to continue trading with and why critics of US foreign policy are attacked far more aggressively than critics of its domestic policy.

Manipulators understand that wealth control is a means to power and not an end in itself; that’s why you see things like Zuckerberg hurting his own profit margins by making changes to Facebook which make the platform less fun to use but shore up establishment narrative control.

Power trumps profit every time. Manipulators are driven ultimately by the desire to control as many humans as possible to the greatest extent possible. Money is a useful tool for accomplishing that, but in a pinch they’ll swap it out for military/police force or censorship etc.

Wealth is a narrative construct and can be gained or lost or made obsolete in a new narrative paradigm. Elite manipulators understand that it’s hard, nonconceptual control over hard, nonconceptual objects that gives them their actual alpha status over the rest of the humans.

~

“A newly democratized media environment has made it difficult for people to distinguish fact from fiction.”

‘Oh no! What do we do?’

“Censor everyone except authoritative news sources.”

‘Authoritative news sources? Like who?’

“The ones who lied about Russiagate and all the wars.”

~

As a general rule, indie media should not attack other indie media. If you’re not punching up, you’re punching down.

~

People ask me “Well, what should we do? How do we fix this thing?” And of course my only possible answer is, “Do what I’m doing! Or your version of it.” Of course I’m doing the thing I think we should do to solve the problems of our species. Why would I be doing anything else?

~

Revolution is an inside job. This is not an egoically pleasing fact, but it is a fact. It’s much more fun for egoic mind to believe both the problem and the solution exists in other people, but in reality the changes you can make in yourself will have far greater effects on the world.

There are vast, vast depths within all of us, and we are capable of making vast, vast changes to those depths. We are in fact far more capable of doing this than we are of changing the outside world through force of will. And interestingly when we do this, we do change the world. And we do it far more efficaciously than we can by trying to will it to conform with the noises in our babbling thinky brain.

* * *

Thanks for reading! The best way to get around the internet censors and make sure you see the stuff I publish is to subscribe to the mailing list for my website, which will get you an email notification for everything I publish. My work is entirely reader-supported, so if you enjoyed this piece please consider sharing it around, liking me on Facebook, following my antics onTwitter, checking out my podcast on either Youtube, soundcloud, Apple podcasts or Spotify, following me on Steemit, throwing some money into my hat on Patreon or Paypal, purchasing some of my sweet merchandise, buying my books Rogue Nation: Psychonautical Adventures With Caitlin Johnstone and Woke: A Field Guide for Utopia Preppers. For more info on who I am, where I stand, and what I’m trying to do with this platform, click here. Everyone, racist platforms excluded, has my permission to republish, use or translate any part of this work (or anything else I’ve written) in any way they like free of charge.

Bitcoin donations:1Ac7PCQXoQoLA9Sh8fhAgiU3PHA2EX5Zm2

Tyler Durden

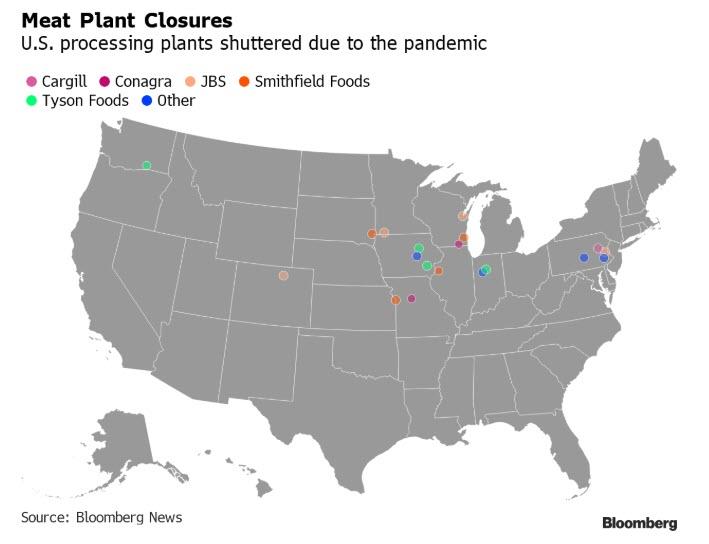

Sat, 05/02/2020 – 23:00 - Get Ready For Slaughterhouse Robots To Ease America's Meat Processing Crisis

Get Ready For Slaughterhouse Robots To Ease America’s Meat Processing Crisis

America’s meat processing crisis, mainly triggered by labor shortages and plant closings due to coronavirus spread, is set to unleash a new wave of automation across plants to ease labor and health woes.

Bloomberg Law reports JBS SA, the world’s largest meat producer, is preparing to install robots in slaughterhouses to mitigate the spread of COVID-19 among human employees working on the production line.

JBS SA CFO Guilherme Cavalcanti recently said the Brazilian processing company expects to expand automation at its facilities across the world.

Cavalcanti said the adoption of automation started before the pandemic as labor tightened at US plants due to a decline in immigration sparked by the Trump administration. He said labor shortages have developed in the US as the virus infects workers and shutters plants.

Watch this video of meatpacking robots already in a JBS SA plant:

The fast-spreading virus has so far infected 4,900 workers (across the entire industry) and left 20 dead at 115 meatpacking plants across 19 states, according to CDC data from April 9-27.

In a JBS SA webinar on how it has handled its pandemic response, Cavalcanti said automation is more important than ever considering labor and health issues.

JBS SA has closed two US meatpacking plants due to the virus outbreak. There have been at least 22 plant closings in the US. We’ve noted, the closures have resulted in a 25% reduction in pork-processing capacity and beef by 10%. This has crushed farmers with overcapacity as they have limited options in selling livestock, resulting in mass cullings and plunging livestock spot prices. As for the consumer, soaring food inflation and shortages have been the result of plants reducing output or closing.

And at Zero Hedge, we have not been shy at telling you how things might pan out when it comes to a nation that is becoming automated, which means millions of jobs will be eliminated entirely by 2030. And, for some more uncomfortable truths, corporate America will speed up their adoption of automation and artificial intelligence, because robots can’t be infected by coronavirus.

Tyler Durden

Sat, 05/02/2020 – 22:35 - "Go Buy Guns First" – John McAfee Warns Governments "Are Deceiving You" About Virus

“Go Buy Guns First” – John McAfee Warns Governments “Are Deceiving You” About Virus

Authored by Amy Castor via DeCrypt.co,

The government is deceiving you. The pandemic is a ploy spread by the fake-news media, and if you care about your lives, go out and buy guns now.

That was the message of John McAfee. Between evil laughs and dark chucklings, the tech guru, tax fugitive, and general wild man shared his suspect views on the “state of the world” during COVID-19 last night at Virtual Blockchain Week.

“We are living in a paradigm the world has never seen before,” the 74-year-old crypto advocate and antivirus-software pioneer said, speaking from God knows where.

(He’s kept his whereabouts a secret since fleeing Belize in 2012 after suspicions grew that he killed his neighbor.)

“One-third of the planet is in lockdown,” he said, adding that most of those people are sitting at home, watching TV, and not doing much of anything, while the US government “pulls money out of thin air.” The situation is not sustainable, he argued.

He was especially disturbed by a recent $2 trillion stimulus package in the US, which appears to be backed by nothing other than the good graces of the US government.

“You can’t pull money out of the air and expect everything to be okay. Money is based on something called industry, production, service. We haven’t increased any of that,” he said, with a deep, unsettling chuckle. He predicted the money-printing will lead to a collapse of the US dollar.

It’s too late for crypto

Bitcoin and blockchain were meant to “save us from financial slavery, and from the overburdened government that creates the fiat currency that we are forced to use,” McAfee said.

But he doesn’t think crypto will save us this time.

“We are not going to jump into crypto,” he said, because it’s not easy enough to use.

“It is not like opening a bank account. You have to spend days understanding what it is and how it works.”

But as far as the markets go, he predicts that the price of Bitcoin will spike ahead of the halving event on May 12. He recalled that in 2016, the last halving event, there was a huge rise in the price of Bitcoin, and then a huge drop. And he believes history will repeat because the same people populate the cryptosphere, and they’re just as greedy as they were four years ago.

More people die of diarrhea

As far as the threat of COVID19, McAfee thinks the number of deaths are skewed because they are presented out of context. It is certainly not worth shutting down entire economies, he believes.

Repeatedly, he said more people die of diarrhea and of the flu. But both comparisons, common attempts to downplay the severity of the virus, have been widely dismissed as reckless by leading epidemiologists.

But the way McAfee, who is known for his drug use and paranoia, sees it—just before opening his talk, he jokingly commented he was getting ready to shoot up with heroin—we are being lied to by the government and stirred up by the media.

“If you use your head and common sense, you can see you are being deceived,” he said.

Due to the global shut down and the money printing, he believes dark times ahead for our species.

The solution?

“Go buy guns, and guns first,” he said.

“Because if you just have the food and you don’t have the guns, your neighbors are going to take it because your neighbors have the guns.”

And then McAfee, who appears to enjoy it when people think he is on edge, pulled out an AK-47 assault rifle and began praising its sturdiness.

“This sucker will always fire,” he said.

Tyler Durden

Sat, 05/02/2020 – 22:10 - "The US Doesn't Own The UN" – Furious Beijing Blasts UN Mission's Taiwan Tweets As "Political Manipulation"

“The US Doesn’t Own The UN” – Furious Beijing Blasts UN Mission’s Taiwan Tweets As “Political Manipulation”

President Trump is going all-in on antagonizing China as a crux of his 2020 campaign strategy (since clearly a large segment of his base, and many undecided voters, blame China for unleashing the virus on the world whether it came from a lab or not). And in keeping with the stepped-up antagonisms – since President Trump’s agreement to “cooperate” with President Xi to fight the virus is 100% meaningless – the US late Friday tweeted its support for Taiwan’s participation in the UN.

Kelly Craft

The tweet, sent by the US Mission to the UN, said the 193-member organization should allow space for “all voices” and welcome “a diversity of views and perspectives” to promote human rights. “Barring #Taiwan from setting foot on UN grounds is an affront not just to the proud Taïwanese people, but to UN principles,” it continued. It was retweeted by US Ambassador Kelly Craft, who succeeded Nikki Haley as US ambassador to the UN.

.@UN was founded to serve as a venue for all voices, a forum that welcomes a diversity of views & perspectives, & promotes human freedom. Barring #Taiwan from setting foot on UN grounds is an affront not just to the proud Taiwanese people, but to UN principles. #TweetForTaiwan

— U.S. Mission to the UN (@USUN) May 1, 2020

https://platform.twitter.com/widgets.js

The U.S. believes firmly that #Taiwan belongs at the table when the world discusses #COVID19 and other threats to global health. Before 2017, Beijing didn’t object to Taiwan joining the World Health Assembly as an Observer. What’s changed? #TweetforTaiwan

— IO Bureau @ State (@State_IO) May 1, 2020

https://platform.twitter.com/widgets.js

Is the health of Taiwan’s 23 million people less important now than it was before 2017? Or, is the #PRC punishing Taiwan voters for freely choosing their own leader? #TweetforTaiwan

— IO Bureau @ State (@State_IO) May 1, 2020

https://platform.twitter.com/widgets.js

We all know Taiwan has long been committed to global health and boasts one of the finest health and research networks in the world, and that Taiwan promotes scientific cooperation and transparency on threats to #health. #TweetforTaiwan #TaiwanModel

— IO Bureau @ State (@State_IO) May 1, 2020

https://platform.twitter.com/widgets.js

.@iingwen, the contrast with the #PRC is striking. China’s response to the outbreak of #COVID19 has been to hide the facts, muzzle its scientists, and censor discussion. #Taiwan‘s response has been and continues to be a model for the world. #TweetforTaiwan #TaiwanModel https://t.co/KADqwnLsrr

— IO Bureau @ State (@State_IO) May 1, 2020

https://platform.twitter.com/widgets.js

Sympathy for Taiwan has been running high since the country masterfully handled the coronavirus outbreak. Another boost came when eporters exposed the WHO’s bias toward Taiwan and refusal to even acknowledge the de facto independent state (legally viewed in China as an errant province).

Never one to mince words, President Xi has threatened retaliatory violence against any nation state that dares assist Taiwan on the road to sovereignty, a role that the US under President Trump has consistently flirted with. Trump’s overall hawkishness toward China – a huge component of his political appeal – is why there’s little doubt that China is actively trying to hurt Trump’s election chances (we suspect their intelligence indicates Joe Biden’s level of cognitive decline is more serious than most Americans realize).

Unsurprisingly, China’s Mission to the UN – a body where China enjoys tremendous clout as a permanent voting member of the UN Security Council – responded that the US Mission was way out of line and should probably calm the fuck down before these twitter fingers turn to trigger fingers.

The spokesperson for China’s U.N. Mission called the U.S. Mission tweet “a serious violation” of the General Assembly resolution that gave China the U.N. seat, three U.S.-China joint communiques and China’s sovereignty and territorial integrity.

“It gravely interferes with China’s internal affairs and deeply hurts the feelings of the 1.4 billion Chinese people,” said the spokesperon, who was not named. “There is only one China in the world. The government of the People’s Republic China is the sole legal government representing the whole of China, and Taiwan is an inalienable part of China.”

China’s mission accused the United States of ”hypocrisy” for citing the U.N.’s welcome of diverse views while repeatedly using its power to issue visas to block or delay U.N. member states and civil society organizations from attending activities at the United Nations.

China strongly urged the United States to abide by the one-China principle, the three joint communiques between the two countries and the General Assembly resolution “and immediately stop backing the Taiwan region, politicizing, and undermining international response to the pandemic.”

“While the coronavirus is raging across the world, people of all countries are calling for international solidarity in fighting the pandemic,” the Chinese spokesperson said. “Political manipulation by the United States on an issue concerning China’s core interests will poison the atmosphere for cooperation of member states at a time when unity and solidarity is needed the most.”

And the icing on the cake: Global Times editor Hu Xijin whining that the US “doesn’t own” the UN.

The US, for its own agenda, often puts together Five Eyes Alliance and some other Western countries, pretending to be international community. It is just a small gang, with combined population much smaller than China’s or India’s. The UN is not a holding company of the US. pic.twitter.com/keHORO6v1p

— Hu Xijin 胡锡进 (@HuXijin_GT) May 2, 2020

https://platform.twitter.com/widgets.js

Now get ready to do this all again tomorrow when the Pentagon sends a US carrier strike force through the Strait of Taiwan (we’re joking of course…but on a more serious note…it wouldn’t be so far-fetched).

Tyler Durden

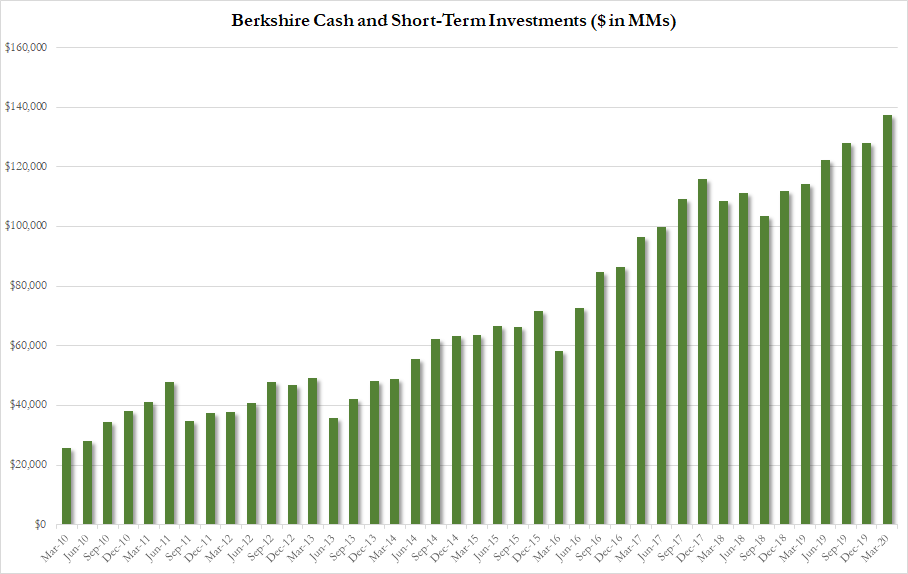

Sat, 05/02/2020 – 21:45 - Brace For A Monday Massacre: Buffett Liquidates All Airline Holdings As Berkshire Sees Another Leg Lower

Brace For A Monday Massacre: Buffett Liquidates All Airline Holdings As Berkshire Sees Another Leg Lower

Well, it’s official: there won’t be any “Buy American” op-eds by the Oracle of Omaha this time around. In fact, if anything, they will be titled simply “Sell.“

Warren Buffett, who turns 90 in 4 months, had an unpleasant surprise for the permabullish Berkshire faithful during their

annual pilgrimage to Omahalive-stream of Berkshire’s annual meeting: one month after Berkshire surprised investors by selling parts of its Delta and Southwest Airlines stakes – both of which had previously been above a 10% ownership level and speculation was rife that Berkshire could purchase an airline outright in the near future – the Oracle of Omaha said that, 4 years after Berkshire took major stakes in the four largest US airlines, he had liquidated the sold the entirety of its equity position in the U.S. airline industry which included $6.5 billion worth of stock in United, American, Southwest and Delta Airlines.Assuring that Monday will be a bloodbath for Trannies (that would be the transportation stocks you perverts), Buffett justified his decision as follows: “The world has changed for the airlines. And I don’t know how it’s changed and I hope it corrects itself in a reasonably prompt way,” he said. “I don’t know if Americans have now changed their habits or will change their habits because of the extended period.”

But “I think there are certain industries, and unfortunately, I think that the airline industry, among others, that are really hurt by a forced shutdown by events that are far beyond our control.”

“When we bought [airlines], we were getting an attractive amount for our money when investing across the airlines,” he said. “It turned out I was wrong about that business because of something that was not in any way the fault of four excellent CEOs. Believe me. No joy of being a CEO of an airline.”

““I don’t know that 3-4 years from now people will fly as many passenger miles as they did last year …. you’ve got too many planes.”

Realizing that he won’t be alive by the time a turnaround eventually happens, he clarified that he made the decision and that he lost money on his investments. “That was my mistake.”

Highlight: “The value of certain things have decreased,” Warren Buffett says. “Our airlines position was a mistake. Berkshire is worth less today because I took that position… There are other decisions like that.” #YFBuffett pic.twitter.com/W1ZqRzsfmv

— Yahoo Finance (@YahooFinance) May 3, 2020

https://platform.twitter.com/widgets.js

Asked by CNBC’s Becky Quick to clarify if Berkshire had sold all of its airline holdings, Buffett answered “yes” and explained: “When we sell something, very often it’s going to be our entire stake: We don’t trim positions. That’s just not the way we approach it any more than if we buy 100% of a business. We’re going to sell it down to 90% or 80%.”

“The airline business — and I may be wrong and I hope I’m wrong — but I think it’s changed in a very major way,” Buffett said. “The future is much less clear to me.”

As Bloomberg reminds us, Buffett has had a complicated relationship with the airline industry over the years. After a troublesome investment in USAir, Buffett joked that he would call an 800 number to declare he was an “air-o-holic” if he ever got the urge to invest in airlines again. Then in 2016, Berkshire dove into the industry again, amassing stakes in the four largest airlines. His renewed faith in the industry prompted speculation that he might one day own one of the carriers.

There is a more simplistic explanation of Buffett’s style of investing at least in recent years: he will buy the stock of companies that engage in massive buybacks, such as Apple, even though his annual letter bashes companies that buybacks stocks, and he will dump all companies that halt buybacks, of which IBM is the most famous example. And since the quasi-bailed out airlines won’t be repurchasing stock for years and years to come, it was only a matter of time before Buffett dumped them.

It also means that Buffett may soon liquidate many more sector holdings, starting with the banks which have also suspended buybacks for the near future and may be forced to extend said suspension indefinitely unless there is a V-shaped recovery in the global economy. The banks will then be followed by consumer discretionary, railroads, and many more. In fact, it would explain why unlike 2008, Buffett has not only not been buying any stocks despite major “bargains” but has actually been aggressive in liquidating his holdings, hardly an endorsement of the broader market.

Amusingly, after wasting much digital ink bashing buybacks in his annual letters, Buffett went off on a rant defending buybacks during the annual videocast: “It’s very politically correct to be against buybacks now,” he said. “There’s a lot of crazy things being said about buybacks. Buybacks are so simple. It’s a way of distributing cash to shareholders,” especially when that shareholders is Warren Buffett. The “oracle” then noted that share repurchase programs should be executed in a price and need-sensitive manner, but “when the conditions are right, it should also be obvious to repurchase shares and there shouldn’t be the slightest taint to it anymore than there is to dividends.” Yes, well, good luck with all that Warren because for the next 2 years, you can kiss buybacks goodbye from all companies except perhaps the FAAMGs.

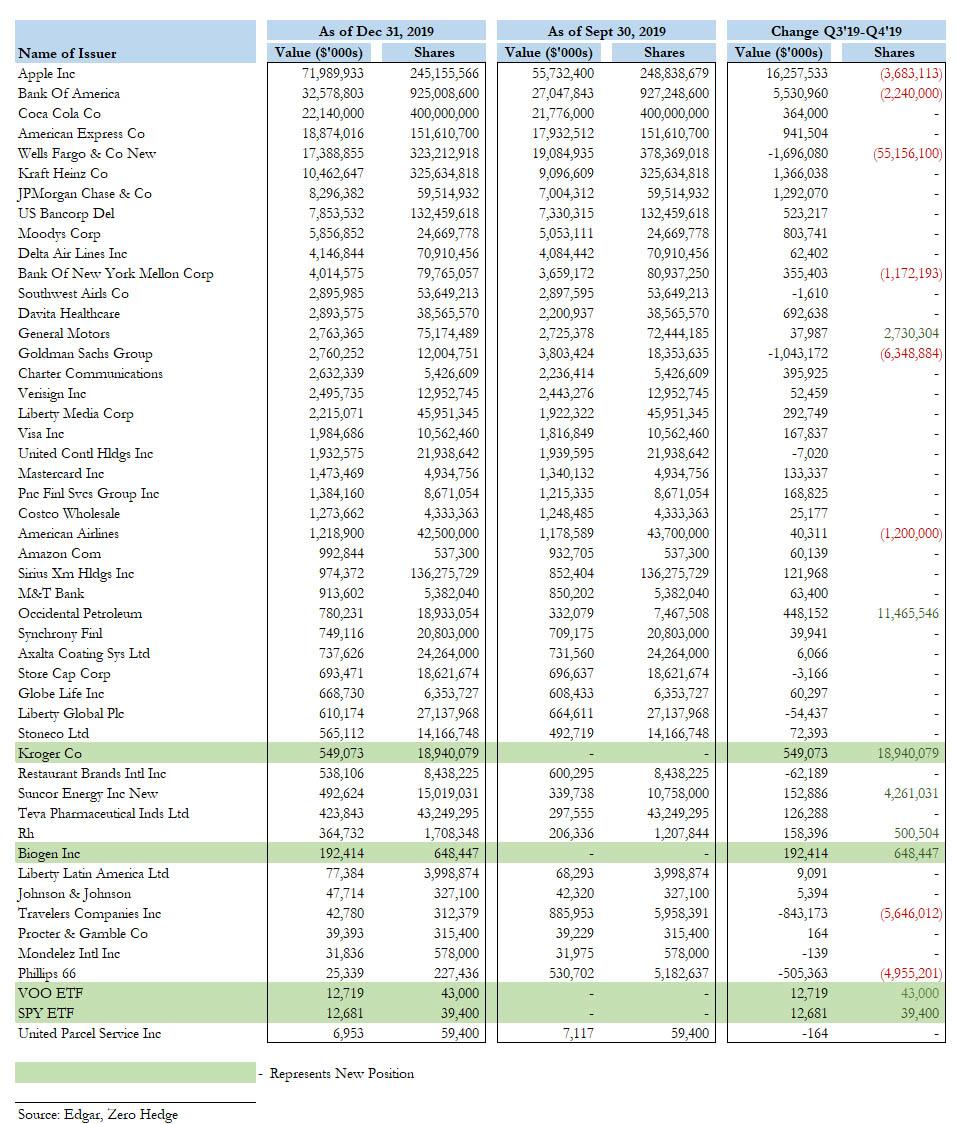

For those curious what Buffett will sell next, here is a full summary of Berkshire’s most recent equity holdings:

“If we like a business, we’re going to buy as much of it as we can and keep it as long as we can,” he added. “And when we change our mind we don’t take half measures.”

His comments Saturday afternoon came after Berkshire reported a $50 billion Q1 loss and only nibbled at equities during the violent stock market rout in March, mostly on his investment portfolio, even as the conglomerate’s cash stockpile rose to a record $137BN (more net cash than AAPL has) and up $10 billion from the $127 billion it reported at the end of 2019.

As we reported earlier, the company spent just $1.8 billion buying stocks and just $1.7 billion repurchasing Berkshire Hathaway shares during the first quarter of 2020, suggesting not only that Buffett could not find any of his hallmark bargain, value opportunities in the market sell-off, which took the S&P 500 down more than 30%, but that Buffett sees the current market rebound as nothing more than a dead cat bounce as he prepares to snap up the real bargains after the next crash.

#WarrenBuffett sold $6.5 in equities in april20, mostly Airlines and admits: “I was wrong” on the sector. He bought very little & didnt buy back any shares in #BRKH. Meaning: #Buffett (a long term bull) is NOT very bullish on stocks right now! #berkshire2020 #BerkshireHathaway pic.twitter.com/DV1DhHN2N7

— peterpauldevries (@peterpaul_vries) May 2, 2020

https://platform.twitter.com/widgets.js

Explaining why he didn’t repurchase more Berkshire Hathaway shares during the sell-off in the first quarter, Buffett said “the price has not been at a level where it really feels way better to us than other things, including the option value of money, to step up in a big way.” Which is a long way of saying it remains too expensive.

Worse, explaining why he still hasn’t made a major acquisition despite the recent 35% drop in the market, the billionaire investor said “we have not done anything because we haven’t seen anything that attractive,” adding that “we are not doing anything big obviously. We are willing to do something very big. I mean you could come to me on Monday morning with something that involved $30, or $40 billion or $50 billion. And if we really like what we are seeing, we would do it.”

The fact that he hasn’t done it yet means one thing: Buffett, or rather the banks that advise the soon-to-be-90 year old investor are convinced that a next leg lower in stocks is coming, and he should conserve his ‘dry powder’ for when it comes.

And what may be scariest for the bulls, is that in justifying his lack of buying, Buffett practically blamed the Fed, saying that “the Fed acted too quickly and too strongly for Berkshire to may any big deals right now.” Not only that, but even Buffett – whose entire fortune is the result of enjoying sequential bailouts from either governments or central banks time and again – appears to be becoming a measured Fed skeptic: “you can look at the Fed’s balance sheet and you will see some extraordinary changes there in the last 6 or 7 weeks. And we don’t know the consequences of that.” And while he adds that Powell took Draghi’s “whatever it takes squared… we are prepared at Berkshire that maybe the Fed will not have a chairman that acts like that” which explains Berkshire’s $137 billion in cash, which in other words is a hedge for when the Fed finally fails to prop up stocks.

Highlight: “We do know the consequences of doing nothing,” Warren Buffett says. “That would’ve been the tendency of the Fed many years past… We do never wanna be dependent on the not only the kindness of strangers but the kindness of friends.” #YFBuffett pic.twitter.com/gfrqLaShsU

— Yahoo Finance (@YahooFinance) May 2, 2020

https://platform.twitter.com/widgets.js

Translation: according to none other than the most admired investor in the world, the Fed’s unprecedented bailout of capital markets has not only disconnected prices from fundamentals but has led to a market so overvalued that there are still no bargains despite the recent crash (and subsequent dead cat bounce).

We were all waiting for Buffett to buy preferred stock in the airlines or Boeing as he did in some banks in ‘08. He didn’t. Does it mean he thinks this crisis is far worse than the Great Recession and not easily reversible? My bet is absolutely yes.

— Scott Wapner (@ScottWapnerCNBC) May 3, 2020

https://platform.twitter.com/widgets.js

And now we prepare for the Monday bloodbath in the trannies, and perhaps across the entire market, as investors – notorious for being unable to think for themselves and always blindly following the actions of a 90-year-old man – furiously imitate what Berkshire has already done. And, if the bulls are unlucky, the selling could be the catalyst for the next major market drop… which would of course be delightfully ironic if Buffett’s own actions catalyze the crash that he hopes to benefit from and finally put his record cash hoard to use.

Tyler Durden

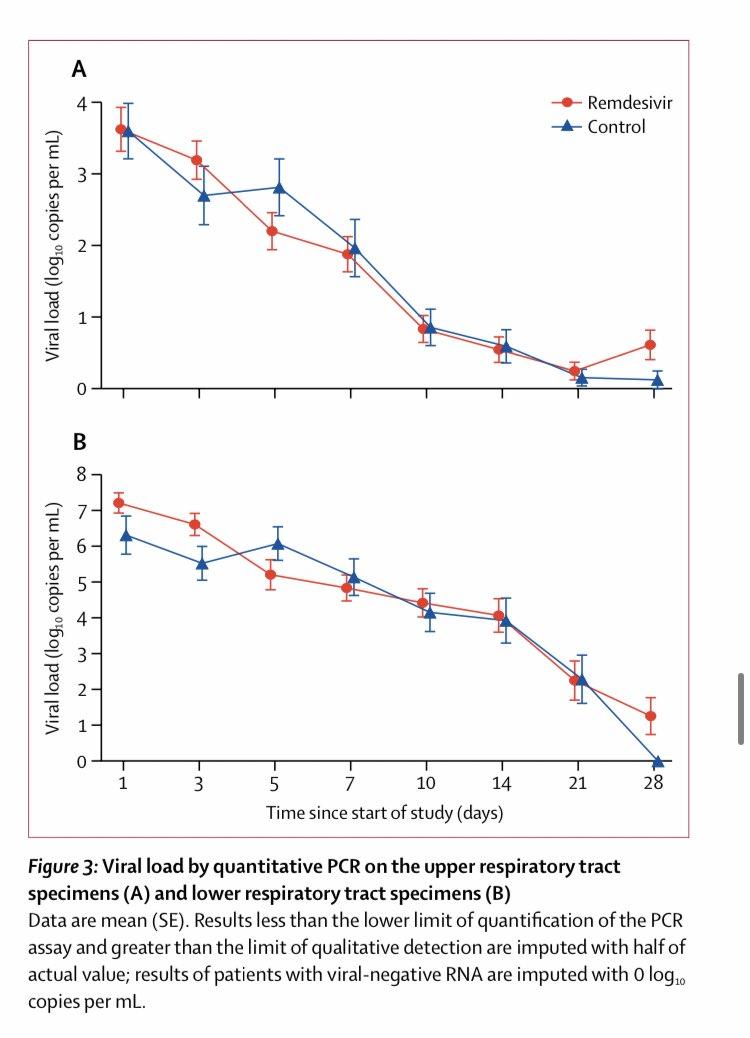

Sat, 05/02/2020 – 21:25 - "Remdesivir Is Probably Worthless" – A Trauma Surgeon Exposes "Drug Company's Shenanigans"

“Remdesivir Is Probably Worthless” – A Trauma Surgeon Exposes “Drug Company’s Shenanigans”

Markets got very excited (briefly) this week about a study finding a Gilead Sciences drug helped coronavirus patients heal a little more quickly.

But that was all the trial found: remdesivir isn’t the miracle cure that will get us all out of lockdowns tomorrow, unfortunately.

Worse, as Bloomberg’s Faye Flam writes, the trial was rushed to get quick FDA approval, without getting helpful information on what kinds of patients it helps or hurts the most; and now that the study is over, we’ve forever lost a chance to help doctors treat virus patients better.

All of which raises a significant number of questions and Acute Care Surgeon (and Asst Professor of Surgery at Wash U.) Mark Hoofnagle warns “I am truly sorry to say, Remdesivir is probably worthless…”

In an excellent Twitter thread, Hoofnagle details what he calls “some fascinating drug company shenanigans.”

First, the pre-test probability that an infused, small-molecule inhibitor of a virus would improve mortality in symptomatic patients was already pretty low. Unfortunately, antivirals work poorly in acute disease. This has to do with their mechanism of action, and host response.

Antivirals usually target some aspect of viral replication/assembly/transmission. Remdesivir is a clever pharmacologic prodrug that inhibits a key piece of RNA viruses that mammals don’t have – the RNA-dependent RNA polymerase, and inhibits viral replication.

Unfortunately, by the time you are symptomatic with a virus, you are usually already high/peak viral load. So, when you give an antiviral to someone who is already ill, the damage from the virus is largely done.

It’s there in big numbers and in the cells.

Pick your metaphor. The cat is out of the bag. The damage is done. At this point the host response to virus is activated, and your body is suppressing replication through a variety of mechanisms (which also make you feel terrible).

So how could inhibiting RDRP after the fact help? The answer is, it probably doesnt. It certainly didn’t in this trial – no difference, not even a trend in mortality, but in subgroup analysis maybe shortened disease duration in early/mild disease.

Now, critics of stupid drugs that should never have been stockpiled by govts say, “sounds like Tamiflu!”

Yes. This is the same as Tamiflu, which also maybe shortens flu by a day, but otherwise is a largely useless antiviral (and actually harmful with bad side effect profile).

Fortunately, side effects of remdesivir did not seem severe in this trial with only about 3x as many patients stopping than placebo, some rashes, nothing life threatening.

Where do the Shenanigans come in?

Well, remember how maybe this Chinese trial showed a shortened course in a subset of patients? Like tamiflu? But didn’t change mortality?

Well a month ago the NIAID trial changed their endpoints to remove death and instead look at dz duration.

No really.

They changed the destination half way through the race to match the only positive outcome of another trial, that they (or Gilead at least) certainly had a copy of the paper once it was submitted to Lancet.

Shenanigans! Get a broom!

Since NIH remdesivir trial is in the news…

was there an explanation about why the primary outcome (now positive) was changed last month to ‘time until clinical recovery?’ @matthewherper https://t.co/fCTc1EGI1d pic.twitter.com/W1hAACnO1r

— Walid Gellad, MD MPH (@walidgellad) April 29, 2020

https://platform.twitter.com/widgets.js

This is like declaring a race and then when you realize you’re not going to win, declaring the destination was actually wherever you are standing at the moment.

Then, even more fishy, *the same day* as this Lancet trial is release, Gilead and NIAID claim a “positive trial” and they’ve “shortened the course of the disease significantly”. Notably, the mortality benefit did not reach significance.

By the end of the day, reports that FDA is going to emergently approve remdesivir for treatment of COVID.

Gilead gets what they want. No one will want to be in a control arm in further trials and they will argue all future trials must be non-inferiority.

Before we have the answer whether this drug actually changes anyone’s destiny, it’s going to become the gold standard therapy. We will likely now never know if (the unlikely possibility) it changes mortality.

Absolute genius. You have to salute them. On the day a negative trial of their drug is reported, based on a press release they took over the news cycle, and with some midstream edits to their endpoints their now “positive” trial wins them FDA approval and a halted trial.

It’s an infusion, once symptomatic, you need an admission, a test, etc., really even symptoms are probably too late a goal for such a therapy to work. Prophylaxis (like Gilead’s Truvada/PreP) would be better – but unworkable in its current form.

Either way, a big win for Gilead, but I’m unimpressed with any if the evidence presented so far that this is a game changer.

* * *

How long before Hoofnagle is banned from Twitter?

Hoofnagle is not alone in his skepticism.

Naked Capitalism’s Yves Smith exclaims, it is disturbing to watch the push to con the public into seeing remdesivir as the only promising treatment for coronavirus, and points to a new study that found and tested 47 old drugs that might treat the coronavirus: Results show promising leads and a whole new way to fight COVID-19

Tyler Durden

Sat, 05/02/2020 – 20:55 - 6 Reasons Why This Is (Or Isn't) The Worst Economy Since The Great Depression

6 Reasons Why This Is (Or Isn’t) The Worst Economy Since The Great Depression

Authored by Daniel Nevins via Nevins Research,

When the NBER’s Business Cycle Dating Committee draws the boundaries on the current recession, it’s unlikely to stand out as an especially long one. In fact, by the time the committee publishes the official start date, it could be past its end date.

Why?

Because it’s front-loaded. Spending has dropped so sharply in such a large portion of the economy that many types of activity have nowhere to go but up. And once activity starts increasing, even from nothing, that’s expansion, not recession.

But the eventual business-cycle dates tell us little about our current situation. We could hit bottom in 2020 but then expand so weakly that we don’t restore vitality for several years. So let’s consider how the economy might unfold over a fixed horizon—say, three years from 2020 to 2022—rather than fixating on business-cycle dates.

First, I’ll look at the reasons why our situation is really, really bad, and then I’ll consider why it might not be that bad, after all. I’ll benchmark my calculations against the post–World War II period, but especially against the economic destruction from 2008 to 2010.

Why this is the worst economy since the Great Depression

I have six reasons.

Reason #1: This is a “double-recession.”

Consider that our last ten recessions were shaped mostly by four categories of spending: business equipment, commercial real estate, home building and consumer durables. If you isolate only the ups and downs of those four categories (but throw in changes in inventories to account for milder, inventory recessions), your partial business-cycle history would be almost indistinguishable from the actual history.

Moreover, those four categories typically amount to less than a quarter of the economy. In 2019, they composed 19.5% of GDP, as shown below:

-

Business equipment: 5.8%

-

Commercial real estate: 2.9%

-

Home building: 3.7%

-

Consumer durables: 7.1%

So a 19.5% chunk of the economy explains the first part of the double-recession, and we know it’s currently recessionary because the usual precursors are back—collapsing business profits, tightening loan standards, widespread job losses and rising delinquencies. With the usual precursors in place, we can expect a sharp contraction in all four categories noted above.

But the second part of the double-recession is separate. Consider the 2019 GDP weights for the additional spending categories below, totaling 11.3%:

-

Transportation services: 2.2%

-

Recreation services: 2.7%

-

Food services and accommodations: 4.8%

-

Gasoline and other energy goods: 1.6%

Now we’ve reached the piece that’s completely new—it has no precedent in past business cycles. Each of the four categories shown above has contracted far more than ever before. In each case, activity is only a fraction of what it was just three months ago—probably less than half, and maybe even less than a quarter. Considering the severity of the contraction, together with the GDP weights, the destruction in these items alone is enough to establish a recession, even without the usual fixed investment and consumer durables categories discussed earlier.

So that’s what I mean by a double-recession. The first part includes the fixed investment and consumer durables categories (totaling 19.5% of GDP). The second part includes the additional categories (totaling 11.3% of GDP) that imploded during the last two months, even as they’re normally only bit players in the business cycle.

Reason #2: Pandemic-related business costs could last for years.

Businesses will have to manage through some combination of the following:

-

Migration to more secure but higher cost suppliers (in response to supply chain fragilities exposed by the pandemic)

-

Measures to facilitate social distancing, including larger business premises in some cases

-

More frequent and thorough cleaning of business premises

-

Personal protection equipment for employees and, in some cases, customers

-

COVID-19 testing costs

-

Potentially greater contributions to employee health insurance (when insurance companies build COVID-19 into their cost structures, premiums can only go up)

-

Potentially greater absenteeism (employees being told to stay home with even mild illnesses, employees relying on public transportation facing greater challenges getting to work safely)

-

Potential work stoppages when employees test positive

-

Potential hazard pay

We can only guess how widespread and persistent these costs will be. But across the whole economy, they’ll surely add to a significant, positive number. They’re bad news for business profits, inflation and probably both (more on inflation in a moment).

Reason #3: The Fed only had two bullets in the interest-rate chamber (the two March rate cuts).

After cutting the fed funds rate in March from 1.6% to just above zero, the Fed can’t reduce it further without entering the Twilight Zone of negative rates. (Sure, other countries have tried negative rates, but it’s still the Twilight Zone.) By comparison, here are the fed funds rate changes during the last five recessions, from business-cycle peak to business-cycle trough: –4.8%, –9.8%, –2.0%, –3.2% and –4.1%. So this year’s change of –1.5% is only a fraction of the interest rate stimulus we normally see in recessions.

Reason #4: Bankruptcies could be more severe than in any other post-WW2 recession.

I wrote “could be” because we don’t know for sure, but record bankruptcies seem consistent with three things we do know.

-

First, business shutdowns within the 11.3% of GDP noted above (the second part of the double-recession) will surely result in record destruction in that particular portion of the economy.

-

Second, activity has already contracted more sharply than at any time since the 1933 national bank holiday, and in that instance, widespread business stoppages only lasted a week.

-

Third, nonfinancial businesses are loaded up with record amounts of debt. As of Q4 2019 and relative to GDP, nonfinancial businesses were more indebted than ever before on a gross basis (74% of GDP), and they also carried more debt than in any prior expansion after netting out interest-earning assets and cash (55% of GDP). In short, nonfinancial businesses could hardly have entered this crisis with a riskier aggregate balance sheet.

Reason #5: Meet the zombies—next generation.

Stimulus programs are helping forestall economic destruction, but they’re also propping up companies that wouldn’t be viable without cheap financing backed by the Federal Reserve and Treasury Department. Some of those companies will still go bust, despite public support. Others will become zombies, dependent on loans that can only be paid back by obtaining more loans. To those who pointed to the zombie companies of the last decade as one reason for a less-than-vibrant global expansion, you haven’t seen anything yet.

Reason #6: Inflation risks are unusually high for a recession.

As noted above, the pandemic has lifted business costs by adding procedures and complexities that didn’t exist before. Rising business costs damage profitability, at first, but should eventually have some effect on inflation. And that’s not all. Inflation is normally a policy choice (either intentional or inadvertent), and policy makers are more inclined to risk it than at any time in the last four decades. Notably, current policies include direct injections of Fed-financed spending power into the Main Street economy. Moreover, those injections appear to be augmenting rather than just supplanting spending power supplied by commercial banks. (I’ve shown several times that past QE programs merely substituted Fed financing for commercial bank financing, without having a significant effect on the total.)

Note that I’m not using the flawed logic of monetarist economists who predicted rising inflation during the Fed’s earlier QE programs, nor did I join those predictions (just the opposite, as shown here, for example). Also, the inflation outlook is hardly one-directional, since certain items, such as housing costs, are now less likely to inflate than they are to deflate or remain stable.

But the factors discussed above should threaten the benign inflation of recent decades. After remaining below 3% for the last 24 years, an increase in core inflation to just 4% would be a major event. And if we get there, fiscal and monetary policies would become more challenging, to say the least. After many years of disinflation, policy makers would again be forced to choose between snuffing out inflation and sustaining growth.

Why this isn’t the worst economy since the Great Depression

I have six reasons, once again, the first three of which compare 2020 to 2008.

Reason #1: The big-4 “home” risks—home prices, home mortgage debt, home building and home equity extraction—are relatively nonthreatening.

The mid-2000s housing bubble brought unsustainable prices alongside unsustainable growth in mortgage debt, home building and home equity extraction. Just before the pandemic, by comparison, house prices and housing activity appeared sustainable. Here’s a rundown of 2019 data versus “peak” housing boom data:

-

Home prices: Grew 3% in 2019 versus –19% in 2008 (after peaking in mid-2006)

-

Home mortgage debt: 49% of GDP in 2019 versus 72% in 2007

-

Home building: 3.7% of GDP in 2019 versus 6.6% in 2005

-

Home equity extraction: 1% of DPI in 2019 versus 8% in early 2006 (according to Bill McBride’s calculations)

We can link each of the items above to a significant drop in household spending power or housing activity in the 2008-9 recession and the years that followed, whereas the data show much lower risks today. Clearly, the big-4 home risks are unlikely to wreak as much destruction in the current recession as the destruction caused by the housing bubble.

Reason #2: Sterilization? What’s that?

In 2008, the FOMC fretted for months before dropping long-established central banking orthodoxies. But such lengthy deliberations have long since gone out of style. The committee now crams money without hesitation into every financial-sector crevice that appears to be leaking. The new policy “normal” invites both moral hazard and zombification of wide swathes of the economy, as noted above. But the immediate upside is significant—the Fed’s interventions short-circuited the financial crisis that appeared to be unfolding in March.

Reason #3: Banks have more capital than they did in 2008.

We’ve all heard the story about the better capitalized banking system, and it’s true. But higher capital ratios won’t stop banks from slowing or even shuttering their lending operations. (They’ve already done that.) So the capital cushion is larger, and that’s nice to have, but it won’t save the economy. The main benefit is that measures to bail out the banks won’t need to be as large as they would otherwise be.

Reason #4: Some areas of the economy are seeing stellar demand.

I noted above that spending has evaporated like never before in portions of the economy that total 11.3% of GDP. Now consider three other types of spending:

-

Food and beverages purchased for off-premises consumption (4.8% of GDP)

-

Other consumer nondurables (5.6% of GDP)

-

Health care (11.5% of GDP)

Solid spending in these areas, which total 22% of GDP, doesn’t negate the destruction in the transportation, recreation, restaurant, hotel and energy sectors. But it’s important to recognize that some of the spending lost through health fears and business shutdowns is being redirected, not extinguished. It’s flowing strongly into other parts of the economy. And the jobs market demonstrates that point—many recently jobless workers are finding new positions at Amazon, Instacart, CVS or one of a smattering of other companies whose outlook has brightened. So the double-recession I noted above might net out to more like a recession-and-a-half.

Reason #5: Furloughs, not layoffs.

Of the newly jobless workers who don’t find jobs elsewhere, many remain on their employers’ payrolls, retaining certain benefits but not working or receiving wages. One survey shows that 78% of employees who lost their wages due to the coronavirus expect to return to their former jobs. That might prove more hopeful than realistic, but it’s a less bearish recession story than the more typical story of companies slashing labor unconditionally.

Reason #6: Helicopter money!

Now for the elephant in the room. Fiscal policy makers are intent on providing “what it takes” to overcome the crisis. For that, they’re tapping into the Fed’s unlimited capacity to finance government spending with newly created money. They’re tapping it like never before. To highlight just two data points:

-

Roughly half of unemployment claimants will have more income than they had while working (through July, at least), thanks to an extra $600 weekly of CARES Act benefits on top of their normal state benefits.

-

Millions of working Americans will also make more than they would have without COVID-19, thanks to CARES Act stimulus payments.

It shouldn’t be surprising that the survey linked above shows people feeling better about their finances than they did a month ago, despite weekly unemployment claims averaging over five million between the two survey dates.

So helicopter money gives us yet another surreal and unprecedented development to ponder. In the short-term, it’s certain to blunt the pandemic’s economic impact. In the long-term, we’ll face consequences, but I won’t delve into that in this article. I’ll only suggest tuning out pundits who claim that “advanced” nations with their own currencies can drop helicopter money without repercussions. In fact, the advanced nations of today reached their advanced status long ago after enduring tumultuous periods of fiscal profligacy, learning from those experiences, and then maintaining relatively sound finances thereafter. And if they didn’t learn from experience? Well, that’s one of the biggest reasons that many countries fail to advance.

(My book supports that argument with an examination of every recorded instance of governments accumulating a higher debt-to-GDP ratio than America’s debt-to-GDP as of 2018. For anyone interested in the general idea without the historical detail, I published an excerpt here.)

Conclusions

The eventual COVID-19 wreckage pivots on many unknowns, and future policies are among them. But the biggest unanswered question—at least when it comes to the economy—is this:

For how much longer will the pandemic prevent vulnerable businesses from operating profitably (or operating at all)?

Optimistically, new COVID-19 cases will descend downward until they hit bottom in a few months, allowing businesses to restore profitability. That’s the scenario the President’s task force includes in its slideshows—it shows virtually no new cases by July. And the more political voices on the task force have reinforced that message, playing up the idea that we’ll be back to normal by this summer. If their prediction proves accurate, the economy should perform better in 2020–22 than it did in 2008–10, for these reasons:

-

With a COVID-19 resolution in the summer, the housing market would be in far better shape than it was in 2008.

-

The financial sector would recover relatively quickly—banks would still be cautious but not as cautious as they were during and after the Global Financial Crisis.

-

Many depressed businesses would bounce back at least partially and rehire furloughed employees.

-

Some businesses boosted by the pandemic would continue to thrive.

-

Exiting the recession, household spending power would be unusually strong, thanks to the recession’s short duration as well as generous government handouts.

So that’s the outcome we’re hoping to see, but it has an obvious weakness. That is, it presumes the coronavirus remains dormant after the economy restarts. A different theory says the virus revives whenever it finds an opening. Evidently, that’s a common feature. Epidemics tend to attack in waves. Until vaccines become available, the challenge in snuffing out this epidemic is that it only takes a handful of infected people going about their normal lives to reseed it.

In other words, a future resurgence of COVID-19 seems the most likely outcome. It’s the scenario many experts warn us to expect, and not just any experts but the ones who’ve been most accurate to date.

Where does that leave the economy?

The worst case combines a historically deep recession with a disappointing recovery that feels more like continued recession. If future COVID-19 waves prove as dangerous as the first wave, the recession could be an early 1980s–style double-dip. But other possibilities are less severe. For example, medical discoveries could make the virus less risky, restoring confidence in normal business activities. (Note that Dr. Fauci was citing “quite good news” on remdesivir trials as I write this.)

So the possibilities run from one extreme to the other. We need to be ready for anything, unfortunately, from a mid-2020 rebound to a prolonged crisis more severe than any since the Great Depression.

Tyler Durden

Sat, 05/02/2020 – 20:30 -

- 50 Dead, 60 Wounded After Venezuela Prison Uprising: Live Updates

50 Dead, 60 Wounded After Venezuela Prison Uprising: Live Updates

Summary:

-

Italy sees 76% surge in new COVID-19 deaths as single-day total hits 11-day high

-

New York sees first rebound in deaths since April 25th.

-

12.3% of New York state tested positive for COVID-19 antibodies

-

Spain allows outdoor exercise

-

Russia reports another record jump in cases

-

Video shows Mexican hospitals hiding bodies of COVID-19 patients as hallways packed with the sick

-

More EU countries back plan to waive law requiring airlines give cash refunds

-

IMF lends another $642 million to Ecuador as coronavirus ravages country

-

France extends state of emergency order until July 24

-

Singapore eases some lockdown measures as domestic cases decline

-

US case total tops 1.1 million

-

Japan joins US in fast-tracking remdesivir

* * *

Update (1725ET): In what has been a relatively quiet day for virus news, South American newspapers are reporting on a prison riot in Venezuela that has left almost 50 prisoners dead. The riot reportedly started on Friday, according to local newspaper Ultimas Noticias and Reuters.

Prison riots have occurred in Italy, China and elsewhere as prisoners, forced to live in crowded conditions, rebel over prohibitions against visitors while outbreaks are virtually left unchecked.

Opposition lawmakers reportedly blamed the riots on new rules banning visitors from bringing food for the inmates. The riot took place at Los Llanos Penitentiary Center in Guanare in the western state of Portuguesa.

To date, Venezuela has confirmed 335 coronavirus cases and 10 deaths from the virus, but the outbreak is believed to be much more widespread. And the further plunge in oil prices caused by the outbreak has only exacerbated one of the world’s worst humanitarian crises.

At least 46 prisoners are believed to have died, along with another 60 who were injured, many seriously.

In a local media interview, Prisons Minister Iris Varela said the riot resulted from an escape attempt. On twitter, local accounts claimed guns and grenades were used by the prisoners, and that the Warden of the prison had been shot and badly wounded.

The Venezuela Prisons Observatory posted photos of what appeared to be bodies lying on a blood-stained concrete patio.

It said there were 2,500 prisoners in the jail, which is designed to hold 750.

* * *

Update (1325ET): As Italy and Spain continue to tiptoe toward reopening, France has decided to take a U-turn and extend its “State of Emergency” – an order that undergirds the strict legally-enforced lockdown in France – until July 24, an unprecedented two-month extension that will almost certainly infuriate thousands of French citizens.

Though, to be sure, fear of the virus runs deep in France, just like it does in Italy and Spain where many residents – especially the vulnerable – express trepidation about reopening. But French Health Minister Olivier Véran said Saturday that the a bill to extend the deadline will be put to France’s parliament on Monday.

“We are going to have to live with the virus for a while,” Interior Minister Christophe Castaner said after a cabinet meeting.

Travellers to France, including French citizens returning home, will face a compulsory two-week quarantine and possible isolation when they arrive in the country to help slow the spread of coronavirus, the health minister said.

Véran said the duration and conditions of the quarantine would be defined in a decree to be published. Decisions to isolate people would be scrutinised by judges to ensure they are justified and fair, he added.

To be sure, France is still planning on easing some conditions on May 11, and then some more on May 17. But some measures – like ensuring restaurants and retailers don’t allow the number of customers to reach full capacity – will likely persist for a couple more months, according to France 24.

President Macron said Friday during a ‘May Day’ address that the French people shouldn’t expect life to go back to normal immediately after the first restrictions are lifted on May 11.

Norway recently announced plans to extend a ban on large gatherings through the summer until summer, and many officials, including NYC Mayor de Blasio and NY Gov. Cuomo have warned that concerts, shows and music festivals might not return for some time.

In other news, Reuters reports that Germany, Italy and Spain have joined a call by 12 EU governments to suspend rules requiring airlines to offer full cash refunds as more airlines – including Ryanair – implement mass layoffs or file for bankruptcy.

“I’m glad a very large majority of member states are supporting my request to authorise airlines and maritime groups to temporarily use vouchers when trips are cancelled, so as to relieve their cash reserves while protecting passengers’ rights to a refund,” French transport minister Jean-Baptiste Djebbari told Reuters in a statement.

Finally, the IMF said Saturday it would lend another $643 billion to Ecuador as it grapples with one of the deadliest outbreaks in the region while also struggling with the financial whiplash caused by the global drop in oil prices.

* * *

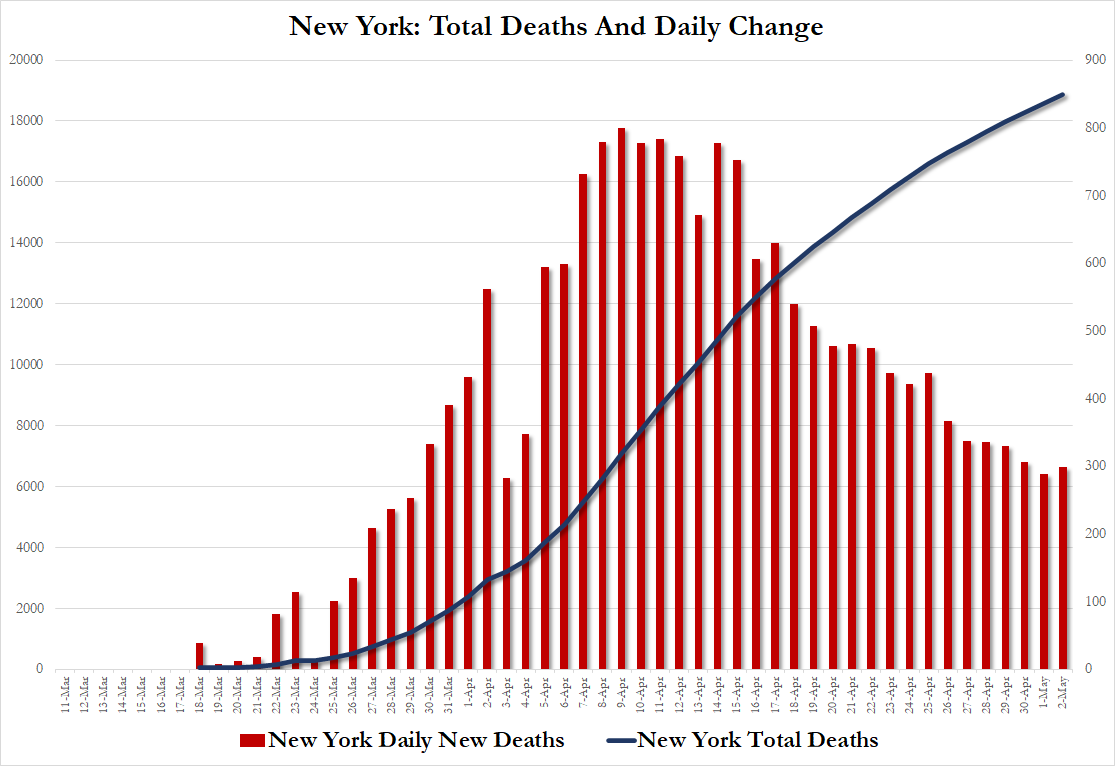

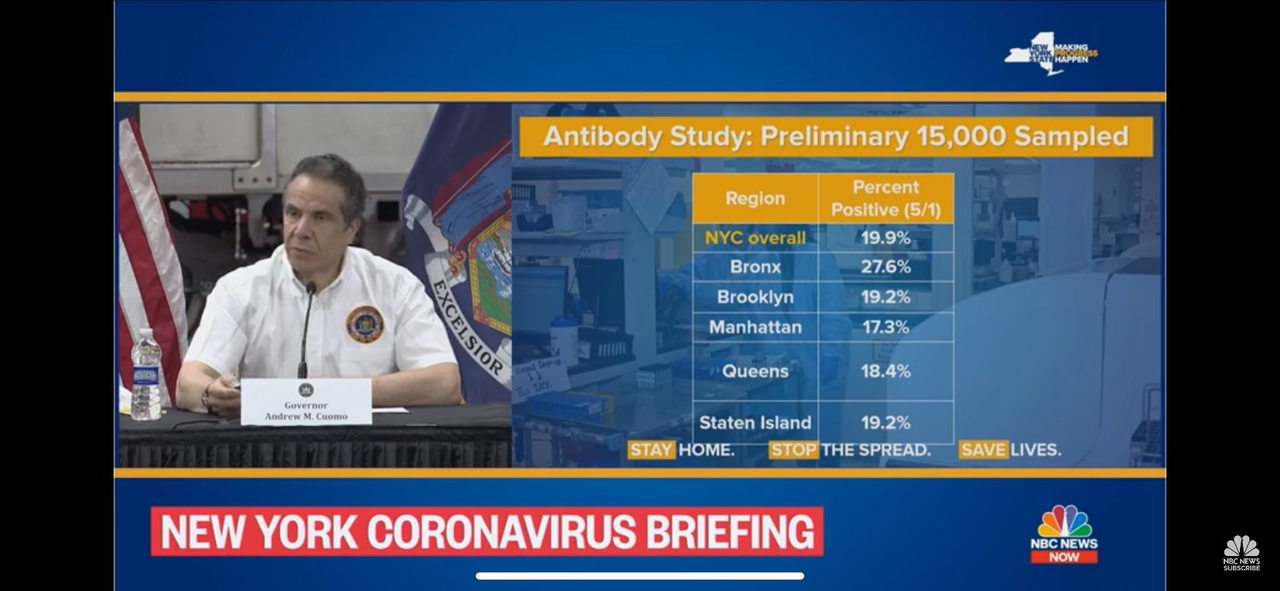

Update (1130ET): New York suffered its first rebound (to 299) in COVID-19 deaths since April 25th. Governor Cuomo says this is “bad news” though added optimistically that hospitalizations declined further.

Additionally, 12.3% of New York state has tested positive for novel coronavirus antibodies, Gov. Andrew Cuomo said at a briefing on Saturday.

As a whole, 19.9% of New York City has tested positive for antibodies, the preliminary study found. At 27.6%, the Bronx is reporting the highest rate of infection, which Cuomo said the state would further investigate.

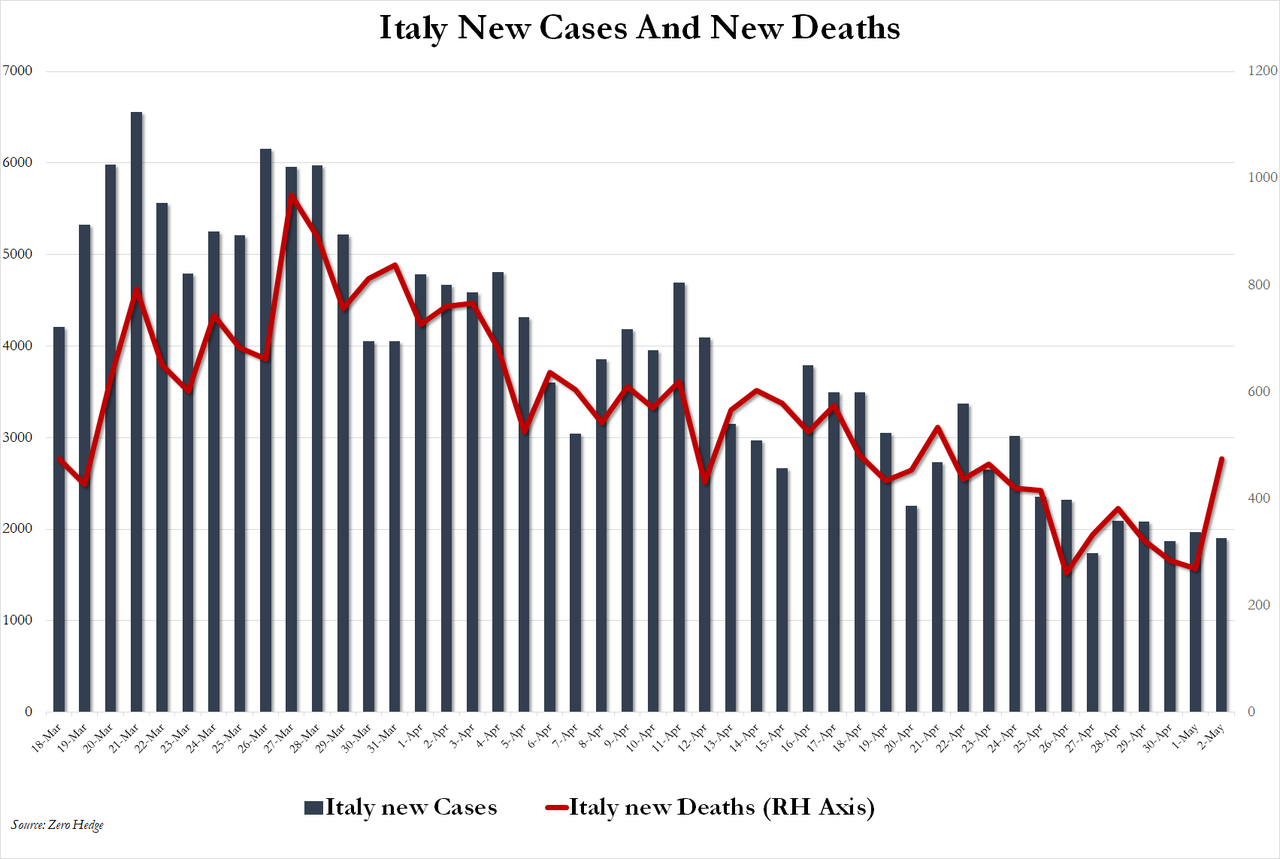

Italy also suffered a surprise resurgence in COVID-19 deaths…adding 474, the most since April 21st.

* * *

For the first time in seven weeks, adult Spaniards are enjoying a jog or a bike ride outdoors as PM Pedro Sanchez lifted restrictions on outdoor exercise.

Spain’s death toll and case count have been trending lower (interspersed with a handful of one-day spikes) for more than two weeks. A week ago, the government lifted restrictions requiring children to remain indoors, allowing young children to leave their homes (accompanied by an adult) for the first time in a month and a half.

Spain’s lockdown has been among the most strict in the world (in some ways, it approximated the lockdown faced by the tens of millions of Chinese residents of Hubei).

Of course, that remains to be seen: One of the biggest stories of the past week has been the uptick in Germany’s ‘infection rate’ – known as “R” – which approximates the average number of people infected by an infected patient. So long as the ratio stays below 1, then the outbreak is slowing. But mid-week, Germany revealed that its ‘R’ rate had jumped from 0.70 to 0.96 in the week since some more shops were allowed to reopen.

However, now that people are back out and about, Spain is imposing a new restriction: the government is requiring masks to be work on all public transport as of Monday, the prime minister said earlier this week as he outlined plans to relax the lockdown.

To ensure that nobody is unable to comply, the government will hand out millions of masks to reduce the risk of contagion, Pedro Sánchez said in an address to the nation on Saturday afternoon. He pleaded with Spaniards to exercise responsibility when the next phase towards ending the lockdown begins on Monday.

Sánchez said Saturday that 6 million masks would be handed out at transport hubs, while 7 million would be handed out by local councils, and 1.5 million would be distributed by the Red Cross and other NGOs. He added that the success of Spain’s phased emergence from lockdown would depend on “social and personal responsibility,” adding, “the key to the de-escalation isn’t just about personal decisions. The key will be tens of thousands of decisions taken at home, on public transport, at work, and in free time.”

Spain’s Health Ministry said Saturday there have been 216,582 confirmed cases of the virus in the country, and 25,100 deaths.

In Italy, concerns about the reopening are intensifying have led to deep political divisions about how the process should be conducted, as millions worry about another devastating spike in deaths.

As Spain and Italy prepare to lift all remaining restrictions, Russia is finding that its national lockdown, which was extended to mid-March last month by President Putin, might not be long, or strict, enough.

It’s becoming increasingly clear that the virus has already deeply penetrated Moscow society, and spread far and wide enough to create a serious problem in the massive country of 144 million. New daily nfections in Russia have risen by 20% as officials worry that hospitals across the country – but particularly in Moscow – might be overrun.

More than 9,000 new infections were reported on Saturday, another daily record. Once again, they were mostly in Moscow, where the mayor said earlier this week that the government might establish temporary hospitals in sporting arenas or shopping centers to help manage the flow of seriously ill patients, following several other European countries, including Spain and the UK.

Russia has 124,054 confirmed cases, including Prime Minister Mikhail Mishustin, who had been charged with leading the country’s response. Russia’s death toll stood at 1,222.

Its death toll stood at 1,222 as of Saturday morning, although many suspect that the true number of cases is likely much larger, as is the number of deaths.

Over in North America, the government of AMLO, the far-left anti-establishment leader who has been skeptical of the virus from the beginning, has just been exposed for actively trying to cover up the extent of the crisis.

In the US, the number of confirmed cases climbed to 1,104,345 as of Saturday morning, while the number of deaths hit 239,236.

And here’s a rundown of where every country stands re: ‘the virus curve’.

Relatives of patients burst into a Mexican hospital on Friday night and discovered bodies in bags on stretchers crammed into a room. Several of the families discovered the bodies of their loved ones, deaths that hadn’t officially been reported in Mexico’s numbers.

Watch the video below:

En Hospital General de Ecatepec Las Américas , familiares de paciente, entran a buscarlo, y descubren que falleció y encuentran los restos de otros fallecidos

Esto es un cuadro dantesco digno de un Apocalipsis, que tienen que decir @HLGatell y @lopezobrador_ ?

⚠️ Fuertes imágenes pic.twitter.com/ctA6X3n5R4— Aprendiz de Brujo 💎(No Soy Periodista) (@JoseAntonioLo06) May 2, 2020

Finally, Singapore said it will start easing some of its distancing measures after reporting a drop in locally transmitted coronavirus cases. The average daily number, excluding migrant workers living in dormitories, of locally transmitted cases has dropped to 12 in the past week from 25 the week before, as the country’s outbreak has been almost entirely confined to impoverished migrant workers who represent a kind of second-class caste in Singaporean society.

As more scientists question the wisdom of the US going all in on remdesivir, Japan said Saturday that it woud fasttrack a review of the antiviral drug remdesivir so that it can hopefully be approved for domestic COVID-19 patients. We suspect US investors will be watching for results of that study.

Tyler Durden

Sat, 05/02/2020 – 20:22 -

- US Embassy: Israeli West Bank Annexation Can Move Forward Without A Palestinian State

US Embassy: Israeli West Bank Annexation Can Move Forward Without A Palestinian State

The recently established US Embassy in Jerusalem (moved from Tel Aviv last year as part of Trump’s plan) has confirmed that the world will soon see the most controversial element of Trump’s peace plan put into effect: Israeli annexation over broad swathes of the West Bank, particularly the Jordan Valley.

“As we have made consistently clear, we are prepared to recognize Israeli actions to extend Israeli sovereignty and the application of Israeli law to areas of the West Bank that the [Trump peace plan] foresees as being part of the State of Israel,” a top US Embassy official told the Times of Israel on Friday.

Prime Minister Benjamin Netanyahu with US Ambassador to Israel David Friedman (center). Image source: US Embassy/Times of Israel. The statement made clear that “Israeli actions” will be validated with or without recognition of a Palestinian state, something which on paper at least Trump’s ‘deal of the century’ offered.

Though the deal offers statehood, the Palestinians have rejected the US-Israeli brokered Trump peace plan from the start, given they simply had no involvement or were not fundamentally consulted.

Ultimately such a brazen annexation, which as we noted before PM Netanyahu said will take place as early as within two months, or likely early summer, will essentially end the path to statehood.

But maybe this was the whole point to begin with: design and orchestrate a ‘peace plan’ which ultimately preempts any real path to statehood all while charging the Palestinian side with not being on board, or as has been heard many times before: the Israelis can claim “we don’t have a partner for peace”.

Should Israeli annexation indeed move forward by this summer, as Netanyahu envisions, it could potentially unleash protests and violence on the level of a third Intifiada. Palestinian Authority leaders as well as Hamas have vowed that such an extensive new Israeli land grab will be resisted by call costs.

Tyler Durden

Sat, 05/02/2020 – 20:05 - SpaceX: Camel's Nose Under The Tent Of Rapid Space Militarization

SpaceX: Camel’s Nose Under The Tent Of Rapid Space Militarization

In the last several decades, and certainly in the post-9/11 environment in which the previous restrictions on the militarization of the American society largely disappeared, the US national security establishment has expand not only by creating new programs and agencies, but also by co-opting non-state actors. Many a US think-tank is now little more than an extension of some US government agency, conducting research to validate previously arrived-at conclusions in furtherance of a specific institutional agenda. Likewise many corporations have gone beyond being mere defense or intelligence contractors. Rather, their business activities are from the outset designed to be readily weaponizable, meshing seamlessly with the armed services and intelligence agencies.

It is not entirely clear how the process works, for there does not appear to be a system of contract awards for specific deliverables. Rather, it seems these capabilities are developed on the initiative of specific businesses which speculate their efforts will be utilized by the US national security establishment ever on the lookout for technological “game-changers”. Moreover, given the unchecked growth of the US national security budget, these entrepreneurs can operate in high confidence their efforts will also be financially rewarded by the intelligence and defense establishments, even if they are not commercially viable.

Falcon 9 launch in November 2019, which carried 60 Starlink satellites, via SpaceX. There have been numerous examples of initially civilian applications being put to use for the benefit of US national security institutions. Facebook has made its databases available to various agencies to test facial recognition technologies, for example. Google and Amazon make their cloud capabilities available to the Pentagon and the intelligence communities. The opposition to China’s Huawei 5G networks and cell phones appears to be motivated by the concern these systems do not have backdoors installed for the benefit of US national security state.