- Greek Brothels To Reopen But Hookers And Clients Required To Wear Masks And Gloves

Greek Brothels To Reopen But Hookers And Clients Required To Wear Masks And Gloves

In Greece the discussion about “essential businesses” appears to have gone in a different direction than in the United States. While Americans are bickering over when to reopen malls, restaurants and casinos, Greece has managed to get its “most essential” businesses up – so to speak – and running. By which we of course mean brothels.

Brothels in Greece – where a global pandemic can’t possibly stop the local men from getting their dose of sex-for-sale – are set to re-open soon, however with a set of new laughably absurd protection measures, on top of the precautions one would already expect when visiting a brothel, according to The Newspaper.

Customers at brothels will be required to wear plastic masks and gloves while having sex, according to the Greek press. And in addition to the robust security already needed in a brothel, the additions of thermometers, disposable sheets and “frequent periodic disinfection” of the business will all be a part of post-coronavirus brothel life (it wasn’t immediately clear how s temperatures of both hookers and clients would be taken).

It does however beg the question: why weren’t disposable sheets and “frequent periodic disinfection” used to begin with?

But, we digress. This is just another example that no matter what the circumstances, sex sells and capitalism adapts. Back in March, we noted that one company had launched a “solution” to the loneliness of quarantine by offering antibacterial sex dolls.

The lesson for the US? If the Greeks are this insistent on going back to work, maybe there’s a win/win scenario: convert all those vacant WeWork offices into brothels and get all those millions of women “seeking arrangements” with wealthy sugar daddies to “work” legally: who knows, it could be the basis for a truly modern “New Deal” aimed at pulling the US out of its current depression.

Tyler Durden

Mon, 05/04/2020 – 02:45 - Three Reasons Why The Eurozone Recovery Will Be Poor

Three Reasons Why The Eurozone Recovery Will Be Poor

The Eurozone economy is expected to collapse in 2020. In countries like Spain and Italy, the decline, more than 9%, will likely be much larger then emerging market economies. However, the key is to understand how and when will the eurozone economies recover.

There are three reasons why we should be concerned:

-

The eurozone was already in a severe slowdown in 2019. Despite massive fiscal and monetary stimulus, negative rates, and the ECB balance sheet above 40% of GDP, France and Italy showed stagnation in the fourth quarter and Germany narrowly escaped recession. The eurozone weakness started already in 2017 and disappointing economic figures continued throughout the next years. Many governments blamed the weakness on the Brexit and Trade War cards, but it was significantly more structural. The eurozone abandoned all structural reforms in 2014 when the ECB started its quantitative easing program (QE) and expanded the balance sheet to record-levels. Manufacturing PMIs were already in contraction, government spending remained too high and the elevated tax wedge weighed on growth and jobs. In 2019, almost 22% of the eurozone GDP gross added value came from Travel & Leisure, a sector that will unlikely come back anytime soon, while the exporting sector is also likely to suffer a prolonged weakness.

-

The banking sector is still weak. In the eurozone, 80% of the real economy is financed via the banking channel (compared to less than 15% in the United States). Eurozone banks still have more than 600 billion euro in non-performing loans (3.3% of total assets vs 1% in the U.S.), an almost unprofitable business with a poor return on tangible assets (ROTE) due to negative rates, and a significant challenge ahead, as most of the growth investments, in LatAm in particular, may reduce capital strength significantly in the next months. Most of the eurozone governments are relying on leveraging the banks’ balance sheets in their “recovery plans”. A massive increase in loans, even with some form of state guarantee, is likely to cause significant strains on lending capacity and solvency in the next years, even with massive TLTROs and capital requirement reductions.

-

Most of the recovery plans go to government current spending, and tax increases will surely impact growth and jobs. The eurozone tax wedge on jobs and investment is already very high. According to the Paying Taxes 2019 report, the majority of eurozone economies show widely uncompetitive taxation levels. As most governments will massively increase deficits to combat the Covid-19 crisis, there is a high likelihood of a massive increase in taxes that will make it more difficult to attract investment growth and jobs. Most of the recovery plans are also aimed at bailing out the past and letting the future die. There are massive bailout packages for traditional conglomerates and industries, but investment in technology and R&D continues to have high burdens and no support. Considering that the eurozone was already in contraction in the middle of the massive Juncker plan (that mobilized more than 400 billion euro in investments) and the large green policies implemented, it is safe to say that relying on a Green New Deal will unlikely boost growth or reduce debt. The main problem of these large investment plans is that they are politically directed and, as such, have a large tendency to fail, as we saw with the Jobs and Growth Plan of 2009.

Almost 30% of the eurozone labor force is expected to be under some form of unemployment scheme, be it temporary, permanent, or self-employed cessation of activity. After a decade of recovery from the past crisis, the eurozone still had almost double the unemployment rate of its large peers, the US, or China. Germany may recover jobs fast, but France, Spain or Italy, with important rigidities and tax burdens on job creation may suffer large unemployment levels for longer.

The eurozone also faces important challenges into a recovery due to its lack of technological and intellectual property leadership. Those two factors will help China and the U.S. recover faster, as well as the reality of having more flexible jobs market and higher support for entrepreneurial activity through attractive taxation. Considering the severity of the crisis, the eurozone is likely to need at last 10% of its GDP o rebuild the economy, but that figure is almost completely absorbed by the traditional sectors (airlines, autos, agriculture, tourism). Furthermore, the New Green deal initiative includes severe restrictions to travel and energy-intensive industries that may act as a brake on future growth.

The ECB policy was already unnecessarily expansionary in the past years, and now it runs out of tools to address the unprecedented challenge of recovery post-Covid-19. With negative rates, targetted liquidity programs, asset purchases of private and public debt, and a balance sheet that exceeds 42% of GDP of the eurozone, the best it can do is to disguise some risk, not eliminate it. We should also warn of adding massive monetary imbalances when demand for euros globally is acceptable but shrinking according to the Bank of International Settlements, and risk of redenomination remains in a politically unstable eurozone.

Our estimates show that, even with large fiscal and monetary stimulus, the eurozone economy will not recover its output and jobs until 2023, and rising debt to record highs as well as monetary imbalances due to massive supply of euros in a diminishing demand environment, may cause significant problems for the stability of the eurozone.

The eurozone needs to understand that if it decides to increase taxes to address the rising debt due to the Covid-19 response, its ability to recover will be irreparably damaged.

Tyler Durden

Mon, 05/04/2020 – 02:00 -

- China Faces "Economic Reckoning" As COVID-19 Turns World Against Globalisation

China Faces “Economic Reckoning” As COVID-19 Turns World Against Globalisation

Authored by Cary Huang, op-ed via The South China Morning Post,

-

Trump, Brexit, trade war… the forces against globalisation have been gathering pace since 2008. Now the coronavirus threatens the knockout blow

-

That’s bad news for an economic giant that is one of its biggest beneficiaries

One of the more worrying consequences of the coronavirus is that it looks likely to become a catalyst for deglobalisation.

At the centre of this will be the decoupling of the Chinese economy with developed economies and the US in particular. The world’s three largest free economies – the European Union, the United States and Japan – are all drawing up separate plans to lure their companies out of China.

European Union trade commissioner Phil Hogan has called on companies to consider moving away from China; US President Donald Trump’s top economic adviser Larry Kudlow has said the government should pay the costs of American firms moving manufacturing back from China onto US soil; and Tokyo has unveiled a US$2.2 billion fund to tempt Japanese manufacturers back to Japan or even to Southeast Asia.

Coronavirus: Can China overcome global mistrust to lead the fight against Covid-19

Meanwhile, bills are piling up in the US Congress aimed at reducing America’s reliance on Chinese supply chains and pushing for a decoupling of the world’s two largest economies.

While these are recent moves, the truth is the debate on globalisation – and deglobalisation – began more than a decade ago in the wake of the global financial crisis of 2008.

After decades of globalisation in trade, capital flows and even people-to-people exchanges, the trend has reversed over the past decade as trade and financial integration stalled.

Protectionist tendencies are on the rise. Since 2008, G20 countries have added more than 1,200 restrictions on exports and imports. Britain’s decision to leave the EU, the election of Trump on a protectionist agenda, and the rising popularity of right-wing political parties in France, Italy and elsewhere are all examples of rising public discontent with the status quo.

Deglobalisation gained steam when Trump launched tariff wars against many of American’s trade partners, China in particular. Since the advent of the US-China trade war in the past two years there has been growing evidence of a sharp decrease in merchandise, capital and people-to-people flows.

Conventional wisdom suggests globalisation makes the world a better place to live as a whole, as free trade generally promotes global economic growth. Economic liberalisation creates jobs, makes companies more competitive, and lowers prices for consumers. Advances in technology and communications have made it easier than ever for people and businesses to stay connected.

Chinese farmers see livelihoods threatened by coronavirus pandemic and related economic slump

But globalisation is a complicated issue and its benefits and disadvantages are not equally shared. Globalisation is good for multinational corporations and Wall Street as it opens up opportunities to sell goods and services to much larger markets with greater profits. They also benefit from moving assembly lines to developing countries where production costs are lower.

The biggest problem for developed countries is that jobs are lost in the process. Supporters of globalisation point out that it has brought about cheaper imported goods. But this benefit does not offset the decline of jobs and therefore wages.

Another problem for developed countries is that they lose domestic fiscal revenue when countries move production elsewhere. In the US, the process has cost not only many jobs but also steadily increased the trade deficit and debt.

China has been the biggest beneficiary as its economic rise has come hand in hand with globalisation.

Since it joined the World Trade Organisation in 2001, China has leapfrogged France (in 2005), Britain (in 2006), Germany (in 2007) and Japan (in 2010) to become the world’s second-largest economy. This rise was thanks largely to open access to international markets and billions of dollars of foreign direct investment (FDI). China has for some years been the world’s top destination for FDI and this has played a critical role in making the country a global economic powerhouse, turning an agricultural backwater into the world’s manufacturing hub and largest merchandised goods exporter in just a few decades.

The flip side is that deglobalisation poses a very real risk for China, as its economic prospects have become so deeply intertwined with world markets.

US colleges face US$15 billion hit as Chinese students stay away amid coronavirus pandemic

Exports of goods and services accounted for 19.51 per cent of China’s GDP last year, according to the World Bank. While that figure is declining, it is still sizeable. Based on this, a 10-percentage-point decline in China’s exports might mean a decline of about 2 percentage points in GDP growth on average.

Exports employ 180 million workers, so any hit to the sector would also have a knock-on effect on investment, incomes, consumption and employment.

The outbreak of Covid-19 has further convinced the sceptics of globalisation by highlighting a flaw in supply chains. Developed economies have been made painfully aware that decades of deindustrialisation have resulted in greater risks in the areas of public health, national security and geopolitics.

Politicians, policymakers and business executives in developed economies have come to realise the hazard involved in overreliance on China for critical supplies, particularly for medical equipment, pharmaceuticals and medicines.

What has upset many in the West is the realisation that they were wrong to assume globalisation and democracy would go hand in hand. China’s meteoric economic rise, its pivot to more authoritarian rule and a more assertive stance on the international stage in recent years have proved such assumptions completely wrong.

Coronavirus: How badly is Covid-19 disrupting the oil industry in the US and beyond?

For China hawks in the West, the globalisation of the past few decades has seen the free West help create a communist monster, one that now poses the most severe challenge to established universal values and the global order.

That is why the Trump administration’s December 2017 National Security Strategy classified China as a strategic rival that aimed to “undermine the American economy, values and interests”. The EU has made a similar policy statement, identifying China as a “systemic rival”

The global economy as a whole will suffer from deglobalisation and the decoupling of the world’s largest economies if the flow of capital, investment and trade becomes less dynamic. But the escalating trade war and rising strategic competition between the US and China were fostering the deglobalisation trend even before the outbreak of the coronavirus pandemic. Covid-19 is only likely to accelerate the decoupling and therefore may well prove to be a historic turning point.

It seems unavoidable that the coronavirus will usher in a new era of economic development, both for China and the rest of the world.

Tyler Durden

Mon, 05/04/2020 – 00:00 -

- Majority Of Americans Don't Trust Tech Companies With Contact-Tracing

Majority Of Americans Don’t Trust Tech Companies With Contact-Tracing

With the idea of contact tracing as a plan to help re-open businesses and stop the spread of the COVID-19 virus, many Americans are skeptical about their privacy and how much data these tracing tools will collect on their lives.

In a joint survey between the Washington Post and the University of Maryland, only 43 percent of respondents said they trust the tech companies responsible for creating these contact tracing tools – specifically Apple and Google.

Health insurance companies didn’t fare much better at 47 percent, while universities and public health agencies held a majority of trust with 56 percent and 57 percent, respectively.

You will find more infographics at Statista

As Statista’s Willen Roper notes, contact-tracing has been touted as one of the only plans that would allow people in the U.S. to begin re-opening measures without causing further outbreaks. Experts suggest around 60 percent of the population would need to participate in contact tracing in order to stop the spread of the virus. But in the same survey, only 50 percent of respondents said they would use a contact tracing app, with only 17 percent of those people saying they would definitely use it.

Many are weary of privacy concerns surrounding companies having access to location data and health records, despite Google and Apple creating strict privacy guidelines around their contact tracing tools. Encrypted data and a plethora of safeguards are said to exist within these contact tracing tools, but with large data breaches occurring almost annually with top tech companies, many are still cautious.

Tyler Durden

Sun, 05/03/2020 – 23:35 - Dems' Rehabilitated Hero: Online Disgust Follows Glowing Praise For George W. Bush's COVID-19 Message

Dems’ Rehabilitated Hero: Online Disgust Follows Glowing Praise For George W. Bush’s COVID-19 Message

Authored by Andrea Germanos via CommonDreams.org,

George W. Bush’s record in office became the subject of numerous tweets after a video message released Saturday from the former president elicited praise from some Democrats.

A Message from President George W. Bush@TheCalltoUnite pic.twitter.com/FIn9wuOPTF

— George W. Bush Presidential Center (@TheBushCenter) May 2, 2020

https://platform.twitter.com/widgets.js

In the video statement, shared on Twitter by the George W. Bush Presidential Center, Bush called on people to come together to face the “shared threat” of the coronavirus pandemic.

Good morning. George W Bush belongs in The Hague.

— Benjamin Dixon (@BenjaminPDixon) May 3, 2020

https://platform.twitter.com/widgets.js

The former president said “we have faced times of testing before,” referencing the post 9/11 period when he said the nation rose “as one to grieve with the grieving” — a time period his administration rolled out its war on terror, which included a torture program.

Various progressive journalists pushed back, however, against those who appeared to be sanitizing Bush’s record and suggesting he was preferable to President Donald Trump.

Like what is wrong with you? pic.twitter.com/YjVSp4wG9y

— Sana Saeed (@SanaSaeed) May 3, 2020

https://platform.twitter.com/widgets.js

Writing in 2018, Andy Worthington, investigative journalist and author of The Guantanamo Files, criticized…

“the bizarre propensity, on the part of those in the center and on the left of U.S. political life, to seek to rehabilitate the previous Republican president, George W. Bush.”

If you had told me four years ago that George W Bush would be a hero to Democrats I would have had you committed. This is absolute insanity. The man is a war criminal who also let thousands die during Katrina. https://t.co/6WunURPQzY

— Farron Cousins (@farronbalanced) May 3, 2020

https://platform.twitter.com/widgets.js

The nice little painter man who passed mints to Michelle Obama at a funeral is actually a mass murderer who belongs in front of a war crimes tribunal, not being praised for releasing web videos.

— jeremy scahill (@jeremyscahill) May 3, 2020

https://platform.twitter.com/widgets.js

Worthington pointed to a Pew poll as Trump took office showing that 48% of American backed the use of torture in some circumstances, saying it was “a sign of the enduring power of the Bush administration’s bellicose pro-torture maneuverings in the wake of the 9/11 attacks.”

* * *

And Trump himself joined in the pile-on, but for different reasons.

.@PeteHegseth “Oh bye the way, I appreciate the message from former President Bush, but where was he during Impeachment calling for putting partisanship aside.” @foxandfriends He was nowhere to be found in speaking up against the greatest Hoax in American history!

— Donald J. Trump (@realDonaldTrump) May 3, 2020

Tyler Durden

Sun, 05/03/2020 – 23:10 - Future Economy Class Cabins In Post-Corona World Could Look like This…

Future Economy Class Cabins In Post-Corona World Could Look like This…

The future of economy class cabins on commercial jets could be reshaped because of the COVID-19 pandemic. New cabin seating arrangements have already been conceptualized by an Italian design firm this week that shows plastic shields and backward seats.

Aviointeriors has designed a “hygienic screen to cocoon passengers and keep them separate from their neighbors. Let’s take a look at Glassafe, a potential post-COVID-19 economy cabin modification,” reported Simple Flying.

Glassafe is a kit-level solution for airlines that can be installed on existing seats to make close passenger seating a reality while abiding by social distancing rules.

The company has also rolled out another concept. It is called Janus, a row of three seats where every middle seat is positioned backwards.

As shown in this view, Janus has a “wrap-around transparent barrier envelopes each passenger, providing a big plastic cocoon that protects from germs, bad breath, and fights for the armrest,” said Simple Flying.

The biggest challenge at the moment for major airlines is to make customers feel safe in a closed environment. And perhaps by restructuring the cabin with social distancing in mind, plastic shields and backwards seats could be the solution.

We noted on Friday morning that Ryanair CEO Michael O’Leary was unhappy with “idiotic” in-flight social distancing rules. He said Irish authorities forced his planes to eliminate the middle seat to comply with new regulations.

Perhaps O’Leary should give Aviointeriors a call about the Janus seating arrangement…

Tyler Durden

Sun, 05/03/2020 – 22:45 - Leftists Fume As Michael Moore Turns On Fraudulent "Green" Movement In Latest Movie

Leftists Fume As Michael Moore Turns On Fraudulent “Green” Movement In Latest Movie

Executive produced by activist and filmmaker Michael Moore, 21stCentureWire.com points out that the new documentary Planet of the Humans, dares to say what no one else will say on this Earth Day – the leading ‘green’ environmental activists, including Al Gore, have taken their followers down the wrong road – selling out the real environmental movement to some of wealthy corporate interests in America and he world.

This film is the wake-up call to the reality we are afraid to face: the mainstream environmental movement is pushing lies in the form of various techno-fixes and band-aids – all of which are reliant and use large quantities of fossil fuels and rare earth minerals. Have environmentalists fallen for a “green” illusion? More than any other documentary to date, this film exposes the wholesale fraud behind subsidized industries like biomass fuels, wind turbines, and even not-so ‘green’ electric car…

…and that is why Moore’s typical leftist cult following has turned on him so aggressively – facts don’t fit their narratives and cognitive dissonance is not a safe space.

In fact, as 21stCenturyWire.com reports, ever since Moore released the new documentary, leftwing green activists have leveled a furious attack against the filmmaker for daring to blow the whistle on the “green energy scam.” Moore, a hero of the political left, has now cast serious doubt over the efficacy of ‘renewables’, including solar and wind energy. Incredibly, many green groups and political operatives are now trying to get the film banned.

A recent report from Sky News in Australia talks about how the new film presents a number of inconvenient truths.

Watch:

As VoxDay notes, who would have expected Michael Moore would take on one of the biggest shibboleths of the Left, the so-called Green movement and its massive globo-corporate charade of “renewable energy”:

Examples include a zoo that claims to power itself on ‘renewable’ elephant dung but only produces enough to heat the elephant house.

They film a supposedly solar-powered music festival that quietly plugs into the grid and a similar arrangement at General Motors’ HQ at the launch of a hybrid, plug-in car, where the electricity grid powering the vehicle is ’95 per cent’ fed by coal.

The film also takes issue with solar panels, highlighting their limited shelf-life and that they are made from non-renewable quartz and coal.

In another sequence, joshua trees are chopped down in California so a huge solar facility can be built.

Moore’s documentary is particularly damning of ‘biomass’, the supposedly-renewable energy created by burning organic matter. The film shows huge piles of trees that have been chopped down to feed a power plant, its chimney belching out smoke that appears far from environmentally sound.

Viewers are told biomass is the biggest single source of renewable energy around the world, and – nonsensically given it is supposed to be about energy conservation – has involved wood chips being shipped to Europe from North America, Brazil and Indonesia.

‘Our anxiety over [global] warming has panicked us into embracing anything green or alternative without actually looking too closely at what is involved,’ the film states. With plans to turn animal fat into biomass fuel, the film asks: ‘Is there anything too terrible to qualify as green energy?’

The film suggests that mega-rich businessmen – including Sir Richard Branson and British timber investor Jeremy Grantham – and banks such as Goldman Sachs – are keen to invest in green energy because they want to make a quick buck rather than because they are worried for the planet. According to Moore, Toyota, Citibank and bulldozer giant Caterpillar becoming sponsors of Earth Day provided final confirmation that Big Business has taken over the green movement.

When they had picked their jaws off the floor, the first response from some of the climate scientists and environmental campaigners who have been enthusiasts for renewable energy delighted their opponents – they wanted to ban it.

Finally, while this documentary is groundbreaking in the sense that it is one of the first ever comprehensive exposures of the environmental fraud which underpins ‘sustainable energy’ and the much celebrated Green New Deal, we note 21stCenturyWire.com’s warns that towards the end of the film director Jeff Gibbs veers into extremist ‘depopulation’ rhetoric, and infers that a radical social engineering agenda must be pursued in order to achieve population control – which he believes will somehow stop a ‘human-caused extinction event’ due to man-made CO2-induced ‘climate change.’

Putting aside that radical ideological segue by Gibbs, on balance, the film remains a powerful piece of investigative journalism which goes a long way towards challenging the green orthodoxy on widely held assumptions surrounding ‘green’ energy and sustainable development – which is crucial in advancing a fact-based discussion on how the world will realistically meet its energy needs in the future, as well as shining a light on the transnational profiteers who are pushing Wall Street’s ‘Green New Deal’ speculative energy market.

Tyler Durden

Sun, 05/03/2020 – 22:20 - "We Had 2 Customers All Weekend" – Georgia's Small Businesses Gripe About "Disastrous" Reopening

“We Had 2 Customers All Weekend” – Georgia’s Small Businesses Gripe About “Disastrous” Reopening

A few days back, we shared an interesting piece of “real time” data suggesting an increase in foot traffic to retail “hot spots” across Georgia last weekend, the first that certain businesses in the state were allowed to reopen.

But since the “anonymized” cellphone location data didn’t offer any indication of spending, we speculated that consumers desperate for freedom after being cooped up inside for weeks might simply be taking advantage of the excuse to ramble and roam the retail landscape and window-shop, even if most of the stores in any given strip mall remained closed. Since consumer spending drives 70% of the American economy – an oft-quoted stat – if nobody was buying, then no economically productive activity was occurring and the “green shoots” were really just a mirage.

Over the weekend, we learned Warren Buffett has jettisoned his airline stocks and decided to sit this crisis out (laying most of the blame for his decision at the Fed’s doorstep). A report in Bisnow looking back on the first week of Georgia’s reopening found that it was mostly “a disaster” for small businesses.

Bad Axe CEO Mario Zelaya expected business to be bad, maybe 10% of the hundreds of customers he would expect to see throw axes and drink beer on a typical weekend. “That was the worst-case scenario, especially with all the marketing we did,” Zelaya said. “The reopening weekend was a disaster. We had two customers all weekend.”

Despite the public health and political debate, one thing is clear: The longer retailers and restaurants stay closed, the harder it will be for them to survive. “I think every small-business owner is in the same position as we are where they’re nervous, and they’re worried, and they’re scared of public backlash,” Zelaya said. “Our only decision right now is to survive. We’ll take measures to ensure that.”

Commercial landlords mostly confirmed that about 50% of the rent from their retail tenants has been collected since the crisis began. And in states like Georgia and Texas, landlords have been mostly understanding with small businesses and even smaller chains, allowing them enough wiggle room to wait to reopen until they have a better shop at operating profitably.

Atlanta-based real estate firm Ackerman & Co. collected about 50% of its rents from its retailers in April. Retail President Leo Wiener said he doesn’t expect May to be much different. Wiener said Ackerman continues to be understanding with tenants who choose not to open despite Kemp’s decree that they can legally do so. “At this point, it just doesn’t make business sense to push a tenant open. I’ve got to trust that the restaurateur knows their customer,” he said. “I just think it’s too early for landlords to start pushing tenants.” Bob Prosen, the CEO of small to midsized business crisis consultant The Prosen Center for Business Advancement, said many mom-and-pops don’t have enough revenue to remain shuttered much longer. “It certainly is not their landlords that are driving this. I understand it’s a problem, but that’s not the primary driver,” Prosen said. “They are going to lose their businesses.” About a third of Atlanta-based Coro Realty Advisor’s retail tenants reopened over the past weekend, Coro President Robert Fransen said. Most others expect to reopen over the next two weeks, he said. But even with the lifting of the shelter-at-home order, Coro hasn’t demanded any of its tenants turn the lights back on. “We don’t want to treat our tenants that way. Our personal opinion from the company is [the reopen decree] was too soon,” Fransen said. “So we did feel it was unfair to box tenants in on a decision we didn’t agree with.”

Because otherwise, businesses – who aren’t getting the same relief that employees get when they’re laid off (employees collect unemployment whereas small businesses are getting zero-interest loans, though at least most of the ‘PPP’ loans should convert to grants) – are just adding to the “L” tab that they’re going to need to pay back later.

Zelaya said his Atlanta Bad Axe Throwing location is a “canary in a coal mine” to see how things may return for the chain once other locations open. This weekend, it plans to reopen in Oklahoma City and soon after, it plans to restart locations in Texas. His landlords have put little pressure on him to open before he is ready, let alone permitted by state law. Zelaya said he has been given rent concessions on many of his locations. “Our [Atlanta] landlord is an extremely phenomenal person. From the very beginning when it all went down, essentially his words were, ‘I feel for you man, we’ll figure it out. Just be safe,’” he said of Gartland Long, who owns Bad Axe’s location at 1257 Marietta Blvd. NW. “He’s been arguably the easiest landlord we have to work with.” But when Zelaya can, he is trying to reopen locations in hopes of just making some money again. Not only did Bad Axe lose revenue from walk-in customers, but it had to refund money from groups that booked events ahead of time. “When someone on staff gets laid off, they get unemployment insurance and they get relief from the government. When a small business is forced to shut down, we get offered loans. We don’t get the relief,” Zelaya said. “It’s not like we’re vicious, money-hungry large corporations. We have families to feed, too.”

Even the businesses that are allowed to reopen won’t be be running at full capacity for months. In other words, investors might want to wait for a few more weeks of spending data before making any conclusions about what letter this rebound will most closely resemble.

Tyler Durden

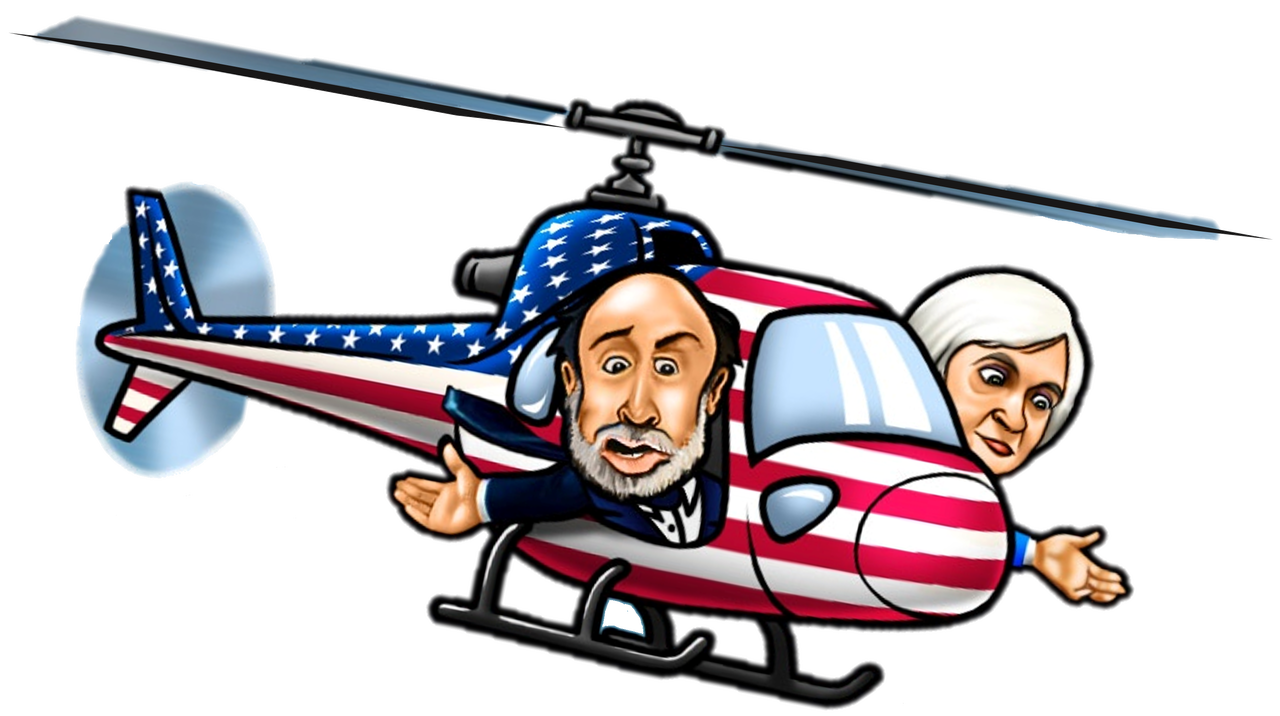

Sun, 05/03/2020 – 21:55 - QE Defender – Stop The QE Insanity: Helicopter Money And The Risk Of Hyperinflation

QE Defender – Stop The QE Insanity: Helicopter Money And The Risk Of Hyperinflation

Submitted by BullionStar.com,

In 2016 at FreedomFest in Las Vegas, BullionStar first launched the QE Defender game.

With the central banks going all in on debasement of money by all means of quantitative easing and money printing, the QE Defender Game is more relevant than ever. We have therefore updated the characters of the game which can be played for free without registration here.

“There’s an infinite amount of cash in the Federal Reserve” – Minneapolis Fed President Neel Kashkari, March 23

“When it comes to this lending, we’re not going to run out of ammunition, that doesn’t happen” – Federal Reserve Chairman Jerome Powell, March 26

QE COVID

Over the last two months, major central banks and governments across the globe have unleashed a series of monetary and fiscal interventions on markets and economies which are unprecedented in their magnitude and which are bordering on the destruction of the current financial system.

While the global spread of coronavirus COVID-19 provided the trigger and the pretext for the current full-spectrum quantitative easing, money printing, asset purchases and economic bailouts, the size and scope of the current assault on free markets makes all previous central bank and government interventions look insignificance in comparison.

Markets are now officially broken. In some cases, the US Federal Reserve and the European Central Bank have become the markets, such is the scale of their asset buying, and their actions are making the bailouts of 2008 and 1998’s Long Term Capital Management (LTCM) look like a walk in the park.

From quantitative easing to zero bound interest rate cuts and beyond, from helicopter money to economy wide bailouts, the combined monetary and fiscal interference in markets and economies over recent weeks has now distorted everything from market prices to risk preferences to the time value of money, while shattering the concept of freely trading markets and free enterprise.

All of this in an environment of locked down economies, minimal economic activity, huge job losses, shrinking tax revenue and economic stagnation, as well as the impending approach of an unprecedented global recession, that if long lasting, will become a depression.

On the monetary side, the renewed and limitless quantitative easing – with central banks creating money out of thin air to buy up financial assets across all risk categories – combined with interest rate distortions, is both prolonging the very asset bubbles that the same central banks themselves created, while also leading to explosive increases in money supply. This in turn is leading to the destruction of currency values, and most worryingly, setting the scene for the real possibility of hyperinflation.

On the fiscal side, government stimulus packages of direct payments and loan and tax write-offs across vast swathes of economic sectors is not only creating a future dependence on income support and a pretext for the introduction of direct transfers to individuals, but is burdening the very same workforces with future tax burdens and even more debt.

Helicopter Drops

In this scenario, helicopter money, analogous to a helicopter dropping cash directly to the population, comes into play. Essentially helicopter cash represents direct methods of boosting consumer demand by the distribution of currency directly to the public into their bank accounts and into their pockets. Like quantitative easing, direct cash drops pave the way for destruction of currencies and can be the touch-paper to trigger hyperinflation.

Importantly, on both the monetary and fiscal fronts, the sheer flood of official interventions across markets and economies is now creating the largest moral hazard problem the world has ever seen, with investors and economic actors being conditioned to the expectation that central banks and governments will always come to the rescue by propping up asset prices and bailing out entire sectors (think banks, airlines and real estate), thus creating an environment that encourages a lack of individual consequences for future risky behavior, but at the same time creating dire consequences for the collective financial and economic system.

While the scale of what is happening right is daunting and difficult to keep track of, a ballpark estimate suggests that the total size of interventions from just some of the world’s largest monetary and fiscal authorities is currently more than US $10 trillion and counting. For a taste for how uncharted and dangerous this QE is becoming, a quick look at the US and Europe is instructive.

Quantifying QE – USA: Whatever it takes

After cutting interest rates to zero via two emergency decisions during March (March 3 here and March 15 here), the US Federal Reserve then announced on 15 March that over the coming months it would ramp up QE by buying at least $500 billion of US Treasury securities and at least $200 billion of agency mortgage-backed securities.

That’s $700 billion of Fed debt buying from banks and the Treasury across a cross section of widening of risk categories. At the same time, the Fed begun flooding the Fed system with credit in an attempt to boost liquidity, including $1 trillion in repurchase operations per day.

When this didn’t placate markets, the Fed then went ‘all in’ on 23 March and announced the start of open-ended quantitative easing (QE) in unlimited amounts, to buy an even wider range of debt from low to much higher risk classes, promising to:

“purchase Treasury securities and agency mortgage-backed securities in the amounts needed…including purchases of corporate and municipal bonds.”

The Fed then also established swap lines with a whole range of major central banks around the world, providing these central banks with dollar funding in exchange for US Treasuries. This in essence expands the money supply of US dollars all over the world.

Then on 9 April the Fed was back, announcing another $2.3 trillion in QE, in the form of $600 billion purchases of bank loans of individuals and businesses, $500 billion buying of municipal bonds and loans (states, cities etc), and $850 billion in QE related to credit facilities of US corporates and asset-backed vehicles. Incredibly, this includes junk bonds and junk bond ETFs, with such market euphemisms as high yield, extended yield, and beyond investment grade. There is therefore, it seems, no limit to the depths the US Fed will go in its quest to prop up prices, bail out Wall St banks and hedge funds, and destroy financial markets.

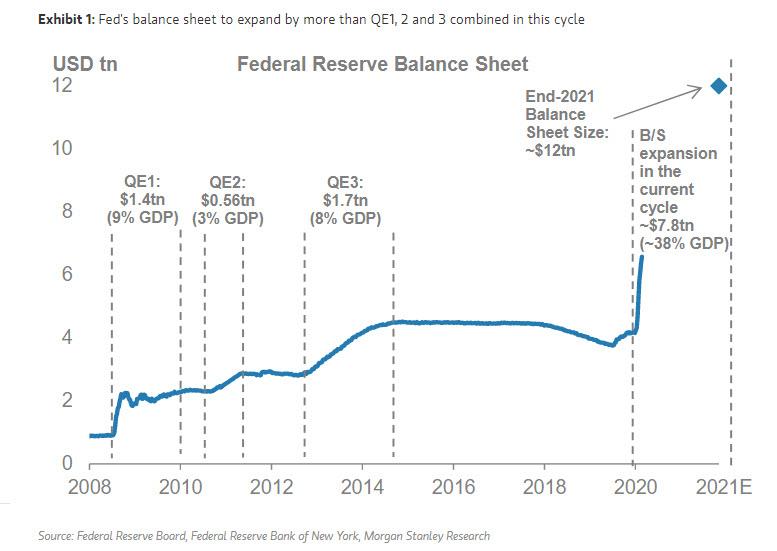

Not surprisingly, this new unprecedented and unlimited QE by the Fed over March and April can already be seen in the huge explosion in US money supply, where the monetary aggregate measure M2 (which includes cash, demand deposits, time deposits and money market mutual funds) has rocketed higher from the new money “out of thin air” that has no bearing on underlying economic growth. This can be seen in the below Federal Reserve chart. As a closely watched indicator in forecasting future inflation, this M2 chart speaks volumes.

M2 – A broad money supply measure – Date range 2016 -2020 – To infinity and beyond Q 1 2020. Source – Fed St Louis In the same vein, as architect of this rampant QE, the money out of thin air hits the Fed’s bottom line,showing up in the rapid expansion of the Fed’s balance sheet, which has ballooned from $ 4.17 trillion at the end of February to $6.4 trillion now. That’s an insane $2.2 trillion added since the start of March, or in other words, a 50% expansion in the Fed’s balance sheet since the end of February. This is neatly illustrated in the blow out of the Fed’s total assets since early March.

Balance sheet (total asset) of the US Federal Reserve – last 5 years. Source: Fed St Louis Turning to US fiscal interventions, at the end of March the US federal government pushed through a staggering $2.2 trillion economic bailout package titled the Coronavirus Aid, Relief, and Economic Security Act (CARES Act), an intervention so large that it’s equivalent to 10% of US GDP. This CARES Act (which was ready and waiting in the wings) covers everything from loans to large and small corporations ($750 billion), the bailout of the US airline industry ($26 billion), loans to states and local governments ($340 billion), and most controversially, direct payments to individuals ($300 billion).

This last category is literally ‘helicopter money’, with every taxpayer in the US set to receive a $1200 payment, plus an additional $500 per child, with the transfers being made via stimulus checks (cheques) and direct deposits to bank accounts. The US IRS calls these Economic Impact Payments, but they are really direct cash injections, literally the long predicted helicopter cash drops. This money is printed out of thin air, directly distributed to the population, and most importantly raises the money supply while diluting the purchasing power of all existing currency.

An image from the original version of BullionStar’s “QE Defender’ video game launched in 2016 and featuring the Fed chairs Ben Bernanke and Janet Yellen

Quantifying QE: Europe – ECB

After cutting one of its key refinancing rates to -0.75% in early March, the European Central Bank (ECB) then announced new monetary QE interventions on 12 March in the form of €120 billion of bond buying (quantitative easing) to complement its existing bond buying programme. On the same day, the ECB also announced an intent to flood cheap liquidity to European banks using longer-term refinancing operations (LTROs).

A week later on 18 March, the ECB ramped up the QE and went practically unlimited, announcing an enormous €750 billion Pandemic Emergency Purchase Programme (PEPP), a fancy name for even more QE that aims to buy government and corporate bonds (debt), including non-financial commercial paper (short-term loans). In total, that’s €870 billion in monetary QE interventions from the ECB.

Extraordinary times require extraordinary action. There are no limits to our commitment to the euro. We are determined to use the full potential of our tools, within our mandate. https://t.co/RhxuVYPeVR

— Christine Lagarde (@Lagarde) March 18, 2020

On the fiscal side, Europe is leading the way with the largest fiscal bailout by any economic bloc so far, totaling a massive €3.2 trillion in fiscal bailouts across the continent. This includes emergency packages of individual European countries such as Germany, Spain and France, but also an EU wide bailout fund of €540 billion to which the European Union has agreed, consisting of €240 billion in credit for Eurozone countries via the European Stability Mechanism (ESM), €200 billion in loans for small businesses via the European Investment bank, and €100 billion in loans for job support.

The sheer scale and unprecedented nature of these European union interventions motivated one of its countless bodies, the European Economic and Social Committee, to proudly comment on 16 April that:

“In less than 4 weeks, the EU has done more than in the four years following the 2008 crisis, with interventions already decided that are estimated at over EUR 3 trillions.”

As to how the EU will pay for all of these bailouts, the EU Commission claims to have the answer, saying that it will, surprise, surprise, “propose borrowing to finance the recovery plan“.

With the US government introducing helicopter money, can Europe be far behind? While the European Central Bank claims that helicopter money is not an option that’s being considered, would you believe them? In a recent letter responding to a member of the European Parliament (dated 21 April), the ECB’s Christine Lagarde avoids the question of whether helicopter money is a fiscal or monetary in nature, only saying that it has never been discussed by the ECB’s Governing Council. But in the infamous words of another fellow Europhile Jean-Claude Juncker, “When it becomes serious you have to lie.“

Helipad – Letter dated 21 April 2020 from Christine Lagarde, president of the European Central Bank, about helicopter money Beyond the Fed and the ECB, all other major monetary authorities and governments around the globe are also engaging in massive QE and economic bailouts, from the Bank of Japan and Bank of England to the Chinese and the International Monetary Fund (IMF), from Australia to Brazil and from South Korea to Singapore. For example, the Bank of England has its own £645 billion QE programme buying UK government bonds and sterling corporate bonds, and has now moved to directly finance the spending the UK Treasury, a form of helicopter money.

Meanwhile, the Bank of Japan has just announced that it will now consider unlimited bond buying of government and corporate bonds – “Bank of Japan mulling unlimited bond buying at next meeting: Nikkei“. Everywhere one looks, the evidence is there, it’s QE to infinity, buying up all debt of all types and all risk categories at any price, in the process destroying the financial system and setting the scene for hyperinflation.

100 trillion Zimbabwean dollars Hyperinflation

In an interview in 2010, then Fed chairman Ben Bernanke tried to dissuade concerns over Fed money printing, QE and market interventions, saying that:

“This fear of inflation I think is way overstated …What we’re doing is lowering interest rates by buying Treasury securities. And by lowering interest rates, we hope to stimulate the economy to grow faster.

The trick is to find the appropriate moment when to begin to unwind this policy. And that’s what we’re going to do.”

Fake words then from Bernanke, fake words now. There was no real unwind. Tapering was trick and a distraction. This is the same Bernanke who explained how the Fed’s lending is merely electronic printing, creating money out of thin air, and in so doing, inflating the money supply.

Fed’s Ben Bernanke in 2009: “To lend to a bank we simply use the computer to mark up the size of the account” https://t.co/pFLm5FxqM6 #QE

— BullionStar (@BullionStar) April 23, 2020

Quantitative easing, despite the complicated name, is a simple case of massively expanding the money supply. Helicopter money ditto, is also a simple case of massively expanding the money supply.

By artificially boosting demand in a scenario of lower production and constrained supply using the printing press and its electronic equivalent (QE and helicopter money), more fiat currency is entering the existing system. This can lead to product shortages, hoarding, and higher consumer prices, i.e. rising inflation, which is the economic textbook situation of too much money chasing too few goods.

Rising inflation in turn leads to lower purchasing poor and eroding value for a paper currency, loss of confidence in that currency, and in a downward spiral, faster spending to get rid of the increasingly worthless currency, which in turn leads to even higher prices, hoarding and inflation. And all this in an environment of economic stagnation and recession. This then leads to higher inflation expectations, and ultimately hyperinflation.

And what are we seeing right now in the global economy, led by the large central banks and the largest economies? Explosions in money supply brought on by quantitative easing. Increasing experiments of directly transferred helicopter money to artificially boost consumer demand. Supply side shortages and hoarding. Economic turmoil and economies in stagnation due to covid-19 lock downs with massive unemployment and economies slipping into recession and possible depression.

Hyperinflation is essentially a rapid and accelerating inflation amid a collapsing currency value, and it can arrive rapidly in an environment where frequent price rises have already begun to take hold. In such scenarios, national cash becomes worthless and precious metals and reserve currencies become stores of values. For some of the more prominent hyperinflationary events in recent times just look at the hyper inflationary experiences of Argentina, Zimbabwe and Venezuela. See “The Power of Gold in Times of Crisis” for details.

For example, in 1989, prices in Argentina rose by an annualized 500 percent. In 2008, Zimbabwe’s annual inflation rate at one point reached 231 million percent. Annual inflation in Venezuela, which is still in the midst of hyperinflation, is currently over 2300%.

But what if hyperinflation hits major economics such as the US and Europe and their ‘strong’ fiat currencies in the form of the US dollar and Euro? In the current environment of full-scale quantitative easing and the emerging popularity of helicopter money, this is something which populations may soon be about to find out.

Under this possible scenario, physical gold will become one of the few trusted assets to remain a secure store of value and wealth preservation when paper currencies crash and burn. Universally trusted as a safe harbor in times of crisis and emergency, physical gold is both the proven last man standing and the go to asset in a world at risk of hyperinflation.

This article was originally published on the BullionStar.com website under the same title “QE Defender – Stop the QE Insanity | Helicopter Money and the Risk of Hyperinflation”

Tyler Durden

Sun, 05/03/2020 – 21:30 - Watch: Video Of NYPD Officer Brutalizing Bystander During 'Social Distancing' Arrest Sparks Outrage

Watch: Video Of NYPD Officer Brutalizing Bystander During ‘Social Distancing’ Arrest Sparks Outrage

We’ve been covering the NYPD’s ‘War on Barbecuing’ since news first broke that the NYPD – presumably at the behest of Mayor de Blasio – was ordering 1,000 more cops to patrol the city’s parks and public space to crack down on any ‘social distancing’ violations with tickets, summonses and arrests.

The same mayor who once dismissed the threat posed by the virus is flexing his muscles after the ultra-orthodox Jewish community in Williamsburg openly defied him last week by gathering for the funeral of a Rabbi, prompting Hizzoner to threaten a crackdown (eliciting an immediate backlash and accusations of anti-semitism).

On Sunday, ABC 6 shared a video of a New York City cop arresting a man and violently taking him down over an alleged social distancing violation.

The video, filmed by a bystander, showed the plainclothes officer, who was not wearing a protective face mask, slapping 33-year-old Donni Wright in the face, punching him in the shoulder and dragging him to a sidewalk after leveling him in a crosswalk in Manhattan’s East Village.

Wright was allegedly filming the officer making an arrest for a social-distancing violation before he turned on the bystander instead and threatened to taze him then attacked him, while another bystander filmed the incident.

De Blasio called the video “unacceptable” and said the officer involved has been placed on “modified duty” while internal affairs investigates

Saw the video from the Lower East Side and was really disturbed by it. The officer involved has been placed on modified duty and an investigation has begun. The behavior I saw in that video is simply not acceptable.

— Mayor Bill de Blasio (@NYCMayor) May 3, 2020

NYC is of course the hardest hit area in the entire US, with as many as 20% of the city’s population suspected of having been infected with the virus. We suspect the mayor will announce tomorrow that he plans to “ease up” on ticketing and arrests for these types of violations.

Tyler Durden

Sun, 05/03/2020 – 21:05 - Epstein Had Extensive Ties With Harvard University

Epstein Had Extensive Ties With Harvard University

Authored by Zachary Stieber via The Epoch Times,

Sex offender Jeffrey Epstein had extensive ties with Harvard University, which admitted him as a Visiting Fellow and later gave him his own office, according to a review conducted by Harvard attorneys and an outside law firm.

Epstein was awarded the title of Visiting Fellow, which goes to independent researchers, in 2005 despite the fact he “lacked the academic qualifications Visiting Fellows typically possess and his application proposed a course of study Epstein was unqualified to pursue,” according to the review (pdf).

Dr. Stephen Kosslyn, the chair of the Psychology Department at the time, recommended Epstein’s admission. Epstein donated $200,000 to support Kosslyn’s work between 1998 and 2002.

Epstein told the university in his application that he wanted to “study the reasons behind group behavior, such as ‘social prosthetic systems,’ and their relationship to a changing environment,” using a term invented by Kosslyn.

“That is, other people can act as ‘prosthetics’ insofar as they augment our cognitive abilities and help us to regulate our emotions—and thereby essentially serve as extensions of ourselves. I wish to understand how the brain both allows such relationships to develop and how those relationships in turn take advantage of key properties of the brain,” Epstein wrote.

Jeffrey Epstein appears in court in West Palm Beach, Fla., on July 30, 2008. (Uma Sanghvi/Palm Beach Post via AP)

Epstein paid tuition and fees to become a Visiting Fellow but “did very little to pursue his course of study,” according to the review. He was readmitted for a second year after saying in an application he wished to “find a derivation of ‘power’ (Why does everybody want it?) in an ecological social system” but withdrew following his arrest in 2006.

Epstein was accused of molesting dozens of underage girls that year. He ended up pleading guilty to one count of soliciting minors for prostitution in 2008.

Kosslyn admitted to the attorneys conducting the review that Epstein wasn’t qualified to conduct the research outlined in the application. Epstein’s educational background, lacking a college degree, was highly unusual for a Visiting Fellow.

Kosslyn in his recommendation for Epstein called the financier “extraordinarily intelligent, broadly read, and very curious.”

“Jeffrey has been a spectacular success in business, and it is clear why: He’s not just intelligent and well-informed, he’s creative, deep, extraordinarily analytic, and capable of working extremely hard,” he added.

Harvard University in Cambridge, Massachusetts, on April 22, 2020. (Maddie Meyer/Getty Images)

Had His Own Office

Epstein’s involvement with Harvard didn’t stop with his criminal conviction.

The sex offender was given an office with his own telephone line in Harvard’s Program for Evolutionary Dynamics (PED), which he helped establish in 2003 with a $6.5 million donation. He also received a keycard and passcode access to the program’s offices.

Epstein is believed to have visited Harvard offices dozens of times between 2010 and 2018 after being released from jail.

“Epstein was routinely accompanied on these visits by young women, described as being in their 20s, who acted as his assistants,” the review states. According to prosecutors, many women who spent time with Epstein were underage.

Epstein would give Martin Andreas Nowak, a professor of biology and mathematics, the name of professors he wanted to meet with. Either Epstein or Nowak would invite the academics to meet with Epstein at the PED offices.

The meetings usually took place on weekends.

“Taken as a whole, the documents suggest that Epstein viewed the PED offices as available for his use whenever he wished to gather academics together to hear scholars talk about subjects Epstein found interesting,” lawyers wrote in the review.

Nowak, who lawyers said took no steps to conceal Epstein’s activities, was placed on paid administrative leave on May 1 after the review was published. Officials are probing whether Nowak violated university rules.

The visits came to an end only after a number of PED researchers objected to the situation.

Not only Epstein, but his “assistants” received cards and keypad codes that let them access PED buildings whenever they wanted. When Harvard tightened security in 2017 by installing a different card reader system, several cards designated for temporary visitors were mailed to an assistant of Epstein.

Nowak’s chief administrative officer (CAO) informed the professor of the arrangement, calling it “easier” because Epstein “would have go go get photo [sic] taken” if he instead was given different, more specific type of card.

“Epstein’s permanent possession of a visitor keycard; his knowledge of the passcode to the PED offices; and his possession of a key to an individual Harvard office all gave him unlimited access to PED. It appears that this circumvented rules designed to limit access to Harvard space to individuals with legitimate reasons to be there,” the review stated.

“In effect, Professor Nowak and his CAO permitted Epstein to use PED’s offices as his own whenever he came to campus. Moreover, they did so without due regard for Harvard’s security rules.”

A protest group called “Hot Mess” hold up signs of Jeffrey Epstein in front of the federal courthouse in New York City on July 8, 2019. (Stephanie Keith/Getty Images)

Gifts, Links

Harvard accepted four gifts after Epstein’s arrest but no further donations were accepted after his conviction, under a decision by President Drew Faust. Several faculty members, including Nowak, tried to convince Faust to revise the order.

Epstein bypassed the order by getting others to donate to the university. Those donations included $7.5 million to support the work of Nowak. Leon Black, who donated millions with his wife or through their foundation, told lawyers he was introduced to the professor through Epstein.

Nowak also allowed links to the websites of Epstein’s foundations on PED’s website at the request of Epstein’s publicist. A full page featuring Epstein was also published on PED’s website. It was removed in 2014 after complaints from a sexual assault survivor’s group.

Epstein also regularly received communications from Harvard’s development offices, including an invitation to attend the start of the university’s Capital Campaign in 2013.

The review of Epstein’s ties with Harvard was conducted by Diane Lopez, the university’s general counsel, Ara Gershengorn, a Harvard attorney, and Martin Murphy of Foley Hoag LLP.

They recommended to Harvard President Lawrence Bacow that Harvard develop clearer procedures for reviewing potentially controversial donations, revise its procedures for appointing Visiting Fellows, and consider whether any further actions should be taken based on Epstein’s unfettered access to PED.

Bacow said in a letter to the Harvard community that he’s instructed members of his team to begin implementing the recommendations “as soon as possible.”

“The report issued today describes principled decision-making but also reveals institutional and individual shortcomings that must be addressed—not only for the sake of the University but also in recognition of the courageous individuals who sought to bring Epstein to justice,” he concluded.

Tyler Durden

Sun, 05/03/2020 – 20:40 - China Hid Severity Of Coronavirus To Hoard Supplies, New Intelligence Shows: Live Updates

China Hid Severity Of Coronavirus To Hoard Supplies, New Intelligence Shows: Live Updates

Summary:

- Russia reports 4th straight record new cases

- Spain sees lowest deaths since March 18

- Zimbabwe asks IMF for $2 billion rescue loan

- Moscow Mayor warns 2% of city likely already infected

- NYPD issue ‘dozens’ of summonses, make several arrests for ‘social distancing’ violations

- New York case total: 316,415

- Roche receives emergency auth from FDA for COVID-19 tests

- MIT study says only 1/3 Chinese KN95 masks work as well as US N95s

- New Intel leak says US believes China lied about the virus to buy time to grab up PPE

- New Jersey reports another~200 deaths

- Northeastern states join together to buy PPE

- LA County coronavirus cases pass 25k

- Pompeo doubles-down in a tweet

- Niger reports polio outbreak as vaccinations halted

- UK, NY see lowest deaths in weeks

- France’s controversial ‘StopCovid’ app nearly ready

- Boris Johnson names son after doctors who saved his life

- Global COVID-19 confirmed cases passes 3.5 million

* * *

Update (2000ET): Though the number has no actual bearing on reality, President Trump said Sunday evening that he expects between 75,000 and 100k deaths from COVID-19 in the US, goal posts that have been steadily moved higher, eliciting howls of anger from liberals, even as the rate of doubling slows and states begin reopening.

Trump says we’re going to lose anywhere from 75,000-80,000 to 100,000 people, then, a bit later, says it’s 80,000 or 90,000. He’s steadily moved the number up from the 50,000-60,000 total he cited on April 20.

— James Mitchell Ⓥ (@MesMitch) May 4, 2020

* * *

Update (1750ET): Across the five boroughs, police are busy writing tickets, issuing summonses and – in at least a few cases, we’re told – making arrests.

While the Americans who are able enjoy a beautiful Sunday in the sun, here are a handful of the most important coronavirus-related headlines from the last few hours;

The number of coronavirus cases in LA County surged past 25,000 Sunday as public health officials confirmed another 791 cases, along with another 21 deaths, the Baldwin Park, CA Patch reports.

There are now 25,662 cases of COVID-19 and 1,229 deaths related to the disease caused by the virus, according to the Los Angeles County Department of Public Health.

“The people lost to COVID-19 are mourned by all of us in L.A. County, and to their loved ones, we wish you peace and healing,” Barbara Ferrer, the county’s public health director, said Sunday.

As has been the case throughout the pandemic, 92% of the people who died from the virus had underlying health conditions, and the virus continued to have a slightly disproportionate impact on communities of color.

For the 1,121 deaths for which data was available, 38% were Latinx, 29% white, 19% Asian, 13% black and 1% Native Hawaiian or Pacific Islander, according to the Los Angeles County Department of Public Health.

The confirmed cases include 745 in Long Beach and 417 in Pasadena, which have their own health departments.

Los Angeles County continues to represent about half of the cases and deaths across the state. Officials in Sacramento reported Saturday that the state had 53,616 cases and 2,215 deaths.

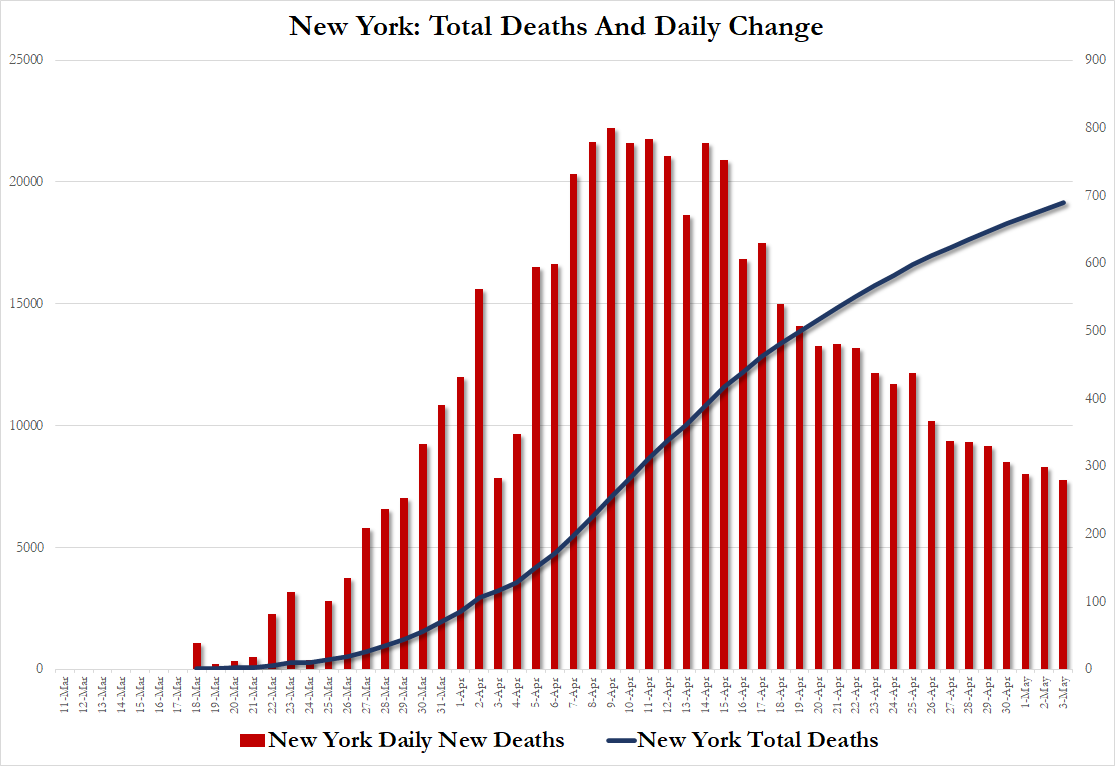

New York on Sunday reported another 3,438 new cases of coronavirus, slightly higher than the recent average, as well as the 280 new deaths we mentioned earlier (the lowest single-day total in weeks). That brought New York’s total to 316,415 cases and 19,189 deaths.

And as more states prepare to reopen during the coming week, Mississippi Gov. Tate Reeves on Sunday defended the steps his state has taken to reopen its economy despite not meeting the White House guidelines recommendation of 2 weeks of declining cases. Mississippi reported its largest single-day total of new cases on Friday, with 397. Gov Tate argued this was an “anomaly” and that his state simply hasn’t seen enough cases to warrant continuing with the lockdown.

“You have to understand that Mississippi is different than New York and New Jersey,” Reeves said on “Fox News Sunday.” “What we have seen is for the last 35-40 days, we’ve been between 200 and 300 cases without a spike. Our hospital system is not stressed, we have less than 100 people in our state on ventilators.”

Watch a clip from the show below:

The governors of NJ, Conn., NY and several other northeastern states (remember that whole alliance thing?) announced on Sunday that they were forming a consortium to buy PPE together.

Combining the efforts several states into a regional purchasing initiative will help our states obtain needed PPE, tests, and other medical equipment without competing against each other.

Thanks to our neighbors in NY, NJ, RI, MA, PA, and DE for joining us in this initiative. https://t.co/yRKBrcMlWr

— Governor Ned Lamont (@GovNedLamont) May 3, 2020

New Jersey Gov Phil Murphy congratulated New Jerseyans for “behaving” this weekend after he opened the parks for what was expected to be a beautiful day. However, Murphy said if he gets reports of “bad behavior” or if cases spike over the next 2 weeks, he “won’t hesitate” to close the parks again.

Across the state, hospitalizations continued to decrease while the rate of doubling of new cases continued to slow.

UPDATE: We’ve received 2,912 additional positive #COVID19 test results, bringing our statewide total to 123,717. pic.twitter.com/xy2Fn9qos0

— Governor Phil Murphy (@GovMurphy) May 2, 2020

Unfortunately, even with the positive trends we’re seeing, we continue to lose too many residents to #COVID19.

With heavy hearts, we must report an additional 205 deaths from among our New Jersey family.

We’ve now lost 7,742 blessed souls to this virus. pic.twitter.com/j57wNMcIwn

— Governor Phil Murphy (@GovMurphy) May 2, 2020

On Sunday, health officials in Beijing reported just 2 new cases for the entire country over the last 24 hours – one of which was imported. That was great news for China, but you know what wasn’t so great? The results of an MIT study, published Sunday, finding only one-third of Chinese KN95 masks work as effectively as N95 masks.

All this comes following another US intel leak to the AP claiming something many already widely suspected: Chinese leaders lied about the outbreak during the early days to buy time to grab up all the PPE and other critical supplies to ensure the safety of the Chinese people, while leaving the rest of the world to fend for itself.

This hoarding behavior was behind the global shortages of PPE that left hundreds of thousands of medical professionals working with garbage bags instead of gowns and ineffective clothe masks. Thousands contracted the virus and hundreds of health-care workers died unnecessarily all around the world because China chose to hoard supplies.

Which also means Beijing could have said a lot more than they did about how widespread the virus might already be, which is why we’re only just now finding out that there was community spread in the US as early as January.

China didn’t just stock up on PPE being produced in the country; officials ordered PPE being manufactured all across Asia and cleaned them out.

U.S. officials believe China covered up the extent of the coronavirus outbreak — and how contagious the disease is — to stock up on medical supplies needed to respond to it, intelligence documents show.

Chinese leaders “intentionally concealed the severity” of the pandemic from the world in early January, according to a four-page Department of Homeland Security intelligence report dated May 1 and obtained by The Associated Press. The revelation comes as the Trump administration has intensified its criticism of China, with Secretary of State Mike Pompeo saying Sunday that that country was responsible for the spread of disease and must be held accountable.

The sharper rhetoric coincides with administration critics saying the government’s response to the virus was slow and inadequate. President Donald Trump’s political opponents have accused him of lashing out at China, a geopolitical foe but critical U.S. trade partner, in an attempt to deflect criticism at home.

Not classified but marked “for official use only,” the DHS analysis states that, while downplaying the severity of the coronavirus, China increased imports and decreased exports of medical supplies. It attempted to cover up doing so by “denying there were export restrictions and obfuscating and delaying provision of its trade data,” the analysis states.

The report also says China held off informing the World Health Organization that the coronavirus “was a contagion” for much of January so it could order medical supplies from abroad — and that its imports of face masks and surgical gowns and gloves increased sharply.

All of this comes as Beijing once again trades rhetorical barbs with Secretary of State Pompeo, who told ABC on Sunday that US intel agencies have “enormous evidence” that SARS-CoV-2 likely leaked from a biolab in Wuhan.

The secretary doubled down in a tweet sent 3 hours ago from his official account.

The Chinese Communist Party continues to block access to the Western world, the world’s best scientists, refusing to cooperate with world health experts, to figure out exactly what happened. This unacceptable during an ongoing threat, an ongoing pandemic. pic.twitter.com/qa156CfTAB

— Secretary Pompeo (@SecPompeo) May 3, 2020

Watch the latest video at foxnews.com

More Republicans have embraced the “China hawk” position since the advent of the outbreak…for obvious reasons. Speaking Sunday on Fox News Channel’s “Sunday Morning Futures” with Maria Bartiromo Ted Cruz said he believes China “is the most significant geopolitical threat to the United States for the next century.”

Watch the latest video at foxnews.com

China’s efforts to fabricate its economic resurgence narrative has come under a lot of pressure this weekend. In Italy, the Italian press has been pushing back against reports in Chinese press claiming Italians have been chanting “Grazie Cina” over Beijing’s “donations” of PPE and other assistance in fighting the virus.

Classic.

Consumer confidence is collapsing in most major countries in Asia Pacific, but not in China.

Fabricated data.…. CCP at its finest. pic.twitter.com/VslzmXKer3

— Otavio (Tavi) Costa (@TaviCosta) May 1, 2020

Finally, Bloomberg reports that the EU Commission will not unveil its proposal for a recovery fund this week as expected…extending the interminable delay for a recovery package that Christine Lagarde warns was needed yesterday.

Just imagine what will happen to the euro area when there are no tourists across the periphery nations this summer and fall?

* * *

Update (1345ET): The UK Department of Health and Social Care just confirmed the death-toll figures we reported earlier, as well as the latest batch of new cases.

As of 9am 3 May, there have been 1,206,405 tests, with 76,496 tests on 02 May.

882,343 people have been tested of which 186,599 tested positive.

As of 5pm on 02 May, of those tested positive for coronavirus, across all settings, 28,446 have sadly died. pic.twitter.com/801yyNWcr3

— Department of Health and Social Care (@DHSCgovuk) May 3, 2020

Update (1312ET): As we reported yesterday, the NYPD dispatched some 1,000 additional officers to patrol city parks on Saturday and issue tickets to anyone found barbecuing, drinking and violating social distancing rules prohibiting “crowds”.

And while the chief of police said he hoped no summonses would be issued, given the vast drop in city coffers, it appears the cops went on a ticketing frenzy, issuing dozens of summonses for lax social-distancing in city parks on Saturday, the nicest day of the year so far, as shell-shocked New Yorkers emerged from their shells.

“In parks specifically yesterday, we issued 43 summonses,” Shea said Sunday in a joint press briefing with Mayor Bill de Blasio.

An additional eight summonses were issued outside of parks for a total of 51, said Shea, who noted that while “not every single one” of the write-ups was for failing to maintain a social distance “the majority were.”

In addition to the summonses, the NY Post reported that three arrests were made citywide.

Meanwhile, although JHU hasn’t gotten there yet, at least one tally of international confirmed cases is saying we’ve passed the 3.5 million mark.

NEW: Number of confirmed coronavirus cases has reached 3,500,000 worldwide.

— Norbert Elekes (@NorbertElekes) May 3, 2020

* * *

Update (1200ET): The UK reported 315 new coronavirus deaths on Sunday, its smallest daily increase in more than a month, bringing its countrywide total to 28,446.

In NYC, Mayor de Blasio said during his Sunday briefing that the “vast majority” of New Yorkers are complying with social distancing rules (obeying social-distancing rules, despite flocks of people who went outside this weekend to enjoy the early spring weather. The city issued a total of 43 summonses in parks and eight outside.

The city is a step closer to performing its own coronavirus tests, the mayor said. He said that by Friday 30,000 swabs for testing would be ready, ramping up to 50,000 full tests later this month.

In Albany, Gov Cuomo is starting his Sunday press briefing by reporting 280 new deaths over the last 24 hours, the lowest number since March 30. The hospitalization rate has also fallen again.

Holding a briefing with updates on #Coronavirus. Watch Live: https://t.co/5IukEpYock

— Andrew Cuomo (@NYGovCuomo) May 3, 2020

The governor announced plans to sign a law requiring all hospitals in the state to have 90 days worth of PPE on hand at all times.

NEW: New York State will require all hospitals to have on hand a 90-day supply of PPE at quantities sufficient to meet the rate of use during the worst of this crisis.

— Andrew Cuomo (@NYGovCuomo) May 3, 2020

“Those who don’t learn from history are doomed to repeat it.”

The 1918 Influenza Epidemic lasted over 10 months and came in three waves.

The 2nd wave was worse than the first wave.

We must be cautious. The war isn’t won yet.

— Andrew Cuomo (@NYGovCuomo) May 3, 2020

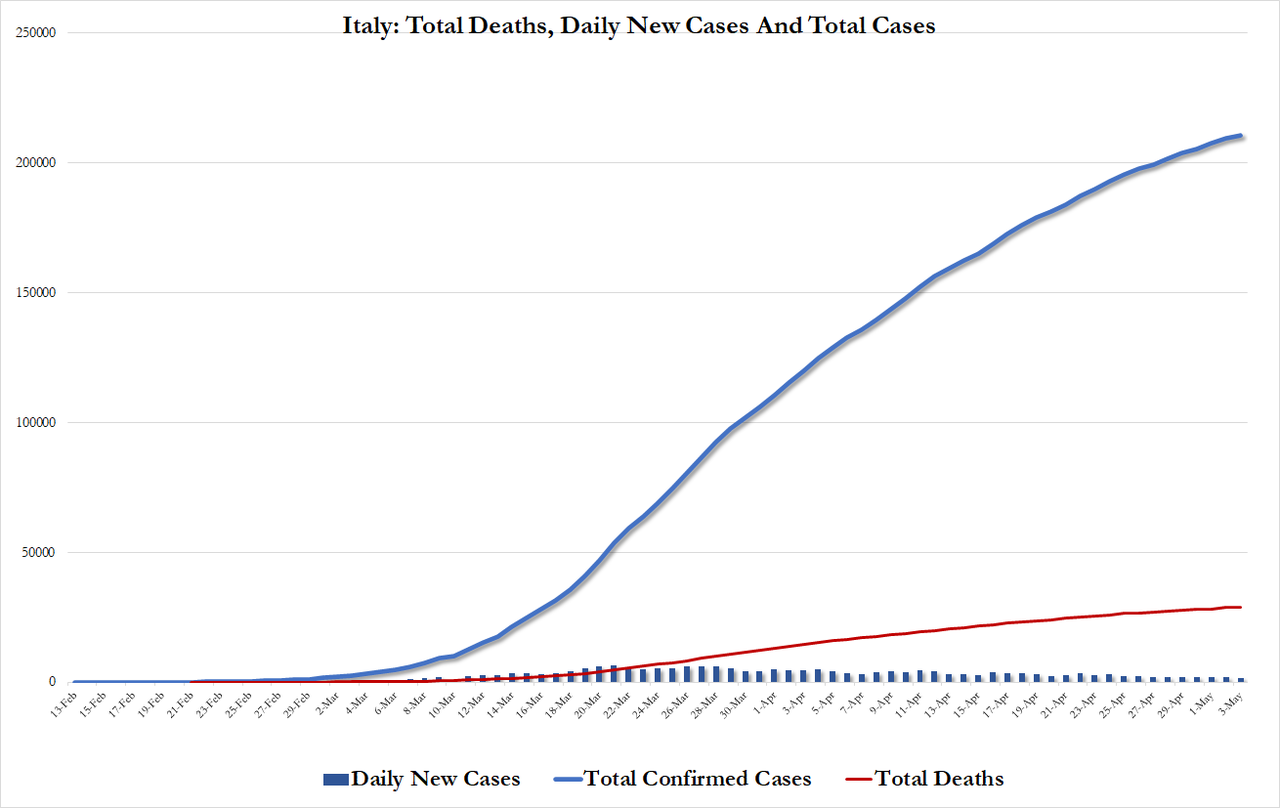

Italy also saw some good numbers today, reporting its lowest number of deaths since early March.

BREAKING: Italy reports 1,389 new cases of coronavirus and 174 new deaths.

Total of 210,717 cases and 28,884 deaths.

— Norbert Elekes (@NorbertElekes) May 3, 2020

NEW: Number of recovered coronavirus patients in Italy has reached 80,000.

— Norbert Elekes (@NorbertElekes) May 3, 2020

Continuing the trend of both deaths and new cases declining, along with net hospitalizations and…

…yet another day where the number of recovered patients outnumbered the newly diagnosed.

NEW: For the 7th time since coronavirus outbreak, Italy has reported more new recovered patients than new cases.

— Norbert Elekes (@NorbertElekes) May 3, 2020

NEW: Number of recovered coronavirus patients in Italy has reached 80,000.

— Norbert Elekes (@NorbertElekes) May 3, 2020

Singapore reported a good number.

NEW: Singapore reports 657 new cases of coronavirus, 18,205 cases in total.

647 of new cases are foreigners.

— Norbert Elekes (@NorbertElekes) May 3, 2020

And Portugal also reported its best numbers in 6 weeks as it prepares to reopen on Monday.

NEW: Portugal reports 92 new cases of coronavirus, 25,282 cases in total.

Portugal’s lowest increase since March 16.

— Norbert Elekes (@NorbertElekes) May 3, 2020

NEW: Portugal ended coronavirus state of emergency, begins reopening on Monday.

— Norbert Elekes (@NorbertElekes) May 3, 2020

As more doctors around the world warn about the dangers of halting vaccination campaigns – particularly in impoverished parts of the developing world – to focus on the coronavirus, Niger has reported its first outbreak of polio this year as vaccinations were rolled back.

AFRICA: Niger reports new polio outbreak after vaccination suspended during coronavirus pandemic. – WHO

— Norbert Elekes (@NorbertElekes) May 3, 2020

Letting its vaccination programs lapse is just the latest blow to the WHO’s credibility.

Before we go: According to JHU, we;re only about 50k confirmed cases away from the 3.5 million mark. The latest number was 3,452,285.

* * *

Every day, it seems, Russia sets a new record for the largest number of new COVID-19 cases confirmed in a day. As we reported yesterday, Health officials in Moscow announced more than 9k new cases. On Sunday, they announced more than 10k new cases, another record sum. In the span of just two weeks, Russia has gone from having a relatively inconsequential number of positive cases to housing one of the largest outbreaks in the world. Of course, the infections didn’t just happen overnight. It’s merely the latest evidence that by the time Russia closed its Far Eastern border back in January the seeds of domestic transmission may have already been planted.

That would jive with evidence that the first COVID-19 death in the US might have occurred as early as Feb. 6, meaning parts of New York, California and Washington were probably already suffering from local human-to-human transmission.

Russia added 10,633 cases of Covid-19, the highest daily number for the nation so far, increasing for a fifth day in a row. The total number of cases has risen to 134,687, according to the government’s virus response center. Around a half of the new cases are asymptomatic and Moscow accounts for nearly 56% of new infections. Russia’s total Covid-19 fatalities rose to 1,280.